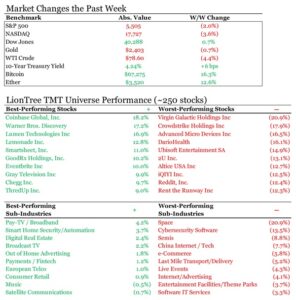

What a week. Aside from TMT earnings season kicking off, we saw a major rotation in the markets with small caps and laggards like industrials rallying, while the tech-laden Nasdaq sold off. (Russell 2000 +1.7%, Dow +0.7%, Nasdaq -3.7%). We’ve been talking about the market concentration for some time, so this reversal was quite notable. The equal weighted S&P outperformed the official index by ~190bp this week, and the Russell 2000 logged its fourth up week out of five. Also of note this week was the massive global systems outage stemming from a defective Windows update (see more in Theme #2).

There was certainly a lot to talk about fundamentally this week, and we focused on the below (all links are clickable)

- It Was Déjà Vue Quarter For Netflix, As The Co’s Eyes Remain On The Prize

- Outages & Cyberattacks Highlight Dependence On Tech Infrastructure

- The Streaming Popularity Contest Continues With Big Budgets, Tech Upgrades, And More

- Activists Continue To Gravitate To TMT… Match & BuzzFeed Feel More Heat

- New Forecasts For Global Entertainment & Media Revenues Through 2028… Digital Advertising, Gaming, And APAC Are All Key Growth Drivers

- More Updates From The Digital Ad Space + Ad Agency Holding Co Earnings

- A Mid-Year Look At Key Music KPIs

- Some Pluses And Some Minuses With Consumer Retail/E-Commerce Spending Trends

- Grab Bag: Online Grocery Delivery Sale Surge / Trump’s Take On TikTok / Potential M&A Chatter At VZ And GOOG

Have a great weekend.

Best,

Leslie

It Was Déjà Vue Quarter For Netflix, As The Co’s Eyes Remain On The Prize

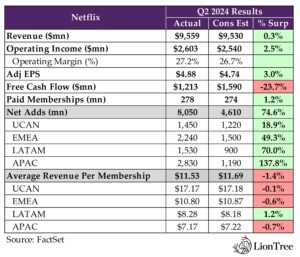

As the poster child for the Streaming Entertainment sector, all eyes were on Netflix’s earnings report this week. What stood out the most to us? The Co blew it away on net adds (+8mn vs cons +4.6mn), attributing the growth to stronger customer acquisition and healthy retention. However, Netflix also cautioned that Q3 paid adds will be lower q/q due to tough y/y comps from Q3:23, which had the first full qtr impact from paid sharing.

As has been the case for the past five quarters, while net adds have seen double or triple-digit beats versus estimates, there hasn’t been that much of a flow-through to revenue, as Q2 sales beat by a miniscule +0.3%, which is a continuation of the recent pattern in which revenue for the most part has been generally in-line with estimates, despite the blockbuster subscriber net add beats.

Live event programming, advertising, and gaming are some of the incremental offerings that Netflix has been working on to boost financials, and the company provided updates on all those fronts. Live entertainment is proving to be a significant engagement driver (Q2’s The Roast Of Tom Brady attracted its largest live audience yet), and advertisers are also enthusiastic about the opportunity. Mgmt continues to be optimistic about their event-based sports strategy, in which they’re able to avoid the risk associated with the high costs of big league sports rights and renewals but still benefit from the inherent popularity of these games.

Progress in advertising is also moving along, with ad-supported now making up over 45% of all sign ups in Netflix’s ad markets. While scaling inventory continue to be a priority, Netflix has now reached a point where the company is scaling faster than its ability to monetize its inventory, so Netflix is making investments to build out those capabilities. Advertising won’t be a primary driver of revenue growth in 2024 or 2025, but it will be a “key component” in the longer-term revenue and profit growth picture. In a similar vein, gaming is also still ramping up, and while investment levels remain “quite small” compared to overall content spend, progress is accelerating, with plans to launch about one new title per month based on Netflix IP in Netflix Stories starting this month.

Finally, to quickly flag on the financials, Q2 op margins were a standout at 27.2%, beating the Street’s 26.7% estimate and mgmt raised FY24 op margin guidance from 25% to 26%. Investors should expect growing margin each year (though the rate of expansion will vary year to year). The company also raised its FY24 rev growth outlook to +14-15% y/y growth, up from previous +13-15% y/y, reflecting “solid” membership growth trends and business momentum.

See below for more regarding our key thoughts and takeaways from Netflix’s qtr.

-> NFLX share have had a nice run and despite falling -1.5% post its Q2 print, the stock is still up +31% YTD

Much Better Paid Adds And Better Margins Were The Key Drivers In Q2 But Paid Adds Should Be Lower Y/Y in Q3

- Rev growth of +17% y/y (+22% y/y ex-FX), slightly beat consensus: This was driven primarily by +16% y/y increase in avg paid memberships

- But ARM growth of +1% y/y (+5% y/y ex-FX) missed consensus of +2.3% y/y

- Q2 paid net adds came in almost double vs expectations:05mn vs cons 4.6mn; Drivers included “a little stronger than [..] expected” acquisition and continued “very healthy” retention across all regions

- Op margin of 27.2% was strong: Up from 22% last yr and beat cons 26.7%

- Outlook – Q3 subscriber and ARM:

- Paid net adds will be lower y/y due to paid sharing impact comps: Q3:23 had the first full qtr impact from paid sharing

- Global ARM will be ~flat y/y in Q3 due to ongoing FX headwinds and plan and country mix

- Expects total Q3 rev growth of +14% y/y (+19% y/y ex-FX) due primarily to price changes in Argentina and the devaluation of the local currency relative to the US dollar

The Co Raised Full Year The Revenue And Margin Outlook

- Incr’d FY24 rev growth outlook: Expected growth of +14% to +15% y/y (up from previous +13% to +15% y/y)

- Reflecting “solid” membership growth trends and business momentum, partially offset by the strengthening of the US dollar vs. most other currencies

- Also incr’d FY24 op margin outlook: To 26%, up from prev 25%

- Driven by improved rev outlook and ongoing expense discipline

- Pace of margin expansion going forward? Reiterated commitment to grow margin each year, though rate of expansion will vary year to year

- Continue to expect FY24 FCF of $6bn

Further Leaning Into “Eventized Programming” – “We’ve Been Amazing At Film And Series For A Long Period Of Time, But Now Increasingly We’re Adding Live Events Into It.”

- Reiterated $17bn content spend target for the year

- Looking ahead “that $17bn will grow as our revenue grows. It won’t grow as fast as our revenue grows, but it will grow to accommodate that”

- “Our goal and our mission here is we have to spend the next $1bn of programming better than anyone else in the world, and there’s no one better at doing it than Netflix.”

- Q2 had strong content across series and films

- Series: Bridgerton S3, Baby Reindeer, Queen of Tears and The Great Indian Kapil Show

- Films: Under Paris, Atlas and Hit Man and The Roast of Tom Brady

- Upcoming content slate –

- 2024 – several big releases on the way through the end of the year: Including new seasons of Squid Game, Emily in Paris, Selling Sunset, Lincoln Lawyer, The Diplomat, Virgin River, Love Is Blind

- 2025: New seasons of Wednesday, Stranger Things, The Night Agent

- On live entertainment strategy – “we’re in live because our members love it. And it drives a ton of engagement and it drives a ton of excitement…advertisers like that too…so, everyone’s interests here are perfectly aligned”

- In Q2, The Roast of Tom Brady attracted Netflix’s largest live audience yet

- Building out their event-based sports viewing model, which helps mitigate the risk of high costs and low profitability associated with broadcasting entire sports seasons

- Focused on generating excitement with high-quality games (i.e., hosting two NFL games on Christmas Day)

- Limiting the # of games to maintain a special event atmosphere

- Continue to be “in love” with the “very profitable” storytelling version of sports – “if you can’t wait for those football games on Christmas Day, you can watch Receiver right now”

Making “Steady Progress” Scaling Ads Biz But Still Don’t Expect It To Be A Primary Growth Driver Through 2025

- Ads tier membership grew +34% q/q, driven by attractiveness of offering ($6.99/mo in the US, with two streams, high definition and downloads), along with the phasing out of the Basic plan in the UK and Canada, which Netflix will now start in the US and France

- Ads tier now accounts for over 45% of all signups in Netflix’s ads markets

- Making improvements to service they offer to advertisers

- In the UK, starting September, Barb will measure Netflix’s ad supported plan, making it easier for clients to plan campaigns and understand their audiences on Netflix

- New features like “pause” or “keep watching” ads and in the two months since the launch of the beta in May, have closed 60+ pause ad campaigns with brands, like Expedia, Coca-Cola, Ford, L’Oréal and McDonald’s

- On the programmatic side, will expand capabilities this summer to include The Trade Desk, Google DV 360, and Magnite

- In-house ad tech platform is coming soon: Testing in Canada in 2024 and launching more broadly in 2025; Will give advertisers new ways to buy, insights to leverage, and ways to measure impact

- “On track” to achieve critical scale goals for all their ad countries in 2025, creating a “strong” base from which their can further increase ad membership in 2026 and beyond

- Have reached a point where they can shift some focus from scale to effectively monetizing their “rapidly-growing” inventory: Through adding more sales and ad operations personnel and building overall capabilities to meet advertisers; Giving advertisers more effective ways to buy; Building their own ad server

- BUT don’t expect advertising to be a primary driver of rev growth in 2024 or 2025

