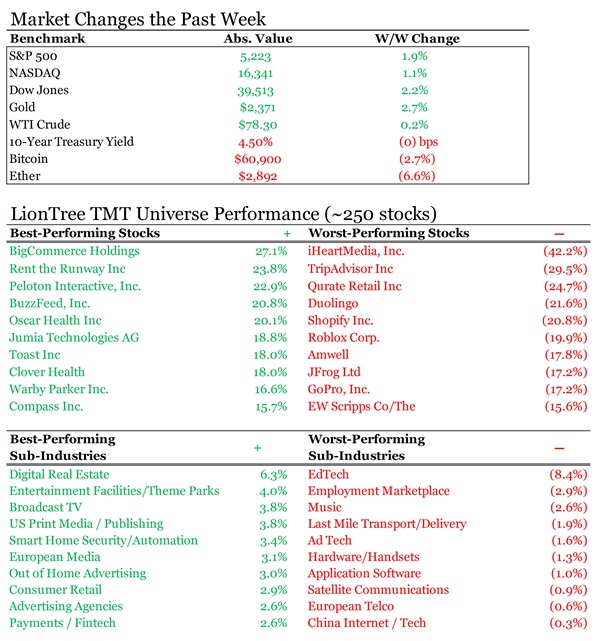

It was an incredibly busy week on the earnings front once again in the TMT sector, with 77 companies in our LionTree Universe reporting! That might be a weekly record. We have key updates across Big-Cap Media, Last-Mile & Grocery Delivery, Music, Video Games, and More. On the markets side, we had another up week, as the S&P rallied +1.9% and Nasdaq rose +1.1%. All eyes will be on the CPI numbers due out next week.

See below for key perspectives and updates in this edition (all are clickable links):

