This was a big week for the connectivity sector with earnings across the big three incumbent telcos, not to mention some other updates on the deal front as well. The rest of the ad agencies also reported. Theme #1 details the earnings scorecard thus far.

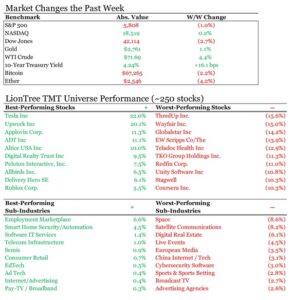

The overall market was a bit mixed, with the S&P down about -1%, while Nasdaq squeaked out a gain (its 7th straight up week – helped by Tesla’s +22% rally).

See below for what we focused on in this week’s edition (all links are clickable):

- Earnings Scorecard – Week 1 & 2

- US Telcos Bet On Broadband As Core Postpaid Phone Trends Diverge

- TKO Makes A Move To Augment Its Position In Premium Sports

- Some Key Updates & Milestones Regarding Next Gen Transport

- Several “Major Forces” That Are Shaping The TMT Sector Are…

- MORE Pushback On The Frontier/Verizon Deal Struck This Week

- Strategic Predictions For IT Organizations & Users Through 2029, Per Gartner

- Ad Agency Holding Co Earnings Follow-Up – It Was A Tale Of Two Cities Between IPG & WPP

- Grab Bag: Netflix Shutters AAA Game Studio/Ray-Ban Meta Glasses Are Seeing “Strong Demand”/ Amazon Reportedly Working On Low-Cost Storefront

Also, I wanted to flag that LionTree served as the exclusive financial advisor to Grandview on its sale to TPG’s Initial Group.

Enjoy the read.

Best,

Leslie

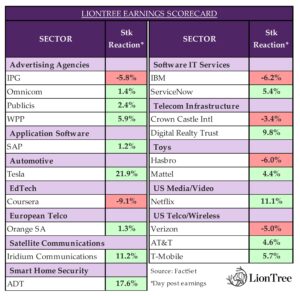

Earnings Scorecard – Week 1 & 2

Twenty companies in our LionTree Universe have already reported their third quarter results. Stock price reactions were biased to the upside, with 14 companies (70%) trading up in reaction to their numbers and 6 companies (30%) trading down. The best performer was Tesla, which was up a +21.9% post its report, and the worst performer was Coursera, which fell -9.1% in reaction.

Netflix kicked off earning on a strong note last week, with the stock up +11.1% (see Theme #1 from last week for the recap). Ad agency reports were spread out over this week and last, with Omnicom and Publicis both trading up +1.4% and +2.4%, respectively (see Theme #4 from last week), while market reactions were more divergent for WPP and IPG’s reports this week, up +5.9% and down -5.8%, respectively (see Theme #8 ).

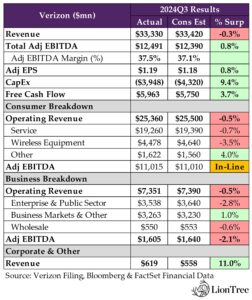

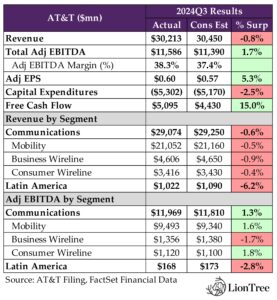

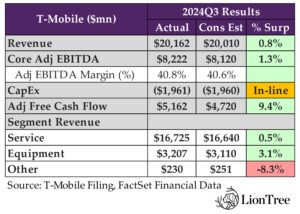

The highlight of this week came from the connectivity sector, as the three big telcos shared their quarterly results. Verizon saw the toughest reaction from the Street, down -5.0%, while AT&T and T-Mobile were received more positively, trading up +4.6% and +5.7%, respectively (see Theme #2).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe.

US Telcos Bet On Broadband As Core Postpaid Phone Trends Diverge

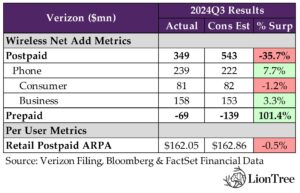

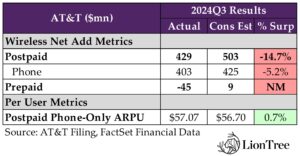

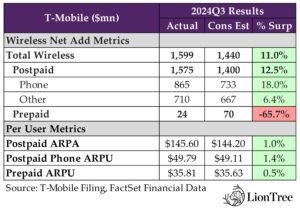

The earnings cycle kicked off in the connectivity industry, with the US incumbent telcos batting lead-off this week and cable companies Comcast and Charter on-deck to publish their results next week. T-Mobile performed the best relative to expectations, beating on all fronts while Verizon and AT&T’s headline numbers were mixed. In the core postpaid phone segment, T-Mobile recorded its best Q3 net adds in a decade with +865k (a wide +18.0% ahead of cons). Verizon’s +239k postpaid phone net adds also surprised to the upside by a solid +7.7%, driven by stronger than expected contributions from Business and a turnaround in Consumer. In contrast, AT&T’s +403k postpaid phone net adds missed sell-side estimates by -5.2% (the first miss on postpaid phone net adds by one of the major incumbent telcos in the last six quarters!). Looking ahead, commentary suggests that Verizon and AT&T’s postpaid phone net adds will improve sequentially in Q4, though T-Mobile’s could take a step down on an absolute basis.

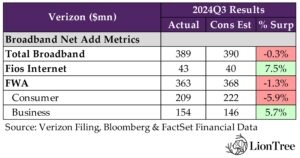

On the broadband side, T-Mobile, again, stood out from the pack, beating expectations for its high-speed Internet net adds by +4.0% and continuing to acquire most of its new FWA customers from cable companies and existing T-Mobile cohorts. Verizon’s total broadband net adds were a slight -0.3% below consensus estimates, but the bigger story was its plan to cover well over 100mn homes with its broadband offerings in the combined Verizon- Frontier footprint and new FWA subscriber targets of 8-9mn by 2028. For AT&T, better than feared non-Fiber subscriber net losses were unable to offset a -11.9% miss on Fiber net adds, though this was primarily due to a one-month work stoppage in the Southeast and the impact of the recent hurricanes on the company’s pace of fiber installations in the region. Internet Air has been an incremental source of net new broadband subscribers for AT&T, though deployments remain “strategic.”

Regarding some puts & takes on FCF and returns to shareholders, despite some obstacles from higher cash taxes and other factors, all three telcos generated higher than expected FCF in Q3. However, T-Mobile’s buybacks were lower than expected after multiple run-ups in its share price caused the company to rethink its approach, and Verizon communicated that its CapEx levels will be higher in 2025 to account for its fiber investments. Moreover, there was also some discussion about the upcoming 6G cycle…

A few other key comments to flag upfront include: 1) In response to a question about possibly raising the bid for Frontier, given all the pushback from Frontier shareholders, Verizon emphasized that its agreement with Frontier followed a “competitive process”, reflected its “best and final” offer, and that it would be “fair and good for all shareholders”; 2) T-Mobile expects that its fiber JVs and agreement to acquire USCellular will all likely receive final regulatory approval at various points throughout 2025; and 3) AT&T surprised some sell-side analysts when it said it “won’t rule out” the possibility of opening its network to wholesale.

See below for more details on our key takeaways from the telcos’ latest round of earnings calls.

-> AT&T is hosting an Analyst and Investor Day on December 3

-> Verizon shares dropped -5.0% in reaction to earnings and closed the week down -5.9%; AT&T shares rose +4.6% in response to earnings but ended the week ~flat; T-Mobile shares were up +5.7% post-earnings but finished the week up just +1.4%; YTD, Verizon stock is still trading up +9.8%, AT&T stock is up +30.1%, and TMobile stock is up +41.2%

There Were Some Puts & Takes W/ Headline Results, Though T-Mobile Was A Clear Standout

- Verizon printed MIXED headline numbers, missing on rev but slightly beating forecasts on adj EBITDA: Rev was ~flat y/y in Q3 (vs +0.6% y/y in Q2) and closed -0.3% below cons; Adj EBITDA grew +2.1% y/y (vs +2.8% y/y in Q2) and topped cons by +0.8%; Adj EPS of $1.19 beat by +0.8%; FCF came in +3.7% ahead of cons

- Consumer (~76% of total rev) – IN-LINE TO BELOW: Q3 rev was up +0.4% y/y (vs +1.5% y/y in Q2) and missed cons by -0.5%; Adj EBITDA rose +1.8% y/y (vs +2.8% y/y in Q2) and ended ~in-line w/ cons

- Business (~22% of total rev) – MISS: Rev fell -2.3% y/y in Q3 (vs -2.4% y/y in Q2) but closed -0.5% behind cons; Adj EBITDA was down -3.7% y/y (vs -3.5% y/y in Q2), missing cons by -2.1%

- AT&T – Headline results were MIXED, w/ a shortfall on the top-line and a beat on adj EBITDA: Q3 rev was down -0.5% y/y (vs -0.4% y/y in Q2) and missed cons by -0.8%; Adj EBITDA rose +3.4% y/y (vs +2.6% y/y in Q2) and topped cons by +1.7%; Adj EPS beat cons by +5.3%; FCF finished +15.0% above cons

- Mobility (~72% of Communications rev) – MIXED: Rev grew +1.7% y/y in Q3 (vs +0.8% y/y in Q2) but missed cons by -0.5%; Adj EBITDA was up +6.7% y/y (vs +5.3% y/y in Q2) and beat cons by +1.6%

