It was another week where concerns about AI disruption reverberated through the markets and dominated many of the earnings call across the sector. In most cases it has been a shoot and ask questions later mentality for investors and it can be difficult for many mgmt teams to disprove an AI bear thesis given we are at the very early stages of even understanding all the upstream and downstream implications.

Stock reactions to earnings this week continued to skew negative, with only 39% of companies in our LT TMT & Consumer universe trading higher following their reports. See Theme #1 for more details on that and the full list of what we focused on this week is below.

- Earning Scorecard – Week 4

- SPOT Refutes The AI Bear Case, Easing Some Investor Angst

- Agentic Shopping Disruption Risk Further Weighs On Shopify’s Shares

- DraftKings Resets Street Expectations While Pushing Ahead On The “Huge” Predictions Opportunity

- AppLovin’s & Unity’s Mgmt Were Not Able To Ease Investor AI + Meta Competition Concerns

- Big Retailer Exposure Disproportionately Weighs On Pinterest…Diversifying & Improving Go-To-Market = The Key Focus

- Expedia & Airbnb Show Strength In Q4 But See Diverging Reactions To Forward Positioning

- Instacart Executes Despite Fears Of Heightened Competition

- T-Mobile’s Growth Framework + More Shareholder Returns Appeased The Street This Week

- Quick Earnings Takes: Roku, & Lyft

As always, comments and feedback is always welcome and enjoy the long President’s weekend.

AND Happy Valentine’s Day!

Best,

Leslie

Earning Scorecard – Week 4

Week 4 of earnings has come to a close. In total, 28 stocks in our LionTree Universe reported. Stock reactions were skewed negatively again this week, with 17 stocks trading down and only 11 trading up. The best performer in reaction to earnings was Coinbase, which was up +16.5%, while the worst performer was Unity, which fell -26.3% (see Theme #5).

Media & streaming had some winners with Spotify closing up +14.7% after reporting (see Theme #3) and Roku rose +8.1% in reaction to its print (see Theme #10). Connectivity giant T-Mobile was also in the green post its Q4 results, rallying +5.1% (see Theme #9).

Consumer internet companies that reported this week had mixed performance in reaction to results, with last-mile grocery delivery Co Instacart shares’ trading up +8.6% (see Theme #8) while ride-sharing Co Lyft fell -17% (see Theme #10). Similarly mixed, OTA companies Airbnb and Expedia closed up +4.5% and down -6.7% respectively in response to their results (see Theme #7).

Aside from Unity, other application software companies that had a tough week include Applovin and Shopify, which were down -19.7% and -6.7% respectively the day after reporting (see Theme #5 and Theme #3). Also dragged down were DraftKings, whose shares fell -14.3% in reaction to earnings (see Theme #4) and Pinterest, whose stock declined -17% (see Theme #6).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

SPOT Refutes The AI Bear Case, Easing Some Investor Angst

Software SaaS stocks have not been the only ones severely sold off on concerns about AI disruption. From the all-time high of $772.60 at the end of June 2025, Spotify shares fell to a 52-week low of $412.75 (-47%) last Thursday when AI fear hit a new level across the market. Not surprisingly, mgmt fielded A LOT of AI related questions on its earnings call this week! (As did most other companies that we focused on this week in other Themes below).

Mgmt did voice some concern about AI risk for SaaS companies but is not concerned with its own subscription/ad model. They emphasized that Spotify is building a unique dataset mapping language to music, to podcasts, and to audiobooks that LLMs cannot replicate, and argued that this personalized understanding of user tastes will become more critical as AI accelerates the volume of “spammy” tracks flooding the platform. Also, regardless of where the music is made, “the cultural moment always happens on Spotify” given its “large reach and monetization opportunities.”

Internally, the Co is seeing very strong AI productivity gains, with their “best” developers not writing a single line of code since December (only supervising AI-written code) and they launched AI-enabled product features that they were unable to do before. Overall, mgmt envisions an AI flywheel where “AI leads to better personalization, better personalization creates more engagement. More engagement leads to more retention. More retention leads to lifetime value, and boom, more lifetime value leads to more enterprise value.

Regarding their actual results, FX was a headwind, but underlying results were a clean beat. FX-neutral (FXN) revenue growth accelerated from +12% y/y in Q3 to +13% y/y in Q4 and that is expected to further accelerate to +15% y/y in Q1. Q4 margins also topped expectations and are anticipated to further expand in 2026 y/y. MAUs grew +11% y/y, helped by the global launch of the mobile free tier enhancements and strong Wrapped campaigns (300mn+ users engaged globally, +20% y/y), and the former positions the Co to drive paid subscribers looking ahead.

One area that is still a work in progress is the advertising business. FXN ad-supported revenue rose +4% y/y, similar to Q3, but further improvement is anticipated in H2.

All in all, Q4 and the outlook paint a picture of a very healthy business, but investors will be watching for evidence that personalization and dataset advantages translate into durable competitive moats as AI lowers the cost of music creation and distribution.

Spotify’s May 21st investor day will be the next opportunity for the Co to convince the Street that it will fall into the long-term AI winner camp.

-> Spotify jumped +14.7% on the back of its reports as a bit of a relief and supportive mgmt comments, but is still down -41% from its all-time high at the end of June 25

Despite FX Headwinds, Q4 Topped The Street

- Total revenue BEAT by +0.2%: Up +7% y/y (+13% FXN) vs +7% y/y in Q3 (+12% FXN in Q3)

- GM expanded +83bp y/y to 33.1%…due to content cost favorability

- Premium GM gains were driven by rev growth outpacing music costs net of marketplace programs and audiobooks costs, largely offset by video podcast costs

- Ad-Supported GM gains driven by improved contribution from podcasts and music

- Operating income BEAT by +9.5%: Up +47% y/y, due to lower Social Charges (€67mn below their expectations) and gross margin strength

- Op Margin BEAT cons: 5% vs 14.2%

- FCF reached €834mn…LTM FCF hit €2.9bn

- MAU slightly BEAT expectations…added +38m in Q4 (a record), reaching 751mn total (up +11% y/y vs +11% y/y in Q3), driven by…

- y/y and q/q growth across all regions, w/ outperformance led by RoW, LatAm & Europe

- Global launch of mobile free tier enhancements

- Strong holiday demand + Spotify’s Wrapped campaigns (300mn+ users engaged globally, +20% y/y)

FX-Neutral Q1 Guidance Implies Accelerating Growth & Stronger-Than-Expected Margins

- FXN Q1 revs guidance implies growth accelerates to +15% y/y from +13% y/y in Q4 (reported Q1 revenue guidance MISSED cons by -1.7% due to a bigger FX headwind of ~670 bps vs ~580 bps in Q4)

- Guidance includes pricing implementations and in-line churn

- Forecasts ARPU growth of +5-6%

- Q1 operating income guidance BEAT cons by +1.7%: Incorporates €10mn in Social Charges

- Q1 gross margin guidance BEAT cons by 6bp: Driven by y/y favorability in their Premium segment

- Q1 total MAU guidance BEAT cons by +0.9%: Implies ~+8mn net new MAUs in the qtr (vs +38mn in Q4)

- Q1 Premium subs guidance slightly MISSED cons by -0.3%

- Implies ~3mn net adds in the qtr

- Q1 Premium subs guidance slightly MISSED cons by -0.3%

- For 2026, mgmt. is “confident” in the gross margin trajectory… operating & gross margins should be “up y/y” but could see “variability” on a qrtly basis

- Price increases will outpace net content costs in 2026

- The ads biz is improving slowly and will pick up in H2

- Marketplace adds to margins

- Expanding new verticals w/in countries helps drive margins

- Also in 2026, expect continued “healthy” MAU and subs growth throughout the year & expect to maintain low churn

- The enhanced free tier positions SPOT for conversion of subs

- 2026 FCF should “meaningfully” exceed 2025 levels (progressing to normalized tax rate)

Mgmt Fielded A LOT Of Questions On AI & Refutes Market Concerns

- “Like any significant global shift, we know that there will be winners and losers, but there is no question in my mind that we will continue to be one of the big beneficiaries of AI”

- “Significant disruption happens when new technologies enable new asymmetric business models” …i.e.,

- What Spotify did to music downloads

- What Uber did to taxi service

- Etc.

- Mgmt sees risk to SaaS but not SPOT’s subscription/ad model

- The pivotal question: “The question everyone should be asking is does this evolution create new business models, or are we mostly just seeing new technologies?”

