Week one of earnings season for the sector started with a positive tone, given Netflix’s better than expected results. The Co continued to grow subscribers while also beating profitability estimates. See Theme #1 for our key takes and perspectives. The major indices also ended the week on a positive note, with the Dow, S&P and Nasdaq all up almost 1%, marking the 6th consecutive week of gains. The strong September retail sales report was the main macro update as well.

See below for what we focused on in this week’s edition (all links are clickable):

- Lights, Camera, Action – Netflix Delivers The Right Balance

- Will Verizon Have To Up The Ante For Frontier? Frontier Shareholders Are Pushing Hard

- Higher Prices For Essentials Will Take A Cut Out Of Holiday Shopping + Other Spending Updates

- Ad Agencies – Publics & Omnicom Outperform Despite Macro Pressures

- Positive Comments On The Consumer Out Of The Big Banks…

- Premium Sports Rights Continues To Play A Pivotal Role In The Sector

- Grab Bag: The FTC’s New Click-To-Cancel Rule/Uber Explores A Deal For Expedia/Video Game Strike Negotiations Set To Resume

Enjoy the read.

Best,

Leslie

Lights, Camera, Action – Netflix Delivers The Right Balance

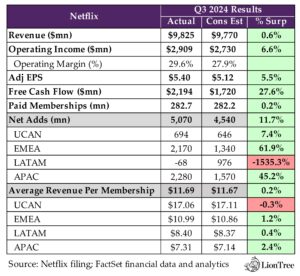

Netflix kicked off earnings season on the media side with strong results across the board. The Co beat on both its Q3 numbers as well as its Q4 guidance, and profitability continues to shine under the spotlight. Q3 op margins topped consensus for the 12th quarter in a row, and Q4 op margin guidance also came in higher than Street estimates. While the 2025 op margin guide implies a +1ppt y/y improvement, which is a deceleration from the +6ppt y/y “outsized margin improvement” forecasted for 2024, this is part of Netflix’s strategy to balance margin growth with investments in the business, and they continue to see “plenty of room” to increase margins over the long term.

Netflix also beat on Q3 revenue and Q4 revenue guidance, though 2025 guidance was in-line and bakes in a deceleration of growth to +11-13% y/y (vs +15% y/y expected for 2024), driven predominately by a “healthy” increase in paid memberships, followed by increases in average revenue per membership (ARM).

It’s still early days for the ads business, and it won’t be a primary driver of revenue just yet in 2025, as the company is still at a point where it’s scaling its audience and inventory faster than its ability monetize them. That being said, adoption of the ad-supported plan continues to accelerate seq, and engagement patterns of viewers on ad plans vs non-ad plans are largely the same.

In terms of the content slate, Q4 will see the return of key series like Squid Games S2, Outer Banks S4, and Love is Blind S7, as well as new dramas and films. Most notably, Netflix will expand its offerings to include live events, including the Mike Tyson and Jake Paul boxing match on November 15 and two Christmas Day NFL games. While H1’s lineup was lumpier due to the strikes (and hit UCAN the hardest), output has been more normalized in H2, though it will not fully recover until 2025.

See below for more detail on the above, along with what we thought were key comments on the pricing strategy, bundling, the competitive landscape, gaming, and more.

-> Netflix’s stock jumped +11.1% the day after its report and ended the week up +5.7%; YTD, the stock is up +56.9%

Clean Beats Across Q3 Headline Results

- Q3 rev growth of +15% y/y (or +21% y/y ex-FX) beat consensus, but was a decel from +16.8% last qtr

- ARM was flat y/y (or +5% y/y ex-FX) and also slightly beat consensus

- Q3 op margin of 29.6% showed a nice step up: Compared to 27.2% in Q2 and was up +7ppts y/y

- Came in above guidance due to “slightly” higher revenue and the timing of spend

- Q3 paid net adds beat by +11.7%: 07mn vs cons 4.5mn; Beat across all regions w/ the exception of LATAM

- International dynamics –

- Rev growth rate in APAC (+19% y/y) was the highest

- UCAN and EMEA both saw rev growth rates of +16% y/y; UCAN (most mature market) was driven by +10% y/y and +5% y/y growth in avg paid memberships and ARM, respectively; EMEA’s growth was consistent with the increase in avg paid memberships

- LATAM rev was up +9% y/y

- What drove the LATAM member net loss in Q3?

- Primarily due to recent price changes in some of their bigger LATAM markets, “which always dampens near-term member growth”

- Already seeing “a nice rebound” so far in Q4, and noted that is qtr had lasted one more day, net adds would have been up, not down

- Underlying biz trends remain “healthy”, as YTD rev growth is in-line with 2023 growth, despite “much more significant” currency headwinds in 2024 vs 2023

- Have an “incredible slate” upcoming in Q4

- Rev growth rate in APAC (+19% y/y) was the highest

Q4 Guidance Topped Estimates / Initial Projections For 2025 Imply Some Seq Slowdown In Rev And Op Margin Growth

- Q4 guidance higher than cons across the board

- Q4 rev – higher by +0.8%: $10.128bn vs cons $10.04bn

- Q4 op income – higher by +3.3%: $2.19bn vs cons $2.12bn

- Op margin of 22% beat cons 21.2% (implies a 5ppt y/y improvement)

- Q4 EPS – higher by +8.5%: $4.23 vs cons $3.90

- Q4 paid net adds are expected to be higher in Q4 vs Q3, due to “normal seasonality and a strong content slate”

- Provided initial 2025 guidance w/ revs in-line

- 2025 rev guidance at mid-pt was in-line with estimates: $43-44bn vs cons $43.51bn

- Implies seq deceleration in growth: +11-13% y/y rev growth in 2025 vs expected +15% y/y in 2024

- Drivers of growth: Majority expected to come from membership growth from full year impact of 2024’s “strong” net adds and “solid” paid net adds expected in 2025 ; Increase in ARM will also contribute

- Expect y/y increase in op margin, but at a slower pace: Targeting 2025 op margin of 28% (+1ppt increase y/y) vs 27% forecasted for 2024 (+6ppt increase y/y)

- “After delivering outsized margin improvement in 2024, we want to balance near term margin growth with investing appropriately in our business. We still see plenty of room to increase our margins over the long term”

- 2025 rev guidance at mid-pt was in-line with estimates: $43-44bn vs cons $43.51bn

- No change to capital allocation strategy despite expectations to generate substantial FCF over the next several yrs

- No plan to increase leverage to buy back stock or to issue a dividend

- Continue to prioritize profitable growth by reinvesting in biz, maintaining “ample” liquidity, and returning excess cash to shareholders beyond minimum cash on balance sheet

- “We put a real premium on balance sheet flexibility…to be clear, no minimum leverage targets”

There’s Still Quite A Bit Of Wood To Chop W/ Advertising Monetization, But It Is A Huge Oppty

- Ad-supported plans accounted for over 50% of signups in ads countries in Q3, up from “over 45%” in Q2

- Ads plans membership base was up +35% q/q in Q3, vs +34% q/q in Q2

- Ad plans members are watching a similar amount of hours and similar titles relative to non-ads plan members

- Reiterated in-house ad tech platform launch timeline: On track to launch in Canada in Q4, with broader launch to all ads countries in 2025

- Have expanded programmatic capabilities with The Trade Desk and Google DV360, which is “going well”

- Live with 1-to-1 private marketplaces in UCAN and LATAM

- Have some always-on agency deals in the US and Australia

- Will be adding more programmatic capabilities next month in UCAN and LATAM and building from there

- “Going to take us a while to catch up to that significant inventory expansion we’ve been able to drive”

- How important are partnerships vs Netflix building its own walled garden? “We’ve learned not to be too rigid in our position… we’ll evolve based on how our business is evolving and frankly how the ecosystem is evolving around us, but we believe these partnerships are very positive for us”

- Will see further improvement in ad biz in 2025, but still some ways off before it’s a significant contributor to revenue

- Still scaling audience and inventory faster than their ability to monetize it, which creates a short-term drag on ARM

- Saw over a +150% increase in ad sales commitment in this year’s US upfronts

- “Roughly doubling” ad rev in 2025, “but it’s off a small base”

- “It starts to become a material contributor of revenue over the next several years”

- But highlighted “tremendous upside” in opportunity: $600bn+ in consumer spend in the areas and countries Netflix operates in, of which they’re only capturing 6-7% today

- “We’ve got a roadmap for more formats, for more features, for more measurement that’s all coming. So, while we’ve got lots of work to do, we are very confident in our ability to execute and grow our ad business, much like we did with the paid sharing initiative”

Pricing Strategy Continues To Be A Balance Of Choice With Value

- What is Netflix’s reasoning for only raising prices of non-ad tiers, while keeping ad-supported plan prices the same?