- Business Wireline (~16% of Communications rev) – MISS: Q3 rev fell -11.8% y/y (vs -9.9% y/y in Q2) and missed cons by -0.9%; Adj EBITDA decr’d -20.0% y/y (vs -13.9% y/y in Q2) and closed -1.7% below cons; “Cont’d industry-wide secular declines in legacy voice svs” were a headwind

- Consumer Wireline (~12% of Communications rev) – MIXED: Rev incr’d +2.6% y/y in Q3 (vs +3.0% y/y in Q2), ending -0.4% below cons; Adj EBITDA grew +8.6% y/y (vs +3.0% y/y in Q2) and beat cons by +1.8%, benefiting from broadband growth and ongoing cost transformation efforts

- T-Mobile – Headline numbers broadly BEAT: Q3 rev incr’d +4.7% y/y (vs +3.0% y/y in Q2) and beat cons by +0.8%; Core adj EBITDA grew +8.9% y/y (vs +9.4% y/y in Q2) and topped cons by +1.3%; FCF came in +9.4% ahead of cons

- Service rev (~83% of total rev) – BEAT: Rev grew +5.1% y/y in Q3 (vs +4.4% y/y in Q2) and closed +0.5% ahead of cons

- Equipment rev (~16% of total rev) – BEAT: Q3 rev was up +4.3% y/y (vs -2.0% y/y in Q2) and topped cons by +3.1%

Verizon And AT&T Are On Track To Achieve Their FY24 Guidance, While T-Mobile Set Its Sights Higher

- Verizon maintained its initial FY24 outlook –

- Total wireless svs rev is still expected to grow +2.0-3.5% y/y

- Reiterated profitability targets:

- Adj EBITDA growth between +1.0-3.0% y/y, vs cons +1.9% y/y

- EPS range of $4.50-4.70 vs cons $4.59

- AT&T remains “on pace to deliver” on its original FY24 guidance –

- Wireless svs rev growth in the +3% y/y range

- Broadband rev growth of over +7% y/y

- Adj EBITDA growth in the +3% y/y range

- Adj EPS between $2.15-2.25, which was in-line w/ cons at the mid-pt

- T-Mobile raised its FY24 guidance –

- Postpaid net adds were upped by +150k at the mid-pt: Now projects +5.6-5.8mn (vs +5.4-5.7mn prior)

- Core adj EBITDA was incr’d by +$50mn at the mid-pt: Now expects between $31.6-31.8bn (vs $31.5-31.8bn prior), which was ~in-line w/ cons

- The ACP impact on adj EBITDA is now expected to be toward the higher end of the $350-450mn range: This has been driven primarily by declines among the Co’s wholesale providers

- Hurricane-related costs will also be incurred in Q4

T-Mobile Outperformed The Most On Postpaid Phone Net Adds / Business Adds Strong Across The Board / An iPhone Upgrade Super Cycle Is Unlikely In The Near Term

- Verizon – Postpaid phone net adds showed a “significant improvement y/y” and topped expectations: Q3 total retail postpaid phone net adds of +239k (vs +100k in the prior yr qtr and +156k in Q2) beat cons by +7.7%

- Consumer postpaid phone net adds turned positive but slightly missed: Posted +81k net adds (vs -51k the prior yr qtr and -8k in Q2), missing cons by -1.2%

- Growth in gross adds slowed seq: Q3 gross adds grew +5.9% y/y (vs +12.0% y/y in Q2); This was still the Co’s seventh straight qtr of y/y growth in gross adds, driven by local mkting efforts, structural changes to sales orgs, and myPlan

- Verizon is “not seeing a big upgrade cycle right now”: The Co’s total wireless upgrade rate of 3.00% (vs the prior yr qtr’s 3.40% and Q2’s 2.80%) was below cons 3.10%; “Customers are choosing to hang onto their phones [for] a lot longer”, upgrading every “40 months or so”, on avg

- The Co still projects positive Consumer postpaid phone net adds in FY24: Implies at least +85k Consumer net adds in Q4; Notably, this will be with and without contributions from second numbers

- The Business segment posted “another qtr of solid growth”: Business postpaid phone net adds incr’d +4.6% y/y in Q3 (vs +8.3% y/y in Q2) and beat cons by +3.3%; Noted “sustained buying activity throughout the qtr” as well as “contributions from SMBs, enterprises, and public sector customers”

- Churn incr’d seq and more than anticipated: Q3 total retail postpaid phone churn was down -10bps y/y to 0.89% (vs 0.85% in Q2) but was higher than cons’ 0.87%; Churn from the past yr’s 4-5 price hikes was lower than Verizon expected and will start falling over time, w/ cont’d efforts to “earn the trust of customer[s]”

- Consumer postpaid phone net adds turned positive but slightly missed: Posted +81k net adds (vs -51k the prior yr qtr and -8k in Q2), missing cons by -1.2%

- AT&T – Postpaid phone net adds decr’d seq and finished below forecasts: Postpaid phone net adds were down -13.9% y/y to +403k in Q3 (vs +419k in Q2) and missed cons by -5.2%

- The Co’s performance was “consistent w/ [its] wireless mkt normalization expectation”: Despite this environment, AT&T “grew efficiently w/ lower y/y postpaid phone churn and upgrade rates”

- Still, a “technology shift” has resulted in “a lot of [growth] coming from business”: Bizs that “traditionally purchase wireline svs… are now migrating certain products and svs to wireless”

- FirstNet has also been seeing “sustained growth”: FirstNet ended Q3 w/ ~6.4mn total connections (vs 6mn+ exiting Q2)

- AT&T’s postpaid upgrade rate fell even further below last yr’s levels: Q3 postpaid upgrade rate of 3.5% was down -40bps y/y (vs -20bps y/y in Q2) and missed cons’ 3.8%

- iPhone sales have been “down slightly over last yr’s levels on an introduction”: The Co is still waiting for the software release, though “whether or not that… drives interest in the consumer base to accel [sales] remains to be seen”

- Churn ticked down on a y/y basis: Postpaid phone churn was down -10bps y/y to 0.78% in Q3 (vs 0.70% in Q2) but was slightly higher than cons’ 0.77%; The Co expects to deliver the best postpaid phone churn in the industry for 13th time in 15 qtrs

- A seasonal pickup in activity is expected in Q4: Including seasonally higher phone purchasing activity, upgrades, and promo cycles

- The Co’s performance was “consistent w/ [its] wireless mkt normalization expectation”: Despite this environment, AT&T “grew efficiently w/ lower y/y postpaid phone churn and upgrade rates”

- T-Mobile delivered its best Q3 postpaid phone net adds in a decade: Q3 postpaid phone net adds incr’d +1.8% y/y to +865k (vs +777k in Q2) and beat cons by a wide +18.0%, driven by “cont’d y/y growth” in gross adds and “record low” Q3 postpaid phone churn

- T-Mobile cont’d to lead the industry in share of switchers: Grew its share of households in both top 100 & smaller mkts in rural areas and still has “lots of room to run in [its] under-penetrated areas and segments”

- T-Mobile’s NPS score in rural mkts is +20% higher than the next highest competitor: This helps the Co build on its “overall growth momentum” in smaller mkts and rural areas, where it has a number one win share

- The Business segment saw “positive trends in all segments”: Posted its “best activations on record” in enterprise, double digit q/q growth in net adds in govt, and “a lot of wins” w/ retail multi-site during the qtr

- Postpaid phone churn was lower than expected: Postpaid phone churn was down -10bps y/y to 0.86% in Q3 (vs 0.80% in Q2), ending below cons’ 0.90%

- Upgrade rates remained “low”: Consumers have devices “that generally work better” and “that are becoming more expensive and lasting longer”

- 2024 postpaid phone net adds are now forecast to be ~+3mn: Implies +826k postpaid phone net adds in Q4, which would represent a -100k y/y drop from the prior yr qtr; The guide was “cautious”, given Q4 has the two biggest months of the yr for the Co

- T-Mobile cont’d to lead the industry in share of switchers: Grew its share of households in both top 100 & smaller mkts in rural areas and still has “lots of room to run in [its] under-penetrated areas and segments”

T-Mobile Led The Group In Wireless Svs Rev Growth

- Verizon – Wireless svs rev growth decel’d seq: Q3 wireless svs rev rose +2.7% y/y (vs +3.5% y/y in Q2), as a full qtr’s impact of ACP’s conclusion as well as promo amortization posed headwinds

- It was a tale of two cities between Consumer and Business: Consumer wireless svs rev growth decel’d to +2.9% y/y (vs +3.7% y/y in Q2), while Business wireless svs rev incr’d +2.9% y/y (vs +2.4% y/y in Q2)

- “Seq growth” in wireless svs rev is expected in Q4: Driven by volume improvements, incr’d contributions from FWA, and recently communicated pricing actions, though partially offset by promo amortization

- AT&T – Mobility svs rev growth accel’d seq: Mobility svs rev incr’d +4.0% y/y in Q3 (vs +3.4% y/y in Q2), driven by “strong execution” in the Co’s “balanced go-to-mkt strategy”

- A ~$90mn adjustment boosted svs rev: This followed the Co’s efforts to align the timing of certain administrative fees

- T-Mobile’s svs rev growth and postpaid svs rev growth led the industry “by a wide margin”: Postpaid svs rev was up +8.3% y/y in Q3 (vs +6.9% y/y in Q2); Highlighted that this was ~+2x higher than peers’ svs rev growth

- FY24 svs rev growth is still expected to accel over 2023’s levels: YTD, T-Mobile’s svs rev is tracking +4.0% higher y/y, which is above the +3.1% y/y growth across 2023

