TGIF… the avalanche of key TMT earnings this week was a bit overwhelming, and we had to pick our spots (70% of the S&P 500 constituents have reported Q3 results thus far). Needless to say, there was an incredible amount of new information and updates to make sense of and piece together. The market backdrop during the week was a bit volatile as well, with the major indices ending in the red (the S&P 500 down -1.4% and Nasdaq down -1.5%).

While there will be a continued onslaught of earnings next week, the US Presidential Election is obviously going to be the main event. I’ll leave it at that!

Enjoy the weekend and the read (this is a more fulsome update than usual!)

- Earnings Scorecard – Week 3

- GOOGL & META: The AI Spending Trajectory Took Center Stage Over Core Fundamentals…

- Amazon Looks To Be Firing On All Cylinders

- Snap Makes Progress, But Its Platform Transformation Is In Transition

- Comcast & Charter Showcased The Strength Of Their Converged Offerings

- Is A Corporate Action Coming In Legacy Media? Will Comcast Spin-Off Cable Nets?

- Roku Follows In Netflix’s Footsteps With Less Disclosure Going Forward

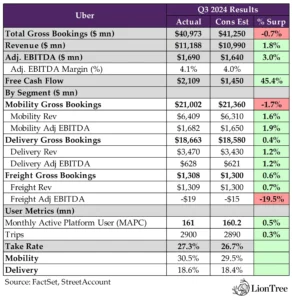

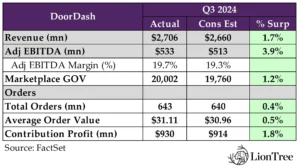

- Uber’s Mobility Gross Bookings Growth Bumps Into The Curb, Though Both Uber And DoorDash Deliver On Delivery

- Public Cloud Providers Ride The AI Wave To New Heights

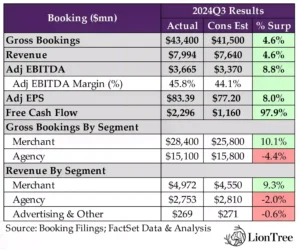

- Booking – Resilience In Travel Demand Reinvigorated Growth In Room Nights

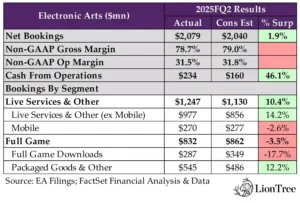

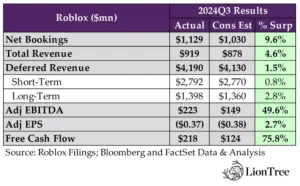

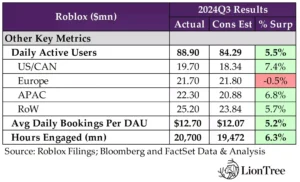

- EA & Roblox’s Prints Point To Underlying Strength In Interactive Entertainment

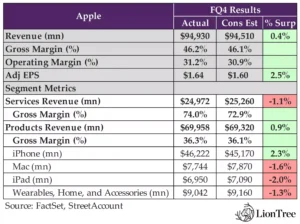

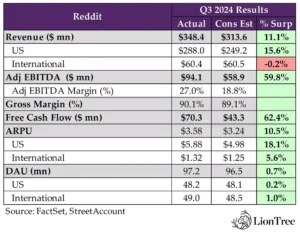

- Quick Takes On Additional Key Prints – Apple & Reddit

Best,

Leslie

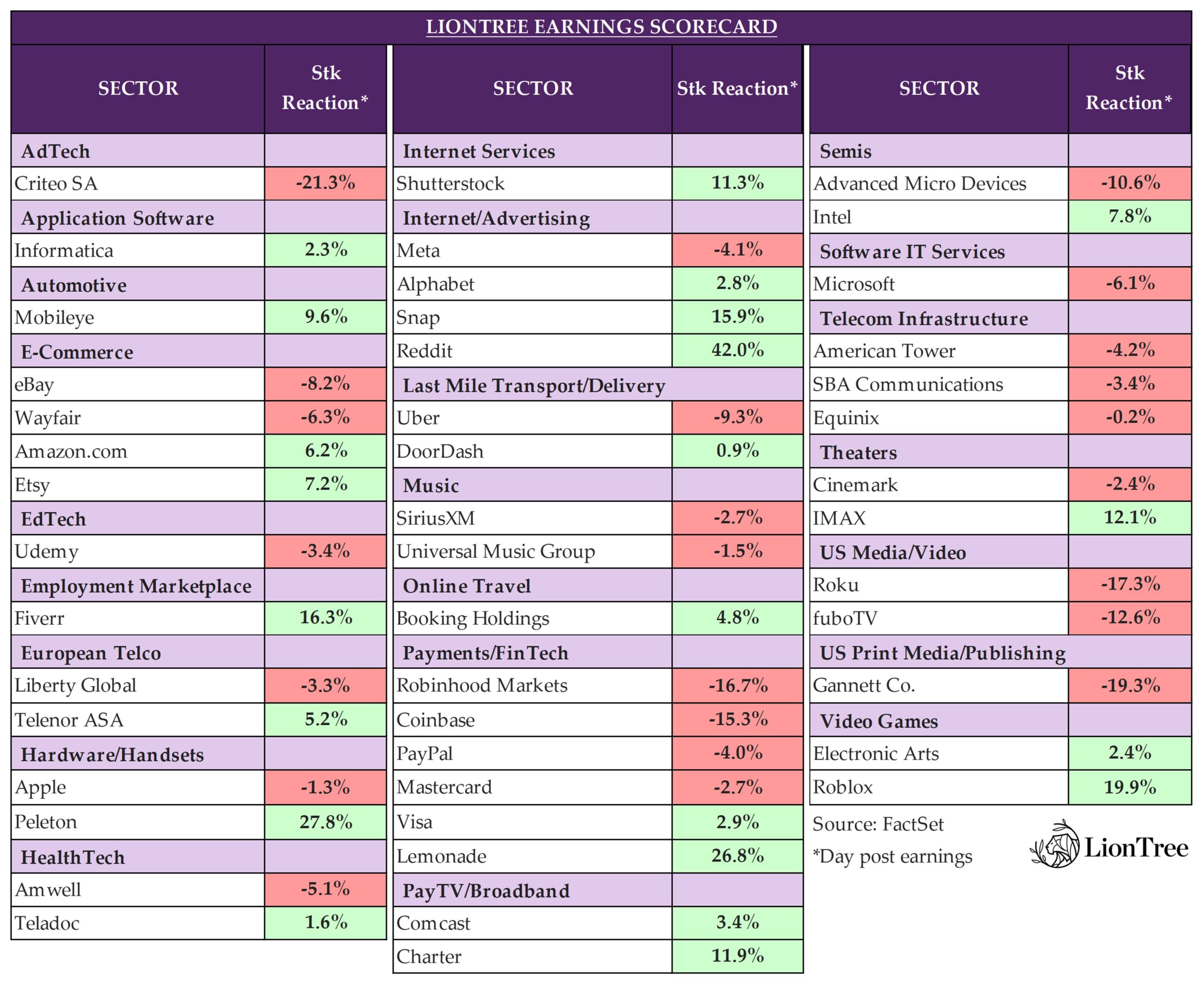

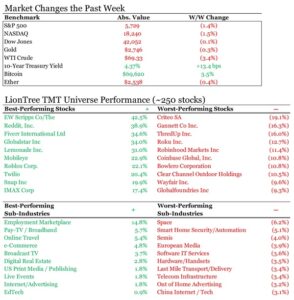

Earnings Scorecard – Week 3

It was a non-stop earnings blitz on the circuit this week, as 46 companies in our LionTree Universe reported their third quarter numbers, a big step up from the 15 that reported last week. Similar to last week, stock price reactions were biased to the downside, as 24 companies (52.2%) traded down in reaction to their prints, while 22 companies (47.8%) traded up. Criteo SA was the worst performer of the group, down -21.3% post its report, while Reddit was the best performer, jumping +42.0% (see Theme #12).

In addition to Reddit on the social media front, Snap put out its numbers this week, and the stock was up +15.9% in reaction (see Theme #4). The digital duopoly of Meta and Alphabet were also up this week, though Street reactions diverged, with the former trading down -4.1% and the latter trading up +2.8% (see Theme #2 for the deep-dive on both and Theme #9 for Google’s Cloud results). The mixed reactions followed through across Big Tech, as Amazon’s stock jumped +6.2% in reaction, while Apple fell -1.3% (see Theme #12 for the quick takes) and Microsoft was down -6.1% (see Theme #9 for more on Azure’s performance).

The digital duopoly wasn’t the only duo to report this week, as both cable juggernauts Comcast and Charter went up +3.4% and +11.9%, respectively, on the back of their prints (see Theme #5 for the deep-dive on the cable bizs and Theme #6 for updates from Comcast’s Content & Experiences business). On the interactive entertainment front, Electronic Arts and Roblox followed a similar pattern and also traded up +2.4% and +19.9%, respectively (see Theme #11). Also in media, but on the video streaming side, Roku posted its biggest one-day loss since mid-February, plummeting -17.3% (see Theme #7 for more color).

