A staggering 44% of the S&P 500 reported this past week (per MarketWatch data), and Big Tech was well represented, but was met with divergent reactions. Alphabet’s +10% move on the back of its earnings was a major standout. The markets also moved higher (S&P 500 +0.9% and Nasdaq +1.1%) despite continued geopolitical tensions.

Also, while no surprise, rate actions emerged at Wednesday’s Fed meeting, listening to Fed Chairman Powell’s last official comments felt bitter-sweet…the end of an era!

The full list of what we focused on in this edition is below:

- Earning Scorecard - Week 3

- Alphabet’s Big Capx Investments Are Showing Clear Signs Of Returns

- All In, Amazon Continues To Execute Across Its Businesses

- Meta Beats Across The Board But The AI ROI Debate Dominates As Capx Moves Up AGAIN

- Price Hikes Help Spotify’s Q1 But Its Investment Ramp Spooks Investors

- UMG’s Business Faces A Multitude Of Moving Parts

- Verizon’s Early Progress With Its Turnaround Strategy

- T-Mobile’s Growth Vectors Remain In Place

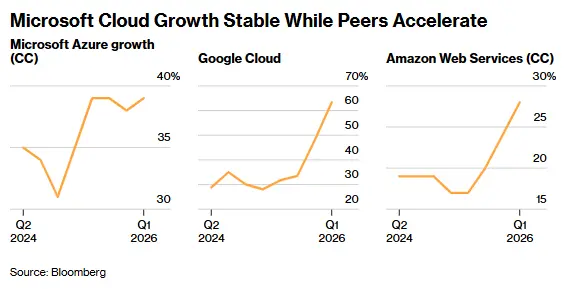

- MSFT’s Combo Of Decelerating FQ4 Top Line Growth Y/Y + Higher CapEx Underwhelmed

- Apple Beats Across the Board But Memory Costs & Supply Constraints Will Be Key Watchpoints Ahead

- AI Disruption Fears Remain, But Booking Sees Resilient Underlying Travel Trends Ex The Middle East Conflict

Lastly, LionTree Advisors is proud to have served as exclusive financial advisor to PlayMetrics, a leading provider of operations management software for youth sports organizations, on its acquisition of substantially all the assets of SportsEngine from Versant Media Group, Inc.

Have a nice weekend.

Best,

Leslie

Earning Scorecard - Week 3

Week 3 of earnings was large cap heavy! A total of 38 stocks in our LionTree Universe reported and stock reactions were slightly biased to the negative side this week, with 20 (53%) stocks trading down and 19 (47%) stocks trading up. The best performer in reaction to earnings was Fiverr, which was up +17%, while the worst performer was Roblox, which fell -18%.

It was a pivotal week for large-cap Tech with Alphabet up +10% in reaction to earnings (see Theme #2), Amazon up +0.8% (see Theme #3), and Apple up +3.3% (see Theme #10). Meta was down -8.6% in reaction (see Theme #4) while Microsoft also down -3.9% (see Theme #9). See our deep dives for more color.

Music was also represented with Spotify down -12.4% in reaction to its earnings (see Theme #5), while UMG was flat (see Theme #6). In telcos, Verizon rose +1.6% in reaction (see Theme #7) and T-Mobile rallied +6.1% (see Theme #8). Booking was down -0.3% in reaction (see Theme #11) and was also the first OTA to shed light on travel trends, especially given the geopolitical climate.

Other notable prints that we wanted to highlight, but were not able to do our usual deep dives for include:

- eBay: Traded down flattish in reaction to results despite a strong Q1 (GMV, revenue, and adj EPS all beat consensus), slightly stronger than expected active buyers of 136mn, and Q2 GMV guidance of $21.3bn-$21.7bn that was +2% above cons at the mid-pt

- Reddit: Traded up +13.1% in reaction to strong Q1 w/ revenue (+69% y/y) and adj EPS both topping expectations, and Q2 rev & adj EBITDA both ahead of cons (by +1.3% and +5.2% respectively)

- Roku: Traded up +6% in reaction to strong Q1 (revenue and adj EBITA both beat cons by +4.2% and +13.1% respectively), strong Q2 guidance (at the mid-pt, revs beat by +1.2% and adj EBITDA beat by +28.1%) as well as better 2026 guidance (at the mid-pt, revs beat by +0.6% & adj EBITDA beat by +6.3%)

- Roblox: Traded down -18.1% in reaction to mixed Q1 results (bookings and revenue missed the Street while adj EPS beat), softer user trends (132mn DAUs and 31bn hours engaged both missed), and a cut FY2026 bookings outlook by -11%, at the mid-pt; Q2 bookings guidance was also -14% below consensus

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Alphabet’s Big Capx Investments Are Showing Clear Signs Of Returns

Big Tech earnings drove a volatile week with diverging stock reactions, but Alphabet stood out as its heavy capex most clearly translated into broad-based returns across its businesses in Q1. The Co’s HUGE beat in Cloud revs (grew +63% y/y with AI solutions as the primary driver) and cloud margins (32.9% vs cons 23%) coupled with a MASSIVE backlog (nearly doubled to $462bn) were all major positives. Search revenue’s acceleration to +19% y/y also topped expectations. Clearly the investments in AI are paying off and the Co wants to stay ahead of the curve. Q1 capx was +$200mn higher than consensus and 2026 capx was raised by +$5bn at the mid-pt (to $190bn) to now include investments related to the acquisition of Intersect Power (closed in March). 2027 capx is still a wild card, and is guided to be “up significantly,” but investors are giving the Co the benefit of the doubt (at least at the moment) given the strong ROI that they have been generating on incremental spend.

In addition, five of our other top takeaways from the Co’s results include: 1) Cloud revenue growth would have been even higher if they were still not capacity constrained; 2) The Co is selectively starting to sell their TPUs externally, which is a big deal (though this will be more of a 2027 story); 3) Gemini enterprise Q1 paid MAUs in subscriptions grew +40% q/q and Q1 was the strongest qtr ever for consumer AI plans, primarily driven by Gemini app adoption; 4) AI experiences are driving search usage and queries to all-time highs (including commercial queries); and 5) Agentic commerce is gaining real adoption (moving to implementation).

See more color below on all the above, in addition to other key updates across Alphabet’s businesses including YouTube, Waymo and more. Overall though, the Co’s full stack approach appears to the working…

-> GOOGL shares rallied +10% post its print, lifting Google to its best month on Wall Street since 2004 (+34% in April); YTD, the stock is up +22.1%, outperforming YTD performances of MSFT down -14.2%, META down -7.78%, and AMZN up +16.2%

-> See Themes #4, #3, and #9, for thoughts on Meta, Amazon, and Microsoft’s results, respectively

A HUGE Beat In Cloud & Upside In Search Drove A Strong Q1…Strong Operating Leverage Stood Out

- Revenue BEAT: By +2.8%, up +22% y/y (+19% FXN) vs +12% y/y in Q1:25

- Driven by stronger Search, Cloud, and Subscriptions growth

- 11th consecutive qtr of double-digit growth

- Q2 FX guidance…the FX tailwind will be ~+1pt to consolidated revs vs a +3pt FX tailwind in Q1

- Adj op Income materially BEAT: By +9.6%, up +30% y/y

- Adj op margin of 36.1% was WELL ABOVE cons 33.9%, reflecting strong topline leverage in Services + Cloud despite higher AI infra, marketing, and AI talent spend

- Adj EPS BEAT: By +6.8% to $2.81

- FCF MISSED cons by -13.8% at $10.1bn

- The Co incr’d the qtrly dividend by +4.8% to $0.22/shr

Capx Is Likely To Take Another Leg Up In 2027 Y/Y Given Strong Demand & Return On Investment

- Q1 capx came in slightly above cons: $35.7bn vs $35.5bn, but up over 100% y/y

- The overwhelming majority of spend is going to technical infrastructure; ~60% of technical infra spend was in servers and ~40% in data centers/networking

- CAPX OUTLOOK…an increase in 2026 guidance due to its recent acq, and 2027 is likely another step up

- 2026: The Co raised guidance by +$5bn at the mid pt ($180-190bn) to now incl investment related to the acq of Intersect (closed in March)

- 2027: Capx is guided to be up “significantly” y/y

- As the Co sees “unprecedented” internal + external compute demand

- The investments in AI are delivering “strong growth” …i.e., record revenue and backlog growth in Google Cloud, strong performance in Google Services

- Reminder that higher capx means higher depreciation + energy/data center operating costs

It Was A Blow-Out Quarter For Google Cloud…AI Solutions Were The Primary Growth Driver For The 1st Time, Backlog Nearly DOUBLED, And External TPU Sales (1st Time) Open A New Leg Of Growth

- Q1 Cloud revenue growth accelerated to an impressive +63% y/y, from +48% y/y in Q4 and +34% y/y in Q3 due to “strong demand for our AI products and infrastructure”

