It remains a week-by-week market with ebbs and flows along with trade/economic headlines, and this week was another ebb higher (S&P 500 +1.5% and Nasdaq +2.2%) despite the very public spat between President Trump and Elon Musk.

See below for the key updates/developments/themes that we focused on in this edition:

- The Sports Betting Industry Loses A Bet On New Tax Hikes…

- How Much Is Your Data Worth? Brazilian Citizens Could Find Out Soon

- Several Provocative Comments Out Of VC + PE Execs This Week

- Power Is The New Gold… AI Demands Spur Big Tech To Push Further Into Nuclear

- TikTok’s Ad Event & Other Key AI Ad Updates

- What % Of Consumer ONLY Carry A Digital Wallet? + A Few New Stats On Consumer Retail Preferences

- Grab Bag: Anthropic Reached $3bn ARR / Are Ad Budgets Shifting From TTD To AMZN? / Temu Is Seen As Losing ~50% Of DAUs Due To Tariffs

Also, I’d also like to congratulate my colleagues on several deals announced this week:

- LionTree is proud to have served as the exclusive financial advisor to Wonderbly on its sale to Penguin Random House

- LionTree is proud to have served as the exclusive financial advisor to Likewise on its sale to Watchlist

- LionTree is proud to have served as the exclusive financial advisor to DICE on its sale to Fever

Have a nice weekend. It is finally getting hot here on the East Coast!

Best,

Leslie

The Sports Betting Industry Loses A Bet On New Tax Hikes…

Illinois legislators last weekend surprised investors when they voted to finalize a $55.2bn budget which includes additional taxes on sports betting. Essentially, sportsbooks will be taxed 25c per bet for the first 20mn wagers and 50c per bet beyond that. Note that this tax is on top of the tiered 20-40% tax structure that was increased from 15% just last year. Once Gov J.B. Pritzker signs the budget, it will go into effect for the fiscal year starting July 1st. See below for some Street estimates on the impact, as well as the status of other proposed state changes in sport betting taxes. Potential changes in tax rates have been a hot button for sports betting investors…

-> DraftKing’s stock dropped -6% on the back of the news and Flutter Entertainment fell -2.7%; YTD, their stocks down -3.7% and -3.4%, respectively

How Much Will This Addtl Illinois Tax Hurt Sports Betting Companies? (link/link)

- Per the WSJ, DraftKings and FanDuel (owned by Flutter) have a ~75% combined market share in Illinois

- The Citizens Bank team est’d a 2026 impact of (excluding any mitigation efforts) –

- DraftKings will take a $79mn hit (5.4% of EBITDA)

- FanDuel will take a $86mn (2% of EBITDA)

- The Sports Betting Alliance (SBA) warned that customers will bear the cost of this new tax & argues these customers will be pushed into the illegal market

- They instead were pushing for a proposal to legalize online casinos in Illinois w/ est’d taxes up to $800mn per year

Other Recent Updates Regarding States’ Increasing Tax Sports Betting Taxes (link/link/link/link)

- Maryland: In May, Governor Wes Moore signed the Maryland budget, which included a 5ppt increase to the sports betting tax rate from 15% to 20% (but note that the rate was lower than the 30% rate first introduced)

- Online casino legislation has not advanced

- Ohio: In April, Governor Mike DeWine’s proposal to double the sports betting tax from 20% to 40% (just 2 yrs after increasing it from 10% to 20%) did NOT move forward; In May, a lawmaker instead intro’d a 2% handle tax on top of the existing 20% tax on revenue (West Virginia and Kentucky both previously floated handle taxes, but each proposal was denied)

- New Jersey: In Feb, Governor Phil Murphy proposed increasing the sports betting tax from 13% to 25%

- Lawmakers have a June 30 deadline to pass the budget

Louisiana: In May, a sports betting price hike from 15% to 21.5% was passed in the House and it is awaiting Senate action which is expected shortly

How Much Is Your Data Worth? Brazilian Citizens Could Find Out Soon

One update that we were intrigued to see this week was that Brazil is piloting dWallet, which is a project that lets citizens earn money from their data. When the federal bill is passed it will be the first of such in the world. (link)

- How will it work? The pilot involves a small group of Brazilians who will use data wallets for payroll loans

- When users apply for a new loan, the data in the contract will be collected in the data wallets, which companies will be able to bid on

- Users will have the option to opt out

- It works much like 3P cookies, but instead of simply accepting or declining, people can choose to make money

- After a user accepts a company’s offer on their data, payment is cashed in the data wallet, and can be immediately moved to a bank account

- Some concerns about the project include: 1) it could harm small businesses who may not be able to bid high enough for data and that 2) vulnerable socioeconomic groups could be negatively impacted

- In 2023, Brazil drafted a bill that classifies data as personal property

- The global data market is currently valued at $4bn and is expected to grow to $40bn+ by 2034

Several Provocative Comments Out Of VC + PE Execs This Week

There were several provoking soundbites from VC and PE execs this week, covering everything from unicorn survival rates, to global investing shifts, to AI’s impact on the workforce. Accel and CapitalG shared that they expect only a small percentage of today’s tech unicorns are likely to see successful exits, with many expected to stall, sell for less, or shut down entirely. In Europe, CVC Capital Partners pointed to both the opportunities and challenges in the region’s PE market, citing cultural differences, less efficient dealmaking, and rising competition. Additionally, Vista and Thoma Bravo weighed in on AI, with some warning of major disruption to white-collar jobs, but also enthusiasm about boosting productivity.

See below for more on the above.

VC Execs Expect Only A Fraction Of Unicorns Will Thrive (link)

- Accel Partners partner Rich Wong –

- Of the 1k+ tech unicorns (VC-backed Cos worth $1bn+), at least 1 in 5 of are those likely to fail

- “I think maybe out of that thousand, 20% fully die”

- About half of the remaining companies will be stuck, unable to grow bigger or go public

- Some of those may “ultimately have reality set in,” and sell themselves for lower prices than once seemed feasible

- Others, not quite failing, “will be a bit zombie-ish and grind on”

- The remainder ~20-25% of unicorns will “ultimately succeed in some form,” whether that’s a successful sale, or a public offering

- Of the 1k+ tech unicorns (VC-backed Cos worth $1bn+), at least 1 in 5 of are those likely to fail

- CapitalG managing partner Laela Sturdy –

- While some startups will take off, only “a small minority” of current tech unicorns “are going to be standalone public companies”

- The biggest and most successful Cos will be able to choose when and if they go public

- “I think there will be a time when most generational technology companies will choose to go public. There are still advantages”

- While some startups will take off, only “a small minority” of current tech unicorns “are going to be standalone public companies”

European PE Is Both A Challenge & A Catalyst (link)

- CVC Capital Partners CEO Rob Lucas – investing in Europe can be challenging, and investors will need to navigate large cultural and economic differences, and find value amid the region’s less efficient markets

- “It’s just difficult to come here and to really understand all the nuances of each of the different markets”

- On heightened level of interest and activity in Europe – “I’m not sure I would call it a renaissance, only because I really just don’t think Europe’s ever really gone away”

- “Sure, GDP and the stock market indices have lagged over the last decade. But actually the ability for the private markets to generate returns has been very strong”

- “And certainly, we have seen across CVC, the returns we’ve been able to generate within Europe have been impressive”

- Expects that as investors in PE become more demanding, firms are likely to pursue consolidation

- “What our LPs, our strategic partners, are looking for from us at any given time is more and more demanding…groups coming together is a natural part of that”

- Looking forward – PE has “very strong tailwinds” behind it and remains a “super strong” asset class

- “We have cycles, and clearly we’re going through one of those at the moment…these periods of instability and dislocation, they are the periods when you can make the best investments”

PE Execs Weigh In On Expected AI Impacts (link)

- Vista Equity Partners’ CEO Robert F. Smith – while speaking at the SuperReturn International private capital conference in Berlin, predicted that 40% of people in attendance will have an AI agent and 60% will be looking for work next year

- “There are 1 billion knowledge workers on the planet today and all of those jobs will change…I’m not saying they’ll all go away, but they will all change”

- “You will have hyper productive people in organizations and you will have people who will need to find other things to do”

- Marathon Asset Management CEO and founder Bruce Richards – “Not all those companies will make the AI adjustment and there will be creative destruction that comes their way”

