This week seemed like it would never end with the last full-on barrage of earnings prints within the sector! In the background (or foreground for that matter) was the incredibly volatile market environment. The VIX (a key metric for market expectations of volatility) closed at $20/share but spiked to an intra-day high of $66/share on Monday on the back of the global market meltdown. After ebbing and flowing throughout the week, the major indices ended almost flat versus last Friday’s close (the Dow -0.60%, S&P -0.04%, and Nasdaq -0.18%). Whether or not we are headed into a recession was the pivotal debate all week. The most current tally seemed to be that the market is pricing in a -50bps cut during the Fed’s September meeting.

There was an incredible amount of new information to digest and make sense of this week. There was actually more out than we could even take a look at!

In addition to the media earnings-palozza, which was a big focus, we spent time on last mile & grocery delivery, online travel, music, and more. See below for the key focus themes in this edition (all links are clickable):

- Earnings Scorecard – Week 4

- Disney’s Entertainment Division Takes The Torch For The Next Near-Term Leg

- What Is The Value For Linear Networks? WBD & PARA Take Big Write-Downs

- Fox Came Out On Top Vs Peers This Qtr And Is Well Positioned For The Political & Sports Cycle Ahead

- WMG Pulls Ahead With A Favorable DSP Mix Vs Peers

- Instacart Holds Its Lead In The Highly Sought After Online Grocery Delivery Market

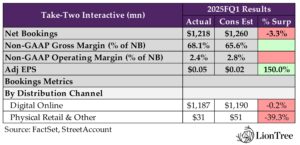

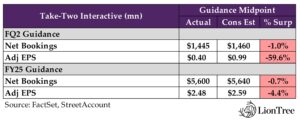

- Take-Two Is Laying The Foundation For “Tremendous Growth” In FY26 & FY27

- After Q1’s Net Income Detour, Uber Is Back On Course

- EXPE/ABNB: Further Data Points Regarding Slowing Travel Demand Heading Into H2:24

- Some Additional Quick Hits From This Week’s Earnings

This is another jam-packed edition. I personally will need the weekend to recover 😊

I hope you have a nice weekend.

Best,

Leslie

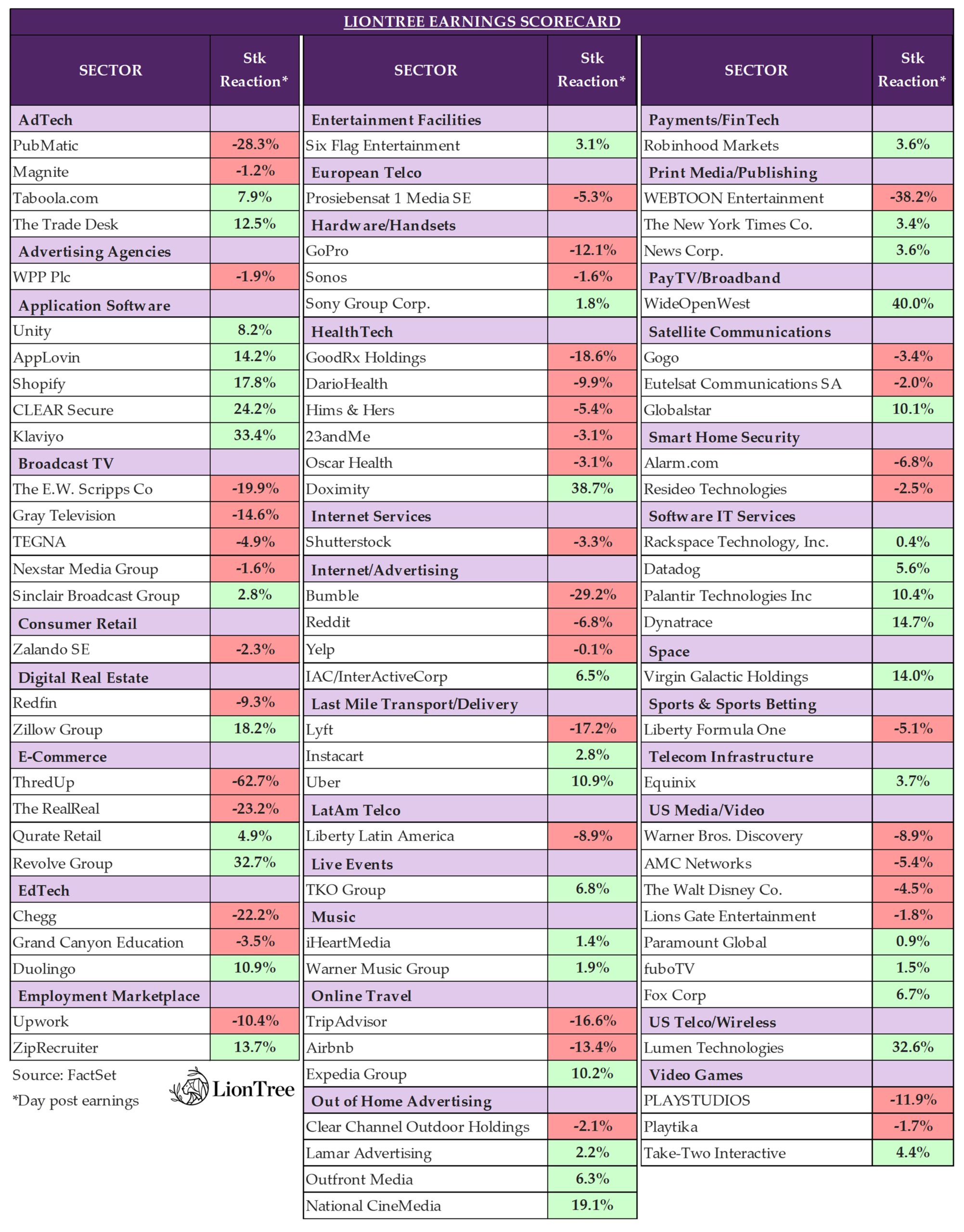

Earnings Scorecard – Week 4

People living in the northeast of the US weren’t the only ones to witness a downpour this week – it was also raining cats and dogs on the earnings front this week, with a record 84 companies in our LionTree Universe reporting their results (which was even more than the massive 56 companies that reported last week). Price reactions were almost split down the middle, though slightly balanced to the downside, with 43 companies (51.2%) trading down post their prints, and 41 companies (48.8%) trading up. Doximity was the best performer, trading up +38.7% the day after it reported, while ThredUp was the worst performer, down -62.7%.

Media dominated the earnings circuit this week, with several big prints hitting the tape. Fox was the first to report and was the best performer in the sector, trading up +6.7% in reaction (see Theme #4) followed by Disney the next day, which went the other direction and traded down -4.5% (see Theme #2). Warner Bros. Discovery was the worst performer in the group and traded down -8.9%, and Paramount closed out the week, up +0.9% (see Theme #3). Also in the media space, but on the music side, Warner Music Group traded down -0.9% (see Theme #5) after its print.

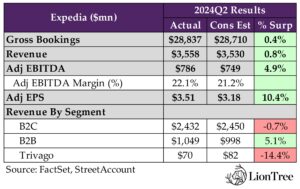

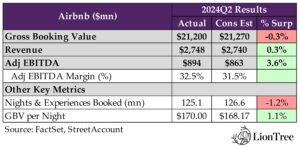

There were also a couple big prints in the last-mile/delivery sector this week, with Uber and Instacart both trading up +10.9% and +2.8%, respectively, in reaction to their earnings (see Theme #8 and Theme #6). Over in online travel, Expedia and Airbnb went in different directions, with the former trading up +10.2% and the latter trading down -13.4% (see Theme #9). In interactive entertainment, Take-Two’s earnings report led the stock to rise +4.4% (see Theme #7).

