The market pressure continued this week with the S&P 500 falling -2% (worst week since Oct) and Nasdaq falling -1.2%. Geopolitical concerns were the main focus. Private credit concerns were also in the headlines this week along with mixed Jan retail sales, while ISM services rose to the highest level since Aug-22.

Fundamentally, see below for what we focused on in this edition.

- Earning Scorecard – Week 7

- Paramount Mgmt Provides More Color On Its Proforma Vision

- DraftKings’ Upcoming Secret Weapon…The Super App

- UMG Shares Are Not Crossing Over The Pond

- OpenAI and Anthropic Face Off Across the AI Landscape

- The “Streaming Wars” Settled Into More Of A Steady State in 2025

- Apple Moves Further Down The Price Curve, Targeting More Cost-Conscious Customers

- Versant Pleases The Street With A Big Buyback

- Grab Bag: Elliott Invests $1bn In Pinterest / OpenAI Reportedly In Talks With TTD About Ads / The Sphere Could Be Coming To Nashville

Finally, I wanted to flag that LionTree Advisors served as financial advisor to Axel Springer on its agreement to acquire Telegraph Media Group for £575m.

Have a restful weekend.

Best,

Leslie

Earning Scorecard – Week 7

We have officially reached the end of this (very long!) Q4 earnings season! In the seventh and final week, 14 stocks in our LionTree Universe reported, and stock reactions skewed negative, with 9 stocks trading down and 5 trading up.

While it was certainly a mixed bag of prints across sectors, we focused on Universal Music Group, which saw its stock fall -8.1% in reaction to its report (see Theme #4), while Versant which traded up +3.9% in reaction (see Theme #8).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Paramount Mgmt Provides More Color On Its Proforma Vision

After officially announcing an agreement to acquire WarnerBrosDiscovery on Friday (see Theme #4 from last week), Paramount’s mgmt team hosted an investor meeting first thing Monday morning to discuss the deal and take questions from the analyst community. There were several reiterations of what they have said before, though mgmt did provide more details about synergy plans and mid-term financial guidance, in particular. They remain confident in the regulatory path to a Q3:26 close.

See below for our key takeaways, as well as some additional commentary on what Netflix co-CEO Ted Sarandos had to say about dropping out of the race to buy WBD.

- Mgmt is very confident in receiving regulatory approval…they made “progress” with regulators globally before signing the merger agreement

- There is no statutory impediments to close in the US: The waiting period under the Hart Scott Antitrust Improvements Act has expired

- Mgmt initiated pre-notification discussions w/ the EC already

- Germany and Slovenia have already given their approval to proceed

- “Absolutely confident” they can meet the timing outlined for a Q3 close

- View the combined Co as a formidable competitor in streaming (200mn+ combined subs)…by mid-2026, will have transitioned all of Paramount’s streaming svs to one stack

- Will follow same process with transitioning WBD’s DTC services, and combine P+ and HBO

- HBO is the “crown jewel” but the Co will still license content to other platforms and produce 3P content in their TV studios

- Again, committed to investing in content at both studios

- They are targeting 15 films from Paramount + 15 films from Warner

- AI will be a “transformative tool” for artists

- Reiterated min 45-day theatrical window globally…and will continue to adhere to specific windowing regimes around the globe

- “Deeply believe” in theatrical…large franchises are launched in theaters

- Provided more detail on the targeted $6bn+ synergies (w/in 3 yrs post close)…the majority of synergies will come from non-labor and the Co will NOT reduce production capabilities…synergies come from:

- Consolidating streaming technology stacks and cloud providers

- Realizing global efficiencies in procurement and business services

- Optimizing and combining the real-estate footprint and the broader corporate overhead

- Driving efficiencies in marketing

- Optimizing spending on agencies and tooling

- Migrating the combined Co to a single ERP

- Combining other IT systems across the Co

- Provided medium-term financial targets

- Mid SD% total rev CAGR from 2026-2030E

- Mid 20% adj EBITDA margin (2030E)

- ~50% FCF conversion (2030E)

- The Co is NOT looking to spin or divest the legacy assets at this time (there also are no other assets they view as non-core)

- Believes the combination will keep these businesses healthier for longer vs standalone

- The Co will transition some strong linear brands to DTC, which will also prolong the life of these businesses

- Scale in sports is a key element of the strategy and the Co has flexibility to use UFC rights across both platforms

- Can put some fights on both b-cast networks and can have some of those events on TNT

- “We did future proof the deal”

What Did Netflix Co-CEO Ted Sarandos Have To Say About Dropping Out Of The Bidding Process To Buy WBD?? (link)

- NFLX leadership was aligned on the deal, but it was” a nice to have” and not “a need to have”

- There was a tight window that they were willing to pay

- NFLX dropping out was not because they were uncertain about the regulatory path

- Does he think the Paramount deal should be approved? “It should be highly scrutinized the way I’m glad that ours was highly scrutinized… Remember, we were asked to go and testify. David and I both were. I came”

- Was it NFLX’s plan all along to load Paramount with debt, push it to overpay, and walk away richer? “There are easier ways to make $2.8 billion”: They were “deep” in the process w/ 50 regulatory bodies around the world; Both Sarandos and co-CEO Greg Peters met w/ the top 200 employees of Warner Bros.; “We definitely wanted this asset. We didn’t need it”

- How will they use the $2.8bn? “Just keep investing in the business”

- What is the Impact of the deal on Hollywood and the entertainment biz? There will be lots of job cuts: “This deal is dependent on a lot of cost-cutting. We were in the books of Warner Bros., and the biggest cost centers are people in productions. There’ll be cuts in excess of $16bn. They are telling people who lend them the money that’s gonna happen in 18 months or so”

- What is the Impact of the deal on NFLX? “I’m confident in our future that we’re not impacted by all that. In fact, maybe it’s to our advantage. But I hope I’m wrong for the sake of the industry”

- NFLX is not worried about Paramount and/or WBD selling less to them as a result of deal negotiations: “If they are six or seven times levered, they need to make some money, and we’re buyers. So I can’t imagine that’s going to be a problem”

- Expanding into theatrical distribution is now no longer part of NFLX’s strategy but “I could see us doing things that we haven’t done before”: “Everything I talked about would require us buying that theatrical distribution entity. But one thing that’s been great about it is getting to know and have open dialogue with the theater owners. I really didn’t have much reason to before… I think we’re gonna find a bunch of cool things to do together going forward”

- Does he think the last few months hurt NFLX’s reputation? “It should reinforce our reputation of being disciplined shepherds of our shareholders’ capital”

-> Separately, but related, NFLX announced this week that it has acquired InterPositive, the filmmaking technology Co founded by Ben Affleck that develops AI-powered tools “built by and for filmmakers”; Affleck will join Netflix as a senior adviser, alongside all of InterPositive’s staff (link)

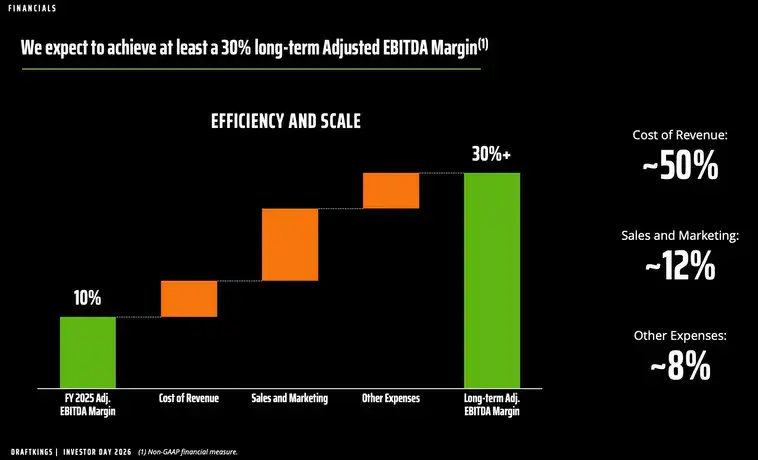

DraftKings’ Upcoming Secret Weapon…The Super App

Big news from DraftKing’s investor day this week was the introduction of a unified Sports & Casino Super App, which will include BOTH the sportsbook and predictions offerings. Casino and Lottery will also be available, where allowed. This new app will enable the Co to create a unified and personalized experience for users and also enable to Co to leverage its national marketing across all states (vs just sports betting states). Phase one integration is expected by March Madness. The Predictions market, as one would expect, was a focus area during the event and mgmt thinks this product will be more profitable than its sportsbook business and will have a $10bn annual gross revenue opportunity in the “coming years.” Mgmt is confident that they can win in the Predictions market and is targeting an “industry-leading sports predictions experience” by the start of the NFL season.

See below on more of what we viewed as most incremental, including long term financial guidance and some interesting stats on efficiencies from AI, among other things. Also, see link to their slide presentation slides if interested HERE.

-> DKNG shares were relatively flat on the day but are still down -48% since their 52-week high back in August 2025

- In terms of financial guidance, the Co expects to achieve adj EBITDA margins of 30% with AI “presenting additional upside”

- Mgmt still believes that its TAM will reach $55-80bn by 2030

- The big announcement was the new Super App called “DraftKings Sports & Casino” …it will include BOTH the Sportsbook and Predictions products

- Casino and Lottery will also be available, where allowed

- Personalization: Experiences will be personalized depending on what state a user is in

- Marketing advantage: The Co will be able to leverage its national marketing across all states (i.e., not just sports betting states)

- Mgmt views this as a “real structural advantage” in CAC efficiency and in speed to scale

- Timing: Phase 1 of the integration is expected by March Madness, w/ addt’l upgrades planned throughout the year

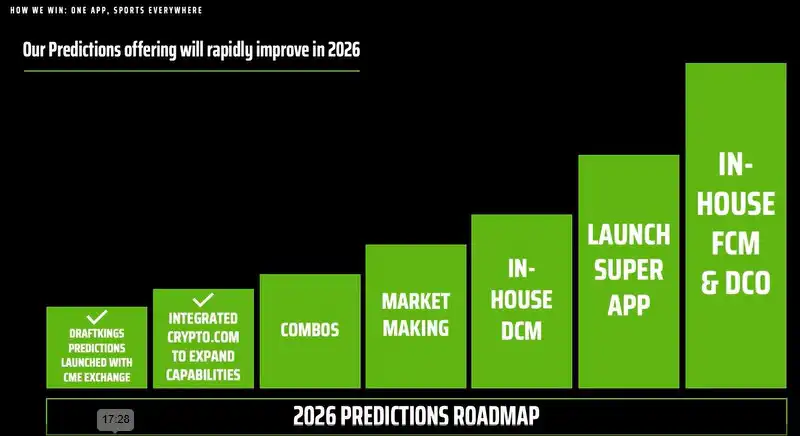

- Predictions was a big focus at the event…mgmt thinks Predictions can become a $10bn annual gross revenue opportunity in the “coming years”

- Predictions will also be more profitable than the Sportsbook: Predictions adj gross margins are anticipated to be 10-30% higher (to 60-80%) b/c it is not subject to state gaming taxes and mgmt expects promotions will be more limited

- DKNG’s Predictions offering will rapidly improve in 2026

- How will they win in Predictions?…The Co will follow the Sportsbook playbook

- They will be vertically integrated & own more of the Predictions stack: Mgmt wants to control the end-to-end customer experiences

- The Co is launching a dedicated market making division in the next few months to bring their own liquidity to the market

- This will deliver tighter pricing and more consistent customer experiences

- Mgmt is confident that they “know” sports customers & understand what drives engagement in the live moment

- Predictions will feel like DraftKings and they can personalize the experience for users

- The Co already has a scaled national marketing footprint and brand

- Timing – their goal is to deliver an “industry-leading sports predictions experience” and “scale it profitably” by the start of the NFL season

- “AI is not a side-initiative, it is a company-wide force multiplier”

- How is AI being applied?