- Those that can’t make the AI transition face a “Blockbuster Video moment” (referring to the home video rental chain that lost out to streaming svs and filed for bankruptcy)

- Thomas Bravo founder Orlando Bravo on Anthropic CEO Dario Amodei’s comment that AI could wipe out half of all entry-level white-collar jobs in the next few yrs – “It’s a very futuristic point of view”

- “But I think it will make white collar jobs more productive and people a lot smarter. I use ChatGPT and all kind of models all the time. I said, hey write me a paper on this topic, and then I can think more thoughtfully and more deeply about that topic and improve it”

Power Is The New Gold… AI Demands Spur Big Tech To Push Further Into Nuclear

A couple weeks ago we talked about the issue of how much energy these proliferating and increasingly complex AI queries require (see Theme #2 from May 23rd Weekly Update) and along this same theme, Meta’s 20-year deal with Constellation Energy Group (CEG) was an important development this week. Meta will be buying nuclear energy for its data centers from CEG’s existing plant in Illinois and this deal reportedly could also lead to the construction of a new nuclear plant. This was good news for CEG, as that Illinois plant was set to be shut down in 2027, but it will now operate until 2047, if approved by regulators. Some key details are below, along with other recent pushes by Big Tech into nuclear to help shore up the much-needed energy demands that will be skyrocketing as we look ahead. (link/link)

- Timing: June 2027

- How much energy will Meta be using? Meta will fund ~1.1 gigawatts, which is the entire output from the site’s sole reactor

- For context, 1 gigawatt is enough to power almost 1mn homes

- How much is Meta paying? A Jefferies analyst est’d Meta is paying ~$80 per megawatt hour (vs the CEG-Microsoft deal priced ~$110 per megawatt hour)

- This is Meta’s first foray into nuclear power…other Big Tech recent deals include –

- Microsoft: In September, the Co signed a 20-yr agreement w/ CEG to restart Three Mile Island

- Google: In May, the Co partnered w/ Elementl Power to fund 3 new nuclear sites; Last year Google partnered w/ Kairos Power on small modular reactors

- Amazon: The Co has invested $500mn+ to develop small modular reactors and bought a data center powered by the Susquehanna nuclear plant

- Trump is also spurring nuclear plant construction: Last month, he signed four executive orders aimed at speeding up the building of nuclear power plants, including small modular reactors

- The White House also set a goal to 4x the # of nuclear power plants in the US from ~100 gigawatts to 400 gigawatts by 2050

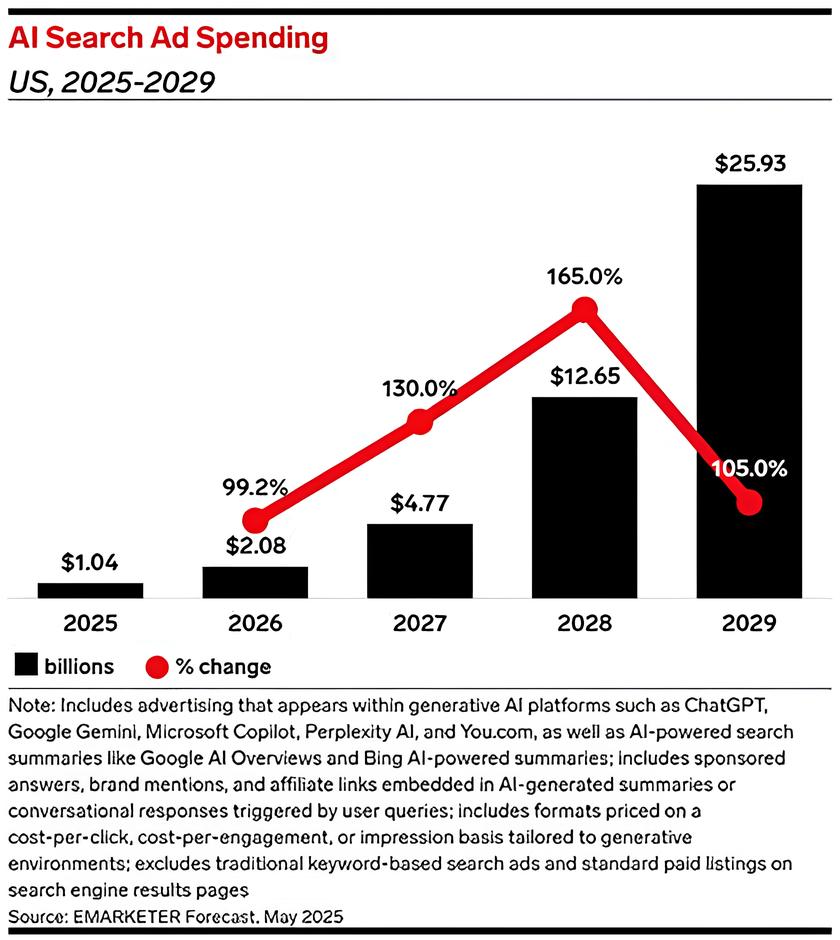

TikTok’s Ad Event & Other Key AI Ad Updates

TikTok shared at its TikTok World event this week that 1 in 4 TikTok users start searching within 30 seconds of opening the app – a stat that shows how quickly users move from passive viewing to active discovery. Now, both TikTok and Meta are racing to turn that intent into action with a new wave of AI-powered ad tools. TikTok is leaning into its growing role as a full-funnel platform, rolling out new AI tools that help brands reach users, drive discovery, and boost sales all within the app. Meanwhile, Meta is planning to let advertisers hand over the reins entirely, using AI to generate and target ads based on just a product image and budget.

As both platforms double down on AI to streamline and scale digital ads, eMarketer projects AI-driven search ad spend will surge from $1bn this year to $26bn by 2029. a massive ramp-up that reflects how quickly AI is becoming a core part of the advertising toolkit.

See below for more on this theme.

TikTok Shared Some Key Search & TikTok Shop Engagement Stats (link)

- Searches per session are up 40%+ y/y

- 1 in 4 TikTok users start to search for something within the first 30 seconds of opening the app

- 76% of TikTok users are likely to consider a brand because of content seen on the platform

- 64% of TikTok shoppers have made a purchase directly from content or from ads that they saw on the platform

- TikTok Shop now has 15mn+ sellers globally

- TikTok Shop partners collectively generated $100mn+ in sales on Black Friday

Capitalizing On The Growth In Engagement…TikTok Annc’d New AI-Powered Ad & Creator Tools At Its Ad Summit This Week (link)

- TikTok emphasized its role as a full-funnel marketing platform, offering tools that support every stage — from brand awareness to conversion — through AI, automation, and creative solutions

- TikTok One Insight Spotlight: A tool that allows brands to plug in specific industries, viewing history, and user demographics in order to see which videos and keywords are being engaged with by a particular audience on the app

- The tool then automates suggestions for what kind of content a brand should produce to capture an audience’s attention in real-time

- TikTok One Content Suite: Enables marketers to easily find and access all user-generated videos mentioning their brand or products on TikTok and turn them into high-performing ads, “in an instant”

- Compared to searching in the app, Content Suite surfaces 40x+ more relevant results that are impactful for a brand

- Market Scope: A tool TikTok began testing in select markets last month that tracks where users are in the funnel re: awareness, consideration, and conversion

- The analytics dashboard was developed to help advertisers tweak campaigns based on where users are in their purchasing journey.

