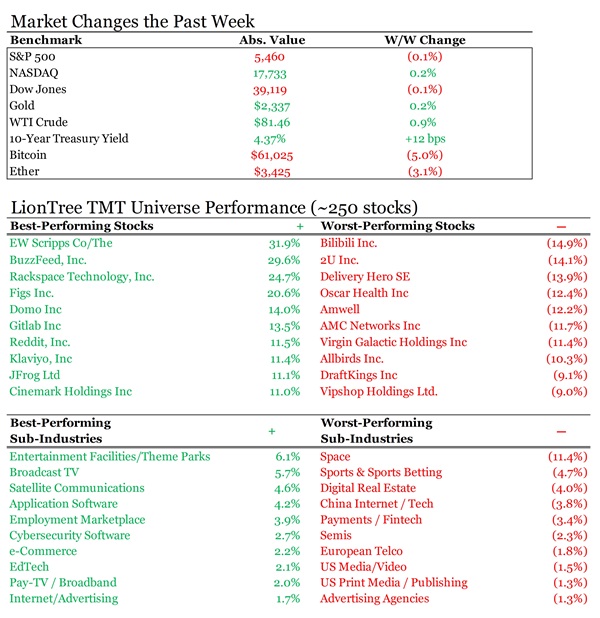

Q2 is now officially in the rearview mirror with today being the last trading day of the quarter. The big tech names were the key drivers of Nasdaq’s +8.3% and the S&P 500’s +~4% upward move for the period with names like Nvidia, Apple, and Amazon up by +37%, +22% and +21% respectively for the quarter. However, the unweighted S&P 500 index was actually down -3% which points to the continued high level of market concentration.

For this week’s edition, we focused on the below key updates and developments (all are clickable links):

- It’s A Wrap On Q2…Who Were The Best & Worst Performers?

- The E-Commerce Industry Is “Primed” For Another Major Summer Sales Event

- More Rationalization Is Coming To Video Streaming…

- The European Commission Leads The Tech Regulation Drumbeat This Week

- Big Tech’s AI Arms Race Heats Up

- Where Do Things Stand For Paramount Now?

- T-Mobile’s 5G Network Performance Continues To Lead The Pack + Other Connectivity Updates

- Grab Bag: DoorDash-Deliveroo Deal / Dungeon & Fighter Tops Charts / AI Broadcasting At Olympics

Also, it was a busy week for LionTree with a couple announcements that I wanted to highlight:

LionTree served as a co-manager on WEBTOON’s IPO (NAS: WBTN), which was priced at $21/share, the high end of its range, to raise $315mn. WEBTOON is a leading global entertainment company and home to some of the world’s largest storytelling platforms. LionTree served as the exclusive financial advisor to Boat Rocker on the sale of Untitled Entertainment to TPG.

Enjoy the read and have a nice weekend.

Best,

Leslie

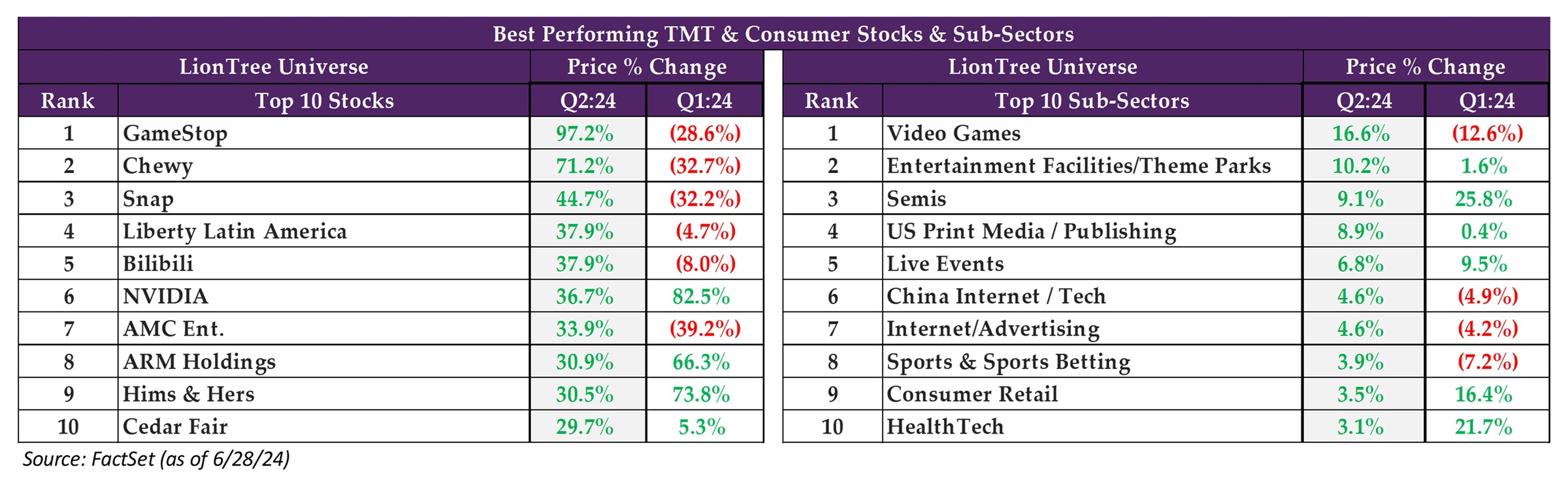

It’s A Wrap On Q2…Who Were The Best & Worst Performers?

The major indices posted another quarter of strong gains, although not quite as strong as last qtr. After two quarters of double-digit growth, with the S&P 500 up +11.2% in Q4 and +10.2% in Q1, the index decelerated to single digits growth in Q2, up +3.9% over the qtr. Nasdaq rallied harder, up +8.3%, but compared to +9.1% in Q1 and +13.6% in Q4. However, high levels of market concentration remain a key theme.

Within the S&P 500, Information Technology was the best-performing sector, up +3.2%, on avg, though down from last qtr’s +7.7%. Utilities (+2.1%) and Communication Services (+0.7%) were the only other sectors that traded up in the qtr. Consumer Staples and Consumer Discretionary were the two worst performing sectors in the S&P 500, down -7.0% and -6.2%, respectively, in Q2 (vs +4.8% and +8.1%, respectively, in Q1).

Internationally, it was a mixed bag across the board. In Europe, DAX was down -1.4% (vs +10.4% in Q1) and CAC was down -8.9% (vs +8.8% in Q2), while Euronext was up +1.1% (vs +12.3% in Q1) and FTSE was up +2.7% (vs +2.8% in Q1). It was a mixed picture in Asia as well, with the Nikkei and SSE Composite down -2.0% (vs +20.6% in Q1) and -2.4% (vs +1.2% in Q1), while the Hang Seng was up +7.1% (vs -3.0% in Q1).

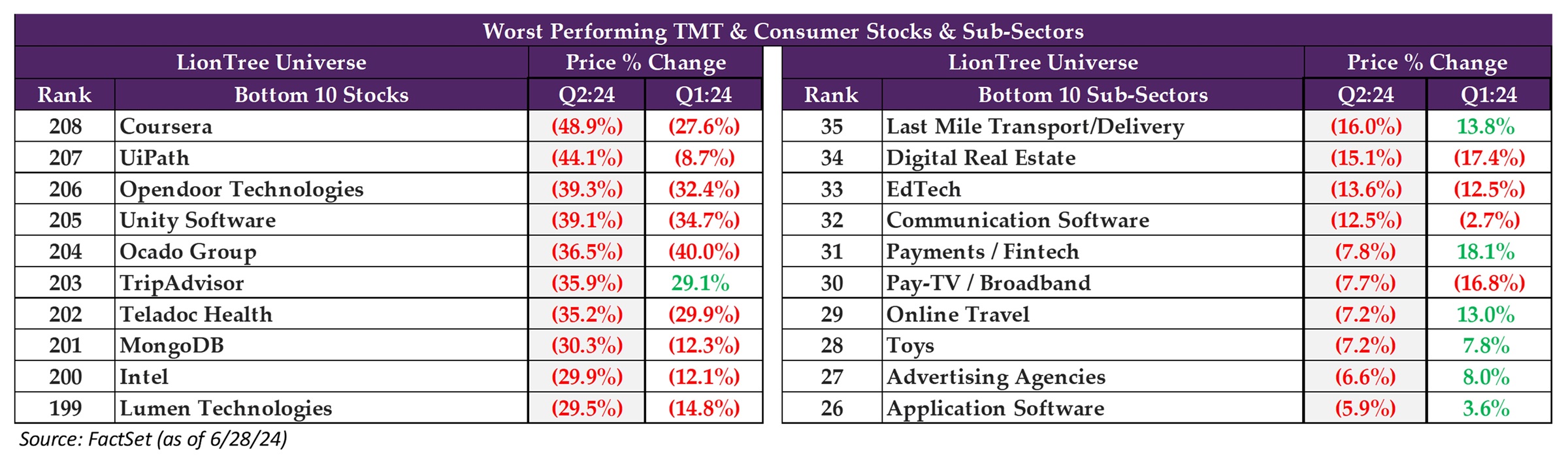

Looking at performance across our LionTree Universe of ~200 stocks in the TMT and Consumer sector with $1bn+ market cap, it was tough going, with just 43% of stocks trading up in the quarter, vs 52% in Q1 and 77% in Q4. More interestingly, almost a third (~32%) of stocks traded down double-digits, which is even higher than last qtr’s 29% and Q4’s ~10%.

Who was the best performer in Q2? It was GameStop, which was up +97% in the quarter driven by a meme rally. It was followed by Chewy, up +71%, and Snap, up +45%, to make up the Top 3 best performers of Q2.

On the other hand, which stocks fared the worst in Q2? It was Coursera, down -49% in Q2. UiPath and OpenDoor were down -44% and -39%, respectively, to round out the Bottom 3 worst performers of Q2.

