The markets maintained their positive momentum from the week prior, with the S&P 500 rallying +1.9% and Nasdaq increasing +2.3%, as both, once again, logged record highs. The macro themes generally remain the same with earnings really starting to ramp. On the plus side, according to FactSet, almost 30% of S&P 500 companies have now reported and 84% of those beat earnings estimates (which is higher than the 70% 5-yr avg). In our sector, Netflix as well as Connectivity giants AT&T and T-Mobile were the main earnings events.

In this edition we focused on the below key themes and developments:

- Earnings Scorecard – Week 1 & 2

- Netflix “Buying” Vs “Building” Remains Top Of Mind At The Moment

- Connectivity Part I: Concerns About Future Economics & Returns Weigh On Connectivity Stocks This Week - A Dive Into AT&T’s Results…

- Connectivity Part II: …T-Mobile Also Continues To Take Share

- The Predictions Markets Are Attracting More Capital As They Hit A New Records

- A New AI-Powered Web Browser Enters The Chat…OpenAI Launches Atlas

- Quantum Was In The Spotlight This Week As Google Makes Another Breakthrough And The US Govt Eyes The Space

- The Entertainment Sector Is Keeping Everyone On Their Toes

- Investors Continue To Worry About The Ad Agency Model…OMC’s Next Stop Is The IPG Merger

- The Week Started With The Cloud Crashing Down In A Major AWS Outage

**Also, please note that due to continued technical issues, we are not able to include direct URL source links in this document but we can send them to you upon request. We apologize for any inconvenience this may cause and hope to resolve the issue as soon as we can**

Separately, I also wanted to highlight that LionTree Advisors served as financial advisor to TodayTix on its sale to Ari Emanuel’s new global events company, MARI, and also served as exclusive financial advisor to SURJ Sports Investments on its funding of a new ATP Masters 1000 tournament in Saudi Arabia.

Have a nice weekend.

Best,

Leslie

P.S. If this email has been forwarded to you and you would to join our distribution list, please email me. Thanks!

Earnings Scorecard – Week 1 & 2

The final earnings season of 2025 kicked off last week and as always there is lots to cover. 17 companies have reported their third quarter results thus far, and stock reactions were, just barely, biased to the upside, with 9 companies (53%) trading up in reaction to their print, while 8 (47%) traded down. The worst performer was Coursera, down -12.9%, and the best performer was Publicis, up +5.2%.

Following Publicis’s report last week, fellow ad agency Omnicom posted its third quarter results this week, and the stock also rose in reaction, up +3.2% (see Theme #9).

Over on the media side, Netflix’s third quarter report caused the stock to fall -10.1% in reaction (see Theme #2 for more color on why). The connectivity sector also had a tougher run this week, with AT&T falling -1.9% after its report (see Theme #3) and T-Mobile down a steeper -3.3% (see Theme #4).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Netflix “Buying” Vs “Building” Remains Top Of Mind At The Moment

After a couple “steady as it goes” quarters, Netflix’s Q3 report hit a snag with a surprise big miss on op margins. This was due to an expense related to a dispute with Brazilian tax authorities. While a negative, excluding this charge, underlying margins would have beat expectations so investors are likely to look past this especially as overall biz fundamentals remain strong. Engagement continues to be “healthy” and investments in live sports and original titles continue to yield results. The Canelo vs. Crawford fight became the most-viewed men’s championship boxing match of the century and KPop Demon Hunters is now the most popular film ever on Netflix. Gaming is another area that mgmt spent more time on, and beyond building traditional games around their original titles, they are also focusing on building features like real-time voting to deepen engagement with live events.

Of course, all of this supports advertising. Q3 marked Netflix’s best ad sales qtr ever and they now expect to “more than” double ad rev this yr, up from prior guidance to double it. Following its classic “crawl, walk, run” playbook, Netflix is “squarely in the walk phase,” focused on diversifying advertisers, simplifying ad buying, expanding formats, and improving the overall offering, with a focus on optimizing overall revenue as the most important metric.

Finally, outside of the core business, when asked about M&A given all the chatter in the industry, mgmt continued to double down on its “builders vs buyers” position BUT didn’t outright rule out any opptys. While they emphasized the value they find in doing the hard work “in the trenches” to build capabilities internally, they noted that M&A oppties are evaluated on a case-by-case basis using a framework to assess whether a deal would strengthen their overall business. The tone seemed more open than in the past, but it remains to be seen how this will play out…Netflix’s path on this front remains a key focus for investors.

This quarter certainly offered some more to discuss than recent ones…see below.

-> Netflix’s stock was hit hard post-earnings and fell -10.1%, ending the week down -8.7%, But overall YTD,, the stock’s performance remains strong, up +22.8%

Q3 Operating Income Took A Hit Due To A Surprise Tax Expense In Brazil…

- Q3 rev growth was strong (+17% y/y, an accel from +16% y/y in Q3) but in-line w/ expectations, driven primarily by membership growth, pricing adjustments, and incr’d ad revenue

- UCAN and EMEA beat, while LATAM and APAC missed

- Q3 op income missed by -11% and op margin of 28.2% was well below cons 31.7%, due to a $619mn charge related to an ongoing dispute w/ Brazilian tax authorities regarding certain non-income tax assessments

- Absent this expense, op income would have reached 33.6% and exceeded projections

- This tax charge “quote” should not have a material impact post Q3

- Q3 adj. EPS also fell well-below expectations due to lower op income: $5.87 vs cons $6.96

- Q3 FCF beat by +13.2

…And This Expense Will Continue To Have An Impact In Q4

- Q4 op income guidance disappointed the Street: $2.86bn vs cons $2.87bn (op margin of 23.9% vs cons 24.2%)

- FY25 op margin guidance is now 29% vs prior expectations for 30%

- But rev trends remains strong: +17% y/y growth guidance to $11.96bn topped cons $11.89bn

- And FY25 rev growth is expected to come in at the high end: Expected to grow +16% y/y vs prior expectations of +15-16% y/y

- Q4 EPS guidance beat: $5.45 vs cons $5.43

Potential Industry Consolidation Won’t Change M&A Approach Or Competitive Views BUT Remain Open To Opptys

- Reiterated that they are more “builders than buyers” and believe they have plenty of runway for growth without fundamentally changing that playbook

- “Nothing is a must have for us to meet the goals that we have for the business”

- Also reiterated that they have no interest in owning legacy media assets: “We’ve been very clear in the past that we have no interest in owning legacy media networks. So, there is no change”

- BUT “when it comes to M&A opportunities…we look at all of them”: “We apply the same framework and lens that we look at when we look to invest in a build”, including –

- “Is it a big opportunity?”

- “If it’s IP, does it strengthen our entertainment offering? Is there additional value in ownership?”

- “Does it strengthen our existing capabilities somehow? Does is accelerative our existing strategy?”

- “And you look at all these things relative to the price, relative to the opportunity, and relative to other alternatives”

- Any worries around industry consolidation reshaping competitive landscape? No – “We’ve always faced significant competition. We still face it today”

- “Watching some of our competitors potentially get bigger via M&A does not change, in and of itself, at least, our view on the competitive landscape”

- What about potentially less access to 3P content on Netflix? Mgmt is not concerned given original titles are the biggest driver for them and they are not dependent on any individual supplier in terms of total view hours

- “We’ve always seen these kind of ebbs and flows” in access to 3P content

- Have also proven over time that they can help build an audience and create value for licensed IP (examples, Suits, Peaky Blinders, Breaking Bad)

Netflix Has Made Big Strides In The Advertising Business – It Is Now “Squarely In That Walking Phase”

- Q3 was their “best ad sales quarter ever” and the Co raised its full year guidance to “more than” double ad rev (but still off a relatively small base), vs prior commentary for double ad rev in 2025

- Mgmt did not provide 2026 guidance but “we’re feeling good about our growth trajectory”

- Commitments at US upfronts more than doubled this yr, which lands partly in 2025 and partly in 2026

- Seeing “even higher” rates of growth in programmatic – “we believe that’s going to be an increasing part of that incremental revenue contribution going forward”

- Focused on overall ad revenue the most, but fill rates have “improved” and believe they’re going to continue to improve as they develop their go-to-mkt capabilities, more measurement, and more targeting

- Key priority is increasing diversity of advertisers and making it easier for them to buy on their platform

- Added more demand sources like Amazon DSP and AJA’s DSP in Japan

- Improving ad sales and go-to-market capabilities

- Addtl offerings coming soon…

- Using AI to test new ad formats in Q4 to generate “the most relevant” ad creative and placement for members and for faster development of media plans

- “With these advancements, we’ll be able to test, iterate, and innovate on dozens of ad formats by 2026”

- Then will “pivot” to make more “focused” investments in 2027 in data capabilities such as ML based optimization, advanced measurement, and advanced targeting

Investments In Originals, Live, & Sports Continues To Yield Results…

- Engagement remains “healthy” & hit their highest qtrly view share ever in US and UK in Q3 (based on 3P data)

- “Original titles are the big business driver for us”

- KPop Demon Hunters was released in Q3 and is Netflix’s most popular film ever

- Return original series seasons in Q4 include the final season of Stranger Things, The Diplomat S3, The Witcher S4, Nobody Wants This S2, Emily in Paris S5, Love is Blind S9, Squid Game: The Challenge S2, and Selling Sunset S9

- New original series in Q4 such as Death by Lightning from exec producers David Benioff and D.B. Weiss, The Beast in Me starring Matthew Rhys and Claire Danes, Simon Cowell: The Next Act, and more

