Markets RALLIED in this heavy earnings week. Nasdaq was up +4.5% while the S&P 500 rose +2.3%, which is the 6th-straight weekly gain and both indices ended at fresh record highs. Software was a leading sector (IGV +5.2%) and was also higher for a 4th-straight week. Optimism regarding a diplomatic solution with Iran was a key driver, in addition to earnings continuing to broadly come in stronger than expected. Per Factset, 89% of S&P 500 companies have reported and the blended earnings growth rate of +27.7% is the fastest pace since Q4:21 and well ahead of the 13.1% expected at the end of the quarter.

This is another heavy earnings-oriented edition, so we had to pick our spots!

- Earning Scorecard - Week 4

- It Was A Strong Opening Act At Disney, Though Little Changed In The Script

- No Chg To PSKY’s 2026 Outlook & The Co Is Progressing Structural Changes Ahead Of The WBD Deal Close

- WBD Makes Some Progress Ahead Of The PSKY Deal Close

- WMG’s Execution Is Matching The Long-Term Growth Algorithm

- Live Nation & TKO Keep Hitting Play As Live Entertainment Dismisses The Macro Backdrop

- DKNG Is Going All-In On Predictions In H2

- Shopify’s Higher Investment Adds More Fuel To The AI Worries Fire

- Pinterest and Snap Navigate a Shared Playbook, But With Diverging Outlooks

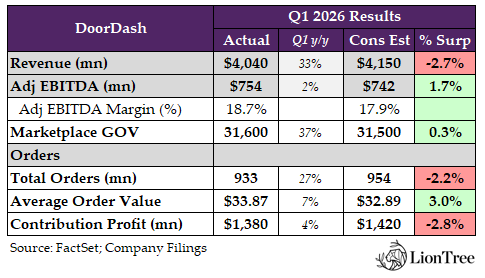

- Uber, DoorDash & Instacart’s Results All Point To Resilient Last Mile Demand, But Forward Signals Show Different Paths

Lastly, LionTree Advisors is proud to have served as financial advisor to Siris Capital Group on the $4.2bn sale of Equinti, a leading global transfer agent, to Bullish.

Enjoy the weekend, especially all my fellow mothers! I hope that you will all be pampered! 😊

Have a nice weekend.

Best,

Leslie

Earning Scorecard - Week 4

A whopping 74 stocks in our LionTree Universe reported in this Week 4 of earnings! Stock reactions were slightly biased to the positive side, with 37 (51%) stocks trading up and 35 (49%) stocks trading down. The best performer in reaction to earnings was Rackspace, which was up +55.1%, while the worst performer was Criteo, which fell -21.2%.

It was a pivotal week for Media Entertainment with Disney, Paramount, and Warner Bros. Discovery all reporting (see Themes #2, #3, and #4, respectively) and the former led with a +7.5% positive reaction to results. Warner Music Group rallied +7.2% in reaction (see Theme #5), and Live Nation and TKO were also in focus, with Live Nation up +6.7% and TKO down -1.6% in reaction (see Theme #6).

Sports betting was represented by DraftKings, which was up a modest +1.6% in reaction to earnings (see Theme #7). In Commerce and Consumer Internet, Shopify fell -15.6% (see Theme #8), while Pinterest and Snap were up +6.9% and down -2.1%, respectively (see Theme #9) post their earnings reports. Rideshare / last-mile was also in focus, with Uber up +8.5%, DoorDash up +2.0%, and Instacart down -8.2% in reaction to earnings (see Theme #10).

Other notable prints that we wanted to highlight, but were not able to do our usual deep dives for include:

- AppLovin – traded up +6.4%: The Co delivered a strong Q1, with results ahead of cons across the board

- Q1 revs beat by +4.0%, adj EBITDA beat by +4.7%, and adj EPS beat by +3.5%

- The Q2 outlook was also above cons, with rev and adj EBITDA guidance ahead by +2.1% and +2.5%, respectively.

- The Trade Desk – traded down -2.8%: Q1 results were mixed, and the weaker-than-expected Q2 guidance spooked investors

- Q1 rev and adj EBITDA beat by +1.5% and +4.5%, respectively, but adj EPS missed by -11.1%

- The bigger issue was guidance as Q2 revs was -2.7% below cons and adj EBITDA guidance was -10.9% below cons

- Airbnb – traded up +0.7%: Q1 was solid and the Co raised its FY rev/adj EBITDA outlook

- Q1 rev beat cons by +2.3%, while adj EBITDA was ahead by +7.1%; Q2 rev guidance at the midpoint was +3.2% above cons

- In terms of key KPIs, Q2 GBV is expected to grow low DDs y/y, driven by growth in Nights and Seats Booked and a moderate ADR increase, though Nights & Seats Booked growth is expected to slightly decelerate from Q1 due to an est’d ~100bps headwind from the Middle East conflict and a significantly lower FX tailwind

- For FY26, Airbnb raised rev growth guidance to low-to-mid teens y/y vs prior guidance of at least double-digit growth and cons of +12.0%

- The Co also expects adj EBITDA margin of at least 35%, up from prior guidance for margins to remain stable with 2025

- Expedia – traded down -8.9%: Q1 was in-line to better but Q2 guidance underwhelmed

- Q1 bookings beat by a modest +1.5% but rev beat cons by +2.4%, adj EBITDA beat by a strong +19.8%, and adj EPS beat by +30%

- In terms of the Q2 guidance…

- The mid pt of the rev guidance was only +0.7% above cons

- The mid pt of the bookings guidance was -0.4% below cons

- The expected adj EBITDA margin expansion of 0.5-1% was below cons 0.8%

- 2026 guidance was reaffirmed

- The Co annc’d a new $5bn repurchase authorization

- CoreWeave – traded down -11.5%: in-line to better Q1 but Q2 guidance disappointed

- Q1 rev beat cons by +5.6%, while adj EBITDA was in line and the adj EPS loss of ($1.40) narrowed by $0.09

- Q2 guidance disappointed

- Mid pt of revenue guidance was -6.5% below cons

- Mid pt of adj. op income guidance was -61.2% below cons

- Mid pt of capex guidance was +3.9% above cons

- 2026 guidance was re-affirmed for revenue and op income while capex guidance was raised to $31-$35bn from the prior $30-$35bn

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

It Was A Strong Opening Act At Disney, Though Little Changed In The Script

It was smooth sailing in Josh Amaro’s inaugural quarter since taking the helm as CEO of Disney. The Co solidly beat Street expectations and raised some of its FY26 guidance metrics. The playbook has not changed though…it is all about executing on the existing strategy that has been put in place. Investing in great content, as well as product & technology, plus advancing ESPN DTC all remain in the forefront of the plan, and are expected to drive accelerating growth for the Co in H2.

Five other important things that we learned from Disney’s results/call are: 1) FQ2 Streaming OI margins hit 10.6% (up +88% y/y), effectively reaching double-digits ahead of the FY26 guidance target (which was reiterated); 2) The Experiences business is not seeing any negative consumer behavior due to higher energy prices (at least yet) and mgmt expects domestic attendance in FQ3 to be BETTER than FQ2’s -1% y/y decline; 3) While the Co raised the FY2

Sports OI growth outlook (low DD to mid DD) , it was all due to the addition of the NFL Network (no underlying change); 4) Disney+ will evolve into a super-app, connecting streaming, sports, parks, and gaming; and 5) The Co raised the FY26 buyback target to $8bn from $7bn.

So all in all, this quarter was more about “steady as she goes”, and looking forward, it will all be about continuing to execute on the Co’s core priorities.

Below are more details on these most important points, in addition to some others…

-> Disney share rallied +7.5% on the back of results but is still down -5% YTD

Solid FQ2 Results…With the Only Drags Being Entertainment OI and Lower Than Expected FCF

- Total FQ2 rev BEAT cons by +1.3%: Up +7% y/y

- Upside was driven by strength in Entertainment and Experiences (Sports in-line)

- Operating income BEAT cons by +4.5%: Grew +4% y/y

- Upside in Experiences was the main driver, followed by Sports

- Entertainment OI missed cons by -1.6%

- Adj EPS BEAT cons by +5.4%: Up +8% y/y

- FCF MISSED cons by -5.9%: Reflecting elevated capex and content investment

FY26 Guidance Still Reflects DD Adj EPS Growth & FQ3 Op Income Growth Guide Implies A H2 Acceleration

- FY26 adj EPS guide is +12% y/y excl. the 53rd week / +16% y/y incl. 53rd week

- Previously guided for “DD growth”

- Raised the FY26 buyback target to at “least $8bn” from $7bn

- FQ3 op income guide of ~$5.3bn implies continued H2 acceleration, BUT mgmt flagged “macroeconomic uncertainty” for consumers

- FY27: Continue to expect DD growth in adj EPS, ex the impact of the 53rd week (FQ4:27 will lap the impact of the 53rd week in FQ4:26

The Macro Dynamics Are Not Impacting Disney’s Experiences Business, Incl At International

