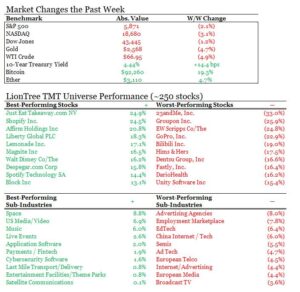

After the huge stock market surge last week, the major indices gave back some of those gains, though asset classes like crypto advanced their momentum. Investors continue to assess the winners and losers as the picture regarding the new administration further unfolds. The S&P 500 and Nasdaq fell -2% and -3.2%, respectively, this week.

While there are still a few stragglers set to report next week, we are finally past the bulk of this very busy earnings season. This week we delved into Entertainment, Theme Parks, Streaming, Music, Concerts, Online Grocery, and China Tech, plus some key updates out of Liberty Media’s Investor Day. It is never a dull moment!

Have a nice weekend.

- Earnings Scorecard – Week 5

- Disney’s New Multi-Year Guidance Paints A Picture Of Accelerating Earnings Growth

- Spotify’s Playbook Is Working… 2025 Becomes The Year Of Growth WITH Profitability

- It’s Never A Dull Moment When Talking About The Liberty Media Complex…

- Expect An Even “Bigger Year” For Live Nation In 2025

- Deepening Relationships With Retailers Is Instacart’s “Secret Sauce” But Is Also “Under-Appreciated”

- China Tech Received A “Significant” Benefit From Stimulus Measures… BUT Concerns Remain

- Grab Bag: Microsoft Gaming Is Open To M&A/Trump Plans To Halt TikTok Ban/Netflix Ad Biz Hits 2-Yr Mark With 70mn MAUs

Best,

Leslie

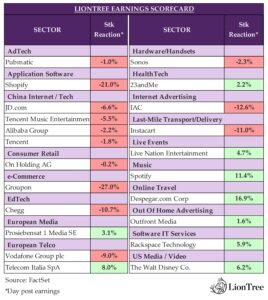

Earnings Scorecard – Week 5

We are finally reaching the tail-end of earnings season, and the pace of reports has started to tick down, with 21 companies in our LionTree TMT and Consumer Universe reporting their quarterly results (down from a record 98 last week). Similar to the last three weeks, stock price reactions were biased to the downside, as 11 companies (52%) traded down after their prints, while 10 companies traded up (48%). Groupon was the worst performer of the week, down -27.0%, while Shopify was the best performer, up +21.0%.

After Fox, Paramount, and WBD reported last week, Disney’s earnings this week rounded out this quarter’s media earnings, and it ended on a strong note, with the stock up +6.2% in reaction (see Theme #2). It was also a strong showing on the music side, with Spotify popping +11.4% post its report (see Theme #3), as well as on the live entertainment front, with Live Nation trading up +4.7% (see Theme #5).

That being said, market reactions weren’t all positive. Instacart was also on deck this week, and the stock fell -11% in reaction (see Theme #6). It was also tough going for the China Tech companies that reported this week, with JD.com down -6.6%, Alibaba down -2.2% and Tencent down -1.8% (see Theme #7).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Disney’s New Multi-Year Guidance Paints A Picture Of Accelerating Earnings Growth

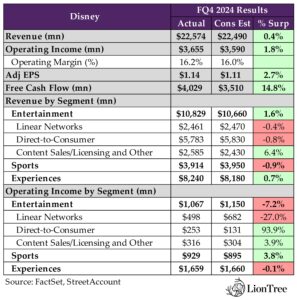

After the success of Inside Out 2 and Deadpool vs Wolverine (the only two $1bn+ movies globally YTD), Disney posted another blockbuster – this time on the FQ4 results front. The company’s headline numbers across revenue, op income, and EPS all beat. Notably, despite some areas of weaknesses across segments, the standout performance came from the DTC segment, which posted an op income beat that was nearly double the Street’s expectations, marking Disney’s second consecutive quarter of DTC profitability.

That wasn’t the only big topic of conversation on the call, as analysts were drilling down on the new and in-depth multi-year guidance, which painted a picture of accelerating earnings growth through FY27.

Regarding the quarter and starting with the Entertainment segment, DTC’s strength was driven by growth in subscribers (added +4.4mn in the qtr vs +0.7mn last qtr) as well as the advertising tier’s performance (~60% of new US Disney+ subscribers are choosing the ad tier). Looking ahead, growth is expected to come from a balance of subscriber growth and pricing, with a little more leaning towards pricing, with expectations of pricing-related churn being somewhat reflected in the FQ1 outlook for a “modest” decline in Disney+ subs vs FQ4. Also related to streaming, Disney announced that the ESPN+ streaming tile will be available starting December 4. The ESPN flagship product will also be launching in early fall 2025, and the payback is expected to come “relatively quickly” in 2026.

Another point of emphasis from the Co was that it continues to see strength in linear, particularly across its live offering, and despite overall declines, streaming is its “natural hedge” for when consumers ultimately decide to switch. In the meantime, integrations between linear and streaming platforms are viewed as a way to gain share in advertising.

Finally, on the Experiences front, while it was a good qtr for domestic, international was a drag on the segment due to region-specific dynamics that seemed to fall into the qtr. That being said, Disney is seeing strengthening in the consumer and is anticipating a gradual acceleration in the business going forward. However, Experiences op Income was guided for one more negative quarter (due to Hurricane impact and new Cruise ship launch next week) before turning positive in FQ2.

As always, there’s a lot to dig into from the quarter…see below for what we thought was most important.

-> Disney shares jumped +6.2% post-earnings and finished the week up +16.2%; YTD, Disney stock is trading up +27.5%

While FQ4 Beat Across The Top-Line, Results Were Mixed Under The Hood / DTC Profitability Beat Was A Standout

- FQ4 rev – BEAT by +0.4%: Increased +6% y/y (vs +4% y/y in FQ3) to $22.6bn

- Content Sales/Licensing & Other and Experiences were the upside areas to revenue

- BUT all other business lines missed expectations

- FQ4 op income – BEAT by +1.8%: Grew +23% y/y (vs +19% y/y in FQ3) to $3.7bn

- DTC profitability upside stood out with op income at $253mn vs cons $131mn

- BUT Linear Networks op income was -27% below expectations

- Adj EPS – BEAT by +2.7%: $1.14 vs cons $1.11

- FCF – BEAT by +15%

Mgmt Provided A Plethora of Optimistic Guidance Across The Business Over The Next Two Years

- Expect accelerating EPS growth through FY27: Expect to continue to drive “healthy” growth beyond this year

- FY25: High single digit growth y/y, which is BETTER than cons +4.4%

- FY26: Double digit growth vs cons +12.0%…driven by –

- Entertainment seg op income: Double digit % growth due to growth in Entertainment DTC biz and a 10% op margin for Entertainment SVOD DTC biz (ex, Hulu Live DMVPD service)

- Sports segment op income: ~+Lsd% growth

- Experiences segment op income: ~+Hsd% growth

- FY27: Double digit growth vs cons +11.4%

- FY25 advertising rev: Expected to be “at or stronger” than FY24’s +3% y/y

- FY25 CapEx came in higher than expectations: ~$8bn vs cons $6.54bn, driven primarily by fleet expansion at Disney Cruise Line and new guest offering at theme parks around the world

- Cash from operations –

- FY25 – BEAT: ~$15bn vs cons $14.81bn

- FY26: Double digit growth

- FY25 stock repurchases: Targeting $3bn in stock repurchases

- FY25 dividend growth: Targeting increases to divided at a rate that tracks Co earnings growth

Streaming Profitability Improved Seq In FQ4 (After Reaching Profitability For The First Time In FQ3) / The Push For Ad-Supported Sign-Ups Is Working, With Majority Of New Subscribers Choosing The Tier

- FQ4 overall Entertainment segment BEAT on rev by +1.6% but missed on op income by -7.2%: Rev grew +14% y/y (vs +13% y/y in FQ3); Op income grew from year-ago $236mn to $1.1bn

- Linear Networks – dragged down the segment on both rev (-0.4% miss) and op income (-27% miss): Rev fell -6% y/y and op income was down -38% y/y due to higher marketing costs, lower affiliate rev, and a decline in ad rev

- DTC – had a standout qtr for profitability (+94% beat), but missed on rev (-0.8% miss): Rev grew +15% y/y, and op income went from year-ago -$420mn to $253mn, driven by growth in subscription and ad rev

- Content Sales/Licensing & Other – beat on both rev (+6.4% beat) and op income (+3.9% beat): Rev grew +14% y/y and op income went from year-ago -$149mn to $316mn, reflecting the theatrical success of Inside Out 2 and Deadpool & Wolverine

- Combined DTC biz profitability improved in FQ4: Op income reached $321mn (up from $47mn in FQ3)

- Consists of the Direct-to-Consumer line of business at the Entertainment segment and ESPN+ at the Sports segment

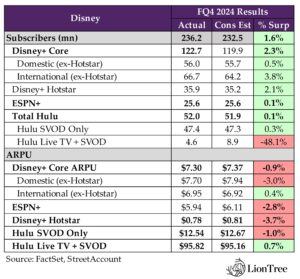

- Disney+ Core BEAT on subscribers, but MISSED on ARPU…FQ1 subs should see modest decline seq

