It was a bit of an up and down week with the major indices closing Friday roughly flat w/w. However, big cap tech is buoying the markets as the equal-weighted S&P 500 index (RSP) was down -1.2%. One macro update that was particularly in the headlines (in addition to Trump/China news) was the higher than consensus core readings for both April CPI and PPI.

There were a couple of key earnings stragglers this week (Fox, Versant, and Alibaba) and we focused on several other interesting developments across the sector as well. See below for what is included in this edition.

- Earning Scorecard - Week 5

- Fox Ends Large Cap Media Earnings On A High Note

- BABA’s FQ4 + Outlook = Better Than It Looked At First Blush

- Versant Accelerates Its Shareholder Return Strategy & Benefits From Licensed Content

- The Connectivity Sector Looks Skyward

- Total Web Usage Continues To Fall Despite Strong Growth In AI Referrals

- Waymo Is Expanding, But Not Without Growing Pains

- Google’s Android I/O Edition Provided A Sneak Peak To The Real I/O Event Next Week

- US Digital Video Ad Spend Is Projected To Grow +11% Y/Y In 2026

- Grab Bag: eBay Rejects GME’s Takeover Proposal / TikTok Expands Into Experiences / GTA 6 Pre-Orders Next Week?

Nvidia’s earnings will certainly be a market catalyst next week as well.

Have a nice weekend.

Best,

Leslie

Earning Scorecard - Week 5

16 stocks in our LionTree Universe reported in Week 5 of earnings. Stock reactions were heavily skewed to the negative side, with 11 (69%) stocks trading down and only 5 (31%) stocks trading up. The best performer in reaction to earnings was Versant, which was up +9.9% (see Theme #2), while the worst performer was Doximity, which fell -23%.

Also in Media, Fox reported this week (see Theme #4) and was up +8.1%. China Tech was active with Alibaba (see Theme #3), JD.com and Tencent Music all reporting, but with mixed reactions. For a quick take on the latter two companies:

- JD.com – Traded up +3.1%: The Co delivered a strong Q1, especially on profitability

- Q1 revs beat by +1.3%

- Non-GAAP EBITDA beat by a massive +69.9%

- Non-GAAP EPADS beat by +40.7%

- Tencent Music – Traded down -1.3%: The Co reported a modest Q1, with results in-line to only slightly ahead of cons

- Q1 revs were inline w/cons

- Music-related services revs slightly beat by +0.5%

- While Social entertainment svs and other revs missed by -2.1%

- Gross margin of 44.9% beat cons by +20bps

- Non-IFRS EPADS beat by +2.8%

- Q1 revs were inline w/cons

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Fox Ends Large Cap Media Earnings On A High Note

While Fox had tough comps due to the Superbowl, FQ3 results handily beat expectations, especially on profitability (with revs +6% ahead, adj EBITDA +27% ahead, and adj EPS 35% ahead). The headline beat was broad-based across Cable Nets and TV. Fox’s favorable positioning in News and Sports continues to be a differentiator and has made the Co more immune to some of the sector headwinds in general entertainment. Our top 5 key learnings from Fox’s results include: 1) Core advertising was much stronger than expected…b-cast ad revs BEAT cons by +10.4% and cable networks ad revs BEAT cons by +8.6%…ex-the Super Bowl, ad revenues grew double-digits y/y and momentum is “continuing” into FQ4; 2) Tubi revs incr’d +23% y/y and it was the 3rd straight quarter at break-even or better…investment intensity related to Tubi is also starting to moderate; 3) The World Cup is expected to be EBITDA accretive at the total company level with revenue split evenly across FQ4:26 & FQ1:27; 4) Fox One “exceeded expectations” and mgmt believes that those subscribers are incremental… churn has also been lower than expected; and 5) In Distribution, cable subscriber declines have been stable (at under -6.5% y/y)…and Fox One is not included in this metric (i.e., would make it better).

So overall, FOX has been executing well during this seasonally tough comp period, and looking forward, over this fiscal year, the Co should benefit from the World Cup and political.

-> FOX shares closed the day up +8.1% following its earnings report, though they are still down -11.2% YTD

FQ3 Was Another Broad Beat

- Revenues BEAT cons by +5.6%: Down -9% y/y vs up +2% y/y in FQ2

- The decline is primarily due to the absence of last year’s Super Bowl LIX broadcast, partially offset by continued digital growth led by Tubi, an addtl NFL Wild Card game, higher sports sublicensing rev, and +3% distribution growth

- Adj EBITDA BEAT cons by a large +26.6%: Grew +11% y/y vs a -11% y/y decline in FQ2 and margins hit 23.9% vs cons 19.9%

- Growth reflected lower sports programming rights amortization and production costs from the Super Bowl comp, partially offset by the addtll NFL Wild Card game and Fox One launch costs

- Adj EPS BEAT cons by +34.7%: Grew +20% y/y

- Cable Networks outperformed

- Revs BEAT by +4.8%, rising +6% y/y vs +5% y/y in FQ2

- Adj EBITDA BEAT by +12.2%, rising +1% y/y vs +5% y/y in FQ2

- Rev growth was partially offset by higher sports rights amortization

- Television also outperformed

- Revs BEAT by +4.8% but declined -19% y/y vs -1% y/y in FQ2

- Primarily due to the absence of the Super Bowl

- Adj EBITDA of $191mn was well ahead of cons $78mn and up over 3x y/y, with expenses down -24% y/y due to lower sports programming rights amortization and production costs

- Revs BEAT by +4.8% but declined -19% y/y vs -1% y/y in FQ2

- FQ3 FCF of $1.77bn was consistent with the 2H seasonal reversal of sports rights payments and advertising receivables

- Fiscal YTD buybacks were $1.95bn (cumulative repurchases since 2019 are $8.5bn+ or ~36% of shrs, incl completion of the $1.5bn ASR)

Ad Revs Ex Superbowl Were UP Double-Digits W/ Momentum Continuing

- Headline FQ3 ad rev decl’d -24% y/y due to the Super Bowl comp, BUT ex Super Bowl & other NFL postseason schedule changes, total Co ad revs would have grown DD y/y… and that “momentum continues into our fiscal fourth quarter”

- TV Advertising revs declined -30% y/y due to the absence of Super Bowl LIX, partially offset by an addtll NFL Wild Card game and cont’d Tubi growth

- Cable Ad revs grew +5% y/y, driven by higher news pricing and World Baseball Classic, partially offset by lower ratings

- The upfront setup appears strong heading into FQ4 / FY27

- Seeing “healthy” scatter

- Pharma, tech, and finance were called out as growth categories

- Political expected to layer in toward the autumn

- “The combination of a strong underlying ad market leading into these upfronts and also, the political revenue that’s, you know, already beginning to flow in, gives us great confidence in the ad market moving forward”

Fox News Ratings Comps Were Tough Given Last Year’s Presidential Inauguration, But April Is “Very Positive” / Sports Ratings Were Also Strong

- Fox News achieved its highest FQ3 ad rev ever…Fox News digital also delivered DD growth in both YouTube and social views

- Given the comps against the presidential inauguration a year ago, ratings were down -57% y/y in FQ3

- BUT the Co is seeing “very positive” y/y growth in April

- Fox News added 200 premium ad clients thus far in FY26 on top of the 350 added in FY25, taking new clients to 500+

- Fox News national pricing / CPMs are up over 45%, but mgmt still sees “a great upside opportunity” to narrow the gap between Fox News and b-cast CPMs

- Given the comps against the presidential inauguration a year ago, ratings were down -57% y/y in FQ3

- Strong FQ3 sports ratings

- World Baseball Classic avg ratings were up over 150% vs the 2023 tournament and the final drew 10mn+ viewers

- MLB opening weekend on Fox was up +45% y/y and IndyCar ratings were up +37% as of qtr-end

- NFL regular season games on Fox reached 170mn+ viewers during the 2025-26 season and the NFC Championship averaged 46mn+ viewers

There Is A Lot Of Excitement About The World Cup

- FIFA Men’s World Cup is seen as the largest upcoming catalyst, with the tournament spanning 104 matches over 5 weeks and the event will be split 50/50 financially across FQ4:26 / FQ1:27

- The event should be EBITDA accretive at the total Co level (due to b-cast)

- Revenues will skew to the b-cast side, where it should also be EBITDA accretive

- On the cable side, there will be less rev and will likely NOT be EBITDA accretive

- World Cup should help drive Fox One and Tubi

- Fox One should benefit from addtl sports content and could see a seasonal lift similar to the start of other sports seasons

- Tubi will simulcast opening matches and host a FIFA World Cup hub, giving the platform a brand / engagement opportunity across ~100mn MAUs

Tubi Continues To Be A Growth Driver & Investment Levels Are Moderating

- Tubi revs grew +23% y/y, accelerating from +32% y/y in FQ2, while total view time (TVT) grew +19% y/y vs +17% y/y in FQ2

- Tubi remained “break-even or better” for the 3rd straight qtr

- Mgmt highlighted the mix of library content, Tubi originals and creator-led titles as key engagement drivers

- Tubi now has 220+ creators and over 17k episodes, with plans to expand this creator universe to attract younger audiences and drive higher retention

- Investment levels (related to launch, marketing & tech costs) into Tubi are starting to moderate as the platform grows

- The two World Cup games that will be simulcast on Tubi won’t impact Tubi’s revenue because that revenue will be recognized by FOX Sports

- BUT… it will be additive to Tubi’s brand and audience metrics

Distribution Trends Are Stabilizing, With Skinny Bundles & Fox One Improving The Pay-TV Debate

- Distribution revs grew +3% y/y vs +4% y/y in FQ2

- Cable distribution was up +5% y/y vs +5% y/y in FQ2, as pricing gains outpaced the impact from net subscriber declines

- TV distribution was down -1% y/y vs +1% y/y in FQ2

- Continues to be in-line with expectation for TV distribution revenue to be ~ flat for the full year before returning to growth in fiscal 27

- Cable sub declines remained at under -6.5% and have stabilized for several qtrs…Fox One subs are also NOT included in this number as well

