It has been a choppy market lately, but the major indices bounced back a bit from last week’s sell-off and both the S&P 500 and Nasdaq closed up ~ +1.7%. Nvidia’s results were the main event (see Theme #2), as TMT sector earnings finally wound down this week. Among other interesting updates and developments, we did our usual deep dive analysis of key earnings trends for the sector (see Theme #1) and also included an analysis of 13F shareholder position changes from last week.

The full list of what we focused on in this edition is below (all links are clickable):

- Earnings Wrap: The Magnitude Of Profitability & Sales Beats Takes A Step Down And Stock Volatility Increases

- NVIDIA Doesn’t Disappoint High Expectations / AI Chip Demand Will Exceed Supply For At Least “Several” Quarters

- WMG’s Particular Focus On Wholesale Pricing & The India Opportunity Stand Out

- Five Key Insights Regarding Gen AI In The Enterprise…

- Hedge Funds Pile Into Non-Tech, As Per The Latest 13-Fs

- The DoJ Looks To Breakup Google + Other Regulatory Updates

- Pinduoduo Continues To Prioritize The Long-Term, Despite Near-Term Choppiness

- It’s Official… Comcast Cable Nets Will Forge Their Own Future And Media Consolidation Is A Potential Path

- Streaming Sports Hits A New Milestone…Momentum Is Accelerating BUT QoS Can Be A Challenge

- Grab Bag: WBD-NBA Reach Rights Resolution/ TTD Introduces Ventura/ Thanksgiving Weekend Consumer Spend Projections

Have a nice weekend.

As always, let me know if you have any feedback or comments.

Best,

Leslie

Earnings Wrap: The Magnitude Of Profitability & Sales Beats Takes A Step Down And Stock Volatility Increases

As the frenzy of earnings season winds down, we analyzed Q3 results across our LionTree TMT and Consumer Universe, spanning ~200 companies across 32 sub-sectors with market caps of $1bn+ to spotlight some key trends as well as the quarter’s best and worst performers.

As has been the case for several of the past quarters, profitability continues to be a metric that companies are honing in on, with 83% outperforming expectations (which was basically in-line with 82% from last qtr). That being said, the magnitude of these beats took a big step down in Q3, with just 40% exceeding consensus estimates by double, triple, or quadruple digits, vs 55% in the prior qtr.

Companies also continued to outperform Street expectations on revenue, with 68% beating estimates, which was a dip from Q2’s 70%. Similar to adj EBITDA, the magnitude of beats tapered down in Q3, as only 2% of the companies that beat estimates beat by 10%+ (vs 4% in Q2 and 7% in Q1), and 22% of companies that beat on adj EBITDA missed on sales (up from 20% in Q2 and 18% in Q1).

Looking into stock performance, there was more volatility on the back of results than the last two quarters. While 50% of stocks traded up post their reports (which was down from 53% in Q2 and 51% in Q1), 20% traded UP double-digits in reaction to earnings, up from 18% in Q2 and 13% in Q1. Also, 16% of stocks traded DOWN double-digits, which is up from 10% in each of the prior two quarters.

Finally, digging into company-specific performance, ThredUp was the best performer in response to earnings, jumping +58.5%, followed by Applovin and Reddit, up +46.3% and +42.0%, respectively. On the other end, The E. W. Scripps Co. saw the biggest stock plunge post earnings, down -35.5%, followed by Figs and Groupon, falling -28.3% and -27%, respectively.

See below for additional insights on the Q3 financial and stock performance of companies and sub-sectors within our LionTree Universe of TMT and Consumer stocks…

Of The Companies & Sub-Sectors That BEAT Expectations…

- EBITDA – Of the companies in our LionTree Universe that report adj EBITDA, 83% beat on consensus adj EBITDA, and 40% had double, triple, or quadruple-digit beats

- Hardware/Handsets had the highest avg adj EBITDA beat of +121.8%, which was mostly driven by GoPro (+235.0% beat; $5.4mn vs cons -$4.0mn) and Peloton (+106.8% beat; $115.8mn vs cons $56.0mn)

- EdTech, which had the highest avg adj. EBITDA beat in the prior four qtrs, was pushed down to the second spot and had an avg beat of +106.1% in Q3; Similar to last two qtrs, the substantial avg beat was mostly driven by Coursera(+375.0% beat; $13.3mn vs cons $2.8mn) and Udemy (+127.5% beat; $11.6mn vs cons $5.1mn)

- Smaller beats from Duolingo (+11.8%), Chegg (+10.9%), and Grand Canyon Education (5.4%) also propped up the avg

- E-Commerce hasd an avg beat of +98.6%, which was largely driven by The RealReal’s adj. EBITDA beating expectations by +560.0% ($2.3mn vs cons -$0.5mn)

- Double-digit beats from Revolve Group (+73.3%), Groupon (+43.7%), and ThredUp (+34.2%) also drove up the sector avg

- There were some Cos that did drag down the sector avg, including MercadoLibre (-22.6% miss) and Wayfair (-1.6%)

- Sales – Overall, 68% of the companies in our LionTree Universe beat consensus on sales, but only 2% of those companies beat expectations by double-digits or more

- Satellite Communications had the highest avg sales beat in our Universe, topping cons by +8.8%, on avg, which was mostly driven by Globalstar (+19.9% beat)

- Gogo and Iridium Communications both also beat by +3.3% and +3.2%, respectively

- European Telco stocks had an aggregate sales beat of +4.6%, largely driven by Telenor ASA (+28.2% beat)

- Smaller beats were posted by Liberty Global (+1.6% beat), Telefonica SA (+0.4% beat), and Orange SA (+0.2% beat)

- There were some misses in the sector, including from BT Group (-2.5% miss) and Telecom Italia SpA (-0.3% miss)

- Digital Real Estate stocks beat by +4.1%, on average, driven by Opendoor Technologies (+8.7% beat) and Zillow Group (+4.6% beat), though Redfin came in below expectations (-1.0% miss)

- Satellite Communications had the highest avg sales beat in our Universe, topping cons by +8.8%, on avg, which was mostly driven by Globalstar (+19.9% beat)

Of The Companies & Sub-Sectors That MISSED Expectations…

- Sales – Of the companies in our LionTree Universe that reported adj EBITDA, 17% reported numbers in-line/lower than consensus adj EBITDA

- Video Games saw the largest avg miss amongst the sectors, down -17.2%, driven by some tough misses from Roblox (-63.2% miss) and Skillz (-23.0% miss)

- The sector did see some beats, however, including from PLAYSTUDIOS (+12.3% beat) and Playtika (+5.2% beat)

- China Internet/Tech stocks were down -2.9%, on avg, which was largely driven by Alibaba’s miss (-14.4%), but partially offset by com’s beat (+8.6% beat)

- Music stocks had the third largest adj EBITDA miss, down -1.3%, on avg, which was mostly driven by iHeartMedia’s miss (-4.3% miss)

- The sector saw some small beats, including from Universal Music Group and SiriusXM, which both beat by +0.2%

- Video Games saw the largest avg miss amongst the sectors, down -17.2%, driven by some tough misses from Roblox (-63.2% miss) and Skillz (-23.0% miss)

- Sales – Overall, 32% of the companies in our LionTree Universe reported sales in-line/lower than consensus

- Telecom Infrastructure stocks had the highest sales miss in our Universe, with the sector missing expectations by -1.7%, in aggregate, which was mostly driven by American Tower’s miss (-9.0%)

- SBA Communications also missed (-0.3%)

- That was partially offset by Equinix and Digital Realty Trust, which were in-line with expectations, and Crown Castle Intl’s beat (+0.6%)

- US Print Media/Publishing missed expectations by -1.2%, on avg, which was largely weighed down by Gannett missing expectations (-3.6% miss)

- Both The New York Times and News Corp came in mostly flat

- China Internet/Tech took the third position in the Bottom 3 and missed expectations by -0.7%, on avg, with the biggest miss coming from Alibaba (-1.2% miss) and Tencent (-0.4% miss)

- com, iQIYI, Baidu and Tencent Music Entertainment came in mostly flat

- Telecom Infrastructure stocks had the highest sales miss in our Universe, with the sector missing expectations by -1.7%, in aggregate, which was mostly driven by American Tower’s miss (-9.0%)

NVIDIA Doesn’t Disappoint High Expectations / AI Chip Demand Will Exceed Supply For At Least “Several” Quarters

The world’s largest company by market cap shined though once again, delivering results and outlook that was enough to illicit cheers from the investment community despite the bar being VERY high.

Top of the mind was NVIDIA’S next-generation Blackwell chip, and going into the call, there was some chatter about a delay in its release. But those concerns were assuaged given that production of the AI GPU is “in full steam”. The Co will deliver “more Blackwells than we had previously estimated” in the current qtr and will build on that into the year ahead. Demand for Blackwell is expected to exceed supply for several quarters in fiscal 2026, which will put pressure on margins in the near-term, but will ultimately settle in the mid-70s range once fully ramped. The crossover from Hopper to Blackwell is expected to happen in April, but Hopper demand is expected to continue at least for several quarters.

Drilling down a little more. Data Center rev grew triple-digits (though at a slightly slower pace vs the prior qtr) and reached a new record in Q3. The segment, which makes up 88% of total Co rev, beat expectations, alongside all the other biz segments, which also all posted beats. Looking into Q4, revenue is expected to continue to decel in growth, but will still be material, as Blackwell is “on track” to exceed its previous sales target of “several billion dollars.”

See below for some high-level takeaways from the call.