- Are currently scaling faster than their ability to monetize their growing ad inventory, which is both a near-term challenge and a medium-term oppty

- “We’re confident that advertising will be a key component of our longer-term revenue and profit growth”

- Ad-free vs ad-supported dynamics

- Engagement on ad-supported vs ad-free is roughly the same, at ~2 hrs of viewing per member, per day

- Ad-supported ARM is currently lower than ad-free ARM, as they’re “racing behind” trying to fulfill increasing inventory; As it scales, represents an oppty to accelerate rev growth

- Considering raising prices of ad-supported tier in the future? Think about it similar to how they think about pricing in general, “which is it’s our job to increase the value that we are delivering to all of our members… we’ll think about that in the ads context just like we would in the non-ads context”

- Investments to ramp the ads business are embedded in guidance

- Early results from phasing out basic $11.99/mo ad-free tier in select markets and replacing with $6.99/mo ad-supported tier? “I’ll just let our actions speak for ourselves. When those things go well, we typically roll it out, and we’ve had the confidence to move forward with that change in the US and France. So, that’s an indicator of how it’s going”

Competition Remains Fierce But Netflix Still Sees Plenty Of Room To Increase Penetration

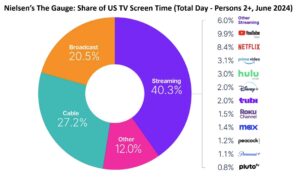

- Streaming accounted for 40% of total US TV screen time in June, which was a first:

- Netflix and YouTube collectively accounted for almost 50% of all streaming TV watch time in the US

- Netflix generated more view hours in the Nielsen Top 10 across film, series, and licensed titles than all the other streamers combined In H1

- This was despite headwinds from paid sharing

- “The challenge for so many of our competitors is that while they are investing heavily in premium content, it’s generating relatively small viewing on their streaming services and linear continues to decline”

- Mgmt reiterated comments that Netflix is ~10% of TV time in every country they operate in “so, still lots of room to grow…very pleased with our engagement, but not fully satisfied”

Improvements To Netflix Home Page Are In The Works

- “Our biggest update in a decade”

- Began testing a new, simpler, and more intuitive TV homepage in June, which will “significantly” improve the discovery experience on Netflix

- What are some of the changes?

- More visible title information at a glance, including synopsis, genre, and ratings

- Title previews are larger and more dynamic, w/ more immersive trailers and bigger box art to make browsing easier

- Simplified the navigation war and moved it to the top of the page to create quicker, easier short cuts

- Includes My Netflix, which has everything members have saved or watched and was previously only available on mobile

-> Separately but related, see Theme #3 for updates Disney is making to its own tech infrastructure

- Rollout of new home page will be “a long iterative journey” and “we’re trying to take that first step and set us up for that”: “Our expectation is that this new structure will allow us to deliver, as the old structure did for a decade, multiple repetitive material benefits to users in terms of engagement, which would lead into retention and then revenue”

Still Early Days In Gaming, But The Ramp Up Is Accelerating

- Have launched 100+ games so far, and have 80+ games currently in development

- “We’ve calibrated the growth in investment [in gaming] with the growth in business impact, so we’re being disciplined about how we scale that”: Engagement and impact of gaming on overall biz at its current scale is “still quite small”, and investment level in games relative to overall content spend is “also quite small”

- “Now obviously, the job is to continue to grow that engagement to the place where it has a material impact on the business”

- Particular emphasis on “Netflix Stories”, which are interactive narrative games based on Netflix IP: Will launch about one new title per month in Netflix Stories starting in July; Launched games based on Virgin River and Perfect Match in Q2, and games based on Emily is Paris and Selling Sunset are in the works

- “I think the idea of being able to take a show and give the super-fan a place to be in between seasons… It’s a really great opportunity and a rare one where one and one equals three here”

Outages & Cyberattacks Highlight Dependence On Tech Infrastructure

Developments this week underscored how dependent society has become on IT and software services maintained by multiple vendors. In what has been deemed by many to be the largest-ever global outage, a “defect” in an update for Windows issued by CrowdStrike crippled IT organizations worldwide and forced many industries to a standstill. Along with causing TV stations to go down and nearly 1,400 flights to be canceled, the outages have severely impacted healthcare and other emergency services. As of right now, there doesn’t appear to be an easy fix to the problem either, unfortunately.

In a similar vein, the past few years have seen an almost universal push across industries to collect increasing amounts of data and then to leverage those datasets to develop better customer and operational insights. However, in aggregating and storing that massive amount of information, companies have also created some potential vulnerabilities that can be exploited by bad threat actors. This week, it was reported that Disney was targeted by a “hacktivist” group that claims to have taken issue with how the company handles its contracts with artists, its “approach to AI”, and its “pretty blatant disregard for the consumer”. Although the hacktivist group, which calls itself Nullbulge, says that it leaked sensitive information containing computer code and details about upcoming projects, these claims couldn’t be verified. As of now, it is still unclear just how widespread the group’s access to Disney’s internal systems was.

There were also more updates related to the high-profile Snowflake hack that affected “nearly all” of AT&T’s customers, which was previously disclosed last week. To rectify one of the worst security breaches of a US telco in history, the company apparently paid ~$380,000 – a relatively low amount compared to other recent ransom payments and a mere “drop in the ocean” for AT&T.

See below for more details.

- A “defect” in CrowdStrike’s software update for Windows caused widespread IT outages (link): Bizs across the world began reporting that devices running Windows OS started showing Blue Screens of Death early Friday morning; Hours later, CrowdStrike CEO George Kurtz said his Co found a “defect” in a Windows update it issued

- “This is not a security incident or cyberattack”: Per Kurtz, who added that “the issue has been identified, isolated, and a fix has been deployed”

- Issues appear to stem from CrowdStrike’s Falcon Sensor product: According to the Co, the Falcon system is part of CrowdStrike’s security tools and can block attacks on systems

- Only Windows devices appear to be impacted: Kurtz confirmed that Mac and Linux hosts haven’t been impacted by the update

- It’s unclear exactly how extensive the issues are and how long it will take to resolve them: Microsoft issued a statement that it believes that a “resolution is forthcoming”

- It looks like there isn’t an automated way to fix the issues: A cybersecurity researcher reviewed a copy of the CrowdStrike update and said that the file isn’t properly formatted, which “causes Windows to crash every time”

- “Millions” could be lost by organizations b/c of the outages: Swaths of bizs across a wide variety of industries, including healthcare, hospitality, banks, TV stations, and airports, among others, have had to stall operations or shutdown entirely

- Some noteworthy examples of affected bizs: Sky News was forced to go offline, the US emergency alert system said there were various 911 outages in a number of states, hospitals have canceled nonurgent surgeries, and even the Paris Olympics was impacted in a “limited” way

- Almost 1,400 flights have been canceled globally: United, Delta, and American Airlines all issued a “global ground stop” on all flights

- “This is not a security incident or cyberattack”: Per Kurtz, who added that “the issue has been identified, isolated, and a fix has been deployed”

-> Microsoft has also been dealing w/ unrelated outages of Microsoft 365 and Azure cloud svs this week; Microsoft 365’s status page warns that customers may not be able to access SharePoint Online, OneDrive for Business, Teams, Intune, PowerBI, Microsoft Fabric, Microsoft Defender, and Viva Engage; However, as of Friday morning, the Co said that “svs availability is gradually returning to a healthy state”; In contrast, the Azure team appears to be a step behind and is “currently applying mitigation [to the underlying cause] through multiple workstreams” (link)

- Disney reportedly had sensitive data leaked online by a hacktivist group (link/link): An anonymous hacking group that calls itself Nullbulge revealed in a blog post that it published online data from thousands of Disney’s internal Slack workplace channels; It’s not clear how widespread the group’s access to Disney’s Slack system was

- Nullbulge cited several reasons for targeting Disney: Including “how [the Co] handles artist contracts, its approach to AI, and it’s pretty blatant disregard for the consumer”; Nullbulge promotes itself as a hacktivist group that advocates for artist rights

- “In a duel, you better fire first”: A spokesperson for Nullbulge said that the group believed that making demands of Disney would be ineffective, so it released the data first

- The scope of the data that was leaked was broad, per Nullbulge…: Includes 1.1TB of data, w/ every msg and file from nearly 10,000 slack channels, including computer code, details about unreleased projects, as well as booking and rev data from Disneyland Paris

- … Though these claims couldn’t immediately be verified: Files viewed by the WSJ includes conversations about maintaining Disney’s website, software dev, hiring assessments, programs for emerging leaders within ESPN, and pictures of employees’ dogs

- The group likely used a Trojan horse to comprise a Disney manager’s PC: Nullbulge claims to have twice compromised the computer of a Disney manager of software dev – once using a video game add-on, and a second time using another, undisclosed method

- Nullbulge cited several reasons for targeting Disney: Including “how [the Co] handles artist contracts, its approach to AI, and it’s pretty blatant disregard for the consumer”; Nullbulge promotes itself as a hacktivist group that advocates for artist rights

- AT&T reportedly paid a hacker group ~$380,000 to delete stolen customer data (link/link): The Co reportedly negotiated the payment through an intermediary named Reddington, which acted on behalf of the ShinyHunters hacking group

- The hack was one of the worst security breaches of a US telco in history: The breach was tied to a security incident at Snowflake and involved call and text msging records of “nearly all” of AT&T’s customers over a six-month stretch in 2022; The Co is in the process of notifying ~110mn affected individuals

