The wait is FINALLY over! The -50bps interest rate cut was the main event and comes after much debate all year. Data that I have seen points to expectations of a further -50bps drop in the benchmark borrowing rate this year and another -100bps worth of cuts in 2025. Investors have been getting comfortable with a soft-landing scenario, and the S&P (+1.4% this week) and the Dow (+1.6%) both hit all-time highs, while Nasdaq also rallied in step (+1.5%).

Within the sector, it was a heavy week for investor days with Universal Music Group, Electronic Arts, and T-Mobile US all showcasing updated strategic visions and providing new guidance for shareholders and analysts. Overall, we focused on the below key themes, developments, and updates in this edition (all links are clickable):

- UMG’s Unveils Its Multi-Faceted Growth Strategy In The Evolving Music Sector

- EA Declares That Gen AI Is Poised To Drive “Another Tectonic Shift” In The Interactive Entertainment Industry

- T-Mobile’s Next Chapter – “Challenger to Champion”

- Some Key Callouts From The Connectivity Corner

- Snap Is Going All In On “Chatting, Snapping, And Watching Entertaining Videos”

- FX Takes The Top Spot At The Emmys

- Corporate Restructurings Across The TMT Circuit – WMG, Paramount, And Amazon

- Grab Bag: Walmart Offering Instant Bank Payments/Microsoft’s New Buyback Program/MAGNA Raises 2024 US Ad Growth Estimates

Hope you have a nice weekend.

Best,

Leslie

UMG’s Unveils Its Multi-Faceted Growth Strategy In The Evolving Music Sector

Coming off a tough last qtr where Universal Music Group (UMG) negatively surprised, with slower than expected subscription streaming revenue growth due to the mix shift to DSPs (despite Spotify having better-than-expected results and Warner Music Group reporting strong results), UMG’s Capital Markets Day (which was one of many Investor events this week!) was squarely focused on engendering support and confidence in the long-term growth trajectory for the company.

UMG’s new mid-term growth targets point to at least +7% total revenue growth on a compounded basis through 2028 (including +8-10% subscription streaming revenue growth) and +10% adj. EBITDA CAGR during the period. Integral to the plan is balancing continued subscriber growth with improved monetization through price increases, the super-premium tier, and also improved monetization of ad supported tiers. There has been some investor debate about the magnitude of runway left for subscriber growth, especially in developed markets, though mgmt. refuted these concerns with estimates from internal research efforts. But regardless, penetrating its “high potential markets” (such as China and India) will be a big component of the subscriber growth strategy and will consist of both organic and inorganic growth. Big picture as it relates to streaming, UMG sees the industry moving from Streaming 1.0, which was achieving scale and a focus on subs growth, to Streaming 2.0, which emphasizes innovation, customer segmentation, and ARPU growth.

UMG compared the evolution of music streaming to that of SVOD, where market segmentation and product tiering, enhanced premium features, and improved account sharing has helped to propel growth. As we’ve heard from many players in the music ecosystem for some time, UMG believes that music, in general, is still significantly under-monetized relative to other forms of entertainment. The avg US monthly household SVOD spend of ~$61 is 4x that of music spend.

UMG sees long-term growth opportunities from superfans, direct-to-consumer (D2C) products, and new revenue streams like music in gaming, fitness, health, and wellness. See below for more details.

-> UMG shares were down -1.0% in reaction to the event and finished the week down -3.6%; YTD, UMG stock is down -11.9%, which compares to WMG stock trading -14.9% lower and Spotify stock trading +94.3% higher

-> Separately but also in Music, Warner Music Group announced a revised strategic restructuring plan this week… See Theme #7 for more color

UMG Sets Forth Mid Term CAGR Guidance Through 2028

- Total revenue CAGR of over +7% through 2028 (does not include M&A)

- Scaling SuperFan business

- Penetrating high potential markets

- Reinvesting in the business

- Subscription rev CAGR +8-10% through 2028

- Cont’d subscriber growth

- Improved monetization from price increases & segmentation

- Adj EBITDA CAGR of +10% through 2028

- Full implementation of operational redesign

- Improvements in operating leverage

- FCF before investment conversion ratio of 60%-70%

- UMG is committed to paying a significant dividend while maintaining financial flexibility for further investment

Future Growth Will Be Balanced Across Both Subscriber Additions & Improved Monetization

- Subs penetration will be driven by:

- Demographic tailwinds

- Tech & streaming adoption in high potential mkts

- Streaming innovation and value enhancement

- Ad supported migration to paid

- Monetization will be driven by:

- Price increases aligned with value

- Price increases have been dramatically below inflation

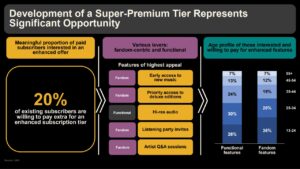

- Very bullish on the Super-Premium tier

- The Co is in advanced talks with Spotify about what the Super-Premium tier will look like

- Believe that 20% of paid subscribers would be interested in paying for a premium tier

- 20% to 30% of music listeners are in a category of superfans and maybe somewhere in the region of 20% are interested in a Super-Premium platform that would include products like early access

- Better monetization of ad supported tiers and family plans

- While ad-supported revenue has been variable, UMG believes that as consumer engagement in short-form video grows, monetization will follow; The Co is confident that it will be able to capitalize on the incr’d ad revenue from social and video platforms as better ad products are developed

- UMG is focused on innovating its ad-supported offerings: The Co is exploring new ways to monetize free-tier users by potentially segmenting and creating enhanced tiers of service, similar to how subscription services use premium tiers

Sees The Shift From Streaming 1.0 -> Streaming 2.0

- UMG expects continued growth in streaming, with a transition from Streaming 1.0 of achieving scale and a focus on subs growth to Streaming 2.0 of maximizing customer value and a focus on subs AND ARPU growth

- Streaming 2.0 will focus on developing super-premium tiers, price optimization, and geographic expansion

- Partnerships with platforms like Apple, Amazon, and Spotify are essential to the Streaming 2.0 strategy

Still Ample Room To Support More Streaming Growth

- Consensus predicts 1bn+ subscribers by 2028

- UMG’s research indicates there are ~220mn addt’l subs already in the consideration set (~75mn established markets and ~145mn high potential markets)

- 61% of US weekly audiobook listeners currently don’t have a music subscription

- Spending on streaming is ~50% of peak us recorded music rev per capita spending in 1999 (adj for inflation)

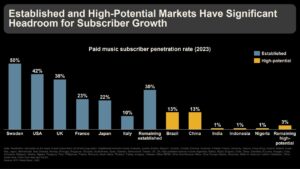

High Potential Markets Will Drive Much Of Future Growth, And M&A Is A Key Strategic Component

- High-potential markets (e.g., China, India, Southeast Asia), which is ~85% of the global population, will drive much of UMG’s future growth due to their large populations and increasing subscription penetration

- China: It is the largest paid subscriber market with only 13% penetration; ARPU has been increasing with product innovation and there is more room to go with pricing tiers

- India: Huge potential given #1 size population; Seeing meaningful ad-supported growth and longer-term subscription opportunity with only 1% penetration of paid subs

- Will be aggressively investing in high potential markets over the next 3-5 years

- Have a repeatable & scalable model to drive growth in high potential markets:

- Local A& R Teams

- Distribution via Virgin Music

- M&A

- M&A will focus on acquiring local labels and catalog rights, partnering with independent entrepreneurs, and leveraging the Chord investment vehicle for opportunistic catalog acquisitions

- Deals in these high-potential markets are typically small but highly strategic: Like with deals the Co has done in markets like Nigeria, Lebanon, and Thailand to strengthen its presence

- M&A is NOT required to meet the projected revenue growth of more than +7% CAGR

Superfan Engagement & D2C Strategy

- UMG aims to unlock superfan spending through premium products and experiences (e.g., merchandise, vinyl, artist collectibles)

- D2C sales have been growing at a +33% CAGR, and UMG has built a substantial owned audience of 100mn+ fans through online stores

- The Co believes its D2C capabilities provide a competitive advantage in attracting and retaining artists

EA Declares That Gen AI Is Poised To Drive “Another Tectonic Shift” In The Interactive Entertainment Industry

Continuing on the theme of investor meetings this week, EA hosted an event in New York to shed some light on its long-term growth strategy, showcase upcoming launches, and highlight other key strategic priorities. EA CEO Andrew Wilson opened up the three-hour presentation by speaking to the “tectonic shift” that was occurring during the company’s last Investor Day eight years ago, when the interactive entertainment space was just beginning to transition from CDs to digital. Now, Wilson believes that the industry is in the midst of other major inflection point, one prompted by the emergence of generative AI. He stressed that AI isn’t “merely a buzzword” for EA, as the company has 100+ active novel AI projects along with plans to further integrate generative AI features across its business to enhance its key franchises. One interesting use case will be on the user-generated content side. By employing gen AI to simplify and remove friction from the creation process, EA will look to open the floodgates on the amount of content being released on its platforms and rapidly accelerate the growth of its massive online communities.

