The tech landslide continued this week with Nasdaq falling -1% (the S&P 500 fell -0.4%). February was Nasdaq’s worst month since March of 2025 and the carnage on Monday was of particular note (see Theme #2).

Earnings was a focal point yet again (Week 6!) with all eyes on Nvidia’s print in particular (see Theme #3). We also had key updates out of Media Entertainment, Ad Tech, Live Events, among others.

See below for what we focused on in this edition.

- Earning Scorecard – Week 6

- AI-Fear Hits A New Level Given The Perfect Storm Of Updates While AI Valns Reach New Highs

- Will Nvidia’s Huang Be Right In That “More Compute = More Revenue”?

- Paramount Is Now Positioning For Its Next Act…Paramount + WBD

- Not To Be Forgotten Amongst It All, WBD Also Reported Its Q4 Numbers

- The Trade Desk Remains Under The AI + Heightened Competition Microscope

- TKO Continues To Shift Towards Higher Margin, Contractual Media Rights & FIPs

- A Few Other Quick Earnings Takes…Salesforce, CoreWeave, & CLEAR Secure

Also to flag, see our SPOTLIGHT section below for a new LionTree Podcast conversation between Tarek Mansour, Founder and CEO of Kalshi, and Rich Kleiman, Founder and CEO of Boardroom. It is worth a listen!

Lastly, LionTree Advisors is proud to have served as financial advisor to Paramount Skydance on the announced all cash acquisition of Warner Bros. Discovery, valued at $110bn. This continues the firm’s long-standing advisory relationship with Paramount, following its roles in the combination of CBS and Viacom in 2019, the sale of Simon & Schuster to KKR from Paramount Global in 2023 and the merger between Paramount Global and Skydance Media in 2025.

Have a nice weekend.

Best,

Leslie

Spotlight

On a special episode of The LionTree Podcast, we explore how prediction markets are re-shaping the way we understand uncertainty, truth and decision-making. In partnership with Boardroom, the media brand at the intersection of sports, business and entertainment, we present a conversation between Tarek Mansour, Founder and CEO of Kalshi, and Rich Kleiman, Founder and CEO of Boardroom. Watch now HERE.

Earning Scorecard – Week 6

This was Week 6 of the TMT earnings storm (are we almost done??!). In total, 48 stocks in our LionTree Universe reported. Stock reactions skewed positive despite the markets selling off, with 26 stocks trading up and 22 trading down.

Probably the most widely followed print was NVIDIA, which fell -6% in reaction (see Theme #3) while the best performer in reaction to earnings was Rackspace, which was up +69%, and the worst performer was CoreWeave, which fell -19% (see Theme #8 for the quick take).

Media giants were in the headlines this week and, in addition to deal announcements, Paramount and WBD also reported their qtrly results and were up +10% and -0.3%, respectively, in reaction (see Theme #4 for Paramount and Theme #5 for WBD).

Elsewhere in the sector, The Trade Desk was down -5% in reaction (see Theme #6) and TKO Group was up +8% (see Theme #7). CLEAR Secure rallied +39% (see Theme #8), and Salesforce rose +4% (see Theme #8).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

AI-Fear Hits A New Level Given The Perfect Storm Of Updates While AI Valns Reach New Highs

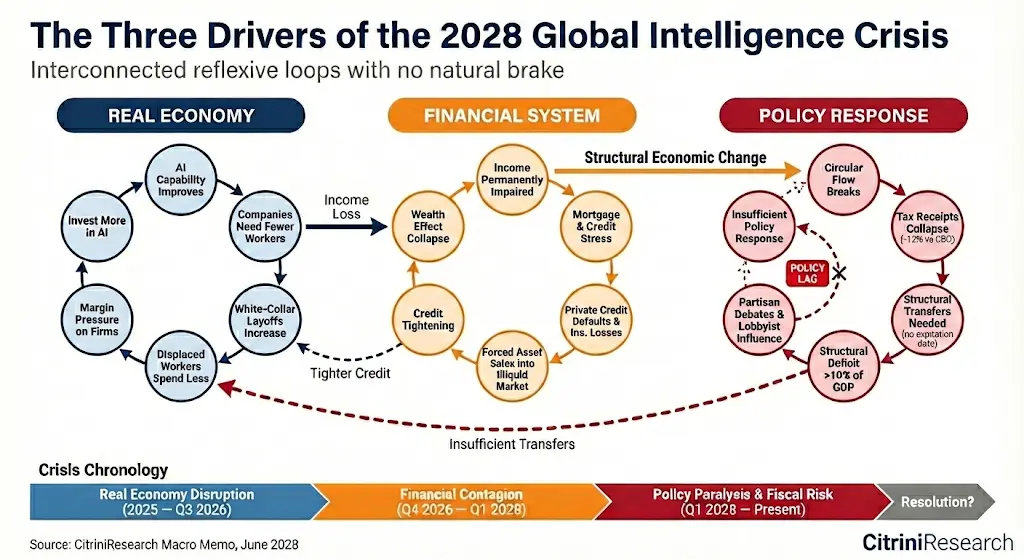

The AI disruption fear snowball turned into more of an avalanche on Monday, spurred by a trifecta of inputs that yet again spooked already jittery investors. First, over the weekend, Citrini Research released a report depicting a very unfavorable macro scenario fast forwarding to June 2028. AI’s impact on the jobs picture has already been an ongoing debate, and the report exasperated that fear in addition to fear about the potential domino impact from a “major unwind of the premium that currently exists on human intelligence” which puts us in unchartered territory as it relates to a new equilibrium. By 2028, the firm’s scenario included a recession, high unemployment, and a falling stock market.

To add to the negativity, on Monday morning, Anthropic’s blog post highlighting that Claude Code can now help modernize COBOL caused another software scare as it is seen as highly disruptive to IBM’s mainframe business (IBM’s shares dropped -13%). The nail in the coffin on Monday was Black Swan’s Nassim Taleb warning that markets are underpricing structural risks and overestimating the durability of today’s AI leaders, noting that early pioneers are often displaced. He highlighted that investors should brace for escalating volatility and potential bankruptcies in the software sector as the AI rally enters a more fragile phase.

Following the Monday carnage, Anthropic’s Enterprise event actually helped to quell further concerns given broad-based partnerships announced in conjunction with the new connectors and plugins aimed to “turbo charge” capabilities of individual workers in Finance (including investment Banking & Private Equity) as well as an Enterprises’ HR or Operations. The event provided more comfort that Anthropic and other LLMs are positioning themselves to be an “orchestration layer” on top of existing and incumbent systems, rather than a full replacement.

Lastly, in a splash at the end of the week, OpenAI’s announced a $110bn round (at a $730bn valuation!), which is the largest round in history and also included Amazon as a key investor.

Overall, the volatility being created by uncertainty about where the world is headed as it relates to AI implications is intense and investors continue to choose a “shoot first and ask questions later” approach. Unfortunately, we believe that this volatility will persist for a while as it will take time to prove or disprove the bull or bear case…

Citrini Research Over The Weekend Sparks More Concerns About AI’s Future Impact On The Economy (link to report)

- In the firm’s report called “The 2028 Global Intelligence Crisis: A Thought Exercise in Financial History, from the Future”, it shows the possible progression of AI’s impact on companies and the economy over the next 2 years

- The overarching theme is that there will be a major unwind of the premium that currently exists on human intelligence which puts us in unchartered territory as it relates to a new equilibrium

- Reaching this new equilibrium could come with a lot of pain ahead

- The report was written AS IF it were 2028

- This AI cycle could create a negative feedback loop with “no-brakes”: AI improves → need fewer workers → lead to more layoffs → leads to less spending → drives more margin pressure → drives more AI spend à AI improves (“human intelligence displacement spiral”)

- What does this hypothetical progression of AI’s impact look like in this report?…

- Improvements with agentic coding in late 2025 makes “build vs buy” real and mid-market SaaS can be replicated in weeks which forces repricing

- Software SaaS repricing: By mid-year, SaaS contracts are being renewed at -30% discount but the long tail of SaaS, like Monday.com, Zapier, and Asana have it “much worse”

- Imagined headline: ServiceNow Q3:26 net new ACV growth decelerates to 14% to 23% and the Co announces a -15% workforce reduction

- An initial AI boom and stock market rally in 2026 masks a broken consumer economy: By Oct 2026, the markets rally (S&P ~8,000 and Nasdaq >30,000) as early-2026 layoffs expand margins and profits get recycled into AI compute, even as real wage growth collapses and “Ghost GDP” emerges (output in accounts, not in household circulation)

- Agentic commerce is in full force in 2027…LLM usage is the default and every major AI assistant has integrated some agentic commerce feature

- These models are able to run on phones and laptops so the marginal cost for inference comes down significantly

- Agents start to make decisions in the background and commerce “stopped being a series of discrete human decisions”

