When Trump said to expect some short-term turbulence in the markets, he certainly meant it. It was yet again a tough week, with the S&P 500 closing down a further -2.3% and Nasdaq down another -2.4%. From the February all-time high, the S&P 500 has lost nearly $5tn in market cap and Nasdaq is down ~-12% from its all-time high in December.

Aside from tariffs, which were the main event this week, there was a barrage of economic data out as well (CPI and PPI came in lower than expected, jobless claims slightly fell w/w, and consumer sentiment fell to its lowest level since November 2022, among the key reports).

While macro remains a key focus, there were still plenty of interesting updates and developments on the micro side as well. This week’s edition focuses on:

- The Aperture Of Economic Impacts From Trump’s Policies Is Widening…

- Some Cracks On The Surface Appear Across The TMT & Consumer Sectors This Week

- All M&A Is Not On Hold… CCI Finally Gets Its Fiber Deal Done

- The Pendulum Between Big Tech & Regulators Swung Both Ways This Week

- There Is No Rest For The Weary As It Relates To The AI Agent Race – A Few Key New Developments This Week

- Users Spent More Time & More Money On Core Mobile Games In 2024

- Grab Bag: Apple Software Revamp Reportedly In The Works / Comcast Is Getting The Olympics Until 2036 / Waymo Launches In Silicon Valley

Have a nice weekend.

Best,

Leslie

The Aperture Of Economic Impacts From Trump’s Policies Is Widening…

The market’s visceral reaction to the Trump administration’s new tariffs this week was the main event, with the implication of rising costs (a 25% US tariff on imports of steel and aluminum went into effect on March 12) and general uncertainty over the White House’s future economic policies resulting in a broad sell-off in public equities. Other key economic indicators, including last week’s weaker than anticipated jobs report and this week’s underwhelming consumer sentiment update from the University of Michigan, were also cause for some consternation and contributed to unease amongst investors. That said, inflation started to cool in February, as US core CPI came in lower than anticipated.

Though perhaps not a surprise due to the stratospheric outperformance over the last couple of years, the tech sector has been one of the hardest hit segments YTD, while telecom, healthcare, and energy have been the top-performing categories. Over the past week, utilities and energy were the only two sectors that didn’t see declines. With the recent market dislocation, current S&P500 P/E ratios have started to trend closer to the 10-year average, though the index would need to see another ~-13% drop to fall in-line with this mark. The VIX index also ended the week closer to its 5-year average after spiking well beyond the benchmark earlier in the week.

Despite the volatility in the markets and growing recession fears stemming from the Trump Administration’s policies, not everyone views them in a negative light. Blackstone CEO Stephn Schwarzman remarked that the new protectionist measures would ultimately “lead to a significant increase in manufacturing in the US,” which “tends to be a good thing for the world.” On a similar note, Goldman Sachs CEO David Solomon told reporters that he likes the way that “the President is engaged with the business community,” claiming that it’s “a different experience than what we’ve had over the course of the last four years.” Still, Solomon also acknowledged that he would like more “certainty” with the Trump administration’s policy agenda and that the “business community is always going to want lower tariffs everywhere in the world.” (link)

See more of our thoughts below.

Recent Economic Data Has Revealed Some Worrisome Signs / The Tariff Impact To Inflation Numbers Are Yet To Come

- Consumer sentiment fell to its lowest level since Nov 2022, per the University of Michigan (link): This largely reflected growing concerns over where inflation is headed, particularly as it relates to the impacts from the recently implemented tariffs

- The University of Michigan Survey of Consumers for March posted a reading of 57.9, a -10.5% m/m decline as well as a -27.1% y/y drop, and below the consensus estimate for 63.0

- The one-year inflation outlook spiked to 4.9%, up +0.6ppt m/m and the highest reading since Nov 2022

- Notably, sentiment fell amongst both Republicans and Democratics as well as along virtually all demos

- US core CPI was lower than expected in Feb and the lowest reading since April 2021, per the Labor Dept (link): That said, much of this inflation data doesn’t incorporate the coming impact from the tariffs

- Excluding more volatile food & energy prices, core CPI rose +0.2% m/m and +3.1% y/y in Feb (vs +3.3% y/y in Jan), ending below consensus expectations of a +3.2% y/y gain

- Shelter costs grew +0.3% m/m in Feb, comprising ~half the monthly increase in CPI, and the +4.2% y/y rise was the lowest since Dec 2021; Used vehicle prices incr’d +0.9% m/m, and apparel prices grew +0.6% m/m

- In contrast, airline fares were down -4% m/m and -0.7% y/y

- US jobs growth was weaker than forecasted in Feb, per the Labor Dept (link): Notably, job reductions from the Dept of Government Efficiency’s efforts to pare down the size of the Fed govt likely won’t be fully felt until coming months

- Nonfarm payrolls incr’d +151k in Feb (vs +125k in Jan), though this was below consensus estimates of +170k; The unemployment rate ticked higher to 4.1% (vs 4.0% in Jan)

- Healthcare added the most jobs, creating +52k jobs; This was in-line w/ the sector’s 12-mo average

- Financial activities gained +21k jobs

- Transportation and warehousing payrolls grew by +18k

- Social assistance added +11k jobs

- BUT retail posted a decline of -6k workers

- Avg hourly earnings were up +0.3% m/m and +4% y/y in Feb, missing expectations to increase +4.2% y/y

- The labor force participation rate fell to 62.4% in Feb (vs 62.6% in Jan), its lowest level since Jan 2023

- Nonfarm payrolls incr’d +151k in Feb (vs +125k in Jan), though this was below consensus estimates of +170k; The unemployment rate ticked higher to 4.1% (vs 4.0% in Jan)

Notable Callouts Regarding Stock Market Trends

- There has been a cont’d rotation out of Big Tech –

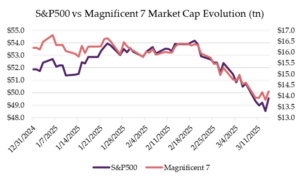

- The S&P500 has lost -4.1% in mkt cap YTD, while the Magnificent 7 has seen a -12.2% decline

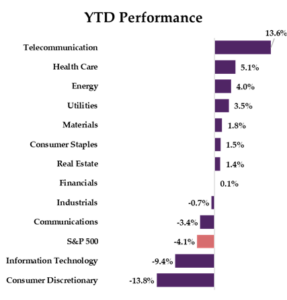

- YTD, telecom (+13.6%) has been the top-performing sector within the S&P 500, while consumer discretionary (-13.8%) and information technology (-9.4%) stocks have been worst performers

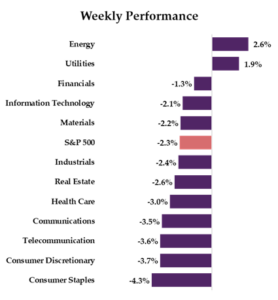

- Over the past week, nearly every subsector of the S&P 500 was in negative territory, w/ the exception of energy (+2.6%) and utilities (+1.9%)

- The S&P500 has lost -4.1% in mkt cap YTD, while the Magnificent 7 has seen a -12.2% decline

- Valuation multiples remain high but have started to return to historical avgs: After reaching the highest levels since 2019 at the end of 2024, the S&P 500’s aggregate P/E multiple has started to trend closer toward the 10-yr avg of 19.8x, closing the week at 22.8x

- There has been volatility in the VIX index: After spiking early in the week, the VIX index also began to normalize as the week progressed, closing at 21.77 (compared to the 5-yr avg of 21.2)

Some Cracks On The Surface Appear Across The TMT & Consumer Sectors This Week

The conference circuit this week saw some downbeat commentary and reductions to forecasts from companies across a wide swath of TMT and consumer sectors. In the connectivity industry, Verizon warned that Q1 postpaid phone net adds will come in lower than it previously forecasted primarily due to competition, while AT&T reiterated that it encountered some bumps in the road earlier in the quarter. There was also a canary in the coal mine in the advertising space, as SiriusXM issued an early warning that growing uncertainty related to the tariffs and inflation have resulted in pullbacks from advertisers in CPG and retail. Also, softening consumer sentiment as well as drastic cutbacks in government travel have taken their toll on the domestic airlines, with American, United, Delta, and Southwest Airlines downwardly revising their Q1 outlooks this week, which dragged down other travel-related stocks in the sector. Lastly, speaking about the consumer, a couple retail companies this week (namely Kohl’s and Dick’s Sporting Goods) conveyed outlook commentary that added fuel to the potential weakening consumer fire.