- The scope and details of the data could present national security risks: Given that peoples’ locations could be ascertained w/ the data; That said, the hacker said that they didn’t believe the info stolen from AT&T was valuable

- BUT AT&T believes that stolen call and text logs haven’t been made public: The Co reportedly received a video from the hackers proving that all stolen data was deleted

- The alleged payment is relatively low when compared to ransom demands from other high-profile breaches: For example, Colonial Pipeline paid a hacking group $4.4mn after a ransomware attack in 2021, while UnitedHealth Group paid a cybercrime group $22mn in Feb of this yr

- ShinyHunters reportedly initially demanded a payment of $1mn: Though AT&T was able to talk the group down to a lower price, which was paid on May 17 in BTC

- The hack was one of the worst security breaches of a US telco in history: The breach was tied to a security incident at Snowflake and involved call and text msging records of “nearly all” of AT&T’s customers over a six-month stretch in 2022; The Co is in the process of notifying ~110mn affected individuals

-> On a related note, Imperva’s new network security report revealed that the telecom industry has been seeing the highest y/y increases in DDoS attacks; In H1:24, telcos experienced a +548% y/y increase in application layer attacks; Per the report, the fast-increasing rate of DDoS attacks reflects telcos’ “crucial role in maintaining internet connectivity and the high stakes in disrupting their svs”; Still, The financial industry still accounted for the highest percentage of attacks, at nearly 24% compared to telecom’s 12.3% (link)

The Streaming Popularity Contest Continues With Big Budgets, Tech Upgrades, And More

In addition to Netflix’s earnings report this week (see Theme #1), we also came across several data points on the various other streamers. YouTube’s content being greater than any other VoD-first player this year, Disney making improvements to its tech infrastructure, and Peacock emerging as the fastest riser in popularity amongst the streamers are just some of the key highlights. And what % of viewers are considered “quick churners” (i.e. signed up for a new platform and then dropped it within 6 months of signing up)? See below to find out.

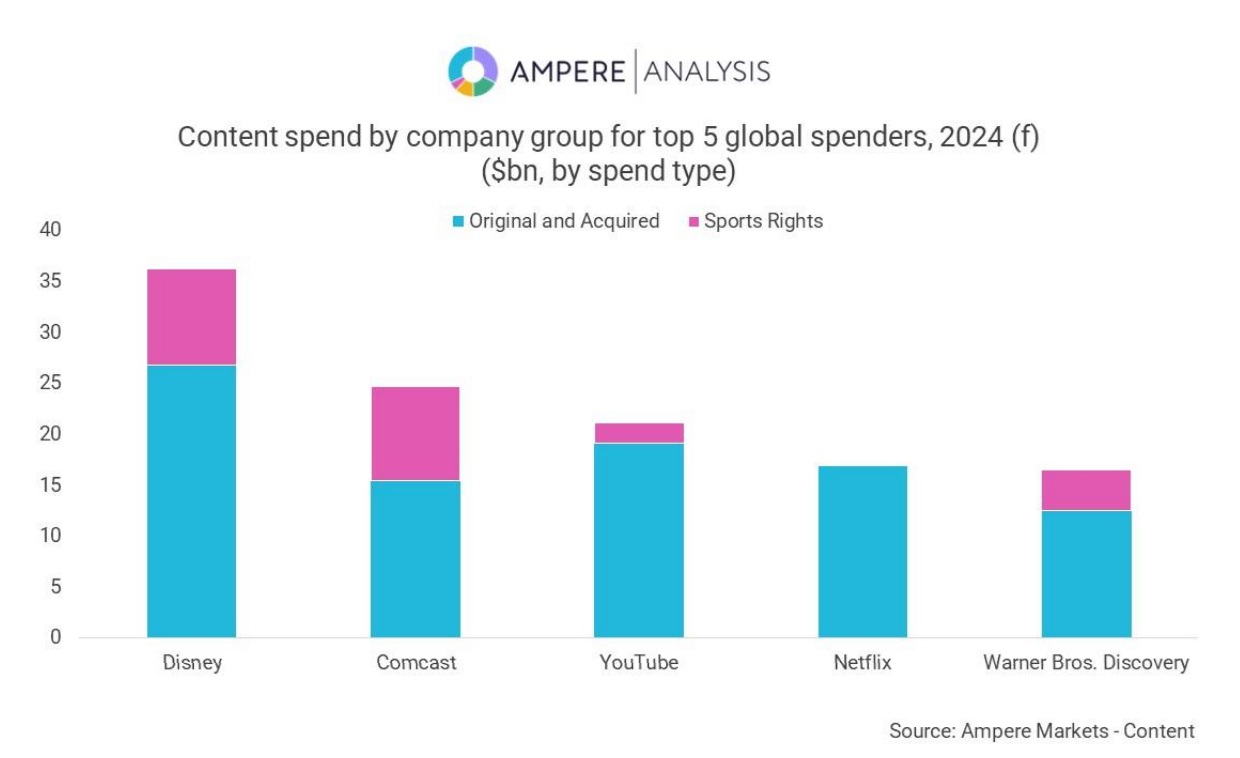

A Deep Dive On YouTube’s Content Spend Relative To Other Streamers,Per Ampere Analysis (link)

- At nearly $20bn, YouTube’s content spend this year will be greater than any VoD-first player

- YouTube will have the second largest non-sports content spend globally in 2024, coming in behind Disney

- YouTube’s total expenditure will be the third largest worldwide this year for the fourth consecutive year, when taking into account sports right spend, coming in behind Disney and Comcast (both forecasted to spend just over $9bn on sports rights in 2024)

- Some other quick facts on YouTube:

- YouTube’s ad rev alone, forecasted at $35bn in 2024, exceeding Disney+ and Amazon Prime Video’s total earnings and falling just shy of Netflix’s total revenue (unlike SVoD platforms, YouTube’s main source of revenue is advertising, not subscription fees

-

- YouTube is the #1 platform for online video viewing globally and its ad rev is driven by its large user base: 83% of respondents were monthly active users of the platform in Q1:24, ahead of monthly active video viewers for Netflix at 57% and Instagram at 4

Disney Is Reportedly Working On “Netflix-Style” Updates For Disney+ (link)

- New Disney+ features are in the works and some of which could roll out in the next 6 mos, including –

- Customized promotional art for new shows and movies based on subscriber’s tastes and usage history

- Emails sent to viewers who stop watching in the middle of a series reminding them to finish

- Disney is moving towards a more “Netflix-like” model that relies on user data to drive Disney content suggestion algorithms vs human-curated content recommendations

- What is the current process? Disney employees manually curate and drag-and-drop suggested tiles into rows that viewers see near the top of their screens when they log in based on themes (i.e., Halloween, Pride Month) or new releases

-> Disney has been shifting focus from attracting new subscribers to increasing viewing time spent; The goal is to reduce churn and generate more revenue from advertising sales; On the Co’s last earnings call, CEO Bob Iger said Netflix is the “gold standard” in streaming

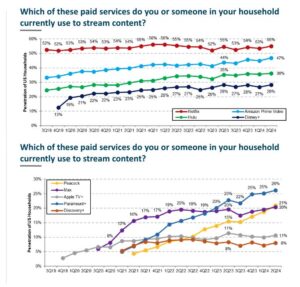

Peacock’s Popularity Has Risen The Most Y/Y Amongst The Streamers, Per MoffettNathanson (link/link)

The research firm asked 8,500 US households, “Which paid service do you or someone in your household currently use to stream content?” (Q2:23 -> Q2:24)

- By Streamer:

- Netflix (in-line): 55% -> 55%

- Amazon Prime Video (up): 44% -> 47%

- Hulu (up): 35% -> 36%

- Disney+ (in-line) 28% -> 28%

- Paramount+ (up): 23% -> 26%

- Max (in-line): 20% -> 20%

- Peacock (up): 15% -> 21%

- Apple TV+ (in-line): 11% -> 11%

- Who was the biggest gainer? Peacock, which along with being the fastest riser ALSO surpassed Max; Peacock was also the only streamer that released the same number of new original seasons in Q2 as it did a year ago

Some New Data On Streaming Service Spending, Churn, And Preferences Trends From Hub Entertainment Research (link)

- Consumers are maxed out on TV subscription spending, with little more room for increased expenditure: Avg spend in 2024 is around $82/mo, while maximum willingness is at $87/mo (vs avg spend in 2023 of $85/mo and maximum willingness of $88/mo)

- Cancellation reasons are as much about lack of content as about wanting to save money: 50% of respondents who cancelled a service within 6 months of signing up cited “not enough value” or “financials reasons”; 48% said there were “no more shows of interest” while 42% cited that there was “one show only”

- About half of viewers churn in and out of services

- 44% are “quick churners”: Have signed up for a new platform and then dropped it within 6 months of signing up

- 50% are “serial” churners: Have signed up, canceled, then resubscribed to the same svs (so they are only paying when there is something they want to watch)

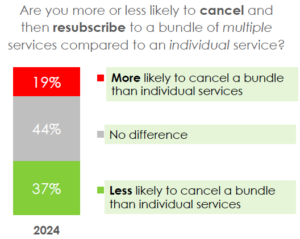

- But bundling reduces “revolving door” churn: 37% of respondents said they are less likely to cancel a bundle than individual services (vs 44% who said there would be no difference and 19% who said they would be more likely)

- Free ad-supported (FASTs) svs are perceived as more valuable than paid platforms: 34% associated “Excellent” value from FAST svs (vs 25% for SVOD w/ no ads and 22% for SVOD w/ ads)

- But users report slightly stronger loyalty to more expensive ad-free svs: 52% of respondents said they “definitely will” have/use an ad-free svs a year from now vs 40% for ad-supported svs

Activists Continue To Gravitate To TMT… Match & BuzzFeed Feel More Heat

We’ve been highlighting the increased level of activist activity within TMT over the last year, and once again, activist activity spiked this week, as Starboard joined two other activist funds in pressuring Match to make some strategic changes that they believe will unlock value. Also this week, the Pulte Family disclosed an activist stake in Buzzfeed and publicly supported Vivek Ramaswamy, who outlined his plan for changes at the company back in May.