- Agents optimize all commerce transactions for consumers…

- Subscriptions and memberships won’t passively renew despite lack of usage

- The average LTV of the subscription economy declines

- Agents will price match for every transaction

- …this leads to significant impacts across businesses in 2027

- OTAs: Travel booking platforms will be “a casualty” as by Q4 2026, agents are assembling complete itineraries faster and cheaper

- Insurance: Agents re-shop insurance policies annually and dismantle the 15-20% premiums that insurers earn from passive renewals

- Other professional services: Financial advice, tax prep, routine legal work are all disrupted

- Real estate: The median buy-side real estate commissions in major metros compress to under 1%, and a growing share of transactions are closing with NO human agent on the buy side at all

- Buying behavior: Agents “destroy habitual intermediation” (“I always just order from here”)

- Last mile/delivery: More apps enter the last mile areas…the gig workers market is fragmented overnight and multi-app dashboards let these workers tracking incoming jobs from 20-30 platforms at once…and margins compress

- Credit card fees: In machine-to-machine commerce settle most transactions using stablecoins via Solana or Ethereum L2s, where settlement is near-instant and the transaction cost was measured in fractions of a penny (vs the 2-3% card interchange rate)

- Private credit grows < $1tr (2015) to > $2.5tr (2026) and Moody’s in Apr 2027 downgrades $18bn across 14 issuers

- “Smoking gun scenario”: Zendesk misses debt covenants, $5bn direct lending facility marked to 58 cents

- Contagion risk escalates via life-insurer “permanent capital” structures; regulators tighten capital treatment (Nov 2027)

- The economy hits recession by Q2:2027

- June 2028, the Zillow Home Value Index falls -11% y/y in San Francisco, -9% in Seattle and -8% in Austin

- This follows Fannie Mae flagging higher early-stage delinquency from jumbo-heavy ZIP codes – areas that are populated by 780+ credit score borrowers and typically “bulletproof”

- The mortgage market cracks in H2

- Stocks correct along the lines of the Global Financial Crisis (down-57% peak-to-trough)

- Brings the S&P500 to ~3500

- Other macro stats at that time (2028)

- Labor’s share of GDP declines from 64% in 1974 -> 56% in 2024 -> 46% in 2028

- Unemployment hits 10.2%

Source: Citrini Research

Anthropic’s New Claude Code Tool That Modernizes COBOL Sparks Another Sell-Off, Esp In IBM (link)

- What is COBOL? It is an antiquated programming language and most of the mainframe computers that run on COBOL are made by IBM

- COBOL handles ~95% of ATM transactions in the US

- Hundreds of billions of lines of COBOL run in production every day, powering critical systems in finance, airlines, and government

- The problem: The # of people who understand it shrinks every year

- Modernizing a COBOL system once required armies of consultants spending years mapping workflows BUT now w/ Claude, teams can modernize COBOL codebase in “quarters instead of years”

- What was IBM’s response? Per IBM’s SVP & Chief Commercial Officer Rob Thomas (link/link)…

- “The value IBMmainframe delivers has nothing to do with COBOL, It has to do with what the platform is”

- “Translating code is one thing. Modernizing a platform is something else entirely. The two are not the same, and the gap between them is where most enterprises run into trouble”

- Reasons why Thomas thinks the “translation argument” falls short:

- Translation captures almost none of the actual complexity: The modernization challenge is not a COBOL language problem, it is everything the application runs on and integrates with

- Decades of hardware-software integration cannot be replicated by moving code: An analogy is the iOS and iPhone: someone could build an alternative, but it is unlikely to displace a billion iPhones

- AI strengthens the mainframe case, it does not weaken it: It compresses timelines and addresses the skills gap as experienced COBOL developers retire

- SaaS-only solution does not hold up under scrutiny: “Given everything happening around digital sovereignty and data residency, would an organization make its most critical transactions dependent on a provider operating in a jurisdiction it does not control?”

- Some of this conversation is not about the mainframe

- Most of the headlines are about the code, but the engineers know the code is the starting point

- The real modernization work is what the application runs on, how it scales, how it recovers, how it is encrypted, and how it integrates with everything around it

-> Despite IBM’s response and rationale, the Co’s shares had their biggest drop in 25 years, down -13% in reaction to the news but finished the week down -6.7%

Also On Monday, Nassim Taleb Warned That Investors Should Brace For Escalating Volatility And Bankruptcies In The Software Sector (link) Watch the full video interview HERE

- Nassim Taleb warned that markets are underpricing structural risks and overestimating the durability of today’s AI leaders, noting that early pioneers are often displaced

- Bankruptcies in parts of the software sector are likely to come due to technological instability, intense competition, and geopolitical shifts

- Taleb argues “tail-risk across sectors is structurally underpriced” and the danger is not a small correction but “a large drawdown”

- The AI rally has been driven by a narrow group of stocks, leaving indexes vulnerable if leadership rotates

- Big Tech’s borrowing to fund AI infrastructure could also take years to pay off

- Taleb stresses investors should maintain hedges because large drawdowns are hard to predict

- He highlights broader macro risks, including persistent US deficits, sanctions reducing dollar appeal, tariff uncertainty, and potential oil-shock stagflation

On Tuesday, Anthropic launches New Enterprise Offerings Which Quelled Some Of The Market Concerns (link/link/link/link/link)

- Admins can now set up plugins from starter templates or build them from scratch, with Claude guiding users through setup

- A new unified menu called “Customize” consolidates plugins, skills, and connectors so admins can see and manage everything in one place

- Anthropic launched new Finance Specific plugins

- Financial analysis: Supports baseline workflows across market research, financial modeling, and PowerPoint template creation and quality checking

- Investment banking: Helps in reviewing transaction documents, building comparable company analyses, and preparing pitch materials

- Equity research:Accelerates research workflows, parsing earnings transcripts, updating financial models with new guidance, and drafting research notes

- Private equity: Can review large document sets, extract standardized financial data, model scenarios, and score opportunities against investment criteria

- Wealth management:Helps advisors analyze portfolios, identify drift and tax exposure, and generate rebalancing recommendations at scale

- In addition, the Co annc’d two new Model Context Protocol (MCP) connectors, which give Claude direct access to institutional data platforms

- MCP is Anthropic’s universal plug that lets an AI assistant safely connect to a customers’ data

- FactSet connector brings real-time market data, fundamental analysis, earnings estimates, and research insights into Claude

- MSCI connector brings MSCI’s index data into Claude, enabling users to access MSCI’s proprietary index data

- Anthropic also noted several partners are launching their own plugins included S&P Global and LSEG

- The Co also released plugins for other areas of Enterprises

- HR: Helps draft offer letters and build onboarding plans as well as write performance reviews and run compensation analyses

- Design: Accelerates workflows by generating critique frameworks, drafting UX copy, running accessibility audits, and structuring user research plans

- Engineering: Streamline tasks like writing standup summaries, coordinating incident response, building deploy checklists, and drafting postmortems

- Operations: Helps in process documentation, vendor evaluations, change request tracking, and runbook creation

- Brand voice (by Tribe AI): Analyze existing documents, marketing materials, and conversations to distill your brand’s voice into clear, enforceable guidelines

- Anthropic also annc’d partnerships to integrate Claude into major workplace apps including: (link/link/link)

- Slack

- Intuit

- DocuSign

- LegalZoom

- FactSet

- Gmail

- Several sell-side analysts walked away believing that concerns about AI’s negative impact on software is overblown (link/link)

- Deutsche Bank: “After watching Anthropic’s enterprise agents briefing event, we have even greater conviction that model providers are unlikely to displace software incumbents and are instead positioning themselves and their agents to be an orchestration layer (control pane or conductor) on top of existing and incumbent systems”

- William Blair: The enterprise event “suggested that Anthropic sees its opportunity not in replacing enterprise software but in becoming the intelligence infrastructure that makes existing software dramatically more capable”

- RBC Capital: “We believe the event highlighted Anthropic’s need/willingness to partner with existing software companies, rather than a rip-and-replace scenario”

- Wedbush Securities: “The reality is that these new AI tools will not rip and replace existing software ecosystems and data environments”

-> Salesforce shares jumped +4% in reaction to Anthropic’s event while Docusign and LegalZoom each gained more than +2%; FactSet shares rose +6%. Intuit stock was relatively flat, closing down -0.2%; Other stocks to note include Okta and Cloudflare which rose +2%; Zscaler and Tenable each gained +4% and SentinelOne climbed +3%

Last But Not Least – The Largest Funding Round IN HISTORY…OpenAI $110bn New Investment At A $730bn Valuation, W/ Amazon As A Key Investor, Closed Out The Week (link/link)

- OpenAI’s $110bn funding round this week marks the largest private financing IN HISTORY

- OpenAI first broke the record last year with a $40bn fundraise led by SoftBank

- Anthropic has the next highest total, bringing in $30bn in its latest round

- xAI last raised $20bn

- Valuation step-up: The round values it at $730bn pre-money, up from a $500bn valuation in an Oct secondary financing

- Investors: The round included Amazon at $50bn, Nvidia at $30bn, and SoftBank at $30bn

- Amazon’s $50bn is structured as $15bn upfront + $35bn in the coming months “when certain conditions are met”

- Alongside the financing, Amazon annc’d a multiyear strategic partnership with OpenAI to build customized models for Amazon customer-facing apps

- OpenAI is expanding an existing $38bn AWS agreement by $100bn over the next 8 years

- AWS will be the exclusive 3P cloud provider for OpenAI’s enterprise platform Frontier

- OpenAI said nothing changes regarding the terms of its partnership with Microsoft, calling it “strong and central

- OpenAI will use 3 gigawatts of dedicated inference capacity and 2 gigawatts of training capacity on Nvidia Vera Rubin systems

- CNBC reports OpenAI is now targeting about $600bn in total compute spend by 2030, after earlier talk of $1.4tr in infrastructure commitments

- OpenAI is reportedly projecting 2030 total revenue greater than $280bn, split roughly evenly between consumer and enterprise

- The transaction is being viewed in the market as a key step towards a potential IPO as early as late 2026

Will Nvidia’s Huang Be Right In That “More Compute = More Revenue”?

