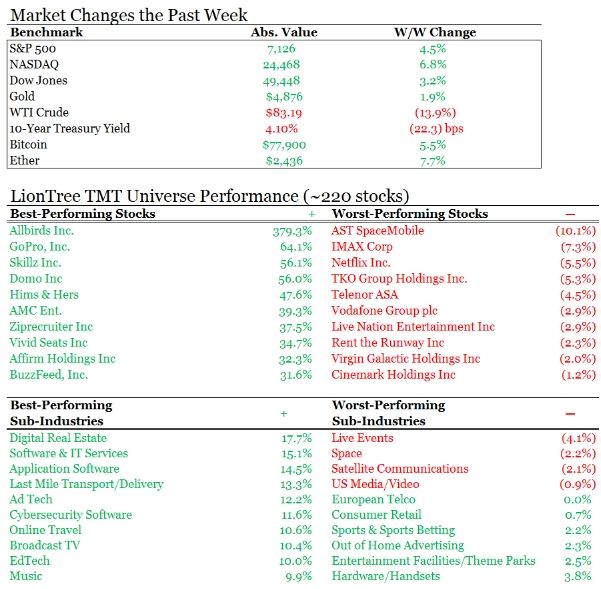

Nasdaq posted its 13 straight up session, which is the 15th longest winning streak on record! That is thanks to favorable Trump comments about movement towards the end of the Iran war. Importantly, crude oil prices were pushed to multi-week lows. Let’s hope for no surprises over the weekend.

Re-assuring comments regarding consumer spend resiliency and limited impact thus far from the geopolitical backdrop from key bank earnings this week also helped the market. TMT earnings also kicked off with heavy-weight Netflix reporting, though investors had hoped for more (see Theme #1). Sector prints will start to ramp next week.

See below for our focus areas in this edition. I especially wouldn’t miss Theme #3 where we dove into an incredible Stanford University AI-related dataset report.

- Netflix Is Heads Down In Execution Mode

- Snap ’s New Actions To Right The Ship

- AI Can Code But Can’t Tell Time?!

- State-Level Pushback Against Data Center Expansion Is Growing

- This Week’s Most Impactful AI Updates …The Battle Intensifies

- TikTok, Instagram, and Snapchat Play Very Different Roles in Teens’ Lives

- Amazon Officially Pushes Harder Into Satellite Ambitions W/ Globalstar Deal

- Grab Bag: Uber Commits $10bn To AVs, Apple Is Actively Testing New Glasses , & Allbirds Transitions To AI Compute

**Last call-out for our most recent quarterly report, LionTree’s Lens – Spring 2026… CLICK HERE to access our report and video narration**

Have a great weekend. We’ll unfortunately be back to the 50o+ here in NYC vs the summer weather this week!

Best,

Leslie

Netflix Is Heads Down In Execution Mode

It was another tough quarter for Netflix. While Q1 was essentially in-line with lowered expectations when excluding the WBD termination fee windfall, Q2 guidance fell below Street projections. With that said, mgmt still believes that it is on track to hit the FY2026 outlook, albeit back-end loaded with operating margins.

On the plus side, the recent price hike has been well received, and their price / value ratio remains compelling. In the US, Netflix subs are paying “the least per hour of viewing compared to other SVOD offerings” and “in some case, you’d have to pay two times per hour to get a competitive service.”

Investors have also been very focused on the Co’s engagement trends and, while not transparent, mgmt’s KPI of “member quality” hit an all-time high. More traditional measures like view hours were also up and the Co saw positive retention across regions y/y. All of this supports the argument that incremental products like gaming (still viewed as a huge opportunity), podcasts, and live events are enhancing stickiness rather than cannibalizing core viewing.

Speaking about live content, it was interesting to hear Netflix confirm that it is currently in discussions with the NFL, but still within a sports strategy of tent-pole events which has not changed.

The advertising business is on track to double y/y in 2026, and programmatic is expected to grow to over 50% of non-live advertising revenue over time.

AI also remains a cornerstone to the narrative and NFLX thinks they will be leading the charge with AI production, and their recent acquisition of InterPositive will bolster their capabilities on this front.

Lastly, Reed Hastings’ decision to not stand for Board re-election post his current term (expires at the Annual Meeting in June) also stood out. It is the end of an era.

Overall, investors were hoping for more, but little has changed with the yearly outlook and in our mind it is all about mgmt executing on the playbook and new initiatives looking ahead.

-> NFLX shares fell -10% in reaction but the stock is still up +4% YTD

Q1 Was Essentially ~In-Line Though WBD Termination Fee Was A Windfall To Adj EPS & FCF

- Rev BEAT cons by +0.6% and grew by +16% y/y (+14% y/y FXN)

- Growth was driven primarily by membership growth, higher pricing, and increased ad revenue, with additional upside from favorable F/X and stronger-than-expected subs

- Op margin MISSED cons (32.3% vs cons 32.4%)

- +60bps y/y due to op leverage

- Adj EPS BEAT cons by +61.8%

- Driven by higher op income & a $2.88bn termination fee related to WBD transaction

- FCF BEAT cons by +67%

- Driven by stronger operating performance and the termination fee

- Repurchases resumed following the termination of the Warner Bros. transaction…Q1 buyback was $1.3bn, leaving $6.8bn remaining on the authorization

Q2 Guidance Disappointed Investors BUT Mgmt Reiterated The Full Year 2026 Outlook…Margin Growth Remains H2 Weighted

- Q2 guidance MISSED cons… still implies moderating growth and margin pressure

- Rev guidance of $12.57bn MISSED cons by -0.1%…implies +13.5% y/y growth (+12% FXN) vs cons of +14.1%

- Growth reflects cont’d membership and pricing growth but decelerating vs Q1

- Op margin guidance of 32.6% MISSED cons 33.4% but is up from 34.1% y/y and reflects higher content amortization

- EPS guidance of $0.78 MISSED cons of $0.84

- Reflects normalization vs Q1’s non-recurring benefit

- Rev guidance of $12.57bn MISSED cons by -0.1%…implies +13.5% y/y growth (+12% FXN) vs cons of +14.1%

- 2026 guidance UNCHANGED

- Rev guidance at the mid-pt is +0.3% ahead of cons and implies +12-14% y/y growth (+11-13% FXN), vs +16% y/y in 2025

- Growth will be driven by membership growth, pricing, and a projected ~2x increase in ad revenue

- Op margin guidance of 31.5% (includes ~$275mn of acq-related expenses) remains below cons 32.7%, but is up from 29.5% in 2025

- Margin progression remains back-end loaded due to higher content amortization growth in H1, with moderation in H2

- Rev guidance at the mid-pt is +0.3% ahead of cons and implies +12-14% y/y growth (+11-13% FXN), vs +16% y/y in 2025

- 2026 FCF guidance RAISED to ~$12.5bn (vs prior $11bn), driven by the WBD termination fee and strong underlying cash generation

“Member Quality” KPI Hits An All-Time Highs Based On Mgmt’s Data

- Total Q1 view hours growth was consistent with H2’25 trends despite external competition (e.g., Olympics) but mgmt. reiterates how that is not the only engagement metric

- Their primary engagement KPI of “member quality” hit another all-time high…retention improved across all regions y/y

- They don’t disclose their “Member Quality” calculation for competitive reasons

Growth In The Advertising Business Remains ON TRACK…Programmatic Is Also Expected To Increase To Over 50% Of Non-Live Ads Mix Over Time

- Mgmt reiterated expectation to ~2x ad revenue y/y to ~$3bn in 2026

- The Co’s advertiser ecosystem is scaling rapidly

- The advertiser base grew +70% y/y to 4,000+ and expect further expansion

- But NFLX is still concentrated in the top advertiser accounts

- Their strategic path for ad revenue growth…

- Have been making it easier for advertisers to buy on their platform

- Added more DSP integrations which also provides more ways to buy

- Improving go-to-mkt capabilities

- Increasing the sales force

- Continuing to build ad products

- Leverage AI w/in the Netflix ad suite which will make it easier to design new creative formats, custom ads, improved contextual relevance, etc

- Programmatic ad buying will increase…it is expected to exceed 50% of non-live ads revenue over time

- Ad tier traction remains strong

- >60% of sign-ups in ads markets are coming from ad-supported plan

The Co Maintained Its Cash Content Spend Ratio

- Continue to expect an annual cash content spend-to-amortization ratio of ~1.1x

- The vast majority of their content budget remains on core series and films…highlights in the slate:

- Films

- Here Comes the Flood with Denzel Washington

- Greta Gerwig’s Narnia

- Series

- Will Ferrell’s The Hawk

- One Hundred Years of Solitude S2

- Lupin Part 4

- Films

Live Content Is Still Small BUT Demonstrating Disproportionate Impact…Discussions With The NFL Are Underway

- The Co aired 70+ live events in Q1, compared to 200+ across all of FY2025, ie, already accounting for ~35% of last year’s total…Q1 successes include:

- World Baseball Classic which was exclusively for members in Japan was a huge hit

- Delivered 31.4mn viewers

- 3rd most-watched program ever on Netflix in Japan

- Led to the largest day of sign-ups in the country (Japan was the largest contributor to member growth in Q1)

- BTS The Comeback Live also had a strong showing

- Delivered 18.4mn global viewers

- Reached the weekly Top 10 in 80 countries

- Coming up…UK fight between Tyson Fury and Anthony Joshua

- World Baseball Classic which was exclusively for members in Japan was a huge hit

- The Cos sports strategy is “unchanged” as they are most interested in those “big breakthrough events, less so in the regular season packages”

- Ramping up sports events globally and locally

- Multiyear deal with CONCACAF for rights in Mexico

- The Women’s World Cup in US and Canada

- The M&A event with Ronda Rousey and Carano

- Ramping up sports events globally and locally

- NFLX is “in discussions” with the NFL right now as they “think there’s an opportunity to expand the relationship”

- “We’ve learned a lot about how what works and how to value the NFL and live generally over the last couple of years”

- “And this is going to inform how we have those discussions and help us be much even more disciplined”

Bullish On The Expansion Into Gaming & Podcasts Are Showing Incremental Engagement

- Continue to see gaming as a “significant” market opportunity…”we’re still really just scratching the surface today in terms of what we can ultimately do in this space”

- Launched a new “Playground” kids app

- ~10% of kids’ profiles have played NFLX games and almost 50% of kids’ profiles view content on mobile and table

- Expect to add more kids’ games in “the coming months”

- Seeing “promising traction” for their cloud TV games

- “We believe game play can have a positive impact on member retention”

- Launched a new “Playground” kids app

- Podcasts are showing early signs of incremental engagement (not substitution)…this can be seen given the Co is over-indexing on daytime viewing (which is normally lighter) and higher mobile usage

“Netflix Is Going To Remain At The Forefront In The Exploration And Innovation Of AI In The Creative Process”

- The Co focuses generative AI investment where it has “differential or unique capability to deliver returns to the business”

- Content: “Content production is a big one” and “member experience is another big one”

- User experience: “We’ve been in personalization and recommendation for two decades” but still see “tremendous room and opportunity to make it even better by leveraging some of these newer technologies”

- New model architectures in recommendation systems are already “driving increased engagement with the service” and act as a “force multiplier” on content investments

- On the content side, “it takes a great artist to make great art and AI won’t change that”

- AI will give those artists better tools to bring those visions to life

- The tools will help with “references, previsualization, visual effects, sequence prep, shot planning”

- The acq of InterPositive accelerates NFLX’s Gen AI capabilities b/c it’s a proprietary tech that was created specifically for filmmakers

- Even though ownership of InerPositive is new, there have been a “bunch of interest” with their creators

Several Other Key Points

- Netflix still has a big TAM for future growth …they currently have:

- <45% penetration of broadband households

- ~5% global TV view share globally

- ~7% share of their addressable revenue pool

- Price increases have “gone well” and just annc’d price adjustments in Spain

- Subscribers are still getting great value:

- In the US, Netflix subs are paying “the least per hour of viewing compared to other SVOD offerings”

- “In some case, you’d have to pay two times per hour to get a competitive service”

- Subscribers are still getting great value:

- The Co is launching vertical video at the end of the month

Snap ’s New Actions To Right The Ship

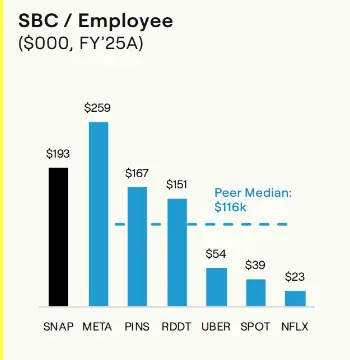

Just two weeks after activist investor Irenic Capital Mgmt’s public letter to Snap CEO Evan Spiegel advocating for employee cuts, changes to stock comp frameworks, and increased use of AI for internal efficiencies (plus several other proposed actions that it thought would get the stock to $26.37/share), Spiegel officially announced employee and cost guidance changes this week. 16% of the workforce is being eliminated, which will lead to $500mn+ in annualized savings. The Co also reduced its 2026 cost guidance for adj operating expenses and stock-based comp. Preliminary Q1 adj EBITDA is also 26% ahead of current consensus, with Q1 revenue trends on track (was a sigh of relief post last qtr’s trends).

Given Irenic’s argument that Snap’s stock based comp (SBC) per employee is too high, we did a quick calculation using Snap’s new lower headcount and the new SBC 2026 guidance, and SBC/employee actually goes from $193k in 2025 to an estimated $237k in 2026, so some investors could argue that the SBC cuts could have been higher.

Regardless, the Co’s cost base is coming down as Snap navigates being “squeezed between giants with enormous resources and nimble startups moving fast.” It is focused on its structural pivot toward “profitable growth” which mgmt. began talking about on their Q3:25 earnings call in November.

We expect additional color on this announcement during the Co’s May 6th earnings call, along with updates on the future direction of the Spectacles business (Irenic was pushing the Company to either sell it or shut it down), the Perplexity deal (which is reportedly “dead” – link), and any competitive pressure from OpenAI’s new advertising launch.