- The Experiences segment outperformed expectations in FQ2…revs BEAT by +1.1% and OI BEAT by +3.1%

- Segment rev grew +7% y/y and OI grew +5% y/y, both fiscal Q2 records

- Upside was from the Core parks revenue…and it was broad-based with admissions, F&B, and merchandise

- World of Frozen / Disney Adventure pre-opening costs weighed on OI growth by ~2 pts (non-recurring)

- Segment rev grew +7% y/y and OI grew +5% y/y, both fiscal Q2 records

- The Co has “NOT seen any change in consumer behavior from elevated gas prices thus far and aren’t currently seeing a material impact on the remainder of the fiscal year”

- Domestic parks per capita spending grew +5% y/y

- Based on forward bookings, Disney World bookings are pacing “up strongly”, and even with the 40% increase in cruise capacity, booked occupancy remains in line y/y

- “However, we’re mindful of the macro uncertainty consumers are facing and we’re not immune to the impacts, including how a significant further rise in fuel prices from current levels could eventually lead to changes in consumer behavior if that possibility were to occur”

- Global guests grew +2% y/y in FQ2 and have a bullish outlook looking ahead

- AND expect growth to improve in the back half and “forward bookings are very encouraging as we look to the rest of the year”

- The segment beat even though domestic park attendance declined -1% y/y due in part to cont’d softness in intl visitation (it would have been up y/y excluding that)

- Looking ahead, mgmt expects FQ3 domestic park attendance to improve vs FQ2 given the healthy current domestic demand, but mgmt. also notes that consumer macro uncertainty remains a risk

- The Co is beginning to lap the attendance headwinds in the domestic parks from the opening of Epic Universe and expects international visitation to stabilize

- Current demand at domestic parks and resorts is healthy but mgmt is “mindful of the macroeconomic uncertainty consumers are facing today”

- Disney is bullish about its new experiences coming online

- The Disney Adventure was launched in March (expands penetration in Asia and bookings have been “very strong”)

- The Co opened the World of Frozen at Disneyland Paris, and guest response has been “positive”

- Plans re Experiences capx?

- In 26: Have the new ship and the ramp of major new expansions at Walt Disney World in Orlando, Disneyland in Anaheim, and Shanghai Disney Resort

- Over the next decade: The majority of capx is earmarked for investments to expand capacity

SVOD Growth Accelerated Y/Y In FQ2 & The Segment Is On Track For “At Least 10%” SVOD Margins In FY26

- FQ2 SVOD rev grew +13% y/y, accelerating from +11% in FQ1, driven by improved monetization from rate adjustments, volume growth, intl wholesale agreements and FX

- Saw double-digit advertising revenue growth y/y

- FQ2 SVOD OI margin surpassed the FY26 target, but the FY26 guidance was still reiterated – i.e., do costs ramp in H2 or is this conservative?

- FQ2 SVOD OI grew +88% y/y, reaching a 10.6% margin (1st DD SVOD margin qtr)

- But mgmt. reiterated “at least 10%” SVOD margin in FY26

- The main focus areas for future SVOD growth

- Focused on driving Disney+ outside the US and are seeing early success with local originals (Battle of Fates in Korea and Rivals in the U.K.)

- Highly focused on churn (the integrated Disney+ and Hulu experience is benefiting retention)

- “Reducing churn on Disney+ might be the single most significant opportunity that we have”

- Product improvements that reduce user friction, allow more intuitive discovery, and help users decide what to watch and to decide sooner

- Their Video and Browse initiative launched in the US in January

- It lets subscribers preview content directly while still browsing, so they don’t have to click in and out of titles

- Launched Verts on Disney+ in March… short-form / vertical video and interactive features are being intro’d to meet evolving consumer behavior and increase platform stickiness

- The Co is looking to build Disney+ beyond a premium SVOD services (see section below)

- In the meantime, the Co revamped the user interface and is improving personalization

- What is mgmt’s view regarding content licensing to 3P’s? No change to the strategy

- We’ve always distinguished between franchise IP and general entertainment. So franchise and branded IP stays on the platform and general entertainment. That library content can find audiences elsewhere. And that’s it’s been working pretty well for us financially”

Disney+ Is Evolving Into A “Digital Centerpiece”…Driving A More Connected, Superapp-Like Ecosystem Across Streaming, Sports, Games & Experiences

- Disney+ is seen as the “primary relationship between Disney and its fans…where everything comes together—entertainment, sports, experiences”

- This reflects a strategic shift from a standalone streaming service to a central hub connecting the broader Disney ecosystem

- Disney has “passionate fans”…a lot of park customer are Disney+ subs and there are millions of Disney+ subs that don’t go to parks…“we’re building Disney+ to serve as the immersive, interactive digital centerpiece of the company”

- Mgmt emphasized the shift from “a subscriber” to “a relationship with the company…that spans years and generates value across every part of our business”

- Early product and UX investments are foundational to enabling this broader platform strategy

- Focused on improving the consumer experience, reducing friction and increasing engagement through personalization and discovery tools

- Product enhancements (UI improvements, preview features, personalization) are explicitly tied to increasing engagement and reducing churn

- Focus on “hyper-personalized” content feeds, AI-driven recommendations and customized experiences across Disney+ and ESPN

- The goal is to create a single, unified touchpoint that drives engagement, retention and ultimately lifetime value

- Bundling & integration across owned services is a key step toward the super-app model

- The Disney+ and Hulu integration is driving “higher engagement” and “lower churn than…the services on their own”

- ESPN DTC is being integrated into the broader offering, with sports positioned as a key engagement and acquisition driver within the ecosystem

- The Co’s strategy emphasizes internal bundling first, with selective 3P partnerships only where they enhance the Disney+ experience

- How does Epic Games tie into Disney’s eco-system? “Disney+ is the hub, but the hub needs spokes. Epic gives us an interactive gaming native environment to reach audiences that we don’t currently own. And by the way, particularly younger audiences”

The Higher Sports FY26 OI Growth Guidance Reflects The Addition Of The NFL Network, Not An Underlying Change

- The Sports segment also out-performed, especially on operating income…revs BEAT cons by +0.2% and OI BEAT by +9.6%

- Sports rev grew +2% y/y, while OI declined -5% y/y (higher programming costs)

- ESPN advertising rev decl’d -2% y/y due to fewer impressions, fewer NBA games and lapping 4 Nations hockey

- ESPN subscription / affiliate rev grew +6% y/y, supported by DTC growth and NFL transaction contribution (+3 pts)

- Sports rev grew +2% y/y, while OI declined -5% y/y (higher programming costs)

- High priority is shifting ESPN to DTC… “it’s just the beginning”: The strategy includes cont’d product innovation, a focus on adding content partners, and distributing product through both direct and wholesale channels

- “This strategy is already yielding results as revenue generated by our digital subscribers in Q2 more than offset secular declines in the linear subscriber universe”

- The F3Q Sports OI decline guidance of -14% y/y (worse than cons -8% y/y) is due to DD programming expense growth and timing of new rights agreements

- But for FY26, Disney now expects MSD growth in OI , up from prior LSD, given the inclusion of the NFL transaction

- BUT the NFL deal is ~3c dilutive to FY26 adj EPS due to higher non-controlling interest

- Have been making enhancements to the ESPN app

- Multi-view

- Verts

- Sportscenter for You

- Regarding NFL re-opening media rights deals? Disney has “not started conversations about an early renewal but are always willing to have a conversation with NFL”

- “Expect to be in the business with the league for years to come”

- “Sports rights are expensive and can be dilutive without scale, but we have scale in our most important market, the US and the biggest sports media brand in the world”

Disney Is “Embracing” Emerging Technology BUT Human Creativity Will Remain “At The Center”

- The Co wants “to be a leader with leveraging tech for content creation but at the same time, we’re committed to implementing AI in a way that keeps human creativity at the center of everything that we do, and, of course, respects creators and the tremendous value of our own intellectual property”…the Co will use AI to:

- Make the production process more efficient

- Increase the volume of content that they put out in streaming

- Develop a “hyper personalized recommendation engine” across Disney+ and ESPN

- Enhance ad targeting capabilities

- On the Experience side, there’s a significant opportunity to make it easier for families to plan their trip to optimize all their time with Disney and to personalize their experience

- Also, the Co is implementing precision labor demand forecasting across theme parks

Other Key Updates & Comments Across Film, Linear, & Content

- Changes since Dana Walden took over the unified Entertainment content biz…

- Centralized TV programming w/in Disney Entertainment DT

- They are now programming for Disney Plus and Hulu “while being smart about windowing content to linear so that we can expand reach and maximize monetization”

- Integrated the games biz into Disney Entertainment

- This creates new opportunities to cross-promote franchises and use games to extend storytelling and ultimately develop new IP

- “Dana is making sure that every decision we make in content from development all the way through how we distribute that, it’s optimized for the fan and for the long term strength of our brands”

- Centralized TV programming w/in Disney Entertainment DT

- Short form content has exploded and the Co will continue to experiment

- The Co is making sure IP shows up across social platforms

- They intro’d vertical video on D+ (as mentioned above) and it is already driving deeper engagement and on ESPN