- Mgmt has been taking a conservative approach by excluding Fox One subs from the sub decline metric

- Fox One was a “significant contributor” to subscriber growth…overall “it has exceeded expectations, but it is early days”

- Mgmt is confident the subs are additive to the ecosystem

- Churn has been lower than expected

- In FQ3, over ½ of viewership was for news

- Sports is helping to bringing in new subs as well

- Skinny bundles are “helping the eco-system”…but it is still early days”

- ~1/3 of their distribution income is up for renewal in fiscal 2027 and that’s skews towards TV

- But mgmt feels very good about both Cable distribution and TV distribution growth in FY27

Fox Annc’d New NFL Games But Has Not Started Any Re-Negotiations On Current Packages

- Fox annc’d rights to 2 addt’l NFL regular season games in national windows for the coming season

- A week 10 Munich game that creates a Sunday triple-header (the 1st triple header on broadcast TV in history)

- A week 15 Saturday game

- Are there tensions with the NFL as per press reports? “There is no tension really with the NFL…we’re partners for 30 years” and “we look forward to being partners for the next 30 years”

- Fox has 4 years remaining on the current NFL deal and has had no “substantive” discussions around renegotiation / extension of their current rights despite press speculation

- Mgmt would like to broaden and deepen the NFL relationship but only in a “disciplined” way

A Few Other Key Comments / Updates

- The Co remains bullish on sport betting…but no new news was provided:

- Mgmt reiterated:

- That the Co retains a 2.5% equity stake in Flutter and an 18.6% option in FanDuel

- Mgmt has over 4 years to exercise the FanDuel option and is going through licensing processes so that they can exercise it

- Mgmt reiterated:

- YTD, digital investment spend is pacing lower y/y…

- In FY25, they spent $290mn

- At the start of FY26, they guided for ~$350mn of digital investment spend for the year

- But now, mgmt. expects FY26 to be “comfortably inside that $290mn”

- For FY27 they are “not anticipating any surprises”, but if we see opportunities, “we won’t be shy about investing”

BABA’s FQ4 + Outlook = Better Than It Looked At First Blush

While US TMT earnings have started to slow down, Asia Tech results were in focus this week with Alibaba the main heavy weight to report their FQ4. At first blush, the print didn’t look that inspiring with total revenue missing cons by -1.5% and much more dramatically, adj EBITDA missed by -28% given the high level of investment intensity, but positives emerged under the hood and in relation to mgmt. commentary and forward guidance. One of those being that Core China Commerce Mgmt revenue (CRM) growth was better than it looked given an accounting change…ex that CMR was up +8% y/y vs +1% y/y in FQ3.

The Top 5 list of other things that we learned include: 1) The Cloud business has a lot of momentum…external cloud customer revenue accelerated from +35% last qtr to +40% this qtr and AI-related product rev reached RMB8.97bn, up triple-digit y/y for the 11th consecutive qtr, and represented 30% of external Cloud rev…and mgmt expects this to cross 50% in ~1 yr and be the “primary engine” of Cloud rev growth; 2) Model and Application services (MaaS) ARR incr’d more than 10x from Nov/Dec last yr to May, already surpassing RMB8bn and mgmt guided for that to surpass RMB10bn in the June qtr and RMB30bn by year-end as enterprise customers accelerate their shift to production-scale complex workloads; 3) Quick commerce rev growth was strong at +57% y/y vs +25% y/y in FQ3 BUT still MISSED cons by -6.8%…on the plus side, mgmt expects quick commerce unit economics to turn positive by the end of FY:27; 4) China E-commerce adj EBITA fell -40% y/y due to quick commerce, user experience and technology investments…BUT ex Quick Commerce losses, China E-commerce adj EBITA would have been stable y/y; and 5) AIDC adj EBITA loss narrowed to RMB138mn, which was a large beat vs cons loss of RMB591mn, and narrowed sharply from a RMB2.0bn loss last yr.

So overall, results were in parts better than it looked at first blush and the outlook points to improvements in key areas looking ahead.

-> After initially trading down -4% pre-mkt, the stock closed the day up +8% as investors more fully digested the results; But YTD, the stock is down almost -10%

-> JD.Com also reported this week, in addition to Tencent Music Entertainment (see Theme #1)

FQ4 Was Another Tough Qtr For Alibaba, With Profitability MUCH Lower Than Consensus…

- FQ4 revs MISSED cons by -1.5%: Grew +3% y/y (+11% y/y ex-Sun Art/Intime)

- With weaker than expected results across all segments except All Others

- Adj EBITDA MISSED cons by -28.1%: Declined -61% y/y… but a lower adj EBITA loss in Intl Digital Commerce was a key upside driver

- Adj EBITDA margin of 6.8% was ~250bps below cons 9.3%

- Adj EPDAS of RMB0.60 was well below RMB6.14

- CapEx was RMB26.9bn vs cons RMB31.1bn, up +11% y/y

…But Core Customer Mgmt Rev (CMR) Slightly Beat & Accelerated Y/Y On An Underlying Basis & China E-Comm Grp EBITDA Would Have Been “Stable” Y/Y Excluding The Losses From Quick Commerce

- FQ4 China E-Comm business overall performed below expectations: Revs MISSED by -3.2% (grew +6% y/y) & adj EBITA MISSED cons by -6.2% (declined -40% y/y)

- Under the top-line hood, while core Customer Mgmt rev was a tad better than cons, Direct sales, logistics and others rev, Quick commerce revs, and China commerce wholesale revs were all below projections

- But excluding the losses from Quick commerce, China E-Comm grp EBITDA would have been “stable” y/y

- But it will fluctuate q/q due to significant investment in merchant retention and the user experience

- Underlying Customer Management rev (CMR) was better than it looked…CMR grew +1% y/y (a tad better than cons) but excl the contra-rev impact from the upgraded merchant business development program, CMR would have grown +8% y/y (vs +1% y/y in Q4)

- Platform subsidies directly tied to merchant marketing spend are now recorded as contra-rev rather than sales and marketing expense

- AI is becoming more directly embedded in commerce workflows

- Taobao/Tmall e-commerce services have been integrated into the Qwen app

- Taobao launched Qwen Shopping Assistant, an agent covering idea generation, product discovery, in-sale support, order mgmt and post-purchase services

- Wukong, an AI-native enterprise agent, was rolled out to merchants to improve operating efficiency and bring agentic capabilities into merchant workflows

- Direct sales, logistics and others rev declined -6% y/y and MISSED cons by -8.9%

- 88VIP members (most valuable customers) surpassed 62mn and grew double-digit y/y

…AND Quick Commerce Losses Are Expected To Narrow Substantially Over The Next 2 Yrs & Unit Economics Are Expected To Turn Positive By The End Of FY27

- FQ4 Quick Commerce rev MISSED cons by -6.8% but did grow +57% y/y vs +56% y/y in Q4

- The business maintained stable market share and improved unit economics

- Order volume was up 2.7x y/y and non-food orders were up 3x from April onward

- AOV incr’d q/q and unit economics improved due to fulfillment/logistics efficiency plus order mix

- Quick commerce is contributing to traditional e-comm customer acquisition, user engagement, diverse demand fulfillment, transactions, monetization and logistics infrastructure

- Mgmt expects unit economics to turn positive by the end of FY27 and expects quick commerce to achieve overall profitability in the future

- Quick commerce losses are expected to narrow substantially over the next 2 yrs, helping offset the near-term drag from continued investment

- Unit economic improvements are coming from enhanced fulfillment/logistics efficiency and order mix optimization

Cloud Revenue Growth Accelerated Y/Y But Was Slightly Lower Than Street Projections

- FQ4 Cloud Intelligence Group revs grew +38% y/y vs +35% y/y in Q4 and +34% in Q3 but MISSED cons by -1.5%

- External customer rev accelerated to +40% y/y vs +35% y/y in Q4

- AI-related product revs continue to grow at a very rapid pace

- AI-related product rev grew triple-digit for the 11th straight qtr and annualized AI-related product rev surpassed RMB35.8bn

- AI-related products now account for 30% of Cloud external rev…and mgmt expects this to cross 50% in ~1 yr…and will be the “primary engine” of Cloud rev growth

- Model and Application services (MaaS) ARR has incr’d more than 10x from Nov/Dec last yr to May, already surpassing RMB8bn

- And mgmt expects that to exceed RMB10bn in the June qtr and RMB30bn by year-end as enterprise customers accelerate their shift to production-scale complex workloads

- MaaS growth is primarily driven today by API calls on their platform, followed by AI software subscriptions to a lesser degree

- Demand for MaaS is outstripping supply with many customers waiting to access the services and mgmt. expects continued price improvements

- MaaS inherently has higher margins vs IaaS

- Model Studio customer base grew +8x y/y and token consumption volumes grew substantially q/q

- Qwen 3.6-Plus launched with “significant” gains in coding and agentic programming, up to 1mn token native context window and improved multimodal perception/reasoning

- Specialized models HappyOyster and HappyHorse are being commercialized in phases, adding world model and video generation capabilities to the model portfolio

- Regarding agentic AI, mgmt described the industry as at a “pivotal inflection point” from conversational chatbots to autonomous agents, driving growth across training, inference and agent orchestration

- T-Head (the Co’s chip business) has over 100k Zhenwu parallel processing unit (PPUs) deployed on Alibaba Cloud public cloud with 30+ leading automakers and autonomous driving companies using the chips for intelligent driving R&D

- T-Head proprietary GPU chips have achieved scaled mass production, with 60%+ of compute capacity already serving external customers across internet, financial services and autonomous driving verticals

- “As the only AI cloud provider in China capable of delivering self-developed AI chips at-scale, we’ve secured autonomy over our compute supply-chain while providing customers with highly competitive AI inference and training services. In an environment of compute scarcity, this structural advantage is favorable to our revenue growth and gross margin improvement”

- Cloud Intelligence Group adj EBITA grew +57% y/y and was ~INLINE w/ cons

- Adj EBITA margin was relatively stable at 9.1%

- Cloud gross margins are expected to start improving in the next 1-2 qtrs and to be significantly higher over the next 2-3 yrs

