It was a brutal week on many fronts. Guess how much the Magnificent 7 lost in market cap this week?? Almost $400bn. The market sell-off however spread beyond the big tech names and small caps, which have been outperforming, and took it on the chin with the Russell 2000 falling almost -7%. Emerging concerns about economic growth and a potential recession stemmed from weak employment and manufacturing data that was out this week. The move in Treasury yields was also a standout as the 10-yr yield has solidly dipped below 4%.

Aside from the consternation about the market and outlook, it was an insane earnings week with a huge swath of companies deciding to all report on Thursday night, making for a tough end to the week! Overall, 75% of S&P 500 have now reported.

See below for the key focus themes in this edition (all links are clickable):

- Earnings Scorecard - Week 3

- Digital Advertising – Part I: Meta Would “Rather Risk Building [AI] Capacity Before It Is Needed, Rather Than Too Late”

- Digital Advertising – Part II: Challengers PINS & SNAP Feel Some Heat

- Amazon’s Results Feed Into Worries About The Consumer

- Cloud Investments Should Support Strong Top-Line Growth Into H2

- Roku’s Diversification Strategy Is Starting To Bear Fruit

- Video Games – EA & Roblox Shined In Q2, But All The Focus Was On Their Near-Term Outlooks

- Apple Returns To A Path Of Positive Revenue Growth

- DraftKings Plans To Take To the Offensive In H2:24

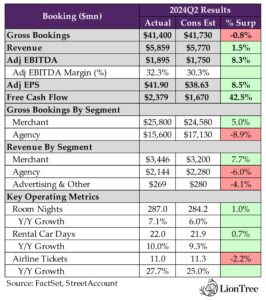

- Booking Confirms That The Travel Market Continues To “Normalize”

- Quick Takes On A Couple Other Key TMT Prints…Live Nation & T-Mobile

Be forewarned, this is a heavier than normal report!

Have a nice weekend and I’d love to hear about any additional thoughts you have a key updates, expectations, and themes as well. There was certainly A LOT to digest and make sense of.

Best,

Leslie

Earnings Scorecard - Week 3

A whopping 56 companies in the LionTree Universe reported their second quarter results this week, more than double the 23 companies that reported last week. Unlike last week, stock price reactions were biased to the downside, as 32 companies (57.1%) traded down in reaction to their results, while 24 companies (42.9%) traded up. Amwell was the best performer of the group, trading up +40.2% the day after it reported, while Snap was the worst performer, down -26.9% (see Theme #3).

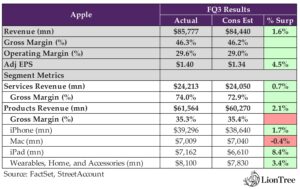

Along with Snap, Pinterest was the other digital advertiser to get hit post its print, falling -14.5% (see Theme #3). On the other hand, Meta traded up +4.8% after its results (see Theme #2). It was a big week for Big Tech, and market reactions were mixed, with Apple trading up +0.7% (see Theme #8), Microsoft trading down -1.1% (see Theme #5 for color on its Cloud business), and Amazon falling –8.8% (see Theme #5 for AWS results and Theme #4 for its core Consumer business).

There were also some key reports out of the interactive entertainment sector this week, with Electronic Arts and Roblox reporting and seeing divergent reactions, up +1.2% and down -6.4%, respectively (see Theme #7). Also in media but on the streaming/digital entertainment side was Roku, which fell -4.0% the day post its report (see Theme #6).

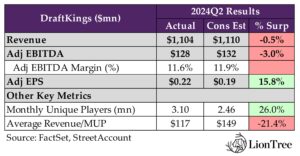

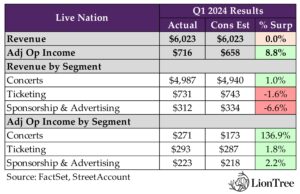

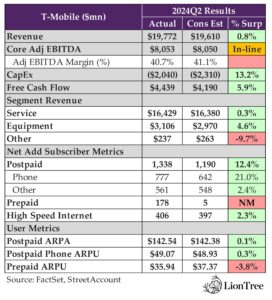

Booking Holdings kicked off online travel earnings this week and declined -9.2% (see Theme #10). DraftKings was also a key report out from the sports betting sector and fell -9.8% (see Theme #9). T-Mobile also finished out the big 3 connectivity reports this week and rose +3.9% (see Theme #11 for the quick hits), while Live Nation gave us a read into live entertainment trends and was up +1.7% (see Theme #11 for key points).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Digital Advertising – Part I: Meta Would “Rather Risk Building [AI] Capacity Before It Is Needed, Rather Than Too Late”

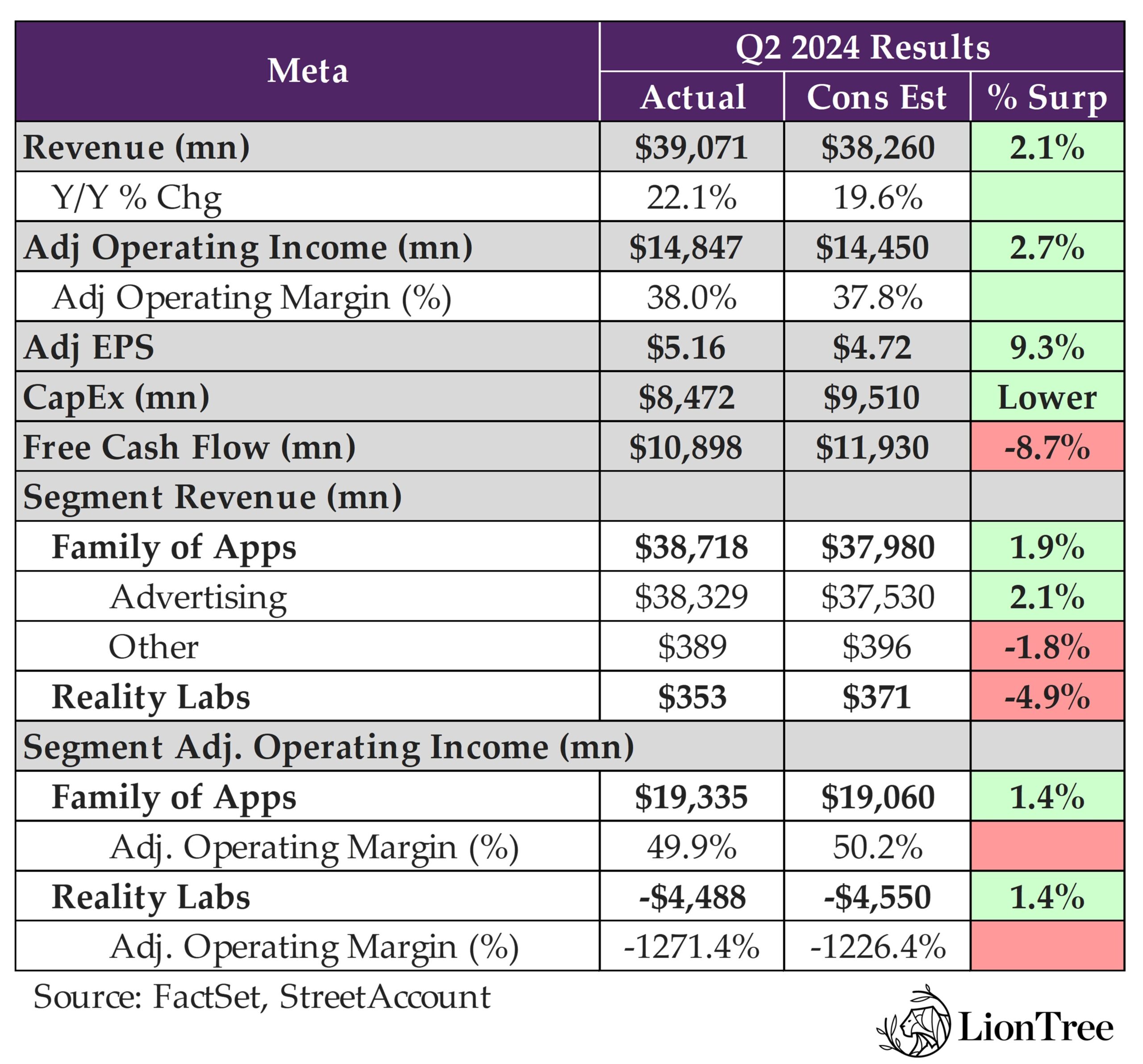

Surprise, surprise, capital spending was one of the biggest focus areas on Meta’s earnings conference call this week, especially given the commentary and tone regarding future spend, which drove the stock down -10% post Q1 results. While the Co posted another step up sequentially, Q2 CapEx came in almost -$1bn below Street estimates. But that doesn’t mean the spending spree is over. Mgmt raised the bottom end of the existing 2024 CapEx guidance and continues to prep investors for “meaningfully higher” CapEx in 2025. Also, in a similar vein to Alphabet CEO Sundar Pichai’s comments last week on Alphabet’s earnings call, Mark Zuckerberg said, “At this point I’d rather risk building [AI] capacity before it is needed, rather than too late.”

In regard to when AI products like Meta AI and AI Studios will begin to contribute to revenue, expect the Co to follow its tried and tested playbook of introducing a new product, scaling it, and only then focusing on monetization (most recently used this with Reels). While genAI products won’t be a meaningful driver of revenue in 2024 or 2025, they are expected to open up new revenue oppties over time that generate a “solid” return on investment. Alternatively, for those looking for more immediate monetization benefits from AI initiatives, AI integrations in existing products that are already at scale (like Instagram and Facebook) are already showing “lots of upside” by making advertising experiences more effective with tools like Advantage+, helping to drive revenue growth and conversions w/o increasing the # of ads or reducing ad load.