Similar to last qtr, earnings became a sell-the-news event for Nvidia. On the plus side, the Co’s FQ4 revenue topped Street expectations due to Data Center upside (where revenue growth accelerated to +75% y/y and grew +22% seq) given strength in Networking in particular. FQ1 revenue guidance was also +7% ahead of consensus and revenue growth should be up sequentially every qtr in the calendar year 2026 (and notably this guidance doesn’t include any revenue from China). What also stood out was that the Co has inventory and supply commitments in place to address future demand, including shipments extending into calendar 2027, and FQ4 gross margins were slightly better projected and are guided to remain stable for the full year. The one nit-pick was that FQ4 adj op income was a tad light.

Bigger picture, Nvidia mgmt was very positive on the sustainability of the AI demand environment and while the Co has strong visibility through F27, investors & analysts have been concerned about growth thereafter if hyperscaler capx slows. CEO Jensen Huang’s answer was consistently that ”more compute equals more revenue” and companies will have to spend. Why? Because over the last 2-3 months we have reached “the inflection point” with agentic AI and AI is now generating profitable tokens that are productive for customers. But in order to generate more tokens, they need more compute capacity and the amount of computation necessary for Agentic AI is “far, far greater” than what was needed in classical compute. Hence, as Jensen sees it, more compute capacity translates directly to growth…and that translates directly to revenues. “I think people are increasingly starting to understand that as well.”

Overall, it was a solid quarter, but the bar continues to be high for the Co and investors are still jittery about the sustainability of the massive amount of spend that is being invested in AI infrastructure by companies far and wide but, in particular, the hyperscalers (the top 5 hyperscalers still account for ~50% of Nvidia’s data center revenue) and Jensen’s new equation needs to be proved out.

See more of our key takeaways from NVIDIA’s results and conference call commentary.

-> Nvidia shares fell -5.5% on the back of results and essentially has been stuck in a trading range since last November

A Generally Positive FQ1 W/ Better Revs (Data Center), GM, & Adj EPS But Lower Adj Op Income

- Total revs BEAT cons by 3.1% due to upside in Data Center revenue: Total revs growth accelerated to +73% y/y from +62% y/y in Q3 and grew +20% q/q

- Data Center revs (92% of total) BEAT cons by +2.7%: Grew +75% y/y (from +66% y/y in Q3) and grew a material +22% q/q

- Networking was the key driver, generating $11bn in revs and rising 3.5x y/y

- ProViz revs also BEAT by +75% (though it is a small part of the biz) and grew +159% y/y and +74% seq

- Gaming and Auto & Robotics revenue all MISSED estimates: Grew +47% y/y and +6% y/y respectively

- Data Center revs (92% of total) BEAT cons by +2.7%: Grew +75% y/y (from +66% y/y in Q3) and grew a material +22% q/q

- Non-GAAP gross margin SLIGHTLY BEAT cons projections

- But non-GAAP op income SLIGHTLY MISSED cons projections

- Adj EPS BEAT by ~6%

- FCF was MARGINALLY HIGHER

FQ1 Guidance Was More Favorable Than Street Projections

- FQ1 rev guidance was +7% ahead of the Street ($78bn, +/- 2%)

- Like this qtr, Data Center will be the main driver

- The Co is NOT assuming any compute revenue from China

- The Co expects seq revenue growth throughout calendar 2026, exceeding what was included in the $500bn Blackwell & Rubin revenue opportunity they previously talked about

- Mgmt stressed that they have inventory and supply commitments in place to address future demand, including shipments extending into calendar 2027

- FQ1 non-GAAP gross margin guidance at 75% (+/- 50bp) was essentially in-line

- FQ1 non-GAAP OpEX $7.5bn (incls $1.9bn stock-based comp)

- FY2027

- Reiterated mid 70s gross margins target for the full yr

- Expect non-GAAP op expense to growth in the low 40s y/y

The AI Demand Environment Remains Strong Which Should Sustain Given That More Compute = More Revenue For Customers

- AI demand continues to “strengthen” as inference deployments grow in addition to training

- However, every data center is power-constrained

- “The transition to accelerated computing and the infusion of AI across existing hyperscale workloads continue to fuel our growth”

- Agentic & physical AI applications built on increasingly smarter and multimodal models are beginning to drive financial performance

- The Co has demand visibility further out than what is usual…they strategically secured inventory and capacity to meet demand beyond the next several qtrs (grew inventory +8% q/q)

- Mgmt also stressed that the demand profile is diverse and NOT just chatbots, and ROIs have been strong

- There is “strong evidence of ROI” as hyperscalers upgrade massive traditional workloads to genAI including search, ad generation, and content recommendation systems

- This is “encouraging” their largest customers to accelerate capx

- There was some analyst focus on how the Co will continue to grow the business if the major hyperscalers pull back on their massive capx spend (the Co’s the top 5 cloud providers and hyperscalers collectively account for a little over 50% of Data Center revenue) BUT Jensen is confident given in this new AI world, “AI Compute = Revenue” and essentially, customers across the eco-system will have to spend…Why?

- Mgmt believes we have reached “the inflection point” with agentic AI (see section below) and that AI is generating profitable tokens that are productive for customers

- In order to generate tokens, they need compute capacity

- The amount of computation necessary for Agentic AI is “far, far greater” than what was needed in classical compute

- More compute capacity translates directly to growth…and that translates directly to revenues

- “Without investing capacity today, without investing in compute, there cannot be revenue growth and that I think everybody understands. Compute equals revenues”

- “The wave that we’re seeing now is the agentic AI inflection and the next inflection beyond that is physical AI”…there’s a “giant opportunity ahead”

Within The “Last Couple Of Months” Agents Have Hit A Real “Inflection Point” & “The Floodgates Are Open” For Enterprise AI

- Frontier agentic systems have “reached an inflection point”

- Claude Code, Claude Cowork & OpenAI Codex have “achieved useful intelligence”

- Adoption is skyrocketing

- Tokens are profitable

- This is all driving “extreme urgency to scale up compute”

- “The agents are super smart. They’re solving real problems. Coding is obviously supported by agentic systems now. And all of our coders here at NVIDIA are using agentic systems”

- Jensen thinks Anthropic’s revenue will be up “10x” in a year even though they are “severely capacity constrained because demand is just incredible”

- OpenAI’s demand is “incredible”

- Anthropic’s Claude Cowork agent platform is “revolutionary” and has “opened the floodgates” for enterprise AI adoption between Claudie Cowork and OpenClaw

- Compute demand is skyrocketing and “the ChatGPT moment of Agentic AI has arrived”

The US Vs China AI Fight Remains A Big Focus

- Nvidia has yet to generate revenue from H200 products from China-based customers and the Co does “not know” when any imports will be allowed into China

- Chinese competitors are “making progress” and have the “potential to disrupt the structure of the global AI industry over the long term”

- “To sustain its leadership position in AI Compute, America must engage every developer and be the platform for choice for every commercial business, including those in China”

- The Co assumes NO compute revenue from China-base customers in its FQ1 guidance

The Co Continues To Make Strides In Innovation & Price Performance

- Mgmt stressed Nvidia’s price performance lead…and it plans to stay there

- “Nvidia produces the lowest cost per token”

- The GB300 NVL72 achieved up to 50x performance per watt and 35x lower cost per token vs Hopper

- CUDA architecture is “more effective, more efficient, delivers more performance per flop, per watt, than any computing architecture out there”

- Data centers that run on Nvidia “generate the highest revenues”

- Nvidia’s R&D budget approaching $20bn annually is “unmatched”…the Co intend to deliver x factor leaps in performance per watt every generation

- The new Vera Rubin platform (unveiled last month and can train MoE models w/ ¼ the # of GPUS and reduce inference token costs by up to 10x vs Blackwell)