See our thoughts/takes below.

Starboard Joins The Match Activist Bandwagon

- What happened? The investment firm disclosed a 6.6% position, making them the largest shareholder, and sent a letter to the Co’s CEO and CFO this week highlighting the view that Match is a “growing, high quality business in a secularly growing industry” AND is “deeply undervalued”; It outlined some broad areas it believes will help close that gap

-> Other activists, Elliot Investment Mgmt and Anson Funds Mgmt have also taken stakes in the Co, and the Co has already appointed 2 new members to the board and named a new CEO for Tinder

- Starboard points to share price declines since the split from IAC: “Over the last four years since the separation from IAC, Match’s share price has declined by nearly 70%, significantly trailing the broader market”

- It believes that there needs to be more product innovation at Tinder: Starboard believes that overall revenue growth has been hindered at Tinder (Match’s largest app) because of lack of product innovation, which they believe has driven the user and payer declines at Tinder

- They think that Match can meaningfully improve profitability/margins

- The investment firm argues that Match has produced cumulative incremental margins below its consolidated margins – “This does not make sense”; They expect incremental margins for Match to be in excess of 50%

- Starboard believes the Co can increase its adj op margins to 40%+ and sees it as “a highly achievable goal, as Match generated 38% adj op margins in 2019 with ~40% less revenue than it has today”

- Match should be more aggressive and systematic w/ its capital return program: “At or around the current valuation, we believe Match should be using 75% or more of its free cash flow, plus some or all of the ~$900mn of available capacity under its 3.0x net leverage target, to repurchase shares”

- Match is expected to produce $1bn+ of FCF in 2024 and even greater amounts in the future, so it should be able to significantly reduce its share count, given its currently “depressed” valuation

- Believe Match can generate $5.50 or more of FCF/share in 2026

- Match is expected to produce $1bn+ of FCF in 2024 and even greater amounts in the future, so it should be able to significantly reduce its share count, given its currently “depressed” valuation

- Starboard is pushing for a sale of the Co if it cannot close the valn gap

- See link to Starboard letter to mgmt if interested

-> The stock rose +7.5% on the back of the Starboard news but is still down -5.0% YTD

The Pulte Family Backs Ramaswamy With Respect To BuzzFeed

- What happened? (link): The Pulte Family disclosed less than 1% stake but publicly supported Vivek Ramaswamy’s (BuzzFeed’s second largest shareholder w/ ~9% stake) plan to seek mgmt changes; A spokesman for the family indicated that it might increase its stake in the “days/weeks ahead”

- What is Ramaswamy’s plan? An excerpt from its letter to mgmt. on May 27, 2024 (link to view Ramaswamy’s letter)

- Get back to startup size: Face the harsh reality that staff cuts and restructuring thus far have only been “catching the falling knife.” BuzzFeed needs a complete ground-up restructuring to right-size itself for the coming AI-driven changes to your business

- Focus on audio & video content: After getting back to startup size, invest further in places where BuzzFeed has a competitive advantage: creator-led audio & video content

- Make BuzzFeed a bold, distinctive brand: Distinguish yourself from competitors by openly admitting your past journalistic failures and redefine BuzzFeed’s brand around the pursuit of truth.

- The board: Ramaswamy also put forth 3 more conservative-leaning nominees to the board, Chris Balfe, Patrick Bet-David, and Clay Travis

-> BuzzFeed went public via a SPAC in December 2021 in a 1.5bn deal; It has never traded higher than its $38.48/shr price when the deal closed, and has since fallen to $2.73/share or $105mn market cap

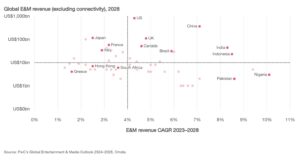

New Forecasts For Global Entertainment & Media Revenues Through 2028… Digital Advertising, Gaming, And APAC Are All Key Growth Drivers

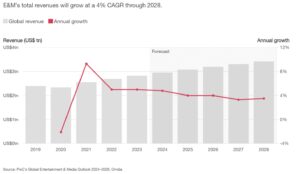

Taking a step back to frame the overall Media & Entertainment TAM and revenue market opportunity, we took a deep dive into PwC’s annual report, Perspectives from the Global Entertainment & Media (E&M) Outlook 2024-2028, which was released this week. While the themes discussed in the report are consistent with many of those that we have been talking about for some time (growth in CTV & retail media, streaming bundles, evolving business models, etc.), their projections provide helpful guideposts.

Overall growth in global E&M has been outpacing overall economic growth and is expected to increase +3.9% CAGR from 2024-2028, thanks in large part to digital advertising, w/ CTV and retail media being critical growth drivers. Gaming, not surprisingly, is also one of the fastest expected areas of growth in the sector, with AsiaPac being the main regional driver. Across all of global E&M, while the US remains the largest market, India and Indonesia standout as large markets with stronger growth, and China is also closing the spend gap vs the US, though the country does have its own challenges.

See below for our main takeaways from the data and report and see the link to PwC report if interested in more.

- The overall Global E&M industry revenues incr’d +5% y/y to $2.8tn in 2023 and is projected to hit $3.4tn in 2028

- Growth has outpaced overall economic growth cited by the IMF

- Looking forward, Global E&M revenue is forecasted to increase at a +3.9% CAGR from 2024-28

- Advertising “is poised to become a more important part of companies’ business models — even for those that had previously avoided ad revenues”

- Ad spend is expected to surpass $1tn in 2026 and will grow at a +6.7% CAGR through 2028, when ad spending will be almost 2x the 2020 total

- Advertising will account for 55% of total E&M industry growth over the coming five years

- A large portion of the fastest growing areas within the Global E&M industry outlook are within digital advertising: Total digital advertising is forecast to increase +10.1% in 2023, adding $52.5bn in new revenues and rising +9.5% CAGR through 2028, accounting for 77.1% of total spend

- Retail//other display internet advertising revenue is the fastest growing area: This pool is growing especially fast in more mature e-commerce markets like the US, where it will rise at a CAGR of +21.6% to $31.7bn in 2028, from $11.9bn in 2023

- Retail media players are increasingly experimenting with “shoppable TV” advertising, which makes it possible for consumers to buy products direct from ads on television and on videos

- Online connected TV (CTV) ads is projected to double, from $20.5bn in 2023 to $41.2bn in 2028

- Retail//other display internet advertising revenue is the fastest growing area: This pool is growing especially fast in more mature e-commerce markets like the US, where it will rise at a CAGR of +21.6% to $31.7bn in 2028, from $11.9bn in 2023

-> See Theme #6 for more on some key updates in digital advertising this week

- Despite expected increases in Global OTT SVOD services from 2023-2028, average revenue growth per user is expected to be muted on average, hence new business approaches will be critical: Global OTT SVOD subscriptions are expected to rise from 1.6bn in 2023 to 2.1bn in 2028 (+5% CAGR), but avg rev per OTT SVOD is anticipated to only increase from $65.21 in 2023 to $67.66 in 2028

- The focus is on ad-based tiers, password crackdowns, and “appointment viewing” content, such as live sports, to attract both subscribers and advertisers

- Global AVOD rev will continue to grow at double-digit rates through 2028 for a five-year CAGR of +14.1%; By 2028, advertising will account for ~28% of global streaming revenues, up from 20% in 2023

- Consolidation in intl streaming, plus the return of the bundle are key themes looking ahead

- The focus is on ad-based tiers, password crackdowns, and “appointment viewing” content, such as live sports, to attract both subscribers and advertisers

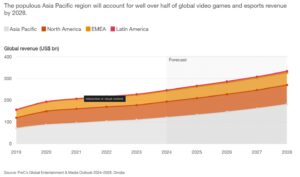

- Gaming remains one of the fastest-growing E&M sectors, driven largely by Asia Pacific, w/ revenues expected to top $300bn in 2028: Global video games revenue (includes esports which is still small), reached $227.6bn in 2023, up +4.6% y/y, and revenue is on track to top $300bn in 2028, more than 2x 2019; In 2028, gaming will account 9% of the entire E&M industry

-

- App-based social/casual gaming revenue ($82.9bn) was narrowly ahead of in-app games ad revenue ($72.4bn)

- By 2028, the latter will rise at a +15.4% CAGR globally to $147.9bn in 2028, while the former will grow at just a +5.15% CAGR, to $106.6bn

- By 2028, social/casual gaming will account for more 75% of the overall global video games and esports market

- Asia Pacific is the biggest region globally for total video games and esports revenue: In 2023, video gaming in the region generated revenues of $109.6bn, 48.1% of the segment’s global total; By 2028, the region will account for $181.8bnlion in gaming revenues, or 54.4% of the total.