- Risk to SaaS: “In SaaS, there is currently a lot of fear that the perceived business model will be challenged by more outcome-based models, which is reasonable”

- Spotify’s business model will “excel”: “However, in the consumer space that we are in, we believe the dominant business model will continue to be ads plus subscription, both places where Spotify excels”

- “Our job then just becomes leveraging these new technologies to our benefit”

- For consumer products, mgmt cites the Internet analogy…

- “When the internet came along, everyone thought that we would all have our own web pages”

- “What actually happened was there ended up being very few web pages”

- “In times of lower friction, things actually tend to aggregate, not disaggregate”

- “And that’s the opportunity we see in front of us”

- “I think companies such as us are simply going to produce massively more software, up until our limiting factor or the amount of change that consumers are comfortable with”

- Spotify is building a data set that doesn’t exist elsewhere…the data set of language to music, language to podcast, and language to books

- “We’ve all had the song-to-song data set, but no one had the language-to-song data set”

- “And I want to drive home a point here, which is this is a very specific data set”

- A personalized understanding of individual user tastes will become more and more critical as AI accelerates the amount of “spammy” tracks

- AI will drive a flywheel of value for the Co…

- AI leads to better personalization for users

- Better personalization leads to more engagement

- More engagement leads to more retention

- More retention leads to lifetime value

- “And boom, more lifetime value leads to more enterprise value”

- The Co is at “just at the beginning of capturing AI efficiencies” with internal processes BUT Spotify has realized significant internal efficiencies on the software engineering front

- Example: “An engineer at Spotify on their morning commute from Slack on their cell phone can tell Claude to fix a bug or add a new feature to the iOS app. And once Claude finishes that work, the engineer then gets a new version of the app pushed to them on Slack on their phone so that he can then merge it to production all before they even arrived at the office”

- Their “best” developers “haven’t written a single line of code since December”

- They only generate code and supervise it

- “It is a big change. It is real and it’s happening fast”

- AI is enabling new products and more’s to come

- Users can now ask SPOT a question like:

- “What was the first track I ever listened to on Spotify” and they can get an answer

- “Please take the ones I listened to more than 3x and match them against what was popular at the time”

- Mgmt will provide more AI product details at its investor day on May 21st

- Users can now ask SPOT a question like:

- Tech companies that have not already been investing in AI are going to be left behind (vs SPOT who has been investing in AI for years)

- Mgmt is not concerned about competition from music created on other AI platforms

- “Regardless of where the music is made, the cultural moment always happens on Spotify. That is where all music charts and finds an audience […] because Spotify has long been the place that delivers both the large reach and monetization opportunities”

- What % of music is AI-generated and how much is being uploaded? Mgmt wouldn’t share that information but does not want to dictate what tools creators want to use

- HOWEVER, the Co does think consumers will want to know if content is AI-generated…they are focused on providing that

Q4 Premium Biz Was Mostly IN-LINE With Cons…Not Seeing Any Neg Impact From Jan Price Hike

- Q4 Premium revs grew +8% y/y (+14% y/y FXN vs +13% last qtr): Subs growth was the driver

- Premium subs grew +10% y/y to 290mn…all regions grew both y/y and q/q

- Driven by strong holiday promotional campaign intake

- Premium ARPU declined -3% y/y to €70 (or up +2% y/y FXN)

- Driven by price increase benefits, partially offset by product/market mix

- Premium subs grew +10% y/y to 290mn…all regions grew both y/y and q/q

- A few key enhancements to Premium include –

- Launched music videos: In beta for users in North America, available in 111 markets

- Smarter Live Events discovery: All within the app, listeners can discover nearby spots and explore upcoming lineups

- Prompted Playlist: Puts the algorithm directly into the hands of listeners, allowing users in select markets to describe exactly what they want to hear

- Thus far in Q1, the Co is not seeing a negative impact on the recent price increase implemented in Jan

- “No surprises at all”

- Churn was “in-line”

Underlying Ad Revenue Growth Should Improve In H2 2026

- Q4 Ad-Supported rev declined -4% y/y (or incr’d +4% y/y FXN) vs -6% y/y in Q3 (+4% FXN): Ex effects of the podcast optimization strategy, ad revs were up +7% FXN (vs +mid SD growth y/y in Q3)

- Ex FX, growth in music advertising was driven by growth in impressions sold, partially offset by softness in pricing (ARPU was weaker than expected)

- Podcasting growth was led by sponsorship gains, partially offset by optimization of podcasting inventory in Owned & Licensed portfolio

- Automated sales channels = the largest contributors to overall ad growth

- Ad-Supported GM of 19.5% rose +441bps y/y, (+525bps in Q3) driven by improved contribution from podcasts and music

- Advertising biz is set to “improve” in H2:26

- Still “have work to do” w/ the ad tech stack but “definitely making good progress and seeing positive signs”

- “Encouraged” by new ad tools adoption

A Few Other Updates/Comments That We Would Call Out

- Podcasting is at scale: There are now 530k+ video podcast shows on the platform; Consumption on SPOT has incr’d by more than 90% since the launch of the Spotify Partner Program

- Why enter the physical books business? Audiobooks and physical books are the same market…consumer preferences drove them to get into physical books

- Mgmt is still very bullish on audio books…“there’s so much upside there”

- In ~2 yrs, have more than tripled their catalog to 500m+ titles and expanded into 14 global mkts (there are “so many more” markets to go from here)

- Also note that the Co is not holding inventory in physical books

- SPOT subscribers still account for only 3.5% of the world’s population…“it’s not implausible to imagine us converting 10% or even 15% of the world’s population to subscribers”

- The Co paid $11bn+ to the music industry in 2025 vs $10bn+ in 2024

Agentic Shopping Disruption Risk Further Weighs On Shopify’s Shares

Going into Shopify’s Q4 print, there was already a lot of fear in the market around how Agentic AI will potentially disrupt the Co’s commerce platform, and mgmt’s comments on the call did little to ease those concerns. Investors remain worried about the implications of discovery, product selection, and checkout increasingly shifting to AI agents and how that will change the economic model for merchants and Shopify.

Mgmt repeatably stressed that commerce is complicated and while agents may address the front end of a customer’s commerce journey, the back end remains the hard part of the process, and that is defensible for Shopify.

Shopify’s orders coming from AI-driven search were up 15x over the past year, albeit off a limited base, and the Co stressed that in an AI agent world, these flows still route through its back-end stack. Shopify characterizes the Universal Commerce Protocol (UCP), which is co-developed with Google), as the “common rails” for any agent to connect with any brand on the internet. It is the only protocol that covers the full commerce journey from end to end (search-> cart-> checkout-> post order) and it can handle complicated requirements. Merchants will get “instant access” to “millions” of potential buyers who are actively looking for their products. Importantly, merchants do not have to rebuild customizations for UCP and when asked by the analyst community in different ways on the call, mgmt point blank said that merchants’ economics remains the same relative to a direct storefront sale.

These AI concerns dramatically overshadowed what was a strong Q4 result. GMV and revenue both beat expectations (the Q4 revenue rate was more than ALL OF 2020!), European merchant GMV growth was especially strong, and payments penetration continued to climb. Gross margin in Merchant Solutions was the only Q4 blemish due to mix, but pressures should ease starting in Q1.

Shopify now powers 14%+ of the US e-commerce market and has more room to grow, but over the next few quarters, investors will be carefully tracking agent-driven commerce traffic and monetization impacts/implications.

See below for more of what we viewed as most incremental from Shopify’s Q4 results and conference call.

-> Shopify shares fell -6.7% in reaction to results and it down ~35% from its all- time high in late Oct 2025

Shopify Q4 Exceeded Street Projections…The Only Weakness Was Merchant Solutions Gross Margins

- Q4 GMV BEAT cons by +2%…it rose +31% y/y (+29% FXN) vs +32% y/y in Q3 (+30% FXN in Q3): Growth was led by 2024 and 2025 cohorts (outperforming older cohorts)

- N.Amer: Outperformed their expectations

- Intl: Almost 50% of incremental GMV dollars came from outside N. Amer

- European merchants’ GMV rose +45% y/y or 35% y/y FXN

- Offline: Incr’d +27% y/y (vs +31% y/y in Q3)

- B2B: Rose +84% y/y (vs +98% y/y in Q3)

- Vertical strength (similar to prev qtrs)

- Apparel and accessories

- Health and beauty

- Home and garden

- Food and beverage

- Q4 total revenue BEAT by +2.2%…it rose +31% y/y (+29% FXN) vs +32% y/y in Q3 (+32% FXN in Q3): Seeing growth in both existing and new merchants

- N.Amer: Up +28% y/y vs +29% in Q3 (now powers 14%+ of US e-commerce market)

- Intl: Up +36% y/y vs +39%y/y in Q3 (nearly half their merchant base is now located outside of North America)

- Offline: Grew +27% y/y

- Q4 Merchant Solutions posted mixed performance with BETTER revenue but WORSE margins

- Revs grew +35% y/y (vs +38% y/y in Q3): Driven by the strength in GMV and incr’d penetration of Shopify Payments

- Shopify Pay – key stats:

- GMV processed on Shopify Payments reached $84bn, up +38% y/y and accounted for 68% of GMV (four pts higher than Q4:20): Reminder – Q4 is a big qtr seasonally for Shop Payments

- More than 50% of their US payment volume in Q4 flowed through Shop Pay

- Gross margins of 36.8% fell y/y due to the mix shift to payments rev, decreases in 3P referral and transaction fees, and the y/y impact PayPal had to GM comparability

- Outlook: Have now “largely moved past the more temporary y/y comparability headwinds in gross profit, like the changes in pay trials”

- Q4 Subscription Solutions slightly BEAT consensus

- Revs grew +17% y/y (vs +15% y/y in Q3): Driven by a larger % of subscriptions coming from higher priced plans and higher variable platform fees

- Q4 MRR grew +15% y/y, w/ cont’d growth in each of Standard, Plus and Offline (Plus was only one highlighted in Q3)

- MRR Plus accounted for 34% of MRR in Q4 (vs 33% Q4:25)

- Outlook – headwinds in Q1: Y/Y growth rate in MRR will continue to have comparability headwinds until Q2:26 given the rollout of 3-month trials, particularly in their largest mkts, did not incur until Q1:25.

