Nasdaq and the S&P 500 continued to edge higher, once again hitting fresh new record highs during the week (Nasdaq was up +1.5% while the S&P 500 rallied +0.6%). Concerns about the Fed’s independence and the rate cut trajectory, especially in light of the stronger economic indicators such as better-than-expected June retail sales figures, were key macro areas of focus, along with the continued trade talks/negotiations.

Within the sector, earnings is off and running with Netflix and the ad agencies the main prints this week. Our view on the most important themes/updates/developments in TMT this week are below:

- Netflix: Another Steady As She Goes Qtr, Though Some Investors Were Hoping For More

- Ad Agencies: The Cloud Of Uncertainty Remains But Some Agencies Are Faring Better Than Others…

- Company Spotlight: AST SpaceMobile Is Pushing Forward The Next Iteration Of Consumer Connectivity…Satellite Direct To Device

- America’s Infrastructure Revival Continues To Accelerate

- Recent Consumer Spending Trends Surprise On The Upside

- Retail Vacancy Rates Ticked Up, But Demand Remains Healthy In High-Traffic Areas

- Grab Bag: OpenAI Launches ChatGPT Agent / Uber-Lucid-Nuro Robotaxi Deal / Peacock Raises Prices Yet Again

Have a nice weekend.

Best,

Leslie

Netflix: Another Steady As She Goes Qtr, Though Some Investors Were Hoping For More

While Netflix’s better-than-expected headline Q3 results and higher 2025 guidance was a good outcome, some investors had hoped for a cleaner beat given most of the upside and improved outlook was due to favorable FX moves, hence the knee jerk negative stock reaction. With that said, the underlying business is showing nice growth with revenues accelerating from +13% y/y (or +16% y/y FX-neutral) in Q1 to +16% y/y (+17% FXN) in Q2, which slightly beat cons by +0.2%. UCAN in particular posted an impressive y/y rev growth acceleration from +9% to +15%, respectively, given the effects of a full qtr of price increase. Operating margins at 34% also stood out, and FCF came in well ahead of consensus. The Co doesn’t provide subscriber details any more but mgmt indicated that member growth was ahead of their plan, albeit back-end loaded so it had a limited impact on Q2 performance.

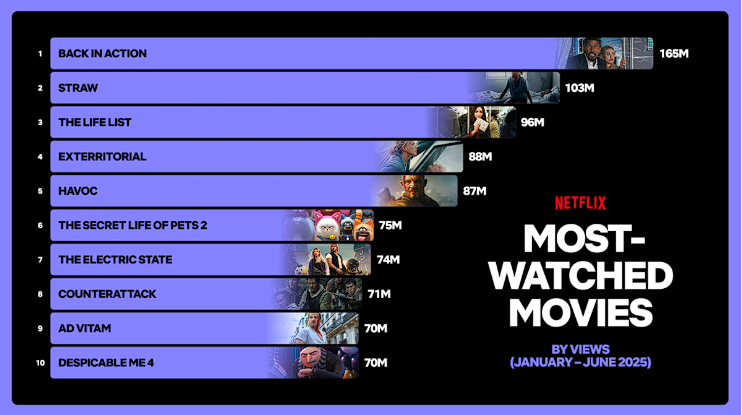

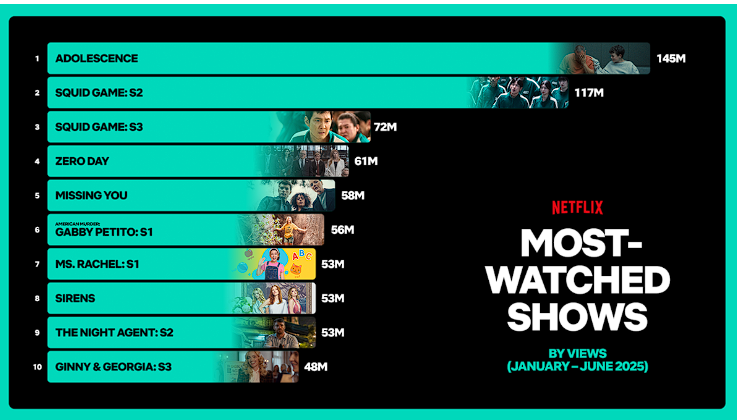

Progress with the Co’s ads business is moving right along and the Netflix Ad Suite being rolled out across all markets was a key milestone. Advertisers will now find it much easier to buy on the platform. Positive early feedback coupled with a strong US upfront gives confidence that the Co will hit its goal of doubling ad revenue this year. The content slate also continues to deliver with several global hits in Q2 and a strong pipeline into H2 and 2026. Concurrently with earnings, Netflix published its H1 bi-annual engagement report which breaks out the most watched shows & films and is always interesting to peruse (I’ve added a couple to my watch list! Here’s the link).

AI was a point of conversation, and the Co anticipates a positive impact across the board – for its creators, customers, and business. There was some concern on the conference call about “stagnating” member engagement numbers, but mgmt believes H2 engagement will improve from H1 on the back of the strong slate.

Overall, Netflix has been one of the top performers in the sectors and with that comes high expectations. Even with the pull-back in reaction to this print, the stock is still up +35.7% YTD, vastly outperforming Nasdaq’s +8.2%. In our mind, this qtr was more of a steady as she goes qtr (similar to last qtr) and the Co will remain squarely focused on the 80% of TV viewing that neither YouTube nor Netflix is winning right now. The Co is also insulated from many of the macro sensitivities that have, or will have, an impact on other companies and industries, at least in the near-term.

-> NFLX shares initially fell slightly in reaction to earnings but closed the day post earnings flat; As noted, the stock is still up +36% YTD, making it one of the best performing stocks in our Universe

Q2’s Beat Was Mainly Driven By Favorable FX In The Period

- Rev growth accelerated to +16% y/y (+17% FX-neutral) from +13% y/y (+16% y/y ex-FX) in Q1 & slightly beat cons by +0.2%

- However, the beat vs guidance was “primarily” b/c of favorable FX

- Member growth was “ahead of plan”, though back-end weighted in the qtr so it didn’t have much of an impact in Q2

- The Co has not seen any change in consumer behavior / key consumer metrics…retention, plan take rate, and plan changes are all ~ the same and stable

- Op margin of 34% was a standout (up +7bp y/y) due to rev upside and expense timing and easily topped cons 32.8%

- Adj EPS (+47% y/y) beat cons by 1.7% and FCF was 7.4% ahead of cons

- All regions posted y/y growth (all posting DD FXN increases) and UCAN rev growth, in particular, accelerated to +15% y/y, from +9% in Q1 given the benefit of a full qtr of price increases

- In addition to UCAN, EMEA revs came in stronger than expected

- Latam and AsiaPac both missed Street projections

The Higher 2025 Guidance Was Also Mostly FX Driven

- Q3 guidance topped Street ests

- Revs: $11.53bn (+17% y/y growth both reported and FXN) was above cons $11.28bn

- Op margin: 31% compared to cons 30.8%

- Adj EPS: $6.87 was above cons $6.69

- Raised 2025 guidance BUT primarily reflects the weakening of the US dollar vs. most other currencies

- Incr’d rev guidance from $43.5-$44.5bn to $44.8-$45.2bn (above cons $44.55bn): Implies +15-16% y/y growth (+16-17% FXN)

- The majority of the increase in rev guidance was due to FX moves (weakening $ vs other currencies) with the rest was due to biz momentum

- Incr’d FXN op margin guidance from 29% to 29.5% (or 30% on a reported basis)

- However, the H2 op margin will be lower than H1 due to higher content amortization and higher Sales & Mkting costs given the larger slate in the period (op margins will still be up y/y in both Q3 & Q4)

- Incr’d 2025 FCF guidance from ~$8bn to $8-8.5bn due to higher revs & op margins

- Incr’d rev guidance from $43.5-$44.5bn to $44.8-$45.2bn (above cons $44.55bn): Implies +15-16% y/y growth (+16-17% FXN)

The Co Is Still On Track To Double Ad Revenue In 2025

- As a key milestone, the Co completed the rollout of Netflix Ad Suite across all ad markets & early results are in-line w/ expectations: The “main benefit” is that it will make it easier for advertisers to buy on the platform

- It positions the Co to offer better measurement, enhanced targeting, innovative ad formats and expanded programmatic capabilities

- Netflix will also roll out other demand sources like Yahoo

- The US upfront is nearly complete w/ the major agencies & results have been in-line to slightly better and consistent with the goal of roughly doubling the ads business this year

- Other planned ad features –

- Improved targeting and measurement

- Leveraging advertiser and 3P data sources

- Improve ad experience for members with personalization and relevance

- Interactivity will be intro’d in H2

Netflix’s Deep & Diverse Content Slate Continues To Propel The Service But The Co Needs To Continue To Deliver A String Of Hits…

- Key content drivers in Q2 include:

- Hit series: Squid Game S3, Sirens, Ginny & Georgia S3, The Eternaut and Secrets We Keep

- Hit films: Tyler Perry’s STRAW and Exterritorial

- Concurrently with its earnings, the Co released its H1 bi-annual engagement report with the most watched shows & films – see top 10 lists below (link to report)

- Members watched 95mn+ bn hours on Netflix in H1, +1% y/y

- Non-English language TV & films represented more than 1/3 of all Netflix viewing in H1

- Almost 50% of viewing on Netflix Originals came from titles launched in 2023 or earlier

- Members watched 95mn+ bn hours on Netflix in H1, +1% y/y

- The Co has a strong H2 slate, which includes:

- Wednesday S2

- The Stranger Things finale

- The Canelo-Crawford live boxing match

- Happy Gilmore 2

- A House of Dynamite

- Frankenstein

- This strong slate rolls into 2026, which includes:

- The Rip w/ Ben Affleck and Matt Damon

- Enola Holmes 3 w/ Millie Bobbie Brown

- Great Gerwig’s Narnia

- Return of Bridgerton, One Piece, Avatar: The Last Airbender, The Gentleman, The Four Seasons, Running Point, Beef, 3 Body Problem, Love is Blind, Outer Banks

- New content like Man on Fire, reimagining of Little House on the Prairie, The Boroughs (new show from The Duffer Brothers)

