I first wanted to pause to remember all those impacted by September 11th and honor the lives lost, the courage shown, and the enduring spirit of unity that continues to inspire us. It is hard to believe that it was 24 years ago, yet may its influence continue to shape how we live, lead, and come together.

Turning to our Weekly Update, we knew it was going to be a busy start to September – and we were not proven wrong this week. The tech sector continues to be on a tear with Oracle’s +26% move and AI enthusiasm helping to propel Nasdaq up +2% on the week and drive the S&P 500 up +1.6%. The media sector was also a key focal area with media consolidation speculation emerging. Wall Street conference season also continued this week. Net, there was not a shortage of important updates and developments that we wanted to analysis and flag.

In this edition, we focused on the below themes:

- Oracle Moved Into The AI Infrastructure Spotlight With Its Landmark OpenAI Deal

- Are We Finally On The Brink Of Large Media/Entertainment M&A??

- Crypto & FinTech Lead the Charge In The IPO Revival

- SpaceX Pours More Fuel On The Connectivity Competition Fire

- Snap Is Prepping For 2026 To Be “The Most Consequential Year Yet”

- Apple’s Not Exactly “Awe Dropping” Event

- Global Mobile Data Traffic Per Smartphone Is Expected To Grow +11% CAGR From 2024-2030

- AI’s Ongoing Push Into Hollywood’s Creative Scene

- A Steady Stream Of Next Gen Transport Updates This Week

- Grab Bag: Amazon-Netflix Ad Tie-Up / Murdoch Succession Resolution / YouTube’s NFL Broadcast Breaks Platform Record

Lastly to highlight, LionTree served as exclusive financial advisor to Areim on its €600m debt financing of EcoDataCenter.

Have a restful weekend. We are bracing for another busy week looking ahead.

We’re also excited to spotlight an innovative launch from our friends and partners at The Baer Faxt, the definitive multi-channel media platform for the global art market. This week they unveiled NoReserve, a new weekly newsletter crafted for both established and emerging art collectors, as well as discerning luxury-market consumers. Curated by subject-matter experts, NoReserve delivers actionable intelligence and timely insights—helping readers confidently navigate the traditionally opaque world of auctions, international art fairs, galleries, and emerging trends—while keeping them at the forefront of the latest news shaping the global art ecosystem. Check the link for more info.

Oracle Moved Into The AI Infrastructure Spotlight With Its Landmark OpenAI Deal

This was an incredible week for Oracle and the rest of the AI sector as the Co’s market cap skyrocketed by ~$240bn on the back of a $300bn, 5-year deal with OpenAI for cloud computing and a surge in Remaining Performance Obligations (RPOs). Oracle’s +36% share gain in reaction to the news was reportedly the largest since 1992 and helped Larry Ellison dethrone Elon Musk as the richest man in the world.

While the quarter itself was mixed and the guidance was ho-hum, the +359% y/y surge in RPO to $455bn was a main highlight and was attributed to the Co signing four contracts with three large customers during the qtr. Mgmt also cited the expectation of exceeding $500bn in RPOs in a few months’ time given other deals in the pipeline. Oracle Cloud Infrastructure (OCI) revenue is now expected to grow at a ~70% CAGR from FY25 to FY30.

All in all, Oracle joined the short list of AI golden children this week and looking ahead, all eyes will be on the new financial plan which is expected to be outlined at the Co’s upcoming Analyst meeting on October 13-16 in Las Vegas.

See below for more color (link/link/link)

-> Oracle’s stock closed up +36% in reaction to the deal and ended the week up +25.5%; YTD, the stock is up +76.8% which compares to Nvidia +32.4%; The AI group performed well on the back of this news, with CoreWeave’s +17% gain being of note

Cloud RPOs Skyrocket…The $300bn OpenAI Deal Is A Massive Driver

- FQ1:26 headline results were mixed w/ total revs (+12% y/y in CC) below cons by -0.7%, op margins 60bp better than expected, & adj EPS missing forecasts

- FQ2:26 revenue guidance implies +12%-14% y/y growth in CC & non-GAAP EPS is expected to grow +8-10% y/y

- Cloud rev (IaaS plus SaaS) growth is the key driver…growing +27% y/y in CC in FQ1 and expected to accelerate to +32-36% y/y growth in CC in FQ2

- The Co raised FY2026 CapEx guidance from $25bn+ to ~$35bn

- The “vast majority of our CapEx investments are for revenue-generating equipment that is going into the data centers and not from land or building”

- A key standout was that FQ1 Remaining Performance Obligation (RPO) of $455bn was up +359% y/y in both USD and CC… “we signed four multi-billion-dollar contracts with three different customers in Q1”

- Cloud RPO growth of ~+500% was on top of the +83% growth last year

- Expect RPO to exceed $500bn over the next few months, as they anticipate adding more multi-billion customers over the period

- Also guided for Oracle Cloud Infrastructure (OCI) revenue to grow +77% to $18bn in FY2026, w/ projections to reach $32bn, $73bn, $114bn, and $144bn over the next four years, representing ~70% CAGR

- Most of the rev in this 5-yr forecast is already booked in their reported RPO

- “Oracle is off to a brilliant start to FY26″

- “We have signed significant cloud contracts with the who’s who of AI, including OpenAI, xAI, Meta, NVIDIA, AMD and many others” – the quick terms on the OpenAI deal

- Size: $300bn over five years (starting 2027)

- Scale: Requires 4.5 GW of power capacity (same amount consumed by ~4mn homes)

- OpenAI annc’d in July that it struck a 4.5 GW deal w/ Oracle, but didn’t disclose the size of the contract

Are We Finally On The Brink Of Large Media/Entertainment M&A??

Larry Ellison was not the only Ellison in the headlines this week! Investors have been asking, for what seems like years and years, when large scale Media/Entertainment assets will consolidate. It was hard to miss the barrage of press reports citing that Paramount Global’s new owner David Ellison is preparing a bid to acquire all of Warner Bros. Discovery, which includes the linear networks, the movie studio, and the streaming assets. This also comes ahead of WBD’s planned split into two separate businesses, which is expected in Q2 of next year.

The move is viewed as an effort to get ahead of possible rival bids from tech or other media Cos for WBD’s most sought after assets once the split is complete. If pursued, it would represent one of the largest media consolidation plays since Disney’s acquisition of Fox in 2019. With chatter that a bid could be submitted as soon as next week, another potential blockbuster deal may soon be on the docket.

See below for what’s been speculated in the press…

-> WBD surged +29% on the day of the report (the stock’s best day ever),and ended the week up +56% while Paramount Global also rallied +16% on the day and closed the week up +25%; YTD, WBD is up +79% and PARA is up +81%; Disney, Fox, and Netflix closed the week -1.6%, -5.6%, and -4.4%, respectively

Paramount Skydance Is Reportedly Preparing A Bid To Acquire Warner Bros. Discovery (link)

- What is the bid for? Paramount’s bid will reportedly be for the entire company, including its linear networks and movie studio

- This comes after WBD annc’d in June that it would separate into two Cos (one focused on the legacy cable-TV biz and the other on streaming and studios) by Q2 of 2026

- Preempting a potential bidding war for WBD’s streaming & studios biz? There is speculation that Paramount Skydance is trying to acquire the Co before the split, aiming to get ahead of possible bids from tech players like Amazon.com and Apple

- Not the first time a WBD-PARA merger has been explored: Prior to Skydance securing a deal in July 2024 for Paramount Global, WBD CEO David Zaslav and Paramount then-CEO Bob Bakish had reportedly discussed the possibility of a merger in late 2023, but those talks did not progress beyond an initial exploratory meetup (link)

- Financing: The majority of the planned bid for Warner will reportedly be made up of cash, but a specific mix of cash vs stock is not known

- Timeline: Per sources, a bid has NOT yet been submitted, but could come as early as next week, though plans could still fall apart

- Impact to the legacy media competitive landscape: A merger would shrink the number of legacy media studios to four from five and mark the biggest consolidation in Hollywood since Walt Disney Co. bought the entertainment operations of Fox Corp. for $71bn in 2019

WBD CEO David Zaslav Is Reportedly Looking To Set Up A Bidding War (link/link)

- Zaslav has reportedly been gauging bidding interest from other media and tech Cos, including Amazon, Apple, and Netflix

- For reference, Paramount Skydance’s market value was $16.4bn before news of the potential offer broke, and WBD’s was ~$30bn (WBD has worked to cut its debt, it still has net debt of ~$35bn as of June 30th)

A Potential Deal Is Likely To Involve Regulatory Scrutiny (link)

- With the proposed bid spanning a large portfolio of media properties, the deal is likely to face close review from the US Department of Justice on regulatory and antitrust grounds

- It would likely not require approval from the Federal Communications Commission (FCC), since WBD doesn’t hold TV broadcast licenses and Paramount would not be transferring their CBS-held licenses to WBD

- As a reminder, the FCC’s scrutiny of CBS broadcast licenses were the primary reason for a prolonged delay in Paramount’s merger with Skydance

- Senator Elizabeth Warren posted on X – “This media merger must be blocked as a dangerous concentration of power” (link)

Paramount Skydance Has Been On A Deal-Making Spree (link/link/link)

- Shortly after completing the merger of Paramount and Skydance, the newly combined Co has…

- Struck A 7-yr deal for the US rights to UFC

- Signed an exclusive contract with the Duffer brothers, who created Stranger Things

- Agreed on deal with video games publisher Activision to produce a movie based on the Call of Duty franchise

- CBS is also confirmed to be in talks with Bari Weiss to acquire her news site, The Free Press, and give her a senior editorial role at the company, per Axios

Analysts Share Some Initial Thoughts On The Speculated Deal (link/link)

- MoffettNathanson’s Robert Fishman on how M&A may have been part of the Skydance strategy all along

- The idea would be “to consolidate media assets during a period of industry-wide instability and build a conglomerate with a streaming-first focus wrapped with TV and film studios and potentially a larger linear television portfolio”

- And the advantage of moving now is that it could “preempt a potential bidding war for only the Warner Bros. Streaming & Studios assets post-split”

