What a week. It was pretty much all dominated by AI in one form or fashion. Panic selling on the “AI is eating software” theme hit a new level this week (the IGV software ETF is now down ~30% since late Oct) and also spilled over into other related sectors as well. AI capx going up dramatically at companies like Alphabet and Amazon was another big focus as well.

However, the massive Friday rally helped the S&P 500 to recover its losses earlier in the week and Nasdaq closed down only -1.8% (vs steeper lows earlier). On the macro side, the weaker-than-expected jobs report caught investors’ attention, but at least for S&P 500 companies that have reported, Q4 earnings growth is close to +13% y/y which is well above the +8.3% expected which is a very positive sign.

It is another earnings heavy edition, please see below for what we focused on this week:

- Earning Scorecard – Week 3

- The Claude Cowork Market Meltdown

- The Capx Overhang Returns, Though Google Shows All Signs Of Successful Execution At Least Thus Far

- Ditto For Amazon…The Massive Capx Ramp Sparks Concerns, But The Co Is Realizing Strong Returns

- Disney Sets Sail With New Leadership During A Fiscal H2 Pickup

- Fox Is Executing Well In This Cyclically Slower Year

- WMG Is Hitting The Right Notes On Margins And AI Partnerships

- AI Concerns Overshadow Take-Two’s Strong Beat & Raise Qtr

- Snap Navigates A Self-Inflicted DAU Dip…While Still Aimed At Its Long-Term Goals

- Uber Keeps Driving While Building For An Eventual Driverless Future

- Other Quick Earnings Takes: Reddit & Roblox

**Also, LAST CALL if you would like to participate in LionTree’s 8th Annual TMT Sector Themes Survey. It consists of 25 simple questions about the market, sector developments, and company outlooks and takes less than 10 minutes. We are closing the survey at the end of the weekend and will send results only to those that participate! CLICK HERE for the survey**

Enjoy the weekend and rest up before the next wave of earnings reports next week, with Spotify kicking things off Tuesday morning.

Best,

Leslie

Earning Scorecard – Week 3

Week 3 of earnings has come to a close. In total, 36 stocks in our LionTree Universe reported (though it felt like more!). Stock reactions were skewed negative this week with 26 stocks trading down and only 10 trading up. The best performer in reaction to earnings was Roblox, which was up +10.3% (see Theme #11), while the worst performer was Peloton, which fell -25.7%.

It was a tough week for Big Tech with Amazon down -5.6% in reaction to results (see Theme #4) though Alphabet’s shares closed almost flat after being down as much as -8% intra-day (see Theme #3), Elsewhere in digital media, Snap closed down -13.4% following results (see Theme 9), while Reddit fell -7.4% (see Theme #11)

Media conglomerates were under pressure with Disney and Fox shares down -7.4% and -3.6%, respectively (see Themes #5 and #6) and in music, WMG shares rallied +3.6% (see Theme #7).

In Last-Mile Transportation Uber fell -5.1% in reaction (see Theme #10), Lastly, gaming stock Take-Two (see Theme #8) dropped -5.4% post earnings.

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

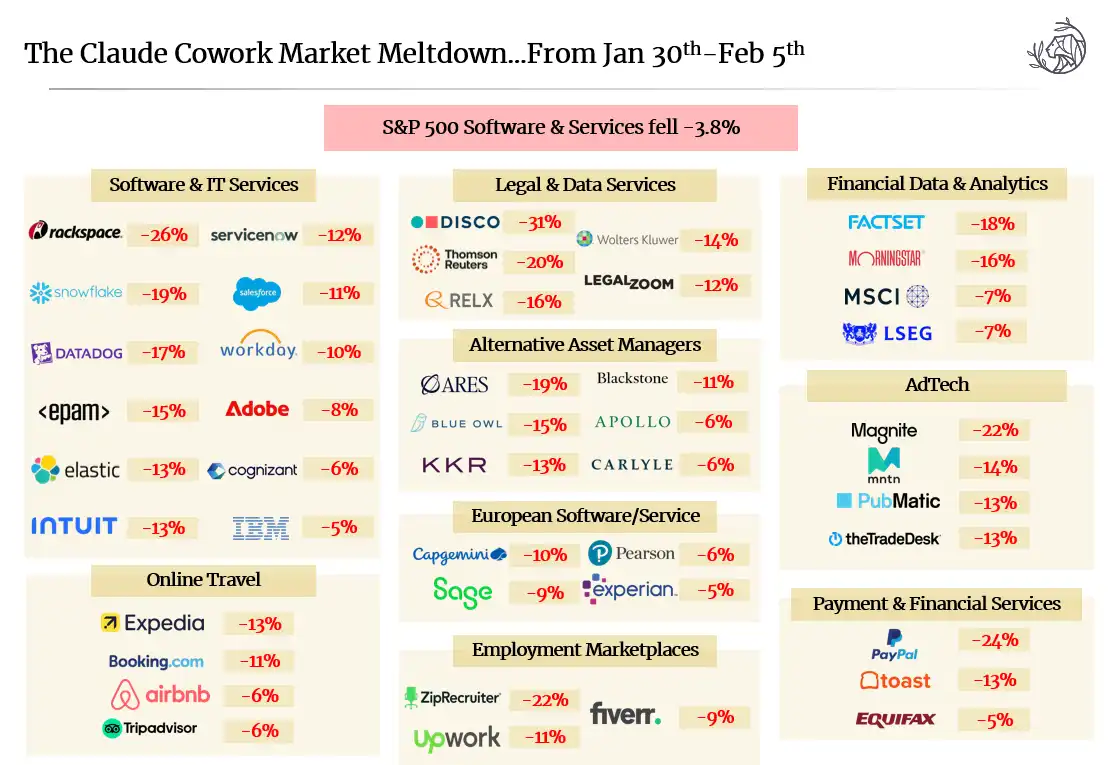

The Claude Cowork Market Meltdown

Who knew that the addition of a couple of plug-ins could trigger a global stock selloff? While a gross oversimplification, that is essentially how Anthropic drove an ~trillion-dollar selloff after it released a set of industry-specific add-ons to its Claude Cowork product, expanding its abilities across productivity and finance to marketing and operations. In reaction, investors hit the sell button not just for software companies, but also software-adjacent and software-exposed businesses, as fears about its potential to disrupt existing tools and workflows reached a new level.

Despite the carnage in the market (up until Friday), several industry leaders argued that the sell-off was an overreaction. Nevertheless, this week’s stock reactions were a continuation of growing investor uncertainty around how AI will reshape the tools and platforms that companies rely on every day.

See below for the quick drill-down of what happened this week. We anticipate this debate will persist for a while, with software survivors at some point emerging out of the rubble.

The Market Meltdown Catalyst…Anthropic Announces Plugins For “Cowork”

- On January 12th Anthropic launched Claude Cowork (link)

- Cowork is essentially a user-friendly version of Claude Code and is designed to manage files, research, and execute multi-step workflows

- Claude Cowork works like a “proactive teammate” rather than a chat bot: Once given access to a specific folder, it independently plans and executes tasks (i.e., reading, creating, and organizing files) while keeping the user in the loop; Instead of constant back-and-forth, users can assign it work, queue feedback, and let Claude steadily carry it through with more autonomy and context

- Example use cases: Reorganize downloads by sorting and renaming each file; Creating a new spreadsheet w/ a list of expenses from a pile of screenshots; Producing a first draft of a report from a user’s scattered notes

- Then on January 30th, Anthropic rolled out a series of plugins that could be added to Cowork (link)

- The plugins bundle skills, connectors, slash commands and sub-agents so people can use Cowork as a specialist for specific roles, teams and companies

- The Co launched with 11 plugins spanning a wide range of use cases –

- Productivity: Manage tasks, calendars, daily workflows, and personal context

- Enterprise search: Find information across your company’s tools and docs

- Plugin Create/Customize: Create and customize new plugins from scratch

- Sales: Research prospects, prep deals, and follow your sales process

- Finance: Analyze financials, build models, and track key metrics

- Data: Query, visualize, and interpret datasets

- Legal: Review documents, flag risks, and track compliance

- Marketing: Draft content, plan campaigns, and manage launches

- Customer support: Triage issues, draft responses, and surface solutions

- Product management: Write specs, prioritize roadmaps, and track progress

- Biology research: Search literature, analyze results, and plan experiments

What Followed Was Carnage Across The Market…But Particularly Across Software, Software-Adjacent, And Software-Exposed Names

- Stocks plunged in response to the announcement given fears that the new plugins will take a bite out of business for many software, data, and professional services companies

- Software stocks almost across the board were indiscriminately sold

- Legal & Data Service Cos saw some of their highest daily losses on record on Tuesday

- Thomson Reuters, which owns the Westlaw legal database, fell -16%, its biggest daily loss on record and lowest close since June 2021

- RELX and Wolters Kluwer, both providers of legal analytics services, fell -14% and -10%, respectively; RELX’s plunge was its biggest since 1988

- The drop in software valuations fed directly into the private credit market, as alternative asset managers with significant exposure to software borrowers fell between 6-19% from last Friday to Thursday

- Blue Owl, for example, was down ~15% over the same time period and is now down ~50% over the past yr, as part of that repricing of risk tied to software-linked loans and broader market jitters

Source: FactSet; All stock performance data is from 1/30/26-2/5/26

But There Are Some Who Think The Sell Off Is An Over Reaction

- NVIDIA CEO Jensen Huang said its “illogical” to think AI will replace software tools (link)

- On Tuesday, Huang said, “there’s a whole bunch of software companies whose stock prices are under a lot of pressure because somehow AI is going to replace them…it is the most illogical thing in the world”

- He argued it makes sense for AI to use existing tools to accomplish tasks, rather than reinventing them, using the examples of ServiceNow, SAP, Cadence and Synopsys – “would you use a hammer or invent a new hammer?”