- The Co shipped the 1st Vera Rubin sample to customers this week

- Remain “on track” for production shipments in H2 of the year

- “Expect every cloud model builder to deploy Vera Rubin”

A Few Other Updates & Developments We Viewed As Important

- Supply constraints will be a headwind for Gaming in F27

- FQ4 gaming revs rose +46% y/y (vs +30% y/y in FQ3)

- Outlook: “Looking ahead, while end demand for our products remains strong and channel inventory levels are healthy, we expect supply constraints to be the headwind to gaming in Q1 and beyond”

- Can gaming grow y/y in F27? Mgmt didn’t explicitly answer but just said supply will be tight for a couple of qtrs

- “Physical AI is here”: Contributed $6bn+ to revs in FY26

- Regarding self driving…the 1st passenger car featuring Alpamayo built on Nvidia Drive will “soon” be on the road in the new Mercedes-Benz CLA

- Rototaxi fleets are expected to scale from thousands of vehicles in 2025 to millions over the next decade

- The market will be hundreds of billions of dollars in revenue

- Automotive revs were up +6% y/y in FQ4

- Space datacenters? The economics are poor today but they will improve over time

- “Artificial intelligence in space will have very good, very interesting applications”

- Why not launch a huge share repurchase? Supporting the eco-system is one of the most important things they can do right now and will remain an important priority… at the same time, the Co is committed to the buyback and the dividend (but didn’t say anything about increasing the pace of shareholder returns)

Paramount Is Now Positioning For Its Next Act…Paramount + WBD

Paramount’s pursuit of Warner Bros Discovery has been a long and winding road that finally came to an end with the deal being made official on Friday, after Netflix bowed out post Paramount’s upped bid. The proforma company is now the main event but Paramount’s Q4 standalone performance should not be set aside.

It’s been six months since Skydance completed its takeover of Paramount, and while Q4 was somewhat mixed, mgmt is clearly in the weeds, transitioning and executing. Q4 rev came in roughly in-line with Street expectations, as strength in TV Media offset softer results in DTC and Filmed Entertainment. Adj OIBDA beat by a solid +9%, driven primarily by outperformance in TV Media and DTC losses that were slightly better than expected.

UFC was a focus on the call and by all measures, mgmt view performance of these new rights as a success. The debut UFC 324 event is now Paramount+’s largest exclusive live event to date. Advertiser demand has been stronger than anticipated, and mgmt noted that UFC viewers are engaging with other Paramount+ content. The Co’s Paramount One initiative is helping drive that success by activating its full ecosystem across linear, streaming, and sports to build momentum around the launch.

On streaming, improving profitability remains a priority, including exiting uneconomic hard bundles. While that will weigh on subscriber growth this year, it should improve overall unit economics and underlying growth should be positive. Filmed Entertainment had a tougher qtr due to weaker theatrical performance and tougher y/y comps, though a ramp of the 2026 film slate will make the segment “significantly” more profitable, with a more meaningful step-up in 2027–2028 as major franchises return.

Looking ahead, mgmt reiterated FY26 rev and adj. OIBDA guidance, with rev weighted more toward H2 and profitability roughly evenly split through the year. The Co remains “firmly on track” to deliver “at least” $3bn in efficiencies through 2027, including more than $2.5bn in run-rate savings by the end of 2026. But ending where we started, the forward picture is now driven by the combination of Paramount + WBD, which is expected to close in Q3.

-> Paramount shares rose +10.0% post its print, and then jumped an even more dramatic +20.8% after the deal with WBD was finally announced

-> After Netflix said that it was walking away from the deal, its stock jumped +13.8% in reaction; On the other hand, WBD shares fell -2.2% in reaction but are up +38.6% from Oct 2025, when the Co annc’d it was “exploring a potential sale of all or some of its media holdings” and +196% from Jun 2025 when it officially annc’d plans to split into two separate, publicly traded Cos

Paramount Rewrites The Ending Of The WDB Deal Saga

- Post market-close on Friday, February 27th, Paramount annc’d it will be acquiring Warner Bros Discovery “to form next-generation global media and entertainment company” (link)

- Final valuation: Paramount will acquire 100% of WBD for $31/shr in cash, plus the “ticking fee” (if applicable), valuing WBD at $81bn in equity value and $110bn in enterprise value

- Multiple: On a fully synergized basis, values WBD at 7.5x 2026 EBITDA; At closing, expect to have a net debt-to-EBITDA of 4.3x on a synergized basis, with “a clear path” to investment grade credit metrics within three years of closing

- Funding: The transaction is funded by $47bn in equity, fully backed by the Ellison Family and RedBird Capital Partners

- Paramount expects that the acq will yield $6bn+ in synergies, which are driven by a combination of technology integration, corporate-wide efficiencies, optimizing the combined real estate footprint, and otherwise streamlining operational efficiencies

- Expected to close in Q3 2026, subject to customary closing conditions, including regulatory clearances and approval by WBD shareholders, with a vote expected in the early spring of 2026

-> Netflix bowed out of the bidding war shortly after WBD’s Board on Thursday determined that Paramount’s revised proposal is a “Company Superior Proposal” under the terms of WBD’s merger agreement with Netflix

Turning to Paramount’s Q4 Results…The Qtr Was A Bit Of Mixed Bag, As The TV Media Segment Boosted Overall Co Performance

- Q4 rev was IN-LINE: Grew +2% y/y (accel from -0.4% y/y in Q3)

- TV Media was the main upside driver

- DTC & Filmed Entertainment missed by -3.4% and -0.3%, respectively

- Q4 adj OIBDA BEAT by +9.0%: Grew +8% y/y (decel from +11% y/y in Q3)

- TV Media boosted overall adj OIBDA and beat by +24%

- DTC saw a smaller beat of +1%

- Filmed Entertainment missed by a significant -118%

- Q4 adj EPS of -12c was well BELOW cons -1c

- Q4 FCF of $101mn BEAT by a significant +128%

Q1 Guidance Was Mixed…Revenue Guidance Disappointed While Adj. OIBDA Guidance Was Well Ahead

- Q1 rev guidance was -1.9% BELOW cons at the mid-pt: It is expected to grow b/w -1 to +2% y/y to reach b/w $7.1-7.35bn

- Overall revenue growth will be driven by DTC, partially offset by decline in TV Media and a “slight” decline in Studios rev due to comps

- Q1 adj EBITDA guidance was +28% ABOVE cons at the midpt: It is expected to reach b/w $900mn-$1bn, or a 13.1% margin at the midpt, w/ ~$75mn of SBC in the qtr

- Mgmt anticipates transformation costs of “several hundred million” in Q1, which will impact reported FCF

BUT Reiterated The FY 2026 Guidance…Framing It As A Key Investment Year On The Path To Long-Term Value Creation

- Reiterated FY26 rev and adj. OIBDA guidance, which is in-line and +8.6% ahead of cons, respectively

- Rev will be relatively more weighted to H2 and profitability “roughly” evenly weighted

- Rev will grow +4% y/y (vs -3% y/y in 2025) to reach $30bn, w/ DTC being the primary driver

- Adj. OIBDA expected to reach $3.8bn, up +24% y/y (vs -1.3% y/y in 2025)

- “Firmly on track” to deliver “at least” $3bn in efficiencies through 2027, w/ more than $2.5bn in run-rate efficiencies expected by the end of 2026

- Continue to expect FCF conversion of ~5% before ~$800mn of transformation costs, noting that despite $300mn+ of debt paydown in Q1, underlying conversion (ex-restructuring) is tracking at ~5%, though still below target levels

- “Absolutely committed” to achieving investment-grade credit metrics by 2027 (on a standalone basis)

- Expect FCF conversion to improve meaningfully into 2027 and beyond, as 2026 is an “important” yr for investing in the transformation of the biz and ramping up their content slate, with returns expected to drive growth and bring FCF back to, and “hopefully” above, industry norms

- Did not provide guidance beyond 2026 but noted that they are “investing for long-term value creation and we expect that to show through over the next many years”

- More specifically called out medium-term financial goal of transitioning to “sustainable” topline growth driven by DTC, w/ increasing margins and FCF conversion, while managing their balance sheet to regain investment grade debt metrics

UFC Had A “Hugely Successful Launch”

- Debut UFC 324 fight was Paramount+’s largest exclusive live event to date, reaching ~7mn households in the US and LatAm

- Ad demand for UFC has been “strong” and ad rev has been “much more promising than we expected”

- “Overall, the partnership has really started ahead of expectations”

- Also…UFC fans have been engaging with other Paramount content: “They’re watching Landman. They’re watching other series, so we’re really seeing that flywheel work for us, and we also are really seeing it work well with Zuffa Boxing”

The Co Continues To Take Steps To Improve DTC Monetization

- Q4 DTC rev grew +10% y/y, fueled by +17% growth at Paramount+, though Non-Paramount+ was down -16%