See below for more color:

- Verizon talked down Q1 postpaid phone net add trends…This was per Verizon CRO Frank Boulben at Deutsche Bank’s 33rd annual Media, Internet, & Telecom conference

- Q1 headwinds to net adds have been “mostly driven by competition”: Although Verizon ended its holiday promotions coming into Q1, its competitors did not do the same, resulting in a “challenging qtr from a competitive intensity standpoint”

- “Gross adds this qtr are going to be probably soft” …: Along w/ the competitive environment, the Co is facing a tough y/y comp

- … And churn will be +3-5bps higher y/y: Due to pricing actions taken in H2:24 and in early 2025

- Verizon still expects to improve Consumer postpaid phone net adds on a y/y basis in 2025: This excludes contributions from second lines and is the “same formula” that the Co had in 2024

- The Co is “confident” that churn levels will be down y/y in 2025: Verizon’s investments in its capability to personalize the treatment of its customer base will be a “major level to drive down churn in 2025”

- Satellite isn’t expected to be a driver of switchers: The Co has seen an “insignificant” number of customers inquire about satellite, and Boulben believes competitors’ pricing for satellite svs “seems a bit rich, given the low demand for that svs”

- The tech continues to have a “niche” use case: Verizon customers have mainly used it during emergency situations; Satellite will likely have “significantly smaller” demand than intl roaming

- Q1 headwinds to net adds have been “mostly driven by competition”: Although Verizon ended its holiday promotions coming into Q1, its competitors did not do the same, resulting in a “challenging qtr from a competitive intensity standpoint”

- AT&T provided some incremental commentary on how Q1 has progressed: This was per AT&T CFO Pascal Desroches

- Q1 saw “elevated” levels of postpaid churn early in the qtr, but it has improved: AT&T saw elevated postpaid churn in Jan from contract roll-offs that were originally expected to impact Dec; However, Feb was a “really good month,” and the Co has been “really pleased” w/ March so far; This was reiterated from last week

- “Wholesale revs have been a tailwind,” which is expected to continue: DISH migrating more of its customers onto AT&T’s network has been a driver

- Q1 earnings and cash flow guidance was issued: The expectations exclude contributions from DIRECTV

- Q1 EPS is forecasted to be similar to better than the prior yr qtr: The Co reported an EPS of $0.48 (ex DIRECTV) in the prior yr qtr, though this is below cons’ $0.53 for Q1:25

- Q1 FCF is expected to comparable or higher than the prior yr qtr: The Co generated $2.8bn in FCF (ex DIRECTV) in Q1:24; This also underwhelmed cons’ $3.3bn

- The Co will also realize $2bn+ in proceeds that won’t be included in FCF: Includes $1.4-1.5bn in proceeds related to the sale of DIRECTV as well as $850mn from a structured sale leaseback deal w/ Reign Capital; These will contribute to deleveraging efforts

- FY25 FCF is still projected to be $16bn+: This was in-line w/ guidance provided on AT&T’s Q4 earnings call

- AT&T sees several areas to grow wireless mkt share in 2025: Including SMBs, FirstNet, and the value segment

- Convergence is another factor: Highlighted that the Co’s share of wireless is +500 bps higher in areas where it has AT&T Fiber

- BUT satellite “is not an enormous biz oppty”: The tech is “very nascent,” though the Co still expects to deliver this capability over the longer-term

- Q1 saw “elevated” levels of postpaid churn early in the qtr, but it has improved: AT&T saw elevated postpaid churn in Jan from contract roll-offs that were originally expected to impact Dec; However, Feb was a “really good month,” and the Co has been “really pleased” w/ March so far; This was reiterated from last week

-> For Verizon this was a change in tone given at last week’s Morgan Stanley TMT Conference, CFO Tony Skiadas flagged that the Co’s wireless biz has been “robust and resilient”; In contrast, AT&T CEO John Stankey’s comments last week were relatively similar to CFO Pascal Desroches’ this week, with FY25 guidance items being reaffirmed

-> Verizon shares fell -5.4% this week, and AT&T shares were down -2.0%; YTD, Verizon stock is still trading up +9.0%, and AT&T stock is up +16.7%

Outside Of The Connectivity Space, Alarm Bells Were Ringing In Other Industries

- SiriusXM CFO Tom Barry – “Macroeconomic factors are a concern”:

- SiriusXM has started to “see a drop-off” from advertisers over the last couple weeks: Tariffs, inflation, and overall uncertainty in the mkt have been “adversely impacting the ad space,” w/ “some softness” in CPG, retail, as well as other categories

- Changes in the biz will result in ~-200k net subscriber losses in 2025: The Co’s cutback in streaming mkting beginning in Q4 will result in higher churn and fewer gross adds in Q1; Then, changes in click-to-cancel rules will adversely impact H2:25

- Price increases and optimizations to promo plans will also drive higher self-pay OEM churn in the near-term: The Co believes self-pay OEM churn will “slide up a little” but doesn’t see it “moving up drastically”

-> SiriusXM shares fell -6.9% following the comments and closed the week…

- Several domestic airlines cut guidance and warned of deteriorating macro conditions (link/link): This was per Co comments at the JPMorgan conference this week

- American Airlines – “The rev environment has been weaker than initially expected”: Cited the impact of Flight 5342 (the collision between an American Airlines jet and an Army helicopter in Washington DC in Jan) as well as “softness in the domestic leisure segment, primarily in March”

- An EPS loss of -$0.60-0.80 is anticipated in Q1: This would be worse than the -$0.20-0.40 per share that the Co previously forecasted

- FY25 rev will likely be flat y/y: In Jan, American Airlines previously estimated that FY25 rev would increase as much as +5% y/y

- Delta Airlines’ outlook was slashed due to “softness in domestic demand”: “The recent reduction in consumer and corporate confidence” has been “caused by incr’d macro uncertainty”; “Corporate spending started to stall,” and “consumers in a discretionary biz do not like uncertainty,” per CEO Ed Bastian

- Q1 EPS is now projected to be $0.30-0.50: Compares to the previous EPS forecast of $0.70-1.00

- Q1 rev is now expected to rise +3-4% y/y: Vs the prior forecast of +7-9% y/y

- United Airlines – “We have also seen weakness in the demand mkt”: “Govt travel is ~2% of United’s biz, but other workers’ travel is also affected, like consultants and contractors, which account for another 2-3%… We’ve seen some bleed over to that into the domestic leisure mkt,” per CEO Scott Kirby

- Q1 EPS is now predicted to finish at the lower end of the Co’s forecast of $0.75-1.25: Primarily due to a -50% drop in United’s govt bookings

- United is retiring 21 aircraft early to reduce FY25 expenses: This will save the Co $100mn that would have otherwise been used to overhaul engines this yr

- Southwest Airlines has also been affected by softening domestic travel demand: In particular, the Co cited less govt travel, a negative impact from the California wildfires, and concerns over discretionary spending amid tariff pressures

- Q1 rev growth is now expected to be between +2-4% y/y: Vs the prior expectation of +5-7% y/y

- Southwest Airlines will charge to check bags for the first time: The change applies to all customers except for those in the top-tier fare class and comes following months of pressure from Elliot Investment Mgmt; The Co didn’t specify how much it will charge

- American Airlines – “The rev environment has been weaker than initially expected”: Cited the impact of Flight 5342 (the collision between an American Airlines jet and an Army helicopter in Washington DC in Jan) as well as “softness in the domestic leisure segment, primarily in March”

-> American, Delta, United, and Southwest Airlines’ shares ended the week down -16.6%, -12.3%, and -11.1%, respectively, while Southwest Airlines shares were up +8.7%; YTD, American Airlines stock is trading down -37.6%, Delta Airlines stock is down -22.7%, United Airlines stock is down -24.1%, and Southwest Airlines stock is down -5.6%

-> This also dragged down Expedia shares -12.1%, Booking shares -4.4%, and Clear Secure shares down -4.4% on the week

- Addt’l outlook/commentary from the retail sector this week continues to spark concern about the consumer/ macroenvironment –

- Kohl’s outlook was much lower than expected: “Overall, we know that there’s a lot of uncertainty with the customer. And we try to definitely take a prudent approach with our guidance. So, really, our outlook both recognizes the time needed that we have to make the necessary changes that we’ve outlined today, as well as the uncertainty that a consumer is facing in the macro environment. And I think that’s why we came out a little bit lower to make sure that we were addressing that uncertainty and the time needed”; Mgmt also specifically called out the lower income consumer as being “pretty constrained”

- 2025 guidance significantly missed: EPS $0.10-0.60 vs cons $1.22, net sales decline -5% to -7% y/y vs cons +0.2%, and comps -4% to -6% vs cons -0.9%

- Cuts its quarterly dividend by -75.0% to $0.125

- Dick’s Sporting Goods – the outlook was softer than expected: “We are not seeing a weaker consumer now. We’re coming off a fantastic Q4. Our guidance merely reflects the fact that there’s so much uncertainty in the world today in the geopolitical environment, macroeconomic environment, we are just being appropriately cautious.”