- The Co still need a steady drumbeat of shows/films and “eventually games”…each content hit success drives <1% of total viewing

- Quality of content is important: Netflix received 120 Primetime Emmy nominations across 44 titles

- No changes to overall philosophy on sports content and live strategy

- TF1 partnership goes live in the summer of 2026 and will be an oppty to learn

Netflix Anticipates That AI Will Bring Significant Benefits All Around

- Mgmt is “convinced” AI is a tremendous oppty for creators to make films and series “better” and “not just cheaper”

- Their creators are already seeing the benefits with pre-visualization and shot planning work and certainly visual special effects (which used to be just for big studios)

- These tools are expanding the possibilities of storytelling on screen

- See “tons” of oppties with the member experience

- Personalization still has a lot of room for improvement

- The Co is piloting conversational experiences for consumers

- Advertising is another “great area” to be enhanced with AI

Other Key Comments/Updates

- The Co is focused on growing engagement: In response to analyst questions about “stagnating” viewing share domestically, mgmt flagged that the main engagement metric they track is “per owner household engagement” which has been steady over the last 2 years throughout the rollout of paid sharing – but they want that to grow

- Outlook: Mgmt thinks engagement growth in H2 will be better than H1

- The Co believes that the full bundle will remain its approach for the foreseeable future but “never say never” regarding moving to some type of tiering for the services and not making all content available to everyone

- Ultimately, the Co is balancing giving users choice, providing good accessibility & attractive price points, and driving reasonable returns for the business

- Regarding the new UI on the homepage, the Co is seeing better performance than the pre-launch testing which gives incr’d confidence it will drive better performance

- Netflix remains squarely focused on the 80% of TV viewing that neither YouTube nor Netflix is winning right now

- Not much new was said regarding the gaming initiative – strategy remains the same

- Continue to invest in immersive, narrative games based on their IP

- Need to get more scale before monetization becomes a “materially relevant” consideration

- The TAM remains large

- Mgmt reiterated that they have no interest in legacy media assets but consolidation on that front is likely to occur

Ad Agencies: The Cloud Of Uncertainty Remains But Some Agencies Are Faring Better Than Others…

WPP’s surprise negative pre-announcement last week, and the resulting -15% stock drop, sparked renewed concern about the health of the ad market and agency landscape. That put extra focus on Omnicom’s (OMC) and Publicis’s (PUB) earnings this week to see whether they’d confirm a broader slowdown.

The quarters themselves for both OMC and PUB were in-line to better-than-expected with the former reporting slightly higher than expected Q2 organic revenue growth of +3% (led by strength in the Media business) and in-line adj EBITDA margins (15.3% flat y/y). Meanwhile, Publicis’s +5.9% organic growth was well ahead of cons +4.6% and driven by gains in Connected Media plus a rebound at Publicis Sapient. The Co also posted an “industry-leading” operating margin of 17.4%.

The outlook, however, was a little squishy. OMC acknowledged some delays in client decision-making, though framed them as temporary and emphasized continued strong engagement with clients and business pitches (and seemed to take a dig at WPP). Publicis echoed a similar sentiment, noting clients remain “very combative, but also cautious.” At the same time, client investment levels held steady through Q2 which was a plus, but the Co did caution that new business activity is expected to slow down in Q3 vs Q2, which caused some investor angst especially after WPP’s comments last week. Even with a layer of cautiousness, unlike WPP, both OMC and PUB maintained or raised their 2025 guidance, with OMC reiterating prior targets and PUB raising its organic growth outlook to “close to” 5%, vs prior guidance of +4-5%.

Regarding the pending OMC/IPG merger, the recent approval in the US was a critical milestone and OMC is confident in securing approval from the 5 remaining jurisdictions (the biggest being the EU). The deal is still seen as on track for a H2 close. Commenting on the merger, PUB is not worried about a changing competitive landscape and noted that “the reason why we are winning today is not because we are the second biggest in term of scale of media, it’s because we are the first in term of innovation.” The Co also threw out that the merger is an opportunity for them to potentially poach talent.

AI was a big focus on the earnings call with more than one analyst raising concerns about the potential dilutive impact to the industry. Both firms dismissed those concerns, viewing AI as a tool to enhance efficiency, creativity, and client returns and believing it will ultimately drive greater marketing spend rather than reduce it. Time will tell and this is likely to remain a hot button for investors as we see how this unfolds in practice.

See below for more on what we found most incremental from OMC’s and PUB’s results and earnings.

-> OMC shares rallied +4.6% on the back of results but ended the week down -2.3%; Publicis closed the day post results flat but fell -6% for the week; IPG also fell -2.3% this week while WPP didn’t recover from its free fall last week; YTD, Publicis is down -8%, IPG -14%, OMC -17%, and WPP -46%

Both Omnicom & Publicis Report Better Than Expected Q2 Results

- OMC – Q2 results were slightly better than expected w/ +3% organic revenue growth vs +2.8% (after slightly missing in Q1): FX rev impact was a +1.1% increase in reported revenue; Acqs & dispositions impact was +0.1% in Q2

- Verticals

- Media & Advertising: +8%, led by strong media performance & mixed ad performance

- Precision Marketing: +5%, driven by US digital & CRM strength offset by mixed intl

- Public Relations: -9%, primarily in the US, due largely to weaker performance in global networks & some reduction relative to the benefit in 2024 from national election spend; Expect to see a difficult comp for the rest of 2025

- Healthcare: -5%, due to a client loss & brand wind-downs; Continue to expect improved performance as the year progresses

- Branding & Retail Commerce: -17%, pressured by market uncertainty

- Experiential: +3%, U.S. strength offset by declines in China & Middle East

- Execution & Support: +1%, U.S. growth offset by Europe

- Regions – growth across all regions, w/ the exception of the U.K

- US (~52% of rev): +3%

- Other N. Amer: +2.4%

- UK: -2.5%

- Europe: +2.5% (although mixed by mkt)

- Asia Pac: +6.5%

- LatAm: +18%

- ME and Africa: +0.9%

- Verticals

- OMC – Adj EBITDA @ 15.3% was inline w/ cons (and flat y/y); Adj EPS beat by 1.5%

- OMC – On track to repurchase $600mn in 2025: Bought back $142mn in Q2 following $81mn in Q1

- If it weren’t for the IPG agreement, they “would probably be a lot more active in the market than we are currently”

- PUB – The +5.9% organic growth in Q2 easily beat cons +4.6%: This was a seq accel from Q1’s +4.9%; Accelerating ahead of 5-yr CAGR of +4.9% in Q2, despite incr’d macro uncertainty & external pressures

- Verticals

- Connected Media (~60% of rev): Up HSD, driven by Publicis Media’s scale, powered by Epsilon’s proprietary data

- Intelligent Creativity (~25% of rev): Up HSD, supported by “significant” new business wins and scope expansions in production and creative

- Technology (~15% of rev): Returned to growth (saw -MSD decline in Q1) and was “slightly positive” despite ongoing “wait and see” attitudes on CapEx spend affecting every IT consulting firm; Better-than-expected performance at Publicis Sapient drove most of the acceleration in group organic growth in Q2 vs Q1

- Regions

- US (58% of net revs): +5.3% growth, on top of plus +5.3% growth rate from last yr; Also an acceleration vs Q1 due to Publicis Sapient turning positive this qtr

- Europe: +4.6% growth, following +4.2% in prior yr, reflecting “robust” results in Connected Media and Intelligent Creativity, w/ Sapient “practically stable”

- Asia Pac: +5.7% growth, w/ China up +5.2%, driven by mkt share gains

- No material differences in monthly organic performance across Q2, but each month showed sequential improvement in absolute terms, making June the largest month of the qtr

- Verticals

- PUB – operating margin reached “industry high” of 17.4%: Vs 17.3% in H1:24 and +590bps vs peers in H1:25 based on consensus

- Delivered outperformance while making “significant” investments in building and staffing their Core AI platform for €55mn, upgrading their talent pool and investing in new biz and onboarding new clients

- “We are not buying market share”: Have passed on “a couple” pitches both last yr and this yr

And FY25 Guidance Was Either Maintained Or Raised

- OMC – Reiterated 2025 organic growth & adj EBITDA guidance: Though if rates stay where they are then FX would have a +1% benefit in Q3, +2% in Q4 and 1% for FY 2025

- They are “very comfortable” with the guidance they previously gave

- Mgmt believes that Washington will give a lot more clarity to this over the rest of the quarter, hence they will be able to plan better as we move into Q4 and subsequently

- PUB – Raised FY net rev organic growth guidance: Updated to “close to” +5% for the full yr vs prior guidance of +4-5%

- “Despite the lack of visibility in a challenging macro context”: Factors in anticipated reduction in client marketing spend in H2, negative full-year performance at Publicis Sapient, consistent with other IT consulting firms, and a negative impact from year-end adjustment after the positive of 2024

- Will be “more than offset” by “stronger than expected” H1 and 15 material wins since the beginning of the year, some of which are set to progressively ramp up from Q3

- Will be driven by a combination of “a bit over” 200bps from new biz and 300bps from existing client expansion

- Tailwind in 2025 comes primarily from H2:24 wins that are now ramping up, not what was won in H1:25; “Q2’s biggest win…will actually have no contribution for us in 2025”

- “To be honest, 2025 for us is almost behind us. We are thinking about 2026”: Not expecting any new wins or losses to have a material impact on 2025

OMC & Publicis Both Highlight A Positive Competitive Position

- OMC – Seemed to take a dig at WPP competitively: “If you objectively look at the industry, at least for the last two years, out of the people you would consider competitive in the set, two of us continue to win, and the others continue to suffer at one pace or another. By the way, those are the same two that I tried to merge with a decade ago. So I wasn’t wrong then and probably won’t be wrong this time”

- PUB – On client relationships: “We are losing less than competition…not only we are winning more, but we are losing less…we haven’t lost one big client in the last years”

OMC Sees Temporary Client Decision Delays While PUB Reports Relatively Stable Investment Despite Cautious Client Sentiment