Efforts To Expand Relationships W/ Customers Have Been Driving Up Postpaid ARPU/ARPA

- Verizon – Postpaid ARPA came in below forecasts: Total wireless retail postpaid ARPA of $162.05 rose +3.8% y/y in Q3 (vs +4.3% y/y in Q2) but slightly missed cons by -0.5%

- “Targeted pricing actions, FWA expansion, and the further adoption of myPlan are all contributing to ARPA growth”: MyPlan now represents 37%+ of Verizon’s consumer postpaid phone base, w/ the Co more than doubling myPlan subscribers since the end of last yr

- “Addt’ly, [myPlan] perk rev continues to provide a notable benefit”: Upselling customers on perks is creating “a lot of momentum on the price side” and is helping to reduce churn; The Co has 7mn perks in its biz and plans to double that by this time next yr

- “Targeted pricing actions, FWA expansion, and the further adoption of myPlan are all contributing to ARPA growth”: MyPlan now represents 37%+ of Verizon’s consumer postpaid phone base, w/ the Co more than doubling myPlan subscribers since the end of last yr

- AT&T – Postpaid phone ARPU growth topped estimates: Q3 postpaid phone ARPU of $57.07 was up +1.9% y/y (vs +1.4% y/y in Q2) and beat cons by +0.7%; Growth was “largely driven by higher ARPU on legacy plans” as well as efforts to get customers to “buy up and get more… products and svs”

- The ~$90mn one-time adjustment also benefited postpaid ARPU

- Mid-Q3 price increases are still expected to be a tailwind in Q4: These have already been baked into the Co’s guidance

- BUT ARPU growth could start plateauing in 2025: The Co would like to “do a little better at the low-end of the mkt overall” next yr, and this “would naturally come at a little bit of a play on ARPU”; That said, this “wouldn’t bother” the Co

- T-Mobile – Postpaid ARPA was better than anticipated: Postpaid ARPA of $145.60 incr’d +4.1% y/y in Q3 (vs +2.6% y/y in Q2) and beat cons by +1.0%

- ARPA growth has been driven by “a number of factors”: The rate plan optimization was “a very minor component”

- In Consumer, the Co has been “really seeing strength in growth of and expansion of customer relationships”, including w/ 5G home broadband and other connected devices;

- T-Mobile for Business has seen “a lot” of success w/ ARPA expansion across segments

- “Cont’d strength” in ARPA prompted the Co to raise the FY24 guide: Now expects FY24 ARPA in the ~+3% y/y range (currently tracking +2.9% higher y/y YTD)

- Postpaid phone ARPU growth also topped estimates: Q3 postpaid phone ARPU of $49.79 was up +1.7% y/y (vs +0.5% y/y in Q2) and beat cons by +1.4%; That said, this is a “very mix-driven metric”, and the Co tends not to focus on it

- ARPA growth has been driven by “a number of factors”: The rate plan optimization was “a very minor component”

The Telcos Saw Some Divergent Trends In Prepaid, BUT The ACP Impact Is In The Rearview Mirror

- Verizon – Prepaid net losses reflected a “turnaround” in the biz: Q3 total prepaid net losses of -69k (vs the prior yr qtr’s -207k and Q2’s -694k) were better than cons’ -139k

- Excluding SafeLink, prepaid net adds were positive for the first time since the TracFone acq: Delivered +80k prepaid net adds, excluding SafeLink (vs -12k in Q2)

- The Co’s core prepaid brands “continue to perform well”: Excluding SafeLink and the related ACP impacts, Visible, Total Wireless, and Straight Talk combined to drive a total y/y improvement of over +300k net adds

- The headwind from ACP ending was higher than expected: Prepaid rev declined by ~-$40mn in Q3 as a result of the conclusion of the ACP program, representing a -100bps headwind compared to the Co’s prior expectation it would create a -50bps headwind

- BUT ACP pressures are now “firmly behind” Verizon: The Co “further distanced” itself from the effects of the ACP shutdown in Q3 and is “confident that the rigor being applied to [its] prepaid operations will position [it] well going into 2025”

- AT&T’s prepaid biz underperformed expectations: Prepaid net losses of -45k (vs +56k the prior yr qtr and +82k in Q2) were worse than cons’ +9k; Prepaid churn of 2.73% was down -5bps y/y (vs +7bps y/y in Q2)

- Still, the Cricket brand “continues to display remarkable consistency”: The Cricket brand has posted positive phone net adds for 40 consecutive qtrs or a decade straight

- T-Mobile – Prepaid net adds were underwhelming: Q3 prepaid net adds of +24k (vs +79k the prior yr qtr and +179k in Q2) were -65.7% below cons, though commentary was limited

- Prepaid churn was higher than expected: Prepaid churn was down -3bps y/y to 2.78% in Q3 (vs 2.54% in Q2) but still ended above cons’ 2.74%

- Prepaid to postpaid conversion was “consistent” w/ “recent history”: Saw +175k net transfers from prepaid to postpaid in Q3, which was in-line w/ trends seen over the past five yrs and indicative of “vibrant economic times”

Commentary On The Promotional Environment & Go-To-Mkt Trends Was Consistent

- Verizon “continue[s] to be disciplined w/ [its] promo spend”: The Co has been “maintaining [its] targeted and segmented approach to customer retention”

- The go-to-mkt approach for broadband offerings hasn’t changed: Verizon has been using “similar tactics” and “promotions” to support its “strong momentum in sales on Fios and FWA”

- “myHome has been a very successful launch”: “A lot of [Verizon’s] base tends to like the perks” and have been “tak[ing] on new perks” upon sign up, as “they like the ability to share their perks between mobile and phone”

- Verizon is “very disciplined about [its] retention spend”: “It has to be demand-led”, and “customers have to want it”

- The go-to-mkt approach for broadband offerings hasn’t changed: Verizon has been using “similar tactics” and “promotions” to support its “strong momentum in sales on Fios and FWA”

- AT&T – The industry is “competitive”, but players are behaving rationally: AT&T “can understand” what its competitors have been trying to achieve in the mkt and what it has “in terms of [its] long-term ability to compete against [them] in an effective fashion”

- The Co has “a lot of flexibility” to scale up device promos in Q4, if necessary: The Co’s “balanced” go-to-mkt strategy through the first three qtrs of the yr have positioned it “adjust to whatever takes place” in the device mkt

- AT&T is fine-tuning its distribution in the biz mkt: “There’s still some segments in the biz mkt where we can be more present and effective, especially given what we’re able to do on a combined basis, the introduction of Internet Air in addition to selling voice products as well as our fiber footprint”

- The Co has “tried to be disciplined” about not pursuing lower-quality growth: AT&T feels good about “the balance of [its] growth to the quality of [its] growth”

- T-Mobile continues to have a “winning formula”: The Co has a “unique proposition of best network, best value, and best experience; “The Un-carrier stands for superior value”, and T-Mobile will continue to use this as its “North Star” moving forward; Otherwise, commentary on the competitive environment was limited

Telcos, In Aggregate, Posted A Y/Y Decline In Total Broadband Adds, BUT Verizon’s New FWA Targets Were Front & Center

- Verizon’s total broadband net adds slightly missed BUT outlined plans to double its FWA base by 2028: Q3 total broadband net adds were down -22.7% y/y to +389k (vs +391k in Q2) and missed cons by -7.6%; Still, Verizon cont’d its streak of +375k broadband net adds for the ninth consecutive qtr

- FWA net adds missed, dipping seq and y/y: FWA net adds of +363k were down -5.5% y/y (vs -1.6% y/y in Q2) and closed -1.3% below cons, given the shift toward less dense, suburban-rural mkts; W/ nearly 4.2mn FWA subs, Verizon reached its goal of 4-5mn fifteen months ahead of schedule

- Both Consumer and Business FWA net adds took a step down seq: Consumer FWA net adds of +209k were down from Q2’s +218k and missed cons by -5.9%; Business FWA net adds of +154k slipped from Q2’s +160k but beat cons by +5.7%

- Outlook- Verizon now expects to double its FWA base to 8-9mn subs by 2028: The Co also plans to accel coverage to 90mn households over the same period (from 60mn currently) – More details below

- Fios net adds improved seq and were better than anticipated: Fios net adds fell -40.3% y/y to +43k in Q3 (vs +28k in Q2) and beat cons by +7.5%; After softness in Q2, the Fios biz is “back to normal again”

- The Co is aiming for an 80/20 contribution to svs from rev from broadband net adds: The Co recognizes the need to “balance P&Q” in terms of building a “long-term sustainable subscription biz”

- FWA net adds missed, dipping seq and y/y: FWA net adds of +363k were down -5.5% y/y (vs -1.6% y/y in Q2) and closed -1.3% below cons, given the shift toward less dense, suburban-rural mkts; W/ nearly 4.2mn FWA subs, Verizon reached its goal of 4-5mn fifteen months ahead of schedule

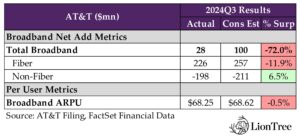

- AT&T – Broadband net adds declined seq and came in below forecasts: Q3 broadband net adds were up +86.7% y/y to +28k (vs +52k in Q2) but were well under cons’ +100k

- Broadband rev growth decel’d further: Consumer broadband rev grew +6.4% y/y in Q3 (vs +7.0% y/y in Q2 and +7.7% y/y in Q1); YTD, broadband rev is tracking +7.0% higher y/y, in-line w/ FY24 guidance

- Fiber net adds were temporarily impacted by a one-month Southeast work stoppage and the hurricanes: Q3 Fiber net adds fell -23.6% y/y to +226k (vs +239k in Q2) and missed cons by -11.9%, as the work stoppage and storms resulted in ~50,000 fewer net adds; Still sees “strong underlying demand for fiber”