These better ad experiences helped drive the Family of Apps ad revenues growth to +22% y/y, which beat consensus by ~2%. Ad strength should continue into Q3, but as a caveat it will decelerate y/y, given the lapping of strong growth from “China-based advertisers” as well as strong Reels impression growth a year prior. There are also “modestly larger” FX headwinds in Q3.

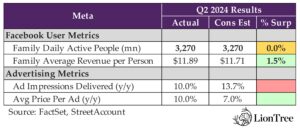

At the core of the platform are the users, and we’d flag several milestones, such as WhatsApp reaching 100mn+ monthly actives in the US, and Threads being close to hitting 200mn monthly actives (vs 150mn last qtr). Facebook is also making a comeback amongst young adults, especially in the US. Overall Family daily active people (DAP) hit 3.27bn on avg for June, which is up +7% y/y.

In terms of other future growth drivers, Reality Labs continues to be a work in progress, with revenue growing +28% y/y (from +30% in Q1) but missing Wall Street estimates by -5%. Investments into this business segment are considerable (Q2 operating loss of -$4.5bn), but were slightly less than expected. Looking ahead, op losses are expected to continue to increase “meaningfully”. Both Quest 3 and the Ray-Ban Meta glasses are seeing better-than-expected demand.

See more of our thoughts/takeaways from Meta’s results below. Also, see Theme #3 for perspectives on Pinterest & Snap’s results, both of which disappointed investors.

-> Meta traded up +4.8% in reaction to earnings and also ended the week up +4.8%; YTD, the stock is up +37.9%

Q2 Headline Results Beat Cons On The Top & Bottom Lines…And The Q3 Top Line Deceleration Was Not As Much As Expected

- Q2 total revs beat cons by +2.1%, though the growth of +22% y/y (+23% ex-FX) decel’d from +27% y/y in Q1

- Family Of Apps Advertising revenue was better than expected and beat by +2.1%

- Reality Labs revenue missed expectations by -5%

- Q2 operating margins of 38% were slightly ahead of cons 37.8% (better performance in both FoA and RL segments)

- Q2 EPS beat by +3%

- Q2 CapEx spending was more than $1bn below cons, but FCF still missed by ~$1bn

- OUTLOOK: Q3 total rev range beat cons by +1.7% at the mid-pt: $38.5-41bn, which assumes foreign currency will be a -2% headwind to y/y growth, vs cons $39.1bn

- Guidance implies a growth rate of +16.4% y/y vs cons +14.5% y/y

- OUTLOOK: Reiterated full-year 2024 total expenses in the $96-99bn range

Advertising Strength Is Expected To Continue, BUT Tough Comps, Among Other Dynamics, Will Weigh On Y/Y Ad Growth In Q3

- Seeing “healthy” global ad demand and delivering ongoing ad performance improvements: Anticipate these trends to continue to benefit Q3

- Family of Apps (FOA) +22% y/y ad revs growth (+23% ex-FX) was broad-based with strength across regions and verticals, with particular strength among smaller advertisers

- Online commerce was the largest contributor to the y/y growth, followed by gaming and entertainment & media

- Family of Apps (FOA) +22% y/y ad revs growth (+23% ex-FX) was broad-based with strength across regions and verticals, with particular strength among smaller advertisers

- But expect Q3 y/y ad revenue growth to slow, as they lap “strong” growth from China-based advertisers, “strong” Reels impression growth from a year ago, and “modestly larger” FX headwinds in Q3, based on current rates

- On a user geography basis, Q2 ad rev growth was strongest in RoW and Europe

- RoW +33% y/y

- Europe +26% y/y

- Asia-Pacific +20% y/y

- North America +17% y/y

- On an advertiser geography basis, Q2 total rev growth cont’d to be strongest in Asia-Pacific at +28% y/y, though growth was below the first quarter rate of +41% y/y, as the Co lapped a period of stronger demand from China-based advertisers

Meta’s Family Of Apps’ Post Impressive User Growth Metrics… AI Is Helping Drive Engagement on Platforms / US And Young Adults Were Key Demographic Callouts

- Family daily active people (DAP) hit 3.27bn, on avg, for June (in-line w/ cons), which is up +7% y/y

- “We’re seeing good y-over-y growth across Facebook, Instagram and Threads… both in the US and globally”

- US and young adults have been bright spots for Facebook: “Particularly pleased” with progress being made and seeing “good results” from focusing apps more towards 18–29-year-olds; “The numbers we’re seeing, especially in the US, really go against the public narrative around who’s using the app”

- Ad impressions across FoA incr’d +10% y/y and avg price per ads incr’d +10% y/y

- Impression growth: Mainly driven by Asia-Pacific and Row

- Pricing growth: Driven by incr’d advertiser demand, in part due to improved ad performance; This was partially offset by impression growth, particularly from lower-monetizing regions and surfaces

- “Quite pleased” with trajectory of Threads: About to hit 200mn monthly actives (vs 150mn last qtr); “Making steady progress towards building what looks like it’s going to be another major social app, and we’re seeing deeper engagement”

- WhatsApp growth in US was a highlight – “Big tailwind if the US ends up being a big market”: Now serves 100mn+ monthly actives in the US; WhatsApp has been leading messaging app in many countries around the world, but not in the US; “We’re starting to make inroads into leading in the US as more and more people use the product and realize that, hey, this is a really good experience”

- More broadly, seeing “particularly promising signs” regarding retention and engagement on WhatsApp

- Monetizing business messaging making progress: “Family of Apps Other revenue was $38mn, up +73% y/y, driven primarily by business messaging revenue growth from our WhatsApp Business Platform”

- Advances in AI continue to improve the quality of recommendations and drive engagement on Facebook and Instagram: “As we develop more general recommendation models, content recommendations get better”

- Seeing “encouraging early results” on Facebook from global rollout of unified video player and ranking systems, which is expected to unlock addt’l growth oppties for short form video as they increasingly make shorter videos into the overall base of Facebook video engagement

- Instagram Reels engagement continues to grow through ongoing enhancements of recommendation systems, part of which includes increasing the share of original posts within recommendations so people can discover content from emerging creators; Now, more than half of recommendation in the US come from original posts

- Over time, looking to move towards a single, unified, recommendation system that powers all the content, including things like people you may know across all svs

- Video is expected to remain a source of impression growth in H2

- On Instagram, expect Reels to continue to drive growth

- On Facebook, expect to grow overall video time while increasing the mix of short-form video, which creates more impression growth oppties

CapEx Plans Remain In Focus… Meta Raised The Low End Of The Full Year 2024 Capex Guidance Despite Q2 Spend Materially Below Expectations

- Q2 CapEx of $8.5bn was -11% below cons but a sizable step up from Q1’s $6.72bn: Due to investments in servers, data centers and network infrastructure

- For 2024, raised the bottom end of the CapEx range to $37-40bn from $35-40bn

- For 2025, currently expect “significant CapEx growth” – “We are not in a position to quantify this yet” but will give further guidance “as appropriate”

- Will be investing in core AI as a part of the infrastructure growth next year

- And investing in training capacity for Gen AI efforts will be a big driver of future CapEx needs

- Different expectations for CapEx for Core AI investments and Gen AI investments

- Core AI investments: Take a very ROI-based approach; Still seeing strong returns as improvements to both engagement and ad performance have translated into revenue gains

- “It makes sense for us to continue investing here”

- Gen AI investments: Don’t expect gen AI products to be a meaningful driver of revenue in ’24 or ’25, but “do expect that they’re going to open up new revenue opportunities over time that will enable us to generate a solid return off of our investment while we’re also open sourcing subsequent generations of Llama”

- Core AI investments: Take a very ROI-based approach; Still seeing strong returns as improvements to both engagement and ad performance have translated into revenue gains

Investing Big In AI To Stay Ahead Of The Curve And Avoid Falling Behind Later

- Big picture investment philosophy – It is better to risk building capacity before it is needed than risk not doing so

- “We’re planning for the compute clusters and data we’ll need for the next several years. The amount of compute needed to train Llama 4 will likely be almost 10x more than what we used to train Llama 3 — and future models will continue to grow beyond that. It’s hard to predict how this will trend multiple generations out into the future, but at this point I’d rather risk building capacity before it is needed, rather than too late, given the long lead times for spinning up new infra projects”

- Released Llama 3.1 in Q2 – “I think we’re going to look back at Llama 3.1 as an inflection point in the industry where open-source AI started to become the industry standard, just like Linux is”

- 405B model has better cost performance relative to the leading closed models

- Already starting to work on Llama 4 “which we’re aiming to be the most advanced in the industry next year”:

- Despite investment philosophy, remain committed to operational efficiency across the Co

- Llama underscores Meta’s bullishness on open source: “My view is that open source will be safer, will enable innovation that improved all of our lives faster and will also create more shared prosperity…this approach has consistently worked for us and I expect it will work here too”

While Gen AI Use Cases Are Limitless And Meta AI Is The Talk Of The Town, Near-Term Benefits Will Be Seen On Meta’s Existing Advertising Biz

- Focused on 4 primary areas in genAI oppties –

- Enhancing the core ads biz

- Helping grow business messaging

- Oppties around Meta AI

- Oppties to grow core engagement over time

- Bullish on Meta AI, which is “on track” to becoming the most-used AI assistant by the end of the year

- Quick stats:

- Meta AI has been used for “billions” of queries since first being introduced

- Meta AI can now be used in 20+ countries and 8 languages

- Integration with WhatsApp – seeing “particularly promising signs” in terms of retention and engagement, which has coincided w/ India becoming their largest mkt for Meta AI usage

- “Still uncovering the wide range of use cases that it’s valuable for”: Including utilitarian use cases like searching for information or role-playing conversations, as well as creative use cases like the new “Imagine Yourself” feature that lets you create images of yourself

- “Bottom line here is that Meta AI feels like it is on track to be an important service and it’s improving quickly both in intelligence and features”

- Quick stats:

- Launched AI Studio, “which lets anyone create AIs to interact with across our apps”

- Allows creators to create an AI agent that can channel them to engage more w/ their community, answer people’s questions, create content, and more

- Not specific to just creators, anyone can built their own AI based on their interest that they can then engage with or share with their friends

- Business AIs “are the other big piece here” and has potential to “dramatically accelerate” business messaging rev: Still in alpha testing with increasing # of bizs, and feedback so far has been positive; Think that over time, bizs will pull all of their content and catalog into an AI agent that customers can interact with, which will help drive sales and saves them money

- AI initiatives that could be potential biz drivers in 2025 and 2026? AI integrations in existing products that are already at scale

- “Lots of upside” in AI initiatives that are helping users find better content through improved recommendations, as well as making the advertising experiences more effective

- Monetization of AI products will likely follow path of prior products (most recently Reels): “I think you all know this from following our business for a while, but we have a relatively long business cycle of starting a new product, scaling it to something that reaches 1bn people or more, and only then really focusing on monetizing at-scale…the early signals on [Meta AI and AI Studios] are good”

- GenAI products will NOT be a meaningful driver of rev in 2024

Meta’s Is Making Progress With Monetization Efficiency

- The Co is getting better at determining the best ads to show and when to show them during a person’s session across both Facebook and Instagram

- This is enabling the Co to drive revenue growth and conversions w/out increasing the number of ads, or in some cases, even reducing ad load

- “Continue to see opportunities to grow ad supply on lower monetizing surfaces like video, including within Facebook as the mix of overall video engagement shifts more to shorter videos over time, which creates more ad insertion opportunities”

- Pleased with progress at enhancing marketing performance: AI is playing an “increasingly central role”

- Advantage+: Making it easier for advertisers to maximize ad performance and automate more of their campaign set up; These tools continue to unlock performance gains, with a study conducted this year demonstrating +22% higher return on ad spend for US advertisers after they adopted Advantage+ Shopping campaign

- Advertiser adoption of these tools continues to expand

- Intro’d Flexible Format to Advantage+ Shopping, which allows advertisers to upload multiple images and videos in a single ad that Meta can select from and automatically determine which format to serve, in order to yield the best performance

- Expanded the list of conversions that businesses can optimize for using Advantage+ Shopping to include an additional 10 conversion types, including objectives like “add to cart””

- Advantage+: Making it easier for advertisers to maximize ad performance and automate more of their campaign set up; These tools continue to unlock performance gains, with a study conducted this year demonstrating +22% higher return on ad spend for US advertisers after they adopted Advantage+ Shopping campaign

- “We’ve seen promising early results since introducing our first generative AI ad features – image expansion, background generation, and text generation – with 1mn+ advertisers using at least one of these solutions in the past month”

Seeing Some Very Early Benefits From Investments In Reality Labs, But Still A Long Ways To Go

- Reality Labs Q2 headline results were mixed: Rev grew +28% y/y to reach $353mn, missing cons by -4.1%, driven primarily by Quest headset sales; Reality Labs operating loss is still large at -$4.49bn but was slightly above cons -$4.55bn

- Looking ahead – expect Reality Labs op losses to increase “meaningfully” y/y due to ongoing product development efforts and investments to scale their ecosystem

- Prior Reality Lab investments are helping pull forward timelines for some products: A few years ago, the Co had predicted that holographic AR would be possible before smart AI, but now it looks like those technologies will be ready in the opposite order

- “We’re well-positioned for that because of the Reality Labs investments that we’ve already made”

- Quest 3 is “selling well” and “outpacing our expectations”

- “Think that’s because it is not just the best MR headset for the price, but it’s the best headset on the market”

- In addition to gaming, users are increasingly using it for its capabilities as a general computing platform, using it to watch videos, browse website, extend their PC via virtual desktop, and more

- Ray-Ban Meta “continue to be a bigger hit sooner than we expected thanks in part to AI”: Now on the second generation of the glasses; Demand is still outpacing ability to build them, but “hopeful we’ll be able to meet that demand soon”

- “Showing very promising traction with the early signals that we are seeing across demand, usage, and retention, increasing our confidence in the long-run potential of AR glasses”

- Other oppties to deepen relationship with EssilorLuxottica? “Great company that has a lot of different products that we hope to be able to partner with…I think there’s a lot more to go from here”

Digital Advertising – Part II: Challengers PINS & SNAP Feel Some Heat

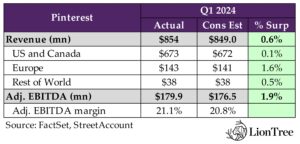

It has been a bit shaky out of the gate regarding digital ad trends, with Alphabet’s YouTube reporting weaker than expected revenue growth last week (decelerated from +21% y/y in Q1 to +13% y/y in Q2) and seeing some pressure in Q3 (see Theme #2 from last week), but Meta and Amazon reporting strong ad revenue results this week (see Theme #1 and Theme #4, respectively). Finishing out the major digital advertisers this week were Pinterest and Snap, which both felt some heat on the back of a volatile environment for brand advertising, especially with consumer advertisers. Starting with Pinterest, while the Co’s Q2 revenue results were actually a tad ahead of Wall Street forecasts, investors reacted negatively to the Q3 guide for a sharper deceleration in y/y revenue growth (from +21% in Q2 to +17% in Q3 at the mid-pt). Mgmt cited a “stable” ad market and some incremental FX headwinds BUT noted that there is also some softness in CPG, and namely food & beverage. Pinterest believes it is still gaining share, and while some of the macro dynamics may be out of its control, big picture, the Co continues to execute on its path to serve advertisers’ full funnel needs and has been successfully building lower funnel capabilities that are showing tangible results. It was a positive to hear that ad demand for the Co’s solutions is starting to come from the next tier of advertisers and broadening out. Performance+ should also help accelerate adoption from that segment of advertisers. The Co’s 3P partnerships with Amazon and more recently Google have been doing well, and the Co is able to address under-monetized RoW countries. This will remain a key part of the growth story along with monetization in the Co’s mature markets. Importantly, monthly active users (MAU’s) hit a record high, and engagement remains strong on the platform.

Moving onto Snap, the volatility of brand advertising, particularly in N. America with certain consumer discretionary verticals, was the swing factor with Snap’s performance in Q2. This came as a surprise after strong sequential rebounds in both Brand and Direct Response (DR) last qtr. For context, Snap’s Brand revenue growth went from a -3% decline in Q4:23 to +12% in Q1:24 but now fell -1% in Q2. However, DR performance was more resilient, rebounding from +3% in Q4:23 to +17% y/y in Q1 and posting +16% in Q2. The total number of active advertisers on Snap’s platform more than doubled in Q2 on the back of strong traction with small and medium size businesses (SMBs). Similar to Pinterest, as well as Meta for that matter, overall user growth and engagement was strong, with daily active users (DAUs) up + 9% y/y to 432mn, hitting an all-time high, though the strength came from lower monetization regions. North America was impacted y/y by optimization changes to the “go-to-market organization”, but this has started to see some improvements. Overall, the better-than-expected adj EBITDA in Q2 was more than offset by the weaker Brand revenue trends and weaker Q3 guidance. Going forward, the Co remains focused on improving results in N. America, growing the community and engagement, investing in DR advertising products, and diversifying revenue growth with Snapchat+. More details to come at the Snap Partner Summit on Sept 17.

See the below two sections for what we thought were the key themes, updates, and takeaways from 1) Pinterest and 2) Snap.

-> Pinterest shares fell -14.5% on the back of results and ended the week down -22.5%, while SNAP fell -26.9% in reaction to its print and ended the week down -29.8%; YTD, PINS is down -21.4% and SNAP is down -44.7%

1) PINTEREST – See below for details on what we thought were the key themes, updates, and takeaways

PINS – Another Quarter Of Better-Than-Expected Headline Results

- Q2 revenue: Beat by +0.6%, Grew +21% y/y (vs +23% y/y in Q1) to reach $854mn

- Q2 adj EBITDA: Beat by +2.4%; Reached $180mn (21% margin, ~+600bp y/y

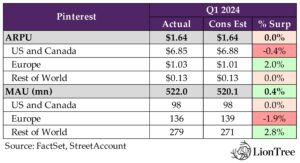

PINS – User Growth/Engagement Trends: Growth In MAU Sequentially Was Driven By RoW

- Global MAUs reached another record high of 522mn, growing +12% y/y (vs +12% y/y in Q1)

- Deeping engagement per user: Reflected in steady improvement in the WAU to MAU ratio in 2024

- Users continue to grow y/y across all of geographic regions in Q2

- US and Canada MAU +3% y/y

- Europe MAU +9% y/y

- ROW MAU +17% y/y

- What has driven better MAU growth?