- Brand Consideration Ads: Being rolled out now and is a new mid-funnel campaign objective that leverages Market Scope data to target users showing signs of engagement and exploration

- TikTok’s Smart+ suite (recently launched): In March, TikTok said that Smart+ campaigns received a 5.1x higher incremental ROAS and a 2.2x higher relative purchase lift compared to regular campaigns (link)

-> Separately, related to TikTok Shop, per press reports, the Co made some changes whereby brands will have to pay for TikTok ads to maintain and/or increase the number of views they were previously receiving on the video-sharing app for free; Apparently the lapse of free views began last year, but has since become more dramatic; Within less than 2 years, TikTok Shop has become the 4th-most popular social commerce platform in the U.S., per Capital One, w/ Americans spending ~ $32mn per day on TikTok; In 2024, the # of shoppers on TikTok rose 34.2% y/y w/ projections showing a 5.91% annual increase through 2027 (link)

Meta’s Big Move To Offer Soup To Nuts AI Ads (link)

- Meta is planning (per WSJ) to provide brands with the ability to fully create and target ads w/ its AI tools by the end of this year, which created a bit of stir out of the gate on Monday

- Sources cited said that brands would just have to provide a product image and their budget and then voila, Meta’s AI will generate the ad (image, video, text) and figure out what users to target on Facebook and Instagram

- Advertisers also would have the ability to personalize ads (same ad, different version) based on factors like location

-> Ad agencies fell on the news, with WPP closing the day down -2.5%, Publicis -3.3%, OMC -4.0% and IPG -4.6%

AI Search Ad Spend Is Forecast To Reach $26bn By 2029 Per New eMarketer Projection (link)

- In 2025, ad spend for AI-based search is expected to reach $1bn

- Accounting for 0.7% of total search ad spending

- By 2029, it is projected to hit ~$26bn

- Google is expected to “hesitate to fully implement AI search at a large scale until they have clearer data on its net economic benefit and user engagement outcomes”

- Due to AI-driven search tools significantly reducing the need for users to click through multiple traditional search results

- eMarketer also flags that Companies also concerned that AI will cannibalize established search ad revenue streams

What % Of Consumer ONLY Carry A Digital Wallet? + A Few New Stats On Consumer Retail Preferences

We came across a survey conducted by Ayden (covering 41k consumers and 14k retailers across 28 global markets) on consumer retail preferences as it relates to shopping that we thought made the cut this week. See the stats that we found most interesting below. These are further broken out by demo (along with other insights) in the full report if you want to dig in more: Retail Report 2025 – The Adyen Index – Adyen

- Online vs In-Store

- 37% of consumers prefer to shop in the store while 24% prefer to shop online

- 40% of consumers value both online and in-store equally

- Importance of social media

- 38% of Gen Z choose retailers that let them shop on social media

- 45% of Gen Z has shopped on social media

- Findings regarding consumers’ payment preferences

- 38% used digital wallets in the past year

- 49% prefer to use credit or debit cards

- 23% of consumers ONLY carry a digital wallet

- 46% of consumers will abandon the cart if they can’t pay how they want to

- Mixed consumer views on AI

- Regarding interacting w/ AI when shopping

- 46% of consumers DO NOT like to interact with AI while shopping online

- But 63% understand that retailers use AI to help recommend products

- Regarding views on tracking purchases & browsing history to deliver personalized offers and ads –

- 40% say it is helpful

- 38% say it is invasive

- Regarding using AI assistants

- 37% of consumers have used ChatGPT or AI assistants to shop

- Regarding interacting w/ AI when shopping

- AI is a top priority for retailers

- 34% of retailers will invest in AI to support sales & marketing

- 33% of retailers will invest in AI to support their product

Grab Bag: Anthropic Reached $3bn ARR / Are Ad Budgets Shifting From TTD To AMZN? / Temu Is Seen As Losing ~50% Of DAUs Due To Tariffs

- Anthropic reaches $3bn in annualized revenue (link/link)

- The Co crossed $2bn at the end of March, which was up from nearly $1bn in December 2024

- What’s driving the growth? Enterprise demand…: “Companies are moving from AI pilots to production-level deployment, and Anthropic is positioned well for that shift,” per a source cited by Reuters

- Anthropic’s rev comes largely from selling AI models as a svs to other Cos

- …which is a key differentiator from OpenAI –

- OpenAI is shaping up to be a consumer-oriented Co, as the majority of its rev comes from subscriptions to its ChatGPT chatbot

- In comparison, Anthropic’s Claude has seen less adoption than OpenAI, and traffic was ~2% of ChatGPT’s in April

- OpenAI has not reported enterprise-specific rev but said in May that paying seats for its ChatGPT enterprise product have grown to 3mn, up from 2mn in February

- Anthropic vs OpenAI val’n: Anthropic closed a $3.5bn fundraise earlier this yr that valued the Co at $61.4bn; OpenAI is currently valued at $300bn

- Press reports cite advertisers shifting millions of dollars in ad budgets from The Trade Desk’s DSP to Amazon’s (per an Ad Week report) (link)

- Examples –

- A global auto brand moved ~$80mn annually to Amazon DSP by Q1, partly because it can now sell cars directly on Amazon

- A global tech brand shifted ~$5mn for a single campaign but still uses TTD for other spend

- Why the shift? Amazon’s lower fees, improved user interface, greater measurement visibility, exclusive live sports, Prime Video’s growing reach, and a more collaborative partnership model

- TTD comments that its value prop to clients is “very different” –

- “Amazon can offer very cheap reach because it directs advertiser demand to its own platform, notably Amazon Prime”

- “TTD doesn’t own or operate any media…advertisers objectively decide between all ad impressions on the open internet”

- TTD’s spokesperson also flagged that the Co has seen “solid growth” and is “growing faster than Amazon”: As a reference, Amazon’s ad rev grew +18% y/y to $13.9bn in Q1, while The Trade Desk reported a +25% y/y increase, generating $616mn in the same qtr

- Examples –

-> TTD ended down -6.4% the day the report was published; The stock has had a tough going and is down -39.2% YTD

- PDD’s Temu is seen as losing almost half of US daily users following end of “de minimis” loophole (link)

- Daily US users of fell by -48% in May compared to March, according to market intelligence firm Sensor Tower

- Temu slashed ad spending in the US and shift its order fulfilment strategy after the White House on May 2 ended the practice known as “de minimis” (allowed Chinese companies to ship low-value packages to the United States tariff-free)

- Last week, PDD’s Q1 earnings fell short of growth estimates and mgmt told analysts on a post-earnings call that tariffs had created significant pressure for its merchants

Stock Market Check

This Week's Other Curated News

Artificial Intelligence/Machine Learning

- Alphabet CEO Sundar Pichai said the Co will cont’d hiring engineers despite AI-driven efficiencies. He emphasized the need for top talent to build & refine AI models. While AI boosts productivity, Pichai noted it also creates new roles. Alphabet is investing in infra & safety to scale responsibly. The Co aims to balance innovation w/ workforce evolution, even as some roles shift or phase out (Bloomberg)

- Reddit sued Anthropic, alleging its AI bots accessed Reddit over 100,000 times since Jul 2023, violating its terms of service. The lawsuit claims Anthropic scraped Reddit content to train Claude AI models without a license. Reddit argues this undermines its API monetization strategy and user privacy. The Co seeks damages and an injunction. (The Verge)

- China is experiencing an AI agent boom, w/ startups rapidly deploying autonomous agents for customer svs, finance, & education. Fueled by gov’t support & VC funding, firms like MiniMax & 01.AI are racing to commercialize AI agents that can reason, plan, and act independently. Unlike US rivals focused on foundational models, Chinese cos emphasize real-world applications. However, concerns persist over data privacy, hallucinations, & regulatory gaps (MIT Technology Review)

- Alibaba annc’d its Qwen3 Embedding series as open-source AI models, aiming to strengthen its global lead in text-embedding tech. These models support 100+ languages (incl. code), enabling multilingual, cross-lingual, and code retrieval. Ranked top by Hugging Face and 3rd globally in LLMs per Stanford’s 2025 AI Index, Alibaba’s move boosts dev access and AI capabilities (South China Morning Post)

- Codex, OpenAI’s cloud-based software engineering agent, now has internet access, but it’s off by default due to security risks like prompt injection and data exfiltration. Users must enable it manually and can restrict access via domain allowlists and HTTP methods. OpenAI advises caution, highlighting risks through examples. The rollout extends to ChatGPT Plus users, expanding from prior Pro-only access (net)

- Microsoft made OpenAI’s Sora available via Bing Video Creator on its mobile app for iOS and Android. Users can generate 5-sec videos from text prompts in 9:16 format (16:9 coming soon). Each user gets 10 “Fast” generations; more can be redeemed w/ Microsoft Rewards. Up to 3 videos can be queued. Videos can be downloaded or shared and are stored for 90 days. The feature isn’t yet available in Copilot or on desktop (MediaPost)