- “By acting now, [Paramount Skydance] positions itself to secure the entire company before rivals can cherry-pick the most attractive assets”

- “Overall, we would expect material cost synergies from the overlapping cable networks”

- There are “presumably a high level of synergies from combining CBS News with CNN plus the long-term existing partnership between CBS and Turner with the NCAA’s March Madness Final Four”

- Wolfe Research’s Peter Supino on scale advantages and cost synergy estimates

- “Strategically, a deal would create the world’s largest film and TV studio and a top 5 global streamer with the content, subscribers, and fixed cost leverage to compete with industry leaders on the basis of content, technology (AI, streaming UI, ad tech), and marketing”

- Expects initial cost synergies of ~$3bn

- $1.5bn from the elimination of duplicative costs at Streaming & Studios

- $1.2bn from the elimination of Warner Bros.’ corporate costs

- ~$250mn from WBD’s stable of linear networks

- “The company could also choose to consolidate what would be an excess of film studio real estate”

- Guggenheim Securities’ Michael Morris on the combined biz oppty

- Estimates that Paramount+ has ~50mn domestic subscribers and Warner Bros. has ~58mn in the US across HBO and HBO Max

- The global streaming tallies stood at 77.7mn for Paramount and 125.7mn for WBD as of the end of the most recent qtr

- “The amount of overlap (or lack thereof) is critical to the combined business opportunity…a bundled P+/HBO/WBD streaming product that reaches subscribers currently on only a single service should represent the highest incremental margin opportunity”

- Estimates that Paramount+ has ~50mn domestic subscribers and Warner Bros. has ~58mn in the US across HBO and HBO Max

- Bernstein Research’s Laurent Yoon on weight of an Ellison bid vs other potential buyers

- “Could there be another bidder? We wouldn’t rule that out just yet… However, the backing of the Ellison family — with a war chest that just got bigger by $100 billion … might make others hesitate. No one else may show up, but everyone’s thinking.”

- CFRA Research’s Kenneth Leon noted some financial and strategic hurdles for the deal

- “We think the high debt leverage of WBD is an impediment to a high bid for WBD’s shares”

- He suggested that, even if Paramount Skydance wins a deal for WBD as a whole, it may “be only interested in the businesses that will become Warner Bros. and not see meaningful value creation from the Discovery Global media portfolio”

Separately But Related…Prior To The Potential Deal Speculation Hitting The Tape, WBD CEO David Zaslav Shared Some Incremental Company Comments At The GS Communacopia Conference…

- Price hikes will come in the future, driven by confidence in quality of their content: “The fact that this is quality…we all think that gives us a chance to raise price. We think we’re way underpriced. We’re going to take our time because we’re really growing now and people […] are spending more and more time with us, but we think that there’s real upside to that”

- “It’s hard to replace quality content that people love”

- “And we’re less and less dependent on sport”

- “And I think the more we can be dependent on our IP – and I think that’s a big differentiator in terms of our ability to capture margin and growth”

- [We are] “in a really formidable position to split the company”

- “All of this happening when we paid $20 billion of debt down… as of last quarter, we were net $3.3 billion of debt with $20 billion paid down”

- “The company is outperforming pretty aggressively, which I think will help us.”

- “By being split, there’ll be a real focus… CNN… sports portfolio… free-to-air business in Europe… It’s an exciting time as we become global, global in terms of production and global in terms of streaming”

Crypto & FinTech Lead the Charge In The IPO Revival

$4.4bn in proceeds was raised in the IPO market this past week, which was more than the proceeds raised in each MONTH so far this year. What has been a major driver for the surge? Crypto/FinTech IPO deals. Klarna, Figure, and Gemini all priced their respective IPOs this week and collectively raised $2.6bn in proceeds. That accounted for 59% of the total proceeds raised this week and bigger picture, Crypto/FinTech IPOs have accounted for 31% of total proceeds raised Q3-to-date.

This burst of activity comes after a prolonged dry spell, with very few Crypto/FinTech IPOs making it onto the market in recent quarters. The pickup in new issuance in this sector began in May with eToro’s IPO, and momentum accelerated in Q3. Circle and Chime priced in June, followed by Bullish in August, and now this week’s slate of offerings, marking one of the more concentrated stretches of IPO activity the sector has seen in some time.

The positive performance of these deals, both on their first day of trading and from IPO-to-date (with the exception of eToro and Chime), has been a key catalyst for the strong momentum seen in overall IPO activity, along with a more favorable regulatory backdrop.

See below for a deeper look into the above.

3 Mega FinTech/Crypto IPOs Priced This Week & Raised $2.6bn (59% Of The Total)

- Buy-now-pay-later lender Klarna raised $1.4bn at an $15.3bn market cap

- The deal priced at $40/shr, which was above its range of $35-$37

- The stock popped +14.6% on its first day, but gave up some of those gains to close the week up +7.3%

- Blockchain-powered lending platform Figure raised $788mn at a $6.1bn market cap

- The deal priced at $25/shr, which is above its range of $20-$22

- The stock was up +24.4% on its first day and ended the week up +30.0%%

- Crypto exchange Gemini Space Station raised $425mn at a $3.5bn market cap

- The deal priced at $28/shr, which was above its range of $24-$26

- The stock began trading on Friday and ended the day up +14.3%

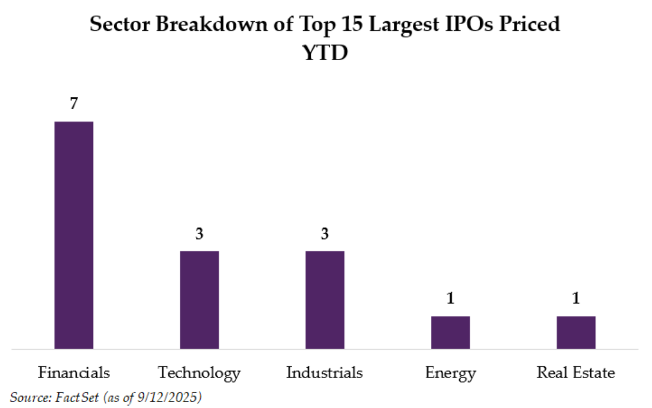

The Majority Of The Top 15 Largest IPOs YTD Have Come From The Crypto/FinTech Sector

- Financials (7)

- Crypto/FinTech (6): Klarna ($1.3bn); Bullish ($1.1bn); Circle ($1.1bn); Chime ($864mn); Figure ($788mn); eToro ($620mn)

- InsurTech (1): Accelerant ($724mn)

- Technology (3): CoreWeave ($1.5bn); SailPoint ($1.4bn); Figma ($1.2bn)

- Industrials (3): NIQ Global Intelligence ($1.1bn); Firefly Aerospace ($868mn); Legence ($728mn)

- Energy (1): Venture Global ($1.75bn)

- Real Estate (1): SmartStop Self Storage ($810mn)

How Have Crypto/FinTech IPOs Done Relative To Other Sectors In The Top 15?

- Of the 9 deals that priced above their respective ranges, 6 were in the Crypto/FinTech sector

- Crypto/FinTech IPS outperformed the broader Top 15 group on first day trading performance….

- Crypto/FinTech deals: +60%

- Non-Crypto/FinTech deals: +35%

- …as well as overall IPO-to-date performance

- Crypto/FinTech deals: +59%

- Non-Crypto/FinTech deals: +22%

SpaceX Pours More Fuel On The Connectivity Competition Fire

In late August 2025, when AT&T annc’d the $23bn purchase of 50 MHz of low- and mid-band wireless spectrum from EchoStar, it was widely reported that SpaceX and T-Mobile were also in the mix with respect to evaluating purchase of additional SATS’ spectrum (link). And voila, this Monday, SpaceX annc’d that it will be buying $17bn in wireless spectrum licenses from EchoStar as well. This fueled the fire in regard to increasing levels of competition in the Connectivity sector and weighed on stocks in the space. With that said, AT&T CEO John Stankey is not worried about SpaceX as a competitor, per comments this week as well.

Key details on the deal are below. (link/link/link/link/link/link)

-> After rallying 15% after the AT&T deal was announced, the stock rallied further this week by +11.4% (YTD it is now up +224%; The Connectivity sector was under pressure in reaction to Echo’s purchase with Charter down -2.5%, Comcast down -0.9%, AT&T down -0.6%, Verizon down -0.6%,and T-Mobile down -0.2%; AST SpaceMobile also traded down -8.7% this week.

- Value: ~$17bn (up to $8.5bn in cash and up to $8.5bn in stock) for Echostar’s full portfolio of AWS-4 and H-block spectrum licenses

- Plus other financial obligations: SpaceX will cover ~$2bn in EchoStar’s interest payments through 2027

- Includes a long-term commercial agreement: EchoStar’s Boost Mobile customers will be able to use Starlink’s direct-to-cell satellite service

- EchoStar will retain Dish TV, Sling, HughesNet, and Boost Mobile

- EchoStar’s deals w/ SpaceX & AT&T resolves the FCC’s concerns over its spectrum use – FCC Commissioner Carr reportedly confirmed this just hours after this deal was annc’d

- President Trump previously prodded EchoStar and FCC Chair, Brendan Carr, to reach a deal for the Co’s wireless spectrum licenses

- SpaceX had urged FCC to reallocate underused spectrum, accusing EchoStar of “failing to meet certain obligations”

- SpaceX’s purchase will allow it to deploy “next-generation, laser-linked Starlink satellites designed to boost cell network capacity more than 100x”

- “With exclusive spectrum, SpaceX will develop next generation Starlink Direct to Cell satellites, which will have a step change in performance and enable us to enhance coverage for customers wherever they are in the world”

- But phones supporting the new EchoStar spectrum likely won’t ship for ~2 years

- Chipsets still need to be modified to use the spectrum, and satellites using the frequency also need to be launched

- Musk hinted at potentially building a Starlink-branded phone as a “forcing function” if manufacturers resist supporting the spectrum

- SpaceX has launched 8,000+ satellites since 2020, creating a low-Earth orbit network used by militaries, transportation firms, and rural consumers

- ~ 600 of these satellites launched since Jan 2024 are “cell towers in space”