- Q1 DTC outlook…

- “Strong” rev growth, accelerating “nicely” q/q (grew +10% y/y in Q4), driven by Paramount+ ARPU growth and domestic subscriber adds, partially offset from the exist of intl hard bundles that accounted for 1mn+ paid subs at the end of 2025

- Continued y/y improvement in total DTC profitability

- “Flattish” q/q sub growth, due to the exit of hard bundles

- Paramount+ reached 9mn paid subs, which was below cons 80.2mn (up from yr-ago 77.5mn)

- Churn is trending in “the right direction” BUT there are areas for them to continue to improve

- Historically, churn has been seasonal, rising the summer after the Masters and declining when the NFL returns

- Now, expect that yr-round UFC programming and a larger film slate (which feeds Paramount+) will help smooth that seasonality and reduce churn, alongside the other initiatives

- “We’ve seen accelerating growth in Paramount+, doing better, and better every quarter. The key now is to get ongoing engagement”

- Churn is trending in “the right direction” BUT there are areas for them to continue to improve

- Monetization of Pluto is a headwind, as engagement on the platform is up

- Pluto is a profitable platform but was, in their perspective, underinvested in by the previous owners, both on a content and product standpoint

- Have brought in new leadership to help on the advertising side and they are working “hand-in-hand” to make sure that they improve the product and improve monetization

- More broadly – “big believer in the FAST space. And I think when you really look at globally, FAST is something that is only going to grow in importance”

- Making “focused” investments in tech and innovation across the streaming biz, “recognizing that sustainable growth is driven not only by what audiences watch, but by the quality of the end-to-end user experience”

- Expect overall tech stack streaming convergence to be done in the coming qtrs: Currently have three separate stacks that are running on multiple clouds, all independent of one another

- Looking ahead – expectations for 2026:

- DTC rev growth to accelerate y/y (vs +12.5% y/y in 2025): Driven by continued “healthy” sub growth (which is also expected to accel in 2026), better ARPU from price increases and mix shift, and stronger DTC advertising

- DTC ad rev to grow y/y: “We expect to meaningfully recover DTC ad growth in the yr”

- DTC profitability to improve y/y as they both grow rev and manage their investments

- Paramount+ to have “healthy, accelerating” underlying sub growth y/y (vs +1.8% y/y in 2025) BUT will be impacted by exiting of hard bundles: The decision to exit ~4-5mn hard bundle subs with unattractive economics (accounting for <2% of Paramount+ rev in 2025) will result in only “modestly higher” total paid subs vs 2025

TV Media Is Still On The Decline, But Are Managing For Stable Profitability

- Q4 TV Media rev declined -5% y/y (though an improvement from -12% y/y in Q4): Driven by…

- Ad declines of -10% y/y, including a 7ppt impact form political spending and Big Ten Championship in Q4:24

- AND affiliate rev decline of -7% y/y due to lower payTV subscriber volume

- Partially offset by +10% y/y growth in licensing

- Looking ahead – expectations for 2026:

- “Some declines” in TV media revs, “mostly in line” with industry headwinds around pay TV

- BUT ad rev decline will be “more moderate”, but w/ some caveats: Feel “really good” about upfronts coming up this yr and also have some tailwinds from political spending in 2026

- Will also have “some” impact from the sale of Telefe in Chilevisión

- While TV Media revs will decline, expect overall 2026 profitability in the biz to be stable on both a profit dollars and a margin basis

It Was A Tough Qtr In Filmed Entertainment, But Have A Plan To Reinvigorate The Biz

- Q4 Filmed Entertainment rev was propped up by consolidation (otherwise would have declined y/y): Increased +16% y/y (vs +30% y/y in Q3), primarily due to the consolidation of Skydance licensing and other rev, partially offset by a “significant” decline in theatrical rev vs Q4:24 slate

- Q4 Filmed Entertainment adj OIBDA “did not meet our expectations”: Fell -183% y/y, which was largely attributed to weak theatrical performance

- 2026 slate…scaling from 8 movies to 15+ movies releasing and they are going to be “significantly” more profitable

- Have greenlit 11 movies and 11 original series since taking over six months ago

- Also reiterated that they will be at “steady state” of 15+ movies per yr

- But the real step-up in box office and profits comes in 2027–2028 when major franchises return: Including films like A Quiet Place, Sonic and Call of Duty

- Looking ahead – 2026 expectations:

- Theatrical rev to decline y/y BUT profitability will be up y/y: The Co is increasing the # of film releases, but tough y/y comp due to Mission Impossible release last yr, which will drive the y/y rev decline

- In a “real rebuild phase” of the biz

- As they execute that rebuild, some of that will come through in the 2026 slate, but mostly that will come through in future yrs

- So even w/ theatrical rev dropping down, expect better cost mgmt and benefits from their licensing deals to drive “significant improvement” in the profitability of the film slate

- Overall Studios rev to growth y/y, driven primarily by licensing and combining Skydance into the segment

- Theatrical rev to decline y/y BUT profitability will be up y/y: The Co is increasing the # of film releases, but tough y/y comp due to Mission Impossible release last yr, which will drive the y/y rev decline

With Renewals Coming Up, Feel “Confident” About Relationship With NFL

- “We talk to the NFL almost daily. We have a great relationship with the NFL…[and] this past year was our most watched year ever”

- Mgmt didn’t talk specifics about upcoming renewals but said “we feel pretty confident we’re going to be in business with the NFL for a long time”

- NFL games on Paramount+ will continue to mirror the Co’s linear regionalized broadcast model

- Regionalizing games maximizes total viewership across the country, which drives the NFL’s flywheel of ratings and revenue

- Paramount+ will follow the same regionalized approach as linear TV and CBS expects Fox to do the same on its streaming platform

Other Quick Comments On Paramount One And AI Implementation Across The Co

- The Co will be activating Paramount One ecosystem “across a lot of our tentpole franchises [and] our series launches as we really integrate this business to operate as one company”

- Paramount One initiative “propelled” success of UFC 34: “We really activated all of our linear channels, our DTC platforms and really the entire ecosystem, to deliver billions of impressions, which really helped drive that launch of UFC 324, which again came in ahead of our expectations and really helped us create the largest live event in the history of Paramount+”

- Have a “robust” portfolio of planned offerings around the Teenage Mutant Ninja Turtles franchise, including two major theatrical releases, a partnership w/ Mattel for franchise-themed toys, and much more

- “One of our core goals is to become the most technologically capable media company”

- AI is a tailwind for the Co: “We really view artificial intelligence as an unbelievable tool for artists that will be a significant unlock on creativity”

- On internal AI investments: Expect to increase headcount of engineers by 10x to work on these initiatives

- Does AI commoditize content production? No: “I don’t think there’s anything that’s going to replace artists. I don’t think there’s anything that’s going to replace the creativity of original storytelling”

Not To Be Forgotten Amongst It All, WBD Also Reported Its Q4 Numbers

With the Paramount / Warner Bros Discovery deal now official (see the final terms in Theme #4), the latter’s Q4 results seem a bit like an afterthought or anti-climactic. With that said, it didn’t stop us from digging in. WBD’s Q4 rev and adj EBITDA beat expectations by +1.6% and +4.7%, respectively. DTC was a bright spot, with both segment rev and adj EBITDA exceeding forecasts, and streaming ad rev growth accelerated sequentially. DTC subscribers came in ahead of expectations, putting the company “well on the way” to reaching 150mn+ subs by year-end. However, ARPU remains under pressure, primarily driven by domestic factors related to a previously disclosed deal renewal, though these headwinds do not derail mgmt’s internal forecasts of roughly tripling streaming profits by 2030. The international biz is a key component to growth (it is already profitable and does not require significant increases in local content spend to sustain growth). Not that it will matter given the Co will no longer be standalone, mgmt had planned to stop reporting DTC subscriber and ARPU metrics as others in the sector have done.

On the Studios front, 2026 has started strong with Wuthering Heights being the ninth consecutive theatrical release from the Co to open at #1. While 2026 Studios profitability is expected to be relatively in-line with 2025, 2027 is anticipated to be an inflection point, with a slate of tentpole and franchise “powerhouses” on the horizon. A similar story is expected for the Gaming biz, in which 2026 is expected to follow a similar trajectory as 2025, serving as a reset year, and then an acceleration in 2027 and 2028.

On the Networks side, seq ad revenue acceleration was a highlight, despite NBA-related headwinds. US ad sales remain healthy, driven by new upfront deals, good scatter premiums, and strong audience delivery across sports, news, and entertainment. International ad sales have outperformed the US, and the Co expects continued stability and growth. CNN All Access launched in Q4, and Europe’s Olympic Winter Games were the most streamed ever, with linear viewership up 50%+. They remain open to investing “strategically and opportunistically” in sports rights across all their platforms,

Overall, the message was one about execution, though that execution will now be in the hands of Paramount!