- Q4 MRR grew +15% y/y, w/ cont’d growth in each of Standard, Plus and Offline (Plus was only one highlighted in Q3)

- Gross profit grew +18% y/y (margins 81%): Growth is due to a reduction in support costs given operating leverage

- Revs grew +17% y/y (vs +15% y/y in Q3): Driven by a larger % of subscriptions coming from higher priced plans and higher variable platform fees

- Adj op income BEAT by a larger +10.2%…due to content cost favorability

Q1 Guidance Points To Another Period Of Strong Quarterly Growth Though GMs Are Held Back

- Q1 revenue guidance of “low 30%s” was ABOVE cons +25%…drivers:

- Payments growth led by shop pay

- Cont’d success of existing merchants

- Adding more new merchants

- Strong int’d growth, especially in Europe

- Cont’d expansion of more products

- Q1 gross profit dollars growth will continue to impact…it is guided to increase “high 20s%” due to:

- Cont’d mix shift btw the growth rates of merchant solutions & subscription solutions

- This should narrow vs 2025

- Cont’d strength of payments

- Q1 operating expenses guidance of 37-38% of revenues, reflecting a cont’d improvement of a couple of points y/y

- Q1 FCF margin guidance is in the “low to mid-teens”, slightly down y/y

- Q1 is typically the lowest GMV quarter, affecting both revenue and CF

- Expect a slightly higher effective tax rate as well

- Approved a share repurchase program of up to $2bn

Mgmt Stressed That AI Can’t Displace The Complicated Commerce Journey

- Shopify wants to sell everywhere…2026 will unlock “a huge new surface area – AI shopping”

- Merit based discovery is going to happen with agentic

- Products will be surfaced based on relevance

- “We’ve been building for this new era of AI shopping for a long time, and it’s now here”

- Over the last 12 months, orders coming to Shopify stores from AI search are up 15x, but off a small base

- AI powers the long tail of commerce, surfacing smaller merchants and buyers who might otherwise have never discovered them

- This is merit-based discovery at scale for buyers

- Mgmt thinks Agents will “bend the curve of e-commerce penetration by stripping out friction, pulling late adopters in, and moving more everyday purchases online”

- BUT “commerce is complex, it’s dynamic, and it’s also easy to get wrong. It’s so much more than just a transaction”

- That is why Universal Commerce Protocol (UCP) is so important…it’s the “common rails agentic commerce runs on… it’s an open standard for any agent to connect with any brand on the internet”

- It is the only protocol that covers the full commerce journey from end to end (search->cart=->checkout->post order)

- It can handle complicated requirements: White glove shopping, Subscriptions, etc

- Expands merchants’ reach: Merchants can sell on every major AI platform and get instant access to millions of potential buyers who are actively looking for their products

- Oppty w/ non-Shopify merchants: Merchants who are not even on Shopify can also syndicate their products as well

- It is the only protocol that covers the full commerce journey from end to end (search->cart=->checkout->post order)

- When asked about OpenAI and Stripe’s competing ACP initiative…mgmt. didn’t directly comment other than to say that merchants do not have to rebuild customizations with UCP and that UCP is more than just for the transaction

- But what about the economics for Shopify merchants in Agentic UCP transaction vs their online store? “They are the same”

- Shopify runs both the front end and the back end today

- Under UCP, Shopify still powers the overall experience, but the merchants keep their own checkout system on the back end

- With ChatGPT, for example, OpenAI will run the front end (the screens and the forms that the buyer uses), but Shopify still runs the back end

- “LLMs do not bypass Shopify’s checkout. And in fact, I think this is really where Shopify shines. The complex, the back end of commerce will always flow through Shopify

- Shopify’s AI assistant sidekick is providing merchants with tangible results (the assistant uses “everything it knows about your business, and it proactively tells you which tasks to prioritize, and it will even help you execute those tasks”)

- Key stats: 3 weeks after launch of the latest edition, Sidekick generated almost 4k custom apps, created 29k+ automations w/ Shopify flow, built almost 355k task lists, & edited 1.2mn+ photos

- Good example: For one of Shopify’s jewelry brands, Sidekick Pulse made a recommendation to bundle 4 separate products & sell them together as a stack b/c it knew that those 4 products were already best sellers, and it also knew that bundles tend to convert better and drive-up cart value

A Few Other Notable Points To Mention

- Growing offline retail is also a priority in 2026

- They will bring subscriptions in-store

- The Co’s unified commerce philosophy drives them to “make it fast, easy, and intuitive for a merchant to reach buyers everywhere, whether that’s online and AI chats or in person”

- ShopApp is “reimaging” how the discovery process works: The home feed provides tailored content, exclusive offers and interactive experiences from their network of brands, matched to shoppers’ interest

- Advertising gained taction in 2025 and the Co “will build” on that momentum in 2026

- Shop Campaigns revenue doubled and merchant adoption tripled in 2025

- Merchants only pay if they make a sale…they can advertise across 8 channels (X, Snapchat, Bing, Google, Instagram, Facebook, and their Shop app and Shopify storefronts)

- AI is also helping with product development: By leveraging AI automation and proprietary project mgmt and talent mgmt systems, Shopify has been able to “accelerate” its product development w/out growing the size of team

DraftKings Resets Street Expectations While Pushing Ahead On The “Huge” Predictions Opportunity

The predictions market has been the rage as of late and investors have been trying hard to assess its potential impact on the entire sports betting industry. Not surprisingly, it dominated the discussion on DraftKings’ Q4 earnings call and while Q4 profitability was well ahead of the Street, Q4 revenues were only in-line and the 2026 guidance was set much lower than the Street projections. There were several moving parts.

On predictions, mgmt remains VERY bullish on this opportunity and views it as largely incremental, bringing in new customers in existing states as well as customers in states where they do not offer their traditional sportsbook (~50% of the population). Mgmt sees a potential $10bn annual gross revenue TAM for the predictions market over time, with DKNG generating “hundreds of millions” in annual revenue “in the years ahead”. Early engagement metrics for the Co’s prediction offering, including strong downloads and trading activity around the Super Bowl, were encouraging, but the Co is waiting for its product to be more competitive before it aggressively pushes it (which should be “relatively soon”). Importantly, mgmt has NOT seen any meaningful cannibalization from the predictions market on their existing customers, with any overlap concentrated among lower‑margin customers. For 2026, while there will be some increased customer acquisition costs for this new product, predictions revenue is not included in the new 2026 revenue guidance, hence it would be upside.

Touching on Q4 more broadly, adj EBITDA was very strong (~28% ahead of consensus) while revenue was in-line (rose +43% y/y). Sportsbook revenue increased ~64% y/y as handle growth accelerated seq, net revenue margins expanded, and parlay mix continued to rise. While sports outcomes fluctuate qtr-to-qtr, they were more sportsbook friendly in Q4.

One other Q4 metric of focus was monthly unique players (MUP) which was ~9% below expectations. This is a continuation of the MUP normalization from an unusually strong 2024. Ex‑Jackpocket, MUPs grew ~+5% y/y, roughly in line with Q3, while ARPU modestly exceeded expectations.

The strong negative stock reaction was predominately driven by the new 2026 guidance which was well below Street expectations. It implies revenue growth of ~+11% y/y, which is a sharp deceleration from the +27% y/y reported in 2025. We view this guidance as conservative and a deliberate reset given prior guidance “self‑inflicted” missteps. Per CEO Jason Robins, “for me, missing numbers again is just not acceptable.” Also, as mentioned above, predictions revenue is not factored into the guide, while incremental associated costs are.

Regardless, the lower-than-expected guidance, drove the stock sell-off as the Co resets expectations to a level that we would wager they can beat. Also, please note that the Co is holding a virtual investor day on March 2nd.

-> DKNG shares fell -14.3% in reaction to earnings and is down -59% from its 52-week high almost 1 year ago.

