Putting aside all the geopolitical tensions, Artemis II’s successful launch on Wednesday was an exciting milestone (in addition to my son’s 15th birthday on that day😊). What was really mindboggling to hear was how fast the rocket was going! Over 17,000 mph! And that is just on the way up. In addition to being the first crewed lunar flight in 50+ years, some stunning stats are: (link)

- At 17,000 mph, one could get from Los Angeles to New York in ~ 10 minutes and speed is 22x the speed of sound

- The speed for reentry will be even faster at 25,000 mph!

- The Artemis II rocket and capsule, when fully stacked, is taller than the Statue of Liberty

- Artemis II will be ~ 250,000 miles from Earth at its furthest

- The total journey (around the moon and back) is ~685,000 miles

- The rocket thrust at liftoff was 8.8mn pounds

Back on earth, the markets finally bounced (the S&P 500 up +3.4% and Nasdaq up +4.4%) in this shortened holiday week given hopes that the Iran war is winding down, though fears somewhat emerged again today. Investors jumped into tech laggards and energy sold off this week, though crude was up 12% (highest level since mid-2022)

There were a lot of interesting updates and developments fundamentally this week and we focused on the below in this edition.

- LionTree Lens: Spring 2026 - *NEW REPORT*

- TMT Stocks Took It On The Chin In Q1…Though Connectivity Bucked The Trend

- Snap Comes Into Scope For The Activist Community

- The Macro Uncertainty Didn’t Stop Big M&A…& More Is Likely To Come

- The AI Customer Is Reshaping Retail

- Key AI Updates Around Security Concerns, Model Launches & Record $ Raises

- Enticements For Large Private Co’s To IPO Emerge This Week, Just In Time For SpaceX

- The Road Ahead For Robotaxis Is Not Without Its Bumps, But Progress Continues

- Grab Bag: Netflix Looking For More NFL / Meta Testing Instagram+ / AT&T Launches OneConnect

Lastly, I wanted to highlight that LionTree Advisors is proud to have served as financial advisor to The Rip City Rising ownership group on the completed acquisition of a majority ownership position in the Portland Trail Blazers, the Rip City Remix, and Rip City Management, and to have also served as exclusive financial advisor to Pro Football Focus (PFF) on its sale to Teamworks, the Operating System for Sports™ powering more than 7,000 elite sports organizations globally. Congrats to all involved!

Have a nice long weekend. 🐰🥚

Best,

Leslie

LionTree Lens: Spring 2026 - *NEW REPORT*

In case you missed our email yesterday, we wanted to highlight our latest LionTree’s Lens: Sector Insights & A Look Ahead, Spring 2026 perspectives, which details what we viewed as the most significant market trends and thematic shifts across the TMT and consumer sectors over the past quarter, along with some forward-looking expectations.

AI emerged as the defining theme of this edition, dominating the narrative across a broad range of sub-sectors. Its influence is reshaping coding, gaming, music, commerce, and even Hollywood, and investors have been trying to navigate these stormy waters. Beyond AI, this edition is also packed with updates across live entertainment, M&A, streaming, regulation, predictions markets, disclosures, and more…

-> As always, we’re happy to discuss any of these topics in more detail, and we’d appreciate your thoughts and/or feedback.

CLICK HERE FOR THE FULL VIDEO (~20min) AND DECK

Table of Contents

TMT Stocks Took It On The Chin In Q1…Though Connectivity Bucked The Trend

Following a tough Q4, stocks in the sector had a similarly tough Q1. A very high 70% of companies in our LionTree Universe of ~170 stocks in the TMT and Consumer sector with $1bn+ market caps posted a share price decline during Q1 (65% did the same during Q4).

And even more, of those stocks that traded down, 83% traded down double-digits, which was noticeably higher than the 61% that traded down double double-digits in Q4.

Which stock bucked the trend and saw the largest Q1 gain in our Universe? It was DigitalOcean, up +78% in the qtr. The Co reported strong Q4, beating consensus revenue, adj EBITDA, and adj EPS, posting a record $51mn ARR (up +123%y/y) and raised their 2026 and 2027 revenue outlook “on the back of top customer growth and growing AI traction.”

Sub-sector wise, as detailed in our new quarterly LionTree’s Lens (just published yesterday – link to access HERE), Telecommunications benefitted from the flight to safety in the period.

Which stock had the toughest Q1? It was FuboTV, which fell -69% in the period, followed StubHub, down -54% and Unity, down -50%, to make up the bottom 3.

How did the “Magnificent 7” do in Q1? They were all DOWN: The “Magnificent 7” all posted negative returns in Q1, a notable reversal from the more mixed performance seen in Q4. Microsoft led the group lower, falling -23.5%, and Apple and NVIDIA were comparatively more resilient but still finished the qtr in negative territory, down -6.6% and -6.5%, respectively

Snap Comes Into Scope For The Activist Community

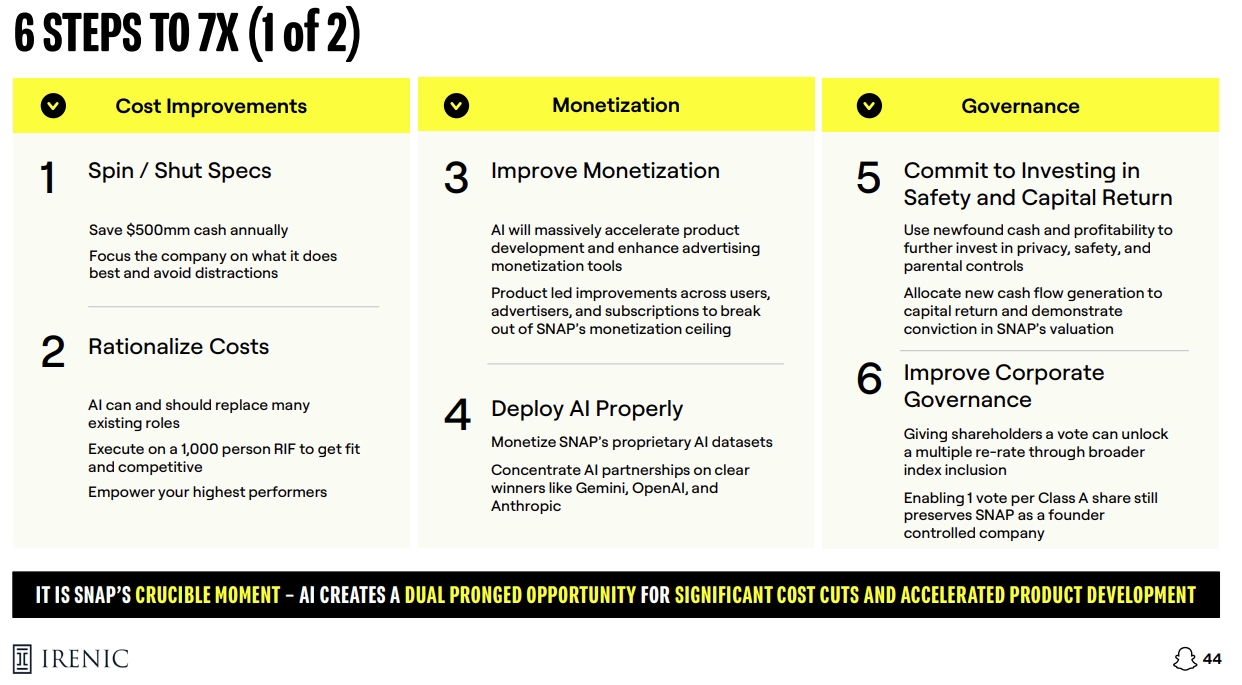

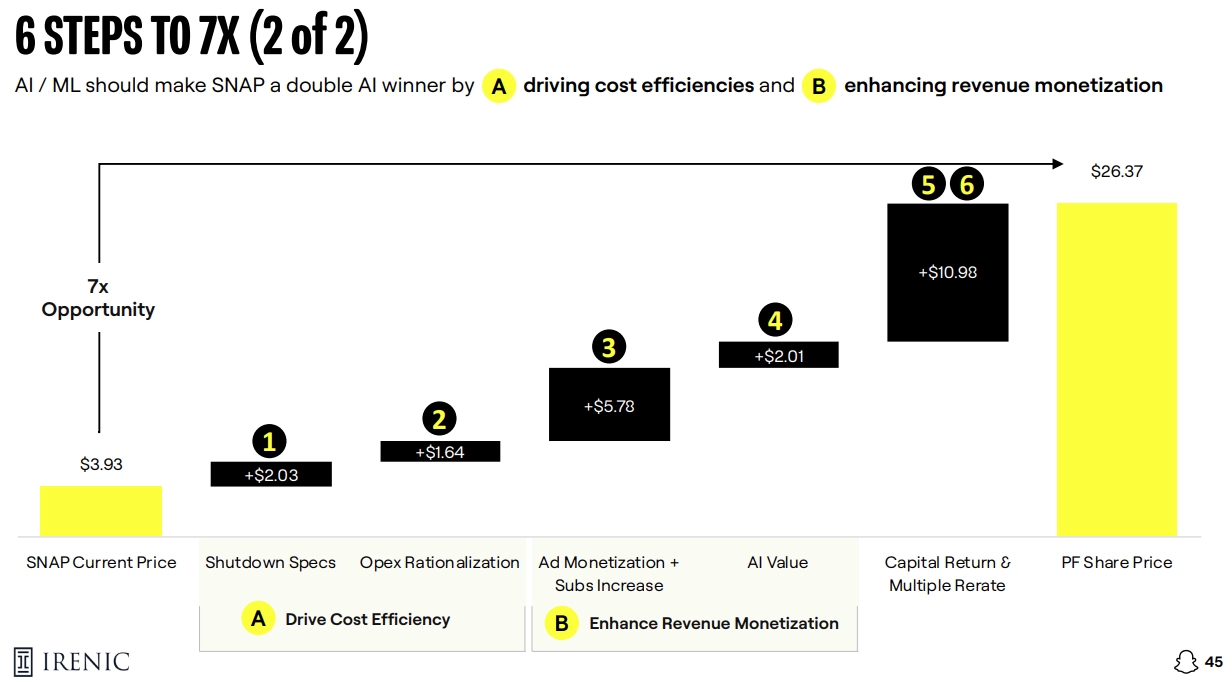

Another activist action came into play this week. Irenic Capital Mgmt’s (now owns ~2.5% of Snap shares) public letter to Snap CEO Evan Spiegel outlined what it sees as the path to $26.37/share, or 7x above the share price before this communication.