- OMC – While mgmt acknowledged some delays in client decision-making, they framed it as temporary: “Some decision processes have gotten delayed or a little slower than what we might have expected in prior years. But again, that’s a temporary phenomenon from my perspective”

- PUB – Have not seen any change in Q2 vs Q1 in client investment levels

- Clients are “very combative, but also cautious”

- “Clients perfectly understand that they have to keep investing in marketing to preserve and grow their market share”

- Expecting “some” impact in H2 but “so far so good”

OMC Remains Active In Pitches Even Through The Summer Though PUB Cautions About A Slower H2

- OMC – The Co is still making pitches: “We continue, along with at least one competitor, to be invited to, I think, every single pitch of any size, because clients are curious about how our services differ from those of maybe one other in the group, primarily. So it’s business as usual, I think”

- Mgmt also highlighted that some active pitches are going on during the summer which is “somewhat unusual, because people typically delay some of those decisions until the autumn”

- PUB – Pace of pitching is expected to slow in H2 which “honestly for us it’s almost a good thing because our primary focus is really to integrate what we have won”

- It was a “particularly intense H1 for the industry…I think I spent 80% of my time pitching”

- “it seems that H2 will be a bit less busy in term of big pitches. And from what we are seeing so far, there is not that much”

OMC’s IPG Merger Is “On Track” For H2 Close / PUB Is Not Worried & Sees The Merger As Oppty To Potentially Poach Talent

- OMC – DOJ approval in June was a big milestone and regulators in other regions look to the US: Mgmt is confident it will get approval from the remaining 5 (of 18) jurisdictions w/ the EU being the largest

- Clients are positive on the deal and OMC agencies in the meantime have not been distracted

- Reiterated the $750mn synergy target; Are “highly confident” and “we’re certainly working on plans to exceed it as well”

- PUB – Regarding the upcoming OMC-IPG merger: “Being the biggest doesn’t mean that you’re going to grow market share”

- “Scale gives you access to the stadium…”: “The three main players would all have access to the stadium”

- …but after that clients want to see innovation: “The reason why we are winning today is not because we are the second biggest in term of scale of media, it’s because we are the first in term of innovation”

- Impact on talent from OMC-IPG merger or challenges at WPP? “I don’t think the takeover of Omnicom or even the change that will happen at WPP will mean that clients will run out the door tomorrow, but talent might. And this is where we have a big opportunity and this is what we are playing at the moment”

OMC Seeing Little Impact from RFK Jr’s Spotlight On Pharma Ads & Tariffs Talks Are Fading In Client Conversations

- OMC – Have not seen changes to Pharm ad trends on the back of RFK Jr’s focus: “There is very little change or action going on. And many of the things that are being suggested don’t seem to have…caught much traction in terms of the way behavior is occurring”

- “The medium possibly could change in which that information gets relayed, but the need to get that information to the consumer, that only gets more complex every day and that benefits us”

- OMC – Tariffs are no longer dominating conversation with clients: At Cannes, it was so noticeable that it [tariffs] wasn’t a word that was being bantered around. It was kind of refreshing”

Publicis Is Sees Outperformance At Sapient (But Mostly Due To Easier Comps), Stable Remuneration Models, and Confidence In Talent Retention

- PUB – “Better performance than expected on Sapient” in Q2 but that was mostly due to an easier y/y comp

- “Where we have to be careful is on the CapEx spend”: IT consulting sector has adopted a “wait and see” attitude for the last 18 months and that’s expected to continue

- But growth is expected to turn back to negative: Sapient was negative in H1 (despite slightly improving in Q1) and H2 is expected to be in-line w/ H1

- “But what is very important is this is fully baked in our guidance”

- PUB – No “significant evolution” in remuneration models: Most contracts still based on retainers, some performance-linked components (mainly in media and production), and the rest structured as project or term-based fees

- PUB – On talent retention: “We are home […] that is growing, a home that is innovating, a home that is growing enough not to fire people, but to make them progress and grow. And so, we are doubling down on that”

- Some key stats: Have a “fairly stabilized attrition” at around 18%; Have added “slightly over” 3,000 new recruits, which directly supports ramp-ups from wins at the end of last yr and Q1

- “We are absolutely not worried about staffing our new business and staffing our new clients. We just need to make sure…that we pitch the right people vs. having the choice in the people”

- Spent ~€60mn in restructuring costs in H1:25, +up €22mn y/y, primarily for talent upgrades

There Was A Big Focus On AI At Both OMC And PUB…Will Propel The Business & Won’t Be Dilutive

- OMC – Believe that the Co is differentiated in how they use AI: Have an “elite” data set

- Phase 1: Focused on ideation, copy generation, and distilling audience insights

- Phase 2 (now): Development of an agentic framework — rolling out AI agents across workflows and campaign lifecycles

- Examples include synthetic focus groups, multi-agent reasoning engines in health, & product launch support in commerce

- In terms of financial impacts, “there’s a book yet to be written”: The Co believes that their compensation models will “increasingly shift to outcomes, however defined”

- “We’re not caught in time — we can evolve how we get paid as our tools and client ROI improve”

- “If a customer saves 10% using our AI tools, they’re likely to plow that back into marketing and advertising — so we don’t lose out”

- “The more we can prove ROI, the more comfortable clients are spending more to generate that return”

- PUB – Have invested ~€12bn in data, technology and AI BUT “we are not planning to become and we are definitely not an AI company…we are a service company that is…leveraging AI pretty well”

- On hiring AI talent – “we are looking for people that can help us make AI an immediate positive impact on our current business”: “We are looking to make sure that we can improve the efficiency of our organization through AI and we are doubling down in acquisition”

- “AI is great, but AI has no taste”

- PUB – Sapient is a “unique competitive advantage” for them – “have some of the most advanced capabilities in AI-driven business transformation”

- “We are exactly at the right place in an environment that is still difficult due to this uncertainty”

- “…have absolutely no exposure to business process outsourcing, which is where we expect AI to severely disrupt”

- “We have to wait for this wait-and-see attitude to change, but we are very confident in the ability of Sapient not only to grow but to be an incredible differentiator in new business”

- “You would remember that we moved from €1.5bn to €2bn in roughly three years when we repositioned Sapient. We are expecting very soon to see this kind of growth”

OMC and Publicis See AI Ad Tools from Google, Meta, and Others Boosting Creativity and Client Growth & NOT Threatening Their Business

- OMC – on concerns about next-gen video tools (e.g., Google’s Veo3, OpenAI’s Sora) cannibalizing agency work

- “We incorporate all those major models… and use them across all workflows”

- “It’s absolutely driving a certain degree of efficiency as it relates to content creation”

- “It’s not about creating the same content for cheaper — it’s about creating more content to drive mass personalization at scale”

- “All of the advancements in this technology is supercharging our capabilities and actually adding greater value to what we deliver for our clients, which are outcomes on a regular basis

- “Allowing our creative teams to explore […] uncharted creative territories, and that is really expanding the aperture of our creativity that we already believe that we have an unfair share of within Omnicom”

- PUB – “I have been hearing that platforms will eat us for breakfast basically since I started. And since then, we have […] doubled our revenue and more than doubled our market cap”

- “We feel very confident in where we are and the uniqueness of our model”

- “Thinking that a single tech platform, however good is the platform…could deliver an end-to-end solution for a big client is actually misunderstanding the intelligence of our clients”

- “They perfectly understand that they need to leverage AI, that they need the best platform, but they need a partner that can connect the entire ecosystem and help them to grow in this very, very complex AI-driven world”

- “This is about making sure that they own their data and don’t give it to the walled garden. It’s about connecting the entire media ecosystem…It’s about making sure that we, as a partner, preserve their brand value”

Company Spotlight: AST SpaceMobile Is Pushing Forward The Next Iteration Of Consumer Connectivity…Satellite Direct To Device

Satellite-based mobile connectivity is gaining traction as operators and technology companies explore new ways to fill coverage gaps and extend coverage to remote and underserved areas. Recent developments underscore the growing activity in space, from Apple’s partnership with Globalstar for emergency satellite texting, to Amazon’s ongoing buildout of its Project Kuiper constellation, and SpaceX’s collaboration with T-Mobile to enable satellite messaging via Starlink.

Against this backdrop, we had the pleasure of hosting a conversation with AST SpaceMobile President Scott Wisniewski who covered a broad range of topics, including a comprehensive update on the company’s path to commercialization, its near-term launch cadence, and the roadmap to achieving continuous global mobile coverage.

To date the Co has secured ~50 mobile network operator partners globally including Verizon (who also invested $100mn) and AT&T in the US, Vodafone in Europe (also just announced a JV), and Ratuken in Japan, and it is currently in the midst of starting its first preliminary launch campaign which will involve five satellite launches over the next 6–9 months, opening the door to commercial services in 2026. AST plans to have ~45-60 satellites up by the end of next year which will enable 24/7 coverage across the “key markets that matter” like the US, Europe, Japan, and select strategic markets (not yet announced), as well as US govt customers.

Notably, Scott framed regulatory approvals as procedural rather than prohibitive, aided by a supportive FCC, existing frameworks from other players like SpaceX and OneWeb, and close coordination with operator partners. He also provided insights into AST’s pricing strategies, integration with mobile operators, and how they see the mix between commercial and government revenue evolving over time.

See below for our key takeaways from the discussion and let us know if you have any questions or would like to speak further about our meeting.