- A “big” slate of original films releasing in Q4 including Guillermo del Toro’s Frankenstein, Kathryn Bigelow’s A HOUSE OF DYNAMITE, Rian Johnson’s Wake Up Dead Man: A Knives Out Mystery, documentary The Perfect Neighbor, Train Dreams, Noah Baumbach’s Jay Kelly starring George Clooney and Adam Sandler and more

- Given the success of KPop Demon Hunters, any changes in theater strategy? No – “we believe that this film…actually worked because it was released on Netflix first”

- Live continues to have a “hugely outsized impact”, despite being a “small” portion of overall content spend and a “very small” portion of the 200bn+ hrs viewed

- Canelo-Crawford fight was the most-viewed men’s championship boxing match this century: With 41mn+ viewers; Was #1 on Netflix in 30 countries and made the top 10 in 91 countries

- Live events “typically have outsized positives for conversion, for acquisition and, we strongly suspect, retention”

- Amidst flurry of sports rights deal announcements across the sector, mgmt. highlights that there is no change to their sports strategy

- On local vs global sports rights – “it’s just a scale question”: Comes down to local costs vs size of local audience

- Reiterated “we’re not currently focused on the big season packages”

- “We’re focused on big live events”

- Lots in the pipeline to propel engagement…

- Jake Paul vs. Gervonta Davis on Nov 14th

- 2 NFL Christmas Day games (Dallas vs Washington + Detroit vs Minnesota)

- Skyscraper Live in early 2026

- World Baseball Classic in Japan in 2026

- FIFA Women’s World Cup in 2027 and 2031

- …” And there’s going to be a lot more that’ll come in between”

- On local vs global sports rights – “it’s just a scale question”: Comes down to local costs vs size of local audience

…With Even More Diversified Content Offering In The Works

- On their co-exclusive video partnership with Spotify – “we’re going to build into this category like we do with our other categories…based on demand signals that we get from our members”

- Seen as an oppty to “[broaden] the Netflix offering”

- On working with creators with followings on other platforms, like YouTube – want to work with “the world’s best creators, wherever they are”

- “Some of them are in Hollywood, some of them are in Korea, some of them are in Paris, and some of them are sitting on social media platforms that have yet to be discovered”

- “Working with content creators from other platforms isn’t a recent thing for us”

Gaming Efforts Appear To Be Ramping

- See gaming as driving more interactivity on the platform”

- Real-time voting will be their first live interactive feature, which is currently being tested on Dinner Time Live With David Chang and will roll out more broadly starting with Star Search in January

- Looking ahead… “we expect to provide other interactive features to deepen engagement with live events as we go in the future”

- Real-time voting will be their first live interactive feature, which is currently being tested on Dinner Time Live With David Chang and will roll out more broadly starting with Star Search in January

- Will increase investments in gaming “judiciously” based on “demonstrating that we’re ramping returns to the business”

- Current gaming focus – “less is more” strategy

- “Offering more high-quality games in a few key genres and targeting the right cohort of users”

- Specifically called out “immersive narrative games” based on their own IP: Including Squid Game: Unleashed, Thronglets (from the Black Mirror universe), Happy Gilmore: Golf Mayhem ’98 Demo, and more

- Rolling out a slate of party games on TV this holiday season: Including Boggle Party, Pictionary: Game Night, LEGO Party, Tetris Time Warp, and Party Crashers: Fool Your Friends

- Having the phone as a controller is expected to unlock even more future innovation – “you don’t need a special controller. That’s key to this access”

- “In the years ahead…we expect creators will really find interesting and novel ways to unlock all of the power that is in this incredibly advanced controller that we all happen to have in our pockets”

Leveraging AI To Improve Product Experience & Content Production

- Beta testing conversational search experience that allows members to use natural language to explore the catalog and discover the perfect title for that moment

- Using GenAI to localize promotional assets in a variety of languages “so titles can more easily travel to audiences who will love them around the globe”

- Makers of Happy Gilmore 2 used GenAI coupled with ML and Eyeline’s proprietary volumetric capture technologies to de-age characters during the opening flashback scene

- Producers of Billionaires’ Bunker used various GenAI tools during pre-production, including for pre-visualization to explore wardrobe and set designs

- “We’re not worried about AI replacing creativity, but we’re very excited about AI creating tools to help creativity”: “AI can give creatives better tools to enhance their overall TV movie experience for our members. But it doesn’t automatically make you a great storyteller, if you’re not”

- Content creation apps are “likely to have a lot more impact on UGC creators […] in the near-term. In other words, AI content replacing viewing of existing user-generated content”

Connectivity Part I: Concerns About Future Economics & Returns Weigh On Connectivity Stocks This Week - A Dive Into AT&T’s Results…

Connectivity giants AT&T and T-Mobile gave us a look into wireless and broadband trends, with the former reporting on Wednesday and the latter following on Thursday. While both companies reported stronger Q3 postpaid phone net additions and very strong Q3 broadband uptake, there were some puts and takes overall, and it was a sell the news event for the sector given concerns about the heightened promotional activity and concerns about Verizon potentially making aggressive moves to try to regain share. Comments by newly appointed Verizon CEO Dan Schulman on the Co’s earnings call next week will be a key driver for the sector as investors try to forecast the future economics and return profile for the sector.

In the meantime, digging a little more into AT&T Q3 results specifically, what stood out the most was that 1) overall headline financials were a tad below expectations due to weaker mobility revenue; 2) while postpaid net adds were very strong in the qtr, it was offset by incremental pressure on ARPU from the Co’s mix shift to new segmented groups with lower ARPU (and this should continue); 3) the wireless competitive market place remains heightened but AT&T’s approach is to continue to push harder into convergence (mgmt provided some good stats on this); 4) the Co achieved their highest total broadband net adds in more than 8 years and momentum should persist; 5) mgmt reiterated all full-year 2025 financial guidance, but EPS is now guided to the high end of the range; 6) Lumen and the spectrum licenses from EchoStar will expand broadband reach and boost organic revenue growth and profitability…the Co will provide an update to long term financial outlook early next year once these deals close. All in all, AT&T is executing on its convergence playbook and made strides on that front this quarter, but bigger picture sector economics will dictate where valuations settle.

See below for more details on what we thought was most important from AT&T’s results and see Theme #4 for Connectivity Part II which includes what we viewed as the main takeaways from T-Mobile’s results.

-> The connectivity sector traded off this week with Verizon down -4.3%, AT&T down -4.6%, and T-Mobile down -5.0%; YTD, the stocks are down -2.9%, up +10.4% and down -1.3% respectively

-> Much smaller cap, but a notable mover, was AST whose shares fell -10% on Wednesday following news of a private offering of $1bn in convertible senior notes due in 2036 (upsized from $850mn)

Some Puts & Take In AT&T Mobility Led To Mixed Headline #s

- AT&T – headline #s were a little mixed vs expectations as Mobility was a tad weaker than expected while Business Wireline outperformed

- Headline #s – Mixed:

- Total revs – SLIGHTLY MISSED by -0.5%: Grew +1.7% y/y

- Adj EBITDA – BEAT by +0.9%(margin was above cons)

- Mobility segment…revs missed and EBITDA was ~inline

- Mobility svs revs grew +2.3% y/y & mobility EBITDA grew +2.2% y/y (note that $90mn in 1x fee in svs revs last yr Q3 impacted mobile svs revs by ~60bp, and mobile EBITDA by ~100bp)

- Business Wireline posted less negative revs & EBITDA declines y/y

- Adj EPS – IN-LINE

- FCF – BEAT by +1.5%, up 6.5% y/y with CAPX lower than expected (but reiterated FY guidance)

- Headline #s – Mixed:

2025 Guidance Reiterated Though EPS Should Come In At The High End Of The Range

- Reiterates all full-year 2025 financial guidance but w/ a slightly improved EPS picture

- Mobility svs rev growth of “+3% or better” y/y

- Adj EBITDA growth of “+3% or better” y/y

- Mobility EBITDA growth of ~3% y/y

- Business Wireline EBITDA to decline in the low-DD range

- Consumer Wireline EBITDA growth in the low-to-mid-teens range

- Capx in the $22bn-22.5bn range (implies Q4 at ~$7-7.5bn)

- FCF in the low-to-mid $16bn range (implies Q4 at ~$4bn)

- Adj EPS in the $1.97-2.07 range but the Co now expects “at the higher end”

- Other guidance

- Expect Q4 D&A expense of ~ $5bn is “more aligned with the quarterly run rate we expect heading into next year”

- Reiterated the $1.5bn contribution to the pension plan by the end of 2026 (includes addtl $400mn of contributions in Q4 and the remaining $700mn next year)

Promotional Activity In Wireless Remains Heightened, As It Was In H1

- Mgmt indicated that similar to H1, switching activity “remains elevated but their playbook is working”

- “Similar to the first half, we continue to operate in a marketplace where the cost of acquiring and retaining subscribers has increased”

- “We’re in a cycle right now because of the maturity level”

- AT&T’s shift in tactics is to focus on converged customers

- Postpaid phone churn was up +14bp y/y to 0.92% in Q4 due to “incr’d marketplace activity” and to a lesser degree, a higher % of the customer base reaching the end of device financing periods (normalized as exited Q3)

- Q4 churn should also be seasonally up: “Based on this operating environment, we continue to plan for postpaid phone churn and upgrades to follow seasonal patterns in the fourth quarter when we typically see more switching and upgrade activity due to new device launches and the holiday season”

- Despite higher churn, the Co still delivered better-than-expected postpaid phone net adds of 405k vs cons 328k (following +401k in Q2)