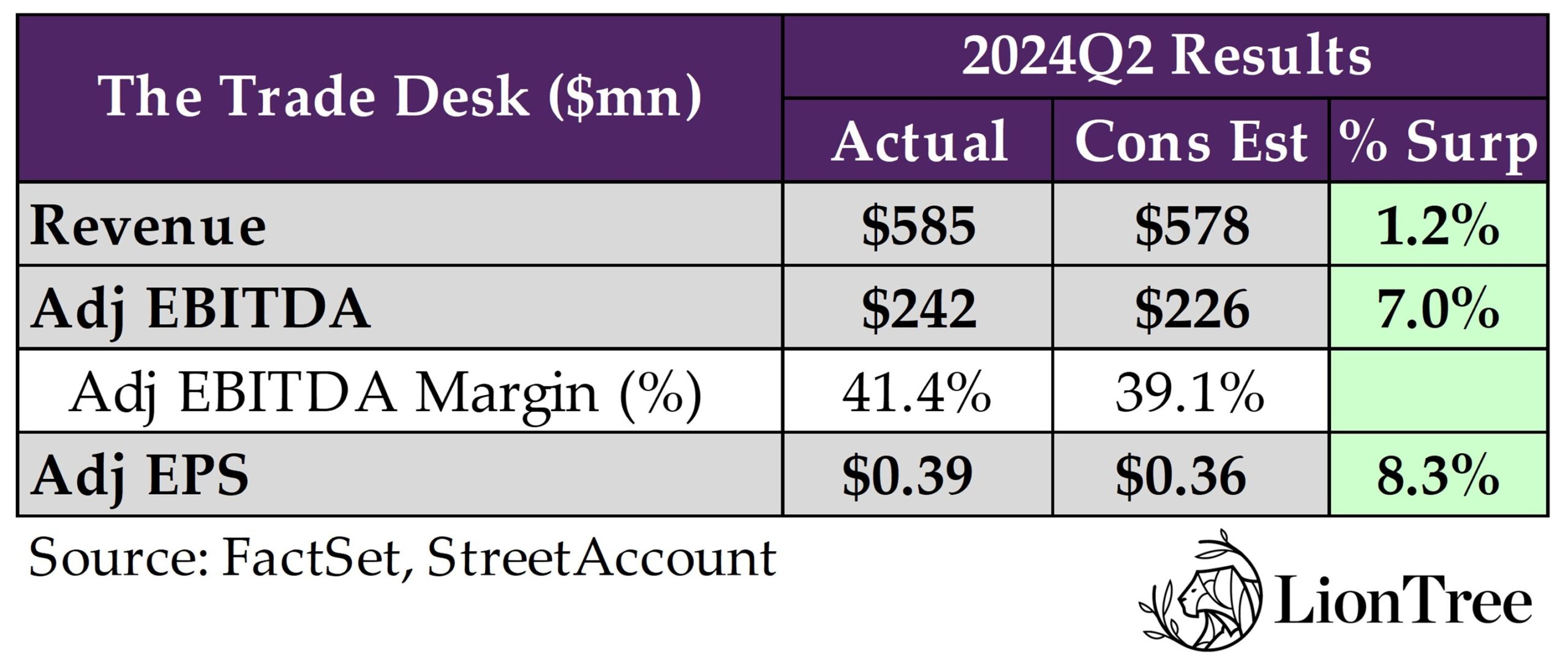

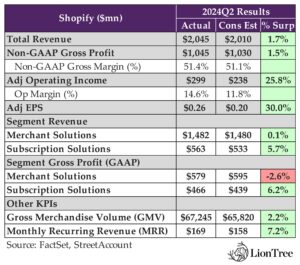

We also took a quick look at Shopify and The Trade Desk, which soared +17.8% and +12.5%, respectively, after their reports (see Theme #10).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Disney’s Entertainment Division Takes The Torch For The Next Near-Term Leg

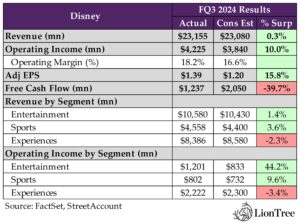

It was certainly the earnings storm in Large Cap Media this week with Disney, Warner Bros Discovery, Fox, and Paramount all reporting results. Starting with Disney, one of the biggest focus areas from its FQ3 update was the disappointing domestic parks trends, which dragged down the Experiences business (segment revenues and adj op income missed by -2.3% and -3.4%, respectively), and these headwinds are expected to persist over the next couple of qtrs. Experiences op income is guided to drop by ~-msd% in FQ4 due to the softening of demand in the domestic theme parks, a slowdown in Paris due to the Summer Olympics, and cyclical softening in China. This was a hot button for investors, as the update was on the heels of Comcast’s Universal Studios Parks’ weaker than expected results and near term outlook, which was mostly due to lower domestic park attendance (see Theme #7 from July 26th Weekly). But also, like Comcast, Disney mgmt remains bullish on the business return profile within this segment longer term and continues to invest.

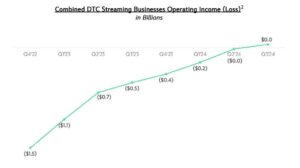

With the Theme Parks business in a bit of the doldrums, the Co is now relying on the Entertainment segment to carry the torch in the near term, and a highlight on that front was that the Co’s combined streaming businesses reached profitability for the first time since launching in the fall of 2019 (posted FQ3 op income of $47mn vs a loss of -$512mn in the year-ago period). We’d note that better profitability in ESPN+ helped Disney get over the finish line. Without it, the DTC streaming unit would have seen a loss of -$19mn. Importantly, streaming profitability is expected to continue into FQ4, and Disney continues to work towards achieving double-digit margins, which will be helped by another round of price hikes that the company is implementing across nearly all of its streaming plans in October, in addition to other initiatives like password sharing crackdown, improvements to technology features, and more. A standalone ESPN streaming offering remains on track for the fall of 2025.

Also, it looks like Disney’s strategy to focus on quality over quantity in its studio business is starting to work. Disney’s theatrical film division posted its first profit since early 2022. Pixar’s Inside Out 2’s performance has become the highest-grossing film globally of all time. Disney expects other hits in the coming quarter with the release of Deadpool & Wolverine, which generated the highest-ever box office gross for an R-rated movie when it opened last month and has earned $824mn in the global box office thus far. They have a full slate looking out the next several years and are particularly excited about Moana 2 and Mufasa: The Lion King in the nearer term.

Based on the qtrly results, Disney raised its full-year EPS growth guidance to +30% from the prior +25% and continues to make progress on its $7.5bn+ annual cost saving initiatives.

In addition to the above highlights, there were several additional updates across advertising, sports rights, and more that we thought were important. See below. For thoughts and perspectives on Warner Brothers Discovery and Paramount, see Theme #3, and for more on Fox, see Theme #4.

-> It was a mixed bag in terms of reactions to large cap media results… Disney shares fell -4.5% post-results and Warner Bros Discovery fell -9%, but Fox was up almost +7% and Paramount was up almost +1%

Disney’s Headline FQ3 Beats (Especially On Profitability) & The Co Raised FY EPS Guidance Once Again, BUT…

- Profitability came through with ~in-line revs: Total op income beat by +10% while total revenue was +0.3% ahead of consensus; Adj EPS beat by +16%

- The revenue and op income beat was driven by Entertainment and Sports; Experiences missed on both fronts

- Raised the full year adj EPS growth target again: To ~+30% y/y, up from the prior guidance provided last qtr of over +25% and the two-qtr prior guidance of “at least” +20% y/y

- Maintained FCF guide of $8bn for the fiscal year

- Regarding the $7.5bn+ annual cost saving initiative: “Continue to focus on driving incremental cost savings above and beyond our previously stated target as we deliver on our strategic priorities”

The Bigger Focus Was On The Softness In Domestic Parks, Which Is Expected To Persist In The Near-Term

- The Experiences business disappointed on both revenue and op income in FQ3: Revs incr’d +2% y/y and missed cons by -2.3%, and op income fell -3% y/y and missed cons by -3.4%: Parks and Experiences op income fell -4.4% y/y, while Consumer Products op income incr’d +2% y/y

- What happened? Rev growth was impacted by moderation of consumer demand at domestic parks towards the end of FQ3 that exceeded previous expectations, though Disney Cruise Line, Consumer Products, and some int’l sites improved y/y

- FQ3 Parks & Experiences breakdown by geography –

- Domestic rev grew +3% y/y but op income fell -6% y/y

- While results decreased “modestly” in the qtr, attendance was comparable y/y and per capita spending was slightly up

- What drove the op income decrease? Higher costs driven by inflation, increased technology spending and new guest offerings, partially offset by the comparison to depreciation in the prior-yr qtr related to the closure of Star Wars: Galactic Starcruiser and cost saving initiatives

- International rev grew +5% y/y, while op income grew +2% y/y

- Domestic rev grew +3% y/y but op income fell -6% y/y

- FQ4 outlook – Expect that the demand moderation seen in the domestic businesses in FQ3 could impact the next few quarters

- Expect FQ4 Experiences segment op income to decline by ~-msd% y/y: This decline reflects underlying dynamics that impacted FQ3, as well as impacts at Disneyland Paris from a reduction in normal consumer travel due to the Olympics, and some cyclical softening in China

- On consumer trends: “The lower income consumer is feeling a little bit of stress. The high-income consumer is traveling internationally a bit more. I think you’re just going to see more of a continuation of those trends in terms of the top line”

- Are “actively monitoring attendance and guest spending and aggressively managing our cost base”

- Also expect “a flattish revenue number in FQ4” for the Experience segment

- Expect FQ4 Experiences segment op income to decline by ~-msd% y/y: This decline reflects underlying dynamics that impacted FQ3, as well as impacts at Disneyland Paris from a reduction in normal consumer travel due to the Olympics, and some cyclical softening in China

- Looking past FQ4 – “I don’t think I’d refer to it as protracted, but just a couple of quarters of likely similar results… I would just call this as a bit of a slowdown that’s being more than offset by the Entertainment business”

- In the long-term – “Despite recent economic uncertainty that is impacting consumers, we remain confident about the long-term opportunities before us”

- New cruises line offerings – The Co will debut the Disney Treasure and Disney Adventure in FY25 and the Disney Destiny in FY26

- Have continued to see strong demand at Disney Cruise Line so far this qtr, though results in FQ4 will reflect pre-launch expenses for Disney Adventure and Disney Treasure

- Further expanding cruises across Asia: Disney Adventure will be based out of Singapore; Also recently announced an agreement with the Oriental Land Company to bring their Cruise Line to Japan

- “Do have some expenses attached to our ships coming in and that will affect us a bit in 2024 and a bit in 2025”

On A Positive Note, Streaming Turned A Profit For The 1st Time In FQ3 And Is Expected To Sustain in FQ4 / The Paid Sharing Initiative Has Started

- FQ3 overall Entertainment segment rev grew +13% y/y, while op income nearly tripled y/y in FQ3 due to “significantly” improved results at both DTC and Content Sales/Licensing and Other

- Results at Entertainment DTC were “stronger than anticipated” with rev up +15% y/y and op income improving by ~+$500mn y/y to a loss of -$19mn, driven by growth in subscription and ad rev, in addition to “strong” cost mgmt

- Content Sales/Licensing and Other results came in “well above” guidance, as despite rev being down -4% y/y, op income was up ~+$350mn y/y, primarily due to the performance of Inside Out 2

- The combined streaming biz reached profitability in FQ3 (ahead of guidance): Driven by “better-than-expected” performance in DTC Entertainment, combined with profitable results at ESPN+

- Expect profitability across the overall Entertainment segment in FQ4 as well

- The combined streaming biz is on track for profitability to improve in FQ4

- Content Sales/Licensing and Other is expected to see profitability in FQ4 that’s “roughly similar” to FQ3 and further expect profitability for the full fiscal yr 2024

