Before we dive into this earnings-heavy edition, I wanted to give a quick reminder to please participate in our 8th Annual TMT Sector Themes Survey if you haven’t yet had the chance to do so. It consists of 25 simple questions about the market, sector developments, and company outlooks. It will take less than 10 minutes and we only send results to those who participate – CLICK HERE. Thanks!

Turning to the week, after a lot of ups and downs, the major indices closed mostly flat (S&P 500 up +0.3%, Nasdaq down -0.2%). A notable stat out this week was US consumer confidence, which fell to its lowest level in 12 years on more pessimistic views from Americans worried about the nation’s economy, inflation and a weakening labor market. Trump also officially named former Fed governor Kevin Warsh to succeed Jay Powell as Fed chair.

On the earnings front, it was a heavy skew toward Big Tech and the Connectivity sector. See below for what we focused on this week.

- Earning Scorecard – Week 1 & 2

- The Meta Narrative Does A 180…The Co Is Yielding Strong ROI From AI Investments In The Core

- Volume Growth Will Be A Key Driver To AT&T’s New, Better-Than-Expected Long-Term Plan

- Comcast’s NBCU Delivers & There’s A Clearer Line Of Site Out Of Its Connectivity Investment Period

- Has Charter Finally Reached The Broadband Inflection??

- Verizon Is Full Steam Ahead On Its Turnaround Journey

- Microsoft’s Results Bring “The AI Investment Vs Returns” Question Back To The Forefront

- iPhone Demand Drives A Strong FQ1 For Apple, Though Supply Hurdles Persist

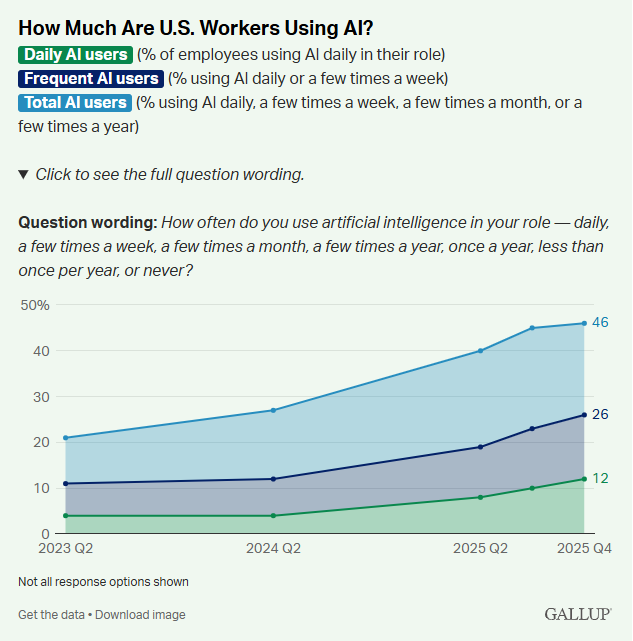

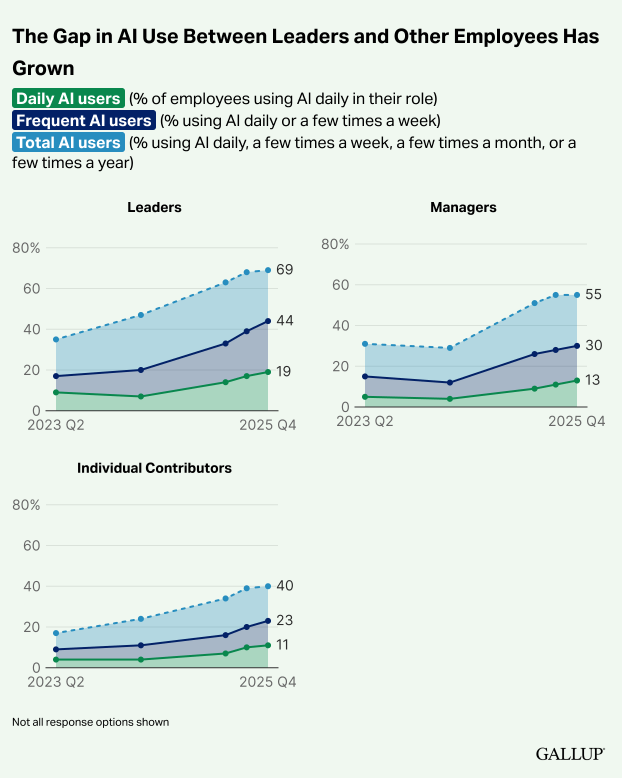

- Successful AI Organizational Adoption Likely Follows The Hockey-Stick Growth Pattern

- Grab Bag: Nvidia Invests More Into CoreWeave / Amazon Is Further Expanding Groceries / Pinterest, Along With Others Announce Job Cuts

Enjoy the weekend and rest up before the next wave of earnings reports next week, with Disney kicking things off Monday morning.

Best,

Leslie

Earning Scorecard – Week 1 & 2

Week one and two of earnings have come to a close. In total, 16 stocks in our LionTree universe reported. Stock reactions were even this week with (8) stocks trading down and (8) trading up. The best performer in reaction to earnings was Verizon, which was up +11.7% (see Theme #6), while the worst performer was Intel, which fell -17.0%.

There was mixed performance elsewhere in Big Tech with Meta shares rallying +10.4% in reaction to earnings (see Theme #2), Microsoft closing down -10% (see Theme #7), and Apple shares up just +0.5% (see Theme #8).

It was a favorable week in the Connectivity sector given that in addition to Verizon mentioned above, Charter shares rose +8.4% in reaction to earnings (see Theme #5), followed by AT&T, and Comcast trading up +4.7% and +2.9%, respectively (see Theme #3 and Theme #4).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

The Meta Narrative Does A 180…The Co Is Yielding Strong ROI From AI Investments In The Core

While Meta CEO Mark Zuckerberg isn’t saying “I told you so,” Q4 results and the 2026 guidance made it hard to argue that all the AI investment is not having a profound impact on the Co’s core business trajectory. Last quarter the stock sold off -11% in reaction to higher investment levels and this qtr, the stock rallied +10% on better-than-expected results. 2026 capx guidance was still +13% above consensus, but the y/y rate of growth is slowing.

In addition to the higher capx in 2026, operating expense guidance pointed to a ~40% y/y increase (at the midpt) but even so, op income is still expected to exceed 2025 levels, supported by accelerating Q1 rev growth y/y (fastest rate in 5 years) and a disciplined approach to reinvesting in AI and other strategic priorities while maintaining a focus on long-term profitability.

The core advertising biz is showing persistent strength as AI-driven enhancements are driving stronger engagement and monetization across ad products. Meta is expanding ads to new surfaces, including Threads and WhatsApp, while improvements in AI model consolidation and backend systems drove a +12% increase in ad quality in Q4. AI-powered tools for advertisers and creative workflows are also accelerating performance, with features like incremental attribution and click-to-message ads yielding meaningful gains.

Looking ahead, mgmt framed 2026 as the year AI “accelerates even further.” A key focus is personal superintelligence, where AI understands an individual’s context, interests, and behavior to deliver more relevant and adaptive experiences across platforms, recommendations, and commerce. New AI-driven media formats are expected to pave the way for Meta glasses, which will be the primary focus for Reality Labs (marking a shift away from the metaverse-heavy investments of past years).

Lastly, detail on internal AI-driven efficiency gains among Meta employees was also interesting. Since early 2025, AI coding tools have driven a +30% increase in output per Meta engineer, with “power users” seeing even stronger gains of 80%+ y/y. This power AI user dynamic that Meta is seeing internally was also echoed more broadly in a Gallups recent AI in the workforce survey that we separately detailed in Theme #9 as well.

Net net, investors are feeling more comfortable that Meta is executing on and investing in its long-term strategy in a disciplined way.

See our deep-dive regarding the points we saw as most important/incremental from Meta’s results below.

-> Meta was up +10.4% on the back of its print and is up 8.5% YTD, after being up +10% in 2025

Meta Posted A Strong Q4

- Q4 total revs BEAT cons by +2.5% and grew +24% y/y (vs +26% y/y growth in Q3)

- Family of Apps (FOA) revs BEAT w/ ad revs ~2% better than expected and Other beat by +10%

- Reality Labs BEAT by +1.5%

- Q4 adj op income BEAT by +3.4% (margin of 41.3% vs cons 40.9%)

- FOA adj op income BEAT 52.2% vs cons 51.9%

- Reality Labs adj op income MISSED -630.4% vs cons -624.6%

- Q4 EPS beat by +8%

- Q4 FCF BEAT by +10%, while CapEx was slightly higher than expected

2026 Is Positioned For Strength…Q1 Rev Guidance Implies The Fastest Growth In ~5 Yrs / Despite 2026 Being Another Investment Year, Op Income Is Expected To Be Above The 2025 Level

- For Q1…the mid-pt of REVENUE guidance was ~7% ahead of cons ($53.5-56.5bn vs cons $51.4bn), implying a +30% y/y growth (largest growth in the last 5 yrs)

- What’s driving the acceleration? “Strong” demand seen through the end of Q4 that is continuing into the start of 2026; Q1 guidance also assumes ~4% FX tailwind to y/y rev growth (vs ~1% in Q4) as they lap the strengthening of the US dollar a year ago

- BUT for full yr 2026… REVENUE growth y/y will be “below” Q1 levels – why?

