The start of the week marked the quarter-end, and while it didn’t look like it was going to be case earlier in the period, the quarter ended in positive territory, continuing the hot streak. What was different though was that there was some broadening of performance overall, which is a healthy development. In Theme #1, we took a deeper dive more specifically into the winners and losers in the sector for Q3.

See below for the full list of what we focused on in this week’s edition as the most important themes and updates across the sector (all links are clickable):

- Q3 Stock Wrap – Lumen, Clover & Redfin Take The Top Spots

- The AI Arms Race Dominates Big Tech

- The Consolidation Frenzy In Connectivity Continues…

- Will Hybrid Carriage Agreements Change The Trajectory Of Pay-TV Subscriber Declines?

- The State Of Global Venture Capital Investments In 3 Slides (Spoiler – It’s Not Great)

- The Streamers’ Rapid Push Into Live Remains In Focus

- Grab Bag: Apple Pivots On Film Strategy/Spotify Raises Prices In Canada/California Rejects AI Safety Bill

Enjoy the weekend.

Best,

Leslie

Q3 Stock Wrap – Lumen, Clover & Redfin Take The Top Spots

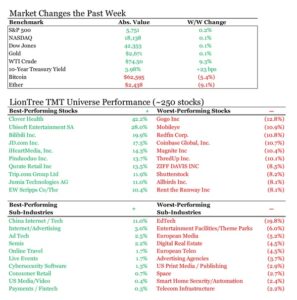

While in negative territory for part of the quarter, stocks eventually rebounded, and Q3 ended up being another quarter with strong positive q/q returns, with the S&P 500 taking leadership over the tech-heavy Nasdaq (the S&P 500 was up +5.4% in Q3 vs +3.9% in Q2, while Nasdaq was up +2.6% vs +8.3% in Q2).

Within the S&P 500, all sectors were up in the quarter with the exception of Energy, which was down -5.0%. Utilities led the way and was the best-performing sector, up +17.5, on avg, which was on top of a +2.1% gain last quarter. Information Technology was up +3.6%, on top of the +3.2% gain back in Q2. Consumer Discretionary and Consumer Staples both rebounded, with Consumer Discretionary up +9.8% (vs -6.2% last qtr) and Consumer Staples up +5.6% (vs -6.9% last qtr), respectively.

In Europe, performance was positive across the board. DAX was up +5.6% (vs down -1.4% in Q2), and CAC was up +2.1% (vs down -8.9% in Q2). Euronext was up +11.0% (vs +1.1% in Q2), and FTSE was up +0.9% (vs +2.7% in Q2). It was mostly positive in Asia as well, with the SSE Composite up +12.4% (vs -2.4% in Q2) and Hang Seng up +19.3% (vs +7.1% in Q2). However, Nikkei was down -4.2% (vs -2.0% in Q2)

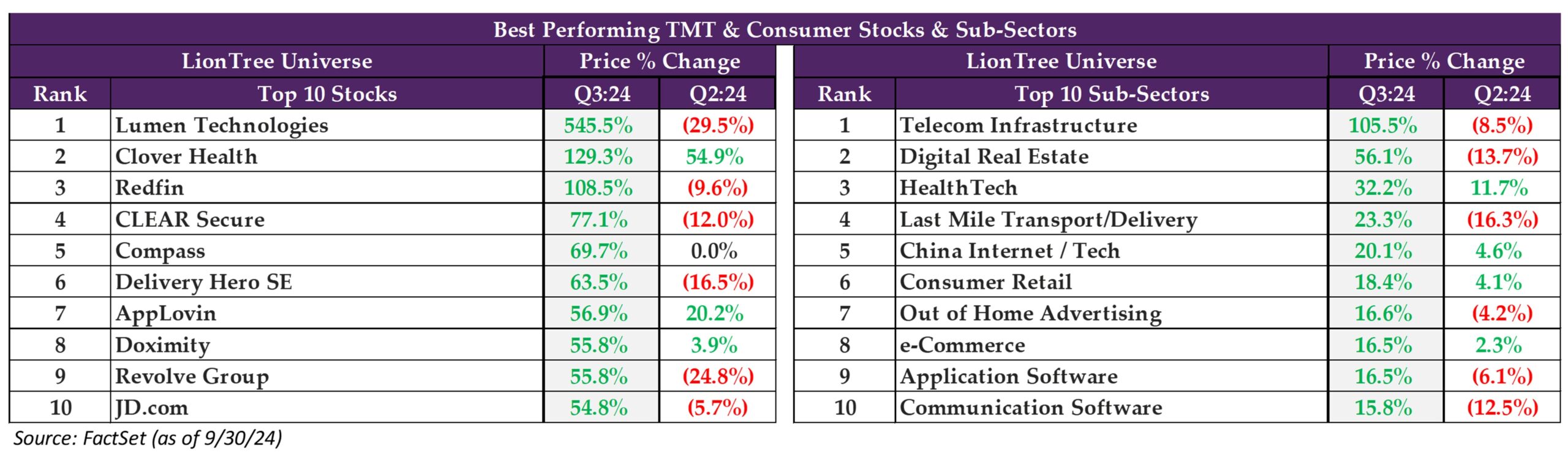

Looking at performance across our LionTree Universe of ~200 stocks in the TMT and Consumer sector with $1bn+ market cap, rallies this quarter were actually much more broad-based, with 71% of stocks trading up, a significant step up from the just 43% in Q2 and 52% in Q1. That being said, 44% traded up double-digits, which is about in-line with last quarter’s 46%.

Which stocks saw the largest gains in Q3? It was Lumen Technologies, up a gigantic +546% in the quarter, as the Co announced several new business wins amid surging AI demand. It was followed by Clover Health, up +129%, and Redfin, up +109%, to round out the Top 3 best performers of Q3.

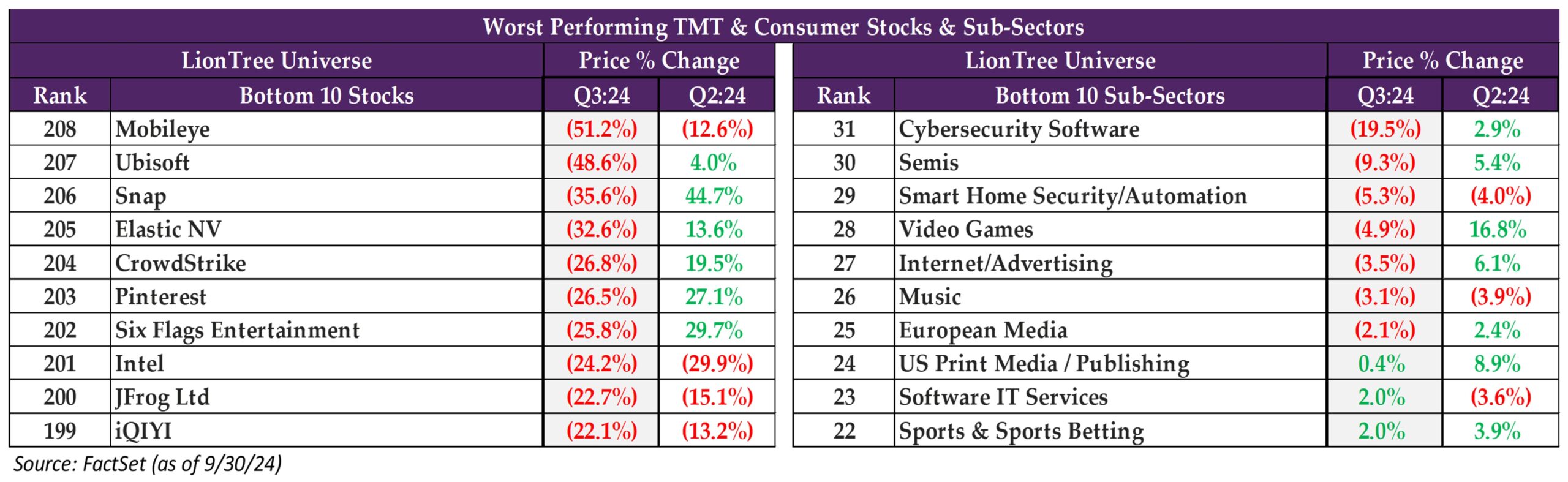

On the other hand, which stocks had the toughest in Q3? It was Mobileye, down -51% in Q3, as the Co reduced its full year outlook. Ubisoft and Snap were down -49% and -36%, respectively, to make up the Bottom 3 worst performers in Q3.

The BEST Performing Sub-Sectors in Q3

- #1 = Telecom Infrastructure: After falling -8%, on avg, in Q2, the sector reversed course in a big way and was up +106%, on avg, in Q3

- Lumen Technologies’ +546% jump in the quarter drove most of the sector’s performance

- Crown Castle, SBA Communications, American Tower, and Equinix also benefitted the sector’s performance, as all four companies posted double-digits gains in the quarter

- Digital Realty Trust was also up a modest +6% in Q3

- #2 = Digital Real Estate: The sector also reversed course in Q3 and was up +56%, on avg, which was a turn-around from the -14% avg decline it posted in Q2

- Redfin’s +109% gain in the quarter headlined the sector’s performance

- That being said, Compass and Zillow Group also posted strong double-digits performances of +69.7% and +38%, respectively

- Opendoor Technologies was also up +9% in the quarter

- #3 = HealthTech: The sector saw continued growth in Q3, up +32%, on avg, which was an acceleration from Q2’s avg of +12%

- Clover Health was up a significant +129% in Q3

- Doximity and Oscar Health saw double-digit gains in the qtr, up +56% and +34%, respectively

- That being said, there were some drags in the sub-sector, asTeladoc, Hims & Hers, and GoodRx were all down -6%, -9% and -31%, respectively, in the qtr

The WORST Performing Sub-Sectors in Q3

- #31 (last place) = Cybersecurity Software: The sector saw an unfavorable turnaround, going from a +3% gain, on avg, in Q2 to a -20% loss, on avg, in Q3

- Most of the names in the sector were down double-digits, including CrowdStrike, down -27%, Okta, down -21%, and Zscaler, down -11%

- #30 = Semis: The sector also saw a reversal of fortunes, going from a gain of +5%, on avg, in Q2 to a loss of -9%, on avg, in Q3

- Intel and GlobalFoundries were the worst performers in the sector, down -24% and -20%, respectively

- QUALCOMM and ARM Holdings were also down double-digits, falling -15% and -13%, respectively

- NVIDIA was down -2% in Q3

- That being said, there were some gainers in the qtr, including Advanced Micro Devices and Broadcom, which were up +1% and +7%, respectively

- #29: Smart Home Security/Automation: The sub-sector saw a greater degree of red in Q2, down -5%, on avg, after falling -4%, on avg, in Q2

