The tough sell-off on Friday pushed the major indices solidly down for the week with the S&P 500 falling -2.4% and Nasdaq declining -2.5%. Tension with China and the threat of a “massive” increase in tariffs on Chinese products caused major angst with investors.

It was also another big week in AI, headlined by OpenAI’s Developer Day and a big contract with AMD. In this edition we focused on:

- *NEW DECK* LionTree's Lens: Sector Insights & A Look Ahead, Fall 2025

- Software Development Shifts From MONTHS To MINUTES

- The U. S. Consumer Is Expected To Show Up For The Holidays…

- Short Sellers Stick With Their Key Bets Despite The Market Rally

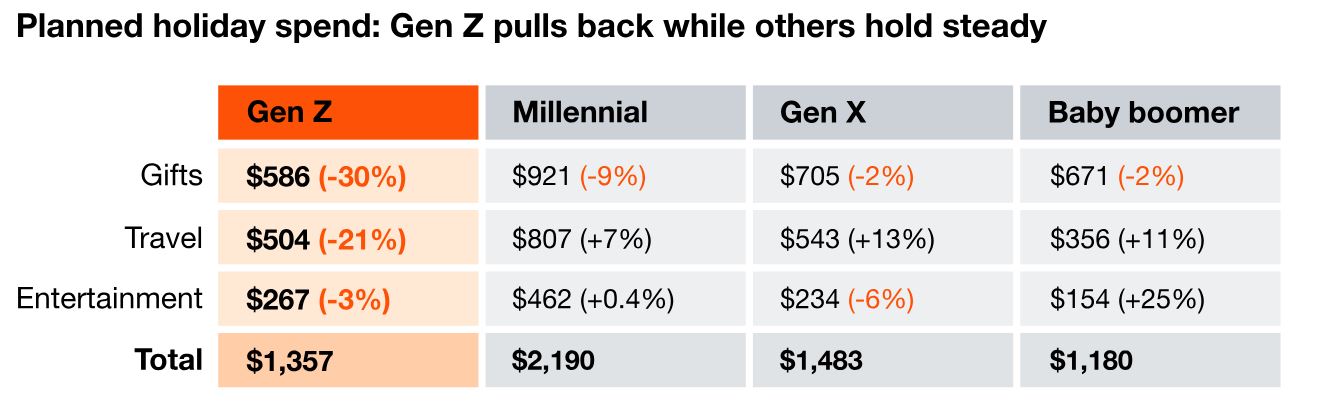

- Teens Are Spending LESS, But Coach Is Winning Big, While Nike and iPhone Lose Steam, Per Piper Sandler Report

- New U.S. Streaming Share Data Points To Heighted Competition

- Platforms, Partnerships, & New Formats Were Just Some Of The Updates Out Of The Advertising Sector This Week

- Grab Bag: Ticket Price Hikes At Disney Parks / AI Could Erase 100mn US Jobs / Netflix Aug Engagement Stats

Also to highlight, LionTree Advisors served as financial advisor to MARI, a new global events and experiences company founded by Ariel Emanuel, following its acquisitions of IMG’s portfolio of international tennis events, Frieze, and a majority ownership interest in Barrett-Jackson.

Enjoy the weekend and brace for the start to TMT earnings season next week! It always seems to come so quickly.

Best,

Leslie

*NEW DECK* LionTree's Lens: Sector Insights & A Look Ahead, Fall 2025

In case you missed our email earlier this week, we wanted to flag our latest LionTree’s Lens: Sector Insights & A Look Ahead, Fall 2025 deck, which highlights what we view as the most important market trends and thematic shifts across the TMT and consumer landscape during the last quarter, and some perspectives as we look ahead.

Click HERE for our slide deck and the ~20-minute video presentation.

Markets have largely held their ground through Q3, even as investors continue to weigh mixed economic signals and shifting policy expectations. Dealmaking momentum has strengthened, with large-cap tech, media, and consumer names driving a rebound in both IPO and M&A activity.

In this edition, we look at how the AI story is evolving from infrastructure to monetization, the growing overlap between sports, streaming, and media rights, the new era of wireless connectivity, the staying power of live events, the growing rollout of robotaxis and autonomous mobility platforms, and much more.

-> As always, we’re happy to discuss any of these topics in more detail, and we’d appreciate your thoughts and/or feedback. Feel free to reach out.

Key Themes

Macro & Markets

- The Stock Market Is Incredibly Resilient But Multiples Hit A High

- The Media/Entertainment Sector Led The Market In Q3

- The Interest Cut Cycle FINALLY Begins, Though With Some Caution

- IPOs Breakout Thanks To Tech & Crypto/FinTech…

- …And Larger Deals In General Made A Comeback, While Smaller Deals Struggled

Key Themes Across The Sector

- Media/Entertainment Dealmaking Accelerates Around Scale and IP

- AI Demand Continues To Challenge Data Center Capacity And Drive CapEx…

- …But Will Returns On This Unprecedented Level of Investment Be High?

- And Some Of The Sharpest Minds Are Warning Of An AI Reality Check

- We Are At A Pivotal Moment For Sports Streaming

- Individual Consumer Subscriptions Are Fatiguing… As Bundling Is Gaining Traction

- Live Entertainment Demand Is Showing No Signs Of Slowing Down, But There Are Some Shifts In Consumer Habits

- The 800 Pound Gorilla Ups The Ante In Online Grocery

- The Big Beautiful Bill = A Wind Fall For The Connectivity Sector

- Wireless Connectivity Is Entering A New Era Given High Penetration Rates

- Expect Robotaxi & AV Investments To Continue At A Rapid Clip

- Meta’s Metaverse Makes Scientific Breakthroughs, But Are People Ready?

- Prediction Markets Are Taking Betting Opportunities To A New Level

Wall Street Sentiment

- Wall Street’s Top TMT Picks & Pans

- New Price Targets Imply More Upside Across The Sector

Software Development Shifts From MONTHS To MINUTES

OpenAI’s 2025 Dev Day underscored just how rapidly the AI sector is evolving, with the company’s latest announcements enabling a new pace for both innovation and adoption of AI products and tools. The Co’s developer ecosystem and user base have seen exponential growth, now at over 4mn developers and 800mn+ weekly ChatGPT users, which is up 2x and 8x, respectively, from just two years ago. API usage has also surged, currently processing 6bn tokens per minute vs only 300mn 2 years ago, highlighting the scale at which AI is now being integrated into real-world applications. Yet, as CEO Sam Altman remarked, “we are still so early on this train.”

In terms of the major product launches, the new Apps SDK allows 3P apps to be integrated directly within ChatGPT, creating seamless user experiences and broadening app reach. AgentKit simplifies the creation and deployment of autonomous AI agents, making it easier to move from prototype to production. The upgraded Codex, now generally available, accelerates software development with advanced code generation and collaboration tools. Meanwhile, new APIs for GPT-5 Pro, Sora 2, and gpt-realtime-mini deliver enhanced reasoning, multimedia generation, and expressive voice capabilities, supporting a wide range of innovative applications across industries.

Overall, Altman’s bold statement that “this is the biggest change to how software gets created that I have ever seen” sets the bar high but this could mark a fundamental shift in the industry, where software that used to take months or years to build can be created in minutes. On a simplistic level, the Co highlighted an 89-year-old Japanese retiree who taught himself to code using ChatGPT and went on to develop 11 iPhone apps specifically designed for elderly users! The day was a big one for OpenAI and also for some public companies that were cited during the presentation, as well as for AMD who secured a multi-year, multi-gigawatt chip partnership with OpenAI.

See below for our main takeaways from the keynote and, if interested in more, see Link To Keynote.

OpenAI’s New Stats, New Product Updates, And New Features

- OpenAI released impressive user & developer growth statistics…from DevDay in 2023 to today –

- Number of developers who have built w/OpenAI has incr’d 2x to 4mn+

- Weekly active ChatPGT users has incr’d 8x to 800mn

- The number of API tokens per minute has incr’d 20x to 6bn (from 300mn)

-> Separately, but related to the demand side, NVIDIA CEO Jensen Huang said this week on CNBC that, “this year, particularly the last six months, demand of computing has gone up substantially”, which also caused some excitement. (link)

- Intr’d Apps SDK …This enables integration of 3P apps directly w/in ChatGPT: It essentially connects data, triggers actions, and renders an Interactive UI for apps directly in ChatGPT and enhances user experience by consolidating functionalities

- OpenAI called out several specific apps that users can interact with in ChatGPT & moved a few of the stocks on the day:

- Booking.com: -0.1%

- Canva: Private

- Coursera: +0.4%

- Expedia: +2.1%

- Figma: +7.4%

- Spotify: -0.3%

- Zillow: -3.6%

- Availability:

- Apps SDK is now available in preview to start building

- Later this year, developers can submit apps for review and publications

- OpenAI called out several specific apps that users can interact with in ChatGPT & moved a few of the stocks on the day:

- Intr’d AgentKit…This is a toolkit to make building AI agents simpler and more effective: Provides resources for creating, testing, and deploying AI agents, hence taking them from prototypes to production

- Available now

- Launch partners include (with stock price reaction where applicable):

- Ramp: Private

- LY Corporation: Not listed in the U.S.

- Canva: Private

- Box: +1.6%

- HubSpot: +2.6%

- Intr’d Codex…This is an upgraded AI coding assistant… “anyone with an idea can build apps for themselves”

- Availability: Codex is now officially out of research preview and into GA

- Runs on GPT-5-Codex model…improves code generation, refactoring, and review processes: It works everyone that developers code now; GPT5 Codex has become one of their fastest growing models ever

- Since its release, they have already served 40T+ tokens

- Almost all new code written by OpenAI today is written by Codex users

- Intro’d a new set of features to make Codex more helpful for engineering teams and promote collaboration: 1) have a slack integration; 2) a new codex SDK to extend and automate codex in a team’s workflow; 3) new admin tools and reporting; Expect to see more improvements soon

- Use case example: Cisco rolled out Codex across its entire engineering and now they are able to get through code reviews 50% faster and reduce the avg project timeline from weeks to days

- New models in API…

- gpt-realtime-mini…A compact, low-latency voice model: Offers expressive voice interactions at 70% reduced cost vs previous models; Enables developers to incorporate voice capabilities into their products efficiently; Available now via API

- GPT-5 Pro…Supports developers in building more reliable and sophisticated applications

- Sora 2 …Includes enhanced video & audio generation: Produces realistic, synchronized video and audio content; Empowers creators with improved tools for multimedia content generation

-> There was also quite a bit of focus and controversy regarding Sora this week…it was disclosed that the app hit 1mn downloads less than 5 days after its launch in late Sept, which is a faster rate than ChatGPT, despite still only being available on iOS devices and invite-based; But also, the Motion Picture Association said on Monday that “videos that infringe our members’ films, shows, and characters have proliferated on OpenAI’s service”…and “OpenAI needs to take immediate and decisive action to address this issue”; AND, per sources, Disney has opted out of having its IP appear in the Sora app; OpenAI is reportedly working to address all of this (link/link)

OpenAI Also Annc’d A Strategic Partnership With AMD (link / link)

- Length: “Multi-year”

- Terms: AMD to deliver 6 gigawatts of Instinct GPUs, starting with the MI450 series in H2 2026

- The collaboration grants OpenAI access to current and future AMD chips

- Promotes enhanced software-hardware integration and accelerates OpenAI’s AI capabilities