- They “did the same thing on our ESPN app and the early performance of the ESPN verts…has been really promising”

- Mgmt doesn’t sounds interested in separating the linear cable nets and the linear business is getting smaller and smaller…

- The Co monetizes content across multiple distribution platforms and “separating those monetization platforms into discrete businesses is highly complex and, in our view, unlikely to create incremental value for shareholders, especially given where linear networks are valued in today’s marketplace”

- “The linear earnings base is becoming smaller and smaller every quarter within our P and L”

- “Yes, linear revenues are declining, but Disney Entertainment as a segment is growing nicely”

- Excited for the upcoming theatrical releases of The Mandalorian & Grogu, Toy Story 5, and the live-action Moana

No Chg To PSKY’s 2026 Outlook & The Co Is Progressing Structural Changes Ahead Of The WBD Deal Close

While PSKY shares popped at first blush given the much better profitability reflected in the Co’s Q1 adj EBITDA results (beat cons by +29.4%) and the better Q2 adj EBITDA guidance (beat by +10%), the stock gave back gains on commentary that timing benefits were at play and H2 spending will ramp, hence no change to the full year 2026 adj EBITDA outlook (and no change to the rest of 2026 guidance for that matter). With that said, we’d note that Wall Street analysts had been taking a more conservative view on 2026 profitability, so they might revisit that at the least.

Aside from that, the 5 most interesting incrementals that we learned from PSKY’s results include: 1) Better streaming profitability was the largest driver to the adj EBITDA beat (reached $251mn versus cons $69mn) but again, some of this was due to timing; 2) Paramount+ benefited from +14% y/y ARPU growth (with no negative impacts to the Jan price increase) and the Co added 2mn underlying subs, which was offset by over 1mn international low-ARPU hard bundle exits; 3) The streaming tech stack convergence remains on track for mid-year launch; 4) Studios materially outperformed as well vs the Street in Q1 (revs and adj EBITDA beat by +44% and +134%, respectively) given licensing and a stronger-than-expected film contribution, but the division faces tough comps in the rest of 2026; and 5) Linear revenues declined at a faster pace than expected (Licensing & Other was the biggest drag vs projections) but mgmt showed better cost discipline.

Bigger picture, mgmt conveyed confidence in closing the WBD deal by the end of Q3 and is structurally preparing where it can. In advance of that, investors are assessing whether PSKY’s DTC subscriber ad growth can meaningfully accelerate growth in H2, whether TV Media declines can stabilize; and whether cost discipline can translate into durable FCF as transformation costs ramp.

See below for more details on the above, as well as other key updates.

-> Theme #4 is a deep-dive into WBD’s results as well

Much Higher Profitability Was A Main Upside Surprise In Q1… While TV Media Revs Were A Bigger Than Expected Drag

- Q1 total revenues BEAT cons by +1.1% (grew +2% y/y) with Studios the biggest upside driver (+43.7% ahead of expectations), followed by Streaming subscriptions (+2.7% ahead of cons)

- On the flipside, much lower Licensing & Other revs ($540mn below cons) was the biggest drag

- The bigger surprise was Q1 adj. EBITDA BEATING cons by +29.4%: It grew +59% y/y but was helped by timing benefits

- Better profitability was posted across all businesses, but DTC was the biggest upside driver followed by Studios

- “Expenses were a bit lighter than we had planned for. This is primarily around a slower pacing of hiring and…some of the shift in timing of content” spend

- Adj EBITDA upside did not flow through to adj. EPS though, which was IN-LINE vs cons

- FCF of $96mn BEAT cons by +133% (but declined -22% y/y)…reflects improving profitability BUT still impacted by transformation costs and content investment

Q2 Guidance Was Mixed & The Full Year 2026 Guidance Was Reiterated As Costs Ramp In H2

- Q2 revenue guidance MISSED cons by -3.1%…reflects ~flat y/y growth driven by:

- Growth in DTC, and Studios to a lesser extent

- But tough comps from Mission Impossible & NCAA + cont’d TV Media pressure

- While Q2 adj EBITDA guidance BEAT cons by +10.2% at the mid-pt…

- …mgmt now expects profitability to skew toward H1 as content cost timing shifts to H2

- The Co anticipate transformation costs of “several hundred million” in Q2, which will impact their reported FCF

- Mgmt reiterated 2026 guidance

- The Co reiterated 2026 adj EBITDA despite beating in Q1 and higher than expect Q2 guidance…this is due to costs shifting to H2 (note that the Street had been taking a more conservative view on adj EBITDA guidance by 5.3%)

- In H2, there will be “some margin hit” in DTC based on when the slate launches in Q3 and Q4

- The revenue guidance implies +4% y/y growth

- Hence a strong revenue growth ramp in H2

- Continue to expect $3bn+ efficiencies through 2027 and $2.5bn+ run-rate efficiencies by YE26

- Continue to expect ~5% FCF conversion before ~$800mn transformation costs

- The Co reiterated 2026 adj EBITDA despite beating in Q1 and higher than expect Q2 guidance…this is due to costs shifting to H2 (note that the Street had been taking a more conservative view on adj EBITDA guidance by 5.3%)

Core DTC Trends Are Strong & DTC Ad Growth Is Expected To Drive A H2 Acceleration

- DTC was the biggest profitability upside driver in Q1

- Rev grew +11% y/y and BEAT cons by +2.0%

- And more materially, adj. EBITDA of $251mn beat cons by $69mn (higher by +264%)

- Q1 Paramount+ revenue growth of +17% y/y (in-line w/ Q4) was driven by higher ARPU + higher quality subscriber adds

- Q1 ARPU rose +14% y/y driven by price increases + mix shift

- Reaction to the price increases across Essential and Premium tiers in the U.S., Canada, Australia and LatAm was “in-line” w/ expectations

- Q1 Subs grew +2% y/y…with reported sub adds of 700k q/q…BUT underneath that, the Co added ~2mn subs and exited a little over 1mn low-ARPU intl hard bundle subs (“less than $1 ARPU”)

- Bundles represented <2% of revenue but inflated subs

- Getting rid of these hard bundles is the right decision economically

- Paramount+ subs in total reached 79.6mn

- Q1 DTC advertising returned to growth and is expected to drive an H2 acceleration

- Mgmt “expects to meaningfully recover DTC ad growth”

- 2026 outlook…mgmt expects continued “healthy underlying subs” growth (especially as the content slate builds throughout the year), and will continue to see improvement in ad monetization

Content Investment & Tech Improvements Are Central To The Co’s Strategy

- Sports remains a core driver of DTC engagement and subs acquisition, and also the Linear segment

- Paramount+ offers ~14k hours of sports content annually

- Q1 included NFL playoffs, UEFA competitions, UFC, and March Madness coverage

- CBS delivered the most-watched final round of the Masters in over a decade

- NCAA March Madness was the second-most watched since 1994

- NFL on CBS had its most-watched year ever (from prior quarter context, still referenced as baseline momentum)

- Paramount+ offers ~14k hours of sports content annually

- UFC has exceeded mgmt expectations “across the board”

- Strong viewership

- Avg UFC viewership across Paramount platforms is 15x the avg PPV event over the past two years

- UFC 326 / 327 main fight cards on CBS avg’d 2.8mn viewers, ~50% higher than ABC’s NBA primetime game that night

- High engagement, including cross platform

- 10mn+ households have watched UFC programming on Paramount+

- 100mn+ hours of UFC content has been consumed across the platform

- UFC is driving cross-content engagement (users staying on platform to watch other shows like South Park)

- Improving demo mix

- New UFC subs are 15 yrs younger than avg Paramount+ viewer

- Better advertising demand

- UFC ad demand exceeded expectations and was a meaningful Q1 ad contributor

- Strong viewership

- The Co is in the midst of its sales re-tooling…& the streaming tech stack convergence remains on track for mid-yr launch

- BET+ content transition onto Paramount+ was completed ahead of the broader service integration

- Consolidated the national sales org into a single client-centric structure under unified leadership

- Launched Paramount Media Labs

- The Co is accelerating Precision+, an AI-powered targeting / optimization product combining 1P and 3P data

- Precision+ is driving performance efficiency gains above benchmarks also using AI driven QA

- New streaming product features are already rolling out, which are designed to deepen engagement

- Mgmt is working on improved personalization,recommendations, discovery and monetization

- Short-form video clips just rolled out on Paramount+ mobile app

- They enhanced the mobile experiences – like live stats for live sports

- The Co is planning gaming, polling and additional interactive features

- Pluto will get its “most significant” product update since inception this summer

- 65% of U.S. Pluto viewing minutes now come from registered users, up nearly +60% y/y

- OD TV hours per user up +60% after recent updates

Studios Is Rebuilding With Some Early Wins But The Real Slate Step Up Comes In 2027+

- Studios significantly BEAT expectations, with EBITDA +134% above cons and strong y/y growth