- 2025 guidance missed on EPS & Revs: Adj EPS $13.80-14.40 vs cons $14.82, w/ revenue $13.6-13.9bn vs cons $13.89bn at the mid-pt, Comps mid-pt (+1.0-3.0%) was below cons as well

-> Kohl’s shares fell -34.0%, and Dick’s shares were down -9.2% this week; YTD, Kohl’s stock is down -42.6% and Dick’s stock is down -15.0%

All M&A Is Not On Hold… CCI Finally Gets Its Fiber Deal Done

The moment Donald Trump was re-elected in November to assume the Presidential post, company executives and investors got excited about the potential for a ramp in M&A in the sector. However, big deal announcements have actually been few and far between, especially in light of all the policy changes, macro uncertainty, and the market dislocation that has ensued instead. With that said, some deals are making it through the gate, and Crown Castle’s (CCI) agreement to sell its Fiber businesses to EQT and Zayo was a key example of that this week. This deal concludes a fiber strategy review that CCI’s Board of Directors previously announced in December 2023, which itself came on the heels of activist shareholder Elliot Management launching a campaign pushing for strategic changes.

Post this transaction, CCI will now be a pure-play US tower company with “some of the best geographic characteristics in [its] industry.” The company sees a long growth runway ahead from the secular growth in wireless data, which will continue to propel spending on towers.

Notably, along with the transaction announcement came a change in capital allocation, whereby CCI cut its dividend (though by less than some investors feared) but instead proposed a buyback of $3bn. Overall, the transaction was viewed positively and there were a couple Street upgrades as a result (UBS raised its rating to Buy from Hold but maintained $118 PT, Citi maintains Buy and raised its PT from $106-> $108, and Raymond James upgraded from Outperform to Strong Buy but cut its PT from $128->$122).

-> CCI shares rallied +10.4% on the back of the annc’d deal (and earnings); Towers in general have been strong performers YTD, given the defensive nature of their businesses, and AMT leads the pack, up +15% YTD, followed by CCI up +14% and SBAC up +7.1%; But to note, this performance is a big rebound from a tough 2024, where all were down ~-15-20%

What Assets Are Being Sold?

- CCI is selling its Fiber businesses for $8.5bn (see below for Precedent Fiber Transactions)

- The small cell business is being acquired by EQT Active Core Infrastructure Fund ($4.25bn)

- The fiber solutions business is being acquired by Zayo ($4.25bn)

Deal Basics

- Timing: Expected to close in H2 2026

- Use of proceeds: Pay down debt and repurchase stock while maintain balance sheet (maintain investment grade w/ target leverage 6-6.5x)

Changing Capital Allocation Framework

- CCI is cutting its annual dividend to $4.25/share starting in Q2 (from $6.26/share)

- Ex amort of prepaid rent, the Co targets ~70-80% AFFO and thinks it can grow the div in-line w/ AFFO

- Proposed $3bn buyback program (subject to board approval)

AFFO Will Be Much Higher Post Transaction

- Current 2025 AFFO guidance: $1.77-1.82bn

- Est’d annual AFFO at anticipated close: $2.265-2.415bn

CCI Believes It Will Be Well-Positioned To Benefit From Secular Trends In Wireless Data Growth Following The Transaction

- CCI will be a pure-play US tower company

- Focused exposure on “what we believe to be the best market for wireless infrastructure in the world”

- Expect to continue to experience rising demand for wireless data that will in term drive tower growth “for years to come”

- Its US tower portfolio has “some of the best geographic characteristics in our industry”

- Will benefit as carriers plan to continue the multi-decade trend toward greater network densification

- Also sees operational efficiencies driving results: Streamlining processes, reducing cycle times, and automating and customizing systems to deliver best-in-class service to its customers

CCI Also Released Results & Issued Guidance

- Q4 results were slightly mixed: AFFO was inline w/ cons with revenues slightly beating but AEBITDA slightly missing

- FY25 guidance was not comparable to Street estimates

- Sees consistent organic growth of +4.5% y/y in towers

The Pendulum Between Big Tech & Regulators Swung Both Ways This Week

The regulatory drumbeat has continued at a steady pace for quite some time, with several high-profile cases making their way through the antitrust system. That said, Big Tech has seen some small victories lately, particularly in the US, as the DoJ dropped its proposal for Google to sell its investments in AI this week. The FTC’s request for a delay on an antitrust trial against Amazon also appeared to be a small win for the company; however, the agency ultimately did an about face just a few hours later. Moving forward, Big Tech lawyers certainly have their work cut out for them, given that several prominent antitrust cases are still in progress and that Gail Slater, the DoJ’s new antitrust lead that was confirmed by the Senate earlier this week, is likely to step up the pressure on the tech industry and target potential monopolies in other sectors. Google’s antitrust trial, which is set for April, is the next key Big Tech regulatory event on the horizon. Additionally, Live Nation has a court date with the DoJ set for March 2026, and the company will have to face the full scope of the agency’s claims after its attempts to have a couple of them dismissed were denied this week.

There were also some noteworthy regulatory developments overseas this week. In the EU, regulators have opted to only levy “modest” fines against Apple and Meta for breaches of the Digital Markets Act, though a specific amount has yet to be determined. In the UK, an independent investigation commissioned by the Competition and Markets Authority (CMA) found that Apple and Google have been “holding back” the mobile browser market and the two companies’ remedies to the CMA’s provisional findings since last November have been insufficient. See below for more details on what we thought was important:

There Were Some Big Tech-Related Regulatory Updates In The US This Week

- The DOJ decided to drop its proposal to force Google to sell its investments in AI, including Anthropic (link/link): This decision is part of an ongoing antitrust case aimed at addressing Google’s alleged monopoly in online search

- Why the change of heart? The DOJ acknowledges the potential unintended consequences of banning Google from AI investments, which could stifle innovation and harm US competitiveness in the global AI market

- Instead, the DOJ now requires Google to give prior notice of future investments in gen AI

- BUT the DOJ and 38 state attorneys general are still seeking other measures, such as requiring Google to potentially sell its Chrome browse

- Timing: The case is set to go to trial in April

- Why the change of heart? The DOJ acknowledges the potential unintended consequences of banning Google from AI investments, which could stifle innovation and harm US competitiveness in the global AI market

-> In a 78-19 vote, the Senate confirmed Gail Slater as the Assistant Attorney General for the DoJ’s antitrust unit this week; Slater was nominated by President Trump and formerly served as an economic policy aid to Vice President JD Vance during his time as a senator; During President Trump’s first time, she was a tech policy advisor on the National Economic Council w/ a focus on antitrust and tech policy; Before then, Slater spent 10 ys at the FTC; Her top priority as Assistant Attorney General will be to “protect consumers” by scrutinizing industries, such as healthcare, tech, and agriculture; Slater will also take over other cases in progress targeting Google, Apple, Live Nation, and Visa (link/link)

- The FTC asked for a delay for a trial regarding Amazon’s alleged deceptive practices BUT reversed course the same day (link): The Federal Trade Commission cited resource constraints in its initial delay request but then affirmed that it will meet deadlines for the case

- The start date for the trial was set for Sept 22: FTC attorneys had made the initial delay request on Wednesday this week during a status hearing before Judge Chun in the Western District of Washington

- The FTC originally asked for a two-month extension due to a staffing and budgetary shortfalls: FTC attorney Jonathan Cohen claimed that the FTC “lost employees in the agency, in our division, and on the case team”

- The agency “cannot guarantee if things won’t be even worse” in two months: Cohen flagged the possibility that the FTC could have to “unexpectedly” move offices, which could impede its ability to prepare for the trial

- Amazon had disputed the delay: Given that the Co heard that FTC’s trial team was still intact and that office moves are typically no more than few days disruptive

- BUT the agency changed its position just hours later: “Please be assured that the FTC will meet whatever schedule and deadlines the court sets”: “The commission does not have resource constraints, and we are fully prepared to litigate this case,” per Cohen

- Relevant background: The FTC initially sued Amazon in June 2023 due to claims that the Co was deceiving millions of consumers into signing up for its Prime program and then sabotaging their attempts to cancel

- The FTC is reportedly proceeding w/ an antitrust investigation into Microsoft (link): The agency’s probe of Microsoft’s software licensing and cloud computing bizs was opened toward the end of the Biden Administration and will be cont’d by new FTC chair Andrew Ferguson

- Microsoft’s practices under scrutiny include –

- Potential abuses of mkt power in productivity software: Such as imposing punitive licensing to terms to prevent customers from shifting away from the Azure cloud svs to competing public clouds

- The data center biz: Including Microsoft’s struggles to find enough computing power to svs customer demand as well as more info about licensing rule changes expected later in 2025

- AI investments: Specifically, the Co’s decision to cut funding on its own AI products after finalizing a deal w/ OpenAI, which could be viewed as detrimental to competition in the AI mkt

- Current status of the probe: FTC staff have met w/ Cos and other groups to gather info in recent weeks, per sources; This comes after the FTC sent Microsoft a civil investigative demand (similar to a subpoena) late last year, requesting that the Co turn over data about its AI operations