See below for our drill down of key takeaways from WBD’s Q4 and conference all and see Theme #4 for more on Paramount’s Q4 performance as well (as well as quick final deal terms).

-> WBD’s stock was down -0.3% post its print and closed down -2% on the week

Headline Q4 Beat, Though Results Were A Bit Mixed Under The Hood

- Q4 consolidated revs beat by +1.6% (driven by Networks and Studios), while adj EBITDA beat by +4.7%

- Studios – missed on rev, but beat on adj EBITDA

- Networks – beat on rev, while in-line on adj EBITDA

- Streaming – beat on both rev and adj EBITDA

- FCF of $1.38bn was below expectations of $1.94bn

The DTC Build Out Is Steady As It Goes, Despite Near-Term Headwinds, Supporting The Medium- to Long-Term Profitability Outlook

- Q4 total Streaming revs were up +4% y/y (vs flat y/y in Q3) and adj EBITDA decr’d -7% y/y (vs +19% y/y in Q3), both ahead of analyst expectations

- Q4 Streaming ad rev incr’d +17% y/y (vs +15% y/y in Q3)

- Primarily driven by an increase in ad-lite subscribers

- Partially offset by the absence of the NBA in the current yr qtr

- Note that the absence of the NBA in the current year negatively impacted the y/y growth rate by -3% ex-FX

- DTC subs reached 131.6mn, beating cons 131mn and surpassing 130mn target the Co established back in Aug 2022

- The beat was driven by domestic subs (intl subs were ~in-line)

- Looking ahead…expect a strong update on subs and to finish Q1 at 140mn+, which is “well on our way” to 150mn+ subs target by yr-end: This is augmented by recent launches of HBO Max in Germany and Italy, as well as the upcoming launches in the UK and Ireland on Mar 26th

- DTC ARPU remains under pressure: Overall ARPU fell -9% y/y to $6.80 vs cons $6.86, primarily attributable to a -11% decrease in domestic streaming ARPU to $10.45 (also -3.6% below cons) and growth in lower ARPU intl mkts (beat by +6.1%)

- The decrease in domestic streaming ARPU was primarily driven by the impact of the domestic distribution deal renewal with a former related party that was previously disclosed in Q2

- HBO Max content highlights in Q4 –

- IT: Welcome to Derry delivered the fourth strongest debut season in HBO history, averaging 27mn+ global viewers per episode

- Heated Rivalry became the #1 first-run acquired scripted series in HBO Max history with an avg of 13mn global viewers per episode

- Heaven in Poland is now the second most watched HBO Max local original series ever in Poland.

- And HBO Max is off to a “strong” start in 2026 –

- Return of Industry and The Pitt, each growing season over-season viewership by 30% and 50%, respectively, and demonstrating steady week-over-week audience growth

- A Knight of the Seven Kingdoms, the third installment in the Game of Thrones franchise, is currently averaging 24mn+ viewers per episode globally and growing.

- Coming soon…House of the Dragon, Euphoria, The Gilded Age, Dune: Prophecy, and Hacks are all returning this year, along with the premiers of Lanterns and Stuart Fails to Save the Universe

- On intl expansion… international streaming is already profitable, and they don’t need a big increase in local content spending to sustain growth or profitability

- Most mkts have hit profitability 1-2 yrs post launch (vs internal expectations of 3-4 yrs)

- And those mkts that have been around for a couple of yrs (i.e., LatAm) are “meaningfully profitable”

- Global IP reduces need for heavy local spend, as big franchises like DC and HBO brands already have global appeal

- Enables them to only have to invest in local content where it makes sense

- Looking ahead…expect another “strong” yr for the Streaming segment for both rev and adj EBITDA: Expect subscriber-related rev growth to continue accelerating throughout 2026, driven by…

- Another yr of “healthy” subscriber growth, including those on the ad-supported tier and the corresponding ad rev benefits

- Full yr benefit of subscription price increases, particularly ones like in the US that took effect in Q4

- Strongest content slate yet, which has launched them into 2026 ahead of expectations

- Continued product enhancements and feature improvements that drive further engagement and retention improvements

- The upcoming lapping of two one-time resets –

- The H1 impact of the NBA on ad revs (4% ex-FX and 15% ex-FX headwind in Q1 and Q2, respectively)

- The previously disclosed domestic distribution renewal with a former related party partially through Q2

- By 2030, the Co is internally forecasting streaming profits to roughly triple, driven by…

- Strengthening content: “Never been clearer” about the kind of content they need and the customer segments they have to go after and strengthen

- Subscriber volume and penetration growth: Growth from recent launches in large European mkts, deeper penetration in existing mkts, sharper marketing, and early innings of password-sharing enforcement (global rollout beginning in 2026)

- Product enhancements: Went from “not good to good,” but still got “ways to go to get to great” w/ hundreds of small enhancements aimed at improving engagement and overall user experience

- Retention/churn reduction: “Significant” oppty to continue to improve churn and retention and have # of initiatives going forward this yr and next to continue to drive that lower

- Monetization upsize: Combination of both price on the subscription side and ad sales; Still launching in new mkts w/ ad tiers and think there’s further upside in the yrs to come

After Years Of Restructuring And Recalibrating The Studios Biz, The Fruits Of Labor Are Starting To Show Through

- Q4 total Studios rev fell -11% y/y (vs +24% y/y in Q3) and adj EBITDA fell -27% y/y (vs +126% y/y in Q3)

- Note that there were no theatrical releases in Q4

- But the Co has theatrical momentum into Q1…Wuthering Heights is its 9th consecutive theatrical release to open at #1: Has generated $160mn+ at the global box office in two weeks, including an $83mn opening weekend

- And the films are getting recognition at awards shows –

- Won nine Golden Globe Awards, including Best Picture – Musical or Comedy for One Battle After Another, and Cinematic and Box Office Achievement for Sinners

- Received 30 total Academy Award nominations, the most of any studio this yr, including a record-breaking 16 nominations for Sinners, 13 for One Battle After Another, and one for Weapons

- The 2027 film slate is set to deliver “a truly monumental year” for Warner Bros, w/ tentpole and franchise “powerhouses” on the horizon, from Godzilla vs. Kong 3, Superman: Man of Tomorrow from James Gunn, Minecraft 2, Conjuring: First Communion, Batman Part II from Matt Reeves, Gremlins, and Lord of the Rings: The Hunt for Gollum

- 2026 will be the first yr that WBTV will deliver more episodes to streaming platforms than to broadcast and cable combined

- Notable projects for 3Ps include Ted Lasso (Apple TV), Bad Monkey (Apple TV), Shrinking (Apple TV), and Running Point (Netflix)

- Key titles produced in association with HBO for HBO Max include the series premiere of Lanterns and the award-winning series The Pitt, which was already renewed for a third season

- The Co will “confidently” invest this yr for 2027 and beyond to support a more robust slate of theatrical and television titles, the opening of the Harry Potter experience in Shanghai and Abu Dhabi, and the rebuilding of their video game pipeline

- Looking ahead…expect Studios segment 2026 adj EBITDA to be “relatively in-line” w/ 2025, even as they lap “strong” box office success and a “sizeable” TV licensing deal renewal in 2025

- Looking ahead longer-term…continue to make progress towards segment adj. EBITDA target of “at least” $3bn

2026 Will Still Be A Reset Year For The Gaming Biz Though An Acceleration Is Expected Starting In 2027

- 2024 saw some unsuccessful launches…

- “We had allowed ourselves to sort of get distracted to going after too many IPs with a too broad a set of studios”

- …so 2025 became a “reset” year for the games biz

- “The core of last year’s reset was around getting back to proven studios with proven games and proven players”

- As a result, “we didn’t really replenish the pipeline”

- 2026 will generally look similar to 2025 BUT will have two big IPs launching

- LEGO Batman series launching in May on the console PC side

- Dragonfire, which is the second game in the Game of Thrones: Conquest franchise, which will be launching this summer on mobile; Predecessor is still delivering “significant” financial returns and expect a “similar trajectory” for this game

- “The real fruits will start coming in 2027 [and] 2028, when we return to some of our biggest franchises”… which are still to be announced

Networks Ad Recovery and Strategic Sports Investments Are Offsetting Near-Term Headwinds

- Q4 Networks rev fell -13% y/y (accel from -22% y/y in Q3) and adj EBITDA fell -27% y/y (decel from -20% y/y in Q3)

- Distribution revs fells -8% ex-FX (in-line w/ Q4)

- Ad rev decr’d -14% y/y ex-FX (improvement from -20% y/y in Q3), primarily driven by…

- Domestic audience declines of -22%

- And the absence of the NBA in the current yr, which negatively impacted the y/y growth rate by -4% ex-FX

- Content rev decr’d -32% ex-FX, primarily due to the timing of third-party licensing deals

- Digging a bit deeper into Networks ad rev improvement (-14% y/y ex-FX was an accel from -20% y/y in Q3) … US ad sales are healthy despite some NBA-related headwinds, and international ad sales are even stronger