- Revenue BEAT cons by +43.7% and grew +11% y/y

- Scream 7 surpassed $200mn globally and became the highest-grossing installment in the franchise’s 30-year history

- Also Skydance / TV studio licensing was a key driver

- Adj EBITDA also doubled y/y to $164mn, driven by licensing deals, and BEAT cons by $94mn

- Revenue BEAT cons by +43.7% and grew +11% y/y

- 2026 theatrical rev is expected to decline y/y due to tough Mission Impossible comps but mgmt reiterated its commitment to 15 film releases in 2026 vs 8 in 2025

- Key upcoming releases: Billie Eilish – Hit Me Hard And Soft: The Tour, Passenger, Scary Movie and jackass: best and last

- Mgmt is very focused on ROI analysis for content they are underwriting (has been an investor concern)

- A step-function increase is expected in 2027–2028 from franchise reactivation

- Key franchises: Sonic, A Quiet Place, Call of Duty

TV Media Revs Declined Y/Y More Than Expected Though Cost Discipline Remains Strong

- TV Media was the primary revenue drag in Q1 vs cons and y/y, mostly due to Licensing & Other

- Revenue MISSED cons by -9.7%, declined -6% y/y (vs -5% y/y in Q4)

- Advertising rev decl’d -6% y/y: Including 2ppt impact from intl exits, partially offset by 1ppt political benefit

- Affiliate rev decl’d -6% y/y: Reflecting continued pay TV sub erosion

- Licensing & Other fell -3% y/y and missed cons by a large $540mn

- Revenue MISSED cons by -9.7%, declined -6% y/y (vs -5% y/y in Q4)

- But Q1 profitability in TV Media was materially better than expected

- Q1 TV Media adj EBITDA BEAT cons by +14.0% and grew +21% y/y

- Margin expanded to 29% vs 24% in Q1’25

- Q1 TV Media adj EBITDA BEAT cons by +14.0% and grew +21% y/y

- And mgmt expects stable-to-improving FY26 TV Media margins, while payTV sub erosion continues to weigh on revenue

A Few Other Key Comments

- Mgmt expects total Co ad rev to return to growth in H2, driven by DTC acceleration more than offsetting TV

- Q1 total ad rev decl’d -3% y/y but improved vs Q4

- DTC ads returned to growth in the qtr

- Q1 total ad rev decl’d -3% y/y but improved vs Q4

- Mgmt remains very confident in the WBD deal close by the end of Q3

- AI efficiencies…~ 80% of their engineering organization is using code assisted tech which is driving “meaningful production gains and really cutting approval times by more than in half”

WBD Makes Some Progress Ahead Of The PSKY Deal Close

The clock is ticking for WarnerBrosDiscovery (WBD) to be acquired by Paramount Global (expected during Q3) but in the meantime, the Co continues to move forward with its key initiatives which are basically “scaling HBO Max globally, returning our Studios to industry leadership, and optimizing our Global Linear Networks.”

The quarter itself reflected much better profitability, with in-line revenue (when adjusting for inter-company transactions). Digging deeper, the top 5 most incremental points in our mind from WBD’s results include: 1) Stronger growth in the Studios business was the largest upside driver in the qtr, though we would note that the Co benefited from inter-company licensing due to the Intl HBO launches…with that said, Q2 is a tough Studios comp qtr; 2) Better Streaming profitability was also a standout (Streaming adj EBITDA beat cons by ~29%) and subscriber-related revenue growth accelerated +400bps sequentially, with contributions from pricing (still no negative impact from the price hikes in Dec), the ad-tier mix (50% of gross adds are now ad-supported), and international; 3) While HBO Max’s global launches are largely complete, further penetration and monetization is the next leg of growth; 4) Streaming advertising grew +19% y/y FXN despite the NBA headwind; and 5) The Networks biz outperformed expectations (i.e., less bad), with ad declines improving sequentially and distribution holding in better than feared but revenue s and EBITDA are still declining high single digits, and the NBA absence remains a headwind.

With all that said, the next big catalyst is the close of the PSKY deal, but the core debate about whether streaming can scale fast enough to offset the linear erosion and volatile qtr-to-qtr Studios performance, and if the Co can at the same time improve profitability and de-lever the balance sheet, remains in place.

See below for more details on the above, as well as other key updates.

-> Our deep-dive on PSKY’s results are in Theme #3

Upside In Profitability Was The Main Headline Highlight In Q1

- Q1 revs IN-LINE w/ consensus: Down -1% y/y (-3% y/y FXN)

- Posted ad rev decline of -8% y/y ex-FX, as ad-lite streaming growth was more than offset by the absence of NBA and domestic linear audience declines

- Adj EBITDA BEAT cons by +11.7%: Grew +5% y/y, driven by better profitability trends in Streaming + Studios

- Adj EBITDA margin expanded to 24.7% vs cons 22.2%

- BUT FCF MISSED cons by -269.5% at -$476mn loss vs cons +$807mn …driven by:

- ~$100mn transaction/separation costs

- Higher content investment, higher tax pmts & working capital timing, partially offset by lower interest pmts

- Transaction costs will remain a FCF headwind through 2026

- The biz continues to operate in the historical 33-50% FCF conversion range on an underlying basis but there will be addtl transaction-related cash costs through the closing of the PSKY transaction

- Also, the Co ended Q1 with net leverage of 3.4x

Streaming Momentum Accelerated In Q1…Intl Roll-Outs Are Complete & Focus Now Shifts To Greater Penetration & Monetization

- Upside in Streaming profitability was a stand-out in Q1, on slightly better revenue trends as well

- Revs BEAT cons by ~+1.7%: Grew +9% y/y (+7% y/y FXN), driven by global expansion and subscriber growth

- Adj EBITDA BEAT cons by a large +28.8%: Grew +29% y/y (+17% y/y FXN) reflecting strong operating leverage

- Subscriber-related rev growth accelerated +400bp seq to +8% y/y FXN in Q1, supported by pricing, ad-tier mix, and international expansion

- OUTLOOK – mgmt guided for a “healthy acceleration in subscriber-related revenue growth…picking up pace through Q2 and rest of year”

- Q1 Distribution revenue growth accelerated to +7% y/y FXN (from +2% y/y FXN in Q4) given strong subscriber growth both in existing and new markets, as well as the benefit of the Q4 2025 US price increase

- And continue to see limited churn impact from that Q4 price increase

- Q1 Advertising rev growth also accelerated to +19% y/y FXN (despite the NBA headwind), highlighting strength in the ad-lite tier and monetization scaling

- 50% of global retail gross adds took the ad-supported tier

- The HBO Max global roll-out is largely complete w/ its launches in UK, Germany, Italy and Ireland: To date, the U.K. and Germany launches have gone “particularly well w/ retail subscriber acquisitions trending ahead of internal expectations, while Italy has been in-line”

- But the intl launches are still nascent and mgmt “sees substantial runway for continued penetration growth in existing markets”

- The Co is “on track” to surpass its 150mn global streaming subscriber target by the end of 2026

- In Q1, they exceeded their guidance of more than 140mn global streaming subscribers

- HBO Max has more active shows averaging over 20mn global viewers than ever before…

- Q1 streaming content drivers include:

- The Pitt which averaged more than 20mn viewers an episode in Q1

- A Knight of the Seven Kingdoms which averaged 36mn viewers per episode (among the most popular debut series in HBO history)

- Rooster

- DTF St. Louis

- Like Water for Chocolate (Mexico) and Maxima (Argentina) were 2 intl hits

- In EMEA, this year’s Olympic Winter Games was their most streamed Olympic Winter Games ever

- Content drivers into Q2 and beyond:

- Euphoria Season 3 is off to a “great start”

- House of the Dragon Season 3 (June)

- Stuart Fails to Save the Universe (July)

- Lanterns (Aug)

- Harry Potter and the Philosopher’s Stone (Xmas Day)

- Q1 streaming content drivers include:

- Mgmt is a big believer in the bundle…some of the Co’s highest LTV subs come from bundled subs

- Bundles are “obviously hugely beneficial to churn and ultimately it’s a very healthy and growing part of the business that I think will be an increasingly important part of the entire ecosystem”

- In 2026, mgmt expects another “strong year” for both Streaming revenues and adj EBITDA

- But 2 factors are impacting y/y growth in Q2:

- The absence of the NBA, representing a 16% ex-FX headwind to ad revenues

- The previously disclosed domestic distribution renewal w/ a former related party, which has weighed on distribution revenue growth, will be lapped by the end of this month

- But 2 factors are impacting y/y growth in Q2:

Higher Intercompany Licensing Was A Key Driver For Studios In Q1…Q2 Comps Are Tough But 2026 Adj EBITDA Should Be “Relatively Flat” Y/Y

- Studios significantly outperformed, driven by higher intercompany licensing tied to HBO Max Intl launches

- The Co continues to shift from heavily externally focused content licensing to a more internal utilization model, though it takes a little longer to positively hit the P&L…” it’s going to be a very, very helpful driver for us”

- Revenue BEAT cons by +18.8%: Grew +35% y/y (+31% y/y FXN)