- Disney+ Core subscribers beat by +2.3%: Incr’d seq by +4.4mn (vs +0.7mn q/q in the prior qtr)

- Domestic: Added +1.3mn subs q/q (vs +0.8 subs q/q in prior qtr)

- International: Added +3.2mn subs q/q (vs -0.1mn subs q/q in prior qtr)

- Disney+ Core ARPU missed by -0.9%:

- Domestic: Fell from $7.74 in FQ3 to $7.70 in FQ4 due to a higher mix of subscribers to ad-supported and wholesale offerings, partially offset by a higher ad rev

- International: Incr’d from $6.78 in FQ3 to $6.95 in FQ4 due to higher retail pricing, partially offset by a higher mix of subscribers to ad-supported and wholesale offerings and an unfavorable FX impact

- FQ1 outlook – Expect “modest” decline in Disney+ subs vs FQ4, driven by the expected temporary uptick in churn from both the recent price increases and the end of a recent promotional offer

- Disney+ Core subscribers beat by +2.3%: Incr’d seq by +4.4mn (vs +0.7mn q/q in the prior qtr)

- Entertainment DTC ad rev grew +14% y/y (vs +20% y/y in FQ3), driven by Disney+

- ~60% of new US Disney+ subscribers are choosing the ad tier

- ~37% of total US subs and ~30% of global subs are AVOD subs

- Expect advertising will continue to be a driver of DTC rev going forward

- “It’s not just about raising pricing… the pricing that we recently put into place, which is increased pricing, was actually designed to move more people in the AVOD direction, because we know that the ARPU and interest in it from advertisers and streaming has grown”

- A deeper drill down of the Entertainment op income outlook –

- FY25: Double digit op income growth compared to FY24’s +172% y/y, weighted to H1 of the yr

- Entertainment DTC op income increase of ~$875mn versus FY24, which includes a comparison to an adverse impact of the India DTC business of ~$200mn on FY24 Entertainment DTC results

- Expect growth to come from a balance of pricing and subscriber growth, with a little more tilt towards pricing

- FQ1 Content Sales/Licensing and Other op income “relatively in-line” with FQ4

- Entertainment DTC op income increase of ~$875mn versus FY24, which includes a comparison to an adverse impact of the India DTC business of ~$200mn on FY24 Entertainment DTC results

- FY26: Entertainment: Double digit op income growth compared to FY25 guidance

- 10% op margin for the Entertainment SVOD DTC bizs (excl. Hulu Live DMVPD service), driven by –

- Growing subscribers (each incremental subscriber has “very, very” high margins attached to them)

- Increasing pricing in-line w/ content value

- Increasing engagement and reducing churn, including improving the recommendation engine

- Increasing ad monetization

- International, which continues to be a “significant” opportunity

- 10% op margin for the Entertainment SVOD DTC bizs (excl. Hulu Live DMVPD service), driven by –

- FY25: Double digit op income growth compared to FY24’s +172% y/y, weighted to H1 of the yr

- “View international as a terrific opportunity” to grow streaming biz and will be doing some “selective investing” in EMEA and APAC

- BUT have slowed down investments in those markets until technology to maximize returns and reduce churn is improved: “We don’t want to spend on the content side until we’re confident that we can get the necessary returns on those investments”

- Noted that investments won’t be “enormous in nature by any stretch of the imagination”…: Have modeled in “some incremental growth” in content spend as a result, but “not enough to be significantly disruptive to the overall cash flow or algorithm for the company”

- … B/c making content with global appeal and franchise value remains the priority and is what gives them a competitive edge: Had the only two $1bn+ movies so far this year and that was generated from across the world; “And if you look at some of our competitors who don’t have movies of basically that quality or that level of success, they have to spend more in local content, because they don’t have that”

- Have several initiatives in process to boost engagement, reduce churn, and improve the overall user experience – “We’re already seeing increased engagement in a very short period of time”

- Improving streaming tech

- Enhancing personalization through better recommendations

- Addressing password sharing (has launched in ~130 countries)

- Unifying tech and ad stacks across Disney+ and Hulu

Gearing Up For ESPN+ Launches… The Tile On Disney+ In Dec And Flagship DTC In 2025

- FQ4 Sports missed on rev, but beat on op income

- Rev – MISSED by -0.9% Flat y/y (vs +5% y/y in FQ4)

- Domestic ESPN ad rev was up +7% y

- Op Income – BEAT by +3.8%: Fell -5% y/y (vs -6% y/y in FQ4), driven by Domestic ESPN, as higher college football rights costs were partially offset by ad rev growth

- Rev – MISSED by -0.9% Flat y/y (vs +5% y/y in FQ4)

- Sports op income outlook – growth will accelerate in FY25, but decel again in FY26

- FY25: +13% op income growth compared to FY24’s -2% y/y; Adjusting for the impact of the India biz on Sports’ FY24 results, op income is expected to decrease ~10%

- FY26: Low single digit op income growth compared to FY25

- College Football is driving fan engagement on both ABC and ESPN

- College Football on ABC is off to its best start since 2009, with rating up +45% y/y

- Announced that the ESPN+ streaming tile will be available on Disney+ beginning Dec 4: Will provide Trio Bundle subscribers full access to all of the ESPN+ sports content while inside Disney+ (similar to experience offered to bundle subscribers with Hulu on Disney+)

- Will also make select ESPN content available all Disney+ subscribers, including certain live sports events and games, as well as studio shows, series, and documentaries

- ESPN flagship will be available on Disney+ and within the ESPN App in early fall 2025: Subscribers to the flagship product and Disney+ will have access to the full suite of ESPN and ESPN+ content within Disney+

- The flagship experience within the ESPN App will give subscribers access to an enhanced array of digital features, such as fantasy sports, integrations, enhanced statistics, betting features, and e-commerce to accompany ESPN’s full package of sports programming

- In addition to viewers, will also be a “very compelling” offering for advertisers: Offers a combination of live sports, which is “extremely attractive” to advertisers, as well as ad tech that Disney already has built and continues to improve

- Will be an investment in 2025 which mgmt. expects to pay back “relatively quickly” in 2026

Still Seeing Strength In Linear TV, Especially in Live, And Is Complimentary To Streaming Offering / No M&A Or Divestiture Plans On The Horizon

- Didn’t provide specific guidance on Linear biz outlook but gave some incremental commentary – “We modeled that it would continue to decline” BUT “we have a bit of a natural hedge in the way that our portfolio operates”

- “Well-positioned” regardless of whether consumer decides to stay in linear longer or move over to the streaming side

- “I think in many ways, we’re sort of a must-have platform inside of most households”

- While linear TV faces challenges, it is “very strong” right now and, in conjunction with streaming, provides a compelling offering to advertisers

- Integrating linear and streaming platforms (i.e., simulcasting NFL games on both ESPN and ABC) creates value by offering advertisers access to broader, differentiated audiences

- Additionally, proprietary adtech stack and ability to serve targeted ads more effectively to consumers, esp in the streaming biz, is a competitive advantage

- Also “working well” selling inventory with Google and YouTube, allowing advertisers to reach differentiated audiences through The Trade Desk platform, which Disney’s adtech enables

- “We certainly feel optimistic about our ability to gain share in advertising based on that”

- Given Comcast’s plans to spin off its cable networks, would Disney consider a similar move? “We don’t really need more assets right now, either from a distribution or from a content perspective”

- Highlighted 20th Century Fox acquisition in 2017, which boosted content and distribution for streaming (came w/ control and ultimately ownership of Hulu

- While I think we’ll always look opportunistically at opportunities…we, in many respects, have already consolidated”

- Also “absolutely did not see” see an oppty to create value through divestitures

- Highlighted 20th Century Fox acquisition in 2017, which boosted content and distribution for streaming (came w/ control and ultimately ownership of Hulu

- Clarified that the DirecTV deal structure is not indicative of the future structure of deals: Deals are tailored to the unique circumstances of each partnership

Experiences Was Slightly Weighed Down By International In FQ4 / But Seeing The Consumer “Strengthening” in FQ4 And Expect That Continue Into FY25

- FQ4 Experiences beat on rev but slightly missed on op income

- Rev – BEAT by +0.7%: Increased +1% y/y (vs +2% y/y in FQ3)

- Op income – MISSED by -0.1%: Decreased -6% y/y (vs -3% y/y in FQ3)

- FQ4 Parks & Experiences breakdown by geography – Growth in domestic op income was more than offset by a decline in international

- Domestic rev grew +3% y/y, and op income was up +5% y/y

- Op income growth was driven by higher guest spending, partially offset by higher OpEx and costs related to new guest offerings driven by Disney Cruise Line pre-opening costs associated with recent fleet expansion

- International rev fell -5% y/y, and op income was down -32% y/y: Decrease in op income reflected –

- Op income was impacted by Shanghai Disney Resort driven by lower attendance, Disneyland Paris reflecting the impact of the Olympics, and higher costs related to new guest offerings