- AST SpaceMobile is on the cusp of seeing an inflection in its business trajectory on the back of a steady stream of satellite launches and subsequent revenue generation

- The Co is on track for commercial service in 2026

- Satellite launch & coverage guidance –

- Plan 5 launches over the next 6–9 mos

- Which they view as conservative

- Plan orbital launches every 1-2 months on avg during 2025 and 2026

- Target ~45-60 satellites by the end of 2026

- 45-60 satellites will provide 24/7 coverage in the markets that matter like the US, Europe, and Japan, the US government, and other strategic markets

- “45 to 60 target is our religion” and will “burn the house down to get to”

- Contracted launch capacity is now close to 70 satellites

- Plan 5 launches over the next 6–9 mos

- Mgmt is very confident in receiving all necessary approvals

- Regulatory approval is a “fascinating piece of alpha” that’s misunderstood and is seen as procedural rather than gating factors for launches and service approval

- Operate a Low Earth Orbit (LEO) network that avoids many political and spectrum conflicts typical of GEO satellites

- Benefit from precedent set by industry leaders like SpaceX and OneWeb,

- More efficient approval process under the current FCC chairman Brendan Carr

- Also partner closely with major MNOs who bring their own regulatory influence and experience

- Regulatory approval is a “fascinating piece of alpha” that’s misunderstood and is seen as procedural rather than gating factors for launches and service approval

- How many subscribers or capacity can the network support? Under some conservative math…

- Each satellite can serve ~1mn gigabyte users per month

- With 45-60 satellites in operation providing continuous service to the markets that matter

- “That’s 50mn gigabyte users per month”

- “That’s 500mn users if they’re only consuming 100 megabytes each”

- “You could do that in a developing country — for talk and text only”

- In the US, AST has strong partnerships and backing from Verizon and AT&T, who prefer AST’s solution over competitors

- Competition from Apple/Globalstar and EchoStar/Boost is seen as limited due to their narrower focus on basic texting or lack of advanced direct-to-device strategies

- T-Mobile partnered early with SpaceX/Starlink, but AST believes their solution is more advanced and better integrated with operators

- AST’s core differentiator vs other satellite providers is satellite size

- AST’s satellites: ~2,000 square feet of aperture — “by far the largest thing that’s ever been put up”

- Bigger aperture = bigger field of view: One AST satellite covers an area roughly half the continental US or a 2,800 km diameter circle

- AST’s satellites: ~2,000 square feet of aperture — “by far the largest thing that’s ever been put up”

- AST still expects pricing to follow a flexible, market-driven model similar to international roaming

- While premium bundle inclusion is being explored, expect most of the revenue to come from a 50/50 split add-on pricing model

- The Co has guided for $50-75mn in revenue in 2025 (back-end loaded)

- Gateway revenue should be the “lions share” in 2025 and the rest is govt contractual milestones and some service revenue from commercial services

- For the next couple of yrs, mgmt expects the majority of rev to come from the US govt

- Defense/govt business may stabilize to lower levels in steady state, with the shift toward commercial dominance happening possibly around the Co’s first $1bn rev yr

- Other key comments –

- Not planning to pursue Residential broadband at this point

- They have over 50 operator partners that have almost 3bn subs, which is a large TAM to sell into

- Engaging cable US MVNOs directly is technically and commercially feasible

- Not planning to pursue Residential broadband at this point

America’s Infrastructure Revival Continues To Accelerate

Infrastructure investment remains a key focus of the Trump administration, and this week, Trump announced over $90bn in corporate commitments tied to AI, technology, and energy at the inaugural Pennsylvania Energy and Innovation Summit. The event, hosted Tuesday in Pittsburgh by Senator Dave McCormick, aimed to position the state as a hub for artificial intelligence and industrial growth. “We’re building a future where American workers will forge the steel, produce the energy, build the factories and really run a country like… this country has never been run before,” Trump said.

Underpinning Trump’s new commitment, a plethora of companies, including Google, CoreWeave, Meta, Anthropic, Blackstone, and more, announced sizeable infrastructure investments. Google announced a $3bn hydropower agreement with Brookfield. Blackstone pledged $25bn toward data centers and energy infrastructure in Northeast Pennsylvania, alongside a joint venture with PPL Corporation. CoreWeave committed $6bn to a new AI data center, and Westinghouse aims to have 10 new nuclear reactors under construction by 2030. That’s just to name a few of the many companies that committed to investing (full list HERE).

Separately, but related, Apple announced a $500mn deal with MP Materials to source rare earth minerals and build two US-based facilities. This is part of its earlier pledge to invest $500bn+ in the US over the next 4 years. Additionally, Meta unveiled plans to bring its first AI supercluster online next year (Meta was also a participant in the $90bn investment in Pennsylvania, committing $2.5mn to support Carnegie Mellon–affiliated startups in advanced technologies in Pennsylvania).

See below for more on this key development this week.

As Part Of The $90bn in Investment Announced For AI and Energy In Pennsylvania…

- Google makes the world’s largest $3bn hydropower deal with Brookfield (link/link/link)

- Announced a “first-of-its-kind” Hydro Framework Agreement (HFA)

- Under the HFA, Google has the ability to procure carbon-free electricity from up to 3,000 MWs of hydroelectric assets that will be relicensed, overhauled, or upgraded to extend the asset’s useful life and continue adding power to the grid

- The first contracts executed under the HFA are for two hydropower facilities in Pennsylvania that Brookfield is relicensing

- The power will come from the Holtwood and Safe Harbor plants, about 75 miles southwest of Philadelphia, with 670 megawatts of generating capacity for 20 years

- Google said it plans to expand the deal eventually beyond those sites to other parts of the Mid-Atlantic and Midwest

- The deal is part of an effort to “responsibly grow the digital infrastructure that powers daily life for people, communities and businesses”, Google said.

- Announced a “first-of-its-kind” Hydro Framework Agreement (HFA)

- CoreWeave announces $6bn investment in Pennsylvania AI data center (link)

- Plans to invest as much as $6bn to set up an initial 100 MW data center in Pennsylvania

- The data center will be able to expand to 300 MW

- Drive job creation in the area: Project is expected to create ~600 “skilled, competitively waged” jobs during the build phase, w/ ~70 full-time technical and operational roles at launch, and scaling to ~175 over time

- The facility will add to CoreWeave’s network of 33 AI data centers, including 28 located across the United States

- Plans to invest as much as $6bn to set up an initial 100 MW data center in Pennsylvania

- Blackstone announced a $25bn investment in data center and energy infrastructure development in Northeast Pennsylvania along with a new joint venture with PPL Corporation for power generation

- This investment is expected to create 6,000 construction jobs along with 3,000 new permanent jobs

- Westinghouse Electric Company is working to have 10 new, large nuclear power plant reactors under construction by 2030, generating what is currently estimated to be $6bn in economic impact and 15,000 new jobs in southwest Pennsylvania

- Meta committed to support promising early-stage Carnegie Mellon University-affiliated startups, in partnership with the Swartz Center for Entrepreneurship, with a $2.5mn gift

- This initiative will provide funding to high potential startups in advanced technologies, including those working in areas critical to the energy, infrastructure, health care and defense industries which will create economic opportunities in Pennsylvania

- Anthropic invests in cybersecurity and energy research education in Pennsylvania

- Committed $1mn over three yrs to support the PicoCTF program that provides cybersecurity education to middle and high school students.

- Announced $1mn over three yrs to support energy research at Carnegie Mellon University

- And many more…for the full list of companies and investments announced at the Pennsylvania Energy and Innovation Summit, click HERE

Apple & Meta Expand US Infrastructure Investments In Rare Earth Minerals And AI Compute

- Apple makes $500mn deal to buy rare-earth minerals from MP Materials Corp. (link/link/link)

- MP Materials is the only fully integrated rare earth producer in the US

- Spending on rare-earth minerals is part of Apple’s earlier pledge to invest $500bn+ in the US over the next 4 yrs

- The deal includes building two new US facilities –

- In Mountain Pass, California, for recycling rare earths

- In Fort Worth, Texas, to produce magnets for Apple products

- MP plans to produce 10,000 metric tons of rare-earth magnets a year by 2028, up from the current output of 1,000 tons

- MP will reportedly start shipping these magnets to Apple by 2027, and they’re expected to go into hundreds of millions of Apple devices

- Incr’d production will support “dozens of new jobs” in advanced manufacturing and R&D

- Both Cos will provide extensive training to develop the workforce, “building an entirely new pool of US talent and expertise in magnet manufacturing”

- Aligns with Trump’s push to reduce US reliance on China for critical minerals

- Just days earlier, the Department of Defense also invested $400mn in MP Materials, calling it a major step in creating a domestic rare earth supply chain

- Right now, China dominates over 90% of the global rare earth magnet production, a critical part in devices like iPhones, AirPods, and Macs.

- MP Materials is the only fully integrated rare earth producer in the US

- Another quick update from Meta CEO Mark Zuckerberg – Meta plans to bring its first supercluster online next yr (link/link)

- “We’re going to invest hundreds of billions of dollars into compute to build superintelligence. We have the capital from our business to do this”

- “Meta is on track to be the first lab to bring a 1GW+ supercluster online. We’re actually building several multi-GW clusters”

- First one is called Prometheus and will come online in 2026

- Also building Hyperion, which will be able to scale up to 5GW over several yrs

- “We’re building multiple more titan clusters as well. Just one of these covers a significant part of the footprint of Manhattan”

- “Meta Superintelligence Labs will have industry-leading levels of compute and by far the greatest compute per researcher. I’m looking forward to working with the top researchers to advance the frontier!”