- Utilizing AI to drive incr’d relevance and personalization

- Upgraded the search ranking algorithm in Q2 to incorporate new signals; Resulted in a significant increase in global search fulfillment rate (i.e., users are finding more of what they’re looking for when they search on Pinterest)

- Doubling down on curation through boards and collages to help users navigate their inspiration to action journey

- Increasing actionability, particularly for shopping

- More than doubled the number of outbound clicks sent to advertisers y/y for the third qtr in a row

- More new filters like price, retailer, and brand on high shopping intent search queries across fashion and home decor verticals; Experimenting w/ other filters

- Introduced video shopping ads

- Utilizing AI to drive incr’d relevance and personalization

PINS – BUT Slower Than Expected Q3 Revenue Guidance (Partially Impacted by FX) More Than Offset The Better Q2

- The Q3 revenue guidance was -1.8% below the Street at the mid-point: Implies +16-18% y/y growth (vs +21% y/y in Q1)

- FX will be a -1ppt headwind

- From a seq comp perspective, Q1 growth also benefited from seasonal factors, like Easter timing and leap day

- Also, comps last year did start to become more difficult in Q3, and the Co is experiencing further softness in food and beverage, as noted

- Addt’ly, the Co doesn’t accept political ads, which investors need to consider when comparing platform ad performance

- Q3 OpEx is expected to grow +17-20% y/y (which is a step up from the +13% y/y in Q2): Guidance is b/w $485-500mn, driven by ongoing infrastructure optimization efforts and investment increases in R&D; Anticipate flat Q3 non-GAAP cost of revenue

- Reiterated margin expansion expectations for 2024: Though implies a more modest level than the +660bp delivered in 2023

- Expansion will be modest in H2 vs the significantly higher expansion in H1 as the Co laps the strengthening of adj EBITDA margins in H2:23

PINS – Cites A Stable Ad Market & Strong Positioning + Monetization Trends

- Mgmt characterizes the ad market as relatively stable vs last qtr and are confident in their competitive position

- “We’re gaining share with some of the largest and most sophisticated advertisers in the world”

- More than doubled the number of clicks to advertisers y/y for the 3rd straight qtr

- Their larger, more sophisticated advertisers continue to lean into the platform as they have adopted our lower funnel tools and are seeing continued success but are now seeing signs of value capture from the next tranche of advertisers

- Believe Performance+ will help accelerate lower funnel adoption for that next tier of advertisers

- Advertisers who use upper and lower funnel objectives see +2x higher conversion rates than those who use one objective alone

- Nearly 100% of lower funnel revenue is covered by direct links or Mobile Deep Linking, hence it takes just one click to lead the user directly to an advertiser’s product or purchase page; This is more than double the amount of clicks to advertisers y/y for the third quarter in a row

- Vertical performance

- Saw strength in the Retail category due to the lower funnel improvements and also in emerging verticals, like Tech, Autos and Financial Svs, but this was partially offset by softness w/in CPG, esp food and beverage advertisers

- Q2 ad impressions grew 35%, while ad pricing declined 11% y/y: These dynamics were similar to Q1, with ad impressions being driven both by increases in total impressions as well as increases in ad load

- See more room to increase ad load due to the synergies between users’ commercial intent and relevant ads

- In Q2, saw a greater mix shift to ad impressions w/ lower avg pricing or eCPM: Started to serve ads in previously unmonetized markets, mostly in the RoW region, many of which have lower eCPMs than existing monetized markets

PINS – 3P Partnerships/Resellers Are Performing Well And Will Be Growth Drivers For RoW

- Acceleration in RoW revs was due to ramping the Google 3P partnerships (annc’d in Q1 and ramped in Q2)

- Partnership allows the Co to monetize previously unmonetized markets, and the Co is starting to expand into other relevant RoW countries

- The Amazon partnership is also “ramping nicely”

- Resellers are another lever to monetizing those regions: Launched these reseller partnerships in Q2, so “that’s still in early days, but we expect this to start to modestly contribute to the RoW segment over the course of the next year as well”

- Seeing some synergies between the resellers and the 3P partnerships

2) SNAP – See below for details on what we thought were the key themes, updates, and takeaways

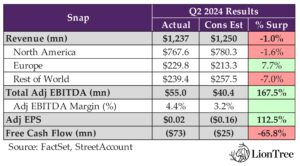

SNAP – Adj EBITDA Was The Positive Driver With Headline #s in Q2

- Adj EBITDA of $55mn, well above cons $40.4mn and up strongly from last yr’s -$38mn (+243% y/y)

- Sets up well for cont’d improvement in op leverage as the year progresses

- Adj EBITDA flow through was 55% in Q2, up from 22% in Q1

- Adj gross margin was relatively stable at 53% in Q2

- Q2 revenues slightly missed cons by -1%, growing +16% y/y vs +21% y/y in Q1

- Regional Dynamics – Revs in Europe was an upside driver, more than offset by lower rev in N. Amer and RoW

- America rev up +12% y/y: Lower growth due to weaker brand demand which was concentrated in the region; DR was a bright spot in North America due in part to the SMB customer segment

- To accelerate growth in the Americas, made changes in Q2 to optimize the go-to-market organization to better support clients where they see the best product market fit and greatest opportunity going forward

- Europe rev grew +26% y/y: Cont’d progress on DR, and a relatively more stable demand environment for Brand, fully offset the impact of more challenging y/y comps

- Rest of World rev grew +20% y/y: Driven by cont’d progress of DR, while the deceleration seq was primarily due to the timing of holiday periods shifting out of Q2 this year

- America rev up +12% y/y: Lower growth due to weaker brand demand which was concentrated in the region; DR was a bright spot in North America due in part to the SMB customer segment

- FCF was – $73mn vs -$119mn in the prior year

SNAP – Q3 Profitability Guidance & The Y/Y Rev Deceleration Rate Were Negative Focus Areas

- Mid-pt of adj EBITDA guidance at $85mn was -22.6% below cons of $109.8mn

- Mid-pt of revenue guidance was -0.4% below cons $1.36bn and reflects +12-16% y/y growth

- But this also implies seq growth of +8-11%, which is very strong historically

- On a 2-year stack, this implies +18-22% vs +11-12% in H1:24

- Expect more of the growth to come from DR and contribution from Snapchat+ (over 100mn per qtr run rate); Have not assumed a big rebound in Brand in Q3

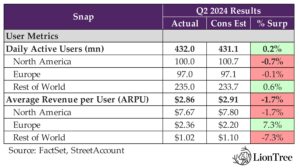

SNAP – Strong Daily Active Users Driven By RoW & ARPU Upside Driven By Europe

- DAUs grew + 9% y/y to 432mn to an all-time high and beat cons by +1mn; This was also up +10mn seq

- Amer DAU at 100mn was down by less than -1% y/y but up seq, as initiatives to improve the way Snapchatters communicate are showing early signs of progress

- Europe DAU at 97mn was up +1mn y/y and +3mn seq

- RoW DAU at 235mn was up +16% y/y and +4% y/y seq

- Europe drove the upside to total ARPU while performance in N. Amer was below expectations

- While RoW brought in more users on lower-than-expected APRU…

- Europe was the sole driver for upside to total ARPU

- OUTLOOK: Guiding for Q3 DAU of ~441mn, +8.6% y/y and +2% seq

- ~ 80% of Snapchatters are above the age of 18

SNAP – Advertising Performance Is Being Weighed Down By Brand Weakness… Direct Response (DR) Has Been Gaining Traction

- Total ad revs grew +10% y/y in Q2, down from +16% y/y in Q1 due to weakness in Brand advertising, which was down -1% y/y (down from +12% y/y in Q1), driven by –

- Particularly weak demand from certain consumer discretionary verticals, including retail, technology, and entertainment

- Also the timing impact of holidays shifting out of Q2 in the current year

- Direct response ad revs grew +16% y/y (similar to +17% y/y in Q1) driven by –

- Total active advertisers more than doubling y/y (seeing strong traction with SMBs)

- Cont’d progress w/ the 7-0 Pixel Purchase Optimization

- Early contributions from product improvements delivered for app-based advertisers

- Making progress on three foundational advertising platform initiatives –

- Larger ML models

- Improved signals

- More performant ad formats

- Other key advertising KPIs –

- Global impression volume grew ~+13% y/y, driven in large part by expanded advertising delivery within Spotlight

- Total eCPMs were down ~-3% y/y, as inventory growth exceeded ad demand growth in Q2

SNAP – Continue To Invest In & Focus On Platform Improvements and Content Engagement

- Delivered a number of new communication features and user experience enhancements in recent months –

- Map Reactions

- Editable Chats

- My AI Reminders

- Investing to enhance iOS app performance

- Working to combine stories and spotlight

- Continue to invest in ML models to improve content ranking and personalization as well as in Gen AI models and automation for the creation of ML and AI Lenses

- Seeing a significant improvement in content engagement –

- Global time spent watching content grew +25% y/y and +10% seq in Q2, driven by strong growth in total time spent watching Spotlight and Creator Stories

- But made some disruption changes in N. America; This led to mixed results on time spent with content, which declined by just under -2% y/y but did increase nearly +6% seq

- As the Co moved through the qtr, North America content engagement trends “improved”, and time spent w/ content incr’d y/y in the month of June

- Global time spent watching content grew +25% y/y and +10% seq in Q2, driven by strong growth in total time spent watching Spotlight and Creator Stories

- Making it easier for creators to submit and subsequently share compelling content: The number of creators submitting Spotlight content grew over +20% y/y in Q2

- Excited about growth in Spotlight time spent and think have headroom, given time spent on competitive short form video content

SNAP – Other Key Updates

- Infrastructure cost per DAU came in lower than expected: Was 81c, which is up from 80c in Q1 but below guidance of 83-85c due to a combination of greater than expected engineering efficiencies and a more moderate ramp in ML and AI investment

- Making progress with non-advertising revenue streams: Other revenue was up +151% y/y to reach $105mn in Q2 – the majority of which is Snapchat+ subscription revenue

- Now have 11mn+ Snapchat+ subscribers vs 9mn in Q1

Amazon’s Results Feed Into Worries About The Consumer

While Amazon’s AWS business is a key driver for the Company and outperformed this qtr (see Theme #5), concerns that arose surrounding the consumer took center stage and dragged down Amazon shares on the back of results. Amazon’s core N. American Stores business was negatively impacted by consumers “trading down” on price and looking for lower ASP items, and this dynamic has continued into Q3. On the heels of Amazon’s results Thursday night were the weak employment numbers that hit on Friday morning, which also stoked the developing recession fears.