- Revenue exceeded $20bn for the 1st time

- AND “our Cloud revenue would have been higher if we were able to meet the demand”

- The backlog also nearly doubled q/q to $462bn from $240bn

- The majority of the backlog is still GCP agreements, but it also includes TPU hardware sales

- Just over 50% of backlog should convert to revenue in the next 24 months

- Enterprise AI solutions became the primary growth driver for Cloud for the 1st time in Q1: Driven by strong demand for their key models, including Gemini 3, and strong growth in infrastructure due to cont’d deployment of TPUs and GPUs in core

- Revenue from products built on Google’s AI models grew nearly +800% y/y vs nearly +400% y/y in Q4

- Growth in GCP cont’d to grow at a rate much higher than Cloud’s overall revenue growth rate, driven by demand for infrastructure and other svs such as cybersecurity and data analytics

- Workspace delivered strong DD revenue growth: Driven by an increase in the # of seats and the avg rev per seat

- New customer & deal momentum is strong

- New customer acquisition doubled y/y

- The number of $100mn to $1bn deals doubled y/y, and the Co signed multiple $1bn+ deals

- Customers outpaced initial commitments by +45%, accelerating from +30% last qtr

- External TPU monetization is a new theme: Google will begin delivering TPUs directly into select customer data centers, not just via Cloud

- This as “opportunistic” and ROIC-driven, targeted at use cases like frontier AI labs and capital markets/HPC customers that want TPUs on-prem

- The Co will begin recognizing a small % of TPU hardware sales later in 2026, with the vast majority of rev recognized in 2027 (TPU hardware sales will fluctuate qt rot qtr)

- Seeing strong demand for their Agentic defense cyber security offerings

- Closed the acq of Wiz, a leading cloud and security AI platform, in March

- “The performance of this so far has exceeded our expectations”

- Closed the acq of Wiz, a leading cloud and security AI platform, in March

- Q1 Cloud adj operating income BEAT by a large 38%, w/ margins expanding to 32.9% from 17.8% a yr ago

- Mgmt attributed this to topline leverage plus operating efficiency across technical infra + the org (to note, the market has been concerned that AI cloud revenue is lower margin)

- Outlook: Cloud margins will now include a low-SD pt headwind for the balance of 2026 from the Wiz acq

- Mgmt stressed its vertical optimized AI stack differentiation: “We are unique in the market because of our vertically optimized AI stack and the way we co-develop the components from our infrastructure and models to platforms and the tools to applications and agents”

- Owning frontier models and silicon “helps us stay ahead of the curve”

- Deep investment in the security layers “keeps everything safe”

- “I think we are the only provider in the market that offers all of these in a vertical stack”

Google AI Models Have “Great Momentum” & Gemini Adoption In Both Enterprise & Consumer Stood Out

- 1st party models now process more than 16bn tokens per minute vs 10bn in Q4

- Gemini 3.1 series of models offer more choices for developers

- Speech to text is now available in 70 languages and with 3.1 Pro

- Generative AI media models are “incredibly” popular

- Lyria 3: Generated over 150mn songs since launching on the Gemini app

- Nano Banana 2: Reached 1bn images in nearly half the time of Nano Banana 1

- Veo 3.1 Lite: The most cost-efficient video model to date

- GEMA 4 (the Co’s “most intelligent” open model) has been downloaded 50mn+ times in just a few weeks

- The Co’s open models have now been downloaded over 500mn times in total

- Gemini enterprise Q1 paid MAUs in subscriptions grew +40% q/q: That includes major global brands like Bosch, Citi Wealth, Merck, and Mars Incorporated

- Saw 9x y/y growth both in seats sold w/ partners and in the # of partners adopting it for internal use

- Q1 was the strongest qtr ever for consumer AI plans, primarily driven by Gemini app adoption

- Personal intelligence is now in the Gemini app, AI mode, and Gemini in Chrome… “early traction has been good”

- Also integrated Nano Banana 2 to make personalized image creation possible in the Gemini app

- Maps recently got its “most significant upgrade” in over a decade with Gemini…users can now have a conversation with Maps and get more personalized suggestions and intuitive directions

Search Growth Accelerated Y/Y More Than The Street Expected As AI Overviews + AI Mode Drive More Queries & Better Commercial Intent

- Q1 Search revenue growth accelerated to +19% y/y from +17% y/y in Q4 and +15% y/y in Q3 and BEAT cons by +2%: The Retail + Finance verticals were the biggest contributors…”AI Overviews are driving overall Search”

- AI Is helping with:

- Ad quality

- Advertiser tools

- Reinventing ads in new AI experiences

- AI Is helping with:

- AI experiences are driving search usage and queries to all-time highs (including commercial queries)

- Reiterated that it is still an “expansionary” moment in search

- AI is improving engagement & monetization in a more tangible ways

- Smart bidding now uses Gemini to match user intent to an advertiser’s product & services more accurately and further drive performance…this level of granularity was “previously impossible to achieve at scale”

- Gemini helps advertisers drive more efficient and effective campaigns, people no longer search in fragments

- AI has “significantly expanded” its ability to deliver ads on longer, more complex searches that were previously difficult to monetize

- More than 30% of customer search spend now uses AI-enabled campaigns through AI Max or Pmax and they are seeing more conversion for the same spend

- Direct Offers in AI Mode are “resonating with users” and getting positive customer feedback

- The Co is testing new ad formats that show retailers selling the organically recommended products surfaced in AI Mode

- AI Search is getting cheaper & faster at scale

- Search latency has fallen >35% over the past 5 yrs despite a more complex results page

- Since upgrading AI Overviews + AI Mode to Gemini 3, the cost of core AI responses has fallen >30%

- Mgmt sounded open to AI search monetization via subscriptions vs just ad-supported, but down the road

- As higher-value use cases emerge, there may be cases where users want the most powerful models but “today in the Gemini app, we’re focused on the free tier and subscriptions”

- “We’re not rushing anything here”

Also, Agentic Commerce Is Now Becoming More Of A Real Near-Term Catalyst

- UCP appears to be gaining more ecosystem traction…Amazon, Meta, Microsoft, Salesforce, and Stripe joined the UCP Tech Council this qtr

- Mgmt has received “tremendous feedback” from hundreds of tech cos, payment partners, and retailers

- Merchant adoption is moving from concept to implementation

- Sephora and Macy’s joined the companies rolling out UCP

- Ulta Beauty launched commerce inside AI Mode in Search and the Gemini app, letting shoppers review recommendations, compare options, and complete streamlined checkout for eligible purchases directly within Google’s AI experiences

- “Agentic experiences are additive” and can transform shopping from discovery to decision…by removing the “grunt work” of shopping and making the process more assistive, personal, and fluid

YouTube Ad Revs Slightly Trailed Expectations But Y/Y Growth Still Accelerated… Subscriptions Rev Was A Key Growth Driver

- YouTube (YT) ads revenue growth re-accelerated to +11% y/y from +9% y/y in Q4, though it was still a slight miss (-1.1%) vs cons

- Direct Response remained the key driver, followed by Brand

- AND YT subscriptions revenue is growing FASTER than Ads, particularly YouTube Music + Premium.

- Q1 delivered the largest quarterly increase in non-trial YouTube Music + Premium subscribers globally and in the U.S. since launch in 2018

- Premium Lite was fully launched in 23 countries by the end of Q1, with another dozen+ countries planned for Q2

- Q1 engagement/use cases remained very strong

- U.S. viewers are now watching 200mn+ hours of YouTube content daily

- 10mn+ channels were publishing Shorts each day as of March

- YouTube has led streaming watch time in the U.S. for 3 consecutive yrs

- The Co continues to build more commerce + creator tools into the platform

- Gemini now powers YT Creator Partnerships directly inside YouTube Studio and Google Ads

- The Co is curating top podcast inventory into premium ad offerings

- Supergoop’s campaign w/ creator Liza Koshy drove a +93% lift for Glowscreen and a +55% overall brand lift, highlighting the brand-commerce opportunity

- Subscriptions Platforms & Devices revenue rose +19% y/y and BEAT by +3.3%

- Paid subscriptions reached 350mn, up from 325mn last qtr

- Strong growth in both YT subscriptions, as noted above, & Google One subscriptions (given incr’d demand for AI plan)

Waymo Continues To Scale… While Portfolio Simplification Elsewhere Makes Other Bets Cleaner

- Waymo remains an important growth initiative and surpassed 500k fully autonomous rides per week, doubling in less than a year

- Nashville launched a few weeks ago, bringing six new cities so far in 2026 and operations in 11 major U.S. cities overall

- Other Bets operating loss improved seq to -$2.1bn from -$3.6bn in Q4, though still worse y/y

- The broader Other Bets portfolio is becoming more streamlined

- Verily completed an external capital raise and was deconsolidated

- GFiber annc’d plans to combine w/ Astound Broadband & is expected to deconsolidate upon close in Q4

All In, Amazon Continues To Execute Across Its Businesses

While there were a lot of positives with Amazon’s Q1 results, there were also a couple of offsets that left the stock relatively unchanged. Big picture, Q1 results showed momentum across its cloud, AI, infrastructure, and consumer businesses, but Q2 op income guidance disappointed (after beating in Q1). Also importantly, Q1 capx was ~in-line and the Co didn’t further raise the $200bn 2026 guidance provided last qtr (which we view as a plus). Our other top five takeaways from results are: 1) AWS’s growth of +28% y/y was the highest growth in 15 qtrs and a big number for a segment that has an ~$150bn annualized revenue run rate; 2) AWS’s chips biz is scaling quickly with Q1 revenues up ~40% q/q (the annual rev run rate is now over $20bn) and mgmt flagged again that there is a “good chance we’re going to sell racks over the next couple of years”; 3) The Stores’ network efficiencies also continues to improve with fulfilment network costs growing slower than unit growth; 4) Rufus (Amazon’s AI personal assistant) MAUs were up ~115% and engagement was up ~400% y/y but 3P horizontal agents have more work to do; and 5) Advertising growth remained strong at +22% y/y.

