It was a choppy week in the market, with Monday’s sell-off triggered by some cautionary valuation comments by Fed Chairman Powell, followed by economic data that led investors to dial back interest rate cut expectations. While the major indices on Friday recovered from lower levels earlier in the week, they still broke their recent streak of positive returns (4 weeks in a row) with the S&P falling -0.3% and Nasdaq declining -0.7%.

It was another very busy week with meaningful updates across the sector. This week we focused on the below key themes and developments:

- AI Infrastructure Spending Is Accelerating Into Unchartered Territory

- TikTok Is Still Inching Towards A Conclusion, With A Jump Step This Week

- The Video Game Juggernauts End On A High Note After A Tough Week, While Google Is Pushing Harder Into Game Play

- The NFL Is Likely To Set A New Media Rights Record Sooner Rather Than Later + Other Key Sports Developments

- Meta Shakes Up The Dating App World This Week

- A Stream Of Other Important AI Updates & Developments

- A New “Put Your Phone Down” Incentive Hits The US Wireless Market

- Entertainment Content Spend Has Still NOT Peaked

- Prices Move Up AGAIN In The Streaming Video Space

Also to mention, LionTree served as exclusive financial advisor to Semler Scientific on its merger with Strive, Inc.

As always, let me know if you have any questions and I hope you have a nice weekend

Best,

Leslie

AI Infrastructure Spending Is Accelerating Into Unchartered Territory

AI infrastructure (and a lot of it) was all the rage this week as we saw a sweeping set of initiatives that collectively mark a turning point in the economics and scale of AI compute deployment. NVIDIA kicked off by announcing that it will invest up to a massive $100bn into OpenAI with the goal of creating 10 gigawatts of AI datacenters running off NVIDA systems.

Later in the week, OpenAI separately revealed that it has 5 new US based data centers in the pipeline which are part of a broader expansion of the Stargate initiative. While Stargate was off to a “slow start”, SoftBank CFO Yoshimitsu Goto is not worried, stating “we want to deliberately spend time to build the first model successfully.” These 5 new sites, plus Stargates’ flagship site in Abilene, Texas, and ongoing projects with CoreWeave put Stargate on a “clear path” to securing the full $500bn, 10-gigawatt commitment “ahead of schedule”

Bigger picture, OpenAI is laying the groundwork for $1 trillion+ in infrastructure spending given that EACH gigawatt of capacity is expected to cost ~$50bn, and 20+ gigawatts of capacity is expected to be needed. Obviously, that would require another step function increase in investment!

Below, we broke down the key updates on this theme this week, including deployment timelines, financing strategy, and the implications for hyperscale AI infrastructure.

-> NVIDIA shares closed up +1% this week

NVIDIA Intends To Invest Up To $100bn In OpenAI, Tied To At Least 10 Gigawatts Of NVIDIA Systems (link/link/link/link)

- Scale: Partnership will enable OpenAI to build at least 10 gigawatts of AI datacenters w/ NVIDIA systems that will be built and deployed for OpenAI’s next-gen AI infrastructure

- Per NVIDIA CEO, Jensen Huang, this is equal to 4-5mn GPUs which the Co will ship in total this year and twice as much as last year (7.5mn homes simultaneity)

- OpenAI will work with NVIDIA as a preferred strategic compute & networking partner

- They will work together to co-optimize their plan for OpenAI infrastructure software with NVIDIA hardware and software

- Timeline: First gigawatt to go live in H2:26, It will be built on the Co’s Vera Rubin platform

- NVIDIA’s first investment of $10bn will be made after the first gigawatt is complete

- NVIDIA estimated in Aug. 2025 that it would cost $50–60bn to build each gigawatt of capacity, with ~$35bn of that for NVIDIA chips/systems

- NVIDIA’s first investment of $10bn will be made after the first gigawatt is complete

- OpenAI is now at 700mn active weekly users

- Reported 400mn back in Feb. 2025 and 500mn in Jul. 2025

OpenAI Is Also Teaming With Oracle & SoftBank To Build Five New Stargate Data Centers (link/link/link)

- OpenAI also annc’d plans to build 5 new US data centers under its Stargate initiative

- As a reminder, in January 2025 at the White House, OpenAI, Oracle, and SoftBank annc’d the Stargate initiative, aiming to invest $500bn and deploy 10 gigawatts of AI over the next five yrs

- How were the 5 new sites chosen? Through a nationwide process launched in Jan, in which OpenAI, Oracle, and SoftBank reviewed 300+ proposals and 30+ states

- 3 of the new facilities are being developed in partnership with Oracle

- Locations: Shackelford County, Texas; Doña Ana County, New Mexico; and an undisclosed Midwestern site

- Expected to create thousands of jobs: Together, these sites are expected to create 25k+ onsite jobs, and “tens of thousands” of addtl jobs across the US

- OpenAI and Oracle’s agreement represents a partnership that exceeds $300bn between the two Cos over the next 5 yrs

- The other 2 addtl sites are being developed with SoftBank

- Locations: Lordstown, Ohio and Milam County. Texas

- These sites can scale to 1.5 gigawatts over the next 18 months

- The combined capacity brings Stargate to ~7 gigawatts of planned capacity and to $400bn+ in investment over the next 3 yrs: Coming from the 5 new sites – along with their flagship site in Abilene, Texas (see below), and ongoing projects with CoreWeave

- On a “clear path” to securing the full $500bn, 10-gigawatt Stargate commitment “ahead of schedule”

OpenAI Has Plans For A $1 Trillion Build-Out Of Computing Power (link)

- OpenAI is planning a $1tr build out for computing warehouses across the US and abroad

- Their first “Central-Park sized” flagship site in Texas will bring online ~900 megawatts of capacity

- New jobs are being created, some of which will be permanent –

- 6,000+ workers are on the project every day, alternating between two 10-hr shifts, 7 days/wk

- 1,700+ permanent jobs are expected to remain after construction ends, per an Oracle executive

- OpenAI calls it “the largest AI supercomputing complex in the world”…: Building out 8 “hyper-futuristic data centers” across the 1,100-acre site

- …but they still need more: OpenAI said that it would ultimately need more than 13x the computing power of its first site

- New jobs are being created, some of which will be permanent –

- How did OpenAI get to the $1tr figure? EACH gigawatt of capacity is expected to cost ~$50bn, and 20+ gigawatts of company capacity is expected to be needed to meet the increasing ChatGPT demand

- Looking even further ahead…demand is likely to reach closer to 100 gigawatts, one Co exec said, which would equate to $5tr (that exceeds the annual GDP of Japan or Germany)

- How will OpenAI finance these investments? “I don’t think we’ve figured out yet the final form of what financing for compute looks like,” per OpenAI CEO Sam Altman

With All This Spending, OpenAI CEO Sam Altman Had A Lot To Say In His Latest Blog Post (link)

- “As AI gets smarter, access to AI will be a fundamental driver of the economy, and maybe eventually something we consider a fundamental human right”

- “We are putting the groundwork in place to be able to significantly expand our ambitions for building out AI infrastructure”

- Both to build out inference compute to run these models, as well as for training compute to keep making them “better and better”

- What would be the potential use cases?

- “Maybe with 10 gigawatts of compute, AI can figure out how to cure cancer”

- “Or with 10 gigawatts of compute, AI can figure out how to provide customized tutoring to every student on earth”

- “Our vision is simple: we want to create a factory that can produce a gigawatt of new AI infrastructure every week”

- BUT “the execution of this will be extremely difficult”

- “It will take us years to get to this milestone”

- “It will require innovation at every level of the stack”

- “We are particularly excited to build a lot of this in the US”

- “Right now, other countries are building things like chips fabs and new energy production much faster than we are, and we want to help turn that tide”

- Plans for financing these investments? “We have some interesting new ideas”: “Later this year, we’ll talk about how we are financing it; given how increasing compute is the literal key to increasing revenue”

TikTok Is Still Inching Towards A Conclusion, With A Jump Step This Week

On the back of a surge in press reports, Trump finally signed an executive order that would enable an American-led group of investors to acquire TikTok from ByteDance. But while Trump’s tone was triumphant, it seems that several loose ends still remain. The most pressing is that China has yet to say publicly whether it has granted approval, and ByteDance itself has not acknowledged that a transaction is underway. The composition of the buyer group is also fluid. Oracle, Silver Lake, and Abu Dhabi’s MGX are reportedly involved, while names like Rupert Murdoch and Michael Dell have also been floated. A final purchase price has also not been disclosed, though Vice President JD Vance, who led negotiations, put the value of the new US entity at ~$14bn, far below analyst estimates of $35–40bn. Questions also remain over how licensing and revenue-sharing with ByteDance would be structured, and how government involvement might influence content oversight and algorithm monitoring going forward.

While TikTok’s future is still in a bit of a limbo, Meta has been pressing ahead with new social media features and products. Instagram surpassed 3bn MAUs (the third Meta app after Facebook and WhatsApp to reach that milestone) and is planning on rolling out changes to its app to prioritize private messaging and Reels. The platform is also preparing an algorithm update that lets users directly choose topics they want to see more often, a shift powered by advances in Meta’s AI models. Lastly, the Co has also released “Vibes”, which is a feed specifically for AI-generated short-form videos where users can create, remix, and share across Meta’s platforms.

All taken together, short-form content has certainly become a central feature in the social media ecosystem, and with the advancements in AI, both on the recommendation side and now the content generation side, it will remain an important medium to keep an eye on.

See below for what we thought were the important updates.

Trump Signs Executive Order Facilitating The TikTok Deal, But How Exactly It Will Work Is Still Unknown (link/link)

- Trump’s order will enable an American-led group of investors to buy the app from China’s ByteDance

- It also provides a 120-day window to finalize the details

- The executive order itself is a declaration by the president that the proposed deal meets the security concerns laid out in that law

- Details on who exactly would be buying TikTok were vague – “we have American investors taking it over, running it, highly sophisticated”

- Oracle is going to play “a big part,” Trump said at the signing

- It has been reported that Oracle, private equity group Silver Lake and Abu Dhabi’s MGX will control ~45% of TikTok US

- Trump had also said over the weekend that Rupert Murdoch and his son Lachlan Murdoch could be involved in the TikTok deal, along with Dell Technologies CEO Michael Dell

- Overall, the deal Trump is seeking to finalize will spin out TikTok’s US biz into a new, US-based venture owned mainly by American investors, w/ ByteDance’s stake shrinking to < 20%

- BUT it seems the deal is not yet finalized and it will also require China’s approval

- No representatives from ByteDance were present at the signing

- ByteDance hasn’t acknowledged that a transaction is taking place

- No purchase price was mentioned

- There’s no indication that the Chinese govt has made changes to laws that would be necessary for a deal to take place

- “There was some resistance on the Chinese side,” VP JD Vance said, “We’re going to keep on working at it”

- However, Trump said at a White House signing ceremony that he “had a good talk” with the Chinese president, Xi Jinping, who “gave us the go-ahead”

- Vice President JD Vance, who led the team to find a solution for TikTok, said the US entity would be valued at ~$14bn which created a bit of a stir

- The value of the US biz is far lower than the value for ByteDance overall, which is estimated to be ~$330bn

- It is also far below the $35-$40bn estimate analysts had expected

- But Vance said that it would “ultimately” be up to the investors to figure out its price

- There has also been speculation that ByteDance will be getting ~50% of TikTok US profit under the deal

- Under the current proposal, TikTok US would pay ByteDance a licensing fee (some speculate ~20%) on the revenue it takes in for use of its algorithm

- On top of that, ByteDance would take ~20% of the profit from the remaining revenue, in line with its remaining equity stake

- With the govt facilitating the deal, how will that impact the type of content available on the app and how it will be monitored?