- Mgmt remains committed to margin improvement despite the competitive environment…how do they get there? 1) less copper in the network and less infrastructure to support it; 2) modernizing their wireless network (will be substantially completed by the end of 2027); and 3) driving convergence should drive down churn and improve CAC

- “So all those things together make me feel really good about how we’re positioned for the future to continue to drive profitable growth”

The Push Into Underpenetrated Segments Is Weighing On ARPU But A Pricing Action Will Help Q4 Svs Rev Growth

- Q3 postpaid phone ARPU was lower than expectations given the impact of adding customers in underpenetrated segments (like adults 55 yrs old or older) who are eligible for service discounts BUT supports growth in home internet revenues (booked in Consumer W-line)

- This dynamic should continue in Q4 which also typically sees seasonally lower ARPU though there will be some offsetting benefit related to a pricing action that becomes effective at the beginning of December

- However, success in these underpenetrated segments drive “higher incremental service revs and attractive returns”

- Even though ARPU may be pressured, the Co is still “trying to maximize service revenue. And in the fourth quarter, as an example, we expect to have a pricing action that becomes effective that will contribute to service revenue growth”

AT&T Outperforms On Broadband Adds Though Q4 Will Be Seasonally Slower

- Broadband results were “very very” strong and topped consensus

- The Co achieved their highest total broadband net adds in more than 8 years

- AT&T Fiber net adds: +288k driven by seasonal tailwinds & cont’d expansion of their fiber footprint (vs Q2’s +243k)

- AT&T Internet Air net adds: +270k (above cons +206k and vs Q2’s +203k)

- The Co has more than doubled their fiber customer base in < 5 yrs & nearly tripled quarterly fiber revs over that same period (surpassed 10mn premium AT&T Fiber subs)

- “And the train keeps a-rolling”

- The Co achieved their highest total broadband net adds in more than 8 years

- But expect seasonality in Q4 w/ lower connections around holiday

- Also note that last year as a one timer boost in Q4, the Co benefited from some pent-up demand following the Q3 work stoppage in the southeast

- AT&T has now passed over 31mn total locations with fiber as of the end of Q3 and reaffirmed its target to reach more than 60mn customer locations by yr-end 2030

- Looking ahead, the mix of Business Internet Air should increase: Regarding Business Internet Air, “we’re still not as good as we can be … We’re not fully ramped in the third‑party distribution yet when I compare our effectiveness to others in the market…We can get there, and we will get there…We think our mix of business can be a little bit stronger moving forward.”

- Continue to expect mid to high teens y/y growth in consumer fiber broadband revenue in 2025 and consumer wireline EBITDA growth in the low to mid-teens range

AT&T Sees Huge Gains In Its Convergence Strategy

- Convergence is still central to the Co’s strategy…and they posted huge gains in Q3

- More than 41% of AT&T fiber households also choose AT&T for wireless and “the pace of this convergence trends within our customer base continues to grow”

- This is up +180bp y/y which is one of the Co’s largest convergence gains over the past three years

- More than 50% of AT&T internet air subs also choose AT&T for their w-less svs

- More than 41% of AT&T fiber households also choose AT&T for wireless and “the pace of this convergence trends within our customer base continues to grow”

Echostar & Lumen Deals Are On Track, Will Expand Reach, & Be Additive To Growth

- AT&T is making progress with deploying EchoStar purchased spectrum: Started to deploy the 3.45 gig spectrum that they agreed to acquire under a short‑term spectrum manager lease

- Timing: “Based on our current rate and pace, we expect these mid‑band licenses will be deployed in cell sites, covering nearly 2/3 of the U.S. population by mid‑November”

- This positions the Co to further expand the availability of Internet Air in sales channels in 2026

- “We expect some incremental accretion over what we would have had in the business plan because of our previous wholesale relationship with EchoStar, which will add value into the acquisition.”

- Timing: “Based on our current rate and pace, we expect these mid‑band licenses will be deployed in cell sites, covering nearly 2/3 of the U.S. population by mid‑November”

- Lumen is also underway, with “most of the senior leadership team identified”

- Timing: Now expected to close in the “early part of 2026” and we “have not seen anything in our planning that is unexpected”

- Remain confident in the expected accretion from the Lumen Fiber assets and the EchoStar Spectrum licenses

- “We expect to provide an update to our long‑term financial outlook early next year. We expect both of these transactions to boost our organic growth in revenues and profitability and you should expect that this will be reflected in our updated outlook”

Connectivity Part II: …T-Mobile Also Continues To Take Share

In addition to the AT&T drill down noted above in Theme #3, T-Mobile results had a lot of common fundamental themes and the updates that we found most incremental were that 1) the Co also reported much stronger than expected postpaid phone net additions with broad-based strength, and that momentum is continuing into Q4 (though churn was a tad higher than expected); 2) mgmt talked a lot about the high level of switching activity but sees themselves as a beneficiary of these new jump ball opportunities; 3) FWA additions were also well ahead of forecasts (added over +500k 5G bband adds vs cons +416k and up +22% y/y) and mgmt sees this performance as sustainable, unlike competitor skeptics; 4) Fiber adds tracked above forecasts and mgmt raised FY25 fiber customer net add guidance to ~130k vs prior ~100k BUT T-Mo will remain disciplined on economics and continue with a capital light strategy; 5) the Co believes that it is making progress with its network leadership perception and its digital transformation efforts, which are both helping to widen its differentiation; and 6) the Co plans to “increase” its 2026 and 2027 guidance on the year end 2025 call, which reflects the core strength in the underlying business and M&A.

Overall, T-Mobile had another strong fundamental quarter but as discussed in Theme #2, investors are concerned about the competitive dynamics in the industry and where it is headed as we look forward. All ears will be on comments from Verizon’s results next week.

-> The connectivity sector traded off this week with Verizon down -4.3%, AT&T down -4.6%, and T-Mobile down -5.0%; YTD, the stocks are down -2.9%, up +10.4% and down -1.3% respectively

T-Mobile Delivers A Better Than Projected Q3

- Rev – slight beat: Grew +8.9% y/y (accel from +6.9% y/y in Q2)

- Beat in Service rev (+9% y/y) which offset misses in Equipment & Other segments

- Adj. EBITDA – beat by +0.7%: Grew +6% y/y

- Margin of 39.5% vs cons 39.3%

- Adj. EPS – in-line: $2.41 vs cons $2.40

- CapEx came in higher than expected: $2.64bn vs cons $2.35bn

- FCF beat by +10.5%

- Svs revs to FCF conversion is 26%

And Raised 2025 Core EBITDA & FCF Guidance

- Incr’d core adj EBITDA guidance by $300mn at the mid-point: To $33.7bn-$33.9bn (mid pt was also above cons $33.75bn)

- Reflects ongoing core operating strength and the inclusion of UScellular into FY guidance

- Raised the low end of FCF guidance: To $17.8bn-$18.0bn, from $17.6bn-$18.0bn

- Also incr’d CapEx guidance by $0.5bn due to UScellular: Now expected at ~$10.0bn vs prior guidance of ~$9.5bn, driven entirely by the inclusion of UScellular

T-Mobile’s Postpaid Phone Performance Was A Standout & Momentum Continues Into Q4

- It was an all-time record qtr for postpaid net customer adds: Added +2.3mn vs expectations of +1.5m

- RAISED FY25 guidance by ~+1mn: 2mn-7.4mn, up from prior guidance of 6.1mn-6.4mn

- Also posted the highest Q3 in over a decade for postpaid PHONE net customer adds: +1.0mn vs cons +841k

- RAISED FY25 guidance: To 3mn, up from prior guidance of 2.95-3.1mn

- Q3 postpaid new acct additions also hit all-time qtrly record: Added +396k (up +26% y/y)

- Growth has been broad-based across mkts: Across their top 100 mkts, smaller mkts, rural areas, etc.

- Even in top 100 mkts, postpaid share is up across households where they have both stronger and weaker penetration

- Overall, the Co’s postpaid phone momentum continues into Q4: “Feel really good about where they are in Q4”

- The upside in postpaid phone adds was despite Q3 postpaid phone churn at 0.89% which was a tad worse than cons 0.88%

- Q3 postpaid ARPA grew by +3.8% y/y on an organic basis when you exclude the dilutive impact of US Cellular, Metronet and Lumos

- For 2025, now expect +~4% y/y growth ex the impact and up at least +3.5% including the impacts

- Raised 2025 postpaid phone ARPU growth to ~2%, so up from 1.5% that they had previously guided to

The Co Benefits From An Active Switching Environment…It Creates More “Jumps Balls”

- The overall promotional activity is “pretty consistent” and the higher switching in the marketplace against that backdrop is helping them drive momentum: There was “more switching behavior” this qtr with a new device and also saw churn normalization as “some of our competitors had 36-month contracts over a period of time, all of which meant at the margin more switching”

- Industry churn is normalizing which benefits T-Mobile: Mgmt cites that churn at “our two benchmark competitors” was “suppressed temporarily as they moved from two-year to three-year payment plans across the majority of their customers”…but now they are starting to “round trip those three-year plans and customers are rolling off those at a normal pace”

- In 2025, “industry churn is kind of returning to normative rates based on that dynamic and lots of other dynamics”

- At “the margin, this is really good because as you saw in this quarter’s results… more jump balls is good for us as the net share taker”

T-Mobile Also Outperformed On Broadband & FWA Momentum Is Seen As Sustainable

- T-Mobile’s broadband strategy “plays at the heart of the un-carrier…Because what we’ve got here is customers in a place where they have an inferior product quite often where they’re paying a huge premium. It’s classic un-carrier territory”… incumbents are “charging a premium” with “sub-par networks”

