Going into the long weekend, the major indices were modestly up (the S&P 500 rose +0.9% this week, while the NASDAQ rose +0.45%), during quite a busy week of new sector developments and updates along, with a few last earnings results.

See below for what we focused on in this edition.

- NVIDIA’s Growth Vectors Continue To Expand

- Is TTWO’s Net Bookings’ Guidance Conservative?

- Q1 Earning Wrap- The Vast Majority Of TMT Stocks Beat The Street

- Google I/O: New AI That Creates “Any Output From Any Input”

- Spotify’s New 2030 Targets Caught Investors’ Attention This Week

- SpaceX Drops Is S-1!

- Publicis Makes A Big Push Into Agentic AI W/ Its $2.2bn LiveRamp Deal

- 13-Fs Point To A Rotation Back Into Big Tech In Q1

- Grab Bag: Walmart Sparks Concern / Minnesota Prediction Mkts Ban/ Airbnb “Super App” Push

Also, LionTree is proud to have served as exclusive financial advisor to Vox Media on the sale of Vox Media Podcast Network, New York Magazine, and Vox to Lupa Systems, James Murdoch’s media and technology holding company. Congrats to all involved.

Enjoy the Memorial Day long weekend!

Best,

Leslie

NVIDIA’s Growth Vectors Continue To Expand

All eyes (as usual) were on Nvidia’s earnings this week and while the Co delivered FQ1 and FQ2 guidance ahead of Street expectations (and the guide doesn’t include China so there could be further upside), reiterated several longer-term guidance targets, and dramatically increased shareholder returns (raised the qtrly div 25x to 25c and announced an incremental $80bn buyback), it was not enough to move the stock higher given what was already priced in.

With that said, there were still a lot of other positives from earnings, and our top five learning include: 1) Demand commentary was extremely bullish, with mgmt saying that AI infrastructure demand has gone “parabolic” and that the buildout is “accelerating”…mgmt emphasized that compute capacity equates to revenue and profits for hyperscalers and that customers are generating profitable revenue beyond the depreciable life of their GPUs; 2) The Co expects its revenues to grow faster than hyperscaler capex, which analysts project will increase ~90–100% this year (and mgmt. reiterated its projection for $3–4tn in annual hyperscaler capx by the end of decade; 3) Mgmt reaffirmed it CY2025–27 visibility of $1tn from Blackwell/Rubin, and re-confirmed that Vera CPU would be incremental to that figure; 4) The new ACIE segment ($37.4bn in FQ1 revenue, +74% y/y), which is AI clouds, industrial, enterprise, sovereign AI and AI factories, is expected to grow faster than Hyperscale revenue and become the larger long-term opportunity, suggesting that Nvidia is not just a hyperscaler capex story; and 5) Vera will open a new $200bn TAM and give Nvidia another major growth driver beyond GPUs, with visibility to nearly $20bn of CPU revenue this year…Vera also is expected to be incremental to GPU demand because agentic AI requires CPUs for orchestration while the actual “thinking” still happens on GPUs.

See below for more details on the points we cited above but also other incremental updates from Nvidia’s results (including Physica AI, among other things). All in all, the fundamentals remain intact in our view.

-> Nvidia shares were relatively flat in reaction to results and are up +15.4% YTD

FQ1 Was Broadly Better Than Street Projections

- This was the 3rd consecutive qtr of y/y acceleration, and the 14th straight qtr of seq growth

- Total revs BEAT cons by 3.4%: Grew +85% y/y (vs +73% y/y in FQ4 and +62% y/y in FQ3) and was up +20% q/q

- Growth was driven by the Blackwell ramp across hyperscalers, frontier model builders, AI cloud providers and sovereign customers

- Mgmt changed the reporting segments… it split the biz into Data Center and Edge Computing, w/ Data Center split btw Hyperscale and ACIE

- Data Center

- Hyperscale = public clouds and the largest consumer internet companies

- ACIE = AI Clouds, Industrial & Enterprise, and incls AI purpose-built data centers and AI factories across industries/countries

- Edge = devices for agentic and physical AI, incl PCs, game consoles, workstations, AI-RAN base stations, robotics and auto

- Why make the change? To better reflect the business given that AI and the applications are diverse, where it runs are diverse, how it is governed is diverse

- Data Center

- Non-GAAP gross margin was IN-LINE: Flat-ish q/q vs 75.1% in FQ4

- Non-GAAP op income BEAT cons by 3.9%

- Non-GAAP op margin was 65.9% vs 65.7% cons

- Adj EPS BEAT cons by 6.9%

- FCF BEAT cons by 28.4%…reached a record

- CapEx was HIGHER than cons: It grew +25% y/y

FQ2 Guidance Also Topped Expectations W/ No China Contribution Assumed…BUT Mgmt Incr’d FY27 Cost Growth Guidance

- FQ2 rev guidance at $91bn (+/- 2%): Implies +95% y/y growth and +12% q/q, with seq growth expected to be driven primarily by Data Center

- The Co is NOT including any DC compute revenue from China (similar to last qtr’s assumption)

- The US gov’t approved licenses for H200 shipments to China-based customers, BUT Nvidia has not generated any related rev and remains uncertain whether imports will be allowed into China

- FQ2 GAAP and non-GAAP gross margins guide is 74.9% and 75%, respectively (+/- 50bp):

- For FY2027: The Co maintains its target for mid-70s gross margins

- FQ2 GAAP and non-GAAP OpEx guide is $8.5bn and $8.3bn, respectively

- For FY2027: Mgmt INCR’D OpEx growth to the upper 40s y/y from the prior low-40s expectation

- Driven by higher R&D and accelerating use of AI tools to enhance productivity

- For FY2027: Mgmt INCR’D OpEx growth to the upper 40s y/y from the prior low-40s expectation

- FY2027 tax rate guidance was revised LOWER: GAAP/non-GAAP tax is now expected at 16-18% vs prior 17-19%, driven by geographic mix

- Mgmt reiterated confidence in $1tn of Blackwell/Rubin revs from CY2025 through CY2027

Shareholder Returns Step Up Materially, While The Co Still Invests

- Co returned a record ~$20bn to shareholders in FQ1 through repurchases and dividends

- The Board approved an incremental $80bn share repurchase authorization, in addition to the $38.5bn remaining under the prior authorization at qtr-end

- The Co significantly raised the quarterly dividend to $0.25/share from $0.01/share

- Mgmt reit’d guidance to return roughly 50% of FCF to shareholders this yr

- The higher shareholder returns are not at the expense of investing in the business/eco-system

- “We will make investments necessary to deliver the industry’s lowest cost per token and the highest token throughput, which will help our customers and partners scale and expand the AI frontier”

Demand Has Gone “Parabolic…The AI Infrastructure Build Out Is “Accelerating”…And Nvidia Should Grow Faster Than Hyperscaler Capx Increases

- Demand for AI infrastructure continues to expand at an “unprecedented pace”…AND mgmt asserts that ”customers are generating profitable revenue beyond the depreciable life of their GPUs”

- “The build-out of AI factories is accelerating. The value of NVIDIA AI infrastructure is rising”

- The price of renting an H100 has risen 20% YTD

- A100 cloud pricing is up almost 15%

- “AI is no longer a nice to have. AI is now a necessity for enhancing productivity across all industries and roles”

- Mgmt. cites 2 primary drivers behind the accelerating AI infrastructure build out:

- Search and advertising are among the largest hyperscale workloads that are transitioning from CPU to GPU- computing

- The adoption of products and services native to AI is also inflecting

- Revs are also accelerating across all layers of “the AI cake”, incl energy chips, infrastructure models and applications

- “Growth in the model layer, particularly at Anthropic and OpenAI, has been incredible with momentum continuing to accelerate, including breakout growth in Open AI codex since the launch of GPT 5.5”

- Analysts project hyperscaler capx growth of ~+90-100% this year (exceeding $1 trillion) and mgmt. reiterated its guidance that AI infrastructure spend will reach $3-4 trillion annually by “the end of this decade”

- “I have every expectation it’s going to grow from here”… given that if hyperscalers “don’t have the compute, they won’t have the revenues. It is very clear. Compute is revenues. Compute is profit”

- Software Cos didn’t use to use as much compute but AI requires a tremendous amount of compute

- Mgmt said customers are generating profitable revenue beyond the depreciable life of their GPUs, which should support financing the AI infrastructure spend across the ecosystem

- Mgmt expects the Co to grow faster than those capx forecasts b/c…

- They are taking share w/ the hyeprscalers and Anthropic is a big new partner for them

- Growth in AI native clouds will need a lot of inferencing and Nvidia is well positioned (w/ its full stack) to capture share in this fragmented market

- And they “are the only Co serving Physical AI today”, which will also be a big growth driver

Hyperscaler Demand Continues To Propel Data Center Rev Growth But ACIE Revenue Is Expected To Grow Faster & Be A Much Larger LT Opportunity

- Data Center revs (92% of total) BEAT cons by 2.9%: Grew +92% y/y (vs +75% y/y in FQ4 and +66% y/y in FQ3) and was up +21% q/q driven by cont’d strength in Blackwell architecture & demand for GB 372 was particularly strong

- Ex-China, DC revenue grew ~120% in the quarter

- The new DC revenue segments are ~50/50 of the total, showing the diversity of the business

- Hyperscale revs were $37.9bn: Grew +115% y/y and +12% q/q and represented ~50% of Data Center revs

- Includes public clouds and the world’s largest consumer internet companies

- Nvidia is gaining share at hyperscalers given expanded support from Anthropic (for whom Nvidia will being on a “significant” amount of capacity this year) and continued deployments across OpenAI, Gemini, xAI, Meta, Microsoft AI and other frontier labs

