Nvidia’s FQ3 turned into a sell the news event and led to a massive intra-day swing in the major indices on Thursday as investors continue to debate the AI bubble narrative. Per FactSet, Goldman Sachs noted the S&P 500 closing negative after gapping up more than +1.4% at the open has only happened two other times: 7-Apr-20 (after Covid crash) and 8-Apr-25 (following Liberation Day crash). Bitcoin’s free fall was also a main focus this week as well.

Overall, thanks to Friday’s rebound, Nasdaq only fell -2.7% and the S&P 500 was only down -2% (which is still a notable hit but it could have been worse).

With Nvidia and Warner Music Group results bringing up the rear of TMT earnings, we did take a look at the aggregate sector performance during the results season relative to expectations (see Theme #1).

The key themes/developments that we focus on this week include:

- Q3 Earning Wrap: TMT Beats Expectations But To A Lesser Degree

- It Was A Sell The News For Nvidia & The Market…The AI Bubble Debate Continues

- WMG Enters F2026 On A Stronger Note

- Despite AI Angst, Innovation & Investment Continues To Push Forward At A Record Pace

- Media M&A Remains Front & Center As Potential Deals Expand

- New 13-F Filings Show That Tech Moved Back Into Favor During Q3

- Grab Bag: More Sports Media Deals / More Entrants Into Prediction Mkts? / Live Nation & StubHub Take A Hit As UK Plans To Ban Ticket Reselling

Have a nice weekend.

Best,

Leslie

Q3 Earning Wrap: TMT Beats Expectations But To A Lesser Degree

As we have finally reached the end of the Q3 earnings season (stragglers this week were Nvidia and Warner Music Group…see Theme #2 and Theme #3, respectively), we looked across our LionTree TMT and Consumer Universe of ~200 companies covering 37 sub-sectors with market caps of $1bn+ to evaluate financial performance relative to Wall Street projections.

Overall, while the vast majority of companies in our Universe beat Q3 expectations on both sales and profitability, the percentage that beat eased from last qtr. More specifically, on profitability, 80% of companies beat consensus Q3 projections but this was down from 83% in Q2, and on sales, 74% of companies topped estimates, which was down from 78% in Q2.

What was the Street’s reaction to these results? It was neutral, with 50% of companies trading up in reaction to results and 50% trading down.

See below for more on Q3 financial and stock performance of companies within our LionTree Universe of TMT and Consumer stocks relative to Street expectations.

It Was A Mixed Bag Stock Performance-Wise With 50% Of Companies Trading Up and 50% Trading Down In Reaction To Q3 Results

It was 50/50 with the number of companies that traded up and the number of companies trading down in reaction to results, BUT more companies traded up double-digits than traded down double-digits.

Top 3 Best & Worst Performers In Reaction To Q3 Results…

Fewer Companies BEAT Q3 Expectations But It Was Still The Majority

- Take Two, Roblox, & Palantir had the largest % beats in sales

- Overall, 74% of Cos in our LionTree Universe beat cons on revenue (down from ~78% in Q2)

- Only 1.4% of those companies beat by double digits, down from 5% in Q2

- Though the median sales beat rose to +3%, up from +2.3% in Q2

- Sonos, iQIYI, and Liberty Braves Group had the largest % beats on adj EBITDA

- Overall, 80% of companies in our Universe beat consensus on adj. EBITDA, (vs 83% in Q2) and 34% had double-digit beats (down from 39% in Q2)

- However, the median adj EBITDA beat rose to +8%, up from +6.2% in Q2

More Companies MISSED Revenue Expectations In Q3…

- Lions Gate, DraftKings, and Mattel had the largest % misses on sales

- Overall, 26% of the companies in our Universe reported sales in-line/lower than consensus, up from 22% in Q2

- FuboTV, Clover Health, and JD.com had the largest % misses on adj EBITDA

- Overall, ~16% of the companies in our Universe were in-line or missed consensus on adj. EBITDA, down from ~17% in Q2

It Was A Sell The News For Nvidia & The Market…The AI Bubble Debate Continues

Whether we are, or are not, in an AI bubble has been causing a lot of angst and volatility in the market and while Nvidia’s FQ3 results and guidance topped Street estimates and CEO Jensen Huang addressed that concern on the Co’s Wednesday evening earnings call, it was not enough. What did he say? “There’s been a lot of talk about an AI bubble” but “from our vantage point, we see something very different.” He highlighted three simultaneous platform shifts that are currently happening instead – 1) the move from CPUs to accelerated computing, 2) the transition from classical machine learning to generative AI, and 3) the emergence of agentic AI. Each shift is expanding workloads, accelerating adoption, and driving entirely new categories of demand, and GPU deployments are broadening beyond hyperscalers into enterprises, industries, and sovereigns.

Digging more specifically into the Co’s results, FQ3 revenue set a new record and guidance for FQ4 was above estimates. Gross margins held in the mid-70s, a level they expect to sustain next yr despite rising component costs, thanks to continued mix benefits, faster production cycles, and NVIDIA’s ability to tightly manage a highly complex supply chain amid demand that remains consistently above plan. They reiterated that the Co remains “on track” for ~$500bn in revenue from Blackwell and Rubin over 2025–2026, and they may even top that given continued strength in the order pipeline.

So overall, it was a solid quarter but expectations were high and when the stock started to faulter, it turned into not only a sell the news for Nvidia, but a sell the news on the broader tech market. The AI bubble debate is far from over, but in the meantime, AI developments/innovation remain in full force (see Theme #4).

See below for what we viewed as most important regarding Nvidia’s FQ3 results.

-> Nvidia was initially up ~5% post earnings but ultimately fell -3.2% post earnings due to broader market concerns around AI and took the market down with it; With that said, the stock continues to outperform YTD it is up +33%

NVIDIA Tops FQ3 Street Expectations

- FQ3 total rev was another record: Saw “record” seq growth of +22% (vs +6% q/q in Q2) and was also accelerated to up +62% y/y (vs +56% in Q2)

- “Record” Data Center rev (90% of total rev) beat: Grew +66% y/y (vs +56% in Q2) and beat estimates by +4.4%

- ProViz and OEM & Others revs also beat by +25.2% and +8.7%, respectively, while Gaming and Automotive & Robotics missed by -2.7% and -4.1%, respectively

- Non-GAAP gross margin came in slightly ahead @ 73.6% vs cons 73.4%

- Increased seq due to Data Center mix, improved cycle time, and cost structure

- Non-GAAP op income was up +62% y/y (vs +51% y/y in Q2) and also beat cons by +4.1%

- Non GAAP op margin of 66.2% easily beat cons 65.7%

- Adj EPS of $1.30 beat cons $1.26

- However, FCF of $22.1bn was well below cons $27.5bn

FQ4 Guidance Was Also Ahead Of Projections

- FQ4 rev – BEAT: $65bn +/- 2% vs cons $62.2bn

- Implies +14% q/q growth at the midpt, driven by continued momentum in the Blackwell architecture (not assuming any Data Center compute rev from China, similar to last qtr)

- FQ4 non-GAAP gross margin – BEAT: 0% vs cons 74.1%

- FQ4 non-GAAP OpEx – HIGHER: $5.0bn vs cons $4.58bn

- Expect to hold margins in the mid-70s for both this yr and next

- For this yr, they improved costs and product mix enough to push gross margins into the mid-70s, and expect to end the year there

- For next yr, some component costs across the industry are rising, but the Co plans to offset those through more cost improvements, faster production cycles, and product mix

- Non-GAAP OpEx is guided to grow to ~$5bn in FY27

- Nvidia has a new architecture coming out that will require cont’d investments in engineering, software, and systems, etc.

- NVIDIA could generate ~$500bn in FCF over the next couple of yrs – how would they use it?

- Cash for funding growth and supply chain

- Stock buybacks

- Ecosystem investments (i.e. invested in OpenAI, Anthropic, etc.)

Mgmt Highlighted That “The World Is […] Undergoing Three Massive Platform Shifts At Once”

- “There’s been a lot of talk about an AI bubble. From our vantage point, we see something very different”

- Shift #1: CPUs -> GPUs

- Traditional computing is moving from CPUs to GPU-accelerated computing because CPUs aren’t getting much faster anymore (Moore’s Law slowing)

- “The transition to accelerated computing is foundational and necessary, essential in a post-Moore’s Law era”

- Shift #2: Classical ML -> GenAI

- GenAI is replacing older machine-learning systems in things like search ranking, recommender systems, ad targeting, etc.

- “The transition to generative AI is transformational and necessary, supercharging existing applications and business models”

- Shift #3: GenAI -> agentic AI

- New AI systems can reason, plan, use tools, and act (like coding assistants, legal AI, medical AI, self-driving, etc.)

- “The transition to agentic and physical AI will be revolutionary, giving rise to new applications, companies, products and services”

- “NVIDIA is chosen because our singular architecture enables all three transitions”

AI Infrastructure Demand Refuses To Relent Across Generations

- Demand for AI infrastructure “continues to exceed expectations”…

- Clouds are sold out

- GPU installed base, both new and previous gens, including Blackwell, Hopper, and Ampere, are fully utilized

- …and expect $3tn-$4tn in annual AI infrastructure build estimates by end of 2030 for which NVIDIA will be the “superior choice”

- Blackwell “gained further momentum” in FQ3, as GB300 crossed over GB200 and contributed ~2/3 of total Blackwell rev

- Transition to GB300 has been “seamless”

- Hopper recorded ~$2bn in rev in FQ3 (but could have been more if China orders had materialized)

- H20 sales were ~$50mm

- Sales “disappointed” due to missed oppty in China: “Sizable” purchase orders never materialized in the qtr “due to geopolitical issues and the increasingly competitive market in China”

- BUT “committed to continued engagement with the US and China governments and will continue to advocate for America’s ability to compete around the world”

- Some addtl color on Rubin CPX product which is “on track” to ramp in H2:26

- Designed for “long context” type of workloads: Tasks where AI must read and absorb large amounts of data (PDFs, videos, 3D images, etc.) before generating an answer

- Has “excellent” performance per dollar and per watt

- Remain “on track” for $500bn of rev from Blackwell and Rubin AI chips for CY 2025 + 2026 (and there’s a chance they may top that)

- Shipped $50bn in FQ3

- Demand is strong enough that they’ll probably exceed it

Some Additional Color And Commentary

- Currently ~40% of shipments are tied to AI inference but see oppty ahead to scale even more

- “Our leadership there is surely multiyear” – Grace Blackwell and the NVLink 72 network deliver 10–15× higher performance than competitors and “It’s going to take a long time before somebody is able to take that on”

- There is no single bottleneck that will constrain growth…despite supply chain constraints given NVIDIA’s scale, emphasized the Co has strong planning, control, and partnerships to manage it

- “We have great partners that we’ve worked with for 33 years… We plan up the supply chain, down the supply chain. We have established a whole lot of partners. And so, we have a lot of routes to market.””

