Political headlines caused quite a bit of choppiness in the market this week, though the major indices ended close to flat when all was said and done (the S&P 500 fell -0.4% and Nasdaq was down -0.06%). It also stood out that gold was up another +8.4% this week and silver rallied +14%, both hitting a fresh new high.

Netflix kicked off earnings season on Tues with some puts and takes (see Theme #2) and this week’s other key updates & developments that we focused on include:

- Please Participate In Our 2026 Sector Themes Survey!!

- Engagement Trends & Deal Uncertainty Remain Front & Center For Netflix

- Important AI-Related “Need To Knows” This Week

- A Picture Says A Thousand Works When It Comes To Streaming Series & Production Trends

- Some Surprises Emerge Regarding 2025 Mobile App Trends

- Prediction Market Activity Continues To Scale Despite Regulatory Headwinds

- VC Investments Accelerate In 2025 Thanks To AI & Late-Stage Tech Growth

- Short Form Video Continues To Gain Growth & Ad Monetization Momentum

- Grab Bag: Amazon CEO Comments On Tariffs / Ubisoft Shares Fall After Restructuring News / Blue Origin Announces Deployment Of Satellites

Have a nice weekend (though we are slated to have a major snow storm!)

Next week’s earnings barrage includes heavyweights such as META, MSFT, and TSLA Wednesday after the close, and AAPL Thursday after the bell, among many many others!

Until then, see below.

Best,

Leslie

Please Participate In Our 2026 Sector Themes Survey!!

In case you missed my email earlier this week, we’re excited to share that we kicked off our **8th Annual LionTree Sector Themes Survey.**

It consists of 25 quick questions about the market, sector developments, and company outlooks.

It should take less than 10 minutes to complete.

The full survey results will be distributed in late February, and to ONLY those who take it!

CLICK HERE To Complete The Survey

(For reference, last year’s survey results can be accessed here)

Engagement Trends & Deal Uncertainty Remain Front & Center For Netflix

After the long weekend, Netflix kicked off the core earnings season for the sector with a few puts and takes that caused a pull-back in the stock. While Q4 financials modestly topped expectations, the Q1 guidance was disappointing, especially on operating margins and 2026 op income growth will be back-half weighted given a ramp in content spend in H1. Investor concerns about user engagement have been an overhang on the stock and was a big focus of analyst questions on the call. It was encouraging to hear that viewed hours for branded originals rose +9% y/y in H2:25, up from +7% y/y in H1:25 (and accounts for ~50% of total viewing) but non-branded viewed hours declined y/y in H2:25 due to a lower volume of licensed, 2nd run content across most regions, after an elevated period post the 2023-24 WGA strike.

So where does the Co go from here? They aim to increase engagement with not only a broad line up of originals, but also an expanded portfolio of licensed titles (recently announced several partnerships on this front). The Co is also investing more in podcasts and cloud-TV games to further drive engagement. But it is worth noting that not all viewed hours are created equally. Live entertainment is still a small percentage of overall viewed hours, but it has a disproportionately positive impact and Netflix will further its offering on this front in 2026, especially internationally.

Netflix’s ad business has also been scaling nicely. The Co grew ads revenue by more than 2.5x y/y in 2025 (to $1.5bn) and aims to again double ad revenue in 2026. Closing the monetization gap with standard plans without ads is a clear objective that mgmt believes can be achieved by improving ad capabilities.

A couple other points to highlight include that Netflix will roll out a new mobile UI later in 2026 and the Co is pausing their buyback to help fund the pending acquisition of WBD’s assets.

Overall, there were a few areas to pick on within Netflix’s results, Driving engagement is critical for the long-term investment thesis, but this requires some additional investment in H1. There is also uncertainty about the outcome of the WarnerBrosDiscovery transaction. With that said, mgmt is still asserting that it “feels good” about the long-term internal targets that were previously cited in the press, which doesn’t include M&A activity.

See more details on our key takeaways below.

-> Netflix shares fell as much as ~6% on the back of results, but slightly rebounded through the day to end down -2.2%; The stock is still down -36% from its high back in June

Q4 Modestly Tops Consensus Expectations, Despite Unfavorable F/X Movements

- Q4 rev BEAT cons by +0.7% and grew by +18% y/y (+17% y/y FXN)

- Growth was driven primarily by membership growth, higher pricing, and increased ad revenue

- Q4 op margin BEAT cons (24.6% vs cons 24.4%)

- +2pts y/y due to operating leverage of higher revs

- Q4 adj EPS BEAT cons by +1.8%

- Q4 FCF BEAT cons by +38%

- Q4 paid subs hit 325mn+, which is up +8% y/y…but a decel from +16% y/y in 2024

- Q4 buyback was $2.1bn, leaving $8bn remaining on the authorization

But 2026 Guidance Reflects Decelerating Y/Y Growth & Op Margins Missed Projections (Acq Related Expenses & Ramping Content Spend In H1)

- Q1 guidance was below consensus, especially regarding op margins

- Rev at the mid-pt missed cons by -0.3% ($16bn vs cons $12.19bn)

- Op income margin of 32% was below cons 34%

- EPS of $0.76 missed cons $0.81

- 2026 guidance reflects decelerating y/y growth and a ramp in content spend

- Rev at the mid-pt slightly beat cons by +0.3% ($50.7-$51.7bn vs cons $51.03bn)…with ad revenue a greater driver of growth

- This represents +12-14% y/y growth (or +11-13% y/y FXN), which is down from +16% y/y in 2025 (or +17% FXN)

- Growth will be driven by increases in membership and pricing plus a projected rough doubling of ad rev in 2026 y/y (hence, advertising will have more of a relative impact to growth)

- 2026 op margin guidance of 31.5% (includes ~$275mn of acq-related expenses) was below cons 32.7%, but up from 29.5% in 2025…2026 y/y margin expansion will be back-end loaded

- The margin forecast reflects content amortization growth of ~10% y/y in 2026 (which is a step up from growth of ~7% y/y in 2025)…higher content amort growth is expected in H1 than H2 due to the timing of title launches

- Hence, op income growth y/y will be higher in H2 vs H1

- Rev at the mid-pt slightly beat cons by +0.3% ($50.7-$51.7bn vs cons $51.03bn)…with ad revenue a greater driver of growth

- 2026 FCF guided is for $11bn, which assumes a cash content spend to content amortization ratio of ~1.1x

- Netflix is pausing their buyback to help fund the pending acq of WBD’s assets

Engagement Levels Were A Big Focus On The Conference Call…It Was Up For Originals But Down For Licensed Content

- Viewed hours in H2 incr’d +2% y/y (up by +1.5bn hours to 96bn in total) which was a faster rate than the +1% y/y in H1

- This was driven by a +9% y/y rise in viewing of branded originals in H2, which is up from +7% in H1 (and accounts for ~50% of total viewing)

- A couple call outs of content with 100mn+ views include…

- Massive final season of Stranger Thngs (120mn views)

- Frankenstein (102mn views)

- BUT engagement was partially offset by a y/y decline in non-branded view hours in H2 due to lower volume of licensed, 2nd run content across most regions post an elevated period post the 23-24 WGA strike

- Viewing hours is an important KPI but it is not the only metric and not all hours are created equally

- Total view hours is “overly simplified” as it is a broad metric and there are a lot of mixes in that (Japan watches 50% to 2/3 as much TV as US users), plan mix, etc.…so mgmt. looks at engagement at a portfolio level

- Retention is amongst the best in the industry – customer satisfaction is at an all-time higher and churn was down y/y

Expect Netflix To Invest More In Licensed Content, Podcasts & Cloud-TV Games To Drive Engagement

- Looking ahead, the Co aims to increase engagement across both core series & films, including both originals and 2nd run titles): It will have a broad line up of originals and also will expand licensed titles…efforts on that front include:

- New US licensing partnership with Universal kicks in for live action films

- Licensed ~20 shows from Paramount for both US and international territories

- Expanded pay-1 film pact with Sony Pictures from a US to a global deal (will reach full global availability in early 2029)

- Expect the Co to also broaden the set of creators that they work with (recently intr’d video podcasts)

- “Super pleased” with early results of the podcasts on the platform

- Will bring “more and better” games to members across all devices in 2026

- Brought their cloud delivered TV-based party games to 1/3 of members and early results are “encouraging”

- The Co will be expanding their cloud game line-up in 2026… “very bullish on the opportunity side” and are “seeing progress”

- They will ramp investment based on returns to the business

- “Super confident [Netflix] will grow engagement and the value of that engagement”

Live Continues To Be An Area Of Expansion (Esp Internationally)…Its Still Small As A % Of View Hours But Has A Disproportionate Positive Impact

- In live, have executed 200+ events and will do more outside the US

- Live accounts for a small proportion of total view hours, but can have an outsized positive impact around conversation and acquisition and the Co is seeing some benefits from retention as well

- In 2026, mgmt remains excited about expanding their live offer, especially outside the US:

- The Co will deliver their 1st local live event outside the US…which is the World Baseball Classic (WBC) in Japan

- Netflix will stream all 47 games of the 2026 WBC live and on demand

- Other expansions:

- A new show called Star Search, with live fan voting

- Skyscraper Live

- Three MLB events including an exclusive Opening Night game and the Home Run Derby

- The Co will deliver their 1st local live event outside the US…which is the World Baseball Classic (WBC) in Japan

Reiterated Comments About The WBD Deal Rational & Remain Confident In The Regulatory Approvals

- Continue to see “a tremendous opportunity” with the WBD deal

- “When we got under the hood saw things that are very exciting”

- Netflix had previously debated internally whether they should build a theatrical business but were focused on other areas at the time…they are very excited to enter theatrical via WBD’s film business

- The TV studio is complementary and the Co will continue to be a supplier to others in the industry

- HBO is a premium brand…customer love it and knows what it means…it’s complementary and allows them to adjust tier structures