- Hyperscale revs were $37.9bn: Grew +115% y/y and +12% q/q and represented ~50% of Data Center revs

- ACIE revs were $37.4bn: Grew +74% y/y and +31% q/q

- AI cloud revs more than tripled y/y

- The number of partner data centers that exceed 10MW nearly doubled in one yr to 80+ sites

- Sovereign revs incr’d 80%+ y/y…Nvidia AI infrastructure is now deployed across nearly 40 countries representing ~$50tn of GDP

- Looking ahead, ACIE is expected to grow faster the Hyperscale and become larger over time…“that is where the economics are going to be”

- Industrial/enterprise represents ~$50-80tn of the world’s economy and is where future economics will be generated for the Co

- There are 250k enterprise companies globally and “many of them will have to build or want to build AI factories for themselves to operate”

- This segment is very fragmented…requires a well-integrated platform solution and a very large go to market

- “Custom chips just don’t apply because these data centers want to buy systems. They want to operate systems. They don’t want to design, they don’t want to build it themselves”

- “This second category, is fairly, fairly, poorly understood”… very few companies aside from Nvidia have exposure

With The Shift To Agentic, Mgmt Remains Very Bullish On Vera Which Opens A New $200bn TAM

- Vera is arriving just in time to meet this inflection and “Vera opens a brand new $200 billion Tam for NVIDIA a market we have never addressed before. And every major hyperscaler and system maker is partnering with us to deploy it”

- The Co has “visibility to nearly $20bn in total CPU revenue this year”

- Mgmt reiterated the Vera Rubin launch in H2…starting in Q3, Q4 will ramp more, and Q1 will ramp significantly

- Reminder that the $1 trillion visibility of Blackwell/Rubin platforms from 2025 through cal 27 does not include any Vera CPU standalone

- Vera Rubin will be “even more successful” than Grace Blackwell

- “Every model Co will jump on Vera Ruben from the get-go which wasn’t true for grace Blackwell”

- Agentic AI makes CPUs incremental rather than cannibalistic to GPUs

- CPUs run agent harnesses, orchestration, and tools

- Mgmt expects billions of agents over time and agents will spin out subagents using browsers, compilers, simulators, databases and other tools

- Every time they spin off, inferencing will be needed and “all of the thinking happens on GPUs”

- “All of the orchestration essentially runs on CPUs and the subagents, when they’re spun off, they, when they’re thinking they use GPUs”

- Mgmt expects Vera demand to be supply constrained throughout Rubin’s life

Physical AI Is Expected To Also Be A Major Future Growth Driver (W/In Next 5 Yrs)

- Edge Computing revs of $6.4bn (8% of total) grew +29% y/y and +10% q/q, with strong Blackwell workstation demand offsetting “modest” consumer weakness from higher memory/system prices

- Physical AI revs exceeded $9bn over the last 12 mos and mgmt believes it will be the next wave after agentic AI

- “NVIDIA is practically the only company serving physical AI today”

- “In the next 5 years, physical and robotics AI will grow incredibly fast”

- Auto / robotics partnerships continue to expand

- Mgmt is bullish on the Uber partnership in particular which will power robotaxi fleets across nearly 30 cities and four continents by 2028

- “Yesterday’s computing was largely about personal computing. In the future, it’s going to be about personal AI and that personal AI. One example of it is the self-driving car. It’s a car. It’s a robotic system. That’s essentially your personal AI”

Is TTWO’s Net Bookings’ Guidance Conservative?

That is a key question from Take-Two’s FQ4 earnings report. Net bookings guidance for FQ1 and FY27 was -9% and -11% below the Street, respectively, and adj EPS was below by even more. Investors are asking if the guidance is conservative given the highly anticipated launch of GTA VI which is still slated for Nov 19th (thank goodness it remains on schedule). While very excited and bullish about the release, mgmt declined to provide any color on expectations, pre-orders, pricing, etc, which some analysts were hoping for. However, it was good to hear that GTA momentum into the launch remains strong w/ GTA V selling nearly 230mn units, GTA Online RCS growing +5% y/y in FQ4 (vs mgmt’s prior guide for a modest decline), and GTA+ saw significant y/y growth. Rockstar’s GTA VI marketing is starting “this summer” so that will certainly be a key catalyst looking ahead.

Other key standouts that we would call out from results include: 1) The qtr itself was better than expected with Net Bookings beating cons by +1.9% and topping the high end of mgmt’s guide due to better-than-expected performance from the GTA series, mobile titles and Red Dead Redemption series…adj EPS also exceeded cons by +43%, with a larger margin vs top-line beat; 2) Mobile was strong with RCS up +7% y/y with several titles ahead of expectations BUT FY27 mobile RCS y/y decline guidance reflects tough Color Block Jam comps and an expected moderation across mature Zynga titles… mgmt is not assuming to “continually beating expectations” across the mobile business; 3) The pipeline remains strong with 29 title releases through FY29, with potential upside because many mobile games in development / testing are not yet included unless specifically scheduled for worldwide launch; 4) It sounded like mgmt was more open to selective accretive acquisitions as cash flow improves (the Co is guiding for over $1bn in operating cash flow this fiscal year); and 5) Mgmt continues to view AI as an enabler vs a disruptor for their business.

See below for more color on what we found most incremental from results.

–> TTWO closed down -4% post results and is down -11% YTD

TTWO Delivers A Modest FQ4 Net Bookings Beat (Driven By GTA, Mobile And Red Dead) & Greater Upside To Margins

- FQ4 Net Bookings BEAT cons by +1.9%: Flat y/y and at $1.58bn, was above the high-end of mgmt’s $1.51-$1.56bn guide

- Upside driven by better-than-expected performance from the GTA series, several mobile titles and the Red Dead Redemption series

- During the qtr, the Co launched Sid Meier’s Civilization VII for Apple Arcade, PGA TOUR 2K25 for Switch 2, and WWE 2K26

- RCS grew +7% y/y (in line with mgmt’s prior +7% guide) but decelerated from +23% y/y in FQ3; It accounted for 82% of Net Bookings

- Mobile RCS grew +7% and GTA Online RCS grew +5%, both ahead of mgmt expectations

- NBA 2K RCS grew +10% but was softer than expected after extreme Q2 / Q3 growth

- Gross & operating margins were both ahead of the Street: OpEx decr’d -2% y/y due to lower marketing spend, with some spend shifting out of the qtr

- Non-GAAP gross margin BEAT cons by +170 bps at 65.5% of NB vs 63.8%

- Non-GAAP operating margin BEAT cons by +310 bps at 12.5% vs 9.4%

- Adj EPS BEAT cons by +43%

But The FQ1 & FY27 Net Bookings Guidance & Adj EPS Fell Short Of Street Expectations

- Net Bookings fell well short of consensus

- FQ1 was -9.1% below the cons

- FY27 was -11% below cons (implies +20% growth y/y)

- Adj EPS fell well short of consensus

- FQ1 was -9% below the cons

- FY27 was -26% below cons

- Other key points on FQ1 guidance

- Net Bookings’ largest contributors to are expected to be NBA 2K, GTA series, Toon Blast, Match Factory!, Empires & Puzzles, Red Dead Redemption series, Color Block Jam, Words With Friends and Zynga Poker

- Expect RCS to decline ~-3% y/y, assuming:

- High-single-digit growth for NBA 2K

- Declines for Mobile and the GTA series

- On a mgmt basis, OpEx is expected to grow by ~ 3% y/y

- Other key points on FY27 guidance

- Net Bookings’ largest contributors are expected to be Grand Theft Auto Series, NBA 2K, Toon Blast, Match Factory, Empires, and puzzles, the Red Dead Redemption series, words with Friends, Color Block Jam, and Zynga Poker

- Label mix is expected to be Rockstar Games 36%, Zynga 35%, and 2k 29%

- Expect RCS to be flat y/y and represent 65% of Net Bookings vs 78% in FY26

- Assumes NBA 2K up high-single-digits

- GTA series “up” and mobile “down” due to last year’s Color Block Jam success and moderation across several mature Zynga titles

- On a mgmt basis OpEx is expected to grow ~+8% y/y

- Largely from GTA VI / new mobile marketing and higher R&D

- About half of the ~$300mn non-GAAP OpEx increase is for S&M

- Net Bookings’ largest contributors are expected to be Grand Theft Auto Series, NBA 2K, Toon Blast, Match Factory, Empires, and puzzles, the Red Dead Redemption series, words with Friends, Color Block Jam, and Zynga Poker

GTA VI Remains The Primary FY27 Catalyst…But Mgmt Kept Details & Expectations Under Wraps

- Mgmt reiterated the Nov 19th release date for GTA VI (console-only)

- GTA VI’s release is “arguably the most anticipated entertainment property of all time” and will be a major catalyst for FY27 Net Bookings

- The Co is “extraordinarily excited about the release but will not opine on the numbers”

- Rockstar marketing campaign will start “this summer”

- TTWO is seeing strong performance of GTA into the launch

- GTA V sold-in nearly 230mn units

- GTA Online RCS grew +5% y/y in FQ4, materially better than the Co’s prior guide for a modest decline

- Growth was driven by A Safehouse in the Hills, one of GTA Online’s best-performing updates, with mansion properties, Michael de Santa, new missions, vehicles, GTA+ benefits and the Rockstar mission creator

- GTA+ saw significant y/y growth, helped by holiday update benefits and inclusion of NBA 2K26 in its games library