See below for more thoughts on the above, as well as other important points on key parts of the business.

All in all, we viewed results more positive than not.

-> AMZN shares closed up almost +1% after its report and ended the week up +16.3%; YTD, the stock is up +16.2%

-> See Themes #2, #4, and #9 for our takes on Alphabet, Meta, and Microsoft’s results, respectively

Amazon Delivers A Strong Q1 BEAT, Especially On Profitability & Earnings…

- Q1 revs, op income and adj EPS all BEAT cons

- Revs BEAT by +2.4% and grew +17% y/y (+15% y/y FXN) vs +14% y/y (+12% y/y FXN) in Q4

- NA segment BEAT by +1.7%: Sales grew +12% y/y vs +10% y/y in Q4

- Intl segment BEAT by +3.9%: Sales rose +19% y/y (+11% FXN) vs +17% y/y (+11% FXN) in Q4

- AWS BEAT by +2.6%: Rose +28% y/y vs +24% y/y in Q4

- Op income BEAT by +14.7%…with op margin of 13.1%, up +130bp y/y (highest op margin ever)

- NA op income of $8.3bn BEAT by +21.7%

- Op margin reached 8% up +160bp y/y

- Intl op income of $1.4bn BEAT by +30.8%

- Op margin reached 3.6% up +60bp y/y

- AWS op income of $14.2bn BEAT by +10.6%

- Op margin reached 37.7% down -180bp y/y

- NA op income of $8.3bn BEAT by +21.7%

BUT Q2 Guidance Was Mixed…Better Revs & Worse Op Income Vs Expectations

- Q2 rev guidance was +4.3% AHEAD of cons and implies +16-19% y/y growth, vs the +17% y/y in Q1

- Anticipates an unfavorable impact of ~10bp from FX rates

- Strong sales trends are carrying into Q2

- Q2 op income was -2.9% BELOW the Street

- The Q2 guidance given assumes 3 things…

- That Prime Day occurs in Q2 in most of the largest geos (incl the US) and occurs in Q3 in Australia, Brazil, India and Japan

- Note that in 2025, Prime Day was in Q3 for all countries

- The seasonal step up in stk-based comp expense in Q2

- ~$1bn cost increase due to Amazon Leo (to manufacture and launch more satellites) booked in Amer

- Leo’s commercial services are on track to launch in Q3

- Expect to begin capitalizing certain costs in Q4, including production & launch costs

- Higher transportation costs related to fuel inflation, which is partially offset by the recently implemented fuel & logistics related FBA surcharge

- That Prime Day occurs in Q2 in most of the largest geos (incl the US) and occurs in Q3 in Australia, Brazil, India and Japan

Q1 Capx Was ~IN-LINE, Though Forward Spend Is Still A Question

- Q1 capx of $43.2bn was just slightly below cons

- What about the capx outlook? There were no specific comments re the previous $200bn 2026 capx guidance but when asked about capx spend looking ahead…

- Amazon already has customer commitments for a “substantial” portion of the 2026 capacity coming online

- “We still view today’s environment as a once in a lifetime opportunity…expect that we will invest a significant amount of capital over the coming years to pursue that opportunity”

- “Our customers, our shareholders and Amazon in general are going to be much better off down the road because we did so”

- The faster AWS grows, the more short-term CapEx the Co will spend

- Reminder that monetization typically lags investment by 6-24 months BUT…

- Data centers can have 30+ year useful lives

- Chips, servers, and networking gear typically have 5-6 year useful lives

- Near-term FCF can be pressured during rapid growth, but the Co expects attractive cumulative returns once capacity is utilized

- Reminder that monetization typically lags investment by 6-24 months BUT…

- The cost of memory has skyrocketed as everyone has seen but are working with partners to secure supply

- Mgmt believes this situation also pushes companies to shift faster to cloud as well

AWS’ Revenue Acceleration Was A Big Positive W/ The Print

- Q1 AWS revenue BEAT cons by +2.6% and is up +28% y/y (the fast growth rate in 15 qtrs) driven by both core and AI services (mgmt sees strong correlation btw the two and expect this to increase over time)

- Op margins reached 37.8% vs cons 35.0%

- Q1 AWS AI rev is growing “triple digits” y/y and they are bringing more capacity online: AI momentum is driven by,,,

- Broad AI capabilities across the stack

- Proximity of AI workloads to customers’ existing apps and data

- Ability to bundle AI with AWS’s broader cloud services

- Enterprise-grade security, reliability, and operational performance

- Q1 AWS backlog reached $364bn (+93% y/y) and this does NOT include the recently annc’d the $100bn Anthropic deal

- The backlog also has “reasonable breadth” and is not concentrated in just one or two customers

- AI labs are spending “an incredible amount” on compute on AI and the core side but the Co is also seeing “quite a bit of enterprise spend on AI”

- On the platform side…

- SageMaker can reduce training time by up to 40%

- Bedrock offers access to frontier models for inference

- Used by 125k+ customers

- ~80% of Fortune 100 companies are using Bedrock

- Customer spend grew +170% q/q

- Processed more tokens in Q1 than in all prior years combined

- Bringing OpenAI models to Bedrock is “a big deal”:

- GPT-5.4 was added this week

- GPT-5.5 is expected soon

- Also began previewing Bedrock managed agents powered by OpenAI

- Believe agents will drive much of the value companies get from AI, and is pushing several offerings in that area…

- Customers can build agents using proprietary data and Strands, which has been downloaded 25mn+ times and saw 3x q/q download growth

- Can also deploy agents using Agent Core, with some customers deploying an agent as often as every 10 seconds

- AWS also offers turnkey agents/products for coding, migrations, business operations, and knowledge work

- Customers can build agents using proprietary data and Strands, which has been downloaded 25mn+ times and saw 3x q/q download growth

- Other key AWS AI products stats:

- On Kiro, the number of developers using it more than doubled q/q

- Enterprise customer usage incr’d ~10x

- Transform has helped customers save over 156mn hours of manual migration/modernization effort

- Quick saw the number of new customers grow more than 4x q/q

- Recently annc’d Quick Desktop, which can query email, calendar, Slack, local files, summarize information, compose communications, and automate tasks

- On Kiro, the number of developers using it more than doubled q/q

Amazon’s Chips Story Remains A Hidden Gem (Was A New Narrative Last Qtr)

- AWS’s chips biz is scaling quickly…revs grew ~40% q/q in Q1

- Annual rev run rate is now over $20bn (vs ~10bn in Q4)

- If the biz were accounted for like a standalone chip vendor, the run rate would be $50bn

- The Co believes its custom silicon biz is now one of the “top three data center chip businesses in the world”

- Annual rev run rate is now over $20bn (vs ~10bn in Q4)

- And Trainium is maintaining its momentum… “customers always want choice “

- AWS has $225bn+ in revenue commitments for Trainium

- Trainium 2 offers ~30% better price-performance than comparable GPUs and is largely sold out

- Trainium 3, which started shipping at the start of 2026, offers 30–40% more price-performance than Trainium 2, and is nearly “fully subscribed”

- Much of Trainium 4, still ~18 months from broad availability, has already been reserved

- On the cost side, Trainium provides major cost savings

- Could save the Co “tens of billions” of dollars of capx per year

- Could provide “several hundred bp” of operating margin advantage versus relying only on 3P chips for inference

- As also signaled earlier, mgmt stated there is a “good chance we’re going to sell racks over the next couple of years”

- Bedrock runs most of its inference on Trainium

- AI is not just a “GPU story” but is also a “CPU story”…regarding Amazon’s Graviton CPU chip

- Meta has committed to using “tens of millions of Graviton cores”

