This week, the major US indices took a bit of a breather following the recent surge. Nasdaq ended the week ~flat and the S&P 500 fell a modest -0.3% (though both did hit a fresh new record high during the week). On the macro front, tariff news flow was the main event but investors took the updates in stride in the big scheme of things. Next week’s June CPI will be a key event along with the start of earnings (!). It was also notable that Nvidia became the 1st company with a $4 trillion market cap (after passing $3 trillion in June 24, $2 trillion in Feb 24, and $1 trillion in May 23…

In terms of the most important developments/updates in TMT this week, our focus was on the below:

- An Advertising Canary In The Coal Mine? WPP Negatively Pre-Announces

- Prime Day Becomes Prime WEEK!

- VC’s Continue To Plow $ Into AI, Though Q2 Levels Are Down From Q1

- Short Sellers Change Positioning The Most In AST SpaceMobile & Redfin In Q2

- AI First Web Browsing Is Gaining Momentum

- Tech Giants Still See A Bright Future For Mixed Reality Wearable Tech

- Streamers Are Clamoring For More Sports Content…

- Consumers Are Increasingly Turning To Bundles For Streaming Services

- Grab Bag: Delta Gets Back On The Flight Path In Q2/NVIDIA Reportedly Working On China-Specific AI Chip / Big Beautiful Bill Speeds Up AT&T’s Fiber Rollout

I hope you have a nice weekend.

Best,

Leslie

An Advertising Canary In The Coal Mine? WPP Negatively Pre-Announces

It was a downer at the start of the week with WPP surprising the Street with a H1 trading update that signaled much worse than expected trends in Q2 (especially in June) due to a “challenging” trading environment with macro pressures “intensifying” and lower than expected net new business. These trends were also guided to persist in H2. As such, mgmt slashed revenue and margin guidance for H1 and for the full year 2025 (net new business losses and the macro deterioration contributed roughly the same to the negative revision). Also, on the heels of this trading update, the Co announced that CEO Mark Read will step down at the start of September and will be replaced by Cindy Rose. She will join from Microsoft, where she has been the COO, Global Enterprise, but has held numerous senior leadership positions in her last 9 years there, amongst other appointments.

All in all, the picture looks a bit cloudy for the ad agencies but we’ll certainly hear more from the other large players during the upcoming earnings cycle, and WPP mgmt will provide additional guidance when it reports its 1H25 results on August 7th.

In the meantime, see more details below on WPP’s H1 trading update this week.

-> WPP share fell a sharp -18% in reaction to the statement and closed the week down -23%…it also dragged down the rest of the sector with IPG, OMC and Publicis all down -3%, -3, and -4% this week; All the major ad agencies have struggled YTD but WPP has trailed the group (IPG -11%, OMC -15%, Publicis -2%, and WPP -46%)

WPP Pre-Announces Disappointing H1 Trends Due To A “Challenging” Trading Environment W/ Macro Pressures “Intensifying” And Lower Net New Business

- Cut H1 revs guidance: Expects like-for-like revs less pass-through costs to decline by -4.2% to -4.5%, with a decline of -5.5% to -6.0% in Q2

- Stripping out one-off factors, the underlying run rate like-for-like would be closer to -3.6% to – 3.9% in H1, and -4.5% to -5% in Q2; In absolute terms, revenue less pass-through costs is projected at ~£5bn

- Cut H1 op profit margins: Expects headline op profit in the range of £400-425mn, which is consistent w/ a margin decline of 280-330 bps y/y (ex-FX) to 8-8.5%

- Drivers include the lower rev less pass-through costs plus severance action at WPP Media

- Cut FY 2025 outlook…given “the expectation of continued macro uncertainty weighing on client spend and weaker net new business than originally anticipated”

- Cut 2025 like for like revenue less pass-through costs guidance to -3% to -5%, from flat to -2%

- Cut headline op margin y/y decline guidance to 50- 175bps (ex- FX), vs the previous ~flat

- Restructuring actions help margins but plan to continue to invest

- What happened?

- Mgmt cites a “challenging” trading environment w/ macro pressures “intensifying” and lower net new business

- Performance in June was worse than anticipated and the Co believes these trends from H1 will continue into H2

- The Co saw a deterioration of performance as Q2 progressed

- Saw a greater degree of caution on client spending than expected (esp in CPG)

- Saw weaker net new business

- The Co has seen this weakness not just from sectors impacted by tariffs… “We’ve just seen more caution from clients”

- This is exacerbated by 1-time factors which impacted WPP Media’s performance in the qtr

- The Co indicated that “the latest convergence tracker shows that new business opportunities in media y/y are running about a third of the level in 2025 as they were in 2024”

- Expect higher severance in H1: H1 total severance costs will be ~£100mn, which is an incremental ~£65mn or 120bpy/y

- Bridging the ORIGINAL vs NEW guidance –

- ORIGINAL guidance…anticipated a headwind from net new business in H1, and a tailwind in H2, leaving the full-year impact broadly neutral

- This reflected known wins and losses at that time & an expectation on the volume of new business and WPP’s win rate

- NEW guidance…anticipates a negative impact from net new business for the year as a whole, reflecting “incremental client losses and a lower level of new business conversion”: About half of the delta is from net new business and half is from the weaker macro

- Mgmt ests the impact to be ~100- 150bp

- This includes some “pull-forward” of client losses which they would have originally expected to impact 2026

- The impact of the macro & current client spending has been more pronounced in Q2 than anticipated and more than had been assumed at the bottom end of their original guidance

- ORIGINAL guidance…anticipated a headwind from net new business in H1, and a tailwind in H2, leaving the full-year impact broadly neutral

- What’s the color on regions and segments?

- Regionally: Saw a q/q deterioration in N. Amer which is expected to be down lsd% across H1

- Other regions “have remained weak despite an easing comparative”

- Segments: Expect the Global Integrated Agencies business growth to decline from -2.8% in Q1 to a mid-sd% decline in Q2 (H1 decline mid-sd%) w/ lower client spend & net new business impacting WPP Media & Ogilvy in particular

- Regionally: Saw a q/q deterioration in N. Amer which is expected to be down lsd% across H1

Prime Day Becomes Prime WEEK!

What began as Amazon’s summer sales event has evolved into a full-blown retail moment across the industry. Amazon’s Prime Day, which runs through the end of today (Friday) was extended to four days this year, up from two in prior years. But Amazon is not alone. Walmart, Target, Best Buy, Costco, and Kohl’s are all running major sales this week, many of which are longer than their respective events held last year. Adobe estimates that US consumers will spend nearly $24bn online across all retailers by the time all the shopping events wrap up, roughly equivalent to two Black Fridays.