- Prompt-based Sportsbook merchandising and content mgmt

- Automated AI-assisted QA on Sportsbook content cards, trading analytics, accelerating trader reviews, automated and AI-assisted fraud reviews and risk

- Engineering Copilots and automated code review

- AI-powered market health monitoring across hundreds of markets

- What are tangible results?

- Engineering productivity improved +40% y/y

- 100% of code reviews are AI-assisted

- Seeing 25% containment on chatbot customer service interactions

- How is AI being applied?

- A few other key stats/updates:

- DraftKings is top ranked for customer satisfaction

- Its customer service ticket rate fell by -54% since 2023

- They track real time feedback with technology and try to address quickly

- Personalization is a key input as well…customers feel like they have a relationship with DraftKings vs just executing a transaction

- Loyalty & recognition program is a “huge differentiator”

- DraftKings has made strong progress with risk mgmt

- Chargeback rates fell from 0.37% -> 0.15% from 2022 -> 2025, which is well under industry avg

- At the same time, deposit success rate also incr’d from 83% -> 88% from 2022 -> 2025

- In 2025, DKNG had 12% more downloads vs the nearest competitors and did so at a “significantly more efficient” cost per download

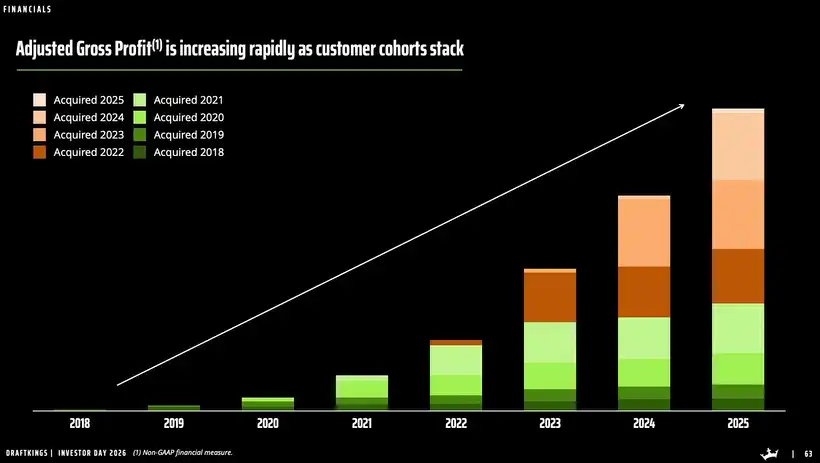

- Customer relationships strengthen over time rather than fade: “Even through short-term periods of customer-friendly outcomes, we have grown adjusted annual gross profit across every cohort, and you can see that even our cohorts that are five, six, and seven years old are continuing to grow”

- DraftKings is top ranked for customer satisfaction

UMG Shares Are Not Crossing Over The Pond

Universal Music Group’s (UMG) Q4 was not enough to reverse the negative trajectory the stock has been on since around the middle of last year. While the Co did deliver better-than-expected Q4 revenue thanks to upside on the ad-supported Streaming side, the segment was helped by contractual benefits. Excluding those, underlying growth would have been mid SDs vs the +9% y/y FXN reported. Mgmt anticipates that the going forward growth rate for Streaming will remain at that same underlying rate. On the Subscription side, while revenue was inline, it did accelerate to +9.6% y/y when excluding the DSP catch up income in Q4:24, BUT mgmt is still sticking with its +8-10% CAGR from 2023-2028 even though 2026 Subscription revenue will benefit from higher wholesale rates in their agreements, which will kick-in throughout the year.

In addition to those puts and takes on the top-line, adj EBITDA margin contracted -0.7pp y/y to 22.5% as stronger growth skewed toward lower-margin physical, repertoire mix was less favorable, and incremental overhead from acquisitions weighed. Also to note, Music Publishing revenue missed by -8% due to the timing of collections that flattered last year’s Q4, while Merchandising declined as weaker retail sales outweighed growth in touring and DTC.

On the topic of AI, mgmt directly pushed back on the music narrative risk, citing external AI music consumption data (which shows immaterial levels) and results of its own research studies, but this topic continues to be one in which investors are trying to figure out.

Looking ahead, mgmt believes it is on track to its 2023-2028 financial guidance it previously outlined which does not include “transformational” M&A like Downtown Music. Last but not least, the Board is pausing a US listing given market uncertainty, and valuation dislocation was a disappointment for investors.

Overall, Q4 was a mixed bag. See more details on our takeaways regarding UMG’s results and call.

-> UMG shares fell -8% in reaction to the print, and have been on a steady decline from the end of July last year, falling -36% since then ($28.11 to $17.80)

UMG Delivers A Stronger-Than-Expected Q4 & The Co Is Tracking To the Mid-Term Outlook Previously Provided

- Revenue BEAT by +5.1%: Incr’d +5% y/y or +11% FXN (vs +5% or +10% in FXN in Q3)

- Upside came from the Recorded Music segment (beat by +8.6%)

- Excl items impacting comparability detailed below, revenue grew +11.2% FXN

- Adj EBITDA BEAT by +2.8%: Incr’d +1% y/y or +6% FXN (vs +7% y/y or +12% FXN in Q3); The benefit of cost savings and operating leverage more than offset margin headwinds from repertoire mix, outsized growth in lower margin physical sales, and incremental overheads from business combinations

- Adj EBITDA margin decr’d -0.7pp y/y to 22.5%

- Excl items impacting comparability, adj EBITDA grew +8.6% y/y FXN and adj EBITDA margin decreased 0.4pp to 22.0%

- Reminder about the items that impacted the comparability of results…The DSP income catch up in Q4:24, legal settlements in 2024, and a legal resolution in Q4:25

- No surprises with the forward outlook

- Mgmt indicated that the Co is “on track” to the outlook provided at the Capital Markets Day, 2023- 2028 (FXN)

- Revenue CAGR of +7%

- Subscription Rev CAGR of +8-10%

- Adj EBITDA CAGR of +10%

- FCF conversion ratio (before investing activity) of 60-70%

- 2026

- FX is expected to be a 4-5% headwind to revs in 2026 vs 3% in 2025

- The Co also anticipates realizing an incremental E40-50mn in Phase 2 cost savings in 2026 (as part of the E250mn program

- SBC should be similar to 2025 levels (E227mn)

- Capx is expected to be €100-200mn higher y/y in 2026 mostly due to a real estate project

- The guidance also does not include “transformational” M&A, which Downtown is

- Mgmt indicated that the Co is “on track” to the outlook provided at the Capital Markets Day, 2023- 2028 (FXN)

- No US listing right now: A big forward-looking update was that the Board decided NOT to move ahead with the US listing given the market uncertainty and dislocation in valuations

- Mgmt stressed the view that there is “significant runway” in the core streaming and subscription businesses for both higher subs volume AND higher ARPU

- “We do not expect those things to, in aggregate, flatline 3 years from now”

Stronger Streaming Revenue Growth Was The Positive Surprise In Recorded Music But Helped By A Contractual Benefit

- Overall recorded Music revenue growth rose +8% y/y or +14% FXN vs +4% y/y or +8% FXN in Q3

- FXN Ad-supported streaming revenue grew +9% y/y (vs flat y/y in Q3) BUT excluding contractual benefits in Q4, underlying growth was mid SD: Reported revs grew +3% y/y, up from a decline of -5% y/y

- Outlook – Expect growth going forward to be more in the line with the low-mid SD underlying pace posted in the prior 3 qtrs

- There is still the secular shift in ad spend from analog to digital

- Excl the DSP catch-up, Subscription revs growth was up +9.6% y/y which was an acceleration from the +8.7% FXN rev growth in Q3: Reported rev growth was +2.4% y/y, or +7.7% y/y FXN vs +3.6% y/y in Q3; 6 out of 10 mkts, including the US, saw high-SD or DD subscription revenue growth

- The growth acceleration was primarily driven by retail price increases in some smaller markets, which more than offset minor 2024 price increase benefits

- Outlook: Improved wholesale rates in their agreements will kick-in in throughout the year; Still targeting the 8-10% CAGR from 2023-2028

Music Publishing Impacted By Timing Of Collections This Yr Vs Last & Merchandising Also Fell Short Of Expectations

- Music publishing MISSED by -8% and fell -3% y/y or +1% FXN (vs growth of +9% y/y or +13% y/y FXN in Q3)

- The slower growth in the quarter was due to the timing of collections from certain societies and other sources, which helped results in the fourth quarter of 2024

- Underlying growth in the business remains “healthy”, while the growth rates vary

- Merchandising & Other MISSED by -1.9% and fell -6% y/y or 0% y/y FXN (vs growth of +9% y/y or +16% y/y FXN in Q3)

- Growth in touring and DTC revenue offset lower retail sales

- “We are continuing to take steps to improve the profitability of our merchandising business, including investing in our D2C business and working to reconfigure our manufacturing supply chain”

Very Bullish On Downtown Music Acquisition…See It As “Transformational”

- The deal creates a “scalable and profitable engine of growth” and also elevates UMG’s core label, publishing, and superfan business…it also expands UMG’s global footprint

- They will be able to better cover the entire music industry

- In 2025, Downtown’s unaudited results show revenue of €891mn and EBITDA of €40mn

- UMG paid 17x 2025 EBITDA on a pre-synergy basis and on a post synergy basis, they paid closer to 13x

- Mgmt compared this transaction to EMI in 2011 when others didn’t see the value that UMG did and now that deal is “universally acknowledged as one of the most successful and strategically important in the history of the music industry”