- Within Asia Pacific, total video games and esports revenue in Indonesia is projected to rise at a CAGR of +16.0% through 2028, which makes it the third-fastest-growing video games market (tied with Pakistan)

- US is the largest E&M market, but Indonesia and India stand out as large markets w/ higher growth

- US: Represented more than one-third of global E&M spending in 2023, but growth is expected at only +4.3% CAGR through 2028, which is below the global rate of +4.6%

- India will be the world’s fastest-growing OTT video-streaming market over the forecast period: Demand for sports is high in the region

- China’s continued strong growth means it’s steadily closing the gap on the US in terms of market size: Projects a +7.1% CAGR, and by 2028, China’s advertising and consumer spending revenues ($362.5bn) will be less than half of those in the US ($808.4bn); But tight govt regulation “can make investing there more complex than in other territories”

- Smaller markets with high expected growth:

- Nigeria -> E&M growth of +10.1% CAGR through 2028

- Turkey -> E&M growth of +9.5% CAGR through 2028

More Updates From The Digital Ad Space + Ad Agency Holding Co Earnings

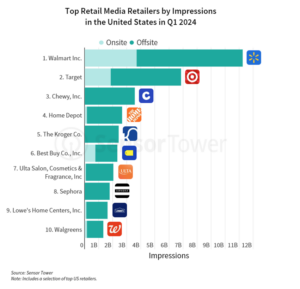

Along with the digital advertising forecasts from PwC in its annual Entertainment & Media report that we flagged in Theme #5, there were several other updates this week from the digital advertising space that we wanted to highlight. Specifically, a new forecast from the Interactive Advertising Bureau predicts that spending on digital video advertising will jump +16% y/y to $62.9bn in 2024 and comprise the majority of overall annual advertising budgets for the first time. An increasing number of media buyers now consider social media and CTV to be “must-buy” channels, and they have been reallocating ad dollars from national/local broadcast and cable TV platforms accordingly. In addition to CTV, retail media has been another rapidly growing area of advertising recently. This week, Sensor Tower published findings that revealed that the reach of Walmart’s retail media network is unparalleled amongst its retailer peers, delivering 11bn impressions in Q1 compared to second place Target’s fewer than 7bn impressions. Notably, Walmart also enjoyed a wide lead in onsite impressions, which appear on a company’s own website instead of on others’.

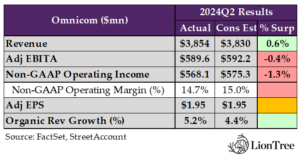

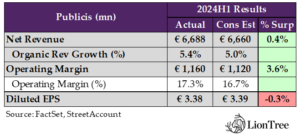

On a related note, Omnicom and Publicis, two of the major advertising agencies holding companies, reported earnings this week. Both reported slight top-line beats that were supported by solid organic growth across geographies, though each was impacted by more difficult comps in some key regions. Looking ahead, while Omnicom opted to maintain its prior organic growth guidance, Publicis raised its range by +100bps to +5-6%, as the company now expects to hit the high-end of its prior guidance despite acknowledging persistent macroeconomic challenges.

See below for more details:

-> Omnicom shares fell -4.0% following earnings and ended the week down -2.5%; Publicis shares were down -1.5% in response to earnings, closing the week down a slight -0.8%; YTD, Omnicom stock is still trading up +5.2% and Publicis stock is up +17.4%

- Digital video ad spend is predicted to rise +16% y/y to $62.9bn in 2024 and account for the majority of total annual ad spend for the first time, per the IAB (link): This jump will outpace growth in the total advertising spending as well as 2023’s +15% y/y increase in digital video ad spending, per the Interactive Advertising Bureau

- The majority of ad spending is expected to be on digital for the first time: Spending on digital video ads is projected to account for 52% of total ad spending, compared to a 48% share for linear TV; In 2023, digital video ads comprised 48%, while linear TV made up 52% of overall spend

- More advertisers and media buyers are considering social media and CTV a “must-buy”: Buyers indicated ad dollars being spent on CTV were being reallocated from national/local broadcast and cable TV channels as well as other nonvideo digital ads

- Three-quarters of CTV buying is now being done programmatically: This makes it easier for advertisers to optimize campaigns, improve returns on ad spending, and achieve scale

- Media buyers are now evaluating campaigns based on outcomes: Such as sales and store visits

- The adoption of alternative currencies has also picked up: 89% of advertisers have either transacted, tested, or discussed the use of alternative currencies; 28% have transacted on non-demographic metrics

- BUT there have been some challenges: Including that they’re too expensive, lack standardization as well as historical benchmarks, and involve more complexity if planning for multiple currencies

- Walmart’s retail media network delivers the most ad impressions amongst its peers (link): Sensor Tower’s new report revealed that Walmart’s retail media network saw 11bn impressions in Q1, which was far ahead of Target in second-place w/ fewer than 7bn impressions

- More specialized retailers hold the other top spots: After Walmart and Target, Chewy was #3 w/ 3-4bn impressions, while Home Depot and Kroger were #4 and #5, respectively, both w/ between 2-3bn impressions

- Walmart also holds the top spot for onsite retail media impressions: For reference, onsite ads appear on a Co’s own website instead of other channels; Target and Best Buy were the only other top 10 retailers w/ a significant share of onsite impressions

- Personal care was the leading category for US retail media impressions in Q1: This includes products such as fragrances/perfumes, makeup, and haircare; Ulta and Sephora were the leading retailers in the space

- Though top categories varied significantly between retailers: General retailers like Walmart, Target, and Walgreens covered a wide range of categories, while specialized ones like Chewy and Home Depot were more focused

Separately, A Couple Of The Ad Agency Holding Cos Reported This Week…

- Omnicom printed mixed headline results: Q2 rev incr’d +6.8% y/y (vs +5.4% y/y in Q1) and beat cons by +0.6%, as organic rev growth of +5.2% y/y (vs +4.0% y/y) surpassed cons +4.4% y/y; Adj EBITA grew +5.5% y/y but missed cons by -0.4%, and non-GAAP op income closed -1.3% below cons as well

- Geographically, the Co had a “solid qtr across regions” …: Organic y/y rev growth in the US accel’d to +6.3% (vs +4.3% in Q1), growth in LatAm improved to +24.5% (vs +22.3% in Q1), growth in the UK accel’d to +6.9% (vs +3.2% in Q1), and growth in Euro mkts ticked up to +4.5% (vs +3.5% in Q1)

- … Though APAC was up against more difficult comps: APAC’s organic rev declined -0.1% y/y (vs +3.0% y/y in Q1), given the strong growth in the Co’s Experiential biz in China in Q2:23

- Clients have been “conservative in forecasting”: Cited cont’d uncertainty surrounding the trajectory of the Fed’s rate cuts, the upcoming US elections, as well as snap elections in the UK and France as the main reasons for this

- Geographically, the Co had a “solid qtr across regions” …: Organic y/y rev growth in the US accel’d to +6.3% (vs +4.3% in Q1), growth in LatAm improved to +24.5% (vs +22.3% in Q1), growth in the UK accel’d to +6.9% (vs +3.2% in Q1), and growth in Euro mkts ticked up to +4.5% (vs +3.5% in Q1)

- Omnicom maintained its full-yr organic growth guidance…: The Co still anticipates an organic y/y rev growth range of +4-5% in FY24 and has posted a +4.6% y/y rate to-date

- BUT expects “stronger second half results”: Driven by new wins and project spend in Precision Marketing returning to a normal level;

- Publicis’ headline results mostly beat, though EPS slightly missed: Net rev was up +5.9% y/y in H1:24 (vs +4.2% y/y in FY23) and topped cons by +0.4%, w/ organic rev growth of +5.4% exceeding cons +5.0%; Op margin expanded +6.1% y/y (vs +4.3% y/y in FY23) and beat cons by +3.6%; However, EPS missed by -0.3%

- The Co “performed well in all of [its] regions”…: Organic y/y rev growth in North America accel’d to +5.2% (vs +4.8% in Q1), rev growth in APAC stepped up to +7.7% (vs +6.2% in Q1), rev growth in the Middle East & Africa accel’d to +9.1% (vs +4.0% in Q1), and rev growth in LatAm improved to +18.9% (vs +7.8% in Q1)

- … Though Europe was setback by some tougher comps: Noted a “very challenging comp” vs Q2:23, when the Co reported +15.2% y/y growth in the region

- Most of the Publicis’ client industries “posted positive growth”: The TMT sector (13% of the Co’s net rev) saw over +11% y/y organic growth, and healthcare posted +26% y/y organic growth on top of difficult comps; Also highlighted contributions from automotive and food & bev

- The Co “performed well in all of [its] regions”…: Organic y/y rev growth in North America accel’d to +5.2% (vs +4.8% in Q1), rev growth in APAC stepped up to +7.7% (vs +6.2% in Q1), rev growth in the Middle East & Africa accel’d to +9.1% (vs +4.0% in Q1), and rev growth in LatAm improved to +18.9% (vs +7.8% in Q1)

- Guidance for FY24 organic net rev growth was raised: Now expects a range of +5-6% y/y (vs the prior +4-5% range); 5% is the “new floor” even w/ the “current global context” and “ongoing delays in client biz transformation projects”; The 6% “stretch” target will be dependent on an “improved macro context”

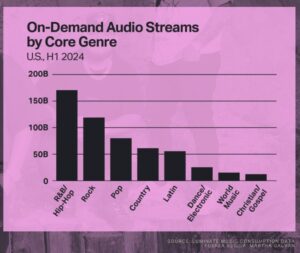

A Mid-Year Look At Key Music KPIs

Within the music sector, Luminate’s 2024 Midyear Music Report has a lot of granularity about trends pertaining to artists, genres, demos, and regions, but we outlined a few higher level metrics below that looked most interesting to us (here is the link if you want to peruse the additional detail in the report – Luminate Report