Roku wasn’t the only stock that suffered a notable drop, as Uber saw its biggest drop since Oct 2022, down -9.3% after its print, though delivery competitor DoorDash saw a more favorable reaction and traded up +0.9% (see Theme #8 for more on those dynamics). Finally, Bookings kicked off the OTA prints on a favorable note, trading up +4.8% (see Theme #10).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

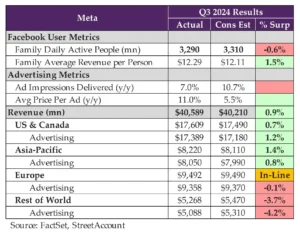

GOOGL & META: The AI Spending Trajectory Took Center Stage Over Core Fundamentals…

Higher capital spending in the AI arms race has been a key theme in the Big Tech sector, as companies scramble to build the necessary AI infrastructure to solidify a leading position in this technological revolution that is underway. Last qtr, the message from Alphabet and Meta was that it was too risky to under-spend then over-spend, which spooked investors. This qtr, Alphabet reassured the Street, pointing to an expected deceleration in CapEx y/y growth in 2025 relative to 2024’s increase. On the other hand, Meta’s capital spending trajectory is not as clear, other than the Co continuing to say that 2025 CapEx spend will be up “significantly” from its raised 2024 guidance (see Theme #3 for Amazon’s update on its CapEx outlook). This topic will continue to be a hot button for investors, who are eager to see the financial benefits from these investments. But some of those are starting to show through…

Both Alphabet and Meta delivered better than expected results relative to expectations (especially regarding profitability), though y/y top line growth rates were impacted by tough comps (as previously discussed). Alphabet’s advertising ad revenue growth of +10% and Meta’s Family of App ad revenue growth of +19% still reflect healthy performances. Alphabet’s Search business has not seen a negative impact from GenAI standalone platforms and, in fact, has seen AI “supercharging” search. People are expanding how they are using search. Regarding YouTube, ad revs were more or less in-line, as Short’s monetization improved again this quarter with higher watch time. For Meta, the Co has been able to achieve its advertising results with fewer impressions and higher growth in avg price per ad, which was a key point. Looking ahead, higher engagement and monetization is Meta’s strategic formula, and using AI to improve recommendations is a core tenant of both of those objectives. Threads is growing nicely (reached almost 275mn MAUs) and is expected to be the next major social app for the company (though monetization is not a priority now). Meta AI is seen as a critical engagement driver as well, with monetization to follow.

Outside of core advertising, Alphabet’s Cloud business had a blockbuster qtr, with accelerating revenue growth and much stronger operating margins (see Theme #9 for more). Meanwhile, Meta continues to spend a lot on Reality Labs, though traction remains a work in progress. We’ll see how well the newly released Quest 3S performs over the holiday season.

Net-net, Alphabet and Meta performed well in many aspects this quarter but their bigger picture progress regarding this AI technology wave will remain front-and-center. Alphabet started off a little slowly with Gemini compared to its peers. However, the Co has been integrating Gemini across its core products, and there is now “a lot of velocity” in the underlying models. Alphabet is working on the third generation and has an aggressive roadmap ahead for 2025, so more to come. For Meta, CEO Mark Zuckerberg thinks “this may be the most dynamic moment” that he’s seen in the industry, and Meta is moving forward full speed ahead. One last thing to note is that Meta’s management bypassed a question regarding recent press about Meta developing its own AI search engine (link).

See below for what we thought were the key themes and updates out of Alphabet and Meta’s results and conference calls. Also, see Theme #9 for thoughts on performance in the Cloud and Theme #4 on perspectives on Snap’s results.

-> Google shares rose +2.8% post-earnings and ended the week up +3.6%; Meta shares fell -4.1% in response to earnings and closed the week down -1.1%; YTD, Google stock is trading up +22.6%, and Meta shares are still up +60.2%

-> Also, note that Alphabet’s upcoming DOJ antitrust trial remains an overhang

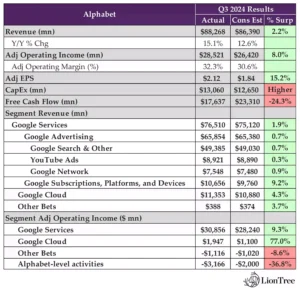

Alphabet & Meta’s Qtrly Headline Results Topped Expectations & Reflect Strong Growth In The Core And Much Better Than Expected Operating Margins

- GOOGL – Headline numbers topped expectations across the board: Consol revs growth accelerated to +15% y/y (+16% ex FX) from +14% growth in Q2 and beat cons by +2.2%; Op margins of 32.3% was also stronger than cons’ 30.6% (margins expanded by +4.5ppts y/y); EPS beat by +15% (and was up +37% y/y)

- Google Services revs beat by +1.9% (up +13% y/y) and op income was +9.3% ahead of cons

- Total Google Advertising beat by +0.7% (+10% y/y)

- Subscription, platform and devices revs beat by +9.2% (rose +28% y/y); YT TV and YT Music Premium were strong contributors to subscription revenue growth, in addition to Google One, plus the launch of Made by Google devices in Q3

- Cloud revs beat by +4.2% (posted accelerated growth to +35% y/y) due to performance in GCP; 17% op margins was significantly above cons 10%

- Google Services revs beat by +1.9% (up +13% y/y) and op income was +9.3% ahead of cons

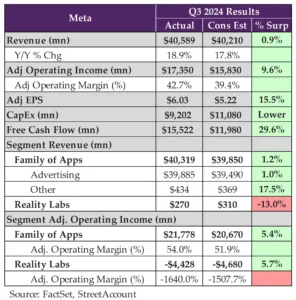

- META – Strong Q3 results relative to expectations w/ lowered FY expense outlook

- Total revs beat cons by +0.9% and grew +19% y/y (ex FX +20%), though decelerated from +22% y/y in Q2 and +27% y/y in Q1: Family of Apps Ad rev beat by +1%, while Reality Labs rev disappointed

- OUTLOOK: Mid-pt of Q4 revs guidance ($45-48bn) was +0.7% above cons

- Adj op income beat by +9.6% (much stronger margin of 42.7% vs cons 39.4%)

- OUTLOOK: Lowered top end of the 2024 total expenses guidance: From $96-99bn to $96-98bn

- EPS beat by +15.5%; FCF was +30% higher due to lower CapEx spend

- Total revs beat cons by +0.9% and grew +19% y/y (ex FX +20%), though decelerated from +22% y/y in Q2 and +27% y/y in Q1: Family of Apps Ad rev beat by +1%, while Reality Labs rev disappointed

Hefty CapEx Spend Remains A Theme For Big Tech Though Alphabet’s Y/Y CapEx Growth Should Peak In 2024

- GOOGL – Q3 CapEx was once again higher than expected, but the y/y increase in 2025 should ease

- Q3 – Similar to Q2, CapEx in Q3 was higher than expected, which weighed on FCF: Spent $13bn (+3% above expectations, and guidance was “at least $12bn”), and FCF missed by -24%; The majority of spend is on tech infrastructure (~60% of that on servers and ~40% on data center and networking equip)

- And expect Q4 CapEx to be similar to Q3 levels (previous guidance was “at least $12bn”)

- 2025 – Expect an increase y/y, but “likely not the same percent step up that we saw between ‘23 and ‘24”: Will provide more color on the Q4 call

- Q3 – Similar to Q2, CapEx in Q3 was higher than expected, which weighed on FCF: Spent $13bn (+3% above expectations, and guidance was “at least $12bn”), and FCF missed by -24%; The majority of spend is on tech infrastructure (~60% of that on servers and ~40% on data center and networking equip)

- META – Q3 CapEx was lower than expected but will ramp significantly in Q4 and in 2025

- Q3 CapEx of $9.2bn was much lower than cons $11.08bn but was impacted in part by the timing of Q3 server deliveries, which will be paid for in Q4

- 2024 – The Co raised FY CapEx range from $37-40bn to $38-40bn

- 2025 – Anticipate “significant” CapEx growth in 2025: With a focus on AI infrastructure expansion

- “We expect a significant acceleration in infrastructure expense growth next year as we recognize higher growth in depreciation and operating expenses of our expanded infrastructure fleet”

Alphabet’s & Meta’s Ad Growth Was Impacted By Tough Comps But Not By As Much As Expected & Still Reflected Healthy Rates

- GOOGL – Tough comps continue to weigh on ad revenue growth: While Google Total Advertising beat expectations, it did decelerate to +10.4% y/y vs +13.6% in Q2, given the impact of tough comps y/y due to APAC based retailers

- Search & Other Ad revs up +12%, which was a slight decel from +14% y/y in both Q1 and Q2: Growth was broad-based across verticals led by fin svs due to strength in insurance, followed by retail

- YouTube Ad revs grew +12% y/y which was a slight decel from +13% in Q2 and well below Q2 +21%: Growth was driven by brand, closely followed by direct response (DR)

- Had a slight tailwind from election-related ad spend in Q3, which was “a little bit more pronounced in YT ads”

- Network revenues were down -2% y/y

- H2 commentary – Comps get tougher as H2 progresses: Due to APAC-based retailers and a headwind y/y from growth in subscription platforms and devices revenue in Q4 due to the pull forward of the Made by Google launch in Q3

- META – Family of App ad revenue was strong at up +19% (ex FX +20%) and beat cons by +1% and as expected slightly decelerated from Q2’s +22% y/y due to touch comps/FX impact: FoA adj op margins of 54% were materially ahead of cons’ 51.9%

- Online commerce vertical was the largest contributor to y/y growth, followed by healthcare and entertainment & media

- Ad growth by user geography / and by advertiser geography:

- ROW +23% / 17%

- Europe +21% / 21%

- Asia Pac +18% / 15%

- N. Amer +16% / 21%

- Delivered fewer impressions but higher growth in avg price per ad:

- Total impressions incr’d 7% (driven by Asia Pac and ROW) vs cons’ +10.7%

- Avg price per ad incr’d +11% (due to advertiser demand partially offset by impression growth esp from lower monetizing regions and surfaces) which was better than cons’ 5.5%

Alphabet’s Search Business Is Being “Supercharged” By AI Vs Cannibalized

- GOOGL – AI is transforming and expanding how people use Search and is “supercharging” the business: With AI, the Co can understand intent better and connect users to the most relevant ads; There are no signs of negative impact from standalone GenAI platforms like ChatGPT; Users are coming to Seach more often

