The exciting Nasa Moon Mission is slated to come to a close, with Artemis II expected to touch down on the West Coast tonight. We will be watching for that!

In the meantime, optimism regarding war de-escalation boosted the markets this week with Nasdaq’s +4.7% rally leading, followed by the S%P 500’s +3.6% increase. AI was once again a main driver for stocks across the sector, both positively and negatively. On the latter in particular, cyber security stocks took it on the chin on the back of AI disruption concerns stemming from an Anthropic update (see Theme #2).

Big picture, we focused on the below developments and themes in this edition:

- Pershing Lays Out A Path To UMG’s Value Creation

- AI Developments Span Cybersecurity, Competition, and Compute This Week

- Amazon’s Chip Business Is “On Fire” & “Will Be Bigger Than [People] Think”

- Cybercrime Losses Hit New Highs While AI-Related Fraud Becomes a Meaningful Category

- Shorts Sellers Generally Hold Onto Their Top Picks In Q1

- Falling Global Worker “Engagement” Doesn’t Bode Well For AI Productivity

- Grab Bag: Greece Social Media Ban / Nexstar-Tegna Merger Hits Another Bump / Prediction Mkt Updates

** Also, in case you have not had a chance to take a look, CLICK HERE to see our recent quarterly report, LionTree’s Lens – Spring 2026 **

Lastly, I wanted to highlight that LionTree Advisors is proud to have served as exclusive financial advisor to Bregal Sagemount on its strategic growth investment in Redgate Software.

Have a nice weekend.

Best,

Leslie

Pershing Lays Out A Path To UMG’s Value Creation

Pershing Square’s proposed combination of Universal Music Group (UMG) and SPARC Holdings (its SPAC) was a main event this week. Bill Ackman’s fund has been a long-time shareholder of the Co and seemingly got tired of watching the stock decline from ~€29/share in mid Feb 2025, to a low of €15.5/share towards the end of last week. Public music-oriented stocks have been under a lot of pressure, stemming from some company-specific factors, but also from general fears about the long-term impact of AI on the labels’ business model. Pershing is not worried about the latter, and in fact, similar to what we have heard from UMG’s mgmt, they believe that AI will be a net positive.

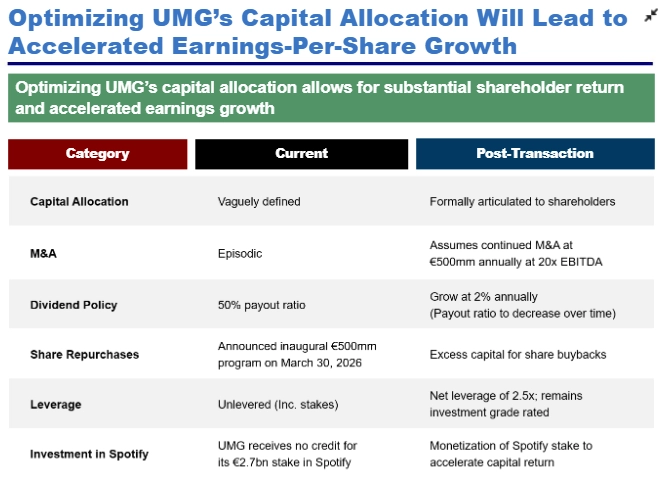

On company specific factors, the fund believes that shares of the NEW UMG will re-rate by 1) optimizing capital allocation and the balance sheet; 2) improving financial disclosures, expanding investor access, and publishing a “long term algorithm with a focus on per share EPS growth”; 3) enhancing corporate governance…including refreshing the board, and 4) listing in the US. In addition, the stock appreciation that would come from projected adj EPS growth of +15-19% CAGR over the next 6 years and assumed multiple expansion.

In this transition, Pershing estimates that UMG shareholders will receive an estimated value of €30.40/share, or a 78% premium to UMG’s last closing price pre-announcement. While UMG shareholders will get fewer shares in the NEW UMG, the Pershing Team argues that the newCo will be much more valuable.

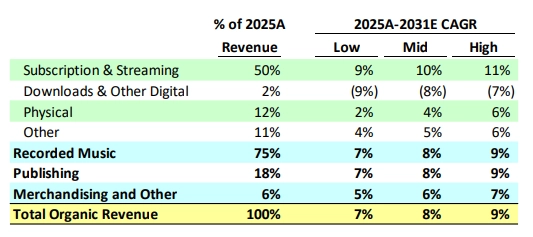

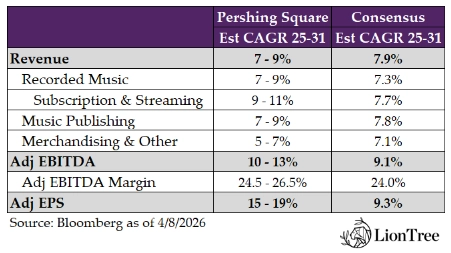

How do the fund’s 2025-31 financial projections compare to current Wall Street consensus expectations? They are more bullish. Pershing’s adj EPS CAGR assumptions for the NEW UMG at +17% (at the mid-pt) are much higher than cons +9.3%. Their 2031 adj EBITDA margin estimate of 25.5% (at the mid pt) exceeds cons 24%. Lastly, their Streaming & Subscription CAGR projection of +10% (at the mid-pt) compares to cons +7.7%.

All in all, Pershing Square sees UMG as a high quality, capital light royalty on the LT growth of global music. Streaming penetration and appropriate price hikes are anticipated to support long term high-SD revenue growth for the next decade+ and growth is projected to accelerate this calendar year due to wholesale price increases (music is still the lowest cost form of media entertainment). A lot still needs to happen for this deal to proceed but, at minimum, it puts more pressure on UMG mgmt to more aggressively look for ways to create value for shareholders.

See more color below on the points we viewed as most important in this proposal. If you want to see Pershing Square’s full presentation, it can be found after registering on their webcast page HERE.

-> UMG shares rallied as high as +24% on the back of the news but closed the day up +11%; However, the shares are still down -30% from late July last year; YTD, WMG is also down -7% and SPOT is down -18%

Pershing Square’s Proposal Basics

- Transaction structure: Pershing Square is proposing that UMG merge with Pershing Square SPARC Holdings

- Timing: The deal is expected to close by Q4:26

- Total consideration of cash + stock (based on their assumed value of NEW UMG) is €30.40/shr

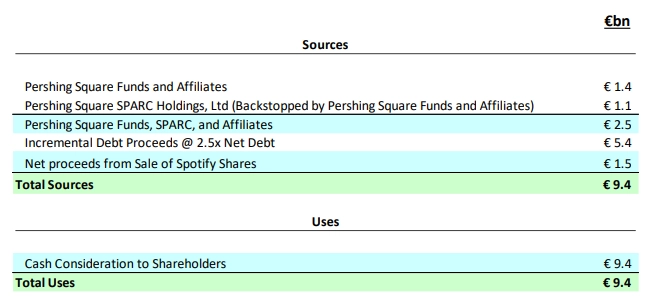

- Cash: €5.05/shr in cash (worth €9.4bn)

- Stock: 0.77 shares in NEW UMG (which they value at €32.90/shr) for each share of UMG owned by a shareholder (though shareholders may elect to receive all cash, all stock or a mix)

- How does Pershing get to their €90/shr for NEW UMG? By estimating €1.32 EPS in 2027 and assuming a 25x NTM PE multiple

- The proposal implies that current UMG shareholders will own a slightly lower % of a “much more high-quality company”

- The €9.4bn of cash consideration will be funded by:

- €2.5bn from Pershing Square Funds, SPARC, & Affiliates

- €5.4bn from incremental debt (net debt to EBITDA of no more than 2.5x)

- €1.5bn of net proceeds from the sale of the Co’s stake in Spotify (post tax/artists share)

- UMG artists will receive up to €750mn in proceeds from the sale of SPOT shares

- Pershing Square will waive its right to receive SPARC sponsor warrants

- Pershing also proposes that 17% of UMG outstanding shares will be cancelled: The 2.5x net debt at inception will be used to repurchase shares at €22/share

- Proforma ownership…Pershing Square would own 11.7%

Pershing Square Thinks The Stock’s Underperformance Is Due To…

- Uncertainty regarding Bolloré Group’s 18% stake in the Co

- Cyrille Bolloré’s resignation from UMG’s board at the end of July 2025 sparked more concern on this front

- The postponement of a US listing (annc’d in March of this year)

- The underutilization of UMG’s balance sheet, which has led to reduced returns on equity

- The absence of a publicly disclosed capital allocation plan and of an earnings algorithm

- The lack of investor credit for UMG’s €2.7bn stake in Spotify

- Suboptimal shareholder investor relations, communications, and engagement

…And They Believe They Can Close The Gap On Those Concern By Doing These Things

- Optimizing capital allocation & the balance sheet will lead to €14.9bn of total FCF capital allocation over the next 6 years

- Sell the Co’s ~3% Spotify stake:

- That would net €1.5bn to shareholders (post €480mn in taxes & €750mn in artist payments)

- Adopt a consistent 2.5x net debt /adj EBITDA leverage target

- This compares to 0.9x today (0.1x net of stakes)

- WMG is already at 2.5x levered, even though UMG is the market leader

- Pershing is confident UMG can maintain investment grade at this leverage level

- Reduce the dividend…Pershing argues that too much is being given back to shareholders via dividends right now (the current policy is paying 50% of net income for the dividend)

- Instead, increase the div by 2% annually which would reduce the payout over-time

- This would free up €3bn in incremental cash

- With these changes, the Co would generate total FCF for capital allocation at €14.9bn over the next 6 years: This leaves a lot of room for strategic investments AND also buybacks

- The Co will be disciplined & thoughtful on any catalog purchases and associated structuring (vs some of the other deals that are being done in the market)

- Sell the Co’s ~3% Spotify stake:

- Improve shareholder engagement…Pershing will work with the Co to enhance financial disclosure, expand investor access, and publish a “long term algorithm with a focus on per share EPS growth”

- Pershing proposes that the Co provides new guidance (see below)…

- …INSTEAD of what UMG provided at its Capital Markets Day

- Pershing proposes that the Co provides new guidance (see below)…

- Boost corporate governance…including refreshing the board

- The fund proposes Michael Ovitz as Chairman and 2 reps from Pershing Square

- Change the listing location to the US…this should be a significant positive change

- The Co should be US-based given more than 50% of revenue and profits come from the US and they are based operationally in CA

- A US listing provides incr’d liquidity, a broader investor base, broader index inclusion, US research analyst coverage (but the fund is also open to maintaining a dual listing)

- NEW UMG would also be eligible for S&P 500 and other major indices inclusion, making the stock ownable for many funds.