EA’s Investor Day presentation also provided an in-depth look at how the company’s key franchises have been performing and its plans for each moving forward. There was certainly a lot to cover, and we did our best to highlight the key takeaways below. Some updates that really stood out to us were EA’s lofty growth targets for The Sims and EA SPORTS, a new Sims movie in collaboration with Amazon MGM Studios, and an upcoming beta test of a new EA SPORTS app. The latter two underscore how the company is starting to look beyond gaming and to engage players even when they aren’t in EA experiences. Sports, in particular, will play a central role in this push, and the company will aim to “blur the line between virtual interactive sports, where the vast majority of the next-generation audiences [lie], and real world sport, where the vast majority of the current value lies”.

The culmination of all the milestones that were touted over the course of the presentation, especially the progress that EA has seen its American football business, was that the company now expects to reach the high-end of its guidance for its second fiscal quarter and FY25. Moreover, EA now believes that it can “significantly outpace market growth through FY27” while concurrently expanding operating margin. These appear to be some ambitious targets, but if the company can execute on its AI-driven strategy over the next few years, they certainly seem achievable. See below for more details on the Investor Day.

-> EA shares fell -2.7% following the Investor Day, closing the week down -4.3%; YTD, EA stock is trading up +2.0%

Highlights On The Evolution Of The Overall Biz + Guidance Updates

- The Co is “on track” to achieve the high end of its Q2 and FY25 net bookings guidance: For reference, expects FQ2 net bookings between $1.95-2.05bn (implying a -9.8% y/y decline), as well as a net bookings range of $7.3-7.7bn across FY25

- EA believes it can “significantly outpace mkt growth through FY27”: Cited the Co’s start to FY25 as well as “confidence in the breadth of experiences” shared at the Investor Day

- EA also has plans to expand its op margin in 2025-2027: Via a combination of top-line growth and op leverage; Will expense R&D, and the upcoming pipeline has a “favorable mix of high margin digital and owned IP”

- New biz models will drive margin improvements beyond FY27: This will be supported by ongoing efforts to enhance content delivery and developer productivity through tools, technology, and gen AI

- Expects to return $1.5bn to shareholders in FY25: Plans to further scale the stock repurchase program through FY27

- EA has made significant progress since its last Investor Day 8 yrs ago…

- Live services and other net bookings have more than doubled from $2.3bn to $5.4bn

- Digital bookings now represent 90% of the Co’s biz

- EA has 5 of the top 25 HD experiences in the West, and it expects to add to this w/ Battlefield

- The Co has more than doubled the amount of content offerings that it delivers

- Has returned ~70% of FCF to shareholders, amounting to ~$8bn over the last 8 yrs

- … And this has cont’d over the LTM:

- There have been 13bn+ hrs played in EA’s experiences

- 60mn hours of content have been created

- 3bn hrs have been watched on social platforms

AI “Is Not Merely A Buzzword” For EA

- EA has 100+ active novel AI projects across three strategic pillars – efficiency, expansion, and transformation: The Co manages 100+ ML and LLMs on its central platform and handles 1bn+ AI requests daily; These models power various in-game features

- Efficiency means “driving more iterations, more testing, and higher quality-content”: The Co will also use gen AI to remove obstacles for its game devs and help culturalize content across geos; “The lowering of these friction points leads to deeper gameplay experiences”

- EA believes “AI will greatly expand and transform the entertainment experience for UGC”: “It will accelerate how innovators and creators in entertainment are building and delivering experiences rooted in self-expression, content creation, curation and instant gratification”

- Centralizing assets “has become more and more critical in this new age of AI”: The Co is in a “multi-yr process” of centralizing decades of high-quality 3D data and assets, which will enable rapid prototyping and provide devs w/ “game-ready assets they can quickly modify to go directly in their game”

Updates On Key Franchises

- EA’s massive online communities were front and center: Includes Apex, Battlefield, The Sims, and SKATE; These appeal to broad audiences, are available on multiple platforms, have diverse biz models, regularly release new game content, and offer a variety of ways to play and create content and connect w/ friends

- Apex Legends “will continue to deliver for many yrs to come”: 170mn+ people have played to-date, and the Co will continue to “bring new modes of play and great updates” in the months to come, including the second drop of Season 22 this week

- “Battlefield is one of the most valuable franchises in the world”: The franchise has acquired 25mn+ players over 7 seasons of content, and it has seen 250mn+ hours played over the LTM; The Co is “building a connected universe… filled w/ Battlefield experiences”

- EA plans to introduce a new “large-scale community testing program” early next yr: As part of a push to gain more feedback for Battlefield experiences

- SKATE has been “revitalized” into a “truly community-driven platform that transcends the traditional skate game”: The open-world skate game will be accessible across PC, console, and mobile devices, w/ the full experience of the title set to become available in early access next yr

- EA believes it can “more than double” annual net bookings for The Sims over the next five yrs: Along w/ a new experience, a standalone mobile game, and a Nintendo Switch spinoff on the way, “major shifts in tech, especially AI” will enable the Co to “scale this experience beyond anything [it’s] done before”

- Annc’d a Sims movie in partnership w/ Amazon MGM Studios: Kate Herron will direct and co-write w/ Briony Redman; LuckyChap and Vertigo Entertainment will produce alongside The Sims’ team w/ Herron and Redman executive producing; More details to come nexst yr

- 1.2bn+ hours have been played in The Sims 4 over the LTM: Players have spent 210mn+ hours watching Sims content over the past yr, and there have been 1bn+ downloads from the gallery since Sims 4 launched

- EA SPORTS’ TAM oppty is far larger than its current player network: EA SPORTS’ has 265mn+ players today, which is still a fraction of the 4bn+ sports fans around the world, of which 1bn+ are from “younger generations who are still growing their fandom”, per the Co’s estimates

- The biz has a strong track record: EA SPORTS has seen a +11% CAGR in total session days of engagement across its largest HD franchises over the past 10 yrs; In the last 18 months, the Co has launched 13 new HD games across 9 different franchises

- Key EA SPORTS franchises have achieved some noteworthy milestones:

- EA SPORTS FC is now the “biggest video game franchise in the western world” on a TTM basis: Fans have spent 8bn+ hours playing FC experiences over the past yr

- “The Madden franchise has just had its strongest yr”: Reached all-time highs for unique players, monthly and weekly active users, as well as net bookings this yr; The equivalent of ~23,000 NFL seasons are played in Madden every day, and players have incr’d nearly +50%

- College Football was the “largest launch of a new console game in North America in 2024”: It has also “arguably become the biggest moment in US sports entertainment this yr”

- EA is working on building “connected ecosystems” across its main sports franchises: The Co is also developing “tools for the entire community to create and share content and contribute to the value across each of these ecosystems”

- The Co also sees oppties beyond sports: The global sports mkt is expected to grow to $600bn+ annually over the next 5+ yrs, per multiple sources, and EA is “preparing [its] biz to aggressively pursue this new value” and drive

- The EA SPORTS app is the Co’s first product beyond gaming: The Co provided a first look at the new app, which “empower[s] fans to come together, share their passion, and celebrate the sports they love all around the world”; Provides a way for EA to reach fans outside of games

- EA has “clear advantages” in action RPGs: Including IP that attracts massive online communities and “the production capabilities to deliver at scale”; Notably, action RPGs have “one of the highest player bases and addressable markets at $20bn+”

- Bioware’s Dragon Age is already generating “strong demand on all platforms”: The game, which “looks great on console and PC alike” is coming on Oct 31; “The Dragon Age community is buzzing and the press reception has been really positive”

- Highlighted Iron Man, EA’s first title in partnership w/ Marvel: The AAA action-adventure game is being developed by Motive in Montreal and “will feature an original narrative and a unique take on one of Marvel’s most popular heroes, Tony Stark”

- Another Marvel collab, Black Panther, “will be a love letter to fans”: Being developed by Cliffhanger Games and will combine “vibrant characters, the world of Wakanda, an original story, and all new technology… that will actually transfer across many [of EA’s] games and studios”