- Do NOT thinking about pricing relative to competitors (who have been raising prices for both non-ad and ad-supported tiers)

- Rather from the value being delivered to customers

- Want to have a range of price points be able to deliver different features for different consumers, w/o adding too much complexity

- “We love the low price point and increased accessibility that comes with our ad plan”

- Also focused on optimizing long-term revenue rather than ARM

- “We’ll continually try to offer consumers a spread of plan choices, the right features at the right price point, and evaluate that and evolve it based on what we think works”

- Phase out of Basic Plan across UCAN, UK, and France has gone well and “in-line with our expectations” / Will be starting phase out in Brazil later in Q4

- “It’s a good example of…how we…continue to evolve plans and pricing, thinking about expanding that range, especially the low end in our ads plan, but also keeping the number of choices manageable”

Netflix Is Building Its Own Playing Field In The Competitive Landscape

- Focused on building out Netflix’s offerings vs bundling with competitors to drive growth

- Bundling is familiar and comfortable for legacy media Cos, and “makes sense for them” given the “narrow scope of the libraries on these services and the fairly limited engagement”

- Netflix is focused on adding more value to its own offering –

- Which already includes first-run films, original series from around the world, unscripted shows, competitions shows, animated series, and films, and live events, with

- And building capabilities in ads, games, and more live content

- “We’re really betting on our ability to reach consumers and on our ability to continue to grow value of this package”

- View on YouTube’s growing share of TV consumption? “While we do compete for that time, we’re interestingly complementary as well”

- “We put up our trailers on YouTube and they get a lot of viewing, which is great, because it drives a lot of viewing on Netflix”

- “We have very different strengths”: Netflix assumes the financial risk when creators make content; Netflix’s subscription model generates higher returns for creators, which lets them make more ambitious investments in their next project

- “It’s hard to imagine how those […] big, creative bets will be possible with YouTube’s model”

- “Netflix fulfills an important and different role for both consumers who want these great movies and TV shows, but also for creators who want partners that can share in the risk”

- “We are really focused on the 80% of watching what happens not on YouTube or Netflix yet. So, we’ve still got plenty of work to do”

Tone On Content Slate Remains Upbeat – “We Could Not Be More Excited About Where We Sit Right Now And Where We’re Heading”

- Have maintained “very healthy” engagement so far this yr

- Averaging ~2hr of viewing per member per day

- Engagement on a per-owner household is up through the first three qtrs of 2024

- Total hours were up ~1% y/y in H1

- Increasingly seeing a “steady drumbeat” of hits internationally, driven by “decades-plus” investment in respective creative communities and working with local storytellers

- Specifically called out that Q4 will have “big titles” from the US, Brazil, Korea, UK, and Germany

- Some lingering impacts from strike related work stoppages, but should be back to normal by 2025

- Series are “a little more” on track than film, but neither are fully recovered

- Film also had a leadership change, “which changed the cadence of releases a bit”

- H1 content lineup was “much lumpier than we like” and hit UCAN the hardest (though impacts were felt in production around the world)

- By the end of Q3, content lineup was a lot more normalized

- Q4 will see things getting “much steadier”

- Will be “largely back to normal” starting in 2025

- Series are “a little more” on track than film, but neither are fully recovered

- “Finished Q3 with some big hits”, including –

- The Union (111.9mn views)

- Rebel Ridge (104.7mn views)

- Beverly Hills Cop: Axel F (87.5mn views),

- The Perfect Couple (65.2mn views)

- Monsters: The Lyle and Erik 4 Menendez Story, by Ryan Murphy (54.6mn views) and The Menendez Brothers documentary in October (24.2mn views)

- Emily in Paris, S4 (51.0mn views)

- Nobody Wants This (37.0mn views)

- In addition to “finish[ing] the year strong with a great Q4 slate”, Q4 will mark Netflix’s initial steps into live content expansion

- Squid Game, S2

- Outer Banks, S4

- Love is Blind, S7

- 100 Years of Solitude in Columbia

- Senna in Brazil

- Aaron Rodgers: Enigma

- Mike Tyson and Jake Paul boxing match on Nov 15th

- Two NFL games on Christmas Day

- 2025 slate “showcases the scale and the ambition and reflects the investment that we’ve made in the steady cadence of programming”

- 52 weeks of WWE starting in January

- New seasons of Wednesday andStranger Things

- New shows from Shonda Rhimes and Ryan Murphy

- New Knives Out film

- Guillermo del Toro’s Frankenstein

- New Happy Gilmore movie

- Russo Brothers’ The Electric State

- Reiterated that they are NOT looking to change talent compensation model / Both creators and Netflix benefit from paying upfront

- For creators, Netflix takes all the financial risk that they can focus on making “the best possible version” of their content

- For Netflix, the model enables them the attract “the best talent in the world”

- Have been and continue to be open to open to more bespoke deals where talent is interested, but “they rarely happen, because typically, the talent chooses the upfront model”

Other Initiatives Remain In The Works

- Continue to build out pipeline of games

- From Netflix IP (Squid Game, Virgin River, The Ultimatum) as well as “storied game classics” (like Monumental Valley 3)

- Have also been working to improve overall core Netflix product experience, including a new, more intuitive version of the TV home page

- “We’re excited with the progress that we’ve seen there. So, we’re polishing it up and we’re excited to bring that to our subscribers around the world

- View on AI – “Needs to pass a very important test…can it help make better shows or better films?”

- “We benefit greatly from improving the quality of the movies and the shows much more so than we do from making them a little cheaper…any tool that can go to enhance the quality, making them better, is something that is going to actually help the industry a great deal.”

Will Verizon Have To Up The Ante For Frontier? Frontier Shareholders Are Pushing Hard

Deal M&A in the Connectivity sector has been fast and furious as of late but could be running into some speed bumps, particularly as it relates to Verizon’s $20bn offer to buy Frontier Communications. A string of unhappy shareholders have voiced concerns, and some have even conveyed intent to vote against the transaction. Glendon Capital Markets and Cerberus Capital Mgmt (almost 10% and 7.3% shareholders, respectively) have both reportedly expressed that Verizon’s $38.50/share offer undervalues Frontier. In a more public fashion, Cooper Investors Pty (Australian-based global asset manager with ~$7bn AUM) sent a formal letter to Frontier’s board that said shareholders would “benefit far more from Frontier remaining as a standalone company rather than being acquired by Verizon for $38.50 per share,” adding that the “offer is too low, and shareholders don’t get compensated for potential synergies.” They plan to vote against the transaction.

Frontiers response? “As you would expect, we are actively engaging with our shareholders ahead of our Nov 13 special meeting, and are always open to hearing their feedback,” per a Frontier spokesperson

Some Wall Street analysts have had mixed views regarding the transaction as well (link). New Street Research citied a low deal valuation last month when they calculated that the deal is accretive to Verizon shareholders with conservative synergies up to a price of $71/share. On the other side, MoffettNathanson and KeyBanc analysts have argued that acquiring Frontier is a poor use of capital by Verizon and that the size of Frontier’s fiber footprint is too small to move the needle on Verizon’s wireline/wireless convergence strategy.

Next key date…Frontier shareholders are set to vote on the proposed deal on Nov 13.

See below for our take on Cooper’s main arguments – Cooper’s full letter can be accessed HERE.

- Background: Copper Investors have been shareholders of Frontier since 2021 and currently own ~800k shares

- Frontier is a compelling investment as a standalone Co: Since the Jan 2021 Investor meeting, Frontier’s mgmt has made “significant progress in executing their strategy, substantially de-risking the investment across key dimensions” (with respect to capital spending, funding, and fiber penetration)

- “The business is on the cusp of entering the most rewarding period for stockholders as the fiber deployment risks decline and cash flows increase”

- “Surprised the Board decided to sell the Company at this juncture at a price that does not appear to fully account for the significant future value we believe is about to begin accruing to stockholders”

- Frontier should be valued on 2026 metrics: Given that the Co is on track to complete the network upgrade in mid-2026

- It will have an expected 10mn fiber passings and $2.6bn in EBITDA in 2026

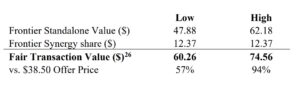

- Low end valuation for Frontier standalone is $47.88/share based on a 10x 2026 EV/EBITDA multiple

- The merger proxy used 2026 EV/EBITDA ranges of 5.5x – 10.6x and 7.25x – 8.50 to generate valn ranges for Frontier, but “legacy” cable comps are not the right comps… fiber transactions point to a much higher valn

- The avg EV/EBITDA multiple of precedent fiber transactions is 14.6x, and fiber assets seldom trade for < 10x EBITDA

- At a 10x 2026 EBITDA multiple, Frontier should be worth $47.88/share on a standalone basis at the time the transaction is closed, or ~ 24% above the current Offer Price

- Higher end valuation for Frontier standalone is $62.18/share, based on $3,000 per passing 2026

- The current Offer implies standalone Frontier is being valued at $2,399 per passing

- But Frontier’s assets are worth a “premium” to those of “legacy cable” peers given growth profile

- Even a modest premium of $3,000 per passing (below Frontier’s own funding and precedent fiber deals) values equates to $62.18/share, which is +62% above the current Offer Price