Some early data points have already emerged. Adobe reported a +9.9% y/y increase in US online sales on July 8, the first day of Prime Day, making it the biggest e-commerce day of the year so far. However, 3P data from Momentum Commerce suggested that Amazon-specific Prime Day declined -41% y/y on the first day of the event, likely due to the longer shopping window. Amazon pushed back on those figures, calling them inaccurate.

More complete numbers will come into focus after the weekend once all major events conclude and final sales are tallied. In the meantime, see below for the initial updates and read throughs.

Prime Day Is Expected To Spark A Surge In Online Sales, Per Adobe (link)

- Initial estimates – Adobes estimates that the Prime Day event (running from July 8-11) will drive $23.8bn in online spend across US retailors, up +24.8% y/y or +$9.6bn y/y (link)

- This is approx. equivalent to two Black Fridays, which drove $10.8bn in online spend during the 2024 holiday shopping season

- Shopping on mobile devices is set to hit an all-time high, driving 52.5% of online sales (vs desktop shopping) at $12.5bn

- This continues to be a growth driver for US retailers, with more impulse shopping happening on mobile devices

- Discounts are expected to remain at historically high levels, as overall, discounts across US retailers will be in the range of 10%-24% (off listed price)

- Apparel expected to have the biggest deals at 24% (vs 20% last year)

- Electronics at 22% (vs 23%)

- Televisions at 17% (vs 16%)

- Appliances at 16% (vs 14%)

- Toys at 15% (vs 15%)

- Furniture at 14% (vs 16%)

- Computers at 12% (vs 11%)

- Sporting goods at 10% (vs 11%)

- Consumers are expected to “trade up” to higher-ticket items, driven by strong discounts; The share of the most expensive goods is set to increase by 18% (vs to avg levels YTD)

- In electronics, the share of the most expensive goods is expected to rise by a significant 52%

- Sporting goods, up 32%

- Appliances, up 29%

- Furniture, up 28%

- Toys, up 18%

- Personal care, up 15%

- Apparel, up 9%

- Categories with a drop include home and garden (down 4%) and grocery (down 6%), as consumers embrace lower-priced products

- Consumers are getting a head start on back-to-school shopping (which generally begins in mid-August to early-September)

- Categories expected to see the biggest boost are backpacks & lunchboxes (up 225% compared to the daily average in June 2025), kid’s apparel (up 200%), and general school/office supplies (up 180%)

- Shopping for college essentials is also expected to see strong growth, including in twin/full mattresses & toppers (up 55%), bedroom/bathroom linens (up 49%), microwaves (up 75%), headphones & speakers (up 150%), and computers (up 140%)

- Traffic from genAI sources is expected to increase by +3,200% y/y

- Material acceleration from the 2024 holiday shopping season (between Nov. 1 and Dec. 31, 2024), when traffic from genAI sources increased by 1,300% y/y

- In a recent Adobe survey of 5k US consumers, the shopping tasks respondents said they used genAI for include conducting research (per 55% of respondents), receiving product recommendations (47%), seeking deals (43%), getting present ideas (35%), finding unique products (35%) and creating shopping lists (33%)

- Buy Now Pay Later (BNPL) usage is expected to see a sligh uptick

- Expects BNPL to drive between $1.8bn-$1.9bn of overall online spend, which represents an 8% share, up from 7.6% last yr

- Strong spending during the Prime Day event will be driven by net-new demand, as opposed to higher prices

- E-commerce prices have fallen for 33 months, down -2.01% y/y in May 2025, per the Adobe Digital Price Index, which tracks online prices across 18 product categories

A Whole Host Of Retailers Followed Amazon And Are Having Big Sales Events This Week (link)

- New this year – Amazon’s annual Prime Day summer sale has been extended to 4 days, up from 2 days in previous years and will run from July 8-11

- Amazon said it doubled the length of the annual sale b/c shoppers have indicated they wanted more time to navigate the deals

- Walmart Deals 2025 will run from July 7-13

- Walmart+ members got early access to the sale at 7pm ET Monday; The sale starts at midnight ET Tuesday online for all shoppers and in stores when they open

- First time the sale will be available both in stores and online

- Target Circle Week is going from July 6-12

- The sale started even earlier for members of the paid Target Circle 360 program

- There will be early back-to-school and college shopping deals and the return of Target’s “Deal of the Day”

- Best Buy’s “Black Friday in July event” is running from July 7-13

- The retailer is calling it one of its “biggest sale events of the summer”

- The sale was three days last year, but like Amazon’s, increased in length

- Costco’s five-day sale is running from July 7-11

- The sale is online-only and while supplies last

- Kohl’s Summer Cyber Deals runs from July 7-10

- The sale ran for 4 days this yr (up from 2 days in 2024)

- New daily deals were added each day in-store and online (included free shipping on all online orders)

Mixed Initial Data Points On Consumer Spend

- On Tuesday (July 8), the first day of Amazon’s Prime Day event, US online sales were up +9.9% y/y to $7.9bn – “the biggest e-commerce day so far this year” (link)

- Also eclipsed total online spending during Thanksgiving last year, when sales on the holiday reached $6.1bn

- Walmart’s six-day deals event also started Tuesday, while Target Circle Week kicked off on Sunday and Best Buy’ Black Friday in July event began Monday

- That said, Amazon Prime sales were down -41% y/y on the first day of Prime Day, per Momentum Commerce, which manages sales for 50 sellers on Amazon accounting for $7bn in spending on the online platform (link)

- Why the decline? “Likely explained by consumers ‘treasure hunting’ across Amazon, adding products to cart but being slower to purchase in case new deals show up” across the longer event period, Momentum CEO and founder John Shea wrote in a LinkedIn post

- Also found that the avg rate of discount on the first day was 21% vs 24% during Prime Day 2024

- In response, Amazon said that Momentum’s numbers are “highly inaccurate” and typical “of statements made by third-party consultancies that don’t have access to the actual data”

- The Co is “really pleased by the engagement that we’re getting from our customers and our members,” per Amazon Prime VP Jamil Ghani

Preliminary Prime Day Stats From Numerator As Of 4pm On July 11th (link)

- 154,807 Prime Day orders

- 52,807 households shopping

- 307,746 items purchased

- $53.34 avg order size

- $156.37 avg household spend

- Many Prime Days shoppers also shopped or planned to shop other retailer deals, including –

- Walmart Deals (49% of shoppers)

- Target Circle Week (37%)