- Arm CEO Rene Haas said fears about AI hurting software companies are a “micro-hysteria” that exceeds the reality of how businesses are actually using the tools (link)

- Mark Murphy, head of U.S. enterprise software research at JPMorgan, said it “feels like an illogical leap” to say a new plug-in from an LLM would “replace every layer of mission-critical enterprise software” (link)

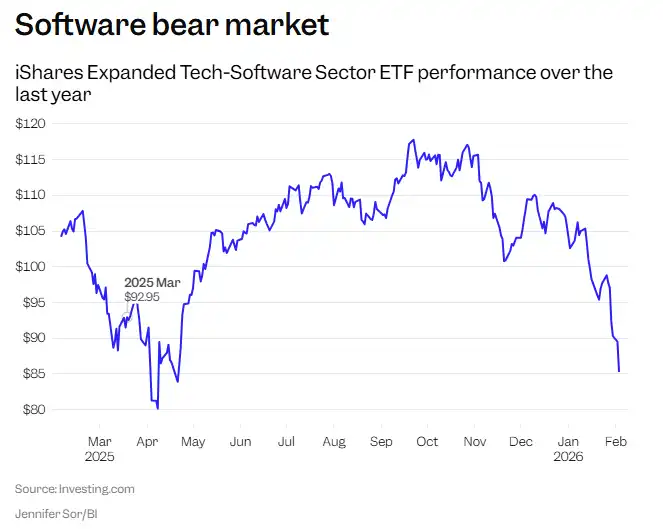

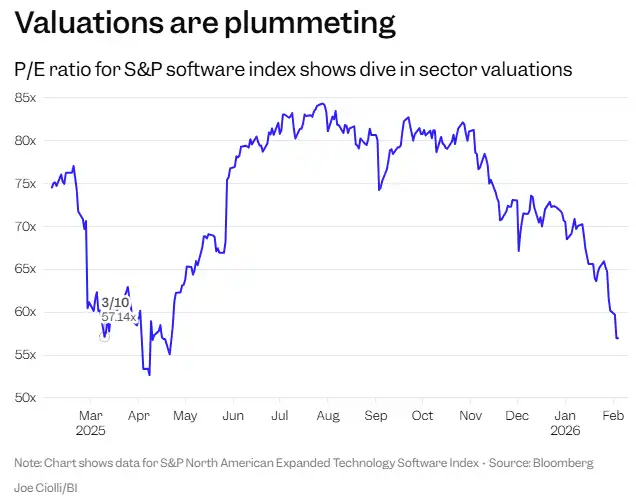

But This Is Not A New Worry … Software Stocks Have Been On The Decline (link)

- Software stocks officially entered a bear market last week, the iShares Expanded Tech-Software Sector ETF (IGV) is now down -27% (as of Feb 5th) from its Sept 2025 peak

- The average multiple of Cos on the IGV index has fallen from 39x forward earnings to about 21x as of Feb 4th

Source: Business Insider

- The P/E ratio in the S&P software index dropped to below 60x, down from a peak of around 85x last summer

Source: Business Insider

The Capx Overhang Returns, Though Google Shows All Signs Of Successful Execution At Least Thus Far

Capx took another leg higher (AGAIN) when Alphabet issued 2026 capx guidance of $175-185bn, which was +55% above Street forecasts and, at the mid-point, is DOUBLE the full year 2025 level. When the Co said on its last year’s call that 2026 capx would be “significantly” higher, they certainly meant it!

The question is whether all this investment will be well spent, and at least thus far, one can certainly argue that it has been. Google’s Search and Cloud revenue growth both accelerated, and on the latter that was despite being in a supply constrained environment and not able meet all the demand.

Regarding Search, it wasn’t that long ago that the Street thought that Google’s core Search business would be disintermediate by AI platforms. Instead, the Co is seeing increased usage and better monetization. Q4 Search revenue beat the Street by +2.6% and accelerated to +17% growth y/y. Mgmt framed this as an “expansionary moment” with Q4 daily AI mode queries per user doubling in the US and queries 3x longer than traditional search (though some analysts focused on how monetizable this higher‑complexity usage really is).

Cloud outperformance was the other positive surprise with Q4 revenue beating the Street by +9.1% and operating income beating by a huge +45%. Growth accelerated to +48% y/y from +34% y/y in Q3 despite, as mentioned above, demand still outstripping supply. The backlog being up +50% q/q and doubling y/y to $240bn is also a good indicator of future demand. Enterprise AI adoption has been ramping with 75% of Cloud customers using Google’s vertically optimized AI stack and those customers are using nearly 2x as many products.

It was also impressive that Gemini hit 750mn MAUs and is now embedded across Search, Chrome, consumer apps, and enterprise workflows. Enterprise adoption was a standout with more than 120k companies using Gemini and 8mn paid enterprise seats were sold in 4 months. To the question about AI eating software, CEO Sundar Pichai said that AI is an “enabling tool” like it has been for Google and companies that are “seizing the moment” have the same opportunity ahead.” This remains an open question and a key debate for the sector (see Theme #2)

On the negative side, YouTube ad revenue fell ~4% below cons (grew +9% y/y), with brand weakness tied to lapping the US election cycle. However, to be fair, YT subscription revenue was strong, hence it makes more sense to look at the segment holistically.

Overall, the Co has made a lot of progress levering AI inside and outside the company to drive better results but the much higher capx, plus the general concerns about downstream AI implications for their software customer base dragged on the stock in reaction.

-> Google shares fell -0.5% in reaction to earnings, is up +3% YTD, following a huge +63% rally in 2025

Search & Cloud Drove Better Overall Q4 Results…Though YouTube’s Ad Rev Weakness Stood Out

- Revenue BEAT: By +2.2%, up +18% y/y vs +16% y/y in Q3 2025

- Acceleration driven by Search & Cloud

- Expect FX tailwind to consol Q1 revenue

- Adj Op Income MISSED: By -2.5%, up +32% y/y vs +31% in Q3 2025

- Adj Margin MISSED: 6% vs cons 33.1%

- Adj EPS BEAT: By +7.2% up +31% y/y vs +35% y/y in Q3 2025

- Capex came in higher than cons: $27.85bn vs $27.80bn

Google’s Search Is Enhanced & Not Disrupted By AI…Its An “Expansionary Moment”

- Google’s Search revenue beat cons by +2.6% and continues to accelerate to +17% y/y in Q4 from +15% y/y in Q3 and +12% y/y in Q2

- Retail was particularly strong

- Search saw more usage in Q4 than ever before as AI continues to drive an expansionary moment

- AI is being integrated into Search …it is improving ad quality, advertiser tools, and user experiences and also making it easier to deliver ads on longer, more complex searches, which was difficult to monetize before

- Shipped over 250 product launches within AI Mode and AI Overviews

- Last quarter, integrated Gemini 3 directly into AI Mode in Search and last week upgraded AI Overviews to Gemini 3

- Once people start using these new experiences, they use them more

- In the US, daily AI Mode queries per user doubled since launch and AI Overviews continue to perform very well

- Queries in AI Mode are 3x longer than traditional search (the Co is also in the early stages of experimenting with AI Mode monetization)

- Also seeing sessions become more conversational, w/ a significant portion of queries in AI Mode now leading to a follow up question

- Mgmt is very bullish on its Universal Commerce Protocol (UCP) dramatically improving the commerce experience: People can soon use a new checkout experience to buy directly in AI Mode and Gemini from select merchants

- The Co has received “tremendous feedback from the industry”

- “There’s an oppty to improve the experience”…“there can be a foundational uplift here”

- “It makes it easier for users to complete transaction but also allows merchants to help showcase the range of their offerings” (i.e., if they want to make a promo)

- “Excited about a future whereas people are going through discovery, searching, finding new things, if they’re interested in acting upon it, all of that is seamless”

- “So, it overall creates an expansionary moment”

- UCP is the core foundation for interoperability for agentic commerce and “this is the year” that consumers will actually be able to use agents for shopping

- People are also searching in new ways beyond text

- Nearly 1 in 6 AI Mode queries are now non-text using voice or images

- Circle to Search is now available on over 580mn Android devices

YouTube Ad Revs Fell Short But Subscriptions Grew

- YT Q4 ad revenue fell ~4% short of cons expectations, growing only +9% y/y vs +15% in Q3 and +13% in Q2…DR was strong while brand advertising was weaker

- YT Q4 ad revenue drill-down

- Brand: Growth y/y was most negatively impacted by lapping the strong spend on US elections, though the Co saw a slight impact in some other brand related verticals as well

- Going forward: Excited about the CTV opportunity, more innovative ad formats, and shoppable

- DR/Performance: There’s a lot of momentum w/ demand gen adoption across SMB and the Co is excited about cont’d ad innovation in DR (like shoppable formats, incl in the living room) which will drive strength in retail, Shorts, etc.)