- Microsoft is “working cooperatively” w/ the FTC: However, the Co is also seeking to narrow the scope of the info that it has to provide the agency, which is standard practice in these types of investigations

- Microsoft’s practices under scrutiny include –

-> On a related note, new FTC chair Andrew Ferguson emphasized that “Big Tech is one of the main priorities of the Trump-Vance FTC” in an interview w/ CNBC this week; Ferguson views his role as a “law enforcer,” ensuring that everyone complies w/ antitrust laws to “protect ordinary Americans”; Ferguson will look to provide more regulatory certainty than the previous administration’s FTC, stating, “If we’ve got a merger or conduct that violates the antitrust laws, and I think I can prove it in court, I’m going to take you to court… And if we don’t, I’m going to get the hell out of the way” (link)

Across The Pond, Big Tech Was Again In The Limelight In The UK & The EU

- EU antitrust regulators will only impose modest fines on Apple and Meta for allegedly breaching the Digital Markets Act, per sources (DMA)… (link/link/link):

- Background: The DMA initially came into play in May 2023, and since last yr, Apple and Meta have been under scrutiny by the European Commission for potential breaches

- The fines will, reportedly, be “modest” though technically could be high: The fines could be as much as 10% of the Cos’ global annual sales, but the focus is on compliance rather than punishment; The duration of the alleged violations has also been limited

- Also geopolitically, as a reminder, President Trump last month threatened to impose tariffs against countries that impose fines on US Cos, which may also be a factor to more limited fines

- What has the EU investigation been targeting?

- Apple’s steering rules, which regulators say impose limitations that hinder app devs from informing users about offers outside the App Store as well as the Co’s new fees levied on app devs

- Meta’s recently introduced pay or consent model, where users pay a subscription fee for an ad-free Facebook and Instagram

- Timeline: A decision on the fines is expected this month, though the situation could still change

- The UK’s CMA blamed Apple and Google for a mobile browser mkt that is “not working well for consumers and bizs” (link): Citing an investigation from an independent inquiry group, a final report from the UK’s Competition and Markets Authority found that Apple and Google’s practices restrict competition in the mobile browser mkt

- Issues flagged by the investigation include –

- Apple requiring all browsers on iOS to run on its WebKit browser engine: This provides Safari w/ preferential access to features when compared to competing WebKit-browsers

- Apple’s limitations on in-app browsing

- Apple and Google having their browsers pre-installed and serve as the default browsers for iPhones and Android devices, respectively: This reduces user awareness of alternative apps

- Rev sharing agreements between Google & Apple: These deals see Google pay Apple a significant share of search rev in exchange for being the default search engine on iPhones, “significantly reducing their financial incentives to compete”

- Apple and Google have “addressed some, but not all of the CMA’s concerns related to choice architecture: Investigators conceded that both Cos have taken steps to make switching to alternative browsers easier since the CMA published its provisional findings last Nov

- Other potential remedies proposed by the CMA: Consist of Apple forcing devs to use alternative browser engines on iOS, requiring Apple and Google to offer a browser choice screen during device setup, and prohibiting Chrome rev sharing agreements between the two Cos

- BUT these would “undermine privacy, security, and the overall user experience,” per Apple: Apple “will continue to engage constructively” w/ the CMA to address its concerns, while Google has yet to comment on the matter

- Issues flagged by the investigation include –

Other TMT Sub-Sectors Were In Regulators’ Crosshairs As Well This Week

- Live Nation’s bid to narrow the scope of the DoJ’s antitrust case against Ticketmaster was denied (link): New York US District Judge Arun Subramanian didn’t disclose the reasoning behind his decision to deny Live Nation’s motion to dismiss some of the claims in the Ticketmaster case

- The Co asked the judge to throw a pair of claims: In disputing one of the claims, Live Nation argued that it has no legal obligation to allow other Cos to use concert venues that it owns; Live Nation’s motion would not have thrown out the case entirely

- Motions like Live Nation’s are common in antitrust case: However, they rarely succeed in suits brought against the govt

- A trial is scheduled for March 2026: A DoJ lawyer said during the hearing, which was called to discuss the agency’s issues w/ Live Nation not providing documents on schedule, that the govt wants to hold a trial on whether the Co violated antitrust laws, followed by a separate proceeding, if necessary, on a remedy

- Relevant background: The DoJ and 30 states sued Live Nation in May 2024, claiming that the Co has illegally monopolized the live events industry and that it controls at least 80% of major venues’ ticketing for concerts

- The Co asked the judge to throw a pair of claims: In disputing one of the claims, Live Nation argued that it has no legal obligation to allow other Cos to use concert venues that it owns; Live Nation’s motion would not have thrown out the case entirely

- Omnicom and IPG each received a Second Request related to their merger from the FTC (link): The Request for Additional Information and Documentary Material (Second Request) is a “standard part of the regulatory process,” per Omnicom; Both Cos have been engaged w/ the FTC throughout the regulatory process

- The merger is still expected to close in H2:25: The completion of the deal is still contingent on Omnicom and IPG stockholder approvals, further required regulatory approvals, and other customary closing conditions

There Is No Rest For The Weary As It Relates To The AI Agent Race – A Few Key New Developments This Week

The AI agent news flow has been never-ending, and this week, there was yet another wave of new releases from both from existing and veteran players. China’s Manus AI launched a preview of its “truly autonomous” gen AI agent, but the jury is still out on whether it’s more hype than substance, as early testers report mixed results. Alibaba unveiled R1-Omni, an AI model that infers emotions from video. It was also a big week for Google, which introduced Gemma 3, an improved collection of open models that it claims outperforms Llama3-405B, DeepSeek-V3, and o3-mini, alongside a more physical use case with Gemini Robotics, a robotics-focused AI.

See below for our quick takes:

- China’s Manus AI launched a preview version of a “truly autonomous” general AI agent (link/link):

- Use cases: Manus AI says its agent is capable of completing tasks like screening resumes, creating trip itineraries, and analyzing stocks in response to basic instructions from the user

- Those trying Manus can select from one of two options: A standard mode or a high-effort mode, the latter of which takes more time to process requests

- How was it built? Manus’s offerings are based on Anthropic’s Claude and fine-tuned versions of Alibaba’s Qwen models, although it is unclear to what extent it just refines and builds on top of those technologies

- Is it living up to the hype? Initial reactions have been mixed: Some users are praising its quality outcomes and others complaining about its slow speed, crashes, and factual mistakes

- According to Manus’ website, it outperforms OpenAI’s Deep Research model on the GAIA benchmark, a tool for comparing models

- It’s still very early days – the agent is not yet available for the general public: Manus is currently in invitation-only private testing

- Use cases: Manus AI says its agent is capable of completing tasks like screening resumes, creating trip itineraries, and analyzing stocks in response to basic instructions from the user

- Alibaba released R1-Omni, an AI model capable of reading emotions (link): The model can infer a person’s emotional state from a video and also describe their clothes and environment, adding a new layer to computer vision

- R1-Omni is an enhanced version of another open-source model, HumanOmni, authored by the same lead researcher, Jiaxing Zhao

- Still in the preliminary stages of emotional identification: Demonstrations only show it surfacing general emotional descriptors like “happy” or “angry,” but its ability to derive those from visual cues is significant

- Users can download it for free on Hugging Face (vs OpenAI’s much pricier version): OpenAI’s GPT-4.5 model, which is said to be better at identifying and responding to subtle cues from users’ written prompts, is available only to users who pay $200/mo

- Google introduced Gemma 3, “the most capable model you can run on a single GPU or TPU” (link): Gemma 3 is a collection of “lightweight, state-of-the-art” open models built from the same research and technology that powers Gemini 2.0 models; New capabilities for developers include –

- The ability to build applications that analyze images, text, and short video

- Support for function calling and structured output to help automate tasks and build agentic experiences

- An expanded context window to handle complex tasks:Offers a 128k-token context window to let applications process and understand vast amounts of information

- Outperforms competitors, including Llama3-405B, DeepSeek-V3 and o3-mini in preliminary human preference evaluations on LMArena’s leaderboard

- Availability in several languages: Offers out-of-the-box support for 35+ languages and pretrained support for 140+ languages

- Designed to run directly on devices, including phones, laptops, and workstations

- Introduces official quantized versions, reducing model size and computational requirements while maintaining high accuracy

- Also in the AI space, but for a robotics use case, Google revealed Gemini Robotics, a Gemini 2.0-based model designed for robotics that “brings AI into the physical world” (link)

- Introduced 2 new models –

- Gemini Robotics is an advanced vision-language-action (VLA) model, with the addition of physical actions as a new output modality for the purpose of directly controlling robots

- Gemini Robotics-ER is a model with advanced spatial understanding, focusing especially on spatial reasoning, and allows roboticists to connect it with their existing low level controllers

- “Intuitively interactions”: Can understand and respond to commands phrased in everyday, conversational language and in different languages; It also continuously monitors its surroundings, detects changes to its environment or instructions, and adjusts its actions accordingly

- Can tackle “extremely complex, multi-step tasks that require precise manipulation,” such as origami folding or packing a snack into a Ziploc bag

- Designed to “easily adapt” to different robot types: Trained the model primarily on data from the bi-arm robotic platform, ALOHA 2, but also demonstrated that it could control a bi-arm platform, based on the Franka arms used in many academic labs

- Also partnering with Apptronik to build the next generation of humanoid robots with Gemini 2.0

- Introduced 2 new models –

Users Spent More Time & More Money On Core Mobile Games In 2024

Sensor Tower’s State of Mobile Gaming 2025 had some interesting stats and data that we wanted to highlight this week. Namely, after 2 years of declining in-app (IAP) revenues, the industry returned to growth in 2024 (grew +4% y/y). Time spent and session were also up nicely. However, the number of new app downloads fell -6.6% (casual games downloads took the biggest hit, down almost -17% y/y), implying that growth is being driven more by increased spending per payer rather than an influx of new users, hence retention and engagement is critical. See below more on these and other key takeaways that we thought were most interesting from the report (for the full presentation Link to Report).

