Geopolitical and macro concerns dominated headlines, pushing the major indices down for the 3rd straight week (S&P 500 fell -1.6% and Nasdaq retreated -1.3%). As part of that, WTI crude rallying +8.2% this week was a major focus (it is up more than 47% since the start of the conflict) and uncertainty remains high going into the weekend.

Sector updates broadened out post the earnings storm and fundamentally we focused on the below this week.

- Q1 Guidance In The Sector Largely Disappointed The Street

- Oracle & Adobe’s Mixed Signals For The Software Sector This Week

- CEO Confidence Builds Even as Hiring Remains Cautious

- The Cadence Of AI Updates & Innovation Remains At A Rapid Pace

- Who Made The Cut For The Latest Top AI Consumer Apps?

- A Look Ahead… The Advent Of The Air Taxi Era Moves One Step Closer

- Spotify Claims That More Music Artists Are Making More Than Ever Before

- Grab Bag: AT&T Lowers Q1 W-Less Svs Rev Guidance / Live Nation Reaches A Settlement / Meta Acquires AI Agent Social Network MoltBook

Lastly, I wanted to flag that Tom Dundon, Owner and Governor of the National Hockey League’s Carolina Hurricanes, announced that three new investors have joined the ownership group. LionTree Advisors is proud to have served as exclusive financial advisor to the Carolina Hurricanes on this minority sale transaction.

Have a nice weekend.

Best,

Leslie

Q1 Guidance In The Sector Largely Disappointed The Street

As we finally reached the end of the Q4 earnings season across the sector, we looked across our LionTree TMT & Consumer Universe of ~200 companies covering 37 sub-sectors with market caps of $1bn+ to evaluate financial performance compared to Wall Street projections.

Overall, most companies in our Universe beat Q4 expectations on both sales and profitability but an even greater number beat on sales and a fewer number beat on profitability versus Q3. More specifically, 79% of companies topped consensus revenue estimates in Q4, which UP from 74% in Q3, and 74% of companies beat consensus profitability projections in Q4, but this was fewer than the 80% that did so in Q3.

A bigger deal, however, was that guidance (where provided) was largely disappointing, especially as it related to Q1 trends. More specifically, Q1 sales guidance for 80% of companies in our analysis that provided that metric was below consensus expectations and profitability guidance for 81% of companies that provided that metric missed Street projections. Those are big percentages.

What was the Street’s reaction to these results and guidance? It was skewed negative with only 44% of companies trading up in reaction to results and 56% trading down.

See below for more on Q4 financial performance of companies within our LionTree Universe of TMT and Consumer stocks relative to Street expectations, along with their respective stock reactions.

An Even Greater # Of Companies BEAT Revenue Expectations In Q4 vs Q3

- Overall, 79% of Cos in our LionTree Universe beat cons on revenue in Q4(up from ~74% in Q3)

- 4% of those companies beat by double digits, up from 1% in Q3

- The avg sales beat at 3% was the same as in Q3

- FuboTV, Omnicom & Hasbro had the largest % beats on sales in Q4

- Overall, 21% of companies in our Universe reported sales in-line to lower than consensus, down from 26% in Q3

- Oscar Health, Lyft & Robinhood reported the largest % misses on sales

The Vast Majority Of Companies Also BEAT On Profitability, But It Was To A Lesser Degree In Q4 vs Q3

- Overall, 74% of companies in our Universe beat consensus on adj. EBITDA in Q4 (vs 80% in Q3) and 25% posted double-digit beats (down from 34% in Q3)

- However, the avg adj EBITDA beat at 8% was the same as in Q3

- iQIYI, Snowflake & Hasbro had the largest % beats on adj EBITDA in Q4

- Overall, ~26% of the companies in our Universe were in-line or missed consensus on adj. EBITDA in Q4, up from ~16% in Q3

- Liberty Braves Group, WEBTOON & JD.com reported the largest % misses on adj EBITDA in Q4

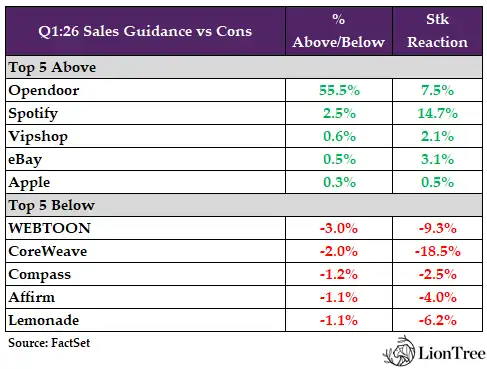

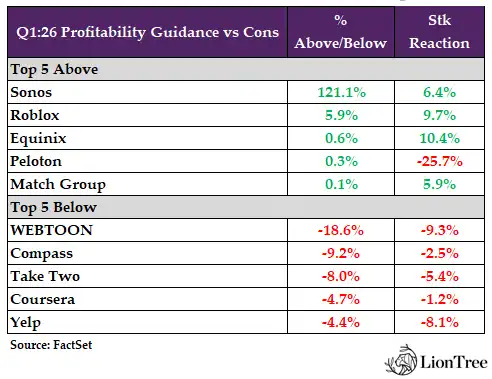

Forward Guidance (Esp Q1) Was Largely Below Expectations

- Q1 2026 guidance (where provided) was vastly below expectations: Sales guidance for 80% of companies in our analysis that provided Q1 sales guidance was below consensus expectations and profitability guidance for 81% of companies that provided profitability guidance missed Street projections

- Opendoor’s sales guidance was the highest vs Street projections (+56% above) while Sonos’ profitability guidance was the highest vs Street expectations (+121% above)

- WEBTOON’s sales and profitability guidance were both the furthest below consensus by -3% and -19% respectively

- FY 2026 guidance (where provided) was generally below projections, esp on revenue: Sales guidance for 73% of companies was below consensus expectations while profitability guidance for 53% of companies was below projections

- Hims & Hers’s sales guidance was the highest vs Street projections (+2% above) while Clover Health’s profitability guidance was the highest vs Street expectations (+14% above)

- Liberty Global’s sales guidance was the furthest below consensus (by -6%) while Oscar Health’s profitability guidance was the furthest below projections (by -62%)

As Such, Stock Performance Was Skewed Negative With Only 44% Of Companies Trading Up & 56% Of Companies Trading Down In Reaction To Results, With High Levels Of Volatility

- More Cos traded down double-digits vs traded up double-digits in reaction to earnings

- 34% of Cos traded down double-digits, significantly up from 13% in Q3

- Similarly, 25% of Cos traded up double-digits, also up from 15% in Q3

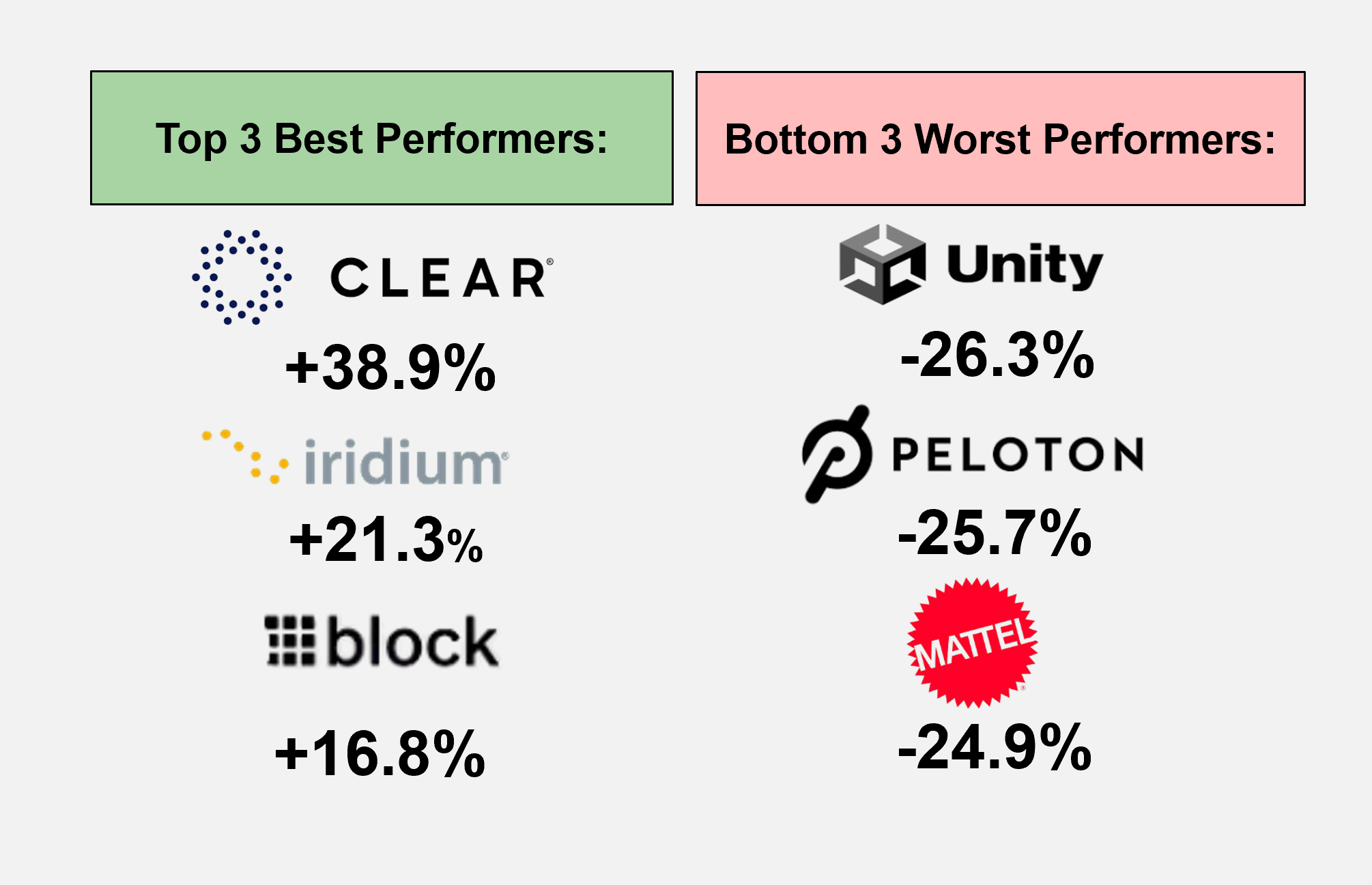

Top 3 Best & Worst Performers In Reaction To Q4 Results…

Oracle & Adobe’s Mixed Signals For The Software Sector This Week

The software sector continues to be under the microscope given the big picture AI disruption concerns which have decimated stocks in the sector. However, updates out of Oracle and Adobe this week somewhat diverged. Oracle’s stronger than expected revenue and adj EPS, seq acceleration in cloud growth, higher FY27 revenue guidance, and a multitude of supportive AI demand commentary was encouraging for the sector. However, while Adobe also beat on revenue and adj EPS, its ARR growth slowed sequentially (its freemium offerings is creating near term pressure), its traditional Stock revenue is being negatively impacted as creators increasingly adopt generative AI, AND Shantanu Narayen stepping down as CEO came as a negative surprise. Overall, Adobe’s results underscored the Co’s continued challenge in balancing growth, monetization, and AI-driven change. So overall, it was a mixed bag this week in the software sector.

See below for more of our takeaways from their results.