- This deal is an “accelerator of strategy”

- “Confident will secure all of the approvals”… “its pro consumer, pro growth, pro innovation”

- “Will need those teams as these are 3 businesses that they do not have”

- “Will expand US production capacity”

- “This is a vertical deal”

- Combined PF post close, 85% of the revs is from the core Netflix business

Other Key Comments On Pricing, Innovation/Product Features, Mobile, Advertising, & LT Targets

- On pricing, mgmt cited that there is not a change in the Co’s approach given the WBD pending deal

- Expect more innovation with product features in 2026

- Interactive experiences such as live voting w/ Moments

- Convenient and seamless connectivity to play games on TV using a phone or controller

- Real time personalized recommendations that respond to moods and interests in the moment

- New discovery and viewing experiences

- The Co is pursuing a broader upgrade of its mobile experience…a new UI is coming

- The Co has been testing vertical video for mobile for 6 months and the feed (with short, swipeable clips drawn from popular Netflix original series, films, and other programming optimized for portrait-mode viewing on handheld devices link/link) has been available over the last 3 months

- Netflix is also working on a new mobile UI and will roll out later in 2026

- Netflix’s ad rev grew by more than 2.5x y/y in 2025 (to $1.5bn) and as mentioned above, the Co aims to again double ad revenue in 2026…Netflix is working on reaching parity between standard without ad ARM and ad tier ARM: The gap is narrowing as they improve ads capability

- “So now that we’ve grown to relevant scale, meaning consumer reach in all our ads countries, our main focus is on increasing the monetization of that growing inventory. It’s likely to remain our focus for at least the next several years. So, we believe we can close that gap. And that means upside in terms of ad revenue growth”

- Still feel good about the long-term internal targets previously cited in the press (and those didn’t include any M&A)

- It was previously reported that by 2030, Netflix aims to double revenue from $39bn in 2024, generate ~$9bn in global ad sales, and triple operating income from $10bn in 2024(link)

Important AI-Related “Need To Knows” This Week

The pace of innovation and key developments related to AI continues at break-neck speeds. We highlighted below what we viewed as most important in AI this week across funding updates, leaked company financials, new product related updates, datapoints regarding supply constraints due to strong AI CPU demand, China vs the US on AI dominance, AI monetization plans, and a few other comments from Davos on AI’s impact on jobs as well as the AI bubble debate.

See below for our quick takes on all of these “need to knows” that emerged this week.

Yet Again, More Funding Is Going Into The Large AI Companies

- Anthropic’s $10bn funding round is reportedly oversubscribed, w/ a valuation at $350bn (link/link): The round is now expected to exceed $10bn; Recall that the Co also has $15bn in total prior funding commitments from Nvidia & Microsoft

- At the same time, The Information reported that Anthropic lowered its 2025 profit margin expectations due to the rapidly growing cost of running large models

- Anthropic now reportedly projects a 40% gross profit margin in 2025, which is 10% below its previous internal estimates

- Costs of third-party cloud infrastructure from Google & Amazon has climbed ~23% more than anticipated

- On the top-line. Anthropic’s rev run rate hit ~$9bn at the end of 2025, according to people familiar with the details (run rate was $4bn in July of last year)

- At the same time, The Information reported that Anthropic lowered its 2025 profit margin expectations due to the rapidly growing cost of running large models

- OpenAI also met with investors in hopes of a $50bn funding round (link)

- Sam Altman has been meeting with investors in the Middle East to line up funding for a new investment round that could total at least $50bn

- The Co is looking to raise at a valuation of about $750bn-$830bn, according to people familiar with the matter

- OpenAI was most recently valued at $500bn in the fall of 2025

-> Also, this week, OpenAI revealed that its API business alone added over $1bn in annual recurring revenue in the past month. To diversify monetization further, management is now openly exploring ads in ChatGPT and revenue-sharing model licensing, signaling a shift from its historically consumer-only mindset (link)

This Week Included A Multitude Of Key New Product Related Updates

- Meta’s new AI Team has delivered its first key models internally this month (link): Meta’s CTO Andrew Bosworth annc’d that the models “showed a lot of promise” but the work is not done

- He highlighted the importance of bringing consumer products to market over the next 2 years

- Apple is reportedly planning to revamp Siri this year (link): The chatbot, code-named Campos, will be embedded into the iPhone, iPad and Mac operating systems and replace the current Siri interface, according to people familiar with the plan; It will have both voice & typing modes

- Timing? The chatbot capabilities will come later in the year, according to sources

- The Co reportedly aims to unveil the tech in June at its Worldwide Developers Conference and release it in Sept

- Note that the previously promised, non-chatbot update to Siri is planned for iOS 26.4, which is due in the coming months

- Something to highlight –

- The Co is designing Campos so that its underlying models can be swapped out over time

- That means the Co will have the flexibility to move away from Google-powered systems if it desires

- Timing? The chatbot capabilities will come later in the year, according to sources

->Apple stock was up +2% in reaction to the news

- OpenAI is reportedly planning its first AI device in 2026…which could be an AI earbud (link/link): The physical product is being developed in collaboration with Jony Ive, the former legendary Apple design chief

- Timing: “We are looking at something in the latter part of 2026,” Chris Lehane (OpenAI’s Chief Legal Officer) told Axios, but did not confirm if it will be for sale this year

- What is the device? It is rumored to be a pair of AI earbuds, code-named “Sweetpea” internally

- The earbuds reportedly use a two-nanometer processor capable of running AI tasks locally

- The Co is reportedly working on a design to “stand out” from other ear buds

- Baidu’s AI assistant Ernie reaches 200mn MAUs, according to sources, after launching in Q3 2025 (link)

- Ernie Assistant is integrated into its flagship Baidu search-engine app and on personal computers

- To flag: Last week, Alibaba said it is connecting its Qwen chatbot into its consumer ecosystem and allowing it to carry out tasks on users’ behalf

- The Qwen app surpassed 100mn MAUs within 2 months of its Nov launch

Supply Constraints Due To Strong AI CPU Demand Comes Into Play This Week W/ Intel’s Numbers

- Intel issues out a weaker than expected Q1 outlook given supply constraints that are holding the Co back from capturing significant server CPU demand: “In the short term, I’m disappointed that we are not able to fully meet the demand in our markets” (link/link)

- Q1 2026 outlook:

- Revenue: $11.7-$12.7bn (down -$0.5bn y/y) vs cons of $12.54bn

- Gross margin: 5% (down -4.7ppts y/y) vs cons of 36.6%

- EPS: $0.00 (down -$0.13 y/y) vs cons of $0.06

- Mgmt sees some relief in supply beginning in Q2

- Q1 2026 outlook:

->Intel stock fell a significant -13% in reaction to the news

US Firms Are Blasting China AI Companies

- Anthropic CEO Dario Amodei on Tues said Trump’s decision to allow the sale of AI chips to China is like “selling nuclear weapons to North Korea” (link)

- What is his argument? The U.S. is many years ahead of China when it comes to making chips, and sending them there could help Beijing catch up”

- Referring to building AI models, Amodei posed: “I’ve called where we’re going with this, a country of geniuses in a data center”

- “So imagine 100mn people smarter than any Nobel Prize winner, and it’s going to be under the control of one country or another”

- What is his argument? The U.S. is many years ahead of China when it comes to making chips, and sending them there could help Beijing catch up”

- At the same time, DeepMind’s CEO commented this week that Chinese AI firms are behind the West (link)

- CEO Demis Hassabis said Chinese AI Cos haven’t been able to innovate beyond the cutting edge of tech and remain ~6 months behind the frontier AI of the leading western labs

- He believes that there was a “massive overreaction” when DeepSeek’s R1 model was released a year ago

- “They’re very good at kind of catching up to where the frontier is, and increasingly capable of that. But I think they’ve yet to show they can innovate beyond the frontier”

On The AI Monetization Front, DeepMind Has No Plans To Bring Ads To Gemini

- Following press last week that OpenAI’s ChatGPT is testing advertising on the platform, Alphabet’s DeepMind CEO Demis Hassabis, speaking at the World Economic Forum in Davos, made it clear that Google’s Gemini chatbot won’t be adding ads anytime soon (link)

- “It’s interesting they’ve [OpenAI] gone for that so early,” Hassabis said when asked about OpenAI’s decision to roll out sponsored content in ChatGPT

- “Maybe they feel they need to make more revenue”

- “It’s interesting they’ve [OpenAI] gone for that so early,” Hassabis said when asked about OpenAI’s decision to roll out sponsored content in ChatGPT

A Few Other Key AI Related Comments From Davos That Sparked Our Interest This Week

- Palantir CEO, Alex Karp, said AI “will destroy” humanities jobs BUT there will be “more than enough jobs” for people with vocational training (link/link)

- But employers need different ways to test aptitude beyond just academic degrees

- Karp pointed to the former police officer who attended a junior college, who now manages the U.S. Army’s Maven system, a Palantir-made AI tool that processes drone imagery and video

- “In the past, the way we tested for aptitude would not have fully exposed how irreplaceable that person’s talents are”

- But employers need different ways to test aptitude beyond just academic degrees

- Microsoft CEO Satya Nadella explained that if AI growth spawns solely from investment, then that could be a sign of a bubble (link): “A telltale sign of if it’s a bubble would be if all we are talking about are the tech firms”…“If all we talk about is what’s happening to the technology side then it’s just purely supply side”

- BUT… Nadella offers a fix: Calling on business leaders to adopt a new approach to knowledge work by shifting workflows to match the structural design of AI

- “The mindset we as leaders should have is, we need to think about changing the work—the workflow, with the technology”

- Corporate structures need to change: Nadella argues that AI creates a “complete inversion” of how information moves through a business, replacing slow, hierarchical processes with a view that forces leaders to rethink their organizational structures