-> NVIDIA was up +0.5% the day after its report, and ended the week flat; YTD the stock is up +186.7%

Q3 Was A Clean Sweep Qtr Of Beats

- Easy beat on Q3 revenue: Grew +94% y/y to reach record quarterly rev of $35.1bn, though this is down from +122% y/y in Q2, +262% in Q1, and +265% in Q4

- Beat across all segments

- Q3 gross margins were a tad better than expected and increased y/y: Reached 75% vs cons 74.9% and in-line w/ yr-ago 75% on a non-GAAP basis; Reached 74.6%, which was up from year-ago 74% on a GAAP basis, with the increase due to a higher mix of Data Center rev

- But gross margins decr’d seq (75.7% non-GAAP and 75.1% GAAP in Q2) primarily driven by a mix shift from H100 systems to “more complex and higher cost” systems within Data Center

- Q3 EPS and FCF also beat expectations

Q4 Guidance Was Marginally Ahead Of Expectations & Incorporates The Early Stage Of Blackwell Rollouts, Which Weighs On Margins Near-Term

- Q4 rev guidance was modestly above expectations at the midpt and implies cont’d seq decel in y/y growth: $37.5bn + / – 2% (implies range of $36.75bn – 38.25bn) which beat cons by +1.1% at the mid-pt; This implies growth between +66-73% y/y (vs +94% y/y in Q3)

- Data center rev –

- “On track” to exceed previous Blackwell rev estimate of “several billion dollars” as visibility into supply continues to increase

- Networking rev expected to grow sequentially in Q4 with continued data center expansions and Blackwell integration

- Gaming rev will decline seq in Q4 due to supply constraints (sell through was “strong” in Q3)

- Data center rev –

- Q4 GAAP and non-GAAP gross margins are expected to be 73.0% and 73.5%, respectively, +/- 50 bps: Non-GAAP gross margin was +10bps above cons

- Looking ahead – As Blackwell ramps, expect gross margins to moderate to the low 70s, and when fully ramped, will be in the mid-70s

- “Reasonable assumption” for that to be in H2:FY26 but “we’ll just have to see how that mix of ramp goes”

- “Our current focus is on ramping to strong demand, increasing system availability and providing the optimal mix of configurations to our customer”

- Looking ahead – As Blackwell ramps, expect gross margins to moderate to the low 70s, and when fully ramped, will be in the mid-70s

- Q4 GAAP and non-GAAP OpEx are expected to be ~$4.8bn and $3.4bn, respectively, which was above cons estimate of $3.2bn

Hopper Demand Remains “Strong” Ahead Of Crossover And Rollout Of Blackwell / “We Are Racing To Scale Supply To Meet The Incredible Demand” For Blackwell

- Data center rev reached a new record: Grew +112% y/y (decel from +154% y/y in Q2) to reach a record $30.8bn and beat cons by +6.8%

- Both compute and networking rev decel’d q/q –

- Compute rev was $27.6bn, up +132% y/y (vs +162% y/y in Q2)

- Networking rev was $3.1bn, up +20% y/y (vs +114% y/y in Q2); Though networking rev was seq down -15% y/y, networking demand is “strong and growing”

- Drivers of growth? Demand for Hopper computing platform for training and inferencing of large language models, recommendation engines, and generative AI applications

- Cloud service providers represented ~50% of Data Center rev, and the remainder was represented by consumer internet and enterprise Cos

- Both compute and networking rev decel’d q/q –

- Demand for Hopper architecture is “strong” and H200 offering grew “significantly” in the qtr

- Hopper and Blackwell (NVIDIA’s next Data Center architecture) crossover expected to happen in April

- Hopper demand will continue through next year, “surely the first several quarters of the next year”

- is it possible for Hopper to grow b/w Q3 and Q4? “It’s possible, but we’ll just have to see”

- Completed a successful mask change for Blackwell that improved production yields

- Hopper demand will continue through next year, “surely the first several quarters of the next year”

- Blackwell shipments scheduled to begin next qtr (Q4:FY25) and will continue to ramp in FY26

- Will be shipping both Hopper and Blackwell system in Q4:FY25 and beyond

- Blackwell demand is “staggering” and expected to exceed supply for “several qtrs” in FY26

- “Every customer is racing to be the first to market. Blackwell is now in the hands of all of our major partners, and they are working to bring up their data centers”

- Shipped 13,000 GPU sample to customers in Q3, including Oracle, Microsoft, OpenAI, and many more

Agreeable Regarding Potential Tariff Impacts Under Incoming Trump Administration / Bullish On China Market, While Highlighting Progress Across Other Key Geographies

- “Whatever the new administration decides, we’ll, of course, support the administration. That’s our highest mandate”

- “And then after that, do the best we can and just as we always do…we will comply with any regulation that comes along fully and support our customers to the best of our abilities and compete in the marketplace. We’ll do all of these three things simultaneously.

- “We expect the market in China to remain very competitive going forward. We will continue to comply with export controls while serving our customers”

- Data Center rev from China in Q3 grew seq, due to shipments of export-compliant Hopper products to industries

- As a % of total Data Center rev, China remains “well below” levels prior to the onset of export controls

- Other geographic callouts –

- India: Tata Communications, Yotta Data Services, Infosys, CSC, and Wipro are driving a ~10x increase in NVIDIA GPU deployments and training 500,000 developers on NVIDIA AI Enterprise

- Japan: SoftBank is building the nation’s most powerful AI supercomputer with NVIDIA DGX Blackwell and transforming telecom networks into AI-driven systems alongside firms like Fujitsu, NEC, and EY Strategy and Consulting

- United States: NVIDIA is collaborating with T-Mobile to implement AI-driven telecommunications solutions, similar to its AI-powered network transformation efforts in Japan

- Sovereign AI initiatives also “continue to gather momentum as countries embrace NVIDIA accelerated computing for a new industrial revolution powered by AI”

- Particularly in regions like Europe and Asia-Pacific, with investments in AI factories and regional clouds

Growth Continues Across Other Business Segments

- Gaming rev was up +15% y/y (vs +16% y/y in Q2), driven by sales of GeForce RTX 40 Series GPUs and game console SoCs

- Notebook, console, and desktop rev all grew seq and y/y

- Professional Visualization rev was up +17% y/y (vs +20% y/y in Q2), driven by the continued ramp of RTX GPU workstations based on NVIDIA’s Ada architecture

- Automotive rev was a record, up +72% y/y (vs +37% y/y in Q2), driven by their self-driving platforms

WMG’s Particular Focus On Wholesale Pricing & The India Opportunity Stand Out

While Spotify has outperformed its plan over the last couple of quarters with rebounding user growth in combination with strong execution on monetization, the big labels have had more choppiness with their results. Last quarter, Universal Music Group (UMG) surprised the Street with lower-than-expected streaming subscription growth, while this quarter, Warner Music Group’s (WMG) results, despite beating forecasts overall, lagged as it relates to its digital and streaming performance. This was more than offset by better trends in Artist Services & Expanded Rights, Licensing, and Physical within Recorded Music as well as Sync within Music Publishing.

The Co posted its fourth straight quarter of double-digit growth in streaming subscription revenue (ex-FX & one-time items), but growth rates have been moderating and the outlook calls for high single digit growth for FY25 and beyond. Management is confident in sustaining that level of subscriber growth due to 1) still low penetration rates of music streaming services in both mature as well as emerging markets (called out India in particular); 2) lots of areas to benefit from price increases and optimization (a big focus on wholesale price increases among other things); and 3) expected market share gains.

Another aspect that investors harped on was that ad-supported streaming revenue growth went from +1% (ex-FX) to a decline of -6%. Meta’s discontinuation of using premium music videos and the TikTok deal renewal in the prior year both impacted the business and were previously flagged. Mgmt also pointed to macro as a headwind to the business, but underlying growth is up low to mid-single digits.

On the positive side, WMG has successfully been re-engineering the business, creating more efficiency and driving margins. Mgmt now sees more cost savings stemming from the re-org and pointed investors towards an improving margin profile and strong CF conversion looking ahead.

Overall, there were puts and takes this qtr, and it will be incumbent upon mgmt to block and tackle and show the Street that future streaming growth will accrue to the labels and not just Spotify, which has been a main current beneficiary. Mgmt’s confidence is also reflected in the board’s authorization of a new $100mn share repurchase program.

See below for what we thought was most incremental from WMG’s results and earnings call.

–> WMG shares were down -7.4% in reaction to the print but recovered slightly to end the week down -3.3%; YTD, WMG stock is trading down -11% and UMG stock is down -12.5%, while Spotify’s stock is up +152.8%

FQ4 Headline Numbers Were Better Than Expected…

- Strong FQ4 numbers relative to consensus: FQ4 total revs were up +2.8% y/y (or 2.9% ex-FX) vs down -0.6% y/y (or up +1% ex-FX in FQ3) and beat cons by +2.5%; Adj OIBDA grew +11.4% y/y (the same ex-FX) vs +6.4% y/y (or +8% ex-FX in FQ3) and also beat cons by +2.3%; FCF fell -10% y/y

- Recorded Music – BEAT: Revs were up +3.9% y/y ex-FX (vs -1% y/y ex-FX in FQ3) and beat cons by +4.5%; Adj OIBDA was marginally ahead of expectations

- Weaker than expected performance in Digital (BMG digital rev roll-offs had a $23mn unfavorable impact, and the renewal of an int’l digital partner had a $4mn unfavorable impact) was more than offset by upside in other revenue segments of Recorded Music

- Music Publishing – MIXED: Revs were up +5% y/y ex-FX (vs +9% y/y ex-FX in FQ3) and missed by -4.9% while adj OIBDA beat by +4.3%

- Digital was again impacted by the CRB Rate benefit of $17mn in the prior yr qtr; The only revenue area that beat consensus was Sych

- Recorded Music – BEAT: Revs were up +3.9% y/y ex-FX (vs -1% y/y ex-FX in FQ3) and beat cons by +4.5%; Adj OIBDA was marginally ahead of expectations

…BUT The Deceleration In Subscription Streaming Revenue Growth Continues

- Recorded Music total streaming revenue growth of +6% on a normalized and ex-FX basis is down from +10.2% in FQ3 and +11% in FQ2

- Subscription streaming growth slowed down to +10.6% on a normalized and CC basis (4th consec qtr of DD growth) from +14% y/y in FQ3 and +13.5% in FQ2

- Last qtr the company guided for “continued strength in subscription streaming revenue,” hence the qtr’s performance was a disappointment

- Subscription streaming growth slowed down to +10.6% on a normalized and CC basis (4th consec qtr of DD growth) from +14% y/y in FQ3 and +13.5% in FQ2

- Outlook – Subscription streaming is expected to increase “high single digit” growth for fiscal 2025 on a “multi-year basis”

- …Though they are lapping price increases in H2, so there will be some moderation during the period

And Ad Supported Streaming Revenues Showed More Challenging Trends Given Some 1x Items

- Normalized ad-supported rev fell -5.6% ex-FC, which is down from comparable growth of +1% in FQ3 and +5% in FQ2

- The qtr was impacted by Meta discontinuing the use of premium music videos and the TikTok deal renewal in the prior year, which had been previously flagged

- The business also continues to be impacted by “macro” trends as well though the “underlying core advertising there is stable and growing”

- Seeing low to mid-single digit growth at the moment

Mgmt Remains Very Confident In Three-Prongs Underpinning The Growth Strategy

- What are the key drivers for growth looking ahead?