- Graviton delivers up to 40% better price-performance than other x86 processors

- It is now used by 98% of the top 1,000 EC2 customers

- “Nobody has a better set of chips across AI and CPU workloads than AWS with Trainium and Graviton, and we’re unusually well positioned for this AI inflection”

The Stores Business Has Not Maxed Out On Broader Selection, Faster Speed, & Greater Efficiencies

- Unit growth in Stores reached +15% y/y vs +12% y/y in Q4 (the highest since the tail end of COVID lockdowns)

- The Co cont’d to expand selection, including 600+ new notable brands

- More items are being shipped faster (~1bn items were shipped via same-day or overnight delivery so far this year and delivery speeds are still improving) …

- Recently intro’d 1-hour & 3-hour delivery options on ~90k items

- 1-hr delivery is available in hundreds of cities and towns

- 3-hr delivery is available in more than 2,000 cities and towns

- The Co is continuing to expand Amazon Now, which offers delivery in 30 minutes or less on “thousands of items”

- The svs launched last year in India and orders there are increasing 25% m/m

- Prime members 3x their shopping frequency once they begin using the service

- Amazon Now is available to tens of millions of customers across 9 countries, with further expansion planned

- Recently intro’d 1-hour & 3-hour delivery options on ~90k items

- Amazon’s grocery biz remains a key priority across both perishables and non-perishables (it is now the 2nd-largest grocer in the US)

- The Co offers same-day delivery of perishables alongside mns of other items across more than 2,300 US cities and towns, w/ further expansion planned

- Perishable sales grew more than 40x y/y

- Perishables now account for 9 of the top 10 most-ordered same-day delivery items where the service is available

- Customers who shop same-day perishables build larger baskets, adding ~3x more items and spending 80%+ more than customers who do not

- The Co offers same-day delivery of perishables alongside mns of other items across more than 2,300 US cities and towns, w/ further expansion planned

- The Co remains focused on price competitiveness…in Q1, the avg prices of products offered on Amazon.com “declined” y/y

- Prime Day will take place in most countries in June, with addtl member savings across categories

- Network efficiency also continues to improve (fulfilment network costs grew slower than unit growth)

- Outbound shipping costs grew +12% y/y and fulfillment expense grew +9% y/y (FXN)

- “We’re able to deliver items faster and improve the customer experience, while at the same time lowering our cost to serve”

- See “meaningful opportunities” to further enhance productivity across the global fulfillment network while still increasing delivery speed (optimizing inventory placement to shorten distance traveled, reduce touches for package, and improve consolidation rates)

- Robotics and automation are creating step function efficiencies

- Whole Foods Market also continues to expand…the Co currently it has ~550 stores and plans to expand by ~100 “over the next few years”

Mgmt Is Very Bullish On What Agentic Commerce Looks Like, But 3P Agents Still Need Some Work

- Rufus (Amazon’s AI shopping assistant) has “substantially” improved and continues to gain adoption

- Monthly active users were up ~115%

- Engagement was up ~400% y/y

- But Amazon also expects to do a lot with 3P agents as well, though the experience “just hasn’t gotten great with these third-party horizontal agents yet”

- They often do not get pricing or product info right

- They don’t have any personalization data or any shopping history

- The Co is “having conversations” with these companies to “try to make that better and find something that works for customers and all the companies”

- Mgmt thinks advertising “will do well” w/ agentic commerce despite some analysts thinking otherwise (see more below on Q1 advertising performance in general)

- It will be so much easier to do advertising so there will be a lot more advertisers

- Agentic experiences tend to be interactive with multi-turns when relevant products (sponsored and non-sponsored) can be surfaced

- And will also have sponsored prompts

Advertising Growth Remains Consistently Strong

- Q1 advertising revenue reached $17.2bn in the quarter, up +22% y/y vs +22% y/y in Q4

- The Co is expanding its AI tools for advertisers

- It expanded Creative Agent, an AI tool that helps plan and execute the ad creative process

- The tool is now available in Canada, France, Germany, India, Italy, Spain, and the UK

- Intro’d new AI tools for sellers

- Intro’d a new AI experience in Seller Central and early feedback has been “strong”

- The product dynamically generates personalized data visualizations, insights, and scenarios tailored to seller goals

- A couple highlighted partnerships…

- Deepened their Netflix partnership with Amazon Audiences

- Enables advertisers to apply Amazon’s exclusive signals from shopping, browsing, and streaming to Netflix’s viewers to reach the right audiences

- Partnered with Comcast Advertising to expand local advertising to “thousands of brands”

- Expanded interactive video ad capabilities to partners, starting with Samsung TVs

- Deepened their Netflix partnership with Amazon Audiences

Several Other Notable Updates Across Prime Video, Alexa+, Leo, Zoox, & Health

- Prime video remains a key pillar for Prime membership growth and “is profitable” in its own right

- Project Hail Mary hit ~$615mn in global box office to date, and its opening weekend was the 2nd biggest for any non-sequel, non-franchise film in the last decade

- Also surpassed 100mn viewers globally for the Culpables movie trilogy, with all 3 films reaching #1 in ~170 countries at launch

- Total viewership of exclusive coverage of the NBA, SoFi play-in tournament was up +18% vs last year on cable

- Alexa+ early access expanded to “millions more” Prime members in Mexico, the UK, Italy, and Spain and stats are positive…customers are:

- Talking to Alexa Plus 2x as much and for longer durations across a wider breadth of topics

- Completing 3x more purchases on devices

- Streaming ~25% more music

- Using smart home features ~50% more often than Alexa Classic

- Very bullish on Amazon Leo w/ commercial service on track to launch in the next few months…see this as a “many billion dollar” revenue business with an attractive return profile

- The Co said Leo should offer roughly:

- ~2x better downlink performance

- ~6x better uplink performance

- Amazon said it has 20+ launches planned in 2026

- 30+ launches planned in 2027

- Mgmt believes that it will have a cost advantage

- The combination of LEO and Cloud is also very attractive for customers

- The Globalstar deal will bolster service capabilities

- The Co said Leo should offer roughly:

- Zoox has now driven ~2mn miles and carried more than 350k riders; It is publicly available in Las Vegas and San Francisco, is testing in 8 addtl cities, and will also be available through the Uber app in Las Vegas, with Los Angeles planned

- The Co launched Health AI, a 24/7 AI-powered personal health agent backed by One Medical clinicians

- Health AI can provide clinical guidance and, with customer permission, take actions such as booking appointments, managing prescriptions, and facilitating care with a One Medical provider

Meta Beats Across The Board But The AI ROI Debate Dominates As Capx Moves Up AGAIN

As mentioned above, Alphabet delivered the clearest, strong, broad-based returns on its high capx spending across its businesses, and while Meta is also reaping benefits from AI in its ads business, investors do not see the ROI on its heavy capx investments as clearly visible. That said, the core business is performing well with Q1 revenue accelerating from +24% y/y in Q4 to +33% y/y in Q1 (but this was largely expected), adj op income margin of 40.6% well ahead of cons 35.0%, EPS of $10.44 nearly double expectations, and FCF of $12.4bn was almost 3x cons. Our top 5 other takeaways from Meta’s results are: 1) While Q1 capx was $7.7bn below expectations, mgmt. raised 2026 guidance by $10bn and it sounds like 2027 could be a major step up as well given comments about previously underestimating their compute needs; 2) The Muse Spark launch is a meaningful milestone though exact timelines on future releases will remain fluid as the Co prioritizes quality over a fixed cadence; 3) the ad business continues to benefit from AI, with performance gains across the ad stack, Gen AI creative tools are now used by 8mn+ advertisers, and newer surfaces like Threads and WhatsApp Status are beginning to contribute; 4) Users were weaker than expected in Q1, but purely due to the Middle East conflict (growth would have been up q/q excluding that impact); and 5) AI glasses “continues to be one of the fastest growing categories of consumer electronics ever.”

Net net, the fundamentals of the core business remain strong (though somewhat baked into estimates), CapEx is moving higher (again), when the longer-term return profile on its AI investments is still an open question, hence, the path forward is not without uncertainty in investors’ minds.

See below for more details on the above as well as key updates on content recommendations, partnership ad product revenue, Meta AI, agents, workforce efficiency, and more.

