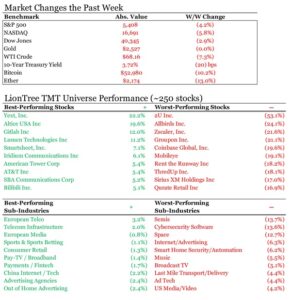

The first week of September didn’t start on the best footing with the markets taking it on the chin. Friday’s weaker than expected payroll numbers capped off the week of worries and fed into concerns about the economy. Nasdaq led the sell-off (especially semiconductors), down a massive -5.8% which was its worst week since Jan 2022. Nvidia’s stock fell -9.5% on Tuesday alone, losing $279bn in market value, which is now the record for the biggest single day drop for a US company. The S&P 500 did relatively better but was still down -4.3%.

Next week’s August CPI numbers will be a key catalyst looking ahead.

Fundamentally, it was also a very busy week with lots of key updates and developments. We dove into the below themes in this edition (all links are clickable):

- TV Channel Bundling Practices Moves Further Into The Spotlight

- Verizon Ups The Ante On Its Position In Convergence With The Frontier Acquisition

- The Upcoming Sports Season Is Set To Propel Sports Betting Activity In H2

- More Worries About Consumer Spend & Fraudulent Transactions

- Nvidia Was In The Regulator Spotlight This Week Along With A Few Other Regulatory Updates

- Big Investments Don’t Always Yield Big Successes In Gaming

- Key Platform Updates Across Snap Maps, Spotify “Daylists” And IG Stories

- Experimentation With Merging Sports & Entertainment…The UFC Take To The Sphere

- Digital Ad Market Forecasts Get An Upgrade

- Grab Bag: Amazon-Bally Sports Potential Deal / Nordstrom Take Private Submits Another Take-Private Bid / WBD’s New Global Experiences Division

Hope you have a nice weekend.

Best,

Leslie

TV Channel Bundling Practices Moves Further Into The Spotlight

On the heels of FuboTV winning its injunction again Disney, Fox and Warner Bros Discovery for launching their sports JV Venu, in which part of the argument was that they are disadvantaged economically because they are “forced” to buy long tail channels that subscribers don’t want so that they can get access to the valuable content like key sports…DTV and Disney are locking horns regarding their carriage renewal agreement and had similar arguments emerge. DTV doesn’t want to pay for a traditional full bundle of programming that its customers don’t care about and they do not want to be held to minimum penetration requirements. The Co instead wants to offer flexible lower cost genre bundles where consumers “only pay for the channels that they want to watch”. DTV also wants to provide subscribers with an aggregated experience. In their mind, this dispute is “really about changing the model in a way that gives everyone confidence that this industry can survive.”

Disney says it is seeking a fair agreement and contends that they have engaged in discussions about more flexible packages and that higher prices reflect the heavy investment they make for their top tier talent. Disney pulled the plug on its channels on DTV’s platform and DTV says it will endure as long as it takes given this is about “changing the model” of how networks are licensed and distributed to ensure the “survival” of the pay-tv industry. It sounds like this may not be a quick fix…

However, not all deals are contentious, and Charter and AMC Networks quietly announced an early renewal of their carriage agreement this week as well. It has some similar terms that where a part of the final Charter/Disney agreement last year.

Net net, there is a brightening spotlight on the industry practice of programmers requiring a portfolio of channels be packaged or bundled together (like sports with potentially less-watched entertainment networks) and minimum subscriber penetration guarantees regardless of if consumers want them or not. The outcome of this new DTV/Disney battle (in addition to the FuboTV/Venu situation) could set an important precedent for the industry going forward. See link for DTV detailed argument & slide deck and also other sources (link/link/link/link)

Below are more details on DTV/Disney, Charter/AMC Network, and the pay-tv ecosystem.

DTV Vs Disney – Round 1

DirecTV’s Stance –

- This is an “existential” fight: DTV argues that the industry’s current model is unsustainable, with high carriage fees driving up costs and leading to higher consumer churn

- “Video is all we have…and video is what makes up our future”

- The Co wants Disney to unbundle low demand channels so packaging aligns by genre vs having to buy traditional large packages with minimum penetration requirements “so consumers only pay for the channels that they want to watch”

- The Co wants to provide subscribers w/ “skinny, genre-based” bundles that are lower cost offerings, closer in price to DTC streaming options

- DTV says the pay-tv bundle should only have between 10-50 of the “most engaging” channels, which is a fraction of the “hundreds” of offerings in “bloated,” high-priced packages

- DTV data shows that only 6% of its customers are willing to pay more than $11 for ESPN and that programming costs related to Disney equates to ~$270/sub

- …DTV says Disney is seeking rates “north of that”

- DTV disclosed that on avg, only two-thirds of its customers watch a combined three hours or more across Disney’s portfolio of 16 channels, yet the agreement requires nearly all of its customers to pay for the full slate

- DTV also released data suggesting that the pay TV audience is somewhat segmented and niche, with less than 40% of users regularly tuning into live sports, and less than 40% of the audience regularly watching pure entertainment channels

- In total, DTV’s content costs for Disney alone amounts to ~$2bn per yr per the Co

- DTV also wants to be able to provide subscribers with an aggregated video experience: The Co wants to pair third party DTC services with its product as well

- Consumers are increasingly cutting the cord b/c they are frustrated with the number of services they must pay for and navigate to access content

- DTV is interested in the ability to incorporate the DTC apps consumers want at their choosing but not forced on a majority of subscribers

- The Co pointed to Disney’s recent decision to shutter TV Everywhere apps (which provide free streaming access using pay TV provider login credentials) for apps like Watch ABC, DisneyNow, Freeform, FXNow and Nat GeoTV as further restricting options for pay TV consumers and hurting the value proposition, while bolstering its own DTC apps

- DTV is committed to changing the industry model

- This dispute is “really about changing the model in a way that gives everyone confidence that this industry can survive”

- DTV will endure “as long as it needs to” to secure fundamental changes in the way networks are licensed and distributed; “We’re prepared to take this as long as it needs to.

- Other key comments

- DTV alleges that Disney demanded that it waive future claims of anti-competitive behavior as part of the negotiation, which DirecTV rejected

- DTV supports FuboTV’s lawsuit against the Venu JV, viewing it as a challenge to the industry’s longstanding bundling practices

- DTV also argues that programmers are shifting their best content away from linear while still raising programming rates, which drives more pay-tv subscriber declines and that they are devaluing content within the cable bundle by making premium content exclusive or available at lower cost on their own DTC apps, where consumer would need to pay twice

- DTV alleges that Disney demanded that it waive future claims of anti-competitive behavior as part of the negotiation, which DirecTV rejected

Disney’s Position –

- Disney claims it is seeking a fair agreement and accuses DTV of denying subscribers access to content during crucial sporting events like the US Open, college football, and the NFL season

- “DirecTV chose to deny millions of subscribers access to our content just as we head into the final week of the US Open and gear up for college football and the opening of the NFL season”

- Disney rejects DTV’s claims that it refused to engage in discussions about more flexible packages, labeling these accusations as “blatantly false”; “While we’re open to offering DirecTV flexibility and terms which we’ve extended to other distributors, we will not enter into an agreement that undervalues our portfolio of television channels and programs”

- DTV acknowledged that Disney offered some sort of skinny bundling or flexibility during ongoing negotiations but indicated they were still tied to minimum penetration guarantees and other terms that DTV felt had too many negative implications for its business to agree to

- Disney argues that they invest heavily in top-tier content, which justifies their pricing and packaging strategies

Current Status –

- Disney has gone dark on DTV: Disney blacked out its channels on DTV just before a major college football game, which DTV argues was a deliberate move to pressure them during negotiations

- DTV says it is willing to endure the blackout as long as necessary to secure these changes, despite the approaching NFL season.