- Global On-Demand Audio streaming was up +15.1% y/y in H1:24 to 2.29tn

- In the US…

- Total album consumption was up +7.4% y/y in H1

- Total digital music consumption was up +7.5% in H1

- On-demand Streaming- Audio volume was up +8% y/y in H1

- R&B / Hip-hop has the highest # of streams, followed by Rock

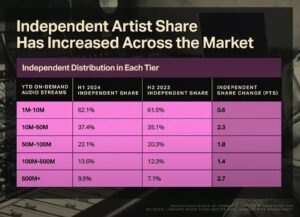

- The share of indie artists is ticking up:

- Indie artists made up 62.1% of all artists who accumulated between 1-10mn US On-Demand Audio streams in H1 (62.3% of artists to reach 10-50mn US on demand streams have major distribution)

- The share of indie artists who earned 500mn+ On-Demand Audio streams incr’d by more than +2% y/y in H1

- What matters most on music streaming services? Consumers at risk of churning prioritize the following features when compared to the average paid music streamer:

- 48%+ exclusive artist content

- 49%+ additional content outside of music

- 50%+ live streaming of events/concerts/live performances

- GenZ is spending the most on concerts: Live music makes up 64% of monthly music spend, and GenZ spends 23% MORE per month than the average US music listener

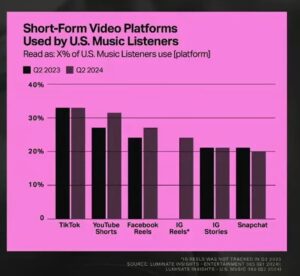

- TikTok is the short form video platform most used by US music listeners

- YouTube Shorts follows closely behind

Some Pluses And Some Minuses With Consumer Retail/E-Commerce Spending Trends

It was a big week for the retail/e-commerce sector, as sales during Amazon Prime Day, which ran from July 16-17, hit “record-breaking” levels and sparked a flurry of online shopping activity that exceeded Adobe Analytics’ optimistic expectations. While Adobe Analytics initially predicted that online spending would grow +10.5% y/y and reach a record $14bn during the 48-hour period around Amazon’s shopping event, the company later revealed that online sales surged past this high bar, increasing +11% y/y to $14.2bn. Notably, Amazon touted that “millions more” Prime members shopped the event compared to 2023, and this appeared to be the main driver behind the significant y/y jump in spending, based on Numerator’s findings that the average order size and spend per household actually dropped from last year. In terms of products, electronics and back-to-school-related items were highlighted as the best performing categories during this year’s Prime Day.

Still, despite the strength of back-to-school-related sales during Prime Day, a separate Deloitte survey published this week suggests that parents expect to spend less on back-to-school related items this year. In total, $31.3bn of back-to-school spending is forecasted in 2024 (vs $31.9bn in 2023), representing an average per child outlay of $586 (vs $597 in 2023). In particular, one trend to monitor is that low- and middle-income families have been pulling back on spending due to struggles with finances and concerns about the economy. Interestingly, Commerce Department data released this week indicated US retail sales were much stronger than anticipated in June, though one economist attributed this to “openhanded spending by affluent consumers… keeping the economy as a whole moving forward”. This could be the case throughout the remainder of 2024, as another report by FTI Consulting predicts that US online retail sales growth will accelerate slightly this year over 2023.

See below for more details on what we thought was most important:

Amazon Prime Day Sales Continues To Reach New Heights, Surpassing Estimates

- Amazon touted “record-breaking” sales during Prime Day 2024 (link): Prime Day 2024 saw more items sold during the two-day event than any previous Prime Day; This was the fourth consecutive yr that Amazon has set new sales record during the event

- “Millions more” Prime members shopped Prime Day 2024 than last yr: The Co indicated that the “oppty to save big” drove a “record-breaking” number of customer sign-ups for Prime in the three weeks leading up to Prime Day, w/ “millions of new members worldwide”

- Details on overall sales weren’t provided: Previously, Amazon said that its customers purchased 375mn+ items and saved $2.5bn during Prime Day 2023

- Independent sellers sold 200mn+ items during the event: As Prime members in the US were able to “shop more deals on small biz products than ever before”

- Both popular brands and SMBs saw success w/ deals: Flagged TruSkin, ALOHA, Blueland, and Native Pet as examples of SMBs that performed well w/ deals; In terms of more popular brands, the Co highlighted deals from Apple, Sol de Janeiro, Dyson, and Ring

- Prime members also “took advantage of incredible savings” on Amazon devices and subscriptions: Highlighted Amazon Music Unlimited, Kindle Unlimited, and Audible, as well as Amazon Fresh and Whole Foods Market grocery delivery, plus food delivery from Grubhub+

- An estimated 10mn trips were saved by customers choosing to consolidate orders: Resulting in lower carbon emissions, on avg

- “Millions more” Prime members shopped Prime Day 2024 than last yr: The Co indicated that the “oppty to save big” drove a “record-breaking” number of customer sign-ups for Prime in the three weeks leading up to Prime Day, w/ “millions of new members worldwide”

-> In advance of Prime Day 2024, Amazon expanded access to Rufus, its Gen AI shopping tool, to all its US customers; Rufus is a gen AI-powered conversational shopping assistant designed to help customers save time and make more informed purchase decisions, and it is now available in the Amazon Shopping app in the US; According to Amazon, Rufus helped millions of customers shop and discover items during Prime Day (link)

- Amazon Prime Day boosted US online sales to record-setting and higher than expected levels, per Adobe Analytics (link/link): Adobe Analytics found that online spending in the US rose +11% y/y to $14.2bn during this yr’s 48-hour Prime Day event, topping the Co’s estimates of $14bn

- The strong performance was driven by BTS shopping…: Back-to-school related spending was up +216% across both days compared to avg daily sales levels in June 2024

- … As well as an “apparent product refresh cycle”: Online sales for the electronics category grew +61% across retailers, given strong demand for tablets, TVs, and Bluetooth speakers this yr

- But avg order sizes were lower y/y during Amazon Prime Day 2024, per Numerator (link): Numerator’s preliminary findings revealed that the avg order size was $57.97 during this yr’s Prime Day, a decline from 2023’s $58.67 and 2022’s $60.73 avg order values

- Spend per household also dropped from last yr: The avg household spent $152.33 during Prime Day 2024 compared to $181.72 in 2023 and $176.71 in 2022

- Order frequency per household was down y/y as well: In 2024, 60% of households placed 2+ separate orders, whereas 73% placed 2+ orders in 2023

- The top selling items on Prime Day 2024: Amazon Fire TV Sticks were the top-selling item (by number of units), followed by Premier Protein Shakes, Liquid IV Packets, Glad Trash Bags, and COSRX Snail Mucin Serum

However, Deloitte Expects Overall BTS Spending Levels To Be Down Y/Y

- 2024 back-to-school spending levels are expected to decline from last yr (link): Per a new Deloitte survey of 1,198 parents of K12 students, parents plan to spend $586 per child on back-to-school (BTS) items this yr, a drop of -$11 from 2023 levels; In total, $31.3bn of back-to-school spend is projected in 2024 (vs 2023’s $31.9bn)

- Low- and middle-income families are pulling back on spending: BTS spending by low- and middle-income families is forecasted to drop -4% y/y and -9% y/y, respectively, due to struggles w/ finances and concerns about economic conditions

- Clothing & accessories will account for most of BTS spending: Clothing & accessories are predicted to account for ~40% of total BTS spending; Tech products and school supplies are projected to respectively comprise ~27% and ~24% of overall spending

- BTS spending on tech products is projected to be down -11% y/y: This will be offset partly by higher spending on personal hygiene and home furniture; Otherwise, spending clothing & accessories as well as school supplies are both expected to be flat y/y

- Shopping for the BTS season is expected to occur earlier this yr: As 66% of planned BTS spending is predicted to occur by the end of July 2024, an uptick from 59% in 2023

- 59% of respondents believe the best deals occur earlier in the season: Notably, 48% plan to shop Amazon Prime day sales compared to 39% in 2023

- Gen AI is becoming more integral to the shopping journey: 18% of parents plan to use Gen AI for BTS shopping, and 23% say their children are using in their schoolwork (vs 15% in 2023)

- Parents are expected to similar amounts on extracurriculars: 86% of respondents enrolled their children in extracurricular activities, and they expect to spend $582 per child on these (includes fees and equipment)

Several Other Notable Updates On The Retail/E-Commerce Space Also Hit The Tape This Week…

- US retail sales were much better than anticipated in June (link/link): Per the Commerce Dept’s new data, US retail sales were flat m/m in June (vs +0.3% m/m in May), beating expectations of a -0.3% m/m decline; On a y/y basis, US retail sales were up +2.3%, though this was down from Jan’s +7.7% gain

- Core retail sales also topped Street forecasts: Excluding autos and gas, US retail sales incr’d +0.8% m/m in June, exceeding estimates for a +0.2% m/m rise

- Category-specific color – Online store sales led the way: Non-store retailers saw a +1.9% m/m jump in sales in June; Addt’ly, building material & garden equipment store sales rose +1.4% m/m, clothing retailer sales incr’d +0.6% m/m, and sales at food svs & drinking establishments grew +0.3% m/m