-> Meta fell -8.6% post its print, it’s worst day since October

-> See Themes #2, #3, and #9 for our thoughts on Alphabet, Amazon, and Microsoft’s results, respectively

Easy Headline Beat In Q1, Driven By Much Better Profitability

- Q4 total revs BEAT cons by +1.3% and grew +33% y/y (vs +24% y/y growth in Q4)

- Family of Apps (FOA) revs BEAT w/ ad revs ~1% better than expected and Other beat by +15%

- Reality Labs MISSED by -18%

- Q4 adj op income BEAT by +8% (margin of 40.6% vs cons 35.0%)

- FOA adj op income of 48.1% BEAT vs cons 5%

- Reality Labs adj op income also MISSED -5% vs cons -986.1%

- Q4 EPS of $10.44 was well ABOVE cons $6.67

- Q4 FCF of $12.4bn was a BIG BEAT vs cons $4.4bn

- Q4 CapEx of $19.84bn was much LOWER vs cons $27.6bn

Q2 Revenue Guidance Was In-Line But All Signs Point To A Further Substantial Capx Ramp Looking Ahead

- For Q2…the mid-pt of REVENUE guidance was in-line w/ cons ($58bn-$61bn vs cons $59.48bn), implying +25% y/y growth

- Guidance assumes FX is an ~2% tailwind to y/y total rev growth, based on current exchange rates

- For 2026…reiterated EXPENSE guidance of $162bn-$169bn (vs $118bn in 2025)

- On Capx…

- For 2026…even though Q1 capx was $7.7bn below expectations, mgmt. raised the FY capx guidance by $10bn, or +8.0% at the midpt ($125bn-$145bn vs prior guidance $115bn-$135bn): This was +10% higher than cons $122.6bn

- Reflects expectations for higher component pricing this yr and, to a lesser extent, addtl data center costs to support future yr capacity

- “But every sign that we’re seeing in our own work and across the industry gives us confidence in this investment”

- For 2027…mgmt. did not provide specific CAPX guidance but noted that they are “undergoing a very dynamic planning process” as they work through what their capacity needs will be over the coming yr

- “Our experience so far has been that we have continued to underestimate our compute needs”

- “Expectation is that compute will become even more central to the business going forward”

- “If we end up not needing as much as we anticipate, we can choose to bring it online more slowly or reduce our spending in future years as we grow into the capacity that we’re building now.”

- For 2026…even though Q1 capx was $7.7bn below expectations, mgmt. raised the FY capx guidance by $10bn, or +8.0% at the midpt ($125bn-$145bn vs prior guidance $115bn-$135bn): This was +10% higher than cons $122.6bn

- A quick comment on the regulatory front… “we continue to monitor active legal and regulatory matters, including headwinds in the EU and the US that could significantly impact our business and financial results. For example, we continue to see scrutiny on youth-related issues and have additional trials scheduled for this year in the US, which may ultimately result in a material loss”

Users Were Slightly Below Expectations Due To Regional Disruptions (Though Underlying Engagement Trends Remain Strong)

- Ended Q1 w/ 3.56bn Family DAPs using at least one of Meta’s apps everyday, which was a touch below cons 3.62bn

- Saw a “small” decrease in Dec total family DAPs due to internet disruptions in Iran and a restriction on access to WhatsApp in Russia

- Absent these impacts, growth in family DAPs would have been positive q/q

- Daily and monthly actives on Instagram and Facebook continue to grow, with video driving all time high engagement across both apps

- WhatsApp “continues to see strong momentum too, including in the US”

- Threads “continues on its trajectory to be the leading app in its category”

Muse Launch Highlights Early Progress As Meta Builds Toward Agents & Personal Superintelligence But The Product Release Cadence & Monetization Timeline Remains Vague

- Meta’s “biggest milestone so far this year” – release of Muse family of models, including their first model, Muse Spark, along w/ a “significantly” upgraded new version of Meta AI

- First release from Meta Superintelligence Labs… “it shows that our work is on track to build a leading lab”

- “Our focus this year is validating the model architectures and techniques in these domains before we scale them out in future years”

- Spark has already made Meta AI “a world-class assistant” that leads in several areas related to their vision of personal super intelligence, including visual understanding, health, shopping, social content, local, creating games and more

- Hearing “very positive” feedback on it so far

- Seeing double-digit % increases in Meta AI session per user + the Meta AI app has consistently been near the top of the app stores

- Also working on using Spark in their upcoming models to improve their recommendation systems and core business in Facebook, Instagram and advertising

- Currently…Meta’s apps primarily help 1) connect people 2) learn about the world, and 3) entertainment

- What Meta is working towards… “to understand more of people’s goals so we can help improve their lives in all of the ways that they want”

- Using their new AI models, for the first time in Meta’s history, the Co will be able to develop a first principles understanding of what users care about

- Enables them to both show and create more personalized content specifically for what people are trying to achieve

- Since Meta’s recommendation systems are operating at such a large scale, the new research and technology will be phased in “over time”

- Another key focus is to deliver agents that understand goals and work “day and night” to help achieve them

- Personal agents are focused on helping people achieve the diverse goals in their lives

- On monetization… “we think there will be clear monetization opportunities over time. You can imagine commission structures or a premium offering”

- Business agents are focused on helping entrepreneurs and bizs use Meta’s tools to grow their efforts, reach new customers and serve existing customers better

- On monetization…currently free for most bizs but expect to work towards establishing a longer-term monetization model

- Looking ahead… “these agents will work together to form an ecosystem…I believe that the future will see a massive increase in entrepreneurship from people creating new things that they’ve always wanted to exist, but previously didn’t have the tools to bring into the world”

- Already testing an early version of business AIs and weekly conversations have grown 10x since the start of this yr

- Personal agents are focused on helping people achieve the diverse goals in their lives

- The overall view is that AI is NOT going to replace people, but rather amplify people’s ability to do what they want (i.e., improve health, learning, relationships, ability to achieve career goals, etc.)

- “People will be more important in the future, not less”

- Reiterated monetization strategy for investments in models and products… “the formula for our company has always been build experiences that can get to billions of people and focus on monetizing them once you get to scale”

- On expected timeline of future releases… prioritizing quality over a fixed timeline, making exact cadence unpredictable

- “We are trying novel things. You don’t exactly know when they’re going to land…. getting to like that quality bar is something that I care about more than hitting a specific week for launching”

- Quickly on the compute side…rolling out more than 1 gigawatt of their own custom silicon being developing with Broadcom + a “significant amount” of AMD chips to complement the new NVIDIA systems that they’re rolling out as well

- “One of the primary goals of our Meta Compute initiative is to lead the industry in efficiency of building Compute. And we expect that will be a strategic advantage over time”

Advertising Momentum Continues With Surface Expansion, AI Model Advancements, And Scaling AI Tools For Businesses

- Family of App ad revs accelerated to +33% y/y (vs +25% y/y in Q4, +26% y/y in Q3, and +22% y/y in Q2) and beat cons by +1.0%; FOA adj op margins of 48.1% came in more materially ahead of cons 44.5%

- Q1 ad impressions were up +19% y/y (vs +18% y/y in Q4): Growth was healthy across all regions, driven primarily by engagement and user growth, as well as ad load optimizations

- Q4 avg price per ad was up +12% y/y (vs +6% y/y in Q4): Saw broad-based growth driven by benefits from ad performance improvements, better macro conditions vs Q1:25 and currency tailwinds in intl regions, partially offset by strong impression growth, including from lower monetizing regions

- Expanded availability of ads on newer surfaces in Q1

- Threads: Brought ads to people in more mkts

- WhatsApp: Making “good progress” w/ rollout of ads in Status, w/ hundreds of millions of people now viewing them daily

- Continue to deliver performance gains within their ad systems by deploying more complex and predictive models

- Enhancements made to Lattice’s modeling and learning techniques in Q1, along with advances in Meta’s GEM model architecture, drove a more than 6% increase in conversion rate for landing page view ads

- Also expanded coverage of their adaptive ranking model in Q1 to support off-site conversions, which drove a +1.6% increase in conversion rates across the major surfaces on Facebook and Instagram

- Also leveraging AI to make it easier for businesses to manage their customers, develop ad creative, and engage with customers

- Now have 10mn+ conversations each week being facilitated through business AIs, up from 1mn at the start of the yr

- Continue to expand access of business AIs globally

- In Q1, expanded on WhatsApp to SMBs across LatAm and Indonesia, as well as on Messenger in APAC

- Will further expand access to more countries in Q2, while adding more capabilities to the AIs

- Meta AI Business Assistant has now been fully rolled out to all eligible advertisers on supported Meta buying svs, providing personalized recommendations to advertisers, resolving account issues and servicing campaign insights to help optimize results

- Since they began testing the Assistant in Q4, common account issues have been resolved at a 20% higher rate

- Also introduced Meta Ads AI connectors in open beta, providing advertisers the ability to connect their Meta Ad account directly to an AI agent

- Usage of ad creative tools is also scaling with 8mn+ advertisers using at least one of Meta’s Gen AI ad creative tools and particularly strong adoption among small- and medium-sized advertisers

- These tools are benefiting performance as well with advertisers using the video generation feature seeing more than 3% higher conversion rates in tests

- Will also continue to invest in the value optimization suite, which helps advertisers maximize their return on ad spend by prioritizing the highest value conversions rather than optimizing solely for the most conversions at the lowest cost

- Adoption by businesses has been strong following performance improvements made over the past yr, w/ ARR now over $20bn, more than doubling y/y