- Other consideration = OpenAI gets AMD warrants and could acquire ~10% of AMD if exercised in full: AMD issued OpenAI a warrant for up to 160mn shares of AMD common stock that will vest as –

- The first tranche vests w/ the initial 1 gigawatt deployment

- Additional tranches vest as purchases scale up to 6 gigawatts

- Vesting is further tied to AMD achieving certain share-price targets and to OpenAI achieving the technical and commercial milestones required to enable AMD deployments at scale

- Deal size? OpenAI said the deal was worth billions, but declined to disclose a specific dollar amount

-> AMD shares traded up +23.7% and is up +80% YTD

The U. S. Consumer Is Expected To Show Up For The Holidays…

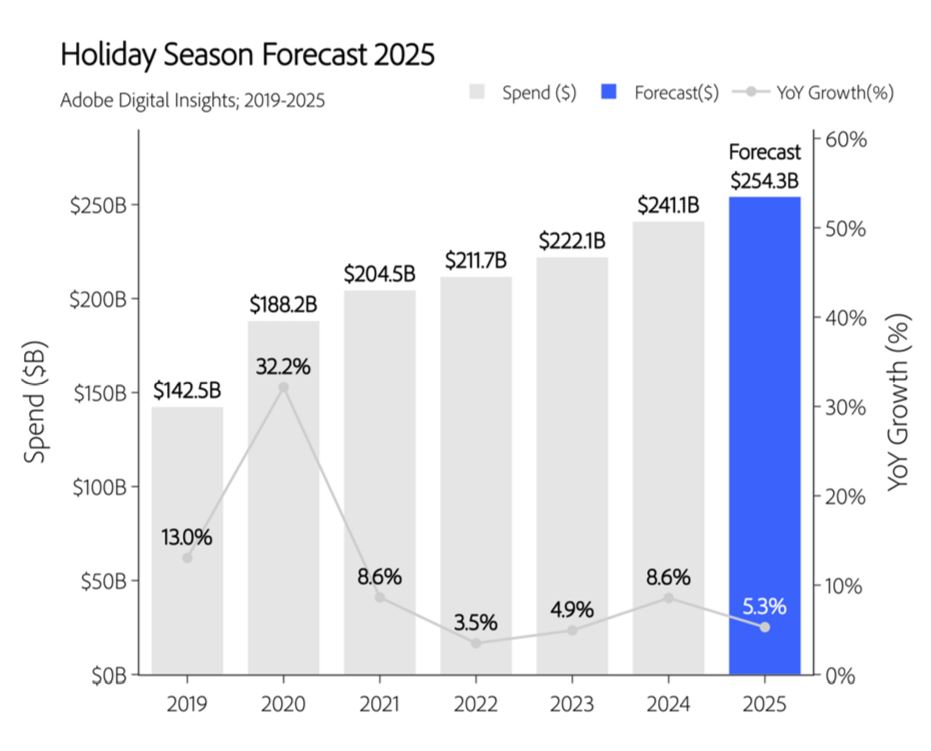

Adobe’s widely followed U.S. holiday shopping forecast for 2025 was a focal point this week, setting a confident tone. Total U.S online spending is expected to surpass $250bn this season, up a solid +5.3% y/y, though moderating from last year’s +8.6%. The firm expects over half of online purchases to happen on mobile for the first time, and “buy now, pay later” usage is projected to hit new highs, including a record-breaking $1bn+ on Cyber Monday alone. Demand overall will likely still concentrate around Cyber Week but GenAI is expected to reshape the top of the funnel. How accurate was Adobe’s estimate going into the holiday’s last year? Pretty close. The Co initially forecast +8.4% y/y growth and the actual was +8.7% y/y.

In other related reports published this week, PwC cites how Gen Z is shifting behavior favoring discounts and in-store discovery, while Circana highlights inflation concerns pushing consumers to shop earlier and lean into promotions.

Taken together, the data points point to a holiday selling season that’s digitally driven, mobile-first, and shaped by a more intentional, though still resilient, consumer.

See below for more details on what we thought was most incremental from these holiday spending reports.

Adobe Forecasts 2025 Holiday Season Online Spending To Cross $250bn But Y/Y Growth Will Normalize (link/link)

- A record $253.4bn (up +5.3% y/y) is anticipated to be spent online this holiday season (Nov-Dec): Although it could fluctuate between $250.3bn-255.9bn

- This is a deceleration from last yr’s very high +8.6% y/y to $241.1bn

- Category breakdown – electronics will generate the most sales while groceries will drive the most y/y growth

- Electronics: $57.5bn, up +4% y/y

- Apparel: $47.6bn, up +4.4% y/y

- Furniture and Home goods: $31.1bn, up +6.5% y/y

- Grocery: $23.5bn, up +9.3% y/y

- Toys: $8.8bn, up +7.3% y/y

- Cosmetics: $8.4bn, up +9.1% y/y

- Sporting Goods: $8.2bn, up +5.1% y/y

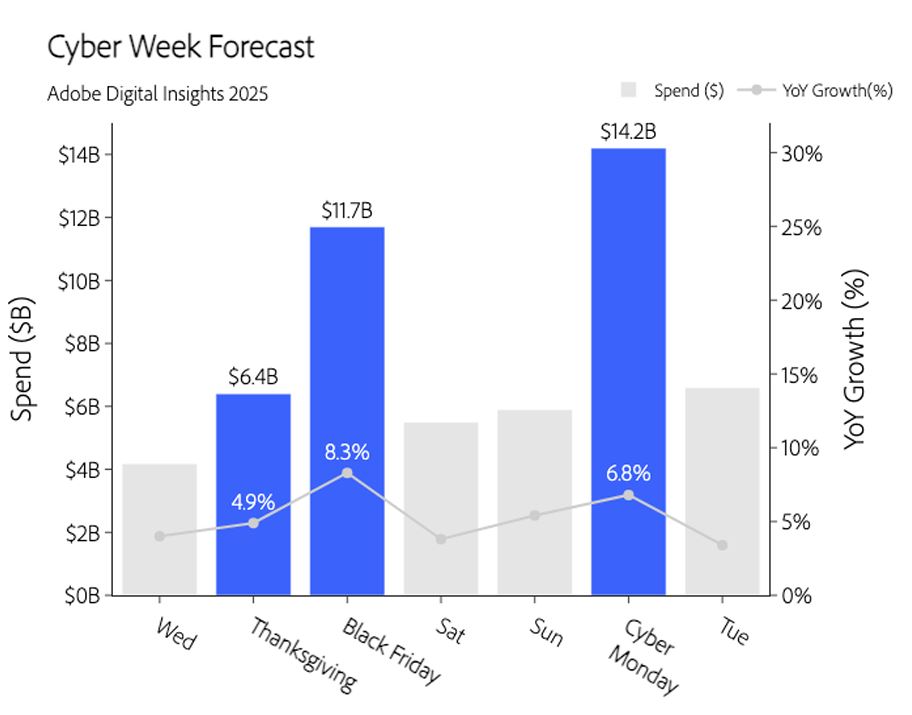

- Cyber Week (Thanksgiving to Cyber Monday) is projected to hit $43.7bn, up +6.7% y/y (deceleration from last yrs +8.3% y/y to $41.1bn) (link)

- Black Friday will see the highest growth over the Cyber Week at $11.7bn, up +8.3% y/y

- Compared to the $10.7bn spent in 2024, up +9.2% y/y

- Cyber Monday growth is projected to hit $14.2bn, up +6.3% y/y

- Compared to the $13.3bn spent in 2024, up +7.3% y/y

- Black Friday will see the highest growth over the Cyber Week at $11.7bn, up +8.3% y/y

- 2025 is positioned to become the first full yr w/ more than 50% of online spending happening on mobile devices

- Mobile rev share is projected to hit a record 56.1% for the holiday season w/ 7 out of 10 online retail visits happening on mobile devices

- A record $142.7bn will be spent via mobile this holiday season, up +8.5% y/y

- Consumers are less sensitive to price changes, likely due in part to consumer willingness to purchase full-price items or even items that have incr’d in price w/ the expectation that prices may be much higher in the future

- Sensitivity to price change has decreased by -12.8% on avg so far in 2025

- The decline in sensitivity to discounted prices has been slightly steeper at -13.2%

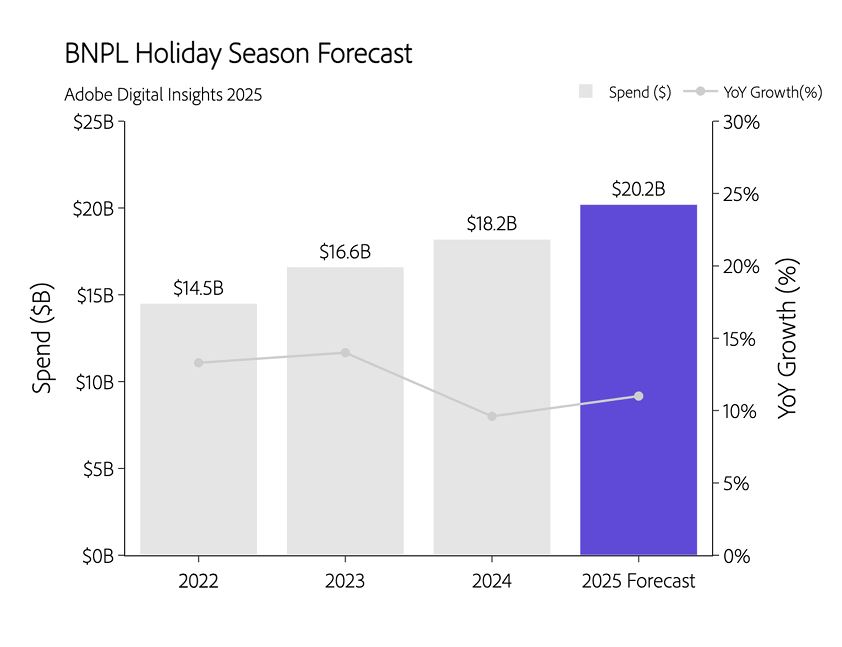

- Buy now, pay later momentum is also building heading into the holiday: Forecasted to see $19.8bn-20.4bn in BNPL spend (up +9-12% vs the 2024 holiday season)

- Black Friday is forecasted to see between $748mn-775.5mn in BNPL spend, up +9-13% y/y

- Cyber Monday is expected to set a record for the most spent on a single day through BNPL w/ a forecast of $1.02bn-1.06bn (up +3-7%)

- Projected to be the first day to cross $1bn in BNPL spend

- The majority of BNPL is being driven by people on their smartphone, rather than a desktop, tablet or laptop