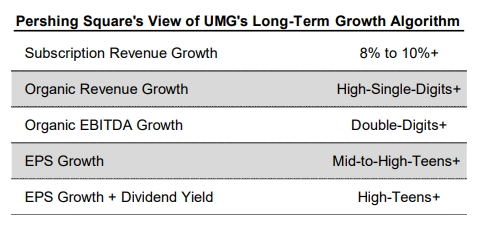

What Are Pershing’s Long Term Financial Expectations For NEW UMG?

- REVENUE – expected in the high SD annual range over the next 6 years…driven by Subscription & Streaming revenues (half of overall revenue) growing at a DD rate over the period

- The shift to wholesale pricing will be a driver

- And streaming services are still underpriced

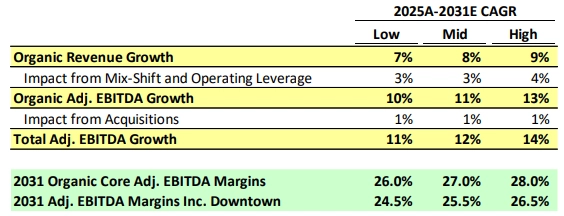

- ADJ EBITDA MARGINS – expected to expand significantly from 22.5% in 2025 to mid-to-high 20s% by 2031

- Acq of Downtown Music and higher growth in independent svs will be a modest headwind to margins (though there could be synergies with the deal, which are not factored in) BUT…

- The revenue mix shift (normalization of physical and merchandising, shift to streaming and catalog listening) will be positive

- Also expect operating leverage (AI efficiencies and A&R costs do not need to scale proportionately w/ rev growth – though an analyst on the conference call pushed back on the latter)

- Margins should inherently be higher than peers b/c of UMG’s scale

- ADJ EBITDA GROWTH – if margins expand to 24.5-26.5% by 2031…

- It can drive EBITDA growth of 10-13% CAGR over the next 6 years

- And w/ acquisitions should result in adj EBITDA growth of 11-14% CAGR

- Adj EPS – project will growth 15-19% CAGR, and with addtl ~1% div yield, the total return would be 16-20% CAGR

How Do These Projections Compare To Current Wall Street Consensus? …They Are Much Higher Especially On Adj EPS Growth & Adj EBITDA

- We compared Pershing Square’s long-term NEW UMG estimates with the current UMG bberg consensus expectations through 2031

- Pershing’s adj EPS CAGR projection is dramatically higher (+17% at the mid-pt vs cons +9.3%), followed by adj EBITDA CAGR (+12% at the mid-pt vs cons +9.1%)

- Subscription & Streaming revenue CAGR is more bullish as well (+10% at the mid-pt vs cons +7.7%)

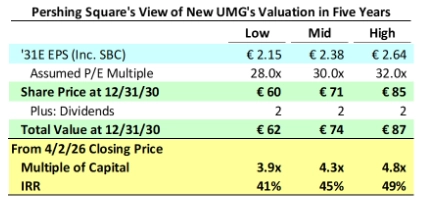

Where Does Pershing Square Think The Stock Can Rerate To? …between €62 – 87/shr In 5 Years

- The stock was trading at a P/E of 15.6x (pre-this announcement) … near an all-time low

- Pershing Square expects P/E multiple expansion to 28-32x in 5 years

- Based on its adj EPS growth estimates and anticipated P/E multiple expansion, this implies the stock will hit between €62-87/shr, offering an IRR of 41-49%

What About Risk From AI? Will That Negatively Impact The Plan? No, Pershing Sees It As A Positive (Similar To What UMG Mgmt Has Already Been Saying)

- Interestingly, Pershing Square didn’t bring up AI at all in its pitch until asked on the call directly by an analyst

- The fund argues that AI will be a net positive (similar to what UMG mgmt. has been saying) b/c of:

- The labels will become more important as a curation engine & platform for artists to stand out from the noise

- Most music is not actually listened to and they think this will be the same with AI music

- The majors are gained shr of listening in 2025 despite total content proliferation

- AI enables new monetization opportunities beyond DSPs

- AI enhances creativity and improves human artistry…artists are using it today

- AI will help UMG be more efficient (automate A&R and predictive talent sourcing, artist & fan engagement, generating marketing content, activation of catalog, rationalize costs and automate process)

- AI artists will be a niche…fewer than 1% of songs are “commercially relevant” and fewer than 0.2% of songs are culturally relevant

Pershing Square Is “Very Confident That This Transaction Addresses Everyone’s Concerns”

- What are next steps? Pershing Square needs –

- UMG’s and SPARC’s board approval

- Pershing Square owns 100% of SPARC

- 2/3rds vote in favor of the Transaction by UMG shareholdings that attend the meeting

- Pershing has “spoken to” the Bolloré Group and they are “intrigued which was music to our ears but the devil is in the details”

- The fund expects that “Tencent will find this attractive”

- “We don’t see a reason” why we won’t get the support for this”

- The customary regulatory approvals

- UMG’s and SPARC’s board approval

- Other proposed changes

- A new employment contract for Lucian Grainge… “Lucian’s contract is too complicated”

- Pershing believes that there is a change of control in his contract but does not know of any other contract affected by change in control

- A new employment contract for Lucian Grainge… “Lucian’s contract is too complicated”

AI Developments Span Cybersecurity, Competition, and Compute This Week

Every time we thought we had all the impactful AI updates covered, another one seemed to come up! This week included a wide range of announcements across AI’s implications on cybersecurity, new model releases, enterprise tools, escalating competition between OpenAI and Anthropic, and a continued surge in infrastructure investments.

Digging in, arguably the announcement that reverberated through the market the most was Anthropic’s Project Glasswing, which came about because of capabilities observed in its Claude Mythos, a new frontier model that has already identified thousands of high severity vulnerabilities across major operating systems and web browsers. Project Glasswing is a limited access program that brings together a group of large tech and cybersecurity Cos that exclusively have access to the model to identify and fix vulnerabilities. The development not only triggered a sharp decline across cybersecurity stocks, but also prompted an urgent meeting between Fed Chair Jerome Powell, Treasury Secretary Scott Bessent, and major bank CEOs to discuss potential risks and preparedness. Later in the week (and not to be overlooked), it was reported that OpenAI is developing a similar cybersecurity-focused product that will similarly be restricted to a small group of partners. Needless to say, cyber security stocks had a touch week.

Elsewhere in AI…1) Meta introduced Muse Spark, its first model from a broader overhaul of its AI efforts; 2) Anthropic expanded access to Claude Cowork with new enterprise features and launched Managed Agents, a suite of tools designed to help developers build and deploy agents more quickly; and 3) Competition between OpenAI and Anthropic also intensified, with Anthropic reporting ARR surpassing OpenAI and OpenAI sharing some sharp comments on Anthropic’s positioning in an internal memo.

In addition, across infrastructure, several large-scale investments and partnerships were announced, including Meta expanding its agreement with CoreWeave, a new CoreWeave deal with Anthropic, and additional compute partnerships involving Google, Broadcom, and Intel. Amazon also continued to expand its data center footprint.

Please see more details below, and also see Theme #3 for other important AI related updates from Amazon CEO Andy Jasey’s annual shareholder letter.

It Was A Tough Week For Cyber Security Stocks

- Anthropic announces “Project Glasswing”, which is meant for “securing critical software for the AI era” (link/link)

- What brought about Project Glasswing? Anthropic has observed capabilities in Claude Mythos Preview, a new frontier general-purpose model trained by Anthropic, that they believe could reshape cybersecurity for better and worse, with concerns that such a powerful vulnerability-finding model could cause serious harm if widely released

- “AI models have reached a level of coding capability where they can surpass all but the most skilled humans at finding and exploiting software vulnerabilities”

- Claude Mythos has already found thousands of “high-severity vulnerabilities” in every major OS and browser…in some cases, these vulnerabilities have “survived decades of human review and millions of automated security tests”

- “Given the rate of AI progress, it will not be long before such capabilities proliferate, potentially beyond actors who are committed to deploying them safely”

- Project Glasswing brings together a limited # of Big Tech names as launch partners “in an effort to secure the world’s most critical software”: Cos include Amazon, Apple, Broadcom, Microsoft, Cisco, CrowdStrike, Palo Alto Networks, and the Linux Foundation

- Have also extended access to a group of 40+ addtl orgs that build or maintain critical software infrastructure so they can use the model to scan and secure both first-party and open-source systems

- Why not do a general release? Anthropic has said that frontier AI models are approaching a point where keeping the strongest systems tightly held, while giving select defenders early access, may be safer than broad release (more on that below)

- Launch partners will be the only ones to have access to Claude Mythos Preview: Anthropic is NOT currently planning to publicly release the model due to security concerns

- Launch partners will use Mythos Preview in their defensive security work, and Anthropic will share findings with industry: The partners will use the model to analyze their system to spot high-stakes vulnerabilities and help patch them up

- Access is restricted to keep those same adversaries from using it to find weak points and conduct attacks

- Within 90 days, Anthropic said it will publish what the program has learned, including vulnerabilities fixed and improvements that can be disclosed

- What brought about Project Glasswing? Anthropic has observed capabilities in Claude Mythos Preview, a new frontier general-purpose model trained by Anthropic, that they believe could reshape cybersecurity for better and worse, with concerns that such a powerful vulnerability-finding model could cause serious harm if widely released

- On the back of that…Fed Chair Jerome Powell and Treasury Secretary Scott Bessent met w/ Wall Street bank CEOs in an urgent meeting on concerns around the incr’d cyber risk from Anthropic’s Claude Mythos (link/link)

- The mtg was reportedly arranged on short notice to make sure banks are aware of possible future risks raised by Anthropic’s Mythos and are taking precautions to defend their systems

- All the banks summoned to the mtg are classified as “systemically important” by top regulators, meaning their stability is a priority for the global financial system

- Reportedly in attendance: The CEOs of Citi, Morgan Stanley, BOA, Wells Fargo, & Goldman Sachs; JPM was reportedly unable to attend

- As a reminder… last week, Anthropic said it was in ongoing discussions with US govt officials about the model’s “offensive and defensive cyber capabilities” and the Co reportedly proactively briefed senior US govt officials and key industry stakeholders on Mythos’s capabilities ahead of its release

- Another update that might add more fuel to the fire looking ahead = OpenAI is reportedly in the process of finalizing a product with advanced cybersecurity capabilities that will also only be released to a small set of partners (link)

- The product will reportedly be distributed through “Trusted Access for Cyber,” a pilot program OpenAI launched in February alongside the release of GPT-5.3-Codex