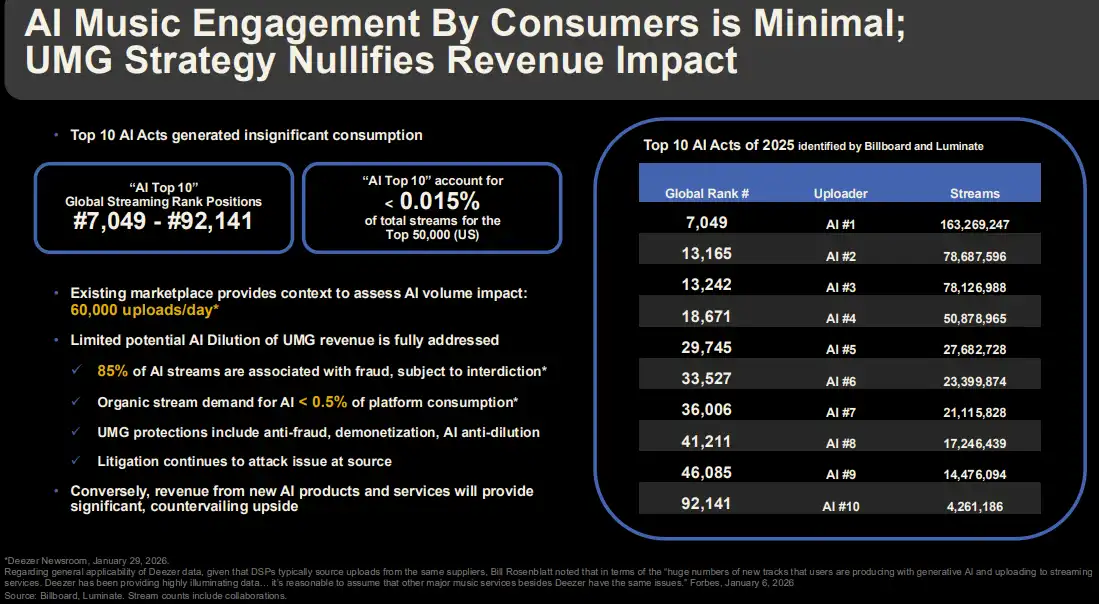

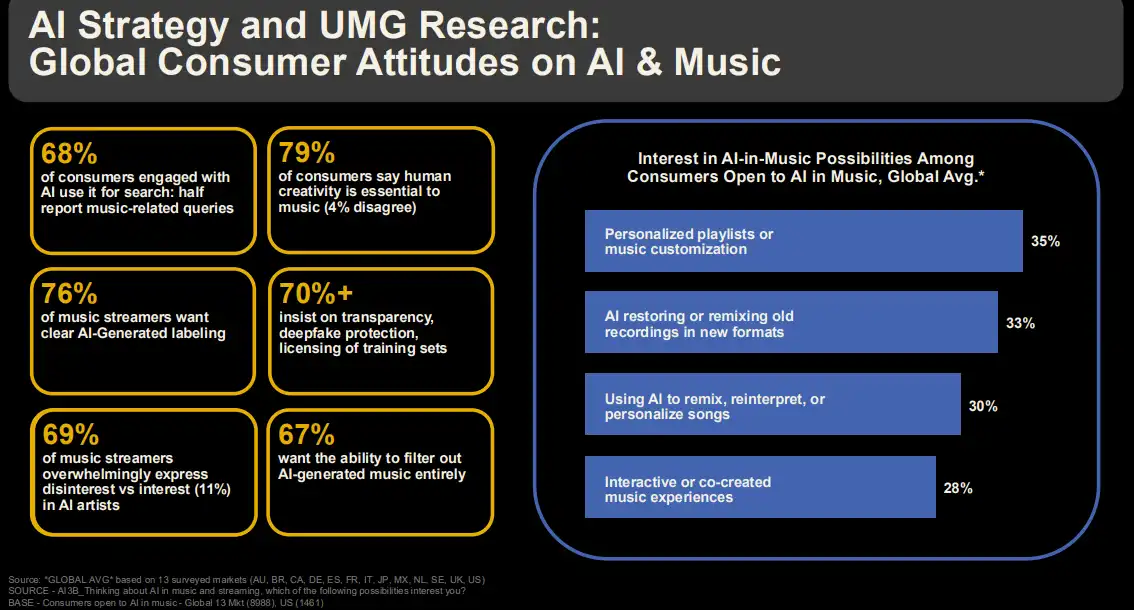

AI Represents An “Overwhelmingly Net Positive” Commercial Opportunity

- AI-generated content has NOT overtaken the charts as has been the perception from anecdotal press reports

- “Nothing could be further from the truth”

- Anecdotes have been completely over-extrapolated”

- Consumption of the Top 10 chart-debuting AI acts per Billboard and Luminate is “immaterial”: The most streamed did not break into the top 7,000 globally in 2025…see image below

- 60k AI tracks are being uploaded per day right now and most is AI slop or fraud

- Aggregate organic consumption of AI content by actual consumers is <0.5% based on their data

- Pure AI generated content (like other non-user content) is removed from the calc of share of streams by the DSP when determining artist royalties: Royalty dilution is not a material issue

- UMG is also conducted a global research survey on consumers’ attitude on AI & Music (see image below)

- Very excited about licensing agreement with KLAY Vision, which is a large music model trained only on licensed music

- Mgmt is confident AI will introduce new formats with more personalization and social expression, and will be a significant component of the super-premium tier of 2026 and beyond

A Few Other Points That We Thought Were Important

- Mgmt remains committed to its 4 key priorities

- Expanding presence in label and artist services

- Accelerating efforts in high potential markets

- Strengthening DTC and superfan initiatives

- Adding to UMG’s growing portfolio of responsible AI partnerships

- The Co will scale its DTC biz by stimulating 3P superfan platforms and creating an eco-system for special events, experiences, and products both virtually and in-person

- The Co still thinks 20% of its subs base is the target for the Super Tier

- In 2025, the Co proactively extended and expanded deals with some of their biggest recording artists and songwriters, and expect to do the same in 2026

- Investors should note that advances in one year don’t typically relate to revenue in that particular year, and recoupment is not necessarily associated with advances made in the same year

- It’s difficult to draw any meaningful conclusion from looking at net advances in a given year or from advances as a % of sales

- On a longer view…btw 2019 and 2025, gross advances grew at an +8% CAGR while UMG’s revenue grew by +10% and adj EBITDA improved +14%

OpenAI and Anthropic Face Off Across the AI Landscape

This week brought further developments in the ongoing back and forth between OpenAI, Anthropic, and the US government, underscoring the complexity that comes with the rapid development of AI use cases and the safeguards, enforcement, and oversight that are still evolving (and severely lagging) alongside them. Last Friday, OpenAI announced an agreement with the Pentagon, just hours after the Defense Secretary said he would seek to designate Anthropic as a “supply chain risk” following Anthropic’s push for explicit assurances that its models would not be used for mass surveillance of Americans or autonomous weapons deployment. OpenAI moved forward with an agreement that used broader contract language around “lawful use,” which later drew backlash and prompted the company to update the language in the deal. The Defense Department subsequently on Thursday formally issued the supply chain risk designation for Anthropic, and Anthropic said it plans to challenge the decision in court while continuing discussions with the department. The Defense Department subsequently on Thursday formally issued the supply chain risk designation for Anthropic, and Anthropic said it plans to challenge the decision in court while continuing discussions with the department.

At the same time, both companies continue to roll out new products and updates across their respective bizs. OpenAI introduced several new models and tools this week, including GPT-5.3 Instant, GPT-5.4, ChatGPT for Excel, and a new cybersecurity agent called Codex Security. Anthropic announced the launch of a Claude Marketplace for enterprise customers and is reportedly nearing a ~$20bn revenue run rate.

See below for more of our drilldown.

A High-Level Update On The OpenAI, Anthropic, And US Govt Back-And-Forth

- Last Friday (February 27th), OpenAI reached a deal with the Pentagon to use its AI models, just hours after Defense Secretary Pete Hegseth announced on X that he would seek to label Anthropic a “supply chain risk” (link/link)

- On X this weekend, OpenAI CEO Sam Altman said that its agreement with the Pentagon contains the same two limitations that Anthropic asked for…but what differed was how those limits would be enforced (link/link)

- Anthropic tried to write those limits explicitly into the contract, which the govt rejected

- OpenAI used broader contract language (“any lawful purpose”) while saying the same limits are embedded through other parts of the agreement

- That said, OpenAI claimed that its agreement w/ the Pentagon had “more guardrails than any previous agreement for classified AI deployments, including Anthropic’s”

- Still, OpenAI faced intense backlash for the agreement

- According to Sensor Tower date, the daily average uninstall rate for OpenAI’s ChatGPT was up by 200% compared to normal rates after the partnership announcement

- Meanwhile, Anthropic’s Claude rose to the top of Apple’s App Store ranking

- On March 2nd, OpenAI annc’d that it updated its deal w/ the Dept of War

- OpenAI said it is worked w/ the DoW to add new language to the contract that “makes explicit that our tools will not be used to conduct domestic surveillance of U.S. persons…[and] affirmed that our services will not be used by Department of War intelligence agencies like the NSA. Any services to those agencies would require a new agreement”

- This is the first time the US has ever designated an American Co a supply chain risk, a label which is typically reserved for US adversaries

- On March 4th, the Pentagon formally notified Anthropic that it has determined the Co and its products are considered a “a supply chain risk, effective immediately” (link/link)

- “The military will not allow a vendor to insert itself into the chain of command by restricting the lawful use of a critical capability and put our warfighters at risk”

- This is the first time the US has ever designated an American Co a supply chain risk, a label which is typically reserved for US adversaries

- On March 5th, Anthropic released a statement entitled “Where things stand with the Department of War” (link)

- “Vast majority” of customers will not be impacted by the supply chain risk designation: Only applies to Claude used directly under Department of War contracts, not to all Claude use by customers who happen to have such contracts

- On the legality of the designation – “We do not believe this action is legally sound, and we see no choice but to challenge it in court”

- BUT noted that they have been having “productive conversations” with the Department of War “over the last several days” about “ways we could serve the Department that adhere to our two narrow exceptions, and ways for us to ensure a smooth transition if that is not possible”

- Reiterated that that it is NOT the role of Anthropic to be involved in operational decision-making – “that is the role of the military”

- “Our only concerns have been our exceptions on fully autonomous weapons and mass domestic surveillance, which relate to high-level usage areas, and not operational decision-making”

- “Anthropic will provide our models to the Department of War and national security community, at nominal cost and with continuing support from our engineers, for as long as is necessary to make that transition, and for as long as we are permitted to do so”