The BEST Performing Sub-Sectors in Q2

- #1 = Video Games: After falling -13%, on avg, in Q1, the sub-sector reversed course and was up +17%, on avg, in Q2

- GameStop’s +97% gain in the quarter drove most of the sub-sector’s performance; Playtika also posted a double-digit gain (though to a much lesser degree) of +11%, while Take-Two and Ubisoft’s more modest gains of +5% and +5% further propped up the sector

- The sector’s performance was slightly offset by Nintendo and Roblox’s -2% and -3% drops over the qtr

- #2 = Entertainment Facilities/Theme Parks: The sub-sector saw accelerated growth in the qtr, up +10%, on avg, on top of a +2% average increase in Q1

- Sub-sector performance was driven by Cedar Fair and Six Flags Entertainment, which were both up +30% and +26%, respectively, in Q2 (note, the two companies are set to merge in early July); Bowlero was also up +6% in the qtr; Vivid Seats was the only exception in qtr, down -4%

- #3 = Semis: The sub-sector was up +9.1%, on avg, in Q2, which was a deceleration from Q1’s avg of +25.8%

- Not surprisingly, NVIDIA and ARM Holdings were the drivers of the sub-sector’s performance, up +37% and +31% over the qtr, respectively; Broadcom and QUALCOMM also posted double-digit positive performance, up +21% and +18%, respectively

- That being said, there were some drags in the sub-sector, as GlobalFoundries, Advanced Micro Devices, and Intel were all down -3%, -10% and -30% in the qtr

The WORST Performing Sub-Sectors in Q2

- #35 (last place) = Last Mile Transport/Delivery: The sector fell -16%, on avg, in Q2, a reversal from +14%, on avg, in Q1

- Several companies in the sector posted double-digit losses in Q2, including Ocado Group (down -37%), Lyft (-27%), DoorDash (-21%), JustEatTakeaway.com (-18%), Delivery Hero SE (-17%), and Instacart (-14%); Uber was also down -5%

- Deliveroo was the exception in the sub-sector, up +11%

- #34 = Digital Real Estate: The sub-sector fell one spot further in Q2 (was the third worst-performing sector in Q1, vs second worst-performing in Q2), down -13.1%, on avg, which is a decel from Q1’s -17.4%

- Companies in the sector continued to have it tough, with OpenDoor down -40% in the qtr, and Zillow down -6%; Compass ended the qtr flat

- #33 = EdTech: The sub-sector saw a greater degree of red in Q2, down -14%, on avg, after falling -13%, on avg, in Q1

- Sub-sector performance was largely driven by Coursera and Udemy, both of which fell -49% and -21%, respectively, in Q2; Duolingo was also down -5.4%

- That being said, PowerSchool Holdings and Grand Canyon Education were up +5% and +3%, respectively

The E-Commerce Industry Is “Primed” For Another Major Summer Sales Event

It was an exciting week in the e-commerce industry, as Amazon annc’d the dates of its tenth annual Prime Day with an original song, “It’s Prime Day”, by Megan Thee Stallion (link). Along with offering Prime members exclusive access to “millions of great deals” and bringing back invite-only sales, Prime Day 2024 will also see select influencers begin releasing deals on various products on Amazon’s marketplace beginning on July 8. That said, Amazon won’t be the only major retailer hosting a large sales event in July, as news of Prime Day was followed closely by announcements from Walmart and Target that each is separately planning its own “biggest sale of the season” during the month. Like Amazon, both Walmart and Target will provide exclusive benefits for members of their premium subscription offerings. However, with all of the concurrent summer sales events and the fact that consumers have likely come to expect that these will occur on annual basis, it is questionable how effective they will be in driving incremental sales…

There were also a few other impactful e-comm updates and developments this week outside of the upcoming summer sales events. Data published by Route revealed that TikTok Shop’s growth actually accelerated after the Biden administration signed a divest-or-ban law in April. Furthermore, Route’s findings suggest that TikTok Shop has been taking a bite out of Amazon’s e-commerce market share in the US. That said, this trend may not continue for long as Amazon reportedly plans on creating a discount section on its website that will ship products from Chinese warehouses directly to customers overseas to better compete against the likes of TikTok Shop and Temu. Also, Target, which this week announced a partnership with Shopify to expand its third-party marketplace, could be more of a threat to Amazon on the domestic front moving forward.

See below for more on this week’s key updates from the e-commerce space

- Amazon is planning to host Prime Day 2024 from July 16-17 (link/link): The tenth Prime Day event starts at 12:01 PDT on July 16 and runs through July 17, providing Prime members w/ exclusive access to “millions of great deals”

- Prime Day will be available to customers in 23 countries: Including the US, UK, Canada, Spain, Australia, Germany, Mexico, Japan, the Netherlands, Saudi Arabia, and Turkey, among others (India will get its own Prime Day later this summer)

- New deals will drop as often as every five minutes during select periods during the event: This will incentivize Prime members to “come back and shop often”

- There will also be deals on digital goods & svs: Such as five free months of Amazon Music Unlimited, up to 50% off select movies and shows to rent or own, and discounts on Prime Video Channels, such as Starz and Crunchyroll, as well as grocery delivery svs

- Certain influencers will begin dropping deals on various products starting on July 8: Participating influencers include Jess Sims, Alyssa McKay, Monet McMichael, Jared McCain, Millie Bobby Brown, Meredith Duxbury, and Alix Earle

- Amazon is bringing back invite-only deals: After requesting an invitation, members that are selected will be notified via email during Prime Day w/ instructions on how to purchase the item at the exclusive deal price

- The Co highlighted some of the top invite-only deals for Prime members: Including up to -40% off Sony Wireless Headphones and up to -30% off Peloton products

- Other stats underscored the magnitude of Amazon customers’ savings: Over the last yr, Amazon customers saved nearly $24bn from deals and coupons, w/ Prime members enjoying the vast majority of those savings, including $2.5bn+ during Prime Day 2023

- Other major retailers also annc’d big sales events slated for July this week

- “Walmart Deals” will be the Co’s “largest savings event ever” (link): The event starts Monday, July 8th at 5 pm EST and runs through Thursday, July 11th at 11:59 pm EST; All customers will have the oppty to shop “thousands of deals on popular items”, though Walmart+ members will get a five-hour head start

- Target is hosting “its biggest sale of the season” during Target Circle Week (link): From 2 am CST on July 7 through the end of July 13, Target will offer more deals for members of Target Circle, the Co’s free-to-join loyalty program, including deep discounts and personalized Target Circle bonuses

-> Google has also been looking to capitalize on the incr’d shopping activity around Prime Day by launching new shopping features and expanding existing shopping features in its search engine; In addition to rolling out a special deals section to highlight discounted items across the Web, the Co has expanded its price comparison tools, including a feature that will show shoppers special pricing that a retailer might be offering members of their rewards or loyalty programs; Google’s aim is to make it “fiscally irresponsible” for people to start their online shopping anywhere else behinds Google’s website (link)

- TikTok Shop has cont’d to grow rapidly, despite the potential looming US ban (link): New data from Route shows that the orders placed on TikTok Shop grew +13% m/m from April to May – almost double the Co’s +7% avg monthly gain in orders since the beginning of 2024

- The accel in order growth comes despite a slowdown in go-to-mkt efforts: After initially covering the costs of steep discounts to incentivize customers to buy and larger brands to join, TikTok eased off those subsidies and began taking a larger cut of merchants’ sales in Apr

- TikTok Shop had already been on a hot start in 2024…: In Q1, the Co’s customers were even higher than in Q4:23, which benefited from seasonally elevated holiday shopping activity

- … After ending 2023 on a high note in the US: Per TikTok, the Co closed 2023 w/ 500k+ Shop sellers in the US; Entering 2024, TikTok Shop was targeting to grow its US biz tenfold to ~$17.5bn in sales

- TikTok has been hiring hundreds of employees to its US operations: Even after the Biden administration signed a divest-or-ban law in Apr, ByteDance has poured resources into tightening its grip on the US

- TikTok Shop has been taking share from Amazon: From Q4:23 to Q1:24, Route’s data shows that the Co’s mix of orders from Amazon shifted from 65% to 61% over the period, w/ total orders from Amazon growing +1% (vs an avg of +7% for TikTok Shop)

-> In response to growing competition from overseas competitors such as TikTok Shop and Temu, Amazon reportedly plans to launch a section on its website that will ship cheap items from warehouses in China directly to overseas consumers, per The Information; The new mktplace will offer unbranded fashion, home goods, and daily necessities, w/ orders taking an avg of 9-11 days to be delivered to customers; Amazon reportedly told Chinese sellers that it would begin signing up sellers in the summer and begin accepting inventory in the fall (link)

–> PDD shares fell -4.6% in response to news that Amazon is planning a discount section, ending the week down -7.6%; YTD, PDD stock is trading down -9.1%

- Target and Shopify annc’d a partnership that will significantly expand Target’s third-party mktplace (link): Shopify sellers can now apply to join Target Plus, Target’s 3P mktplace where merchants can sell and manage orders; This will provide them access to millions of Target shoppers

- This is Shopify’s first collab w/ a major retailer: The initial group of Shopify sellers to have products featured at Target include True Classic and Caden Lane, among others

- Target Plus currently has a fraction of the scale that its competitors possess: Before the Shopify partnership, Target Plus counted ~1,200 sellers compared to Amazon’s nearly 2mn sellers and Walmart’s ~135,000

-> Shopify also broadened access to its AI-powered tools this week, making them available to more users; Customers can now use Shopify’s editing tool on their smartphones to enhance images used in promotional materials, including emails; The feature was previously restricted to only editing product images online; Shopify also expanded access to Sidekick, its chatbot that helps merchants w/ queries, including insights on customer behavior, that was in testing since last year w/ 2,000+ users (link)

