TGIF to another very busy earnings week! We have thoughts and updates out across Cloud/AI, E-Comm, Online Travel, Sports Betting, Tech Hardware, Food Delivery, and Live Entertainment, among other areas!

In the meantime, the markets continued their rebound, with the S&P 500 and Nasdaq closing up +0.55% and +1.43%, respectively, as Big Tech registered some nice gains, despite concerns on the consumer coming out of retail earnings.

See below for key perspectives and updates in this edition (all are clickable links):

- Earnings Scorecard – Week 3

- Amazon Follows Suit By Stepping Up CapEx Spend To Meet AI Demand

- The NBA Media Rights Deal Suggests The Market Is Not Past Peak Sports Rights Values

- UMG Sees A “Substantial Improvement” In Total Value From The New TikTok Deal

- Pinterest’s Platform Transformation Is Delivering “Compounding Benefits”

- Live Nation’s Results Point To No Slowdown In Live Entertainment

- DraftKings: The Odds Are Still In Favor Of Growth + Profitability In Sports Betting

- Apple’s Record $110bn Buyback Takes Center Stage

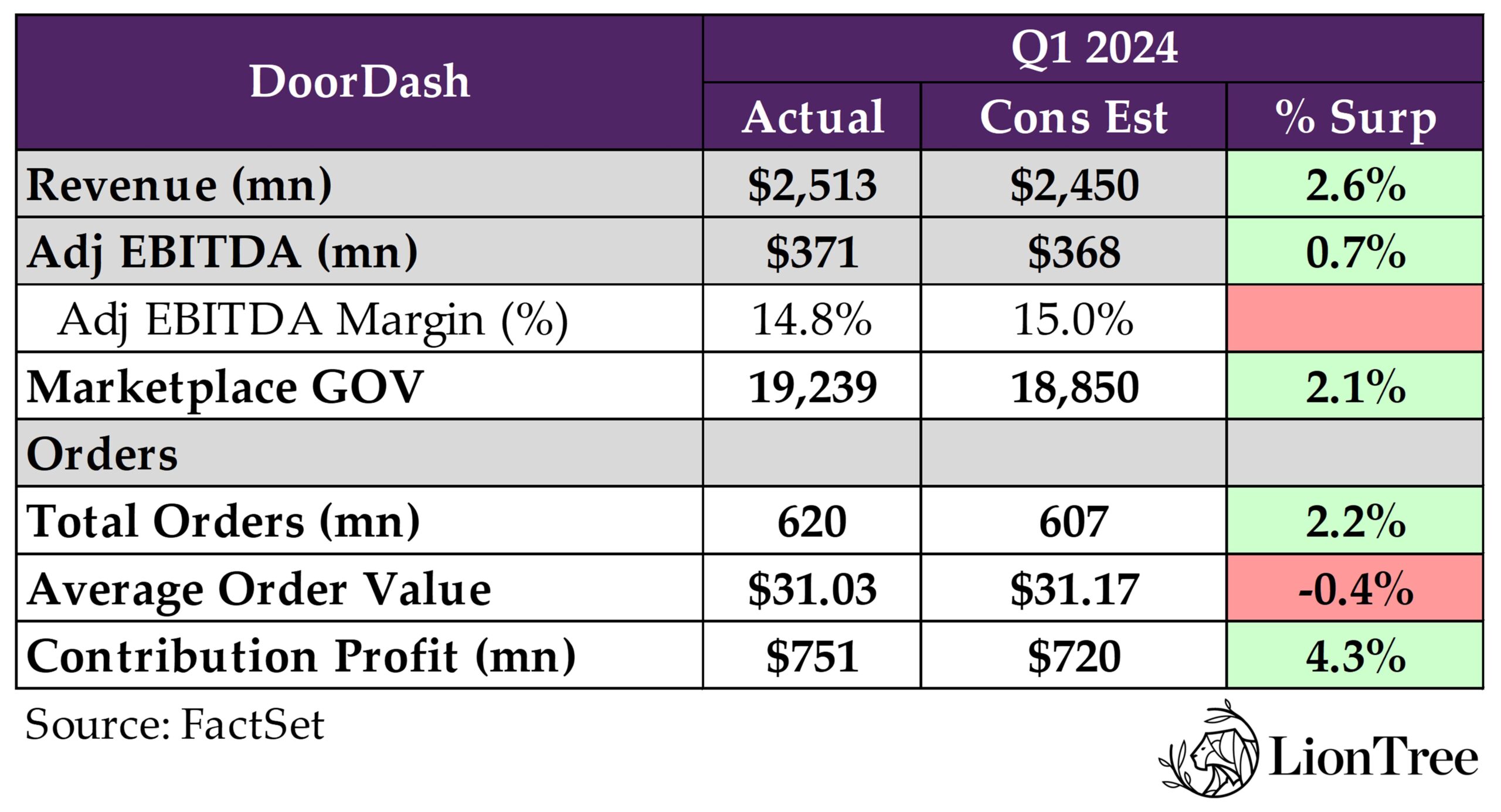

- DoorDash Expects To Be Dashing More Strongly In H2

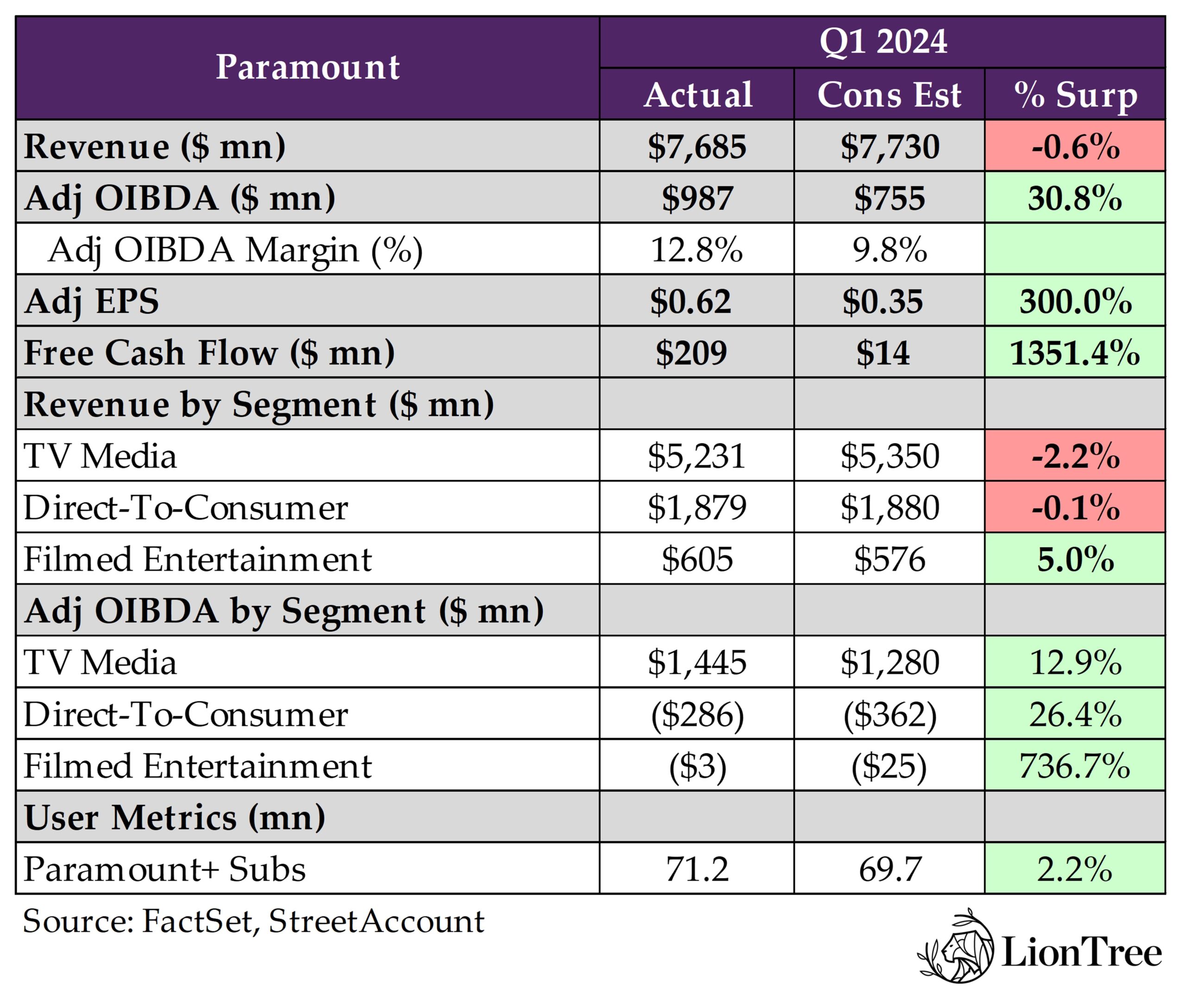

- Paramount’s Story Continues To Unfold

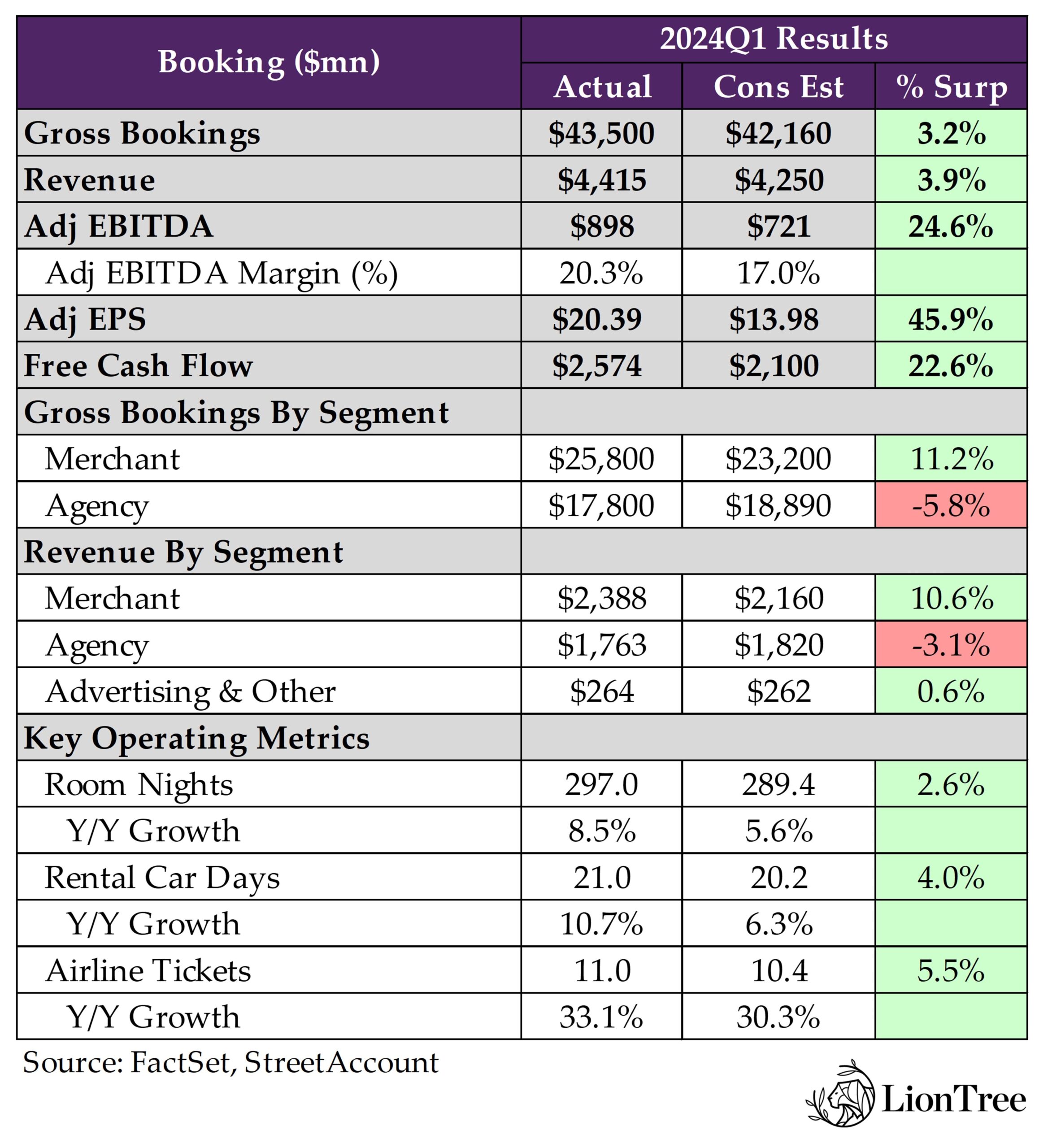

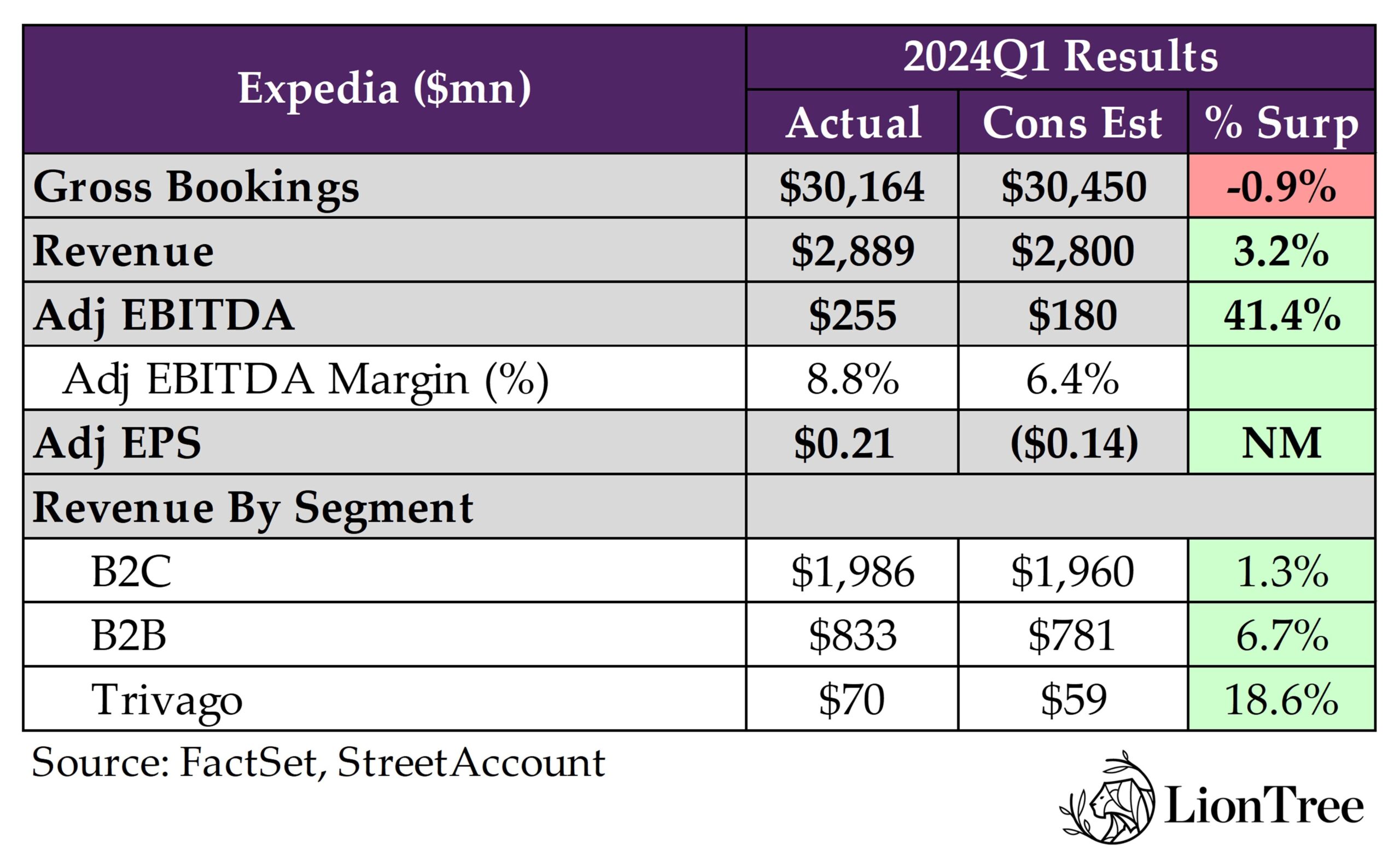

- OTAs Offer Divergent Views Of The Travel Landscape

This is a pretty dense edition. Enjoy the read and let me know if you have any questions or comments.

Best,

Leslie

P.S. Quick question – How much has Apple spent on stock repurchases over the last decade (hint: it is more than any other tech company)?? The answer is… $650bn since 2012!

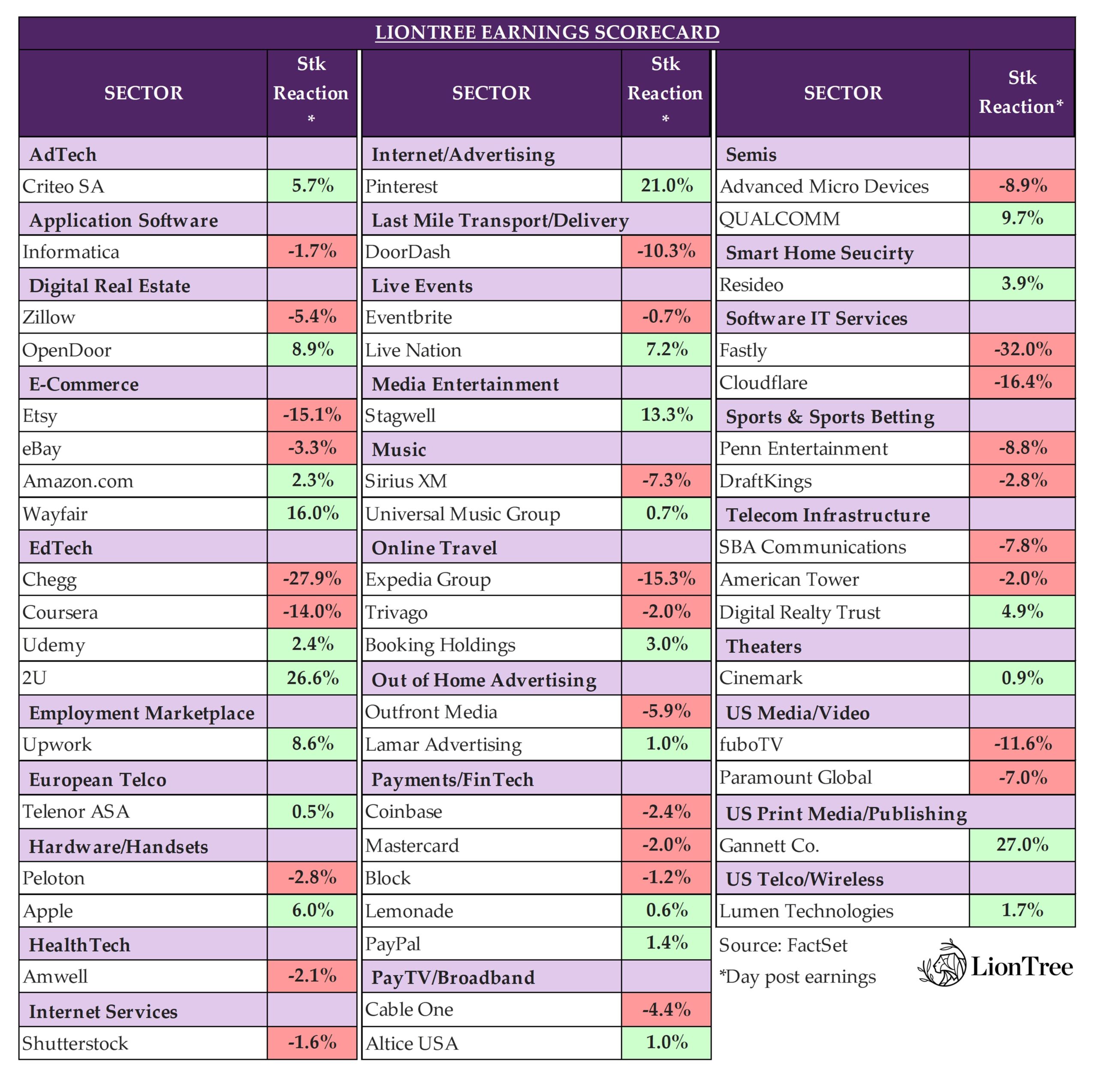

Earnings Scorecard – Week 3

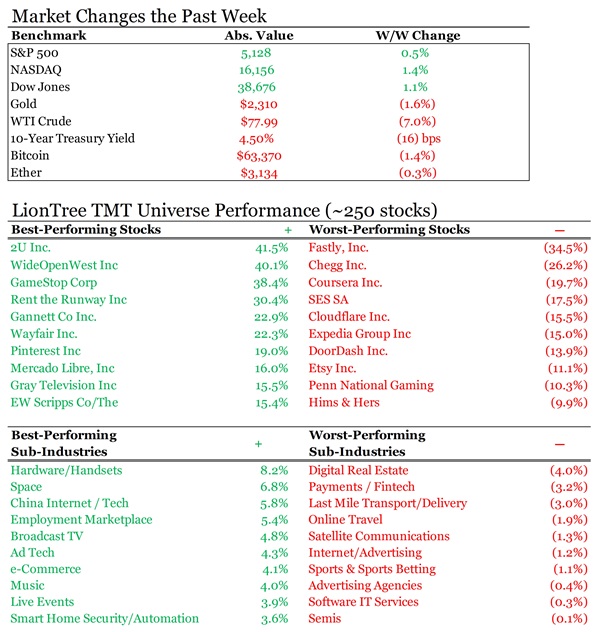

There was a deluge of earnings prints that came out this week, as 52 companies in the LionTree Universe reported results (more than double the 25 companies that reported last week). Similar to last week, stock price reactions were biased to the downside. 28 stocks (53.8%) traded down, and 24 stocks (46.1%) traded up. Fastly was the worst performer of the week (down -32.0%), while Gannett was the best performer (up +27.0%)..

Amazon (see Theme #2) and Apple (see Theme #8) finished out the MAANG reports for the quarter, with the stocks trading up +2.3% and +6.0%, respectively, in reaction to their results. Also finishing out their sector’s reports was Pinterest (see Theme #5), which was the last of the major digital media Cos to share its results and soared +21.0% in reaction.