- Fiber ARPU growth slowed slightly: Fiber ARPU of $70.36 was up +3.2% y/y in Q3 (vs +3.4% y/y in Q2), w/ an intake ARPU of ~$75 (vs “above $70” in Q2); The Co continues to see “solid uptake in higher-speed fiber tiers and healthy underlying pricing trends”

- Q3 was the first full qtr in which ARPU was impacted by the rollout of Autopay changes: Views Autopay as a long-term benefit for customers as well as operationally

- Fiber ARPU growth slowed slightly: Fiber ARPU of $70.36 was up +3.2% y/y in Q3 (vs +3.4% y/y in Q2), w/ an intake ARPU of ~$75 (vs “above $70” in Q2); The Co continues to see “solid uptake in higher-speed fiber tiers and healthy underlying pricing trends”

- Internet Air FWA net adds were ~consistent seq and is still being used strategically: Net adds of +135k in Q3 (vs +139k in Q2) brought the Internet Air base to nearly 500,000 total consumer subs; Although the offering is in more mkts, the Co has been using it “very strategically”

- The biz mkt is an “attractive mkt” for the product: Given the Co can bring in other products and svs, such as handsets, in the account to justify usage characteristics; Expects to continue scaling distribution in the mid-biz mkt

- The pace of Consumer net adds “is never going to rival what you’re seeing w/ anybody else”: Will use Internet Air selectively to migrate customers off copper and occasionally in mkts where there’s “surplus spectrum… in place for many, many years”

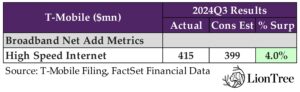

- T-Mobile – High speed internet (HSI) net adds improved seq and beat estimates: Q3 HSI net adds were down -25.5% y/y to +415k (vs +406k in Q2) but still came in +4.0% above cons

- In terms of drivers, “the broad trend lines haven’t changed much”: The majority of the Co’s new HSI customers continue to come from cable and existing T-Mobile customers

- “Customers just love this product”: The Co’s FWA offering is the “highest net promoter score, by some measures, product in the country”

- Avg speeds “are just like cable avgs” and are “rapidly improving”: The avg speed experience is 3x what it was three yrs ago; “It matches cable, but… it’s differentiated vs other fixed wireless offerings as well”

- Usage is at 0.5 TB/mo and growing

- T-Mobile for Business had “one of [its] strongest qtrs ever” for HSI net adds: Highlighted govt and DoD as areas where the Co had particular success w/ HSI

- “Churn trends have looked very nicely”: The Co has been “pleased” w/ the levels of churn it has seen over the past yr and a half

- The Co is now halfway to its long-term target of 12mn HSI customers by 2028: In Q3, T-Mobile crossed the 6mn threshold in just three yrs

- In terms of drivers, “the broad trend lines haven’t changed much”: The majority of the Co’s new HSI customers continue to come from cable and existing T-Mobile customers

Investment Updates – The Focus Was On Fiber Expansion Initiatives & Spectrum Plans / VZ’s New Bband Coverage Targets / AT&T Is Getting Stronger Than Expected Returns In Fiber Out Of Region

- Verizon set new broadband coverage targets, w/ plans to cover 100mn+ homes “in the future”: This is combined between the fiber and FWA networks, w/ the Co planning to accel FWA coverage to 90mn households (from 60mn currently) by 2028 and eventually pass 35-40mn homes w/ fiber

- Will reach coverage of 90mn FWA homes and bizs via “three key things”: Including the “aggressive deployment” of C-band and mmWave (ultra wideband), a new, 1 gig mmWave MDU solution rolling out in 2025, and leveraging its “vast small cell network”

- The Co will cover 80-90% of its planned footprint w/ ultra wideband by the end of 2025: Verizon plans to end 2024 w/ 70% coverage and will accel its deployment pace next yr

- Verizon sees a “clear path” to 35-40mn fiber passings “over time”: Expects 30mn+ fiber passings in the combined Verizon/Frontier footprint by 2028 (vs ~25mn currently) and 35-40mn fiber passings beyond that

- A “very small percentage” of those passings will be funded by BEAD: Verizon expects to reach 35-40mn passings with or without the program

- The Co is on track for ~500k Fios passings in 2024: The Co is targeting an expansion to +650k Fios passings in 2025 and believes it can grow that to over +1mn after the Frontier deal closes; Frontier is on pace to pass 10mn homes w/ fiber by the end of 2026

- The Co is targeting having 70% of its sites on C-band by the end of 2024: As well as 80-90% of sites on C-band by the end of 2025

- Verizon also further expanded its satellite capabilities: Partnered w/ Skylo, adding to Verizon’s ongoing work w/ AST SpaceMobile and extending the Co’s network to previously underserved areas

- Will reach coverage of 90mn FWA homes and bizs via “three key things”: Including the “aggressive deployment” of C-band and mmWave (ultra wideband), a new, 1 gig mmWave MDU solution rolling out in 2025, and leveraging its “vast small cell network”

- AT&T has now passed 28mn+ consumer and biz locations w/ fiber: The Co remains on track to pass 30mn+ fiber locations by the end of 2025 and doesn’t expect its pace of deployments to “dramatically change” next yr

- The Co has been seeing “better-than-expected returns” on its out-of-region fiber investment…: AT&T “can safely say [that] everything at the front end, customer acquisition, ARPUs, [its] rate of penetration… are looking very, very similar to what’s happening in region”

- … Which contributed to the potential expansion of its initial build target by ~10-15mn addt’l locations: Will provide more details on plans for AT&T Fiber at its Analyst and Investor Day on Dec 3

- “There’s things that we can do to start to moderate our capital intensity”: Particularly as the Co gets “better and better [at] driving costs down” and gets “some of these things behind [it] over time”

- BUT AT&T is “interested in the secondary mkt” for spectrum: Sees oppties to “pick up attractive spectrum that is harmonized w/ [its] existing holdings” as a “good move” for both shareholders and customers; Has the balance sheet “latitude and flexibility to do those kinds of things”

- The Co has been seeing “better-than-expected returns” on its out-of-region fiber investment…: AT&T “can safely say [that] everything at the front end, customer acquisition, ARPUs, [its] rate of penetration… are looking very, very similar to what’s happening in region”

- T-Mobile “expect[s] to extend” its 5G network lead “over time”: Evidenced by the fact that its “margin of superiority is greater today than it was two yrs ago”

- The Co has “so much more room to run” on its mid-band 5G upgrades: T-Mobile has only deployed ~60% of its mid-band spectrum (3.45 GHz) for 5G and is primarily targeting mkts “where there could potentially, over time, be a need to expand [the Co’s] capacity”

- Outlined the customer-driven coverage approach: The Co assigns to a CLV value to a grid across the country w/ 4mn+ 165-meter-wide hexagons, so it can know where it can build to please customers

- The 6G cycle may be “fundamentally more efficient to roll out than prior cycles”: Given that “the promises of open RAN may finally be realized at scale in the AI RAN era, allowing the Co to “offset potential future cost of replacement of future technologies w/ fundamental efficiencies”

- T-Mobile “intend[s] to be a Co that drives the future of 6G”: This is why it has partnered w/ Ericsson, Nokia, and NVIDIA to help invent AI-RAN

- T-Mobile “[doesn’t] really see any barriers to progress” w/ direct-to-cell tech: The Co has 200+ satellites in the air w/ Starlink and thinks the process w/ the FCC “will work itself out”; Received temporary authorization during the hurricanes and successfully completed hundreds of thousands of text msgs

- 800 MHz spectrum could be used as an alternative to PCS spectrum for this: The Co is no longer required to sell 800 MHz as a result of its merger and doesn’t currently have plans to use it

- The Co has “so much more room to run” on its mid-band 5G upgrades: T-Mobile has only deployed ~60% of its mid-band spectrum (3.45 GHz) for 5G and is primarily targeting mkts “where there could potentially, over time, be a need to expand [the Co’s] capacity”

Verizon Sounded More Upbeat On Convergence Than Before, While AT&T And T-Mobile Maintained Their Views

- The Verizon model of convergence is “demand-led” and accretive to the Co: The Co’s convergence model is accretive to both rev and margins and “has a very attractive ROIC”

- Highlighted four ways that “this convergence comes to life”: Including the launch of both myPlan and myHome, the new Verizon app for both mobility and home, transparent pricing, and the Co’s large distribution network of stores as well as its digital footprint

- The Co expects penetration “well north of 40%” in its convergence biz: Every new cohort that Verizon has brought on “actually gets to that [40%] a little faster than the previous cohort”

- Having a fiber presence provides competitive advantages for the wireless biz: In some of Verizon’s “big” mkts where it has fiber, the Co’s wireless mkt share is +500bps better than ones where it doesn’t possess fiber; Will capitalize more on this dynamic w/ the ability to cross-sell mobility to Frontier’s base

- Bundling mobility w/ fiber has resulted in a -50% reduction in mobility churn: On the other side of the coin, mobility-fiber bundles have also driven a -40% drop in fiber churn; Sees churn benefits on FWA as well

- AT&T’s “strategy remains the same – To lead the industry in converged connectivity through 5G and fiber”: “It’s increasingly clear that customers prefer to purchase mobility and broadband together as a converged svs”

- “Only AT&T can offer [convergence] at scale w/ benefits from owners’ economics”: The “true benefit” of owning and operating both 5G and fiber networks at scale is “the ability to drive higher share in both mobility and broadband through converged svs penetration”