- “If I could make it 100% MAGA I would, but it’s not going to work out that way unfortunately. No… every group, every philosophy, every policy, will be treated very fairly,” Trump told reporters

- A White House official said Monday the algorithm would be “continuously monitored” to ensure it is “not being unduly influenced”

- “This deal really does mean Americans can use TikTok but actually use it with more confidence than they had in the past because their data is secure and it won’t be used as a propaganda weapon like it has in the past,” VP Vance said

- Also to note, earlier this week, the Trump administration said that the US will NOT hold a golden share or equity position in the new entity that will control TikTok’s American operations (link)

- The new board will not have a member selected by the US government, and Americans will hold six of the seven board seats for TikTok US

While TikTok Dominates Headlines, Meta Has Been Working To Keep Its Social Media Innovation Engine Running

- Instagram hits 3bn users + changing its home screen to prioritize DMs and Reels (link/link)

- Instagram now has 3bn monthly active users: Meta last disclosed Instagram’s user figures in October 2022 when Zuckerberg said during an earnings call that the app had crossed 2bn monthly users

- Changes are coming to the home screen navigation bar –

- Will highlight private messaging and Reels, making those features easier to find

- Also running a test in India where the app will open directly into Reels instead of the traditional feed, a design the company also employed for a newly released iPad app

- How are users using Instagram?

- Private messaging is the most popular way people share on the app, followed by disappearing Stories

- More than 50% of the time spent on Instagram comes from people watching videos, and most of those videos are recommended to users from outside the accounts they follow

- “People think of us — they think of a feed of square photos, but that’s just not how people use Instagram and it hasn’t been for a long time now,” said Adam Mosseri

- On competition w/ TikTok – it is “top of mind,” per Mosseri…esp in India

- India is particularly crucial for Instagram b/c TikTok is currently banned in the country

- BUT “it’s very possible that TikTok ends up back in India, and so we want to make sure that we are not being complacent in one of our most important countries,” which is likely to drive growth in the next few years,” Mosseri said of the upcoming test

- Also coming soon…an algorithm update that will let users choose topics they want to see more often in their Reels feed: Allows users to go into setting and type in their interests

- Meta has mostly relied on implicit signals (like who they follow, the videos they like or share, they videos they hide, etc.) to show people relevant content

- This new option is more explicit and primarily possible b/c of advancements in AI, as Meta’s LLMs have gotten better at identifying and labeling content in a video so recommendations can be more specific

- AI videos are also getting their own feed…Meta Introduced “Vibes” which is “a new way to discover and create AI videos” (link)

- What is “Vibes”? A new feed in the Meta AI app and on meta.ai where you can create and share short-form, AI-generated videos

- The feed will become more personalized over time

- If something catches a user’s eye, they can create their own video, remix what they see, and share it with friends and followers

- How does content creation and editing work? Users can start from scratch, work with content they already have, or remix a video from the feed to make it their own

- Can also add new visuals, layer in music, and adjust styles to match their taste

- Where can the content be shared? It can be posted directly to the Vibes feed, DM’d to friends, or cross-posted to Instagram, Facebook Stories and/or Reels

- Meta has partnered with AI image generators Midjourney and Black Forest Labs for the early version of Vibes, while the Co continues developing its own AI models

- What is “Vibes”? A new feed in the Meta AI app and on meta.ai where you can create and share short-form, AI-generated videos

The Video Game Juggernauts End On A High Note After A Tough Week, While Google Is Pushing Harder Into Game Play

Late Friday afternoon, headlines surprised the gaming world…Electronic Arts is reportedly nearing a ~$50bn deal to go private! The reported buyers are a group of investors including PE firm Silver Lake, Saudi Arabia’s Public Investment Fund, and Jared Kushner’s Affinity Partners, and if completed, the deal would likely become the largest leveraged buyout ever. EA’s stock reacted immediately, jumping +15% to close at a record high of $193.35, giving the company a market value of ~$48bn, and Take-Two traded up in sympathy.

Before the news hit, it was actually a tougher week for the video game giants. Early players of the just-released EA Sports FC 26 have been underwhelmed, while the Switch 2 release of Take-Two’s Borderlands 4 has been delayed with no new date announced. Although the company says it needs more time to “polish” the game, it’s hard to ignore that its release on other consoles has also faced complaints.

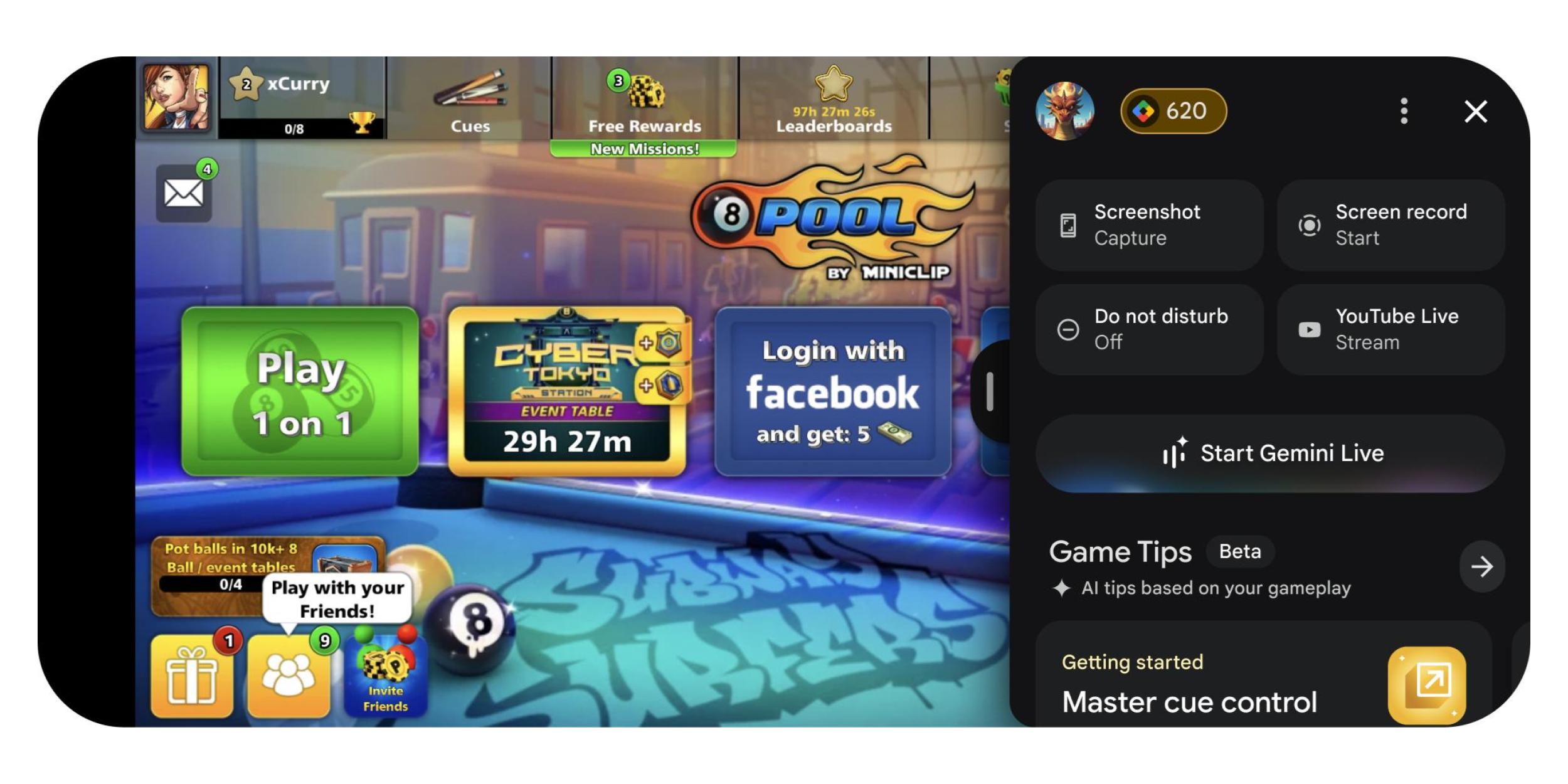

Meanwhile, Google also made videogame headlines this week with a harder push and a wave of updates to Google Play, introducing new personalization tools, AI-driven features, and expanded content offerings designed to deepen user engagement across devices. Highlights include the debut of a centralized “You” tab for account management and recommendations, the launch of Gemini Live overlays to bring real-time AI assistance into gameplay, and enhancements ranging from Gen AI avatars and expanded Play Points rewards to new community and competitive features like Play Games Leagues. With Google Play Games on PC now officially out of beta and additional regional entertainment initiatives underway, the updates underscore Google’s push to make Play a more integrated hub for gaming, media, and discovery.

See below for more on our quick takes on these updates.