- And this valn places no value on the Co’s remaining 5mn copper passings

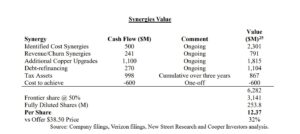

- Frontier’s share of the deal synergies (listed below and total $6.3bn) should equate to an addt’l $12.37/shr

- Net-net, the fair transaction value for Frontier is +57-94% above the Offer Price

- “We reiterate our strong opposition to the Proposed Transaction at $38.50/share and intend to vote our shares against its approval”

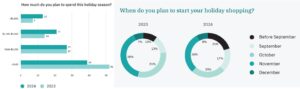

Higher Prices For Essentials Will Take A Cut Out Of Holiday Shopping + Other Spending Updates

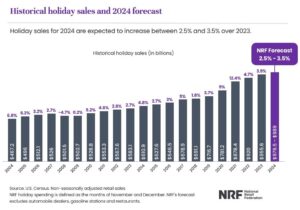

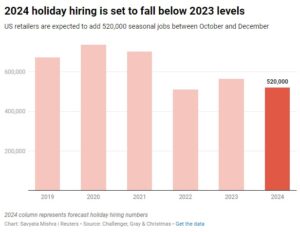

Although many companies have cautioned that “significant market uncertainties remain” (see Theme #4 ), the recent stronger than anticipated retail sales reports from the US Commerce Department as well as the Fed (finally) beginning to cut borrowing rates have fueled the debate about whether the economy is headed for a soft landing, and these mixed views have also been reflected in divergent holiday sales forecasts. This week, a new report from the National Retail Federation forecast that holiday spending will grow at the slowest pace in six years, increasing just +3% y/y at the mid-point following a +3.9% y/y increase in 2023. Accordingly, the NRF also predicts there will be a downtick in seasonal hiring, with retailers expected to bring on 400-500k seasonal workers after employing 509k last year. This is similar to Challenger & Gray’s prediction, which sees 520,000 seasonal jobs being added in Q4 – the second-lowest total it has counted since 2009.

In contrast, other outlooks on the upcoming holiday shopping season were more constructive. A recent ESW survey found that 61% of shoppers plan to spend more than $600 (an increase from last year’s 48%), with nearly double the number of shoppers starting their shopping earlier in the year. That said, while budgets are growing, inflation remains a major concern, as almost half of respondents that plan to spend less will be cutting back due to higher prices for essentials, like gas and groceries.

See below for more of what we thought was important regarding this theme.

Holiday Spending Is Expected To Grow At The Slowest Pace In Six Yrs, Per The National Retail Federation (link)

- Winter holiday spending is projected to grow +2.5-3.5%y/y to $979.5-989bn in 2024: This is a slowdown from 2023’s +3.9% y/y increase in holiday sales to $955.6bn

- E-commerce is predicted to be the primary driver of sales growth for the upcoming season: Online and other non-store sales are expected to increase +8-9% y/y (vs +10.7% y/y in 2023) and account for between $295.1-297.9bn of the total spending

- Retailers are expected to hire between 400-500k seasonal workers this yr: Some of these may have been pulled into Oct to support retailers’ holiday buying events this month; This marks a decline from last yr’s 509k seasonal hires

- Key differences w/ this yr’s holiday season: The shopping window between Thanksgiving and Christmas will be 5 days shorter this yr, and the economic impact of Hurricanes Helene and Milton as well as the presidential election cycle could impact consumer spending as well

While Holiday Budgets Are Increasing Overall, High Prices On Essentials Are Still Driving Spending Cutbacks, Per ESW (link/link)

- Shoppers will spend more this year…

- 61% of shoppers plan to spend $600+ this year, vs 48% last year

- The %age of shoppers planning to spend $1,800+ nearly doubled y/y

- … And will spend it over longer periods of time

- The %age of shoppers who started holiday shopping before September also nearly doubled y/y

- Of those who will spend less this holiday season, nearly half (47%) said they’re cutting back due to rising prices on essentials like gas and groceries

- The oldest and youngest shoppers have the lowest budgets

- 51% of Baby Boomers and 52% of Gen Z have holidays budgets of <$600

- 31% of Millennials and 33% of Gen Z have holidays budgets of $901-$1,500

- Holiday shoppers are hesitant to pay for shipping and returns

- 57% of respondents said free shipping was mostly to influence their decision to make a purchase

- 60% of shoppers of all ages will pay up to $9 for expedited shipping

- More than half of Baby Boomers will not pay extra for expedited shipping

- 49% of shoppers will only purchase items that they can return for free

- But, in exchange for free shipping, shoppers are willing to be more patient

- 41% of shoppers will wait 4-7 days for their packages to arrive

- 27% of shoppers will wait 8-10 day for their packages to arrive

- Shoppers who started early were more likely to say that they would only buy if returns are free

- But, in exchange for free shipping, shoppers are willing to be more patient

- 57% of respondents said free shipping was mostly to influence their decision to make a purchase

- “I plan to shop online less” – Younger shoppers are more likely to reduce their ecommerce activity this year compared to older consumers

- Gen Z – 21%

- Millennials – 17%

- Gen X – 9%

- Baby Boomers – 7%

- Which major shopping sale days do consumers plan to shop the most at?

- Black Friday – 35%

- Amazon Prime Big Deal Days – 24%

- Cyber Monday – 15%

- Thanksgiving – 10%

- Columbus Day – 7%

- Singles’ Day – 5%

- Almost half of consumers (49%) will use TikTok for gifting this holiday season

- Will buy directly on TikTok Shop – 11%

- To search for gifts – 15%

- To get inspiration – 23%

- Don’t plan to use TikTok for holiday gifting – 51%

Holiday Hiring Is Starting To Ramp Up, But 2024 Hiring Levels Are Expected To Come In Lower Than 2023

- Several Cos have annc’d hiring plans for the holiday season so far… (link)

- Amazon: 250,000 seasonal, full-time, and part-time workers (same as 2023)

- Target: 100,000 seasonal workers (same as 2023)

- Macy’s: 31,500 full-time and part-time seasonal workers (down from 38,000 in 2023)

- Bath & Body Works: 32,700 workers (a slight increase from last year’s 32,500)

- UPS: 125,000 workers (up from 100,000 in 2023)

- 1-800-Flowers.com: 8,000 workers (same as 2023)

- Dick’s Sporting Goods: 8,000 seasonal workers (down from 8,600 in 2023)

- Kroger: 25,000 (said it was “seeking to hire thousands of associates” in 2023)

- Burlington: 24,500 seasonal, full-time, and part-time workers (did not specify in 2023)

- JCPenney: 10,000 seasonal associates (did not specify in 2023)

- … Though retailers are expected to add fewer seasonal jobs this year vs 2023 due to softer labor market and tighter consumer spending, according to forecast from Challenger, Gray & Christmas in September

- Predicts that retailers will bring on 520,000 new jobs in Q4, the second-lowest total since 2009 and well below last year’s roughly 564,000

Ad Agencies – Publics & Omnicom Outperform Despite Macro Pressures

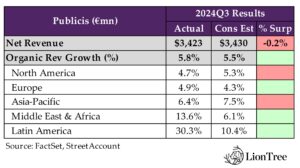

Publicis and Omnicom, two major ad agency holding companies, reported earnings this week, providing a glimpse into how competitive dynamics in the space have been shaking out. For the most part, it was a strong showing for both. The pair beat consensus estimates on organic revenue growth and appeared to successfully navigate through a worsening macroenvironment that was more challenging than Publicis anticipated, suggesting both were net takers of market share during the quarter. Publicis, in particular, highlighted that it again outperformed the industry by an average of +300bps, driven by new business the company added during the summer and YTD as well as its “ability to capture a disproportionate share” of client spend on personalization at scale. Publicis’ confidence in these trends led it to raise the floor of its FY24 organic revenue growth guidance range by +50bps to +5.5-6.0%. Interestingly, Publicis refuted the notion that principal trading has been a key contributor to its outperformance and that the practice suffers from a lack of transparency. US principal media activity represents less than 1% of the Publicis’ net revenue, and the company asserted that it never uses a client’s data for other clients or for its own purposes.

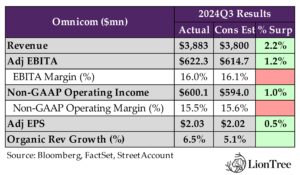

Turning to Omnicom, the Co’s headline numbers were mostly better than anticipated, as its reported revenue and adj EBITDA were +2.2% and +1.2% ahead of expectations, respectively, but operating margins were lower than expected which was a major focus for sell-side analysts during the Q&A portion of the call but recent new business wins did have a margin drag and that should start to improve once the Co begins servicing that revenue later in Q4 and early 2025. However, mgmt’s comment that the impact of investments in AI is still “unknown”, given the costs associated with developing those tools, certainly raised some eyebrows. Notably, one of Omnicom’s new business wins included Amazon’s media business in the Americas, which was “the biggest pitch of the year” and the company’s “largest win in quite a while”. This success demonstrates that Omnicom’s decision to acquire Flywheel is already starting to pay significant dividends by helping to land these types of accounts. Nonetheless, Omnicom conservatively maintained its FY24 organic y/y revenue growth outlook of +4-5%, implying Q4 growth in the ~low-4% range, due to lingering uncertainty in levels of year-end budget flush, which did disappoint investors.