Recent Consumer Spending Trends Surprise On The Upside

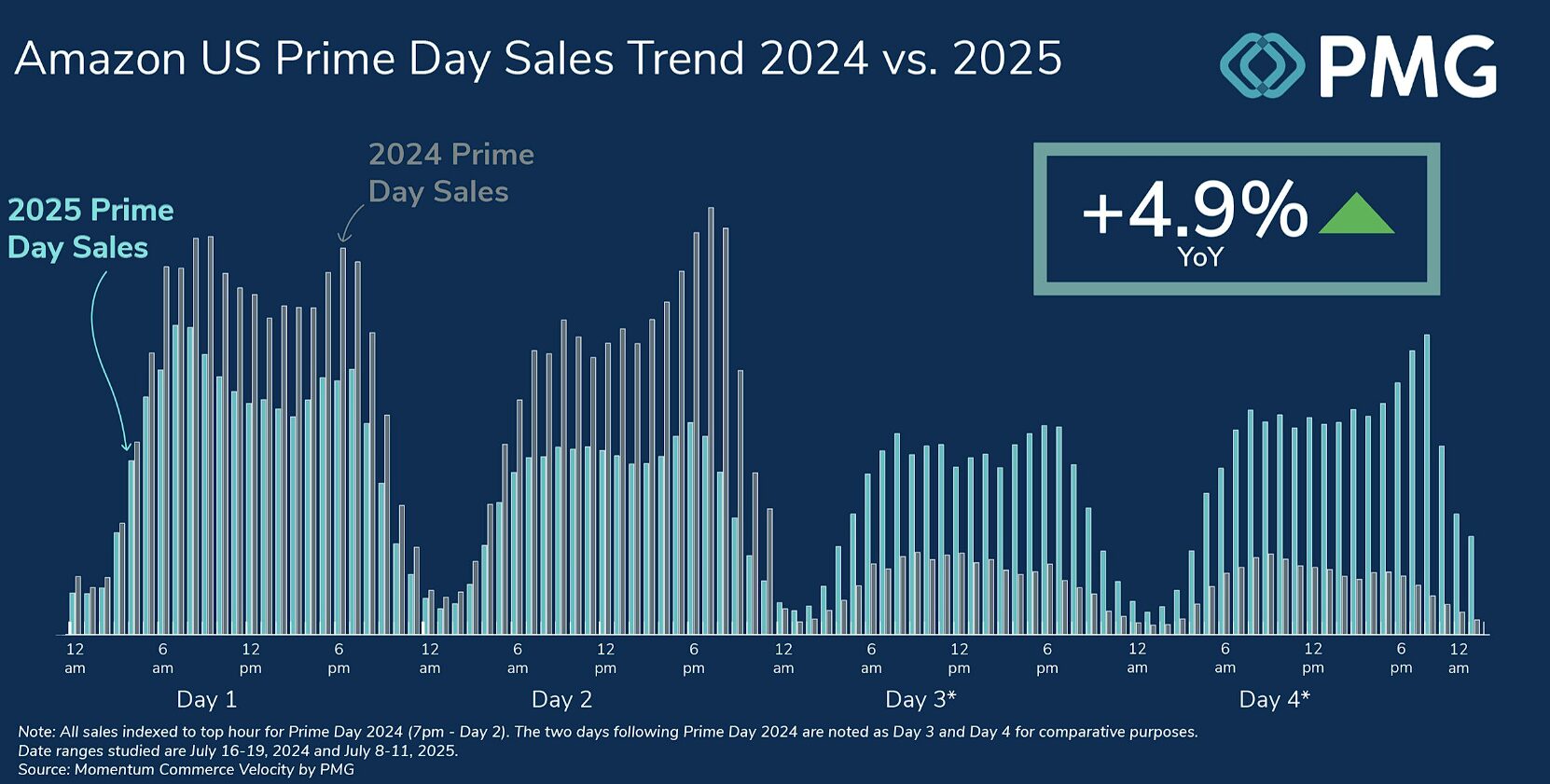

As a follow up our update last week where we took look at the early reads from last week’s Prime Day event, which ran from July 8-11, Amazon subsequently gave more color, saying that this year’s event was its “biggest ever”. With that said, that is a familiar refrain that we’ve heard them use to describe previous Prime Day events. Once again there wasn’t much shared in the way of concrete figures, but data from third-party trackers like Momentum Commerce and Numerator seem to support that it was a strong shopping event.

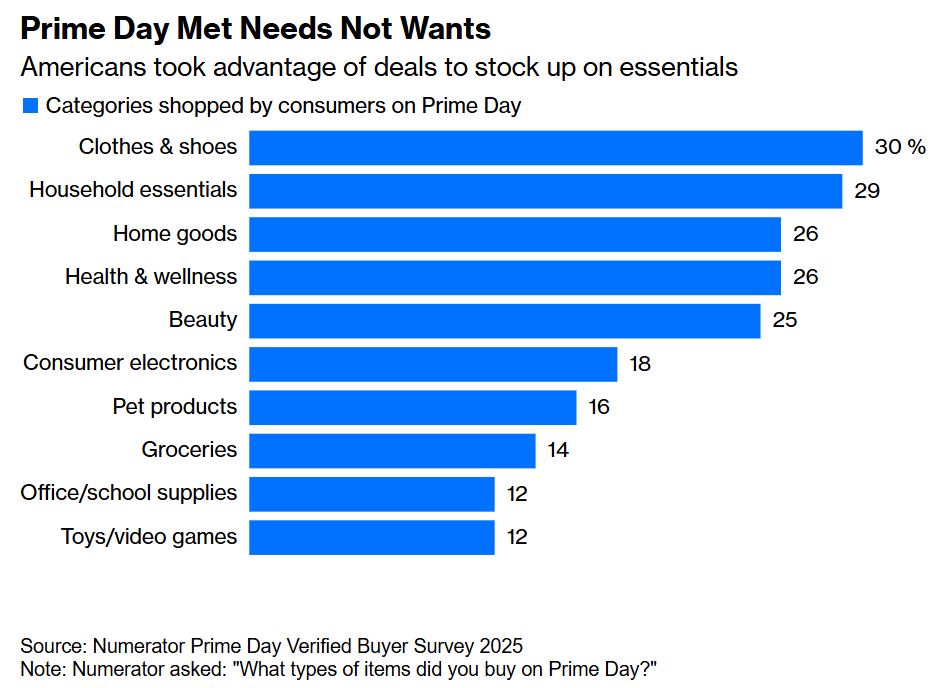

Per Momentum Commerce’s Tracker, total sales during the four-day event grew +4.9% y/y, with over 25% of products on Amazon US featuring discounts, an increase from 23.6% in 2024. While everyday essentials drove a lot of the shopping activity, Numerator reported a 20% lift in purchases of higher-priced goods relative to YTD avgs, which suggests some consumers used the deals to “trade up.”

More broadly, US online spending during the Prime Day window jumped +30.3% y/y to $24.1bn, per Adobe. Mobile shopping continued to grow, accounting for 53.2% of online sales. And shoppers increasingly turned to generative AI-powered tools, as click-through traffic from AI assistants surged more than 3,000% y/y.

See below for the recap of what we found was most interesting.

As Per Usual, Amazon Said Its Prime Day Event Was Its Biggest Ever (But Didn’t Share Much Detail Beyond That) (link)

- Prime Day 2025 was Amazon’s biggest Prime Day event ever

- Customers saved “billions” on deals across 35+ product categories, “more savings than any previous Prime Day event”

- This year’s Prime Day event was bigger than any previous four-day period that included a Prime Day event, with record sales and more items sold during the four days

- Independent sellers, most of which are small and medium-sized businesses, also achieved record sales and a record number of items sold

- What items were bought?

- “Members saved big on best-selling brands like Dyson, medicube, and Philips Sonicare”

- “Members scored deals across categories including electronics, beauty, and household essentials”

- There were deals on best-selling products like Apple AirPods Pro 2, BIODANCE Bio Collagen Real Deep Mask, and Dawn Platinum Powerwash Dish Spray

- “Millions” of Alexa-enabled devices were purchased

- Ring Battery Doorbell and Fire TV Stick HD were two of the event’s best-selling items

- Deals weren’t limited to just amazon.com

- Whole Foods offered 50% off all ice cream and frozen desserts for Prime members (if only we had known!)

- Amazon Fresh offered $30 off purchases of $150+

Amazon Prime Day Event Sales Grew +4.9% y/y, Per Momentum Commerce’s Tracker (link)

- Total sales grew +4.9% compared to the combined performance of 2024’s two-day Prime Day and the two days immediately following

- 25.6% of products on Amazon US featured discounts, representing an 8% increase from 2024’s rate of 23.6%

- Discount breadth increased progressively from Day 1 (22.7%) to stabilize on Days 3 and 4 (26.7%)

- While more products were on sale, the avg discount depth decreased to 21.7%, down 11% from a rate of 24.4% in 2024

- Avg discount depths grew incrementally each day (21.4%, 21.6%, 21.8%, 21.9%), suggesting retailers strategically deepened discounts to maintain momentum

* Momentum Commerce tracked $750mn+ in Amazon U.S. sales during the 2025 Extended Prime Day, based on data from its Velocity platform covering $7bn+ in annual GMV across hundreds of brands.

More Essential Purchases Made During Prime Day, Despite Some Trade Up to Pricier Items (link/link)

- Rather than splurging on expensive electronics or luxury items, many shoppers used the sale to stock up on household essentials

- 2/3 of the items purchased cost <$20, and the avg household spent $156, according to research firm Numerator

- That said, consumers did gravitate towards pricier goods: Discounts during the Prime Day event drove many shoppers to “trade up” to higher-ticket items

- Across all categories tracked by Adobe, the share of the most expensive goods increased by 20% (vs avg levels YTD)

- Some brands, particularly ones with pricier products from high tariff countries, faced a tougher challenge and decided to skip the event this year or decrease the number of deals they offered

- Only 3% of items purchased on Prime Day cost more than $100

How Did Overall Online Sales Shape Up? (link)

- Online spending across all retailers in the US was up +30.3% y/y to $24.1bn, per Adobe

- This came in above their estimate of +28.4% y/y growth

- Overall discounts across US retailers were between 11-24%

- This came in above prior forecast range of 10-24%

- Shopping on mobile was the dominant transaction channel, driving 53.2% online sales, above Adobe’s forecast of 52.5%

- Shoppers are increasingly using genAI-powered chat svs and browsers as a shopping assistant

- GenAI traffic to US retail sites (measured by shoppers clicking on a link) increased +3,300% y/y

- Buy Now Pay Later usage saw an uptick: BNPL orders accounted for 8.1% of online orders (up from 7.4% in 2024)

- BNPL was used most in the apparel, electronics, home goods, and health & beauty categories

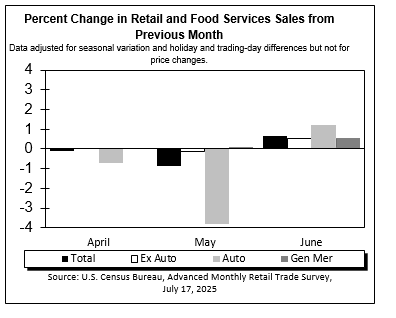

How Has Consumer Spending Been Shaping Up Overall? Retail Sales Actually Rebounded In June (link)

- Retail sales increased +0.6% in June after two straight monthly declines (-0.9% drop in May and -0.1% drop in April)

- Also came in above consensus of +0.2%

- Core sales (ex-Autos) were up +0.5% in June, up from May’s -0.2% reading

- Also ahead of expectations of +0.4%

- Category callouts –

- Auto sales +1.2% (saw the highest growth amongst the categories)

- Car manufacturers, however, reported a decline in unit sales in June, so the rise in receipts was due to higher prices

- Building material garden equipment store sales +0.9%

- Clothing retailers +0.9%.