Big News Hit The Tape Friday Afternoon…Electronic Arts Is Reportedly Nearing An ~$50bn Deal To Go Private (link/link)

- Who are the reported buyers? A group of investors including PE firm Silver Lake, Saudi Arabia’s Public Investment Fund and Jared Kushner’s investment firm Affinity Partners

- PIF already holds an ~10% stake in EA

- A deal could be announced as early as next week

- If the deal comes together, it will likely be the largest leveraged buyout ever (not adjusting for inflation)

- Would surpass the agreement to take TXU Energy private for ~$45bn back in 2007 (w/ debt, the deal totaled ~$70bn in enterprise value)

- And then there was one? Comes just two years after Activision Blizzard’s $75bn sale to Microsoft in one of the tech industry’s biggest-ever deals; EA is one of the world’s largest independent games publishers outside China, alongside Grand Theft Auto maker Take-Two Interactive

-> EA had a mkt cap of ~$43bn before the news hit; After the report, the stock jumped +15% and shares closed at $193.35, a record high, giving the Co a mkt value of ~$48bn; The stock was already up ~+17% over the year before the news; Take Two traded up +4.5% on Friday as well

Before The EA News Hit, It Was Shaping Up To Be A Tougher Week For The Video Game Giants

- EA Sports FC 26 has been facing some early technical issues and has had a lukewarm reception (link/link)

- The game is currently sitting at 3 stars on Steam, with just 52% of comments being “positive”; Reviews are from those who had paid for early access (the game officially launches Sept 26th)

- The EA FC Mobile servers were also down for maintenance on Sept 24th, during which players were unable to access the game

-> EA shares fell as much as -4.6% (the biggest intraday decline since Apr 4th) in reaction and closed down -3.9% on the day (but per the above, rallied on Friday given the deal speculation)

- Take-Two Interactive’s Borderlands 4 Switch 2 release has been delayed (link/link/link)

- No new release date has been set: Gearbox said it will update the “release timing” for Borderlands 4 once it has “fully adjusted [its] plans”

- Was supposed to be released on Oct 3rd

- Reason for the delay? “Committed to ensuring we deliver the best possible experience to our fans, and the game needs additional development and polish time to do that”

- One of the improvements? Cross saves: “Our hope is to also better align this release with the addition of cross saves, which we are working on and recognize is very important”

- Release on other consoles has been met with several complaints: Borderlands 4launched on September 12th for PC, PS5, and Xbox Series X / S, but came under scrutiny for performance issues; Gearbox subsequently released a patch that “improves stability” on PCs

- Also the game reportedly demoed poorly on Nintendo Switch 2 at Gamescom and PAX West (major video game conventions)

- No new release date has been set: Gearbox said it will update the “release timing” for Borderlands 4 once it has “fully adjusted [its] plans”

-> Take-Two’s stock fell -3% the day of this news (but rallied on Friday as mentioned)

Google Is Pushing Harder Into Gaming With Several Key Updates To Google Play (link/link/link)

- Google is rolling out a new “You” tab for a personalized hub

- The new tab will serve as a homebase for account info, housing stats, rewards, subscriptions and updates

- Beyond gaming, recommendations extend to audiobooks, novels, and podcasts, with features to resume content where users left off

- The “You” tab begins rolling out this week in select Play Points markets, with a broader expansion to additional countries on Oct. 1st

- The new tab will serve as a homebase for account info, housing stats, rewards, subscriptions and updates

- Launched alongside the “You” tab is a Gemini Live overlay for games, letting players ask for hints without leaving their game

- How it works: Players can drag a handle to open tools (screenshots, recording, YouTube streaming, DND) and tap “Start Gemini Live” to share their screen and get AI-driven advice

- Rollout: Launching in select games over the coming months; Developers must support Sidekick by July 2026

- Other Play Games enhancements –

- Added Gen AI Avatars to customize gaming identity

- Expanded Play Points rewards across mobile + PC, plus perks like merch and VIP experiences

- Launch of Play Games Leagues (first one: Subway Surfers, Oct 10–23)

- Enhanced Game Detail Pages with events, updates, progress, and a new Q&A community feature (launching next month in select markets)

- Google Play Games on PC is now officially out of beta, with 200k+ titles available

- Regional launches like entertainment hub in Korea and short-form dramas/webcomics in the U.S.

- Guided Search powered by AI, organizing apps by user goals (“find a home,” “deck-building games”)

The NFL Is Likely To Set A New Media Rights Record Sooner Rather Than Later + Other Key Sports Developments

The NFL is the most valuable sports league in the world and it’s about to get even more valuable. Despite already commanding the largest media rights package in history ($111bn over 11 years), new comments from Commissioner Roger Goodell this week suggest the league may begin renegotiating as early as 2026, four years ahead of schedule. That could unlock a major step-up in annual fees, with some Wall Street analysts estimating a jump from $10bn to $18bn per year. The timing reflects a strategic recalibration given the fact that despite the NFL continuing to dominate viewership metrics, rival leagues are securing richer deals on a per-viewer basis. The NFL would also like more flexibility with streaming partners.

See below for more details on Goodell’s comments, other potential implications of a new NFL deal, plus a couple additional key sports related updates this week.

The NFL Could Be Renegotiating Its Media Rights Deals Sooner Than Expected…And See A Big Step Up In $s (link/link/link)

- While the NFL’s current $111bn, 11-yr deal media rights deal (signed in 2021) runs through 2033, with an opt-out after 2029-30 (2030-31 for Disney), Roger Goodell told CNBC this week that talks could begin as early as 2026 (four years ahead of schedule)

- Wall Street analyst cites that the NFL’s media rights could increase from $10bn per year to $18bn per yr: This could potentially begin with the 2027 season

- Why does the NFL want to begin talks ahead of schedule?

- Despite the NFL having better TV ratings, other leagues have secured more lucrative deals

- 72 of the top 100 programs in 2024 (93 of 100 in 2023) were NFL games

- NFL regular-season games average 17.5mn viewers, vs. NBA at ~1.6mn

- In terms of viewer hours, the NFL has 8bn while the NBA has 2bn

- NFL gets $1.27mn per viewer hour compared to the $3.55mn per viewer hour of the NBA

- Goodell says NFL is “leaving money on the table”

- The NFL league also wants flexibility to add partners like YouTube and Netflix, which have already streamed select games

- Despite the NFL having better TV ratings, other leagues have secured more lucrative deals

- But to note, the ESPN/NFL stake deal (NFL acquiring 10% of ESPN) is seen as potentially complicating 2026 negotiations due to conflicts of interest

- Other implications from a new deal include –

- It could increase the league’s salary cap in future seasons, giving teams more money for players and possible roster expansions

- It could also drive team valuations higher (the avg team now worth $7.65bn, up +18% y/y)

- It could pressure MLB (set to renegotiate after 2028), forcing media companies to prioritize NFL spend or help MLB argue for higher fees

Netflix Adds Addt’l Exclusive Sports Games (link)

- The Yankees Opening Day 2026 will be a Netflix exclusive on March 25th, per The Athletic

- 21 Yankees games this season have been streamed on Amazon Prime Video

- The Yankees have already been part of Apple’s exclusive Friday Night Baseball and a Sunday Roku stream

- This season, the Yankees are also expected to feature in ~1 Peacock-exclusive game next year under MLB’s new rights deal with NBC

Also, To Flag…Lawmakers Have Been Raising Antitrust Concerns About ESPN’s MLB & NFL Deals (link)

- A group of lawmakers, including Senators Bernie Sanders (I-VT), Elizabeth Warren (D-MA), and Representatives Joaquin Castro (D-TX) and Pat Ryan (D-NY), sent a letter to Disney, ESPN, the NFL, and MLB raising antitrust concerns about ESPN’s pending deals with both leagues

- NFL Deal: ESPN to acquire NFL Media properties (including NFL Network), with the NFL also taking a 10% ownership stake in ESPN; Lawmakers warn this could create preferential treatment for ESPN and disadvantage other distributors

- MLB Deal: ESPN is negotiating to license the MLB.TV out-of-market streaming service, which lawmakers fear could make it harder and more expensive for current subscribers on other platforms to access games