- TV rev rose +58% y/y FXN (higher internal licensing + externally licensing)

- Theatrical rev rose +21% y/y FXN (higher internal licensing)

- Games rev decr’d -30% ex-FX (lower library rev)

- Adj EBITDA BEAT cons by +88.6%: Grew +199% y/y (+156% y/y FXN)

- While Studios faces tough comps in Q2, 2026 adj EBITDA should be “relatively in-line” with 2025

- Q2’s tough comps are due to strong performance of A Minecraft Movie, Sinners, and Final Destination: Bloodlines and also WBTVG renewed an internal content licensing deal for a tentpole library title last year

- There will also be qtr-over-qtr fluctuations of content sales which leads to bumps

- Mgmt thinks they are “well-positioned” to achieve the goal of at least $3bn in annual WB Studios adj EBITDA

- 2026 is seen as an inflection point as streaming should represent “a greater portion of first-run deliveries than broadcast and cable combined for the first time”

- Selling ~80 shows to over 20 streamers

- Notable Q1 deliveries include:

- Memory of a Killer (renewed for a 2nd season)

- Rooster (HBO)

- Shrinking (renewed for a 4th season and is the 2nd most watched Apple TV comedy behind only Ted Lasso)

- The Pitt (HBO Max)

- The Voice (NBC, renewed for its 30th season)

- Notable additional Q1 orders include:

- The next seasons of Abbott Elementary (ABC) and Georgie & Mandy’s First Marriage (CBS)

- A new Netflix series, I Suck at Girls

- WBD is ramping theatrical releases… from 11 in 2025 to 14 in 2026 and up to 18 in 2027…key titles include:

- Dune: Part III

- The Lord of the Rings: The Hunt for Gollum

- DC franchises like Supergirl, Clayface

- The Batman: Part II

- A Superman sequel Man of Tomorrow

- Original stories like The Great Beyond, Panic Carefully, and Digger

- In horror, Evil Dead Burn and The Conjuring: First Communion

- In animation, The Cat in the Hat later this year, followed by Bad Fairies and Margie Claus next year

Linear Network Declines Were Slightly “Less Bad” Than Expected …Ad Trends Improved Seq But Mgmt Is Mindful Of The Macro

- The Networks business topped Street estimates and y/y declines improved sequentially

- Rev BEAT cons by +2.7%: Decl’d -8% y/y (-9% FXN) which is an improvement from -12% y/y (-13% FXN) in Q4

- Distribution fell -8% y/y FXN (ongoing pay-TV subscriber declines)

- Advertising fell -12% y/y FXN (NBA absence + audience declines): NBA absence was a -7% ex-FX ad rev headwind but +16% ex-FX cost benefit

- Content fell -9% y/y FXN (timing-related)

- Adj EBITDA BEAT cons by +1.5%: Decl’d -9% y/y (-10% FXN) which is also an improvement from -21% y/y (-21% FXN) in Q4

- Rev BEAT cons by +2.7%: Decl’d -8% y/y (-9% FXN) which is an improvement from -12% y/y (-13% FXN) in Q4

- Underlying ad revenue trends improved…Q1 reported ad revs were down -12% y/y FXN, a +200bp improvement sequentially but mgmt is also mindful of the macro

- Q1’s improvement was despite an incremental 300 bps headwind from the absence of the NBA relative to Q4

- The overall advertising market remains “healthy with scatter CPMs commanding a strong premium to upfront”

- But “visibility remains limited given broader macro uncertainty”

- “We are actively monitoring the geopolitical and macro environment” and will take any appropriate actions if need be

- Delivery trends are improving…general entertainment networks delivered a 16% seq improvement in y/y delivery trends, finishing the qtr down -8% y/y

- And for Q2, mgmt expects underlying domestic delivery trends to be roughly similar to Q1

- But reminder on Q2 factors:

- Expect the absence of the NBA to result in a 20% ex-FX negative impact to y/y ad revs partially offset by a net 400 bps ex-FX benefit to ad revenue related to the b-cast of the NCAA March Madness Final Four and Championship games, and the absence of the NHL Stanley Cup Final in the current year

- The absence of the NBA is expected to be a benefit to adj EBITDA in H1 as reduced opex will more than offset the reduction in ad revenues

- With the key U.S. distribution renewals in H1:25, secured low SD digit affiliate rate increases (including a flat affiliate rate for TNT, despite the loss of the NBA)

A Few Other Notable Comments/Updates From The Call

- Know “the power of sports” but mgmt wants to prove their ability to streaming sports profitability which is trickier

- The Co will experiment but will be disciplined

- The PSKY deal is still expected to close during Q3

- Thoughts on what happens with the rest of the media sector? “Your guess is as good as ours in terms of what happens to the overall universe”

WMG’s Execution Is Matching The Long-Term Growth Algorithm

WMG shares have been dragged down by AI disruption fears (as has the music sector), but the Co certainly delivered a stronger than expected Q1, easing some of those concerns. WMG’s accelerating revenue growth (total revenue growth re-accelerated to +12% FXN from +7% last quarter and beat consensus by +7.5%) and robust margin expansion (adj OIBDA beat by +10.6%) was a strong combination. Growth in the qtr was underpinned by an increase in recorded music subscription streaming revenue of +15% y/y (on an FXN & adj basis) due to subscriber growth, market share gains, pricing increases (PSM), and also easy comps. AI has also been a key enabler across the company’s priorities driving tangible growth and cost results.

Five of our other top learnings from WMG’s results are: 1) Margin expansion has been ahead of plan (+250bp seq in Q1 to 22.9%) and mgmt raised the FY guidance to the high-end of the +150-200bp expansion target; 2) US streaming share incr’d +1.1pts y/y and mgmt see gains as sustainable, though APAC is still a work in progress; 3) Monetizing and growing Catalog remains a key focus (AI is helping here)…it now represents ~65% of streaming revenue; 4) Ad-supported streaming revenue growth also accelerated (to +11% FXN from +4% last quarter) and is expected to maintain a healthy trajectory; and 5) Similar to other commentary in the music sector, WMG has not seen any dilution from AI music’s increased volume.

Net net, Q1 was the 4th consecutive quarter where the Co posted growth “in line with or above” their sustainable growth model and execution is now matching the long-term algorithm mgmt. has been underwriting. While the AI worries have not disappeared, the qtr likely helps ease some of those concerns.

See below for more details.

-> WMG shares rallied +7.2%…and is up +9.5% YTD (UMG and SPOT are down -11 & -28% respectively YTD)

FQ2 Reflects Another Stronger Than Expected Qtr, With Streaming Growth A Key Contributor

- Total FQ2 revs BEAT cons by +7.5% and adj OIBDA BEAT by a larger +10.6%

- Total revs grew +17% y/y (+12% FXN), accelerating from +10% y/y (+7% FXN) in FQ1

- Adj OIBDA grew +31% y/y (+24% FXN)…this was the second consecutive qtr where margin expansion was ahead of the high end of the full-yr target

- Adj OIBDA margin of 22.9% BEAT cons 22.3% and expanded +250bps y/y (+230bps FXN)

- Big UPSIDE with Recorded Music…led by subscription streaming growth accelerating to +15% y/y FXN on an adj basis

- Revs BEAT cons by +7.0% and grew +17% y/y (+13% FXN)

- Adj OIBDA of $346mn BEAT cons by +8.1% and grew +28% y/y (+22% FXN)

- And Music Publishing was also slightly ahead of the Street

- Revs BEAT cons by +2.3% and grew +14% y/y (+10% FXN)

- Adj OIBDA BEAT cons by +2.1% and grew +14% y/y (+10% FXN)

Margin Expansion Is Ahead Of Plan…Hence, WMG Raised Margin Expansion Expectations To The High-End Of Its FY26 Target

- WMG RAISED its FY26 margin expansion target to the “high end” of +150-200bps

- The strategic reorganization, focused investments in tech, and the rollout of the financial transformation program are all contributing to the margin improvement

- The Co reiterated the short-term margin target of mid-20s and longer-term target of high-20s (YTD it is at 24%)

- Key drivers: profitable growth, cost savings and op leverage, with incremental help from catalog growth, DSP pricing / tiering and accretive AI rev starting FY27

- “I’m very confident that we can get to the high-20s target in the medium to long term”

- Productivity is now being “embedded into the culture”

- The Co is leveraging AI more effectively for process automation and better real time decision making

- This is freeing up more resources for value-added work, leading to incremental growth at a lower cost

- Its Finance dept is the initial use case for AI-enabled operating leverage…advanced real time forecasting & reporting has “significantly” accelerated decision making

- WMG plans to use AI-driven tools to further streamline finance and other functions

- “These tools in combination with our relentless focus on profitable growth, will contribute to our margin targets of mid-20s in the short term and high-20s over the longer term”

- Mgmt reiterated its sustainable growth model

- High-single-digit total revenue growth

- Double-digit adj OIBDA and adj EPS growth

- 50-60% operating CF conversion as a % of adj OIBDA

- FQ2 OCF grew +83% y/y and first-half conversion was 66% of adj OIBDA, above the 50-60% model

Streaming Growth Stepped Up Sharply …And Advertising Growth Also Accelerated

- Both subscription and ad supported streaming benefited from “healthy” market growth and global market share gains plus subscription streaming also saw the benefit of PSM increases

- Recorded Music subscription streaming revs accelerated sharply to +20.9% y/y (+15.4% FXN) on an adj basis vs +12.0% y/y (+8.7% FXN) in FQ1

- Drivers for the +15.4% FXN adj subscription streaming rev growth?

