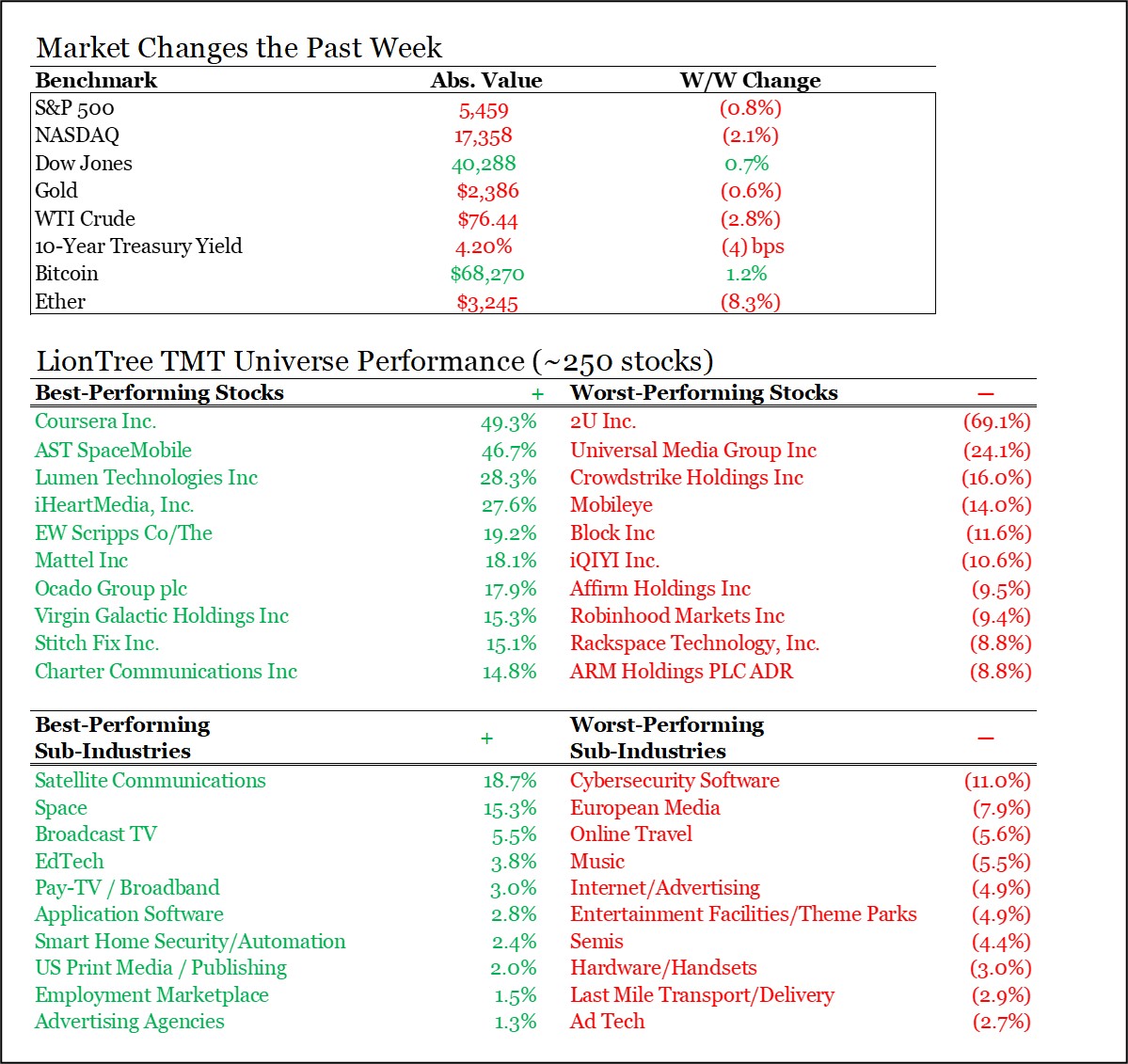

The big market rotation continued this week. Nasdaq fell -2% (though partially recovered on Friday from lower levels), while the Dow rose +0.8% and the Russell 2000 rose +3%. The “Magnificent 7” is collectively down ~13% since peaking July 10, while the small call Russell 2000 is up almost +10% for that period. Next week will be pivotal with the Fed meeting…

In the meantime, earnings is in full swing, and 41% of the S&P 500 has now already reported. Within our sector, it was a huge week for Connectivity (Verizon, AT&T, Comcast and Charter all reported), Digital Advertising, Cloud, and Music, among other sub-sectors. There was certainly a lot to digest and think about.

See below for the key focus themes in this edition (all links are clickable):

- Earnings Scorecard- Week 1 & 2

- Alphabet Says It’s Better To Over-Invest In AI, Than Under-Invest…

- Connectivity – Part 1: Verizon & AT&T Somewhat Diverge In Q2

- Connectivity: Part II – Cable Companies Are Weathering The ACP Storm Better Than Expected

- Investors Cheer Spotify’s Year Of Monetization + Better Paid Subscription Growth

- UMG’S Results Were Impacted By Varied DSP Performance, But Its “Entire Mentality Is To Grow The Pie”

- A First Look At Media Entertainment Trends Raised Concern On Theme Parks

- Grab Bag: Reddit Strikes Sports Partnerships / Apple Cuts Content Spend / Prop 22 Is Upheld

There is a lot packed in so you might need a little extra time this weekend!

Best,

Leslie

Earnings Scorecard- Week 1 & 2

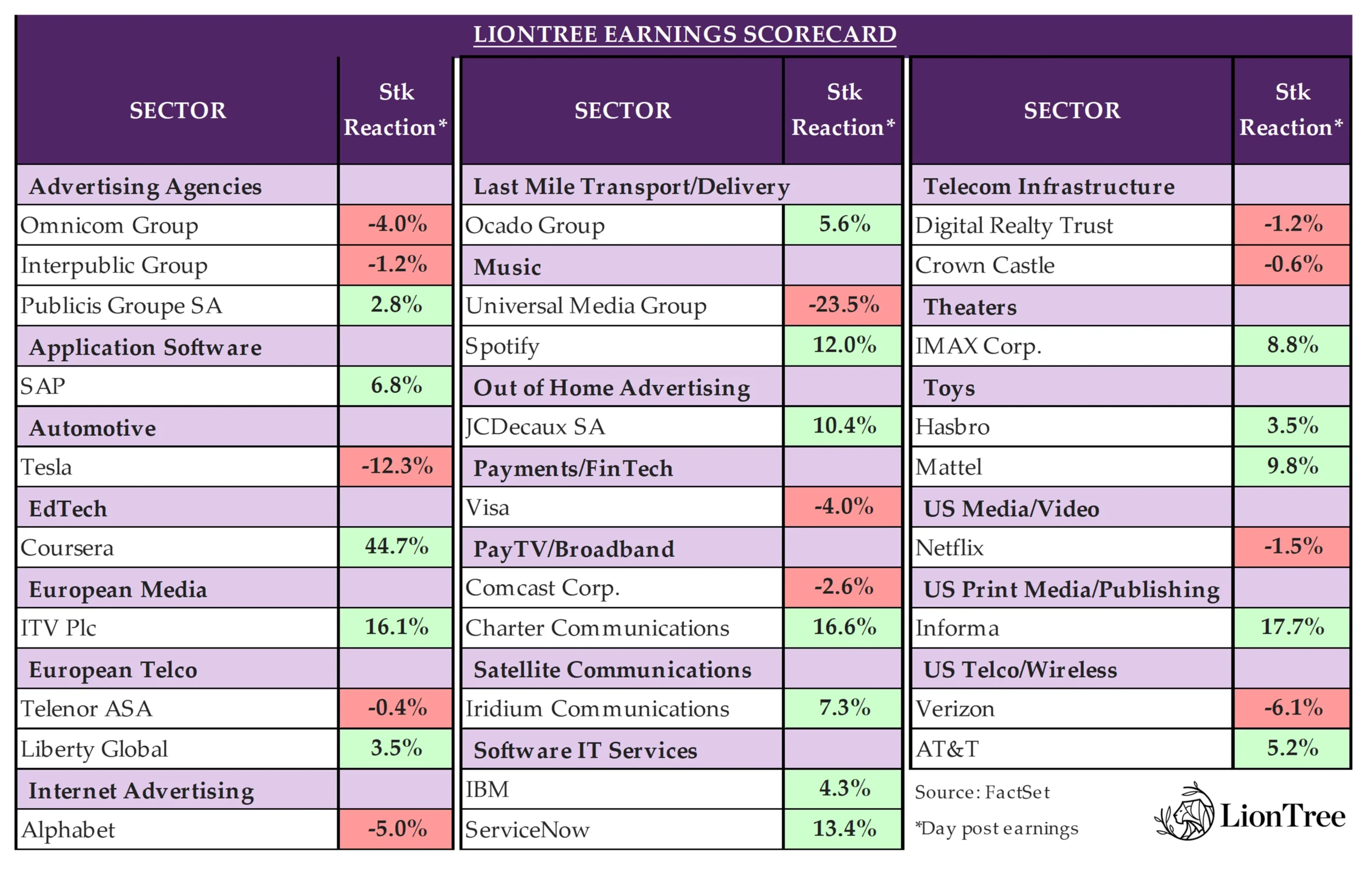

It’s that time of the year again when earnings season descends down en force. Over the last two weeks, 29 companies in our LionTree Universe reported their second qtr results, and stock price reactions were biased to the upside, with 18 companies (62.1%) trading up and 11 companies (37.9%) trading down following their prints. The worst performer in the group was Tesla, which traded down -12.3% in reaction to its report, and the best performer was Coursera, up +44.7%.

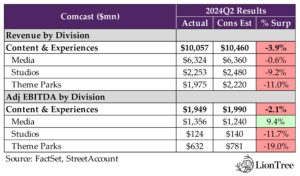

Connectivity names dominated the earnings circuit this week, with both telco and cable names reporting. On the Telco side, AT&T led, trading up +5% in reaction, while Verizon went the other way and traded down -6% (see Theme #3). Within Cable, Charter saw a huge jump and ended the day up +17%, while Comcast fell -3% (see Theme #4). Comcast’s results also included a first look into the Media sector through its media arm, NBCUniversal (see Theme #7 for more color).