- Expect that FX tailwinds will dissipate later in the yr based on current rates

- Will be lapping stronger periods of growth later in the yr that benefited from 2025 ad performance investments and the strong macro landscape

- Expect there could be some headwinds from introducing a revised, less personalized ads offering in the EU (begins rolling out later in Q1)

- For 2026…the EXPENSE guidance was $162-$169bn (vs $118bn in 2025)

- The majority of expense growth will be driven by infrastructure costs, which includes 3P cloud spend, higher depreciation, and higher infrastructure OpEx

- The 2nd largest contributor to total expense growth is employee compensation, driven by investments in technical talent

- At the segment level…expect expense growth to be driven by FOA, w/ Reality Labs op losses remaining similar to 2025 levels

- For 2026…expect OP INCOME to be “above” 2025 levels

- Will still be investing in AI infrastructure and talent

- Reiterated framework of growing consolidated op profit over time to guide these investments

- For 2026…the CAPX guidance was ~13% above expectations ($115-135bn vs cons $110.74bn)

- Y/Y growth will be driven by incr’d investment to support Meta Superintelligence Labs efforts and the core business

- Capx growth rates: +84% y/y in 2025 & +73% y/y in 2026 at the mid-pt

- Will continue to be “opportunistic” about share repurchasing but “first order use of capital” for the Co is investing in resources to position themselves as a leader in AI

- On ongoing regulatory chatter –

- Recently aligned with the European Commission on further changes to their less personalized ads offering, which they will begin rolling out this qtr

- Continue to monitor legal and regulatory headwinds in the EU and the US that could “significantly” impact business and financial results

- I.e., continue to see scrutiny on youth-related issues and have several trials scheduled for this yr in the US, which may ultimately result in a material loss

The Core Advertising Business Continues To Operate On All Cylinders

- Family of App ad revs grew +25% y/y (vs +26% y/y in Q3 and +22% y/y in Q2) and beat cons by +2.7%; FOA adj op margins of 52.2% also came in ahead of cons 51.9%

- Q4 ad impressions were up +18% y/y (vs +14% y/y in Q2): Growth was healthy across all regions, driven primarily by engagement and user growth, and to a lesser degree, ad load optimizations

- Q4 avg price per ad was up +6% y/y (vs +10% y/y in Q2): Benefiting from increased advertiser demand, largely driven by improved ad performance

- Saw “healthy” y/y growth across all verticals in Q4 (w/ the exception of politics, due to lapping US presidential election last yr)

- The online commerce vertical was the largest contributor to y/y growth, followed by professional services, and technology

- Ended Q4 w/ 3.58bn DAUs using at least one of Meta’s apps everyday (up +7% y/y and in-line w/ cons)

- Includes 2bn+ DAUs each on Facebook and WhatsApp and “just shy” of $2bn on Instagram

Recommendation Optimizations In Q4 Drove Incremental Engagement Across Platforms

- On Instagram…

- Reels watch time was up 30%+ y/y in the US

- Grew the prevalence of original content in the US by +10ppts in Q4, with 75% of recommendations now coming from original posts

- On Facebook…

- Video time cont’d to grow double-digits y/y in the US

- Saw a +7% lift in views of organic feed and video posts on Facebook in Q4, resulting in the largest qtrly rev impact from a Facebook product launch in the past two yrs

- Now surfacing 25% more Reels published that day than in the prior qtr

- On Threads…

- Optimizations made in Q4 drove a +20% lift in Threads time spent

- Other key platform updates…

- Now support 9 different languages w/ “hundreds of millions” of people watching AI-translated videos everyday: Already driving incremental time spent on Instagram, and plan to launch support for more languages over the course of 2026

- ~10% of the Reels people view each day are now created in the Edits app, which is almost triple from last qtr

- Looking into 2026…“we see a lot of opportunity to drive additional [engagement] gains”

- Includes scaling the complexity and amount of training data used in their models, while continuing to make the systems more responsive to people’s real time interests

AI-Driven Enhancements Are Also Driving Stronger Engagement & Monetization Across Ad Products

- Continue to make progress in bringing ads to Threads and WhatsApp

- On Threads – beginning to expand ads to all remaining countries this month, including the UK, European Union and Brazil

- On WhatsApp – expect to complete the rollout of ads and status throughout the yr

- On monetization efficiency – seeing “very strong” results from ad performance investments as model size and complexity continue to scale

- In Q4, learning improvements drove a +3.5% lift in ad clicks on Facebook and a 1%+ gain in conversions on IG

- Looking ahead…expect ad performance investments in 2026 will drive further gains

- Consolidation of models + a series of back-end improvements drove a +12% increase in Ads quality in Q4

- Saw “strong” success from consolidating Facebook feed and video models in H1:25, and extended the effort in Q4 by folding Stories and other services into the core Facebook model, driving the increase

- Looking into 2026…expect to consolidate more models than they have in the prior 2 yrs

- Q4 biz ad product updates – continue to invest in helping bizs leverage AI

- Started testing Meta AI business assistant w/ advertisers, which helps with tasks like campaign optimization and account support; Will make available to more advertisers in the coming months

- AI in ad creative – combined revenue run rate of video generation tools hit $10bn, with q/q growth outpacing the increase in overall ads rev by ~3x

- Click-to-message ad rev growth accel’d in Q4, with the US up 50%+ y/y, driven by “strong” adoption of website to message ads; Paid messaging within WhatsApp also continues to scale, crossing a $2bn ARR in Q4

- Incremental attribution feature is driving a +24% increase in incremental conversions vs their standard attribution model: Has already achieved a multibillion dollar ARR just 77 months since launch

- Other incremental commentary on business AIs …

- Will expand availability to more mkts; Mexico and Philippines has reached 1mn+ weekly conversations b/w people and business AIs on Meta’s messaging platforms

- Also extending their capabilities beyond just finding information to also completing tasks directly within WhatsApp

- Longer-term…working on improving larger scale models as a way to drive ads biz scale

- Typically don’t use larger model architecture for inference b/c their size and complexity would make it too cost prohibitive

- Instead, they drive performance from these models by using them to transfer knowledge to smaller, lightweight models used at runtime

- BUT scaling up the compute available to these larger models over time is expected to drive gains across the different stages of ads ranking and recommendation

2026 Is The Year AI “Accelerates Even Further”

- Over the next few months, the Co will start shipping their new models and products…

- These first models will be “good” but “more importantly…will show the rapid trajectory that we’re on”

- …then over the course of the yr will “steadily push the frontier” as they continue to release new models

- May take a few iterations to find product-market fit but think they’re starting off early enough in the yr that they expect to see “some” success by the end of the yr

- Continue to be capacity constrained and that’s expected to continue through “much” of 2026…

- …but highlighted the Meta Compute initiative, which is based on the belief that engineering, investment, and partnership efficiency in building infrastructure will be a strategic advantage

- Will focus on long-term investments in silicon and energy

- Will advance their own silicon program while working with key partners to design flexible systems

- Expect cost per gigawatt to decrease “significantly” over time through technology and supply chain optimization

- Quick update on Meta AI…

- Now available in 200+ mkts

- # of daily actives generating media tripled y/y in Q4

- Looking ahead into 2026… expect upgrades to media generation models and new features that improve the product experience

Starting To See The Early Innings Of Their Vision To Build Personal Superintelligence

- “We’re starting to see the promise of AI that understands our personal context, including our history, our interests, our content, and our relationships”

- On recommendation systems – Meta’s “world-class” recommendation systems are “primitive” compared to what will be possible soon and improving recommendations is a key focus in 2026

- Plan to continue scaling up their models and increasing the amount of data they use, including a longer history of content interactions to further improve the overall quality of recommendations

- Will continue to make recommendations even more adaptive to what a person is engaging with during their session, so the recommendations surfaced are more relevant to what they’re interested in at that moment

- Will work on more deeply incorporating LLMs into their existing recommendation systems, which will be useful for content that has been more recently posted since there’s less engagement data to base recommendations off of

- On commerce – integrating AI-driven commerce across both feeds and business messaging, which will “significantly” increase WhatsApp’s capabilities over time

- For customers, new agentic shopping tools will allow people to better find the specific products they are looking for

- For sellers, ads will help bizs find the specific people who are interested in their products

- New kinds of content will soon be possible as well – expect an “explosion” of new media formats that are driven by an AI vs an algorithm…

- Feeds will become more interactive as AIs will understand the user and be able to show and/or generate personalized content for the user

- …and glasses will be the “ultimate incarnation” of that vision

- Will be able to see what a user sees, hears, says, and help as they go through their day

- Will also be able to show information and generate custom UI right in the user’s vision

Glasses Are The Primary Focus Area For Reality Labs

- Reality Labs Q4 revs fell -12% y/y (vs +74% y/y in Q3) and beat cons by +1.5%; Reality Labs Q4 op loss of -$6.0bn was more than cons -$5.7bn