Net-net, Publicis and Omnicom performed well in a tough environment and set a high bar for the other ad agency holding companies slated to report later this cycle (IPG is scheduled for Oct 22, WPP is set for Oct 23, and Dentsu for Nov 14).

See below for more of our key takeaways from Publicis and Omnicom’s prints:

-> Publicis shares gained +2.0% in reaction to the print and ended the week up +3.5%; Omnicom stock rose +1.4% following the print and closed the week up +1.6%; YTD, Publicis stock is trading up +19.5% and Omnicom stock is up +20.8%

Both Publicis & Omnicom BEAT Organic Rev Growth Expectations Though OMC Margins Were Softer

- Publicis’ net rev fell slightly short of estimates…: Reported net rev rose +5.6% y/y in Q3 (vs +6.8% y/y in Q2), missing cons by -0.2%

- …BUT organic rev growth was nicely above consensus: Organic rev incr’d +5.8% y/y in Q3 (vs +5.6% y/y in Q2) and beat cons’ +5.5% y/y

- FX became a headwind: There was a net negative impact of -1.2% or -€36mn (vs a “small positive impact” of +€13mn in Q2) due to the depreciation of the US dollar and the Argentinian peso, partially offset by of the increase of the pound sterling vs euros

- Confirmed that 2024 financial ratios will be “maintained” at “industry-leading levels”:

- Still sees an operating margin of 18% (flat w/ 2023) and €1.8-1.9bn in FCF before changes in working capital

- Also expects to sustain its “industry-high bonus pool” and including a €100mn OpEx investment in its AI plans

- The $1bn acquisition of Influential and Mars United will be “in-line” w/ the Co’s current margins

- Omnicom beat on top-line and adj EBITA, but margins were underwhelming: Q3 reported rev grew +8.5% y/y (vs +6.8% y/y in Q2) and topped cons by +2.2%; Adj EBITDA rose +7.9% y/y (vs +5.5% y/y in Q2) and beat by +1.2%, but adj EBITA margin of 16.0% was below cons’ 16.1%; Adj EPS was +0.5% above cons

- Organic rev growth was also better than anticipated: Q3 organic rev was up +6.5% y/y (vs +5.2% y/y in Q2), surpassing cons +5.1% y/y

- The FX impact was “nominal”: Resulted in just a -0.1% decline in reported rev (vs a -1.0% headwind in Q2)

The Strong Organic Growth Performance Was Despite A Seq Deteriorating Macroenvironment

- Publicis – It has been a “more challenging than expected macroeconomic context”: The macroenvironment “has not been doing any better” and, “in many cases, [has] gotten worse”

- “There is a wait-and-see attitude that we clearly see”: Given that clients require “CapEx investments to truly transform”

- BUT “the tone of [the Co’s] client is still a tone of tone of confidence”: This is b/c “everyone has understood now that it’s all about biz transformation and making sure [they] adapt to this new world”

- “Media and the media landscape has been changing way faster than the creative landscape”: “Agencies and clients had to adapt to this new model… which create[s] more oppty”

- Production is a “very big source of growth for the mkt in general and for [Publicis]”: The Co has made “huge progress” in using AI to deliver more content faster and cheaper as well as w/ more agility and quality; More innovation on this front will be unveiled at the beginning of 2025

- Publicis again outperformed the industry by more than +300bps, on avg: Cited two reasons for this –

- Publicis had a “particularly strong” new biz track record over the summer and YTD

- The Co has an “ability to capture a disproportionate share” of client spend on personalization at scale

- “There is a wait-and-see attitude that we clearly see”: Given that clients require “CapEx investments to truly transform”

- Omnicom – “Significant mkt uncertainties remain”: Given the upcoming US elections as well as the ongoing conflicts in Ukraine and the Middle East

- That said, the elections “won’t really significantly impact” project spend in Q4: Similar to past yrs, the Co will gain more visibility into levels of Q4 project spending as it works through Q3 – “That number goes from some number to $250mn, depending on client activity”

- “The industry is in better shape than it was in the last five or six yrs”: Enhanced measurement has been one key reason, as clients will typically “sit and give you a very fair hearing about where to invest that money” when the Co can provide measurement capabilities

- Agencies also have access to budgets that they didn’t have in the past: Clients have been converging or merging certain budgets, allowing agencies oppties to provide svs to clients’ CIO and sales organizations

Despite Macro Risks, Publicis Is Optimistic About The Rest Of FY24, While Omnicom Is More Conservative

- Publicis raised the low-end of its FY24 organic growth guidance range: Now anticipates +5.5-6% y/y organic rev growth in FY24 (vs +5-6% y/y previously and +4-5% y/y initially); This is ahead of the Co’s 4-yr CAGR of +4.7%

- The outlook accounts for “current macro uncertainties” …: These “continue to weigh” on the Co and are expected to “impact clients’ EOY budget adjustments”

- BUT Publicis has been showing its “ability to win mkt share and outperform the industry”: The Co “cont’d to win mkt share in Q3” and is “planning to keep the momentum until the end of the yr”

- “Q4 is always a qtr of adjustments”: Acknowledged a “risk for instability depending on how the election will go”

- The outlook accounts for “current macro uncertainties” …: These “continue to weigh” on the Co and are expected to “impact clients’ EOY budget adjustments”

- Omnicom maintained its FY24 outlook despite the Q3 beat –

- The Co is “on track” to hit the high-end of its +4-5% y/y organic growth target: This implies organic growth in the low +4% y/y range in Q4, which was due to uncertainty around levels of project spend

- Recent client wins will start to benefit financial performance moving forward…: Expects a “full contribution” from new client wins in Precision Marketing in Q4 and “beyond”, while recent wins in Public Relations will start to be reflected in 2025

- … BUT have weighed on margins thus far: The most expensive time of the Co’s relationship w/ clients is when it wins new biz, given that it is “staffing up without the rev”

- Flywheel “will contribute very strongly” to Omnicom’s growth: Believes Flywheel is “a decade ahead of the next closest thing” and that it will help the Co expand within the retail media space

- Recent client wins will start to benefit financial performance moving forward…: Expects a “full contribution” from new client wins in Precision Marketing in Q4 and “beyond”, while recent wins in Public Relations will start to be reflected in 2025

- FY24 EBITA margin is still expected to be “close to flat w/ 2023”: YTD EBITDA margin is 15.1% (vs 15.2% at this time last yr)

- The Co has “a number of things going on” to improve margins: Including finding efficiencies in its production and advertising bizs as well as efforts to incorporate more automation; But the impact of its investments in AI is still “unknown”, given the costs associated w/ developing those tools

- The Co is “on track” to hit the high-end of its +4-5% y/y organic growth target: This implies organic growth in the low +4% y/y range in Q4, which was due to uncertainty around levels of project spend

Performance Highlights By Region/Discipline

- Publicis has been “accel’ing on growth” throughout 2024: The Co’s +5.8% y/y rise in organic rev in Q3 was a step up from H1’s +5.4% growth

- “Creative accel’d in Q3, delivering ~+msd% y/y growth”: Compares to ~+lsd% y/y growth in Q2; Strength in Q3 was driven by “solid momentum on production and new biz wins, including scope expansions”

- Publicis (mostly) “performed well in all regions” –

- Growth in North America was a bit underwhelming: North America organic rev was up +4.7% y/y (vs +5.2% y/y in Q2) but below cons’ +5.3% y/y, as Publicis Sapient “posted a slight organic decline due to the cont’d wait-and-see attitude from clients”

- Europe accel’d seq: Europe organic rev incr’d +4.9% y/y (vs +4.2% y/y in Q2), beating cons’ +4.3% y/y; Strong growth in France, Germany, and Central & Eastern Europe offset declines in the UK

- APAC growth slowed seq: APAC organic rev rose +6.4% y/y in Q3 (vs +7.7% y/y in Q2) but missed cons’ +7.5% y/y; Despite the slowdown, growth in China accel’d due to mkt share gains

- Growth in the Middle East & Africa improved seq: Middle East & Africa organic rev incr’d +13.6% y/y (vs +9.1% y/y in Q2) and beat cons’ +6.1% y/y, “largely driven by Media activities and Publicis Sapient”

- LatAm growth picked up further seq: LatAm organic rev grew +30.3% y/y (vs +18.9% y/y in Q2) and far exceeded cons’ +10.4% y/y; Organic growth was strong in Brazil, Mexico, Colombia, and Argentina, though this was “partly due to inflation”

- Omnicom – Organic rev growth was “very strong”:

- Breakdown by discipline –

- Advertising & Media growth accel’d seq: Advertising & Media organic rev growth of +9.4% y/y (vs +7.8% y/y in Q2) “reflected cont’d strong growth in media and improved performance in advertising”, including positive contributions from the production initiative