- AI Overviews transition is “working well”, including for ads: Started to rollout to 100+ new countries and will reach 1bn users on a monthly basis; Seeing strong engagement; People are learning that Google can answer more of their questions; Started showing search and shopping ads w/in the overview for mobile users in the US

- For AI overviews overall, the Co is seeing monetization at the ~same rate

- Circle to Search is now available on 150mn+ Android devices, w/ people using it to shop, translate text, and learn more about the world around them: A third of the people who have tried circle to search now use it weekly

- Lens is now used for 20bn+ visual searches per month, w/ 25% of these searches having commercial intent: It is “one of the fastest growing query types we see on Search”

- Annc’d the rollout of shopping ads above and alongside relevant lens visual search results to help better connect consumers and businesses

- “All these AI features is just the beginning”

- AI Overviews transition is “working well”, including for ads: Started to rollout to 100+ new countries and will reach 1bn users on a monthly basis; Seeing strong engagement; People are learning that Google can answer more of their questions; Started showing search and shopping ads w/in the overview for mobile users in the US

Alphabet’s YouTube Shorts Monetization Is Improving

- GOOGL – YouTube (YT) YouTube’s total ads and subscription revenues surpassed $50bn over the past four quarters for the first time

- Using AI to greatly improve recommendations on YouTube

- Seeing robust watch time growth of YT: Particular strength in Shorts and in the living room; 70bn+ YT shorts are watched every day

- Short’s monetization improved again this quarter: Cont’d to significantly close the monetization gap with in-stream video, particularly in the US and other more highly monetizing markets

- Of all the channels uploading to YouTube each month, 70% are uploading Shorts; Now have the ability to upload Shorts up to 3min long

- Advertisers now able to book first position on Shorts

- YT Subscription growth is strong: YT- Together, YouTube TV, NFL Sunday Ticket and YouTube Music Premium are driving subscription growth; “Leaning into” the living room experience with Multiview and a new option for creators to organize content into episodes and seasons, similar to traditional TV

- Google DeepMind’s most capable model for video generation video is coming to YouTube shorts to help creators later this year

Other Ways That AI Is Transforming Alphabet’s Business

- GOOGL – AI will revolutionize every part of the marketing value chain

- On creative: Advertisers now use Gemini powered tools to build and test a larger variety of relevant creatives at scale

- Their most advanced text-to-image model, Imagen 3, helps customers produce high quality imagery for their campaigns

- On media buying: AI-powered campaigns help advertisers get faster feedback on what creatives work

- On measurement: Meridian is helping to scale measurement of cross channel budgets to drive better business outcomes

- On creative: Advertisers now use Gemini powered tools to build and test a larger variety of relevant creatives at scale

- GOOGL – Gen AI is helping to make the Co more efficient

- Today, more than a quarter of all new code at Google is generated by AI, then reviewed and accepted by engineers

Meta’s User Engagement Remains A Key Focus & Threads Is Slated To Become The Next Major Social Media App

- META – 3.2bn people use at least one of its apps per day in Sept

- WhatsApp just passed 2bn calls made globally every day

- Facebook continues to see positive trends with young adults esp in the US

- Have seen a +10% increase in time spent within the Facebook video player since the global rollout of the unified video player

- Instagram growth remains strong globally

- “Reels continues to see good traction, and we’re making ongoing progress with our focus on promoting original content, more than 60% of recommendations now coming from original posts in the US”

- Threads is on track to become the Co’s next major social app: It has almost 275mn MAUs and has seen more than +1mn sign ups per day; Engagement is growing as well

- But won’t be a driver to 2025 revenue – goal is to drive growth & deepen engagement

Meta – AI Is Having A Positive Impact On Core Business Engagement & Monetization And The Long Term Road Map

- Meta’s core revenue growth strategy is centered around…

- Deliver engaging experiences to users

- Improving recommendations is a key focus

- Gen AI, Threads, and Meta AI will also drive more engagement

- Monetizing that engagement over time

- Oppty to grow ad supply on lower monetizing surfaces like video – think shift to short form will continue

- Continuing to optimize when and where to show ads w/in a person’s session

- Enhance marketing performance

- Deliver engaging experiences to users

- AI is expected to accelerate their core business and should have strong ROIs over the next few years “so I think we should invest more there”; The AI investments require serious infrastructure, and the Co expects to continue investing significantly there too

- What are the biggest opportunity sets for AI on the platform? Making Feed, Reels, and ads more relevant, helping advertisers generate better ads, helping people create the content that they want, and helping with the integrity of operations and compliance; It is also going to enable completely new types of services; Expect people to interact with a variety of AI agents on both consumer and business side

- Meta AI has 500mn+ MAUs: On track to be the most used AI assistant in the world by the end of year; Focused on making Meta AI more valuable to user which will lead to monetization over time (not now); What do people use it for?

- Info gathering

- Help with how to tasks (largest use case

- Go deeper on interest or look for content on services

- Image generation

- Improvements to AI driven feed and video recommendations have led to an +8% increase in time spent on FB and a +6% increase on Instagram this year alone

- 1mn+ advertisers use Meta’s genAI tools to create 15mn+ ads in the last month

- Estimate that businesses that use image generation see a +7% increase in conversion (and thinks there’s more upside to this)

- Great momentum with Llama: Released Llama 3.2 this qtr, and Llama 4 is well into its development; Expect the smaller Llama 4 models will be ready sometime early next year and are very excited about this launch

Meta’s Business Messaging In Gaining Momentum, While Realty Labs Remains A Work In Progress

- META – Business messaging monetization was better than expected: Family of Apps Other revenue, which is primarily business messaging rev growth from the WhatsApp Business platform, was up +48% y/y to $434mn; This was +18% above consensus

- Significant spending continues in Reality Labs, while revenues come in shy

- RL revs grew +29% y/y to $270mn (-13% below cons), and operating loss was $4.4bn (cons $4.68bn)

- Demand for Ray-Ban Meta glasses continues to be “very strong”

- Look forward to seeing how well Quest 3S does this holiday season

- Orion (full holographic AR glasses) is where they are ultimately going

- Outlook – 2024 Reality Labs operating losses will “increase meaningfully” y/y; The Co is not sharing guidance for 2025 yet

- RL revs grew +29% y/y to $270mn (-13% below cons), and operating loss was $4.4bn (cons $4.68bn)

Alphabet’s Waymo Surprised On The Upside

- GOOGL – Waymo (the biggest part of Other Bets) is now “a clear technical leader within the autonomous vehicle industry and creating a growing commercial opportunity”

- Surprised on the upside how much people love the product

- Each week, Waymo is driving 1mn+ fully autonomous miles and serves 150k+ paid rides

- Waymo has multiple paths to market and growth will come through its partnership with Uber in Austin and Atlanta, plus a new multi-year partnership with Hyundai

- Drones: Another new bet Wing (drone delivery) passed the 1-year anniversary of scaling its partnership with Walmart in the Dallas Fort Worth area and now operates in 11 stores serving 26 cities and towns

Amazon Looks To Be Firing On All Cylinders

There were a lot of pluses with respect to Amazon’s results this qtr. The Co delivered very strong profitability upside on slightly better revenue, and the mid-pt of Q4 guidance was more-or-less in-line on revenue but reflected higher margins than expected. The level of profitability in both the international business and AWS stood out in particular. For international, Q3 adj operating income of $1.3bn easily topped consensus $206mn. Factors driving the improvements are the same that have been driving N. America profitability, meaning lower cost to serve, greater contribution from advertising, improved selection, and faster delivery speeds (which help drive consumer demand). There is now a clear profitability trajectory in the international segment, and it was encouraging to hear that over time, the Co believes this business can reach N. American profitability levels (which continue to press higher as well).

In the retail business, Amazon’s approach remains the same – providing customers with a very broad selection, low prices, fast and free delivery, and a range of compelling Prime member benefits. The Co is on track to deliver its fastest speeds ever for Prime members globally for the second year in a row. Mgmt does still see some price consciousness on the part of consumer but also sees that they are buying more everyday essentials from the Co, which leads to a stickier and more valuable customer over time.

As another top-line and profitability driver, Amazon’s advertising business continues to post strong y/y growth of +19%, and there are more levers for growth going forward, with both sponsored links as well as Prime Video.

AI and capital spending, of course, was a big focus on the call. Amazon’ 2025 CapEx will be higher y/y (as Alphabet and Meta also noted), but mgmt did a great job at reassuring investors that they are not overbuilding capacity and will see strong returns and higher margins as the AI business matures. AI is having a big impact not only in AWS, but also on other areas of the company.

Lastly, Amazon shared some stats that were good reminders about the company’s large opportunity in the retail business. Amazon is only ~1% of the market segment share of worldwide global retail, and ~80- 85% of that market segment share still lives in physical stores: “If you believe that equation is going to flip in the next 10 to 20 years, which, which we do, there’s just a lot of opportunity, not just for us, but for several players”.

See below for more details on what we thought was most incremental from the Co’s results and conference call.