- Y/Y decline in Reality Labs rev is due to the lapping of the introduction of Quest 3S in Q4:24, as well as retail partners procuring Quest headsets during Q3:25 to prepare for the holiday season, which was recorded as revenue in Q3

- Reality Labs 2026 losses are expected to be similar to 2025 and will likely be the peak

- Sales of Meta glasses more than tripled in 2025 …Meta thinks that glasses are reaching a smartphone-level inflection point

- Most of Reality Labs’ investment will go towards glasses and wearables going forward

- And on other Reality Lab initiatives…will also focus on making Horizon a “massive” success on mobile and making VR a profitable ecosystem over the coming yrs

2026 Is Also The Year Meta Employees Are Going To See AI “Dramatically” Change The Way They Work Internally

- Investing in AI native tooling, so individuals at Meta can get more done

- They are elevating individual contributors and flattening teams

- Also starting to see projects that used to require big teams now get done by a “single very talented person”

- AI coding tools have been driving an increase in output per Meta engineer

- Since the beginning of 2025, the Co has seen a 30% increase in output per Meta engineer

- Majority of that growth is coming from the adoption of agentic coding, which saw a “big jump” in Q4

- Seeing “even stronger” gains with “power users” of AI coding tools, whose output has increased +80% y/y

- Looking ahead…expect this productivity growth to accelerate in H2

- Since the beginning of 2025, the Co has seen a 30% increase in output per Meta engineer

- Bigger picture, there is a “big delta” b/w those who use AI and use it well and those who don’t, and that’s likely to create a “profound” dynamic across the whole economy in terms of the productivity and efficiency with which Cos are run

Volume Growth Will Be A Key Driver To AT&T’s New, Better-Than-Expected Long-Term Plan

AT&T’s new 3-year guidance pointing to higher growth than the Street was expecting, coupled with a better-than-anticipated Q4 was met with analyst and investor cheer. Big picture, the Co expects to grow adj EBITDA by +3-4% y/y in 2026 (ahead of cons +3%) and to accelerate that growth to +5% y/y in 2028 (vs cons +3%). What is driving this growth? Volumes & greater penetration of the fiber footprint as well as convergence are critical to the plan, plus integrating Lumen’s fiber assets will create “pretty significant” upfront costs in 2026, but as the asset penetration increases and the legacy declines fade, adj EBITDA growth is expected to accelerate. Adj EPS is expected to grow at a double-digit CAGR through 2028 (vs cons +10%).

While Q4 headline results impressed, there were some puts and takes under the hood with w-less subscriber phone adds and churn both falling short of projections and broadband adds were a mixed bag with fiber additions beating the Street while FWA additions missed. With that said, convergence gains accelerating in Q4 (up +200 bp to 42% penetration) was a key highlight and mgmt’s 50% penetration target is not likely the future cap.

Looking ahead, it will be more of a volumes game. Mgmt will be taking a consistent, disciplined approach to pricing in both w-less and home internet, balanced by gains in underpenetrated categories such as value focused customers and converged customers, as mentioned (where they take an upfront ARPU hit). Mgmt is expecting to see higher device upgrades in the year ahead which will also be a headwind to ARPU. Overall mgmt believes that they can still grow advanced home internet services revs organically by 20%+ per year through 2028 given this expected growth in customer relationships.

A few other important outlook assumptions include capital intensity coming down once the major capital projects are substantially completed by the end of 2030, cost savings accelerating y/y in 2026, and the Co returning $45bn+ to shareholders over the next 3 years (almost 30% of AT&T’s mkt cap). At the same time, net debt will return to the 2.5x target within ~3 years post close of its pending acquisitions

Lastly, as a heads up the Co is reorganizing its reporting segment to separate out the legacy assets starting in Q1:26.

See below for much more detail plus a few more points we viewed as important.

-> AT&T share rallied +4.8% on the back of results and the connectivity sector was generally up in sympathy; However, AT&T share are still down -3% YTD (following being up +9% in 2025)

Q4 Headline Numbers Accelerate Growth & Top Street Expectations

- Rev BEAT by ~2% & grew +3.6% y/y (an accel from +1.6% y/y in Q3) – the upside came from higher-than-expected Equipment rev, Business W-line rev, and Latam rev

- W-less svs revs growth of +2.4% (in-line w/ cons but slightly up from +3% in Q3)

- Adj EBITDA BEAT by ~1% & grew +4.1% y/y (an accel from +2.4% y/y in Q3)

- Expanded adj EBITDA margins by 20bp (though the Street expected a little more)

- Adj EPS BEAT by 13% & grew +21% y/y (was up ~9% in 2025)

- The upside to guidance came from a lower-than-expected effective tax rate & stronger growth in adj EBITDA

- FCF BEAT by 7.4% & grew +2% y/y (reached $16.6bn total in 2025 which was at the higher end of guidance):

- The Co paid lower than expected cash taxes but accelerated pension contributions in Q4…but these combined were effectively neutral to FCF in the qtr

AT&T’s New Long-Term 2026-2028 Growth Guidance Topped Street #s

- Svs rev growth guidance is in LSD range annually from 2026-2028…how will they achieve this? Growth in consumer & biz customer relationships is the primary driver as they expect to gain wireless subscriber share through convergence in areas where they offer fiber & FWA

- This compares to Street expectations at +2.3% y/y for 2026, +2.1% y/y for 2027, and +1.6% y/y in 2028

- Adj EBITDA growth is guided in the +3-4% range in 2026, improving to +5% or better in 2028 (and is above cons expectations of +3% y/y every yr over the forecast period), as growth in Advanced Connectivity increasingly more than offsets declines in Legacy

- What’s driving the inflection in 2028? Integrating the Lumen assets will create “pretty significant” upfront costs in 2026, but as asset penetration increases and legacy declines fade, EBITDA growth is expected to accelerate

- Expect “strong and sustained” growth in Advanced Connectivity segment from 2026-2028…

- Rev growth in the MSD range annually

- Includes expected growth of 5%+ y/y in 2026, which bakes in ~100bps of growth from Lumen’s retail fiber subscribers

- EBITDA growth in the MSD-HSD range annually

- Includes expected growth of 6%+ y/y in 2026

- Does NOT expect planned acquisition of retail fiber subscribers from Lumen to materially impact EBITDA in 2026

- Rev growth in the MSD range annually

- …as well as “sustained” declines in the Legacy segment as the Co phases out the large majority of its copper network by end of 2029 and upgrades customers to 5G and fiber

- Rev expected to decline 20%+ y/y in 2026 and will be immaterial by the end of 2029

- EBITDA expected to be negative after 2027 until direct costs associated with operating the copper-based network are “substantially eliminated”

- Adj EPS guidance of $2.25-$2.35 in 2026 (which is up +7% y/y at the mid-pt and is +4% above cons $2.21) w/ a double-digit 3-yr CAGR through 2028 (vs cons +10% CAGR)

- The outlook anticipates that Lumen and EchoStar acqs will “modestly” dilute adj EPS in 2026-2027 and be accretive beginning in 2028

- For 2026 specifically…Outlook includes ~5c of dilution from stand up costs and higher interest expense related to Lumen and EchoStar transactions and an effective tax rate in the 22% range

- Capital investment guidance in the $23-24bn range annually during 2026-2028 (vs $22bn in 2025)

- Looking further out, capx intensity will be coming down: The Co expects that major capital projects will be “substantially completed” by the end of 2030 or sooner

- As they complete these investments, expect capital intensity to decline from high-teens % of rev to mid-teens

- Looking further out, capx intensity will be coming down: The Co expects that major capital projects will be “substantially completed” by the end of 2030 or sooner

- FCF of $18bn+ in 2026 (in-line w/ cons), $19bn+ in 2027 (vs cons $18.9bn), and $21bn+ in 2028 (vs cons $19.2bn): Y/Y increases are driven primarily by growth in adj EBITDA

- Specifically for 2026…FCF drivers = growth in adj EBITDA, lower pension contributions and lower legal settlements, partially offset by higher capital investments and cash interest

- Also expect greater cash tax savings under the One Big Beautiful Bill Act than the Co expected back in Q2, and plan to use the incremental tax savings to fund working capital and growth initiatives

- Expect annual cash taxes of ~$1-$1.5bn through 2028, which primarily reflects further assessments of expected savings due to this legislation

- “Our goal is to put these savings to work over the next three years to fund working capital and growth initiatives”

Also Provided Incremental Q1 Guidance, Which Will See An Impact From Upfront Costs Of Long-Term Investments

- Q1 adj. EBITDA y/y growth is expected to be below the run rate expected for the FY26 (which is +3-4% y/y)

- Have plans to “accelerate and scale” the execution of their strategy across 5G and fiber this year, so expect some upfront investments to be reflected in Q1 results

- Includes incremental spend to integrate and scale expected Lumen retail acqs + investments to accelerate fiber deployment

- Also lapping ~$100mn of 1x benefits disclosed in Q1:25

- Also expect Q1 FCF to be in the $2-$2.5bn range

While Q4 Headline #s Exceeded Expectations, It Was A Bit Of A Mixed Bag W/ Q1 Unit KPIs…Though Fiber Additions Were A Source Of Upside

