While geopolitical headlines were hard to ignore (and remained obviously very active this week once again), the earnings ramp refocused investors on fundamentals and the S&P 500 and Nasdaq notched their 4th straight weekly gain and closed at new all-time highs.

It was a big week in the Connectivity sector in particular with mixed reactions to results, especially as the sub-sector previously benefited from a rotation away from potential AI disrupted companies.

The full list of what we focused on in this edition is below:

- Earning Scorecard - Week 1 & 2

- Investors Patiently Await AT&T’s Growth Acceleration

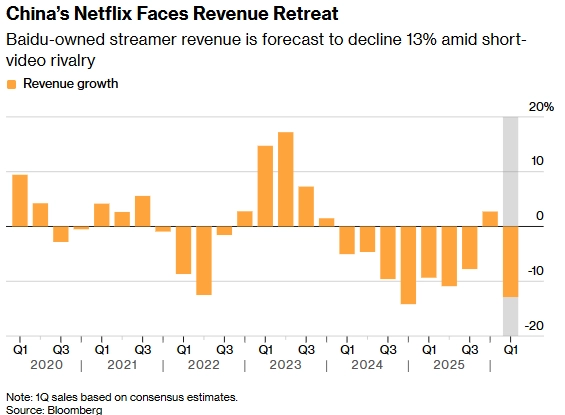

- Comcast Sees Early Fruit From Its Connectivity Pivot, While Media Outperforms

- Charter’s Q1 Is A Reminder That Improvement Is Not Always A Straight Line…

- This Week’s “AI Need To Knows” …One Of Which Is iQiyi Expecting AI To Create The BULK Of Its Films & Shows In 5 Years!

- AI Coding Is Democratizing App Creation…But Will Quality Control Become A Bigger Issue?

- Humanoid Robots Win The Gold, Silver & Bronze Metals!

- Grab Bag: DT/TMUS Combo? / Tesla Paid Robotaxi Miles Nearly 2x / MSFT’s Game Pass Gets Cheaper

Enjoy the read and brace for next week’s significant earnings ramp, with 180 S&P constituents set to report, including 5 of the Mag 7 names (AMZN, GOOGL, META, MSFT and AAPL), along w/ other key prints including VZ, SPOT, BKNG, TMUS, UMG, RDDT, and ROKU.

Best,

Leslie

Earning Scorecard - Week 1 & 2

Weeks 1 and 2 of earnings have wrapped and in total, 13 stocks in our LionTree Universe reported. Stock reactions were slightly positive, with 7 stocks (54%) trading up and 6 stocks (46%) trading down. The best performer in reaction to earnings was Intel, which was up +23.2%, while the worst performer was Charter, which fell -25.4% (see Theme #4)

Comcast also reported this week and rose +7.7% in reaction to its earnings (see Theme #3), though it gave back those gains by the end of the week. Also in connectivity, AT&T was up +0.4% in reaction to its print (see Theme #2).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Investors Patiently Await AT&T’s Growth Acceleration

After unveiling its 3-yr plan last qtr, AT&T kicked off connectivity earnings this week with a few surprises, but the Top 5 most important incrementals in our mind include: 1) Q1’s top line and adj EBITDA growth rate y/y slowed from Q4’s level but are expected to accelerate in Q2 and throughout the remaining quarters in 2026 to reach the reiterated full year guidance (driven by wireless pricing actions, improving convergence trends, and scaling contributions from Lumen assets); 2) Convergence penetration ex-Lumen reached ~45%, which is up +3ppts y/y and continues to climb; 3) Near-term ARPU dilution should persist given value focus (convergence/One Connect offer) but mgmt remains confident in the long term economics; 4) The pressure on the Legacy business is expected to also persist for several more quarters but the copper shutdown is progressing (30%+ wire centers are on a definitive schedule for shutdown and the Co has a path to more); and 5) AT&T might expand the number of satellite relationships as new LEO constellations are deployed.

Quickly touching on the headline numbers, total Q2 revenue growth reached +2.9% y/y, core Advanced Connectivity revenue growth over-indexed at +5% y/y, offsetting the strong -25% y/y decline in the Legacy business. Q2 adj EBITDA was in-line, but margins slipped -30bps y/y to 37.4% given last year’s ~$100mn vendor settlement benefit, and also the absorption of the -40% decline in Legacy EBITDA y/y. Below the line items drove upside to adj EPS vs consensus and FCF declined -20% y/y on elevated capex of ~$5.1bn tied to fiber buildout.

Bigger picture, strategically, AT&T’s emphasis on building an “open” and software-defined network architecture, alongside optionality in satellite partnerships, was interesting and suggests a longer-term effort to reposition AT&T as a more flexible connectivity platform (analogous to the hyperscalers’ infrastructure) rather than a traditional telco. With that said, the nearer term narrative has not changed.

See below for more details of what we thought was meaningful.

-> AT&T shares were roughly flat in response to its earnings print and are up +5.5% YTD, outperforming T-Mobile US’s –6.5% but under-performing Verizon’s +13.8%

-> Also in connectivity, see Theme #3 and Theme #4 for our thoughts on Comcast and Charter results

Q1 Results Were Marginally Ahead Of Street Projections

- Rev slightly BEAT by +0.8% & grew +2.9% y/y vs +3.6% y/y in Q4: Driven by Advanced Connectivity strength & Lumen contribution, partially offset by Legacy declines worse than expected

- Advanced Connectivity BEAT by +0.7% & grew +5% y/y

- Adj EBITDA IN-LINE & grew +2.3% y/y vs +4.1% y/y in Q4 but margins slightly missed (decr’d 30bps to 37.4%) due to Q1:25 results including a benefit to just EBITDA of ~$100mn related to the resolution of vendor settlements

- Adj EPS BEAT by +3.6% & grew +12% y/y vs +21% y/y in Q4: Driven by EBITDA growth and ongoing cost efficiencies

- FCF BEAT by +3.3% but declined -20% y/y vs +4.2% y/y in Q4: Reflects higher capital investment (~$5.1bn) to accelerate fiber deployment

An Acceleration In Svs Revenue & Profitability Growth Is Expected Through The Rest Of The Year To Reach The Reiterated 2026 Guidance

- The existing 2026 outlook was maintained

- Svs rev growth in the low-single-digit range y/y

- Advanced Connectivity svs rev growth of 5%+ y/y (Advanced Connectivity w-less svs rev growth of 2-3% y/y)

- Legacy svs rev decline of -20%+ y/y

- Adj EBITDA growth in the 3 – 4% range

- Advanced Connectivity EBITDA growth of 6%+

- Adj EPS of $2.25 – 2.35 / shr

- Capx of $23 – 24bn

- FCF of $18bn+

- Incl cash taxes of $1-1.5bn & cash contributions to its employee pension plan of ~ $350mn

- Stock buyback of ~$8bn (and to maintain a consistent pace of buybacks through 2028)

- Net leverage ratio will decline to ~3x by the end of the year (from ~3.2x following the Echostar transaction)

- And return to the 2.5x range w/in ~3 yrs following the transaction

- Svs rev growth in the low-single-digit range y/y

- Guidance implies a “meaningful” acceleration in both svs revs and adj EBITDA growth in Q2 and the rest of 2026: Drivers include…

- Growth in converged relationships

- Wireless pricing actions begin in April (the Co benefitted for the majority of the qtr)

- Lumen scaling – will see improvement in fiber net adds and converged relationships

- EBITDA growth supported by cost actions, digitalization, and AI efficiencies

- “I feel really good about where we are and the pacing for the rest of the year”

- Mgmt also reiterated the $4bn annual cost savings target by 2028

Strategically, The Co Wants To Operate The “Most Advanced & Open Communications Network In The US” By The End Of The Decade

- What does that mean?

- First is regarding the wireless network architecture, where AT&T is opening parts of the network to better manage “supply chain costs and performance of equipment and the architecture over time”

- “As we close the EchoStar transaction,” investors should see the “first instantiation of that” when AT&T starts deploying newly acquired spectrum

- Second is the “complete re-engineering of the core of the network”

- First is regarding the wireless network architecture, where AT&T is opening parts of the network to better manage “supply chain costs and performance of equipment and the architecture over time”

- A long but telling quote: “Just as hyperscalers opened up the ability to spin up compute and storage through touching parts of a terminal, there’s no reason why our routing infrastructure and what we turn out to customers shouldn’t have that same software based capability that is digitally driven through API structures and allow not only our end users, but partner network customers to be able to control aspects of the network moving forward at a much lower internal operating cost”

- Mgmt believes they will be able to reach more end users than the competition due to the “dense metro fiber” and “deep nationwide spectrum”

Q1 Subscriber KPIs Were Mixed, With Wireless Phone Net Adds The Positive Standout Vs Projections…

- Q1 wireless unit KPIs were mixed vs. Street expectations

- Postpaid phone net adds BEAT by +9.4%, but broader subscriber trends were weaker as total postpaid adds MISSED by -19.6% & prepaid adds were also softer (MISSED by -43.2%)

- Churn trends were worse than expected

- Postpaid phone-only ARPU was in-line

- Q1 Fiber & FWA additions were in-line to lower than cons

- Fiber adds of 292k were roughly in-line (-0.3% vs cons)

- FWA adds of 239k MISSED by -1.1% (though mgmt expects “cont’d growth” in FWA sales volumes looking ahead)

- Overall, it was the 6th consecutive qtr of total consumer and business net ads adds >500k

…But Convergence Penetration Continues To Grow, And Creates Long-Term Economic Benefits Despite A Short Term ARPU Hit

- Q1 convergence penetration was ~45% ex Lumen (~42% incl Lumen), which is up +3ppt y/y (fastest y/y growth rate)