Meanwhile Charter Quietly Moves Forward With An Early Carriage Renewal With AMC Networks

- Not too much detail was disclosed but the agreement includes streaming apps similar to the deal with Disney (link): Charter will be including AMC’s ad-supported AMC+ at no addtl cost to Charter’s Spectrum TV Select customers; Charter will make AMC+ available for purchase to its millions of Internet-only customers

- With the addition of AMC+, Charter, through its programming deals, will be providing its Spectrum TV Select Plus customers more than $40/month in retail value for streaming apps, and over $30/month in retail value for Spectrum TV Select/Select Signature customers

- Financial terms of the agreement were not disclosed but term length = “multiple years to come”

An Update On The Current Status Of The Pay-Tv Eco-System

- In Q2, the US pay-tv industry lost another 1.62mn subs to 68.76mn; It fell -6.9% y/y vs -6.8% y/y in the yr-ago qtr (link): This is per MoffetNathanson research; Ex vMVPDs, the rate of decline among “traditional” pay-tv providers (cable, satellite and telco) was -12.6% y/y, worse than -11.3% y/y a year earlier which is the tenth consecutive quarter of double-digit declines

- US cable lost -1.03mn in Q2

- Satellite lost -495k

- Telcos lost -144k

- vMVPDs (YouTube TV, Fubo, Sling TV, etc.) added 49k, an improvement from a yr-ago loss of -6k subs, reaching 19mn

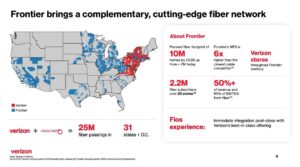

Verizon Ups The Ante On Its Position In Convergence With The Frontier Acquisition

In a surprise move, Verizon announced the acquisition of Frontier Communications this week in an all cash $20bn deal. Verizon’s broadband bias has been fixed wireless access (FWA) but this firmly adds more size and scale to its fiber portfolio in a complementary way. This will set the stage for the company to be more competitive in offering both premium broadband and wireless to its customers, as it sees strong financial results from these multi-product offerings given the lower churn benefits that convergence brings (also note that the Co’s philosophy is not to discount the individual components of a converged offering given the critical nature of both wireless and broadband).

The transaction will be immediately accretive to both revenue and EBITDA growth upon close and will be accretive to EPS and FCF in the 1st yr post close. Verizon also expects at least $500mn of run rate operating cost synergies by year three.

Collectively, Verizon and Frontier currently have ~10mn fiber customers across 31 states and Washington, D.C., with their fiber networks passing ~25mn premises. Its fiber passings are expected to grow to 30mn at the time of close (in 18 months).

Overall, this certainly bolsters the Co’s fiber broadband position but it also doesn’t reflect any change in commitment to FWA as well. Per CEO Hans Vestberg, Verizon has “unparalleled strength in broadband and wireless, the best wireless network and the best customer base, we’re differentiated from our competitors in a significant way.”

We included more details below on what we found most important regarding the transaction.

-> This announcement was a big stock driver…In the days from the leak to through the formal announcement, Frontier rallied +38.0% closing Wednesday night at $38.68, which is +0.5% above the offer price; Lumen Tech rallied +14.2%, Altice +13.39%, and AT&T was up +0.4%, while Verizon fell -3.4%

- Transaction basics –

- Total offer: $20bn in cash or $38.50/shr for Frontier, a ~44% premium to the 90-Day volume-weighted avg share price on September 3rd (before media reports emerged)

- Timing: Expected to close in ~ 18 months

- Refinancing/tax losses: Expect to refinance Frontier’s existing debt and inherit its existing net operating tax losses

- Modest impact to leverage ratio: Expect a modest increase in net unsecured debt to adjusted EBITDA ratio of ~0.2x to 0.3x at close

- No chg to capital allocation priorities

- Accretive to both revenue and EBITDA growth upon closing: It will be accretive to EPS and FCF in the 1st yr post close

- Expect at least $500mn of run rate operating cost synergies by year 3: Synergies driven by network integration, third-party contract synergies and customer experience improvements, go-to-market savings on marketing and advertising, as well as incr’d efficiencies and savings from duplicative functions and other efficiencies in wholesale and small business groups

- About half of the synergies are in the network: Access costs/transport, etc.

- The other half is around go-to-market and some redundant costs: Marketing, advertising, and customer experience improvement

- Also see the opportunity for revenue synergies from mobile and home convergence, including cross-selling benefits: But this is not baked in

- Significantly expands Verizon’s fiber footprint, accelerated delivery of premium mobility and bband services; It will also power VZ’s intelligent edge network

- “We already have a rapidly growing customer base in fixed wireless access. We have the best mobility customer base in the industry. Now, we’re adding size and scale to our best-in-class fiber offering”

- Frontier has invested $4.1bn over 4 years to upgrade its network

- Frontier derives more than 50% of its revenue from fiber products

- It has Net Promoter Score “6x higher than the closest cable competitor”

- Complementary footprint: Frontier’s customer base is in markets that are highly complementary with Northeast and Mid-Atlantic focus

- Frontier intends to maintain its plan to build out 2.8mn passings and reach its goal of 10mn locations by 2026

- Frontier expands VZ’s fiber footprint in 22 new states

- Fiber over FWA? Verizon is still very committed to BOTH FWA and fiber; The deal does not reflect anything different to that

- It doesn’t sound like additional fiber acquisitions are in the plan given the scale and distribution Verizon gets with the deal

- Why now? “The economics of this deal and the time to market was, of course, very, very appealing for us”

- Will now have one of the largest bband footprints available and have owners’ economics on that as well

- Proforma fiber position will be 30mn homes passed by 2026

- Verizon is a little north of 60mn FWA homes passed currently

- Still believe in convergence without discounting individual product components and that leads to attractive financial accretion: “Two great products should not be discounted…wireless and broadband are critical”

- They see 50% reduction in mobility churn when they bring the two products together and a 40% reduction in fiber churn when they do that as well; They see similar numbers on the FWA side as well

- That translates into accretion both on revenue and EBITDA immediately

- They see 50% reduction in mobility churn when they bring the two products together and a 40% reduction in fiber churn when they do that as well; They see similar numbers on the FWA side as well

- Also reaffirmed previous full year 2024 guidance

Additionally, There Were A Couple Other Key Updates On The Connectivity Front This Week…

- AST SpaceMobile sets Sept. 12th target date for its first commercial satellite launch (link/link)

- What will the launch entail? The goal is to send up five “BlueBird” satellites so they can relay high-speed internet to unmodified smartphones on the ground; The Co is using a Falcon 9 rocket from SpaceX for the launch

- The launch will enable AST SpaceMobile to start beta tests of its cellular satellite system for mobile phones as soon as December

- This will be the largest ever commercial communications arrays to be deployed in low Earth orbit

- What will coverage look like?