More Rationalization Is Coming To Video Streaming…

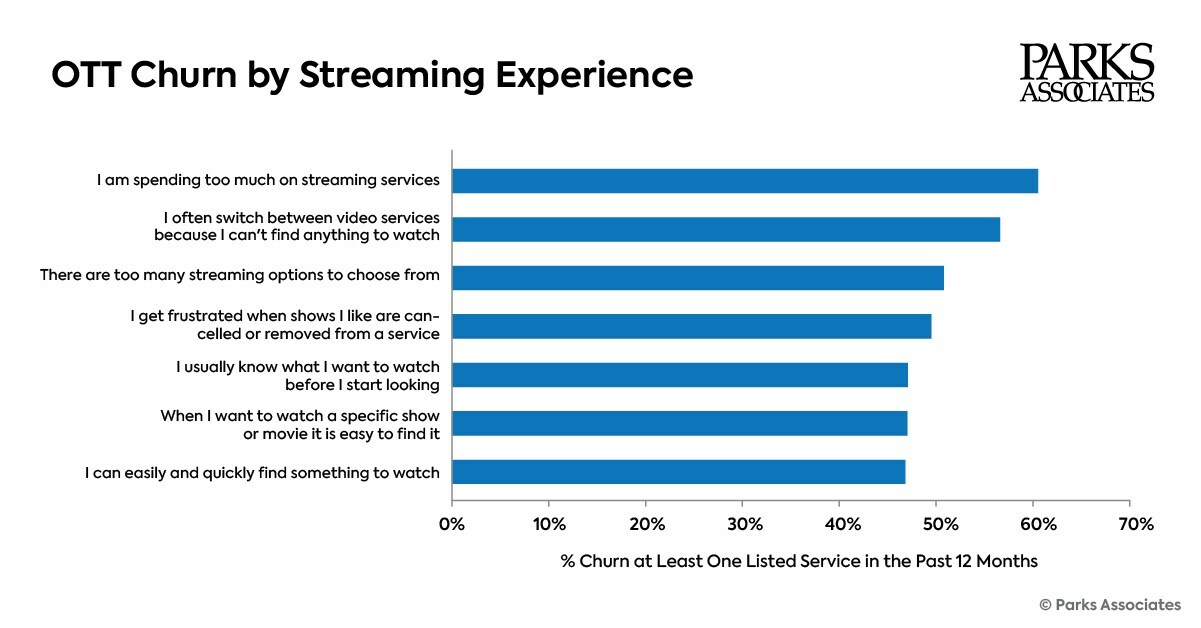

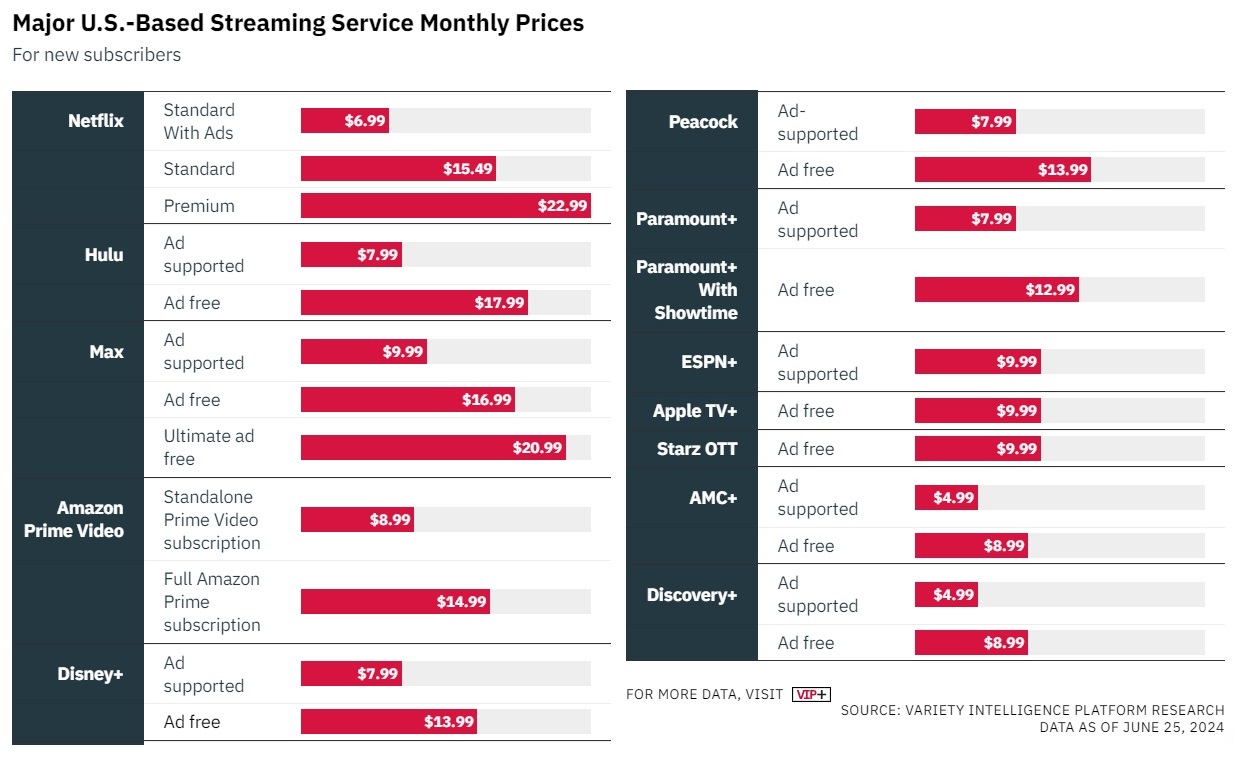

There was a consistent stream of streaming updates this week across the gamut, as the tug of war between streamers increasing prices and consumers spending less on streaming continued. On the consumer side, new research out from Park Associates found that US SVoD spending has dropped -30% since 2021 as consumers have been reducing the number of paying services that they subscribe to and moving down to ad-based tiers. That was a particularly interesting data point considering some reports out this week and that Netflix is considering launching a free ad-supported plan in select markets across Europe and Asia.

Also on the Netflix front, Dish became the latest pay-TV provider to bundle in the service in an attempt to slow the cord-cutting bleeding, announcing a new deal that offers a $6.99/mo credit towards a Netflix plan (Netflix’s Standard w/ Ads costs $6.99/mo). Also on the bundling front, Verizon expanded its “myPlan” streaming perks to home internet customers with the launch of “myHome.”

On the pricing front, Paramount annc’d plans to raise prices for its streaming plans, just about a year after the last price hike. On the other hand, Spotify brought down the entry price for ad free music. After raising prices across all its subscription plans just a couple of weeks ago, the Co annc’d its new “Basic” streaming plan in the US, which is a music-only, no audiobook offering. It marks the return of a $10.99/mo tier which is a lower price point than the $11.99/mo Premium Individual tier that was previously the cheapest option.

See below for the drilldown on all the above…

US SVoD Spend Has Dropped, per Park Associates (link/link)

- There has been a -30% drop in spending for streaming SVoD services since 2021, with the avg US internet household spending ~$63/mo, down from $90/mo in 2021

- “Consumers are spending less, but rather than go without, many are using ad-based alternatives to save on costs”

- Households are stacking fewer streaming svs

- The overall avg # of streaming video svs subscriptions per household has dropped below 5

- In Q1:24, 20% of US internet households report paying for 9+ svs, down from 29% in Q3:23

- 48% of US internet households cancelled a streaming video service in the past 12 months

Other Key Updates Out This Week On Streaming Price Hikes, Bundles, And More…

- Paramount Global to raise prices for its streaming plans (link/link)

- Paramount+ Essential will increase by $2 to $7.99/mo

- BUT the price increase will only impact new subscribers starting Aug 20: Current users of the plan will continue to pay $5.99/mo

- Paramount+ with SHOWTIME will increase by $1 to $12.99/mo

- This price increase will impact all users: Will go into effect Aug. 20th for new users and Sept. 20th for existing customers

- The new price is still below that of the ad-free versions of Netflix, Disney+ and WBD’s Max

- Pricing of annual subscription plans for both tiers will remain UNCHANGED: Paramount+ With Showtime is $119.99/year; Paramount+ Essential is $59.99/year

- Legacy Paramount+ Limited Commercial plan will also see price increase by $1 to $7.99/mo

- While the plan has been discontinued, Paramount continues to offer it to subscribers with an active account who signed up while it was still available

- While the plan has been discontinued, Paramount continues to offer it to subscribers with an active account who signed up while it was still available

- Paramount+ Essential will increase by $2 to $7.99/mo

- Netflix reportedly considering launching a free ad-supported plan in select markets (link)

-

- The markets being considered are in Asia and Europe where other TV networks also have free plans

- There are no plans to offer a free svs in the US

- Talks are still in the VERY early stages

- The Co has experimented with a free plan in the past (link): Back in 2021, Netflix launched a free plan in Kenya, in which viewers could watch a selection of Netflix content ad-free on Android mobile phones; If viewers enjoyed the content, they could upgrade to a paid plan to watch the full catalog on a TV or laptop

- But it discontinued the plan last year

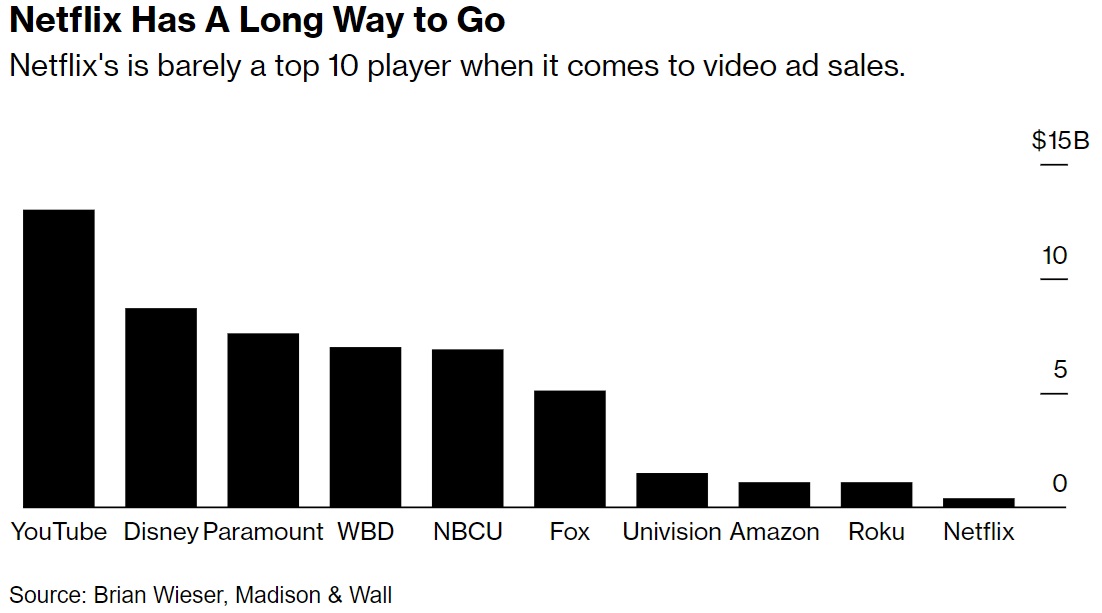

- A new free ad-supported plan could potentially help address one of the Co’s biggest challenges – creating more ad inventory: Per an ad exec cited by Bloomberg, “They’ve been slow to scale” and “there is not a clamoring for them” given that Netflix is at best the ninth or tenth biggest player in online video advertising, and has been trying to charge as much as twice as the competition

- The markets being considered are in Asia and Europe where other TV networks also have free plans

- Dish bundles Netflix for free with a new 2-yr offer (link)

- The Co will include Netflix’s Standard plan with Ads w/ a Dish TV subscription for no addtl cost for 2 years: The plan regularly costs $6.99/mo in the US and requires new or existing customers to lock in to a 24-month commitment, with early termination fees if they cancel before the term expires

- Dish TV customers can also choose to upgrade to the $15.49/mo Netflix Standard (no ads) or the $22.99/mo Netflix Premium plans, while receiving the $6.99 monthly credit

- The Co will include Netflix’s Standard plan with Ads w/ a Dish TV subscription for no addtl cost for 2 years: The plan regularly costs $6.99/mo in the US and requires new or existing customers to lock in to a 24-month commitment, with early termination fees if they cancel before the term expires

-> Other pay-TV operators have also been leaning into streaming bundles…Charter includes Disney+, ESPN+ and Paramount+ for many Spectrum TV users; Last month, Comcast launched StreamSaver, a package that includes NBCU’s Peacock Premium (w/ ads), Netflix Basic (w/ ads) and Apple TV+ for a discounted price of $15/mo

- Verizon extends its bundled “myPlan” streaming perks to home internet customers with launch of myHome (link/link/link)

- Had previously been available only to those who subscribe to Verizon’s postpaid wireless Internet svs

- “A one-stop shop for internet, entertainment, and connected home offerings”: The new “myHome” feature will allow customers of Fios-branded wireline internet, as well as Verizon 5G Internet fixed-wireless-access users (67mn subscribers in all) the option of instantly adding various bundled streaming perks for $10/mo per perk with no contract obligations

- MyHome currently supports Netflix & Max (with ads), Disney Bundle (including Disney+, Hulu, and ESPN+), YouTube Premium, and Walmart+ membership with an included Paramount+ subscription; Apple One and Apple Music Family are coming later this summer

- How does it work? Customers can choose from Fios, 5G Home, or LTE Home internet, then decide if they want add-ons, like streaming services or bundles, a connected home product, and a live TV option

- Spotify launches a new “Basic” streaming plan in the US (link/link/link/link)

- How does Basic differ from Premium? Music-only, no audiobooks: Priced at $10.99/mo, the plan provides the same ad-free music listening perks as on the $11.99/mo Premium Individual tier, but w/o the 15 monthly hours of audiobook listening that’s included w/ Premium; The plan is only available for individual subscribers (not to couples or families)