Also within Media, Music was a sector of focus, and on the platform side, Spotify traded up +12.0% after posting its results (see Theme #5), though the going was tougher on the label side, with Universal Music Group plunging -24% after its report (see Theme #6).

We also got a first glimpse into Big Tech earnings with digital advertising juggernaut Alphabet, which fell -5% in reaction (see Theme #2). Also to flag in the advertising space, agencies Omnicom and Publicis reported last week, and reactions diverged, down -4.0% and up +2.8%, respectively (see Theme #6 from last week’s Weekly). Netflix was the other big print from last week and fell -1.5% (also covered in Theme #1 of last week’s Weekly).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Alphabet Says It’s Better To Over-Invest In AI, Than Under-Invest…

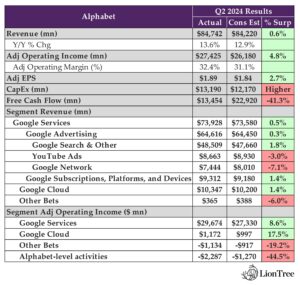

“When you go through a curve like this, the risk of under-investing is dramatically greater than the risk of over-investing.” That was a notable quote from Alphabet CEO Sundar Pichai on the Co’s Q2 earnings call, through which he rationalizes the Co’s Q2 y/y CapEx growth of +91.4% y/y to $13.2bn (following the +91% y/y growth in Q1 to $12bn). This came in ~+$1bn higher than Street estimates, and Alphabet expects to spend at least $12bn per quarter on CapEx through the end of the year. While this spending will weigh on FCF, management reassured investors that they continue to count on operating margin expansion in FY24 relative to FY23, despite some expected choppiness in Q3.

To provide some comfort regarding these investments, management made a point to highlight all the ways they’re starting to see AI benefits across the company’s segments, particularly advertising. Importantly, ad revenue in the Co’s core Search business came in stronger than expected, as the rollout of AI Overviews in the US has been driving higher engagement from younger users and increasing traffic to businesses. However, investors homed in on the disappointing YouTube advertising revenue, which was due to tougher y/y comps that will persist into Q3. That being said, new advertising features and products continue to be built to help advertisers leverage AI relevant products, and given that Gemini has been “natively multimodal from the ground up”, the Co expects to see it becoming “deeply relevant to YouTube” in the near future.

In addition to the strong results in Search, Cloud was a key upside driver and stood out with growth accelerating to +29% y/y, given an increasing contribution from AI. The segment set threshold records, as revenue crossed the $10bn mark for the first time (and beat by +1.4%), while operating profit passed the $1bn mark for the first time (and beat by +17.5%).

Other key updates from Alphabet included a $5bn multi-year investment in its Other Bets division, walking back on cookie deprecation (guess the cookie won’t be crumbling after all!), and more.

See below for more of what we viewed as most important.

-> Alphabet fell -5.0% in reaction to its print and further fell to end the week down -6.0%; YTD, the stock is still up +19.7%

-> AdTech names PubMatic and Criteo ended the week up +5.3% and +11.2%, respectively, while Magnite ended the week down -3.7% in in reaction to the press early in the week that Google was abandoning its cookie deprecation plans; The Trade Desk also ended the week down -3.7%, and was down -11.5% post Alphabet results, weighed down by the weaker YouTube ad rev; Roku also fell -10.5% in reaction

Q1 Beat On Headline Results, Though CapEx Investments Continue To Weigh On FCF

- Consol rev was up +14% y/y or +15% ex-FX (vs +15% y/y or +16% ex-FX in Q1) and beat cons by +0.6%

- Search remained the largest contributor to growth, and Cloud followed

- Op income beat cons by +4.8% w/ margins of 32%

- Y/Y margin expansion reflects ongoing efforts to durably reengineer the cost base and rev strength

- EPS beat by +2.7%

- CapEx came in higher than expected, and FCF of $13.5bn missed by -41.3%

- CapEx was driven “overwhelmingly” by investment in technical infrastructure with the largest component being for servers, followed by data centers

- On investment strategy – “When you go through a curve like this, the risk of under-investing is dramatically greater than the risk of over-investing”

Some Choppiness Is Coming In Q3, But Remain On Track For FY24 Margin Expansion

- Continue to expect to deliver FY24 op margin expansion relative to FY23, BUT Q3 will be under pressure, reflecting 1) increases in depreciation and expenses associated w/ the higher levels of investment in their technical infrastructure; And 2) the increase in cost of revenues due to the pull forward of hardware launches into Q3

- Similar to Q2, FCF y/y growth in Q3 will be depressed due to a timing benefit in last year’s Q2 and Q3 from a $10.5bn deferred cash tax payment

- Continue to expect qtrly CapEx through the year to be roughly at or above $12bn, keeping in mind that the timing of cash payments can cause variability in quarterly reported CapEx

Search Ads Had A Strong Qtr, While YouTube Ads Were Weighed Down By Tough Comps (Which Will Continue Into Q3)

- Google Search & Other revs beat cons by +1.8% and grew +14% y/y (in-line w/ Q1), led by growth in Retail, followed by the financial svs vertical

- YouTube ad revs missed cons by -3.0% and sharply decelerated to +13% y/y (vs +21% y/y in Q1): Growth was driven by brand, followed by direct response advertising; The seq decel primarily reflected tougher comps when YouTube was lapping negative y/y growth from Q1:23 and benefitted from the extra day from a leap year; Y/Y comps were impacted by a ramp in APAC-based retailers that begin in Q2:23, as well as FX headwinds

- Q3 will also see some pressure from lapping increasing strength in ad revs in H2:23 – in part from APAC-based retailers – as well as FX headwinds

Alphabet Is Building Out AI Use Cases Across Biz Segments

- 2mn+ developers are using Gemini across their developer tools

- Comes in four sizes with each model designed for its own set of use cases

- Offers the longest context window of any large-scaled foundation model-to-date at 2mn tokens

- All six Google products w/ 2bn+ monthly users now use Gemini

- Announced 30+ new ads features and products in Q2 to help advertisers leverage AI across Search, PMax, Demand Gen, and Retail

- Beta testing virtual try-on and shopping ads and plan to roll it out widely later this yr; Feedback shows this feature gets 60% more high quality views than other images and a higher click out to retailer sites

- AI-driven profit optimization tools have been expanded to PMax and standard shopping campaigns: Advertisers that use profit optimization and smart bidding see an avg +15% uplift in profit compared to revenue-only bidding

- Demand Gen is rolling out to Display and Video 360 and Search Ads 360 in the coming months with new generative image tools that create high quality image assets for social marketers: When paired w/ Search PMax, Demand Gen delivers an avg of 14% more conversions

- On AI integrations within YouTube – “Gemini has been natively multimodal from the ground up. But most of the use cases today that have been unlock have been around the tech side… but over time obviously it will be deeply relevant to YouTube”

- Where is Google seeing “faster than expected” traction in AI? Where are there oppties?

- Consumer: “Seeing progress on the organic side. Obviously, monetization is something that we would have to earn on top of it”

- Enterprise: “I think we are at a stage where definitely there are a lot of models. I think roughly the models are all kind of converging towards a set of base capabilities. But I think where the next wave is working to build solutions on top of it. And I think there are pockets, be it coding, be it in customer service, etc., where we are seeing some of those use cases, seeing traction. But I still think there is hard work there to completely unlock those”

AI Is Helping Deliver Better Responses In Search

- Seeing positive trends from the roll out of AI Overviews in the US, including increases in Search usage and increased user satisfaction w/ results

- Seeing even higher engagement from younger users aged 18 to 24 when they use Search with AI Overviews

- AI Overviews is driving traffic to bizs, as ads appearing above or below AI Overviews provide “valuable” options for people to take action and connect with bizs

- Looking ahead, AI Overviews will scale over the course of the year to more countries

- Will also start testing Search and shopping ads, giving advertisers the oppty to appear within the Overview in a section labeled as “Sponsored” when they’re related to both the query and information in the AI Overview

- Relentlessly” driving efficiencies and quality improvements in AI models

- Doubled the core model size for AI Overviews, while at the same time improving latency and keeping costs per AI Overviews

- Focused on matching the right model size to the complexity of the query in order to minimize impact on costs and latency

- In six months, AI-driven improvements to quality, relevance, and language understanding have improved Broad Match performance by +10% for advertisers using Smart Bidding

- Advertisers who adopt PMax to Broad Match and Smart Bidding in their Search campaigns see an average increase of over +25% more conversions or value at a similar cost

Reversal of Cookie Deprecation Plan Highlights User Choice as the Best Path Forward for Improving Privacy

- “We are super committed to improving privacy for users in Chrome… but on third-party cookies, given the implications across the ecosystems and considerations and feedback across so many stakeholders, we now believe user choice is the best path forward there”

- “We’ll both improve privacy by giving users choice, and we’ll continue our investments in privacy-enhancing technologies”

-> Earlier this week, Google annc’d plans to keep third-party cookies in its Chrome browser for those who don’t disable them; However, to enhance user privacy while preserving advertising effectiveness, Google plans to roll out a new solution: a one-time prompt that enables users to set preferences that will apply across Google browsing experiences; In Jan 2020, Chrome promised to phase out the technology “within two years”, but since then, the Co has pushed back its deadline two more times – most recently, in April of this year, citing regulatory concerns about Google’s Privacy Sandbox, the Co’s suite of proposed cookie alternatives (link/link)

While YouTube Ad Revs Missed Given Tough Comps, The Ads Biz Remains In A Strong Position

- YouTube continues to lead in viewership

- YouTube is the most watched streaming platform on TV screens in the US for the seventeenth consecutive month, per Nielsen

- Second most watched after Disney across all media Cos and their combined TV viewership

- Growth is happening in multiple verticals, including sports, which has seen CTV watch time on YouTube grow +30% y/y

- CTV on YouTube is continuing to benefit from combination of “strong” watch time growth, viewer and advertiser innovation, and a shift in brand ad budgets from linear TV to YouTube

- Shorts continues to see improvement in monetization, particularly in the US

- Seeing “very encouraging” contribution from brand advertising on Shorts, which was launched in Q4:23

- Shopping remains “a key area of investment”: Last year, viewers watched 30bn hours of shopping-related content, and there was a +25% increase in watch time for videos that helped people shop

- Rolled out several product updates to YouTube Shopping, including product tagging, product collections, and a new affiliate Hub