-> Amazon shares traded up +6.2% on the back of results and closed the week up +5.4%; The stock is up +30.3% YTD

Amazon Delivers A Stronger Than Expected Qtr Esp On Profitability

- Q3: Operating margins beat cons by a wide +18% on a +1% revenue beat

- Total revenue growth slightly accel’d to +11% y/y from +10% y/y (or +11% ex-FX) in Q2

- Op income grew +56% y/y to $17.4mn, the highest qtrly op income ever, and was +$2.4bn above the high end of the guidance range

- Adj EPS beat by +25%

- Q3: N. Amer and Intl revs and op income both topped expectations, while better AWS profitability was the main area of upside (with ~in-line revenues)

- Amer revs rose +9% y/y (in-line with +9% in Q2), w/ op margins of 5.9% (vs +5.6% in Q2), which was up +100bp y/y due to cont’d improvements in the fulfillment network cost structure

- Intl revs grew +12% y/y and profitability was MUCH better than expected

- Q4: Mixed – Rev guidance was slightly lower, and op income was better at the mid-pt

- Revenue guidance of $181.5-188.5bn was -0.7% below cons at the mid-pt

- Operating income guidance of $16-20bn was +3.9% above cons at the mid-pt

Making More Gains On Lowering Cost To Serve

- More gains to capture with outbound regionalization and getting items closer to customers: Early in re-architecting the way they inbound items and spread them to regional fulfillment nodes, but already improved ability to spread inventory across fulfillment centers by +25% y/y

- Expect these changes will further improve inventory placement, offer faster delivery times, save transportation costs, and increase units per ship per box

- Expanding same-day delivery facilities: W/ 40mn+ customers receiving free same-day delivery this past qtr, a +25% increase y/y

- Innovating in robotics to speed up delivery, reduce costs, and improve safety in the fulfillment network: Launched their 12th generation fulfillment center design (Shreveport, Louisiana), which reduces fulfillment processing time by up to -25%, increases the number of items the Co can offer for same day or next day delivery, and is expected to drive a +25% improvement in cost to serve during peak

CapEx Will Be Increasing In 2025, But Returns Seem Visible

- YTD total CapEx (cash CapEx + capital leases) reached $51.9bn and are on pace to hit $75mn in 2024

- The majority of the spend to support the growing need for technology infrastructure relates to AWS but also incls tech infrastructure to support the North America and international segments

- Continuing to invest in fulfillment and transportation network to support the growth of the business, improve delivery speeds and lower cost to serve (incls investments in same day delivery facilities in the inbound network and as well in robotics and automation)

- Spend will “spend more” in 2025: Really driven by gen AI

- Need to invest in infrastructure ahead of demand but have good visibility: The AI biz is a multi-billion business growing at triple digit percentages y/y and growing 3x faster in its stage of evolution than AWS did itself and AWS grew very fast

- The faster they grow demand the faster they need to invest in the infrastructure upfront

- But they can make this an attractive ROC business

- “I believe we have more demand that we could fulfill if we had even more capacity today… we want more capacity and supply to be able to provide them”

- Gen AI is a once in a lifetime oppty: “I think our customers, the business and our shareholders will feel good about this long term that we’re aggressively pursuing it”

Still Seeing Some Consumer Price Consciousness & Trading Down But Units Sales Were Up

- “Customers have been looking for deals and are price conscious”

- Strength in everyday essentials rev is a positive indicator: Customers who purchase these types of items build bigger baskets, shop more frequently and spend more on Amazon; Will take a short-term degradation in ASP b/c of the long-term value of the customer

- Speed delivery is a key factor for growth in this category

- Worldwide paid units accelerated to +12% y/y growth (vs +11% y/y in Q2)

- Lower pricing and shipping more quickly, and it is resonating, as unit growth continues to be strong and outpace rev growth

- Prime remains a core contributor to the y/y growth: Prime membership growth accel’d in Q3 both in the US and globally

- “We’re encouraged by the start of the holiday season, which kicked off in October with a strong Prime Big Deal Days”

Have Reached A Clear Positive Trend Line With International Profitability

- Intl profitability is at $2.5bn YTD

- Seeing strength in established countries like the UK and Germany, as they drive efficiencies through improved productivity in the transportation network and better execution in fulfillment centers

- Have seen fluctuations but starting to see clear trend lines that are moving positive: Have seen y/y improvement in op margin For each of the last 7 qtrs

- Driven by the same factors as N. Amer: Lower cost to serve, greater contribution from advertising, improved selection, and faster delivery speeds, which help drive consumer demand

- Different countries are at different stages, but over time, the Co thinks intl margins should reach US levels, which are not static either

Still More Room To Go With Advertising

- Ad revenues growth (ex-FX) rose +18.8% y/y to reach $14.3bn: This compares to +20% in Q2 and slightly beat cons by +0.4%

- Provide all types of brands with full funnel advertising at scale

- Still believe there are many opportunities to further expand like w/ sponsored products, newer areas like prime video ads

- Entering the first broadcast season for prime video advertising following a very strong showing In the upfronts

- Supporting brands of all sizes w/ their gen AI powered creative tools across display video and audio, incl video generator

- “While we’re generating a lot of advertising revenue today, there remains considerable upside”

Gen AI Across The Business Ex-AWS

- Using gen AI “pervasively” across Amazon’s other businesses (more on AI in AWS in Theme #9): Have hundreds of apps in development or launch

- Expanded Rufus, the gen AI-powered expert shopping assistant, to the UK, India, Germany, France, Italy, Spain and Canada; Added more personalization in the US

- Recently debuted AI Shopping Guides for Consumers, which simplifies product research

- Recently launched Project Amelia and their AI assistant

- Are re-architecting the brain of Alexa with a new set of foundational models and are adding AI into all of their devices

- Next gen AI assistants will be better at not just answering questions as well as summarizing, indexing, and aggregating data, but also taking actions…”and you can imagine us being pretty good at that with Alexa”

Other Key Call Outs & Initiatives

- Early sales of recently launched new Kindle lineup has significantly outperformed expectations: It includes the AI-powered Kindle Scribe for enhanced note-taking; 20bn+ avg monthly pages are read on Kindle devices worldwide

- Significantly improving the customer Pharmacy experience:

- Amazon Pharmacy now delivers to 95% of first-time customers within two business days and 20% of Prime members within 24 hours

- Next year, plan to expand to 20 new cities, enabling nearly half the US to receive medications within hours

- Still very early in robotics in fulfillment network: AI is going to be a big piece of what they do in their robotics network; Just hired some key people; Customers are monetizing the resources, but these investments will be useful asset for many years

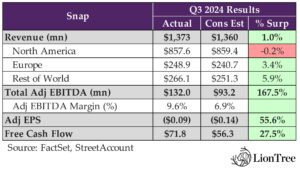

Snap Makes Progress, But Its Platform Transformation Is In Transition

Profitability took the center stage in Snap’s Q3 report, reaching $142mn (up from year-ago $40mn) and beating estimates by +42%. Revenue was a modest +1% ahead of expectations and grew +15% y/y, which marked a slight deceleration from Q2’s +16% y/y, as N. America’s growth continues to be tempered by weaker brand-oriented demand, while Europe and RoW continue to make progress on the DR ad platform front. More specifically, ad rev grew +10% y/y (in-line w/ Q2), which was primarily driven by direct response as Snap made “meaningful progress” in its lower funnel DR biz. The combination of more performant DR products, go-to-market operations optimized for SMB customers, and easier onboarding and integration tools are helping to expand Snap’s SMB customer base. As a result of these efforts, total active advertisers more than doubled y/y. However, brand advertising remains a drag and is not expected to rebound in Q4.

A big focus on the call was on roll-out of Simple Snapchat, the Co’s new and simplified version of Snapchat. The Co is taking a slow and steady approach and is currently testing with ~10mn Snapchatters across “dozens” of countries. Early feedback suggests that Simple Snapchat is driving the greatest content engagement gains among “more casual users”, which is encouraging. Rollout of the new interface will be gradual and focused on understanding inventory shifts and monetization impacts, but some potential near-term disruption is baked into the Q4 guidance.

Looking ahead, the mid-pt of the Q4 profitability guidance range came in above cons, while the mid-pt of the Q4 rev guidance was weaker than expected (includes some risk associated with the Simple Snapchat roll-out) and reflects a deceleration in growth seq. Overall, there are signs of progress in the core ad business, but the turnaround remains a work in progress.

Commentary on Snap’s augmented reality initiatives was relatively light and mostly reiterated commentary from its Partner Summit back in mid-September. Lastly, to flag, Snap announced a $500mn stock repurchase program (though only 2% of the mkt cap).

See below for more details on what we thought was most incremental.

-> It was a sigh of relief with Snap results/guidance and the stock closed the day up +15.9% in reaction to earnings and ended the week up +19.9%; With that said, the stock is still down -26% YTD

Q3 Saw A Clean Sweep Of Beats On The Top-Line, With Profitability Being The Highlight + The Annc’d Buyback Program…

- Q3 rev – BEAT by +1.0%: Grew +15% y/y (but a slight decel from +16% y/y in Q2)

- N. Amer rev grew +9% y/y (vs +12% y/y in Q2), with the relatively lower rate of growth due to the impact of weaker Brand-oriented demand being relatively concentrated in the region (similar commentary made last qtr)

- Europe rev grew +24% y/y (vs +26% y/y in Q2), as continued progress on their DR ad platform fully offset the impact of more challenging prior year comparisons

- RoW rev grew +32% y/y (vs +20% y/y in Q2), driven by the continued progress with Snap’s DR ad platform

- Q3 adj EBITDA – BEAT by significant +41.6%: Reached $132mn compared to $40mn in prior-yr qtr, reflecting higher revenue and operating expense discipline

- Adj. EBITDA flow-through was 50% in Q3, down from 55% in Q2

- Q3 FCF – BEAT by +27.5%: Reached $71.8mn vs cons $56.3mn

- Authorized $500mn share repurchase program

…BUT Q4 Headline Guidance Came In Mixed

- Q4 rev guidance – BELOW @ the mid-pt: $1.51-1.56bn vs cons $1.56bn, implying +11-15% y/y growth (vs +15% in Q3)

- Bakes in risk of near-term disruption from early testing of Simple Snapchat in Snap’s most highly monetized mkts and upper funnel advertising from large enterprise clients that has been underperforming the overall ads biz in recent qtrs and has historically been an important component of demand in Q4

- Q4 adj EBITDA guidance – ABOVE @ the mid-pt: $210-260mn vs cons $231.8mn (+1.4% beat at mid-pt)

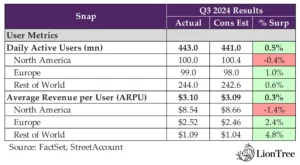

Overall User Trends & Guidance Were Better Than Expected, Despite N. America Not Performing As Well As Anticipated