- Are custom AI chips a threat to NVIDIA? No, workloads are now so diverse and system-level that only NVIDIA’s full-stack GPU platform (which can “run every single model”) can support them

- Modern AI systems require entire integrated computing systems (racks, networking, memory, software), not just chips

- Custom AI chips may work for narrow tasks, but they can’t handle the complexity, variety, or rapid evolution of AI the way NVIDIA’s architecture can

WMG Enters F2026 On A Stronger Note

After a tough first half, Warner Music ended its FQ4 with strength, posting its strongest quarterly top-line growth rate (+13% y/y) in nearly two years, and surprising the Street with an +11% revenue beat and an +8% adj OIBDA beat. This level of growth reflected nice sequential improvement from +7% y/y last qtr, driven by a sharp rebound in recorded music streaming and a 64% surge in artist services as WMX leaned into merch campaigns for legacy acts. The only area that analysts harped on was a drop in adj OIBDA margins y/y but that was due to a mix shift to lower margin other services revenues.

After reorganizing and investing in its core music business, the Co retook market share (+0.6ppts in the U.S., and similar trends globally) and looking into fiscal 2026, mgmt. expects a year of “strong” top line growth. That will be underpinned by 1) price increases in calendar 2026 given that the Co locked in new wholesale price hikes across four of the five largest DSPs; 2) a robust pipeline of “accretive“ M&A; and 3) a contribution from adjacent areas such as distribution & DTC offerings.

On the cost side, despite the FQ4 miss on adj OIBDA margins, mgmt. is confident in its margin accretion guidance of +150–200bps in FY26. They get there by 1) accelerating their high-margin streaming business; 2) increasing prices which improves margins; 3) finalizing M&A with higher-margin, accretive businesses; and 4) staying on track with their cost-saving plan (will deliver $200mn of savings in fiscal 2026 and up to $300mn in fiscal 2027… and savings will increase sequentially through the year). Mid-to-long term, the Co is targeting margins in the mid-to high 20s.

Lastly, there was a lot of focus on potential AI disruption on the conference call but the Co instead sees AI as incremental upside, with licensing deals already in place and opt-in protections for artists. Mgmt believes that history favors incumbents who adapt. Net net, the Co is entering FY26 with more visibility given the pending price increases, identifiable accretive M&A, and a strong release slate. Executing on the margin accretion narrative will also be key, as will growing distribution. The AI risk question is likely to persist until we have a clearer picture of the industry impacts.

-> WMG shares fell -2.7% (but also due to the market sell-off on Thursday) and the shares are still up +1.4% YTD

Big BEAT On FQ4…WMG Accelerates Top & Bottom-Line Growth

- FQ4 total revs beat cons by 11.3% and adj OIBDA beat cons by 8%

- Total revs grew +13% y/y, the highest y/y growth in nearly two years and vs +7% y/y in FQ3

- Reflects seq improvement in recorded music streaming growth and 64% growth in artist services as WMX led merch campaigns for Oasis and My Chemical Romance

- Adj OIBDA grew +12 y/y

- Only disappointment was on margins (due to higher low margin other service revenue mix)

- Total revs grew +13% y/y, the highest y/y growth in nearly two years and vs +7% y/y in FQ3

- Recorded music subscription streaming revs rose +8.4% y/y on an adj basis vs +8.5 y/y on adj basis in FQ3

- Due to subscriber growth and market share performance

- Ad supported streaming revs grew +3% y/y on an adj basis vs -2% y/y on adj basis in FQ3

- Due to performance of their music and the timing of certain DSP payments

- Music publishing revs grew +13% y/y (vs +9.4% y/y in FQ3), driven by double-digit growth across performance, mechanical and sync

Over The Year, The Co Has Focused & Simplified Its Organization And… “It Has Been Working”

- The Co is fostering closer collaboration and alignment between Atlantic and Warner Records in the UK and their counterparts in the US

- Organized operations in Italy into two frontline labels, Atlantic and Warner Records, mirroring the label structure in the US and the UK

- Unified Australasia and Southeast Asia businesses to create bigger opportunities in this region

- Streamlined operations and strengthen the impact for artists in Central Europe by merging Benelux with Germany, Switzerland and Austria

- Also modernized the infrastructure: Including strengthening the global digital supply chain, implementing tools to help artists and songwriters make faster, smarter, data-driven decisions about their careers, as well as tools for employees to be better informed and more effective

Posted A “Notable” Improvement In Market Share in H2 Across Flagship Labels & Key Regions…

- US market share incr’d +0.6ppts y/y (per Luminate), and the Co saw “similar improvement” around the world in EMEA, LatAm and APAC

- The Co also has a higher new release mkt share at Atlantic and posted a “jump” in global catalog share…global share of Spotify Top 200 rose +6 ppts vs fiscal 2024 and for the entire qtr the Co had #2 market share

- What are you doing differently? The share improvements were driven by cont’d focus on artist development, also their focus on distribution and catalog

New Deals With Top DSPs Include Higher Wholesale Pricing, Which Goes Into Effect In Cal 2026

- Since the start of 2025, WMG signed renewals with 4 of the largest 5 DSPs

- All deals have wholesales price increases and include monetization models for future use cases

- The price increases will go into effect in calendar 2026

- There’s much more standardization in place with their DSP deals than was the case in the past

- The price increases will help drive revenue growth and margins

Mgmt Is Confident In Accretive M&A in 2026

- Mgmt is “committed to driving incremental growth and value creation through accretive M&A”

- The Co has a “robust” deal pipeline and “will share updates in the near future”, including via the JV with Bain

- They are focused on a few large opportunities where they, as a publisher, can add value in a way that creates value not just for artists and songwriters, but also in a way that delivers a strong return for them

- The key focus is their catalog business as they are highly accretive and will do it in a capital efficient way

- Very confident M&A can help accelerate growth

“Tremendous Opportunity” To Accelerate Growth In Distribution & Direct-To-Consumer

- Distribution is a big focus: Brought on new leadership and have been spending time building new capabilities that enable them to provide better customer service but also to integrate clients faster and more efficiently, so that “we can grow this business profitably”

- Think growth will accelerate here in 2026

- There are “opportunities to capitalize on the passionate demand from fans all over the world for physical music and direct-to-consumer offerings”

- Other drivers to future growth: Premium offerings from DSPs and AI is an opportunity

- “See tremendous potential in new incremental growth areas, particularly in AI licensing deals, which we plan to discuss in future calls”

Overall, Mgmt Is Bullish On Fiscal 26…Expects Strong Top-Line Growth & Despite FQ4 Lower Y/Y Margins, Remains Confident In Margin Accretion Going Forward

- Excited about the forward slate

- In Q1: Will have new albums from Fred Again, FkA Twigs, Not for Radio, Aya Nakamura and Robert Plant, along with deluxe album additions from Ed Sheeran, Cardi B and PinkPantheress…also have new singles from Charli xcx, Charlie Puth, Jisoo, Hilary Duff, Ciesco. Alex Warren, David Guetta, Anthony Spence and more…

- Expect “strong” top line growth in fiscal 2026…which will be driven by price increases, M&A as well as contribution from adjacent areas such as distribution & DTC offerings (mentioned above)

- Any more color on streaming growth expectations? “These [FQ4] results are pretty much reflective of what we should expect in the first quarter of 2026”

- “Very very comfortable” in the margin accretion guidance in fiscal 2026 of +150-200bp of adj OIBDA margin improvement

- What gets them there?

- Will accelerate high margin streaming business

- Higher prices will help margins

- Envision M&A with higher margin accretive businesses

- On track with cost saving plan (will deliver $200mn of savings in fiscal 2026 and up to $300mn in fiscal 2027… and savings will increase sequentially through the year)

- What gets them there?

- Long term margin targets? In the mid-to long term, targeting margins in the mid-to high 20s

- “Over time, the adj OIBDA will approach the adj EBITDA margins to the mid-20s and then we’re starting to maintain and grow margins”

- FQ3 operating CF conversion was 12% but mgmt continues to target 50-60% over a multi-yr period

There Was A Lot Of Analyst Focus On AI (Won’t It Negatively Impact?)…But Mgmt Is Leaning In & Views It As An “Incremental” Opportunity

- Generative AI is “an incremental opportunity because the past has shown us that changes like this always create one”

- See AI as the “democratization of creation” … and they “need to be proactive and lean in”

- BUT the Co will only make agreements w/ partners who commit to licensed models and if they can secure economic terms that “properly reflect the value of music”; The deal terms are tied to usage and revenue growth

- The Co has already done deals with partners like Audio, Stability AI and Clay along these lines

- Also, their artists and songwriters will have a choice to “opt in” to any use of their name, image, likeness or voice in new AI generated songs

- Why not a threat? “With every change, every technology change, there’s always a threat and an opportunity. The market position and distribution was a threat. Everybody was predicting our demise and sidestepping the major music companies. And obviously the opposite has proven to be true over time. And we believe the same happens here”

Despite AI Angst, Innovation & Investment Continues To Push Forward At A Record Pace

In the midst of all the focus and debate regarding a potential AI bubble given Nvidia’s results (see Theme #2) and also other cautionary comments from the likes of Alphabet CEO Sundar Pichai that added fuel to the fire this week, there was still an impressive array of key updates and innovations across the space this week that we wanted to highlight. More specifically, there was a wave of major product launches, strategic partnerships, and funding announcements from the sector’s biggest players. Google unveiled Gemini 3 and a broad suite of new AI capabilities spanning search, coding, imaging, and travel; Meta introduced SAM 3 and SAM 3D for next-generation content manipulation; Cloud and semiconductor giants deepened their ties with Anthropic; and xAI pursued another multibillion-dollar raise.