Q4 Reflects Much Greater Profitability But Monthly Unique Players Were Weaker Than Expected

- Q4 revs were in-line w/ expectations but adj EBITDA was +28% ahead (17.2% margins vs cons 13.5%)

- Revenue: Rose +43% y/y vs +4% y/y in Q3

- Adj EBITDA: Up 4x (margin expanded 100bp+ y/y to 17%

- Q4 EPS of 25c beat cons 10c

- Q4 monthly unique players (MUP) was -9% below cons (flat y/y): Ex the Jackpocket impact, it was up +5% y/y vs up +6% y/y in Q3; Overall 2025 MUP came back “down to earth” from an unusually strong 2024

- Avg rev/MUP was a tad better that projected (up +43% y/y vs +3% y/y in Q3)

- Bought back 8mn shares and expect to “remain active “in the market

2026 Guidance Fell Well Short Of Street Expectations As DraftKings Invests In Predictions AND Bakes In A High Level Of Conservatism

- Total 2026 revenue guidance was -8% below cons and adj EBITDA guidance was -18.4% below cons

- What drives the strong slow-down in expected top line growth in 2026? The mid-pt of +11% y/y growth compares to +27% y/y in 2025

- Mgmt explained that they were very conservative w/ guidance when they went public but got away from that philosophy… then the stock got killed on what mgmt viewed as still a strong outcome

- This was “self-inflicted”

- They “like the playbook of being more conservative”

- The 2026 guidance that they put out to the Street had been shaved more than once

- “For me, missing numbers again is just not acceptable, and so it’s not something we’re willing to do…let’s make sure we put something out there that we feel really good about”

- Mgmt explained that they were very conservative w/ guidance when they went public but got away from that philosophy… then the stock got killed on what mgmt viewed as still a strong outcome

- Predictions revenue would be upside to the 2026 guidance…other key guidance drivers / assumptions –

- Investments: Expects investment in DraftKings Predictions, line of sight jurisdiction launches, and disciplined planning

- Taxes: Assumes state tax rates remain consistent

- Sports outcomes: Does NOT include the modest benefit of YTD sports outcomes

- Mgmt projects 1 standard deviation of variance would impact revs by +/-~$150mn & adj EBITDA by +/-~$100mn

DraftKings Sees Predictions As A Huge And INCREMENTAL Opportunity

- “Predictions is developing into a massive, incremental opportunity”…the Co “expects to emerge as a leader”

- CFTC leaning into Predictions markets is what made DKNG accelerate efforts in this area

- “Anything that creates a stable regulatory environment that allows us to operate more freely is a great upside thing for us”

- How big could Predictions be? Predictions could represent a $10bn annual gross revenue opportunity in the years ahead

- Mgmt expects the volume growth on DraftKings Predictions to “accelerate through 2026 and beyond”

- The Co believes it can generate “hundreds of millions” in annual revs from Predictions in the “years ahead” and there is “much more” upside over the longer term

- The Co has NOT seen any “discernible impact” from Predictions on their Sportsbook revenue…it is “not largely incremental” to their EXISTING customer base

- In Missouri (newest launch state)…Sportsbook adoption was higher than in any state launch in their history through the first 2 months and activity/customer has been strong

- Q4 sportsbook handle growth accelerated and in Jan it has incr’d +4% y/y even after 2 consecutive months of Sportsbook friendly outcomes and as parlay handle mix continues to increase

- The Co also cited 3P data showing Predictions had only a “slightly impact” to Jan handle and primarily impacted low-margin customers

- DKNG’s Predictions product will bring in new customers in existing states and customers from other states were they are not present in OSB but now have predictions

- CA, TX, and Florida in particular are “huge opportunities”

- DKNG is able to launch predictions in half the country population-wise

- Early signals are strong for DKNG Predictions: On Super Bowl Sunday, DKNG Predictions had the 2nd most downloads in its category and delivered 3x its prior record for daily trading volume

- Customer retention is also strong so far, even w/ a product that is in its early stages

- The Co wants to have the best Prediction product before pushing it more aggressively… and they are “not that far off” from that

- Mgmt cites a huge advantage in marketing with their national approach

- It can drive value in both of their products

- The Co will lay out more of their marketing strategy at the upcoming investor day (Mar 2nd)

- Mgmt cites a huge advantage in marketing with their national approach

- In 2026, investors should expect a step function improvement in DKNG Prediction, and the Co believes they can be highly differentiated

- Plan to integrate Railbird mid 2026 (will improve economics as they will own more of the stack)

- Launching market making for sports contract in 2026

- DKNG should be able to be one of the largest market makers

- Over time…the Co will also introduce exclusive combo trading options that could be a major differentiator given their data advantage

- As noted above, Predictions revenue is all upside to DKNG’s 2026 guidance: The Co will spend more on Predictions customer acquisition but there will “probably be some revenue” as well

The Co’s Core Sportsbook Had A Strong Qtr & Benefited From Sportsbook Friendly Outcomes

- Sportsbook had a “standout” Q4…revs incr’d +64% y/y to $1.4bn

- Handle growth accelerated to +13% y/y from +10% y/y in Q3

- Sportsbook net revenue margin incr’d 250bp y/y to 8%

- Parlay handle mix incr’d almost +500bp y/y

- Sports outcomes were sportsbook friendly in Q4, and overall Sportsbook hold percent was slightly above 12%

- For the 2025-2026 NFL season, their NFL hold percent was 16%

- Mgmt believes there is upside in the 2026 guidance from its core sportsbook as well…”everyone gets hung up on handle and we’ve tried to educate people that you can’t look at that in isolation”

- From Jan through Oct, DKING net rev margin was ~6.5%

- Since then (Nov, Dec, Jan, Feb to date), net rev margin has been 9% (40% higher)

- At the start of NFL season when customers were winning, the Co had “really high” team handle growth for a few weeks in Oct

- Then DKNG started to do a little better and was more efficient with promo

- Handle growth will slow when they are winning that much

- But the Co did great in Q4 despite handle slowing a little

- Also, handle for EVERY single sport outside of the NFL is growing (by DD%)

A Few Other Key Comments From Our Point Of View (Promo Environment & Taxes)

- It has been a “very rational” environment from a promo standpoint right now: Promo is also “not a huge thing” in predictions

- Mgmt cited that they have cushion w/ the conservative guide and are “prepared” if things change and they need to deploy more

- On potential state tax increases? “In my view, states would be absolutely crazy right now to raise OSB taxes with everything going on with predictions. So [we are] definitely getting some good traction on both that and on future legalization”

- “I wouldn’t be surprised if that’s the difference between getting a state or two done this year or no”

AppLovin’s & Unity’s Mgmt Were Not Able To Ease Investor AI + Meta Competition Concerns

Ad technology players have faced a double whammy with concerns about AI disruption to the video gaming business (from the likes of Google’s recent Genie announcement) PLUS fears of increased competition in video game advertising from Meta, who became more competitive in iOS mobile games at the end of January after years of being quieter on this front (the concerns emanated from a recent LinkedIn post – link).

Both companies proactively tried to ease investors’ concerns…stating that AI will actually be a tailwind for the videogame ecosystem given the content explosion that is coming (and the need for discovery/curation) and will be complementary to gaming engines like Unity. Both companies also downplayed the bear case that Meta will cause significant competition pressure on the advertising side.

This issue is that these bear concerns can’t be disproved at this stage. Investors want to more fully understand the implications of this very quickly changing AI landscape and are choosing to remain on the sidelines in the meantime. The fact that both companies also beat Q4 results didn’t carry much weight given that is in the rear-view window.

See below for more of what we thought was most important from both AppLovin’s and Unity’s Q4 earnings, especially as it relates to AI / Meta competition concerns.

APPLOVIN: The Co delivered better Q4 results as well as stronger Q1 guidance BUT that was overshadowed by persistent investor concerns about AI disruption and increased competition from Meta, despite mgmt’s comments and arguments that were meant to ease these worries.