- 4 out of every 10 AT&T Fiber households also choose AT&T as their wireless provider: This compares “nearly 4 out of every 10” last qtr

- The Co’s share of postpaid phone subs within the AT&T Fiber footprint is ~+500bps higher than its national avg: Similar to stats shared last qtr

- “Only AT&T can offer [convergence] at scale w/ benefits from owners’ economics”: The “true benefit” of owning and operating both 5G and fiber networks at scale is “the ability to drive higher share in both mobility and broadband through converged svs penetration”

- T-Mobile’s comments on convergence were sparse: The Co previously emphasized that its “mobile biz stands strongly alone” but also acknowledged that many of its broadband customers have bundled wireless and broadband together and have “realized discounts by doing so”

It Was A Mixed Qtr For CapEx Relative To Sell-Side Forecasts

- Verizon – CapEx was lower than forecasted: CapEx was down -3.6% y/y in Q3 (vs -10.1% y/y in Q2) and finished +9.4% better than cons; Through the end of Q3, Verizon’s CapEx levels were tracking -15.1% below the prior yr, as the Co remains at BAU levels

- The reaffirmed FY24 CapEx range of $17.0-17.5bn was +0.5% above cons at the mid-pt

- 2025 CapEx is projected to be in the $17.5-18.5bn range: This is “all-in” number that includes all of the Co’s growth initiatives, including investments in both C-band and fiber

- AT&T – CapEx was higher than anticipated: Q3 CapEx incr’d +14.1% y/y (vs +1.2% y/y in Q2) and was -2.5% worse than cons; YTD, CapEx is tracking +1.3% higher y/y

- FY24 CapEx guidance of $21-22bn was reaffirmed: Though “higher capital investment” is expected in Q4, as the Co ramps up its wireless network modernization

- AT&T’s pace of building has been “more level loaded” than some of its peers: AT&T has been already been investing in fiber for four yrs and plans to continue introducing new footprint at a “ratable” pace in 2025

- T-Mobile – CapEx was ~in-line w/ expectations: CapEx fell -19.1% y/y in Q3 (vs -26.9% y/y in Q2) and closed ~on-par w/ cons; YTD, CapEx is pacing -19.3% lower y/y

- Narrowed the range for FY24 CapEx: Now anticipates $8.8-9.0bn (vs $8.7-9.1bn prior)

FCF Was A Highlight For All

- Verizon – FCF exceeded expectations: Q3 FCF of $6.0bn was down -10.8% y/y (vs +3.0% y/y in Q2) but still topped cons by +3.7%; To-date, the Co has generated $14.5bn of FCF, which is “consistent w/ the prior yr”

- YTD cash taxes are tracking $2.5bn higher y/y: Higher cashes taxes will continue to pose a headwind to FCF heading into 2025, and the Co is waiting to “see what happens on the legislative front”

- Capital allocation priorities remain unchanged: The top priority remains investing in the biz, followed respectively by the commitment to the dividend, having a strong balance sheet, and share buybacks

- The Co updated its long-term leverage target: Verizon is now aiming for a net unsecured debt to adj EBITDA ratio of 2.0-2.25x (ended at Q3 at 2.5x)

- AT&T – FCF finished well ahead of estimates: FCF of $5.1bn decr’d -1.7% y/y in Q3 (vs +8.7% y/y in Q2) but still beat cons by +15.0%; YTD, FCF of $12.8bn is tracking +23.3% higher y/y, as the Co has been working to drive “higher FCF that is more ratable on a qtrly basis”

- Q3 FCF was impacted by a $480mn payment: This was previously disclosed on the Co’s prior earnings call and was related to its wireless network transformation and the cont’d paydown of vendor financing obligations; Will continue to pay down vendor balances in Q4

- Reiterated FY24 FCF between $17-18bn: The Co is currently tracking to the mid-pt of this range

- There will be some tailwinds and headwinds in 2025: Will be better positioned w/ vendor financing balances, but the absence of DIRECTV and higher cash taxes will be offsetting factors

- T-Mobile – Adj FCF was better than projected: Adj FCF of $5.2bn was up +29.0% y/y in Q3 (vs +54.3% y/y in Q2), topping cons by +9.4%; YTD, FCF of $12.9bn is tracking +39.5% higher y/y

- A “strategic change” caused the Co to pause buybacks: After the Q2 call, there was a “run-up” in the share price that was faster than anticipated and that the trading plan didn’t account for; After stepping back to “re-think strategically” its approach to buybacks, T-Mobile has been “in the mktplace consistently”

- FY24 guidance for adj FCF, including payments for merger-related costs, was raised by +$50mn at the mid-pt: Now forecasts $16.7-17.0bn (vs $16.6-17.0bn prior); This doesn’t assume any material net cash inflows from securitization

- Net cash provided by operating activities incr’d by +$150mn at the mid-pt: Now expects between $22.0-22.3bn (vs $21.8-22.2bn prior)

Other Highlights – Commentary On Recent M&A & Potentially Wholesaling Fiber

- Verizon – prospects to raise the price? The Frontier deal was a “competitive process”: The Co gave its “best and final” offer, and it now has a signed agreement and a contract for a merger; Feels “really confident” that this offer is “fair and good for all shareholders”

- Verizon’s spectrum deal w/ US Cellular is “going to take some time” to close: The deal is “hanging on another acquisition”, and Verizon doesn’t expect cash outflows from the transaction until 2026; The aim is really just “adding capacity”, as “it’s a buy vs build in that region”

- AT&T “won’t rule out” the possibility of wholesaling fiber in its territory: Acknowledged “that it is a high fixed cost industry” and that “there’s been an element of wholesale that has played [out] over time in virtually every piece infrastructure that’s been built”; The “day could arrive” when “it may be accretive to the overall returns of the biz”

- T-Mobile on wholesaling fiber – “We’re open-minded to all future constructs”: That said, cautioned that the Co’s main priority is being “first to fiber” in the places it targets and has teamed up w/ “some of the fastest moving players” in the industry to do so; The Co “wouldn’t speculate more on the future than that”

- T-Mobile – The processes around all of the Co’s transactions “are going really well”: There’s been “good progress through the whole regulatory process”, though approval is still needed from several different groups

- Lumos is expected to close in the first part of 2025, and Metronet is also projected to close in 2025: Both have cleared the DoJ review process and are still pending the FCC’s approval

- USCellular is expected to close in middle part of 2025: It’s a transaction that “very clearly will result in both lower prices and better network”

TKO Makes A Move To Augment Its Position In Premium Sports

There was some moving and shaking in the sports entertainment world this week, as TKO Group, the Endeavor-owned company that runs the Ultimate Fighting Championship (UFC) and World Wrestling Entertainment (WWE), agreed to buy three major businesses, including sports marketing agency IMG, live events business On Location, and Professional Bull Riders (PBR), from its parent company. The transaction consolidates Endeavor’s key sports assets into a single publicly traded company, while the rest of Endeavor continues its ongoing process to become private through a deal with PE firm Silver Lake.

In conjunction with the acquisition, TKO authorized a share repurchase program and initiated a quarterly cash dividend program.

Also to flag, while the Co is reporting its Q3 results on November 6, management gave a preview to their results, noting a “solid quarter” as business at TKO, UFC, and WWE “remain[s] strong.” On the heels of that performance, the company plans to guide to the upper end of its previously disclosed full year range for revenue and adj. EBITDA.

See below for more details on our key takeaways.

-> Shareholders reacted negatively to the transaction, with TKO shares trading down -8.7% on the back of the announcement due to concerns about dilution, among other things

TKO To Acquire IMG, On Location, And Professional Bull Riders From Endeavor Group (link)

- What are the assets that are being acquired?

- IMG is one of the world’s largest global distributors and producers of sports content, packages and sells media rights and brand partnerships, and provides strategic consultancy, digital services, and event management for 200+ rightsholders

- The acquisition of IMG does not include businesses associated with the IMG brand in licensing, models, and tennis representation, nor IMG’s full events portfolio

- On Location is a hospitality provider offering event access, VIP services, and packages for sports, music, and cultural events

- Professional Bull Riders (PBR) is a professional bull riding league that organizes 200+ events annually, reaching 285mn households in 65 territories

- IMG is one of the world’s largest global distributors and producers of sports content, packages and sells media rights and brand partnerships, and provides strategic consultancy, digital services, and event management for 200+ rightsholders

- Endeavor’s ownership of TKO will increase from ~53% to ~59% on a fully diluted basis, pro forma for the transaction; TKO shareholders will own the remaining 41%

- Transaction details: The all-stock transaction is valued at $3.25bn, which is “subject to purchase price adjustments to be settled in cash and equity”

- Anticipated synergies: Expects to generate $30mn in run-rate synergies in connection with the deal

- Timeline: Transaction is expected to close in H1:25

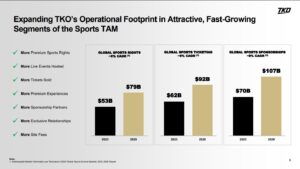

- Reasoning for the deal? “In addition to complementing TKO’s existing core UFC and WWE businesses, the strategic acquisition of these sports and hospitality assets from Endeavor expands TKO’s operational footprint in the fast-growing premium sports market and enables direct participation in the upside from partner leagues and events”

- UFC and WWE will still be TKO’s primary assets…: “I want to underscore that TKO, without question, is and will continue to be fueled by UFC and WWE, which we anticipate will clearly represent the vast majority of TKO’s adjusted EBITDA”

- Tough market reaction to the deal: TKO’s stock fell -8.7% in reaction to the deal announcement