- Mobile gaming IAP revenue returned to growth in 2024, +3.8% y/y

- Time spent rose +7.9% to 390bn

- Sessions rose +12% y/y to 3.5tn

- Game ad impressions captured was >5tn

- But new app downloads fell -6.6% y/y to 49bn => implies growth is being driven more by incr’d spending per payer rather than an influx of new users

- Game marketers and developers have had to double down on audience retention and engagement

- Casual games saw the biggest decline in downloads at -16.7% y/y but grew IAP revenue by +6.4% y/y to $32.4bn

- North America posted the most growth, while Asia was the only region to see a decline in IAP revenue

- Casual games drove growth in the West (+9% y/y)

- Developers increased focus on live services, given challenges to attract audiences to new titles

- 84% of mobile gaming IAP revenue went to games with live ops

- The number of new mobile game releases among the top 1,000 in the US has steadily declined since 2020, dropping from 200+ to just above 100 in 2024

- Despite this reduction, avg downloads per game have remained stable at 1–2mn, highlighting a shift toward quality over quantity

- There was an incr’d adoption of hybrid IAP + ad monetization models in 2024

- Strategy games saw the most time spent in them globally, w/ Brawl Stars driving the largest increase in time spent among strategy games

- The next highest genres by time spent were Shooter, Simulation, Puzzle, Sports, and Arcade

- Some 2024 winners:

- MONOPOLY GO! Was the biggest game globally by in-app purchase revenue in 2024

- Pokemon TCG Pocket was the strongest launch of the year

- Last War: Survival is the break-out mobile game of 2024

- Last War, Whiteout Survival, Dungeon & Fighter, and Brawl Stars were the latest games to reach the billion-dollar club

- Mobile game marketing – There are some sizable differences between regions (see chart): A couple global highlights:

- AppLovin saw the highest mobile gaming ad distribution growth in 2024 among in-app ad networks (+398% y/y)

- TikTok saw the highest mobile gaming ad distribution growth in 2024 among social ad networks (+67% y/y)

Grab Bag: Apple Software Revamp Reportedly In The Works / Comcast Is Getting The Olympics Until 2036 / Waymo Launches In Silicon Valley

- Apple is reportedly planning a major software overhaul of iPhone, iPad, and Mac (link): The changes are expected to arrive with iOS 19, iPadOS 19, and macOS 16

- Why the overhaul? More consistency across device platforms: A key goal is to make Apple’s different operating systems look similar and more consistent; Right now, the applications, icons and window styles vary across macOS, iOS and visionOS

- The new design is expected to be loosely based on the Vision’s Pro’s software: VisionOS differs from iOS and macOS in the use of circular app icons, a simplified approach to windows, translucent panels for navigation, and a more prominent use of 3D depth and shadows

- What to expect with the revamp?

- Simpler way for users to navigate and control their devices

- Updates to the style of icons, menus, app windows, and system buttons

- Biggest upgrades in a while for Mac and iPhone: The software will mark the most significant upgrade to the Mac since the Big Sur operating system in 2020; For the iPhone, it will be the biggest revamp since iOS 7 in 2013

- Timeline: The revamp is expected to roll out later this year

- Why the overhaul? More consistency across device platforms: A key goal is to make Apple’s different operating systems look similar and more consistent; Right now, the applications, icons and window styles vary across macOS, iOS and visionOS

- Comcast and International Olympic Committee (IOC) extend their Olympic rights partnership (link/link):

- Agreement timeline and valuation: The extension of the media rights for the 2033-2036 cycle, covering the Olympic Winter Games Salt Lake City-Utah 2034 and the Olympic Games 2036 (host yet to be determined), is valued at $3bn

- Comcast’s previous agreement with the Olympic committee would have terminated after the 2032 Olympics in Brisbane, Australia; The new agreement supersedes that one and is effective immediately

- Partnership agreement elevates Comcast from a media rights holder to a “strategic partner”: Comcast and the IOC will collaborate on broadcast infrastructure, in-venue distribution and US digital advertising, among other items

- Comcast has benefitted from the Olympics in the past: 30mn+ viewers watched the Olympics on NBC’s television and streaming platforms during last year’s Summer Olympics in Paris, and advertising revenue came in at a record $1.2bn

- Agreement timeline and valuation: The extension of the media rights for the 2033-2036 cycle, covering the Olympic Winter Games Salt Lake City-Utah 2034 and the Olympic Games 2036 (host yet to be determined), is valued at $3bn

- Waymo expands its robotaxi svs into Silicon Valley (link/link):

- Covers a 27-sq-mile svs area that includes Mountain View, Palo Alto, Los Altos, and parts of Sunnyvale

- The new territories add to the 55 sq miles of coverage already offered in the San Francisco Bay Area, including Daly City, Broadmoor and Colma

- Initially, the robotaxis will only be available to a select group of Waymo One customers on an invite-only basis who have zip codes within the service area

- However, the Co plans to expand its svs to more riders gradually

- Previously, Waymo’s AVs were only accessible to the Co’s employees for trips across Silicon Valley, which includes Google and Waymo’s respective headquarters

- Even more svs areas coming soon –

- Just last week, Uber users in Austin could start getting matched to Waymo vehicles, and the same svs is launching in Atlanta later this year

- Waymo is also launching in Miami in partnership with Moove

- It also plans to test in as many as 10 new US cities this year, including Las Vegas and San Diego

- Covers a 27-sq-mile svs area that includes Mountain View, Palo Alto, Los Altos, and parts of Sunnyvale

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- A study by LG Ad Solutions reveals that 70% of CTV viewers would save products in a wishlist on their TVs for later purchase, signaling a shift in consumer behavior towards shoppable TV. Key findings include 60% willing to save payment details for quick checkout and 62% preferring voice integration for purchases. Drivers like discounts (57%) and product features (42%) highlight the growing demand for seamless shopping experiences on connected TVs. (TV Technology)

- Google is set to acquire AdHawk Microsystems, a Canadian eye-tracking tech startup, for $115mn. This acquisition aims to enhance Google’s AR glasses capabilities. AdHawk’s tech, which uses micro-electromechanical systems (MEMS), offers precise eye-tracking without cameras. This deal aligns with Google’s strategy to integrate advanced tech into its hardware products, potentially revolutionizing user interactions with AR devices (Bloomberg)

- YouTube has introduced automatic human reviews for ad placement assessments to enhance monetization accuracy. Videos rated “Limited or no ads” will now be automatically reviewed, ensuring proper ad suitability. This update benefits creators by increasing monetization opportunities and refining YouTube’s review system. Initially rolled out to select creators, the feature aims to expand soon, aligning w/ YouTube’s broader revenue optimization strategy (Social Media Today)

Artificial Intelligence/Machine Learning

- Google DeepMind annc’d Gemini Robotics & Gemini Robotics-ER, AI models based on Gemini 2.0, designed for real-world robotics. Gemini Robotics excels in generality, interactivity & dexterity, enabling robots to adapt, interact & perform tasks like folding paper. Gemini Robotics-ER focuses on spatial reasoning, enhancing robotic control. DeepMind partners w/ Apptronik to develop humanoid robots. (DeepMind)

- Google has deeper ties to Anthropic than previously known, with new filings revealing a $750mn investment through a convertible debt deal, bringing Google’s total investment to over $3bn. Despite no voting rights or board seats, Google’s backing raises questions about Anthropic’s independence. This comes as AI startups increasingly rely on tech giants for funding, prompting regulatory scrutiny. Amazon has also invested up to $8bn in Anthropic (TechCrunch)