- The first five BlueBird satellites will be enough for it to offer a “non-continuous” cellular broadband svs across the US and in select markets globally; It is planned to support beta test users for AT&T and Verizon (AST SpaceMobile’s two major investors on the project) and will target ~100% nationwide coverage w/ 5,600+ coverage cells in the US

- Will need to launch between 45 to 60 satellites before AST SpaceMobile can offer “continuous” coverage in the US

- Launch is happening after a bit of a delay: The Co originally planned launch the first batch of BlueBirds in Q1, but a supply chain issue delayed work on the satellites

- What will the launch entail? The goal is to send up five “BlueBird” satellites so they can relay high-speed internet to unmodified smartphones on the ground; The Co is using a Falcon 9 rocket from SpaceX for the launch

-> AST SpaceMobile’s stock was up +12.5% on the back of the news, but still ended the week down -10.1%

- SoftBank to launch Eutelsat OneWeb satellite connectivity services in Dec. 2024 (link)

- Based on its partnership with Eutelsat Group, SoftBank will offer eight different service plans with high communication speeds and low latency under the “Eutelsat OneWeb” name to businesses, government agencies and local governments in Japan

- Will enable “high quality, highly secure satellite communications services in maritime and mountainous areas, where connectivity is difficult to provide with ground-based mobile networks”

- Potential applications: Remote control and monitoring of construction machinery, video transmission and remote operations using consistent communication speeds with guaranteed bandwidth, and the provisioning of secure communication lines when disasters occur

- Part of SoftBank’s goal to build a “Ubiquitous Network” that combines ground-based terrestrial networks and non-terrestrial network (NTN) solutions to bring connection to the most remote locations

The Upcoming Sports Season Is Set To Propel Sports Betting Activity In H2

As the NFL season kicks off, the stakes are higher than ever – not just on the field, but in the betting world as well. The NFL is poised to see a record $35bn in gambling this season, marking a +30% increase from last year. Meanwhile, DraftKings and White Hat Gaming face fines in Connecticut after a glitch made an online slot game impossible to win, with DraftKings also required to implement stricter internal controls. As legal gambling continues to surge, both opportunities and regulatory challenges are on the rise, which will definitely be shaping the future of the rapidly evolving industry. See below for the updates.

- NFL is expected to see record $35bn in gambling this season, per the American Gaming Association (link)

- That’s a ~30% increase from the amount bet on the NFL last year and is based on data released by some states on the amount wagered on pro football

- More than 95% of that betting will be done online

- Three states have launched legal online betting markets since last NFL season, and they are Maine, North Carolina and Vermont; Overall, 38 states and the District of Columbia have legal betting markets entering the NFL season

- For comparison, the NFL’s power in the gambling world is ~12x times greater than that of March Madness, for which the AGA projected $3bn in wagers (link)

- That’s a ~30% increase from the amount bet on the NFL last year and is based on data released by some states on the amount wagered on pro football

- Connecticut fines DraftKings and White Hat Gaming over impossible-to-win game (link/link): The Connecticut Department of Consumer Protection’s (DCP) Gaming Division has fined both operator DraftKings and the game’s supplier White Hat Gaming after finding that a glitch was stopping an online slot from producing wins

- What was the glitch? Deal or No Deal Banker’s Bonanza ran 20,000+ plays without producing a single win over the course of seven days following the game’s launch; ~522 players in Connecticut wagered a combined total of ~$24,000 without a win being handed out

- False advertising: The game was advertised as paying out almost 95c for every dollar wagered

- What caused the glitch? The problem was a technical flaw, as a computer glitch had incorrectly set the odds to zero, meaning the game was unable to register wins

- What was the fine? DraftKings was fined $19k, while White Hat was fined $3,500; While White Hat Gaming “responded swiftly” to investigators’ inquiries, DraftKings’ response “was not satisfactory” hence the higher fine

- DraftKings also refunded back players the money from their plays during the affected week

- DraftKings will also have to make procedural changes: “As a result of the DCP investigation, [DraftKings] was instructed to implement greater internal controls for their products, submit regular reports for new games to DCP, and make improvements to their consumer complaints process,” a spokesperson for the DCP said

- Not the first fine for DraftKings: In July, the New Jersey Division of Gaming Enforcement fined DraftKings $100,000 for “gross errors and failures” in reporting inaccurate sports betting data

- What was the glitch? Deal or No Deal Banker’s Bonanza ran 20,000+ plays without producing a single win over the course of seven days following the game’s launch; ~522 players in Connecticut wagered a combined total of ~$24,000 without a win being handed out

More Worries About Consumer Spend & Fraudulent Transactions

A swath of retailers have been issuing results over the last few weeks with mixed commentary on the consumer and this week we had a couple more datapoints that signal more pressure on consumer spend. Also, consumers are getting more worried about fraud and fraudulent credit card transaction hit a new high. See more details below…

More Data Pointing To Consumer’s Feeling Pressure…

- Dollar Tree Q2 earnings disappoint and the FY outlook is cut

- Q2 headline misses: Rev of $7.37bn missed cons by -1.6%; EPS of 97c was below cons $1.04

- Lowered FY guidance: Net sales now expected to be b/w $30.6bn-$30.9bn (vs prior $31bn- $32bn); EPS b/w $5.20-$5.60 (vs prior $6.50 to $7.00)

- Seeing weaker sales, particularly on the discretionary side of the biz: “Dollar Tree has a broader customer base that includes more middle and upper-income households and beginning this quarter, we started to see inflation, interest rates and other macro pressures have a more pronounced impact on the buying behavior of these customers. This impacted our second quarter comp performance and is the primary driver of our revised full year outlook”

- Comes after Dollar General also cut its FY sales and profit outlook, citing “a core customer who feels financially constrained”

-> Dollar Tree plunged -22.2% post its print and ended the week down -21.3%; YTD, the stock is down -53.2%

- Dick’s Sporting Goods beat Q2 cons estimates, but issued cautious guidance

- Q2 headline results beat: Rev of $3.47bn beat by +0,9%; EPS of $4.37 came in above cons $3.86

- Some mixed results across FY guidance –

- Raised EPS of $13.55-13.90 which beat cons $13.84 and was up from prior guidance $13.35-13.75, but at the midpt was only an 18c raise, even though Q2 EPS beat by 51c

- Reaffirmed rev $13.1-13.2bn which was below cons $13.26bn

- Raised comp sales growth to +2.5-3.5% vs prior guidance +2.0-3.0% and cons +2.9%

- “The difference between the high end of the range or the low end of the range is balancing the macroeconomic uncertainties that exist, as the consumer continues to be under pressure and we are balancing our optimism and our confidence in our core strategy against the macroeconomic backdrop”

-> Dick’s Sporting Good fell -4.9% post its report and further fell through the week to end down -12.2%; That being said, YTD the stock is still up +41.6%

Consumer Concern On Identity Theft And Fraud Is Up Y/Y, Per Experian (link)

- 84% said they worry about identity theft, up +20ppts y/y

- 80% said they worry about bad actors acquiring their card information, up +19ppts y/y