- OpenAI annc’d new ChatGPT productivity features incl cloud storage integration (Google Drive, Dropbox, OneDrive, Box, SharePoint) for querying docs directly. A new record mode transcribes meetings via mic, generating summaries, key points, action items & time-stamped citations. Action items convert to Canvas docs. Beta MCP connectors link w/ HubSpot, Linear for autonomous research. Cloud tools are for paid users; MCP for Pro, Team & Enterprise (MacRumors)

- AI coding startups like Magic, Cognition, and Augment are drawing sky-high valuations, fueled by investor hype and demand for dev productivity tools. Magic raised $200mn at a $1.5bn valuation; Cognition’s AI agent Devin secured $175mn at $2bn. These cos promise to automate software dev, but many lack rev. VCs are betting on future dominance despite unclear biz models. Critics warn of a bubble forming in AI dev tools (Reuters)

- Google-backed AI startup Limitless, founded by ex-Evernote CEO Phil Libin, unveiled a wearable AI recorder and assistant focused on personal—not general—intelligence. The device captures meetings and conversations, offering searchable transcripts and summaries. Unlike general AI, Limitless emphasizes user-controlled data and productivity. The Co aims to redefine AI utility through privacy-first, user-centric design (MediaPost)

- Elon Musk’s xAI is launching a $300mn share sale valuing the group at $113bn, enabling staff to sell shares to new investors. The Mar. acquisition of X by xAI priced the AI Co at $80bn and X at $33bn. A larger equity round is expected to follow. xAI is also seeking $5bn in debt financing via Morgan Stanley. Musk aims to integrate AI, compute, and distribution across X, xAI, and Tesla (Financial Times)

- Elon Musk’s xAI is launching a $5bn debt sale, led by Morgan Stanley, to fund its AI infrastructure expansion, including the Colossus supercomputer. The move follows xAI’s merger w/ X under xAI Holdings, valued at $113bn. xAI, which operates 200K+ GPUs, aims to scale to 1mn chips. The sale supports Musk’s renewed focus on tech ventures amid rising AI competition (SiliconANGLE)

- Apple is set to unveil major AI upgrades at WWDC, incl. “Apple Intelligence,” a system integrated into iOS 18, iPadOS 18 & macOS 15 (Tahoe). Features incl. AI-generated emojis, enhanced Siri, & smart recaps for notifications, web pages, docs, etc. A new Passwords app & gaming enhancements are also expected. Apple aims to balance AI utility w/ privacy (Bloomberg)

Audio/Music/Podcast

- Spotify laid off 15 employees across The Ringer&Spotify Studios, marking a 5% staff reduction. The eliminated roles will be reallocated to support Spotify’s video podcast push. No podcast shows are being canceled. The layoffs follow previous cuts in 2023 when 200 podcast staffers were let go. CEO Daniel Ek emphasized video podcasts as a strategy to boost engagement rather than a full pivot to video (MSN)

- Spotify and United Airlines have partnered to bring 450+ hours of free audio content—including podcasts, video podcasts, audiobooks, and playlists—to in-flight entertainment across 680+ aircraft. This marks Spotify’s first onboard offering of audiobooks and video podcasts. Starting 2026, passengers can sync personal devices to seatback screens for full Spotify access. The new “Spotify” category replaces the old “Audio” section in United’s IFE system. (Simple Flying)

- Major record labels incl. Universal Music Group, Sony Music & Warner Music are in talks to license music to AI cos like Udio & Suno. These startups use genAI to create songs mimicking real artists. Labels seek licensing deals to avoid litigation & monetize AI-generated content. Talks are early-stage, w/ no final agreements. (Bloomberg)

- Taylor Swift now controls her full music catalog after buying back the master rights to her first six albums. This move marks a major milestone in her long-running battle for ownership, which began after her original masters were sold without her consent. Swift had previously re-recorded her early albums to regain control. The buyback solidifies her authority over her legacy and future rev streams (MSNBC)

Cable/Pay-TV/Wireless

- MultiChoice expects higher FY earnings due to one-off asset sales, despite a drop in underlying profit. Core headline earnings per share will rise by >100%, mainly from selling its stake in BetKing. However, underlying biz performance weakened due to currency volatility, inflation, and lower consumer spending. The Co continues cost-cutting and digital transformation to stabilize ops. Full results to be released later in Jun (Telecompaper)

- Rogers has received all major league approvals to acquire Bell’s 37. 5% stake in MLSE for C$4.7B, increasing its ownership to 75%. The deal awaits final CRTC approval for a minor media asset. (Street Account)

Cloud/DataCenters/IT Infrastructure

- Amazon annc’d a $10bn investment in North Carolina to expand AWS cloud & AI infra. The project will create 500 high-skilled jobs & support thousands more in the data center supply chain. Since 2010, Amazon has invested $12bn in NC, contributing $13.1bn to GDP. New roles include data center engineers, network specialists, & ops managers. Amazon also launched a $150K community fund for STEM, workforce dev, & sustainability (About Amazon)

- AWS annc’d up to 45% price cuts for EC2 NVIDIA GPU-accelerated instances (P4d, P4de, P5, P5en), effective for On-Demand from Jun 1 and Savings Plans from Jun 4. Reductions vary by instance type and term, e.g., P5 sees up to 45% drop. This move aims to offset GPU scarcity and support genAI workloads. AWS also expands On-Demand capacity in key global regions and introduces P6-B200 via Savings Plans for large-scale ML deployments (AWS News Blog)

- CoreWeave stock rose ~3% after it reported record-breaking MLPerf Training v5. 0 results using Nvidia’s GB200 Grace Blackwell GPUs. Partnering w/ Nvidia & IBM, CoreWeave deployed 2,496 GPUs—30x larger than any other cloud participant—to train Meta’s Llama 3.1 405B model in just 27 mins. The Co claims its infra enables clients to deploy AI models months ahead of rivals, cutting dev time & cost (Yahoo Finance)

- Snowflake annc’d plans to acquire Crunchy Data to integrate its enterprise-grade Postgres tech into the AI Data Cloud. Snowflake Postgres will offer full Postgres compatibility, robust governance, and security for AI apps. The move supports regulated workloads and expands Snowflake’s transactional data capabilities. Partners like Blue Yonder and LandingAI will benefit from faster deployment and improved efficiency (Street Account)

Crypto/Blockchain/web3/NFTs

- Uber is exploring stablecoins to enable faster settlements & cut FX costs across global ops. CEO Dara Khosrowshahi said dollar-pegged stablecoins could streamline cross-border payments, reduce banking intermediaries, & enhance liquidity mgmt. The move aligns w/ broader blockchain adoption trends. Challenges include regulatory compliance & digital asset security. (AInvest)

- Meta shareholders overwhelmingly rejected a proposal to explore Bitcoin as a treasury asset, w/ <1% support. Submitted in Jan. by Ethan Peck, the plan cited Bitcoin’s 124% 2024 surge as a hedge vs. inflation & weak bonds. Despite backing from Strive Asset Mgmt’s CEO Matt Cole, nearly 5bn shares voted no. The proposal ranked last among 14 on the ballot. GameStop & Metaplanet have pursued similar Bitcoin strategies (DL News)

Cybersecurity/Security

- AT&T suffered a massive data breach exposing PII of ~44mn subscribers. Data—names, DoBs, emails, addresses, phone numbers, & 43,989,219 SSNs—was leaked on a Russian forum. Hackers decrypted the data, heightening ID theft risks. Linked to Apr 2024 Snowflake breach, ShinyHunters claimed responsibility. AT&T hasn’t confirmed if this is a new breach. Experts urge credit freezes, MFA, & account monitoring to mitigate threats (Cord Cutters News)

- Oregon Gov Tina Kotek signed a law banning cos from selling precise location data (within 1,750-ft radius) and restricting targeted ads to users under 16. The law amends the 2023 privacy act, which only required opt-in consent. Ad industry groups opposed the bill, citing marketing challenges, while privacy advocates like EPIC and Consumer Reports supported it, citing safety and data misuse concerns (MediaPost)

- CrowdStrike’s Q1 results beat estimates, showing strong demand for its cybersecurity svs despite recent cost cuts. Rev rose 33% Y/Y to $921mn, topping forecasts. Adj EPS hit $0.93. However, FY rev guidance of $3.98bn–$4.01bn fell short of expectations. CEO George Kurtz said the Co remains focused on profitable growth, leveraging AI to enhance threat detection and customer value (Bloomberg)