- Disney+ Core BEAT on subscribers and ARPU; Expect modest growth next qtr

- Disney+ Core subscribers beat by +0.7%: Incr’d seq by +0.7mn (vs +6.3mn q/q in the prior qtr)

- Domestic: Added +0.8 subs q/q (vs +7.9mn q/q in prior qtr)

- International (ex-Hotstar): Lost -0.1mn subs q/q (vs -1.6mn q/q in prior qtr)

- Disney+ Core ARPU beat by +1.5%: Decr’d seq by -$0.06 (vs +$0.44 q/q increase in prior qtr)

- Domestic: Fell from $8.00 in FQ2 to $7.74 in FQ3 due to the impact of subscriber mix shifts (bundling and shift to ad model)

- International (ex-Hotstar): Incr’d from $6.66 in FQ2 to $6.78 in FQ3 due to increases in retail pricing, partially offset by an unfavorable FX impact

- Disney+ Hotstar: Incr’d from $0.70 in FQ2 to $1.05 in FQ3 due to higher ad rev

- FQ4 Outlook – Expect Disney+ Core subscribers to grow “modestly” in FQ4

- Disney+ Core subscribers beat by +0.7%: Incr’d seq by +0.7mn (vs +6.3mn q/q in the prior qtr)

- Hulu SVOD Only beat on subscribers, while Hulu Live TV + SVOD missed / Both beat on ARPU

- Total Hulu subscribers were in-line with expectations at 51.1mn

- Hulu SVOD Only: Added +0.9 subs q/q (vs +0.7mn q/q in prior qtr)

- Hulu Live TV + SVOD: Lost -0.1mn subs q/q (vs -0.1mn q/q in prior qtr)

- ARPU beat in both segments

- Hulu SVOD Only: Incr’d from $11.84 to $12.73 due to higher ad rev

- Hulu Live TV + SVOD: Incr’d from $95.01 to $96.11 due to higher ad rev

- Total Hulu subscribers were in-line with expectations at 51.1mn

- ANOTHER set of price hikes are coming in October – “We’re seeing growth in consumption and the popularity of our offerings, which gives us the pricing leverage that we believe we have… We do feel like we’ve earned that pricing in the marketplace”

- Prior price increases have been successful: Have only seen “modest churn” and “nothing we would consider significant” from previous price increases

- Pricing levers have and will continue to increase: “We believe that as we add these new features like the channels that we’re going to be adding later this year… and the success of our movie slate …that the pricing levers that we have has actually increased”

- Confident in the journey to double-digit margins… have “multiple building blocks” for improving margins over the coming years (did not specify a timeline), including but not limited to –

- Increasing pricing this fall “to further align with the value we are providing to consumers”

- Product updates and features designed to increase engagement and reduce churn, including playlists, adding News, the ESPN tile on Disney+, and bundles (“bundling has had a positive impact on churn”)

- Technology enhancements, including improving their recommendation engine and making their marketing more efficient

- Continuing to grow their subscriber base, including by operationalizing paid sharing, which started in June and kicks in “in earnest” in September (“we’ve had no backlash at all”)

Strength In ESPN+ Drove Combined Streaming Biz Profitability / Renewed Deal W/ NBA & WNBA Will Bring “Tremendous” Value

- Sports FQ3 rev grew +5% y/y, while op income fell -6% y/y: Op income would have grown by +4% y/y ex-Star India results, which were lower y/y driven by the timing of the ICC linear rights costs

- Domestic ESPN rev was up +5% y/y

- ESPN+ generated positive results and contributed towards profitability of the combined streaming biz

- Expected to be profitable in Q4 as well

- Key FQ3 ESPN watch stats –

- ESPN was the #1 cable network for adults 18-49 in total day audience for the 13th consecutive qtr

- Had the most watched FQ3 in primetime in a decade among adults 18-49

- Disney was responsible for 46% of total sports viewing minutes among adults 18-49 in FQ3

- On the 11-yr right extension w/ NBA and WNBA – did not go into specifics about profitability in the early yrs, “but there’s tremendous value in this deal”

- Still have one more yr on the current deal – “We have the finals for 12 years, and they drive significant value for us”

- “Deal reflects the value of live programming… also reflects the growing value of basketball and the growing value of women’s sports as a large WNBA component to this”

- “It secures our ability to bring ESPN in the digital direction, particularly as we look to launch flagship sometime at the end of 2025”

- “We believe that by the time this kicks-in in a year from now, that a lot of the pieces will be in place in terms of driving more advertising revenue, more distribution revenue, moving to digital”

- “We’ve [also] secured international rights particularly to the finals not in every market around the world, but in most markets. And that will drive some added revenue as well”

- Interest in the NBA is growing “significantly” across the globe, in part b/c of growth in intl player representation across NBA teams – “We look forward to presenting NBA games, including the Finals, in many markets around the world”

- Will distribute NBA games on ESPN-branded platforms in several intl mkts…: Including LatAm, sub-Saharan Africa, Oceania, and the Netherlands

- … As well as via Disney+ in select markets in Asia and Europe

- Will launch ESPN tile onto Disney+ in December: “Will serve as another access point for our sports content and allow for greater audience expansion. We see this as a first step to bringing ESPN to Disney+ viewers”

- “Broken record” on strategic partnership talks for ESPN: “Believe it or not we’re still having conversations about it. We thought and continue to believe there may be opportunities to partner with others, particularly on the content side and that’s why we’ve continued to add to explore it. But nothing more to add”

- Update on standalone ESPN streaming offering? “Continue to ready the launch of our enhanced standalone ESPN flagship streaming service for the fall of 2025”

- Subscribers to the svs will be able to see ESPN’s full package of sports programming, including NBA and WNBA live events and programming, in addition to digital features such as fantasy sports, enhanced statistics, betting, and e-commerce

Saw “Strong” Upfront Results And Views The Ad Market As Healthy

- “The ad market is really, really strong and healthy for us” – Overall ad rev was up +8% y/y: In terms of categories, financial services and consumer products, consumer services and technology are all doing “very well”, while auto “is a little bit softer”

- DTC ad rev was up +20% y/y, reflecting growth across Disney+ Hotstar, Disney+ Core, and Hulu

- # of domestic streaming advertisers grew by more than 20% y/y, largely driven by automation, while programmatic revenue growth increased by 80%+

- ESPN domestic ad rev grew +17% y/y

- DTC ad rev was up +20% y/y, reflecting growth across Disney+ Hotstar, Disney+ Core, and Hulu

- Overall upfront rev rose +5% y/y, driven by sports and streaming

- 40%+ of total upfront dollars committed this year are addressable, inclusive of streaming and digital

- Introduced a Disney Streaming Entertainment ad offering, which matches advertising oppties with impressions that are served across their family of streaming apps, maximizing supply against premium audiences and outcomes

- “We’re selling audiences rather than just selling streaming channels, which enables advertisers to more effectively target the audiences that they’re seeking”

Studios Had A Blockbuster Qtr As “Focus On Improving Quality Has Yielded Tremendous Success”

- Released the #1 titles in May, June, and July – Pixar’s Inside Out 2, Marvel’s Deadpool & Wolverine, and 20th Century Studios’ Kingdom of the Planet of the Apes earned a collective $2.8bn at the global box office

- Inside Out 2 has grossed $1.5bn+ globally, making it the highest-grossing animated film ever and among the top 10 biggest movies of all time

- Deadpool & Wolverine had the biggest opening weekend for an R-rated film ever ($444mn globally) and has grossed $850mn+ globally in less than 2 weeks

- This gives Disney five of the top six opening weekends of all time

- Full slate of films in the docket in 2024, 2025, and 2026

- Later in 2024: Moana 2; Mufasa: The Lion King

- 2025: Captain America: Brave New World; Thunderbolts; The Fantastic Four: First Steps; Zootopia 2; Avatar 3

- 2026: Avengers: Doomsday; A new Star Wars movie featuring the Mandalorian and Grogu; Toy Story 5 (the first Toy Story movie since 2019)

- Since 2005, Disney has released more films that have earned $1bn+ (27) than the rest of the entertainment industry combined (22)

- Theatrical successes are causing “a multiplier effect” that “contribute to our growth and improved financial performance in streaming [and] should also positively impact churn and engagement”

- In the lead-up to and following the theatrical release of Inside Out 2, millions of viewers turned to Disney+ to watch the original Inside Out film from 2015, driving 1.3mn+ Disney+ sign-ups and generating 100mn+ views of the original film globally since the first Inside Out 2 teaser trailer dropped

- Saw “heightened viewership” of the original Deadpool films with the release of Deadpool & Wolverine

- Expect similar engagement with the upcoming releases of Moana 2 and Mufasa: The Lion King

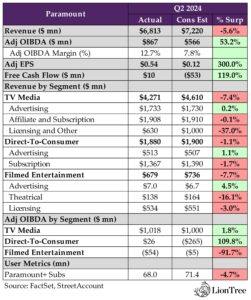

What Is The Value For Linear Networks? WBD & PARA Take Big Write-Downs

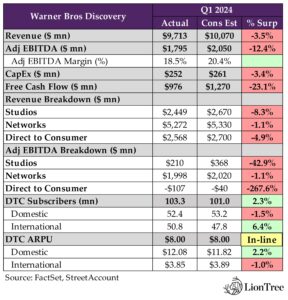

The downpour of media earnings post Disney’s results continued through the week, and our next deep dive is into Warner Bros Discovery (WBD) and Paramount’s results. One of the biggest focus areas and common threads was the revised valuations of their respective cable businesses, with WBD taking an enormous $9.1bn goodwill impairment charge on its Networks business and Paramount taking a $6bn charge in its TV Media business. Clearly this raises a lot of questions about further write-downs in the space and what the ultimate valuations of these businesses will be.