- 40mn+ fans have connected w/ the Star Wars Jedi franchise: The Co is “working hard” on the final chapter of the Star War Jedi series

- Touted EA’s “successful history w/ Lucasfilm and Star Wars”: To-date, EA’s Star Wars games have accounted for $5bn+ in net bookings

Sell-Side Reactions Were Mostly Upbeat (link)

- Bank of America emphasized EA’s strong positioning to outpace industry growth in FY26 and FY27:

- Highlighted EA’s ability to leverage its vast resources and tech, including gen AI, to build higher-quality content faster

- Underscored EA’s increasing moat through its large online community, which supports scaling, engagement, and monetization

- Acknowledged ambitions beyond gaming, such as advertising and sponsorships but caveated that it’s hard to underwrite these opportunities until proven

- Deutsche Bankwas upbeat, w/ EA trending towards the high end of its FY25 bookings guidance:

- Noted EA’s strong performance in College Football and Madden, though slightly offset by weaker-than-expected results from Apex Legends

- Appreciated EA’s multi-year financial framework, highlighting accel’ing growth and op margin expansion through FY27

- Encouraged by EA’s $5bn share buyback program but remained cautious about near-term execution

- Morgan Stanley was focused on potential catalysts: Including the upcoming beta test of EA’s new Sports App and key game launches, like Battlefield and The Sims

- Views successful execution in non-sports titles as a critical driver of sentiment and earnings, maintaining a balanced view on the stock

- Jefferies echoed long-term optimism but raised concerns about the timing of the game pipeline

- Acknowledged the solid outlook but noted that investors seeking near-term assurances might have been left wanting more, especially regarding FY26 bookings

T-Mobile’s Next Chapter – “Challenger to Champion”

T-Mobile’s Capital Markets Day rounded out the trifecta of investor meetings this week! With 3.5 years elapsing since T-Mobile’s last Investor Day, this year’s event was devoted to the company’s plan and vision for the next 3-year period, a timeframe in which it intends to transition from “challenger to champion” and lead its rivals in both postpaid net adds and broadband. Other key priorities involve extending T-Mobile’s lead as “the nation’s best network” as well as undergoing an AI-driven transformation that will reimagine the customer experience and result in higher levels of satisfaction. Partnerships will be integral to T-Mobile’s efforts to further incorporate AI into its business, and OpenAI CEO Sam Altman and NVIDIA CEO Jensen Huang joined T-Mobile CEO Mike Sievert to discuss how these new collaborations will work. Ultimately, T-Mobile believes that these initiatives will culminate in 100% of handset upgrades and at least half of activations being done digitally.

The juiciest tidbits of the presentation for investors were likely T-Mobile’s forward-looking comments on its broadband business. The company expanded its FWA subscriber goal to 12mn by the end of 2028 from its prior target of 7-8mn by the end of 2025 and also revealed a plan to pass 12-15mn homes with fiber across its various JVs, wholesale relationships, and its own T-Fiber brand. Network capacity isn’t a concern for T-Mobile in establishing these new milestones, given that its faster than expected spectrum deployments have resulted in “areas of fallow capacity across the country”. The Co’s fiber-to-the-home (FTTH) strategy will supplement the FWA business, opening up more available slots for FWA as customers upgrade to fiber offerings. It sounds like demand for these spots is fairly high as well, with T-Mobile touting a waitlist of 1mn+ potential FWA customers in pockets across the country.

Looking at the numbers, T-Mobile’s outlook for the next 3 years as well as its FY25 guidance were mostly in-line with the Street’s expectations, though some believe that the forward-looking comments on capital returns left some room to be desired. Interestingly, T-Mobile’s Capital Markets Day provided a greater uplift to another company’s stock than its own, as Apple traded up +3.7% on the day following the event after Sievert remarked that T-Mobile’s iPhone sales are “higher than last year” though he still doesn’t envision an imminent supercycle. See below for more details:

-> T-Mobile shares were down -1.5% following the event and ended the week down -1.7%; YTD, T-Mobile stock is still trading up +24.4%

Regarding The Current iPhone Upgrade Cycle – T-Mobile “Think[s] This One May Unfold A Little Differently”

- T-Mobile’s iPhone “sales are higher than last yr” …: Sales have been “vibrant” and better than last yr, and this is “saying something b/c sales last yr were quite strong”

- … And there is more upside to come: Believes the “word-of-mouth value” will take off later “b/c the principal differentiating feature is coming in a later software release”

- BUT “this probably isn’t” going to be a “supercycle”: T-Mobile suspects the cycle “will be drawn out over time… as people get the Apple Intelligence features later, start showing their friends and generate later excitement as opposed to in prior yrs”, which were driven by hardware updates

The Co Outlines Financial Targets Out To 2027…

- T-Mobile’s concept of “Challenger to Champion” will “create incredible momentum”: As part of this push, the Co identified the following priorities –

- Extend its lead as “the nation’s best network”: The Co believes its network lead is greater than two yrs ago and that it will be “even further ahead” in 2027 by leveraging and expanding its “durable advantages”

- Sustain its industry-leading growth “between now and 2027 and likely beyond”: Sees T-Mobile being “the leader in postpaid net adds this yr, next yr, and every yr”

- Continue to lead in broadband: More details on the Co’s new targets for its FWA and fiber bizs are below

- Redefining T-Mobile into a “deeply data-informed, AI enabled, digital-first Co”: Aims to do 100% of handset upgrades digitally by 2027, “sometimes w/ the assistance of people or AIs”, w/ “at least half of activations done digitally”

- Another priority – A -75% reduction in inbound contacts, while still increasing customer satisfaction

- Forward-looking comments on 2025:

- 2025 will be a “low point” for svs rev growth: Anticipates another yr of “exciting +4% y/y growth” in svs rev, driven primarily by T-Mobile hitting an “inflection point around wholesale rev”, given “a full yr of runoff of ACP” as well as the “planned transitions” of some of the Co’s MVNO partners

- Postpaid svs rev will continue to grow at a +6% y/y rate

- Core adj EBITDA is projected to grow ~+5% y/y: Cited, again, the “inflection point” of wholesale svs rev “as well as very prudent ongoing enhanced investments in 2025”

- One-time “artifacts” are responsible for the implied margin dilution: Emphasized that the dilution is not related to the Co’s fiber investments but, rather, one-time items such as the “long anticipated declines in the wholesale biz”

- Set financial targets for 2027:

- Svs rev will accel from a ~+4% CAGR “over the past few yrs” to “closer to +5%” between 2023-2027

- Forecasts 2027 EBITDA of $38-39bn: This represents a ~+$10bn increase over 2023’s EBITDA of $29bn

- CapEx is expected to remain in the $9-10bn range annually through 2027

- FCF is forecasted to be between $18-19bn in 2027: Representing a +8% CAGR over the period; This doesn’t include any of the Co’s pending M&A deals

- Expects to convert 25% of svs rev into cash by 2027: The Co plans to extend its ~4% lead to a 7-12% lead over its benchmark competitors

- Anticipates $80bn of “cumulative cash flexibility” between now and 2027: Plans to allocate this “massive firepower” in the following manner –

- The first $10bn will be dedicated to the previously annc’d US Cellular, Lumos, and Metronet

- $50bn will be earmarked for “shareholder remuneration” via dividends and buybacks over that period

- The remaining $20bn will be left for “further investments in [the] biz organically or inorganically, for potential de-levering, or for incr’d shareholder remuneration beyond the $50bn”

T-Mobile Sets Its Sights On A New FWA Target

- T-Mobile has a new goal of 12mn FWA customers by the end of 2028: Compares to its former target of 7-8mn FWA customers by the end of 2025; The Co ended Q2 w/ 5.6mn FWA customers that use an avg of 0.5TB per month

- Fallow capacity gives T-Mobile “confidence” in the new 12mn target: The Co’s end-to-end 5G network, fully dedicated 5G mobile core, and faster than expected spectrum deployment has resulted in “areas of fallow capacity across the country that are beyond even [its] initial forecasts”

- The FTTH strategy will supplement the FWA strategy: Given that when a FWA customer upgrades to fiber, it “also opens up a new incremental slot for addt’l 5G broadband customer” within the Co’s fallow capacity sectors

- Demand for FWA has been outstripping supply: The Co has a waitlist of 1mn+ customers for 5G broadband located in “pockets across the country” and plans to roll fiber into these mkts to take advantage of that demand

- The Co has better data on which customers to target w/ FWA: Over the last 3.5 yrs, the Co has collected data that combines location info w/ “actual insights about usage” to help it target customers and sell more FWA svs in areas where it has fallow capacity