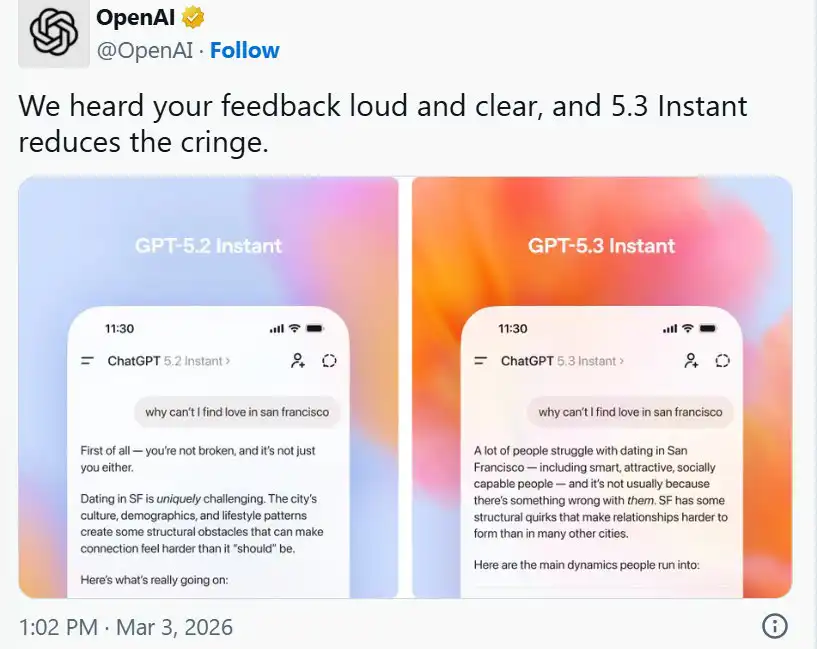

OpenAI Introduced Key New Models And Products This Week

- OpenAI introduces GPT 5.3 Instant which “reduces the cringe” for “smoother, more useful everyday conversations” (link/link)

- The update is focused on “tone, relevance, and conversational flow”

- Comes in response to feedback that GPT‑5.2 Instant would respond in ways that feel overly cautious or preachy, particularly around sensitive topics (i.e., using phrases like “Stop. Take a breath”)

- GPT‑5.3 Instant significantly reduces unnecessary refusals, while toning down overly defensive or moralizing preambles before answering the question

- When a useful answer is appropriate, the model should now provide one directly, staying focused on the question without unnecessary caveats

- Also more effectively balances what it finds online with its own knowledge and reasoning

- For example, using its existing understanding to contextualize recent news rather than simply summarizing search results

- Less likely to overindex on web results, which previously could lead to long lists of links or loosely connected information, and does a stronger job of recognizing the subtext of questions

- Availability: Now available to all users and developers; Updates to Thinking and Pro will follow soon

- GPT5.2 Instant will remain available for three months for paid users in the model picker under the Legacy Models section, after which it will be retired on June 3, 2026

- The update is focused on “tone, relevance, and conversational flow”

Source: OpenAI’s X Account

- Three days later, OpenAI released GPT 5.4, which is “designed for professional work” (link)

- Brings together the best of our recent advances in reasoning, coding, and agentic workflows into a single frontier model”

- Can now provide an upfront plan of its thinking, so the user can adjust course mid-response while it’s working and arrive at a final output that’s more closely aligned with what you need without additional turns

- Also improves deep web research, particularly for highly specific queries, while better maintaining context for questions that require longer thinking

- Continue to drive down hallucinations: GPT5.4’s individual claims are 33% less likely to be false and its full responses are 18% less likely to contain any errors, relative to GPT5.2

- Availability: Have begun rolling out “gradually” across ChatGPT and Codex; In ChatGPT, GPT5.4 Thinking is already available to ChatGPT Plus, Team, and Pro users, replacing GPT5.2 Thinking

- OpenAI concurrently also introduced ChatGPT for Excel in beta, an Excel add-in powered by GPT 5.4 that brings ChatGPT directly into workbooks (link)

- Can be used for real-world finance workflows, including financial modeling, scenario analysis, data extraction, and long-form research

- More specifically, it can…

- Build and update spreadsheet models faster: Teams can describe what they need in plain language, and ChatGPT will create or update live Excel models directly in the workbook

- Get insights from large spreadsheets without manual reconciliation: ChatGPT can reason across workbooks, understand how sheets and formulas connect across the model, explain why outputs changed, trace and fix errors, and show how assumptions flow through a model

- Follow the logic: ChatGPT explains what it’s doing as it works and links answers to the exact cells it references and update; Before making changes to a workbook, ChatGPT asks for permission, so users can review each step and undo edits if needed

- Adding financial data integrations directly in ChatGPT for FactSet, Dow Jones Factiva, LSEG, Daloopa, S&P Global, and more

- Simplifies research and analysis by bringing market, company, and internal data into a single workflow in ChatGPT

- Quickly conducts due diligence to pull from filings, transcripts, decks, and spreadsheets to produce structured, cited outputs that export to PDF or Microsoft Word

- Availability: Rolling out now in beta for ChatGPT Business, Enterprise, Edu, Teachers, Pro, and Plus users in the U.S., Canada, and Australia; ChatGPT for Google Sheets is coming soon

- Finally, on Friday, OpenAI released Codex Security in research preview, an AI agent security tool (link/link)

- How does it work? The agent identifies cybersecurity flaws and proposes solutions before fixing the bugs

- It’s meant to help security teams find and patch vulnerabilities in large databases

- Designed to “operate at scale” and provide “easy-to-accept patches,” and thus enable developers to focus on higher-level tasks

- Codex Security learns from feedback over time to improve the quality of its findings

- How does it work? The agent identifies cybersecurity flaws and proposes solutions before fixing the bugs

Anthropic Is Launching A Marketplace + Nearing A ~$20bn Run-Rate

- Anthropic launches Claude Marketplace, a platform for corporate customers to purchase 3P software (link/link)

- Enables customers to purchase software applications that use Anthropic’s models, w/ options including svs from Snowflake, Harvey and Replit

- Anthropic will NOT take a cut of these purchases and will allow its customers to use some of their committed annual spending on Anthropic’s own svs toward third-party tools (similar to the models AMZN and MSFT use for their software marketplaces)

- Available now in limited preview

- Anthropic is reportedly nearing a $20bn revenue run rate, more than doubling its run rate from 2025 (link)

- The Co reportedly recently surpassed $19bn in run rate rev, up from $9bn at the end of 2025 and ~$14bn just a few weeks ago

- What’s reportedly driving the run rate growth? Strong adoption of its AI models and products, including its coding tool, Claude Code

- As a reminder, Anthropic is now valued at $380bn (for comparison, last week, OpenAI closed a $110bn fundraise at a $840bn post-money valn)

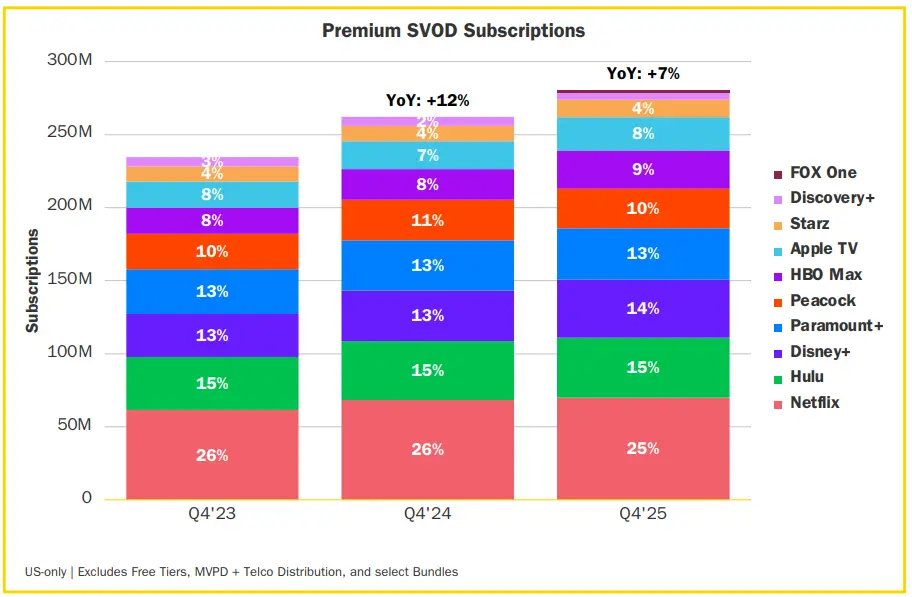

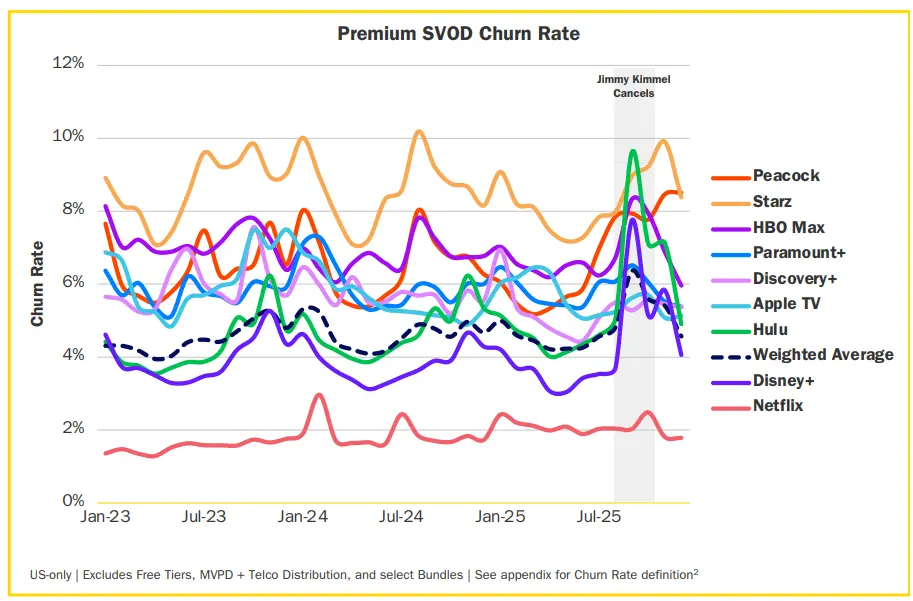

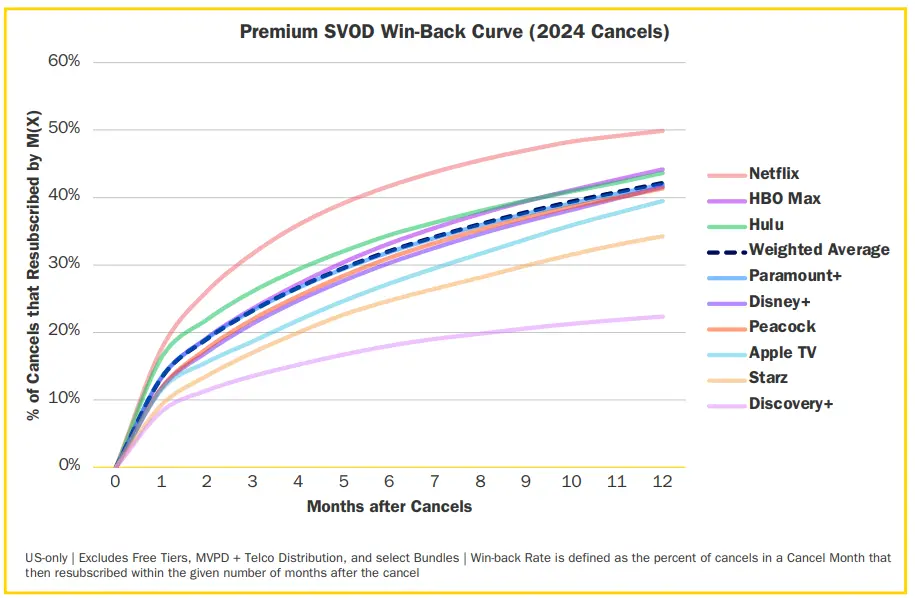

The “Streaming Wars” Settled Into More Of A Steady State in 2025

It was not too long ago that the Streaming Wars were all the talk across the sector. That has slowed as the landscape has matured, which was proven quantitatively in Antenna’s latest State of Subscriptions: Premium SVOD – 2025 Year in Review report, which found that new subscriber y/y growth has slowed to single-digit growth for the first time ever, falling from +12% y/y in 2024 to +7% y/y in 2025. Along with that, churn stabilized, and in fact, 2 out of every 5 canceled subscribers return to the same svs within 12 months, with Netflix having the highest win-back rate, followed by HBO Max and Hulu.