- ~6-7ppts subscriber growth

- ~3ppts pricing / PSM

- ~3ppts market share

- Also ~2-3ppts easier prior-yr comp

- On an apples-to-apples basis, subscription streaming growth was around ~12-13%

- Drivers for the +15.4% FXN adj subscription streaming rev growth?

- Expect more room for growth ahead…

- There is more pricing to come

- M&A is not in numbers

- Acquired distribution Co will show up in the numbers later this calendar year

- WMG has done deals with AI companies and are in the process of doing more deals with DSPs

- …mgmt. is “very confident that we can continue to deliver numbers that are consistent with our sustainable growth model”

- Recorded Music ad-supported streaming revs also accelerated sharply to +12.9% y/y (+11.3% FXN) on an adj basis vs +7.7% y/y (+4.4% FXN) in FQ1

- Driven by a “strong overall ad environment” and global market share gains

- Mgmt noted that ad growth differed by partner, w/ some platforms growing “very, very strong” while another partner has not yet contributed as much, but has strategic intent to improve (confident they will)

- On the social side, a new deal also contributed to growth (but mgmt. did not quantify)

- Mgmt is confident that advertising growth will continue to be strong looking ahead

- “One of our partners will do a much better job”

- Music Publishing streaming revs grew +20% y/y (+16% FXN), accelerating from +12.8% y/y (+10.4% FXN) on an adj basis in FQ1

- Driven by new deals / renewals and continued market growth

Market Share Gaina Are “Not Short-Term” …But APAC Remains The Main Area To Fix

- WMG US streaming share grew +1.1ppts y/y and US new release share grew +2.7ppts y/y in FQ2

- This compares with ~+1ppt US streaming share growth in FQ1

- The gains were broad-based across labels, regions, and channels EXCEPT APAC which lagged behind

- WMG recently appointed a new leader and continues to see the “most amount of work to do”

- What is driving the mKt share gains? And is it sustainable? The drivers were strong pipeline mgmt, catalog optimization, and a disciplined focus on distribution… long-form programming will be a new share driver

- Creative momentum remained strong across established and emerging artists globally

- High-profile wins included Bruno Mars dominating four Billboard charts simultaneously, PinkPantheress securing her first Global 200 #1 and Don Toliver scoring his first #1 album

- Additional breakout / chart-topping artists highlighted included sombr, Black, The Marias, Alex Warren and Junior H, with local #1s in Italy, Poland, Sweden, France, Spain and Mexico

- Incr’d monetization of catalog plus high margin accretive catalog (leveraging Bain JV)

- See more below

- Incr’d focus on distribution to serve the independent artists community “profitably”

- Recent deal with Two Stream and acq of Revelator enhance capabilities

- Long-form programming emerged as a new share driver

- After last qtr’s multi-year first-look documentary deal with Netflix, WMG annc’d a multi-year first-look deal with Paramount to produce theatrical live-action and animated feature films

- WMG has “hit our stride,” is “firing on all cylinders” and the market share gains are “not short term” but the result of long-term foundational work

PSM Increases Are Now Flowing Through…With More DSP Step-Ups & AI Premium Tiers Expected To Drive Value-Led Growth

- After more than a decade of volume-led growth, mgmt emphasized that growth is now shifting toward volume + value, with greater certainty around economics “irrespective of retail pricing”

- The Co is pursuing “innovative partnerships” w/ traditional DSPs & emerging AI platforms through several avenues, including

- PSM increases on existing tiers

- Licensing agreements w/ emerging AI platforms

- Collaborating with DSP partners on the AI-centric premium tiers

- PSM increases began in FQ2 and contributed ~3ppts to subscription streaming growth of +15% on an FXN adj basis

- More PSM increases across other DSPs will roll in throughout the balance of FY26, providing further support for subscription streaming growth

- WMG is engaged with their traditional DSP partners regarding AI-centric premium tiers that would allow fans to engage more deeply w/ music and support higher ARPU

- Mgmt believes that consumers will like offerings that “blend creation and consumption”

- They are also focused on AI licensing partnership agreements like with Suno, who it sees as the near-term proof point for incremental AI monetization

- Suno is generating ~$300mn of annualized rev and plans to launch a fully licensed offering later this yr

- Suno’s 2mn subscribers are paying an avg of $12.50/mo

- WMG expects AI platform deals to begin contributing materially to future streaming rev growth starting in FY27 “Our industry leading and thoughtful approach to AI will drive one of the biggest incremental value creation opportunities for our industry”

- AI dilution remains a key investor concern, but mgmt said WMG has not seen dilution (like others in the industry have said)

- Per Deezer data, AI-generated tracks are ~44% of daily uploads but only ~1-3% of streams and a much smaller share of royalties, with ~85% of those streams deemed fraudulent

- Apple data shows AI music is less than 0.5% of listening

Catalog Monetization Remains A Major Priority & AI Is Becoming A Bigger Enabler

- WMG’s catalog is home to over 1mn tracks from more than 70,000 artists

- Catalog remains a major strategic focus, representing ~65% of Recorded Music streaming rev and growing across “shallow and deep vintages”

- WMG is using an always-on marketing approach to continuously revitalize repertoire

- The Co is introducing iconic artists to younger audiences through new release

- Madonna is a great catalog case study

- Ahead of Confessions II (her 14th album), WMG’s catalog marketing campaign drove Madonna weekly streams up +24% vs baseline, with under-20 fans accounting for 35% of Spotify streams

- Her new duet “Bring Your Love” w/ Sabrina Carpenter was Madonna’s highest-charting track yet on Spotify and fueled her biggest-ever streaming day on the platform

- AI tools are enabling WMG to monetize deeper parts of its catalog more efficiently

- AI enables quick / cost-effective creation of motion art, visualizers, lyric videos and other engagement assets

- WMG is also using a proprietary model to determine where marketing activity should be focused, enabling better and deeper monetization

- On catalog acquisitions, Bain JV has now deployed $650mn of its ~$1.65bn capacity to acquire catalogs

- Acquisitions are focused on iconic high-margin catalogs with growth potential and attractive return profiles

- WMG continues to maintain a “strong pipeline” of potential catalog oppties

- Return thresholds are similar as for A&R

Live Nation & TKO Keep Hitting Play As Live Entertainment Dismisses The Macro Backdrop

Live Nation and TKO are two sets of results that always provide a window into the health of the live entertainment sector. What did we learn this qtr? Live Nation delivered a broad-based beat across all segments in Q1 and record deferred rev signals a strong back half of the year. TKO beat on the headline numbers but results were a bit mixed under the hood, and guidance was reaffirmed but not raised.

That said, both companies paint a consistent picture that live entertainment demand remains resilient. Both saw no slowdown across genre, demographic, or geography, and both dismissed any impact from Middle East tensions. Fans are showing up in record numbers, pricing power remains intact, and the pipeline of events and content continues to grow heading into what is shaping up to be a strong back half of the year. The big focus is really on operational execution.

See below for more color on the points we thought were most incremental from both Q1 earnings results.

That said, both companies paint a consistent picture that live entertainment demand remains resilient. Both saw no slowdown across genre, demographic, or geography, and both dismissed any impact from Middle East tensions. Fans are showing up in record numbers, pricing power remains intact, and the pipeline of events and content continues to grow heading into what is shaping up to be a strong back half of the year. The big focus is really on operational execution.