Paramount (see Theme #10) kicked off legacy media earnings this week and traded down -7.0%. On the music side, Universal Music Group (see Theme #4) was up +0.7%, and on the Live Entertainment side, Live Nation (see Theme #6) was up +7.2%.

It was also a big week for the online travel names, and reactions diverged between the two big players, with Booking Holdings trading up +3.0% but Expedia falling -15.3% (see Theme #11). Also see a tough market response was DoorDash (see Theme #9), which fell -10.3% the day after posting its results.

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe.

Amazon Follows Suit By Stepping Up CapEx Spend To Meet AI Demand

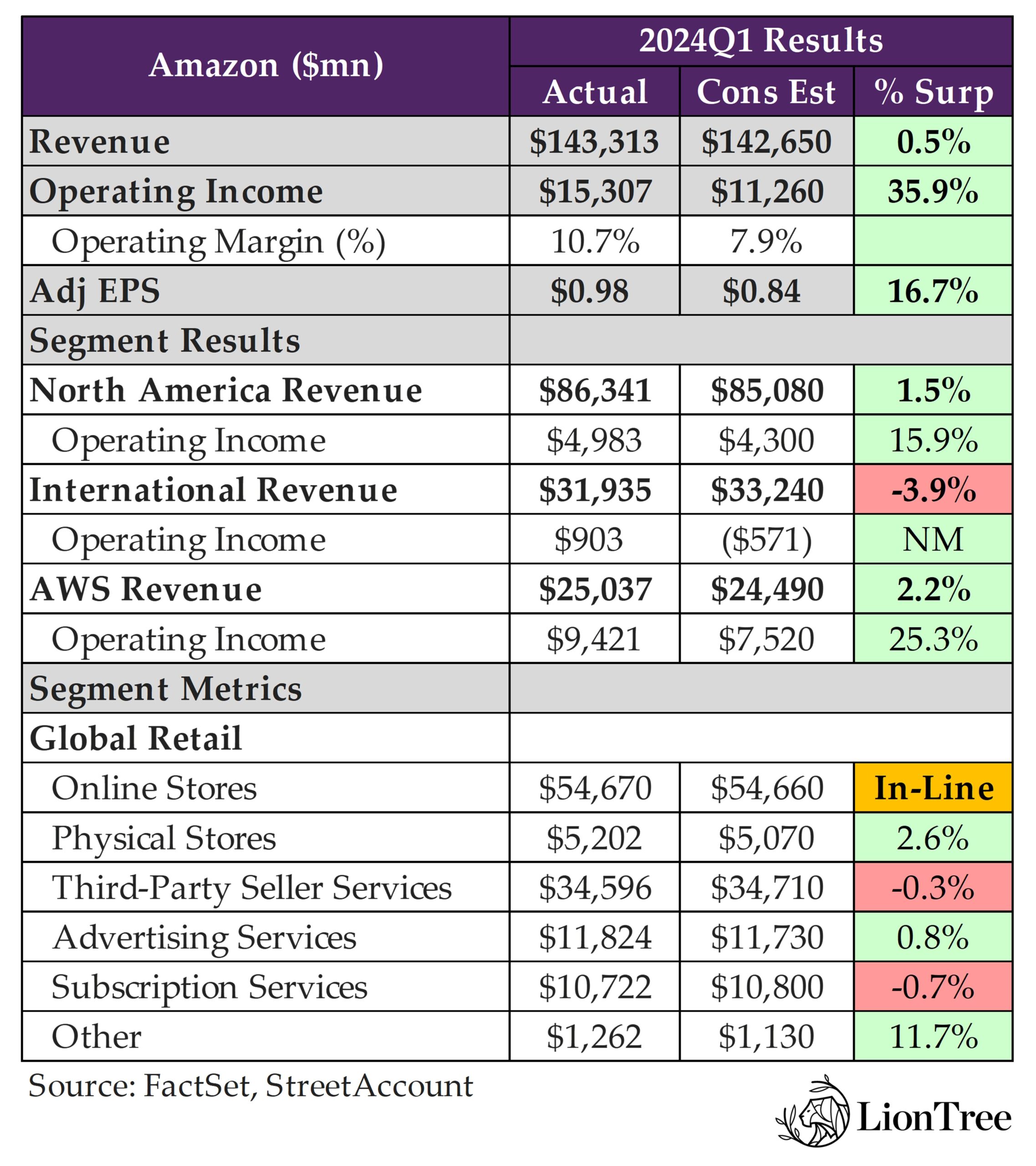

The impact and focus on AI and higher CapEx spending to support tech infrastructure has been the key theme for Big Tech this earnings season (see last week’s Theme #2 on Meta and Theme #3 on Alphabet). Now, Amazon has followed the lead of its other Big Tech peers by guiding for more spending to support customers’ capacity needs in AWS. Q1 CapEx of $14bn will be the low point for the year. While this means more upfront costs, visibility to generating returns on these investments is high, so the company should get support from Wall Street. Amazon’s accelerating top-line growth in AWS (from +13% y/y to +17% y/y, and the biz is now at a $100bn+ annual revenue run rate) also indicates success with its AI products and capabilities. AWS customers are through the cost optimization phase and are now renewing their infrastructure modernization efforts. The step up in AWS’s growth rate coming in combination with higher margins is notable as well (AWS op income margins at 2.8%, up +710bp y/y).

The core Stores business performed solidly (+6.9% y/y in Q1 vs +8.9% y/y in Q4), and Amazon is further expanding selection, focusing on providing value and accelerating delivery speed (setting another record on speed for Prime customers in Q1), while lowering cost to serve, which importantly has more to room to go. North American operating margins at 5.8% also have not likely arrived at a ceiling.

Overall, the strength across Amazon’s businesses came through in Q1, and costs efforts have been working. While the pendulum is shifting to investment again, we’d expect the company to better balance these efforts with maintaining a focus on profitability vs what we’ve seen in previous investment cycles.