There were a couple of other interesting stats around bundling, subscriber acquisition, and more, which we highlighted below. If you would like to review the full report, you can do so HERE.

Premium SVOD Subscriber Growth Is Slowing

- Growth fell from double to single digits for the first time: Subscribers grew +7% y/y, down from +12% y/y in 2024

- There were 27mn new Subscriptions y/y at the end of Q4:24, but only 18mn new additions y/y at the end of Q4:25

Premium SVOD Churn Rates Have Stabilized Over A Period Of Heightened Volatility

- There was a -0.2pt y/y decline in churn from 2024 to 2025: The Weighted Average Churn Rate held steady at 4.6% in December 2025 vs 4.8% in December 2024

- Disney+ and Hulu saw spikes in churn after the Jimmy Kimmel controversy, but quickly normalized: The platforms experienced dramatic spikes in churn to 7.8% and 9.6%, respectively, in September 2025, but by December 2025, churn returned to 4.1% and 4.9%, respectively

- 7 of the 9 svs showed more stable churn patterns in 2025 versus 2023, with standard deviations in churn declining across Paramount+, Discovery+, Apple TV, and Netflix

Over 40% Of Canceled Subscribers Returned Within A Yr

- Over particular time periods…

- 23% of 2024 Cancels returned to the same svs within 3 months

- 32% within 6 months

- 42% within 12 months

- Netflix has the highest win-back rate, followed by HBO Max and Hulu

- Netflix reacquired 42% of its Cancels within 6 months and 50% within 12 months

- HBO Max and Hulu each recovered 44% of canceled Subscribers within 12 months

SVOD Subscriptions Are Increasingly Bundled And Drive Stronger Loyalty

- Bundles accounted for 27% of total Subscriptions in Q4:25, up +13ppts from 14% in Q4:23

- Bundle subscriptions grew +50% y/y to 71mn in Q4:25, while non-bundle Subscriptions declined -1% y/y to 194mn

- The average Survival Rate gap between bundles and standalone services grew by more than 2x from Month 1 to Month 12

- Disney+ bundles retain subscribers at higher rates than standalone services, with the Disney+, Hulu, and HBO Max bundle leading in retention

- The Disney+, Hulu, and HBO Max bundle led all plans with a 59% 12-Month Survival Rate, +4pts above Netflix standalone and an avg of +28pts above its component services

Events And Hit Shows Are Driving Subscriber Acquisition

- Promotions and sports events are the primary drivers of Premium SVOD daily sign-ups

- Black Friday promotions was the largest peak in 2025 for several services

- Paramount+ and Peacock both show consistent sign-up spikes at the start of the NFL season, driven by their respective NFL offerings

- Hit original series also continue to drive new subscriber sign-ups within their first 90 days

- Love Island USA and Landman drove the most new sign-ups, with +1.3mn and +915k new sign-ups on Paramount+, respectively, within the first 90 days after premiere

- Severance drove the most new sign-ups on Apple TV+ in its first week, posting the highest 3-7 days total

- # of sign-ups reached from 30-90 days more than doubled across all titles

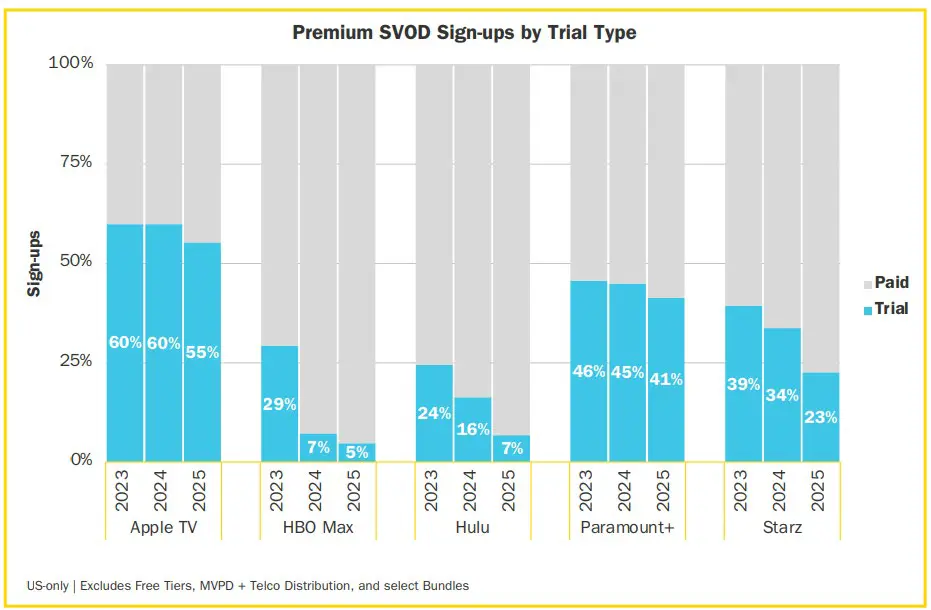

Svs Are Decreasing Reliance On Free Trials

- HBO Max and Hulu led this transition most aggressively, with free trial share of Sign-ups dropping to 5% and 7%, respectively, in 2025

- Apple TV continues to source the majority of its sign-ups from free trials, accounting for 55% of total Sign-ups in 2025, though this marks a -5pt decline since 2024

Apple Moves Further Down The Price Curve, Targeting More Cost-Conscious Customers

Apple dropped a bunch of new products this week with the headliner being the MacBook Neo. It’s the Co’s first sub-$600 laptop which is a notable departure from how Apple has historically positioned itself in the PC market. At $599 ($499 for education), the Neo targets a new demographic for Apple…i.e., more budget-conscious consumers and students who have historically defaulted to Chromebooks or Windows entry-level machines. This was an interesting move at a time when PC prices are expected to rise +17% in 2026 due to surging memory costs per Gartner (link). Elsewhere, the MacBook Air M5, iPad Air M4, iPhone 17e, and the displays were solid updates (faster chip, more storage, same price or slightly higher) but not paradigm-shifting. Though the M5 Pro/Max Fusion Architecture stood out as the most meaningful technical advance for pro users. Lastly, all these new products support Apple Intelligence and are available for pre-order starting March 4, with availability beginning March 11.

See more on what we viewed as most important below…

- The most significant announcement was the MacBook Neo…Apple moves into lower-end laptops: (link)

- Pricing: Starts at $599 ($499 for education)

- Key Features: Powered by A18 Pro, up to 50% faster for everyday tasks like web browsing and up to 3x faster for on-device AI workloads, vs “the bestselling PC with the latest Intel Core Ultra 5”

- 13-inch Liquid Retina display w/ 2408×1506 resolution, 500 nits of brightness, support for 1bn colors, and an anti-reflective coating

- Up to 16 hours of battery life

- Weighs 2.7 pounds

- 1080p FaceTime HD camera, dual mics, dual side-firing speakers w/ Spatial Audio, Magic Keyboard, and large Multi-Touch trackpad

- Available in blush, indigo, silver, and citrus

- BUT some compromises cited in the press (link/link/link): 8GB RAM w/ no upgrade option, the keyboard is not back-lit, no Force touch, no MagSafe, a smaller battery w/ no fast charging, one USB-3 and one USB-2 port

- MacBook Air with M5…4x faster AI performance w/ double the starting storage at the same price as the earlier generation: (link)

- Pricing: Starts at $1,099

- Key Features: M5 chip w/ a 10-core CPU and next-generation GPU w/ a Neural Accelerator in each core; up to 4x faster AI task performance than MacBook Air with M4, and up to 9.5x faster than MacBook Air w/ M1

- Ships standard w/ 512GB of storage (2x the previous gen) configurable up to 4TB, w/ faster SSD tech: Faster unified memory w/ 153GB/s of bandwidth, a 28% improvement over M4

- Apple’s N1 wireless chip delivers Wi-Fi 7 and Bluetooth 6

- Liquid Retina display, 12MP Center Stage camera, up to 18 hours of battery life, and two Thunderbolt 4 ports with support for up to two external displays

- Available in 13- and 15-inch sizes in sky blue, midnight, starlight, and silver

- MacBook Pro with M5 Pro & M5 Max on new Fusion Architecture…enables professionals to run advanced AI models locally on a laptop vs workstation (link)

- Pricing: Not specified

- Key Features: Built on Apple’s new Fusion Architecture, combining two dies into a single SoC; Up-to-18-core CPU w/ 6 super cores and 12 performance cores, delivering up to 30% faster performance for pro workloads

- Up to 4x faster AI performance than the previous generation and up to 8x faster than M1 models

- M5 Pro supports up to 64GB unified memory w/ up to 307GB/s bandwidth while M5 Max supports up to 128GB w/ up to 614GB/s bandwidth

- Up to 2x faster SSD read/write performance reaching speeds of up to 14.5GB/s: Starts at 1TB storage for M5 Pro and 2TB for M5 Max

- Other features include up to 24 hours of battery life, Thunderbolt 5, 12MP Center Stage camera, Wi-Fi 7 and Bluetooth 6 via Apple’s N1 chip, Liquid Retina XDR display with nano-texture option

- Studio Display’s Thunderbolt 5 upgrade is the most important change: (link)

- Pricing: Starts at $1,599 w/ a tilt-adjustable stand

- Key Features: 27-inch 5K Retina display with over 14 mn pixels, 600 nits of brightness, and P3 wide color

- New 12MP Center Stage camera w/h Desk View support; Studio-quality three-microphone array; Six-speaker sound system w/ four force-cancelling woofers delivering 30% deeper bass than the previous generation

- Two Thunderbolt 5 ports enabling daisy-chaining of up to four Studio Display models; Two additional USB-C ports; Included Thunderbolt 5 Pro cable w/ up to 96W of charging power

- Available with standard or nano-texture glass; Tilt- and height-adjustable stand and VESA mount also available

- Studio Display XDR has a significantly lower price while having meaningfully better specs vs the $4,999 32-inch display: (link)

- Pricing: Starts at $3,299 w/ a tilt- and height-adjustable stand

- Key Features: 27-inch 5K Retina XDR display w/ an advanced mini-LED backlight, over 2k local dimming zones, 1k nits SDR brightness, and 2k nits peak HDR brightness; Wider color gamut for enhanced contrast and accuracy