- Starlink reported 6.2mn+ global subs as of July, w/ 2mn+ just in the US

- The FCC’s response = it brings more competition: The “deals that EchoStar reached with AT&T and Starlink hold the potential to supercharge competition, extend innovative new services to millions of Americans, and boost U.S. leadership in next-gen connectivity”

- Competitor comments? AT&T says that it is not worried about SpaceX as a direct rival

- CEO John Stankey downplayed the risk of SpaceX becoming a true competitor when speaking on the Wall Street conference circuit this week

- “Does 40 MHz allow for a robust terrestrial replacement?” Stankey said “No”

- But he believes that SpaceX might be capable of providing some “fundamental basic connectivity” w/ EchoStar’s spectrum and agrees that SpaceX’s future platform could help out in rural areas and possibly open up some wholesale opportunities

- Analyst Phillip Burnett from New Street agreed services will have limited reach indoors/urban, but that it could add value in rural markets, where Starlink might complement existing fixed satellite offerings

- He believes 40-50 MHz of spectrum is not enough to replace traditional carriers that each hold ~300+ MHz

- CEO John Stankey downplayed the risk of SpaceX becoming a true competitor when speaking on the Wall Street conference circuit this week

Snap Is Prepping For 2026 To Be “The Most Consequential Year Yet”

As it reaches its 14th year, Snap CEO Evan Spiegel shared a note with team members reflecting on the company’s current moment, which he described as a “crucible.” In the letter, he outlined the challenges Snap is facing and the steps the company is taking to address them while positioning itself for long-term success. Key initiatives include focusing on medium-sized advertisers to reaccelerate advertising growth, returning to a startup-style approach by organizing small, highly accountable squads around the company’s biggest bets, investing in AI and direct revenue opportunities, strengthening reliability and overall performance, and building Specs to reimagine the future of computing.

See below for the drilldown. If you would like to read the full letter, the link is HERE.

-> Snap was up +0.4% for the week, but is still down -32% YTD

-> Also to flag in social media, Pinterest traded down this week by -7.7% on the back of comments at GS Communicopia, in which management described a macro environment with “puts and takes”, noting that small businesses may need to raise prices due to tariff risks while large retailers face margin pressures from higher tariff-related costs

Snap Is In A “Crucible” Moment

- The Co “stumbled in Q2” (ad rev growth was +4% y/y vs +9% y/y in Q1)…BUT “we have an enormous opportunity to re-establish momentum and enter 2026 prepared for the most consequential year yet in the life of Snap”

- “Poised to reach one billion Snapchatters, introduce Specs to the world, and generate record revenues diversified across direct revenue (meaning in-app purchase and subscriptions) as well as advertising”

- “We’re not far from achieving Fortune 500 status”

- Called out that “the cutoff for inclusion in the Fortune 500 was $7.4 billion in revenue in 2025” and “analyst estimates [suggest] Snap could reach nearly $6 billion in revenue in 2025”

- “Snap currently occupies a unique position, with significantly more scale and engagement than smaller players, but with less scale and market power than our larger competitors”

- “Our largest competitors are worth trillions, invest hundreds of billions in capital each year, and are being sued for monopolistic practices”

- “We also face smaller, nimbler competitors growing ad revenues faster off a smaller base with leaner cost structures and higher gross margins”

Will Reaccelerate Advertising Growth By Focusing On Medium-Sized Customers

- Penetration is still below half a percent with “high-fit customers”…: Who often spend at the scale of large accounts and retain at high rates

- …BUT biz development efforts have already brought in 2k+ new activations this yr, with each of these sellers each contributing ~$6mn in annualized rev on avg in the US

- “By rebalancing our sales coverage and product roadmap around these customers, we have a durable path to faster growth”

- “Doubling down” on foundations of their ad platform which are improving competitiveness in the lower funnel: Over the past year, have –

- Stabilized marketplace dynamics

- Launched tCPA v2

- Rolled out the App Power Pack, which bundles performance-driving features (i.e., Sponsored Snaps, Playables, etc.)

- Early pilots in the Americas and India are delivering a 25% lift in app installs with unique converters up 18%

- Sponsored Snaps and Promoted Places are “proving to be unique, high-impact formats”

- Sponsored Snaps drive up to 22% more conversions and ~20% lower CPAs when included in campaigns

- Promoted Places have already shown double-digit visitation lifts in early testing, “opening up an entirely new opportunity for advertisers”

- “These products work because they are built on the core of Snapchat’s product value: communication, maps, and friends”

- Remain under 1% share of a global digital ad market that is growing +13% y/y: Closing that gap requires –

- Consistent delivery against lower funnel objectives

- Reigniting brand dollars with differentiated formats like Sponsored Snaps

- Strengthening 3P measurement

- Telling a sharper story through their new “Say it in a Snap” narrative

- Continuing to invest in AI to compound performance over time in ranking, creative generation, and personalization

Also Plan To Accelerate Direct Rev Efforts, Which Is “One Of Snap’s Fastest-Growing Opportunities”

- Expanding Snapchat+ with new, premium features, and “bolder” merchandising

- Planning to introduce livestreaming and launch new tools “to help creators build deeper relationships with their biggest fans”

- “By investing in a stronger payments infrastructure, better lifecycle management, and creator monetization tools, we can make direct revenue a durable multi-billion dollar growth driver for Snap”

- Snapchat+ currently stands at 15mn+ subscribers and $700mn+ in ARR

Focusing On Closing Gross Margin Gap With Competitors

- Snap’s gross margin of 52% is “meaningfully below” many of its competitors

- “Largely because of our higher infrastructure costs as a share of revenue and the meaningful portion of revenue we share with creators, publishers, and platforms”

- Focusing on a set of initiatives to “improve efficiency, reduce costs, and better monetize the depth of engagement with our core products”

- Infrastructure – hold spending flat from 2025 to 2026

- Content – evolving revenue sharing arrangements with creators and publishers

- Payments – oppty to reduce platform fees by building their own 1P wallet

- “We believe these efforts can improve gross margins by several percentage points, creating a path to 60% gross margins and putting us on stronger footing to scale profitably while continuing to invest in our community”

N.America Growth is Lagging, And Investments Across Core Snap Features Will Be Critical To Driving Engagement

- Path to reaching 1bn MAUs by 2026 is “clear” …

- Reach 75%+ of 13–34 yr olds in 20+ countries

- … BUT growth has lagged in N. America

- DAUs fell -2% y/y to 98mn in Q2

- Content engagement globally continues to climb, but N. America is challenged by declines in Friend Stories that haven’t yet been offset by enough growth in Spotlight

- “We need to embrace this transition fully… we’re making significant investments to improve Spotlight”

- Also have “tremendous” headroom to continue growing w/ new Snapchatters around the world

“Our Vision For AI Enhances Your Relationships, Instead Of Replacing Them”

- Focused on 5 priorities –

- Building a partner platform that makes Snap an easy and valuable distribution channel for AI agents

- Developing the personalization layer, creating experiences that strengthen friendships and deepen connections by learning from interactions across Snapchat

- Unlock direct revenue with subscriptions, giving people access to premium AI tools through Lens+ and Platinum bundles

- Roll out Sponsored AI Chats so people can experiment with AI tools from brands directly in chat

- Continue innovating in social AI experiences, showing the world what’s possible when AI isn’t just a solo tool but something you can share with your friends

- At the enterprise level – strategy is moving from experimentation w/ genAI tools to scaled, outcome-driven adoption

- Immediate priority is to double down on four key functions – Engineering, Sales, Trust & Safety, and Customer Support – where AI is already delivering “measurable” impact

- “We’re also experiencing friction between teams eager to accelerate with AI tools and our security teams”

- “We’re putting strong guardrails in place and articulating a clear framework to determine what’s fine, what’s OK with caution, and what’s too risky, so teams can move quickly and safely”

Reliability Has Been a Pain Point, And Structural Changes Are Underway

- “Over the past few quarters, we’ve encountered reliability issues…we are addressing these issues head-on”

- “In 2026, we will complete the core rewrites, expand safe-rollout coverage to 100% of Tier-0 services, adopt freshness SLAs across all critical ML models, and set clear targets for incident reduction and performance gains”

Returning Back To A Start-Up Style Approach

- “Our current stock price reflects doubt. At this valuation, there’s startup-style return potential”

- “Willingness to move fast, risk failure, and build the impossible is the only way we’re going to win against competitors ten times our size and startups ten times more fearless”

- “We’re going to try a new way of organizing around a handful of our big, new bets” – what does that look like?

- “Five to seven teams—squads of 10 to 15 people—will run like startups inside Snap, with single-threaded leaders accountable for outcomes”

- “Weekly demo days, 90-day mission cycles, and a culture of fast failure will keep us moving”

- “We have the platform, the distribution, the data, and the vision to reinvent personal computing itself. What we need now is to prove it”

Building Specs To Reimagine Computing And Move Towards An AI-First Experience

- “The need for Specs has become urgent… they represent a shift away from the app paradigm to an AI-first experience”

- “People spend over seven hours a day staring at screens. AI is transforming the way we work…and the costs of manufacturing physical goods are skyrocketing”

- “Specs address all three challenges with eyes-up computing, a new AI-native operating system that understands your context, and the replacement of physical products with photons”

- Also an “enormous” business opportunity…“Specs are how we move beyond the limits of smartphones”

- “One pair of Specs can substitute for many screens”

- “Our operating system, personalized with context and memory, compounds in value over time”

- “A marketplace of digital goods, from spatial Lenses to virtual tools, has near-zero marginal cost”

Apple’s Not Exactly “Awe Dropping” Event

When “Awe Dropping” was used as the official tag line for Apple’s annual event this week, it conjured up lofty ideas of what truly would fit that bill and while what was introduced had some interesting technology and features, we didn’t think it lived up to the title. Despite iOS 26 and watchOS 26 leading the “Apple Intelligence” era, the hardware announcements leaned heavily on design, cameras, displays, and battery life rather than AI breakthroughs, which was somewhat disappointing. The iPhone 17, Air, and Pro models, along with Apple Watch Series 11, SE 3, and Ultra 3, do offer on-device Apple Intelligence features like Live Translation, smarter call/message screening, and AI-enhanced camera styles, but these are largely incremental quality-of-life upgrades vs transformational. Apple also mostly kept its starting prices the same, except for the iPhone 17 Pro.