- Mgmt expects converged penetration to improve to 50% and higher

- While there is an ARPU hit in the near-term, expect economic benefits longer term

- Q1 postpaid phone ARPU was flat y/y (as expected)…as they gain customers in underpenetrated categories and grow the converged account base that receive discounts

- As a greater portion of customers purchase wireless and internet connectivity from AT&T, they “will demonstrate improved trends in churn and additional improvement in account growth

- The Co sees increasing penetration of the value segment from 40% to 50% as “economically rational and value creating” even if it means “we take some ARPU dilution to do that”

- The Co’s fiber expansion will enable more convergence opportunities and net adds should ramp over the course of the year (“while still considering typical seasonality”)

- The Co has 37mn+ fiber locations currently

- Mgmt continues to expect to grow its fiber reach by ~8mn locations in 2026 (incl over 4mn from Lumen)

- And maintains the path 60mn+ by 2030

- Mgmt wants to be “a man for all seasons and handle every customer”

- AT&T One Connect (single subscription service for fiber + wireless at a flat monthly rate) was of particular focus on the call; It helps the Co push into the lower-end segment; The BYOD segment is increasing

- It will be iterative roll-out…the Co does NOT expect big volumes in “the 1st couple of weeks”

- It will become an “important” part of the portfolio over time

- One Connect will help the Co shift from device subsidies and focus on service…people will not be “clouded” by what they pay for the network and what they pay for devices

- Other Q1 product evolutions include –

- Expanded the AT&T guarantee to cover Internet Air

- Launched a new flagship app to deliver a simple digital 1st experience

- Refreshed the unlimited Yourway plans to deliver more value

Satellite Was Framed As A Consumer Connectivity Opportunity, With Multiple Wholesale Partners Likely Over Time Vs The One Now…

- Regarding satellite / LEO, the Co sees it as “great innovation for consumers” that will “help grow the market in total”

- In the next 18-24 months, the US could have “always on connectivity”

- The Co expects customers will want that, and the Co will “integrate those offerings into our services”

- AT&T is putting “most of our R&D” and commercialization work into the AST SpaceMobile relationship

- BUT… there will be “probably at least three” capable providers serving the US over time (i.e., AST SpaceMobile, SpaceX, and Amazon LEO)

- The Co’s goal is to have a “good, strong wholesale relationship,” and “it may not just be with one of them, it may be with more than one of them”

- The Co pushed back on the idea that satellite direct to device is a major near-term threat, saying the tech development is not likely to be a “straight line from here to there” with hurdles including –

- Getting satellites up

- Keeping them up

- Securing the right spectrum

- Managing “power levels and interference”

- Tuning devices properly

- Customers have high service level expectations, and it doesn’t work well indoors

Business Connectivity Service Revenue Finally Stabilized Y/Y…Suggesting Fiber/FWA Growth Is Starting To Offset Legacy Drag

- Advanced Connectivity revs grew +5% y/y which is below the expected full year run rate

- Svs rev growth of +3.6% y/y

- W-less svs rev growth of +1.7% y/y was driven by growth in volumes

- Equip rev growth of +9.3% y/y was from higher wireless device sales volumes

- Svs rev growth of +3.6% y/y

- Expect Advanced Connectivity w-less svs rev growth y/y to improve in Q2 from the +1.7% in Q1 (and maintain the 2-3% growth guidance for 2026) …driven by –

- Expectations for “customer gains from the new unlimited & converged subscription plan, and our expanding opportunity to sell wireless and home internet services together”

- It also reflects the recent price increase in Q2

- Advanced home internet service revenue grew +27.3% y/y, but that INCLUDES new customers acquired from Lumen (added ~650bp of growth in Q1)

- Organic growth was mainly driven by customer adds

- Advanced Connectivity Business svs revenues stabilized y/y for first time ever based on better sales execution & the expanding fiber reach: Business Fiber + Advanced Connectivity revs grew +7.2% y/y

- Outlook: Expect Advanced Connectivity Business svs revs to remain “stable” near term and grow low SD CAGR though 2028

- Advanced Connectivity EBITDA rose +5.6% y/y and mrgns rose 30bp despite headwinds

- High SD growth in low margin equip revs

- The inclusion of revenues in geographies acq’d from Lumen (but did not make a material contribution to EBITDA in the qtr)

- 40% of the adj EBITDA benefit from vendor settlements was incurred in this segment

- The outlook reflects an immaterial EBITDA contribution in 2026 from Lumen assets

- FWA is enabling broader enterprise penetration: Previously they were limited to fiber-only coverage (~65–70%)

- Improves competitiveness in enterprise segment

- The Co’s convergence strategy is also extending into enterprise

The Legacy Business Remains A Drag But Is Winding Down / The Copper Shutdown Is Materially Progressing

- The legacy business is declining rapidly w/ revs down ~-25% y/y and EBITDA down ~-40% y/y due to the cost lag during this transition

- Expect this lag dynamic to persist for the “next several qtrs.”

- But that copper shutdown is progressing materially: “This FCC order that came out is a very strong order In my view…it gives a good roadmap”

- 30%+ wire centers are on a definitive schedule for shutdown and have a path to more

- They have no new legacy orders in most footprints

- They are migrating customers to fiber and FW

Comcast Sees Early Fruit From Its Connectivity Pivot, While Media Outperforms

Comcast appears to be hitting an inflection regarding its investment cycle, i.e., its strategic go-to-the market shift with new connectivity pricing and packaging and new customer experience initiatives. While still early days, much better broadband subscriber trends in Q1 were a key standout, with POSITIVE net adds of +65K (vs cons DECLINE of -169k), which represents an increase of +117k y/y. Even with more than half of the y/y improvement coming from its “Legendary February” promotion, the numbers would have topped the Street without it. Along with the better broadband additions, w-less net additions also surged given the strong uptake of free lines (30% of postpaid connects). This all occurred despite a still “intense” competitive environment in the connectivity sector all around. The near-term costs and dilution from this strategic shift weighed on ARPU and adj EBITDA (as expected) and will show the same trend in Q2, but mgmt is confident that pressure will ease as the Co exits the year.

While the Connectivity & Platforms (C&P) segment works through its transition and remains in negative growth territory, the Content & Experiences (C&E) segment beat the Street almost across the board. The Olympics and Super Bowl drove a step change in revenue and advertising, and Peacock saw strong engagement and revenue growth (though subscriber adds fell short of expectations). The NBA rights costs (that have been pressuring EBITDA) peaked this quarter, and Peacock is guided to approach break even in Q2 (but the sustainability of that profitability remains an open question given the seasonality of sports costs). Trends at Domestic Parks remain strong, with no significant negative impact from geopolitical / macro issues (at least thus far) and the Studio business is also performing well.

How did this all translate to the Co’s overall Q1 results performance? Revenue beat by +3.5%, adj EBITDA beat by +2.7% and adj EPS beat by +9.7%, though the latter two were still down meaningfully y/y. Looking ahead, the next few quarters are critical, and key deliverables will be a continued positive trajectory of bband additions, evidence that the free wireless base is converting to paid in H2, and a favorable profitability picture at Peacock.

Lastly, regarding the potential for more cable M&A, which has been topical, mgmt essentially said that they are happy with their asset mix and see ample opportunities as is, but they are also open to “benefit ourselves through scale in partnership terms” and they are “open to strategic possibilities to create value.” But the focus “is really on what we can do ourselves. And the list is long, and we’re underway on that.”

See below for more detailed thoughts and updates.

-> Comcast shares rallied +8% on the back of results but gave back those gains post Charter’s results and a Street rating downgrade on Friday which drove the stock down -13%; YTD the stock is now down -2%.

-> See Theme #2 and Theme #4 for our thoughts on AT&T and Charter results (including additional cable M&A comments)

Some Signs Of Life Emerge In Q1

- Rev BEAT: Rose +5% y/y (vs +1% y/y in Q4) and BEAT cons by +3.5%

- 60%+ of total revs come from their “6 major growth drivers” vs 50% 3 years ago

- The connectivity pivot is gaining traction with broadband losses improving y/y and record wireless adds

- Media strength driven by Olympics + Super Bowl, with strong Peacock and advertising growth

- 60%+ of total revs come from their “6 major growth drivers” vs 50% 3 years ago

- Adj EBITDA BEAT by +2.7%: Fell -17% y/y (vs -10% y/y in Q4)

- Adj EBITDA margin slightly MISSED: 25.2% vs 25.4%

- Decline y/y reflects continued investments in go-to-market strategy, customer experience, and pressure from NBA rights + higher sports programming costs, partially offset by growth in Business Services and Theme Parks

- Adj EPS BEAT by +9.7%: But was down -28% y/y

- Capx was LOWER than cons (~-10%): Grew +4% y/y

- Connectivity & Platforms capx incr’d (customer premise equipment + network investment)

- Content & Experiences capx declined (-20% y/y, post Epic Universe opening)

- But FCF of $3.9bn BEAT cons by +28% (down -28% y/y)

- Capex incr’d +4.4% to $2.4bn, which fell below cons

- Connectivity & Platforms’ capex incr’d +13.4% to $1.8bn

- Primarily reflecting higher spending on customer premise equipment, scalable infrastructure and support capital

- Content & Experiences’ capex decr’d -20.1% to $481mn

- Reflecting the opening of Epic Universe in May 2025

- Connectivity & Platforms’ capex incr’d +13.4% to $1.8bn

- Leverage reached ~2.3x w/ cont’d focus on shareholder returns (~$2.5bn returned in Q1…$1.3bn in buybacks, $1.2bn in dividends)

The Connectivity & Platforms (C&P) Business’ Slightly Better Than Expected Results Reflects Early Signs Of Progress With Comcast’s Strategic Broadband Pivot