- Older generation is more concerned: Of those aged 55-69, 86% said they were concerned about someone stealing their credit card information, compared with 71% of respondents aged 25-29

- 71% said they worry about criminals using AI to commit fraud

- Growth in concerns mirror a surge in losses to fraudulent credit card transactions: Consumers lost $10bn to fraud in 2023, up +14% y/y and the highest dollar amount the agency ever recorded

Nvidia Was In The Regulator Spotlight This Week Along With A Few Other Regulatory Updates

Nvidia was in the regulatory spotlight this week but it ended being a little bit of a he said-she said situation. It started with Bloomberg reporting that NVIDA received a subpoena from the DoJ in an antitrust investigation, citing sources. The gripe was reportedly that Nvidia is making it very hard for customers to change suppliers and penalizing buyers who use other companies’ AI chips in addition to Nvidia’s. The regulatory officials apparently are trying to determine if Nvidia gives preferential treatment to customers who either use its technology exclusively or buy its complete systems. Nvidia’s acquisition of Run:ai is cited as part of the investigation as well (link/link).

While an official inquiry is clearly not confirmed, it is confirmed that the DoJ is doing work around Nvidia’s market position and we suspect we are likely to hear more about this looking ahead.

Aside from the back and forth on the status of a DoJ investigation on Nvidia, there were a couple other key regulatory oriented updates out this week:

- The Competition and Markets Authority (CMA) has launched an investigation into Ticketmaster regarding the sale of tickets for the upcoming Oasis reunion tour (link): The investigation focuses on whether Ticketmaster breached consumer protection laws, particularly concerning the use of ‘dynamic pricing’, which may breach consumer protection or competition laws in certain circumstances.

- Timing/next steps: The CMA is in the initial stages of its investigation and is collecting evidence from Ticketmaster, the band’s mgmt, event organizers, and consumers; The CMA issued a call for evidence from consumers by 5pm on Thursday, September 19, 2024

-> Separately but related, Live Nation’s President, Joe Berchtold, expressed confidence at an investor conference this week that they will prevail against the DOJ lawsuit alleging anti-competitive practices tied to its Ticketmaster acq, despite acknowledging the potential political challenges; He emphasized that Live Nation and Ticketmaster operate separately but complement each other, enhancing profitability from concerts; While the trial may not begin until early 2026, the Co remains focused on improving customer experience, transparency, and addressing issues like bot enforcement in ticket sales (link)

- The CMA also provisionally found that Google may have breached competition law by favoring its own ad tech services in the open-display ad market, causing harm to “thousands” of UK publishers and advertisers (link): Similar investigations are being conducted by the US Department of Justice and the European Commission

- Key concern:

- Google is accused of “self-preferencing” its ad exchange, AdX, by using its dominant mkt position in both publisher ad servers and ad-buying tools

- The CMA believes Google’s practices have restricted competition, disadvantaging rival ad exchanges and publisher ad servers

- Next Steps: The CMA will consider Google’s representations before making a final decision and the CMA is exploring measures to ensure Google stops these practices and prevents future anti-competitive behavior

- Key concern:

Big Investments Don’t Always Yield Big Successes In Gaming

The hit-driven nature of the video game industry is still at play and was underscored this past week as two highly anticipated games underperformed despite significant investment. Ubisoft’s newly released Star Wars Outlaws failed to meet sales expectations despite significant marketing investments, while its ongoing title XDefiant continues to struggle with player retention. Meanwhile, Sony’s Concord, which was in development for 8 years, faced such poor reception that it was pulled just two weeks after launch. Similar to many other industries, substantial spend doesn’t always guarantee success. See below for details.

- Analysts cut Ubisoft sales forecasts following poor performance of Star Wars Outlaws and declining players interest in XDefiant (link/link/link/link)

- “Star Wars Outlaws has struggled to meet our sales expectations despite positive critical reviews,” said JPMorgan analyst Daniel Kerven.

- Star Wars Outlaws was released on PlayStation 5, Xbox Series X/S, and PC on August 30, 2024 and was the first open-world Star Wars video game

- Lowered sales expectations by -2mn: Down to 5.5mn units sold through March 2025

- The game had the highest marketing budget for any game released by the studio to date: The game reportedly cost 30% more than Assassin’s Creed Mirage, but was underperforming that game by 15%, according to Twitch data

- Xdefiant has also come in under expectations, according to Midcap Partners analyst Charles-Louis Planad

- Despite a successful launch with 11mn+ unique players, the free-to-play shooter game has reportedly been struggling to retain the audience and barely reaches 20k peak concurrent players across all platforms (down from a record of 1mn uniques and 8mn total in its first week)

- Assassin’s Creed Shadows release on Nov 15 will be Ubisoft’s next test

- “Star Wars Outlaws has struggled to meet our sales expectations despite positive critical reviews,” said JPMorgan analyst Daniel Kerven.

-> Ubisoft’s stock has fallen to a 10-yr low, with the stock falling -5.1% on Monday and continuing to fall on September 3rd, ending the week down -15.2%; YTD, the stock is down -37.0%

- Sony to shut down multiplayer shooter game Concord following poor sales of the game (link)

- Concord launched as a $40 game after eight years of development

- But it will go offline only 2 weeks after launch: The first-person hero shooter launched exclusively on PS5 and PC on Aug, 23rd, and will be taken down on Sept. 6th

- Sales have come in at <25k and reached an all-time peak of 697 players on Steam, which is lower than the launch peak of The Lord of the Rings: Gollum (widely regarded as the worst game of 2023)

- “While many qualities of the experience resonated with players, we also recognize that other aspects of the game and our initial launch didn’t land the way we’d intended”

- Players who purchased the game will be issued a refund and once refunded, will not longer have access to the game

- Was entering an extremely competitive genre, where incumbents like Overwatch are free to play

- Could re-launch w/ different model: Will “explore options, including those that will better reach our player…while we determine the best path ahead”

Key Platform Updates Across Snap Maps, Spotify “Daylists” And IG Stories

Arguably the biggest challenge that media platforms face is not just growing, but maintaining user engagement, and platforms have been ramping up efforts through feature updates in order to keep the user on their respective apps. There were several innovative updates out on that front this week. Snap circulated an internal memo on its 13th anniversary, which touched upon several initiatives that are in the works, including testing a simplified version of the Snapchat app. Spotify has also expanded its dynamic “daylist” playlists globally, and Instagram now allows public comments on Stories. More on all this below.