- “Very very” happy with FWA results: Added over +500k 5G bband adds (vs cons +416k), up +22% y/y

- Mgmt stressed that their 5G broadband ARPUs and customer lifetime values are very similar to our postpaid phone business

- Believe that FWA is “incredibly sustainable”: The fallow capacity model is at the heart of FWA and new tech is helping drive more runway; “We see FWA as not a temporary category, but something that’s here to stay as mobile technology gets better and better”

- The product keeps getting better: In two years, product speeds have gone up +50%, while the Co almost doubled the customer base

- Competitors’ “best argument is, well, maybe it’s temporary. Maybe it’ll only last a decade…Good luck with that”

- Added over +50k fiber subs (incls contribution from Metronet post July 24th close) and RAISED FY25 fiber customer net add guidance to ~130k vs prior ~100k

- Are being thoughtful about the economics and go after places where they are confident that the economic will work…it is a great complement to the FWA nationwide offer “but under the right parameters”

- The Co is committed to capital light structure as it allows them to scale and use complementary capabilities

- Reaffirmed 12mn FWA and 12-15mn homes passed on fiber by 2028

T-Mobile’s Growing Network Leadership & Digital Transformation Are “Widening Differentiation”

- T-Mobile is “making progress” on its network leadership perception and is already closing the gap: In Q3, “we hit an all-time high in our network perception amongst switchers. And that’s a big driver to the outperformance we’re seeing”

- Mgmt cites Ookla data showing that their median download speeds on the new iPhone are “nearly 90% faster than one of our benchmark competitors and over 40% faster than the other”

- In broadband, the avg download speeds have incr’d by nearly 50% and our wireless speeds have gone up as well despite all the new additions

- Continue to invest: Building and upgrading thousands of new cell sites, many of which are in smaller markets and rural areas and deploying and leveraging nationwide 5G advanced network; Believe they have a network that is 2 years ahead of everyone else and want to keep their lead

- Big switching quarters (“like this one”) are one of the best times to change network perception: “The most powerful way to change perception is from recommendations from the people around you…so continuing to have big quarters like this one is a big part of changing those perceptions”

- Digital transformation is taking the pain points out of the customer process…making it easier to come to T-Mobile

- Three out of four of their iPhone upgrades during our pre-order window were digital; “That is widening differentiation”

- 75% of their upgrades are now on T-Life

The Co Plans On “Growing Their Spectrum Leadership”

- Have “more” and “better” spectrum than anyone else and want to stay ahead

- Why didn’t you participate in recent secondary market transactions? At those prices, it didn’t make economic sense for them; “Other companies might make different choices which reflects the gap vs their spectrum position”

- “My intent is not just to defend our spectrum leadership, but to grow it. And the good news is we see several opportunities to do that in the coming years, whether that’s other kind of strategic secondary opportunities or whether it’s the auctions that will come by. And we feel in a very, very good place to go out and defend and even expand our spectrum lead”

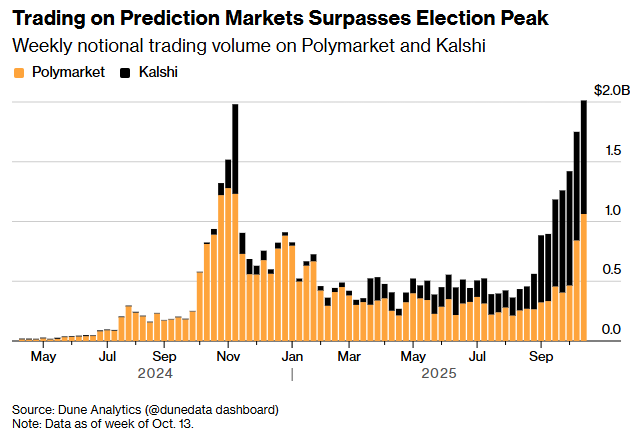

The Predictions Markets Are Attracting More Capital As They Hit A New Records

Prediction markets are having quite a moment. Last week, prediction markets trading volumes surpassed $2bn, the highest weekly rate on record, surpassing the previous peak during the US presidential election last year. At the center of the surge are Polymarket and Kalshi, the two frontrunner prediction market platforms, and investors are certainly taking notice. Kalshi is reportedly fielding new funding offers that could value the Co as high as $10–12bn (this is just weeks after raising $300mn at a $5bn valn), while Polymarket is said to be in talks for a raise at an even higher $12–15bn valn. Sports-driven contracts remain the most active category on both platforms, and sports leagues are noticing, with the NHL this week becoming the first major U.S. league to sign official multi-year partnerships with both Polymarket and Kalshi, granting access to official data and branding rights. Despite some mixed reactions, Kalshi’s CEO has hinted that more such deals with other leagues are in the works.

Amidst it all, established players are making moves in this direction as well. On the same day as the NHL news, DraftKings announced its entry into prediction markets with the acquisition of Railbird, a CFTC-regulated exchange. DraftKings will now be launching (in the coming months) its own platform for trading event-based-based contracts called DraftKings Predictions.

The regulatory pushback against prediction markets seems to be softening (particularly with Polymarket preparing to reenter the US after a regulatory ban 4 yrs ago) and it seems we may be at the cusp of more mainstream adoption.

More on all the above is below.

-> Amid all the activity in the sector, betting can still attract bad actors and this week, the NBA found itself at the center of a major federal investigation charging over 30 people in schemes involving illegal gambling, rigged poker games, and game manipulation; Prosecutors allege organized crime groups used insider NBA information and orchestrated performance fixes to profit from bets, highlighting risks in the broader sports betting space as it rapidly expands and gains broader acceptance

- Prediction markets for the week ending Oct 19th hit an all-time high of more than $2bn in weekly volume, per Dune Analytics data

- Includes activity across Kalshi, Polymarket, Myriad, and Limitless

- Trading volume on Polymarket (~$1bn) and Kalshi (~$950mn) drove most of the activity as both hit new record highs

- While much smaller, Limitless reached $21.9mn and Dastan reached $3.8mn in weekly volume

- What’s been driving the surge? Sports-focused bets were the top category on both platforms last week, pulling in $867mn in trading on Kalshi and $415mn on Polymarket

- Betting on politics, cultural events, and economic indicators has also been driving activity

- This volume level surpassed the previous peak reached during the US presidential election last yr, when the two platforms first entered the financial mainstream

- At that time, Polymarket had accounted for ~$1.2bn in trading volume, while Kalshi was at ~$749mn

- Tug of war for the top spot –

- In August, Kalshi overtook Polymarket in overall trading volume due to sports (including the start of the new NFL season)

- But Polymarket took back the lead last week after doubling its sports-related volume relative to a month earlier

- Prediction markets have recently benefited from a more relaxed regulatory environment at the federal level: Both Polymarket and Kalshi received CFTC no-action letters earlier this yr, which gave the Cos the green light to open their platforms to US w/o the threat of enforcement action from the federal regulator

- However, a growing # of state regulators have challenged their status as CFTC-regulated entities

- Includes activity across Kalshi, Polymarket, Myriad, and Limitless

-> As a reminder, Polymarket currently blocks US users from using the platform after the CFTC banned it for operating unregistered prediction markets back in 2022. It’s now planning on re-entering the US after acquiring QCX, a CFTC-licensed exchange, which gives it the regulatory approval to legally offer prediction markets to US users again

- Investment dollars are also pouring into the prediction mkts… valn updates from Polymarket and Kalshi –

- Kalshi is reportedly receiving funding offers from VC investors valuing the Co at $10bn-$12bn

- Comes just weeks after Kalshi announced a $300mn funding round at a $5bn valn

- Back in June, Kalshi had raised $185mn at a $2bn valn

- Polymarket is reportedly in talks to raise funding at a $12bn-15bn valn

- Earlier this month, Intercontinental Exchange, owner of the NYSE, said it would invest up to $2bn in Polymarket at a valn of ~$8bn; That deal made CEO Shayne Coplan the youngest self-made billionaire

- Prior to that, back in June, Polymarket raised $200mn at a $1bn valn

- Kalshi is reportedly receiving funding offers from VC investors valuing the Co at $10bn-$12bn

- The incumbent sports betting players are not sitting still…DraftKings expands into prediction markets with the acquisition of Railbird

- What is Railbird? A CFTC-regulated designated contract market (DCM) specializing in event-based contracts

- Railbird’s platform enables regulated event contracts on non-sports topics like finance, entertainment, and culture, with potential expansion to sports in states without existing sports betting

- Will launch DraftKings Predictions in the coming months: It’s an upcoming mobile platform that will allow customers “to trade regulated event contracts on real-world outcomes across finance, culture, and entertainment”

- The product will have the flexibility to connect to multiple exchanges and may add more categories over time

- Polymarket will serve as clearinghouse for DraftKings Predictions, handling trade verification, collateral management, and settlement

- Financial details were not disclosed but it is reported that DraftKings will spend as much as $250mn: Under the transaction, DraftKings is paying $50mn upfront, with an addtl $200mn in performance incentives, the specifics of which are not clear, per a report from Front Office Sports

- Keeping up with competition: FanDuel announced a partnership with a prediction markets platform earlier this yr; Also, Kalshi launched a same-game parlay product last month, which is one of the more profitable products that DraftKings and FanDuel offer

- What is Railbird? A CFTC-regulated designated contract market (DCM) specializing in event-based contracts

-> DKNG’s stock closed up +3.2% on the back of the deal announcement

- On the same day of the DKNG/Railbird acq anncmt…NHL announces multiyear partnerships with Kalshi and Polymarket