- C&P results were slightly ahead of consensus w/ revenues down -1% y/y or -4% FXN and adj EBITDA down ~4.3% or -4.7% FXN y/y (vs -4.3% or -4.5% FXN in Q4)

- Convergence revs decl’d -2.8% y/y (vs +2% in Q4): Pressure on broadband revenue was partially offset by 15% growth in wireless svs revenue

- Pressure continues to be driven by ARPU declines + elevated marketing, product & customer service costs tied to the go-to-market pivot BUT these new go-to-mkt & customer experience initiatives are showing some early signs of success relative to Street expectations

The Y/Y Improvement In Broadband Subscribers Was A Major Standout BUT Near-Term ARPU & EBITDA Pressure Remains Before The H2 Inflection

- Q1 broadband losses improved by +117k y/y to positive ~65k …cons was bracing for a decline of -169k: “Our new go to market offerings are clearly resonating with customers”

- Connect volumes improved for the 1st time since Q4 2020 w/ lower voluntary churn, a step up in the take rate on gig plus speeds, and improving NPS

- BUT NOTE that over 50% of the improvement in y/y subscriber losses came from “Legendary February” promotions (even excluding that, the numbers would have been better than the Street)

- Monthly data usage on the network is up 10% y/y this qtr

- ~40% of the residential broadband base is now on simplified pricing w/ the majority expected to migrate by YE

- In addition to the bband subscriber improvements, the Co also achieved record Q1 w-less net adds of +435k vs cons +357k (~22% beat) and marked a record quarter: 30% of connects net adds are coming from existing mobile customers adding more lines

- W-less free line offers are performing well (drove ~50% of residential postpaid connects): They build awareness, increase attachment and are expanding the top of the funnel

- Mgmt is confident they can covert a “meaningful portion” of free w-less lines to paid in H2: Early cohorts are showing strong conversion to paid relationships

- Also gaining traction w/ Premium unlimited plans (~30% of postpaid phone connects and since launch the base is up ~5x)

- Along these lines, launched a premium Mobile Plus plan this week which adds lifetime device protection for all devices (no one else offers this so mgmt. sees it as a big differentiator)

- The 9.7mn total w-less lines base still only accounts for ~16% penetration (vs ~15% in Q4) so there is plenty of room for growth

- This positive Q1 bband & w-less subscriber performance was despite a competitive environment that remains “incredibly intense” and mgmt is not expecting any improvement for the rest of the year: Interestingly, mgmt indicated that Q1’s better connects and disconnects were across all their competitive environments

- Fiber overbuild continues to accelerate (55% overlap with the base)

- FWA remains aggressive

- Satellite is “getting more promotional”

- Wireless competition remains elevated

- The strategic pivot is weighing on ARPU as previously guided…it was down -3.1% y/y (vs +1.1% in Q4) driven by no rate increases, new go to market pricing (including the Legendary February offers), & free wireless lines, which are initially dilutive to bband ARPU

- This incremental ARPU & EBITDA pressure is expected to persist into Q2 but mgmt “anticipates some relief” exiting the year as they begin to lap the initial investment pressures & more fully monetize the free lines at the 1 year anniversary from the launch

- Comcast’s convergence rate, or avg revenue per account, currently stands at roughly $85 which “for context, our telecom competitors are roughly double this amount on the same metric”

- “This really underscores the significant growth opportunity in front of us, especially as we stabilize broadband and look to accelerate growth through wireless”

- “We do maintain our pricing flexibility so we can adjust the rate and acquisition pricing as the market evolves”

“Legendary February” Was A Big Beneficiary To The Media Biz In Q1

- Q1 Media rev outperformed, driven by the significant boost from “Legendary February” (which also boosted broadband subscribers per the above): Segment rev and adj EBITDA both topped Street forecasts by +7% and +19% respectively

- Media revs grew +60% y/y, driven by strong contributions from the Milan-Cortina Winter Olympics and Super Bowl, which together drove $2.2bn of incremental rev

- Media rev ex those events grew +13% y/y, driven by +21% y/y growth in Distribution and +5% y/y growth in Advertising

- Q1 Media adj EBITDA loss of -$426mn was as expected and represented peak EBITDA dilution from NBA costs

- Underlying demand in advertising remains “strong”, supported by a record upfront and a strong sports lineup (including the NBA)

- Looking into Q2…the Co will continue to benefit from sports, including the NBA playoffs and the FIFA World Cup on Telemundo and Peacock

- 225mn+ Americans watched across the Milan Cortina Winter Olympics, Super Bowl 60 and the NBA All-Star game…driving record advertising sales (~$2bn over the 17 days) and helping accelerate momentum at Peacock

- Milan Cortina was the most watched games since Sochi, avging 23.5mn viewers

- NBC closed out prime time #1 on the closing ceremony night, marking the Co’s 143rd consecutive Olympics night at the top

- Peacock was also a benefactor… streamed a record 16.7bn minutes, more than 2x all prior winter games combined

- The Super Bowl averaged 125.6mn viewers, the most watched in the Co’s 100-yr history and the second most watched program ever

- NBA All-Star game delivered its largest audience since 2011 w/ 8.8mn viewers across NBC, Peacock and Telemundo, peaking at 10mn

Peacock Is Expected To Be Profitable In Q2 (But Whether That Sustains After That Is Still TBD)

- Peacock rev grew +71% y/y (vs +20% y/y in Q4) and surpassed $2bn for the first time

- Peacock is on track to approach profitability for the first time next qtr

- Will Peacock profitability persist after Q2? Mgmt was vague: “…because of our straight-line amortization of NBA rights, as we look to the next season, so to speak, of NBA lapping itself, I think the prospect for ongoing and durable profitability for Peacock is what we have our sights set on”

- Peacock subs grew +2mn q/q (vs +3mn q/q in Q4) to reach 46mn, which was BELOW cons 48mn

Studios Delivers A Solid Beat Driven By Licensing, With Cont’d Box Office Momentum And A Strong Pipeline Ahead

- Q1 Studios biz came in well ahead of expectations: Rev beat by +21% and adj EBITDA beat by a substantial +106%

- Rev and adj EBITDA growth was due to higher content licensing rev, driven by the renewal of The Office on Peacock

- Super Mario Galaxy movie crossed $750mn globally and is the biggest title of the yr worldwide

- The franchise has now grossed $2bn at the global box office

- The Co has a “strong” lineup for the rest of the yr w/ Steven Spielberg’s Disclosure Day, Illuminations, Minions & Monsters, Christopher Nolan, the Odyssey and Universal’s Focker-In-Law, among others

Domestic Parks Remain Strong with No Meaningful Geopolitical Impact (Yet) Though Intl Is Seeing Some Pressure

- Q1 Theme Parks rev was +3.6% ahead of cons while adj. EBITDA was ~in-line

- Domestic parks continue to perform well…

- Orlando continues to perform “extremely well” w/ Epic driving “strong” resort attendance and higher per cap spending

- Have NOT seen any pullback in the Parks biz from higher oil prices, BUT that could change: Depending on duration of the effect on price of gas, airline tickets, etc.

- Also flagged that inbound intl travel to the US Parks has never gotten back to pre-COVID levels, so that is also a factor that continues to exist

- …BUT feeling some pressure at Intl parks

- Osaka is seeing some impact from China-related inbound travel trends, which is putting pressure on attendance

- Beijing is navigating a more challenging macroeconomic environment

- Are continuing to invest behind a pipeline of growth…

- Opened Fast and Furious Hollywood drift in Universal Hollywood this yr

- Opening their first ever kids’ Park in Frisco, Texas this summer

- UK park is progressing through final planning approvals, as site stabilization begins

- Building on their strength in Japan, w/ immersive Pokémon experiences

Charter’s Q1 Is A Reminder That Improvement Is Not Always A Straight Line…

After Charter delivered much lower-than-anticipated broadband losses in Q4, investors were expecting those improved trends to be part of the Co’s Q1 narrative as well, especially post Comcast’s better than expected bband results earlier this week (see Theme #3). However, that was not the case with Charter’s Q1 broadband losses of-120k falling below cons -95k. Competition remains high but “the level of promotional activity was not a fundamental change.” Gross adds weakened due to a top-of-funnel issue driven by lower sales activity (churn actually improved). Mgmt does NOT believe that the weakness indicates a product issue and remains “focused on clearly messaging and delivering our superior value, utility and service to both new and existing customers.” This has been a work in progress.

On the mobile side, net adds also trailed expectations as higher disconnects tied to promotions and device subsidies offset solid gross additions. Also, after positive video ads in Q4, Q1 video losses were modestly worse than expected, but to be fair, still improved significantly y/y, supported by bundled streaming products that are reducing churn (but adding higher streaming costs).

On the plus side, the Cox transaction is on track for a summer close (just waiting on California’s approval) and mgmt raised the run rate opex synergy targets from $500mn to $800mn and indicated that there could be more to come (plus revenues synergies are not factored in as well).

Mgmt still expects to have “slight” adj EBITDA growth in 2026 ex transition costs, helped by the political tailwind, and with capx coming down meaningfully post 2026, FCF will start to ramp (the capx reduction from ~ $11.7bn in 2025 to < $8bn in 2028 is worth more than $28/shr of incremental FCF based on today’s share count per mgmt.). That said, investors are not giving the Co the benefit of the doubt and want to see a sustainable recovery in the bband business.

Also, what did CHTR mgmt say about further potential cable M&A (which has been on investor’s minds)? “There is a significant rationale for cable M&A but there’s nothing that we’re looking at today or doing today other than finish the Cox transaction, but I think the opportunities there to do more over time, and we’ll evaluate it when it’s available.”