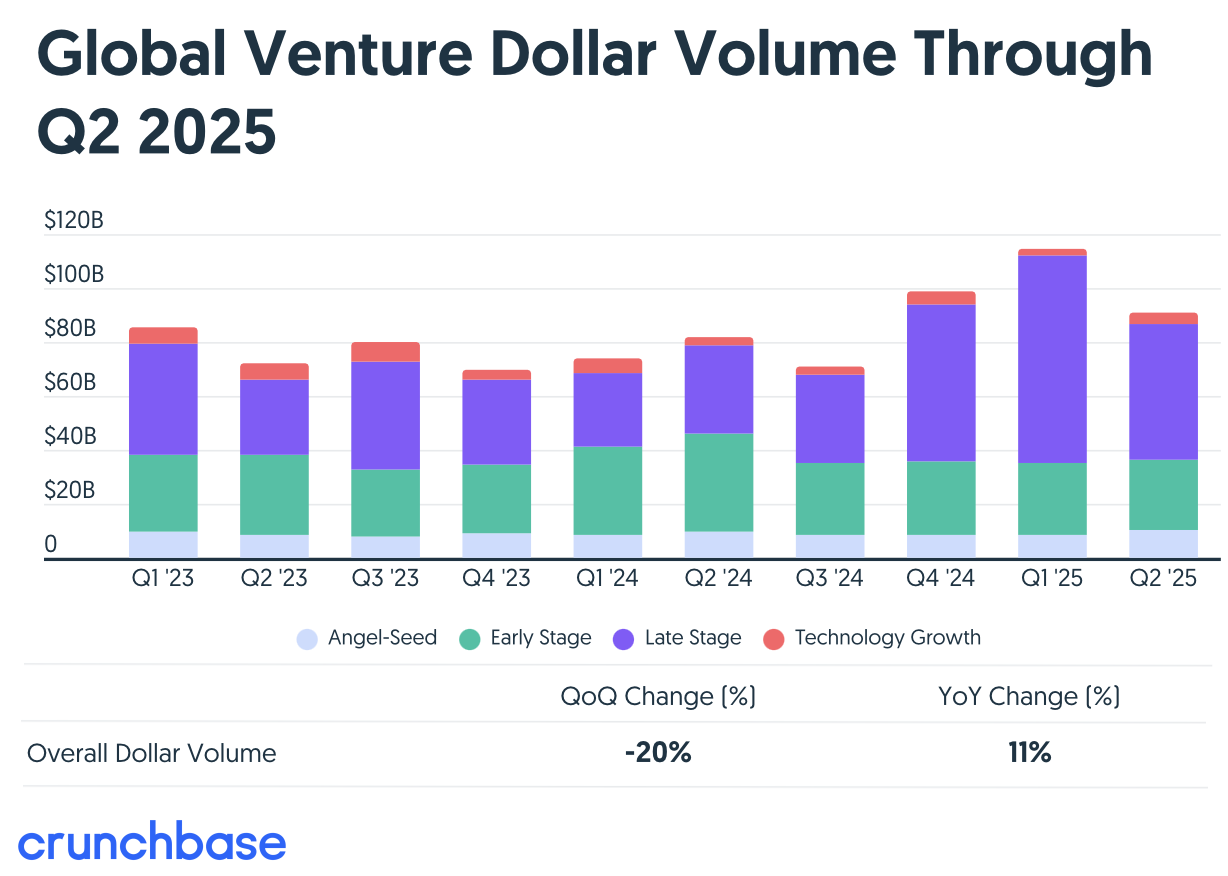

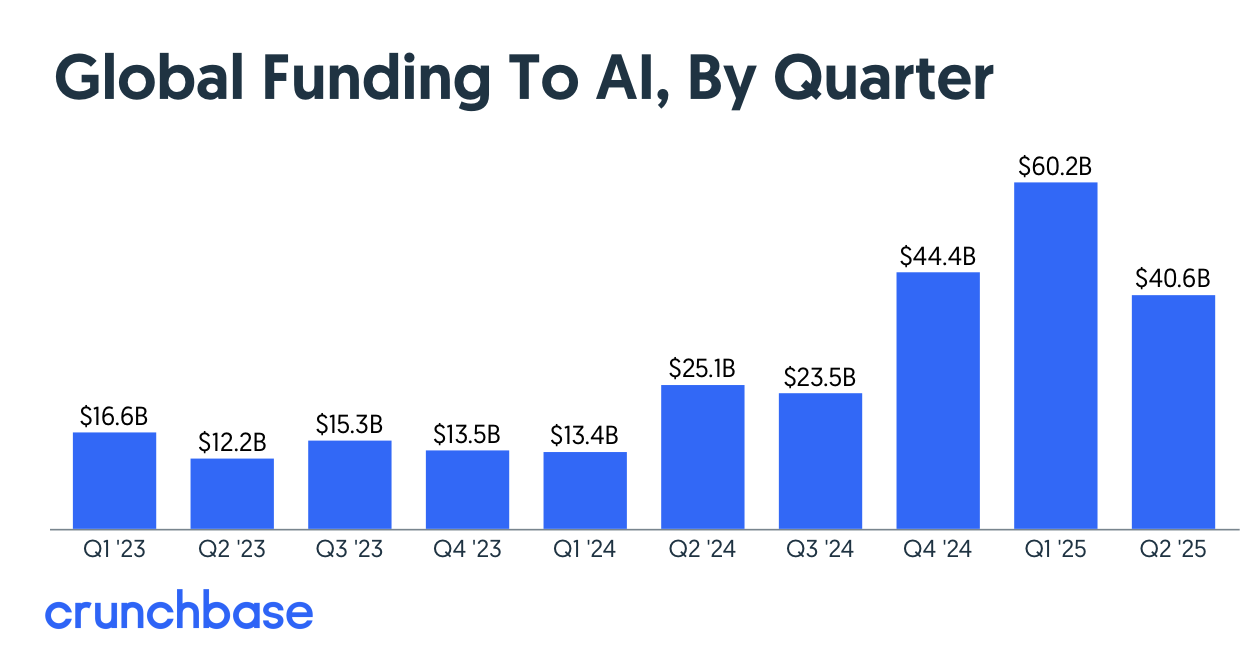

VC’s Continue To Plow $ Into AI, Though Q2 Levels Are Down From Q1

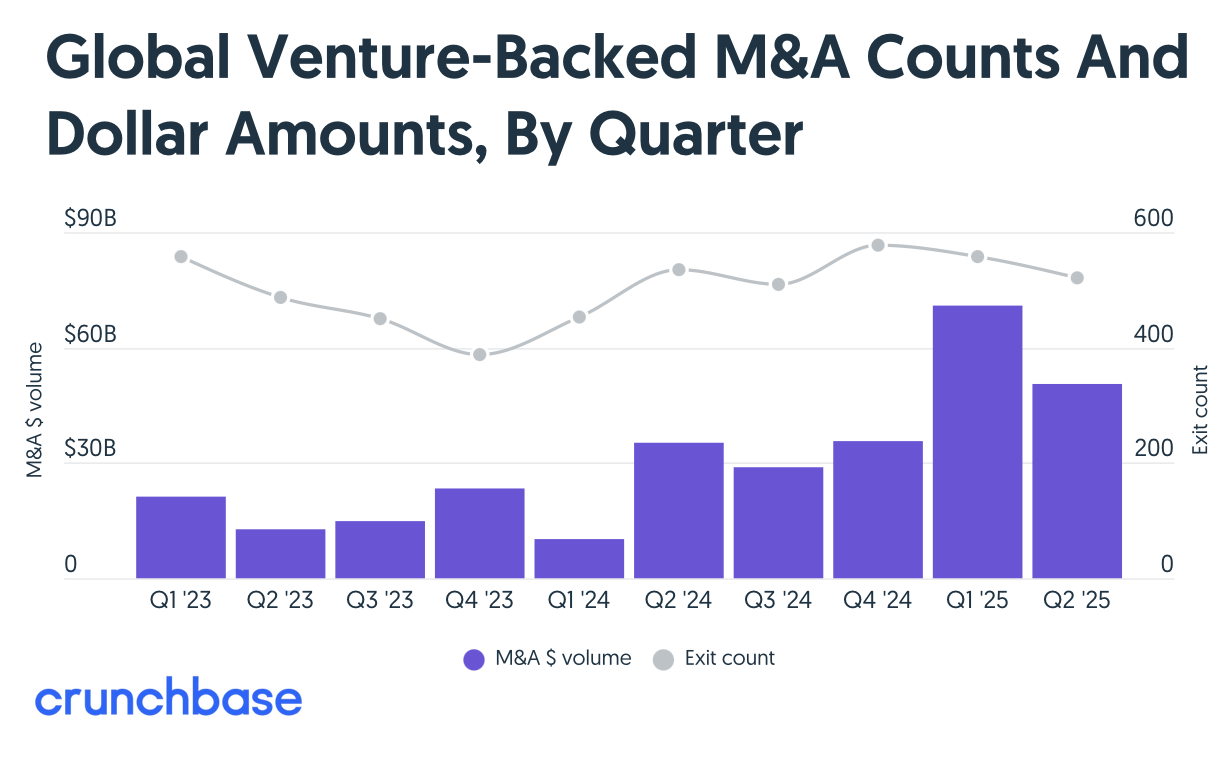

Per Crunchbase data this week, we got an update on global venture capital funding trends. Overall, Q2 was a strong qtr for capital funding (incr’d +11% y/y) but levels were down from the blockbuster and record setting Q1 levels. Investments into AI dominated and accounted for ~45% of all VC funding in Q2. Healthcare/BioTech and Financial Services were distant 2nd and 3rd in terms of sectors that VC’s funded in the period. In terms of exits, M&A was also up for the second qtr in a row, rivaling peak M&A amounts in 2021.

See more details below on what we thought was most incremental. (link)

-> Related, other data out this week pointed to at least 36 new tech unicorns being crowned thus far YTD; The full list can be found HERE

- Q2 global venture capital funding incr’d +11% y/y to $91bn but fell -20% from Q4’s $114bn (highest qtr for funding since Q3 2022)

- The y/y increase over the last 3 qtrs has been driven by billion-dollar-plus rounds into AI research labs as well as data and infrastructure providers in the sector

- Funding in AI has been sky-high and the most active sector for VC capital in Q2 at $40bn, ~45% of total global funding in the period