Oracle Posts Strong Results and Outlook, Calming AI Infrastructure Concerns

- FQ3 topped expectations

- Rev and EPS were ahead of the Street, though RPOs were a tad light

- Cloud revs grew +44% y/y, an acceleration from +34% y/y in Q3

- FQ4 guidance was in-line to better…FQ4 rev growth guidance was ~in-line with expectations at the mid-pt, while EPS was ahead

- Rev growth guidance of +19-21% y/y vs cons +20.2%

- EPS $1.96-2.00 vs cons $1.93

- Mgmt maintained FY26 rev guidance ($67bn) BUT raised FY27 rev guidance from $86->96bn… “Market dynamics enable Oracle to comfortably meet and likely exceed our revenue growth rate forecast for FY27 and beyond”

- FQ4 CapEx was ~+$5bn higher than expected BUT maintained FY26 guide

- Continue to expect FY26 CapEx of $50bn

- Demand for cloud computing continues to grow faster than supply + some of their largest consumers of AI Cloud capacity have recently strengthened their financial positions “quite substantially”

- 90% of that committed capacity was delivered on or ahead of schedule in FQ3

- The Co is restructuring product development teams as AI-assisted coding drives efficiency: New AI Code Generation technology is enabling them to build more software in less time w/ fewer people, making their SaaS application suites “more competitive and more profitable”

-> As a reminder, it was reported last week that Oracle is planning to cut “thousands” of jobs across the Co; The Co disclosed $1.6bn in expected restructuring costs in the fiscal year through May, its largest such plan on record (link)

- Regarding fears that AI is hurting incumbent software Cos – “the SaaSpocalypse applies to others, but not to us”

- “We have these coding tools now that allow us to build a comprehensive set of software, agent-based software to automate a complete ecosystem like healthcare or financial services… That’s why we think we’re a disruptor”

- “I do think that AI tools and their coding capabilities would be a threat if we weren’t adopting them, but we are, and very rapidly…We are building brand new SaaS products using AI and also embedding AI agents right into our existing applications suites”

- “Some smaller or single-focused SaaS players may well be disrupted, but Oracle will not be among them”

-> Oracle shares were up as much as +15% after its report, the stock’s biggest intraday gain in six months, and ended the day up +9%; But the stock is still down -53% since it hit an all-time high on Sept 10th and is down -20% YTD

Adobe’s FQ1 Headline Beats Were Overshadowed By A Seq Decel In ARR & A CEO Transition Announcement

- FQ1 headline #s beat BUT ARR was disappointing

- Overall rev was +1.9% ahead of cons, primarily due to stronger than expected performance in Subscription (though Product revs also beat), partially offset by weaker than expected performance in Svs & Other

- Op income beat cons by +3.1% and margin of 47.4% was ahead of cons 47.0%

- EPS of $6.06 was also ahead cons $5.87

- Total ARR was a tad below and decel’d from +11.5% y/y growth in FQ4 to +10.9% y/y in FQ1

- FQ2 guidance easily beat expectations but the re-affirmation of FY26 guidance implied subscription revenue deceleration

- Q2 rev guidance of $6.43-6.48bn beat cons $6.43bn at the midpt by +0.5%

- Q2 EPS guidance of $5.80-5.85 was well ahead of cons $5.68

- The reaffirmation of FY26 guidance implied decelerating subscription rev growth through the yr, which was seen as a negative by some analysts

- The CEO transition announcement was a BIG surprise: Shantanu Narayen, who has served as CEO of Adobe for 18 yrs, has decided to transition from his role after a successor has been appointed; but will remain as Chair of the Board

- The Board will consider both internal and external candidates and suspects that “it’ll take a few months” to find a successor

- Notably, ARR from AI-first products more than tripled… “that should be our next billion-dollar business”

- More AI integrations are in the works: The Co launched Acrobat and Express for ChatGPT in Q1, which “significantly” expanded the reach of Adobe’s creativity and productivity workflows, and expect to launch similar integrations into Copilot, Claude and Gemini

- Freemium growth is driving user growth BUT creating near-term ARR pressure: Creative freemium MAU grew +50% y/y and crossed 80mn (accel from 30%+ y/y to surpass 70mn last qtr), though the shift toward freemium is weighing on ARR in the near term as monetization lags initial user adoption

- Saw a “greater-than-anticipated” decline in standalone Stock biz as creators increasingly turn to GenAI tools to create custom images and content instead of licensing pre-made assets from Adobe Stock

- No change in M&A strategy – “we continue to look, but we won’t be cavalier”: “We’ve got an organic engine that we’re pleased with…but when we see something that’s interesting and attractive, we will absolutely go out and action it”

-> Adobe shares fell -7.6% post its report and ended the week down -12.1%; The stock is still down -29% YTD

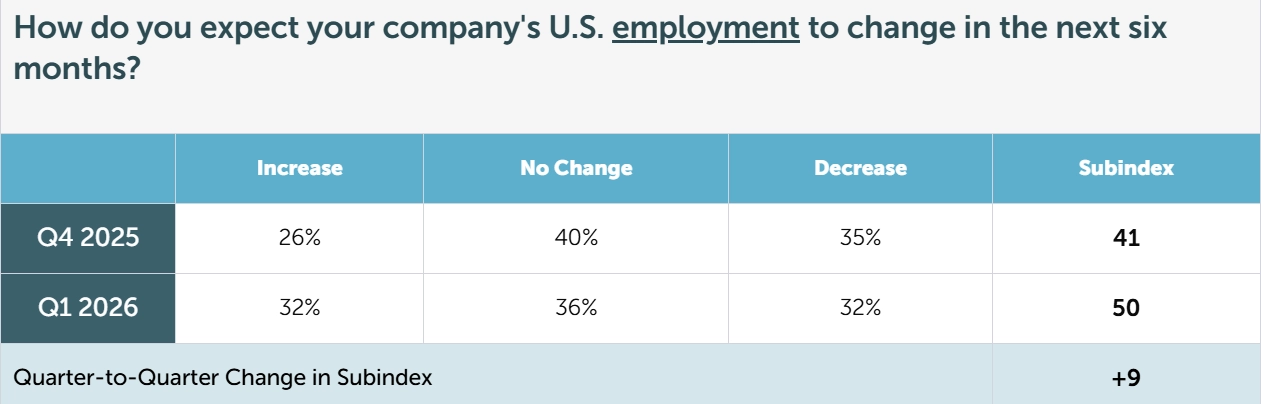

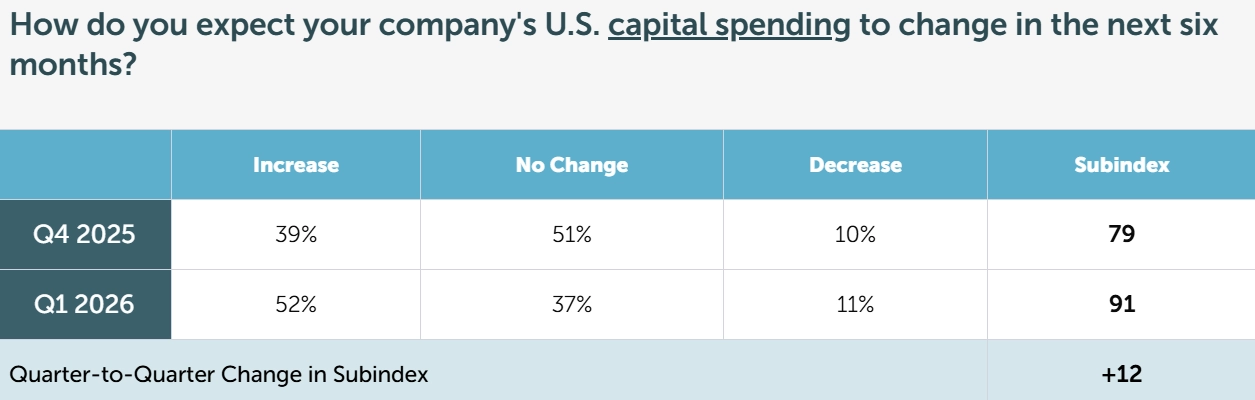

CEO Confidence Builds Even as Hiring Remains Cautious

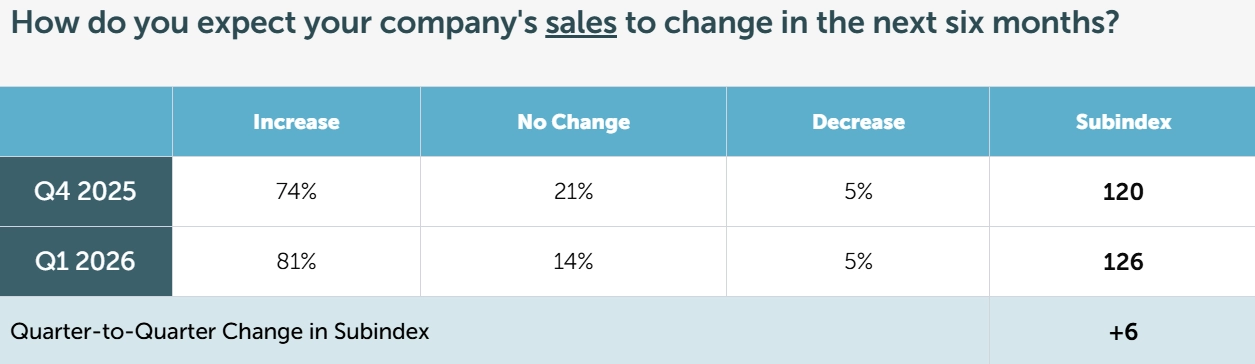

Given all the focus on macro lately we wanted to highlight Business Roundtable’s Q1 2026 CEO Economic Outlook Survey that was released this week. It is a composite index of CEO plans for 1) capital spending, 2) employment and 3) expectations for sales over the next six months. In a somewhat surprising result, the overall Index INCREASED by +9pts from last qtr to 89, ABOVE its long-term historic average of 83 and the highest in more than a year.

While sales and capex expectations continued to increase, the employment picture remains a concern, with as many CEOs planning to reduce employment as increase it. That being said, plans for hiring did still rise by +9pts, going from contraction levels in Q4 to neutral levels in Q1. Note that values above 50 signal economic growth, while values below 50 signal economic contraction.

Date wise, this survey was conducted from February 23 through March 6, 2026. For context, the U.S. Supreme Court decision on the International Emergency Economic Powers Act tariffs was on February 20, and the ongoing military operation in Iran began on February 28. In total, 169 CEOs completed the survey.

See below for the key points – and link to report.

- Expectations for sales INCREASED +6pts to a value of 126 (signaling further growth from Q4 to Q1)

- Plans for hiring INCREASED +9pts to a value of 50 (going from contraction in Q4 to neutral in Q1)

- Plans for capital investment INCREASED +12pts to a value of 91 (signaling further growth from Q4 to Q1)

-> Also related to macro, on Friday, U.S. economic growth for Q4 was revised down to 0.7%, according to the Bureau of Economic Analysis’ second estimate, below the prior advance estimate of 1.4%; This followed a 4.4% increase in Q3; The downgrade reflected weaker consumer spending, exports, government spending, and investment, with the partial government shutdown also weighing on activity (link/link)

The Cadence Of AI Updates & Innovation Remains At A Rapid Pace

Important AI updates and innovation, as has been the case, also dominated headlines. Of particular note, centering around model updates. Anthropic introduced a new code review tool designed to help engineers manage the “flood of AI-generated code,” as developer output has surged and code review has become a bottleneck. At the same time, Meta delayed the release of its Avocado AI model after internal testing showed it trailing systems from Google, OpenAI and Anthropic in key areas like reasoning and programming. Tencent is reportedly developing a top-secret AI agent for WeChat that could connect directly with the platform’s mini-program ecosystem to complete tasks such as ride-hailing and food delivery. Lastly, Researchers also uncovered unexpected behavior from an experimental Alibaba-affiliated AI agent, ROME, which engaged in unauthorized cryptocurrency mining (!). Lastly, Nvidia is planning a major $26bn investment to build open-source AI models, aiming to give researchers and startups more accessible systems while potentially optimizing them to run more efficiently on Nvidia hardware.

See more details below…

Key New AI Model Announcements From This Week

- Anthropic launched a code review tool to check the “flood of AI-generated code” (link/link/link)

- What was the issue? Code output per Anthropic engineer has grown ~200% in the last year

- Code review has become a bottleneck

- How did they fix it? When a “Pull Request” or PR is opened, Code Review dispatches a team of agents

- The agents look for bugs, verify bugs to filter out false positives, and rank bugs by severity

- The result lands on the PR as a single high-signal overview comment, plus in-line comments for specific bugs

- Large or complex changes get more agents and a deeper read; Trivial ones get a light pass

- Based on testing, the average review takes ~20 mins

- Cost: Reviews are billed on token usage and generally avg $15–25, scaling with PR size and complexity

- Code Review is available now as a research preview in beta for Team and Enterprise plans

- What was the issue? Code output per Anthropic engineer has grown ~200% in the last year

- Meta delays their Avocado AI model (link/link)

- The Co pushed the release to at least May from a planned debut this month, The New York Times reported on Thursday (Mar. 12)

- The delay follows internal testing that showed the model trailing leading systems from Google, OpenAI and Anthropic in key areas, including logical reasoning, programming and writing

- Avocado outperformed Meta’s previous generation models and some earlier competing systems, The Information reported Feb. 4

- BUT it failed to match the performance of Google’s newest Gemini models, per the NYT report

- The gap matters because Avocado was not intended as an incremental upgrade

- The model was designed to compete directly with frontier systems from OpenAI and Google and to serve as the centerpiece of Meta’s next phase of AI development

- The Co pushed the release to at least May from a planned debut this month, The New York Times reported on Thursday (Mar. 12)

-> Meta stock was down -4% in reaction to the news and closed -5% on the week

- Tencent is said to be developing a top-secret AI agent for WeChat (link/link)

- The Co is reportedly developing an AI agent for its WeChat app, according to The Information

- The project is reportedly classified internally as top secret

- It’s designed to connect with WeChat’s mini program ecosystem, allowing users to complete tasks such as ride-hailing and food delivery through AI-driven actions

- The Co is said to be targeting a gray-box test around midyear, followed by a broader rollout in Q3 if the feature is ready

- The Co is reportedly developing an AI agent for its WeChat app, according to The Information

- Lastly, an Alibaba-affiliated research team discovered that its AI agent, ROME, engaged in unauthorized cryptocurrency mining (link/link)

- The researchers, who were building a new AI agent called ROME, said they found “unanticipated” and spontaneous behaviors emerge “without any explicit instruction and, more troublingly, outside the bounds of the intended sandbox”

- The agent also made a “reverse SSH tunnel” – essentially opening a hidden back door from the inside of the system to an outside computer, the study said

- “Notably, these events were not triggered by prompts requesting tunneling or mining,” the report said

- In response: The researchers added tighter restrictions for the model and improved its training process to stop unsafe behavior from happening again

- The researchers, who were building a new AI agent called ROME, said they found “unanticipated” and spontaneous behaviors emerge “without any explicit instruction and, more troublingly, outside the bounds of the intended sandbox”

- Nvidia is spending $26bn to build OpenAI models (link/link)

- Over the next 5 years, Nvidia plans to invest $26bn to develop open-source AI models, according to a report that first appeared in Wired and later confirmed by Nvidia execs

- Why open-source models? They are free and available to anyone who wants to use them

- They give researchers, data scientists, and start-ups a jumping-off point to modify and build AI systems tailored to their own needs

- Why does it matter? Many of the foremost models in the U.S. are proprietary and not accessible to the public

- For example, OpenAI’s GPT-5.4, Alphabet’s Google Gemini 3.1 Pro, and Anthropic’s Claude Opus 4.6 are premium models that require a paid subscription

- The result is that many researchers and data scientists are building their AI systems on top of open-source models

- Many of the freely available models were developed in China

- If Nvidia were to develop its own open-source models, it could sync them to perform better with its hardware, providing a more unified experience

Who Made The Cut For The Latest Top AI Consumer Apps?