- Google warned that hackers are exploiting Salesforce flaws to steal sensitive cos data, targeting misconfigured integrations between Salesforce and third-party apps. Attackers use phishing and session hijacking to access CRM systems. Google’s Threat Analysis Group said multiple industries are affected, urging cos to audit access controls. Salesforce stated it’s working closely w/ impacted clients to mitigate risks (Bloomberg)

- CrowdStrike revealed it received inquiries from DOJ and SEC regarding its accounting practices. The focus is on revenue recognition and customer contracts. Co stated it’s cooperating fully and believes its practices comply w/ GAAP. The disclosure comes amid broader scrutiny of tech cos’ financial reporting. Analysts say the probe could weigh on investor sentiment despite strong biz fundamentals (Bloomberg)

eCommerce/Social Commerce/Retail

- US toy sales rose 6% YoY (Jan–Apr), w/ unit sales up 3%. Adults (18+) drove growth, spending $1.8bn in Q1—12% more YoY—becoming the top spending group. Sales surged for toys priced <$15 & $20–$69.99, while mid-tier toys lagged. Collectibles like Pokémon & sports cards fueled demand. Consumers are either “trading up or pulling back.” Despite rebound, tariffs & e-comm disruptions challenge cos. Nearly 80% of US toy imports come from China (Retail Dive)

- Procter & Gamble plans to cut ~7,000 jobs globally over 2yrs, mainly in non-manufacturing roles, as part of a cost-saving strategy amid automation & AI adoption. The move aims to streamline ops & boost productivity. P&G expects to save $1.3bn in labor costs. Cuts will span multiple regions & functions, but frontline manufacturing roles are largely unaffected. (Reuters)

- Lululemon beat Q1 expectations w/ EPS of $2. 60 (vs. $2.58 est.) & rev of $2.37bn (vs. $2.36bn est.), but cut FY EPS guidance to $14.58–$14.78 (from $14.95–$15.15) citing a “dynamic macroenvironment.” Net income was $314mn. Shares fell ~20% Tariffs & economic uncertainty pressured outlook. Q2 rev forecast: $2.54–$2.56bn; FY rev unchanged at $11.15–$11.3bn. CEO said Lululemon will “play offense” despite headwinds (CNBC)

- Dollar General raised its annual outlook after Q1 results beat expectations, signaling resilience amid tariff pressures. The Co now expects same-store sales to rise up to 2.5% this fiscal yr, up from Mar guidance of 2.2%. EPS forecast was also lifted. CEO Todd Vasos said the Co is attracting more higher-income shoppers, reflecting shifting consumer behavior. DG aims to offset much of the tariff impact through strategic sourcing and pricing (Bloomberg)

- Dollar Tree warned of a profit hit due to inflation, reduced gov’t aid, and rising theft, causing shares to fall ~14% (Wed, Jun. 4). Co plans to close ~600 Family Dollar stores in H1 FY24 and another 370 Family Dollar & 30 Dollar Tree stores as leases expire. Despite 12% rev growth, Family Dollar saw a 1.2% drop in same-store sales. Co also plans to introduce items priced up to $7 to boost margins. Shrink remains a key headwind (Bloomberg)

- Costco held prices on tariff-impacted staples like bananas and pineapples by absorbing margin hits and working w/ suppliers to protect members. CFO Gary Millerchip said the Co prioritized essentials over discretionary items like flowers. Strategies included rerouting goods, pulling forward purchases, and expanding Kirkland sourcing. Q3 net income rose to $1.9bn, w/ net sales up 8% to $61.96bn despite macro headwinds (Retail Dive)

- Despite expectations, tariffs haven’t yet triggered major price hikes. Fashion retailers are absorbing costs to retain customers, fearing demand loss. Many stocked up pre-tariff to delay impact. Price sensitivity keeps pricing stable, while low svs inflation (e.g., travel, dining) offsets pressure. However, signs of inflation are emerging as large cos like Walmart and Macy’s begin raising prices. Long-term, strategic hikes or cost cuts are inevitable (Business of Fashion)

- NJ strip malls are reinventing to become “Amazon-proof” by adding gyms, med spas, pickleball courts, and entertainment to attract foot traffic. Developers are shifting from retail-only to mixed-use formats, integrating dining, wellness, and svs. Leasing demand is strong, w/ vacancy rates falling. Cos like Urban Edge and Onyx Equities are leading the trend. Experts say experience-driven tenants are key to long-term viability (com)

- Off-price retailers face more tariff pressure than expected, despite earlier beliefs they were shielded due to indirect sourcing. Evercore ISI est. ~40% of TJX’s U.S. imports last yr came from China. Retailers pivoted quickly—stockpiling before Apr.2 tariffs, pausing at 145%, then resuming at 30%. Fast-boat shipping may raise costs. Legal uncertainty remains after a court injunction Jun 4 was paused Jun 5 (Retail Dive)

Electric & Autonomous Vehicles

- China’s tightening grip on rare earth exports is disrupting global EV & defense supply chains. US automakers warn delays in export approvals could halt assembly in weeks. China refines 99% of heavy rare earths like neodymium & terbium, vital for EVs, turbines, & electronics. (Environmental Health News)

- Amazon is preparing to test humanoid robots for package delivery, marking a major step in its automation strategy. The robots, developed in partnership w/ Agility Robotics, aim to enhance last-mile logistics efficiency. Trials will begin in controlled environments before expanding. The move aligns w/ Amazon’s broader push into robotics and AI to reduce labor costs and improve delivery speed. Full rollout timeline remains undisclosed (The Information)

- Toyota has invested $250mn—the first half of a planned $500mn—into Joby Aviation to deepen their alliance in electric air mobility. The funding supports Joby’s scaled manufacturing plans near Dayton Intl. Airport. The Co has built 5 aircraft in Calif. & aims to expand w/ Toyota’s production expertise. The partnership strengthens their shared vision for sustainable, short-hop air travel (Dayton Daily News)

Film/Studio/Content/IP/Talent

- “Ballerina,” a spinoff from the John Wick universe starring Ana de Armas, is projected to open at $30–34mn, below the $73. 8mn debut of “John Wick 4.” Despite Keanu Reeves’ cameo, Lionsgate sees this as a test of the franchise’s reach. With an $80mn budget and 75% Rotten Tomatoes score, the film emphasizes stylized action. It’s part of a broader Wick expansion incl. “John Wick 5,” an animated prequel, and a Vegas immersive experience. (TheWrap)

- AMC Networks signed a deal w/ genAI firm Runway to use its tech for marketing images and pre-visualization of unproduced shows. AMC aims to cut content costs while maintaining quality across platforms like AMC+, Shudder, and Acorn TV. The AI tools won’t be used in final content but will aid creative planning and promo material generation. Execs see AI as a pivotal tech shift amid cord-cutting and profit pressures (The Hollywood Reporter)

- Mattel is merging its film & TV units to form Mattel Studios, aiming to streamline content dev & boost IP monetization. The move consolidates leadership under Josh Silverman, who will oversee franchise mgmt, content, and licensing. The Co seeks to expand its entertainment footprint following the success of the Barbie film & other IP-driven projects (Reuters)

FinTech/InsurTech/Payments

- Venmo annc’d a major commerce expansion w/ its Debit Mastercard & Venmo Checkout, enabling users to spend balances in-store/online w/ enhanced rewards. Q1 rev rose 20% YoY; Pay w/ Venmo volume up 50%+. Cardholders now earn 15% cashback at brands like Sephora, Lyft & McDonald’s. New features incl. tap-to-pay, auto top-ups, intl use, & FDIC pass-through. (Street Account)

- Chime Financial is targeting an $11. 1bn valuation in its IPO, aiming to raise up to $673.4mn by selling 32mn Class A shares at $24–$26 each. Existing investors plan to sell 6.1mn shares (~$158.6mn). On an undiluted basis, the Co would be valued at ~$9.5bn. 2024 rev hit $1.67bn (up 31% YoY), w/ net loss narrowed to $25.3mn. Chime had 8.6mn active accounts as of Mar.31. The IPO could pave the way for other fintechs like Klarna & Revolut (Axios)