- Subscriber growth: Rising penetration rates in both developed and emerging markets (see more color below)

- Pricing optimization: Includes audience segmentation and superfans, higher ARPU across DSPs, as well as wholesale pricing optimization, improving the family plan and multiuser discounts, per subscriber minimums, trying to move the industry more progressively on the wholesale side as music is an anchor tenant driving high engagement

- And more innovation

- Market share: Increase market share through a strong release slate and ongoing investments in artist development and catalog acquisitions.

Subscription Trends In Cable TV/SVOD Support Higher Expected Penetration In Music & Markets Like India Are A Key Call Out

- See room for music subscriber penetration growth in both Mature and Emerging markets: US cable TV penetration is a little over 50% and SVOD penetration is approaching 50%… vs Music which is much lower

- Mature markets music subscriber penetration: Expect to increase from ~35% to nearly 50% by 2030

- Emerging markets music subscriber penetration: Expect to increase from single to low-double digits by 2030

- India is a particularly attractive market

- Market dynamics

- 4bn population and the 5th largest GDP, but it’s still only the 14th largest music market in the world

- That gap will continue to close in the coming years

- Paid subscribers In India have incr’d by almost +40% y/y, but it still has less than 2% penetration

- WMG launched in India in 2020 and have:

- Partnered with most important local players and has bought stakes in and acquired outright local music companies, such as E-Positive, Vevo, and Global Music Junction

- Also just bought a stake in Skillbox, a leading ticketing and live events platform

- Building local stars and Indian fan bases for local talent

- Saw 100%+ revenue growth in India in FY24

- Expect to keep taking share

- Market dynamics

Lots Of Releases “In The Hopper” For FY2025 BUT Reminder That Q1 Faces Tough Comps (Previously Disclosed)

- Great release slate: Exciting release slate that includes projects from Rose, Dua Lipa, Teddy Swims, Jack Harlow, Enson Boone, Mike Towers, David Guetta, Burna Boy, and more

- FQ1 tough comps

- Streaming growth will be impacted by the BMG digital distribution roll off, the digital license renewal in the prior year and the lapping of Spotify price increases

- BMG digital distribution roll-off ~-$16mn rev impact vs prior yr qtr: Was originally planned to roll off by the end of fiscal ’24 will now continue into fiscal ’25

- Digital license renewal added $27mn to prior yr qtr: This will not recur in the current year

- Physical distribution relationship with BMG –$15-20mn neg impact in FQ1: Largely rolled off, leading to an expected unfavorable revenue.

- Licensing revenue will reflect the $68mn catalog licensing agreement extension disclosed in Q1 2024

- Artist services revs will reflect the exit of O&O media properties, which contributed $20mn in the prior year qtr

- Streaming growth will be impacted by the BMG digital distribution roll off, the digital license renewal in the prior year and the lapping of Spotify price increases

Expect A Long Runway For Margin Improvement

- FQ4 total adj OIBDA margin incr’d +7 ppts y/y to 21.7% from 20.0% (ex-FX)

- Strong operating performance and savings from the Co’s restructuring plans, of which a majority has been reinvested in the business

- Outlook – remain committed to +100bp increase in margins per year over a multi-year period & 50-60% operating CF conversion

- There will be qtr-to-qtr fluctuations due to timing of releases and marketing and how and when savings are redeployed but continue to see margin expansion oppties as the business shifts more to digital and streaming and diversifies

Recorded Music Re-Org Should Yield Greater Cost Savings Than Earlier Expected

- Some core benefits of the re-org –

- Simplifies structure

- Creates regional leadership

- Better aligns key business lines

- Addresses foundational infrastructure issues

- Improves leadership structure in the US and supports global expansion

- Enhances artist development

- Now anticipate pre-tax cost savings of $260mn from the restructuring plan (vs $200mn previously): A significant majority of the savings will be achieved by the end of fiscal 2025

Another Interesting Comment

- The gaming industry is a good case study on the super-fan: Music is monetized the same way if you are a fan or super-fan, so this is under-exploited

- 80% of gaming revenue comes from 20% of users, but that’s more of a transactional model rather than a subscription model

- “Adding features that drive engagement, give people higher quality, more interactions, all of that, like learning from the gaming industry is a really good place to go”

Five Key Insights Regarding Gen AI In The Enterprise…

We are always on the lookout for good reports on AI and its development, and this week, we came across Menlo Ventures’ new report, 2024: The State of Generative AI in the Enterprise. Menlo’s research reveals that overall enterprise spending on AI is expected to reach $13.8bn this year, up +6x from 2023 levels, as companies shift from experimentation to execution with respect to integrating AI into business strategies. However, AI in the enterprise is still in the early days. 72% of decision makers anticipate broader adoption of gen AI tools in the “near future,” but more than one-third don’t have a clear vision about how gen AI will be implemented across organizations.

The findings were based on a survey of 600 enterprises, and the report has good details on emerging companies in the space as well as helpful sector heat maps that you can access HERE, though we wanted to pull out our Top 5 takeaways/insights from the report upfront. See below.

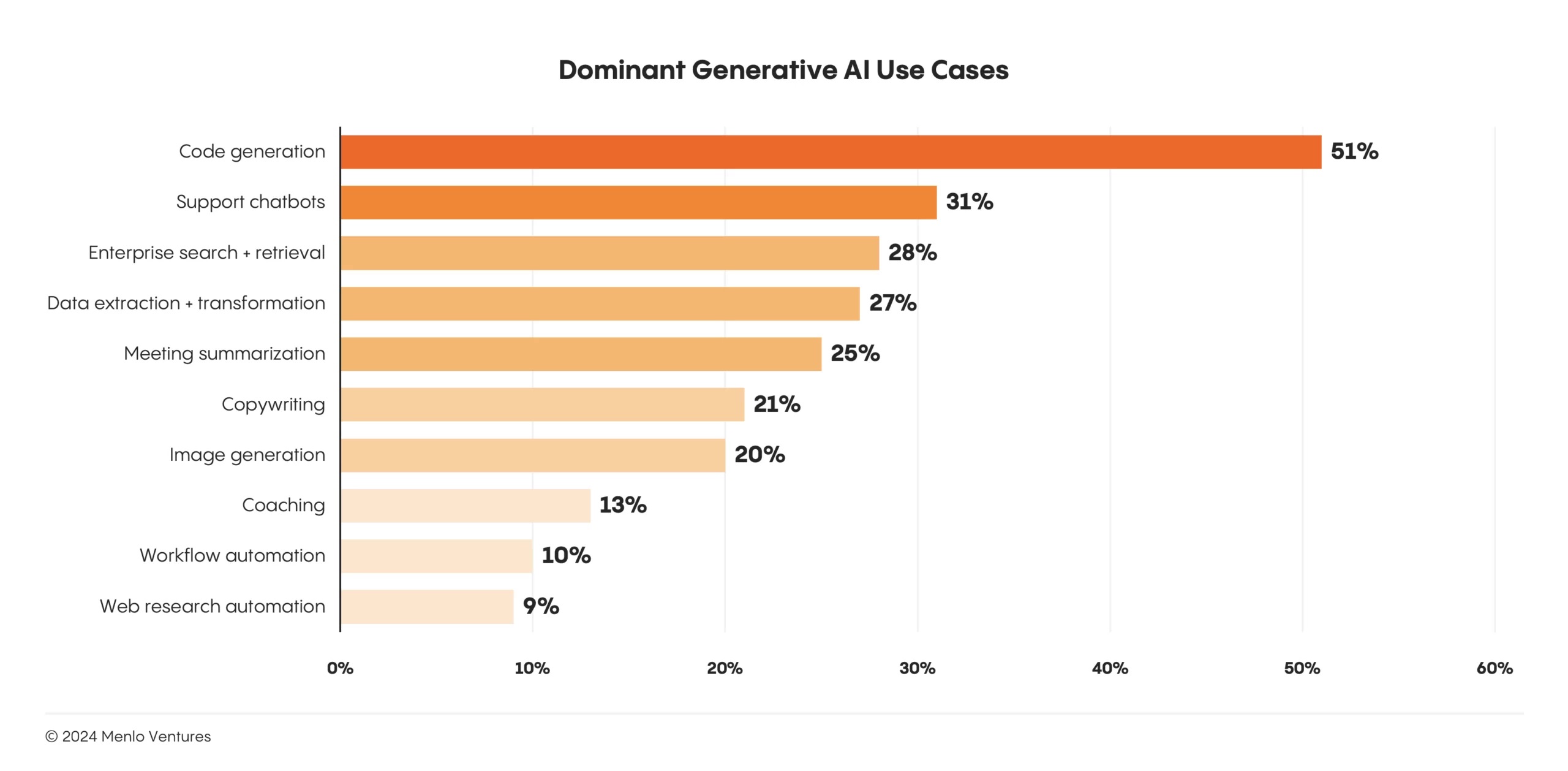

- What are the predominate use cases? -> A question that comes up all the time when talking about AI implementation

-

- Coding (51% adoption per survey results)

- Support chatbots (34% adoption)

- Enterprise search + retrieval (28% adoption)

- Data extraction + transformation (27% adoption)

- Meeting summarization (24% adoption)