- CPE enhancements have also helped “the cost curve come down”: The newest routers cost the same as the prior generation but are “much more powerful”, enabling the Co to approve more customers in areas w/ fallow capacity than it could beforehand

- Fallow capacity gives T-Mobile “confidence” in the new 12mn target: The Co’s end-to-end 5G network, fully dedicated 5G mobile core, and faster than expected spectrum deployment has resulted in “areas of fallow capacity across the country that are beyond even [its] initial forecasts”

The Co Is Also Aiming To Become A “Scaled Fiber Provider”

- T-Mobile plans to cover 12-15mn homes w/ fiber: This number accounts for the combined fiber passings across the Co’s JVs, wholesale relationships, and its own T-Fiber brand

- The Co expects to “achieve marginally higher penetration than a standalone over-builder” …: Didn’t provide a specific number or range but noted that its pure-play fiber partners each have a penetration of 35%+

- … And to “get there more cost effectively”: T-Mobile will “serve those customers subsequently more cost effectively” but didn’t elaborate on how

- The target implies that T-Mobile’s JV partners will have to accel fiber deployments: Highlighted that Metronet is building 65k fiber locations this month and that Lumos “is right there behind them; Expects these rates to rise as these Cos work closer w/ T-Mobile and its financial partners

- The JVs will “certainly” contribute svs rev and EBITDA: The Co modeled these as “being at or potentially slightly above +20% IRRs, including the ability for $1bn+ in distributions back from Metronet; T-Mobile plans to provide “a more wholesome picture around svs rev” and other financial metrics after the deals close

- “We’re not doing this to defend our mobile biz”: But also acknowledged that “there’s some evidence… that there could be churn benefits and other benefits to the mobile biz as well” from having fiber

- The Co expects to “achieve marginally higher penetration than a standalone over-builder” …: Didn’t provide a specific number or range but noted that its pure-play fiber partners each have a penetration of 35%+

T-Mobile Is Pushing Towards AI-Enabled “Transformative Customer Experiences”

- “We live in an era of AI”: Along w/ already using AI to progress towards its goal of reducing inbound contacts by -75%, T-Mobile believes that it can use AI to “unlock individualized experiences for customers informed by data in the way humans can never do in real-time”

- “AI can ascertain what went wrong and why and actually prevent those problems”: If users call customer svs about a dropped call, AI can perform a “real-time interrogation” of the network to understand the issue and explain to callers about why it happened and how the problem is being fixed

- Months ago, the Co “quietly launched” T-Life, a new lifestyle app: T-Life is “one of the foundational investments” in the Co’s future, and is “more than an app”, allowing users to check their bills at T-Mobile, manage their magenta status benefits, and redeem rewards

- The app is on pace to have 40mn active users in 2024

- A “unique partnership” w/ OpenAI will “create a new kind of engagement model for customers”: OpenAI Sam Altman CEO joined the event to discuss the new partnership, which will see the two Cos launch the IntentCX decision-making platform in 2025

- IntentCX will use OpenAI’s LLMs to determine “the next best action” for a customer: IntentCX will “listen to the customer’s actual intentions… and then choose a treatment based on massive pools of data that will optimize their success journey w/ T-Mobile”

- T-Mobile also extended its partnership w/ NVIDIA, Nokia, and Ericsson to create a research center: The research center will focus on a new wave of networking tech called AI-RAN; NVIDIA CEO Jensen Huang joined the event to discuss these efforts and how the Co has “fused signal processing and AI into one computing platform”

Other Highlights – T-Mobile Annc’d A New Svs For First Responders

- T-Priority will offer the “world’s first 5G network slice for first responders”: The svs will provide “lower latency, faster speeds, and priority across… all the lanes”; The City of New York plans to implement it within their svs, and T-Mobile is already working w/ other first responder agencies nationwide

Some Sell-Side Reactions (link)

- Goldman Sachs highlighted T-Mobile’s “ambitious targets” for broadband growth” and both rev and cost initiatives around AI:

- BUT while the Co’s financial guidance was “broadly in line with elevated expectations heading into the event,” it was modestly disappointing for capital returns

- Still, GS “came away from the event with increased confidence in the sustainability of T-Mobile’s growth trajectory, particularly with respect to its broadband initiatives”

- Oppenheimer was positive on T-Mobile’s AI initiatives:

- “The Co has transformed to the leading wireless carrier in spectrum depth, network performance, growth, and FCF margins, and is taking the lead in GenAI on both networks and CX”

- Underscored that T-Mobile aims to “reduce inbound calls by -75% and resolve 100% of upgrades and 50%-plus of activations digitally”

- Highlighted that T-Mobile partnered w/ OpenAI for its upcoming IntentCX platform to increase customer engagement and has also working w/ NVIDIA to “accel the development of AI-RAN”

- KeyBanc Capital Markets viewed the fiber strategy favorably

- T-Mobile’s 2027 guidance has “a number of upside levers from the contribution of Metronet, Lumos and US Cellular, plus the execution of ‘Hero Projects’ and growth in underpenetrated Small Markets and Rural, Business and now First Responders”

- T-Mobile has set targets that would make it “a larger Home Broadband provider by customer count” than both AT&T and Verizon, which highlights that the Co is “not at a strategic disadvantage despite lower Fiber home passed targets”

Some Key Callouts From The Connectivity Corner

Along with T-Mobile’s Capital Markets Day (see Theme #3), there were also a handful of noteworthy updates in the connectivity and pay-TV spaces that we wanted to highlight this week. Along with Dish and DirecTV re-sparking merger talks that were originally kindled in 2002 but ultimately blocked by the US Justice Department, the battle between Disney-DirecTV finally reached a conclusion, with a hybrid and flexible + DTC carriage agreement being the outcome. Also, Charter announced new low pricing for internet plans when bundled with mobile plans, introduced a “first-of-its kind” customer commitment, and launched a new brand platform across its 41-state footprint this week. See below for more details:

- Satellite TV consolidation? Dish and DirecTV are reportedly in early talks again about a possible merger (link /link): Both companies have been in similar merger discussions in the past w/out success given antitrust concerns so this is not a slam dunk but the sector is also in a different place competitively vs where it was in the past

- Both DTV and Dish have been losing subscribers rapidly: In Q2 2024 alone, they lost a combined 495k subscribers, while the overall pay-TV sector lost 1.62mn; DTV’s subs base has dropped from 15.4mn in 2021 to ~11mn

- The regulatory environment may be more favorable this time, given the declining market power of the satellite TV industry: Wall Street analyst from MoffettNathanson Research commenting “it’s hard to imagine that regulators would block this deal”

- But analysts expects that synergies would be limited: This is because they operate on different technologies

- Skeptics question that a deal sustains the satellite TV industry: The merger might only extend the life of satellite TV for ~ a year and is not likely to change the landscape for the industry

- A DirecTV official declined to comment on the rumors

- The Disney/DTV fight is over…a hybrid and flexible linear + DTC carriage agreement was the conclusion (link): The two Cos reached a preliminary agreement, ending a nearly two-week blackout, and Disney’s networks were restored to DirecTV customers; The deal includes:

- DTV can offer “genre-specific” channel bundles, allowing customers to choose from sports, entertainment, and family packages at lower prices

- The structure includes Disney’s full portfolio of networks and offers access to Disney’s streaming services like Disney+, Hulu, and ESPN+ at no extra cost to subscribers in select packages and will be made available on an a la carte basis

- DTV will be able to offer the ESPN standalone streaming service for free when it launches in 2025

- The companies are finalizing a multi-year contract

- Charter introduced new pricing for Spectrum, along w/ more bundling options and faster internet speeds (link): The Co will also begin offering credits for svs outages and is promising heightened reliability for customers

- Spectrum will charge as low as $30/mo for its 500Mbps internet plan, or $40/mo for 1GB svs: Specifically, these prices will be available to those that bundle the plans w/ two mobile lines or cable TV

- The Co is also raising the baseline internet speed for current customers at no addt’l cost

- The Co also annc’d a “first-of-its-kind Customer Commitment”: The new Customer Commitment provides performance and service benchmarks to Spectrum customers

- Life Unlimited, a new brand platform, encapsulates Charter’s new commitments: The platform offers “customers access to a life of ‘unlimited’ oppty and possibility when seamlessly connected through Spectrum’s Internet, Mobile, and Video svs”

- Charter will also be more transparent w/ customers about costs: The Co is including taxes and fees within its “whole dollar pricing”, and there are now no annual contracts for any residential svs

- The launch took place this week: The new Customer Commitment, pricing plans, speed increases, and brand platform will roll out across its 41-state footprint this week

- Spectrum will charge as low as $30/mo for its 500Mbps internet plan, or $40/mo for 1GB svs: Specifically, these prices will be available to those that bundle the plans w/ two mobile lines or cable TV

Snap Is Going All In On “Chatting, Snapping, And Watching Entertaining Videos”

Outside of the Investor & Capital Markets meetings this week mentioned above, Snap hosted its sixth annual Snap Partner Summit on Tuesday, unveiling a series of updates across both its platforms and products.