HealthTech/Wellness

- 23andMe set a new auction after ex-CEO Anne Wojcicki submitted a $305mn bid to take the Co private. The offer, made via her firm Altos Labs, tops the previous $280mn bid from Francisco Partners. The auction will allow other bidders to respond. Wojcicki, who stepped down in 2024, still holds a significant stake. The Co has struggled w/ declining sales & data privacy concerns. Final bids are due later in Jun (Bloomberg)

- Peloton CEO Peter Stern stated he has no interest in selling the Co, emphasizing focus on reigniting innovation and leveraging AI to personalize fitness experiences. Speaking at Bloomberg Tech Summit, Stern highlighted initiatives like Personalized Plans, already used by 600K+ members, and tech-driven coaching to boost results. He reaffirmed Peloton’s long-term strategy centers on product, software, and human coaching integration. (Bloomberg)

- Hims & Hers annc’d plans to acquire European telehealth platform Zava, expanding into Ireland, France & Germany. The deal, set to close mid-yr, will grow its active customer base by ~50%, adding 1.3mn to its 2.4mn users. CEO Andrew Dudum said the move accelerates global expansion. Zava CEO David Meinertz will lead intl biz post-deal. Zava will retain branding for a few quarters before rebranding (CNBC)

- Neuralink, Elon Musk’s brain-computer interface Co, closed a $650mn Series E round led by ARK Invest, Founders Fund, Sequoia Capital & Thrive Capital. The Co has implanted brain chips in 5 individuals w/ severe paralysis & received FDA breakthrough device designation in May. The deal values Neuralink at ~$9bn pre-money. The Co aims to accelerate clinical trials & tech dev (TechCrunch)

Last Mile Transportation/Delivery

- China’s Didi reported Q1 rev of $5. 7bn, up 8.5% YoY, driven by domestic ride-hailing recovery & overseas expansion. Net loss narrowed to $100mn from $200mn YoY. Total ride orders rose 17% to 3.3bn. Didi’s int’l biz grew 25%, w/ strong demand in Latin America. The Co is investing in AI & autonomous driving to boost efficiency. Regulatory headwinds have eased since its 2021 crackdown, aiding gradual recovery (Reuters)

- Uber & DoorDash settled their legal dispute w/ NYC over delivery fee caps. Under the deal, the city will revise its permanent cap of $1.50/order to a tiered system based on restaurant size & order volume. In return, the cos will drop lawsuits filed in 2021. The agreement aims to balance fair pay for platforms & sustainability for local eateries. NYC Council will vote on the new structure later this summer (Bloomberg)

- Walmart & Wing annc’d expansion of drone delivery svs to Atlanta, Charlotte, Houston, Orlando and Tampa, making Walmart the first retailer to scale drone delivery across five states. The new svs will launch at 100 stores, building on existing operations in Northwest Arkansas&Dallas-Fort Worth. Wing operates w/in FAA guidelines, flying drones up to a 6-mile range. (The Verge)

- Lime renewed its multiyear agreement w/Uber, ensuring its shared bikes & scooters remain available on Uber’s app across the US, Canada, Europe, Australia & New Zealand. Uber One members will get 10% cashback on Lime rides. Lime, which saw 30%+ growth for four consecutive yrs, plans expansion into Mexico & Barcelona. The deal strengthens Lime’s position as a leading micromobility Co, w/Uber holding a 29% stake (The Verge)

- Meituan’s Keeta brand is expanding drone delivery svs in Dubai Marina, marking a significant overseas push. The Co secured regulatory approvals for Beyond Visual Line of Sight (BVLOS) operations, enabling wider coverage. The initiative aligns w/Dubai’s smart mobility goals, aiming for 33% drone delivery coverage by 2030. (Bloomberg)

- Deliveroo launched drone food delivery in Dublin via a pilot w/ Manna, enabling 3-min drop-offs at up to 80km/h. Operating in Blanchardstown, it serves diners within 3km from restaurants like Musashi & Boojum. Food is lowered via biodegradable tether, tracked in-app. The 6-month trial aims to expand to more eateries & retail, targeting hard-to-reach areas. Manna has completed 170K+ flights; expansion depends on regulatory approval (The Caterer)

Macro Updates

- Fed’s Beige Book showed US economic activity rose slightly, w/ 8 of 12 districts reporting modest growth. Consumer spending dipped, esp. in retail, while manufacturing stayed flat. Price pressures persisted but inflation showed signs of moderating. Cos face difficulty passing on higher costs as consumers grow more price-sensitive. Labor mkts eased slightly—more applicants, easier hiring. Global freight disruptions had limited impact on supply chains (Bloomberg)

- US trade deficit narrowed by a record $14bn in Apr to $68. 9bn, driven by a sharp 7.6% drop in imports—the steepest since Apr.2020. Imports of consumer goods, vehicles, & industrial supplies fell, reflecting cooling domestic demand. Exports slipped 0.5%, led by declines in food & capital goods. Economists say the plunge may be temporary, tied to shipping disruptions & inventory adjustments. The data could influence Fed’s inflation outlook (Bloomberg)

- Canada’s trade deficit hit a record $4. 3bn in Apr, as exports plunged 5.6%—the steepest drop since 2020—largely due to Trump-era tariffs on autos, aluminum, & lumber. Exports to the US fell 7.2%, while imports declined 1.4%. Energy exports dropped 8.5%, and auto shipments fell 6.9%. Economists warn prolonged tariffs could deepen the imbalance. The Canadian dollar weakened slightly post-release (Bloomberg)

- CBO projected Trump’s proposed tariffs could reduce the US budget gap by ~$2. 8tn over 10yrs, assuming full implementation and no policy reversals. The estimate is being used by GOP lawmakers to justify extending tax cuts, arguing tariff rev would offset deficit increases. Critics argue the burden would fall on US consumers and cos, not foreign entities, and question the long-term feasibility of such projections (Bloomberg)

- US hiring slowed to its weakest pace in 2yrs, w/ private payrolls rising by just 37,000 in May, per ADP data. This marked the 2nd straight month of underwhelming job growth, missing all economist estimates. Sectors like biz svs, education & health shed jobs. Analysts cite Trump’s trade policies as a growing concern for staffing. Labor mkts are expected to cool further, raising concerns over economic momentum (Bloomberg)

- US svs activity unexpectedly contracted in May for the 1st time in nearly a yr, w/ ISM index falling to 49. 9 from6, signaling contraction. New orders dropped sharply to 46.4, while prices paid rose to 68.7, indicating inflationary pressure. Employment edged up slightly to 50.7. The data suggests higher tariffs and economic uncertainty are weighing on the svs sector, aligning w/ weak ADP hiring figures (Bloomberg)

Media Conglomerates

- WBD shareholders rejected CEO David Zaslav’s $52mn 2024 pay in a nonbinding vote, amid a ~60% stock drop since the 2022 merger. Critics cite misaligned incentives and past $247mn stock-heavy awards. Despite debt reduction from $55bn to $38bn, S&P downgraded WBD’s credit rating. (Financial Times)

- Paramount Global nominated three new board directors as it awaits approval for a potential merger w/ Skydance Media. The nominees include former FCC chair Tom Wheeler, ex-Disney exec Angelique Brantley, and investment banker Charles Phillips. The move follows the exit of four directors and signals strategic alignment ahead of a possible deal. (Reuters)

- Disney laid off several hundred employees globally, impacting TV, film, marketing, publicity, casting, development, and corporate finance teams. The Co framed the move as a step toward operational efficiency. No departments were eliminated. This follows prior rounds of layoffs in Mar., Oct. and Sept. 2024. Despite cuts, Disney projects strong FY25 growth, incl. 16% EPS rise and double-digit gains in entertainment and sports segments (Variety)

- WBD initiated targeted layoffs across linear TV networks incl CNN, TNT, TBS, TCM, Discovery, and Food Network, affecting <100 staff. The move follows a 7% rev drop in linear TV biz to $4.7bn in Q1, driven by 12% ad & 9% distribution rev declines. Adj operating income fell 15% to $1.79bn. Layoffs aim to boost efficiency amid cord-cutting & streaming shift. Affected staff to receive severance & support. (Cord Cutters News)