- “We have an organization, we have departments, we have these specializations, and the information trickles up,” Nadella said; “No, no, it’s actually—it flattens the entire information flow. So once you start having that, you have to redesign structurally”

- Large organizations need to move faster: “For large organizations…there’s a fundamental challenge: Unless and until your rate of change keeps up with what is possible, you’re going to get schooled by someone small being able to achieve scale because of these tools”

- BUT… Nadella offers a fix: Calling on business leaders to adopt a new approach to knowledge work by shifting workflows to match the structural design of AI

- NVIDIA CEO Jensen Huang described AI as the foundation of “the largest infrastructure buildout in human history,” driving job creation across the global economy (link)

- Huang framed AI not as a single tech but as a “a five-layer cake”: Spanning energy, chips and computing infrastructure, cloud data centers, AI models and, ultimately, the application layer

- AI will create jobs: Since every layer of AI’s five-layer stack must be built and operated, the platform shift is creating jobs across the economy, from energy and construction to advanced manufacturing, cloud operations and application development

- The application layer will see the most economic benefit: Where AI is transforming industries such as healthcare, manufacturing and financial services

- “AI is infrastructure”: Arguing that every country should treat AI like electricity or roads

- AI literacy is becoming essential: “It is very clear that it is essential to learn how to use AI, how to direct it, manage it, guardrail it, evaluate it”

- For developing countries, AI offers a chance to narrow long-standing technology gaps

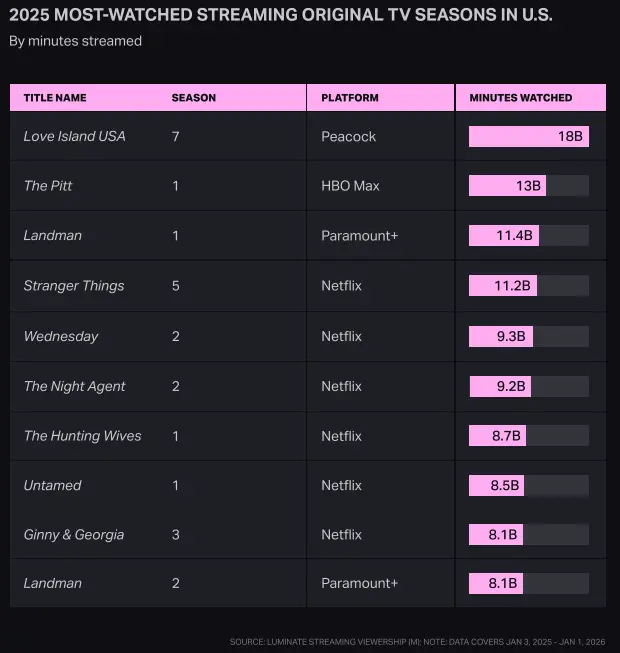

A Picture Says A Thousand Works When It Comes To Streaming Series & Production Trends

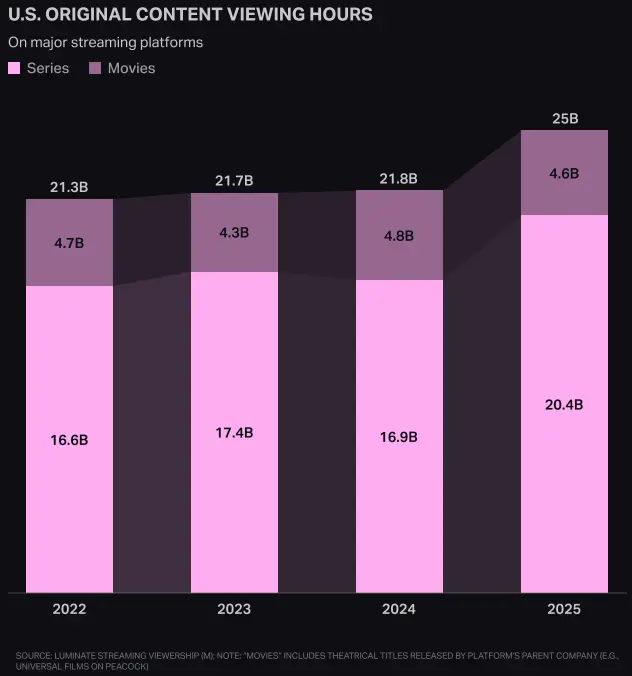

Luminate’s 2025 Film-TV Year End Report made our top themes cut this week given the multitude of revealing stats and charts outlined in the reports. Big picture, 2025 was the year where steaming and TV shifted from a focus on volume as the value driver to a focus on quality and reliability of engagement. Overall US TV production continues to fall from previous oversupply (-11% y/y in 2025) but on the flipside original streaming content consumption grew +15% y/y in 2025.

The report also points to Netflix losing its place regarding the top US streaming original TV season. For the first time since Luminate started tracking this data, a Netflix show was not in lead in 2025. Instead, it was Peacock’s Love Island USA (grew viewership +150% y/y).

We detailed our six most-favorite charts and takeaways below. If you would like to see the entire presentation which includes some additional observations, you can request it HERE

US TV Production Continues To Decline Across The Board As The Industry Corrects From Oversupply In The Early 2020s

- US TV production overall was down -11% y/y in 2025

- B-cast series were down -21% y/y (though the prior yr strike had created a comp challenge)

- Cable series were down -10% y/y

- SVOD series were down -8% y/y

- Production locations have also meaningfully shifted as LA live action production is down more than -50% from the historical peaks (and down -26% y/y in 2025)…production is shifting overseas

- Unscripted streaming & linear TV volumes were down -31% y/y: The declines were broad-based across sub-genres though unscripted sports documentaries and series was one of the few to post volume increases

The Number Of Netflix US Produced SVOD TV Premieres Continued Its Downward Trajectory In 2025 Y/Y Though A Couple Other SVOD Plays Ramped Production

- Declines in US produced SVOD TV premieres in 2025 y/y –

- Netflix (but is still by far producing the most)

- Hulu

- Paramount+

- HBO Max

- Peacock

- Increases in US produced SVOD TV premieres in 2025 y/y –

- Disney

- Prime Video

The Video Streaming Eco-System Is Becoming More Diversified…The Top 3 Most Watched Streaming Original TV Seasons In The US Were All Non-Netflix

- The most watched US streaming original TV season of the year was Peacock’s Love Island USA (grew viewership +150% y/y)

- This was the 1st time in history since Luminate started tracking the data that a Netflix show didn’t lead

- This was also the 1st time an unscripted streaming original led the annual rankings

- The #2 and #3 most watched US streaming originals were on HBO Max and Paramount+

- Netflix still accounts for 6 of the top 10 slots in the overall ranking

Original Streaming Content Consumption Grew +15% Y/Y In 2025, While Film Streaming Viewing Fell

- US original content viewing hours incr’d from ~22bn in 2024 to 25bn in 2025

- Driven by major original hits on multiple services

- US Film viewing hours fell from 4.8bn in 2024 to 4.6bn in 2025

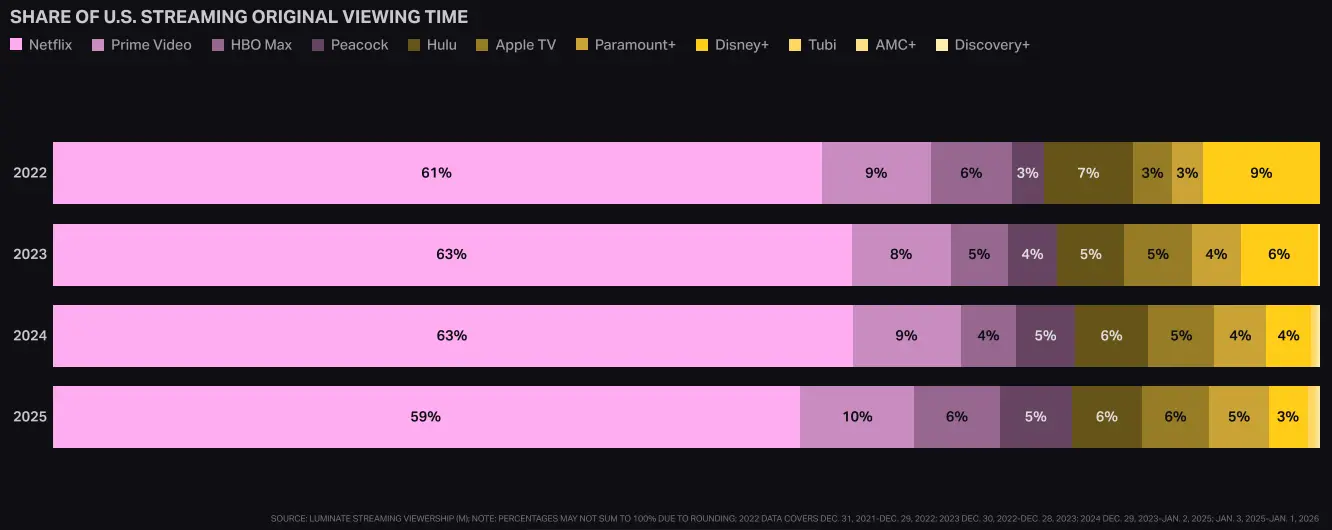

While Overall Original Streaming Content Viewing Hours Rose, Netflix’s Share Fell

- Netflix’s share of US original content viewing dropped below 60% for the 1st time