- Q4 wireless unit KPIs fell below Street expectations almost across the board

- Postpaid phone net adds (missed by -9%), postpaid phone churn was higher than expected, & prepaid adds were also weaker

- The only minor upside came from postpaid phone-only ARPU

- Mixed bag w/ bband adds given Q4 fiber adds BEAT while FWA adds MISSED the Street: Though achieved ~500k combined advanced home internet net additions for the second consecutive qtr

- Fiber adds of 283k BEAT by +6.6%

- Consumer Wireline fiber rev: $2.2bn, up +13.6% y/y

- FWA adds of 221k MISSED by -14%

- Fiber adds of 283k BEAT by +6.6%

Looking Ahead, AT&T Expects To Take More Share On The Back Of Continuing To Expand The Fiber Footprint & Convergence

- AT&T maintained guidance to ramp the annual pace of fiber construction from 3mn new locations in 2025 to a run rate of 4mn by the end of 2026: The acq of Lumen’s fiber assets & build capabilities including Giga power will also expand beyond this

- Total fiber customer locations at the end of 2025 = 32mn

- Total fiber customer locations at the end of 2026 = ~40mn

- NEW GUIDANCE…beyond 2026, the Co plans to expand fiber reach by ~5mn locations annually through the end of this decade

- …BUT over the past 2 yrs given inflation, their avg deployment cost per fiber passing has incr’d by ~2% annually, and they expect a similar trend over the next 3 yrs

- Accelerated convergence gains also stood out in Q4

- The fiber convergence rate rose +200bp y/y to 42% (their fastest annual increase since they began tracking this metric)

- “I do expect the convergence rate to continue to improve” … “we’re going to drive that to 50% [target] and feel very comfortable” … BUT it will go higher…”I don’t expect it to stop there”

- Mgmt continues to stress that while there is an initial investment in converged customers, the long-term economics with lower churn and purchasing of addt’l services will be more than offsetting

- Churn has gone up with unbundled customers

- The fiber convergence rate rose +200bp y/y to 42% (their fastest annual increase since they began tracking this metric)

- Also, mgmt remains positive on oppty with the Lumen fiber assets as the network that they are acquiring only has 25% customer penetration which is well below AT&T’s fiber penetration of 40%

- And there is plenty of room for new converged customers: AT&T ests that < 20% of these customers also subscribe to their w-less service

- This is less than 50% of the convergence rate that AT&T achieved in their current fiber footprint

- And there is plenty of room for new converged customers: AT&T ests that < 20% of these customers also subscribe to their w-less service

What Are The Key W-Less & Broadband Assumptions Underpinning The New 3-Yr Guidance? Volume Growth Is A Main Driver

- Postpaid phone ARPU…assume a “relatively stable” trend

- Will have a “consistent, disciplined approach” to pricing

- Balanced by gains in underpenetrated categories such as value focused customers

- Plus growth in converged customer relationships

- Similar to the approach in w-less, mgmt. will maintain a “consistent approach” to pricing in home internet, balanced by gains in under-penetrated customer categories at different price points as they materially expand the availability of home internet services

- LT outlook assumes a lower contribution from bband ARPU growth than they have posted over the past few years

- Expect higher device upgrades…continue to plan for an operating environment with “elevated levels of new and existing customers that are eligible for device offers”

- Given that they amortize a portion of device offers through w-less svs rev, expect ~90bp headwind to postpaid ARPU growth in 2025 (which is the same impact in 2025)

- Expect advanced home internet service revs to grow organically by 20%+ per yr through 2028 (in-line w/ the annual rate over the past 2 yrs)

- The primary driver is growth in customer relationships that will come given the expanded reach of AT&T fiber and the availability of Internet Air

- “Expect to sell more [FWA] this year than last year”

- In 2026…w/ the addition of Lumen, expect 30%+ y/y growth in advanced home internet rev: Lumen fiber assets (deal expected to close in Q1) will add ~$900mn of annualized fiber revs

- The outlook factors in the portion of the convergence discount that they allocate to internet services as they grow the converged customer base

What Else Is Assumed In The New Long-Term Guidance?

- Cost savings are expected to accelerate in 2026: Achieved $1bn+ of cost savings in 2025 and expect to accelerate in 2026

- How? By leveraging AI, moving more customer transactions to digital, and achieving greater operating leverage as they grow their customer base

- Also expect D&A expense of ~$20bn annually through 2028

- As incremental depreciation from growth investments is offset by the roll off of depreciated assets that have reached the end of their useful lives

Expect AT&T To Bring Leverage Down Even W/ Significant Shareholder Returns

- The Co expect to return $45bn+ to shareholders over the next 3 yrs, representing almost 30% of AT&T’s mkt cap or 75%+ of expected FCF: The Co plans to maintain the current common stock dividend and continue share repurchases at a consistent pace through 2028

- Includes ~$8bn of buybacks in 2026 + board authorized an addtl $10bn after the current buyback authorization is completed

- Longer-term… “we expect that our improved growth, declining capital intensity and higher free cash flow will provide us with even greater flexibility to support enhanced shareholder returns”

- Even with strong shareholder returns, net leverage is still expected to return to ~2.5x target within ~3yr post close of Lumen + Echostar acqs

- Immediately post-close (early this yr): Expected to increase to ~3.2x

- By year-end: Should fall to ~3x as they grow adj EBITDA and FCF; Also expect to receive cash from an equity partner that will also co-invest in the acquired Lumen fiber assets

- Within ~3 yrs post-close: Expect to return to ~2.5x

The Co Is Restructuring Operating Segments Around 5G & Fiber Connectivity Starting In Q1:26

- Advanced Connectivity segment: Primarily includes the Co’s domestic 5G & fiber based wireless, internet and other advanced connectivity services

- On a recast basis, this segment contributed ~90% of consol revs & over 95% of adj EBITDA in 2025

- Segment results will be reported in aggregate, w/ supplemental disclosures on consumer and business performance

- Legacy segment: Represents results from the Company’s domestic legacy voice and data svs provided over its copper-based network to consumer and business customers

- Latin America segment: Will continue to represent results for the Co’s wireless biz in Mexico

Other Points We Wanted To Call Out

- Both the Lumen fiber asset deal and the Echostar spectrum license deals are expected to close by end of yr: Lumen acq is expected to be completed in Q1, while Echostar is supposed to close “early this year”

- The long-term outlook does not anticipate a material contribution to EBITDA growth from the pending acqs until 2028, which is also when they expect these investments to become accretive to adj EPS

- Bad debt/health in the consumer? Not seeing any notable changes in customer payment patterns

- The Co does not expect a new foldable iPhone to become a broadly adopted form factor

- Mgmt believes that the Echostar deal will allow them to be more strategic on what they are doing with spectrum going forward

- They believe industry spectrum demand is not all centered around the same bands, which is a positive dynamic

Comcast’s NBCU Delivers & There’s A Clearer Line Of Site Out Of Its Connectivity Investment Period

2025 was certainly a transition and investment year for Comcast as it implemented a strategic go-to-the market shift with new connectivity pricing and packaging and new customer experience initiatives. The aim is to stabilize the broadband customer base and position for subsequent growth. We are always a fan of companies effecting these shifts as quickly as possible, and that is what Comcast appears to be doing.

The Q4 results reflected this transition with pressure on Connectivity ARPU plus elevated marketing, product & customer svs expenses. Connectivity & Platform (C&P) adj EBITDA fell -4.5% y/y. Q4 subscriber additions across broadband and wireless were also below expectations. Nonetheless, mgmt was “encouraged” by what they are seeing thus far with the new go to market strategy & investments in customer experience (more color below). Investors should expect continued pressure from the Co’s strategic shift in H1, but H2 is positioned for tailwinds as they lap this investment cycle.

On the Content & Experiences (C&E) side of the business, results in the core Media segment were essentially in-line with expectations, with the key driver being Peacock (revs up +20% y/y growth). The Co is absorbing the cost of the new NBA contract but these sports rights appear to have helped drive subs (up +8mn y/y and up +3mn q/q). Another highlight was theme parks where revenue growth accelerated to +22% y/y (from +19% y/y in Q3) and EBITDA rose +24% y/y (crossing the $1bn level for the 1st time). Epic Universe’s performance stood out and importantly drove higher per capita spend & attendance across the entire Orlando resort.

So net net, trends in the Co’s media and theme parks segments paced ahead and while the connectivity business remains in transition, pressure will ease in H2.