See below for more color on the key announcements and new products (link/link).

-> Apples shares fell –1.5% on the day of the announcement and is up -6.2% YTD, vs Nasdaq’s +14.8%

- Apple iPhone 17

- Price: Starts at $799.99 (same price as previous model); storage options 256GB / 512GB

- Release Date: Pre-orders start Fri., Sept. 12th; Available in stores starting Fri., Sept. 19th

- Battery: All-day battery; Up to 30 hours video playback; 50% in ~20 minutes with high-wattage USB-C adapter

- Key Features:

- Camera: New Center Stage front camera (first square sensor, 18MP), wider FOV, landscape selfies without rotating, Dual Capture video: record with front + rear cameras simultaneously

- Chip: A19 chip (3nm, 6-core CPU, 5-core GPU, Neural Accelerators in GPU cores)

- AI Updates: Live translation In Messages, FaceTime and Phone; Visual intelligence: Screenshot Search

- Protection: Ceramic Shield 2 front cover, 3× better scratch resistance, anti-reflection

- Other: Starts at 256GB storage (double last gen’s base), Bigger 6.3-inch Super Retina XDR display w/ ProMotion (120Hz)

- Apple iPhone Air

- Price: Starts at $999.99; Storage options 256GB / 512GB / 1TB

- Release Date: Pre-orders start Fri., Sept. 12th; Available in stores starting Fri., Sept. 19th

- Battery: All-day battery life, optimized by A19 Pro + Adaptive Power Mode; extended life with optional MagSafe Battery (up to 40 hours video playback)

- Key Features:

- Camera: Same Center Stage front camera (18MP square sensor, AI auto-frame, Dual Capture)

- Chip: A19 Pro chip (fastest CPU + 5-core GPU, Neural Accelerators for on-device AI)

- AI Updates: Same Apple Intelligence suite as iPhone 17 (translation, visual intelligence, call screening, etc.)

- Protection: First iPhone with Ceramic Shield 2 on front AND back (4× crack resistance, 3× scratch resistance)

- Other: Breakthrough thin design – only 5.6mm thick (thinnest iPhone ever), eSIM-only design (no physical SIM tray)

- Apple iPhone 17 Pro & 17 Pro Max

- Price: iPhone 17 Pro starts at $1,099.99; iPhone 17 & Pro Max starts at $1,199.99. (this is up +$100 from the 16 Pro, but the Pro Max did not see a price change); Storage options –

- Pro: 256GB / 512GB / 1TB

- Pro Max: 256GB / 512GB / 1TB / 2TB (largest ever)

- Release Date: Pre-orders start Fri., Sept. 12th; Available in stores starting Fri., Sept. 19th

- Battery: Best battery life in iPhone history

- Pro Max delivers up to 39 hours video playback; Both models charge 50% in 20 minutes with a high-wattage USB-C adapter

- Key Features:

- Camera: 3× 48MP Fusion cameras (Main, Ultra-Wide, all-new Telephoto) = 8 lens equivalents, Digital zoom up to 40×, Pro video features: ProRes RAW, Apple Log 2, genlock, open gate recording

- Chip: A19 Pro chip (6-core CPU, 6-core GPU w/ Neural Accelerators in each core, larger cache, 16-core Neural Engine), Supports local large AI model performance + hardware ray tracing for AAA gaming

- AI Updates: Full Apple Intelligence suite (translation, visual intelligence, call/message screening)

- Protection: Ceramic Shield 2 front and back (3× scratch resistance, 4× crack resistance)

- Other: New 2TB storage option (first for iPhone, on Pro Max), New thermal system for higher sustained performance

- Price: iPhone 17 Pro starts at $1,099.99; iPhone 17 & Pro Max starts at $1,199.99. (this is up +$100 from the 16 Pro, but the Pro Max did not see a price change); Storage options –

- AirPods Pro 3

- Price: $249.99 (same price as previous model)

- Release Date: Pre-orders already available; Available in stores starting Fri., Sept. 19th

- Battery: 8 hours w/ Active Noise Cancelltion (ANC), 10 hours without

- Key Features:

- Audio: 2× ANC, multiport acoustic design, Adaptive Audio

- Fit: Enhanced fit (5 foam tip sizes), IP57 rating

- Health: First-ever heart rate sensor, Workout Buddy integration

- AI Updates: Live Translation, Adaptive EQ, Personalized Volume, Voice Isolation, Hearing tools

- Apple Watch Ultra 3

- Price: Starts at $799.99 (same price)

- Release Date: Pre-orders already available; Available in stores starting Fri., Sept. 19th

- Battery: 42 hours (72 hours in low battery mode / 20 hours of battery with all features active)

- Key Features:

- Protection: Rugged titanium body with WR100 certification

- Health: New – nightly quality scoring with breakdown (duration, consistency, awakenings, stages), New – passive BP signs alerts (30-day data)

- AI Updates: Workout Buddy: An AI-driven fitness companion that delivers real-time, personalized spoken motivation, using your heart rate, pace, distance, Activity rings, and historical milestones

- Other: Includes a unique Waypoint watch face with live compass, satellite shortcut, and Night Mode, Also the only Apple Watch with built-in, two-way satellite communications

- Apple Watch Series 11

- Price: Starts at $399.99 (same price)

- Release Date: Pre-orders already available; Available in stores starting Fri., Sept. 19th

- Battery: 24 hours

- Key Features:

- Protection: Aluminum (and titanium options); Ion-X with ceramic coating (“Ceramic-X” equivalent)—2× more scratch-resistant than SE’s Ion-X

- Health: Same new features as the Ultra 3

- AI Updates: Also includes Workout Buddy coming with iOS 26

- Apple Watch SE 3

- Price: Starts at $249.99 (40mm and 44mm sizes), (same price)

- Release Date: Pre-order available today (9/9), in stores Friday, September 19th

- Battery: 18 hours, charges 2x faster than previous, 15 mins can add 8 hours of battery (80% in 40 mins)

- Key Features:

- Protection: Aluminum case; Ion-X front glass, now 4× more crack-resistant than SE 2. No sapphire or ceramic coating

- Health: Does not get BP sign alerts but does get the new nightly quality scoring. Also gets new sleep apnea notifications and ovulation estimates

- AI Updates: Also includes Workout Buddy coming with iOS 26

- Apple Final Cut Camera 2.0

- ProRes RAW supported: First time ever on smartphone, lets you record raw sensor data for maximum control in editing — adjust exposure, color temperature, tint, etc. after the fact

- Genlock Supported: Lets iPhones sync perfectly with other pro cameras or iPhones in a multi-cam shoot

- Center Stage Front Camera: Works with the Co’s new 18MP front camera, allowing portrait or landscape recording without rotating your phone

- Free on App Store, release coming later this month

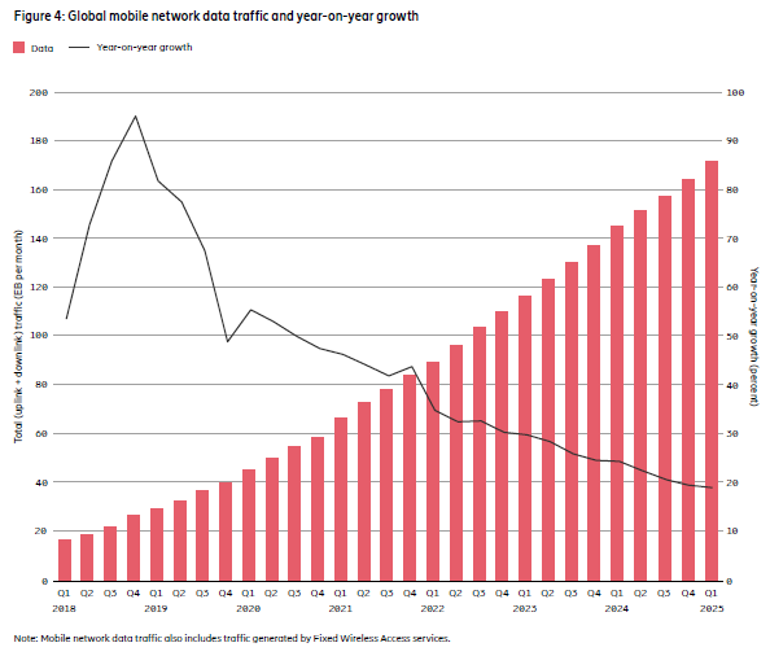

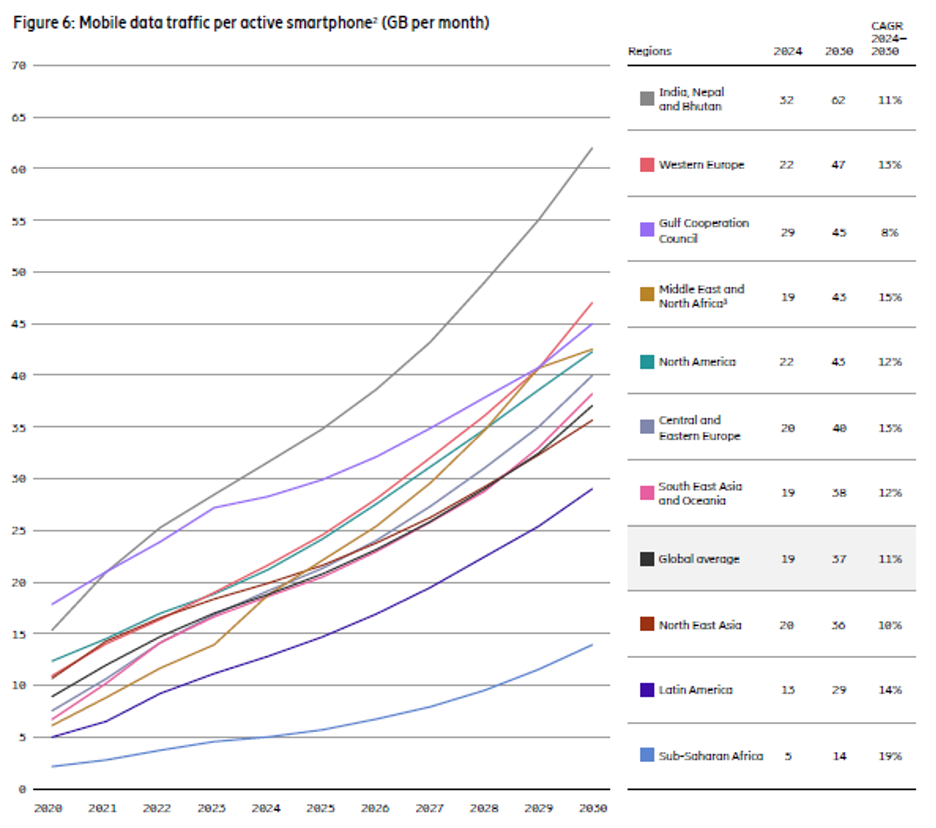

Global Mobile Data Traffic Per Smartphone Is Expected To Grow +11% CAGR From 2024-2030