-

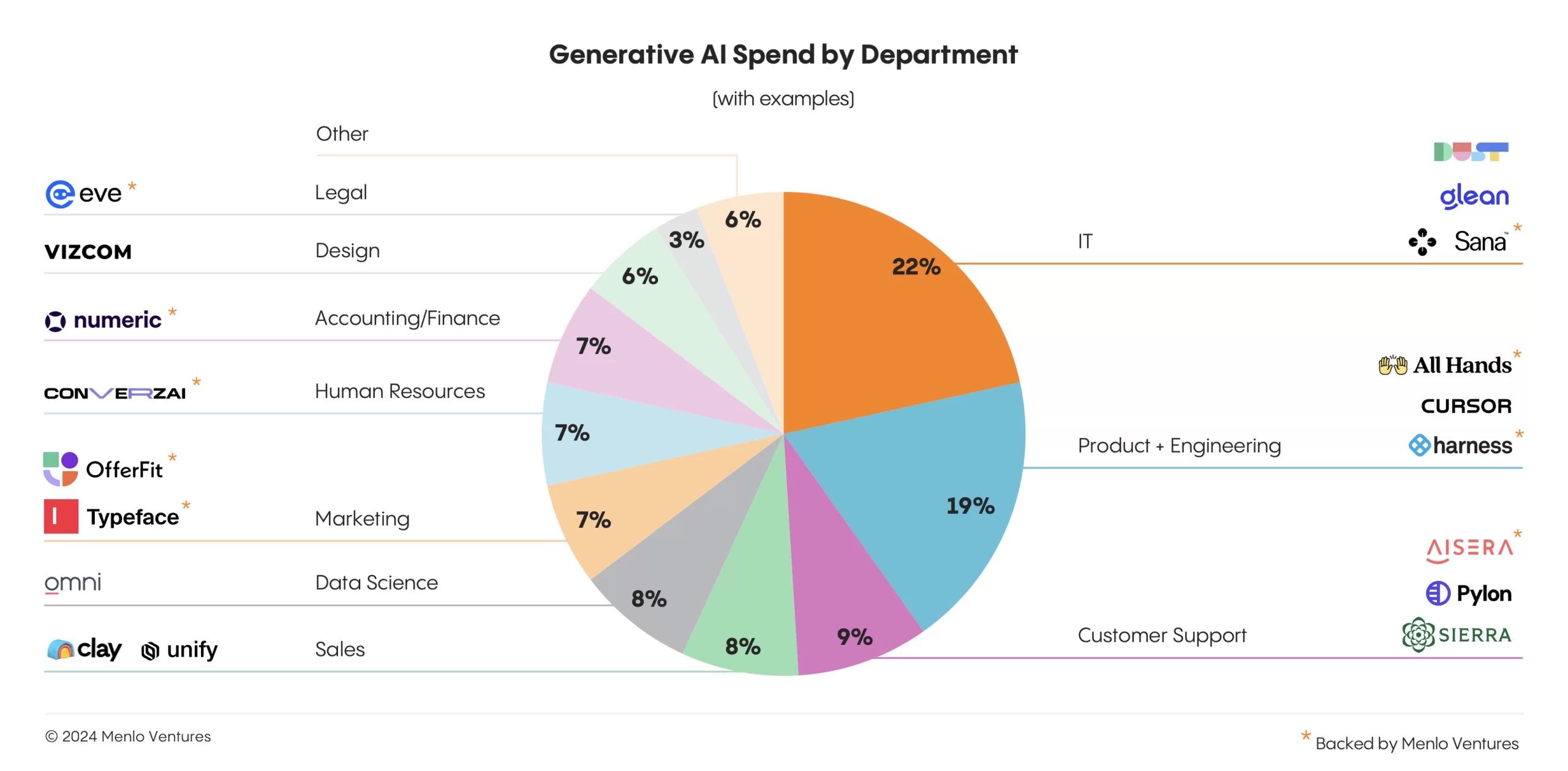

- What departments account for the largest share of AI spending? -> not a shocker to see the breakdown but interesting detail nonetheless

- Technical departments command the largest share of spending, w/ IT (22%), Product + Engineering (19%), and Data Science (8%) together accounting for nearly half of all enterprise generative AI investments

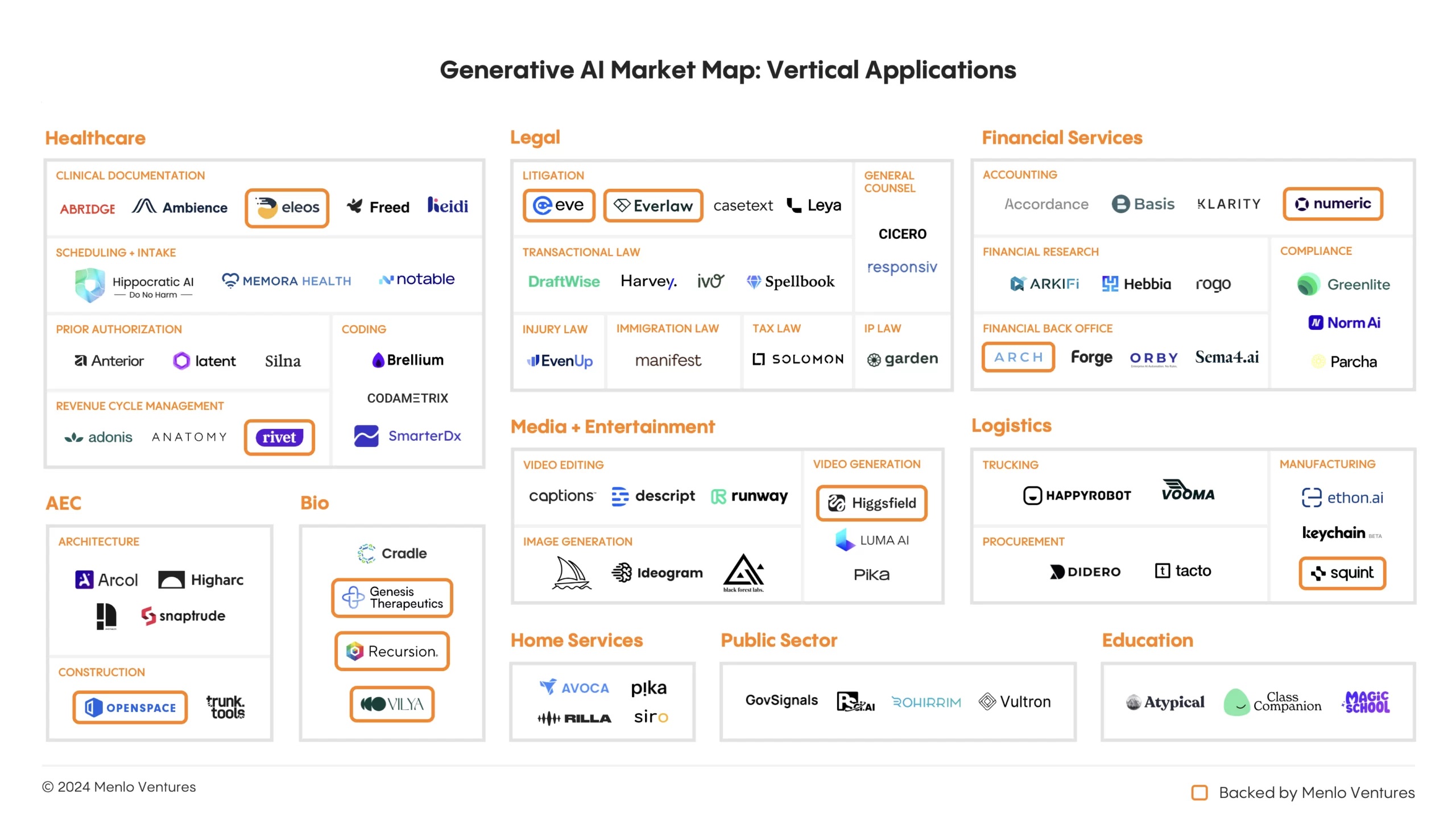

- What verticals are leading adoption?

- Healthcare: $500mn in enterprise AI spend

- Legal: $350mn in enterprise AI spend

- Financial Services: $100mn in enterprise AI spend

- Media & Entertainment: $100mn in enterprise AI spend

- What are the market share shifts with LLMs?

- OpenAI has been the market leader by far, but has ceded market share to Anthropic; Google has also gained share

- Enterprises have typically deployed 3+ foundation models in their AI stacks

- When moving to a new LLM, organizations most commonly cite security and safety considerations (46%), price (44%), performance (42%), and expanded capabilities (41%) as motivations

- THREE key forecasts looking ahead –

- Agents will drive the next wave of transformation

- Advanced agents could disrupt the $400bn software market—and eat into the $10 trillion US services economy

- This shift will demand new infrastructure: agent authentication, tool integration platforms, AI browser frameworks, and specialized runtimes for AI-generated code

- David beats Goliath: More incumbents to fall

- Chegg saw 85% of its market cap vanish, while Stack Overflow’s web traffic halved

- Other categories are ripe for disruption

- IT outsourcing firms like Cognizant and legacy automation players like UiPath should brace for AI-native challengers moving into their market

- Over time, software giants like Salesforce and Autodesk will face AI-native challengers

- No relief in sight: The AI talent drought intensifies

- We are on the brink of a massive talent drought

- Agents will drive the next wave of transformation

Hedge Funds Pile Into Non-Tech, As Per The Latest 13-Fs

Given the huge earnings storm last week, we were not able to cover all the 13-F updates that hit the tape, so we wanted to include some thoughts and perspectives this week instead in light of some interesting stock ownership changes across the sector.

At the forefront of the updates is always Warren Buffett’s Berkshire Hathaway, which was a LARGE net seller across its portfolio in Q3, selling ~$36bn of stocks while purchasing only ~$1.5bn. It took just two new positions in Q3, which were in Domino’s Pizza and Pool Corp and, similarly, only increased its positions in two companies, which were Heico (+0.5% increase after taking a new position last qtr) and SiriusXM (+691% increase on top of a +262% increase last qtr). It decreased its positions in Bank of America and Charter (after maintaining positions in both Cos last qtr) and Ulta Beauty (cut by ~97% after initiating a position just last qtr) and further decreased its positions in Capital One by -7% (on top of -21% last qtr) and Apple by -25% (after cutting in half last qtr). Despite cutting its position in Apple from ~$175bn in the start of the year to ~$70bn at the end of Q3, the Co still accounts for about a qtr of Berkshire’s equity portfolio. It offloaded its position in Liberty SiriusXM and maintained positions in Ally Financial, Amazon, American Express, Atlanta Braves, Chevron (after cutting by -3.6% last qtr), Chubb, Citi, Coca-Cola, Jeffries, Kraft Heinz, Kroger, Liberty Latin America, Liberty Media, Liberty Formula One, Mastercard, Mitsubishi, Moody’s, Occidental Petroleum, T-Mobile, Verisign, and Visa.