Meta Shakes Up The Dating App World This Week

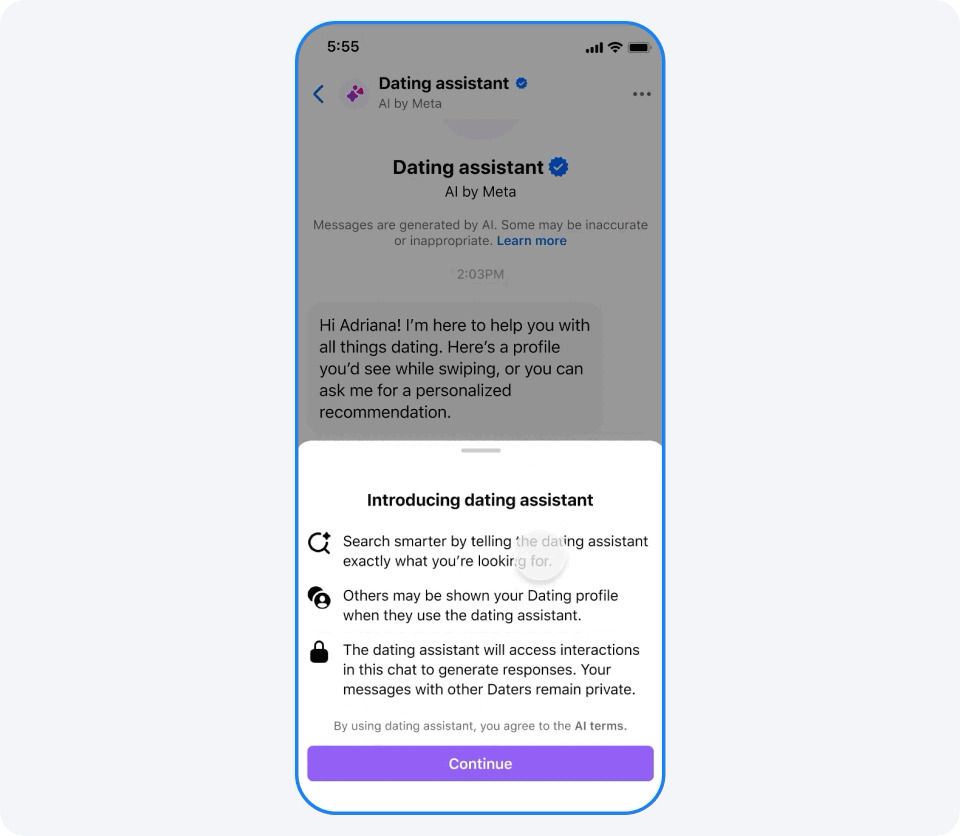

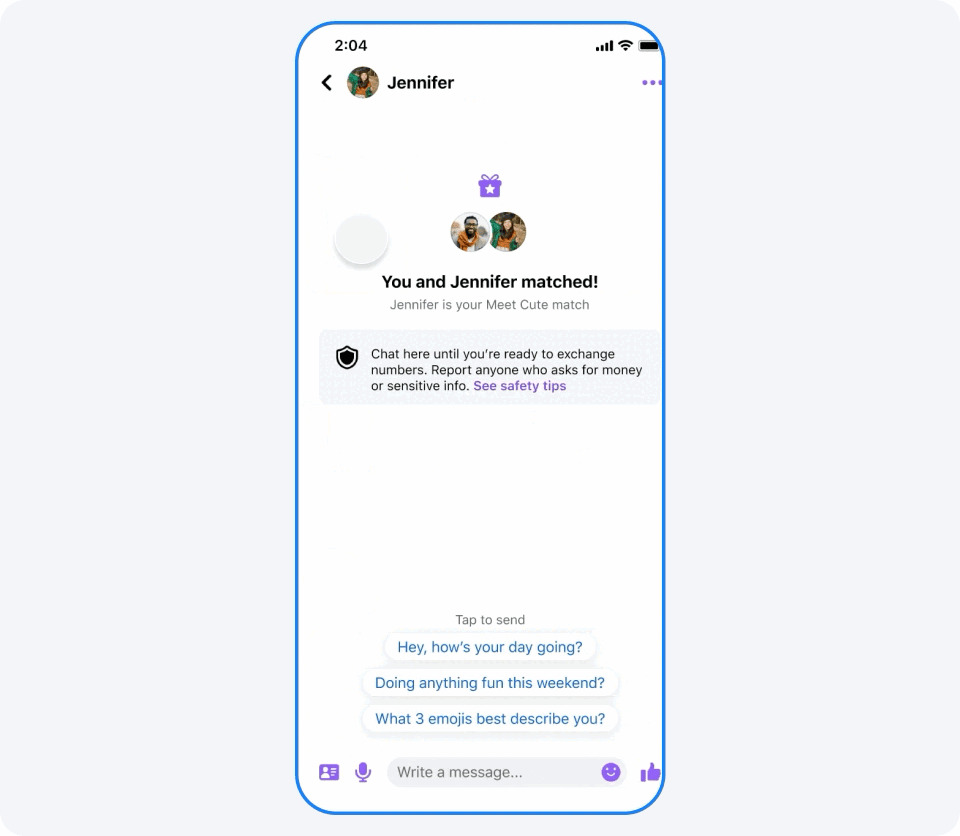

Meta first launched its Facebook Dating feature in 2019, which was aimed at offering a more integrated dating experience within the Facebook app by connecting users based on shared interests, events, and groups rather vs just swiping. Fast forward, this week Meta made a splash in the dating world by introducing some new features that caught investors’ attention, particularly those that own Match and/or Bumble.

The two key new announcements were 1) an AI-powered “Dating Assistant” and 2) a “Meet Cute” feature. While Facebook Dating users are reportedly miniscule next to Match’s ~14.9mn users and Bumbles ~50mn users, Facebook is in a very advantageous position given that it has a huge pool of 2.1bn DAUs to tap into, though not all would be looking for dates 😊.

See our quick take below…(link/link)

-> Bumble and Match Group traded down-3% and -5% respectively in reaction to the announcement

- Dating Assistant:

- Helps users find better matches based on interests & preferences

- Let’s users search for matches through natural prompts (e.g., “find a Brooklyn tech bro who goes to EDM concerts”)

- The chatbot can provide dating advice, like what to say to a match or where to go on a first date, based on publicly available profile information

- Will be rolled out gradually in the US and Canada

- Meet Cute:

- Automatically pairs users with a weekly match using the Co’s algorithm, with the option to un-match

- The Co may rollout other frequencies of matches as well

- This feature is aimed at ending swipe fatigue

- Other info about Facebook Dating …

- The Co has been focused on younger users, reporting a +10% y/y increase in matches among young adults, and hundreds of thousands of new accounts monthly in the US and Canada

- The app is positioning itself as a free alternative to Hinge or Bumble

A Stream Of Other Important AI Updates & Developments

While we included several AI enabled product updates in some of the other themes we discussed this week (online dating and gaming for example), there was a barrage of other similarly important AI updates this week that touched on personalization, real-time interactivity, multimodality, and accessibility. Alibaba debuted a fully open-source multimodal AI model, while OpenAI, Perplexity, and Microsoft 365 Copilot introduced personal-assistant capabilities, including ChatGPT Pulse, an AI inbox assistant, and with flexible model choices between OpenAI and Anthropic Claude models. Google continues to embed AI into daily life with Search Live for real-time voice-and-camera guidance, Gemini TV for personalized recommendations and learning, and Gemini Robotics 1.5 for multi-step physical tasks. Finally, OpenAI expanded access with ChatGPT Go, a low-cost subscription in India and Indonesia offering higher usage limits and improved memory.

Innovation is happening at lightning speed! See below for more on these key AI product updates this week…

Alibaba Enters The Multimodal AI Race (link/link)

- Alibaba debuts Qwen3-Omni: A fully open-source multimodal AI model

- What can it do? It accepts text, image, audio, and video inputs, and outputs text and audio

- Closest competitor? Google’s open source, Apache 2.0 licensed Gemma 3n, which accepts video, audio, text, and images as inputs, but only outputs text

- Accessibility: Can be downloaded, modified, and deployed for free under an enterprise-friendly Apache 2.0 license, even for commercial applications.

- While OpenAI’s GPT 4-0 and Gemini are also omni models, they are closed source, so users have to pay to use it

- Introduced three distinct versions, each serving a different purpose –

- Instruct: Full capabilities (can handle text, audio, and video inputs; generates both text and speech outputs)

- Thinking: Focused on reasoning tasks and long chain-of-thought processes (accepts multimodal inputs buts outputs only text)

- Captioner: “Fine-tuned” variant built specifically for audio captioning (producing “accurate, low-hallucination” text descriptions of audio inputs)

- How does performance compare to other models? Across 36 benchmarks, Qwen3-Omni got “state-of-the-art” on 22 and leads open-source models on 32

-> Separately, but related, Alibaba’s shares were up +9% in premarket trading on Wednesday after the Co said it plans to increase spending on AI models and infrastructure development, on top of the 380bn yuan ($53bn) over 3 yrs it announced in Feb (link)

AI Is Increasingly Becoming A Personalized Assistant

- OpenA introduces ChatGPT Pulse (link)

- What is Pulse? New experience where ChatGPT proactively does research to deliver personalized updates based on user chats, feedback, and connected apps (i.e., calendar, email)

- Pulse surfaces insights through visual topical cards designed to be scanned or expanded for more detail

- How does It work? Each night, ChatGPT synthesizes information from your memory, chat history, and direct feedback to learn what’s most relevant to you, then delivers personalized, focused updates the next day

- Each update is available for that day only unless you save it as a chat or ask a follow-up question, which adds it to your conversation history

- Example use cases: These could look like follow-ups on topics you discuss often, ideas for quick, healthy dinner to make at home that evening, reminder to buy a buy a birthday gift, etc.

- Pulse is still in preview and may “miss the mark” but it remembers feedback for next time and improves as it learns from real use

- What comes next… “by combining conversation, memory, and connected apps, ChatGPT is moving from answering questions to a proactive assistant that works on your behalf”

- “Over time, we envision AI systems that can research, plan, and take helpful actions for you—based on your direction—so that progress happens even when you are not asking”

- Availability: Available to Pro users on mobile; “We’ll learn and improve from early use before rolling it out to Plus, with the goal of making it available to everyone”

- What is Pulse? New experience where ChatGPT proactively does research to deliver personalized updates based on user chats, feedback, and connected apps (i.e., calendar, email)

- Perplexity introduces Perplexity Email Assistant – “a personal assistant for your inbox” (link)

- Exclusively available for Perplexity Max subscribers

- Which email platforms does it work with? Connects w/ Gmail and Outlook

- How does it work? Email Assistant connects directly with your email account across your phone and computer; It drafts replies, organizes messages, schedules meetings, and more

- Learns your communication style and priorities

- Drafts responses matching your tone

- Suggests meeting times based on your calendar preferences, saving time on routine tasks

- Security features: SOC 2 and GDPR compliance by default and never trains on your data

- Microsoft is expanding model choice in Microsoft 365 Copilot w/ introduction of Claude Sonnet 4 and Claude Opus 4.1 (link)

- Users will be able to switch b/w OpenAI and Anthropic models easily: Copilot will continue to be powered by OpenAI’s latest models, while also giving customers the flexibility to select Anthropic models

- How Anthropic models are showing up in Microsoft 365 Copilot today –

- Researcher agent: Now lets you choose between OpenAI or Anthropic Claude models for deep reasoning, enabling complex, multistep research across web data, emails, chats, meetings, and files

- Copilot Studio: Claude Sonnet 4 and Claude Opus 4.1 can now power enterprise agents, letting you build, manage, and mix models from Anthropic, OpenAI, or the Azure Model Catalog for reasoning, automation, and specialized tasks

Google Continues To Integrate AI Into Everyday Use Cases & Real-Time Interactions

- Google rolls out Search Live, which lets user talks directly with Google Search in real time (link/link)

- How does it work? Built into the Google app, it lets users talk with Search and share camera views for AI-powered answers, context, and links in real time

- What’s new? Unlike earlier versions that only had a talk-and-listen mode, this release includes both voice and camera input

- Use cases –

- Scan board games at once to get advice on rules, best choices, or game suggestions for your group

- Get step-by-step help setting up devices, identifying cables, or fixing issues by showing your setup

- Point your camera at tools or ingredients to get guidance, substitutions, or step-by-step tips for activities

- Google launches Gemini for TV (link/link)

- How does it work? Users can “engage in free-flowing conversations” just by saying “Hey Google” or pressing the microphone button on the TV to engage the assistant

- Variety of use cases for watching television –

- “Find me something to watch with my wife. I like dramas, but she likes lighthearted comedies”

- “What happened in the last season of ‘Outlander’”

- “What’s the new hospital drama everyone’s talking about?”

- As well as for learning –

- For school projects: “Explain why volcanoes erupt to my third grader.”

- For new skills: “How do I learn guitar as a beginner?”

- For the kitchen: “What’s a dessert I can make in less than an hour?”

- Availability: Now available on the TCL QM9K series, and later this year will expand to Google TV Streamer, Walmart onn. 4K Pro, Hisense U7, U8, UX, and TCL QM7K, QM8K, and X11K models

- Also an update on the robotics front…Google DeepMind unveiled Gemini Robotics 1.5 and Gemini Robotics-ER 1.5 (link/link)

- What is it? An upgraded AI model that allow robots to go beyond single-step commands and perform multi-step, real-world problem-solving — even pulling information from the web to complete tasks

- How does it work?