- Earnings Scorecard – Week 4

- DIS - Jitteriness About Parks Shakes The House Of Mouse

- WBD Is Pushing Harder On Streaming Profitability & Bundles

- FOX’s Fundamentals Moved In The Right Direction, Excluding Seasonal Factors

- WMG Is Focused On Ensuring The Sanctity Of Its Pricing Across The DSPs

- Uber’s Core Fundamentals Remain Intact

- Instacart Hitches Its Cart To Uber To Drive Another Avenue Of Growth

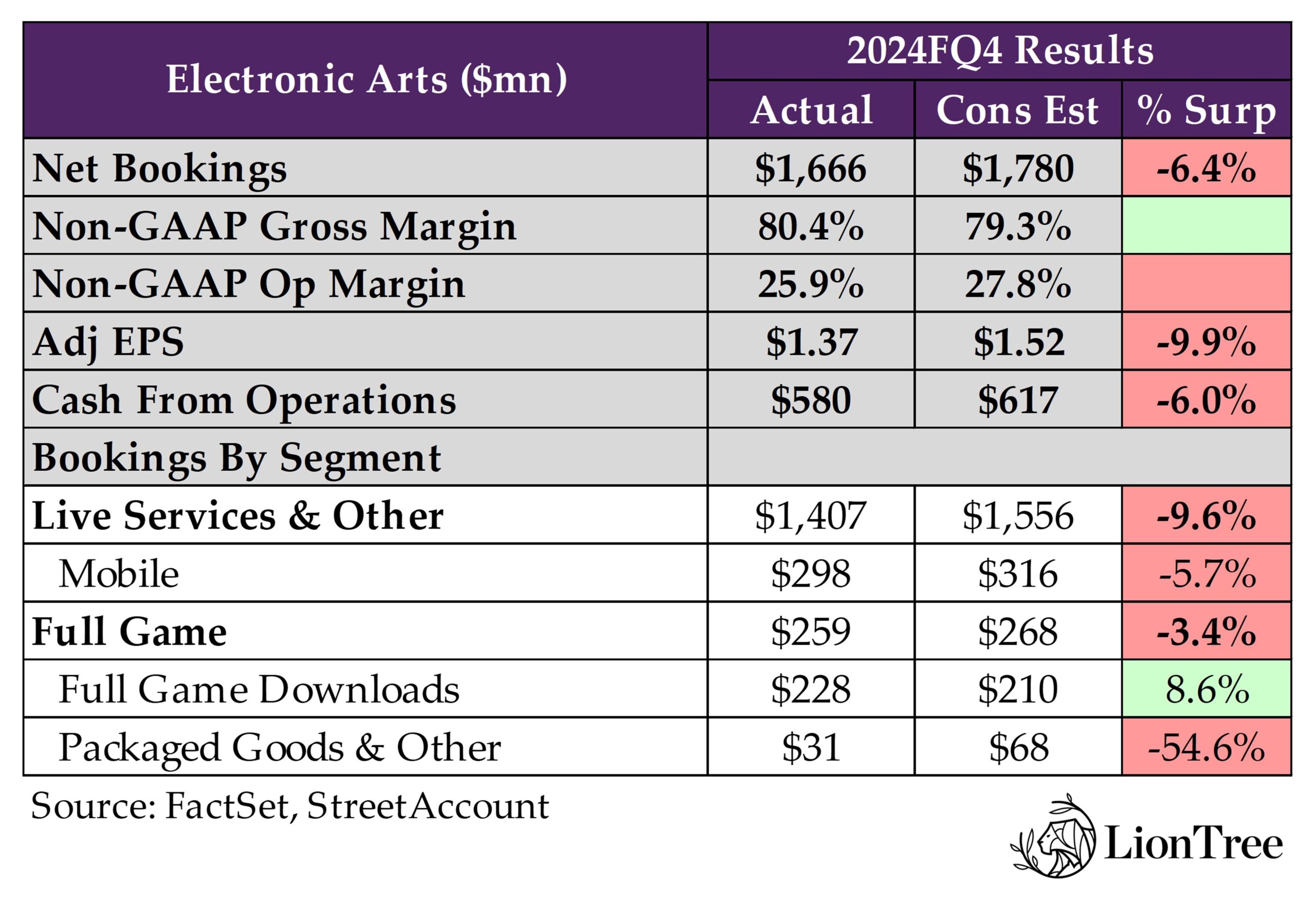

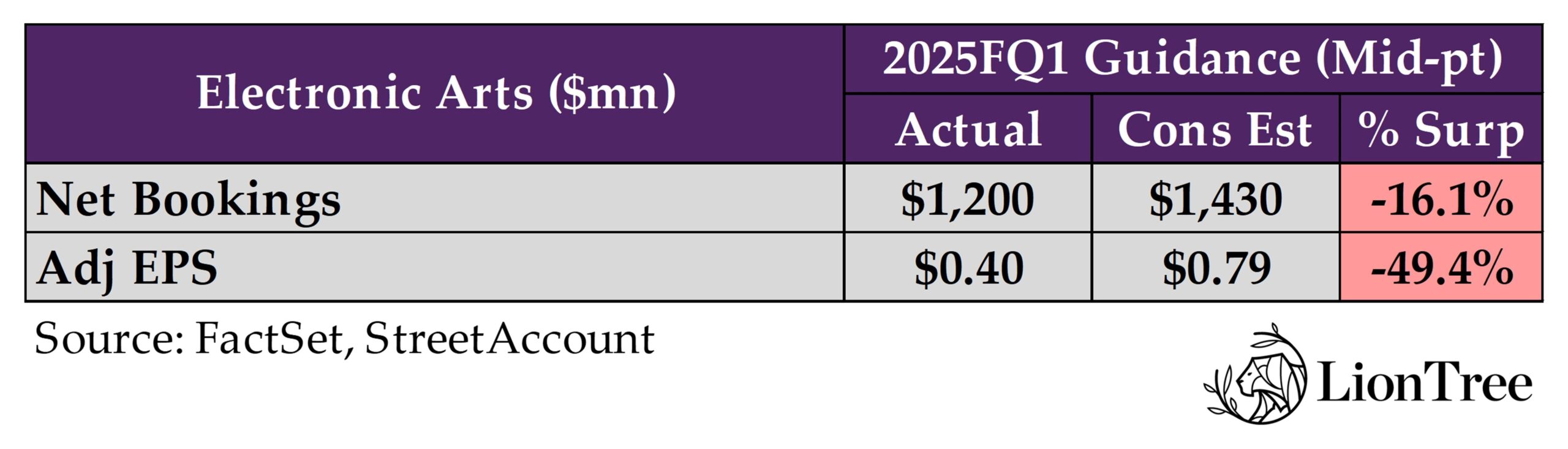

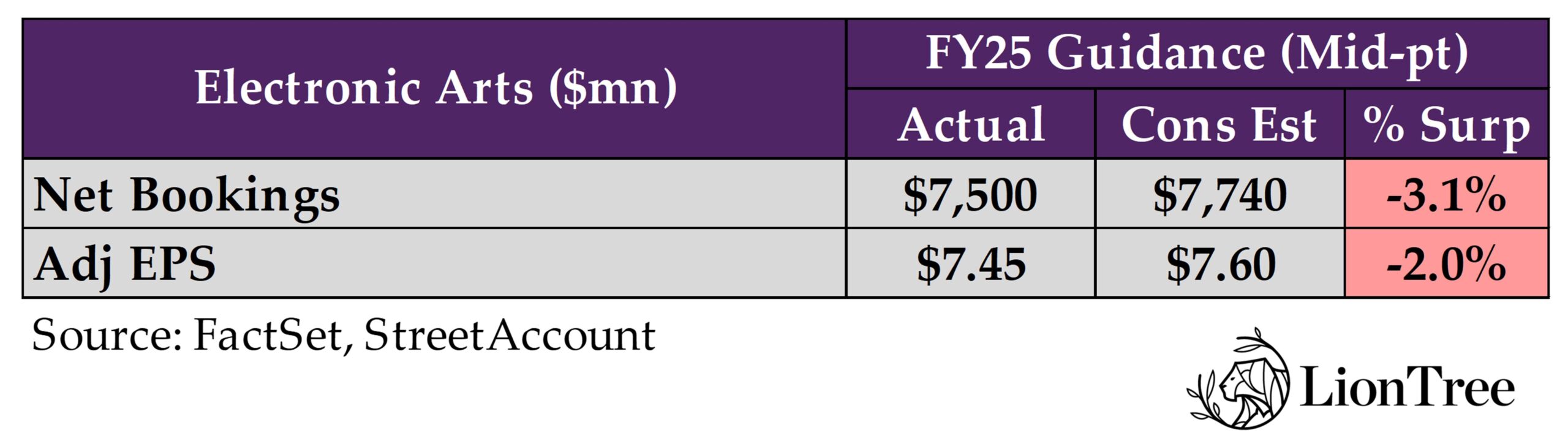

- EA Continues To Point To Greener Pastures On The Horizon

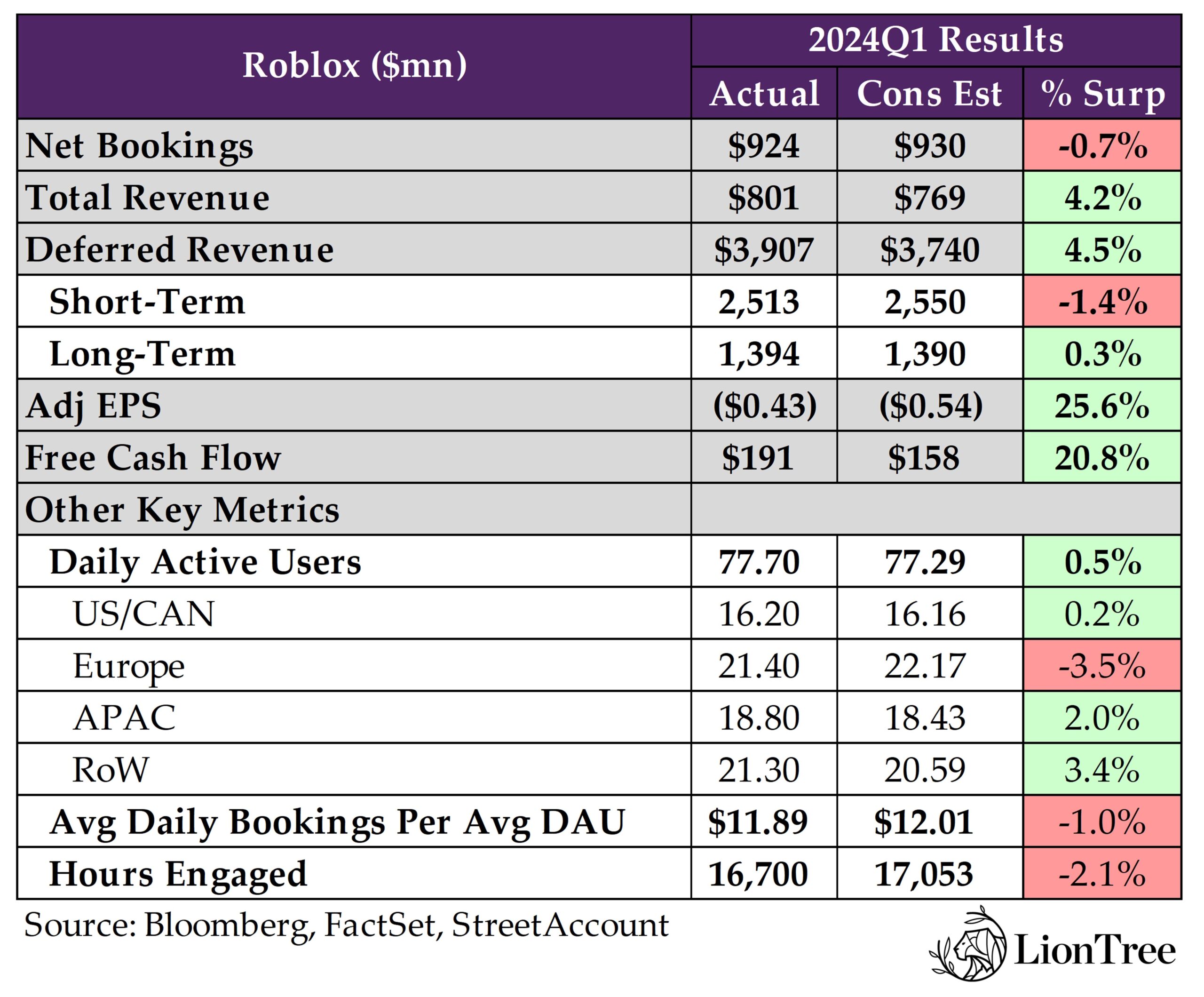

- Forward Outlooks Cast A Shadow Over The Video Game Infrastructure Space

- The Trade Desk Continues To Benefit From “Major Disruption” In Advertising

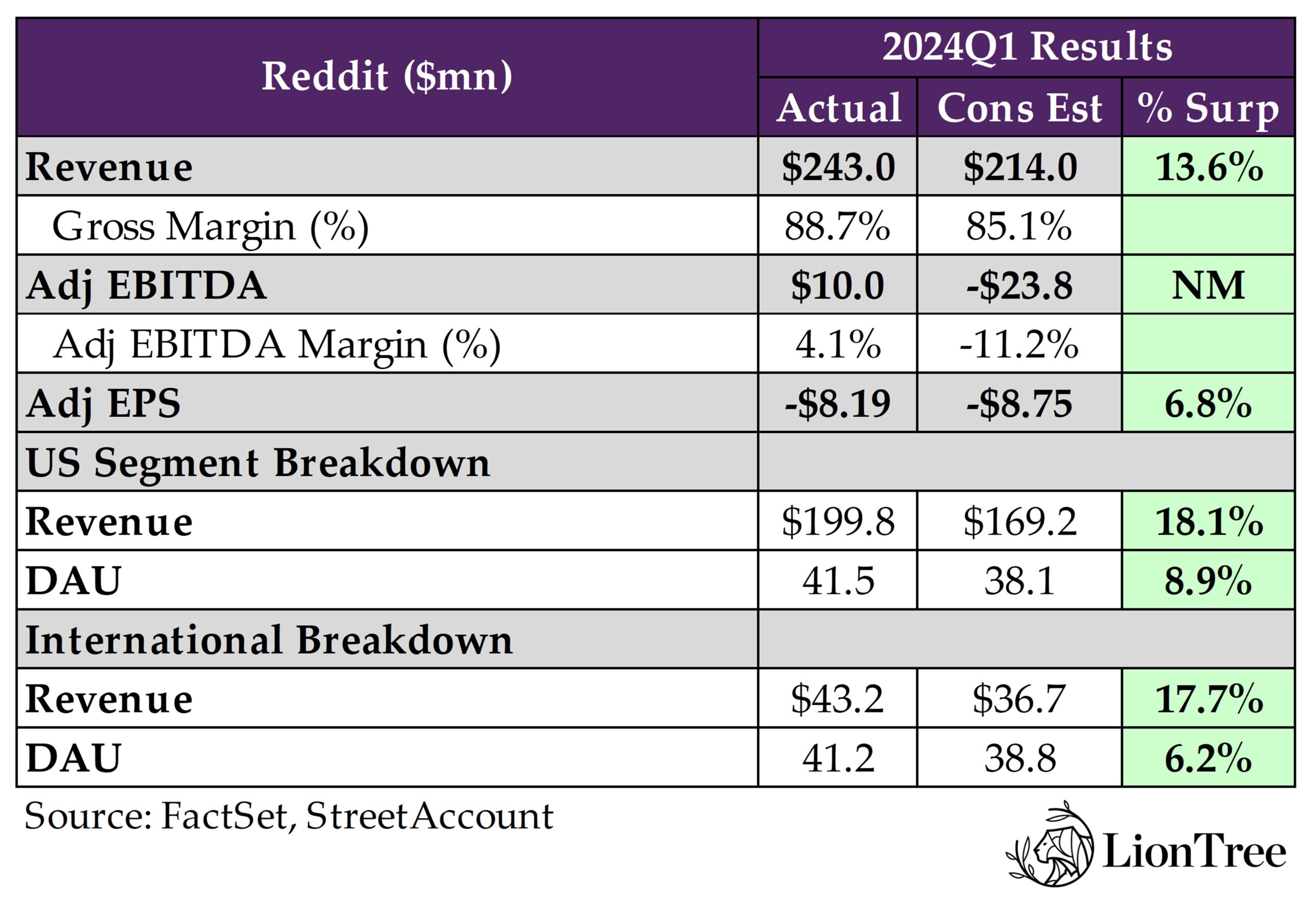

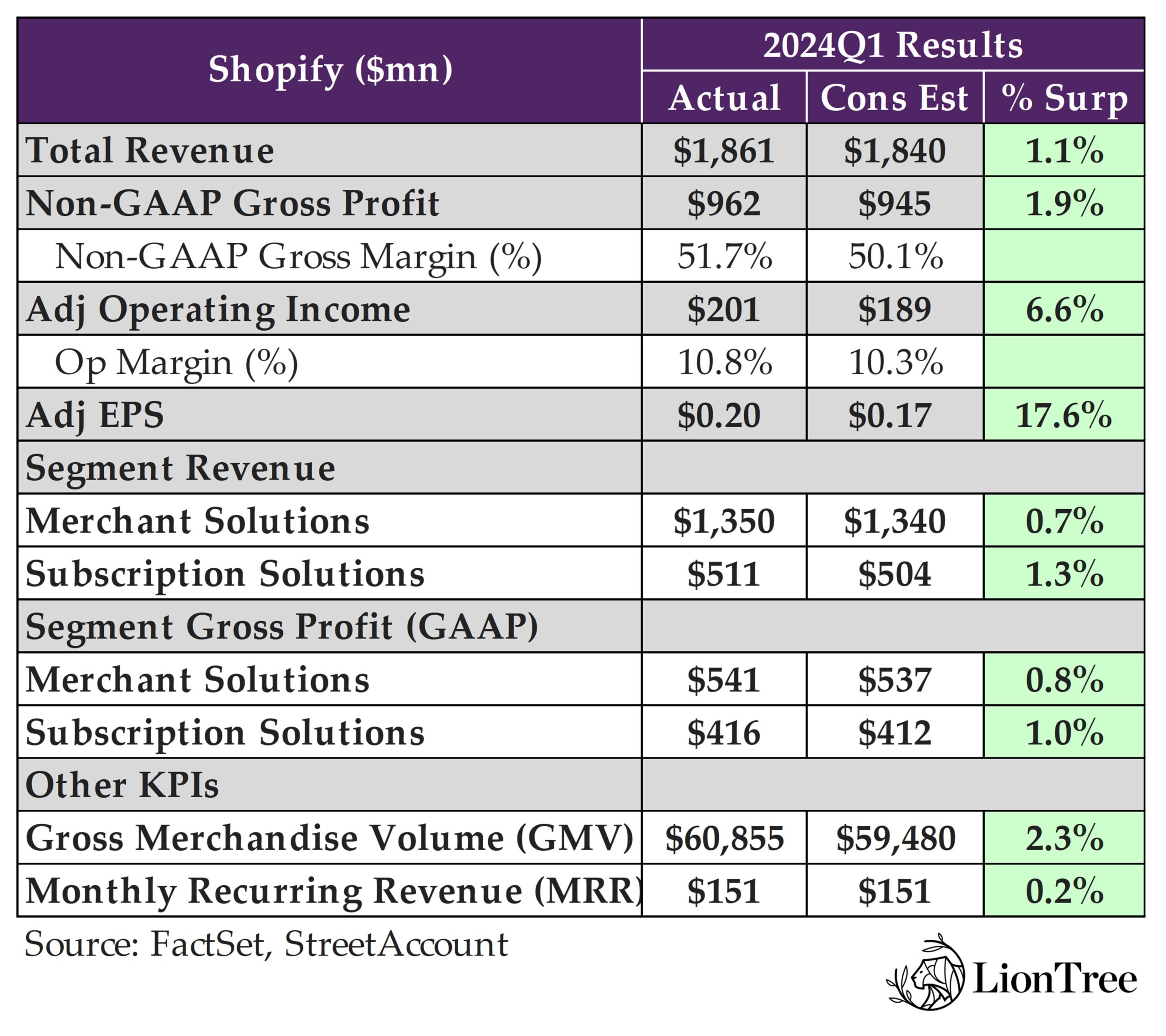

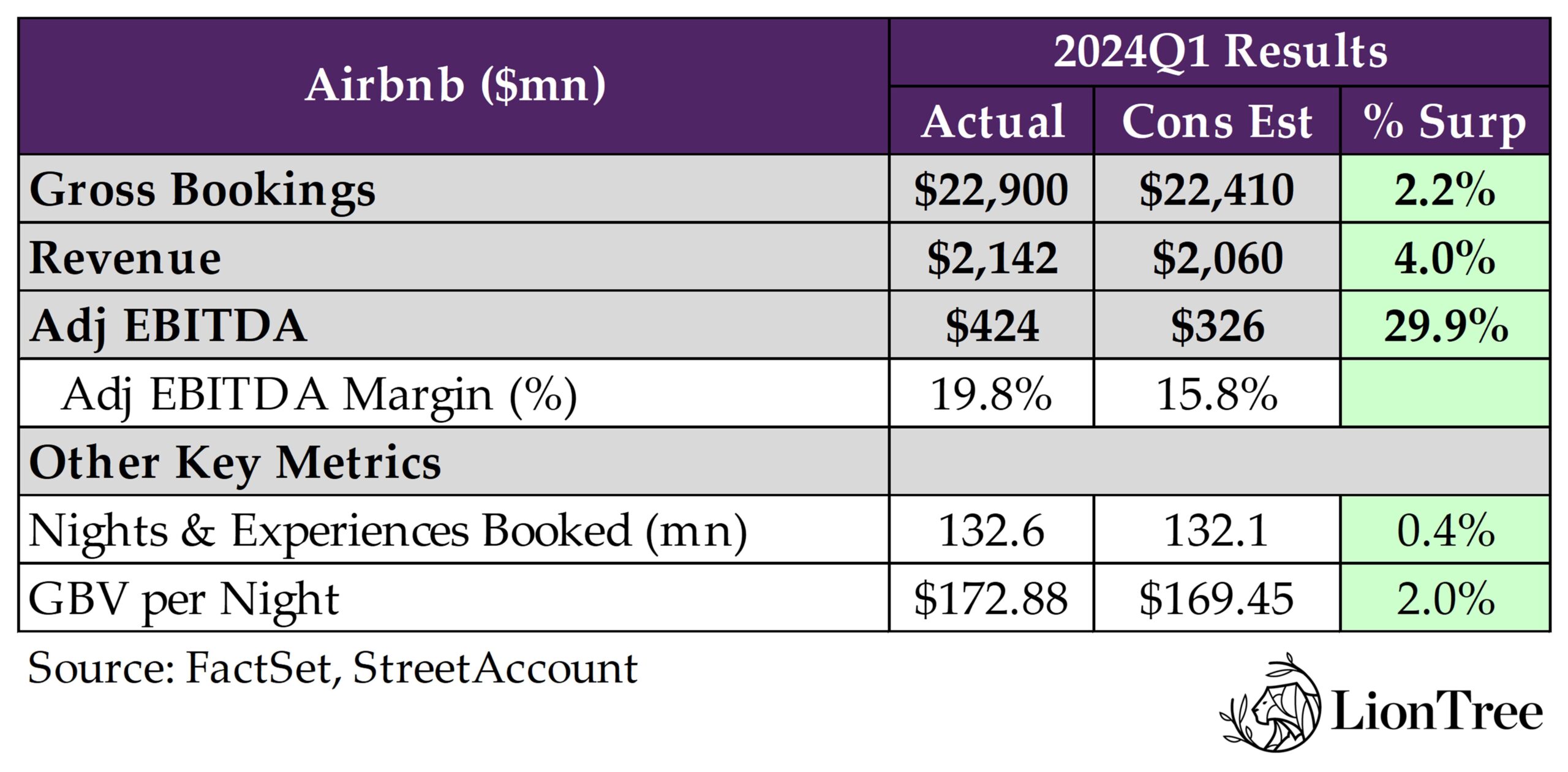

- Earnings Grab-Bag: Reddit / Shopify / Airbnb

This is another jam-packed report. There was a lot to distill and analyze.

Have a nice weekend.

Best,

Leslie

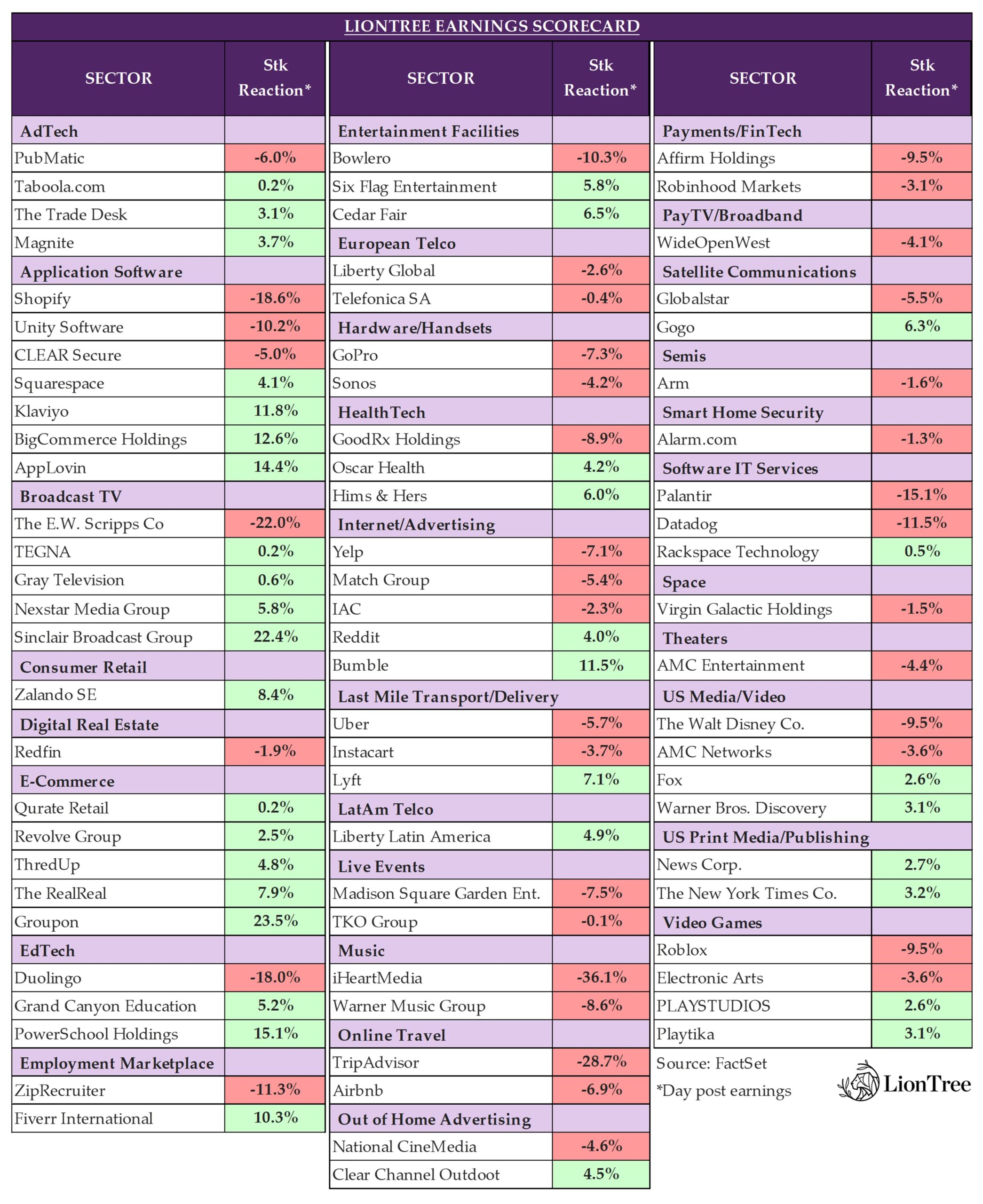

Earnings Scorecard – Week 4

The fourth week of earnings saw a week-high of 77 companies reports in the LionTree Universe report their first quarter results (up from an already high 52 companies that reported last week). Similar to the last two weeks, stock price reactions were biased to the downside. 40 stocks (51.9%) traded down, and 37 (48.1%) traded up. iHeartMedia was the worst performer (down -36.1% post its print), while Groupon was the best performer (up +23.5%).

The media companies dominated the earnings circuit this week, and while Warner Bros. Discovery traded up +3.1% (see Theme #3) and Fox was up +2.6% (see Theme #4) in reaction to its results, Disney fell -9.5% (see Theme #2 for more on why). On the Music side, Warner Music Group also got a tough reaction from the Street and fell -8.6% (see Theme #5).