- Details beyond the press reports remain limited at this point

-> The HACK ETF rose slightly (up +0.3%) on Tuesday, the day of the Project Glasswing announcement, but then subsequently fell almost -10% over the remainder of the week; Cybersecurity stocks that were hit hard including Okta down -21.5%, Cloudflare down -21.1%, Zscaler down -14.8%, Check Point Software down -8.8%, Fortinet down -7.1%, and CrowdStrike down -5.0%

Other New Disruptive AI Models Releases This Week…

- Meta’s new Muse Spark, “the first product of a ground-up overhaul” of Meta’s AI efforts, was met with enthusiasm (link)

- The initial Muse Spark model is “small and fast by design”, though capable enough to reason through complex questions in science, math, and health

- “It is a powerful foundation, and the next generation is already in development”

- Muse Spark is purpose-built for Meta’s products: It will power a smarter and faster Meta AI, and over time unlock new features that cite recommendations and content people share across the platforms

- Where is Muse Spark being deployed? It currently powers the Meta AI app and website, and will be rolling out to WhatsApp, Instagram, Facebook, Messenger, and AI glasses in the coming weeks

- What’s changed w/ the Meta AI app and meta.ai: Both are getting an upgrade, along w/ a new look; Meta AI can now provide a quick answer or help with complex problems that need strong reasoning; Users can switch b/w modes depending on the task and Meta AI can launch multiple subagents in parallel to tackle the question

- Unlike Meta’s previous AI models, Muse Spark is a primarily in-house tool for Meta (for now): Earlier models were released as “open weight” models, meaning anyone could download the models for free and run them on their own equipment, as well as modify and fine-tune them as they wished

- The initial Muse Spark model is “small and fast by design”, though capable enough to reason through complex questions in science, math, and health

-> Meta’s stock was up +6.5% on the day of the announcement and ended the week up a strong +9.6%

- Anthropic opens Claude Cowork up for general availability + introduces enterprise capabilities (link/link)

- Claude Cowork for macOS and Windows is now generally available for all paid subscribers across Pro, Team, and Enterprise plans

- Was previously only available in research preview

- Also, Claude Cowork now includes six features built especially for enterprise use –

- Role-based access controls to define what different teams can do

- Group spend limits to manage costs per team

- Usage analytics for tracking adoption and activity

- Expanded OpenTelemetry support for monitoring system events

- Zoom MCP connector for meeting insights

- Per-tool connector controls to limit actions, like write access

- Who is the rollout targeted towards? Mainly organizations looking to move beyond individual AI chat interactions toward delegating entire workflows to autonomous agents

- Per Anthropic, non-engineering teams (i.e., operations, marketing, finance, and legal) now account for the majority of Cowork usage within early enterprise adopters

- Claude Cowork for macOS and Windows is now generally available for all paid subscribers across Pro, Team, and Enterprise plans

- Anthropic launches Claude Managed Agents, “a suite of composable APIs for building and deploying cloud-hosted agents at scale” 10x faster (link/link)

- Aims to help developers build and deploy AI agents much faster

- With Managed Agents, developers can now “go from prototype to launch in days rather than months”: Up until then, creating AI agents meant handling complex backend work such as secure infrastructure, state mgmt, setting permissions and constantly updating systems when models changed

- How does it work? Developers only need to describe what the agent should do, what tools it can use, and what guardrails should be in place; A built-in orchestration system then decides when to use tools, how to manage context and how to recover from errors

- Managed agents include –

- Production-grade agents with secure sandboxing, authentication, and tool execution handled

- Long-running sessions that operate autonomously for hours, with progress and outputs that persist even through disconnections

- Multi-agent coordination so agents can spin up and direct other agents to parallelize complex work

- Trusted governance, giving agents access to real systems with scoped permissions, identity management, and execution tracing built in

The OpenAI Vs Anthropic Battle Intensifies

- The OpenAI vs Anthropic feud escalates…OpenAI takes another swing at Anthropic in an internal memo saying they are “operating on a meaningfully smaller curve” and are compute constrained (link/link/link)

- OpenAI says that they are outpacing Anthropic by “rapidly and consistently” adding computing capacity to support wider adoption of its software… “that gap matters because compute is now a product constraint”

- OpenAI plans to have 30 gigawatts of compute by 2030, while it expects Anthropic to have ~7 to 8 gigawatts by the end of 2027

- “Even at the high end of that range, our ramp is materially ahead and widening

- OpenAI is also benefitting from “compounding advantage,” with better infrastructure and models lowering costs, and superior products leading to higher rev

- “This leverage also enables OpenAI to continue democratizing AI by making our tools available to hundreds of millions of people for free and being more generous with builders, passing that capacity on to the people who are creating and solving problems with our tools”

- Also characterized Anthropic CEO Dario Amodei as miscalculating the market’s appetite for more AI products…

- “In hindsight […] that caution looks less like discipline and more like underestimating how fast demand would arrive”

- ….and took a swipe at Anthropic’s more conservative spending approach vs OpenAI’s view that heavier infrastructure investment is self-reinforcing

- Cheaper costs follow from stronger models and hardware, and those savings in turn fund product improvements that attract more customers and revenue.

- “Each new generation of infrastructure lets us train more capable models, making every token more intelligent than the one before… at the same time, algorithmic gains and hardware improvements reduce the cost to serve each token, lowering the cost per unit of intelligence”

- OpenAI says that they are outpacing Anthropic by “rapidly and consistently” adding computing capacity to support wider adoption of its software… “that gap matters because compute is now a product constraint”

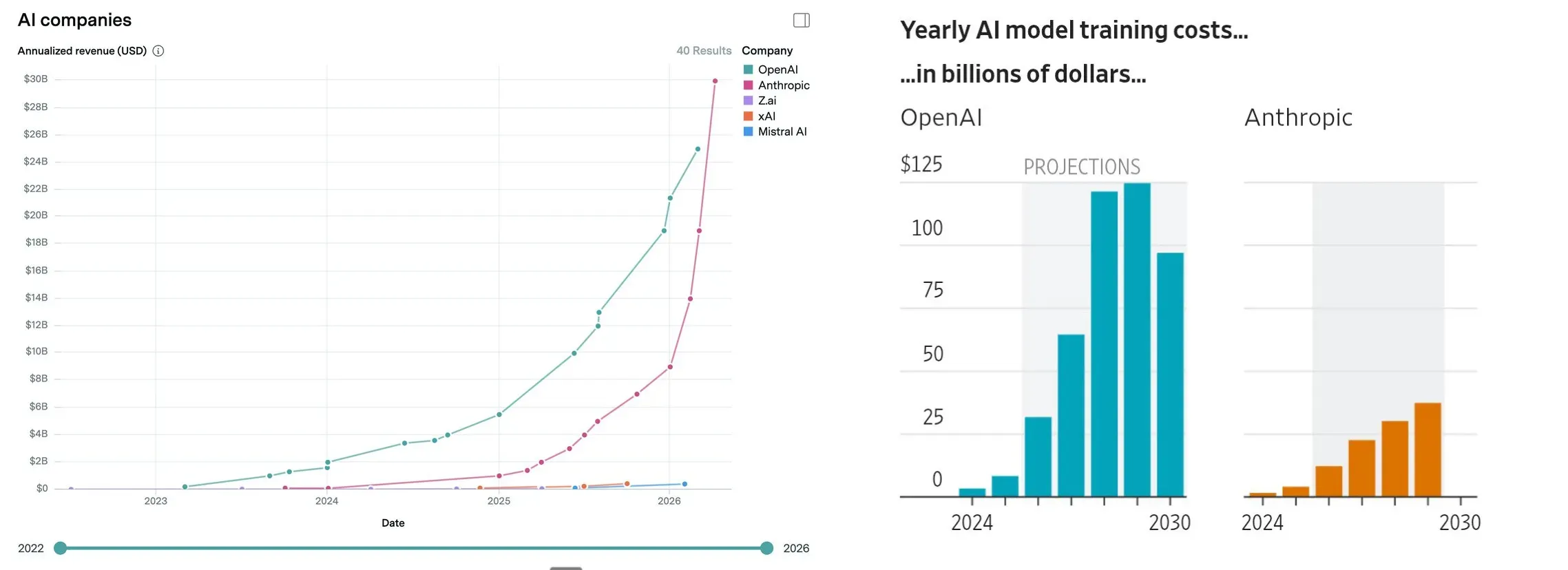

- At the same time, Anthropic’s ARR has reached $30bn, surpassing OpenAI’s $25bn (link/link/link): Note that Anthropic’s latest ARR figure is from this week, vs OpenAI’s is from late Feb 2026

- Anthropic’s ARR incr’d +$11bn in just a month…: and is up from $19bn in February

- When the Co annc’d their Series G fundraising in Feb, it had 500+ biz customers that were each spending $1mn+ on an annualized basis

- Today, that # exceeds 1,000, ie, doubling in <2 mos

- …and has incr’d +$21bn YTD: Up from ~$9bn at the end of 2025

- Anthropic’s large enterprise base is a significant advantage over OpenAI

- 80% of Anthropic’s rev comes from biz customers vs OpenAI’s more consumer-heavy composition

- Enterprise rev tends to carry higher retention rates, better expansion economics, and lower churn

- Some other key OpenAI vs Anthropic financial differentiators…

- OpenAI is spending 4x more to train models that generate less revenue: OpenAI is heading toward $125bn in yearly training costs by 2030, while Anthropic’s is projected at ~$30bn for the same period

- Anthropic is expected to reach profitability three yrs before OpenAI, while also generating more rev: Anthropic projects positive FCF by 2027, while OpenAI expects to reach breakeven in 2030

- Anthropic’s ARR incr’d +$11bn in just a month…: and is up from $19bn in February

Source: The AI Corner

-> Also on the topic of AI platform KPIs but on a much smaller scale, Perplexity’s revs have jumped +50% in the last month, pushing its ARR past $450mn, after the launch of a new agent tool and a shift to usage-based pricing; Perplexity was last valued at $20bn in September, up from $500mn at the beginning of 2024 (link)

A Whole Host Of Capacity And Infrastructure-Related Updates This Week…

- Meta commits to spending an addtl $21bn w/ CoreWeave in an expanded AI infrastructure agreement (link/link/link)

- CoreWeave will provide AI cloud capacity through December 2032 for approximately $21bn

- The dedicated capacity will be deployed across multiple locations and will include some of the initial deployments of the NVIDIA Vera Rubin platform

- The distributed approach is designed to optimize performance, resilience, and scalability for Meta’s AI operations.