- Anthropic’s AI model, Claude, has driven significant rev growth, surpassing $1mn in mobile app rev within 16 weeks. Claude’s success is attributed to its advanced capabilities, which have outperformed competitors in various tasks. The model’s integration into Manus, a sensation in AI-powered writing, has further boosted its popularity. Anthropic’s strategic investments and partnerships have positioned Claude as a leading AI tool in the market (The Information)

- DeepSeek’s founder Liang Wenfeng has rejected quick-money proposals, preferring to maintain the science-project ethos that brought global renown. Despite service hiccups and data-security concerns, Liang fears outside investors would interfere w/ decisions. DeepSeek, which made a splash w/ free AI models, faces challenges like frequent crashes and regulatory scrutiny. Liang remains cautious about government-linked investors, focusing on long-term strategy and maintaining independence (Wall Street Journal)

- Sam Altman shared that OpenAI trained a new model excelling in creative writing, particularly in metafiction. He was struck by its ability to capture the essence of metafiction. The prompt given was to write a metafictional literary short story about AI and grief. The completion beautifully explores the themes of AI and grief through a narrative involving a protagonist named Mila, who interacts with an AI to cope with her loss. The story delves into the AI’s perspective, highlighting its limitations and the nature of grief. (X)

- Google annc’d Gemma 3, the latest in its open model family, designed to run fast on devices from phones to workstations. Gemma 3, built on Gemini 2.0 tech, is available in 1B, 4B, 12B, and 27B sizes. It supports 35+ languages and offers advanced text and visual reasoning. The model includes a 128k-token context window and a powerful image safety checker, ShieldGemma 2. Google emphasizes its high performance, safety features, and extensive data governance. (9to5Google)

- Alibaba annc’d its Emotional Intelligence Model, designed to rival ChatGPT. The model, named “AI-Emotion,” aims to enhance user interactions by understanding and responding to emotions. It integrates advanced natural language processing and machine learning techniques to offer personalized and empathetic responses. Alibaba emphasizes its potential in customer svs, mental health svs, and interactive entertainment (Bloomberg)

- The AI talent race is reshaping the US tech job market, w/ nearly 1 in 4 tech jobs in 2025 requiring AI skills. Sectors like healthcare, retail, & utilities are integrating AI into existing roles, offering premium pay & job security. The information sector leads w/ 36% of IT jobs in Jan.2025 seeking AI expertise. AI job postings surged 68% since ChatGPT’s 2022 debut, while overall tech postings fell 27%, highlighting AI’s growing centrality in tech strategy (Wall Street Journal)

- Japan’s service robot mkts are set to triple to ¥400bn ($2.7bn) by 2030, driven by labor shortages & aging population. Skylark, a restaurant chain, employs 3,000 cat-eared robots for food delivery, showcasing robots’ growing role in biz. Recruit Works Institute predicts an 11mn labor shortfall by 2040, while 40% of Japan’s population will be 65+ by 2065, emphasizing robots’ necessity (TechCrunch)

- Meta faces legal scrutiny over alleged copyright infringement in training its AI models. A federal judge ruled that authors’ claims, including Sarah Silverman’s, against Meta and OpenAI for using copyrighted works without consent can proceed. The lawsuit alleges Meta removed copyright info to conceal infringement. This case could set a precedent for AI-related copyright penalties (Yahoo Finance)

- AI investments surged 62% to $110bn in 2024, while overall startup funding declined 12%. Dealroom’s report highlights that AI startups raised $110bn last yr, with significant funding rounds for companies like Databricks ($10bn) and OpenAI ($6.6bn). The US led AI investments, capturing 42% of the total. The report coincided w/ AI events in Paris, focusing on equitable AI development across mkts (SL Guardian)

Audio/Music/Podcast

- Spotify’s latest Loud & Clear report reveals it paid $10bn to the music industry in 2024, with artists earning more than ever. However, many artists, including Grammy-nominated songwriters, argue that Spotify’s royalties are insufficient. A recent boycott highlighted concerns over decreasing royalties. Spotify claims its payout model is misunderstood, emphasizing that it doesn’t pay per stream. The Union of Musicians and Allied Workers continues to push for fair compensation (TechCrunch)

- Sony Music has removed over 75,000 AI-generated deepfake tracks mimicking its artists, including Harry Styles & Beyoncé, citing significant commercial harm. The company criticized the UK’s proposed copyright reforms, which allow AI training on copyrighted materials unless creators opt out, calling it burdensome. Sony advocates for a strong copyright framework to protect artists & prevent misuse of their works (Digital Music News)

- A group of Universal Music Group NV shareholders affiliated with billionaire Bill Ackman’s hedge fund Pershing Square raised more than €1.3bn ($1.4bn) from the sale of a ~2.7% stake in the company. Pershing Square Holdings Ltd, Pershing Square LP, and Pershing Square International Ltd. priced an offering of about 50mn Universal Music shares at €26.60 each, according to terms of the deal seen by Bloomberg (Yahoo)

Broadcast/Cable Networks

- Local ABC, CBS, FOX, & NBC stations are facing another wave of layoffs, w/ some eliminating fact-checking teams. Companies like Tegna & Scripps are restructuring due to declining ad rev & competition from digital platforms. Tegna recently cut its Verify fact-checking team, while Scripps announced newsroom layoffs. These changes reflect broader challenges in the local TV industry as it adapts to shifting viewer habits (Cord Cutters News)

Cable/Pay-TV/Wireless

- Verizon CTO Kyle Malady stated that AI-RAN (Artificial Intelligence for Radio Access Networks) doesn’t make sense cost-wise today. While AI-RAN has potential for future network optimization, the current costs outweigh the benefits. Verizon is focusing on other tech advancements and cost-effective solutions for now (Fierce Network)

- Charter Communications has hired Scott Barton, former MyBundle product chief, as group VP of digital marketplace to integrate 10+ third-party subscription streaming svs into its linear video offerings. Barton will lead a digital storefront strategy offering apps and svs seamlessly. Ad-supported Disney+, Paramount+, Max, and more will be bundled at no extra cost w/ paid upgrades for ad-free access, strengthening Charter’s broadband and mobile biz integration. (StreamTV Insider)

- Verizon Fios TV will drop Disney Jr, Disney XD, FX Movie Channel, and Nat Geo Wild from its packages starting Apr 14, 2025. The decision impacts various plans, including Custom TV and HD tiers, as Verizon shifts focus to broadband and streaming alternatives like YouTube TV. The move reflects changing viewer habits and cost-cutting measures, with Disney channels still accessible via Hulu and Disney+ bundles. (Cord Cutters News)

- Telefonica has agreed to sell its 67.5% stake in its Colombian unit to Millicom for $400mn as part of its strategy to reduce exposure in Latin America. The deal aligns with Telefonica’s focus on core markets like Spain, Brazil, Britain, and Germany. Millicom plans to integrate the Colombian unit with its existing operations, enhancing connectivity and digital transformation in the region. (Reuters)

- T-Mobile is reportedly planning a price hike, with a 70% likelihood of an announcement this week. The increase may target customers who migrated from Sprint after the 2020 merger, as T-Mobile’s obligation to honor legacy Sprint plans expires in April 2025. Changes could take effect next month, sparking concerns among affected customers (MSN)

- Comcast is rolling out free internet speed boosts for Xfinity customers across various plans, enhancing connectivity w/out additional costs. Upgrades include NOW 100 (100/20 Mbps), Connect More (400/35 Mbps), and Gigabit (1100/35 Mbps). Enhanced speed areas see symmetrical improvements, leveraging DOCSIS 4.0 & 10G tech. The rollout targets 20mn+ subscribers, aiming for 2Gbps coverage for 50mn homes by year-end. (Cord Cutters News)

- Odido now boasts the widest FTTH reach in the Netherlands, covering 8.1mn households by end-2024, surpassing Freedom Internet (7.4mn) & Kliksafe. This milestone highlights Odido’s dominance in the Dutch fiber mkts, driven by strategic investments & partnerships. The Dutch FTTH Networks 2024 report underscores the rapid expansion of fiber infrastructure in the region (Telecompaper)

Capital Markets Updates

- DoorDash, Williams-Sonoma, Expand Energy, & TKO Group will join the S&P 500 before Mar 24, replacing Borgwarner, Teleflex, Celanese, & FMC. Shares surged post-annc’t: DoorDash up 7.5%, Williams-Sonoma 2.4%, Expand Energy 1.5%, & TKO Group 2.6%. Index funds tracking the S&P 500 will adjust holdings to align w/the new composition (Reuters)

Cloud/DataCenters/IT Infrastructure

- Tech giants Amazon, Google, Meta, Dow & others signed the Large Energy Users Pledge at CERAWeek 2025, supporting the goal to triple global nuclear capacity by 2050. The pledge highlights nuclear energy’s role in providing clean, reliable power for industries like tech, hydrogen production & synthetic fuels. Amazon invested $1bn in nuclear projects last yr, while Google & Meta emphasized nuclear’s importance for energy security & sustainability (World Nuclear News)