- Brings back a $10.99/mo tier: Last year, Spotify bumped up the cost of Premium from $9.99/mo (the price the svs launched at in the US more than a decade ago) to $10.99/mo; Now, the Premium tier costs $11.99/mo, a dollar more than the new Basic tier

- The Co had already launched a similar offering in the UK at the beginning of June (link)

- How does it compare to competition? Creates a music-only offering that’s the same price as the $10.99/mo plans for Apple Music and Tidal

- Spotify already offers an audiobooks-only plan in the US that is priced at $9.99/mo and includes 15 hours of audiobook listening time, plus ad-supported music

- Brings back a $10.99/mo tier: Last year, Spotify bumped up the cost of Premium from $9.99/mo (the price the svs launched at in the US more than a decade ago) to $10.99/mo; Now, the Premium tier costs $11.99/mo, a dollar more than the new Basic tier

- Comes just weeks after Spotify raised prices for all of its subscription plans: Increased Premium Individual plans by +$1 to $11.99/mo, the duo plan rising by +$2 to $16.99/mo, and the family plan rose by +$3 to $19.99/mo

- How does Basic differ from Premium? Music-only, no audiobooks: Priced at $10.99/mo, the plan provides the same ad-free music listening perks as on the $11.99/mo Premium Individual tier, but w/o the 15 monthly hours of audiobook listening that’s included w/ Premium; The plan is only available for individual subscribers (not to couples or families)

-> On May 16, the US-based Mechanical Licensing Collective sued Spotify for allegedly underpaying royalties to songwriters and publishers as a result of it reclassifying its Premium services as bundles; The new $10.99/mo tier will pay the existing, higher level of mechanicals, but listeners will need to actively choose to switch to it if they were automatically put on the $11.99/mo plan

The European Commission Leads The Tech Regulation Drumbeat This Week

The European Commission published preliminary views that found both Apple and Microsoft to be in non-compliance with antitrust laws, paving the way for rulings that could potentially assess fines of up to 10% of each company’s annual global revenues. However, regulators hope that an ongoing dialogue will bring Apple and Microsoft’s business practices in adherence with the rules, as the two have already made moves to address the issues.

Separately, there were also some other updates related to other ongoing antitrust cases against Apple and Google.

See below for more details.

- The EU found Apple to be in breach of the Digital Markets Act (DMA) (link): In preliminary findings, the European Commission said it believes that Apple’s rules of engagement do not comply w/ the DMA, “as they prevent app devs from freely steering consumers to alternative channels for offers and content”

- The EU flagged three separate issues w/ Apple’s policies:

- Apple’s matchmaking fees to app devs goes “beyond what is strictly necessary”: Refers to Apple including fees charged to app developers for every purchase made within seven days of linking out to the commercial app

- Apple makes it difficult for customers to find pricing info: Given that the Co requires devs to “link out” to a webpage where customers could then find contract details

- The EU also opened a separate non-compliance procedure against Apple’s “core technology fee”: This relates to a $0.50 charge that Apple demands every time a developer’s app is installed on a phone

- Apple has 12 months to comply or face fines of up to 10% of its global revs: However, the EU hopes that ongoing dialogue will lead to compliance rather than fines; Apple can also appeal the Commission’s preliminary findings

- Apple has already made a number of changes to comply w/ DMA: The Co responded to the EU by saying, “We are confident our plan complies w/ the law, and estimate more than 99% of developers would pay the same or less in fees to Apple under the new biz terms we created”

- The EU flagged three separate issues w/ Apple’s policies:

- The EU charged Microsoft w/ antitrust violations related to its bundling of Teams w/ Office 365 (link): The European Commission’s preliminary view is that Microsoft’s bundling of Teams w/ its productivity suite provided Teams w/ an advantage by not giving customers a choice whether they would get access to the software

- Some background on the investigation: The EU opened a formal investigation into Microsoft last yr after Slack, which is owned by Salesforce, filed a complaint; A second complaint was also filed by German videoconferencing Co Alfaview

- Microsoft’s prior changes last yr weren’t enough to address competition concerns: These first were rolled out in Europe and then worldwide

- The Co now offers a lower-priced version of its productivity suites that doesn’t include Teams

- New, large biz customers now need to purchase the svs separately, while existing ones can choose whether they want to continue to have the products packaged together or not

- The EU also highlighted concerns about the extent to which rival collab tools can integrate w/ Microsoft products: The commission noted that this “conduct may have prevented Teams’ rivals from competing, and in turn innovating”

- Microsoft could receive a fine amounting to 10% of its global revs: Though the Co will have a chance to argue its case and can propose potential remedies to address regulators’ concerns and avoid a fine

- Microsoft’s prior changes last yr weren’t enough to address competition concerns: These first were rolled out in Europe and then worldwide

- Some background on the investigation: The EU opened a formal investigation into Microsoft last yr after Slack, which is owned by Salesforce, filed a complaint; A second complaint was also filed by German videoconferencing Co Alfaview

- There were also some updates in some other ongoing antitrust cases against Big Tech Cos:

- A US District Judge ruled that Google CEO Sundar Pichai and co-founder Sergey Brin cannot avoid being deposed in antitrust case (link): The case concerns a lawsuit brought by Texas and other states accusing Alphabet of unlawfully monopolizing critical parts of the display ads mkt

- Nature of the questions: The plaintiffs want to ask Brin about the 2008 acquisition of DoubleClick, and they want to ask Pichai about an ad mkt deal w/ Facebook in 2018

- Logistics: The trial is scheduled for March 2025; Brin’s deposition will be limited to 2.5 hrs and Pichai’s deposition will be capped at 4 hrs

- The UK’s CMA released a progress update regarding its investigation of mobile browsers and cloud gaming (link): For next steps, the CMA will hold hearings w/ Apple and Google in July before publishing a provisional decision in Oct; Reponses to the working papers can be submitted until July 22

- A US District Judge ruled that Google CEO Sundar Pichai and co-founder Sergey Brin cannot avoid being deposed in antitrust case (link): The case concerns a lawsuit brought by Texas and other states accusing Alphabet of unlawfully monopolizing critical parts of the display ads mkt

Big Tech’s AI Arms Race Heats Up

Big Tech’s rapid push into AI over the past couple of years has created some new fault lines within the space, bringing some players into more direct competition but also potentially fostering new alliances between those once considered rivals. Speaking to the former dynamic, Amazon has reportedly been working on developing a new chatbot to rival OpenAI’s ChatGPT. Codenamed Metis, Amazon’s chatbot will be powered by the company’s most powerful AI model, Olympus, and it may one day have the ability to draw from information beyond just the data it was trained on for its answers – a feature that would significantly differentiate it from other AI models. For its part, OpenAI announced the acquisitions of two startups as part of a strategy to improve its suite of enterprise offerings.

On the other side of the coin, earlier in the week Apple and Meta also reportedly (by the WSJ) held discussions regarding a potential AI partnership, however, a subsequent article by Bloomberg indicated that these talks ended months ago over Apple’s concerns with Meta’s privacy policies.

The debate surrounding just how impactful generative AI will be on creative industries also continued to swirl back-and-forth this week. The major record labels, including Sony, UMG, and WMG, filed lawsuits that accused both Suno and Udio of using their music catalogs without permission to train AI models. Given that damages could amount to nearly $350mn, the lawsuits could have a material impact on Suno and Udio’s nascent businesses. In a related vein, OpenAI CTO Mira Murati also warned that “some creative jobs will go away” but added that “maybe they shouldn’t have been there in the first place”.

More details are below.

- Amazon is reportedly developing an AI chatbot to compete directly w/ ChatGPT (link): Per Business Insider, the chatbot is codenamed Metis (the Greek god of wisdom) but hasn’t officially been named; Like most other chatbots, Metis would be browser-based and provide basic text- and image-based answers in a conversational style

- Metis is powered by Amazon’s AI model Olympus: W/ 2tn+ parameters, Olympus is more powerful than the Co’s publicly available Titan LLM

- A distinguishing factor – Metis could eventually leverage data beyond what it was trained on: By utilizing retrieval-augmented generation (RAG), Metis might be able to offer current information, such as sports scores or stock prices

- Metis will also provide links to source the answers it provides: Enabling users to decide whether to trust the info on their own accord

- Timing: A new chatbot could reportedly launch in Sept 2024

-> On a separate but relate note, Reuters reported that Amazon is working to replace what it refers to internally as “Classic Alexa,” the current free version, w/ an AI-powered one; Sources indicate that Amazon also plans to add another tier that uses more powerful AI software for more complicated queries and prompts, charging either a $5/mo or $10/mo subscription fee to use the more advanced version (link)

- Apple and Meta reportedly discussed an AI partnership… but these talks fell through (link/link): Per sources cited by the WSJ, Apple and Meta discussed integrating its genAI model into Apple Intelligence back in March; However, a separate Bloomberg report indicated talks ceased due to Apple’s concerns w/ Meta’s privacy policies

- Apple is seeking to offer a wide variety of AI models b/c users prefer different models for different tasks: This was per Apple’s senior VP of software engineering Adam Federighi at WWDC; This approach also prevents Apple from becoming overly reliant on OpenAI

- It’s unclear what the financial windfall would be for AI Cos: Although AI Cos will obtain access to massive distribution through an Apple partnership, some are skeptical that many users will upgrade to the premium versions of AI models when the free ones are readily available

- Though a longtime Apple analyst estimates some could earn billions: He anticipates ChatGPT’s usage will double w/ the Apple partnership, but OpenAI’s infrastructure costs will increase +30-40%; Ultimately, 10-20% of Apple users are expected to become premium subscribers to AI models

- Apple is seeking to offer a wide variety of AI models b/c users prefer different models for different tasks: This was per Apple’s senior VP of software engineering Adam Federighi at WWDC; This approach also prevents Apple from becoming overly reliant on OpenAI

- OpenAI has been on a spending spree lately, w/ two new acquisitions this week: Both deals point to OpenAI’s expanding ambitions in the enterprise space

- OpenAI purchased Rockset, a database analytics Co, in a deal worth hundreds of millions (link/link): The Cos didn’t disclose the size of the deal but a source indicated OpenAI used hundreds of millions of dollars’ worth of shares to buy Rockset

- Background on Rockset: Rockset builds real-time search and analytics databases, enabling users, developers, as well as enterprises to better leverage their own data and access real-time info as they use AI products and build more intelligent applications

- Rockset could help enable OpenAI’s models to provide faster and more accurate responses: Given that Rockset’s expertise in real-time data processing and vector search will enhance OpenAI’s ability to quickly access and analyze vast amounts of info

- OpenAI also acquired enterprise video collaboration platform Multi (link): A source indicated that the deal is technically an “acqui-hire” and that most of Multi’s 5-person team will join OpenAI; Multi will shut down after July 24

- Multi is designed to enable remote teams to work together via video chats: Multi is a Zoom-based platform that offers features like the ability to collab across screen shares from up to 10 people, offering customizable shortcuts and automatic deep links for code, designs, and documents

- OpenAI purchased Rockset, a database analytics Co, in a deal worth hundreds of millions (link/link): The Cos didn’t disclose the size of the deal but a source indicated OpenAI used hundreds of millions of dollars’ worth of shares to buy Rockset