- Gemini Robotics 1.5: Vision-language-action model that converts visual inputs and instructions into motor commands, enabling robots to transparently plan and execute complex tasks while transferring skills across different robot types

- Gemini Robotics-ER 1.5: Vision-language model that reasons about the physical world, integrates digital tools, and generates multi-step plans, achieving state-of-the-art results in spatial understanding

OpenAI Is Expanding Accessibility With Low-Cost Offerings In India + Indonesia

- OpenAI launches ChatGPT Go in Indonesia, following last month’s rollout in India (link/link)

- What is ChatGPT Go? “Low-cost subscription plan that provides expanded access to ChatGPT’s most popular features at an affordable price”

- Serves as a mid-tier subscription between OpenAI’s free and Plus options

- Features –

- Users get 10x higher usage limits than the free plan for sending questions or prompts, generating images, and uploading files

- Also allows ChatGPT to remember previous conversations better, enabling more personalized responses over time

- Pricing: Rp75,000 ($4.50/month)

- Competition for Google? Comes as Google launched its AI Plus plan in Indonesia earlier this month, also priced around $5/mo

- Already seeing big uptake in India: Since the launch of ChatGPT Go in India last month, paid subscribers made more than doubled

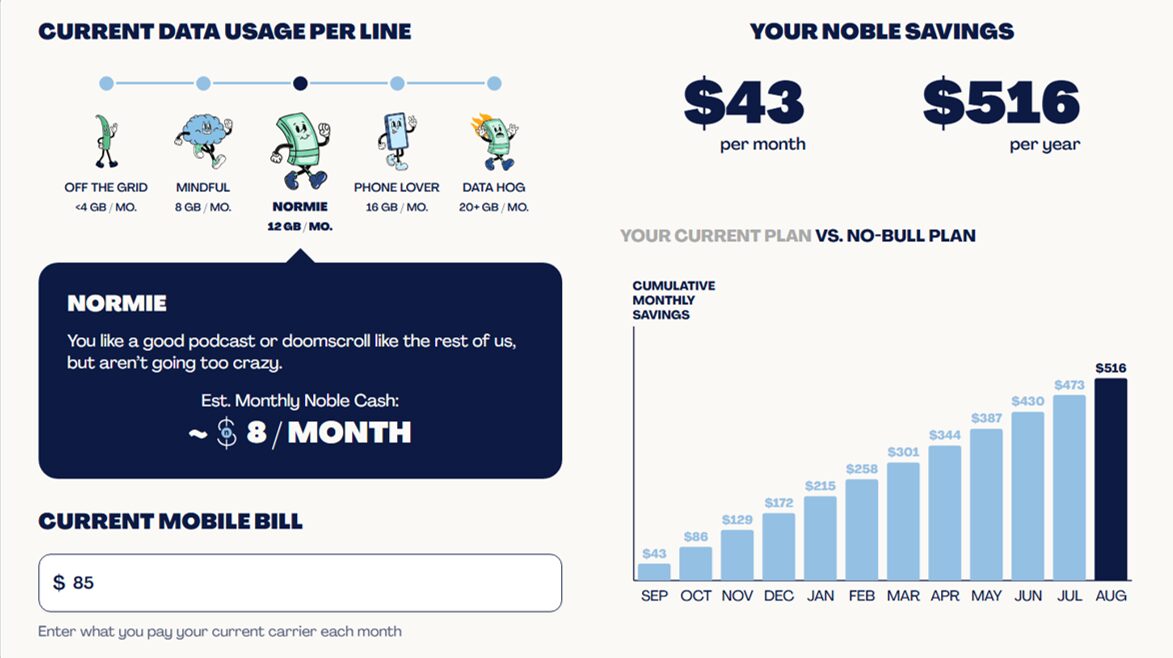

A New “Put Your Phone Down” Incentive Hits The US Wireless Market

We wanted to flag an update that we saw on CNBC this week, given it is an example of a new, innovative, and aggressive US wireless svs prepaid pricing model. Subscribers are only paying $50/month upfront for unlimited data, but will get money back depending on how much data they actually use in the period, essentially creating an incentive for customers to use their phones less. This new challenger is called Noble Mobile, founded by Andrew Yang.

While there was not any color on initial subscriber uptake rates, it seems like it could be attractive to at least some segments of the market, hence worth noting.

See below for details from the CNBC interview below (video clip can be found HERE).

- Nobile Mobile’s founder & CEO Andrew Yang was a former 2020 Democratic presidential candidate and also launched the Forward Party in 2022

- His thesis (link) –

- Americans are paying 2x for wireless data when compared to Europeans, Australians etc. as there is a “data tax” on Americans

- Large carriers have been pricing up the service to pay dividends, and not making big investments in the networks, which have actually reached parity with each other

- Also, many Americans “pay for an all-you-can-eat-data-buffet,” but don’t end up using all of it

- Noble Mobile is an MNVO (mobile virtual network operator) and is running on the T-Mobile network

- How does the pricing work? The Co gives incentives to use your phone less…

- Subscribers pay $50 upfront for the month but can get up to $20 in cash back based on the data they use

- The avg person uses 12GB of data a month and would get ~$8-$10 back per month

- Noble will pay a 5.5% interest rate on the savings customers get back in their account within Noble

- The Co wants to build a “set it and forget it” savings plan, “which is the first of its kind” and customers can use that money to pay their phone bill the next month

- If subscribers use more than 20GB per month, they don’t owe anything more than the $50/month that they paid upfront

- Can you make money charging only $50/mo for unlimited? Yang says yes

- This is a “for profit business”

- He wouldn’t’ disclose any details about the wholesale agreement w/ TMUS but Yang stressed that they are NOT taking losses on new customers, even on day 1

- What is T-Mobile’s reaction since this is lower pricing on their network? They like having different offers in the marketplace

- Yang believes that they will likely take more share from AT&T and Verizon since they tend to be more expensive

- Noble vs Mint Mobile? They are different; Nobile is creating an incentive to use your phone less, while Mint is more of a discount offering phone plan

- A lot was not discussed though, including –

- Data speed and if they would throttle at certain data thresholds…on the website it says “we reserve the right to limit excessive usage if it causes a strain on our network”

- It doesn’t look like there are any family-oriented plans (based on the website)

- What handset upgrade policies may look like

- Subscriber, churn data or expectations, and/or other expected metrics

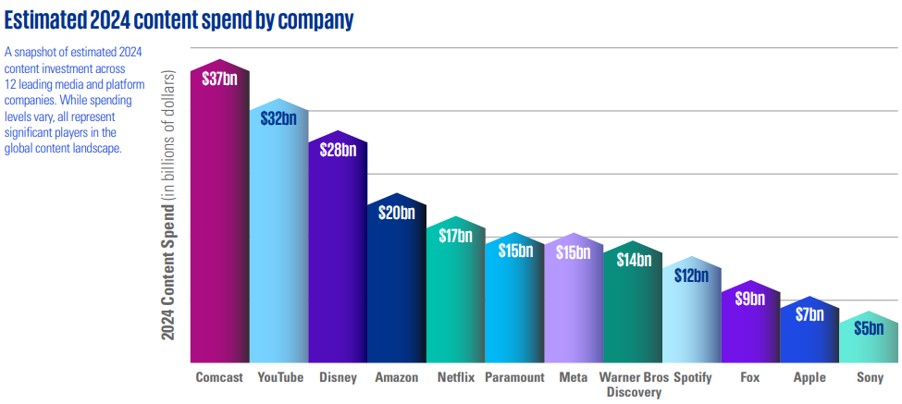

Entertainment Content Spend Has Still NOT Peaked

While there’s been ongoing debate in the industry about whether content spend has already peaked, KPMG’s analysis

published this week titled “Money in Motion: The Future of Content Spend and Business Models in Media” suggests otherwise. The ceiling hasn’t been reached, with growth now coming from a broader mix of formats, platform and audience behaviors. Sports rights remain a major driver, but the most dynamic growth is happening in user-generated content, where creators are becoming as valuable to platforms as top-tier scripted series once were to studios. In a sense, user-generated content has created its own genre.

Who spent the most in 2024? Comcast/NBCU held onto its #1 position yet again.

Below are a few stats we found the most interesting, and if you’d like to delve into the full report, click HERE.

- Annual content spend by the industry’s 12 biggest media and entertainment Cos now exceeds $200bn

- Growing at a 10% CAGR since 2020, w/ some moderation post-pandemic

- In 2024, the group set another new content-spending record, paying out ~$210bn, up +4% y/y

- Comcast/NBCUniversal has maintained its #1 position for the fifth yr in a row, spending $27bn in 2024 (flat y/y)

- “While some argue that ‘peak content’ has been reached, we believe the industry is far from saturation – although the reality is more nuanced”

- Content spend is not growing uniformly across formats and genres

- For example, investments in sports rights have continued to rise, while investments in other areas (like scripted and reality programming) have slowed

- In general, growth is now coming from an expanding mix of content types, distribution platforms and audience preferences

- In particular, the shift toward user-generated content and ad-supported models (such as YouTube and Amazon), as well as the emergence of free streaming svs (such as PlutoTV and Tubi) are poised to drive further content expansion

- Content spend is not growing uniformly across formats and genres

- “No one form of content will dominate the industry”: “We anticipate a future that features a diverse array of content types, from high-budget film and TV series to user-generated content from individual creators”

- BUT the growth of user-generated content has outpaced other segments and will likely see continued expansion, fueled by increased ad dollars and a “robust” creator economy

- “In a sense, user-generated content has created its own genre, which is why it isn’t simply replacing traditional film and TV productions”

- The firm expects that the blending of high production values applied to individual creators’ content will become more prevalent

- “The future landscape will see fierce competition for individual content creators, akin to the historical battle for screenplays and series ideas”

- On AI’s impact on content and media models – “it would be surprising to us if overall content spend changed quickly…in the near term, AI will augment the production process, rather than take it over”

- For example, for large-budget productions, talent fees still make up 20-30% of total production costs and “an AI Tom Cruise is the not the same as the real Tom Cruise”

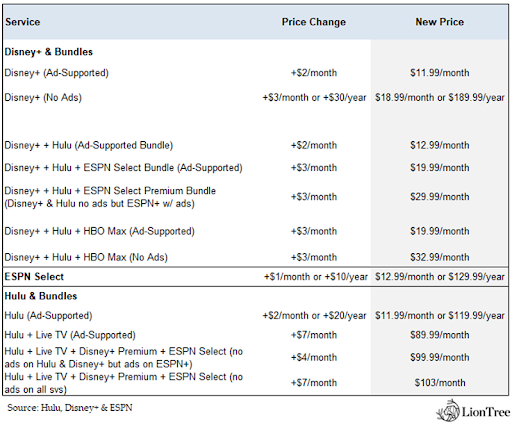

Prices Move Up AGAIN In The Streaming Video Space

Continuing the trend of a greater focus on video streaming profitability, and higher subscription entertainment prices as a way to get there, Disney is now slated to implement another round of streaming price increases starting on October 21st. These increases will be across its entire portfolio including Disney+, ESPN+ (which is also rebranding to ESPN Select), and Hulu, and the magnitude will range from $1 to $7 across monthly and bundled plans.