- com and ADT weighed down on the sector, down -14% and -5%, respectively

However, Resideo was up +3%

The AI Arms Race Dominates Big Tech

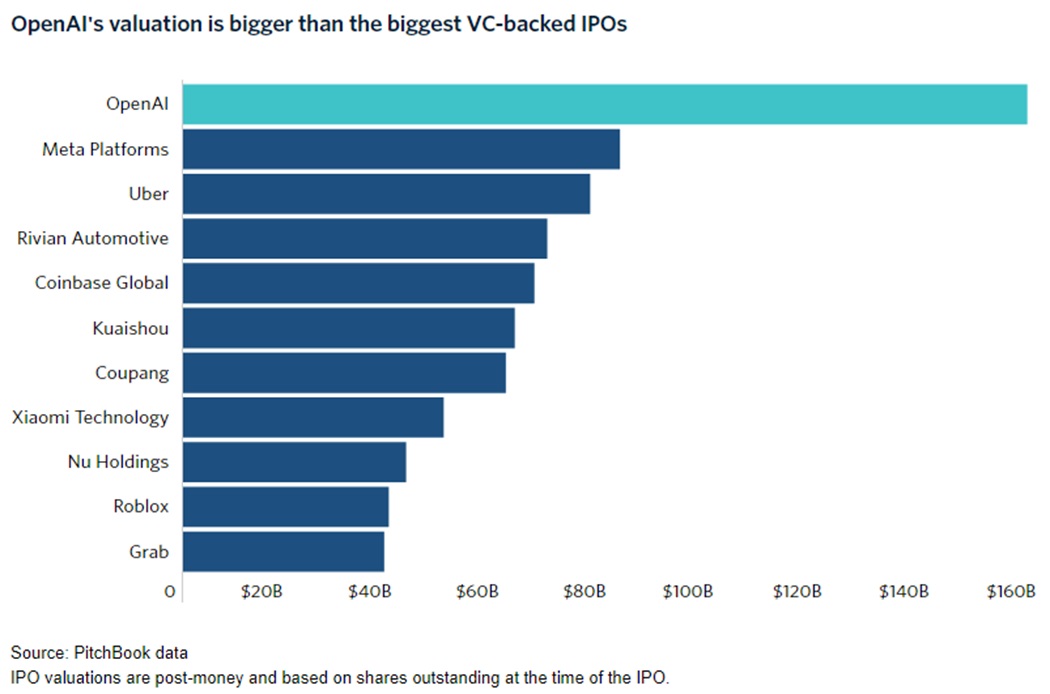

It was certainly an AI-dominated week across the TMT landscape, as OpenAI, Microsoft, and Google made headlines with several noteworthy updates across their respective AI businesses. To keep up in the AI arms race, participants have had to have some deep pockets, and OpenAI significantly expanded its war chest this week. The company raised $10.6bn in fresh liquidity between closing a $6.6bn funding round at an eye-popping $157bn post-money valuation and opening up a $4bn revolving credit facility that includes an ability to borrow an additional $2bn. OpenAI is now the third most valuable VC-backed company in the world behind just TikTok and SpaceX. Moving forward, the additional capital will enable OpenAI to “invest in new initiatives and operate with full agility” as part of the company’s ambitious plans to more than triple its revenue between 2024 and 2025.

One of OpenAI’s largest backers, Microsoft, which also participated in the latest funding round, announced several major upgrades to its own “AI companion”, Copilot, this week. The updates greatly improve Copilot’s functionality for both users and advertisers, though many of these are only rolling out on a limited basis for now. For users, the main theme was personalization, as new features enable Copilot to read users’ screens, speak to them, think through more complex questions, as well as summarize news and weather that’s specific to them. On the advertising side, relevancy was a big focus. Beyond just Copilot, Microsoft also incorporated gen AI into Bing searches and revealed plans to invest $4.8bn into AI and cloud infrastructure in northern Italy over the next two years.

For its part, Google has been matching OpenAI and Microsoft step for step. Along with reports coming out that the company is working on developing software that can mimic humans’ ability to reason, similar to OpenAI’s o1, Google is mirroring Microsoft’s playbook by introducing ads to AI Overviews on search this month. The company is beginning to use AI to organize search pages as well, displaying a custom results page with relevant info to searchers instead of just a list of links. However, the feature is only currently available on mobile in the US for searches related to recipes and meal ideas. Elsewhere, Google also added support for several new languages for Gemini Live, with plans to rollout 40+ languages and extensions “in the coming weeks”.

See below for more details…

-> Next week will likely be another big one for the AI space, w/ AMD’s Advancing AI 2024 event and NVIDIA’s AI Summit both on the horizon

OpenAI Is The Third Most Valuable VC-Backed Co In The World

- OpenAI raised $10.6bn in fresh liquidity (link/ link): This week, OpenAI closed a $6.6bn funding round at a $157bn post-money valuation and also opened up a $4bn revolving credit facility

- The Co has an option to increase its line of credit by an addt’l +$2bn: The loan is unsecured and can be tapped over the course of three yrs

- OpenAI’s interest rate is equal to the SOFR rate + 100 bps: The Secured Overnight Financing Rate (SOFR) was at just over 5% earlier this week, meaning that OpenAI’s rate would be ~6% on funds that it borrows right away

- OpenAI’s funding round included many well-known investment firms and Big Tech Cos: Sources indicated the round was led by Thrive Capital and that Microsoft, Nvidia, SoftBank, Khosla Ventures, Altimeter Capital, Fidelity, MGX, and Tiger Global also participated; However, Apple reportedly passed on the round

- OpenAI plans to use the money to “invest in new initiatives and operate w/ full agility”: The Co will use the money to invest in research and products, expand infrastructure, and expand talent; The new liquidity “also reaffirms [OpenAI’s] partnership w/ an exceptional group of financial institutions”

- Putting the funding round into context (per Pitchbook data):

- OpenAI is now the #3 most valuable VC-backed Co in the world: TikTok owner ByteDance is #1 at $220bn, and SpaceX is #2 at $180bn

- OpenAI is worth a lot more than any VC-backed Co at the time of their IPO (see chart below)

- OpenAI’s closest competitor Anthropic was valued at $19.4bn in Jan

- The Co anticipates ~$5bn in losses on $3.7bn in rev in 2024 and expects to reach $11.6bn in revs in 2025 (link): This was according to a person close to OpenAI

- The Co has an option to increase its line of credit by an addt’l +$2bn: The loan is unsecured and can be tapped over the course of three yrs

-> OpenAI also hosted its 2024 DevDay this week to showcase several new tools to help devs build tools with its AI models; Along w/ unveiling a public beta of its “Realtime API”, which provides devs w/ the oppty to build nearly real-time, speech-to-speech experiences in their apps w/ the choice of using six voices, OpenAI also introduced vision fine-tuning in its API, enabling devs to use images and text to fine-tune their applications powered by GPT-4o (link)

The AI-Related Updates Came Fast & Furious From Microsoft This Week…

- Microsoft launched new Copilot capabilities for all users (link/link): These updates are rolling out to all users on Copilot apps for iOS, Android, Windows, and the web, enabling Copilot to read users’ screens, speak to them, think through more complex questions, and more; Microsoft is also bringing Copilot to WhatsApp

- Introduced Copilot Labs, an exclusive Copilot Pro opt-in program for experimental capabilities: Microsoft plans to trial its most advanced tools with a small subset of users to gather feedback and apply key learnings before releasing them to all users

- Think Deeper is the first feature available in Copilot Labs: Think Deeper provides Copilot w/ the ability to reason through more complex problems using the latest reasoning models; It can help solve difficult math problems or evaluate the cost of managing home projects

- Copilot Vision gives users the option to let Copilot see what they see: Copilot will sit within Microsoft Edge and, upon request, help users understand the page they’re viewing, answering questions, suggesting next steps, and helping them navigate the content; None of the content will be stored or used for training

- Voice will make Copilot feel more like an AI companion: This makes Copilot even more accessible to users; They can, for instance, use it to ask a quick question or to vent at the end of a tough day; There will be four voice options to choose from, adding more of a personal touch

- Copilot Discover will become more personalized: W/ users’ permission, Copilot Discover offers a guide to useful features and conversation starters based on their interactions w/ other Microsoft svs; The feature will be further personalized over time according to users’ conversation history

- Copilot Daily provides a summary of news and weather: This will be read to users in their favorite Copilot Voice, w/ more options like reminders for upcoming events; Daily will only pull from authorized sources

- Daily is only available in the US and UK at launch

- Introduced Copilot Labs, an exclusive Copilot Pro opt-in program for experimental capabilities: Microsoft plans to trial its most advanced tools with a small subset of users to gather feedback and apply key learnings before releasing them to all users

-> Microsoft will pay publishers for content that appears in Copilot Daily; Reuters, Axel Springer, Hearst Magazines, USA Today Network, and The Financial Times are signed on, and there are plans to add more sources over time, along with additional personalization and control features (link)

- Microsoft is adding targeted ads, metrics, and diagnostic capabilities to Copilot (link): The ads will be displayed below Copilot’s organic response in results, w/ a stronger focus on relevancy of the info served

- Users will see fewer ad annotations and extensions: As the updated Copilot tech can now identify relevant and useful content more effectively; Ads will also be triggered based on a user’s entire conversation, not just the last prompt

- “Ad voice” will help make ads feel more natural and inviting to users: Ad voice is a summary that acknowledges the organic response and introduces the message from advertisers, sharing w/ the user how the following ad section connects to their convo

- The ads started to roll out on copilot.microsoft.com in Oct: The experience will expand over time to updated apps on Android and iOS as well as Copilot experiences in Bing and Edge

- A new diagnostics feature will begin piloting this month: The new gen AI-powered diagnostics tools will assist advertisers in inspecting campaign setup, assessing the health of accounts, diagnosing where attention is needed, and proposing next steps; This will all occur in a conversational context

- Performance snapshot will also enter pilot testing in Oct: The feature gives advertisers quick updates on how their campaigns and accounts have been performing during a specific length in time; Advertisers will be able to use natural language to ask Copilot for a summary of key insights, trends, and anomalies

- Users will see fewer ad annotations and extensions: As the updated Copilot tech can now identify relevant and useful content more effectively; Ads will also be triggered based on a user’s entire conversation, not just the last prompt

- Microsoft also incorporated gen AI into Bing searches for all US users (link): The Bing generative search launch comes after a pilot run in July, though the tool is still under development

- Searching “Bing generative search” on Bing is the easiest way to invoke it: Microsoft is also working on introducing an option to more easily trigger Bing generative search for informational queries

- There’s also an option to dismiss AI-generated summaries for traditional search results: This is similar to Google’s AI Overviews feature

- Bing generative search is powered by a mix of AI models: The new experience combines the foundation of Bing’s search results w/ both large and small language models

- Bing generative search will answer queries more reliability than previous iterations of AI on Bing: Microsoft has “refined” its methods to optimize accuracy in Bing, improving the Co introduced LLM-powered

- Searching “Bing generative search” on Bing is the easiest way to invoke it: Microsoft is also working on introducing an option to more easily trigger Bing generative search for informational queries

-> Microsoft is also using AI to enhance Windows search on its new Copilot Plus PCs, including the addition of a new Click to Do feature that’s similar to Google’s Circle to Search; These improvements, among other AI-powered upgrades, will make it easier for users to find and interact w/ images emails, documents, and even videos; The enhanced Windows search will first show up in File Explorer on Copilot Plus PCs starting in Nov (link)…

AND Google Has Been Keeping Up In The AI Arms Race

- Google is reportedly working on AI software that resembles humans’ reasoning ability, similar to OpenAI’s o1 (link): Per sources, multiple teams at Google have been making progress on AI reasoning software, which is more adept at solving multi-step problems in fields such as math and computer programming

- The Co is trying to approximate human reasoning using “chain-of-thought programming”: Google pioneered this technique, in which software will pause for a matter of seconds before responding to a written prompt while considering a number of related prompts behind the scenes and summarizing the best one

- Google employees are no longer as concerned that they’re falling behind OpenAI: Now that Google has debuted some of its own work, the employees are no longer as worried as they were following the launch of ChatGPT, according to one person

- Math reasoning has been another area of focus for the Co: Google showcased math reasoning models AlphaProof and AlphaGeometry 2 in July; The programs aced four of the six problems featured in the International Math Olympiad

- Google is introducing ads to AI Overviews (link): Users will now start seeing relevant products in their Google search’s AI-generated summaries; The launch will only occur in the US on mobile devices