-> Comcast shares actually rallied +3.6% in reaction to earnings despite the mixed Q1 performance and downbeat H1 outlook

Q4 2025 Results

- Rev ~IN-LINE: Rose +1% y/y (vs down -2.7% y/y in Q3)

- But the focus businesses are growing faster:

- The 6 focus growth businesses grew at a +mid-SD rate y/y

- 3 of the 6 key growth businesses (Theme Parks, Peacock, & Domestic Wireless) each grew revenue ~+20% y/y

- But the focus businesses are growing faster:

- Adj EBITDA slightly MISSED by -0.6%: Fell -10% y/y (vs -0.7% y/y in Q3)

- Adj EBITDA margin SLIGHT MISS: 5% vs 24.6%

- Drivers: Decline y/y reflects investments to transition customers to the new packaging & pricing and in customer experience, plus the Co is absorbing the cost of the new NBA contract

- Adj EPS BEAT by +15%: But was down -12% y/y

- Capx was HIGHER than cons by +4.7% (but fell -5% y/y)

- Content & Experiences capx declined -17% y/y (lower investment in Theme Parks)

- Connectivity & Platform capx was stable

- But FCF of $4.4bn BEAT cons $2.3bn but included a $2bn cash tax benefit related to an internal corporate reorg

- Returned $2.7bn in Q4 ($1.5bn in buyback)

The Impact From New Go-To-Market Plus Customer Experience Initiatives Weighed On Q4 Connectivity & Platform (C&P) Results But Early Progress Is Seen As “Encouraging”

- C&P total Q4 revenues fell -1.1% y/y (vs -1.4% y/y in Q3), while adj EBITDA fell -4.5% y/y (vs -3.7% y/y in Q3)

- APRU was under-pressure and the Co had elevated marketing, product & customer svs expenses

- The competitive environment for bband stepped up in Fiber in Q4 (and that continues)…FWA competition was consistent, and the Co flags that it saw “a step up” in wireless competition towards the end of Q4

- Q4 bband losses of -181k were marginally worse than cons -177k… the “early traction” from the new initiatives were “more than offset by the cont’d competitive environment”

- Mgmt expects that market to remain “intensely competitive”

- Q4 bband ARPU grew +1.1% (vs -4% y/y in Q3 and +1.2% y/y in Q2) reflecting the new go to mkt pricing

- This pressure is expected to persist in H1 (see section below)

- Q4 wireless adds reached +364k which missed cons +397k

- Seeing strong uptake of customer uptake of the free wireless line: Nearly 50% of the resi postpaid connects came from customers taking a free line…these will be converted to paying after the 1 yr offer

- The Co is also seeing uptake in the premium unlimited package (targeting the high value postpaid market)

- Comcast now has 9mn+ wireless lines which is still only 15% penetration of the base

- Q4 convergence revs grew 2% y/y in the qtr, driven by 18% growth in w-less

- “Encouraged” by what they are seeing with the new go to market strategy & investments in customer experience

- Voluntary churn continues to trend lower

- Seeing strong adoption of the 5-yr price guarantee

- Seeing a “significant improvement” in take rates of gig+ speeds…~40% of the base is on Gig Plus tiers

- Cont’d uptake of free wireless lines (has been the biggest area of investment)

- NPS is “moving in the right direction”

- Remain focused on transitioning the majority of the customer base to the simplified, market-based pricing plans and are “prioritizing getting to the other side of this transition as quickly as possible”

Connectivity & Platforms Headwinds Will Continue In H1 But Tailwinds Should Emerge In H2

- H1 headwinds

- Near term revenue will continue to be impacted by the rate investments (simplified bband pricing and offering free w-less lines)

- ARPU pressure should continue over the next “couple” of qtrs

- Will not have a bband rate increase

- Will have the dilutive impact from the free wireless lines

- WIll have the ongoing migration of the base to simplified pricing

- This also drives operating costs higher due to customer experience initiatives

- Expect EBITDA pressure over the next couple of qtrs

- H2 tailwinds

- The majority of the base will be on the new pricing and packaging for bband…the ARPU pressure will ease

- Expect to convert the “vast majority” of free lines into paying relationships which will provide a “meaningful” tailwind to convergence revenue growth

- They will have a much higher % of customers on gig + speed plans (more differentiated from FWA and satellite)

- EBITDA pressure will ease as the Co starts to lap the initial investments

- Other important guidance:

- FCF in 2026 won’t include $2bn in 1x time benefit from 2025

- Capx in 2026 should be similar to 2025 and spending at both C&P and C&E to be consistent y/y

- The capital allocation strategy remains unchanged

Network Upgrade & AI Investments Are Bearing Fruit

- Continue to make substantial progress on the network upgrade: ~60% of the footprint is now transitioned to mid split spectrum & a virtualized architecture

- Already seeing benefits from greater automation & the deployment of AI across the network to optimize the end-to-end customer experience

- 20% reduction in trouble calls

- 35% reduction in repair minutes

- As the Co completes upgrades across most of the footprint, they will start marketing multi-gigabit symmetrical speeds and their differentiated capabilities, creating opportunities to move customers into higher value tiers over time

Other Key C&P Updates / Developments

- Within Business Services…revs rose +6% y/y and EBITDA incr’d +3% y/y…Enterprise is a key growth driver looking ahead

- Q4 trends: Seeing modest rev growth in SMB and strong momentum in enterprise solutions business (which has been the trend)

- Competition: Remains elevated especially in FWA

- 2026: Focused on stabilizing small business while accelerating growth in mid-market & enterprise “where demand for advanced, secure and scalable connectivity continues to increase” and will help drive APRU

- The Co will be expanding business mobile relationships w/ T-Mobile MVNO later in 2026

- Mgmt disclosed that the Co “modernized” its VZ MVNO partnership but didn’t provide any more color

- The addition of T-Mobile as a network partner for their business customers starts later in the year

The Media & Theme Parks Segments Outperformed The Street While Studios Fell Short

- The Media segment outperformed consensus: Revenue (+6% y/y) & adj EBITDA both topped Street forecasts (note that results include Versant which was spun on Jan 2nd)

- Peacock was the main top line driver (see section below)

- Total advertising rose +1.5% y/y (strength from NFL and NBA launch, but lower advertising from political)

- Media EBITDA fell (-141% y/y) due to addition of NBA rights but think will offset through ad growth and subs additions & monetization across both linear and Peacock

- Q1 EBITDA guidance: Q4 had 25% of total games for the season but Q1 will be the peak volume period with 50% of games which will result in peak EBITDA dilution

- Theme Parks also outperformed: Revs and adj EBITDA were +2.5-3% higher than cons (see section below)

- Studio performance fell well short of cons expectations: Revenues missed the Street by -9% and adj EBITDA by -15.2%

- While Wicked has grossed well over $1bn WW, the Studio biz was impacted by tough comps y/y, the timing of licensing deals, & higher marketing spend due to higher volume of films this year

- Optimistic on slate going forward: Led by The Odyssey from Christopher Nolan, the Super Mario Galaxy movie, Minions 3 from Chris Meledandri and Disclosure Day from Steven Spielberg

Peacock Was The Biggest Driver To Media Results…Added Subs & Losses Continue To Improve

- Peacock revenue rose +20% y/y to a record $1.6bn

- Distribution revs grew 30%+ y/y

- Ad revs grew almost +20% y/y due to the strong sports lineup

- Peacock losses hit -$552mn in Q4 (NBA addition & exclusive NFL game) but improved by $700mn y/y for the full year

- Outlook – expect Peacock losses to “improve” again y/y

- Peacock subs incr’d +8mn y/y and +3mn q/q to 44mn

Theme Parks’ Growth Accelerated In Q4 As Epic Universe Drove An Uplift Across The Entire Orlando Resort

- Themes parks rev growth accelerated to +22% y/y (from +19% y/y in Q3) and EBITDA rose +24% y/y (crossing the $1bn level for the 1st time)

- “Couldn’t be more pleased” with Epic’s performance: It drove higher per capita spend & attendance across the entire Orlando resort

- The Co will expand ride throughput over the next several qtrs which will lead to higher attendance, strong per caps & addtl op leverage over time

- Bullish on 2026… it will be the 1st full year with Epic plus, will have the opening of Universal Kids Resort in Frisco, Texas, the debut of the first outdoor roller coaster at Universal Studios Hollywood, and a new universal resort in the UK

What About Potential M&A Or Ramifications?

- Mgmt commented that WarnerBrosDiscovery’s international reach “would have been additive” but Comcast was not interested in an all-cash deal

- However, it did “force them to take a look at what they have and what they are building”

- The M&A talk has “stirred the pot” and companies are trying to think about what this means for them and Comcast is open to that kind of thinking

- But mgmt is “very confident and comfortable that they are in the right parts of the industry”

Has Charter Finally Reached The Broadband Inflection??

That is a key point coming out of Charter’s Q4 earnings. While headline financials were mixed (revenue slightly missed consensus while adj EBITDA, adj EPS, and FCF all beat), the big story was significantly lower than expected broadband losses in Q4 (and further improvements are expected in 2026). On top of that, the Co actually added video subscribers given the success of its new video strategy. Also at an inflection is adj EBITDA as the Co is guiding for “growth” in 2026 vs the -1.2% y/y decline in 2025, though as a caveat, it will be more back-half weighted (more color on drivers below).

Mgmt’s capx outlook commentary also provided comfort given 2025 was the peak year for capital spending, and beyond 2026, total capx dollars should be on a “meaningfully” downward trajectory. The Co anticipates returning to normalized capex (sub $8bn/yr) by 2028 which drives the strong FCF growth story. Also standing out was a lowered leverage target post-Cox from 3.5-4x in 2-3 years post the deal close to the “lower end” of a new 3.5-3.75x range to be achieved 3 years post the deal close. Even with that, the Co is firmly committed to their shareholder return strategy.