- Precision Marketing growth was down slightly seq: Precision Marketing organic rev was up +0.8% y/y (vs +1.4% y/y in Q2); “Cont’d strong growth” at Flywheel and in the US was offset by “lower client spending primarily concentrated in a few mkts outside the US”, such as the UK

- Public Relations growth stepped up seq: Public Relations organic rev incr’d +4.3% y/y (vs +0.9% y/y in Q2); Benefited from US election spending but saw a “softer performance internationally”

- Branding & Retail Commerce declines steepened seq: Branding & Retail Commerce organic rev decr’d -5.4% y/y (vs -3.8% y/y in Q2), driven by “reduced client spending” at the Co’s branding agencies and a “flat” performance in Retail Commerce

- Experiential rev growth improved further seq: Experiential organic rev incr’d +35.3% y/y (vs +17.6% y/y in Q2); Activations for the summer Olympics were a tailwind, while execution & support was flat

- Growth accel’d across nearly all geos: The US saw organic rev growth of +6.5% y/y (vs +6.3% y/y in Q2), Europe grew +6.8% y/y (vs +4.5% y/y in Q2), APAC was up +10.9% y/y (vs -0.1% y/y in Q2), the Middle East & Africa rose +24.8% y/y (vs 8.0% y/y in Q2), and LatAm grew +8.7% y/y (vs +24.5% y/y in Q2)

- Breakdown by discipline –

Commentary On Client Verticals

- Publicis – 7 of the Co’s top 10 client sectors again posted positive growth –

- TMT (~13% of net rev) “cont’d to perform very well” but decel’d seq: Grew over +9% y/y (vs +11% y/y in both Q1 and Q2)

- “Healthcare recorded double digit growth”: This was on top of double-digit growth in the prior yr qtr, driven by new biz wins across different activities and scope expansion w/ a number of existing clients

- Healthcare contributed nearly +200bps to organic growth in Q3: YTD, Publicis is performing 3x better than the second-best player in the industry; In Q3, the Co doubled the performance of the second-best player, despite not participating in two big healthcare pitches

- “Retail was slightly down”: Given a lower contribution from Publicis Sapient from delays in DBT projects in Europe and tough comps, particularly in the UK

- Auto faced “a challenging context” but still managed positive growth: The Co remains optimistic on the segment, given that “people will not stop using car anytime soon”

- Food & bev growth decel’d: Growth was flat in Q3 but still up +4.3% YTD; Q3 was impacted by a “very high comparable” as well as customers remaining in a wait-and-see approach

- Omnicom’s rev by industry sector maintained “historical stability”: There were “no significant changes in mix” both in Q3 and YTD; Pharma & Health, Food & Bev, and Auto accounted for 16%, 15%, and 12% of the Co’s rev in Q3, respectively; Each figure was flat w/ the prior yr qtr

Other Highlights – Comments On Principal Trading + Amazon’s Media Biz

- Publicis – “It would be wrong to say that this media platform and this principal of media buying is the reason for outperformance”: For example, US principal media activity represents less than 1% of the Co’s net rev

- “It’s very important to note that those media platform[s] have nothing to do w/ the black box”: Publicis “never ever” uses client data for another client or for itself; The Co also has “zero tolerance for garbage inventory, which is garbage media”

- Omnicom “won the biggest pitch of the yr by being awarded Amazon’s media biz in the Americas”: This was the Co’s “largest win in quite a while” and points to its “solid relationship” w/ Amazon following the Flywheel acquisition and its “extremely strong media offering”; Rev from the deal will start in 2025

- There’s a “real enterprise relationship” between Amazon and Omnicom: The partnership was “instrumental” in enabling Omnicom to directly measure online retail sales generated from media campaigns “across the full advertising journey”

- Other notable wins: Include Michelin’s global media biz, integrated svs for Barclays and Bimbo Bakeries USA, Adobe’s digital experience biz, precision marketing for Princess Cruises, as well as creative for Corona Extra, General Mills, and Pepsi

Positive Comments On The Consumer Out Of The Big Banks…

Outside of our core TMT sector, we do try to keep tabs on relevant updates from other sectors, particularly as it relates to the health of the consumer and consumer spending trends, given the implications across our space. The past two weeks have been big ones for results out of several juggernaut banks (Goldman Sachs, Citigroup, Bank of America, JP Morgan Chase, and Wells Fargo). Overall, the comments on the consumer were broadly positive, which is a good read. See below for more detail and specific commentary…

- Goldman Sachs: “The U.S. economy continues to be resilient”

- Positive tone: “Inflation has been coming down, the recent unemployment data is supportive, and while we’ve seen some softness in consumer behavior, the tone of my recent conversations with clients has been quite constructive”

- Overall, the firm remains cautiously optimistic about consumer trends amidst a complex economic backdrop

- Optimistic on a soft landing: “The beginning of the rate cut cycle has renewed optimism for a soft landing, which should spur increased economic activity”

- Positive tone: “Inflation has been coming down, the recent unemployment data is supportive, and while we’ve seen some softness in consumer behavior, the tone of my recent conversations with clients has been quite constructive”

- Citigroup: The consumer is healthy, and signs of stress are isolated

- The US consumer is healthy & resilient: “The US consumer dynamics remain remarkably consistent with prior quarters. Our customers are healthy but more discerning in their spend with signs of stress isolated to the lower FICOs”

- “Based on what we see, the US consumer continues to remain healthy and resilient. Spend and payment rates continue to normalize, and underlying credit performance remains broadly in line with our expectations”

- Consumer delinquencies declined seq: “Sequentially, net credit losses declined while delinquencies increased both in line with historical third quarter seasonality. Absent this seasonality, we continue to see stabilization in early-stage delinquencies”

- The US consumer is healthy & resilient: “The US consumer dynamics remain remarkably consistent with prior quarters. Our customers are healthy but more discerning in their spend with signs of stress isolated to the lower FICOs”

- Bank of America: Positive comments on the health of the consumer

- Positive comments on consumer spending patterns: Consumer spending “activity is consistent with how customers are spending money in the 2016 to 2019 timeframe when the economy was growing and inflation was under control”

- Areas of consumer concern are not impacting overall activity: “Consumers are wary of the cost of living, worried about higher rates and other matters. But overall, activity is fine. Unemployment is low and wage growth is steady, both of which bode well for the consumer overall and for consumer asset quality”

- Consumer credit losses are down y/y: “On asset quality, a few quarters ago, we told you that consumer credit losses would go down this quarter, given delinquency trends we had seen at the time. We also told you that office losses would be lower. Both of these proved true again this quarter”

- JP Morgan Chase: Spending patterns have normalized / no weakening in retail spending

- Consumer spend is “a little bit boring in a sense” because its normalized: There was a “heavy rotation into T&E as people did a lot of traveling and they booked cruises that they hadn’t done before and everyone was going out to dinner a lot…so you had the big spike in T&E, the big rotation into discretionary spending. And that’s now normalized”

- No weakening in retail spending: “And inside that data, we’re not seeing weakening, for example, in retail spending”

- “So, overall, we see the spending patterns as being sort of solid and consistent with the narrative that the consumer is on solid footing and consistent with the strong labor market, and the current central case of a kind of no landing scenario economically”

- Wells Fargo: Sees resilience in the consumer & spending patterns

- Mgmt highlighted that both consumer and commercial customers have remained resilient: This is supported by a strong labor market and wage growth

- Consumer charge-offs declined, particularly in the credit card portfolio, and overall consumer credit performance remained stable

- Despite some stress in lower-income segments due to inflation, consumer spending on credit and debit cards increased y/y, although the growth pace has slowed

- Sees some potential tailwinds for lower-income: The management noted that the benefits of slowing inflation and easing interest rates should particularly help lower-income customer

- Overall: “We continue to look for changes in consumer health, but we have not seen meaningful changes in trends when looking at delinquency statistics across our consumer credit portfolios.”

- Mgmt highlighted that both consumer and commercial customers have remained resilient: This is supported by a strong labor market and wage growth

Premium Sports Rights Continues To Play A Pivotal Role In The Sector

The central role that sports has assumed for both holding together the linear TV ecosystem as well as attracting new subscribers to streaming platforms continues to be an ongoing theme, with several additional proof points this week. The latest edition of Nielsen’s The Gauge report revealed that the NFL was instrumental in driving an increasing share of TV usage for both Amazon Prime and Peacock in September, which would seem to support a separate report from Guideline that found that the price for a 30-second NFL ad spot is set to increase +9% y/y in October (vs +7% y/y in September). However, the NFL has hit some speed bumps lately, with the Week 6 slate of games dipping in ratings for a second consecutive week after a hot start to the 2024-25 season, per Sports Media Watch, so it will be interesting to see if that affects pricing for an ad spot moving forward.