Stepping back and looking more broadly at the companies’ operational performances, starting with WBD, it was a tough quarter all the way around, with the Co posting headline results that missed consensus across all segments on both revenue and profitability. FCF also missed by -23.1%, and headwinds are expected to persist in H2, driven by several factors, including y/y strike-impacted comps and the Olympics. As a result, the timeline for achieving their 2.5-3x gross leverage target will likely take longer than expected.

Streaming is of course a huge focus area, and Max added +3.6mn subscribers in the qtr, driven by international as domestic actually lost subscribers q/q. While DTC profitability swung to a loss in Q2 (negative surprise), it’s expected to ramp into positive territory in H2, and mgmt remains confident in their target for $1bn+ in DTC adj EBITDA by 2025. They have several levers they can rely on, with the biggest being their international rollouts (expect the “bulk” of total subscriber growth to be international moving forward), as well as a password sharing crackdown, price raises, and more.

One thing in particular that investors were curious about was the speculation about potentially splitting up the company. While management said they are always open to engaging in potential discussions, they emphasized that their focus is on the one Warner Bros Discovery strategy and that it takes time for all the efforts they’ve been making over the past 2.5 years to show through. Over time, they believe that the corporate structure will become a “secondary consideration”.

There were several additional WBF updates that we thought were interesting across the content slate, Olympics, gaming, NBA rights lawsuit, and more, which we outline below.

Moving to Paramount and its underlying financials, the top-line remains in flux in many ways, as total revenue came in -6% below consensus, with lower results across all segments (and was down -11% y/y). Driving higher profitability was the key upside driver (as was the case last qtr as well), with adj OIBDA a huge +55% ahead of Wall Street forecasts. The biggest contributor to that was the Direct-to-Consumer (D2C) business surprisingly breaking into the black, reaching profitability for the first time. However, this won’t sustain into H2, as sports content spend cyclically ramps, but the Co is still confident in achieving P+ domestic profitability for the full year 2024. This will help drive “significant” growth in total company OIBDA for FY24, and FCF will grow y/y in 2024.

Also incremental within the streaming business was that Paramount+ (P+) lost -2.8m subscribers sequentially during the period, as they exited a South Korean partnership and experienced churn from subscribers who had joined in Q1 for the Super Bowl. That said, growth is expected to return in H2. Price increases are helping to drive P+ ARPU (globally was up +26% y/y), and the most recent price increase will positively impact the P&L in Q4. All in all, P+ subscription revenue rose +50% y/y (consistent with the Q1 growth rate). Paramount also provided some details on its recent carriage agreement with Charter.

We highlighted other key points below regarding the Co’s advertising biz, linear affiliate agreements, and more. But it’s also worth noting that while the Paramount/SkyDance deal is not expected to close for some time, the Co is moving ahead with its strategic plan to streamline the organization, transform D2C, and optimize the asset mix. Paramount announced a -15% cut to its US-based workforce, starting the coming weeks, which clearly shows that its cost out plan is aggressively underway. These transformations never take a straight line, and investors will want to see many proof points along the way…

See below for 2 sections…1) a deep dive on Warner Brother Discovery and 2) a deep dive on Paramount…Also, see Theme #2 and Theme #4 for thoughts and perspectives on Disney and Fox’s results, respectively.

-> WBD felt some heat, trading down -9% in reaction to earnings while Paramount was up nearly +1%; In comparison, Disney shares fell -4.5%, while Fox was up almost +7%

1) WARNER BROS DISCOVERY (WBD) – See below for what we thought was most important and incremental from its results and conference call

WBD – A Tough Q2 On All Fronts

- Consolidated revs missed by -3.5%: Fell -5% y/y (vs -7% y/y in Q1)

- All three segments missed

- Adj EBITDA missed by -12.4%: Fell -16% y/y (vs -19% y/y in Q1)

- All three segments also missed

WBD – Expect FCF Headwinds To Persist Into H2 / Increased Timeline To Get To The Gross Leverage Target

- FCF decreased by -$746mn y/y in Q2 and missed expectations by -23.1%

- What drove the decrease? Lower operating profits, partially offset by lower restructuring costs, as well as higher net content investment, in part due to the prior year benefit from the WGA strike

- Some puts and takes regarding FCF in H2 – “Cash conversion will certainly be lower than the very elevated levels last year”

- Will have their normal semiannual cash interest payments in Q3

- Will be comping against the most strike impacted quarters last yr

- Olympics will be a “meaningful” drag on FCF in Q3, including in part due to working capital dynamics

- Primary use of FCF will continue to be debt paydown: “With a weighted average maturity of nearly 14 years and an average cost of 4.6% and with our strong free cash flows significantly greater than our maturities in any given year for the foreseeable future, we have an advantageous capital structure to support our transformation and the growth opportunities ahead”

- Timeline to gross leverage target may be longer than previously expected…: “Have not wavered” in commitment to achieving 2.5-3x gross leverage target, but may come at “a longer timeframe than previously anticipated” (ended Q2 at ~4x)

- … “That said, I remain confident in our ability to continue to both generate meaningful FCF in the second half and pay down debt, and we expect to finish the year at lower net leverage than at the start of the year”

WBD – Takes A Massive $9.1bn Write-down On TV Networks In Q2

- Took a $9.1bn non-cash impairment charge against the carrying value in the Networks segments

- How did they get there? WBD’s balance sheet carries “significant” amounts of goodwill created over a series of past M&A transactions, including the formation of WBD in 2022, and the regular monitoring of the value and use of assets

- Impairment charge was driven by “a number of triggering events”, including the difference between their current market cap and the book value of the Co, continued softness in the US ad market, and uncertainty related to affiliate and sports rights renewals

- How did NBA negotiations play into this? “There is no one factor that is driving this impairment,” though “discussion” around the NBA rights had “come into play as a triggering event;” Ultimately, it was a “full reevaluation” of the value of the networks, “not a response to one individual factor”

- Impairment charge “reflects the value shift across business models”: While they are “certainly not dismissive of the magnitude of this impairment,” it reinforced their “conviction and confidence in the growth and value opportunity” across their Studios and DTC bizs “have never been stronger”

- “This is really a distribution ecosystem in transition, not a content ecosystem in transition”: Using their content increasingly more successfully in the streaming space and less so on the linear side; “The goodwill impairment at the end of the day is the accounting reflection of that state of the industry and our strategy”

- “It’s fair to say that even two years ago, market valuations and prevailing conditions for legacy media companies were quite different than they are today, and this impairment acknowledges this and better aligns our carrying values with our future outlook”

WBD – Always Open To Strategic Partnership Discussions But Remain Optimistic About One Warner Bros. Discovery Strategy

- “You shouldn’t be surprised to see us engaging in partnership discussions… where it makes sense, you have seen us engage in those things”

- On speculation about a potential splitting up the Co – “The focus is on running the business”

- But it takes time for efforts to show through: “You will see as our Studio begins to grow and if our global Direct-to-Consumer business scales the way we believe it’s going to, then that will be very apparent to investors and we expect that that will create shareholder value”

- Studios: Across gaming, film, and TV production, “it takes a little longer to see the results of the very significant changes that the team has been making”

- DTC: “We’re really starting to see the fruits of our labor”

- “The Studio and the DTC segment have… tremendous value opportunity, and once we start seeing more evidence for that and seeing more materialization of that value, I believe that corporate structure is actually a secondary consideration”

WBD – DTC Was The Highlight For Advertising

- Q2 total ad rev fell -3.5% y/y, which was a seq improvement from -6.5% y/y in Q1

- DTC ad revs was up +98% y/y (accel from +70% y/y in Q1), on continued strong demand for Max inventory and the addition of sports content, which drove healthy engagement

- Looking ahead: Expect “meaningful” growth ahead as more subscribers opt for the ad-lite tier, which represented 40%+ of global gross adds in Q2

- Networks ad revs were down -9% y/y (improved from -11% y/y in Q1), as domestic impressions declined -13% during the qtr and were partially offset by strong sports-related pricing

- Looking ahead: Not seeing a lot of change in the linear ad mkt in the US and Q3 is typically a weaker qtr given the timing of sports; Europe is “actually looking almost surprisingly strong in some of the markets. That’s definitely a positive outlier” but visibility is not high enough to give any predictions

- “Tying this back to the impairment conversation, this is another great example of how pressure on one segment goes hand-in-hand with tailwinds in another”

- DTC ad revs was up +98% y/y (accel from +70% y/y in Q1), on continued strong demand for Max inventory and the addition of sports content, which drove healthy engagement

- On upfront – “We performed well relative to the industry”

- Max volume grew by ~50% as “clients continue to see great value in our upscale and younger skewing audience, as well as in sponsorship opportunities in award-winning content”

- In linear, did “especially well” in sports, “strong pricing and double-digit volume growth led by increased demand for our coverage of March Madness, Major League Baseball, NBA, the NHL, including the Stanley Cup Finals, and new properties like NASCAR and The French Open”

- Looking ahead – “While trends across our advertising business continue to reflect the bifurcation in the broader ad market, we remain encouraged by the healthy momentum and growing scale we see in streaming”

WBD – DTC Growth Is Being Driven And Is Expected To Continue To Be Driven By International / Expect Profitability To Inflect In Q3 Onwards

- Max added +3.6mn subs in Q2 to reach 103.3mn (beat by +2.3%): Acceleration from +2mn subscriber adds in Q1

- Intl drove q/q subscriber growth, as domestic lost subs: Domestic subscribers fell by -0.3mn, while intl subscribers grew by +3.9bn

- Saw a “modest” uptick in churn after March Madness and the conclusion of the NDA and NHL season, which was expected