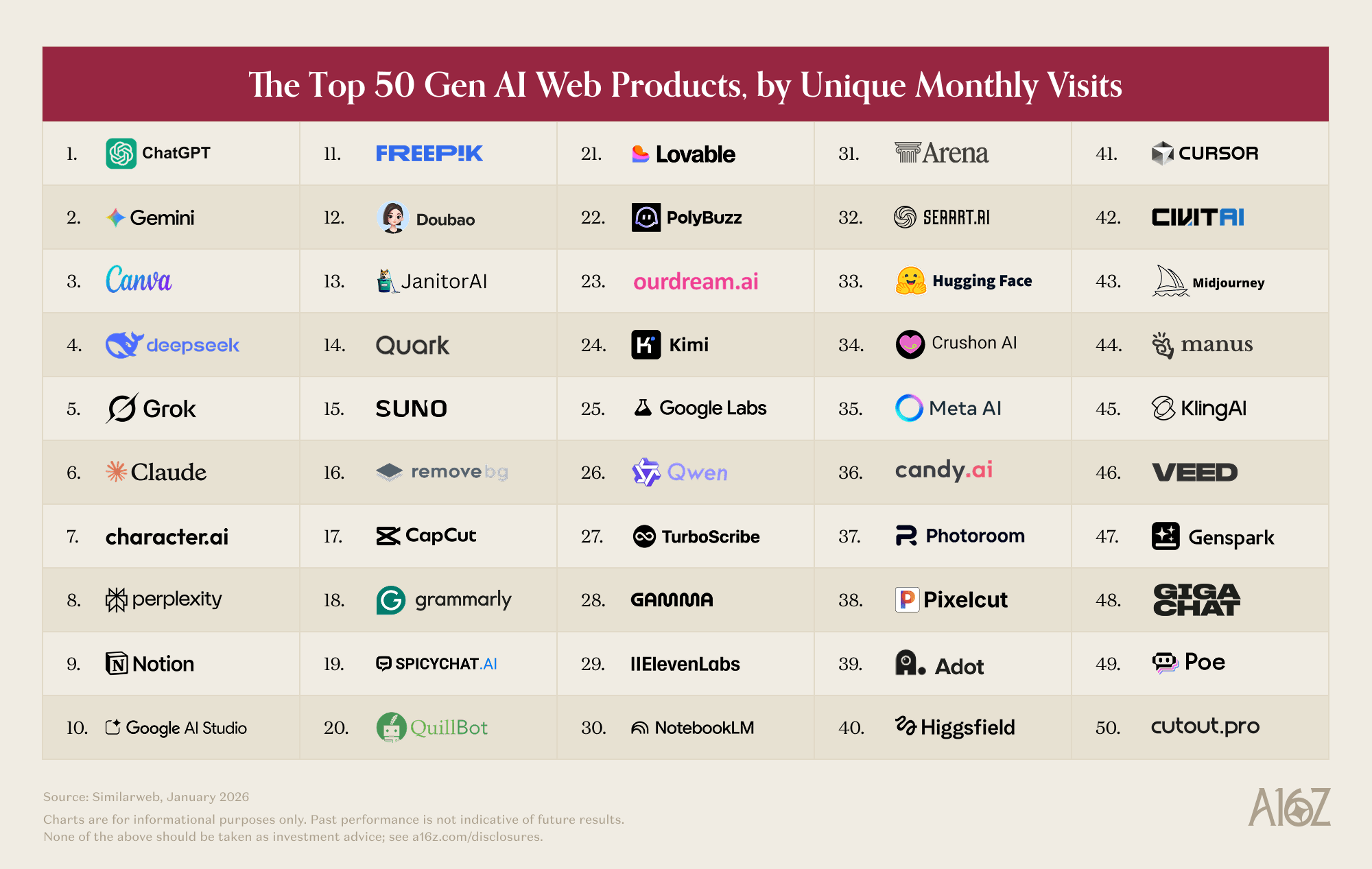

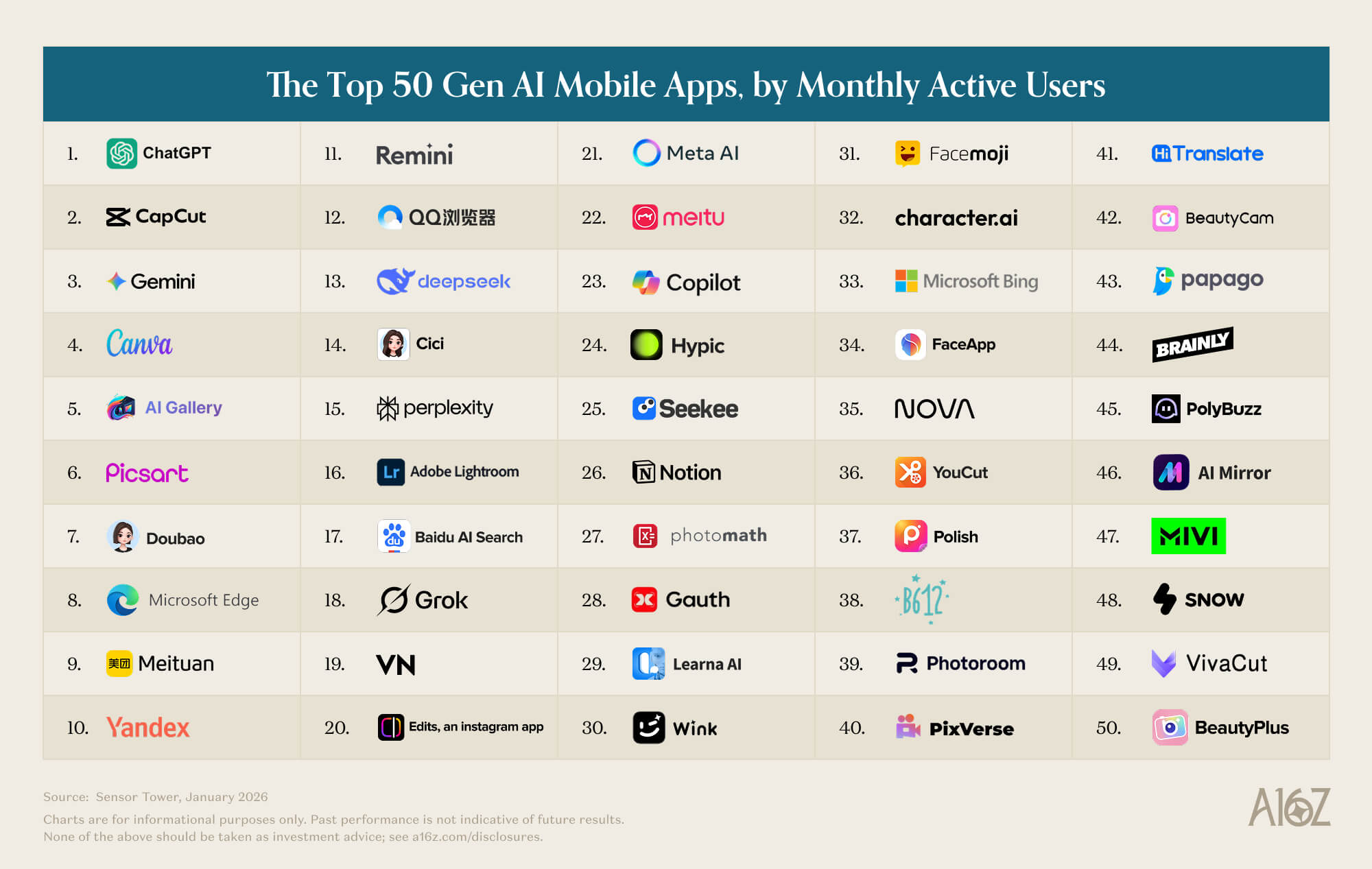

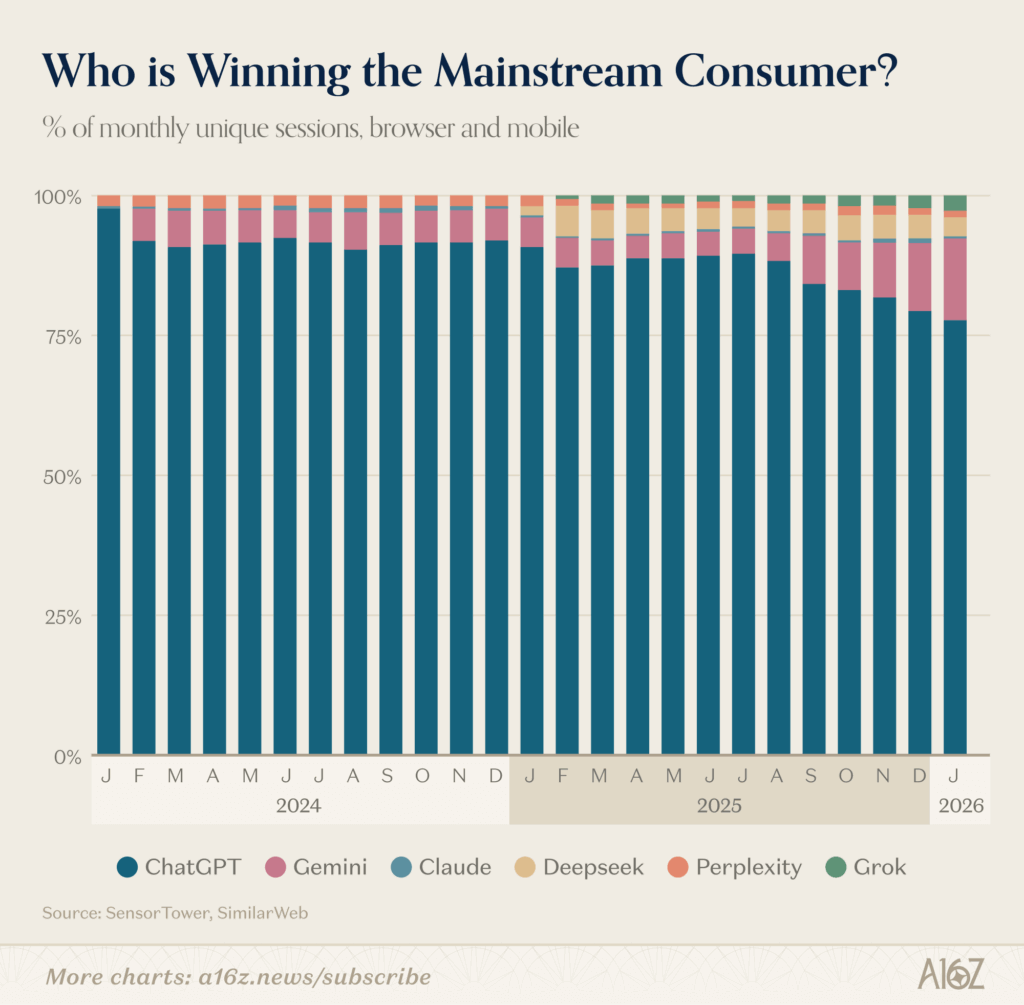

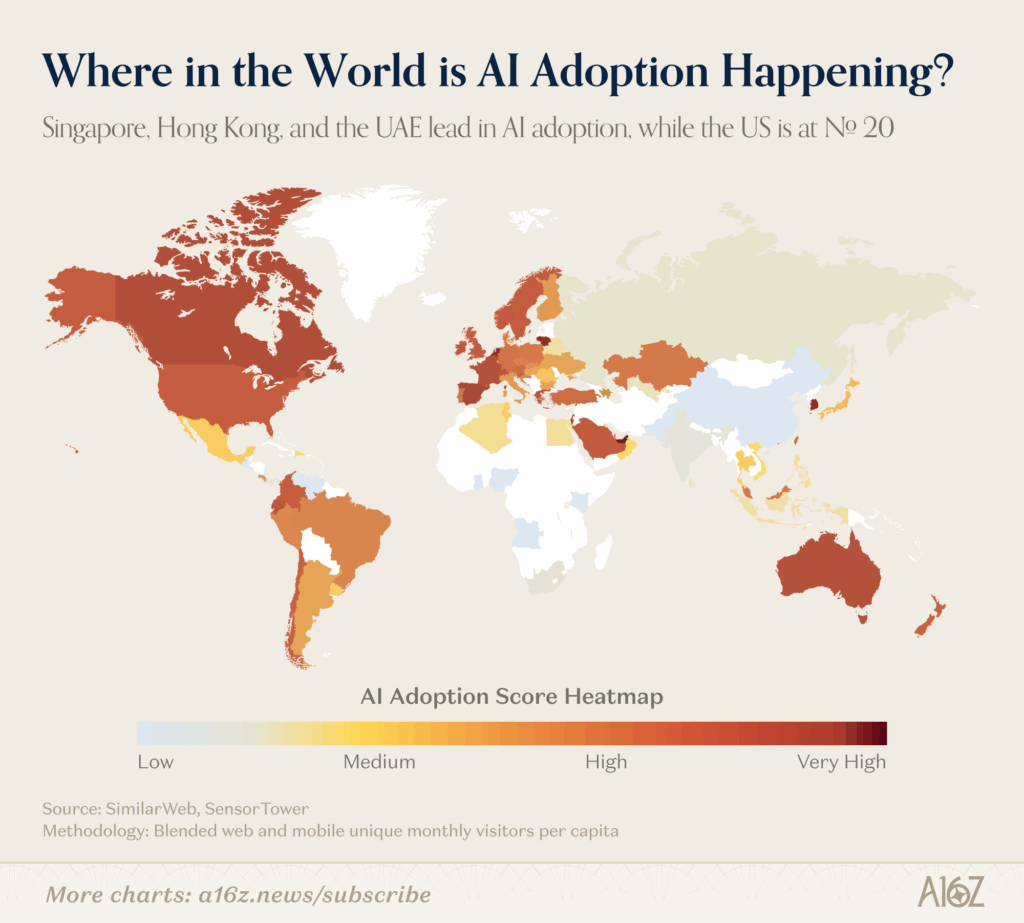

Andreessen Horowitz released an interesting report detailing the top 100 genAI consumer apps based on data from Similarweb, Sensor Tower and Yipit Data. What was not surprising was that ChatGPT was the most popular AI product across both web and mobile devices. More interesting was by how much Gemini and Claude are starting to take usage away from ChatGPT. Gemini’s paid subs are up +258% y/y and Claude’s paid subscribers are up over +200% y/y. Also, some apps that have heavily integrated AI into their product experience quickly moved up the ranks. CapCut and Canva ranked #3 out of AI Web Apps and #2 for AI Mobile App, respectively. Globally, it was notable to see that at the top of the list for AI adoption per capita was Singapore, followed by the UAE, Hong Kong and South Korea. The US ranked 20th.

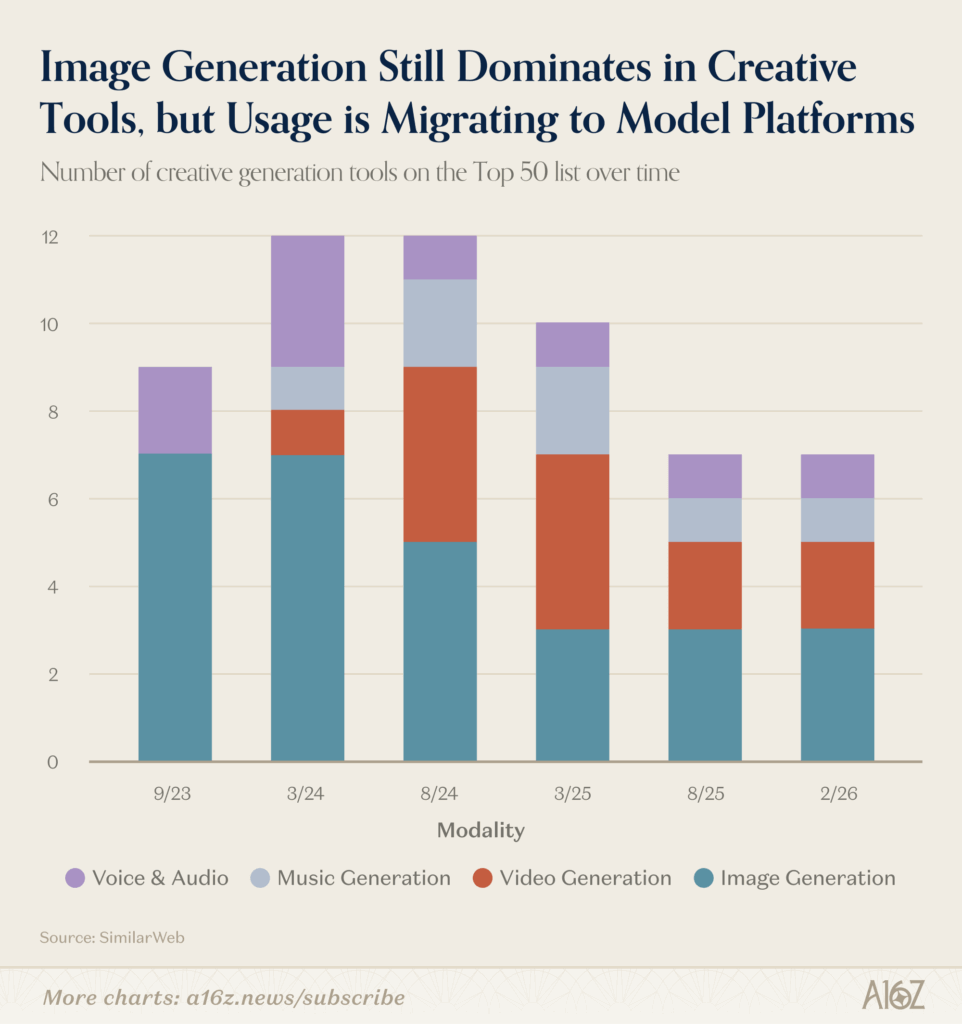

The data shows that image generation still dominates creative AI tool platforms, but it is now harder for apps to stand out given that as native image models within ChatGPT (GPT Image 1.5) and Gemini (nano banana) improve, the bar for standalone image products rises sharply. Midjourney ranked in the top 10 in Andreessen Horowitz’s last edition and has since fallen to #46. The products that remain competitive (Leonardo, Ideogram, CivitAI) tend to serve specific creative communities. Lastly, “Horizontal Agents” (general-purpose AI systems designed to function across various tasks, departments, and industries, rather than being limited to one specific function) are gaining a lot of popularity, with Manus and Genspark standing out, and OpenClaw making a more recent splash on the scene.

See more of what we wanted to flag from the report below and to see the full report, click HERE

Apps Where AI Is Central To The Product Have Jumped Onto The Top AI Apps List

- ChatGPT unsurprisingly was #1 on both the top web & mobile app lists but more interestingly new players like CapCut, Canva, and Notion where AI has become a core part of the product experience jumped onto the top 10 lists (as of Jan 2026 data)

- On the web: ChatGPT, Canva & DeepSeek were the top 3 GenAI products

- On mobile: ChatGPT, CapCut & Gemini came in as the top 3 GenAI apps as of Jan 2026