- Builds on a prior ~$14.2bn commitment…. updated agreement brings Meta’s total contracted spend with CoreWeave to ~$35bn, extending the duration into 2032 (vs the original deal through 2031) and incorporating previously optional capacity

- CoreWeave now holds $35bn in contracts with Meta, making Meta one of CoreWeave’s largest customers

-> Meta and CoreWeave both ended the day of the announcement up +2.6% and +3.5%, respectively

- CoreWeave also annc’d a multi-yr agreement w/ Anthropic to support the development and deployment of Anthropic’s Claude family of AI model (link)

- The multi-yr agreement will bring compute online starting later this yr

- Under the agreement, Anthropic will use CoreWeave’s cloud platform to run workloads at production scale, while benefitting from CoreWeave’s “industry-leading” performance and reliability

- The collaboration will initially focus on a phased infrastructure roll-out with the potential to expand over time

- Financial terms of the agreement were not disclosed, but it’s a “multibillion-dollar contract,” per CoreWeave CEO

-> CoreWeave jumped +10.9% in reaction to the deal and ended the week up +24.0%

- Anthropic also expanded into partnership with Google and Broadcom for “multiple gigawatts” of next-gen TPU capacity that is expected to come online in 2027… (link)

- Strategic rationale? It will power Anthropic’s frontier Claude models and help them serve the “extraordinary” demand from customers worldwide

- The “vast majority” of the new compute will be sited in the United States, making this partnership a major expansion of Anthropic’s Nov 2025 commitment to invest $50bn in strengthening American computing infrastructure

-> Broadcom’s stock was up +6.0% on the back of the announcement, their second-best day of the yr

- …and Anthropic is also reportedly considering building its own AI chips (link)

- The plans are in the early stages and the Co may still decide to only buy AI chips and not design any

- The Co has yet to commit to a specific design or put together a dedicated team to work on the project

- For some context… Anthropic uses a range of chips, including TPUs designed by Google and Amazon’s chips to develop and run its AI software and chatbot Claude

- As a reminder…Meta and OpenAI already have similar projects underway

- Separately, Google expands its partnership w/ Intel for AI infrastructure development in a “multi-year” collaboration (link/link/link): Intel will provide processors across Google Cloud’s infrastructure while co-developing custom chips for data center tasks

- Intel’s Xeon processors will continue to power Google Cloud infrastructure across AI, inference and general-purpose workloads

- For context, Xeon once commanded a market share of more than 99%, but has lost ground over the last few yrs to competitors like Advanced Micro Devices and in-house efforts by customers (such as Google)

- Google will also customize Intel’s infrastructure processing units (IPUs), which is meant to reduce some of the data center burden on CPUs

- How? The programmable accelerators can offload networking, storage and security functions from host CPUs, which Intel says delivers greater efficiency and more predictable performance across large AI environments, enabling Google Cloud to scale without increasing the complexity of its systems

- The two Cos said their collaboration will enable “a more balanced approach to AI system design — one that improves utilization, reduces complexity and scales more efficiently”

- Intel’s Xeon processors will continue to power Google Cloud infrastructure across AI, inference and general-purpose workloads

-> Intel shares were up +4.7% on the day of the announcement

-> Separately, but related, Intel announced this week that it will join Elon Musk’s Terafab AI chip project to make processors powering their humanoid and data center goals; Last month, Musk launched the Terafab project, in which Tesla and SpaceX will work together to produce chips for data centers, robots and autonomous cars; The plan involves building two advanced chip plants at a site in Austin, Texas – one facility will concentrate on supplying chips for electric cars and humanoid robots, while the other is planned to support AI data centers located in space (link/link/link)

- Amazon’s total planned investments in Mississippi data centers has reached $25bn, w/ plans to create 2,000+ “highly-skilled” jobs across all their Mississippi data center operations (link)

- This represents one of the largest corporate investments in Mississippi’s history but is not the first investment Amazon has made in the state:

- 2 yrs ago, Amazon broke ground on its first data center campus in Madison County (the largest capital investment in Mississippi’s history at the time)

- That was followed by a $3bn planned investment in Warren County

- The Co is investing an addtl +$12bn to build two new data centers: Includes an addtl $11bn investment in Madison County (expected to create ~700 new jobs) and a $1bn investment in Hinds County (expected to create ~100 jobs)

- Amazon now has 4 data centers being built in the state

- This represents one of the largest corporate investments in Mississippi’s history but is not the first investment Amazon has made in the state:

Amazon’s Chip Business Is “On Fire” & “Will Be Bigger Than [People] Think”

Amazon CEO Andy Jasey’s annual shareholder letter clearly articulated his forward-looking vision and mgmt philosophy, with several great food for thought comments. An overarching theme throughout was that life and businesses do not move in a straight line…one needs to ebb and flow, adapt, jump into opportunities, and revisit. Amazon over the years has had periods of innovation and periods of retrenchment, but Jasey was adamant (again) that AI is one of these rare once-in-a-lifetime opportunities, and that Company is going to invest heavily. He defended their spending plans, saying that the guided $200bn capx in 2026 is not investing on a “hunch”. AI demand continues to exceed supply, and the Co has commitments for the additional planned capacity. These investment spikes “will invite scrutiny, but the game-changers don’t typically accommodate smoother investment horizons.”

AWS’s AI business is now at a $15bn run rate (Q1) and the chips business is “on fire”. Jasey projects that if standalone, the chips business in aggregate would have an annual revenue run rate of $50bn. He also interestingly previewed that the Co might look at sell chips to third parties in the future.

Regarding the core Retail business, faster delivery, to more places (i.e., rural), can still yield more upside in Jasey’s view. Drone delivery services are expanding as part of that, and non-perishables are also a key investment area that has been showing strong results. Satellite connectivity, autonomous cars, and robotics were also called out as well for driving future growth.

All in all, the letter reinforced much of what mgmt has been articulating but it added some powerful stats and wrapped it within its mgmt philosophy and approach.

See below for more of what we thought was most interesting and impactful from the letter. Also see Theme #2 for more impactful AI related updates out this week.

Underpinning Themes In This Year’s Letter

- “Wherever possible, invent the next inflections”

- Be willing to pursue parallel paths when it’s unclear what’ll best drive the desired trajectory (2 > 0)”

- “If there’s an obvious path to changing your trajectory, take it and run. But, most new jumps forward aren’t like that. There’s invention and experimentation required, and pursuing multiple paths gives you the best chance to find it”

- “When you identify disproportionate inflections, bet big”

- “This will create investment spikes that will invite scrutiny, but the game-changers don’t typically accommodate smoother investment horizons. One of these seminal shifts is AI.”

- “Accept going back to the starting line to redirect the trajectory”

- “Cultivate a culture that can cope with squiggly lines”

Jasey Reiterates That AI Is A “Once-In-A-Lifetime” Opportunity

- Echoing previous comments, “AI is a once-in-a-lifetime opportunity where the current growth is unprecedented and the future growth even bigger”

- “We’re not investing ~$200bn in capex in 2026 on a hunch”

- “When Edison opened his first commercial power station in 1882, most people understood it as a better way to light a room. What they couldn’t see was that electricity would eventually reorganize every factory, home, and industry on Earth. AI may have comparable impact. The difference is that electricity took 40 years to get where it was going. AI appears to be moving ten times faster”

- Amazon has customer commitments for the infrastructure they are building

- Most of the 2026 capx will be monetized in 2027-2028 and the Co already have customer commitments for a “substantial portion” of it

- “We are willing to make large capex investments and endure short-term FCF headwinds for the substantial medium to long-term FCF surplus”

- “Amazon is smack in the middle of this land rush, and companies are choosing AWS for AI”

AWS Demand Exceeds Supply, The AI Revenue Run Rate Is $15bn+, & The Chips Business Is “On Fire”

- AWS could be growing even faster

- Mgmt reiterated that by the end of 2027, AWS will double total power capacity over 2025 (the Co added 3.9 GW)…and that the Co is monetizing that capacity as fast as it’s installed

- “We still have capacity constraints that yield unserved demand”

- “Two large AWS customers have already asked if they could buy *all* of our Graviton instance capacity in 2026…we can’t agree to these requests given other customers’ needs, but it gives you an idea of the demand”

- AWS’s AI revenue run rate is over $15bn in Q1:26

- The chips business is “on fire” and Amazon is set to benefit from the shift to better price-performance

- While Nvidia is the dominant market leader, customers will shift to better price-performance alternatives

- “We’ve seen this movie before”

- “In the CPU space, virtually all of the workloads ran on Intel chips until we invented Graviton in 2018. Graviton, which has up to 40% better price-performance than other x86 processors, is now used expansively by 98% of the top 1,000 EC2 customers”

- “The same story arc is unfolding in AI”

- “Demand for Trainium is booming” & will drive up operating margins: It will save Amazon “tens of billions” of capex dollars per year, and provide “several hundred basis points” of operating margin advantage versus relying on others’ chips for inference

- Trainium2: Has largely sold out

- Trainium3: Started shipping at the start of 2026 (30-40% more price performant than Trainium2) & is “nearly fully-subscribed”

- Trainium4 (~18mo away from broad availability): A significant chunk has already been reserved.

- Their chips business is “on fire” and will be “much larger” than most people think…they might sell to 3rd parties in the future

- Amazon’s chip business’ annual rev run rate is now over $20bn, growing triple digit % y/y

- If it was a standalone biz, the rev run rate would be ~$50bn

- “There’s so much demand for our chips that it’s quite possible we’ll sell racks of them to third parties in the future”

Growth Drivers For The Retail Business Include Expanding Reach, Delivering Faster, & Growing Non-Perishables

- Fast delivery has not reached its peak…the Co is expanding drone delivery & Amazon Now: The Co has delivered 500mn+ same day units in 2026 thus far

- Prime Air now has a scalable design

- They plan to serve communities w/ 30mn customers by year-end

- Expect to deliver half a billion packages by the end of this decade (w/ an aim to deliver is less than 30 min)

- Amazon Now (delivery on thousands of items w/in 20 min) has been very successful in India where orders are increasing 25% month-over-month, w/ Prime members tripling their shopping frequency once they start using it

- The Co is starting to expand Amazon Now in the U.S. and Europe

- Prime Air now has a scalable design

- The non-perishables grocery business continues to “grow quickly”.

- 100 more WFM stores are coming in the next few years (550+ stores now)

- There will be more Daily Shop stores (smaller format)

- Adding perishables into SameDay Delivery network has been a “breakthrough”

- Have Same-Day fresh food delivery in over 2,300 towns and cities across the country.