- Continue to expect the “bulk” of total subscriber growth to emanate from outside the US BUT expect to see monetization gains from all regions “with perhaps the biggest upside opportunity domestically, at least in the near-term”

- Intl drove q/q subscriber growth, as domestic lost subs: Domestic subscribers fell by -0.3mn, while intl subscribers grew by +3.9bn

- DTC profitability swung to a loss in Q2…: Adj EBITDA came in at -$107mn, vs Q1’s $86mn

- This was a big miss vs cons -$40mn

- … But expect a “strong ramp” to positive adj EBITDA in H2 / Remain confident in $1bn+ DTC adj EBITDA by 2025 target – “This is a starting point, not an ending point”: “We’re finally, after two years of heavy investment, hard work, at the point where we’re ready to accelerate…we believe we are going to see an acceleration on the top line”

- “We have significant opportunity across every driver of the business”, including –

- Intl growth and rollouts in more mkts is “by far the biggest”

- “Continued momentum” behind their content slate

- Raising prices in the US and internationally

- Raised domestic ad-free by $1 and saw better-than-expected churn during July, when the price increased rolled through the existing subscriber base

- Changing some rev share agreements outside of the US

- “Historically in some of the wholesale agreements on the HBO side, we feel we’re underpriced”

- Rolling out ad-lite in more markets

- “Rolled it out in 39 markets across LatAm and handful of markets across Europe. We’re looking to roll it out in more markets. So, advertising will become a bigger and bigger play for us”

- Distribution agreements with more partners

- Password sharing crackdown

- Will start at the end of 2024 and bleed into 2025

- Stronger engagement fueled by a more personalized content discovery experience

- Continued expense discipline

- “That said… we will always prioritize investing to secure profitable Max subscribers versus maximizing near-term EBITDA in any given quarter or a year”

- “We have significant opportunity across every driver of the business”, including –

- Significant untapped intl TAM oppty – Max is now in 65 intl markets, but is still not present in almost half of the global addressable mkt, including “sizable” streaming markets where their content and franchises have “significant” fan bases like Australia, Japan, the UK, Germany, and Italy

- “We intend to continue our drumbeat of new market launches over the next 18 to 24 months”

- Will be launching in the UK at the end of 2025

- Have also been tapping into existing partnerships w/ intl distributors of their linear channels for Max: “Very active” in “reimagining” those existing partnerships, which help get Max on the devices of more consumers faster and at a fraction of the acquisition cost

- “Encourag[ing] them to support the distribution of Max in ways that are a true win-win for both parties”: Have done 150+ of these deals to date in Europe and LatAm, and “you’ll begin to see them really pay off and we have more to come”

- By H1:26, expect “the vast majority” of their rollout will have taken place

- On TAM oppty vs competition: “We talk about addressable market and the fact that our two bigger peers are in…100% of those addressable markets, we’re in just over 50% of them today…So, you have to do your own thinking of what our penetration and opportunity could be, but we’re about half of the addressable market today at 103mn subs”

- “We intend to continue our drumbeat of new market launches over the next 18 to 24 months”

- “Continue to lead” in bundling

- Launched a new bundle last month with Claro, the biggest cable distributor in Brazil, which offers Max, Netflix and Globoplay, the largest local streamer in the market, and Claro TV+

- Launched the Ultimate Bundle in the US two weeks ago, which includes Disney+, Hulu, and Max

- Rolling out Venu Sports in the fall with ESPN and Fox

- “We have one of our strongest lineups over the next two-plus years to support our global expansion”

- Q2 content highlights –

- House of the Dragon and the Hard Knocks franchise featuring the Giants have both done “incredibly well”

- Looking ahead –

- “Highly anticipated” HBO series, The Penguin, written and directed by Matt Reeves, premiering in September

- New Dune series coming in November

- “Blockbuster” international titles like the new series, City of God: The Fight Rages On, premiering later this month

- New seasons of hit shows, The White Lotus and The Last of Us coming next year

- Q2 content highlights –

WBD – Olympics Are A Hit And Driving Intl Max Sub Growth / Majority Of Costs Will Hit The Balance Sheet In Q3

- Purposely timed the launch of Max in Europe to capitalize on the attention around the Olympics: “It was a heavy lift and it paid off”

- 141mn people have engaged across their channels and platforms: Spanning linear, digital, social, and streaming; Broadcasting the games on Max and discovery+, on linear TV, and online through their Eurosport channels to 47 markets in 20 different languages

- “Max and discovery+ are the only place to watch virtually every minute of the Olympic Games, and it’s really worked for us”

- Response from consumers has “exceeded our highest expectations”, both in terms of subscriber growth and viewership

- Olympics have been a “huge” driver of growth internationally

- But the Olympics will weigh on financials in Q3 – “All of the costs are essentially recognized in the quarter where the games take place… [while] a lot of the benefits are generated over the entire eight-year period,”

- Expect “just over” -$100mn of negative impact on EBITDA, mostly at Networks

- Expect a “more pronounced” FCF impact on the negative side

- BUT expect better economics moving forward: Final Olympic Games under the agreement struck in 2015; New Olympics rights agreement will begin with the 2026 Winter Games, which is better aligned to their streaming and pay-TV platforms

WBD – Emphasized The Diversity Of WBD’s Sports Offering, Though The NBA Remains The Wild Card

- Added several new sports rights in the last 12 months: Including NASCAR, Roland-Garros Tennis, BIG EAST Men’s and Women’s Basketball, Mountain West Football, as well as College Football Playoff Games

- “All of this will help support the upcoming launch of Venu Sports”

- Details on NBA rights lawsuit were sparce: “We’re in a litigation, and at this point, we’ve handed it off to our lawyers. We have confidence in our position. The judge will decide whether…what we offered matched or not…we’re getting back to work and the lawyers will handle this, and the judge will decide and off we’ll go”

- Potential impact of losing NBA on Networks adj EBITDA? “…we have said in the past that the NBA is a profitable right, and we’ve been very clear about that…this is not the time to go into any level of detail”

WBD – Studios Are Still In The Midst Of A “Multi-Year Turnaround” But Bullish On Upcoming Slate From New Mgmt Team

- Q2 Studios rev and adj EBITDA fell y/y: Down -5% and -31%, respectively

- Looking into H2: While the strike impact will present a favorable y/y comp on adj EBITDA during the second half of the year, it will be a headwind to cash content spend

- On the Warner Bros TV side – Currently have close to 90 live action scripted, unscripted, and animated series for nearly 20 different platforms in production

- Only studio with shows on every major platform industry-wide, including Presumed Innocent on Apple TV+, which is now the number one drama series in the history of the platform.

- Television was down y/y…: “Particularly as we work through the last of the strike delayed delivery”

- … But expect a “big swing up” in H2:

- Strike-impacted comps: “We’re now coming into the part of the year that was deeply impacted by the strike last year, so that should be a helper”

- Not seeing a slowdown in TV content purchases, despite broader slowdown: “On the TV side, which is encouraging, there is quantifiably a lot less investment in the marketplace in purchasing TV content, and we’re not really seeing that. I think it represents the fact that we have very high-quality content. Our content is working very well. We have strong IP, that’s known”

- Content on the theatrical/DC Studios side –

- Seeing “great” response to Twisters,” which they’re 50% partners with Universal Pictures and Amblin; Has made ~$275mn at the box office and is one of the year’s top 10 highest grossing films worldwide

- Kite Man “is doing very well” after premiering in Max in July

- “Beetlejuice 2 and Joker: Folie à Deux is releasing in September and early October, respectively and “excited for what’s ahead”

- Super/Man: The Chris Reeve Story will have a brief run in theaters in September before coming to Max

- The Penguin, a live action series, premieres in September

- Creature Commandos, an original animated series, kicks off in December

- Superman is set to release on July 11th

- Looking ahead into H2 – “We have two big films in the pipeline” (Beetlejuice 2 and Joker: Folie à Deux), which is “a little more beneficial” y/y in terms of release schedule

- “…With only one film in December, whereas last year, we took a lot of marketing expenses and didn’t get a lot of the benefit of some of the late releases in December”

- But caveated that “each one of those are hit-driven and creates some volatility as well”

- Longer term outlook – 2025 will be the year that films green-lit by Warner Bros Pictures Group’s mgmt team will “dominate the slate”, which they are bullish on: “There is no question about it that the Studio can operate at a very, very significantly higher level of performance”

WBD – Games Are Still Struggling From Tough Y/Y Comps, But Remain Optimistic About Strategy Around Leaning Into Franchises And Free-To-Play

- Games are still struggling from tough y/y comps but leaning Into franchises and free-to-play

- Remain confident in franchise IP giving them a leg-up: “Particularly in a world where the gaming industry launching brand new franchises is getting harder and harder for a number of reasons, including IDFA deprecation and more challenges with marketing and customer acquisition”

- And seeing “high demand” for it, which “we’re looking to take advantage of”: “We have 11 studios here and we have a lot of IP, and there’s also a lot of interest among others in coming to take advantage of some of that IP for gaming, which we’re looking at”

- Leaning into free-to-play space w/ Player First deal, which was about strengthening capabilities “because we do think we are subscale and we have more opportunities to grow in that space, which is a big part of the market”

- Will provide more balance to the Games biz from “the inevitable cyclicality” of console-based releases, which have 3–4-year time horizons and “a little bit more” lumpiness

2) PARAMOUNT (PARA)- See below for what we thought was most important and incremental from the company’s results and conference call

PARA – Q2 Reflects Top-Line Dislocation Across The Board But Surprise D2C Profitability Drove Big Adj OIBDA Beat

- Missed on total rev by almost -6% while adj OIBDA beat by a huge +55%:Total revs fell -11% y/y (vs +6% y/y in Q1), while adj OIBDA grew +43% y/y