- Snap circulated an internal memo detailing changes to the Snapchat app + addtl incremental updates (link)

- Adding new ad formats –

- Sponsored Snaps will appear in the chat inbox as a new Snap without a push notification, and opening the message is optional

- Will be the first time that ads will appear in the messaging section of Snapchat

- Promoted Places will enable bizs to use the Snap Map to reach incremental customers who are exploring places nearby, and easily measure the visitation lift with Snap’s closed-loop and privacy-safe measurement

- Will be the first time Snap will monetize its maps features

- Sponsored Snaps will appear in the chat inbox as a new Snap without a push notification, and opening the message is optional

- Testing a “further simplified” version of Snapchat: Aims to improve accessibility and usability; Early tests have been “directionally positive” but “will be thoughtful and deliberate about making a change of this magnitude”

- Key quotes from the letter –

- On share price performance: “You may be wondering why, with all of the progress we’ve made in our business over the last year, our share price performance has lagged the overall market. The answer is simple: our advertising business is growing slower than our competitors”

- On competitive position within smart glasses space: “Unlike in digital advertising, where we were a late entrant in a market with established, scaled players, we are a leader in the market for this new type of glasses and in the development of our augmented reality platform”

- Adding new ad formats –

- Spotify launches “daylist” playlists globally (link)

- What is a daylist? It’s a personalized playlist that evolves throughout the day depending on a user’s listening habits

- How does it work? At the time of launch, Spotify said that it uses data of “niche music and microgenres” that a user listens to at a particular time of the day to suggest tracks and update the daylist

- Now available in all markets –

- Introduced first to English-speaking mkts in Sept ’23, including US, Canada, UK, Australia, New Zealand, and Ireland

- Expanded further in March ’24 to 65+ countries

- Now launching the feature in all markets where Spotify is available

- Also adding support for 14 new languages, including Arabic, Catalan, German, Japanese, Korean, and more

- Have seen initial success in early launches…: After the expansion in March, 70% of daylist users would come back weekly to access the playlist

- …but few other details have been shared: Haven’t specified how many users overall have used this feature or how much music discovery it is driving

- What is a daylist? It’s a personalized playlist that evolves throughout the day depending on a user’s listening habits

- Instagram adds comments to Stories (link)

- Adds a more public way to respond to Stories: Previously, replying to an Instagram story sent a private message visible only to the person who posted the content; With the update, anyone who can view a users’ Stories can also see the comments

- Will be an optional feature: Users will have the option to turn comments on or off for any story they share, and users can preserve comments by saving the story post as a highlight

Experimentation With Merging Sports & Entertainment…The UFC Take To The Sphere

Due to an unexpected course of events with a scheduling conflict with hosting its upcoming MMA event at MGM on September 14th, the martial arts flighting league UFC turned to Las Vegas’ The Sphere to host their event. This will be the first live sporting event to he hosted at the $2.3bn venue. UFC CEO Dana White was inspired by the Sphere’s technology during U2’s residency and envisioned the venue’s potential for live sports.

The “Riyadh Season Noche UFC” event will combine MMA fights with immersive storytelling using the Sphere’s massive 160k sq-ft curved LED screen. Each fight will take place in a different “world” projected on the screen, telling a larger story that celebrates Mexico’s contributions to combat sports. The event includes films directed by Academy Award-nominated Carlos López Estrada, serving as interludes between the bouts.

This will be a costly experiment though, costing UFC over $20mn, while most of the UFC’s PPV fights cost about $2mn and the original budget was $8nm, underscoring the scale and ambition of the project.

Dana White sees the event as a “game changer” that merges sports and entertainment, potentially influencing how future arenas are designed and used but this event might be a one and done event given UFC’s existing deal with MGM to host events at T-Mobile Arena in Las Vegas. Regardless, it could influence how other sporting events are produced if proven to be successful. “If you take what U2 did and multiply it by a million, that’s where we are.” (link)

Digital Ad Market Forecasts Get An Upgrade

Political election ad spend, cyclical events (like the Summer Olympics) and a more resilient economy are all signs that the Interactive Advertising Bureau (IAB) pointed to when it revised its 2024 digital ad market forecast upward, now expecting +11.8% y/y growth, up from the previous +9.5% y/y projection. Upward revisions were broad-based across almost all channels and indicate an H2 growth rate that will more than double that of H1. See below for the details.

IAB Upgrades Its Digital Ad Outlook And Now Expects The Sector To Grow +11.8% In 2024 (link)

- Marks an upwards revision from the earlier +9.5% projected increase from last November

- What’s driving the change?

- An acceleration in the ad market in recent months: Election ad spending and other cyclical events (i.e., Summer Olympics) is driving a +16% jump in the second half of 2024, vs +7.9% in the first half

- Fading worries about the overall economy: “The resilient economy, marked by a 2.3% rise in consumer spending in Q2 2024, has eased buyers’ concerns,” it says; While 49% of buyers said last November they were worried about a slowing economy, today 38% have that concern

- By channel – nearly all are expected to post higher growth rates y/y, with the exception of “Other Traditional Media (Radio, Print, OOH, Direct Mail”

Grab Bag: Amazon-Bally Sports Potential Deal / Nordstrom Take Private Submits Another Take-Private Bid / WBD’s New Global Experiences Division

- Amazon reportedly nearing deal to stream Bally Sports content (link/link)

- Reportedly in late-stage talks for a contract to livestream on Amazon Prime this coming season

- Expected to include all the Bally Sports broadcasts of 13 NBA franchises, as well as five MLB teams and nine NHL teams

- Discussions are supposedly about a non-exclusive deal, which could allow Diamond to further expand its reach by signing deals with other platforms

- Viewers will reportedly pay ~$20/mo for access to their home team’s local games through Prime, which is what is what Bally Sports+ currently charges monthly

- Potential deal could help Diamond emerge from bankruptcy: To emerge from bankruptcy, Diamond needs to convince the judge it will be a feasible company going forward, and through the reported deal, it could argue that it can increase its subscriber base significantly by going through Amazon

- Reports come just weeks after Amazon allegedly walked away from a $115mn deal to acquire streaming rights for certain NBA teams from Bally Sports (link)

- Nordstrom family makes $3.8bn offer to take the retailer private (link)

- Joining with Mexican retail group El Puerto de Liverpool in their bid: The Mexican company, which bought an ~10% stake of Nordstrom in 2022, owns the department stores Liverpool and Suburbia and operates franchise locations for brands that include Gap, Banana Republic, Williams Sonoma and Pottery Barn in Mexico

- Following the proposed deal, the Nordstrom family would own 50.1% of the business, while Liverpool would own 49.9%

- What do the offer details look like? The group is offering $23/shr in cash, a <1% premium over the stock’s recent trading price and less than half of the $50/shr it offered in 2018 during a failed attempt to take the Cod private

- What comes next? A special committee of the Nordstrom board said it would review the proposal

- Joining with Mexican retail group El Puerto de Liverpool in their bid: The Mexican company, which bought an ~10% stake of Nordstrom in 2022, owns the department stores Liverpool and Suburbia and operates franchise locations for brands that include Gap, Banana Republic, Williams Sonoma and Pottery Barn in Mexico

- Warner Bros. Discovery creates a new global experiences division (link/link)

- What groups are being consolidated? Consolidating its “Global Themed Entertainment” licensing group and its “Studio Tours & Retail” group under one umbrella

- What does that cover across WBD’s business? The Co’s worldwide studio tours, retail destinations, touring exhibitions, and all location-based experiences

- What will be the division’s responsibilities? “Will be charged with strategically expanding the company’s fan facing experiences and pursuing new businesses that capitalize on the Company’s world-class intellectual property…and its award-winning operated businesses including Warner Bros. Studio Tours in London, Hollywood, and Tokyo”

- This restructure is “very much an investment and expansion strategy, so no personnel impacts are involved”