–>AppLovin shares fell -19.7% in reaction to earnings and is now down -46% from its 52-high in mid-Dec 2025

- APP Q4 was a nice BEAT vs the Street… “we delivered the strongest operating performance in our history”

- Revenue BEAT by +3%: Up +66% y/y vs +68% y/y in Q3

- Adj EBITDA BEAT by +5.2%: Up +82% y/y vs +79% y/y in Q3

- Q1 guidance was also AHEAD of consensus AND reflects seq growth vs the usual seasonal seq decline

- Revenue guidance BEAT by +3.5% at the mid-pt: Up +19% y/y vs +66% y/y in Q4

- Drivers = Had a strong exit rate w/ mobile gaming performance, the e-commerce launch, and growth in the prospecting model; “Have a high level of confidence” in the guide

- This also implies +5-7% seq growth vs Q1 normally being a weaker seq qtr

- Adj EBITDA guidance BEAT by +5.7% at the mid-pt

- Guiding for ~84% margins

- Revenue guidance BEAT by +3.5% at the mid-pt: Up +19% y/y vs +66% y/y in Q4

- Mgmt disputes the notion that AI is going to displace their business…”there is a real disconnect between market sentiment and the reality of our business”

- Mgmt is NOT concerned regarding AI disruption or incr’d competition from Meta…why?:

- The Co has “successfully operated” in a highly competitive market…AI will just forces more innovation

- It is not a zero-sum auction-based market…as bid density goes up, the pie expands

- APP’s share in the auction might fall, but their economics can actually grow since their model uniquely understands impressions and highly values some of those (but not all of them)

- When competitors (like Meta) win an impression, it is likely one that APP values less

- Instead of winning a low value impression, APP charges the winning bidder 5%

- Mmgt is skeptical that Meta would violate Apple’s terms by attempting deterministic bidding on no-IDFA traffic

- “It makes no logical sense”

- Meta was a significant player in in-game advertising 5 years ago, but post IDFA changes, APP’s AXON 2 has dramatically moved ahead (and the model continuously reinforces itself and gets smarter)

- “We’ve never seen growth in the ecosystem cause harm to our AppLovin bidding environment since we got so good”

- AXON 2 is the “biggest breakthrough model” in this category and is ahead by “a lot”; AXON 2 didn’t exist 5 years ago

- “There is no world where Meta is going to end up becoming that kind of dominant player”…”we’ve got such a strong position”

- “It’s highly unlikely that someone else is going to come in and materially disrupt it”

- Meta’s model is built for social and trained on social…APP’s model and training is built on their gaming eco-system

- Mgmt also argues that AI’s impact on game creation will be a net positive for APP

- AI will make games easier to build which mgmt. believes will INCREASE the value of their eco-system vs DECREASE the value as feared

- Content will “explode” so discovery will be critical

- “The winners will be platforms that can efficiently match the right user to the right content at the right moment. That is exactly that our models are designed to do”

- Also, the Co doesn’t see any decline in mobile gamers…people will always look for entertainment that fits naturally into their day like casual gaming; “What’s changing is how well that attention can be monetized”

- APP only converts a small portion of impressions they serve right now…there is a “big oppty” to grow that

- Separately, the ramp in e-commerce was a key focus on the call as well

- E-commerce has been live for 1.5 years and is “doing really well”

- The Co opened the self-serve platform in Q4 referral only

- They are on track for GA-type launch in H1

- E-comm won’t impact the overall numbers for “a while” but the Co is “seeing great trends”

- They are focused on any transactional web advertising business model, rather than lead gen which they will focus on later

UNITY: Similar to AppLovin, while Q4 results topped Street expectations, AI disruption / Meta competition fears took center stage for investors; That was also coupled with weaker Q1 guidance (including flat growth in Grow Solutions); On the plus side, the drag from ironSource should ease post Q1, which has “masked” growth in Vector but the bigger picture market concerns will take some time to play out.

–>Unity stock fell -26.3% in reaction to earnings and is now down -60% from its 52-high in mid-Dec 2025

- Q4 was a nice BEAT vs the Street, with the most revenue upside in Create Solutions

- Revenue BEAT by +2%: Up +10% y/y vs +5% y/y in Q3

- Adj EBITDA BEAT by +5.9%: Up +18% y/y vs +19% y/y in Q3

- BUT Q1 guidance was WORSE than expected…especially on adj EBITDA

- Revenue guidance MISSED by -1.4% at the mid-pt

- In Grow, expect rev to be flat q/q

- In Create, expect DD y/y rev growth (ex the impact of non-strategic rev)

- Adj EBITDA guidance MISSED by -8.1% at the mid-pt

- Revenue guidance MISSED by -1.4% at the mid-pt

- The negative drag from ironSource should ease…mgmt stressed that throughout 2025 & into Q1:26, the sharp decline in ironSource’s Ad Network has “at times masked this incredible growth in Vector”

- It is “drawing to a close”, which will materially enhance growth rates, and profitability in their ad biz in the years ahead

- The ironSource Ad Network will represent ~6% of total Unity rev in Q1 and will become an even smaller component over time

- In contrast to market fears, mgmt. believes that AI is going to be a “massive tailwind for the video game industry”

- Leisure time will increase “massively”… this will lead to an explosion of time spent in video games

- AI will make game creation more efficient and less expensive, remove drudgery work, and allow creators to focus on differentiation and innovation regarding building new things

- “We believe that’s [AI] just going to have an extraordinary positive impact on our industry over time”

- “World models will be a source of inspiration and assets for creators BUT will not replace game engines”

- Unity will translate rich visual input from these models and they can be refined with deterministic systems that Unity developers are using today

- “We compile the pieces together after those assets are created, and we help creators turn those into real games”

- Mgmt has not seen any impact from Meta and is confident it can compete going forward

- “Meta has been competitive in iOS traffic for quite some time. This wasn’t a new dynamic. It did not have a meaningful impact on us in any way. We are laser-focused on the games industry in our business, not e-commerce”

- Given the “understanding we have in that segment [gaming], we feel very very good about our ability to compete with anyone…and we’ve seen essentially no impact”

- “I would in general caution investors from overreacting to LinkedIn posts”

Big Retailer Exposure Disproportionately Weighs On Pinterest…Diversifying & Improving Go-To-Market = The Key Focus

It was another tough quarter for Pinterest as it is still navigating many of the same headwinds that emerged in Q3, namely the impact of moderating ad spend from larger retailers (where PINS has more exposure than other platforms) given tariff-related margin pressures. This was a headwind in both UCAN and Europe during the qtr and could even be more pronounced of a headwind in Q1 (Q1 revenue guidance missed the Street by -2%). This dynamic puts even more urgency in mgmt’s strategy to diversify its revenue mix towards mid and small businesses in particular.

This pressure resulted in a -7.7% revenue miss in Europe in Q4 (grew +25% y/y, down from + 41% y/y in Q3) along with flat revenue growth (at 9% y/y) in UCAN. In addition to the Q1 revenue headwinds, the Co is also investing more in the business (high ROI areas such as GPU capacity to enable key AI initiatives and building more powerful AI models while also seeing less benefit from the earlier multi-yr infrastructure cost optimization efforts). As such, Q1 adj EBITDA guidance fell -14% below consensus.

User engagement remains a crucial positive with MAUs growing in every region during Q4 but mgmt. argues that the strength of user activity, engagement, and high commercial intent on the platform is not translating to the revenue potential of the company. Looking ahead, investors will be looking for execution of the new mgmt. appointments to accelerate its sales and go to market efforts.

While Pinterest remains committed to its 30-34% medium-term margin targets and mid to high teens revenue growth targets longer term, investors want to see more signals that the business is headed in that direction.

See below for more of what we thought was most important from Pinterest’s Q4 results and conference call…

-> Pinterest’s shares closed down -17% after reporting and is down -60% from its 52-week high at the end of July 2025

Q4 Top Line MISSED, Driven By Lower Than Expected Revenue In Europe

- Q4 rev MISSED by -0.8% and grew +14% y/y (+12% y/y FXN), decelerating from Q3’s +17% y/y (+16% y/y FXN): Growth was driven by retail, though, with “puts and takes within that”; Mgmt was “not satisfied with our Q4 revenue performance and believe it does not reflect what Pinterest can deliver over time”

- The big drag was Europe which MISSED by -7.7% and grew +25% y/y (vs +41% y/y in Q3): Driven by retail but ARPU was much lower than expectations

- Saw a “second order effect” on cross-border spend from certain large global retailers who pulled back ad spend in Europe as well

- UCAN BEAT by +0.7% (last qtr missed by -1.6%) and grew +9% y/y vs (+9% y/y in Q3): Strength came from retail, financial services and telecom

- RoW BEAT by +3.9% and grew +64% y/y (vs +66% y/y in Q3)

- Recalibrated across their global portfolio due to the same tariff and margin pressure

- The big drag was Europe which MISSED by -7.7% and grew +25% y/y (vs +41% y/y in Q3): Driven by retail but ARPU was much lower than expectations

- Adj EBITDA MISSED by -1.6%, up +15% y/y (vs +24% in Q3): Expenses grew at a higher rate y/y, due to certain legal costs not expected to repeat, as well as lapping insurance proceeds received in the prior year

- Adj EBITDA margin of 41% compared to cons 41.4%

Tariffs Caused A Greater Headwind Than Already Expected … The Impact Could Be “More Pronounced” In Q1…AND The Co Is Investing More

- In Q4, the Co’s largest retail advertisers (incl both in UCAN and Europe) created a “more meaningful headwind than we expected” as they sought to protect their margins and pulled back on ad spend

- “We believe this pullback on ad spend from larger advertisers was felt across the industry, but impacted our platform to a higher degree” given their current revenue mix

- Looking ahead to Q1, mgmt expects these headwinds will continue and may become “slightly more pronounced”, including in UCAN and Europe

- Pressures should ease in H2: “We’re not seeing any new factors today beyond what we’ve described that would create more headwinds to our current trajectory”

- Larger retailer headwinds will start to anniversary in H2:26

- Pressures should ease in H2: “We’re not seeing any new factors today beyond what we’ve described that would create more headwinds to our current trajectory”