Metaverse/AR & VR

- Meta is pursuing Hollywood partnerships to boost content for its next-gen VR headset, aiming to rival Apple’s Vision Pro. The Co is in talks w/ major studios to license immersive experiences and 3D films, enhancing its Quest ecosystem. Meta’s strategy reflects a broader push to blend entertainment and tech, positioning VR as a mainstream media platform. The new headset is expected to launch later this yr. (Wall Street Journal)

- Epic integrated MetaHuman Creator into Unreal Engine 5. 6, easing hyperrealistic character creation. New face-to-body tools boost customization. Devs can sell MetaHumans on Fab mkts. Real-time animation via webcam was demoed. Licensing now supports Unity, Godot, Maya, Houdini & Blender (The Verge)

- Meta’s Aria Gen 2 smart glasses feature AI-powered upgrades incl full eye-tracking, 3D hand tracking & a PPG heart rate sensor in the nosepad. Weighing 74–76g, they come in 8 sizes. Four computer vision cameras boost spatial awareness, while a global shutter sensor (120dB HDR) enhances visibility. A contact mic improves voice pickup. Folding arms aid storage. Still a research tool, Aria Gen 2 supports AI/robotics dev, not for commercial use (The Verge)

Online Travel

- Foreign air arrivals to the US have dropped 2. 5% amid growing global unease tied to Donald Trump’s political resurgence and proposed policies. Bloomberg’s analysis highlights how Trump’s rhetoric and potential return to the White House are deterring international travelers, especially from Europe and Asia. Travel industry leaders cite concerns over visa restrictions, geopolitical tensions, and a less welcoming perception of the U.S. as key factors behind the decline (Bloomberg)

Regulatory

- EU unveiled a digital foreign policy strategy to strengthen global tech partnerships, promote democratic values, and counter digital authoritarianism. The joint communication outlines goals to secure supply chains, enhance cyber resilience, and shape global digital rules. It emphasizes cooperation w/ like-minded partners, esp. in AI, 5G, and data governance. (Telecompaper)

- Trump called Elon Musk “CRAZY” and threatened to cut gov’t contracts to his cos, saying it would save “Billions and Billions. ” Musk fired back on X, threatening to decommission SpaceX’s Dragon spacecraft. The feud follows a fallout over a major tax bill. Tesla shares dropped sharply post-comments. Musk accused Trump of ingratitude and even suggested impeachment. (CNBC)

- FCC Commissioner Nathan Simington annc’d his departure by week’s end, leaving only Brendan Carr (R) & Anna Gomez (D) active. W/ Geoffrey Starks (D) also exiting this month, the FCC lacks a quorum (min. 3 members) to act officially. Simington, appointed by Trump in Dec. 2020, focused on free speech, nat’l security & infrastructure. Olivia Trusty is nominated for the GOP seat, pending Senate confirmation. Ownership & streaming rules remain under discussion (MSN)

- Google to appeal EU ruling on antitrust case over Android search practices, arguing the decision ignores how Android fosters competition. EU regulators upheld a $4.3bn fine, claiming Google imposed illegal restrictions on device makers to cement its search dominance. Google cont’d to defend its model, stating it offers choice and supports innovation. The Co plans to challenge the ruling at the EU’s highest court (Reuters)

- EchoStar opted not to pay ~$183mn in cash interest due on 3 DISH DBS note series: $72. 2mn (5.25%, 2026), $71.9mn (5.75%, 2028), and $38.4mn (5.125%, 2029). This constitutes a default under indentures, though a 30-day grace period applies before it becomes an Event of Default. The Co. cited the move as strategic, awaiting FCC relief. The decision highlights EchoStar’s reliance on regulatory intervention amid financial strain (Bloomberg Law)

- Trump admin is expanding its review of federal contracts, now targeting tech cos after previously focusing on consulting firms. The move could impact major players in AI, cloud & defense tech. Officials aim to scrutinize ties between federal spending & firms perceived as politically misaligned. This shift signals a broader strategy to reshape gov’t procurement under Trump’s leadership (Wall Street Journal)

Satellite/Space

- SES annc’d the appointment of Lisa Pataki as new CFO, effective Jul. 1. She succeeds Sandeep Jalan, who steps down after 4yrs. Pataki joined SES in 2022 as Deputy CFO & SVP Group Controller, previously holding senior finance roles at Telenor & PwC. (Telecompaper)

- Orange signed a multi-yr deal w/ Eutelsat Group to use OneWeb’s LEO satellite fleet for enhanced connectivity in remote regions. The agreement supports Orange’s goal to expand high-speed broadband across Europe, Africa, Latin America, and other underserved areas. OneWeb’s LEO tech offers low-latency, high-capacity links, complementing Orange’s terrestrial & satellite networks. Deployment will begin in 2025, boosting digital inclusion efforts (Telecompaper)

- AST SpaceMobile stock climbed after an analyst flagged potential investment interest from Amazon’s Jeff Bezos. The speculation follows AST’s recent satellite success and growing momentum in space-based cellular broadband. While no official confirmation has been made, the market responded positively to the possibility of strategic backing from a high-profile tech figure, boosting investor confidence (Benzinga)

- Elon Musk said SpaceX’s 2025 rev is ~$15. The Co is targeting ~$9bn from Starlink and ~$6.5bn from launches. Musk noted Starlink is nearing breakeven and could be spun off via IPO in the coming yrs. (Bloomberg)

- Telstra has launched satellite-to-mobile messaging in partnership w/ Starlink, enabling text svs in remote areas across Australia. The initial phase supports SMS on select devices, w/ plans to expand to voice & data in 2025. The move aims to enhance connectivity in underserved regions. Telstra is the first in Australia to integrate Starlink’s direct-to-device tech (Telecompaper)

- Eutelsat is seeking €1. 5bn in funding to expand its LEO satellite constellations & better compete w/ Starlink. Talks involve the French govt, Fonds Strategique de Participations, CMA CGM & UK govt. The French govt’s stake could rise from 13.6% to 30% if the deal proceeds. Funds will also support Eutelsat’s role in the EU’s IRIS2 mega-constellation, which needs €2bn+ (Advanced Television)

Social/Digital Media

- Apple lost its bid to pause a court order requiring App Store reforms from the Epic Games case. The US Supreme Court declined Apple’s request , meaning it must allow developers to direct users to external payment options. The ruling stems from a 2021 antitrust suit by Epic. Apple argued the changes could harm users, but courts upheld the injunction. The Co must now comply while continuing to appeal parts of the decision (Reuters)

- A lawsuit filed challenges Florida’s new law banning social media for kids under 14 and requiring parental consent for ages 14–15. NetChoice, a tech trade group, argues the law violates First Amendment rights and is unworkable. Gov. Ron DeSantis defends it as protecting minors from online harm. The law, set to take effect Jan.1, faces scrutiny over enforcement and constitutional validity (AP News)

- Roblox is facing pressure from marketers demanding third-party ad measurement tools. While ad rev remains a small part of its $3.6bn 2024 rev, it’s key to future growth. Agencies say lack of tools like Nielsen/Comscore hinders new brand adoption. Roblox is working w/ partners like Google, Kantar, IAS & Nielsen to improve transparency. Despite progress, buyers warn of a ceiling without verified metrics (Digiday)

- Chinese social app Xiaohongshu reached a $26bn valuation, boosting GSR Ventures’ fund performance. The Co’s valuation rose after a recent funding round, reflecting strong user growth and monetization. GSR, an early investor, saw its fund value surge, aiding LP returns. Xiaohongshu blends eCommerce w/ social content, appealing to Gen Z. The Co is reportedly eyeing a Hong Kong IPO, though timeline remains uncertain (Bloomberg)

Software

- MongoDB beat Q1 expectations w/ adj EPS of $1 vs. est. $0.67 and rev up 22% YoY to $549mn. Atlas rev rose 26%, driving strong performance. Co posted net loss of $37.6mn, improved from $80.5mn YoY. Operating cash flow hit $109.9mn. Customer base grew to 57,100, w/ 55,800 on Atlas. Co raised FY guidance and expanded buyback program. Shares surged 13% after-hours, adding to earlier 3% gain (SiliconANGLE)