- ScaleAI: $14.3bn

- Anduril Industries: $2.5bn

- Thinking Machines Lab: $2bn

- Safe Superintelligence: $2bn

- Grammarly: $1bn

- Anysphere: $900mn

- Helsing: $694mn

- Other active sectors for VC funding in Q2 –

- #2 – Healthcare & biotech companies, raising $14.8bn

- #3 – Financial services, raising $10.8bn

- Q2 was the 2nd-strongest qtr for startup M&A dollar volume since 2021, with $50bn in reported exit value…last qtr was the strongest, at $71bn given the $32bn Google/Wiz deal

- OpenAI was the most-active & largest acquirer by amount in Q2, buying 4 companies including Jony Ive’s io for $6bn & Windsurf for $3bn

- 18 Cos were acq’d for $1bn+ in Q2

- ~50% were acquired by public companies, and 3 by PE firms

- Funding trend by stage…late stage drove y/y gains in Q2

- Late-stage Cos: Funding reached $55bn, +55% y/y (but down q/q by close to a third)

- Early-stage Cos: Funding was flat q/q in Q2 reaching $26bn across 1,600 Cos with the largest rounds at this stage peaking around $220mn

- Seed Cos: Funding reached $10.3bn in Q2

- Thinking Machines raised 20% of that w/ a $2bn seed round that marked the largest on record at that stage

- Excluding the Thinking Machines’ round, seed funding would have been flat q/q and down y/y