- Domestic rev grew +3% y/y, and op income was up +5% y/y

- Drill down on Experiences op income guidance … “We certainly feel like the consumer is strengthening… our expectation going forward is a gradual strengthening in the consumer”

- FY25: +6-8% op income growth compared to FY24’s +4% y/y, weighted to H2 of the yr (bookings in H2:FY24 are positive, and are “optimistic” about how bookings are looking getting into H2:FY25)

- FQ1 op income adversely impacted by ~$130mn due to Hurricanes Helene and Milton and ~$90mn due to Disney Cruise Line pre-launch costs

- Will then turn positive in FQ2 and see further strengthening over the course of the yr, driven by new Disney Treasure cruise ship, overlapping FQ4 labor costs in Disneyland Resort, and expectations of consumer to “gradually strengthen” through the yr

- FY26: Accelerate to high single digit op income growth compared to FY25

- FY25: +6-8% op income growth compared to FY24’s +4% y/y, weighted to H2 of the yr (bookings in H2:FY24 are positive, and are “optimistic” about how bookings are looking getting into H2:FY25)

- Disney Cruise Line growing to 6 ships, with 7 addtl ships currently in development

- Unveiling Disney Treasure next week, growing ship fleet from 5 ships to 6

- “Robust slate of new projects coming to our parks tied to many of our popular franchises” including –

- Magic Kingdom is undergoing the largest expansion ever, including a new area inspirited by Cars and a Villains themed land

- Monsters, Inc. themed land coming to Hollywood Studios

- New areas with attractions themed to Encanto and Indiana Jones coming to Disney’s Animal Kingdom

- Doubling the size of Avengers Campus with two new attractions at Disney California Adventure

- First-ever ride-through attraction themed to Coco at Disney California Adventure

- Avatar-themed destination coming to Disney California Adventure

- First-ever ride-through attraction themed to The Lion King coming to Disneyland Paris

- How much of longer-term return on investments will come from pricing vs attendance? “It’ll be a balance of both” and “we’ll have the ability to flex that as we learn our way into it”

FQ4 Was “One Of The Best Quarters In The History Of Our Studio” / Created The Only Two $1bn+ Movies YTD

- Television branded series and general entertainment programming are performing “exceptionally well”

- Growing new audiences and won a “record-breaking” 60 Emmy awards

- Disney FX received the most awards in its history (36), including 19 awards for Shōgun, the year’s most-awarded series, and 11 for The Bear, which broke its own record with the most comedy series wins in a single year

- Momentum across the film slate – Disney became the first studio to cross $4bn globally in 2024

- “Extremely proud” of summer box office performance, fueled by the top two movies of the year to date, Inside Out 2 and Deadpool & Wolverine

- Closing out 2024 with two other “highly anticipated” titles, Moana 2 later in November and Mufasa: The Lion King in December

- Have “an extremely promising” content slate in 2025, including Captain America: Brave New World, Lilo & Stitch, The Fantastic Four: First Steps, Zootopia 2 and Avatar: Fire and Ash

- Have been seeing viewership of earlier titles of successful or anticipated releases (i.e., Inside Out 2, Moana, and Marvel movies) “spike significantly” on streaming platforms

- With upcoming releases of Zootopia, Avatar, Star War film, Avengers film, etc. in 2025 and 2026, Disney has a “strong sense that they’re going to enable us to strengthen our streaming performance”

Spotify’s Playbook Is Working… 2025 Becomes The Year Of Growth WITH Profitability

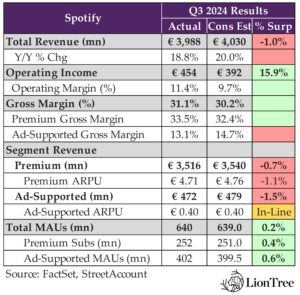

Spotify kept the tempo up and delivered ANOTHER quarter of record operating income, gross margin and FCF. In addition, while missing expectations for MAUs the past two quarters, growth is back in track, as the Co outperformed on that metric this qtr (Premium subscriber adds and ad-supported MAUs both beat forecasts).

However, revenue was the laggard in the quarter, missing consensus expectations by -1.0%, with performance on both the premium and ad-supported side coming in lower than expected due to currency and advertising headwinds. Those headwinds are expected to continue into Q4, causing revenue guidance to come in -3.8% below forecasts. Nevertheless, the company is delivering on its promise that 2024 would be the year of monetization and is setting the stage to evolve into “Growth WITH Profitability” in 2025, which went over well with investors.

Of the several initiatives that Spotify has in the works to build towards that 2025 vision, analysts were particularly interested in updates on the advertising front. The reliance on brand advertising, which is heavily influenced by broader market trends, weighed on Q3. The Co is very focused on diversifying into more performance-based svs advertising through its Spotify Ad Exchange, but it is still in the early days. 2025 will be a year of testing, with a more material impact expected to be seen in 2026. Other initiatives across AI, video, podcasts, audiobooks, courses in the UK, and other new features on the platform continue to drive engagement, and the Co’s underlying relentless focus on the LTV/SAC ratio will ultimately drive future price increases and contribute to a strong sustainable top-line growth profile.

See below for more on what we thought was most interesting from Spotify’s quarter.

-> Spotify shares rose +11.4% following earnings and ended the week up +14.4%; YTD, Spotify stock is trading up +143.9%

Another Qtr Of Record Gross Margin, Op Income, And FCF Far Outweighed The Small Miss On Rev In Q3

- Q3 rev came in slightly below expectations – MISSED by -1.0%: Total revs grew +19% (decel from +20% y/y in Q2) to €4.0bn

- Premium rev (88.2% of total) – MISS: Grew +21% y/y (in-line w/ Q2)

- Ad-supported rev (11.8% of total) – MISS: Grew +6% y/y (decel from +13% y/y in Q2)

- Q3 gross margin sets another record / saw cont’d expansion and outperformance, driven by the premium segment: 31.1% vs cons 30.2%, up +473 bps y/y

- Premium gross margin – BEAT: Grew +436 bps y/y to 33.5% vs cons 32.4%, driven by favorability in music, audiobooks, and Other Cost of Revenue

- Ad-Support gross margin – MISS: Grew +486bps y/y to 13.1% vs cons 14.7%, driven by favorability in music, podcasts, and Other Cost of Revenue

- Q3 op income also set another record – BEAT by a wide +15.9%: Reached €454mn vs cons €392mn (11.4% margin vs cons 9.7%), reflecting lower personnel and related costs and lower marketing spend, partially offset by €54mn in Social Charges

- Q3 MAUs – BEAT by +0.2%: Grew by +14mn (vs +11mn in Q2) to reach 640mn vs cons 639mn

- Posted another all-time record qtr of FCF: €711mn (up from last qtr’s record of €490mn), driven by improved op income profile, as well as net working capital favorability

Premium And Ad-Supported Were Both A Drag On Rev Given Lower Than Expected ARPU / BUT MAUs Outperformed In Q3

- Premium revs growth of +21% y/y or +24% y/y ex-FX (vs +21% y/y or +22% ex-FX in Q2) and missed expectations; Growth was driven by –

- Premium subs growth of +12% y/y, or +6mn, to 252mn (1mn above guidance)

- Reflects q/q and y/y growth across all regions, with outperformance led by Europe and LatAm

- Continued strong promotional campaign performance due to top-of-funnel health

- ARPU growth of +9% y/y or +11% y/y ex-FX (vs +8% y/y or +10% ex-FX in Q2) to €4.71

- Ex-FX, ARPU performance was driven by price increase benefits, partially offset by product/market mix

- Premium subs growth of +12% y/y, or +6mn, to 252mn (1mn above guidance)

- Ad-Supported revs grew +6% y/y or +7% y/y ex-FX (a decel from +13% y/y or +12% ex-FX in Q2) and missed expectations

- Q3 was another qtr of “volatile” marketer spending on brand-related campaigns

- Saw y/y growth across all regions

- MAUs grew +11% y/y (vs +14% y/y in Q2)

- Q3 advertising growth drivers –

- Music advertising was driven by growth in impressions sold, partially offset by softness in pricing

- Podcasting advertising was driven by growth in impressions sold, partially offset by softness in pricing

- The Spotify Audience Network saw high single digit Q/Q growth in participating publishers (saw “seq growth” last qtr)

- What drove the turnaround in MAU from Q2 (missed guidance by -5mn) to Q3 (beat guidance by +1mn)?