On the platform side, Snap is rolling out a major redesign of the app that zeros in on the three central things Snap enables users to do – “chatting, snapping, and watching entertaining videos”. Downsized to just three tabs on the app, Spotlight (Snap’s short-form video and TikTok competitor) is put front-and-center, while the user’s camera and chats comprise the other two tabs. Of course, all this is meant to push users who open the app to send and receive messages from their friends to watch creator content while they’re in the app, which in turn will boost ad engagement. As Snap CEO Evan Spiegel said, “bringing content closer to communication is going to fuel a real flywheel for us”.

On the product side, the company unveiled the fifth generation of the Spectacles AR glasses with a completely redone Snap OS. Similar to its predecessor, the Spectacles 5 are designed specifically for developers, who must be willing to commit to a year-long $99/mo subscription if they want to build AR apps for the device. Snap’s unveiling of the new device precedes Meta’s Connect event next week, where the Co typically unveiled its latest hardware, and there are some speculations that Meta may be releasing its own AR device at the event.

There were a whole host of other key updates from the event that we found interesting. See below for more details. (link/link/link/link/link/link)

New AR Glasses + Rebuilt Lens Studios Is Meant To Enable AR Developers To Create More Robust AR Experiences

- Introduced fifth generation of its AR glasses, which are powered by the new Snap OS

- How are they different from VR headsets? “VR headsets are like sticking a laptop to your face”: “They’re isolating, make you feel motion sick, they’re really heavy, and they can be uncomfortable”

- In contrast, AR glasses “allow you to see the real world through Lenses”: “They allow you to share experiences together with your friends and family, and they’re lightweight and wearable”

- Snap has an advantage when it comes to AR glasses: “Making augmented reality glasses is really hard. And we know that the industry is littered with companies that have tried and we’ve been working for a really long time on these”

- Deliver up to 45 minutes of continuous standalone runtime

- Spectacles will NOT be sold and will only be available to developers: Developers have to apply for access through Lens Studio, the company’s desktop tool for creating AR software, and pay $99/mo to rent a pair for at least one year

- “Our goal is really to empower and inspire the developer and AR enthusiast communities” … “This really is an invitation, and hopefully an inspiration, to create”

- Rebuilt Lens Studio from the ground up

- Revamped Lens Studio, which allows creators to build their own augmented reality (AR) lenses on Snapchat and allows developers to quickly push their projects to Spectacles.

- Easy Lens lets creators generate new Lenses in just minutes by typing a prompt in an LLM chat interface that connects with Lens Studio components and builds the Lenses right then and there

- Partnering with OpenAI to provide access to multimodal LLMs for building Lenses, with the newly rebuilt Lens Studio

- Other GenAI features in Lens Studio will include Animation Blending, Body Morph, and Icon Generation

- 375k+ AR creators, developers, and teams from nearly every country in the world have built 4mn+ lenses; In just the last year, Snapchatters have engaged with Lenses made by the Co’s AR community 4.5tn+ times

Simplified Snapchat UI Centered Around “Communication, Taking Pictures, And Entertainment”

- Rolling out a streamlined and simplified UI to put the focus on short-form videos from creators and Snap’s various partnered media publishers

- Reduces its previous five separate sections to three, putting Spotlight front and center, with an endless swipeable feed of content; The other two tabs are the user’s camera, and their DMs with friends

- “This evolved version of Snapchat aims to simplify the Snapchatter experience by organizing the app around what we use our phones for most: communication, taking pictures, and entertainment”

- Redesign is currently being tested and roll out to full user base is TBD

- Reduces its previous five separate sections to three, putting Spotlight front and center, with an endless swipeable feed of content; The other two tabs are the user’s camera, and their DMs with friends

- Series of new AI features, including –

- New AI Grandparents Lens that lets users to see elderly versions of themselves

- Snapchat+ subscribers can add AI-generated captions to their Snap Memories and Lenses

- MyAI (chatbot integrated with Snapchat) has further been upgraded to analyze Snaps and interpret complex parking signs, translate menus in a foreign language, identify unique plants, and more

- Snapchat community has grown to 850mn+ users globally and they have “a line of sight to reaching over a billion”

More Tools And Features To Build Out And Further Support Creators

- # of creators posting publicly has more than tripled over the past year; 500mn+ people watch Spotlight videos; ~15bn interactions between creators and theirs on Snapchat everyday

- Announced new Snap Star Collab Studio program, which makes it easier for content creators on Snapchat to share their engagement rates and demographic data with brands or advertisers

- New profile design allows Snapchatters aged 16+ to easily toggle between their personal and public

- More tools to make content and build community: Users can pin their favorite Snaps to the top of their Public Profile, use Templates to make it even easier to create and share Snaps, and use Replies to turn messages into a photo and video response to create deeper engagement with fans

- Introducing new AI video-generation tool for creators: Will allow select creators to generate AI videos from text prompts and soon from image prompts

- Tool will be available in beta on the web for a small subset of creators, and for now, Snap doesn’t have any plans to make Snap AI Video available to anyone beyond creators

- All content created with Snap AI Video will include a watermark that will stay visible when content is downloaded and shared

- Snap has now beaten competitors in releasing text-to-video AI generators, including TikTok and Instagram

- Although Meta unveiled a tool called Make-A-Video back in 2022 that enables text-to-video generation, it hasn’t released it to the public

- OpenAI and Adobe plan to release text-to-video AI generators to the public later this year

FX Takes The Top Spot At The Emmys

Over the past several years, the Emmys have undergone a marked transformation, as streamers like Netflix and Disney+ have increasingly made their presence felt at the awards, often outpacing traditional networks in both nominations and wins. We always like to take a look at the Emmys as a gauge of what shows from what networks are resonating, and this year, a surprise winner emerged… See below for which platform, as well as other key highlights from the event.

Network Highlights

- The Walt Disney Company took home 60 Emmys overall, breaking the record for the most wins in a year scored by a single company

- CBS previously set that record in 1974 with 44 wins, which Netflix tied in 2021

- FX had the most wins by a network (36), beating out both Netflix (24 wins) and HBO (14 wins)

- First time in at least 15 years that the top network of the night was not Netflix or HBO

- First time FX has topped all other networks in total wins, as FX’s best year prior to this was in 2016 with 18 wins

Show Highlights

- Top 5 shows by Emmy wins –

- Shogun (18 – FX)

- The Bear (11 – FX)

- Baby Reindeer (6 – Netflix)

- Saturday Night Live (6 – NBC)

- Jim Henson Idea Man (5 – Disney+)

- FX’s Shogun broke the record for most wins by any show in a single season (18)

- FX’s The Bear broke its own record for most wins by a comedy series in a single year (11), topping last year’s 10 wins

Corporate Restructurings Across The TMT Circuit – WMG, Paramount, And Amazon

The increased focus on cost efficiency continues across the sector, and this week, there were announcements and updates out from names across music, media, and e-commerce. Warner Music Group shared plans for an increase in anticipated layoffs and severance payments, Paramount is further cutting its US workforce, and Amazon is looking to flatten its structure and bring back pre-pandemic office attendance policies. See below for the updates.