- Revenue missed across the board…

- TV Media by -7.4% (revs fell -17% y/y)

- D2C by -1.1% (revs grew +13% y/y)

- Filmed Entertainment by -7.7% (revs fell -18% y/y)

- …though adj OIBDA beat was mostly due to D2C breaking into the black ahead of expectations

- TV Media by +1.8%

- D2C posted a profit $26mn vs the large -$265mn loss estimate

- Filmed Entertainment loss was higher than expected at -$54mn vs cons -$5mn

- Revenue missed across the board…

- Adj EPS of 54c was well above cons 12c, and the Co delivered $10mn in FCF, which was much better than cons loss of -$53mn

PARA – D2C Reached Profitability For the 1st Time And While This Won’t Persist In H2, Mgmt Remains Confident In Reaching Profitability Targets in 2025

- D2C was profitable for the qtr (1st time since P+ launched 3.5 years ago)…

- DTC profit growth was $450mn y/y and totaled almost $900mn for the past 4 qtrs

- But one of the reasons that the D2C segment was profitable in Q2 was b/c it was a lighter qtr in terms of, in particular, sports expense, but that picks up in H2

- D2C total revs grew +13% y/y (but down from +24% y/y in Q1)

- BUT expect the segment to generate losses in Q3 and Q4 due to the timing of content expenses

- Notwithstanding, mgmt. believes they are still on track to achieve P+ domestic profitability for the full year 2025

- D2C Subscription revenue grew +12% y/y (a decel from +22% y/y in Q1 and +43% y/y in Q4) due to subs growth and price increases at P+

- P+ subscription revs incr’d +50% y/y (flattish from the +51% y/y in Q1)

- Paramount+ lost subscribers in the qtr due to partnership exit + Super Bowl sub churn but expects to return to growth in H2

- P+ subs fell -2.8mn to 68.4mn due to exiting hard bundle agreement in South Korea, which contributed a lot of subs but limited revenue and profits; Also, domestic sub growth was positive but weighed down by elevated churn from subs that joined for the Super Bowl in Q1

- Outlook: Expect P+ subs to return to net subs growth in H2

- Price increases will continue to propel P+ ARPU: P+ ARPU globally grew +26% y/y due to the price increase in Q3 2023 and shift in intl to higher ARPU markets

- Q4 will feel the benefit from this next price increase: Another price increase goes into effect later this month but don’t expect a meaningful financial impact until Q4 due to the timing to roll out and the price increase only apply to new customers for the ad supported tier

- D2C ad revs grew +16% y/y (vs +31% in Q1 given the Super Bowl): Driven by increased viewing hours across P+ and Pluto in addition to higher CPMs

- Outlook- expect D2C ad growth in Q3 to be “Similar to Q2”

- Pluto consumption hits record: Pluto delivered 3.7bn hours for inH1, +8% y/y and is their highest consumption ever

- On international streaming – The Co wants to take a “thoughtful” approach for each market and that could entail more strategic partnerships with platforms that already have strong reach

- They have interest from “many partners” in this area

- Mgmt clarified the accounting for the deal with Charter:

- Charter subs who activate P+ will count as P+ subs

- When they activate, Paramount will start to allocate a certain amount of the fees they receive from Charter to P+

- Revenue from deals like Charter where they are providing P+ credentials in a bundle will be split or shared between TV media and D2C segment

- “The revenue that we receive is not contingent on whether somebody activates or not, it’s all part of the overall economics of our arrangement with the distributor”

- Around labor day the P+ Essentials ad supported tier will be available to Charter’s linear customers

PARA Takes $6bn Goodwill Impairment Charge In Its TV Media Biz

- TV Media remains under significant pressure; Q2 revs fell -17% and adj OIBDA fell -15% y/y

- Linear ad revs fell -11% y/y

- Domestic ad trends were negatively impacted by sports comprising a smaller share of inventory than in recent qtrs.

- Y/Y growth in non-sports domestic advertising improved vs Q1

- Outlook – expect linear ad trends in H2 to improve with the return of live sports, new fall programming and political

- Affiliate and subscription revs fell -5% y/y due to subscriber “declines” and a 1ppt decrease from the absence of PPV boxing events, partially offset by price increases

- Outlook – expect TV Media affiliate rev growth to decelerate modestly vs Q2 due to “the market dynamics and impact from existing Showtime Sports”

- Licensing and other revs fell -48% y/y due to fewer availabilities and lower licensing volumes in the secondary market

- Linear ad revs fell -11% y/y

- Drivers for the $6bn goodwill impairment charge is for their cable nets reporting unit at TV Media?

- The largest magnitude is from the value implied by the SkyDance transaction and accounting wise. They need to reconcile the value or their individual reporting units with the enterprise value of the whole company that’s implied by the transaction

- Overall linear declines were another factor

PARA – Pleased With Upfront Results All Things Considering

- “Pleased” with upfront results esp in the “context of the evolution of the ad market and scale of new entrants”

- Linear volume trends were inline y/y and CPMs were up on a blended basis due to sports and b-cast which were relatively strong

- The digital marketplace was also strong… secured over $1bn in commitments across the streaming portfolio

PARA – Executing On The Cost Cutting & Optimizing Plans

- Annc’d that the Co is cutting the US-based workforce by ~15% (marketing & comms and corporate structure) and these actions will take place in the coming weeks and be almost fully complete by YE

- This is part of the $500mn annual run rate cost savings plan (part of the $2bn of cost efficiencies identified ny Skydance) that they identified in June

- Mgmt believes they can reach the full $500mn run rate expense reduction as they enter 2025 (and expect to incur a restructuring charge of ~$300-400mn in Q3)

- Reiterated that they will continue to evaluate their asset portfolio

PARA – Focused On Creating “Big Broad Hits” – Looking At The Slate Ahead…

- Are planning “the most ambitious slate yet for Paramount+”: Incls new seasons of Tulsa King in September, Lioness in October, and the new series Land Man in November, as well as the series finales of Evil and SEAL Team

- Rrecent box office hits, the new CBS primetime slate, the new NFL season, and the first full season of Big 10 College football are also headed to P+

- The Showtime slate: Incls a new series the Agency from George Clooney, and in December, Showtime’s biggest franchise ever returns with Dexter Original Sin

- “The next season’s primetime schedule on CBS is one of the strongest I’ve seen”: In addition to 16 returning series, new shows will incl a spin-off of Young Sheldon, a contemporary reimagining of the classic series Matlock and a new addition to the NCIS universe

- And in Filmed Entertainment: Releasing the first animated Transformers film in nearly 40 years, followed by Smile 2, and in November, Gladiator 2 (the trailer was “one of the most viewed ever for Paramount”), the at the end of the yr, Sonic the Hedgehog 3

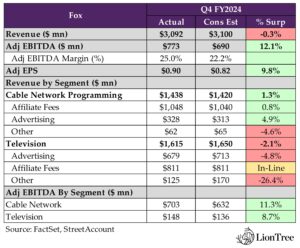

Fox Came Out On Top Vs Peers This Qtr And Is Well Positioned For The Political & Sports Cycle Ahead

Last but not least as it relates to Big Cap Media, Fox pulled away from the pack with a strong positive reaction to its earnings print. It delivered strong upside to Wall Street expectations, especially regarding profitability (adj. EBITDA beat by +12%), which was deja vue to last qtr. The Co importantly executed on its affiliate renewal cycle (completed 1/3 of affiliate renewals in Fiscal 2024) and expects further growth in FY25, but to a more modest degree. The Co ended the fiscal year on a positive note on the ratings front, as Fox News returned to ratings growth and is taking share in this “extraordinary news cycle”. Total ad revs were flat y/y, but on the digital side, Tubi remained a strong growth driver, despite Amazon Prime entering the ad-supported streaming market. Tubi held its ground on pricing, and growth accelerated to “mid to high teens” as the Co exited the qtr. The Co will continue to invest in Tubi during the course of the new Fiscal year but at a slightly lower rate. The goal is for the Co’s combined digital assets to show profitability. Investors are patiently waiting for the sports JV Venu to be launched in the fall, and Fox is “incredibly excited about it”, reiterating its expectation to reach 5mn subs in 2 years.

Investors always remain focused on what the Co will do with financial capacity, and cash returns are certainly on that list (Fox also announced a +3.8% increase to its semi-annual dividend). However, Fox again noted an increasing focus on prudent M&A. Although it has “nothing to update” in that category, it “remains an important lever.”

Looking ahead, CEO Lachlan Murdoch sums it up, “As we enter a very exciting fiscal 2025, we will continue to focus on execution with events such as the US election cycle at our local stations and Fox News Super Bowl 59 on Fox, the renewal of one quarter of our distribution revenue, and the launch of the venue sports streaming service in the fall.”

See more details on what we thought was most interesting/incremental…See Theme #2 and Theme #3 for thoughts and perspectives on Disney, Warner Brothers Discovery, and Paramount’s results.