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- ADWEEK has exclusively learned that Omnicom Media Group and WPP have won Amazon’s media review. “After a comprehensive advertising agency review for our consumer biz, we’ve chosen to partner w/ OMG and WPP,” Amazon spokesperson Margaret Callahan said in a statement. Amazon calls the decision a strategic move to benefit from the best of what both agencies have to offer. (ADWEEK)

- Disney is expected to generate close to $4.5bn in streaming ad rev in 2024, mostly thanks to Hulu, Sahil Patel of The Information reports, citing a person w/ knowledge of the co’s ad biz. Only Alphabet’s YouTube, and possibly Amazon, are bigger in streaming ads, according to the website. (TipRanks Financial)

- Over a quarter of advertisers plan to reduce spending on Elon Musk’s X (formerly Twitter) due to concerns over content and trust, according to Kantar research. Since Musk’s $44 billion acquisition, ad revenue has plummeted, with global revenue forecast to drop to $1.9 billion in 2024. Marketers’ trust in the platform has significantly declined, with only 4% believing X offers brand safety. (the Guardian)

Artificial Intelligence/Machine Learning

- Qualcomm’s exclusivity on Copilot+ PCs is ending, with Intel’s 200V processors and AMD’s Ryzen AI 300 series chips set to support Copilot+ features starting in November. These AI-enhanced PCs include tools like Live Captions, image generation in Paint, and Auto Super Resolution for gamers. Intel’s 200V series boasts up to 48 TOPS for AI tasks, while AMD’s chips offer 50 TOPS. Copilot+ features will be available as a free update for eligible devices. (Engadget)

- Synthetic data is increasingly used to train AI models where real data is scarce, offering scalability and control. While beneficial, it poses challenges like bias and reliability issues. AT&T balances real and synthetic data for AI training, using synthetic data for scenarios like network forecasting. Despite its advantages, synthetic data requires validation with real data to ensure accuracy and effectiveness. (Fierce Network)

- The US, UK, and European Union have signed the first “legally binding” treaty on AI, which is supposed to ensure its use aligns with “human rights, democracy and the rule of law,” according to the Council of Europe. The treaty, called the Framework Convention on Artificial Intelligence, lays out key principles AI systems must follow, such as protecting user data, respecting the law, and keeping practices transparent. (The Verge)

- YouTube annc’d a new set of AI detection tools to protect creators, including artists, actors, musicians and athletes, from having their likeness, including their face and voice, copied and used in other videos. This system will be expanded to include new synthetic-singing identification technology to identify AI content that simulates someone’s singing voice. Other detection technologies will be developed to identify when someone’s face is simulated with AI, the company says. (TechCrunch)

Audio/Music/Podcast

- Spotify won a court case where it was accused of streaming Eminem’s music without proper licensing. Despite finding that Spotify lacked a license, the judge ruled it not liable for lost royalties. The court noted that Kobalt Music Group, which managed royalties for Eminem’s publisher, may be responsible for any penalties. (BBC)

Cable/Pay-TV/Wireless

- AT&T has been awarded a 10-yr contract to support the US Department of Homeland Security (DHS) with Government Emergency Telecommunications Service (GETS) and Wireless Priority Service (WPS). The contract, initially awarded in Mar 2024 and valued at $146mn, was expanded in Aug to include next generation 5G networks. This contract marks the continuation of a more than 30-yr partnership between AT&T and DHS. (THEFASTMODE)

- AT&T has shared new details on its negotiations with the Communications Workers of America (CWA) as the strike enters its third week. AT&T claims to have made a “strong final offer,” including an 18% wage increase over five years and enhanced healthcare contributions. However, the CWA accuses AT&T of bargaining in bad faith. Despite ongoing discussions, the strike continues, with no resolution in sight. (Yahoo News)

- Cable TV viewership continues to decline in 2024, now accounting for just 26.7% of all TV viewership, while streaming has risen to 41.4%, according to Nielsen. Broadcast TV holds 20.3%, and 11.6% comes from other methods. Overall TV viewership increased by 2.3% in July 2024, driven by events like the Summer Olympics in Paris. (Cord Cutters News)

- Dish Network, burdened with over $20 billion in debt, is in talks with creditors to resolve a lawsuit over a controversial asset transfer. The discussions, involving potential extension of a $2 billion bond due in November, may occur this week. The lawsuit demands Dish undo transfers that moved assets out of bondholders’ reach. (Bloomberg Law)

- Emirates Investment Authority, operating under the e& brand, has increased its stake in Vodafone Group to 15.01%, now holding 3.94bn voting rights worth £3bn. This follows a strategic partnership allowing e& to raise its stake to just under 25%. The U.K. government has expressed national security concerns due to Vodafone’s strategic role, leading to the establishment of a national security committee to oversee sensitive activities. (RCR Wireless News)

- The Communications Workers of America have informed AT&T and the Federal Mediation and Conciliation Service that it would no longer be a part of the mediation, it said in a statement. “The co was using the mediation process as another delaying tactic,” said CWA District 3 Vice President Richard Honeycutt. More than 17,000 Workers represented by the CWA union, which include technicians, customer svs representatives, and others who install, maintain, remain on strike which began last month. (Yahoo Finance)

- The FCC approved $9bn to expand 5G internet access to rural Americans, aiming to bring high-speed internet to millions who currently lack options. FCC Chairwoman Jessica Rosenworcel emphasized the urgency of using the 5G Fund to connect rural households and businesses. An auction will allocate the funds to companies to develop 5G services, though widespread availability may take years. (Cord Cutters News)

- The US pay TV industry lost 1.62mn customers in Q2, with YouTube TV showing a seasonal trend, gaining subscribers during the NFL season but losing 150,000 in Q1 and only adding 50,000 in Q2. The vMVPD market overall sees disconnects post-NFL season, with growth expected in Q3. DirecTV Stream gained 86,000 customers, while platforms like Sling TV are capitalizing on the situation. (Yahoo Finance)

- Virgin Media O2 is reportedly seeking outside investors to help fund its £5bn (€4.5bn) newly created network co to challenge market leader BT Group, according to a Bloomberg report. The co, which is also being backed by Infravia Capital Partners, is investing £1bn in the UK’s broadband infrastructure, aiming to reach 5mn premises by 2026. The sale that could represent between 20 and 40% of the co could get underway as soon as Oct. (ADVANCED-TELEVISION)

Cloud/DataCenters/IT Infrastructure

- SK Telecom (SKT) and SK Broadband are set to launch an 800Gb/s next-gen backbone network across South Korea, with a successful test on a 1,200km stretch between Seoul and Busan. They are preparing to meet rising data demands from 5G, AI, and cloud services. SKT also tested a 1.2Tb/s peak rate at its Incheon data center, using advanced optical technology for efficient, reliable traffic transmission. (Mobile World Live)

Crypto/Blockchain/web3/NFTs

- The Federal Trade Commission found the amount of money lost to Bitcoin ATM scams increased nearly 10x from 2020 to 2023, going from $12mn to $114mn. Consumers have already lost $65mn to the ruse in the first half of 2024 alone. (The Verge)

Cybersecurity/Security

- Leaked Disney data this summer included financial, strategy details, and personal info of staff and customers, such as passport numbers and addresses. Over a terabyte of data, including Disney+ revenue, park pricing, and cloud login credentials, was leaked by hacking group NullBulge. The breach involved 44mn Slack messages, revealing computer code and details of unreleased projects. (Yahoo Finance)