Warner Music Group Annc’d A Revised Strategic Restructuring Plan (link)

- Increase in anticipated headcount reduction: Now expecting to reduce ~750 employees (~13% of workforce), up from previously anticipated reduction of ~600 employees (~10% of workforce)

- Continue to expect that a majority of those reductions will be related to the O&O Media Properties, Corporate and various support functions

- Increased severance and termination costs…: Now expect ~$150mn in severance and termination costs, up from the originally expected ~$85mn

- … With an extended timeline: ~$30mn to be paid by FY24, ~$85mn by FY25, and ~$35mn by FY26, extended from the originally expected ~$35mn paid by FY24 and ~$65mn by FY25

- Increased expected pre-tax cost savings: Now expect to generate ~$260mn (significant majority of which will be achieved by the end of FY25), up from originally expected savings of ~$200mn (by end of FY25)

- Increased pre-tax charges: Now expect ~$180mn in pre-tax charges for FY24, up from the originally expected ~$120mn

- Increased non-recurring pre-tax charges: Now expect total pre-tax charges of ~$210mn, up from the originally expected ~$140mn

- Increased non-recurring after-tax charges: Now expect total after-tax charges of ~$135mn, up from the originally expected ~$105mn

- Non-cash impairment charges unchanged with addtl charges: Non-cash impairment charges remain at ~$55mn, primarily in connection with the disposal or winding down of the the O&O Media Properties, with an addtl ~$5mn of other non-cash charges

Paramount Institutes Another Round Of Cuts (link)

- Paramount Global’s advertising group conducted a round of layoffs as part of the Co’s efforts to cut $500mn in annual costs

- Paramount Advertising is the centralized team that manages domestic multiplatform ad sales across CBS, BET, Comedy Central, MTV, Nickelodeon, Paramount+, Pluto TV and other properties

- Exact number of cuts was not disclosed

- Comes a month after Paramount Global officially initiated long-planned layoffs that will see it reduce its US-based workforce by 15%, with 90% of cuts expected to be completed by the end of September

Amazon Releases Memo To Employees From CEO Andy Jassy Regarding Simplifying Organizational Structure and RTO Full-Time (link)

- “Feel good about the progress we’re making together”

- “Stores, AWS, and Advertising continue to grow on very large bases”

- “Prime Video continues to expand”

- “New investment areas like GenAI, Kuiper, Healthcare, and several others are evolving nicely”

- “And at the same time we’re growing and inventing, we’re also continuing to make progress on our cost structure and operating margins, which isn’t easy to do”

- Implementing a series of changes to “remove layers and flatten organizations more than they are today” – “We want to operate like the world’s largest startup”

- Asking each s-team organization to increase the ratio of individual contributors to managers by at least 15% by the end of Q1:25

- “If we do this work well, it will increase our teammates’ ability to move fast, clarify and invigorate their sense of ownership, drive decision-making closer to the front lines where it most impacts customers (and the business), decrease bureaucracy, and strengthen our organizations’ ability to make customers’ lives better and easier every day”

- Requiring employees to be back in the office 5 days a week starting Jan. 2nd, 2025

- Will bring back assigned desk arrangements in locations that were previously organized that way and for locations that had agile desk arrangements before the pandemic, including much of Europe, will continue to operate that way

- Asking each s-team organization to increase the ratio of individual contributors to managers by at least 15% by the end of Q1:25

-> Separately, but related, Amazon also annc’d this week that it would be making its biggest ever investment of $2.2bn+ in pay and benefits for its employees; 800k+ members of Amazon’s front-line worker team will be getting an additional $1.50/hr starting this month, which will bring their avg base wage to more than $22/hr and avg total compensation to more than $29/hr when including the value of elected benefits; This represents an increase of $3,000/yr on avg for full-time employees who work a 40-hr week; Hourly team members in the US will have Prime added to their benefits package at no addtl cost; The Co also annc’d a few other compensation changes, including more flexible scheduling, more choices in the employee education program known as Career Choice and the elimination of the 90-day requirement before new workers are eligible for those benefits (link/link)

Grab Bag: Walmart Offering Instant Bank Payments/Microsoft’s New Buyback Program/MAGNA Raises 2024 US Ad Growth Estimates

- Walmart reportedly planning to offer instant bank payments (link):

- Customers will reportedly soon have the option to pay directly from their bank accounts with instant transfers for online purchase, meaning the purchase will be reflected in the customer’s bank account balance instantly and Walmart will receive the funds immediately

- Walmart has offered pay-by-bank through Walmart Pay since earlier this year: Until now, the transactions were similar to digital checks and took ~3 days to finalize when being processed through The Automated Clearing House, the same network often used for bill payments or paycheck deposits

- The advantage of using instant pay-by-bank over debit cards for customers: Customers can avoid stacked pending transactions; For customers carrying low balances, pending transactions can open them up to the risk of overdraft or non-sufficient funds fees from their bank

- The benefit for retailers: The move allows them to bypass card networks and potentially reduce merchant processing fees

- Expected to roll out in 2025, and the transactions will occur over bank technology provider Fiserv’s NOW Network, which integrates with The Clearing House’s Real Time Payments network and the Federal Reserve’s FedNow

- Microsoft annc’d a new $60bn share repurchase authorization program (link): The new share repurchase program, which has no expiration date, may be terminated at any time

- The Co also revealed a seq increase in the qtrly dividend: Declared a qtrly dividend of $0.83 per share, reflecting an +$0.08 or +10% q/q increase

- The dividend is payable Dec. 12, to shareholders of record on Nov 21; The ex-dividend date will be Nov 21

- A date was set for the 2024 Annual Shareholders Meeting: The meeting will be held on Dec 10, and shareholders at the close of biz on Sept 30 will be entitled to vote their shares

- The Co also revealed a seq increase in the qtrly dividend: Declared a qtrly dividend of $0.83 per share, reflecting an +$0.08 or +10% q/q increase

- MAGNA Global raised its 2024 US ad growth estimate (link): The Co raised underlying 2024 ad rev forecasts from +8.2% y/y -> +8.9% y/y (and including cyclical events raised from +10.7% y/y growth -> +11.4% y/y)

- Smaller declines in National TV ad rev helped drive stronger-than-expected total US ad rev in Q2:

- National TV fell -1.1%

- Linear networks fell -6.4%

- AVOD, CTV, and FAST grew +19.6%

- Outlook for the remainder of 2024:

- National TV ad revs are forecasted to decline -1.7% y/y (vs -3% y/y prior)

- Linear TV is expected to fall -6.8% y/y (vs -7.5% y/y prior), while AVOD, CTV, and FAST will increase +19.3% y/y (vs +15.3% y/y prior)

- Local TV revs are expected to increase +25.4% y/y with cyclical events (but drop -3.9% excluding)

- Cyclical events driving 2024 ad rev: Include $9bn from the election as well as $1.5bn from the Olympics ($1.1bn linear and $400mn digital/streaming)

- Digital pure-play ad revs are expected to grow +14.2% y/y (grew +16% y/y in H1)

- National TV ad revs are forecasted to decline -1.7% y/y (vs -3% y/y prior)

- The ad market is expected to remain strong in 2025: Sees underlying revenue growth of +6.3% y/y to $291bn (+3.9% y/y when including cyclical events)

- Digital ad revs are expected to rise +8.7% y/y

- Traditional media ad revs are expected to decline -1.5% y/y

- The ad market is predicted to surpass $400bn in 2026

- Smaller declines in National TV ad rev helped drive stronger-than-expected total US ad rev in Q2:

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Google took a major step this yr to end an EU antitrust investigation w/ an offer to sell its AdX advertising marketplace. However, European publishers rejected the proposal as insufficient, per sources. Google has never before offered to sell an asset in an antitrust case, according to three lawyers involved in antitrust cases who did not have permission to speak publicly. (Yahoo Finance)

- Publicis annc’d an acquisition of Mars United Commerce for an undisclosed sum. Formerly the Mars Agency, Mars United Commerce (MUC) is an independent commerce marketing Co that helps guide marketers on how to best reach consumers in online and offline shopper ecosystems. MUC’s abilities will join Publicis in three primary areas, including Strategy and insights, Media and activation, and Performance and measurement. (Digiday)

- Roku launched Roku Ads Manager, a self-svs platform designed to attract performance marketers that use social media & search and enable them to buy connected TV. Performance marketers will be able to create campaigns using shoppable ads linked to the Shopify accounts and interactive ads using Ads Manager. There is no minimum budget for Roku Ads Manager users. (Broadcasting Cable)

- Spectrum Reach, the ad-sales arm of Charter Communications, has reached a deal w/ Amazon to become a local reseller of streaming Amazon Ads. The collab will enable Spectrum Reach to offer small, local biz clients campaigns that include linear inventory and a broader range of streaming inventory, enabling advertisers to reach more households in their region. Spectrum Reach said its streaming inventory reaches ~90% of viewers in its footprint. (Broadcasting Cable)

- VideoAmp said that $1bn in media buys have already been guaranteed using its measurement as a currency this yr. VideoAmp is on track to reach $1.5bn by the end of the yr, the Co added, and is growing at a rate of 651% y/y. VideoAmp said the gains were coming as more ad buyers and advertisers invest in data-driven, audience-based campaigns and use measurement from Cos other than Nielsen. (Broadcasting Cable)

- YouTube confirmed that advertisers can broadly serve up pause ads to users, which show users an ad alongside their content when they hit the pause button. YouTube started piloting pause ads in 2023 w/ a limited selection of advertisers, and Google chief business officer Philipp Schindler revealed this April that they were unsurprisingly a big hit w/ ad firms and lucrative for Google. (The Verge)