See below for more details and updates on other key Amazon business areas, such as advertising, Amazon Prime Video, Healthcare, and more…

-> Amazon shares rose +2.3% in reaction to earnings and ended the week up +3.7%; YTD, Amazon stock is trading up +22.6%

Amazon’s Q1 Beat The Street, With AWS Profitability Being The Biggest Positive Delta Vs Expectations

- Total revs at +13% y/y (vs +14% in Q4) was a tad better than expectations, but profitability was the standout vs cons:

- Some rev growth dynamics: Revenue had an impact from the leap year, which added +120bp to qtrly revs growth rate, but had an unfavorable FX impact vs plan, which was a -50bp headwind

- Op income was the highest qtrly number ever: Up +221% y/y and reached a 10.7% margin vs cons 7.9%

- EPS beat… 98c vs cons 84c

- Segment-Wise

- N Amer – BEAT: Revs (+12% y/y vs +13% in Q4) and op income (5.8% margin, up 460bp y/y) were both ahead of cons

- Intl – MIXED: Revs (+11% y/y FXN vs +13% FXN in Q4) were light but actually reported positive $903mn op income vs cons negative -$571mn

- AWS – BEAT: Revs (+17% y/y vs +13% in Q4) and op income (2.8%, up 710bp y/y) were both ahead of cons

- Other KPIs

- 3P svs revs up +16% FXN

- 3P seller unit mix was 61%, up +200bp y/y

- Paid units +12% y/y, similar to Q4

However, Q2 Guidance Was Lackluster Vs Estimates

- Mid-point of Q2 revenue guidance was -2.5% below cons: Growth range implies +7-11% y/y, which is a deceleration from the +13% y/y in Q1

- Assumes ~-60bp unfavorable impact from FX

- Also, Q1 growth was helped by ~+120bp y/y from the leap yr

- Mid-point of Q2 op income guidance is -5.7% below cons: But still up +55.8% y/y from the prior yr qtr’s $7.7bn

- Includes the impact from the seasonal step-up in SBC, given timing of the annual compensation cycle

Amazon Continues To Drive Faster Delivery & Broader Selection In Online Stores & Expanding Capabilities In Grocery

- Gunning for even faster delivery as it leads to higher shopping frequency

- 2bn+ global units arrived same or next day in Q1

- Amazon delivered to Prime members at its fastest speeds ever; In March, across the top 60 largest US metro areas, ~60% of Prime member orders arrived the same or next day, and in London, Tokyo, and Toronto, 3 out of 4 items were delivered the same or next day

- When customers received items quickly, they use Amazon more frequently

- Adding even more selection for customers: Added new brands incl Clinique, Parade and CIDER in the US; Annc’d collaboration w/ Hardly Ever Worn It in Europe to offer customers pre-owned items from luxury brands

- Are also making it easier for 3P sellers to add products to their store by just providing a URL to the seller’s website, Gen AI tools automatically create product detail pages on Amazon

- 100k+ of selling partners have used one or more of their GenAI tools

- Are also making it easier for 3P sellers to add products to their store by just providing a URL to the seller’s website, Gen AI tools automatically create product detail pages on Amazon

- Results show that “customers are shopping but remain cautious”: Focused on offering everyday low prices which is “important to our customers in this uncertain economic environment”; Customers are trading down on price when they can and seeking out deals

- Continue to expand capabilities in Grocery

- Launched a grocery subscription for unlimited delivery on orders over $35 from Whole Foods Market, Amazon Fresh, as well as local grocery and specialty retailers

- The subscription benefit is available to Prime members in 3,500+ towns and cities in the US, as well as customers using a registered Electronic Benefits Transfer card

- Annc’d Whole Foods Market Daily Shop: Provides customers in urban neighborhoods a quick, convenient shopping experience; Being launched on the Upper East Side in Manhattan, w/ more NYC locations to follow

- Launched a grocery subscription for unlimited delivery on orders over $35 from Whole Foods Market, Amazon Fresh, as well as local grocery and specialty retailers

Expect To See Further Improvements In Cost To Serve

- Have already made progress with regionalization efforts but think there are addt’l opportunities in the fulfillment network to lower costs more while improving customer experience: Avenues for efficiencies incl…

- Consolidating units into fewer boxes

- Allowing for better inventory placement closer to customers

- In fulfillment network, focusing on investing in the inbound network, streamlining and standardizing process paths, and adding robotics and automation

AWS Widely Outperformed Expectations And Higher Capx Will Lead To More Revenue

- AWS revenue growth posted a strong acceleration from +13% y/y in Q4 to +17.2% in Q1: Companies have largely completed cost optimization efforts and are turning attention to newer initiatives; Companies are modernizing infrastructure and leveraging GenAI to change their customer experiences and businesses

- AWS op income incr’d +83% y/y to $9.4bn: But reminder, the change in the est’d useful life of servers primarily benefits the AWS segment, and AWS op margins will “fluctuate” driven in part by the level of investments

- On the AI front, the Co has already “accumulated a multi-billion revenue run rate” and continue to add capabilities to all three layers of the GenAI stack

- Bottom layer (for developers and Co’s building models themselves): Have the broadcast selection of Nvidia compute instances, but demand for their customer chips, Trainium and Inferentia, is “quite high”; Larger quantities of Tranium 2 is coming in H2:24 and early 2025; Companies are seeing “eye popping” results with SageMaker (managed end to end svs for developers in preparing their data for AI, managing experiments, training models faster, lowering inference latency and improving developer productivity

- Middle layer (for developers and companies who want to leverage existing LLMs and customize with their own data): This is where Amazon Bedrock has the broadest selection of LLMs available to customers, plus model evaluation, retrieval augmented generation, guardrails, etc

- Bedrock already has tens of thousands of customers; A week ago, Bedrock launched a series of other features, but perhaps most importantly, Custom Model Import; Makes it simple to import models from SageMaker or elsewhere into Bedrock before deploying their application

- Top of the stack (Gen AI applications): Annc’d general availability of Amazon Q, the most capable Gen AI-powered assistant for accelerating software development and leveraging companies’ internal data

- Q has the highest known score in acceptance rate for code suggestions, outperforms all other publicly benchmarkable competitors on catching security vulnerabilities, and leads all software development assistants on connecting multiple steps together and applying automatic actions

- CapEx is going “meaningfully” up y/y in 2024, which bodes well for future growth: The more demand AWS has, the more the Co has to procure new data centers, power, and hardware

- Amazon doesn’t spend the capital without very clear signals that it can monetize

- Q1’s $14bn of CapEx will be the low qtr for the year

- Remain “very bullish: in AWS: The biz is at a $100bn+ annualized rev run rate, but 85%+ of the global IT spend remains on-premise; Plus, the Gen AI that will be created on the cloud represents “a very large opportunity”

Other Initiatives – Advertising, Prime Video, Autonomous Car, Healthcare, Satellite Efforts

- Advertising revenue growth was strong at up +24% y/y FXN: Compares to +26% y/y FXN growth in Q4

- Driven by sponsored products (improvements in relevancy and measurement) and more room to grow

- Just starting with Prime Video ads and “encouraged by the early response”

- Prime Video continues to build content slate:

- Released 20 films and series from Amazon MGM Studios

- “Fallout” is the latest big hit (65mn+ viewers worldwide in its first 16 days) on the heels of the very successful Road House movie (50mn+ viewers worldwide)

- Annc’d that Prime Video will stream its first NFL Wild Card playoff game in January 2025

- Internationally have 30+ local Amazon Originals

- Hazbin Hotel had the most total global viewers on its opening weekend for a new animated series on Prime Video

- The Beekeeper ranked in the top-10 of theatrical releases by revenue globally in Q1

- Annc’d plans to create a new series from Mr Beast; Beast Games is set to have 1,000 contestants competing for $5mn; The series will premiere on Prime Video in 240+ countries and territories

- Expanded the company’s health care offerings: Providing customers in the US more convenient access to medical care and medications

- Launched same-day delivery of prescription medications to customers in 8 cities, incl LA and NYC, with plans to expand to more than a dozen cities by the end of the year; Customers are now getting first filled medications +75% faster y/y nationwide

-> While Amazon is moving forward with its healthcare offering, Walmart annc’d it is shutting down all of its 51 health clinics as well as its telehealth offering, as the company grapples with increasing costs and reimbursement issues, though its in-store pharmacy and vision centers will remain open (link)

- Hitting milestones with robotaxis: On the path toward commercializing Zoox, Amazon’s self-driving robotaxi, which is expected later this year

- Received Zoox’s California PUC Driverless Autonomous Vehicle Pilot permit, which allows Zoox to carry members of the public in Foster City w/out charging a fare

- Expanded driving capabilities to include higher speeds, night driving, and driving in light rain in both California and Nevada

- Expanded the virtual boundary where Zoox can operate its robotaxis in Las Vegas, helping prepare for the first public riders in the city later this year.

- Kuiper is getting closer to having its production satellites in space and is entering commercial beta

The NBA Media Rights Deal Suggests The Market Is Not Past Peak Sports Rights Values

In our most recent annual survey, we polled our readers for their views on how much the value of the NBA’s media rights would rise during the upcoming negotiations, and the largest segment of respondents (~45%) thought they would increase +50% from the $2.6bn that Disney and Warner Bros Discovery currently pay the league annually, implying ~$3.9bn. Well, that pales in comparison to press reports this week suggesting that the value of the NBA’s media rights could nearly triple to a whopping ~$7bn per year, underscoring just how valuable premium live sports are becoming within the broader media ecosystem.

There were some other noteworthy developments elsewhere across the sports space as well this week, including a couple of fallouts over carriage renewal discussions that ultimately resulted in consumers losing further access to sports programming and even greater fragmentation. Separately, it was also reported that Fox is asking for $7mn for a 30-second ad spot in the 2025 Super Bowl as a starting point with would-be advertisers, potentially positioning the company to command an even greater premium than Paramount received during this year’s record-breaking Super Bowl event.

See below for more details:

- The NBA is reportedly targeting $76bn in total rights fees over 11 yrs, a +3x increase over its current deal (link): The NBA has apparently agreed to the general framework of deals w/ Disney and Amazon worth $2.6bn/yr and $1.8bn/yr, respectively; Both agreements are subject to change but are expected to be signed

- The winner of a third package still has yet to be decided: Sources indicate that the race has boiled down to Warner Bros Discovery and Comcast, which has proposed a deal worth ~$2.5bn annually, or double the amount WBD pays under its current contract

- Comcast appears to the favorite to win the rights: Given the size of its offer and its ownership of the NBC broadcast network, which will help the NBA reach as many people as possible, despite the ongoing declines in linear viewership

- Turner’s four-decade relationship w/ the NBA is at stake: If Comcast wins the rights, WBD will lose the NBA rights after the 2024-25 season, likely leading to a loss of viewers for its TNT network; Notably, WBD signed a 10-yr deal w/ NBA legend Charles Barkley as a host in 2022

- Adopting the NFL’s fragmentation playbook has benefited the NBA: By splitting the league’s rights up into three packages (instead of the two offered previously), the NBA is set to secure a record payday of close to $7bn annually, underscoring the extremely high demand for live sports

- The NBA emphasized bringing in a third partner rooted in technology: Amazon is reportedly discussing a package of games for Prime video that would include some of the conference finals, though specifics will depend on the outcome of the third rights package

- Disney is expected to keep the NBA finals: In the past, Disney has also had one of the two conference finals, while Turner has had the other; Disney will air games on ABC and ESPN as well as stream them

- The winner of a third package still has yet to be decided: Sources indicate that the race has boiled down to Warner Bros Discovery and Comcast, which has proposed a deal worth ~$2.5bn annually, or double the amount WBD pays under its current contract

There Were Also Some Other Notable Updates Across The Sports Media Landscape This Week…

- Fubo dropped Discovery networks after reaching an impasse w/ Warner Bros Discovery (link/link): Fubo said it had not received a response from WBD in recent carriage talks and removed 19 Discovery networks from its svs in response to WBD’s refusal to negotiate

- Fubo and WBD have a history of carriage disputes: Fubo hasn’t carried nearly a dozen networks from the Warner side of WBD, including TNT and CNN, since it was unable to renew a carriage agreement with the former WarnerMedia networks in 2020

- Fubo believes it negotiated in good faith: Fubo said that it offered WBD mkt rates for its content but didn’t receive a counteroffer from the Co

- Flexibility in sports bundling is at the heart of the current standoff between the two: Fubo accused WBD of denying Fubo customers the choice of accessing Turner sports content through a more affordable, skinny sports bundle

- Fubo also criticized WBD’s role in the sports streaming JV w/ Disney and Fox: Fubo took issue w/ WBD’s decision to make sports content that available in the JV that it otherwise wouldn’t have broken out as a separate offering; Fubo also recently filed an antitrust lawsuit against the JV

- Diamond Sports failed to renew its distribution deal w/ Comcast (link): Diamond’s prior deal w/ Comcast expired the night of April 30, impacting local coverage of several MLB games and an NHL playoff game between the Nashville Predators and the Vancouver Canucks

- Diamond has been successful in its negotiations w/ other cable networks: Diamond agreed to a carriage deal w/ Charter, the largest US cable video distributor, last month and is close to finalizing a deal w/ DirecTV, the country’s third largest cable TV provider; The Co also renewed a deal w/ Cox this week

- Diamond “declined multiple offers”, per Comcast: Notably, Comcast recently reached new distribution deals w/ the Mid-Atlantic Sports Network and SportsNet Pittsburg after the two agreed to be placed on more expensive and less broadly distributed tiers

- The stakes are high for Diamond…: The Co’s prior deals with Charter, Comcast, and DirecTV collectively represent ~81% of its total distribution rev

- … While Comcast can bide its time: Comcast has kept several sports channels dark on its systems indefinitely amid carriage negotiations; For example, New York’s MSG Networks has been off of Comcast in New Jersey and Connecticut since 2021

- Fox is reportedly seeking at least $7mn for a 30-second commercial in its 2025 broadcast of Super Bowl LIX (link): This was per sources w/ insight into the Co’s early talks w/ potential advertisers; The $7mn price tag marks a slightly higher starting point than Paramount’s initial request for between $6.5-7mn for a half-minute ad

- Fox is also seeking addt’l payments from potential sponsors that aren’t regular media buyers w/ the Co: This is standard practice by most networks each yr; Fox will likely insist on a commitment from advertisers to buy other parts of its portfolio, including Tubi, Fox Broadcasting, or other parts of Fox Sports

- Media buyers are taking a more measured stance during talks…: One buying exec doubted that some advertisers would be “chomping at the bit” to pay $7mn for an ad

- … Though execs at Fox have been optimistic: The Super Bowl has reached record audiences in each of the last two yrs, w/ an estimated 123.7mn viewers tuning in to watch the Kansas City Chiefs beat the San Francisco 49ers in overtime on Feb 11 in the most recent game

- Fox won’t host its next Super Bowl until 2029: Disney recently joined the rotation of Super Bowl rights holders, extending the period that each network has in between hosting the games

UMG Sees A “Substantial Improvement” In Total Value From The New TikTok Deal

Finally, the UMG and TikTok standoff ended, and the two came to a meeting of the minds with regard to a new agreement. While characterized as a win-win, UMG stressed that it would see a “substantial improvement” in total value derived from the relationship, which included a revenue component that wasn’t part of the last deal and includes other aspects that don’t necessarily show up in the revenue line, including e-commerce, ad credits, data marketing programs, and other things. Also, UMG indicated that TikTok addressed its concerns regarding AI and “protecting the integrity and value of human artistry”.