See more thoughts below,

-> Charter shares fell -25% in reaction to results and are now down -14% YTD.

-> See Theme #2 and Theme #3 for our thoughts on AT&T and Comcast results (including additional cable M&A comments)

Mixed Q1 Headline Results But Still Expects “Slightly Positive” Adj EBITDA Growth For The Year (Ex Transition Costs)

- Total revs slightly BEAT cons by +0.4% (fell -1.0% y/y)

- Ex advertising & programmer app allocation, total rev grew +0.1% y/y

- Adj EBITDA was roughly IN-LINE w/ cons (fell -2.2% y/y, and down -1.8% ex transition expenses)

- But adj EPS MISSED cons by -7%

- Capx was HIGHER than expected by $210mn: Given timing of spend, with higher upgrade/rebuild (primarily network evolution) and CPE, partly offset by lower line extension spend

- But FY26 capex GUIDANCE was MAINTAINED at $11.4bn

- FCF MISSED by -17%: Higher capx was partly offset by a “less unfavorable change in accrued expenses related to capx and higher net cash flows from operating activities”

- The Co continues to expect EBITDA to grow “slightly” in 2026 excluding transition costs, helped by political advertising

A Big Focus Was On Disappointing Subscriber Trends Vs Street Expectations

- Broadband losses were worse than anticipated (total Internet losses of -120k vs cons -95k)…driven by lower connects y/y, partly offset by slightly lower churn …the operating environment remains competitive

- See details in the next section

- Mobile net additions of +368k were well below cons +436k…reflecting ongoing competitive intensity

- Gross adds improved y/y, BUT higher disconnects on a larger base due to elevated promotional activity and device subsidies which weighed on net adds

- With that said, the base reached 12.1mn lines and grew +17% y/y

- Video subscriber losses were slightly worse than expected (-60k vs cons -57k) BUT showed the cont’d trend of y/y improvement (Q1:25 loss was -181k): The value proposition around bundled streaming apps is helping to mitigate declines

- Over 50% of expanded basic video customers have activated at least one included streaming app, w/ activated customers taking nearly 4 apps on avg

- Churn for expanded basic customers who activate is one-third lower, w/ improvement visible across all tenure cohorts

- Video is still being used to support broadband acq & retention BUT $218mn of streaming app costs were netted w/in video rev vs $47mn last year as the mix continues to shift toward lower-priced packages

- Over 50% of expanded basic video customers have activated at least one included streaming app, w/ activated customers taking nearly 4 apps on avg

Top-Of-Funnel Weakness And Competition Continue To Pressure Bband Adds & Better Messaging Is Still Required To Unlock Growth

- Regarding bband macro and competitive headwinds…

- Low move activity persists

- Seeing cont’d mobile substitution

- Saw “expanded” FWA competition (AT&T is increasingly active)

- The fiber overlap growth persists (but consistent so “nothing new”)

- What about satellite competition? CHTR is not seeing any meaningful share loss today from satellite in rural mkts but the Co could have been doing better in some cases

- It is a “great product”

- Mgmt sees the potential for partnership opportunities: “There are ways to attach satellite and to become a seller of that product to the extent that they were willing to have us as a reseller and bundle that together with our broadband service”

- They could be “more friend vs foe”

- But “the level of promotional activity was not a fundamental change” … “Charter’s issue is top of funnel”

- Bband churn remains at very low levels and improved y/y, indicating core customer satisfaction and product stickiness remain intact

- BUT gross adds weakened due to a top-of-funnel issue driven by lower sales activity

- Mgmt thinks they can get back to broadband growth and it sounds like they could use pricing if it was the right move: Mgmt has “not made any determination of pricing increases”…but are mindful that “we are still in an inflationary environment“

- Mgmt continues to argue that the Co’s product quality is ahead of reported customer results, and that the main bottleneck is not the product set but market perception and go-to-market execution

- “Our results don’t yet reflect that reality given the legacy reputation of cable. So we remain focused on clearly messaging and delivering our superior value, utility and service to both new and existing customers”

- “The ability to cut through and message to customers around our value and utility is actually the thing that’s creating pain for us”

- “It really comes to doing a better job of messaging our value and utility”

- “I don’t think we need to spend anything more in marketing”

- ~45% of the residential customers are in the new pricing and packaging launched in late 2024

- Other key product and services updates:

- Saw much stronger than expected attach w/ Invincible WiFi launched in February, which created short-term supply constraints

- The product adds battery backup and a 5G failover connection, materially increasing utility during outages or disruptions

- By year-end 2026, about 50% of the Spectrum network is expected to be upgraded to symmetrical and multi-gig service, with significant work on the remaining also in process

- The Co deployed new AI tools now used by our service agents, driving higher customer satisfaction and reducing call times with higher job satisfaction for our employees as well

- Saw much stronger than expected attach w/ Invincible WiFi launched in February, which created short-term supply constraints

- Mgmt remains focused on returning to broadband ARPU growth, BUT in 2026, it “could go either way” in terms of it turning positive, depending on offer tuning, balancing competitiveness, and external conditions

The Cox Deal Is On Track & Charter Raised Synergies Targets, While Remaining Confident In The Customer Economics

- The Cox deal close is still set for the summer…all approvals are in hand except California

- W/in a “couple of months” of closing, the Co will launch the Spectrum brand and pricing and packaging within the legacy Cox footprint

- The Co is going to enter into Cox’s footprint with a “big bang”…“I think we’re going to make a splash because we’re new”, then will need to back that up with service

- Mgmt raised the run-rate opex synergies guidance from $500mn to “at least” $800mn

- The uplift reflects better visibility into procurement synergies including programming, and more visibility into financials and what CHTR can achieve with Cox’s cost structure

- Mgmt also suggested there is still potential upside to that new target

- These new estimates also do not include the benefits of applying Charter’s operating strategy to create revenue and operating cost synergies over time, or CapEx savings

- “We believe those operating synergies will also be significant”

- Even though Cox has higher bband ARPU which will be coming down standalone, “customer” ARPU and EBITDA margin is not that different: “Higher sales of broadband… lower churn of broadband…significantly higher attach rate for mobile and video… preserves your overall customer margin… and more operating and CapEx cost synergies along the way allow you to fund that growth”

- There is also incremental upside from field sales, stores, service model changes, and highly complementary B2B capabilities

CapEx Is Near Peak Levels…& Will Drive $28/Shr+ Of Incremental FCF Using Today’s Share Count

- Q1 capex was $2.9bn, up $456mn y/y, driven by timing of network evolution spend and higher CPE tied to WiFi 7 / Invincible WiFi

- Maintained 2026 capex guidance at ~$11.4bn, with spend thereafter expected to meaningfully decline

- The Co still expects to hit a normalized capx level in 2028

- Mgmt highlights that the capx reduction from ~$11.7bn in 2025 to < $8bn in 2028 is worth more than $28/shr of incremental FCF based on today’s share count

- “If we take consensus 2026 free cash flow and substitute our expected 2028 CapEx for 2026 CapEx, our current stock price would imply a free cash flow multiple of only about 3.8 times, and a free cash flow yield of over 25%.

- $963mn of buybacks were completed in Q1 while leverage targets remains the same

- Mgmt reiterated leverage targets post transactions (the low end of the 3.5- 3.75x leverage range within 3 years of deal close) and will continue ongoing capital returns to shareholders despite the deleveraging

Quick Update On Financial Reporting Post The Deal

- Post-deal close, results will reflect a full qtr for Legacy Charter + a stub period for Legacy Cox

- The Co will report similar customers, PSU and revenue data for both legacy entities for several qtrs to enable investors to track individual company performance

- CHTR will not break-out expenses or capx by legacy entities

- Will continue to report transition expense and capital related to the integration and will provide updates on certain items, including estimates for the synergies realized

- At close, the outstanding share count will increase as they will issue the equivalent of just over 46mn CHTR shares to Cox Enterprises

- Comprised of common and preferred partnership units, partly offset by net Charter share reduction of ~ 6.8mn shares associated with the Liberty Broadband transaction

- That 6.8mn figure is lower now than when the Co annc’d the Liberty Broadband transaction, due to their ongoing share repurchases from Liberty Broadband

- If they had closed on March 31st, the standalone share count at close on a “as converted as exchanged basis” would have been ~179mn

This Week’s “AI Need To Knows” …One Of Which Is iQiyi Expecting AI To Create The BULK Of Its Films & Shows In 5 Years!

The biggest AI updates this week were widespread across the ecosystem. OpenAI and DeepSeek are releasing models that can more independently handle tasks like coding, research, and data analysis, while Google, Amazon, and Meta are building out the infrastructure to support them, including new TPUs, expanded Trainium capacity, and large-scale Graviton deployments. At the same time, Big Tech is doubling down on Anthropic, with Google and Amazon committing tens of billions to expand their partnerships.

AI is also becoming more embedded in day-to-day work and content creation. Tools like Delivery Hero’s coding agent and Adobe’s marketing products are taking on tasks that previously required significant human effort, while iQiyi is launching an AI filmmaking platform and shifting toward a model where creators produce and monetize AI-generated films directly. In music, the volume of AI-generated tracks is rising quickly BUT consumption remains low.

Also, more regulatory US- China AI tensions emerged this week. See below for details on what we viewed as the most important AI developments this week.