In their Snap Back To Reality: Save Snap Now 6-point plan, spinning off/shutting down Specs seems like the easiest step to execute and create value IF mgmt decides that they want to pursue that change. This area has been near and dear to CEO Evan Spiegel’s heart and his long-term vision so it would be quite a pivot. Also more clear-cut to potentially implement is further cost rationalization, including revamping employee incentives. Improving ad monetization and leveraging AI has already been a priority area of focus for the Co but this public pressure could spur a different approach that might yield quicker results. Investing in child safety also makes sense as this is something that all the social platforms are going to need to do more of given the heightened regulatory and community focus. But Irenic’s biggest individual per share value creator (42% of the total) would come from changing the corporate governance structure and giving public shareholders 36% vote share, which is hard to handicap at this point (maybe the predictions market will transact on this!).

Irenic’s deck is 70 pages (DECK LINK) but we streamlined what we saw as the key points to their argument. See below.

-> Snap share rallied +14% in reaction to Irenic’s public letter and closed the week through Thursday up +18%, though it is still down -43% YTD.

First off…who is Irenic Capital?

- It was founded in 2021 by Adam Katz (formerly at Elliott Mgmt) and Andy Dodge (formerly at Indaba Capital Mgmt)

- Irenic is an event-driven, special situations firm that invests across the capital structure, and based on a YE filing, they have ~$2.4bn AUM (link)

Irenic Acknowledges That Snap Has Some Amazing Assets…With Users, Engagement, & Proprietary Data…

- The Co has scaled subscribers & strong reach to attractive demos

- 1bnn MAUs and 474mn DAUs

- That reaches 75% of users aged 13-34 globally

- Users have high levels of engagement

- 350mn of users are engaging w/ AR tools

- 400mn+ MAUs engage with Snap Maps

- 200mn users play games

- Time spent on the app is 30 min daily

- Users are opening the app 40x a day

- Snap+ has 25mnn paying subs, approaching $1bn of ARR

- The Co has a ton of proprietary data

- Social graphs

- 5bn+ snaps are created daily

- More than 1 trillion memories have been saved since 2016

- 17bn engagements w/ gen AI lenses capturing unique facial & object data sets

- Proprietary real-time interest, location, and commerce data

- Ad conversion feedback through proprietary measurement platforms

…BUT That The Current Strategy Is Not Working (Stock Is Down, KPIs Are Below Peers, Etc.) And The Firm Needs To Do These 6 Things To Create Value – SEE IMAGE BELOW

A Deeper Drill Down On Their 6-Points…

- Spin-out or shut down Specs… and save $500mn of est’d cash cost yearly

- $3.5bn has been invested over 11 years and the biz is highly unprofitable with no visibility to that changing

- Snap can’t compete in this area w/ better capitalized peers like Meta and players like Google, Apple, Microsoft, and MagicLeap have all deprioritized the space, while China competition is heating up

- Rationalize costs…cut employees, change stock comp, and drive more AI efficiencies

- Ex Specs, core Snap headcount is 60% above pre-COVID levels

- Personnel cost/employee at Snap is +31% higher than peer median ($485k vs $372k)

- Though Meta is higher at $535k

- SBC/employee cost at Snap is 67% higher than peer median ($193k vs $116k)…Irenic is pushing Snap to move from a purely time-based approach to 2/3 performance vested w/ $10 and $15 share price targets

- Though Meta is higher at $259k

- 3-yr change in gross profit/employee is 83% lower than the peer avg

- Improve ad monetization…Meta has 7x ROAS and 70%+ Rated Higher ROI, while Snap has 2.3x and <10%

- Improve targeting, automation, and AI-assisted set up

- Provide advertisers with more AI capabilities across campaigns and optimizing ROAS

- Increase ad loads (they think Snap can increase ARPDAU by 30%+ with ads alone)

- Raise load on existing surfaces (Spotlight and Discover) to align with peer benchmarks (20-25% range)

- Improve adtech capabilities, including:

- End-to-end automation capabilities (optimize audience, bidding, budgets, placements, etc.)

- Improve lower-funnel signal capture (deepen Pixel / CAPI / server-side data integrations for targeting optimization)

- Upgrade measurement and reporting (better in-platform dashboards, stronger attribution, etc.)

- Provide users with fewer features as Irenic argues that they are confusing and yielding limited time spent

- Monetize surfaces that deliver content to high-intent users and lean into further monetizing high frequency user surfaces like Chat and Maps (~60% of time spent is on Chat and Camera)

- On Chat: Drive creation of Company pages with shoppable products; Facilitate “click to buy” features directly within the chat interface

- On Maps: Focus efforts on working w/ local businesses to drive addtl “Promoted Places” and “Business Profiles” to drive user traffic; Further curate the maps community to be a trusted guide for users to find places with friends and feed its identity graph to increase monetization across its network

- Drive subscriber growth given the view that Snap+ can reach 10% of DAUs

- Deploy AI properly…MyAI has posted a strong increase in users (fast climb to 100mn) but the fund thinks Snap has the wrong partners (Microsoft and Perplexity) and is pushing for other partnerships

- Commit to invest in safety and capital returns

- Improve corporate governance…Irenic highlights that all other Cos give a public shareholder a vote, which is not the case for Snap

- One class A share should = 1 vote so that public investors get 36% vote share (in-line w/ Meta, Google, and others)

- this would also allow for Russell Indices inclusion

…And If Snap does This, Irenic Argues That The Stock Will Go Up To $~27/Share

- The buckets that create the MOST value and would drive an addt’l ~$11/shr combined are:

- # 5- Commit to investing in safety and capital return and

- #6 – Improving corporate governance projected to generate the largest increase in value

- The next largest bucket to create addt’l value of ~$6/shr is:

- #3 – Improve ad monetization and grow subscribers

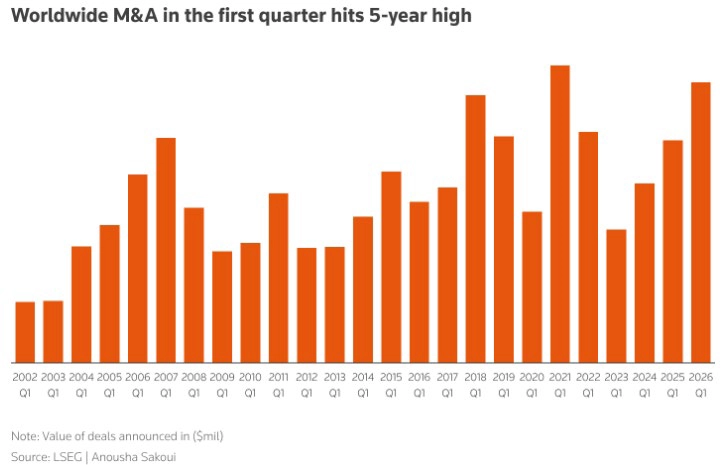

The Macro Uncertainty Didn’t Stop Big M&A…& More Is Likely To Come

After being up an exceptional +45% y/y in 2025, global M&A activity grew a strong +26% y/y in Q1, reaching $1.2tn despite all the macro volatility. Mega-deals and AI-linked transactions were the main drivers, with a record 22 deals above $10bn and multiple large equity stake transactions tied to OpenAI and Anthropic funding rounds. Cross-border activity was also a standout, up +47% y/y to its highest Q1 level in over two decades, with the U.S. capturing more than half of inbound value.

The backdrop suggests corporates and financial sponsors are leaning into scale and long-term positioning rather than waiting out near-term uncertainty, though regulatory risk remains an active constraint, as seen in the late-stage block (temporary restraining order) of Nexstar’s $6.2bn Tegna acquisition. At the same time, strategic competition is intensifying across key TMT verticals, including satellite connectivity, where Amazon is widely reported to be exploring a potential Globalstar acquisition to accelerate its Kuiper business, and gaming where Disney is reportedly considering a full takeout of Epic Games “at the right moment”, despite mixed internal views and weakening Fortnite engagement. Lastly, Warner Music Group also announced a small transaction this week to expand distribution and label services.

See below for more on what we viewed as the most important updates on this front.

Macro Uncertainty Did Not Dampen Big Deals In Q1, per LSEG data (link/link)

- Q1 global M&A value across all industries exceeded $1.2tn, up +26% y/y despite deal count down -17% y/y (i.e., avg deal sizes were larger)

- Deal pipelines at some of the bulge bracket banks have also reportedly strengthened by value and volume

- There was a surge in mega-deals and AI-driven capital concentration in Q1

- The 22 $10bn+ deals in Q1 was a qtrly record w/ the largest being:

- McCormick’s acquisition of Unilever UK food business at a $45bn enterprise value

- Engie’s acquisition of UK Power Networks at a GBP15.8bn enterprise value

- 4 of the top 6 deals were linked to AI leaders and were equity stake purchase transactions:

- OpenAI $110bn funding round (accounts for 3 of top deals in Q1)

- Anthropic $30bn fundraise (tied for 4th-largest transaction)

- The 22 $10bn+ deals in Q1 was a qtrly record w/ the largest being:

- Cross-border deal activity also stood out, w/ value rising +47% y/y to $454.7bn (highest Q1 since 2002)

- US was the most targeted country, accounting for 52.4% of these deals

- Followed by the UK at 11.5%

Competition In Satellite Connectivity Looks Set To Intensify (link/link/link/link/link)

- Amazon is widely reported to be looking to expand its LEO satellite business w/ a potential acq of Globalstar: This is not confirmed but key points in the press + background on Globalstar is below:

- Globalstar is a LEO satellite operator (voice, data, asset tracking) serving enterprise, gov’t, consumer end markets

- Mkt cap before this rally was ~$8.6bn (market cap today is ~$10bn)

- 2025 revenue: $273mn, up +9% y/y

- 2026 revenue guidance: $280-305mn, up +7% y/y at the mid-pt

- 2025 adj EBITDA: $136.1mn (50% margin)

- 2025 adj FCF: $171.1mn

- Strategic logic: The acq would create more scale and accelerate Amazon’s LEO buildout (Project Kuiper / “Leo”) and vertical integration of satcom capabilities

- However, deal complexities exist given Apple’s ~20% stake in GSAT (Apple invested $1.5bn in Globalstar in 2024) which requires parallel negotiations b/w Amazon and Apple

- Apple uses Globalstar to provide the ability for users to send text messages, call emergency assistance, and seek roadside help in areas where cellphone service isn’t available

- What is the current LEO competitive positioning?