See below for more of the key points in our mind from Snap’s update.

-> Snap shares rallied +6.5% on the back of the update and are up +53% from its $3.93 low on March 27th, 2026; With that said, it is still down -39% from its 52-wk high of $10.40 back in July 2025

- Q1 preliminary numbers are ABOVE cons, especially on profitability:

- Rev of $1.53bn was a slight +1% above cons (and is at the high end of the prior guidance of $1.50-1.53bn)

- Adj EBITDA of $233mn BEAT cons by +26% (and prior guidance of $170-190mn)

- Cutting ~1,000 employees or ~16% of the full-time base (note that Irenic had advocated for ~1.5k total cuts…1k core + 500 Spectacles)

- Est’d annualized cost savings is $500mn+ (based on H2:26)

- Restructuring costs: ~$95-$130mn (the majority expected to be incurred in Q2)

- Mgmt updated the FY 2026 cost structure guidance, with a bias towards reductions:

- Maintained FY guidance for:

- Infrastructure costs: $1.6-1.65bn

- All other adj cost of rev (ex-Infrastructure costs): 16–17% of rev

- Lowered FY guidance for:

- Adj operating expenses: Cut by $250mn to ~$2.75bn

- Stock-based compensation: Cut by $150mn to ~$1.05bn

- Maintained FY guidance for:

-> Back of the envelope, based on a new est’d employee count of 4,419 after the 16% reduction, and the new $1.05bn stock-based comp, that implies $237k SBC/employee which would be an increase from $193k in 2025; Aside from cuts to SBC/employee, Irenic was also pushing Snap to move from a purely time-based approach to 2/3 performance vested w/ $10 and $15 share price targets

Irenic’s previous analysis circulated on March 31st

Source: Irenic Presentation

- Mgmt reiterated 60%+ gross margins guidance for 2026, which is slightly above cons 59% and up from 55% in 2025…how to get there:

- Monetizable growth focus (higher-value geos / users)

- Mix shift to higher-margin ad placements

- Scaling subscriptions (Snapchat+ + direct rev streams)

- The Co has been “significantly scaling” AI across product + engineering workflows enabling teams to focus more on strategic priorities and move faster

- 65%+ of new code is generated by AI

- AI agents are delivering measurable productivity

- 1mn+ support queries/month have been handled

- 7,500+ bugs have been identified via code review agent

- Mgmt reiterated their long term strategic goals

- 1bn MAUs

- Revenue growth pillars

- Accelerate direct response advertising share gains

- Increase content engagement to drive monetization

- Scale subscriptions + diversify revenue

- Financial goals

- Sustained EBITDA profitability + positive FCF

- A clear path to net income profitability

- Strategic positioning

- Lead the next computing platform transition

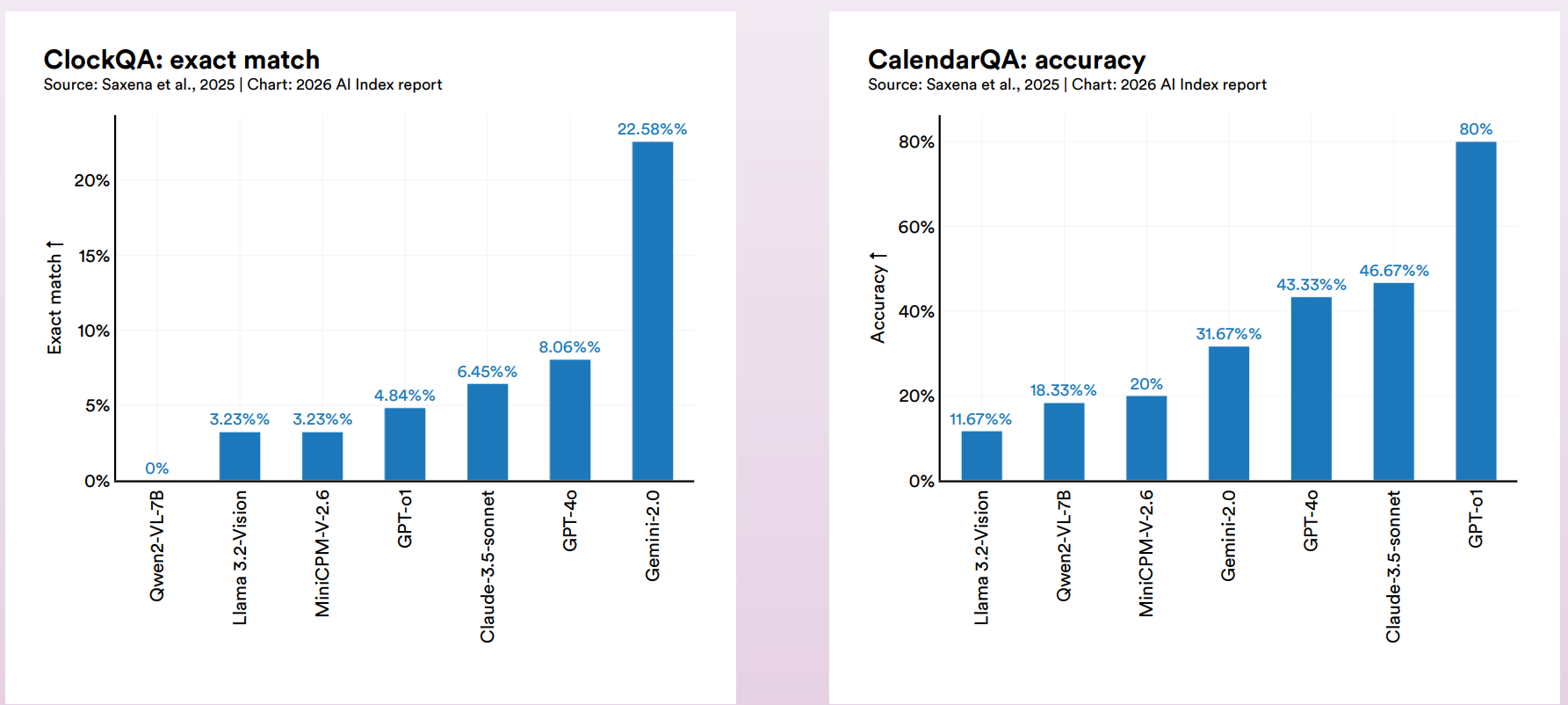

AI Can Code But Can’t Tell Time?!

Stanford University’s 2026 AI Index Report was one of the most comprehensive data reports that we have seen, maybe ever! The 423-page report (!) has AI data related to technical performance, infrastructure, environmental impact, jobs and workforce, investment levels, impact on science/medicine, and more. The authors pride themselves in being a 100% neutral party trying to provide the public, corporations, researchers, and governments data on which to come to their own strategies and conclusions about AI. Big picture though, the data shows that AI is scaling faster than systems around it can adapt.

It was hard to pick our Top 15 insights, given there are many, many, more, but see below. (One of most fascinating was that was that top models read analog clocks correctly just 50.1% of the time vs 90.1% for humans!).

The full report can be accessed HERE

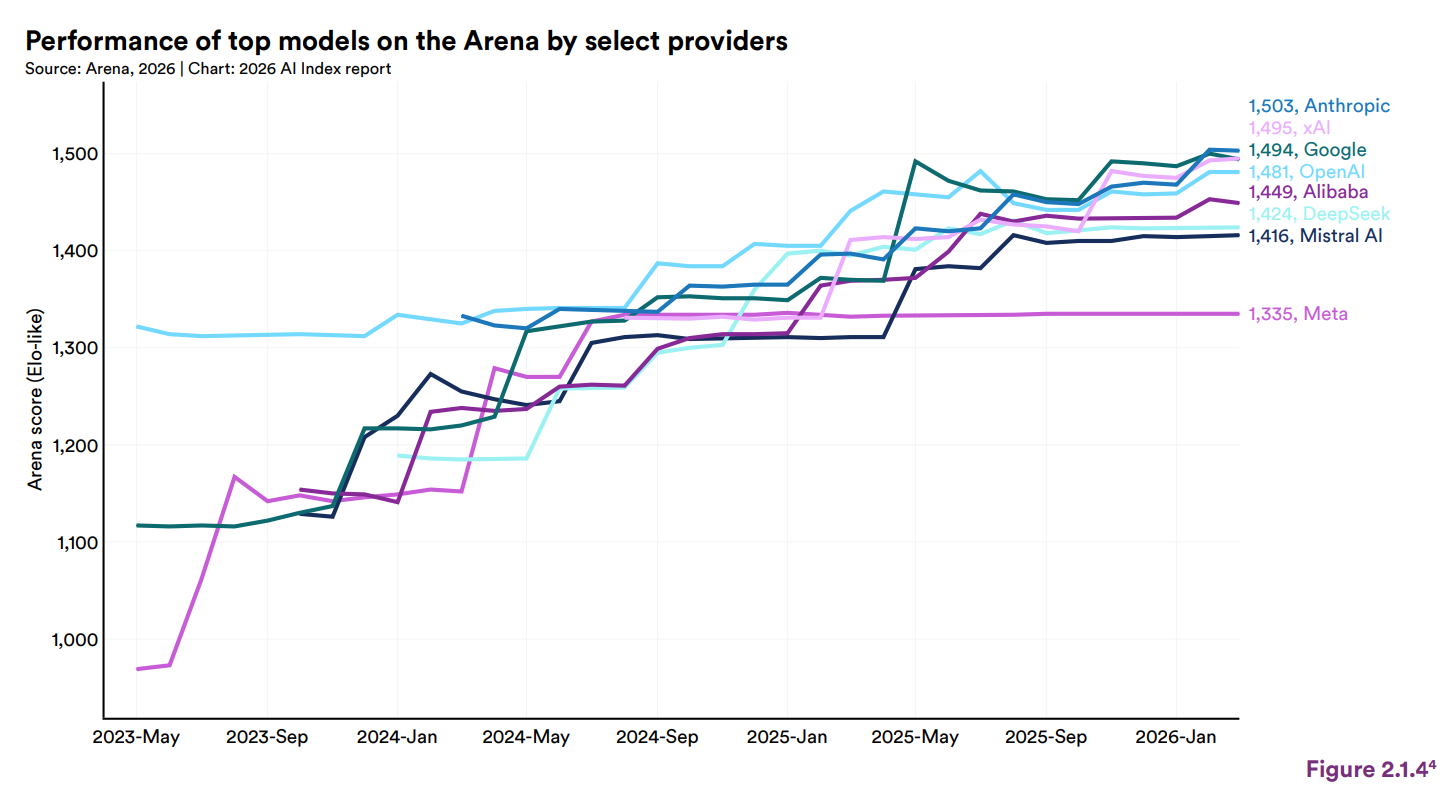

- Top model performance is converging, w/ 4 companies now clustered within 25 Elo points (inspired by chess ratings) when rated against one another by human voting in the Arena Leaderboard and benchmark

- The AI gap between the US and China has closed…

- In February 2025, DeepSeek-R1 briefly matched the top U.S. model, and as of March 2026 Anthropic’s top model leads by just 2.7%

- China leads in publication volume, citations, and patent grants, while the U.S. retains higher-impact patents and produced 50 notable models in 2025 vs China’s 30

- South Korea leads in AI patents per capita, and China’s share of the top 100 most-cited AI papers grew from 33 in 2021 to 41 in 2024

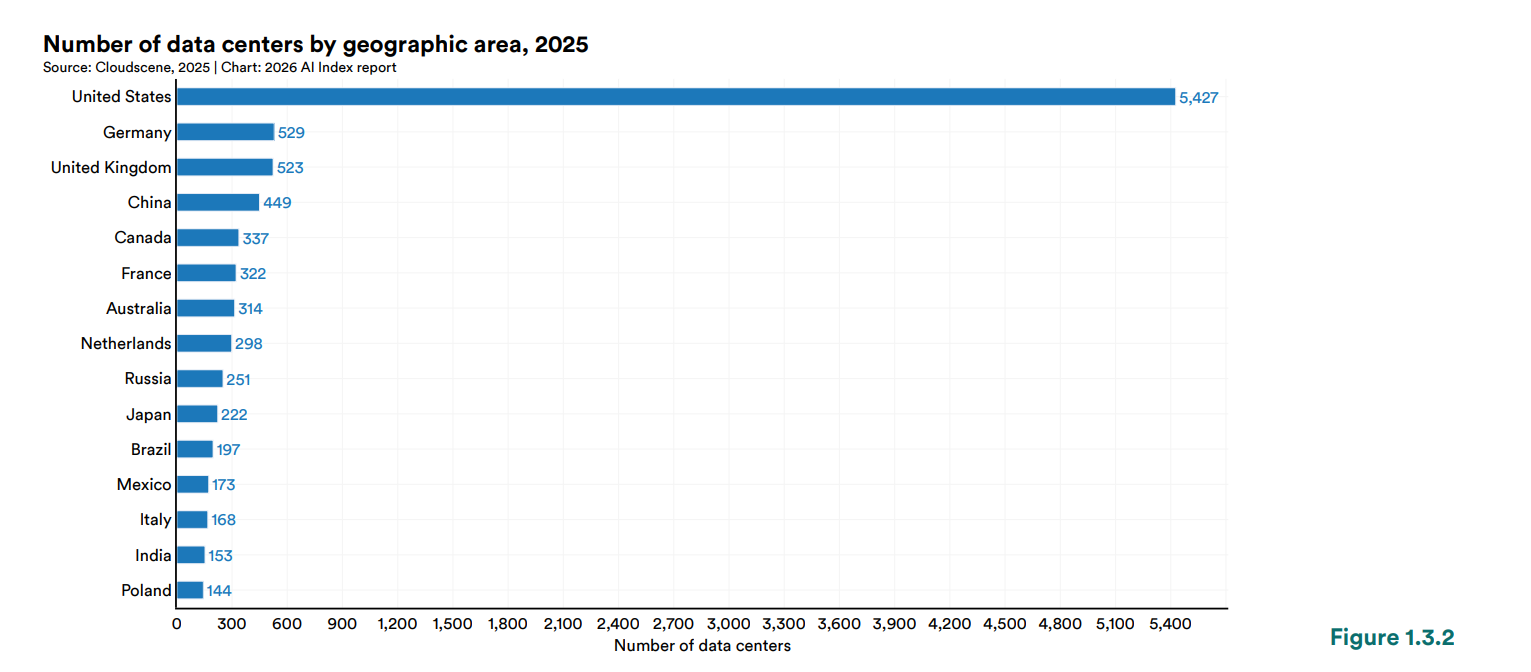

- The US has 10x as many datacenters (5,427) and consume more energy than any other country