While the NFL has seen some recent relative ratings softness, other leagues have posted impressive viewership numbers. The MLB playoffs, particularly on the National League side, has achieved several viewership milestones, and audiences for the WNBA Finals saw a material +85% y/y increase through the first two games of the series. These further proof points likely haven’t gone unnoticed by streamers, as NBCUniversal is reportedly planning to add its RSNs to Peacock, which would bring games from high-profile teams such as the Golden State Warriors, Boston Celtics, and Philadelphia Phillies onto the platform. ESPN Chairman Jimmy Pitaro also shared some details about the vision for ESPN’s upcoming standalone streaming service but didn’t provide any updates on timing or pricing.

See below for more details.

- NFL TV ratings were down in Week 6, per Sports Media Watch (link): This past weekend’s ratings dip marked the second consecutive week that ratings declined; Only two windows outperformed their 2023 Week 6 counterparts, w/ the rest being down y/y

- Thursday Night Football: Amazon Prime Video’s showing of the 49ers-Seakhawks game was down -5% y/y

- Sunday early afternoon: Fox’s 1pm EST games were down -13% y/y

- Sunday mid-afternoon: The Lions-Cowboys matchup on Fox drew 24.06mn viewers, a -8% y/y decline from the Eagles-Jets game last yr

- Sunday Night Football: The Bengals-Giants game, hosted by NBC, was the least watched Sunday Night Football broadcast since 2020 w/ 15.44mn viewers

- Monday Night Football: The 17.3mn viewers for the Bills-Jets game was down -12% y/y from last yr’s Cowboys-Chargers game

- Looking ahead – viewership could improve in Week 7: Given that the Chiefs, which didn’t play in Week 6, have a matchup against the 49ers

-> The price for a 30-sec NFL ad spot is set to increase +9% y/y in Oct (vs +7% y/y in Sept), per advertising intelligence Co Guideline; The top three product categories advertising in NFL games season were Entertainment & Media, Financial Services and Technology, while Wellness (+42% y/y) and Pharmaceuticals (+39% y/y) were the categories w/ the most significant spending increases; This comes as the NFL is avg’d 17.22mn viewers through Week 5, a +1% y/y increase, per Nielsen (link/link)

-> Separately, news emerged this week that former quarterback Tom Brady will finally have a long-delayed bid to become a 10% stakeholder in the Los Angeles Raiders, along w/ biz partner Tom Wagner, brought before NFL ownership for approval; The vote is expected to be a formality after the NFL’s finance committee unanimously cleared Brady’s proposal (link)

- But other sports leagues touted strong viewership numbers –

- MLB – Game 1 of the National League Championship Series (NLCS) was the most-watched LCS Game 1 since 2009 (link): The first game of the NLCS between The Mets and The Dodgers’ avg’d 8.5mn viewers across Fox, Fox Deportes, and streaming

- There were a peak of 10.1mn viewers on Fox, per Anthony Dicomo, who covers The Mets for MLB.com

- Fox Sports also recorded the most-watched National League Divisional Series (NLDS) since 2015 (link): The Dodgers-Padres and Mets-Phillies series combined to avg 4.1mn viewers across nine games

- WNBA – Game 2 of the Finals drew its largest audience since 2001 (link): Last Sunday’s (Oct 13) WNBA Finals game between the Lynx and Liberty avg’d 1.35mn viewers, marking a +93% rise vs the avg of 2023’s WNBA Finals; Through two games, viewership for the WNBA Finals is up +85% y/y

- MLB – Game 1 of the National League Championship Series (NLCS) was the most-watched LCS Game 1 since 2009 (link): The first game of the NLCS between The Mets and The Dodgers’ avg’d 8.5mn viewers across Fox, Fox Deportes, and streaming

-> The WNBA is evaluating 10-12 cities as candidates to host a sixteenth WNBA franchise by 2027-2028, per commissioner Cathy Engelbert; A sixteenth team would tie the record high number of franchises that the league had from 2000-2002 and would come in addition to the three expansion teams that were annc’d last Sept; Philadelphia, Nashville, Denver, and somewhere in South Florida have all been mentioned as possibilities in the past (link)

There Were Also Several Sports-Related Streaming Updates Out This Week…

- ESPN Chairman Jimmy Pitaro divulged new details about ESPN’s new standalone streaming svs (link): Pitaro spoke this week at Columbia University Sports Management Conference

- The new offering will be a comprehensive platform that integrates all of ESPN’s capabilities: Including live sports, news, analysis, fantasy sports, betting, ticketing, and merchandise

- It will also feature a range of innovative features: Including the below-

- Multi-screen viewing: Watch multiple games or events at the same time

- ESPN Bet integration: Place bets directly w/in the streaming experience

- Ticketing and merchandising: Purchase tickets and merchandise seamlessly

- Fantasy sports tools: Manage fantasy teams and access real-time data

- Personalized content: Receive customized recommendations and curated content feeds

- Advanced statistics: Dive deep into real-time data and analytics

- ESPN+ inclusion: Access the existing ESPN+ library w/in the flagship service

- The exact launch date and pricing for the new svs remain undisclosed

- NBCUniversal reportedly plans to add its RSNs to Peacock as early as 2025 (link): Sources indicate NBCUniversal is still completing details of the plan and that the rollout could be delayed

- The four NBC Sports networks that will be added have local broadcast rights in Boston, Philadelphia and across Northern California, per sources: This means that games for high-profile teams, such as the Golden State Warriors, Celtics and Phillies, will be included

- Games will still be available on TV: One option being discussed is to make the channels available as add-ons in the local mkts, so that fans in them can pay extra to stream games

- Amazon Prime Video recorded the largest m/m growth in share of TV usage in Sept, largely thanks to the NFL (link): Nielsen’s latest edition of The Gauge found that Prime Video’s share of TV usage incr’d +12% m/m in Sept, driven by Thursday Night Football as well as Lord of the Rings: Rings of Power

- Peacock also got a boost from the NFL: Peacock’s coverage of the Packers-Eagles game in Sao Paolo, Brazil was the eleventh most-streamed program in Sept w/ 2.6bn minutes viewed

Grab Bag: The FTC’s New Click-To-Cancel Rule/Uber Explores A Deal For Expedia/Video Game Strike Negotiations Set To Resume

- The FTC’s new “click-to-cancel” rule will make it easier for consumers to cancel subscriptions (link): Under the US Federal Trade Commission’s new rule, bizs cannot force customers to cancel a subscription using a different method than the one that they used to sign up

- The rule applies to any automatically renewing subscription: Ranging from gym memberships to magazine subscriptions, as well as monthly payments for svs (i.e., Amazon Prime)

- Other types of plans that it covers: Include free trials that charge if customers don’t cancel in time as well as continuity plans, where consumers receive periodic product shipments until canceled

- Timing: Most of the provisions in the “click-to-cancel” rule will go into effect 180 days after it’s published in the Federal Register

- The rule is part of the FTC’s broader crackdown on questionable subscription practices: Earlier this yr, the FTC sued Adobe for offering “deceiving subscriptions” and making it difficult for customers to cancel these; Amazon and Microsoft’s practices have also been under scrutiny by the agency

- The rule applies to any automatically renewing subscription: Ranging from gym memberships to magazine subscriptions, as well as monthly payments for svs (i.e., Amazon Prime)

- Uber reportedly explored a potential bid for Expedia (link): After the idea was put forward by a third-party, Uber reportedly approached advisers in recent months to examine whether such a deal would be possible and how it would be structured, per sources

- Uber’s interest was at a very early stage: People familiar w/ the matter cautioned that no formal approach to Uber has been made and that there are no current discussions; It is possible that a deal might not transpire

- Uber’s capacity for M&A has been strengthened over the past yr: Uber’s stock price has risen ~+85% over the past yr, giving it a mkt cap of $173bn; In comparison, Expedia’s mkt cap sits at ~$20bn

- Uber CEO Dara Khosrowshahi was previously Expedia’s CEO from 2005-2017: Khosrowshahi also remains a non-executive director on Expedia’s board, meaning that any approach would likely be friendly and that he would recuse himself from deal discussions

- Acquiring Expedia would further Uber’s ambitions of creating a “super app”: “Anywhere you want to go in your city and anything that you want to get, we want to empower you to do so,” per Khosrowshahi

- Uber’s interest was at a very early stage: People familiar w/ the matter cautioned that no formal approach to Uber has been made and that there are no current discussions; It is possible that a deal might not transpire

- SAG-AFTRA is set to resume negotiations w/ video game Cos next week (link): After commencing strikes three months ago, SAG-AFTRA will return to discussions surrounding a new video game contract w/ signatories of the Interactive Media Agreement (IMA) on Oct 23

- The Cos involved include Disney, Activision, EA, and Warner Bros Games, among others: This week, the actors’ guild also staged a picket at the offices of Warner Bros Games

- Disagreements over AI are at the center of the impasse: Although the strikes started in July, there had already been a yr of on-and-off again talks, where both sides had agreed on nearly all points except for protections for AI replication of actors’ voices, movements, and likenesses

- SAG-AFTRA is seeking to ensure that video game performers are guaranteed consent and compensation for any use of their work in AI models: The union claims that IMA Cos only offered protections for motion capture performers whose characters have a likeness resembling their own