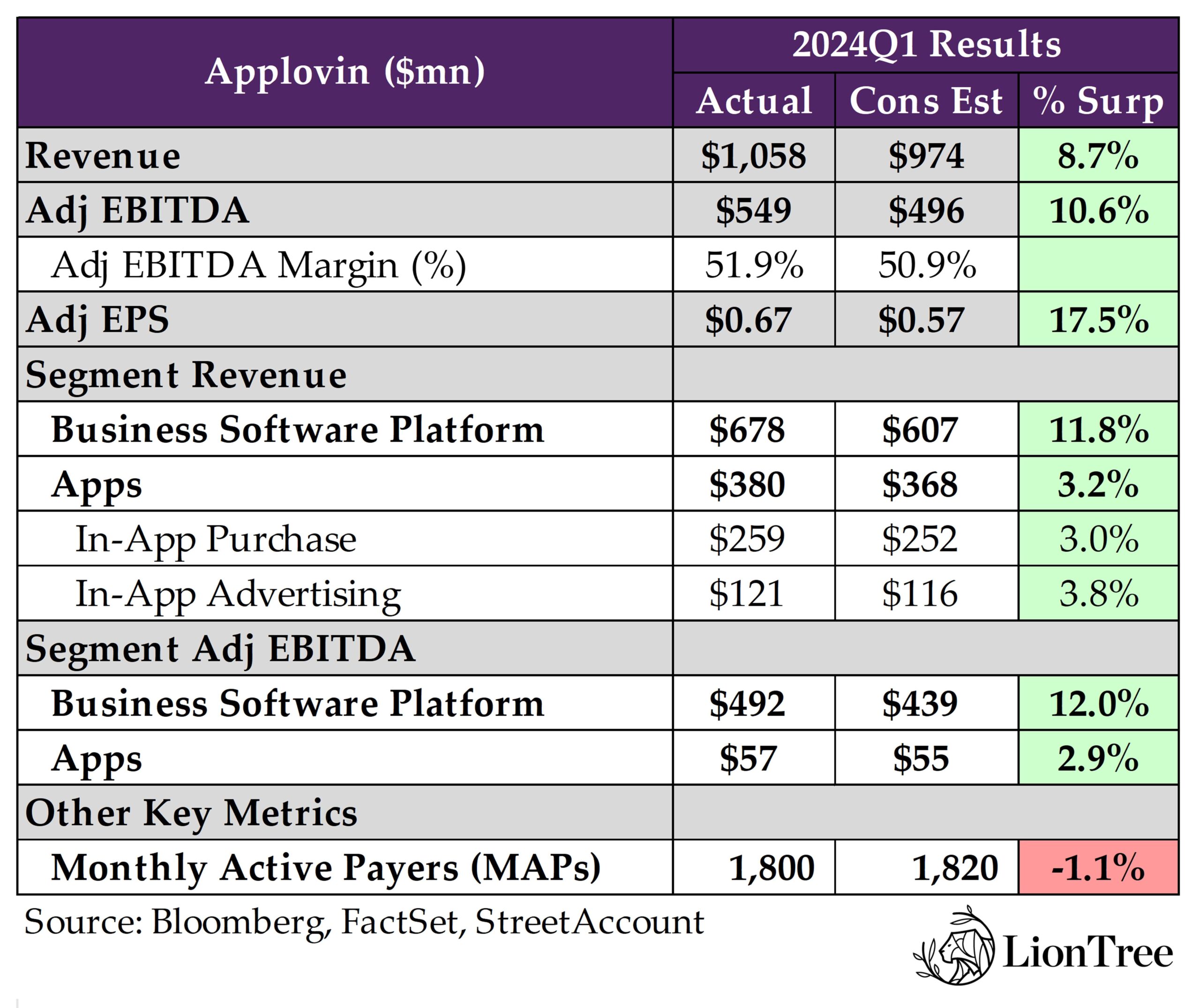

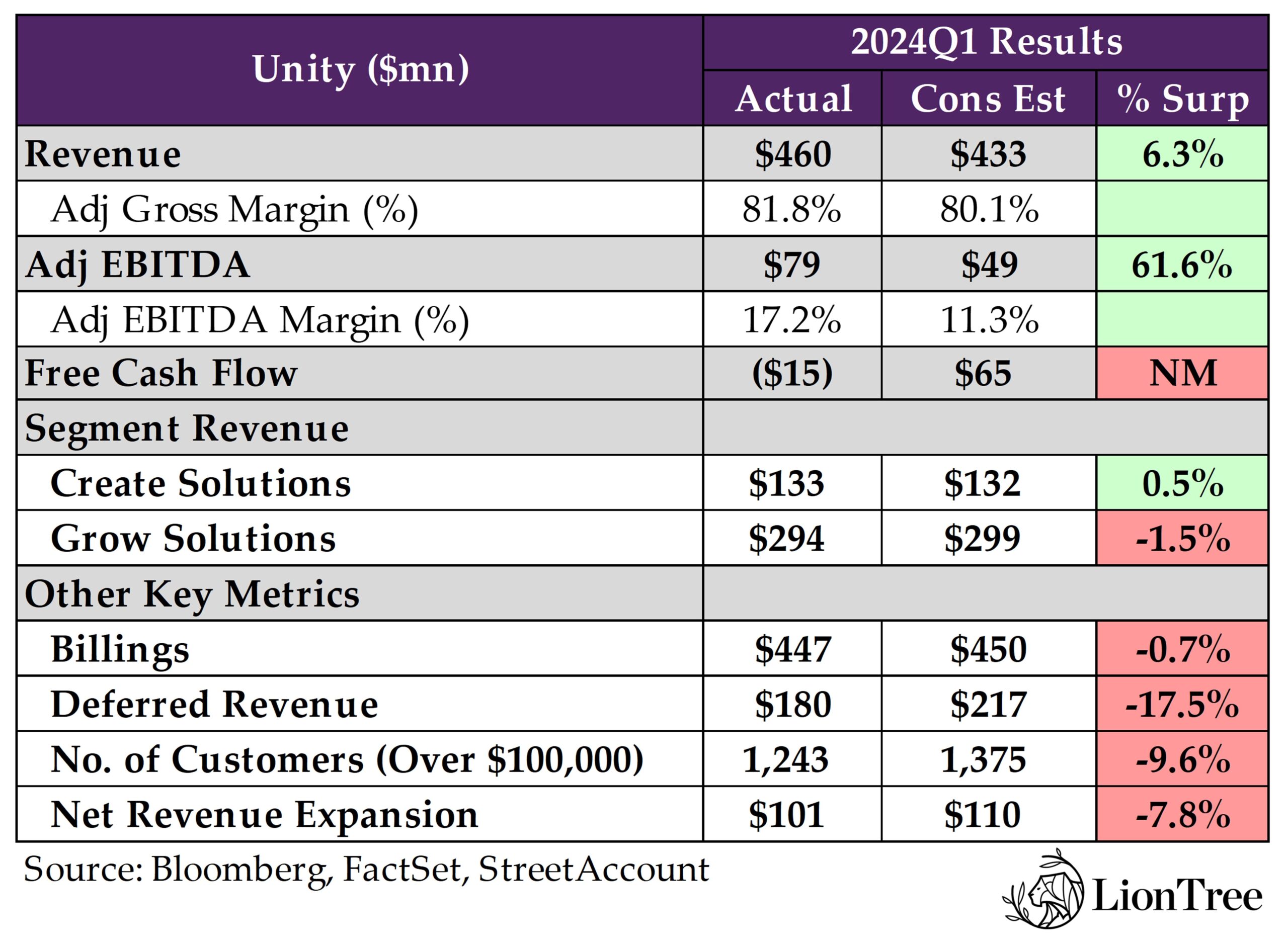

Moving to interactive entertainment, Electronic Arts fell -3.6% in reaction (see Theme #8), while on the video game infrastructure side, Roblox and Unity fell -9.5% and -10.2%, respectively, and AppLovin traded up +14.4% (see Theme #9).

In Last Mile/Delivery, the two ride-sharing companies saw their stocks take opposite routes, as Uber’s stock went south, down -5.7%, and Lyft’s went north, up +7.1% (see Theme #6). Instacart also had a rough ride on the day after its report and ended the week down -3.7% (see Theme #7).

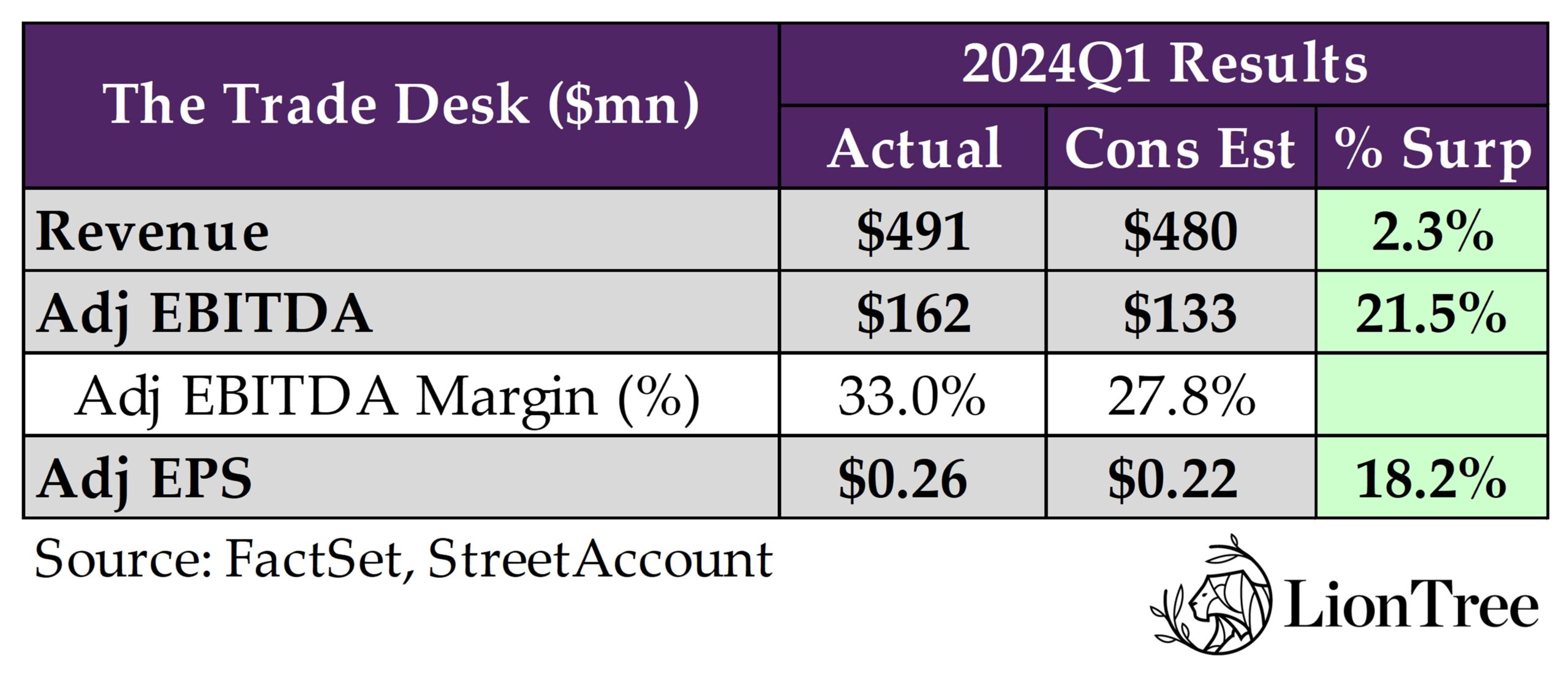

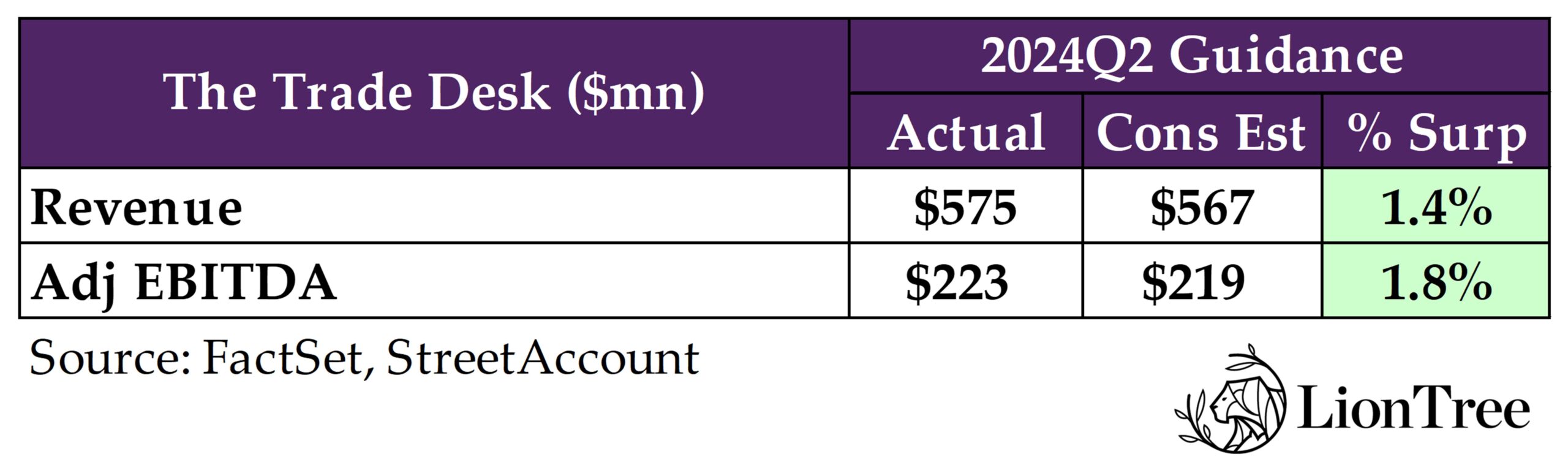

Finally, AdTech leader The Trade Desk’s print also hit this week, and the stock was up +3.1% in reaction (see Theme #10). Also seeing some moves in their stocks were Reddit, up +4.0%, Shopify, down -18.6%, and Airbnb, down -6.9%, following their reports (see Theme #11).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe.

DIS - Jitteriness About Parks Shakes The House Of Mouse

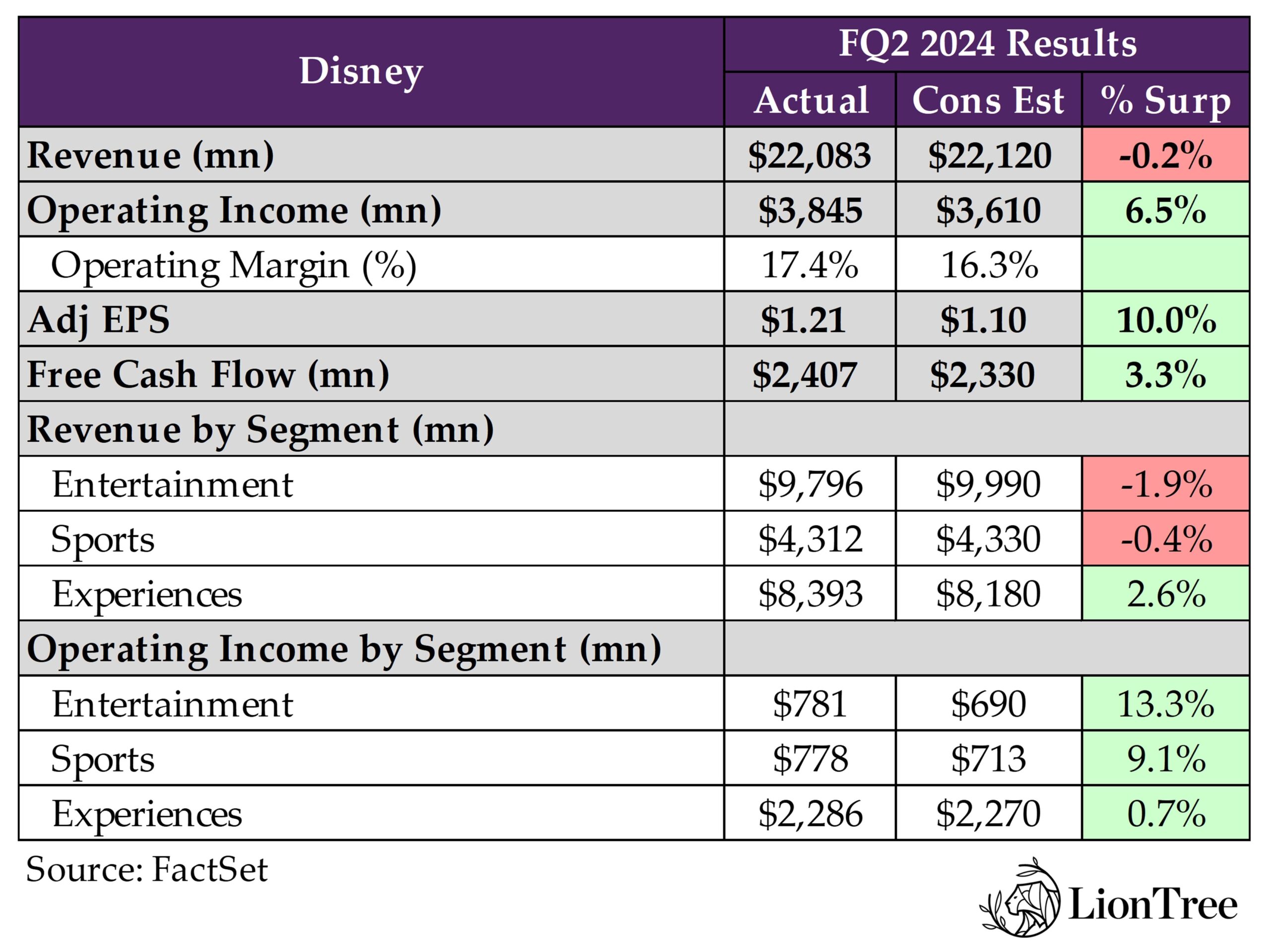

In the midst of Disney’s linear to streaming transition, the Parks business has been a Rock of Gibraltar supporting growth and profitability along the way. Attendance bounced back strongly post-COVID, given all the pent-up demand; however, there appears to have been some dislocation recently. Following Comcast NBCU’s comments last week that it saw some pullback late in Q1 from the “unprecedented” attendance in Orlando following the pandemic due to timing of new attraction openings and “some incr’d competition” from other entertainment venues, Disney comments regarding its parks segment caught our attention. Specifically, the Co indicated that “while consumers continue to travel in record numbers” and it continues to see “healthy demand”, it has observed “some evidence of a global moderation from peak post-COVID travel”. This is one of the reasons why the Co guided for ~flat operating income in the Experiences business in FQ3, which took investors by surprise. Disney is still investing heavily in the Parks business and expects strong returns on this investment, but this update does raise the question about how long this normalization will last. Management also indicated that wage pressure was a factor to the disappointing operating income guidance.