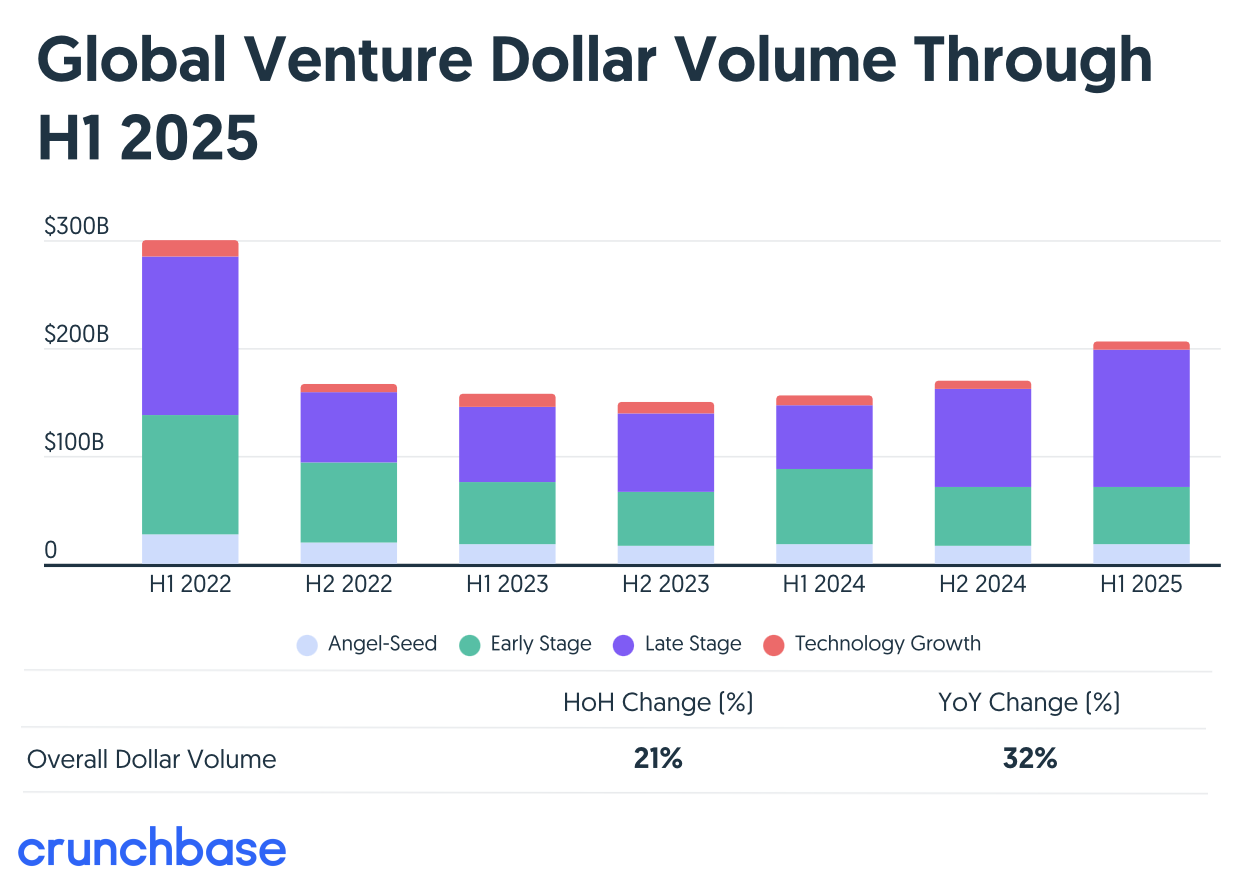

- In total, $205bn was raised via VC in H1, up +32% y/y and up +21% vs H2:24

- More than 1/3 of H1 funding went to just 11 companies that raised rounds of $1bn or more

- Both of the 2 largest venture fundings on record were raised this year…

- Scale AI, with $14.3 billion in Q2

- OpenAI with $40 billion in Q1

Short Sellers Change Positioning The Most In AST SpaceMobile & Redfin In Q2

Short interest data for the period ending June 30 was made available this week, giving us a look at where sentiment stands across the LionTree Universe of ~150 publicly traded TMT and Consumer companies with $1bn+ market caps. While there weren’t any major changes in the list of most shorted names, there was some reshuffling at the top. Groupon moved into the #1 spot, followed by Hims & Hers and Gogo. A few names rotated in and out of the Top 20, including new entrants like GameStop, Oscar Health, Lyft, AMC Entertainment, Paramount and Magnite.

Even with elevated short interest across the group, Q2 was a tough period for short sellers. Only 7 of the 20 most shorted stocks underperformed the S&P 500’s +10.6% gain, while the Top 20 group overall climbed an average of +39.1%. AST SpaceMobile, which saw the largest increase in short interest last quarter, posted the largest decrease in Q2. On the flip side, Redfin had the biggest jump in short interest but still managed to rally +21.5% in the qtr.

See below for more details on our analysis.

Most Shorted Stocks (As % Of Float) – Groupon

- The Top 3 Most Shorted – #1 is Groupon, #2 is Hims & Hers, & #3 is Gogo -> Groupon ascended from the #2 position in Q1 to take the top spot; Hims & Hers also rose from the #4 position last qtr to take the #2 spot; Gogo, which was the most shorted stock in Q1, fell to the #3 position

- AST SpaceMobile fell out of the Top 3 from last qtr, but remained within the Top 20, coming in at the #5 position

- Stocks that dropped out of the Top 20 most shorted: Outfront Media, Teladoc Health, Charter Communications, Penn National Gaming, Fiverr International, Omnicom Group

- Stocks that joined the Top 20 most shorted: GameStop, Oscar Health, Lyft, AMC Entertainment, Paramount Global, Magnite

-> It was a rough qtr for short sellers in Q2… only 7 of the Top 20 most shorted stocks underperformed the S&P 500’s +10.6% during the period and the Top 20 most shorted stocks traded up +39.1% on avg in Q2, also significantly outperforming the S&P 500

Largest Decrease In Short Interest (As % Of Float) – AST SpaceMobile

- AST SpaceMobile went from seeing the largest increase in short interest in Q1 to the largest decrease in Q2: The Co saw a -10.3ppt decrease in Q2 to 25.4% (vs a +12.1ppt increase in Q1 to 35.7%)

- It went from being the #3 most shorted stock in Q1 to #5 in Q2

- Gogo also saw a sizable decrease in short interest of -10.2ppt to 30.7%

Largest Increase In Short Interest (As % Of Float) – Redfin

- The largest increase in short interest was seen by Redfin: The Co saw a +10.0ppt increase in Q2 to 23.1% and was also the #10 most shorted stock at the end of Q1 -> The stock traded up a significant +21.5% in Q2, easily outperforming an already strong S&P 500 performance of +10.6%

- 4 of the Top 10 increases in short interest are companies in the Consumer Internet sector: Redfin, Etsy, Wayfair, and Lyft -> All the companies outperformed the S&P 500’s +10.6% performance, with the exception of Etsy