- Stronger engagement, which translated to more MAUs through –

- Product improvements (main change) – “lots of small tweaks that have been driving good results”

- “Things in the past that probably weren’t smart, we reversed”

- Added new features

- Improvements in marketing strategy, due to –

- Increased marketing spend due to improved efficiency in its advertising approach, as reflected in favorable SAC-to-LTV ratios

- If these favorable ratios continue, Spotify will strategically invest in marketing to further accelerate growth

- Stronger engagement, which translated to more MAUs through –

On Track For First Full Yr Of Op Income Profitability / 2025 Will Be A Yr Of “Growth WITH Profitability”

- Q4 revenue guidance – MISSED by -3.8%: €4.1bn vs cons €4.26bn

- FX rate headwinds expected to continue into Q4 and impacted outlook by ~€80mn

- Y/Y ARPU growth expected to “slightly reduce” y/y: While new pricing will contribute towards ARPU growth in Q4, the impact of last year’s price increases in 63 markets will slightly reduce ARPU growth by ~4% y/y ex-FX

- Q4 gross margin guidance – BEAT: 31.8% vs cons 30.8%

- Q4 op income guidance – BEAT by +10.3%: €481mn vs cons €436.1mn

- Q4 MAU guidance – BEAT by +0.9%: 665mn vs cons 659.3mn; Implies addition of ~+25mn net new MAUs in Q4

- Total premium subscribers expected to reach 260mn, implying the addition of ~+8mn net subs in Q4

- Guidance drivers: Incorporates the “very low levels of churn” expected in the 6 markets that they recently announced price increases in, as well as ongoing actions to drive better subscriber monetization

- Incremental guidance commentary beyond Q4 –

- FY24 expected to be SPOT’s first full year of positive op income of €1.4bn

- In the long run, see “substantial runway” to grow margins and income, which will be driven by continuing focus on improving their product and bizs via targeted investments, disciplined management and improving monetization

- 2023 was about efficiency, 2024 was about monetization, what will 2025’s story be? “Growth WITH Profitability”

- “It’s really proven that it’s not just about growth or just about profitability, but that we can deliver both at the same time”

- Drivers in achieving the long term +20% annual revenue growth goal set out in 2022 Investor Day?

- Room for continued market penetration: Spotify currently has 640mn users, and there are 3bn+ people worldwide interested in music

- Price Increases: Spotify has successfully raised prices in the past, and “nothing” indicating they can’t in the future

- Improving monetization strategies and closing the gap between value and price

- More variations/SKUs in subscription biz

- Faster advertising growth

Big Initiatives Are Underway In Spotify’s Advertising Business Which Should Impact The Biz In 2026

- Still “early days” for Spotify Ad Exchange – 2025 will be a year of testing, and the Co will see the impact going into 2026

- Current ad biz is “heavily reliant” on direct sales and top funnel brand spend, which are influenced by broader market trends

- To diversify into more performance-based svs instead of brand, have created the Spotify Ad Exchange and are testing integration with The Trade Desk

- “We are new to the auction environment, and it’s important that we are very deliberate and careful about how we roll out and supply into these channels”

- Ad rev is growing slower than MAUs (+6% y/y vs +11% y/y in Q3, respectively) – Is programmatic the only solution to fill the gap? Programmatic is a “big part” of the solution, but Spotify is also working on –

- Self-serve platforms like SPOT’s Ads Manager and launching a new supply-side platform (SPOT’s Ads Exchange)

- Improving measurement and diversifying ad formats

- Auctions, which comes with programmatic and is a new approach for Spotify and will be important for the ad strategy moving forward

- Thoughts on charging a small subscription fee to ad-supported users in more mature markets? “Always open to considering how we evolve our opportunity”

- BUT regulatory restrictions around music are a consideration…: Unlike video, where ad-supported models with fees are more common, the music industry has unique regulatory challenges, including widespread ad-supported music that’s already available (i.e. radio) and likely not going to change

- … And differ from those around video: “I don’t think we can just overlay what happened in video and say, hey, let’s do the same thing in music because it’s a very, very different regulatory environment and very different industry environment.”

- Already playing a “pretty big role” on the sports advertising side and is a “great driver” for Spotify with advertisers and consumers

- The Ringer is an example of a podcast that’s doing “phenomenal” on the podcasting side

Unrelenting Focus On Deepening Consumer Value Underpins SPOT’s Initiatives Across Price Increases, Platform Features, Subscription Product Offerings, Partnerships With Labels, And More

- “We feel really good about the proposition of Spotify and our value-to-price”

- Are the price leader in many markets

- Strategy is to continue to focus on LTV to SAC ratio in the near- to mid-term… and price increases will follow: “How do we constantly and relentlessly add more and more value to our consumers? Because we know that if we focus on that, eventually price will be there for us to take, as I think we’ve proven this year”

- Adding new ways for people to engage with Spotify, as well as making smaller incremental improvements, both of which are driving “great results”

- AI, video, podcasts, audiobooks, courses in the UK, and other new features are all contributing to more ways for users to engage with the platform

- AI DJ and music videos in particular are “exceptions” in driving user engagement and are “moving averages”

- People who are using music videos have “significantly higher” engagement and retention than ones that don’t

- Similar pattern with AI DJ – seeing “amazing” results, “not just on quantitative metrics, but also on quality metrics”

- “Excited” about upcoming “super-premium” product offering that “creates something that consumers love, but…also delivers value back to creators”

- Didn’t share specifics, but implied that the product will focus on things superfans value, like closer connections to artists and higher sound quality

- “This higher-priced music tier of Spotify is certainly one that I think will have a lot of growth for the music industry and something that consumers will love too”

- Also open to exploring partnerships with record labels considering launching superfan apps

- Vague commentary on speculation of record labels wanting a per-subscriber model vs Spotify’s variable pricing: “We have a very healthy relationship with our partners, and we’re constantly discussing what the future of the model will be and how this can provide growth for the music ecosystem”

Updates On SPOT’s Other Initiatives – Podcasts, Audiobooks, And Marketplace

- Audiobooks – The Co reached 1-yr mark since launching audiobooks offering and is “very excited” about ongoing progress

- Have more than doubled # of titles available since launch

- Seeing “strong, strong, strong” adoption across the board, and adoption per user is also growing “very nicely”

- In the US, among the audiobook users, seeing 5+ hrs more consumption per Spotify users

- Podcasts – Views on competitive landscape and regulatory restrictions

- Spotify’s competitive position vs YouTube in the video podcasting space? Spotify has always faced competition from larger platforms, but instead of focusing on that, they focus on understanding the needs of creators and consumers

- Not seeing a winner-take-all dynamic: Creators often want to be on multiple platforms

- Working to have established creators share more of their content on Spotify: Many creators are already on Spotify, but they often only share part of their content, and Spotify wants to enable more ways for them to add more content to Spotify

- Oppty for Spotify to earn rev when podcasters use paywalls on Spotify? Challenges in the near-term in ability to do so

- Held back by app store rules, which currently limit Spotify’s ability to support direct upsells and offer addt’l paid options within the app

- “But in theory, we could, and I think our partners would like for us to help drive their businesses, and we obviously would love to do so too”

- Spotify’s competitive position vs YouTube in the video podcasting space? Spotify has always faced competition from larger platforms, but instead of focusing on that, they focus on understanding the needs of creators and consumers

- Marketplace – “Very pleased” with it, with growth being driven by –

- Near-term growth being driven by increased # of artists and label teams using Marketplace and product updates including giving marketing teams more control over campaigns and better integration with their existing tools

- Long-term growth initiatives include improvements on the merchandising front, especially around how the music releases and Marketplace products show up to user (i.e., have been adding music videos on a product, which has shown to drive a “significant uptake” in streaming share)

Recognize That What’s Unfolding With AI Is An “Inflection Point” And Are “Building For A Future Full Of Possibility”

- In the near term, see potential for “transformative” shifts in music discovery and “new, innovative ways” to connect artists and fans “like never before”

- Approach to investments in long-term AI growth? “This is not reckless spending…we’re going to be highly disciplined in what we do”

- “Unlike other AI companies, this is not CapEx intensive for us. This is purely based on usage when we find it”

- “If we see something that we think will drive meaningful engagement or retention uplifts, it is in the best interest of Spotify…to pursue that. And if that means that there are shorter-form trade-offs, where numbers on a margin perspective will go down for a little bit of a while, we’re still always happy to make that trade-off”

It’s Never A Dull Moment When Talking About The Liberty Media Complex…

Liberty Media likes to have something new to talk about at its annual investor meeting every November, and this year seemed to take that to a new level. Not only was there the surprise announcement that the Co is spinning off Liberty Live, but also the surprise news that Liberty Media CEO Greg Maffei was stepping down after almost two decades at the company. The Charter deal to acquire Liberty Broadband was also announced but was somewhat expected, given previous disclosures. All-in-all, the aim of the asset shuffling is to simplify the structure, help reduce trading discounts, and enhance trading liquidity.

Regarding other updates from the almost full day analyst meeting, there was certainly a lot covered, but we wanted to highlight a few comments that we thought were particularly incremental regarding potential consolidation and AI impacts… see below.

Simplifying Structures… Key Announcements

- Greg Maffei is stepping down from CEO & President of Liberty Media

- Will leave at the end of the year

- Will transition into an advisory role

- John Malone, the company’s chairman, will serve as interim CEO

- Liberty is spinning-off Liberty Live Group

- The new entity Liberty Live will hold ~69.6mn shares of Live Nation shares and Quint will be reattributed from the F1 group in exchange for certain private assets

- Why?