- Amazon Kuiper: Currently has ~180 satellites in orbit (and has been behind schedule)…and plans for ~7.7k

- SpaceX Starlink: Currently has over 9.5k satellites and over 9mn users globally; The biz is est’d to account for ~50–80% of SpaceX total revenue and has key gov’t/national security exposure (Starshield)

-> GSAT shares rallied +13% on the back of this deal speculation but before that, the stock was up +276% since its deal with Apple

-> Also related this week, Amazon struck a deal with Delta to provide in-flight WIFI services to, initially, 500 aircraft starting in 2028; Kuiper would provide Delta with internet speeds 3-4x what it currently offers; Terms were not disclosed. (link)

US Local TV Station Consolidation Hits A Roadblock (link/link/link/link)

- Late last week, a federal court temporarily blocked the $6.2bn Nexstar / Tegna deal (creating the largest local TV stations operator in the US): This comes after legal challenges from DTV and several state attorneys

- Due to potential antitrust concerns the judge ordered a temporary restraining order (TRO) which prevents the Cos from integrating operations for at least 2 weeks

- The ruling came after the deal was approved by the FCC on March 19th

- Pres Trump also endorsed the deal last month

- U.S. Senate Commerce Committee also questioned the FCC Chair Brendan Carr & criticized his approval of the deal w/o a vote from the full commission, per Bloomberg

- Next steps – April 7th: There will be a hearing regarding extending the TRO

- Nexstar’s response? The Co said certain aspects of the closed transaction “cannot be reversed” and that the restraining order “creates immediate operational harm to Tegna and Nexstar, regulatory conflicts, and a governance vacuum”

- “It is difficult to freeze integration that was already taking place… complying with certain aspects of the TRO is impossible”

-> Nexstar fell -13% on the back of the ruling

Disney May Make A Much Bigger Push Into Gaming…(link/link/link)

- Disney is mulling a potential full acq of Epic Games at the “right moment” as per press reports this week

- Note that Epic remains founder-controlled (Tim Sweeney holds full voting control), making any transaction highly dependent on his willingness to sell

- This would follow Disney’s prior $1.5bn minority investment (Feb 2024) which was apparently supported by now Disney CEO Josh D’Amaro (former parks/gaming advocate)

- Last week on CNBC, former Disney exec Kevin Mayer also publicly endorsed a potential acquisition or similar gaming asset addition for the Co

- However, internally, there is reportedly mixed views at Disney about moving in this direction (some execs supportive; others are opposed to deal economics/strategy)

- Strategic logic? The acq would materially accelerate Disney’s gaming/metaverse strategy and position Fortnite as Disney’s primary interactive platform

- There is already a deep existing partnership: With extensive Disney IP integrations (Star Wars, Marvel, Pixar, etc.) + an upcoming Disney-dedicated Fortnite mode (a virtual “Disneyland”-like experience) thought timing of that launch is still unclear

- As background, Epic’s biz has been under operational and competitive pressures

- The Co annc’d ~1k employee layoffs last week (~20% of its workforce) tied to declining Fortnite engagement since 2025 + broader cost pressures

- Epic has seen waning interest in non-core Fortnite modes (LEGO, racing, music)

- Competition has been on the rise (Roblox)

WMG Further Expands Distribution & Label Services (link)

- Warner Music Group is buying Revelator which is an independent-focused music platform providing distribution, analytics, and royalty/accounting tools: The Co specializes in digital music distribution, rights management, royalty accounting, and real-time analytics

- Timing: The deal is expected to close next quarter

- Financial terms: Not disclosed

- Strategic rationale: Enhance the suite of services that WMG labels & ADA offer to artists and the independent community, while scaling WMG’s reach

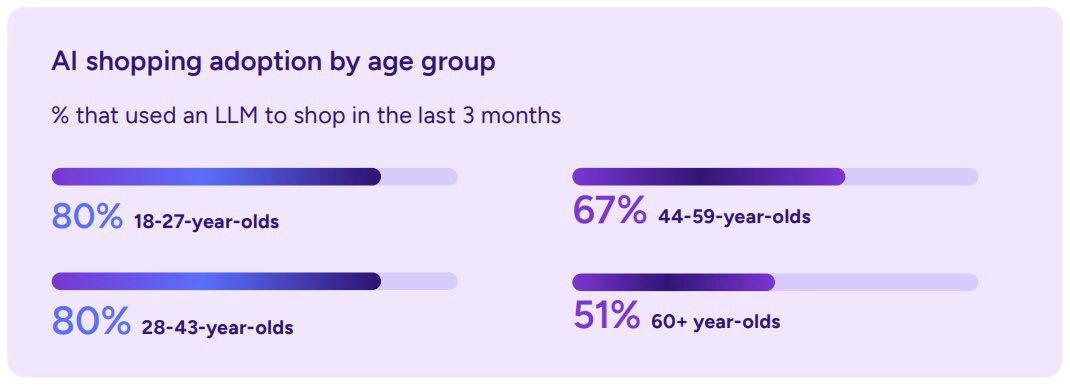

The AI Customer Is Reshaping Retail

We have been talking for some time (and also touched on in our new LionTree’s Lens – LINK) that agentic shopping is at an inflection point and Rithum and Studio’s Retail Dive report, titled The New Discovery Engine, published this week, suggests that consumers’ adoption of agentic shopping is higher than some might have thought. And retailers need to move faster to catch up…

Based on a survey of 1,046 U.S. and U.K. shoppers, the majority are already using AI for shopping purposes, and the most desirable demographics, higher-income and younger shoppers, are not only using it the most but also trusting it the most. In these cases, instead of selling to people, retailers are selling to agents, and one mis-step can put brands into the vortex.

On the other side, unknown brands can emerge on short lists, when historically they would not have. Essentially, brand recognition and customer loyalty alone will not be enough to win purchases and AI will decide on products based on the accuracy and consistency of data that brands’ provide plus data that is outside of a brand’s control like reviews on Reddit or other sources.

When AI has good information, it works in a retailer’s favor. When it doesn’t, 58% of shoppers say their trust in that brand goes down and nearly one in five abandon the purchase altogether.

So, all in all, in the age of AI, retailers are finding that their product data is becoming their most important salesperson.

See below for what we thought were the key takeaways, and if you would like to access the full report, you can do so HERE.

A High % of Shoppers, Especially Younger & Wealthier,Are Already Using AI For Purchases

- The majority of shoppers across ALL age groups are already using AI for shopping

- But adoption amongst the younger demo is significantly higher…

- 80% of 18- to 43-yr-olds have used AI for shopping in the last 3 mos, vs 51% of 60 and older have done the same (but this still seems pretty high)

- Gen-Z and Millennials don’t think of AI as a nice-to-use option, but rather an essential infrastructure that’s woven into how they shop

- Similar to how Google Maps had become an essential navigation tool for more people

- …AND higher income shoppers are also heavily leaning into AI

- Lower-income shoppers use AI to find the best price

- Higher-income shoppers use it to skip research entirely, and they’re 2x as likely to trust AI without visiting another site

- Higher-income and young shoppers also trust AI the most and verify it the least

- 80% of households earning $150k+ say they’re “extremely” or “very” confident in AI’s accuracy, vs 63% of those earning <$30k

- 64% of 18 to 27yearolds are likely to make a purchase w/o verifying an AI recommendation, while only 31% of those aged 60 and older do the same

- LLMs are making shoppers more confident…

- 43% compare more options

- 36% make faster decisions

- 34% feel more confident about their purchases

- …and less loyal

- 19% now buy from brands or purchase products they haven’t heard of before simply b/c AI recommended it

- 13% are more likely to switch retailers or products based on AI suggestions

- Rather than ceding control to AI, most shoppers are leveraging it as a tool to refine and filter their options

- Research product information: 90%+ of AIactive shoppers use LLMs to dig into product details

- Compare products and prices: 90%+ use them to compare options side by side

- Decide where to buy: More than half (53%) rely on AI to choose the retailer once they’ve decided what to buy

- What are shoppers using AI to buy?

- Electronics leads by a significant margin: 45% of shoppers use an LLM to help on electronics purchases in the last six months

- Apparel, shoes, and jewelry: 37% of shoppers

- Groceries: 36% of shoppers

Relying On Brand & Customer Loyalty Will No Longer Work For Retailers As They Start “Selling” To AI

- Before, e-commerce winners were driven by brand recognition and customer loyalty…now they’re being determined by who provides LLMs the best product and pricing information in addition to external reviews

- A new brand can displace a household name when its product data gives AI better information along the lines that it is looking for, and/or its products have more positive reviews

- For example, a brand can drop from a top citation to near-invisible in a matter of weeks when a competitor publishes a more structured product page, a Reddit thread surfaces full of complaints, or a pricing inconsistency makes AI stop trusting the data

- When AI gets it wrong, the retailer takes the blame

- When an LLM provides incorrect product information, 58% of consumers say their trust in the product or brand decreases; Nearly 1 in 5 (16%) walk away from the purchase entirely

- Consumer are also getting more comfortable with fully agentic AI for shopping as well …

- 50% of AI power users are “very likely” to hand purchasing decisions over to AI

- 67% of shoppers who fully trust AI accuracy say they’re ready to let it buy for them

Key AI Updates Around Security Concerns, Model Launches & Record $ Raises

It feels like ground hog day when it comes to the barrage of interesting and important AI advancements, but this week also surfaced some high-profile growing pains as well. As AI models grow more capable and more widely adopted, the risks around security, privacy, and competitive intelligence are becoming more apparent, and this week continued to offer reminders of that. Anthropic suffered its second accidental leak in as many weeks, this time exposing nearly 500,000 lines of Claude Code’s source code, and Perplexity is now reportedly facing a new proposed class-action lawsuit alleging that it shared users’ private conversations with third parties without their consent (though the Co said it has not received said lawsuit).

On the model front, it was a busy week of releases, with Google dropping Gemma 4 and a new cost-effective video model (just a week after OpenAI announced it would be shutting down its Sora video-making app), and Alibaba releasing several updates across its Qwen lineup.

Rounding out the week, OpenAI closed Silicon Valley’s largest ever funding round, raising $122bn at an $852bn valuation, and shared a few notable Co updates including details on a unified superapp that’s in development.