- Salesforce acquired Own Company, a data management and protection firm, for $1. 9bn in cash. This marks Salesforce’s largest deal since acquiring Slack in 2021. Own, founded in 2015, provides enterprise data backup, security, and recovery solutions. The acquisition aims to enhance Salesforce’s data protection offerings, supporting its commitment to secure, end-to-end solutions for its customers. (TechCrunch)

EV/ Autonomous Vehicles

- Tesla has launched the long-awaited “Actually Smart Summon” feature, allowing owners to summon their car to a specific location via the Tesla app. Additionally, the “Dumb Summon” feature lets users move the vehicle forward or backward. “Actually Smart Summon” is currently available only on vehicles with Hardware 4, with potential future availability on Hardware 3. The features are intended for use in parking lots or driveways. (TESLARATI)

Film/Studio/Content/IP/Talent

- According to Samba TV, 902,000 U.S. households watched the premiere of The Lord of the Rings: The Rings of Power Season 2 within four days, a significant drop from the 1.8mn who watched Season 1’s premiere within three days. Despite this sharp decline, the show is expected to still appear on Nielsen charts. Amazon has not released its own data, and the full impact will be clearer with delayed Nielsen reports. (Deadline)

- Warner Bros is set for a significant release with the sequel “Beetlejuice Beetlejuice,” directed by Tim Burton and starring Michael Keaton. The film is projected to open with $100M-$110M domestically and a global start of up to $145M, marking the first September release in seven years to surpass $100M in its opening weekend. Strong presales and the inclusion of Jenna Ortega are contributing to high expectations. (Deadline)

FinTech/InsurTech/Payments

- Alibaba Group plans to launch a US credit card, the Business Edge Credit Card, to encourage small businesses to buy products on Alibaba. Developed with Cardless on Mastercard’s network, the card offers 3% cash back or 60-day interest-free terms on purchases up to $40,000. It has a $199 annual fee and aims to boost confidence in buying from China-based suppliers as Alibaba seeks international growth amid domestic challenges. (Yahoo Finance)

- Alibaba’s Taobao and Tmall will soon accept Tencent’s WeChat Pay, marking a significant collaboration between China’s largest tech firms. This move allows Chinese consumers to use WeChat Pay, the country’s second-largest mobile payment system, on Alibaba’s e-commerce platforms, which had previously relied on Alipay. The cooperation follows the end of China’s antitrust review of Alibaba and aims to enhance market reach, especially in lower-tier regions and among elderly users. (South China Morning Post)

- Vodafone Germany partnered w/ messaging co Horisen and Dimoco Payments to develop a public transport ticketing concept based on Rich Communication Services and Direct Carrier Billing (DCB), a solution the trio claimed will be the first of its kind. In an annc’mnt, Horisen stated it will provide its own biz messenger platform for the svs, which allows commuters to book transportation tickets through Vodafone’s RCS messaging and pay directly through their phone bills. (Mobile World Live)

HealthTech/Wellness

- Carlyle Group has selected banks for an initial public offering of Acrotec Group, which could be valued at as much as 4bn Swiss francs ($4.7bn), according to people familiar w/ the matter. Beyond the Seine Bank of America Corp., Morgan Stanley and USGroup AG are working on the potential Zurich listing of the luxury-watch parts maker. Deliberations are ongoing and details of the IPO including valuation, timing and the bank lineup could still change, the people said. (Bloomberg law)

Last Mile Transportation/Delivery

- Delivery Hero has hired banks to work on the listing of its Talabat unit in Dubai, preparing to cash in on a flood of IPOs in the Gulf. The German food delivery co has lined up Emirates NBD Bank PJSC, Morgan Stanley and JPMorgan Chase & Co for the deal, people familiar w/ the matter said, asking not to be named discussing confidential information. The share sale could raise about US$1bn (RM4.35 bn), they said. (The Edge Malaysia)

- Lyft will sell some assets related to its bike and scooter rental operations and cut jobs, the ride-sharing svs provider said, as part of a restructuring plan to rein in costs. The co, which offers the popular Citibike svs in NYC and runs similar operations in other US cities, had in Jul. 2023 said it was exploring options for the unit after having received “strong inbound interest”. Lyft did not provide details on the operations it would retain but disclosed about $34mn-$46mn in charges. (Yahoo Finance)

- Uber and Turo have announced a multi-year partnership allowing Uber customers to rent vehicles from Turo’s extensive selection directly through the Uber app, starting in 2025. This collaboration will expand Uber Rent’s offerings in key markets, boost Turo hosts’ entrepreneurial opportunities, and support shared transportation goals, targeting a $150B+ market across the US, UK, Canada, Australia, and France. (NEWSWIRE)

Macro Updates

- Job openings data released showed the labor market continued to cool in July. New data from the Bureau of Labor Statistics showed there were 7.67mn jobs open at the end of July, a decrease from the 7.91mn seen in Jun. (AP News)

- The Bank of Canada cut key interest rates by a quarter of percentage point, bringing its overnight rate down to 4.25%. “If inflation continues to ease broadly in line with our Jul. forecast, it is reasonable to expect further cuts in our policy rate. We will continue to assess the opposing forces on inflation, and take our monetary policy decisions one at a time,” said Bank of Canada Gov. Tiff Macklem in an opening statement at a news conference following the decision. (MarketWatch)

- US manufacturing activity shrank in Aug for a fifth month, reflecting faster rates of declines in orders and production. The Institute for Supply Management’s manufacturing gauge edged up 0.4 point to 47.2, data out showed. A reading below 50 indicates contraction. The group’s measure of production slid for a fifth month, deeper into contraction territory, to the lowest level since May 2020. (Bloomberg)

Online Marketplaces/Learning (Real Estate/Education/Jobs)

- Rupert Murdoch’s News Corp REA Group said that it was considering a possible cash and share offer for Rightmove, but that it had yet to have any discussions with the company, in statements to the Australian and UK stock markets. Shares in Rightmove surged by 27% to £7.08 after the news, making it the top riser on the FTSE 100 and giving it a market value of £5.8bn. Rightmove is the UK’s leading property portal market, and estate agents across Britain use the site to advertise properties for sale and rent. (the Guardian)

Social/Digital Media

- A federal judge has ruled that social media cos can’t be required to block certain types of content from teens. The ruling will prevent some aspects of a controversial social media law in Texas from going into effect. The ruling came as the result of tech industry groups’ challenge to the Securing Children Online Through Parental Empowerment (SCOPE) Act, a Texas law that imposes age verification requirements and other policies for how social media cos treat teenage users. (Engadget)

- The Supreme Court confirmed an order to ban X in Brazil and fine those who don’t comply with it by using a virtual private network, or VPN. All five judges on the top court panel voted in favor of the decision to shut down the platform. X can still appeal the decision, after the conclusion of the hearing. (Yahoo Finance)

Software

- Salesforce has entered into a definitive agreement to acquire Tenyx, a co specializing in artificial intelligence-powered voice agents. This move is expected to augment Salesforce’s customer svs by creating more natural and engaging conversational experiences. The cos did not reveal the financial details or other terms of the transaction. The completion of the acquisition is anticipated for the Q3 of Salesforce’s FY 2025, which concludes on Oct. 31, 2024. (Yahoo Finance)