Looking ahead, returning to positive broadband net additions is a key focus and a “game of inches”. It is not likely to happen this year but investors should expect to see a positive trajectory. While the mobile business was held back by not participating in the “flood of subsidies” in the market, the convergence strategy remains a top priority and focus is on further building brand recognition and driving strong word of mouth. The mobile adoption penetration curve in Cox’s territories post close should also be an improvement from Spectrum Mobile’s adoption curve in Charter’s footprint. Cost attention and efficiency remains a top priority and an improved trajectory in adj EBITDA is within sight.

All in all, this was a sigh of relief quarter. The business is moving in the right direction but execution remains the name of the game.

-> Charter’s shares rallied +10% on the back of results, recovering from the share declines out of the gate in January; The stock was down -42% in 2025

Mixed Q4 Headline Result

- Q4 total revs missed cons by -1% (fell -2.3% y/y)

- Q4 adj EBITDA beat cons by +1.6% (fell -1.2% y/y)

- Q4 adj EPS beat by +5%

- Q4 FCF beat by ~+3% despite Q4 capx being $140mn higher than the Street

2025 Was The Peak CapEx Yr & The Co Expects To Return To Normalized CapEx Sub $8bn Annually By 2028

- 2025 was the peak year of capx and beyond 2026, expect total capx dollars to be on a “meaningfully” downward trajectory

- FY25-28 cumulative capx guidance INCLUDING BEAD is $40-40.5bn (the prior guidance of $39.5-40.5bn EXCLUDED BEAD)

- BEAD spend is expected to total ~$230mn, mostly in 2027- 2029

- By year…will hit a normalized capx level in 2028

- FY26: ~$11.4bn

- FY27: ~$9.5bn

- FY28: $7.5-8bn (reaching 13-14% capital intensity level for Charter, should be able to do the same incl Cox)

- NEW – FY29: $7.5-8bn (flat y/y)

Lowered Target Leverage Post Cox But Remain Committed To Shareholder Returns

- The Co also adjusted post Cox transaction target leverage to the low end of the new 3.5-3.75x range, which they expect to achieve within 3 years post the close (before expected 3.5-4.0x in 2-3 yrs post close)

- The Co believes this will help attract more potential investors

- Despite that, mgmt still expects significant capital returns to shareholders

- Note that in Q4, bought back $750mn of stock in the qtr at avg price of $259/shr

- Debating how to allocate FCF is a “first class problem” but mgmt remains committed to the buyback program

Expect EBITDA to “Grow” In 2026, With Strength Moreso In H2

- Adj EBITDA will “grow” in 2026 but H1 will be “more challenged” than H2 due to a 1x benefit from Q1:25 and political advertising in H2

- Could adj EBITDA grow higher than 1% this year? “Maybe”…EBITDA growth is challenged in 2026 given the headwind from broadband subscriber declines, BUT mgmt. believes they can overcome that w/ the combo of:

- Mobile growth and changing mix of internet driving positive ARPU growth

- Cont’d operational improvements

- “Attentive” expense mgmt

- Political advertising being a driver

- Cost of service coming down again y/y (excl bad debt, cost to serve customers declined -3.2% y/y in Q4)

- Growth in Marketing & Sales will also be down y/y

- Continue to look for ways to drive down costs: Investing in tech, incl AI, to increase customer satisfaction through self-service where customers want it, and also enhancing employee service capabilities across sales, call center services, field operations and the network itself

Significant Upside In Customer Volumes… Broadband Losses Lower Than Expected While Video Subs GREW

- Broadband losses were much lower than anticipated (total Internet losses of -119k compared to cons -136k)…churn improved y/y given last year’s ACP related impact…but headwinds to growth include:

- Internet competition for new customers remains high

- Low move rates and higher mobile substitution

- Expanded FWA competition & fiber overlap growth, similar to earlier in the yr

- Video subscriber adds was also a positive surprise (+44k vs cons for -63k loss)

- Spectrum TV Select subscribers now receive up to ~$117 per month (soon will be $129/mo) of streaming apps at no extra cost

- BUT mobile net additions of +428k were lower than expected… due to heavy device subsidies activity by the big telco competitors, including the new iPhone 17, through the holiday sales cycle (gross adds were higher)

- “The convergence strategy is working”

- The market was “flooded” with subsidies that they didn’t follow

What Should Investors Expect For Broadband, Mobile, & Video Trends In 2026+?

- Getting back to positive broadband net additions is a “game of inches”…not expecting bband volume growth this year but expect to see a positive trajectory

- Focused on more clearly messaging the greater value and utility and providing the best quality of svs in the mkt

- What is the sustainability of video gains? The north star is not to just have net video gains, but want video to support bband acq and retention

- The video eco-system remains challenged…programming costs continue to go up

- There is only a slight difference between Q4 vs Q3, and KPIs could fluctuate back

- Selling DTC apps a-la-carte will be an increasing component of their video offer

- Outlook comments on product ARPU for 2026

- Internet ARPU should grow in 2026 but more slowly than prior years: As they drive Spectrum pricing & packaging through the footprint

- End of 2025, 40% had the new pricing and packaging

- Expect that to increase to 60% by the end of 2026

- Mobile ARPU had been declining but has bottomed: As more customers take the gig product, which includes Unlimited plus and Unlimited pricing…and as they see some contra revenue from the phone balance buyout plan, ARPU has been pressured… there might be addtl mobile ARPU declines y/y but “I think that we’re at a low point there” and that it has “bottomed” seq

- Video ARPU has multiple headwinds: Programmers streaming app allocation, unfavorable bundled revenue allocation, and a higher mix of skinnier video tiers…but also passing some programming increases to customers

- Internet ARPU should grow in 2026 but more slowly than prior years: As they drive Spectrum pricing & packaging through the footprint

- Spectrum Mobile brand is gaining momentum but is still in the early stages

- It is still a relatively new brand and concept to get cellular from a cable Co

- Spectrum Mobile’s reputation and word of mouth is “improving” but will “take some time” to develop

- They are on “a steady path” to increase brand awareness

- Most customers have NOT picked up that when they move around the country, they are getting faster speeds via WiFi; Charter “needs to show this better”

- Nearly 90% of Spectrum mobile traffic goes over their network

- What will mobile penetration curve in Cox territories look like? An improvement to the Spectrum Mobile penetration curve at Charter is a “good starting point”: “Our platforms, our sales channel, our marketing, our national brand awareness, it’s all in a much better place”

A Few Other Call-Outs

- Total commercial revs grew by +0.3% y/y with mid mkt and large business rev growth of +2.6% (ex wholesale revs, it was up by +3%); Small biz revs fell by -1.3%

- The Co generated +46k net customer adds in their subsidized rural footprint and grew subsidized rural passings by 147k and by 483k+ in the last 12 months (vs 450k target)

- Expect subsidized rural passings growth of ~450k in 2026 (the last large build year)

- Regarding the updated Verizon MVNO agreement – similar to Comcast and Verizon, no details were provided

- “It is a very good deal for both companies”

- The “structural” agreement has not changed

- Improvements/progress the Co has delivered in customer service commitments:

- Internally, moved the service window target to 2 hours and 1 hour for business (no competitors do this)

- Backing the customer service guarantee w/ credits beginning in February

- If they don’t hit the guarantees $1,000 of savings/yr when customers take internet and 2 lines of mobile from Spectrum they will credit the difference

- Gig speed availability:

- By the end of 2026, 50% of the current Spectrum network will be upgraded to symmetrical and multi-gig service

- It will be 100% in 2027

Verizon Is Full Steam Ahead On Its Turnaround Journey

The first 100 days have now passed at Verizon under new CEO Dan Schulman’s leadership and a lot has taken place in this first chapter of Verizon’s turnaround story. While Q1 results at the top-line were mixed, the focus is more on what’s coming ahead in 2026+, as mgmt framed the yr as a “step-function” improvement vs recent history. The focus is on pushing towards volume-based growth across both mobility and broadband, with the goal of exiting 2026 on much stronger financial ground. The year ahead is transitional, but the building blocks for more durable growth and improved financial performance are being put in place.

At the core of this reset is a sharper focus on growth areas alongside aggressive efforts to simplify the organization and improve efficiency. Verizon is actively streamlining the business, exiting pockets of underperformance, and working toward a $5bn OpEx savings target by 2026, with a portion of those savings set to be reinvested back into the business. Early signs of progress are already visible, as Q4 delivered 1mn+ mobility and broadband net adds, which has been the Co’s strongest quarterly net add performance since 2019.

In particular on the wireless side, Q4 postpaid phone net adds reached their highest level in six years, though churn remains elevated due to prior price increases without increases in value (which Schulman reiterated multiple times is not part of the going forward strategy). Reducing churn is a key priority in 2026 and the Co will be investing in the customer experience and deepening convergence to drive higher CLTV. On the topic of convergence, on the broadband side, Frontier is a central focus following the close of the acq, unlocking significant cross-sell opportunities. They are particularly bullish on the fiber oppty and actually raised their medium-term fiber passing targets from 35-40mn to 40-50mn.