Meanwhile, Creative Industries Have Been Grappling W/ The Downstream Implications Of The AI Push…

- The major record labels all filed lawsuits accusing both Suno and Udio of mass copyright infringement (link): In federal lawsuits, Sony, UMG, and WMG alleged Suno and Udio copied music without permission to teach their systems to create music that will “directly compete with, cheapen, and ultimately drown out” human artists’ work

- The labels complained that Suno and Udio users have been able to recreate elements of popular songs…: Including The Temptations’ “My Girl,” Mariah Carey’s “All I Want for Christmas Is You” and James Brown’s “I Got You (I Feel Good)”

- … As well as create vocals that are “indistinguishable” from famous musicians: Such as Michael Jackson, Bruce Springsteen, and ABBA

- The combined damages could amount to nearly $350mn: The labels requested statutory damages of up to $150,000 per song that Suno and Udio allegedly copied; They accused Suno of copying 662 songs and Udio of copying 1,670

- Suno’s response – “Our tech is transformative”: Suno CEO Mike Shulman explained that the Co’s tech is “designed to generate completely new outputs, not to memorize and regurgitate pre-existing content”

- The labels complained that Suno and Udio users have been able to recreate elements of popular songs…: Including The Temptations’ “My Girl,” Mariah Carey’s “All I Want for Christmas Is You” and James Brown’s “I Got You (I Feel Good)”

- “Some creative jobs will go away,” per OpenAI CTO Mira Murati (link): Speaking in an interview, Murati added, “But maybe they shouldn’t have been there in the first place”

- “Using [AI] as a tool for education, creativity, will expand our intelligence and creativity and imagination”: Murati noted, “The first step is to… help people understand what these systems are capable of, what they can do, integrate them in their workflows, and then start predicting and forecasting the impact”

- Though Murati couldn’t define just how impactful AI will be: ““I’m not an economist, but I certainly anticipate that a lot of jobs will change”…“Some jobs will be lost, some jobs will be gained”

- The jobs most likely to be impacted are ones that are “strictly repetitive”: These are ones that are not “advancing further” creativity or problem-solving

Where Do Things Stand For Paramount Now?

At a town hall on Tuesday, Paramount’s trio of co-CEOs provided an update for the Co’s 20,000+ employees on where things stand with plans they laid out at their June 4th annual shareholder meeting, including cutting more than $500mn in costs annually through layoffs and other cost-reduction measures, pursuing a joint venture to gain streaming scale for Paramount+, and potentially selling some assets to strengthen the balance sheet. The town hall meeting had originally been set for June 5 but the co-CEOs rescheduled it for June 25, citing “ongoing speculation regarding potential M&A.” On June 11, Shari Redstone, Paramount Global’s controlling shareholder, ended negotiations with David Ellison’s Skydance Media about a prospective merger. (link)

See below for the key updates from the meeting. (link/link/link)

- On M&A chatter – “We’d like to take a moment to acknowledge the challenges of all the M&A speculation surrounding our company. We know what a difficult and disruptive period it has been. And while we cannot say that the noise will disappear, we are here today to lay out a go-forward plan that can set us up for success no matter what path the company chooses to go down”

- Commentary on layoffs were sparce: Execs did not discuss timing of when mass layoffs might hit across the company or how large the cutbacks will be; They were asked if they had a timeline for job cuts, but didn’t provide one

- Have already begun to transform the cost base of the company, with work “well underway across corporate functions” like legal and corporate marketing / Modernizing the organization “so we can move faster — and be more nimble”

- “To be clear, $500mn in cost savings is just the beginning” and that they expect to provide more details on the Q2:24 earnings call in August

- Have definite plans to unload “certain Paramount owned assets” and have “already hired bankers to assist us in this process – and we’ll use the proceeds to help pay down debt and strengthen our balance sheet”

- “A 61% decline in profits is simply unacceptable…we need to act now to reverse this trend”

- On Paramount+ international expansion: “We are advancing talks with potential partners that will significantly transform the scale and economics of the service making it profitable and driving long term value. This approach could also serve as a model for the US”

T-Mobile’s 5G Network Performance Continues To Lead The Pack + Other Connectivity Updates

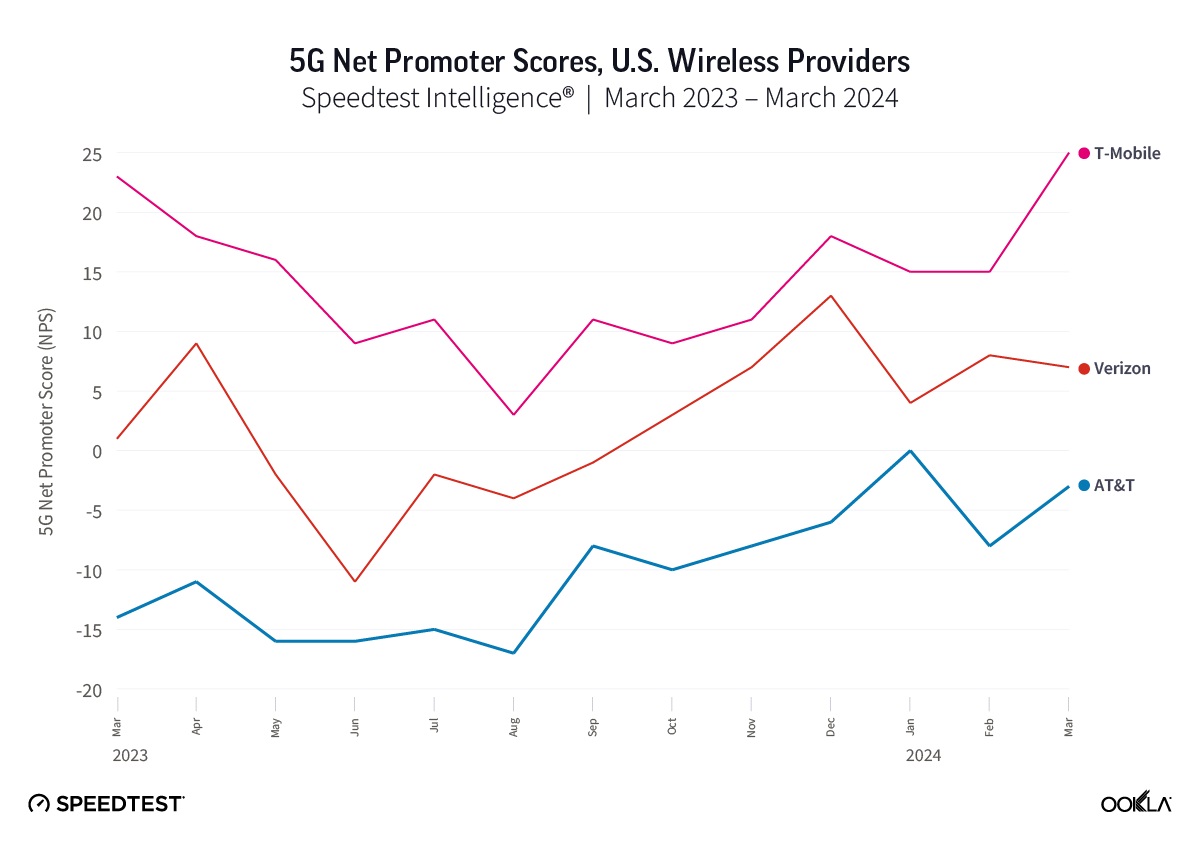

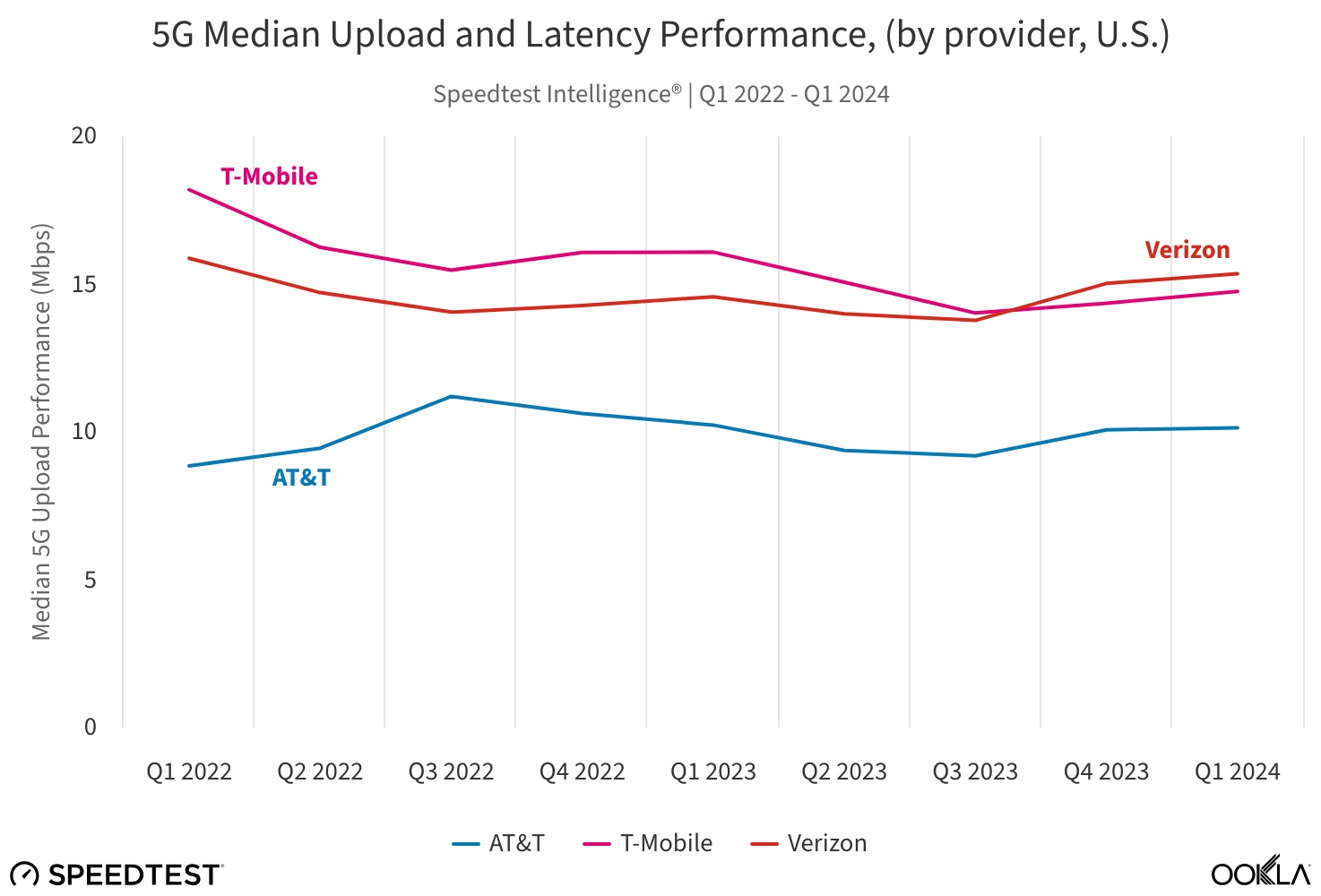

There were also a few connectivity-related updates that we wanted to flag this week. For starters, Ookla published its quarterly report on 5G network performance and revealed that T-Mobile boasted the highest 5G median download speeds in Q1, while Verizon possessed the fastest 5G median upload speeds, continuing a trend from Q4:23. Sequentially, the most incremental change in the report was a sizable improvement in T-Mobile’s 5G NPS scores, which Ookla attributed to the company’s deployment of additional mid-band spectrum.