- Additionally, Benchmark removed its price target while downgrading the stock to Hold from Buy (link)

- It specifically pointed to On Location’s 6% adj. EBITDA margin and IMG’s complicated fit with TKO’s existing operations

- PBR’s $40mn contribution to adj. EBITDA was also labeled as “insignificant” by the analysts

- A Seaport Research analyst reiterated his Buy rating, but reduced his price target from $137 to $135

- The deal is a “logical recombination of assets… we think there is nearly +20% upside in TKO shares, and would be buying this pullback””

- The PT reduction was to account for the impact of issuing $3.25bn of equity to Endeavor.; “Operational synergies should have more room to grow with the sports assets concentrated at TKO, while [Endeavor] will continue to participate in that upside with its stake that will increase to ~59% when that sale closes in 1H25” (link)

- Additionally, Benchmark removed its price target while downgrading the stock to Hold from Buy (link)

- Other Endeavor assets are up for sale –

- Back in August, Endeavor has said it is seeking a buyer for its sports gambling and technology businesses OpenBet and IMG Arena (link)

- Hours after the TKO agreed to buy IMG, On Location, and PBR, Endeavor also announced that it was launching a review of the events within its IMG portfolio and may sell off certain assets (link)

- Events under review include the Miami Open and Madrid Open, two ATP Masters 1000 and WTA 1000 tennis tournaments, and art organization Frieze

- This review follows the announcement in April 2024 of Silver Lake’s agreement to take Endeavor private, which includes provisions related to the potential sale of certain businesses, excluding company TKO Group Holdings and entertainment agency WME

TKO Also Authorized A Share Buyback Program And Initiated A Quarterly Cash Dividend Program

- Share repurchase program of up to $2bn of TKO’s Class A common stock over the next 3-4 yr period

- Approved initiation of quarterly cash dividend program of $75mn, commencing in 2025

- The share repurchase program authorization and approval to initiate a quarterly cash dividend program are separate from and are not conditional upon TKO closing the acquisition of PBR, On Location, and IMG

Some Key Updates & Milestones Regarding Next Gen Transport

Elon Musk’s comments on Tesla’s earnings call about the company’s robotaxi services plans made some waves in the ride-sharing industry this week. Additionally, in another interesting update related to next-gen transportation, we wanted to flag a regulatory update out of the FAA as it pertains to “flying” vehicles.

See below.

- New competition in ridesharing coming as soon as 2025? Elon Musk’s comments regarding Tesla’s soon-to-be-launched autonomous ride sharing services spooked the likes of Uber and Lyft this week…

- “We’re building out the early stages of our ride-hailing network

- “We do expect to roll-out ride-hailing in California and Texas next year to the public”

- ”I’d say like, we’ll definitely have it available in Texas and probably have it available in California, subject to regulatory approval” (it is a long process)

- “… And maybe some other states actually next year as well, but at least California and Texas”

- “We’ll be able to have driverless Teslas doing paid rides next year, sometime next year”

-> Uber shares ended the week down -1.9%, while Lyft shares closed the week down -4.1%; YTD, Uber stock is still trading up +26.1%, while Lyft stock is down -10.5%

- What about the development of “flying” taxis? The electric vertical takeoff and landing aircraft (eVTOL) industry hit a milestone this week when the FAA cleared the path for “powered-lift” vehicles to share US airspace with planes and helicopters (link)

- “Powered-lift” vehicles will be the first completely new category of aircraft since helicopters were introduced in 1940

- These aircraft will be used for a variety of services, including air taxis, cargo delivery, and rescue and retrieval operations

- The regulatory agency published its final ruling on the integration of “powered-lift” vehicles into the airspace; The ruling included pilot training guidelines and operating rules, charting the path for the “air travel of the future”

-> Startups like Joby Aviation and Archer Aviation have been expected to launch air taxi networks commercially in 2025 and 2026 (link/link)

Several “Major Forces” That Are Shaping The TMT Sector Are…

Activate recently released its 10th Annual Technology and Media Outlook report, which is an in-depth analysis into the “major forces” shaping the years ahead in technology, internet, media, entertainment, eCommerce, sports, live events, generative AI, and more. It is an extensive deck that draws on large scale consumer insights, industry, and economic analysis, combined with Activate Consulting’s proprietary knowledge, experience, and perspective in these industries.

We detailed below what we thought were the 10 most interesting insights and forecasts from the report, and if you want to dig into the entire 206-page deck (!), the link is HERE.

- Consumer time and attention… by 2028, people will spend an addt’l 9 minutes each day with technology and media…: From 13:08 hours to 13:17 hours, with increases in time spent on messaging & social media, gaming, and video

- … And those addt’l 9 minutes will add $10bn+ to the US consumer technology and media industry

- Super users are key… compared to all other users, Super Users spend substantially more time engaging in all major technology and media activities, at 18:49 hours vs 9:24 hours for all other users

- Generative AI… will change how people search online

- Generative AI is rapidly transforming search and discovery, already addressing 60% of search activity today

- 15mn US adults begin their searches on a dedicated generative AI platform, which is forecasted to grow to 36mn by 2028

- Audio… paid subscriptions to music streaming svs will continue to increase, albeit at a slower pace than before

- Media companies will begin to charge for top podcasts

- Audio streaming svs will add partnerships and collaborations to capture value from artist engagement

- eCommerce… global eCommerce merchandise volume will continue to be dominated by the top 10 companies, but there will be oppties for a large set of other retailers (see chart below)

- eCommerce is a marketplace business, with 3P sellers generating ~85% of online GMV for the top 10 eCommerce players

- Retailers are becoming media companies, and retail media revenue is expected to nearly double over the next 4 years, reaching $100bn+ by 2028

- Consumer internet and media revenues… subscriptions will make up the vast majority of the growth in consumer spend, adding $136bn by 2028

- Sports media & betting… sports betting will be a significant driver of sports fan engagement and the total amount wagered in sports betting is forecasted to reach ~$200bn by 2028

- Sports betting operator revenue will exceed $20bn by 2028 and will grow faster than the amount wagered as operator margins continue to expand

- Live events… stadium and arena investment is booming to meet the demand from sports and large-scale artists concerts; New stadium and arena technology will raise the bar for fan experience, requiring increased investment and design innovation

- The Sphere’s investment in technology and innovation has showcased the realm of possibility within live experiences

- Video gaming… active gamers are expected to reach 3.5bn+ by 2028, up from 2024E’s 2.7mn, and global consumer video game rev will reach $200bn+ by 2028, up from 2024E’s $172bn

- Super Gamers (34% of US gamers, who spend nearly four hours/day playing across platforms) will be a growth driver for the industry

- The majority of top earning PC/console games are installments in existing game franchises, with very few new games breaking into the top 10

- Generative AI will lower the barrier to entry for in-game creation for both users and developers

- Spatial computing… spatial computing’s iPhone moment is within sight; Much of the required technology, device, AI, and ecosystem is already in the pipeline

MORE Pushback On The Frontier/Verizon Deal Struck This Week

Following Theme #2 from last week, there were more disgruntled Frontier shareholder’s that came out of the woodwork this week – namely Carronade Capital and Glendon Capital. The arguments were similar to what we heard last week, i.e., the belief that Frontier standalone (excluding the value of synergies) is worth more than Verizon’s offer price based on their comps analysis and forecasts for the business. The funds this week also pushed back on Frontier’s Board’s decision to set the record date before it was announced in the proxy and then to “rush a shareholder vote.”

See below for some key aspects of these shareholder’s valuation arguments. As a reminder, the shareholder vote is scheduled for November 13.

-> Frontier shares were up a slight +0.9% this week and are trading +42.1% higher YTD

- Carronade Capital (owns ~2mn shares of Frontier) thinks Frontier is worth $43.60/share standalone (BEFORE synergies) vs the $38.50 offer (Carronade Capital letter)

- Cites recent estimates ranging from $47.88-60.00+ per share before any synergy value

- Points to fiber transactions valuations (Metronet/T-Mobile, Lumos/T-Mobile, and Horizon/Shenandoah), which have been valued in the low to mid-20x TEV/EBITDA

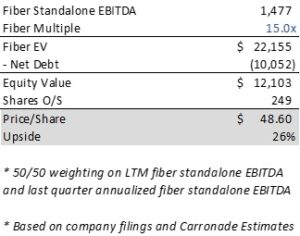

- Valuing Frontier’s Fiber only EBITDA at a “substantial discounted multiple of 15x” implies $48.60/shr before synergies (this excludes any value on the existing non-fiber business, which generated $756mn of LTM EBITDA, NOL benefits)

- Glendon Capital (~10% holder) – Believes that Frontier’s enterprise value (“EV”) is worth at least $26bn ($61/shr) today, which is +30% higher than the current $20bn deal value (Glendon letter)

- Deal undervalues Frontier on EV/EBITDA: The $20bn deal value is 8.5x 2025 Wall Street consensus EV/EBITDA, but the firm views T-Mobile as the closest comp, which trades at ~11x

- Also, the “appropriate private market multiple range is 15-20x”

- Deal undervalues Frontier on a per passings basis: Using the value per fiber passing established by the Metronet and Lumos deals as well as assigning zero value to copper assets, the firm arrives at “a minimum enterprise value for Frontier of $26bn (or $61 per share)”

- The firm pushed back on the financial advisors’ terminal growth rate assumption

- The proxy DCF uses a range of +0.75-1.75% for terminal growth

- The firm believes a realistic growth rate to be +2.5-3.5%, resulting in an EV for Frontier of $24-28bn ($53-68/share)

- A modest terminal growth rate range of +2.0-2.5% after a 3-year phase in period, plus a WACC of 8% in the DCF analysis yields an EV of $24-26bn ($53-61/share)

- Deal undervalues Frontier on EV/EBITDA: The $20bn deal value is 8.5x 2025 Wall Street consensus EV/EBITDA, but the firm views T-Mobile as the closest comp, which trades at ~11x

Strategic Predictions For IT Organizations & Users Through 2029, Per Gartner

Gartner this week outlined its top strategic predictions for IT organizations and users through 2028, which include their crystal ball on how generative AI will impact industries. We listed these predictions by the greatest percentage of expected adoption, though the time frames vary. It is food for thought… CLICK HERE if you want to see the full deck.