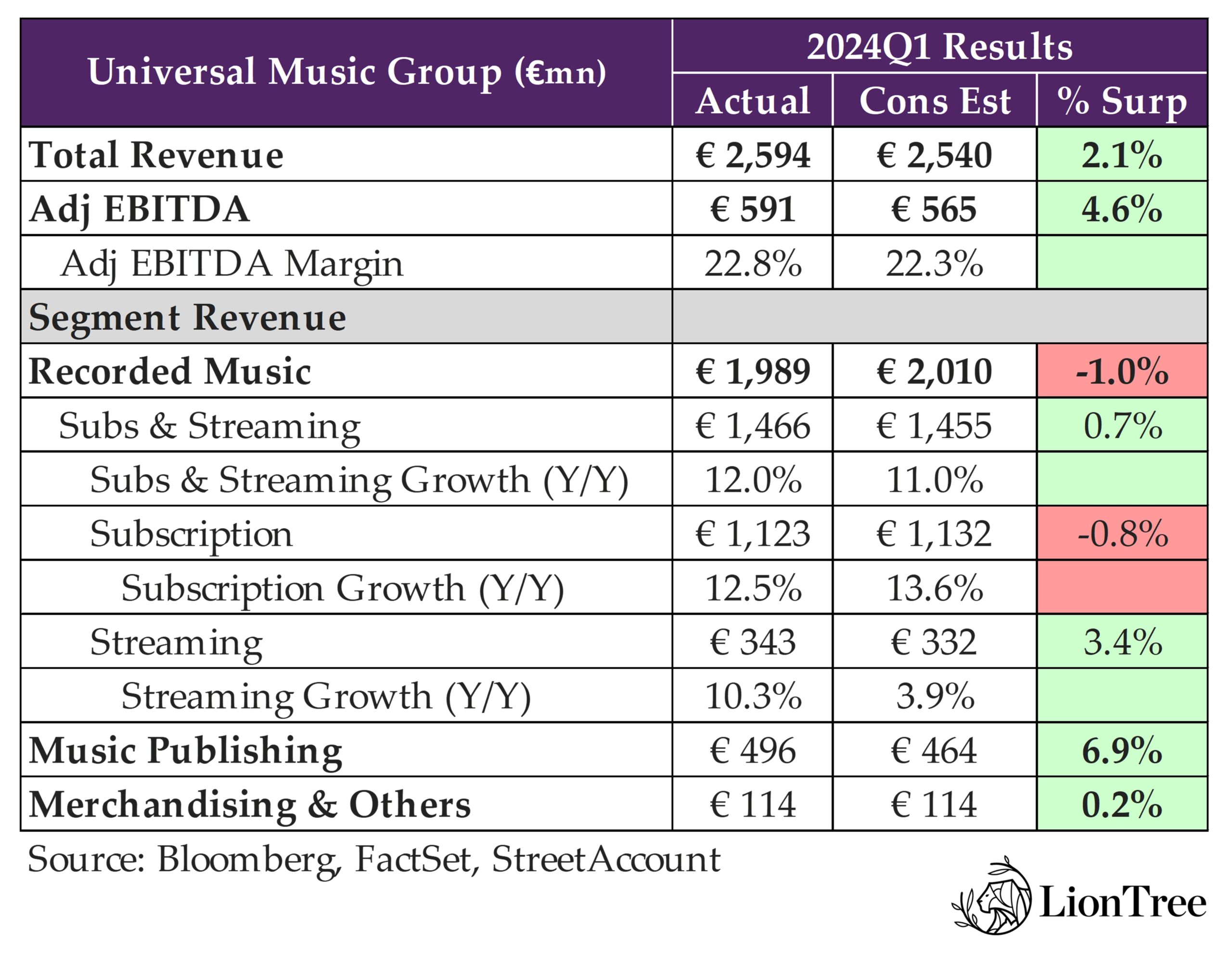

With respect to UMG’s quarterly results, the company delivered a strong Q1 relative to expectations, with total revenues up +8% y/y FX-neutral and adj EBITDA up +16% y/y, driving significant margin expansion. The upside to the numbers came from Recorded Music Ad supported streaming revenue growth accelerating from +5.6% y/y in Q4 to +10.3% y/y FXN in Q1 and easily beating cons +3.9%. This was encouraging; however, mgmt cautioned to “not get ahead of ourselves too far too quickly” after just one quarter. On profitability, adj EBITDA margins of 22.8% topped cons 22.3%, but mgmt reminded investors that there will be quarterly fluctuations and that trends should be assessed annually. The company also reiterated guidance of adj EBITDA margins in the mid-twenties in the medium term.

In the core Recorded Music Subscription business, revenues are still growing double-digits, but there was some focus on the deceleration from +15.0% y/y FXN growth in Q4 to +12.5% y/y FXN growth this qtr. While the Spotify price increase helped during the qtr, growth on some other platforms has not been as fast, given that UMG has lapped the one-year mark from earlier price adjustments, eroding their positive impact on the company’s P&L.

Lastly, mgmt stressed that the new terms with DSPs on premium bundles do not change UMG subscriber economics and that the company views Spotify’s experimentation with different pricing tiers positively because they believe it will ultimately attract more subscribers into the ecosystem, retain existing ones, and increase the customer lifetime value.

All-in-all, the music industry has been able to enact structural change with more of a win-win partnership mindset, a unique dynamic, and the trend toward monetization and harvesting in the music sector continues.

See below for more on our key takeaways and thoughts from UMG’s results and conference call.

-> UMG shares were up +3.6% in response to earnings, closing the week up+4.9%; YTD, UMG stock is trading +12.0% higher

UMG’s Agreement With TikTok Is At A “Substantially” Better Total Value

- Tiktok agreed to key changes and addressed concerns about gen AI on its platform; The new deal better aligns with the values of other comparable partnerships

- Saw a “substantial improvement” in total value derived from the relationship: Multifaceted deal on compensation

- Revenue: “Revenue under this new deal does mark an improvement for our last deal”

- Other economic value: There are also “other aspects and economic value that don’t necessarily show up in the revenue line, including things like e-commerce, ad credits, data marketing programs, other important facets of the platform relationship that we have with TikTok”

- AI: Also, “can’t emphasize enough the strategic significance in the area of AI… TikTok will also protect the integrity and value of human artistry by ensuring that fake artist AI content uploaded by third parties that misappropriates the identities of our artists, infringes on their right of publicity, can be removed. Collectively, these and other commitments we’ve secured regarding generative AI represent what we think is a dramatic improvement from where things stood just a few months ago”

- Saw a “substantial improvement” in total value derived from the relationship: Multifaceted deal on compensation

- Other efforts in social media:

- Have been working to accelerate engagement with music on Snapchat, Insta, and Youtube shorts

- Recent new agreement with Spotify makes available a range of new features that were previously only found on social media platforms and broadened the definition of the social music category

UMG Q1 = Better Streaming Revenue & Better Margins

- Revs and adj EBITDA beat expectations:

- Revs: Grew +7.9% y/y FXN (actual +5.8%), which beat cons +7%

- Adj EBITDA: Beat by +4.6%; Adj EBITDA up +13.2% y/y or +15.9% FXN (margins expanded +1.5ppts to 22.8%)

- Recorded Music (77% of total rev) … Streaming rev growth was the key upside driver offsetting slower Subscription rev growth

- Total Recorded Music revs grew +3.4% y/y or +6% FXN but slightly missed consensus

- Subscription revs incr’d +10.7% or 12.5% FXN (driven primarily by subscriber growth but also price increases) but missed cons +13.6% FXN

- Streaming revs incr’d +8.9% y/y or +10.3% FXN and beat cons +13.6% FXN

- Physical revs decr’d -18.5% y/y or -14.4% FXN (largely due to a very difficult y/y comp in Japan and expect tough comps for the year)

- License & other revs decl’d -1.8% y/y, or -0.4% FXN (due to a timing-related decline synch revs)

- Downloads & other digital revs decr’d -16.4% y/y, or -13.2% FXN (download sales cont’d the industry-wide decline

- Total Recorded Music revs grew +3.4% y/y or +6% FXN but slightly missed consensus

- Music Publishing (19% of total rev)… Beat by +7%

- Revs grew +16.7% y/y, or +18.4% FXN

- Digital revs incr’d +22.9% y/y, or +24.6% FXN, driven by continued growth in streaming and subscription revenue

- Performance rev incr’d +26.7% y/y, or +28.1% FXN, due in part to higher society payments in the US, as well as greater than anticipated live activity in Europe

- Synchronization rev fell -10.1% y/y, or -7.5% FXN, as a result of timing; Mechanical rev grew by +8.7% in both reported and FXN

- Revs grew +16.7% y/y, or +18.4% FXN

- Top sellers: Taylor Swift, Noah Kahan, Morgan Wallen, Ariana Grande, and Olivia Rodrigo

Recorded Music Subscription Revs Benefited From The SPOT Price Increase In Q1 But Growth On Other Platforms Lagged Due To Comps

- Recorded Music Subscription revs growth decelerated from +15.0% in Q4 to +12.5% FXN in Q1: While the Co saw the full benefit from the Spotify price increase, “several other platforms did not grow as quickly”, UMG began to anniversary the positive 2023 impact on price increases at Apple and Amazon

- New terms on premium bundles do not change UMG’s subscriber economics: As previously discussed, “the new terms have some incentive structures around kitting KPIs that might relate to margin, but there is no change to what we previously said in terms of those impacts to our subscriber economics”

- “We’re of course going to stay vigilant in looking after the interest of our songwriters as we stay in close dialogue with all parties and all constituencies. We’re pretty good at coming up with solutions that benefit all of us. Our entire mantra is win, win. And I think we should add that Spotify has been an incredibly good partner

- UMG is positive on Spotify experimenting with different pricing tiers: “They’re looking to maximize the optimization of customer value, we think ultimately attracting more subscribers into the ecosystem and retaining the subscribers and increase the customer lifetime value”

- Market share is stable and healthy, and UMG “remain[s] encouraged by the total subscriber growth throughout the market”

Encouraged By Co’s Ad Supported Performance But Not Ready To Call It A Trend Yet

- Recorded music ad supported streaming rev growth accelerated to +10.3% y/y in Q1 from +5.6% in Q4 FXN: “Really encouraged” by the improvement in the ad supported streaming growth, but they are still cautious at the moment with regard to the entire marketplace for advertising

- “Need to see consistent, broad-based improvements across all partnerships and across all geographies and probably over a more consistent longer term time frame”; One qtr is encouraging, but “let’s not get ahead of ourselves too far too quickly”

Co Advocates Looking At The Margin trajectory On An Annual Vs Qtrly Basis & Reiterated Medium-Term Guidance

- Margins can vary qrtr to qtr, so investors should focus on annual trends: “Be very careful about any individual quarter”; Q1 came from op leverage but also revenue mix given the decline in physical sales and increase in the higher margin streaming and subscription rev plus €12mn savings from cash compensation from the equity plan

- Reiterated guidance of adj EBITDA margins in the mid-twenties in the medium-term

- Positive impact from cost savings initiatives is still to come: These savings began to roll out in April

- Remains on track for the €75mn in cost savings as previously guided for 2024

Remain Focused On More Fully Monetizing SuperFans

- Very encouraged by the “positive reaction” regarding prospects of a super-premium tier at a higher price point: That would involve an even more advanced value proposition for customers to take advantage of the potential 10-20% of the subscriber base that UMG’s research suggests could be the target market for a higher value, higher priced subscription tier;

- The research suggests that one in five paid music subscribers would be willing to pay for a premium tier – That’s enticing