In terms of other areas of the business, better operating income within Entertainment along with better operating income in Sports drove the profitability beat in FQ2. The Entertainment DTC business (which includes Disney+ and Hulu) broke into the black this quarter, and the Co reiterated the consolidated streaming business will reach profitability in FQ4. However, this path will not be linear, some softness is expected in FQ3. Core Disney+ subscriber growth beat consensus, but it was helped by adds that came from the Charter agreement (which, by the way, Disney doesn’t necessarily see as a template for other deals), while ARPU was lighter than expected. Also, the Co does not expect to see Core Disney+ subscriber growth in FQ3 (due to the non-renewal of Disney+ Hotstar’s ICC Cricket rights) but then anticipates sub growth will return in FQ4. Subs growth of other services, including ESPN+, missed consensus, but the Co will have the ESPN+ tile launched at the end of the calendar year and is on track to launch its standalone ESPN app in 2025. Lastly, given the strong earnings performance, management also raised EPS guidance for the FY, despite the weak Experiences guidance.

Was there any update on the CEO succession plans? Not really. Bob Iger only commented, “I’m confident that they will choose the right person at the right time and that to the extent that I can, we’ll participate in a smooth transition.” The activists quieted down post the shareholder vote after all board members were re-elected, though the topic could certainly re-surface to the extent stock performance doesn’t bounce back. Disney shares remain up +17% YTD.

See below for more detailed key points regarding Disney’s results and see Theme #3 and Theme #4 for the drilldown on Warner Bros Discovery and Fox’s results as well.

-> Disney plunged -9.5% after its report and ended the week down -6.9%; YTD, the stock is still up +17.2%, vs WBD’s -28.4% and Fox’s +11.9%

Better Profitability In Entertainment & Sports Drove FQ2 Beat / Raised FY EPS Guidance

- The profitability push persisted in FQ2, though rev slightly missed consensus: Total op income beat by +6.5% and adj EPS grew +30% y/y and beat by +10.0%

- Revenue misses in both Entertainment and Sports segments was partially offset by a beat in Experiences

- Profitability beat across all segments, but most materially in Entertainment followed by Sports

- Raised adj EPS growth target to +25% y/y for the FY (from prior guidance of “at least” +20% y/y)

- Continue to expect to generate $8bn+ in FCF for the FY

- Continue to make “good progress” on cost efficiency initiatives: Remain positioned to exceed $7.5bn annualized target

Overall DTC Subscriber Adds Missed, While DTC Profitability in Remains On Track For FQ4 / FQ3 Will Be Soft

- Entertainment segment FQ2 rev fell -13% y/y, while op income flipped positive primarily due to “expense savings”

- Reiterated streaming profitability guidance but “path to profitability will not be linear”: Expect a softer FQ3 due in large part to the seasonality of its India sports offering, but continue to expect profitability in FQ4 and further improvements in profitability in FY25

- FQ2 total subscribers grew +4.1mn seq but missed expectations by –0.3% / ARPU mostly missed, with the exception of Disney+ International and ESPN+

- Disney+ Core beat: Increased seq by +6.3mn

- Region drivers –

- Domestic: Added +7.9mn subs q/q, driven by Charter entitlements

- International: Lost -1.6mn subs q/q, driven by the impacts of wholesale deal changes and price increases

- Ad tier subscribers reached 22.5mn globally, partially driven by the recent Charter deal

- Disney+ Core ARPU incr’d seq by $0.44 (but missed by –2.0%), reflecting price increases for the domestic premium tier as well as international ARPU growth, partially offset by lower ad supported ARPU domestically driven by dilution from Charter entitlements

- Early takes on Charter partnership? “Very early days…that said, we’re happy with it so far”

- “Obviously have gotten added subscribers”

- “Cannibalization has not been very high”

- “Overall, the engagement has been good”

- “It’s been a successful deal for us and for Charter, so we feel good about it”

- Do NOT view the deal it as a template for the future, as each deal needs to be architected for the specific needs of the partner

- FQ3 & FQ4 outlook – Do NOT expect to see core subscriber growth at Disney+ in FQ3 but anticipate sub growth will return in Q4: The vast majority of subscriber losses in FQ3 will be due to the non-renewal of Disney+ Hotstar’s ICC Cricket rights

- Region drivers –

- ESPN+ missed on subscribers (-5.3% miss) but beat on ARPU (+5.2% beat)

- Both Hulu SVOD-only and Hulu Live TV + SVOD missed on subscribers and ARPU

Sees Path For Further DTC Subscriber, Engagement, And Advertising Growth

- Drivers for further subscriber growth and engagement

- In March, successfully launched Hulu on Disney+ and are “encouraged by early results”

- At the end of this calendar year, will be adding an ESPN tile to Disney+, giving all US subscribers access to select live games and studio programming within the Disney+ app

- Will launch the enhanced standalone ESPN streaming service in the fall of 2025

- Password sharing beginning next month-in very select markets: Will roll-out more broadly across the globe in September; “We feel quite bullish about it”

- Improved tech, including recommendation engines

- Will build out international more strongly

- The Co believes they are in a “good spot” regarding DTC advertising, but there is some new supply to work through: The ad market is “pretty healthy” as they head into the upfront and live and sports are playing out well

- The challenge is that there is more supply in the market as a competitor entered the ad tier: But regardless, think DIS “is in better place than last year”

- “Demand is out there and it’s pretty high. So, as we lap our way out-of-the supply increase, I think we’re going to be in a good spot as we enter next year”

- The challenge is that there is more supply in the market as a competitor entered the ad tier: But regardless, think DIS “is in better place than last year”

Provided Healthy Outlook For Sports Trends In FQ3 To-Date

- FQ2 Sport rev grew +2% y/y (vs +4% y/y in FQ1), but Sports op income decr’d slightly y/y, reflecting the timing impact of College Football Playoff games at ESPN, offset by improved results at STAR India Sports

- Domestic ESPN rev grew +4% y/y, reflecting higher programming and production costs from the timing of an addt’l College Football Playoff game in the quarter versus the prior year, which were only partially offset by higher ad revenue

- Domestic ESPN ad sales increased by over +20% y/y, or ~+hsd% y/y when adjusted for the College Football Playoff timing shift of an addt’l game as well as a new NFL divisional playoff game in Q2

- Domestic affiliate revs also decreased in the qtr, driven by fewer subscribers, partially offset by contractual rate increases

- Outlook – Q3TD, seeing healthy demand driven by the NBA playoffs, as well as domestic ESPN cash ad sales pacing up

- Expecting to incur linear ICC rights expense at Star India in Q3

- DIS is being selective with international sports rights to drive international growth for ESPN or Disney+: “Being selective about adding international rights right now where possible, where the opportunity exists, we’re doing so, but we’re not investing heavily at this point in growing our international rights, except again where we can buy them along with the rights that we’re licensing for the United States”

- “It’s an opportunity for us to plant the seeds for more growth for ESPN outside the United States, but we’re walking before we run-in that regard”

- Believes NBA rights are important but would not talk about potential costs: Thinks it is a sports product with growth ahead and believes will get long term NBA deal

Next Qtr Guidance For The Experiences Business Spooked Investors; Parks Demand Is Strong But Seeing Some “Normalization”

- Experiences revs incr’d +10% y/y & op income rose +12% y/y (mrgns expanded +60bps y/y)

- Parks and Experiences OI incr’d +13% y/y and Consumer Products OI incr’d +7%

- FQ2 Parks & Experiences breakdown by geography –

- Domestic grew +7% y/y, driven by Walt Disney World and the cruise business

- Disneyland saw a y/y decline due to cost inflation, including from higher labor expenses

- International grew +29% y/y, driven by Hong Kong Disneyland resort

- Domestic grew +7% y/y, driven by Walt Disney World and the cruise business

- Outlook – Continue to expect robust op income growth at Experiences for the full-year, BUT FQ3 op income is expected to come in ~flat y/y due to several items; FQ4 will see some pressure as well (but easing)

- 1x items, incl timing of media and tech expenses and timing of Easter

- Higher wage expenses and pre-opening expenses related to the Disney Treasure and Adventure cruise ships as well as Disney Cruise Line’s New Island, Lookout Kay

- Demand at Parks is still “healthy” but seeing some normalization: “While consumers continue to travel in record numbers and we are still seeing healthy demand, we are seeing some evidence of a global moderation from peak post-COVID travel”

- Pressures from wages, pre-opening costs, and demand impacts are expected to persist in FQ4, but do expect y/y Experiences op income growth to “rebound significantly” in FQ4 due to fewer comparability or timing factors

- Backing-out one-timers both for FQ3 and FQ4, expect OI to be in the mid to-high single-digit range for Q3 and to be double-digit for Q4

- Parks & Experiences has a lot of runway to generate strong returns on investment: “There is lots of opportunities to continue to grow attendance, both domestically and internationally. And the cruise business, frankly, is one that has an enormous number of opportunities for us over-time and that is why we’re leaning more heavily into that business”; Expect to get “excellent returns” out-of-the business, in particular in Cruises

Bullish On IP Slate…The Focus Has Been On Quality Vs Quantity

- Content Sales/Licensing and Other revenues fell -40% y/y and lost -$18mn

- Studio profitability has some cyclicality, but that business should get back to profitability

- Key new theatrical releases arriving over the next few months: “So I feel really good about what’s coming up”

- Friday: Kingdom of the Planet of the Apes

- This summer: Pixar’s Inside Out 2, Marvel’s Deadpool and Wolverine, and 20th Century Studios Alien Romulus

- Later this year: Moana II and Mufasa the Lion King

- 2025: Captain Brave New World, Fantastic Four, Elio, Zootopia 2 and Avatar 3

- “We’ve been working hard with the studio to reduce output and focus more on quality” …particularly at Marvel: Going to decrease volume and go to ~ two TV series a year instead of ~ four and reduce film output from ~ four a year to ~ two or max three; “We’re working hard on what that path is”

- The Co is balancing sequels w/ originals, particularly in animation: “We had gone through a period where our original films in animation, both Disney and Pixar were dominating. We’re now swinging back a bit to lean on sequels”; Sequels are “known” and takes less in terms of marketing

- In terms of Marvel specifically, actually have both: Thunderbolts is coming up in 2025 as an original, have Deadpool sequel is coming this summer and Avengers, and Captain America is coming out in 2025

- Continue to look opportunistically into the 20th Century Fox library to see what can be mined

- Open minded on licensing off platform but don’t expect a significant amount: Limiting their own product to their own platforms “definitely does have some value”, but “we’re also watching as some studios have licensed content to 3P streamers and that creates more traction, more awareness and in effect increases not only the value of the content from a financial perspective, but just in terms of traction”

- “So, we’re going to — we’re looking at it with an open mind, but I don’t think you should expect that we’ll do a significant amount of it”

WBD Is Pushing Harder On Streaming Profitability & Bundles

In between Disney’s Tuesday morning print and Warner Bros Discovery’s Thursday morning print came a big announcement – the two legacy media players would be partnering to launch a Disney+, Hulu, and Max bundle. This is certainly a step in the right direction to fix the fragmented DTC customer experience. The offer will be launched this summer, will be priced attractively, and clearly could help drive subs and increase retention. Expect WBD to engage in more of these bundles in the future, which will also include partnerships with telcos and mobile broadband players (as already being seen in Europe, LatAm, as well as the Netflix-Disney bundle with Verizon).

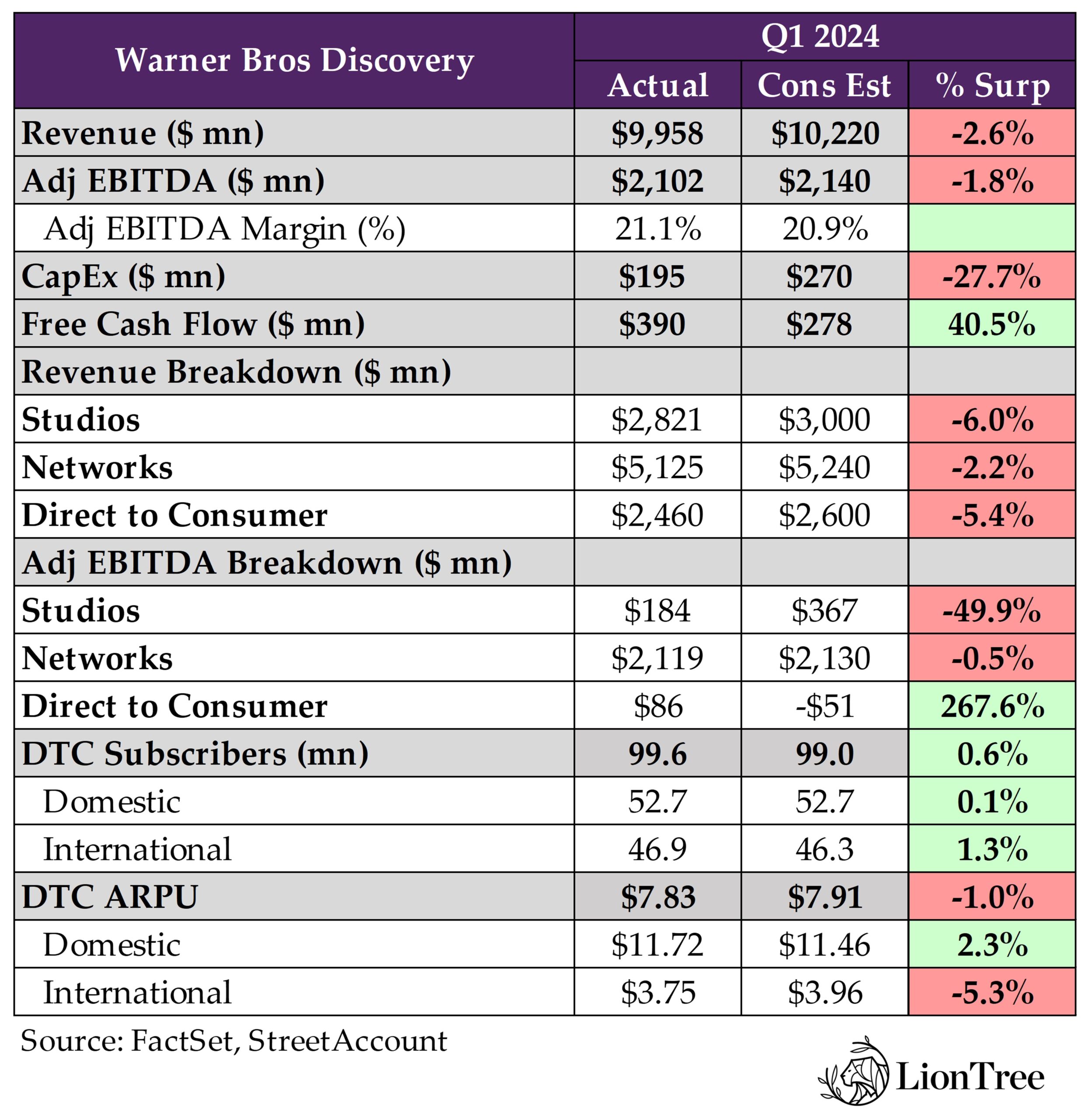

In terms of Q1, WBD’s total revenue and adj EBITDA came up short of expectations, with misses across all segments except DTC, where ad. EBITDA swung to a positive $86mn vs consensus expectations for a loss of -$51mn. This is a key milestone, and the segment is expected to remain profitable in 2024 and achieve its $1bn+ adj. EBITDA target for 2025.