We also took a quick look at Michael Burry’s Scion Asset Management (as a reminder, Michael Burry famously predicted the 2008 financial crisis and was one of the main characters in the book and movie, The Big Short), and this quarter, the fund further increased its exposure in China (nearly 50% of his portfolio is invested in the country). It doubled its position in JD.com (after decreasing last qtr), making it Scion’s top holding, and further increased its positions in Alibaba by +29% (making it Scion’s second largest holding) and Baidu by +67%. It also increased its positions in Olaplex and Shift4 Payments (after taking initiating positions in both companies last qtr), as well as Molina Healthcare. It further decreased its position in The RealReal and sold out of its positions in BioAtla and Hudson Pacific Properties. It total, the firm now holds 8 positions (down from 10 in the prior qtr).

Where are the top hedge funds investing, in aggregate? Each quarter, WhaleWisdom tracks the stocks that were most bought and sold during the quarter across 150 of the top hedge funds (link). It ranks the “hottest” stocks based on a formula that takes into account the number of buyers adding and initiating new positions vs sellers, the change in average ranking that the stock had in the portfolios, and the number of times the stock appears in the top 10 holdings of the portfolios. The biggest takeaways were:

- TMT took a big step back in Q3 – only 1 of the Top 10 was a TMT stock: This is down from 4 in Q2, 2 in Q1, and 4 in Q4

- What was the TMT stock that made it to the Top 10? It was ServiceNow, which actually took the #1 position (and had never been ranked before)

- 4 of the MAANG names made it to the Top 100 list (up from just 2 last qtr): Apple (#17), Alphabet (#42), Meta (#46), Amazon (#56); Netflix was the only name that didn’t make it on the list

- Breakdown by sector: Energy companies took the top spot again, as 34 of the Top 100 companies were in the sector (down from 35 in Q2 and 40 in Q1); Also like last qtr, information technology was the second most popular industry, with 15 of the Top 100 Cos in the sector (up from 12 in Q2 and 9 in Q1), followed by 12 in Finance and 11 in Consumer Discretionary; Communications rounded out the Top 5, with 8 Cos making the Top 100

- Increases and decreases in popularity

- There were some gainers this quarter that were worth flagging (Q2:24 -> Q3:24) …

- Mercado Libre (Not ranked -> #3)

- Mastercard (#7 -> #4)

- Wells Fargo & Co (#123 -> #5)

- Costco (#111 -> #10)

- NVIDIA (#92 -> #12)

- UnitedHealth Group (Not ranked -> #13)

- The Walt Disney Co. (#67 -> #16)

- Apple (#126 -> #17)

- com (#137 -> #18)

- Walmart (#74 -> #21)

- Coca-Cola (Not ranked -> #22)

- Eli Lilly & Co (#37 -> #35)

- American Express (#100 -> #36)

- Micron Technology (#88 -> #37)

- Tesla (#71 -> #38)

- Alphabet (#134 -> #42)

- General Motors (#182 -> #48)

- Citigroup (#153 -> #49)

- PayPal (#160 ->#51)

- com (#64 -> #56)

- JPMorgan Chase & Co (#110 -> #68)

- Broadcom (#107 -> #71)

- Alibaba (#168 -> #73)

- Applied Materials (#135 -> #76)

- Alphabet (#139 -> #79)

- Palantir (Not ranked -> #84)

- Johnson & Johnson (Not ranked -> #87)

- Taiwan Semiconductor Manufacturing Co. (#130 -> #95)

- Salesforce (Not ranked -> #96)

- Visa (#114 -> #100)

- …as well as some losers

- Meta (#4 -> #46)

- Advanced Micro Devices (#49 -> #86)

- Microsoft (#38 -> #88)

- Adobe (#13 -> #99)

- There were some gainers this quarter that were worth flagging (Q2:24 -> Q3:24) …

Where are activist/event investors placing their bets, in aggregate? After four consecutive quarters of being net sellers, the top 9 activist funds were net buyers, though just by a difference of $14bn, buying $$2.747bn of stocks (vs ~$1.2bn last qtr) and selling $2.733bn (vs ~$4.6bn last qtr)

- Inflows: Financial stocks saw the most inflows (+$1.3bn) which was a reversal from last quarter, when the sector was -$460mn in outflows; Transportation saw the second largest inflows (+$1.1bn), followed by Media (+$239mn), Consumer (+$108mn) and Healthcare (+$42)

- Financial inflows were largely driven by Pershing Square and Third Point both taking positions of +$1.4bn and +251mn, respectively, in Brookfield Corp.

- Transportation inflows were almost entirely driven by Elliott Investment Management increasing its in Southwest Airlinesby ~$1.1bn

- Outflows: Information Tech was the sector that saw the most outflows in Q3 (-$1.0bn), which was a continuation of -$251mn in outflows that the sector saw last qtr; Real Estate (-$545mn) saw the second largest outflows, followed by Industrials (-$494mn), Telecom/Cable/Satellite (-$401mn), Technology Hardware (-$233mn) and Utilities (-$97mn)

- Information Tech outflows were largely driven by Third Point selling out of its position in Alphabet (-$328mn), Meta (-$317mn), Microsoft (-$306mn), and Amazon ($261mn)

Drilling Deeper Into Individual Activist Funds…

- ValueAct increased its position in Roblox by +341%, further increased its position in Disney by +22% (after increasing by +13% last qtr), and initiated positions in Liberty Live, Live Nation, Meta, and Visa; The fund maintained its position in Salesforce, decreased its position in Expedia by -24%, and sold out of its positions Flutter Entertainment, KKR, New York Times, and Spotify

- Starboard Value took a new position in AutoDesk, and maintained its position in News Corp (after increasing last qtr), Rogers Corp., and Wix (after decreasing by -23% last qtr); It decreased its position in Match Group (after initiating a position last qtr), Salesforce (after increasing last qtr) and further decreased its positions in GoDaddy and Humana

- Sachem Head increased its position in CVS Health (after taking a new position last qtr) and maintained its positions in Deliveroo and Twilio; It decreased its position in Sprinklr by -9% (after increasing by +16% last qtr) and sold out of its positions in Lamb Weston, Liberty Global and Seagate Technology

- Trian Fund increased its position in U-Haul (after initiating a position last qtr), decreased its position in Wendy’s (after increasing last qtr) and Unilever, and further decreased its positions in Invesco and Allstate -15% and -70%, respectively (after decreasing by -20% and -10%, respectively, last qtr); The fund sold out of its position in The Walt Disney Co

- Third Point initiated positions in Clear Channel Outdoors, CVS Health, Flutter Entertainment, and Tesla; The fund increased its position in Live Nation (after initiating last qtr), and maintained its positions in Cinemark, Hertz, and USCellular; It decreased in Apple (which it took a new position in last qtr), as well as Amazon and Apollo Global (both positions it maintained last qtr) and further decreased its positions in Bath & Body Works, Meta, Microsoft and PG&E; It also sold out of its positions in Advance Auto Parts, Alphabet, Micron Technology, Uber, and Verizon

- Pershing Square increased its position in Nike (after initiating last qtr), maintained its position in Alphabet, Chipotle and Universal Music Group, and further decreased its position in Hilton by -18%; It did not sell of out any positions

- Icahn Associates increased its position in Centuri Holdings and Icahn Enterprises by +39% and +7%, respectively; It maintained its remaining positions across its portfolio and did not take any new positions, nor did it decrease or sell out of any

- JANA Partners increased its position in Rapid7 (after initiating last qtr) and further increased its position in Trimble; It took a new position in Lamb Weston and further decreased its position in Frontier Communications

- Elliott Management increased its position in Southwest Airlines (after taking a new position last qtr), and further increased its positions in Etsy, Liberty Broadband, and Match Group; The fund maintained its positions in Arm Holdings, Bausch Health, Cardinal Health, Crown Castle, Pinterest, and Vantage Towers

The DoJ Looks To Breakup Google + Other Regulatory Updates

There were also some notable updates across the globe on the regulatory front this week, particularly as it relates to Big Tech. In the US, the Justice Department formally proposed a breakup of Google after a federal judge ruled in March that the company’s search business had violated antitrust law. In addition to a sale of the Chrome browser, government lawyers also urged the judge to force the company to syndicate its US search results to other rival search engines, among other restrictions. Over in the EU, Amazon also found itself in the crosshairs of regulators, as its online marketplace will be reportedly investigated by the European Commission next year to assess whether or not the company’s conduct has violated the Digital Markets Act. Lastly, Australia’s parliament is also starting to consider landmark legislation that would ban social media for children under age 16 and put the onus on social media platforms for preventing them holding accounts. The bill already has wide political support and could set a precedent for other governments around the world.

See below for more details on this week’s key regulatory news.