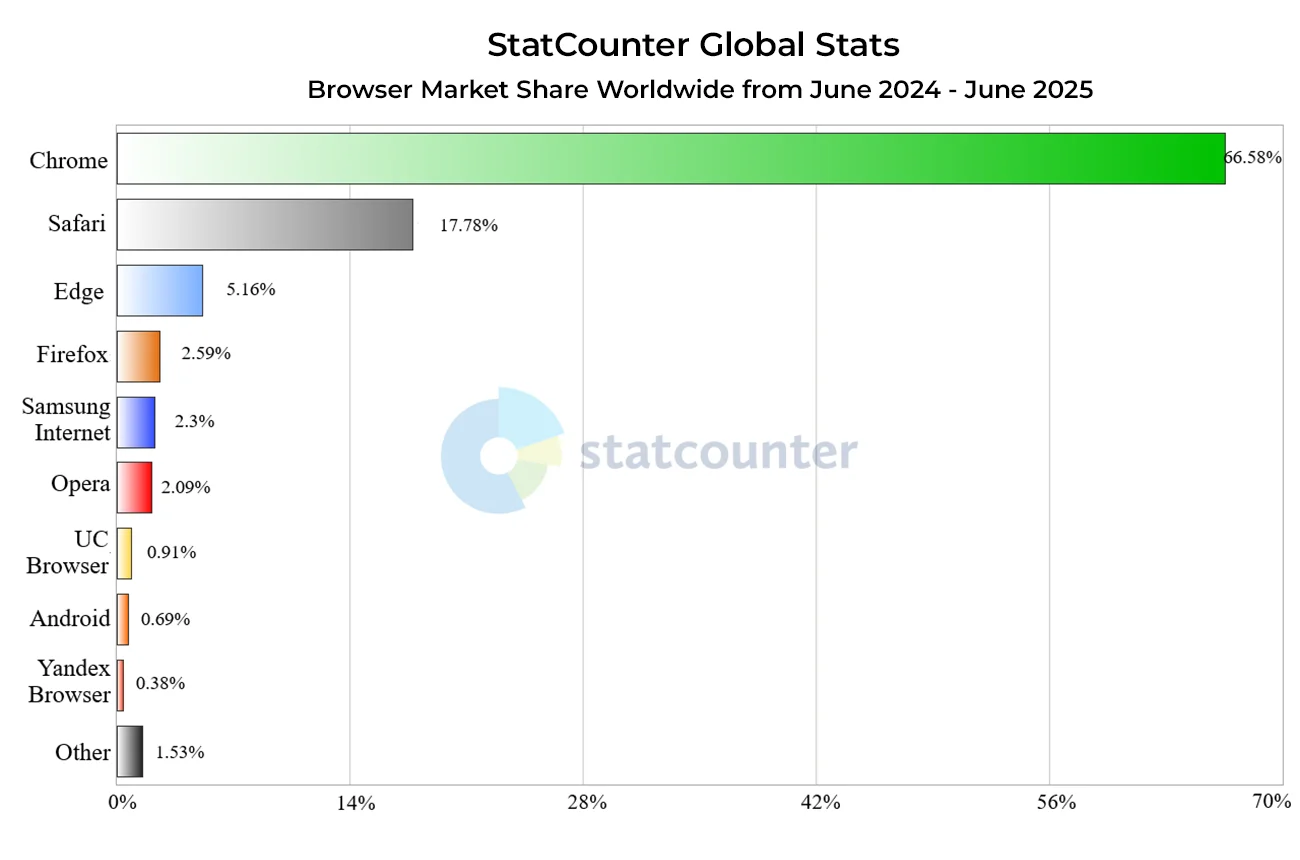

AI First Web Browsing Is Gaining Momentum

As the AI landscape evolves, browsers are emerging as the next key interface and one which AI companies are increasingly seeing as ripe for innovation. Perplexity is the first amongst the major AI names to make a formal move this week with the launch of Comet, an AI-native browser. Designed around Perplexity’s conversational search engine, Comet integrates an assistant that helps users research, summarize, compare, and complete tasks in a single interface. The browser is currently available to Perplexity Max subscribers, with broader (invite-only) access rolling out over the summer.

While Perplexity may be the first major AI company to launch an AI-powered browser, it isn’t the first overall, as startups like The Browser Company and Brave have already rolled out AI-powered browsers with varying levels of integrated assistance. But momentum is clearly building as, also this week, OpenAI is reportedly preparing to debut its own browser in the coming weeks. That said, all of these companies face an uphill battle in a landscape where Google Chrome maintains an ironclad grip, powering more than two-thirds of the global browser market.

See below for more on these updates.

- Perplexity launches Comet, an AI-powered web browser “for today’s internet” (link/link/link)

- Perplexity’s search engine is set as the default option for users

- Enables users to ask questions, perform tasks, and conduct research in a single, unified interface

- Integrates a built-in assistant that can compare products, summarize content, book meetings, and transform complex workflows into simple, conversational experiences

- Comet is based on Chromium, the open-source software engine that underpins Chrome

- Will support Chrome extensions and allow users to bring over their bookmarks

- Chromium is also widely supported by websites, which avoids compatibility-related technical issues

- Currently, the browser can run on Windows and macOS, and plan to add support for more operating systems in the coming months

- Availability: Available now to Perplexity Max subscribers (Perplexity Max costs users $200/mo)

- Broader invite-only access will roll out to their waitlist over the summer

- New users will also receive a limited number of invites to share

- Plan to “continue to launch new features and functionality for Comet” in the future

- OpenAI is also reportedly close to releasing its own web browser (link)

- It is expected to launch in the coming weeks, according to people familiar with the matter, cited by Reuters

- The browser is reportedly designed to keep some user interactions within a ChatGPT-like native chat interface instead of clicking through to websites, per the sources

For context…what does the browser landscape look like now?

- Chrome dominates: Google Chrome, which is used by 3bn+ people, currently holds ~2/3 of the worldwide browser market, according to web analytics firm StatCounter; Apple’s Safari lags far behind with a ~18% share

- What other AI browsers are out there? Two other AI startups, The Browser Company and Brave, have released AI-powered browsers capable of browsing and summarizing the internet

Tech Giants Still See A Bright Future For Mixed Reality Wearable Tech

While progress of virtual and augmented reality (VR/AR) has been disappointing vs earlier rosy projections, tech giants like Meta and Apple remain focused on investing in this area to help develop and eventually lead this potentially big market opportunity. There were press updates out this week pertaining to both companies’ investments or new product plans which highlights the continued steadfastness to foster growth and consumer adoption. Meta reportedly acquired just under 3% of Essilor Luxottica (with potential to buy more), signaling a deeper commitment to making smart glasses a mainstream product. Meanwhile, Apple reportedly is refining its approach to mixed reality with updates to the Vision Pro lineup, balancing performance enhancements in the near-term with a longer-term push toward broader market penetration through lighter, more affordable hardware. We are still a way off from an inflection point in consumer adoption, but big tech remains on that path…more color on these developments are below.