- Drivers: Rising MaaS/inference mix, reasoning/inference optimization that increases output per card, and scaling of T-Head chips

- Mgmt’s primary objectives are growth, token consumption and market share, with margins being a “secondary” consideration as AI penetration across industries remains early

- On capex…compute infrastructure demand is expected to increase 10x from 2022 to 2033 and the Co now says it might “overshoot” the original RMB380bn guidance over the next three years (2025-2027)

- But the Co “can also acquire compute capacity through opex, selling AI servers with proprietary T-Head chips, or co-building computing centers”

Other Key Updates On International Digital Commerce & Shareholder Returns

- FQ4 Intl Digital Commerce is expected to move from loss to profitability over the next 2 yrs

- AIDC revs MISSED cons by -1.3% but grew +6% y/y

- But the adj EBITA loss narrowed +96% y/y to RMB138mn and BEAT cons

- Driven by a combination of logistics optimization and operating efficiency

- Positive AliExpress stats:

- The “Brand+” program further accelerated brand onboarding, and the penetration of quarterly transacting consumers for “Brand+” surpassed 30%

- The unit economics of the AliExpress’ Choice biz continued to improve “substantially on a sequential basis”

- The Board approved an annual dividend of US$1.05/ADS for FY26, equal to an aggregate payout of ~$2.5bn

Versant Accelerates Its Shareholder Return Strategy & Benefits From Licensed Content

It was the second quarter in a row where Versant surprised the Street with new shareholder return news. This time it was a $100mn accelerated buyback that should be completed in Q2. This follows the $100mn worth of stock that they bought back in Q1 as part of the $1bn share buyback authorization that was announced last qtr. The Co also declared a $0.375/shr quarterly dividend. All of this was received well. Turning to fundamentals, Q1 topped expectations, most materially on the profitability side, with a key positive being the benefits of a licensing deal that was fully recognized in the qtr. Looking forward, however, programming expanse will be weighted towards H2 (especially Q4) and SG&A will also be modestly up, hence the overall 2026 guidance previously outlined was reiterated, despite the Q1 beat.

Five of our other key learnings from the Co’s results include: 1) The declines in the Linear business were largely in-line with the previous trends (though were a tad better than cons) and the Co’s news and sports focus positions them well regarding skinny bundles; 2) While advertising revenue missed Street projections (by -3.9%), the trend improved materially to a decline of -5% y/y from -9% y/y in Q4 and -12% in Q1 last year; 3) Platforms rev growth was a key standout, beating cons by almost +8% and growing +9.5% y/y, driven by Fandango ticketing / VOD / Fandango1 and GolfNow bookings, payments and GolfPass subs, 4) MS NOW DTC and Fandango AVOD remain on track to launch later this yr; and 5) The bar for M&A remains high.

See more details below.

-> Versant shares rallied +9.9% on the back of results and buyback news but they are still trading down -4.5% YTD

Versant Posted Another Stronger-Than-Expected Qtr Though Maintained The FY Guidance Despite The Beat Given Timing Considerations

- Q1 revenue BEAT cons by +4.3%…the -1% y/y decline improved from the -7% y/y in Q4 thanks to Platforms & Content Licensing & Other revs

- Linear distribution BEAT cons by +1.0%: Decl’d -7% y/y vs the -6% y/y in Q4

- Advertising MISSED cons by -3.9%: Fell -5% y/y vs the -9% y/y in Q4

- Platforms BEAT cons by +7.9%: Grew +10% y/y vs -1% decline in Q4

- Content licensing & Other grew +113% y/y to $121mn

- Due to the timing of licensing agreements incl a large Keeping Up With the Kardashians deal

- Q1 adj EBITDA BEAT cons by +15.8%: Grew +5% y/y

- Adj EBITDA margin of 41.7% was +420bps above cons, reflecting lower entertainment programming expense, reduced SG&A and operating efficiency, partially offset by rev declines and higher costs tied to content licensing deals

- Programming / production costs were down -5% y/y; total cost of rev was $638mn, down -3% y/y; SG&A was $346mn, down -9% y/y

- Q1 adj EPS BEAT cons by +25.9%: Fell -22% y/y

- Q1 FCF reached $558mn vs cons of $389mn

- For 2026, the Co maintained the existing guidance despite the Q1 beat…

- Revs btw $6.15-6.4bn

- Adj EBITDA btw $1.85-2.0bn

- FCF btw $1.0-1.2bn

- …Because there will be quarterly fluctuations in the business w/ content licensing and working capital timing and higher programming costs in H2, particularly Q4

- Content licensing rev can vary materially q/q and y/y because rev is recognized when content is delivered

- Programming costs are expected to be higher in H2 (esp Q4) due to sports rights timing

- Q1 FCF benefited from working capital timing incl A/R collections and payable processing

- Mgmt expects these items to normalize as the yr progresses

- …and SG&A is also expected to incr modestly to support growth initiatives incl DTC offerings, while capx should also incr modestly over the remainder of the yr

Versant Continues To Scale Shareholder Returns & The Bar For M&A Remains High

- The Co repurchased $100mn of Class A shares in Q1 (of the $1bn authorization), declared a $0.375/shr qtrly dividend, and annc’d a new $100mn ASR expected to complete in Q2

- Mgmt “likes to make those [capital market] decisions in the context of the market environment and opportunities we see to add value. And that’s going to be our approach going forward as well”

- Regarding M&A, “clearly we’re looking in a variety of areas. And obviously I can’t be too specific here”…but mgmt. has “a very high threshold”…

- “If it makes a lot of sense and it adds a lot of value, we’ll pursue”

- “But if it doesn’t, we really like the hand that we have”

Strong Ratings & KPIs For The Co’s Key Networks…And Mgmt Sees Likely Oppties To Expand Its Sports Right Selectively

- CNBC delivered its highest-rated qtr in 4 yrs w/ DD y/y growth

- MS NOW delivered its most-watched qtr since 2024, with DD y/y growth in total day and primetime viewers across key demos

- Reached 30mn+ avg weekly viewers among key demos

- Viewers watched avg 9 hrs weekly, the 2nd-highest engagement across all cable networks and nearly double the next closest competitor

- Digital also inflected, with the strongest Q1 on record for the website / app, 1.6bn+ YouTube + TikTok views YTD and original podcast downloads up 60%+ y/y

- The Golf Channel drew its largest Players Championship audience in two decades, reaching 13.5mn unique viewers during Masters week

- Golfnow delivered broad growth across tee time, bookings and payments

- GolfPass reached its highest subscriber count ever, helped by the Rory McIlroy partnership

- Sports / entertainment engagement was strong

- Milan Cortina Olympics on USA Network / CNBC delivered the largest Olympics audience in USA Network history, reached ~75% of US Pay TV HHs and secured the #1 rank among sports / entertainment cable networks

- League One Volleyball’s first season delivered record viewership incl the most-watched match in league history, while WNBA coverage recently kicked off

- E! Live from the Red Carpet doubled viewership y/y across key events incl the Oscars, Grammys and Critics Choice Awards

- Mgmt believes there will be opportunities to pick up sports rights given the pressure on some of their larger competitors will be under “to retain or grow their NFL expense” which will force decisions on other content that VSNT can “selectively look at”…but in a “judicious” way

- Since the spin was announced, Versant has extended USGA, extended PGA of America Ryder Cup, expanded WNBA and added League One Volleyball

Linear Subs Declines Have Been Relatively Consistent & Mgmt Feels Well Positioned With Skinny Bundles

- Linear revs BEAT cons by +1% and declined -7% y/y, which compares to -6% y/y declines in Q4

- Co is “well-positioned” in skinny bundles because 4 of 7 linear networks sit in news / sports, incl MS NOW, CNBC, Golf Channel and USA Network

- The entertainment networks remain the bigger debate, but mgmt pointed to stability and flexibility

- Oxygen is available as both a Pay TV network and free OTA multicast, illustrating their willingness to use alternative distribution where additive

- Mgmt said the Co can be creative as a standalone company without damaging MVPD relationships

- DTC is intended to complement rather than replace MVPDs, creating a “circular” audience flow across platforms and helping reduce the impact of linear sub declines over time

Ad Revenue Declines Have Meaningfully Improved, Though Underperformed The Street

- While advertising revs were below the Street and decl’d -5% y/y, it was a “significant improvement” from the -12% decline in prior-year Q1 (and -9% y/y in Q4)

- The improvement was driven by organic portfolio strength rather than new initiatives like Free TV Networks

- The marketplace has been strong and news and sports have been “resilient”

- “Our partnership with NBCU representing us in the market has proven to be fruitful for both parties and we believe that this is sustainable”

- To call out, the Olympics was NOT a meaningful ad halo in Q1 b/c NBC just buys the time from Versant

- Rev diversification outside Pay TV will also help advertising revenue…incl DTC, free TV, digital platforms and Fandango AVOD

- Fandango AVOD will be free w/ ads and use data from ticketing / home video users to serve relevant ads

- Mgmt sees customer data from Fandango / GolfNow as a targeting and programmatic advantage as more ad inventory moves outside linear

Platforms Growth Was A Bright Spot & DTC / AVOD Launches Are Still On Track

- Platforms rev BEAT cons by +7.9% and grew +9.5% y/y vs -1% decline in Q4: Growth was primarily organic, with self-promotion across linear helping drive awareness for Fandango, GolfNow, GolfPass and Rotten Tomatoes

- CNBC DTC strategy will be enhanced via the acq of StockStory, an AI-driven financial insights platform that supports real-time actionable investment intelligence and the next phase of CNBC’s DTC product development

- MS NOW DTC and Fandango AVOD remain on track to launch later this yr

- DTC / AVOD investment should not be “substantial” b/c the Co can leverage existing Fandango video infrastructure and CNBC streaming capabilities

- Incremental spend is mostly marketing / awareness plus bespoke UX design and this is already embedded in the FY26 outlook through modest SG&A and capx increases

- Versant is testing vertical video and launched a new Golf Channel app built for vertical video

- Mgmt said it is working with multiple companies and expects to extend vertical video into other genres

Content Licensing’s Strength In Q1 Was Driven The Kardashian Deal …The Business Will Be Lumpy Qtr-To-Qtr

- Content licensing & Other revs grew +113% y/y to $121mn, driven by the multi-yr licensing of Keeping Up With the Kardashians and other library titles

- Reminder that licensing deals are fully recognized when the content is delivered so Q1 can’t be extrapolated for the full year performance

- The content sales are profitable and generate “very good margins,” although residual costs vary by deal depending on talent participation

- Mgmt is confident in further monetizing its broader library across true crime, unscripted and newly created originals

- Third parties have already reached out about licensing shows the Co is currently creating

The Connectivity Sector Looks Skyward

The connectivity sector was full of notable updates this week, with the major US wireless carriers, satellite operators, and Big Tech all pushing further into space-based connectivity. AT&T, Verizon, and T-Mobile announced plans to launch a JV aimed at reducing cellular dead zones by pooling spectrum to support satellite-based phone service in rural and remote areas. Also, the FCC approved EchoStar’s ~$40bn spectrum sale to SpaceX and AT&T, with the transactions expected to expand 5G coverage, support Starlink’s device-to-device ambitions, and help ensure Boost Mobile’s continued viability through a hybrid MVNO arrangement with AT&T. Lastly, SpaceX and Google are reportedly in talks around orbital data centers, highlighting growing interest in space-based infrastructure despite questions around cost and feasibility versus terrestrial data centers.