- The DoJ formally proposed a partial breakup of Google (link): The request by the Justice Department and a group of states could lead to the most significant antitrust penalties for a tech giant in a generation and comes after a landmark ruling earlier this yr that found that Google had violated antitrust law w/ its search biz

- Antitrust enforcers urged District Judge Amit Mehta to force Google to sell the Chrome browser…: The DoJ reasons that a spinoff of Chrome, which is used on billions of devices worldwide, could help prevent a monopoly from recurring

- … And ban the Co’s exclusive search agreements: Including Google’s exclusive, multi-yr contract w/ Apple, Samsung, and others that made Google the default search engine on their devices

- “The playing field is not level b/c of Google’s conduct”: “And Google’s quality reflects the ill-gotten gains of an advantage illegally acquired,” per govt lawyers; “The remedy must close this gap and deprive Google of these advantages”

- Govt lawyers also believe that Google should be required to syndicate its US search results to other rival search engines for the next decade: This could put other search alternatives on more even footing w/ Google

- The DoJ also called on Meta to impose a range of other restrictions: Some of these are aimed at preventing future harm; One such request would require Google to give websites the option not to have their data collected for training the Co’s AI tools

- Google’s response – The govt proposal is “extreme”: In a blog post, Google President and Chief Legal Officer Kent Walker added that the proposal would undercut Americans’ security and privacy by making Google share its user data w/ others

- Antitrust enforcers urged District Judge Amit Mehta to force Google to sell the Chrome browser…: The DoJ reasons that a spinoff of Chrome, which is used on billions of devices worldwide, could help prevent a monopoly from recurring

-> Alphabet shares were down -4.7% in reaction to the news and ended the week down -4.5%; YTD, Alphabet stock is still trading up +17.9%

There Were Also Some Other Big Tech-Related Regulatory Updates Overseas This Week…

- Amazon is reportedly likely to face an EU investigation into its online mktplace next yr (link): Per Reuters, European antitrust regulators plan to investigate whether the Co favors its own brand products on its online mktplace, which would be a violation of the EU’s Digital Markets Act

- Amazon could face a fine of up to 10% of its global annual sales: BUT the Co said it is compliant w/ the DMA and has engaged constructively w/ the European Commission

- Incoming EU antitrust chief Teresa Ribera will make the final decision on the investigation: Including whether it proceeds as well as its timing; Ribera is set to take up her post next month, replacing outgoing Margrethe Vestager

- The European Commission has been building a case against Amazon since March: In March, the Commission said it was gathering facts and info on Amazon’s treatment of its own brand products on the Amazon Store

- Australia’s parliament is considering a law that would ban social media for children under age 16 (link): Michelle Rowland, Australia’s communications minister, introduced the world-first law this week, stating that online safety is one of parents’ toughest challenges

- The bill targets TikTok, Facebook, Snapchat, Reddit, X, and Instagram: According to Rowland, these platforms would be subject to fines of up to 50mn Australian dollars (~$33mn) for systemic failures to prevent young children from holding accounts

- These platforms would have one yr to work out how to implement the age restriction: If the bill passes

- Messaging svs and online gaming platforms won’t be subject to the age restrictions: Given that their users “do not face the same algorithmic curation of content and psychological manipulation to encourage near-endless engagement”

- The legislation has wide political support: “There is wide acknowledgement that something must be done in the immediate term to help prevent young teens and children from being exposed to streams of content unfiltered and infinite,” per Rowland

- “For too many young Australians, social media can be harmful”: The following stats are from Rowland and the Australian govt’s research –

- Almost two-thirds of 14- to 17-yrs-old Australians have viewed extremely harmful content online, including drug abuse, suicide or self-harm as well as violent material

- One quarter have been exposed to content promoting unsafe eating habits

- 95% of Australian care-givers find online safety to be one of their “toughest parenting challenges”

- The bill targets TikTok, Facebook, Snapchat, Reddit, X, and Instagram: According to Rowland, these platforms would be subject to fines of up to 50mn Australian dollars (~$33mn) for systemic failures to prevent young children from holding accounts

Pinduoduo Continues To Prioritize The Long-Term, Despite Near-Term Choppiness

This week saw Temu owner Pinduoduo (PDD) release its latest earnings, and for the 2nd consecutive quarter, the Co’s print revealed relatively disappointing results. Under pressure from “intensified competition and external challenges,” which echoed commentary from other big China tech names (see Theme #7 from 11/15/24 Weekly), PDD’s top-line growth decelerated sequentially to +44.3% y/y (vs +85.7% y/y in Q2) and missed consensus estimates by -3.4%. These headwinds, combined with the Co’s “substantial investments” in its merchant ecosystem, also led to its non-GAAP operating profit finishing -5.1% short of expectations. Nonetheless, PDD has no plans to deviate from its current course and is “committed to making more meaningful, long-term investments” to support its merchants. Thus far, these efforts have received “notable positive feedback,” helping to drive “significant order volume growth” from consumers in rural areas as well as a successful Double 11 Shopping Festival that contributed to a tenfold sequential increase in sales by national brands.

In contrast to its investment strategy, PDD did not see as much of a benefit from the Chinese government’s recently introduced stimulus policies. Although these measures have provided “significant support to industries and fuel to consumer demand,” PDD was unable to “fully leverage” these “new opportunities” to the same extent as its competition. Mgmt explained that the Co’s status as a third-party platform forced it to “incur much higher costs” in order to “stay competitive with similar products.” Moving forward, the financial impacts of this could “further increase,” given PDD’s expectations that it will remain at a disadvantage relative to its peers “for some time.”

As always, commentary on Temu and the global business was high-level. Much of the discussion was focused on the Co’s efforts to “continuously enhance [its] svs standards and compliance posture” in response to increasing pressure from both regulators and consumers in its overseas markets. Despite this adversity, PDD’s “commitment remains unchanged” with its global business, and recent setbacks “will not deter” it from “exploring the way forward”. All said, it appears that PDD is planning to stick to its guns amid an operating environment that has become increasingly complex to navigate.

-> Pinduoduo shares dropped -10.6% following the print and finished the week down -12.2%; YTD, Pinduoduo stock is trading -31.6% lower YTD

Worse Than Expected Headline Results Reflected Mounting Competition & “External Challenges”

- Headline numbers revealed decel’ing growth and broadly disappointed relative to the Street’s expectations

- Rev incr’d +44.3% y/y in Q3 (vs +85.7% y/y in Q2) and closed -3.4% below cons, as a +0.6% beat on Online Mkting Svs rev was more than offset by a -7.7% miss on Transaction Svs rev

- Non-GAAP op profit was up +47.7% y/y (vs +139.5% y/y in Q2) but fell -5.1% short of cons

- Non-GAAP EPADS of CNY18.59 missed cons by -5.1%

Macro Commentary – PDD Has Been Disadvantaged By China’s Recent Stimulus Measures

- There has been a “steady” recovery in consumer spending and “strong growth in online consumption” in H2:24: Recent shopping festivals have also driven increases in consumer activities on the Co’s platform

- The new stimulus policies have “opened up new oppties”: These measures “have brought significant support to industries and fuel to consumer demand”

- BUT PDD was “unable to fully leverage [these] macroeconomic shifts”: Given that it operates solely as a third-party platform, the Co was forced to “incur much higher costs than peers” in order to “stay competitive w/ similar products”; Will continue to adversely impact profitability in the near-future

- The Co “may continue to experience disadvantages relative to [its] peers for some time”: The “limitations imposed by [its] platform biz model,” plus “the operational mindset shaped by [its] previous experience and “shuffles in [its] capabilities,” could “further increase the financial impacts”

- Shifting consumer preferences has imposed “new demands on supply chain innovation”: Indicated that consumers currently have a “greater focus on quality and personalization”

- The overall level of competition in the e-commerce mkt also “remains intense”: The “highly dynamic” mkt is characterized by “constant changes, diverse biz models, and intensifying competition”

- The new stimulus policies have “opened up new oppties”: These measures “have brought significant support to industries and fuel to consumer demand”

Go-To-Mkt Color – PDD’s Newly Launched Merchant Support Programs Have Received “Notable Positive Feedback”

- Growth in sales & mkting expenses decel’d seq: On a non-GAAP basis, sales & mkting expenses rose +40% y/y in Q3 (vs +48% y/y in Q2), as the Co remained focused on giving back to consumers throughout its promotional campaigns and continuing to invest in mkting to promote its platform

- BUT sales & mkting expenses accounted for a higher percentage of revs seq: Comprising ~30% of total rev in Q3 (vs ~26% in Q2)

- PDD “made substantial investments in the merchant ecosystem,” launching several new initiatives: These measures are intended to drive efficiency gains to improve cost savings and svs quality for merchants

- A new RMB10bn fee reduction program rolled out in late Aug: The program includes multiple measures to improve cost savings and svs quality for merchants, such as svs fee refunds, a fee reduction for BNPL svs, lower security deposits, an easier fund withdrawal process, and after-sales support upgrades

- The RMB10bn program covers all product categories on PDD’s platform

- “Many merchants… saved hundreds of thousands of RMB a yr”

- The Co also launched a “high-quality merchant support program”: This aims to “empower merchants and brands that demonstrate product and tech innovation capabilities”; PDD offers comprehensive support in product development, mkting, operations, and operations mgmt.

- The high-quality merchant support program has already been implemented in dozens of agricultural regions and industrial zones

- Introducing “logistic support drivers” has helped promote e-commerce across western China: The Co’s first upgrade to its fulfillment experience helps merchants penetrate underserved mkts and builds on its earlier initiative to provide free shipping to some villages in western China

- The Co also eliminated trans-shipment fees for merchants on shipments to western regions: Enabling merchants to reach a broader base of customers at a lower cost

- A new RMB10bn fee reduction program rolled out in late Aug: The program includes multiple measures to improve cost savings and svs quality for merchants, such as svs fee refunds, a fee reduction for BNPL svs, lower security deposits, an easier fund withdrawal process, and after-sales support upgrades

- The Co is “committed to making more meaningful, long-term investments in this direction” moving forward: So far, these policies have received “notable positive feedback” from merchants

The Core E-Commerce Biz Was Under Pressure

- Multiple factors caused a “moderation in rev growth” and profits to have “trended lower”: Including –

- The “intensity” of the competition in the e-commerce sector: As well as other “various challenges faced by [the] biz”

- Ecosystem investments had an “expected impact” on profitability: The Co warned last qtr that profits would start to “gradually trend down” starting in Q3 b/c of these investments, and the financial impact has been “within [its] expectation

- BUT PDD has been seeing “significant order volume growth” from rural regions: As the Co’s logistic support measures have cont’d to benefit consumers in remote areas

- The Harvest Festival helped “seasonal agricultural products reach urban mkts”: During the festival, the Co allocated RMB1bn to subsidies and RMB2bn to mkting resources to support its high-quality agricultural merchants

- The Double 11 Shopping Festival helped drive a +10x seq increase in national brands’ sales: PDD’s RMB10bn program partnered w/ numerous national brands to launch customized, high-quality products during the festival

The Global Biz (Temu) Has Been Under More Regulatory Scrutiny, BUT PDD Has Been Responding

- The Co’s “commitment remains unchanged”: “The goal has always been to deliver our unique value to consumers across the different countries”; To achieve this, the Co will “continue to strengthen [its] capabilities” by improving its supply chain and upgrading its svs