- Meta is reportedly plowing more money into AI-powered smart glasses (link): The Co apparently invested $3.5bn in Essilor Luxottica this week, which is aimed at accelerating the development & global rollout of AI-powered smart glasses

- Meta reportedly acquired just under 3% of Essilor Luxottica (the world’s largest eyewear manufacturer and parent company of Ray-Ban and Oakley)

- The investment was made at market value & could potentially increase to 5% over time, per sources

- Meta has been collaborating w/ Essilor Luxottica since 2019…they have developed –

- Ray-Ban Meta Smart Glasses

- Oakley Meta HSTN

- The deal is part of a broader vision by CEO Mark Zuckerberg to make wearable AI a central pillar of Meta’s future, alongside its investments in the metaverse and custom AI infrastructure

-> Essilor Luxottica shares jumped +5.5% in reaction to the press reports and Warby Parker shares also rallied +4.5% (Warby has a partnership with Google to develop AI glasses)

- Apple is reportedly planning two major updates to its Vision Pro headset…the more significant one being in 2027 (link/link)

- Vision Pro 2 is expected to launch later in 2025 – it’s a refreshed version of the current Vision Pro, and will –

- Be Faster: It will have the M4 chip which is 2x faster than the older M2

- More comfortable: The strap will be redesigned, which will improve comfort, especially for long-term wear

- Weigh the same: The overall design & weight (~1.4 pounds) will remain mostly unchanged

- Pricing is expected to remain the same: $3,499

- A lighter & more affordable version is expected to be introduced in 2027 – it is reportedly internally dubbed the “N100” or possibly named Vision Pro Air; Key features:

- It will be a complete redesign to reduce the weight & cost

- It will use cheaper materials like plastic

- It will have fewer sensors and possibly the removal of the EyeSight display to cut costs

- This version is aimed at broader consumer adoption, addressing complaints about the current model’s price and comfort

- Vision Pro 2 is expected to launch later in 2025 – it’s a refreshed version of the current Vision Pro, and will –

Streamers Are Clamoring For More Sports Content…

As we flagged in Theme #8, 88% of consumers are watching the same or more streaming content than last year, and 30% find live content, like sports, “very appealing.” Streaming viewership certainly isn’t going anywhere (unless up), and sports rights activity is reflecting this sustained demand.

This week, Apple reportedly submitted a bid of between $150mn-$200mn for the US Formula 1 rights, which is more than double what ESPN currently pays. Meanwhile, Fox Nation made its first move into live sports with a deal to stream Professional Bull Riders’ weekly events, launching “PBR Friday Night Live” this August. Also, after a couple year gap, ESPN renewed its partnership with the BIG EAST in a 6-yr agreement that will bring 300+ live events annually to ESPN+. Finally, DAZN secured exclusive and non-exclusive rights to Italy’s Serie A for the 2025/26 season across the U.K., Ireland, and US, which adds to the Co’s ongoing broadcast of all 63 matches of this summer’s FIFA Club World Cup.

See below for more details on the slew of sports streaming developments this week.

- Apple reportedly bid on Formula 1’s US broadcast rights (link/link/link)

- Success of Apple’s recent F1 movie at the box office is seen as a key driver for the bid: The film was an Apple Original Films project and has grossed over $300mn worldwide-to-date, making it Apple’s highest-grossing film ever

- The Co is said to have offered “between $150mn and $200mn per year” — far above the reported $85mn to $90mn that ESPN is currently paying per annum, and far beyond what ESPN can rationally afford”

- The league’s current deal w/ ESPN expires at the end of this yr

- ESPN let its exclusive bidding period for the rights lapse, citing higher costs, however, it remains in the mix, alongside Apple and other bidders

- If a deal materialized, Apple would stream F1 in the US starting w/ the 2026 season

- What sports rights does Apple have currently? Apple TV+ features exclusive MLB matches with Friday Night Baseball, and the Apple TV app is the exclusive streaming home of all Major League Soccer games

- Fox Nation makes its first sports rights deal with Professional Bull Riders (link/link/link)

- This will be the first time Fox-News owned streaming platform has offered weekly live sports coverage

- Fox CEO Lachlan Murdoch recently estimated that Fox Nation has surpassed 2mn paying customers

- Will air the “PBR Friday Night Live” series: The series will launch on Aug 8 in Sunrise, FL, and continue through the fall, finishing with the league’s championship opener on Oct. 24 at T-Mobile Arena in Las Vegas

- In a lead-up to the live coverage, starting July 11th, Fox Nation will debut Season 2 of the reality series Last Cowboy Standing: Over the span of 10 weekly episodes, the series features a group of amateur bull riders competing for a chance to join a PBR team

- PBR’s primary rights partner is Paramount Global; The deal with Fox is the first new rights deal for PBR since it was acquired by TKO Group earlier this yr

- This will be the first time Fox-News owned streaming platform has offered weekly live sports coverage

- ESPN and BIG EAST reunite w/ 6-yr media rights deal (link/link)

- ESPN+ will stream 300+ BIG EAST events annually

- Adds hundreds of live BIG EAST events to ESPN’s college sports portfolio

- At least 25 non-conference BIG EAST Men’s basketball games, a minimum of 75 women’s basketball and 200 Olympic sport events will stream on ESPN+ annually beginning in the 2025-2026 academic season

- Deal does NOT include a linear component, as those deals were struck a year ago with Fox, NBC, and TNT Sports

- ESPN had the rights to the Big East from 1980 to 2013; The revived partnership comes after ESPN lost Big Ten media rights to Fox, NBC and CBS in 2022

- ESPN+ will stream 300+ BIG EAST events annually

- DAZN secures rights to Italy’s Serie A football in UK and US markets (link/link)

- Exclusive and non-exclusive rights to Lega Serie A (Italy’s top football league) competitions

- In the 2025/26 season, DAZN will stream every Serie A championship match in the UK and Ireland and the US…

- In the UK & Ireland, have exclusive rights for up to 8 matches per round and non-exclusive rights for the remaining 2

- In the US, 5 matches per round will be broadcast exclusively, and 5 matches per round will be available non-exclusively

- …alongside highlight rights across most global territories

- Also acquired highlight rights for the Serie A Championship, Coppa Italia and Supercoppa Italiana across nearly every country worldwide, excluding Italy, Republic of San Marino, Vatican City, and the MENA region

- Comes as DAZN continues its global broadcast of all 63 matches of the FIFA Club World Cup this summer

Consumers Are Increasingly Turning To Bundles For Streaming Services

As the global streaming landscape matures, consumer behaviors and expectations are shifting – driven by rising costs, evolving content preferences, and growing competition from alternative platforms. There were two survey results out this week that that we wanted to highlight as they shed some more light along these lines. First, the Global Streaming Study 2025 by Simon-Kucher showed that while 88% of users are watching the same or more content than last year, 42% feel they’re spending too much, and 35% plan to cancel at least one subscription, though nearly half would reconsider if offered cheaper, ad-supported options. With that said, bundles are gaining strong traction and live content, such as sports and concerts, are resonating especially with younger audiences. Lastly, the results point to social media increasingly competing for screen time. The second survey, conducted by Horowitz Research, also highlights strong consumer interest in unified service bundles and centralized subscription management.