Artificial Intelligence/Machine Learning

- A redditor posted a peculiar screenshot that appeared to show OpenAI’s ChatGPT reaching out proactively, instead of responding to a prompt. The bizarre exchange would suggest that OpenAI is working on a new feature that allows its chatbots to reach out to users, instead of other way around — a potentially effective way to gin up engagement. When we reached out to OpenAI, the Co acknowledged the phenomenon and said it had issued a fix. (Futurism)

- Alibaba has released 100+ open-source AI models and boosted the capabilities of its proprietary tech as it looks to ramp up competition w/ rivals. The newly-released models, known as Qwen 2.5, are designed for use in applications and sectors ranging from automobiles to gaming and science research, Alibaba said. They have more advanced capabilities in math and coding, it added. (CNBC)

- Aramco Digital and AI startup Groq annc’d plans to construct what they say will be the world’s largest AI inferencing data center in Saudi Arabia. The partnership, unveiled on stage at the Global AI Summit 2024, marks a significant step in Saudi Arabia’s push to become a global AI hub. Set to launch by yr-end, the facility will initially house 19,000 of Groq’s Language Processing Units, eventually expanding to 200,000. (Maginative)

- California governor Gavin Newsom signed two bills that will protect performers from having their likeness simulated by AI digital replicas. The two SAG-AFTRA supported bills, AB 2602 and AB 1836, were passed by the California legislature in Aug and are part of a slate of state-level AI regulations. The two bills’ signing may bode well for the fate of the arguably biggest legal disruption to the AI industry: California’s SB 1047. (The Verge)

- Google in the next few months will begin to flag AI-generated and -edited images in the “About this image” window on Search, Google Lens, and the Circle to Search feature on Android. Crucially, only images containing “C2PA metadata” will be flagged as AI-manipulated in Search. According to one estimate, there was a 245% increase in scams involving AI-generated content from 2023 to 2024. (TechCrunch)

- Meta’s Mark Zuckerberg, Spotify’s Daniel Ek, and Stripe’s Patrick Collison wrote an open letter slamming Europe for its “fragmented and inconsistent” regulation of data privacy and AI. The letter called for decisions from data privacy regulators across the EU to be faster, clearer, and more harmonized “to enable European data to be used in AI training for the benefit of Europeans”. (Fortune)

- Microsoft, BlackRock, Global Infrastructure Partners, and Abu Dhabi’s MGX teamed up to launch the Global AI Infrastructure Investment Partnership. The Global AI Infrastructure Investment Partnership aims to mobilize up to $100bn in total investment potential, including debt financing. W/ a focus on AI innovation and economic growth, the partnership will primarily invest in the US and its partner countries. (Yahoo Finance)

- OpenAI is turning its Safety and Security Committee into an independent “Board oversight committee” that has the authority to delay model launches over safety concerns, per a blog post. The committee made the recommendation to make the independent board after a recent 90-day review of OpenAI’s “safety and security-related processes and safeguards.” The committee will “be briefed by Co leadership on safety evaluations for major model releases”. (The Verge)

- OpenAI’s latest fundraising is nearing completion, w/ prospective investors set to find out whether they’ll be part of the deal, according to people familiar with the matter. The $6.5bn funding round for the Co is oversubscribed. One of the people said that the excess demand was in the billions of dollars. At least one notable existing OpenAI investor won’t be participating, Sequoia Capital, the people said. (The Economic Times)

Broadcast/Cable Networks

- Fox News Media annc’d that Fox Weather, a free ad-supported streaming TV svs, is now available to DirecTV customers. Available to all DirecTV customers w/ the Entertainment package or higher, Fox Weather will now be accessible to millions of satellite subscribers w/ an internet-connected set top box on channel 363 and by using the DirecTV App. The network continues to be available to customers who stream DirecTV satellite free. (TVTechnology)

Broader Media & Entertainment

- The Guardian’s parent Co annc’d that it is in formal negotiations w/ Tortoise Media over the potential sale of the Observer, the world’s oldest Sunday newspaper. Guardian Media Group (GMG) told staff it was in exclusive negotiations w/ Tortoise after being approached with an offer that was significant enough to look at in more detail. (the Guardian)

Broader Technology

- The once-booming tech job mkt has contracted sharply, w/ software development postings down over 30% since Feb 2020. Tech Cos have shed ~137,000 jobs since Jan 2024. Cos are pivoting from growth-at-all-costs strategies to profit-focused approaches, cutting entry-level positions and redirecting resources towards AI development. (SLASHDOT)

Cable/Pay-TV/Wireless

- AT&T and its JV partner TPG are in early-stage talks to merge their DirecTV satellite TV svs w/ EchoStar owned Dish, a person familiar w/ the matter told Reuters. The two Cos first attempted to merge back in 2002, though the US Justice Department blocked the tie-up. The combined entity would create the largest pay-TV svs provider in the US at ~16mn subscribers if the talks are successful. (Yahoo Finance)

- Charter Communications CEO Chris Winfrey aims to enhance the company’s reliability and credibility. Charter is rolling out changes, including new bundles, increased internet speeds, credits for service outages, and simplified pricing with no annual contracts. The “Life Unlimited” initiative seeks to improve customer perceptions and address challenges like declining broadband growth and cable TV defections. (AOL)

- Comcast is charging some customers $32.75 a month for broadcast TV fees, and local RSN costs are $22.65 a month. Put these two fees together and you pay $55.40 a month extra for the channels they advertise as a part of the TV package. These are the highest total fees for broadcast TV and RSNs that Cord Cutters has ever seen. These fees are Comcast and others passing on the costs of these networks to customers. (Cord Cutters News)

- CWA reached tentative agreements w/ AT&T Southeast and AT&T West for new union contracts, ending the 30-day Southeast strike. The new, five-yr contract for Southeast employees includes across the board wage increases of 19.3%, w/ addt’l 3% increases for wire technicians and utility operations. Hurricane Francine just made landfall and is zeroing in on the area, where 17,000 AT&T Southeast US employees have been on strike for nearly a month. (Fierce Network)

- Dell’Oro Group analysts are still hot on private RAN, expecting a 21% growth rate over the next five yrs, while public RAN rev is set to decline at a 3% CAGR over the same time period. The growing private wireless opportunity is a massive yet “largely untapped,” Stefan Pongratz, Dell’Oro Group VP, said in the Co’s latest private wireless Q2 report. The sector presents a stark contrast to public wireless, which has suffered a recent downturn. (Fierce Network)

- T-Mobile told the FCC that it plans to use the spectrum acquired from UScellular to expand its fixed wireless access svs to rural mkts. It also claims the deal will help it compete w/ cable operators expanding into mobile svs. “The transaction will expand T-Mobile’s fixed wireless service offering and thereby increase competition for in-home broadband svs,” T-Mobile said to the FCC. = (NextTV)

- Vodafone is signing up for an extra 68,000 new Microsoft Copilot licenses to boost worker productivity and collaboration. In an extension of Vodafone’s 10-yr strategic partnership w/ Microsoft and following a successful trial period across the biz, the former will roll out the latter’s enterprise-specific Gen AI solution, Microsoft 365 Copilot, to up to 68,000 of Vodafone’s ~100,000 employees across several countries. (UC Today)

Cloud/DataCenters/IT Infrastructure

- BT Group, Equinix, and Toshiba annc’d that they will provide quantum secure connectivity at two prime colocation Equinix data centers located in London’s Canary Wharf and Slough. Customers using the Equinix data centers will be able to connect to BT Group and Toshiba’s quantum-secured metro network and trial the transmission of data, protected using Quantum Key Distribution (QKD). (THEFASTMODE)

- NTT Group plans to enter the electricity transmission and delivery biz using a system that centrally controls renewable energy within power grids. NTT Anode Energy developed the grid-control system w/ communications tech. It analyzes the power output from renewable sources and stores electricity in batteries when necessary. The amount of electricity generated by solar and other renewable sources varies widely depending on weather conditions. (Mobile Europe)

Cybersecurity/Security

- The FBI led an operation to disrupt a global botnet w/ connections to the Chinese govt, FBI Director Christopher Wray said. A group tracked as Flax Typhoon infected “hundreds of thousands” of devices worldwide as part of an operation to compromise organizations and exfiltrate data, Wray said, adding that Flax Typhoon is associated w/ Integrity Technology Group, a Chinese Co that has publicly acknowledged its connections to China’s govt. (THERECORD)

eCommerce/Social Commerce/Retail

- 32% of US consumers plan to start their holiday shopping “between July and Oct,” per a recent survey by Gartner. 29% plan to start in Nov, the Co said. However, just 14% of those surveyed said they plan to spend more on holiday shopping this yr compared to last yr. Most of those polled — 64% — said they plan to maintain their prior spending level, while 21% said they’re reducing their spending. (Retail Dive)