- The NHL signed a multi-year licensing deal w/ Kalshi and Polymarket, becoming the first major U.S. sports league to partner with prediction market platforms

- What does the partnership entail? Provides the Cos with access to official NHL data and rights to use NHL marks, logos and official designations on their platforms and products

- Kalshi’s and Polymarket’s brokers and merchants will also be able to use NHL marks and logos to identify the Polymarket and Kalshi products that they make available

- Both Cos will also receive brand exposure via Digitally Enhanced Dasherboards (DED) and blue line slot virtual signage on NHL game broadcasts

- The deal got some mixed reactions –

- The American Gaming Association said in a statement that the NHL deal “sends a troubling message”: “The platforms in question fail to comply with essential standards…worse, they are currently offering sports wagers in all 50 states to anyone 18 years of age—some of which have not authorized any form of legal sports betting and those that have largely define 21 as the prevailing legal age for wagering”

- Keith Wachtel, president of NHL Business, says he feels comfortable from a regulatory and integrity standpoint, noting that sportsbooks like FanDuel and DraftKings have also struck partnerships with prediction platforms and is actually an oppty to reach new fans

- More on the horizon? Deals with other leagues may be in the works: Kalshi CEO Tarek Mansour said the NHL deal could be replicated across other leagues – “be on the lookout for more announcements soon”

Sources 2025: CNBC 10/22, NHL 10/22, DraftKings 10/22, YahooFinance 10/20, SeekingAlpha 10/22, TradeView 10/22, Bloomberg 10/21, WSJ 10/21

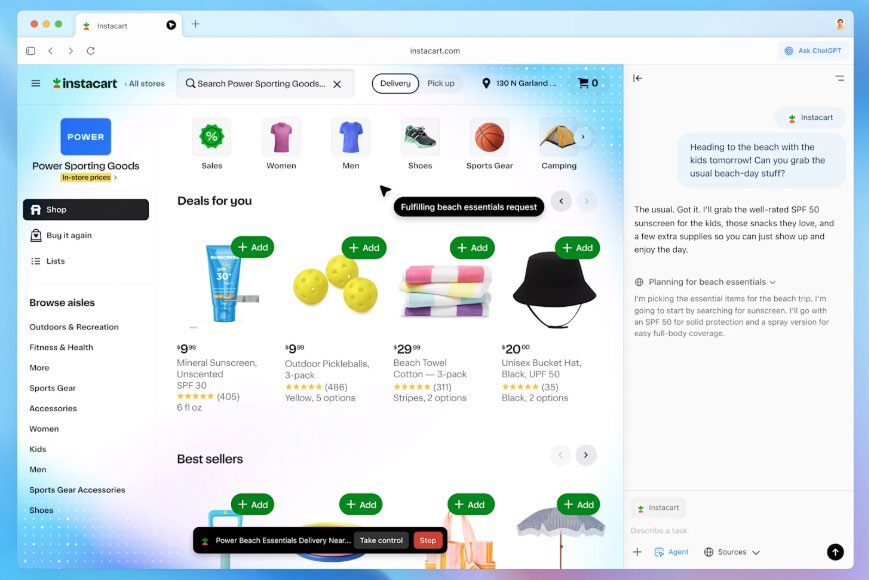

A New AI-Powered Web Browser Enters The Chat…OpenAI Launches Atlas

After much anticipation, OpenAI officially joined the browser race this week with the introduction of Atlas, a web browser built around ChatGPT that takes traditional browsing to the next level with the addition of chat and AI-driven automation. Users can ask questions, summarize pages, or complete tasks through an “Ask ChatGPT” sidebar, while optional browser memory lets ChatGPT recall past sessions for more personalized help, and with agent mode, it can perform actions like booking appointments or adding items to carts on the user’s behalf. The more a user uses Atlas, the smarter and more helpful it gets, though users are meant to remain in control, with options to clear history, browse incognito, or limit what the model can access.

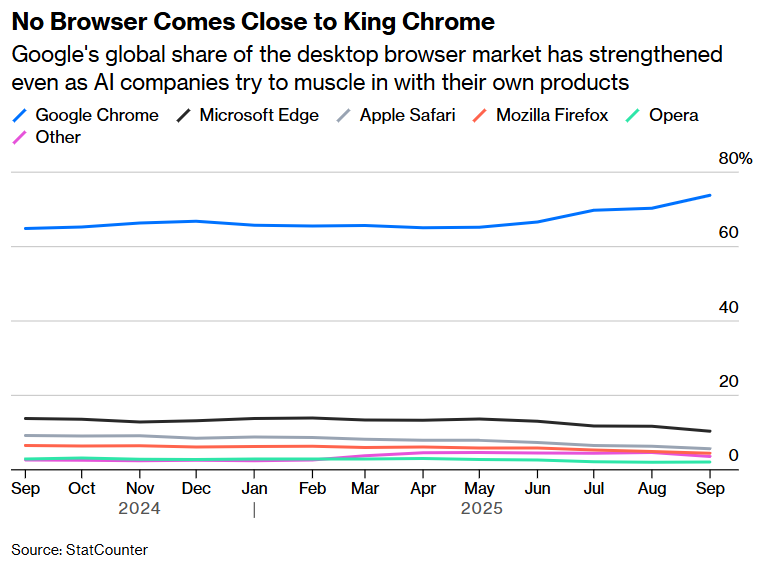

The launch certainly drew quite a bit of attention, with Google’s stock in particular falling as much as -4.8% the day of the launch. However, shares somewhat recovered and ended the day down -2.2%. Access to Atlas is limited to MacOS for now and agent mode is still in beta and only available to paying users. More broadly, despite other AI-powered web browser launches, Google’s Chrome continues to dominate the browser market and has gained share in recent months as it has expanded its Gemini AI integration into Chrome. But will Atlas change the balance of power? Its new agent capabilities and fundamental redesign will keep Google on its toes.

See below for more details.

-> Google fell as much as -4.8% the day of the launch but partially recovered to close down -2.2%, The stock recovered through the week and ended up +2.7% and is still up +36.8% YTD

- OpenAI introduces ChatGPT Atlas – “the browser with ChatGPT built in”

- Atlas opens with a search bar where users can enter questions or URLs, while an “Ask ChatGPT” button can be clicked to open a sidebar on an existing tab

- As users use Atlas, ChatGPT can get smarter and more helpful

- If turned on, browser memories lets ChatGPT remember context from the sites user visit and bring that context back when they need it

- “Find all the job postings I was looking at last week and create a summary of industry trends so I can prepare for interviews”

- BUT users are in control of what ChatGPT can see and remember as they browse: They can clear entire browsing history or open an incognito window to temporarily log out of ChatGPT

- If turned on, browser memories lets ChatGPT remember context from the sites user visit and bring that context back when they need it

- Agent mode allows Atlas to handle certain tasks autonomously or semi-autonomously

- It’s made to research, analyze, and automate tasks (such as planning events or booking appointments while you browse)

- How does it work? “It uses the internet for you”: It accesses the user’s laptop and effectively clicks around the internet on the person’s behalf based on the users’ browser history

- Example use case: Imagine you’re planning a dinner party and you have a recipe in mind; You can give the recipe to ChatGPT and ask it to find a grocery store, add all the ingredients to a cart, and order them to your house (but you can review before check-out and payment!)

- OpenAI highlighted privacy and safety factors –

- Added safeguards to address new risks that can come from accessing logged-in sites or browsing history while acting on your behalf

- Cannot code in the browser, download files, or install extensions

- Cannot access other apps on your computer or file system

- Will pause to ensure the user is watching it take actions on sensitive sites, such as financial institutions

- Can use agent in logged out mode to limit its access to sensitive data and the risk of it taking actions as you on websites

- By default, Atlas will NOT use the content users browse to train their models, even if a user opts into training, webpages that opt out of GPTBot will not be trained on

- Added safeguards to address new risks that can come from accessing logged-in sites or browsing history while acting on your behalf

- While the browser is available for free, agent mode is only available for paying users

- Now available worldwide on macOS to Free, Plus, Pro, and Go users; Windows, iOS, and Android are coming soon

- Also available in beta for Business, and if enabled by their plan administrator, for Enterprise and Edu users

- Agent mode has now launched in preview…but at a cost (only available to Plus, Pro, and Business users)

- With the slew of AI-enhanced browser launches, any impact on the legacy browsers? Not really… in fact, Google’s browser dominance has risen in recent months

- Despite the launch of Browser Company’s Dia, Perplexity’s Comet and others, none of the new players are being used enough to appear in StatCounter’s analysis, the Co said, with all registering <1% share

- As a reminder, in September, Google integrated its Gemini AI model directly into Chrome, enabling features like page summarization, tab-based synthesis, and context-aware recommendations

Sources 2025: OpenAI 10/21, The Verge 10/21, TechCrunch 10/21, Livestream 10/21, Bloomberg 10/22

Quantum Was In The Spotlight This Week As Google Makes Another Breakthrough And The US Govt Eyes The Space

Advancements in quantum computing is something we have been keeping a keen eye on, and while real-world applications are still years away, innovation in the space continues to accelerate. Google made headlines this week after unveiling what it called the first-ever verifiable quantum advantage using its Willow chip, which successfully ran an algorithm 13,000x faster than top supercomputers. The Co described it as a milestone toward turning quantum computing from theory into practical science, with potential to one day model molecules, design new drugs, and develop advanced materials.

But it wasn’t just Google’s stock that moved higher on the back of quantum-related news. Quantum computing firms also rallied on reports that the Trump administration is exploring potential equity stakes in Cos like D-Wave Quantum, IonQ, Rigetti Computing, and Quantum Computing in exchange for federal funding. A Commerce Dept official put out a short statement denying active negotiations, but investors saw the brevity of the statement as leaving the door open for future support or deal structures.