- Investments are also set ramp in 2026…the Co will reinvest ~50% of the $100mn annualized non-GAAP opex savings from Jan restructuring…the cost of revenue investment will be ~100bp impact in 2026

- Investing in high ROI areas such as GPU capacity to enable key AI initiatives

- Continue to build more powerful AI models

- The Co has also already captured much of the benefit of their multi-yr infrastructure cost optimization efforts so that is starting to reach “diminishing returns”

- Mgmt expects “modest headwinds from cost of revenue as a % of revenue in 2026”

Q1 Guidance Missed Across The Board

- Q1 revenue guidance was WEAKER by -2% at the mid-pt…it implies +11-14% growth y/y (vs +14% in Q4)

- Assumes a ~3 pt tailwind from FX

- Q1 adj EBITDA guidance MISSED by a wider -14.1%: $176mn vs cons $205mn

- Q1 non-GAAP cost of rev should grow seq by low SD%…“we’re making deliberate investments in GPU capacity to enable key AI initiatives”

- These investments will allow them to train and serve visual foundation and conversation models

- Q1 non-GAAP cost of rev should grow seq by low SD%…“we’re making deliberate investments in GPU capacity to enable key AI initiatives”

- Despite anticipated y/y pressure in H1:26, excluding the tvScientific acg, mgmt guides for flat adj EBITDA margins in 2026 vs 2025 (at ~30%):

- tvScientific is expected to close in Q1 or Q2 and will have a roughly 100bps negative impact to adj EBITDA margin

- Mgmt reiterated adj EBITDA margin targets of 30-34% over the medium term

- The Co is “moving with urgency” to return “over time” to the mid to high teens revenue growth or better

- The Co will get there by broadening its revenue mix and accelerating its sales and go-to-mkt transformation

On The Positive Side, User Growth Remains Strong & Notably Hits A Record For The 10th Consecutive Qtr

- Q4 global MAUs reached 619mn, growing +12% y/y (vs +12% y/y in Q3) for the 10th consecutive quarter of record high users

- Posted growth across all regions

- UCAN: 105mn MAUs growing +4% y/y (+4% y/y in Q3)

- Europe: 158mn MAUs growing +9% y/y (+8% y/y in Q3)

- RoW: 356mn MAUs growing +16% y/y (+16% y/y in Q3)

- Posted growth across all regions

- The Co doesn’t believe its current revenue growth reflects the strength of user activity, engagement, and high commercial intent on the platform

AI Is “Central” To The Co’s Strategy…And Mgmt Is Not Worried About ChatBots

- How does Pinterest fit into an increasingly competitive digital ad landscape, specifically w/ ChatGPT launching ad products and the industry moving toward AI-driven automation?

- PINS has higher commercial intent: 50% of Pinterest’s 80bn monthly searches have commercial intent, which is a much higher mix than typical AI prompts

- PINS has better curation: The Co uses a unique “curation signal” (how users save and organize pins) to train its AI, resulting in recommendations that are 30% more relevant than standard off-the-shelf AI models

- PINS’ monetization beyond the App: Through the tvScientific acq, the Co is starting to monetize its intent data on other “surfaces” like CTV

- By combining visual discovery (Pinterest) w/ CTV (tvScientific), Pinterest becomes a “full-funnel” solution, capturing a user’s intent on their phone and closing the sale on their TV

- Today the Co sees 80bn monthly searches on the platform (vs ChatGPT’s 75bn monthly prompts) but with much higher commercial interest at over 50% (vs ~2% for ChatGPT)

- Competing for user engagement “is not new to us”

- During the period when AI chatbots were scaling, PINS reported ten consecutive qtrs of record high MAUs as noted above, 100% of which are logged in and reached 105mn UCAN MAUs

- The Gen Z population “are also flocking to Pinterest” representing ~50% of the users today, and they remain the fastest growing user cohort

- PINS’ AI model introductions have shown tangible gains on the platform

- OmniSage (core AI model intro’d in 2025) drove a 450bps lift in sitewide saves

- PinFM (proprietary foundation ranking model recently launched) distills lifetime user actions into the recommendations on home feed, driving personalization

- Have seen a 240bps increase in saves across the platform

- Navigator One is in development and will allow the Co to fine-tune open-source models to power their newest AI experiences

- This framework reduces latency and delivers ~90% reduction in cost versus utilizing a leading 3P proprietary model

- Pinterest Assistant usage (beta launch in Q4) is resulting in 25ppts higher share if commercially oriented questions

- The Co expects to meaningfully broaden access to US users in the “coming months”

- ~50% of their new code is AI generated

SMBs Are Their Fastest Growing Market & Remain A Key Priority To Diversifying Their Revenue Mix Beyond Large Retailers

- The Co is seeing strong performance in their SMB biz (these advertisers represent ~15% of revenue today)…The rev growth rate of this group nearly doubled y/y in 2025

- Mgmt sees this as an opportunity over a multi-year period

- SMBs who are adopting Performance+ campaigns to automate and simplify campaigns set up with AI are seeing stronger performance and are spending more on our platforms

- Mgmt believes it can accelerate growth of this advertiser group “over time”

- PINS will continue to focus on driving Performance+ campaign adoption, as well as simplifying the advertiser onboarding experience

- “Lee and the team are focused on bringing a new level of sophistication to our go to market efforts, including how we sell to a broader range of advertisers, particularly with SMBs”

- SMB advertisers on PINS have a 12% higher monthly revenue growth rate versus non-adopters

Expedia & Airbnb Show Strength In Q4 But See Diverging Reactions To Forward Positioning

OTA giants Expedia and Airbnb also reported this week, giving us a glimpse into travel trends which were strong in the fourth quarter. More specifically, Expedia posted strong Q4 bookings growth, margin expansion, and B2B upside, though full-year 2026 guidance, while slightly above the Street, reflected a cautious approach given macro uncertainty. Airbnb also exceeded expectations across Q4 gross bookings, revenue, and nights booked, and highlighted initiatives, from services and experiences to AI-driven enhancements, though 2026 guidance was more in-line.

Online travel is another sector where AI disruption concerns remain front and center, though Airbnb managed to provide more comfort to investors than Expedia was able to do, likely in part due to Airbnb’s new CTO hire, Ahmad Al-Dahle, who recently led the genAI team at Meta that built the Llama model.

See more detail below on what we viewed as most important from Expedia’s and Airbnb’s results.

Expedia: Despite Expedia delivering a better than expected Q4 and stronger than anticipated Q1 guidance, the full year 2026 outlook baked in a level of conservative given the macro environment; Mgmt has been executing on its strategic plans (bookings growth accelerated, B2C margins expanded, B2B revenue grew DD y/y across all regions, etc) but AI disruption concerns (plus the sub-dude 2026 guidance) ended up overshadowing what were strong results and outlook for Q1.

->Expedia shares fell -6.4% in reaction to earnings and is down -28% from its 52 week high in Jan this year

Q4 Was Another Positive Qtr For Expedia…

- In Q4, the Co posted accelerated bookings growth & expanded margins

- Gross booking beat by +3% and accelerated to +11% vs +12% y/y in Q3…B2B is a key growth driver

- B2C +5% y/y

- B2B +24% (DD growth across all regions)

- Adj EBITDA beat by +11%

- B2C margins at 31.5% reflect 6pps increase y/y (helped by direct sales & marketing leverage)

- B2B margins at 24% fell 1 ppt

- Adj EPS beat by +13%

- Gross booking beat by +3% and accelerated to +11% vs +12% y/y in Q3…B2B is a key growth driver

- Q4 room night growth also exceeded expectations…up +9% y/y vs +11% y/y in Q3

- US rose high SD

- EMEA and RoW rose low DD (though geopolitical issues in Asia)

- Grew share in the US for both hotel and Vrbo and held lodging share globally

- Expedia’s partner-funded promotions were 30%+ of bookings in Q4, up 10pts+ seq

- ~70% more properties participated in their Black Friday sales

- Bought back $255mn of stock and raised the qtrly div by 20% to $0.48/shr

- The Co will “continue opportunistic share repurchases at a pace similar to recent years:

Strong Upside In B2B & Advertising…Consumer Bookings Grew DD% Outside The US

- Q4 B2B revenue growth was an area of particular upside in Q4 (beat cons by +7.5%)

- B2B bookings rose +24% y/y vs +26% y/y in Q3

- The Co posted DD% growth across all regions

- They gained share w/ existing partners & realized benefits of incr’d marketing to large partners

- Also added new partners and travel agents were more active than in prior Q4s

- Expedia will continue to invest in new lines of biz

- Ad revs grew +19% y/y, an accel from +16% y/y in Q3

- Expedia is a “high return channel

- AI integrations are helping ads performance

- Consumer spending remained healthy in Q4, w/ longer bookings windows and lengths of stay y/y