Key Model Updates This Week From OpenAI And DeepSeek

- OpenAI releases GPT 5.5, which is its “smartest and most intuitive to use model” yet (link)

- Available in two variants – GPT-5.5 and GPT-5.5 Pro: The standard version serves as the versatile flagship for general intelligence tasks, while the Pro model is built for more demanding work such as legal research, data science, and advanced business analytics where accuracy is paramount

- The model “understands what you’re trying to do faster and can carry more of the work itself”: Excels at writing and debugging code, researching online, analyzing data, creating documents and spreadsheets, operating software, and moving across tools until a task is finished

- “You can give GPT‑5.5 a messy, multi-part task and trust it to plan, use tools, check its work, navigate through ambiguity, and keep going”

- “Especially strong” gains in areas where progress depends on reasoning across context and taking action over time, like agentic coding, computer use, knowledge work, and early scientific research

- GPT‑5.5 delivers this step-up in intelligence w/out compromising on speed: GPT‑5.5 matches GPT‑5.4 per-token latency in real-world serving, while performing at a much higher level of intelligence

- GPT 5.5 was released w/ the Co’s “strongest set of safeguards to date”, designed to reduce misuse while preserving access for beneficial work

- BUT to flag…GPT-5.5 is significantly more expensive than GPT-5.4: Those using the model through an API will pay $5 per million input tokens and $30 per million output tokens, a 2x increase from GPT-5.4

- It will only be available to paying subscribers, including ChatGPT Plus, Pro, Business, and Enterprise users, with GPT-5.5 Pro access starting at the Pro tier and upwards

- OpenAI’s new model rollouts have been back-to-back: OpenAI released its last model only last month, with a previous release in December and, before that, November

- DeepSeek launches new-generation V4 models (link/link): This is the 1st new-generation model that DeepSeek released since its R1 model became a global sensation in Jan 2025

- The Co annc’d two new models, DeepSeek-V4-Pro, a large-size model w/ 1.6 trillion parameters, and the smaller V4-Flash

- Similar to DeepSeek’s previous model releases, the latest upgrades are open-source, allowing developers to download the code, run it locally and modify it in most cases

- Both V4 Flash and V4 Pro support text only, unlike many of its closed-source peers, which offer support for understanding and generating audio, video, and images

- Both models are also more efficient and performant than DeepSeek V3.2 due to architectural improvements, and have almost “closed the gap” with current leading models, both open and closed, on reasoning benchmarks

- On pricing, DeepSeek V4 is much more affordable than any frontier model available today

- The smaller V4 Flash model costs $0.14 per million input tokens and $0.28 per million output tokens, undercutting GPT-5.4 Nano, Gemini 3.1 Flash, GPT-5.4 Mini, and Claude Haiku 4.5

- The larger V4 Pro model costs $0.145 per million input tokens and $3.48 per million output tokens, also undercutting Gemini 3.1 Pro, GPT-5.5, Claude Opus 4.7, and GPT-5.4

-> Separately, but related, Tencent and Alibaba are reportedly in talks to invest in DeepSeek as part of its first ever funding round at a valn $20bn+; The talks are still underway and both the valn and the amount of capital to be raised could still change (link)

Big Tech’s Big Investments In Anthropic This Week…

- Google plans to invest up to $40bn in Anthropic (link/link)

- Committing to invest $10bn now in cash at a $350bn valn (the same amount it was valued at in a funding round in Feb, not including the recent money raised)

- Will invest another $30bn if Anthropic hits performance targets

- Anthropic and Amazon also expand their partnership (link)

- Amazon will invest $5bn in Anthropic today and up to an addt’l $20bn in the future tied to certain commercial milestones

- This is in addition to the $8bn Amazon previously invested in Anthropic

- Anthropic committed to spending $100bn+ over the next 10 yrs on AWS technologies

- This encompasses current and future generations of Trainium (Amazon’s custom silicon) and tens of millions of Graviton cores (Amazon’s widely-adopted CPU chip)

- Anthropic will secure up to 5 gwgigawatts of capacity to train and power its advanced AI models

- A portion of which will include significant Trainium3 capacity expected to come online this yr

- Overall, the commitment includes Trainium2, Trainium3, Trainium4, and the ability to purchase future generations of Trainium as they become available

- Amazon will invest $5bn in Anthropic today and up to an addt’l $20bn in the future tied to certain commercial milestones

AI Infrastructure Continues To Scale To Meet The Demands Of The Agentic Era

- Google introduces two new TPUs designed for the “agentic era”…its eighth-generation TPU 8t (training) and TPU 8i (inference) (link/link)

- This is the first time the Co has split its TPU line into two distinct chips optimized for separate workloads

- A step up from previous generations: Up to 3x faster AI model training, 80% better performance per dollar, and the ability to get 1mn+ TPUs to work together in a single cluster

- Google is using these chips to supplement the Nvidia-based systems it offers in its infrastructure and it NOT just flat-out replacing Nvidia

- In fact, Google Cloud will have Nvidia’s latest chip, Vera Rubin, available later this year (link)

-> Also worth flagging on the Google Cloud front, Google annc’d this week that processing capacity has incr’d to over 16bn tokens per minute via direct API use by customers, up from 10bn last qtr, as the shift toward agentic enterprise use continues to accelerate (link)

- Meta has signed an agreement to deploy AWS Graviton processors at scale (link)

- The deployment starts with tens of millions of Graviton cores, with the flexibility to expand as Meta’s AI capabilities grow

- The chips will power various workloads at Meta, including supporting the Co’s AI efforts: That work requires infrastructure that can handle billions of interactions while coordinating complex, multi-step agent workflows, which is “exactly the kind of CPU-intensive work Graviton is designed for”

AI Is Continuing To Become A Bigger Part of How Work Gets Done

- Delivery Hero unveiled Herogen, an autonomous software delivery agent that unlocks 130-person engineering output (link)

- Built in-house, Herogen is already delivering an annual coding output equivalent to 130 senior engineers (or an est’d 250k hrs of manual coding annually), and its capacity is expanding rapidly

- How does it work?

- Product and engineering teams assign tasks in natural language and Herogen then writes, tests, and iterates on the code, before submitting the result as a proposal

- A “council of agents” (built on a number of leading LLMs from different providers) reviews the code from various perspectives before a human does a final check

- Herogen operates autonomously, unlike previous generations of AI coding assistants that require constant manual oversight and revisions

- Currently, Herogen demonstrates an 85% success rate, measured as the ratio b/w merged and rejected pull requests

- The “vast majority” of tasks require zero or one interaction with the human in the loop, with built-in safeguards enabling intervention when needed

- Although currently adopted by only 18% of the company’s developers, Herogen is already responsible for 9% of all code change requests across Delivery Hero

- The Co plans to continue expanding Herogen’s reach, with a goal of having it handle 20% of all code change requests by yr end

- Herogen is “a tool for job evolution, not job elimination”: It “changes how our engineers spend their days, but it does not move them away from their craft…as the software engineering profession changes, Herogen enables engineers to have more impact in a shorter time than ever before”

- Adobe launched a suite of AI products to help corporate customers automate and personalize digital mkting functions (link)

- CX Enterprise is an AI agent-based platform that can be used to help bizs boost areas like customer engagement, sales and loyalty

- CX Enterprise Coworker is an AI-based solution designed to help organizations manage and orchestrate customer experiences more efficiently

- Designed to monitor signals, recommend actions, and execute cross-channel experiences based on established organizational goals

- Will be generally available in the coming months

- Teaming up w/ 30+ AI platforms and other Cos to set up the broadest agentic AI ecosystem in the industry, per Adobe

- Includes Amazon Web Svs, Microsoft, Anthropic, OpenAI and Nvidia, allowing customers to use AI agents across those Cos platforms for digital mkting tasks

- Comes after Anthropic released Claude Design last week

AI Expands Across Content & Music Creation As Volume Rises, Though AI Music Consumption Is Still Minimal

- China’s iQiyi now expects AI to create the bulk of its films and shows in 5 years (link/link/link/link): The Co is pivoting to an AI-first, creator-led platform model…it includes:

- A move from a centralized platform to a creator marketplace…converting iQiyi’s video app and website into more of a social media destination that hosts mainly AI-generated content

- Creators will decide independently what to produce, fund projects themselves, and upload finished works to compete directly for audience attention; Rev will be tied to actual performance, w/ no stated ceiling

- iQiyi will focus on providing the technology stack, distribution system, and basic governance rules, while stepping back from most editorial decisions

- The debut of the Nadou Pro suite, iQiyi’s AI-native production platform that can handle almost every aspect of filmmaking

- Integrates ~70 AI agents, covering scriptwriting, directing, visual design, editing, and more, into a unified workflow that resolves key AIGC challenges like character and scene consistency while enabling creators to produce film-grade content with improved efficiency

- Creators using Nadou Pro can license from iQiyi’s IP library, collaborate with affiliated talent, and draw on a shared digital asset library of virtual sets, props, and AI-rendered characters, with direct access to iQiyi’s distribution and monetization systems

- Rev sharing is linked to performance, and iQiyi is offering a 20% subsidy for AI-generated mid-form series through yr-end 2026

- The Co expects AI to create the bulk of its films and shows in 5 yrs

- Starting w/ debut slate of 16 Nadou-produced films spanning sci-fi and anime + aiming to release a commercially successful AI-generated film as soon as this summer

- The Co will still maintain investment in professionally produced content, but will reallocate a portion of its capital to bolster its AI svs, and will pay AI content creators an addtl cut of advertising and membership fees

- There will also be an AI actor “database” which was met with significant industry backlash…

- The database is designed to connect filmmakers with actors willing to have their likeness used in AI-generated content

- iQiyi addressed the controversy… “we are not currently licensing the likeness of actors. Rather, we are enabling AI creators and actors to more quickly establish connections through Nadou Pro,” said iQIYI SVP Liu Wenfeng

- The platform stressed that “the performers agreeing to join only means they have willingness to cooperate on AI film and television projects; Whether they would participate in a specific project or play a particular role would still require separate negotiations and authorization

- A move from a centralized platform to a creator marketplace…converting iQiyi’s video app and website into more of a social media destination that hosts mainly AI-generated content

- AI-generated music tracks now account for 44% of new uploads on Deezer, BUT listener demand remains negligible, and most of the content is found to be fraudulent (link/link/link)

- Nearly 75k AI-tracks are uploaded every day, which amounts to 2mn+ AI-generated tracks uploaded per month

- Deezer reported receiving around 60k AI tracks per day in January, up from 50k in November, 30k in September, and just 10k in January 2025, when it first launched its AI-music detection tool

- BUT consumption of AI-generated music on the platform is still very low, between 1-3% of the total streams

- ALSO, a majority (85%) of these streams are detected as fraudulent and are demonetized by Deezer

- For context… Deezer has had its AI detection tool in place since the beginning of 2025, and more than 13.4mn AI-generated tracks were detected and tagged on the platform that yr

- How are other music streaming svs dealing with the explosion of AI tracks?