In terms of streaming subscribers, in addition to the international launches (will be rolling out Max to 25+ additional markets across Europe in the next several weeks, with more to follow), another driver of growth will be this just-announced bundle with Disney. All-in-all, there is a greater line-of-sight to sustained profitability and subscriber growth in DTC.

However, it continues to be a tough advertising environment, though the Co’s y/y ad rev losses did improve sequentially. Overall ad rev was down -7% y/% (which is an improvement from -9% y/y in Q4), as growth in DTC ads started to offset linear ad declines. That being said, linear is far from being completely down and out, as WBD continues to see opportunities in the space, particularly internationally in free-to-air channels. Looking to Q2, the Co expects to see continued sequential improvement in total ad rev growth, led by what is expected to be its biggest DTC quarter ever.

Lastly to flag, despite having generated $1.8bn in global box office since the start of the year, the Studios segment was dragged down by games, with “Suicide Squad: Kill the Justice League” underperforming, especially compared to last year’s “Hogwarts Legacy” release. Quickly to note on the sports side, while commentary on the NBA was limited, conversations are ongoing, and WBD is “hopeful” for a deal “that makes sense for both sides.” The outcome of this negotiation certainly will have implications for the Co.

See below for more on all of the above and see Theme #2 as well as Theme #4 for the deep-dive on Disney and Fox’s results as well.

-> WBD climbed +3.1% in reaction to its print and ended the week up +2.3%; YTD, the stock is down -28.4% vs Fox’s +11.9% and Disney’s +17.2%

Better Than Expected FCF & DTC Positive Adj EBITDA Were Main Q1 Highlights / Expect To “Meaningfully Exceed” Cost Saving Target

- Consolidated rev missed by –2.6%: Fell -7% y/y (vs -7% y/y in Q4)

- All three segments missed

- EBITDA missed by –1.8%, but DTC was better: Fell –19% y/y (vs –5% y/y in Q4)

- Studios and Networks both missed, but DTC came in positive $86mn vs expectations of a loss of -$51mn

- FCF beat by +40.5%, despite being in the Co’s “seasonally weakest FCF generation qtr”: Improved by +$1.3bn y/y to $390mn in Q1 and $7.5bn in TTM FCF

- Drivers:

- Continued to benefit from the many initiatives to improve working capital, which the Co is still in the “early innings of realizing”

- “More disciplined and analytical approach” to content investment and allocation

- “Meaningfully lower” cash restructuring costs

- Lower cash interest expense, as a result of $6bn+ of debt repaid over the past 12 months

- Primary use of FCF remains delivering the balance sheet and are committed to gross leverage target range of 2.5-3x: “Confident that we will continue to make progress towards further delivering this year”

- Drivers:

- See a path to “meaningfully exceed” the $1bn+ of remaining cost savings that they have previously guided to, which is on top of the $4bn+ already realized through the end of 2023

Despite Linear Ad Declines And DTC Ad Increases, Expect To See “A Very, Very Long Period Of Co-Existence”

- Q1 total ad rev fell -7% y/y (vs -9% y/y in Q4), helped in part by a record March Madness Men’s Basketball Tournament and steadier overall ratings

- Networks were down -11% y/y (improved from -14% y/y in Q4), primarily driven by audience declines in domestic general entertainment and news networks, as well as the soft linear ad mkt in the US and LatAm; The decline was partly offset by growth in EMEA; The AT&T SportsNet exit was a modest headwind to ad rev

- DTC was up +70% y/y (accel from +51% y/y in Q4), primarily driven by higher engagement on Max in the US, which in part was due to the launch of B/R Sports on Max in October 2023, and ad-lite subscriber growth

- Looking to Q2 – expect to see continued seq improvement in total y/y ad rev growth, led by what is expected to be their biggest DTC qtr ever: Cited the following drivers for the seq improvement –

- Launched international ad-lite offering in LatAm, with EMEA coming soon, which will be “critical” in enhancing their portfolio offerings

- Continue to see “select” opportunities in linear despite “obvious secular challenges”

- EMEA continues to be a standout bright spot, particularly from free-to-air channels, which outperformed in Q1 with positive rev growth (primarily driven by “robust” rev growth in Poland, Italy, and Germany) and they are seeing a continuation of their trend in Q2

- Except for the UK and the Nordics, advertising revs were flat to up in virtually all EMEA markets in Q1

- Linear cash pacing in the US continues to improve “modestly” QTD, even excluding the positive impact of the NCAA Men’s Final Four and the Championship Games

- Will benefit from having these games exclusive to WBD this year, but do not have the Stanley Cup finals and the exit of the AT&T SportsNet will continue to be a headwind to revs with marginal profit impact through the end of Q3

- Though materially smaller, LatAm has been and continues to be a different story, particularly given cyclical and secular headwinds in Brazil and Mexico, their two largest mkts in the region

- Unlike Europe, where they are a scale broadcaster in several markets, they are more exposed to the less resilient pay-TV ecosystem that is experiencing a more pronounced secular shift of ad dollars to streaming (but are now better positioned to capture a share of this migration with launch of Max in the region)

- Taking an increasingly more holistic portfolio approach to monetizing viewership in both linear and Max, supporting their ability to offer their partners incremental reach and more customized ad solutions spanning all platforms, particularly in the US

- EMEA continues to be a standout bright spot, particularly from free-to-air channels, which outperformed in Q1 with positive rev growth (primarily driven by “robust” rev growth in Poland, Italy, and Germany) and they are seeing a continuation of their trend in Q2

- On upcoming upfront – It’s a “little early” to discuss but “definitely hope to continue some of the momentum that we’ve seen last year”

- “Operating in a much more constructive environment this year than we did last year”

- Convergence of DTC and linear is “working very well right now” and the way they take their inventory to the market is “fully harmonized”

- Seen “some nice growth rates” for DTC inventory and taking it to market with more data-driven products

Despite Launch Costs From Max’s International Rollout, Continue To Be Disciplined And Expect DTC To Remain Profitable In 2024 And Achieve $1bn+ Adj. EBITDA Target In 2025

- Max added 2mn subscribers in Q1 to reach 99.6mn subs (beat by +0.6%)

- Gaining subscriber traction in all regions

- Looking to Q2 –

- Content rev expected to be down y/y: Similar to Q1, when content rev was down -46% y/y, will have a more difficult comp in Q2, both of which are a product of timing of output deals renewed last year, availability of content, as well as content utilization choices

- Some slowdown in US, but growth continues in int’l: US subs will be impacted by some seasonality, particularly related to sports, but on track for continued “robust” international growth

- Expect new subscriber highs through the remainder of the year

- Expect to remain profitable in the DTC segment during 2024, despite heavy launch investments, and remain “fully confident” in the path to achieve $1bn+ adj. EBITDA target for 2025 and growth ambitions thereafter

- 2024 is “a pivotal and critical year for Max with an aggressive relaunch and rollout underway that will meaningfully expand our global presence and growth potential”

- “Off to a strong start” with ~$86mn in adj EBITDA generated this qtr, despite absorbing some of the launch costs of LatAm

- Highlighted “three key metrics” that “underpin our strategic and financial objectives” for DTC

- Subscriber growth: Nearing 100mn subscribers and see “strong indicators” of continued growth through rest of the year

- Putting more partnerships in place to accelerate rollout, an enhanced subscriber migration experience that reduces one-time churn, and more optimized marketing investment

- Engagement and monetization:

- Engagement reached an all-time high in Q1 through a combination of stronger content and product enhancements, and the Co is taking “meaningful” steps to grow it further

- Global ARPU grew +4% y/y in Q1 (vs +7% y/y in Q4), which in part reflects a greater mix shift of lower ARPU intl subs vs US subs

- US ARPU grew +8% y/y in Q1 (vs +8% y/y in Q4)

- Churn: Still above their longer-term target but cont’d to trend downwards and hit an all-time low in the US at the end of Q1

- Saw “continued healthy improvements” in habituality and diversity of viewing in Q1, which are the most correlated inputs to churn

- Subscriber growth: Nearing 100mn subscribers and see “strong indicators” of continued growth through rest of the year

- International expansion of Max is underway: YTD, have expanded from single market in the US to 39 countries and territories

- Successfully migrated HBO Max subscriber base in LatAm over the past couple of months: Now able to offer more consumer-friendly pricing and packaging across ad-lite, ad-free- and premium tiers, with more flexibility and subscription options and addt’l paths to monetize the base

- Will rollout svs to 25+ addt’l mkts across Europe in the next several weeks, including their first new mkts, France and Belgium, with more to follow

- Max will be the only place where viewers across Europe will be able to watch every part of the Olympics

- The content lineup on Max over the next 12-18 months is “one of the strongest ever”

- Coming in Q2: S3 of Hacks, Streaming premiere of The Iron Claw and Dune: Part Two, Champions League in LatAm, and the S2 premier of House of Dragon, “just to name a few”

- Over the next 18 months: S2 of The White Lotus, S2 of The Last of Us, S3 of And Just Like That, along with tentpole original series including The Penguin Doom Prophecy, Welcome to Derry, A Knight of the Seven Kingdoms, a Spinoff of the Game of Thrones franchise, plus an ongoing slate of fresh new Warner Brothers theatrical releases such as Godzilla, Ex-Con, Furiosa, Beetlejuice, Joker 2, and more

“Need To Fix” The DTC Consumer Experience, And Bundling Will Help Do That

- Partnering with Disney to launch a streaming bundle, which will include Disney+, Hulu, and Max: “First of its kind offering that gives US consumers the option of an ad-lite or ad-free package that includes Max, Disney+, and Hulu”

- Will go live later this summer

- Will be priced “very attractively”, working off of the Max standalone and the existing Disney+ and Hulu package bundle

-> On the news of streaming partnerships, there was a report out this week from The Hollywood Reporter that Paramount might attempt a combination of its streaming service, Paramount+, with Comcast’s streaming service, Peacock; Details are very sparse as neither of the companies have made a formal announcement about the talks, and no pricing, naming, or other details have been decided; According to the report, the feasibility of a partnership would depend on several factors, including whether or not Comcast gets an NBA package, if Byron Allen or another bidder takes a swing at acquiring BET, who would even control the combined service, and whether a combination would be enough to compete against the upcoming Disney-Fox-WBD sports JV (link/link)

- Disney bundle is expected to help increase retention, lower churn, and in turn support higher customer lifetime values, as customers will have to retain all three streaming svs to take advantage of the price value in the offering

- As the bundle gets more traction, will benefit from increased efficiencies (including with marketing)

- Any plans to add other svs to the Disney+, Hulu, and Max bundle? Current bundle gives “the greatest offering of kids and family content, the greatest offering of adult fare, the greatest offering of scripted and non-scripted content. So, we don’t think we need anybody else in that package to make it incredibly compelling”

- “We do think this package can be an anchor tenant of every household’s entertainment experience. And we don’t think there is a need at this point for anything more”

- Update on bundle Max-Netflix bundle with Verizon? Doing “much better than expected… it’s another example where there’s more strength together… it’s just more efficient”

- Expect more bundles in the future, including w/ telcos: As they roll out in Europe, have partnership with Canal, Free, Orange, SFR, “all the big mobile Telco players”; “That’ll continue to be our strategy. Then partnerships with other programmers and other streamers, we will continue to explore, and I think you should see that in our roadmap in the quarters to come”

- “We need to come together ourselves and provide a better consumer experience…or there’ll be other companies [that] will do it for us”

- Cos like Roku and Apple and Amazon “are doing a terrific job of aggregating services in the quest to provide a better consumer experience” BUT “it’s much more efficient, better ARPU and a much better business if we can do it ourselves”

- Bundling will allow the legacy media players to “[get] back to all being great at what we do and swim in the lane that we were great at”

- Vs back in the 2010s, when “the industry went down the very dangerous financial path of trying to invest in every type of content, in every genre to try and be something for everyone”

- Now, with the new bundles, they can “go back to investing in the areas that we really are great at”

- “Disney, obviously, is incomparable and a world leader in kids and families”

- “We are world leaders in premium drama, scripted drama, comedy, nonfiction verticals”

- Consumers benefit because at a “very attractive price” they get a combination of products and don’t feel the need to switch in and out of services month to month

- “The key for us is, we need to be prominent in all of the major bundles because we want to be in front of all consumers”

Limited Commentary On NBA, But Discussions Are Ongoing

- Currently in active negotiations: “We’ve enjoyed a strong partnership with the NBA for almost four decades. We’re in continuing conversations with them now, and we’re hopeful that we’ll be able to reach an agreement that makes sense for both sides”

- Under current deal with the NBA, WBD has matching rights that allow them to match third party offers before the NBA enters into an agreement with them

- Had “a lot of time” to prepare for this negotiation and have strategies in place for the various potential outcomes

Have Been Taking “Meaningful” Steps To Rebuild Studios, Though Gaming Weighed On Results In Q2

- Q1 financials were overshadowed by tough gaming comps: $400mn+ y/y decline in rev was primarily due to the “very tough comp” following the success of Hogwarts Legacy last year, in conjunction with the disappointing Suicide Squad release in Q1, which has a $200mn impact to adj EBITDA

- Striving to “return the luster to Warner Brothers Pictures”, but it “takes time and it’s not something that can be accomplished overnight”

- “The heavy lifting taking place…isn’t something that you see fully reflected yet in our financials. However, we are confident it will become more apparent with time”

- Currently stand at the #1 spot for box office share this year: Making it the first studio this year to reach $1bn in both overseas and worldwide box office

- Dune: Part Two and Godzilla x Kong: The New Empire have grossed $1.2bn+ in global box office; Dune: Part Two is the highest grossing movie of 2024 to date with $700mn+ in global box office

- Have generated $1.8bn in global box office since start of the year

- Continue to lean on franchises as they develop new projects: “It’s a core value and a key advantage for us. We have the characters and stories people love and yearn for everywhere in the world, in every language”

- In the early stages of script development of the first of the new Lord of the Rings movies, which are expected to release in 2026; “Lord of the Rings is one of the most successful and revered franchises in history and presents a significant opportunity for our theatrical business”

- Harry Potter, Lord of the Rings, Superman, and many other parts of the DC universe are “largely underused. We are hard at work fixing that”

Looking To Leverage AI Across The Co To Run Bizs More Productively And Effectively

- “We recognize that AI is going to have an increasing impact on society and our industry, and we intend to take full advantage to enhance the products and experiences we deliver to consumers and to achieve greater efficiency companywide”

- Focused particularly on improvements to ad targeting and recommendation algorithms: AI-based understanding of their customers and content is being activated across product, marketing, and ad sales

- Since the initial launch of Max, have been using AI and ML to personalize content discovery, and have continuously innovated to improve models and present the right content in front of consumers at the right time

- Using AI to identify and optimize ad break oppties in premium HBO content more efficiently and swiftly, which typically does not have natural ad breaks, enabling them to offer premium content on their ad light tier and create variable ad load for content as they monetize it using multiple tiers and platform

- Have “dozens of other experiments” ranging from corporate and developer efficiency to marketing optimization and targeting