See below for more.

As AI Scales, So Does Its Vulnerabilities… Another Anthropic Leak and a New Lawsuit for Perplexity (link/link/link/link/link/link/link)

- Last week Anthropic accidentally leaked an unreleased AI model…this week Anthropic accidently leaked Claude Code’s source code!

- Anthropic accidentally released part of the internal source code for its AI-powered coding assistant, Claude Code, due to “human error” and NOT a security breach, the Co said

- No confidential information was leaked: The exposed code was related to the tool’s internal architecture

- What exactly was leaked? The leak revealed commercially sensitive information, including Anthropic’s proprietary techniques, tools and instructions for guiding its AI models to work as coding agents

- An internal-use file mistakenly included in a software update pointed to an archive containing nearly 2,000 files and 500,000 lines of code, which were quickly copied to GitHub

- The leaks could help competitors…: Like OpenAI and Google, better understand how Claude Code’s AI system works w/o needing to reverse engineer them

- …as well as hackers: Hackers now have a large amount of new information to probe for bugs they could use to exploit the Claude Code software, or manipulate its Claude AI model into helping w/ their cyberattacks

- How many people accessed the leaked info? A post on X sharing a link to the leaked code had 29mn+ views a day after the leak, and a rewritten version of the source code quickly became GitHub’s fastest-ever downloaded repository

- What were some of the leaked features?

- Kairos, a collection of updates that will allow Claude to work in the background, sending updates about its progress to a customers’ phone and using a “dream mode” to automatically consolidate Claude’s memories from past sessions; The updates also include a “proactive” feature that prompts Claude to “Take initiative — explore, act, and make progress without waiting for instructions”

- “Buddies” or virtual duck avatars to visualize coding agents

- Anthropic accidentally released part of the internal source code for its AI-powered coding assistant, Claude Code, due to “human error” and NOT a security breach, the Co said

- Perplexity AI is reportedly facing a lawsuit over allegedly sharing users’ data without consent

- The proposed class-action lawsuit alleges that Perplexity AI used hidden tracking mechanisms to let third parties access sensitive user interactions

- Filed by John Doe from Utah, the lawsuit alleges that users’ private conversations with Perplexity AI are being accessed by Meta and Google, even when the users are in Incognito mode

- The complaint further claims that as soon as users land on Perplexity’s homepage, tracking tools are installed on users’ devices without their knowledge or consent

- BUT Perplexity says it has NOT received any lawsuit: “We have not been served any lawsuit that matches this description so we are unable to verify its existence or claims,” said Jesse Dwyer, a Perplexity spokesperson

- A Meta spokesperson pointed to a Facebook help page which says it’s against the Co’s rules for advertisers to send the Meta sensitive information

- This would not be Perplexity’s first privacy related lawsuit…the Co is currently facing another lawsuit from Amazon: Amazon sued Perplexity in November 2025, alleging the startup took steps to “conceal” its AI agents so they could continue to scrape the online retailer’s website without its approval; A federal judge recently temporarily blocked Perplexity from accessing Amazon through its Comet browser

- The proposed class-action lawsuit alleges that Perplexity AI used hidden tracking mechanisms to let third parties access sensitive user interactions

More Key LLM Updates From OpenAI & Alibaba…

- Google released Gemma 4, a family of open models built off of Gemini 3 (link/link/link)

- The big update – Google is releasing the Gemma 4 family under an Apache 2.0 license

- The Co made previous Gemma models available through its own Gemma license

- The move will give people a greater deal of freedom to modify the new systems to their needs

- Gemma 4 comes in four sizes that go beyond chatbots to building agents and autonomous AI use cases running directly on-device

- The “workstation” tier includes a 31B-parameter dense model and a 26B A4B Mixture-of-Experts model, both supporting text and image input with 256K-token context windows

- The “edge” tier consists of the E2B and E4B, compact models designed for phones, embedded devices, and laptops, supporting text, image, and audio with 128K-token context window

- Model has been trained on and can support 140+ languages

- The big update – Google is releasing the Gemma 4 family under an Apache 2.0 license

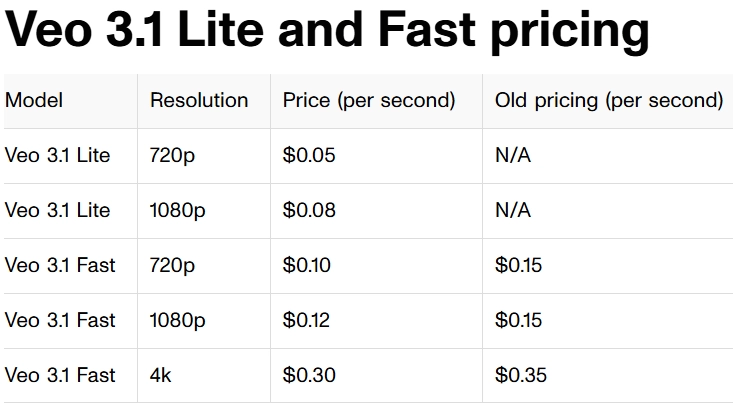

- On the back of OpenAI announcing it was shutting down its Sora video-making app last week…Google this week intro’d its most cost-effective AI video model “Veo 3.1 Lite” AND is reducing the price of its Fast model

- The new model “balances practical utility with professional capabilities”

- Supports Text-to-Video and Image-to-Video

- Offers flexible framing for landscape (16:9) and portrait (9:16) ratios and 720p and 1080p video resolutions

- Can also customize duration at 4s, 6s or 8s, with cost adjusting accordingly

- How does it compare to Veo 3.1 Fast? Its usage costs are 2-3x lower than those of the Veo 3.1 Fast version, but with the same speed

- Availability: The rollout of Veo 3.1 Lite began on Mar 31st and is accessible to developers through the paid tier of the Gemini API and Google AI Studio, including Google’s filmmaking studio, Flow

- ALSO…the price of Veo 3.1 Fast will be REDUCED on April 7

- The new model “balances practical utility with professional capabilities”

Source: CNET

- A big week of releases for Alibaba…the Co released closed-sourced “Qwen 3.6-Plus: Towards Real World Agents”… (link/link/link/(link/link)

- It represents a “massive” capability upgrade over its predecessor (Qwen3.5 series released in February)

- Practical engineering performance includes mainstream code repair, complex terminal operations and automated task

- Multimodal improvements applied to reasoning, document understanding, physical world visual analysis, and visual coding

- Optimization for “genuine business scenarios”: “We believe the future of multimodal AI lies not just in isolated task performance, but in providing holistic support for workflow-oriented operations”

- Compatibility with OpenClaw

- Also includes support for Anthropic API protocol for use with Claude Code

- The model’s closed-sourced approach is different than other Chinese developers including MiniMax Group and DeepSeek, who have open models

- The model will be integrated into Alibaba’s Qwen chatbot app for consumers, as well as its recently launched Wukong app that offers work productivity AI agents for enterprise users

- It represents a “massive” capability upgrade over its predecessor (Qwen3.5 series released in February)

- Also this week… Alibaba had a dual release of Qwen3.5-Omni and Wan2.7-Image: 5-Omni turns sketches and voice into working code, while Wan2.7-Image fills in the visuals

- Qwen3.5-Omni allows users to code by demonstration

- Its standout feature, “Audio-Visual Vibe Coding,” enables developers to code by demonstration rather than writing from scratch

- Users can show a sketch and describe functionality verbally, eliminating the need for boilerplate code

- The model automatically generates functional UIs for websites, apps, and mini-games

- Wan 2.7 handles the visual design process

- Through a new “color palette” feature, users can input specific color codes and proportions directly into their prompts

- The model also allows creators to fine-tune specific physical attributes, such as eye shape and bone structure, to generate truly unique and lifelike characters tailored to a specific project

- Qwen3.5-Omni allows users to code by demonstration

Notable OpenAI-Specific Updates…OpenAI’s $122bn Raise + KPIs (link)

- OpenAI closes Silicon Valley’s largest-ever funding round – raised $122bn at a post money val’n of $852bn

- Extended participation to investors through bank channels for the first time ever, raising $3bn+ from individual investors

- Also annc’d that OpenAI will be included in several ETFs managed by ARK Invest

- ARK’s flagship $6bn Innovation ETF will have a ~3% exposure to OpenAI following the investment, and is the first private Co the fund will hold, per reports

- OpenAI shares are already a small part of mutual funds and ETFs run by T. Rowe Price and Fidelity

- The round was anchored by Amazon, NVIDIA and SoftBank, along w/ continued participation from Microsoft

- OpenAI also shared some quick Co KPIs…

- OpenAI now generates $2bn in rev per month, up from $1bn per qtr at the end of 2024 and $1bn annually just a yr after launching ChatGPT in Nov 2022

- It is now growing rev 4x faster than the Cos “who defined the Internet and mobile eras, including Alphabet and Meta”

- Its enterprise segment is on track to reach parity w/ consumer by the end of 2026: Enterprise makes up more than 40% of OpenAI’s rev

- The Co is working on building a unified AI superapp that will bring together ChatGPT, Codex, browsing, and their broader agentic capabilities into one agent-first experience

- “This is not just product simplification. It is a distribution and deployment strategy… a single product surface allows us to improve faster, ship more coherently, and capture more of the value created by agentic workflows”

- OpenAI now generates $2bn in rev per month, up from $1bn per qtr at the end of 2024 and $1bn annually just a yr after launching ChatGPT in Nov 2022

Enticements For Large Private Co’s To IPO Emerge This Week, Just In Time For SpaceX

One of the key themes we flagged in our most recent LionTree’s Lens (published yesterday – link to access HERE) is that larger deals (outside of TMT) are starting to make a comeback, accounting for ~72% of IPO proceeds in Q1 vs just 28% in Q1 last year. That is a welcomed dynamic but overall activity is far from the 1990s peak levels, which saw 400+ IPOs annually, vs the ~150-200 seen in recent years (link).

Part of the reason is that companies are choosing to stay private for longer (the # of public Cos listed on US exchanges has shrunk by more than a third since 2000, according to a white paper from Nasdaq last yr). Being a public company adds a lot of additional time and resources. Given that, a couple of developments this week that would entice large private companies to go public, caught our attention. Namely, index providers are making moves to rework the rules around how quickly newly listed large-cap companies can enter their flagship benchmarks (Nasdaq being the first) and the SEC’s proposal to shift from quarterly to semiannual reporting advanced to the White House for review.