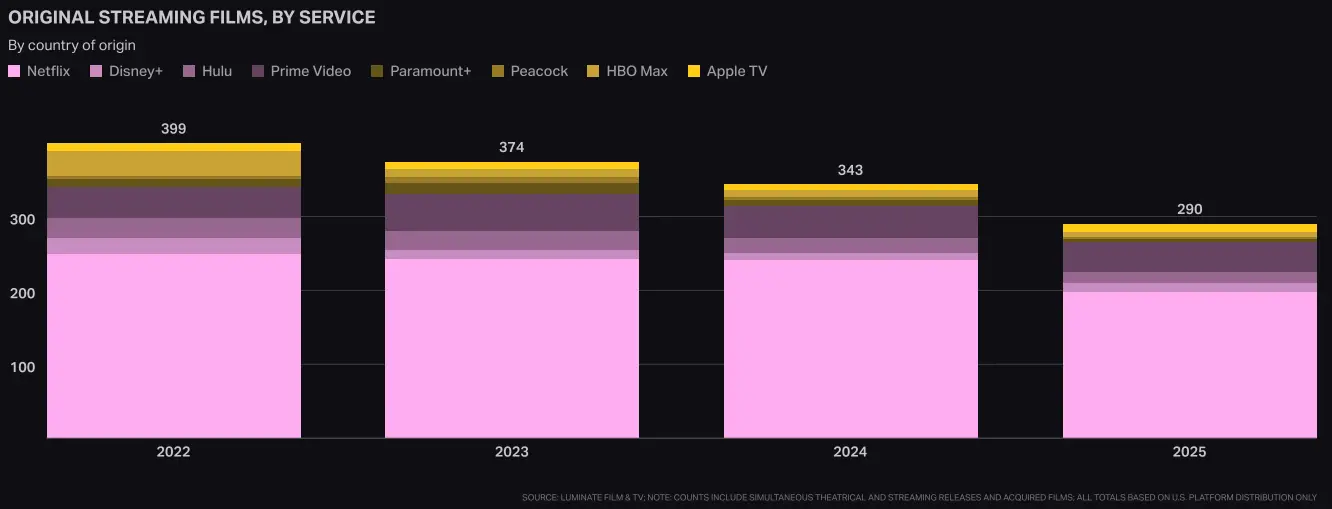

Furthermore, Streaming Film Output Continues To Fall, With Strong Declines At Netflix

- Streaming film output has dropped from 343 in 2024 to 290 in 2025

- Netflix’s 2025 slate was down by almost 20% y/y

Some Surprises Emerge Regarding 2025 Mobile App Trends

What was the top downloaded video streaming app in 2026? It wasn’t Netflix, Disney+, or Prime Video…it was actually DramaBox, a short-drama app that helped make short dramas the breakout subgenre of 2025. This was one of the many key insights we found interesting in Sensor Tower’s State of Mobile 2026 report, which took a deep-dive into the trends and milestones that shaped the mobile landscape in the past year across sub-sectors like social media, video streaming, retail, travel, and much more.

See below for what we thought were the key incrementals, and if you would like to peruse the full report, you can download HERE.

2025 Rankings – Top 5 Apps By…

- Downloads

- ChatGPT

- TikTok

- WhatsApp Messenger

- IAP (In-App Purchase) Revenue

- TikTok

- Google One

- ChatGPT

- YouTube

- Disney+

- Monthly Active Users

- YouTube

- Google Chrome

- WhatsApp Messenger

- Gmail

- Also to flag…three apps surpassed $1bn in global IAP rev for the first time in 2025 – ChatGPT, CapCut, and WeTV

- ChatGPT reached $3.4bn, ranking as the 3rd-highest-grossing app of the year behind TikTok and Google One

Sub-Sector Callouts

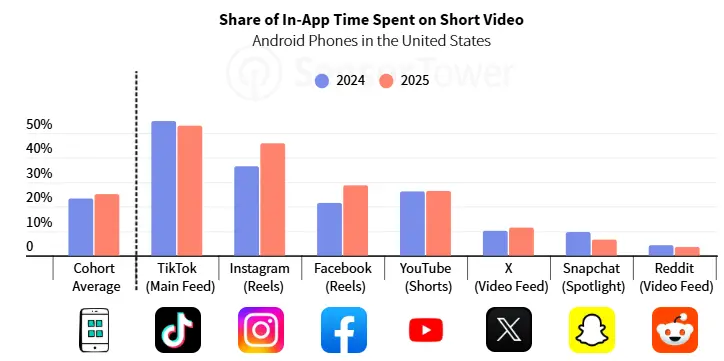

- Social Media – the increase in short-form video usage was driven by Instagram and FB, as TikTok time spent actually declined y/y: Overall, short-form video represented an avg of 25% of time spent across seven key social apps in 2025, which is UP +1.8ppts y/y

- Reels now accounts for a substantial share of engagement…46% of time spent on Instagram and 29% on Facebook

- Video Streaming – short dramas were the breakout subgenre of 2025: Total time spent on short drama apps grew by +311% y/y in Q4:25; Additionally, streaming downloads of short drama apps grew +186% y/y, overtaking traditional OTT streaming downloads for the first time, which fell -7% y/y over the same period

- Short drama app share of total video entertainment time has been growing quickly in the last 2 yrs: Jumped from <1% share in Q1:24 to 10%+ in Q4:25

- And the competitive landscape continues to diversify: While DramaBox and ReelShort maintain their dominant stronghold, securing the top two spots worldwide and across N. America, LatAm, and Europe, 35+ different platforms surpassed 10mn+ global downloads each in 2025

- 3 of the Top 5 most downloaded video streaming apps in 2026 were short drama apps:

- DramaBox (short drama)

- ReelShort (short drama)

- Netflix

- Kuku TV (short drama)

- JioStar

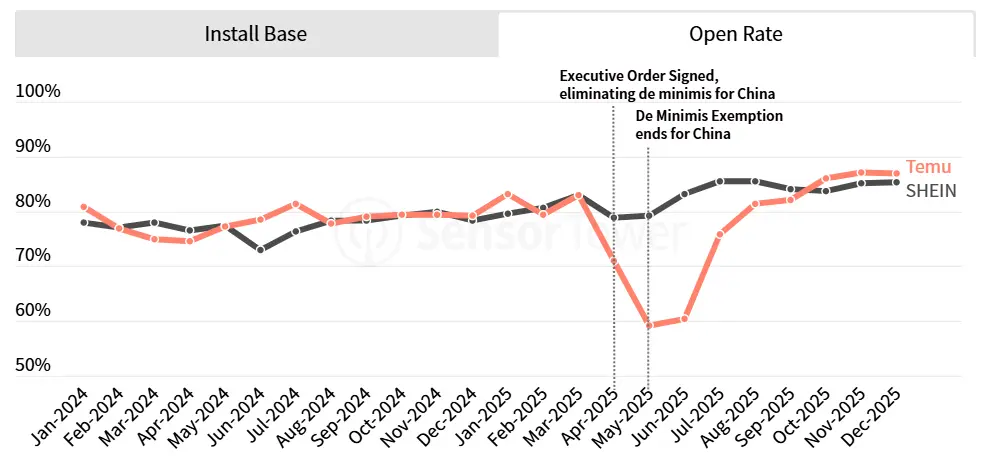

- Retail – the elimination of the de minimis exemption in Q2:25 highlighted the precariousness of relying on paid acq b/w Temu and Shein

- Following the elimination of the exemption, Temu cut ad impressions by -97%, which led to its open rate plummeting from 82% to 64%

- Temu’s direct-from-factory model preserved its low-cost edge and ultimately drove its recovery back to its pre-tariff scale of 91mn by Oct 2025

- Conversely, despite Shein reducing ad impressions by -30%, SHEIN’s open rate remained above 80%, signaling a more resilient, brand-loyal audience capable of weathering the tariff shock organically

- Following the elimination of the exemption, Temu cut ad impressions by -97%, which led to its open rate plummeting from 82% to 64%

- Food & Drink – emerging mkts are driving growth as US adoption stalls: Worldwide downloads for Food and Drink apps reached a record 2.4bn in 2025, up +13% y/y, driven largely by a surge in emerging regions

- India led this expansion with a +56% y/y surge in downloads

- Travel – growth is increasingly driven by emerging mkts while, in contrast, the US represents a highly consolidated mkt: The travel sector continued its steady upward trajectory, with both global downloads and time spent up +3% and +8% y/y in 2025, respectively

- Travel infrastructure and digital adoption are rapidly expanding in emerging mkts, w/ Vietnam (+21%) and the United Arab Emirates (+17%) currently leading the world in new app downloads

- US growth is mainly driven by increased session depth and user retention within existing apps, rather than new user acquisition: While US downloads in 2025 are up only +2% vs 2022, total time spent has surged by +29% over the same period

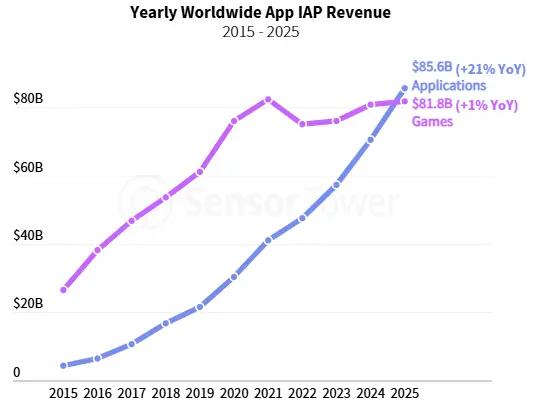

- Gaming – consumers spent more in non-game apps than games apps for the first time ever: Consumers spent ~$85bn in non-game apps in 2025, up +21% y/y and 2.8x the amount spent five years earlier; That compares to Games, where consumers spent $81.8bn, up +1% y/y

- Generative AI led this revenue growth, but it was not the only driver, as nearly all app genres recorded positive IAP revenue growth in 2025, underscoring the broad-based strength of app monetization beyond games

Prediction Market Activity Continues To Scale Despite Regulatory Headwinds

Activity in the predictions markets continues to scale rapidly. Overall, trading volumes on Kalshi and Polymarket were in aggregate up +13% seq from November, reaching a new high, and trends so far suggest that January will be an even bigger month. All of this is happening at the same time that regulatory pressure continues to build and Massachusetts, Portugal, and Hungary all jumped on that bandwagon this week.