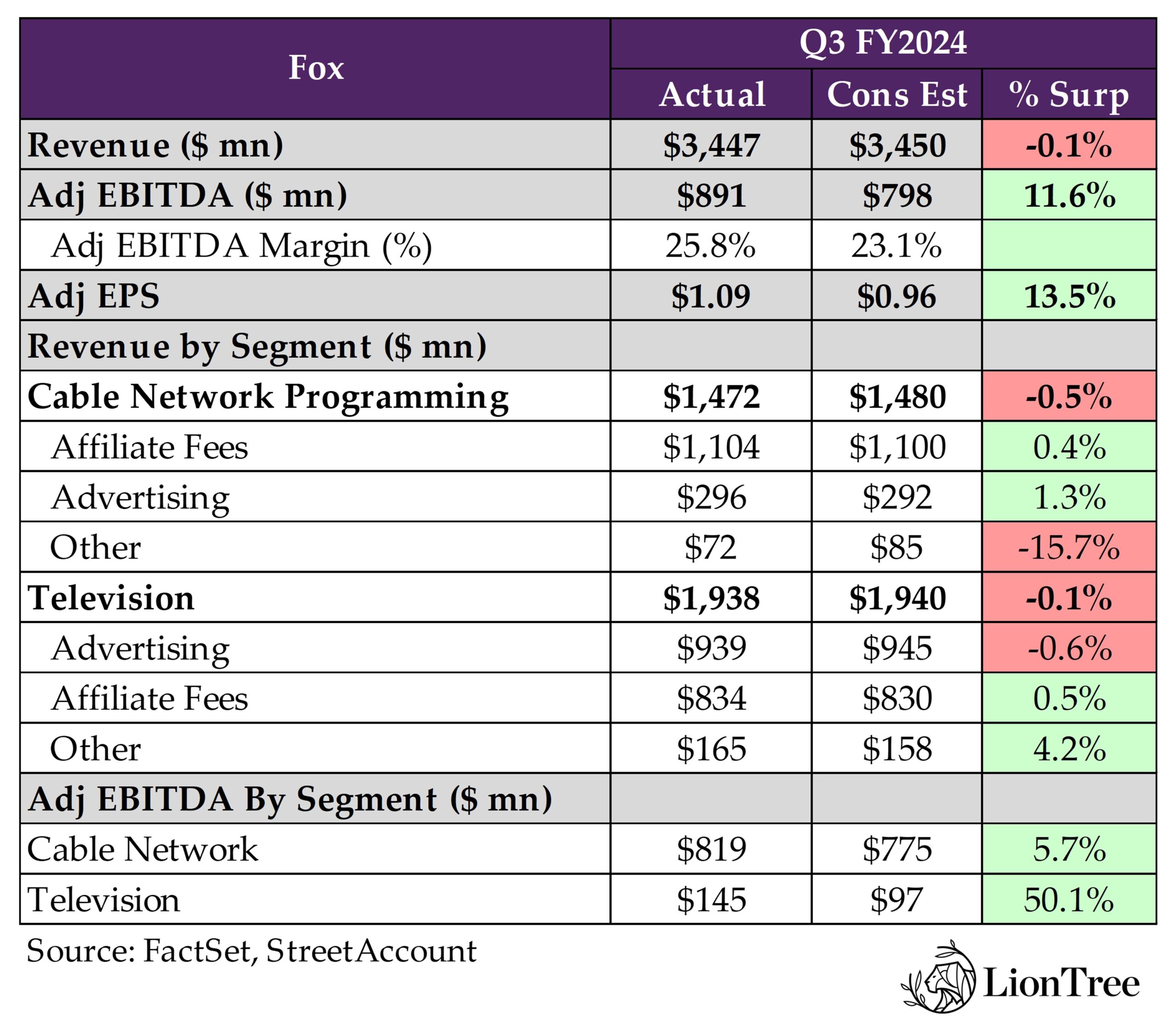

FOX’s Fundamentals Moved In The Right Direction, Excluding Seasonal Factors

Investor reactions to the Media earnings-palooza over the past couple of weeks have been quite bifurcated, with Fox and Warner Bros Discovery trading up but Disney and Paramount trading down post-earnings. There have been a lot of moving parts and company-specific dynamics, but at least in terms of Fox, much better profitability (adj EBITDA ~+12% ahead) was the key upside driver, given that revenues were more or less in-line. Tubi remains a shining star and has been growing to scale. It delivered +22% y/y rev growth in the quarter, driven by a +36% y/y increase in total view time (TVT) and +20% y/y growth in monthly active users (to just under 80mn). Tubi’s share of total US TV view time also grew +60% y/y, which was faster than any other streaming service over that same period. The proactive nature of Tubi users’ viewing behavior is also attractive to advertisers, and the Co is not concerned with weakness in CPMs, despite increased supply from Amazon Prime Video’s ad-tier. With that being said, Tubi’s revenue comps will be tougher next qtr.

The price increases in the carriage renewals helped affiliate revenues to grow this quarter and while total advertising revs fell a meaningful -34% y/y, it was seasonally due to the absence of the Super Bowl and 2 fewer NFL playoff broadcasts than in the prior year. EXCLUDING these items, total ad revs were up ~+lsd% y/y, and comments were constructive on the scatter and upfront market. Also, Fox’s political ad revs should ramp in Fiscal H2. Lastly, questions about the commitment to the Sports JV also emerged, but Fox remains enthusiastic and is excited about how the beta is looking.

See below for more thoughts on the above as well as insights into other key Fox comments and updates. Also, see Theme #2 and Theme #3 for a respective drill down into Disney and Warner Bros Discovery’s results this week, and see Theme #10 from last week for some perspectives on Paramount’s latest earnings update.

-> Fox ended the day of its report up +2.6% and built on those gains to close the week up +4.6%; YTD, the stock is up +11.9%, vs WBD’s -28.4% and Disney’s +17.2%

Much Better Profitability Drove Upside Vs FQ3 Expectations

- Total revs were ~in-line with consensus, but adj EBITDA was ~+12% ahead: The +7% y/y growth in adj EBITDA came despite tough comps with the Super Bowl; EPS of $1.09 (+16% y/y) also beat by +13.5%

- Cable Network: Revs (down -6% y/y) a tad light but adj EBITDA beat (grew +3% y/y)

- Expenses were down -16% y/y, primarily due to the timing of the associated sports sub-licensing expenses, lower costs at Fox News, and the de-consolidation of the USFL

- TV: Revs were in-line (down -22% y/y), but adj EBITDA beat (incr’d +24% y/y)

- Expenses were lower, primarily due to the impact of the NFL schedule, along with fewer hours of original scripted primetime content, including the impact of the industry labor disputes

- Cable Network: Revs (down -6% y/y) a tad light but adj EBITDA beat (grew +3% y/y)

- FQ3 to date, the Co repurchased $300mn and returned ~$125mn via the dividend: Total cumulative buyback activity since the launch of the program in 2019 now amounts to $5.4bn, or 26% of total shares outstanding; Fox remains committed to fully utilizing the current $7bn authorization

Tubi Remains A KEY Growth Driver / Total Viewing Time Was Up +36% Y/Y / Not Concerned About CPM Pressure

- Tubi posted +22% rev growth in FQ3, driven by a +36% increase in total view time (TVT) and +20% growth in monthly active users (to just under 80mn)

- Tubi’s share of total US TV view time grew +60%: This was than any other streaming svs over that same period

- 60%+ of Tubi’s users are classified as cord-cutters or cord-nevers

- 90% of those users’ time watching is “proactively on-demand” as opposed to passively watching

- This is much more valuable to advertisers

- This positions Tubi very well as an important part of the growing digital streaming advertising marketplace

- No concerns about CPM pressure for Tubi (was flagged by Disney as a headwind): Think they are already efficient with CPMs vs others; “I think some of our competitors priced themselves when they entered the AVOD market over the past 12 and 18 months very high. And we’re seeing in the marketplace them having to drop CPMs as new entrants add supply to the market. So that’s affecting the market overall”

- But note that next qtr, Tubi will face tough comps (revenues grew +40% y/y FQ4 last year)

Underlying Ad Trends Are Moving In The Right Direction

- Total advertising revs fell -34% y/y due to the absence of the Super Bowl and 2 less NFL playoff broadcasts than in the prior year… BUT ex these items, total ad revs were up ~+lsd% y/y

- Cable ad revs fell by -6% y/y… lapping issues with direct response

- National sports networks ad revs were down due to the absence of last year’s Super Bowl-related programming and the World Baseball Classic

- Fox News ad revenues were impacted by moderating direct response (DR) pricing declines and lower digital traffic, partially offset by higher national pricing

- TV ad revs fell -40% y/y on a reported basis due to sports schedule

- As noted above, Fox felt the impact of the absence of last year’s Super Bowl and two less NFL playoff games

- Overall advertising trends at Fox are “clearly moving in the right direction, both in the scatter market and in early upfront discussions”

- Fox is confident it will see strong political ads in H2 F25: They know how much money has been raised, and the stations are well-positioned

Renewals Continue To Grow Affiliate Revenues

- Total affiliate fees incr’d +4% y/y (vs +4% y/y in FQ2), with growth in both TV and cable segments supported by a recent cycle of affiliate renewals

- Cable affiliate fee rev were up +1% y/y (vs +0.5% y/y in FQ2)

- Growth in pricing outpaced the impact from industry subscriber declines running in the mid-8% range

- TV affiliate fee revs grew +9% y/y (vs +10% y/y in FQ2)

- Price increases across O&O and 3P FOX-affiliated stations more than offset the impact from subscriber declines

- Cable affiliate fee rev were up +1% y/y (vs +0.5% y/y in FQ2)

FQ4 Will Be Quieter In Sports But Excited By The Beta Version Of The Sport JV Product

- Key content plans during the quieter FQ4 sports calendar

- Launching Summer of Soccer: 200+ hours of live soccer coverage across the platform, starting with the UEFA European Football Championship on June 14 and Copa America on June 20

- A new schedule from Fox Entertainment: Gordon Ramsey’s Food Stars and new shows, like the 1% Club

- Focused and making progress on the Sports JV

- Have 150 engineers and executives

- Focused on sports fans outside the traditional bundle

- Have been trialing the beta and “can’t wait to launch this fall”

- Regarding the NBA…FOX is very happy with the sports portfolio they have and that is why they “didn’t pursue NBA in this negotiation”

A Few Other Key Comments

- Not looking to monetize the FanDuel option or Studio Lot

- M&A – “We obviously don’t want our balance sheet to go to waste, but we haven’t found anything yet that we’re going to do or follow. But it is something we are keeping a close eye on”

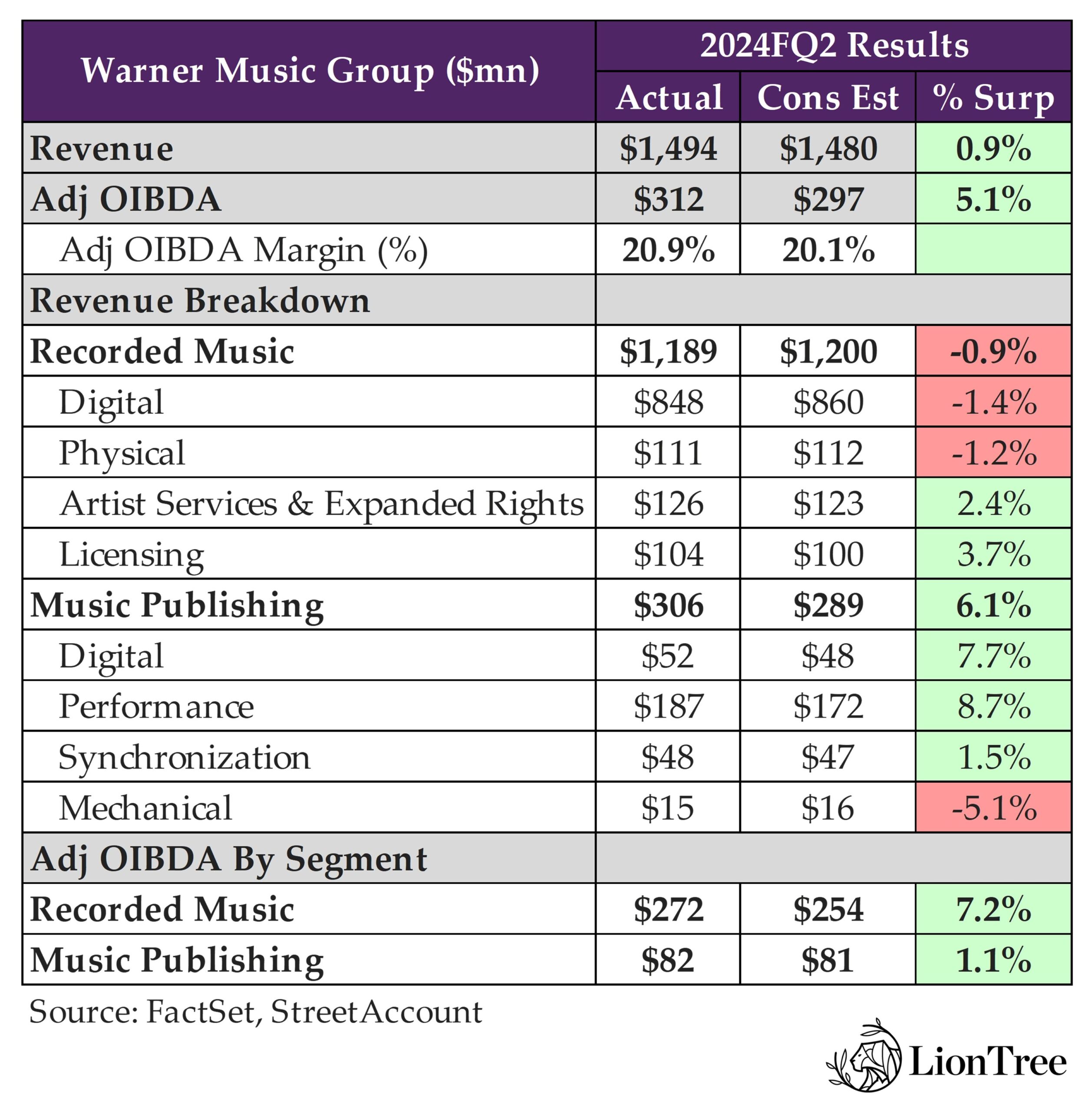

WMG Is Focused On Ensuring The Sanctity Of Its Pricing Across The DSPs

Warner Music Group’s FQ2 headline numbers were better-than-expected, with adj OIBDA closing +5.1% ahead of consensus expectations on a ~+1% revenue beat, though there were some puts and takes. Upside to the top-line was driven by Music Publishing, but there was some disappointment that Recorded Music missed primarily due to lower-than-expected digital revenue. Streaming revenue growth in the quarter came in at +11% y/y, representing a sequential acceleration that was supported by +13.5% y/y growth in Subscription revs (up from +12% in FQ1), as the company benefited from stronger music performance, subscriber growth, and subscription price increases. However, Ad-Supported revs grew +5% y/y, decelerating from +10% y/y in FQ1 due to “platform mix.”

There were a couple of questions from analysts on the call trying to assess whether WMG will participate in incremental revenue from Spotify’s bundled offer… but it sounds like won’t necessarily be the case. WMG said its job is to make sure the “sanctity” of their pricing is moving up as appropriate. However, it doesn’t mean that there won’t be higher-priced bundled offerings that are allocated for those additional content providers. WMG CEO Robert Kyncl commented, “The job of wholesalers, like music companies [and] like ourselves, is to ensure that the sanctity of our pricing across the different services, whether individual subscriptions, standalone subscriptions, or bundled offerings, are in line with each other. So, you can expect us to pursue that strategy.” The Co does continue to support further price increases and optimization especially where it thinks the offers will bring in more subscribers. That helps everyone.

WMG is on track with its restructuring plans and is set to deliver $200mn in annualized run rate cost savings, which is a plus. That said, investors grumbled about forward comments suggesting that organic streaming growth may not accelerate over the next couple of quarters despite the strong H2 slate, given comps with last year’s DSP price increases. Overall, WMG is focused on growing the Music revenue opportunity and its share of that pie, and it plans to do so via driving more engagement with its music, increasing the value of its music, and evolving how the company works together.

See below for more on what we thought was most incremental from results and the conference call.