However, when is enough, enough? Recent surveys suggest as many as 40% of households plan to cancel at least one service in 2026 due to affordability concerns.

See below for more details on Disney’s coming price hikes. (link/link/link/link)

- Effective date of price hikes: Oct. 21st

- A few key points:

- The Co is raising Disney+ “no ads” more than “with ads” (+$3/mo vs +$2/mo, respectively)

- Consumers continue to get a lot more value with the various bundles

- ESPN+ will officially rebrand as ESPN Select: The name change is meant to reflect the platform’s focus on delivering selective sports content tailored to dedicated fans, distinguishing it from broader sports media offerings

- A few other industry price hikes in 2025:

- Netflix basic: $9.99 to $11.99 (Jan 2025)

- YouTube TV: $73 to $83/month (Jan 2025)

- Discovery+ ad-tier: $4.99 to $5.99 (Jan 2025)

- Peacock ad-tier: $5.99 to $7.99 (Jul 2025)

- Apple TV+: $9.99 to $12.99 (Aug 2025)

- A recent survey indicated 40% of streamers plan to drop at least one service in 2026 due to costs (link)

- Average US household streaming spend now rivals/exceeds $80/mo, echoing traditional cable bills

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Google faced fresh antitrust heat as Business Insider sued for damages, alleging monopoly abuse in ad tech. Exec Tim Craycroft revealed Google considered selling its ad biz twice—2021’s Project Sunday and again in 2024. US DOJ seeks AdX divestiture; EC fined Google €3.5bn for favoring its own svs. Publishers claim forced use of DFP/AdX depresses rev. Judge Brinkema demands clarity on divestiture feasibility. (CXOToday)

- Meta staffers are in early-stage talks w/ Google Cloud to use Gemini and Gemma models to enhance ad targeting. The move highlights Meta’s AI scaling challenges despite heavy investment. Choosing Google’s AI over in-house tech reflects strategic shifts in its ad biz. Both cos reported AI-driven ad rev growth in recent earnings. Meta also explored partnerships w/ OpenAI for chatbot and social media AI features. (Reuters)

- The Trade Desk & Acxiom annc’d True Intelligence, enhancing their UID2 partnership. Built on Snowflake & integrated w/ TTD’s Kokai AI platform, it links digital/CTV ad impressions to real-world outcomes using Acxiom’s data. Unlike walled gardens, advertisers get log access & CRM integration. The goal: smarter, incremental measurement across open internet mkts. (AdExchanger)

- Best Buy annc’d new ad svs at its “We Got Next” showcase, incl takeover packages for in-store/exterior branding. Sports tie-ups w/ NFL & TGL were expanded, tapping into its shopper base, 26% more likely to be sports fans. Best Buy Ads, launched in 2022, connects 93% of rev to customer IDs. (Retail Dive)

- Netflix & AB InBev inked a global mktg deal making AB InBev’s beer brands title sponsors of Netflix content & live events. Co-branded campaigns will span NFL games, boxing, Women’s World Cup, w/custom packaging & potential new products. The multiyear pact leverages both cos’ global scale to create culturally relevant, consumer-centric experiences across mkts. (The Hollywood Reporter)

- Clear Channel Outdoor rose ~8% in premarket trading after a Bloomberg report said activist investor Anson Funds urged the Co to pursue a sale. Anson and Legion Partners—both top 10 shareholders—have pushed for this move since May 2023. Clear Channel gave 5%–9% Q3 rev growth guidance and is advancing debt reduction. (MSN)

Artificial Intelligence/Machine Learning

- AI coding start-ups raised ~$7. 5bn in 3 months as investors bet coding will be AI’s “killer app.” Factory, backed by Sequoia, NEA, JPMorgan & Nvidia, annc’d $50mn funding. Cognition, Anysphere & Replit raised $1.6bn since Jun. Google paid ~$2.5bn for Windsurf tech. Factory aims for $20–25mn annual rev by end-2025. Cursor’s rev exceeds $500mn. Market could hit $10tn+, but competition from OpenAI & Anthropic looms. (Financial Times)

- OpenAI annc’d GDPval, a benchmark testing AI vs. humans across 44 jobs in 9 top GDP-contributing industries. GPT-5-high matched or beat experts in 40.6% of tasks; Claude Opus 4.1 hit 49%, aided by strong visuals. While limited to report-writing, OpenAI sees this as progress toward AGI. GPT-4o scored just 13.7% last yr. More robust tests are planned to better reflect real-world workflows. (Tech Crunch)

- CoreWeave expanded its OpenAI partnership w/a new $6.5bn deal, totaling $22.4bn in agreements. The move reflects rising AI infra demand and rev diversification, shifting from Microsoft, which made up 60% of 2024 rev. OpenAI’s Stargate project nears 7GW capacity, backed by ~$400bn investment. Nvidia, owning >5% of CoreWeave, annc’d a $100bn OpenAI investment and $6.3bn hardware order, sparking antitrust concerns. (Reuters)

- AI agents in logistics fail >50% of the time, as shown by Anthropic’s vending machine fiasco. To reduce failure, cos must scope agent boundaries, add human-in-the-loop checks, and apply deep logistics knowledge. (Forbes)

- Amazon’s AI coding assistant Q Developer saw modest rev of ~$16. 3mn ARR in its 1st yr, lagging rivals like Cursor ($500mn) & Windsurf ($82mn). Despite 9x daily usage growth, internal demand favors external tools. Amazon plans Q brand revamp; Q Biz to relaunch w/ Quick Suite. CEO Jassy cited $260mn in efficiency gains but acknowledged Cursor’s impact. (Business Insider)

- SoftBank cut 23% of its subsidiaries in 2024, incl. selling Fortress to a UAE fund, to refocus on AI. It annc’d $2bn investment in Intel and added stakes in Nvidia, TSMC. This streamlined strategy doubled its stock, making it one of Japan’s top cos. Investors favor its AI-centric pivot, signaling broader mkts may reward clarity over diversification. (Finimize)

- Fidji Simo, OpenAI’s CEO of Applications, is seeking a leader to drive monetization, incl. ads on ChatGPT. The role will manage all rev efforts—ads, subs, etc.—and report directly to Simo, who joined OpenAI last month from Instacart. She oversees most of the biz except research, infra, consumer hardware & safety, which report to Sam Altman. Talks w/ candidates, incl. ex-Facebook execs, are ongoing. (Sources News)

- Google will receive warrants for ~24mn shares (5. 4% stake) in Cipher Mining under a 10-yr AI hosting deal w/ Fluidstack. Google will backstop $1.4bn of Fluidstack’s lease obligations. The $3bn agreement includes two 5-yr extensions, potentially raising total rev to ~$7bn. Cipher to deliver 168 MW IT load (max 244 MW capacity) at Lake Barber, TX by Sept. 2026, retaining 100% project ownership and tapping capital mkts as needed. (Investing.com)

- Microsoft is in talks w/ U. S. publishers to launch a two-sided AI marketplace, starting w/ Copilot, to compensate for content use. This move marks a milestone in building sustainable biz models for content cos in the AI era. Rising copyright concerns and lawsuits are pushing tech cos to strike stronger deals. Publishers seek control, consent & rev as AI platforms multiply. (Axios)

- Meta annc’d a super PAC to oppose AI/tech policy bills it views as burdensome. W/ federal regulation stalled, cos face challenges in active state legislatures. Anthropic plans D.C. expansion to guide lawmakers on AI’s rapid impact. Meanwhile, Democrats craft an AI playbook ahead of midterms, warning tech may deepen economic divides—criticizing GOP’s lax stance on regulation. (Axios)

- Despite rising gen AI adoption, most cos report no measurable ROI. A BetterUp–Stanford study blames “workslop”—AI-generated content that looks polished but lacks substance, shifting effort to recipients. ~40% of U.S. employees received workslop recently, costing ~$186/month per person and harming trust, collaboration, and productivity. Leaders must guide purposeful AI use aligned w/ biz goals. (Harvard Business Review)

- The DOJ will retry its case to break up Google’s ad tech biz, arguing the Co illegally monopolized mkts. Judge Brinkema may order divestiture of Google’s ad exchange, unlike Judge Mehta’s prior ruling on search mkts, which denied major remedies. DOJ sees stronger grounds here as the contested product was central to trial. Google calls proposals “radical,” while publishers cite lack of viable alternatives. (The Verge)

Audio/Music/Podcast

- Major record labels escalated their lawsuit against AI music startup Suno, alleging it illegally “stream ripped” songs from YouTube to train its models. The amended complaint filed claims Suno bypassed YouTube’s encryption, violating DMCA rules. RIAA seeks $2,500 per circumvention and up to $150K per infringed work. Suno defends its actions as fair use, but hasn’t disclosed its training data. (The Verge)

Broadcast/Cable Networks

- ABC annc’d Jimmy Kimmel Live! will return Tues. after a brief suspension due to controversial comments. The move sparked debate over free speech, gov’t pressure, and FCC involvement. Nexstar & Sinclair pulled the show, citing public interest. Protests followed, w/ 400 artists & ACLU backing Kimmel. His contract ends in May, as linear late-night faces viewership declines. (StreamTV Insider)

- Shareholders of DallasNews Corp approved its merger w/ Hearst. Hearst will acquire The Dallas Morning News & its sister Co, Medium Giant, for $16.50/share in cash. MNG Enterprises had bid up to $18.50/share, but Hearst won. Hearst aims to strengthen local media in growing mkts. (WFAA)

Cable/Pay-TV/Wireless

- Altice France is exploring a sale of its SFR Business unit to cut debt, per Bloomberg. The unit offers fixed/mobile connectivity, cloud svs, and cybersecurity to cos, and may be valued at several bn euros. Potential bidders include Free (Iliad SA), Bouygues SA, and PE firms. The move could reshape France’s B2B telecom mkts, where Orange SA leads. Sale talks are ongoing; Altice may still opt out. (Investing.com)

- Comcast plans job cuts at its largest unit housing Xfinity internet, mobile & pay TV to centralize ops & boost broadband biz. Starting Jan., a mgmt layer will be removed, w/ regional leaders reporting to a new nationwide exec. While front-line svs won’t be impacted, roles to be centralized are still being identified. The move follows prior shifts to national pricing & centralized marketing, legal & finance. (Reuters)

- T-Mobile annc’d Srini Gopalan will succeed Mike Sievert as CEO, marking a planned leadership shift. Sievert becomes Vice Chairman, advising on strategy and innovation. Gopalan, ex-Deutsche Telekom CEO, led T-Mobile’s tech, consumer & biz units, driving 5G/fiber growth. The Co aims to cont’d its Un-carrier strategy, scaling AI-enabled, digital-first svs for superior customer experience and mkts share. (Street Account)