- Healthy & personal car stores +0.5%

- Online retail sales +0.4%.

- Dining out +0.6%.

- Furniture stores -0.1%

- Electronic & appliance stores -0.1%

- Auto sales +1.2% (saw the highest growth amongst the categories)

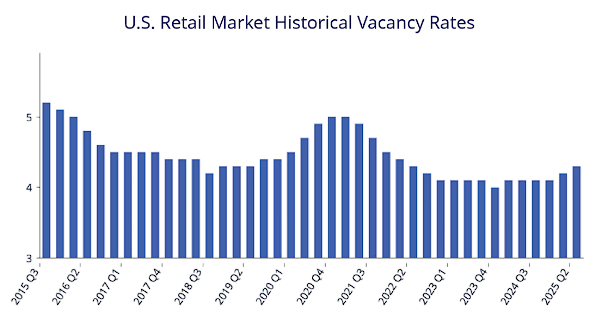

Retail Vacancy Rates Ticked Up, But Demand Remains Healthy In High-Traffic Areas

On the topic of shopping and retail, we also wanted to highlight an updated report on Q2 US Retail Market Statistics published by real estate firm Collier this week…a couple quick stats from the report that stood out to us include…(link)

- Retail vacancy rates were 4.3% in Q2, up +10bp from Q1

- Net absorption turned negative in Q2 w/ 6.4mn sq ft returning to the market and leasing activity was down -2%, largely due to store closures and limited high-quality space

- As of the end of June, 5,822 US store closures were tracked, totaling 123.7mn sq ft of space (per Coresight Research)

- But much of the available space is older and lower quality (40% rated 2 Stars or below; less than 25% built after 2000)

- More space is available now than at the start of the year, driven by closures annc’d in late 2024. Despite this, demand remains healthy, especially in high-traffic areas

- Construction has been limited – only 6mn sq. ft. were delivered in Q2 (to 47.9mn total sq ft under construction)

- New development is limited by high costs and competition from other sectors

- Since 2020, just 21mn sq ft of new retail space has been listed — less than 5% of national availability

- Texas leads in new space, with nearly one-third of first-generation listings

- Sales efficiency was strong – asking rents dipped slightly to $25.46/sq. ft. (down 0.39%) but monthly sales per sq ft hit $24.96, up 30%+ from pre-pandemic levels

- Some landlords are achieving 40%+ rent premiums on re-leased space

Grab Bag: OpenAI Launches ChatGPT Agent / Uber-Lucid-Nuro Robotaxi Deal / Peacock Raises Prices Yet Again

- OpenAI launches ChatGPT Agent (link)

- Can now ask ChatGPT to handle requests like –

- “Look at my calendar and brief me on upcoming client meetings based on recent news”

- “Plan and buy ingredients to make Japanese breakfast for four”

- “Analyze three competitors and create a slide deck”

- Combines capabilities from OpenAI’s previous agentic tools, including Operator’s ability to interact with websites, deep research’s skill in synthesizing information, and ChatGPT’s intelligence and conversational fluency

- ChatGPT carries out these tasks using its own virtual computer, fluidly shifting between reasoning and action to handle complex workflows from start to finish, all based on the user’s instructions

- But the user is always in control: ChatGPT requests permission before taking actions of consequence, and you can easily interrupt, take over the browser, or stop tasks at any point.

- Equipping the agent with a suite of tools –

- Visual browser that interacts with the web through a graphical-user interface

- Text-based browser for simpler reasoning-based web queries

- A terminal

- Direct API access

- Agent can also leverage ChatGPT connectors, which allows you to connect apps like Gmail and Github so ChatGPT can find information relevant to the user’s prompts and use them in its responses

- Available to Pro, Plus, and Team users

- Can now ask ChatGPT to handle requests like –

- Uber partnering w/ EV-maker Lucid and self-driving tech startup Nuro to launch robotaxi svs (link)

- Uber announced that it or its 3P fleet partners will purchase and operate Lucid Gravity SUVs outfitted with Nuro Driver technology

- Will leverage the Lucid Gravity, an all-electric SUV w/ a 450-mile EPA estimated range

- Autonomy will be powered by the Nuro Driver Level 4 self-driving system

- These vehicles will be made available to rides exclusively on Uber’s platform

- Uber aims to deploy 20,000 or more Lucid vehicles equipped with the Nuro Driver over 6 yrs

- Expected to first launch later next yr in a major US city

- The inaugural Lucid-Nuro robotaxi prototype is already in operation at Nuro’s proving grounds in Las Vegas

- Uber also said it would be making separate multi-hundred-million dollar investments in both Lucid and Nuro

- Uber announced that it or its 3P fleet partners will purchase and operate Lucid Gravity SUVs outfitted with Nuro Driver technology

-> Lucid closed up +36% on the day of the announcement, its biggest gain in 2.5+ yrs; Uber was flat

- NCBU’s Peacock is raising subscription prices for the third time in three yrs + testing new tier (link/link)

- NBCU last increased Peacock pricing in July 2024, after hiking prices a yr earlier for the first time since Peacock’s 2020 launch

- Increase of $3/mo (biggest in Peacock’s 5-yr history) for monthly plan

- Premium (includes ads) will increase from $7.99/mo to $10.99/mo

- Premium Plus (has limited ads in live programming) will increase from $13.99/mo to $16.99mo

- Increase of $30/yr for annual plan

- Premium will increase from $79.99/yr to $109.99/yr

- Premium Plus will increase from $139.99/yr to $169.99/yr

- According to NBCU, Peacock will stream more live sports in 2026 than Amazon Prime, Paramount+, Hulu, HBO Max, Apple TV and Netflix combined

- Comes ahead of the NBA’s return to NBC (and Peacock) in the fall of 2025 after a 23-yr absence on the network

- Also have return of the NFL’s “Sunday Night Football” this fall

- Also the NBA, WNBA, Premier League, Big Ten, the FIFA World Cup in Spanish

- NBC also has Super Bowl LX, and next year’s NBA All-Star Weekend, as well as the Milan-Cortina Winter Olympics and Paralympics in February 2026

- The new pricing now makes Peacock more expensive than the ad-supported and ad-free tiers at Netflix, Disney+, HBO Max and Paramount+

- Also beginning to test a new Peacock “Select” tier, which will feature NBC and Bravo current seasons and an assortment of library titles

- Will be priced at $7.99/mo and $79.99/yr

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Nearly 90% of advertisers are using or planning to use GenAI for video ads, per IAB’s 2025 report. GenAI is key for SMBs (small and mid-tier brands) to scale creative affordably. (TvTech)

- Trade Desk shares surged 14% after S&P Global annc’d it will replace Ansys in the S&P 500, following Synopsys’ expected $35bn Ansys acquisition closure. This cont’d index reshuffle follows Datadog’s recent entry. Despite a 36% YTD drop, Trade Desk’s $37bn market cap secures its spot. (CNBC)

- Health Sec Kennedy Jr and Sen Sanders & King are targeting the $10bn pharma ad mkt. Kennedy eyes stricter disclosure rules or ending tax write-offs for ads. Sanders & King’s bill—End Prescription Drug Ads Now Act—would ban such ads across TV, radio, print, digital & social. The move could hit linear TV hard as it cont’d to lose biz to digital mkts. (The Wrap)

- NBCUniversal annc’d record 2025–26 Upfront ad sales, driven by live events, NBA addition, and Peacock’s growth. Tentpoles like the Olympics, Super Bowl LX & FIFA World Cup surpassed past benchmarks. Peacock saw a 20% YoY rev boost, now ~⅓ of total commitments. Telemundo, BravoCon & SMB clients hit highs. Programmatic topped $1bn. NBCU’s One Platform sold across all linear & streaming under VERSANT. (NBCUniversal)

Artificial Intelligence/Machine Learning

- A coalition of funders, incl Gates Foundation & Ballmer Group, will spend $1bn over 15 yrs to develop AI tools for public defenders, parole officers, social workers, etc. The funders annc’d the creation of NextLadder Ventures to offer grants & investments to nonprofits & for-profits. The goal is to spur economic mobility by helping frontline workers manage huge caseloads. NextLadder will partner w/ AI Co Anthropic, which will offer tech expertise. (AP News)

- Google’s Veo 3 video generation model is now available via the Gemini API, targeting developers for advanced video creation. Veo 3 generates high-res video w/ synchronized audio from text prompts, including visuals, dialog, music, and sound effects. Access costs $0.75/sec for 720p video w/ audio. (The decoder)

- Bharti Airtel has partnered with Perplexity, an AI-powered answer engine, to offer a free 1-yr Perplexity Pro subscription to its 360mn prepaid, postpaid, and broadband customers. This marks Perplexity’s first partnership w/ a telecom operator in India, aiming to boost adoption in the world’s second-largest internet mkt. Airtel customers can avail this offer via the Airtel Thanks app until Jan. 17, 2026). Perplexity Pro typically costs $20 (~₹1,731) per month. (Moneycontrol)

- AI search startup Perplexity raised $100mn, boosting its valuation to $18bn. Backed by Nvidia, SoftBank, NEA & IVP, the Co’s rev surged from $35mn (Aug. 2023) to $150mn (Jul. 2025). (AI Invest)

- Scale AI cut 14% of staff (~200 roles) weeks after Meta’s $14. 3bn investment and hiring of founder Alexandr Wang as chief AI officer. Interim CEO Droege cited overexpansion and bureaucracy. Despite layoffs, Scale AI plans to grow its enterprise/public sector units. Co also ended work w/500 contractors. (CNBC)

- ChatGPT has hit 900mn downloads globally, far ahead of rivals with Gemini (200mn), DeepSeek (127mn), and Copilot (79mn). Experts say its lead stems from engaging convos, fast answers, and frequent updates. Despite Google and Microsoft’s multi-bn AI investments, ChatGPT remains the top choice for users, dominating the AI chatbot space. (Money Control)