See more details below.

In Contrast To Nvidia CEO’s Positive Comments On AI Demand (See Theme #2), Alphabet’s CEO Makes Cautionary AI Bubble Comments This Week…

- Alphabet CEO Sundar Pichai made several cautionary AI comments during an exclusive BBC interview

- While the growth of AI investment has been an “extraordinary moment”, there is some “irrationality” in the current AI boom

- Will Google be immune to the AI bubble burst? “I think no company is going to be immune, including us”

- For the first time, he also said Google would “over time” take a step to “train our models” in the UK

- “We are committed to investing in the UK in a pretty significant way”

- However, he also warned about the “immense” energy needs of AI, which made up 5% of the world’s electricity consumption last year, according to the International Energy Agency

…But At The Same Time, Google Announces “A New Era Of Intelligence” w/ The Launch Of Gemini 3

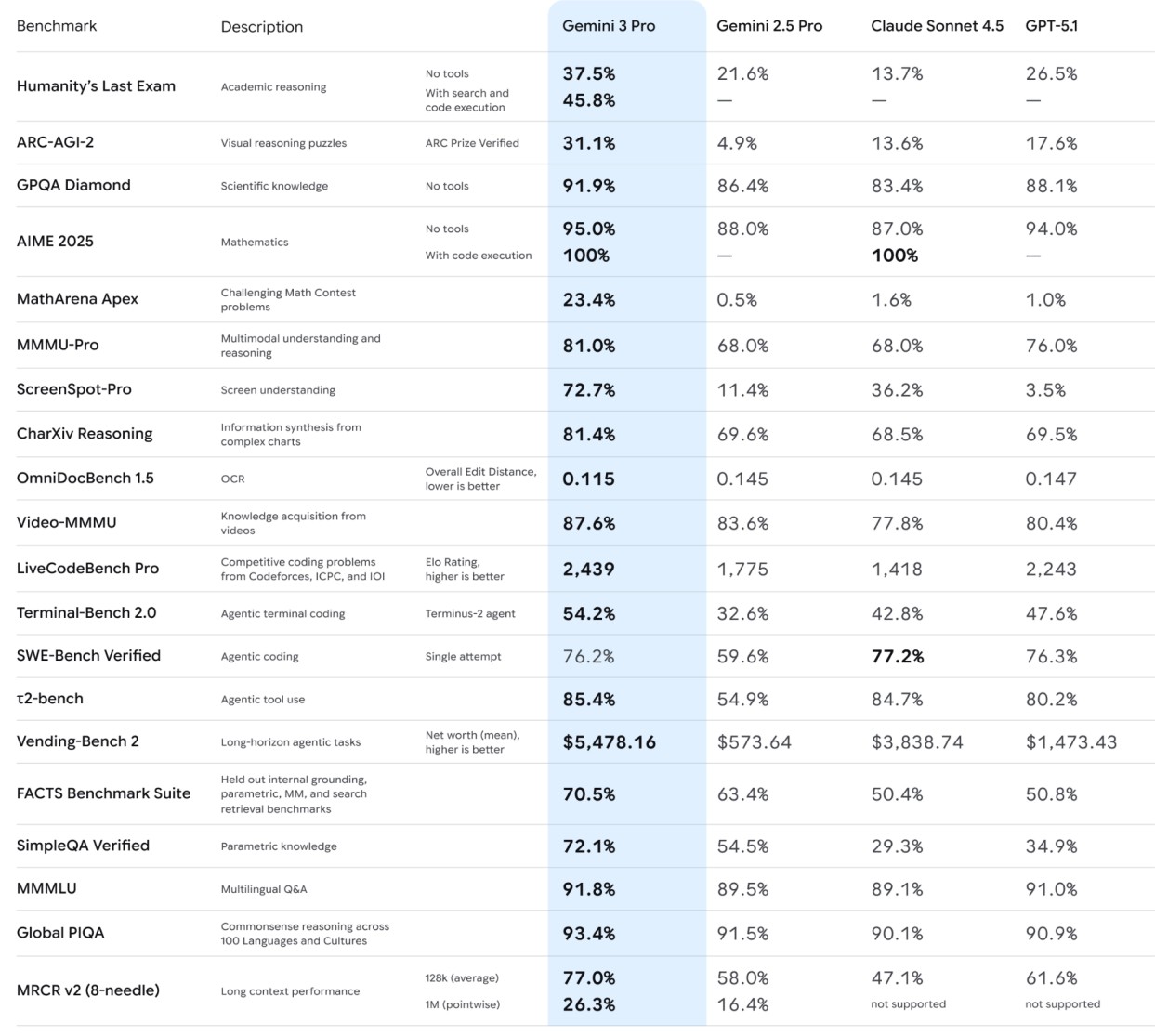

- Google’s new Gemini 3 Pro (rolled out Tues) topped the boards against other competing models

- Gemini 3 Pro also introduces Deep Think

- It achieved an unprecedented 45.1% on ARC-AGI-2, demonstrating its ability to solve novel challenges

- Other key features include:

- Learn: Generative UI

- The Co highlighted learning capabilities that can decipher a handwritten family recipe or even analyze people’s pickleball matches and make suggestions to improve

- AI Mode in Search now uses Gemini 3 to enable new generative UI

- These experiences include immersive visual layouts and interactive tools and simulations

- Build: Google Antigravity

- You can now build with Gemini 3 in Google AI Studio, Vertex AI, Gemini CLI and their new agentic development platform, Google Antigravity

- It’s also available on third-party platforms like Cursor, GitHub, JetBrains, Manus, Replit and more

- Plan: Gemini Agent

- A new tool that orchestrates and completes multi-step tasks on people’s behalf, rolling out to Google AI Ultra members first

- Learn: Generative UI

- Google also released Nano Banana Pro

- This is the updated version of the Co’s generation and image editing model

- The platform uses advanced reasoning from Gemini 3 to provide images with real world facts and real time information

- The Co also said that the model is “best” for creating images with text directly rendered on them, and can blend up to 14 single images into one

- Nano Banana Pro is available in the U.S. for Google AI Pro and Ultra subs

- This is the updated version of the Co’s generation and image editing model

- Google’s Gemini app now has 650mn MAUs and AI Overviews has 2bn MAUs

- As a comparison, OpenAI said in Aug that ChatGPT hit 700mn weekly users

- ~70% of their Cloud customers use their AI, 13mn developers have built with their generative models

Google Also Pushes Harder Into Travel & Coding

- Google annc’d Canvas this week as part of its AI Mode features in Search and Gemini: It gives you a place to organize plans and can be used to build travel plans that are customized for specific needs

- How does it work?

- Once asked, you’ll get a plan in the Canvas side panel that brings together real-time Search data for flights and hotels

- You also get details from Google Maps like photos and reviews and relevant information from sites across the web

- To refine the plan and make it your own, you can ask follow-up questions, like choosing a hotel that’s closer to brunch but a bit further from hiking trails

- Travel planning with Canvas is available on desktop in the U.S. for those opted into the AI Mode experiment in Labs

- How does it work?

- The Co also annc’d the expansion of Flight Deals

- What is it? An AI-powered search tool within Google Flights that recently launched in the U.S., Canada and India

- It’s designed for flexible travelers who want to quickly find affordable destinations and save money on their next trip

- To get started, just describe where, when and how you’d like to travel

- Flight Deals has started rolling out to 200+ countries and territories worldwide, including the U.K., France, Germany, Mexico, Brazil, Indonesia, Japan and Korea

- What’s next?

- They are working to make it possible to finish booking flights and hotels directly in AI Mode

- What is it? An AI-powered search tool within Google Flights that recently launched in the U.S., Canada and India

- Coding was also at the center of attention with Google’s announcement of Antigravity: It supports multiple agents and gives them direct access to the editor, terminal, and browser

- One of the key components of Antigravity is how it reports on its own work

- As it completes tasks, it will produce Artifacts: Task lists, plans, screenshots, and browser recordings that are intended to verify both the work it’s done and what it will do

- Antigravity’s other big change is that it offers two main usage views

- The default Editor view and the new Manager view

- Manager is designed for controlling multiple agents at once, allowing each to work more autonomously

- Antigravity is available in a public preview now, compatible with Windows, macOS, and Linux

- It’s free to use, with what Google calls “generous rate limits” for Gemini 3 Pro, though it also supports Claude Sonnet 4.5 and OpenAI’s GPT-OSS

- One of the key components of Antigravity is how it reports on its own work

Meta Annc’d SAM 3 and SAM 3, Their AI Content Manipulation Tools

- What is it & how does it work?

- SAM 3: Enables detection and tracking of objects in images and video using text and visual prompts

- SAM 1 & 2 were focused on visual prompts while 3 added text

- SAM 3D: Enables 3D reconstruction of objects and people based on a single image

- SAM 3D Objects enable object and scene reconstruction

- SAM 3D Body enables human body and shape estimation

- Currently being implemented on Facebook marketplace so customers can virtual see items in their home before buying

- You can experiment with both models now on their new platform, Segment Anything Playground

- SAM 3: Enables detection and tracking of objects in images and video using text and visual prompts

Another Circular Funding Deal Was Also Annc’d This Week

- Microsoft, NVIDIA and Anthropic annc’d new strategic partnerships: Anthropic is scaling its Claude AI model on Microsoft Azure, powered by NVIDIA

- This will broaden access to Claude and provide Azure enterprise customers with expanded model choice…this partnership will make Claude the only frontier model available on all 3 of the world’s most prominent cloud services

- Anthropic committed to purchase $30bn of Azure compute capacity and to contract additional compute capacity up to one gigawatt with NVIDIA Grace Blackwell and Vera Rubin system

- Microsoft committed to continuing access for Claude across Microsoft’s Copilot family, including GitHub Copilot, Microsoft 365 Copilot, and Copilot Studio

- As part of the partnership, NVIDIA and Microsoft are committing to invest ~$10bn and ~$5bn respectively in Anthropic