See more below…

AT&T, Verizon and T-Mobile Plan To Launch A JV To Help End Dead Zones (link/link)

- The JV is designed to support satellite-based phone svs in cellular dead zones, enabling customers to remain connected in rural and remote areas

- The JV will “pool” the carriers’ spectrum to support the satellite svs, which require radio frequencies to deliver the data; Another key goal is to provide consumers with “greater choice”

- Collectively, satellite svs functions as “supplementary components to the core wireless svs customers depend on”

- The JV is expected to deliver customer benefits across highlighted areas –

- Will help reduce US dead zones and reach previously unserved areas

- Will provide backup connectivity when ground networks are disrupted by natural disasters or other unusual events

- Will give customers more consistent performance and easier access to satellite svs across providers

- The combined investment is expected to improve D2D access, expand provider options, and support new customer experiences

- A unified approach will create more consistent customer experience across the industry

- Additionally, the Cos highlighted Industry benefits –

- Creates more oppties for satellite providers to compete, invest, and grow, while helping rural MNOs bring new products to customers

- Helps MNOs launch new customer svs more quickly

- Helps improve utilization of scarce, nationally licensed spectrum resources

- Will support a standards-based approach across operating systems, apps, and device manufacturers to improve satellite network user experience

- CEO soundbites underscore the JV’s focus on expanding reliable connectivity, reducing dead zones, and strengthening U.S. communications infrastructure

- AT&T CEO John Stankey… the goal is to make staying connected simple “no matter where you are” by accelerating access to “reliable, and always-on coverage everywhere”

- T-Mobile CEO Srini Gopalan… the JV will use expanded satellite capacity to deliver service with “fewer dead zones” and broader direct-to-device experiences

- Verizon CEO Dan Schulman… the partnership is about “building resilient digital infrastructure” and giving customers “more options” while strengthening U.S. infrastructure

–>AT&T, Verizon and T-Mobile stocks were down -0.4%, -0.3% and -1% respectively

The FCC Approved A Sale Of EchoStar Spectrum To SpaceX & AT&T (link/link/link)

- The $40bn sale of wireless spectrum was approved because the move would “boost connectivity across the country”

- The Co is selling ~50 megahertz of its nationwide spectrum to AT&T for its 5G network for $23bn

- 30 MHz of mid-band spectrum

- 20 MHz of low-band spectrum

- Additionally, ~65 megahertz of its spectrum is being sold to SpaceX for $17bn

- The FCC is requiring EchoStar to establish an escrow account of $2.4bn that would cover any amounts that they may owe in connection with disputes over work under the licenses

- The FCC also said it had received comments that EchoStar has indicated it will not pay companies for construction of a new 5G network

- EchoStar is “analyzing this requirement and evaluating next steps”

- The Co is selling ~50 megahertz of its nationwide spectrum to AT&T for its 5G network for $23bn

- AT&T and EchoStar will create a hybrid MVNO (Mobile Virtual Network Operator) arrangement that ensures the continued viability of Boost Mobile

- The FCC also said it is requiring AT&T to build its network “years faster” than the Co originally requested and the FCC’s rules ordinarily require for builds after auction

- AT&T’s low-band spectrum will expand coverage across the US, especially in rural and underserved areas

- SpaceX is gaining access to exclusive-use spectrum for a Starlink device-to-device service and other offerings

- The FCC is also granting waivers for SpaceX to address convergence of wireless and satellite broadband

- The announcement allows SpaceX to use its new spectrum flexibly for terrestrial, space-based and hybrid network architecture

- The FCC is also granting waivers for SpaceX to address convergence of wireless and satellite broadband

- EchoStar said it expects to receive ~$22bn in total from the deal, including up to $11bn in SpaceX stock and ~$2bn in interim financing to cover payments tied to debt through at least Nov. 30, 2027

->EchoStar’s stock was up +2.4% in reaction

SpaceX and Google Are Also Reportedly In Talks To Launch Orbital Data Centers (link/link/link)

- Google was an early SpaceX investor and owned 6.1% of the Co at the end of 2025, per regulatory filings

- The Co is also reportedly talking to other rocket-launch Cos as well

- It also plans to launch prototype satellites by 2027 as part of an initiative called Project Suncatcher, annc’d late last year

- The Co is also reportedly talking to other rocket-launch Cos as well

- Elon Musk has created hype for orbital data centers, claiming they are cheaper to operate

- Advocates also point out that they are free from the local backlash that US ground-based buildouts attract

- However, according to others on the matter, terrestrial data centers are much cheaper than those in orbit once satellite construction and launch costs are factored in

- Andrew McCalip, a space engineer, calculated that a 1 GW orbital data center might cost $42.4bn, ~3x its ground-bound equivalent

->Space stocks jumped higher following the report, with Rocket Lab trading up +6%, Firefly Aerospace up +2%, Voyager Technologies up +15% and Intuitive Machines up +11%

Total Web Usage Continues To Fall Despite Strong Growth In AI Referrals

While AI is driving usage to certain parts of the web, it was not enough (by a long shot) to offset declining overall web usage in 2025 and into Q1. That was our main takeaway after looking at Sensor Tower’s inaugural 2026 State of Web report. Big picture, people are spending more time offline, and more digital time has shifted to mobile apps. Gen AI referrals are growing very quickly, but they still make up less than 1% of total web traffic. Direct visits remain the main way people reach websites. AI related-traffic will certainly continue to grow and Commerce is one of the more interesting areas to watch given some proof points such as Amazon’s Rufus-assisted shoppers converting at nearly 2x the rate of non-Rufus shoppers.

See below for what we thought were the top 6 most interesting stats from the report (the full report can be accessed here).

- Overall web usage ticked down y/y in 2025…and that’s continued into Q1:26

- Total web visits, including desktop and mobile across 56 mkts, fell -1.8% y/y

- Time spent fell even more sharply across those mkts, down ~-5% y/y

- Why is usage falling? In-person activity continues to rebound post-pandemic + mobile apps capture a growing share of digital attention

- Some geographic callouts –

- US, Japan, and Western Europe are all expected to continue to see web time spent drifting downward

- India and Vietnam were the only major mkts to see y/y growth in both visits and time spent in 2025

- Brazil, Indonesia, and South Korea all saw relatively flat web traffic

Source: Sensor Tower

- But there are areas of the web that are seeing incr’d usage…namely, Generative AI websites dominated the top 10 breakout website by visits list

- ChatGPT.com led the way and saw a staggering +60bn visit increase y/y

Source: Sensor Tower

- Gemini and Claude are steadily challenging ChatGPT’s market dominance

- Despite intensifying competition, ChatGPT remains the undisputed leader, commanding a 53% share of total AI time spent as of Mar 2026

- BUT this dominance is increasingly challenged by Gemini and Claude, both of which have maintained a consistent upward trajectory to collectively secure over 35% of the mkt’s engagement

Source: Sensor Tower

- With that said, Generative AI is still a very, very small fraction of website visit traffic

- Direct traffic remains the dominant source of web visits across desktop and mobile

- Although Gen AI referral traffic is growing rapidly, it still represents a very small share of overall web traffic, accounting for just 0.7% of total visits across most websites

Source: Sensor Tower

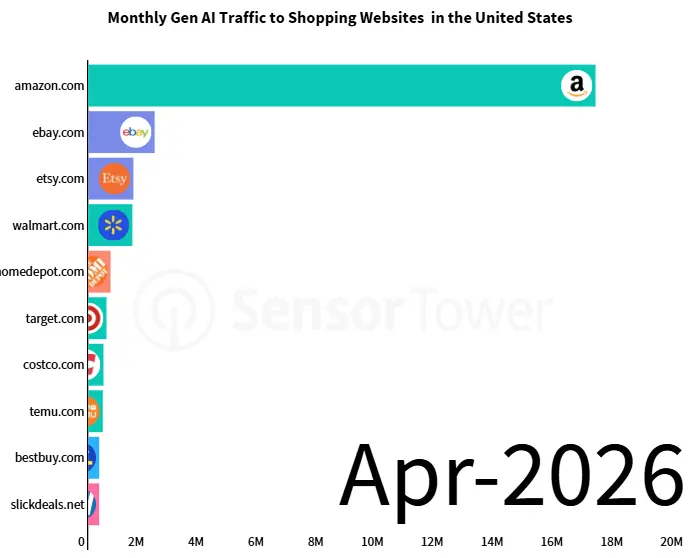

- Amazon leads the small, but growing, race for AI traffic

- By Apr 2026, top shopping websites in the US generated 33mn+ visits from Gen AI sources, up 600%+ from Apr 2023