- The grocery business has grown to over $150bn in gross sales in 2025, making Amazon the second-largest grocer in the U.S

- Remain committed to the rural delivery network build

Other Key Comments / Updates

- Robotics use has scaled at Amazon but is still in its infancy

- The Co now have over 1mn robots operating in fulfilment centers…and at the same time have been one of the largest job creators in the US

- Amazon is “still in the early stages of leveraging robotics”

- Amazon Leo is scheduled to launch mid-2026…it will launch w/ “meaningful” revenue commitments

- Performance will be stronger than what is available now to underserved customers and geos and at a lower cost and seamlessly integrated with AWS

- The Alexa revamp has been successful & there’s more to come…customers are:

- Talking to Alexa 2x as much (and for longer durations across a wider breadth of topics)

- Completing purchases on devices 3x more

- Streaming music 25% more

- Using smart home functionality 50% more

- “Alexa is still early in its journey to be the world’s best personal assistant. But, it wouldn’t be on its way again without going back to the start”

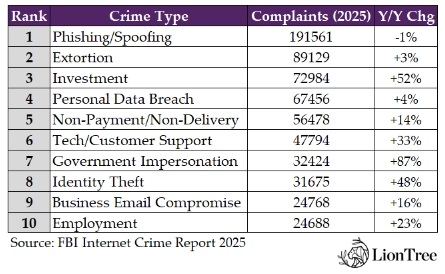

Cybercrime Losses Hit New Highs While AI-Related Fraud Becomes a Meaningful Category

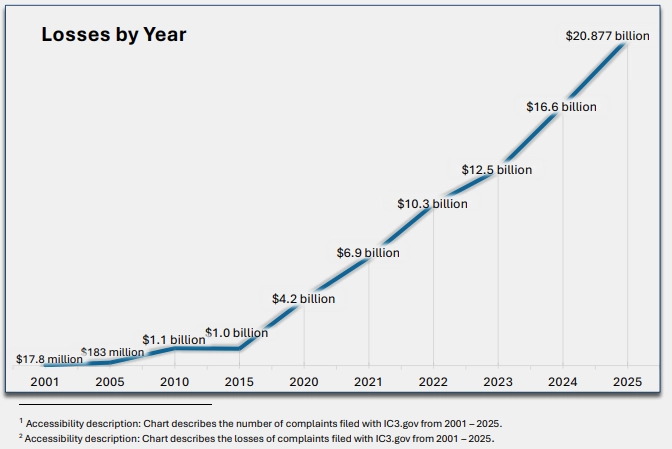

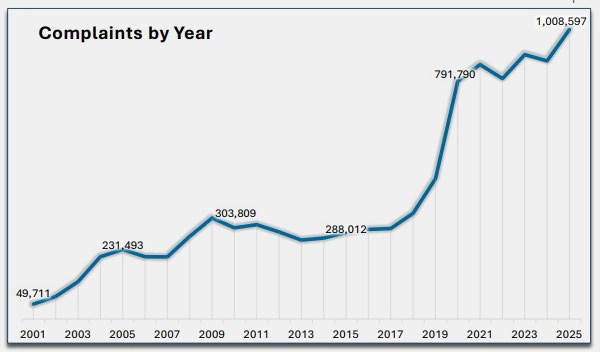

We came across the FBI Internet Crime Complaint Center’s (IC3) annual 2025 Cybercrime report this week which was a stark reminder that alongside all the technological advances and innovation, new cyber safety risks are emerging as well.

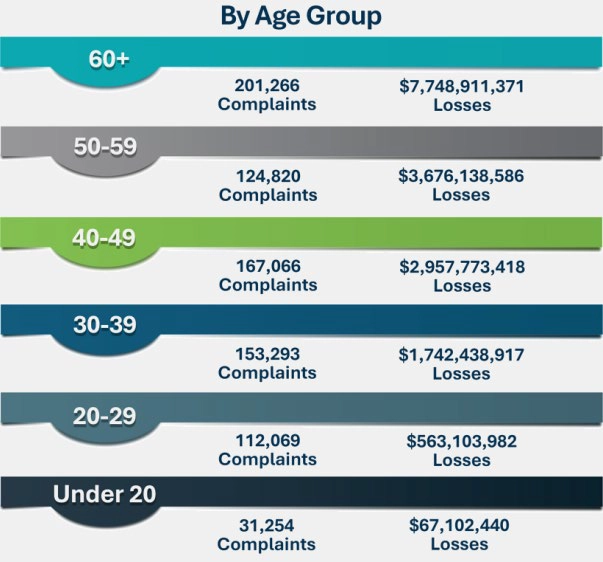

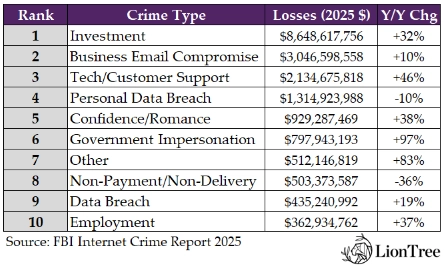

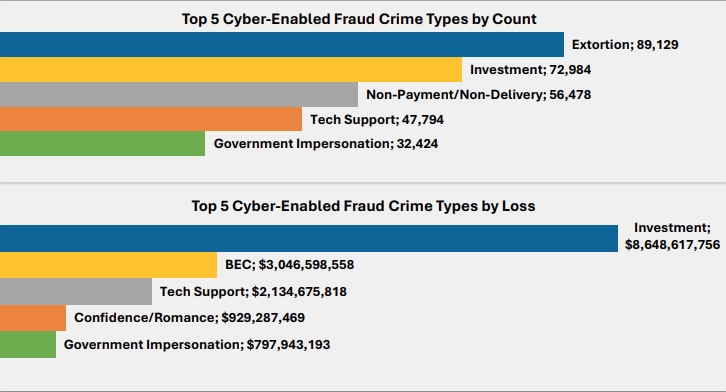

To put this into perspective, the IC3 receives an average of ~3,000 Cybercrime complaints PER DAY. A few stand-out stats from their report include: 1) US cyber-enabled crime reached a new high in 2025, with losses rising to ~$21bn (+26% y/y) and the average loss per incident also increased (suggesting that individual attacks are worsening in magnitude); 2) The 60+ demo is the most vulnerable; 3) By Cybercrime type, Investment losses are by far the highest (over $8bn); 4) Cryptocurrency-related Cybercrime also accounted for $11.4bn in losses; and 5) AI-related Cybercrime is also on the rise (reached $893mn in losses, with the majority stemming from investment scams). Looking ahead to 2026, we strongly suspect that AI-related Cybercrime will show a meaningful step up…

See below for a deeper dive into the key stats: (link/link/link)

- U.S. victims lost ~$21bn to cyber-enabled crimes in 2025, up +26% y/y which is down from the +33% y/y in 2024

- BUT… the average loss of $20,699 was an acceleration from $19,372 in 2024

- Total complaints in 2025 reached 1,008,597 up from 859,532 in 2024

- People of 60+ are by far the most vulnerable demo, accounting for:

- 20% of total complaints in 2025

- 37% of total losses

- What were the most common complaints by number in 2025?

- Phishing/Spoofing, which although the #1 crime type, was down -1% y/y (and was the only category that was down y/y)

- Government Impersonation saw the largest increase, up +87% y/y, followed by Investment complaints, up +52% y/y

- What were the most common losses by dollar value in 2025?

- Investment losses were, by far, the highest and were up +32% y/y

- Government Impersonation losses saw the largest increase, up +97% y/y

- Non-Payment/Non-Delivery losses were down -36% y/y

- In terms of the medium or tool used to facilitate complaints or losses in 2025…Cryptocurrency-related were meaningful

- Cryptocurrency-related accounted for:

- 181,565 complaints (vs 149,686 in 2024)

- $11.4bn in losses ($9.3bn in 2024)

- AI-Related (new category) accounted for:

- 22,364 complaints

- $893mn in losses (~$632mn came from “investment”, ~$30mn from BEC & ~$19mn from Tech/Customer Support)

- Cryptocurrency-related accounted for:

- Regarding Cyber-enabled fraud (responsible for 85% of all losses reported to IC3 in 2025, vs 83% in 2024)

- Cyber-enabled fraud in 2025

- 452,868 complaints, up from 333,981 in 2024

- $17.7bn in losses, up from $13.7bn in 2024

- Cyber-enabled fraud in 2025

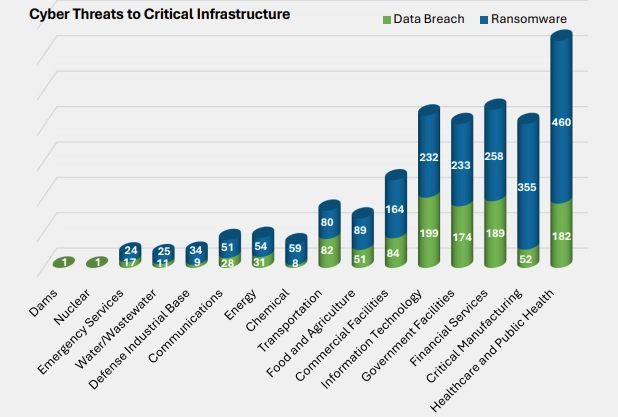

- The top 5 most targeted Cyber threats to critical infrastructure sectors in 2025 were the same as in 2024

- Healthcare

- Manufacturing

- Financial services

- Government facilities

- Info Tech

- IC3 received complaints from ~200 countries in 2025, and these accounted for almost $1.6bn of the overall annual losses

- The top 3 countries that submitted complaints:

- Canada

- India

- Japan

- The top 3 US states remained that same as last year:

- CA ($3.6bn)

- TX ($1.8bn)

- FL $1.6bn)

- The top 3 countries that submitted complaints:

Shorts Sellers Generally Hold Onto Their Top Picks In Q1

In analyzing the short interest data (made available this week) for ~150 stocks in our LionTree Universe across the tech, media, telco, and consumer sectors, with $1bn+ in market cap, 12 of the top 20 most-shorted stocks underperformed the S&P 500 this past quarter. There was not too much movement on the most shorted list. Of the Top 20 most shorted stocks in Q1, 17 were also on the top 20 most shorted list in Q4. The Top 3 most-shorted stocks at quarter end were Hims & Hers and AST SpaceMobile, which maintained their #1 and #2 most-shorted rank, respectively, while TripAdvisor edged up from #4 to #3 this qtr

In terms of the biggest changes in Q1, fuboTV saw the shortest covering, while Pinterest topped the list for largest increase in its short position.