- Spotify announced new policies around slop, impersonation, and disclosing whether AI was used to create the music

- Apple Music is asking artists and record labels to label songs made with AI

- Bandcamp has banned AI music altogether

- Qobuz has started automatically detecting and labeling AI music

- Nearly 75k AI-tracks are uploaded every day, which amounts to 2mn+ AI-generated tracks uploaded per month

US-China AI Tensions Rise As Both Sides Restrict Tech and Investment

- The Trump administration published a memo accusing China of “industrial-scale” theft of AI technology and said it will crack down on the “exploiting” of AI models made in the US (link/link)

- “The US govt has information indicating that foreign entities, principally based in China, are engaged in deliberate, industrial-scale campaigns to distill US frontier AI systems,” Michael Kratsios, director of the White House Office of Science and Technology Policy, wrote in a memo

- Chinese campaigns were “leveraging tens of thousands of proxy accounts to evade detection and using jailbreaking techniques to expose proprietary information”

- To address the threat, the Trump Administration will…

- Share information with US AI Cos concerning attempts by foreign actors to conduct unauthorized, industrial-scale distillation, including the tactics employed and actors involved

- Enable the private sector to better coordinate against such attacks

- Work together with private industry to develop best practices to identify, mitigate, and remediate industrial-scale distillation activities and build strong defenses against such activities.

- Explore a range of measures to hold foreign actors accountable for industrial-scale distillation campaigns

- China responded by calling the accusations “pure slander” and said it opposed “the unjustified suppression of Chinese companies by the US”: “China has always been committed to promoting scientific and technological progress through co-operation and healthy competition. China attaches great importance to the protection of intellectual property rights,” said a Chinese the embassy spokesperson

- “The US govt has information indicating that foreign entities, principally based in China, are engaged in deliberate, industrial-scale campaigns to distill US frontier AI systems,” Michael Kratsios, director of the White House Office of Science and Technology Policy, wrote in a memo

- On the other hand…Chinese regulators are planning to restrict technology firms from accepting US capital without govt approval (link)

- What has been conveyed? Agencies including the National Development and Reform Commission have told several private firms in recent weeks they should reject capital of US origin in funding rounds unless explicitly approved, according to people familiar with the matter

- Moonshot AI, which is considering an IPO, was reportedly among those that got the guidance, along w/ fellow Chinese startup StepFun

- Regulators have also reportedly decided on similar restrictions for ByteDance, as they don’t want the Co to approve secondary share sales to US investors without govt approval

- The move stems from the $2bn acq of Manus by Meta earlier this year, which triggered a Beijing probe into illegal foreign investment and tech exports after its December announcement (link)

- The deal was first seen as a model for startups with global aspirations, but critics now argue it gave valuable AI technology to a geopolitical rival

- What has been conveyed? Agencies including the National Development and Reform Commission have told several private firms in recent weeks they should reject capital of US origin in funding rounds unless explicitly approved, according to people familiar with the matter

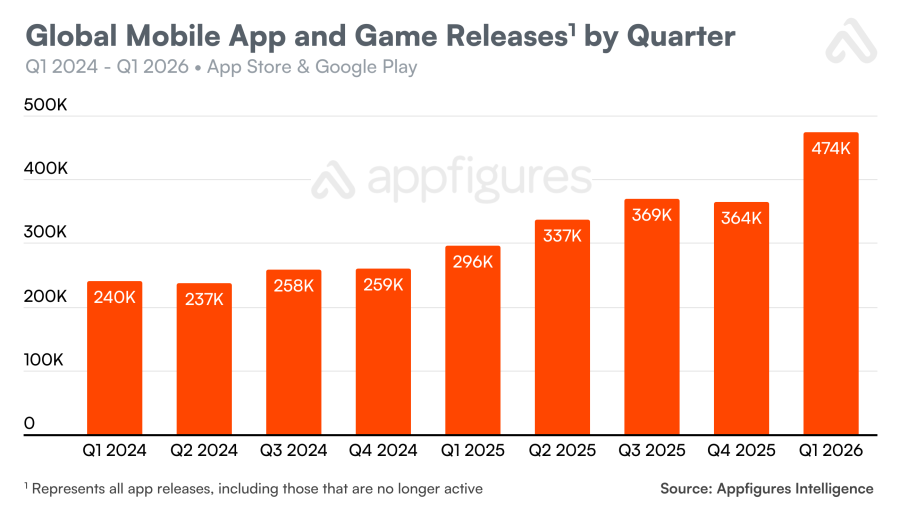

AI Coding Is Democratizing App Creation…But Will Quality Control Become A Bigger Issue?

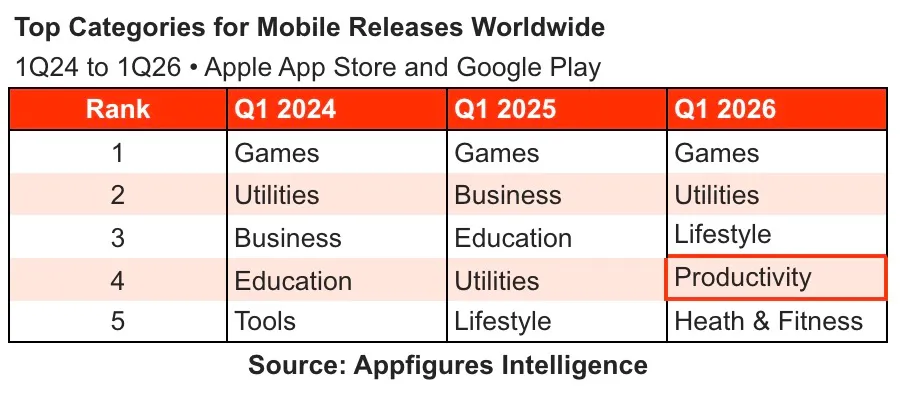

With AI coding capabilities reaching new highs, it is making it easier and less expensive for people to create their own apps, and we saw this play out in data from Appfigures this week, which shows that worldwide app releases surged in Q1 2026 (after a step up in 2025), with growth significantly outpacing prior quarters. This spike was especially pronounced on Apple’s App Store, while Google Play also contributed to the broader upward trend.

As part of this, the composition of new apps is also evolving. While mobile games continue to dominate overall release volumes, categories like productivity, utilities, and lifestyle are climbing the ranks.