Lastly, it sparked our interest when Schulman hinted on the call that a new value proposition is launching in H1:26. While there was limited detail, the expected impact is already embedded in 2026 guidance. Alongside these operational initiatives, a $25bn share repurchase program to be completed over the next three years was also announced, as well as a pull forward in the Co’s annual dividend increase.

There is clearly a lot in motion at Verizon, and little time has been wasted in turning strategy into action. See below for more of what we thought was most important.

-> Verizon’s stock jumped +11.8% on the day of its report and ended the week up +12.7%; The shares were up +1% in 2025

Verizon’s Q1 Results Were A Bit Of A Mixed Bag

- Total revs – BEAT by +0.9%: Up +2% y/y (in-line w/ Q3)

- Both Consumer and Biz segments beat by +1.2% and +1.0%, respectively

- Adj EBITDA MISSED by -1.3%: Down -1% y/y (vs up +2% y/y in Q3)

- Both Consumer and Biz segments missed by -1.0% and -1.8%, respectively

- Margin of 32.6% was below cons 33.3%

- Adj EPS BEAT: $1.09 vs $1.05

- FCF was +2.3% ahead of cons

Verizon’s 2026 Guidance “Reflects The Beginning Of Our Turnaround” & Is A “Step Function Change From Recent Historical Performance”

- Note that 2026 financial guidance includes Frontier from January 20, the closing date of the acq

- Provided guidance for postpaid phone net adds for the first time ever: Expect to deliver 750k-1.0mn postpaid phone net adds in 2026, or ~2-3x what they delivered in 2025 and the highest since 2021

- That is “only 10-15%” of the new adds to the industry, which is a “doable” target in yr 1 of the transition

- Will not require overutilizing promotions or pricing to achieve those targets; If churn is reduced by 5bp, they will already be halfway to their target

- Will also continue to invest in the overall customer experience, and the $5bn in OpEx savings gives them flexibility to do that

- And will leverage all their convergence oppties, including in FWA and across new Frontier mkts

- Anticipate 2026 to be a “transitional” yr for rev and will see ~180bp headwind as they lap prior yr price increases, absorb promotional amortization, and await the benefits from churn reduction and increased volumes

- Guided for mobility and broadband svs rev growth of 2-3%, equating to ~$93bn, even as they lap billions of dollars of price increases from last yr that they will not repeat

- Wireless svs rev growth is expected to be ~flat as the Co transitions to sustainable volume-based growth

- 2026 adj EPS guidance of $4.90-$4.95 was +3.7% ahead of cons $4.75 at the midpt

- Implies growth of +4-5% y/y (which is a significant accel from -1.9% in 2025 and significantly higher than the 5-yr historical avg of ~-1% y/y growth)

- Expect 2026 adj. EBITDA to grow FASTER than adj EPS

- Have line-of-sight to delivering ~$5bn in OpEx savings in 2026: With a “substantial” portion realized by headcount reductions, alongside marketing efficiencies, real estate rationalization, contract renegotiations and more

- Will reinvest a portion of those savings to drive a higher quality rev profile

- 2026 CapEx guidance of $16-16.5bn was less than cons expectations of $18.05bn and below 2025’s $17.0bn

- 2026 FCF guidance of $21.5bn+, growing ~7% or more from 2025 (above the ~-1% y/y over the last 5 yrs), which will mark the highest FCF generated since 2020

- Given all the efficiency work being done, Frontier acq is no longer expected to be cash flow dilutive in 2026

Outlined 4 Key Priorities In Allocating Capital Spend…Which Included Pull Forward In Dividend Increase + $25Bn Share Repurchase Program

- Investing in the biz

- Applying the same rigor towards CapEx as they are on OpEx efficiencies

- Focused “squarely” on growth areas –

- In mobility, they are focused on the completion of their C-Band buildout and increasing investments to maintain reliability

- In broadband, they are focused on reaching 40mn-50mn fiber passings over the medium-term

- Firmly committed to VZ’s dividend

- Pullingforward their annual dividend increase to May, which represents an annualized increase of $0.07 or +2.5%/shr from their prior annual dividend rate

- Marks their 20th consecutive year of dividend increases

- Goal is to put the board in a position to continue to increase that dividend

- Maintaining a strong balance sheet

- Remain committed to paying down debt and returning to a target leverage range of 2.0-2.25x in the 2027 timeframe

- Returning cash to shareholders

- Announced up to $25bn of share repurchases, which they expect to complete over the next 3 yrs, with at least $3bn of repurchases in 2026.

- Expect to “significantly increase” their total return of capital to shareholders over the next three years

Update On The First 100 Days Of The “New” Verizon Turnaround Story

- Emphasized that “no company ever cost cuts its way to greatness” and they are “examining every dollar of OpEx and CapEx to ensure it is being spent on initiatives that will drive customer loyalty and brand trust”

- “Already a leaner, more efficient and intense organization” + “bringing in talent with new skill sets to complement our workforce”

- “We aim to be the most efficient telecom company in our industry” – “every single year, we will become more efficient, more agile, more outcomes-oriented and our speed of decision-making and product deployment will meaningfully increase”: How?

- Continue to reduce complexity

- Eliminate structural inefficiencies

- Divest non-core assets

- Deploy automation at scale

- What will drive financial success?

- Subscriber growth driven by convergence

- Value-based pricing strategy

- Superior value-added services

- Fully revamped end-to-end customer experience

- What will NOT? Price increases that drive short-term rev and earnings – “that is not a sustainable financial model, nor an engine of long-term growth”

- Mgmt is also “determined” to be an AI-first Co and deploy AI at scale: “Eventually, every individual customer will have a tailored proposition”

- Leveraging AI to simplify offers, personalize interactions, and reduce churn through “smart, consistent” marketing

- Using predictive models to anticipate customer pain points before they happen

The Co Reported Notable Q/Q Jumps In Net Adds Across The Wireless Segment, Particularly In Postpaid Phone

- Q4 total postpaid phone net adds was the highest in 6 yrs: +616k (huge jump from +36k in Q3)

- Consumer postpaid phone net adds were a hefty beat: +551k (vs -7k in Q3) and beat cons by +44%

- Driven by “strong” demand as they leveraged their financial strength and flexibility to fund growth oppties

- Business postpaid phone net adds missed: +65k (vs +51k in Q3) and missed cons +68k

- Continued to see growth in the SMB and enterprise sectors.

- Public sector results were impacted by residual disconnects from govt efficiency efforts and the federal govt shutdown

- However, public sector performance improved from the prior qtr and w/ the “vast majority” of these related disconnects behind them

- Outlook – expect to see further improvements in public sector wireless volumes in H1

- Consumer postpaid phone net adds were a hefty beat: +551k (vs -7k in Q3) and beat cons by +44%

- Q4 prepaid phone net adds were also a big beat: +109k vs cons +43k

- 6th consecutive qtr of positive subscriber growth

- Completed a comprehensive, long-term agreement with Comcast and Charter to continue their partnership: Didn’t share any details, but said that partnership is “on very solid footing…financially, operationally and strategically”

Postpaid Churn & ARPA Both Disappointed In Q4… “We Have A Large Opportunity To Address Churn”

- Q4 postpaid phone churn incr’d to 1.32% (up from 0.98% in Q3) and was higher than cons 1.23%

- This is largely from prior pricing actions, as well as competition

- Churn is a “pivotal” oppty in 2026 and expect investments in the customer and increased convergence oppties to benefit retention and LTVs over the next few qtrs

- Q4 postpaid ARPA missed by -1.2%: Grew +1.0% y/y (decel from +2.0% in the last 2 qtrs) to reach $170.61

Strength In Broadband Will Now Be Supercharged With The Closing Of The Frontier Acq

- Total Q4 broadband net adds came in ahead of cons: +316k vs cons +275k

- Total Q4 FWA net adds beat, again driven by Consumer: +319k (up from +261k in Q3), which was +14% ahead of cons

- Consumer beat by +25.0%, while Business missed by -33.3%

- Q4 Fios internet net adds were the high fourth qtr net adds since 2020: +67k (up from +61k in Q3) and beat cons +55k

- On the fiber front…Frontier acq has now closed and are full speed ahead on leveraging “huge” cross-sell oppty

- In Q4, generated +125k fiber net adds (up +29% y/y)

- In 2026, want to add “at least” 2mn fiber passings organically

- RAISED medium-term fiber passings goal from 35mn-40mn to 40mn- 50mn (whether that be organically or inorganically)

- Expect to realize $1bn+ of run rate operating cost synergies by 2028, double their initial estimate: Savings will be derived from network integration, 3P contract efficiencies and GTM savings across marketing and advertising

- Intend to “aggressively” seize incremental net adds and share of both mobility and broadband svs within Frontier mkts

Finally To Flag…Coming Soon in H1 Is A Brand-New Value Proposition

- Shared very few, vague details about what exactly the value prop is – “we are not going to show our hand until the day we launch”

- BUT the expected impact has already been incorporated into guidance: Based on “significant” mkt input and data analytics of how it will impact their volumes and financials

- Targeting launch for H1:26

- Currently in “deep” mkt research with a “very sophisticated” conjoint analysis…: Providing them w/ detailed customer feedback, projected market dynamics and associated financial and operational metrics

- …and feedback is “quite positive”

- Now in the fine-tuning stage of how the value prop will work

Microsoft’s Results Bring “The AI Investment Vs Returns” Question Back To The Forefront

It was not all smooth sailing for big tech this week (like it was for Meta in Theme #2). Microsoft lost over $350bn in market cap at one point on Thursday following its results.