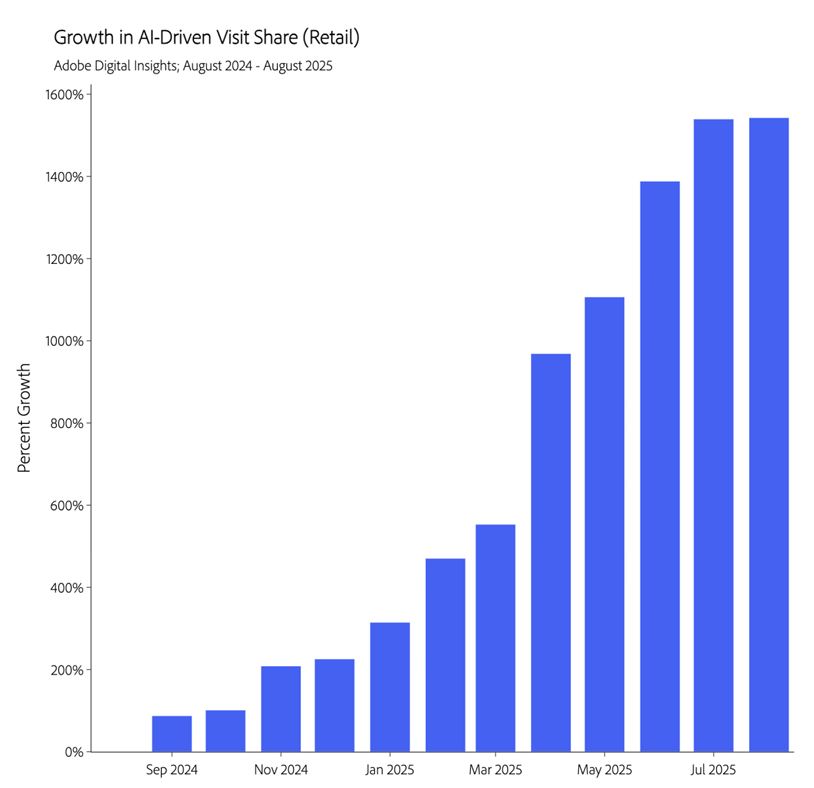

- GenAI is expected to play a much greater part in holiday shopping this season

- In August, traffic from GenAI sources to retail sites is up +1500% y/y, w/ nearly +300% growth since Jan

- This holiday season, traffic is expected to rise +515-520% y/y, w/ Thanksgiving alone growing an expected +725%-730% y/y

- 75% of consumers are familiar w/ AI assistants, ~33% have used them for online shopping

- ~80% of consumers say they use AI assistants more frequently during or leading up to high-stakes shopping events

- 72% of consumers who have used AI for online shopping said they are less likely to return items purchased

- This holiday season, traffic is expected to rise +515-520% y/y, w/ Thanksgiving alone growing an expected +725%-730% y/y

- Methodology: The have a robust dataset from over 1 trillion US retail sites, 100mn product SKUs and 18 different categories; The survey was based on the responses from ~5,000 U.S. consumers, fielded between Sept 9th – Sept 16th, 2025

PwC’s Latest Report States Gen Z Is Pulling Back The Most This Season (link/link)

- ~ 79% of Gen Z will wait for products to go on sale, and only 21% regularly pay full price

- Searching for discount codes is up +14%, while browsing is up +17%

- 59% still prefer known brands but 41% are willing to buy less expensive, private-label alternatives and 49% want customized products

- But Gen Z isn’t spending less across the board, they’re reallocating

- When asked where they’d cut back over the next 6 months, Gen Z pointed to restaurants and take-out (51%), clothes (33%), and alcohol (29%)

- Few said they would cut out “high value” items

- When asked where they’d cut back over the next 6 months, Gen Z pointed to restaurants and take-out (51%), clothes (33%), and alcohol (29%)

- Also, the assumption that Gen Z would live entirely online is outdated

- 61% now prefer to discover new products in-store

- 37% plan to shop in-store more frequently than usual this holiday season (up from 27% in 2024)

- 43% of Gen Z is expected to use social media to discover gifts this holiday, compared to 30% overall

- They also use it to research (39% vs 27%) and compare items before purchasing (32% vs. 22%)

- 11% of Gen Z say that BNPL is one of their top 3 payment methods for this holiday season, up +5% y/y

A Report By Circana Shows Consumers Are Bracing For Higher Prices

- 80% of shoppers expect prices to rise, driven by tariffs and inflation (link/link)

- This is pushing many to shop earlier and lean harder on promotional events, like those from Amazon, Walmart and Target

- 34% of holiday shoppers say they will take advantage of more deals this yr

- On avg, consumers plan to spend $796 on holiday shopping this yr, which is up 3% y/y

- 31% of shoppers say they will buy fewer items this holiday

- Holiday shoppers have also expanded the timeframe of their shopping season

- ~50% of consumers plan on starting their holiday shopping before Thanksgiving, and 24% have already started or even finished, up +~4% y/y

- Black Friday remains the most popular of the traditional shopping days, w/ 19% planning it as the kick-off

- The number of consumers planning to wait until Dec, thereby getting a late start to holiday shopping, is 19%, the lowest it has been in recent yrs

Short Sellers Stick With Their Key Bets Despite The Market Rally

It has been a while since we combed through short interest data, so we decided to do so for the period ending September 30, which was made available this week. Given all that has transpired over the last 6 months, it was interesting to see where the shorts have been placing their bets as we head into the rest of the year, and where they have gotten more bearish, and where they have been covering positions. The analysis includes ~160 stocks in the LionTree Universe with $1bn+ in market cap across the tech, media, telco, and consumer sectors.

Short sellers generally stuck with their positions. The Top 3 most shorted stocks at quarter end were Hims & Hers, Lemonade, and The RealReal, and the first 2 were also on the Top 3 list last qtr. Of the Top 20 most shorted stocks in Q3, 14 were also on the top 20 most shorted list in Q2.

In terms of the biggest changes in Q3, Cinemark saw the most short covering, while Six Flags Entertainment topped the list for largest increase in its short position.

See the bullets below and table for more detail…

Most Shorted Stocks (As % Of Float) – Hims & Hers

- The Top 3 Most Shorted – #1 is Hims & Hers, #2 is Lemonade, & #3 is The RealReal -> Hims & Hers ascended from the #2 position in Q2 to take the top spot; Lemonade also rose from the #4 position last qtr to take the #2 spot; The RealReal was not included in the Q2 analysis as its market cap was <$1bn but broke into the list this qtr

- Groupon, which was the #1 most shorted stock in our LionTree Universe last qtr, was not included in our Q3 analysis due to its market cap being <$1bn but still maintains a very high short position

- Stocks that dropped out of the Top 20 most shorted: AMC Entertainment, Cinemark, Groupon, Magnite, Paramount Global, Reddit, Redfin

- Note that Groupon also dropped out of this analysis from last qtr due to its market cap falling below <$1bn

- Stocks that joined the Top 20 most shorted: DigitalOcean, fuboTV, Opendoor Technologies, Reddit, Six Flags Entertainment, The RealReal, TripAdvisor

- Note that The RealReal and Opendoor Technologies were also added to the Top 20 this qtr but not included in last qtr’s analysis due to their mkt cap being <$1bn at the time

-> With the market rallied, it was once again a hard qtr for short sellers in Q3, as only 7 of the Top 20 most shorted stocks underperformed the S&P 500’s +7.8% gain during the period; In fact, the Top 20 most stocks traded up +89% on avg (or +20% on avg ex-Opendoor), also outperforming the S&P 500

Largest Increase In Short Interest (As % Of Float) – Six Flags Entertainment

- The largest increase in short interest was seen by Six Flags: The Co saw a +5.8ppt increase in Q3 to 20.1% and was also the #9 most shorted stock at the end of Q3 -> The stock fell -25.3% in the qtr, underperforming the S&P 500’s +7.8% gain

- Other stocks with notable increases in short interest = Playtika, IMAX, and Mobileye -> Playtika and Mobileye underperformed the S&P 500, while IMAX outperformed

Largest Decrease In Short Interest (As % Of Float) – Cinemark

- The largest decrease in short interest was for Cinemark: The Co posted a -5.8ppt decrease in Q3 to 20.1%; It went from being #7 most shorted stock in Q2 to dropping out of the Top 20 in Q3

- Other stocks with notable decreases in shorts interest = Paramount Global, WEBTOON Entertainment, and Gogo

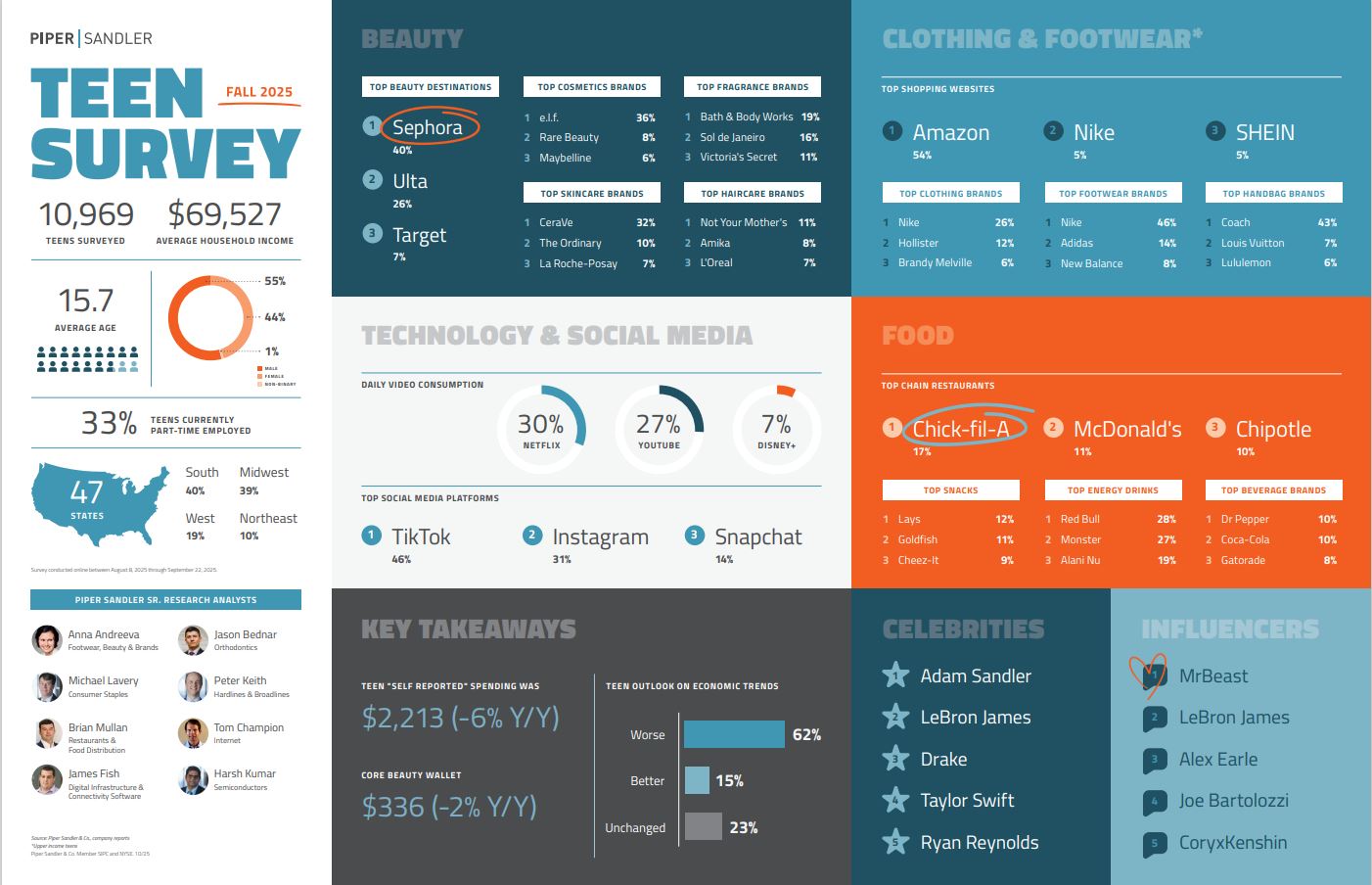

Teens Are Spending LESS, But Coach Is Winning Big, While Nike and iPhone Lose Steam, Per Piper Sandler Report

In addition to all the holiday spending predictions (see Theme #3) we also looked at Piper Sandler’s 50th semi-annual Taking Stock With Teens survey, which gathers insights from 10k+ teens (w/ an avg age of 15.7 yrs) on their spending habits, fashion choices, tech usage, and brand and media preferences.