- However, greater scale has meant “higher requirements” from consumers and external stakeholders:

“Regulatory trends in various mkts [have] placed higher demands on [PDD’s] compliance capabilities”; In response, the Co has been “actively engaging with external stakeholders” in mkts where it operates

- However, greater scale has meant “higher requirements” from consumers and external stakeholders:

- PDD has made an effort to “continuously enhance [its] svs standards and compliance posture”: Has “carefully listen[ed]” to external stakeholders’ feedback and suggestions and then will “promptly incorporate” these into the Co’s daily operations

- The Co has “invested heavily in building a strong expert compliance team”: The team closely tracks regulatory changes and industry trends across its mkts, which allows the Co to “translate insights into actional compliance guidance

- The Co also “further streamlined” its merchant onboarding and product listing processes: The Co has “invested substantial resources” into proactive product quality checks as well as combining tech and menu screening to promptly detect and address potential productivity risks

- Recent setbacks “will not deter” the Co from “exploring the way forward”: Although “challenges from the outside”, including “the impact of the intensifying competition in the global mkts” and regulatory concerns “will bring ups and downs” to the Co’s biz, this adversity motivates PDD to continue to strengthen its capabilities

PDD Cont’d To “Make [Its] Own Contributions” To The Field Of Agriculture

- PDD has had a “particular focus” on advancing research and tech innovation in agriculture: Hosted the Smart Agriculture Competition to explore cutting-edge tech in agricultural digitization as well as the annual Global Agrilnno Challenge to allow young entrepreneurs to present innovative digital solutions to global agriculture challenges

It’s Official… Comcast Cable Nets Will Forge Their Own Future And Media Consolidation Is A Potential Path

Following recent comments about its intention to explore a spin-off its cable assets, Comcast made it official this week. Overall, the transaction is expected to take ~1 year to complete, but it sounds like the plan is to both build scale while also initiating an “attractive” capital return policy. Does this start the clock on media consolidation? Speculation certainly has emerged.

We detailed the key aspects of the transaction below.

- What assets are being spun-off? NBCU’s cable TV networks, including USA Network, CNBC, MSNBC, Oxygen, E!, SYFY and Golf Channel along w/ digital assets including Fandango and Rotten Tomatoes, GolfNow, and Sports Engine

- What remains? NBCUniversal b-cast and streaming media properties, including NBC and Bravo – which all power Peacock – along with Telemundo, the theme parks business and film and television studios

- Transaction Details –

- Will be a tax-free spin-off / SpinCo will have the same dual-class share structure as Comcast

- Financial impact: Expected to be accretive to revenue growth at Comcast and ~neutral to Comcast’s leverage position

- Do not expect any change to its credit profile or ratings as a result of this transaction

- Timing: Expect to complete the spin in ~1 year

- Who will lead the SpinCo?

- CEO: Mark Lazarus (current Chairman of NBCUniversal Media Group)

- CFO & COO: Anand Kini (current CFO of NBCUniversal and EVP of Corp Strategy at Comcast

- Looking ahead / strategy –

- “Establishing SpinCo as a potential partner and acquirer of other complementary media businesses”

- “We see a real opportunity to invest and build additional scale”

- “Our financial strength will also provide capacity for an attractive capital return policy while allowing for investment in the growth of these businesses”

- Increased operational focus

- What about addtl consolidation? Per sources, the SpinCo will look at merging w/ other cable channels and potentially create its own streaming services to grow after separating from its parent (link)

- Channels specializing in documentaries or food-related shows are among the options to bolster the portfolio

Streaming Sports Hits A New Milestone…Momentum Is Accelerating BUT QoS Can Be A Challenge

In one of our first Weekly Updates at the start of 2024, we laid out our view that sports streaming was hitting an inflection point and that it was just a matter of time until it starts to deliver more attractive reach to sports leagues & advertisers. Fast forward… we are well on our way in this direction, but it has come with some growing pains as streaming platforms are still bolstering infrastructure to be able to handle the huge spikes in traffic demand… (link/link/link)

- During 2023, the Super Bowl LVII broadcast on Fox Entertainment was the most watched telecast, garnering 114.3mn viewers

- BUT two of Amazon Prime’s Thursday Night Football games made the Top 100 most watched US Telecasts list for the first time (though ranked at the very bottom at #98 and #100 w/ 15.3mn and 15mn viewers, respectively).

- In January 2024, Peacock’s NFL AFC Wild Card Game between the Kansas City Chiefs and Miami Dolphins became the most-streamed event in US history, reaching 27.6mn total viewers.

- Last week, Netflix’s Mike Tyson vs Jake Paul match drew 108mn viewers worldwide making it the “most streamed global sporting event ever” per Netflix (the event peaked at 65mn concurrent streams with 38mn concurrent streams in the US); Also, the Co’s streaming broadcast of Katie Taylor vs Amanda Serrano became the most-watched professional women’s sports event in US history, averaging an estimated 74mn live viewers.

- Plus out of home viewing: 1mn+ viewers were estimated to have watched the Netflix fight from over 6k bars and restaurants in the US, per Joe Hand Promotions

-> Given the high viewership levels during the Paul-Tyson livestream, viewers faced several technical issues, including frequent lags, low video resolution, buffering, server connection issues, inability to login to the platform, and more during the livestream, and Downdetector.com reported that there were ~100k reports of disruptions in the service during the broadcast (link)

-> The fight wasn’t the first time Netflix faced technical issues a live event: Last year, the live reunion for S4 of Netflix’s Love In Blind was plagued with glitches and was ultimately made available nearly 24 hours later on the platform as a taped event

- To finish out the year, Netflix will air two live NFL games on Christmas Day 2024, and the Co is bringing in some star power, announcing this week that Beyonce will perform at halftime during the Ravens-Texans game (link)

Overall, we’d expect to see sports broadcasts on streaming platforms rise further up the top telecast list for 2024 but streaming platforms, Netflix in this case, need to continue to ensure quality of service with these live b-casts.

Grab Bag: WBD-NBA Reach Rights Resolution/ TTD Introduces Ventura/ Thanksgiving Weekend Consumer Spend Projections

- Warner Bros Discovery and NBA resolve lawsuit and sign 11-yr global rights deal (link/link): The new rights deal goes into effect next year and will end TNT’s more than three decades as a home for NBA games

- What was the lawsuit? In July, WBD sued the NBA after the league rejected its matching rights and cut WBD out of in its new TV deal, which it has set with Disney’s ESPN as well as Amazon and NBCUniversal

- What are the terms of the new agreement?

- Live NBA telecast rights in the Nordics and parts of LatAm: WBD will carry live telecasts of NBA games in the Nordics (Denmark, Finland, Norway and Sweden), Poland and Latin America (excluding Brazil and Mexico)

- Warner Bros. Discovery will lose rights to the regular and postseason games for its TNT network in the US after this season

- TNT Sports will now televise an exclusive slate of Big 12 football (13 games each season) and men’s basketball (15 games each season) starting with the 2025 season, which it will sublicense from ESPN

- That agreement follows a similar five-year deal the two struck in March to share College Football Playoff games, starting with the current season

- TNT Sports will continue to fully create and produce Inside the NBA and will be distributed on ESPN and ABC

- WBD also plans to develop new content with the talent of “Inside the NBA” for its own platforms

- Expanded global content and highlight rights for TNT Sports, Bleacher Report and House of Highlights, with the ability to produce and distribute NBA content across the WBD portfolio, along with meaningful promotion, sales and creative commitments across both NBA and WBD platforms

- Live NBA telecast rights in the Nordics and parts of LatAm: WBD will carry live telecasts of NBA games in the Nordics (Denmark, Finland, Norway and Sweden), Poland and Latin America (excluding Brazil and Mexico)

- WBD and the NBA confirmed that they have resolved all disputes relating to the NBA’s recent media agreements

- The Trade Desk annc’d Venture, a new TV operating system (link): The Trade Desk will partner with smart TV OEMs and other streaming TV aggregators to deploy Ventura

- Reasoning – existing OS providers have a conflict of interest because they own content, (i.e., Roku, Amazon’s Fire TV and Google’s Android TV) which has muddled the ad ecosystem for everyone, per TTD CEO and founder Jeff Green (link)

- “We’re looking at a concentration around a handful of players that lack objectivity…We think we’re in a unique position to make the ecosystem better”

- NOT competitive to Roku: TTD has a strong ad partnership w/ Roku, and Green believes that Roku’s ad biz will benefit from the stronger ecosystem

- TTD will benefit financially from a more transparent ecosystem b/c it lacks a conflict of interest, per Green: Ventura will be successful if it drives more pricing transparency and stronger measurement for the CTV advertising ecosystem at large; “Ultimately, the measure of success will be, do we have an ad auction that is so transparent that we can predict outcomes?”