- BUT despite this rapid growth, AI referrals remain relatively small vs to the 2bn+ visits recorded by the top 100 shopping sites in Apr 2026

Source: Sensor Tower

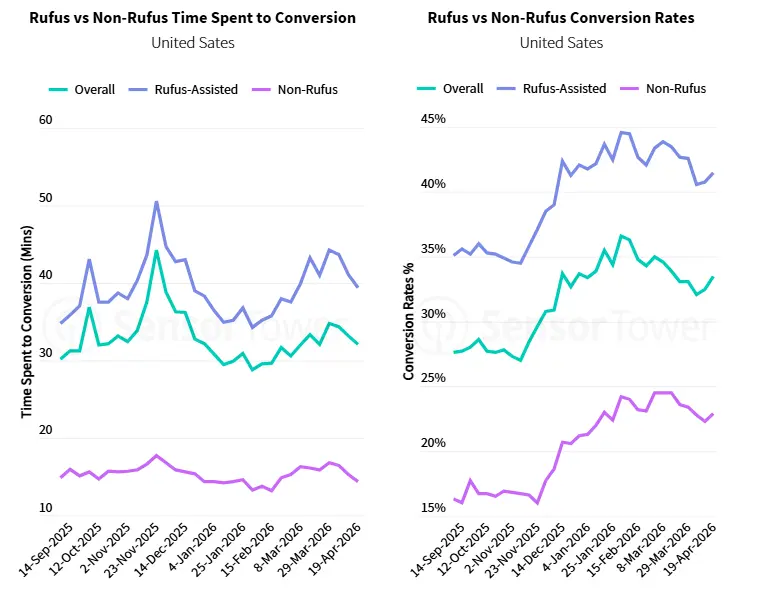

- An interesting AI-assistant callout = Amazon shoppers utilizing Rufus convert at nearly 2x the rate of non-Rufus shoppers

- While Rufus-assisted sessions maintained a conversion rate above 40% throughout Q1 2026, non-Rufus shoppers hovered around 20%, suggesting that the AI effectively reduces purchase hesitation by providing the specific information necessary to finalize a sale

Source: Sensor Tower

Waymo Is Expanding, But Not Without Growing Pains

Waymo has been the robotaxi leader in the US and is now deepening its US robotaxi service coverage in 11 existing markets by 300 square miles to over 1.4k in total (a 27% increase from their estimated square miles coverage as of April).

At the same time, Waymo announced a voluntary recall of ~3,800 robotaxis this week which was tied to a software issue involving flooded roadways, so it has not all been smooth sailing with this burgeoning technology (see the April 8th edition of The Weekly, Theme #8 for some recent bumps in the Asia Robotaxi landscape as well).

See more color below…

Waymo Annc’d Expansion Plans Across Existing US Markets (link/link)…

- Waymo annc’d a major expansion of its autonomous robotaxi svs area, growing to over 1,400 square miles across 11 US cities

- That a 27% increase from the est’d ~1,100 square miles of coverage as of April 2026

- The expansion is about growing the svs area WITHIN cities where they have already proven the model works

- The expansion starts in Miami, with Austin, Atlanta, Houston, and the San Francisco Bay Area up next for deeper coverage

- Waymo now serves over 20mn trips and is still targeting 1mn trips per week by the end of 2026

- The Co expanded to 10 US cities in Februaryand has laid the groundwork for 20+ cities, including its first international markets in London and Tokyo

…BUT Their Growth Is Not Without Growing Pains (link/link)

- The Co also this week recalled ~3,800 robotaxis in the US to fix a software issue that could allow vehicles to drive onto flooded roads

- AVs in Austin, Texas were recently seen on camera driving onto a flooded street and stalling

- Similar incidents have occurred in other locations

- Per a Co statement on Tuesday… it’s “identified an area of improvement regarding untraversable flooded lanes specific to higher-speed roadways,” and opted to file a “voluntary software recall” with the NHTSA

- The Co added that it’s working on “additional software safeguards” and has put “mitigations” in place, limiting where its robotaxis operate during extreme weather, so that they avoid “areas where flash flooding might occur” in periods of intense rain

- The voluntary recall is for Waymo vehicles that use the Co’s fifth and sixth generation automated driving systems (or ADS)

Google’s Android I/O Edition Provided A Sneak Peak To The Real I/O Event Next Week

Google I/O is still a week away, but the Co already started making announcements with The Android Show: I/O Edition. The Android-focused presentation previewed several updates across Google’s ecosystem, from new Gemini-powered Android features to expanded integrations for creators and even new hardware. One of the biggest reveals was the Googlebook. It was described as a laptop “designed from the ground up for Gemini Intelligence,” Googlebook is not intended to replace Chromebooks. Instead, it appears to be built around AI-first workflows, with Gemini helping users handle more complex tasks.

Speaking of Gemini Intelligence, it’s set to transform the Android experience in several ways. For example, you’ll be able to create widgets on your phone to meet your exact needs. It’s also being integrated into Android Auto, where you can perform complex tasks by simply speaking. Lastly, Google announced another key integration with Instagram that will make content creation even better with Android phones.

See more of the need to knows below…

->Alphabet’s stock was up +4% on the day of the event and is up +25.3% YTD

Highlighted Releases At The Google’s Android Show: I/O Edition (link/link/link)

- A big announcement was Google’s Googlebook, a new line of laptops built around Gemini Intelligence

- Development partners including Acer, Asus, Dell, HP, and Lenovo

- It is expected to launch this fall in multiple shapes and sizes

- Key features include:

- “Magic Pointer”, a new cursor with Gemini built in

- Android phone compatibility, allowing users to run phone apps from their Googlebook

- Custom widget creation

Source: TechCrunch

- Gemini expands across Android w/ agentic actions, Chrome integration, form filling, and smarter dictation

- Gemini Intelligence will be able to take information from one app and perform multistep actions across other apps

- Use cases include taking a photo of an event flyer and asking Gemini to find the event on sites like Expedia

- Gemini in Chrome will also come to Android

- Users will be able to summarize web pages or ask questions about what they are viewing

- Users also get an experimental auto-browse feature, which can navigate websites and complete tasks, such as booking a ticket, on the user’s behalf

- Gemini will help users fill out forms on mobile

- The feature will use data from Personal Intelligence

- It will be available through an opt-in feature

- The Co intro’d a new Gboard (the Co’s keyboard app) feature called Rambler

- Rambler turns speech into cleaned-up text, removing filler words such as “um” and “ah”

- It can also understand corrections in speech, such as “Let’s meet at 3 p.m. … um, 2 p.m.” and posts “Let’s meet at 2 p.m.”

- Gemini Intelligence will be able to take information from one app and perform multistep actions across other apps

- Android Auto is being redesigned with a more personalized interface

- Updates include:

- New widgets that can appear alongside navigation

- New designs that adapt to different car screen shapes and sizes

- Supported cars will be able to play YouTube videos in 60 fps full HD later this year

- Launch partners include BMW, Ford, Genesis, Hyundai, Kia, Mahindra, Mercedes-Benz, Renault, Škoda, Tata, and Volvo

- Gemini is rolling out broadly on Android Auto, enabling hands-free questions, brainstorming, learning, and food ordering, starting with DoorDash

- Updates include:

Source: TechCrunch

- The Co rolled out new Android Creator Tools

- Android is launching Screen Reactions, which records the user and their screen at the same time

- The format is designed for social-style content, similar to TikTok and Instagram Reels

- Screen Reactions will first roll out on Pixel devices this summer

- The Co partnered with Meta to improve Instagram on Android

- Improvements include:

- Ultra HDR, native stabilization, night mode and better photo and video quality from capture to upload

- Android is also getting exclusive tools in Meta’s Edits app, including:

- Smart enhance for photo upscaling and sound separation to boost or remove sounds

- Google annc’d Create My Widget, a feature that lets users create custom Android widgets using natural language

- Users can describe what they want, and Android will generate a widget for the home screen

- Example: Asking for “three high-protein meal prep recipes every week” could create a personalized recipe dashboard

- The Co refreshed all ~4,000 Android emojis, calling it 3D Emoji

- Continuing to expand Quick Share’s compatibility with Apple’s AirDrop

- Last year, Pixel phones gained the ability to share files with iPhones through Quick Share/AirDrop support

- This year, the feature will expand to more Android manufacturers, including:

- Samsung, Oppo, OnePlus, Vivo, Xiaomi and Honor

- Users without a compatible device will be able to generate a QR code through Quick Share to send files to an iPhone via the cloud

- Quick Share will also become available inside apps such as WhatsApp

- Introduced a new transfer flow for users switching from iPhone to Android

- Users will be able to import passwords, photos, messages, favorite apps, contacts, eSIM and home screen layout

- The feature will launch on Samsung Galaxy and Google Pixel devices this year

- Annc’d Pause Point, a feature designed to reduce distracting app usage

- When opening an app marked as distracting, users will see a 10-second pause before entering the app

- During that pause, Android will suggest alternative actions, such as opening Google Play Books to read

- Users can also set a timer to limit how long they spend in the distracting app

- Expanding default-on theft protections to Android users globally

- They will be enabled by default on: New Android 17 devices, freshly reset devices and devices upgraded to the latest OS

- Key theft-protection features include things like Remote Lock, Theft Detection Lock, fewer PIN/password guessing attempts and longer wait times between failed unlock attempts

- Law enforcement will be able to access a device’s IMEI from the lock screen on Android 12 and higher to help verify stolen devices

- Theft protections will also expand to Android 10+ devices in select markets, including:

- Argentina, Chile, Colombia, Mexico and the UK

Source: TechCrunch

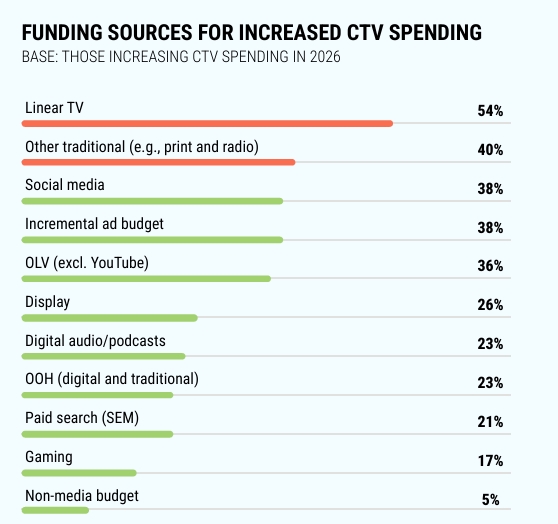

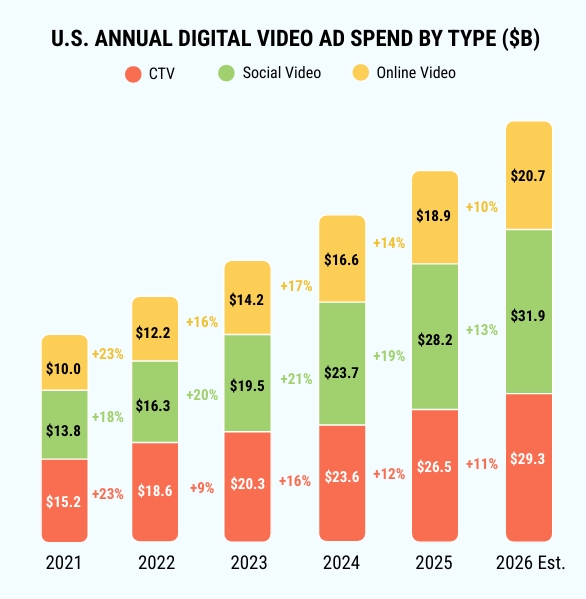

US Digital Video Ad Spend Is Projected To Grow +11% Y/Y In 2026

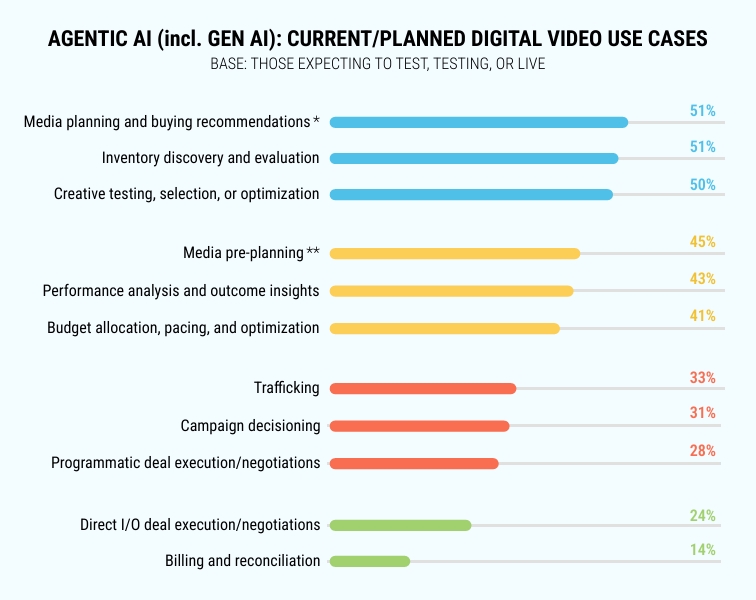

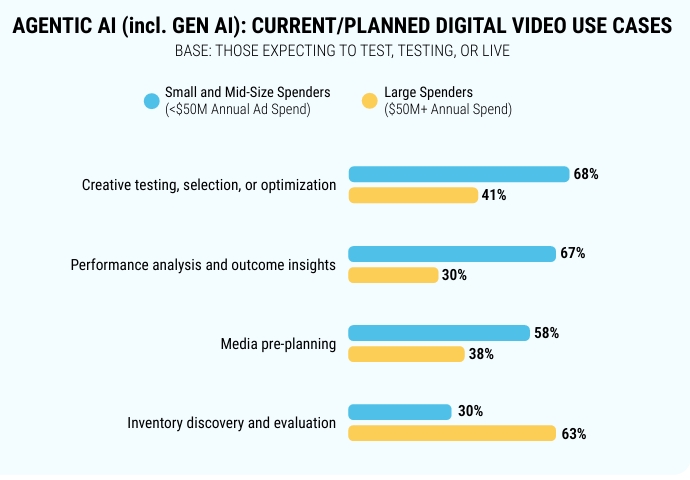

We took a look at IAB’s 2026 Digital Videos Ad Spend & Strategy – PART 1 report this week, which was centered around US market size and growth projections. Our top 5 takeaways of what was most interesting from the report are: 1) US digital video ad spending will reach ~$82bn this year, up +11% y/y; 2) CPG and retail continue to lead digital ad spend, followed by tech, pharma, and entertainment, while Auto is the only category to decline; 3) Digital video is expected to account for more than 60% of total TV and video ad spending for the first time; 4) Overall, social video ad spend overtook CTV in 2025 and will likely extend that lead in 2026, with social video rising +7% y/y to lead all formats as a “must-buy,” while CTV declined -7% y/y; and 5) Small-to-mid-size advertisers are leaning into agentic AI for execution-heavy use cases, as they often lack the infrastructure these tools replicate, while larger spenders are focusing on inventory discovery and evaluation.

To see the full slide deck, click HERE…but our main takeaways are below.

-> Separately but also related to digital advertising, it was disclosed this week that Netflix’s ad-supported tier reached 250mn monthly users …which is up substantially from 94mn in 2025 and 70mn in 2024; Netflix will also launch the ad-supported plan in 15 more countries next year (link)

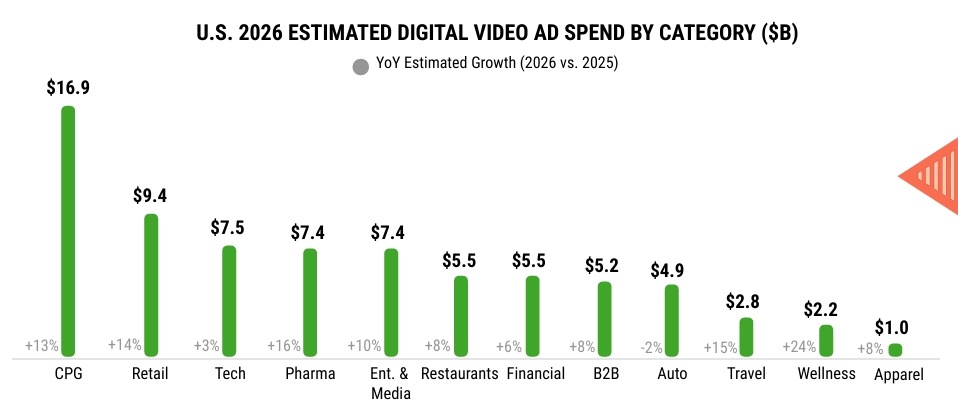

Digital Video Ad Spend Is Est’d To Grow +11% y/y In 2026 & Exceed 61% Of Total TV/Video Ad Spend

- Digital video ad spend is projected to hit $81.9bn, up +11% y/y in 2026 vs $73.6bn, up +15% y/y in 2025

- Growth is roughly half its 2022 peak as the market normalizes from the post-COVID acceleration

- CPG and retail continue to lead investment, followed by tech, pharma, and entertainment

- Auto is the lone exception, declining -2% y/y amid elevated prices and interest rates, a softening job outlook, and tariff pressures

Source: IAB Report

- Digital video is projected to account for 61% of the total TV/video ad spend in 2026 vs 58% in 2025 and 51% in 2024

- It will continue expanding in 2026 despite major cyclical events, incl. the Olympics, World Cup, and midterm elections, which typically anchors spend in linear

- Further accelerating the shift is that these major events are becoming more widely available on streaming platforms

- There is greater investment from small spenders as the number of them investing in CTV has increased from 60% in 2024 to 85% in 2026 with self-serve platforms lowering the entry barrier

Source: IAB Report

- BUT… overall, social video ad spend overtook CTV in 2025 and will likely extend that lead in 2026

- Compared to 2025, social video ad spend rose +7% y/y to lead all formats as a “must-buy”, while CTV declined -7% y/y

Source: IAB Report

Agentic AI Is Making Inroads With Respect To Digital Video Advertising, But In Different Ways

- 2 out of 3 buyers are already live, testing, or planning to use agentic AI for digital video campaigns

- When factoring in the ~28% who are “actively investigating”, nearly all buyers in the market are on a near-term path to adopting agentic AI

- Agentic AI adoption is currently centered on decision support rather than the purchase decision itself

- Agentic AI adoption is concentrated in internal-facing workflows (planning, inventory discovery, and creative optimization)

- AI usage declines as processes become more external facing

Source: IAB Report

- Small-to-mid-size spenders are using agentic AI in different ways than large spenders

- Small-to-mid-size spenders are using agentic AI for execution-heavy use cases as they often lack the infrastructure that these tools replicate

- Larger spenders, by contrast, are using AI for inventory discovery and evaluation

Source: IAB Report

Grab Bag: eBay Rejects GME’s Takeover Proposal / TikTok Expands Into Experiences / GTA 6 Pre-Orders Next Week?