Elsewhere across the telco space, Verizon rebranded its logo, opting for a warmer, more “approachable” color for its “V”-branding. The company also announced a new home internet bundle that simplifies the purchasing experience for customers and could potentially attract more customers to Verizon’s FWA and fiber services. That said, the FWA market could be in for a slowdown in net adds moving forward, at least according to New Street Research, which estimated that the incumbent telcos ended Q1 w/ ~half the total FWA subscribers that their networks have the capacity to accommodate. Separately, AT&T faced a setback in its efforts to wind down its legacy copper network this week, as the California Public Utilities Commission ruled that the company’s status as a “carrier of last resort” means that it must maintain its copper plant in the state, despite it being lightly used and expensive to upkeep. See below for more details on all of the above:

Ookla Released Its Qtrly Update On 5G Median Upload/Download Speeds This Week (link)

- T-Mobile continues to possess the fastest 5G median download speeds: This data was as of March 31, 2024

- T-Mobile: 14 Mbps

- Verizon: 67 Mbps

- AT&T: 36 Mbps

- T-Mobile has also experienced a strong uplift in NPS scores: The Co’s sizable increase in NPS score in March was correlated w/ its deployment of addt’l mid-band spectrum

- Verizon continues to boast the fastest upload speeds: That said, upload speeds among all three incumbent telcos have remained fairly stagnant over the last couple yrs, remaining between 10-20 Mbps (see below)

- The relative importance of upload speeds & latency performance is expected to grow: As 5G download performance begins to exhibit diminishing marginal returns, and increasing importance is given to improving the experience of latency-sensitive use cases such as video calling, mobile gaming, and augmented reality

There Were Also Some Other Interesting Updates Within The Telco Space This Week…

- Verizon rebranded its logo and annc’d a new home internet package (link): The Co’s new “V”-branding is still in red, but now contains warmer yellow hues meant to help consumers connect w/ the brand more intimately; Verizon’s previous logo was “very elegant” but “a bit cold”, per Verizon’s Chief Revenue Officer Frank Boulben

- New advertising around the brand refresh is intended to make Verizon’s brand more “approachable”: The Co wants to consumers to become more “emotionally connected” w/ its brand and view it as “the remote control of [their lives]”

- Verizon’s myHome bundle will make things simpler for customers: W/ myHome, customers will receive svs completely over fiber or 5G, depending on their address; The package also allows them to select from various streaming svs for a fee that is guaranteed for four yrs

- The telco incumbents have enough network capacity for 16mn FWA subscribers, per new estimates (link): New Street Research applied T-Mobile’s FWA growth framework (the Co aims for 7-8mn FWA subs) to the other top 3 US wireless operators to arrive at the figure; Total FWA adoption ended Q1 at 7.8mn, per Parks Associates

- A breakdown of each telco’s estimated FWA capacity:

- T-Mobile: 7-8mn subs

- Verizon: 4-5mn subs

- AT&T: 3-4mn subs

- Dish: 1mn subs

- FWA net adds are predicted to slow sharply over the next couple of yrs: New Street analysts “expect net adds for T-Mobile and Verizon to slow as gross adds flatten and disconnects continue to grow with the base”; Net adds are projected to slow further in 2025 or 2026, w/ both reaching capacity thresholds

- Carriers could increase network capacity to accommodate 19mn FWA subs, but this is unlikely: Given that “a significant change in network technology or spectrum availability would be required to increase capacity by more under the current model; neither is likely in the next five years”

- A breakdown of each telco’s estimated FWA capacity:

- California ruled that AT&T can’t shut down portions of its copper DSL network in the state (link): The California Public Utilities Commission (CPUC) argued that AT&T’s status as a “carrier of last resort” in the state obligates the Co to maintain its aging copper network, despite its relatively light use and high maintenance costs

- AT&T’s plans to shutter its copper network are an integral part of its cost savings initiative: Analysts estimate the Co serves ~60mn customer locations w/ copper and that after efforts to turn off the aging network end, at least 15mn AT&T copper locations won’t be offered a fiber replacement

- Other states have been making similar moves: Regulators in Utah recently moved against CenturyLink’s request to shutter its own copper network in the state, for example

Grab Bag: DoorDash-Deliveroo Deal / Dungeon & Fighter Tops Charts / AI Broadcasting At Olympics

- DoorDash reportedly discussed a takeover of Deliveroo, but no deal was reached (link): Sources indicate DoorDash approached Deliveroo, but talks ended after disagreement on valuation; There are currently no ongoing talks, according to people familiar w/ the matter

- However, there could more cross-border M&A in the delivery space soon: Following the publication of the Reuters report, Jeffries analysts wrote that the valuation gap between US and European food delivery Cos could be a catalyst for cross-border M&A this yr

- Amazon is Deliveroo’s largest shareholder w/ a 13.32% stake: DST Global is the second-largest shareholder w/ 7.54%, followed by Deliveroo CEO Will Shu w/ a 6.46% holding, per LSEG data

-> DoorDash shares were down -0.9% in reaction to the news and closed the week down -4.5%; Delieroo shares rose +1.2% following the report and finished the week up +1.8%

- Tencent’s Dungeon & Fighter (DnF) Mobile earned $270mn in the first month of its China release, per Sensor Tower (link): Since launching on May 21, DnF Mobile has held the top positions for the iOS charts in all categories, a “very impressive start”, per Sensor Tower’s senior director of Asia-Pacific mkting

- DnF Mobile crossed the US$100mn mark just 10 days after launching: The title contributed to a +12% rise in Tencent’s mobile gaming rev in May

- The game is also outperforming Tencent’s long-time blockbusters: DnF Mobile’s 11-day sales run in May surpassed the combined revs of Honour of Kings and Peacekeeper Elite over the same time period

- DnF Mobile has benefited from a pre-established gamer base: The game has attracted attention from Chinese gamers who were fans of the multiplayer “beat ‘em up”, action role-playing PC game that initially debuted in mainland China in 2008

- BUT there have been some setbacks w/ the release: Last week, Tencent pulled DnF mobile from Android app stores run by Chinese smartphone Cos, including Huawei, Oppo, and Vivo due to disagreements over rev sharing; However, this isn’t expected to affect the games’ sales

- The 2024 Paris Olympics will be narrated by an AI-version of Al Michaels (link): NBCU execs annc’d that a customized, daily highlight reel for the Olympics will be available to Peacock subs; The reel will feature the voice of Al Michaels, the 79-yr-old American broadcaster that first covered the Olympics decades ago

- Peacock’s program has been trained from Michaels’s NBC clips: Michaels joined NBC in 2006 and was the longtime announcer for “Sunday Night Football”; Michaels approved the use of his voice after being persuaded by a demonstration of the tech

- AI will be used to create customized collections of highlights for viewers: After subscribers select the Olympic events that interest them most, Peacock’s AI machines will get to work compiling the most notable moments in a customized package narrated by Michaels’ voice

- If this is successful, AI could be leveraged in other ways on the Peacock platform: Including possibly Andy Cohen AI recaps for Bravo shows, per Kelly Campbell, the president of Peacock; Ultimately, Campbell “want[s] to do this for every sporting event and show… on Peacock”

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Toys R Us is embracing gen AI tools that have become the focus of the marketing and media industry. Toys R Us Studios relied on Native Foreign and Chief Creative Officer Nik Kleverov, who has alpha access to Sora, to create a one-minute photo-realistic video about the retailer’s origin. “Through Sora, we were able to tell this incredible story with remarkable speed and efficiency,” said Kleverov. (Retail Dive)

Artificial Intelligence/Machine Learning

- A group of record labels such as Universal Music Group (UMG), Sony Music Entertainment, and Warner Records are suing two of the top names in generative AI music making, alleging the companies violated their copyright “en masse. ” The two AI Cos, Suno and Udio, use text prompts to churn out original songs. Suno is available for use in Microsoft Copilot though a partnership with the tech giant. Udio was used to create “BBL Drizzy,” one of the more notable examples of AI music going viral. (The Verge)

- More US Cos are about to flip the “on” switch when it comes to automating tasks w/ artificial intelligence. Large Cos are leading the stampede into AI, w/ 76% saying they will use it to automate in the coming yr. That’s up from the 55% that used AI during the previous yr. (Fortune)

- The new Voice Mode the AI co showed off for ChatGPT is officially being delayed by at least one month from its planned rollout date of late Jun. The Co disabled that AI voice. But despite the critics and setbacks, the co continues to impress and gain new adherents, such as the makers of new music videos and commercials w/ its unreleased video AI model Sora, healthcare startup Color which is integrating GPT-4o into a cancer screening app for clinicians, and signing lots of new enterprise accounts. (VentureBeat)

Audio/Music/Podcast

- YouTube is reportedly offering to pay Sony, Warner, and Universal “lump sums of cash” in exchange for licensing their songs to legally train its new AI music tools. The platform is aiming to license music from “dozens” of artists, which will instead be used to train new AI tools planned to launch later this yr. The fee that YouTube is willing to pay will likely be one-off payments rather than royalty-based arrangements. (The Verge)

- KKR has a long history in the music industry – Its latest move focuses on a different sector of the biz though: live music. KKR has acquired Superstruct Entertainment, which runs more than 80 festivals in Europe and Australia. Boardmasters, Sónar and Wacken Open Air are among its events. Although terms of the deal were not announced, the Financial Times reported that the price was €1.3bn ($1.39bn at current exchange rates). (Music Ally)

Broader Connectivity

- America Movil will be consolidating ClaroVTR into its ongoing operations. As previously disclosed, AMX has been providing funding to ClaroVTR through convertible notes to support the execution of its biz plan and for the refinancing of certain bank debt existing at the formation of the JV and Liberty LatAm had the right to catch-up its respective portion of such funding commitments by the middle of this yr for ClaroVTR to continue as a 50:50 JV. LLA will continue to own approx. 9% of the equity of ClaroVTR. (BUSINESSWIRE)

- AT&T CEO John Stankey said that Congress should give the FCC the power to require Big Tech firms to contribute to a gov’t fund that subsidizes access to telecom and broadband svs. Under current law, fees are levied on cell phone and landline svs subscribers to support the Universal Service Fund, which spends about $8bn a yr. Since 2020, Congress had allocated a total of $17bn to help lower-income families and people impacted by COVID get free or low-cost internet. (AOL)

- BT Group has implemented energy-saving ‘cell sleep’ technology across its EE mobile sites nationwide, following trials in each of the UK’s home nations. ‘Cell sleep’ software works by putting certain 4G LTE capacity carriers to sleep when the capacity is not needed, based on predicted periods of low traffic which have been established for each site through machine learning. The system then automatically wakes up during busy periods, and is also configured to react to unexpected surges which might occur during scheduled sleep modes. (VanillaPlus)