With the mixed Q2 results, investors quickly homed in on the weaker-than-expected Q3 guidance, which was -1.2% below consensus on revenue and a significant -46% below on operating income. Granted, there are some historical headwinds to Q3 operating margins, but this was still a disappoint, especially with spending levels being a hot button for investors as of late. H2 CapEx is also expected to be up “meaningfully” up vs H1.

On the plus side, the $1.2bn y/y positive swing in Amazon’s Intl segment’s operating income is a key call out, in addition to the continued strong growth in the Co’s high margin advertising business (+20% y/y). Big picture, Amazon added $2bn+ in ad revenue y/y and has generated more than $50bn in ad revenue in the trailing 12 months. Sponsored products have been the primary driver, but Prime Video ads will certainly be a growth vector ahead.

Amazon also had positive things to say about the progress of Prime Video and emerging business areas, such as Pharmacy and Satellite connectivity.

See below for more details on what we found most interesting regarding the Co’s non-AWS business.

-> AMZN share fell -8.8% in reaction to earnings (and the broader tech melt-down on Friday) and ended the week down -8.0%; The stock is now up +10.5% YTD, slightly underperforming Nasdaq’s +11.6%

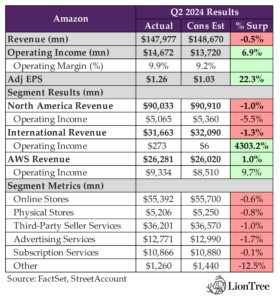

Q2 Headline Results Were Mixed And Q3 Guidance Disappoints

- Q2: Slight miss on overall revenue but much better operating income

- Total revenue grew +10% y/y (+11% ex-FX) vs +13% in Q1, but missed by -0.5%

- Operating income grew +91% y/y and beat by +7%

- Q2: N. America and Intl rev fell short of expectations, while AWS beat and intl profitability was much better than expected

- America revs rose +9% y/y and op margin of 5.6% incr’d +170bp y/y but was down -20bps seq due to some investment areas, incl Kuiper, where they are starting to manufacture satellites for launch in Q4

- Int’l revs grew +10% y/y (ex-FX)

- Regionalization has been working – saw improvements in cost to serve: Driven by efforts to place inventory more regionally, closer to where customers are

- More consolidated shipments w/ higher units per box shipped

- Also saw packages traveling shorter distances to customers, and this led to better on-road productivity in the transportation network

- FORWARD LOOKING: “I think we have a lot of opportunities”

- Q3: Guidance was below expectations

- Revenue guidance of $154-158.5bn is -1.2% below cons at the mid-pt

- Operating income guidance of $11.5-15bn is -46% below cons at the mid-pt

- Historically have seen a headwind to Q3 op margins due to Prime Day deals, plus marketing spend surrounding the event

- Also beginning to ramp up capacity to handle Q4 holiday volumes in fulfillment network

- Also expect CapEx to be up in H2: H1 CapEx was $30.5bn and will be “higher” in H2

- The majority of the spend will be to support the growing need for AWS infrastructure as they continue to see strong demand in both generative AI and non-generative AI workloads

A More Careful Consumer Is A Headwind To The Core N. Amer Stores Business Extending Into Q3

- N.America Stores business rev growth rate (+9% y/y, which was a decel from +12% y/y in Q1) was impacted by customers trading down, which is likely to be a headwind in Q3

- Consumer headwinds: Seeing lower avg selling prices b/c customers continue to trade down on price when they can, “Consumers being careful with their spend…looking for lower ASP products, looking for deals that continued into Q2”; Higher ticket items like computers or electronics or TVs are growing faster for them vs what they see in the industry but more slowly than what they see in a more robust economy

- OUTLOOK: “We’re seeing signs of it continuing in Q3”

- But did have very strong unit volume growth that slightly accelerated when adjusted for leap year in N. America; Overall unit sales grew 11% y/y, which is consistent with growth rates in Q1 after ~100bps adjustment for leap year

- A few considerations impacting N. America Stores rev growth rates

- Last quarter’s Leap Day added ~+100bps of y/y growth

- Seller fees are a little lower than expected given behavior changes from the latest fee changes

- Believe Stores margins can continue to increase over time: “It’s not going to happen in one quarter…or one fell swoop. It’s going to take work over a long period of time”

Intl Segment Makes Strong Progress W/ Profitability (Op Income Up +$1.2bn y/y)

- Intl Stores revs incr’d +10% y/y (ex-FX) and were profitable again w/ op income of $300mn: That is an improvement of +$1.2bn y/y (margin was 0.9%, up +390bp y/y); Driven by established countries, where they are improving their cost structure with better inventory placement and more consolidated shipments

Bullish On Advertising…Still At The Early Stages Of What’s Possible In Video Advertising

- Advertising revenue growth (ex-FX) was strong at +20% y/y in Q2 (to $12.8bn), though decelerated from +24% y/y in Q1

- Advertising remains an important contributor to profitability in N. America and Int’l

- Saw strong growth on an increasingly larger revenue base this quarter

- Continue to see opportunities that further expand their offering in sponsored products (drives the most today) as well as newer areas like Prime video ads

- Added over +$2bn in ad revenue y/y and generated more than $50bn in ad revenue in the trailing 12 months

- “Even with this growth, it’s important to realize we’re at the very beginning of what’s possible in our video advertising”

- Had first Upfront appearance in May and were “encouraged” by feedback on the differentiated value via content, reach, signals, and ad tech

- “While ads have become the norm in streaming video, we aim to have meaningfully fewer ads than Linear TV and other streaming TV providers”

Continue To “Like The Progress” Of Prime Video

- “Our storytelling is resonating with our hundreds and millions of monthly viewers worldwide”: Amazon MGM Studios recently received 62 Emmy nominations

- Fallout is the second most-watched original title ever for Prime Video

- The Idea of You attracted nearly 50mn viewers worldwide in the first 2 weeks on Prime Video

- Season 4 of The Boys reached #1 on Prime Video in 165 countries in its opening 2 weeks

- “See momentum in live sports” and highlighted 11-year “landmark deals” with the NBA and the WNBA: When combined w/ their original films and shows, partner streaming services, licensed content and rent or buy titles, “Prime Video continues to evolve into the best destination for streaming video”

Other Updates On Key Initiatives

- Pharmacy continues to grow “really quickly” and to get more resonance with customers: This is a “natural extension for us to build a pharmacy offering from our retail business”

- Accelerating satellite manufacturing of Project Kuiper (low-Earth orbit satellite constellation):

- Annc’d a distribution agreement w/ VRIO who distributes DIRECTV Latin America and Sky Brasil

- Continue to “feel significant demand for the service” from enterprise and government entities

- Expect to start shipping production satellites late this year

- Continue to believe this could be a “very large business for us”

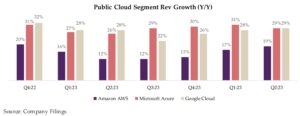

Cloud Investments Should Support Strong Top-Line Growth Into H2

Following Alphabet’s Q2 report last week, which showed accelerated sequential Google Cloud growth and set all-time records on both revenue and operating profit (see Theme #2 from last week’s Weekly), all eyes were on Amazon and Microsoft to see if their Cloud divisions would bring sunshine or rain.

Interestingly, Amazon’s AWS and Microsoft’s Azure showed divergent paths in Q2. AWS followed Alphabet and posted its third straight quarter of accelerating growth. AWS now boasts an annualized revenue run rate of $105bn+ and with 90% of global IT spend still on-prem, growth is aplenty looking ahead. In particularly, businesses of all sizes are increasingly leveraging AI, and Amazon’s AI business is achieving a multibillion-dollar revenue rate, with growth expected to outpace traditional AWS growth. Unlike traditional infrastructure, generative AI is built directly in the cloud, offering significant new opportunities.

On the other hand, Microsoft went the other way and posted a seq deceleration in revenue growth, and a further deceleration is expected in FQ1, but mgmt anticipates Azure growth to re-accelerate in FH2 as capital investments create an increase in available AI capacity to serve more of its growing demand. Azure’s slowdown in the qtr was partly due to high demand for AI svs outstripping available capacity and slightly lower than expected growth in certain European regions. While gross margin decreased, it is expected to improve seq in the next qtr. Despite these challenges, Microsoft reported strong commercial bookings and record commitments to its cloud platform, and cloud security solutions and tools like Azure Arc continued to show strong adoption and revenue growth.

Overall, it wasn’t an across the board beat for Cloud this Q2, but the demand outlook remains strong. The expanded capacity from higher capital investment should enable strong top line growth across the board looking into H2.