See below for details on these key developments.

Predictions Market Volumes Reach A New High

- Overall trading volumes on the platforms are trending up, with Jan on track to beat Dec

- In Dec 2025:

- Kalshi made up $6.5bn (up from $5.8bn in Nov 2025)

- Polymarket made up $2.2bn (up from $1.9bn in Nov 2025)

- In Dec 2025:

Source: Block Data

New Legal Troubles Emerge For Kalshi & Polymarket

- Kalshi cannot operate a sport-prediction market in Massachusetts (link/link)

- What happened? Suffolk County Superior Court Judge Christopher Barry-Smith granted MA Attorney General Andrea Campbell’s request for a preliminary injunction against Kalshi

- Campbell sued Kalshi in Sept trying to stop them from offering sports wagering without a sports betting license

- Timeline: The injunction is scheduled to go into effect on Friday (Jan 23rd)

- There could be a hearing held the same day if either party requests one

- For reference, this is not the only suit Kalshi is facing: They are in the middle of litigation in 12 states

- What happened? Suffolk County Superior Court Judge Christopher Barry-Smith granted MA Attorney General Andrea Campbell’s request for a preliminary injunction against Kalshi

-> Online betting sites, DraftKings, Flutter, and Penn Gaming all traded down by -1%, -2%, and -4%, respectively on the news

- Also this week, Portugal & Hungary ordered Polymarket to be blocked (link/link/link)

- What happened? Both the Hungarian Supervisory Authority for Regulated Activities and the Portuguese Gaming Regulatory Authority issued bans, accusing Polymarket of illegal gambling activity

- Portugal gave Polymarket 48 hrs to halt activity

- This came after ~€4mn ($4.3mn) was wagered on the presidential markets in the hours before results were annc’d

- In total, trading volume exceeded 110mn euros (~$119mn)

- In Hungary, they issued a temporary order requiring domestic internet service providers block access until further decisions were made

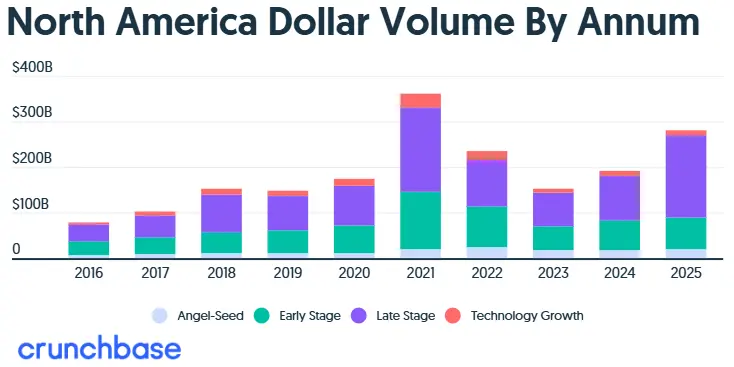

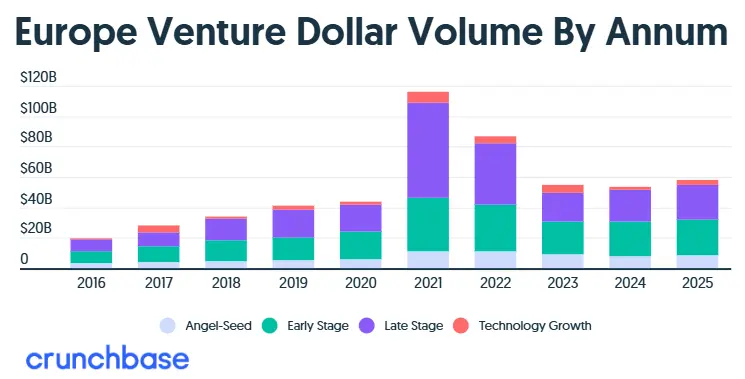

VC Investments Accelerate In 2025 Thanks To AI & Late-Stage Tech Growth

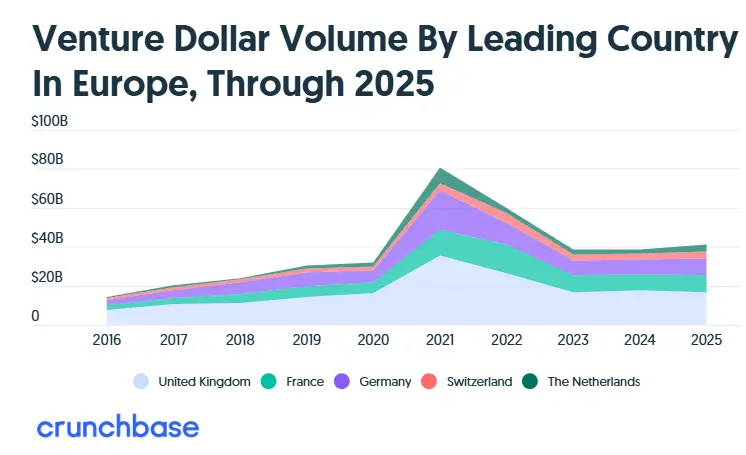

The final numbers are in regarding N. America and Europe’s venture capital investments for the full year 2025, per Crunchbase data. VC investments overall saw accelerated y/y growth in both regions, driven by continued momentum in AI and late-stage tech-growth investments (obviously not too much of a surprise). On the other side, it did stand out that investment in seed companies in N. America fell ~-9% y/y in 2025. It was also interesting to see that in Europe, the UK remained the largest recipient of venture capital by total investment dollars, but to a lesser degree than last year as investment into other European countries increased.

What can we expect in 2026? AI-related investments are likely to still dominate but one other headline that caught our attention this week on the topic of private investments was that PE giant Thoma Bravo sees the huge drop and carnage in software stock valuations as a “huge buying opportunity” per the FT, citing co-founder Orlando Bravo (link).

See below for more color on what we thought was most relevant.

2025 Showed Accelerated Y/Y Growth In Total Venture Capital Dollar Investments In Both N. Amer & Europe, With AI Being A Key Driver

- Overall VC funding in North America & Europe for the full year 2025 accelerated y/y, with Europe seeing strong dollar investment in Q4 (link/link)

- North America – 2025: Reached ~280bn, up +46% y/y (accel from +25.9% y/y to $191.8bn in 2024)

- North America – Q4: Reached $67bn, up +3% q/q and +3% y/y (but deal count declined ~-16% y/y and declined ~-14% q/q

- Europe – 2025: Reached ~$58bn, up +9% y/y (a big turnaround from the -2.4% y/y decline to $53.5bn in 2024)

- Europe – Q4: Q4 2024 saw $16.6bn, up +20% q/q and +27% y/y

- North America – 2025: Reached ~280bn, up +46% y/y (accel from +25.9% y/y to $191.8bn in 2024)

Source: Crunchbase Data

Source: Crunchbase Data

- AI (not surprisingly) was a huge category in VC funding for the year

- North America: ~$168bn, or ~60% of all startup funding went to AI-related companies in 2025 (in Q4 it was also more than 50%)

- In Q4: The largest AI deals were $2.3bn Series D for Anysphere and a $2bn Series B for software development AI startup Reflection AI

- For 2025: The largest AI rounds were OpenAI’s $40bn SoftBank-led financing in March & Anthropic’s $13bn Series F in Sept

- Europe: ~$17.5bn of all startup funding went to AI-related companies in 2025, up from ~$10bn in 2024

- Paris-based Mistral AI raised the largest round in the year, close to ~$2bn

- North America: ~$168bn, or ~60% of all startup funding went to AI-related companies in 2025 (in Q4 it was also more than 50%)

- In Europe, the U.K. led VC funding, raising ~$17bn in 2025 which was ~29% of total European VC funding BUT this is also down from the UK VC funding accounting for ~33% of all Europe VC spend in 2024

- #2 = France: Startups raised $8.5bn

- #3 = Germany: Startups raised $8.4bn

- #4 = Switzerland: Startups raised $3.6bn

- #5 = The Netherlands: Startups raised $3.4bn

- #6 = Spain: Startups raised $2.9bn

- #7 = Finland: Startups raised $2.2bn

- Except for the U.K., each of those countries raised more VC funding in 2025 than in 2024

Source: Crunchbase Data

- Late stage & tech growth has seen a flood of investment

- North America: Investments in late-stage & tech-growth was up +75% y/y to $191bn in 2025

- In Q4, investments were relatively flat (at ~$41bn)

- Europe: Investment grew +65% y/y to $9.2bn in Q4 (reached the highest level in two years)

- North America: Investments in late-stage & tech-growth was up +75% y/y to $191bn in 2025

- Early-stage funding showed mixed trends

- North America: Investment was up ~5% y/y to $69bn in 2025

- And hit a high point in Q4, w/ $21.6bn of investment (large deals included a $700mn Series B for identity security provider Saviynt and a $600mn Series B for AI robotics startup Physical Intelligence)

- Europe: Investment was down -4% y/y in Q4 to $5.3bn

- North America: Investment was up ~5% y/y to $69bn in 2025

- Seed funding was down to in-line y/y

- North America: Investment fell -9% y/y to $20.4bn in 2025

- In Q4, deal count also ticked lower, hitting a low w/ ~1,300 reported seed financings

- Europe: Investment was flat y/y at $2bn in Q4 and seed funding reached $8.5bn in 2025

- North America: Investment fell -9% y/y to $20.4bn in 2025

Short Form Video Continues To Gain Growth & Ad Monetization Momentum

As we highlighted in our most recent LionTree’s Lens, Winter Edition (see slide #17 of the deck), the shift of video usage to short form has been underway and we anticipate that trend to continue. 95% of consumers regularly watch short‑form videos, with 71% doing so daily per a recent Clutch report in November (link). There was a time when TikTok’s fate was in question, but that debate came to rest with the formal announcement about the TikTok USDS Joint Venture LLC this week. The deal structure was previously widely reported, hence while an important milestone, it was a bit anticlimactic. Elsewhere in short form, YouTube CEO Neil Mohan published his annual letter, highlighting key 2026 priorities for the platform (AI and commerce stood out to us), and Threads’ ad monetization expansion globally also rose to the top this week. Lastly to flag, Netflix has also been experimenting with the vertical screen which could bring more short form competition as we progress in 2026 and into 2027 (see Theme #2).