- Q3 – DAUs BEAT by +0.5%: Grew +9% y/y (in-line w/ Q2) to reach 443mn (incr’d +11mn seq); Overall ARPU also topped estimates

- N. Amer DAUs were flat y/y but up seq to reach 100mn, as initiatives to increase user engagement began to show early signs of progress (Co shared similar commentary last qtr); But missed consensus

- N. Amer ARPU was also lower than expected

- Europe DAUs were up +2mn seq and +4mn y/y to reach 99mn

- RoW DAUs were up +9mn seq and +33mn y/y to reach 244mn

- N. Amer DAUs were flat y/y but up seq to reach 100mn, as initiatives to increase user engagement began to show early signs of progress (Co shared similar commentary last qtr); But missed consensus

- Q4 DAU Outlook – HIGHER by +0.5%: Expected to grow +9% y/y to reach ~451mn vs con 448.7mn

- AI-enabled features and investments in content platform helped drive user engagement in Q3

- Spotlight reached 500mn+ MAUs on avg in Q3, up +21% y/y

- Global time spent watching content incr’d +25% y/y (in-line w/ Q2) and +6% q/q (vs +10% q/q in Q2)

- N. Amer time spent watching content was down -1% y/y (vs -2% y/y in Q2) and up +2% q/q (vs +6% q/q in Q2)

- Relatively higher rate of growth outside N. Amer is due in part to the greater mix of content viewing being driven by Spotlight in these regions, as Spotlight reach and depth of engagement continues to grow “rapidly” across regions

- # of people sharing Spotlight content with friends is up over +60% y/y

- # of creators posting content grew ~+50% y/y

- # of Snaps sent to My AI (Snap’s AI-powered chatbot) in the US more than tripled q/q

Seeing Ongoing Momentum With DR Products And Growth In SMBs / Brand Advertising Is Not Expected To Make A Comeback In The Near-Term

- Q3 total ad rev grew +10% y/y (in-line with Q2) to reach $1.25bn

- Driven primarily by growth from DR ad rev

- Q3 brand-oriented ad rev was down -1% y/y (in-line w/ Q2)

- Continued to see weak demand from certain consumer discretionary verticals including technology, entertainment, and retail

- Looking to Q4 – Snap is “not expecting any significant recovery”: Have been down -1% y/y in last two qtrs and “not anticipating a major shift there” going into Q4; “Obviously, that’s an important component of revenue in the final quarter of the year. Our product execution is the key that we’re focused on there in terms of igniting growth long term”

- Focused is on reaccelerating upper funnel brand revenue growth

- Launched First Lens Unlimited in Q3, which offers advertisers the first impression of the day in the first slot of the AR Lens Carousel, allowing them to reach Snap’s community at greater scale

- During testing, First Lens Unlimited drove an average increase of over +35% in incremental impressions for advertising partners

- Launched State-specific First Story, which allows US advertisers to target First Story takeover campaigns to individual states or to reach the entire country with different creative for each state

- Also experimenting with two new ad placements, Sponsored Snaps and Promoted Places, which are on track to launch in certain geographies in Q4

- Both of these placements are designed to leverage their existing full-screen vertical video Snap Ad format so that advertisers can automate placement across their service without having to develop bespoke creatives

- Launched First Lens Unlimited in Q3, which offers advertisers the first impression of the day in the first slot of the AR Lens Carousel, allowing them to reach Snap’s community at greater scale

- Q3 direct response ad rev grew +16% y/y (vs +15% y/y in Q2)

- Driven by continued “strong” demand for Snap’s 7-0 Pixel Purchase optimization (up more than +160% y/y) and growing contribution from App Purchase optimization

- “Rapidly” expanding Snap’s SMB customer base through a combination of more performant DR products, go-to-market operations optimized for SMB customers, and easier onboarding and integration tools

- Total active advertisers more than doubled y/y

- Looking into Q4 and beyond: “Focused on continued execution there [specifically lower funnel DR], continued CAPI adoption, continued rollout of the app optimizations and client performance”; Focused on growing and building momentum with the SMB customer segment

- Other key advertising KPIs –

- Global impression volume grew +19% y/y (vs ~+13% y/y in Q2), driven in large part by expanded advertising delivery within Spotlight and Creator Stories

- Total eCPMs were down ~-7% y/y (vs ~-3% y/y in Q2), as inventory growth exceeded ad demand growth in Q3

- Further improving go-to-market operational optimizations for SMBs

- Continue to enhance the advertiser onboarding experience by personalizing and automating the buying process from end-to-end so that SMB’s can optimize their campaigns faster and enhance performance

- Recently launched automated in-flight campaign recommendations, adaptive templates for campaign set-up, and scaled creative editing

- Expansion of 7-0 Optimization to app install and app purchase is driving better performance for advertisers

- Early results are showing cost-per-install decreasing -24% and cost-per-purchase decreasing -27% compared to 28-1 optimization

- Introduced new Landing Page View optimization goal to help advertisers drive “high-quality” traffic to their websites

- Through improvements in ML models that optimize for this specific objective, observed lower cost for some advertisers versus traditional click engagement models.

Early Testing Of “New And Simplified” Snapchat Is Driving Incremental Engagement, But The Co Has Some Ways To Go Before Broader Rollout

- The new interface organizes Snapchat into 3 core experiences focused on communicating w/ friends, using the camera, and watching entertaining content

- For Snapchatters: Offers a more personal, relevant, and easy to use interface

- For Creators: Unlocks greater discovery and enhances the ability for content to reach new audiences

- Initial observations arounds Simple Snapchat (introduced selectively in Q3) …

- ~10mn Snapchatters using Simple Snapchat across dozens of countries

- Driving the greatest content engagement gains among more casual / “new and less engaged” users

- “Important input to community growth and advertising inventory”

- Seeing “particularly positive” impacts on Android devices

- Including incr’d time spent with content, incr’d story views, and more replies to friends’ stories

- Also seeing an increase in content active days on iOS, BUT impacts to other top engagement metrics are not yet as broadly positive as on Android

- This is due in part to the differences in engagement across these platforms

- “Encouraged” by the early progress BUT “we definitely have a lot of work to do to iterate and test before we begin a broader rollout […]

- “Still early in the journey on understanding the monetization dynamics and some of those inventory shifts and how that could impact revenue”

- “We certainly want to take the time to work through those sorts of changes and make sure advertisers and our partners, for example, are prepared for those sorts of changes”

- Have begun limited testing of Simple Snapchat in Snap’s top markets and may expand this testing throughout Q4, but don’t anticipate a full rollout until Q1 at the earliest

- “I think the North Star is going to be the community engagement and then thinking about how we can best manage this transition so that our advertising partners and content partners can benefit from it as well”

On Augmented Reality – “Going To Stay Focused On Our Strategy And Keep Executing”

- Introduced fifth-gen of Spectacles in Q3

- Addressing the “chicken and egg” challenge of providing appealing lens experiences for first-time buyers of Spectacles

- Continue to focus on supporting developer ecosystem to help build Lenses for Spectacles for when the consumer product is made available

- 375k+ AR creators, developers, and teams from nearly every country have built 4mn+ lenses

Continue To Make Progress In Diversifying Revenue Streams (Snapchat+ Subscriptions Makes Up The Majority)

- Other rev “more than doubled” y/y to reach $123mn: Includes all non-advertising rev, the majority of which is Snapchat+ subscription rev

- Snapchat+ subscribers “more than doubled” y/y to exceed 12mn+ (vs 11mn+ in Q2)

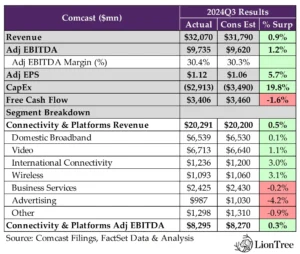

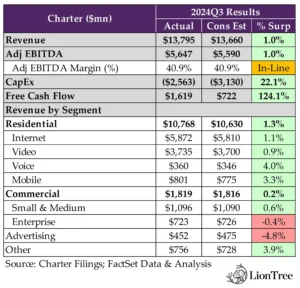

Comcast & Charter Showcased The Strength Of Their Converged Offerings

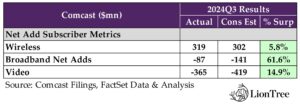

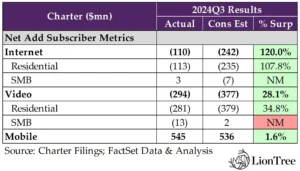

Following the earnings sprint from the incumbent telcos last week (see Theme #2 from 10/25/24 Weekly), the cable companies stepped up to the plate this week to round out earnings for the connectivity space, and they certainly had a strong showing. Along with mostly stronger than anticipated headline results, another key highlight was that Comcast and Charter posted fewer than expected net losses in their core broadband segments in Q3. Each has been managing through the end of ACP well, and without the impact from the program’s conclusion, both would have seen positive broadband net adds during the quarter. This was partially due to the seasonal uplift that the cable companies received from back-to-school activity, though the two also benefited from AT&T’s 30-day work stoppage in the Southeast. However, outside of these one-time drivers, the broadband market remained “competitively intense”. Fixed wireless has “taken a toll”, and both Comcast and Charter downplayed the impact that future fiber overbuilding will have on their businesses. Other near-term headwinds in Q4 include the impact from the recent hurricanes in addition to further ACP-related churn. Still, Charter sees a “better unit growth setup” on the horizon in 2025.

Results on the wireless side of the cable companies’ businesses also outperformed consensus forecasts in Q3, and convergence remains at the heart of both companies’ strategies to grow their mobile segments, with each claiming that it is uniquely “positioned to win.”. While Comcast plans to continue experimenting with new converged offers moving forward, Charter’s recent brand refresh, which included new pricing and packaging for its converged bundles, have already been “showing promising results” in its early stages, driving more mobile lines per sale, among other benefits. Looking ahead, there is still a “very long runway of growth” left in the two cable companies’ mobile businesses. Comcast has only penetrated ~12% of its broadband subscriber base with wireless offerings, while Charter only sells mobile to ~8% of its internet-only customers.