- Brand: Growth y/y was most negatively impacted by lapping the strong spend on US elections, though the Co saw a slight impact in some other brand related verticals as well

- Strong momentum with YT Shorts

- Shorts now averages 200bn+ daily views

- In a number of countries (incl the US) Shorts earns more rev per watch hour than traditional in-stream YT

- However, investors should look at YT revenue holistically given that when an ad supported user moves to subscription, it has a neg impact to ads but positive impact to subscriptions

- And it was a strong Q4 for YT subscriptions, especially w/ YT Music and premium category

- Premium will soon launch new YouTube TV plans

- And it was a strong Q4 for YT subscriptions, especially w/ YT Music and premium category

- In 2025, YT total rev passed $60bn across both ads and subscriptions

- Google has 325mn paid subs across consumer services w/ strong uptake of Google One (strong demand for AI plans) + YT Premium

- Creators & viewers are using the Co’s AI tools: In December, 1mn+ channels used their new AI creation tools to enhance creativity and 20mn+ viewers used their new ask tool powered by Gemini to learn more about the content they watched

- Mgmt was “blown away” by Google’s Genie (just annc’d & caused a big sell-of with videogame stocks – see Theme #8)

- Google has spent a lot of time creating these worlds

- Think it will have a wide level of applicability

- Google shines with multi-modal and real-world representation and Genie furthers that

Capx To Rise Much More Than Expected In 2026 …Demand Continues To Outpace Supply

- Q4 capx at $27.85bn was just modestly above cons, but grew +90% y/y

- The bigger focus was on 2026 capx guidance of $175-185bn, which was a significant +55% above cons $116bn and up almost +100% y/y at the mid-point (after a +74% y/y increase in 2025)

- Investments should ramp over the course of the year

- Expect the growth rate of 2026 depreciation to accelerate in Q1 and meaningfully increase for the full year

- Continue to be supply constrained and there is a time delay from when previous investments were made to when they can close the gap

- The time horizons are increasing in the supply chain

- Mgmt expects demand across the board will be “exceptionally strong” and that they will go through the year in a supply constrained way

- In 2025, ~60% of capx went towards machine investment (shorter term) and the rest went to long duration assets…It should be similar in 2026

- For 2026, just over half of their ML compute is expected to go towards the cloud business

- What keeps you up at night? “Compute capacity is the top question” (power, land supply chain constraints)… “how do you ramp to meet demand and get investments right for the long term”

Google Cloud Is Performing MUCH Better Than Expected Despite This Constrained Environment

- Google Cloud revs beat cons by +9.1% and adj OI beat by +45% (margins hit 30.1% vs cons 22.6%)

- Cloud revs growth significantly accelerated to +48% y/y (hitting over $70bn annual run rate) vs +34% y/y in Q3 and +32% y/y in Q2

- GCP continues to grow faster than Cloud’s overall revenue growth rate

- Strong growth in Enterprise AI infrastructure

- Double digit growth in Workspace (posted increase in avg rev/seat and in the # of seats)

- The Co posted strong backlog growth as well: Up +55% q/q (and doubled y/y) to $240bn w/ AI demand from wide breadth of customers

- Exited the year w/ 2x the new customer velocity compared to Q1

- Signing larger customer commitments: The # of deals in 2025 over $1bn surpassed the previous 3 yrs combined

- 75% of Google Cloud customers have used their vertically optimized AI (from chips to models to AI platforms) and enterprise AI agents

- These AI customers use 1.8x as many products as those who do not

- Outlook – expect to continue to drive “strong growth” despite the tight supply environment

See Extraordinary Growth Of Gemini Including In The Enterprise…Software Co’s Need To Seize The AI Moment

- Gemini app has 750mn MAUs vs 650mn in Q3

- Gemini is also seeing a sharp increase in engagement per user on the app, especially with Gemini 3 users

- All metrics showed progress globally

- The introduction of Gemini 3 in AI Mode was a very positive driver as well

- Seeing strong enterprise adoption of Gemini

- More than 120k enterprises use Gemini

- 95% of the top 20 and over 80% of the top 100 SaaS companies use Gemini

- Google sold 8m paid seats of Gemini enterprise (launched 4 months ago)

- Gemini enterprise managed 5bn+ customer interactions in Q4, growing 65% y/y

- Revenue from AI solutions built by Google’s partners incr’d nearly 300% y/y, and commitments from their top 15 software partners grew more than 16x y/y

- But are software companies losing seat and pricing power? Are their businesses being undermined by Gemini adoption? “See very, very good SaaS customers who are leaders in their respective categories successfully incorporating Gemini deeply in critical workflows, improving product experience and driving growth or using it to drive efficiency within their organizations”

- “It is an enabling tool” like it has been for Google

- Companies that are seizing the moment have the same oppty ahead”

- “Excited” about their partnerships

- Tokens, usage, growth etc. has been “very robust” in Q4

- A couple other telling AI related stats:

- In Q4, revenue from products built on their gen AI models grew nearly 400% y/y, significantly accelerating from the prior qtr

- ~50% of their codes are written by coding agents (which are then reviewed by our own engineers)

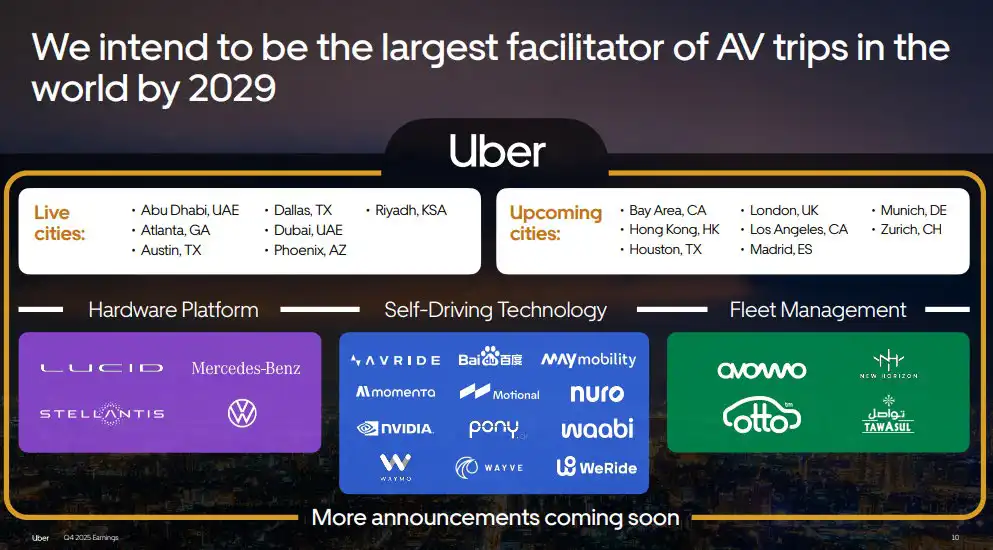

A Few Other Key Comments On Waymo

- Waymo continues to scale

- New funding: Waymo raised its largest investment round to date this week (raised $16bn at $126bn valuation)

- Google funding a significant portion of the round

- Scaling rides: In Dec, the Co surpassed 20mn fully autonomous trips and are now providing more than 400k rides every week

- Waymo continues to expand its service territory

- Miami (6th mkt) launched 2 weeks ago

- The Co will expand its service to multiple cities across the US and in the UK and Japan

- Making progress on opening services to airports and freeways

- New funding: Waymo raised its largest investment round to date this week (raised $16bn at $126bn valuation)

Ditto For Amazon…The Massive Capx Ramp Sparks Concerns, But The Co Is Realizing Strong Returns

Alphabet was not the only one to spook the Street with higher capx…Amazon followed suit when it guided for $200mn in capx in 2026 which is +52% higher than 2025 (which itself was up +59% y/y). Amazon added 1.2 gigawatts of power q/q in Q4 (more than any other datacenter company in the world) and added 3.9 gigawatts over the last 12 months, which is 2x what they had in 2022. The Co expects to double it again by the end of 2027.

Last quarter the debate centered on AWS’ reacceleration and whether the early AI lift was sustainable. This quarter AWS growth accelerated again, up +24% y/y (from +20.2% in Q3), its fastest pace in 13 quarters, and backlog surged +40% y/y. Even with the massive investments that the Co has already made in capacity, it has not been able to keep up with supply. As soon as new capacity comes on-line at AWS, they sell it.

Interestingly, mgmt believes that the AI market demand right now is a barbell, BUT the middle (for Enterprise workloads) will be the biggest and most durable users of AI capacity longer term. Bottom line, mgmt is VERY confident in generating strong returns sustainably on this investment, and like Google, that has been reflected in the strong business performance thus far.

Outside AWS, the core retail story is steady as she goes. Worldwide paid units improved to 12% y/y, delivery speeds hit new highs for Prime members, and Amazon continues to press selection, price competitiveness, and cost-to-serve efficiency. Advertising maintained strong momentum, growing +22% y/y to $21.3bn (following +22% y/y in Q3), helped by continued traction in Prime Video ads and live sports.

While most of the focus was on the longer term and future returns on the capx spend, nearer term, Q1 sales guidance was in-line but op income guidance missed by -14% (which was a disappointment) as Amazon factors in roughly $1bn in incremental Leo launch costs (commercial launch is in 2026) along with continued investments in quick commerce and sharper pricing in the stores business.

Net net, the key question for Amazon (and other Big AI Tech companies in the sector) is whether the Co can translate its unprecedented capacity build into sustained AWS revenue acceleration, margin leverage, and improvements in the core retail business. Signs point in that direction in our opinion.