See details below on this key theme.

“TikTok USDS Joint Venture LLC” Is Now Official

- The TikTok USDS JV is largely as previously reported but as a reminder on key points… (link/link/link/link)

- Data protection:S. user data will be protected by USDS JV in Oracle’s secure U.S. cloud environment

- Algorithm security: The JV will retrain, test, and update the content recommendation algorithm on U.S. user data

- The content recommendation algorithm will be secured in Oracle’s U.S. cloud environment

- Software assurance: The JV will secure U.S. apps through software assurance protocols, and review and validate source code on an ongoing basis, assisted by Oracle

- Trust & safety: The JV will safeguard the U.S. content ecosystem and have decision-making authority for trust and safety policies and content moderation

- The JV framework: Oracle, Silver Lake & MGX will collectively own 45% of the U.S. entity

- Nearly one-third of the Co will be held by affiliates of existing ByteDance investors

- 20% of the JV will be retained by ByteDance

- New investors include Michael Dell’s family office, NY -based investment firm Alpha Wave and Revolution, a Washington D.C.-based VC firm

- While the final valuation of the US entity has not been formally disclosed, JD Vance previously referenced a figure of about $14bn

YouTube CEO Neal Mohan Shares YouTube’s 2026 Priorities…AI & Commerce Stand-Out

- YouTube CEO Neal Mohan shares priorities for YouTube in 2026 (link)

- AI will be used as a “new creative frontier”: This yr, creators will be able to create a Short using their own likeness, produce games with a simple text prompt, and experiment with music; AI will remain a tool for expression, not a replacement

- The Co will be further building out AI transparency & protections: By clearly labeling content created by YouTube’s AI products, requiring creators to disclose when they’ve created realistic altered or synthesized content, equipping creators with new tools to manage the use of their likeness in AI-generated content, and supporting related legislation

- The Co is focused on driving commerce: The aim is to make YouTube a premier shopping destination because viewers trust product and brand recommendations from creators

This Week’s Short Form Ad Monetization Updates

- Threads now moves to a global roll-out of ads (link/link/link/link)

- History of the ads rollout:

- Jan 25: Started initial tests w/ select advertisers in the US and Japan

- April 25: Wider availability was launched

- Next week: Ads will be rolled out to all users globally

- User growth: Threads has 400mn+ MAU’s, with execs saying it could reach 1bn in a few years

- After the July 2023 debut, reached 200mn users in mid-2024

- Then reached 320mn in Jan 2025

- The added another 30mn April 2025

- In addition, Meta expanded the third-party verification already available on Facebook and Instagram (including feed and Reels) to the Threads feed through Meta Business Partners

- History of the ads rollout:

- Most of Instagram’s ads ran on Reels in 2025, per Sensor Tower (link/link)

- More than half of all ads on Meta’s Instagram ran in the service’s short-form video product Reels in 2025, up from 35% in 2024

- Reels usage in the US:

- On Instagram, Reels accounted for 46% of time spent in 2025, up from 37% in 2024

- On the Facebook app, Reels accounted for 29% of time spent in 2025, up from 22% in 2024

Grab Bag: Amazon CEO Comments On Tariffs / Ubisoft Shares Fall After Restructuring News / Blue Origin Announces Deployment Of Satellites

- Amazon’s CEO said Trump’s tariffs have started to “creep” into prices (link): Amazon and many of its third-party merchants pre-purchased inventory to try to get ahead of the tariffs and keep prices low for customers, BUT… most of that supply ran out last fall, Jassy said in a Tuesday interview with CNBC

- “So you start to see some of the tariffs creep into some of the prices, some of the items, and you see some sellers are deciding that they’re passing on those higher costs to consumers in the form of higher prices, some are deciding that they’ll absorb it to drive demand and some are doing something in between,” Jassy said. “I think you’re starting to see more of that impact”

- The comments are a notable shift from last year, when Jassy said Amazon hadn’t seen “prices appreciably go up” a few months after Trump annc’d tariffs

- Ubisoft shares fall after game cancellations, reduced guidance & a reorganization (link/link)

- Game cancellations: Effected 6 games, while also allocating more time to 7 titles

- The Co is lowering its fixed cost base: By an additional €200mn over the next 2 years

- This brings the total reduction in fixed costs since FY2022-23 to around €500mn

- This new objective is expected to bring total fixed costs to €1.25bn on a run-rate basis by March 2028, compared to €1.75bn in FY2022-23

- For FY2025-26 the Co now expects:

- Net bookings: ~€1.5bn, translating into -€330mn gross margin reduction

- Non-IFRS EBIT: -€1bn, mainly reflecting both the impact of the updated FY26 net bookings assumptions above and the following transformation related decisions that led to a one-off accelerated depreciation of around €650mn

- FCF: Between -€400mn and -€500mn

- Non-IFRS net debt: Between €150m and €250mn as of YE FY26, with a cash and cash equivalents position of between €1.25bn and €1.35bn vs. prior guidance of €1.5bn

- The Co no longer considers its previously communicated FY2026-27 guidance to be an appropriate reference and will therefore update it in May 2026

–>Ubisoft shares fell a dramatic -34% in reaction to the news

- Bezos’ Blue Origin to deploy thousands of satellites for new ‘TeraWave’ communications network (link/link)

- What was the announcement? The TeraWave architecture consists of 5,408 optically interconnected satellites in low Earth orbit (LEO) and medium Earth orbit (MEO)

- Timeline: Deployment of satellites is planned to begin in Q4 2027

- User parameters: The network is meant to serve a maximum of ~100k customers

- Speed targets:

- Globally distributed customers can each access speeds of up to 144 Gbps delivered using Q/V-band links from a constellation of 5,280 LEO satellites

- Up to 6 Tbps can be accessed via optical links from 128 MEO satellites

Stock Market Check

This Week's Other Curated News

Artificial Intelligence/Machine Learning

- Survey data shows a wide divide on AI’s impact: workers say AI saves little time and often adds an “AI tax” from rework, while C-suite leaders report major gains. Many staff feel anxious or overwhelmed, w/ limited use beyond drafts or search. Some cos that annc’d AI-driven cuts later restored human roles as promised efficiency hasn’t hit rev or ops yet. (The Wall Street Journal)

- Google annc’d Personal Intelligence for AI Mode, letting it tap Gmail and Photos to give tailored responses. The opt‑in feature helps plan trips, shop, and create personalized recs by using hotel bookings, memories, prefs, and past buys. Google says data isn’t used to train models, and users can toggle the feature anytime. (TechCrunch)

- Adobe annc’d Firefly Foundry, an AI platform using “commercially safe” models to help creators generate high‑fidelity media while preserving artistry and rights. Major partners incl. CAA, WME, UTA, B5 Studios & top directors. Launch comes as Hollywood faces AI concerns amid guild talks. Adobe says the tool supports end‑to‑end creative workflows; ~85% of Sundance picks used its tech. (Deadline)

- The Human Artistry Campaign annc’d a push claiming big tech cos are training gen‑AI on copyrighted works w/out permission. Backed by ~700 creatives, it argues artists’ careers are at risk and urges licensing + opt‑out rules. Supporters say real innovation comes from humans, while only a few Hollywood cos, incl. Disney, have begun sanctioned licensing for AI tools. (The Hollywood Reporter)

- Saudi Arabia’s National Infrastructure Fund and Humain annc’d a financing pact of up to $1. 2bn to expand AI and digital infra. The non-binding deal supports up to 250 megawatts of AI data centre capacity for customers and was annc’d in Davos. The move backs the kingdom’s push to diversify away from hydrocarbons. (Reuters)

- Meta CTO said the Co’s new Meta Superintelligence Labs team, formed last yr, delivered its first high-profile AI models internally in Jan. , calling them “very good.” The lab was created after leadership changes and criticism of Llama 4. Speaking at Davos, the CTO said more work is needed post-training, but Meta is starting to see returns from 2025 investments and expects consumer AI trends to firm up in 2026–2027. (Reuters)

- A blog post analyzes the electricity use of AI coding agents vs a ‘median query. ’ Drawing on Epoch AI and pricing data, the author estimates a typical Claude Code session consumes ~41 Wh, ~138x a 0.3 Wh median prompt, while a day of heavy use hits ~1,300 Wh. (Simon P Couch)

- Thousands of students will get college decisions faster as admissions offices adopt AI to read essays and review transcripts. Facing funding pressure, schools aim to streamline staff workloads w/ tech already used to screen job applicants. (Bloomberg)

- ServiceNow annc’d a multi‑yr strategic collaboration w/ OpenAI to accelerate enterprise AI outcomes. The deal enables customers to access frontier models, custom AI solutions, and scalable deployment w/out bespoke development. (ServiceNow)

- OpenAI annc’d rollout of age prediction on ChatGPT consumer plans to identify users likely under 18 and apply added safeguards. The tech uses behavioral and account signals to estimate age, defaulting to safer experiences. Teens get protections limiting sensitive content, while misclassified users can verify age via selfie. (OpenAI)

- News Corp annc’d a partnership w/ Symbolic. ai to deploy AI newsroom tools, starting w/ Dow Jones Newswires. The tech supports research, transcription, fact-checking, SEO and newsletter creation, aiming to cut fragmented workflows. (MediaPost)

- OpenAI Co outlines how ChatGPT evolved from research preview to core infra powering daily life and work. Broad adoption drove subscriptions, usage-based APIs, ads and commerce, w/ monetization scaling to value. Compute grew 3x YoY to ~1.9 GW by 2025, while rev rose 3x to $20bn+. A flywheel links compute, research, products and biz. (OpenAI)