- Mgmt also declined to answer analyst questions about pre-orders and specific pricing plans as well

TTWO Has A “Ground Breaking” Pipeline, With Potential Upside

- The Co is slated to release 29 titles through Fiscal 2029 BUT there could be more

- The pipeline only counts mobile games specifically scheduled for worldwide launch within the three-year window but the Co continues to develop and test many new titles that are NOT reflected in the outlook, “some of which may be added to our multiyear count”

- YTD… the Co released Sid Meier’s Civilization VII for Apple Arcade, PGA TOUR 2K25 for Switch 2 and WWE 2K26 across PS5 / Xbox Series X|S / Switch 2 / PC

- FY27 will be a “milestone” year led by the GTA VI launch plus six additional titles which include:

- Two mobile titles, NBA 2K27, PGA TOUR 2K27, WWE 2K27 and one platform extension

- Expect more content & experiences as well to drive engagement and RCS across existing titles

- FY28-FY29 includes 22 titles

- One mobile title, five sports titles, three core new IPs and 13 core existing IPs, including seven sequels and six remakes / remasters / platform extensions

Mobile Cont’d To Outperform …But Lower FY27 Guide Reflects Moderating Growth From Existing Titles

- Zynga achieved its highest level of Net Bookings since TTWO acquired the business in 2022

- FQ4 mobile performance was broad-based

- Toon Blast grew ~+25% y/y

- Empires & Puzzles grew +5%

- Color Block Jam grew +15%

- Top Eleven had its strongest qtr ever after 16 years in market

- FQ4 mobile performance was broad-based

- 2K mobile also contributed, with WWE SuperCard reaching nearly 39mn lifetime downloads, NBA 2K26 Arcade Edition maintaining a top-5 Apple Arcade position and NBA 2K All-Star in China nearing 10mn registered users in just one year

- But FY27 mobile RCS is expected to be “down” y/y due to tough Color Block Jam comps and assumed moderation in mature Zynga titles

- Mgmt. is being prudent and is “not prepared to guide to continually beating expectations at any business unit”

- Some titles that were new last year, are older this year

- The guidance “doesn’t include some massive new releases”

- The DTC channel continues to drive net booking and margin growth as the Co integrates addtl mobile titles and increases player engagement and conversion

- Mgmt thinks the competitive and regulatory environment will be favorable regarding overall distribution cost

- DTC costs are materially lower than third-party distribution costs, but TTWO will still meet consumers where they are and “values “third-party retailers when they provide marketing value

NBA 2K Delivered Record FQ4 BUT Monetization Normalized After Extreme Early-Year Growth

- FQ4 NBA 2K RCS grew +10% y/y, one of the strongest Q4s in franchise history, but softer than mgmt expected as high-engagement players concentrated spend in Q2 / Q3

- NBA 2K26 sold-in 10mn+ units to date, +5% vs NBA 2K25, with RCS growth driven by higher DAUs and games played per user

- The FY27 guide assumes NBA 2K RCS grows high-single-digits despite lapping FY26 records

- The new expansion into College basketball was a focus

- Visual Concepts launched Season 5 for NBA 2K26, its first college-themed offering, featuring 16 universities

- The release is a “glimpse of what’s to come in college basketball for the next year and beyond”

- Other sports franchises contributed engagement upside

- WWE 2K26 was well received by critics and consumers, with RCS +20% y/y and 85mn+ matches played

- 2K is supporting WWE 2K26 with multiple updates through its Ringside Pass

- PGA TOUR 2K25 had a resurgence from Season 5 and PS Plus, with 60mn rounds played in FQ4, +110% q/q, and more content updates planned

A Few Other Key Comments / Updates (AI, Potential M&A, Consumer Behavior)

- Mgmt sees AI as an enabler, not a disruptor to their business…in response to a question about Google’s Genie and AI disruption, mgmt is not concerned:

- “Confusion surrounds a belief that somehow more efficient asset creation puts us at some disadvantage or creates a competitive advantage for someone else. And I just don’t believe that’s the case”

- “No one exclusively licenses technology for video games…so if a competitor has access to AI and that allows someone to do something better, quicker, um, cheaper than we would have access to the same thing”

- “Asset creation is not the same thing at hit creation”

- Do you have buy-in at the studios regarding these tools? Yes- “everyone has bought into the possibility of new tech”

- Mgmt sounded more open to future inorganic growth:

- Mgmt highlighted that all acquisitions over the past ~two decades have been accretive and successful

- “You are not going to see us doing deals hand over fist, but assuming our balance sheet continues to improve, I think you could imagine more inorganic growth in the future as well”, also stressing when it is accretive

- Lower-priced / Roblox-style experiences are not viewed as a structural risk to AAA games, as posed by an analyst on the call

- Mgmt’s view is that kids often age out of children’s programming and that mature rated TTWO titles address a different audience

- Mgmt is not worried about the next generation not being interested in their more mature and expensive titles

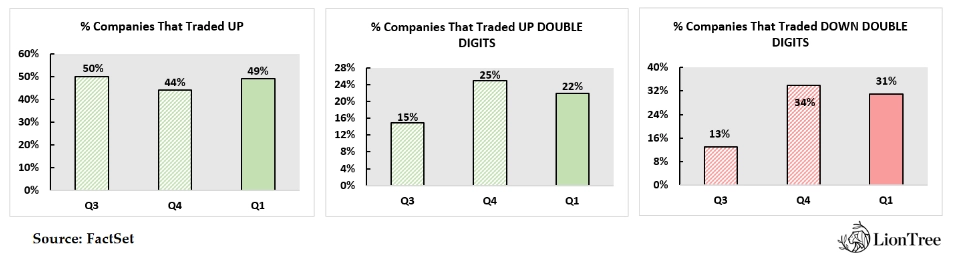

Q1 Earning Wrap- The Vast Majority Of TMT Stocks Beat The Street

These strangler earnings this week finally put an end to Q1 earnings season across the sector, hence we looked across our LionTree TMT & Consumer Universe of ~200 companies covering 37 sub-sectors with market caps of $1bn+ to evaluate the qtrly financial performance compared to Wall Street projections.

Overall, the vast majority of companies exceeded consensus revenue and profitability forecasts, but to a slightly lessor degree vs Q4 regarding revenue, and to a greater degree regarding profitability. More specifically, 74% of companies topped consensus revenue estimates in Q1, but that is down from 79% in Q4, and 88% of companies beat consensus profitability projections in Q1, up from 74% in Q4.

What was the Street’s reaction to these results? It was slightly skewed negative with 51% of companies trading down in reaction to results and 49% trading up.

See below for more on Q1 financial performance of companies within our LionTree Universe of TMT and Consumer stocks relative to Street expectations, along with their respective stock reactions.

The Vast Majority Of Companies BEAT Revenue Expectations In Q1, But To A Lessor Degree Than In Q4

- Overall, 74% of Cos in our LionTree Universe beat cons on revenue in Q1(down from ~79% in Q4)

- 2% of those companies beat by double digits, down from 4% in Q4

- The avg sales beat was 2%, down from 3% in Q4

- Affirm, Intel and Nexstar had the largest % beats on sales in Q1

- Overall, 20% of companies in our Universe reported sales in-line to lower than consensus, down from 21% in Q4

- Robinhood, Coinbase & Oscar Health reported the largest % misses on sales

Even More Companies BEAT On Profitability In Q1 vs Q4

- Overall, 88% of companies in our Universe beat consensus on adj. EBITDA in Q1 (vs 74% in Q4) and 37% posted double-digit beats (down from 25% in Q4)

- The avg adj EBITDA beat at 15% was up from 8% in Q4

- fuboTV, WEBTOON and Compass had the largest % beats on adj. EBITDA in Q4

- Overall, ~29% of the companies in our Universe were in-line or missed consensus on adj. EBITDA in Q1, up from ~26% in Q4

- JD.com, Alibaba & Coinbase reported the largest % misses on adj. EBITDA in Q4

Stock Performance Was Skewed Negative With 51% Of Companies Trading Down & 49% Of Companies Trading Up In Reaction To Results

- Fewer Cos traded down double-digits and traded up double-digits in reaction to earnings

- 31% of Cos traded down double-digits, down from 34% in Q4

- Similarly, 22% of Cos traded up double-digits, also up from 25% in Q4

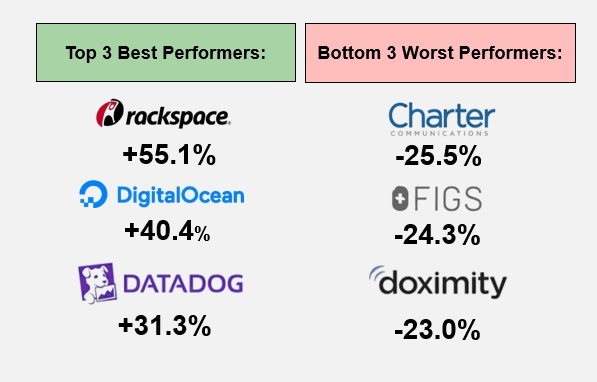

Top 3 Best & Worst Performers In Reaction To Q1 Results…

Google I/O: New AI That Creates “Any Output From Any Input”

Google’s I/O always comes with a slew of interesting updates, and this year did not disappoint. First and foremost, growth in AI usage/engagement has been staggering with the Co’s total tokens processed increasing from 480 trillion a year ago to 3.2 quadrillion today, and AI Mode crossed 1bn MAUs in under a year. An overarching theme that stood out to use was the significant increase in conversational capabilities that are now available (or coming soon) across Google’s many surfaces. It is becoming easier and easier to use and instruct AI. Google’s new Gemini Omni was a major new release at the event, with the model being able to basically create “any output from any input.” That pretty much says is all! Google is also significantly amping up its agentic development and management capabilities with the introduction of Gemini 3.5 Flash & Antigravity 2.0. The former is a much faster model vs other frontier models (4x the output tokens per second) at less than half the cost, per mgmt. These new capabilities also underpin Google’s new Gemini Spark which is an impressive 24/7 personal AI agent that will help people navigate their life, but in a safe way. Agentic capabilities will also be coming to Search this summer, and we were also excited by Google’s new Universal Cart that can be filled across merchants and Google surfaces…its “shopping with superpowers.”