-> Amazon shares closed down -5.6% in reaction to earnings and was down -12% on the week; YTD, it is down -8.9%

Q4 Slightly Exceeded Street Expectations

- Q4 revs and op income slightly top expectations while adj EPS slightly misses

- Revs grew +14% y/y (+12% y/y FXN) vs +13% y/y (+12% y/y FXN) in Q3

- North Amer segment sales grew +10% y/y

- Intl segment sales rose +17% y/y (+11% FXN)

- AWS rose +24% y/y

- Op income grew to $25bn from $21.2bn Q4:24

- North Amer op margin reached 9% up 100bp y/y

- Into op margin 1% (excl charge would have been up y/y)

Q1 Op Income Guidance Disappoints As It Factors In Incremental Costs For Leo’s Launch

- Q1 revenue guidance was in-line w/ cons and implies +11-15% y/y growth (assumes ~180bp tailwind from FX), vs the +14% y/y in Q4

- Q1 op income guidance missed the Street by -14.4%…mainly b/c it now includes ~$1bn y/y increase in Amazon Leo costs, plus also investment in quick commerce and “sharper prices” in the stores biz

- Reminder re accounting for Leo…

- Right now, the Co expenses Leo costs as incurrent

- Later this yr, many of these costs (satellite manf & launch svs) will be capitalized within the intl segment

- Reminder re accounting for Leo…

The Pace Of Capx Investments Is Still Much Higher Than The Street, BUT Mgmt Is VERY CONFIDENT In Returns

- Q4 capx at $39.5bn was +15% ahead of cons, ending the year at $131.8bn (vs the guidance in Q3 for $125bn in 2025)

- For 2026, the Co guided for ~$200bn in capx (+52% y/y following +59% y/y in 2025)

- Most of the spend is going towards AWS b/c of the “very high demand”

- Most of the spend is for AI but some for core workloads

- Mgmt stressed repeatedly that they are confident in generating strong returns on this capital spend

- The Co is monetizing capacity as soon as it gets online

- “We have deep experience understanding demand signals in the AWS business and then turning that capacity into strong return on invested capital. We’re confident this will be the case here as well”

- The Co is seeing “strong return on invested capital” and “seeing strong demand”

- “These investments will yield strong returns on invested capital”

- Amazon is trying to seize this “once in a lifetime” moment

- This is an “extraordinarily unusual opportunity to forever change the size of AWS and Amazon as a whole”

- It is an “extraordinary opportunity for companies to change their customer experiences and for start-ups to be able to build brand new experiences / businesses that would have taken much longer to try to accomplish before then can right do now

- The Co “will invest aggressively here”

- Over the last 12 months, Amazon added 3.9 gigawatts of power…that’s 2x what they had in 2022 when the Co was at an $80bn annual run rate business…expect to double it again by the end of ’27

- They added 1.2 gigawatts of power q/q in Q4… which is more than any other data center company in the world

- “We’ll add a lot more [capacity] in ’26, in ’27, and in ’28 for that matter”

AWS Posted Its Fastest Growth In 13 Qtrs

- AWS results were better than expected…revs beat cons by ~1% and AWS op income beat by 4.7%

- AWS revenue grew +24% y/y to $142bn annualized revs run rate (it was up +$2.6bn seq and up $7bn y/y)

- Mgmt reminded investors that their growth performance can’t be compared to companies w/ higher growth but much smaller bases

- Amazon is adding more incremental revenue and capacity than others

- The Co is seeing strong growth in core non-AI workloads as enterprises move from on premise to cloud

- The Co’s business remains capacity constrained…as soon as new capacity comes online, they sell it

- The backlog is at $244bn, up +40% y/y and up +22% q/q

- Have “a lot” of deals in the pipeline

- “There is a lot of demand for AWS right now in AI and core AWS space”

- New AWS deals: OpenAI, Visa, MBA, Blackrock, Perplexity, Lyft, United Airlines, DoorDash, Salesforce, US Air Force, Adobe, Thomson Reuters, AT&T, S&P Global, National Bank of Canada, the London Stock Exchange, Choice Hotels, Accenture, Indeed, HSBC, CrowdStrike and many more…

The Biggest Long-Term Demand Source For Capacity Is Still To Come

- Who is taking all this capacity? The vast majority of the capacity they have is being consumed by external customers (vs internally used)

- The AI market demand right now is a barbell…but the middle will be the biggest and most durable user of AI capacity longer term

- AI labs are spending “gobs and gobs” on compute on a couple runaway applications (they are consuming a lot of capacity for training and inference)

- On the other side, enterprises are getting value from AI doing productivity & cost avoidance types of workloads (customer service or biz process automation and some fraud pieces)

- Then all the enterprise production workloads are in the middle of the barbell and enterprises are at various stages of figuring out how to move those and put them into production

- AI demand is “so huge” already but “the lion share of demand will come from the middle barbell” and that will come over time as…

- More and more AI talent is added

- Inference becomes less expensive

- And as companies start to have success at moving workloads to run on top of AI

“I Don’t Think Folks Have Realized How Strong A Chips Company We’ve Become Over The Last 10 Years”

- AWS’s chips biz (including Graviron and Trainium) has reached a $10bn+ annual rev run rate growing at triple digits % y/y…and “it’s still very early”

- Graviton delivers up to 40% better price performance than leading x86 processors, and is used extensively by over 90% of AWS’s top 1000 customers

- Graviton itself is a multi-billion dollar annualized run rate business, growing more than 50% y/y

- Trainium is “taking off” and is at a multi-billion annualized rev run rate

- Trainium 2: Sold over 2.4mn chips (fastest ramping chip launch ever); Trainium is underpinning Bedrock usage today

- 30-40% more price performance vs comparable GPUs

- Trainium 3: Seeing “strong demand”; Expect nearly all of T3 chips supply to be committed by mid-2026

- 40% more price performance vs Trainium 2;

- Trainium 4: They are in the process of building and seeing “strong interest already”…coming in 2027

- Trainium 5: Having “conversations” about T5

- Trainium 2: Sold over 2.4mn chips (fastest ramping chip launch ever); Trainium is underpinning Bedrock usage today

The Stores’ Business Strategy Remains Steady As She Goes…Faster Speeds, Greater Selection, Value Prices & Greater Operational Efficiencies

- Q4 Online Stores revenue slightly beat Street projections and grew +8% y/y while Physical Stores revenue was modestly below consensus and grew +5% y/y

- WW paid units grew +12% y/y FXN (highest qtrly rate in 2025) vs +11% in Q3

- For the third year in a row globally in 2025, the Co achieved both their fastest ever delivery speeds for Prime members while also reducing cost to serve

- Amazon continues to expand selection –

- Amazon Haul grew selection to over 1mn items under $10 and are now serving customers in more than 25 countries/regions

- The Co is seeing a strong response to everyday essentials (grew 2x the rate of all other categories in the US in 2025) and grocery including perishables (for 150mn Americans mostly online and whole foods)

- With $150bn in gross sales, Amazon is a larger grocer

- They remain committed to staying “sharp on price” and meet or beat other retailers’ prices (they are 14% lower than avg other major online retailers, per 3rd party study)

- Driving for even higher delivery speeds continues to be a priority –

- Delivered +70% more items same day y/y

- Have incr’d the speeds for rural customer w/ almost 2x more monthly customers in rural areas receiving same day delivery y/y in 2025

- Customers that buy perishables delivered same day shop more than 2x customers that don’t

- Amazon will expand to more communities in 2026 and open 100+ new Whole Foods stores in the next few years

- Launched Ultra-fast delivery in India, Mx, and the UAE…it is 30min or less for thousands of items

- Testing in the US and the UK

- Offering later cut-off times for same day delivery

- “Add to Delivery” made up ~10% of all Prime volumes fulfilled each week

- Delivered +70% more items same day y/y

- See further opportunities to enhance productivity in the global fulfilment network

- Optimize inventory placement

- Reduce touches per package

- Improve package consolidation

- Lever robotics and automation

- The Stores business has also seen success innovating with AI

- Rufus is improving: More than 300mn customers used it in 2025 (and customers who use Rufus are 60% more likely to complete a purchase),

- Lens saw usage incr’d 45% y/y

- Mgmt is “very optimist” about agentic shopping making it easier for customers and believe that their own agent will be best positioned vs 3rd parties

- 3rd party horizontal agents will be able to enable shopping as well BUT they won’t have any shopping history and they will get product & pricing details wrong, so the customer experience will need to be refined

- The value exchange between Amazon and 3rd parties will also have to “make sense to both sides”

- “Horizontal agents are good at aggregating selection, but retailers [like Amazon] are much better at delivering the best experience”

- Mgmt is “optimistic” that people will use their shopping agent but also expect to work with other 3P agents “over time”

A Few Other Important Updates & Developments (Advertising, Satellites)

- Advertising revs grew +22% to $21.3bn led by sponsored products in stores

- Saw cont’d growth in Prime Video ads (contributing meaningfully to revenue)

- Prime Video has an avg ad-supported audience of 315mn viewers globally

- “Great success” w/ live sports: Thursday Night Football (4th season broke viewership records – avg 15mn+ viewers, +16% y/y); Packers v Bears Wild Card Game was the most streamed NFL game in history (31.6mn viewers)

- AI innovation: Recently annc’d ads agent (advertisers research, brainstorm, and generate full funnel ad campaign from concept to completion using conversational guidance – takes weeks long process to hours)

- Saw cont’d growth in Prime Video ads (contributing meaningfully to revenue)

- Leo is moving to commercialization in 2026 –

- Launched 180 satellites thus far

- 2026: Will launch 20 more and expect to launch commercially during the year

- 2027: Will launch more than 30

- Partners: Have “dozens” of commercial agreements already signed, including w/ AT&T, DirecTV, Latin America, JetBlue and Australia’s National Broadband Network, and “have many more on the way”

Disney Sets Sail With New Leadership During A Fiscal H2 Pickup

Disney’s earnings report on Monday morning ultimately proved not to be the main event for the Co this week, as its FQ1 results were sidelined by its CEO succession announcement on Tuesday morning. Disney Experiences Chairman Josh D’Amaro will become the next CEO, succeeding long-time CEO Bob Iger. Concurrent with D’Amaro’s appointment, Dana Walden, Co-Chairman of Disney Entertainment and widely viewed as a final contender for the role, has been named President and Chief Creative Officer. Both appointments will be effective March 18. As for Bob Iger’s next steps, he will continue to serve as Senior Advisor and a member of the Board until his retirement on December 31, 2026.