See our analysis below for more details…

Most Shorted Stocks (As % Of Float) – Hims & Hers…Again For The Third Quarter In A Row

- The Top 3 Most Shorted = #1 is Hims & Hers (3rd qtr in a row), #2 is AST SpaceMobile (same as Q4), & #3 is TripAdvisor (up from #4 in Q4)

- WEBTOON fell from #3 in Q4 to the #4 in Q1

- Stocks that dropped out of the Top 20 most shorted: CLEAR Secure, Teladoc Health, Reddit & Etsy

- Stocks that joined the Top 20 most shorted: TKO Group, USA TODAY, Opendoor & Pinterest

Largest Increase In Short Interest (As % Of Float) – Pinterest

- The largest increase in short interest was seen at Pinterest: The Co saw a +11ppt increase in Q1 to 15.6% of the float short -> The stock fell -29.2% in the qtr

- Other stocks with notable increases in short interest = Hims & Hers, Omnicom & TripAdvisor -> all of which underperformed the S&P 500 in the period

Largest Decrease In Short Interest (As % Of Float) – fuboTV

- The largest decrease in short interest was for fuboTV: The Co posted a -16.8ppt decrease in Q1 to 1.3% -> The stock was down -68.7% in the qtr, significantly underperforming the S&P 500

- Other stocks with notable decreases in shorts interest = The RealReal, CLEAR Secure, and Compass -> The RealReal & Compass underperformed the S&P 500, while CLEAR Secure was up +38%

-> The S&P 500 was down -4.6% in Q1 and 12 out of the top 20 most-shorted stocks underperformed the index over the period; On avg, the top 20 most-shorted stocks traded down -14% in Q1, compared to Q4’s average of -10%

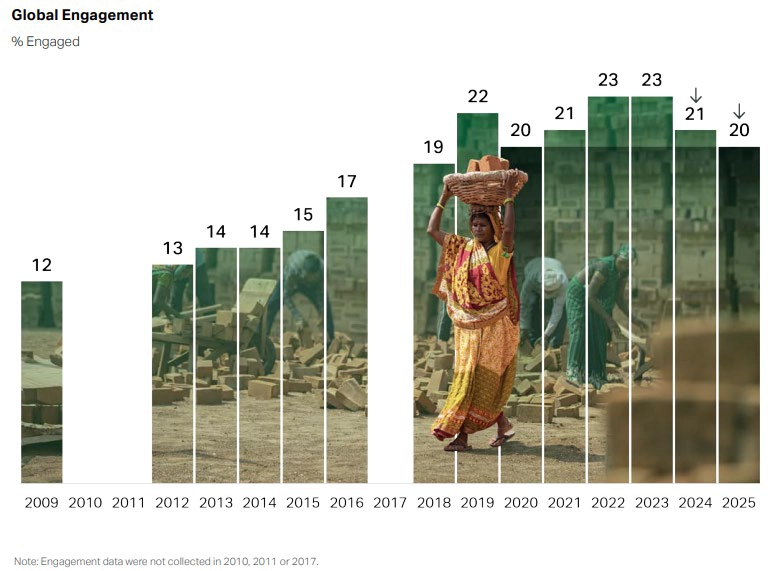

Falling Global Worker “Engagement” Doesn’t Bode Well For AI Productivity

Gallup released two reports this week, first being the State of the Global Workforce: The Human Side of the AI Revolution which had a couple of telling stats that we wanted to highlight. This report is essentially an ongoing study of how employees feel about their work and lives, which has a high correlation to workforce performance. The second was their AI Paradox report, which was a deep dive into Gen Z and their stance on AI.

Our biggest takeaways from the first report was that 1) employees are becoming “less engaged” in work, which has negative implications for productivity; and 2) while AI is being technically integrated into organizations, direct managers are not proactively enough championing AI with their staff. The largest takeaway from Gallups AI report was that while organizations are expanding their AI use, adoption among the younger generation remains uneven and is not growing on its own.

See below for more details. stats & key observations:

Global Workforce Engagement Falls, Potentially Impacting Productivity

- Global engagement is down for the 2nd year in a row though the US & Canada showed more positive trends

- The largest drop was in South Asia, primarily India, coinciding with a reduction in mgmt roles, likely linked to organizational flattening and slower hiring in the IT sector (potentially due to AI)

- Engagement in the US & Canada over-indexed the Global average (31% vs 20% respectively) and was flat from the prior year period

- Employee engagement is as a measure of readiness for change, hence high engagement means a greater ability to manage the disruption from AI

- Employees see AI as having a “somewhat” or “extremely” positive impact on their productivity but only 12% strongly agree that AI has transformed how work gets done in their organization

- Manager engagement has also fallen sharply since 2022 (-9pts) and the engagement gap with employees is significantly reduced

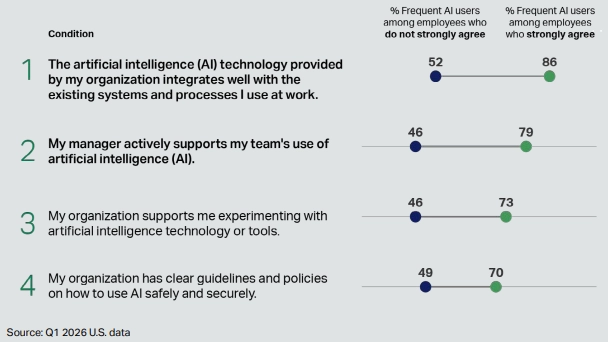

- Manager’s advocating for AI is a huge driver for employee adoption: W/in U.S. organizations that are investing in AI technology, employees who strongly agree that their manager actively supports their team’s use of AI are:

- 98.7x as likely to strongly agree that the AI has transformed how work gets done in their organization

- 97.4x as likely to strongly agree that AI gives them more opportunities to do what they do best every day

- Less than a third of U.S. employees in organizations that have begun implementing AI technologies strongly agree their manager actively supports their team’s use of the technology

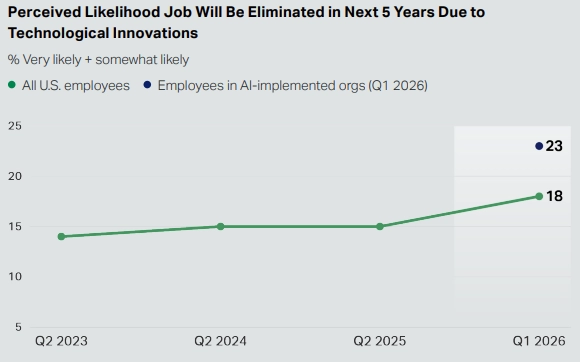

- Large U.S. employers are more likely to reduce their workforce after implementing AI; Smaller employers are more likely to expand their workforce

- While AI is reconfiguring organizations, the effects so far on employment are not uniformly negative

While AI Infrastructure Is Growing, Gen Z Adoption Remains Uneven (link)

- While organizations are expanding AI infrastructure, meaningful adoption among younger people remains uneven and is not growing on its own

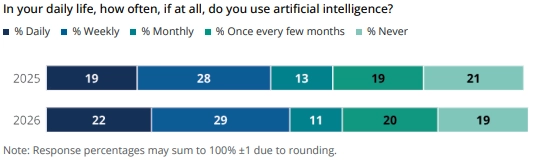

- Just over half of Gen Z report using generative AI at least weekly, essentially unchanged from 2025

- This level off stands in contrast to broader market trends –

- Worker access to AI rose by 50% in 2025 and the share of work hours spent using generative AI climbed from 4.1% to 5.7% in the same period

- Gen Z’s use of AI in everyday life has remained largely stable over the past year

- Just over half of 14- to 29-year-olds say they use AI either daily (22%) or weekly (29%), while 11% report using it monthly, 20% every few months and 19% say they never use it

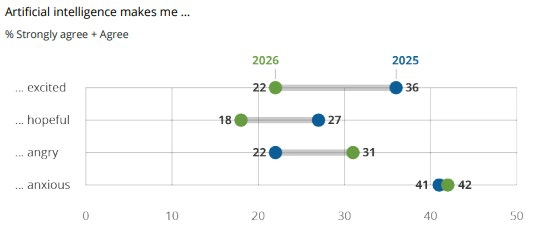

- The excitement (22%) and hopefulness (18%) that Gen Zers feel about using AI were already low last year and declined sharply this year, while anger (31%) increased and anxiety (42%) remained steady

- Curiosity about AI (49%) is the most strongly felt emotion of the five measured

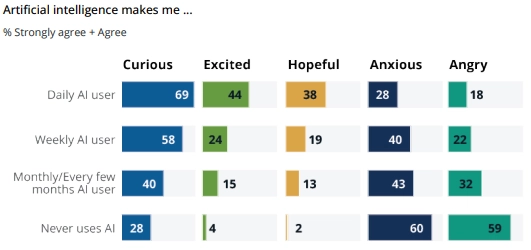

- Frequent Gen Z AI users report much more positive emotions toward AI than non-users, though even daily users have grown less positive over the past year

- Among daily users, 69% say AI makes them feel curious, 44% excited, and 38% hopeful, compared with 28%, 4%, and 2%, respectively, among non-users

- Gen Z remains skeptical about AI’s positive impact on core skills and productivity

- They are split on whether AI helps them search for accurate information, and some believe it will do more harm than good for creativity (38%) and critical thinking (42%)

- Confidence in AI-driven efficiency has also fallen: Agreement that it helps people complete work faster is down -10 points to 56%, while agreement that it speeds up learning is down -7 points to 46%

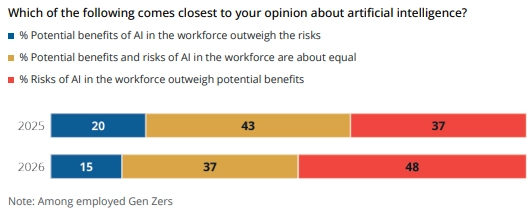

- Young adults in the workforce are significantly more likely to view AI as a risk than a benefit in the workplace

- Nearly half (48%) say the risks outweigh the benefits, compared with just 15% who say the opposite, while 37% see the risks and benefits as equal

- 52% think they will need to know how to use AI for postsecondary education, marking a five-point increase since 2025

- 48% believe AI skills will be necessary for their future career’s vs 45% in 2025

Grab Bag: Greece Social Media Ban / Nexstar-Tegna Merger Hits Another Bump / Prediction Mkt Updates

- Greece will ban social media for children under 15s starting Jan 1, 2027 (link/link)

- Starting Jan 1, 2027, platforms will need to be able to restrict users or face fines described in the EU Digital Services Act (DSA) reaching up to 6% of their global turnover

- Once the legislation is enacted, social media platforms will be responsible for reverifying the ages of all users in the country to exclude those who are 15 years or under

- Which platforms will be impacted? The new law will target social media platforms that enable the user to create profiles, interact with others and share content, such as Facebook, Instagram and TikTok

- What was the sentiment around the ban? An opinion poll by ALCO published in Feb. showed ~80% of those surveyed approved of a ban

- The Greek gov. has already outlawed mobile phones in schools and set up parental control platforms to limit teenagers’ screen time