- Ads will only appear if a question or query has a “commercial angle”: For example, if a person searches for ways to get a grass stain out of their pants, Google’s AI-generated response will offer some tips and suggest some products that could help remove the stain

- Google has been testing ads in AI Overviews since May: The Co moved forward w/ a full rollout b/c the ads help people “quickly connect with relevant businesses, products, and svs to take the next step at the exact moment they need them”

- No action is required from advertisers for their ads to appear on AI Overview

- The Co is also making some formatting changes to AI Overviews: Cited webpages will now appear more prominently on the right side of the summary, as tests showed that this “has driven an increase in traffic to supporting websites compared to the previous design”

- Google is launching AI-organized search pages as well: This feature displays a custom results page w/ relevant info instead of just showing a list of links; It’s currently only available in the US on mobile for searches related to recipes and meal ideas

- Ads will only appear if a question or query has a “commercial angle”: For example, if a person searches for ways to get a grass stain out of their pants, Google’s AI-generated response will offer some tips and suggest some products that could help remove the stain

-> Another new update from Google this week allows Lens users to take a video and use their voice to ask about what they’re seeing in the video; The feature, which rolled out in Search Labs on Android and iOS, will surface an AI Overview and search results based on the video’s contents and their question; Google Lens is also updating its photo search feature w/ the ability for users to ask a question using their voices (link)

- Gemini Live will now support several other languages beyond English (link): The conversational AI voice chat has started to support French, German, Portuguese, Hindi, and Spanish, and these will be available to all users in a “couple of weeks”

- Support for 40+ other languages is launching in “the coming weeks”: The Co also plans to add Gemini extensions for Calendar, Tasks, and Keep in “the coming weeks” as well as expanded capabilities for the Gemini virtual assistant

- The Gemini Live rollout has been progressing rapidly: Gemini Live was first unveiled as a subscriber-only feature as part of the Pixel 9 series launch in mid-Aug; The Co then opened it up as a free feature for all Android users in mid-Sept

The Consolidation Frenzy In Connectivity Continues…

We spotlighted the seemingly incessant deal flow within the connectivity space last week, and this week brought a continuation of that trend, as a couple more deals that were previously in the news came into fruition, plus some additional announcements.

In the pay-TV space, DirecTV and Dish officially announced a merger, whereupon the former will acquire EchoStar’s video distribution assets (Dish DBS) for $1 and the assumption of ~$9.75bn in net debt to become the largest pay-TV provider in the US with ~20mn subscribers. Concurrently, TPG plans to buyout AT&T’s 70% stake of DirecTV, though AT&T and DirecTV will still maintain “an ongoing commercial relationship” moving forward. Along with potentially generating a $1bn/year run-rate in cost synergies by the third anniversary of the deal’s close, which is expected in late 2025, the transaction could also provide “the new DirecTV” with more leverage with programmers. More specifically, the company will aim “to better work with programmers to deliver smaller packages at lower price points” during upcoming carriage renewal discussions. Ultimately, the new DirecTV aspires to be a “one-stop service to consumers”, integrating linear, SVOD, AVOD, and PVOD together and ensuring that people only pay for the genres they want to watch. With better access to capital and an “improved financial profile”, the company will also look to accelerate investment in the customer experience around its offerings in an effort to stem the pay-TV industry’s losses to the cord-cutting trend.

On the EchoStar side of the equation, the transaction will eliminate debt, reduce the company’s financing needs for the next 24-36 months, and free up other resources that will be put to use in enhancing its mobile business and 5G open RAN network. In aggregate, EchoStar has raised $5.5bn of capital to invest and still has “plenty of dry powder” left over to create a “very, very attractive number four position” in the US telco industry. However, in contrast to recent moves from its peers, the company does not intend to invest in fiber or other non-wireless assets. Instead, EchoStar will deploy its capital “very prudently” and “much more efficiently that the other providers [and] operators” by not deviating from a wireless-only approach. Overall, the company touts a strengthened position as the fourth US facilities-based carrier.

Elsewhere within the connectivity space, Verizon shook things up this week, negotiating a deal to sell and lease back over 6,000 towers to Vertical Bridge on 10-year terms as part of a broader strategy to “drive down tower-related costs”. It was also reported that Zayo and TPG are the final remaining bidders to purchase Crown Castle’s fiber and small cell assets, though a deal likely isn’t coming soon and isn’t guaranteed, according to sources. Finally, Gogo made some waves in the in-flight connectivity space, reaching an agreement to acquire Satcom Direct in a move that that will enable to expand within the business aviation market and provide an entry point into the military/government space.

Needless to say, there was a lot to digest this week on the connectivity front – See below for more details:

-> Echostar shares rallied +35% from the day before the initial press speculation emerged about a deal (Sept 13) to an intra-day high on Sept 27, following subsequent reports that emerged; However, it turned into a sell-the-news event, w/ Echostar stock closing the week up just +5% from the unaffected share price ($22.27/shr), as there is still a long execution road ahead operationally

Key Takeaways From DirecTV And EchoStar’s Calls Regarding The Transaction

- DirecTV will acquire Dish TV and Sling TV from EchoStar after being in advanced talks last week: The deal still needs to be approved by regulators and is expected to close in Q4:25 if all moves forward as planned

- The deal involves a debt exchange transaction: DirecTV will pay EchoStar $1, plus the assumption of ~$9.75bn in Dish DBS net debt; DirecTV will acquire 100% of EchoStar’s pay-TV biz

- Echo Star will be allowed to access ~$1.5bn cash from Dish DBS through Sept 2025, subject to operating covenants

- Certain outstanding Intercompany Loans held by Dish will be release

- Concurrently w/ the M&A transaction, TPG Angelo Gordon and other lenders, including DirecTV, provided $2.5bn of financing to full refinance Dish DBS’ 2024 debt maturity

- Exchange offer: EchoStar launched an exchange transaction to holders of five different series of Dish notes, w/ a total face value of ~$9.75bn

- Dish debtholders need to agree to a haircut for the deal to close: The M&A close is contingent on obtaining $1.568bn of discount to face value on Dish DBS debt

- Separately, AT&T cut a deal to get out of the DirecTV biz: TPG also said that it agreed to acquire the 70% of DirecTV currently owned by AT&T; However, DirecTV will still have “an ongoing commercial relationship” w/ AT&T around the sale of other svs

- The deal involves a debt exchange transaction: DirecTV will pay EchoStar $1, plus the assumption of ~$9.75bn in Dish DBS net debt; DirecTV will acquire 100% of EchoStar’s pay-TV biz

- The new DirecTV will be the largest pay-TV provider in the US: Together, DirecTV and Dish DBS have ~20mn pay-TV subs, while Charter and Comcast each have a little over 12mn pay-TV subs

- Added scale will provide w/ more leverage w/ programmers: “Incr’d scale [will] allow new DirecTV to better work w/ programmers to deliver smaller packages at lower price points, which is what consumers want”

- An “improved financial profile” will improve access to capital: This will enable further investment in the user experience

- DirecTV estimates that the merger could create cost synergies of at least $1bn/yr: Including in lowering content cost, efficiencies in SG&A and customer support resources, and tech; Expects to achieve these by the third anniversary of closing

- The new DirecTV wants to become “a simple, one-stop svs to consumers”: Imagines a “different kind of packaging concept, keeping the price down to where they only pay more or less the genre or type of content that [people[ want”

- The new Co will have better aggregation capabilities: The Co plans to aggregate a “small, genre-based-specific choice of linear, combined w/ SVOD and/or AVOD, or FAST channels, [and] a whole host of other things that will wrap around the user interface”

- The deal allows EchoStar to focus resources on building out its 5G open RAN network: The deal “significantly delevers” the Co and “provides capital… to strengthen [its] position as the number four US facilities-based carrier and a much stronger competitor”

- EchoStar is “refocusing” its portfolio on the growth part of its biz: The Co has access to “significant addt’l capital” to develop its Boost Mobile nationwide 5G O-RAN network

- The Co is “focused on wireless” only at the moment: EchoStar will use its capital “very prudently” and won’t invest in fiber or other infrastructure, like its competitors have

- EchoStar “[does] not intend to miss any obligations or deadlines” from the FCC: This will be true both immediately and in the longer-term, given the improved liquidity profile

- The Co’s terrestrial 3.45 GHz C-band spectrum “now becomes unencumbered”: The transaction will eliminate a $2.8bn spectrum-backed obligation on EchoStar’s 3.45 GHz spectrum

- EchoStar is also “well-positioned” to take advantage of its satellite-based spectrum: The Co is the only operator that has rights to the same spectrum in the US as it does globally, w/ 30 MHz of S-band rights globally and 40 MHz of S-band rights in the US

- In total, EchoStar has raised $5.5bn of investment capital: The Co will “invest in [its] mobile biz and continue to build and enhance [its] nationwide 5G open RAN network”; Some of the funds will also be earmarked for “general corporate purposes

- This reduces the Co’s financing needs for the next 24-36 months: Also pointed out that the Co can “address those financing needs at the end of those windows w/ “addt’l firepower from collateral” that was used to raise the $5.5bn

- EchoStar has access to $13bn in capital today through the deal: This could go up to $15bn in the next couple yrs, based on the assessment of the value of its spectrum

- EchoStar is “refocusing” its portfolio on the growth part of its biz: The Co has access to “significant addt’l capital” to develop its Boost Mobile nationwide 5G O-RAN network

Verizon & Vertical Bridge Also Finalized A Tower Deal This Week… Among Other Transactions Across The Space

- Verizon and Vertical Bridge agreed to a $3.3bn transaction involving 6,339 towers across all 50 states (link): Vertical Bridge will obtain the exclusive rights to lease, operate, and manage the wireless towers from subsidiaries of Verizon; The sale is expected to close by the end of 2024

- The $3.3bn amount includes certain commercial benefits: The deal is structured as a prepaid lease w/ upfront cash proceeds of ~$2.8bn

- Verizon will lease back capacity on the towers as the anchor tenant: Verizon’s lease agreements w/ Vertical Bridge have 10-yr terms, w/ options that could extend them for up to 50 yrs

- There are also provisions allowing for Verizon to expand capacity on the towers: Access to addt’l space on the towers will enable Verizon to hang more equipment on the towers in future upgrade cycles

- “This agreement… will support Verizon’s efforts to drive down tower-related costs”: The Co’s existing build-to-suit agreement w/ Vertical Bridge is another example of these efforts

- Some background on Vertical Bridge: The Co was founded in 2014 and is the largest private owner and operator of communications infrastructure and locations in the US, w/ 500,000+ sites, including 11,000+ owned and master-leased towers

-> Verizon shares were relatively ~flat in reaction to the news and ended the week down -1.6%; YTD, Verizon stock is trading up +17.2%

- Zayo Group and TPG are reportedly competing to acquire Crown Castle’s fiber and small cell assets (link): Zayo, which is owned by EQT and Digital Bridge, and TPG are the two remaining bidders for the assets, though Crown Castle could choose to sell only one of the bizs

- Both units are worth less $5bn each: If both assets are sold, the deal is likely to be valued between $8-10bn, according to people familiar w/ the matter

- A deal likely isn’t imminent and isn’t guaranteed: Sources indicated that a deal is still several weeks away and a transaction may not necessarily occur; Another suitor could also approach Crown Castle

- Crown Castle has been exploring options for its fiber biz: The Co initiated a review of its fiber biz last Dec after reaching a deal w/ Elliot Investment Mgmt; This June, Crown Castle cut its annual profit forecast and annc’d it would lay off -10% of its workforce as a result of this review