Back to fundamental trends…the back-half weighted narrative for F2026 that we talked about last qtr remains intact. On the Entertainment side, this qtr marked the first time Disney stopped breaking out revenue and operating income across its linear TV networks, streaming, and theatrical businesses, making it more difficult for investors to assess. Disney also discontinued reporting streaming subscriber numbers, following Netflix’s lead from last year. The segment delivered a +3% revenue beat, driven by two $1bn+ box office releases and strength in its SVOD svs, but operating income declined -35% y/y for a second consecutive qtr, reflecting higher production and marketing costs tied to those releases. Looking ahead, given the slate they have in the works, segment OI is expected to grow double-digits for the full year, weighted in H2.

Within Experiences, it was a record qtr with both qtrly rev and op income reaching all-time highs, which was driven by continued strength in domestic parks. BUT international visitation remains an overhang which will impact FQ2 op income growth (will be “modest”) with higher growth in H2 after the March launch of Disney’s eighth cruise ship, the Disney Adventure, in Singapore.

More broadly, investors have been focused on what a post-Iger Disney will look like. Iger addressed this on the earnings call (prior to the succession announcement), noting that the Co is in “much better shape” than when he returned three years ago, when there was “a tremendous amount that needed fixing.” His successor will take over a biz that is now “well positioned” in both Entertainment and Experiences and looking ahead there is now a “healthy competition” at the Co between the two businesses to see which “is going to essentially prevail as the number one driver of profitability for the company.”

-> Disney shares fell -7% on the back of the print and ended the week down -4%

Disney’s FQ1 Beat On The Top-Line & EPS But Segment Results Were Mixed Under The Hood

- Total FQ1 rev BEAT by +1.1%: Up +5% y/y (accel from flat y/y in FQ4)

- Entertainment and Experiences BEAT, while Sports missed

- Total op income BEAT by +0.9%: Fell -9% y/y (decel from -5% y/y in FQ4)

- Sports and Experiences BEAT, while Entertainment missed

- Adj EPS of $1.63 beat cons $1.57: Down -7% y/y, reflecting lower Entertainment results driven by film slate comparisons, partially offset by higher results at Experiences

- FCF loss -$2.8bn was below cons gain of $2.6bn

The Co Reaffirmed FY26 Guidance

- Reaffirmed double digit adj EPS growth y/y vs cons +11.5%

- Entertainment – reaffirmed double digit segment OI growth y/y, weighted to H2:26 (vs +19% y/y in FY25)

- Sports – reaffirmed LSD segment OI growth y/y (vs +20% y/y in FY25)

- Experiences – reaffirmed HSD segment OI growth y/y, weighted to H2:26 (vs +8% y/y in FY25)

- On track to repurchase $7bn of stock

- Note that Q4 FY26 includes a 53rd week of operations…guidance for fiscal yr segment op income, SVOD op margin, and adj EPS excludes the benefit of the addtl week, while other guidance points include the 53rd week

Higher Op Expenses Continues To Weigh On The Entertainment Segment, But A Reacceleration Is Still Expected In H2 / SVOD Is Increasingly Contributing To Overall Segment Results

- Entertainment – FQ1 headline results were mixed vs consensus (+2.7% rev beat, -6.0% OI miss)

- Revs were up +7% y/y (accel from -6% y/y in FQ3)

- But op income fell by -35% y/y (in-line w/ FQ3)

- Reflecting higher programming and production and mkting costs driven by more theatrical releases in the qtr (9 releases vs 4 in the prior yr)

- SVOD rev incr’d +11% y/y and op income reached $450mn (8.4% op margin)

- Rev growth reflects a 1 ppt adverse impact from the inclusion of Star India rev in the prior-yr qtr

- Op income grew +$189mn to reach $450mn, driven by subscription and ad rev growth, partially offset by higher programming and production and mkting cost

- For FQ2…expect SVOD OI of ~$500mn, up +$200mn y/y, as investments in content and technology and improved user experience drive subscription and ad rev growth

- For FY26…remain on track to reach a 10% SVOD op margin for the yr

- Key drivers = Zootopia 2 & Avatar: Fire and Ash will be released on streaming by the end of this fiscal year

- Advertising rev decr’d -6% y/y, and reflects a net adverse impact of 11pts from the inclusion of Star India ad rev in the prior-yr qtr, lower political advertising vs Q1:25, and Fubo ad rev

- For FQ2…segment OI expected to be roughly comparable to Q2 last yr (~$1.7bn)

- For FY26…continue to expect double-digit segment OI growth weighted to H2:26, driven by Disney’s theatrical release slate and continued growth from its SVOD svs

- How does the new Entertainment segment disclosure better align w/ the Co’s goals for the biz? Talking about streaming, theatrical, linear networks, etc. “creates a lot of complexity that’s just not reflective of the reality”

- “We manage the Entertainment business as a single entity”

- “For us to […] get into a lot of depth […] I don’t think it’s terribly informative to investors and it’s not the reflective of the way that we create or distribute content

- “It’s just a level of nuance that may have been relevant in the past, but just isn’t relevant anymore”

- A “one-app” bundled experience could be coming by the end of the calendar year: Bundled subscribers churn out less; While consumers will always to be able to buy Disney+ or Hulu on its own, they believe “by and large” that the “great majority” of consumers will buy both for a fully integrated experience

- Regarding the partnership with OpenAI…plan to introduce a “curated” slate of Sora-generated content on Disney+

- Did not specify how UGC from Sora will show up on Disney+ – “we’re working through all the technical details of that”

- Do you expect overtime to grow beyond the 30-sec videos in the current agreement? “For now, we’re sticking to the 30-second limit on videos created down the road, not sure, but we’re not really focused on that at this point”

Blockbuster Qtr For Studios Biz

- Studios delivered two $1bn films in FQ1: Both Zootopia 2 and Avatar: Fire and Ash crossed the $1bn mark at the global box office

- Several titles in the works for a 2026 release –

- The Devil Wears Prada 2

- The Mandalorian and Grogu

- Toy Story 5

- Moana (live-action)

- Avengers: Doomsday

Mixed Regional Performance In The Experiences Segment & Reiterated That Pre-Opening / Pre-Launch Costs Will Weigh On FQ2

- Experiences – delivered record qtrly rev and OI (rev beat by +0.9%, OI beat by +2.8%)

- Qtrly rev exceeded $10bn for the first time

- Domestic Parks & Experiences drove the increase in overall segment OI and was up +8% y/y (vs +9% y/y in FQ25)

- Driven by higher guest spending, an increase in passenger cruise days due to the Disney Treasure and Disney Destiny, and 1% growth in attendance at Disney’s domestic parks, partially offset by an increase in costs for new guest offerings (including expansion costs for Disney Cruise Line)

- On Walt Disney World specifically…had a “very good” quarter that benefitted from the overlap of the hurricane

- Outlook: Bookings are up +5% for the full yr, weighted more toward H2

- International Parks & Experiences OI and was up +2% y/y (vs +25% y/y in FQ25) – “international visitation was softer”

- Reflecting higher attendance and guest spending, partially offset by higher costs

- “We continue to monitor international visitation to our domestic parks and adjust our strategy”

- For FQ2…expect “modest” Experience OI growth, driven by –

- International visitation headwinds at Disney’s domestic parks

- Pre-launch costs for the Disney Adventure at Disney Cruise Line

- Pre-opening costs for World of Frozen at Disneyland Paris

- For FY26…segment growth is expected to be H2-weighted

- Reiterated HSD segment OI growth weighted to H2, which will benefit from the launch of their two new cruise ships and the opening of World of Frozen at Disneyland Paris

- Room bookings at Walt Disney World are pacing up +5% y/y, weighted to H2

- Have expansion projects underway at all theme parks –

- New World of Frozen at Disneyland Paris opening next month

- New experiences feat. Bluey

- Activations planned around the release of Toy Story 5

- A new mission featuring the Mandalorian and Grogu inside Millennium Falcon: Smugglers Run coming soon

- Disney Cruise Line fleet now stands at eight cruise ships, w/ another five scheduled for launch beyond FY26

- Recently launched the Disney Destiny, which has received “outstanding” reviews from guests since its maiden voyage on Nov 20th

- The Disney Adventure, Disney’s first ship homeported in Asia, is on its way to Singapore for its maiden voyage on Mar 10

Sports Segment Results Were Impacted By YouTube TV Blackout & Higher Expenses From New Sports Rights

- Sports – headline missed on rev but beat on op income (-1.0% rev miss, +6.1% OI beat)

- OI fell -23% y/y, as ad rev growth of +10% y/y was more than offset by higher programming and production costs and a decrease in subscription and affiliate fees

- Temporary suspension of YouTube TV carriage had an adverse impact to segment OI by ~$110mn

- For FQ2… expect comparable rev vs prior yr and higher rights expenses for college (including the reversal of the timing benefit for Big 12 programming) and new WWE rights costs to drive a y/y decrease in segment OI of ~-$100mn

- For FY26…continue to expect LSD OI growth

- ESPN captured 30%+ of all sports viewership across networks

- Season-to-date, ESPN has delivered its third most-watched NBA regular season

- Still early days for ESPN Unlimited but “pleased” w/ engagement and adoption: “We are encouraged by ESPN app authentication from pay-TV subscribers, the pace of new signups, and the engagement patterns that have followed”