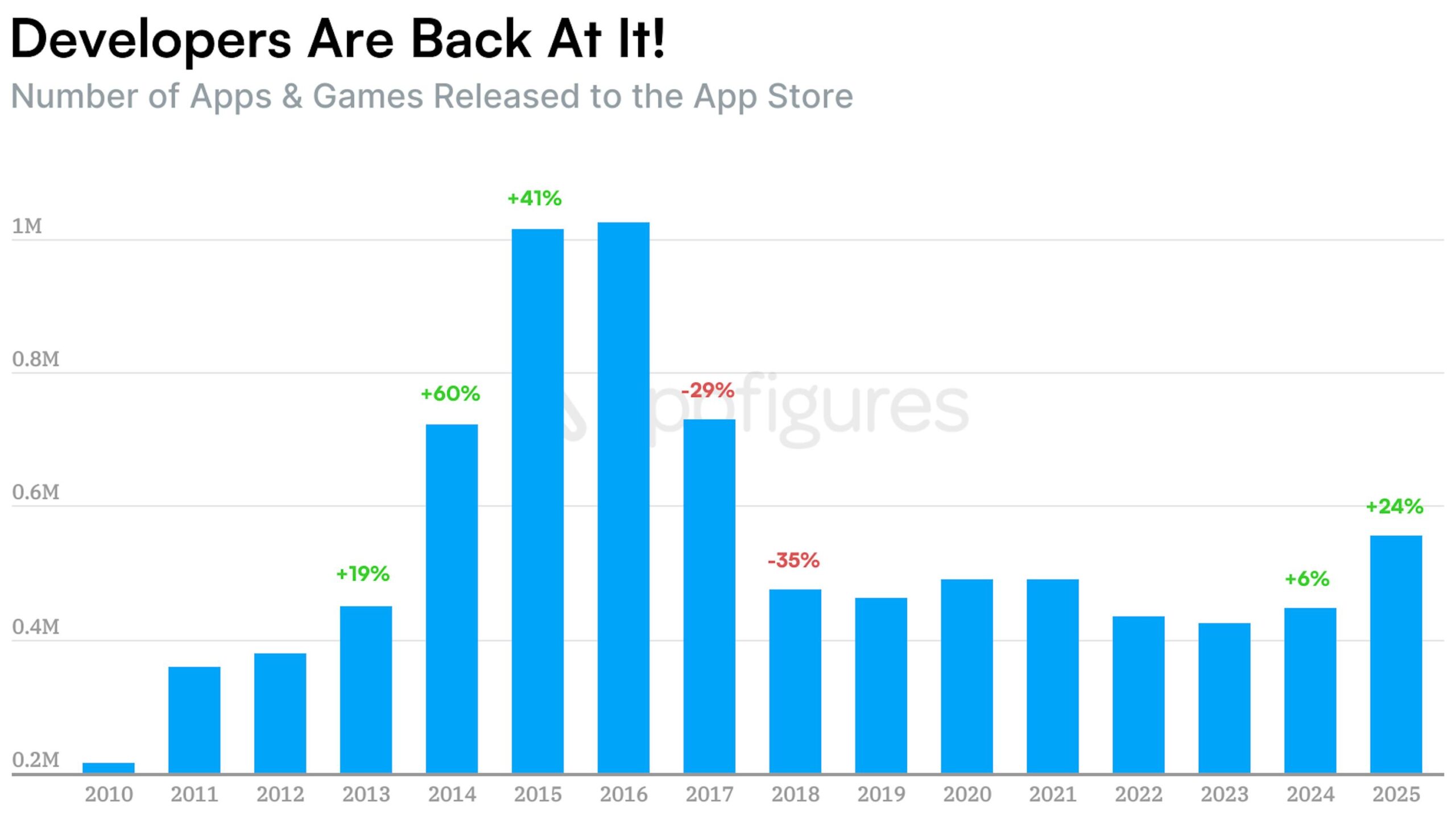

But this explosion of new apps could also create more challenges with quality control. On April 13th, Apple removed Freecash from the App Store following concerns around data practices and misleading incentives, with similar enforcement on April 15th on Google’s Play Store. As app creation becomes more accessible, platforms may face increasing pressure to implement tighter oversight. Based on data from February this year, despite the surge in new app releases in 2025, the total number of apps on the App Store actually slightly declined from 2.475mn to 2.42mn, indicating that a high number of apps were removed or “cleaned up” (link).

See more details below on the data we found most important on this theme…

- Worldwide app releases in Q1 were up +60% y/y (accelerating from +41% y/y in Q4:25 & +43% y/y in Q3:25) across both the App and Google Play Stores, per Appfigures (link)

- In Q1, app releases on the App Store were up +80% y/y alone

- In the month of April so far…the total # of app releases is up +104% across both stores’ y/y, and up +89% y/y on iOS

Source: TechCrunch

-> Looking back to 2025, Appfigures data showed that the number of apps released to the App Store that yr rose +24% y/y which was a strong step up vs the growth rate over the prior 7 yrs (but a far cry from peak levels in 2016)…see chart below (link)

Source: Appfigures

- In Q1, there was also a shift in the categories of new apps…Mobile games still account for most of the new app releases worldwide, as they have in prior years

- BUT… “productivity” apps have moved into the top 5 this year

- The “utilities” category has also moved up to #2 from #4

- “Lifestyle” apps are now #3, up from #5

- BUT… “productivity” apps have moved into the top 5 this year

Source: TechCrunch

-> To note from last week, Freecash, a data-harvesting app marketed heavily on TikTok, surged to the top of the App store charts (peaking at #2 in the US) after downloads jumped from ~876K in Oct 2025 to 5.5mn in Jan 2026 and nearly ~6mn in Feb 2026; Despite claims of paying users for simple activities, it primarily incentivized game installs while collecting highly sensitive personal data, according to Malwarebytes; The app also allegedly used deceptive marketing and may have bypassed prior bans by reappearing under a different developer account; Following scrutiny, Apple removed it on Apr 13th from the App Store, and Google later pulled it from Google Play on Apr 15th (link)

Humanoid Robots Win The Gold, Silver & Bronze Metals!

What also caught our attention this week was that a humanoid robot took the world record for a half marathon that was held in Beijing this past weekend, which is a major milestone and reflects strong advances over the last year in terms of structural reliability and cooling of the technology. See below for key needs to knows from this development: (link/link)…YT Video Clip

- The winning robot was a “Lightening” model developed by Chinese smartphone brand called Honor and ran the race autonomously

- Despite crashing into a railing near the end of the race and having to be picked up, Lightening finished the half-marathon in 50 min and 26 secs, which is faster than the half-marathon world record set by Jacob Kiplimo from Uganda last month (57 min and 20 secs)

- In last year’s Beijing half-marathon race, the fastest robot finished in 2 hours and 40 min, so this was a big leap forward

- The 2nd and 3rd place winners were also Honor robots

- There were over 100 robots that competed in this race (60% were remote controlled during the run vs autonomous)

- Last year, only 6 of the 21 robots completed and passed the finish line

-> Separately but related, this update also follows a crazy viral video last week of humanoid robots’ martial arts performance (Quick Clip)

Overall, China remains at the forefront of the robotics industry and as per the impressive Stanford University’s 2026 AI Index Report that we delved into in last week’s edition, in 2024, China accounted for 54% of industrial robots installed globally, up from 51.1% in 2023. But adoption has been measured. Global y/y growth of industrial robots was flat, and several major markets, including the United States, Germany, and Italy saw declines. Taiwan was an exception, recording the highest y/y growth at 33%. Also, capabilities across use cases are still limited in certain areas. While robots excel in controlled environments, they succeeded in only 12% of household tasks based on Stanford’s data. So overall, we continue to see a strong future for robotics, and major advances technologically are underway, but the industry is still at the infancy of the growth curve, and China is at the forefront (for reference, Stanford’s full report can be accessed HERE).

-> Separately but related to humanoids, Tesla’s first large-scale Optimus factory will begin shortly in Q2 (see image below). Tesla’s existing Fremont facility will replace the Model S and Model X production in Q2:26 and instead be producing 1mn Optimus robots. They are also preparing a Gigafactory Texas for the second-generation line of the robots, which is being designed for long-term annual production capacity of 10mn robots (link)

Source: Tesla Earnings Slides

Grab Bag: DT/TMUS Combo? / Tesla Paid Robotaxi Miles Nearly 2x / MSFT’s Game Pass Gets Cheaper

- Deutsche Telekom AG is reportedly discussing a potential combination with T-Mobile US (link)

- Background: DT already holds a ~53% stake in TMUS

- A holding Co would reportedly be created that would make a stock bid for both Cos shares, per sources

- The new Co would have a single corporate layer that would control DT and TMUS’s operations and be jointly owned by current investors

- The combined entity may seek a listing on a US and a major European exchange, though the details are still being worked out

- The transaction would be complex and faces significant obstacles, including the need for political support in Berlin and Washington

- The German govt and state-owned lender KfW own a combined stake of ~28% in DT, making them the top two shareholders and giving them major sway in any deal

- US Congressman Jim Jordan, chairman of the House Judiciary Committee, said that the US govt would look at the details of any deal: “A foreign company taking over T-Mobile will get our staff’s attention”

- Citigroup analysts said they don’t immediately see obvious benefits for TMUS shareholders

- It raises the question as to whether DT would be willing to pay a significant premium to consolidate ownership

- “Especially since DT could argue its non-US operations are already undervalued within the DT share price,” the analysts wrote

- Background: DT already holds a ~53% stake in TMUS

-> In reaction to the news, T-Mobile fell -1.5% and Deutsche Telekom shares fell -4.9% in Frankfurt

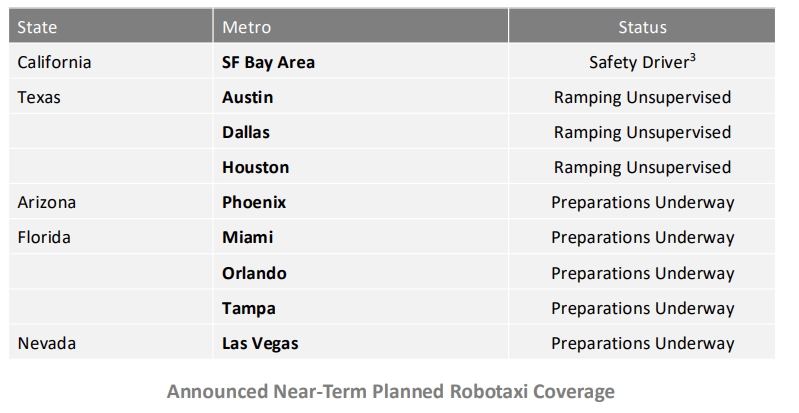

- Key callouts from Tesla’s Q1 earnings about AVs (link)

- In Q1, paid robotaxi miles nearly doubled sequentially

- Once in production, they expect that Cybercab will begin to replace the existing Model Y fleet

- It will be the largest volume vehicle in the fleet “over time”

- The Co began moving its fully self-driving (FSD) cars (but supervised) to subscription-only

- Adoption & penetration both cont’d to grow, with record net new subscriptions in Q1

- A “major focus” is increasing awareness of the safety and convenience provided by FSD as “we evolve our sales strategy to position FSD” as the product

- The Co received approval to deploy FSD in the Netherlands in April, which clears the path for potential approval in other EU countries

- Continue to make progress on approval in China

- Version 14.3, which was launched in April, “was a major architectural update”, and they have a whole pipeline of major improvements

- There’s a version 15 coming “hopefully by the end of this year, but certainly by early next year”

- It will be a complete “overhaul of the software architecture”

- The Co is working on “automating digital workloads, building an intelligence layer that will complement the real-world AI we have built to operate vehicles and humanoid robots”

- Hardware 3 does not have the capability to achieve unsupervised FSD

- Relative to Hardware 4, it has only one eighth the memory bandwidth

- Memory bandwidth is one of the key elements needed for unsupervised FSD

- The version of Robotaxi “running in Austin, Dallas, Houston, etc.” are essentially 14.3 variants