- eBay rejected GameStop’s $56bn takeover proposal, calling the unsolicited bid “neither credible nor attractive” (link/link/link)

- As a reminder: GameStop CEO Ryan Cohen last week unveiled a bid for eBay, offering to acquire the online marketplace for $125 per share in a cash-and-stock deal

- They had a $20bn financing commitment from TD Securities and have ~$9bn in cash on hand

- Paul Pressler, the chairman of eBay’s board, wrote in a letter “The Board has thoroughly reviewed your proposal and has determined to reject it” highlighting 6 factors…

- eBay’s standalone prospects

- Uncertainty regarding the financing proposal

- The impact of the proposal on eBay’s long-term growth and profitability

- Leverage, operational risks, and leadership structure of a combined entity

- Resulting implications of these factors on valuation

- GameStop’s governance and executive incentives

- The financing letter, also released by eBay, stated that TD’s offer assumes that the combined Co maintains an investment-grade creditprofile from at least 2 of the top 3 ratings agencies

- Moody’s Ratings said last week that the acquisition would be “credit negative” for eBay because of the substantial increase in leverage implied by the deal structure

- As a reminder: GameStop CEO Ryan Cohen last week unveiled a bid for eBay, offering to acquire the online marketplace for $125 per share in a cash-and-stock deal

- TikTok is broadening its app to include experiences…TikTok GO is a new way for people in the US to discover and book local services, including hotels, attractions, and tours, directly on TikTok (link/link)

- TikTok GO surfaces lodging and things to do across videos, search, and location pages

- When users find something, they like, they can view details, check availability, and complete a booking in just a few simple steps

- Partners include Booking.com, Expedia, Viator, GetYourGuide, Tiqets, and Trip.com

- Users must be at least 18 years old to book an experience

- GTA 6 pre-orders to open next week, according to Best Buy leak (link/link)

- Early on Thur. morning a Best Buy email was sent out to select people

- YouTuber Frogboyx1Gaming was the first to report the supposed email, even going live on stream to show it

- According to his screenshot, the Best Buy promotion reads:

- GTA 6 Pre Order (Physical Game)

- Duration: May 18, 2026 – May 21, 2026

- Online Sale: 5%

- Several other people within the Best Buy affiliate program also provided screenshots from the same email that they received

- There is also speculation that the 3rd trailer for GTA 6 will be released alongside the pre-order

–>Take-Two’s stock was up +5% in reaction to the news

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Meta is forecast to generate ~$240bn in ad rev in 2026, up 22. 3% YoY, per WARC, after reaching $196bn in 2025. AI-driven tools boosted impressions 19% and prices 12%, improving returns and lowering costs. Facebook will drive 60% of rev. Heavy AI spend (~$600bn by 2028) supports growth, though user growth has plateaued, raising investor concerns. (MediaPost)

- YouTube is stepping up efforts to connect creators w/ sponsors, aiming to retain talent amid competition from Netflix and TikTok. Instead of only sharing ad rev after hits, the Co now helps secure funding before launch. Creator Kareem Rahma expanded to YouTube, gaining support for a new show and chances to pitch it to advertisers at a major event, boosting production ambitions. (The New York Times)

Artificial Intelligence/Machine Learning

- Verizon annc’d it joined Anthropic’s Project Glasswing to boost AI‑driven cybersecurity, testing Claude Mythos Preview to detect complex vulnerabilities in critical infrastructure. The Co says the partnership enhances its ability to secure networks, share cross‑industry insights, and maintain high safety standards while evaluating emerging tech w/ strict oversight. (Verizon)

- China is seeing a reverse brain drain as “sea turtles” return from U. S. tech firms, boosting Beijing’s push in AI and advanced tech. Headhunters target talent from firms like Meta and Google, offering pay matching or exceeding Silicon Valley despite lower costs. Fierce global competition has driven soaring salaries, as China seeks to challenge U.S. dominance in key tech sectors. (Wall Street Journal)

- Apple’s partnership w/ OpenAI has frayed as the AI Co weighs possible legal action over alleged contract breaches. OpenAI claims Apple limited ChatGPT integration and failed to drive subscriptions despite expectations of deeper Siri and system use. Tensions add to broader tech rifts, w/ privacy concerns and device ambitions also straining ties, though talks may still resolve without court. (Yahoo Finance)

- Pershing Square, led by Bill Ackman, annc’d a new Microsoft stake, calling it a bargain as mkts underprice AI upside. The fund began buying shares in Feb. amid weakness after softer cloud rev and rising capex. Ackman sees Azure and M365 (w/ Copilot) driving enterprise AI growth. He said ~$190bn 2026 spend will boost future rev, while competition fears are overstated. (Yahoo Finance)

- SoftBank annc’d a ~$46bn Vision Fund gain for FY ended Mar. , largely driven by surging value of its >$30bn OpenAI stake, which delivered ~$45bn in gains; quarterly gains hit $20bn, mostly from OpenAI. Losses in holdings like Coupang, DiDi and Klarna weighed on performance, while rising exposure raised debt concerns and led S&P to shift outlook to negative amid heavy AI-focused strategy. (CNBC)

- Meta annc’d an “incognito” mode for AI chats on WhatsApp, enabling private sessions processed in a secure environment. Messages aren’t saved, disappear on exit, and lose context once closed or device locked. The feature uses Meta’s latest model and will roll out over coming months, expanding prior privacy-focused AI infra amid rising concerns over sensitive data use. (TechCrunch)

- Musk’s xAI is pushing Wall Street firms to adopt its Grok chatbot to boost rev ahead of SpaceX’s IPO. Cos like Morgan Stanley and Apollo are testing it, though usage remains limited. xAI relies heavily on Musk-linked deals and trails rivals in finance tech. Burning ~ $1bn monthly, it is expanding sales and leveraging ties, even as leadership shifts with its CRO moving to an advisory role. (Yahoo Finance)

- Apple explored allowing AI agent apps on App Store, aiming to balance new AI-driven features w/ strict security rules. It had blocked some “vibe coding” apps that self-modify code. AI agents pose risks, incl. unintended actions. Apple is also upgrading Siri w/ AI, partnering w/ firms like Google, while discussing integrations w/ devs amid concerns over future fees. (MacRumors)

- Cerebras priced its IPO above range, raising $5. 55bn at $185/share, valuing the Co at ~$56.4bn. The AI chipmaker’s debut signals strong demand amid a broader chip rally. The Co is shifting toward cloud svs while reducing reliance on key customers, and faces competition from major tech players. CEO stake ~ $1.9bn, w/ backing from major investors. (CNBC)

- OpenAI could save ~$97bn by 2030 after renegotiating its Microsoft deal, cutting rev share from 20% to ~8–10% w/ caps on payouts. The new terms remove AGI-linked payment spikes and end Azure exclusivity, letting OpenAI use AWS/Google Cloud. Microsoft retains 27% stake, IP access to 2032, while OpenAI plans potential IPO. (MSN)

- Anthropic is in early talks to raise at least $30bn at a valuation above $900bn, w/ round possibly closing by end‑ May. The deal isn’t final. The Co is seeking funds amid heavy spending on AI compute infra and may pursue an IPO as soon as Oct. Google and Amazon have pledged major investments, while prior cloud deals commit over $300bn for long‑term capacity. (Tech in Asia)

- OpenAI annc’d it will give the EU access to GPT-5. 5-Cyber, rolling out the cyber model in limited preview to vetted security teams. EU businesses, governments and the AI Office will review deployment to address safety concerns. OpenAI said the step supports shared cyber defense via its EU Cyber Action Plan. (CNBC)

- Microsoft CEO Satya Nadella testified in the Musk v. Altman OpenAI trial, saying Elon Musk never raised concerns to him about Microsoft deals. Nadella detailed the cos strategic partnership, said investments were commercial, not donations, and cited discounted computing w/ marketing benefits. Microsoft has invested ~$13bn since 2019; execs said ~$9.5bn rev recognized by Mar. 2025. (CNBC)

- Elon Musk’s AI model Grok is falling behind faster-growing rivals, raising doubts about its ability to catch up. Grok, released in late 2023 and integrated into X, reached mn users but growth has flattened. Adoption slowed as parent SpaceX annc’d a deal in early May to rent all computing capacity at a key data center to Anthropic, highlighting intense competition for scarce AI computing power. (The Wall Street Journal)

- AI chipmaker Cerebras Systems Inc. upsized its US IPO, seeking up to $4.8bn as demand builds, per filings annc’d. The Co plans to sell 30mn shares at $150–$160, vs 28mn at $115–$125, valuing it at ~$34.4bn. Orders exceed supply by >20x, w/ pricing set for May 13. It may be the largest US listing this yr. (Yahoo Finance)

Audio/Music/Podcast

- Spotify annc’d it will adopt Apple’s HLS tech for video podcasts, enabling creators to distribute shows across Apple Podcasts and Spotify w/o changing setups. The move supports cross-platform reach and future monetization on Apple’s platform. Spotify also expanded video support via partners like Libsyn and Audioboom, boosting distribution and rev options, w/ further monetization tools planned later this yr. (9to5Mac)

- Spotify annc’d a limited-time feature marking its 20th yr that extends its Wrapped recap across users’ full listening history. It highlights join date, first song, favorite artists, and total unique tracks, plus a playlist of top 120 songs w/ play counts. Users can share stats like Wrapped. Available globally for ~6 weeks, it builds on Wrapped’s strong engagement driving user activity. (TechCrunch)

Capital Market Updates

- Anduril, a defense tech Co, annc’d raising $5bn, valuing it at $61bn, up from $30. 5bn a yr earlier. Backed by Thrive Capital and Andreessen Horowitz, total funding reached $6.82bn. Founded in 2017, it builds A.I.-driven weapons incl. drones, subs, and AR helmets, expanding from border surveillance into battlefield tech amid U.S. military modernization push. (The New York Times)

- ServiceNow Inc. seeks to raise about $4bn via a potential US high-grade bond sale being considered, linked to the software Co’s recent acquisitions. Barclays Plc, Citigroup Inc., JPMorgan Chase & Co. and Wells Fargo & Co. arranged investor calls on Mon., people w/ knowledge said, requesting anonymity because they’re not authorized to speak publicly. (Bloomberg)

- Alphabet plans its first yen bond sale to widen funding as AI competition lifts spending. The Google parent raised its 2026 capex outlook to ~$190bn and has issued euro, Canadian dollar, sterling and Swiss franc notes, raising ~$17bn recently. Analysts say strong demand gives low‑cost capital as total debt topped $100bn. (Yahoo Finance)

- Amazon annc’d its debut Swiss franc bond sale, launching six tranches due in 3–25 yrs to raise at least CHF1. 9bn (~$2.4bn). The deal shows Big Tech tapping non‑US mkts to fund heavy AI spending, w/ strong demand seen in recent euro issues. Amazon plans ~$200bn of 2026 capex within ~$725bn forecast by peers, though some investors worry AI rev may lag. (Yahoo Finance)