Lastly, Demis Hassabis from Google DeepMind highlighted that all of these innovations are paving the way for artificial general intelligence (AGI) which he sees as “just a few years away”…the timing of that would be a good question for Kalshi to add to the platform!

Overall, it was a long keynote, but the updates that we viewed as most important are below.

-> GOOGL share was flat in reaction to its event and the stock is up +21% YTD

-> Just ahead of I/O, Blackstone & Google annc’d a JV to create a new U.S.-based AI cloud infrastructure Co; Blackstone is committing $5bn in equity capital and holding a majority stake while Google will supply its proprietary TPU chips; The first 500 mw of compute capacity is targeted for 2027 w/ plans to scale significantly beyond that; This follows a similar Blackstone/Anthropic deal earlier this month LINK

Key AI Usage & Engagement Stats

- The Co has seen massive growth in tokens processed across all its surfaces

- Has gone from 9.7T (May 24) -> 480T (May 25) -> 3.2 quadrillion (May 26)

- 8.5m+ developers are building with Google’s models monthly (vs the 7mn at last yr’s I/O)

- Model APIs processing has also seen massive growth

- Tokens per min processed has gone from 10bn in X -> 16bn (a month ago to) -> ~19 billion now

- 375+ Google Cloud customers each processed over 1 trillion tokens individually in the past 12 months (up from 330 customers at Cloud Next last month)

- 13 Google products have over 1bn users each; 5 of those have over 3bn users

- More people are using Google products, and using them more frequently

- No competitor has this breadth of 1bn+ user surfaces

- AI Overviews: 2.5bn MAUs

- AI Mode: Reached 1bn+ MAUs in under a year

- The Gemini app now has over 900mn MAUs, representing 2x growth y/y

- And daily requests are up 7x y/y sowing that engagement is deepening

Google Has Made Significant Progress With World Models…”Ai Is Going From Predicting Text To Simulating Reality”

- Google’s new Gemini Omni was a major new release…the model can basically create “any output from any input”

- The first model in the Onmi family is Gemini Omni Flash…it combines Gemini with their generative media models

- It provides a new level of world understanding, multimodality and editing and Gemini Omni allows you to make a video with conversational language

- Essentially Veo, Nano Banana and Genie are all able to now create even more realistic videos, images and interactive simulations (though it is still not “perfect”)

- Avail: Today in the Gemini app, Google Flow, and YouTube Shorts

- API access for developers is avail in the coming weeks

- With all this new AI created content, Google is also focused on AI content transparency (people can identify high quality deep fake videos only 1/4th of the time)

- Google’s SynthID has watermarked over 100bn images & videos and 60k years of audio assets

- “Millions” of people use SynthID detector to find out if it is AI gen content and the Co is now making it avail in the Gemini app)…they will be expanding to search and chrome

- Partners: OpenAI, Kakao, and ElevanLLabs, follow Nvidia who signed on last year

Google Amps Up Its Agentic Development & Mgmt Capability W/ The Intro Of Gemini 3.5 Flash & Antigravity 2.0

- The new Gemini 3.5 Flash combines “frontier intelligence with action”

- This new model beats Gemini 3.1 Pro across almost all benchmarks, with particular gains in coding

- It is a much faster model vs other frontier models (4x the output tokens per second) AND less than half the cost, per mgmt

- Top companies in Google Cloud are processing about 1bn tokens per day…if they shifted 80% of workloads from other frontier models to 3.5 Flash that would save them $1bn+ annually

- Avail: Today across all products and APIs.

- Gemini 3.5 Pro…is coming in the next months

- The Co also released Antigravity 2.0 which expands Google’s agent-first coding platform to develop and manage multiple autonomous AI agents with a new standalone desktop app

- An optimized version of Flash runs at 12x the speed of other frontier models within Antigravity (vs. 4x in the standard model).

- Antigravity internal token processing has incr’d from 500bn tokens/day in March to 3T+ tokens/day now, doubling every few weeks

- Avail: Today for developers

- “Gemini 3.5 and Antigravity are unlocking a new world of agents and agentic capabilities”

The Co Is Aiming To Also Bring Agentic Capabilities To Consumers

- Google’s new Gemini Spark is a 24/7 personal AI agent helping people navigate their life…in a safe way

- It takes action on users’ behalf but “under their direction”

- And works behind the scene (people can close their computers)

- It runs on dedicated machines on Google cloud

- It is powered by 3.5 and Google Antigravity

- It integrates with Google products and in the coming weeks will integrate with 3P tools

- Later this summer it will operate within Chrome

- Android Halo will bring this to the phone later this summer

- Avail: Rolling out to AI Ultra subscribers (see below on pricing changes) in the US next week

- It takes action on users’ behalf but “under their direction”

- Launched a new Ultra plan for $100/month

- And for its top tier plan, Google cut pricing from $250/mo->$200/mo

Google’s New Search & Commerce Capabilities…

- “Google Search is AI search”

- The Co upgraded AI Mode with Gemini 3.5

- A new search box is rolling out today that gives users the best of AI and get the best of the web

- It is a seamless experience

- A new search box is rolling out today that gives users the best of AI and get the best of the web

- Agentic capabilities will be coming to Search this summer (w/ Gemini 3.5 & Antigravity)

- In the background 24/7, it will monitor the web and real-time data sources (news, finance, sports, social) for changes relevant to users’ specific questions/requests…examples:

- It will surface fresh content that users were looking for

- It will surface real estate listings based on users’ criteria when they come available

- It will alert users when there are celebrity sneaker drops

- Avail: Rolling out this summer for AI Pro and Ultra subscribers

- In the background 24/7, it will monitor the web and real-time data sources (news, finance, sports, social) for changes relevant to users’ specific questions/requests…examples:

- Updates with UCP:

- It is expanding to Canada, Australia and the UK in the coming months

- AP2 is designed to make sure agents are under users’ control with payments: Agents will make the purchase only within set parameters, the data is private and secure

- Avail: AP2 in Gemini Spark is available in the “coming months”

- Google also annc’d the Universal Cart across merchants and Google surfaces…its “shopping with superpowers”

- Users can check out with Google pay or go to the brand’s website

- Universal Cart is also intelligent…it can find hidden savings, make sure you are buying the right products based on known needs, etc

- Avail: Rolling out across search and the gemini app this summer and YT and gmail will follow

Notably, Google Is Bringing Voice Conversation Capabilities To More Products

- As mentioned above,

- Gemini Omni Flash accepts voice/audio as an input type and supports conversational editing via voice commands, including editing characters, backgrounds, and other elements in generated video

- Antigravity 2.0 includes native voice command support which lets developers talk to their agents rather than type

- Maps got its biggest upgrade recently w/ Ask Map

- Users can ask more complex, longer conversational questions

- With Docs Live users can create a document verbally (and even as stream of mind)

- Avail: Rolling out to AI Pro and Ultra subscribers this summer

- The Co is launching Ask YouTube, a conversational AI search w/in YT that handles complex queries, surfaces the most relevant videos, and jumps directly to the relevant moment within a video

- Avail: Testing now, rolling out broadly in the US this summer.

- Voice capabilities are also coming to Gmail and Google Keep

A Couple Other Interesting Updates

- Google Pics is a new standalone AI image creation and editing tool built on Nano Banana, treating every element in an image as an individual object rather than a flat static image

- Avail: Rolling out to AI Pro and Ultra subscribers in Workspace later this summer.

- Google annc’d that its first audio glasses will arrive this fall

- Gemini speaks into users’ ear from the glasses

- Partners: Gentle Monster, Warby Parker, Samsung

- Avail: This fall

- It will pair with android and iOS devices

Spotify’s New 2030 Targets Caught Investors’ Attention This Week

Another headlining event this week was Spotify’s Investor Day and the Co made a splash with new 2030 guidance that track well above consensus 2026 and 2027 estimates and also several new partnership agreements, including a UMG licensing agreement for AI-powered covers and remixes and Reserved by Spotify with Live Nation regarding concert tickets. Additionally, stats regarding the effectiveness of Co’s proprietary Large AI Taste model also stood out.

See more below about the stock moving new guidance and company partnerships. See HERE for the Co’s full day summary.