- In the US, seeing strong seq growth despite NBA headwinds, driven by new upfront deals, good scatter premiums, and “real health” in terms of audience delivery across sports (MLB, NHL), news (CNN, which is seeing an “even more pronounced uptick”), and entertainment (TLC, HGTV, Food Network, Discovery)

- Intl has been outperforming relative to the US, led by EMEA, with trends pointing to stability or potentially “a little bit” of growth in ad sales going into 2026

- Launched CNN All Access in Q4, “an important milestone in building a modern, digital first news platform, to adapt to how audiences consume news”

- “Encouraged by the early performance of CNN All Access, and expect subscribers and engagement to continue to grow as we enter the midterm election cycle and look ahead to the 2028 presidential election”

- Kicked off 2026 as the home of the Olympic Winter Games in Europe, with linear viewership up 50%+ across Europe’s largest markets: Including France, Germany, Italy, Poland and the UK vs Beijing 2022

- This yr’s Olympic Winter Games were the most streamed ever with viewers more than tripling compared to Beijing 2022

- Will continue to “strategically and opportunistically” invest in sports rights across all their platforms

- Reinvested some of the NBA cost savings, including in expanded College Football Playoff rights with coverage expanding to 5 of the 11 games starting in Q4

- “Well underway” in developing their TNT Sports app, which will serve as a centralized destination for their sports portfolio in the US

- Plan to launch the product in 2026 and make it available standalone and through distribution and bundling partnerships

- Expect sports viewership as a %age of the total portfolio to grow “meaningfully”.

- Looking ahead…expect a 7% ex-FX and 20% ex-FX headwind to ad rev in H1 from the absence of the NBA in Q1 and Q2, respectively, which will be more than offset by an associated improvement in operating expenses

- Also expect continued ad revenue growth in key scaled intl markets including Poland and Italy, and across the EMEA region as a whole

- On a net basis, expect FY26 OpEx to improve in the HSD %age range

- Looking ahead…remain focused on sustaining “healthy” adj EBITDA and FCF for “years to come”, driven by their “strong” assets and disciplined investment strategy

Some Incremental Commentary On Discovery Global Spinout

- Note that these comments were made prior to the announcement that Paramount would be acquiring Warner Bros. Discovery

- On Discovery Global spinoff and leverage – will come out the gate w/ 3.3x net leverage which is “absolutely sustainable and supportable”

- Driven by scale (reach ~1bn people), intl ad trends that are expected to be flat-to-slightly up this yr, a “high-impact” sports portfolio (140 events reaching 2mn+ viewers), profitable Discovery+ with millions of regularly engaged viewers, CNN’s digital expansion (CNN All Access), and anticipated Single B to low BB credit ratings

- Expect to see Single B or maybe low BB ratings for Discovery Global

- “Continue to have appetite for sports rights” and are “open for business” BUT will be disciplined

- “It is one of the important strategic pillars”

- “We’re not going to be doing deals that don’t make financial sense for us”

- “You will always see us involved in every process that’s ongoing, and we will know what the value is, and we’ll continue to be great partners”

- “We’re very happy with the partnerships that we have. And there will certainly be continued appetite as we go forward, even after separation into Discovery Global”

The Trade Desk Remains Under The AI + Heightened Competition Microscope

The Trade Desk continues to be under pressure given concerns about the macro/ad market, as well as ongoing AI and competition worries, and the Co’s weaker than expected Q1 guidance provided no relief. While Q4 revenue grew +14% y/y, roughly in line with expectations, it follows a deceleration trend from +18% y/y in Q3 and +19% y/y in Q2. Q4 adj EBITDA grew +47% y/y and topped consensus by +14% but the Q1 adj EBITDA guidance was -13% below Street projections due to investments being made in the business. Of focus was that the pull-backs from CPG and global auto advertisers (~25% of TTD’s business) has not abated and mgmt is taking a cautious view in the quarter ahead, with Q1 revenue growth guidance of only +10% y/y.

While investor concerns on AI persists, mgmt views it as an accelerant vs disruptor for their business (though some software companies with a focus on “generic processes or low-grade data” are seen as at risk). Platforms that have “earned the trust of their clients and partners, and have amassed data that is scaled, unique, refined, and actionable, are in the perfect position to leverage advances in AI to add more value” (i.e., TTD sits here). “AI companies without access to scaled, quality data or amazing levels of trust will not last long.” Mgmt also refutes the notion that increased competitive intensity is at play with the Co’s decelerating growth.

Despite all these moving parts, the Co is pushing forward with product innovation and simplification and are particularly excited about Audience Unlimited and Deal Desk, where early signs are positive. Mgmt is also revamping its go to market. Over the next few quarters, the market will be watching for stabilization in CPG and autos and clearer evidence that new AI driven products and workflow changes translate into faster spend growth. Putting a floor on the decelerating top-line growth is a critical first step…

-> TTD shares were down -4.8% in reaction to earnings and closed down -5.1% on the week. YTD the stock is down -37%

Q4 Was Marked By Much Better Than Expected Profitability (Rev Growth Was In-Line)…

- Revenue BEAT by +0.7%: Up +14% y/y, decelerating from +18% y/y in Q3

- Driven by strong growth across CTV and audio from a channel perspective, as well as in regions outside of the US

- Video (~50% of their biz): Continues to grow as a % of the channel mix; CTV grew at a faster rate than the overall business despite lapping strong political CTV spend

- Mobile (~30% of their biz): Display represented a low double-digit share

- Audio (~6% of the biz): Grew y/y at a rate higher than any other channel in Q4

- Geographically: The US represented ~84% of rev in Q4 and international represented ~16%

- Growth across the international biz continues to outpace growth in NA

- Driven by strong growth across CTV and audio from a channel perspective, as well as in regions outside of the US

- Adj EBITDA BEAT by +13.9%: Up +47% y/y vs +23% y/y in Q3

- Adj EPS BEAT by +14.7%: Up +8% y/y vs +21% y/y in Q3

- Bought back ~$423mn of stock in Q4 (~$1.4bn for all of 2025)

- The board approved an addtl $350mn authorization (the total amount available for future repurchases is now $500mn)

- FY25 customer retention remained ~95% during the year, as it has for the past 12 consecutive years

…BUT The Macro & Advertising Environment Still Has Its Challenges, Esp In CGP & Autos

- The trend of weak CPG & global autos (over 25% of TTD’s business) that started in Q2:25 continues to be the case into Q1

- These verticals have seen “levels of uncertainty… [not seen] for most of the last 15 years”

- Many had “tough choices” in 2025 and “still have tough choices ahead,” some “shrunk branding spend” and focused on “cost cutting” vs “growing”

- On their earnings calls recently, “several global brands have talked about pulling back on advertising budgets, driven by the month-to-month volatility caused by these macro forces”

- At CAGNY last week, “many of the large global brands spoke about consumer pressure, slower volume recovery, and ongoing input cost volatility, reinforcing what we are seeing in our data”

- While CPG & auto companies “remain challenged starting this year, we are encouraged by how many of those same global brands are talking about more objective decision-making”…there is “growing skepticism of the cheap reach dynamics of walled garden platforms” and that “cheap reach does not drive growth”

- The advertising industry has “became enamored with scale over substance, equating impressions with effectiveness”

- “This outdated approach creates a false sense of efficiency, masking the true ineffectiveness of these buys”

- But “2025 was fantastic” for “tech spend… travel spend… pharma spend… [and] communication spend”

- AND the Co estimates “more supply was added to the global market than in any year before”…which they view as a “huge validation” of their model

- When there’s “more supply than demand,” it’s “a buyers’ market,” which puts clients “in an incredibly powerful position”

- Their advantage: “Objectivity… by not owning inventory” is “more valuable than ever”

- For advertisers using data-driven “decisioning” to find “the most relevant and valuable impressions across all channels,” “they’ve never had it better” and “have more choice than ever”

…AND Q1 2026 Guidance Disappointed

- Q1 revenue guidance MISSED by -1.6%: Represents +10% y/y growth vs the +14% y/y reported in Q4

- The Q1 guide reflects “prudence” regarding CPG & Autos as noted above and “does not reflect a diminished long-term opportunity”… it’s “a macro” issue” …“dialogues…are as strong in most cases as ever” and mgmt is “very optimistic about the future”

- Q1 adj EBITDA guidance MISSED by an even larger -12.6%: Due to infrastructure investment

- But expect FY2026 adj EBITDA margin % to be approximately in-line with 2025

- Headcount growth should remain below rev growth

- Mgmt will be deliberate in prioritizing investments that directly support rev growth and AI-driven innovation

Mgmt Is Confident That AI Platforms Won’t Displace What TTD Is Doing…But That It Will Enhance It

- AI might “compress” or “disaggregate” some software companies, “especially those that deal with generic processes or low-grade data”…