See below for more details

AWS Was A Bright Spot Within Amazon’s Q2 Results

- AWS rev growth accelerated for the third straight qtr and beat expectations: Grew +18.8% y/y (up from +17.2% y/y in Q1) to $26.3bn and beat cons by +1.0%

- AWS is now at a $105bn+ annualized run rate (vs $100bn+ last qtr)

- AWS op income also beat estimates: Incr’d +72.2% y/y (vs +83% y/y in Q1) +to $9.3bn and beat cons by +9.7%, driven by a continued focus on cost control, including a “measured” pace of hiring

- AWS op margin includes an ~+200bps favorable impact from the change in the estimated useful life of servers instituted in Q1; Continue to expect AWS op margins to fluctuate over time, driven in part by the level of investments being made at any point in time; Remain focused on driving efficiencies across the biz, which enables them to invest to support the “strong” growth they’re seeing in AWS, including genAI

- Continue to see three macro trends drive AWS growth –

- Cos have completed “the significant majority” of their cost optimization efforts and are focused again on new efforts

- Cos are spending their energy again on modernizing their infrastructure and moving from on premises infrastructure to the cloud

- Builders and Cos of all sizes are excited about leveraging AI (Amazon’s AI biz continues to grow “dramatically” with a multibillion-dollar revenue run rate, despite it being early days)

- Generative AI and AI as a whole are expected to grow rapidly, potentially outpacing the traditional AWS growth rate: Unlike the traditional infrastructure, which involves migrating on-premises systems to the cloud, a process that takes time, genAI will be built directly in the cloud from the start, presenting significant new opportunities for AWS, and potentially expanding its market more quickly than traditional cloud services

- See a long road of growth ahead: “We’ll see where the growth rate nets over the next number of years…about 90% of the global IT spend is still on premises. And if you believe that equation is going to flip, which I do, there’s a lot of growth ahead of us in AWS”

- In the past 18 months, AWShas launched more than twice as many machine learning and generative AI features into general availability than all the other major cloud providers combined

Microsoft’s Cloud Miss Overshadowed The Co’s Overall Top-Line Beat

- Azure’s FQ4 seq decel in y/y growth spooked investors…: Rev was up +29% y/y (vs +31% y/y in FQ3 and +30% y/y in FQ2), coming in below cons +30.2%; Ex-FX, Azure’s y/y rev growth of +30% y/y (vs +31% y/y in FQ3 and +28% y/y in FQ2) also came in below cons +31.2%

- …as did guidance for FQ1: Ex-FX, +28-19% y/y vs cons +30.6% y/y

- Expect Azure growth to re-accelerate in H2, as capital investments create an increase in available AI capacity to serve more of the growing demand

- What drove the slowdown in FQ4? Azure growth included 8pts from AI svs, where demand remained higher than available capacity; Also, in June, saw “slightly lower-than-expected” growth in “a few” European geos

- Microsoft Cloud gross margin was down seq (as Co had expected)…: FQ4 Microsoft Cloud gross margin percentage decreased ~2pts y/y to 69% (vs 71% in FQ3), in-line with Co’s expectations

- … But expected to improve seq in FQ1 (still down y/y): Should be ~70%, which is still down y/y, driven by the impact of scaling AI infrastructure

- Commercial bookings were “significantly ahead” of expectations but decel q/q, up +17% y/y (+19% y/y ex-FX) vs FQ3’s +29% y/y (+31% y/y ex-FX)

- Had “record commitments” to Microsoft Cloud Platform, driven by growth in the # of $10mn+ and $100mn+ contracts for both Azure and Microsoft365, as well as “and consistent execution across our core annuity sales motions”

- Continue to see “sustained” rev growth from migration, as Azure Arc is helping Cos to streamline their cloud migrations and now have 36k+ Arc customers, up +90% y/y

- Cloud security use case reached a milestone, as MSFT’s cloud security solution, Defender for Cloud. Surpassed $1bn in rev over the past 12 months

- Reiterated that FY25 CapEx is expected to be higher than FY24 to meet growing demand signal for AI and Cloud products: Reiterated that it will increase on a seq basis. though there may be quarterly spend variability from cloud infrastructure buildouts and the timing of delivery of finance leases

- Cloud and AI related spend represents nearly all of total CapEx, with ~half for infrastructure needs and the remaining ~half for servers

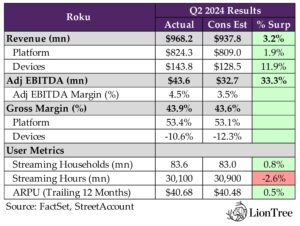

Roku’s Diversification Strategy Is Starting To Bear Fruit

It was a strong quarter for Roku, with sweeping beats across the top and bottom line, as well as its fourth consecutive quarter of positive adj. EBITDA and FCF. The beats were driven by both the Devices and Platform segments, and top of mind remains the Co’s goal of accelerating Platform revenue (85.1% of total revenue in Q2). While y/y growth decelerated seq in Q2 and is expected to continue to decelerate in Q3, a turnaround is expected in Q4 onwards.

Diversification has been a key word across several of the company’s revenue objectives. More specifically in advertising, its diversified offerings kept Roku insulated from market-driven pricing changes that are impacting other streaming services. Y/Y growth of advertising across the Roku platform, excluding M&E, outperformed the overall ad market and OTT ad market in the US. While the M&E vertical continues to be challenged, as streamers have been pulling back spend on marketing over the past few years, Roku has been diversifying. M&E is now a “significantly” smaller % of the overall platform business, and the company is not reliant on that vertical for future growth. The Roku Home Screen is also a big oppty that they continue to drill into, particularly for advertisers looking to reach their ad-free SVOD users. In terms of accessibility, partnerships with 3P platforms, most recently with Trade Desk, are helping them to grow demand for all the supply they have to offer.

We’d also flag that Roku’s sports offering is one of its fastest growing features, with streaming hours from the Roku Sports Experience more than tripling y/y. They recently launched an MLB zone, in addition to its NFL and NBA Zones, and also secured exclusive multi-year rights to the MLB’s Sunday Leadoff live games, which are available for free on The Roku Channel (TRC). TRC remained the #3 app on the Roku platform in Q3, with streaming hours accelerating seq to +75% y/y, as viewership of key events like the presidential debate move from traditional TV to streaming. They are also collaborating with NBCU to create an Olympics zone, which provides a single, simplified destination for the 2024 Paris Olympics and allows viewers to subscribe to Peacock directly through the Roku platform, a win-win for both Roku and Comcast.

Looking ahead into the next quarter, revenue guidance was in-line with expectations, with y/y growth expected to decelerate seq across both segments, with Platform rev in particular impacted by a challenging y/y comp. That being said, adj. EBITDA guidance was a big beat, as they continue to focus on operational discipline.

Overall, it was a good qtr relative to expectations.

See below for more on all the above.

-> Roku shares opened in positive territory this morning after reporting its results last night but was dragged down by the market sell off to close -4% lower on the day; The stock is still down -40% YTD

Clean Beat Across Q2 Headline Numbers / Achieved Fourth Consecutive Qtr Of Positive Adj. EBITDA and FCF

- Total revenue – BEAT by +3.2%: Total rev grew +14% y/y (vs +19% y/y in Q1)

- Devices revenue – BEAT by +11.9%: Grew +39% y/y (vs +19% y/y in Q1), driven by the retail distribution expansion of Roku-branded TVs

- Platform revenue – BEAT by +1.9%: Grew +11% y/y (vs +19% y/y in Q1), reflecting contribution from streaming services distribution and advertising activities, despite continued softness within M&E

- EBITDA – BEAT by +33.3%: $43.6mn vs cons $32.7mn (margins at 4.5% vs cons 3.5%), driven by Platform segment

- Gross margins were also a beat (43.9% vs cons 43.6%)

- Devices gross margin of -10.6% was up +6.4pts y/y and beat cons -12.3%

- Platform gross margin of 53.4% was up +0.1pts y/y and beat cons 53.1%

- Fourth consecutive qtr of positive adj. EBITBA and FCF was a result of top-line growth and ongoing operational efficiencies

Q2 Users KPIs Were A Positive As Roku Continues To Scale Internationally

- Streaming Households – BEAT by +0.8%: Added +2.0mn in Q2 (up from +1.6mn in Q1) to 83.6mn globally, driven by both TVs and streaming players

- Making “good progress” growing streaming households in the countries they are prioritizing, across the Americas, and the UK

- Streaming hours – MISSED by -2.6%: Up +20% y/y (vs +23% y/y in Q1) to 30.1bn

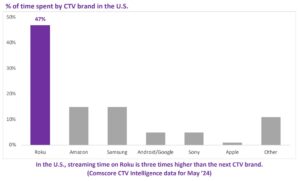

- Avg Streaming Hours per Streaming Household per Day = 4.0hrs in Q2 (down from 4.2hrs in Q1, but up from 3.8hrs in Q2:23)

- Streaming time on Roku in the US is 3x high than the next streaming CTV brand, per Comscore

- ARPU – BEAT by +0.5%: Was flat y/y (similar to Q1) at $40.68 on TTM basis, reflecting an increasing share of Streaming Households in intl markets, where they are currently focused on scale and engagement w/ monetization efforts in the early stages

Q3 Profitability Guidance Was A Highlight Coupled With An In-Line Revenue Outlook

- Q3 total revenue – in-line: Will grow +11% y/y (decel from +14% y/y in Q2) to reach 1.01bn, which was in-line with cons

- Q3 Devices rev will grow +24% y/y (decel from +39% y/y in Q2), reflecting continued expansion and investment in the Roku-branded TV program

- Q3 Device margins will remain in the negative low-double digits

- Q3 Platform rev will grow +9% y/y (decel from +11% y/y in Q2), which takes into account a challenging y/y growth rate comparison within streaming services distribution along with elevated positive 606 adjustments in Q3:23