Sports/Sports Betting

- Banks led by Goldman Sachs Group launched an $850mn leveraged loan to help fund Formula 1 owner Liberty Media Corp’s acquisition of MotoGP World Championship, according to a person familiar w/ the matter. A lender call was held at 2 p.m. New York time and commitments are due, the person said. Initial discussions call for a spread 200bps over the Secured Overnight Financing Rate offered at a discounted price of 99.5 to 99.75 cents on the dollar. (Liberty Media)

- DAZN and the NFL are expanding their 10-year partnership, offering the 2024 NFL season on NFL Game Pass via DAZN in 200+ markets, alongside YouTube and Amazon in select regions. Following a successful first year with a 61% Super Bowl viewership increase and 30% subscriber growth, the 2024 season promises more games with local commentary, ad-free replays, and interactive features, aiming to broaden the NFL’s global fan base. (ADVANCED-TELEVISION)

- ESPN announced it will use generative AI to write recaps for Premier Lacrosse League and NWSL matches, starting Friday. Each AI-generated story will be reviewed by a human editor and labeled as “ESPN Generative AI Services.” The decision sparked outrage on social media, with critics questioning its benefit. ESPN defended the move, stating it allows staff to focus on in-depth coverage while ensuring all matches are covered. (Front Office Sports)

- Roku has annc’d a multi-yr renewal of its deal w/ the NFL that brings back The NFL Zone on the Roku platform in the US just in time for the 2024-25 season. Within the NFL app, fans can subscribe to NFL, which includes access to live out-of-market preseason games, live audio from every game, a 24/7 stream of NFL Network, or NFL Premium to access NFL RedZone. This yr, NFL can be purchased using Instant Signup and Roku Pay, making it easier for users to subscribe to NFL. (TVTechnology)

- Steph Curry is considering NBA team ownership as part of his post-basketball plans. The four-time NBA Champion and 10-time All-Star expressed interest in owning a team, inspired by former superstar Michael Jordan’s ownership of the Charlotte Hornets. Curry believes he could contribute to sustaining the NBA’s success and is keeping ownership on the table as a future goal after his playing career ends. (CNBC)

- The Los Angeles Rams are valued at $8bn, while the Chargers are worth $5.83bn, largely due to stadium economics. Rams owner Stan Kroenke owns SoFi Stadium, keeping 85% of its revenue, including from non-NFL events, while the Chargers, mere tenants, receive only 15%. This revenue disparity, rather than team performance, drives the $2bn value gap between the teams. (CNBC)

- Vizio is launching a new Sports Zone hub on its TV home screen, making it easier for users to find and stream live and on-demand sports content from various apps. The Sports Zone organizes games by sport, offers event pages with all streaming options, and allows users to create personalized watchlists. This feature enhances Vizio’s home entertainment experience, just in time for the fall sports season. (Broadcasting Cable)

- Warner Bros Discovery is suing the NBA to reclaim broadcasting rights after being excluded from a new deal that awarded rights to Amazon, ESPN, and NBC. WBD claims its contractual right to match Amazon’s offer was improperly disregarded. The lawsuit’s expedited schedule could still extend past the start of the 2025-26 NBA season if not dismissed by the New York Supreme Court. A resolution could disrupt future NBA broadcasts if WBD wins. (The Streamable)

Tech Hardware

- China spent more on chipmaking equipment in the first half of the yr than South Korea, Taiwan and the US combined amid a frantic push to localize chip supplies and mitigate the risk of further Western export restrictions, according to global chip industry association SEMI. China spent a record $25bn on chip tools in the first six months of 2024, SEMI data showed. China maintained robust spending into Jul. and could be on track for another full-yr record. (Nikkei Asia)

- Intel is exploring options for its stake in Mobileye Global as part of a strategic overhaul. Mobileye shares hit a record low after Intel’s potential move was revealed. Intel may sell part of its 88% stake amid ongoing financial struggles for both companies. Mobileye’s value has plummeted due to declining automotive demand, leading to significant revenue and income losses. (Bloomberg)

- Telefonica, Ericsson, and MATSUKO have successfully integrated holographic calls into a smartphone dialer using IMS Data Channel technology. The collaboration between Telefonica, Ericsson, and MATSUKO has culminated in one of the most complex demonstrations of IMS (IP Multimedia Subsystem) Data Channel technology to date. IMS Data Channel is a cutting-edge, standards-based technology that enhances existing IMS voice networks, enabling mobile network operators to deliver improved svs to millions of users. (THEFASTMODE)

Towers/Fiber

- Nokia agreed to a multi-yr deal to provide AT&T w/ its next-generation fiber access technologies across the US operator’s current footprint and for future expansions. While financial terms of the five-yr agreement were not disclosed, it is a large customer win for Nokia after AT&T opted for rival Ericsson’s open RAN equipment in 2023. AT&T executives have touted the co’s fiber deployment plans as being key for its long-term success, which includes the convergence of mobile and fiber-based svs. (Mobile World Live)

- Total global revenue for the Broadband Access equipment market decreased to $4.2bn (€3.1bn) in Q2 2024, down -8% y/y, according to a report from Dell’Oro Group. Spending, however, did improve by 4% from Q1 2024, which saw the lowest total spending in nearly three yrs. “Cable operators continue to feel squeezed between fiber ISPs and Fixed Wireless providers who are siphoning away their valuable residential subscribers,” said Jeff Heynen,VP with Dell’Oro Group. (ADVANCED-TELEVISION)

Video Games/Interactive Entertainment

- As the SAG-AFTRA video game strike continues, the union announced that 80 games have signed agreements allowing them to continue using union performers during the dispute. These agreements ensure proper compensation and AI protections for actors. Notable studios like Studio Wildcard and Lightspeed LA have signed on, supporting the union’s demands for AI consent and wage increases, while major companies remain in a standoff with SAG-AFTRA. (The Hollywood Reporter)

Video Streaming

- Rakuten TV is now available on Virgin TV in the UK, offering over 8,000 on-demand titles, 150+ FAST channels, and new releases to rent or buy. Virgin TV customers can access Rakuten TV directly without a subscription, enjoying free content with ads, live TV channels, and premium movies. The partnership enhances Virgin TV’s entertainment options, providing diverse content at no extra cost. (ADVANCED-TELEVISION)

- VIZIO has annc’d that its WatchFree svs has been expanded to the VIZIO mobile app for iOS and Android devices in the US. Users can now take over 300 channels on the go, even if they don’t have a VIZIO. WatchFree users can watch the latest local sports, news and a variety of entertainment programming. WatchFree+ allows users to pick up where they left off on their VIZIO TV at home directly on their phone, so they never miss a second of their favourite content. (ADVANCED-TELEVISION)

- YouTube is expanding its existing set of parental controls w/ a new feature that would allow a parent to link their account to their teen’s account in order to gain insight into the teen’s activity across the video-sharing platform. Once linked, parents will be alerted to their teen’s channel activity, including the number of uploads, subscriptions, and comments — not the content. The new experience builds on the parental controls YouTube introduced back in 2021. (TechCrunch)