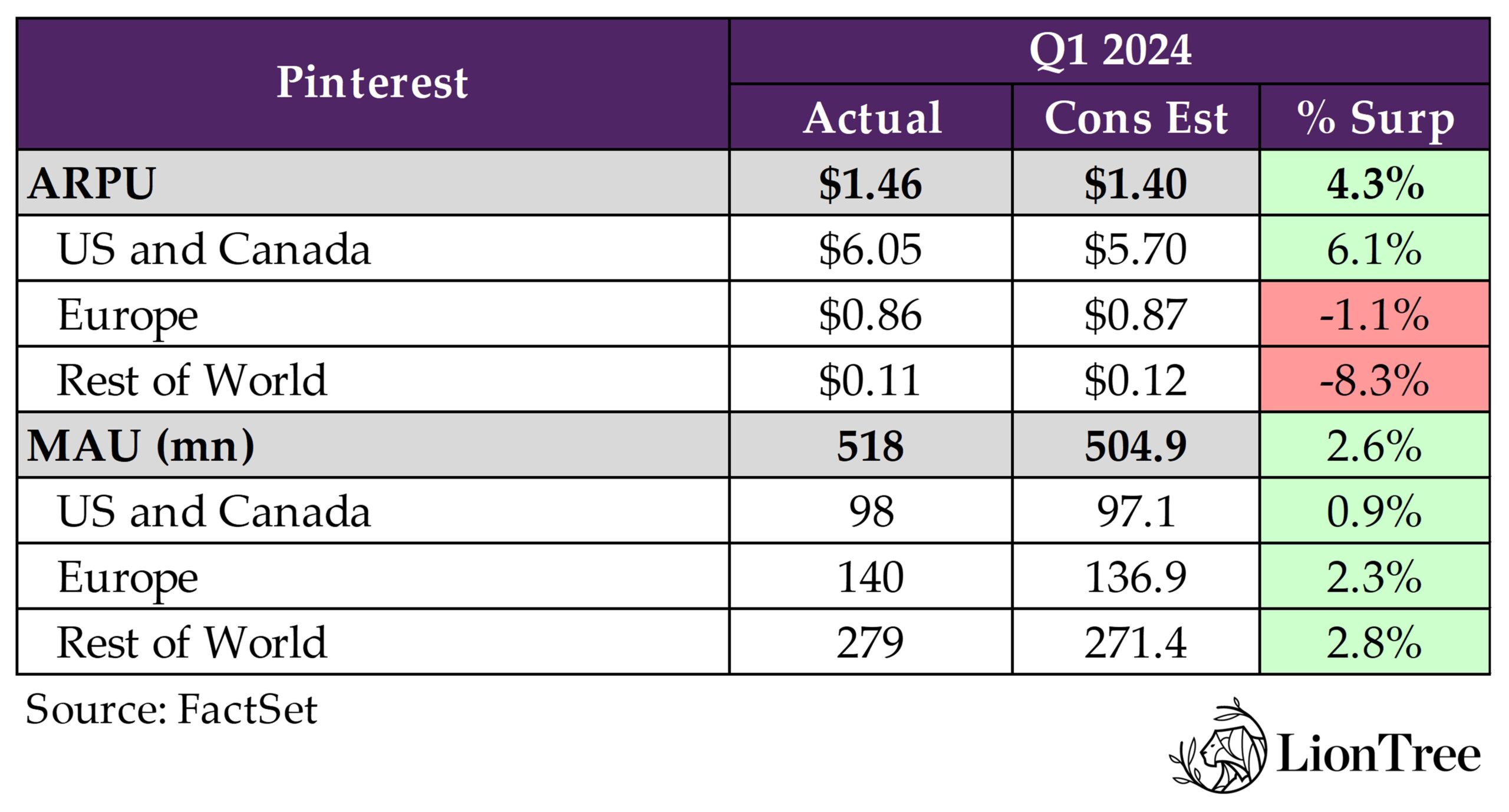

Pinterest’s Platform Transformation Is Delivering “Compounding Benefits”

With Meta and Alphabet accelerating growth in their advertising businesses last year, a key discussion in the sector has been whether the axiom of “the bigger will get bigger” in digital advertising will persist to the extent that smaller digital advertising players are completely edged out. In other words, is there room for smaller platforms like Snap and Pinterest to establish a significant presence in a market overwhelmingly dominated by the “digital duopoly” of Meta and Alphabet?

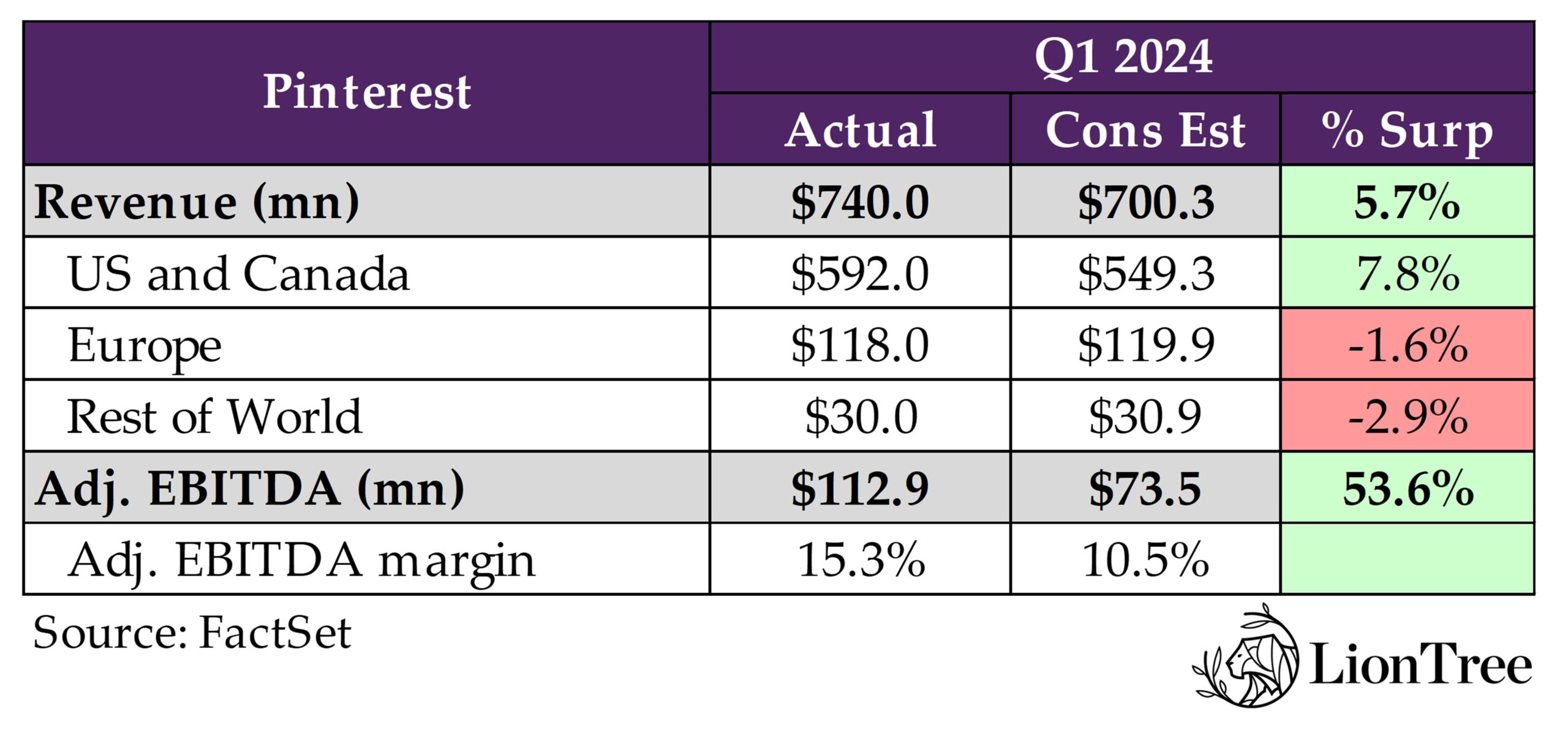

On the back of Snap’s report last week (see Theme #4 from last week’s Weekly), which saw the stock rally +27.6% in reaction to revenue growth accelerating more than expected, coupled with much better profitability and favorable guidance, all eyes were on Pinterest to see if a similar trend would emerge. And Pinterest delivered, coming in above expectations both on Q1 results as well as Q2 guidance. The Q1 beat was driven by UCAN, which saw accelerating revenue growth q/q and also beat expectations, while Europe and RoW decelerated q/q (was the same q/q on a FXN basis, as FX was a headwind) and missed. However, focus has been on the home market, which is also Pinterest’s largest, and now that the company has been seeing results, it’s starting to focus on growing revenues more strongly internationally.

Solid MAU and engagement growth, ad load synergy, and monetization strength in the lower funnel all helped Pinterest achieve its fastest revenue growth since 2021 in Q1. Complementing the strong growth in 1P demand was the emerging contribution in Q1 from Pinterest’s 3P partnerships with Amazon and Google, which have been ramping and helped to round out gaps in the company’s auctions and bring more auction density. It’s still very early days, and they’re just getting start with Google on the international side, so there are “more […] opportunities in front of [them] than behind”

The growth and acceleration seen in the quarter is “a result of months and quarters of compound effects” from the initiatives that Pinterest been acting on to deliver more click and conversion to advertisers, giving them more measurement capabilities, and making it easier for them to create campaigns that deliver great ROI. We’d expect these “compounding benefits” to continue to build heading in Q2 and throughout the rest of the year.

-> Pinterest soared +21.0% post its print and ended the week up +19.0%; YTD, the stock is up +9.1%

Easy Beats In Q1 – The Co Posted Its Fastest Rev Growth Qtr Since 2021 And Continues To Drive Improvements In Profitability

- Q1 revenue – BEAT by +5.7%: Grew +23% y/y or +22% ex-FX (accelerating from +12% in Q4) to reach $740mn

- The upside was all driven by UCAN, as Europe and RoW missed

- Reported revenue did have +2pts of y/y growth benefit from Easter, the leap year, and FX

- Q1 adj EBITDA – BEAT by +53.6%: Grew +319% y/y (vs +86% y/y in Q4) to reach $113mn (15% margin, ~+1,000bp y/y)

Guidance Supports Compounding Benefits Of Growth Initiatives

- Q2 revenue guidance – BEAT by +1.8% at the midpoint: $835-$850mn vs cons $827.2mn

- Implied growth is roughly consistent w/ Q1: When adjusted for the 2pts of y/y growth benefit in Q1 from the Easter timing shift and leap day as well as an addt’l +1pt benefit from FX, which they do not expect to continue into Q2 based on current spot rates, revs are expected to grow +18-20% y/y (vs +23% y/y in Q1)

- Q2 OpEx is expected to grow 11-15% y/y (vs +10% y/y in Q1): Expected to be between $490-505mn, driven by investment increases in R&D, where the Co is investing in headcount for AI talent across their biz

- Reiterated margin expansion expectations for 2024, which are forecast to come in at a more modest level than the +660bp delivered in 2023, as the Co balances investing in growth and flowing profitability through to the bottom line

- Expected the expansion to be more front-end loaded, as they lap the strengthening adj EBITDA margins driven in H2:22

- Some early puts-and-takes when thinking about 2024 rev growth –

- Tough comps going into H2

- Addt’l uncertainties from the ramping deprecation of 3P cookies through this year into early 2025, though the Co feels “well-positioned”

- More value capture on direct links is ahead of the Co vs behind

- 3P ad demand will continue to contribute to growth and grow off the base Pinterest is seeing in Q1

Global MAUs Set Another Record, As User Growth Continues To Accelerate

- Global MAUs surpassed 500mn+ for the first time, as y/y growth accelerated for the seventh consecutive qtr: Up +12% y/y (vs +11% y/y in Q4) to reach 518mn

- User growth accelerated across all regions and beat across all regions, esp ROW and Europe

- ARPU was also better than expected ($1.46 vs cons $1.40), with the upside coming exclusively in the UCAN region

- Deepening engagement per user, w/ engagement growth outpacing user growth

- What has been driving the accelerating growth rate of MAUs?

- Using AI to drive relevance and personalization

- Doubling down on curation through boards and collages

- Driving actionability through core surfaces

- Create a more positive alternative to traditional social media

- Pinterest is aging down as it is “winning with Gen Z”: Largest and fastest-growing demographic at more than 40% of Pinterest users

- Save more pins than any other demo and also find value in new content formats

- View Pinterest as a “distinct and separate destination from other social media apps”

- Rates Pinterest higher on promoting and preserving well-being metrics vs other social media apps

- Connecting with Gen Z through “culturally relevant” moments (i.e., hosted an immersive activation at Coachella)

Improving Curation Tools Like Boards And Collages To Enhance User Experience

- Saw an ~+30% lift in boards created after adding auto organization features to help remove the friction for users to begin creating board

- Users are ~+3x more likely to save Collage Pins vs other Pins on Pinterest: “This is an entirely new, highly engaging, and highly shoppable content format”

- A “significant” portion contain clickable products

- Gaining traction with Gen Z, who are ~70% of collage creators

Starting To See Advertisers Shifting Budgets More Assertively Towards Pinterest

- Saw “broad strength” in retail in Q1, as well as “nice growth” in emerging categories, including financial svs and technology

- Q1 ad impressions accelerated to +38% y/y (vs +33% y/y in Q1) …: Driven by increases in total impressions and ad load

- … While pricing fell –1% y/y (vs –16% y/y in Q1): Largely as a result of accelerating ad demand, but still a y/y decline as the Co continues to drive increased value to advertisers in the form of more clicks and greater efficiency

- “Feel great” about their competitive positioning – advertisers are moving them into “always on” budgets vs “experimental” budgets that Pinterest historically played in

AI Is Driving The Flywheel Effect For Further Relevance In Content Recommendations

- Transitioned from CPU to GPU serving, allowing them to serve models that are 100x larger in size

- This was the first step to unlocking a better product experience by improving their ability to surface more personalized content for their users

- With GPU serving capabilities, they are now developing and deploying even more complex models to drive further gains in relevancy and personalization

- Optimizing recommendation models to focus more on engagement vs view time

- Previously, recommendation models were focused on serving content to drive greater view time in the immediate moment

- Now, as they’ve advanced AI and sharpened focus on user intent, have incorporated more proprietary signals into their recommendation models to optimize for depth of engagement and satisfaction of intent, including driving actionable outcomes (i.e., saves, clicks, and conversions)

- On the advertising front – seen “a lot of success” w/ current optimization tools and investing to build out the suite in order to give advertisers an array of tools to build, optimize, manage, and measure campaigns

- See “significant room” for the Co to drive further rev coverage for entire automation suite: Saw revenue coverage above 80% for automated bidding in Q1, with over half of revenue coverage utilizing either expanded targeting or flexible daily budgets

- Building out a more robust suite of automation tools drive further uptake: Will release these features in stages and will go through a typical product ramp as they develop, test, and scale

- Plan to launch a campaign creation tool that simplifies setup for their automated offerings and remove friction for advertisers to leverage those tools

- Launching a dynamic creative optimization solution set, which will allow advertisers to use genAI to optimize the creatives for their ads

- Introducing ROAS bidding, which is meant to increase advertiser return on ad spend by automatically optimizing campaigns in real-time to prioritize users or products that drive the highest ROI

Much More Value Capture Ahead Through Execution Of Lower Funnel Roadmap

- Solving for the actionability in the lower funnel through mobile deep linking and direct links, enhanced ad platform capabilities, and improved adoption of foundational measurement capabilities

- Adoption of lower funnel formats and tools has been a “critical” part of their monetization strategy

- Lowest funnel conversion objective was their fastest growing, with particular strength coming from the shopping ads format as advertisers turned to Pinterest to drive sales