Also, the cable companies’ video net losses weren’t as steep as the Street had anticipated in Q3. Comcast indicated that churn in its video business has been “stabilizing for a while” and pointed to the introduction of mobile into video bundles as a key reason why. The company also benefited from “high engagement levels” around the Olympics, highlighting that the viewing of Olympics content in Xfinity markets was double the national averages for the same content. Charter’s upcoming “reconstituted” video offering was also a major focus on its earnings call. With efforts to transform all of its major programming agreements in the rearview mirror, the company now has the ability to include its programming partners’ streaming apps within Spectrum TV Select plans, with paths for customers to upgrade to the ad-free version of these apps. Although some work still needs to be done to operationalize the new offering, once it is rolled out in early 2025, Charter will be able to provide TV Select customers with up to $80/month of retail streaming value at no additional cost.

On the investment side, the key update was Charter’s decision to push-out the second phase of its network evolution initiative into 2026 and 2027, marking the second time the company has announced a delay in its original timeline. The move will save Charter ~$500mn in CapEx in 2024, though it also expects an incremental ~$100mn outlay in Q4 to rebuild its network after the hurricanes. For its part, the pace of Comcast’s passings and network upgrade plans remains on track, though there will likely be a “little bit of catch-up” in CapEx spending in Q4.

See below for more details on our key takeaways from Comcast and Charter’s print… and see Theme #6 for our thoughts on Comcast NBCUniversal’s earnings.

-> Comcast shares rose +3.4% post-earnings, ending the week up +4.6%; Charter shares were up +11.9% following the print and closed the week up +9.1%; YTD, Comcast stock is trading down -0.7% and Charter stock is down -5.7%

The Cable Cos’ Strength In Headline Numbers Reflected Broad Outperformances Across Segments

- Comcast – Headline numbers outpaced expectations, outside of a slight miss on FCF: Q3 consolidated rev grew +6.5% y/y (vs -2.7% y/y in Q2) and beat cons by +0.9%, driven by the Olympics; Consolidated adj EBITDA fell -2.3% y/y (vs -0.7% y/y in Q2) but still topped cons by +1.2%; FCF fell short of cons by -1.6%

- Connectivity & Platforms (~63% of total rev) – BEAT: Rev was up a slight +0.1% y/y in Q3 (vs -0.7% y/y in Q2) and closed +0.5% ahead of cons; Adj EBITDA incr’d +0.9% y/y (vs +1.6% y/y in Q2) and beat cons by +0.3% y/y; Residential rev topped cons by +0.9%, while Business Services missed cons by -0.2%

- Net add subscriber metrics for broadband, wireless, and video all broadly outperformed

- Charter – Headline results mostly surprised to the upside: Rev incr’d +1.6% y/y in Q3 (vs +0.2% y/y in Q2) and topped cons by +1.0%; Adj EBITDA was up +3.6% y/y (vs +2.6% y/y in Q2) and beat cons by +1.0%, though adj EBITDA margin was in-line w/ cons’ 40.9%; FCF finished a material +124.1% ahead of cons

- Residential rev (~78% of total rev) – BEAT: Q3 residential rev was up +0.3% y/y (vs -0.6% y/y in Q2) and beat cons +1.3%; Customer relationships fell -1.8% y/y (vs -1.3% y/y in Q2), while monthly rev per customer incr’d by +1.8% y/y (vs +0.4% y/y in Q2)

- Commercial rev (~13% of total rev) – slight BEAT: Commercial rev rose +2.0% y/y in Q3 (vs +2.1% y/y in Q2) and ended a slight +0.2% above cons; SMB rev incr’d +1.0% y/y (vs +0.6% y/y in Q2), and Enterprise rev grew +3.7% y/y (vs +4.5% y/y in Q2)

- Broadband and Video net losses were better than feared, and Wireless net adds also came in ahead of forecasts

Competition In The Broadband Mkt Remains High, As Move Activity Continues To Be Slow

- Comcast – “The underlying mkt… remains competitively intense”: Flagged a “cont’d competitive backdrop” that “hasn’t changed” from prior qtrs

- “Fixed wireless has obviously taken its toll”: The Co “think[s] that’s a mkt that’s going to continue to exist”, as FWA has “carved out a niche in the mkt” for the “value-conscious consumer”

- Comcast doesn’t have a “crystal ball” when it comes to FWA’s longer-term penetration rates, “whether its 10% [or] 15%”

- “Fiber… is the real long-term competitor”: This has been the case for the last ~20 yrs, and Comcast continues to see a “steady increase” from fiber in its footprint

- Comcast is 50% overbuilt w/ fiber, but “that will go higher”: Given that “the carriers have annc’d plans to take that higher”

- Eventually, the Co sees “the competitive environment sort of leveling out”: Highlighted that early fiber mkts saw some “initial uptake” but ultimately resulted in a “relatively even share between [the Co] and fiber”

- Comcast’s ARPUs in overbuilt mkts are “very consistent” w/ overall ARPU: This “goes back to [the Co’s] playbook in terms of segmentation” as well as its ability to provide “the best Wi-Fi in the mktplace” and content offerings

- “Fixed wireless has obviously taken its toll”: The Co “think[s] that’s a mkt that’s going to continue to exist”, as FWA has “carved out a niche in the mkt” for the “value-conscious consumer”

- Charter – “We are still very much in an atypical low churn environment when you exclude ACP”: That said, the Co “expect[s] mkt activity and selling oppties to pick up over time”

- However, “it’s still a competitive environment for new sales”: Charter “continue[s] to compete well against both wireline overbuild and cell phone internet, each w/ expanded footprints”

- “There’s not a great financial return for wireline overbuilds”: This is true w/ a single overbuilder, and the returns become “terrible” when there’s multiple; Overbuilders “can put up a few points of penetration” in the first 18-24 months, but then “the mkt kind of settles out”

- Charter believes we’ve seen the “peak cell phone Internet impact”: Given that the cell phone Internet (FWA) providers will “face challenges” as data usage continues to rise

- The Co is “thinking about the long-term for the biz”: Looking ahead, one of the “big questions or variables” is if a lower interest rate environment “impact[s] mortgages in a way that drives higher move rates”

- However, “it’s still a competitive environment for new sales”: Charter “continue[s] to compete well against both wireline overbuild and cell phone internet, each w/ expanded footprints”

Lower Than Expected ACP-Related Churn Contributed To Better Than Anticipated Broadband Net Losses

- Comcast – Q3 broadband net losses weren’t as steep as anticipated: Reached a net losses of -87k (vs -18k the prior yr qtr and -120k in Q2) were better than cons’ -141k; Comcast lost a net -79k residential customers (vs -110k in Q2) and -8k biz customers (vs -10k in Q2)

- Excluding ACP, broadband net adds would have been positive +9k:

- ~One-third of ACP-related churn were direct losses experienced in Q3: The remaining ~two-thirds reflects a reserve taken for the number of subs predicted to churn in the coming months due to a non-pay or delinquency status

- Three other factors “were unique” to the qtr: Without these drivers and the ACP impact, the Co estimates broadband net adds would have been “slightly worse” than the prior yr qtr

- Comcast performed “well” in back-to-school: The Co performed ~ the same level as last yr in back-to-school activity

- The Olympics was “good for cable”: The Co leveraged the Olympics “by investing in incremental nationwide brand mkting behind [its] Olympic-related offers”; Olympic audiences were “highly engaged”, w/ viewership in Xfinity mkts double the national avgs

- AT&T’s work stoppage was a benefit: The 30-day stoppage was “not a major driver, but it did have an impact” in a “limited” part of Comcast’s footprint

- SMB “continues to be a competitive mkt”: The Co has been focused on increasing rev via ARPU growth and expanding relationships w/ SMB customers by driving higher adoption of a suite of addt’l products

- Comcast has been “taking share” at the enterprise level: Growth in enterprise rev has outpaced growth in SMB rev as the Co continues to scale the enterprise biz

- Excluding ACP, broadband net adds would have been positive +9k:

- Charter – Internet net losses were better than feared: Reported net losses of -110k in Q3 (vs +63k in the prior yr qtr and -149k in Q2) were far better than cons -242k; Residential Internet net losses of -113k beat cons’ -235k, and SMB net adds of +3k surpassed cons’ -7k

- Without the impact of ACP ending, Internet customers would have grown: The end of the program resulted in ~-200k Internet losses, w/ “incremental non-pay disconnects” driving more than half of those losses and voluntary churn being the primary reason for the rest

- There was also a “small impact” from lower connects related to the program’s conclusion

- Otherwise, Charter has “cont’d to do a very good job in managing the end of the program”: The Co has retained most of the customers that were previously receiving an ACP benefit

- Other temporary tailwinds benefited net adds during the qtr: Including a seasonal back-to-school uplift in activity and one of the Co’s competitors (AT&T) experiencing a work stoppage; These won’t be factors in Q4

- Net adds in the subsidized rural footprint ticked up seq: To +41k in Q3 (vs +36k in Q2)

- Without the impact of ACP ending, Internet customers would have grown: The end of the program resulted in ~-200k Internet losses, w/ “incremental non-pay disconnects” driving more than half of those losses and voluntary churn being the primary reason for the rest

Forward-Looking Commentary – The Recent Hurricanes Will Impact Q4

- Comcast – “The underlying environment remains the same” and “very competitive” in Q4: Also acknowledged “some impact” from the two hurricanes but didn’t have numbers to share on the call; Otherwise, churn is expected to remain at low levels, and activity is expected to seasonally tick up in the Southeast