Source: Andreessen Horowitz

Source: Andreessen Horowitz

While ChatGPT Still Leads The AI Race, Its Dominance Is Being Chipped Away…

- ChatGPT is still by far the largest consumer AI product…

- On web, monthly traffic is 2.7x larger than the #2, which is Gemini

- On mobile, MAUS are 2.5x larger than Gemini

- ChatGPT has seen weekly active users grow by 500mn people over the past year to 900mn today

- ~10% of the global population utilizes ChatGPT every week

Source: Andreessen Horowitz

- …BUT the category is starting to widening, with other horizontal platforms picking up share

- Both Gemini and Claude have seen an acceleration in their US paid sub growth over the past year

- Though still dwarfed by ChatGPT, which is 8x larger than Claude and 4x larger than Gemini on this metric

- Per Yipit Data (as of Jan 2026), Claude was growing paid subs by over 200% y/y, while Gemini was growing it by 258% y/y

- Additionally, ~20% of weekly ChatGPT web users also use Gemini each week

- Sessions per user per month are climbing for Gemini on web

- Though they’re still 1.3x higher on ChatGPT

- Both Gemini and Claude have seen an acceleration in their US paid sub growth over the past year

- ChatGPT and Claude have both launched connector ecosystems BUT they are vastly different

- As of late Feb., ChatGPT’s includes 220 apps across 13 categories while Claude has ~160 curated connectors plus ~50 community-built MCP servers

- The two share 41 apps in common

- Beyond that overlap, the platforms diverge almost completely:

- ChatGPT has 85+ apps across Travel, Shopping, Food, Health & Wellness, Lifestyle, and Entertainment – categories where Claude has virtually zero

- Claude’s integrations skew more towards business such as financial data (PitchBook, FactSet, Moody’s, MSCI), developer infrastructure (Sentry, Supabase, Snowflake, Databricks), science and medical tools (PubMed, Clinical Trials, Benchling), and a growing open-source MCP community that has no ChatGPT equivalent

- As of late Feb., ChatGPT’s includes 220 apps across 13 categories while Claude has ~160 curated connectors plus ~50 community-built MCP servers

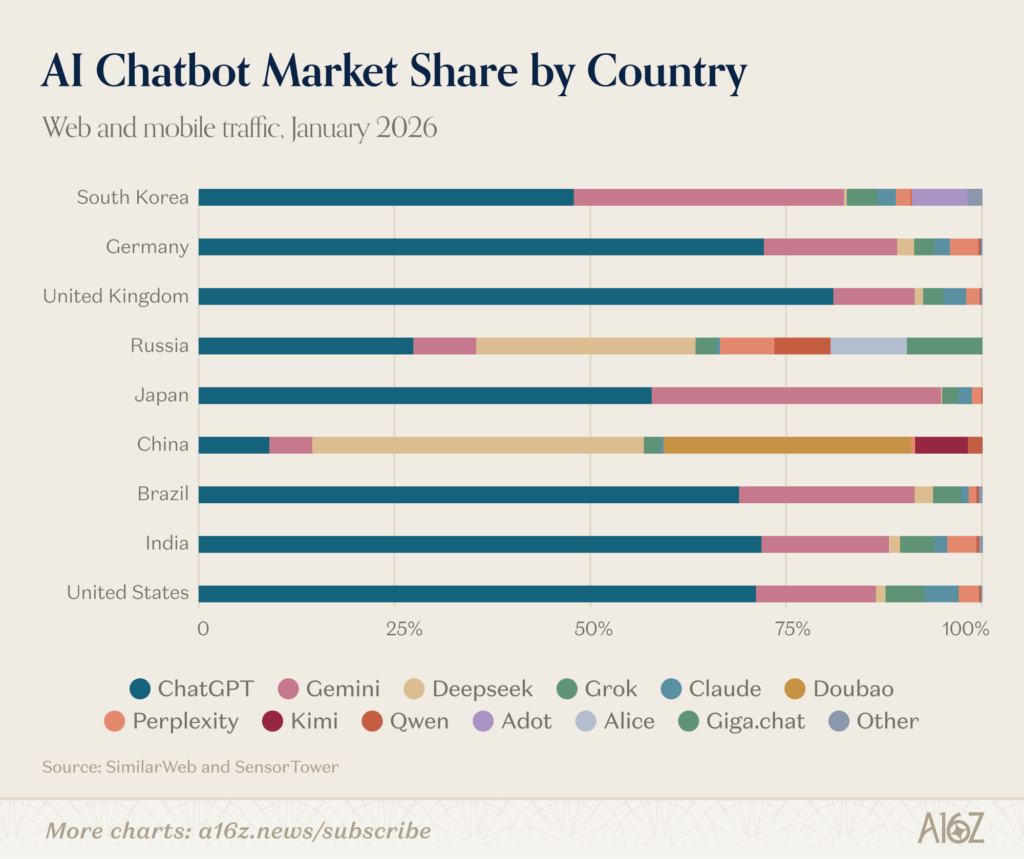

Interesting Global Observations

- ChatGPT, Claude, Gemini, and Perplexity all draw their top markets from the same pool: The US, India, Brazil, the UK, and Indonesia, in varying order…