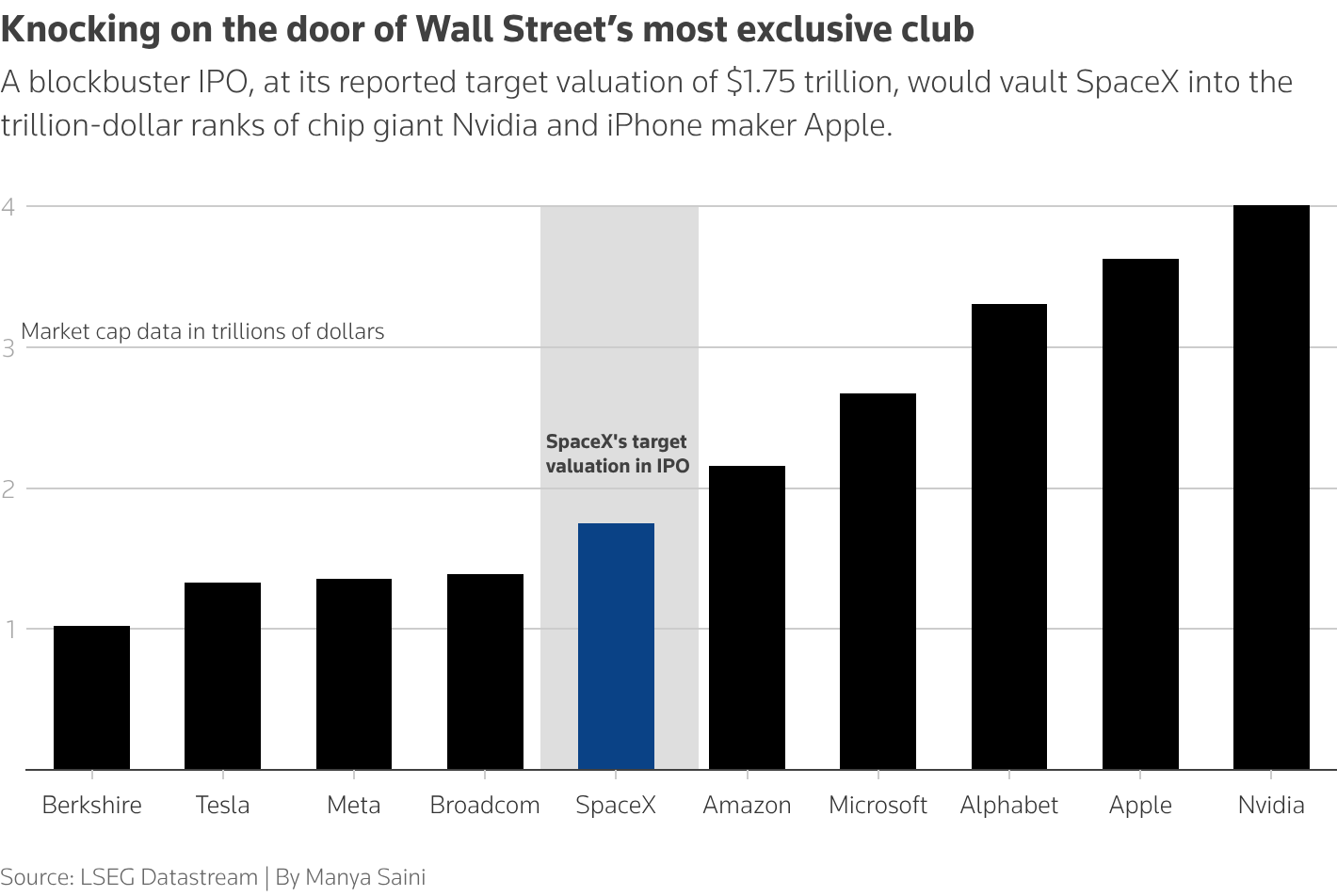

This is just in time for SpaceX, which was in focus this week given press reports that it filed confidentially for what could be the largest IPO in history. The transaction could happen as early as June/July.

See below for more key points from our view.

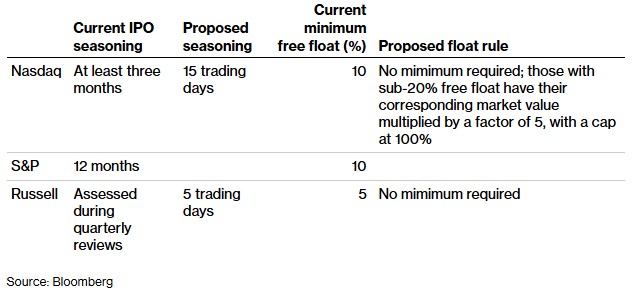

Newly-Public Large Companies Stand To Benefit From New Index Inclusion Changes (link/link/link/link/link link)

- This week, Nasdaq became the first index to enact a change to its inclusion rules

- Its “Fast-entry” rule shortens the time to trading from 3 mos to 15 days: Nasdaq will evaluate newly listed stocks for potential entry by ranking their market cap on the 7th trading day and assessing whether they would rank within the top 40 index members; If a Co meets all the eligibility criteria, it will be fast-tracked into the Nasdaq-100 after the 15th day of trading

- The timeline is shortened from the previous at least three months currently

- The exchange also removed the minimum 10% float requirement for eligibility

- The revisions, annc’d after an industry consultation last month, will take effect on May 1, though most updates are not expected to affect the benchmark’s composition until June

- Its “Fast-entry” rule shortens the time to trading from 3 mos to 15 days: Nasdaq will evaluate newly listed stocks for potential entry by ranking their market cap on the 7th trading day and assessing whether they would rank within the top 40 index members; If a Co meets all the eligibility criteria, it will be fast-tracked into the Nasdaq-100 after the 15th day of trading

- Nasdaq is not the only index to consider changes…

- Russell, which started its own consultation in February and proposed to shorten an IPO’s seasoning period to five trading days, has extended the deadline for feedback to April 3

- S&P Dow Jones Indices are engaging with stakeholders to determine whether there’s demand for changing rules, but no decision has been made and S&P would still have to launch a formal consultation that would last several weeks before any change can be made

- Why are these changes being evaluated?

- Expediting the entry of large IPOs would ensure that the indexes “are more representative of the US equity market sooner,” Russell said in a statement accompanying its consultation

- It would also help incentivize more Cos to go public: The # of public Cos listed on US exchanges has shrunk by more than a third since 2000, according to a white paper from Nasdaq last yr

- But what are critics saying?

- A shortened timeline would expose index-tracking funds to outsized price swings that newly-public stocks typically experience

- It would also push index funds closer to buying before the mkt has established a reliable price, as index funds, in theory, are supposed to passively accept the prices that the mkt gives and buying on or before the IPO doesn’t give enough time for that price discovery to happen

- Which companies would be set to benefit? Some very large IPOs that are said to be on the docket, including SpaceX, OpenAI, Anthropic, Databricks, Stripes, and others

- If the 10 largest US venture-backed Cos were to IPO and join the S&P 500, they would collectively represent ~4.5% of the index, more than the entire energy sector, according to S&P’s own analysis

- SpaceX alone, targeting a val’n of ~$2 trillion would be larger than all but five current members of the S7P 500 (more on that below)

- Both OpenAI and Anthropic’s latest rounds were at val’ns of $122bn and $30bn, respectively

- BUT the standard requirements is that Cos trade publicly for at least 12 mos before than they can be considered for S&P 500 inclusion hence that means that index funds that track the benchmark can’t invest in them and could miss out in the interim

- If the 10 largest US venture-backed Cos were to IPO and join the S&P 500, they would collectively represent ~4.5% of the index, more than the entire energy sector, according to S&P’s own analysis

Source: Bloomberg; Note that since the publication of the graphic, Nasdaq has confirmed that it would be moving forward with its proposed seasoning and minimum free float rule

More Visibility To The Largest IPO Ever Emerges (link/link/link)

- Speaking of SpaceX, it made big headlines this week when, reportedly, it confidentially filed for what would become largest-ever IPO

- The Co apparently submitted its draft IPO registration to the SEC, putting it on track for a June/July listing

- SpaceX is speculated to seek an IPO valuation of more than $2 trillion

- As a reminder…the Co acquired CEO Elon Musk’s AI startup xAI in a deal that valued the enlarged entity at $1.25 trillion ($1 trillion val’n for SpaceX and $250bn val’n for xAI)

- The rumored deal size is as much as $75bn

- At that size, it would dwarf the current record holder, Saudi Aramco’s $29bn debut in 2019

- As a comparison, last yr, the US IPO market raised $44 billion altogether from 202 listings

- The IPO is expected to have a large retail component, with SpaceX potentially allocating as much as 30% of the offering to small investors

- That would be at least 3x the typical retail allocation in major IPOs

- SpaceX is reportedly hosting an analyst day on April 21

- SpaceX had also reportedly made early index inclusion a condition of its choice of listing venue (link)

-> Space stocks jumped on the news, with AST SpaceMobile and Rocket Lab both ending the day up +12%, as well as Planet Labs up +10% and Intuitive Machines up +9%

-> Also see Theme #4 for thoughts on Amazon’s reported interest in acquiring GlobalStar, which would make them more competitive to SpaceX

Source: Reuters

The SEC’s Proposal To Reduce The Number Of Earnings Disclosures Moves One Step Forward (link/link)

- Also, a quick follow-up for Cos already public…the SEC’s proposal to shift from quarterly to semiannual reports has advanced to the White House for review on March 27th

- What happens now? Once the review is finished, the commission can then vote to release the plan and take public feedback; Commissioners would then need to vote again on a final version for the rule to take effect

- Historically, SEC rulemaking efforts have averaged ~18 mos from proposal to final rule

- For some context…

- The SEC has been working on this potential earnings disclosure overhaul since last yr following President Donald Trump’s call to shift to semiannual reports from quarterly ones

- SEC Chairman Paul Atkins has vowed to fast-track the potential plan…:

- He said the change could save Cos significant time and money

- And also flagged that foreign private issuers who trade on US exchanges only have to submit twice-yearly reports, so a proposal for domestic Cos could bring those disclosure requirements into alignment for some Cos

- …but advocates of the disclosures say the transparency helps investors make key decisions

- Atkins has also recently proposed scaling the frequency of corporate disclosures to a firm’s size

- What happens now? Once the review is finished, the commission can then vote to release the plan and take public feedback; Commissioners would then need to vote again on a final version for the rule to take effect

The Road Ahead For Robotaxis Is Not Without Its Bumps, But Progress Continues

Robotaxi safety concerns were in focus this week with Baidu suffering a mass robotaxi outage in China that left passengers stranded in live traffic, and Tesla revealed that its robotaxis are, in rare cases, being remotely operated by human employees, which also raised concerns.