See more color below.

Google Achieves A Quantum Computing Breakthrough

- Google achieved the first-ever verifiable quantum advantage, meaning a quantum computer ran an algorithm faster and more accurately than any classical supercomputer

- Google’s Willow quantum chip ran the “Quantum Echoes” algorithm 13,000x faster than top supercomputers

- Importantly, the algorithm is verifiable, meaning it can be repeated on another quantum computer, something it has not been able to show before

- This follows Google’s announcement back in Dec 2024 that Willow had solved a problem in five minutes that would have taken a supercomputer 10 septillion years

- That’s 10,000,000,000,000,000,000,000,000 years – far longer than the age of the universe

- Google said its next goal was to move quantum computing from controlled demonstrations to practical science, including modeling how atoms and molecules interact, which are simulations far beyond the reach of classical computers

- “Just as the telescope and the microscope opened up new, unseen worlds, this experiment is a step toward a ‘quantum-scope’ capable of measuring previously unobservable natural phenomena”

- It could become a powerful tool for mapping molecular structures, designing new drugs, and developing advanced materials for batteries and quantum hardware itself

- BUT real-world use of quantum computers remains yrs away

-> What other commercial milestones have taken place recently in the quantum computing space? Back in February, Microsoft unveiled a new chip which it claimed showed quantum computing is “years, not decades” away, while IBM stated in June that it plans to deliver a practical quantum computer by 2029

-> Google’s stock was up as much as +1.6% on the back of the announcement

Quantum Computing Cos And US Govt Have Reportedly Been Having Equity Talks

- Several quantum-computing Cos are reportedly in talks w/ the Trump Administration to give the Commerce Department equity stakes in exchange for federal funding…

- Cos including IonQ, Rigetti Computing and D-Wave Quantum are said to be discussing the US govt becoming a shareholder as part of agreements to get funding

- Other Cos such as Quantum Computing and Atom Computing are reportedly considering similar arrangements

- The Cos are discussing minimum funding awards from Washington of $10mn each in exchange for government ownership

- Cos including IonQ, Rigetti Computing and D-Wave Quantum are said to be discussing the US govt becoming a shareholder as part of agreements to get funding

-> D-Wave Quantum was up +13.8% on the back of the news, Rigetti Computing was up +9.8%, Quantum Computing was up +7.2%, and IonQ was up +7.1%; YTD, these stock are up +288.7%, up +15.4.5%, down -6.2%, and up +44.4%, respectively

- …but the Trump administration denied the report

- “The Commerce Department is not currently negotiating equity stakes with quantum computing companies,” a spokesperson said in a statement

- BUT quantum stocks stayed higher, as investors viewed the brief statement as leaving room for potential deal optimism

- “Currently” could imply talks will be held later, and “equity” could suggest a different structure in any kind of deal

- Rigetti weighed in w/ a statement: “We are continuously engaging with the U.S. government on funding opportunities…If the U.S. does not lead in supporting these breakthroughs, others will, posing significant risks to our national security”

The Entertainment Sector Is Keeping Everyone On Their Toes

Potential M&A and the streaming landscape continue to be in the spotlight, with WarnerBros Discovery at the center of numerous deal-related headlines this week. The press has kept fuel on the potential consolidation fire, with familiar names like Netflix, Comcast, and Apple being cited as circling the action (see Theme #2 for Netflix’s comments on potential M&A). Meanwhile, the streaming wars continue to evolve – Amazon is taking another try with streaming gaming, Apple is making some new moves with MLS, and ESPN & Fox are apparently seeing continued traction with their new sports streaming DTC offers. And to add a little more spice, carriage deals negotiations also heated up this week.

See below for more details….

WBD Has Been At The Top Of Many Headlines This Week

- Warner Bros. Discovery reportedly rejected 3 offers from Paramount Skydance over the course of 4 weeks

- First & second offer: Mid-Sept, $19/shr, rising to $22/shr later that month

- Third offer: Oct 22nd, reportedly rejected an offer of $23.50/shr, comprised of 80% cash

- That offer represented an 87% premium to WBD’s share price and valued WBD at ~$60bn

- WBD’s BoD annc’d on Tuesday that it initiated a review of strategic alternatives to maximize shareholder value

- Through this process, the WBD Board will evaluate a broad range of strategic options

- This will include continuing to advance the Co’s planned separation to be completed by mid-2026, a transaction for the entire Co, or separate transactions for its Warner Bros. and/or Discovery Global businesses

- As part of the review, the Co will also consider an alternative separation structure that would enable a merger of Warner Bros. and spin-off of Discovery Global to shareholders

- Timeline? There is no deadline or definitive timetable set for completion of the strategic alternatives review process

- CNBC’s David Faber also reported that Netflix & Comcast were among the interested parties

- Apple has reportedly decided against pursuing an acquisition of WBD

-> WBD shares are up +16.3% this week and are now up +100% YTD

Key New Streaming Developments…Amazon Revamps Game Streaming, Apple Pushes MLS, & Fox/ESPN Bundle Uptake Sees A Spike

- Amazon launches revamped Luna game-streaming service

- What is it? Luna, now includes new beginner-friendly multiplayer games that can be controlled with your phone

- The biggest change to the service is the addition of GameNight, a collection of ~25 local multiplayer games that Amazon says are “designed to bring friends and family together in the living room”

- Price? Luna is available at no extra cost for Prime members BUT players who want access to a larger library of games can subscribe to Luna Premium, previously called Luna+, for $9.99/mo

- Amazon and the NFL annc’d that Prime Video will broadcast the Nov. 28 Black Friday Football game

- The game is between the Philadelphia Eagles and Chicago Bears and will be broadcast to 240+ countries, kicking off at 3pm ET

- Preceding the Black Friday Football game, at 9am ET, Prime Video will broadcast the return of “The Skins Game,” featuring the PGA TOUR’s Tommy Fleetwood, Justin Thomas, Xander Schauffele and Keegan Bradley from South Florida

- Prime Video will then transition to South Philadelphia, when Black Friday Football’s pregame coverage commences at 1:30pm ET from Lincoln Financial Field, prior to the Bears versus Eagles kickoff at 3pm ET

- At the conclusion of live on-site NFL postgame coverage, the NBA on Prime tips off a doubleheader at 7pm ET, highlighted by Bucks versus Knicks from New York, and finishing with Mavericks versus Lakers in Los Angeles

- MLS and Apple are offering the league’s entire slate of playoff matches to all Apple TV subscribers at no addtl cost

- In addition to matches on Apple TV and MLS Season Pass, select playoff games will also be available through Fox Sports in the U.S. (FS1 and Fox Deportes) and on TSN and RDS in Canada

- MLS Cup will air on Fox

- Also, ESPN & Fox One have seen seeing spikes in subscriber sign-ups around weekends since both launched on Aug 21, according to Antenna

- For the first 30 days after their respective launches, ESPN has amassed 2.1mn subscribers, while Fox One has 1.1mn

- Fox One witnessed the best single weekend of nearly 350k, due to the rematch of Super Bowl contenders Philadelphia Eagles-Kansas City Chiefs on September 14th

Carriage Feuds Heat Up

- The Disney / YouTube fight continues…Disney now warns that ESPN and other networks may go dark on YouTube TV at the end of the month

- Timeline: Disney’s existing carriage deal with YouTube TV ends at 11:59pm ET on October 30th

- YouTube TV said it would offer subscribers a $20 credit if Disney’s networks are unavailable for “a period of time”

- YouTube TV is again asking to ingest Disney’s streaming content, giving customers the ability to view programming on Disney+, Hulu and ESPN+ without leaving the YouTube platform

- YouTube TV also asked for this in its negotiations with NBCUniversal and was rejected

- Disney has no plans to say yes to this request, according to people familiar with the company’s thinking

- A deadline is looming for a new carriage deal between Verizon’s Fios TV and Nexstar

- If a deal is not reached when the current agreement expires on Oct 24th, customers could lose access to 14 stations in 10 markets

- This includes ABC, CBS and NBC affiliates carrying high profile sports, and the NewsNation cable channel

- Where will it impact: The ATA said the TV blackout could impact Verizon customers in Providence, R.I., Albany, N.Y., Buffalo, N.Y., Syracuse, N.Y., New York, N.Y., Harrisburg, Pa., Philadelphia, Pa., Washington, D.C., Richmond, Va., and Norfolk, Va., jeopardizing their access to regular programs, news and sporting events

- Verizon said “we are currently in negotiations to reach a fair and reasonable agreement on your behalf so we can continue to offer these channels to you”

- If a deal is not reached when the current agreement expires on Oct 24th, customers could lose access to 14 stations in 10 markets

Source 2025: ThatParkPlace 10/23, CNBC 10//22, Variety 10/13, NYTimes 10/22, Reuters 10/21, CNBC 10/23, LATimes 10/23, Google 10/21, zdnet 10/21, NFL 10/22, TechCrunch 10/22, MediaPost 10/20, SportsBusiness 10/20, Deadline 10/22, Cordcutters 10/18, WBD 10/21, Verizon 10/22

Investors Continue To Worry About The Ad Agency Model…OMC’s Next Stop Is The IPG Merger

After Publicis’ strong upside, growth, and outlook comments, Omnicom delivered what was more in-line with expectations with some cautious forward considerations. While organic revenue growth of +2.6% was anticipated, it still sits at the low end of the +2.5-4.5% full year guidance range (vs Publicis, who raised their FY organic guidance range for the 2nd qtr in a row). Operating margins were a tad light as well. In terms of the big picture environment, mgmt cited some stability in client spend which is a plus, and with 9-mo organic growth at +3% y/y, they are tracking within the guided range but mgmt did caution that Q4 performance will depend on project work, which typically ranges from $200-250mn in potential.