- Also, TSMC fabricates almost every leading AI chip, making the global AI hardware supply chain dependent on one foundry in Taiwan (though a TSMC-U.S. expansion began operations in 2025)

- Regarding AI’s environmental footprint in 2025:

- Grok 4’s est’d training emissions reached 72,816 tons of CO₂ equivalent

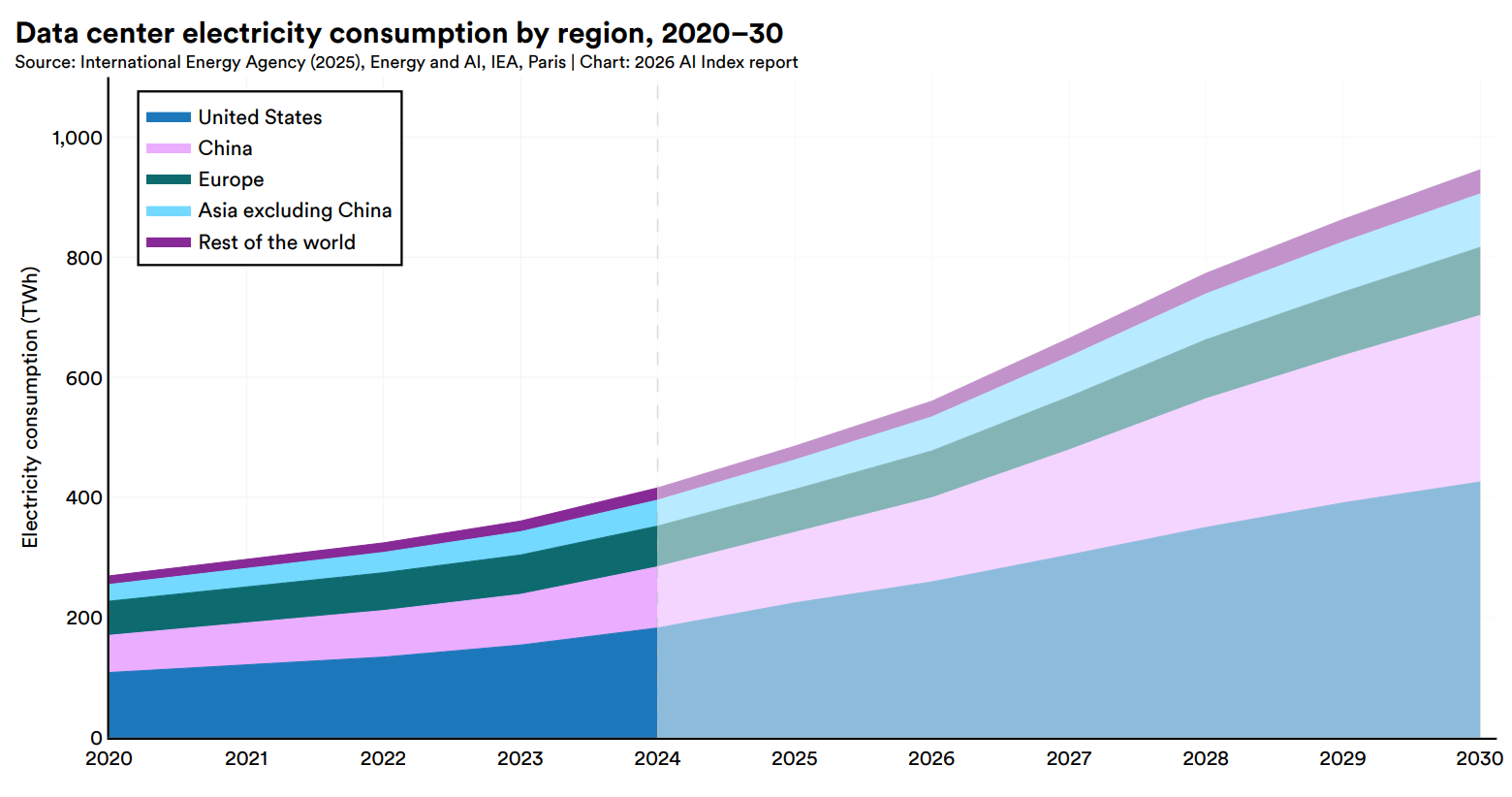

- AI data center power capacity rose to 29.6 GW which is comparable to NY state at peak demand

- Annual GPT-4o inference water use alone may exceed the drinking water needs of 12mn people

- See below for est’d data center electricity consumption by region through 2030

- AI models can win a gold medal at the International Mathematical Olympiad BUT CANNOT reliably tell time

- Researchers call this jagged frontier of AI

- Gemini Deep Think earned a gold medal at IMO

- BUT top models read analog clocks correctly just 50.1% of the time vs 90.1% for humans (who failed this?!)

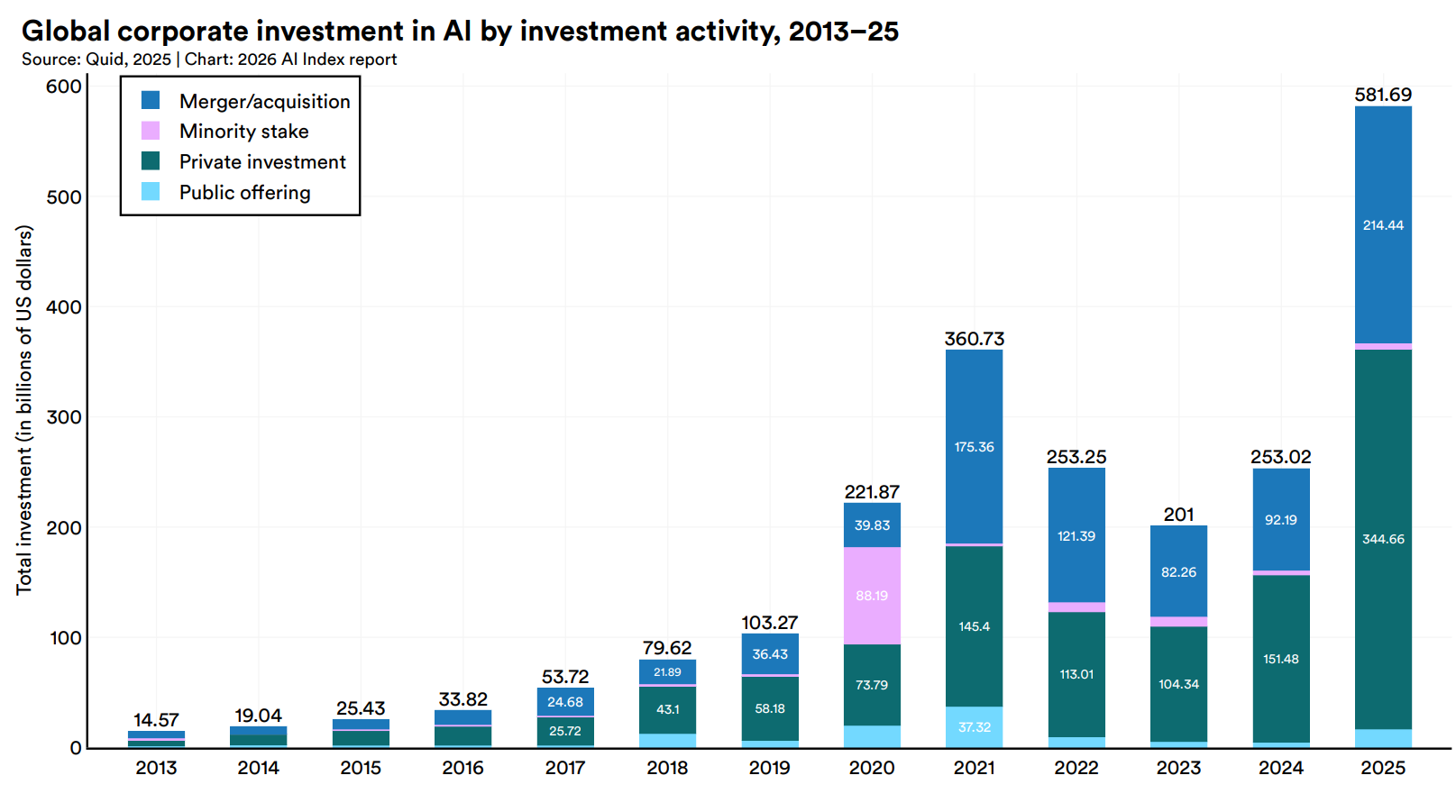

- Global corporate AI investment more than doubled y/y in 2025

- Private investment grew fastest at 127.5% y/y and now accounts for 60% of the total

- Generative AI investment grew more than 200% y/y and captured nearly half of all private AI funding

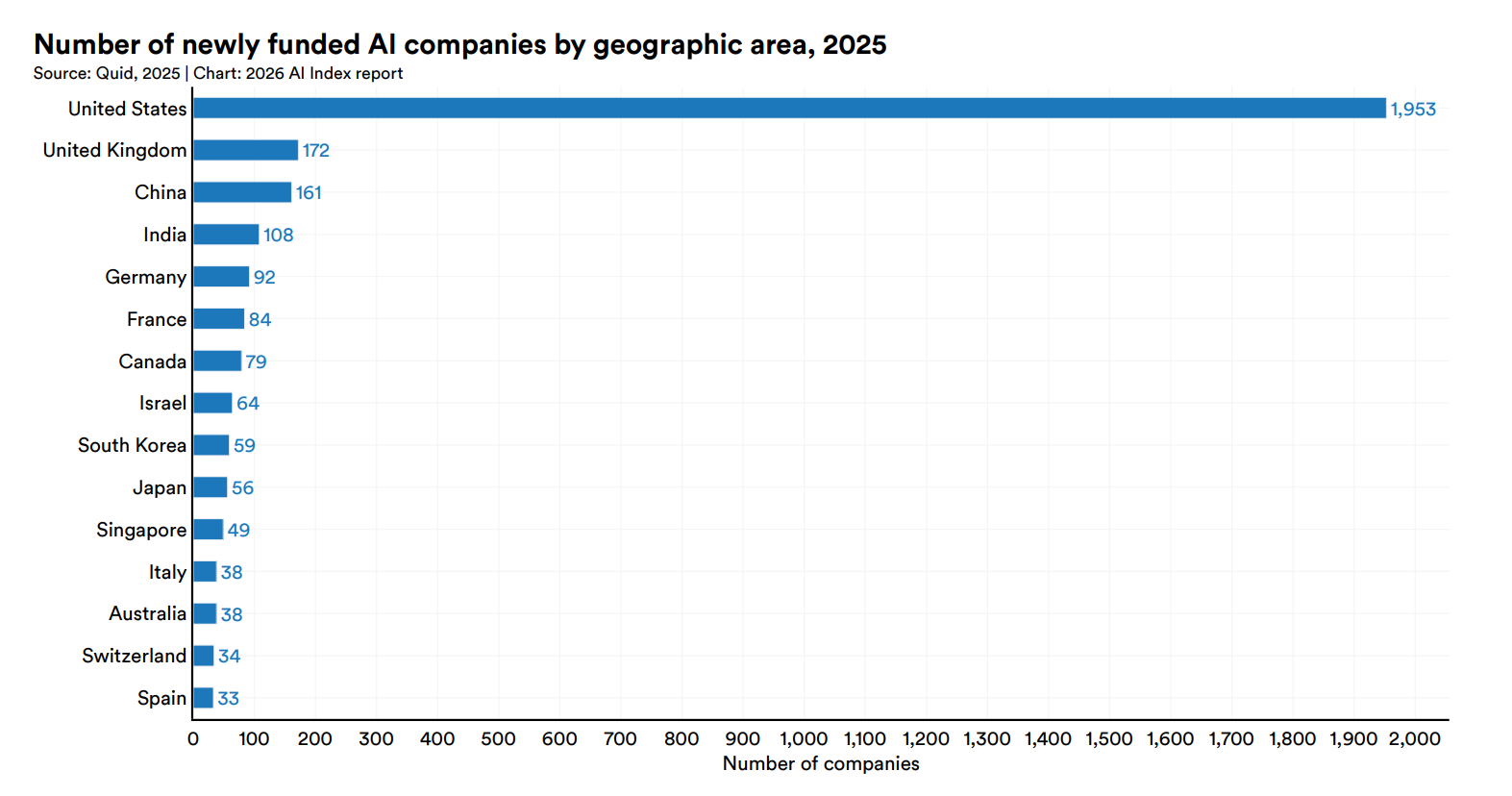

- The U.S. also led in entrepreneurial activity with 1,953 newly funded AI companies in 2025, more than 10x the next closest country

- BUT the number of AI researchers and developers moving to the U.S. has dropped 89% since 2017, with an 80% decline in the last year alone

- With that said, the U.S. is still home to more AI talent than any other country

- BUT the number of AI researchers and developers moving to the U.S. has dropped 89% since 2017, with an 80% decline in the last year alone