- Comcast Business annc’d a strategic agreement w/ Starlink, to provide connectivity solutions to Comcast Business enterprise customers. The collaboration enables advanced satellite capabilities in Comcast Business’ Managed Connectivity portfolio to deliver fast and reliable connectivity that supports a range of biz applications for enterprise customers, including those w/ locations in underserved regions. Starlink is excited to work w/ Comcast Business to deliver reliable connectivity to customers. (THEFASTMODE)

- India’s Bharat 6G Alliance has recently signed a Memorandum of Understanding (MoU) w/ 6G Smart Networks and Services Industry Association and 6G Flagship-Oulu University to boost research activities in the 6G field. The entities noted that the work will encompass aligning research and development priorities that support a common 6G vision and creating secure and trusted telecommunications as well as resilient supply chains. The two will work together to create a shared vision and roadmap for 6G. (RCR Wireless News)

- Over the last few months Spectrum has been laying off customer svs and call center employees. Columbus, Ohio, 175 svs center workers lost their jobs earlier this month. In Walker, Michigan, 240 call center employes lost their jobs this month. In Milwaukee, Wisconsin, 173 call center employees are losing their jobs. In Northern Kentucky, 215 employees lost their jobs. And 230 call center employees lost their jobs at a Austin, Texas, call center. (Cord Cutters News)

Broader Media & Entertainment

- Disney’s efforts to have an antitrust class action from streaming subscribers dismissed has been denied one more time, but the Co will now not be on the hook for any cash. “The Court once again finds Plaintiffs’ allegations sufficient to plead Disney’s market power in a well-defined SLPTV market in the US,” wrote US District Judge Edward J. Davila. (Deadline)

- CNN CEO Mark Thompson said he hopes that by the end of this yr, “There are meaningful things out in the market that you can see which represent change,” to the Co’s subscription product strategy. By the numbers: Of the ~ 170mm digital CNN monthly users, there are ~ 17mm–20mm who are “really engaged,” he said. (Editor and Publisher)

- Disney has started to roll out a new update that will show you on the main menu how far into a show you are on its continue-watching menu. This is a great feature to show you if that episode you are seeing is one that is almost done or just started. Here is what the new Disney update looks like:This all comes as Hulu is now built into Disney, which recently merged w/ Hulu. (Cord Cutters News)

- Disney is expanding its audience graph and clean room tech outside of the US, plus integrating w/ Mercado Ads DSP. The enhanced ID data is meant to help improve targeting while doing so in a privacy-focused way through Disney clean room technology. The partnership includes a direct connection between Mercado Ads demand-side platform (DSP) and Disney’s in-house Real Time Ad Exchange so brands can activate on biddable Disney inventory for programmatic buying, w/ data connections to the Audience Graph via BridgeID. (StreamTV Insider)

- Nielsen released their second monthly Media Distribution Gauge Report which finds Disney continues to garner the most viewers, followed by YouTube, Paramount & WBD. This new report offers cross-platform measurement of total TV consumption aggregated by parent media Cos. In May, Disney, with ABC, several cable networks and the Disney streaming bundle garnered the highest audience share at 11.5%. (In Apr. Nielsen noted that Disney+ and Hulu accounted for 42% of Disney’s total viewing.) (Forbes)

Broader Technology

- Google is adding support for 110 new languages to Google Translate. Before, Google Translate supported 133 languages, so this expansion, which the Co says is its biggest ever, marks a significant jump. Google’s PaLM 2 AI language model helped Translate learn these new languages, and it was especially good at learning ones that were related to one another. Most of the new languages are spoken by at least 1mn people. (The Verge)

- Italy is asking Google to pay 1bn euros ($1.07 bn) in unpaid taxes and penalties seven yrs after the Co settled a landmark tax dispute with Rome authorities. The sources said Italy’s Revenue Agency has started an adversarial process w/ Google which may end either w/ a settlement or w/ the opening of a judicial litigation. The investigation was launched in Dec 2022, and the claims cover the years 2018 to 2022. (The Economic Times)

- A new report from The Information details Apple’s efforts to automate more of the iPhone production process. The report explains that Apple has told managers to “reduce the number of workers on iPhone final assembly lines by as much as 50% over the next few yrs.” The machinery necessary to automate iPhone production can sometimes cost hundreds of millions of dollars each yr. (9to5Mac)

- Facing new competition from startups like Arc, Google annc’d that it’s bringing five new features to the Chrome browser on mobile devices, each designed to enhance the search experience. These include new shortcuts for local search results, a refreshed address bar for easier navigation, trending search suggestions, live sports cards for fans, and more personalized search recommendations to cater to users’ browsing habits. The features will roll out soon for both Android and iOS devices. (TechCrunch)

- Oracle Corp. warned investors that a new law potentially banning TikTok in the US threatens to hurt its financial results. TikTok uses Oracle’s cloud infrastructure to store and process US user data, and is considered by many Wall Street analysts to be one of the Austin-based Co’s largest customers for that closely watched biz. Oracle’s annual rev from the popular video app may be in the range of $480mm to $800mm, estimated Kirk Materne, an analyst at Evercore ISI. (Yahoo Finance)

Cable/Pay-TV/Wireless

- Ericsson’s latest Mobility Report added 300mn to its previous 2029 forecast for 5G. The upward revision is owing to a more positive outlook for Africa. According to the report, 5G subscriptions increased by 160mn during Q1 2024 to total 1.7bn. Nearly 600mn new 5G subscriptions are expected to be added this year as a whole. In 2029, 5G mobile subscriptions are set to reach nearly 5.6bn. (Fierce Network)

- Pay TV executives of a nervous disposition may want to look away now as new figures from a respected Wall Street analyst show the brutal levels of cost cutting ongoing in the US. The US pay-TV industry saw a record 6.9% decline in subscriptions during Q1 2024, w/ 2.37mm households cancelling their svs, according to SVB MoffettNathanson analyst Craig Moffett. This marks a significant acceleration from the previous yr’s decline of 2.0mm subscribers and “the fastest pace ever recorded”. (CSIMAGAZINE)

- Research from TV manufacturer and Official Partner of the tournament, Hisense, has revealed that one fifth of UK adults haven’t upgraded their TV for more than ten yrs. Less than half of Brits (41%) have a soundbar setup in their home for that authentic matchday atmosphere and what’s more, almost half (48%) of the UK haven’t changed their TV settings since they bought their TV, meaning many are missing out on the optimal viewing experience w/ Sports mode on many new models. (ADVANCED-TELEVISION)

Capital Market Updates

- PitchBook’s mid-yr update to its 2024 US Venture Capital Outlook pretty clearly suggests that, for lots of fundraising VCs right now, it is brutal out here. But there are nuances to this. Avg fund size this year is already bigger than last, hitting $153.5mn, as compared to $149.4mn in 2023. At the time PitchBook pulled this data, 181 funds had been closed in 2024, putting this yr on pace for the lowest total in a decade. (Yahoo Finance)

Crypto/Blockchain/web3/NFTs

- A new survey by Nomura Holdings and its digital asset subsidiary Laser Digital paints a bullish picture for cryptocurrency adoption among Japanese institutional investors. What Happened: The survey, conducted in Apr. 2024, reveals that 54% of respondents intend to invest in cryptocurrencies w/in the next three yrs, according to Coinpost. (Benzinga)

eCommerce/Social Commerce/Retail

- An entity affiliated w/ investment firm L Catterton raised a total of $756mn dollars in the sale of 14mn ordinary shares linked to footwear specialist Birkenstock. BK LC Lux MidCo, which oversees 9.9mn shares, and employees of the Birkenstock Group, who hold power over 4.1mn shares, are to take part in the secondary public offering, w/ a price set at $54 per share. (FashionUnited)

- Nike shares dropped after the Co reported weaker than expected sales in its FQ4. The Co’s FQ4 revs hit $12.6bn, down 2%, and its direct-to-consumer sales fell 8% to $5.1bn (£4.3bn). Revs for the Converse brand were down 18%, due to declines in North America and Western Europe. For the current qtr, Nike expects sales to decline by 10% due to a slowdown in its Chinese market and waning consumer demand around the world. (Retail Gazette)

- Revolve, which also operates luxury site FWRD, will acquire Alexandre Vauthier, the French haute couture house, out of administration. The deal will allow Aleandre Vauthier to retain its 29 employees and return to the Paris couture calendar, the Cos said. Financial terms of the court-supervised deal were not disclosed. This marks the first time Revolve has acquired a fashion label since 2015. (The Business of Fashion)

- Temu is facing a consumer protection lawsuit brought by Attorney General of Arkansas Tim Griffin, per court documents. Griffin said in a statement that Temu wasn’t an online marketplace but instead “a data-theft biz that sells goods online as a means to an end.” The complaint names Temu holding Cos PDD Holdings and Whaleco and references reports stating that Temu collects users’ personal information w/out permission. (Fashion Dive)

- Walgreens plans to close a “significant portion” of its ~8,700 stores in the US, CEO Tim Wentworth told investors. The Co didn’t share a specific figure, but said it is reviewing one-quarter of its stores that are underperforming financially. Walgreens has already closed hundreds of stores over the past few yrs. Walgreens also plans to reduce its stake in value-based medical chain VillageMD. (Retail Dive)

- Amazon opened its second Amazon Fresh store in New Jersey, the Co said in an emailed annc’mnt. The new supermarket in Eatontown features the updated brick-and-mortar format that the retailer unveiled at stores in Chicago and Southern California last yr. With the addition of the new Eatontown store, Amazon’s website now lists 42 Amazon Fresh locations across eight states. (Retail Dive)

- Meituan is considering raising funds via a bond offering this yr, people familiar w/ the matter said, as the Chinese food delivery and shopping platform seeks to repay some existing debt and fund its expansion. Meituan, founded in 2010 and led by billionaire Wang Xing, is working w/ investment banks to lay the groundwork for an offering, the people said, asking not to be identified because the matter is private. The size of the bond could be more than $1 bn, according to the people. (Yahoo Finance)

- Northern New Jersey is a proving ground for a strategy the toymaker is banking on – entertainment venues featuring Hasbro brands like Nerf, Tinkertoys and Transformers. A key component of toymaker Hasbro’s long-term growth strategy is unfolding at two malls in New Jersey. The two Northern New Jersey malls, Westfield Garden State Plaza and American Dream, are launch pads for three in-person play experiences – Planet Playskool, The Gameroom powered by Hasbro, and Nerf Action Xperience. (Forbes)

- Ocado said it employed 18,869 people globally in its latest annual report, down from 19,744 the yr prior. A significant amount of the staff cuts were in relation to “headcount rationalisation” w/in its head office and support functions, helping cut costs by around £17m, the Times reported. Earlier this month, the retail and technology firm officially fell out of the FTSE 100, after 6 yrs on the list as its valuation fell from a £22bn high in the pandemic to £3.1bn. (Retail Gazette)

- Retailers in China face a daunting near-term future after a disappointing mid-yr online shopping festival. E-commerce sales declined for the first time during the so-called 618 festival that ended last week, reports said, reflecting the pressures building up on retailers who are already locked in a gruelling price war. The festival, named after the Jun 18 founding date of e-commerce provider JD.com but embraced by all platforms, is China’s second-biggest annual sales event after ‘Singles Day’ in Nov. (Yahoo Finance)