And YouTube Continues To Drive Most Of Subscription Revenue + More Announcements On Android And Pixel Are Coming Soon

- Subscriptions, Platforms and Devices beat cons by +1.4% and grew +14% y/y (vs +18% y/y in Q1)

- Subscriptions (the majority of revenue for the segment) continues to see “significant” growth: Both YouTube TV and YouTube Music Premium are key drivers, as well as Google One

- Outlook: The anniversary impact of the price increase for YouTube TV, which drove the seq decline in y/y growth, will persist through the balance of the year

- Platforms – “Pleased” w/ performance in Play, driven by an increase in buyers

- Devices will see a tailwind in Q3:24, as Made by Google launches had been pulled forward into Q3 from Q4

- Subscriptions (the majority of revenue for the segment) continues to see “significant” growth: Both YouTube TV and YouTube Music Premium are key drivers, as well as Google One

- Samsung’s new devices will include the latest AI-powered Google updates on Android

- Recently introduced a new Pixel 8a, powered by the latest Google Tensor G3 chip, which provides AI experiences like Circle to Search, Best Take, and a Gemini-powered AI assistant

- Will have more to share around Android and the Pixel portfolio of devices at the Made by Google event in August

Cloud Acceleration Driven By Continued AI Demand From Partners

- Cloud revs beat cons by +1.4% and were up +29% y/y (accel from +28% y/y in Q1), reflecting “significant” growth in GCP, which was above growth for Cloud overall, and includes an increasing contribution from AI as well as “strong” Google Workspace growth, primarily driven by increases in avg rev per seat

- Q2 was a qtr of milestones on both rev and operating profit: Google Cloud rev crossed the $10bn mark for the first time, while operating profit passed the $1bn mark for the first time

- “Really pleased” with Cloud margin improvement, which reflects the efficiency efforts they’ve implemented and the rev strength they delivered; Looking into Q3, expect the same seasonal pattern they saw last year

- “Majority” of top 100 customers are already using their genAI solutions

- Latest NVIDIA Blackwell platform will be coming to Google Cloud in early 2025

- Key AI partnership callouts –

- Momentum w/ AI infrastructure: Providing AI start-ups like Essential AI with leading cost performance for models and high-performance computing applications

- Advances since Cloud Next

- Trillium: A3 Mega powered by NVIDIA H100 GPUs, doubles the networking bandwidth of A3

- Vertex Enterprise AI Platform: Helps customers like Deutsche Bank, Kingfisher, and the US Air Force build powerful AI agents

- New announcements during the qtr

- Gemini Pro 1.5 and Gemini Flash 1.5: Used by Uber and WPP for customer experience and marketing

- Broadened support for 3P models: Includes Anthropic’s Claude 3.5 Sonnet and open-source models like Gemma 2, Llama, and Mistral

- Only Cloud provider to offer grounding with Google Search: Expanded capabilities with Moody’s, MSCI, ZoomInfo, and more

- AI-powered application portfolio: Helping win new customers and drive upsell

- Conversational AI Platform: Used by Best Buy and Gordon Food Service

- Gemini for Workspace: Helps Click Therapeutics analyze patient feedback for targeted digital treatments

- AI-powered agents: Helping customers develop better quality software, find insights from their data, and protect their organization against cybersecurity threats using Gemini

- Software Development: Used by Wipro with Gemini Code Assist to develop, test, and document software faster

- Data Analysis: Used by Mercardo Libre with BigQuery and Looker to optimize capacity planning and fulfill shipments faster

- Cybersecurity: Helps protect organizations against threats

- Security Portfolio

- Mandiant Teams: Manage cybersecurity risks and breaches

- Q2 AI Infusion: Helps TELUS strengthen its proactive security posture

Progress In Waymo Is Driving A Fresh Round Of Multi-Year Investment In Other Bets

- Alphabet Is committing to a new $5bn multi-year investment in Other Bets: “Continue to focus on improving overall efficiencies as we invest for long-term returns”

- “This new round of funding, which is consistent with recent annual investment levels, will enable Waymo to continue to build the world’s leading autonomous driving technology Co”

- “Really pleased” with progress Waymo is making

- 2mn+ trips serviced to date

- 20mn+ fully autonomous miles driven on public roads

- Now delivering 50k+ weekly paid public rides, primarily in SF and Phoenix

- Removed the waitlist in SF in June, so anyone can take a ride

- Fully autonomous testing is underway in other Bay Area locations

-> Also in the self-driving space this week, General Motors annc’d that it would be “indefinitely suspending” work on Origin, the autonomous vehicle produced by GM’s self-driving subsidiary; GM CEO Mary Barra said in a letter to shareholders that the change will lower Cruise’s costs and “addresses the regulatory uncertainty” around the vehicles’ lack of manual controls such as a steering wheel or pedals; Cruise will instead focus their efforts on the next generation of the battery-run Chevrolet Bolt; The decision to “pause” production of the Origin triggered a $605mn charge in Q2; Cruise has been under scrutiny since an October crash involving a pedestrian on the streets of San Francisco (link/link)

Connectivity – Part 1: Verizon & AT&T Somewhat Diverge In Q2

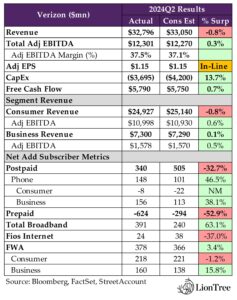

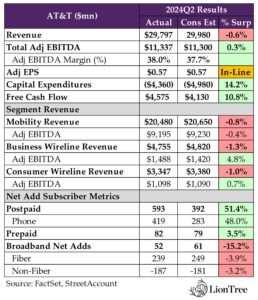

It was eventful week in the telco space, as Verizon and AT&T both reported Q2 results. In a continuation from the previous two quarters, the two incumbents printed mixed headline results, with each posting top-lines that fell short of consensus estimates and adj EBITDA numbers that exceeded expectations. Nonetheless, both reiterated their outlooks for FY24. What was particularly top of mind on the earnings calls was the potential for higher upgrade/switching activity in the back half of the year with the upcoming handset upgrade cycle. In particular, Verizon CEO Hans Vestberg believes that “we’re going to see some excitement around AI” with Apple’s upcoming iPhone launch, though AT&T CEO John Stankey cautioned that it remains to be seen “whether or not there’s something more compelling” in this year’s cycle, given that other AI devices have come into the handset ecosystem over the last couple of months but haven’t seemed to be “world-changing”. In any case, the emergence of generative AI should represent significant longer-term drivers for both Verizon and AT&T. The former has dimensioned the Verizon Intelligent Edge Network to be the “backbone of the GenAI economy”, while the latter’s “dense fiber assets” could also be utilized to support more data intensive AI applications.

The telco incumbents also sustained momentum across their core postpaid phone businesses in Q2. Despite “ongoing wireless market normalization”, Verizon and AT&T each saw sequential and y/y improvements in postpaid phone net adds that respectively surpassed consensus forecasts by a wide +46.5% and +48.0%, respectively marking the fifth consecutive quarter the two companies’ postpaid phone net adds topped estimates. The business segment was one of the main reasons for their outperformance, with both Verizon and AT&T highlighting successes with large enterprises and public sector customers. Verizon’s numbers were also augmented by second line additions (to which investors did not give as much credit). In contrast, their performances on the prepaid sides were more divergent. Verizon lost more prepaid customers than the Street anticipated with ACP ending, while the effect of the program’s conclusion on AT&T was more in-line with expectations. Looking ahead, it sounds like ACP will not materially impact the incumbents’ results, as the “vast majority” of ACP-related disconnects are now behind them.

There were also some puts & takes for the telcos on the broadband sides of their businesses. On one hand, lower move activity remained a persistent headwind throughout the quarter and contributed to worse than expected sequential declines in Verizon Fios and AT&T Fiber’s net adds. On the other hand, FWA net adds picked up sequentially in Q2, with Verizon adding +378k (vs +354k in Q1) and AT&T adding +139k (vs +110k in Q1), as more customers looked to migrate from legacy copper-based internet connections to FWA alternatives. Interestingly, while AT&T emphasized the importance of convergence within its broader go-to-market strategy, Verizon’s tone on convergence was a bit more muted, as management is skeptical that the US market will approach the levels of convergence seen in Europe.

Speaking of capital allocation, FCF was a standout from both incumbent’s prints in Q2, driven by their lower than anticipated levels of CapEx. Although AT&T’s CapEx was still a bit higher than its spend the prior year, both telcos appear to be following through on their commitments to return capital to shareholders after the peak 5G investment cycle.

See below for more detail on what we thought were the most incremental items from Verizon and AT&T’s Q2 earnings, and see Theme #4 for more on Connectivity perspectives from Comcast and Charter results…

-> Verizon shares fell -6.1% following the print but recovered some losses to end the week down -3.7%; AT&T shares rose +5.2% in reaction to earnings but ended the week down a slight -0.6%; YTD, Verizon stock is still trading up +6.3% and AT&T stock is up +13.2%

–> On a related note this week, T-Mobile annc’d a $4.9bn JV w/ KKR to acquire MetroNet, a provider of fiber connectivity svs; T-Mobile plans to use Metronet’s digital and fiber infrastructure to expand to more households w/ fiber broadband svs; Metronet’s fiber network reaches 2mn+ households in 17 states, and the Co is expected to reach 6.5mn homes by the end of 2030; The transaction is expected to close in 2025, subject to customary closing conditions and regulatory approvals (link)

Both Telcos Out-Delivered On Adj EBITDA But Missed On The Top-Line

- Verizon – Headline results were mixed, w/ a shortfall on rev but a beat on adj EBITDA: Q2 rev was up +0.6% y/y (vs +0.2% y/y in Q1) but missed cons by -0.8%; Adj EBITDA rose +2.8% y/y (vs +1.4% y/y in Q1) and topped cons by +0.3%; Adj EPS of $1.15 was in-line w/ cons; FCF beat by +0.7%; Postpaid phone and broadband net adds both beat

- Consumer (~87% of adj EBITDA) – Mixed: Rev growth accel’d to +1.5% y/y in Q2 (vs +0.8% y/y in Q1) but fell -0.8% short of cons while adj EBITDA incr’d +4.0% y/y (vs +3.6% y/y in Q2) and beat cons by +0.6%; Gains in svs rev were partially offset by declines in wireless equipment rev