Ericsson’s annual Mobility Report (June 2025) was released this week and, as always, has all sorts of interesting stats and estimates regarding mobile subscriptions and data traffic trends. There was a lot to digest, but two stats that we thought were worth flagging were: 1) total global mobile network traffic growth remains strong but does continue to decelerate given the law of large numbers. With that said, it is still expected to grow at +17% CAGR through 2030. And 2) total data traffic per smartphone is expected to grow +11% CAGR from 2024-2030. Net net, the capacity demands on global wireless networks will continue to increase over the foreseeable future…

See more below and see link to report for more information if interested.

Global Mobile Data Traffic To Grow +17% From 2024-2030

- Global mobile network traffic grew +19% y/y in Q1 2025 and it was up +5% seq…and while growth is expected to decline to +15% by 2030, that still represents a CAGR of +17% over the full forecast period

- Total monthly global mobile network traffic reached 172EB in Q1

- Growth will be driven by rising smartphone subscriptions & increasing avg data vol per subscription due to incr’d viewing of video content

- Video traffic accounted for 74% of all mobile data traffic in 2024

- Global mobile network data traffic is expected to grow from 164 EB/month in 2024 to 431 EB/month in 2030

Monthly Data Traffic Per Smartphone Is Expected To Grow +11% CAGR On Avg From 2024-2030

- Monthly data traffic per smartphone will increase from 19 GB in 2024 to 37 GB in 2030 globally

- America data traffic per smartphone is anticipated to increase +12% CAGR from 2024-2030

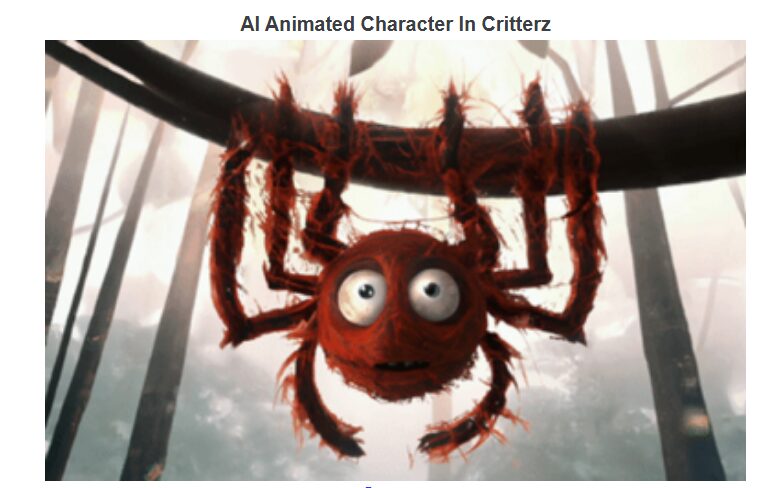

AI’s Ongoing Push Into Hollywood’s Creative Scene

AI is in the process of revolutionizing the film and video industry by streamlining production, enhancing creativity, and personalizing viewer experiences. In pre-production, AI can help analyze scripts, forecast audience reactions, and optimize casting decisions. During production, it can enable advanced visual effects, virtual cinematography, and even synthetic actors. Post-production benefits include AI-powered editing, sound design, and localization tools. On the distribution side, AI can personalize recommendations and marketing strategies. But it is not yet off to the races and serious issues like protecting IP and copywrite still need solution

In the meantime, technological innovation is happening at a rapid clip and there were a couple notable updates this week along this theme with news that OpenAI is supporting the creation of an animated feature-length movie called “Critterz” and Alphabet announced a few updates to it Veo 3 AI video platform as well.

See details below for more details (link/link/link):

- OpenAI is supporting the creation of an animated feature-length movie “Critterz”

- Budget: $30mn, which is much less expensive than typical animated film costs

- Time frame: Production has begun; Aiming to be complete in 9 months vs the typical 3 years

- Process

- Humans will be writing the script

- Human actors will be cast for character voices

- Artists will create sketches which will be enhanced by AI

- New monetization: Developing a profit-sharing model for ~ 30 people working on the film, reflecting new ways of compensating creative teams in AI-driven projects

- Copyright: While AI output can’t be copyrighted, the film’s human-created voice work and artwork likely qualify it for protection

- Distribution & marketing remain unclear

-> Traditional media companies have also been experimenting with AI but have been a bit cautious due to concerns regarding the impact on actors and the writer guilds.

- Google also annc’d Veo 3 and Veo 3 Fast updates

- Veo 3 is the Co’s “state-of-the-art model for generating high-fidelity, 8-second 720p or 1080p videos from a text prompt, featuring stunning realism and natively generated audio”

- Lowered the price: Veo 3 is $0.40 / second, was $0.75. Veo 3 Fast dropped to $0.15 / second from $0.40

- New capabilities: Veo 3 or Veo 3 Fast videos can now be done in vertical 9:16 aspect ratio and up to 1080p HD resolution

A Steady Stream Of Next Gen Transport Updates This Week

The commercialization of autonomous vehicles has been one of the key sector themes that we have been highlighting since we saw an inflection developing in July 2024 which coincided with Alphabet announcing an incremental $5bn investment in Waymo. A lot has transpired since and this week was littered with a litany of key developments in this still emerging next generation transport industry – see below. We expect the pace of updates to remain robust as we look ahead.

Amazon’s Zoox Officially Enters The Robotaxi Scene (link/link)

- Amazon-owned Zoox officially launched robotaxi services by offering free rides to the public on/around the Las Vegas Strip starting Sept 10th

- The Co has a fleet of 50 vehicles mainly located in Las Vegas but is currently waiting for the state’s approval to collect fare

- Next launch? San Fran, where it has been testing for months and has riders on the wait list

- As we have highlighted before, Zoox vehicles are different than competitors as they have no manual controls and passengers sit facing each other

- Amazon bought Zoox for $1.3bn back in 2020

Uber Expands Robotaxi Svs Tests To Germany & Will Now Add Helicopter Transport To The App (link/link/link)

- Uber & Momenta will begin testing Level 4 driverless robotaxis in Munich, Germany in 2026

- Vehicles will initially use safety monitors, transitioning to fully driverless once validated

- If Munich goes as planned, the Co will expand to other European cities

- Shanghai-based Momenta already runs a robotaxi svs in China; Investors include SAIC Motor, GM, Toyota, Mercedes-Benz, and Bosch; They also supply driver-assistance software to automakers like Mercedes and BMW (~400,000 vehicles)

- Uber will offer Blade helicopter rides in its app starting in 2026, through its expanded partnership with Joby Aviation

- Comes after Joby’s $125mn acq of Blade in August (excluding Blade’s medical organ transport division)

- Blade flew ~50k passengers last year across 12 terminals

- “Integrating Blade into the Uber app is the natural next step in our global partnership with Uber” said Joby founder and CEO JoeBen Bevirt

- Joby intends to expand air taxi services to Dubai, New York, Los Angeles, the U.K., and Japan

- Comes after Joby’s $125mn acq of Blade in August (excluding Blade’s medical organ transport division)

Lyft Officially Rolling Out Its First Robotaxi Pilot In Atlanta Updates (link)

- Lyft is officially rolling out its first robotaxi pilot in Atlanta, partnering with May Mobility (backed by Toyota & BMW): Pilot details –

- Toyota Sienna minivans w/ cameras, radar, & lidar operating in a 7-square-mile service area around Midtown Atlanta

- Cars will have “standby operators” (safety drivers) to take control if needed, answer questions, and ensure rider comfort

- The Co has several other partnerships that are in the works

- Lyft is working w/ Benteler Mobility to launch a self-driving shuttle service that is planned to hit in late 2026

- Additionally, the Co is working w/ Intel’s Mobileye to launch “thousands” of robotaxis in Dallas, and will move into addtl markets in the months that follow

Grab Bag: Amazon-Netflix Ad Tie-Up / Murdoch Succession Resolution / YouTube’s NFL Broadcast Breaks Platform Record

- Amazon & Netflix advertising tie-up created a bit of buzz this week…Netflix’s ad-supported tier inventory will be available through Amazon’s DSP: The deal further consolidates Amazon’s reach as it now has programmatic access to all major U.S. streaming services, in addition to its own Prime Video, and also gives Netflix enhanced targeting and flexibility for its global advertising base (link/link)

- Timing: Starting in Q4

- Market availability: 11 global markets…U.S., U.K., France, Spain, Mexico, Canada, Japan, Brazil, Italy, Germany, Australia

- Other Amazon ad partners: NBCU (Peacock), WBD (Max), Fox (Tubi, Fox One), Paramount (Paramount+, Pluto), and Disney (Disney+, Hulu, ESPN)

-> The Trade Desk’s stock fell -12% in reaction to the news given concerns that this new deal could limit The Trade Desk’s access to Netflix’s ad inventory

- Murdoch family resolves succession dispute (link): A protracted legal battle over the future of the Murdoch family trust was resolved this week

- In a newly established trust Rupert Murdoch’s son Lachlan Murdoch will stay in control of both legacy companies

- His three older children, Prudence, Elisabeth, and James, will receive cash payouts for their shares and will step away from their roles at both Cos

- The agreement also prevents them and their affiliates from acquiring shares of either company moving forward.