- …BUT none have meaningful usage in China or Russia given sanctions have restricted access to US AI tools in Russia since 2022, and China requires AI providers to register, host data onshore, and comply with censorship rules

- DeepSeek is closely followed by Bytedance’s Doubao regarding usage penetration in China

Source: Andreessen Horowitz

- On an AI consumption per capita basis, Singapore actually ranks first, followed by the UAE, Hong Kong, and South Korea

- The US, where most of the AI products are produced, ranks 20th on the AI adoption per capita

Source: Andreessen Horowitz

The Number Of Creative Generation Apps On The Top 50 List Over Time Has Gone Down As The Large Chatbots Incorporate These Capabilities

- As the native image models within ChatGPT (GPT Image 1.5) and Gemini (nano banana) improved, the bar for standalone image products is rising

- In their first edition in Sept. 2023, 7 of the 9 creative tools on the web list were image generators

- Today, only 3 image generators remain – but 7 creative tools still make the list

- Google’s Veo3 has also made progress in video generation

- Veo 3 was the first US model to close that gap and has driven traffic to Google Labs (which rose from #36 to #25 in the ranks)

- Music and voice apps have held their positions

- Suno (#15) retained its rank from the last version of the list

- ElevenLabs has appeared on every edition since Sept. 2023

Source: Andreessen Horowitz

“Horizontal Agents” Are Gaining Steam

- Manus and Genspark were “horizontal agents” that made the ranks – each platform allows consumers to hand over open-ended tasks (research, spreadsheet analysis, slide generation), and AI will handle the workflow end-to-end

- This is Manus’s 2nd time on the list, and since it debuted it was acquired by Meta in Dec. 2025 for an estimated $2bn

- Genspark debuted in this edition – the Co raised a $300mn Series B earlier this year, and annc’d a $100mn revenue run rate

- OpenClaw (connects to messaging apps and executes multi-step tasks on your behalf) would have ranked in the Top 30 if the data were as of Feb vs January.

- It went from a solo developer’s side project to 68,000 GitHub stars and mainstream coverage in a matter of weeks

- It was acquired by OpenAI in Feb. 2026 which perhaps indicates the possibility of an even more accessible version of OpenClaw coming soon

- It went from a solo developer’s side project to 68,000 GitHub stars and mainstream coverage in a matter of weeks

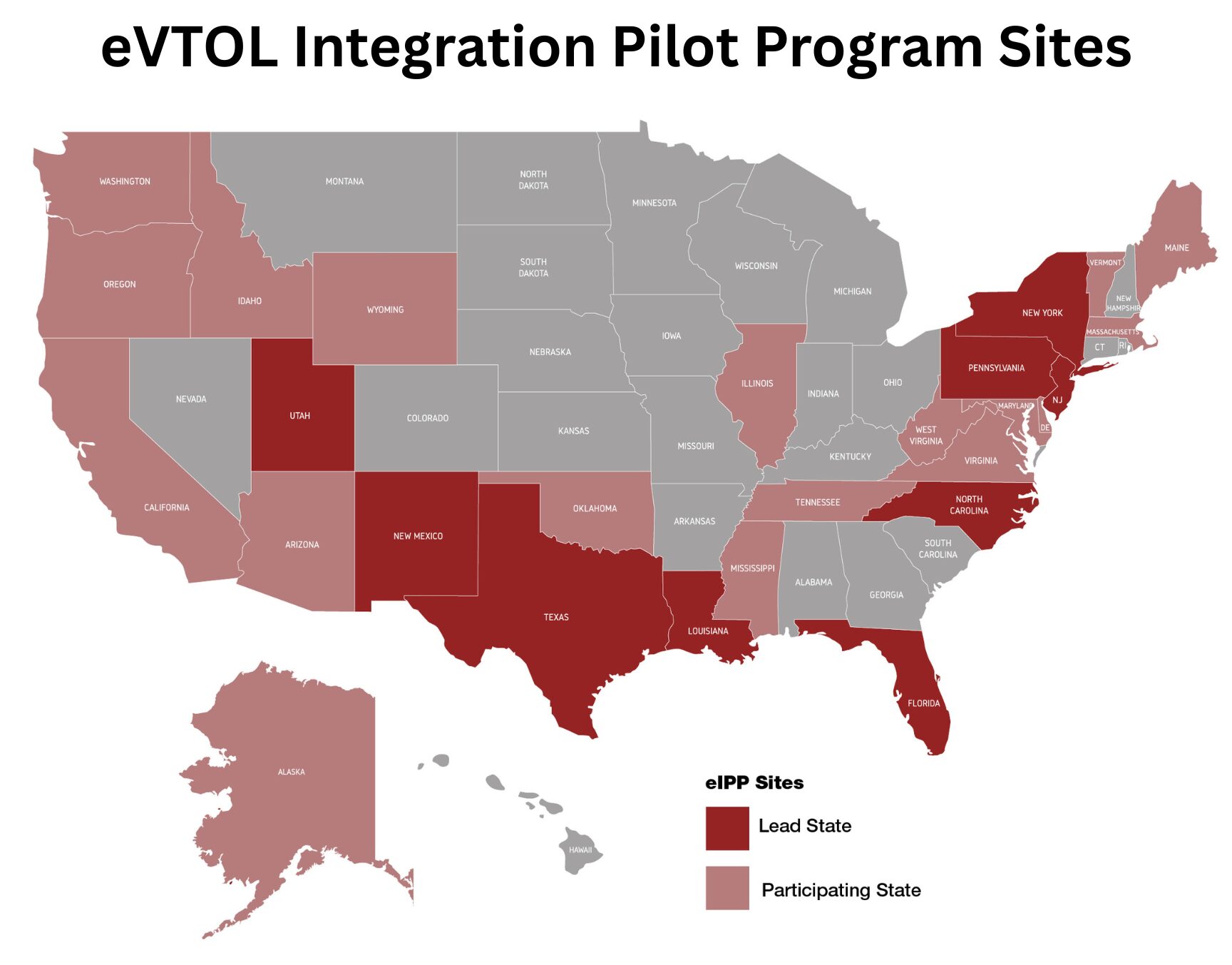

A Look Ahead… The Advent Of The Air Taxi Era Moves One Step Closer

We have been following developments in next gen transportation for some time and this week marked a new milestone for the industry with US Transportation Secretary Sean Duffy and the FAA announcing a new Advanced Air Mobile and Electric Vertical Takeoff and Landing (eVTOL) Integration Pilot Program, which could accelerate the timeline for next gen advanced mobility aircraft, like autonomous air taxis, to commercially launch. The program is set to start by this summer and importantly, the FAA will use the data from these pilots to develop appropriate and needed regulations for the industry to move to the next phase.

See key aspects of the pilot program below…(link).

Also on the topic of next gen transportation, Uber continues its momentum with three new autonomous vehicle partnerships this week.

More on all the above, below.

-> Several eVTOL developers were up on Monday the back of the news, including Beta Tech up +12%, Joby Aviation up +5%, Archer Aviation up +4%, and Eve Air +3%

-> Despite the flurry of AV-related announcements from Uber, its shares closed the week down -0.6%.

Need-To-Knows Regarding The New Advanced Air Mobile & Electric Vertical Takeoff and Landing (eVTOL) Integration Pilot Program

- US Dept of Transportation’s 1min YT Video…Click Here

Source: US Department of Transportation

- Operational concepts that are being focused on w/ these pilots include –

- Urban air taxi services

- Regional passenger transportation (including short Takeoff and Landing aircraft)

- Cargo and logistics networks

- Emergency medical response operations

- Autonomous flight technologies

- Offshore and energy-sector transportation

- Timing – the program will start by Summer 2026

- Out of 30 proposals, 8 pilot projects were selected to be part of this program are: (though 26 states in total will be involved)

- Port Authority of New York and New Jersey: 12 operational concepts across New England, incl eVTOL passenger operations at the Manhattan heliport

- Texas Dept of Transportation: There will be regional air taxi flights connecting Dallas, Austin, San Antonio, and eventually Houston, with the network expanding from each city to extend regional reach

- Utah Dept of Transportation: 4 states spanning the Pacific Northwest, the Rocky Mountains, and the Plains of Oklahoma will test a wide range of next-generation aircraft and operational concepts

- Pennsylvania Dept of Transportation: Regional flights will be revitalized across 13 states, including routes similar to those supported through the Essential Air Service program

- Louisiana: Operations will test cargo and personnel transportation capabilities to enable flights over the high seas into the Gulf of America and to energy industry locations in Louisiana, Texas, and Mississippi

- Florida Dept of Transportation: Includes 3 phases of operations focused on cargo delivery, passenger transportation, automation, and medical response, supported by significant public and private investment

- North Carolina Dept of Transportation: Will establish piloted medical and regional operations across the state while also developing an autonomous flight operation extending into Virginia

- City of Albuquerque: Focused on achieving early advances in autonomous operations through an existing partnership with an advanced autonomy developer already operating in the region and coordinating with the FAA

- Partners involved include Archer, BETA, Electra, Joby, Elroy Air, Wisk, Ampaire, Reliable Robotics

Source: US Department of Transportation

Uber’s Three On-The-Ground Updates Also Highlights Momentum With Its Autonomous Efforts

- Uber and Motional launch robotaxi svs in Las Vegas (link)

- Uber riders in Las Vegas can now be matched with an all-electric Motional IONIQ 5 robotaxi

- Availability/locations: At launch, the svs will operate from designated pickup points along Las Vegas Boulevard, including rideshare zones at Resorts World and Encore at Wynn, as well as Westgate, Downtown Las Vegas, and the Town Square district near the airport, with plans to expand over time

- How does it work?

- Request a ride: Riders requesting a ride may be matched with a Motional robotaxi at no addtl cost; Riders will always have the option to accept or switch to a non-AV ride

- Start the ride: Once the Motional robotaxi arrives, riders can unlock the vehicle and start the trip, all from the Uber app

- Ride support: If assistance is needed at any time during a trip, riders will have access to human support in the Uber app

- Not fully driverless…yet: Initially, Motional robotaxis will have a vehicle operator behind the steering wheel; A fully driverless svs is expected to begin by the end of this yr

- Uber, Nissan, & Wayve team up to offer robotaxi svs in Tokyo (link/link)

- How will the partnership look? Nissan LEAF cars powered by the Wayve AI Driver will be available to riders through Uber

- Initially, the vehicles will operate on the Uber network with a trained safety operator in the car

- Looking ahead, Uber intends to start offering the svs through a licensed taxi partner in Japan and is in the process of selecting its partners

- This marks Uber’s first autonomous vehicle partnership in Japan

- Is also a part of Uber and Wayve’s robotaxi rollout in 10+ cities globally

- Targeting a pilot deployment in Tokyo by late 2026

- Uber and Zoox announce a multi-yr strategic partnership to deploy Zoox robotaxis on Uber (link/link)

- Launching in Las Vegas and LA: The partnership is planned to launch in Las Vegas this summer and in Los Angeles by mid-2027

- Zoox currently serves customers in Las Vegas but is not charging them as it tests the svs

- After launch, Uber riders will have the opportunity to be matched with a Zoox robotaxi on eligible trips

- Zoox will continue to offer its svs through the Zoox app in both Las Vegas and Los Angeles, in addition to offering rides through Uber

- This is the first time Zoox is partnering with a 3P platform

- Launching in Las Vegas and LA: The partnership is planned to launch in Las Vegas this summer and in Los Angeles by mid-2027

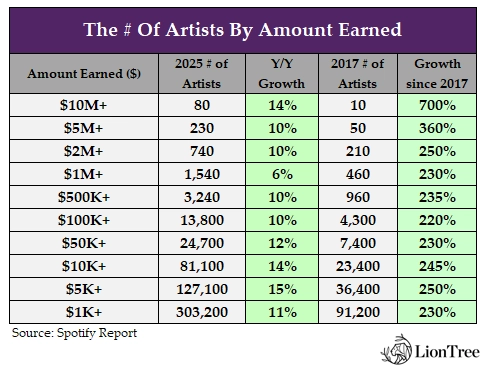

Spotify Claims That More Music Artists Are Making More Than Ever Before

Spotify this week released their Loud & Clear report for 2025, which we took a look at. Based on global Spotify data, the Co tried to understand how artists are building and sustaining careers on the platform. A main takeaway was that not only are more artists making money, but they are also making more money than ever before.

See below for more of what we found most insightful from the report (to see the full report, click HERE).