- By 2027

- 70% of new contracts for employees will include licensing and fair usage clauses for AI representations of their personas

- Employees’ personal data that is captured by enterprise LLMs will remain part of the LLM not only during their employment, but after their employment

- 70% of healthcare providers will include emotional-AI-related terms and conditions in technology contracts or risk billions in financial harm

- Using emotional AI on tasks such as collecting patient data can free up healthcare workers’ time to alleviate some of the burnout and frustration they experience with increased workload

- 20% of organizations will use AI to flatten their organizational structure, eliminating more than half of current middle management positions

- AI will take over automating and scheduling tasks, reporting and performance monitoring for the remaining workforce, enabling the remaining managers to focus on more strategic, scalable and value-added activities

- 70% of new contracts for employees will include licensing and fair usage clauses for AI representations of their personas

- By 2028

- 70% of organizations will implement anti-digital policies, given technological immersion will impact populations with digital addiction and social isolation

- 40% of large enterprises will deploy AI to manipulate and measure employee mood and behaviors, all in the name of profit

- 40% of CIOs will demand “Guardian Agents” be available to autonomously track, oversee, or contain the results of AI agent actions

- 30% of S&P companies will use GenAI labeling, such as “xxGPT,” to reshape their branding while chasing new revenue As the GenAI landscape becomes more competitive, companies are differentiating themselves by developing specialized models tailored to their industry

- 25% of enterprise breaches will be traced back to AI agent abuse, from both external and malicious internal actors

- ~1bn people will be affected by digital addiction, which will lead to decreased productivity, increased stress and a spike in mental health disorders such anxiety and depression; Additionally digital immersion will also negatively impact social skills, especially among younger generations that are more susceptible to these trends

- Fortune 500 companies will shift $500bn from energy opex to microgrids to mitigate chronic energy risks and AI demand

- By 2029

- 10% of global boards will use AI guidance to challenge executive decisions that are material to their business

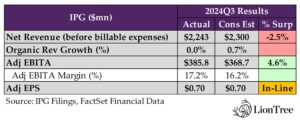

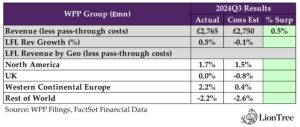

Ad Agency Holding Co Earnings Follow-Up – It Was A Tale Of Two Cities Between IPG & WPP

As an addendum, of sorts, to our theme on Publicis and Omnicom’s earnings last week (see Theme #4 from last week’s Weekly), we included some brief takeaways on IPG and WPP’s Q3 prints this week. Along with some interesting high-level commentary on client sentiment and the macroenvironment, there were also noteworthy comments on the ad agency holding companies’ key client wins and M&A plans. Big picture, IPG disappointed investors, while WPP surprised to the upside. See below for more details.

-> IPG shares fell -5.8% post-earnings and finished the week down -7.0%; WPP shares rose +5.4% in response to earnings, closing the week up +3.5%; YTD, IPG stock is trading down -8.7%, while WPP stock is up +15.4%

- IPG – Q3 organic growth disappointed: Q3 rev before billable expenses decr’d -2.9% y/y (vs -0.1% y/y in Q2) and closed -2.5% behind cons; Organic rev growth was flat y/y, missing cons’ +0.7% y/y; Adj. EBITDA was down -2.9% y/y (vs +2.6% y/y in Q2) but still beat cons by +4.6%

- Q3 numbers included a $232mn, non-cash goodwill impairment charge: This was related to the Co’s Digital Specialist agencies and its progress in the sale process of R/GA and Huge

- IPG saw “very strong growth” from consumer-facing Cos: Particularly those in food & bev as well as consumer goods

- Other posted “solid growth”

- Healthcare, retail, and financial svs saw “modest increases”

- Autos & Transportation as well as tech and telecom declined: Mainly due to the Co’s account losses in in late 2023

- The Co “definitely gets “the sense that things are improving” in the macroenvironment: Clients “seem to be looking past” the global situation and fiscal policy in the US has been moving in a “positive direction”;

- BUT “economic and political uncertainty” in the US and IPG’s largest intl mkts “remains a significant consideration”: “This is especially relevant given the relatively high levels of discretionary project spend that characterize Q4 and the holiday season”

- IPG is seeing a “very active pipeline” of project work for Q4: The Co will be focused on “capitalizing on those oppties”, given that it will “facing top line headwinds” heading into 2025 following some recent account reviews

- “Principal buying has clearly impacted our [Media] biz”: IPG continues to scale its practice in principal media buying, “which has been a decisive factor in some large pitches”; Represents both an “incremental option for value creation” for prospective clients and an oppty for growth w/ existing clients

- On potential further divestitures – “There is a bit of addition by subtraction when you’ve got things that are holding you back”: IPG will “look at what makes sense” and will consider changes that “improve [its] growth profile”

- FY24 guidance was unchanged: Still anticipates organic rev growth of ~+1% y/y as well as an adj EBITA margin of 16.6%

- WPP’s Q3 trading update revealed a broad top-line beat and a return to growth: Q3 rev less pass-through costs was down -2.6% y/y (vs -2.3% y/y in Q2) but still topped cons by +0.5%; LFL rev growth of +0.5% y/y was better than cons’ -0.1% y/y

- Growth was stronger than anticipated across all core operating regions: The following numbers are on a LFL basis

- North America decel’d seq: Grew +1.7% y/y (vs +2.0% y/y in Q2)

- The UK improved seq: Growth was flat y/y (vs -5.3% y/y in Q2)

- Western Continental Europe accel’d seq: Incr’d +2.2% y/y (vs +0.3% y/y in Q2)

- Rest of World was similar seq: Dropped -2.2% y/y (vs -2.2% y/y in Q2)

- The Co saw an accel across most key client sectors: The following numbers are on a LFL basis –

- CPG grew +7.3% y/y (vs +5.1% y/y in Q2)

- Tech & Digital Svs was up +1.3% y/y (vs -1.0% y/y in Q2)

- Healthcare & Pharma was down -7.7% y/y (vs -9.7% y/y in Q2)

- Auto incr’d +5.8% y/y (vs +3.6% y/y in Q2)

- Retail fell -5.9% y/y (vs -10.7% y/y in Q2)

- Telecom, Media, & Entertainment was down -2.3% y/y (vs +5.1% y/y in Q2)

- Highlighted WPP winning Amazon’s media biz outside the US…: Contributing factors included GroupM’s “very strong team”, the demo of WPP Open, a “very close collab” w/ VML throughout the pitch, and the global strength of GroupM’s biz

- … As well as acquiring more of Unilever’s biz: WPP came out “ahead of where [it] started” after Unilever’s recent competitive review, consolidating the retail media biz it previously lost; Demonstrated a “strong, very integrated approach” across media & commerce

- FY24 guidance was reiterated: The Co’s two major wins (above) won’t kick in until 2025

- Still sees LFL rev less pass-through costs y/y growth of -1% to 0%, w/ Q4 facing a tougher comp than Q3 and macro uncertainty

- Improvement in headline operating profit margin of +20-40bps (excluding FX impact)

- Growth was stronger than anticipated across all core operating regions: The following numbers are on a LFL basis

Grab Bag: Netflix Shutters AAA Game Studio/Ray-Ban Meta Glasses Are Seeing “Strong Demand”/ Amazon Reportedly Working On Low-Cost Storefront

Netflix Appears To Be Re-Working Its Gaming Strategy…

- Netflix shuts down AAA game studio Blue (link): The “Blue” team was formed in late 2022 and focused on developing “AAA” games under Chacko Sonny, who previously worked on the hit multiplayer shooter Overwatch and worked at Blizzard before leaving for Netflix

- Blue was looking to hire engineers just four months ago: But now, Sonny, as well as former Halo creative lead Joseph Staten and ex-Sony art director Rafael Grassetti, are now no longer working for Netflix after the Blue studio was shut down

- Netflix’s bet on gaming may not be paying off…yet: CNBC data from late 2023 indicates that <1% of Netflix subs play its games on a daily basis

- BUT Netflix isn’t throwing in the towel on games: Despite shuttering Blue, a Netflix spokesperson said that the Co still has a long-term commitment to games more broadly

- AAA games can take 5-7 yrs and $80mn+ to develop: This suggests that Blue’s projects were still in earlier stages when the studio was shut down

Ray-Ban Meta Glasses Are Seeing “Strong Demand”, Per EssilorLuxottica’s CFO Stefano Grassi

- EssilorLuxottica is “very happy about the performance” of Ray-Ban Meta: The glasses are “an overall success story”, according to EssilorLuxottica’s CFO Stefano Grassi on the Co’s Q3 Sales and Rev Call

- Ray-Ban Meta is the bestseller in 60% of Ray-Ban stores in Europe…: “It’s not just a success in the US, where it’s obvious, but it’s also [a] success here in Europe”

- … And has experienced “strong demand” everywhere else: Ray-Ban Meta has seen “success” in “every geography… where it’s commercialized and sold”