- Amazon annc’d an increase in wages for its hourly warehouse workers along w/ other benefits, including a Prime subscription at no extra cost. In a statement, the Co said the hourly members of the front-line team will be getting at least an addt’l $1.50/hour starting this month. This will bring their avg base wage to more than $22/hour and avg total compensation to more than $29/hour when the value of their elected benefits is being included. (RTTNews)

- Amazon is leveraging gen AI to boost efficiency in deliveries. Use cases include delivery route optimization and warehouse robot technology, per an interview w/ Steve Armato, VP of transportation technology and svs at Amazon. Technologies like gen AI have fueled growth in same-day and next-day deliveries, w/ 60% of March Prime deliveries falling in the category for the top 60 metro areas in the US, according to Armato. (www.retailcustomerexperience.com)

- Amazon is rolling out an AI tool designed to help 3P sellers quickly resolve issues w/ their accounts and fetch sales and inventory data. The Co said that it’s launching the product, called Amelia, in beta for select US sellers before introducing it more broadly later this yr. Amazon describes it as an “all-in-one, generative-AI based selling expert,” and is making it accessible through Seller Central, the internal dashboard for 3P merchants. (CNBC)

- Amazon’s second Prime Day event of the yr will take place at the beginning of Oct. The two-day shopping event, which Amazon is calling Prime Big Deal Days for the second yr in a row, will begin at 12:01AM PT / 3:01AM ET on Tuesday Oct 8 and run through Wednesday Oct 9). Like last yr, Amazon is running the 48-hour promo in an attempt to jumpstart the holiday shopping season. Amazon says it will offer up to 55% off select Amazon devices. (The Verge)

- Chewy annc’d the commencement of an underwritten offering of $500mn of shares of its Class A common stock, par value $0.01 per share, by Buddy Chester Sub LLC (the “Selling Stockholder”), which is an entity affiliated w/ funds advised by BC Partners, Chewy’s largest shareholder. The Selling Stockholder intends to grant the underwriters a 30-day option to purchase up to an addt’l $75 mn of shares of Class A common stock. (Investing.com)

- Ocado Retail launched Ocado Ads in partnership w/ Australian unified retail media platform Zitcha. Ocado’s online-first operating model will allow Ocado Ads to drive measurable growth for its brand partners, while delivering relevant advertising and a personalized experience for customers, allowing them to find the brands they want and discover new products. (https://www.retail4growth.com)

- Ocado Retail, the JV between the online grocer and M&S, incr’d its sales forecast for the yr following a strong performance in its first three qtrs. The Co’s online supermarket sales rocketed 15.5% to £658mn in the 13 weeks to Sept 1. Avg orders per week rose 14.7% to 437k, and volumes were up 15.4%, thanks to a 10.3% increase in active customers to 1.06mn. (Retail Gazette)

- Sam’s Club will bump its starting wage to $16 and accelerate pay increases for nearly 100,000 front-line workers, Chris Nicholas, president and CEO, said. Employees’ avg hourly rate will be ~$19 – a figure that has incr’d nearly 30% in the past five years. Associates will receive increases from 3-6% “based on yrs of svs,” Sam’s Club said. (Retail Dive)

- Shein’s executive chairman Donald Tang said the US’ move to close a loophole that allows low-value shipments to enter the country duty free won’t be a problem for it. The US proposed rules to crack down on a trade exemption for packages that fall under the $800 “de minimis” threshold. However, Tang said, “Shein has a competitive advantage because of its on-demand model and not the de minimis rules”. (Retail Gazette)

- Target is pulling back the curtain on its seasonal hiring strategy. Heading into the holiday season, Target says it is offering current team members the oppty to work extra hours during the season and is leveraging its On Demand team, which includes team members who pick up shifts as they choose. The Co is also planning to add ~100,000 seasonal team members across its stores and supply chain facilities. (Progressive Grocer)

- Tesco chief Ken Murphy revealed the Co is considering using its Clubcard data to “nudge” customers towards healthier and cheaper alternatives. Murphy said the supermarket was using AI to monitor how its customers were shopping to provide suggestions on what products to buy next in an effort to deliver better value to consumers. Murphy noted: “It can start nudging you to say if you wait another week to buy this, this is coming on deal”. (Retail Gazette)

- The US consumer remained choosy in Aug, but nevertheless cont’d to spend on discretionary goods, sending retail sales in the sectors covered by Retail Dive up 4.3% y/y. A major factor was ongoing strength in e-commerce, which rose 5.6%, per to numbers released by the US Dept of Commerce. The National Retail Federation found that Aug retail sales, excluding restaurants, fuel, and autos rose 1.93% y/y. (Retail Dive)

- Whole Foods Market is opening its first smaller format store, called Whole Foods Market Daily Shop, in NYC’s Lenox Hill neighborhood. The store is 9,101 sq feet and offers grab-and-go meals as well as weekly essentials, p;er a press release. The first 300 customers in line on opening morning, on Sept18, will receive a limited-edition tote bag, complimentary cold brew coffee from Nguyen Coffee Supply, and muffins from Abe’s. (www.retailcustomerexperience.com)

EV/ Autonomous Vehicles

- Intel issued a statement regarding its Mobileye stake. “As the majority shareholder in Mobileye, Intel has an unwavering focus on value creation and are excited about the future of its biz. We currently do not have any plans to divest a majority interest in the Co,” Intel wrote, adding, “By providing Mobileye w/ separation and autonomy, we have enhanced its ability to capitalize on growth oppties and accel its path to creating even greater value”.” (Intel Corporation)

Film/Studio/Content/IP/Talent

- Amazon will become the newest member of the Motion Picture Association, adding its tech industry clout to the Hollywood lobbying group. Its decision to join the MPA is a symbol of the convergence of entertainment and Big Tech, which were separated by a sharp divide not that long ago. Amazon will become the seventh member of the MPA, which already includes Disney, Netflix, Warner Bros, NBCUniversal, Paramount, and Sony. Netflix joined in 2019. (Variety)

- Runway, an AI startup, made a name for itself building generative models seemingly trained on unlicensed content from the internet. Now, the Co has signed a deal with Lionsgate that will give it access to the studio’s massive portfolio of films and TV shows. Lionsgate annc’d that it is partnering w/ Runway to create a new customized video generation model intended to help “filmmakers, directors and other creative talent augment their work.” (The Verge)

- The eight biggest theater chains in the US and Canada annc’d that they plan to invest $2.2bn+ to modernize and upgrade 21,000+ screens over the next three yrs. The investment will cover everything from improved sound and projection to upgrading dining experiences plus, in some locations, investing in attractions like pickleball and ziplines. (Variety)

FinTech/InsurTech/Payment

- Abu Dhabi’s Mubadala Investment Co has taken a significant stake in Revolut, one of the fastest-growing digital banks. The sovereign wealth fund invested through a share sale, marking a pivotal moment as Revolut continues its rapid expansion after securing a UK banking license in July 2024. This move underscores the confidence in Revolut’s growth trajectory and the increasing importance of digital banking in today’s financial landscape. (LINKEDIN)

- Affirm’s BNPL svs is now available as an option for qualified iOS 18 users when checking out w/ Apple Pay. Affirm lets approved users make purchases w/ biweekly payments or monthly payments. While Affirm is already a well-established buy-now-pay-later svs, integrating the feature into the Apple Pay checkout process will present the svs to even more users. (9to5Mac)

- JPMorgan Chase could take over as the backer of Apple’s credit-card program after the Apple and Goldman Sachs moved to part ways last yr, per The Wall Street Journal. Goldman and Apple have reportedly had discussions w/ a number of other banks, including Synchrony Financial, Capital One, and American Express about taking over as Apple’s banking partner. (Investopedia)

Handheld Devices & Accessories/Connected Home

- Apple annc’d California residents can add their driver’s licenses and state IDs to Apple Wallet on their iPhones and Apple Watches as part of the state’s mobile driver’s license (mDL) pilot program. Up to 1.5mn pilot participants can add the docs to Apple Wallet by scanning their driver’s license or state ID card using their iPhone and then providing a scan of their face using a “series of facial and head movements” as an added security measure. (The Verge)