- Simplifies Liberty Media’s capital structure

- Reduces the discount to net asset value of Liberty Live stock

- Enhances trading liquidity at both entities

- Post spin-off, Liberty Media will hold motorsport businesses and related sports investment

- Liberty Media and Liberty Live will be separate publicly traded companies, and Liberty Media will no longer have a tracking stock structure

- Liberty Media expects to complete the split-off in H2:25

- Charter Communications has reached a deal to acquire Liberty Broadband in an all-stock transaction

- Liberty Broadband owns 26% of Charter shares

- Will spin off the GCI business to Liberty Broadband shareholders before the deal closes

- The transaction is expected to close on June 30, 2027

A Few Key Snippets From Liberty’s Investor Day Q&A

- More industry consolidation should happen, per John Malone: “The world has changed”

- Cable is limited by its footprint, while tech has no limitations: Charter is limited, as it only covers 30% of the US terrestrial footprint, while the big tech guys cover the globe

- “Charter should be allowed to merge with Comcast or Cox or T-Mobile or anybody… That would reduce capital intensity, improve efficiency, maintain competition, and improve the quality and cost effectiveness of the services they provide”

- “And I think tying an industry’s hands behind its back and allowing big tech to run wild in every direction that they choose to run in, I think, is inappropriate.”

- AI is having a tangible impact… Charter CEO Chris Winfrey provided some great color about AI utilization in their call centers today:

- The customers’ voice is their ID when they call in

- AI-driven conversational interactive voice response are taking 10% of calls -> that will increase to 50% at the end of this year

- These bots are “doing a great job”; Customers are “thanking them”…”the AI is that good”

- When a human agent fields the call instead:

- The AI gets them the right information on the screen

- “The AI is listening to the phone call with the customer in parallel and checking the telemetry, last billing call, last repair call, and prompting the agent based on the tone of the call, based on what the customer’s saying with real live voice-to-text translation feeding to the agent says this is the next best action.”

- The AI provides a summary of the call so when a field tech goes out, they have all the notes as well

- “We deal with millions and millions and millions of transactions every day. We don’t need to have an agent trying to figure each individual, one of those transactions. The machine can, for the most part, do that and provide better service; get the customer off the call faster which is in the customer’s interest…The agent finishes the call happier.”

- “But most of what we’re seeing, the benefit is to make the job better, easier and more effective for the call center agents and the field techs as well. I mean, I could go on and on, I won’t, but applications are pretty limitless”

- Will you have more F1 races? No – 24 races is the max practical limit due to the strain it places on teams and logistics

- Competitive risk from Starlink in the broadband area? Right now, it works well in low-density areas but faces congestion issues in denser areas, making it less competitive with fiber in urban regions

- Timing of MotoGP deal close? Mgmt feels confident it will close by the end of the year

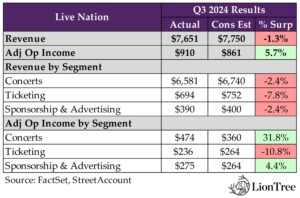

Expect An Even “Bigger Year” For Live Nation In 2025

Live Nation’s “highest ever” quarter of Concert profitability (Concert AOI beat consensus by +32%) was a key highlight, along with bullish commentary about the profitability AND demand picture for 2025. Overall AOI growth for 2024 is pacing toward a double-digit rise, and 2025 should be an even higher growth year. That more than offset any disappointment about the greater than expected y/y decline in Concert revenue due to fewer stadium shows.

Activity YTD is demonstrating a win-win situation on both the fan and artist side, as fans are not only coming out to concerts (up +3% YTD), but artists are making more money (+30% more per show when playing the same amphitheater this year vs 2022/2023). Activity looking ahead continues to be robust, with tickets sold globally in Sept and Oct up +20% y/y. It was also positive to hear that the 2025 show pipeline is “up double digits.”

On the venue front, Venue Nation is expected to host ~60mn fans and is expected to grow by an incremental +8mn in 2025 as it adds/refurbishes 14 additional venues through 2025. A particular area of focus is the “premium” experience, as premium inventory is always high in demand and the first to be sold out, and an increase in supply will in turn bring about a “much better return.” Three-fourths of CapEx is being driven by Venue Nation, and to flag, 2024 CapEx guidance was increased from $650mn that was guided last qtr to $700mn due to the addition of an amphitheater project.

It was a tougher quarter for Ticketmaster, as the segment missed on both revenue and AOI, but a turnaround is expected starting in Q4 as it enters a period of “unprecedented level of activity” (200+ stadium and arena shows are going on sale just next week). This will continue through next year, given that 2025 is expected shake out like 2023. While Ticketmaster continues to be the subject of a DOJ lawsuit, mgmt expressed hope for “a return to the more traditional antitrust approach” with the new administration.

Lastly, Sponsorships & Advertising had mixed performance, as revs missed by -2.4%, but AOI beat by +4.4%. Globalization will be a key factor in driving Sponsorship revenue in the future.

See below for what we thought was most incremental from Live Nation’s qtr. Also, see Theme #4 for Liberty Media’s announcement on Liberty Live.

-> Live Nation traded up +4.7% on the back of results which is the fifth qtr in a row w/ a positive stock reaction to results; YTD, the shares are up +37.8%

Q3 Missed On Revenue (Across All Segments), But Concerts Propelled Top-Line Profitability

- Revenue – missed by -1.3%: Down -6% y/y (vs +7% y/y in Q2) to $7.7bn

- Missed across all segments due to the reduction in stadium show volume this year

- Adj op income – beat by +5.7%: Up +4% y/y (vs +21% y/y in Q2) to $910mn

- Concerts and Sponsorship & Advertising segments beat, while Ticketing missed due to the reduction in stadium show volume

FX Headwinds & Increased CapEx Will Not Have Substantial Impact To Q4

- FX impact to rev is expected to accelerate in Q4 and weigh on AOI (YTD, FX impact to rev, op income and AOI has been ~1%)

- Acceleration is notably due to exposure from LatAm currencies, and could impact operating income by more than -30% and AOI by ~-mid-teens% for the qtr

- But “don’t think it’s a material 2025 issue at this point”

- Raised 2024 CapEx guidance from $650mn to $700mn

- What drove the increase? Finalized a formal agreement to co-develop an amphitheater w/ a partner, which required shifting the project’s CapEx onto its book; $50mn expected CapEx increase includes $30mn from the partner, so Co’s net cash contribution is lower than the full CapEx

- Three-fourths of total CapEx driven by Venue Nation: 5 venues account for ~45% of total venue spend

- Now have $130mn in committed capital from third parties (up from $100mn guided in last qtr), including sponsorship agreements, JV partners, and other sources, reducing cash flow

- Pacing toward double-digit AOI growth for the year, which will be impacted by one-time accruals

Bullish On The Year Ahead…Expect “Even Bigger” Growth 2025

- “Leading indicators point to more growth in 2025”

- 20mn+ tickets already sold for Live Nation concerts in 2025, pacing up double-digits

- Concerts pipeline in large venues is growing, up double-digits vs this point in 2023 (include stadiums, arenas, and amphitheaters)

- Stadium pipeline up double-digits vs this point in 2022

- Recent 2025 stadium onsales are delivering double-digit avg growth in show grosses relative to past tours

- 2025 onsales called out include Coldplay, Rüfüs Du Sol, and Shakira

- Sponsorship momentum continues, with commitments pacing up double-digits

Posted “Highest Ever” Concert Profitability While Hosting Fewer Stadium Shows In The Qtr / Expect “Strong” Concert Revenue & AOI Growth In 2024

- Concerts missed on rev, but posted a notable beat on the profitability front

- Rev missed by -2.4%: Fell -6% y/y (vs +8% y/y in Q2) to $6.6bn

- Adj op income beat by +31.8%: Grew +39% y/y (vs +61% y/y in Q2) to $474mn

- Saw “record” AOI margin of 7.2% (vs 5.4% in Q2) and is on track to deliver 2024 margins towards pre-pandemic levels

- The y/y revenue decline was driven by fewer stadium shows and fans in Q3

- The total number of events was ~12.8K, up +6% y/y

- The number of fans was 50mn, down -4% y/y: Due to fewer stadium shows partially offset by more fans attending arena shows as well as theaters and clubs

- Saw double digit arena fan growth globally, most notably in the US

- YTD artists grossed +30% more per show, on avg, when playing the same amphitheaters this year vs 2022 / 2023, offsetting rising show costs

- Tickets sold globally in Sept and Oct are up 20%+ y/y, reflecting “continued strong demand”

- FY24 concerts outlook: Expect “strong” revenue and AOI growth, driven by continued growth across arenas, amphitheaters, and stadiums

- Margins are expected to land around 2019 levels

-

Lots In The Works On The Venue Front, With Premium Experiences A Particularly Beneficial Growth Oppty

- For 2024, Venue Nation expects to host ~60mn fans, up +8% y/y (vs +13% y/y in 2023)

- Made 3 “major enhancements” to venue portfolio this year…

- Estadio GNP (Mexico City) reopened this summer, with avg net per fan spending up +20% compared to pre-renovation levels

- Northwell at Jones Beach amphitheater (New York) reopened after a successful renovation; Season seat and box suite sales were up +50%, food and beverage net per fan spending are up double-digits, and VIP club sales are up +50%

- Brooklyn Paramount (New York) opened earlier this year, and its VIP Club is generating +30% more rev per show relative to VIP clubs at other top performing theaters in the US