At the same time, international expansion accelerated this week, with WeRide and Grab launching Singapore’s first autonomous public ride service and Dubai officially kicking off commercial autonomous taxi operations in partnership with Apollo Go and WeRide.

Taken together, this week captured both sides of the roads that the AV industry is on right now…expanding into new markets and geographies at a rapid clip, while still working through the safety and regulatory challenges that come with deploying these systems at scale.

See below for more on the above.

Robotaxi Safety Concerns Were In Focus This Week… (link/link/link/link/link/link)

- Passengers were stranded in moving traffic after Baidu robotaxi outage in China’s Wuhan – the FIRST time a mass shutdown of robotaxis has been reported in China

- A preliminary investigation indicates more than 100 Apollo Go robotaxis came to a halt b/c of a “system malfunction,” per the Wuhan police

- What happened with passengers?

- After the robotaxi stopped, instructions on a screen read, “driving system malfunction. Staff are expected to arrive in 5 minutes”…which apparently was not the case

- Some passengers got out of the cars themselves, and others were afraid to get out in the middle of busy roads

- No injuries were reported

- A similar incident happened last yr in the US: In December, many of Waymo’s self-driving cars came to a stop in San Francisco because of a power outage

- For context… Apollo Go is the largest robotaxi provider in China; Baidu operates more than 1,000 robotaxis, mostly in China, started a svs in Abu Dhabi and Dubai this year and is working with partners to launch service in Britain and Switzerland

- Tesla has admitted that its robotaxis are, in “rare cases”, being driven remotely by real humans

- This was revealed through letters submitted by seven AV Cos to Massachusetts Senator Ed Markey in an investigation into self-driving vehicle technology

- What exactly did Tesla share? “As a redundancy measure in rare cases … [remote assistance operators] are authorized to temporarily assume direct vehicle control as the final escalation maneuver after all other available intervention actions have been exhausted,” Karen Steakley, Tesla’s director of public policy and business development, shared in the letter

- In those situations, operators are reportedly able to take over Tesla’s robotaxis when they’re moving at speeds ~2mph or less, and then drive the car at up to 10mph if software permits it

- “This capability enables Tesla to promptly move a vehicle that may be in a compromising position,” Steakley wrote, adding that it helps avoid waiting for a first responder or a field worker to come and retrieve the car

- Tesla’s remote assistance operators are in-house employees working from two locations: Austin, Texas and Palo Alto, California

- Why is this a point of concern? Direct remote control comes with inherent risks, from network latency delaying signals and therefore the remote worker’s ability to react in real time to a lack of complete situational awareness

- In comparison, Waymo’s Driver software can call on human help to offer context and answer questions to help it navigate complicated driving situations, but the Co says these workers never drive the robotaxi themselves

- Markey called Tesla’s refusal to share more specific information regarding how many takeovers occur “especially concerning,” since the remote workers “are permitted to teleoperate the vehicle”

- Steakley said in her letter that divulging such information “would necessarily reveal highly sensitive trade secrets and confidential business practices” that Tesla needs to maintain its “competitive position in the AV industry”

AV Launches Continue Full Speed Ahead, With The Latest Launches In Singapore And Dubai

- WeRide and Grab launched Singapore’s first autonomous public ride svs called Ai.R (Autonomously Intelligent Ride) (link/link)

- How does it work?

- Operating hours: The Ai.R fleet operates on weekdays (Monday–Friday) from 9:30 AM to 5:30 PM

- Routes: Riders can choose between two full AV shuttle routes; A 20-min “Mini Route” will also be offered for those looking for a shorter AV experience

- Fares: Rides will be free until commercial svs begins in mid-2026, allowing more passengers to share their feedback, as well as gathering insights into usage patterns, to help to fine-tune service and pricing standards for the introductory discounted fare

- Transition to public svs follows a “rigorous” community engagement phase: Since Jan 2026, 1,000+ passengers trialed the svs and provided feedback to improve ride experience

- To date, the Ai.R fleet has safely clocked 30,000km of autonomous mileage

- WeRide and Grab have framed workforce development as a central component of the rollout…

- During the initial phase of public rides, Safety Operators will be onboard the AVs to help ensure a seamless journey

- To date, 14 Grab driver-partners have successfully completed specialized training with WeRide and GrabAcademy to become certified Safety Operators and another batch of Grab driver-partners are currently undergoing training and assessments

- WeRide and GrabAcademy have also commenced Remote Operator training, where participants learn how to monitor the fleet remotely from the Ai.R Operations Command Centre

- How does it work?

- Dubai Roads and Transport Authority (RTA) launched commercial autonomous taxi svs, in partnership w/ Apollo Go and WeRide (link/link)

- The launch follows a supervised trial that began in Dec 2025 and a driverless vehicle permit granted by the RTA in Feb 2026

- The svs is currently limited to the cities of Umm Suqeim and Jumeirah

- But the RTA permit covers planned expansion into addtl districts including Dubai Silicon Oasis, Dubai Investment Park, and Al Hamriya Port

- Passengers can now book rides through two apps: WeRide via Uber and Apollo Go via the Apollo Go app

- During this first phase, RTA will deploy 100 taxis within Dubai’s transport network, with gradual expansion expected in the coming yrs

- Follows the rollout of driverless Uber taxis on Abu Dhabi’s Yas Island in Nov 2025: The UAE capital became the first city in the Middle East to operate fully driverless robotaxis, and the only city outside the US to offer such vehicles on Uber’s platform

- Pilot programs are also underway in Ras Al Khaimah in the UAE

- More deployments across the region are in the works… WeRide and Uber committed in Feb 2026 to deploy at least 1,200 robotaxis across Dubai, Abu Dhabi and Riyadh

- Specifically for Dubai, the city is targeting 25% autonomous journeys by 2030

Grab Bag: Netflix Looking For More NFL / Meta Testing Instagram+ / AT&T Launches OneConnect

- Netflix is reportedly evaluating moving deeper into franchise sports with addtl NFL packages…its current 2-game Christmas package is under 3-year deal that ends this final year (link)

- The Co is exploring expansion to ~4-game package, incl.:

- NFL Thanksgiving Eve game (new inventory)

- International game (league-controlled inventory)

- NFL…

- Reportedly is currently restructuring rights w/ all b-cast partners to create smaller 4–5 game packages to offer streamers

- And recently got back rights to ~5 games that could be potentially split across multiple buyers

- The Co is exploring expansion to ~4-game package, incl.:

- Meta is testing a premium subscription on Instagram, called Instagram+, that gives paying users access to exclusive features (link/link)

- Where are the tests happening and how much are users being charged? Subscriptions are currently being tested in Mexico (costs ~$2.20/mo), Japan (~$2/mo) and the Philippines (~$1.07/mo)

- What could some of those perks look like?

- Viewing another person’s Story without them knowing

- Creating unlimited audience lists; Seeing how many people rewatched their Stories

- Extending a Story for an extra 24 hours and choosing to spotlight a Story up to once per week

- Searching through the Story viewer list to quickly see if a specific person looked at their Story, instead of having to scroll through the entire list

- Meta says it’s going to continue testing the Instagram premium subscription before rolling it out further

- As a reminder…Meta is also considering premium subscriptions for Facebook and WhatsApp, which the Co said back in Feb

- AT&T launches OneConnect, a new all-in-one plan for internet and wireless (link): “The first-ever single subscription to deliver unlimited connectivity that powers all devices—wearable, smartphones and tablets at home and on the go”

- Includes both 1 Gig fiber home internet and unlimited mobile svs that can be shared across various devices

- Allows users to manage both mobile and internet usage under one account and removes the need for separate billing systems and plans

- OneConnect pricing vs existing AT&T offerings

- $90/mo for an individual plan on OneConnect vs ~$155 (wireless $90 + fiber $65)

- $120/mo for two people on OneConnect vs ~$225 (2x wireless + fiber)

- $225/mo for 3+ people

- BUT the plan is only available to new customers, and there doesn’t seem to be a comparable plan for existing users at the moment

- Includes both 1 Gig fiber home internet and unlimited mobile svs that can be shared across various devices

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Publishers saw mostly double‑digit CPM and rev gains from The Trade Desk’s OpenPath over the past six months, despite volatility and sharp dips. Several said duplicate bids tied to OpenAds trials lifted yields, prompting faster integrations. Smaller and mid‑size pubs trimmed resellers and improved CPMs, while others flagged transparency gaps, buy‑side friction and fluctuating spend. (Digiday)

- IAB annc’d a whitepaper on agentic AI reshaping video planning, buying, measurement and creative. Autonomous systems can optimize performance in real time, but full end-to-end automation is ~1–2 yr away due to data standards, interoperability and governance gaps. The report says ~69% of analytics teams are scaling AI, shifting measurement to active, learning systems across CTV, OLV, social and FAST. (MediaPost)

- The Trade Desk is overhauling Identity Alliance payouts, shifting from volume-based fees to payments tied to incrementality, rewarding partners whose data adds unique value. The change, taking effect in early 2026 w/ a Q2 transition, aims to cut duplicative signals but has sparked concerns over transparency, abrupt terms, and near-term rev impact. (Digiday)

- Roku annc’d Howdy™ as a U.S. mobile app for iOS and Android, expanding its affordable, ad‑free SVOD offering. Priced at $2.99/mo, the app gives on‑the‑go access to thousands of titles and 10,000+ hours from partners incl. FilmRise, Lionsgate, Sony and Warner Bros. Discovery. (Roku)

Artificial Intelligence/Machine Learning

- Meta is assembling an elite AI research team, MRS Research, inside its recommendation systems to enhance Facebook and Instagram algorithms, per job posts and LinkedIn. Formed during an Oct. reorg, the unit targets long‑term AI research and publishing to “leapfrog” current systems and works closely w/ ads. Led by VP Yang Song, hires include talent from TikTok and Amazon, as Meta doubles down on AI to boost its core biz. (Business Insider)