–>Spotify’s stock was up +13% in reaction to the news and is down -10.5%

Key New Financial Targets & Partnerships From The Investor Day

- Since the 2022 Investor Day…

- +18% FXN revenue CAGR

- 32% gross margin in Q2 2022

- Over 18ppts of op margin expansion

- ~€3bn in FCF in 2025

- The Co initiates 2030 targets which track well above consensus 2026/2027 estimates…

- Mid-teens revenue CAGR (vs cons +10.3% in 2026 and +12.2% in 2027)

- Gross margin of 35-40% (vs cons +33.3% in 2026 and +34.3% in 2027

- Operating margin above 20% (cons +15.6% in 2026 and +17.6% in 2027)

- Strong growth in FCF

- …And is also targeting 1bn subscribers, €100bn in revenue and 40% gross margins by 2030

- Spotify and UMG annc’d a recorded music and music publishing licensing agreement: It enables the launch of a new generative AI-powered tool allowing fans to create covers and remixes from participating artists and songwriters; The tool will be launched as a paid add-on for Spotify Premium users

- The deal opens additional revenue streams and new ways to drive discovery

- Artists and songwriters can directly share in the value generated through AI-driven licensed covers and remixes

- The initiative is artist-centric, rooted in responsible AI, and designed to bring artists and fans closer together

- The deal opens additional revenue streams and new ways to drive discovery

- The Co annc’d Reserved by Spotify with Live Nation as a launch partner

- For the first time, an artist’s most dedicated fans on Spotify Premium will have two tour tickets held just for them before they go on sale to the general public

- Reserved by Spotify arrives this summer with Live Nation as launch partner

- Spotify is the exclusive audio streaming service offering this type of reserved access to Live Nation tickets

- The feature will help fans access many of the most anticipated tours in the U.S., with more markets coming fast

- Spotify’s proprietary Large AI Taste Model which is trained on trillions of behavioral signals across music, podcasts, and audiobooks is showing early success:

- Early AI deployments are driving:

- 9% growth in Autoplay song saves

- 9% improvement in podcast discovery from Home

- Nearly 20% more interaction with DJ messages

- 99% of Spotify engineers use AI weekly

- More than 73% of code contributions are AI-assisted

- Spotify introduced Studio by Spotify Labs, a standalone desktop app for private, personalized audio experiences like daily briefings

- Studio will be available soon as a Research Preview for Premium users in more than 20 markets

- Early AI deployments are driving:

SpaceX Drops Is S-1!

SpaceX’s publicly filed S-1 was another big update this week. The almost 300-page report obviously has an enormous amount of information but we wanted to pull out some key stats that we think are “need to knows” about their businesses…see below. The link the full filing can be found HERE as well.

Overall Company / Financials

Overall Market Opportunity / TAM

- TAM by segment:

- Space: $370bn

- Connectivity: $1.6tn

- AI: $26.5tn

The Connectivity Business KPIs

- Connectivity TAM break-down:

- $870bn Starlink Broadband

- $740bn Starlink Mobile

- Additional enterprise and government opportunities

- Segment financials:

- The Co has ~ 9,600 Starlink broadband and mobile satellites in Low-Earth Orbit

- Starlink satellites accounted for ~75% of all active maneuverable satellites in orbit as of March 31, 2026

- As of March 31, 2026, Starlink served ~10.3mn Starlink Subscribers across 164 countries, territories, and other markets

- Speeds: Starlink residential users had median peak-hour download speeds of 225 Mbps and median latency of ~25 milliseconds as of March 31, 2026

- The Co expects V3 satellites to offer one Tbps of downlink capacity per satellite

- The Co expects to begin deploying V3 satellites using Starship in the second half of 2026

- A single Starship launch is expected to deploy up to 60 V3 satellites to LEO, representing a potential 20x increase in Starlink downlink capacity deployed relative to a Falcon 9 launch

- Since 2023, “no Starlink Enterprise customer having contributed more than $750k of annual revenue has voluntarily discontinued their service”

- Starlink Mobile provides satellite-to-mobile connectivity, “supplementing terrestrial networks and substantially reducing mobile ‘dead zones’ across ~30 countries”

- As of March 31, 2026, dedicated satellite-to-mobile constellation included ~650 V1 Mobile satellites

- Starlink Mobile served ~7.4mn monthly unique devices across ~30 countries

- The Co has partnerships with ~30 MNOs on 6 continents, covering an area home to ~1.9bn people

- MNO partners include T-Mobile, One NZ, Optus, Telstra, Rogers, KDDI, Salt, Entel, Kyivstar, and VMO2

- Capabilities:

- Current V1 capabilities include “light data, text messaging (SMS), and over-the-top voice services”

- V2 Mobile satellites are “designed to provide more comprehensive satellite-to-mobile services, including broadband data and IoT connectivity” and are expected to begin deploying on Starship in 2027

- The Co expects Gen2 service using V2 Mobile satellites to enable 5G-like connectivity

- The EchoStar spectrum acq is expected to close in November 2027

- “The expansion of our satellite-to-mobile connectivity services depends substantially on our ability to secure and maintain partnerships with mobile network operators and on the adoption of necessary hardware and software modifications by device manufacturers”

Space / Launch Stats

- Segment financials:

- As of March 31, 2026, SpaceX had launched ~7,400 metric tons to orbit

- Completed ~650 orbital space launches

- Over 540 launches were completed by a flight-proven Falcon rocket

- In 2025, SpaceX completed 170 missions across Falcon and Starship vehicles

- 159 flight-proven booster launches

- The Co has now launched over 2,200 metric tons, representing over 80% of mass to orbit for the world

- Falcon 9:

- Payload capacity to LEO of ~23 metric tons when fully expendable

- First stage has demonstrated the ability to refly 34 times

- Over 99% mission success rate

- Falcon Heavy:

- Payload capacity to LEO of ~64 metric tons

- 11 launches as of March 31, 2026

- 100% mission success rate

- Dragon:

- Since 2020, Dragon has safely flown 78 crewmembers from 20 countries

- SpaceX was the primary launch provider for the U.S. government; in 2025, launched 11 of 12 National Security Space Launch medium and heavy lift missions and all five U.S. crew and cargo missions to the ISS for NASA

- 2025: ~1/5 of revenue was attributable to agencies within the US federal government

Starship Snippets

- Starship is “designed to be the world’s first fully and rapidly reusable spacecraft”

- Starship V3 is designed to deliver 100 metric tons to Earth’s orbit in a fully reusable configuration

- Future Starship generations are designed to double this payload capacity

- The Co expects Starship to commence payload delivery to orbit in H2 of 2026

- SpaceX has invested over $15bn in Starship

- SpaceX has executed 11 Starship flight tests and scheduled a 12th flight test to debut the next-generation Starship vehicle and Super Heavy booster

- The Co plans to demonstrate “catching the upper stage and demonstrating in-orbit propellant transfer capabilities”

- Starship is expected to reduce the cost to reach orbit by 99% or more relative to the historical average launch cost

- The Co says Starship is “the key enabler of our long-term growth strategy by unlocking entirely new categories of missions”

- Risk: current Falcon 9 and Falcon Heavy rockets “are not capable of deploying V3 satellites and V2 Mobile satellites”

- Risk: “AI compute satellites at scale need full Starship reusability to be economically compelling”

The AI Business Segment

- AI TAM:

- $2.4tn AI infrastructure

- $760bn consumer subscriptions

- $600bn digital advertising

- $22.7tn enterprise applications

- AI segment includes AI compute, Grok, and X

- SpaceX acquired xAI in February 2026

- Segment financials:

- COLOSSUS and COLOSSUS II collectively provide ~1.0 gigawatt of compute power, with additional power capacity available for data center operations

- The next phase of COLOSSUS II expected to bring online at least 220k additional GB300 processors and over 400 additional MW of compute power

- Grok model: Since Grok-1 in November 2023, the Co released four major versions and notable variations, culminating in Grok-4.3 in April 2026

- Grok achieved frontier-level performance in scientific reasoning within 2 years of initial release, as measured by GPQA Diamond score

- Next-gen models expected to scale toward multiple trillions of parameters

- X / Grok usage:

- Over 1.3bn supported accounts active in last twelve months ended March 31, 2026

- ~550mm MAUs

- ~350mm daily posts

- ~117mm MAUs used Grok’s AI features as of March 31, 2026

- Paid subscribers:

- ~6.3mm active paid subscribers as of March 31, 2026

- ~4.4mm X Premium and Premium+ paid subscribers

- ~1.9mm SuperGrok, SuperGrok Heavy and SuperGrok Lite paid subscribers

- Imagine generated ~10bn images and over 2bn videos per month, on average, for Q1 2026

- The Co plans to evolve X into an “Everything App” integrating “real-time information, communications, media, payments, banking, commerce and more”

Orbital AI Compute / Space Data Centers KPIs

- “We expect to begin deploying our orbital AI compute satellites as early as 2028”

- The Co believes reusable rockets, satellite manufacturing, and operational expertise can enable deployment of “massive AI compute satellite constellations, with potentially millions of satellites, for orbital data centers”

- Orbital AI compute is expected to use:

- Sun-synchronous orbit

- Space-based solar power

- Radiative cooling

- Starlink low-latency global connectivity

- The Co’s goal: “to launch 100 gigawatts of compute to space each year”

- Deployment of 100 GW per year would require:

- “Thousands of launches per year”

- Transport of “~1mn metric tons to orbit annually”

- Satellites carrying “over 100 kilowatts of compute power per metric ton”

- The Co says 100 GW of compute, if operated continuously, would require generation resources equal to ~1/5 of annual US power production in 2025

- Deployment of 100 GW per year would require:

- The Co believes orbital AI can lower cost per token because “the marginal cost of energy for our AI compute satellites will be minimal because our satellites are powered by solar arrays in space”

- The Co says orbital AI compute “is an incredibly difficult technical challenge that only we can solve at scale in the near term”

- Risk: orbital AI compute is unproven; no one has previously operated orbital AI compute, and space conditions on such infrastructure “have not been tested”

Moon / Mars / Future Markets Highlights

- Mission: “to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars”

- Growth strategies include:

- “Establish the lunar economy, including cargo transport, manufacturing, and energy production on the Moon”

- “Deploy orbital AI compute at scale”