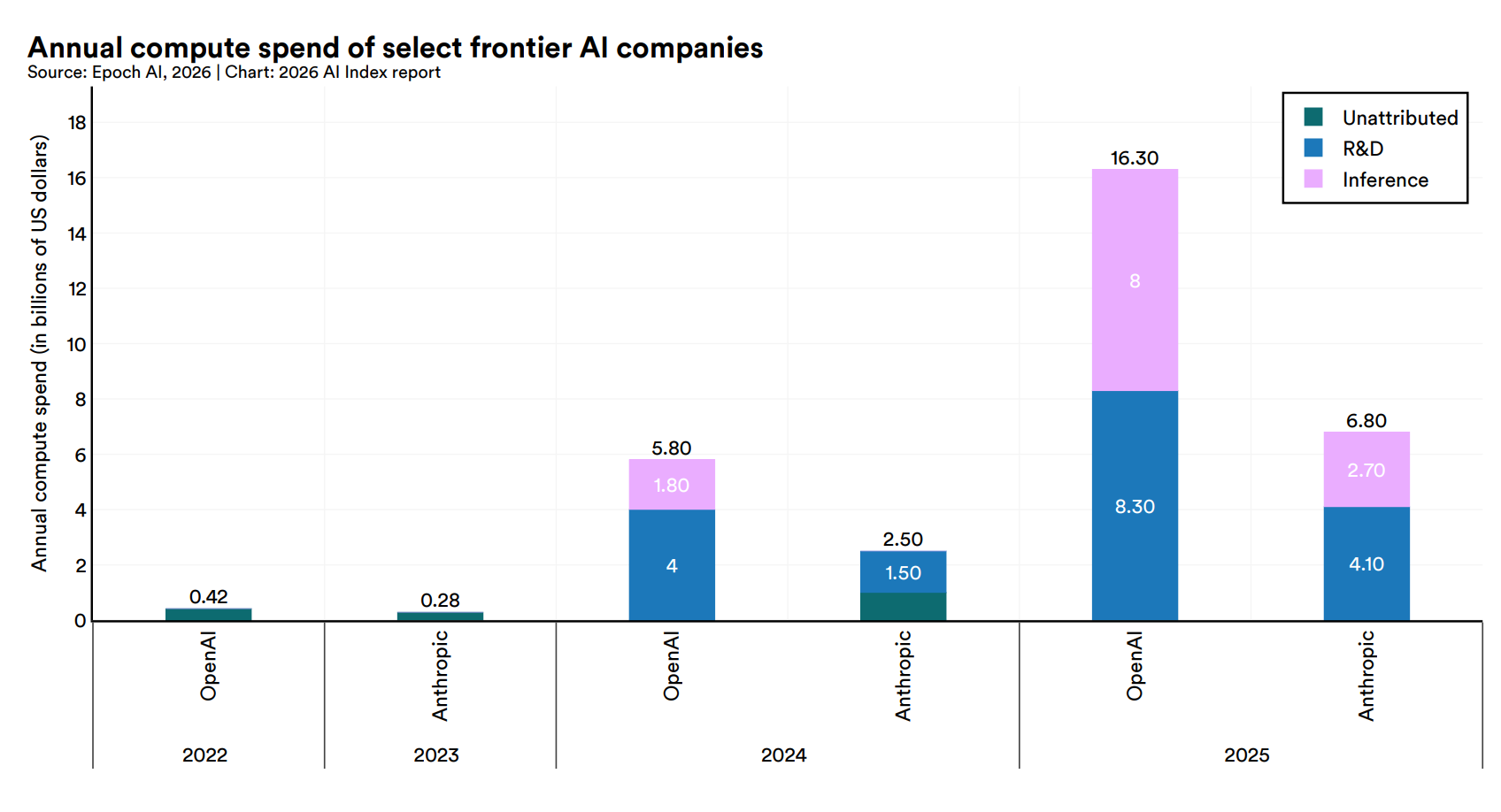

- OpenAI’s compute spend towers over all other and incr’d significantly from 2024 to 2025, as did Anthropic’s

- Video generation models are starting to capture how objects behave

- Google DeepMind’s Veo 3, tested across more than 18k generated videos, demonstrated abilities like simulating buoyancy and solving mazes without being trained on those task

- See below image showing how visual generation has improved over time…

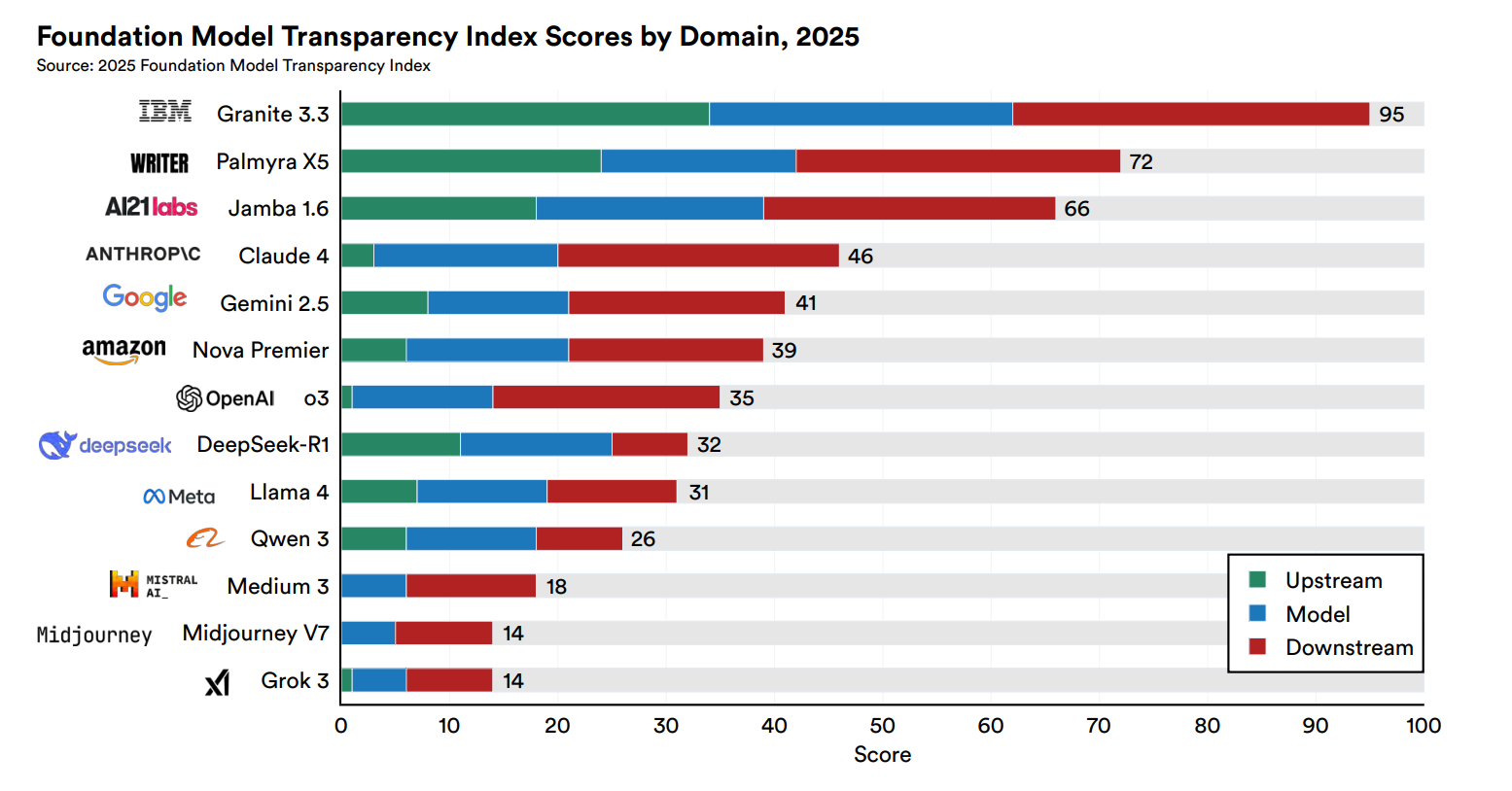

- AI companies grew less transparent this year

- After rising on the Foundation Model Transparency Index from 37 to 58 between 2023 and 2024, the avg score dropped to 40 in 2025

- Training code, parameter counts, dataset sizes, and training duration are no longer disclosed for several of the most resource-intensive systems, including those from OpenAI, Anthropic, and Google

- AI models struggle to tell the difference between knowledge and belief

- When a false statement is presented as something another person believes, models handle it well

- When the same false statement is presented as something a user believes, performance collapses

- AI models perform better in business domains like tax, mortgage processing, corporate finance, and legal reasoning BUT have challenges in fields with where high competency and reliability are required

- Studies report gains of 14% to 15% in customer support, 26% in software development, and 50% in marketing output

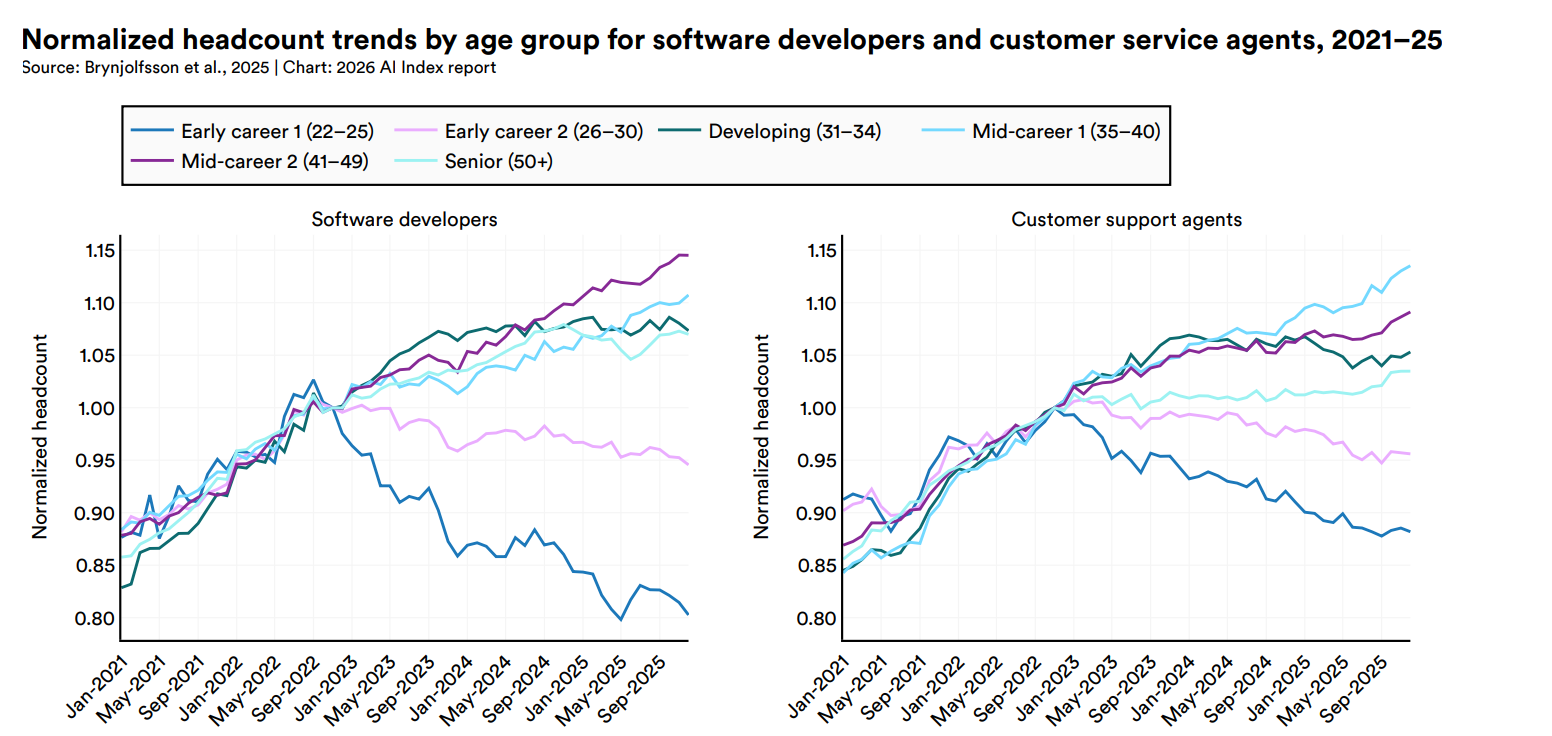

- In software development, where AI’s measured productivity gains are clearest, U.S. developers ages 22 to 25 saw employment fall nearly 20% from 2024, even as the headcount for older developers continues to grow

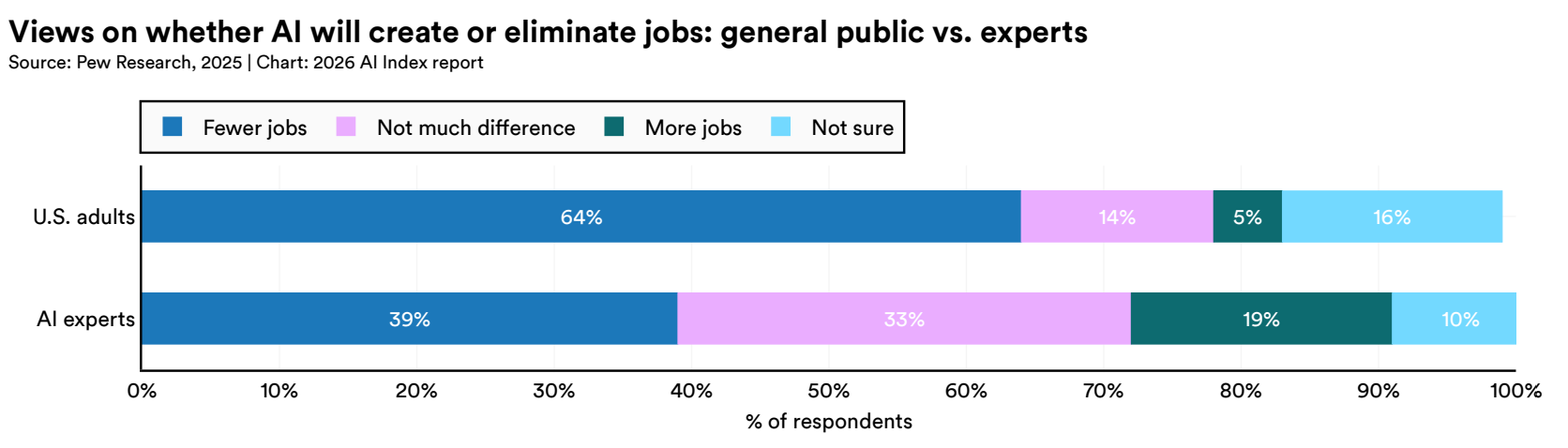

- Nearly two-thirds of Americans (64%) expect AI to lead to fewer jobs over the next 20 years, while only 5% expect more