- Google annc’d its $19. 99/month AI Pro now includes 5 TB storage, up from 2 TB, w/ no price increase, adding 3 TB for all users globally. Storage works across Gmail, Drive, and Photos. Pricing tiers stay unchanged, w/ upgrades at $49.99 for 10 TB and up to 30 TB on Ultra. (9to5Google)

- Q1 2026 saw global venture funding hit a record ~$300bn as the AI boom drove massive investment. About 6,000 startups raised capital, up over 150% QoQ and YoY, w/ AI taking ~$242bn, or 80% of total. Four mega-rounds led by OpenAI, Anthropic, xAI and Waymo made up 65%. U.S. cos captured 83%, valuations surged, late-stage deals dominated, while IPOs lagged and M&A stayed strong. (Crunchbase)

- NVIDIA annc’d a strategic partnership w/ Marvell Tech to expand its AI ecosystem via NVLink Fusion. The tie-up links Marvell’s custom XPUs and networking to NVIDIA’s AI factory and AI-RAN platforms, delivering greater choice and flexibility for customers building rack-scale infrastructure. NVIDIA also invested $2bn in Marvell and both will collaborate on silicon photonics and optical interconnects. (NVIDIA)

- Apple is testing a Siri upgrade that can process multiple commands in one query, aligning it w/ newer AI assistants, Bloomberg News reported. The feature is being built into iOS 27, iPadOS 27 and macOS 27, due later this yr. Apple plans to highlight the revamp and new Apple Intelligence tools at its WWDC on Jun. 8 as it tries to catch up in the AI race after a muted 2024 rollout. (Reuters)

- China’s DeepSeek AI chatbot suffered its longest outage since its viral rise in early 2025. The cos status site showed a “major outage” lasting ~7 hours, from early morning to 10:33 a.m. local time. No cause was disclosed, though problems can stem from servers or updates. Earlier API svs outages occurred in Jan. 2025, but the main user site had avoided prolonged disruptions. (Reuters)

- Last yr, OpenAI unveiled a plan letting partners like Spotify tech SA and Booking Holdings Inc. launch mini apps inside ChatGPT, echoing Apple Inc.’s App Store to make an all in one platform. Six months later, app makers say progress is slow: 300+ integrations are hidden, features are limited as partners resist ceding customer ties and payments, and devs cite tedious approvals, buggy tools, and scant usage data. (Bloomberg)

- Microsoft annc’d Copilot Cowork is now available via the Frontier program. The new capability extends Microsoft 365 Copilot to handle long‑running, multi‑step workflows by planning tasks, reasoning across files and tools, and carrying work forward w/ visible progress. (Microsoft)

- OpenAI’s push to build a ChatGPT app store, annc’d as a challenge to Apple’s App Store, has struggled six months in. Developers cite a slow approval process, bugs, and limited data, while partners resist sharing payments and customers. Over 300 apps exist but offer thin functionality, forcing users off-platform to complete purchases. (Bloomberg)

- French AI start-up Mistral raised $830mn in its debut debt financing to fund Nvidia-powered data centres across Europe, amid rising demand for sovereign European alternatives to US tech groups. The Co previously outlined plans to spend €4bn on AI infrastructure in France and Sweden. (Financial Times)

Broadcast/Cable Networks

- Fox and Sinclair told the FCC that live sports should remain free on broadcast TV, arguing streaming paywalls violate the 1961 Sports Broadcasting Act. Fox warned paywalled streaming raises costs and limits access, while Sinclair said leagues w/ antitrust perks are shifting games off public airwaves. (Bloomberg)

- US broadcast station owners urged the FCC to curb Big Tech buying sports rights, arguing it could erode local TV news. Filings said streamers use live sports as loss leaders, shifting events from free over‑the‑air TV to paywalled svs. Fox and Sinclair warned access to the World Series, NFL and Olympics could suffer. (Reuters)

Cable/Pay-TV/Wireless

- T-Mobile cont’d layoffs, confirming IT job cuts as it realigns to support future growth and innovation, while still investing in select roles. The Co said it eliminated roles this month and is offering support to affected staff. In Washington state, 446 jobs were cut in Feb., following 532 in Aug., per WARN data. The carrier had ~75,000 employees as of Dec. 31. (Fierce Network)

- A US judge in Manhattan granted Verizon Wireless a preliminary injunction blocking T‑Mobile’s “Save Over $1,000” ad campaign, ruling the apples‑to‑oranges comparison was literally false and caused irreparable harm. The court said truthful ads serve public interest, cutting claimed savings to ~$229/yr. (Reuters)

- KDDI Co annc’d a Special Investigation Committee report on fictitious circular ad transactions at subs BIGLOBE and G-PLAN. Two employees ran non-substantive trades from ~2018; the probe found no mgmt awareness or similar cases. The impact forces restatements totaling ~¥246.1bn rev and losses, incl external outflows and impairments. (KDDI)

- Iliad’s Free annc’d the Free Max mobile plan, claiming the first offer w/ unlimited data in France and 135+ destinations. Priced at €29.99/month, or €19.99 for Freebox subs, the no‑contract plan includes unlimited 5G/5G+ data in France, unlimited 4G/5G abroad, unlimited calls, SMS and MMS in Europe and other regions. A Free Max Pro biz version at €29.99 excl. VAT is also available. (Iliad)

- AT&T agreed to a deal worth up to $2bn to upgrade the federally subsidized FirstNet emergency cellular network it runs for the Commerce Dept. , promising system upgrades and lower rates in exchange for faster federal approvals. CEO John Stankey reached new terms after months of talks w/ Commerce Sec. (The Wall Street Journal)

Capital Market Updates

- Morgan Stanley’s E*Trade is in talks to lead retail distribution for SpaceX’s planned IPO, potentially securing most small-investor allocation. Sources say Robinhood and SoFi pitched roles but could be excluded, w/ Fidelity also vying. SpaceX may set aside up to 30% of shares for retail, though most would go to banks’ wealthy clients. (Reuters)

- Podcast host Eric Newcomer reports on secret Jan. 2026 Coatue slides shared w/ investors, outlining how the invest Co values Anthropic, one of the most valuable private tech cos. Coatue proj a $1.995trn valuation in 2030, citing ~$18bn rev and a $14bn EBITDA loss in 2026, ~ $30bn run-rate rev, and ~$19bn ARR. (Newcomer)

Cloud/DataCenters/IT Infrastructure

- CoreWeave raised $8. 5bn from banks and investors to fund expansion of its cloud computing capacity, calling it the largest chip-backed debt deal. The investment-grade loan is secured by GPUs and customer contracts, per a statement. Bloomberg said the debt is backed by cont’d contracts w/ Meta Platforms Inc. worth at least $19bn. (Bloomberg)

- Microsoft, Chevron and hedge fund Engine No. 1 annc’d an exclusive pact to develop power generation and supply for data centers, as big tech races to secure electricity for gen AI svs. No commercial terms are finalized. The plan builds on Chevron–Engine No. 1 efforts to site gas-fired plants near U.S. data centers using GE Vernova turbines, tied to a proposed ~$7bn West Texas facility producing ~2,500 MW to support a large campus, w/ first output targeted by 2027. (Reuters)

- France’s public sector ordered €84mn in public cloud svs in 2025, up 62% yr-on-yr, according to a report by the Interministerial Digital Directorate (DINUM). The increase mainly benefitted European-based providers in the public sector, which together held a 70% share of total spending. (Telecompaper)

- Google plans to help finance a ~$5bn Texas data center leased to Anthropic as AI infra competition intensifies. The project, run by Nexus Data Centers, could exceed $5bn in its initial phase, w/ Google providing construction loans alongside bank financing. (MSN)

Crypto/Blockchain/web3/NFTs

- Google Research warns future quantum computers could break elliptic curve cryptography securing cryptocurrencies w/ far fewer resources than thought. A whitepaper outlines new estimates, urges blockchains to migrate to post-quantum cryptography, and recommends short-term defenses. (Google)

- Event-wagering mkts face scrutiny after concentrated trades ahead of a Trump post on Iran moved crude and equities. A study of Polymarket found patterns consistent w/ insider use of nonpublic info, estimating ~$143mn profits over two yrs. Linked accounts earned ~$1.6mn betting on Iran and Venezuela, prompting calls in Congress to rein in the biz amid limited oversight. (Yahoo Finance)

eCommerce/Social Commerce/Retail

- Nike beat Q3 FY2026 EPS and rev estimates but annc’d a weaker near‑term outlook, sending shares down ~9%. Rev was flat at $11.28bn, EPS was $0.35, while net income fell 35% to $520mn. Mgmt expects Q4 sales down 2%–4% and a ~20% China decline, partly offset by 3% growth in N. America; margins were pressured by tariffs amid a cont’d turnaround. (CNBC)

- Macy’s annc’d Ask Macy’s, an AI-powered shopping assistant rolled out across its digital platforms. The conversational tool helps shoppers discover brands, trends and personalized recommendations, plus virtual try-on. Powered by Google Gemini, the feature lifted rev per visit 4.75x in beta vs non-users. (Retail Dive)

Electric & Autonomous Vehicles

- A major outage hit one of China’s biggest robotaxi operators, stranding riders and halting cars on busy highways. Baidu Co operates self-driving vehicles across dozens of cities; users in Wuhan said cars abruptly stopped in fast lanes, w/ some passengers stuck ~90 minutes. WIRED reported at least three accidents. (Yahoo)

- Tesla disclosed that its robotaxis are at times driven by remote human operators, saying it occurs rarely and only at speeds below 10 mph. The admission came in letters to US Sen. Ed Markey as part of an inquiry into self‑driving tech. Submissions from seven AV firms, including Tesla, Amazon‑owned Zoox and Uber‑ and Nvidia‑funded Nuro, outlined “remote assistance,” sparking calls for greater transparency. (WIRED)

Film/Studio/Content/IP/Talent

- Universal Music Group NV annc’d plans to repurchase €500mn ($575mn) of its shares, representing the record label’s first-ever buyback since it was listed in 2021. The Netherlands-based Co said the buyback program, detailed in a statement on Monday, will be used for its incentive compensation plan and to reduce the Co’s overall share capital following its public listing in 2021. (Bloomberg)

FinTech/InsurTech/Payments

- Visa annc’d six new AI tools to modernize credit card charge disputes, CNBC reported. Tools target merchants, issuers and acquirers, using generative and predictive AI to prevent disputes, streamline cases and cut costs. Most svs will launch later this yr. (CNBC)