- Aand have plans to add or refurbish an addt’l 14 venues through 2025, which is expected to increase capacity by an incremental +8mn fans

- Fans continued to seek premium offerings in Q3…

- Rev from premium VIP tickets at major festivals (100k+ fans) are up over +20%

- Rev from amphitheater VIP clubs increased by +19%

- … And serving the “premium” fan continues to be an ongoing focus: Expect percentage of premium fans at a show to grow to be up to exceed 20% of a show

- “But we always sell out of the boxes, sell out of the premium inventory first. We never have a problem selling”

- “Premium experiences [are] a big underpin to our entire growth forward… We think that is a big part of our CapEx”

- On refurbishments: Several refurbishments they’ve been doing at venues have been around taking regular seats and turning them into premium experiences

- On new building: Starting new buildings with a mandate that they must have a certain higher %age of premium seats, lounges, and experiences; “So those venues start with a much better return”

- Average net per fan spend has been pacing up YTD

- At Live Nation amphitheaters, avg net per fan spending grew over +$3 per fan (up +9%) for the same artists’ shows in 2024 relative to 2022/2023

- Globally, major festivals (100k+ fans) avg net per fan spending was up double-digits for repeating events

- What’s been driving the growth? Improvements in food and beverage offerings across new, high-end venues; Upgraded stadiums and arenas now offer more points of sale (POS), premium food options, mocktails, and non-alcoholic drinks

- Expect to continue growth of ~+$2/head annually by enhancing selections, POS, and premium choices in amphitheaters, theaters, and arenas, with “significant” potential for further gains

After A Weaker Than Expected Q3, Ticketmaster Is Entering A Period Of “Unprecedented Activity” in Q4 (Which Will Continue Into 2025)

- Misses across rev and profitability for ticketing

- Rev missed by -7.8%: Fell -17% y/y (vs +3% y/y in Q2) to $694mn

- Adj op income missed by -10.8%: Fell -33% y/y (vs flat y/y in Q2) to $236mn

- The “unprecedented” volume of stadium sales last year weighed on Ticketmaster’s Q3 rev and ticket sales

- Fee-bearing tickets sold in Q3m was ~83mn, down from 89mn in the prior yr qtr

- Despite the venue mix change, Q3 was the fourth highest ever in terms of sales volume and the third highest ever with respect to GTV

- International Ticketing also had its single biggest sales day ever in Sept 2024, driven by outstanding demand for Coldplay tickets in Europe

- What investments is Ticketmaster making to reinforce and extend its competitive position technologically? Spent “tens of millions of dollars” in capital, including on –

- Advanced pricing tools for venues and promoters to assess ticket market value

- Enhanced marketing capabilities to promote shows

- High-demand on-sale management for a better buying experience

- Digital ticketing innovations and anti-bot technology for consumer protection

- Ongoing tech development for both enterprise and consumer-facing solutions

- “We think Ticketmaster is the best in the world and seen a number of on-sales recently where Ticketmaster has been able to deliver a much better experience and sell tickets at a volume that others have been unable to handle”

- Looking ahead into Q4 and next year –

- Q4 will be “very strong”

- Oct transacted ticket sales were up +15% on all ticket volume and up +23% for concert events, including Live Nation shows

- 2025 will “look more like 2023”; FY AOI margin is expected to be similar to last year

- Q4 will be “very strong”

Globalization Will Help Drive Future Growth In Sponsorships

- Sponsorship rev missed, but profitability beat

- Rev missed by -2.4%: Grew +6% y/y (vs +3% y/y in Q2) to $390mn

- # of strategic partners who generate $1mn+ per year increased by 20% and drove majority of the rev growth

- Adj op income beat by +4.4%: Grew +10% y/y (in-line w/ Q2) to $275mn

- Growth largely driven by on-site platforms, international markets, and ticket access deals

- Rev missed by -2.4%: Grew +6% y/y (vs +3% y/y in Q2) to $390mn

- Most of the growth in # of partners generating $1mn+ is coming from the existing customer base

- Most expansion has come from current customer base of 900-1000 sponsors and growing with them, as well as expanding outside markets

- Have been able to upgrade customers once they’ve gotten into the Live Nation ecosystem and been able to understand their brand needs

- Expanded beauty and fashion portfolio at more global festivals, including brands such as American Apparel, Wrangler, Ulta Beauty, and American Eagle in Mexico

- FY24 sponsorships outlook: Full-year AOI margin expected to be “similar” to last yr

- One of the “foundational drivers” is globalization: As they do more shows around the world (i.e., LatAm, India, Middle East, Singapore, Australia), it provides more inventory to open “new borders and new relationships”; “As our global pipe continues to grow, so will our sponsorship, and we’ll see continued growth”

Anticipate Regulatory Environment To Ease Up With New Administration / But No Changes To M&A Strategy

- No changes in M&A strategy – “Nothing’s changed over the last two years, and don’t think anything changes going forward”

- “We don’t have any sizable M&A targets that we would do with or without where the regulation stands in America”

- Impact of Trump presidency on biz? “We are hopeful that we’ll see a return to the more traditional antitrust approach”

- Request to breakup Live Nation and Ticketmaster is a “highly interventionist approach”, which is generally unlike a Republican administration, “where the agencies have generally tried to find ways to solve problems they see with targeted remedies that minimize government intervention in the marketplace”

- Continue to hope for better regulation around secondary mkt: “America seems to be a market where secondary is free to run” and there “seems to be more and more attention around the secondary market”; The Co “hope[s] over time [that] better regulations get put in place to help the consumer”

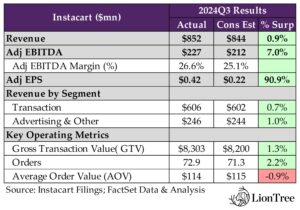

Deepening Relationships With Retailers Is Instacart’s “Secret Sauce” But Is Also “Under-Appreciated”

Competition concerns for Instacart recently resurfaced following news that Amazon in experimenting with new formats to drive deeper into the grocery delivery business (link); however, Instacart continues to deliver upside to Street estimates. For the third consecutive quarter, the Co’s Q3 headline results broadly surpassed sell-side expectations, as “very strong customer demand” helped drive a +1.3% beat on gross transaction value (GTV), which flowed into +0.9% and +7.0% respective beats on revenue and adj EBITDA. Notably, Instacart has not seen any evidence of “meaningful trade down” despite a focus on increasing affordability to attract more price-conscious consumers (savings per order on the company’s platform rose +18% y/y to $5.35 in Q3). This contributed to a sequential acceleration in GTV growth to +10.8% y/y from +9.7% y/y in Q2, and a recent integration with Kroger, combined with the solid uptake that the Super Saver fulfillment option has seen, should provide further opportunities for the company to grow in the value segment ahead.

On the advertising side, revenues also outperformed estimates, though growth was flat sequentially amid continued pullbacks from certain large CPG brands. Nonetheless, “strength among emerging brands”, ongoing efforts to diversify supply & demand, ad format innovation and new measurement tools, plus encouraging progress with the Carrot Ads retail media network are all signs that the ads business has been building momentum towards accelerating growth.

Looking past Instacart’s stronger than expected Q3 results, the Q4 outlook disappointed investors. The GTV growth guidance implies a sequential slow down to +8-10% y/y (vs +10.8% y/y in Q3), given tough y/y comps from last year’s “meaningful” step-up in incentive spend as well as a “small impact” from Ahold Delhaize’s recent outage. The Q4 adj EBITDA guidance was also -3.1% below consensus, as “positive seasonality” is expected to be offset by investments in service enhancements. Still, Instacart believes that it is well-positioned competitively. The scope and depth of the company’s retailer integrations are really its “secret sauce” and “create a really big competitive advantage compared to other platforms,” based on the “slow” integration process and the necessity of becoming “deeply embedded” with retailers’ IT departments. CEO Fiji Simo believes these dynamics are “under-appreciated”, but Instacart still needs to prove to the market that it can sustainably increase its growth rate and capture a greater share of the $1.1tn grocery market laid out in the company’s S-1. Instacart’s other initiatives, including the nascent and “promising” restaurant business, will also drive growth moving forward, and although the “operationally heavy” Caper Carts will “take time” to roll out, they open up another big opportunity.