-> Also related this week, Disney closed its deal with the NFL, valuing ESPN at ~$30bn and giving the league a 10% non-controlling stake; The agreement deepens ESPN’s NFL partnership by transferring full ownership of NFL Network, adding exclusive game inventory, and integrating RedZone and other NFL media assets across ESPN’s linear and streaming platforms; Disney retains the option to buy back the NFL’s stake beginning in 2034, while the league has the right to increase its ownership at a discounted valuation (link)

Quick Point To Flag On WBD Transaction Implications

- Brief comments re the ongoing WBD transaction – “I think more than anything, it illustrates the value of that IP beyond the big screen”

- It “should emphasize or cause investors to appreciate the tremendous value of our assets, particularly our IP,” as well as “our brands and our franchises” and “let’s not forget, ESPN”

- Any plans to acquire more IP? “I don’t really feel that we have a need to buy more IP. We’re just going to continue to create our own and we’ve got an unbelievable bedrock of stories already told to grow from”

Fox Is Executing Well In This Cyclically Slower Year

It feels a little like Groundhog Day as Fox once again delivered a better-than-expected set of quarterly numbers. Its relative positioning in news and sports continues to enable the Co to outpace peers. FQ2 Cable Network ad rev growth of +7% y/y was a standout and total ad rev growth was up +1% y/y despite tough comps. Per mgmt, since 2021, media peers’ total advertising including streaming is down ~4% CAGR while Fox’s advertising revs, including streaming, has increased +8% CAGR.

Tubi continues to operate on all cylinders and the Co posted strong rev growth of +19% y/y in FQ2 (though down from +27% y/y in FQ1) and did so profitably for the 2nd quarter in a row. The +27% y/y increase in Tubi’s total viewing time in the qtr is also a good leading indicator looking ahead.

The launch of Fox One was a focus and uptake has exceeded expectations. Importantly, the Co has not seen any cannibalization of its traditional linear bundle subscriber (though this is something to look out for) and is tracking to the previously outlined subscriber targets. Another important point was that Fox benefited from improving video subscriber trends and will be a net beneficiary of the shift to skinnier bundles.

Fox remains committed to shareholder returns and since launching its buyback program in 2019, has cumulatively bought back $8.4bn or 35% of total shares, including the $1.5bn accel share repurchase.

All in all, it was a solid quarter, and the Co is executing well during this period of tough comps. See below for more of what we thought was most important from the Co’s results and conference call.

-> Despite the strong beat, Fox share were relatively flat; The shares remain down -10% YTD after being up +40% in 2025

FQ2 2026 Was A Standout Quarter For the Company

- Revenue BEAT by +2.4%: Up +2% y/y, a decel from +5% y/y in Q1

- Adj EBITDA BEAT by +53.2% but still down -11% y/y (vs +2% y/y in Q1): Includes growth driven digital growth initiatives spend & higher sports programming and production costs, partially offset by lower entertainment programming and production costs

- Adj EBITDA Margin BEAT: 4% vs cons 8.9%

- Segment performance BEAT across the board except with Content & Other revenue (mostly due to the timing of deliveries in TV)

- Cable Networks outperformed

- Revs BEAT by +4%, rising +5% y/y, vs +4% y/y in FQ1

- Adj EBITDA BEAT by 23.4%, increasing +5% y/y

- Television outperformed

- Revs BEAT by +2.7% but was down -1% y/y vs +5% y/y in FQ1

- Adj EBITDA of $143mn was well ahead of cons $14mn, but was still down -30% y/y (vs +7% y/y in FQ1) due to higher sports programming rights amortization and production costs and higher digital content costs, partially offset by lower entertainment programming rights amortization and production costs

- Bought back $1.8bn (since launched the buyback program in 2019, have cumulatively bought back $8.4bn or 35% of total shares, including the $1.5bn accel share repurchase)

- Annc’d a 28c semi-annual div

Total Advertising Revs Y/Y Grew Despite Tough Political Comps Last Year

- Grew total Co ad revs +1% y/y despite political last year

- Cable advertising revs grew +7% y/y (vs +7% y/y in Q1), due to higher news & sports pricing, partially offset by lower ratings

- TV advertising revs were flat y/y (vs +6% y/y in Q1) as cont’d digital growth led by the Tubi’s AVOD svs, the impact of addtll MLB postseason games, and higher sports pricing were offset by lower political ad revs & lower ratings

- News hit its highest FQ2 ad rev ever: News, business, further demographic expansion & pricing growth in both direct response and national advertising all contributed to this result

- Ad market for Fox News has been “incredibly robust”

- Added 200 new advertisers (on top of 350 added last your)

- Demand for the audience is very strong

- Scatter pricing for news is up 46-47%

- Direct response pricing is “strong”

- “Couldn’t be more pleased with Fox News”

- Starting to see growing appetite for national political advertising and think Fox News will benefit

- Fox is well positioned as 94% of national ad sales comes from sports, news and streaming vs only 6% from Entertainment

- Of that top 10 categories for national advertising, 8 are up significantly with financials in the lead (insurance)

- Entertainment is modestly down along with some govt and political

- At Fox, Fox News Media had highest ad revs, Tubi had the highest qrtly, weekly and daily ad revs, Fox Sports ad revs are hitting records, and Fox Entertainment ad revs were up y/y for the 1st time in 4 years

- Of that top 10 categories for national advertising, 8 are up significantly with financials in the lead (insurance)

- Local advertising is more mixed given Super Bowl and Olympics but still “feel good”

- Mgmt highlights that since 2021 media peers’ total advertising growth including streaming is down ~4% CAGR while Fox’s ad revs including streaming has incr’d +8% CAGR

Strong Performance At Tubi Was A Standout

- Tubi posted strong revs growth of +19% y/y (though down from +27% y/y in FQ1): Strong upfront for Tubi, “healthy” direct response & partner trends

- Tubi total viewing time (TVT) growth was up +27% (good leading indicator): This is the strongest engagement growth in 7 qtrs

- On demand viewing is over 95% of consumption on Tubi

- Tubi achieved EBITDA profitability for the 2nd qtr in a row

Fox One Has Exceeded Expectations & Not Seeing Any Cannibalization

- Fox One (launched 5 mos ago) is performing better than expected on both direct signups as well as partnerships

- “Have not seen any cannibalization of traditional subscribers”…targeted marketing to cord cutters and cord nevers has been “successful”

- 2/3 of the audience on Fox One are sports fans and 1/3 are news fans

- News viewers engaged w/ the platform 2x as many days per week as non-news viewers and watched nearly 3x as many mins per week on avg

- The Co is “well on track” to hit their low to mid-SD millions of subs over the next 3-4 yrs: Though the impact of sports seasonality is a wild card

- Where is Fox One accounted for on the P&L?

- Platform costs run though the corporate segment (where EBITDA loss fell from -$81mn to -$138mn)

- Then it pays an affiliate fee to the networks for the programming which is recorded in Cable and TV

No Big Affiliate Deals Renewals On The Horizon

- Distribution revs grew +4% y/y during the quarter, with subscriber declines notably improving sequentially even when excluding the contribution from Fox One

- Cable distribution revs grew +5% y/y (+3% y/y in Q1) as contractual price increases were partially offset by the impact of net sub declines

- Distribution rev rose +1% y/y (+2% y/y in Q1), driven by higher avg rates at the Co’s owned & operated TV stations and increases in fees from 3rd-party FOX affiliates

- Renewals are “pretty much done for the [fiscal] year” but will ramp in F27 and F28

- F27 will be more skewed towards TV

- F28 will be more skewed towards Cable

The Trend Of Improving Video Losses Due To Skinny Bundles Is Likely To Continue

- The -6.3% y/y decline in video subs was a strong improvement from the “below 7%” y/y posted last qtr

- That also excludes Fox One sub additions (i.e., would be better if included)

- Looking ahead, mgmt believes that skinny bundles will play a factor at improving sub declines

- Many of these skinny bundles are just now launching and this should be a positive for Fox

- Fox sells its channels as a bundle but distributors have flex on how they market those channels to their consumers…so mgmt believes that they have “downside protection” from this skinny bundle shift

A Couple Other Key Comments Related To Sports & Sports Betting

- Looking ahead, the Daytona 500 and Indy 500, FIFA Men’s World Cup (June)

- There’s a lot of excitement around the World Cup and a robust advertising market

- Will the World Cup be profitable this year? “Yes it will”

- Mgmt was confident that they can manage an increase in an NFL renewal: They believe they can offset any cost increases given they will rebalance their overall portfolio; “Feel pretty comfortable”

- Mgmt believes its stakes in sports betting are worth $2.8bn and are not reflected in the stock price

- 5% stake in Flutter is worth $700mn

- The valuation of the 18.6% in FanDuel is ~$2.1bn

- Combined that is worth ~ $6-7/shr, “which we don’t think is reflected”

- The Co is “watching the predictions market with interest”

WMG Is Hitting The Right Notes On Margins And AI Partnerships

The fruits of Warner Music Group’s restructuring are continuing to pay off. The Co posted a strong FQ1 print, with revenue +4% ahead of expectations and adj OIBDA beating by an even stronger +12%. Margins were a standout, up +310bps y/y to 25.2%, easily surpassing Street estimates of 23.4%, and that margin level should be sustained in the short term and expand to high-20s longer-term. WMG is also gaining momentum in market share, up +1ppt in US streaming (accelerating from +0.6ppts in the prior qtr). Looking ahead, the Co has a strong upcoming release slate and expanded catalog acquisition capacity, as both WMG and Bain each increased their equity commitments by $100mn in their JV, boosting total capacity from $1.2bn to ~$1.65bn. There will be “exciting announcements” ahead as they plan to deploy a “significant portion” of this capacity by the end of FY26.