- Amazon annc’d it will drop American Express and move its small-biz credit cards to Mastercard’s network. Two new cards offer 5% back for Prime members and 3% for non-Prime, w/ no annual fee. Amex cards will transition by Aug. 14, w/ existing limits and rates unchanged. Shift follows an eight-yr partnership and excludes consumer cards. (Payments Dive)

- The Labor Dept proposed a rule easing use of alternative investments in 401(k)s, following a Trump executive order. Alts incl private equity, private credit, real estate and crypto. A fiduciary safe harbor aims to curb lawsuit risk via factors on performance, fees, liquidity and valuation. The plan opens a 60-day comment period. (CNBC)

Handheld Devices & Accessories/Connected Home

- Samsung annc’d Hearapy, a free Android app that claims to ease motion sickness using sound, according to The Verge. The app plays a 100Hz sine wave via headphones for ~60 seconds to stimulate the inner ear’s balance system, with relief said to last up to two hours and sessions repeatable. Duration can be set from 40–120 seconds. (The Verge)

- Samsung annc’d blood pressure monitoring for Galaxy Watch users in the US, cont’d rollout after regulatory delays. Feature requires calibration w/ a traditional upper-arm cuff, Samsung Health Monitor app, and recalibration every 28 days. Not FDA-cleared, it’s for wellness only, on-demand readings. Compatible w/ Galaxy Watch 4+ paired to Galaxy phones on Android 12+, rolling out in phases. (CNET)

- Google is developing a fitness band under its Fitbit brand to compete w/ screenless wearables from firms like Whoop Inc. and Oura Health Oy, according to a person familiar. The device is planned for release later this yr and will offer basic features, requiring a paid subscription to unlock additional functionality, mirroring the biz model used by rival screenless wearables. (Bloomberg)

- Meta annc’d its first prescription-optimized AI glasses, launching Ray-Ban Meta Blayzer Optics and Scriber Optics (Gen 2). The frames support nearly all prescriptions, focus on all-day comfort, and start at $499 w/ US pre-orders open, followed by wider mkts Apr. 14. (Meta)

Last Mile Transportation/Delivery ]

- Uber annc’d an agreement to acquire global chauffeur Co Blacklane, expanding its premium travel biz. Founded in Berlin in 2011, Blacklane operates in 500+ cities across 60+ countries, offering planned luxury svs. The deal supports Uber’s move into the chauffeur sector, w/ Uber Elite and Reserve growth, combining Blacklane’s service expertise w/ Uber’s global scale and tech, and is expected to close by end-2026 subject to approvals. (Uber)

Macro Updates

- Private-sector hiring rose by 62,000 in March, topping expectations, ADP said. Gains were slightly below Feb., as education and health svs added 58,000 and construction 30,000, driving nearly all growth. Info svs, mining and leisure posted smaller gains, while trade, transport and utilities and manufacturing lost jobs. Small biz led hiring; wage growth held at 4.5% for stayers and 6.6% for job changers. Govt roles are excluded. (CNBC)

- US job openings and hiring weakened in Feb, per Labor Dept data published. Open roles fell to 6.9mn from a rev’d 7.2mn in Jan., w/ the openings rate easing to 4.2%. Hiring slid to the lowest level since Apr. 2020, at ~4.8mn workers, pushing the hires rate to 3.1%. (The Wall Street Journal)

- Trump’s tariffs annc’d failed to reshore US electronics manufacturing, instead accelerating supply-chain shifts from China to Vietnam. Bloomberg data shows Vietnam overtook China as top US laptop and console supplier as firms moved final assembly to avoid higher levies. (Bloomberg)

Regulatory

- EU institutions banned staff from using fully AI‑generated images or videos in official communications, citing risks of deception, deepfakes and eroding trust, POLITICO reported. The European Commission, Parliament and Council allow limited AI use for optimization only, stressing authenticity and accountability, even as critics warn the ban could weaken online relevance w/ fast‑moving geopolitical crises. (Politico)

- A global ban on taxing cross border digital streaming and downloads expired, after W. T.O. members ended their annual meeting without extending it. The U.S. pushed to cont’d the ban barring digital duties across e commerce, but Brazil and Turkey blocked a longer extension. (The New York Times)

- Federal prosecutors in Manhattan are exploring whether lucrative prediction-mkt bets could violate insider-trading and other laws, escalating scrutiny of a fast-growing biz largely untouched by regulators. Officials met w/ Polymarket to discuss applying existing rules amid high-profile trades tied to geopolitics and TV outcomes. (CNN)

- The UK CMA annc’d a package targeting biz software and cloud svs to boost choice, prices and resilience for UK biz and the public sector. It will open an SMS probe into Microsoft’s biz software ecosystem in May, citing licensing impacts on cloud mkts as AI reshapes productivity tools. (GOV.UK)

- Australia is investigating Meta’s Facebook and Instagram, TikTok and YouTube for possible breaches of its under-16 social media ban, saying big tech has failed to obey world-leading laws aimed at protecting children from harmful content. (Yahoo)

Satellite/Space

- Delta Air Lines annc’d it struck a deal w/ Amazon to use the cos nascent Leo satellite‑internet svc for in‑flight Wi‑Fi, marking Amazon’s highest‑profile win in the sector. The airline plans to equip an initial 500 aircraft starting in 2028, targeting speeds three to five times faster than current offerings. (The Wall Street Journal)

- SpaceX said it lost contact w/ a Starlink satellite after an unexplained anomaly that appears to have caused it to explode. Space tracker LeoLabs detected dozens of objects near the craft, but SpaceX said debris poses no risk to the ISS or NASA’s Artemis II. The satellite broke up ~560km above Earth and fragments should burn up soon. (The Verge)

Social/Digital Media

- UK social media users are becoming less active on tech platforms as video-focused apps grow and concerns rise that old posts could harm personal or professional life. Ofcom research shows 49% of adults now post, share or comment, down from 61% in 2024, while those exploring new websites fell from 70% to 56%, reflecting a broader shift in online behaviour, the watchdog said in findings released. (The Guardian)

Software

- Oracle said it is cutting thousands of jobs as it ramps AI tech spending, according to people familiar w/ the move. The Co employs ~162,000 and faces mkts pressure over debt used to fund data center buildouts for AI workloads, while its stock is down ~25% this yr. Oracle annc’d in Jan. plans to raise $50bn, and pointed to surging contracted rev, including $455bn in remaining performance obligations, amid strong AI demand. (CNBC)

- Slack annc’d 30+ new AI capabilities, adding desktop‑based meeting transcription and notes that work across apps like Zoom and Google Meet. W/ the Slack desktop app, Slackbot can listen in, create summaries, flag action items and draft follow‑ups. (The Deep View)

- Logan Bartlett outlines Redpoint’s 2026 market update, arguing AI ≠ Dotcom Bubble 2. 0. Unlike 2000, demand is pulling infra, w/ $20bn+ ARR at leading cos and data centers pre-committed. Software selloff is uneven: vertical SaaS +3% LTM due to moats; infra ~+2%; horizontal SaaS -35% as AI solves coordination. (X)

Sports/Sports Betting

- DraftKings won dismissal of a patent suit over micro-betting tech after a New Jersey federal judge ruled the patents were abstract ideas. Judge Zahid N. Quraishi tossed Micro-Gaming Ventures LLC’s claims w/ prejudice, ending allegations that DraftKings’ Sportsbook site and app infringed five patents tied to in-game wagering, video playback, and location-based betting. (Bloomberg)

- NFL annc’d plans to launch a flag football league for women’s and men’s teams by 2028, aiming to boost the sport’s popularity ahead of its debut at the 2028 Los Angeles Summer Olympics. The league will work w/ media and sponsorship partners. Partners include TMRW Sport, a media and tech Co, while the NFL’s venture arm is contributing up to $32mn. Flag football is a non-contact, five-player format with ~4.1mn participants across 39 states. (MediaPost)

Tech Hardware

- Intel said it will spend $14.2bn to buy back the 49% stake in its Ireland factory from Apollo, regaining full ownership as finances improve and AI demand lifts processor sales. Apollo bought the stake for $11.2bn in 2024. Intel said the deal will be funded w/ cash and ~$6.5bn in new debt, boost profit from 2027, and strengthen its credit profile. (Reuters)

- Sony annc’d TCL will buy a 51% stake in its TV biz via a new JV, Bravia Inc. , for ~¥75.4bn (~$473mn). Sony keeps 49%. Using TCL display tech and scale, the Co will sell Sony- and Bravia-branded TVs. The unit, based in Tokyo, starts Apr. 2027 and absorbs R&D, design, mfg, and support for TVs and home theater, plus a Malaysia plant, w/ talks cont’d for a Shanghai factory, as the cos target global growth. (The Verge)

- Micron Tech shares fell 10%, extending a sharp post-earnings sell-off that has erased ~30% since its Mar. 18 report. The Co said surging AI chip demand has outpaced supply, leaving key customers w/ only half to two-thirds of needs. Despite strong AI-driven rev momentum, 2026 losses have cut most prior gains. (CNBC)

Towers/Fiber

- Fibre drove Dutch consumer broadband rev in 2025, w/ FTTH rev up 14. 7% to €1.45bn over the last 12 months, giving FTTH a 51.7% share of the residential broadband market, up from 47% in 2024. This means fibre accounted for over half of rev. By contrast, total consumer broadband market rev grew at a slower 4.2% pace to €2.81bn. (Telecompaper)

Video Games/Interactive Entertainment

- Rec Room, a Roblox-like social gaming platform, will shut down June 1 after reaching 150mn players and creators. In a blog post, the Co said it never built a sustainably profitable biz, as costs overwhelmed rev, citing VR mkts shifts and gaming headwinds. Once valued at $3.5bn, Rec Room cut half its staff in Aug. (The Verge)

Video Streaming

- Global streaming subscription rev tripled in five yrs, topping $150bn in 2025, Ampere Analysis said. Rev rose 14% yr over yr to $157.1bn, driven by price hikes, ad tiers and international expansion. Including ads, svs generated $177bn, w/ ~$20bn from ads. (The Hollywood Reporter)

- Tubi CEO Anjali Sud said the Fox‑owned AVOD will not pivot to shorts, despite a creator push, and remains committed to long‑form VOD. Speaking in NYC, she said differentiation comes from curated, free, premium storytelling vs FASTs and UGC. (StreamTV Insider)