- Ray-Ban Meta won the prestigious 2024 Silmo d’Or for technological innovation in eyewear: Also points to EssilorLuxottica’s “leadership in product innovation”

- The partnership w/ Meta “has a certain aspect of exclusivity”: Though Grassi couldn’t elaborate further; The partnership “will last quite a few yrs” and take both Cos into the next decade

- The collab will also encompass other brands “presumably”

- Ray-Ban Meta is the bestseller in 60% of Ray-Ban stores in Europe…: “It’s not just a success in the US, where it’s obvious, but it’s also [a] success here in Europe”

Amazon Reportedly Working On A Low-Cost Storefront To Rival Asia-Based Retailers

- Amazon reportedly setting price caps on what merchants can charge on its low-cost platform (link/link): Amazon has reportedly shared a list of 700 items with merchants that include a maximum price they are allowed to charge for each item, including an $8 limit for jewelry, $9 for bedding sets, $13 for guitars and $20 for sofas, according to messages from Amazon to merchants seen by The Information

- Significant departure in strategy for Amazon, which historically hasn’t set hard-and-fast price limits for merchants selling on its platform

- And a slightly different strategy from Temu, which typically determines what prices are displayed on its website and pays merchants a set price per sale

- How will fulfillment work? Amazon reportedly plans to ship orders to US customers from a facility in Guangdong, China, and is charging sellers significantly lower fulfillment fees for items sold through the new storefront than it does when shipping items domestically

- Lower shipping costs: Amazon would charge a seller between $1.77-$2.05 to ship a Low-Cost Store item that weighs between 4-8 oz, compared to $2.67-$4.16 for most items of the same weight shipped from domestic warehouses through its regular Fulfillment by Amazon service

- Longer shipping times: Amazon previously told a group of merchants it expects Low-Cost Store orders to arrive in 9- 11 days, compared to the one- or two-day delivery times that are common for its regular site

- Shorter return windows: Customers who shop on the Low-Cost Store will have 15 days to make returns from the day they’re delivered, compared to 30+ days for most items sold through its regular site, according to the seller documents; Items <$3 won’t be eligible for returns at all, while others will be “eligible by default” for “return less resolutions” (customers get a refund while keeping an item)

- Amazon has not set a hard launch date for what it’s calling the “Low-Cost Store”

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Fox Corp has reorganized its ad sales, marketing, and brand partnerships group, resulting in a 3% workforce reduction while hiring several senior executives. President Jeff Collins described the “strategic realignment” as a way to enhance advertiser service amid a shifting marketplace. New roles include Ebony Moore and Brian Schepis, who will focus on client services and yield management, respectively. The new structure aims to create a unified approach for scalable ad products and improved data capabilities across Fox’s diverse properties. (Deadline)

- The IAB Tech Lab has launched the Ad Format Idol initiative to standardize ad formats in the fragmented connected TV (CTV) ecosystem. With major players like Hulu and Netflix setting varied ad specs, advertisers face challenges in adapting creative content. The initiative aims to create a “build once, serve everywhere” model to simplify deployment across platforms, enhance measurement, and improve campaign performance. Stakeholders are invited to submit ad formats for evaluation by January 22, 2025. (The Drum)

- uBlock Origin users may face issues as Google starts disabling the popular ad blocker due to its transition to the Manifest V3 extension framework, phasing out the older Manifest V2. Developer Raymond Hill confirmed this on social media after users reported the ad blocker being disabled in Chrome. Although some users can still download it, Google aims to limit V2 extensions for security reasons, prompting criticism and a potential migration to alternative browsers like Brave or Firefox. While Google asserts that over 85% of extensions are already using Manifest V3, Hill warns that its Lite version lacks the full capabilities of uBlock Origin. (PCMAG)

Artificial Intelligence/Machine Learning

- AI search engine Perplexity is in fundraising talks and hopes to raise ~$500mn at an $8bn valuation, according to the Wall Street Journal. If a deal happens w/ those terms, it would more than double Perplexity’s valuation from its $3 bn valuation when it raised from SoftBank over the summer. The WSJ reports that the co currently receives about 15mn queries a day and brings in ~$50mn in annualized rev. (TechCrunch)

- Anthropic has released an upgraded Claude 3.5 Sonnet model with a “Computer Use” API that lets it interact with desktop apps by imitating keystrokes and mouse gestures. Aimed at automating tasks like research and emails, this model supports Anthropic’s goal of becoming a next-gen AI assistant. Though it shows promise, it still struggles with tasks like scrolling and may pose risks related to misuse and security. (TechCrunch)

- Britain’s competition watchdog has opened a merger inquiry into Alphabet’s partnership w/ artificial intelligence safety start-up Anthropic. The Competition and Markets Authority, which invited comments on the partnership earlier this yr, said on Thursday it has “sufficient information” to allow it to begin an investigation. Alphabet invested $500m (£385m) in Anthropic in 2023, w/ the promise of an additional $1.5bn (£1.2bn) over time. (CityAM)

- Gartner predicts that by 2028, at least 15% of day-to-day work decisions will be made autonomously through agentic AI (up from 0% in 2024). Further emphasizing the technology’s potential, the firm has named it a top strategic technology trend in 2025. “Agentic AI has the ability to plan and sense and take action,” said Gene Alvarez, distinguished VP analyst with Gartner. “Instead of having something just watching systems, agentic AI can do the analysis, make the fix and report that it happened.” (VentureBeat)

- Gen AI startups are getting 40% of all the VC funding that flows into cloud Cos, according to Accel. In its latest annual Euroscape report, Accel said that venture funding for cloud startups based in the US, Europe, and Israel is projected to rise to $79.2bn this yr. It comes after OpenAI earlier this month raised $6.6bn in a mammoth funding round that valued the startup at $157bn. (CNBC)

- Google Photos is adding a new “AI info” section to clearly label when images were edited w/ AI or contain elements of several different pictures. The “AI info” section will be found in the image details view of Google Photos both on the web and in the app. These labels won’t be limited strictly to generative AI, either. Google says it’ll also specify when a “photo” contains elements from several different images. (The Verge)

- Meta is striving to make its popular open-source LLMs more accessible w/ the release of “quantized” versions of the Llama 3.2 1B and Llama 3B models, designed to run on low-powered devices. The Llama 3.2 1B and 3B models were annc’d at Meta’s Connect 2024 event last month. Now it’s releasing quantized, or lightweight, versions of those models, which come with a reduced memory footprint and support faster on-device inference, w/ greater accuracy. (SiliconANGLE)

- Midjourney is planning to release an upgraded web tool that’ll let users edit any uploaded images from the web using Midjourney’s generative AI. The upgraded tool, which Midjourney CEO David Holz said will be released “early next week,” will also allow users to retexture objects in images to “repaint” their colors and details according to captions. (TechCrunch)

- OpenAI plans to launch Orion, its next frontier model, by Dec. Unlike the release of OpenAI’s last two models, GPT-4o and o1, Orion won’t initially be released widely through ChatGPT. Instead, OpenAI is planning to grant access first to Cos it works closely w/ in order for them to build their own products and features, per a source. While Orion is seen inside OpenAI as the successor to GPT-4, it’s unclear if the Co will call it GPT-5 externally. (The Verge)

- Perplexity AI is rolling out two new features to enable newer ways of using the AI search platform’s capabilities. The co has introduced Internal Knowledge Search and Spaces capabilities. The former allows users to search prompts and get responses based on an internal knowledge base while the latter is a collaboration tool that allows users to invite others into a search project. Both features are currently available to paid subscribers of Perplexity AI, including Perplexity Pro and Perplexity Enterprise Pro users. (Gadgets 360)

- Qualcomm and Google have announced a multi-year collaboration to advance generative AI in the automotive sector. This partnership will leverage Qualcomm’s Snapdragon Digital Chassis and Google Cloud to create a standardized reference platform for AI-enabled cockpit solutions. The initiative aims to enhance in-car experiences through intuitive voice assistants and real-time updates. Both companies emphasize that this collaboration will drive innovation, streamline software development, and improve user experiences in software-defined vehicles. (THEFASTMODE)

- Spirent Communications’ report reveals that AI and generative AI are accelerating optical networking speeds, particularly with 400G Ethernet adoption in telecoms and enterprises. Tier 1 operators are upgrading to 400G as part of IP core refresh efforts and standalone 5G launches, while also employing 25G and 100G at various network edges. There’s a rising interest in AI-driven services, prompting enterprises to transition to 200G and 400G Ethernet, with a focus on enhancing data center capabilities and supporting AI applications. (Mobile World Live)

- Stability AI has launched the Stable Diffusion 3.5 series, featuring three image-generation models: Stable Diffusion 3.5 Large (8 billion parameters), Large Turbo (faster but lower quality), and Medium (optimized for edge devices). These models aim to generate more diverse outputs and offer improved performance. Stability AI maintains free use for non-commercial purposes, but businesses must license for commercial use. The series builds on the previous generation with some improvements but may still face issues with prompt accuracy. (TechCrunch)

Audio/Music/Podcast

- Spotify is launching the Spotify Ad Exchange, a supply-side platform aimed at enhancing automated video advertising. This platform will improve ad spending efficiency for larger brands and increase revenue from small to medium-sized businesses. The Trade Desk is the first demand-side partner, connecting its North American customers to Spotify’s video ad inventory. Spotify will also adopt The Trade Desk’s OpenPath for direct access to premium ad inventory and join the Universal ID 2.0 for cookie-less targeting. The platform is currently in a testing phase. (GURUFOCUS)

Broadcast/Cable Networks