- Conversely, gas station sales fell the most: Sales at gas stations dropped -3.0% m/m, driven by lower prices and likely freeing up spend elsewhere; Motor vehicles and parts dealers also saw a -2% m/m decline

- US consumer spending is now expected to have accel’d seq in Q2: Economists now estimate that consumer spending (accounts for ~two-thirds of the US economy) expanded +2.0% y/y in Q2; Previously, forecasts had called for Q2 consumer spending to match Q1’s +1.5% y/y rate

- US online retail sales are projected to grow +9.8% to $1.2tn in 2024, per FTI Consulting (link): This represents a slight accel over 2023’s rate of growth; Now that the post-pandemic transition is over, FTI sees e-commerce sales settling down to more predictable growth and mkt share gains

- E-commerce is forecasted to grow at 2x+ the expected rate of total retail sales (excluding autos & gas) in 2024: This rate of growth would also represent 3x+ the estimated store-based total sales growth

- Online sales growth accounted for 57% of total US retail sales in Q1, its highest rate since 2017 excluding the pandemic period

- E-commerce mkt share is expected to grow to 22.7% by yr-end: This compares to 21.6% at the end of 2023; Moving forward, FTI anticipates share gains of +100bps in 2024 and 2025 (a decel of +125-150bps gains in the pre-COVID period)

- US e-commerce mkt share of total retail sales will plateau near 35% by next decade: This means that the US e-commerce mkt share is approaching two-thirds of its projected ceiling, w/ several product categories already reaching that level

- 45,000 net retail store closures will occur in the US by 2028, per UBS: This represents nearly 5% of the total retail store base if e-commerce mkt share reaches 26% by 2028

- E-commerce is forecasted to grow at 2x+ the expected rate of total retail sales (excluding autos & gas) in 2024: This rate of growth would also represent 3x+ the estimated store-based total sales growth

Grab Bag: Online Grocery Delivery Sale Surge / Trump’s Take On TikTok / Potential M&A Chatter At VZ And GOOG

- Online grocery delivery sales surged +18% y/y to $2.9bn in June (link): This was according to Brick Meets Click and Mercatus’ Grocery Shopping Survey

- A spike in MAUs and incr’d order activity drove growth in online delivery: These factors more than offset a decline in value of orders

- Online grocery delivery captured 38% of online grocery sales in June: This marked a +325bps y/y increase

- Delivery’s outperformance “likely benefited” from promo offers from Instacart and Walmart: This was per David Bishop, a partner at Bricks Meets Click, who added that “these promos focused on delivery ad offered deep discounts on each svs’ annual membership fees”

- Otherwise, overall online grocery sales grew +8% y/y to $7.7bn in June

- Trump says he wouldn’t ban TikTok if he became President – “I’m for TikTok” (link/link)

- Necessary for competition: “Now that I think about it, I’m for TikTok because you need competition…if you don’t have TikTok, you have Facebook and Instagram”

- Trump has criticized Facebook and Instagram for suspending him for two years from both platforms after the Capital Hill incident on Jan 6

- Previous calling it a threat, Trump joined TikTok late last month: Four years after attempting to ban TikTok through an executive order while he was in office after claiming it posted a national security risk

- Support comes at a time when a ban on TikTok is looming: In Sept, a US Appeals Court will hear arguments on a new law signed by current US President Biden requiring ByteDance to sell TikTok’s US assets by January 19 or face a ban

- Necessary for competition: “Now that I think about it, I’m for TikTok because you need competition…if you don’t have TikTok, you have Facebook and Instagram”

- Potential M&A in the works?

- Verizon is reportedly exploring selling thousands of towers in the US (link/link): VZ has reportedly hired advisers to gauge interest from potential buyers for a package of roughly 5,000-6,000 towers; A sale could bring in $3bn+, according to reports, though deliberations are preliminary and there’s no guarantee they’ll result in a sale

- Telcos have historically sold towers to raise cash: In 2015, Verizon sold the rights to lease and operate ~11,000 towers to American Tower Corp for $5bn as part of a deal that help it raise funds for airwave purchase and pay down debt; In 2013, AT&T agreed to sell 9,700 towers to Crown Castle International in a $4.8bn deal, which AT&T then used to begin an upgrade of its network

- Google is reportedly planning to acquire Wiz for $23bn (link/link/link)

- What is Wiz? Wiz enables businesses to conduct comprehensive threat assessments on their IT infrastructure, including the Cloud, and individual software, which is particularly valuable as more enterprises transition to the Cloud

- Has grown at a rapid clip: Wiz was founded in 2020 and hit $100mn in annual recurring revenue after 18 months, and then achieved $350mn in annual recurring revenue in 2023; It raised $1bn back in May at a valuation of $12bn

- Could be Google’s largest-ever deal: A Wiz acquisition would dwarf the size of Google’s largest deal to date, its $12.5bn purchase of Motorola Mobility in 2012; Google also spent $2.1bn on Fitbit in 2021 and $3.2bn on Nest Labs in 2014; Other acquisitions over the years have included YouTube, DoubleClick, Looker, and Waze

- Verizon is reportedly exploring selling thousands of towers in the US (link/link): VZ has reportedly hired advisers to gauge interest from potential buyers for a package of roughly 5,000-6,000 towers; A sale could bring in $3bn+, according to reports, though deliberations are preliminary and there’s no guarantee they’ll result in a sale

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Taboola.com has secured a deal w/ Apple to integrate native advertising into the Apple News and Apple Stocks apps, the digital advertising co said, sending its shares up almost 11%. The agreement strengthens Taboola’s portfolio of reselling contracts and gives Apple an opportunity to expand its advertising biz. The co will manage native advertising across both platforms globally and has been authorized as an advertising reseller. (Yahoo Finance)

Artificial Intelligence/Machine Learning

- A California state bill has emerged as a flashpoint between those who think AI should be regulated to ensure its safety and those who see regulation as potentially stifling innovation. The bill, which heads to its final vote in Aug, is sparking fiery debate and frantic pushback among leaders from across the AI industry—even from some companies and AI leaders who had previously called for the sector to be regulated. (Yahoo Finance)

- Anthropic launched its Claude Android app to bring its AI chatbot to more users. This is Anthropic’s latest effort to convince users to ditch ChatGPT by making Claude available in more places. The Claude Android app will work just like the iOS version released in May, including free access to Anthropic’s best AI model, Claude 3.5 Sonnet, alongside upgraded plans through Anthropic’s Pro and Team subscriptions. (TechCrunch)

- Mistral, a French AI startup, launched a new LLM that can help generate longer tranches of code comparatively faster than other open-source models, such as CodeGemma-1.1 7B and CodeLlama 7B. The Co tested Codestral Mamba on in-context retrieval capabilities up to 256k tokens — twice the number seen in OpenAI’s GPT4o — and found its 7B version performing better than open source models in several benchmarking tests. (InfoWorld)

- TrendForce’s latest industry report on AI servers reveals that high demand for advanced AI servers from major CSPs and brand clients is expected to continue in 2024. Meanwhile, TSMC, SK hynix, Samsung, and Micron’s gradual production expansion has significantly eased shortages in 2Q24. Consequently, the lead time for NVIDIA’s flagship H100 solution has decr’d from the previous 40–50 weeks to less than 16 weeks. (TrendForce)

- Workday’s survey of workers and leaders across the UK suggests bosses think AI could help them save 50% more time than their employees. The poll of 700 workers and 500 business leaders at large organizations in the UK found bosses thought AI could save them 4.4 hours each working day. Employees, on the other hand, believe AI could save them 2.9 hours a day. (Yahoo Finance)

Audio/Music/Podcast

- Record labels, including UMG Recordings, Warner Music, and Sony Music, filed a lawsuit accusing Verizon of intentionally ignoring its customers’ copyright violations for profit. The plaintiffs say they are entitled to as much as $150,000 per violation under the Digital Millennium Copyright Act (DMCA), which could add up to as much as $2.6bn. The lawsuit includes a list of 17,335 tracks from artists or bands. (The Verge)

- YouTube Music is making official sound search, while acknowledging that it’s testing the “AI-generated conversational radio” for US Premium subscribers. The Hum to Search-adjacent capability is called “sound search” in YouTube Music. It simply lets you query YTM’s “catalog of 100mn+ official songs by sound.” Some users had it in May before the feature was rolled back for whatever reason. (9to5Google)

Broader Media & Entertainment

- BBC Studios and Samsung Plus are to expand two BBC FAST channel brands in EMEA. BBC Drama will make its debut in MENA on Samsung TV Plus, whilst Top Gear launches on Samsung TV Plus across MENA, Italy, Spain, France, Germany, Norway, Sweden, and Denmark. Already available in Spain, Italy, and France on Samsung TV Plus, BBC Drama makes its debut in MENA, featuring the BBC’s award-winning British BBC drama. (ADVANCED-TELEVISION)

- Discovery reportedly is slashing 1,000 jobs as the struggling Co faces calls to sell off assets that include ratings-challenged CNN. The layoffs, which began earlier this month, will hit the finance, biz affairs and production departments and at streaming provider Max. The cuts come during a chaotic period for the Co, which last week annc’d that CNN will chop 100 jobs under a major restructuring by new boss Mark Thompson. (Yahoo Finance)

- Mario Gabelli’s investment firm is seeking more details about the valuation of National Amusements assets, signaling the firm may challenge a landmark entertainment industry deal inked. Gabelli Funds, which owns nearly 4.9mn Class-A voting shares in Paramount, is seeking greater transparency around the National Amusements deal, according to another source at Gabelli. (Yahoo Finance)