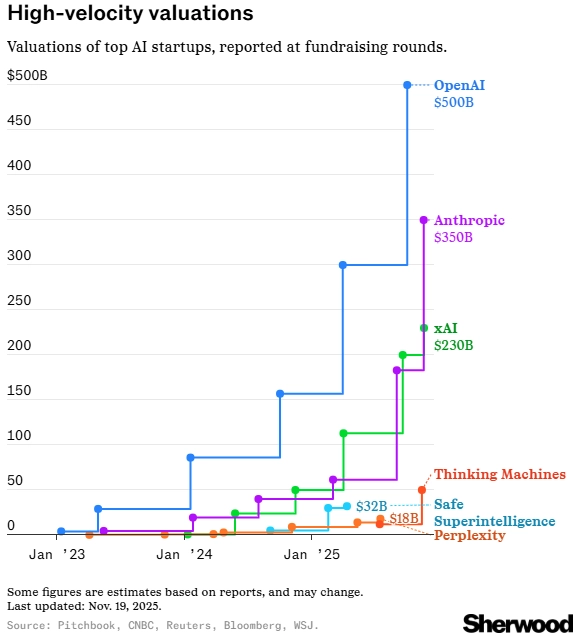

- Anthropic is valued in range of $350bn following the deal (more valn updates are below)

More Data Centers Were Also Annc’d As AI Valuations Continue To Skyrocket

- xAI annc’d a new data center project in Saudi Arabia

- Musk said the 500-megawatt data center for xAI would be powered by Nvidia’s computing chips

- In comparison, xAI’s Colossus 1 data center in Memphis represents ~300 megawatts of computing power

- xAI is reportedly in advanced talks to raise $15bn at a $230bn val’n, per WSJ

- The new val’n would more than double xAI’s $113bn it disclosed when it merged with CEO Elon Musk’s social-media platform X back in March

- A report from back in Sept found that Grok had 64mn monthly users, vs ChatGPT’s 800mn weekly users

Sources: BBC 11/19, Business Times 11/19, Google Press Release 11/18, CBS 11/20, CBS 11/18, WSJ 11/19, Yahoo Finance 11/16, Sherwood 11/19, The Verge 11/18, Meta Press Release 11/19

Media M&A Remains Front & Center As Potential Deals Expand

Outside of AI, this week was dominated by updates on the theme of Media M&A, led by developments in the Warner Bros. Discovery sale process, with multiple bids now reportedly in and shaping investor expectations around one of the largest potential media transactions in years. Paramount Skydance, Comcast, and Netflix all reportedly submitted offers, ranging from full-company acquisitions to targeted bids for film and streaming assets. However, the emerging bid dynamics come against the backdrop of heightened regulatory scrutiny, including early antitrust concerns around Netflix’s involvement. WBD is reportedly targeting a mid- to late-December completion of the process, setting up a potentially decisive end-of-year window for one of the industry’s most closely watched M&A situations.

At the same time, consolidation pressures are surfacing across the broader legacy media ecosystem. Sinclair disclosed an 8.2% stake in E.W. Scripps and said scale is increasingly necessary in the broadcast TV industry to compete against other media and tech Cos. Starz is also exploring a potential tie-up with A+E to bolster its streaming library. Even the advertising sector is potentially consolidating further: WPP has reportedly attracted takeover interest from strategic rivals, including internal discussions at Havas, driving WPP shares up double digits despite the very early stage of talks.

See more details on this key theme below.

First Round Bids For Warner Brothers Discovery Are Reportedly In

- Paramount Skydance, Comcast and Netflix have reportedly all submitted non-binding bids for all or parts of Warner Bros. ahead of Nov 20th first-round offer deadline

- Comcast reportedly bid just for the film and streaming assets: The offer would reportedly see NBCU become the parent of the WBD assets and is not expected to involve a spinout of NBCU as some had speculated

- Similarly, Netflix also reportedly bid solely for the film and streaming assets, and included that it would continue releasing WBD movies in theaters

- Netflix’s offer was expected to be “disciplined”

- But antitrust concerns were already raised before the bid was even submitted – on Nov 13th, Darrell Issa (R-CA) sent a letter to Trump officials saying that a Netflix acq could harm consumers

- “With more than 300mn global subs and a vast content library, Netflix currently wields unequaled market power”

- “Adding both HBO Max’s subs and Warner Bros.’ content rights would further enhance this position, reportedly pushing the combined entity above a 30% share of the streaming market: a threshold traditionally viewed as presumptively problematic under antitrust law”

- Meanwhile, Paramount Skydance submitted its reported fourth bid to date for the entire Co

- Its most recent bid was reported to be $23.50/shr (80% cash, 20% stock), which WBD rejected

- According to recent reports, WBD is looking to get at least $30/shr: That would value the Co at $74.34bn, which is up from Paramount’s offer of $58.23bn

- There was also speculation that Paramount held early talks with Middle Eastern sovereign-wealth funds about forming an investment consortium, but the Co denied it

- The Co was reportedly tying up with the sovereign wealth funds of Saudi Arabia, Qatar and Abu Dhabi

- ““The information Variety published is categorically inaccurate,” a rep for Paramount Skydance said in a statement. “This is a confidential process, which we respect and, as such, will not be commenting until the process is over.””

- What comes next? Another round of bids is expected to occur in the coming weeks when bidders will be asked if they want to submit final, binding offers

- WBD is reportedly aiming to have the sales process wrapped by mid- to late- December

It Wasn’t Just The Conglomerates…Other Instances Of Consolidation Across The Media Names Emerged This Week

- Sinclair is building its stake in E. W. Scripps as it pushes for a potential takeover deal

- Back in August, Sinclair said its board signed off on a strategic review of its broadcast biz, which included examining potential sales and acquisitions.

- Soon after, Sinclair proposed merging its broadcast TV biz w/ Tegna BUT Tegna ended up agreeing to sell to Nexstar ($6.2bn all cash deal)

- In a filing on Monday (Nov 17th), Sinclair disclosed that it has taken an 8.2% stake (~$15.6mn) in E.W. Scripps’ Class A shares as it pushes to combine with the smaller broadcaster

- Sinclair, the third-largest local broadcast Co in the US, has ~185 local stations across the country while E. W. Scripps owns ~61

- Also in the filing, Sinclair said it has engaged in “constructive discussions” with Scripps “for several months regarding a potential combination of the two companies”

- It believes scale, at both the national and local levels, is increasingly necessary in the broadcast TV industry to compete against other media and tech Cos

- Sinclair estimates Scripps’s investors could have the value of their shares triple over time if the two combined

- Also, based on trading multiples, Sinclair has calculated an expected $300mn in synergies if a merger were to take place

- It has structured its takeover proposal to require no external financing, with the goal of bringing down Scripps’s debt load

- And they believe a deal could close within 9-12 mos

- But E. W. Scripps doesn’t seem to be on receptive

- In a statement that same day, Scripps said its board “will take all steps appropriate to protect the company and the company’s shareholders from the opportunistic actions of Sinclair or anyone else”

- BUT the board continues to evaluate “any transactions and other alternatives that would enhance the value of the company and would be in the best interest of all company shareholders”

- Broadcasters are taking advantage of what could be a potentially more favorable regulatory environment

- Sinclair is among broadcasters who have pushed the FCC to relax rules that prohibit a broadcaster from owning TV stations that reach more than 39% of the US TV households

- FCC Chairman Brendan Carr has been public about his belief that restrictions should be loosened, and many expect that ownership cap to be removed in 2026

-> E. W. Scripps jumped a massive +40% on the day of the filing, while Sinclair was up +5%

- Starz is reportedly interested in acquiring A+E

- A+E, which is jointly owned by Hearst and Walt Disney Co., put itself on sale earlier this yr

- Starz has reportedly expressed interest in buying some or all of A+E Global Media

- Execs from both Cos have reportedly held informal talks about a possible tie-up, which would likely involve Starz making an offer and not the other way around

- BUT talks reportedly haven’t progressed very far as A+E is holding out to see if it can get bids from a larger entity

- Both Starz and A+E have very different content: While Starz primarily focuses on premium scripted shows and movies, A+E has historically leaned into fact-based documentaries and reality-based series

-> Starz’s stock was up +11% after the report hit

Plus More Consolidation May Be Happening Amongst The Advertising Agencies…This Time WPP Is At The Center Of Discussions

- WPP is reportedly attracting takeover interest, from both competitors and PE firms

- For some background, WPP is currently valued at ~£3bn, down from a peak of £24bn in 2017

- Havas, considered to be a French rival to UK-based WPP, is reportedly holding internal talks about a potential bid for the Co

- The two sides are reportedly in “very serious” discussions centered on how to value WPP and suggest that Havas was looking at a minority stake in the biz vs a full merger

- Despite its recent step backs, WPP still dwarfs Havas: WPP has 110k employees and a $4.1bn market cap vs Havas’s 23k employees at $1.6bn market cap

- PE firms Apollo and KKR have also reportedly taken a look at WPP’s assets

- But there are some reports that Apollo has ruled out making a bid

- Also, as a reminder, KKR acquired WPP’s PR operation FGS Global last yr

- Where do things stand now?

- Bidders could seek to buy the Co in its entirety, take large stakes in the Biz or attempt to pick off parts of the holding group

- That said, it is not clear whether any formal bids for WPP will actually materialize

-> WPP’s stock rose as much as +13% on the back of the speculation; The stock has had a tough run, down -61% YTD

Sources: Bloomberg 11/16, Cord Cutters 11/17, Hollywood Report 11/17, MediaPost 11/16, Variety 11/20, Media Play News 11/20, TIPRANKS 11/20, New York Post 11/18

New 13-F Filings Show That Tech Moved Back Into Favor During Q3

Just as Q3 TMT earnings was coming to a close last week, the new 13F ownership changes were filed as well and we finally had a chance to take a closer look (as a reminder, this is for the period ending September 30, 2025).

What Were Some Of The Most Notable Changes In Positions?