Lastly, the Co authorized another $250mn increase to its buyback program. See below for more of what we thought was most interesting and incremental from Instacart’s Q3 print:

-> Instacart shares fell -11.0% in response to earnings, ending the week down -12.0%; YTD, Instacart stock is still trading up +79.0%

Headline Results Were Broadly Better Than Anticipated…

- Rev growth decel’d seq but still topped estimates: Q3 rev incr’d +11.5% y/y (vs +14.9% y/y in Q2) but ended a slight +0.9% above cons

- Transaction rev (~71% of total) – BEAT: Incr’d +11.8% y/y in Q3 (vs +16.7% y/y in Q2) and beat cons by +0.7%; Represented 7.3% of GTV (similar to Q2); Recent improvements in transaction rev have been more related to efficiencies on the shoppers side and not related to retailer rev

- Advertising & Other rev (~29% of total) – BEAT: Grew +10.8% y/y in Q3 (vs +10.7% y/y in Q2) and closed +1.0% ahead of cons

- Adj EBITDA growth also slowed seq but exceeded expectations: Adj EBITDA rose +39.3% y/y in Q3 (vs +89.1% y/y in Q2) but still beat cons by +7.0%; The Co has been “very aggressively managing overall costs” and has the ability to pull “multiple levers… to drive leverage”, which delivered “strong profitability results across the board”

- Adj sales & mkting expenses incr’d to 2.4% of GTV (from 2.1% in Q2): The Co saw oppties to “lean into” paid mkting w/ the Olympics and other seasonal events but caveated that this uptick was not “particularly systemic in nature”

- Adj EPS of $0.42 finished a wide +90.9% above cons

… Reflecting An Outperformance On Most KPIs

- GTV growth accel’d seq and was BETTER than projected: Q3 GTV rose +10.8% y/y (vs +9.7% y/y in Q2) and beat cons by +1.3%

- Order volume OUTPACED the Street’s forecasts: Orders of 72.9mn were up +10.1% y/y in Q3 (vs +6.8% y/y in Q2) and came in +2.2% above cons

- BUT AOV FELL SHORT of expectations: Q3 AOV incr’d +0.6% y/y to $113.90 (vs $115.73 in Q2) and missed cons by -0.9%

BUT There Were Some Puts & Takes W/ Q4 Guidance

- GTV growth is expected to decel seq: Anticipates GTV btw $8,500-8,650, which would mark a +8.7% y/y increase at the mid-pt (vs +10.8% y/y in Q3); Will comp against last yr’s “strong holiday season”, given a “meaningful seq step-up in incentive spend” in the prior yr qtr

- Guidance also accounts for a “small impact” from Ahold Delhaize’s recent outage (a grocer partner)

- And the adj EBITDA outlook was underwhelming vs the Street ests: Guided for an adj EBITDA range of $230-240mn, representing a +18.1% y/y gain and missing cons by -3.1% at the mid-pt; Adj OpEx leverage will be the primary driver y/y growth in adj EBITDA (as a % of GTV)

- Advertising & Other rev is projected to grow largely in line w/ GTV guidance on a y/y basis: On a seq basis, Advertising & Other rev will improve seq due to “positive seasonality”

- SBC will also begin to normalize: Given that the Co has lapped its IPO qtr and doesn’t anticipate any further “notable one-time reversals”, such as those experienced in Q1 and Q3 2024

- Continues to expect a seasonal “step-up” in SBC in “every Q2”: Due to the timing of the Co’s annual equity refresh grants

Consumer Color – The Focus On Affordability Has Cont’d… BUT Instacart Hasn’t Seen Evidence Of Trade Down

- “We are seeing very strong customer demand”: The Co hasn’t seen “meaningful trade down” on a per item or type of item basis; There also hasn’t been trade downs across different types of retailers, though “clubs being very strong” has been a “notable exception”

- “We are also not seeing different behaviors across income segments”: Including across both the EBT customer and the non-EBT customer

- “The fundamentals remain really strong”: Given that order growth and frequency have been “going up”

- “Instacart+ subs are cont’ing to grow and outpace the growth in monthly active orders”: Instacart+ engagement has also been rising

- Instacart has been “incredibly focused” on driving affordability for more price-sensitive new customers: Savings per order incr’d +18% y/y to $5.35, as the Co’s “multi-pronged” strategy for having “the most affordable product” has been delivering returns

- The Co has cont’d to “rely on integrations w/ grocers into their loyalty programs”: Highlighted that Instacart just launched flyers w/ Kroger and that every featured item will be at parity w/ in-store prices

- The Super Saver offering has done “a really good job”: Price-sensitive new users that have used this new fulfillment option (offers a $0 delivery fee for scheduling in advance) for 1 out of every 5 orders; Has helped drive “better conversion” and “better retention”

Have Been Successful At Increasing Efficiency Of Existing Shoppers

- Shopper numbers were ~flat seq: Reported ~600k Instacart shoppers on the platform in Q3, which was similar to the figure provided last qtr

- This does not reflect an issue with shopper supply…it is “incredibly healthy”: The Co has a waitlist of shoppers in “many, many cities”

- Shopper tenure is at an “all-time high”: The majority of Instacart orders are now being delivered by tenured shoppers

- “We are simply being more efficient w/ the shoppers we already have”: Including by batching as well as adding faster times of delivery and other optimizations; “The game is not to grow the total number of shoppers” but to “actually utilize [the] shopper supply really efficiently”

- 45% of orders are now delivered by a shopper that is inside the store or within 1 mile of the store

- This does not reflect an issue with shopper supply…it is “incredibly healthy”: The Co has a waitlist of shoppers in “many, many cities”

On The Competitive Environment – Retailer Integrations Provide Instacart W/ A Deep Competitive Moat

- Instacart’s retailer integrations are “really [its] secret sauce”: Instacart is “relentlessly focused” on extending its competitive advantage “by deepening [its] retailer integrations”; This one of the Co’s “most important predictors of growth”

- Being a first-mover “creates a really big competitive advantage compared to other platforms”: Although the integration process is “slow”, given the depth of the integrations and the necessity of getting “deeply embedded w/ the retailers’ IT depts”, Instacart gets “first dibs” on their IT resources

- The Co has invested “enormously in tech” to extend its advantage in retailer integrations: Including in the following areas –

- New, “big” svs: Such as pickup, virtual convenience, bringing alcohol to the platform, and SNAP EBT; Retailers that have adopted at least one of those in the last yr have grown twice as fast as retailers that haven’t

- A new underlying tech platform is also in the works: Will enable Instacart to connect w/ more systems from retailers and to build storefronts as well as other features on the same infrastructure as the Co’s mktplace

- 2025’s tech investments will help “generate a lot of efficiencies in the biz”: The Co will leverage these efficiencies and reinvest them in other areas, including its restaurants platform, Caper Carts and other in-store tech, as well as AdTech

- Longer-term – “The grocery mkt is still vastly penetrated online”, w/ 87% of the industry still offline: Instacart is positioned to capitalize on this as “a leading online grocery mktplace” and the “clear category leader” in both small basket fill-up orders (25% of the industry) and large weekly baskets (75% of the industry)

Efforts To Create A “Virtuous Cycle” In Advertising Are Still Underway

- Ad rev growth was ~flat seq: Grew +10.8% y/y in Q3 (vs +10.7% y/y in Q2) and beat cons by +1.0%

- The Advertising & Other investment rate was 3.0%: This was consistent w/ the prior yr qtr and up from Q3’s 2.8%

- Nearly 220 retailer banners now use Carrot Ads to power their retail media biz: Compares to “over a hundred” retailer banners exiting Q2

- Instacart’s base of active brand partners was flat seq: The Co ended the last two qtrs w/ 6,000+ active brand partners

- Instacart is “making a lot [of] progress” in diversifying supply & demand in its ads biz: On the supply side, Instacart has been increasing the number of different sites where its ads appear, including ones that it doesn’t partner w/ on fulfillment; On the demand side, the Co has been “seeing strength among emerging brands”

- Emerging brands outgrew Instacart’s overall platform during the qtr: In contrast, “certain large CPGs” have cont’d to pull back on spend “for their own specific reasons”

- The Co has “very high confidence” in the performance of ads: Highlighted “direct correlations” between how much a brand spends on its platform and “how this influences their sales and mkt share”

- Ad innovations “could get ad rev to re-accelerate”: There are ongoing initiatives “to further drive demand”; The Co is cont’ing to invest in more ad formats, measurement, and targeting capabilities, as well as campaign mgmt tools

- Deeper retailer integrations have been driving growth in advertising: Every new integration expands Instacart’s scale and makes the Co’s ad network “even more attractive for brands”, given that many brands “do not want to work w/ sub-scale networks”

- Instacart expects to “further increase supply… in 2025 and beyond”: Specifically, by expanding its retail media partnerships and introducing more ad formats to Caper Carts screens, such as shoppable recipes

- Emerging brands outgrew Instacart’s overall platform during the qtr: In contrast, “certain large CPGs” have cont’d to pull back on spend “for their own specific reasons”

- The Co is “really pushing for standardization”: Was one of the first retail media networks to receive MRC accreditation and has done work w/ DoubleVerify; More standardized measurements will help “prove that [Instacart’s] ads are actually working so much better than other platforms”

Other Initiatives – Caper Carts, Restaurants, Businesses

- The number of Caper Carts available in stores has quadrupled over the last six months: Caper Carts now have been deployed across more than a dozen national, regional, and local grocers

- The Co will continue to scale Caper Cart deployments next yr: However, the “biggest bottleneck” is that it will “take time” to integrate them at grocers’ locations, given that they’re “operationally heavy”

- The Co has been seeing increases in basket sizes from Caper Cart adopters: Which has helped w/ “proving the case w/ more retailers and cont’ing to scale”

- Restaurants are seeing “promising early results” on Instacart’s platform: The thesis has been “playing out”, as when people adopt restaurants on the Co’s platform, they show better retention and spend more frequently on grocery; There’s also been “especially high engagement” from Instacart+ members