- His two youngest children, Chloe and Grace Murdoch, are included in the new trust, but voting control with respect to Fox Corp. and News Corp will rest solely with Lachlan Murdoch

- Rupert Murdoch will continue in his role as chairman emeritus of both Cos

-> Fox ended the week down -5.7%, while News Corp was down -0.7%

- YouTube’s first exclusive NFL broadcast averaged 17.3mn global viewers, the most concurrent viewers of a livestream on the platform (link/link): Based on the avg minute audience for Friday’s game between the Kansas City Chiefs and the Los Angeles Chargers taking place in São Paulo, Brazil

- Per YouTube and Nielson data –

- US:16.2mn viewers

- Intl:1.1mn viewers

- Aired on Sept 5th across 230 countries

- How does that compare to other broadcasts?

- Amazon said that its Thursday Night Football averaged 13.2mn US viewers per game for 2024

- Netflix’s Christmas Day games averaged 26.5mn US viewers, per Nielsen Big Data + Panel

- Per YouTube and Nielson data –

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Shares of Omnicom, WPP & IPG fell after Trump annc’d a memo requiring pharma ads to disclose more risk info. The move may disrupt ad spending worth billions, impacting major ad cos. Memo directs HHS to boost transparency in direct-to-consumer drug ads. Omnicom & IPG dropped ~3% to $75.46 & $25.81; WPP slid ~1% to $26.94. (MSN)

- U.S. ad rev rose 10.3% in Q2 2025 (ex-political), per Madison & Wall. Digital ad spend grew 15.8%, now ~70% of total. TV fell 1.7%, though CTV saw gains. Outdoor rose 3.6%; audio, publishing dipped 0.4% & 0.8%. Direct mail up 0.8%. Wieser notes digital-first cos have ad-heavy biz models. Full-yr forecast: 8% growth to $417.5bn; digital up 14% to $293.8bn; TV to drop 3% to $62.3bn. (MediaPost)

- PubMatic sued Google in Virginia, seeking billions over alleged illegal monopoly in ad tech. The suit follows an Apr. ruling that Google monopolized ad exchanges and servers. DOJ wants Google to sell AdX; Google proposes tech fixes w/ 3-yr monitor. PubMatic CEO said Google’s monopoly stifled innovation. Google had considered buying PubMatic in 2011 but chose AdMeld instead. Another trial is set for Sept. (Mint)

Artificial Intelligence/Machine Learning

- OpenAI and Nvidia CEOs plan to pledge support for multi-bn UK data center investments next wk, teaming w/ London-based Nscale Global Holdings. The move, coinciding w/ U.S. President Trump’s visit, highlights rising demand for AI and cloud infra. Several U.S. cos are also expected to annc’d tens of bn in UK investments. Nvidia declined comment; OpenAI and others didn’t respond. (Reuters)

- OpenAI annc’d a recapitalization plan where its nonprofit will retain control of the PBC and gain an equity stake exceeding $100bn. This move aims to boost funding for its mission to ensure AGI benefits all. A $50mn grant initiative was launched to support AI literacy, community innovation, and economic opportunity. The nonprofit will guide safety decisions, w/ support from CA and DE AGs. (Open AI)

- Perplexity, an AI search startup rivaling Google, raised $200mn at a $20bn valuation, per The Information. This follows a $100mn raise in Jul. at $18bn. Total funding now stands at $1.5bn. ARR is nearing $200mn, up from $150mn last month. In Aug., Perplexity offered $34.5bn to buy Chrome amid DOJ’s antitrust push, but a judge ruled Google can retain its search biz. (Tech Crunch)

- Meituan annc’d Xiaomei, an AI agent built on its LongCat model, to enhance food delivery and local svs in China. Users can order via voice, get meal suggestions, and book restaurants. Facing rising competition from Alibaba’s Ele.me and JD.com, Meituan’s move follows rivals’ pledges to avoid price wars. AI voice tech, proven viable by cos like Chipotle, offers ~25% labor cost savings in order-taking. (Tech in Asia)

- Alibaba annc’d Qwen3-Next, a new ultra-efficient model architecture w/ hybrid attention and sparse MoE, enabling 10x inference throughput vs. Qwen3-32B. The 80B-param model activates just 3B during inference. Also launched: Qwen3-ASR-Flash, a multilingual ASR model excelling in noisy settings, and previewed Qwen3-Max, a 1T-param non-thinking model ranked #6 in Text Arena for linguistic precision and reasoning. (Alizila)

- OpenAI & Microsoft have reached preliminary terms on a revised partnership, paving the way for ChatGPT maker to restructure. The deal addresses OpenAI’s complex structure amid its rapid rise as AI’s standard-bearer. The cos said Thurs. the agreement marks a key step in redefining their collaboration, potentially impacting future AI biz strategies & tech mkts. (Axios)

- The FTC annc’d probes into OpenAI, Alphabet, Meta, xAI, Snap & others over AI chatbot safety for kids. Concerns include simulated relationships, data use, monetization & compliance. Since ChatGPT’s 2022 launch, ethical/privacy issues have grown. Meta & OpenAI face scrutiny after reports of inappropriate bot behavior. Cos pledged cooperation; FTC aims to balance innovation w/ child protection. (CNBC)

- ByteDance annc’d Seedream 4.0, an AI image tool rivaling Google DeepMind’s Gemini 2.5 Flash Image. Seedream 4.0 merges Seedream 3.0’s text-to-image w/ SeedEdit 3.0’s editing, offering 10x faster inference. Though not yet ranked, ByteDance claims superior prompt adherence, alignment & aesthetics. Priced at $30 per 1,000 gens, it’s live on Jimeng, Doubao & Volcano Engine; global use via Fal.ai at $0.03/image. (South China Morning Post)

- Latin American musicians say AI-made tracks are flooding Spotify, Deezer & YouTube Music, shrinking rev & visibility. Artists like Nekki & Carri struggle as bots steal streams, shorten song lifespans & dilute cultural value. AI music rose to 18% of Deezer uploads by Apr. Platforms are reacting, but artists fear losing income & identity. Some turn to live shows, vinyl, & teaching to survive. (Rest of World)

- Nvidia launched a lobbying blitz opposing new Senate rules that would restrict A.I. chip sales to China, potentially impacting ~$50bn in rev. The Co criticized the proposal—backed by Sen. Jim Banks—as driven by “A.I. doomers.” The debate reflects a clash between accelerationists and doomers over A.I.’s future. (The New York Times)

- AI agents are disrupting travel booking as Booking.com, Expedia & Airbnb partner w/OpenAI to integrate AI tools. These agents may bypass platforms, letting users book direct, reducing 15–20% commission fees. While cos see potential, limitations persist—AI lacks emotional intelligence & struggles w/complex itineraries. Airbnb plans more “agentic” features in 2025. (Wizcase)

- Google annc’d Veo 3 & Veo 3 Fast updates, incl. 1080p HD, vertical format (9:16), & lower pricing—Veo 3 now $0.40/sec (was $0.75), Fast at $0.15/sec (was $0.40). Devs can build w/ Gemini API for scaled use. Platforms like Invisible Studio, Saga & Mosaic use Veo 3 for AI-native video workflows, boosting productivity & enabling longer, coherent generations up to 64 secs. (Google Blog)

- Anthropic annc’d support for California’s AI safety bill SB 53, which mandates frontier AI cos like OpenAI, Google, and xAI to publish safety reports and frameworks pre-deployment. SB 53 targets catastrophic risks, offers whistleblower protections, and excludes third-party audits. Despite pushback from tech groups, experts say the bill shows legislative restraint and has a solid chance of passing. (Tech Crunch)

- Quantum tech firm Infleqtion annc’d a $1.8bn merger w/ Churchill Capital Corp. X, aiming to raise $540mn incl. PIPE. Funds will boost its neutral atom quantum computer, scale adoption, and strengthen its balance sheet. Infleqtion posted ~$29mn rev in trailing 12 mos, expects $50mn biz by end-2025. Deal offers faster listing vs. IPO, w/ completion eyed by late 2025 or early 2026. (Bloomberg)

- Databricks annc’d a $1bn funding round at a $100bn valuation, w/ rev run rate >$4bn as of Jul., up 50% YoY. AI product sales alone will drive ~$1bn rev. CEO Ali Ghodsi said ~650 customers pay $1mn/yr. New clients incl. Honda, Peet’s Coffee & Princeton Univ. Co had positive free cash flow over past yr. Funds will aid talent retention amid AI hiring wars. (The Wall Street Journal)

- Nebius shares surged 50% after annc’d a $19.4bn AI infra deal w/ Microsoft, incl. $17.4bn in dedicated capacity through 2031. The Co, spun off from Yandex post-Ukraine war, marks a comeback for CEO Volozh. Microsoft seeks to ease AI cloud shortages. Nebius will supply from a new NJ data center, boosting its AI biz in 2026. Financing will be via deal cash & debt, w/ more options under eval. (MSN)

- OpenAI execs are alarmed by growing scrutiny over its for-profit shift, facing pushback from CA philanthropies and nonprofits. Regulators in CA and DE are probing if the restructure violates charitable trust law. Investors tied ~$19bn to the plan, vital for funding AI infra. CEO Sam Altman leads the effort; failure could derail OpenAI’s future. Co has no current plans to exit CA but relocation is a last-ditch option. (The Wall Street Journal)

- Infleqtion, a quantum computing & sensor Co, annc’d a $1.8bn SPAC merger w/ Churchill Capital Corp X , aiming to accelerate quantum tech commercialization. The deal brings $540mn funding, incl. $125mn PIPE. Infleqtion plans to scale neutral atom quantum computers & sensors, w/ ~$29mn rev in trailing 12 mos & ~$50mn biz expected by 2025. (Cryptopolitan)

- CoreWeave annc’d CoreWeave Ventures, aiming to back AI-focused founders w/ capital, tech expertise & compute. The initiative supports scaling via CoreWeave’s AI-optimized cloud, testing clusters, and strategic insights. It enables innovation through capital models, compute-for-equity, and deep tech partnerships. CoreWeave Ventures is already working w/ diverse AI cos across infra & vertical apps. (CoreWeave)