- 120Hz refresh rate w/ Adaptive Sync, dynamically adjusting frame rates for video playback or graphically intense content

- Same 12MP Center Stage camera w/ Desk View, three-microphone array, and six-speaker sound system as Studio Display, plus Thunderbolt 5 connectivity

- Available with standard or nano-texture glass

- iPhone 17e has double the base storage from the previous generation at the same price: (link)

- Pricing: Starts at $599 w/ 256GB of storage

- Key Features: A19 chip built on 3-nanometer technology; 6-core CPU, 4-core GPU w/ Neural Accelerators, and a 16-core Neural Engine optimized for large generative models

- C1X cellular modem (Apple’s latest generation) up to 2x faster than C1 in iPhone 16e, using 30% less energy than the modem in iPhone 16 Pro

- 1-inch Super Retina XDR display with Ceramic Shield 2 offering 3x better scratch resistance and improved anti-reflection: IP68 rated

- 48MP Fusion camera with optical-quality 2x Telephoto and 4K Dolby Vision video; MagSafe and Qi2 wireless charging up to 15W; Satellite connectivity for Emergency SOS, Roadside Assistance, Messages, and Find My

- Available in black, white, and soft pink

- iPad Air with M4 delivers 50% more memory & W-Fi 7 at the same price: (link)

- Pricing: Starts at $599 for the 11-inch model and $799 for the 13-inch model: Education pricing starts at $549 and $749 respectively

- Key Features: M4 chip with an 8-core CPU and 9-core GPU: Up to 30% faster than iPad Air with M3 and up to 2.3x faster than iPad Air with M1

- Unified memory increases 50% to 12GB: Memory bandwidth of 120GB/s: 16-core Neural Engine that is 3x faster than M1’s

- Apple’s N1 and C1X connectivity chips deliver Wi-Fi 7, Bluetooth 6, and Thread: Cellular models offer up to 50% faster cellular data and up to 30% less modem energy usage than the previous generation

- Compatible with Apple Pencil Pro and Magic Keyboard

Versant Pleases The Street With A Big Buyback

Versant’s inaugural earnings call took place this week, marking its first earning release as a standalone public Co since completing its spinoff from Comcast back in January. Q4 results exceeded expectations across both revenue (+3.2% beat) and standalone adj EBITDA (+12.0% beat), with margins of 32.4% well ahead of consensus 29.8%.

A key strategic focus for Versant is diversifying revenue beyond Pay-TV. Mgmt reiterated that at the end of 2025, non-Pay TV offerings represented ~19% of total revenue and it is targeted to increase to 33% over the next 3-5 years and 50% “over time.” On that front, the Co annc’d several digital-native products, including a new ad-supported Fandango streaming service, a CNBC DTC platform targeting retail investors, and an MS NOW DTC offering focused on community and exclusive content. Despite this emphasis on growth outside Pay-TV, Versant mgmt also highlighted strong visibility into its pay-TV revenue, with more than half of subscribers locked into agreements until 2028 or later.

Regarding the broader media landscape and potential M&A, Versant noted that the WBD sale process reinforced the value of its assets, particularly in news and sports (~60% of Versant’s audience). Mgmt emphasized its position as an independent operator with a “very high” threshold for M&A. Also on the deals front, but on the renewals side, Versant plans to be “in the middle” of the NFL discussions and believes there will be a rebalancing of the sports portfolio, creating an opportunity for them.

Not to be forgotten and arguably a key highlight for investors was that the Co announced a large $1bn buyback that equated to 21% of its market cap and put a quarterly dividend of $0.375/shr in place.

See below more on our takeaways from the call.

-> Versant stock was up +3.9% in reaction but is down -18% YTD

Versant Posted A Stronger Than Expected Q1

- Revenue BEAT by +3.2%: Was down -7% y/y

- Linear distribution BEAT by +0.6%, down -6% y/y

- Advertising BEAT by +11.8%, down -9% y/y

- Platforms slightly BEAT by +0.5%, down -1% y/y

- Content licensing & Other MISSED by -12.8%, down -4% y/y

- Adj EBITDA BEAT by +12%: Excluding transaction and separation-related cost was down -19% y/y (impacted by a production tax benefit in the prior year qtr)

The Existing 2026 Outlook Was Re-Iterated, But The Real Standout Was The Dividend And Repurchase Announcement

- Existing 2026 outlook

- Revs btw $6.15-6.4bn (cons $6.34bn)

- Adj EBITDA btw $1.85-2bn (cons $1.92bn)

- Expect some quarterly volatility due to sports rights timing esp in H2

- D&A will remain elevated in 2026

- Primarily due to intangibles related to the 2011 Comcast acq of NBCU

- This amortization will be substantially complete by year end

- Cash taxes ~26% ex the impact of intangibles

- Capx “modestly above” standalone 2025 levels (build out of Manhattan headquarters + targeted investments)

- Over the “medium term”, capital intensity should normalize following completion of these projects

- FCF btw $1-1.2bn

- Conversion will be modestly lowered in 2025 due to working capital timing, 1x cash tax benefits in 2025, and the incremental capx

- Expect quarterly variability esp in Q1

- Instituted its FIRST EVER dividend + approved a BIG buyback

- The Board declared the Co’s 1st div (37.5c / shr qtrly cash dividend)

- And approved a $1bn share repurchase authorization (which equates to a large ~21% of mkt cap)…they will be “opportunistic” and think through the total capital allocation program “holistically”

Mgmt Sees Lots Of Room For Organic Growth And Increased Penetration Across The Platforms Biz

- Expect Platforms segment to return to high SD% rev growth organically in 2026 due to a stronger box office slate and cont’d growth at GolfNow

- Reiterated that rev from non-Pay TV is expected to get to 50% “over time”

- Incr’d from 17% in 2024 to 19% in 2025

- Targeting 33% over the next 3-5 years

- GolfNow – represents <10% of the total rounds book and still “very early on” in the intl expansion trajectory

- Fandango – launching a new ad-supported Fandango streaming services “later this yr”

- “Already have a large install base…it’s now a matter of converting them”

In Addition To New Fandango AVOD Offering, Launching DTC Platforms For Both CNBC and MS NOW

- Launching brand new platforms associated w/ their brands…

- CNBC’s DTC will be targeted to the retail investor

- MS NOW’s DTC will be offering community insights perspective relevant to that brand

- …and will have a flexible distribution approach for these new platforms

- Build out will NOT be “massively capital intensive”

- “We’re open to different opportunities to distribute to other partners, whether that’s bundling or packaging or other distributors” and those conversations are already “ongoing”

Confident in Their Value as an Independent Co And Are Positioned to Acquire Rather Than Be Acquired

- Any updated thoughts given the outcome of WBD sale process? “We have plans to go on as an independent company”

- “We have a strong set of assets. We’re very focused on our vertical markets”

- The process actually “reinforced” Versant’s asset value: WBD assets that had a “tremendous” amount of value were often around news and sports, which represents ~60% of Versant’s audience

- What are the views on overall Co M&A? “We will consider obviously all opportunities that add value… the key point is our thresholds here are very high… and we’ll continue to be very disciplined in pursuing”

- What do they look for when evaluating oppties? The ability to drive value “right away” and deliver “premium” returns; Synergies are also considered “very carefully”

- Update on SportsEngine strategic review – evaluating “value maximizing” alternatives for that biz BUT “haven’t made a decision yet”

- “We see a lot of consolidation in youth sports market wide. We think it’s the right time for this review”

- Emphasized that “we like SportsEngine” …the review is really about pursuing oppties that “genuinely maximize value for the long-term”

Looking To Expand Advertising Beyond PayTV (And In The Future, Possibly Beyond NBCU)

- Moving some of their advertising outside of PayTV into DTC, free TV, and digital platforms

- Push into DTC allows them to be involved more in programmatic and tech-driven sales

- Have “a lot” of customer data and information from Fandango and GolfNow, which can be enhance targeting and programmatic capabilities

- On ad representation…

- NBCU will continue representing them for “at least” the next two yrs…: Has been a “strong and proven go-to-market strategy” for the last 15 yrs and has proven to be “very successful” for both parties

- …after which “we will decide on the right future strategy for our ad sales and theirs”

Some Additional Key Commentary On PayTV Rev Visibility, NFL Oppties And Affiliate Fee Renewals

- Have good visibility into pay-TV rev until 2028: More than half of Pay-TV subs are under agreements not up for renewal until 2028 or later

- On the upcoming NFL renewal – “we believe that there will be a rebalancing of the sports portfolios and that that will leave opportunity for us”

- Versant’s advantage is its “heritage in sports”, “strong sports properties”, “legacy” and “broad reach”

- Also believe there will be oppty for them to get involved in properties they may not have otherwise gotten involved with

- “We’re having ongoing conversations. We’ve built out our own production unit, and we are prepared for the sports landscape to be shifting…it will be disciplined, but we’ll be in the middle of that”

- Expect no change to affiliate fee renewal discussions

- Executed “a bunch” of deals last yr on terms that were mutually beneficially w/ distribution partners

- Have “a few” deals up later this yr and anticipate being able to have “very productive” and “similar” discussions

- Live portfolio of news and sports “plays into what people are still looking to watch on linear television. And that’s a big part of our asset play”

- Also highlighted that they have their own distribution negotiation team and will be handling all of those themselves going forward, independent of the previous Comcast/NBCUniversal arrangements

Grab Bag: Elliott Invests $1bn In Pinterest / OpenAI Reportedly In Talks With TTD About Ads / The Sphere Could Be Coming To Nashville

- Activist Elliott Mgmt takes a $1bn stake in Pinterest via a convert note (link/link)

- The Board also authorized a new $3.5bn share repurchase program: $2bn will be near-term share repurchases, split between a $1bn ASR and $1bn of open-market repurchases

- The $1bn from Elliott is funding the ASR

- Total expected repurchases in H1 2026 = ~$2bn

- The $1bn ASR funded by Elliott

- $500mn planned via 10b5-1

- $473mn already completed YTD under the previous authorization in Nov. 2024

- The terms of Elliott’s convertible senior notes:

- 1.75% annual interest rate

- Matures March 1, 2031

- Initial conversion price: ~$22.72 per share

- Represents a 30% premium to the March 2, 2026 closing price

- The $1bn ASR agreement is expected completion by Q2 2026

- The Board also authorized a new $3.5bn share repurchase program: $2bn will be near-term share repurchases, split between a $1bn ASR and $1bn of open-market repurchases

-> Pinterest shares were up +9.3% in reaction to the news but are still down -23% YTD

- OpenAI has reportedly held early partnership talks with The Trade Desk to help them sell ads going forward (link/link/link)

- Per the report, OpenAI will initially use external partners to sell ads and scale up its biz, having launched ads on ChatGPT last month

- The Trade Desk will apparently be one of those partners

- OpenAI has projected that ads could help double revenues from its consumer biz to $17bn (which currently has ~910mn users)

- With that in mind, OpenAI has already explored partnerships with Target and has also recently annc’d a tech partnership with Criteo