- The restaurants and grocery bizs are “essentially intertwined”: Instacart “really runs the biz as just one biz w/ multiple use cases”; Penetrating the restaurant use case also enables the Co to penetrate the grocery use case, which has been a “real positive”

- Instacart sees ”much higher basket sizes than other restaurant delivery platforms”: This reflects having customers that are “habituated… to larger baskets w/ grocery” as well as “being very strong w/ families”

- “More and more biz customers [are] placing orders on Instacart”: The Co has received 1mn+ orders from biz customers over the past yr and is cont’ing to build more solutions for them, such as the ability to export receipts, tax exemptions, and more robust biz profiles

- There’s also an advertising oppty w/ Instacart Business: By enabling brand partners to advertise on B2B platforms to influence purchasing decisions at foodservice, restaurants, bars, and SMBs in general

Capital Allocation

- Share repurchases stepped up seq: Bought back $357mn worth of shares in Q3 (vs $324mn in Q2), bringing the Co’s cumulative YTD repurchases to just over $1.4bn for 47mn shares, which represents a weighted avg price of $30.27

- The Co authorized a +$250mn increase to its buyback program: This was Instacart’s second extension of the yr, and the Co now has $318mn of buyback capacity entering Q4 (had $68mn remaining from its previous $500mn extension to the original $1bn that was authorized coming into 2024)

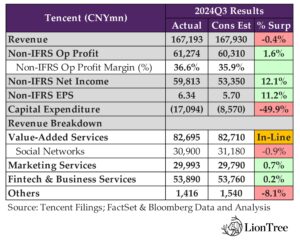

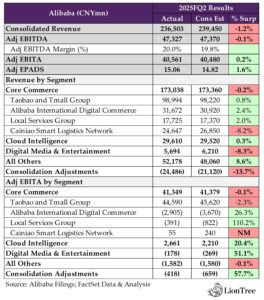

China Tech Received A “Significant” Benefit From Stimulus Measures… BUT Concerns Remain

It was a relatively somber week for the China Tech sector, as Tencent, Alibaba, and JD.com’s latest earnings results were met with a negative reaction from the market. Weak domestic spending trends had been a notable headwind during the group’s last round of earnings calls, and although management teams from all three companies offered constructive comments about the positive impact of the Chinese government’s recent stimulus measures, none of them outperformed consensus estimates on the top-line at this point. Furthermore, competition in China’s e-commerce space remains “intense”, and Tencent, Alibaba, and JD.com each have plans to continue investing in improvements to their respective e-commerce platforms to get a leg up on their peers. In contrast, trends on the bottom-line were more favorable in Q3, as all three reported better than anticipated adj EPADS. Nonetheless, the group’s prints ultimately weren’t able to assuage concerns that investors had going into the results, and the companies’ “cautiously optimistic” views of the economy failed to provide reassurance that domestic consumption trends in China are on track for a sustained recovery.

See below for more details as well as our key takeaways from their results.

-> Tencent shares were down -2.8% post-earnings, closing the week down -2.9%; Tencent Music shares fell -5.5% in response to the print but recovered slightly to end the week down -2.8%; YTD, Tencent stock is trading up +36.7%, and Tencent Music stock is up +22.9%

-> Alibaba shares fell -2.2% in reaction to earnings and ended the week down -5.9%; YTD, Alibaba stock is still trading up +14.3%

-> JD.com shares fell -6.6% in reaction to the print and closed the week down -8.7%; YTD, JD.com stock is up +21.1%

>Tencent Saw “Consistent Performance” From Its Evergreen Titles

- Tencent posted MIXED headline results: Q3 total rev was up +8.1% y/y (vs +8.0% y/y in Q2) but missed cons by -0.4%; Non-IFRS op profit incr’d +18.6% y/y (vs +26.9% y/y in Q2) and beat cons by +1.6%; Non-IFRS net income rose +33.2% y/y (vs +52.6% y/y in Q2) and topped cons by +12.1%; Non-IFRS EPS beat cons by +11.2%

- Value-Added Svs (~49% of total rev) – ~IN-LINE: Rev grew +9.3% y/y in Q3 (vs +6.2% y/y in Q2) and closed ~on-par w/ cons; Gross margin incr’d +2ppts y/y to 57% (flat w/ Q2 & Q1)

- Social Networks (~37% of VAS rev) – MISS: Q3 rev rose +4% y/y (vs +2% y/y in Q2) but fell -0.9% short of cons; Incr’d rev from music subscriptions, app-based game item sales, and mini games platform svs fees was partly offset by decr’d rev from music and games-related live streaming svs

- Marketing Svs (~18% of total rev) – BEAT: Rev was up +16.6% y/y in Q3 (vs +19.5% y/y in Q2), beating cons by +0.7%; Gross margin was up +1ppt y/y to 53% (vs 56% in Q2); The “strengthened” games and e-commerce categories outweighed “weakness” in real estate and food & bev

- FinTech & Biz Svs (~32% of total rev) – BEAT: Q3 rev incr’d +2.0% y/y (vs +3.7% y/y in Q2) but still finished +0.2% ahead of cons; Gross margin rose +7ppts y/y to 48% (flat w/ Q2)

- Value-Added Svs (~49% of total rev) – ~IN-LINE: Rev grew +9.3% y/y in Q3 (vs +6.2% y/y in Q2) and closed ~on-par w/ cons; Gross margin incr’d +2ppts y/y to 57% (flat w/ Q2 & Q1)

- Tencent is “optimistic about the economic revival” in the macroenvironment: The Chinese govt’s recent stimulus policy direction has been “very constructive”; Following gradual declines throughout Q3, the Co’s y/y growth in transaction value saw an “uptick” in Oct after the stimulus policy was annc’d

- BUT “the economic recovery [will] take some time”: Over the “long run,” Tencent “believe[s] it would definitely be re-accel’ing” b/c “there’s a very strong resolution by the govt to revive the economy”

- “There’s actually… positive structural factors in the economy”: Cited “a very strong work ethic among the workers in China, including a very deep engineering pool… entrepreneurs among Cos of all sizes… and also there’s a vast and comprehensive supply chain”

- “Younger users in China disproportionately favor first-person action games vs older users”: First-person action games have become the “dominant genre” among younger players in China and will become the dominant genre “for the China mkt as a whole”

- New first-person action games have NOT cannibalized existing ones: This is “b/c there’s so much difference… between them in terms of user tastes”; These technical differences are “too big for any single game to transcend”

- BUT “the economic recovery [will] take some time”: Over the “long run,” Tencent “believe[s] it would definitely be re-accel’ing” b/c “there’s a very strong resolution by the govt to revive the economy”

- Domestic Games rev growth accel’d seq, as flagship evergreen games “achieved healthy growth results”: Rev grew +14% y/y in Q3 (vs +9% y/y in Q2); Growth in gross receipts also benefited from “proactive adjustments” made earlier this yr

- The Co’s evergreen games delivered a “consistent performance” globally –

- Honor of Kings grew gross receipts y/y: Benefited from a Chinese Valentine-themed event in collab w/ Tencent Comics IP, Fox Spirit Matchmaker, and a “top-tier martial arts-themed outfit”

- Peacekeeper Elite incr’d gross receipts at a double-digit% rate y/y: The title “cont’d its recent rebound,” driven by items related to the Neon Gensis Evangelion anime

- Naruto Mobile grew gross receipts “robustly” y/y: This reflected higher paying user penetration for season passes; The title also achieved a “historical high” of 10mn+ qtrly avg DAUs

- New games are also showing “evergreen potential” –

- DnF Mobile ranked second in gross receipts among all mobile games in Q3: Although Q4 will be a “consolidation period” for DnF Mobile, Tencent plans to release a major content update for Chinese New Year that is “intended to further enhance user engagement and monetization”

- Delta Force is “achieving good avg user daily time spent and player retention rates”: After launching in China in Sept, the game already has several million DAUs; Plans to add a “content-centric” campaign mode and to launch the game in intl mkts “in the coming months”

- The Co’s evergreen games delivered a “consistent performance” globally –

- International Games rev growth was flat seq: Rev was up +9% y/y in Q3 (similar to Q2’s rate), though rev growth “substantially lagged” gross receipt growth b/c improved retention rates for certain titles led to elongation of their rev deferral periods; Title-specific call-outs are included below –

- PUBG Mobile incr’d gross receipts by a double-digit% y/y to a “record high level”: The title saw another “robust performance,” as Egyptian-themed outfits and Lamborghini-braded car costumes “monetized well”

- Brawl Stars’ gross receipts rose “several times y/y”: Brawl Stars remains among the Top 3 mobile games by DAU across the industry and intl mkts, w/ growth being driven by a limited time Mega Boxes even and an IP collab w/ SpongeBob SquarePants

- Valorant incr’d gross receipts over +30% y/y: The title was Tencent’s largest PC game by gross receipts, capturing share in the “reviving” PC mkt; A Chinese Team winning the Valorant Champions Tournament helped attract new players and drive gross receipts to “record high levels”

- The game also benefited from the launch of a console version and esports-themed weapon items: The Co extended Valorant to PlayStation and Xbox in North America, Europe, Japan, and Brazil in early Aug, which expanded the game’s user base