Expanding Commerce Efforts Beyond Just Ads

- Partnerships ads product rev run rate more than doubled y/y in Q1 to $10bn, as brands increasingly turning to creators to promote their products

- Expanding beyond ads to support the product discovery and purchasing happening through creators

- Rolled out affiliate partnerships offering on Facebook last month to more test partners, so creators can tag products from participating retailers on their posts and earn a commission when someone makes a purchase

- Have also started testing similar experiences on Instagram

- “We see a real opportunity to help people more easily discover and buy products within our services, particularly as we incorporate AI deeply across our platforms”

Recommendation Gains Continue As AI And Next-Gen Models Scale

- Continue to see “significant” gains from content recommendation initiatives

- Instagram ranking improvements made in Q1 drove a 10% lift in real-time spent

- Facebook total video time increased 8%+ globally in Q1, the largest q/q gain in four yrs

- Within the US and Canada, ranking improvements drove a +9% increase in video watch time on Facebook in Q1

- Increasing the diversity and recency of recommended content, with same day posts now representing 30%+ of recommended reels on both Instagram and Facebook, more than double the levels from a yr-ago

- What’s driving the gains? Advances being made across the full stack

- On the data front, doubled the length of user interaction sequences used for training on Instagram in Q1, and increased the richness of how each user interaction is described, enabling their systems to develop a deeper understanding of user interests

- Within their models, have “significantly” increased speed with which their ranking models index new posts, which is enabling them to recommend sooner after they are published

- Also applying more advanced content understanding techniques, enabling them to quickly identify posts that may be interesting to someone, even if they haven’t engaged with a lot of similar content

- Using AI to auto translate and dub videos into a viewer’s local language

- Over half a billion users on each of Facebook and Instagram are now watching AI-translated videos weekly

- Looking ahead…making several investments that are expected to deliver more valuable recommendations

- Will continue to scale up their models in several dimensions this yr, including their size and complexity, while incorporating LLMs to deepen content understanding across our platform, enabling Meta to better match users to a wider variety of content aligned to their interests

- Will also execute their longer-term efforts to develop the next-generation of recommendation systems, including building foundation models that power organic content and ads recommendations, as well as developing LLM-based recommender systems

Strong Growth In AI Glasses Are Reality Labs Primary Focus As VR Takes A Back Seat

- Reality Labs Q4 revs fell -2% y/y (vs -12% y/y in Q4) and missed cons by -18%; Reality Labs Q4 op loss of -$4.0bn was more than cons -$4.8bn

- Y/Y loss in rev was due to lower Quest headset sales, which were partially offset by continued strong growth in AI glasses rev

- AI glasses “continues to be one of the fastest growing categories of consumer electronics ever”

- All glasses are designed to easily update to use Meta’s newest AI models and features

- # of people using AI glasses daily tripled y/y in Q1

- ReleasedRay-Ban Meta Optics in Q1, which are designed for all-day wear vs primarily sunglasses

- Later this yr… have some “exciting” new partnerships and styles that “are going to have the potential to reach even more people”

- Looking further ahead…expect for glasses to evolve from being able to just answer questions to becoming a personal agent

- On the broader metaverse / VR strategy…

- Meta still says it remains the biggest investor in VR across the industry

- BUT focus is on making the VR biz “sustainable” as they invest more in areas like AI and glasses

Building a Leaner Workforce to Support AI-Driven Productivity And Faster Execution

- On upcoming plans to reduce workforce… “we believe a leaner operating model will allow us to move more quickly, while also helping to offset the substantial investments we’re making”

- Seeing continued AI-driven workforce efficiencies: Witnessing “more and more” examples where 1-2 people are building something in a week that would have previously taken dozens of people months

- Building “the next evolution” of the Co

- Building the best infrastructure for creating and delivering products at scale

- Streamliningteams so they aren’t bigger than they need to be

- Recognizing and rewarding people who are having outsized impacts

- Setting themselves up to try many more ideas and take on many new projects in the future

- Expectations for ideal workforce size? “We don’t really know what the optimal size of the company will be in the future”

- “Overall, I think, the future is about building many more, higher quality things than we’ve ever built before”x

Price Hikes Help Spotify’s Q1 But Its Investment Ramp Spooks Investors

Over the last 18 quarters, 78% of the time Spotify’s shares moved double digits (up or down) in reaction to earnings, so the type of volatility we saw post Q1 results is certainly more the norm vs the exception. The strong sell-off this quarter was due to the surprise, higher than expected operating expense spend guidance and an ads business that is yet to see the rays of light. Investors are particularly sensitive given the AI disruption narrative and concerns. The most interesting updates on what we learned from Spotify’s results include: 1) The Co is increasing spend on compute and on higher sales & marketing for their new product features, which will weigh on opex over the “next qtr or two”, but mgmt. reiterated y/y op margin expansion for the full year; 2) The Co positively benefitted from its Jan price hike and did not see any negative impact from subscribers; 3) In the ads business, pressure will continue in the “near term” but mgmt still expects improved performance in H2 as billable channels continue to scale; 4) AI remains a key debate but the Co’s proprietary data is seen as a “competitive advantage”; and 5) The new Fitness vertical likely follows the same monetization path as audiobooks.

See below for more details and reminder that the Co is holding an investor day on May 21st

–> SPOT shares fell -12.4% in reaction to results and are now down -24.0% YTD

–> See Theme #6 for our perspectives on UMG’s results

Q1 Results Topped The Street…

- Total revenue BEAT by +0.2%: Up +8% y/y (+14% FXN) vs +7% y/y in Q4 (+13% FXN in Q4)

- GM expanded +133bp y/y to 33.0%…due to Premium strength and revenue mix

- Premium GM gains were driven by rev growth outpacing music costs net of marketplace programs, audiobooks costs and video podcast costs

- Ad-Supported GM declined y/y driven by higher music and other content costs from elevated engagement, partially offset by podcast contribution

- Op income BEAT by +5.8%: Up +40% y/y, due to higher costs driven by marketing, as well as cloud and AI spend (excluding social changes)

- Operating expense included €39mn in Social Charges

- Op margin BEAT: 15.8% vs 15.0%

- FCF reached €824mn…LTM FCF hit €3.2bn

- MAU slightly BEAT by +0.3%…added +10m in Q1, reaching 761mn total (up +12% y/y vs +11% y/y in Q4), driven by…

- Broad-based regional growth, with outperformance led by RoW and N.Amer due to mobile free tier rollout

…BUT Q2 OpEx Spending Guidance Disappointed The Street & Could Remain Pressured Over “The Next Qtr Or Two”

- Q2 revenue guidance BEAT cons by +0.8%: Assumes ~80 bps headwind to growth y/y (vs. ~600 bps in Q1) due to FX rate movements

- But the price hike will be a net benefit in the qtr

- Q2 gross margin guidance IN-LINE: Primarily driven by y/y favorability within the Premium segment

- BUT Q2 op income guidance MISSED cons by -6.8% which was a big focus from analysts

- Incorporates €10mn in Social Charges based on a Q1 close share price of $484.91

- Where is the Co increasing investment? Higher compute and higher sales & marketing of their latest features

- The Co is spending more compute per employee b/c “we’re seeing tremendous return in terms of productivity”

- Are also training on their proprietary data which has an upfront cost

- The Co is further accelerating their ability to ship products during the late fall

- But need to “tell our users about those features” hence the increase in sales & marketing spend (related to the Premium tier)

- The spend should remain around these elevated levels for “the next quarter or two” but mgmt continues to expect both GM and Op Margins to improve y/y in 2026 on a full year basis

- On users, Q2 total MAU guidance was ~inline w/ cons: Implies +17mn net adds q/q to 778mn

- But Q2 Premium subs guidance MISSED by -0.3%: Implies +6mn net adds to 299mn

- 2026: Mgmt reit’d the expectations for a full year of healthy subscriber growth, weighted more to H2

- Continue to expect meaningful y/y growth in FCF into 2026, reflecting improved profitability and working capital profile “while we are also progressing towards a normalized tax rate in 2027”

Q1 Premium Biz Benefitted From The Jan Price Hike

- Q1 Premium revs slightly beat cons by +1% due to higher ARPU: Revs grew +10% y/y or +15% FXN

- Premium subs grew +9% y/y to 293mn…in-line with cons

- Premium ARPU grew +6% y/y to €4.74…AHEAD of cons

- Premium GM of 34.8% was in-line with cons

- Mgmt called out that it has not seen any negative subscriber reaction to the price increases

- Engagement and churn trends remain stable

But The Ad Biz Remains A “Work In Progress” As Monetization Still Lags Engagement

- Q1 ad-supported rev MISSED cons by -7% as ad-supported ARPU was lower than expected: Revs decl’d -5% y/y (but still grew +3% FXN)