Capital Market Updates

- S&P annc’d a ‘BB+’ rating for Paramount Skydance Corp. post-merger of Paramount Global & Skydance Media. Stable outlook reflects plans to cut debt, boost FOCF to debt >6% via streaming rev growth, $2bn cost efficiencies, & $1.5bn cash commitment. Co aims to unify tech platforms, but linear TV EBITDA declines persist. Ratings may shift based on leverage & DTC profitability. (S&P Global)

- StubHub Holdings Inc. has lost ~$2.2bn in market value since its IPO last week, w/ investors facing ~25% loss. This marks the worst debut wk for a US Co raising over $500mn since Sculptor Capital in 2007. StubHub’s performance highlights volatility in IPO mkts, despite recent optimism. (Bloomberg)

- Mortgage demand stalled last week despite falling rates. Total apps rose 0.6%, w/ refi demand up just 1% but 42% above last yr. VA refis surged 15%, now 80% higher than 4 wks ago, making up 60% of activity. Purchase apps were flat, up 0.3% weekly, 18% YoY. ARM demand dipped after prior surge. Avg 30-yr fixed rate fell to 6.34%. Fed speeches, incl. Powell’s, didn’t shift mkts. (CNBC)

Crypto/Blockchain/web3/NFTs

- Cloudflare annc’d NET Dollar, a USD-backed stablecoin to enable instant, secure microtransactions for AI-driven web platforms. Aimed at the “agentic web,” it supports real-time payments by personal/biz agents. The Co seeks to replace ad-based models w/ fractional rev streams rewarding originality. Open standards like x402 and Agent Payments Protocol ensure global interoperability. (Blockworks)

- Circle, the world’s #2 stablecoin issuer, is exploring reversible transactions to allow refunds in fraud/dispute cases—marking a shift from crypto’s immutability ethos. Its new blockchain, Arc, enables counter-payments akin to credit card refunds. Circle also plans encrypted transfers w/confidentiality layers. Arc faces criticism for centralization. USDC could grow by $77bn by 2027 amid a “stablecoin gold rush.” (Financial Times)

- Tether seeks to raise $15–$20bn via private placement, valuing the Co near $500bn. The deal, led by Cantor Fitzgerald, involves new equity. Tether, issuer of USDT (~$172bn mkt cap), reported $4.9bn Q2 profit w/ ~99% margins. Plans include launching USA₮ and reentering US mkts amid shifting policy. Investors are reviewing governance, risks, and growth. (XT.com)

- Coinbase CEO Brian Armstrong told Fox Business the Co aims to be a financial “super app,” integrating crypto w/ traditional svs. He cited bipartisan momentum in Congress, new stablecoin rules, and ETF flows. Armstrong predicted BTC could hit $1mn by 2030. Despite bank lobbying, he defended crypto rewards and partnerships w/ JPMorgan. (CoinDesk)

eCommerce/Social Commerce/Retail

- Birkenstock raised its FY2025 rev outlook to €2. 09bn ($2.45bn), citing strong demand for clogs/shoes despite 15% U.S. tariffs. Q4 rev expected at €520mn, up 18% YoY. Full-price demand led to Q3 profit beat. Co acquired €18mn Dresden facility to expand production by FY2027. Adj EBITDA growth target remains 31.3%–31.8%. Shares rose ~6% premarket. (Yahoo Finance)

- Costco topped Q4 earnings/rev estimates, posting $5. 87 EPS on $86.16bn rev. E-comm sales rose 13.5% YoY; full-yr e-comm rev hit $19.6bn. Membership fee income jumped 14% amid more signups, esp. under-40s. Same-store sales rose 6.4%. Inflation stayed low-mid single digits. Costco opened 27 new warehouses, plans 35 more. Full-yr rev reached $275.24bn, up 8.1% YoY. Shares up ~2% YTD. (CNBC)

- H&M’s Q3 profit rose 40% to $523mn, beating forecasts due to strong autumn collections and tighter cost control. CEO Erver, in role since Jan. 2024, revamped marketing w/ celeb campaigns and trendier styles to rival Zara and Shein. Despite 10% share surge, U.S. tariffs may impact margins. Inventory fell 9%, signaling more in-season full-price shopping. Sept. sales expected flat y/y. (Reuters)

- Online spend has plateaued at 53%, same as last yr, per VML’s Future Shopper report. Consumers now expect 57% online spend in 5 yrs vs. last yr’s 60% forecast. 62% prefer brands w/ both physical & online stores. Political instability affects buying: 66% feel anxious, 60% avoid major purchases. ~70% use AI tools like ChatGPT; 52% want personal AI agents. 45% abandon carts due to poor UX; brands must improve to grow in an AI-first mkts. (MediaPost)

- Instacart annc’d its Consumer Insights Portal (CIP), a self-serve platform offering real-time data from ~100K stores and 1,800+ retail partners. CIP helps brands track SKU-level sales, search behavior, substitutions, and promo impact. Core features include trial/repeat rates, regional vs. national performance, and keyword optimization. The tool aims to boost Instacart Ads and omnichannel biz decisions. (Progressive Grocer)

- Walmart & Target annc’d Oct deals events to kick off holiday shopping early. Walmart Deals runs Oct. 7–12, w/ Walmart+ early access on Oct. 6; Target’s Circle Week spans Oct. 5–11, w/ Circle 360 perks. Discounts include toys, decor, electronics, & essentials. Walmart Q2 rev rose 4.8% to $177.4bn; Target saw a 0.9% drop to $25.2bn. (Retail Dive)

- NikeSKIMS, a collab between Nike and Kim Kardashian’s Skims, is set to launch this week after spring delays. Featuring 3 core collections—Matte, Shine, Airy—plus seasonal drops, it targets female shoppers w/ ~40 styles blending performance and lifestyle. Backed by top athletes, it aligns w/ CEO Hill’s strategy to reclaim mkts. Skims gains Nike’s dev. power; brand last valued at $4bn. (CNBC)

- ODP Corp annc’d its $1bn sale to Atlas Holdings for $28/share, a 34% premium, w/ unanimous board approval. Deal to close by end of 2025, making ODP private. Atlas aims to boost ODP’s B2B growth via cos like ODP Biz Solutions & Veyer. Q2 rev fell 7.6% YoY to $1.6bn due to 60 fewer stores & lower traffic. CEO cites Atlas’ industry expertise & confidence in ODP’s momentum. (Retail Dive)

- Amazon to shut all 19 UK Amazon Fresh stores, converting five to Whole Foods amid waning demand for contactless shopping post-COVID. The concept, launched in 2021, failed to rival Tesco/Sainsbury’s. Staff may be reassigned. Amazon aims to double UK Prime grocery access via Morrisons, Co-op, Iceland & Gopuff. Fresh groceries to be sold on its site from next yr. (The Guardian)

- Amazon’s trial began over FTC claims it duped users into Prime sign-ups. FTC alleges Amazon ignored user confusion to protect rev, violating consumer law. Execs rejected clearer disclosures till 2022 despite internal warnings. Prime’s cancellation flow—dubbed “Iliad”—was complex, deterring exits. Amazon denies wrongdoing, citing clear terms. (Reuters)

- Stitch Fix annc’d Q4 FY2025 results, showing ~4% rev growth to $311mn and adj net loss narrowing to $8. 6mn ($0.07/share). Both beat analyst estimates. However, active client count fell ~8% YoY to 2.3mn, raising concerns over core Fix svs demand. Despite financial improvements, mkts reacted negatively, sending stock down ~17% week-to-date. (MSN)

Electric & Autonomous Vehicles

- Baidu annc’d plans to expand Apollo Go robotaxi svs to Australia & SE Asia after achieving per-vehicle profitability in China. It received 50 new trial licences in Dubai, doubling its UAE fleet to ~100 cars. Despite unit-level profits, the division hasn’t broken even. Baidu has invested billions in self-driving tech since 2013 & partnered w/ Lyft to enter Europe in 2026. (Investing.com)

- Alphabet’s Waymo annc’d Waymo for Biz, enabling cos to set up robotaxi accounts for staff travel in LA, Phoenix, SF, Austin & Atlanta. The Co completes ~1mn rides/month, w/ 1 in 6 riders commuting in key mkts. Features include admin portals, promo codes & ride tracking. Early adopters include Carvana. Waymo is expanding airport access, incl. Phoenix, San José & testing at SF Intl. More features to come as biz use cont’d. (Reuters)

Film/Studio/Content/IP/Talent

- Sony/Crunchyroll’s “Demon Slayer: Infinity Castle” stayed number 1 at the US box office w/$17. 3mn in its 2nd weekend, despite a 76% drop. It’s now the top-grossing anime film ever w/$104mn domestic, $555mn worldwide. Sony’s highest-grossing 2025 film in Crunchyroll mkts ($269mn). “Him” debuted at No.2 w/$13.5mn, while “A Big Bold Beautiful Journey” bombed w/$3.5mn. Overall wknd gross hit ~$77mn. (The Wrap)

FinTech/InsurTech/Payments

- PhonePe, backed by Walmart, has confidentially filed its DRHP w/ Sebi for a $1. 5bn IPO, valuing the Co at ~$15bn. In FY25, net loss narrowed 13.4% to ₹1,727.4cr, while operating rev rose 40.4% to ₹7,114.8cr. Despite diversifying into credit, insurance & wealth mgmt, payments remain core biz.(Economic Times)

- Stripe is in talks to repurchase shares from VC backers at a $106. 7bn valuation, up from its post-pandemic $50bn dip. The Co hasn’t finalized how much stock it’ll buy or if employees are included. This move offers liquidity w/o public mkts. Sequoia previously bought $861mn in Stripe shares at $70bn. (Axios)

- Revolut annc’d its new global HQ in London, reinforcing UK roots and global ambitions. It targets 100mn customers by mid 2027, backed by $13bn in investments over 5 yrs, incl. $4bn for UK. Revolut Biz hit $1bn in annualised rev. Expansion cont’d across Latin America, APAC, Africa & Middle East. Product innovation, strategic partnerships, and tech hubs drive growth in 30+ mkts by 2030. (Revolut)

Last Mile Transportation/Delivery

- Uber & ALDI annc’d a nationwide collab to offer on-demand grocery delivery via Uber Eats. Over 2,500 ALDI stores now on the app, incl. wine & beer at select locations. ALDI becomes 1st retailer to accept SNAP-EBT on Uber Eats from launch. Promo: 40% off $30+ orders (max $25) w/ code ALDIUBER25. Pop-ups in NYC, Miami & Chicago in Oct. highlight ALDI Finds. A win for smart shoppers seeking value & convenience. (StreetAccount)