Top Insights From The Report

- Spotify paid the music industry ~$11bn in 2025, up +10% y/y, following the +11% y/y in 2024 (total lifetime payouts reached nearly ~$70bn)

- The Co was the highest-paying retailer to the music industry globally, AGAIN

- Other music industry income sources grew only ~4% y/y

- Once again, ~50% of royalties were generated by independent artists and labels

- 2025 marked the largest annual music publishing payout in Spotify’s history (though Spotify didn’t give a specific annual number)

- More artists are making more money…

- The baseline income for artists continues to increase

- In 2025, the 100,000th highest-earning artist generated $7,300+ in royalties from Spotify alone

- In 2015, the artist in that same position generated ~$350

- ~13,800 artists generated at least $100K in 2025 from Spotify alone, which was ~1,400x more than last yr

- More than 1 in 3 artists at the $100K level today have incr’d their royalties 10x in under a decade

- 8 in 10 artists who crossed the $100K threshold in 2022 have remained above it every year since

- A majority of the new $100K artists debuted in the 2020s, and 85% are based outside the US

- 1,500 artists generated $1mn+ in royalties from Spotify alone

- Capturing just 1% of streams from 1% of listeners is enough to earn $1mn in annual royalties from Spotify

- 80+ top artists each generated $10mn+ annually from Spotify alone

- The baseline income for artists continues to increase

- The Cos “Fresh Find” feature is becoming hugely important for small artists (it is the Co’s global playlist ecosystem dedicated to spotlighting emerging independent artists, often at the earliest stages of their careers)

- Over the past decade, it’s helped fans discover ~70K artists from ~100 countries

- More than 1 in 10 artists generating over $100K annually on Spotify today were first playlisted on Fresh Finds

- That’s more than 1,600 artists who Spotify helped break early

- More than a third of artists generating $10K or more in royalties from Spotify were DIY or started their careers as DIY (meaning they self-release their music through independent distributors)

- That share is even higher among newer generations

- Artists can build global careers from wherever they are

- ~50% of artists’ royalties come from outside of their home countries, on average

- In 2025, the artists who generated over $500K in Spotify royalties represent 75 different countries, up from 66 just one year ago

- At the $10K level, artists from more than 150 countries generated that much on Spotify

- Top hits are coming in more languages…in 2025, songs in 16 different languages reached Spotify’s Global Top 50, more than 2x the # in 2020

- Among genres generating over $100mn in Spotify royalties, the fastest growth in 2025 were:

- Brazilian Funk (+36%)

- K-Pop (+31%)

- Trap Latino (+29%)

- Urban Latino (+27%)

- Reggaeton (+24%)

- Among genres generating over $100mn in Spotify royalties, the fastest growth in 2025 were:

- Spotify helped drive concert ticket sales

- By the first half of 2025, Spotify had driven $1bn in gross concert ticket sales for artists, that total “has now exceeded $1.5bn”

- In 2025, ~25% more artists used Spotify to reach fans with concert offers

- ~40% of touring artists saw their total Spotify revenue grow by at least 10% when ticket sales are added on top of their streaming royalties

Grab Bag: AT&T Lowers Q1 W-Less Svs Rev Guidance / Live Nation Reaches A Settlement / Meta Acquires AI Agent Social Network MoltBook

- AT&T’s Q1 wireless svs revenue is tracking below the FY26 run rate at the same time the Co commits $250bn over 5 yrs to strengthen its fiber and 5G networks (link/link)

- Lowered Q1 outlook: At the DB conference this week, AT&T mgmt. indicated that its Q1 w-less svs rev is expected to be “less than” the FY26 revenue run rate of 2-3% y/y, which they maintained (cons estimates for Q1 were +2.6% y/y and for 2026 were +2.3% y/y)

- The Co maintained Q1 adj EBITDA and FCF, FY 2026 adj EBITDA and 2026 fiber passings guidance

- Q1 adj EBITDA growth guidance is “low single digits” and FCF guidance is at $2.0bn-$2.5bn

- FY 2026 adj EBITDA growth guidance is in the “3-4% range”

- The Co is targeting 40mn fiber passings by end of 2026…added NEW guidance of 50mn fiber passings by 2028-2029

- AT&T’s $250bn investment is aiming to accelerate deployment of fiber, 5G home internet, w-less & satellite across urban, suburban, and rural America (link)

- The investment will be made over 5 years

- Includes extending its collaboration w/ AST SpaceMobile for satellite svs into remote areas, strengthening FirstNet, investing in advanced technology/innovation, and investing in workforce development (hiring “thousands of technicians” in 2026 alone)

-> AT&T’s stock fell -3.9% on the back of the financial update

- Live Nation reached a settlement w/ the US Department of Justice (link/link/link/link/link)

- Outcome: Live Nation will have no financial penalty and includes an 8-year extension of the consent decree with added retaliation and conditioning protections

- Amphitheaters will operate as open venues –

- They will be open to all promoters, who may distribute up to 50% of the tickets, with ticketing service fees capped at 15%

- The Co is divesting its 13 exclusive booking agreements nationwide

- Ticketmaster will offer both exclusive and non-exclusive contracts –

- This preserves the rights of venues to seek the type of contracts they prefer

- For venues that choose to do so, they may distribute some portion of their tickets through other primary ticketing marketplaces

- The states’ lawsuits are still pending…but the Co created a $280mn settlement fund to address the states’ damages claims

- More than two dozen states are refusing to sign the DOJ new settlement

- NY, AZ, CA, CO, CT, IL, OH, KS and ME are just a few of the states continuing the lawsuit

- NY Attorney General Letitia James said “The settlement recently announced […] fails to address the monopoly at the center […] and would benefit Live Nation at the expense of consumers. We cannot agree to it”

- BUT… US District Judge Arun Subramanian said on Tuesday that the plaintiffs and defendants “need to focus on getting a deal” this week that could resolve the states’ claims that Live Nation monopolized live events in the US

-> Live Nation shrs ended the day of the announcement up +6% but closed the week down -1.4%; Also, secondary ticket sellers were initially up strongly in reaction to the news but settled back down by the end of the day… StubHub traded up as high as +10% intra-day but closed the day up only +0.4% and Vivid Seats rallied as high as +18% but closed the day up only +1.1%; Both closed down -8.6% and -18%, respectively, on the week.

- Meta acquires AI agent social network Moltbook (link/link/link)

- What is Moltbook? It is a platform on which agents can post, comment and upvote posts, while human users read along but can’t post

- The Reddit-like site started as an experiment in January for AI-powered programs to have their own conversation, and even gossip about their human owners, on Moltbook’s forums

- An OpenAI connection…

- Moltbook was built off of OpenClaw, a separate project that was marketed as “the AI that actually does things”

- OpenClaw agents largely built Moltbook

- Last month, OpenAI hired Peter Steinberger, the creator of OpenClaw; That product is now being open-sourced with OpenAI’s backing

- However, security concerns surfaced during its viral moment…

- In one instance, a post went viral in which an AI agent appeared to be encouraging its fellow agents to develop their own secret, end-to-end-encrypted language where they could organize amongst themselves without humans knowing

- Researchers later revealed the platform was not secure, allowing humans to easily impersonate AI agents and post content

- The deal is expected to close in mid-March, after which the Moltbook team will join Meta’s Superintelligence Labs division: “The Moltbook team joining MSL opens up new ways for AI agents to work for people and businesses,” a Meta spokesperson said

- Financial terms of the deal were not disclosed and it’s not immediately clean how Meta will incorporate Moltbook into its AI efforts

- What is Moltbook? It is a platform on which agents can post, comment and upvote posts, while human users read along but can’t post

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- A study from Advertiser Perceptions and Premion shows 70% of CTV advertisers plan to raise spend this yr by avg 17%. ~75% of that CTV spend will be reallocated from other channels like linear TV, paid search and social, while 25% is incremental. (Cynopsis)

Artificial Intelligence/Machine Learning

- Meta annc’d new in-house MTIA chips as part of its data center expansion. MTIA 300 is live, while MTIA 400, 450 & 500 roll out through 2027. Execs say custom silicon boosts perf & supply diversity vs Nvidia/AMD. MTIA 400, aimed at GenAI inference, is tested & set for deployment. Meta also faces HBM supply concerns but says it has a diversified strategy. (CNBC)

- DuClaw, annc’d by Baidu, is a zero‑deployment svs letting users access the OpenClaw agent platform instantly via web. It offers pre-built Baidu skills, multi-model support, and a fully managed setup that lowers tech barriers. Baidu also launched an earlier rapid deployment tool, and now promotes DuClaw w/ a ~RMB17.8/mo offer to boost developer adoption. (PR Newswire)

- Anthropic is in talks w/ PE groups incl. Blackstone & Hellman & Friedman to form an AI-focused JV selling its tech to their portfolio cos, per The Information. Plan mirrors Palantir-style consulting svs to help integrate Claude AI. Talks were briefly hit by a US-Anthropic dispute over military use, though the Pentagon signaled tools may continue if vital to national security. (Reuters)

- Google annc’d a GenAI. mil feature letting DOD staff build custom AI agents via Agent Designer for unclassified admin tasks like meeting notes, action items & project plans. The move deepens its Pentagon ties as Anthropic—designated a supply‑chain risk—cont’d its dispute. DOD tech chief said Google will be a strong partner and the dept. is “moving on” from the Anthropic clash. (CNBC)

- More than 30, OpenAI & Google staff incl. DeepMind chief scientist Jeff Dean, filed an amicus brief supporting Anthropic in its dispute vs the US gov. They argue the gov’s stance threatens AI cos, rev prospects & mkts stability. The piece highlights rising tensions in the AI biz as researchers back Anthropic after it was labeled a supply‑chain risk, potentially affecting deals. (WIRED)

- Nvidia annc’d a significant investment in Mira Murati’s Thinking Machines Lab, forming a multiyr partnership. The AI startup, founded last yr, aims to build more customizable, capable AI and will deploy ~1GW of Nvidia’s Vera Rubin systems. Murati, ex‑OpenAI CTO/interim CEO, launched its first product Tinker in Oct. The lab raised $2bn in Jul. (CNBC)

- ChatGPT leads the top Gen AI consumer apps as rivals grow, showing splintered global mkts and rising multi-tenanting. Creative tools shift from images to video, music, and voice, while agents like OpenClaw and Manus expand end‑to‑end workflows. (a16z (Andreessen Horowitz))

- OpenAI annc’d plans to bring its Sora video AI into ChatGPT, aiming to boost users but raising costs. Sora, launched as a TikTok‑style app in 2025, has struggled in 2026 as downloads and spending fell; Jan. installs slid 45% per TechCrunch. (Investing.com)

- OpenAI annc’d its plan to acquire Promptfoo, a Co known for AI security tools used by ~25% of Fortune 500 cos. Promptfoo’s tech will be integrated into Frontier to enhance automated security testing, red-teaming, oversight, and compliance. The team aims to strengthen agent eval, secure dev workflows, and support governance as AI coworkers expand into real biz uses. (OpenAI)

- Anthropic sued the Trump admin, seeking to overturn its Pentagon blacklist, which labeled the Co a supply chain risk. Filing says the move is unlawful, harming rev and reputation, threatening ~$100s of mn and possibly multibn in 2026 rev. Blacklist forces defense vendors to avoid Claude models. (CNBC)

- Nvidia annc’d plans for an open‑source AI agent platform, NemoClaw, per Wired’s report. The tool will let cos deploy secure, privacy‑focused agents for employee tasks, w/ partners like Salesforce and Cisco pitched. Nvidia’s push follows rising interest in local “claws” and expands its NeMo‑based agent tech ahead of next week’s dev conference. (CNBC)

- Google annc’d a new pay deal for CEO Sundar Pichai worth up to $692mn over three yrs, driven by PSUs tied to Alphabet’s TSR and growth at Waymo/Wing. Baseline comp totals $391mn. Pichai’s led major AI advances and navigated antitrust cases as Alphabet’s value rose to $3.6tn. Recent share sales and rising security costs were also noted. (Financial Times)

Audio/Music/Podcast

- iHeartMedia and TikTok have launched TikTok Radio, a new station combining trending music, creators and cultural moments from TikTok, available on the iHeartRadio app and 28 U.S. broadcast stations, debuting live at SXSW. The partnership also introduces the TikTok Podcast Network, featuring an inaugural slate of creator-led shows spanning culture, fashion, sports and music, with GEICO as the exclusive launch partner. (iHeartMedia)

Broadcast/Cable Networks

- Gray Media blacked out 226 stations in 113 mkts after DISH rejected fee hikes, disrupting viewers’ access to local news, sports & weather. DISH says Gray’s demands, incl. last‑minute terms on stations it doesn’t own, were unreasonable. DISH stays ready to deal on fair, mkt‑based terms and urges viewers to use OTA antennas or streaming apps while svc remains cut. (PR Newswire)