Audio/Music/Podcast

- Spotify annc’d the rollout of its Prompted Playlist beta to US & Canada. The feature uses users’ full listening history + real-time world data to build playlists from natural-language prompts, w/ options for daily or weekly refresh. Tracks include context notes. It expands on AI Playlist by adding deeper personalization, world knowledge, and editable prompts for more dynamic curation. (9to5Mac)

- NetEase Cloud Music and Universal Music Group annc’d a strategic, multi-yr licensing agreement for China. The deal lets NetEase distribute UMG’s global catalog—mn of tracks from Chinese and international artists—across its streaming platform and digital svs. Cos will co-operate on marketing, product innovation, SVIP tiers, and artist-first AI rules to enhance fan experience and link China’s mkts w/ the global music biz. (Universal Music Group)

Cable/Pay-TV/Wireless

- Rakuten Mobile and Rakuten Bank annc’d a joint programme tightening links between the group’s telecoms and financial svs biz. Starting Feb., Rakuten Mobile subscribers w/ a Rakuten Bank account who meet set conditions can earn bonus interest on yen denominated ordinary deposits. (Telecompaper)

Capital Market Updates

- IPOs are set for a 2026 rebound as mkts look for bigger deals. Sports cos like SeatGeek, Hudl, Fanatics, New Era and Eagle Football may pursue listings amid investors’ need for liquidity. 2025 saw ~200 IPOs raise $44bn, but sports IPOs remain limited. StubHub’s weak post-IPO showing adds caution, and experts say a true surge in sports/tech listings may still be yrs away. (Sportico)

- Hedge funds saw ~$116bn in net inflows last yr, lifting industry assets past $5tn as performance added $527bn. Avg return hit 12.5%, the best in 16 yrs. Rising investor interest comes as uncertainty cont’d, pushing managers toward flexible, tactical strategies. HFR said this momentum is expected to accelerate into 2026, signaling stronger demand for hedge fund biz. (MSN)

- Japan’s bond selloff deepened as fiscal fears drove yields to record highs. The 40‑yr rate jumped past 4%, while 30‑ and 40‑yr yields rose >25 basis points, the biggest move since Apr. tariffs turmoil. Investors balked at PM Sanae Takaichi’s tax‑cut plans, citing unclear funding and higher bond issuance. (Yahoo Finance)

- Quant hedge funds started the yr in losses after crowded US equities sank, renewing worries about volatile returns. In early Jan., systematic long-short equity managers logged their worst 10-day stretch since Oct., w/ losses of ~1%, Goldman Sachs Group Inc. data showed. (Bloomberg)

- Bridgewater Associates said it remains bullish on Chinese stocks in 2025 after a local mkt rally lifted its onshore hedge fund by 45%, the best performance in at least five yrs. After strong gains last yr, the Co’s Shanghai-based arm said equities remain attractive as profit expectations improved, making it moderately optimistic on absolute returns and relative performance vs other assets. (Bloomberg)

- US blank-check bankers are active in Jan. as 2025 delivered a strong IPO yr, testing the importance of SPACs as a dealmaking tool. Investors have put over $2bn into SPAC IPOs this month, per SPAC Research. That follows ~$30bn raised across 144 firms last yr—the most since 2021—leaving nearly 200 SPACs seeking deals. (Bloomberg)

Cloud/DataCenters/IT Infrastructure

- OpenAI annc’d plans to pay for energy needs and limit water use at its Stargate data centers, saying it aims to be a “good neighbor” amid community pushback over utilities. The AI firm pledged to fund grid upgrades or secure its own power so ops don’t raise prices, and to cut potable water use via cooling tech and AI design tweaks. (The Verge)

Crypto/Blockchain/web3/NFTs

- Big US crypto players turned against the Clarity Act, a sweeping bill to regulate digital assets, after Coinbase CEO Brian Armstrong withdrew support, delaying Senate action. Infighting among crypto firms, banks, and DeFi groups over stablecoin rewards, oversight, and compliance risks stalling passage before midterms, despite White House backing and industry pressure. (Financial Times)

- Donald Trump’s family fortune reached ~$6. 8bn as his second term began. By the Jan. 2025 inauguration, his assets had shifted beyond real estate and licensing into a social media Co, a co‑founded crypto platform and a Trump memecoin. Digital assets added ~$1.4bn over the past yr, making crypto ~20% of the family’s wealth for the first time. (Bloomberg)

eCommerce/Social Commerce/Retail

- Store openings slowed in 2025 as net retail growth hit 0.7% amid tariffs and macro uncertainty, w/ many cos cutting capex and remodels. Telsey’s report sees 2026 accelerating to 1.4% led by beauty, off‑price and apparel, while luxury and dept. stores post net closings. Bankruptcies like Saks Global create real estate openings for expanding retailers, w/ Target and Walmart growing footprints. (Retail Dive)

- Xfinity annc’d a new membership program giving eligible customers automatic access to weekly perks, discounts, and exclusive experiences. The launch features VIP access to the BAHC Live! concert series in SF ahead of The Big Game. Members get rotating perks, savings on svs, and tiered benefits based on tenure and number of Xfinity svs, replacing the prior rewards program. (Comcast)

- Shopify annc’d merchants will pay a 4% fee on ChatGPT checkout sales starting Jan. 26th, while Google/Microsoft AI modes stay free. Via a data‑sharing program, products appear in AI chats by default unless cos block indexing. Agentic Storefronts routes orders into Shopify checkout. OpenAI’s Instant Checkout expands to Shopify. AI traffic up 7x, AI‑linked orders up 11x. (PYMNTS)

- Nike annc’d a regional leadership shakeup as CEO Elliott Hill pushes a turnaround. Carl Grebert and Angela Dong will exit, w/ César Garcia stepping into EMEA on Feb. 2 and Cathy Sparks named VP/GM Greater China; Cristin Campbell will serve interim in APLA. The changes, shared in a note on [Wed., Jan. 21], follow broader reforms since 2024. (Retail Dive)

- China has widened a probe into PDD Holdings Inc. , owner of Temu, after a physical altercation between staff and regulators at its Shanghai HQ, sources said. More than 100 investigators from SAMR and the STA conducted inspections in recent weeks over alleged fraudulent deliveries and tax issues. (Tech in Asia)

- An article examines Reliance’s claims of quick commerce growth. The Co says daily orders on its hyper-local svc peaked at 1.6mn in the Dec. quarter, vs Blinkit’s 2.4mn daily in Sept. Industry leaders and investors remain unconvinced, noting JioMart’s limited presence in tier 1 mkts and slower 30-min delivery vs 15-min rivals, raising doubts over metrics and narrative. (India Dispatch)

Electric & Autonomous Vehicles

- Waymo annc’d its robotaxi launch in Miami, marking its 6th U. S. mkt and expanding its lead as rivals lag. The svc covers a 60‑sq‑mi area, w/ airport access coming soon. ~10,000 residents signed up as Waymo partners w/ Moove for fleet svs. The Co plans broader 2026 U.S. expansions after ending 2025 w/ 450k weekly rides and 14mn trips. (CNBC)

- Tesla annc’d robotaxi rides in Austin w/ no safety driver, marking a shift from its initial supervised launch last Jun. The fleet now includes a few fully driverless cars, per Tesla AI lead, w/ the ratio set to rise. Riders are being charged, and some trips still use chase cars. Earlier tests in Dec. showed progress as Tesla pushes its AI-driven mobility strategy forward. (TechCrunch)

FinTech/InsurTech/Payments

- PayPal annc’d it will acquire Cymbio to boost its agentic commerce svs, making merchants’ catalogs discoverable on AI platforms like Copilot and Perplexity. Cymbio’s tech will power Store Sync, enabling seamless product + order mgmt w/ merchants staying merchant-of-record. Deal expected to close in H1 2026; terms undisclosed. (PayPal)

- PhonePe updated its IPO filing, showing Tiger Global & Microsoft will fully exit while Walmart keeps majority stake, selling ~45. 9mn shares. Total 50.66mn shares offered. Valued at ~$12bn in 2023, targeting ~$15bn. PhonePe leads India’s digital payments mkts, processing 9.81bn UPI txns in Dec. 2025. In the 6 mos to Sept. 2025, ops rev rose 22% to ₹39.19bn, though losses widened to ₹14.44bn. (TechCrunch)

Live Entertainment/Theme Parks/Concerts/Experiential

- Sphere Entertainment Co, w/ the State of Maryland, Prince George’s County and Peterson Cos, annc’d intent to build a smaller-scale Sphere at National Harbor, its second US venue. The project would use ~$200mn in state, local and private incentives, support ~2,500 construction jobs and 4,750 roles once open, and generate >$1bn in annual impact. (Sphere Entertainment Co.)