- Have “no intention of getting into the hardware business”: Instead, it will partner with other hardware Cos, such as smart TV manufacturers, as well as various television distributors, such as airlines, hotel chains, and gaming companies, to bring its OS to their devices

- Called out “major” benefits of Ventura, including –

- “More intuitive, engaging user experience”, including cross-platform content discovery, personalization, subscription management, and ultimately fewer (more relevant) ads

- “Much cleaner supply chain” for streaming TV advertising, minimizing supply chain hops and costs – ensuring maximum ROI for every advertising dollar and optimized yield for publishers

- Enable advertisers to value and price ad impressions across all streaming platforms more accurately, while finding relevant audiences with greater precision, by incorporating advances such as OpenPath and Unified ID 2.0 (UID2)

- Timeline: Will be rolled out to the market in H2:25

- Reasoning – existing OS providers have a conflict of interest because they own content, (i.e., Roku, Amazon’s Fire TV and Google’s Android TV) which has muddled the ad ecosystem for everyone, per TTD CEO and founder Jeff Green (link)

-> TTD’s stock was up +3.8% on the day of the announcement, while Roku fell -6.7% in reaction

- Consumers are expected to spend $5bn less during Thanksgiving weekend vs last season (link/link): According to a survey from ICSC, consumers plan to spend ~$125bn during the five-day period between Thanksgiving and Cyber Monday vs projections in 2023 of $129.5bn

- Millennials and Gen X shoppers are expected to lead spending, with avg spend amounting to $628 and $629, respectively; Baby boomers are expected to spend an average of $444

- Breakdown of expected spend: 84% plan to spend on holiday gifts for others, followed by spending on dining (76%), other holiday-related items (73%), entertainment and activities (56%), and personal services (56%)

- 57% of shoppers citing deals and discounts as their primary motivators for shopping over the long weekend

- 68% plan to research products ahead of time to find the best deals

- 66% plan to do all or most of their holiday shopping during those five days

- 80% plan to shop on Black Friday and Cyber Monday

- 66% said they will use deals and discounts to stock up on necessary items unrelated to holiday shopping

- Physical stores remain “central” to the shopping experience –

- 88% of respondents said they plan to visit physical stores over the five days

- 82% anticipate visiting a mall or shopping center to shop and take advantage of offerings like dining, entertainment, and holiday experiences

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- OpenAI has recently considered developing a web browser that would combine w/ its chatbot, the Information reported. The Co also has separately discussed or struck deals to power search features. OpenAI has spoken about the search product w/ website and app developers such as Conde Nast, Redfin, Eventbrite and Priceline, the report said, citing people who have seen prototypes or designs of the products. (New York Post)

- Perplexity, an AI-powered search engine, is venturing into e-commerce. The Co debuted a new shopping feature for its paid customers in the US that offers shopping recommendations within Perplexity’s search results as well as the ability to place an order without going to a retailer’s website. W/ the move, Perplexity is taking on Google and Amazon, intending to capture a portion of shopping search results. (TechCrunch)

Artificial Intelligence/Machine Learning

- Amazon is reportedly in discussions w/ several Cos, including Uber, Instacart, and Ticketmaster, to collab on the development of its new AI-powered Alexa. The Co is looking to integrate advanced AI features into Alexa to make the voice assistant smarter and efficient. According to reports, these talks focus on how Cos like Uber and Instacart can enhance Alexa’s capabilities. (LatestLY)

- Biz spending on AI surged by 500% this yr, reaching $13.8bn, per Menlo Ventures. The report also found that OpenAI ceded mkt share in enterprise AI, declining from 50% to 34%. Anthropic doubled its mkt share from 12% to 24%. Meta’s mkt share stayed at 16%, and Cohere’s share remained at 3%. The results came from a survey of 600 enterprise IT decision-makers from Cos w/ 50+ employees. (CNBC)

- Elon Musk’s AI startup, xAI, has been valued at $50bn following a new funding round that raised $5bn. This valuation has doubled since the spring, surpassing the $44bn Musk paid for Twitter. Investors in this round include Sequoia Capital and Andreessen Horowitz2. xAI plans to use the funds to purchase 100,000 Nvidia chips for training AI models. (Business Insider)

- Google’s Gemini chatbot can now remember things like info about your life, work, and personal preferences. As flagged by posters on X (and Google’s official account), a “memory” feature has begun rolling out to certain Gemini users, including this reporter. Like ChatGPT’s memory, Gemini’s adds context to the current conversation. Memory is only available for subscribers to Google’s $20-per-month Google One AI Premium plan. (TechCrunch)

- Microsoft has quietly built the largest enterprise AI agent ecosystem, w/ 100,000+ organizations creating or editing AI agents through its Copilot Studio since launch. This is a milestone that positions the Co ahead in one of enterprise tech’s most closely watched and exciting segments. “That’s a lot faster than we thought, and it’s a lot faster than any other kind of cutting-edge technology we’ve released,” a spokesperson said. (VentureBeat)

- The European Central Bank issued a warning about a potential “bubble” in stocks related to AI, which could burst if investors’ high expectations are not met. This warning was part of the ECB’s Financial Stability Review, highlighting various risks, including geopolitical tensions, and banking system vulnerabilities. The ECB noted that the stock mkt, especially in the US, has become increasingly reliant on a few large AI-focused Cos. (Amwal Al Ghad)

Audio/Music/Podcast

- Spotify is enhancing the audiobook experience for premium users through three new experiments: video clips, author pages, and the ability to add visuals that appear while users listen. These initiatives are part of Spotify’s effort to improve its audiobook offering and bring listeners closer to their favorite authors and stories. One notable new feature is the option for authors or publishers to submit a short video for their audiobooks. (TechCrunch)

Broadcast/Cable Networks

- Nielsen’s Oct 2024 report highlights a significant rise in broadcast viewership, driven by sports and drama programming. Broadcast TV saw a 7% monthly growth, reaching 24.0% of total TV viewing time, its highest share since Jan. This growth marks the third consecutive month of increased viewership, showcasing the strong appeal of sports and scripted dramas to audiences. (Nielsen)

Cable/Pay-TV/Wireless

- Deutsche Telekom is bringing AI Cos into its portfolio and making it available to all customers. Under the name “Magenta AI”, an innovative offer is moving into the MeinMagenta app. This is an answer engine based on AI. Magenta AI offers up-to-date articles in the “Discover” section, which are selected by the AI and can be used to build up knowledge in various areas in a playful way. Magenta AI is launched in cooperation w/ Perplexity. (TELEKOM)

- Orange Egypt showcased its latest digital transformation solutions at the Cairo ICT’24 exhibition. A highlight included the $135mn “New Administrative Capital Data Centre” project, which plays a crucial role in Egypt’s economic and digital transformation. The event, held from Nov 17-20, featured innovations in 5G and AI for smart cities, emphasizing Orange Egypt’s commitment to advancing technological fields. (THEFASTMODE)

- The growth rate of mobile internet users worldwide has slowed significantly, w/ only a 2% increase in 2024 compared to previous yrs. This decel is attributed to mkt saturation in developed regions and economic challenges in emerging mkts. Despite this, mobile internet remains a crucial tool for connectivity and access to information, especially in areas w/ limited infrastructure. (Rest of World)

Capital Market Updates

- Goldman Sachs Chairman David Solomon said there will be more robust levels of both capital raising and M&A in 2025 w/ the new US administration. “Given where we are at the moment, … you’re starting to unleash some of those animal spirits, and you’re seeing a pick-up in equity actuals pick-up in M&A activity,” Solomon said at the Global Financial Leaders Investment Summit hosted by the Hong Kong Monetary Authority. (MarketScreener)

- Madhu Namburi, global chair of technology investment banking at JPMorgan, says there are “~750 quality Cos in tech alone that want to get out,” as he explains why his firm expects a strong return of the IPO and M&A mkts for 2025. He speaks w/ Sonali Basak on “Bloomberg Markets.” (MarketScreener)

Cloud/DataCenters/IT Infrastructure

- Baidu posted a 3% annual drop in Q3 rev, nevertheless beating market expectations amid AI cloud growth. The rev print came in at $4.78bn for the qtr. Net income for the period rose by 14% to $1.09bn. Baidu noted a 12% surge in its non-online marketing rev to the equivalent of $1.1bn, mainly driven by its AI cloud biz. In contrast, online ad spend from SMBs remained weak in Q3 without noticeable improvement in the weeks since, mgmt said. (CNBC)

Crypto/Blockchain/web3/NFTs

- Charles Schwab’s incoming CEO, Rick Wurster, said the Co is looking to offer spot cryptocurrency trading once US regulations make doing so easier – something that’s more likely once President-elect Donald Trump takes office. “We will get into spot crypto when the regulatory environment changes, and we do anticipate that it will change, and we are getting ready for that eventuality,” Wurster, currently Schwab’s president said. (The Business Times)

- Robert F Kennedy Jr made headlines once again w/ his statement that he had “invested most of his wealth” in Bitcoin. The former independent candidate described Bitcoin as the “currency of freedom” in a Nov 16 online post, reiterating the digital asset’s power to hedge against currency inflation. Kennedy has been an outspoken proponent of Bitcoin BTCUSD for some time. (TradingView)

- SEC Chair Gary Gensler will resign on Jan 20, the agency annc’d, paving the way for President-elect Donald Trump to immediately select a replacement. Under Gensler’s leadership the commission has taken an ambitious but controversial approach to several regulatory issues, including cryptocurrencies. Trump has not annc’d his pick to lead the SEC, but the expectation is that the next chair will be friendlier to Wall Street and crypto. (CNBC)

- The UK is set to create an all-encompassing regulatory framework to govern the crypto sector in early 2025. Economic secretary to the treasury Tulip Siddiq confirmed that the new rules would include cryptocurrency and stablecoins, which are pegged against a more stable asset such as a fiat currency. The UK also recently introduced a new bill that, if passed, would give greater legal protections to crypto assets such as Bitcoin and NFTs. (TechCrunch)

- US President-elect Donald Trump wants Cantor Fitzgerald CEO Howard Lutnick, a vocal cryptocurrency enthusiast who has been stablecoin giant Tether’s (USDT) Wall Street banker for years, to serve as his Commerce Secretary, not Treasury Secretary. Lutnick was one of many vying for the powerful Treasury Secretary role, but reports over the past few days suggested his stock had fallen in Trump’s eyes. (COINDESK)

Cybersecurity/Security

- T-Mobile is the latest telecom Co targeted in a Chinese cyber-espionage operation, joining AT&T and Verizon. The “Salt Typhoon” group exploited vulnerabilities, potentially using AI to spy on U.S. officials and access surveillance systems. T-Mobile claims no customer data was compromised but continues to monitor the threat. The breach underscores urgent cybersecurity risks to critical infrastructure. (Cord Cutters News)

eCommerce/Social Commerce/Retail

- Amazon is debuting its Black Friday sales more than a week ahead of the official Black Friday date of Nov 29. Its Black Friday sales event will kick off Nov 21, starting at 12:01 am PST and run through Nov 29, ending at 11:59 pm PST, according to a press release. The sales event is available to Amazon’s Prime membership members, and the Co is already giving peeks at top Black Friday Week deals. (www.retailcustomerexperience.com)

- Charli XCX and H&M hosted a surprise concert, drawing fashion’s “it-girls” to Times Square and then to the Chelsea Hotel. The concert was free and open to any passerby. Fans were given less than an hour’s notice from Charli and H&M to descend upon the center of the city, which was, of course, lit up with Brat green billboards. She performed a 15-minute set, wearing custom pieces by H&M. (L’Officiel USA)