-> Crown Castle shares dropped -2.8% following the report and finished the week down -4.4%; YTD, Crown Castle stock is trading down -3.2%

- Gogo will acquire Satcom Direct to offer multi-band, multi-orbit in-flight connectivity (link): The transaction, which is still subject to regulatory approval, is expected to close by the end of 2024

- Satcom Direct will receive a total compensation of $600mn+: Including $375mn in cash and 5mn shares of Gogo stock (worth ~$34mn as of mkt close 10/1) at closing as well as up to an addt’l $225mn in payments tied to certain performance thresholds over the next four yrs

- The potential addt’l consideration is based on retaining and growing broadband customers: Exceeding the performance thresholds will result in a royalty earnout from 2025-2028 and a buyout earnout tied to 2028 results

- The transaction will be financed w/ cash-on-hand and $275mn in committed new debt: Gogo expects net leverage to be in the 4x range post-closing and anticipates returning to its target range of 2.5-3.5x two years post-closing

- The deal will expand Gogo’s TAM within the biz aviation (BA) and military/govt mobilty mkt…: Satcom Direct generates ~80% of its rev from the BA mkt and ~20% from the military/govt space, and following the deal, Gogo’s Tam will include 14,000 biz aircraft outside North America

- … As well as the Co’s efforts to expand internationally: Satcom Direct already has “an extensive international sales and svs footprint”

- The transaction is expected to be immediately accretive to earnings and FCF per share: Satcom Direct is projected to deliver ~$485mn in rev w/ adj EBITDA margins of ~17% in 2024, and the deal is expected to generate $25-30mn in annual run-rate cost synergies two yrs after closing

- The combined Co will be able to offer a “unique” product line: Gogo will be able to sell its Galileo low-earth orbit (LEO) solution integrated into Satcom Direct’s geostationary and L-band offerings, enabling it to “satisfy the performance and cost needs of every segment” of the global BA and gov’t mkts

- Satcom Direct will receive a total compensation of $600mn+: Including $375mn in cash and 5mn shares of Gogo stock (worth ~$34mn as of mkt close 10/1) at closing as well as up to an addt’l $225mn in payments tied to certain performance thresholds over the next four yrs

-> Gogo shares was down -0.8% in response to the news but closed the week down -12.2%; YTD, Gogo stock is trading down -37.2%

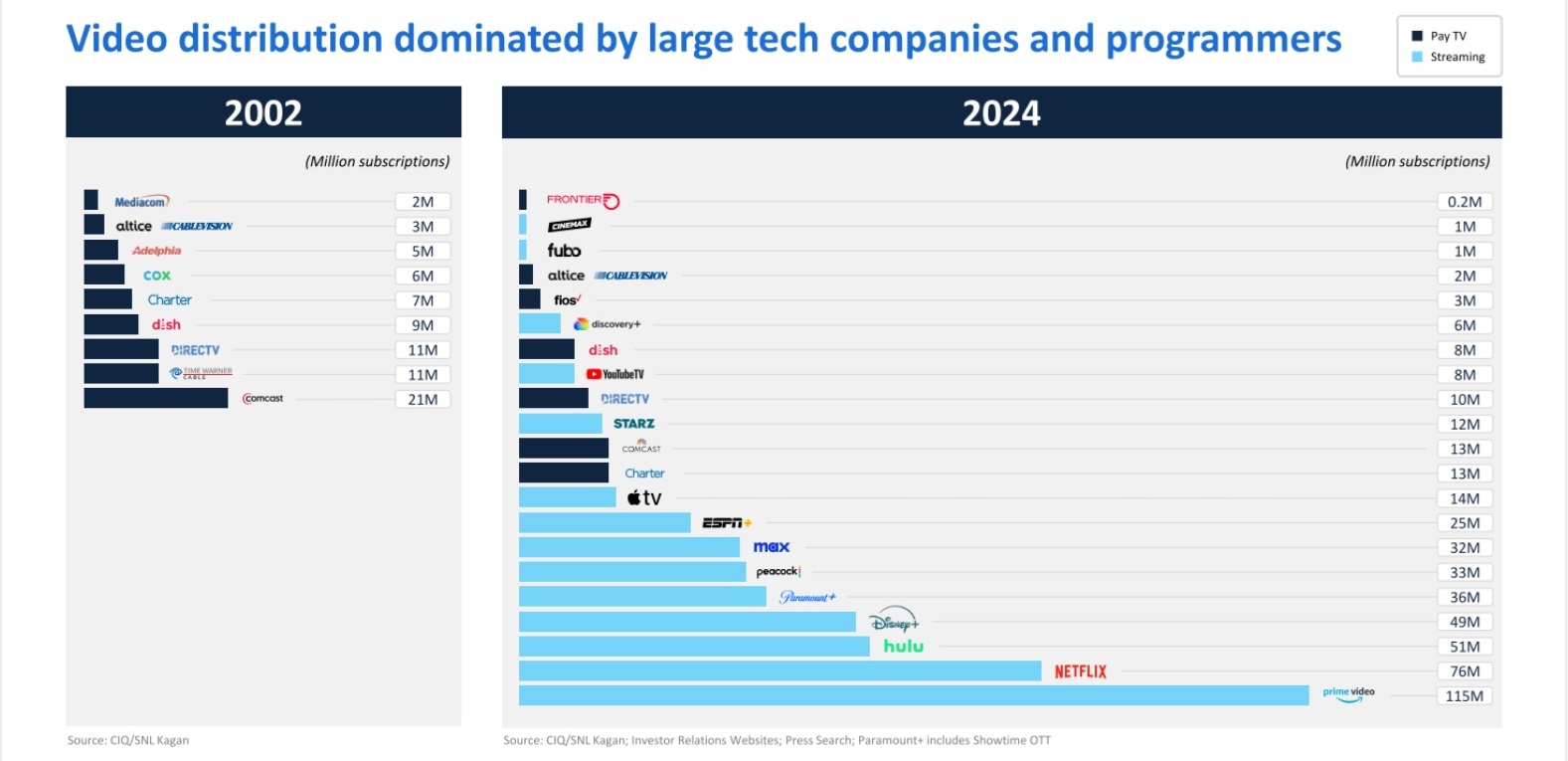

Will Hybrid Carriage Agreements Change The Trajectory Of Pay-TV Subscriber Declines?

That is at least what Charter Communications is aiming for. In its continued effort to integrate streaming platforms into its traditional pay TV network packages, Charter announced this week that it has secured a new multi-year TV network carriage deal with NBCUniversal to include its streaming service Peacock. With the deal, Charter has now completed deals with every major programmer, providing “better flexibility and greater value to [its] customers by including DTC streaming apps with their Spectrum TV service, at no extra cost”.

- NBCUniversal and Charter announce multi-year renewal agreement, which now includes Peacock (link)

- New addition – NBCU’s streaming svs Peacock will be free for Spectrum TV Select video customers

- Will also allow video customers to upgrade to Peacock Premium+, which is ad-free, and will make both Peacock products available for purchase to its broadband-only customers in 2025

- The agreement will continue to include the “full portfolio” of NBCU’s broadcast, entertainment, Hispanic, news and sports networks, including NBC Television Network and Telemundo (through NBC-owned TV stations), USA Network, Bravo, CNBC, and more

- The announcement comes after Charter made similar deals to include Disney+ and ESPN+, Warner Bros. Discovery’s Max and Discovery+, Paramount Global’s Paramount+ and BET+, AMC Networks’ AMC+, and TelevisaUnivision’s Vix

- According to Charter, the programming deals reached over the past year will soon provide Spectrum TV Select video customers up to $65 per month of retail DTC streaming value

- New addition – NBCU’s streaming svs Peacock will be free for Spectrum TV Select video customers

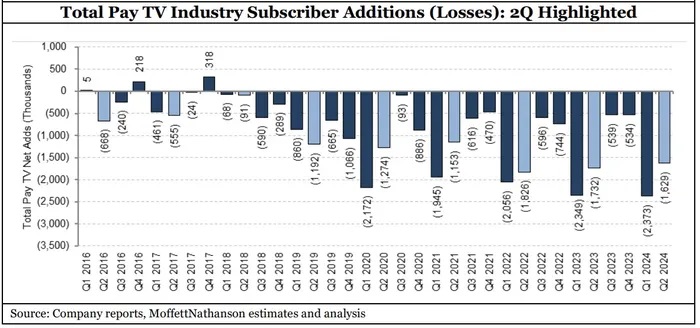

-> As has been known for a while, the pay-TV universe has been bleeding subscribers for the past several years, and in the most recent quarter lost -1.6mn subscribers, ending Q2 w/ 68.76mn subscribers, down -6.9% y/y; And when vMVPDs aren’t included, that rate of decline rises even higher, to -12.6%, marking what would be the tenth consecutive qtr of double-digit declines (link/link)