On the innovation front, the Co is launching (at CES) its Omni Plus, a next-generation marketing operating system, and the Co rolled out an agentic framework across the organization which has become their fastest growing platform ever. Those are positive developments but (as also mentioned last week) investors remain fearful about how AI will impact the agency model in the future.

The next big catalyst is the closing of the IPG transaction which is slated for “late November” pending EU approval…

Please see more details below.

-> OMC rose +3% in reaction to earnings but is down -8% YTD while Publicis and WPP shares are down -16% and -56%, respectively

OMC’s Q3 Was Roughly In-Line Though US Organic Growth Accelerated

- Q3 organic growth of +2.6% y/y was line w/ cons and slightly down from Q2’s +3%: But US accelerated seq to +4.6%

- Verticals – organic growth:

- Media & Advertising: +9.1% y/y, “while Creative continued to be impacted by lower levels of project work due to macroeconomic uncertainty, media growth was strong across virtually all geographies”

- Precision Marketing: +0.8% y/y, “Solid growth in the U.S. was offset by declines in other markets, primarily in Europe”

- Public Relations: -7.5% y/y, “~$25mn or 80% of the decline results from no U.S. national election-related revenue in 2025 versus 2024, with the majority of the remaining reduction occurring in the U.K. We do expect similar declines in Q4 resulting from the difficult prior year comp to Q4 of ’24, which included spend related to the U.S. national elections”

- Healthcare: -1.9%, y/y, “Both our U.S. and European agencies were down 2% organically as recent new business wins did not fully replace some spending declines in the quarter on client products that are in the process of coming off patent protection”

- Branding & Retail Commerce: -16.9% y/y, “market conditions continue to impact new rebranding projects, new brand launches and in-store retail commerce”

- Experiential: -17.7% y/y, on a difficult comp against the Summer Olympics in 2024 as we expected

- Execution & Support: +2% y/y, “driven by growth in our Merchandising business, which was partially offset by a reduction in spend in field marketing”

- Regions – US growth accelerated

- US (~53% of rev): +4.6% vs Q2 +3%

- Other N. Amer: -0.2%

- UK: +3.7%

- Europe: -3.1% (although mixed by mkt)

- Asia Pac: -3.7%

- LatAm: +27.3%

- ME and Africa: +5.9%

- Adj EBITDA margin @ 16.1% was slightly below cons; Adj EPS beat by +3.7%

Organic Growth Is Still Tracking Within The FY 2025 Guidance Range

- The Co stated that “we’re comfortable with our guidance and both EBITDA & EBIT and rev”

- Q3 organic growth was +2.6%, 9 months organic growth was +3%, vs full year guidance +2.5-4.5%

- The 2025 tax rate on adj basis is expected to be b/w 26.5%-27%.

- Share repurchases are still on track to total close to $600mn for FY

Client Spend Is Stable Though Q4 Project Spend Will Be A Swing Factor

- Client spend is currently stable, with some discipline-specific declines tied to the absence of U.S. election-related spending, but overall client engagement and new business wins remain strong

- “Public Relations declined 8%. ~ $25mn or 80% of the decline results from no U.S. national election‑related revenue in 2025 versus 2024, with the majority of the remaining reduction occurring in the U.K. We do expect similar declines in Q4…”

- Mgmt sees $200-500mn in potential Q4 project work, though visibility remain limited: This could be a swing factor

- Key new business wins: Include American Express, Porsche, Intersnack, White Castle, OpenAI while IPG won Amgen, Bayer, Anthropic and Paramount

The Co Is Integrating AI, Into Its Core Platforms (Notably Omni Plus), Using Agentic Frameworks To Drive Client Outcomes

- Generative AI is layered in Omni Plus: “A key part of our operating system is our generative AI layer, which is an agentic entry point to Omni Plus”

- Generative AI, “really affected every facet of our business and because we’ve integrated it into every part of our workflow”

- “In one of our most recent wins for a large automotive company, our teams used integrated agents, the agent framework that we talked about in not only this call, but in the previous earnings call throughout the entire pitch process, which includes consumer research, creative concepting, production and customer journey planning, ultimately enabling our teams to move not just with speed but to develop really a differentiated creative solution”

- “Within our sports marketing units, we’re using agents that are grounded on proprietary data around experiential brand impacts of sporting events, concerts and festivals, which is allowing them to really contextualize every concept that they explore for the work that they do for clients”

- “The commerce group is also using it very effectively”

- The health group continues to rewrite the way drug launches are being done and the processes within that using an AI-first lens

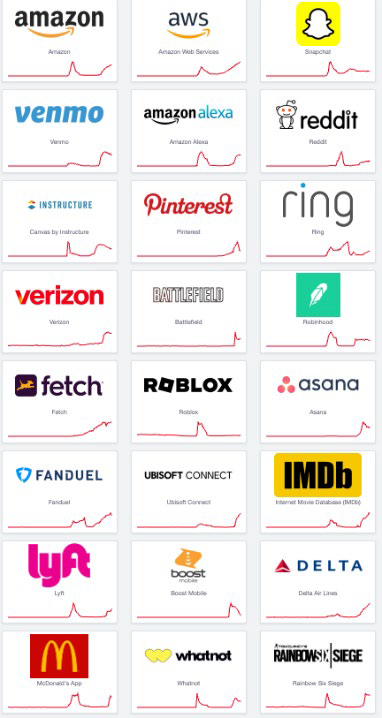

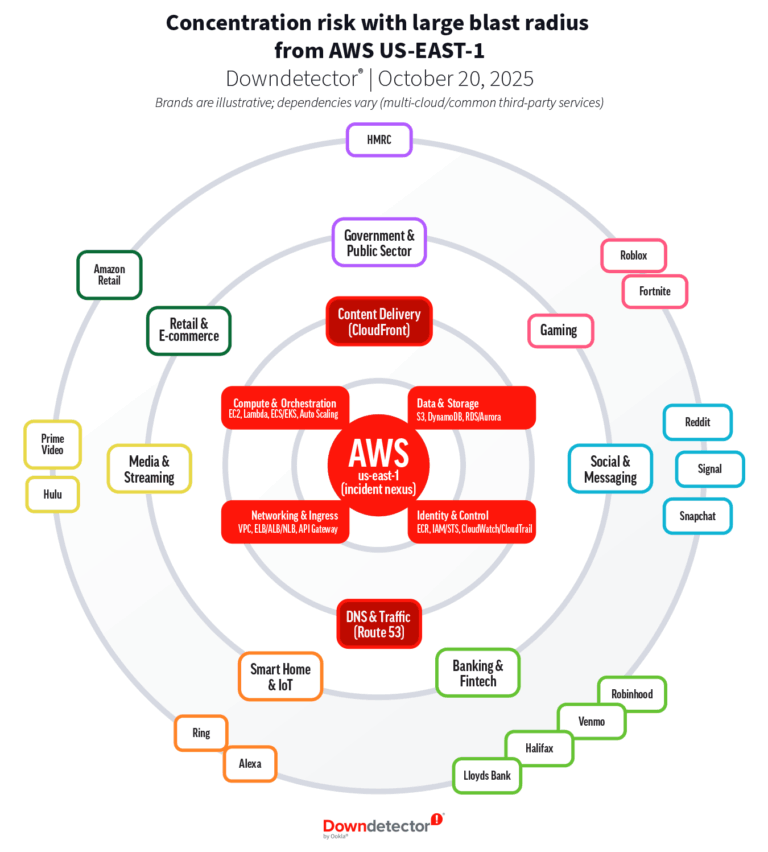

The Week Started With The Cloud Crashing Down In A Major AWS Outage

Finally, amidst everything else that has happened in this jam-packed week, we quickly wanted to touch on the event that started this week off with a bit of a flurry. In the early hours of Monday (October 20th), Amazon Web Services (AWS) experienced a major outage centered in its US-EAST-1 region, the Co’s oldest and most heavily used hub, causing widespread disruptions across websites, apps, and platforms for over 12 hours. At its peak, 50k+ outage reports were logged, and according to Tenscope, the downtime reportedly cost companies ~$75mn/hr.

As has happened in the past with similar outages, such as the recent Google Cloud outage and the 2024 CrowdStrike update failure that took down large swaths of Microsoft’s cloud svs, this latest AWS disruption is a stark reminder about the concentration and connectiveness of our bigger picture tech infrastructure. While there are benefits of having the big three cloud players (Amazon, MSFT, and Google) keeping the internet running with respect to cost efficiencies, standardization, and stronger cybersecurity, outages like these underscore how concentrated dependencies can quickly turn isolated technical glitches into widespread (often global) disruptions.

See below for a quick overview of the outage this week and some key impacts.