- Will continue to expand based on the V 14.3 base “for a while”, until V 15 lands and “V 15 is going to be a major upgrade”

- In Q1, paid robotaxi miles nearly doubled sequentially

Source: Tesla Earnings Slides

- Microsoft lowers Game Pass prices and drops Call of Duty from “day-one offerings” (link/link/link)

- The Co’s subscription gaming svs is getting a price drop, just 6 months after getting its biggest price increase

- The head of Xbox, Asha Sharma said on X that the “Game Pass had become too expensive”

- Game Pass Ultimate: Originally $19.99 à was raised to $29.99 in Oct. 2025 à then was lowered to $22.99 this week

- PC Game Pass: Originally $11.99 à was raised to $16.49 in Oct. 2025 à then was lowered to $13.99 this week

- The new prices start the next billing cycle

- Also … titles in the “Call of Duty” franchise will no longer be part of the two subscriptions immediately when they come out

- Instead, gamers can purchase CoD at launch or choose to wait until the following holiday season, playing older versions in the meantime

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- SiriusXM annc’d a deal w/ Alphabet’s YouTube to sell YouTube audio ads exclusively in the US. The move supports YouTube’s push to monetize its growing podcast and music listening base beyond video ads. Advertisers can buy podcast, music and talk audio inventory via SiriusXM Media, alongside SiriusXM, Pandora and other streaming svs. (Reuters)

- Midterm spending for the 2026 cycle is on track to top $10bn, per Kinetiq cos The $10 Billion Midterm, sitting 8% below the 2024 presidential cycle ($11. 2bn) and 16% above the 2022 midterms ($8.9bn). Broadcast leads ad outlays w/ 46.2% of spend, while streaming captures ~25%. (Cynopsis)

Artificial Intelligence/Machine Learning

- SpaceX annc’d a deal granting it the right to buy AI coding startup Cursor later this yr for $60bn, or pay $10bn for joint work. Cursor, built by Anysphere, has raised $3bn+. The partnership combines Cursor’s coding tech w/ SpaceX’s AI compute as Elon Musk pushes the Co toward becoming an AI-focused biz ahead of a planned IPO. (Yahoo Finance)

- Robinhood Ventures Fund I (RVI) annc’d a ~$75mn investment in OpenAI, buying common stock on Apr. The move marks one of RVI’s largest bets and supports its mission to broaden retail access to private mkts. RVI, a NYSE-listed closed-end fund launched in Mar., offers exposure to late-stage private cos w/ no accreditation, minimums, or performance fees. (Robinhood)

- Wall Street law firm Sullivan & Cromwell said an AI-assisted court filing in the Prince Group case contained errors from hallucinations. Inaccurate citations misquoted US bankruptcy code and cases. The Co apologised to a New York judge, said AI policies weren’t followed, filed corrections, and said lawyers must ensure accuracy. (The Guardian)

- Anthropic plans to provide European banks access to its Mythos AI model soon, after initial rollout to U. banks, according to sources. The move comes amid regulator warnings that the tech poses cybersecurity risks to banks’ legacy systems. Rollout checks may mean access in days or weeks. (Reuters)

- OpenAI annc’d a Codex for Mac feature called Chronicle that expands memory by using recent on-screen context. The tool helps Codex understand references like “this” or “that,” learning workflows over time. (9to5Mac)

- GitHub annc’d changes to Copilot plans for individuals to ensure service reliability. New signups for Pro, Pro+, and Student are paused, while Free stays open and upgrades cont’d. Usage limits are tighter, w/ Pro+ offering >5× Pro, plus warnings and tracking coming. Opus models are removed from Pro, w/ Opus 4.7 staying on Pro+ and earlier versions being retired. (GitHub)

- The National Security Agency is using Anthropic’s latest AI model, Mythos Preview, despite the Defense Department having blacklisted the Co as a supply‑chain risk, according to two sources. The move highlights tensions w/in the Pentagon, which oversees NSA, as cybersecurity demands appear to outweigh internal disputes over the AI biz and vendor trust, Axios reported. (Axios)

Audio/Music/Podcast

- Texas AG Ken Paxton annc’d an investigation into major music streaming platforms, incl. Spotify, Apple Music, Pandora, Amazon Music and YouTube Music, over alleged payola. The probe examines whether undisclosed payments were accepted to boost playlists or recommendations, distorting competition and misleading users. (Texas Attorney General’s Office)

- TV Tech reports video podcasting is surging as podcasts hit record reach. Edison Research says 58% of Americans 12+ listened in Feb. 2026 (~167mn people), the highest yet. While listening leads, video adoption is rising: 80% of adults both watch and listen. (TV Technology)

- TheWrap reports that iHeartMedia is in talks to merge with SiriusXM in a deal being facilitated by Irving Azoff, though discussions are ongoing and there is no guarantee an agreement will be reached. If it happens, it would combine the largest U.S. radio broadcaster with SiriusXM’s satellite and streaming business, creating a much bigger audio and podcast platform. (The Wrap)

Broadcast/Cable Networks

- Nexstar CEO Perry Sook blasted DirecTV for opposing the $6. 2bn Tegna merger after a federal judge blocked it. He argued claims that Nexstar would be a broadcast behemoth ignore competition from far larger tech cos and accused DirecTV, linked to 83% of recent retrans blackouts, of political tactics. Sook warned local TV faces consolidation, w/ two or three cos likely surviving. (Deadline Hollywood)

Cable/Pay-TV/Wireless

- T-Mobile US annc’d its Board approved a $3. 6bn increase to the 2026 shareholder return program, taking total authorization to $18.2bn through Dec. 31, 2026. The program includes share repurchases and cash dividends, such as $1.02 per share paid Mar. 12 and another scheduled Jun. 11. (Investing.com)

- Major wireless cos AT&T, Verizon and T‑Mobile may avoid paying FCC fines over yrs of selling sensitive user location data. Proposed $196mn penalties face court delays as carriers argue fines require jury trials, aided by recent rulings weakening regulatory authority. Even if upheld, FCC plans to make fines nonbinding until court action, likely letting cos off the hook. (Techdirt)

- Telia Co said Q1 was a strong start to 2026, reporting 2. 1% growth in svs rev on a like-for-like basis, driven by solid trends in Sweden and Lithuania. Adj EBITDA rose 4.0% like-for-like as rev expanded across most mkts and operating costs declined. CEO Patrik Hofbauer said headcount fell 5% in the quarter, cutting opex by 2%. (Telecompaper)

- Rogers Communications reported Q1 2026 results showing total svs rev of CAD 4. 9bn, up 10%, while adj EBITDA rose 5% to CAD 2.4bn. Total rev reached CAD 5.48bn, driven by wireless at CAD 2.59bn, cable at CAD 1.95bn, and media at CAD 988mn. Free cash flow increased 32% to CAD 0.2bn during the quarter. (Telecompaper)

- Orange raised its outlook for annual EBITDA after leases growth to above 3%, up from ~3%, aided by a one-time fibre financing boost in France in Q1. In the first three months of the yr, EBITDA after leases climbed 4.9% to €2.601bn, while rev increased 1.9% to €10.095bn, reflecting steady operating performance. (Telecompaper)

- America Movil reported a strong start to 2026, adding 3mn+ postpaid customers and ~600,000 fixed broadband subs. Rev rose 2.1% YoY to MXN 237bn, while EBITDA climbed 3.8% to MXN 95bn. Excluding forex, rev jumped 6.1%, w/ svs rev up 4.6% and equipment rev up 11.3%. (Telecompaper)

- Tele2 reported 3% YoY growth in turnover in Q1 2026, citing success in offering the right product at the right time. Underlying EBITDAaL increased 11%, driven by strict cost control and higher end-user svs rev growth. Net profit from total operations was boosted by a SEK 5.1bn capital gain from the transaction to create the Baltic tower Co. (Telecompaper)

- Omdia said global telecom connectivity rev rose 4% YoY to $1. 3tn in 2025, w/ Q4 mkts reaching $333bn, up 5%. 5G surpassed 3bn connections, growing 34% YoY, led by Asia at 69%, though 4G remains larger at 8.3bn. Fixed broadband hit 1.6bn, w/ FTTx at ~1.169bn. India topped 5G FWA. (Omdia)

Capital Market Updates

- Oracle’s ~$300bn AI data-center megadeal w/ OpenAI is straining Wall Street lending as banks hit exposure limits, clogging balance sheets and slowing new projects. JPMorgan and peers struggled to syndicate billions in construction loans in TX and WI, prompting some developers to switch tenants. (MSN)

- US IPO activity remains weak as >150 execs surveyed by Bloomberg Intelligence say fear of post-IPO lawsuits and regulatory red tape deter listings. Class actions ranked the top concern, ahead of process complexity and disclosure burdens, contributing to a ~50% drop in US public Cos since 1996. Executives also cited short-term mkts pressure and ample private capital as pushing tech and other biz to stay private. (Yahoo Finance)

- Global M&A value rebounded after an Iran war slump, as cos pushed ahead w/ large deals despite volatility. Weekly deal value fell to ~$39bn in early Mar. but averaged ~$117bn in the four weeks from Mar. 15, led by Pershing Square’s $68bn UMG bid and McCormick’s $45bn Unilever food merger. (Reuters)

- Blackstone-backed Liftoff filed for a US IPO, moving closer to public mkts amid renewed listing optimism. The mobile app marketing Co had earlier delayed plans after software stock volatility tied to genAI concerns. Liftoff, formed via a 2021 merger w/ Vungle, posted a $23.1mn loss on $685.7mn rev for 2025 and plans to list on Nasdaq as LFTO. (Reuters)

Cloud/DataCenters/IT Infrastructure