- Verizon Communications Co has raised ~$12bn via global hybrid bond sales over ~6 months to support investment‑grade ratings and cut leverage after its Frontier Communications deal. The debut US dollar tranche follows euro, sterling and A$ issues. Proceeds fund general corporate purposes incl. debt repayment and buybacks, while hybrids gain equity treatment to help keep ~BBB+ ratings, analysts say. (Yahoo Finance)

Cloud/DataCenters/IT Infrastructure

- A Gallup survey found 70% of Americans oppose data centers in their communities, w/ nearly half strongly against them. Resistance spans both parties but is higher among Democrats. Concerns are so strong that more respondents prefer living near nuclear plants. The findings highlight growing backlash as data centers expand to support rising AI-driven demand. (Washington Post)

- Cisco reported Q3 results above expectations, w/ adj EPS $1. 06 and rev $15.84bn, up 12% YoY. Net income rose to $3.37bn. Shares jumped ~15% as AI-driven orders hit $5.3bn YTD, w/ FY outlook raised. Networking rev climbed 25%. Co also annc’d <4,000 job cuts (<5% staff) amid cost shifts toward AI, booking ~$1bn charges. (CNBC)

Crypto/Blockchain/web3/NFTs

- Ledger, a French crypto hardware wallet Co, is delaying its planned U. S. IPO due to unfavorable mkts and weak investor appetite for crypto listings, per CoinDesk. The Co is reassessing plans and hasn’t filed an S-1. CEO earlier weighed a NY IPO or private funding in 2026. Reports cited a potential $4bn listing w/ banks. (Yahoo Finance)

- Circle Internet Group annc’d it raised $222mn in a presale of Arc, the native token for its new Arc blockchain, valuing the network at ~$3bn. The funding, led by a16z w/ backing from BlackRock, Apollo and others, supports Circle’s expansion beyond USDC into blockchain “operating system” and app biz. Shares rose ~16% despite Q1 rev missing estimates. (CNBC)

eCommerce/Social Commerce/Retail

- Thrive Capital, led by Joshua Kushner, has taken a ~$100mn stake in Shopify, marking a rare bet on a public Co. The firm, known for backing startups like OpenAI, framed the investment as a play on AI-driven gains in e-commerce. The move signals confidence in tech’s growing role in commerce and Shopify’s long-term growth potential. (Bloomberg)

- Ryan Cohen urged eBay’s board not to dismiss his ~$56bn takeover bid, saying shareholders deserve a say. After eBay rejected the $125/share offer as not credible, Cohen signaled he may cont’d pursuing the deal, citing possible next steps. He criticized mgmt pay and strategy, while highlighting plans to cut costs and run the combined Co. Analysts note financing and scale challenges. (Reuters)

- Burberry Co reported better-than-exp sales growth, w/ like-for-like up 2% yr, signaling CEO Joshua Schulman’s turnaround—focused on core scarves & trench coats—is gaining traction. However, a cautious outlook citing geopolitical & econ uncertainty hit sentiment, sending shares down ~6.7%. Growth in China (+10%) offset weaker Europe/Middle East sales amid conflict impacts. (Business of Fashion)

- Alibaba shares rose as Co struck bullish tone on AI despite core adj profit plunging 84% YoY to ~$751mn, hit by heavy tech, cloud, and quick commerce investment. Cloud rev jumped 38% to ~¥41.6bn, driven by AI demand, w/ strong growth in AI-related svs. China e-commerce rev rose 6%, while quick commerce surged 57%, underscoring long-term growth bets despite near-term margin pressure. (CNBC)

- Walmart laying off or relocating ~1,000 tech/product staff as part of global restructure, per May 13 memo. Roles shifting to Bentonville & N. California, w/ some cuts and team consolidation to reduce duplication and clarify ownership. Move supports Co’s globalization push, not tied to AI. (Retail Dive)

- Rent the Runway co-founder Jennifer Hyman said she will step down as CEO, president, and board member after ~18 yrs, staying as adviser until Jan. Nordstrom veteran Teri Bariquit becomes interim CEO. Hyman said the Co is in its strongest position, w/ momentum driven by its marketplace, media, and B2B svs, despite long-term profitability struggles since launch. (Retail Dive)

- On reported record Q1 net sales of $1.06bn, up 14.5%, marking first time topping 800mn Swiss francs. Growth was led by Asia-Pacific (+44%) and EMEA (+23%), while Americas rose ~3%. DTC rev climbed 16.4% vs wholesale 13.3%, lifting gross margin to 64.2%. Net income jumped 82.2%. Apparel rev surged 45.1%, footwear +12%. Co raised outlook despite tariff headwinds. (Retail Dive)

- Birkenstock shares fell ~13% after the Co warned of rising costs from US tariffs and Middle East conflict, which disrupted shipments and cut €6mn from EMEA. Q2 rev missed estimates at €618.3mn, w/ margins hit by FX and tariffs. Despite slower demand, the Co maintained FY outlook, expecting 13–15% sales growth, w/ tariffs to pressure H2 margins. (Reuters)

- Amazon annc’d “Amazon Now,” a fast delivery svs offering fresh groceries and essentials in 30 minutes or less, now available to millions across cities like Atlanta, Dallas–Fort Worth, Philadelphia, and Seattle, w/ rapid expansion planned. The svs features thousands of items, 24/7 availability in most areas, and leverages local fulfillment hubs. (Amazon)

Electric & Autonomous Vehicles

- Ford stock jumped ~19% over two days by Thu. , May 14 as investors bet on its AI-adjacent energy storage biz. Morgan Stanley highlighted its $2bn battery ESS push and CATL partnership as a competitive edge, valuing the unit near $10bn. Growth tied to data center demand could drive strong expansion, though the biz may not post positive EBIT until 2028 despite high projected growth. (Yahoo Finance)

Film/Studio/Content/IP/Talent

- Paramount Skydance defended its $110bn bid for Warner Bros. in a May 7 letter to California’s AG amid a probe and industry backlash. It pledged ~30 films/yr w/ 45-day theatrical runs, countering fears of cuts and streaming shifts. Critics warn the deal could reduce output, despite Paramount arguing wider distribution will boost competition. (Yahoo Finance)

FinTech/InsurTech/Payments

- Klarna reported Q1 rev up 44% to $1. 01bn as it shifts toward long-term, big-ticket loans. BNPL demand remained strong, w/ gross merchandise volumes rising 29%, driven by short-term, mid-tier purchases. (Wall Street Journal)

- Robinhood is preparing a second venture IPO (RVII) after its first fund surged from $21 to $43. 69 post‑ debut, driven by AI enthusiasm. Unlike the first fund focused on late-stage firms, RVII will target early- and growth-stage startups, offering higher risk/reward. The move aims to expand retail access to private mkts, letting non‑accredited investors invest in startups w/ daily liquidity. (TechCrunch)

M&A

- Comcast’s Sky advanced talks to acquire ITV’s Media & Entertainment unit for ~£1. 6bn, w/ ~£200mn earn‑out tied to performance. Deal aims to build a top‑3 UK streamer amid weak ad mkts. ITV Studios would buy a Sky production unit, retain IP, and operate standalone. Talks cont’d despite volatility; agreement could be annc’d soon, though risk of no deal remains. (Reuters)

- Bharti Airtel will raise its stake in Airtel Africa via a $2. 9bn share swap ahead of a planned IPO of its mobile-money biz. Board approved issuing up to 146.8mn shares to group Co Indian Continent Investment on a preferential basis, exchanging them for a 16.3% stake in the UK-listed unit, per filing. (Bloomberg)

- Arm and parent SoftBank explored a preliminary bid to acquire AI chip Co Cerebras Systems weeks before its planned IPO, but talks were rejected. Cerebras is targeting a ~$34bn valuation, w/ strong investor demand driving pricing above range and ~30mn shares raising ~$4.8bn. The listing tests appetite for AI chips beyond Nvidia, as SoftBank cont’d pushing into chipmaking and Arm expands its own chip biz. (Yahoo Finance)

Macro Updates

- U.S. retail sales rose ~7% YoY in Apr., per Commerce Dept data tracked by Retail Dive, w/ gains across several core segments incl. nonstore and select discretionary categories. Growth reflects resilient consumer demand, though results vary by sector. Analysts remain cautious as elevated gas prices could pressure spending ahead, potentially weighing on future retail momentum. (Retail Dive)

- Kevin Warsh won Senate confirmation as Fed chair in a close 54‑45 vote, replacing Jerome Powell. Backed by President Trump, Warsh is expected to favor lower rates despite persistent inflation pressures complicating cuts. A longtime critic of Fed policy, he previously served 2006–11 and has called for major changes. (CNBC)

- U.S. CPI likely rose 0.6% in Apr., pushing yr inflation to ~3.7%, highest since Sept. 2023, driven by Iran war-led oil surge lifting fuel costs. Core CPI seen up ~0.3%, boosted partly by one-time rent adj. Rising prices may keep Fed rates steady into 2027, w/ political pressure mounting as consumers face higher fuel & food costs. (Reuters)

- Consumer prices rose last month by the most in three yrs, signaling mounting inflation pressures. Electricity costs surged 6.1% YoY, far outpacing the overall CPI, which climbed 3.8%, the highest since May 2023, per Bureau of Labor Statistics data annc’d Tue. The sharp increase highlights intensifying tensions between utilities, consumers, and power grids over rising energy costs. (Bloomberg)

- Rising prices for gas, groceries and electricity are pushing even seemingly stable households into deeper reliance on credit. The article profiles Alex Watts, an Ohio hospital nurse raising three children and earning ~$140,000/yr, who w/ his wife is cutting driving and savings as monthly expenses exceed income and card balances grow. (The New York Times)

- Gallup data cited by Axios shows the U. S. has the world’s widest generational job-market optimism gap. Just 43% of ages 15–34 said it was a good time to find work in 2025 vs 64% of those 55+, a 21-pt gap. Younger Americans rank 87th of 141 nations. Axios reports pessimism is linked to AI cutting entry-level roles, intense competition, and surveys of ~1,000 respondents per country conducted Mar.–Dec. 2025. (Axios)

Media Conglomerates