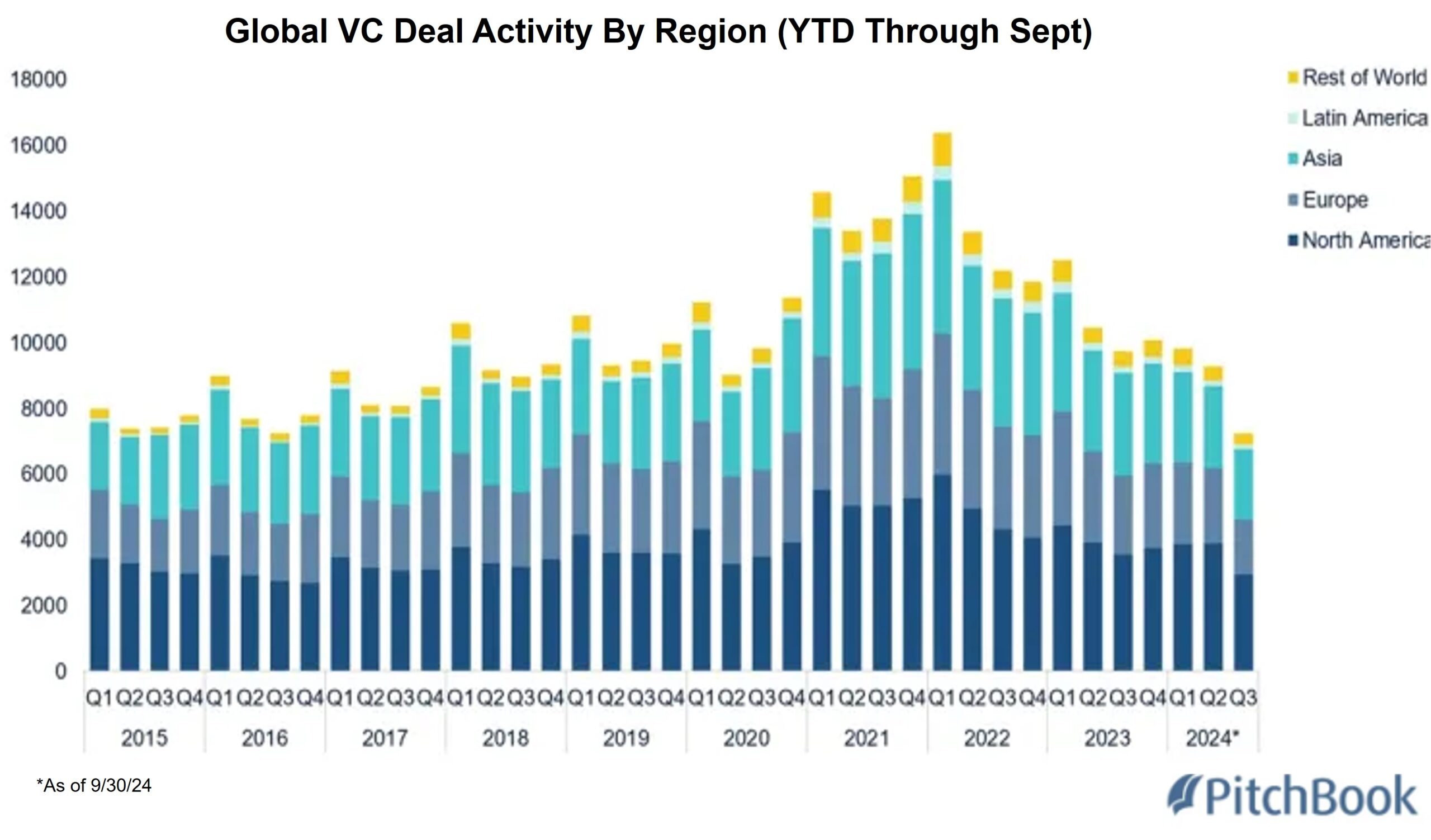

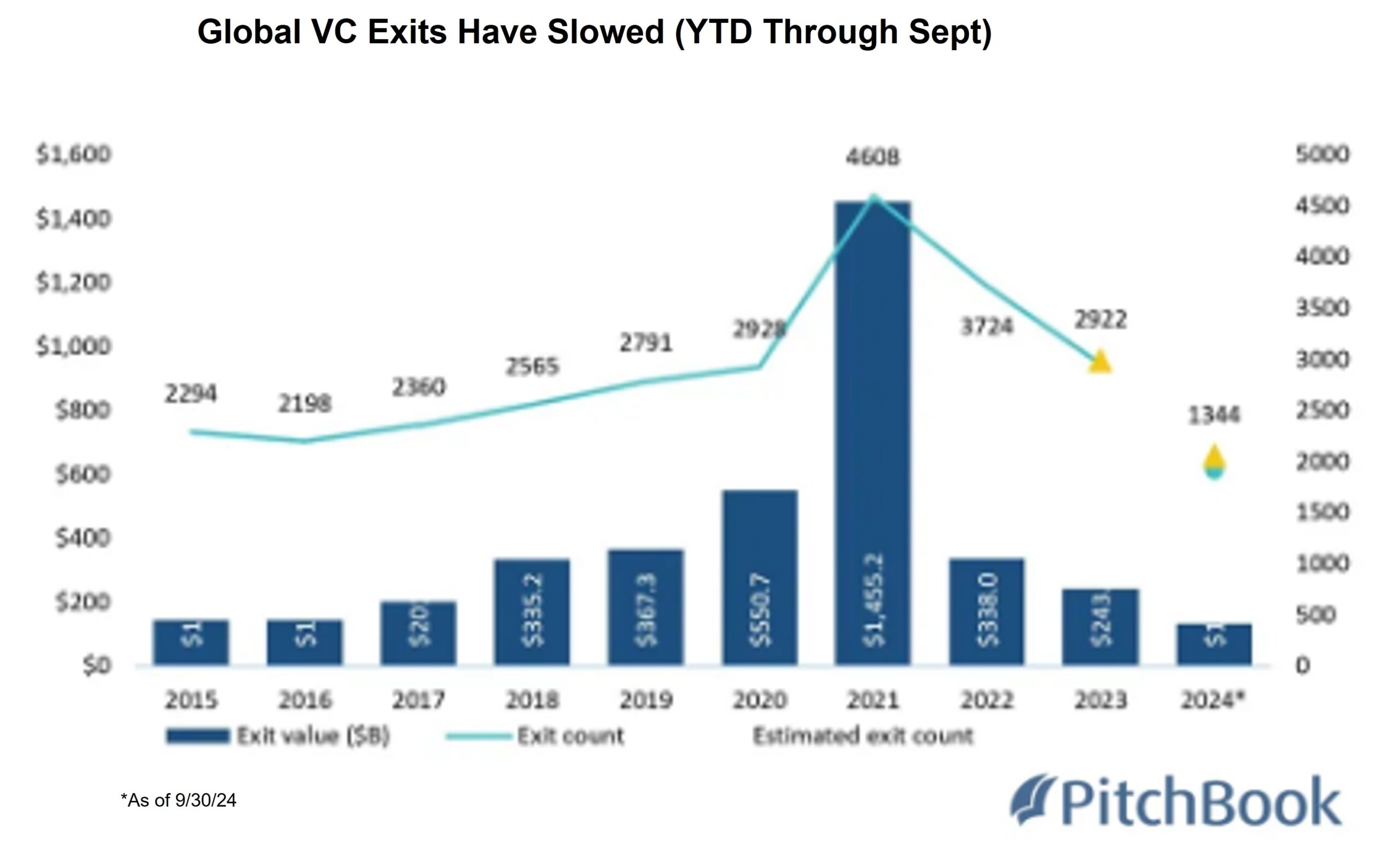

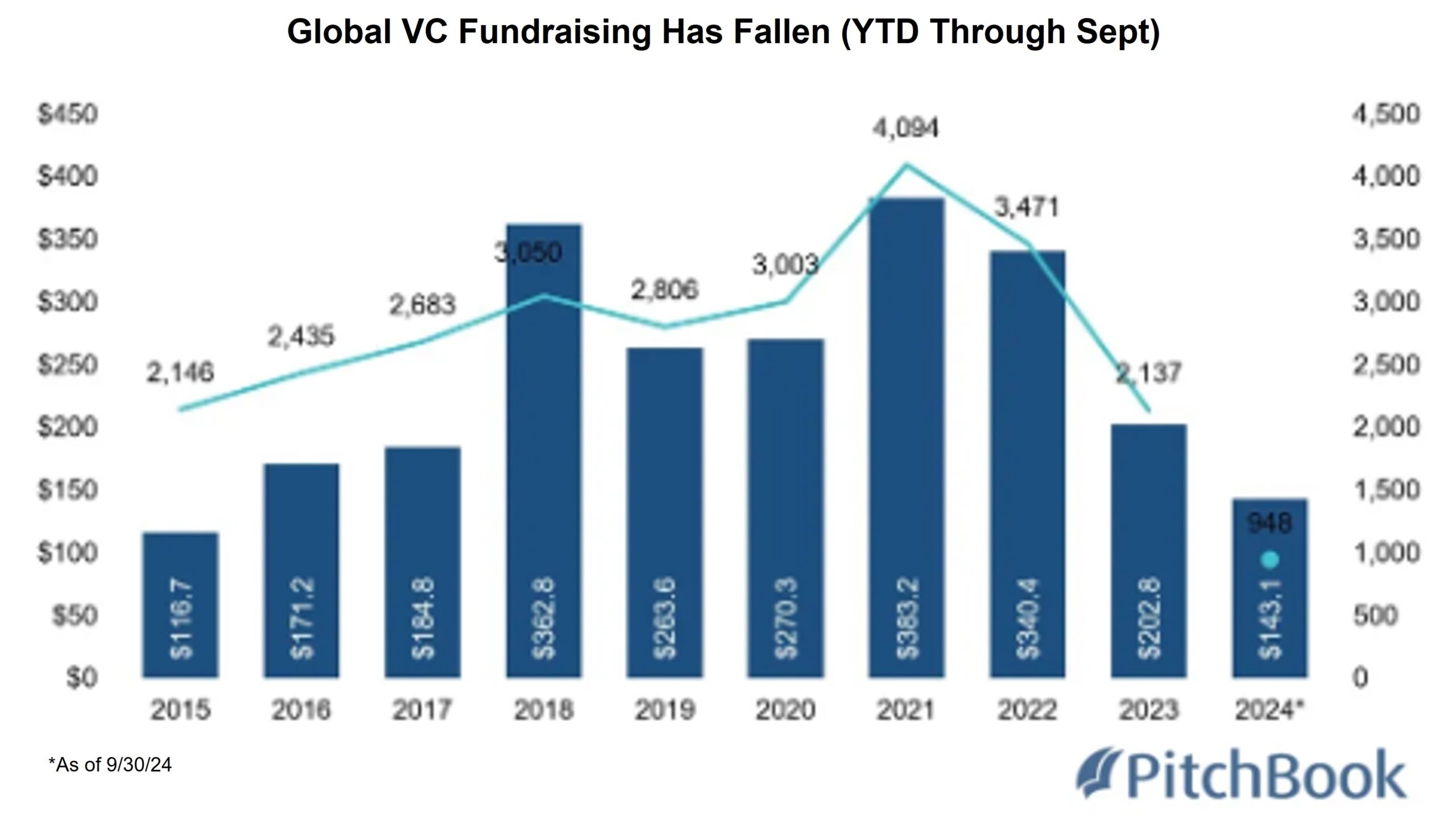

The State Of Global Venture Capital Investments In 3 Slides (Spoiler – It’s Not Great)

Global venture capital activity is still in retrenchment mode following the ballooning of activity in 2021 and 2022. See below for three slides from Pitchbook/National Venture Capital Association Monitor First Look for Q3 that says it all. (link)

- Total global VC deal activity globally YTD through Q3 has fallen below pe-2021 levels: There is one quarter left in the year, but 2024 is currently on pace to be the second-slowest year recorded since PitchBook-NVCA Venture Monitor has been publishing data for VC firm funding

- The slowdown has been across regions

- Deal value during Q3 was the lowest of the year due to few outsized rounds being raised

- Median deal sizes have seen an uptick from 2023, but they remain well below the median from 2021

- VC exits have been limited:

- Only 10 Cos completed IPOs in the US in Q3, resulting in $11.2bn in total exit value

- M&A remains slow due to both regulatory pressures and market conditions

- VC fundraising is also pacing to be another slow year: Only $64bn has been raised across US VC funds

The Streamers’ Rapid Push Into Live Remains In Focus

We are in the middle of a giant value transfer from traditional TV networks to streaming, and the more “must have” content that airs on streaming platforms, the bigger the streaming audience will grow, and the more advertisers are going to want to allocate spend to streaming to attract users… etc. But this is all at the expense of the legacy TV ecosystem.

The big streamers are stepping it up with respect to adding eyeball-grabbing live shows to their slate, and importantly they have also seen proof points that they, too, can simultaneously bring together larger pools of viewers. There were some developments along these lines this week, with Amazon reportedly exploring hosting its first news-related programming related to the election night and the company’s streaming broadcast of the Cowboys-Giants hitting a new viewership record as it relates to a regular season NFL game.