- “Design and manufacture our own chips”

- “Launch digital human augmentation”

- Future markets listed:

- Point-to-point terrestrial travel

- Space tourism

- In-orbit manufacturing

- Passenger and cargo transport to the Moon and Mars

- Energy production on the Moon and Mars

- Manufacturing capabilities on the Moon and Mars

- Asteroid mining

- The Co says many future markets “do not exist today” and may not develop as expected

- “In-orbit refueling of Starship is essential to our lunar, Mars, asteroid mining, and other deep space ambitions beyond geostationary Earth orbit”

- Risk: in-orbit refueling is complex and “we have not yet demonstrated or attempted it”

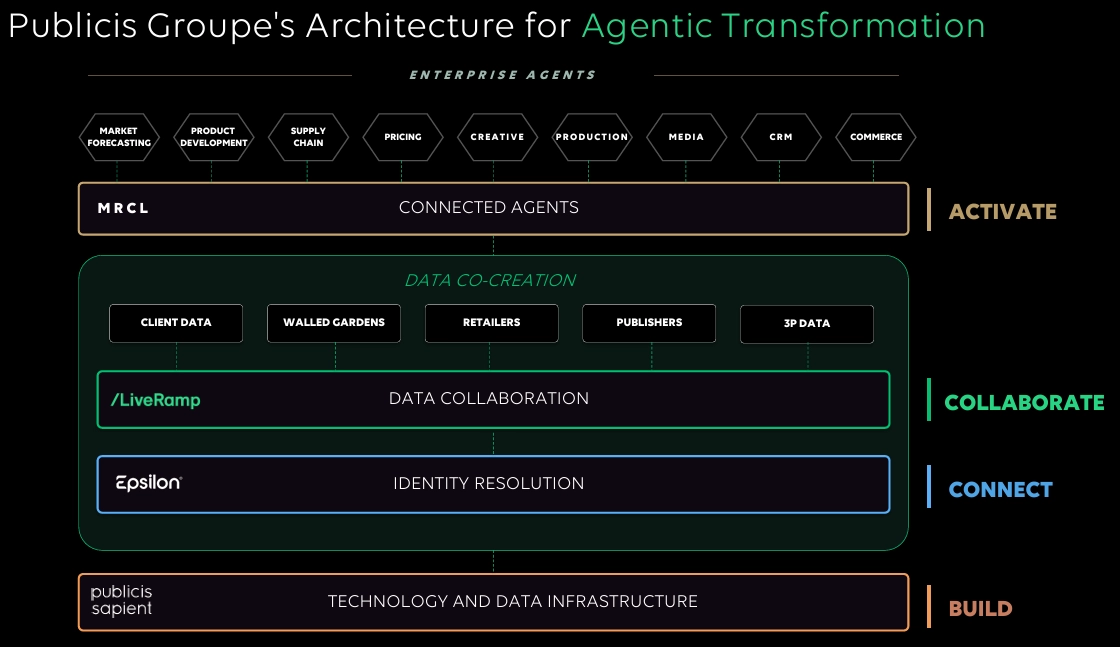

Publicis Makes A Big Push Into Agentic AI W/ Its $2.2bn LiveRamp Deal

Publicis’ acquisition of data collaboration platform LiveRamp for $2.2bn is its largest acquisition since buying Epsilon for $4.4bn in 2019, The deal is rooted in the idea that data co-creation, where a Co can securely combine and activate data across partners, will be a critical enabler of AI agents and agentic business transformation. As Publicis mgmt put it, the acquisition is not about strengthening its traditional marketing offering, but rather about building a broader AI transformation platform across LiveRamp, Epsilon, Sapient and Marcel, while preserving LiveRamp’s neutral and interoperable position in the market.

See below for the key points from the deal announcement. Link to press release HERE and full deck HERE.

-> Publicis jumped +8.2% on the day of the deal announcement but is still down -6.2% YTD

- What is LiveRamp? It is a “global data collaboration that allows companies to connect, unify and activate data throughout the digital ecosystem”

- Enables data activation at scale through plug-and-play connections across an extensive network made up of 25,000 publisher domains and 500+ data and technology partners in 14 mkts

- Its interoperable technology connects data across all major cloud environments w/ robust governance tools and a commitment to shared standards that help customers collaborate with trust and transparency at scale

- The Co has 800+ clients, including 25%+ of the Fortune 500, and covers nearly all segments and verticals, including advertisers, retailers, publishers, platforms and holding Cos

- Financial callouts –

- Rev has grown by +13% CAGR over the trailing 5 yrs

- Non-GAAP EBIT margin of 22% in 2026 improved vs the 4% margin delivered in 2021

- Recurring SaaS subscriptions represent 76% of LiveRamp’s biz

- Customer rev retention has averaged 107%

- Why is Publicis buying LiveRamp? To strengthen the data foundation clients need for effective AI agents

- LiveRamp’s data connectivity, marketplace, collaborative clean rooms, and partner / agent network, combined with Epsilon’s identity, help unify fragmented internal and partner data securely

- This creates proprietary data assets and intelligence that Cos could not build alone, giving clients a more sustainable competitive advantage

- The goal is to close the gap between AI investment and return by continuously training and fueling enterprise-grade AI agents with co-created data

- But why buy LiveRamp if Publicis already had a commercial partnership? To capture the growth of the emerging agentic AI transformation market + “to start building product and services together that no one else could bring”

- Key quote… “We did not need LiveRamp to win in the marketing space…where LiveRamp plus Publicis is going to make a difference is in the agentic space, in this new market where there is huge opportunity because there is a huge barrier created by data”

- LiveRamp will be a complementary layer within Publicis’s broader AI / data stack alongside Sapient, Epsilon, and Marcel

Source: Publicis

- It is an all-cash deal with an enterprise value of $2.2bn… and the $350/shr price was a 29.8% premium to LiveRamp’s closing share price on May 15th

- The implied forward adj EBITDA multiple is 12.3x

- Assuming closing by the end of 2026, the transaction would result in a maximum net financial leverage of ~1.2x in 2027

- The deal will be accretive to Publicis’s headline EPS in Y1 + the Co raised its ’27-’28 CC growth target to +7-8% for net revenue (from +6-7%) and +8-10% for headline EPS (from +7-9%)

- Also confirmed 2026 guidance on all KPIs

- Cost improvement oppties…the Co is targeting a minimum of $50mn of savings on a run rate basis + anticipate LiveRamp to deliver an op margin in-line w/ Publicis Groupe’s margin as of Y1: Will come from…

- The standalone margin improvement plan initiated by LiveRamp w/ its Rule of 40 objective that aims for non-GAAP operating margin of 25% to 30% by 2028

- Post-transaction elimination of all public Co costs at LiveRamp

- Integration of LiveRamp’s back office into Publicis Groupe shared service centers

- Some procurement synergies, including IT, hosting and real estate

- There will be “absolutely no change” in how LiveRamp is led, with Scott Howe remaining CEO (who will report directly to Publicis CEO Arthur Sadoun)

- LiveRamp will also continue to apply its standard commercial practices, with no changes to pricing outside the normal course of business and standard biz practices

- LiveRamp has a “10-year track record of being neutral in the industry,” and said client / publisher feedback after the announcement showed “zero concern” that this commitment would not be upheld

- Timeline: The transaction has been signed and is expected to close before year-end 2026 (subject to regulatory approval and approval from LiveRamp shareholders)

13-Fs Point To A Rotation Back Into Big Tech In Q1

The latest round of 13-F filings covering the period ending March 31, 2026 also hit this week, shedding light on where institutional investors were putting their money last quarter.

As always, we like to start with Berkshire Hathaway’s portfolio changes, and this quarter felt particularly worth digging into as the first quarterly disclosure under new CEO Greg Abel, who officially took the reins from Warren Buffett on January 1, 2026. In Q1, the fund continued its streak as a net seller for the 14th consecutive qtr. The firm’s most significant purchase was a dramatic expansion of its Alphabet position, increasing its Class A stake by ~204%, and also grew its position in The New York Times and Lennar by +199% and 43%, respectively. Berkshire also initiated a new position in Alphabet’s Class C stock, as well as Delta Air Lines and Macy’s. On the selling side, the qtr marked one of Berkshire’s most aggressive single-quarter cleanups in years, with 16 full exits, including Amazon, Charter, Domino’s Pizza, Liberty Latin America, Liberty Media, Mastercard, and Visa. Its position in Chevron was meaningfully reduced (-35%), while its stake in Bank of America was also given a slight trim (-0.7%). As of quarter-end, the fund’s five largest holdings were Apple (22.0%), American Express (17.4%), Coca-Cola (11.6%), Bank of America (9.5%), and Chevron (6.6%), with the top five collectively representing ~68% of the total portfolio.

Berkshire aside, we also took a broader look at institutional activity during the quarter, tracking both aggregate hedge fund positioning across 150 of the top funds as well as where the top activist investors were placing their bets. See below.

Where Are The Top Hedge Funds Investing, In Aggregate?