- Ad MAUs grew +14% y/y to 483mn…roughly inline w/ cons

- Ad ARPU decl’d -18% y/y to €0.27…missing cons by ~-7%

- Ad-supported GM at 13% was meaningfully below cons 16.6%: Higher engagement drove more music and other CoR that more than offset podcast favorability

- GM fell -102bp y/y

- Ad MAUs grew +14% y/y to 483mn…roughly inline w/ cons

- Very encouraged by the new personalized free tier – “it has blown out expectations”

- It has a short-term negative y/y impact on ad biz GM but mgmt is confident that it can monetize the engagement in the coming qtrs

- Seeing more listening/watching days per month

- Mgmt remains confident in converting free subscribers to paid (this is a key deliverable for investors)

- The ads business remains a “work in progress” but mgmt remains confident in closing the engagement vs monetization gap

- The rebuilt ad stack foundation is now in place

- The new automated sales channel represents over 30% of ad supported rev in Q1

- Active advertisers are rising

- Measurement/performance are improving

- BUT legacy direct sales remains choppy

- “This finally lets us better capture the value of our audience”

- Pressure in the ad business will continue in the “near term” but still expect improved performance in H2 as billable channels continue to scale

- “The gap will close. It’s just a matter of time”

AI Remains A Key Area Of Investor/Analyst Debate But SPOT Continues To Believe They Will Be A Beneficiary

- The Co is now integrating AI across “every part” of the platform, shipping more features faster, lowering cost per feature and building a svs that is more personal

- DJ has now been used by 94mn subs and is driving “billions of hours of engagement”

- SongDNA reached 52mn users in just 4 weeks

- Prompted Playlist is expanding into podcasts

- Taste Profile (now in beta) lets users directly edit/refine how Spotify understands their preferences

- SPOT sees its proprietary data as creating a “fair advantage”

- The Co has ~20 years of listening history and is now collecting a new proprietary data set where users are telling Spotify “in plain English what they want”

- This is a “treasure trove of data”

- Its in-house large personalization model, or “taste model,” is trained on Spotify-specific behavior

- Tastes are “not a fact” (which can be more easily commoditized by LLMs) and change by user, market, and culture

- The Co’s sees its data advantage is durable because culture and user taste move so quickly that even a snapshot of behavior across 700mn+ users would lose much of its value within 2-3 weeks

- “The number one reason for why people actually engage more with Spotify is personalization,” hence their investment here

- The Co has ~20 years of listening history and is now collecting a new proprietary data set where users are telling Spotify “in plain English what they want”

- The Co believes there is a big opportunity to use AI for EXISTING artists and creators, not just for creating new music

- “We don’t think existing artists should be left out of AI”

- If you look at other industries, existing IP is the most valuable IP, not the least valuable, but because of how AI music works right now, that is not addressable. That’s the problem we want to solve”

- (UMG commented on this as well in Theme #6)

A Few Other Interesting Updates & Datapoints

- The Co sees fitness as a natural extension of its platform and biz model…their new dedicated fitness hub and bundled Peloton Premium content will be inside Spotify Premium as an ad-free format (like they did with audiobooks)

- The platform can connect creators with user demand

- ~70% of Premium users already work out monthly and users have created >150mn workout playlists

- After launching Spotify Partner Program (SPP) ~1.5 years ago, the Co noticed that many fitness instructors and creators began uploading videos on their own

- The Co expects this vertical to grow further and gave “tennis” as an example: Spotify could recommend stretching videos, instructional content, or even audiobooks to help users prepare for matches

- The platform can connect creators with user demand

- The Co has paid $11bn+ to rights holders

- Live experiences – the Co took Bad Bunny to Tokyo to perform in Asia for the 1st time…then turned around and broadcast that moment to the world

UMG’s Business Faces A Multitude Of Moving Parts

In addition to Spotify’s results (see Theme #5), Universal Music Group (UMG) also shed some light on key trends in music eco-system but from the label side, and provided an update on some company-specific dynamics. The elephant in the room was the Pershing Square merger combination proposal and mgmt is not commenting until its Board makes a decision, but is also taking concrete actions to address many of the suggestions outlined in the plan, with a new €500mn buyback authorization (on top of the €500mn annc’d in March) being one of them. More transparency on business acquisitions/underlying trends, plus the Co is monetizing ½ of its SPOT shares. Five additional key takeaways and learnings from UMG’s results include: 1) Wholesale price increases from multiple Streaming 2.0 deals contributed +3pts to subscription growth in Q1, with some agreements only partially phased in and a full-qtr benefit coming in Q2+ (and more deals are to come); 2) The advertising business continues to lag though mgmt. expects to see “sustained growth over the mid-term”; 3) The Co expects the share reduction experienced in Q1 to gradually recover as the release slate picks up during the year; 4) Artist & Label Services is viewed as an important growth extension, despite the near term margin dilution from the Downtown acq; and 5) The Co is pursuing “responsible” AI partnerships that support existing artist and monetization of catalog.

Overall, there are a lot of moving parts with UMG at the moment between internal strategic decisions and external sector trends which may take some time to play out.

-> UMG shares ended the day flat post its results and YTD is down -20%, vs Spotify down -24%, and WMG down -8%

No Comments On Pershing Proposal But Mgmt Has Been Implementing Some Of The Suggestions

- Mgmt will provide an update regarding the Pershing Square proposal once the board makes a decision

- But the Co has already made shareholder friendly changes in March and is implanting more changes….

- UMG today incr’d its share buyback authorization to €1bn, up from the previously annc’d €500mn

- The Co has already repurchased just over 1.85mn shares for €36mn through Apr. 24

- The Co is monetizing ½ of its Spotify stake (annc’d in March)

- Artists will share in the proceeds

- UMG’s share of proceeds will initially fund the buyback program

- The Co is holding the other 50% since it has “tremendous faith” in the ecosystem

- UMG will execute that sale over the course of the year

- UMG is giving more details to help investors understand their underlying business and investments

- Breaking out the results of the Downtown acq this qtr and the rest of the year

- Providing a look back at Virgin Music’s contribution to Recorded Music results through 2025

- Providing segment EBITDA this qtr and onwards

- On subsequent earnings calls, the Co will provide greater insight into the ways they have evaluated investments in their business, whether or not they be catalogs or other significant M&A activity

Mgmt Is Leaning Harder Into Artist / Label Services…It’s a Growth Vector BUT Dilutive To Near-Term Margins

- The Downtown acq’s inclusion in results (from the Feb 20th close) weighs on margins: The financial inclusions are below:

- Overall

- Revs: €86mn

- Adj EBITDA: €3mn (implying a ~3.5% margin)

- Recorded Music

- Revs: €72mn

- Adj EBITDA: €4mn

- Publishing

- Revs: €14mn

- Adj EBITDA: -€1mn loss

- Overall

- Mgmt details Virgin Music’s business trajectory as a case study…

- Formed Virgin Music Group in late 2022

- Since 2023, it has grown at +16% CAGR

- Finished 2025 w/ €790mn in rev, which represents 8.4% of total Recorded Music rev (up from 7.2% in 2023)

- While UMG’s Recorded Music margins were level from 2024 to 2025, at 25.6%, Virgin’s expanded by ~4ppt in the rev mix from 7.5% to 8.4%, which offset 20bps of y/y margin expansion in the ex-Virgin Recorded Music margin

- “The next phase of our plan for Virgin is focused on empowering independent players, raising the standard of service even higher, and growing our community of dynamic labels and entrepreneurs”

- “We remain confident in our strategy to grow our artists and label services business alongside our label business in order to increase our touchpoints with the fast-growing independent sector”

Q1 Results Reflect Touch Comps & Big FX Headwind

- Please note it is unclear if the following consensus estimates sourced from FactSet include or exclude the Downtown results, so might not be apples-to-apples

- Revenue MISSED cons by -0.7%: Flat y/y as reported, or grew +8.1% FXN

- Ex-Downtown, rev grew +4.9% FXN

- Growth was driven by initial pricing benefits from Streaming 2.0 agreements, strong physical sales, and healthy sync income

- Highlighted Q1 artist drivers

- New releases from BTS and J-Hope in the US, and Frances Theodora internationally

- UK restructuring led to big hits from Olivia Dean, Sam Fender and Mumford & Sons

- Q2 is off to a “strong start”

- With albums from Noah Kahn and a hit single from Olivia Rodrigo

- Adj EBITDA MISSED cons by -3.8%: Fell -4% y/y but grew +3.9% in FXN, excluding Downtown, adj EBITDA grew 3.4% FXN and adj EBITDA margin declined 0.3pp y/y

Slight Outperformance In Recorded Music Subscription Revenue Growth Offset Ad-Supported Streaming Drag

- Overall Q1 Recorded Music segment posted In-line to worse results…impacted by tough comps but the core recorded music business ex Downtown grew mid SD FXN