-> It was a mixed bag with reaction to large cap media results… Disney shares fell -4.5% post results and Warner Bros Discovery fell -9%, but Fox was up almost +7% and Paramount was up almost +1%

- Better profitability was the FQ4 standout on ~in-line revenue

- Total revs grew +2% y/y, with Cable Nets (+2% y/y) outperforming on both affiliate fees and advertising, while TV (+2% y/y) missed on lower ad revenue and other was impacted by lower 3P content sales

- Adj EBITDA (+5% y/y) beat by +12% due to better-than-expected Cable Nets growth of +20% y/y and TV’s less severe than expected decline of -35% y/y

- Executing on affiliate renewal cycles, but annual growth in FY25 will be more modest y/y

- Total affiliate fee revs grew +5% y/y

- Cable Nets grew +2% y/y, as price increases were partially offset by -mid-8% subscriber declines (same as last qtr)

- TV segment grew +9% due to higher fees from 3P FOX affiliates and higher avg rates at O&O TV stations

- Outlook – FY25 is a relatively light year of renewals with ~1/4 of total Co affiliate revs up for up for renewal (more weighted to cable segment): Total affiliate revenue will grow “modestly”

- Total affiliate fee revs grew +5% y/y

- Tubi’s growth accelerated as exited the qtr and remains an area of investment

- Strong competitive positioning and total viewing: “The most-watched TV and movie streaming service in the US” …reached record-high of 2% of total TV viewing at fiscal YE

- Reached all-time high of 81mn MAUs and grew total view time by +17% in FQ4, driven by its expansive library with some unique content

- Total revenue growth decelerated in FQ4: from +22% y/y in FQ3 to +7% in FQ4, given “a complex” digital ad marketplace and a tough y/y comp

- BUT ended the month of June w/ revenue growth in “the mid to upper teens” and that “pace has continued into this quarter with steady pricing, despite increased inventory in the overall market”

- Weathered the huge ad supply when Amazon Prime entered the ad-supported streaming business: This caused other streamers to fight hard and cut pricing, but Tubi didn’t have to cut pricing and expects further growth

- Investments into Tubi will continue but to a lesser degree: For FY24, Tubi was the single largest driver of investment across the growth portfolio, and the level was at a consistent clip to FY23 in the mid-$200mn range, plus the $100mn in other growth assets; This likely goes down to high $200mn in aggregate, given “a little less investment at Tubi,”

- In FY25, the collective digital portfolio is expected to deliver improved EBITDA y/y

- Strong competitive positioning and total viewing: “The most-watched TV and movie streaming service in the US” …reached record-high of 2% of total TV viewing at fiscal YE

- Returned to ratings and share growth at Fox News, which is “taking share in this “extraordinary news cycle”

- FQ4 audience levels return to growth at the Fox News channel, driven by the political coverage and strong primetime lineup

- Fox news exited the fiscal year as the most-watched network in all of cable in total day and in primetime and gained share amongst cable news networks in both prime and total day versus last year

- The rating momentum continued into July…

- In July, total viewers grew nearly +80% and the 25-54 demo grew +120% vs last year

- Fox News had its highest-rated weekend ever in prime-time in July w/ 5.7mn+ viewers watching the extended coverage of the Trump rally in Butler, PA

- Fox News had its highest share of the cable news audience across-the-board in primetime since August 2015

- Fox News channel rated number-one across all linear TV in July for total viewers in weekday prime, beating the nearest broadcast competitor by nearly +10%

- FQ4 audience levels return to growth at the Fox News channel, driven by the political coverage and strong primetime lineup

- Upfront was more successful than they were bracing for & expect a record apples-to-apples political cycle

- Total advertising revenues were flat y/y: Revenue from summer soccer and growth at Tubi was offset by lower ratings and pricing at the Fox Network

- Cable ad revs rose +3% y/y: Primarily due to the b-cast of the CONMEBOL Copa América and UEFA European Championship at the national sports networks and growth in pricing, higher ratings, and lower preemptions, partially offset by lower political ad revs at FOX News

- TV ad revs fell -1% y/y: Lower ratings and pricing at the FOX Network were offset by the broadcasts of the UEFA European Championship and CONMEBOL Copa América at FOX Sports and continued growth at Tubi

- Saw a “much healthier [upfront] market than the nuanced one I referred to six months ago”: Evidenced by “strong” upfront commitments; Saw “y/y growth” in both linear and digital ad commitments as well as “growth” in overall portfolio pricing

- Drivers: This was led by sports and not just football; Fox News saw vol increases at the upfront due to ratings increases; Tubi saw “double-digit” volume growth and stable pricing

- Outlook: “At the local level, we are expecting a very robust election advertising cycle that will be weighted to FQ2”

- The strength in the DR marketplace in the high-teens pricing “bodes well for that line of our business”

- Expect a record political cycle this year ex Georgia run-off 4 years ago

- Total advertising revenues were flat y/y: Revenue from summer soccer and growth at Tubi was offset by lower ratings and pricing at the Fox Network

- Venu is expected to be accretive in short order and will be “revolutionary in the way Americans are going to view sport” … “Remain incredibly excited about it”

- Product update: There’s new beta release “practically every day” and the product is looking “excellent”; It will be “quite revolutionary in the way Americans are going to view sport”

- Pricing: Think the $42.99 as an initial launch price “really hits the right mark”

- Subs targets: No change to the previous guidance for 5mn subs over five years, and it’s “very important that those subscribers are focused on cord-cutters and cord-nevers”

- Timing? Launched date is still “not 100% locked down” but have said this fall

- Economic impact? “We’re a two-sided relationship”, and on a “net-net basis, it should be accretive to us on a pretty quick basis”

- As a shareholder, the business is going to take some time to get to CF breakeven; Share of ownership results will be recorded below EBITDA in equity earnings.

- As a supplier of content, it will benefit affiliate fee revs in both cable and TV

- Content spend will modestly go up, as the pendulum shifts back to more scripted

- Expect to continue to grow content: In FY24, the strike caused a shift to unscripted that was “amplified”; It will now “swing back a little the other way” towards scripted; Also, sports will go up, Tubi will grow content, and News will have modest growth

- Focused on reducing the cost per hour: Think FY25 will be down -10-15% vs F23

- Strategic priorities include an increasing focus on M&A

- Shareholder returns: Returned $1bn of capital through the buyback + a further $250mn in dividend payments

- Raised the semi-annual dividend by +3.8% to $0.27 per share

- Forward strategy on capital allocation? Want to be prudent, organically investment in the business, return capital to shareholders and then increasing focus on M&A

- “Nothing to update in the later category but M&A remains an important lever”

- Shareholder returns: Returned $1bn of capital through the buyback + a further $250mn in dividend payments

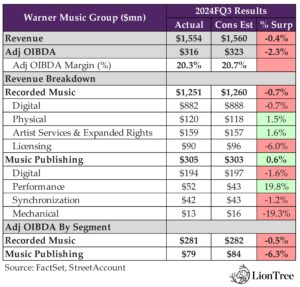

WMG Pulls Ahead With A Favorable DSP Mix Vs Peers

What is going on in the subscription streaming market has been the key question during this earnings season for the Music sector. Earlier this cycle, Spotify reported more Paid streaming music subscribers than expected (see Theme #5 from July 26th WeeklyWeekly 7/26/24), while Universal Music Group missed Subscription streaming revenue growth estimates decelerated (to +7% y/y in Q2 from +12.5% y/y in Q1), as “other large [DSP] partners who have been less successful in driving global adoption have seen a slowdown in new subscriber additions” see Theme #6 from July 26th Weekly). Warner Music Group (WMG) apparently is not exposed to those same large DSPs, given the Co pulled through and delivered stronger than expected results in its subscription streaming business (revs grew +14% y/y in FQ3 on a normalized basis, up from +13.5% in FQ2). Net-net, there are market share shifts going on in the subscription streaming landscape. A key message from WMG was that the relationship between the labels and DSPs is collaborative and that the Co is very open to working with DSPs, as they experiment with new go-to-market strategies aimed at growing the subscriber pie. Similar to trends seen with the rest of the players, WMG’s ad-supported streaming business was impacted by the cont’d “softer” ad market and tough comps.

The market opportunity ahead for subscription streaming is still viewed as robust, given global penetration figures. Price increases and optimization/tiering will also be key drivers looking ahead. AI regulation as it relates to music is moving in the right direction, with the NO FAKES Act introduced in the U.S. Senate last week.

Lastly, the Co talked in more detail about its recent re-org, which was “strategic” and not a “cost cutting exercise”. See below for more details on what we thought were most incremental and important from WMG’s results and conference call.

-> WMG rose almost 2% on the back of results but is still down -21% YTD; This compares to UMG down -14% and Spotify up +89% YTD

WMG’s Headline Results Broadly Underwhelmed Vs Expectations….

- Headline numbers missed: FQ3 total rev was down -0.6% y/y or up +1% ex-FX and missed cons by -0.4%; Adj OIBDA grew +6.4% y/y or +8% ex-FX, falling -2.3% short of cons

- Recorded Music revs decr’d -1% y/y ex-FX and missed by -0.7% and adj OIBDA missed by -0.5%

- BMG digital rev roll-offs was $25mn unfavorable impact, and renewal of an int’l digital partner was $3mn unfavorable impact

- Music Publishing revs incr’d +9% y/y ex-FX and beat by +0.6% while adj OIBDA missed by -6.3%

- The CRB rate incr provided a +$7mn benefit to music publishing digital rev in the prior yr qtr

…BUT Subscription Streaming Growth Was A Relief (Given UMG’s Previous Report)

- Subscription growth once again underpinned overall Recorded Music streaming revenue growth of +10% y/y ex-FX (vs +11% y/y in FQ3)

- Subscription streaming growth accelerated to +14% y/y on a normalized basis from +13.5% in FQ2 and +12% in FQ1

- Driven by subscriber growth that was “pretty consistent across their top DSPs and to a lesser extent price increases; A strong slate was also supportive

- Subscription streaming growth accelerated to +14% y/y on a normalized basis from +13.5% in FQ2 and +12% in FQ1

- Looking to Q4, we see “continued strength in subscription streaming revenue”

- Refutes speculation that labels and DSPs have become adversaries: “I know that investor attention has recently been focused on the dynamics between the labels and the DSPs, with some speculating that we’re adversaries playing a zero-sum game. That’s simply not the case. We’re actively engaged with our partners around ways to drive growth for all of us”

- Believe streaming dynamics remain healthy

- “We’re pleased with the progress that our DSP partners are making” and the demand side is “very resilient”

- “The demand side of our business is very resilient and very strong”

- “We’re not seeing any change in what’s been happening in our revenue mix”