Each quarter, WhaleWisdom tracks the stocks that were most bought and sold during the quarter across 150 of the top hedge funds. It ranks the “hottest” stocks based on a formula that takes into account the number of buyers adding and initiating new positions vs sellers, the change in average ranking that the stock had in the portfolios, and the number of times the stock appears in the top 10 holdings of the portfolios. The biggest takeaways were:

- TMT’s favorability rebounded…7 of the top 10 were TMT this qtr, up from 4 in Q4: They were Lumentum (#2), Toast (#3), EchoStar (#4), Arm Holdings (#5), Tower Semiconductor (#6), Onto Innovation (#9), and Axon Enterprise (#10)

- All of the MAANG stocks remained in the Top 100 and most rose in ranking

- Apple – increased q/q (#58 in Q4 -> #39 in Q1)

- Meta – increased q/q (#50 in Q4 -> #49 in Q1)

- Alphabet – decreased q/q (#38 in Q4 -> #48 in Q1)

- Netflix – increased q/q (#86 in Q4 -> #13 in Q1)

- Amazon – increased q/q (#57 in Q4 -> #38 in Q1)

- All of the MAANG stocks remained in the Top 100 and most rose in ranking

Where Are Activist/Event Investors Placing Their Bets, In Aggregate?

- The top 8 activist funds were net buyers this qtr, buying $7.9bn and selling just $568mn

- Outflows: After seeing the most inflows last qtr, the Industrials sector took a u-turn and saw the most outflows this qtr (-$2.63bn), followed by Media (-$872mn) and Financials (-$866mn) to round out the Top 3

- The Top 3 largest outflows came from Elliott Investment Mgmt selling out of its position in Toyota Industries (-$2.78bn), followed by Pershing Square Capital Mgmt decreasing its position in Alphabet (-$1.68bn) and selling out of its position in Hilton Worldwide (-$921mn)

- Inflows: Real Estate was the only sector that saw an inflow (+$568mn)

- That was mostly driven by Pershing Square increasing its position in Howard Hughes Holding Corp.

- Outflows: After seeing the most inflows last qtr, the Industrials sector took a u-turn and saw the most outflows this qtr (-$2.63bn), followed by Media (-$872mn) and Financials (-$866mn) to round out the Top 3

Drilling Deeper Into Individual Activist Funds…

ValueAct Capital took a new position in KKR, Spotify, and Wix; The fund further incr’d its positions in Toast (+61%) and Visa (+35%) and maintained its position in Salesforce; It decr’d its position in Live Nation (-24%), Blackrock (-21%), Meta (-13%), Roblox (-2%), and Liberty Live (-1%), and further decr’d its position in The Walt Disney Co. (-87%), MongoDB (-25%), and Amazon (-15%); The fund sold out its position in Insight Enterprises

Starboard Value took new positions in CarMax and Lamb Weston; The fund incr’d its position in Riot Platforms (+22%); It decr’d its positions in Tripadvisor (-47%), and further decr’d its positions in News Corp (-42%) and Rogers Corp (-3%); The fund maintained its positions in Bill Holdings, Kenvue, and Match Group; The fund sold out of its positions in Autodesk and Salesforce, both of which it had reduced last qtr

Sachem Head took a positions in Akamai, Bitdeer and ON Semiconductor; The fund incr’d its positions in Carvana (+26%) and further incr’d its position in Dick’s Sporting Goods (+32%); It decr’d its positions in EchoStar (-43%) and Coherent (-40%) and maintained its positions in Six Flags, Sprinklr and Twilio; The fund sold out of its positions in CVS Health, Kenvue, Live Nation, Resideo, Warner Bros. Discovery and ZoomInfo

Trian Fund took a new position in Magnum Ice Cream; The fund decr’d its position in Wendy’s (-51%); It maintained its positions in Invesco, GE HealthCare, GE Aerospace, Janus Henderson, and Unilever; It did not sell out of any positions

Third Point took new positions in Alphabet, ASML, Broadcom, Meta and VanEck Semiconductor ETF; The fund decr’d its positions in Nvidia (-94%) and Live Nation (-73%) and further decr’d its positions in Capital One (-87%), Taiwan Semiconductor (-35%) and Amazon (-10%); It maintained its position in Aurora Innovation and sold out of its positions in Alibaba, Chipotle, Kenvue, Microsoft, Spotify and Wix

Pershing Square took a new position in Microsoft; The fund further incr’d its position in Amazon (+19%); It decr’d its positions in Meta (-1%) and Uber (-1%), and further decr’d its positions in Alphabet (-95%); They maintained their positions in Universal Music Group and Hertz and sold out of its position in Hilton

JANA Partners took no new positions; The fund incr’d its positions in Fiserv (+98%) and Alkami Technology (+11%); It decr’d its positions in Mercury Systems (-17%) and maintained its positions in Rapid7 and Six Flags; The fund sold out of its position in Freshpet, which it had reduced last qtr

Elliott Management took new positions in Norwegian Cruise Line and Transocean; The fund incr’d its position in Hewlett Packard Enterprise (+47%); It further decr’d its position in Southwest Airlines (-48%); The fund maintained its positions in Crown Castle, Equinix, Etsy, and Pinterest and sold out of its positions in Bill Holdings and Toyota Industries

Grab Bag: Walmart Sparks Concern / Minnesota Prediction Mkts Ban/ Airbnb “Super App” Push

- Walmart shrs trade off as mgmt expects consumers to feel more strain

- While Q1 revs were 1.7% ahead of cons (Walmart US comp sales: +4.1%)

- Q2 guidance rev guidance slightly missed by 0.5% and adj EPS was 2.7% below cons at the mid-pt

- However FY guidance was reaffirmed

- Walmart CFO John David Rainey said consumers may feel more strain in Q2 as the effect of tax returns goes away

- Higher tax returns muted some pressure from higher fuel prices, but with refunds largely not coming in now, he expects consumers to feel more pressure (baked into the guidance)

- While Q1 revs were 1.7% ahead of cons (Walmart US comp sales: +4.1%)

–>Walmart’s stock was down -8% in reaction to the news; the stock is up +8% YTD

- Minnesota is first state to ban prediction markets, BUT the CFTC is fighting back (link/link/link)

- The House passed the ban100-32, and the Senate approved it 57-9, before Governor Tim Walz signed it into law

- The law takes effect August 1st, 2026

- The Commodity Futures Trading Commission’s (CFTC) lawsuit seeks to block the law before it goes into effect, arguing the prediction market industry should be exclusively regulated by federal officials

- “This Minnesota law turns lawful operators and participants in prediction markets into felons overnight,” said CFTC Chairman Michael Selig

- “Minnesota farmers have relied on critical hedging products on weather and crop-related events for decades to mitigate their risks

- The Commission has also filed previous lawsuits against Arizona, Connecticut, Illinois, and New York

- They have also filed amicus briefs in the US Court of Appeals for the 6th & 9th Circuits and the Supreme Judicial Court of Massachusetts

- A Polymarket spokesman stated Minnesota’s ban runs counter to the federal gov’s “established framework” for regulating prediction markets

- The House passed the ban100-32, and the Senate approved it 57-9, before Governor Tim Walz signed it into law

- Airbnb is expanding their offering & pushing further into a “super app” (link/link)

- The Co is now offering new services including:

- Grocery delivery

- Airport pickups

- Luggage storage

- Car rentals

- The Co is also expanding “Airbnb Experiences”

- Landmarks: Explore 3,000+ landmark experiences with local experts

- Food culture: Discover 2,500+ culinary experiences, through partners like Chef’s Table and Grand Central Market

- FIFA World Cup 2026: Access once-in-a-lifetime experiences across 6 host cities, from watch parties with Abby Wambach and Julie Foudy to pitch training with Javier Mascherano

- Other Updates:

- AI review highlights: The Co’s AI synthesizes over 1bn guests and host reviews, this helps surface the things customers care about most like location, amenities, family-friendliness, and more

- AI-powered comparison: A new wishlist comparison view helps people choose between homes with AI-generated summaries

- Shared itinerary: A new Trips map shows reservations, nearby restaurants, experiences, things to do, and travel times

- Connections & travel map: People can add friends and family, see where they’ve stayed or are going on Airbnb, review what they booked, and message them for tips

- AI-powered customer support: Airbnb’s AI assistant is now available worldwide in 11 languages, with trip-aware support, interactive issue-resolution cards, and voice support coming later this year

- The Co is now offering new services including:

–>Airbnb shares were up +3% in reaction to the news

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Midterm political ad spend is projected to reach $13. 8bn, up 9% vs 2022, per Madison & Wall, signaling slower growth vs prior election cycles. Digital mkts will capture 50% share, up from 46%, while local TV falls to 36%. Growth is partly driven by GOP funding targeting key races. Other forecasts range ~$10.4bn–$10.8bn, w/ streaming as fastest-growing segment. (MediaPost)

Artificial Intelligence/Machine Learning

- OpenAI generated $5. 7bn in Q1 rev, ~ $1bn ahead of Anthropic, driven by Codex, enterprise sales, and ChatGPT ad tests. Despite this lead, Anthropic’s growth outpaced, w/ annualized rev nearing $45bn vs OpenAI’s $25bn. Anthropic expects Q2 rev to double to ~$11bn w/ $600mn profit. Both cos may pursue IPOs by Q4 2026. (Investing.com)

- Google annc’d Adobe, Canva, and CapCut integrations w/ Gemini AI, enabling users to edit AI-generated content directly. Canva offers layered image editing via Magic Layers, while Adobe plans a creative agent linking 50+ pro tools. CapCut will add image/video editing. Rollouts are staggered, w/ Canva partly live and Adobe coming soon. (PCMag)

- Meta said in Apr. it would cut ~8,000 jobs (10%) as it pivots to AI, w/ 7,000 staff shifted to new initiatives. Layoffs began via early global emails, sparking confusion as employees checked directories and shared reactions online. Some recent hires were also cut, highlighting disruption as the Co accelerates its AI-first transformation and workforce reshaping. (The New York Times)