Overall, teen self-reported spending fell y/y, after growing both in the spring and year-ago fall. Interestingly, teens’ economic outlook is more polarized, w/ a higher percentage expecting conditions to get worse, as well as a higher percentage expecting it to better, compared to spring, though the overall bias remains negative.

Looking into the fashion and beauty side of retail, Amazon remained the #1 shopping website and gained share, followed by Nike at #2. That said, despite leading both as the top clothing brand and top footwear brand, Nike continued to lose mindshare across the board.

Regarding teenage female trends, the core beauty wallet also declined in the fall (after reaching its highest level ever in the spring). We would also flag that Coach has been having a stellar run, reaching 43% share of responses, up from 35% in the spring and just 25% in the yr-ago fall.

On the technology front, it was interesting to see that in the spring (prior to the release of the iPhone 17), 25% of teens expected to upgrade to the iPhone 17. That percentage has now fallen to just 17% in the fall, as it seems some teens have lost excitement around the phone posting its release. Finally, in social media, TikTok remains the most used platform, though Instagram has been gaining share, going from 28% share of responses in the spring to 31% in the fall.

See below for what we thought were the most interesting insights and click HERE/HERE to see the press release.

Teen Spend & Employment Levels Have Fallen Since Spring 2025, But Avg Household Income Is Up

- Total levels of teen spend DECREASED: Teens self-reported spending fell -6% y/y to $2,213 (down from +6% in spring 2025 and +1% y/y in fall 2024)

- But avg household income was up seq: Reached $69,527 in fall 2025, up from $65,995 in spring 2025

- % of teens that are currently employed part-time FELL: 33% (vs 37% spring 2025)

- Teens’ economic outlook is increasingly polarized, with both pessimism and optimism rising, but the bias is negative

- Worse: 62% (vs 57% in spring 2025)

- Unchanged: 15% (vs 23% in spring 2025)

- Better: 23% (vs 19% in spring 2025)

Clothing & Footwear…Amazon Remains The Top Shopping Website And Gained Share, While Nike Lost Share Across Categories

- Amazon retained its #1 spot as the top shopping website (and gained share): Reached 54% share of responses, up from 52% in spring 2025

- Nike remained in the #2 spot (but lost some share): 5% share of responses, down from 6% in spring 2025

- Shein’s remained at #3 (and share was in-line) at 5%

- Nike remains the top clothing brand (but lost share): Fell from 28% share of responses in spring 2025 to 26% share in fall 2025

- Hollister remained at the #2 spot (and gained share): Went from 8% share in spring 2025 to 12% share in fall 2025

- Brandy Melville took the #3 spot: Reached 6% share, knocking out American Eagle, which was #3 in spring 2025 at 6% share

- Nike also continued to lose mindshare amongst footwear brands (but still remains at the top by a large margin): Nike garnered 46% share of top footwear brands, which is a continued downward trend from 49% in spring 2025 and 57% in fall 2024

- Adidas retained its #2 position while also gaining share: Reached 14% share vs 8% in spring 2025

- New Balance dethroned UGG to take the #3 spot: Reached 8% share, bumping out UGG, which was the previous #3 at 6% in spring 2025

- Also in footwear, On Running (#4) overtook HOKA (#5) for the first time in the past six surveys

- “Suggesting On Running is gaining share with all consumers”

- Coach’s share continues to make big moves upwards amongst handbag brands: Reached 43% share in fall 2025, which is up from 35% in spring 2025 and 25% in fall 2024

- Louis Vuitton rose to the #2 spot (and maintained share): Up from the #3 position in spring 2025 at 7%

- Lululemon made a comeback to the top 3: Reached 6% share to take the #3 spot after falling out of the top 3 in spring 2025

Beauty…Spend Fell In The Fall (After Hitting A Record In Spring)

- Core beauty wallet declined -2% y/y to $336

- Comes after core beauty wallet reached the highest level ever at $374 (+10% y/y) in spring 2025

- 85% of female teens reported wearing makeup sometimes or every day, which is up +1pt seq

- Sephora once again continued to gain share as a top beauty destination: Sephora’s share of responses is now at 40%, up from 38% in spring 2025 and 36% in fall 2024

- Ulta maintained share seq at 26% to take the #2 spot

- Target made a comeback to take the #3 spot: After Bath & Body works pushed Target out of the Top 3 in spring 2025, Target returned to the list this time around with 7% share

- e.l.f. maintained its position as the #1 cosmetics brand among all female teens, gaining 1-pt of mindshare seq

Technology & Social Media…iPhone 17 Upgrades Are Expected To Be Lower Than Expected Back In The Spring Timeframe / TikTok Remains The Most Popular Social Media Platform, But IG Is Gaining Share

- A lot fewer teens expect to upgrade to an iPhone 17 this fall/winter: Just 17%, which is a notable step down from 25% in spring 2025

- 87% of teens own an iPhone (vs 88% in spring 2025)

- TikTok remains the most used social media platform, though Instagram is back to gaining share

- TikTok had 46% share of responses in fall 2025 (vs 47% in spring 2025)

- Instagram had 31% share (UP from 28% in spring 2025 after falling from 32% in fall 2024 and 30% in spring 2024)

- Snapchat had 14% share (in-line w/ spring 2025)

- Daily video consumption trends were relatively stable from spring 2025

- Teens spend 30% of daily video consumption on Netflix (vs 31% in spring 2025)

- YouTube was at 27% (vs 26% in spring 2025)

- Disney+ was at 7% (in-line w/ spring 2025 when Hulu was still separate)

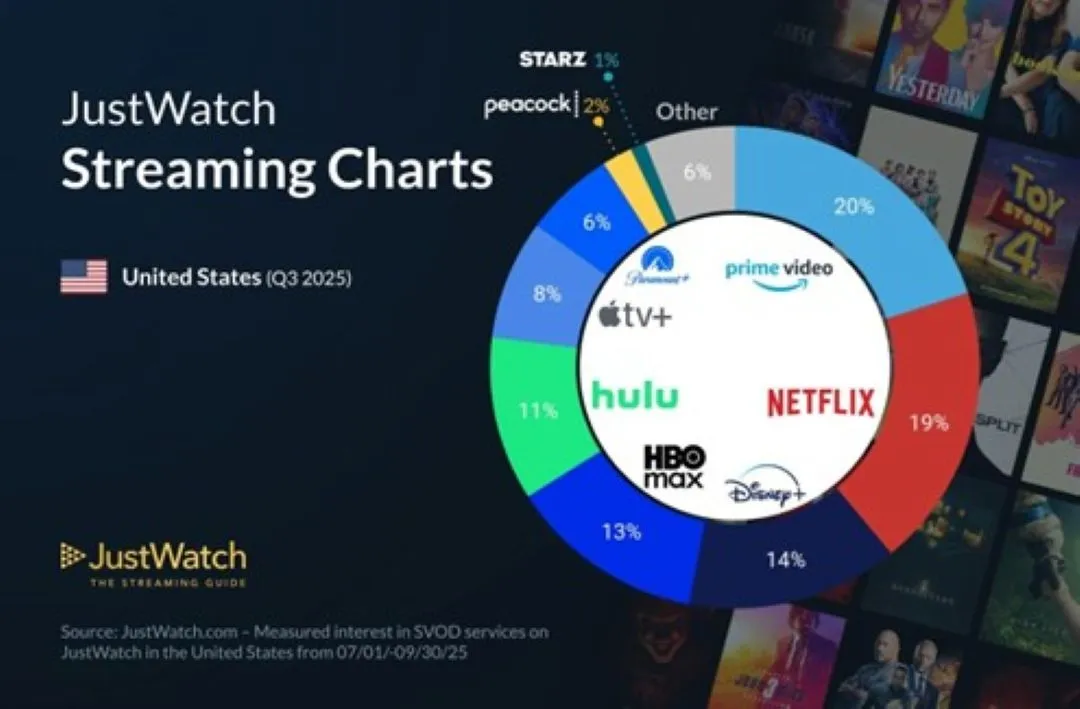

New U.S. Streaming Share Data Points To Heighted Competition

We all know that Amazon Prime Video and Netflix have been the leaders in the US streaming market, but it was interesting to see market share shifts for the major players in Q3, which point to a high level of competitive intensity in the sector.

Based on JustWatch’s Q3 2025 U.S. Streaming Market Share Report published this week, Prime Video and Netflix each saw a 1-percentage point sequential and 2-point y/y decline in market share. Meanwhile, mid-tier platforms like Disney+, Hulu, and HBO Max slightly improved their positions, while Apple TV+ remained steady and Paramount+ lost share.

These insights are derived from user engagement (20mn U.S. users) on JustWatch’s website, TV, and mobile apps. JustWatch calculates market share based on streaming behaviors such as adding titles to watchlists, clicking out to services, applying platform filters, and marking content as “seen.” See a few more details below (link/link).

-> On the topic of streaming, the press also reported this week that on Oct 19th, Apple will finally announce a deal with F1 for $140mn per year, nicely up from the previous $90mn deal w/ ESPN; The fate of F1 TV has apparently been the sticking point and it is still unclear where the sides landed on that (link)

- While Amazon Prime Video & Netflix lead the US streaming video market share-wise at ~20% & ~19%, respectively…

- Both leaders lost traction this qtr with market share down -2% y/y and down -1% q/q

- The largest growth came from the “Other” category, led by BritBox, which recorded the strongest relative growth at +126% YoY

- Paramount+ lost the most market share, down -1% QoQ and down -3% YoY

Platforms, Partnerships, & New Formats Were Just Some Of The Updates Out Of The Advertising Sector This Week

The advertising space was absolutely whirring with activity this week, with updates across adtech, AI, and media. PayPal, American Express, and Duolingo all rolled out new ad platforms, while both Microsoft and Adobe announced partnerships with Amazon. As always, AI is a topic of conversation, and Pubmatic shared that its integration with NVIDIA is delivering 5x faster and smarter advertising decisions, which subsequently sent Pubmatic’s stock up +8%. Separately, but related, a survey amongst CMOs found that while AI adoption in advertising continues to grow, scaling remains a challenge, and most CMOs still use AI for analytics rather than creative workflows.

Outside of adtech and more on the media advertising side, NBCUniversal shared that it has sold out its NBA ad inventory, and Paramount+ introduced show-specific ad placements, letting brands secure fixed positions within individual episodes. Finally, on the regulatory front, the SEC is investigating AppLovin’s data-collection practices.

There was a lot to catch up on with these important developments…see below for more.