- Google annc’d clear Gemini usage limits: free users get 5 prompts/day, 5 Deep Research reports, & 100 AI images. AI Pro offers 100 prompts & 1,000 images; AI Ultra gives 500 prompts. Prior vague terms like “limited access” are replaced w/ exact figures. Changes aim to clarify cos AI svs tiers & encourage upgrades for higher usage. (The Verge)

- OpenAI-backed animated film “Critterz,” aims for Cannes debut in May. Created w/ AI tools like GPT-5, it’s produced by Vertigo Films & Native Foreign. Budget is <$30mn, vs. typical 3-yr timeline, it’s being made in ~9 mos. Script by “Paddington in Peru” team; human actors will voice characters. Co hopes to prove AI can cut costs & time in film biz. (The Wall Street Journal)

- ASML invested $1.5bn in Mistral AI’s $2bn Series C, becoming its top shareholder. The deal values Mistral at $11.7bn, making it Europe’s most valuable AI Co. ASML aims to boost EU tech sovereignty and may gain a board seat. Mistral, backed by Nvidia, competes w/U.S. giants and could help reduce reliance on foreign AI models. (Reuters)

- Apple plans to launch Apple Intelligence in China before 2025 ends, per Bloomberg’s Power On. Despite China being a major iPhone mkts, the AI hasn’t yet arrived due to regulatory hurdles. Apple may release it w/ iOS 26.1 or 26.2, possibly partnering w/ Alibaba. If successful, it’d be the first US Big Tech AI in China, amid ongoing US-China tech tensions and chip sanctions. (Tech Times)

Audio/Music/Podcast

- A collective of 30+ Seattle artists, led by Carolyn Brotherton, pledged to remove music from Spotify, citing its “anti-human” direction. Concerns include AI-generated music, low artist payouts, and CEO Daniel Ek’s AI drone investments. The group criticizes Spotify’s promotion of “ghost artists” and passive listening, urging others to join the boycott to protect artistic integrity and legacy. (MSN)

- U.S. recorded music rev hit $5.6bn in H1 2025, per RIAA report. Growth was <1%, w/ paid streaming up 5.7% to $3.2bn and subscriptions surpassing 100mn. Free streaming fell 3% to $875mn. Digital downloads declined 1.4% to $138mn; physical rev dropped 6% to $576.4mn. Vinyl dipped 1% to $457mn; CDs plunged 22% to $108mn. RIAA shifted to wholesale-only data for global alignment. (The Hollywood Reporter)

Broadcast/Cable Networks

- Warner Bros. Discovery signed a multi-yr deal w/ Nielsen, effective immediately, to use Big Data + Panel as ad currency across linear and streaming. Starting 2026, WBD will adopt Nielsen’s Advanced Audience svs. The pact aims to optimize ad spend via smarter data. Nielsen, accredited for Big Data + Panel in Jan. 2025, remains a top source for streaming TV metrics. Deal enhances WBD’s cross-platform ad solutions. (Nielsen)

- Warner Bros. Discovery sued Dish, alleging Sling TV’s new short-term “Passes” breach their agreement. The lawsuit claims the Day ($4.99), Weekend ($9.99), and Week ($14.99) Passes disrupt cos’ monthly subscription model and threaten WBD’s ties w/ other distributors. WBD seeks to halt Sling’s “unauthorized” use of networks like CNN, TNT, and HGTV via non-subscription access. (Variety)

- Skydance CEO David Ellison, amid merging w/ Paramount, met ex-MTV execs to explore reviving the channel. Ideas included live events and using MTV’s archive. Music industry leaders like Irving Azoff and Lucian Grainge showed interest. Despite rivals spinning off cable assets, the Co aims to reposition MTV as a “music tastemaker” and leverage its legacy to reconnect w/ audiences. (The Wall Street Journal)

Cable/Pay-TV/Wireless

- Global broadband equipment rev hit $4.7bn in Q2 2025, up 1% YoY, driven by fiber and FWA growth. DOCSIS infra spending fell 13%, reaching lows not seen since 2009. Cable cos face delays due to Broadcom’s unified DOCSIS 4.0 silicon. Outside plant spending is rising, expected to hit $10bn by 2028. Harmonic led cable access revs (46%), w/ CommScope (35%) and Vecima (10%). Growth expected to resume in 2026. (Light Reading)

- Charter CEO Chris Winfrey said mobile is “just an extension” of its broadband biz, highlighting its growth potential. Spectrum Mobile hit 10.54mn residential lines in Q2, ~20% of broadband base. Charter revised its buyout offer to cover 2 lines, up to $500/line. A new MVNO pact w/ T-Mobile will allow selling up to 1,000 lines to SMBs starting 2026, expanding beyond the prior Verizon deal’s 10–20 line limit. (Light Reading)

- T‑Mobile annc’d T‑Satellite w/ Starlink connecting 650+ satellites to phones for seamless coverage in dead zones. No extra gear needed; service auto-switches to satellite. Included in Go5G Next/Experience Beyond plans or $10/month. Android pic/voice msg starts Oct. 1; iOS soon. Covers 500K+ sq. mi. T‑Mobile leads U.S. mkts in speed, 5G, and consistency, outpacing Verizon & AT&T. (Variety)

- The FCC annc’d a review to modernize rules on ownership of ABC, CBS, FOX & NBC stations. A Notice of Proposed Rulemaking will assess if current limits—meant to ensure competition, diversity & localism—should be cont’d, changed or scrapped. The move responds to shifts in media mkts due to streaming & tech. Public input will guide decisions amid concerns over consolidation, local voices & minority-owned cos. (Cord Cutters News)

- T-Mobile may shift to a digital-only model, phasing out physical stores and reps per reports. Staff cuts and a push for T-Life app usage signal this move. The Co aims to cut costs and boost margins. CEO Sievert’s $5mn stock sale shows confidence. Though stores remain open, the trend suggests a digital-first future, possibly reshaping the wireless mkts and customer experience. (Cord Cutters News)

- US mobile data traffic rose 32% in 2024 to 132.5 trillion MB, cont’d a 3-yr trend of ~35% growth, more than doubling since 2021. Despite this, <50% of lines are on 5G. 5G investment peaked at $39bn in 2021; operator spend fell to $29bn in 2024 from $30bn in 2023. Over 15,000 new cell towers were added, signaling ongoing infra expansion despite declining capex. (Telecompaper)

- Telefonica CEO Murtra aims to reshape Europe’s telco sector via M&A, targeting assets in Germany, UK, Spain & Brazil, w/ plans to divest Latin American units for ~€3.6bn. He urges regulators to ease merger rules, citing fragmented mkts. Murtra envisions large European tech operators investing in cybersecurity & infrastructure. (Reuters)

Capital Market Updates

- Alibaba Group annc’d a $3.17bn zero-coupon convertible notes offering—2025’s largest—due 2032, convertible into ADRs. Funds will support data center scale-up, tech upgrades & intl. commerce. ADRs fell 1.7% to $141.53 post-annc’t. Prior raises include $5bn in 2024 & HK$12bn ($1.5bn) in Jul. for Alibaba Health. Conversion premium: 27.5–32.5%. Lock-up: 90 days. (The Malaysian Reserve)

Crypto/Blockchain/web3/NFTs

- Gemini crypto exchange, led by the Winklevoss twins, raised $425mn via IPO, pricing 15.18mn Class A shares at $28—above its expected range. GEMI debuted on Nasdaq; Goldman Sachs, Citigroup, Morgan Stanley, and Cantor acted as lead bookrunners. Nasdaq Inc. annc’d a $50mn private placement. ~94.5% voting power remains w/ the twins. Gemini reserved 10% for insiders, 30% for retail investors. (The Block)

- SEC Chair Paul Atkins annc’d Project Crypto at OECD, aiming to end legal chaos in crypto and spark a “golden age” of financial innovation. He said most tokens shouldn’t be treated as securities, marking a shift from past policy. The initiative seeks to modernize rules, attract cos back to U.S. mkts, and enable super-apps, tokenized assets, and DeFi svs under one regulatory umbrella. (MEXC)

- CoinShares annc’d a $1.2bn SPAC merger w/ Vine Hill to shift its listing from Stockholm to Nasdaq. The Co manages ~$10bn in crypto ETPs and holds 34% EMEA mkts share. CEO Mognetti said U.S. listing boosts credibility amid clearer regulation. CoinShares posted 76% adj EBITDA margin in H1 2025. Deal expected to close by end-2025; new parent Co will be Odysseus Holdings Ltd. (Coindesk)

eCommerce/Social Commerce/Retail

- Temu’s frugality-driven model—w/ direct sourcing, localized logistics, and AI—lets it undercut rivals by 30–50%, gaining 17% U.S. discount retail share. Despite $8–$9bn losses and PDD’s 47% Q1 profit drop, Temu expands globally, adapting to tariffs via U.S. warehouses and EU ad shifts. Investors eye GMV growth ($70.8bn in 2024, $100bn+ by 2026) and retention amid regulatory risks. (Ainvest)

- Amazon’s same-day grocery expansion to 1,000+ cities prompted grocers to seek Instacart’s svs, CEO Chris Rogers. Instacart saw increased demand, using the moment to deepen tech use. Despite Amazon’s push, Instacart’s gross transaction value remained steady. Retailers like Walmart and Dollar General also sped up delivery. Rogers noted a similar boost post-Amazon’s 2017 Whole Foods deal. (MSN)

- Albertsons Cos. has annc’d the deployment of Google Cloud’s Conversational Commerce agent in its Ask AI tool across all banner store apps. The AI-powered solution enhances grocery shopping w/ personalized search, natural convos, and real-time answers. Built on Vertex AI, it boosts engagement, rev, and basket size. Early results show >85% of Ask AI convos start w/ open-ended queries, driving smarter, faster shopping. (Progressive Grocer)