-> WMG shares fell -8.6% in reaction to earnings, closing the week down -7.3%; YTD, WMG stock is trading -11.6% lower, while UMG stock is up +8.5% and Spotify stock is up +56.8%

Strong FQ2 With Better Financial (Especially Margins) & User Performance

- FQ2 revenue upside came from Music Publishing, while profit upside came from Recorded Music: Total FXN revs grew +7% y/y (+9% on normalized basis ex BMG/unfavorable renewal) and beat by +0.9%; Adj OIBDA beat by +5.1% (grew +9%, or +10% on a normalized basis)

- Recorded Music revs (+4% y/y and +7% on normalized basis) missed by -0.9% but adj OIBDA beat by +7.2%

- Music Publishing revs (+19% y/y) beat by +6.1% and adj OIBDA beat by +1.1%

WMG Saw Underlying Strength In Subscription & Ad Supported Streaming Revs, While Emerging Platform Revenue Can Be Lumpy

- Subscription revenue growth was the key driver for overall Recorded Music streaming rev growth

- Recorded Music Streaming revenue incr’d +11% y/y on comparable basis vs +4% in FQ1

- Subscription streaming: Grew +13.5% vs +12% in FQ1, which was driven by stronger music performance, as well as subscriber growth and subscription price increases

- Ad-supported streaming: Grew +5% y/y, decelerating vs +10% in FQ1 due to “platform mix”

- Note a few revenue comparability items in Recorded Music streaming revenue

- BMG digital revenue roll-up was -$22mn unfavorable in FQ2

- The renewal w/ an international digital partner that resulted in upfront incremental rev recognition of $27mn last quarter resulted in an unfavorable impact of $4mn this quarter and will have a similar impact in FQ3 and FQ4

- Drivers for the seq decel in ad-supported organic growth

- Saw growth and accelerating trends in the traditional ad-supported

- “But again, underlying strength [was] there in the core subscription streaming and the traditional ad-supported”

- Emerging platform’s organic growth also decel’d seq due to lumpiness

- Cited deal timing, content delivery, as well as mix of platforms for the volatility

- Believe emerging is still a “growing category” and expects it to continue to grow over the long-term

- The Co has seen “encouraging early signs in the evolution of royalty models”, but it will take time: These better align economics with premium content and grow WMG’s participation in the pie; But these shifts to more artist-centric models take time to fully implement, and the Co doesn’t expect an “immediate impact” on results

WMG Is Working To Ensure The “Sanctity” Of Its Pricing Across DSPs

- Does WMG participate in the incremental revenue from Spot’s tiered offer? It sounds like not necessarily in this case… WMG’s response:

- It is great to see price increases after 15 years of no actions by anyone

- It is great DSPs are thinking long and hard about pricing strategies, and bundled services are part of that

- WMG’s job is to make sure “sanity” of their pricing is moving up as appropriate

- But it doesn’t mean that there wouldn’t be higher-priced bundled offerings that are allocated for those additional content providers

- “All of this is, the right direction… this is good news, in my opinion, to push forward”

- “The job of wholesalers, like music companies like ourselves, is to ensure that the sanctity of our pricing across the different services, whether individual subscriptions, standalone subscriptions, or bundled offerings, are in line with each other. So, you can expect us to pursue that strategy”

- WMG will “continue to advocate for further increases, as well as more sophisticated price optimization, especially as DSPs improve their offerings to bring in more subscribers”

Cost Reduction & Tech Plans Are On Track

- Are on track with the restructuring plans set to deliver $200mn in annualized run rate cost savings, but the full savings will not be realized until the end of FY25: Nonetheless, the majority of the changes have already been implemented

- This includes centralizing certain functions and exiting owned and operated media businesses

- Sold the entertainment websites UPROXX and HipHopDX

- Achieved modest cost savings in the quarter, the majority of which were reinvested into tech

- Enhancing Tech capabilities: Made improvements to their royalty systems and the tools used to identify unclaimed revenue; Overhauled their global supply chain, enabling the ability to scale 3P distribution business; Transformed proprietary tools that identify fan trends while building new ways to engage with Superfans

Outlook For The Rest Of The Fiscal Year

- Strong H2 slate…: H2 includes music from Dua Lipa, Twenty-One Pilots, Sia, Gunna, Megan Thee Stallion, David Guetta, Fred Again, Charlie Puth, and Maria Becerra.

- … BUT toned down comments about organic streaming growth accelerating over the next couple of qtrs, despite the strong H2 slate: Have lots of great content coming BUT “keep in mind is that we’ve now seen the full impact of the Spotify price increases in our results and then [in] the second half, we’ll be lapping last year’s price increases with the other DSPs, namely Apple and YouTube”

- “But we’re continually encouraged by the subscriber growth as well”

- BMG will have revenue impact in the -$25-30mn range in both FQ3 and FQ4 (vs -22mn in FQ2), eventually rolling off completely in FY25

- “Our goal continues to be to deliver operating cash flow conversion of 50-60% over a multi-year period, which we expect to achieve for full year 2024”

Other Key Comments On Potential M&A And Super Fans

- What happened with the bid for Believe? Mgmt didn’t provide any color on why they specifically decided not to move forward but did indicate they will continue to look for assets that will augment their strategy

- The Co continues to see plenty of runway on organic investment but “it’s our job to survey the market, and if there’s inorganic opportunities that will accelerate our initiatives, we’ll take those. But I think we’ve always demonstrated to be good stewards financially, and we will continue to do that”

- There are a lot of oppties w/ music content right, but the Co will approach them in a disciplined way: There is more out there than WMG can afford today, and they are diligent about what they go after and associated returns; Higher rates make it more rigorous, but the interest and pricing speaks to the value of music; WMG “still see[s] runway to invest”

- WMG is best to monetize superfans is as “a controlled solution”: The Co has been working on their plan to better monetize super fans – “It’s well-progressed, but nothing new to announce on that”

- The Co is naturally set up “to be the right place to do this and do it cross-platform”; Believes “it has to be a controlled solution” vs developing the strategy with any individual DSP

- WMG can always partner with the DSPs, but through a WMG offering

Uber’s Core Fundamentals Remain Intact

Uber’s stock sank on Wednesday morning, after posting a -$0.32 loss per share in Q1, which was significantly below the $0.22 profit per share that the Street was expecting. That ended Uber’s streak of consecutive profitable quarters, and the $654mn net loss was the steepest quarterly loss since Q3:22, coming in far below the prior Q4’s $1.4bn net profit. Uber attributed the loss to a write down of the Co’s equity investments, with CEO Dara Khosrowshahi stressing on CNBC that the results had “nothing to do with the operating business” (link). That was supported up by the Co’s adj EBITDA, which grew +82% y/y, reaching a record $1.38bn and beating cons by +5.5%.

Digging deeper into Q1 results, gross bookings slightly missed (-0.7% below cons), as holiday timing shifts and FX were headwinds in Mobility, though total revenue still beat by +0.4%. In terms of the Q2 adj EBITDA guidance, it was in-line at the midpoint, while gross bookings guidance slightly missed at the midpoint, as FX will continued to be a headwind. Specifically in Mobility, adj EBITDA margin is expected to be down slightly seq due to expected higher levels of investment and seasonality trends. Overall, Uber is not only seeing growth, but also increased engagement amongst its existing customers. Monthly Active Platform Consumers (MAPC) growth in Mobility is outpacing overall MAPC growth, and order frequency in Delivery is at an all-time high. Uber One members now generate 32% of Mobility and Delivery gross bookings, with members spending +3.4x more than non-members per month.

That being said, Uber is still focused on bringing on new customers via newer use cases, with 20%+ of new customers in Mobility coming from the growth bets category (Hailables, U for Be, Reserve, etc.), and a new partnership with Instacart represents the “addition of a very high quality and highly targeted suburban audience to the Uber Eats ecosystem and to our merchants” on the Delivery side (see Theme #7 for more on Instacart results). Grocery is a particular focus not only on the Delivery side, but also in advertising, which is being seen as an “enormous” and “high-margin” opportunity, given that 15% of monthly actives on Eats bought from grocery in Q1. Non-restaurant advertising is at the point where restaurant advertising was ~3 years ago (now reached 2% of gross booking), and Uber believes non-restaurant can surpass even that.

Overall, while the net loss was a surprise to the Street, the company’s core fundamentals are still strong, and the business segments and new use cases continue to grow. See below for more of what we thought was most important from the Co’s results.

-> Lyft also reported its Q1 results this week, and it was a series of beats across rev of $1.28bn (+10.3% beat), adj EBITDA of $59.4mn (+8.0% beat), and Bookings of $3.69bn (+3.1% beat); Q2 guidance also easily came in above expectations, with adj EBITDA $95-100mn above cons $81.5mn and Bookings of $4.0-4.1bn above cons $3.98bn; The Co also provided some FY24 directional commentary, w/ Ride growth expected to grow in the mid-teens y/y (w/ H2 expected to be ~15%), Gross Bookings growth coming in slightly faster than Rides growth y/y, and adj EBITDA margin of ~2.1%; The Co also remains on track to generate positive FCF for the full year

-> Also to note, Uber will be having its annual “GO-GET” event on May 15; This year’s theme will be “Togetherness”, and will announce new products, features, and partnerships; Lyft also announced that it would hosting its first ever Investor Day on June 6

-> Uber fell -5.7%, while Lyft was up +7.1% in reaction to their respective results; Uber ended the week down -3.2%, while Lyft closed the week down -0.1%; YTD, Uber is up +8.8%, while Lyft is up +14.6%

Uber’s Miss On Gross Bookings Did Not Materially Flow Through To Revenue And Profitability / User Growth Has Been Consistent BUT Write-Off Driving Adj EPS Loss Was Unexpected

- Gross bookings missed by -0.7%: Grew +20% y/y (vs +22% y/y in Q4)

- Trips growth outpaced booking growth for the fifth straight qtr: Trip growth was up +21% y/y (vs +24% y/y in Q4) to 2.6bn, driven by both Mobility and Delivery growth

- Frequency (monthly trips per MAPC) grew +6% y/y to 5.8 (in-line with last qtr), underpinned by 7.1mn drivers and couriers on the platform

- Revenue beat by +0.4%: Q1 rev grew +15% y/y (in-line with last qtr), beating cons by +0.4%

- Take rate beat: Came in at 26.9%, which was above cons 26.6% (Mobility beat, while Delivery missed)

- Adj EBITDA reached a new record and beat by +5%: Grew +82% y/y to $1.4bn (vs +93% y/y to $1.3bn in Q4)

- Adj EPS loss was a big surprise to the Street: Came in at -32c vs cons 22c and -8c in Q1:23

- Net loss of $654mn includes a $721mn net headwind from unrealized losses related to the reevaluation of its equity investments

- Overall user growth was in-line with the last two qtrs: MAPC grew +15% y/y (in-line w/ +15% y/y in Q4 and Q3) to reach 149mm (down from 150mn in Q4)

- Reached new FCF record: $4.2bn for the TTM

Q2 Guidance Accounts For Similar Patterns As Q1

- Q2 adj EBITDA guidance was in-line w/ cons at the midpoint: $1.45-1.53bn vs cons $1.49bn (+58%-67% y/y growth)

- Q2 gross bookings guidance slightly missed at the midpoint: $38.75-40.25bn vs cons $40bn (+18%-23% y/y growth)

- Expect similar trends in Q2 in each of the three variables as seen in Q1

- Audience (how many users of the product)

- Frequency (how often the product is being used)

- Pricing

- FX will also be a headwind: Outlooks assumes ~-3ppt currency headwind to total report y/y growth, including ~-5ppts currency headwind to Mobility’s reported y/y growth (primarily from the Argentine peso)

- “Exactly where they want to be” on 3-yr CAGR outlook: Back in Feb, the Co guided for “mid to high teens” growth

- Expect similar trends in Q2 in each of the three variables as seen in Q1

Mobility Gross Bookings Were Impacted By Timing Shifts And Seasonality / Expect Investments To Ramp Back Up In Q2 Causing Some Margin Lumpiness

- Mobility missed on gross bookings but beat on all other fronts in Q2

- Gross bookings growth decelerated seq to +26% y/y CC, down from +28% y/y CC in Q1 and +30% y/y in Q4, missing cons by -2.8%

- What drove the decel? ~1pt came from deconsolidating the non-ride sharing portion of their Careem biz in Dec, which used to be included in Mobility’s results; Seasonally, LatAm last year saw stronger demand in Brazil around Carnival that did not recur in Q1 of this yr, and Easter and Ramadan shifted between the qtrs, creating some lumpiness on a comp basis

- Revenue growth also decelerated seq to +29% y/y CC, down from +31% y/y CC in Q1 and beat cons by +2.0%; Rev increase y/y was primarily attributable to an increase in Mobility Gross Bookings due to an increase in Trip volumes

- EBITDA margin of 7.9% was a continued step up from 7.5% in Q4 and 7.2% in Q3; Margin improvement y/y was primarily driven by better cost leverage from higher volume

- Take rate of 30.2% came in above cons 28.7%

- Gross bookings growth decelerated seq to +26% y/y CC, down from +28% y/y CC in Q1 and +30% y/y in Q4, missing cons by -2.8%

- Held back some investments in Mobility in Q1 due to seasonality trends, which will ramp back up in Q2: This will cause some lumpiness in Mobility margins, but they remain “very confident” that Mobility is still on a “great trend” for continuous margin improvement

- Active driver growth continued to pace down q/q: Active drivers were up +29% y/y (vs +30% y/y in Q4 and +32% y/y in Q3)

- India crossed 1mn drivers for the first time ever in March, becoming the third country globally to do so

- Where is growth in Mobility coming from?

- “Most significant part of growth is coming from audience”: MAPC growth in Mobility was up +17%, outpacing overall MAPC growth of +15% y/y

- US growth is also “very, very healthy”: Don’t disclose US vs non-US growth, but US is their largest market in terms of gross bookings so “we wouldn’t be able to grow at these rates…without the US growth being very, very healthy”

- New products have been a “particular area of growth” and “introducing a whole new audience to our marketplace”: Looking across Hailables, U for B, Reserve, UberX Share, their new health biz, these new growth bets are growing ~80% y/y, and 20%+ of new customers are coming from the new product category

- Shared Rides gross bookings were up 6x y/y, as they continue to optimize the product

- Further scaled taxi offering in Q1, “significantly” growing taxis in New York City and Los Angeles and officially launching Black Cabs on Uber in London

- Uber Business continues to see “strong adoption” of premium products, with 50% of corporate travel activity on Uber happening on products like Business Comfort, Uber Black, and Reserve

- Work commutes are making a comeback post-pandemic: Workday session growth consistently outpaced leisure, holiday, and late-night session growth, while managed Uber for Business Gross Bookings were up 40%+ y/y

- Airport growth, especially internationally, was “particularly strong”

Being Aggressive, But Strategic, About Building Out Use Cases For Delivery

- Delivery results were a mixed bag in Q2

- Gross bookings grew +17% y/y CC, which was in-line with Q4 and beat cons by +0.9%

- “Our US and Canada growth rates are actually higher than that”

- But revenue grew +4% y/y CC, which was in-line with Q4 and missed cons by -2.0%

- Record adj EBITDA margin of 3.0% was a continued step-up from 2.8% in Q4 and 2.6% in Q3; Margin improvement y/y was primarily driven by better cost leverage from higher volumes and increased Advertising revenue

- Take rate of 18.2% was below cons 18.7%

- Gross bookings grew +17% y/y CC, which was in-line with Q4 and beat cons by +0.9%

- Other key milestones in Q2 –

- Delivery MAPC growth accelerated y/y across many top markets, notably the US, Canada, and Mexico

- Order frequency reached an all-time high

- Reached a milestone of 1mn+ active merchants, up +12% y/y

- What’s been driving accelerating Delivery growth?