- Clicks to advertisers more than doubled y/y again in Q1, after more than doubling clicks y/y in Q4

- Seeing particular strength in US and retail, where they’re taking share and starting to get more access into performance budgets

- Seeing value capture from direct links through increased ad spend from advertisers (97% of lower funnel rev has adopted the direct links format): Advertisers who have seen sustained performance gains from direct links and are able to measure the results have started to increase their share of wallet with Pinterest

- Reaching 5% or more total ad budget with some of their most sophisticated advertisers, implying an even deeper penetration of their digital ad spend

- But much more of the value capture from direct links remains ahead of them, as more advertisers begin to measure and react to the benefits from direct links

- Growing adoption of the API for Conversions to ~40% of total rev (up from 28% at Investor Day last Sept): Provides a server-to-server connection for advertisers to measure and attribute conversions

- Revenue from retail advertisers who have adopted the API for Conversions tends to grow “significantly” faster than revenue from those who have not yet adopted

- Seeing a reinforcing effect take place across lower funnel solution tool set and measurement solutions: As advertisers adopt and see the benefits of shopping ads, mobile deep linking, or direct links, they are more incentivized to adopt their privacy-centric measurement

- Advertisers who have adopted their lower funnel tool sets are also growing much faster than those who have no lower funnel solution adoptions

Integrating More Shoppable Content Into Core Surfaces To Facilitate User Actions

- Outbound clicks to advertisers accelerated q/q and more than doubled y/y, as users take advantage of the improved actionability

- Integrated more shoppable content into core surfaces, including home feed, search, and related items

- Guided shopping modules help users pick up where they left off on prior shopping journeys by resurfacing Product Pins based on past browsing and click history

- Visual shopping modules, such as Shop Similar and Shop the Look, allow users to shop the items they see within lifestyle images right when they discover them

- Brought shoppable video to Pinterest in Q1, expanding Shop the Look to video pins, allowed users to easily shop the items they see in videos

Seeing Emerging Contribution From 3P Partnerships And Now Beginning To Expand That Internationally

- Scaling 3P demand with their two partners – Amazon Ads in the US and Google Ads Manager (recently went live in February) in unmonetized int’l markets

- Amazon partnership is live on all main surfaces in the US, and they are continuing to optimize their respective systems to improve relevance and drive performance for advertisers

- Google partnership is “early” but “is also progressing nicely”

- Saw emerging contribution to revenue from 3P demand, which will be the base from which further 3P revenue will grow throughout the year

- Plans on potentially adding more partners beyond Amazon and Google? Continue to see oppties to expand current partnerships to multiple geographies and continuously evaluating partners that can complement the auction going forward

- In addition to 3P demand from Google, will begin working with resellers to bring in local ad demand, primarily in rest of world markets: Resellers provide a scaled approach to drive demand in markets where they don’t currently have a sales presence and can bring relevant ad content for users in those markets; Demand from resellers will take time to grow in these markets, so they expect this initiative to ramp over the course of the year

- Using a multi-pronged strategy to grow revenue in int’l markets

- In their largest int’l markets, using 1P selling efforts to strategically capture advertiser demand; Also deepening partnership w/ agencies to grow within these markets

- In smaller markets, where they had not monetized or are under monetized, they are introducing addt’l sources of demand to fill in gaps in their auction

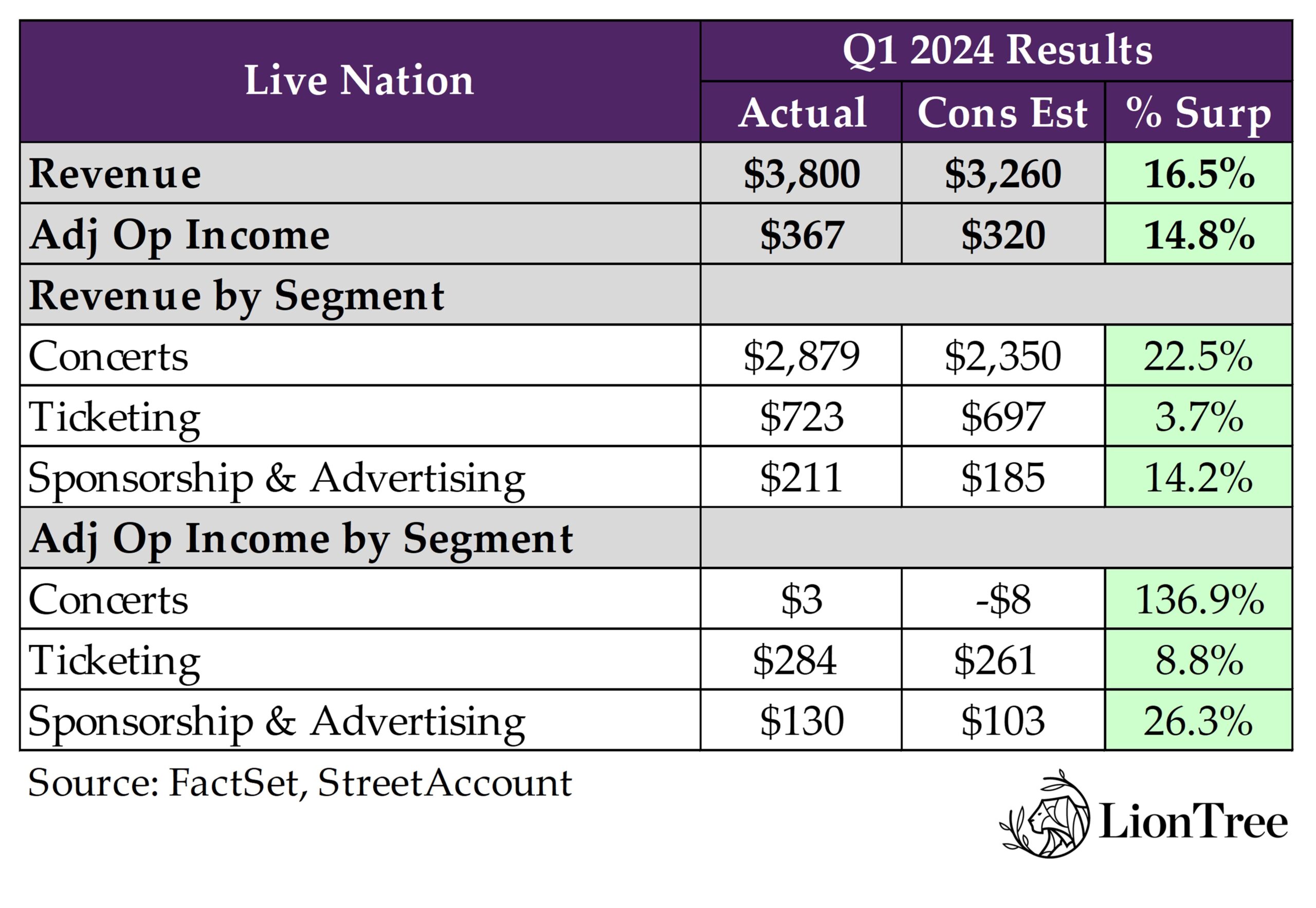

Live Nation’s Results Point To No Slowdown In Live Entertainment

Following the early read into experiential experiences from NBCU last week, in which theme parks saw some declines in attendance in the US (see Theme #9 from Weekly 4/26/24), there was some worry coming into Live Nation’s earnings that a pullback may also be developing in the concert space as well. However, that was far from the case. Results easily topped expectations across all segments. Consumer demand hasn’t shown any weakness, as “global fan demand is stronger than ever, more artists are out on the road, and more venues are being added to bring them together.”

Overall attendance was up +21% y/y to 23mn in Q1, with arenas driving the growth, and ticket sales for shows this year are consistent w/ 2023, despite 2024 not being “a big stadium year.” The ticketing segment will see lower growth as a result of the decrease in deferred revenue associated with stadium tickets, which sell the earliest and are also the highest priced. Historically, that has led to a very high deferred revenue number at this point of the year, but with a shift to more arenas and amphitheaters, that sales cycle is going to come in a bit later. That being said, overall double-digit AOI growth is still expected due to strong consumer demand and sell-through rates.

On the venues side, Live Nation is the leader of the pack, as the company is “the one that everyone wants to partner with.” Live Nation has a good amount of optionality and is executing, with plans to open at least 12 major venues in 2024/25, creating capacity for 8mn+ additional fans and with returns expected to average 20%+. 2024 CapEx was revised up to $600mn (from the prior $540mn) due to “additional venue expansion opportunities”, with three-fourths of that being driven by Venue Nation.

The opportunity in international is also open-ended, particularly on the sponsorship side, and will drive higher growth rates in revenue in Q4 and Q1 of the upcoming years. Sponsorship revenue has historically been more heavily weighted towards Q2 and Q3 due to the summer months in North America and Europe. Putting on festivals in South America and Asia will smooth out the revenue plunges that the sponsorship segment sees in Q1 and Q4, and the company has been “getting real traction building those businesses.”

Finally, on the regulatory front, the company is about to begin discussions with the DoJ about the agency’s ongoing investigations; however, management doesn’t believe a breakup of Live Nation and Ticketmaster is legally permissible. They remain hopeful they can resolve the dispute but are prepared to defend themselves if the case gets to court.

All-in-all, Live Nation is on track to see a record 2024. See below for more.

-> Live Nation traded up +7.2% the day after its print and ended the week up +5.4%; YTD, the stock is up +1.1%

Live Nation Saw Its “Biggest Q1 Ever” As Both Top And Bottom-Line Easily Beat Consensus

- Q1 was a series of beats: Q1 rev was up +21% y/y (vs +36% y/y in Q4) and beat cons by +16.5%; Adj op income rose +15% y/y (vs +20% y/y in Q4) and topped cons by +14.8%

- Revenue and adj op Income beat across all segments

Seeing No Weakness In Consumer Demand

- Q1 fan growth was up +21% y/y to 23mn fans

- Arena led attendance growth, up +40% y/y to ~10mn fans globally

- Festival attendance growth of double-digits, driven by Latin American markets

- “No issues at all” on fan demand relative to last summer

- # of artists that toured last year are in-line w/ the # that are touring again this year

- Those artists are consistently seeing sell-through of those shows at or above where they were last year

- Overall grosses for the artists are also consistently higher, even with a large increase in show count

- Overall arena volume is the largest at this point early on, despite “tremendous growth” in # of arena shows

- Not seeing any cannibalization as a result of increased # of arena shows

- Seeing “strong growth” in on-site spending

Looking Into 2024 – Leading Indicators Point To Another Record Year

- 2024 CapEx estimated to be ~$600mn, an increase from $540mn projected last qtr

- Three-fourths of total CapEx will be driven by Venue Nation; 5 venues account for ~40% of total venue spend

- Most of the CapEx increase relative to their prior projection is due to addt’l venue expansion opportunities, including a stadium in South America to be modeled after Foro So

- Still confident in double-digit AOI growth for the yr: “The story for the year is going to be less of a revenue story, more of a shift in the portion of the fans that are in our venues, higher fan profitability, concert AOI growth through margin expansion”

- Double-digit growth in ticket sales and confirmed shows…

- Live Nation concert ticket sales for overall arena and amphitheater shows are pacing up double-digits

- Confirmed shows for large venues (stadiums, arenas, and amphitheaters) up double-digits, with growth led by arenas and amphitheaters

- 85%+ of full-yr shows at large venues booked, compared to ~75% last yr

- … As demand for global content continues to grow

- Fan count for Q1 shows nearly doubled for int’l artists across top 50 global tours vs 5 yrs ago

- YTD ticket sales per show for Latin shows in the US are up double-digits y/y

- YTD confirmed US show count up +400% y/y for Afrobeats and ~+40% y/y for Latin, with similar trends in Europe

Momentum In Concerts Is Accelerating Into The Summer Season

- Concerts – Big beats: Rev grew +26% y/y in Q1 (vs +43% y/y in Q4) and easily topped cons by +22.5%; AOI grew to $3.1mn vs year-ago $0.8mn and beat cons of -$8mn

- Q1 margins expanded, even with increased arena activity

- What is the driver for bigger step up in North American concert attendance vs international attendance? It is a function of the international stadiums

- Q1 growth in North America was primarily due to fewer international stadium events, particularly in the Southern Hemisphere in Q1:23

- Despite an overall trend towards increasing international growth, this year might see a temporary shift with “disproportionate growth” from North American amphitheaters

- FY24 concert margins expected to be higher than FY23, though still too early to declare exactly what the margin expansion is going to be

- What factors will impact magnitude of growth?

- FX rates

- Arena activity levels, as Q4 is still in the process of being booked; If they have a lot of arena s in Q3, that could bring down margin while bringing up AOI, and “we’ll do that all day long”

- Advertising costs in Q4 related to 2025 stadium shows, as marketing and sales for those shows may begin in Q4; The more stadium tours put on sale in Q4 globally, the bigger the expense hit

- What factors will impact magnitude of growth?