- Swiggy has approved sale of ~12% Rapido stake to Prosus and Westbridge for $270mn. Prosus, already holding 25% in Swiggy, will acquire ~9% stake for $222mn. Westbridge will buy the rest. The deal marks Swiggy’s divestment from the transport platform, w/ both investors boosting their positions. (Investing.com)

Live Entertainment/Theme Parks/Concerts/Experiential

- Jack Antonoff rejected Live Nation CEO Rapino’s claim that concert tickets are “underpriced,” calling resale markups exploitative. He urged banning sales above face value to reduce chaos and reconnect artists w/audiences. Rapino’s remarks came days before FTC sued Live Nation and Ticketmaster for “illegal” resale tactics. DOJ also sued the Co over alleged antitrust violations harming fans, artists, and smaller promoters. (CNBC)

- Danish toymaker Lego annc’d a $269. 5mn deal to acquire 29 discovery centres from Merlin Entertainments, aiming to boost brand engagement. The venues, attracting ~5mn visitors/yr, feature Lego zones, workshops & retail. Lego CEO said the move enhances global retail reach, now at 1,079 stores across 54 mkts. Merlin will cont’d to operate 11 Legoland parks under licence. (Reuters)

M&A

- Blackstone is weighing a sale or IPO of Ancestry. com, which it acquired in 2020 for $4.7bn. Talks are in early stages; no decision yet. Ancestry’s DNA kits and family history svs have built a strong subscriber base. A deal could attract buyers in consumer data and digital health. If mkts remain weak, Blackstone may hold. (Yahoo Finance)

Macro Updates

- Global debt hit a record $337. 7tn at Q2 end, rising $21tn in H1 per IIF. China, France, US, Germany, UK & Japan saw biggest debt increases in USD terms. EM debt rose $3.4tn to >$109tn. Debt-to-GDP ratio hit 242.4% in EMs; global ratio just above 324%. Rising gov’t debt, esp. in G7 & China, strains mkts. Bond redemptions in EMs near $3.2tn for rest of 2025. IIF warns of fiscal pressure & bond vigilantes. (Reuters)

- US GDP grew at 3. 8% annualised in Q2, up from 3.3%, driven by strong consumer spending and falling imports. Consumer spending rose 2.5% y/y to end of Jun., vs. 1.6% prior est. Retail sales rose 0.6% in Aug. despite weak labor data. Job gains slowed to 22,000 in Aug., w/ unemployment at 4.3%. Economists say momentum cont’d, but tariffs and policy uncertainty may slow growth and raise inflation. (BBC)

- Retail seasonal hiring is set to hit its lowest level since 2009, per Challenger, Gray & Christmas. Retailers may add <500K jobs in Q4 2025—an 8% drop YoY. Cos like Target, Macy’s, Aldi haven’t annc’d plans yet. Inflation, tariffs, automation, and high interest rates weigh on mkts. Spirit to hire 50K; Bath & Body Works 32K. PwC sees 5% drop in holiday spend; AlixPartners forecasts 3–5% growth. (CNBC)

- Fed Chair Powell, speaking in Providence, said equity prices are “fairly highly valued” but noted no elevated financial stability risks. Stocks had rallied pre-FOMC rate cut, hitting record highs, but dipped post-speech. Powell emphasized mkts respond to rate expectations and that policy aims to shape financial conditions, not directly target asset prices. (CNBC)

- Retailers face rising challenges as tariffs and softening employment impact consumer spending. Lower-income households prioritize essentials, while wealthier ones continue discretionary purchases. Luxury prices—e.g., denim jackets up 34%—are rising. Retailers aim to protect margins w/ strategic hikes. (Retail Dive)

- Fed Chair Powell, warned of dual risks: rising inflation due to Trump’s tariffs and weakening labor mkts amid immigration policy. He emphasized no “risk-free path” for rate decisions. While some Fed officials push for steep cuts, others urge caution. Powell noted scars from past crises and stressed public service amid political pressure, incl. Trump’s move to fire a Fed Governor. (Investment News)

- Three Fed officials—Milan, Bowman, and Bostic—support shifting from a fixed 2% inflation target to a range-based approach. Milan cited measurement challenges; Bowman noted global use of ranges; Bostic suggested 1.75%–2.25%. Though last yr’s review excluded changes, ongoing discussions persist. (Futubull)

Online Travel

- Navan, formerly TripActions, filed for IPO on Nasdaq (NAVN), reporting $613mn rev (32% growth) and $7. 6bn bookings (34% rise) across 10K+ clients incl Adobe, Geico. Despite $181mn net loss, margins improved to 68%. Founded in 2015, the Co uses AI (Ava assistant, Cognition framework) to streamline travel, payments & expenses. (Tech Funding News)

Regulatory

- Google may face its first EU fine under the Digital Mkts Act in coming months, sources say. The Commission, acting as competition enforcer, is drafting its decision after Google allegedly favoured vertical search engines like Shopping and Flights. Earlier this month, Google was fined €2.95bn under older rules. Despite proposals to address concerns, criticism from rivals persists. EU scrutiny cont’d amid U.S. trade tensions. (Reuters)

- President Trump annc’d a 100% tariff on branded/patented pharma imports starting Oct. 1, unless the Co is building a U.S. plant. Products will be exempt if construction has begun. The move aims to boost domestic pharma mfg. Trump shared the update via Truth Social. (Reuters)

- President Trump annc’d new tariffs targeting heavy trucks, kitchen cabinets, bathroom vanities & upholstered furniture to support domestic cos. Shares in Paccar rose 6% premarket. Analysts say lightweighting may be deprioritized as tariff costs rise. VW paused EV production in Germany due to slow demand & U.S. tariffs. Bosch plans to cut 13,000 jobs amid tough mkts; German auto industry faces deeper crisis. (Automotive News)

- US Judge Alsup preliminarily approved a $1. 5bn copyright settlement against AI Co Anthropic, marking the first such resolution in lawsuits over AI training data. Authors alleged Anthropic used ~7mn pirated books to train Claude. The judge deemed the deal fair, pending final approval. Plaintiffs said it signals accountability; Anthropic aims to focus on safe AI dev. Trial was set for Dec. w/ potential damages in the hundreds of bn. (Reuters)

- Australia annc’d draft legislation to regulate digital asset platforms, extending financial svs laws to crypto cos. The bill defines Digital Asset & Tokenized Custody Platforms under the Corporations Act, requiring licensing, custody standards & dispute systems. Small platforms (<$10mn/yr) are exempt. It also covers staking, wrapped tokens & allows regulatory flexibility. Mulino called it a “cornerstone” for consumer protection & biz clarity. (Yahoo Finance)

- China’s market regulator annc’d draft rules for food delivery svs, aiming to improve quality, ease merchant burdens & ensure rider rights. Key points include fair platform fees, capped working hours, fatigue alerts, & balanced algorithms. Platforms pledged compliance after subsidy battles squeezed profits. Policy promotes fair mkts, tech upgrades & stronger corporate responsibility. (Global Times)

- California Sen. Scott Wiener’s AI safety bill SB 53, now on Gov. Newsom’s desk, mandates AI labs w/ >$500mn rev to publish safety reports on top models. Unlike SB 1047, SB 53 focuses on transparency, not liability. Backed by Anthropic, it targets risks like death, cyberattacks, and bioweapons.(Tech Crunch)

- CMA secured undertakings from Ticketmaster after Oasis ticket sale probe. Fans will get clearer info on tiered pricing, ticket labels, and rev ranges during queues. ‘Platinum’ tickets sold at 2.5x standard price w/o added benefits prompted action. Ticketmaster must report progress for 2 yrs. New UK consumer law from Apr. 2025 allows fines up to 10% of cos’ turnover for breaches. (UK Government)

- Apple’s statement outlines how the EU’s Digital Mkts Act (DMA) is impacting users. DMA has led to delays in features like iPhone Mirroring & Live Translation, increased app risks due to sideloading, and exposure to harmful apps. Apple warns of privacy threats from data-sharing mandates and argues DMA reduces user choice, disrupts cos’ innovation, and creates unfair competition across tech mkts. (Apple Newsroom)

- The Trump admin filed a 49-page brief urging SCOTUS to uphold broad tariff powers under IEEPA. It defends 10–50% levies imposed targeting trade deficits and drug trafficking. Plaintiffs argue overreach; admin claims Congress, not courts, oversees such powers. A ruling favoring Trump could allow presidents to tax w/o prior Congressional approval—raising major constitutional concerns. (Supply Chain Dive)

- SEC Chair Paul Atkins annc’d “innovation exemptions”, aiming to ease crypto regulation by Dec 2025. The move offers conditional relief to firms, enabling faster product launches, fostering DeFi, tokenization, and “super-apps.” It marks a shift from enforcement-led oversight to a pro-innovation stance, boosting U.S. crypto leadership, rev growth, and attracting talent and capital. (FinancialContent)

- Trump annc’d a $100K one-time fee for new H-1B visa petitions, effective Sun. Existing holders re-entering the US won’t be charged. Tech cos like Microsoft, JPMorgan & Amazon urged caution on travel. Indian IT svs cos may face disruptions. Fee aims to protect US workers from lower-paid foreign labor. (Reuters)

Satellite/Space

- United annc’d FAA certification for its first Starlink-equipped mainline aircraft, a Boeing 737-800, w/ first flight from Newark. Starlink, now on ~50% of United’s regional fleet, offers free high-speed Wi-Fi (up to 250 Mbps) to MileagePlus® members. Installations continue at ~50 jets/month. Customers report 90% satisfaction, praising streaming, gaming, and shopping svs onboard. (Street Account)

Social/Digital Media

- Meta annc’d ad-free Facebook & Instagram for UK users at £2. 99/month (web) or £3.99 (apps), citing app store fees. Move aims to boost rev amid EU privacy rules; ads made up 97% of Meta’s rev last yr. UK’s ICO “welcomed” the model, diverging from stricter EU stance. Meta faced €200mn fine in Apr. over EU version, now tweaked. Users 18+ can opt for paid or free w/ ads. Roll-out expected in coming weeks. (The Irish Times)

- Publishers are shifting focus to Reddit, Pinterest & Facebook to offset Google search traffic losses post-AI Overviews. Reddit shows promise for organic traffic via niche content; Pinterest offers discovery but lacks reliable referrals; Facebook sees a traffic uptick but remains volatile. Email boosts engagement, yet isn’t a long-term fix. Execs eye tech investment to future-proof biz strategies. (Digiday)