Live Nation Delivers A Broad-Based Beat As Demand Remains Resilient And All Business Segments Are Firing On All Cylinders

–> Live Nation’s stock was up +6.7% in reaction to earnings and ended the week up +3.2%; YTD, the stock is up +13.3%

- Q1 earnings BEAT across the board

- Revenue – BEAT by +6.2%: Up +12% y/y vs +11% y/y in Q4

- Beat across all segments

- Adj op income BEAT by +10.9%: Up +9% y/y vs +23% y/y in Q4

- All segments were better than expected, but esp Concerts

- Revenue – BEAT by +6.2%: Up +12% y/y vs +11% y/y in Q4

- FY26 guidance was mostly unchanged

- Reiterated FY26 CapEx guidance of $1.1bn-1.2bn

- Reiterated expectations of growing FY26 op income by double-digits, despite op income being impacted by a $450mn legal accrual (will also impact EPS by -$1.93)

- Updated FY26 AOI to FCF-adjusted conversion to be “in-line with or high than” 2025 (vs prior guidance of just “higher” than 2025)

- Overall demand dynamics – seeing NO slowdown across genre, demographic, theater sizes, or region, as Q1 deferred revenue for Concerts and Ticketmaster reached record levels

- Event-related deferred revenue grew +22% y/y to reach $6.6bn, the largest deferred revenue balance in Co history

- Ticketing deferred revenue grew +29% y/y to reach $368mn accounting for $5.5bn in deferred ticketing GTV

- Concerts – broad based demand momentum across geographies and venue is building towards a back half loaded yr

- Expect N. America and intl mkts to perform “very strongly” this yr

- “Very good” qtr in LatAm drove the Q1 outperformance

- Stadiums expected to be up both in the US (“despite a very strong year last year”) and up “strongly” in intl mkts

- Amphitheaters and arenas are up “nicely” in the US, so that should drive solid growth throughout North America

- Stadium and amphitheater growth setting up a strong back half of the yr

- Strong global stadium growth and US amphitheater growth will skew Concerts rev and AOI more heavily toward Q3 this yr vs prior yrs, simply due to venue mix shifting toward larger, seasonal outdoor shows, which by nature bunch up in the back half of the summer calendar

- As a result, Q4 is also shaping up to be a “very strong” margin qtr

- Specifically on amphitheaters…both supply and demand are setting up for a “strong” 2026: Tracking ahead of last yr on show count + ticket sales are up double-digits y/y

- Expect N. America and intl mkts to perform “very strongly” this yr

- Touring – both supply and demand are growing, and tour cancellations are a non-issue / Middle East conflict has had no impact on biz

- Quick comment on Middle East… Middle East disruption has “no material effect” today, as it is a very small touring market with “no tours, no shows planned” in the region

- Seeing no changes in tour cancelation activity… “this year would be no different than any other year”

- Cancellations are tracking “slightly below” the industry: For reference, tend to have 1%-2% cancellation rate historically both at Ticketmaster across the industry and at Live Nation

- “The pie is growing” …: There are more bands on the road on a global basis and that continues to grow

- …and seeing “strong” supply across the globe…: Intl biz growth is potentially stronger than America; LatAm is “on fire”

- …which is expected to continue for “many years to come”

- Ticketmaster – solid underlying momentum and new leadership driving innovation, with near term headwinds from scalper reduction efforts and legal expenses expected to be manageable

- What drove the y/y upside in margins? A lot of the growth on the Ticketmaster side is coming from addtl concert tickets that are being sold; Also adding more clients globally; Underlying biz fundamentals also continue to be in good shape

- New Ticketmaster Global President Saumil Mehta is accelerating innovation across the fan and artist experience on both the front end and global back end

- A top priority remains making the on-sale process smoother and more transparent

- Driving work on a more robust face value exchange program and better on-sale tools for artists (“that’s our biggest pain point”)

- On the back end, rethinking how Ticketmaster enters new mkts using AI and other innovative approaches to move faster without being constrained by legacy platform limitations

- Also remain focused on using the platform’s scale to drive addtl economics, though venue clients will continue to keep the bulk of svs fee economics and the oppty for Ticketmaster is in building incremental value on top of that

- On legal expenses running through ticketing – don’t expect to continue to have same level of elevated expenses going forward: Will continue to have some expenses related to the FTC and “some other activities” but they are expected to moderate over the next few qtrs from where they’re at today

- Ongoing efforts to reduce scalper activity expected to impact FY26 Ticketmaster AOI by MSD

- This is a one-time hit that they expect to grow to offset this yr and fully comp against going forward

- Over time, secondary is expected to gradually decline into single-digits of fee-bearing GTV as “primary will win” and content owners control more inventory

- But overall FY26 Ticketmaster AOI margin expected to be similar to last yr

- Venues – upgraded fan count outlook as Venue Nation accelerates global expansion through innovative financing and capital-light partnerships

- Increased FY26 Venue Nation fan count expectation: Expected to grow double digits this year off the prior 65mm base, implying more than the previously discussed ~5mm increase

- Growth is “pretty evenly distributed” between stronger performance at existing venues and newly added venues

- New venue securitization structure creates a scalable funding engine for long-term venue expansion”

- Live Nation developed a PropCo-OpCo framework, separating its physical venue assets from its operating business, allowing it to borrow against those properties at higher leverage levels without putting pressure on the rest of the balance sheet

- They kicked things off with an initial raise of just over €600mn, using existing venues as collateral, but the structure is designed to be self-reinforcing, so every new venue they add can be folded in as addtl collateral, meaning the funding capacity grows automatically as the portfolio expands

- The end result is a repeatable, scalable financing tool that lets Live Nation continue building out its venue portfolio without having to rely on traditional balance sheet financing each time they want to buy or build a new location

- Partnering with existing stadiums globally offers a capital-light path to venue expansion

- On Live Nation’s agreement with Club Atlético in Argentina for booking and naming rights… “we love that deal, and we absolutely think on a global basis, it’s something we could replicate”: Many stadiums outside the US sit underutilized, making Live Nation a natural partner to drive show volume, bring sponsorship expertise, and inject capital where needed

- “On a global basis, we like building arenas” BUT on the stadium side, they like partnering with them, which is “a little less capital intensive, but locks up a lot of the revenue streams”

- Reiterated oppty in premium: Targeting up to 30% of new arenas in premium capacity, and are retrofitting existing amphitheaters like Indianapolis and Dallas to take premium from as low as 1-2% up to 25%, taking a page out of the sports arena playbook

- Increased FY26 Venue Nation fan count expectation: Expected to grow double digits this year off the prior 65mm base, implying more than the previously discussed ~5mm increase

- Quick update on the regulatory front… what happens next after the DOJ settlement and state case ruling?

- Time scheduled in court for this upcoming Thursday (May 7th) to discuss process

- Three key elements:

- Rulings on evidence-related motions

- Judge to determine the process for DOJ settlement review process

- Remedies portion of the trial that just concluded

- Timing and next steps are uncertain until the judge decides…until then “we have to wait a minute and see how he lays it out”

TKO Continues To See Broad-Based Growth And Demand Across Portfolio While Holding FY26 Guidance Steady

–> TKO fell -1.5% in reaction to its earnings print, but ended the week up +0.5%; YTD, the stock is still down -10.6%

- Q1 total rev BEAT cons by +0.4%, while adj EBITDA BEAT by +0.4% (though margins were a tad light)

- WWE and IMG both beat on rev, while UFC missed

- Adj. EBITDA beat was driven by IMG, as both WWE and UFC both missed

- Also announced an addtl $1bn share repurchase authorization, which is incremental to its previously announced $2bn share repurchase program

- Reaffirmed FY26 guidance

- Rev of $5.675-$5.775bn vs cons $5.77bn (-0.8% below the midpt)

- Adj EBITDA of $2.24-$2.29bn vs cons of $2.27bn (-0.2% below the midpt)

- Performance is expected to be driven by “robust” growth across media rights, live events, including FIPs, and partnership rev

- Both UFC and WWE margins will “meaningfully” outpace 2025

- Continue to see “healthy” demand for premium live events across TKO’s portfolio

- “Firmly moving ahead” w/ scheduled events in Middle East and neighboring mkts AND “we have seen no customer pullback whatsoever”

- TKO doubleheader on June 27th reflect their commitment “to bring world-class events to fans across the region even and despite a challenging environment”

- UFC will return to Azerbaijan with UFC Fight Night Baku + WWE will host Night of Champions from Riyadh, Saudi Arabia

- Following the two events, expect remainder of 2026 slate in Middle East to take place as planned

- Six events inclusive of UFC, WWE, and Zuffa Boxing

- Also noted that following reports of PIF withdrawing funding from LIV Golf, Saudi partners confirmed that this “will not be the case with TKO”

- “Their commitment to our properties in 2026 and beyond is unwavering”

- TKO doubleheader on June 27th reflect their commitment “to bring world-class events to fans across the region even and despite a challenging environment”

- WWE – Q1 rev was up +22% y/y (in-line w/ Q4) and adj EBITDA was up +32% y/y (decel from +44% y/y in Q4)

- Driven by an increases across all categories

- Looking into WWE’s Q2…expected to be the highest rev and adj EBITDA qtr of the yr in terms of absolute dollars, given the timing and mix of the event calendar

- Media rights will continue to benefit from the step-up of their agreement with ESPN

- With respect to live events rev, the Saudi PLE carries a meaningful FIP, but held a similar event in Q2:25

- UFC – Q1 rev was up +12% y/y (decel vs +17% y/y in Q4) and adj EBITDA was up +12% y/y (decel vs +20% y/y in Q4)

- Driven by an increase in media rights, production and content rev, and an increase in partnerships and marketing rev, partially offset by a decrease in live events and hospitality rev

- UFC had 9 total events in Q1:26 compared to 11 total events in Q1:25

- Both Q1:26 and Q1:25 had 3 numbered events

- Q1:26 included 6 Fight Nights vs 8 in Q1:25; Q1:25 also benefited from a Fight Night in Saudi Arabia that carried a meaningful financial incentive package