- Rev were ~IN-LINE: Grew +0.5% y/y, or +8.9% FXN (+5.4% FXN ex-Downtown): Strength in subscription, physical, and sync-led licensing more than offset by softer ad-supported trends and tougher live comps in license & other

- Adj EBITDA MISSED by -1.9%: Margin of 25.1% MISSED by -50bps, though ex-Downtown, margins were flat at 25.7% as Streaming 2.0 pricing / operating leverage offset negative repertoire mix

- Q1 Subscription & Streaming rev were INLINE with cons as better subscription strength offset softer ad-supported performance: Segment growth reached +2.3% y/y, or +10.9% FXN, (+6.4% FXN ex-Downtown)

- Subscription revenue BEAT cons by +1%

- Reported basis: Grew +4% y/y vs +2.4% y/y in Q4

- FXN: Grew +12.5% y/y

- FXN ex-Downtown acq: Grew +7.9% y/y

- Streaming revenue MISSED by -2.6%

- Reported: Fell -4% y/y vs +3.2% y/y in Q4

- FXN: +5.0% y/y

- FXN ex-Downtown: +1.2% y/y

- Subscription revenue BEAT cons by +1%

- The Subscription business benefited from price increases partially offset by tougher comps

- Price increases from Streaming 2.0 deals had a 3pts positive impact (see section below)

- A lighter release schedule caused ~2pts of negative impact to subscription growth vs a strong prior-yr comp / stronger competitive release slate, pressuring frontline market share in Q1

- The ads business remains in a “transitional period”…expect improvement in the “mid-term”

- Seeing uneven performance across major platforms, including ad-rate challenges at one audio platform and ongoing disruption at video from the shift toward short-form consumption

- Continue working closely with partners on better monetization of ad-supported engagement

- “Expect to see sustained growth over the mid-term”

Streaming 2.0 Pricing Is Finally Starting To Show Up…And Mgmt Expects The Benefit To Build Through 2026, Along With A Market Share Rebound

- Wholesale price increases from multiple Streaming 2.0 deals contributed +3pts to subscription growth in Q1, with some agreements only partially phased in and a full-quarter benefit is coming in Q2+

- The three annc’d Streaming 2.0 deals only cover a portion of subs / geographies today, with additional deals expected later this year, which should create further pricing benefit in coming qtrs

- 2025 was their strongest year for market share in more than a decade, and they expect the share reduction in Q1 to gradually recoveras the release slate picks up during the year

- Mgmt was adamant that the Q1 mkt share loss was not due to AI pressures but more so due to new release timing

- “Expect to see further growth in subscription” looking ahead

- How do retail pricing actions by streamers in the US transmit to UMG’s streaming revenue in terms of timing and magnitude? Have a “multi-pronged model with respect to the new deals that we’re doing and our established deals”

- Capture revenue both on the basis of an underlying per sub minimum and also with a % of retail

- “So if there’s a price increase above what’s anticipated based on the wholesale, as you know, translated to through by the per subscriber minimum that we would we would participate”

- “We are, generally speaking, doing deals where we look to fairly and comprehensively participate in the value that our artists content brings to our partners platforms”

- “As we do additional deals, we expect to layer in more benefits from pricing over time”

Mixed To Worse Performance In Music Publishing & Merchandising & Other

- Music Publishing results were MIXED…

- Rev MISSED by -2.5%: Decr’d -1% y/y as reported, but grew +7.0% FXN or +4.3% FXN ex-Downtown

- Growth driven by stronger advertising / trailers / motion picture sync, performance growth, and mechanical strength in Japan

- Adj EBITDA BEAT by +2.3%, up +4% y/y, +11.6% FXN or +12.4% FXN ex-Downtown

- Adj EBITDA margin rose to 24.5%, or 25.3% ex-Downtown, on favorable rev mix, partly offset by higher copyright-enforcement legal fees

- Rev MISSED by -2.5%: Decr’d -1% y/y as reported, but grew +7.0% FXN or +4.3% FXN ex-Downtown

- Merchandising & Other MISSED on topline and profitability…

- Rev MISSED by -9.8%: Decr’d -10% y/y, -1.9% FXN or -1.9% FXN ex-Downtown

- Growth driven by lower DTC due to release timing and weaker retail sales, partly offset by strong touring income

- Adj EBITDA MISSED by -140%: Decr’d -150% y/y, -233% FXN or -233% FXN ex-Downtown

- Due to seasonally lower revenue against fixed overhead, unfavorable revenue mix with proportionally higher touring revenues and higher marketing spend, largely due to timing

- Rev MISSED by -9.8%: Decr’d -10% y/y, -1.9% FXN or -1.9% FXN ex-Downtown

UMG’s AI Focus Is Centered Around Creating New Products And Experiences From Their Existing Catalog Vs. Replacing Artistry

- “Applying AI to preserve, restore and unlock the value of UMG’s vast archives and library. We hold one of the world’s most important music archives”

- The new partnership w/ Nvidia is “exactly the kind of responsible AI partnership we believe in protecting the artists, preserving culture, and creating new value from the amazing assets already within the organization”

- It will create a deeper understanding of the music, video and related materials stored across their vaults across a plethora of formats dating back to the early 20th century

- Accelerates high quality restoration, digitization, and discovery at a scale that would simply not be possible through traditional methods alone

- Emphasized that the partnership is NOT meant to replace artistry or expertise but rather to help protect, understand and responsibly activate their catalogs

- I.e., Uncover recordings and videos that had never been commercially released

- “Over time, we believe this work can preserve irreplaceable assets”

- …while relationship w/ existing DSP partners (like Spotify) is about helping existing artists leverage AI for use cases that will also drive consumer engagement

- Artists want products that allow remixing, mashups, and custom songs that enable hyper personalization and co-creation experience with existing IP, which UMG’s research has found has much more support vs generic AI output

- Consumers want AI that makes music svs work better (i.e., better discovery, better personalization) + gives them a deeper relationship with the artists

- This is directed at the SuperFan opportunity

Verizon’s Early Progress With Its Turnaround Strategy

It has been a volatile earnings season for the major Connectivity companies, with diverging reactions across AT&T, Comcast and Charter last week, but Verizon and even more so T-Mobile were on the positive side of the stock performance ledger this week, especially the latter. First focusing on Verizon, the Co surprised on the upside with better-than-expected profitability performance, offsetting slightly lower than anticipated top-line growth (though the Jan service outage was a 1x drag).

The top 5 most important incrementals in our view from Verizon’s results include: 1) Not only were Q1 postpaid phone net adds much better than expected and mgmt raised its full-yr outlook, but the quality and economics of those subs improved; 2) The Mobility & Broadband service revenue growth rate y/y will accelerate post Q1; 3) The Co expects to remain aggressive in broadband, though prioritizing fiber over FWA where they have coverage; 4) Mgmt thinks the competitive intensity is coming down but “will defend itself” if it needs to; and 5) Verizon has seen some impressive tangible gains from its early AI implementations;

All in all, new CEO Dan Schulman has been in place for ~7 months and has driven some quick wins.

See below for more details.

-> Verizon shares rose +1.6% on the back of results and is leading the Big 3 telcos YTD (Verizon +18.1%, AT&T +5.2%, and TMUS -3.4%); Shares of cable Co Charter also traded down -3.1% in reaction to Verizon’s earnings as well

-> See Theme #8 for our thoughts on T-Mobile USA’s results as well

Verizon’s Weaker Q1 Top-Line Was More Than Offset By Stronger Profitability Momentum

- Total revs MISSED cons by -1.2%: Up +2.9% y/y

- BUT results also included an 80bp impact to wireless svs rev growth due to the Jan. network outage which is one-off

- Adj EBITDA BEAT by +2.1%: Up +6.7% y/y…the highest ever reported adj EBITDA performance

- Margins expanded +140bp y/y to 39.0% (vs cons 37.7%)

- Savings were driven by advertising efficiencies, network cost reductions, third party spend savings, and workforce actions

- By segment – Consumer & Biz rev both fell short of the Street while adj EBITDA beat

- Consumer revs MISSED by -1.0%; Adj EBITDA BEAT by +1.1%

- Biz revs MISSED by -0.7%; Adj EBITDA BEAT by +7.4%

- Adj EPS BEAT by +5.8%: $1.28 vs $1.21 grew +7.6% y/y

- Highest adj EPS growth rate in over 4 YRS

- FCF BEAT by +3.3%: $3.8bn (+4% y/y) despite higher capx

- Driven by better customer experience and operating efficiency

The Co Positively Raised Its 2026 Adj EPS & Net Add Outlook

- Raised 2026 adj EPS guidance to +5-6% y/y ($4.95-4.99) from previous +4-5%

- “The data supports a higher level of confidence”

- But the revised guidance continues to reflect a “prudent view” of competitive dynamics & the macro political and economic environment

- Raised the 2026 total retail postpaid phone net additions guidance to be in “the top half” of the 750k-1.0mn range (see more below)