- FY24 concert AOI growth expected to be primarily driven by Q2 and Q3 activity

Seeing “Strong” Start To Festival Portfolio

- Contrary to press around difficulty selling tickets in the broader festival industry in US and Europe, Live Nation has NOT been seeing challenges

- Benefit from being a global Co and having 100+ festivals around the world

- Ticket sales are up double-digits y/y

- Sponsorship on festivals is up over +20% y/y

- Festival strategy is to launch ~10 new festivals a year internationally, and cut out the weak performers for the next year – “You’re lucky if 50% of them make it the next year”

- “I think this year we started 10, we shut down 6, so you’re always kind of cutting off the weak performers and restarting some new ideas”

- Seeing a shift towards more niche 1–2-day festivals vs massive 3-day festivals

- Organizing large, 100k+ people, multi-day music festivals with unique, high-profile headliner that appeals to all is difficult to deliver year-on-year

- Also, artists are making a lot of money in arenas and stadium, so it’s not as easy to get “that special headliner”

- Seeing “great success” in smaller, ~35k people, 1-2-day festivals that center around a certain genre of music or lifestyle

- Usually have higher per heads and higher sponsorship value

- “If you’re starting a new one, you’re probably starting a more niche strategy and trying to make sure it’s a better experience versus just putting 75,000 people in a field”

- Organizing large, 100k+ people, multi-day music festivals with unique, high-profile headliner that appeals to all is difficult to deliver year-on-year

Ticketing Sales Have Been Consistent Y/Y (Despite Fewer Stadium Shows In 2024)

- Ticketing – beat: Q1 rev grew +13.6% y/y (vs +7% y/y in Q4) and came in +3.7% ahead of cons; AOI was up +5% y/y (vs +4% y/y in Q3) and beat cons by +8.8%

- Saw record Q1 operating metrics

- ~77mn fee-bearing tickets sold, driven by double-digit growth in int’l markets

- Fee-bearing GTV up to ~$8bn, with growth driven by int’l markets

- YTD ticket sales of 86mn for shows this yr are consistent w/ 2023, despite reduced stadium activity / As expected, 2024 will NOT be “a big stadium year”

- Stadium tickets sell earliest and are the highest priced, so they are going to lead historically to a very high deferred rev # at this point of the yr

- With a shift to more arenas and more amphitheaters, the sales cycle is going to come in a bit later

- Will see lower growth as a result of fewer stadium, high-ticket price shows this yr

- FY24 margins are expected to be consistent w/ last yr

Int’l Will Be A Key Driver In Filling In Sponsorship Rev Gaps In The Year

- Sponsorship & Advertising – beat: Rev grew +24% y/y (vs +4% y/y in Q4) and beat cons by +14.2%; AOI was roughly flat (vs +7.2% y/y in Q4) and beat cons by +26.3%

- Was the segment’s highest Q1 rev ever

- 85%+ of expected sponsorship commitments for the year are booked, up double-digits y/y

- By sector: Non-alcoholic beverages, CPG, and retail categories are each up double-digits y/y

- New partners added this year include Jaguar Land Rover’s Defender and U.K. festival headline partners Rockstar Energy and Liquid Death

- Expanded relationships with GNP in Mexico and Cisco and Bacardi in the US

- International festivals, particularly in the southern hemisphere, will drive the higher growth rates in sponsorship rev in Q1 and Q4 this yr

- Balancing out sponsorship rev (which tends to be Q2 and Q3 heavy due to the summer months in N. America and Europe) by putting on festivals in South America and Asia, which they have been “getting real traction building those businesses”

- FY24 Sponsorship & Advertising margins expected to be consistent with last year

Have More Opportunities Than Execution Power On Venue Buildout, “But We’re Building That Muscle Fast”

- Q1 food and beverage spending was up +10% y/y at US theaters and clubs

- Incremental FY24 commentary –

- Venue Nation fan count expected to grow double-digits with more shows at amphitheaters and other operated venues

- Profitability per fan at amphitheaters expected to increase double-digits this year, with these venues delivering over 2.5x the per fan profitability of similarly sized third-party venue

- Venue Nation expanding its global portfolio in 2024 onwards

- Plan to open at least 12 major venues globally in 2024/25, creating capacity for 8mn+ additional fans

- Will also complete “major” refurbishment of two venues in the US and Mexico in 2024

- Expected returns to average 20%+, with a proven track record on recent openings

- “Bunch of ones in the hopper right now” with sports owners – “Everybody that has a sport arena is looking to build out their retail footprint around it”: In potential partnership w/ “a bunch” of different NBA, NHL, or NFL owners, who are building out their concourse/retail area; Will partner with them in capital to help build that out

- Venue strategy when deciding b/w executing independently vs partnering with a third-party? “We do it all”

- Overall – “opportunistic depending on who the developer is”

- Globally – “the pipeline is long” and have “a lot that we’re going to keep rolling out over the next few years”; Can do them almost 100% on their own, but if the economics are there or if there’s a developer, will always look to see which will be a better return on capital

- “We’re the one that everyone wants to partner with, so we have great optionality. We are always kind of the first demand partner that a developer is looking to bring us in and be partners with”

An Overriding Focus Is On The Potential Pending Lawsuit From The Department Of Justice

- About to begin discussions with senior division leadership at DOJ about the issues their staff has been investigating, which is typically in the final phase of an investigation

- Decisions about whether to sue over what and what relief to seek are ordinarily made at the end of that process

- DON’T believe a breakup of Live Nation and Ticketmaster would be a legally permissible remedy

- DOJ’s investigation appears to be focused on specific biz practices, not the legality of the Live Nation-Ticketmaster merger or Live Nation’s overall biz structure

- Live Nation and Ticketmaster came together lawfully through a merger that the DOJ reviewed and approved, subject to divestitures and other remedies

- DOJ has repeatedly stated in court filings that the merger and settlement were in the public interest

- Believe that connection needed to prove Co’s ability to engage in unlawful conduct is lacking, since the conduct under scrutiny falls either within either the ticketing or concert segment, not across

- DOJ’s investigation appears to be focused on specific biz practices, not the legality of the Live Nation-Ticketmaster merger or Live Nation’s overall biz structure

- Remain hopeful they can amicably resolve remaining disputes, but if not, they are prepared to defend themselves in court

- Analysts were still curious…how do they see the relative value of Ticketmaster inside Live Nation vs as a separate standalone Co?

- Run a very decentralized organization

- All four bizs run “incredible core businesses” on their won

- “Long-term, together or sperate, these would all be very successful businesses. We happen to think that we like our portfolio today and plan on keeping it”

DraftKings: The Odds Are Still In Favor Of Growth + Profitability In Sports Betting

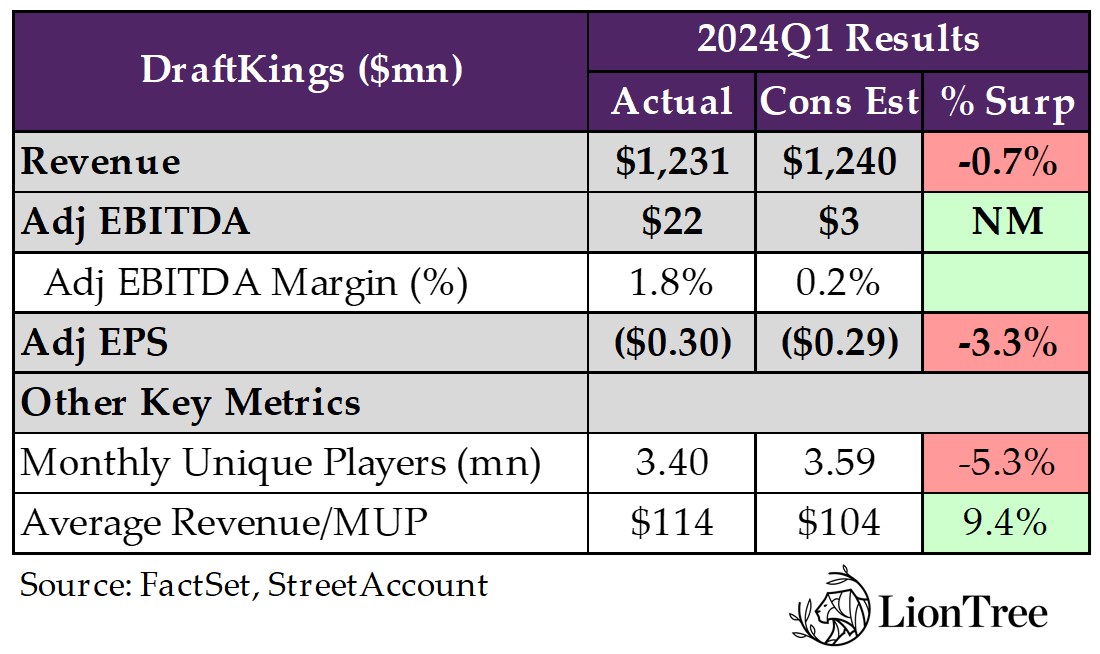

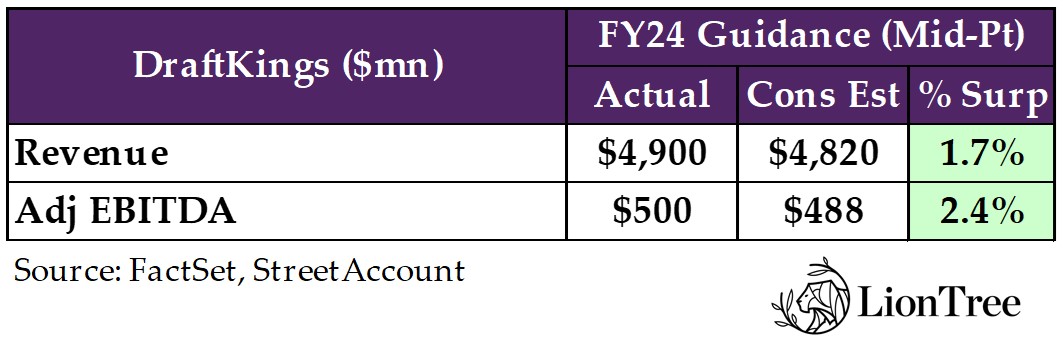

The notion that sports betting continues to be a high growth area within the Entertainment landscape was certainly reflected in DraftKings’ +53% y/y revenue growth in Q1, though Wall Street has caught on and was actually expecting a tad higher growth. The upside in the quarter instead came from better profitability, with adj EBITDA hitting $22mn vs cons $3mn. Also, the Co raised its 2024 revenue guidance by +$125m at the mid-point and its adj EBITDA outlook by +$40mn at the mid-point.

While user metrics were a tad mixed, with lower-than-expected monthly unique players (3.4mn vs cons 3.59mn) but better-than-expected avg rev/MUP ($114 vs cons $104), the Co had a “unbelievably” efficient Q1 for marketing. This continued into April, where DraftKings saw a ~40% y/y decrease in CAC. Also, adj Gross Margin incr’d +550bps y/y to 44% in Q1 due to higher structural sportsbook hold and improved promotional efficiency.

DraftKings is still seeing nice growth in its existing mature markets, and new launches in Vermont and North Carolina have been capturing more value faster (should contribute positively to adj EBITDA in H2:24). Looking ahead to 2025, Texas is a big focus. iGaming should also see momentum pick up once there is some movement legislation-wise, and there will be a lot of state expansions with respect to Jackpocket before the end of the year (the deal is slated to close in mid-2024).

Net-net, while the stock gave back a little in reaction to earnings, underlying market growth and the company’s progression toward profitability appear intact. It also sounds like a shareholder return action could be in the cards in the not-too-distant future, which would certainly be incremental…

See below for more of our key takeaways from DraftKings’s results.

-> DraftKings shares were down -2.8% following the print and finished the week down -3.0%; YTD, DraftKings stock is still up +18.6% after a massive +209.5% rally in 2023

It Was A Little Bit Of A Mixed Q1… But The Co Raised 2024 Guidance

- Q1 total revenue was up +53% y/y but was -0.7% below cons, while adj EBITDA at $22mn was well above cons $3mn

- Adj EBITDA flow through percentage was at 60%

- Adj Gross Margin also incr’d +550bps y/y to 44% as a result of a higher structural sportsbook hold and improved promotional efficiency

- User metrics were mixed: Lower than expected monthly unique players at 3.4mn missed cons 3.59mn, while avg rev/MUP was better at $114 vs cons $104

- Q2, Q3 and Q4 quarterly guidance

- Raised the low end of the rev guidance range for Q2-Q4 to +25-30% y/y: Was +20-30% y/y initially

- Q2 = ~+25% y/y

- Q3 and Q4 = ~+30%

- Reiterated Q2 adj EBITDA of almost $150mn and maintained Q3 guidance of nearly breaking even

- Increased Q4 adj EBITDA guidance: Now expects $325mn+ in Q4 (vs $300mn originally)

- Raised the low end of the rev guidance range for Q2-Q4 to +25-30% y/y: Was +20-30% y/y initially

- Raised 2024 revenue guidance by +$125m at the mid-pt (from $4.65-4.9bn to $4.8-5bn), topping cons by +1.7%, and raised adj EBITDA by +$40mn at the mid-pt (from $410-510mn to $460-540mn), beating cons by +2.4%

- 2024 revenue guidance implies +34% y/y growth

- 2024 adj EBITDA flow-through percentage of 53%

- Includes all existing jurisdictions but excludes proposed acq of Jackpocket.