We always start by taking a look at Berkshire Hathaway, which was a net seller in the qtr, selling ~$13.4bn while purchasing ~$6.7bn. A large chunk of the total purchases came from Berkshire initiating a ~$4.9bn position in Alphabet, which caught a lot of headlines and was also the only new position the fund took on. The fund also increased a number of its positions in its current holdings, including in Chubb by +16%, Domino’s Pizza by +13% and SiriusXM by +4%. On the flipside Berkshire cut its position in Apple by -15% (has sold ~74% of its stake in Apple in the two yrs) and Bank of America by -6%. The only position Berkshire completely sold out of was D. R. Horton. Finally, the fund maintained its positions in Ally Financial, Amazon, American Express, Atlanta Braves, Bank of America, Capital One, Charter, Chevron, Coca Cola, Jefferies, Kraft Heinz, Kroger, Liberty Latin America, Liberty Media, Liberty Formula One, Mastercard, Moody’s, Occidental Petroleum, UnitedHealth, and Visa. Berkshire’s top five holdings (in order of the size of holding) are Apple, American Express, Bank of America, Coca-Cola, and Chevron, which account collectively for ~69.5% of the total portfolio.

Other hedge funds and their positions also made headlines this go around, including Peter Thiel’s fund Thiel Macro, which sold off its entire stake in NVIDIA in Q3, which would have been worth ~$100mn. We would also flag that “Big Short” famed investor Michael Burry, known for predicting the 2008 financial crisis, recently de-registered his hedge fund Scion Asset Management, though Burry said he was “not closing” Scion completely as it was still “active” in markets, but would use it to run other investment ventures.

Where Are The Top Hedge Funds Investing, In Aggregate?

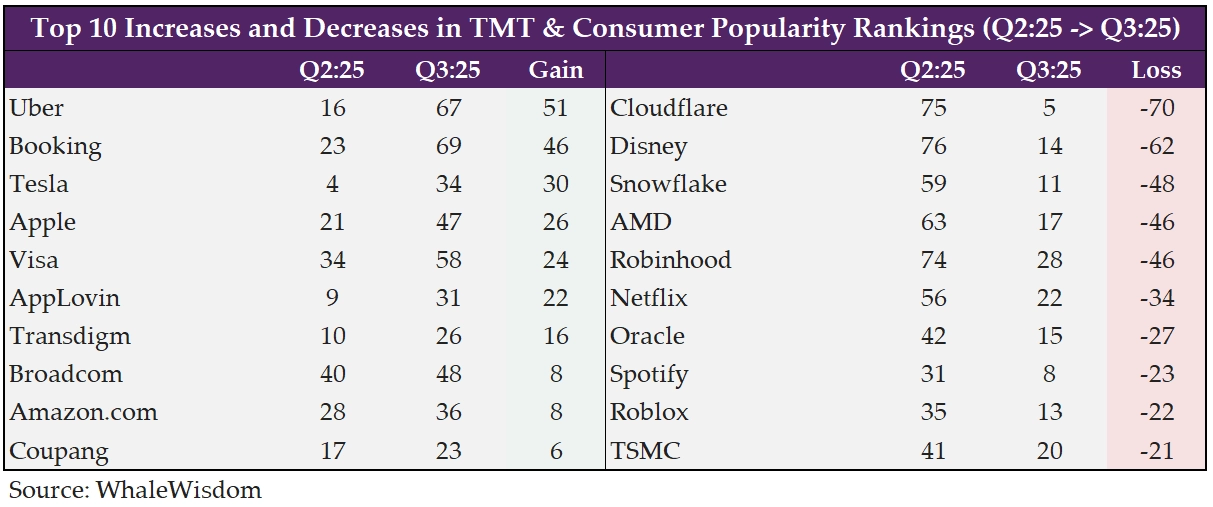

Each quarter, WhaleWisdom tracks the stocks that were most bought and sold during the quarter across 150 of the top hedge funds. It ranks the “hottest” stocks based on a formula that takes into account the number of buyers adding and initiating new positions vs sellers, the change in average ranking that the stock had in the portfolios, and the number of times the stock appears in the top 10 holdings of the portfolios. The biggest takeaways were:

- TMT made a comeback…7 TMT companies were on the Top 10 most bought list (up from 4 in Q2): They were Alibaba (#1), Micron Technology (#2), DoorDash (#3), PDD (#6), ASML (#7), Shopify (#8), and AppLovin (#9)

- ALL of the MAANG Cos returned to the Top 100 list, but most slipped from their Q2 rankings (except Apple)

- Apple – increase q/q (#47 in Q2 -> #21 in Q3)

- Alphabet – decrease (#35 -> #32)

- Netflix – decrease (#22 -> #56)

- Meta – decrease (#39 -> #57)

- Amazon – decrease (#36 -> #58)

- Breakdown by sector – Information Technology continues to dominate the most owned

- Information Technology companies took the top spot again, as 29 of the Top 100 most popular companies were in the sector (a continued step up from 22 in Q2)

- Finance took the second spot for most popular industry, similar to last qtr, w/ 16 of the top 100 Cos in the sector

- 11 Cos in the Communications sector, along with 10 Cos in the Consumer Discretionary sector and 5 Cos in the Industrials sector rounded out the Top 5

- ALL of the MAANG Cos returned to the Top 100 list, but most slipped from their Q2 rankings (except Apple)

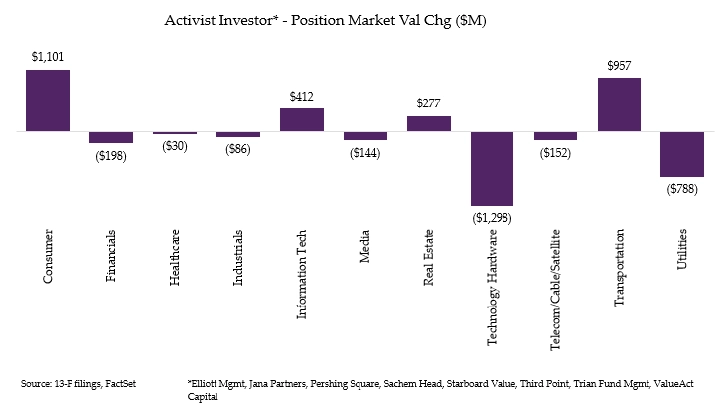

Where Are Activist/Event Investors Placing Their Bets, In Aggregate?

- The Top 8 activist funds were net buyers (but barely) this qtr, buying $2.75bn and selling $2.7bn of stocks

- Inflows: Consumer saw the largest amount of inflows (+$1.01bn), followed by Transportation (+$957mn), Information Tech (+412mn) and Real Estate (+277mn)

- The Top 3 largest inflows came from Third’s Point’s taking a new position +$495mn position in Norfolk Southern Corp, ValueAct Capital Management increasing its position in MongoDB by +$443mn, and Starboard Value taking a +$372mn position in Bill Holdings

- Outflows: Tech Hardware saw the largest outflow of (-$1.3bn) followed by Utilities (-$788mn), Financials (-$198mn), Telecom/Cable/Satellite (-$152mn), Media (-$144mn), Industrials (-$86mn) and Healthcare (-$30mn)

- The Top 3 largest outflows came from Sachem Head selling out of its position in Seagate (-$359mn), ValueAct Capital selling out of its position in Topcon (-$342mn) and Sachem Head decreasing its position in Talen Energy by (-$329mn)

- Inflows: Consumer saw the largest amount of inflows (+$1.01bn), followed by Transportation (+$957mn), Information Tech (+412mn) and Real Estate (+277mn)

Drilling Deeper Into Individual Activist Funds…

- ValueAct took a new position in Toast and increased its position in MongoDB by +207%, Visa by +26% and Meta by +23%; The fund maintained its position in Salesforce; The fund decreased its positions in Live Nation by -18%, The Walt Disney Corporation by -14%, Liberty Media Class C by -12%, Amazon by -10%, Roblox by -10% and Liberty Media Class A by -3%; It sold out of its position in Expedia and Redfin

- Starboard Value took only one new position and it was in Bill Holdings; Similarly, it only increased its position in one Co, which was Riot Platforms (by +89%); The fund decreased its positions in Match by -27%, NewsCorp by -12%, Tripadvisor by -11%, Autodesk by -11% and Salesforce by -0.8%; The fund sold out of its position in Pfizer

- Sachem Head took a new position in Warner Brothers Discovery; They increased their positions in CVS (+4%), Dicks (+55%) and Six Flags (+3%); The fund maintained its positions in Sprinklr and Twilio; The fund sold out of its positions in Vistra, Seagate, and US Foods

- Trian Fund did not take on any new positions; The only Co it increased its positions in was Wendys (by +104%); The fund did not decrease any of its positions and sold out of their holdings in Allstate and UHaul

- Third Point took a new position in Bausch Health; It increased its positions in Microsoft by +175%, Meta by +47%, Kenvue by +6%, Flutter Entertainment by +5%, Amazon by +4%, and Nvidia by +2%; It maintained its position in Hertz; It decreased its positions in Apollo Global by -49%, Live Nation by -32%, Capital One by -23%, Taiwan Semiconductors by -23%; The fund sold out of their positions in Soho House, Workday, and Docusign

- Pershing Square took no new positions and did not increase its position in any Cos; It maintained its positions in Alphabet, Amazon, Chipotle, Hertz, Hilton, and UMG; It decreased its positions in Alphabet by -10% and Uber by -0.1% and did not sell out of any positions

- JANA Partners took a new position in Six Flags; It increased its positions in Rapid7 by +14% and Freshpet by +4%, and decreased their positions in Trimble by -48%; The fund sold out of its positions in Wex

- Elliott Mgmt took a new position in Pepsico; The fund maintained its positions in Crown Castle, Equinix, Etsy, HPE, and Pinterest; The fund decreased its positions in Southwest Airlines by -5% and sold out of its position in Liberty Broadband

Grab Bag: More Sports Media Deals / More Entrants Into Prediction Mkts? / Live Nation & StubHub Take A Hit As UK Plans To Ban Ticket Reselling

- Sports remain at the center of the media entertainment sector and continues to garner top $$s

- The MLB has struck a new 3-year deals with ESPN, NBCUniversal and Netflix: NBC/Peacock will become the new home of “Sunday Night Baseball” and the wild-card round and Netflix will have the Home Run Derby and two additional games

- Price tag? The 3 deals will avg nearly $800mn/yr

- ESPN will still pay $550mn

- The NBC deal is worth $200mn

- And Netflix will pay $50mn

- Changes for ESPN (which has carried baseball since 1990)

- Loses postseason games & the Home Run Derby

- But becomes the rights holder for MLB.TV, which will be available on the ESPN App