- Q3 Platform margin will be ~53%

- Addt’l forward-looking commentary on Platform rev: Anticipate y/y growth rate of Platform rev will accelerate seq in Q4 and remain confident in ability to accelerate Platform rev in 2025

- Q3 Devices rev will grow +24% y/y (decel from +39% y/y in Q2), reflecting continued expansion and investment in the Roku-branded TV program

- Q3 adj EBITDA – BEAT by +72.4%: $45mn vs cons $26.1mm, reflecting ongoing operational discipline

Streaming Services Distribution Is A Key Focus In Accelerating Platform Rev Growth

- Roku is “executing well” against initiatives to accelerate Platform rev growth, which include –

- Maximizing ad demand for Roku

- Leveraging Roku’s Hoe Screen as the lead-in for TV

- Growing Roku-billed subscriptions

- Streaming services distribution activities grew faster than Platform rev overall

- Primarily due to price increases for subscription-based apps on Roku’s platform in H2:23 and H1:24

- Have increased focus on growing the share of subscriptions billed through Roku Pay

- New Content Row on Home Screen is helping to drive Roku-billed subscription sign-ups by highlighting popular titles from SVOD svs on Roku’s platform, and they see upside ahead

- Collaborating with content partners to deliver experiences that benefit viewers, as well as Roku and its partners

- Partnered w/ NBCUniversal to create zone in Roku Sports Experience for the 2024 Olympic Games in Paris, which provides a single, simplified destination for live events, replays, daily primetime shows and more; Viewers can subscribe to Peacock for full Olympics coverage directly through the Roku platform

“Well-Positioned” To Accelerate Ad Biz In H2, Though M&E Is Expected To See Continued Weakness

- Y/Y growth of advertising across the Roku platform, excluding M&E, outperformed the overall ad market and the OTT ad market in the US

- Driven by their broad ad portfolio, reach of Roku Home Screen, and expanding partnerships w/ 3P ad platforms

- Highlighted that they are not impacted by market-driven pricing changes in the same way that streaming svs are – “We have a unique set of ad products and sponsorships that are only possible because we own the platform and we integrate these throughout the viewer experiences…we have flexibility to handle really well the market fluctuations”

- M&E vertical continues to be challenged BUT “we’ve diversified the overall ad business well”

- “We’re really good at M&E and we’re a must have for our M&E partners” BUT “due to the efforts to diversify… M&E is a significantly smaller percent of our overall platform business now versus the last several years”

- How has Roku diversified?

- Increased the # of ad categories and ad units in the viewer experience

- Opened up inventory to new advertisers that used to be reserved almost exclusively for M&E brands and performance advertisers, “and that diversification has worked well”

- “While we’re in a good position to benefit from any M&E rebound and any new M&E entrants into the market, we’re not relying on the vertical for future growth”

- Seeing “good momentum” in the upfront: “It’s been a positive market for us and we’ve been growing our share generally across the board”

- “Hearing a lot of excitement around our new products,” including video ads and the marquee and sports participation

- Getting positive feedback from clients on efforts to make it easier to purchase Roku Media and onboard new clients and measure their performance

- “We’re closing the upfront with poise, we’re building share and we’re having great conversations both about the upfront and establishing client KPIs really well beyond the upfront”

- Roku Home Screen is “highly valued” by advertisers

- Reaches US households w/ 120mn+ people every day (in-line with Q1)

- Provides advertisers w/ oppty to reach ad-free only viewers: Helps to reach the 40% of consumers who only select ad-free versions when given an SVOD ad choice (as per Antenna)

- “For many of our viewers, promotions and advertising in our Home Screen is the only ad they’re going to see”

- In Q2, the percentage of app sessions launched from one of their owned and operated features increased +35% y/y

- Owned and operated features on the Home Screen include Roku’s Content Row, Live TV tile, Sports Experience, and What to Watch

- Recently launched a Content Row that makes personalized recommendations powered by AI, and early results show that these recommendations drove an increase in Streaming Households, avg display ad impressions, and video ad reach of The Roku Channel

- Recently enhanced the marquee ad unit on their Home Screen by adding video

- Limited, invite-only beta for the new video ad unit sold out in the first month, w/ participation from brands such as The Home Depot, Disney, and MINI USA

- Part of ongoing effort to diversity displays ads on the Home Screen beyond M&E advertisers

- Expanding and deepening relationships with 3P platforms to increase demand and make it easier for advertisers to execute campaigns programmatically

- Recently partnered with The Trade Desk so that TTD customers can leverage Roku Media and audience data programmatically to better understand and optimize their campaigns for TV streaming viewers; Expanding relationship w/ Roku’s integration of Unified ID 2.0 (UID2) so Roku advertisers can achieve more precise targeting and means to facilitate data collaboration

- “We’re only a couple of months in, but the partnership with them has been really well received…our relationship is growing…and we look forward to continued innovations ahead”

- Also partnered w/ iSpot so advertisers on the Roku platform can receive best in-class optimization and ad measurement through iSpot’s Unified Measurement solution

- Will continue to partner w/ more 3P DSPs, which along w/ their expanding portfolio of ad products allow Roku to serve the entire demand curve at multiple price points, which will drive incremental rev that will grow over time

- “We’ve got a lot of supply of ads, and we have the ability to grow our supply. So, we’re highly focused on growing demand and third-party partnerships are one way to do that”

- Recently partnered with The Trade Desk so that TTD customers can leverage Roku Media and audience data programmatically to better understand and optimize their campaigns for TV streaming viewers; Expanding relationship w/ Roku’s integration of Unified ID 2.0 (UID2) so Roku advertisers can achieve more precise targeting and means to facilitate data collaboration

- Looking into H2 of 2024, expect these initiatives to help accelerate rev from advertising activities

- For Q3, while M&E is expected to be challenged, anticipate y/y growth of advertising activities to accelerate

Growth Of Streaming Hours On The Roku Channel Accelerated Q/Q

- The Roku Channel remained the #3 app on the Roku platform in Q2 by both reach and engagement, with streaming hours up +75% y/y (vs +66% y/y in Q1)

- Ongoing growth is largely due to its position as the lead-in to TV…:

- …as well as Home Screen’s power to drive viewership: 70%+ of The Roku Channel’s Streaming Hours in Q2 originated from Home Screen features such as the Content Row, Live TV, and What to Watch

- Streaming of news and other live programming continues to grow as viewers cut the cord

- Viewership of June 27th US presidential debate on tradition TV was -30% from the first debate in 2024, TRC’s FAST offering achieved its highest day for both reach and engagement; During the debate, 40%+ of TRC’s viewers watch on their live channels

- While foundation of content spend remains w/ 3P licenses and rev shares, continue to leverage Roku Originals to attract viewers and advertisers

- Reiterated success of Roku Original “The Spiderwick Chronicles,” where they drove viewers from various entry points across the Roku platform, including a takeover the Roku Home Screen, Roku City, and a “Spiderwick” tile (in the app grid), which helped the series achieve the highest reach and engagement of any on-demand title in TRC’s historical during its opening weekend and was sponsored by Airbnb

Roku Sports Experience Is One Of Roku’s Fastest Growing Features

- Nearly half of Americans watch sports on TV every month, and Roku is benefitting from the ongoing shift of sports to streaming by leveraging its position as the lead-in to TV

- In addition to the NFL and NBA Zones, recently launched MLB Zone w/ T-Mobile as a sponsor

- MLB Zone aggregates and organizes live and upcoming games, nightly recaps, game highlight, a fully programmed MLB FAST channel, and more from across the Roku platform

- Also secured the exclusive, multi-year rights for MLB’s Sunday Leadoff live games, which is now available for free on The Roku Channel

- In Q2, Streaming Hours originating from the Roku Sports Experience more than tripled y/y

Quick Updates On Roku Devices And Roku OS

- On Roku Devices –

- Expanded distribution of Roku-branded TVs to Target and other specialty retailers

- New Roku Pro Series hit the market in April, and the higher-performing TVs continue to receive strong reviews

- Expect Devices margin to be in its current range for the next several quarters

- As Roku-branded TVs continue to ramp, component costs will continue to go down, which over time will drive improvement in device margins, but its still early days

- On Roku OS –

- Roku OS was again the #1 selling TV OS in US, with TV unit sales greater than the next two TV operating systems combined

- Roku OS was the #1 selling TV OS in Mexico and Canda, where Roku continues to grow scale through the Roku TV licensing program

Video Games – EA & Roblox Shined In Q2, But All The Focus Was On Their Near-Term Outlooks

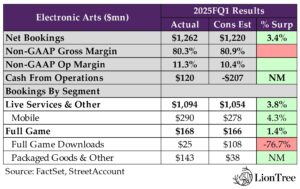

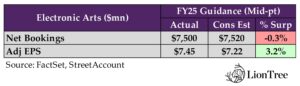

EA kicked off earnings for the interactive entertainment space this week, providing some insight into how the industry has been navigating post-COVID headwinds as well as other ongoing secular shifts. For the most part, EA’s headline results were better than the Street anticipated, with the company’s net bookings closing +3.4% ahead of forecasts and its non-GAAP operating margin of 11.3% topping estimates of 10.4%. The only blemish was a -60bps miss on non-GAAP gross margin, though this wasn’t addressed on the call. The outperformance on net bookings was primarily driven by stronger than expected performances from EA SPORTS FC 24 and Madden NFL 24. These titles, as well as EA’s other key franchises, benefited from “secular tailwinds in social media and sports” that have resulted in consumption “only growing and becoming more concentrated” in them. More specifically, EA CEO Andrew Wilson highlighted that “an expanded definition of play” has been emerging within interactive entertainment as modalities of play that involve “deep connection with… friends [are] becoming more and more important”. In this light, the company is in an “enviable position”, given its “broad portfolio of incredible IP” and “massive player network”, among other competitive advantages.