- Writing separately to the European Commission President, Greece Prime Minister Mitsotakis called for coordinated EU action, arguing that national measures alone would not be sufficient to protect minors from internet addiction

- He proposed establishing an EU‑wide “digital age of majority” at 15, mandating age verification and regular re-verification for all platforms, and setting up a harmonized enforcement and penalty framework

- Starting Jan 1, 2027, platforms will need to be able to restrict users or face fines described in the EU Digital Services Act (DSA) reaching up to 6% of their global turnover

-> Separately, but related, Meta has been removing advertisements from attorneys who were seeking clients that claim to have been harmed by social media while under the age of 18; More than a dozen ads have been found to have been deactivated; Almost all of them ran on both Facebook and Instagram, and some also appeared on Threads and Messenger, plus Meta’s Audience Network, which distributes ads to thousands of third-party sites; Meta defended its actions, saying that they “will not allow trial lawyers to profit from our platforms while simultaneously claiming they are harmful” (link/link)

- The latest on the Nexstar-Tegna merger saga…a federal judge has extended a temporary restraining order against the $6.2bn merger (link/link)

- The move will give U.S. District Judge Troy Nunley until April 17 to prepare a ruling on whether a preliminary injunction is needed to outright block the deal

- The judge also modified the order so both companies could take “reasonable steps” to handle regular business matters like meeting federal debt reporting deadlines

- As a reminder…on March 27th, Nunley put the deal on pause in response to a federal antitrust lawsuit by DirecTV; A group of eight state attorneys general led by California and New York also filed a separate lawsuit seeking to block the merger, which has since been consolidated into one legal action; The legal action came after Nexstar-Tegna was approved by the FCC and DOJ last month and closed just minutes later

- What is the issue? The group alleges the proposed combination would “irreparably drive up consumer costs, reduce local competition, shutter local newsrooms and increase both frequency and duration of blackouts of key local teams and network programming”

- 3 quick prediction mkt updates…

- US Appeals Court rules that New Jersey cannot regulate Kalshi’s prediction mkt (link/link): A 3rd US Circuit Court of Appeals panel ruled on Monday that New Jersey has no authority to regulate Kalshi’s prediction market allowing people to bet on the outcome of sports events; That power rests with the Commodity Futures Trading Commission, the panel ruled 2-1

- But on the other hand, a Nevada judge ruled to continue a ban on Kalshi operating prediction markets in the state (link): A Nevada judge extended a ban on Kalshi from offering event-based contracts that would allow the state’s residents to place bets on sports and other matters without the Co obtaining a gaming license; The judge said he would issue a preliminary injunction sought by the Nevada Gaming Control Board that will bar Kalshi from offering such contracts in the state w/o a gambling license

- FOX is integrating Kalshi forecasts across FOX News Media and FOX One platforms (link/link): As part of the integration, relevant Kalshi data will be incorporated into FOX’s linear and digital content; Kalshi will also work directly with FOX data and production teams to provide real-time access for on-screen graphics and analysis tied to major storylines

- It is paid product placement and Fox will reportedly NOT be using Kalshi data for election coverage, as the channel has its own polling and election teams

- As a reminder… Kalshi has similar arrangements with both CNN and CNBC

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Mobile adtech Co AppLovin is reshaping leadership as CEO and cofounder Adam Foroughi stepped down as board chair, per a SEC filing, while remaining CEO and a director. Wynn Resorts CEO Craig Billings, a board member since 2020, becomes chair. Foroughi said the change lets him focus on strategic execution. (Adweek)

- Microsoft and Publicis Groupe annc’d an expanded strategic partnership to build a full‑stack, agentic AI marketing platform for global biz. The deal unifies Azure cloud, Copilot, AI agents and identity‑based data via Epsilon to modernize legacy systems, personalize campaigns, and better link marketing spend to rev. (Microsoft)

- The Trade Desk is facing a leadership shakeup as three senior executives depart, following the earlier resignation of board member Lise Buyer. Chief marketer and EVP Ian Colley said he is leaving after more than seven yrs to pursue a new opportunity, citing progress in positioning the Co as a leading independent DSP. (Adweek)

Artificial Intelligence/Machine Learning

- OpenAI annc’d a $100/month ChatGPT Pro plan aimed at Codex users who outgrew the $20 Plus tier. The plan offers 5× higher usage than Plus, unlimited Instant and Thinking models, and access to exclusive models, w/ a limited-time boost to 10× Codex usage through May 31. The existing $200 Pro tier remains, offering 20× usage for heavier workflows. (9to5Mac)

- Alibaba annc’d it was behind the once-anonymous AI video model HappyHorse-1. 0, which surged to the top of global benchmarks for text-to-video and image-to-video. The model appeared in early Apr. and was later linked via X to Alibaba’s ATH AI Innovation Unit. News lifted Alibaba shares, w/ Hong Kong stock closing ~2.12% higher, underscoring intensifying AI competition. (CNBC)

- Google annc’d new Google Photos updates for Android, rolling out globally. An “AI Enhance” button offers a one‑tap fix using AI to adjust lighting and contrast, helping users skip manual edits. Separately, video playback speed controls w/ options from 0.25x to 2x are being added via the three‑dot menu. Google says the feature was long requested and is in early rollout. (9to5Google)

- Japan is deploying physical AI robots to fill labor gaps, not replace jobs. Shrinking workforces push cos to use robots in factories, logistics, infra, w/ govt backing to build a domestic sector and target 30% of global mkt share by 2040. (TechCrunch)

- OpenAI CFO Sarah Friar said the Co will reserve a slice of IPO shares for retail investors as it preps to go public, citing strong demand seen in a recent funding round. She declined to annc’d a timeline but said it’s “good hygiene” for an $852bn Co to act like a public Co. CRO Denise Dresser said enterprise now makes up ~40% of rev and is set to reach parity w/ consumer by end-2026. (CNBC)

- European spending on AI products and svs is set to post a 33. 7% CAGR from 2025–2029, per research by IDC. Buyers are forecast to spend $290bn on AI tools in 2029, w/ 54% of total outlay linked to generative AI tech. Tangible gains in cost, efficiency, customer experience and risk management are expected to drive AI deployment despite significant macro headwinds. (Telecompaper)

- Elon Musk, seeks to remove OpenAI CEO and board member Sam Altman amid a legal challenge to the ChatGPT maker’s shift to a for-profit Co. In a Tuesday court filing, Musk said the lawsuit aims to unwind the for-profit conversion and restructuring, remove Altman and President Greg Brockman from leadership roles, and secure a court order restoring OpenAI as a nonprofit research org status. (Bloomberg)

- OpenAI sent letters to California and Delaware AGs urging probes into Elon Musk’s alleged anti-competitive behavior ahead of a trial. Strategy chief Jason Kwon said Musk has tried to undermine the Co by coordinating attacks w/ rivals after leaving OpenAI and founding xAI. OpenAI warned mkts partners of outlandish claims as the case nears. (CNBC)

- Anthropic is in talks to invest $200mn in a new private-equity venture w/ firms incl. General Atlantic, Blackstone and Hellman & Friedman, according to people familiar w/ the matter. The new Co aims to raise ~$1bn and act as a consulting arm, selling AI tech and training portfolio cos to adopt Claude tools. (The Wall Street Journal)

Audio/Music/Podcast

- Spotify annc’d new controls letting users turn off all video across the app, covering music videos, podcasts, vertical video and Canvas clips. Settings roll out worldwide on mobile and desktop, applying to individual and Family Plan accounts. Plan managers can disable video per member, removing the option to switch to video versions of songs or podcasts, expanding earlier Canvas-only controls. (The Verge)

- Spotify annc’d its AI Prompted Playlist feature now works for podcasts, extending a tool first tested for music. Premium users in mkts incl. U.S., Canada, U.K., Ireland, Australia, Sweden can create English-language podcast playlists via prompts and set update frequency. Episodes include notes explaining inclusion. (TechCrunch)

- Talks between top record labels and AI music start-up Suno have stalled, highlighting divisions over how the biz should handle AI-generated music. Universal and Sony have made little progress and rejected Suno’s distribution model, w/ one executive saying there is “no path” under the current proposal. (Financial Times)

Cable/Pay-TV/Wireless

- T-Mobile said it will keep Netflix On Us free for eligible customers despite Netflix raising the Standard w/ ads price to $8. 99/mo. The Co confirmed the benefit remains intact, absorbing the increase so wireless bills stay unchanged after the Apr. move. The perk bundles Netflix into qualifying unlimited plans, with activation through T-Mobile accounts for seamless linking, reinforcing a value focus in competitive mkts. (Cord Cutters News)

- TD Cowen’s yr-end 2025 survey shows T-Mobile topping Verizon on brand/image for the first time in 13 yrs, ranking 1. 96 vs Verizon’s 2.01 and AT&T’s 2.03. Conducted w/ 1,033 respondents, the poll cites T-Mobile’s stronger 5G, better pricing and cx perception overall. Verizon is pushing promos and rural C-band, while AT&T is perceived as highest priced. Price drove 35% of T-Mobile choosers. (Fierce Network)

- ESPN has lost ~40% of cable and satellite subscribers over the past decade, falling from ~100mn homes to ~60mn, pressuring rev and its biz model. The Co signaled new layoffs of ~30 roles, mostly off‑camera, amid cord‑cutting, high sports rights costs incl $2.7bn/yr for MNF, and a prior 15‑day YouTube TV blackout costing ~$100mn. (Cord Cutters News)

Capital Market Updates

- Citi said U. S.-listed ETF assets under management could more than double to ~$25tn by 2030 as investors seek low-cost, diversified access to mkts. AUM stood at ~$10.4tn in Mar. 2025. The bank lifted its outlook from a prior $19tn view and now sees >$40tn by 2035, with active ETFs gaining share vs passive peers on flexible strategies, tax efficiency and lower costs. (Reuters)

- Wealthy investors sought to withdraw $20.8bn from private credit funds in Q1, straining a Wall Street asset class. Groups including Apollo, Ares, Blackstone, Blue Owl and KKR received requests tied to portfolios worth ~$300bn, but funds met just over half, forcing many to wait for later windows. (Financial Times)

- Telefónica informed CNMV that its wholly owned unit Telefónica Hispanoamérica reached an agreement to sell 100% of Telefónica México to Melisa Acquisition, an OXIO-led consortium. The deal values the biz at $450mn (~€389mn) and is subject to customary adj, agreed conditions and regulatory approvals. (CNMV)

- Moody’s cut outlook on U. S. BDCs to negative from stable, citing rising redemption pressure, higher leverage and weaker access to funding mkts. Non-traded BDCs, over 60% of the sector, saw first-ever outflows early this yr after strong 2025 inflows, limiting capital deployment. (Reuters)