- ESPN also gets the in-market streaming rights for the 6 teams whose games are produced by MLB

- NBC will have its own slate of games

- Its first Sunday Night Baseball game starting April 12th

- It will also get a prime-time game on Labor Day night

- As well as the “Major League Futures” game

- Netflix will have the first game of the season on March 25th

- It also has the Home Run Derby and MLB at Field of Dreams in Dyersville, Iowa, on Aug. 13th

- MLB also receives ~$729mn from Fox and ~$470mn from Turner Sports per yr under deals that expire after the 2028 season

- Separately, Paramount won the rights to show the Champions League in the UK and Germany per press reports

- The Guardianwas first to break news of the deal, which is set to run from 2027-2031

- It is reported to have cost the studio well in excess of the current $1.3bn deal in place with WBD’s TNT Sports

- Further shaking things up…Sky also annc’d that it has secured rights to show all Europa and Conference League games from the 2027/28 season

- Coinbase to reportedly launch prediction market powered by Kalshi

- The Co is supposedly preparing to launch a platform that would allow its client to bet on anything from elections to sports based on leaked screenshots

- If true, this is not the first time this has come up as CEO Brian Armstrong had earlier said the Co is exploring prediction markets

- The prediction market biz is becoming increasingly crowded

- Polymarket, which recently received U.S. regulatory approval by acquiring a licensed exchange and clearinghouse, is close to launching its U.S. operations

- More companies, from Crypto.com to President Donald Trump’s Truth Social, are also moving to offer similar products

-> Also this week, Kalshi raised $1bn at a $11bn valuation, up from its $5bn valuation last month; Polymarket, meanwhile, raised up to $2bn from Intercontinental Exchange at an $8bn valuation last month

- Live Nation and StubHub shares drop on a UK ticket resale ban report

- Live Nation stock fell -2.2% and StubHub shares tumbled -6% following a Financial Times report that UK ministers are preparing legislation that would prohibit selling tickets at prices higher than their face value

- The U.K. govs Department for Culture, Media and Sport estimates the move could reduce the average resale ticket price by as much as $48

- The UK would not be the first country to implement such restrictions: Several European nations already have regulations limiting ticket resale prices, including:

- France

- Belgium

- Germany

- Live Nation stock fell -2.2% and StubHub shares tumbled -6% following a Financial Times report that UK ministers are preparing legislation that would prohibit selling tickets at prices higher than their face value

Sources: Investing 11/17, CNBC 11/18, MLB Press Release 11/19, CBS 11/19, The Guardian 11/20, The New York Times 11/21, The Information 11/19, Yahoo Finance 11/19

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- US creator ad spend is set to hit $37bn in 2025, up 26% YoY, growing 4x faster than overall media, per IAB. Legacy formats like linear TV lose share as creators become a “must-buy” for brands. Mid-tier influencers (50K–500K followers) dominate hires at 61%. AI adoption rises, w/ ~75% of brands using tools for editing, briefs, and A/B testing. (Business Insider)

Artificial Intelligence/Machine Learning

- OpenAI annc’d global rollout of ChatGPT group chats, after pilot in Japan & NZ. Feature lets up to 20 users collab w/ ChatGPT in shared convos for planning, docs, research, etc. Personal settings stay private. Users add participants via icon or link; new adds create separate chats. ChatGPT responds when tagged, can react w/ emojis. (TechCrunch)

- Target and OpenAI annc’d a partnership to integrate AI across retail. Target will launch a ChatGPT app enabling curated shopping, multi-item baskets, and flexible checkout options. The Co will cont’d using OpenAI APIs and ChatGPT Enterprise for ~18,000 employees to boost productivity and enhance guest experiences. (OpenAI)

- Google annc’d Gemini app can now verify if images were AI-generated using SynthID watermarking; video/audio support coming soon. Expansion to C2PA credentials will enable detection across more AI tools like OpenAI’s Sora. Images from Nano Banana Pro will include C2PA metadata. TikTok also adopting C2PA. (The Verge)

- Perplexity annc’d launch of its AI-powered Comet browser on Android, bringing most desktop features like AI search, voice mode, tab-based Q&A, and ad blocker. Upcoming updates include conversational agent, quick-action shortcuts, and password manager. iOS version is planned soon. (Yahoo Tech)

- Brookfield annc’d a $100bn global AI infrastructure program, partnering w/ NVIDIA & KIA. The Brookfield AI Infrastructure Fund targets $10bn equity, w/ $5bn already committed. Investments span AI factories, power, compute & adjacencies. Radiant, a new NVIDIA Cloud Partner, will deliver full-stack AI svs. (Brookfield)

- Luma AI CEO Amit Jain said AI innovation will accelerate in 2026, w/ first film “significantly aided by AI” likely short/mid-form. Luma AI, building AI video models, raised $900mn from Humain, AMD & others, bringing valuation to ~$4bn. Deal includes access to Humain’s 2GW GPU supercluster (Project Halo) for world models, key for AGI. (Yahoo Tech)

- Baidu Inc. posted its biggest quarterly rev slide on record as ad biz weakened while it races in AI. Rev fell 7% to 31.2bn yuan ($4.4bn) for Sept. quarter, slightly above projections. Co swung to ~11.2bn yuan net loss due to asset writedowns. Shares dropped ~2% in pre-mkt US trading. (Bloomberg)

- Meta is expanding retail pop-up stores to boost buzz for its Ray-Ban AI glasses, which became a surprise hit last yr. Designed by Matt Jacobson, VP & creative director for AI wearables, the stores aim to create social experiences w/ coffee stations and mirrors for selfies. (The Wall Street Journal)

- Amazon annc’d its first US bond sale in 3 yrs to raise $15bn, aiming to fund AI infra amid surging demand. The six-part deal drew ~$80bn in orders; 40-yr tranche priced at 0.85 pts over Treasuries. Proceeds may go to acquisitions, capex, or buybacks. Meta, Oracle also plan big debt raises as major tech cos eye $400bn AI spend this yr. (Reuters)

- Google annc’d a novel generative UI implementation, enabling AI to create dynamic, immersive interfaces—like tools, games, and apps—tailored to any prompt. Rolling out via Gemini app (dynamic view, visual layout) and Google Search AI Mode for U.S. Pro/Ultra subs. (Google Research)

- Oracle (ORCL) shares plunged 25% in the past month after a bold AI pivot fueled by heavy borrowing. The Co plans to invest hundreds of bn in chips and data centers to support OpenAI, raising investor concerns amid scrutiny of hyperscaler spending. This drop erased ~$250bn in market value since Sept. (Yahoo Finance)

Audio/Music/Podcast

- UMG, Sony & Warner Music have licensed catalogs to AI streaming startup Klay, enabling users to remake songs via AI. Klay, first AI music svc w/ all 3 major labels, licensed thousands of tracks for training while pledging artist & label control. It blends traditional streaming w/ AI remix tools. (Reuters)

Broadcast/Cable Networks

- Disney and Dish face a major dispute as their carriage deal for Dish and Sling TV nears expiration in 2026. A lawsuit over Sling’s short-term “Sports Pass” sparked tensions, w/ Disney claiming contract violations. A judge denied Disney’s injunction, leaving passes active until renewal talks. (Cord Cutters News)

- Fox News Media hired Palantir for the past yr to build custom AI newsroom tools via a commercial deal protecting its IP. Palantir created a “digital twin” of Fox’s biz, embedding engineers to streamline workflows. Tools include topic radar, text editor, and article insights for efficiency. (Axios)

- Nexstar Media Group annc’d filing FCC applications seeking consent for its pending acquisition of TEGNA, including waiver requests to bypass outdated TV ownership rules. Nexstar argues deregulation is vital for local journalism to compete w/ Big Tech and legacy media. (Nexstar)

Cable/Pay-TV/Wireless

- Verizon annc’d its largest layoff, cutting 13,000 jobs (~20% of non-union wage costs) to restructure ops and reduce expenses. Co will convert 179 retail stores to franchises, close one, and expects $1.6–$1.8bn severance charge in Q4. A $20mn fund will aid displaced staff w/ AI-era skills. Shares fell 1% Thurs. (Reuters)

- T-Mobile’s Allan Samson said FWA is no longer rural-focused, w/ ~70% of new customers in top 100 U.S. cities and 65% of quarterly sales from urban/suburban mkts. Avg FWA speed hits 239 Mbps, latency ~34 ms, aided by standalone 5G. Samson admitted limited fiber expertise, citing acquisitions of Lumos & Metronet. (Fierce Network)

- AT&T annc’d deployment of mid-band (3.45 GHz) spectrum from EchoStar to ~23,000 sites, boosting 5G speeds up to 80% across 5,300 cities in 48 states. This cont’d expansion strengthens AT&T’s wireless & home internet svs, enabling more capacity for streaming, gaming & AI apps. (AT&T)

Capital Market Updates

- U.S. small & mid-sized biz owners show optimism for 2026, per BofA survey. 74% forecast rev growth; ~60% plan expansion. Confidence driven by cooling inflation, tariff stability & supply chain recovery. Labor shortages persist, yet 43% aim to hire, only 1% expect layoffs. Over half raised prices due to inflation. (Reuters)

- Corporate insiders are buying shares at the fastest pace since May amid a tech selloff and S&P 500’s 3.1% weekly slide, signaling confidence despite AI-bubble fears. Ratio of buys to sells hit 0.5 per Washington Service. JPMorgan calls drop a “technical washout,” while NVDA’s strong rev forecast post-close lifted sentiment. (Yahoo Finance)

- Mkts reversed as Nvidia-led rally ended amid AI concerns; S&P 500 saw biggest intraday swing since Apr. US sanctions on Russian oil stranded ~48mn barrels, forcing tankers to reroute. Trump-backed Ukraine peace plan offers Russia territorial concessions, NATO block. (Bloomberg)

- SEC staff returned post-longest US govt shutdown to tackle a massive backlog. Supervisors urged “triage”: finish pre-shutdown tasks first, then address the surge of filings received while 90% of workforce was furloughed. The delay risks stalling IPOs as mkts await regulatory clearance amid mounting paperwork. (Bloomberg)