- Charter – Q4 will be impacted by the hurricanes: In addition to extending bill credits to customers in impacted areas, which will weigh on rev, the Co anticipates “some lost customers and passings related to the storm from both suppressed gross adds and the damaged or destroyed plant”

- ACP-related disconnects will also remain a headwind in Q4: Expects ~-100k incremental non-pay disconnects as well as some voluntary disconnects related to the end of ACP in Q4; After this, ACP related effects will be behind the Co

- There’s “certainly a better unit growth setup” for 2025 than 2024: Given that there won’t be ACP and that the Co will have tailwinds from more organic and rural passings; Recent efforts to create addt’l bundles and higher product value packaging as well as a “reconstituted” video product will help as well

Strong ARPU Growth Has Been Helping To Offset Subscriber Declines

- Comcast – Broadband ARPU growth was flat seq: Incr’d +3.6% y/y in Q3 (similar to Q2’s rate), which was “another strong result in the context of a cont’d competitive backdrop”, given ongoing efforts “effectively balance rate and volume through customer segmentation”

- Charter – Residential ARPU growth accel’d seq: Grew +1.8% y/y (vs +0.4% y/y in Q2); Along w/ its new pricing and packaging strategy starting to drive “more sales w/ higher sell-in of [its] best products” the Co saw its highest mix of ads Unlimited+, which drove higher customer value and ARPU

- Y/Y growth benefited from $63mn of customer credits issued in the prior yr period: This was related to the carriage dispute w/ Disney and temporary loss of programming in Q3:23

- Other drivers: Included tailwinds from promo rate step-ups, rate adjustments, and the growth of Spectrum Mobile, partly offset by a higher mix of non-video customers

- Internet ARPU growth took a step up seq: Was up +2.8% on a GAAP basis and +3.1% on a non-GAAP basis (vs +1.7% y/y in Q2); Those two rates will be “coming together” moving forward

- “Mobile ARPU was up and is looking really good”: This was related to the uptake of Unlimited+ plans, which has been driven by the Anytime Upgrade offer; Otherwise, the impact of the Spectrum One roll-off of free lines was “more normalized”

- Y/Y growth benefited from $63mn of customer credits issued in the prior yr period: This was related to the carriage dispute w/ Disney and temporary loss of programming in Q3:23

Go-To-Mkt Color – Comcast Maintained The Status Quo, While Charter’s Recent Changes Have Been Showing Early Returns

- Comcast continues to focus on segmenting the mktplace across its products: The Co’s “fundamental” approach is to “give customers what they want at the right price and the right package”

- Surrounding connectivity w/ “the right package offerings” also remains a focus: Mobile is “front and center” in this strategy, though the Co has been “leveraging everything, including new video products like NOW TV, NOW Latino, and Stream Saver”

- The Co plans to lean into “big sports moment[s]” moving forward: The Olympics was a “unique place” to “drive value for [the] Co across all swim lanes”, and now, “when there’s a big moment in entertainment in any form, look for [Comcast[ to continue to do it”

- Charter’s sales & mkting efforts have been tied to the pricing & packaging for its new bundles –

- The new brand platform, Life Unlimited, is about the Co’s “increasingly converged set of products”: Along w/ “lower promo pricing and lower persistent bundled pricing”, the “new look and feel for the Spectrum brand” are all part of a broader effort to build more trust w/ customers

- The Co’s new pricing and packaging efforts are “showing promising results”, though “it’s still very early”: They are driving “more video sell-in, more mobile lines per sale, and more gig sell-in”; Expects this and broadband sales to accel “over time” as its sales & mkting approach becomes more seasoned

- Further benefits: Include growing customer ARPU at connect, despite lower product pricing, as well as lower billing, svs, and retention calls, while reducing churn; Believes it will also “be really successful in driving addt’l cash flow per customer”

- New bundles have built-in retention mechanisms: For example, customers that take the new double play offer will receive a two-yr price lock, while those that take the triple play will receive a three-yr price lock

- The Spectrum One offering also remains available: The offering, which includes one free mobile line for a yr, now comes w/ a higher starting speed of 500 Mbps

Data Usage Continues To Rise (Though Not Materially On A Seq Basis)

- Comcast – “Broadband usage is skyrocketing”: Comcast’s broadband-only customers are avg’ing 700 gigabytes per month (vs “over 700 gigabytes” per month in Q2), which the Co welcomes, given that its existing network “can handle significant increases in bandwidth consumption at a very low marginal cost”

- Charter – “Customer bandwidth demand continues to grow”

The Cable Cos’ Wireless Net Adds Outperformed But Were A Bit Lower Seq

- Comcast – Wireless net adds were ~flat seq and topped estimates: Reported net adds up +8.5% y/y to +319k (vs +322k in Q2) and beat cons by +5.8%; Comcast ended the qtr w/ ~7.5mn total domestic wireless lines, representing a +19.8% y/y rise

- Highlighted benefits of having converged customers: When wireless and broadband are bundled together, they “drive overall customer relationship ARPU growth, churn benefits for broadband, and higher profitability”; Higher overall customer satisfaction has been another positive outcome

- The Co still sees a “very long runway for growth” ahead: Given that wireless penetration of its broadband sub base remains at ~12% (similar to figures provided on Q2 but up from ~11% as of Q1)

- Comcast plans to continue to test new convergence offers: These will help “capitalize on the significant oppties” ahead of the Co in wireless, including increasing the penetration of its domestic residential broadband base as well as selling addt’l lines per account

- There are other oppties to enhance the Co’s convergence experience: For example, Comcast is rolling out a new feature called WiFi Boost, which automatically increases Xfinity Mobile customer speeds up to 1 gig on the Co’s WiFi network

- Comcast’s convergence strategy “is proving out in [its] financial performance”: Underscored that the Co’s domestic broadband + wireless rev has been growing at a +5% y/y clip, “which consistently leads the industry”

- Charter – Mobile net adds dipped slightly seq but still beat expectations: Mobile net adds were down -8.2% y/y to +545k in Q3 (vs +557k in Q2) but exceeded cons by +1.6%, nonetheless; Charter ended the qtr w/ 9.4mn total mobile lines, a +29.6% y/y uptick

- Charter has been seeing “cont’d success in Mobile”: The Co’s mobile offering “continues to evolve, driving strong results and supporting [its] new pricing and packaging efforts”

- The Co saw its “highest” mix of adds on Unlimited Plus

- Lines per customer “continues to grow nicely”

- Free lines have been converting to paying ones at “very strong rates”:

- Mobile penetration of Charter’s broadband base was similar seq: Highlighted that ~8% of the Co’s total passings currently take its converged offering of Internet and mobile; Charter “remain[s] underpenetrated”

- Charter has been seeing “cont’d success in Mobile”: The Co’s mobile offering “continues to evolve, driving strong results and supporting [its] new pricing and packaging efforts”

Video Churn Has Shown Signs Of Stabilizing / Charter’s New Video Offering Was A Big Focus

- Comcast – Q3 Video losses were better seq and better than feared: Net losses of -365k in Q3 (vs -490k the prior yr qtr and -419k in Q2) beat cons’ -419k

- Churn has cont’d to stabilize and “has been stabilizing for a while”: Introducing mobile into the mix and “high engagement levels” around the Olympics have contributed to “churn reduction”

- The NOW portfolio has boosted video connects: The Co has been offering NOW TV and NOW Latino “surgically” as part of its broader segmentation strategy, and this has “helped video”

- StreamSaver is “profitable, and it makes a lot of sense”: Believes that it offers a “great consumer price point” without subsidizing and that it’s “an example of good video choice”; “Look for more of that from [Comcast] over time”

- Comcast has completed 10 renewals in the past 15 months: These have been w/ “a mix of both traditional and streaming distributors”; The Co most recently signed renewals w/ Charter and Hulu

- Video rev was also better than expected: Down -6.8% y/y (vs -7.8% y/y in Q2) and topped cons by +1.2%; The y/y decline was a function of “cont’d customer losses, coupled w/ slower domestic ARPU growth vs last yr”

- Churn has cont’d to stabilize and “has been stabilizing for a while”: Introducing mobile into the mix and “high engagement levels” around the Olympics have contributed to “churn reduction”

- Charter – Q3 Video net losses were better seq and not as steep as expected: Net losses of -294k (vs -327k in the prior yr qtr and -408k in Q2) were better than cons’ -377k; Resi net video losses of -281k beat cons -379k, while SMB net video losses of -13k were worse than cons’ +2k

- Charter has “transformed all of its major programming agreements” over the past yr: Including most recently an early renewal w/ WBD and then NBCU; The agreements give customers greater overall package flexibility and the ability to include all key streaming apps within Spectrum TV Select plans

- There are also “paths for customers to upgrade to the ad-free version of these apps”: Including the ad-supported versions of Max, Disney+, Peacock Premium, Paramount+, ESPN+, AMC+, Discovery+, BET+ and ViX

- The Co will also sell programmers’ apps on an a la carte basis to broadband and skinny package video customers

- There is still “some work to do to operationalize the new customer prop”: Expects to have the video offering “fully operationalized” in H1:25, or 18 months after starting to enter programming negotiations

- Creating a video mgmt portal is the final priority: The first is programming relationships, the second is launching the DTC app, and the third is implementing a way for customers to upgrade to ad-free versions of streaming apps; Next, the Co will look to put all of that inside a video mgmt portal

- By early 2025, TV Select customers will get up to $80/mo of retail streaming value at no addt’l cost

- New bundling efforts are already generating a “significant uplift” in video sell-in: However, the Co is not forecasting video growth for next yr

- Charter has “transformed all of its major programming agreements” over the past yr: Including most recently an early renewal w/ WBD and then NBCU; The agreements give customers greater overall package flexibility and the ability to include all key streaming apps within Spectrum TV Select plans