- Experts were less pessimistic (39% fewer, 19% more) but forecast far faster adoption

- Frontier models outperform human chemists on avg but CANNOT reproduce published research

- On ChemBench, the best models surpass human expert averages across 2,700+ chemistry questions while struggling with basic tasks

- On ReplicationBench, frontier models score below 20% on paper-scale replication in astrophysics

- On UnivEarth, LLM agents answer Earth observation questions with 33% accuracy, and their code fails 58% of the time

- On end-to-end scientific research tasks, the best AI agents score roughly half of what PhD experts achiev

- On PaperArena, the best agent reaches 38.8% accuracy versus a PhD expert baseline of 83.5%. On BixBench, frontier models achieve roughly 17% accuracy on real-world bioinformatics analysis

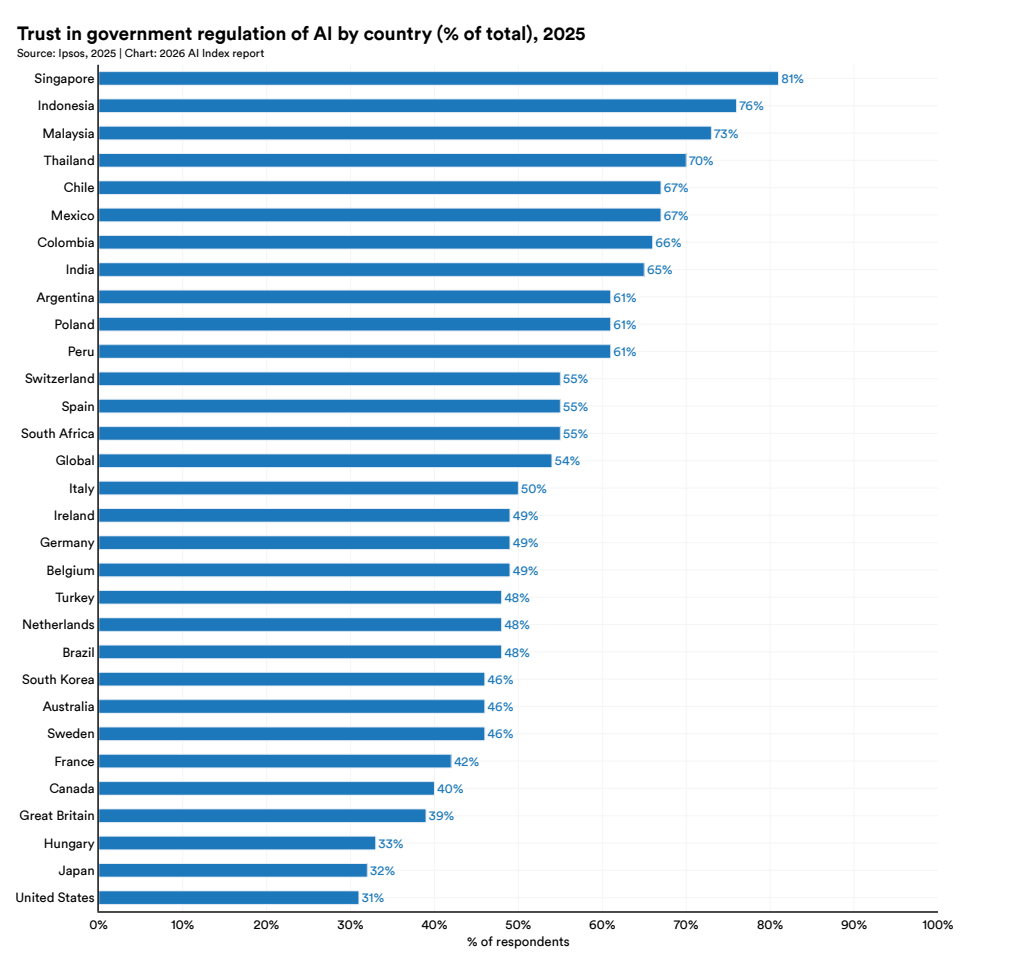

- The US reported the lowest trust in its own govt to regulate AI responsibly of any country surveyed, at 31%

- The global avg was 54%

- Southeast Asian countries are leading (Singapore 81%, Indonesia 76%)

- The EU is trusted more than the US or China to regulate AI effectively

State-Level Pushback Against Data Center Expansion Is Growing

One theme that has been gaining momentum is US state-level push back regarding data center expansion and there were a couple developments on that front this week. In Maine, lawmakers on Tuesday approved a first-in-the-nation, statewide moratorium which would pause the approval of new data centers above 20 megawatts for 18 months, alongside a separate bill removing certain tax exemptions and a new study group to assess environmental and energy impacts. The Governor has 10 days to veto the legislation, sign it into law, or allow it to become law without her signature.

In Virginia, a recent Washington Post–Scar School poll shows support for new data centers falling from 69% in 2023 to 35% in 2026. This comes as Prince William County dropped its legal appeals tied to the proposed “Digital Gateway,” effectively ending years of efforts to revive a 2,100-acre hyperscale campus. The broader region already hosts one of the largest data center hubs in the world, with northern Virginia’s load exceeding 4,900 MW, while the Digital Gateway alone was planned at multi-gigawatt scale.

These updates are not isolated events. There is a long list of other states that have started their own processes dating back to the beginning of the year. More color on the Maine and Virginia updates are below, in addition to other state actions regarding data center expansions on a state-by-state basis …

- Maine could be the 1st state to pause new data center builds as lawmakers passed the first state temporary ban on Tuesday (link/link)

- What would this legislation do? It would pause approvals of new data centers for 1.5 years that require more than 20 megawatts of power for 18 months; It would also establish a study group to examine the impact of such facilities and recommend legislative guardrails

- Separate legislation, also approved, would make data centers ineligible for certain business tax exemptions

- What is next? Governor Janet Mills has 10 days to veto the legislation, sign it into law, or allow it to become law without her signature (see more of amendment LD 307 HERE)

- Why the push back against datacenters? Lawmakers are concerned about the facilities’ use of water and electricity, the risks of pollution and the potential to drive up household energy costs

- What would this legislation do? It would pause approvals of new data centers for 1.5 years that require more than 20 megawatts of power for 18 months; It would also establish a study group to examine the impact of such facilities and recommend legislative guardrails

- Also this week, in Virgina, support for new data centers fell from 69% in 2023 to 35% according to a Washington Post-Scar School poll (link/link)

- This comes one day after Prince William County’s Board of Supervisors voted to drop its appeals defending the “Prince William Digital Gateway”

- The decision ended years of legal effort to revive a 2,100-acre, 37-building campus that, at full buildout, would have been one of the largest data center developments in the country

- More broadly, the region already anchors a large amount of hyperscaler capacity, as northern Virginia’s data center load exceeds 4,900 MW

- The Digital Gateway alone was sized up for multi-gigawatt demand, across some 22mn sqft of building space and 14 dedicated electrical substations

- Data Center Watch, a tracker run by 10a Labs, recorded 48 data center projects blocked or delayed across the US in 2025

- This prevented ~$156bn in planned development, with 57 active opposition groups now operating in Virginia (more than any other state)

- This comes one day after Prince William County’s Board of Supervisors voted to drop its appeals defending the “Prince William Digital Gateway”

- Looking deeper, see below is a quick overview of the other states pursuing moratorium bills as of March 2026 (link)

- Additional moratorium bills are still being discussed in Minnesota and Pennsylvania as well

This Week’s Most Impactful AI Updates …The Battle Intensifies

AI players continue to roll out new models and tools at a rapid pace, while also becoming more explicit about how they see the competitive landscape and their positioning within it. This week, a leaked memo from OpenAI pulled back the curtain on how it’s thinking about its position within the AI landscape, emphasizing a shift toward a more integrated platform, taking direct shots at Anthropic, and sharing more nuanced views on its relationships with Microsoft and Amazon. Additionally, OpenAI followed Anthropic’s cybersecurity push last week and announced its own defensive-focused model, GPT-5.4-Cyber this week. Over at Anthropic, the Co rolled out an upgraded flagship model, Opus 4.7, and a new AI design tool, Claude Design, which lets users create visuals like prototypes, slides, one-pagers, and more using Claude (weighing on share of companies like Figma).

Finally, Microsoft, Meta, and Google each highlighted new efforts across agents, digital avatars, and robotics that we thought were notable.

See below for more of our takes.

OpenAI Shares Candid Thoughts On Anthropic, Microsoft, And Amazon in A Leaked Memo + Releases An AI Model For Defensive Cybersecurity

- A leaked internal memo from OpenAI’s Chief Revenue Officer Denise Dresser gave some interesting insight into the Co’s direction (full memo HERE/link): Key points below…

- Confirms the existence of a new flagship model, codenamed “Spud”, which is described as “an important step in the intelligence foundation for the next generation of work,” focusing on complex reasoning and “intent recognition”

- “Spud will make all of our key products significantly better. It expands the workflows we can own and gives customers another reason to consolidate around us”

- This model is reportedly the engine behind OpenAI’s transition from a chat interface to a “Super App” capable of autonomous agency

- Seemingly favoring AMZN over MSFT…Partnership w/ MSFT has been “foundational” BUT has limited their ability “to meet enterprises where they are – for many that’s [Amazon’s] Bedrock”

- Since announcing a partnership w/ AMZN in Feb, inbound demand from customers for the offering has been “frankly staggering”

- “We are firing on all cylinders to establish this as a scaled distribution channel”

- Some strong words on Anthropic – “their story is built on fear, restriction, and the idea that a small group of elites should control AI”

- How does OpenAI compare? “Our positive message will win over time: build powerful systems, put in the right safeguards, expand access, and help people do more”

- Characterized Anthropic as a “single-product company in a platform war”

- “Their coding focus gave them an early wedge…as AI spreads beyond developers into every team, workflow, and industry, that narrowness can become a real liability”

- And OpenAI has a “real structural advantage” vs Anthropic

- “Their strategic misstep to not acquire enough compute is showing up in the product. Customers feel it through throttling, weaker availability, and a less reliable experience. We saw the exponential compute curve earlier [and] acted on it faster”

- They also allege that Anthropic is inflating its rev figures by ~$8bn: Anthropic is using gross accounting, recording the full price of Claude credits sold via AWS/Google as rev, while OpenAI uses net accounting, only recording what they actually keep after Microsoft takes its cut

- That would put Anthropic’s true run rate at $22bn (vs the currently stated $30bn) and below OpenAI’s ~$25bn

- Also outlined plans to “own deployment” w/ “DeployCo” to “turn product demand into repeatable enterprise transformation”

- “The companies that win enterprise AI will not just have the best models. They will have the best ability to get those models deployed into real workflows, inside real organizations, with real measurable value. We should be the best in the world at that”

- Overall… “we should stop thinking like a company with separate product lines. We should think like a platform company with multiple entry points and one integrated enterprise offering”

- Confirms the existence of a new flagship model, codenamed “Spud”, which is described as “an important step in the intelligence foundation for the next generation of work,” focusing on complex reasoning and “intent recognition”

- OpenAI launched GPT‑4‑Cyber, an AI model for defensive cybersecurity + expanded its Trusted Access for Cyber (TAC) program (link/link)

- GPT-5.4-Cyber is a variant of GPT-5.4 that is fine-tuned specifically for defensive cybersecurity work

- It includes binary reverse engineering capabilities, which allow security professionals to analyze compiled software for malware, vulnerabilities, and security robustness without access to source code

- B/c the model carries higher risk than standard deployments, the model will initially be rolled out on a limited basis to vetted security vendors, organizations and researchers

- Scaling up OpenAI’s TAC program to thousands of verified individual defenders and hundreds of teams responsible for defending critical software

- OpenAI is adding new tiers to its TAC program, which was launched in February, with higher levels of verification unlocking more powerful capabilities

- Users approved for the highest tier will gain access to GPT-5.4-Cyber

- The program’s expansion comes ahead of the release of more capable models in the coming months

- As a reminder…this comes just a week after Anthropic annc’d Project Glasswing, a cybersecurity initiative built around Claude Mythos Preview

- GPT-5.4-Cyber is a variant of GPT-5.4 that is fine-tuned specifically for defensive cybersecurity work

Anthropic Releases Claude Opus 4.7 + Launches Claude Design for AI-Powered Visual Creation

- Anthropic releases its new model Claude Opus 4.7 (link/link)

- Key highlights –

- “Notable improvement” over Opus 4.6 in software engineering: Users report being able to hand off their hardest coding work (the kind that previously needed close supervision) to Opus 4.7 with confidence

- Also has “substantially better” vision: Can see images in greater resolution, and is more “tasteful” and “creative” when completing professional tasks, producing higher-quality interfaces, slides, and docs

- “Substantially better” at following instructions: Where previous models interpreted instructions loosely or skipped parts entirely, Opus 4.7 takes the instructions literally

- Is a more effective finance analyst than Opus 4.6, producing rigorous analyses and models, more professional presentations, and tighter integration across tasks

- Better at using file system-based memory: It remembers important notes across long, multi-session work, and uses them to move on to new tasks that, as a result, need less up-front context

- How does it compare to Anthropic’s most powerful model, Claude Mythos Preview? Its cyber capabilities are not as advanced as those of Mythos Preview; They are releasing Opus 4.7 with safeguards that automatically detect and block requests that indicate prohibited or high-risk cybersecurity uses

- Availability: Available across all of Anthropic’s Claude products, its application programming interface and through cloud providers Microsoft, Google, and Amazon; The new model is the same price as Claude Opus 4.6

- Key highlights –

- On the back of that…Anthropic also intro’d Claude Design, a new Anthropic Labs product designed to simplify visual creation w/ AI (link/link)

- What is it? An AI-powered design tools that enables users to collaborate with Claude to create polished visual work like prototypes, presentations, and marketing assets through simple conversational inputs

- How does it work?