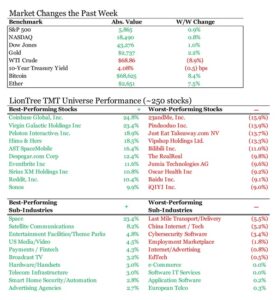

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Adobe annc’d the general availability of Adobe GenStudio for Performance Marketing, a new gen AI-first application that empowers brands and agencies to accelerate the delivery of global advertising and mkting campaigns. The new offering addresses one of the biggest challenges facing bizs today, where the need for highly personalized, on-brand and performant content—across a myriad of channels and geographies—is outstripping available resources. (BUSINESSWIRE)

- Amazon annc’d plans to expand Prime Video ad support to Brazil, India, Japan, the Netherlands, and New Zealand starting next yr. The Co introduced ads on original and library series and film titles in Jan in the US, Canada, Australia, Austria, France, Germany, Italy, Mexico, Spain, and the UK, w/ Prime Video subscribers able to opt out of the ads by paying a monthly fee ($3 in the US). (StreamTV Insider)

- Amazon’s AI generator tool can now create audio ads. Brands can now use gen AI to make audio ads—in addition to images and video—through Amazon Ads’ self-svs tools. That was one of many advertising- and adtech-related developments that the Co annc’d at Amazon unBoxed, its annual advertising conference, as it vies to retain its dominance in digital advertising and retail media. (ADWEEK)

- Donald Trump was asked about Google’s antitrust challenges. Trump said Google “has a lot of power” but didn’t say he favored a breakup. “We want to have great Cos,” he said. “We don’t want China to have these Cos.” The US Department of Justice is weighing asking a federal judge to break up Google after a ruling in August that said the Co illegally acted as a monopoly in its search biz. (Business Insider)

- Global experiential marketing, including both the consumer (B2C) and business-to-business (B2B) sectors, grew 9.7% in 2023 to $116.14bn. While this performance left the industry below the pre-pandemic spending level of $121.87bn in 2019, experiential marketing will surpass pre-COVID spending this yr. Global experiential marketing spending is expected to grow 10.5% in 2024 to $128.35bn, according to new research from PQ Media. (PRWEB)

- Google will block US election ads after the polls close on Nov 5 to prevent voting misinformation, including candidates prematurely claiming victory. Google is implementing the policy “out of an abundance of caution and to limit the potential for confusion, given the likelihood that votes will continue to be counted after Election Day,” a spokesperson says. (TipRanks Financial)

Artificial Intelligence/Machine Learning

- Bain & Co said it will expand its partnership w/ OpenAI to sell the AI startup’s tools, including ChatGPT, to the consultancy’s clients. Last yr, the Cos had set up a global svs alliance to make Bain’s clients aware about OpenAI’s tech. Bain is also investing in establishing an OpenAI Center of Excellence, which will be led by a team of the consultancy. (Yahoo Finance)

- OpenAI and Google have been touting advanced “reasoning” capabilities as the next big step in their latest AI models. However, a new study from six Apple engineers shows that the mathematical “reasoning” displayed by advanced LLMs can be extremely brittle and unreliable in the face of seemingly trivial changes to common benchmark problems. “Current LLMs are not capable of genuine logical reasoning,” the researchers hypothesize. (Ars Technica)

- Toyota Motor’s research unit and Hyundai Motor’s Boston Dynamics are joining forces to speed up the development of humanoid robots w/ AI. The partnership will pair Toyota Research Institute’s expertise in large behavior model learning for machines w/ Boston Dynamics’ humanoid Atlas robot. Boston-based teams from TRI and Boston Dynamics will conduct research on use cases for AI-trained robots in areas such as human-robot interaction. (HT Auto)

- Verizon Business’ fifth annual survey of SMBs found that the number of small-to-medium-sized bizs that are using AI has more than doubled compared to last yr. The survey also found a revival in SMB tech spending, concluding that as SMBs conduct more and more biz online, they are investing more in support of digitalization than they have in the past three yrs. However, four in five SMB decision-makers expressed concerns about the US economy. (RCR Wireless News)

Audio/Music/Podcast

- Spotify said that it is testing music videos for premium users in 85 addt’l mkts. The Co first ran a video experiment in limited markets in March. Spotify originally rolled out music videos in beta in 11 countries, including the UK, Germany, Italy, the Netherlands, Poland, Sweden, Brazil, Colombia, the Philippines, Indonesia, and Kenya. The Co didn’t specify if these 85 new mkts included the US. (TechCrunch)

Broadcast/Cable Networks

- TV2 Média, a Hungarian broadcaster, is being considered as a potential buyer for Warner Bros Discovery’s Polish assets, including the TVN Group, which operates one of Poland’s largest commercial TV networks. This sale is considered to significantly enhance Warner Bros. Discovery’s financial outlook. Other possible buyers include Greece’s Antenna Group and France’s Canal+. TV2 has previously sought to enter the Polish market, indicating its interest in expanding operations there. (dailynewshungary.com)

Cable/Pay-TV/Wireless

- America Movil reported that it more than tripled its net profit in Q3 from a yr ago due in part to a weaker peso boosting its foreign earnings and lower financing costs. Net profit incr’d 217% to 6.43bn Mexican pesos ($326.37mn) but came in below estimates from analysts polled by LSEG. Revs for the Co, controlled by the family of Mexican billionaire Carlos Slim, came in at 223.46bn pesos ($11.35bn) for the period, up nearly 10% y/y. (Investing.com)

- e& UAE annc’d the launch of its groundbreaking team of human-digital advisors at GITEX, each w/ a unique personality representing different nationalities living in the UAE. This innovative customer svs initiative positions e& as the first UAE-based telco to introduce personal digital human advisors, providing a new level of personalized and efficient support to its customers. (ZAWYA)

- e& UAE has achieved a remarkable milestone ahead of GITEX Global 2024 by reaching the fastest aggregated 5G-Advanced speed of 62 Gbps, making UAE residents the first globally to experience such speeds. Utilizing advanced hardware and algorithms like MU-MIMO, e& UAE successfully combined multiple carriers across high- and low-bands. This accomplishment reinforces the company’s commitment to innovation and positions the UAE as a leader in technology and digital connectivity. (THEFASTMODE)

- Jio Platforms posted a 23.4% y/y increase in its consolidated net profit to INR 6,539 Cr in Q2 FY25. Rev from operations jumped 18% y/y to INR 31,709 Cr. Jio’s customer base stood at 47.88 Cr at the end of the Sept qtr, an increase of 4.2% from 45.97 Cr a year ago. Jio Platforms’ ARPU remained unchanged on a seq basis during the qtr at INR 181.7 per month. ARPU grew marginally on a y/y basis from INR 180.5 per month. (Inc42 Media)

- MasOrange hired BNP Paribas to sell its stake in the fiber network it shares w/ Vodafone Spain. The stake is worth between 2.8bn euros ($3.05bn) and 4bn euros. Several infrastructure funds, including France’s Antin and Australia’s Macquarie are interested in the stake, El Confidencial said. (MarketScreener)

- Nokia reported better-than-expected Q3 earnings, mainly on the back of cost cutting measures, but saw its sales dive 8% largely due to a weaker India mkt. The Co reported a net profit of 358mn euros ($389mn) for the period, up 22% from 293mn euros ($318mn) a yr earlier. Nokia’s sales were down at 4.3bn euros ($4.7bn) compared w/ 4.7bn euros ($5.1bn) a yr earlier. Three qtrs of the sales decline was “driven by India due to a strong yr-ago qtr.” (Newsday)

- TCL annc’d the arrival of the groundbreaking TCL LINKPORT IK511, a 5G connectivity device made in collaboration w/ T-Mobile. The TCL LINKPORT IK511 enables devices like laptops and tablets to access T-Mobile’s latest standalone 5G (5G SA) milestone, 5G RedCap, and features the Snapdragon X35 5G Modem-RF System. Launching at T-Mobile stores, this marks a significant milestone in enhancing wireless communication standards across the continent. (THEFASTMODE)

- The FCC annc’d it is formally investigating the use of data caps by broadband providers and their impact on consumers and competition. This inquiry comes as data consumption continues to surge, w/ many consumers facing limitations and potential overage fees on their internet usage. These caps can disproportionately affect small bizs, low-income families, and individuals w/ disabilities who rely heavily on internet access. (Cord Cutters News)

- Wayra, the corporate VC arm of Telefonica, invested an undisclosed sum in Perplexity, a US-based startup that has developed an AI-powered answer engine. Founded in 2022, Perplexity says it uses advanced AI to understand the intent of queries and provide real-time, accurate, and contextual answers to all types of questions using natural language processing (NLP). Customers can ask questions and receive AI-generated answers in real-time. (TelecomTalk)