- Business (~13% of adj EBITDA) – Beat: Rev declines accel’d, falling -2.4% y/y (vs -1.6% y/y in Q1) but coming in +0.1% above cons; Adj EBITDA declines improved to -3.5% y/y (vs -7.2% y/y in Q1) and beat cons by +0.5%; Increases in wireless service rev were more than offset by decreases in wireline rev

- AT&T’s headline numbers were mixed, as top-line underwhelmed while adj EBITDA beat: Rev fell -0.4% y/y in Q2 (vs +2.2% y/y in Q1) and ended -0.6% below cons; Adj EBITDA grew +2.6% y/y (vs +4.3% y/y in Q1) and topped cons by +0.3%; FCF closed +10.8% ahead of cons; Postpaid phone net adds beat, but broadband net adds missed

- Mobility (~78% of Communications adj EBITDA) – Miss: Q2 rev incr’d +0.8% y/y (vs +0.1% y/y in Q1) but closed -0.8% below cons; Adj EBITDA rose +5.3% y/y (vs +7.0% y/y in Q1) but missed cons by -0.4%

- Business Wireline (~13% of Communications adj EBITDA) – Mixed: Rev dropped -10% y/y in Q2 (vs -7.8% y/y in Q1) and missed cons by -1.3%; Adj EBITDA was down -13.9% y/y (vs -16.5% y/y in Q1) but beat cons by +4.8%

- Consumer Wireline (~9% of Communications adj EBITDA) – Mixed: Q2 rev grew +3.0% y/y (vs +3.4% y/y in Q1), missing cons by -1.0%; Adj EBITDA incr’d +7.1% y/y (vs +14.6% y/y in Q1) and beat cons by +0.7%

FY24 Guidance Was Broadly Reaffirmed In Both Cases, Despite The Adj EBITDA Beats

- Verizon is “very comfortable” w/ its rev and adj EBITDA guides for FY24: Reaffirmed forecasts for total wireless svs rev growth between +2.0-3.5% y/y, adj EBITDA growth between +1-3% y/y (below cons +2.1% y/y at the mid-pt), and a full-yr EPS range of $4.50-4.70 (above cons by +0.4% at the mid-pt)

- Seq growth in svs rev is expected in H2:24: Cited “progress on volumes on mobility and FWA”; Headwinds in prepaid are also “improving”; That said, y/y comps will be more difficult in H2:24, given last yr’s pricing changes; The promo environment will be a “wild card” moving forward as well

- The Co’s cost transformation efforts are “on track”: There’s a “lot of work” to reduce costs occurring within IT, real estate, and network decommissioning; A voluntary separation program will also start “manifesting” savings in the tail end of 2024 and into 2025; AI efforts have helped as well

- AT&T is “on pace to deliver on all of [its] full yr financial guidance”: Coming into FY24, the Co forecasted wireless svs rev growth in the +3% y/y range, broadband rev growth of over +7% y/y, adj EBITDA growth in the +3% y/y range, and adj EPS between $2.15-2.25 (-0.9% below cons at the mid-pt)

- A one-time, $480mn payment is expected in H2:24: This is termination fee related to the phasing out of one AT&T’s vendors as part of the Co’s wireless transformation; AT&T expected “some level” of payment related to the occurrence and still plans to hit its original guidance

Verizon & AT&T’s Postpaid Phone Net Adds Topped Estimates (For The Fifth Straight Qtr!) With Second Lines Helping The Former

- Verizon – Postpaid phone net adds beat estimates and showed a “big improvement y/y and seq”: Total retail postpaid phone net adds of +156k in Q2 (up from +8k the prior yr qtr and -68k in Q1) topped cons by a wide +46.5%

- Consumer postpaid phone net losses were better than feared: Declined -8k (vs -136k the prior yr qtr and -158k in Q1) beat cons’ -22k

- Growth in Consumer phone gross adds accel’d seq due to second lines: Consumer postpaid phone gross adds were up +12.0% y/y (vs +5.3% y/y in Q1), the Co’s sixth straight qtr w/ y/y gross add growth

- Excluding contributions from second numbers, gross adds grew +5% y/y: Last qtr, the Co disclosed that second line add-ons comprised a ~+lsd% of total gross adds

- Lower upgrade activity cont’d to weigh on volumes: The Co’s wireless retail postpaid upgrade rate dropped -30bps to 2.4% in Q2 (vs 2.5% in Q1), w/ total upgrades falling nearly -13% y/y; Believes “excitement around AI” could provide a boost to upgrade volumes “over time”

- Reiterated that “positive” postpaid phone net adds are expected in Consumer for the yr: Notably, this will come without the contribution from the Co’s second line offering; Verizon has been seeing improving postpaid phone net adds heading into H2:24

- Growth in Consumer phone gross adds accel’d seq due to second lines: Consumer postpaid phone gross adds were up +12.0% y/y (vs +5.3% y/y in Q1), the Co’s sixth straight qtr w/ y/y gross add growth

- The Co has been “performing extremely well in Business”: Q2 Business postpaid phone net adds rose +8.3% y/y (vs -33.8% y/y in Q1) and came in +38.1% ahead of cons; Saw a “strong seq improvement” in phone net adds across SMBs as well as enterprise and public sector customers

- Churn stepped down seq, as projected: Total retail postpaid phone churn was up +2bps y/y to 0.85% (but down from 0.89% in Q1), matching cons estimates; Verizon believes the majority of its pricing churn is now behind it and continues to expect 2024 consumer postpaid churn to be flat or slightly better y/y

- Consumer postpaid phone net losses were better than feared: Declined -8k (vs -136k the prior yr qtr and -158k in Q1) beat cons’ -22k

- AT&T – Postpaid phone net adds outperformed forecasts, increasing both seq and y/y: Q2 postpaid phone net adds grew +28.5% y/y to +419k (vs +349k in Q1) and beat cons by a wide +48.0%

- “The story really isn’t a whole lot different than it’s been” …: AT&T has been “intercepting customers and channels” where the Co believes it “can make a difference and… add them profitability”; Believes its intercept channels have “gotten a little bit stronger”

- … Though AT&T has been “growing a little bit faster in the biz segment” vs consumer: The Co has been “doing better in some of the govt public safety/first responder structures”; Also benefited from gaining large enterprise relationships

- FirstNet now has 6mn+ total connections: Saw “sustained growth” in FirstNet this qtr

- Postpaid phone net adds have been outpacing last yr’s levels: Despite “ongoing wireless mkt normalization”, the Co delivered +768k net adds in H1:24 compared to +750k in H1:23

- … Though AT&T has been “growing a little bit faster in the biz segment” vs consumer: The Co has been “doing better in some of the govt public safety/first responder structures”; Also benefited from gaining large enterprise relationships

- Postpaid upgrade rates dropped seq, though less than feared: Q2 postpaid upgrade rate of 2.9% (vs 3.1% the prior yr qtr and 3.0% in Q1) was still above cons’ 2.8%; Seasonality was one factor, as “there’s a little bit of suppression that occurs a month or two” handsets are released in the mkt

- BUT the Co anticipates “higher activity levels” in H2:24: This will be “driven by the availability of new devices and features, seasonal purchasing activity, and promo cycles”; “If customers decide that there’s meaningful features in the new devices, [AT&T is] going to respond to it”

- Postpaid phone churn stepped down further seq: Postpaid phone churn fell -9bps y/y to 0.70% in Q2 (vs 0.72% in Q1) and was better than cons’ 0.72%; Converged products have helped “keep customers in the fold”, and similar to last qtr, this is expected to be an industry-leading figure at the time of reporting

- “The story really isn’t a whole lot different than it’s been” …: AT&T has been “intercepting customers and channels” where the Co believes it “can make a difference and… add them profitability”; Believes its intercept channels have “gotten a little bit stronger”

Gains In ARPU/ARPA Were Driven By Higher Value Plans

- Verizon – Postpaid ARPA slightly missed expectations: Q2 total wireless retail postpaid ARPA of $161.20 was up +4.3% y/y (vs +6.2% y/y in Q1) and ended -0.2% below cons

- “myPlan helps drive ARPA growth”: Specifically, through “premium mix adoption and perk rev”; There is further upside in ARPA ahead w/ the percentage of Verizon’s customers using myPlan is expected to “expand meaningfully going forward”

- AT&T – Postpaid phone ARPU was higher than projected: Postpaid phone ARPU of $56.42 grew +1.4% y/y (vs +0.9% y/y in Q1) and beat cons by +0.5%; Upside was “largely driven by higher ARPU on legacy plan[s]”

- The Co still expects “modest” ARPU growth this yr: And it anticipates “greater benefits” from its annc’d pricing actions in Q4 vs Q3

Prepaid – It Was A Tale Of Two Cities W/ The End Of ACP, But Impacts Are In The Rear View Mirror

- Verizon – Prepaid net losses were worse than anticipated w/ ACP ending: Total prepaid net losses of -694k in Q2 (up from -304k loss the prior yr qtr and -216k in Q1), was much worse than cons -294k; The Co had -410k losses related to the conclusion of ACP, the vast majority of which were under the SafeLink brand

- BUT Without SafeLink and the impact from ACP, Verizon would have experienced -12k prepaid net losses

- The impact of ACP’s conclusion on wireless svs rev has been in line w/ forecasts: Last qtr, Verizon indicated the end of ACP would create up to a -50bps headwind to wireless svs rev, and the Co is “tracking inside of that number right now”

- Outlook – Verizon sees “stronger performance” in prepaid in H2:24: “Visible and Total Wireless continue to expand and perform well”, Verizon’s operational execution w/ Straight Talk “continues to improve”, and the “vast majority” of ACP disconnects are now behind the Co

- AT&T – Prepaid phone net adds beat projections: Q2 prepaid net adds of +82k (vs +167k the prior yr qtr and +1k in Q1) beat cons by +3.5%; Prepaid churn of 2.57% was up from 2.50% the prior yr qtr but down from 2.77% in Q1

- As expected, there was “a little bit of an impact” from ACP’s conclusion: There were “some adjustments that were made” as the Co has already transitioned “the vast majority” of its customers, but these effects have been tracking in line w/ expectations to not be “material or significant”

Promotional Environment – The Telcos Appear To Be Avoiding A Race To The Bottom

- Verizon has had a “very disciplined model when it comes to promos”: The Co has been “very consistent” about evaluating price oppties and “aligning price w/ the value proposition for customers”