- A user can describe what they need and Claude builds a first version

- From there, they refine through conversation, inline comments, direct edits, or custom sliders (made by Claude) until it’s right

- When given access, Claude can also apply the team’s design system to every project automatically, so the output is consistent with the rest of the Co’s designs

- Collaboration is a major focus: Users can share designs within their organization, grant editing access, and work together in real time

- Teams have been using Claude Design for…

- Realistic prototypes

- Product wireframes and mockups

- Design explorations

- Pitch decks and presentations

- Marketing collateral

- Frontier design

- Claude Design is powered by Anthropic’s newly-released model, Claude Opus 4.7

- Available in research preview for Claude Pro, Max, Team, and Enterprise subscribers

-> Shares of Figma and Adobe were down -6.8% and -1.5%, respectively, on the day of the release

A Couple Other Notable AI And AI-Adjacent Updates From Microsoft, Meta, and Google…

- Microsoft is building OpenClaw-style agentic AI features within Copilot, aiming to make it more autonomous while addressing the security gaps in the open-source original (link/link/link)

- “Exploring the potential of technologies like OpenClaw in an enterprise context”, including a team of always-on agents that would be able to work 24/7 on a users’ behalf within Microsoft 365 applications

- The always-on version of Microsoft 365 Copilot could reportedly do things like monitor a user’s Outlook inbox and calendar and serve up a list of suggested tasks each day

- Microsoft is also exploring OpenClaw-like agents tailored to certain roles, such as marketing, sales, and accounting, to “limit the permissions the agent needs,” siloing them from other parts of a biz

- Another goal is to make 365 Copilot better at working within Microsoft apps in the background w/o needing direct oversight: For instance, reorganizing one tab of an Excel spreadsheet while users work on other tabs

- Prioritizing enterprise customers, with enhanced access controls to reduce risks

- Reportedly confident that it can implement “safer” versions of the tool

- Timeline is still TBD: Engineers working on those features are reportedly optimistic that some will be ready in time for a preview at Microsoft’s Build developer conference in June, BUT the efforts are still nascent and could change

- “Exploring the potential of technologies like OpenClaw in an enterprise context”, including a team of always-on agents that would be able to work 24/7 on a users’ behalf within Microsoft 365 applications

- Finally…Mark Zuckerberg is reportedly building an AI-powered 3D clone to interact with employees and replace him in meetings (link)

- Zuckerberg is reportedly personally involved in training and testing his animated AI, which could offer conversation and feedback to employees

- The character is reportedly being trained on Zuckerberg’s mannerisms, tone and publicly available statements, as well as his own recent thinking on Co strategies, so that employees might feel more connected to him through interactions with it

- Google introduces Gemini Robotics ER 1.6 that enhances reasoning to help robots navigate real-world tasks (link/link)

- Is a “significant” upgrade to Google’s reasoning-first model that enables robots to understand their environments “with unprecedented precision”

- Is capable of executing tasks by natively calling tools like Google Search to find information, vision-language-action models (VLAs) or any other 3P user-defined function

- This model specializes in capabilities “critical” for robotics, including visual and spatial understanding, task planning and success detection Also unlocked a new capability – instrument reading: Enables robots to read complex gauges and sight glasses

- Availability: Available now to developers via the Gemini API and Google AI Studio

- Is a “significant” upgrade to Google’s reasoning-first model that enables robots to understand their environments “with unprecedented precision”

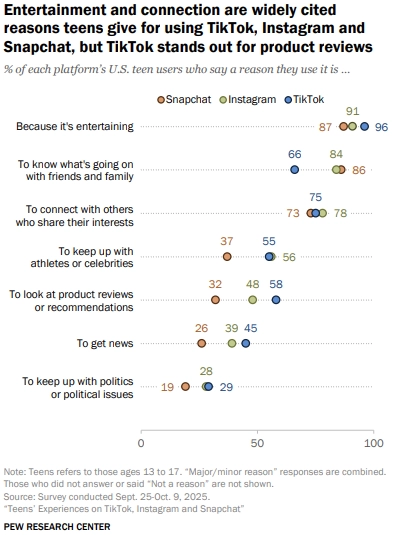

TikTok, Instagram, and Snapchat Play Very Different Roles in Teens’ Lives

In the ever-ongoing battle of social media platforms between TikTok, Instagram, and Snapchat, we thought that a recent Pew Research Center report offers a helpful step back into how teens are actually using and experiencing each platform. While entertainment is the common thread across all three, the roles they play are starting to look pretty different. TikTok has become the go-to for discovery, whether it is content, products, or even news, while Snapchat is much more about staying connected, with teens using it to keep up with friends and communicate throughout the day.

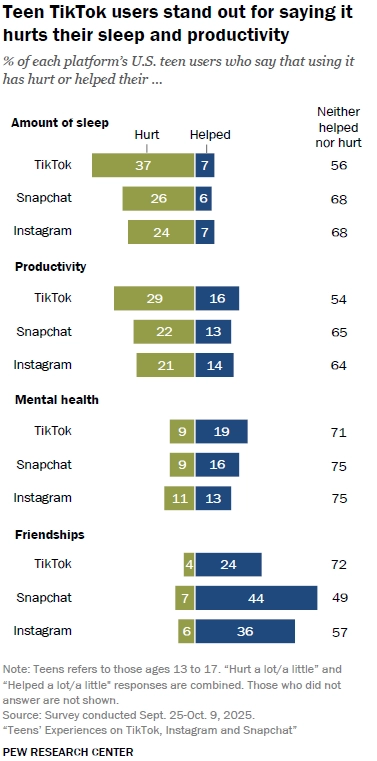

At the same time, most teens say their overall experience on social media is positive or at least neutral, even if there are some clear trade-offs. Concerns around time spent show up most on TikTok, along with more negative views on sleep and productivity. Snapchat, despite its strength in communication, stands out for higher rates of reported harassment. And across all of this, parents tend to see things more negatively than teens, especially when it comes to how much time is being spent and the broader impact of these platforms.

The report was chock full of interesting stats….see below for the ones we found most interesting (and if you would like to access the full report, you can do so HERE).

Platform Use Cases For Teens Are Distinct…TikTok Leads in Discovery, Snapchat in Connection, While Entertainment Dominates Overall

- Entertainment is the top use case across all three platforms, cited by roughly 9 in 10 or more users on each

- TikTok dominates on entertainment…96% cite it as a reason, with 82% calling it a major reason

- Instagram and Snapchat users also cite entertainment, but at slightly lower rates (91% and 87% respectively)

- Staying connected with friends and family is the most prevalent use case for Snapchat

- Two-thirds of Snapchat users say keeping up with friends and family is a major reason they use the app, higher than Instagram (55%) or TikTok (33%)

- TikTok leads in product discovery and news consumption

- ~6 in 10 TikTok users go there for product reviews or recommendations, vs about half on Instagram and far fewer on Snapchat

- ~4 in 10 TikTok and Instagram users cite news as a reason they use the platform; Only ~1 in 4 Snapchat users say the same

- Very few teens use any of these platforms primarily for politics, though TikTok and Instagram edge out Snapchat on this metric

TikTok Draws The Most Time-Spent Concern Amongst Both Teens And Parents

- TikTok users are most likely to feel they spend too much time on the app

- 28% of TikTok users say they spend too much time on it, vs 19% each for Instagram and Snapchat

- Still, the most common response across all three platforms is “about right”… roughly 6 in 10 or more say this for each app

- A significant parent-teen perception gap exists, widest for TikTok

- 44% of parents say their teen spends too much time on TikTok vs only 28% of teens who say the same (a 16-pt gap)

- The same pattern holds for Snapchat (30% parents vs. 19% teens) and Instagram (27% vs. 19%)

- Higher-income parents are more likely to view their teen’s usage as excessive

- Among parents of TikTok users, 47% of those in households earning $75k+ say their teens spend too much time on the app vs 36% of those earning < $75k

- A similar income-based pattern holds for Snapchat but no significant income difference for Instagram

Platform Impacts Diverge…TikTok Skews Negative On Sleep/Productivity While Snapchat Leads On Friendships

- TikTok stands out most for negative effects on sleep and productivity

- 37% of TikTok users say it hurts the amount of sleep they get vs ~24–26% for Instagram and Snapchat

- 29% of TikTok users say it hurts their productivity, compared to ~21–22% on the other two platforms

- Snapchat is the standout platform for positive effects on friendships

- 44% of Snapchat users say it helps their friendships, higher than Instagram (36%) or TikTok (24%)

- Most teens say these platforms neither hurt nor help their mental health, but parents are more negative

- TikTok and Snapchat users lean slightly positive on mental health impact; Instagram users are split evenly between helped and hurt

- Parents are notably more negative – 24% say social media hurt their teen’s mental health overall vs just 8% who say it helps

- Parents also view sleep and productivity impacts negatively BUT are more positive on impact to friendship

- 41% say social media hurts their teen’s sleep; 38% say it hurts productivity

- Friendships are the one bright spot…parents are more likely to say social media helps friendships than hurts them (22% vs. 13%)

Teens Largely Feel Good About Social Media, but Harassment Does Persist, Particularly on Snapchat

- Most teens say these platforms have no impact on how they feel about themselves

- 57–62% across all three platforms say what they see makes no difference to their self-esteem

- When there is an effect, it leans positive (for example, 15% of TikTok users say it makes them feel better vs only 3% who say worse)

- Overall experiences are overwhelmingly positive across all three platforms

- Roughly 7 in 10 teens on each platform describe their experience as mostly positive

- Just 3% say mostly negative on each platform; The rest describe an equal mix of positive and negative

- Snapchat users report the highest rates of personal harassment experiences

- 27% of Snapchat users have experienced at least one of three harassment types (offensive name, rumor, physical threat)

- These shares drop to about 19% on Instagram and 18% on TikTok

- Being called an offensive name is the most common form of harassment on all three platforms

Instagram Feels Safest to Parents While TikTok Drives the Most Unease, Especially Among Parents Of Non-Users

- Parents are most comfortable with Instagram and least with TikTok

- 59% of parents whose teens use Instagram say they are comfortable with it, vs ~51% for TikTok and ~47% for Snapchat

- ~3 in 10 parents are uncomfortable with their teen’s TikTok or Snapchat use and that figure drops to 16% for Instagram

- Discomfort is even higher among parents whose teens don’t currently use these platforms

- 73% of parents whose teens don’t use TikTok say they’d be uncomfortable if they did, which is the highest hypothetical discomfort of any platform

- Smaller but still majority shares say the same for Snapchat (65%) and Instagram (52%)

Amazon Officially Pushes Harder Into Satellite Ambitions W/ Globalstar Deal

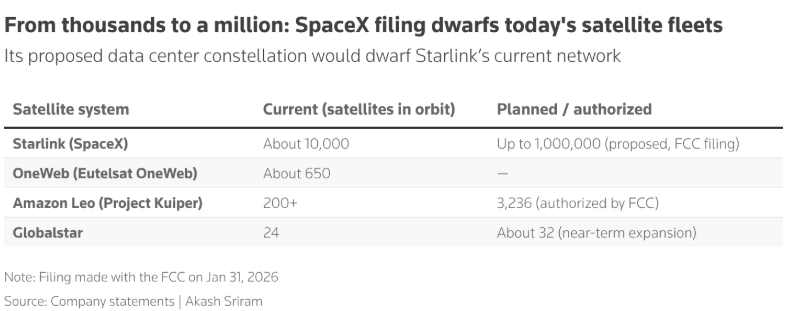

After months of speculation around Globalstar’s fate that started back in October when press reports circulated that the Co was exploring a potential sale with suitors including SpaceX, Amazon was victorious and officially announced this week that it would be acquiring satellite operator Globalstar in a ~$11.6bn deal to help it build out its low-earth-orbit satellite network, Amazon Leo.

Under the agreement, Amazon will acquire Globalstar’s satellite operations, infrastructure, and spectrum assets, which will be integrated with its existing network. Amazon also announced plans to develop a direct-to-device satellite system that is expected to begin deployment in 2028. In parallel, Amazon announced a partnership with Apple to continue and expand satellite connectivity for iPhones and Apple Watches.

While the deal will expand Amazon’s network of ~200 satellites, even with Globalstar’s 24 additional satellites and FCC authorization to build an additional ~3,200, Amazon still has ways to go to match SpaceX’s Starlink constellation of ~10,000 satellites.

See below for the key details on the deal. (link)

-> Globalstar was up +10% on the back of the announcement following the +13% on deal speculation last week, while Amazon was up +4%; Globalstar shares have soared more than +93% since October 29, the last trading day before reports that the Co was exploring a potential sale

-> Also to note, AST SpaceMobile was hit hard in reaction, down -10.5%; Other Connectivity stocks were also down with T-Mobile and American Tower Corp falling -1% and -2.5%, respectively, while AT&T and Verizon were flat.