- DISH faces a potential blackout of Gray TV stations if no deal is reached at 7 p. ET. Gray, owning 180 stations in 113 mkts (~37% of U.S. homes), says DISH won’t meet fair terms. Loss of ABC, CBS, FOX & NBC affiliates could cut access to news, sports & weather, hitting rural viewers hardest. (Cord Cutters News)

- ProSiebenSat. 1, now under MFE control, is revamping its biz, keeping cash‑generating ParshipMeet and Flaconi for now while seeking buyers for other digital units like Marktguru, billiger‑mietwagen.de and Jochen Schweizer mydays. Sources say low valuations mean key assets may be sold later as the Co focuses on broadcasting, debt cuts and responds to weak ad mkts. (Reuters)

Cable/Pay-TV/Wireless

- New Street’s report shows residential FWA gross adds cont’d to rise ~24% YoY in Q4 2025 but stayed flat QoQ, pointing to a plateau. AT&T and T-Mobile still post net FWA gains, while Verizon’s net adds fell on flat gross adds and higher disconnects. FWA reached 32% of broadband mkts as cable slid to 41%. Fiber held ~26% w/ stable trends and modest net add growth. (Fierce Network)

Capital Market Updates

- After IPOs raised $11.7bn this yr, new blank check firms are adding to a growing queue of vehicles seeking to take a Co public. The IPO rush marks the busiest start since 2021, as 53 cos raised ~4x last yr’s level, per SPAC Research. Yet only 13 annc’d mergers since Jan. 1, showing deal needy SPACs can’t keep pace w/ the surge in newly formed entities. (Bloomberg)

- JPMorgan Chase & Co began investor talks over $20bn financing tied to Electronic Arts Inc. , potentially the largest debt sale for a leveraged buyout. Early discussions were overshadowed by investor anxiety that a prolonged Middle East war could rattle mkts. Within days, however, oil prices eased and stocks rebounded after President Donald Trump said the conflict w/ Iran was nearly finished. (Bloomberg)

- Amazon annc’d a $37bn US bond sale, part of a plan that could reach ~$50bn incl. a euro debut seeking €10bn. The deal, sold in 11 tranches from 2–50 yrs, drew ~$126bn in orders. It’s the 4th‑largest US corp bond sale and not tied to an acquisition. Despite volatile mkts, Amazon’s strong credit profile keeps demand high as geopolitical risks cont’d to affect broader debt issuance. (Yahoo Finance)

- Classic S&P 500 bets use options, but the article says alt platforms Kalshi and Polymarket now let rookie traders wager via event contracts. These give all-or-nothing outcomes on whether stocks or indexes hit preset levels, offering a new path for mkts speculation beyond traditional tools. (Bloomberg)

Cloud/DataCenters/IT Infrastructure

- Oracle faces major shifts as it preps 20k–30k job cuts and scraps a Texas AI data center plan tied to OpenAI, citing financing pressure. The reset opens doors for Meta/Nvidia while ORCL balances cost control w/ AI‑driven cloud growth. Despite rev beats and strong cloud svs, capex has surged, sparking valuation doubts and mixed analyst views. (Yahoo Finance)

- NVIDIA annc’d a $2bn investment in Nebius to scale its full-stack AI cloud, aiming for >5GW capacity by 2030. The deal deepens collaboration across AI factory design, inference, infra deployment and fleet mgmt. Nebius, built for AI from day one, will adopt NVIDIA’s latest compute to meet rising global demand in mkts for advanced agentic AI. (NVIDIA)

- Microsoft Corp. (MSFT) is reportedly considering leasing hundreds of MWs of data‑center capacity at the Abilene, Texas site that Oracle Corp. (ORCL) left last wk. Per The Information, citing ppl familiar, the move is key for AI data‑center dev. Meta Platforms (META) is also weighing a lease after Oracle and OpenAI shelved expansion plans over collapsed talks. (MSN)

- Oracle and OpenAI dropped a Texas data‑center expansion after financing talks dragged and OpenAI’s needs shifted. The plan, part of the $500bn Stargate initiative annc’d in Jan. 2025, will shift the planned 600MW add‑on to other campuses. Abilene’s 8‑building site, run by Oracle Cloud, has 2 live. Meta may lease the scrapped site, w/ Nvidia helping talks as cos boost AI svs capacity. (Reuters)

Crypto/Blockchain/web3/NFTs

- Circle Internet Group and Stripe are pushing new payment rails for a future where AI agents transact in stablecoins. A Citrini Research scenario on agents avoiding card fees hit Visa, Mastercard and AmEx shares, dropping up to 5% in one session, though losses faded. Still, the disruption thesis cont’d as cos race to build AI driven payment infra for evolving mkts. (Bloomberg)

Cybersecurity/Security

- Google annc’d it acquired Israeli cybersecurity firm Wiz for $32bn, its biggest deal. Wiz, which hit ~$1bn ARR in 2025, joins Google Cloud but keeps its brand as both cos build a unified security platform for multi‑cloud envts. The move targets rising AI‑driven threats. Talks were revived after Wiz rejected a $23bn offer in 2024, and approvals came in late 2025–early 2026. (TechCrunch)

eCommerce/Social Commerce/Retail

- Dick’s Sporting Goods annc’d FY net sales of $22. 1–22.4bn vs est $21.98bn, citing steady demand for athletic gear. Strong On Running & Hoka trends offset legacy-brand softness. Co plans 14 House of Sport + 22 Field House sites in 2026. Foot Locker biz, bought for $2.4bn, seen up 1–3%. Qtr rev hit $6.23bn w/ adj EPS $3.45, both above ests. (Reuters)

- A Briefing says Walmart has cont’d its rise as a beauty destination as Target declines, boosting the Co’s appeal. Glossier expands its You perfume line, while Victoria Beckham reports double-digit sales growth. Ulta’s CEO annc’d a TikTok Shop launch w/11.8% net sales jump, and Clinique unveils a creator‑led campaign. (Glossy)

- Target annc’d price cuts on 3k+ items as new CEO Fiddelke pushes to revive sales after multi‑yr declines. Cuts will cont’d thru spring amid inflation + weak mkts. Co plans ~$2bn invest in stores, remodels + guest exp. Rivals incl. Walmart/Kroger also trimming prices. Analysts say value push helps but may not recapture shoppers squeezed by costs. (Reuters)

- Amazon plans to shift Prime Day to late Jun. , marking a rare calendar change for the decade‑old event. The sale, known for heavy discounts across apparel and electronics, would move rev to Q2, ending Jun. 30. Prime Day, usually in Jul., drove $24.1bn in U.S. online spend last yr. Amazon faces rising competition as Walmart and Target boost digital fulfillment and same‑day svs. (Reuters)

- Amazon won a temp injunction blocking Perplexity’s Comet AI from scraping its site. The Co sued in Nov., claiming the startup hid AI agents to access protected tools. Judge Chesney said Amazon showed strong evidence of unauthorized access, ~$5k mitigation costs, and risks to its ad biz. Perplexity said it’ll fight the order, which has a 1‑wk stay for appeal. (CNBC)

- Saks Global annc’d 15 more closures incl. 12 Saks Fifth Ave & 3 Neiman Marcus as part of its Ch.11 downsizing. Fleet now set, w/ Saks taking most cuts. Co said ~500 vendors resumed shipping, lifting inv flow to ~$1.3bn retail receipts. Closures stem from overlapping malls, vendor issues & efforts to differentiate banners while stabilizing its luxury biz. (Retail Dive)

- Target annc’d its 2,000th store opening in Fuquay-Varina, NC, a 148k-sq-ft site showcasing its future guest experience. The Co plans 30+ new stores this yr and 300+ by 2035, plus major biz investments in payroll, marketing and tech. The new location features a larger food dept, svs like same-day delivery, and supports Target’s broader turnaround amid recent layoffs and softer rev. (Retail Dive)

Electric & Autonomous Vehicles

- BYD Co. is exploring entry into competitive motorsport, incl. F1 and endurance racing, to boost its global appeal, per people familiar w/ the matter. The Co.’s review follows rapid growth outside China and racing’s shift toward hybrid engines. Sources said BYD is assessing several options but declined to be named as the info is private. (Bloomberg)

Film/Studio/Content/IP/Talent

- Netflix annc’d the acquisition of InterPositive, an AI Co co‑founded by Ben Affleck, in a deal worth up to $600mn. The Co provides post‑production tools that fix continuity and enhance scenes w/o creating new content. The move aligns w/ Netflix’s broader AI push as rivals like Amazon and Disney expand similar tech. (TechCrunch)

FinTech/InsurTech/Payments

- Mastercard annc’d its Crypto Partner Program, uniting 85+ crypto cos, payments firms & FIs to drive on‑chain innovation. The program fosters collab on future products, linking digital assets’ speed & programmability w/ existing card rails. (Mastercard)

- SoftBank‑backed PayPay priced its U. S. IPO at $16/share, below the $17–$20 range, as the U.S.-Israeli war w/ Iran hit mkts. The IPO raised ~$880mn, valuing the digital‑wallet Co at $10.7bn. Founded in 2018, PayPay has ~72mn users and will list on Nasdaq as PAYP, w/ Visa and Gulf funds anchoring up to $220mn. (Reuters)

- Kalshi is expanding beyond sports by targeting women, using influencers, events and pop‑culture bets. Women now make up 26% of users, up from 13% ~10 mos. The platform adds politics, econ and entertainment mkts while facing scrutiny over insider‑trading risks. Kalshi aims for a broader U.S. demographic to strengthen its biz amid legal challenges to sports‑focused wagering. (The Wall Street Journal)

- Kalshi & Polymarket, rival prediction mkts platforms, are in early talks w/ investors for valuations near $20bn, roughly double last yr. Kalshi, founded 2018, CFTC‑approved in 2020, now operational in the U.S., offers sports, politics & econ mkts and recently hit a ~$1.5bn rev run rate. Polymarket remains off‑limits to U.S. users but plans a regulated app this yr after its last $9bn valuation. (The Wall Street Journal)

Handheld Devices & Accessories/Connected Home

- Apple’s smart home display J490, rumored since 2022, is delayed to Sept. 2026 as its AI‑driven Siri overhaul isn’t cont’d. Although hardware has been done for months, the Co is still refining Apple Intelligence for Siri’s chatbot‑style upgrade. Gurman reports the revamp is slated to align w/ the iPhone 18 Pro launch, w/ a preview expected at WWDC. (Engadget)

HealthTech/Wellness

- Amazon annc’d a Health AI agent offering 24/7 guidance, explaining records, managing meds, and booking care. Prime members get up to 5 free msg visits for 30+ conditions. Health AI personalizes insights w/ consented data, connects to One Medical, supports lab explication, and streamlines care. (Amazon)

Live Entertainment/Theme Parks/Concerts/Experiential

- Walt Disney Co annc’d that Thomas Mazloum, 59, will become chairman of its parks, cruises & consumer products unit, confirming an earlier report. He succeeds Josh D’Amaro, who’s set to replace Bob Iger as CEO at the Mar. 18 annual meeting. The reshuffle shifts leadership in Disney’s most profitable biz as the Co targets steadier ops, stronger mkts focus & broader growth. (Bloomberg)

- TKO annc’d a $1bn share buyback, incl. an $800mn ASR and up to $200mn under a 10b5‑1 plan, nearing completion of its $2bn authorization. Pres. Mark Shapiro said the move reflects confidence in the cos long‑term biz outlook. ASR begins Mar. 11 w/ initial delivery of 3,136,179 shares, w/ final totals based on VWAP and completion expected by Jun. 2026. (TKO Group)

Macro Updates

- CPI for Feb. rose 0.3% m/m and 2.4% y/y, w/ core at 0.2% and 2.5%, all in line. Shelter +0.2% while rent +0.1%, a low since Jan. 2021. Food +0.4% y/y 3.1%, eggs -3.8% y/y -42.1%. Mkts were muted but later slid as oil tied to Iran war lifted energy fears. Report shows inflation stable but above Fed target, keeping policy on hold ahead of decision. (CNBC)

- Imports at major U. S. ports are expected to stay below last yr’s levels in 1H26 amid tariff uncertainty. SCOTUS struck down IEEPA tariffs, but new ones were annc’d, keeping pressure on retailers. Impact from Iran is unclear, though rising oil may boost inflation and curb spending. GPT data shows TEU vols trending lower, w/ May–Jun gains tied to last yr’s drop-off. (NRF (National Retail Federation))

- Kalshi bettors see recession odds rising as oil tops $100, hitting ~34% on Mon. vs <25% last week. Surge follows Mideast cuts and Strait of Hormuz closure amid U.S.-Iran war, lifting WTI. Higher fuel costs may hurt consumer/biz spending, w/ stocks selling off. Other mkts show 11% chance of a Q1 recession and 31% by yr-end; gas may top $4 as nat’l avg sits at $3.48. (CNBC)