See details below…

- Amazon is reportedly looking to bring on board Brian Williams, the veteran NBC News and MSNBC anchor, to host a live Election Night special on Amazon Prime Video, per sources (link): This would be the Co’s first entry into news-related programming

- Other reported details on “Amazon’s Election Night Special”

- The show is aimed more toward explaining the news vs than breaking individual pieces of it

- The aim is to be big and accessible and offer a lot of famous guests

- Jonathan Wald, a former exec producer of Williams “11th Hour” on MSNBC, would serve as exec producer of the program

- People familiar with the matter cautioned against viewing the Williams project as a sign that Amazon intended to start producing news programming on a regular basis

- Other reported details on “Amazon’s Election Night Special”

- Streaming hits another milestone as Amazon’s exclusive Cowboys-Giants REGULAR season NFL game hit a new streaming viewership record (link):

- Amazon says 16.22mn viewers were reached, on avg: This was per Nielsen’s Panel Only measurement

- The peak audience of 18.10mn viewers was the largest peak audience ever for TNF

- The previous record was an avg of 15.26mn viewers: For Amazon’s Cowboys-Seahawks regular season game on Nov 30, 2023

- What has been the highest streaming viewership for an NFL playoff game? 23mn viewers on avg for NBCU’s Peacock stream of the Chiefs-Dolphins Wild Card playoff game

- Streaming viewership has been closing the gap on broadcast this season:

- During the first three weeks of the 2024 season, NFL games avg’d 18.6mn viewers across TV/digital, up +10% y/y

- In comparison, over its first three games, TNF on Amazon is avg’ing 14.88mn viewers, up +25% y/y

- Amazon says 16.22mn viewers were reached, on avg: This was per Nielsen’s Panel Only measurement

Grab Bag: Apple Pivots On Film Strategy/Spotify Raises Prices In Canada/California Rejects AI Safety Bill

- Apple is reconsidering its Hollywood strategy after its recent box office disappointments, per press reports last Friday (link/link/link/link):

- Apple reportedly plans to move away from tentpole, high budget films and focus instead on 12 films per year at lower budgets of less than $100mn (link)

- The Co reportedly spent$700mn on the 3 blockbuster movies Killers of the Flower Moon, Napoleon, and Argyle, which grossed $470.4mn globally

- It just recently cancelled the theatrical release of Wolfs (starring George Clooney & Brad Pitt) and instead began streaming the film on Apple TV+ after debuting in limited venues; Apple is considering a similar strategy for subsequent releases, including the World War II drama Blitz

- But Apple’s big budget film F1 is still headed for theatrical release June 2025 (reportedly has a $300mn production budget)

- Spotify is reportedly raising prices in Canada (link/link): This comes after Spotify raised prices to US individual subs from $11/mo to $12/mo in July and after a previous hike in both the US and Canada in 2023

- The price hikes reportedly affect all Spotify Premium plans in Canada:

- Spotify’s Individual plan incr’d by +15% to CAD$12.69/mo (from $10.99/mo)

- The Student plan rose +5% to CAD$6.39/mo (from $5.99/mo)

- The Duo plan jumped +19% to CAD$17.89/mo (from $14.99/mo)

- The Family plan saw the most significant increase of +24%, rising to CAD $20.99/mo (from $16.99/mo)

- The changes come amid the implementation of the Online Streaming Act: The bill sees the Canadian Radio-television and Telecommunications Commission (CRTC) requiring major foreign streamers (those w/ revs of $25mn+) to pay 5% of revs as base contributions into funds for Canadian content

- BUT the price increase wasn’t explicitly linked to the act: “We may also adjust our prices to reflect local macroeconomic factors and meet mkt demands while offering an unparalleled svs,” a spokesperson said

- Spotify is part of a legal challenge to the Online Streaming Act, however: Amazon, Apple, and Spotify filed a legal challenge against the proposed streaming tax in July

- The price hikes reportedly affect all Spotify Premium plans in Canada:

- California Governor Gavin Newsome vetoed a major AI safety bill (link): Newsom cited multiple factors in his decision to veto the Safe and Secure Innovation for Frontier Artificial Intelligence Models Act (SB 1047), including the burden it would have placed on AI Cos, California’s lead in the space, and a critique that the bill may be too broad

- The bill could “give the public a false sense of security”: Newsome noted that “smaller, specialized models may emerge as equally or even more dangerous than the models targeted by SB 1047 – at the potential expense of curtailing the very innovation that fuels advancement in favor of the public good”

- Newsome supports AI safety protocols but believes this bill falls short: Newsome doesn’t think that the state should “settle for a solution that is not informed by an empirical trajectory analysis of Al systems and capabilities”

- The bill would have applied to AI Cos doing business in CA w/ a model that costs $100mn+ to train or $10mn+ to fine-tune: It also added requirements that devs implement safeguards like a “kill switch” and add protocols for testing to reduce the chances of disastrous events, among other things

- Many prominent CA politicians have opposed the bill…: Including former House Speaker Nancy Pelosi, San Francisco Mayor London Breed, and eight congressional Democrats from California

- … While Hollywood has been supportive: Prominent Hollywood names like Mark Hamill, Alyssa Milano, Shonda Rhimes, and JJ Abrams, as well as unions including SAG-AFTRA and SEIU have voiced their support for the AI safety bill

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Disney is aiming to automate 75% of its ad sales by 2027. The Co took a further step toward that end in this yr’s annual TV and streaming advertising upfront mkt. “Of the streaming dollars that came in, of those billions of dollars, more than half of them are transacted programmatically,” Disney’s SVP of addressable sales Jamie Power said. (Digiday)

- JCDecaux announces that its majority-owned subsidiary JCDecaux Top Media SA has acquired from its founders 70% of IMC, a leading OOH co in Central America and the #1 outdoor advertising Co in Costa Rica. As part of the transaction, the remaining IMC’s shareholders contributed their 30% shares in IMC in exchange for a 9% stake in a newly-formed joint-venture regrouping all JCDecaux activities in Central America which include 6 countries. This new joint-venture will be owned by JCDecaux, Publigrafik, Top Partners and former IMC’s shareholders. (GlobeNewswire News Room)

Artificial Intelligence/Machine Learning

- Cisco Systems agreed to invest in CoreWeave, an AI cloud-computing startup, as part of a transaction that values the Co at $23bn. CoreWeave has been discussing a so-called secondary transaction that allows existing shareholders such as employees to tender $400-500mn of their holdings. The deal is reportedly close to being completed. Separately, CoreWeave is mulling an IPO as soon as next yr. (Reuters)

- Nvidia insiders have sold $1.8bn+ in shares this yr, w/ nearly 11mn shares sold, the most since 2020. CEO Jensen Huang sold 6mn shares under a pre-arranged plan, and director Mark Stevens plans to sell 3mn more. These sales come amid investor concerns over Nvidia’s delayed Blackwell chips and AI spending. Despite the sales representing a small percentage of Nvidia’s 24.5bn outstanding shares, they may affect investor confidence. (Bloomberg)

- Nvidia released NVLM 1.0, a powerful open-source AI model that rivals GPT-4 and Google’s systems, marking a major breakthrough in multimodal language models for vision and text tasks. The Co’s new NVLM 1.0 family of large multimodal language models, led by the 72bn parameter NVLM-D-72B, demonstrates exceptional performance across vision and language tasks while also enhancing text-only capabilities. (VentureBeat)

- OpenAI is beta testing a new workspace interface for ChatGPT called Canvas. The Co unveiled its new ChatGPT workspace on its official blog and immediately made it available for ChatGPT Plus and Team users. Enterprise and Edu users will be able to access Canvas sometime next week. Canvas is a virtual interface space for writing and coding projects that allows users to consult with ChatGPT on certain portions of a project. (Engadget)

- OpenAI revealed that “every week, over 250mn people around the world use ChatGPT to enhance their work, creativity, and learning. ” That’s a sharp rise since late Aug, when OpenAI said the chatbot had 200mn weekly users — double the number it had last Nov. As of June, 350mn people were using OpenAI’s tools each month, according to internal documents obtained by The New York Times. (Engadget)

Audio/Music/Podcast

- A number of YouTube videos featuring music from artists such as Adele, Green Day, Bob Dylan, and Nirvana have been unplayable in the US. If users try to play Dylan’s “Like A Rolling Stone” (whether it’s the classic album recording or a live performance), they are instead told: “This video contains content from SESAC. It is not available in your country.” In statements to the press and on social media, YouTube blamed the situation on failed negotiations w/ SESAC, a performing rights group. (TechCrunch)

Broadcast/Cable Networks

- ABC News and the ABC stations group were impacted by layoffs, part of an ongoing round of restructuring at Disney. Some 75 staffers at ABC News and at ABC’s owned local TV stations will be affected, split about evenly between the national news organization and the station group. No programming will be impacted, and no entire teams will be eliminated, but the Co is making the changes to be “sustainable, efficient and future-forward,” per a source. (The Hollywood Reporter)

Broader Media & Entertainment

- CNN annc’d that visitors will soon have to pay to view the website.com will implement a paywall, asking visitors to pay $3.99 a month or a discounted rate of $29.99 a yr for unlimited visits to the news site, exclusive election features, original documentaries, a curated daily selection of their most distinctive journalism, and fewer digital ads. Users will be asked to subscribe after accessing several free stories. (KTLA)

- MFE-MediaForEurope, led by Italy’s Berlusconi family, is considering increasing its nearly 30% stake in German media group ProsiebenSat. 1. CEO Pier Silvio Berlusconi may act next month if ProsiebenSat.1’s Q3 results do not show enough progress on meeting its targets, sources said. (Reuters)

Cable/Pay-TV/Wireless

- Bain Capital annc’d that it will acquire Japan’s largest cellphone sales agent, T-Gaia, purchasing the stakes of major shareholders Sumitomo and Tokyo-based Hikari Tsushin. Bain Capital’s total purchase price in taking the retailer private is expected to exceed 140bn yen. T-Gaia is listed on the Tokyo Stock Exchange’s Prime market, with Sumitomo holding 41.8% of its shares and Hikari Tsushin, along with its subsidiaries, holding a little less than 30%. (Nikkei Asia)

- O2 Telefonica achieved peak download speeds of more than 1.7 Gbps by bundling four frequency bands in 5G Standalone (5G SA) mode. The Co noted that the measurements were taken during a live test on the O2 network in Potsdam. The Co had been offering 5G SA to customers on the entire O2 Telefónica 5G network since Oct 2023. O2 Telefónica carried out the tests in partnership w/ Nokia. (RCR Wireless News)

- T-Mobile US sold more than half-a-billion dollars worth of bonds backed by wireless equipment contracts. This comes after the deal was postponed in Aug, when debt mkts were roiled by a maelstrom of surprise economic, corporate, and central bank news. The Co sold $561.3mn of notes in three parts on Oct 3 following a mkting process that kicked off last week, per sources. The highest-rated tranche carries a coupon of 4.25%, they added. (Reuters)

- Telecom operators are now scaling back their investments in 5G and fixed broadband technologies, per the Dell’Oro Group. Worldwide telecom capex, the sum of wireless and wireline/other telecom carrier investments, declined 10% y/y in the H1:24, partly due to built-up inventory, weaker demand in China, India, and the US, challenging 5G comparisons, excess capacity, and elevated uncertainty. (VanillaPlus – The global voice of Telecoms IT)

- The timeline for BEAD funding remains uncertain, despite most states having their Vol 1 (mapping challenge) and Vol 2 (implementation plan) processes approved by the NTIA. Jade Piros de Carvalho highlighted that states are at different stages, w/ some like Louisiana and Colorado progressing to subgrantee processes. Approval times for final proposals, which must be posted for public comment for 30 days, are still unknown. (Fierce Network)

- Verizon fully restored a network disruption that impacted thousands of customers in the US. The Federal Communications Commission said earlier that it was investigating the Co’s network outage across the US after thousands of users reported outages. According to the tracking website Downdetector.com, the outage began at ~9:30 am ET on Sept 30, w/ Minneapolis, Phoenix, Omaha and Denver among the most affected regions. (Yahoo Finance)

- Verizon reported its engineers had ‘fully restored’ service on Monday, Sept 30th evening following a US nationwide outage that lasted most of the day. Downdetector saw more than 1.6mn user reports of outages by Monday evening, noting that customers of AT&T and T-Mobile “trying to contact Verizon subscribers may also notice issues,” according to a statement from that company. (Fierce Network)

- Vodafone and Three’s response to the CMA’s Notice of Possible Remedies has been published and it disagrees with the CMA’s Provisional Findings. They say the merger will be pro-growth, pro-customer, pro-investment and pro-competitive for the UK and will be “a catalyst for change”. The CMA’s final decision on the merger is not due until December 7th. (Vodafone.com)