- Paramount and Skydance officially annc’d a deal to merge last week, and part of the deal gave the Redstone family 45 days to look for other buyers to beat the Skydance offer. One of the other potential buyers reportedly was Sony, which had looked at Paramount but decided not to follow through on the purchase of Paramount, including its streaming services Pluto TV and Paramount+. (Cord Cutters News)

- Warner Bros Discovery was begged by longtime media analyst Jessica Reif Erlich to do something, anything, from selling the Co, to selling assets, to finding a streaming JV, or merger. “In our view, the current composition as a consolidated public Co is not working,” she said. She had high hopes when Discovery acquired Warner Media in early 2022 but noted the stock has declined more than 70% since then. (Deadline)

Broader Technology

- Net neutrality regulations were supposed to go into effect on July 22, but the US Court of Appeals for the Sixth Circuit said it needs more time to determine if it will allow the rules to go into effect or stay them until it resolves a lawsuit filed by multiple broadband trade groups. The court has postponed the effective date of net neutrality until at least Aug 5. (Fierce Network)

Cable/Pay-TV/Wireless

- America Movil reported a net loss per ADR of 2 cents for Q2 2024 against the net income of 46 cents reported in the prior-year qtr. Total qtrly revs incr’d 1.5% to Mex$205,524mn due to healthy performance in the Service segment biz, offset by poor results from the Equipment business segment. America Movil gained 2.4mn wireless subscribers in Q2. This figure includes 1.8mn postpaid subscribers. (Yahoo Finance)

- AT&T & Verizon are feuding over a plan to boost svs for police, firefighters, and other state and local agencies. AT&T and its allies are asking regulators to provide more wireless frequencies to FirstNet, a cellular network launched in 2017 to connect emergency responders. Verizon called the proposal a giveaway of spectrum valued at ~$14 bn that would give its competitor a “substantial windfall.” (Benton Foundation)

- Comcast and bankrupt Diamond Sports Group have returned to the negotiating table. This comes two and a half months after Diamond’s Bally Sports regional sports networks were pulled off the pay TV operator’s Xfinity TV programming grid in a carriage dispute. The resumption of talks was reported via Puck News last week. (NextTV)

- Deutsche Telekom is offering a new SaaS solution called “Law Monitor”. The AI-based model supports corporate legal departments in quickly recognizing changes to national and, in the long term, international laws. In light of the high density of regulations both in Germany and worldwide, Cos have to monitor more and more laws in order to remain legally compliant. (THEFASTMODE)

- DISH is reportedly at high risk of being unable to pay its bills. DISH has been struggling financially for some time now. Recently, it merged w/ EchoStar in an effort to address these issues but, according to an SEC filing last March, DISH will use a “substantial amount of cash” in the next 12 months. It “raises substantial doubt about [the co’s] ability to continue as a going [sic] concern,” EchoStar said. (Cord Cutters News)

- Maxis, a Malaysian telecommunications co, is considering buying out U Mobile to help it expand in the Asian country. Kuala Lumpur-listed Maxis has expressed interest in U Mobile and talks are at an early stage, sources said. However, pricing could be a hurdle to a potential buyout, w/ U Mobile’s owners seeking a valuation of RM10bn+ (S$2.9 bn). (The Straits Times)

- Mediacom Communications annc’d the launch of Mediacom Mobile, which will rely on Verizon Communications as its MVNO. Designed to be paired with Mediacom Xtream Internet svs, Mediacom Mobile will be available as an unlimited svs for $40 per month per line, plus taxes and fees, or in a pay-as-you-go scheme in which each successively used gig is billed at an addt’l $15 each on top of the $15-a-month base price. (Yahoo Finance)

- Reliance Jio Infocomm is exploring the possibility of a major initial public offering in 2025, per Jefferies. Jeffries also suggested that Jio might debut w/ a valuation ~$112bn, potentially contributing a 5-7% increase in the share price of its parent Co, Reliance Industries. Jefferies also suggested that the IPO could consist of an offer for sale by minority shareholders. (RCR Wireless News)

- T-Mobile emerged as the leader when it comes to mobile KPIs in the US, per Ookla data from Jan through June 2024. The data shows that T-Mobile US has the fastest 5G median download speed at 265.80 Mbps, up from 219.54 Mbps during the same period the previous yr. For median upload performance, T-Mobile and Verizon recorded the same median upload performance while T-Mobile had the lowest latency over 5G. (RCR Wireless News)

eCommerce/Social Commerce/Retail

- 41% of consumers will be splurging on gifts for themselves while tightening their spend elsewhere, per Vericast’s 2024 Holiday Retail TrendWatch report that polled 1,000 US adults. The trend is biggest among Gen z and millennials. The data also revealed 46% said they need to budget more and spend less overall on holiday gifts this yr, according to a press release on the findings. (www.retailcustomerexperience.com)

- A TikTok loophole seems to be allowing some teens access to the TikTok Shop tab, despite offering being restricted to users who are 18+, per TikTok’s policy. The issue occurs when a teen lies about their age when signing up for TikTok, by entering in a date of birth that indicates they are already 18+, but then is later required by a parent to pair the account w/ their parent’s using TikTok’s built-in parental controls. (TechCrunch)

- Back-to-school spending will likely flatten due to financial and economic concerns, per Deloitte’s 2024 Back-to-School Survey, avg’ing ~$586 per student w/ a collective spend of $31.3 bn. Parents expect to spend less on tech products but will increase spend on educational furniture and personal hygiene for students. Clothing and school supplies are expected to account for most of the back-to-school mkt spending. (www.retailcustomerexperience.com)

- Lab-grown pet food is to hit UK shelves as Britain becomes the first country in Europe to approve cultivated meat. The Animal and Plant Health Agency and the Department for Environment, Food and Rural Affairs have approved the product from the Co Meatly. It is thought there will be demand for cultivated pet food, as animal lovers face a dilemma about feeding their pets meat from slaughtered livestock. (the Guardian)

- Luxury goods are being discounted at rates as high as 50% in China, as middle-class shoppers rein in spending on big-ticket items and retailers grapple with overstocking. The discounts in the country are being offered primarily by aspirational brands such as Versace and Burberry, as China’s once-voracious middle-class consumers become more frugal, according to industry insiders and experts. (Australian Financial Review)

- Online spending will reach a record $14bn during Amazon’s Prime Day events, as retailers across the e-commerce universe join Amazon in offering deals, per Adobe’s forecast. Adobe predicts that Prime Day promos this yr will drive record levels of online spending and that sales will be up 10.5% y/y. Adobe expects this yr’s spending growth to significantly outpace last yr’s July Prime Day growth of 6.2% and 2022’s 8.5% gain. (Forbes)

- TikTok is becoming one of the largest e-commerce platforms in Southeast Asia, a market long dominated by local players like Shopee and Alibaba’s Lazada, an annual study showed. The app’s e-commerce platform TikTok Shop incr’d its gross merchandise volume nearly fourfold from $4.4bn in 2022 to $16.3 bn last yr, the fastest growth rate among regional rivals, Momentum Works reports. (Nikkei Asia)

Film/Studio/Content/IP/Talent

- Despicable Me 4 has finally claimed the top spot at the national box office. This comes after being blocked from the top for the past three weeks by the record-breaking Pixar animation, Inside Out 2. Despicable Me 4 brought in a further $4.84mn in its fourth week, enough to pip Inside Out 2’s $4.61mn and take pole position. Inside Out 2 has taken $46.1mn over its five-week run. (Mumbrella)

- Worthe Real Estate, along with QuadReal Property Group and Stockbridge Capital Group, has reacquired Warner Bros Discovery’s Burbank Studios for $375mn, about a year after selling it. The 27-acre, 680,000-square-foot campus will see further development, including five new soundstages. Warner Bros. will lease the studios as the primary tenant. (The Real Deal)

Handheld Devices/Connected Home/Accessories

- Q2 2024 marked the fourth consecutive qtr of growth for the smartphone market, per preliminary qtrly data from IDC. Global shipments are up 6.5% since the same period last yr, translating to ~285.4 mn units during the qtr. However, the Co warned that demand has yet to fully recover and “remains challenged in many mkts”. (RCR Wireless News)

Investor/Market Sentiment

- Across several banks with large wealth-mgmt bizs, a common theme in Q2 earnings was continuing to have to pay higher rates to hang on to brokerage customers’ cash that isn’t invested in things like stocks and bonds. Wells Fargo and Morgan Stanley called out increases in some of the rates they pay on certain brokerage account deposit products, and Bank of America noted a rise in rates paid on wealth-mgmt deposits. (Wall Street Journal)

Last Mile Transportation/Delivery

- Google has become one of the latest investors in Moving Tech, the parent Co of Indian open-source ride-sharing app Namma Yatri that is quickly capturing mkt share from Uber and Ola with its no-commission model. Moving Tech raised $11mn in a pre-Series A funding round co-led by Blume Ventures and Antler. Google, which has pledged to invest $10mn in India, participated in the round. (TechCrunch)

Live Entertainment/Theme Parks/Concerts/Experiential

- The Eagles’ residency at Las Vegas’ Sphere and the legendary band has cont’d to see overwhelming demand and has added four more weekend shows at the immersive venue in Jan 2025. The Rock & Roll Hall of Famers will now play Jan 17, 18, 24 and 25. Tickets for the new dates go on sale 9 am EST July 26 at eagles.com. The residency, which begins Sept 20, is now up to 20 shows. (Pollstar News)