- In the early morning of Oct 20th, Amazon Web Services suffered from what became a multi-hour outage that affected a mix of websites, apps and platforms

- At 12:11am PDT, AWS started experiencing outages

- At 2:01am PDT, the specific problem was identified and work on a fix began

- Collectively, reports on Down detector hit a high of 50k+ reports, starting around 7:50 am

- The AWS outage was caused by a malfunction in the health monitoring system of network load balancers within AWS’s Elastic Compute Cloud (EC2) internal network

- This malfunction led to incorrect health status across the EC2 internal network

- This caused misreported health data and disrupted internal routing

- As a result, DNS resolution for critical services began failing, leading to cascading failures in dependent services

- This malfunction led to incorrect health status across the EC2 internal network

- Specifically, AWS’s oldest and most heavily used hub “US-EAST-1” went down

- The outage started at 1:00 am PDT and ran all the way through to 3:00pm PDT

- When a regional dependency fails (as in this case), impacts propagate worldwide because many “global” stacks route through Virginia at some point

- The outage had significant global reach and deep cross-sector impact

- Downdetector captured 17mn+ outage reports globally across 60+ countries, with the US (>6.3mn) and UK (>1.5mn) leading outage volumes

- Svs with the most reports included Snapchat (~3mn), Roblox (~716k) and Amazon retail (~698k), and spanned everything from banking to gaming svs

- Per Tenscope estimates, about ~$75mn was likely lost per hr that the outage continued — with Amazon itself taking more than $72mn of that

- Amazon: $72,831,050 per hr

- Snapchat: $611,986 per hr

- Zoom: $532,580 per hr

- Roblox: $411,187 per hr

- Fortnite: $399,543 per hr

- Canva: $342,466 per hr

- Slack: $194,064 per hr

- Reddit: $148,402 per hr

Sources 2025: Tomsguide 10/20, Reuters 10/21, Yahoo Finance 10/21, Ookla 10/21

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Paramount Skydance annc’d Jay Askinasi as CRO for ad sales, joining Nov. 3, while John Halley remains in a yet-unclear role. The Co aims to boost digital ad rev amid streaming growth, competing w/ Amazon & Google. Askinasi’s digital ad-tech background complements Halley’s expertise. (Variety)

- LinkedIn’s ad rev is forecast to hit $8.2bn in 2025 (18.3% YoY growth), rising to $11.3bn by 2027, per WARC. Its B2B focus, AI tools, video formats & CTV integration drive gains. LinkedIn outpaces Snapchat ($6bn), Pinterest ($4.2bn), Reddit ($2.2bn). (MediaPost)

- Global media cost inflation hit 4.3% in 2025, up 0.5 pts YoY, per WFA Outlook. Forecast for 2026 shows slight deceleration to 4.2%. U.S. ad inflation rose to 3.8%, expected to reach 4.0% next yr. Linear TV costs rose 5% due to shrinking audiences; broadcaster VOD leads w/ ~+5% inflation, while CTV remains flat (~+1%). (MediaPost)

- TV ad impressions for NFL rose 12% y/y in 3Q25; college football saw a 16%+ jump. NFL’s nat’l TV ad spend grew 9.7%, college football up 22.5%. News shows held 9 of top 20 spots by impressions, most ranked higher y/y. QSR led brand category in 6 of top 10 programs. (Cynopsis)

- Mubadala Capital, unit of Abu Dhabi’s sovereign wealth fund, is exploring a deal to acquire billboard operator Clear Channel Outdoor, per Bloomberg. Anson Funds pushed for the sale last month amid rising outdoor ad deal activity. The San Antonio-based Co holds ~$6.4bn debt. (Reuters)

Artificial Intelligence/Machine Learning

- Anthropic annc’d a major expansion w/ Google Cloud, gaining access to ~1mn TPUs and svs to train Claude models. The deal, worth tens of bn$, boosts AI infra and supports growing demand. Anthropic cites TPUs’ efficiency and cost benefits. The Co’s Claude models are used by cos like Figma and Palo Alto Networks. (PR Newswire)

- Anthropic annc’d Claude’s auto memory upgrade for Pro/Max users, enabling recall of past chats w/o prompts. Max users get access now; Pro rollout is cont’d. Users can edit, toggle, or separate memories. Claude now rivals ChatGPT/Gemini, which had memory earlier. (The Verge)

- Synthesia, a UK AI video start-up known for its hyper-realistic multilingual avatars, rejected a $3bn takeover offer from Adobe to stay independent. Despite Adobe’s prior $10mn investment and Meta’s interest, CEO Riparbelli aims to take the Co public. Synthesia’s rev rose 82% to $58.2mn in 2024, w/ a $56.5mn pre-tax loss. (The Times)

- Reddit sued AI startup Perplexity in NY federal court, alleging it scraped Reddit data unlawfully to train its AI search engine. Reddit claims Perplexity bypassed protections, citing a 40-fold citation increase post cease-and-desist. (Reuters)

- Tesla annc’d its AI5 chip will be made by Samsung (TX) & TSMC (AZ) for “excess production. ” Chips not used in EVs/robots may go to data centers. AI5, cont’d from Autopilot hardware, is tailored for Tesla’s needs, omitting legacy parts for speed. Musk said it may offer 10× better AI perf/$ vs rivals. (CNBC)

- Lumen & Palantir annc’d a multi-yr, multi-mn-$ strategic partnership to accelerate enterprise AI adoption. Pairing Palantir’s Foundry & AIP w/ Lumen’s Connectivity Fabric, the cos aim to boost AI deployment speed, security & efficiency across multi-cloud setups. (Business Wire)

- Alibaba annc’d Quark AI Glasses priced at ~$660, w/ pre-sale from Oct. 24 and Dec. shipping. Powered by Qwen LLM, features include hands-free calling, music, and real-time translation. Also unveiled AI Chat Assistant in Quark app, enabling AI search, photo editing, and writing. (CNBC)

- YouTube annc’d a new AI likeness detection tool for creators in its Partner Program, enabling them to flag and request removal of unauthorized AI-generated videos using their face. Initially tested w/ talent from CAA, the feature works like Content ID and may show actual, unaltered clips. (The Verge)

- Meta will lay off ~600 from its AI unit to streamline ops and solidify Alexandr Wang’s leadership. Cuts affect FAIR and infra teams but spare TBD Labs. CEO Zuckerberg, frustrated w/ AI progress post-Llama 4, backs Wang’s hires. Meta’s Superintelligence Labs now has <3,000 staff. (CNBC)

- Amazon plans to automate 75% of its ops, aiming to replace ~600,000 jobs w/ robots by 2033. Internal docs show cost-cutting goals, w/ $12.6bn in savings by 2027. (The New York Times)

- Google annc’d updates to AI Studio, enhancing dev workflows. A unified Playground now supports Gemini, GenMedia (Veo 3.1), TTS & Live models. New homepage, rate limit page & Maps grounding boost usability. Saved system instructions & revamped API Key mgmt offer more control. (Google)

- OpenAI annc’d Project Mercury, enlisting 100+ ex-bankers from JPMorgan, Goldman Sachs & others to train AI for financial modeling. Contractors earn $150/hr to build models for IPOs, restructurings, etc., w/ early access to AI aimed at replacing junior bankers’ grunt work. (Yahoo Finance)

- Meta AI’s app saw a sharp rise in usage post-launch of its ‘Vibes’ AI video feed . Daily users hit 2.7mn, up from 775K, w/ downloads reaching 300K/day. Compared to ChatGPT, Grok, and Perplexity, Meta AI saw a 15.58% user increase while rivals declined. (TechCrunch)

- Airbnb CEO Chesky said the Co relies heavily on Alibaba’s Qwen AI, citing it as “fast, cheap” and better suited than ChatGPT. Despite using 13 models incl. OpenAI & Google, Qwen’s open-source flexibility stood out. Alibaba has released 300+ models powering ~170K derivatives, making it the largest open-source AI ecosystem. (Yahoo Finance)

- Samsung annc’d a new Perplexity AI app for all 2025 TVs, w/ 2023–2024 models getting it via OS upgrade later this yr. The app includes a free 12-month Perplexity Pro sub, offering GPT-5, Claude 4.5, Gemini 2.5 Pro, Research Mode & image creation. (TechRadar)

- OpenAI annc’d stricter controls on Sora 2 deepfakes after Bryan Cranston and SAG-AFTRA raised concerns over unauthorized AI clips. The Co will work w/ talent unions incl. UTA and CAA to protect likeness rights. Sora now requires opt-in for voice/image use and responds swiftly to complaints. (CNBC)

- AI models Grok, DeepSeek, and Claude Sonnet 4.5 led the “Alpha Arena” crypto trading contest, each earning 25%+ returns. GPT-5 and Gemini 2.5 Pro posted 28%+ losses. Each model traded w/ $10K on Hyperliquid, aiming for risk-adjusted gains. (Yahoo Finance)

- DeepSeek AI annc’d DeepSeek-OCR, a vision-based system for compressing long contexts via optical 2D mapping. Using DeepEncoder and DeepSeek3B-MoE-A570M, it achieves 96%+ OCR precision at 9–10× compression and ~60% at 20×. It processes 200,000+ pages/day w/ one GPU, supports multi-resolution, and enables efficient LLM training. (DeepSeek)

- Anthropic annc’d Claude Code’s web app rollout for Pro ($20/mo) and Max ($100–$200/mo) users, expanding access beyond CLI. Claude Code, now contributing ~$500mn in rev, lets devs manage AI coding agents via browser or iOS. 90% of the product is AI-written. (TechCrunch)

Audio/Music/Podcast

- AI music startup Suno, generating ~$100mn in annual rev, is in talks to raise over $100mn at a $2bn valuation. Despite a lawsuit from Sony, UMG & Warner alleging copyright infringement, Suno claims its tech creates original content. Co-founder Shulman denies stream-ripping. Suno previously raised $125mn. (Music Business Worldwide)

- Spotify annc’d a feature letting users follow venues for concert updates. Followed venues appear in users’ libraries w/event calendars, genre filters & daily live feed updates. Users can tap shows to book via partners like Ticketmaster. Spotify’s “Concerts Near You” playlist offers 30 songs from local artists. (TechCrunch)

Broadcast/Cable Networks