- 30%+ of Verizon customers have myPlan: The Co has been seeing “an incredible adoption rate”, as myPlan’s ability to provide “the most personalized offerings in the industry… deeply resonates w/ customers”

- myHome will incorporate the myPlan’s features to home internet: Thinks this will make the Co’s FWA biz “even stronger”

- Verizon Business Complete just launched as a “new way to serve [the Co’s] SMBs”: Verizon Business Complete is “the industry’s only end-to-end smartphone mgmt system”, and all of the offerings new tiers are “accretive in value” but also give Verizon’s customers better svs

- AT&T maintained its “balanced” go-to-mkt strategy: The Co has demonstrated that it will work w/ customers on a qtr-to-qtr basis to “tweak” its go-to-mkt strategy to make them more successful, instead of driving a race to the bottom w/ “very aggressive, low-ball national offers w/ low-price entry points”

- The Co is “getting incrementally better q/q” at mkting its converged svs: The Co will “continue to take that where [it] can as long as [it] can take it profitably”

- Higher mkting spend is expected in Q3 vs last yr: As AT&T looks to capitalize on higher expected activity levels in the handset mkt in the back half of the yr

Broadband – Low Moving Activity Remains A Headwind But FWA Continues To Be A Key Growth Area

- Verizon is “still taking share” in broadband & FWA beat expectations: Total broadband net adds of +391k were down -6.5% y/y in Q2 (vs -11.0% y/y in Q1) but beat cons by a wide +63.1%; This was Verizon’s eighth consecutive qtr w/ over +375k broadband net adds

- The overall broadband mkt is “very healthy”, despite persistently low move activity: The Co “continue[s] to see healthy demand for reliable broadband, even in the seasonally softer qtr”

- “FWA remains a key driver”: Q2 FWA net adds were down -1.6% y/y (vs -9.9% y/y in Q1) but finished +3.4% above cons thanks to performance in Business; The Co now has 3.8mn FWA subs and is nearing is target of 4-5mn by 2025; It will revisit this target after hitting the range

- Consumer FWA net adds improved seq but missed expectations: Consumer FWA net adds fell -13.1% y/y to +218k in Q2 (vs +203k in Q1) and ended -1.2% behind cons; Along w/ the healthy environment, Verizon has been finding the “right balance” between price and volume

- Verizon Business set a “qtrly record” for FWA net adds: Q2 Business FWA net adds grew +20.3% y/y to +160k (vs +151k in Q1) and beat cons by +15.8%; Demand is “strengthening” as SMBs and enterprises continue to trust its reliability as well as the speed and ease of deployment

- Fios net adds were lower than projected: Q2 Fios net adds fell -48.1% y/y to +28k (vs +53k in Q1), missing cons by -37.0%; Noted a “slight impact” from ACP ending and lower move activity

- AT&T – Broadband net adds were slightly down seq and below expectations: Broadband net adds of +52k in Q2 (vs the prior yr qtr’s -35k and Q1’s +55k) and missed cons by -15.2%; This was the fourth consecutive qtr that the Co has added broadband subs, and the trend is expected to continue

- Broadband rev growth dipped down seq: Q2 broadband rev incr’d +7.0% y/y (vs +7.7% y/y in Q1), as Fiber rev grew +17.9% y/y and offset a -9.0% y/y drop in non-fiber rev (vs -8.2% y/y in Q1)

- Broadband rev growth of over +7% is still projected for FY24

- Fiber net adds were below the Street’s estimates and declined seq: Fiber net adds were down -4.8% y/y in Q2 (vs -7.4% y/y in Q1) and ended -3.9% behind cons; Flagged that the “three primary drivers of net add variability” are the pace of new Fiber deployments, overall broadband mkt dynamics, and seasonality

- Fiber ARPU cont’d to trend upward: Fiber ARPU of $69.00 rose +3.4% y/y in Q2 (vs +4.1% y/y in Q1), as intake ARPU remained above $70

- The broadband mkt has “remained fairly stable”: “Moves are continuing to be a bit suppressed” and beyond normal seasonality, there was “a little bit” of an impact from ACP ending

- Seasonal headwinds are expected to reverse moving forward: Given that Q3 “typically has favorable seasonality” relative to Q2

- Internet Air, AT&T’s FWA product, has seen “early success”: Internet Air is now in parts of 137 mkts, w/ +139k consumer subscribers added in Q2, bringing the product’s total base to nearly 350,000 customers

- The Co isn’t offering Internet Air everywhere to consumers…: AT&T wants to be selective about how it does FWA and plans to use it to help transition customers off of legacy technologies

- … But will make it available nationwide for bizs: Feels “very comfortable” in a nationwide offer for bizs, given that AT&T can acquire the “right customer” that it can “profitably add… to other portfolios”

- Broadband rev growth dipped down seq: Q2 broadband rev incr’d +7.0% y/y (vs +7.7% y/y in Q1), as Fiber rev grew +17.9% y/y and offset a -9.0% y/y drop in non-fiber rev (vs -8.2% y/y in Q1)

AT&T Sees Convergence As An Integral Part Of its Strategy Though Verizon Sees Some Comparative Market Limitations

- Verizon has seen “some uptick” on fixed-mobile convergence: The Co has “economics on wireless and broadband” and continues to see converged products as an “oppty” if customers want them

- BUT it is unlikely the US will reach European levels of convergence: Given that the nature of the mkt is different in Europe vs the US; Nonetheless, Verizon does the see the US moving “further into convergence” to some degree

- The Co’s initial C-band mkts continue to outperform other ones: Reiterated that C-band mkts see better gross add growth, higher uptake of premium svs, and lower churn

- Verizon doesn’t believe in “sort of discounting” its converged product

- AT&T is on a “clear path to becoming the leading provider of converged 5G and fiber svs”: The Co has a “proven ability to drive higher share in both Mobility and Broadband through converged svs penetration”, which is “the true benefit of owning and operating both 5G and Fiber networks at scale”

- “Consumers increasingly prefer to purchase Mobility and Broadband together as a converged svs”: AT&T “believe[s] the success of [its] Fiber biz is driving growth in Mobility and vice versa” in this environment

- Nearly 4 out of every 10 AT&T Fiber households choose AT&T as their wireless provider”: Consequently, the Co’s share of postpaid phone subscribers within its fiber footprint is ~+500bps higher than its national avg

- The ability to sell Fiber to mobile customers has driven faster than anticipated Fiber penetration: Based on publicly available data, AT&T has been able to achieve key penetration milestones “considerably faster” than fiber providers that do not operate wireless networks

- The Co can also reach new broadband customers through its “substantial mobile distribution channels”

- The cont’d expansion of AT&T Fiber will “drive significant growth w/ converge customers”: As a result, the Co sees “a long runway of growth w/ 5G and Fiber together”

Investment Plans Will Support Future Growth

- Verizon’s “network build remains ahead of schedule”: Have deployed C-band on almost 60% of planned sites; As the Co deploys more, this will also open more FWA oppties; The Co has a “great network that can ingest more customers over time”

- Verizon is continuing to expand C-band in suburban and rural areas: Gross adds have been up threefold in mkts w/ C-band

- Verizon’s initial C-band mkts have been outperforming other ones: The Co has been seeing “better gross add growth, higher uptake of premium svs, and lower churn” in its C-band mkts

- Nearly 50% of Verizon’s network traffic is now running on 5G Ultra Wideband: This compares to 36% a yr ago; This percentage will continue to grow as the Co expands its C-band reach

- The previously annc’d partnership w/ AST SpaceMobile will further enhance the Co’s coverage: AST SpaceMobile will provide satellite-to-device connectivity using 850 MHz spectrum and help bring Verizon’s network to unserved communities

- Verizon is continuing to expand C-band in suburban and rural areas: Gross adds have been up threefold in mkts w/ C-band

- AT&T sees “attractive oppties” to expand its fiber network outside its traditional footprint: Including through the cont’d scaling of its Gigapower JV and via capital-light arrangements w/ other providers of commercial open access fiber networks

- The Co is still on track to pass 30mn+ Fiber locations by the end of 2025: AT&T also reiterated that the “better-than-expected returns” on its Fiber investments thus far potentially expands its initial build targets by another ~10-15mn locations

- O-RAN will allow for a “more efficient growth of capacity” in the network moving forward: The Co is aiming to break out the small cell mkt to create a multi-vendor environment; Combined w/ its dense fiber assets, this could be a “match made in heaven” to deal w/ growth in a more cost-effective way

Q2 CapEx Was Broadly Lower Than Projected But Both Co’s Reiterated Their Previous Full-Year Guidance

- Verizon – CapEx levels were lighter than expected, as the Co returns to historic levels of CapEx intensity: Q2 CapEx fell -10.1% y/y to $3.7bn (vs $4.4bn in Q1) and beat cons by +13.7%; Verizon’s H1:24 CapEx spend was -$2bn less than H1:23’s total

- Reiterated FY24 CapEx guidance of $17-17.5bn

- AT&T – CapEx was up y/y but below the Street’s estimates: CapEx incr’d +1.2% y/y in Q2 (vs -13.3% y/y in Q1) but was still +14.2% better than cons; AT&T’s “investment-led strategy” has made it the largest capital investor in the US connectivity infrastructure space since 2019

- Reiterated FY CapEx guidance of $21-22bn: Higher spending in H2:24 will be driven by the Co’s efforts to ramp its wireless network modernization

Lower Capx Helped Drive Better FCF / Capital Allocation Plans Are Broadly InLine

- Verizon – FCF topped estimates: FCF of $5.8bn was up +3.0% y/y in Q2 (vs +16.2% y/y in Q1) and closed +0.7% above cons; Outlined its three capital allocation priorities as follows –

- The Co expects to “generate strong cash flow in the back half of the yr” to support paying down debt: Verizon continues to work toward its long-term target of 1.75-2x net unsecured debt to consolidated adj EBITDA (currently at 2.5x)

- The dividend is “very important”: The Co has been growing its dividend for 17 consecutive yrs, and mgmt is “committed to continue to [putting] the Board in a position to do that”

- Verizon won’t consider buybacks until it gets to a 2.25x net unsecured debt to adj EBITDA ratio

- AT&T – FCF finished well ahead of forecasts: Q2 FCF of $4.6bn grew +8.7% y/y (vs +34.1% y/y in Q1), beating cons by +10.8%; Cited “sustained growth in adj EBITDA, improved conversion of EBITDA into FCF, and lower capital investment as the main drivers