As has been the case across several companies on the earnings circuit this week, AI was a main topic of conversation on the call. WMG has completed deals with several AI music Cos, which will unlock “significant” incremental revenue at accretive economics. In particular, WMG’s partnership with Suno is expected to be a “material” top and bottom-line growth driver starting in FY27. In addition to AI Co partnerships, they are also exploring oppties with their large DSP partners to incorporate AI tools on their platforms to increase engagement. Elsewhere, WMG is deploying AI across operations and hosting workshops to help artists and creator leverage these technologies. AI is at the center of all their initiatives, and mgmt made sure to emphasize that it is being done in a principled way.

All in all, the work WMG put into restructuring is starting to show tangible results. Mgmt remains laser focused on delivery on their three main objectives… growing share, growing the value of music, and driving efficiency.

See below for what we thought was most incremental from WMG’s results and conference call.

-> WMG was up +3.6% post its print, but the stock is still down -5.3% YTD; In 2025, WMG’s stock was down -3.1%

Strong FQ2 Headline Results for WMG Reflect A Third Consecutive Qtr Of Profitability Growth

- Total FQ1 revs BEAT cons by +4% and adj OIBDA BEAT by a larger +12%

- Total revs grew +10% y/y (decel from +13% y/y in FQ4)

- Adj OIBDA grew +28% y/y (big accel from +12% y/y in FQ4)

- Recorded Music subscription streaming revs were up +8.7% y/y on an adj basis vs +8.4% y/y in FQ4

- Ad-supported streaming revs grew +4% y/y on an adj basis vs +3% y/y on adj basis in FQ4

- Driven by “strong” performance from traditional DSPs

- Music Publishing revs grew +15% y/y on an adj basis vs +13% y/y in FQ4

Margins Has Been A Big Focus & WMG Has Been Delivering (And Expects To Continue To Do So In The Short- And Long-Term)

- FQ1 margins were stronger than expected…adj OIBDA margin of 25.2% signif beat cons 23.4%: Up +310bps y/y

- What’s driving the increase? WMG’s reorganization and cost savings related to that, as well as the acceleration of high margin streaming growth and the operating leverage they get behind that

- The ongoing cost savings plan is “delivering on schedule” and “on track” to contribute 150-200bps to margin in FY26

- Reiterated that a margin in “the mid-20s” is sustainable in the short-term, and have a longer-term goal to deliver margins in the high-20s

- As they work to drive “even greater efficiency” through the use of AI and improve op leverage in the biz

- Highlighted some additional drivers for future margin increase: DSP pricing and tiering; High-margin catalog M&A; Accretive AI rev that will continue to accelerate over the next few yrs

- The Co will provide an update on their path to “meaningful margin expansion” as their plans evolve in the upcoming qtrs

WMG Increased The Capacity Of Their JV With Bain

- WMG and Bain have increased their equity commitments by $100mn each

- Expect to maintain the existing equity-to-debt ratio, which will increase the JV’s total capacity from $1.2bn to ~$1.65bn

- Expect “some exciting announcements” coming in the “near future”, as they plan to deploy a “significant” portion of the JV’s total capacity by end of FY26

- “We’ve developed a very, very strong pipeline which we’ll start to announce in the remainder of this calendar year”

Focused On Leveraging AI Across The Biz To Drive “Significant” Top- And Bottom-Line Growth

- Recently completed AI deals with Suno, Stability, KLAY and Udio have the potential to unlock “significant” incremental rev at accretive economics

- Will be compensated on a consumption basis for all of their deals: WMG’s economics will scale as their partner’s bizs grow

- Partnerships will be key to building out the “super fan tiers of the future”, including the ability to create: Creation is “the ultimate expression of fandom…so, for us, the super fan tiers of the future will all include AI functionality to create. And our partnerships with the four companies are key to establishing how we would like to see this market evolve”

- Partner highlight – Suno partnership expected to be a “material” top and bottom-line growth driver starting in FY27: Suno is already earning “several hundred million” dollars in annual rev

- Also exploring oppties w/ their large DSP partners to incorporate AI tools that would enhance the consumer offering

- Including AI tools to accelerate new artist discovery + enhance and automate marketing: Can scale mkting efforts “beyond what’s humanly possible” by “quickly and inexpensively” generating assets like (i.e., motion art, music videos) to better monetize WMG’s music catalog of “over a million” recordings

- “The impact from AI generated assets that spike engagement with the catalog can be a significant one”

- As well as developing tools to amplify the creativity of their artists

- Hosting workshops and songwriting camps to help creators leverage the latest technologies to “hone their work, cut through the noise, and build fandom”

- Emphasized that they are taking an “early and aggressive” approach to embracing these new technologies by authoring ethical AI guidelines

- Enabling WMG to protect and super serve artists and songwriters, while creating incremental opportunities for the entire ecosystem

- Reiterated WMG’s non-negotiable principles –

- WMG’s partners must commit to license models

- Economic terms must properly reflect the value of music

- Artists and songwriters must have a choice to opt in to any use of their name, image, likeness and voice in new AI-generated recordings

- AI will also be advantage on the cost side across WMG’s internal operations

- Have already deployed AI across various depts: “Over the last two years, we have laid the infrastructure foundation for us to effectively deploy AI across many different departments across the company…we have deployed AI across finance, legal, marketing, HR, and more”

- With other use cases in the works: Ranging from “music production, where many of our artists and songwriters are already leveraging these tools, to more analytically-driven, precise deployment of marketing dollars, as well as more real time forecasting and analytic”

Additional Key Biz Updates – Mkt Share Gains, TikTok Deal Renewal, Music Publishing Accelerations

- Seeing “steady” and “broad-based” mkt share improvement – “all of our business units are growing at a very, very healthy clip, and it’s showing up in the results”

- Saw ~1ppt of US streaming mkt share growth over the prior-yr qtr (accel from +0.6ppt in FQ4), w/ strength across new releases and catalog

- Market share on Spotify’s Top 200 chart is up +3ppts FY-to-date

- What’s driving the improvement? Reinvestments from 2024 restructuring into growth through technology and investments into A&R materialized through FY25, which is starting to show through, along with “much, much sharper” capital allocation and “our incredible ability of artist development”

- Where is there room for improvement? Asia: Region where they have “the most amount of work to do”; Have changed leadership across the region; “We got the right people there, but it takes some time and we’ll work on that hard”

- Renewed their deal w/ TikTok, which resulted in improved deal economics

- “Very happy” w/ TikTok partnership

- Did not disclose deal terms but it contains “structural” changes that “better reflect the value of music”

- Flagged that TikTok deal is not material to revenues: Is in the LSD as a % of revs, but “our deals are never just about money. They’re also about data, promotion, insights and all of the things that can help advance our business overall”

- Have “many, many” opportunities to accelerate growth in music publishing

- Will double down on their proven A&R strategy – “we have now more firepower to do that than in the past”

- Further focus on regions where WMG has seen strong tractions behind their investments – specifically called out developing regions and LatAm

- Leverage Bain JV and the increased capacity

- Will also benefit from acceleration and growth of WMG’s AI partnerships

- “We’re really confident that we can continue to deliver double-digit growth in that business…[and] also continue to improve margins…we’re very, very confident about the business and the leadership we have there

“Our Path To Accelerating Growth In 2026 And Beyond Is Clear” …Highlighted Key Drivers

- A “strong” release slate: Anchored by new releases from Bruno Mars, Zach Bryan and many others

- Contractual per stream margin (PSM) increases starting in Q2 and layering in throughout the balance of fiscal 2026

- Will start to see volume-led subscription streaming growth will evolve to volume AND volume-led growth

- “On top of that, we believe this is the best opportunity now with AI to introduce super premium tiers”

- Acquisitions of high-quality accretive catalogs and bolt-on capabilities that will accelerate WMG’s distribution, e-commerce businesses and AI partnerships and initiatives

- Expected to result in a “material” contribution to revenue and margin in FY27

- “In summary, we are very optimistic about the road ahead with greater certainty around DSP deal terms, more consistent market share performance, and a refined approach to capital allocation”

AI Concerns Overshadow Take-Two’s Strong Beat & Raise Qtr

The big story since last Friday (Jan 30th) was a significant spike in concern about Google’s Genie release and more generally AI disrupting the video game industry. Mgmt addressed questions confidently, believing that AI will be an enabler and will not impact the creative part of game development. They see Google’s Genie’s platform as apples to oranges to TTWO’s game development process (see Theme #3 for Google’s comments on its Genie launch).

Nonetheless, these concerns dramatically overshadowed what we viewed as strong quarterly results with another beat and raise. The Co’s business outperformed broadly across all key franchises. Total net bookings grew +28% y/y (vs +33% in FQ3) with recurrent consumer spending up +23% y/y and dramatically exceeding the previous guidance of +8% y/y. The performance was also broad based across their key franchises…NBA 2K grew +30% y/y, Grand Theft Auto Online increased +27% y/y, and Mobile increased +19% y/y (accelerating from mid-teens growth last quarter).

Last but not least, the Co Importantly reiterated the November 19th launch of GTA VI and continues to project record levels of net bookings in Fiscal 2027.

Bottom line, it was a strong quarter but the AI overhang will likely remain in place at least in the short-term.