Cloud/DataCenters/IT Infrastructure

- Alibaba and China Telecom annc’d a new AI data center in southern China powered by 10,000 of Alibaba’s self-developed Zhenwu AI chips, supporting large-scale training and inferencing. China Telecom will own and operate the site, which can scale to 100,000 chips and serve industries from healthcare to materials. (CNBC)

Crypto/Blockchain/web3/NFTs

- Polymarket annc’d its biggest platform upgrade, launching a native stablecoin, Polymarket USD, backed 1:1 by USDC, replacing USDC. The Co is rebuilding its trading system w/ a new order book and updated smart contracts to improve speed, cut costs, and support advanced trading. (Yahoo Finance)

eCommerce/Social Commerce/Retail

- Retailers are increasingly using the First Sale customs rule to reduce tariff costs amid heightened trade volatility. The method lets importers pay duties on earlier supply-chain prices, lowering bills, and is cited by Cos like Target. U.S. Sens. introduced bipartisan legislation to end the practice, arguing it disadvantages domestic producers, while retail groups say it’s a legal, transparent tool. (Retail Dive)

Electric & Autonomous Vehicles

- US used EV sales jumped as petrol topped $4/gal, w/ lease returns swelling supply. Q1 sales rose 12% yr/yr and 17% q/q, per Cox, while new EV sales fell ~28% after a $7,500 credit ended. Off-lease EVs are set to hit 15% of returns in 2026, pushing used EV prices down 8.5% yr/yr and shrinking the petrol gap from $4,923 to $1,334. Analysts say cheaper models may spur adoption despite charging concerns. (Financial Times)

- Waymo annc’d public launch of its fully autonomous ride-hailing svs in Nashville, inviting riders via the Waymo app on a rolling basis to scale safely. The initial 60-sq-mile area spans Broadway, 12 South, Midtown and East Nashville, w/ airport testing underway. Backed by 170mn+ miles of data, Waymo cites ~13x fewer serious-injury crashes vs human drivers and plans Lyft integration later in 2026. (Waymo)

Film/Studio/Content/IP/Talent

- Sony Pictures Entertainment annc’d hundreds of layoffs across film, TV and corporate units as CEO Ravi Ahuja reorients the Co toward core growth areas, calling the move strategic rather than cost cutting. (The Hollywood Reporter)

- The Writers Guild of America annc’d a tentative 4-yr deal w/ major studios a month before its contract expiry, avoiding another strike. The union and AMPTP said the pact protects the guild’s health plan, adds a multimillion-dollar contribution, includes AI safeguards, and raises streaming residuals. (NBC)

- China’s box office is no longer a Hollywood kingmaker as tighter censorship, blackout dates, a lapsed U. S.-China film pact and stronger local films curb access. Only 10 U.S. titles topped $100mn in China over the past five yrs vs nine in 2019 alone, w/ analysts saying Disney’s $650mn “Zootopia 2” run is an anomaly. (CNBC)

- Screenwriters union and studios reached a surprise four-yr tentative deal after ~3 weeks of talks. WGA West said its committee unanimously backed the pact w/ the Alliance of Motion Picture and Television Producers. Terms weren’t disclosed, but expected to bolster health care and add AI protections, building on 2023 gains and curbing free work. (CNBC)

FinTech/InsurTech/Payments

- Visa annc’d Intelligent Commerce Connect, part of its Intelligent Commerce portfolio, to help biz participate in AI‑driven shopping. The platform acts as a network and on‑ramp for agentic payments, enabling secure payment initiation, tokenization, spend controls and authentication via one integration on the Visa Acceptance Platform, w/ support for Visa and non‑Visa cards and major agent protocols. (Visa)

- Kalshi annc’d a partnership w/ Fox Co to integrate real‑time prediction mkts data across FOX News Channel, FOX Business, FOX Weather and the FOX One platform. The sponsored integration adds forecasts on politics, economics, weather and culture to linear and digital coverage, supporting visualization and analysis. (Kalshi)

Handheld Devices & Accessories/Connected Home

- Apple’s first foldable iPhone is on track for a Sept. launch, rebutting earlier claims of major production snags. The device is expected to debut alongside iPhone 18 Pro models during Apple’s usual fall event. (9to5Mac)

HealthTech/Wellness

- Amazon Pharmacy annc’d it will offer Eli Lilly and Cos new GLP‑1 pill Foundayo via Same‑Day Delivery nationwide. Adults w/ obesity or overweight can order w/ a valid prescription, see real‑time availability and transparent pricing, and receive home delivery or in‑office kiosks. Pricing starts at $1/day w/ insurance or $5/day cash; delivery spans ~3,000 cities, expanding to ~4,500 by yr end. (Business Wire)

- Google annc’d updates to its mental health efforts, upgrading Gemini to better connect users to crisis svs. A redesigned “Help is available” module and one-touch access link people to hotlines when chats signal self-harm risk. Google.org will provide $30mn over 3 yrs to scale global helplines, expand work w/ ReflexAI, and offer pro bono tech support. (Google)

Investor & Market Sentiment

- Chegg shares jumped ~14% after activist Galloway Capital annc’d a 5. 44% stake and urged better cos capital mkts communication. A 13D said the stock is undervalued and not in distress, citing a strong balance sheet, net cash and no debt. Galloway backs plans to separate biz units, noting the Skilling segment generates ~$72mn in annualized rev w/ double-digit growth potential, while Academic Svs should deliver cash flow. (Investing.com)

Last Mile Transportation/Delivery

- Amazon and the U. S. Postal Service reached a tentative delivery deal after Amazon threatened sharp cuts. Instead of a two‑thirds reduction discussed earlier, Amazon will trim USPS volumes by 20%, still leaving USPS w/ >1bn packages a yr. Amazon ships ~15% of USPS packages, generating ~$6bn rev, and is its largest customer, so the cut could hurt the agency. (The Wall Street Journal)

Live Entertainment/Theme Parks/Concerts/Experiential

- WWE is reportedly planning to lower upcoming ticket prices after fan pushback and weaker sales, including for WrestleMania 42. Since TKO’s takeover, prices for weekly shows, live events and PLEs climbed as dates and match cards were reduced. Bryan Alvarez said prices could drop through summer, a message echoed on the Apr. 6 RAW when CM Punk openly criticized high ticket costs. (Yahoo Sports)

- Live Nation Entertainment Inc. told a New York jury it has thrived amid strong competition by delivering superior svs to venues and fans, disputing claims by over 30 states that it illegally monopolizes live events. In its federal antitrust trial, the top US concert promoter and ticket seller presented many witnesses to rebut allegations it uses Ticketmaster, promotion biz and owned venues to pressure customers, deter switching or block rivals. (Bloomberg)

Macro Updates

- Fed minutes from March showed officials favoring a wait-and-see stance, holding rates steady amid uncertainty from the Iran war that clouded the outlook. The Fed signaled confidence in keeping policy unchanged for the foreseeable future, extending a pause in cuts that began in Jan. (The New York Times)

- US Q4 GDP growth was revised lower to a 0. 5% annualized rate from 0.7%, per Commerce Dept data. Downgrades to biz investment and inventories drove the cut, while consumer spending was revised to 1.9%. Corporate profits rose $246.9bn. Final sales to private domestic purchasers grew 1.8%. The avg of GDP and GDI rose 1.5% after 4.0% in Q3, signaling softer demand. (Reuters)

Media Conglomerates

- Fox shares rose after a Wall Street Journal report said the U. S. DoJ opened a probe into NFL practices. The DoJ is examining potential anticompetitive tactics that may harm consumers as sports rights fragment across streamers and channels. FOX Class B climbed ~3% and FOXA Class A gained >4%. (Investing.com)

- Disney is expected to lay off as many as 1,000 employees via role eliminations in coming months, with many cuts tied to its marketing unit, Variety reported. The move comes as Josh D’Amaro takes over as CEO, replacing Bob Iger in Feb. and formally assuming the role on Mar. 18. (Variety)

- Paramount has secured signed equity commitments of ~ $24bn from three Middle East sovereign-wealth funds to support its $81bn takeover of Warner Bros. Discovery, according to people familiar w/ the matter. Saudi Arabia’s Public Investment Fund will provide ~ $10bn. The funding helps offset deal costs after Paramount defeated Netflix. (The Wall Street Journal)

Metaverse/AR & VR

- Unity and Meta annc’d an extended multi‑yr partnership to cont’d powering next‑gen VR experiences. Under the agreement, Unity will provide platform and enterprise support for Meta’s VR ecosystem, helping developers develop, deploy and grow apps and games on Meta devices. (Unity)

Regulatory

- StubHub agreed to pay $10mn to settle U. S. FTC charges alleging it failed to clearly disclose total live‑event ticket prices, incl mandatory fees. The Co advertised prices w/o upfront totals, violating the FTC Fees Rule enforced since May 2025. (Reuters)

- Grassley annc’d an inquiry citing new NCMEC data showing major tech cos underreport online child exploitation. Eight firms—incl. Meta, Amazon AI svs, TikTok and Roblox—filed ~17mn reports in 2025, ~81% of CyberTipline total, yet many lacked location or suspect data, hindering enforcement. (Senator Chuck Grassley)

- Kalshi Inc. failed to stop Arizona criminal proceedings against its prediction mkts biz, highlighting widening disputes among states, cos, and the CFTC. A US District Court judge ruled the federal Anti-Injunction Act bars courts from interfering w/ active state cases, denying Kalshi a preliminary injunction and immediate restraining order. (Bloomberg Law)

- A D.C. Circuit appeals panel rejected Anthropic’s bid to pause a Pentagon designation labeling the AI startup a supply chain risk, leaving limits on use of its models in Defense Dept contracts. Judges said potential financial harm to one Co did not outweigh national security interests during active conflict, though they noted likely irreparable harm and urged an expedited ruling. (Politico)

- The US Justice Department’s top antitrust litigator and three senior trial attorneys who led cases against Live Nation Entertainment Inc. , Apple Inc. and Alphabet Inc. cos Google are leaving the agency, people familiar say. Some exits reflect anger over a surprise Mar. 9 settlement w/ Live Nation and worries the division isn’t committed to litigating pending cases. (Bloomberg)

- Florida AG James Uthmeier annc’d a probe into OpenAI and ChatGPT, citing national security and safety risks as the AI Co eyes a potential IPO valued at ~$1tn. He said subpoenas will follow, raising concerns over data falling to foreign adversaries and alleged links to crimes. He cited ChatGPT’s ~900mn weekly users and claimed it aided criminal acts, incl. a Florida State Univ. shooting. (Reuters)