- Q4 Consumer brands bookings rose +5% y/y overall, and DD% outside of the US

- Loyalty members grew mid SDs %, w/ faster growth in silver tiers and above

- All 3 core consumer bands delivered y/y bookings growth for the 2nd consecutive qtr

Guidance Topped Street Estimates W/ Easier Margin Comps In H1…The FY2026 Outlook Bakes In A Level Of Conservatism

- Q1 & 2026 guidance both exceeded the Street (especially with the former)…it “reflects strong bookings momentum as we enter Q1, while remaining appropriately cautious given ongoing macro uncertainty”

- Q1 guidance – DD bookings growth & strong margins expansion given easier comps

- Gross bookings growth +10-12% y/y (FX is 3pt tailwind)

- The upper end implies FX neutral stable growth

- Adj EBITDA margins will be up +300-400bps (Q1 is lowest qtr – so cost out initiatives have an outsized impact to Q1)

- Gross bookings growth +10-12% y/y (FX is 3pt tailwind)

- 2026 guidance – A more conservative full year bookings growth outlook + more moderate margin expansion

- Gross booking growth: +6-8% y/y (FX is 1pt tailwind)

- Upper end implies FX neutral stable grwoth

- 26 outlook assumes a more seasonal cadence similar to what we saw in 2024

- Adj EBITDA margins are expected to expand by +100-125bp

- Reflects a more moderate pace of expansion as they lap the benefits from the 2025 headcount reductions & marketing optimization…those actions to favorably impact H1:26

- Gross booking growth: +6-8% y/y (FX is 1pt tailwind)

Expedia Is Executing On Operational Efficiencies & There’s “More Room” For Margin Expansion Looking Ahead

- Q4 adj EBITDA margins expanded by nearly 4ppts

- The Co realized marketing leverage w/ consumer brands

- Improved targeting & measurement

- Reduced less efficient spend

- Reallocated dollars to higher return marketing opportunities

- Optimized the org structure

- Seeing benefits from AI in product & tech teams

- Shortened design and product cycle times

- The Co is leveraging AI to speed up inventory onboarding teams

- Resolving travel issues faster and more effectively

- Optimizing cloud spend

- The Co realized marketing leverage w/ consumer brands

- How much more upside is there with margin expansion? “There is more to come” (both in B2C and B2B)…but this year, as noted above, will be more front-end weighted, especially in Q1…Drivers for more improvement:

- More marketing efficiency

- Increasing scale

- Growing ads business

The Co Is Driving Product Improvements & Direct Bookings Remains A Key Upside Area

- Areas of key product improvements:

- Site and apps are 30% faster y/y

- Upgraded check out path

- Materially reduced wait times

- Added new payment options

- Are using AI to deliver more personalized experiences

- Enhanced the help center & servicing capabilities

- Expended Vrbo support care

- Working on natural language capabilities

- Expedia is working w/ the LLMs to ensure it shows up in AI searches and function effectively with agentic browsers

- Direct bookings is one of their “biggest” opportunities

- 2/3 of bookings comes from their travelers who begin their planning journey directly with their brands

- Direct bookings are growing faster than indirect bookings

- Mgmt thinks they can continue to deepen direct bookings

AIRBNB: Airbnb ended 2025 on a strong note w/ Q4 results coming in ahead of expectations, and that momentum is expected to continue going into 2026 (though guidance was just roughly in-line); The drive to improve their core offering w/ new features yielded measurable benefits in Q4 and the Co continues to work on diversifying its offerings across every trip-related decision, with Services and Experiences in particular bringing new people to the platform. Underpinning this all is a steadfast focus on leveraging AI across every part of the business, including operationally and across products and the Co has hired Ahmad Al-Dahle, who recently led the genAI team at Meta that built the Llama model, as its new CTO to help the Co be best positioned to succeed in this evolving AI-driven world which comforted some investors.

-> Airbnb was up +4.7% in reaction to its print but still ended the week down -0.7%; The stock is down -10.6% YTD

Q4 Easily Beat The Street (Margins Were The Slight Exception) With Strong Growth Across GBV And Nights & Seats Growth

- Q4 Gross Bookings Value BEAT by +5.2% and was the highest-growth qtr in 2+ yrs: Grew +16% y/y (accel from +14% y/y in Q3)

- Driven by “strong” growth in both bookings and price

- Q4 rev BEAT by +3.3%: Grew +12% y/y (accel from +10% y/y in Q3)

- Q4 adj. EBITDA BEAT by +2.7 but margin of 28.1% slightly missed cons 28.2%

- Q4 Nights and Seats Booked BEAT by +3.7% and grew +10% y/y, marking their strongest growth qtr of the yr

- Driven by strength across all regions

Q1 Guidance Also Beat On The Top-Line, Despite FX Tailwinds & Adj EBITDA Margins Are ~In-Line

- Q1 rev guidance BEAT by +7.4% at the midpt: Implies y/y growth of +14-16%, inclusive of an ~3pt FX tailwind

- Q1 implied take rate expected to be up “slightly” y/y, driven by ADR and FX tailwinds, earlier Q4 bookings, modest timing effects, and the mid-Q1 Easter

- Q1 GBV guidance is expected to increase in low teens y/y

- Driven by HSD growth in Nights & Seats Booked and a “moderate” increase in ADR due to price appreciation and FX

- Q1 adj EBITDA margin guidance is expected to be ~ flat y/y (implying ~18.4% which is ~ in-line w/ Street expectation of 18.5%)

2026 Guidance Is Roughly In-Line W/ Consensus

- 2026 rev growth guidance of “at-least” double digit % y/y was ~ in-line w/ cons +10.2%

- Driven by “sustained” strength in the core biz, “healthy” demand, and continued execution across their key growth initiatives

- 2026 adj EBITDA margin to be “stable” y/y (implied ~ 35.1% which is ~ in-line w/ Street expectations of 35.2%)

- As they reinvest top-line efficiencies to support growth across the biz, primarily in marketing, product, and technology

Feature Improvements For Hosts And Guests Drove The Growth In Q4

- Saw an “immediate” positive response to the US launch of Reserve Now, Pay Later: Allows guests to reserve an eligible stay and pay $0 upfront

- Led to longer booking lead times and a mix shift towards larger entire homes, esp those with 4+ bedrooms, contributing to the increase in ADR and accel in Q4 bookings

- Have now completed testing the feature across addtl mkts, and plan to make it available to even more guests globally in 2026

- Are you seeing an increase in cancellation rates? The overall cancellation rate increased by about ~1% (roughly 16% to 17%), which is not material and is already incorporated into FY EBITDA expectations

- Updated cancellation policies: Hosts can now offer free cancellation up to 14 days before check-in under a new Limited policy; And for guests who book more than a week in advance, a 24-hour grace period after their reservation is confirmed for refunds on shorter stays (under 28 days).

- These changes helped to reduce customer service contacts and increase bookings in Q4

- Simplified fee structure: Starting in October, simplified their fee structure to help hosts price more competitively

- Hosts using property management software moved from a split fee (3% host fee plus a separate guest fee) to a single 15.5% service fee

- By December, most other hosts were also shifted to the 15.5% fee

- While continue to migrate more hosts in 2026

- Hosts can adjust their listing prices to keep the same net earnings, and guests continue to see the full price upfront

- In total, mgmt. estimates that these three features delivered 200bps+ of growth in Nights Booked and ~300bps of growth in GBV in Q4

Large Events Like The Olympics And FIFA Will Help Drive Supply Growth In 2026

- Ended 2025 with 9mn+ active listings around the world (vs 8mn+ at the end of 2024)

- In Q4, active listings grew relatively in-line with y/y increase of Nights and Seats Booked (+10% y/y)

- Continued to see growth in both high-density urban and non-urban destinations, with the most growth in regions with the highest demand, like LatAm and APAC

- Expected impact to financials from Milan Olympics and FIFA this summer? “They are large events on the platform, but in scale are very small portions of the overall business. So we’re looking forward to them. They will be additive in the quarters that they hit.”

- Benefit from these large events is less about bookings and more about raising overall awareness of the brand and driving incremental supply in these mkts

- Many people have no intention of becoming a year-round host

- But when an event comes to town and they list their place to make money for one week, they get introduced to the concept hosting and they realize they like it and want to continue to host

- 40,000 people who listed their homes in Paris during the Olympics have continued hosting

- “The event strategy scales from big global events, down to local events, and we think they’re one of the best ways to recruit supply, and that’s what we’re going to do to grow our supply in Airbnb.”