- Most of the growth last year was on price: Was growing closer to 10% early last yr, now growing in the teens, and “the nature of that growth is improving as well”

- Now, price is a “relatively small portion” of the growth, and audience and frequency are the largest portion of the growth

- Have “a great service” and “a significant selection” (active merchants are up +12% y/y)

- Improving pricing (i.e., merchant-funded promos are up +100bp y/y, lowering effective price to consumer)

- Quality – continue to improve their defect rate

- Continue to spend “aggressively” to market the brand

- Cross-Platform benefits between Mobility and Delivery

- Announced partnership with Instacart – “this partnership is about playing offense”: Uber Eats will not power restaurant delivery on the Instacart app; This is “another growth vector for our US Delivery audience. We’ll be able to reach new consumers who are currently not active on Uber Eats, giving us an opportunity to improve our category position in key areas like the suburbs”

- BUT “make no mistake: we remain committed to executing against our Grocery & Retail strategy

- Expect similar partnerships in the future? Partnerships b/w Instacart and Uber Eats relied on tech already used to integrate Uber Eats into the Uber app; “Going forward, we can leverage this same tech for similar channel partnerships”

- Remain “very positive” on grocery and retail as biz growth “remains quite strong”: Gross bookings are up ~40% y/y, and despite that strong growth, they were still able to expand Delivery EBITDA margins, which was partly contributed to by improvement in the profitability of the grocery biz

- Still not at positive EBITDA margin, but it is improving q/q and y/y

- Continue to expand offerings: Making progress on grocery selection; Consumers can now benefit from grocery loyalty programs while shopping on Uber Eats, with in-app access to member prices and discounts at certain grocery merchants

- “Feel very good about the path we have to getting profitability on grocery” – drivers will be:

- Power of the platform: ~15% of Delivery users are ordering groceries, which is up q/q and y/y

- Continue to see oppties on ads, which are margin accretive as they bring CPG players into the platform for grocery advertising and lowering some of the consumer promotions they have

- “We think that grocery will eventually be a very strong part of the overall portfolio”

- Suburban strategy for Uber Eats? “Very similar” to general strategy for Delivery biz: Generally growing faster in the suburbs than in urban destinations (where they have higher penetration)

- How does Instacart partnership fit in? “Represents the addition of a very high quality and highly targeted suburban audience to the Uber Eats ecosystem and to our merchants. And we think that additional demand from this high-end consumer is going to be welcomed by our merchants… we definitely think that the Instacart deal puts us in a better position for growth going forward in the suburbs”

Push For Continued Uber One Adoption Is Working As Subscription Fees Pass The $1bn Mark

- Uber One membership fees are now in excess of $1bn

- “We think there’s a lot more growth there”

- Uber One strategy is largely the same domestically and globally

- Uber One members now generate 32% of Mobility and Delivery gross bookings (up from 30% in Q4)

- Make up 45%+ of Delivery gross bookings “where generally we’re more highly penetrated”

- Uber One members spend 3.4x as much as non-members per month

- Working on “a bunch of pretty exciting new initiatives”

- Continue to optimize the use of Uber Cash for Mobility: 25% of Uber Cash earned on Mobility in the US is being redeemed on Delivery, which is up from “mid-teens” when they originally rolled out the benefit; Business riders can also get Uber Cash, and they’re seeing 60%+ of Uber Cash on Mobility being redeemed on Delivery as well

- Introducing cash back accelerators, where Uber can increase the cash back amount for any product to the extent they’re trying to drive the product

- More member exclusives coming up, where members have exclusive access to events and experiences “which will surprise and delight our members”

- Moving more members on a global basis to annual pass: Annual pass results in “significantly higher” retention rates (retention increased ~200bps y/y in March)

- Continue to optimize the use of Uber Cash for Mobility: 25% of Uber Cash earned on Mobility in the US is being redeemed on Delivery, which is up from “mid-teens” when they originally rolled out the benefit; Business riders can also get Uber Cash, and they’re seeing 60%+ of Uber Cash on Mobility being redeemed on Delivery as well

Non-Restaurant Advertising Is A Key Area Of Focus, With Grocery Being Viewed As A Particularly Big Oppty

- Expect to beat $1bn advertising revenue target for the year

- Non-restaurant advertising “is still really in nascent stages” vs restaurant advertising (which has reached 2% of gross bookings)

- Think that Uber’s “sponsored items” product can surpass restaurant advertising’s 2%: For example, mgmt. flagged that Instacart is in the mid-2s in terms of advertising as a %age of gross bookings; “Sponsored items is [at the point] where we were in sponsored listings for restaurants three years ago”

- Fully launched sponsored items in UCAN, and it is now being scaled to 8 addtl priority mkts in 2024

- Active w/ ~500 top CPG brands and seeing “very strong retention as we expand”

- “Really, it’s going to be about the growth of the underlying grocery platform…we think it can be an enormous opportunity, and it can a high-margin opportunity as well”

- Increasing grocery audience: ~15% of monthly actives on Eats bought from grocery in Q1, which is up y/y

- New advertising oppties w/ Instacart partnership: When users click through Instacart and they come to the Uber Eats web view app, they are shown Uber’s ads as its Uber’s space to use and monetize

- Remain “quite bullish” on rider ads: Seeing “very strong” engagement from riders, with a click-through rate of 2.5%+, vs the industry avg of <1%; Video ads and tablets “continue to be a very promising growth area for us”

Not Feeling Much Of An Impact From Minimum Wage Regulations As A Co, But Find That It Is Hurting Couriers, Customers, And Merchants

- Update on European gig economy regulation? EU lawmakers “essentially voted to maintain a status quo there with platform worker status continuing to be decided on a country-by-country basis. Member states have until mid-2026 to implement that”

- Uber’s POV: Think that the deal is “really unlikely” to bring major changes to the current situation in “the vast majority” of EU countries

- Impact of minimum wage regulation in Seattle and New York? “Think some of the regulation that we’ve seen has actually been very unpopular with couriers, restaurants, and customers”

- Seattle: Delivery order volumes decreased -45% y/y, which has resulted in courier wait times increasing +50% y/y; Couriers are making more per order, but getting “a lot less” orders, which has resulted in 30% of active couriers leaving the platform

- Seattle city council is bringing forward reform to make the standard “lower and much more viable” for the platforms: “We think we’ll have a positive outcome there”; Believes Seattle’s “poor regulation… has hurt the people that they’re supposed to protect”

- New York: Similarly, have had to slot couriers; Have a waitlist of 20k+ couriers who want to be on the platform, but because of the regulation, have had to reduce the number of couriers on the platform by ~25%

- Seattle: Delivery order volumes decreased -45% y/y, which has resulted in courier wait times increasing +50% y/y; Couriers are making more per order, but getting “a lot less” orders, which has resulted in 30% of active couriers leaving the platform

- Have been able to absorb the financial hits of all these different regulations, as seen in Uber Eats profitability being up +83% y/y

- “We’re a big company with a lot of markets. We’re quite diversified. Our technology continues to drive a more effective marketplace that allows us to absorb these regulations”

- “We’re hoping that…regulators see the path going forward because so far regulation has definitely hurt the people that it’s supposed to protect”

Uber Is Looking To Get In Early And Partner With The Autonomous Vehicle (AV) Industry For The Long-Term

- AV impact on Uber and potential for new competition? “AV technology at maturity is going to be very good for the industry [and] it’ll be great for Uber”

- Will make rides safer

- Will expand the marketplace by lowering prices which usually means higher adoption

- BUT tech will take a long time to develop and a regulatory framework needs to be put in place, making the transition from human drivers to AV “relatively long”

- Individual and fleet owners of AVs will make more money and have a higher ROI if they include their car into the Uber ecosystem and into Uber demand

- Technology – for pricing, matching, routing algorithms, payments, etc. that are already in place on a global level

- Demand – which enables them to partner with these AV providers to drive utilization of their assets

- Have been expanding existing partnerships

- Waymo: Building on their successful Waymo partnership offering fully autonomous rides on Uber in Phoenix, have now expanded to autonomous deliveries on Uber Eats

- Cartken / Mitsubishi Electric: Expanded partnership with Cartken and partnered with Mitsubishi Electric for autonomous robot deliveries in Japan, the first international market to have autonomous delivery on Uber Eats

- “We’re looking to partner with big players and small platforms…as this technology develops, we think we will be a big partner in it”

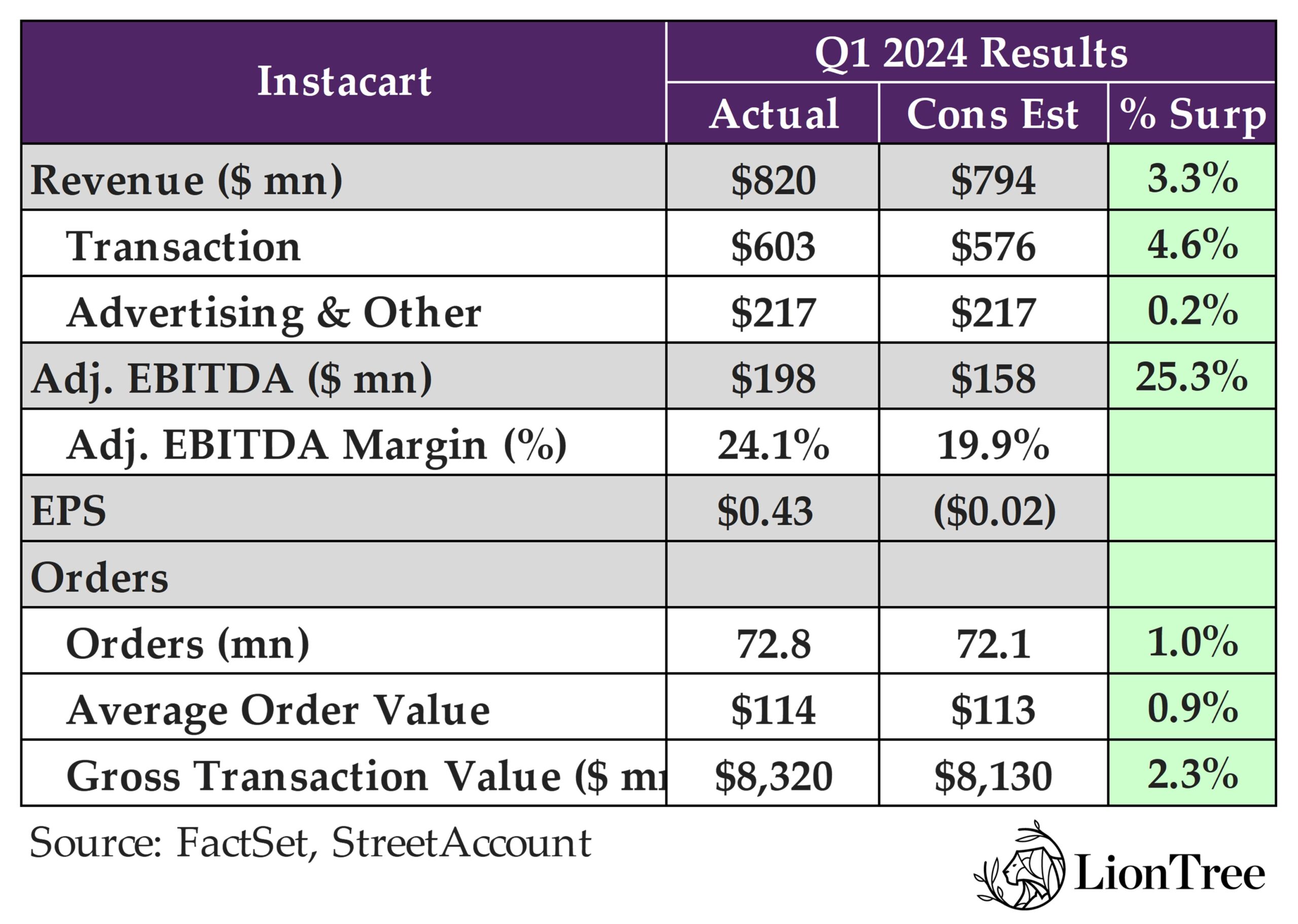

Instacart Hitches Its Cart To Uber To Drive Another Avenue Of Growth

Instacart’s announced partnership with Uber took center stage this week. While most Americans shop for groceries (online or in a store) at least once per week, more than one-third also order takeout or delivery at least once a week, and this partnership helps the Co to service that need as well. While details on the partnership were limited, Instacart gets paid an affiliate fee and will have “positive unit economics” right out of the gate. Its Instacart+ subscribers will also love this, as it provides more value for their current subscription. Progress on this key tie-up will be closely followed…

Regarding Q1 results, they were better-than-expected, especially on the adj EBITDA margin side (24.1% vs cons 19.9%). Gross transaction value (GTV) also accelerated for the fourth consecutive qtr to +11% y/y. The drivers were: 1) improving mature cohort declines and bigger new cohorts than pre-pandemic levels; 2) A lessening of the y/y EBT SNAP headwind, which had the biggest impact in Q4 but a smaller impact in Q1 primarily because of the successful EBT SNAP launches with Kroger and Costco; and 3) Some one-time items. What didn’t go over as well was that GTV growth will likely decelerate sequentially in Q2 to +7-9%, given that the benefit of the leap day is largely expected to be offset by EBT SNAP moving from a modest y/y headwind to a tailwind from Q1 to Q2.

Another focus area was advertising, considering the big opportunity ahead. The guidance that Q2 y/y ad revenue growth will be roughly similar to Q4 and Q1’s levels (+7% and +9%, respectively) was lower than hoped, and it sounds like some large brand relationships pulled back. Given the Instacart’s customer concentration, it was hard for the company to avoid an impact. However, management is working to diversify its advertiser base and is still guiding for an investment rate of 4-5% of GTV over time vs the 2.6% seen in Q1.

Caper Carts are also seen as a significant long-term opportunity for the company. Early customer feedback has been positive, and grocers are excited about the ad options there as well.

The questions about competition always come up on the conference calls, particularly given Amazon’s recent announcement regarding its new grocery delivery subscription for Prime members and EBT cardholders (link). But Instacart still believes it is best positioned in the grocery space due to the company’s technology integrations, breadth of longstanding retailer and brand partnerships, and ability to deliver a great customer experience. The Co also has a significant 1P data advantage. Lastly, along with earnings, Instacart announced a C-suite change with a new CFO, Emily Reuter (former exec at Uber), coming in to replace Nick Giovanni.

See below for more on what we thought was most incremental and interesting from Instacart’s Q1 results and call.

-> Instacart shares pulled back -1.4% in reaction to the print but is still trading up +48.9% YTD; Instacart stock is up +16.5% from its IPO price

Strong Q1 With Better Financial (Especially Margins) & User Performance

- Continued acceleration of GTV y/y growth, which beat cons by +2.3%: Grew +11% y/y in Q1, up from +7% y/y in Q4, +6% y/y in Q3, +6% y/y in Q2, and +3% y/y in Q1)

- Total rev grew +8% y/yand beat cons by +3.3%

- Transaction revenue grew +8.0% y/y and beat cons by +4.4%

- Advertising & other revenue grew +9.0% y/y and was ~in-line with cons

- Adj EBITDA grew +17% y/yand beat cons by +25.0%; It was 2.4% of GTV (vs 2.5% in Q4)

- Order growth y/y also improved for the fourth consecutive qtr:Grew +9% y/y to reach 72.8mn, and average order value (AOV) of $114 was up +2.0% y/y

- Repurchased ~27mn shares worth $751mn: Have total capacity of $249mn left in its existing authorization

- “We plan to opportunistically repurchase shares”

Q1 GTV Outperformance Benefitted From New Cohort Growth, Plus Some 1 Timers…

- Q1 GTV outperformance benefitted from:

- Cohorts: Cont’d improvement in cohort dynamics where mature cohort declines continued to improve, and new cohorts continue to be bigger than pre-pandemic cohorts

- EBT SNAP: Also saw lessening y/y EBT SNAP headwinds, which had the biggest impact in Q4 and a smaller impact in Q1, primarily because of the successful EBT SNAP launches with Kroger and Costco

- One-time items: It included just over 1 %age pt of growth from leap day, in addition to stronger than expected seasonality, as Q1 was an “exceptionally bad winter season”, especially vs the prior yr qtr

…BUT Q2 GTV Growth Will Slow Seq Due To Lack Of One-Timers, While Q2 Adj EBITDA Guidance Is ~In-Line

- Q2 guidance for GTV y/y growth will be in the +7-9% range vs Q1’s +11%: The seq slowdown is primarily due to the not having the benefit of inclement weather, and while Q2 also will not have the benefit of leap day, this will be offset by EBT SNAP moving from a modest y/y headwind to a tailwind from Q1 to Q2

- The guidance is still a step up from Q4’s +7%

- Q2 adj EBITDA guidance is ~in-line: Mid-pt of $180-$190mn compares to cons $184mn

- Implies adj EBITDA as a % GTV at a low of 2.2% and a high of 2.4%; Q2 y/y growth will be driven primarily by transaction revenue and adj OpEx leverage

Advertising Growth Has Yet To Accelerate, But The Opportunity Remains Large

- Q1 Advertising & Other rev growth was flat seq: Grew +9% y/y in Q1 vs +7% in Q4 and +19% in Q3

- Q1 Advertising & other investment rate was +2.6%, down -7 bps y/y, BUT the Co still expects it to reach 4-5% of GTV over time