- …BUT for platforms that have “earned the trust of their clients and partners, and have amassed data that is scaled, unique, refined, and actionable, they are in the perfect position to leverage advances in AI to add more value”

- Advertisers are becoming more selective with their data, “we predict this will continue” and “trust matters more than ever” in an AI fueled world

- “AI companies without access to scaled, quality data or amazing levels of trust will not last long”

- Advertisers “trust us” with their valuable first party data

- “We are convinced that agentic AI will ultimately accrete the most value to companies that already have deep customer trust, that have scaled, refined and objective datasets, and that prioritize objectivity, not by companies with limited data hoping an AI framework becomes their business model”

- TTD sees themselves in this bucket

- Mgmt also thinks their business model is “more conducive” and will “benefit more from AI” than any of their competitors given that “every scaled competitor we have is first and foremost selling their O&O inventory…we don’t have O&O”

- “We have aligned our interests with buyers and that is even more valuable in the AI-fueled ecosystem”

- “The buying platform with the most objectivity and the most trust is the one most likely to create the most scale and win the most market share”

TTD Does Not See An Issue Competitively

- “Has the competitive pressure gone up? … Not really”

- The market is “way more complicated…more fragmented,” and there’s “more noise than ever,” including trade press that “lead[s] with” negative/controversial takes and a “David and Goliath” story (TTD vs Google/Amazon) that’s “not always true”

- TTD believes that it plays “in a different sandbox,” while Amazon is “mostly playing in selling their owned and operated inventory” and trying to win “non-decisioned inventory”

- Amazon “can’t compete on decision” without “hypocrisy” / “channel conflict” (spending on O&O where they make money), plus Amazon “compete[s] with…biggest brands” (especially “CPGs”), which “poses a threat” to their “core business…retail…AWS, especially in an AI-fueled world”

- Mgmt believes they outperform Amazon’s DSP…

- In an example from an appliance manufacturer who tested both for CTV –

- TTD reached 70% more unique households

- At 30% lower total cost

- TTD performed 6x better at delivering campaign goals

- They attribute this to “objective decisioning across the open internet” because “we didn’t prioritize our own impressions because we don’t own any”

- In an example from an appliance manufacturer who tested both for CTV –

Product Innovation Is In Full Force / Simplification & Go-Mkt Improvements Also Remain Priorities

- Audience Unlimited is “one of our biggest innovations ever” and it “will change the usage and value of the data marketplace for both buyers and sellers”; How it works / why it’s different:

- With “a flat cost structure,” Audience Unlimited helps advertisers use “a wider range of the most relevant data” for “an all-in cost where value and impact is clearly understood”

- Agentic AI now lets them “surface the right data segment at the right moment”

- It’s “completely optional”, clients can use it or keep buying data “à la carte”

- Audience Unlimited is part of a broader push to “reform measurement” and enable partners to be “more agentic”

- With “a flat cost structure,” Audience Unlimited helps advertisers use “a wider range of the most relevant data” for “an all-in cost where value and impact is clearly understood”

- Deal Desk is another Kokai-platform innovation…

- As more advertisers pursue “1-to-1 deals” to simplify supply chains, some have “given up buy-side decisioning power” (especially in CTV) and created “inefficient supply chains”

- “90% of deal IDs never scaled” historically

- Deal Desk “centralizes” how buyers “create, manage, and analyze” deals, using AI to “forecast” performance vs the open market and flag issues

- Early read: Deals set up in Deal Desk are performing “meaningfully better,” adoption is “growing”, and it’s rolling out globally (including integrations with “the two biggest SSPs in Germany”)

- TTD is also working on simplification across the platform: They’re working to “simplify the supply chains… measurement… UX… and even simplify the way that we build,” without compromising “transparency”

- This simplification will help compare results and products to walled gardens

- The Co reorganized their go-to-market model around a brand-first, more integrated coverage approach

- They increased the number of advertisers where we have direct relationships, and they eliminated overlapping coverage between advertiser and agency teams

- Joint business plans, or JBPs, are a “good example” of how this shows up in the numbers

- Exiting 2025, JBPs accounted for well over half of their business, and the JBP pipeline is up 2x y/y

TKO Continues To Shift Towards Higher Margin, Contractual Media Rights & FIPs

TKO finished the final quarter of 2025 on a positive note with total revenue and adj EBITDA both ~2% ahead of consensus (though margins were slightly lighter than Street expectations). UFC and WWE were the upside drivers (particularly on profitability), while IMG lagged meaningfully.

We’d call out the strong performance in Partnership & Marketing revenue across the board as a key standout (beat in every segment). UFC partnership revenue surged +39% y/y, WWE grew +57% y/y, and IMG rebounded sharply. Importantly, full-year 2025 global partnerships exceeded the $450mn target and mgmt raised its 2030 partnership revenue target from $1bn to $1.2bn. Nearer-term, mgmt asserts that double-digit growth in partnerships and live events is achievable in 2026.

In contrast, Media Rights performance was in-line to below expectations, with WWE missing modestly despite strong y/y growth tied to Raw and the new ESPN PLE agreement, while UFC was in-line. Live Events and Hospitality also fell short, reflecting timing and mix effects across segments rather than demand issues.

While 2026 guidance was mixed with revenue ~5% below consensus at the midpoint, adj EBITDA was slightly ahead as mgmt is making a deliberate pivot toward higher-margin, contractual revenue, particularly media rights and Financial Incentive Packages. At the midpoint, the outlook implies +21% y/y revenue growth, +43% y/y EBITDA growth, and ~600bps of margin expansion to nearly 40%. Lastly, the Co announced a new $1bn buyback which went over well with investors.

Net net, trends in live sports and events continue to be favorable and are areas that won’t be replaced by AI! The TKO story now hinges on execution and normalization.

See below for more of what we viewed as most important and incremental from TKO’s earnings and conference call …

->TKO stock was up +8% in reaction to results and closed up +6% on the week; YTD the stock is up +7.1%

Q4 Beat, Driven By The UFC and WWE While IMG Lagged

- Q4 Total rev BEAT cons by +2% while adj EBITDA BEAT by +1.7% (though margins were a tad light)

- WWE and UFC both performed better than expected, especially on profitability while IMG fell well short of projections

- UFC – Better than expected…Q4 rev BEAT by +5% (up +17% y/y vs down -8% y/y in Q3) and adj EBITDA BEAT by +6.2% (up +20% y/y vs down -15% y/y in Q3): Adj EBITDA margin at 53% incr’d +100bp y/y

- Had 10 total events, including 4 numbered events (same as last yr’s Q4)

- 4 events were held internationally vs 3 in last yr’s Q4

- UFC 324’s debut on Paramount+ became the largest exclusive live event in Paramount+ history with the broadest reach for a UFC event in nearly a decade

- Had 10 total events, including 4 numbered events (same as last yr’s Q4)

- WWE – Better than expected… Q4 rev BEAT by +3.4% (up +22% y/y vs +23% y/y in Q3) and adj EBITDA BEAT by +11% (up +44% y/y)

- Raw domestic rights deal had favorable impact

- Also had an ~$50mn favorable impact y/y on both rev and adj EBITDA due to their long-term agreement w/ Netflix vs the short-term domestic rights deal that was in place with USA Network in the prior year period

- IMG – Worse than expected…Q4 revs MISSED by -9.5% (fell -9% y/y vs -59% y/y in Q3) and adj EBITDA loss of -$4mn compared to cons gain of $3mn

- As they previewed on our last call, the anticipated decline in rev primarily related to the absence of the Arabian Gulf Cup at the IMG business, which is a biennial event

- Partially offset by an increase in studio rev

- As they previewed on our last call, the anticipated decline in rev primarily related to the absence of the Arabian Gulf Cup at the IMG business, which is a biennial event

- Q4 FCF also fell vs Q3 ($249.4mn vs $416.8mn)

Partnerships Was A Standout Category Across The Board & Should Post DD Y/Y Growth In 2026 / Also Raised LT Targets

- Q4 Partnership & Marketing revenue BEAT expectations in all segments

- UFC – rev BEAT by +20.8% (incr’d 39% y/y vs -4% y/y in Q3)

- Added new partners and renewed existing partners at higher rates

- Making “significant progress” adding new categories and growing existing ones, including recently annc’d deals w/ Ram Trucks, Polymarket & DoorDash

- WWE – rev BEAT by +9.1% (incr’d +57% y/y vs +84% in Q3)

- Due to new partnerships & renewals across multiple categories, incl deals with Riyadh Season, Minute Maid, Comcast and Seagram’s, among others

- IMG – rev BEAT by +123% (incr’d +78% y/y vs down -65% in Q3)

- UFC – rev BEAT by +20.8% (incr’d 39% y/y vs -4% y/y in Q3)

- 2025 Global Partnerships revenue exceeded the $450mn guidance target

- “Expanded renewals with market leading brands like Monster Energy”

- “Innovative new category alliances with Meta, IBM, Polymarket, DoorDash and Ram”