A Whole Host Of New Ad Platform Launches…American Express, PayPal, And Duolingo

- American Express launches digital advertising platform Amex Ads (link/link)

- What is it? Will enable brands to “serve high-spending Card Members relevant, contextual ads in the moments they are likely to engage, shop and spend with the brands they love”

- Examples of how brands are using Amex Ads –

- Marriott Bonvoy used Amex Ads to reach and convert American Express cardmembers who had booked a flight on AmexTravel.com, but had not booked a hotel (achieved 300% ROI increase vs target benchmark, per AmEx)

- Tumi drove sales by reaching card members during and after booking travel using ads on AmexTravel.com and via a post-booking email from Amex Travel (purchases were 30% higher than target benchmark)

- Amex Ads will initially become available on AmexTravel.com, and will ultimately expand to addtl Amex-owned platforms

- PayPal releases advertising platform, PayPal Ads Manager (link/link)

- What is it? “A single, comprehensive platform that allows simple, streamlined management of [small bizs] ad inventory in a platform”, including –

- Monetizing store traffic

- Creating “valuable” new ad inventory (opens up previously unavailable inventory to reach “loyal, high purchase intent” shoppers)

- Unify campaign mgmt

- “Democratizing the power of retail media networks”: Enables small bizs to earn money from their existing store traffic w/ no upfront cost and no minimum commitment

- Will be available in early 2026, starting in the US w/ the UK and Germany to follow

- What is it? “A single, comprehensive platform that allows simple, streamlined management of [small bizs] ad inventory in a platform”, including –

- Duolingo launches its own direct ads sales platform, Duolingo Ads (link/link/link)

- What is it? A new direct ad sales platform that gives advertisers access to premium in-app inventory and creative formats, including character-led campaigns featuring its popular in-app mascots

- The move shifts Duolingo away from relying solely on programmatic ads…: The Co offers interstitials that run after a lesson ends and gaming rewards for watching a video

- …as the Co said programmatic ads did not always align with the app’s brand identity or quality standards: With Duolingo Ads, brands will now have the option to run character-driven campaigns, either fully animated spots starring the company’s mascots or short introductions that lead into the brand’s video content

- Tapping into oppty to grow ad rev: Advertising currently contributes <7% of Duolingo’s total annual rev, which reached $748mn in 2024, vs a much larger share from paid subscriptions

- Since 2015, Duolingo has partnered w/ Google AdMob to monetize its free user base and will continue the partnership in tandem w/ the new platform

- What is it? A new direct ad sales platform that gives advertisers access to premium in-app inventory and creative formats, including character-led campaigns featuring its popular in-app mascots

Amazon Expands Its AdTech Footprint Through New Microsoft & Adobe Partnerships

- Microsoft annc’d Amazon DSP as the preferred transition partner for Microsoft Invest customers (link/link/link)

- In May, Microsoft annc’d a shift in strategy to transition away from media buying through their own DSP

- Why chose Amazon DSP?

- “Because of its ability to deliver exceptional results by leveraging real shopping behaviors, extensive reach, and premium placements across Amazon’s owned sites, apps, and connected TV properties, as well as high-quality third-party publisher inventory”

- Microsoft Monetize will also become a preferred SSP in Amazon’s Certified Supply Exchange program

- Which is intended to give advertisers using Amazon DSP easier access to Microsoft Monetize’s open internet ad inventory and deals

- Advertisers that partner w/ Microsoft Monetize can now use special deal packages, including “Amazon Shopper Insights,” that match Amazon’s shopping data w/ Microsoft’s inventory

- The transition will begin immediately, and Amazon and Microsoft are working together to support the migration of Microsoft Invest customers across countries in the NA, LATAM, EU, and APAC regions

- Adobe and Amazon have formed a partnership to support their mutual customers through media performance (link/link)

- Amazon Marketing Cloud, Amazon’s data clean room for privacy-safe data collaboration, will be plugged into Adobe’s customer data platform, or CDP

- There, the Cos’ joint customers can access aggregated data on how consumers discover, consider, and buy on Amazon, including –

- Audience discovery (finding better prospects)

- Campaign optimization (improving targeting and bidding in real-time)

- Product/consumer insights (understanding how customers move from discovery to purchase across Amazon’s ecosystem)

On The AI Front…In AdTech, PubMatic’s Integration With NVIDIA Is Supercharging Its Ad Buying Platform + Some Key Insights From CMO’s On AI’s Uses In Mkting

- Pubmatic’s integration w/ NVIDIA is delivering 5x faster and smarter advertising decisions (link)

- PubMatic said its use of NVIDIA technology for automated programmatic ad buying across the open internet has resulted in processing that is up to 5x faster than traditional systems

- How does it happen?

- Inference latency is reduced from the industry standard of 5-10 milliseconds to approximately 1 millisecond, achieving 85% fewer auction timeouts and unlocking mns in ad spend lost to tech restrictions

- Using NVIDIA GPUs, PubMatic’s AI-powered decisioning algorithms respond in microseconds, thousands of times faster than consumer AI applications

- Able to process live campaign data 2x and deliver insights 60% quicker by leveraging NVIDIA innovation

- Reduces energy consumption by 30% while delivering better performance

- What’s the overall benefit? “Helping publishers recover ad spend lost to latency and timeouts, while unlocking AI-driven optimization strategies that were previously possible only within walled gardens”

-> Pubmatic jumped +7.5% on the back of the announcements

- Some quick stats from Making Science’s latest report on how CMOs view AI reshaping marketing (link/link): Based on a Forrester Consulting Survey conducted in Aug 2025 of 269 CMOs w/ more than $50mn in ad spending

- Use cases are still heavily skewed towards analytical vs creative workflows

- 55% of CMOs use AI for segmentation, while 51% use it for analytics and 45% use it for media planning

- Vs 11% of CMOs use AI for content creation, and 14% use it for creative testing and optimization

- Integration remains the biggest roadblock, with 76% of CMOs citing it as a barrier

- Until Cos build stronger integration strategies, AI and marketing pilots will keep outpacing the ability to scale enterprise-wide programs

- But regardless, investments have accelerated, with 66% of CMOs saying they are likely to invest in AI-powered marketing platforms within the next 12 mos

- Use cases are still heavily skewed towards analytical vs creative workflows

In Media Advertising… NBCU Has Nearly Sold Out Its NBA Ad Inventory & Paramount Introduces A New Ad Format

- NBCUniversal annc’d it has exceeded its advertising expectations for the return of NBA to NBC (link/link)

- “Nearly all” inventory is sold out…some key stats –

- Nearly 170 partners investing in the property

- 20%+ of advertisers are new to NBCUniversal, broadening the Co’s portfolio-wide partnerships

- NBA’s return to NBCU sparked interest from first-time brands, with nearly 10% new investments into the franchise at large

- “Multi-platform, omni-channel approach” driving demand…70%+ of clients are investing cross-platform

- ~30% of overall NBA investments have gone solely towards digital inventory

- Investments in linear exceeded initial expectations by 20%+

- The Co has officially sold out of all key positions w/ investments across all core categories, including Auto, Finance, QSR, Entertainment, and Retail

- Also making its NBA inventory available programmatically on Peacock, “as part of its ongoing efforts to democratize access to its premium inventory”

- Already seeing a “large” appetite for basketball programming from advertisers, w/ programmatic investments in college basketball up over 100% y/y

- “Nearly all” inventory is sold out…some key stats –

- Paramount+ is letting advertisers buy show-specific streaming ad spots (link/link)

- Developed a new ad format called “streaming fixed units” –

- Allows advertisers to buy a fixed ad placement within a specific episode of streaming television

- For 7 days after the episode goes live, the ad will appear in the exact same position for all viewers who watch on demand

- After 7 days’ elapse, fixed ad placements revert to the individually targeted, dynamic ad insertion formats that run across most Paramount+ inventory

- Although the launch was only announced this week, Paramount+ has already been incorporating streaming fixed units into episodes of “Tulsa King,” which premiered on Sept 21

- It will expand to other shows in 2026

- Developed a new ad format called “streaming fixed units” –

Finally, There Was A Notable Update On The Regulatory Front, As The SEC Is Investigating AppLovin Over Its Data-Collection Practices

- The SEC has reportedly been probing AppLovin’s data collection practices (link/link)

- The SEC is reportedly specifically looking into allegations that the Co violated platform partners’ service agreements to push more targeted advertising to consumers

- Comes in response to a whistleblower complaint and multiple short-seller reports

- Reports accused AppLovin of harvesting proprietary identifiers from other platforms in an unauthorized manner to track users across different websites and apps and retarget them with advertising

- AppLovin CEOAdam Foroughi said that the short reports were “littered with inaccuracies” and denied creating “alternative accurate and persistent identifiers”

- The SEC has not accused AppLovin of wrongdoing, and it was not clear how advanced the review is

- Additionally, SEC probes don’t always result in enforcement actions, but they can lead to fines for Cos or corporate officials if the agency determines there were violations

-> AppLovin’s stock fell -14%, the most since April, on the back of the news

Grab Bag: Ticket Price Hikes At Disney Parks / AI Could Erase 100mn US Jobs / Netflix Aug Engagement Stats

- Disney raises admission prices for Orlando Disney World and Anaheim Disneyland (link/link)

- Tickets for a one-day, single-park visit to Disney World or Disneyland will now cost (for the first time) more than $200 during peak times

- e., the single-day, single-park ticket during the weeks of Christmas and New Year’s will increase +5% in Orlando to $209 and up +8.7% for Disneyland to $224 (up +126% over the past decade)

- The rest of the one-day pricing tiers are increasing between 1.5% and 4.9%, which are notably smaller than last year’s increases (b/w 5.9%-6.5%)

- The steepest increases are on Disneyland’s top-tier tickets

- The Tier 6 one-day pass (purchased on highest-demand days) are jumping +$18 to $224 per adult

- The longest and most expensive Disneyland ticket type, the five-day Park Hopper (lets visitors enter Disneyland Park and Disney California Adventure on the same day for up to 5 consecutive days) climbed +$39 to $655 (up +108% over the past decade)

- Disney parks’ starting and high-end prices for tickets on sale through October 2026 remain unchanged

- Disneyland kept its lowest-priced ticket for its slower season at $104/day (hasn’t changed since 2019)

- Disneyland Resort price increases, overall, are the lowest price increases in several years, per the Co

- Of the seven ticket tiers, five of them are increasing 3% or less

- Demand is still strong for the holiday periods: It recently paused sales on one-day, one-park tickets to Magic Kingdom for this upcoming New Year’s Eve due to expected demand

- Tickets for a one-day, single-park visit to Disney World or Disneyland will now cost (for the first time) more than $200 during peak times

- A new report says AI could erase 100mn US jobs (link)

- As per a report by Senate Democrats released on Monday (Oct. 6th)

- A ChatGPT-based analysis from Sen. Bernie Sanders (I-Vt.), found that AI could wipe out both white- and blue-collar jobs

- The report warns of the rise in “artificial labor,” which it says could “reshape the economy in less than a decade”

- According to the findings, 89% of fast-food jobs, 64% of accounting roles, and 47% of trucking positions could be replaced over the next 10 years

- The other side: Republicans argued that the US should lead global AI development and warned that excessive regulation could give countries like China a competitive edge

- We also came across some estimates on Netflix ad rev and viewership… (link)

- Aug viewership rose +5.1% y/y

- Avg daily viewership returned to growth in Q3: Up +3.5% y/y in Q3, vs -1.8% y/y in Q2