- Shein confidentially filed papers w/ Britain’s markets regulator in early Jun, two sources said, kicking off the process for a potential London listing by the online fast-fashion retailer later in the yr. Shein’s original plan to list in New York came unstuck following opposition from US lawmakers. Shein has updated China’s securities regulator officially about its change of listing venue, said the sources. (Yahoo Finance)

EV/ Autonomous Vehicles

- Waymo is getting rid of its waitlist and opening up its robotaxi svs to all residents of San Francisco. People interested in riding in a driverless car can download the app and request one. In Mar 2022, Waymo began offering driverless rides for its staff. Since then its been giving rides to regular people who sign up for its waitlist, which the company says approximately 300,000 people have done since it first launched. (The Verge)

Film/Studio/Content/IP/Talent

- Indie studio A24 closed a new round of funding led by venture capital firm Thrive Capital. While the amount was undisclosed, the studio’s valuation is now up 40% from its most recent funding round to ~$3.5bn, according to a person familiar with the matter who wasn’t authorized to comment. That first fund raise was in 2022 and consisted of $225mn led by Stripes, which put the studio’s valuation at the time at $2.5bn. (Los Angeles Times)

- Disney/Pixar’s Inside Out 2 keeps on soaring, reaching $799.7mm globally. Within that, its international box office crossed the four-century mark at a running cume of $411.9mm from 44 overseas markets. After 12 days in domestic release, the movie is the No.10 animated film of all time in North America, having passed Minions: The Rise of Gru ($370mm, 2022), Finding Nemo ($381mm, 2003) and Spider-Man: Across the Spider-Verse ($382mm, 2023). The next animated title it will overtake domestically is Disney’s own Frozen (2013). (Deadline)

FinTech/InsurTech/Payments

- A federal judge rejected a $30bn settlement that would have capped the fees Visa and Mastercard charge to merchants for credit and debit card purchases. The decision jeopardizes an agreement that was meant to end two decades of litigation related to swipe fees, which card Cos charge retailers on each purchase a customer makes. Visa and Mastercard will have to either renegotiate the settlement with merchants or go to trial. (Washington Post)

- Flipkart, which is based in India, has quietly started rolling out its own payments app, dubbed Super.money, as it broadens its fintech ambitions more than a yr and half after separating from PhonePe. The Co’s new app, now live in beta on Play Store, allows users to make mobile payments via UPI, an interoperable network that is the most popular way Indians transact online. (TechCrunch)

HealthTech/Wellness

- Amazon is folding its Amazon Clinic telehealth svs into its primary care biz One Medical. The Co explained in a blog post that, to simplify Amazon’s primary care offering for customers, the svs has now been rebranded to Amazon One Medical Pay-per-visit, and now offers more affordable per-visit pricing. Customers can pay $49 for a video call visit or $29 to text message a doctor. (TechCrunch)

Last Mile Transportation/Delivery

- Uber and Lyft will pay Massachusetts drivers some of the highest guaranteed wages in the country under a landmark deal with state prosecutors. Attorney General Andrea Campbell and the Cos agreed on a $175mn settlement that ends the nearly four-yr-old lawsuit against Uber and Lyft, lays out a slew of new wage, benefit and job protection requirements, and sidesteps the legal question at the heart of the case. (WBUR)

- Uber is shutting NYC drivers out of its app during periods of low demand in order to avoid paying them minimum wage, according to a report. The longer the wait time before drivers pick up a passenger, the more Uber and Lyft need to pay in order to meet the TLC-mandated minimum. Since TLC calculates wait times based on industry avg, it requires Uber, the most dominant co in the market, to pay more when Lyft drivers are idle. (New York Post)

Live Entertainment/Theme Parks/Concerts/Experiential

- WALT Disney’s Florida theme parks will let visitors reserve a space for shorter lines on rides as much as one week in advance, in an effort to address complaints about the process. Disney hotel guests will be able to book ride reservations seven days ahead for their entire stay. Disney has made several changes to its parks in recent yrs to cut down on crowding and boost rev. (The Business Times)

M&A

- Financial advisory fees from M&A in Asia dropped to the lowest levels in 11 yrs in H1:2024, w/ little signs of a quick rebound amid declines in both annc’d and completed deals. M&A fees in Asia totaled $1.5bn in the first six months, the lowest since 2013, LSEG data showed. Japan alone accounted for 40% of that. The total value of announced transactions in Asia dropped 25% y/y o $317.5bn, also a 11-yr low. (Yahoo Finance)

Online Marketplaces/Learning (Real Estate/Education/Jobs)

- In 2018, Brookfield Property Partners made a bold move by acquiring full ownership of mall-owner GGP, betting they could transform the Co’s 125 malls into vibrant mini-cities. Six yrs later, only two malls have been redeveloped due to numerous delays, as reported on WSJ. Brookfield initially acquired 34% of GGP, which was bankrupt in 2010, and later bought the rest for $9.25bn in 2018. (CRE Daily)

Satellite/Space

- Amazon’s initial Project Kuiper broadband svs have slipped into 2025 amid plans to launch the Co’s first batch of production satellites on an Atlas V rocket in the last three months of 2024. Amazon had earlier aimed to start deploying 3,200+ satellites in the H1:2024 to begin beta trials w/ potential customers. However, the Co now expects to ship the first production satellites this summer to Florida for the launch. (SpaceNews)

- SpaceX is set to launch a tender offer that would reportedly value the space exploration firm at a whopping $210bn, a record for a privately held US Co. SpaceX will sell shares to employees and other insiders at $112, Bloomberg reported. The round will boost the Co’s valuation up from $180 bn. The projected valuation has surpassed initial expectations due to strong interest from investors, the report added. (New York Post)

Social/Digital Media

- Meta CEO Mark Zuckerberg annc’d that the Co will begin to surface AI characters made by creators through Meta AI studio on Instagram. The tests will begin in the US. The Co’s announcement comes on the same day as a16z-backed chatbot company Character.AI is rolling out the ability for users to talk with AI avatars over a call. Zuckerberg noted that these chatbots will be clearly marked as AI so users are aware. (TechCrunch)

- After a few months of testing during the general elections, Meta is making its Llama 3-powered AI chatbot available to all users in India. Meta AI currently only supports English and no other local languages. The co started testing Meta AI in India across WhatsApp, Instagram, Messenger, and Facebook in Apr. by rolling it out to select users. (TechCrunch)

- ByteDance and Broadcom have discussed a potential collaboration on an AI processor to help bolster the development of that technology. The Cos have talked about a 5-nanometer purpose-built chip, according to a person familiar w/ the discussions. No deal has yet been reached between the two cos, and Broadcom already supplies an older-generation 7nm AI processor for use in ByteDance’s data centers, the person said, asking not to be named as the information is private. (Fortune Asia)

- Linda Yaccarino, the chief executive of X, is under pressure from owner Elon Musk to boost sales and cut costs. Yaccarino fired her right-hand man and head of business operations and communications, Joe Benarroch, this mo, said three people familiar with the matter. The reshuffle comes amid growing tensions between Musk and Yaccarino, stemming from her struggle to steady X’s financial health a yr after Musk poached her from NBCUniversal. (The Irish Times)

Sports/Sports Betting

- FIFA is reportedly seeking to raise as much as $2bn for the expansion of FIFA+, the free streaming svs launched by football’s global governing body to offer live coverage of matches. FIFA is working w/ USGroup AG to raise $1-2 bn. The investment would be for a minority stake in FIFA, sources added, asking not to be named discussing confidential information. (Ad Age)

- The NFL was ordered by a federal jury in LA to pay aggrieved sports fans a total of $4. 7bn after finding the league conspired w/ DirecTV and network partners to increase the price of the exclusive Sunday Ticket games package. The class-action lawsuit, originally filed in 2015, represented 2.4mn+ residential subscribers and 48,000+ commercial establishments that purchased Sunday Ticket when it was still w/ DirecTV. (AOL)

- TNT Sports continues to fill out its portfolio w/ uncertainty clouding its long-term NBA relationship, setting a 6-yr rights deal w/ the Big East Conference for men’s and women’s college basketball. The agreement will bring 65+ regular season Big East college basketball games to lead network TNT as well as TBS, truTV and Max, beginning w/ the 2025-26 season. (Deadline)

- I.-Generated Al Michaels is going to have a voice in NBCUniversal‘s coverage of the Paris Olympics. The reel will feature the voice of Mr. Michaels, the 79-yr-old American broadcaster, who first covered the Olympics decades ago. Mr. Michaels, however, will not be holing up in a broadcast booth each night to briefly summarize the dozens of Olympic events that took place. From there, Peacock’s A.I. machines will get to work each evening cranking out the most notable moments and putting them together in a tidy customized package. (NYTIMES)

- Diamond Must Show Sports Leagues Pay TV Contracts Under Conditions, Bankruptcy Judge Rules. The judge overseeing the bankruptcy restructuring of Diamond Sports Group ruled that the Co must disclose sensitive information from its pay TV contracts w/ its pro-league partners, w/ some conditions, declaring that the NHL and Major League Baseball can’t effectively gauge the viability of Diamond w/out first reviewing firsthand the subsidiary’s biggest rev sources, distribution deals w/ Charter Communications, DirecTV and Cox Communications. (NextTV)

- June is winding down, and WWE is trending up. The Jun. 21 episode of Friday Night Smackdown on Fox drew a significant viewership and rating. Smackdown averaged 2,336,000 viewers and a massive 0.73 P18-49 rating. According to the popular Wrestlenomics Patreon, both the P2+ viewership and 18-49 rating are the highest since Apr. 12, 2024, the Smackdown episode that followed WrestleMania XL. (Awful Announcing)

- UEFA has tapped Genius Sports to provide player-tracking data for some of its club matches, including the Europa League, Nations League and European qualifiers. The partnership w/ European soccer’s governing body, signed on Jun. 15, will span 1,350 matches, according to a Genius Sports regulatory filing. Genius Sports reported rev of $413mm in fiscal 2023, up 21% from the prior yr. (Sportico.com)

Towers/Fiber

- Nokia is reportedly exploring a potential acquisition of Infinera Corp, a maker of optical telecommunications equipment. Nokia has been studying the feasibility of a deal for US-listed Infinera, according to sources. Deliberations are ongoing and there’s no certainty they’ll result in a deal, the people said. (Yahoo Finance)

Video Games/Interactive Entertainment

- Amazon’s gaming division is currently working on eight different game projects. Among the higher-profile games is a new AAA Tomb Raider game from the franchise stewards at Crystal Dynamics alongside a new Lord of the Rings project. Despite the current disruptive macro-economic climate around games (rising costs, mass layoffs, long delays in production pipelines, etc.), Amazon Games has no plans in slowing down. (TweakTown)

- Microsoft is launching its Xbox TV app on Amazon’s Fire TV Sticks in July. The Xbox app will provide access to Xbox Cloud Gaming, allowing subscribers to Xbox Game Pass Ultimate can stream a variety of games directly to Fire TV devices. Microsoft will support the Fire TV Stick 4K Max and Fire TV Stick 4K models for its Xbox app, which will be available in 25+ countries. (The Verge)

Video Streaming