- Amazon Web Svcs annc’d AgentCore, a platform enabling cos to build AI agents for tasks like data analysis and coding, aiming to boost productivity. Unlike rivals, it supports any model. Launched at AWS Summit, it includes a dashboard and marketplace. (Semafor)

- Google, OpenAI, Anthropic & Musk’s xAI won DoD contracts worth up to $200mn each to scale agentic AI for national security. xAI annc’d “Grok for Government” suite incl. Grok 4. The move follows a White House AI push & Trump’s rollback of Biden-era AI rules. (Reuters)

- A report by Internet Matters reveals 67% of kids aged 9–17 use AI chatbots like ChatGPT and Character.AI, w/ 35% saying it feels like talking to a friend. Alarmingly, 12% use them due to lack of real friends. Experts warn these bots blur human-machine lines, posing emotional risks. Some bots even mimic empathy or follow up on sensitive topics. (Futurism)

- AI startup Cognition annc’d it’s acquiring Windsurf, days after Google hired Windsurf’s CEO in a $2.4bn licensing deal. Cognition will buy Windsurf’s IP, product, brand, and talent, though terms weren’t disclosed. The move follows a failed $3bn OpenAI deal. Both cos are backed by Founders Fund. All Windsurf staff will get full vesting and financial participation. (CNBC)

- Tesla has begun rolling out Grok, an in-car conversational AI assistant developed by xAI, to eligible vehicles. Grok, pre-installed on new vehicles, offers hands-free access to a chat-style companion. It supports Tesla models w/ AMD infotainment processors and software version 2025.26 and higher. Grok answers questions and holds conversations but cannot issue vehicle commands. It’s in Beta, requiring no Grok account or xAI subscription. Privacy is maintained as interactions are processed anonymously. (Teslarati)

- SpaceX has committed $2bn to xAI, Elon Musk’s AI venture, marking its first major external investment. This move is part of a $5bn equity round, valuing xAI at ~$113bn. xAI recently raised $5bn in equity and $5bn in debt financing, bringing its total private funding to over $12bn. The investment aims to integrate AI across Musk’s ventures, including Starlink and Tesla. (Tech Funding News)

Audio/Music/Podcast

- Universal’s Virgin Music Group’s $775mn Downtown deal faces a full-scale EU antitrust probe post-July 22, after failing to offer remedies. Critics, incl. Impala & ECSA, say it threatens indie label access in EU mkts. Virgin denies claims, says deal closure still expected in H2 2025. The EU Commission hasn’t annc’d a decision but will launch a 4-month review. (Reuters)

Cable/Pay-TV/Wireless

- Zegona, which acquired Vodafone Spain for €5bn in May 2024, reported customer growth “for the first time in years,” adding 29k broadband and 26k mobile lines in FY25, and more in Q1 FY26. Despite a €82.12mn loss, EBITDAaL rose to €1.24bn. Rev fell to €3.62bn. Zegona implemented 400+ cost-cutting initiatives incl. 28% headcount cut. Focus remains on cash-flow, w/ fiber JV deals aiding turnaround. (Light Reading)

- TIM announces that, as part of the company’s path of deep transformation, it has reached a new agreement with the trade unions – Slc Cgil, Fistel-Cisl, Uilcom-UIL and UGL elecomunicazioni – on labour management. The agreement, which was ratified with an adhesion rate of more than 75%, is divided into three areas: solidarity contract, agile work and result bonus, and represents a concrete step in the transformation process started by the Group, which is following the path traced by the industrial plan to create the conditions for growth. (1INFO)

Cloud/DataCenters/IT Infrastructure

- OpenAI annc’d that it will use Google Cloud for ChatGPT and its API, alongside Microsoft, CoreWeave & Oracle. The move aims to boost computing power amid rising demand. Google’s infra will run in the U.S., Japan, Netherlands, Norway & U.K. Microsoft retains exclusive rights to OpenAI’s APIs. (CNBC)

Crypto/Blockchain/web3/NFTs

- Crypto firm Bitcoin Standard Treasury Co will go public via a merger w/ Cantor-backed SPAC Cantor Equity Partners I. Holding 30,000+ bitcoin, it aims to raise up to $1.5bn in PIPE financing. The combined co will list on Nasdaq as BSTR in Q4 2025. (Reuters)

- The US House, led by Republicans, cleared key steps to advance 3 crypto bills after Trump’s intervention. A stablecoin framework bill, already Senate-approved, is poised for Trump’s signature. Another bill defines crypto mkts structure, while a third-attached to a defense bill—bans a Fed digital currency. GOP leaders faced internal resistance but cont’d efforts secured progress. (Reuters)

- The DOJ and CFTC ended probes into crypto-based betting site Polymarket w/o charges, per notices received earlier in Jul. The investigations, launched under Biden, focused on U.S. user bets despite prior $1.4mn CFTC fine. CEO Coplan, whose devices were seized in a 2024 raid, wasn’t charged. Closure marks another Trump admin rollback of Biden-era actions vs. crypto mkts. (CNBC)

- Grayscale Investments has confidentially filed draft IPO paperwork w/ the SEC, signaling a major US crypto IPO after Circle’s debut. The move follows Grayscale’s GBTC and Ethereum trust conversions into ETFs, pushing AUM past $30bn. The IPO could test investor appetite as crypto cos return to mkts under Trump’s pro-crypto regime. (The Block)

- Bitcoin hit a record $123,153 on Mon, July 14, driven by optimism over US crypto regulation. The House is set to debate bills like the Genius Act, aiming to establish federal rules for stablecoins. Crypto mkts surged to ~$3.8tn. Ether hit $3,081, XRP rose 2.7%. Coinbase, Strategy & Mara stocks gained. Trump’s meme coin dropped 3.4% to $9.45. Dollar weakness also aided bitcoin’s rise. (Reuters)

eCommerce/Social Commerce/Retail

- Target will end its price-matching policy on July 28, citing that most customers compare prices within its own ecosystem. The move, aligning w/Walmart’s strategy, comes amid weak sales, tariffs, and boycotts. (AI Invest)

- Online grocery sales rose 27.6% YoY in Jun. to $9.8bn, while in-store sales dipped. Delivery (+29% to $3.8bn), pickup (+25% to $4.3bn), and ship-to-home (+33% to $1.7bn) all grew. Walmart gained share as supermarkets lost over 2 pts. (Grocery Dive)

- Back-to-school shopping kicked off early in 2025, w/ 67% starting by early Jul, driven by tariff concerns. K-12 families plan to spend ~$858.07, down from 2024, but total spend to hit $39.4bn. College spend avg. is $1,325.85, w/ total at $88.8bn. Online, discount & dept. stores lead. Despite early start, 84% still have half their shopping left, awaiting deals like Prime Day & Target Circle Week. (Chain Storage Age)

- US retail vacancy rose 10 bps in Q2 to 4. 3%, per Colliers, w/ net absorption at -6.4mn sq ft. and leasing down 5.2%. Most available space is older, w/ <25% built post-2000, limiting options in affluent areas. Avg. asking rent dipped ~0.4% to $25.46/sq. ft. Despite store closures, low supply and tight availability—esp. in booming mkts like Texas—mean vacated space is likely to be refilled quickly. (Retail Dive)

EdTech

- McGraw Hill targets a $4.2bn valuation in its IPO, aiming to raise $537mn by offering 24.39mn shares at $19–$22 each. The Co plans to list on NYSE as “MH” and use proceeds to repay debt. A leader in K-12 and higher ed, its tools are used by 99% of U.S. public schools and 82% of higher ed institutions. The Co is expanding digital svs incl. AI tools, but faces risks from generative AI competition. (AInvest)

Electric & Autonomous Vehicles

- Baidu & Uber annc’d a multi-yr strategic partnership to deploy Apollo Go AVs on Uber’s platform outside the US & mainland China. Initial rollouts begin in Asia & the Middle East in 2025. (PR Newswire)

Film/Studio/Content/IP/Talent

- Hollywood faces an AI insurgency as startups like Asteria and Runway AI reshape filmmaking. AI tools now generate scenes, characters, and entire films, promising speed and cost savings. While some embrace the tech’s creative potential, critics warn of lost artistry, job cuts, and ethical concerns. Studios, torn between profit and preservation, face lawsuits and existential questions as cinema’s future is rapidly redrawn. (The Hollywood Reporter)

- ‘South Park’ faces uncertainty as a $3bn, 10-yr deal between creators Parker & Stone and Paramount stalls. Skydance, set to acquire the studio, opposes the terms, citing cash priorities. Park County insists Skydance can’t interfere pre-merger. Streaming rights expired in Jun., intensifying the standoff over rev splits and control. (The Hollywood Reporter)

FinTech/InsurTech/Payments

- Anthropic annc’d Claude for Financial Services to expand its enterprise offerings and boost rev. The platform, built from interviews w/ finance pros, offers enhanced query capacity and integrates w/ svs like Palantir, S&P Global, and Snowflake. Available via AWS and Google Cloud, it aims to transform how finance cos use gen AI in daily ops. (Yahoo Finance)

Last-Mile/Delivery

- JD.com, Alibaba & Meituan are in a fierce race for China’s instant delivery mkts, driven by tech, subsidies & surging demand. Meituan hit 150mn daily orders in Jul. 2025; Alibaba’s Taobao Instant topped 80mn. Each Co pledged ¥10bn ($1.38bn) in promos; Meituan & Alibaba annc’d ¥50bn ($7bn) subsidies. Despite steep losses, cos cont’d expanding logistics to meet 30–60 min delivery norms, reshaping retail & consumer habits. (The Bridge Chronicle)

Macro Updates

- US inflation rose 0. 3% in Jun, pushing the annual rate to 2.7%, per BLS data. Core inflation hit 2.9% y/y. Tariff effects were mixed: apparel (+0.4%) and furnishings (+1%) rose, while vehicle prices fell. Shelter was the largest CPI driver (+3.8% y/y). Trump urged a Fed rate cut, citing “low” inflation. Real wages dipped 0.1% m/m. Mkts reacted mildly; Fed expected to hold in Jul., cut in Sept. (CNBC)