- US stock mkts pullback this month is hitting IPOs hard, complicating cos aiming to go public in the rest of the yr. Prices of recent listings like Gemini Space Station, Fermi, Navan & Stubhub have fallen below IPO levels. Even high-profile debuts incl. CoreWeave, Circle Internet Group & Figma faced declines. (Bloomberg)

- Goldman Sachs is set for its best M&A performance in 24 yrs as megadeals rebound. The bank advised on 34% of the $3.8tn global mergers annc’d this yr, up from 28% in 2024, per LSEG data. W/ less than 7 weeks left, Goldman is on track for its biggest mkts share since 2015, when it hit 34.26%. (FT Chinese)

Cloud/DataCenters/IT Infrastructure

- Tech giants are exploring space-based data centers to meet surging AI energy demands. Bezos touts the moon as ideal for powering energy-hungry ops, while Blue Origin and SpaceX aim to make space travel routine. Current economics don’t add up, but experts say viability could emerge in ~10 yrs. (The Wall Street Journal)

Crypto/Blockchain/web3/NFTs

- Crypto mkts plunged into bear territory, erasing ~$1tn since early Oct. Bitcoin fell 31% from its Oct. 6 high of $126K to $86,398, now down 5% YTD. Massive liquidation on Oct. 10 wiped $19bn–$30bn in leveraged positions. ETFs posted 3 wks of outflows; Thurs. saw $866mn redemptions. (Business Insider)

- Kraken, a major crypto exchange, annc’d it has confidentially filed for a U.S. IPO, aiming for Q1 2026 amid upbeat mkts and Trump admin support. Valued at ~$20bn after recent funding from Jane Street and Citadel, Kraken plans to expand products and global reach. Cos like Circle, Gemini, Bullish also eye listings pre-midterms. (Reuters)

- Bitcoin plunged below $93k, erasing its yr-to-date gains after Trump’s tariff remarks triggered a global mkts sell-off. Crypto’s bear phase deepens as ETFs and cos pull back, w/ institutional outflows and profit-taking. BTC hit a record $126k but reversed amid risk-off sentiment and tech cooling. (Yahoo Finance)

eCommerce/Social Commerce/Retail

- Home Depot missed Q3 earnings for the 3rd straight time and cut its full-yr profit outlook amid weak home improvement demand, slow consumer spend, and soft housing mkts. Rev hit $41.35bn vs. $41.10bn est.; adj EPS $3.74 vs. $3.84 est. Comparable sales rose 0.2%. Full-yr sales seen up ~3%, adj EPS down ~5%. (CNBC)

- Walmart’s US biz is surging amid inflation as shoppers seek affordability. Last qtr sales rose 4.5%, w/ more store visits and higher spend. Co annc’d raised sales & profit guidance, expecting strong holiday season. Investments in wages, stores, and online logistics boosted growth. Gains led by middle- & upper-income households, taking share from Target and dollar stores. (CNN)

- Kroger annc’d major eCommerce updates to boost CX and profitability, targeting ~$400mn improvement in 2026. Plans include expanding Instacart, DoorDash, Uber Eats partnerships for faster delivery, piloting store-based automation, and closing 3 automated facilities in Jan. Impairment charges of ~$2.6bn expected in Q3. (Kroger)

- GameStop annc’d its first “Trade Anything Day”, letting customers swap items like old electronics, scratched discs, toys, or even taxidermy for store credit. Exclusions include hazardous waste, live/dead animals, alcohol, tobacco, drugs, pharmaceuticals, 3D/label printers, VCRs, and DVD players. (Yahoo)

- Nike CEO Elliott Hill annc’d a bold reinvention plan, refocusing on athletes and sport-driven innovation vs lifestyle marketing. Strategy includes restructuring biz by sport, raising prices to protect margins, and rebuilding wholesale ties. (CEO Weekly)

Electric & Autonomous Vehicles

- Waymo annc’d plans to expand robotaxi ops to Minneapolis, New Orleans & Tampa, starting w/ manual drives before testing driverless tech. It already runs in LA, SF, Phoenix, Austin & Atlanta, w/ 2026 targets incl. Dallas, Denver, Miami & more, plus London & Tokyo. Challenges: harsh winters in Minneapolis, tight streets in New Orleans. (TechCrunch)

Film/Studio/Content/IP/Talent

- Lionsgate annc’d MovieSphere Gold, an ad-supported digital network offering films from its 20,000+ title vault, incl. Dirty Dancing, Rambo & Hunger Games. Debuted in ~30mn homes via DirecTV, Dish, Sling & others, reaching 80% of U.S. mkts. CBS Media Ventures will handle ads. (The Hollywood Reporter)

- Universal’s Wicked: For Good scored ~$20M-$22M in Thurs. previews starting 2PM, boosted by Amazon sneaks & Wed. fan shows. Last yr’s previews hit $19.2M, leading to $112.5M opening. Current proj. for weekend: $125M-$150M stateside, w/ global start north of $200M+. Audience score 97% vs. 95% prior film; critics at 70. t time. (Deadline)

- Netflix, once focused solely on streaming, is now diving into merchandising and live events to boost fan engagement and rev. The Co annc’d major licensing deals w/ Hasbro, Mattel & Jazwares for toys tied to hits like “Stranger Things” & “KPop Demon Hunters.” (CNBC)

- “Now You See Me: Now You Don’t” led the box office w/ $21.3mn domestic and $54.2mn intl., totaling $75.5mn globally, signaling Lionsgate’s revival after recent flops. The $90mn film, directed by Ruben Fleischer, reunited original cast and added new stars, boosting appeal. (Variety)

FinTech/InsurTech/Payments

- Klarna annc’d a deal to sell up to $6.5bn loans to Elliott funds over two yrs to boost its BNPL biz in U.S. The $1bn facility uses a forward flow agreement, enabling scalable funding as Klarna ramps merchant base w/ new payment svs integrations. Klarna retains consumer-facing ops incl. underwriting & svs. (Reuters)

- Block annc’d a 3-yr outlook at its investor day, projecting mid-teens gross profit growth to ~$15.8bn by 2028 and adj operating income up ~30% annually to $4.6bn. EPS seen at $5.50 in 3 yrs. For 2026, gross profit est. $11.98bn (+17%), w/ adj income $2.7bn and EPS $3.20. Co expanded share buyback by $5bn (plus $1.1bn remaining). (CNBC)

- Klarna, the Swedish fintech, posted its first earnings post-IPO, reporting Q3 rev of $903mn, up 26% YoY, beating estimates of $882mn. GMV rose 23% to $32.7bn; U.S. mkts drove 43% GMV growth and 51% rev surge. Active customers hit 114mn (+32%). Despite a $95mn net loss vs $12mn profit last yr, Klarna forecasts Q4 rev of $1.07bn. CEO noted AI adoption for product dev but flagged concerns over heavy data center spend. (Reuters)

- BofA annc’d plans to invest $4bn in new tech, focusing on AI to boost productivity and rev. AI tools let bankers cover 50 clients vs 15, automate tasks, and tailor advice using mkts data. Its 18,000 developers report 90% faster software tests. Virtual assistant Erica handled 3bn interactions, replacing work of ~11,000 staff. (Reuters)

Last Mile Transportation/Delivery

- Starship Tech & Uber Eats annc’d a global collab to roll out autonomous sidewalk robot delivery across mkts. Launch starts in Leeds, UK in Dec. 2025, expands to Europe in 2026 & U.S. by 2027. Starship’s 2,700+ robots, scaling to 12,000+ by 2027, have completed 9mn+ deliveries. Robots operate at Level 4 autonomy, enabling 30-min delivery for 2-mile range. Starship raised $50mn in Oct., total funding $280mn. (Starship Technologies)

Live Entertainment/Theme Parks/Concerts/Experiential

- Disney CFO annc’d plans to bring dynamic pricing to U.S. parks, similar to airline model, after success in Paris. Goal: boost incremental rev via ticket, food, merch & svs like Lightning Lane. Rollout likely post-2025. Experiences op income rose 8% to $10bn FY25; attendance fell 1%. Avengers Campus expansion adds two attractions: Infinity Defense & Stark Flight Lab. (Deadline)

- CMA has launched probes into 8 cos incl. StubHub, Viagogo, AA Driving School, Gold’s Gym, Wayfair, Appliances Direct & Marks Electrical over online pricing tactics like drip pricing & pressure selling. New powers let CMA fine up to 10% of global turnover & order compensation. (The Guardian)

- Saudi Arabia will open Six Flags Qiddiya City, marking the first Six Flags outside N. America. Part of Qiddiya Investment Co.’s flagship dev near Riyadh, it aligns w/ Vision 2030 to attract 150mn visitors annually. The park offers 28 rides incl. record-breaking coasters, 18 family rides, dining & retail. (Arab News)

Macro Updates

- Fed minutes signal fading odds for a Dec. rate cut, w/ CME FedWatch showing 32% vs 98.9% last mo. Base rate likely held at 3.75%-4%, despite Trump pushing for cuts amid housing woes. Inflation at 3% vs 2% target splits FOMC; some call for cuts, many for hold. Jobs mkts stagnate, but modest gains (~100K roles) expected, dampening cut hopes. (Fortune)

- US cos shed ~2,500 jobs per week in the four weeks ended Nov. 1, per ADP data, signaling labor mkts lost momentum late Oct. Job cuts slowed into Nov., but planned layoffs hit a 20-yr high, w/ major cos like Amazon & Target annc’d reductions. ADP’s Nov. 5 report showed private employment rose 42,000 after prior declines. (MSN)

- US health care & social assistance plus leisure & hospitality sectors added ~690,000 jobs in 2025, per BLS report. Outside these, total US employment fell by ~6,000 this yr, signaling hiring strength in health care & hospitality while other mkts scale back. (Bloomberg)

- The U.S. labor mkts added 119,000 jobs in Sept., beating forecasts of 50,000, per delayed gov’t data after shutdown. Unemployment rose to 4.4%, highest in 4 yrs, as ~500,000 joined workforce. Gains were led by healthcare, education, leisure & hospitality, but prior months saw downward revisions. (Yahoo Finance)

- Europe’s tech sector shows renewed optimism per Atomico’s report. Ecosystem valuation nears $4tn, contributing 15% to GDP. Funding rebounds to $44bn, w/ AI & defence tech leading; deeptech grabs 36% of VC. Climate tech declines to 18%. Talent hiring eases, but gender funding gap persists. US remains top relocation choice for founders. (Sifted)