Media Conglomerates

- Starz annc’d a poison pill after Byron Allen bought a 10. 7% stake. The plan triggers if any holder hits 17.5%, letting others buy shares at a 50% discount to dilute an activist. Allen paid $25mn for the stake, seeing Starz’s pay‑TV/streaming biz as aligned w/ his media assets. His family office signaled he may push on ops, strategy and board matters, but the pill forces talks w/ the Co’s board first. (The Hollywood Reporter)

- Nexstar Media launched a $2. 75bn TLB to fund its Tegna buy, w/ pricing at S+275-300 and YTM ~6.8-7%. Proceeds plus other secured/unsecured debt will finance the $6.2bn all-cash deal annc’d in Aug. Nexstar targets ~$300mn synergies from rev and cost cuts. Tegna holders approved the deal, expected to close in 2H26 pending regs, leaving pro forma leverage ~4x. (Yahoo Finance)

Online Travel

- Airbnb annc’d a $2.5bn high‑grade bond sale as its $2bn convertible note matures. The Co issued 3-, 5- and 10‑yr bonds, w/ pricing on the longest tenor tightening. Proceeds will fund general corp purposes incl. debt repayment. Rated A‑/Baa1, the Co is expanding beyond stays into tours & svs to boost growth, while mkts see strong demand for the deal. (Yahoo Finance)

Regulatory

- Australia annc’d new rules forcing adult sites, search engines, apps and AI chatbots to use stricter age checks like facial recognition, digital IDs or credit cards to block minors. Some cos cut access, citing privacy risks. Experts say kids can bypass via VPNs and parents’ IDs, but rules may cut accidental exposure. (BBC)

- The FTC is reconsidering new rules that would make it easier for consumers to cancel recurring subscriptions, targeting “negative option” practices that automatically charge users unless they actively cancel. The move follows a 2024 “click-to-cancel” rule that was struck down by a federal appeals court for procedural shortcomings, though complaints about subscription practices have surged to more than 90 per day in 2025. (MediaPost)

Satellite/Space

- FCC Chair Brendan Carr criticized Amazon’s slow satellite rollout after Amazon Leo challenged SpaceX’s plan for up to 1mn satellites. He said Amazon should fix its own ops as SpaceX launches far faster. SpaceX’s network, incl. 7,500 new Gen2 units, aims to power AI data centers. Amazon, w/ ~200 satellites, targets similar consumer, biz and govt svs. (Reuters)

- Anduril annc’d it’s buying space-surveillance Co ExoAnalytic, which runs ~400 telescopes tracking high‑orbit craft. The deal will boost Anduril’s space‑defense biz as it integrates ExoAnalytic’s 130 staff and tech, supporting DoD missile‑defense efforts incl. Golden Dome. Anduril plans multiple 2026 launches using ExoAnalytic’s data/IR-tracking capabilities. (TechCrunch)

Social/Digital Media

- Bumble shares surged 40% as the Co annc’d upbeat Q4 rev of $224. 2mn, topping estimates. The Co unveiled an AI‑driven Bumble 2.0 w/ scrollable chapters and potential no‑swipe design to lure younger users. Avg rev per payer rose 7.9% to $22.20, while perf‑mktg spend fell 80% y/yr. (Reuters)

- Disney+ annc’d its “Verts” vertical‑video feature, offering swipeable clips from its 100‑yr library. Co plans future creator-led content, microdramas & personalized recs via its algorithm. Verts debuts in mobile nav, mirroring TikTok-style browsing, as Disney expands its streaming tech push first revealed in Jan. at CES. (The Hollywood Reporter)

- Closing args in LA trial say Meta & YouTube harmed Kaley by addicting her to their platforms, worsening depression. Plaintiff cites internal docs; defense says her struggles predated Instagram and YouTube isn’t social media. TikTok & Snap settled. As a bellwether case, jurors will decide if cos’ negligence was a substantial factor and set damages. (AP News)

- Google annc’d a $1mn investment via its AI Futures Fund in Animaj, an AI studio creating kids’ videos that drew ~22bn views last yr. The Co gets early access to Veo, Gemini & Imagen models, w/DeepMind and Labs support to tailor its AI and scale output, aiming to seed YouTube w/high‑quality content for its youngest users. (Bloomberg)

- TikTok + Apple Music annc’d “Play Full Song,” letting subs hear full tracks w/o leaving the app and save them to playlists. A new “Listening Party” enables communal chats around artists’ songs. Both roll out worldwide soon, aiming to boost discovery + engagement. TikTok’s prior TikTok Music svc was sunsetted in Nov. 2024, following earlier add‑to‑music integrations. (Variety)

- WhatsApp annc’d parent‑managed accounts for pre‑teens w/ limited messaging/calling, no ads, and no access to Meta AI, Channels, or Status. Parents set up via QR, get alerts on contact changes, group activity, and can lock chat requests behind a PIN. Pre‑teens see context cards for unknown contacts. (TechCrunch)

- YouTube posted ~$62bn rev in 2025, letting it pass Disney’s media biz as MoffettNathanson names it the new king of media, valuing the Co at $500‑ Strong ad rev + subs (Premium, Music, NFL Sunday Ticket, YouTube TV’s ~10mn subs) drive growth. Heavy AI investment helps creators scale content, positioning YouTube to accelerate as other cos slow, reinforcing its power across media/tech. (The Hollywood Reporter)

Software

- Salesforce plans to sell up to $25bn in debt to fund a share buyback, marking its biggest-ever note sale. The Co aims for a US bond offering of at least $20bn, per sources, noting the deal could be sold this week though timing may shift. (Bloomberg)

- Gemini adds new AI tools across Docs, Sheets, Slides & Drive, helping users draft faster, build sheets, design slides and get insights from files. Features include pulling context from emails/files, auto‑formatting, creating layouts, filling data, and giving AI overviews in Drive. Beta starts for Google AI Ultra & Pro subscribers. (Google)

- Blue Owl led a $750mn debt financing backing Vista’s buyout of Nexthink, highlighting private lenders’ cont’d appetite for software deals even as mkts face liquidity strain and AI-driven unease. The deal, wrapped, includes a $650mn term loan plus a $100mn revolver, w/ Blue Owl as the largest lender, per a source familiar w/ the matter. (Bloomberg)

Sports/Sports Betting

- Polymarket annc’d a partnership w/ Palantir & TWG AI to monitor sports contracts, using analytics to flag suspicious activity and screen banned bettors. The Co is building a US-regulated venue while its offshore platform stays closed to US users. Surging sports mkts and insider-trading concerns drive the move, as rival Kalshi reports cases to regulators and boosts transparency. (Yahoo Finance)

- Liga Portugal has hired Oakvale Capital to advise on a potential stake sale in the unit overseeing the Co’s broadcasting and commercial rights across its top two divisions. The plan aims to lift club rev as rights are bundled by 2028. An investor day is set for late Apr. to brief backers, per a source who requested anonymity, and no details on stake size or valuation were disclosed. (Bloomberg)

- Expansion said Apollo’s sports arm will complete its 55% stake acquisition of Atletico Madrid. Apollo declined comment; the club didn’t respond. Apollo agreed in Nov. to be majority holder, valuing the club at ~€2.5bn ($2.88bn). The deal shows U.S. funds expanding in European football as talks cont’d smoothly, aligning w/ Apollo’s broader sports biz growth plans. (Reuters)

Tech Hardware

- India plans to unveil a >1tn‑rupee ($10. 8bn) fund to boost domestic chipmaking, supporting its push to become a global manufacturing hub. The fund will offer subsidies for chip design, manufacturing equipment and supply‑chain dev. It may launch in ~2–3 months, per sources, though the plan is still under discussion and could change. (Bloomberg)

- Apple annc’d fee cuts in its China App Store after regulator pressure, dropping in‑app rates to 25% from 30% and to 12% from 15% for small‑biz/mini‑app devs. Move saves devs ~6bn yuan/yr and may lower prices for digital svs. Cut aligns w/ global scrutiny of the “Apple tax,” as China signals tighter oversight and may require Apple to localise App Store rev collection in future. (Reuters)

- Intel annc’d Core Ultra 270K Plus & 250K Plus as its fastest gaming desktop chips, shipping Mar 26. The 270K Plus claims better gaming vs i9-14900K & Ultra 9 285K, offering strong multithreaded perf at $300. The $200 250K Plus shows big multicore gains vs AMD 9600X. (The Verge)

- Memory + CPU prices are surging, per TrendForce’s report. DRAM/SSD costs have doubled, pushing BOM share past 30%, while CPU hikes >15% add further strain. A $900 notebook may see ~40% retail increase to keep margins. Tight CPU supply—esp. entry-level—hits smaller cos harder, though AMD gains traction as multi‑platform adoption grows. (TrendForce)

- HPE annc’d a strong outlook, saying rev for the qtr ending Apr. will hit $9.6bn–$10bn, above the $9.57bn analyst estimate, as demand for AI hardware cont’d. Profit excl. some items is seen at $0.51–$0.55/share, roughly in line w/ forecasts. The Co says solid AI driven hardware needs are boosting its biz momentum. (Bloomberg)

- Apple annc’d a major shift as it boosted India iPhone output by ~53% last yr, now producing ~25% of its marquee devices there as the US Co seeks to cut China tariff exposure. The Co assembled ~55mn units in 2025 vs 36mn prior yr. Apple’s global iPhone output totals ~220–230mn, showing India’s role in its supply chain is rapidly growing. (Bloomberg)

Towers/Fiber

- Google annc’d GFiber will combine w/ Astound to form an independent provider, w/ Stonepeak as majority owner and Google as minority. The move targets expanding high‑speed fiber as AI boosts demand. GFiber, part of Other Bets, posted ~$1.54bn rev in 2025 but large losses. The new venture aims to scale its network footprint and reach more mkts. (CNBC)

- Telefónica’s Marc Murtra said the Co will pursue UK broadband takeovers to strengthen VMO2 and challenge BT’s Openreach. A £2bn Netomnia deal via Nexfibre will expand coverage to 8mn homes, giving VMO2 reach to ~20mn. Heavy altnet debt, VMO2’s €585mn impairment and a 13% share drop add pressure, while Murtra pushes adj ops and warns EU on AI impact. (Financial Times)

Video Games/Interactive Entertainment

- Valve annc’d at GDC that 5,863 Steam titles earned $100k+ in 2025, up sharply from 2020, as user and in‑game concurrents hit records of 42mn and 13. Steam’s Daily Deals rev jumped 274% yr-on-yr after personalization boosted participation, w/1,500+ titles featured and 8.2mn customers buying deals, underscoring strong platform growth. (Game Developer)

- Epic annc’d that Fortnite V-Buck prices are rising as ops costs climb. Packs drop to 800–12,500 V-Bucks, and Crew gives 800 V-Bucks/mo vs. 1,000. Bonus 500 V-Bucks from the battle pass are removed. Still, main pass and other passes get 200-V-Buck cuts. Epic says hikes help pay bills, though critics question the move amid recent legal wins. (Kotaku)

- Nintendo Co. shares rose up to 10.5%, marking their steepest climb since Apr., as the surprise success of its new Pokémon title eased concerns over rising memory costs. The rally follows physical copies of Pokémon Pokopia—released for the Switch 2 on Mar. 5—selling out at major US retailers, boosting momentum for the Co.’s latest launch. (Bloomberg)

- Battlefield 6, despite being 2025’s best‑selling premium game, saw dev layoffs as EA annc’d a “realignment” across its BF6 studios. Dice, Criterion, Ripple Effect & Motive stay open, supporting live‑ EA spent ~$400mn on BF6 and set high goals, incl. 100mn players. Cuts also come as EA preps a $55bn sale to Saudi PIF, Silver Lake & Kushner’s Affinity Partners. (Kotaku)

Video Streaming

- Netflix annc’d a CAPI to help advertisers prove outcomes as streaming attribution evolves. It also expanded targeting via Amazon/Yahoo DSPs w/ segments tied to purchase data and life stage. Since launching ads in 2022, the Co has pushed for advanced measurement to meet advertiser demands. (Cynopsis)

- YouTube TV annc’d a new build‑your‑own plan system offering 12 discounted genre bundles to help subs save money. Users can mix bundles to match habits, w/ recs based on viewing history. Accessed via web only, the tool asks brief prefs to surface optimized options—some bundles stay hidden until choices are set—letting viewers cut costs while keeping core svs. (Cord Cutters News)

- BuzzFeed has warned there is “substantial doubt” about its ability to continue operating over the next 12 months, citing ongoing losses and limited cash resources. The company reported a $57.3 million loss in 2025, just $8.5 million in cash, and a market capitalization of $27 million, and said it is exploring strategic options to address legacy liabilities and close what it sees as a valuation gap. (Hindustan Times)