- Top 10 title viewership accelerated seq and y/y: Up +19.8% y/y in Q3, vs +9.9% y/y in Q2 and much higher than yr-ago -0.5% y/y decline

- Netflix’s top 4 streaming titles in August generated 22bn minutes collectively

- Netflix’s full-yr 2025 ad rev expected to double y/y: Estimated to reach $2.2bn, which is slightly lower than cons estimates of $2.4bn, but double cons estimates for 2024 of $1.1bn cons

- Aug viewership rose +5.1% y/y

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- The CMA has confirmed Google’s designation w/ strategic market status (SMS) in general search & search advertising svs under the UK’s new digital mkts regime. The decision, based on feedback from 80+ stakeholders, cites Google’s entrenched market power. AI Overviews & Mode are in scope, Gemini is not. SMS allows for future interventions but implies no wrongdoing. Consultations on actions expected later in the yr. (UK Government)

- Boosted by NFL and college football, national linear TV ad rev rose 4% to $8.77bn in Q3, per iSpot. Total ad impressions fell ~3% to 1.7tn; airings dipped 1% to 12.2mn. Live TV gained value, w/ sports & news driving reach. CBS led ad reach (7.04%), followed by Fox News (6.86%), ABC (6.38%), NBC (6.19%), ESPN (3.67%). (MediaPost)

Artificial Intelligence/Machine Learning

- Klarna and Google Cloud announced an AI-first partnership to boost creativity, personalization, and security for Klarna’s 114M consumers. Using Google’s AI stack, Klarna will create dynamic lookbooks, hyper-personalized campaigns, and enhanced visuals, while deploying AI to detect fraud and money laundering, improving both shopping experiences and platform safety. (Google Cloud)

- The US has approved Nvidia chip exports worth several bn dollars to US cos incl. Oracle for AI projects in UAE, under a bilateral deal annc’d in May. Licenses exclude local firms like G42. The move supports a 5GW data center in Abu Dhabi w/ OpenAI, Oracle, Cisco, SoftBank & G42. UAE pledged reciprocal US investment. The deal, Trump-backed, faces scrutiny in Washington over China ties and AI strategy. (Yahoo Finance)

- OpenAI annc’d expansion of its budget ChatGPT Go plan to 16 more Asian countries, totaling 18 incl. India & Indonesia, where pricing is ~$4.50/month. The plan offers GPT-5 access, image gen, file uploads & higher usage limits vs. free tier. By May 2025, adoption in lowest-income nations grew 4× faster than in high-income ones. ChatGPT Go is live on web/Android in Cambodia, Laos & Nepal, but iOS support is pending. (CNBC)

- OpenAI’s Codex edged out Anthropic’s Claude Code in coding benchmarks, scoring 74.3% vs. 73.7%, excelling in debugging and IDE integration. Codex’s rising adoption, fueled by updates and GitHub ties, signals shifting dev preferences. Claude’s long-session support and safety focus contrast Codex’s scale-first strategy. The rivalry drives AI coding innovation but raises job and ethics concerns. (WebProNews)

- Harvard Medical School annc’d a licensing deal granting Microsoft access to its consumer health content on diseases & wellness. Microsoft will pay a fee to use the data to enhance its Copilot AI, aiming to deliver practitioner-like responses. The move supports Microsoft’s strategy to reduce reliance on OpenAI by integrating Anthropic’s Claude & developing its own AI tech. (Reuters)

- The EU Commission annc’d a €1bn ($1.1bn) plan to boost AI in key industries like healthcare, energy, and automotive, aiming to reduce reliance on U.S./China tech. The Apply AI strategy, part of a broader action plan from Apr., seeks to ease regulatory burdens for startups. Funding will come from Horizon Europe & Digital Europe, w/ hopes of matching funds from cos and member states. (Reuters)

- SoftBank annc’d a $5.37bn (€4.62bn) deal to acquire ABB’s robotics biz, aiming to boost its physical AI strategy. ABB Robotics, w/~7,000 staff and $2.3bn rev in 2024, will be carved into a new entity. ABB drops plans to spin off the unit, citing SoftBank’s offer as value-creating. Deal expected to close H2 2026 pending approvals. (Yahoo Finance)

- Nvidia CEO Huang called AMD’s deal w/OpenAI “clever” but surprising, as AMD annc’d a multibn$ partnership granting OpenAI warrants for ~160mn shares—up to 10% of the Co. OpenAI will buy 6GW of chips incl. MI450 series. AMD shares rose 43% this week. Nvidia, investing $100bn in OpenAI, sees AMD as a rising AI chip rival. Huang also confirmed Nvidia’s $2bn investment in Musk’s xAI. (CNBC)

- Nvidia CEO Huang told CNBC that AI demand and computing needs have surged “substantially” in the past 6 mos. Nvidia annc’d a $100bn investment in OpenAI’s data center buildout. Huang warned the U.S. risks falling behind China in AI due to slower energy expansion. He urged cos to build self-powered data centers using natural gas and nuclear to meet AI’s exponential growth. (CNBC)

- 72% of S&P 500 cos disclosed AI as a material risk on 10-Ks in 2025, up from 58% in 2024. Concerns include reputational threats (38%), implementation issues, consumer-facing AI, privacy, hallucinations, bias, and fairness. ~20% cited cybersecurity risks; 41 cos flagged regulatory uncertainty, incl. EU AI Act. AI use has matured across finance, healthcare, IT, and industrial mkts. (Fortune)

- A study published Sept.24 shows most people can’t distinguish real voices from AI clones. While only 41% of generic AI voices fooled listeners, 58% of cloned voices were misclassified as human. Real voices were correctly identified just 62% of the time. Researchers warn of risks to security, ethics, and copyright, as deepfake tech becomes cheap, fast, and accessible w/ just ~4 mins of audio. (Live Science)

- Google DeepMind annc’d the Gemini 2.5 Computer Use model, built on Gemini 2.5 Pro to power agents that interact w/ UIs. It enables form-filling, dropdown control, and login ops, outperforming rivals in browser/mobile UI tasks w/ lower latency. Safety features include per-step checks and system instructions. Early testers report up to 18% better performance and 60% workflow recovery. (Google)

- OpenAI annc’d internal AI tools incl. DocuGPT, sparking concern among software cos. DocuSign CEO Thygesen said the tool, while named similarly, doesn’t rival their svs. The demo was seen as non-material to their biz. OpenAI’s push to embed apps in ChatGPT and expand into humanoid robotics signals broader ambitions, causing ripples across tech mkts. (Wired)

- MrBeast called AI’s rise “scary” for YouTube creators, as tools like OpenAI’s Sora can generate full videos from text. While AI aids production w/ tools like Google’s Veo, concerns over copyright and job loss persist. MrBeast faced backlash after annc’ing an AI thumbnail tool, later replacing it w/ human designers. Experts say creators who embrace AI for quality content may benefit in the short term. (BBC)

- Oracle stock fell 3% after a report revealed thin margins in its Nvidia cloud biz. The Co saw just 14% gross margin on $900mn in sales for the 3 mos ending Aug., far below its ~70% overall margin. Despite forecasting $144bn cloud rev by 2030, concerns rise over profitability due to costly Nvidia chips and aggressive pricing. Oracle’s AI push via Stargate project w/OpenAI remains key. (CNBC)

- Tech stocks are seeing wild swings, w/ AMD’s market cap briefly up ~$100bn after a deal w/OpenAI. Oracle surged 36% last month, adding $255bn on cloud biz guidance. Experts warn of a bubble, likening it to the dot-com era. AI deals, led by Nvidia & OpenAI, spark fears of unsustainable growth. Hedge fund titan Paul Tudor Jones sees parallels to the 1999 crash. (Yahoo Finance)

- Elon Musk’s AI startup xAI is raising $20bn—double its earlier target—w/ backing from Nvidia, which may invest up to $2bn. The funding, split into ~$7.5bn equity and ~$12.5bn debt via an SPV, will buy Nvidia chips for xAI’s Colossus 2 data center in Memphis. The chips will be rented for 5 yrs. The deal structure helps reduce cos’ debt exposure while accelerating AI infra growth across mkts. (Yahoo Finance)

- Adobe (NASDAQ:ADBE) & GitLab (NASDAQ:GTLB) shares slipped Tues. as Mizuho flagged AI’s “severe negative impact.” ADBE’s AI push via Firefly shows promise w/ enterprise clients, but faces rising competition from Canva, Figma & GenAI cos. like Midjourney & Runway. Mizuho cut ADBE’s target to $410 & downgraded GTLB to Neutral, citing uncertain AI impact, monetization risks & competitive pressure. (MSN)

- Deloitte annc’d a deal to deploy Anthropic’s Claude AI to ~470,000 staff across 150 countries—its largest enterprise rollout yet. Claude personas will be tailored for roles from devs to accountants, w/ support from Deloitte’s Claude Center of Excellence. Anthropic, backed by Amazon, cont’d global expansion after unveiling Claude Sonnet 4.5 and closing a $13bn round at a $183bn valuation. (CNBC)

- Google DeepMind annc’d CodeMender, an AI agent that autonomously detects, patches, and rewrites vulnerable code. Built using Gemini Deep Think models, it’s applied 72 fixes across 4.5mn+ lines. CodeMender uses static/dynamic analysis, fuzzing, and an LLM judge for validation. Though still in research, DeepMind aims to release it for devs to secure codebases w/minimal human input. (SiliconANGLE)

- Elon Musk’s xAI is investing ~$40–50bn in Memphis to build Colossus 2, a massive AI data center w/ 550,000 Nvidia chips. The project faces local backlash over pollution, water use, and rebates, despite promises of infrastructure and school funding. xAI raised $10bn, burns cash fast, and relies on SpaceX support. Musk aims to catch up to OpenAI, betting big on speed and scale in the AI arms race. (The Wall Street Journal)

- IBM & Anthropic annc’d a strategic partnership to integrate Claude LLM into IBM’s AI-first IDE, boosting enterprise software dev productivity by ~45%. The IDE supports app modernization, intelligent code review, and security-first workflows. IBM also introduced an ADLC guide for secure AI agent deployment and plans broader Claude integration across its portfolio, reinforcing governance, reliability & open standards. (Street Account)

- European AI founders are increasingly relocating to the U.S. for faster funding, higher valuations, and risk-tolerant investors.S. AI startups raised ~$160bn vs. Europe’s ~$20bn YTD. American investors led 71.1% of European AI deals. Strict EU regulations and slower funding timelines push cos toward U.S. incorporation. (The Wall Street Journal)

Broadcast/Cable Networks

- Fox annc’d it will air 7 games from the 2026 World Baseball Classic, incl. the title game from Miami. Coverage includes 3 Pool B games w/ the U.S. team, 2 quarterfinals, and the final. Other matches will stream on FS1, FS2, Fox Sports app, Fox One, or Tubi. Fox Deportes will broadcast 28 games in Spanish. (AP News)

- WBD’s Q3 ad rev is forecast to drop 17% YoY to $1. 2bn, deepening Q2’s 12% decline, per UBS. TNT lost NBA games, which earned $477mn last season. Viewership is pacing down 27%. Distribution rev to fall 8% to $2.4bn. Streaming (HBO Max, discovery+) sees 3% rise in subs rev to $2.4bn; ad rev up 17% to $239mn. (MediaPost)