Media Conglomerates

- News Corp annc’d a new $1bn stock buyback, raising total authorization to $1. 3bn, w/ ~$303mn still active from its Sept 2021 plan. The Co will accelerate repurchases post-early Aug. after Q4 results, once trading blackout ends. The program has no time limit. (Reuters)

- TelevisaUnivision annc’d a Q2 rev drop to ~$1. 205bn–$1.21bn (vs. $1.257bn in 2024) due to US ad softness & FX impact. Adj OIBDA rose to $395mn–$400mn (from $362mn). Co is in talks to refinance 2027 debt. Cash projected at ~$580mn–$585mn; net debt/OIBDA ratio at 5.5–5.6x. Despite flat subs/licensing rev, linear ratings improved w/ strong sports slate. (Deadline)

Metaverse/AR & VR

- ByteDance is developing lightweight mixed reality goggles under Project Swan, led by its Pico division. The goggles, tethered to a pocket-sized puck for processing, aim to reduce latency using custom chips and spatial sensors. This pivot follows the Pico 5’s weak sales. Competing w/Meta’s Puffin, ByteDance targets comfort, portability, and TikTok integration. (IndianWeb2)

Online Travel

- Delta is shifting from set fares to AI-driven personalized pricing to boost profits. Currently used for 3% of fares, the pilot has shown “amazingly favorable” results. Critics warn it may lead to price-gouging, likening it to “hacking our brains.” (Fortune)

Satellite/Space

- AST SpaceMobile’s subsidiary, Spectrum USA I, LLC, secured a $550mn credit agreement w/ Sound Point Agency LLC. This deal supports payment obligations to Ligado Networks for spectrum access in the US and Canada. (Tip Ranks)

- Amazon is using SpaceX to launch its Project Kuiper satellites, challenging SpaceX’s Starlink in the satellite internet mkts. The KF-01 mission launched 24 satellites from Cape Canaveral. Amazon aims to deploy 3,000+ satellites, w/ 1,600 by Jul. 2026 per FCC mandate. The Co has secured 83 launches, including three w/ SpaceX, investing $10bn+ in Kuiper. (Cord Cutter News)

- The Federal Communications Commission (FCC) just approved SES’s proposed acquisition of Intelstat, a $3.1 billion deal that will allow the Luxembourg-based satcom company to build out its “multi-orbit satellite-based capabilities, spectrum portfolio, and global ground network to serve customers.” The satellite market is forecasted to see explosive growth over the next 10 years, according to Goldman Sachs (Fierce Network)

- Rogers Comm annc’d a beta trial of its satellite-to-mobile text svc, incl text-to-911, via SpaceX’s Starlink & Lynk Global. Free till Oct., it covers most of Canada south of the 58th parallel. The svc aims to boost safety in remote areas. Post-trial, it’ll be free for Rogers Ultimate ($85/mo) users, or $15/mo for others. The tech was first annc’d in Apr. 2023, w/ a test call completed by Dec. 2023. (MSN)

- SpaceX is planning an insider share sale valuing the Co at ~$400bn, per Bloomberg. The per-share price is set at $212, up from $185 in Dec, marking a major jump. This move solidifies SpaceX as the world’s most valuable private Co and top-valued startup. The rocket and satellite biz continues to dominate the private tech mkts w/ strong investor interest. (investing.com)

Social/Digital Media

- Reddit annc’d UK users must verify age via Persona using a selfie or gov’t ID to access mature content, complying w/ the Online Safety Act. Persona won’t retain photos >7 days. (Arc Technica)

- Meta annc’d stricter rules on Facebook to curb “unoriginal” content, targeting accounts reposting others’ text, photos, or videos. ~10mn impersonator profiles and 500K spammy accounts were removed YTD. Offenders face reduced content distribution and loss of monetization. Meta is also testing links to original creators on duplicate videos. (TechCrunch)

Software

- Autodesk shares rose 5.9% to ~$297 on Mon, July 14th after the Co signaled it won’t pursue a PTC acquisition (~$23bn valuation). In an SEC filing, Autodesk emphasized focus on strategic priorities in cloud, platform, and AI; margin-boosting sales/marketing and capital allocation to organic growth, tuck-in deals, and share buybacks. PTC shares fell ~2% to $190. Autodesk stock had dropped 12% last week amid deal speculation. (Proactive)

Sports/Sports Betting

- NBA plans to launch a national streaming svs in the 2027-28 season, aiming to consolidate local media rights for 18 teams into a centralized platform, according to a report by Tom Friend of Sports Business Journal. Teams like the Bucks, Cavaliers, Hawks, and Heat have extended their FanDuel deals through 2026-27, while others may join the national platform. (Cord Cutter News)

- Apollo is in talks to invest in Atletico Madrid via a stake in Atletico Holdco, which owns most of the club. Initial talks focused on financing the club’s €800mn ($929mn) leisure project, w/ €200mn from the club and the rest from private investors. A deal could value the club at up to €3bn. CEO Gil Marin holds >50% of Atletico Holdco; Ares Mgmt and Enrique Cerezo also hold stakes. (Reuters)

- DraftKings is in talks to acquire Railbird Exchange, a newly licensed prediction mkts platform, ahead of football season. While no deal is finalized, the move reflects growing sportsbook interest in federally licensed mkts, which can operate in states like CA & TX. (Front Office Sports)

Tech Hardware

- China’s smartphone mkts declined 4. 0% YoY in 2Q25 to 69mn units, ending 6 quarters of growth. Weak gov’t subsidies and economic uncertainty impacted demand. Huawei reclaimed the top spot after 4+ yrs, while Xiaomi was the only Top 5 OEM to grow, aided by value-focused buyers. Apple narrowed its decline via price cuts making iPhone 16 models subsidy-eligible. (IDC)

- Google annc’d an Aug 20 event in NY to unveil its Pixel 10 lineup, incl. the Pixel 10 Pro Fold with shifted focus toward integrating generative AI deeply into the Android ecosystem. All devices will run Android 16, feature Gemini AI, and use the new Tensor G5 chip by TSMC. While not as slim as Samsung’s Z Fold 7, the foldable will be premium-priced. Google may also debut smartwatches and earbuds. (Indian Express)

- US Commerce Sec Lutnick said Nvidia can resume H20 chip sales to China, calling it the cos “4th best” AI chip. The Trump admin reversed its stance to keep Chinese cos reliant on U.S. tech. Lutnick said the goal is to get Chinese devs “addicted” to the American tech stack. Nvidia’s H20, stripped-down from its top-tier Blackwell chips, could’ve earned $8bn this quarter before the ban. (CNBC)

- The smartphone mkt grew 1% YoY to 295. 2mn units, marking its 8th cont’d growth quarter. Apple shipped 46.4mn iPhones in Q2 2025, up 1.5% YoY, despite a 1% dip in China due to weak demand and ineffective subsidies. Growth in emerging mkts, where Apple targets premium buyers, offset China’s decline. Samsung led w/ 58mn units, driven by AI-enabled mid-range models. (Apple Insider)

Towers/Fiber

- Ofcom annc’d changes to mobile spectrum licence fees, saving operators ~£60mn/yr. Fees for 900 MHz and 1800 MHz bands will be reduced by 26% to £1.032mn/MHz and £0.760mn/MHz, respectively. Fees for 2100 MHz will increase by 6% to £0.722mn/MHz. The changes aim to ensure efficient spectrum use and strengthen operators’ investment capacity in the UK. Ofcom also opened a consultation on amending Mobile Trading Regulations to remove barriers to spectrum trading, w/ responses due by [Fri., Sept. 12]. (Street Account)

- Telenor Group raised its 2025 earnings guidance after strong Q2 Nordic performance. The telecom co now expects high-single-digit organic growth in adj EBITDA in the Nordics, up from mid-single-digit. Group-level guidance revised to mid-single-digit organic EBITDA growth. Free cash flow before M&A projected at ~NOK 13bn for the yr. Q2 svs rev NOK 16.5bn, adj EBITDA NOK 9.3bn. Norway led w/ 3.7% svs rev growth, 16.1% adj EBITDA increase. Telenor signed an 8-yr agreement w/ Hydro for mobile network svs. (investing.com)

- Brookfield Infrastructure Partners plans to acquire ISP Hotwire Communications for ~$7bn, incl. debt, from Blackstone. Hotwire, operating under Fision Fiber, serves nine U.S. states. Blackstone bought it in 2021 and invested $1bn to expand svs. Brookfield’s deal adds to its growing digital infra portfolio, incl. fiber, telco towers, and data centers. T-Mobile & KKR had earlier bid for the co. (Data Center Dynamics)

- EQT, Omers & Phoenix Tower are eyeing final bids for Cellnex’s 72% stake in its Swiss unit, valued up to €2bn. Bids are due by next week. Cellnex, active in 10 countries, entered Switzerland in 2017 via a deal w/ Sunrise. The Co is divesting assets to cut debt. (SWI swissinfo.ch)

- Altice USA annc’d a $1.0bn asset-backed loan facility, secured by HFC network assets in Bronx & Brooklyn. The deal, done w/ Goldman Sachs & TPG Angelo Gordon, matures Jan. 2031 w/ 8.875% fixed coupon. The Co may add debt if conditions met. (Altice)

- CityFibre has secured £2.3bn in new financing, including £500mn in equity from shareholders and £960mn in expanded debt facilities. An £800mn accordion facility will support M&A. This investment will accelerate CityFibre’s growth, enhance its 10Gb XGS-PON network, and boost the UK economy. CEO Greg Mesch highlighted the significant benefits for partners and customers. The UK Chancellor and Secretary of State for Tech praised the investment’s impact on digital infrastructure and economic growth. (CityFibre)

Video Games/Interactive Entertainment

- Roblox annc’d new safety features incl a video selfie-based age-estimation tool to protect its young user base. The in-game “Friends” system is now “Connections,” w/ a new “Trusted Connections” tier for verified users 13+ to chat freely. Teens must verify age via selfie or ID; parental consent may follow. New parental tools include spending alerts, screen time controls & Do Not Disturb mode. (The Seattle Times)