- H1:24 FCF grew +48.1% y/y to $7.7bn: This is “consistent w/ [AT&T’s] goal of driving more ratable FCF”

- FY24 FCF is still expected to between $17-18bn

Other Highlights – Thoughts On AI + AT&T’s Comments On The Recent Data Breach

- Verizon sees itself as a “backbone of the AI economy and the partner of choice for players in the space”: Cited its “portfolio of high-performance spectrum, the capacity of [its] fiber, and [its] ability to deploy and support mobile edge compute”

- The Co is “already seeing the benefits of AI in [its] operations”: The Co has four gen AI products being used by its 40,000 agents to work more efficiently and provide more personalization for customers; “AI is an enabler of efficiencies”

- AT&T is unsure whether “there’s something compelling in this [upgrade] cycle”: “There’s a lot of ways you can experience AI without having to necessarily change out hardware”, and “there have been other AI devices that have come into the handset ecosystem over the last couple months” that haven’t been “world-changing”

- AT&T – “The threat environment we’re in is a really, really difficult environment”: The Co believes “it’s going to get probably more difficult”, given “some of the geopolitical dynamics that are going on”; “Everybody’s dealing w/ this problem”, and AT&T has “handled it about as well as [it] can going through it”

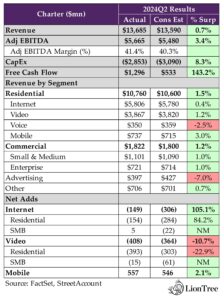

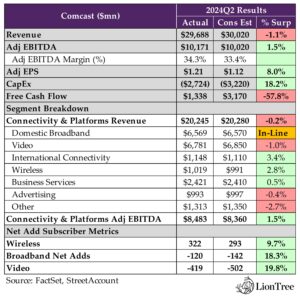

Connectivity: Part II – Cable Companies Are Weathering The ACP Storm Better Than Expected

Alongside the telco incumbents’ prints this week (see Theme #3), the cable sector was also active with earnings, and Comcast and Charter’s Q2 results shed some light on the aftermath of ACP’s conclusion as well as on some of the competitive dynamics in the ongoing convergence battle across the connectivity space. Given that the cable companies, and especially Charter, “put a lot of effort” into ACP, the Street was anticipating a sizable sequential uptick in their broadband net losses during the quarter. However, this wasn’t necessarily the case. While consensus expectations called for -448k broadband net losses combined in Q2, Comcast and Charter only collectively lost a net -269k, as their proactive efforts to manage churn after the program’s end mitigated the impact of the transition more than anticipated. Otherwise, beyond ACP-related impacts, the cable companies highlighted a broadband market that has remained relatively slow due to a lack of moving activity as well as “intensely competitive”, with both fiber overbuilders and fixed wireless continuing to knock on their doorsteps. Moreover, “the bulk” of non-pay churn from former ACP recipients is expected to occur in Q3, so it looks like the cable companies still have some work cut out for them on the broadband front in the near term.

Alongside the telco incumbents’ prints this week (see Theme #3), the cable sector was also active with earnings, and Comcast and Charter’s Q2 results shed some light on the aftermath of ACP’s conclusion as well as on some of the competitive dynamics in the ongoing convergence battle across the connectivity space. Given that the cable companies, and especially Charter, “put a lot of effort” into ACP, the Street was anticipating a sizable sequential uptick in their broadband net losses during the quarter. However, this wasn’t necessarily the case. While consensus expectations called for -448k broadband net losses combined in Q2, Comcast and Charter only collectively lost a net -269k, as their proactive efforts to manage churn after the program’s end mitigated the impact of the transition more than anticipated. Otherwise, beyond ACP-related impacts, the cable companies highlighted a broadband market that has remained relatively slow due to a lack of moving activity as well as “intensely competitive”, with both fiber overbuilders and fixed wireless continuing to knock on their doorsteps. Moreover, “the bulk” of non-pay churn from former ACP recipients is expected to occur in Q3, so it looks like the cable companies still have some work cut out for them on the broadband front in the near term.

Convergence also remains an integral part of Comcast and Charter’s growth strategies, and this was reflected in the stronger than expected performances of their wireless businesses in Q2. The cable companies introduced new pricing plans and converged offers that helped drive a sequential improvement in both of their wireless net adds during the quarter. Comcast gained a net +322k wireless accounts (vs +289k in Q1) and Charter added a net +557k (vs +486k in Q1). Notably, this was also Charter’s “highest port-ins quarter ever” and the first time that the company’s standalone mobile EBITDA was positive. Looking ahead to the back half of the year, there is still much for the cable companies to be “optimistic” about as well. In addition to the upcoming handset upgrade cycle, Comcast and Charter’s mobile product remains “under-penetrated” relative to their overall broadband customer bases, providing their wireless net adds plenty of runway to continue growing as they continue on the path to “establishing a mobile business that is very profitable”.

The cable companies’ results on the video sides of their businesses were more of a mixed bag relative to forecasts. Comcast’s video net losses improved sequentially to -419k and beat consensus estimates by +19.8%, while Charter’s -408k video net losses were slightly worse than Q1’s total and missed cons by -10.7%. Pricing appeared to be one of the main drivers, as Comcast took “slightly less” of a rate increase in its video products this year compared to last year, but Charter‘s decision to pass through increases in programming rates resulted in higher downgrade churn. In particular, this seemed to have an outsized effect on customers coming off ACP, who increasingly prioritized affordability without their monthly internet subsidies. Nonetheless, Charter indicated that the “DTC take-up is going very well”, and the ability to offer hybrid linear-streaming bundles could help slow losses and retain value in its video business on the road ahead.

The big news on the capital allocation front was that Charter trimmed its FY24 CapEx by ~-$300mn at the mid-point to ~$12bn. The company pointed to lower CPE costs from lower than anticipated Internet and Video net adds as the main reason for the reduction. Along with expectations of accelerating EBITDA growth in the back half of the year, this should position Charter well from a FCF standpoint in H2:24 and help it build off of stronger than expected FCF numbers in Q2. For its part, Comcast’s more disappointing FCF performance in Q2 appeared to be tied to a one-time, over +$2bn increase in cash taxes associated w/ the previous payment it received for its stake in Hulu. See below for what we thought was most incremental from Comcast and Charter’s Q2 prints…

-> Comcast shares were down -2.6% in response to the print but recovered slightly to close the week down -1.0%; Charter shares jumped +16.6% in reaction to earnings, finishing the week up +14.8%; YTD, Comcast stock is trading down -9.5% and Charter stock is still down -5.4%

–> On a related note, Consumer Reports’ ISP survey of more than half of its 48k members revealed this week that fiber-optic internet svs received higher overall satisfaction scores than cable-internet providers; Greenlight Networks, EPB, Allo Fiber, Google Fiber, GoNetSpeed, and Sonic all had overall satisfaction scores that landed in the top ratings tier; Scoring worst were satellite broadband providers Viasat Internet and HughesNet, as well as Comcast Xfinity, CenturyLink’s Lumen, Mediacom’s Xtream, and Altice’s Optimum (link)

Comcast & Charter’s Headline Results Diverged In Some Key Areas

- Comcast printed mixed headline results, as rev missed but adj EBITDA surpassed estimates: Consolidated rev dropped -2.7% y/y in Q2 (vs +1.2% y/y in Q1), falling -1.1% short of cons; Consolidated adj EBITDA was down -0.7% y/y (vs -0.6% y/y in Q1) and topped cons by +1.5%; FCF missed cons by a wide -57.8%

- Connectivity & Platforms (~83% of total adj EBITDA) – Mixed: Q2 rev was down -0.7% y/y (vs +0.6% y/y in Q1) and slightly missed cons by -0.2%; Adj EBITDA grew +1.6% y/y (vs +1.3% y/y in Q1) and beat cons by +1.5%; Residential rev missed cons by -0.3%, while Business Services rev ended +0.5% ahead of cons

- In terms of KPIs, wireless, broadband, and video net adds were better than the Street expected

- Connectivity & Platforms (~83% of total adj EBITDA) – Mixed: Q2 rev was down -0.7% y/y (vs +0.6% y/y in Q1) and slightly missed cons by -0.2%; Adj EBITDA grew +1.6% y/y (vs +1.3% y/y in Q1) and beat cons by +1.5%; Residential rev missed cons by -0.3%, while Business Services rev ended +0.5% ahead of cons

- Charter – Headline numbers broadly exceeded expectations: Q2 rev was up +0.2% y/y (vs +0.2% y/y in Q1) and beat cons by +0.7%; Adj EBITDA rose +2.6% y/y (vs +2.8% y/y in Q1), topping cons by +3.4%; FCF finished a wide +143.2% above cons; Internet net losses and Mobile net adds beat, but Video net losses missed

- Residential rev (~79% of total rev) – Beat: Residential rev was down -0.6% y/y in Q2 (vs -0.4% y/y in Q1) but still closed +1.5% ahead of cons; Customer relationships fell -1.3% y/y (vs -0.7% y/y in Q1), while monthly rev per customer grew +0.4% y/y (vs -0.1% y/y in Q1)

- Commercial rev (~13% of total rev) – Beat: Q2 Commercial rev incr’d +2.1% y/y (vs +1.3% y/y in Q1) and beat cons by +1.2%; SMB rev grew +0.6% y/y (vs -0.3% y/y in Q1), and Enterprise rev rose +4.5% y/y (vs +3.8% y/y in Q1)

The Broadband Market Has Been Under More Pressure As Of Late

- Comcast – “The environment for broadband subscribers remains intensely competitive”: This is “particularly felt” at the lower end of the mkt, w/ more “price conscious” customers; However, competition is “no worse” and “no better” than the Co has seen over the past couple of qtrs

- 50% of Comcast’s territories have now been overbuilt by fiber: Expects to be at 60% by yr-end

- Charter – “The broadband mkt actually shrunk as a one-time event”: Growth in the broadband mkt was still “significantly reduced” in Q2 for similar reasons as in Q1, as low move activity, rental vacancies, and the loss of ACP resulted in the mobile-only broadband category reverting back to pre-pandemic levels