- Financial terms – Amazon will acquire 100% of Globalstar in an ~$11.6bn deal: $90.00/shr cash OR 0.321 Amazon shares (w/ value capped at $90/share)

- Premium to GSAT stock price: Represents a +23.5% premium over Globalstar’s Monday closing price ($72.89) and a +36% premium to the share price before deal speculation emerged

- Some caveats to note:

- Only up to 40% of the deal can be paid in cash: If more shareholders choose cash, the extra amount will automatically be converted into stock for everyone proportionally

- Total transaction consideration is also subject to a downward adjustment of $110mn max if Globalstar does not achieve certain operational milestones

- GSAT stockholders holding ~58% of the combined voting power have already approved of the deal

- The deal is expected to close in 2027, subject to…

- Customary regulatory approvals

- Globalstar achieving certain HIBLEO-4 replacement satellite milestones

-> FCC Chairman Brendan Carr told CNBC that the agency will review Amazon’s Globalstar deal, but noted that they are “very open-minded” to the acq and it has the potential to make Amazon a competitor to SpaceX in direct-to-cell svs; “Ultimately, we’ll have to take a look at the paperwork and see, but it’s […] consistent with the long-term vision that we have to make sure that the U.S. leads in this next-gen era of direct-to-cell technologies,” Carr said (link)

- Deal rationale – combines Globalstar’s spectrum, satellite assets, and D2D expertise with Amazon Leo to enable direct-to-device connectivity at scale, extending cellular coverage beyond the reach of terrestrial networks

- Planning to partner with mobile network operators (MNOs) to extend existing cellular networks via satellite, positioning Leo as a complement to traditional telecom infrastructure

- Targets consumer, enterprise, and gov’t use cases, including emergency communications, disaster recovery, remote operations, and IoT connectivity

- Underpins Amazon’s plan to build its own Amazon Leo direct-to-device satellite system, which it expects to start deploying in 2028

- Will deliver voice, messaging, and data services directly to mobile devices

- Offers “substantially higher” spectrum efficiency vs legacy systems, translating to faster speeds and better performance

- The complete Amazon Leo network will include thousands of satellites with capacity to support hundreds of millions of endpoints

- Through the deal, Amazon adds Globalstar’s two dozen satellites to its existing network of more than 200

- Amazon has also been working to ramp up its network by deploying about 3,200 satellites in Earth’s low orbit by 2029, with roughly half required to be in place by a July regulatory deadline

- In comparison, Starlink has a 10,000-unit-strong network

Source: Reuters

- ALSO… Amazon and Apple annc’d an agreement under which Amazon will continue and expand Globalstar’s existing satellite services for iPhones and Apple Watchs

- Currently, Globalstar partners with Apple to power satellite svs on iPhone 14 or later, as well as Apple Watch Ultra 3, allowing users to text emergency services, message friends and family, request roadside assistance, and share their location

- As a reminder… Apple invested ~$1.5bn in Globalstar in 2024 to fund the expansion of its iPhone communication svs, in a deal that also gave Apple a 20% equity in Globalstar

- With the new Amazon-Apple agreement, Amazon will continue to support iPhone and Apple Watch models currently using Globalstar’s existing and planned upcoming low Earth orbit satellite constellations, being manufactured by MDA Space, and collaborate with Apple on future satellite services using Amazon Leo’s expanded satellite network

- Currently, Globalstar partners with Apple to power satellite svs on iPhone 14 or later, as well as Apple Watch Ultra 3, allowing users to text emergency services, message friends and family, request roadside assistance, and share their location

-> Separately, but related from this week , Amazon intro’d its Amazon Leo Aviation Antenna, which allows commercial aircraft and regional jets to offer high-performance, in-flight internet to its passengers; The svs will provide up to one gigabit/sec of download speed and 400 megabits/sec of upload speed to all users aboard the aircraft; Amazon said that the new antenna was designed with no moving parts so that it can hold up under intense temperatures and difficult weather conditions, as well as to reduce maintenance downtime (link/link/link)

Source: Amazon

Grab Bag: Uber Commits $10bn To AVs, Apple Is Actively Testing New Glasses , & Allbirds Transitions To AI Compute

- Uber reportedly is making a big investment ($10bn) into the AV sector (link/link)

- The Financial Times reported the money will be used for buying thousands of AVs and taking stakes in their developers, breaking from its asset-light “gig economy” biz model to avoid disruption from robotaxis

- As a reminder: The Co has partnered across much of the AV industry, including with Baidu, Rivian, and Lucid, and has outlined plans to launch robotaxi svs in ~28 cities by 2028

- The $10bn commitment is reportedly broken down into two main pillars:

- $7.5bn for fleet acquisition

- $2.5bn in equity stakes

- The Financial Times reported the money will be used for buying thousands of AVs and taking stakes in their developers, breaking from its asset-light “gig economy” biz model to avoid disruption from robotaxis

-> Also, this week, Lucid Group is deepening its partnership with Uber, Uber is increasing its purchase commitment to at least 35,000 (from 20,000) vehicles for their future robotaxi service. Uber is adding $200mn more investment (bringing its total to $500mn), while Public Investment Fund affiliate Ayar Third Investment Company is investing $550mn (link)

- According to Bloomberg’s Mark Gurman, Apple is actively testing at ~4 different styles of frames for its upcoming smart glasses project (link)

- As a reminder these glasses are not augmented reality

- They will have integrated cameras, microphones and sensors

- They’ll be able to relay notifications from your phone, capture personal photos and videos, play music, and enable interactions with AI features like upgraded Siri and visual intelligence capabilities

- The 4 designs for the Apple glasses currently in testing include:

- A large rectangular frame, reminiscent of Ray-Ban Wayfarers

- A slimmer rectangular design

- Larger oval or circular frames

- A smaller, more refined oval or circular option

- Reported release date: Later this year or early in 2027, with an actual release in spring or summer 2027

- As a reminder these glasses are not augmented reality

- Allbirds -> NewBird AI: An interesting case study of a high-flying consumer brand that fell into oblivion and is now making a unique 110% pivot

- Allbirds essentially is pivoting from a sustainable footwear brand to now an AI compute infrastructure company!

- It sold the Allbirds brand and footwear assets to American Exchange Group (annc’d at the end of March)

- And just annc’d this week that it raised $50mn in a convert to build its AI compute infrastructure

- They are changing their name to NewBird AI

- In just 5 years, the stock fell from a $4b+ valuation to being sold for $39mn 2 weeks ago

-> On the back of this new raise and strategic pivot announcement, the stock went from $2.49/shr to $17, though it is still a very micro-cap; It closed the week at $10.8 per share

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Google said its 2025 Ads Safety Report shows a shift toward blocking bad ads over banning bad actors. The Co blocked a record 8.3bn ads globally, up from 5.1bn, while suspending fewer advertiser accounts as AI via Gemini catches 99% of policy‑violating ads before display. (TechCrunch)

- IAB annc’d US digital ad rev hit $294. 6bn in 2025, up 13.9% YoY, despite no Olympics, World Cup or elections. Social, video and commerce media drove gains, w/ social at $117.7bn and video at $78bn, while commerce reached $63.4bn. Programmatic rev climbed 20.5% to $162.4bn. Search totaled $114.2bn. AI, creators and performance buying are reshaping the biz, and scaled platforms keep most share. (IAB)

- Disney told advertisers it wants $10mn for 30-sec spots in its 2027 Super Bowl LXI telecast on ABC and ESPN, but the price has slowed sales as marketers push back. Talks are cont’d and may bundle broader sports inventory, incl. Monday Night Football, to close deals. (Variety)

- Alphabet Google faces potential claims running into the bn as advertisers pursue mass arbitration tied to its online search and ad tech biz. Courts have ruled the svs were illegal monopolies, prompting advertisers to band together for payouts. Some cos, incl USA Today Co. and Advance Publications Inc., have sued since 2024, but advertiser contracts require disputes be resolved through mandatory arbitration. (Bloomberg)

- Bango data shows 36% of Americans would accept twice as many ads in streaming svs for cheaper prices. Survey of 2,500 US users found younger viewers more open, rising to 46% of Millennials and 49% of Gen Z. Americans avg 5.2 subs costing $69/month, w/ 23% overspending. (Bango)

- Meta Platforms is expected to overtake Alphabet’s Google as the world’s largest digital-ad Co this yr. Emarketer forecasts Meta net ad rev topping $243.46bn vs Google $239.54bn, after traffic costs. Growth is driven by new ad products such as Reels and broader AI gains. Worldwide Meta ad growth is seen rising to 24.1% from 22.1% in 2025, while Google stays ~11.9%. (The Wall Street Journal)

- Premion’s 2026 CTV/OTT Advertiser Survey shows over 70% of advertisers are boosting CTV ad spend in 2026, w/ budgets up ~17%. The strong momentum raises pressure to turn higher spend into stronger performance outcomes. (Cynopsis)

- BIA Advisory Services lifted its 2026 local ad outlook to $184. 5bn, up from $181.87bn, reflecting 8.1% YoY growth. The firm pointed to stronger performance across mobile, video, streaming and political ads. (Cynopsis)

Artificial Intelligence/Machine Learning

- Qwen annc’d Qwen3. 6-35B-A3B, a fully open‑source sparse MoE model w/ 35B total and ~3B active parameters, focused on agentic coding and multimodal reasoning, per Qwen Team. The model surpasses Qwen3.5 variants on key coding and reasoning benchmarks and rivals larger dense peers. It is available via Qwen Studio, API access, and open weights for community use. (Qwen)

- Google annc’d a Chrome desktop update letting users browse the web side-by-side w/ AI Mode. Clicking links opens pages next to conversational search, enabling comparisons and follow-up questions w/o switching tabs. Google also added multi-tab search, allowing users to pull context from open tabs, images, or files. The feature is live in the U.S., w/ more regions cont’d later. (TechCrunch)

- OpenAI annc’d GPT‑Rosalind, a purpose‑built AI model for life sciences research, aimed at speeding early drug discovery and translational medicine. The model supports evidence synthesis, hypothesis generation, experimental planning and tool‑heavy workflows across chemistry, proteins and genomics. (OpenAI)

- Google is negotiating a classified AI deal w/ the US Department of Defense, citing The Information. The talks would let the Pentagon deploy Google’s Gemini models for all lawful uses across classification levels. Google proposed contract language barring domestic mass surveillance or autonomous weapons w/out human control, while the Pentagon said it will keep using frontier AI via industry partners. (Reuters)

- The UK govt has launched Sovereign AI, a venture fund to back domestic AI startups and cut reliance on foreign tech. The fund will invest ~$675mn across model development, agentic AI, and drug discovery. Portfolio firms get access to supercomputers, free visas for international hires, procurement options, and govt advice. (Wired)

- The White House said it is working to give major US agencies access to Anthropic Co’s Mythos AI model, while adding safeguards over cybersecurity risk. A memo from OMB CIO Gregory Barbaccia said protections are being set so agencies may use the closely held tech, w/ details and timing to follow. (Yahoo Finance)

- ByteDance Seed annc’d Seedance 2. 0, a next-gen video creation model using unified multimodal audio-video tech. The model supports text, image, audio and video inputs, enabling editing, extension and 15-sec multi-shot outputs w/ dual-channel audio. Compared w/ v1.5, it shows higher usability, stronger motion stability, better physical accuracy and improved controllability for complex scenes and pro content creation. (ByteDance Seed)

- Apple is sending many Siri engineers to a multi-week AI coding bootcamp as it prepares a major Siri overhaul ahead of WWDC. About 60 staff will keep working on Siri while another 60 assess safety and performance. The move follows delays to promised Apple Intelligence features, a leadership shakeup, and criticism that the Siri team lagged in using AI coding tools. (MacRumors)

- Anthropic annc’d new ID verification for Claude, asking some users for a gov-issued photo ID and live selfie. The policy applies to limited cases tied to fraud, abuse, or platform integrity, not all users. It follows a surge of privacy-focused users who left OpenAI earlier in the yr. (Yahoo Tech)

- NVIDIA annc’d Ising, the world’s first open AI models aimed at speeding useful quantum computers. The Co said Ising boosts quantum calibration and error‑correction decoding up to 2.5x faster and 3x more accurate than prior methods. The open models let researchers keep data control, integrate w/ CUDA‑Q and NVQLink, and are being adopted by labs, universities, and quantum cos. (NVIDIA)

- Google annc’d Gemini Personal Intelligence launch in India, enabling users to link Gmail, Photos and YouTube to get personalized answers. Initially limited to AI Pro and Ultra tiers, the feature identifies answer sources and warns of context errors. Google plans wider access soon, expanding Gemini’s reach in a key mkt as it rolls out more AI svs locally. (TechCrunch)

- U.S.-based growth and late-stage venture funds drew record inflows as the AI boom narrows investor focus to fast-accelerating startups. According to PitchBook, such funds raised $23.6bn yr to date, already topping any full-yr total in the past dozen yrs. The vehicles back Series C or later rounds, targeting quicker exits amid surging demand for AI exposure. (The Wall Street Journal)

- Google DeepMind annc’d Gemini Robotics-ER 1.6, a reasoning-first robotics tech boosting spatial, multi-view and success detection. The model adds instrument reading for gauges and sight glasses, developed w/ Boston Dynamics, using agentic vision and code execution. It outperforms prior versions on pointing, safety and autonomy, and is available via Gemini API and Google AI Studio for developers. (Google DeepMind)

- Anthropic annc’d a shift to pay‑as‑you‑go pricing for Claude third‑party tools as demand strains compute. Pro and Max subs now pay extra API‑rate usage for high‑volume integrations, ending flat‑fee subsidies. A one‑time credit and prepaid discounts ease the change, while enterprise cos move to lower base fees plus mandatory usage to curb agent‑driven overload and align costs w/ capacity limits. (International Business Times)

- An internal memo from OpenAI rev chief Denise Dresser said the Co is leaning on its Amazon alliance to grow enterprise biz, arguing the Microsoft partnership, while foundational, limited its ability to reach clients via AWS Bedrock. The note follows Amazon’s plan to invest up to $50bn, as OpenAI targets enterprise rev mkts, says enterprise makes up ~40% of rev, and challenges rival Anthropic’s claims. (CNBC)

- OpenAI annc’d it bought AI personal finance startup Hiro in an acquihire, w/ founder Ethan Bloch and staff joining. Terms weren’t disclosed. Hiro, founded in 2023, launched an AI tool ~5 months ago that modeled financial what‑ifs using user data and emphasized accurate math. The Co will shut ops Apr. 20 and delete data May 13, as OpenAI boosts finance-focused tech. (TechCrunch)