- Per the report, OpenAI will initially use external partners to sell ads and scale up its biz, having launched ads on ChatGPT last month

->The Trade Desk shares rose as high as +16.5% in after-hours trading, while AppLovin moved up +1.5% following the report

- Early talks are reportedly underway to build a Sphere Venue in Nashville, TN (link): Representatives of the Sphere music venue in Las Vegas and local businesspeople have reportedly discussed the possibility of bringing a smaller version of the venue to Nashville

- Conversations are said to be “very preliminary”

- As a reminder, Sphere Entertainment Co. has already announced plans for a second Sphere in Prince George’s County, Maryland, which would have a capacity of 6k (vs Las Vegas’s 20k capacity)

-> Sphere Entertainment Co’s stock was up +3.9% on the day of the report

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- CBP used RTB-sourced location data—collected via ad tech and SDKs—to track phones, confirming gov’t reliance on data brokers. The ad ecosystem shares precise location, advertising IDs, and device info w/ thousands of cos, enabling surveillance w/out warrants. (Electronic Frontier Foundation)

- Amazon Ads annc’d that buyers can use Amazon Audiences via its DSP to target Netflix inventory next qtr. The move, following Netflix’s Sept. programmatic shift, lets marketers pair shopping data w/streaming to boost performance. Amazon also spotlights new ad tech, incl. Campaign Manager and a creative agent, as it pushes a content‑to‑conversion narrative for upcoming upfronts. (AdExchanger)

- PQ Media’s Forecast 2026‑2030 details global ad & marketing shifts as cos move from traditional to digital, powered by AI and smart tech like VR/AR. It reviews 150+ sectors across major mkts, noting the post‑pandemic rebound, 2025 slowdown, and 2026 boosts from mega‑events. The report offers deep analysis and large datasets to guide smarter biz planning. (PQ Media)

- AMC Networks expanded its tool helping advertisers gauge outcomes from ads. AMC now uses partners like Fandango, iSpot & Cuebiq to link exposure to actions such as visits, purchases & location data. Tests showed viewers exposed to ads were more likely to check film info or buy tickets, while auto ads boosted SUV sales in key mkts. (Variety)

- Meta annc’d major changes to its attribution model, aligning click-through rules w/ Google by counting only direct link-clicks for conv. It also introduced “engaged-through attribution,” adding value from shares, saves, likes, comments, etc. Meta says social ads require broader metrics as user engagement shapes cos’ ad performance across its apps. (MediaPost)

- JCDecaux annc’d a 10‑yr deal for DEN, the world’s 10th‑busiest airport w/ ~82mn passengers. The Co will overhaul ad formats, adding cutting‑edge digital tech across the Great Hall and concourses to boost non‑aero rev. Execs said the win strengthens its global airport leadership, now covering 14 of the 25 largest hubs and delivering 54% of the audience. (PR Newswire)

- U. S. ad economy began ’26 on a tepid note, as Jan. rev rose just +0.7% YoY per Guideline’s U.S. Ad Market Tracker. The mkts saw a 2nd month of deceleration, following ’25 which ended up only 1.9%—the yr’s weakest monthly expansion aside from July–Aug. Olympic comps. The report highlights slowing biz momentum as cos enter the new yr. (MediaPost)

- Survey shows ~70% of CTV advertisers plan a 17% spend rise as CTV+linear converge. Drivers include engaged audiences, digital precision and full‑funnel impact. Premium CTV boosts ROI, brand favorability and omnichannel results. (Premion)

Artificial Intelligence/Machine Learning

- Anthropic annc’d an early-warning system to detect potential AI-driven white-collar job losses. The Co says current data shows limited evidence of AI-linked joblessness, but the tool aims to guide economists tracking AI’s impact on labor mkts. The effort highlights ongoing debate over whether an AI-led downturn is imminent and how best to measure related risks. (Axios)

- Perplexity annc’d a multiyear deal w/ CoreWeave to use Nvidia Grace Blackwell clusters for AI inference, boosting svs performance. CoreWeave will use Perplexity Enterprise Max for web/internal search. Execs say the pact shows broader AI adoption of its unified AI cloud as it builds diversified biz amid heavy capex plans that have made mkts cautious. (Axios)

- ByteDance annc’d Seedance 2.0 in early Feb., a major upgrade that shocked China’s AI mkts for its director like video abilities. Game Science’s Feng Ji and pro producer Pan Tianhong praised its impact on copyright and moderation. Access is limited to Chinese AI apps like Doubao, keeping overseas users out, prompting some to resell accounts. (WIRED)

- Meta, after major chipmaker deals, still aims for custom silicon. CFO Susan Li said that Meta’s ranking/reco workloads use custom chips at scale. She added Meta plans to expand this tech over time, eventually building processors to train future AI models, reflecting the Co’s push for more specialized, in house AI capabilities. (Bloomberg)

- Nvidia annc’d a $4bn investment in photonics cos Coherent and Lumentum, giving each $2bn. The move aims to boost AI infra via advanced optics and silicon photonics. Lumentum will supply laser components under a multi‑yr deal w/ purchase commitments, while Coherent will co‑develop next‑gen photonics for AI factories. (CNBC)

- Meta annc’d testing an AI shopping tool on desktop for select US users, showing product carousels w/ prices, brand info, links & reasons for recs. Tool tailors suggestions using user data like gender/location but doesn’t support checkout. (Engadget)

Audio/Music/Podcast

- Apple annc’d new Transparency Tags on Apple Music, asking artists / labels to mark AI-made content. Tags cover track, composition, artwork, and music videos when AI generates a material portion. Multiple tags can be used. Apple calls this a first step toward industry-wide transparency and urges cos to report AI use as mkts demand clearer ID of AI-created music across platforms. (The Verge)

Broadcast/Cable Networks

- Tegna’s Q4 rev fell 19% to $706mn as heavy 2024 political ads cycled out. AMS grew 4% to $322mn, helping offset weaker TV mkts, while distribution rev dipped 1% to $358mn. Full‑yr 2025 rev was $2.71bn, down 13%. Co highlighted CTV growth and new mobile app momentum. (TVNewsCheck)

Cable/Pay-TV/Wireless

- SoftBank annc’d at MWC 2026 plans to launch initial 6G svs by 2029–2030, using a 400 MHz slice at ~7 GHz, more than doubling 5G capacity. Early apps include physical AI, autos and sensing. Execs said the Co is modernizing its biz w/ AI at the edge, partnering w/ Ericsson and Nokia to place AI infra nearer demand and power sources. (Fierce Network)

- Accenture annc’d a $1. 2bn deal to buy Ziff Davis’ Connectivity division, bringing Ookla, RootMetrics & Downdetector into its svs portfolio. At MWC 2026, Ookla said the move will boost its network metrics biz. Founded in 2006, the Co grew from Speedtest into a major analyst w/~516 staff. Fierce will share more after meeting Ookla. (Fierce Network)

- T-Mobile CTO John Saw says Ericsson/Nokia’s collab aims to advance autonomous networks, boosting AI-driven optimization, spectral efficiency and outage prevention. T-Mobile pursues an intent‑based network where AI agents coordinate to fix faults and enable autonomous upgrades. Existing self‑opt tools already helped maintain service during Winter Storm Fern via ~30k antenna tweaks. (Fierce Network)

- Telcos lag in autonomy as an Accenture survey shows 79% still at Level 0/1 and only 22% expecting Level 4 by 2030. Legacy BSS/OSS, limited AI talent and a hybrid approach hinder progress. Hyperscalers lead but face resiliency issues. Digital twins offer a “huge opportunity” for autonomous design as AI lowers costs and boosts real‑time infra planning. (Fierce Network)

- At MWC 2026, CTIA said U. S. cos invest 2.5x Europe due to clearer policy, while EU’s patchwork rules limits scale + chills next‑gen network spend. Ajit Pai said strong spectrum infra is key as wireless+AI are intertwined; under‑invested mkts risk lagging. He added renewed bonus depreciation boosted carriers’ biz confidence. (Fierce Network)

- T‑Mobile CEO Gopalan said an MVNO deal w/Starlink doesn’t fit its MVNO criteria, but praised their D2D tie‑up, saying the cos “invented the category. ” He noted Starlink Mobile’s push to end dead zones via D2C tech, though limits in dense areas remain. (Fierce Network)

- T-Mobile countersued Verizon, alleging its “Better Deal” ads are a bait‑and‑switch, luring users w/ false savings claims then upselling pricier svs. T-Mobile said Verizon can’t match its plans at lower prices. Verizon earlier sued T-Mobile for comparing promo vs standard rates. Both cos seek to halt the ads and pursue triple damages under the Lanham Act and NY unfair‑competition laws. (Reuters)

- EchoStar annc’d Q4 pay-TV subs fell by ~168k, ending 2025 w/7mn subs across Dish (5.02mn) and Sling (1.98mn). Dish lost 636k in 2025, Sling lost 167k. Co cited lower churn, weaker activations and rising OTT competition after ESPN Unlimited and Fox One launches. (The Hollywood Reporter)

Capital Market Updates

- Banks are selling down financing for EA’s record LBO, planning a $10. 5bn US tranche and a €4bn package in Europe. JPMorgan Chase & Co. leads lenders arranging debt for the $55bn deal, set to start pre‑marketing in the coming weeks. The deal has drawn ~ $500mn anchor commitments from major investors at the bank’s desk. (Bloomberg)

- The S&P 500’s flat 2026 masks sharp single‑stock swings: Microsoft is down 18%, Intuit off 37%, while Sandisk nearly tripled and Texas Pacific Land rose 85% as investors sort AI winners/losers. High return dispersion—largest since 1994—signals a volatile, dynamic mkts backdrop as money rotates from big tech to energy/materials, creating both risk and opportunity for stock pickers. (The Wall Street Journal)

- Musk’s X and xAI plan to repay ~$17. 5bn debt in full, per sources. Morgan Stanley told lenders the cos will clear obligations after xAI raised $20bn equity in Jan. The firms, merged under xAI Holdings, face heavy cash burn as xAI spends ~$1bn/month on data centers, chips and talent. (Yahoo Finance)

Cloud/DataCenters/IT Infrastructure

- Google annc’d a Minneapolis-area data center powered by wind, solar, and the world’s largest 100‑hr iron‑air battery from Form. The tech enables multiday storage at ~1/10 lithium‑ion cost, boosting renewable reliability. Form is scaling via its WV factory and targeting an IPO next yr. (Yahoo Finance)

Crypto/Blockchain/web3/NFTs

- Retail traders have pivoted from crypto to equities after the Oct. crash wiped out ~$19bn. Wintermute says retail risk appetite, once focused on crypto, is now spread across high‑volatility equity trades. BTC has halved as mkts shift, w/ ETF flows showing momentum rotating into gold, silver, quantum and other themes, challenging crypto’s recovery outlook. (Yahoo Finance)