- Corus Entertainment is nearing a debt restructuring that would give bondholders control via equity and secured debt. The embattled broadcaster, pressured by streaming and ad declines, reported $895mn rev (down 11%) and ~$35mn pretax loss for the 9-mo. ended May 31. Despite setbacks, a restructured Co could yield >$500mn in equity value. (Financial Post)

Cable/Pay-TV/Wireless

- T-Mobile quietly annc’d a late fee hike from $7 to $10. New policy states late fee will be the greater of 5% of monthly charges, $10, or max allowed by law. Autopay users may avoid fees and get bill discounts. Critics question if the Co still fits its “Uncarrier” image amid rising fees. (Droid-Life)

- Verizon annc’d CEO change, naming Dan Schulman to replace Hans Vestberg amid subscriber losses and 18% stock drop. Schulman, ex-PayPal CEO, aims to restore growth w/ cost cuts, capital optimization, and stronger customer value. Vestberg, credited w/ 5G leadership, will aid Frontier integration post $9.6bn deal. (MSN)

- Mobile data traffic in the Netherlands rose 16.1% in Q2 2025 to 719mn GB, per ACM’s mkts monitor—more than double Q1’s 6.5% growth and fastest in 2 yrs. (Telecompaper)

- AMX & Entel annc’d a non-binding agreement to explore a joint offer for Telefónica S.A.’s Chile assets. Any deal would require cos’ approvals & Chilean regulatory clearance. The potential transaction aims to boost telecom competitiveness, investment in high-speed networks, & asset efficiency—key to Chile’s digitalisation. (Street Account)

Capital Market Updates

- JD LOGISTICS annc’d acquisition of JD-SW’s on-demand delivery biz for $270mn, gaining full control of Dajiang & Dasheng. The move boosts last-mile delivery, enhancing fulfillment, efficiency & user experience. It aligns w/ JD LOGISTICS’ strategy for sustainable growth & profitability. Deal strengthens Co’s position in local svs mkts. (AASTOCKS)

Cloud/DataCenters/IT Infrastructure

- Google Cloud annc’d Gemini Enterprise, an AI platform aimed at everyday workers to automate tasks and generate content. Priced at $30/user/month, it unifies Gemini AI, agents, and gen AI tech, connecting w/ biz apps like Salesforce & SAP. It rivals Microsoft’s Copilot & OpenAI’s ChatGPT Enterprise. Google claims $106bn in customer commitments, w/ $58bn expected to boost rev by 2027. Launch supports >12 languages across all Co Cloud mkts. (Financial Post)

- Microsoft is limiting new Azure cloud subscriptions in key US regions due to ongoing data center shortages, expected to persist into 2026. Northern Virginia and Texas are most affected. The shortage impacts both AI and CPU workloads. (Tech in Asia)

- CoreWeave CEO Michael Intrator, in a interview, dismissed circular investment concerns, calling them “fundamentally flawed. ” He cited strong demand from major tech cos like Meta, Microsoft, and Google. CoreWeave, which IPO’d in Mar. raising $1.5bn, has surged 200%+ and inked $22.4bn in deals w/ OpenAI, $14.2bn w/ Meta, and $6.3bn+ w/ Nvidia, emphasizing a major AI infra buildout. (CNBC)

- Since Jan, OpenAI has cont’d a stealth search for Stargate data center sites, led by ex-Meta exec Keith Heyde. ~800 proposals were reviewed, w/ ~20 sites in late-stage diligence. Key factors: power access, scalability, local support. A $17GW buildout was annc’d w/ Oracle, Nvidia & SoftBank. Nvidia pledged up to $100bn. (CNBC)

- AI-driven demand is triggering a “supercycle” in SSD and RAM mkts, w/ analysts warning of NAND and DRAM shortages lasting up to 10 yrs. OpenAI’s deal for 900K DRAM wafers/month may consume 40% of global output. Samsung’s V9 NAND and Micron’s HBM are nearly sold out. While some predict an AI bubble, current trends suggest rising hardware costs. (Yahoo Finance)

Crypto/Blockchain/web3/NFTs

- Coinbase and Mastercard have held advanced talks to acquire London-based stablecoin startup BVNK for ~$2bn, per six sources. The move follows Stripe’s $1.1bn acquisition of Bridge last yr. (Fortune)

- Intercontinental Exchange (ICE), NYSE’s parent, annc’d a $2bn investment in Polymarket, valuing the platform at ~$8bn. ICE will globally distribute Polymarket’s event-driven data, aiding institutional access to real-time sentiment across politics, econ & culture. The move follows Polymarket’s $121mn QCEX acquisition in Jul. 2025 & aligns w/ its US expansion. (CryptoRank)

- Bee Maps, a Solana-based decentralized mapping project, annc’d a $32mn raise led by Pantera, LDA, Borderless & Ajna Capital. Funds will scale infrastructure, deploy devices, enhance AI, and boost $HONEY incentives. Bee’s tech enables real-time map updates via AI dash cams. Co’s new $19/mo Bee Membership slashes entry costs. (CoinDesk)

Cybersecurity/Security

- Google said over 100 cos were likely hit in a hacking campaign targeting Oracle’s E-Business Suite, w/ “mass amounts” of customer data stolen. The attack, possibly active since Jul., is linked to the CL0P group, known for targeting 3rd-party svs. Google noted significant pre-attack research by threat actors. Oracle earlier confirmed extortion attempts; CL0P claimed Oracle’s core product was “bugged.” (Reuters)

- Discord annc’d ~70,000 users may’ve had gov’t ID photos exposed due to a breach at a 3rd-party svs provider. Attackers claim to hold 1.5TB of age verification data, but Discord says figures are inaccurate and part of an extortion attempt. Affected users were contacted; compromised vendor ties were cut. Other impacted data includes names, emails, IPs, and partial credit card info. (The Verge)

- DraftKings annc’d a security breach from credential stuffing attacks. Hackers used stolen credentials from non-DraftKings sources to access user accounts. Exposed data includes names, addresses, birth dates, contact info, last 4 digits of cards, and account details. The Co enforced password resets, MFA for DK Horse logins, and added tech safeguards. Bleeping Computer first reported the incident. (Investing.com)

- Cyber attacks have hit major UK cos like JLR, M&S, and Co-op, causing severe disruption and losses—JLR alone lost ~£50m/week post-Aug. Supply chains, esp. in auto and retail, proved vulnerable due to lean models. Experts warn of rising threats from ransomware, often leased by Western teens. (BBC)

eCommerce/Social Commerce/Retail

- REI Co-op annc’d closures of its NYC flagship, Boston, and Paramus, NJ stores by late 2026 amid a strategic shift led by CEO Mary Beth Laughton. The decision follows a 6.2% drop in 2024 rev to $3.53bn and a $156.4mn net loss. NYC’s SoHo store, opened in 2011 and unionized in Mar. 2022, will cont’d ops till closure. (Chain Store Age)

- Germany’s cartel office is probing Chinese e-com Co Temu, suspecting it of price-fixing on its German mkts. Temu has ~19.3mn users in Germany. The watchdog fears Temu’s pricing terms may harm competition, raising prices elsewhere. (Deutsche Welle)

- Orvis, a Vermont-based outdoor retailer, annc’d closure of 31 stores & 5 outlets by early 2026 due to tariffs. Co will exit lifestyle apparel, refocus on fishing/hunting roots, and relocate HQ to Manchester, Vt. Orvis will retain its website, Orvis Adventures biz, and dealer network (400+). (MSN)

- Amazon’s Oct. 7–8 Prime Big Deal Days offered minimal real savings, w/ some prices even rising. A TV stand jumped 38% to $379, while other items matched prior prices despite “discount” tags. Amazon defended its pricing, but critics say inflated “before” prices mislead shoppers. Tools like CamelCamelCamel help track real deals. (MSN)

- Nike’s online prices rose sharply over the past yr under CEO Hill’s turnaround plan, w/ footwear up 17%, apparel 14%, and equipment 18%. Tariffs on Asian imports and reduced discounting contributed. Despite margin pressure, Nike is leveraging pricing power in core categories. Selective hikes aim to balance brand value and demand. Tariffs may cost the Co $1.5bn in FY26, impacting gross margin by 1.2%. (CNBC)

- Shein, hit w/ €190mn+ fines in 3 months, is boosting internal controls amid slowing growth. Co annc’d a “Biz Integrity Group” to tackle legal risks like IP theft & product safety. (Reuters)

- American Eagle plans to cut tariff costs from $180mn to $70mn by early 2026 via price hikes, supplier negotiations, transport optimization, and sourcing shifts. CFO Mathias said unmitigated costs could hit $150mn next fiscal yr. The Co aims to reduce China/Vietnam sourcing and optimize its supply chain. CEO Schottenstein noted early mitigation efforts have been successful. (Retail Dive)

- Walmart, via South Saturn Ridge LLC, bought Monroeville Mall for $34mn in Jan. and applied for a $7.5mn state grant to demolish it for redevelopment. Plans include new retail, restaurant, entertainment, and public spaces. Tenants like Pickle Parlor and Saga Hibachi face uncertainty. Mayor Gresock said public forums will be held, but no timeline is set. (CBS News)

- Walmart annc’d “Get It Now”, adding a lightning-bolt button for rapid delivery from local stores. W/ Walmart+ ($98/yr), users get 46-min delivery for $10 or free same-day on qualifying orders. The feature taps real-time inventory across 4,600 stores, boosting impulse buys and reducing cart abandonment. Walmart aims to rival Amazon’s speed, leveraging proximity and expanding its 20mn-member base. (Cord Cutters News)

- Rite Aid, after filing its 2nd Chapter 11 in 8 months, has shut all ~1,275 stores and 3 distribution centers, impacting ~24,500 jobs. CVS, Walgreens & Dollar Tree took over ~1,000 stores/leases. The Co cited retail struggles, debt, vendor issues & failed capital as key factors. Prescriptions were transferred to nearby pharmacies, draining resources, per Debtwire’s Sarah Foss. (Retail Dive)

Film/Studio/Content/IP/Talent

- Hollywood talent agency CAA warned that OpenAI’s Sora poses “serious” risks to creators’ rights. Sora, launched in Sept., lets users make AI videos w/ copyrighted content. CAA urged for control, permission, and compensation, calling them creators’ “fundamental right.” OpenAI annc’d plans to add content controls and share rev. Disney has opted out. CAA is engaging w/ cos, guilds, and lawmakers to address concerns. (Reuters)

- Paramount Skydance CEO David Ellison, declined to confirm a bid for Warner Bros. Discovery but emphasized any deal would create “more, not less” for Hollywood. He cited talent, shareholders, and storytelling as priorities. (Deadline)

- Warner Music is nearing a deal w/ Netflix to produce films & documentaries based on its artists, incl. Bruno Mars & Ed Sheeran, Bloomberg reported. CEO Robert Kyncl said partnering w/ a Co like Netflix makes sense to bring legendary song catalogs to life. In Jul., Warner Music & Bain Capital annc’d a $1.2bn JV to acquire music catalogs. Netflix & Warner Music declined comment. (Investing.com)

- The 2025 box office is set for a post-Covid high, nearing $9.2bn in rev, driven by winter hits like “Wicked: For Good,” “Zootopia 2” & “Avatar: Fire and Ash.” Q4 rev may hit $2.7bn, up 7% YoY. Momentum is expected to cont’d into 2026 w/ major IPs like “Toy Story 5,” “Dune: Part Three” & “Avengers: Doomsday.” Disney, Universal & Paramount lead the charge in revitalizing theatrical mkts. (CNBC)