Capital Market Updates

- The market for IPOs of PE-owned cos is improving, w/ four US listings, including StandardAero, raising $1.44bn. JPMorgan says the mkt for sponsor-backed Cos is “very much open,” boosting confidence for next yr’s volumes. YTD IPO proceeds are up 61% from last yr, reaching $35.2bn. The burst of biz will be welcome news for investors sitting on $3.2tn of Cos stuck in PE firms’ portfolios after a choppy three-year stretch for new entrants. (MarketWatch)

Cloud/DataCenters/IT Infrastructure

- BT has said it has “switched on” its network-as-a-service platform Global Fabric, following testing over the last couple of months. Commercial services will launch in early 2025, it said; live testing will continue in the interim. It has established points of presence in over 45 of the “world’s major cloud data centres”, it said. It claimed at the end of last year to have 630 partners for local network connectivity, and 700 partners for local data centre services. (RCR Wireless News)

- Equinix annc’d a JV w/ GIC and Canada Pension Plan Investment Board to invest $15bn to bolster Equinix’s data center buildouts. Equinix will use the investment to expand its xScale data centers, which support AI workloads and are part of a program launched five yrs ago. The newly annc’d $15bn investment will be used entirely on US-based xScale buildouts, ultimately adding more than 1.5 gigawatts of new capacity, said Equinix. (RCR Wireless News)

- Google could one day use nuclear energy to power its AI data centers. Sundar Pichai said the Co is “evaluating technologies like small modular nuclear reactors.” Pichai said that they are looking for energy sources that not only meet its high energy needs but will also fulfill its goal of generating net-zero emissions and aims to achieve net-zero emissions across all of its operations by 2030. (Yahoo Tech)

Crypto/Blockchain/web3/NFTs

- A subcommittee of the CFTC’s Global Markets Advisory Committee approved guidelines for using tokenized shares of money-market funds as collateral in trading. These guidelines support blockchain use for non-cash collateral, aligning w/ CFTC and other US regulators’ margin requirements. The full committee will vote on these recommendations later this yr. If approved, tokenization use could increase, w/ the mkt estimated to reach up to $2tn by 2030. (CoinDesk)

Cybersecurity/Security

- A Russian criminal gang secretly conducted cyberattacks and espionage operations against NATO allies on the orders of the Kremlin’s intelligence svs, per the UK’s National Crime Agency. Evil Corp launched the hacks prior to 2019, the NCA said. The gang has been accused of using malicious software to extort millions of dollars from hundreds of banks and financial institutions in 40+ countries. (Bloomberg)

eCommerce/Social Commerce/Retail

- eBay has scrapped fees for private sellers across almost all of its categories as it attempts to keep fast-growing rivals such as Depop and Vinted at arm’s length. The move means eBay’s UK sellers no longer have to pay transaction fees, except for cars, motorcycles and other vehicles. In Apr. this yr, eBay removed fees for private sellers of pre-owned clothes, and the co said it was “now evolving the experience even further”. (the Guardian)

- A US government lawsuit accusing eBay of selling almost 350,000 polluting and environmentally harmful products, including pesticides and “defeat” devices that let motor vehicles evade emission controls, has been dismissed by a federal judge. District Judge Orelia Merchant ruled that eBay isn’t liable for items that users sell on the digital marketplace due to civil protections that Section 230 of the Communications Decency Act provides for online platforms. (The Verge)

- Amazon is sweetening the pot for its upcoming Prime Big Deal Days sale. Prime members who use their Amazon credit card can earn 10-20% back on select products, making this shopping event even more enticing. The offer applies to a wide range of popular items, including Fire HD 10 tablets, Blink cameras, smart TVs, and KASA smart plugs. Cashback rewards will be automatically applied when Prime members check out w/ their Amazon credit cards. (Cord Cutters News)

- Amazon plans to hire 250,000 transportation and warehouse workers this holiday shopping season, the same number as last yr. This comes as e-commerce spending is expected to outpace overall holiday sales in the final qtr of 2024. It was unclear what percentage of the 250,000 seasonal workers, which include staff in sort centers, fulfillment centers and delivery stations, would be in fulfillment centers or transport employees. (CNBC)

- Authentic Brands acquired athleticwear brand Champion from Hanes Brands for $1.2bn, marking its second-largest acquisition. Champion, generating nearly $3bn in annual sales, will expand under new ownership. Champion’s long-term US collegiate apparel biz will be carried forward under a new license granted to GearCo following the acquisition, which will be managed and operated by Ames Watson w/ Fanatics as an investor. (Retail Bulletin | Daily UK Retail News)

- Costco continues to chip away at the gold mine that is the precious metals market, adding Swiss-made platinum bars to its selection. Costco launched platinum bars on its website for $1,089.99, an addition to the Co’s precious metals selection of gold bars and silver coins. The bars are only sold online, and cannot be delivered to Louisiana, Nevada or Puerto Rico. Interested buyers will also need a Costco membership. (CNBC)

- Costco is the latest warehouse brand to tout its growing popularity with younger shoppers, extending a trend that has become increasingly clear over the past few months. CFO Gary Millerchip said that about half of Costco’s new sign-ups this past yr were under 40, a figure that works out to some 2.5mn millennial and Gen Z households paying for memberships. This percentage has been growing since COVID-19 and has lowered the average age of members over the last few yrs. (Business Insider)

- Costco Wholesale CFO Gary Millerchip said that the Co’s “goal is always to be the first to lower prices” where it sees opportunity to do so. On an earnings call, Millerchip said the Co cut the prices on such items as Kirkland Signature macadamia nuts to $13.99 from $18.99, on 3-liter KS Spanish olive oil to $34.99 from $38.99, and on KS baguette 2-packs to $4.99 from $5.99 during the latest qtr. (Retail Dive)

- European retail is changing dramatically, presenting both challenges and opportunities to optimize sales across ecommerce and physical stores. The profound transformation in European consumers’ spending habits is made clear in The State of Shopping 2024, conducted by ShopFully in collaboration w/ Offerista Group involving 11,000 shoppers that engage regularly w/ the Cos’ marketplaces. (Retail Dive)

- Kohl’s is kicking off its holiday shopping deals in Oct during its “3 Days of Deals” event. Savings will be on thousands of products across home, gifting, fall apparel, footwear, accessories, baby products and other categories. From Oct. 7 to Oct. 9, the co is offering 25% discounts on select purchases with a coupon. Kohl’s will offer discounts on products from brands like Adidas, Nike and Levi’s. The company said it is also offering Kohl’s Rewards members free shipping and triple rewards on nearly everything, including Sephora at Kohl’s purchases. (Retail Dive)

- Mall shoppers are expected to increase 18.7% this yr, and open air shoppers will increase by 10%. Those are findings from JLL’s 2024 Holiday Shopping Report, which polled 1,000+ consumers in Aug and found notable differences in shopping behaviors as compared to 2023, including a 31.7% uptick in holiday budgets in 2024. The report also revealed the avg spending will be $1,261 per shopper for gifts, holiday food and decor, and experiences. (retailcustomerexperience.com)

- Nike reported a rough Q1 that saw revs down 10% y/y to $11.6bn almost two weeks after it revealed its plan to replace CEO John Donahoe w/ longtime veteran Elliott Hill. The DTC biz was hit particularly hard, w/ Nike Direct rev down 13% in the qtr due mostly to a 20% decline in the Co’s digital biz. Wholesale rev was also down, falling 8% to $6.4bn. Nike revoked its full-yr guidance in light of the leadership transition. (Retail Dive)

- Shein is planning informal investor meetings in Europe for its upcoming London IPO, pending UK regulatory approval. During these events, it will address questions from major investors and gauge their interest in investing. Shein aims to launch its float within the current qtr, pending approval from regulator the Financial Conduct Authority (FCA), per a source familiar w/ the situation. (Retail Gazette)

- Simon Property Group launched “Meet Me @themall,” a new advertising campaign targeted at younger customers, specifically members of Gen Z. The Co said it’s partnering w/ 250+ mall-loving influencers and creators to drive awareness and engagement. The campaign is on Netflix, Hulu, and other streaming svs, along w/ Instagram, YouTube, TikTok, and on Simon’s social channels. (Retail Dive)

- Surge pricing on shipping this Black Friday could dampen the profits of independent online electronics stores, making it more difficult than ever to compete with the ecommerce cos. Figures reveal that almost 32% of supply chain firms saw their carrier costs jump in Nov. 2023 compared to the previous month. It comes on top of other pressures facing electronics retailers – including the ongoing ‘cautious spending’ from consumers, who might avoid buying non-essential big ticket items this Black Friday. (ADVANCED-TELEVISION)

- UK retail footfall rose for the first time in over a yr last month, as consumers flocked to the shops during the back-to-school rush. Total UK shopper visitors rose 3.3% last month, up from a decline of 0.4% in Aug, the British Retail Consortium (BRC) reported. Retail parks enjoyed the biggest boost, w/ footfall up 7.3% in Sept, up from a 2.6% rise the month before. (Retail Gazette)

EdTech

- Udemy recently annc’d that it would train generative AI on the classes that its users contribute to the site. In an “Instructor Generative AI Policy” document, it says it plans to offer “Annual Periods designated by us” during which instructors can opt-out of having their classes trained on, and said that when people opt-out of training, it will remove the instructors’ classes from its dataset “by the end of the calendar yr.” (404 Media)

EV/ Autonomous Vehicles

- BYD is recalling 97,000 units due to a technical error that poses fire risks. The Co is recalling Dolphin and Yuan Plus EVs produced in China between Nov 2022 and Dec 2023 for containing a faulty steering control unit. BYD dealers will address the issue at no cost to customers. According to the China Association of Automobile Manufacturers, the recalled models were its best-selling in 2023 and accounted for a qtr of the 3mn cars it sold. (Retail News Asia)

- Hyundai Motor and Waymo agreed to a multi-yr, strategic partnership that includes that the self-driving Co adding Hyundai’s Ioniq 5 EV to its robotaxi fleet. The Cos said that Waymo’s sixth-gen autonomous tech will be integrated in a “significant volume over multiple yrs to support” Waymo’s growing robotaxi biz. The Ioniq 5 EVs will be produced at Hyundai’s upcoming “Metaplant America” in Georgia and equipped w/ Waymo’s self-driving technologies. (CNBC)

- Tesla is no longer selling the sub-$40,000 rear-wheel drive Standard Range version of the Model 3 that has been in the Co’s lineup since 2023. The most affordable trim is now the Model 3 RWD Long Range that starts at $42,490. The change was first pointed out by Electrek and comes as Tesla announces a y/y increase of vehicle deliveries in Q3. (The Verge)

- The National Highway Traffic Safety Administration said that General Motors’ unit Cruise will pay a $1.5mn fine after it failed to disclose details of an Oct 2023 crash involving a pedestrian. Under the settlement, Cruise must submit to NHTSA a corrective action plan on how it will improve its compliance w/ reporting of serious incidents and face enhanced reporting requirements for at least two yrs. NHTSA said Cruise submitted several incomplete reports for crashes involving automated driving systems including two tied to the October crash. (CNBC)

- Uber entered a new deal to offer customers in select cities an option for self-driving vehicles. The partnership is w/ Avride, which used to be the self-driving unit for Russian conglomerate Yandex. The multi-yr deal will begin by introducing Avride’s self-driving robots as a delivery option for Uber Eats orders in Austin, Texas. Later this yr, the robots are expected to become available for delivery orders in Dallas and Jersey City, New Jersey. (Engadget)

- Waymo is set to launch its autonomous ride-hailing service in Austin by early 2025. This week, select public members can access the svs via the Waymo One app, transitioning to Uber next yr. The Co will offer rides across 37 square miles of Austin, initially free for waitlisted users. The fleet includes Jaguar I-PACE AVs. The svs already operates in San Francisco, Los Angeles, and Phoenix. (Yahoo Finance)