Higher Mkting Expenses Weighed On Both Comcast & Charter’s Adj EBITDA Margins

- Comcast – Connectivity & Platforms adj EBITDA margin took a step down seq: Expanded +30bps y/y to 40.9% (vs 41.9% in Q2), which was ~in-line w/ cons

- Residential adj EBITDA margin declined seq…: Incr’d +20bps y/y to 38.6% in Q3 (but down vs 39.9% in Q2); Declines in overall expenses from a mix shift toward higher-margin connectivity bizs and ongoing expense mgmt was offset by higher mkting and promo expense related to the Paris Olympics

- … While Business Services adj EBITDA margin improved seq: Was down -10bps y/y to 57.4% (vs 57.0% in Q2)

- Q4 cost reductions will occur at an “equal” magnitude to last yr

- Residential adj EBITDA margin declined seq…: Incr’d +20bps y/y to 38.6% in Q3 (but down vs 39.9% in Q2); Declines in overall expenses from a mix shift toward higher-margin connectivity bizs and ongoing expense mgmt was offset by higher mkting and promo expense related to the Paris Olympics

- Charter – Adj EBITDA margin was on-par with the Street’s estimates, declining seq: Improved +80bps y/y to 40.9% in Q3 (vs 41.4% in Q2) and closed in-line w/ cons

- Breakdown of expense items –

- Programming costs were down -10.0% y/y (vs -9.8% y/y in Q2): Driven primarily by fewer video customers and a higher mix of lower cost packages within Charter’s video customer base, partly offset by contractual programming rate increases and renewals

- A $61mn benefit related to the temporary loss of Disney programming in Sept 2023 was another offsetting factor

- Cost to svs customers decr’d -0.5% y/y (vs -4.2% y/y in Q2): Productivity gains from 10-yr investments were partly offset by modest y/y growth in bad debt expense

- Sales & mkting expenses grew +4.4% y/y (vs +1.9% y/y in Q2): Related to efforts to drive customer acquisition as well as the Life Unlimited brand relaunch in Sept

- Programming costs were down -10.0% y/y (vs -9.8% y/y in Q2): Driven primarily by fewer video customers and a higher mix of lower cost packages within Charter’s video customer base, partly offset by contractual programming rate increases and renewals

- Tempered comments on Q4 EBITDA growth: “Strong” growth is still anticipated, but “it might not accel the way that [the Co] had hoped”, given that some expense reduction impacts came in a little earlier than expected; There will also be storm impacts that hit in Q4

- There will be “some meaningful headwinds” to EBIT growth in 2025: Including Internet net losses in 2024 and a non-political yr for advertising

- Breakdown of expense items –

Investment Plans – Charter Further Delayed Its Network Evolution Initiative, While Comcast’s Network Upgrades Are “On Plan”

- Comcast expects to maintain its rate of home passings: Similar to last qtr, the Co highlighted that it has driven 1.2mn home passings over the past yr and that it projects to add 1.2mn+ new home passings this yr to “maintain [its] lead” in gig-plus broadband coverage “well into the future”

- The Co’s network upgrade initiatives are also “on plan”: ~50% of Comcast’s footprint has been updated w/ mid-split tech (vs 42% in Q2), and the Co now expects to be “through the vast majority of that effort by the end of next yr”; Previously, Comcast had targeted to be at 50% by the end of 2024

- DOCSIS 4.0 “rides right on the back of that”: The Co remains on a “clear path to offer multi-gig symmetrical speeds” and “really like[s] the roadmap”

- Comcast is already ahead of the curve: The Co is currently “ahead of every single application in terms of broadband capability”

- Comcast “anticipate[s] the activity” is coming w/ BEAD but has “tight thresholds”: It’s still “too early to really comment in terms of how much activity”, though Comcast does “plan to participate w/ reasonable conditions” and w/ “a lot of financial discipline”

- The Co’s network upgrade initiatives are also “on plan”: ~50% of Comcast’s footprint has been updated w/ mid-split tech (vs 42% in Q2), and the Co now expects to be “through the vast majority of that effort by the end of next yr”; Previously, Comcast had targeted to be at 50% by the end of 2024

- Charter’s network evolution initiative is now expected to be completed in 2027: The Co “deliberately slowed” work on step 2 DAA and remote PHY to get the software fully spec’d, pushing back equipment purchasing and deployments

- The network evolution initiative was originally expected to be done in early 2025: The timeline was first pushed back by ~6 months in Q2:23 to the end of 2025 or early 2026

- High-split upgrades should be “largely complete” in all step 1 mkts by the end of 2024: Charter is now broadly mkting its symmetrical speeds in seven of these eight mkts

- The Co has seen “very low incremental $100 per passing”: In-line w/ targets originally laid out as part of the initiative

- Rural passings occurred at a faster pace seq…: Subsidized rural passings grew by +114k in Q3 (vs +89k in Q2 and +73k in Q1)

- … BUT aren’t expected to hit the Co’s 2024 target: Now expects to activate close to +400k in 2024, a +35% y/y increase, though lower than the initial plan of +450k due to shifting construction and labor capacity to rebuilding efforts in hurricane-afflicted areas

- Charter now expects to participate less in BEAD than in RDOF: Given that the most recent broadband map updates have fewer available unserved passings near its network and include “a little less favorable rules framework” when compared to RDOF and state grants

- There’s been “zero difference” in svs quality or competitiveness between HFC and FTTH footprints: Highlighted that 99.5% or 99.8% of the HFC plant consists of fiber, so it’s “essentially the same network”; Conversely, believes “there are some real advantages” to the HFC plant

- The network evolution initiative was originally expected to be done in early 2025: The timeline was first pushed back by ~6 months in Q2:23 to the end of 2025 or early 2026

There Were Some Moving Parts In The Cable Cos’ CapEx Plans

- Comcast – Connectivity CapEx was flat seq: Segment CapEx of $1.9bn dropped -6.5% y/y (vs -12.9% y/y in Q2), reflecting lower spending on scalable infrastructure and CPE, partially offset by higher investment in line extensions and support capital

- Overall CapEx was +19.8% better than expected: Levels of investment in Epic Universe were “significant” but remained “consistent”

- Capital intensity guidance implies “a little bit of catch-up” in Q4: The Co still anticipates similar levels of capital intensity to last yr but was pacing to hit the “low-end” through the first three qtrs of this yr

- Charter – CapEx levels declined seq and were lower than anticipated: CapEx of $2.6bn was down -13.5% y/y in Q3 (vs +0.7% y/y in Q2) and +22.1% better than cons; The drop was driven by declines in core CapEx items, including CPE timing and lower than expected spend on network evolution

- 2024 CapEx is now expected to be ~$11.5bn (vs prior ~$12bn and $12.2-12.4bn originally): The revision reflects full-yr line extension spend of ~$4.3bn (vs prior $4.5bn), partly offset by “slightly higher” core CapEx related to hurricane rebuild activity

- Network evolution spend is now expected to be ~$1.1bn (vs prior $1.6bn): Much of the planned spend for 2024 is being pushed into 2026 and 2027

- The Co expects to incur ~$100mn of incremental CapEx related to hurricane rebuild efforts: That said, Charter is still in the process of assessing impact areas

- 2025 CapEx will not exceed the range originally outlined at the beginning of this yr: Initially projected a $12-12.5bn range for FY25

- “Total capital intensity is now poised to decline significantly after 2025”: Even after accounting for the Co’s plans to expand rural passings

- 2024 CapEx is now expected to be ~$11.5bn (vs prior ~$12bn and $12.2-12.4bn originally): The revision reflects full-yr line extension spend of ~$4.3bn (vs prior $4.5bn), partly offset by “slightly higher” core CapEx related to hurricane rebuild activity

Charter’s FCF Benefited From Lower CapEx, While Comcast’s Slightly Missed

- Comcast – “Significant organic investment” resulted in a slight miss on FCF: FCF of $3.4bn fell -15.5% y/y in Q3 (vs -60.9% y/y in Q2) and missed cons by -1.6%

- Returns to shareholders dipped further seq: The Co returned $3.2bn to shareholders in Q3, w/ repurchases of $2bn (vs $2.2bn in Q2 and $2.4bn in Q1) and dividend payments of $1.2bn

- Charter – FCF came in well ahead of expectations: Q3 FCF $1.6bn rose +47.6% y/y (vs -27.2% y/y in Q2) and topped cons by a wide +124.1%, driven by higher adj EBITDA and lower CapEx

- Share repurchases slowed significantly seq due to ongoing negotiations w/ Liberty Broadband: Bought back $260mn worth of shares in Q3 (vs $854mn in Q2), which was less than originally expected, as Charter became restricted by its negotiations w/ Liberty Broadband

Is A Corporate Action Coming In Legacy Media? Will Comcast Spin-Off Cable Nets?

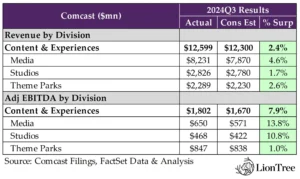

We got a first look at Media sector fundamentals across theme parks, streaming, and the linear ecosystem with Comcast reporting much better than expected results across the board in its Content & Experiences business. With that said, results, to a large extent, were overshadowed by mgmt’s comments that they are in the early stages of exploring if a spin-off of its cable networks to shareholders makes sense and that they are open to a potential streaming partnership. Details were sparse, but it did create some investor enthusiasm.

In terms of some key takeaways with the core fundamentals in Comcast’s Content & Experiences segment, the Paris Olympics was a primary driver across the company’s streaming and linear media businesses. Mgmt did stress that the Olympics was “profitable” (without exactly quantifying) and generated $1.9bn in incremental revenue (including $1.4bn in ad revenue, of which $300mn was for Peacock). The event helped attract new Peacock streaming subs (added +3m in Q3 vs a loss of -0.5mn in Q2). Looking ahead, with the inclusion of the NBA, the Co is confident that they are now a year-long sports destination.