- Taylor Swift’s 89-min “Showgirl” cinematic event earned $33mn domestically and $13mn overseas, totaling $46mn globally over its Oct. 3–5 run. Blending music videos, BTS clips, and lyric vids, it’s a promo for her 12th studio album. Despite booking premium screens, it didn’t hurt Dwayne Johnson’s “Smashing Machine,” which flopped w/$6mn. DiCaprio’s “One Battle” hit $101.7mn globally. (The Hollywood Reporter)

FinTech/InsurTech/Payments

- Block’s Square annc’d a BTC payments + wallet feature for small biz, enabling merchants to convert up to 50% of daily rev into BTC w/ zero fees. The wallet helps manage crypto holdings. Shares rose 2.6%. Block aims to make BTC “everyday money.” Cash App to shut down in UK from Sept. 15. Block also unveiled a BTC mining rig in Aug. to cut costs via swappable parts. (Decrypt)

- Monzo may reapply for a US banking licence, four yrs after its 2021 withdrawal due to OCC resistance and AML concerns. The UK neobank, now profitable w/ ~£1.2bn rev and £60.5mn pre-tax profit, eyes renewed US expansion amid eased regulations. If pursued, Monzo joins fintechs like Checkout.com and Nubank in targeting US mkts. (The Paypers)

- PayPal annc’d U.S. customers will earn 5% cash back on BNPL purchases through Dec. 31. Amid rising holiday financial stress, the Co expands Pay Monthly to in-store, offering flexible payments and rewards. BNPL boosts shopper loyalty and merchant conversion. Customers apply via app, get a virtual card w/in 24 hrs, and manage payments easily. (Street Account)

Handheld Devices & Accessories/Connected Home

- Deutsche Telekom annc’d the AI-phone Pro, launching in Germany & 9 other countries. Priced at €229 or €1 w/ tariff, it features Perplexity assistant, Picsart Pro, triple camera, 6.8″ display, & 88/100 Eco Rating. Includes 18-mo Perplexity Pro & 12-mo Picsart Pro. Aims to make AI accessible via MeinMagenta app & Magenta AI svs. (Telekom)

HealthTech/Wellness

- A Pew survey shows tech is deeply embedded in kids’ lives, incl. TV (90%), tablets (68%), smartphones (61%). YouTube is widely used—85% of kids watch, incl. 62% under age 2. AI chatbots, smartwatches, and voice assistants are part of the mix. 42% of parents say they could manage screen time better. Most believe kids should be 12+ before owning a smartphone. (Pew Research Center)

- TikTok’s algorithm drives compulsive use by serving hyper-personalized content. A WashPost study of 800+ U.S. users found that avg. daily watch time doubled for lighter users over 5 months, reaching 71 mins, while power users stayed near 4 hrs. Swipe speed and app opens rose, indicating habit formation. (The Washington Post)

- Amazon Pharmacy annc’d in-office kiosks debuting Dec. 2025 at select One Medical offices in LA, enabling patients to pick up prescriptions minutes after appointments. Aimed at improving adherence, kiosks offer fast access, video consults w/ pharmacists, and upfront pricing via Amazon app. The service targets ~1/3 of unfilled U.S. prescriptions and pharmacy deserts, streamlining care delivery and reducing delays. (StreetAccount)

Last Mile Transportation/Delivery

- DoorDash & Serve Robotics annc’d a multi-yr partnership to deploy autonomous delivery robots across the U., starting in L.A. The collab supports DoorDash’s multi-modal strategy integrating Dashers, drones & robots to boost efficiency, reduce emissions & traffic. Serve, w/ ~100K deliveries from 2,500+ restaurants, expands its reach via DoorDash’s platform & logistics infra. (DoorDash)

Macro Updates

- Fed officials leaned toward rate cuts in Sept. , split 10-9 on whether two or three were needed by yr-end. Labor mkts showed weakness, prompting concern, while inflation risks persisted. The fed funds rate was cut to 4%-4.25% w/ most expecting further easing. Gov. Miran dissented, favoring a more aggressive path. A gov’t shutdown may hinder data access ahead of Oct. 28–29 FOMC. (CNBC)

- Carlyle Group annc’d its own labor mkts data amid U.S. govt shutdown, estimating just 17,000 jobs added in Sept.—far below Bloomberg’s forecast of 54,000. Using data from 277 cos and 694 real estate investments, Carlyle’s indicators show a resilient but cooling economy. Despite weak payrolls, inflation remains widespread. Fed cut rates last month due to labor softness, impacting mkts. (Detroit News)

- Trump’s new tariffs are driving up US consumer prices as cos pass higher import costs to households. Goods like soup cans, dresses, and car parts are costlier. BLS data shows audio gear up 14%, dresses 8%, tools 5% in 6 mos to Aug. Inflation, flat for 2 yrs, is now rising in import-heavy categories. Despite this, headline inflation in Aug. held at 2.9%. (Moneycontrol)

Online Travel

- Delta Air Lines annc’d adj Q3 earnings of $1.71/share vs. $1.53 expected, w/ rev at $15.2bn. Premium travel rev rose 9% to ~$5.8bn, while main cabin fell 4%. Domestic unit rev grew 2% on 4% capacity rise. Delta forecasts Q4 adj EPS of $1.60–$1.90 and full-yr EPS of $6. CEO sees margin growth in 2026. Strong luxury demand and higher fares buoy outlook despite earlier mkts softness. (CNBC)

Regulatory

- Starting Jan. 1, 2026, Apple will comply w/ Texas’ age verification law by requiring new users to confirm if they’re over 18. Minors must join Family Sharing; parental consent is needed for app downloads & purchases. Apple will update its Declared Age Range API & launch new APIs for parental consent re-requests. Similar laws in Utah & Louisiana will follow. (The Verge)

- Apple and Meta are nearing settlements w/EU regulators over alleged DMA breaches. In Apr., Apple was fined €500M for anti-steering violations; Meta faced a €200M fine over its “pay or consent” ad model. Both cos are negotiating changes to biz practices to avoid further penalties. Apple annc’d App Store policy revamp in Jun.; Meta’s proposals are under review. (MSN)

- New York City filed a federal lawsuit accusing Meta, Google, Snap & ByteDance of gross negligence & creating a public nuisance by addicting youth to social media. The 327-page complaint cites ~1.8mn minors, rising mental health issues, & subway surfing deaths. Google denied claims re: YouTube. NYC withdrew from prior state case to join nationwide litigation w/ ~2,050 similar suits. (Reuters)

- JPMorgan CEO Jamie Dimon backed easing SEC’s quarterly earnings rules, citing pressure on CEOs to meet forecasts. He said JPMorgan would still offer quarterly updates but w/ “less stuff.” Dimon also revealed the Co spends ~$2bn/yr on AI tech, saving nearly the same. He called AI transformative, aligning w/ peers like Goldman Sachs and Morgan Stanley. (Reuters)

- The U. S. Supreme Court declined to halt a judge’s order requiring Google to reform its Play store amid Epic Games’ antitrust suit. The injunction, upheld in Jul., mandates Google allow rival app stores and external payment links. Some changes take effect Oct., others by Jul. 2026. Google, citing security and competitive risks, plans to appeal. (Reuters)

- SCOTUS denied Google’s bid to block a lower court injunction in its case vs. Epic Games. Google must allow 3rd-party app stores, share app catalog w/ rivals, and permit non-Google billing. Injunction bars exclusive deals for Play Store. Epic CEO Sweeney cheered the Oct. 22 change. Google cited security risks, vowed appeal, and said the order jeopardizes safe app downloads. (The Hill)

Satellite/Space

- AST SpaceMobile (NASDAQ: ASTS) stock fell 7% after the satellite comms Co annc’d a $800mn ATM offering. The Co entered an equity distribution deal w/ 10 banks incl. BofA, Barclays, UBS & Deutsche Bank. Shares may be sold via Nasdaq, mkts, or block trades at market prices. The ATM provides capital flexibility while minimizing dilutive impact vs. traditional offerings. (Investing.com)

- AST SpaceMobile annc’d a definitive commercial agreement w/ Verizon to deliver space-based cellular broadband across the U. starting in 2026. The service uses AST’s low Earth orbit tech and Verizon’s 850 MHz spectrum to connect standard smartphones w/o special gear. Successful trials included VoLTE calls via satellite. (Business Wire)

- Airtel Africa, in partnership w/ Eutelsat OneWeb, successfully tested satellite-powered internet on a moving train across a 669km corridor, achieving speeds of 100 Mbps download and 20 Mbps upload. The trial, part of Airtel Satellite for Biz, met adj benchmarks and showed LEO satellites can deliver stable broadband in motion. (Technology Times)

Social/Digital Media

- Instagram is exploring a dedicated TV app to expand its video reach, esp. Reels, amid rising competition w/ TikTok. Instagram chief Mosseri said at Bloomberg Screentime that the Co aims to adapt to shifting user behavior. While no launch is annc’d yet, Mosseri believes existing vertical content suits TV. The Co isn’t pursuing live sports or exclusive Hollywood content. (The Hindu BusinessLine)

- Facebook annc’d an algorithm update to show users 50% more same-day Reels, aiming to boost engagement. New AI-powered search suggestions and friend bubbles enhance Reels interactivity. AI-generated content is treated equally, but users can signal disinterest. Facebook’s VP said authentic, human-driven content still performs best despite rising AI use. (CNET)

- Instagram annc’d Rings, an awards program honoring 25 top creators from its ~3bn users. Winners get a physical ring by Grace Wales Bonner and a digital golden ring for their profile/stories. Judges include Spike Lee, Marc Jacobs, and Adam Mosseri. Criteria focused on creators pushing boundaries across fashion, sports, entertainment, etc. Instagram aims to make Rings an annual tradition. (The Hollywood Reporter)

- Indonesia reinstated TikTok’s license after the Co shared data on live stream activity during deadly Aug. protests. TikTok had initially refused, citing internal policy. The gov’t sought info to trace online gambling tied to monetization. TikTok suspended live streaming on Aug. 30, resumed days later. License was reactivated after obligations were met, per Director Alexander Sabar. (AP News)

- Social media usage peaked in 2022 and has steadily declined, per GWI data from 250k adults across 50+ countries. daily use fell ~10% by end-2024, esp. among teens and 20-somethings. Meta & OpenAI annc’d new AI-driven platforms, but the shift from human interaction to dopamine-rich “slop” content has degraded the experience. (AFR)

Sports/Sports Betting

- NBA has returned to China after a 6-yr rift triggered by Hong Kong protests. The Brooklyn Nets and Phoenix Suns will play pre-season games in Macau. The league annc’d a deal w/ Alibaba Cloud to boost fan engagement and extended its Tencent broadcast deal to 2027. With ~300mn Chinese players, the NBA sees China as its top intl. mkts (Financial Times)

- NCAA annc’d that D-I athletes/staff may bet on pro sports starting Nov. 1, pending D-II/D-III approval. While promoting fairness, risks remain—esp. w/ prop bets. College sports betting, info sharing still banned. 67% of campus students bet; concerns over addiction, debt persist. NCAA vows education-focused harm reduction. Legal issues, state laws, and past sanctions also in spotlight. (Sportico)

Tech Hardware