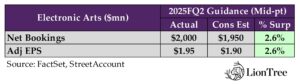

Looking ahead, EA’s FQ2 guidance exceeded expectations on both the top and bottom-line. Along with an “action-packed EA SPORTS quarter” with the recent successful launch of College Football 2025 and the upcoming launches of Madden NFL 25 and FC 25, the company also plans to release season 22 of Apex Legends, which will be more “content-rich” than prior seasons. However, despite forecasting a stronger than expected FQ2, EA stopped short of revising its full-year guidance, preferring to wait to see how its upcoming slate of titles performs. Longer-term, the company is positioning itself for “accelerated growth in FY26 and beyond. EA didn’t provide any details on the progress of its mobile business or its previously stated goal of expanding FY27 GAAP operating margin ~+300-350bps over FY25 but will share more information about its growth opportunities at its upcoming Investor Day on September 17.

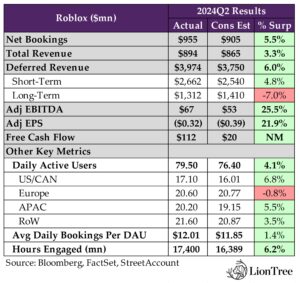

On the infrastructure side of the industry, Roblox also released its Q2 print this week, reporting headline numbers that broadly exceeded consensus expectations. After experiencing “unseasonable” slowness in Q1, Roblox’s initiatives to re-energize net bookings growth appear to have paid off, as growth in the company’s net bookings rebounded above the +20% benchmark set at its Investor Day last November to +22.4% y/y in Q2 (vs +19.4% y/y in Q1) and beat estimates by +5.5%. This result reflected KPI trends that were directionally “strong across all regions”, and with the “very powerful improvements” in user growth and engagement seen exiting Q2 and heading into Q3, Roblox’s management felt comfortable raising its full-year bookings outlook nearly back to levels that were originally projected at the beginning of the year. However, for reasons that weren’t elucidated on the call, the company’s FY24 adj EBITDA guidance range was also lowered, sparking some concerns that recent platform improvements “haven’t put the platform seemingly on stronger footing than it was six or nine months ago”.

Lastly, another update that caught investors off guard was that CFO Mike Guthrie is stepping down to pursue personal interests, though he plans to remain in his role for the time being to assist in finding a successor.

See below for 2 sections which outline what we thought were the key themes, updates, and takeaways from 1) EA and 2) Roblox.

-> EA shares were up +1.2% in reaction to the print and ended the week up +2.5%; Roblox shares fell -6.4% following earnings but recovered slightly to finish the week down -3.6%; YTD, EA stock is trading up +8.8%, while Roblox stock is down -14.6%

1) Electronic Arts – See below for details on what we thought were the key themes, updates, and takeaways

EA – Off To A “Strong Start” In Its FY25 After Adjusting For Tough Comps

- EA’s headline numbers mostly exceeded estimates: Net bookings fell -20.0% y/y in FQ1 (vs -14.4% y/y in FQ4) but beat cons by +3.4%, given comps from last yr’s World Cup benefit to EA SPORTS FC; Non-GAAP gross margin of 80.3% (vs 80.4% in FQ4) missed cons’ 80.9%, while non-GAAP op margin of 11.3% beat cons’ 10.4%

- Live Services (~87% of net bookings) – BEAT: FQ1 net bookings were down -7.1% y/y (vs -13.3% y/y in FQ4) and closed +3.8% ahead of cons; EA “delivered more content to larger audiences, resulting in greater than anticipated engagement and monetization in core live svs”

- Full Game (~13% of net bookings) – BEAT: Net bookings dropped -58.1% y/y in FQ1 (vs +3.6% y/y in FQ4) but topped cons by +1.4%; There were three full game title releases a yr ago, including STAR WARS Jedi: Survivor, EA SPORTS PGA Tour, and Super Mega Baseball 4

EA – Although FQ2 Guidance Surprised To The Upside, FY25 Outlook Was Unchanged

- FQ2 top and bottom-line guidance was better than anticipated: Expects FQ2 net bookings between $1.95-2.05bn, representing a -9.8% y/y decline but beating cons by +2.6% at the mid-pt; Adj EPS range of $1.85-2.05 also topped cons by +2.6% at the mid-pt

- Key assumptions in the outlook: Will be an “action-packed EA SPORTS qtr”, w/ the launch and “strong start” of College Football 25 as well as the upcoming releases of Madden NFL 25 and FC 25; Apex Legends season 22 is also scheduled to launch, but the Co is being “prudent” about its expectations

- Also, FX is expected to have a “minimal impact”

- Addt’l guidance items: Projects GAAP net rev between $1.9-2.0bn, cost of rev between $420-450mn, and GAAP OpEx between $1.19-1.2bn, primarily driven by restructuring-related charges and cont’d investment; This is projected to result in GAAP EPS of ~$0.76-0.93

- Key assumptions in the outlook: Will be an “action-packed EA SPORTS qtr”, w/ the launch and “strong start” of College Football 25 as well as the upcoming releases of Madden NFL 25 and FC 25; Apex Legends season 22 is also scheduled to launch, but the Co is being “prudent” about its expectations

- Reiterated FY25 outlook as EA wants to “get through… major releases” before considering an adjustment to FY25 guidance: Still expects net bookings range of $7.3-7.7bn, which was ~inline w/ cons at the mid-pt though adj EPS between $7.05-7.85 is above cons by +3.2% at the mid-pt

- Key releases: Highlighted Madden 25, FC 25, and Dragon Age: The Veilguard specifically

- Other full-yr metrics were also reaffirmed: Including FY25 net rev between $7.1 – 7.5bn, an OpEx range of $4.35 – 4.44bn, GAAP op margin between 18-20.6%, and a non-GAAP op margin between 29.6 – 31.7%

- EA is positioning itself for “accel’d growth in FY26 and beyond”: The Co expects to “continue to invest w/ sharpened focus” behind its three strategic pillars of entertaining and engaging massive online communities, telling blockbuster stories, and harnessing the power of community in and around its games

- More details about EA’s pipeline long-term growth oppties will be revealed at its Investor Day: Scheduled for Tuesday, Sept 17

EA – Have An “Enviable Position” Amid A Changing Interactive Entertainment Industry

- EA has “cont’d to grow out of COVID”, BUT “that hasn’t been true for the whole industry”: The Co’s “incredible competitive advantage” in its creative talent, production strength, IP portfolio, and “massive player network” have enabled it grow its mkt share in the industry

- A “secular shift” occurring in the industry will benefit EA over the longer-term: Sees “secular tailwinds in social media and sports” as well as a “movement towards the biggest franchises in the industry” that “facilitate an expanded definition of play

- 25-30% of engagement in the interactive entertainment industry is driven by watching content: This correlates to “nearly the same levels” of monetization as playing does “over the course of time”; Fostering “a sense of connection and community is important”

- EA’s franchises will “benefit disproportionately” younger demos: Gen Z and Gen Alpha “continue to grow and age up and fulfill their entertainment needs through interactive games”

- BUT “not all of the industry has been making that transition at the same rate” as EA: The Co has been “working diligently against that transition” and has already “navigated [its] shift in distribution”

- A “secular shift” occurring in the industry will benefit EA over the longer-term: Sees “secular tailwinds in social media and sports” as well as a “movement towards the biggest franchises in the industry” that “facilitate an expanded definition of play

EA – “Consumption Is Only Growing And Becoming More Concentrated” In EA’s Key Franchises

- EA SPORTS FC 24 faced difficult comps but performed “better than expected”: Tailwinds related to the World Cup contributed to double-digit growth the prior yr qtr; To-date, the EA SPORTS FC franchise is up ~+msd% vs the prior FIFA-branded version

- Euro 2024 and Copa America 2024 helped drive “even better than expected monetization”: These major soccer tournaments occurred towards the end of FQ1

- EA SPORTS FC Mobile “delivered a record FQ1 net bookings result: Gameplay improvements and real-life events helped drive double-digit growth in spender acquisition

- “EA SPORTS FC 25 is going to be a giant step forward”: EA is forecasting franchise growth in FY25, seeing “many more oppties to grow its reach, engagement, and impact”

- “FC 25 will feature more innovation, as well more realistic and authentic gameplay”: This will be driven by “tactical sophistication using AI and real-world footballing data”; Will also introduce a new social 5v5 experience, called Rush, as well as new content capture and creation tool

- Madden NFL 24 also posted “greater than expected results”: Madden NFL 24’s “outperformance” is a “strong proof point in the power of [the] thriving community in and around [EA’s] games”

- The Co “saw sustained momentum late in the title cycle”: Both weekly avg use in Ultimate Team and total net bookings grew double-digits y/y, as efforts to deliver fun gameplay, real world connections, and “compelling live content year-round” has driven “deeper engagement”

- Efforts to connect “real-life cultural events to in-game experiences w/ live content” fueled deeper engagement: Including EA’s collab w/ Pat McAfee and its special Michael Vick Edition

- New game modes have also helped attract new younger players: Cited the Co’s efforts w/ Madden Mobile “and the constant evolution of that franchise in its mobile incarnation”

- EA is also “pushing hard” in international geos: Aligning w/ the NFL’s push to build an international fan base by broadening access to the sport w/ via cable and streaming