- This impact is “temporary”, but “it’s hard to predict exactly when”: Believes that the mkt will go back to “a much more normalized environment” when moves come back, housing starts return, and once the ACP impact between Q2 and Q3 is flushed out

- “The lack of ACP will also drive higher levels of mkt churn… over time”: Sees more switching oppties as “more customers [come] in and out of broadband based on affordability”; There will be more transaction volume from a non-pay disconnect and gross adds perspective

- The Co has been facing a “challenging competitive environment”: Competitive overbuilds have cont’d at a “steady pace”, if not “slightly lower” than what it has been; Reiterated that “cell phone Cos will face challenges as the consumer bandwidth demands continue to grow”

- This impact is “temporary”, but “it’s hard to predict exactly when”: Believes that the mkt will go back to “a much more normalized environment” when moves come back, housing starts return, and once the ACP impact between Q2 and Q3 is flushed out

Despite A Difficult Operating Environment, Broadband Net Losses Weren’t As Bad As Predicted

- Comcast – Broadband net losses were better than feared, though seasonally worse seq: Domestic broadband net losses of -120k in Q2 (vs -19k the prior yr qtr and -65k in Q1) beat cons’ -142k; The Co lost a net -110k residential customers (vs -55k in Q1) and -10k biz customers (vs -10k in Q1)

- There was “traditional negative seasonality” during the qtr: When combined w/ intense competition, these factors resulted in the -120k subscriber losses;

- BUT Q3 should be a seasonally stronger qtr: Indicated that “the same things that were headwinds in Q2 largely become tailwinds” moving forward in Q3

- Business Services benefited from “faster growth in mid-mkt and enterprise” …: That has been mainly driven by an increase in customers, as the Co has been investing into this space to build sales & fulfillment and expand its capabilities in other value-added svs

- While the SMB mkt “remains competitive: The Co has been competing aggressively in SMB and driving higher ARPU by pushing additional products that expands its relationships w/ SMBs

- ACP ending had a “minimal impact” on subscriber growth in Q2 but will affect Q3 numbers: “The bulk” of ACP-related subscriber churn is projected in Q3, w/ the “biggest impact” being on non-pay churn

- Otherwise, voluntary churn “continues to perform very well”: Cited Comcast’s superior network, along w/ its better products and extreme focus on competition

- There was “traditional negative seasonality” during the qtr: When combined w/ intense competition, these factors resulted in the -120k subscriber losses;

- Charter – Broadband net losses weren’t as steep as projected w/ ACP’s conclusion: Q2 total Internet net losses of -149k (vs +77k the prior yr qtr and -72k in Q1) were a wide +105.1% ahead of cons; Residential Internet net losses of -154k beat cons by +84.2%, and SMB Internet net adds of +5k came in ahead of cons’ -22k

- There was a “significant drop y/y” in the pool of available gross adds: Given the impact from losing ACP on top of “an already low level” of “overall mkt connect volume”; Q2 also “tends to be a seasonally weaker qtr”

- BUT Charter “performed better” on competitive switching on a seq and y/y basis: As the Co “competed well compared to previous qtrs against both wireline overbuild and cell phone internet, each w/ expanded footprints”

- The Co also posted +36k net adds in its subsidized rural footprint: Compares to +35k in Q1

- ACP-related net losses were “well over” -100k: ~Half was from voluntary churn, while the other half was from lower gross adds, particularly from the “low income segment that had been connecting at a higher rate”

- There will be more ACP-related non-pay disconnects in Q3: “The reality is that the ACP-related non-pay disconnect activity hasn’t started yet”; There will be “sustainable payment trends” through Aug, w/ the “non-pay beginning then and trailing… a little bit into Q4”

- “Overall churn remains at low levels, even w/ the end of the ACP program”: Although “the loss of ACP impacted… churn”, the Co has “retained the vast majority of ACP customers so far”; “Built-in savings” from the Co’s converged bundles and subsidies for former ACP recipients have helped

- There is some momentum heading into Q3: Indicated June was the “best loss” of Q2 and that Internet net adds in July have trended similarly

- There was a “significant drop y/y” in the pool of available gross adds: Given the impact from losing ACP on top of “an already low level” of “overall mkt connect volume”; Q2 also “tends to be a seasonally weaker qtr”

ACP’s Conclusion Was A Headwind To ARPU Growth

- Comcast – ARPU growth decel’d seq but was within the Co’s historical range of +3-4% y/y: Q2 broadband ARPU growth of +3.6% was down from Q1’s +4.2% y/y rate; Despite the downtick, the Co remains focused on effectively balancing rate and volume via customer segmentation

- There was a “little bit” of impact on ARPU from ACP’s conclusion: Consistent w/ Comcast’s approach to normal promo roll-offs, the Co worked w/ customers coming off ACP and migrated them to different products and price levels

- The Co has a “good ability” to increase ARPU on the biz side as well: Comcast is aiming to attach new products to biz relationships as part of transitioning to a “full, managed relationship basis”

- Charter – Residential ARPU growth returned to positive territory: Resi monthly ARPU incr’d +0.4% y/y in Q2 (vs -0.1% y/y in Q1), as promo rate step-ups, rate adjustments, and the growth of Spectrum Mobile were partly offset by a higher mix of non-video customers and lower-priced video packages, plus some Internet ARPU compression

- The end of ACP weighed on Internet ARPU growth: Internet ARPU grew +1.7% y/y in Q2 (flat w/ Q1’s rate), though excluding a $30mn one-time, non-ACP-related charge as well as the impact of extending retention offers to former ACP recipients, Internet ARPU would have risen +2.7% y/y

- The Co’s rev recognition policy for certain post-ACP customers also resulted in “slightly less rev”: For customers w/ a low likelihood to pay after the end of ACP, the Co has been recognizing rev on a cash basis, resulting in slightly lower rev and less bad debt

Go-to-Market Color – New Converged Offers Have Been Gaining Traction

- Comcast’s go-to-mkt strategy in broadband has been “consistent”: The Co has maintained its approach of “striking the right balance between rate & volume and relying heavily on mkt segmentation

- Enhancing offers for the price conscious segment has been a key focus: In Q2, Comcast launched the NOW line of products, which provide internet, mobile, and streaming TV offerings w/ “attractive” all-in pricing w/ no contracts or credit checks; However, it is still too early to gauge the mkt reception to these

- BUT the “vast majority” of Comcast’s base subscribes to more premium products: Consequently, the Co views fiber as its “true long-term competitor” instead of FWA

- Internet Essential tiers have helped mitigate ACP-related losses: Through these plans, customers can get a free line of Xfinity mobile for a yr, and ACP customers get an addt’l free unlimited line for a yr

- The Co has a new, upcoming converged offer that will be tied to the Olympics: The Co has a “great offer” coming that will offer customers the ability to tie broadband and mobile together

- Enhancing offers for the price conscious segment has been a key focus: In Q2, Comcast launched the NOW line of products, which provide internet, mobile, and streaming TV offerings w/ “attractive” all-in pricing w/ no contracts or credit checks; However, it is still too early to gauge the mkt reception to these

- Charter is “very well-positioned competitively” w/ its converged bundle of products: The Co has “cont’d to improve [its] selling capabilities” by rolling out new offers but doesn’t “intend to be in the biz of subsidizing phones”

- Customers increasingly opted for the $40 Unlimited Plus package over the $30 option: New value-added features such as Anytime Upgrade, which allows Unlimited Plus customers to upgrade their phones whenever they want, has helped

- Other new value-added svs have been driving higher take rates: Including the $5/mo repair and replacement plan as well as the phone balance buyout program, where the Co will pay off a switcher’s existing phone lines on purchases of 3-5 lines for up to $2,500

- Spectrum One also “continues to perform well at both connect and at promo roll off”: This is expected to carry into the back half of the yr and drive accel’ing EBITDA growth

- The Co also has a “number of products & offers to assist those that have lost their ACP subsidy”: Including the Spectrum Internet Assist program, the Internet 100 product, and an offer of a free mobile line for one yr

- Customers increasingly opted for the $40 Unlimited Plus package over the $30 option: New value-added features such as Anytime Upgrade, which allows Unlimited Plus customers to upgrade their phones whenever they want, has helped

Charter Saw A Notable Uptick In Data Usage, While Comcast’s Numbers Were Flat Seq

- Comcast – Data usage continues to grow at a double-digit y/y rate: The Co’s broadband-only households consumed 700+ gigabytes of data each month, on avg, w/ ~70% of customers receiving 500+ Mbps speeds and ~one-third getting 1+ Gbps (these are all similar to numbers provided on Q1’s call)

- “These positive consumer trends… will only accel”: Given the shift of live sports to streaming, which when combined w/ entertainment on streaming accounts, accounts for nearly 70% of Comcast’s network traffic today

- 90% of Xfinity mobile smartphone traffic travels over Comcast’s Wi-Fi network: This demonstrates the importance of bundling converged products

- Charter – “Data usage continues to grow, and demand for faster speeds will grow w/ it”: In Q2, ~30% of residential, non-video Internet customers used 1TB+ of data per month (vs nearly 800GB per month reported in Q1)

- The Co also saw the “most additions to [its] gig speed tier ever”: This is area Charter can continue to grow

- 87% of Charter’s mobile traffic is delivered by its Wi-Fi network

Wireless Net Adds Were A Highlight For Both, Driven By New Promos & Pricing Plans

- Comcast – Wireless net adds returned to y/y growth and topped forecasts: Wireless net adds incr’d +1.9% y/y to +322k in Q2 (vs +289k in Q1) and exceeded cons by +9.7%; Comcast now has ~7.2mn total domestic wireless customers, a +20.3% y/y increase

- “Early success w/ new pricing plans launched in April” contributed to the accel in wireless lines: These were specifically targeted at multi-line customers, and the Co saw “cont’d traction” w/ its Buy One, Get One Line offer

- New converged offers also resulted in better overall yield and awareness: Also contributing to higher multi-line attach rates

- There are still “significant oppties” in wireless that Comcast will seek to capitalize on: Including increasing penetration of its domestic residential broadband base, which is currently at 12%, as well as selling more lines per account

- “Biz mobile is just getting going”: Mobile has been “front and center”, as the Co has been working on layering addt’l products and svs on its biz relationships

- Comcast is “optimistic” about a potential handset upgrade cycle: The Co is in a “good position” to be a “switching provider” when an upgrade cycle does occur, given its handset subsidies and trade-in program