- Deeply engaged with their DSP partners in 4 areas:

- Cont’d growth btw emerging and established mkts and taking different approaches w/in those

- Price optimization, which includes family plans and various pricing increases, which “you’ve obviously seen play out over the last year or so and will continue to”

- The evolution of royalty models and how the pie is divided

- Audience segmentation w/ adding non-music content to the music offering

- Very willing to experiment with partners… sometimes it will work and sometimes it won’t

- Still sees a lot of penetration opportunity of music subscriptions…they are still “really low”: “I think they’re overall about 15%. And there’s a lot of headroom there to go from 700mn, 800mn subscriptions today to well over a billion over the next five years”; There’s also still more sophistication and optimization to be done on price, as well as audience and product segmentation/innovation

- Regarding DSP price increases:

- Will still face tough comps: WMG is at the end of lapping YouTube’s price increase but still has a bit of lapping of Spotify (those are the biggest)

- Participation in Spotify’s recent bundled services price increase?“I can tell you that any assumption that a key anchor tenant such as us would not participate is not the best assumption to put it mildly”

Advertising Supported Revenue Will Remain Challenged In FQ4

- Ad-supported revenue incr’d only +1% ex-FX, which is down from +5% y/y in FQ2 and +10% in FQ1

- The deceleration was driven by the “softer” ad market and a “challenging comparison” to the prior year qtr

- Looking to Q4, ad-supported revenue will have challenging comparisons y/y: Similar to what UMG flagged in respect to their business, Meta will no longer be making available premium music videos to WMG users; This change will have a ~$10mn impact per qtr across both recorded music and music publishing starting in Q4

- But optimistic regarding the ad-supported business – “It is a market that you want to be in”:

- “It’s addressable, it’s on mobile devices, it’s on tablets, it’s on computers and it’s on TV screens. It’s not linear advertising that is not effectively targeted and you see the shift from sort of traditional advertising to obviously all the digital platforms”

- “I think we are in the correct advertising market”

- Still view Emerging Streaming as a growth category: Meta changed its offering and moved away from premium music video licensing, but WMG’s underlying relationship w/ Meta “is strong and growing”; Reels and Instagram are “growing well”; Remain excited about the category; TikTok stepped up as well

- “The category continues to be a growth category”

The Executive & Company Re-Org Is A “Strategic Decision”, NOT A “Cost-Savings Exercise”

- The annc’d reorg in recorded music creates a flatter structure:

- Will be 4 major regions in Recorded Music

- Organizing the frontline labels into 2 groups

- Warner Records will expand its responsibilities to oversee Warner Music Nashville

- Atlantic Music Group will fold in recently acquired 10k Projects and Julie Greenwald is taking a new role as Chairman, with Elliot Grainge coming in as CEO

- Strengthening the Co’s central operations and this is a “strategic decision, not a cost-saving exercise”

AI Regulation Is Moving In The Right Direction

- Bullish on the NO FAKES Act which was introduced in the US Senate last week: This act strikes the right balance between propelling the next wave of technology-powered creativity, while safeguarding every American’s right to control the use of their own image and voice in the age of AI

- “We’re making great progress with regulation and governments”

- “You can see a lot more alignment within the music industry, but also within the content industry”

- “We’re very, very focused on this, we’ll religiously defend our IP, our artists and songwriters’ name and likeness”

Other Key Forward Looking Comments

- Have an incredibly strong release slate for Q4 and going forward

- Closing the year with great new music coming from Coldplay, David Guetta, Benson Boone, Myke Towers, Cyril, Fred again, Diljit Dosanjh, and many others

- “But I really want to also say that the performance of our catalog is strong and continues to be strong”

- FY guidance (Sept 2024) reaffirms OCF conversion guidance of 50-60%

- Reiterated that BMG will have revenue impact in the -$25-30mn range in FQ4, eventually rolling off completely in FY25

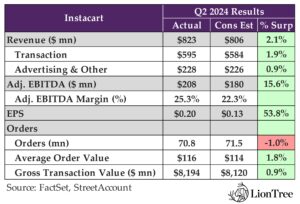

Instacart Holds Its Lead In The Highly Sought After Online Grocery Delivery Market

Despite all the worry about more competition in the under-penetrated online grocery delivery market, Instacart delivered again with a +2% beat on revenue and a +16% beat on profitability (a similar dynamic with Q1 results as well). Importantly, gross transaction value (GTV) beat by +1% and logged a double-digit growth rate, topping the +7-9% growth guidance. Better than expected basket sizes were the main reason given the number of orders was lower than expected. Looking ahead into Q3, the Co’s GTV guidance points to a slight potential deceleration, as there were some non-recurring benefits in Q2, but the top end would still represent double digit growth (+8-10%).

The big picture TAM remains attractive, as the grocery market has been slower than other verticals to digitize. Pursuing new customers remains central to Instacart’s growth plan, but an interesting stat from the conference call was that 25mn people have used the Instacart service over the past year, which provides a huge pool to target for higher utilization. Mgmt is squarely focused on this. Also, normalization of the COVID cohorts seems behind the Co as well, which is a plus.

Advertising is a big part of the investment thesis for Instacart, and on that front, the Co outperformed in Q2. While some of the Co’s large CPG advertising clients have pulled back (like last qtr), Instacart has been able to more than offset that with growth from emerging brands. New ad formats and enhanced measurement are yielding results.

Lastly, Instacart has been very active on the partnership front, and early data shows that the tie up with Uber Eats is working well. While it is not a big contributor to the Q3 guidance, it should help create a future flywheel for the Co.

See below for more of our key takeaways from Instacart’s results and conference call.

-> CART rallied +2.8% on the back of results and is up +36% YTD (and up +6.3% from its IPO)

Instacart Delivers Another Better-Than-Expected Qtr…

- GTV beat cons by +0.9%: Grew +10% y/y in Q2 (slightly down from +11% y/y in Q1, but up from +7% y/y in Q4, +6% y/y in Q3, and +6% y/y in Q2); It also beat guidance of +7-9% growth

- Total rev grew +15% y/y and beat cons by +2.1%

- Transaction revenue grew +17.0% y/y (vs +8% in Q1) and beat cons by +1.9%; driven by fulfillment efficiencies and the lapping of one-time retailer credits and concessions in the prior year quarter, partially offset by ongoing re-investment in consumer incentives

- Advertising & Other revenue grew +11.0% y/y (vs 9% in Q1) and beat cons by +0.9%; Advertising & other investment rate was consistent with the prior year quarter at 2.8%.

- Adj EBITDA grew +89% y/y and beat cons by +15.6%; It was 2.5% of GTV (vs 2.4% in Q1)

- Avg order values surprised on the upside (beat by +1.8%), growing +3% y/y while # of orders was slightly below expectations but grew +7% y/y

- Drivers for higher AOV?

- New Customer Cohorts are reaching bigger baskets faster than prior cohorts

- Existing customers continue to make larger purchases over time

- Q2 saw a higher mix of club orders

- Mgmt doesn’t believe the higher AOVs reflects inflation as they continue to see price per item on an individual basis peaking and number of items troughing

- Drivers for higher AOV?

- Repurchased ~36.5mn shares worth $1bn representing 10%+ of fully digital shares outstanding at the end of 2023; Have total capacity of $425mn left in existing authorization

- Authorized a new $500mn buyback program

Guidance Reflects Continued Strong GTV Growth With The High-End Reaching DD Growth

- Q3 guidance for GTV y/y growth is +8-10% (to $8.1-$8.25bn) and is expected to be driven more by orders than basket size; Reflects ongoing strength in the core service and a modest growth contribution from restaurant orders

- Reminder that H1 GTV outperformance benefitted from a number of one-timers: Including Leap Day in February as well as some one-time seasonal benefits from bad weather

- Q3 adj EBITDA guidance was ~in-line: Mid-pt of $205-215mn range compares to cons $208mn

- Implied adj EBITDA as a % GTV is a low of 2.5% and a high of 2.6%: Q3 y/y growth will be driven primarily by adj OpEx leverage

Take Rates Have Expanded For The Last Couple Of Quarters, Though Q2 Showed A More Modest Expansion

- Shopper Efficiency: Mgmt is seeing shopper efficiencies in terms of the payments that the Co makes to shoppers due to order density and batch rates

- The Co will continue to invest in targeted incentives and leaning into affordability options that allow people to schedule delivery later in the day or pick up orders for free, which shows up in the take rate

Early Data Shows Benefits From Uber Eats Partnership… It Should Help Create A Flywheel

- Instacart fully rolled out restaurants nationwide in mid-June, and Uber is ramping restaurant adoption at a much faster pace than any new entrants be able to accomplish in grocery after years and billions of dollars of investment

- Restaurant orders saw higher average basket size than those on other platforms

- “Early data affirms our belief that restaurants can be incremental to grocery by attracting new customers to our ecosystem and increasing order frequency for existing ones, especially Instacart+ members… Longer term, we believe we can create a flywheel effect where restaurants help grow our grocery orders too”

Positive Cohort Trends & Big Opportunity To Re-engage 25mn Customers That Have Used The Platform In The Past Year

- All the cohorts, both mature and new, are healthy, and their behaviors have normalized as compared to 2023 during COVID: “At this point… we’re really pleased to see that both mature and new [cohorts] are healthy”

- GTV from new cohorts is still higher than pre-pandemic levels

- New customer cohorts are reaching bigger basket sizes faster as compared to existing users

- Focused on deepening engagement with existing AND infrequent customers

- 25mn customers have used the platform in the last year: “This gives us a tremendous opportunity to deepen engagement with infrequent customers while continuing to attract more new users to Instacart”

- The Co is targeting these customers by not just through incentives, but also through promoting Instacart+ and connecting them to all of the affordability options that will build a habit as well.