See more details below on our view regarding what was most incremental with TTWO’s results…

-> TTWO rose +5% after its report and ended the week down 11%; The stock is down -24% YTD

Street Concerns Regarding AI Disruption Dramatically Increased Since Google’s Genie Launch Late Last Week

- What did Google announce? (link)

- On Jan 29, 2026 the Co released Genie 3

- Project Genie is a prototype web app powered by Genie 3, Nano Banana Pro and Gemini, which allows users to experiment with the immersive experiences of worlds model firsthand

- How does it work? Prompt with text and generate or upload images to create a living, expanding environment; Create your characters, your world, and define how you want to explore it

- The “world” can be explored: As you move, Project Genie generates the path ahead in real time based on the actions you take

- You can also adjust the camera as you traverse through the world

- Access to Project Genie begins rolling out to Google AI Ultra subs in the U.S.

- Analysts focused on Genie and the overall impact that AI will have on the interactive entertainment industry…TTWO’s response = they are embracing gen AI and it is an enabler

- The video game biz, since its inception, was built on the back of machine learning and AI

- They create their games in “computers with technology”, ever since questions began about gen AI, ~18 months ago, they have been incredibly enthusiastic about what the future can bring

- The Co has hundreds of AI pilots in implementations across the firm, including with their studios

- They are seeing opportunity to drive efficiencies, reduce costs, and create the opportunity to do what digital tech has always allowed

- This frees up creators to do the more interesting tasks of “making superb entertainment”

- Impact of Genie? “It is early in its iteration at this point, and trying to make a comparison to a game engine is just not even in the same ballpark … Genie is not a game engine but it’s very exciting technology”

- One final note: “There are more elements to gaming than world creation, like story line, mission structure and vibe which cannot be captured with AI”…”AI will make what they do better”

- The video game biz, since its inception, was built on the back of machine learning and AI

Regarding TTWO FQ3 Results…They Were Strong, Driven By Consumer Spend Growth

- FQ3 Net Bookings BEAT by +11.2%: Grew +28% y/y (vs +33% y/y in FQ2)

- Growth was driven by better-than-expected performance from NBA 2K, the GTA series, and several mobile titles, including Toon Blast, Empires and Puzzles, and Top Eleven

- During the qtr, they launched WWE 2K Mobile for Netflix and Red Dead Redemption and Undead Nightmare for several new platforms

- Recurrent consumer spend growth cont’d to accelerate from +17% y/y FQ1 to +20% y/y FQ2 to +23% y/y in FQ3, MASSIVELY outperforming guidance of +8% y/y

- Represents 76% of total net bookings, slightly down from 79% in Q3 2025

- NBA 2K RCS: grew +30%

- GTA Online RCS: rose +27%

- Mobile RCS: incr’d +19%

- FQ3 adj EPS of $1.23 was well ahead of cons $0.83

FQ4 Guidance Topped Estimates As Well

- FQ4 guidance BEAT –

- Net bookings BEAT by +1.3%: $1.54bnbn vs cons $1.52bn

- The release slated for the quarter includes Sid Meier’s Civilization VII for Apple Arcade, PGA TOUR 2K25 for Switch 2, and WWE 2K26. The largest contributors to net bookings are expected to be NBA 2K, the Grand Theft Auto series, Toon Blast, Match Factory!, WWE 2K, Empires & Puzzles, Color Block Jam, Red Dead Redemption Series and Words with Friends

- Adj EPS BEAT by +21.4%: $0.51 vs cons $0.41

- Expect RCS to increase ~+7% y/y assuming –

- A ~20% y/y increase for NBA 2K

- Mid-single digit growth y/y for mobile

- A modest y/y decline for GTA Online

- GAAP net rev to range from $1.57 – $1.62bn vs cons $1.52bn and cost of rev to range from $675 – $692mn vs cons $576mn

- Operating expenses are planned to range from $973-$983mn vs cons of 991mn

- On a management basis, operating expenses are expected to grow by approximately 3% y/y

- Net bookings BEAT by +1.3%: $1.54bnbn vs cons $1.52bn

- Raised FY26 guidance –

- RAISED FY26 net bookings guidance by +18% at the mid-pt: $6.65-$6.70bn vs prior guidance of $6.4-6.5bn and prior guidance $6.05-6.15bn (ahead of cons $6.47bn)

- Reflects Q3 outperformance and higher expectations for several of our key titles in Q4

- Project net bookings breakdown from our labels to be ~46% Zynga, ~38% 2K and ~16% Rockstar Games

- RAISED RCS growth guidance to ~17% y/y from 11%…assuming:

- NBA 2K RCS: grows +37% y/y

- Mobile RCS: grows+13% y/y

- GTA Online RCS: increases slightly y/y

- RAISED OP Cash Flow to ~$450mn which is up from our prior expectation of $250mn vs cons of $266mn

- RAISED FY26 adj EPS guidance by +19.5% at the mid-pt: $3.75-$3.85 vs prior guidance $3.05-$3.30 and prior guidance $2.60-$2.85 (ahead of cons $3.32)

- MAINTAINED: $180mn in capx

- RAISED GAAP net rev, which is now expected to range from $6.55-$6.6bn vs cons $$6.45bn, and cost of revenue, which is expected to range from $2.78-$2.8bn vs cons $2.4bn

- Total operating expenses are expected to range from $3.96 – $3.97bn vs cons $3.87bn

- On a management basis, they now expect operating expense growth of ~8% y/y, which is down slightly from our prior forecast due to a shift of some marketing expenses into next year

- RAISED FY26 net bookings guidance by +18% at the mid-pt: $6.65-$6.70bn vs prior guidance of $6.4-6.5bn and prior guidance $6.05-6.15bn (ahead of cons $6.47bn)

- For FY27 – still expecting to achieve “record” levels of net bookings

Growth In The Mobile Business Was A Key Positive

- Mobile revenue growth accelerated to +19% y/y vs “mid-teens” last qtr: Consumer engagement has been strong

- Toon Blast net bookings grew +43% y/y vs +26% in FQ2, and surpassed $3bn in lifetime net bookings

- Match Factory net bookings grew +17% y/y vs +20% in FQ2

- Color Block Jam remains Rollic’s all-time top performing title and was featured in Apple’s 2025 free games list in the US

- Empires and Puzzles and Words with Friends net bookings grew +11% and +6%, respectively y/y

- The post pandemic rebound has helped mobile –

- The market has rebounded, there are tailwinds and so “as much as I’d like to take credit for all of the team’s success” they are benefiting from consumer engagement with mobile games

- Mobile advertising rev grew +10% y/y vs “an increase” last qtr: Driven by higher avg rev per DAU and mgmt is “highly confident” in mobile looking ahead

- The Co has been adding new ad units to mobile and Zynga has been “very smart” with the way they monetize them

- 2Ks mobile offerings also had another solid quarter

- WWE Supercard, surpassed 38mn lifetime downloads

- NBA 2K mobile continuing to expand its audience

- NBA 2K26 Arcade Edition, held its top 5 position on the Apple Arcade charts

- NBA 2K All-Star in China, grew to nearly 9mn registered users, after less than one year in mkt

- Mobile DTC biz delivered its strongest qtr on record (though mgmt doesn’t disclose how big it is): The Co intro’d recent enhancements that enable more personalized offers, flexible pricing, reduced payment friction, and alternative payment methods with the regulatory environment becoming even more favorable

- DTC should be a meaningful growth driver that will help accelerate net bookings, margins and profitability

Core Segment Saw Growth From A New GTA Online Update As Well As NBA 2K 2026

- GTA 5 recurrent consumer spending grew +27% y/y (exceeding expectations), accelerating from a “decline” last qtr

- Led by GTA Online’s “A Safe House in the Hills” update

- Full game sales of GTA 5 remain strong, with the title now having sold over 225mn units since 2013 launch

- GTA 6 consumer anticipation is huge, and “we will be astonished” by the creativity of the marketing team leading up to its release

- The game is still expected to be released on Nov 19, 2026

- The anticipation of GTA 6 is driving engagement in GTA 5

- After the release of GTA 6, the Co will still focus on GTA 5 Online

- NBA 2K26 delivered stellar results

- To date, the title has sold ~8mn units, representing a high SD % increase over NBA 2K25

- DAUs and MyCAREER DAUs both grew +30% y/y vs +30% and +40% respectively last qtr

- Outlook: It is on track to generate the highest level of annual net bookings and RCS in franchise history

- There is a significant international expansion opportunity

- The NBA continues to be an “amazing partner” for them and they’re expanding internationally

- Basketball is a global sport

- But North America is still a focus of expansion

Other Game Releases Highlighted This Quarter

- In Dec, Rockstar Games expanded Red Dead Redemption and Undead Nightmare onto new platforms

- PlayStation 5, Xbox Series X and S, Nintendo Switch 2, and iOS and Android mobile devices for Netflix subs

- On Jan 14th, 2K and HB Studios annc’d an array of new content for PGA TOUR 2K25

- Including 3 new courses for the 2026 major championships

- The 2026 PGA Championship at Aronimink Golf Club

- The 126th US Open at Shinnecock Hills Golf Club

- The 154th Open at Royal Birkdale Golf Club

- Additionally, they look forward to growing the community with the launch of PGA TOUR 2K25 for Nintendo Switch 2 on Friday

- Including 3 new courses for the 2026 major championships

- Firaxis Games will continue to deliver a steady cadence of updates for Sid Meier’s Civilization VII

- On Feb 5th, 2K launched Civilization VII for mobile devices exclusively on Apple Arcade

- Lastly, On Mar 13th, 2K and Visual Concepts will release WWE 2K26

- Featuring the biggest roster in the series history, (over 400 wrestlers)