- Drivers to the 2024 guidance changes relative to the mid-points:

- $165mn of the rev and $68mn of the adj EBITDA improvement from Customer acq, retention, & engagement, which continue to exceed expectations due to marketing optimization initiatives and product advancements

- $20mn of the rev and $14mn of the adj EBITDA improvement from a higher structural sportsbook hold percentage primarily as a result of momentum into the same game parlay offering

- Now expect the structural sportsbook hold % to approach 10.5% in 2024

- Offset by $60mn of rev and $42mn adj EBITDA headwind from customer-friendly outcomes in late March and April

- Other 2024 guidance:

- Maintained adj Gross Margin in the range of 45-47%, +350bp y/y at the mid pt

- Now anticipates adj Sales & Marketing Expense will decline modestly

- Stock-based comp expense to be flat-to-down in dollar terms and to represent ~ 8% of rev (down from 11% in 2023 and 26% in 2022)

- Incr’d the forecast for FCF, which is now expected at ~ $400mn (vs $310-410mn prior), assuming ~$120mn CapEx and capitalized software development costs

- Expect to consummate the Jackpocket acq near the middle of 2024: “Excited to enter the rapidly growing U.S. digital lottery vertical”

Improving Efficiencies & KPIs

- Strong customer acquisition, retention, and engagement resulted in higher-than-expected handle in Q1:

- Customer acquisition was ~10% higher than had forecast, driven primarily by outperformance in North Carolina, where CAC improved by more than +20% vs CAC in Mass, which had been live for a similar duration in March 2023

- Had a “unbelievably” efficient Q1 for marketing and it continued into April, where the Co had a ~-40% y/y decrease in CAC: They see some opportunities to invest a bit deeper but not significantly

- “We’re not going to have a massive increase. I think this is like optimization around the edges where we see an opportunity”

- Improved structural sportsbook hold percentage: Structural sportsbook hold % was slightly ahead of expectations at 9.8% and incr’d ~+150bp y/y; “So what that really means is that our bet mix came in better than we expected as it relates to projected hold”

- Outlook: Continue to believe that “there’s a lot of upside here” but don’t know what they ceiling

- Handle per active rates all look “healthy” as they continue to drive and increase parlay mix and avg leg count: That will continue to be the focus as long as they continue to see healthy customer metrics and get positive feedback on the product; “So, we’ll see how far we can get it. But right now, we do believe there’s a good bit of upside still remaining”

- Promotional reinvestment for OSB and iGaming cont’d to become more efficient y/y and improved by more than +700bps as a % of GGR: The reinvestment rate also improved on an existing state basis (states that launched between 2018 and 2022)

- Had a lower percentage of the population launch in Q1 this year than last year

- As a drag on the business into Q2, sport outcomes were customer-friendly in the latter weeks of the qtr: The NCAA men’s basketball favorites won a high % of games during the early rounds of this year’s March Madness tournament

See More Penetration Upside In Mature States & New States Capturing Value Faster

- Still seeing growth in existing states: On a same store basis from 2018 to 2022, states grew net revenue ~+40% y/y in Q1, hence healthy growth in existing states

- Expect growth to continue as they improve the product and as the industry evolves and the TAM increases

- Seeing more casual customers coming to the market particularly in the older states

- New launches are capturing more value faster: Vermont and North Carolina’s customer acquisition efficiency is on par with prior launches and both states are expected to contribute positively to adj EBITDA in H2:24; “We’re able to capture a tremendous amount of value in a much shorter period of time with a much more efficient level of investment than we did, say, three or four years ago”

- Texas will be a big focus looking into 2025: “Texas, I think, has a real shot. It got through one chamber last year. And as you may know, the Texas legislature doesn’t meet in 2024. So we’re really gearing up for 2025”

- Expect to see some momentum pick up in iGaming once there is some momentum legislation wise: “Once the states in certain regions start moving on iGaming more, you’ll see a more rapid succession of them. And I also think that the need for tax revenues is going to increase”

- There will be a lot of state expansions with Jackpocket: “You’ll see some additional states come get up and running for Jackpocket before the end of the year”

More Confident Than Ever In FCF and Exploring Capital Return Options

- Have developed more confidence in their FCF trajectory for 2024+:

- Kicked off multi-year planning process

- Exploring capital allocation options given the strong trajectory of FCF

- Will share more in the next qtr

Couple Other Key Comments / Updates

- Have a very high bar for M&A and the organic growth path is really strong right now so “don’t feel compelled” to do M&A for growth

- Media rights partnerships? Amazon has been a great partner for Thurs Night Football and would look to expand the relationship depending on their plans; Have great relationships with a number of different parties rumored to be involved in the bidding on NBA too

- AI “can really be impactful in a significant and transformational way to DraftKings in the future”

- Use multiple tools from 5-10 vendors

- Use AI for things that improve the product, improve efficiency (like code refactoring, code review and marketing, asset creation), and improve customer experience (help model and detect signs of problem gaming so that they can flag things for the player intervention team to go and investigate)

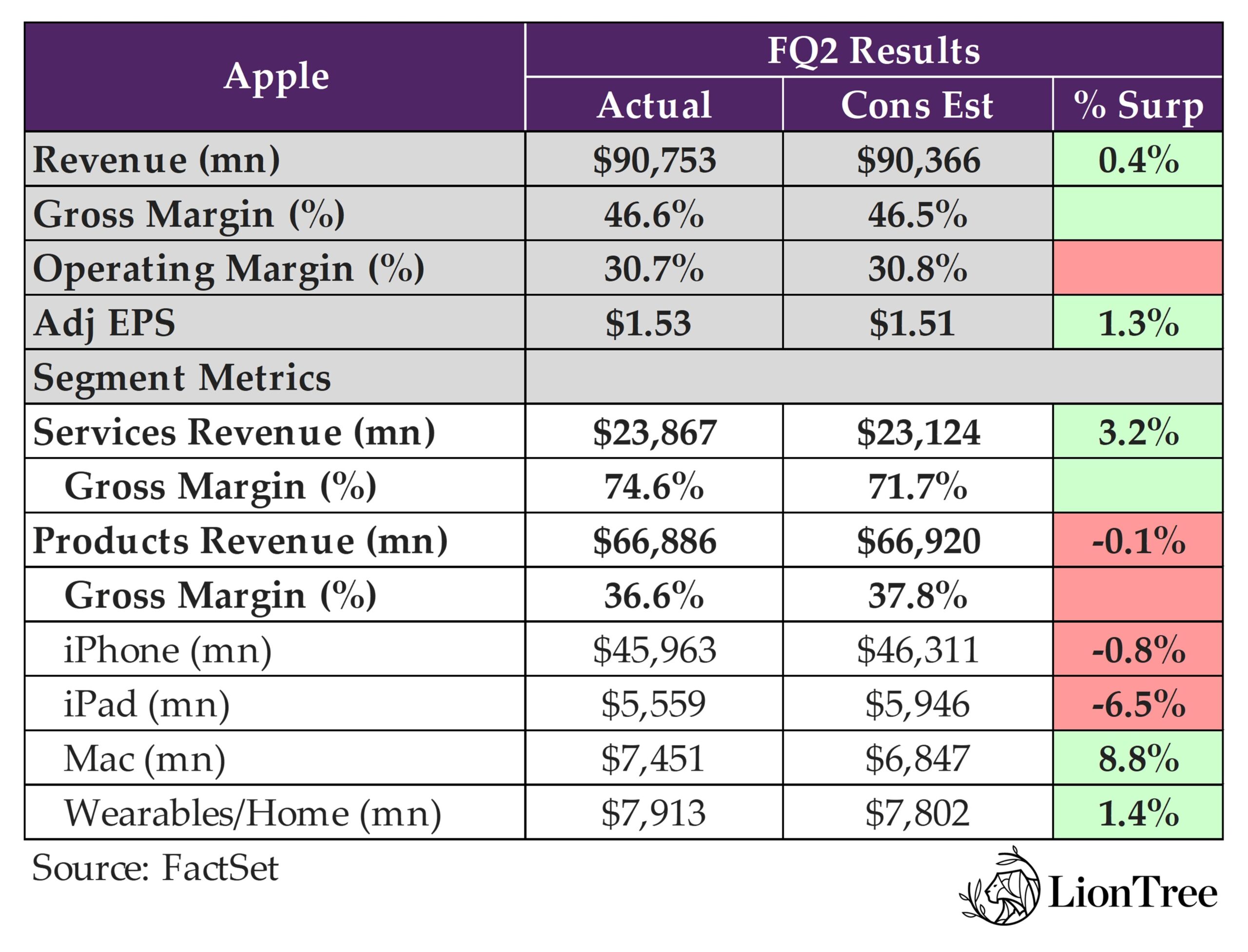

Apple’s Record $110bn Buyback Takes Center Stage

Apple’s triumph of returning to quarterly revenue growth was short-lived, as after finally posting positive revenue growth last quarter (after four straight quarters of revenue declines), revenue once again fell in the most recent quarter, down -4% y/y. That being said, Q1 revenue was +0.4% above consensus, as Services revenue beat by +3.2% (and set all-time high overall Services rev record), but Product rev came in a hair below expectations. Product revenue fell -10% y/y due to tough y/y comps from the benefit of fulfilling pent-up iPhone 14 demand in the year-ago quarter, but ex the impact, Product rev would have been ~flat y/y.

Regionally, Apple saw revenue fall on a y/y basis in each of its geographic segments, excluding Europe. The Greater China market fell -8% y/y, but that was an improvement from -13% y/y in the prior quarter. iPhone 15 and iPhone 15 Pro Max were the best-selling smartphones in urban China, which “means the other products didn’t fare as well”, as was the case last qtr. Overall, the company “maintain[s] a great view of China in the long term”, and outside of China, Apple still achieved revenue records across more than a dozen countries and regions.

Looking ahead, in somewhat of a surprise after 15 straight quarters of just providing “directional insights”, Apple broke its streak to provide formal guidance. FQ3 total revenue is expected to grow low single digits y/y (cons was at +1.5%), while Services rev is expected to grow double digits at a rate similar to the growth seen in FH1. iPad rev is also expected to grow double-digits. The company did not provide guidance for any other segments.

While Apple’s overall results came in above expectations, what really stole the show was the buyback announcement of an additional $110bn – the largest buyback plan in US history, topping the company’s own prior record of a $100bn repurchase authorization back in 2018. Apple has spent the most of any tech company on stock repurchases over the last decade, apportioning $650bn since 2012. At Friday’s stock price, executing Apple’s full buyback authorization would amount to repurchasing nearly 4% of the company’s shares. (link). Also to flag, the company raised its cash dividend by +4%.

Moving forward, there’s lots to look forward to, with an “exciting” product announcement coming next week, followed by the worldwide developers conference next month. Also, similar to last quarter, the company teased “sharing some very exciting things with our customers soon” on the Gen AI front, though what it is and when that will happen is still TBD.

See below for more thoughts and key points.

-> Apple rose +6.0% on the day after reporting its results, posting its best day since November 2022, and ended the week up +8.3%; YTD, however, the stock is still down -4.8%

- FQ2 headline results beat: Total revenue fell -4% y/y (vs +2% y/y in FQ1) and beat cons by +0.4%; Gross margin of 46.6% was up +70bps seq (in-line with estimates of 46.6%), driven by cost savings and favorable mix to Services partially offset by leverage; EPS beat by +1.7%

- Achieved revenue records across more than a dozen countries and regions

- Hit March qtr rev records in Latin America and the Middle East, as well as Canada, India, Spain, and Turkey

- Greater China: Rev fell -8.0% y/y (accel from -13% y/y in FQ1), w/ iPhone being the primary driver (Other products “didn’t fare as well…we clearly have work to do. I think it has been and is through last quarter the most competitive market in the world)

- All-time rev record in Indonesia, “one of the many markets where we continue to see so much potential”

- Hit March qtr rev records in Latin America and the Middle East, as well as Canada, India, Spain, and Turkey

- OpEx came in at the mid-pt of the guidance range: At $14.4bn, in-line with cons, and up +5.0% y/y

- Achieved revenue records across more than a dozen countries and regions

- Product rev missed cons by -0.1%: Fell -10% y/y (vs +0.1% y/y in FQ1); Gross margin of 36.6% was down -280bps seq, primarily due to seasonal loss of leverage and mix, partially offset by favorable costs

- Tough y/y iPhone comp weighed on Product rev growth…: Fulfilling pent-up demand from year-ago December qtr due to COVID-related supply disruptions on the iPhone 14 Pro and Pro Mac added an ~$5bn benefit to March qtr rev last year (ex the impact, Product rev would have been ~flat y/y this past qtr)

- … Partially offset by strength from Mac

- Continue to see “a lot” of interest at the top-end of the range of products: Combination of consumers wanting to purchase the best product offered and Apple’s ability to make those purchased more affordable over time (i.e., financing solutions, installment plans, trade-in programs, etc.); Have seen this trend over the last several year, “which we think is pretty sustainable”

- Total installed base of active devices set a record across all products and geographic segments

- By Segment:

- iPhone rev missed cons by -0.8%: Down -10% y/y (vs +6.0% y/y in FQ1), as segment faced a difficult y/y comp

- iPhone still saw growth in some markets, including Mainland China

- iPhone was the top-selling model in the US, urban China, Australia, the UK, France, Germany, and Japan

- iPhone active installed base reached a new all-time high in total and in every geographical segment

- iPad rev missed by -6.5%: Down -17% y/y (vs -25.3% in FQ1), due to difficult comp with the momentum following the launch of M2, iPad Pro and 10th-gen iPad last FY

- iPad install base reached an all-time high with over half of the customers who purchased iPads during the qtr being new to the product

- Mac rev beat by +8.8%: Up +4% y/y (vs up +1.0% in FQ1), driven by strength of the new MacBook Air powered by the M3 chip

- Mac installed base reached an all-time high with almost half of MacBook Air buyers during the quarter being new to the product

- Wearables, Home, and Accessories beat cons by +1.4%: Down -10% y/y (vs down -11% in FQ1) due to difficult launch compare on Watch and AirPods

- Apple Watch install base reached an all-time high, as ~2/3 of customers purchasing an Apple Watch during the qtr were new to the product

- iPhone rev missed cons by -0.8%: Down -10% y/y (vs +6.0% y/y in FQ1), as segment faced a difficult y/y comp

- Tough y/y iPhone comp weighed on Product rev growth…: Fulfilling pent-up demand from year-ago December qtr due to COVID-related supply disruptions on the iPhone 14 Pro and Pro Mac added an ~$5bn benefit to March qtr rev last year (ex the impact, Product rev would have been ~flat y/y this past qtr)

- Services rev beat by +3.2%: Up +14% y/y (vs +11% y/y in FQ1); Gross margin of 74.6% was up +180bps seq due to a more favorable mix

- Set all-time high overall Services rev record, with record performance in both developed and emerging markets

- Set all-time revenue records in cloud services, payment services, and video

- Transacting and paid accounts reached all-time highs, with paid accounts growing double-digits y/y.

- Paid subscriptions showed “strong” double-digit growth: Have “well over” 1bn paid subscriptions, nearly double the # of paid subscriptions from four years ago (in-line w/ commentary from last qtr)

- Set all-time high overall Services rev record, with record performance in both developed and emerging markets

- FQ3 Outlook: After 15 straight qtrs of providing directional insights in lieu of specific guidance, the Co provided formal guidance under the assumption that the projected macroeconomic outlook doesn’t worsen

- Expect FQ3 total Co rev to grow in the low-single-digits y/y, in spite of FX headwind of ~-2.5ppts (vs cons of +1/5% y/y growth)

- Expect FQ3 Services rev to grow double digits at a rate similar to the growth reported for FH1

- Expect FQ3 iPad rev to grow double digits

- Gross margin: Between 45.5% and 46.5%

- OpEx: Between $14.3-$14.5bn

- OI&E: ~$50mn

- Announced the largest buyback plan in US history: Approved an additional $110bn in share repurchases

- Topped its own prior record: Back in 2018, Apple authorized $100bn in share repurchases, the largest ever up until its latest buyback plan

- Increased quarterly dividend by +4.2%, to 25c from 24c

- Continue to plan for annual increase in the dividend going forward, as they have done for the last 12 yrs

- “Continue to feel very bullish about our opportunity in generative AI”: Making “significant investments” and “looking forward to sharing some very exciting things with our customers soon”