Continued Build Out Of Services And Experiences And Expansion Into Hotels Are Key Components To Execute The Larger Vision For “Airbnb Trip”

- Services and Experiences brought new people to Airbnb in Q4, and almost half of Experiences bookings were NOT attached to an accommodation booking

- Taking a city-by-city approach to grow Services and Experiences globally – “going deep in one place, reaching product market fit and expanding from there”

- Started w/ Paris for Experiences and LA for Services, and seeing “great results”

- Also starting to test new svs like grocery delivery and airport pickups

- Bringing boutique independents hotels onto Airbnb…still early days “but the opportunity with hotels is massive”

- Have started w/ a pilot in cities that are supply constrained due to excess demand or regulation

- In Q4, partnered directly with boutique and independent hotels in New York, Los Angeles, Madrid, and San Francisco

- Why expand into hotels? “We believe bringing more hotels onto the platform can increase our total addressable market, convert more existing guest demand, and drive repeat bookings across both hotels and homes”

- Why not partner with hotel chains? A “large” % of hotels are boutique and independent and want to start there; They tend to pay a higher commission than a chain and have been “aggressive” about reaching out to Airbnb; BUT “we’re not saying what we will or will not do in the futur”

- Will take some time for the biz to scale and have a meaningful contribution to growth but current momentum is “strong”: As of Q4, hotels was a single-digit percentage of total nights booked, but growing nearly double that of the overall platform

- “We’ll be expanding the hotel supply over the course of the year and intend to exit 2026 with hotels being a meaningfully larger percent of the overall business going forward”

- All of these are part of a larger vision…Airbnb Trip

- Because “the big idea here isn’t just building a bunch of standalone businesses” but rather to have a touchpoint across every part of a trip

AI Is Going To Be The Key Driver Of Growth Across Every Facet Of The Company Moving Forward

- Have brought on a new CTO, Ahmad Al-Dahle, who is “one of the world’s leading AI experts”

- Spent 16 yrs at Apple and most recently led the genAI team at Meta that built the Llama model

- Built a custom AI agent to assistant with support issues and already seeing meaningful results

- AI-powered customer support has now been rolled out for English, French and Spanish speaking users across the US, Canada and Mexico.

- Already resolving a third of the support issues w/o needing a live specialist

- Resolution times are also “significantly faster”

- Looking ahead…expect an AI customer svs will not only be chat, but also voice (will be able to call and talk to an AI agent)

- It’s live across N. America and planning to roll it out globally later this yr

- Taking an “iterative” approach to building out AI-powered search

- Early tests are focused on giving guests a more natural way to describe what they’re looking for, and ask questions about the listing and location

- Over time, this will evolve into a more comprehensive and intuitive search experience that extends through the trip

- Expect chatbots are going to be a positive for Airbnb and NOT a competitive threat

- Traffic that comes from chatbots converts at a higher rate than traffic that comes from Google

- “I think these chatbot platforms are going to be very similar to search” and will be top-of-funnel traffic generators for Airbnb

- B/c the underlying AI models are widely available, Airbnb will be able to build its own AI features using its own data

- And Airbnb’s payments, verification systems, customer support, and unique inventory make the core platform difficult to replicate

- Also deploying AI internally…“more than 80% of engineers are now using AI tools. That soon will be 100%”

- What does success in AI look for Airbnb one year from now?

- “AI customer service will be voice and chat across all languages. It will have penetrated many more ticket types”

- “It will massively accelerate our innovation”

- “We’ll be as AI-native as any other company in our space or more”

- “Finally, the experience for guests and hosts will be materially better”

- Financial impact from investments in AI initiatives? “Our investment in AI will not affect the P&L”

Market Specific Updates…APAC Will Be Particular Focus Of International Expansion Strategy In 2026

- N.America saw MSD growth of Nights and Seats Booked (in-line w/ Q3)

- Driven by continued “strong” demand for domestic travel and trips with longer lead times

- ADR in N. America increased +5% y/y (in-line w/ Q3), primarily driven by mix shift

- Growth in short-term stays and entire homes, particularly listings with 4+ bedrooms, continued to outpace long-term stays (trips of 28 days or more) and private rooms, respectively, helping to drive the mix shift

- “Heading into 2026, we continue to see great momentum for North America at large. And it is one of the underpinning points of our optimism around 2026”

- EMEA saw HSD growth in Nights and Seats Booked (accel from MSD growth in Q3)

- Seq acceleration was due to a broad improvement in demand across both core and expansion markets, including key countries like the UK, Spain, and Italy

- ADR in EMEA increased +12% y/y (accel from +10% y/y in Q3), primarily driven by FX

- Latin America saw high-teens growth in Nights and Seats Booked (decel from low-20s growth in Q3)

- ADR in Latin America increased +9% y/y (accel from +4% y/y in Q3), primarily driven by FX and price appreciation

- In Brazil, continued to drive “meaningful growth” across the region, with origin nights booked increasing 20%+ y/y and first-time bookers increasing +17% y/y (second largest contributor to first-time bookers in Q4, behind US)

- In Mexico, saw a strong seq accel of growth in origin nights booked in Mexico and up high-teens y/y

- Asia Pacific saw mid-teens y/y growth in Nights and Seats Booked (in-line w/ Q3)

- ADR in Asia Pacific increased +2% y/y (in-line w/ Q3), primarily driven by price appreciation

- In Japan, saw continued strength in domestic travel

- In India, nights booked on an origin basis grew +50% y/y and first-time bookers grew 60%+ y/y

- “The broad story on APAC is it is stable. We are seeing some very positive signs in particular markets that we’re leaning into and it’s the focus of our international markets expansion strategy going forward”

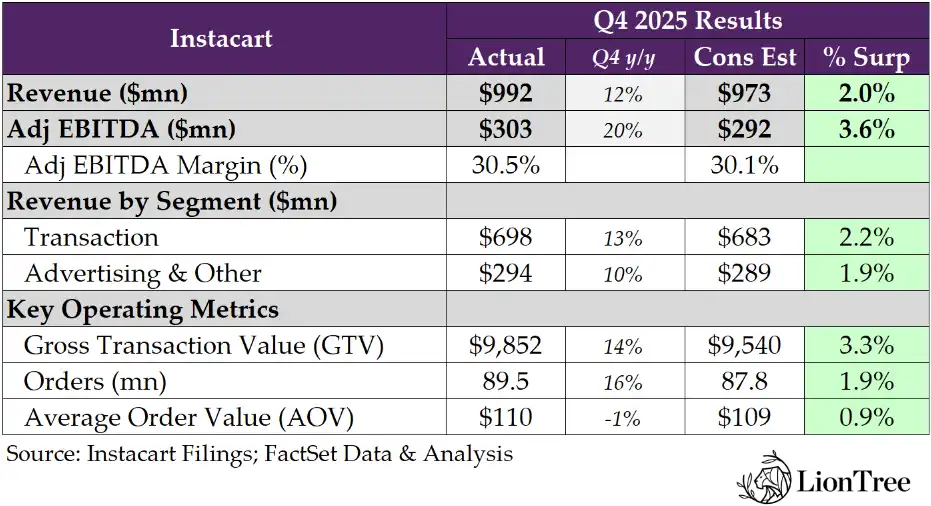

Instacart Executes Despite Fears Of Heightened Competition

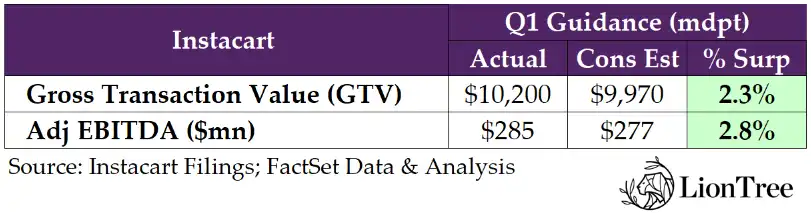

In the face of increased competition concerns, Instacart bagged a blockbuster quarter. In Q4, the Co delivered +14% y/y GTV growth (its strongest in three years and +3% ahead of expectations) alongside revenue and adj EBITDA that beat cons by +2% and +4%, respectively. And growth and profitability are scaling together as orders rose +16% y/y to 89.5mn, engagement reached new highs in December, and margins expanded to 30.5% (up from 29.6% in Q3). That momentum is expected to carry into Q1, albeit with some expected deceleration of GTV growth to +11-13% y/y. On the other hand, Advertising & Other revenue is expected to accel from +10% y/y in Q4 to +11-14% y/y in Q1 and Q1 adj EBITDA guidance was roughly +3% ahead of Street expectations.

Digging into the quarter, it was a story of continued strength in executing their playbook. Strength is ongoing in their core grocery delivery as Marketplace continues to grow, perfect order fill rates continue to improve, and engagement continues to deepen amongst both new and existing customers, all while average order value (AOV) stayed steady at ~$110. Regarding the increased grocery efforts by players like Amazon, Uber and DoorDash, mgmt called the sentiment around the competitive impact “overblown,” with Instacart’s strength in large baskets (75% of the mkt) intact. They’re finding that competitor offerings are “geared towards smaller fill-in orders” and specifically called out that Amazon’s biggest source of grocery customers are from in-store, NOT from Instacart. While they are keeping a close tab on the changing marketplace, mgmt. reminded investors that 80% of their GTV already comes from non-exclusive retailers and multi-platform participation is already embedded in their long-term strategy and guidance.