- UFC deal w/ Paramount+ is off to a roaring start

- Debut on Jan 24th reached more homes than any UFC event in nearly a decade

- First CBS simulcast, UFC 326, was the most watched live UFC event since 2016

- The CBS audience alone was 270%+ above last yr’s UFC avg on linear before counting Paramount+ streaming

- New fans are discovering UFC on CBS and Paramount+, and they are staying

- On Paramount-WBD combination… “we are ecstatic and frankly anxious for them to close this deal and for us to get to the table and start brainstorming what we can do with all their platforms”

- Progress w/ Zuffa Boxing is “exceeding our internal growth plan and timeline”

- Already signed 100+ fighters

- Staged five events w/ “solid” viewership on Paramount+

- Secured a multi-year deal with Sky Sports for the UK and Ireland, “two of the most pivotal and important boxing markets in the world”

- Also signed media rights deals in 15+ addtl territories spanning EMEA and APAC

- “Next phase of our growth plan is underway” with events about to depart the Meta APEX in Las Vegas and go out on the road

- Looking into UFC’s Q2…media rights rev will continue to reflect the step up from the Paramount rights deal + the mix of live events will also impact results

- Expect to stage 11 events in Q2…UFC Freedom 250 at the White House in June + 2 numbered events + 8 Fight Nights

- Expect to lose ~$30mn on UFC Freedom 250, though it is a “once in a lifetime” event that will highlight the brand on the biggest stage possible

- UFC Fight Night Baku carries a “meaningful” y/y financial incentive package, part of a multi-ye renewal at a higher per event fee than they realized in the same mkt in Q2 of last yr

- Expect to lose ~$30mn on UFC Freedom 250, though it is a “once in a lifetime” event that will highlight the brand on the biggest stage possible

- …Vs prior-yr qtr…. which had 4 numbered events + 7 Fight Nights

- Expect to stage 11 events in Q2…UFC Freedom 250 at the White House in June + 2 numbered events + 8 Fight Nights

- IMG – Q1 revs were up +38 % y/y (accel vs -9% y/y in Q4) and adj EBITDA was up +32% y/y (vs -124% y/y in Q4)

- Primarily related to an increase in live events and hospitality revenue

- This increase was primarily related to hospitality sales at On Location from the 2026 Olympics

- On PBR specifically…rev grew +36% y/y to reach $74mn and asset is appreciating

- Opened the yr w/ record performance in seven mkts, including its debut at Boston’s TD Garden and its largest ever attendance at Madison Square Garden in Jan

- PBR’s team series has also approved a two-franchise expansion expected to grow from 10 teams to 12 teams for the 2027 season

- Franchise values are exploding: Growing from ~$3mn at launch → $22mn in 2024 → expected multiples of that in 2027

- Looking ahead…expect continued growth at PBR, and it will be high margin growth, “analogous” to that of the WWE and UFC segments

- Looking into IMG’s Q2…expect results will be driven by On Location with the World Cup starting on June 11, as well as notable events in the qtr like the Final Four and NFL Draft

- Also a “big” qtr for the IMG biz with many of the largest soccer leagues in the final months of their season, the start of Wimbledon, and the first full qtr of the MLS season

- While the World Cup is anticipated to have a positive impact on adj EBITDA, sales efforts for LA28 will have ongoing costs that are expected to partially offset such impact

- TKO is “insulated from AI disruption”: “As AI transforms how content is created and consumed, the value of our IP and properties increases. Our content is live. It’s communal. It’s scarce, and no algorithm can replicate it”

DKNG Is Going All-In On Predictions In H2

DraftKings’ Q1 was a bit of mixed bag with higher expected profitability (adj EBITDA beat by almost 10%) but revenues were ~in-line and monthly unique players (MUPs) were much lower than expected (by -8.5%). Plus, despite the higher Q1 adj EBITDA, the Co re-affirmed the FY adj EBITDA guidance of $800mn at the mid-point. At the same time, mgmt was explicit about the spending plan on its Predictions business that is included in the guidance (it will be a high $200-300mn that will be heavily back-half weighted) and the guidance also includes Alberta & Arkansas launch costs. Adjusting for the assumed Predictions investment spend, the Co’s Core business adj EBITDA is targeted to reach $1bn (which is well ahead of total $620mn reported in FY25). All in all, that’s a plus regarding growth in the Core but investors are focused on the ROI of the large Predictions spend in this competitive market.

Aside from all that, 5 other top takeaways in our opinion are: 1) The SuperApp seems to be working as Predictions CAC declined more than -80% in April after its integration into the app and early traction has been extremely strong with the annualized predictions consumer volume exceeding $1bn and the annualized total volume traded exceeding $2.3bn in April, an increase of +38% & +43% month over month respectively; 2) The World Cup is seen as a “tremendous” customer acquisition event in H2 (especially in non-OSB states)…though it may not be a huge revenue opportunity; 3) The Co’s market making business has been its fastest new business line to reach profitability ever…and the exchange business will be launched in the “coming weeks”; 4) The core OSB performance was strong with revenues growing +24% y/y despite handle up only +1.5% y/y… net revenue margin expanded by +140bp and parlay mix increased +300bp; and 5) April trends were very strong with handle up +6% y/y, revenue up +22% y/y, and $100mn+ EBITDA in a single month.

Overall, DKNG’s core OSB business is performing well and the Co is heavily leaning into Predictions with the user ramp slated to come later this year, which obviously will be a key deliverable as competition in this new market has been a significant investor concern.

See below for more details.

-> DKNG closed the day up just over +1%, though the stock is still down -26% YTD

Higher Than Expected Profitability Was DKNG’s Main Q1 Standout…While Revenue Was In-Line & MUPs Remained Weaker Than Expected

- Q1 revs BEAT by +0.6%: Rose +17% y/y vs +43% y/y in Q4

- Adj EBITDA BEAT cons by a more sizable +9.8%: Grew +64% y/y

- Adj EBITDA margin at 10.2% topped cons 9.3%

- Adj EPS of 20c BEAT cons $2c…DKNG also generated positive net income for the 2nd consecutive qtr

- Monthly unique players (MUP) MISSED cons by -8.5% (fell -4% y/y vs 0% in Q4): This primarily reflects lower MUPs from Lottery following their exit from Texas in 2025; Excl the impact of Lottery, MUPs incr’d by +2% y/y

- Mgmt expects Predictions to drive a “tremendous increase” in MUPs in H2 as DKNG ramps marketing across roughly the other half of the US population (see more below)

- Avg rev/MUP BEAT by +8.5% (up +21% y/y vs +43% y/y in Q4)

- DKNG repurchased almost $100mn of shares in Q1

Despite The Q1 Adj EBITDA Beat, FY26 Guidance Was Maintained And Now Explicitly Includes Predictions Market & New Launch Spend

- FY26 guidance was maintained…

- Mid-pt of rev guidance is -1.8% below cons

- Mid pt of adj EBITDA guidance is +1.1% above cons

- … and mgmt detailed that it includes Predictions investment and expected Alberta & Arkansas launch costs

- Total 2026 Predictions investment is expected to be $200mn-300mn (back-end loaded and largely focused on marketing)

- This implies that the Core business is expected to generate $1bn+ of adj EBITDA this year before the Predictions investment (vs $620mn in total reported adj EBITDA in 2025)

- Mgmt was deliberately disciplined / conservative w/ the initial guidance earlier this year, anticipating potential launches and giving itself room to absorb them

- At the start of the year, the Co knew there was a chance it would “go very aggressive on Predictions”

- Mgmt also contemplated “at least one, maybe multiple launches,” including rumblings in Arkansas and discussions around Alberta

- Alberta is expected to launch “in July”

- The initial guide included “some conservatism,” which was deliberate to help “maintain and hopefully as the year progresses, raise the guide”

- “Not much has changed other than I think we’ve become a little more crystallized in some of these exact numbers. But nothing’s too far off from where we initially thought it would be at the beginning of the year”

DraftKings Expects “Huge” Growth In Users In H2 From Predictions…And The World Cup Is A Key Catalyst

- Given that Predictions is now live in their flagship app their Predictions customer acquisition cost declined more than 80% in April

- Within Predictions, they have more than doubled markets available to trade, which is driving Predictions volume per customer above Sportsbook handle per customer

- In April, the annualized predictions consumer volume exceeded $1bn and the annualized total volume traded exceeded $2.3bn, an increase of +38% & +43% month over month respectively

- As noted above, mgmt expects to invest $200mn-300mn in Predictions this year…the spending ramp starts in Q2 but will be heavily back-end weighted

- Mgmt expects “huge customer acquisition numbers” in the back half if the current regulatory environment hold

- The Co has “very high expectations” for World Cup regarding customer acq and engagement, especially in Predictions states such as CA, TX and FL

- Mgmt does not expect World Cup to be a huge revenue event, BUT it will “be absolutely tremendous for a customer acquisition, starting with these Prediction states”

- Spanish-language functionality launched ahead of World Cup and should help DKNG acquire / engage an incremental audience

- DKNG will “really go for it” but if the numbers don’t support that they will back off…they won’t spend heavily if it is not working