Sports/Sports Betting

- Justin Ishbia reached a deal to acquire controlling interest in the Chicago White Sox. Under the agreement, current owner Jerry Reinsdorf can sell control to Ishbia between 2029–2033, while Ishbia gains the right to buy after the 2034 season. All limited partners may sell to Ishbia in such a transaction. Ishbia, already a minority owner, shifted focus from buying the Twins to increasing his Sox stake. No relocation plans were mentioned (Bleacher Report)

- Vince McMahon sold over 1. 5M shares of TKO stock (~$250mn) to Endeavor earlier this week (Mon, Jun 3), reducing his stake to ~3.25%. This move follows rumors—sparked by Jonathan Coachman’s podcast—that Vince might want to buy back WWE. However, the sale contradicts that idea. Since resigning in Jan.2024 amid legal allegations, Vince has sold nearly $2bn in TKO stock and is reportedly investing in a new entertainment Co, 14th&I. (Cageside Seats)

- NBA Playoffs viewership is up 3% YoY, averaging 4. 5M viewers across ESPN, ABC, and TNT. ABC leads w/ 5.3M avg viewers, boosted by strong Eastern Conference Finals. TNT follows w/ 4.4M, while ESPN trails at 3.9M. The NBA Finals, airing on ABC, are expected to lift overall numbers further. Analysts credit competitive matchups and star power for the uptick in audience engagement. (MediaPost)

- Apple TV is a leading candidate to acquire MLB rights relinquished by ESPN after this season. ESPN opted out of its deal covering Sunday Night Baseball, early playoff rounds, and the Home Run Derby. Apple is eyeing a broader package than NBC, which is targeting Sunday nights. A potential 3-yr deal would bridge to 2028, when MLB’s Fox and TNT deals expire. MLB may split rights to balance reach (NBC) and rev (Apple) (Awful Announcing)

- Fubo and DAZN annc’d a multi-yr integrated partnership, enabling reciprocal distribution of their O&O linear channels in the U. S. Fubo now offers DAZN1, a new channel w/ exclusive boxing & MMA content, available as a stand-alone or add-on. DAZN adds Fubo Sports FAST channel, featuring ~400 live events/yr, to its platform. Fubo will also carry DAZN’s PPV events. Future collabs between cos to be annc’d (Street Account)

- Illinois annc’d a new sports betting tax hike, impacting major operators like DraftKings and FanDuel. The new levy charges $0.25 per bet for the first 20mn wagers, then $0.50 per bet beyond that. Based on TTM data (Apr.24,2024–Mar.25,2025), FanDuel and DKNG would owe ~$77mn and ~$68mn respectively. If implemented, est. H2 impact is ~$40-45mn for FLUT and ~$35-40mn for DKNG. The state expects to raise $36mn in new rev (org)

Tech Hardware

- Apple TV boxes offer stronger privacy than most streaming devices by disabling Siri, location tracking & analytics sharing by default. They avoid ACR tech & require apps to request tracking permission via IDFA. Users can control app access to Bluetooth, photos, music & mic. Apple’s biz model, less reliant on ads, reduces incentive to harvest data. Still, using Apple ID or Apple TV app shares more info (Ars Technica)

- Samsung is nearing a deal w/ Perplexity to integrate AI features into its devices, incl. Galaxy smartphones. The partnership may bring Perplexity’s AI-powered “answer engine” to Samsung’s native apps, enhancing search & productivity tools. Talks are advanced but not finalized. The move reflects Samsung’s push to compete in the AI race amid rising demand for on-device genAI capabilities. (Bloomberg)

Towers/Fiber

- T-Mobile will officially launch T-Mobile Fiber, following its acquisition of Lumos. New plans include Fiber 500 ($60/mo), Fiber 1 Gig ($75/mo), and Fiber 2 Gig ($90/mo), all w/ no data caps, no contracts, and Whole Home Wi-Fi on higher tiers. A special Fiber Founders Club offers 2 Gig at $70/mo w/ a 10-yr price guarantee. Customers also get T-Mobile Tuesdays perks like free MLB.TV and MLS Season Pass (Cord Cutters News)

- Vodafone UK and Three UK completed their £15bn merger after nearly 2yrs, forming VodafoneThree, now the UK’s largest mobile operator w/ ~27mn users. CEO Max Taylor will lead the Co, which plans to invest £11bn over 10yrs to build a next-gen 5G network. £1.3bn will be spent in Yr1 to accelerate rollout. The merger is expected to yield £700mn/yr in cost and capex synergies by Yr5 and boost adj free cash flow from FY29 (Fierce Network)

- BT has launched a new standalone international biz division to serve 1,000+ multinational customers across 180 countries. The unit will operate independently from BT Group’s UK operations, focusing on network, cloud, and security svs. The move aims to streamline operations, enhance customer focus, and drive growth in global mkts. Bas Burger will lead the new division (Telecompaper)

Video Games/Interactive Entertainment

- GTA 6’s delay to May 2026 has reshaped the gaming calendar. During Sony’s State of Play , many publishers locked in Sept/Oct release dates, filling the gap left by Rockstar. Titles like Hirogami (Sept.3), Baby Steps (Sept.8), and Silent Hill F (Sept.25) now headline a crowded fall. Industry insiders say devs waited for GTA 6’s date before finalizing plans. With Rockstar out of 2025, publishers are seizing the open window (Kotaku)

- Nintendo Switch 2 is now officially available. Target restocked consoles offering the Mario Kart World bundle for $499.99 & standard model for $449.99. Other major retailers like Walmart, GameStop, & Best Buy are currently out of stock. (IGN)

- Unity CTO Steve Collins has stepped down just six months after joining from King, citing personal reasons. His exit follows a turbulent period for Unity, including a controversial pricing model change in 2023, CEO resignation, and 25% workforce reduction. While Unity claims Collins’ departure isn’t linked to past turmoil, it marks another exec shakeup as the Co continues its tech transformation (TechCrunch)

- Sony’s State of Play revealed a mix of surprises and updates. Highlights included Marvel Rivals, a team-based fighter from Arc System Works, and a remake of Final Fantasy Tactics. Capcom’s Pragmata got delayed again, now set for 2026. Silent Hill f launches Sept.25. Other reveals: Lumines Arise (Fall 2025), Romeo Is a Deadman (2026), Bloodstained: The Scarlet Engagement, and new Astro Bot DLC. PSVR2 titles also featured (Kotaku)

- Fortnite’s Switch 2 port delivers major upgrades incl. 60FPS, 4K resolution (docked), improved draw distance, and dynamic clothing physics. Epic added mouse support via Joy-Cons, full desktop renderer, and high-detail effects. Players must delete the old version and redownload the new one to access all features. All content transfers remain intact. The upgrade is free and brings parity w/ PS4 Pro/Xbox Series S (Kotaku)

- Activision drew criticism after ads for bundles & battle passes appeared in CoD: Black Ops 6 & Warzone menus post-Season 4 update. Ads showed in loadout/class creation screens, sparking backlash. Activision claimed it was a UI test “published in error” & removed it. Players suspect it was a monetization trial balloon, citing frustration over ads in a full-price game (Kotaku)

Video Streaming

- Fubo expanded its live sports lineup by adding PPV events in Jun, incl CONCACAF World Cup 2026 Qualifiers on Jun 7 & Jun 10, and the Wilder v Herndon boxing match on Jun 27. Events are open to all US viewers—no Fubo sub needed. Soccer matches cost $29.95 each; boxing $24.95. Buyers also get access to Fubo Free’s 200+ FAST channels. Fubo aims to offer flexible, premium sports content at attractive prices (Street Account)

- Netflix’s Tudum fan event in São Paulo highlights its studio-driven global strategy, showcasing stars and content from 20+ countries. The event reflects Netflix’s pivot from licensing to owning IP, with execs emphasizing local production and global reach. With 40% of viewership from non-English titles, Netflix is investing in regional studios and talent to fuel growth and deepen engagement worldwide. (Reuters)

- Netflix and Canal+ signed a landmark deal to distribute Netflix content across 24 Francophone African countries. Starting next month, Canal+ subscribers will access global hits like Stranger Things and Squid Game, alongside African originals like Blood & Water and Blood Sisters. This pact supports Netflix’s strategy to grow in underpenetrated mkts, while Canal+ extends its super-aggregation model beyond Europe. (The Hollywood Reporter)