Film/Studio/Content/IP/Talent

- “Inside Out 2” is a major hit for Disney. “Inside Out 2” is the highest-grossing movie of 2024 so far, and now Disney has annc’d it’s become the biggest film premiere on Disney of the yr as well. “Inside Out 2” garnered 30.5mn views on Disney in its first five days of availability, making it the biggest movie premiere on the svs for the entirety of 2024 and the biggest premiere of all time in the EMEA. (The Streamable)

- Disney’s TV units are undergoing a major reorganization. The Co annc’d that it will shutter its ABC Signature studio, combining its operations w/ 20th Television. Addt’ly, the comedy and drama development teams at Hulu and ABC are merging. Karey Burke, president of 20th TV, will continue to lead the combined studio. The reorganization will also result in ~30 layoffs, Disney says. (The Hollywood Reporter)

- It is a bit of a getting going/holdover situation for the studios this weekend at the international box office. There are two animated films continuing to roll out in the marketplace, both of which are highly scored, and performing to differing degrees. Paramount/Hasbro’s Transformers One added $72mm globally. Universal/DreamWorks Animation’s The Wild Robot also cont’d its staggered release to add 21 mkts this session w/ $53.1mm globally. (Deadline)

- Lionsgate is offering its U.S. employees a voluntary severance and early retirement program amid a contracting media and entertainment landscape that’s resulted in widespread and ongoing industry layoffs. The company, which cut jobs and slashed TV producer deals as it absorbed eOne, is starting now w/ a voluntary approach. (Deadline)

- Teamsters Locals 399 and 817 ratified a new three-yr casting agreement w/ the Alliance of Motion Picture and Television Producers. The deal received a 91.85% approval vote w/ an 83% voter turnout. The agreement covers NY and LA casting directors, associate casting directors, and the newly organized casting assistants. The primary concerns for the union during this negotiation cycle were wage increases and protections. (Deadline)

FinTech/InsurTech/Payments

- SoFi is partnering w/ PrimaryBid Technologies to enhance its IPO share placement business. SoFi’s new directed share platform, which went live on Oct 2, is designed to allow Cos raising capital to allocate a portion of their offering to employees, customers, and other individual investors more efficiently than similar services provided by investment banks that underwrite IPOs, SoFi CEO Anthony Noto said in an interview. (Yahoo Finance)

Handheld Devices & Accessories/Connected Home

- Amazon launched new Fire HD 8 tablets, including Fire HD 8 (2024), Fire HD 8 Kids, and Fire HD 8 Kids Pro. These come w/ upgraded RAM, a 5MP rear camera, and up to 13 hours of battery life. Addt’ly, all three models will have their own collection of colors. New AI features include a wallpaper creator, webpage summarizer, and writing assist tool. Prices start at $99.99, w/ a limited-time offer of $54.99 until Oct 9. (Android Authority)

- Apple is set to announce a new low-end iPhone SE, codenamed V59, early next yr, alongside upgraded iPads and keyboards. This will be the first SE update since 2022, featuring an edge-to-edge screen, moving away from the home button design. The new SE aims to compete in the low-end smartphone mkt, especially in China, and will support Apple Intelligence AI tools. It will resemble the iPhone 14, unlike the current SE, which looks like the iPhone 8. (Yahoo Finance)

HealthTech/Wellness

- Oura annc’d the $349 Oura Ring 4, featuring a slimmer design, improved accuracy, and more sizes. The ring is now fully titanium w/ recessed sensors for comfort. The new algorithm increases signal pathways from 8 to 18, enhancing data accuracy and battery life. It claims a 120% increase in signal quality and a 30% boost in blood oxygen tracking accuracy. The Oura app is also redesigned to better organize new features. (The Verge)

Last Mile Transportation/Delivery

- US asset manager Invesco has raised the value of its stake in Swiggy, ascribing an implied valuation of about $13.3bn to the Indian food-delivery and quick-commerce startup that is on track to go public in about a month. In a disclosure, Invesco’s Developing Markets Fund said it valued the 28,844 shares it owns in Swiggy at $237.24mn as of the end of Jul. 2024. The asset manager bought the shares in Swiggy for $190.47mn. (TechCrunch)

Macro Updates

- Port strikes at East Coast and Gulf Coast ports limited terminal operations, heightening fears of the disruption’s duration and impact. The International Longshoremen’s Association began a strike shortly after 12 am ET on Oct 1 after the union’s master contract w/ the US Maritime Alliance, or USMX, ended. While both the ILA and USMX had exchanged counteroffers 24 hours before the strike was set to start, the union rejected a wage package. (Supply Chain Dive)

- The rocket higher in Chinese stocks so far looks different from the market bubble in 2015, analysts said. Major mainland China stock indexes surged by more than 8% Monday, Sept 30th, extending a winning streak on the back of stimulus hopes. Trading volume on the Shanghai and Shenzhen stock exchanges hit 2.59tn yuan ($368.78bn), surpassing a high of 2.37tn yuan on May 28, 2015, according to Wind Information. (CNBC)

- US private sector hiring rose by 143,000 jobs in Sept, surpassing expectations of 120,000, per ADP. This rebound follows a five-month slowdown, w/ manufacturing adding jobs for the first time since April. Among sectors, svs-providing industries added most jobs, w/ many in the leisure and hospitality segment. Annual pay incr’d by 4.7%, w/ wage gains slightly down. The Federal Reserve’s recent interest rate cuts may further boost the economy. (CNBC)

Metaverse/AR & VR

- Microsoft confirmed that HoloLens 2 production has ended. Now is the last time to buy the device before stock runs out, the Co has been telling its partners and customers. HoloLens 2 will continue to receive “updates to address critical security issues and software regressions” until Dec 31, 2027. As soon as 2028 starts, software support for HoloLens 2 will end. For the original HoloLens headset from 2016, software support will end after Dec 10. (UploadVR)

- Two Harvard students recently revealed that it’s possible to combine Meta smart glasses w/ face image search tech to “reveal anyone’s personal details ”just from looking at them”. In a Google document, AnhPhu Nguyen and Caine Ardayfio explained how they linked a pair of Meta Ray Bans 2 to an invasive face search engine called PimEyes to help identify strangers by cross-searching their information on various people-search databases. (Ars Technica)

Online Marketplaces/Learning (Real Estate/Education/Jobs)

- REA Group has abandoned its attempt to take over the website Rightmove after its fourth offer was rebuffed on Monday, Sept 30th. The co annc’d that it had decided not to make a formal bid, hours after Rightmove’s board rejected its £6.2bn proposal made on Friday, Sept 27. REA told that it was withdrawing its possible offer, having failed to win over the UK property portal’s board. In a statement to the London stock market, REA said it had sought to create a “global and diversified digital property company”, with market-leading positions in Australia and the UK. (the Guardian)

Social/Digital Media

- Texas attorney general Ken Paxton filed a lawsuit against TikTok for allegedly sharing the personal data of minors, which violates the state’s parental consent law known as the SCOPE Act. Paxton accused TikTok of failing to use a commercially reasonable method for a parent or guardian to verify their identity, claiming TikTok’s “Family Pairing” method does not verify their identity or relationship with a minor. (Fox Business)

- The European Commission requested YouTube, Snapchat and TikTok to share more information on their content recommendation algorithms and the role these systems play in amplifying risks to the platforms’ users. The platforms need to submit the requested information by Nov 15. Under the EU Digital Services Act, Cos designated as “very large online platforms” have an obligation to identify, analyze, and assess systemic risks linked to their svs. (Silicon Republic)

- X is now worth less than a quarter of its $44bn purchase price, according to a new estimate from investor Fidelity. The asset manager, which helped Musk acquire the social network formerly known as Twitter, now values its stake in X at ~$4.19mn, based on newly released disclosures from Fidelity’s Blue Chip Growth Fund. For context, Fidelity had initially invested $19.66mn in X through the Blue Chip Fund, as per regulatory filings. (Linkedin)

- YouTube annc’d updates for YouTube Shorts. These include the ability to upload videos up to three minutes long, a redesigned Shorts player, new templates, and a Shorts trends page on mobile. These changes aim to better compete w/ TikTok, which allows longer videos and easy trend participation. The new Shorts player highlights creators’ content by using outlined interaction icons, making more of the video visible. (TechCrunch)

Software

- Microsoft annc’d that it won’t impose a new return-to-office mandate unless mgmt concludes that productivity has dropped. It currently allows employees remotely, w/ many new hires promised the flexibility of working from home at least half the time. Executive VP Scott Guthrie recently told staff at his Microsoft’s Cloud and AI group, which includes Azure, that a policy change isn’t on the cards at present, per sources. (Yahoo Finance)

Sports/Sports Betting

- Diamond Sports said that it plans to drop all MLB teams from its channels except for the Atlanta Braves. Bally Sports networks have been dropping teams during its ongoing bankruptcy process. Last yr, the San Diego Padres and Arizona Diamondbacks exited their regional sports networks. Diamond has reached out to all of the 11 teams on its air w/ amended, proposed contracts to determine the future of MLB on the networks. (CNBC)

- Formula One and LVMH are entering into a 10-yr partnership. The partnership will officially launch at the start of next F1 season and will include “hospitality, bespoke activations, limited editions, and outstanding content”. The official arrangement will not be the first time that LVMH and F1 have worked together. F1 worked w/ one of LVMH’s brands during last yr’s Las Vegas Grand Prix and the team-up was a success. (CNBC)

- The Miami Dolphins are in advanced talks w/ Ares Capital to sell 10% of the team’s parent company for $8.1bn. Joe Tsai, owner of the Brooklyn Nets, is also negotiating to buy 3%. The deal includes Hard Rock Stadium, the Miami Grand Prix, and a stake in the Miami Open. This follows the NFL’s recent rule change allowing private equity investments in teams. The Dolphins, owned by Stephen Ross, are valued at $6.76bn, the seventh-highest in the NFL. (Sportico.com)

- The NBA made its final push to have TNT Sports’ lawsuit dismissed, arguing the network’s purported match of the Amazon rights deal was instead a counteroffer. Responding to TNT Sports’ recent claim that the league inserted a series of “purposely onerous and immaterial” contractual provisions designed to thwart the network and protect Amazon, the NBA said prior case law explicitly allows for extensive customization in its dealmaking. (Front Office Sports)

- The NFL is in talks w/ Skydance Media and RedBird Capital Partners that could result in some of the league’s media assets changing hands, per sources. The talks could include a sale of NFL Media and its NFL Network cable channel, or an acquisition by Paramount Global of the league’s interest in Skydance Sports, a JV that produces movies and TV shows. The NFL has been shopping its media assets for a few yrs. (Bloomberg)

- The NFL retained its nine-yr viewership high through Week 4 of the regular season, and the Chiefs took another notch away from the Cowboys as the league’s most-watched team. In Sept, NFL games averaged 17.9mn viewers (not including the Week 1 Peacock exclusive), which is up 4% compared to the first four weeks of the 2023 season. The NFL was up 10% y/y after three weeks. That was its best avg audience since 2015, which is still the case. (Front Office Sports)

- WBD and All Elite Wrestling reached a multi-yr renewal, shoring up the programming of foundational linear networks TNT and TBS and adding streaming simulcasts on Max. Under the new agreement, WBD’s networks and platforms will remain the exclusive home of AEW Dynamite and AEW Collision. Terms also call for enhanced distribution rights across social platforms as well as “building oppties” for more AEW programming down the line. (Deadline)