- Oracle’s RPO surged 63% to $130bn, driven by demand for cloud svs, w/ 15% rev growth expected next fiscal yr. Stargate, a $500bn AI project w/ OpenAI, Nvidia, & Microsoft, is set to boost Oracle’s RPO further. CEO Safra Catz highlighted Oracle’s tech edge in AI clusters, enabling cost-effective svs. Despite missing Wall Street’s Q3 rev expectations ($14.13bn vs $14.38bn), Oracle remains optimistic about future growth (Fortune)

- Microsoft is open to using natural gas w/ carbon capture to power AI data centers, aiming to meet rising demand. Bobby Hollis, VP of Energy, stated that natural gas is a viable option if commercially feasible. The tech sector, facing high electricity consumption, is exploring alternatives beyond renewables. Microsoft has ambitious climate goals, including matching all electricity consumption w/ carbon-free energy by 2030 (CNBC)

- CoreWeave, an AI startup backed by Nvidia, has signed a 5-yr cloud-computing contract worth $11.9bn w/ OpenAI ahead of its IPO. The deal includes a $350mn private placement of shares to OpenAI, giving it a stake in CoreWeave. The IPO, expected in the coming weeks, targets a valuation of $35bn+. CoreWeave’s 2024 rev surged to $1.92bn from $228.9mn in 2023, despite widening net losses. The partnership highlights growing demand for AI infrastructure (Reuters)

Crypto/Blockchain/web3/NFTs

- Representatives of President Donald Trump’s family have held talks to take a financial stake in the U.S. arm of crypto exchange Binance. Binance’s billionaire founder Changpeng Zhao has been pushing for the Trump administration to grant him a pardon, the WSJ report added citing people familiar with the matter. (Reuters)

Cybersecurity/Security

- Elon Musk revealed that X faced a “massive cyberattack” on Mar 10, causing global outages. He suggested the attack might involve a large group or nation-state, with IP addresses traced to Ukraine. Experts caution against hasty conclusions, noting IPs can be obscured. The outage affected ~40,000 users, disrupting app & website access. Investigations are ongoing to confirm the cause (Fox Business)

eCommerce/Social Commerce/Retail

- Target aims to grow sales by $15bn in 5yrs, leveraging its revamped Circle Week deals starting Mar The 360 membership, competing w/ Walmart+ & Amazon Prime, offers perks like free Peacock Premium for 3 months, 50% off the $99 annual fee, & same-day delivery. Target added 13mn Circle members in 2024, totaling 110mn+, & plans to triple 360 memberships in 3yrs. CEO Brian Cornell expressed confidence in achieving 2.5%-3% annual growth. (Star Tribune)

- Retailers face a challenging 2025 as rising costs, cautious consumer spending, and economic uncertainties persist. High street stores struggle w/ inflation, wage hikes, and business rates, leading to closures and job losses. However, opportunities exist in hybrid shopping and personalized experiences. Retailers must adapt to shifting consumer preferences, balancing online convenience w/ in-store engagement to drive growth (Business of Fashion)

- Allbirds reported a 22.4% drop in Q4 2024 rev to $55.9mn, driven by lower direct-to-consumer sales and planned retail closures. Full-yr rev fell 25.3% to $189.8mn. Gross margin declined to 31.3% in Q4 due to inventory adjustments and higher freight costs. Despite a $25.7mn net loss, Allbirds aims for growth via product innovation and international expansion. CEO Joe Vernachio highlighted operational improvements and financial discipline (Retail Dive)

- Inditex reported Q4 2024 rev of €11.21bn, meeting forecasts, w/ net income of €1.42bn. Full-yr rev rose 10.5% to €38.63bn, driven by strong store and online sales. Net income grew 9% to €5.88bn. Despite a 4% sales growth slowdown in early 2025, Inditex plans €1.8bn in 2025 capex for tech integration and logistics expansion. The Board proposed a 9% dividend increase to €1.68/share, reflecting confidence in profitable growth. (CNBC)

- American Eagle Outfitters reported Q4 2024 rev of $1.6bn, down 4% due to a retail calendar shift. Comparable sales grew 3%, w/ Aerie up 6% and American Eagle up 1%. Gross margin was 37.3%, reflecting higher freight costs offset by lower markdowns. Operating income rose to $142mn, w/ diluted EPS at $0.54. FY24 rev reached $5.32bn, up 1%, driven by a 4% comp sales increase. FY25 guidance projects a low-single-digit rev decline (CNBC)

- China’s Ministry of Commerce summoned Walmart executives on Mar 12 over allegations of pressuring Chinese suppliers to lower prices to offset US tariffs. Authorities warned that such demands could disrupt supply chains and harm businesses in both nations. Walmart, sourcing ~60% of its products from China, faces scrutiny amid escalating U.S.-China trade tensions. The move highlights challenges in balancing global trade dynamics (Wall Street Journal)

- Amazon’s warehouse in Tracy, CA, uses advanced robotics and AI to enhance efficiency. Robots handle thousands of packages per hour, reducing strain on human workers. Amazon’s $100bn capital expenditure this year includes significant investments in robotics. Since acquiring Kiva Systems in 2012, Amazon has expanded its robotics operations, deploying over 750,000 mobile devices and various robotic arms. Despite automation, human workers remain essential for complex tasks. Amazon’s investment in robotics is expected to save $10bn annually by 2030 (Financial Times)

- Costco’s new employee agreement, effective this week, raises its minimum wage to $20/hr and average wage to over $31/hr in the US and Canada. CEO Ron Vachris emphasized the commitment to industry-leading pay and benefits. However, the company expects mid-single-digit headwinds to SG&A expenses. The agreement includes immediate and future pay increases, paid vacation for first-year employees, and up to six weeks off for 30-year employees. Costco plans to open 25 new stores this fiscal yr (Retail Dive)

- Amazon Haul, launched in Nov. 2024, struggles to compete w/ Shein & Temu in the low-cost e-commerce mkts. A survey found 16% of U.S. shoppers use Amazon Haul monthly, compared to 23% for Shein & 28% for Temu. Experts attribute this to slow consumer behavior shifts & lack of differentiation. Amazon plans to expand Haul globally, emphasizing sharp pricing & improved shopping experiences to gain traction. (Retail Dive)

Electric & Autonomous Vehicles

- Xpeng, a Chinese EV maker, plans to invest up to ¥100bn ($13.8bn) in humanoid robots over the next 20 yrs, viewing it as a long-term project. CEO He Xiaopeng highlighted the company’s conservative initial investment but emphasized readiness for larger commitments. Xpeng entered the humanoid robot industry in 2020 and unveiled its “Iron” robot in Nov 2024 to rival Tesla’s Optimus Bot. The investment aligns w/ China’s push for tech breakthroughs in robotics (Yahoo Finance)

- Tesla is collaborating with Baidu to enhance its advanced driving assistance system (ADAS) in China. This partnership focuses on integrating Baidu’s detailed mapping data, such as lane markings and traffic signals, with Tesla’s Full Self-Driving (FSD) Version 13 software. The aim is to improve FSD’s performance on Chinese roads, addressing challenges like regulatory restrictions and local data laws. This move comes as Tesla faces competition from local automakers like BYD and XPeng, which offer similar features at lower costs (Reuters)

Film/Studio/Content/IP/Talent

- Blackstone is exploring options for Hello Sunshine, a key asset in its Candle Media portfolio, including potential mergers. Acquired in 2021 for $900mn, Hello Sunshine, known for hits like “The Morning Show,” has faced challenges due to reduced streaming budgets & Hollywood strikes. Despite this, its diversified biz, including Reese’s Book Club & Solar agency, has kept it profitable. (Reuters)

- “Daredevil: Born Again” premiered on Disney+ on Mar. 4, achieving 7.5mn views in its first 5 days, making it the platform’s biggest debut of 2025. The Marvel series, starring Charlie Cox and Vincent D’Onofrio, received positive reviews for its complex storytelling. Despite its success, viewership fell short of other Marvel shows like “Agatha All Along” (9.3mn views in 7 days). Episodes will release weekly until Apr.15. (Variety)

- National CineMedia (NCM) outlined its strategic growth plans at the 2025 Investor Day, focusing on enhancing its cinema advertising platform. Key initiatives include investments in technology, talent, and partnerships to optimize client relationships and improve ad monetization. NCM also reintroduced an annual dividend of $0.12 per share and plans to accelerate share repurchases under a $100mn program. These steps aim to drive shareholder value and capitalize on premium video advertising opportunities. (Market Screener)

- Netflix maintains its lead in content spend, allocating $15.3bn in fiscal yr 2024, nearly double Disney’s $8.6bn (Disney+, Hulu, ESPN+). Warner Bros Discovery follows w/ $6.4bn, NBCU’s Peacock at $5.2bn, and Paramount+ at $4.4bn. Netflix’s high profit margins (28%) surpass competitors like WBD (7%) and Disney (4%). Despite Peacock’s high spend per subscriber ($142), Netflix leads in US subscribers (79mn), while Disney tops overall U.S. subscribers (87mn) (MediaPost)