Cloud/DataCenters/IT Infrastructure

- Amazon signed three agreements to develop the nuclear power tech around small modular reactors, becoming the latest big tech Co to push for new sources to meet surging electricity demand from data centers. Amazon said it will fund a feasibility study for an SMR project near a Northwest Energy site in Washington state. Energy Northwest, a consortium of state public utilities, will have the option to add up to eight 80 MW modules. (The Star)

- Deutsche Telekom’s T-Systems subsidiary strengthened its cloud clout by ascending into the top-tier of a Broadcom partner program. T-Systems’ designation as a pinnacle-tier VMware Cloud Service Provider means it joins the ranks of Broadcom partners w/ extensive certification, a proven track record in sales, and global coverage. It also pitches the Co deeper into the mkts for private and sovereign set-ups using VMware capabilities. (Mobile World Live)

- Google is turning to nuclear energy to help power its AI drive. On Oct 14, the Co that said it will partner with the startup Kairos Power to build seven small nuclear reactors in the US. The deal targets adding 500 megawatts of nuclear power from the small modular reactors (SMRs) by the decade’s end. The first is expected to be up and running by 2030, w/ the remainder arriving through 2035. (Engadget)

Crypto/Blockchain/web3/NFTs

- Crypto usage hit new highs, according to Andreessen Horowitz, which found record crypto usage amid a maturing biz and tech infrastructure. In its annual “State of Crypto,” the report puts the number of cryptocurrency owners worldwide at a new high of 617mn this yr, w/ between ~30-60mn active users. The report also reveals a significant rise in blockchain activity, w/ 220mn unique crypto addresses engaging with the technology at least once. (Quartz)

- Google has removed live price charts for Bitcoin and other cryptocurrencies from its search results. Users have noticed that queries like “Bitcoin price” or “Ethereum price” no longer display these charts, a feature that has been available since 2018. This change has been in effect for several days, but it’s unclear whether it’s a temporary glitch or a permanent decision. (The Crypto Times)

- Italy’s Deputy Finance Minister Maurizio Leo said the nation will raise taxes on capital gains on cryptocurrencies such as Bitcoin to 42% from 26%. The move comes as Italy decided to strengthen its digital svs tax as part of plans to raise more revs in the 2025 budget. The price of bitcoin remained unaffected by the development, extending its w/w gain to more than 12%, rising above $68,000 for the first time since late July. (Yahoo Finance)

Cybersecurity/Security

- A federal grand jury indictment unsealed charges against two Sudanese nationals for operating and controlling Anonymous Sudan. The cybercriminal group is responsible for tens of thousands of Distributed Denial of Service (DDoS) attacks against critical infrastructure, corporate networks, and govt agencies in the US and around the world. In March 2024, the US Attorney’s Office and FBI seized and disabled Anonymous Sudan’s powerful DDoS tool. (JUSTICE)

- A Pokémon game dev faces a major data leak. Hackers released a collection of leaked data from Game Freak over the weekend, including personal info about employees. Game Freak confirmed the breach, saying that it was the result of “unauthorized access to our servers by a third party” and dated back to Aug 2024. Game Freak said the leaked personal information, which it characterizes as names and Co email addresses, included ~2,600 items. (The Verge)

- China’s cybersecurity agency again rejected claims by the US and Microsoft that Chinese hackers were behind a high-profile attack on critical American computer networks known as Volt Typhoon. Calling the claims a “political farce” orchestrated by the US, China’s National Computer Virus Emergency Response Center said that 50+ cybersecurity experts from around the world agreed that there was insufficient evidence to link Volt Typhoon to Beijing. (Yahoo Finance)

eCommerce/Social Commerce/Retail

- 47% of shoppers plan to shop in physical stores this holiday season, signaling a return to brick-and-mortar shopping, per a new Experian survey. While half of baby boomers said they will shop in physical stores, 46% of Gen Xers and millennials, as well as 44% of Gen Zers, said the same. A third of baby boomers plan to shop online over the holiday season, followed by a quarter of Gen Xers, 23% of millennials, and 20% of Gen Zers. (Retail Dive)

- 63% of consumers will shop for gifts at discount dept stores, per ICSC’s 2024 Holiday Shopping Intentions survey of 1,009 people. Meanwhile, a third will shop at traditional dept stores. On avg, shoppers plan to spend $706 on gifts and other holiday items, the most since 2018. Among the top items on shoppers’ list are gift cards (58%); accessories, apparel and jewelry (52%); and toys, games, sporting goods, and other hobby items (50%). (Retail Dive)

- Ebay unveiled the global expansion of its Circular Fashion Fund (CFF). By the end of 2025, the Co will have committed a total of $1.2mn to foster innovation across mkts, including the UK, Germany, the US, and Australia. In an added incentive for the 2025 cohort, eBay Ventures, the Co’s venture capital arm, will award an addt’l $300,000 dollars to one stand-out biz as the “Circular Fashion Innovator of the Year.” (FashionUnited)

- ESW’s new survey found that holiday budgets are increasing for the consumer, yet high prices, especially for essentials, are prompting half of consumers to cut back on holiday spend. 61% plan to spend $600+ this yr, compared to 48% last yr. However, among consumers who will reduce spending, 47% cited high prices on everyday items such as groceries and gasoline as why they will spend less in the 2024 holiday season. (retailcustomerexperience.com)

- Google Shopping is rolling out a personalized feed that shows users a stream of products they might like. The new feature shows up when they head to shopping.google.com. At the top of the page, they’ll see a carousel of products they’ve recently shopped for, allowing them to jump back into their search. But once they scroll down, Google will surface recommended products and in-line videos related to items they might be interested in. (The Verge)

- Instacart annc’d that it has hired Uber executive Anirban Kundu as its chief technology officer. Kundu, who will join the Co later this month, most recently served as vice president and head of engineering for Uber Delivery. Instacart said Kundu will lead Instacart’s technical team, noting that he brings a deep understanding of multi-sided marketplaces and experience building scaled technical systems that can support long-term growth. (Grocery Dive)

- The LVMH Group Q3 2024 earnings are in. The Co missed mkt expectations w/ a 4.4% drop in revs in Q3, which it blamed on lower growth in Japan and a “marked deterioration” in sales of clothing and accessories to Chinese nationals. Uncharacteristically, the initial press release from LVMH did not include a quote from chairman and CEO Bernard Arnault, w/ the group merely reiterating its guidance for the yr. (WWD)

EV/ Autonomous Vehicles

- Alibaba and Baidu are among the cornerstone investors in the Hong Kong IPO of Horizon Robotics, a Chinese provider of software and hardware used in autonomous driving systems. Rodolphe Saade’s CMA CGM and a Ningbo govt fund are also cornerstone investors. The four have agreed to subscribe for a total of $220mn in shares, sources said. Horizon Robotics is looking to raise as much as $800mn in the IPO. (Yahoo Finance)

- Pony AI filed an IPO prospectus w/ the US SEC, planning to list on Nasdaq under the ticker symbol PONY. The startup, backed by Toyota and Nio Capital, has received seven rounds of funding totaling $1.3bn+ before its planned IPO. Following the IPO, the startup, founded in 2016, will become the first publicly traded Co in the global robotaxi space. (CnEVPost)

Film/Studio/Content/IP/Talent

- Endeavor has consistently felt that Wall Street has underappreciated the bizs’ growth potential. An internal document recently disclosed as part of its going-private transaction w/ Silver Lake details why. Endeavor foresees the biz generating $11.4bn in rev in 2028, a 70% rise from 2023, versus expectations of $10.1bn. The Co sees itself generating EBITDA of $3.1bn, more than double 2023 and also well ahead of outside analysts’ projections. (Sportico.com)

- FilmLA, the quasi-public agency that handles film permits in Los Angeles, reported a weak Q3 2024. Production in the Greater Los Angeles area dropped 5% to 5,048 shoot days. Scripted television producers logged 758 shoot days last quarter across the economically important TV Drama, TV Comedy, and TV Pilot categories. There was an increase in feature film production, some of which cont’d during the strikes. (Variety)

- Legendary Entertainment completed a buyout of Wanda Group’s remaining equity interest in a move CEO Josh Grode said ushers in a new era for the studio. Financial terms weren’t disclosed, but Legendary said it funded the transaction entirely from cash on its balance sheet for the deal led by Grode, without tapping partner Apollo Global. Legendary and Apollo now co-own the Co, and the board will be evenly split between mgmt and Apollo. (Deadline)

FinTech/InsurTech/Payments

- Klarna struck a deal to offload buy-now, pay-later loans that it originates in the UK as it looks for ways to free up capital ahead of its public debut. The deal w/ a subsidiary of the hedge fund Elliott Investment Management will give Klarna £30bn ($39bn) of fresh firepower over the coming years as it looks to grow its biz around the world. Klarna will continue to service the loans included in the agreement. (Bloomberg)

- Robinhood launched its long-awaited desktop platform and added futures and index options trading features to its mobile app. The platform, available at no addt’l cost, will offer advanced trading tools, real-time data, as well as custom and preset layouts. The Co said its desktop trading platform, dubbed “Robinhood Legend”, will focus on active traders. (Investing.com)