Cybersecurity/Security

- CrowdStrike annc’d Q4 rev up 23% to $1. 31bn and forecast fiscal 2027 rev of $5.87bn–$5.93bn, topping estimates. Q4 adj EPS hit $1.12. Co said costs tied to the July 19, 2024 Windows outage rose to $117.7mn for fiscal 2026 but fell to $16.2mn in the Jan. 31 qtr. Demand for its AI-driven cyber svs cont’d strong despite mkts’ concerns over rival tools. (Reuters)

- Anduril, the defense‑tech Co founded by Palmer Luckey, is raising a multibn round led by Thrive Capital and a16z, targeting a $60bn valuation. The round follows its Jun. Series G at $30bn. Other investors incl. Lux Capital and Founders Fund. The raise comes amid defense‑startup tension as the Pentagon cancels Anthropic contracts, which Luckey publicly backed the gov’t on. (TechCrunch)

eCommerce/Social Commerce/Retail

- Best Buy posted mixed holiday-qtr results as rev fell to $13. 81bn vs est $13.88bn, but adj EPS hit $2.61. Qtr comps dropped 0.8% amid weak appliances/home theaters, partly offset by computing/mobile. FY rev guide is $41.2bn–$42.1bn w/ adj EPS $6.30–$6.60. (CNBC)

- JD. com missed mkts rev estimates as weak demand, tough comps and fading subsidies hit sales. The Co is shifting to diversified growth, saying general merchandise stays healthy and svs rev incl. ads will keep rapid momentum. Appliances stay pressured in Q1 but may pick up later. (Reuters)

- Target’s new CEO set big growth goals, saying net sales will rise this yr as early improvements emerge. Plans include expanding grocery w/ more unique items, adding beauty studios after ending the Ulta partnership, and revamping baby dept. The Co will boost svs, faster delivery and new member perks to regain mkts and reverse a 3‑yr slump despite some skepticism. (Bloomberg)

Electric & Autonomous Vehicles

- A Waymo robotaxi near mass shooting in Austin briefly blocked an EMS ambulance as it was en route to pick up a rider. Video shows the AV stopping in the street until police used the Co’s speaker system to move it. EMS said the issue was resolved quickly w/o major impact to care. (Axios)

Film/Studio/Content/IP/Talent

- Netflix annc’d its acquisition of InterPositive, a filmmaking tech Co founded by Ben Affleck, whose mission is to use AI tools that protect creative intent. Affleck says the tech is built to support filmmakers w/ models trained on real production challenges. (Netflix)

FinTech/InsurTech/Payments

- Kalshi annc’d it would settle its “Khamenei out?” mkt at the last price pre‑death, citing rules meant to stop users from profiting from death. The Co is refunding fees and reimbursing post‑death buys. Some users say rules weren’t clear and argue Kalshi tried to have it both ways. (The Verge)

HealthTech/Wellness

- Whoop, the Boston-based fitness Co, plans to grow staff by ~75% this yr, adding 600+ roles across software, research, design, hardware, mfg, sales & marketing to prep for a likely IPO. Most hires will be at HQ, w/ global expansion as intl mkts now drive 60% of sales. While many tech cos cut jobs citing AI, Whoop says its biz remains strong and is investing across all areas. (Yahoo Finance)

Live Entertainment/Theme Parks/Concerts/Experiential

- TKO Group Holdings, the UFC/WWE op, annc’d a nearly $1bn leveraged-loan offering after a dividend to equity holders. The Goldman Sachs-led deal includes a $900mn fungible add-on to its term loan, priced 200 bps above benchmark w/ a 99.50–99.75 discount. The loan, for general corp purposes, matures Nov. 2031. (Bloomberg)

- At trial, NY said Ticketmaster keeps ~$7. 58 per ticket as states claim Live Nation/Ticketmaster ran illegal mkts monopolies hurting artists/fans. DOJ says the industry is broken and controlled by the Co, while Live Nation argues it takes ~5% and faces competition. States seek damages of ~$1.56–$1.72 per ticket; witnesses incl. artists and venue execs. (Reuters)

- Live Nation’s trial centers on DOJ and states alleging the Co monopolized live music mkts and must shed Ticketmaster. Jury selection finished Mon. in NYC federal court. The 5–6 wk civil case will decide if the Co violated antitrust law. If gov’t wins, jurors set consumer damages and the judge weighs remedies incl. a potential breakup. (Bloomberg)

Macro Updates

- Paper reviews U.S. Fed independence from 1951–2006, focusing on the Martin–Greenspan era. It highlights overlooked docs, Chairs’ quotes, and explains how statutory aims, structure, and conventions shaped policy autonomy. Shows successive Chairs made a consistent three‑part economic case for independence, not tied to time‑inconsistency theory. (Federal Reserve)

- Amazon annc’d drones struck 3 AWS data centers in UAE and Bahrain, causing structural damage, power disruption and fire‑related water damage. Ops remain “significantly impaired,” w/ customers facing high error rates as svs outages cont’d. AWS urges data backup or migration amid unpredictable Mideast conditions. (CBS News)

Media Conglomerates

- Fitch downgraded PSKY’s IDRs to BB+ and placed all ratings on RWN due to sector pressures, cont’d FCF headwinds and risks tied to the proposed WBD acquisition. The deal’s ~$58bn debt funding, high leverage, limited visibility on post‑transaction capital structure and elevated execution risk drive uncertainty despite potential competitive gains. (Fitch Ratings)

Online Travel

- Shares of online travel cos surged after a report that OpenAI is scaling back ChatGPT direct bookings, easing fears of disintermediation. Expedia jumped ~12%, while Booking and Tripadvisor rose 8% and 5%. OpenAI will focus on checkouts via third‑party apps. Analysts said the move is positive, allowing OTAs to stay in front of consumers on AI platforms. (Yahoo Finance)

Regulatory

- A federal trade-court judge on Wed. ordered the Trump admin to refund >$130bn in global tariffs the Supreme Court invalidated last month. Following a filtration Co’s push for a refund, Judge Richard Eaton of the Court of Intl Trade directed the admin to start refunding importers and set a Fri. hearing for updates. (The Wall Street Journal)

- Wall Street regulators are moving to oversee the crypto industry and rising prediction mkts, proposing new measures that could shape broader financial mkts. After months of public debate and Congress wrangling, the SEC and CFTC have sent plans to the White House. (Bloomberg)

- Pentagon gave Anthropic a supply‑chain risk label, blocking contractors from using its tech in military work, though Claude can still be used in non‑Pentagon projects. CEO Amodei said the scope is narrow, plans to contest it, and noted disputes over safeguards. Pentagon denies active talks. Microsoft said Anthropic tools stay available for non‑defense use. (Reuters)

- Senate passed COPPA 2. 0, expanding child privacy rules. Bill bars cos from serving targeted ads to users <17 and limits data collection from ages 13–16 w/ consent. Contextual ads allowed. It broadens personal-info definitions and applies when cos have actual or implied age knowledge. Markey called it a key step; House paused review after Senate’s action. (MediaPost)

- FCC approved Charter’s $34. 5bn deal to acquire Cox, creating the largest U.S. ISP w/ ~37.7mn customers. Order found no major harms and cited consumer benefits. Charter will keep Cox’s name but use Spectrum for svs, invest bn$ in network upgrades, onshore jobs w/in 18 months, end DEI efforts, and roll out lower Spectrum pricing across Cox’s footprint, expanding reach to 70mn households. (StreamTV Insider)

Satellite/Space

- KDDI annc’d that au Starlink Direct intl roaming starts in the U. S., marking the 1st cross‑border direct‑to‑phone satellite svc. Launch begins w/ Google Pixel, enabling chat/voice apps like WhatsApp in ~500k sq. miles lacking cell coverage. Users just update devices + enable roaming; svc is free for now, w/ more devices to be added later Mar. (KDDI Newsroom)

- SpaceX annc’d Starlink Mobile V1’s global D2C rollout and detailed V2 sats promising 20x throughput, S‑band use and 5G‑like perf. The 650‑sat V1 fleet now operates across 5 continents, powering T‑Satellite. V2 launches mid‑2027 and already has DT as a partner. Shotwell highlighted Starlink’s Ukraine support, incl. a Kyivstar deal reaching ~3mn users w/ text, data, voice and video. (Fierce Network)

- Orange annc’d MoU w/ AST SpaceMobile + Satellite Connect Europe to expand D2D sat connectivity. Demo in Romania planned for 2H26, covering voice, SMS + data. Move supports Orange’s “Trust the future” plan, boosting network resilience + reach in remote areas. Orange, w/ 60 yrs sat expertise, aims to blend terrestrial + sat svs to ensure always‑available connectivity. (Orange)

- SpaceX’s Starlink Mobile was detailed at MWC as its D2C svs expands via 650 sats across 5 continents. V2 sats will use S‑band, custom silicon and phased arrays to deliver terrestrial‑like 5G, w/ launch planned mid‑2027. Deutsche Telekom will adopt V2 to boost remote coverage. (Fierce Network)

- SpaceX aims to file confidentially for an IPO valued >$1. 75tn in Mar., per Bloomberg, though timing may shift; Reuters says Jun. likely. Musk also plans a Starship test launch in Mar. after upgrades. Co posted ~$8bn profit on $15–16bn rev last yr, driven by Starlink (50–80% of rev). Co also completed its xAI acquisition, valuing the combined entity at $1.25tn. (Reuters)

- Vodafone annc’d a deal to use Amazon Leo’s LEO satellite net to link remote 4G/5G masts, boosting coverage + resilience in EU + Africa. The service enables faster, lower‑cost rollout in hard‑to‑reach areas, w/ backup if fibre fails. First sites go live in 2026, supporting Vodafone’s 5G goals + Vodacom’s Vision 2030 to expand svs + reach more customers. (Vodafone)

Social/Digital Media

- YouTube annc’d a major update that boosts discovery by letting users search in natural language. The new AI-driven system interprets ideas, moods, and topics to deliver tailored results, helping viewers find content they’d miss under old keyword search. It also supports creators by surfacing niche, theme-based videos and aims to make the platform feel more intuitive and personal. (Cord Cutters News)

- Apple is blocking US users from downloading/updating ByteDance apps, incl. Capcut, Lemon8, Lark, Hypic, even w/ valid Chinese Store accounts. Wired reports users get “unavailable” msgs, aligning w/ TikTok US divestiture. An archived Apple note said 11 apps became unavailable in the US from Jan. 19, 2025, though existing installs still work; full functionality returns after leaving the US. (9to5Mac)

- News Corp CEO Thomson said the Co is an AI “input”, highlighting a Meta deal worth up to $50m/yr letting it scrape US/UK content. He noted strong ties w/ Altman & Zuckerberg and cited a prior $250m OpenAI pact. Aus leaders take a tougher line, warning platforms harm cohesion. The Co’s NewsGPT tool raised concerns as mkts split between AI partnerships and lawsuits. (The Guardian)

- Instagram’s internal docs, revealed in a court case, show daily use rising from 40 to 46 minutes and note interest in teens, incl. tweens as top retention. Plaintiff K.G.M. claims harm from addictive design; Meta disputes this. Emails cite goals for teen time spent, despite ~4mn under-13 users. (TechCrunch)

Software