- “Early success w/ new pricing plans launched in April” contributed to the accel in wireless lines: These were specifically targeted at multi-line customers, and the Co saw “cont’d traction” w/ its Buy One, Get One Line offer

- Charter – Mobile net adds improved seq and outpaced estimates: Q2 Mobile net adds fell -14.0% y/y to +557k (vs +486k in Q1) but topped cons by +2.1%; The Co’s total mobile lines ended the qtr up +32.9% y/y to 8.8mn

- Even excluding the benefit of ACP mobile-only retention offers, mobile net adds incr’d seq: Notably, this followed a “very strong” Q1, reflecting Charter’s general momentum” and its efforts to evolve the product w/ new offers and capabilities

- The Co also had its “highest port-ins qtr ever”

- Charter’s mobile product still “remain[s] under-penetrated”: ~8% of the Co’s total passings currently have its converged internet-mobile offering, despite it having “mkt-leading pricing at promotion and retail”

- Standalone mobile adj EBITDA was positive for the first time ever: This comes even when including the headwind of subscriber acquisition costs and without the benefit of GAAP rev allocation to mobile rev; Shows the Co is “on the path to establishing a mobile biz that is very profitable”

- Even excluding the benefit of ACP mobile-only retention offers, mobile net adds incr’d seq: Notably, this followed a “very strong” Q1, reflecting Charter’s general momentum” and its efforts to evolve the product w/ new offers and capabilities

The Cable Cos’ Combined Video Losses Were Less Steep Seq, Even W/ The ACP Impact

- Comcast – Video losses were not as bad as anticipated: Q2 video losses of -419k (vs the prior yr qtr’s -543k and Q1’s -487k) were better than cons’ -502k; The Co took “slightly less” of a rate increase vs last yr, and positioning video alongside broadband has helped as well

- BUT Video rev declines were worse than expected and steepened seq: Video rev fell -7.8% y/y in Q2 (vs -6.9% y/y in Q1), missing cons by -1.0%; Noted cont’d customer losses, coupled w/ slower domestic ARPU growth on a y/y basis

- Charter – Video net losses were ~flat seq but underwhelmed forecasts: Video net losses of -408k in Q2 (vs -200k in the prior yr qtr and -405k in Q1) missed cons by -10.7%; Resi net video losses of -393k missed cons’ -303k, while SMB net video losses of -15k were better than cons’ -61k

- The Video biz was impacted by downgrade churn: Driven by the programming and rate increases that the Co passed through, as well as former ACP customers making decisions based on affordability

- “The DTC take-up is going very well”: The Co began offering Disney+ Basic to its base in late Jan, and it’s been “growing every month”; ESPN+ is also seeing a “very good take-up”, and “penetration is going well”

- The Co expects to have a “fully baked set of product… over the next yr or so” …: The Co just launched ViX and plans to soon roll out Paramount+, Disney+ Premium, and the Disney Duo Basic bundle w/ Hulu; Addt’l features are on the way as well

- … Which will “even further accel the monthly growth”: “The more scale we get there, the more effective it’s going to be”

- The Co isn’t “going to arrest completely the loss of video”: The Video biz “may not be growing”, but “it’s still really important” and “can be very valuable to [Charter’s] converged connectivity relationships”

Expense Mgmt Efforts Have Been Expanding Margins

- Comcast – Connectivity & Platforms EBITDA margin expanded at a higher rate seq: Connectivity & Platforms EBITDA margin of 41.9% was up +90bps y/y (vs +30bps y/y in Q1) and topped cons’ 41.2%

- Residential EBITDA margin incr’d +100bps y/y to 39.9%: Driven by the cont’d mix shift to higher margin connectivity bizs and the Co’s ongoing expense mgmt; The only line expense that incr’d meaningfully over last yr was direct product costs, which are success-based

- … While Business Services EBITDA margin was down -70bps y/y to 57.0%: This reflected the Co’s investments in sales & fulfillment to scale in the mid-mkt and enterprise spaces

- Improvements in legacy cable margin were also more pronounced seq: Legacy domestic cable margin of 48.4% incr’d +110bps y/y in Q2 (vs +70bps in Q1)

- Residential EBITDA margin incr’d +100bps y/y to 39.9%: Driven by the cont’d mix shift to higher margin connectivity bizs and the Co’s ongoing expense mgmt; The only line expense that incr’d meaningfully over last yr was direct product costs, which are success-based

- Charter – Adj EBITDA margin was higher than anticipated and improved seq: Q2 adj EBITDA margin incr’d +100bps y/y to 41.4% (vs 40.2% in Q1) and beat cons’ 40.3%

- Expense breakdown:

- Programming costs fell -9.8% y/y (vs -8.2% y/y in Q1): Driven by -9.5% y/y decline in video customers as well as a higher mix of lighter video packages

- Growth in cost to svs customers declined -4.2% y/y (vs ~flat y/y in Q1): Productivity gains from longer-term investments in workforce & operations resulted in lower labor costs and bad debt expenses

- Sales & mkting expenses were up +1.9% y/y (vs -2.7% y/y in Q1): The Co remains focused on driving customer acquisition

- Adj EBITDA growth is still projected to accel in H2:24: Cited ongoing expense mgmt initiatives, Spectrum One promotional roll-off, and political ad rev

- Expense breakdown:

Investment Plans & Network Build-Outs Remain On Target

- Comcast has expanded its broadband network at the fastest rate in Co history over the last 12 months: The Co has added 1.2mn home passings in the last 12 months and “plan[s] to continue to do that”

- Mid-split deployments have cont’d: The Co now has deployed mid-splits in 42% of its footprint (vs 40% at the end of Q1) and expects to be at 50% by yr-end

- The DOCSIS 4.0 rollout is also “tracking very well”: Comcast has launched DOCSIS 4.0 in multiple mkts thus far but didn’t provide specifics on the final rollout

- The Co has also been virtualizing “huge parts of the network”: This will avoid future node splits

- BEAD is still being figured out on a state-by-state basis: Comcast is “optimistic in a lot of cases” but will “have to look for the guidelines and specifics tied to it”

- Mid-split deployments have cont’d: The Co now has deployed mid-splits in 42% of its footprint (vs 40% at the end of Q1) and expects to be at 50% by yr-end

- Charter’s converged network has been expanding: The Co has been growing its footprint w/ high ROI construction oppties in both rural and non-rural areas

- Network evolution initiatives cont’d: The Co has been upgrading its wireline network to have symmetrical and multi-gig speeds everywhere, and this will support “cont’d growth in data demand from customers and new applications, such as AR, VR, and AI”

- Rural passings seasonally picked up speed seq: The Co grew subsidized rural passings by +89k in Q2, which was above the seasonally slower Q1’s +73k; ~450k rural passings are still expected across 2024, a +50% y/y increase

- RDOF is still projected to be completed by the end of 2026: This would be two yrs ahead of schedule

- The Co’s network offers 43mn+ access points: This number will grow further w/ Charter and its partners’ ongoing Wi-Fi router and CBRS access point deployments

CapEx Spending Was Lower Than Projected Across The Cable Space

- Comcast – Connectivity CapEx fell significantly both seq and y/y…: Connectivity & Platforms CapEx fell -12.9% to $1.9bn in Q2 (vs $2.6bn in Q1), as lower spend on CPE and scalable infrastructure was partially offset by higher investments in line extensions and support capital

- … Which contributed to a wide +18.2% beat on overall CapEx (ie, lower than expected): A reduction in connectivity-related CapEx offset a +4.4% y/y increase in Content & Experiences CapEx, driven by investments in Theme Parks

- The Co “still feel[s] comfortable w/ the capital intensity envelope that [it] gave”: At the beginning of the yr, Comcast indicated that its historic 10% CapEx intensity level is not a constraint and that it would like to “move faster… to the extent [it[ can”

- Also, acknowledged “some timing aspects around equipment purchases within the yr”

- Charter – CapEx levels were relatively flat y/y and lower than expected: Q2 CapEx of $2.9bn was up +0.7% y/y (vs +13.3% y/y in Q1), beating cons by +8.3%; Spend on line extensions grew +3.4% y/y to $1.1bn, driven by while non-line extension CapEx fell -1.0% y/y

- Lowered the FY24 CapEx guide: Now anticipates full-yr CapEx of ~$12bn (vs $12.2-12.4bn prior), reflecting lower CPE costs associated w/ lower Internet and Video net adds, including from the impact of ACP ending

The Cable Cos Posted Similar FCF Levels, Though W/ Widely Different Outcomes Relative To Estimates

- Comcast – “Higher than usual” cash taxes caused a wide miss on FCF: Q2 FCF of $1.3bn was down -60.9% y/y (vs +19.4% y/y in Q1) and missed cons by -57.8%; FCF was impacted by cash taxes that were up +$2bn y/y and associated w/ the payment Comcast received for its Hulu stake and other tax-related matters

- Share buybacks took a step down seq: In Q2, the Co repurchased $2.2bn worth of stock compared to $2.4bn in Q1

- Charter – FCF expanded significantly y/y and far exceeded forecasts: FCF of $1.3bn was up +94.0% y/y in Q2 (vs -46.1% y/y in Q1) and came in a wide +143.2% ahead of cons; Y/Y growth was primarily driven by higher adj EBITDA, lower cash taxes due to timing, and a favorable change in working capital related to expense timing

- Other balance sheet moves have provided better cash flow and incr’d flexibility: The Co has sold its tower portfolio over the last several qtrs to generate almost $400mn in proceeds, launched an EIP securitization program in Q2, and has been working w/ vendors to extend payment terms

- Repurchases were down seq: In Q2, the Co bought back 1.5mn shares for $404mn (vs $567mn in Q1)

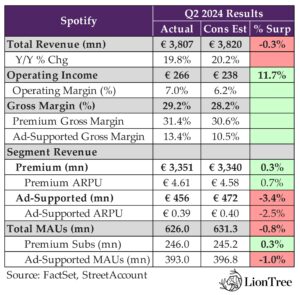

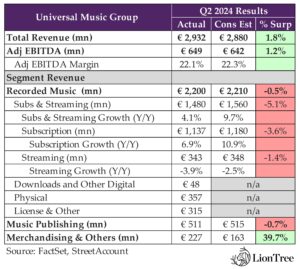

Investors Cheer Spotify’s Year Of Monetization + Better Paid Subscription Growth