- Alibaba annc’d a full AI stack upgrade at its Cloud Summit, spanning infra, chips & models to support agentic AI. New Qwen3.7-Max enables advanced coding, automation & long tasks up to 35 hrs. Cloud upgrades include Panjiu AL128 server for scalable training, while T-Head’s Zhenwu M890 chip boosts performance 3x. (Asia News Network)

- Anthropic expects rev to surge ~130% to $10. 9bn in Q2, marking its first operating profit of $559mn, defying doubts about AI profitability. The startup, once a laggard, reported $4.8bn in Q1 and is growing faster than Zoom during the pandemic and pre-IPO Google and Facebook. The strong outlook comes amid a funding round that could lift its valuation above OpenAI’s. (The Wall Street Journal)

- OpenAI annc’d its reasoning model disproved Erdős’s planar unit distance conjecture, a ~80‑yr problem in discrete geometry. The model produced configs w/ n points yielding n^(1+δ) unit pairs, beating prior n^(1+o(1)). Verified by mathematicians, work links geometry w/ algebraic number theory and marks first major math problem solved autonomously by AI, showing potential for broader research impact. (OpenAI)

- OpenAI, ChatGPT maker, is preparing to file for an IPO within days or weeks, per sources. The AI Co is working w/ bankers at Goldman Sachs and Morgan Stanley on a draft prospectus to be filed confidentially w/ regulators, possibly as early as [Wed., May 20]. The move signals a push toward public mkts as demand for its tech cont’d to grow rapidly. (The Wall Street Journal)

- Paramount annc’d hiring Barak Turovsky as EVP, head of consumer AI on signaling deeper push into AI-driven tech. He will scale AI/ML teams, enhancing personalization, content discovery and monetization across Paramount+ & Pluto TV. CEO David Ellison emphasized tech + storytelling as key to growth, w/ AI seen as boosting creativity, not replacing it, as Co modernizes its biz. (The Hollywood Reporter)

- US backlash against AI is intensifying, w/ rising public skepticism and protests against the fast-growing tech. At a commencement speech, ex-Google CEO Eric Schmidt highlighted AI’s massive impact, but faced boos from graduates. The reaction underscores a widening crisis for the AI industry as negative sentiment grows faster than the biz itself. (The Wall Street Journal)

- Project Genie rolled out globally to Google AI Ultra users, adding Street View integration that lets users create AI-generated 3D scenes grounded in real-world Google Maps locations. The tool builds short, interactive environments from prompts w/ customizable styles and characters. (Engadget)

- KPMG struck a deal w/ Anthropic to embed Claude into its global tax and advisory platform, aiming to boost efficiency and speed. The move marks Claude’s first integration into a Big Four tax system, w/ rollout targeted by end-Sept. Employees and clients can create materials, build agents, and summarize docs, as KPMG builds on Azure-backed infrastructure. (The Wall Street Journal)

- A U. S. jury ruled against Elon Musk in his lawsuit vs OpenAI, finding he sued too late after alleging the Co strayed from its nonprofit mission. The verdict, reached in <2 hrs, clears a key hurdle for a potential IPO reportedly valued near $1trn. Musk plans to appeal, while the judge warned chances are slim. The case highlighted tensions over AI’s purpose, governance and profit motives. (Reuters)

- Chinese AI cos incl. ByteDance & Kuaishou have pulled ahead of US rivals in video-generation tech, leveraging vast short‑video data from apps like TikTok to boost realism, scale, and usability. While US leaders still dominate LLMs, their video tools lag on quality. Rapid adoption across ads, ecommerce, and entertainment signals a shift in AI competition, w/ China’s data edge accelerating gains. (Financial Times)

- Baidu posted a 55% YoY profit drop to $506. 6mn as rev fell 1.1% to ~32.08bn yuan, marking a 4th straight decline. Heavy AI, chips, and autonomous driving investments cont’d to pressure margins while ad biz slumped. AI-related svs showed ~50% growth, offering potential to offset weakness, though returns remain gradual as the Co pushes its AI pivot. (The Wall Street Journal)

- Apple Inc. is prepping AI-driven features for iOS 27 & iPadOS 27, incl. a grammar checker, writing tools, natural-language shortcuts & custom wallpapers, aiming to close gap w/ rivals like Google & Samsung. Updates also bring enhanced Siri, visual analysis via camera & improved Photos editing, ahead of Jun. (Yahoo Finance)

- Anthropic & OpenAI dominate AI startup rev, capturing ~89% share as 34 firms generate ~$80bn annualized rev (~$6. 6bn/month), up 112% in 6 months. Anthropic leads via coding-focused svs. Sequoia says value shifts to app layer as models commoditize. Deals w/ cloud partners impact rev splits. (MediaPost)

- Tencent shares rose over 4% after the Co annc’d plans to shift some AI models from free beta to paid svs. Its Tencent Cloud will commercialize Hy3 Preview and DeepSeek‑V4‑Pro from May 27, adopting usage‑based pricing. The move highlights efforts to monetize AI amid rising competition, as Tencent expands across cloud, ads, and enterprise AI vs rivals like Alibaba and Baidu. (Investing.com)

- Apple is set to launch a standalone Siri app at WWDC w/ iOS 27 preview, featuring chat-based interactions, file uploads, and auto-deleting conversation history after 30 days or 1 yr. The app, powered partly by Google Gemini via private cloud, emphasizes privacy by limiting data sharing. (9to5Mac)

- US roles exposed to AI saw cont’d job losses, per BLS data. 18 occupations (~10mn jobs) fell 0.2% from May 2024–May 2025, vs 0.8% overall growth. Excluding medical roles, declines hit 1.6% for a 2nd yr. Customer svc, secretaries, and sales jobs dropped sharply, w/ AI-linked shifts reshaping hiring as openings lag pre-pandemic levels. (Bloomberg)

Audio/Music/Podcast

- Podcast industry generated ~$9. 2bn in global sales last yr, up 23%, driven by growing shift to video formats. Ads comprise most rev, per Owl & Co report, while subscriptions and other consumer purchases rose 22%. In the US, largest mkts, 73% of 2025 growth came from video-related rev, indicating strong returns from adopting visual podcasting across the biz. (Bloomberg)

- Spotify annc’d a ban on AI-generated podcasts that impersonate creators, reinforcing existing rules to protect identity and trust. The Co said it will remove shows using AI voice cloning or similar methods w/o permission. It also launched “Verified by Spotify” badges for podcasts, highlighting authentic creators based on engagement, compliance, and audience validity, as it seeks a more trusted ecosystem. (Variety)

- Amazon annc’d Alexa+ can now generate AI “podcasts,” featuring two synthetic co-hosts discussing user-requested topics in minutes. The svc draws on partnerships w/ major news orgs to deliver real-time info and lets users customize length and focus. Bundled free for Prime users or $19.99/month otherwise, Amazon says this marks a new way to consume personalized audio content. (Variety)

Broadcast/Cable Networks

- Nielsen data shows Mar. TV trends w/ cable rising 7% MoM to 21.4% due to NCAA, but down YoY from 24.0%. Broadcast slipped to 20.3%. Streaming cont’d growth to 47.6% (43.8% prior yr), led by YouTube 13.2% and Netflix 8.2%. Roku saw biggest gain to 3.0%. Major media cos like Paramount and WBD declined YoY, while Disney held 10.5% share and NBCU rose via strong news viewing. (MediaPost)

- While focus stayed on Nexstar, smaller broadcasters like Gray Media quietly expanded, buying local ABC, CBS, FOX, and NBC stations and forming duopolies. Deals, incl. Lansing, MI, merged newsrooms and resources to boost efficiency and ad reach. Supporters say moves sustain local journalism amid cord‑cutting, but critics warn of layoffs and reduced diversity as consolidation spreads across ~110 mkts. (Cord Cutters News)

- Nexstar Media Group said delays from a court order halting its $6. 2bn Tegna deal have cost tens of $mn, urging an expedited appeal. The Apr. 17 ruling followed challenges from states and DirecTV over competition and pricing. Nexstar warned the pause hurts hiring, relationships, and biz decisions, while a trial may not start until 2027. (Reuters)

Cable/Pay-TV/Wireless

- AT&T annc’d eSIM by AT&T on May 18, 2026, offering intl travelers flexible connectivity across U., Mexico & Canada. Plan includes unlimited data w/ 5GB hotspot, w/ talk & text coming soon. Users can buy 1–30 day passes via app. Service supports 5G, priority data in crowded venues, & aims to simplify travel connectivity during major summer soccer events. (AT&T)

- Iliad reported Q1 organic rev growth of 3. 3% w/ EBITDAaL up 1.2% to €942mn, driven by strong Italy performance where profit rose 25% to €111mn. The Co added 200k subscribers in Italy, while France & Poland saw flat growth despite fibre gains. Free cash flow nearly doubled to €416mn. Iliad also cont’d talks to acquire SFR assets in €20.35bn deal, though outcome remains uncertain. (Reuters)

- FCC filings reveal Amazon’s new home internet hardware for its low‑Earth orbit “Leo” satellite svc, ahead of a planned summer launch. The Wi‑Fi 6 router (model L1LA10) supports mesh networking, Bluetooth LE, and ZigBee, acting as a home hub. W/ ~300 satellites in orbit, the svc targets rural areas, offering multiple terminals, though pricing and rollout details remain undisclosed. (Cord Cutters News)

- T-Mobile CEO said May data shows T-Satellite traffic at just 0. 0002% of total network use, underscoring satellite as complementary, not competitive, to terrestrial svc. Execs framed a new JV w/ Verizon & AT&T as aimed at pooling spectrum, setting standards, and reducing dead zones. (Fierce Network)