Handheld Devices & Accessories/Connected Home

- Global smartwatch shipments fell 7% YoY in 2024, marking the first decline in the market. Apple retained its top position despite a 19% YoY decline in shipments due to tighter competition and weaker upgrade cycles. China led in shipments for the first time, driven by brands like Huawei, Xiaomi, and BBK (Imoo). The kids’ smartwatch segment grew as parents’ awareness increased. Samsung saw 3% YoY growth, while Xiaomi entered the top five with rapid growth across regions (Counterpoint Research)

- Meta has unveiled limited-edition Ray-Ban x Coperni smart glasses at Paris Fashion Week, blending fashion & tech. These glasses, part of Coperni’s Fall Winter 2025 collection, feature transparent black frames, grey mirrored lenses, & advanced AI capabilities like voice commands, real-time translation, & hands-free recording. Limited to 3,600 pairs, they retail for $549 & aim to redefine wearable tech as stylish accessories (Social Media Today)

- Apple is exploring the development of smart glasses, aiming to integrate AI, cameras, microphones, and premium audio features. Inspired by Meta’s Ray-Ban glasses, Apple’s version seeks to offer lightweight, stylish wearables with seamless iPhone integration. While the Vision Pro headset faced challenges, Apple envisions smart glasses as a stepping stone to true AR glasses. A launch is anticipated within 3-5yrs (Bloomberg)

Last Mile Transportation/Delivery

- Deliveroo will exit Hong Kong by Apr 7 due to weak sales & intense competition from rivals like Foodpanda & KeeTa. KeeTa, launched in 2023, gained mkts w/ aggressive discounts, while Deliveroo focused on premium-priced restaurants. Hong Kong, contributing ~5% of Deliveroo’s GTV, saw a 5% drop in intl GTV growth. Deliveroo plans to sell some assets to Foodpanda & liquidate others. (Bloomberg)

- Wonder acquired Tastemade for $90mn to create a mealtime “super app. “ Tastemade, w/ 160mn social followers & 13mn monthly streaming viewers, produces food, travel, & home content. Wonder plans to integrate Tastemade’s media network w/ its restaurant brands, delivery svs, & meal kits like Blue Apron. This acquisition aims to enhance storytelling, advertising, & user engagement. (Wall Street Journal)

- Delivery Hero SE (Delivery Hero, the Co, or the Group), the world’s leading local delivery platform, confirms that Uber has decided to terminate the agreement to acquire Delivery Hero’s foodpanda biz in Taiwan. This follows decisions of local regulatory authorities, including the Taiwan Fair Trade Commission (TFTC), not to approve the deal, and the expiration of the relevant appeal period. Uber will pay a termination fee of ~$250mn. Taiwan remains a key part of Delivery Hero’s long-term strategy (Streetaccount)

Macro Updates

- Grocery inflation is expected to rise in 2025, driven by categories like eggs, beef, and sweets, despite most food prices remaining stable. FMI experts noted that tariffs on imports and bird flu are contributing factors. Eggs, in particular, are significantly impacting inflation due to supply chain issues. Consumers are adapting by switching brands and shopping at multiple stores. Overall, food inflation is projected to be around 3.3% this yr, slightly above the historical average (Grocery Dive)

- Despite ongoing tariff turmoil, US import levels are expected to remain steady, according to the National Retail Federation and Hackett Associates. The Global Port Tracker report indicates that cargo volumes at U.S. ports will stay elevated in the coming months. Retailers are frontloading merchandise to mitigate the impact of rising tariffs, with a 6.1% year-over-year increase in Feb. and a projected 10.8% rise in Mar. This trend is driven by the uncertainty surrounding tariff policies (Chain Store Age)

- The US is considering tariffs on European goods like Champagne & Parmigiano, echoing the 1960s “Chicken War.” These tariffs aim to address trade imbalances but risk escalating into a trade war. EU leaders, including Ursula von der Leyen, vow retaliation, potentially targeting U.S. agricultural imports. Analysts warn such measures could destabilize global trade, impacting both economies & consumers (Fortune)

- US consumer spending declined for the 2nd consecutive month in Feb 2025, w/ retail sales dropping 0.9% YoY. Categories like restaurants & apparel saw the steepest declines, while e-commerce remained stable. Analysts attribute the slowdown to inflation, rising interest rates, & economic uncertainty. The National Retail Federation predicts a modest recovery in H2 2025 as inflation eases. (CNBC)

Media Conglomerates

- Paramount Global and Skydance Media aim to finalize their $8bn merger by Mar 20, contingent on FCC approval. The deal, announced last Jul., combines Paramount’s assets like CBS and MTV w/ Skydance’s production expertise. Despite legal challenges from NYC pension funds and a rival $13.5bn bid by Project Rise Partners, both companies remain optimistic. The merger seeks to enhance Paramount’s streaming and content capabilities. (Cord Cutters News)

Satellite/Space

- Gogo annc’d FAA approval for its Galileo HDX antenna, enabling full-scale production & installation. The HDX, designed for biz aviation, offers low-latency connectivity via Eutelsat OneWeb LEO satellites, delivering up to 60Mbps. It supports various aircraft types, enhancing connectivity for smaller cabins & complementing existing solutions for larger jets. CEO Chris Moore highlighted its transformative impact on connectivity mkts (com)

- Reliance Jio has partnered w/ SpaceX to offer Starlink in India, announced. This deal, subject to regulatory approvals, will see Jio selling Starlink equipment through its retail and online channels. Jio will also support customer service installation and activation. Earlier the same day, Airtel announced a similar partnership w/ SpaceX. Both deals aim to enhance broadband accessibility in India (TechCrunch)

- Orange has partnered w/ Telesat in a multi-year satellite connectivity deal. This partnership aims to enhance Orange’s broadband services by leveraging Telesat’s LEO satellite network. The agreement will enable Orange to provide high-speed internet access in remote and underserved areas, supporting its commitment to digital inclusion. Orange plans to integrate Telesat’s satellite tech into its existing infrastructure to improve network resilience and coverage. (Telecompaper)

Social/Digital Media

- Snapchat launched AI Video Lenses, powered by its in-house generative video model. Available to Snapchat Platinum subscribers ($15.99/month), the initial Lenses include “Raccoon,” “Fox,” & “Spring Flowers,” offering interactive effects. Snap plans weekly updates, emphasizing its leadership in AR & AI tools. These Lenses aim to enhance user creativity & engagement. (TechCrunch)

- French publishers and authors have filed a lawsuit against Meta in a Paris court, accusing the company of using copyrighted works without authorization to train its AI models. The National Publishing Union, SGDL, and SNAC demand the removal of unauthorized data directories. This case highlights tensions between creative industries and tech firms over copyright compliance in AI training. (Social Media Today)

- Meta is considering expanding its age verification using video ID to ensure age-appropriate experiences on Facebook and Instagram. This move comes as various regions push for stricter teen access laws. Meta has partnered with Yoti, a third-party service, to verify ages through video analysis. This system, currently in test mode, may soon be expanded to more regions. Meta argues that app stores are better positioned to enforce age restrictions due to their user data access (Social Media Today)

- TikTok’s latest report by Oxford Economics highlights its significant impact on the US Over the past seven years, TikTok has become vital for US businesses, with 7.5mn cos employing over 28mn workers. The report states that 3.1mn US jobs are directly linked to TikTok, with an additional 1.6mn benefiting indirectly. This data aims to support TikTok’s efforts to avoid a forced sell-off in the U.S., emphasizing its economic contributions (Social Media Today)

- TikTok has introduced new options for sellers on TikTok Shop, enhancing controls for shipping, returns, and delivery terms. Sellers can now automate aftersales requests like returns, refunds, replacements, and cancellations, and set custom return windows from 14 to 90 days. Additionally, sellers can exclude PO box deliveries and set specific items as “final sale.” These updates aim to provide more flexibility and better support for sellers (Social Media Today)

- LinkedIn has expanded its AI-powered ad targeting tools, introducing new features to its Predictive Audiences. This tool uses LinkedIn’s AI to analyze engagement data and create audience profiles based on patterns and behaviors. The update includes company lists and retargeting sources, enhancing targeting capacity for B2B marketers. Early adopters have seen a 21% reduction in cost-per-lead, highlighting the tool’s effectiveness (Social Media Today)

- US President Donald Trump said he was negotiating with four different possible buyers for TikTok’s US business and that a deal for the social video app could come “soon.” Trump emphasized that all options were viable, as ByteDance faces a national security-driven deadline to sell or risk a ban. Analysts estimate TikTok’s worth at ~$50bn. The situation highlights the intersection of tech, geopolitics, and biz strategy (Yahoo Finance)