- Apple is intensifying succession planning as CEO Tim Cook may step down next yr, per FT. John Ternus, SVP of hardware engineering, is seen as the top candidate. The board and execs have cont’d prep for transition after Cook’s 14+ yrs at the helm. A new CEO likely won’t be annc’d before late Jan. earnings, covering holiday mkts. (Reuters)

Media Conglomerates

- Disney projects $24bn content spend in FY26, split 50-50 between sports and entertainment, up from $23bn in FY25. CFO Johnston said growth will cont’d but below prior yrs’ peak when cos overproduced. Focus includes local content in mkts, tech upgrades for Hulu-Disney+ integration, and ESPN Unlimited bundle at $29.99/month. (Variety)

- Paramount Skydance (PSKY. O) annc’d sale of its stake in Chilevision to Vytal Group as part of a strategy to streamline its global portfolio and boost direct-to-consumer svs in Latin American mkts. The deal, led by Tomas Yankelevich, Jorge Carey, and Edgar Spielmann, awaits Chilean regulatory approval. (Reuters)

Metaverse/AR & VR

- Meta annc’d Hyperscape update enabling shared VR spaces via Quest 3/3S or Horizon app. Users can invite friends to photorealistic room replicas; up to 8 ppl per instance, w/ plans to expand. Features include on-device rendering & audio. Rollout is gradual over coming months; rescan needed for shareable worlds. (The Verge)

Regulatory

- EU plans major overhaul of GDPR and AI Act to cut red tape and boost growth. Proposal eases data-sharing rules, lets AI cos use personal data for training under GDPR, and delays high-risk AI compliance until standards exist. Cookie pop-ups will shrink; smaller cos get simplified AI docs. (The Verge)

- Meta annc’d it will start deactivating Instagram, Facebook & Threads accounts of Australian teens aged 13–15, ahead of a social media ban. The ban targets under-16s on major platforms incl. TikTok, YouTube & X. Teens can save content or verify age via selfie or ID. Non-compliance may cost cos up to A$50mn. (BBC)

- Trump lashed out at ABC’s Mary Bruce in the Oval Office, calling her question on Jamal Khashoggi’s killing “horrible” and later branding her “a terrible reporter. ” He also insulted Bloomberg’s Catherine Lucey on Air Force One, saying “Quiet, piggy.” Trump threatened ABC’s license, cited prior $16mn defamation settlement, and reposted NBC criticism. (The New York Times)

- EU Commission has annc’d 3 mkts probes under DMA into Amazon & Microsoft cloud svs to assess gatekeeper status and curb anticompetitive practices. AWS & Azure dominate global cloud mkts; Alphabet also key player. DMA applies to cos w/>45mn users & €75bn cap, requiring interoperability and banning self-preference. (Reuters)

- Washington accused Alibaba of aiding Chinese military ops targeting U. S., per a White House memo cited by FT. The memo includes declassified intel on Alibaba’s tech support to the PLA, raising U.S. security concerns. Alibaba shares fell 4.2% post-news. Alibaba denied claims, calling them false and politically motivated. (Reuters)

Satellite/Space

- AST SpaceMobile annc’d BlueBird 6 launch from India, marking the largest commercial phased array in low Earth orbit (~2,400 sq. ft.), 3.5x bigger than prior models w/10x data capacity. Co plans 5 launches by end of Q1 2026, targeting 45–60 satellites by end of 2026 for global coverage. (Business Wire)

- Orange annc’d “Message Satellite” at Orange OpenTech Paris, enabling SMS & geolocation via satellite when mobile/Wi-Fi is unavailable. Launcing in France & 36 countries, free for 6 months then €5/month. Initially for 5G/5G+ users w/ Google Pixel 9/10, later expanding .(Orange)

Social/Digital Media

- Meta won its antitrust case vs FTC over Instagram ($1bn) & WhatsApp ($19bn) deals. Judge Boasberg ruled FTC failed to prove Meta holds current monopoly in social networking. FTC sought divestiture but lacked evidence amid fierce competition from TikTok, YouTube. (CNBC)

- Americans’ social media use cont’d to evolve in 2025. Pew survey shows YouTube (84%) and Facebook (71%) as top platforms, w/ Instagram at 50%, TikTok 37%, WhatsApp 32%, Reddit 26%. (Pew Research Center)

- Young people increasingly rely on social media for news and shopping, per DoubleVerify’s Global Insights Report. Ages 18–44 favor online video (42%) or social (40%), while 45–65+ lean on TV (59%) and legacy sites (37%). 54% say influencers sway buys; 30% purchased via social in past yr. 57% saw AI content on social vs 26% on search. (Cynopsis)

- TikTok annc’d a new AIGC control in its Manage Topics tool, letting users adjust how much AI-generated content appears in their For You feed. The Co is also testing “invisible watermarking” to improve labeling, alongside existing C2PA Content Credentials. (TechCrunch)

- TikTok annc’d new digital well-being tools incl. an affirmation journal (120+ prompts), calming sound generator, and breathing exercises. Redesigned screen-time page adds creator tips on limiting use. Users earn badges for missions like avoiding night use, setting daily limits, and meditating. (TechCrunch)

Sports/Sports Betting

- George Kurtz, CEO of CrowdStrike and endurance racer, has secured a 15% stake in Mercedes F1’s ownership entity, becoming co-owner alongside Toto Wolff. CrowdStrike has partnered w/ Mercedes since 2019. Kurtz joins the strategic steering committee as tech advisor, focusing on motorsport-data innovation. Governance remains unchanged; Wolff stays CEO & Team Principal. (Formula 1)

- Nielsen’s Oct. Gauge shows NFL cont’d as top driver of TV viewing. Broadcast nets averaged 22% Mon.–Sat., jumping to 27.3% on Sundays w/ CBS, Fox & NBC games. Cable fell 2.7 pts; streaming dipped 1.3 pts on Sundays. Peacock hit 2% vs. 1.5% wkdays; Paramount+ rose to 1.6%. Prime Video surged to 6.4% on Thurs. (The Hollywood Reporter)

- Versant Media Group Inc. , spun off from Comcast Corp., has hired Lazard Ltd. to explore a sale of youth-sports app SportsEngine. The app may fetch $400mn–$500mn. Talks are ongoing w/ suitors incl. cos and sports investors, but no deal is finalized. Versant could still opt to keep the asset. (Bloomberg)

- UC Investments is considering a $2.4bn stake in Big Ten Enterprises, granting 10% of media/sponsorship rights for 15 yrs. The deal, paused for now, faces opposition from Michigan and USC, w/Michigan likening it to a “payday loan” and hinting at leaving post-2036. Big Ten’s current media pact w/Fox, CBS, NBC averages $1bn/yr. (USA Today)

Tech Hardware

- Sunday Robotics annc’d a fully autonomous home robot, Memo, designed to clear tables and load dishwashers. The startup uses a novel training approach for common household tasks and plans to deploy units in homes next yr. (Wired)

- Nokia annc’d a new strategy at Capital Mkts Day to lead AI-driven network transformation. Co will simplify ops into Network Infrastructure & Mobile Infrastructure segments from Jan. 2026. Targets include comparable op profit of €2.7–3.2bn by 2028 vs €2bn now, w/ KPIs like 6–8% CAGR in Network Infra & 48–50% gross margin in Mobile Infra. (Nokia)

- Apple’s N1 chip in iPhone 17 marks a major Wi-Fi upgrade vs. Broadcom-based iPhone 16, boosting global median download to 329.56 Mbps (+40%) and upload to 103.26 Mbps. Pixel 10 Pro leads median download at 335.33 Mbps, while Xiaomi 15T Pro dominates uploads (129.22 Mbps) and latency. (Ookla)

- Apple’s iPhone faces its biggest overhaul yet, impacting features and release timing. The flagship shift aims to reduce reliance on the annual fall spectacle. Mac Pro development is cont’d on the back burner, while Tesla annc’d CarPlay support. Additionally, Apple’s longtime operating chief is wrapping up his tenure at the Co. (Bloomberg)

Towers/Fiber

- Ericsson’s Mobility Report shows 33 operators now offer network slicing-based 5G svs, totaling 65 commercial offerings, incl. 21 launched this yr. Over 90 telcos have rolled out 5G SA, up 30 YoY, w/ 56 working on slicing (118 cases). Europe risks lagging in 6G due to late 5G SA adoption. (Telecoms.com)

Video Games/Interactive Entertainment

- Battlefield 6 became the top-grossing U.S. game in Oct. and the best-selling title of the yr so far, surpassing NBA 2K26, Monster Hunter Wilds, and Borderlands 4. EA annc’d over 7mn copies sold post-launch. It set a 3-yr record for single-month physical & digital sales, beating COD: MW3’s 2023 debut. (Kotaku)

- Unity & Epic Games annc’d partnership to advance open, interoperable future for video gaming. Focus on enhancing dev tools, svs, and cross-platform capabilities. Co aims to empower creators w/ improved tech and shared standards, driving innovation across mkts. (Epic Games)

- EA annc’d a strategic reset for its F1 franchise: no new game in 2026, instead a paid DLC for F1 25 aligning w/ major 2026 season changes like new cars, regs, teams, and drivers. Pricing/timing will be revealed in 2026. A “reimagined” full game launches in 2027, promising an authentic, innovative, and expansive experience as part of EA’s multi-yr investment supported by F1 mgmt and teams. (The Verge)

- Roblox will require age estimation for chat starting early Jan. after scrutiny over child safety and lawsuits against the Co. The process begins Dec. in mkts like Australia, Netherlands, and NZ, expanding globally in Jan. Users will be grouped by age (Under 9, 9–12, 13–15, etc.) and can chat only w/ similar groups. (The Verge)

- Take-Two CEO Strauss Zelnick said consoles aren’t disappearing but gaming is shifting toward PCs and open systems. Mobile gaming, boosted by Take-Two’s $12.7bn Zynga acquisition, now leads rev at 46%, vs. console 41% and PC 13%. Mobile is projected to grow ~10% next qtr, w/global mobile game rev hitting $188.8bn in 2025 (+3.4%). (CNBC)