While the Co actually delivered stronger than expected FQ2 results, the FQ3 guidance was uneventful in combination with market concerns about higher CapEx spending not yielding strong enough returns and OpenAI accounting for 45% of its backlog more than overshadowed.

To give a little more color, CapEx has been on the rise for the Co (and others in the industry) and incr’d +66% y/y in FQ2 but at the same time, Azure Cloud revenue growth y/y has been decelerating and is expected to again decelerate in FQ3. Mgmt stressed that this slower growth is not due to a lack of demand but reflects continued supply constraints as not all of the new incremental CapEx is being allocated to bring on more capacity for Azure. They are also allocating support to accelerate usage in first-party applications like M365 Copilot and GitHub Copilot, which represents incremental businesses which are expanding the TAM, and to fund ongoing R&D and product innovation.

Furthermore, the disclosure that 45% of the remaining performance obligation (RPO) balance is from OpenAI created customer concentration concerns. In defense, mgmt argues that the other ~55% (or ~$350bn) is highly diversified across customers, solutions, industries, and geographies, and is growing ~28% y/y.

Overall, investors’ appetite to underwrite huge AI investment levels continues to become more discriminating. Microsoft will need to show more fruits of their current investment spend to ease these concerns.

-> MSFT shares closed down -10% in reaction and is now down -11% YTD, following up +13% in 2025

Microsoft Tops FQ2 Headline #s

- FQ2 total revs BEAT by 1.2% and grew +17% y/y (+15% FXN), vs FQ1 +18% y/y (+17% FXN)

- PBO rev BEAT: by +2% and grew +16% y/y (+14% FXN)

- Intelligent Cloud rev BEAT by +1.6% and grew +29% y/y (+28% FXN)

- Azure rev growth FXN rose +39% y/y vs cons +39.4% y/y

- MPC rev MISSED by -1%, decel -3% y/y (-3% FXN)

- Microsoft Cloud gross margins decreased due to AI infrastructure investment

- Microsoft Cloud rev of $51.5bn, up +26% (up +24% FXN), vs +26% y/y in Q1:26

- Microsoft Cloud gross margin decreased y/y to 67% driven by continued investments in Al infrastructure and growing Al product usage, offset by efficiency gains in Azure and Microsoft 365 Commercial cloud

- FQ2 Gross margins beat (again) at 68% vs cons 67.1%, op margins were +150bp ahead, and EPS beat by +6% (+24% y/y, +21% FXN vs FQ1 +22% y/y, +21% FXN)

- FQ2 shareholder returns: +12% y/y to $12.7bn total ($6.8bn in dividends & $6bn in share repurchases)

- FQ2 FCF down -9% y/y to $5.9bn reflecting higher CapEx to support cloud and Al offerings

The Overall FQ3 Guidance Was A Non-Event

- FQ3 total rev at the midpt was roughly in-line w/cons, and reflects 15-17% y/y growth (a deceleration from the +17% y/y in FQ2)

- Productivity & Biz processes rev guidance slightly BEAT

- Intelligent Cloud rev guidance slightly BEAT

- Personal Computing rev guidance MISSED

- Some key assumptions underpinning the revenue guidance –

- M365 commercial cloud…accelerating Copilot momentum and ongoing E5 adoption will again drive ARPU growth

- M365 commercial products rev should decline in the low SD q/q, assuming Office 2024 transactional purchasing trends normalize

- Dynamics 365 rev growth to be in the high-teens

- Microsoft Cloud gross margin guidance of ~65% (down y/y) is driven by cont’d investments in AI

- Azure on-premises server rev is expected to decline in the low SD range as growth rates normalize following the launch of SQL Server 2025, though increased memory pricing could create additional volatility in transactional purchasing

- Personal Computing rev growth rates will be impacted as the benefit from Windows 10 to support normalize & as elevated inventory levels come down through the qtr

- M365 commercial cloud…accelerating Copilot momentum and ongoing E5 adoption will again drive ARPU growth

- Expect FQ3 CapEx to decrease on a sequential basis, due to the normal variability from cloud infrastructure build outs and the timing of delivery of finance leases: Expect the mix of short-lived assets to remain similar to Q2

But The Heavy Backlog Exposure To OpenAI Raised Eyebrows

- FQ2 Commercial remaining performance obligation (RPO) of $625bn incr’d +110% y/y (vs +51% y/y in FQ1:26) with a weighted average duration of ~2.5 years (~2 yrs in FQ1)

- ~25% will be recognized in rev in the next 12 months, up +39% y/y

- The remaining portion, recognized beyond the next 12 months, is up +156% y/y

- Notably ~45% of the commercial RPO balance is driven by commitments from OpenAl

- Incudes multi-year demand needs…at the same time it could also cause some quarterly volatility in future bookings and RPO growth rates

- But mgmt highlighted that the majority of capital spend is on GPUs (including for large customers like OpenAI) and is already contracted for most of its useful life

- Excluding OpenAI, ~55% of the RPOs (or ~$350bn) is highly diversified across customers, solutions, industries, and geographies, is growing ~28%, and is larger and more diversified than most peers, which management has very high confidence in

-> Also this week, Perplexity signed a 3-year, $750mn agreement w/ Microsoft to use Azure as a primary platform for accessing frontier AI models through Microsoft’s Foundry program;The deal does not replace Perplexity’s existing AWS usage.(link)

And There Was Ample Analyst Focus On Azure Cloud Y/Y Growth Decelerating While CapEx Grows

- FQ2 CapEx of $37.5bn rose +66% y/y (vs +74% y/y in FQ1) and was above cons $36.3bn: ~2/3 of CapEx was for short-lived assets (primarily GPUs and CPUs), which support Azure platform demand, growing 1st-party applications and Al solutions, accelerating R&D by their product teams, as well as cont’d replacement for end-of-life server and networking equipment

- While at the same time Azure & Other Cloud rev growth decelerated from +40% y/y in FQ1 to +39% y/y in FQ2 and guidance is for further deceleration to +37-38% y/y growth (though mgmt argues that demand is above supply)

- Why isn’t the material increase in CapEx spend leading to higher Azure & Other Cloud revenue growth? Isn’t that level of spend a risk?

- Mgmt clarified that the CapEx investments are not solely to support Azure revenue but also to drive the lifetime value (LTV) of the broader portfolio, including first-party AI applications like M365 Copilot, GitHub Copilot, Dragon Copilot, and Security Copilot, as well as R&D

- Acquiring an Azure customer is super important to them, but so is acquiring an M365 or a GitHub or a Dragon Copilot, which are all incremental biz and TAMs

- Also to note, mgmt stressed that the majority of the current CapEx (esp for GPUs) is fully contracted for most of their useful life so the risk being pointed to “isn’t there” b/c the hardware is already sold

- If all the GPUs that came online in Q1 and Q2 were all allocated to Azure capacity, “the KPI would have been over 40” (while unclear, it sounded like mgmt was referring to what Azure Cloud rev growth would have been in that case)

- “Our customer demand continues to exceed out supply” so mgmt needs to balance the need to have incoming supply to meet Azure’s demand vs other uses noted above

- “Mgmt is working as hard to add capacity as quickly as we can”

- Will add long-lived infrastructure and put more GPUS and CPUs in them as quickly as possible when they are done

Mgmt Outlined Several Bullish Stats To Reflect Strong AI Demand / Adoption Within Enterprises

- AI adoption is compounding across M365, Security, and GitHub, which historically worked well together and are now becoming transformative as AI and agents sit on top of them

- Microsoft 365 data is the most important database for enterprises, because it contains info (people, relationships, projects, artifacts, communications), and Work IQ unlocks this context for workflows and agents

- Agents are the “transformative” layer, where tools like M365 Copilot, GitHub Copilot, and Security Copilot work together

- Demand for specific AI-powered products is robust –

- Microsoft 365 Copilot: +160% y/y increase in seat adds, with accelerating q/q growth, reaching 15mn paid seats; The # of customers with 35k+ seats tripled y/y, and DAUs incr’d 10x y/y

- CoPilot app: DAUs incr’d nearly 3x y/y

- GitHub Copilot: Paid subs reached 4.7mn, up +75% y/y, w/ Copilot Pro Plus subs for individual developers incr’d +77% q/q

- Dragon Copilot (healthcare): Used by 100k+ medical providers & helped document 21mn patient encounters this qtr, up +3x y/y

- Purview: Audited 24bn Copilot interactions this qtr, a 9x increase y/y

Other Points To Highlight

- FQ2 Gaming declined this qtr: Xbox content and svs rev declined -5% (down -6% CC) vs +1% y/y in FQ1:26; Xbox hardware rev declined -32% y/y (down -29% y/y in FQ1:26)

- FQ3 guidance…Gaming rev is expected to decline mid SD y/y due to tough comps, partially offset by growth in Xbox Game Pass and hardware revenue should decline y/y