- Microsoft is testing OpenClaw-like agents for its 365 Copilot, aiming to make the assistant always on and able to complete tasks autonomously, per a report cited by the Co. The execs said the tech could monitor Outlook and calendars, suggest daily tasks, and create role-specific agents for marketing, sales, and accounting, w/ tighter permissions to address security concerns ahead of a June Build reveal. (The Verge)

Audio/Music/Podcast

- Warner Music Group annc’d a strategic minority investment and expansive partnership w/ TuStreams, a leading Música Mexicana platform. WMG will act as global distribution partner for TuStreams’ full catalog and future releases, while collaborating on joint artist signings, A&R and creative development. (PR Newswire)

Broadcast/Cable Networks

- NBCU and Versant captured 13. 1% of Feb. TV viewership, per Nielsen’s delayed Media Distributor Gauge. NBCU held 10% share, w/ spinoff Versant at 3.3%, marking a 48% jump vs Jan. Super Bowl LX drew 125mn+ viewers and boosted Olympics coverage, lifting NBC affiliates 60%. Peacock viewing rose 64% to a 3% TV share, its best to date, while cable news grew 4.4%. (The Wrap)

Cable/Pay-TV/Wireless

- Bouygues, Iliad-Free and Orange lifted their offer for Altice France’s SFR to €20. 35bn (~$24bn), aiming to cut France mobile mkts to three operators. Deal would give Bouygues 42%, Iliad 31% and Orange 27%. It excludes fibre and overseas assets and faces antitrust scrutiny, w/ talks exclusive until May 15. (Reuters)

- TIM said its BoD met in Rome and annc’d the appointment of advisors to examine the full voluntary public tender and exchange offer proposed by Poste Italiane. Evercore and Goldman Sachs were named as financial advisors to support analysis and assessment, while Bonelli Erede and Gatti Pavesi Bianchi Ludovici will serve as legal advisors. (TIM Group)

Capital Market Updates

- Blackstone filed for an IPO of a new data center acquisition vehicle aimed at buying already built, leased assets benefiting from the AI boom. Blackstone Digital Infrastructure Trust Inc. will target newly built properties valued at $250mn–$1.5bn and leased to investment grade hyperscalers, per a US SEC filing Friday. (Bloomberg)

Cloud/DataCenters/IT Infrastructure

- Microsoft said it will take over a Norway data center initially tied to OpenAI’s Stargate plan, renting capacity at an Nscale site in Narvik. The Co will add 30,000 Nvidia chips, building on a prior $6.2bn commitment. OpenAI failed to finalize a deal, paused a UK Stargate effort, is reining in infra costs, and will access Norway compute via Microsoft’s Azure. (Yahoo Finance)

- Oracle annc’d it will buy up to 2. 8 gigawatts of fuel‑cell power from Bloom Energy to supply AI data centers, w/ 1.2 GW already contracted for 2026–27 US projects. Deal highlights rising AI demand straining power mkts. Bloom’s modular tech enables faster buildouts, incl a system delivered in 55 days. (Yahoo Finance)

Crypto/Blockchain/web3/NFTs

- SpaceX holds 8,285 bitcoin worth ~$603mn in custody on Coinbase Prime, per Arkham data. Blockchain records show no change in the stash, w/ the last movement ~4 months ago between SpaceX‑controlled wallets. The Co reported a ~$5bn loss in 2025 as xAI integration costs exceeded $18.5bn in rev, despite earning $8bn profit on $15bn–$16bn rev a yr earlier. (Tech in Asia)

Cybersecurity/Security

- Booking.com said that hackers accessed some customers’ booking data, confirming unauthorized parties may have viewed names, emails, phone numbers, booking details, and info shared w/ accommodations. The Co said it contained the issue, reset reservation PINs, and notified guests. (TechCrunch)

eCommerce/Social Commerce/Retail

- Amazon annc’d its first smart warehouse in Shenzhen, launching a Global Warehousing and Distribution hub to cut Chinese merchants’ storage costs by up to 45% versus holding inventory in the US. The all‑in‑one site handles local storage, customs, cross‑border shipping and transfers, helping sellers target US customers. (South China Morning Post)

- Hundreds of Amazon marketplace sellers staged a 24-hr boycott of ads after Amazon annc’d policy shifts that change ad payments, delay payouts and add a temporary 3. 5% fuel surcharge. Organized by Million Dollar Sellers, whose members generate ~$14bn in rev, merchants say the moves squeeze cash flow and margins across a biz that represents 60%+ of goods sold. (CNBC)

- AI is reshaping how shoppers feel about brands, w/ 80% of consumers under 44 using LLMs before site visits. Over 90% use AI for research and 53% to pick a retailer, often deciding pre-click. One in five bought from a new brand via AI tips. Clear, accurate product data boosts trust, while pricing or info errors cut confidence and can stop a sale. (Retail Dive)

- Instacart annc’d it acquired Instaleap, aiming to speed global expansion of its enterprise platform. The deal adds Instaleap’s grocery tech and fulfillment svs, used by ~100 retailers across ~30 countries in Europe, Latin America and the Middle East. Instaleap will operate as a wholly owned subsidiary while enriching Instacart’s enterprise offerings. (Instacart)

- Amazon Autos now lets shoppers buy a new Chevrolet Corvette on Amazon.com, as the e‑commerce giant quietly expands its car sales biz. What began as an experiment w/ Hyundai Motor cont’d over the past yr and a half, adding Kia, Mazda, Subaru, Chevrolet and Jeep. The svs is active in over 130 cities, highlighting AMZN’s push into auto mkts as shares rose 2.24%. (The Wall Street Journal)

- Walmart-owned Flipkart and Amazon are intensifying pressure on India’s quick commerce startups as competition and costs rise. The Flipkart Co has surpassed 800 dark stores and plans to double by end-2026, w/ 25–30% of orders from small towns. Amazon has ~450–500 stores. (TechCrunch)

Film/Studio/Content/IP/Talent

- Netflix co-CEO Ted Sarandos met theater owners at CinemaCon in Las Vegas, including AMC’s Adam Aron, Regal’s Eduardo Acuna and Cinemark’s Sean Gamble, according to two people w/ knowledge of the Sunday night talks. Discussions focused on putting more Netflix films into theaters, suggesting Sarandos may be changing his tune on theatrical exhibition after years of resistance. (The Wrap)

FinTech/InsurTech/Payments

- Goldman Sachs annc’d plans to launch its first bitcoin ETF after a filing w/ the SEC. The product would give exposure to bitcoin’s price and income from options, marking the cos first crypto ETF push after its Innovator Capital buy. The move follows a rival launch by Morgan Stanley. Analysts caution the volatile mkts and downside risk may limit demand, as bitcoin is down ~15% YTD. (Reuters)

- Kraken co-CEO Arjun Sethi said fears that AI will sharply disrupt SaaS are overblown, arguing most firms already rely on software and AI is simply spreading faster. Speaking at Semafor World Economy in Washington, DC, he said tech-driven disruption is cont’d and uneven. Kraken, which filed confidentially for an IPO, was valued at $13.3bn in Apr., down from a $20bn 2025 peak. (Semafor)

Handheld Devices & Accessories/Connected Home

- Kering annc’d plans to launch luxury Gucci-branded Google smart glasses in 2027, CEO Luca de Meo told Reuters in Florence. The move could make Gucci the first major luxury brand in AI eyewear, competing w/ EssilorLuxottica’s Meta-backed Ray-Ban glasses. (Reuters)

- IDC said global smartphone shipments fell 4. 1% YoY to 289.7mn units in 1Q26 as memory shortages and higher prices hit demand, ending a 10‑quarter growth streak. Samsung and Apple were the only top‑5 cos to grow, up 3.6% and 3.3%, helped by premium focus and supplier leverage. Rising costs are pushing mkts toward higher prices while emerging regions face sharper pressure. (IDC)

- China’s Rokid AI smart glasses outsell Alibaba rivals, beating Meta’s Ray-Ban Display in key features. Rokid’s virtual screen enables teleprompting, navigation and payments, driving demand despite ~$100 higher pricing. The Co ships globally, holds ~3.9% share, sells at $599 overseas vs Meta’s $799, and targets 1mn units in 2026 as AI display glasses remain a niche but fast-growing mkts segment. (CNBC)

HealthTech/Wellness

- AWS annc’d Amazon Bio Discovery, an AI-powered app to speed early drug research. The tool gives scientists access to specialized AI models, an agent to design experiments, and built‑in lab partners, creating a continuous test‑and‑learn loop. AWS said the tech cuts antibody discovery timelines from months to weeks and lowers AI adoption barriers for pharma, biotech, and academic researchers. (Amazon)

Live Entertainment/Theme Parks/Concerts/Experiential

- Canada’s Cineplex, the largest movie-theater chain, is shopping itself to potential buyers in a bid to combine w/ a rival. CEO Ellis Jacob has reached out to peers, including Regal Cineworld Group and Cinemark Holdings Inc., to gauge takeover interest, according to people familiar w/ the matter. Discussions are early, private, and may not result in a deal. (Bloomberg)

M&A

- Prosus annc’d sale of a 4.5% Delivery Hero stake to Uber for ~€270mn ($318mn), selling 13.6mn shares at €20 to meet EU terms tied to its Just Eat Takeaway deal. Uber becomes the fourth-largest holder, with its Delivery Hero stake valued at over $600mn. Shares rose ~2.9% on the news. (Reuters)

Macro Updates

- PwC plans to overhaul its global consulting biz to improve how national firms work together and deliver svs to multinational cos, FT reports, citing sources. The Co aims to standardize training, route demand to best‑qualified teams, and expand shared staff, including in India. (Bloomberg)

Media Conglomerates

- Paramount Skydance staged its first upfront, spotlighting a tech-first rebirth and heavy emphasis on NFL and live sports, w/ CEO David Ellison leading a fast-paced pitch. The Co skipped talk of a potential Warner Bros. Discovery deal, downplayed cable and CBS News, and focused on Paramount+, Pluto TV and adj platform convergence. (Variety)

- An NBCUniversal executive publicly criticized Nielsen after it delayed an update to its Gauge TV‑use report that could have boosted reported broadcast and cable viewing short term. Nielsen postponed integrating Advertising Research Foundation surveys after streamers questioned estimates, then canceled the release. (The Wall Street Journal)

Metaverse/AR & VR

- Meta annc’d price hikes for its Quest VR lineup, citing a global RAM shortage raising costs. The Co will lift Quest 3 by $100 to $599.99, while both Quest 3S models rise $50 to $349.99 and $449.99; refurbished units also jump. Meta said higher memory‑chip prices across consumer tech forced the move, but accessories stay flat, and smart glasses aren’t expected to see increases soon. (The Verge)

Regulatory

- The EC annc’d proposed DMA measures requiring Google to share search engine data w/ third parties on fair, reasonable and non‑discriminatory terms. Data includes rankings, queries, clicks and views, covering eligibility, scope, pricing, anonymisation and access processes, incl. some AI search svs. (European Commission)

- Ohio Casino Control Commission fined online prediction mkts Co Kalshi $5mn for offering unlicensed sports betting, escalating a legal fight over whether its sports contracts are gambling. Regulators said Kalshi ignored cease-and-desist orders issued in Apr. 2025. An Ohio federal judge earlier ruled the contracts are not swaps. (Business Insider)

- The EU said its age verification app for online platforms is ready and will roll out soon as European govts move to curb children’s social media access. EU chief Ursula von der Leyen said enforcement will move “full speed,” w/ platforms held accountable. (Reuters)

- In FCC reply comments, the NAB criticized CTA’s support for streaming, urging policies to keep major sports on broadcast TV. NAB said fans back free, accessible games and oppose paywalled svs that raise costs and confusion. CTA argued mkts should decide distribution and said streaming expands choice and devices. NAB countered broadcast sports drive local news rev and public interest. (TV Technology)

- Anthropic opposes Illinois bill SB 3444, backed by OpenAI, that would shield AI labs from liability if systems cause mass casualties or over $1bn in property damage. The dispute highlights widening divides between US AI cos over regulation as lobbying ramps up. Anthropic has lobbied sponsor Sen. Bill Cunningham to revise or kill the bill, calling talks a possible starting point for future AI law. (Wired)

- Federal agencies are quietly skirting President Trump’s ban on Anthropic to test its new Claude Mythos AI tech, which can uncover critical software flaws. The officials across agencies, Congress, and Commerce Dept.’s AI standards unit sought briefings or testing w/ it for cyber defense, despite litigation and a DOD supply-chain risk label. (Politico)

- European regulators were largely sidelined as U.S. AI Co Anthropic restricted release of its Mythos model, which it says can surpass most humans at finding and exploiting tech flaws. Annc’d last week, access went to 12 U.S. tech cos incl. Apple, Microsoft and Amazon, plus ~40 others unnamed. EU agencies reported limited or no testing, raising security and oversight concerns. (Politico)

Satellite/Space

- SpaceX is arranging multi-day site visits for large potential IPO investors, aiming to showcase facilities in California and Texas as it nears a record-setting public debut. The rocket, satellite and AI Co has filed confidentially and is seeking to raise up to $75bn at a valuation above $2tn. (Yahoo Finance)

Software

- Apple privately threatened to pull Elon Musk’s Grok AI app from the App Store in Jan. after xAI failed to curb creation of nude or sexualized deepfakes, according to a letter Apple sent to U.S. senators and obtained by NBC News. The Co said reviews found Grok and X in violation of App Store guidelines, prompting warnings of possible removal if fixes were not made. (NBC)

- Google annc’d Skills in Chrome, enabling users to save AI prompts as one‑click tools in Gemini in Chrome. The feature lets people reuse workflows across tabs, edit them anytime, and trigger prompts via shortcuts. Google Co said early testers used it for shopping, wellness and productivity. (Google)