M&A

- Activist investors are set to escalate pressure on Cos in 2026, pushing more sales and breakups as M&A heats up. Data show 54% of campaigns in H2 2025 urged deals vs 35% in H1. M&A is viewed as the fastest path to returns, helping some funds deliver double‑digit gains as mkts improve and small‑, mid‑cap targets draw interest. (Reuters)

- CK Hutchison is in advanced talks to sell Three Ireland to Liberty Global, marking another step in the Co’s exit from European telecoms. The deal, valued at up to €1.5bn, would strengthen Liberty’s presence in Ireland, where it currently operates broadband and a virtual mobile svs. (Financial Times)

Macro Updates

- US GDP in Q3 grew at an adj 4. 4% pace, boosted by exports, biz investment and strong consumer spend at 3.5%. Final sales rose 2.9%, signaling steady underlying demand. Economists describe a K‑shape trend, w/ high‑income households and big cos supported by mkts and home prices, while small biz face tariff‑driven costs and tighter labor supply that strain ops. (Reuters)

- Amazon plans new job cuts starting, targeting ~14,000 roles across AWS, retail, Prime Video & HR, matching last yr’s cuts. CEO Jassy says reductions aren’t financial or AI-driven but tied to Co culture + excess layers. Total goal is 30,000 corporate cuts, ~10% of staff, marking Amazon’s largest layoff as AI boosts internal efficiencies. (Reuters)

- Cautious U. S. consumers avoided big-ticket purchases in 2025, favoring smaller items like used goods, apparel and dining out, per Bank of America Institute card data. Researchers cited a split in discretionary spend as jobs and sentiment weakened. Outlook for 2026 hinges on labor mkts, though tax refunds ~18% higher could briefly boost low-income spending and inject ~$65bn. (Retail Dive)

- U.S. stocks rallied after Pres. Trump annc’d a framework for a Greenland deal w/ NATO, easing tariff fears. Dow rose 589 pts (1.2%), while S&P 500 and Nasdaq also gained 1.2%, marking S&P’s best daily % since Nov. Trade‑sensitive shares jumped, volatility fell, Treasurys rose, and the 10‑yr yield slipped to 4.25%, though some caution trade risks cont’d. (The Wall Street Journal)

- The Trump admin projects 4–5% real U. S. GDP growth in 2026, far above current forecasts. Treasury Sec Scott Bessent said strong rev growth, tax refunds of up to $1,000, and gov’t spending shifts could lift demand, while AI adoption may aid productivity. (MSN)

- China’s economic growth slowed in Q4 to 4. 5%, its weakest pace in nearly three yrs, as softer domestic demand weighed on activity, according to official data. Full-yr GDP still rose 5%, meeting Beijing’s target despite trade frictions and a prolonged property slump. Retail sales grew just 0.9% in Dec., while industrial output climbed 5.2%. (CNBC)

- Donald Trump annc’d escalating U.S. tariffs on imports from eight European NATO allies unless a deal is reached for a cont’d push to buy Greenland. Rates start at 10% on Feb. 1 and rise to 25% by June 1, stacking on existing duties. (CNBC)

Media Conglomerates

- Warner Bros. Discovery annc’d via a proxy filing financial projections for CNN tied to its planned Discovery Global spinoff. CNN rev is seen at $1.8bn in 2026, rising to ~$2.2bn by 2030, w/ adj EBITDA ~ $600mn, dipping in 2027 amid (4)% core rev declines. (The Hollywood Reporter)

- Disney Co board is searching for CEO Bob Iger’s successor as his contract ends this yr, w/ chairman James Gorman overseeing the process. Four internal candidates are in contention, led by parks chief Josh D’Amaro, alongside Dana Walden, Alan Bergman and Jimmy Pitaro. (Los Angeles Times)

Regulatory

- Ofcom opened an investigation into Meta’s compliance w/ section 135 info requests issued on 31 Jul 2024 and 19 Jun 2025 for mkts monitoring and the Wholesale A2P SMS Termination review. As a provider of alternative biz messaging svs, Meta’s WhatsApp Business data was required, but evidence suggests responses weren’t complete/accurate. (Ofcom)

- A hearing revealed Epic and Google struck a secret ~$800mn, six‑yr partnership involving Unreal Engine, Fortnite, and Android. Judge Donato questioned if the deal—incl. joint product dev, mkting, and Google using Epic’s core tech—softened Epic’s antitrust demands. CEO Sweeney hinted at metaverse ties as most details stayed sealed. (The Verge)

- China told major tech cos incl. Alibaba, Tencent & ByteDance they can prep orders for Nvidia’s H200, signaling likely import approval. Regulators gave in‑principle clearance, though Beijing may require buys of domestic chips. Move aids hyperscalers building AI svs and is a win for Nvidia, which sees strong AI chip rev. (Yahoo Finance)

- US Supreme Court delayed ruling on challenges to President Trump’s tariffs, heading into a four-week recess w/o decisions. After the hearing, the next session is Feb. 20, keeping disputed duties in force. Tariffs cost importers >$16bn per month and could exceed $170bn by Feb. 20. The court heard arguments Nov. 5, but refunds may be complex, w/ 1,500+ biz cases already filed. (MSN)

- Snap annc’d a settlement to avoid a landmark trial over claims social media platforms engineered features to hook young users. The case, among several vs Meta, TikTok and YouTube, argues tools like infinite scroll caused mental health harm and are inherently defective. Terms weren’t disclosed. (The New York Times)

Satellite/Space

- WSJ reports Elon Musk is racing to take SpaceX public, driven by plans to deploy AI data centers in orbit. Once resistant to an IPO, the Co now sees public mkts as the fastest way to raise tens of bn to fund solar‑powered AI satellites and support xAI, which lags rivals. SpaceX may select banks soon, targeting a July IPO, cont’d ties w/ xAI, including a prior $2bn investment. (The Wall Street Journal)

Social/Digital Media

- Snap annc’d new Family Center tools after settling a suit alleging teen addiction. Parents can track teens’ daily app use, see time spent across features, and view how new friends are known via mutuals/contacts/communities. Updates aim to boost trust, address safety concerns, and follow prior additions like interaction logs, time limits, and blocking My AI. (TechCrunch)

- UK ministers annc’d a consultation on whether to ban social media use for under-16s, amid rising concern over young people’s phone use and online harm. Tech secretary Liz Kendall said existing Online Safety Act measures are not enough, as peers prepare to vote on an amendment to impose a ban within a yr. PM Keir Starmer said he is open to the idea but wants evidence from Australia. (The Guardian)

- A Similarweb report finds Meta’s Threads has surpassed Elon Musk’s X in daily mobile users, reaching ~141. 5mn on iOS and Android vs 125mn for X. Growth reflects longer-term trends, not recent X controversies tied to Grok deepfake probes. Threads’ momentum is driven by Meta cross-promotion, creator focus, and new features, though X still leads on the web. (TechCrunch)

Software

- Private equity firm Thoma Bravo is seeking software deals after a sector sell-off, seeing a “huge buying opportunity,” co-founder Orlando Bravo told the FT. Software mkts fell ~7% in recent weeks amid AI fears, but the Co argues specialised biz w/ deep domain knowledge are insulated. (Financial Times)

- Adobe annc’d new AI tools for Acrobat, expanding document editing and creation. Users can turn files or shared Spaces into presentations via text prompts, using Express themes and images, or generate podcast-style summaries. Acrobat adds prompt-based edits for ~12 actions and AI summaries w/ citations in shared files. (TechCrunch)

- Spotify, w/ Sony, Warner and UMG, won a sealed US court order against shadow library Anna’s Archive, leading to the takedown of its.org domain. A temporary restraining order and later preliminary injunction required domain registries and svs like Cloudflare to disable access, alleging copyright infringement tied to scraped Spotify data. . (Ars Technica)

Sports/Sports Betting

- Paramount annc’d it will sell live, in-game programmatic ads during select marquee UFC events on Paramount+, starting Jan. 24, allowing guaranteed, real-time placements in streamed sports for the first time. The move supports broader mkts access via Amazon, Google, Trade Desk and Yahoo DSPs, while key main cards use fixed units. (Variety)

- Sports Illustrated annc’d SI TV, a free ad-supported streaming channel available 24/7 on multiple FAST platforms. The launch extends SI’s video push w/ original programming, live events, sports lifestyle and archival content, incl docuseries, podcasts and live games. (Business Wire)

Tech Hardware

- Silicon Valley’s biggest tech cos boosted lobbying to $109mn as they courted Trump, aligning AI priorities w/ his agenda. Meta, Amazon, Google, Nvidia, OpenAI and others expanded DC ops, hired Trump allies and praised his policies to ease export limits, cut regs and secure China access. In return, Trump pushed pro-tech moves while expecting major domestic investments. (MSN)

Towers/Fiber

- The consortium of Bouygues Telecom, Free‑iliad Group & Orange annc’d that due‑diligence begun in early Jan. 2026 for a potential deal to acquire major Altice France telecom activities. Terms aren’t agreed, no certainty of completion, & any pact needs party approvals. Orange notes 2024 rev of €40.3bn & 310mn customers as part of its broader biz context. (Orange)

Video Games/Interactive Entertainment

- Nintendo Co shares rose after Circana data showed Switch 2’s Dec. rebound, keeping it 2025’s top US console. Despite a Nov. tariff-hit slump, hardware spending grew 9%. US games mkts were flat at $60.7bn, as svs subs grew 20%. Fortnite led engagement, while Roblox saw 16% rev growth. (Bloomberg)

Video Streaming

- Samsung TV Plus annc’d it surpassed 100mn monthly active users globally, driven by double‑digit viewership growth and a 25% yr‑over‑yr rise in streaming hours in 2025. Growth came from live events, interactive fan experiences like a Jonas Brothers livestream, creator‑led partnerships, and brand deals across music and major sports leagues. (Variety)

- Nielsen said streaming hit a record 47.5% of TV viewing in Dec. 2025, surpassing Jul. highs. A historic Christmas Day drove the surge, w/ 55.1bn viewing minutes, up 8% vs prior record, as NFL games on Netflix and Prime Video and new Stranger Things eps lifted usage to 54% of daily TV. (Nielsen)

- Nielsen data shows Christmas Day 2025 marked the highest streaming usage ever in the U. S., fueled by streaming‑only NFL games and new Stranger Things episodes. Viewers logged 55.1bn minutes, ~54% of all TV use, breaking 2024’s record. The surge pushed streaming to 47.5% of Dec. TV use, while broadcast and cable shares fell. (The Hollywood Reporter)

- Actor Matt Damon said Netflix influences how movies are made, citing viewer phone use at home. Speaking w/ Ben Affleck on the Joe Rogan Experience, Damon said the streamer pushes big action scenes earlier and suggests restating plots “three or four times” in dialogue to hold attention. (Variety)