- Criteo annc’d a partnership w/ Google SA360, becoming the first third-party on-site retail media supply partner. SA360 advertisers can now run sponsored product listings across Criteo’s network of 200+ retailers. This move unlocks new ad budgets, enhances targeting via retailer data, and may expand into other Google tools. Criteo aims to deepen its role in the digital ad ecosystem. (AdExchanger)

- Holiday sales in the U.S. are forecasted to grow 2.9%–3.4% to ~$1.62tn, per Deloitte. E-commerce rev may hit $310.7bn, up 9%. Despite inflation, rising disposable income (3.1%–5.4%) could support spending. Consumers may cut essentials to fund holiday buys. AI use is rising to find deals. Inflation acts as both headwind and tailwind, boosting nominal sales but limiting volume. Forecast covers Nov.–Jan. (Retail Dive)

- Retail theft, once seen as a crisis post-pandemic, is now declining. Retailers admit past exaggeration and cite improved tracking, law enforcement efforts, and harsher laws. Shrink rates—used to estimate losses—are falling due to better inventory processes. NY saw a 12% drop in retail theft after investing $40mn in crime task forces. (CNN)

- Amazon annc’d Lens Live, an AI-powered tool in its iOS app that lets users scan items via camera and browse a swipeable product carousel. Integrated w/ Rufus, Amazon’s AI assistant, it offers summaries and suggestions. Lens Live auto-detects objects, enables tap-to-focus, adds to cart, and saves to wishlists. It’s part of Amazon’s broader AI strategy to reinvent customer experience, first revealed by CEO Andy Jassy last yr. (Retail Dive)

Film/Studio/Content/IP/Talent

- ‘The Conjuring: Last Rites’ scored a massive $83M U.S. debut, ranking 3rd all-time for horror and 2nd globally at $187M. Warners now leads global mkts w/$3.77bn. The film marks the 8th No.1 opening for the Co this yr and sets a franchise record. Strong turnout from female (51%) and Hispanic/Latino (43%) audiences. CinemaScore is B; PLFs/Imax drove 40% of sales. Hamilton also annc’d a $9M theatrical bow. (Deadline)

FinTech/InsurTech/Payments

- Robinhood annc’d Robinhood Social, a platform w/in its app letting users post verified trades, follow investors, and track public figures’ mkts moves. Users can view trading stats, initiate trades via posts, and engage in crypto, options, and prediction mkts. A beta rolls out to ~10K users in Q1 next yr. The Co, now in S&P 500, is expanding into banking, managed accounts, and blockchain amid a strong bull mkts. (The Wall Street Journal)

Last Mile Transportation/Delivery

- Amazon annc’d a strategic partnership w/ Colombian delivery Co Rappi via a $25mn convertible note. The deal includes warrants for up to 12% stake if milestones are met. This move boosts Amazon’s last-mile delivery in LatAm, challenging MercadoLibre. Rappi gains access to Amazon’s tech, logistics & cloud svs, marking a key endorsement from the North American e-commerce giant. (Investing.com)

Live Entertainment/Theme Parks/Concerts/Experiential

- StubHub, backed by Madrone Partners, targets up to $9.2bn valuation in its U.S. IPO, offering 34mn shares at $22–$25 each. Rev rose 3% to $827.9mn in H1 2025, but losses doubled to $111.8mn. Co aims to capitalize on strong mkts and live event demand. Despite investor estimates of $14–$15bn, pricing may be conservative. (Reuters)

- The Sphere in Las Vegas is showing a 70-min. reimagined Wizard of Oz, drawing ~4,000–5,000 fans daily at ~$200/ticket, grossing up to $2mn/day. Execs expect rev to top $1bn. Movies at the Sphere are more profitable than concerts, w/ 70% margins. CEO James Dolan spent $2.3bn on the venue and plans global expansion. Warner Bros. earns a licensing fee; Dolan keeps most profits. (Bloomberg)

- Howard Stern staged a gag, teasing Andy Cohen had taken over his SiriusXM slot amid rumors of show cancelation. Stern, 71, denied being fired, praised SiriusXM CEO, and said he’s “very happy” at the Co. Though no new deal was annc’d, talks cont’d. His current contract, expiring end of 2025, was previously worth ~$100mn/yr. Cohen played along, calling it a “surreal morning.” (Variety)

Macro Updates

- Consumer prices rose 0.4% in Aug., pushing annual inflation to 2.9%. Core CPI hit 3.1% y/y. Jobless claims unexpectedly jumped to 263,000—highest since Oct. 2021. Fed likely to cut rates at its meeting, w/ mkts pricing in further cuts in Oct. and Dec. Shelter, food, and energy costs drove CPI gains. Traders see 100% chance of rate cut, possibly 0.5pt due to labor mkts weakness. (CNBC)

- Initial jobless claims rose by 27,000 to 263,000 for the week ended Sept. 6, highest since Oct. 2021, per Labor Dept. Monthly data showed just 22,000 jobs added in Aug., w/ unemployment at 4.3%. Texas led w/ a 15,304 surge in claims. Continued claims held at 1.94mn. Fed’s Sept. 16–17 meeting may bring rate cuts amid rising employment concerns. CPI excl. food/energy rose 0.3% in Aug., matching forecasts. (Los Angeles Times)

- U.S. economy added ~1.2mn fewer jobs than earlier reported, prompting mkts to expect Fed rate cuts at each of the 3 remaining 2025 meetings. Citigroup’s Hollenhorst said data could justify a 0.5% cut, but a 0.25% cut is most likely coming. Goldman Sachs disputes the job loss figure, estimating ~550,000. White House and mkts pressure Fed amid weak labor data and trade uncertainty. (CNBC)

Online Marketplaces/Learning (Real Estate/Education/Jobs)

- Alibaba’s Amap app has shifted focus from navigation to local biz rankings, intensifying rivalry w/ Meituan, its AI-driven “Street Stars” ranks restaurants, hotels & tourist spots for 170mn users. Launch includes ¥1bn ($140.43mn) in svs coupons across 300 cities. Meituan countered w/ 25mn coupons. Regulators eye pricing wars amid China’s weak mkts & consumer malaise. (Reuters)

Regulatory

- The FTC is probing Amazon and Google over allegations they misled advertisers by failing to fully disclose ad pricing practices—such as reserve pricing and undisclosed cost hikes—amid broader antitrust trials both companies face this month. (Reuters)

- Meta and TikTok won a legal challenge against EU regulators over a supervisory fee under the DSA. The court ruled the fee’s methodology must be revised via a delegated act w/in 12 months. No refund for 2023 fees. Meta, TikTok argued the method was flawed, causing disproportionate charges. Other cos like Amazon, Apple, Google also pay the fee, based on user count and prior yr’s profit/loss. (Reuters)

- Four whistleblowers allege Meta suppressed child safety research post-Frances Haugen leaks. Policy changes discouraged sensitive studies on youth, race, and harassment. Meta allegedly urged vague language or legal shielding. A lawsuit claims Horizon Worlds exposed minors to racism and lacked age safeguards. Meta denies wrongdoing, citing 180+ Reality Labs studies since 2022. (Tech Crunch)

- Treasury Sec. Bessent said ~50% of Trump’s “reciprocal” tariffs may be refunded if SCOTUS rules they exceeded presidential authority. The admin. appealed after a federal court found no IEEPA basis for the tariffs. Despite confidence in a win, BLS data shows 22,000 jobs added in Aug. w/ unemployment at 4.3%. Goods biz hit hardest. US collected $28bn in July tariff rev. Cos like Nike, Walmart warn of price hikes. (CNN)

- The Long-Term Stock Exchange plans to petition the SEC to let public cos share earnings results semiannually instead of quarterly. The move aims to cut costs, reduce pressure on execs, and support long-term biz goals. LTSE met w/ SEC officials and left encouraged. The proposal, which could save cos millions, would apply to all U.S. public cos, not just those listed on LTSE. (The Wall Street Journal)

Satellite/Space

- AT&T CEO Stankey, said SpaceX’s $17bn EchoStar spectrum deal is a smart move but not a threat to terrestrial wireless. He doubts satellite tech can match AI-era demands or indoor coverage. Analysts agree, citing D2C limits. AT&T’s $23bn EchoStar buy aims to boost FWA and biz svs. Stankey also supports open RAN to diversify vendor supply as legacy gear is phased out. (Light Reading)

- Elon Musk annc’d SpaceX’s $17bn deal w/ EchoStar for AWS-4 & H-block spectrum to enable satellite-to-cell svs. Phones supporting this spectrum won’t ship for ~2 yrs. Analysts say SpaceX needs an MVNO deal to reach consumers. Apple’s stance remains unclear, despite its Globalstar ties. The move may reshape D2D mkts, marking a pivotal shift in U.S. telecom. (Fierce Network)

- FCC will end its probe into EchoStar’s 5G obligations after the Co annc’d spectrum deals—$17bn w/ SpaceX and $23bn w/ AT&T. FCC Chair Carr confirmed EchoStar met buildout requirements and retains exclusive rights to key spectrum. The Co, co-founded by Charles Ergen, had faced scrutiny over slow 5G deployment. Deals remain subject to FCC approval. (Reuters)

- Elon Musk’s SpaceX annc’d a ~$17bn deal w/ EchoStar for AWS-4 & H-block spectrum licenses—split between $8.5bn cash & $8.5bn SpaceX stock. SpaceX will pay ~$2bn in interest on EchoStar debt through Nov. 2027. EchoStar’s Boost Mobile users will access Starlink Direct to Cell svs. EchoStar shares rose 19%. (Yahoo Finance)

Social/Digital Media

- Reddit annc’d removal of subreddit subscriber counts, replacing them w/ 7-day metrics: visitor activity (based on a 28-day avg) and contributions (excluding removed content). The shift aims to reflect real engagement vs. passive membership. Mods now face limits—max 5 subreddits w/ >100k visitors. Subscriber data remains in mod-only insights. Change supports better moderation but drew mixed reactions. (The Verge)

Software

- The EU Commission accepted Microsoft’s commitments to address antitrust concerns over tying Teams to Office 365/Microsoft 365. Microsoft will offer suites w/o Teams at lower prices, enable data portability, and improve interoperability. These legally binding changes aim to restore fair competition in EU mkts and will remain in force for 7–10 yrs. (European Commission)