-> On a related note, despite any growing subscription fatigue, it may not be as easy as they had hoped to actually cancel services given a U.S. appeals court this week blocked a rule that would have required businesses to make it as easy to cancel subscriptions and memberships as it is to sign up, saying the agency that created it did not follow protocol; The rule was set to take effect on July 14. Oh well…(link)

Global Streaming Study 2025 By Consultancy Firm Simon-Kucher (link / link)

- Users are watching more: 88% of users report consuming the same or more streaming content vs last year

- A critical mass of users think they are paying too much: 42% of paying subscribers believe they are spending too much on streaming services

- Over 1/3 say they plan to cancel streaming services: 35% of global users plan to cancel at least one subscription in the next 12 months

- This is up 2 ppts vs responses last year

- 48% said they would reconsider if offered a cheaper, ad-supported plan

- The majority of users subscribe via bundles: 51% of global subs now choose bundled streaming packages, often provided through telecom operators

- 30% of users—especially younger audiences—find live content “very appealing”: This includes sports competitions, concerts, breaking news, and cultural events

- Social media is a growing competitor to time spent streaming: 37% of users globally say social media is replacing their streaming time

- In Spain and Sweden, this figure rose from 29% in 2024 to 36% in 2025

- In highly digital markets –

- India: 72%

- Singapore: 56%

- Among users under 40-year-olds, 49% view platforms like TikTok, Instagram, and YouTube as alternatives to traditional streaming

- Sample Size: Over 12,000 users across 11 countries

Horowitz Research (link)

- 66% of consumers say they would likely switch to a bundle from one provider for a wide variety of services, including streaming TV services, home security, fitness, smart home, music and other subscription services

- Interest in bundling all digital services & apps is highest amongst –

- Families with children in the home (76%)

- Younger consumers (75% of 18-to-34-year-olds & 71% of consumers 35-49)

- Streamers (71%)

- Interest in bundling all digital services & apps is highest amongst –

- 56% of consumers wish there was one centralized place for them to manage all their subscriptions

- 41% said that keeping track of their various subscriptions to apps, streaming services, and smart home services is currently a challenge

Grab Bag: Delta Gets Back On The Flight Path In Q2/NVIDIA Reportedly Working On China-Specific AI Chip / Big Beautiful Bill Speeds Up AT&T’s Fiber Rollout

- A first look into travel performance in Q2…Delta Airlines beats estimates as bookings stabilize and the Co reinstates its FY guidance (link/link/link)

- Posted a strong Q2: Record rev of $15.5bn (+0.3% beat vs cons) on 13% op margin; EPS of $2.10 came in above cons $2.06

- Q3 guidance also beat / Reinstated FY guidance: Q2 EPS of $1.25-$1.75 vs cons $1.34; FY EPS of $5.25-$6.25 beating by +7% and FCF of $3-4bn coming in +27% above

- Decision to restore full-year financial guidance is a reflection of “our confidence in the business”

- Since April, “demand trends stabilized …and we continued to see resilience in our diverse, high-margin revenue streams”, Delta president Glen Hauenstein said’

- Corporate travel has also stabilized as bizs have more clarity and confidence than they did earlier this yr, but it’s in line with last yr, not the 5%-10% growth Delta expected at the start of the yr

- “Strong demand” for transatlantic travel pushed rev from flights to European destinations up 2% from last year’s record level

- Premium demand is up, while main cabin demand is still down: While fares have dropped across the US, Delta’s premium-product revenue rose +5% y/y, as sales from the main cabin fell -5% y/y

- The passage of the tax and spending bill and the Trump administration rolling out more trade deals with “less rhetoric and more action” are giving customers more clarity and confidence, said CEO Ed Bastian

-> Delta was up +12% post its Q2 earnings report and ended the week up +11.4%; The stock is still down -6.4% YTD; Travel OTAs also rallied with Expedia up +4.1% this week as well

- NVIDIA reportedly plans to release a new AI chip designed for China (link)

- The chip is a version of Nvidia’s existing Blackwell RTX Pro 6000 processor modified to meet Trump’s tightened export control rules, according to people with knowledge of the plans

- The product would be stripped of the most advanced technologies, such as high-bandwidth memory (HBM) and NVLink, which improves interconnections for faster data transfers

- Could be released as soon as September, as the Co wants to make sure the product complies with the Trump administration’s export restriction and won’t face a ban after launch

- Nvidia’s clients in China have reportedly been testing samples of the chip and expressed interest in significant orders, according to the people with knowledge of the Co’s plans.

- CEO Jensen Huang is reportedly also planning a visit to China, and is expected to reaffirm NVIDIA’s commitment to the Chinese mkt

- The chip is a version of Nvidia’s existing Blackwell RTX Pro 6000 processor modified to meet Trump’s tightened export control rules, according to people with knowledge of the plans

- AT&T says it will accelerate its fiber network expansion following the passage of the One Big Beautiful Bill (link/link)

- The bill means AT&T will be able to deploy fiber to an additional 1mn locations each year starting in 2026

- At present, the carrier has deployed fiber to 30mn locations across the US, though it wants to hit 60mn by the end of 2030

- The bill also “creates a pipeline of midband spectrum that will help meet soaring consumer demand and keep the U.S. technologically competitive with other countries”

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Google’s AI Max is a new suite of ad tools designed to enhance search campaigns. Unlike Performance Max, AI Max offers more flexibility, allowing advertisers greater control over AI integration. Rolling out this summer, AI Max represents Google’s latest effort to modernize search advertising. (Digiday)

- Stagwell annc’d SMP, a centralized team of global media, tech & data experts to optimize trading & investment svs. Matt Adams will lead as Global CEO; Marissa Jimenez joins as Global Chief Trading & Solutions Officer on Mon(Jul.14). SMP aims to streamline ops, boost efficiency & offer creative, media & digital transformation svs across cos (Stagewell)

- Lamar annc’d it acquired Verde Outdoor’s assets in the billboard industry’s 1st UPREIT deal, adding 1,500+ faces incl. 80 digital across 10 states. Verde owners received Lamar LP units, tied to Lamar’s Class A stock. The structure offers tax deferral & future deal potential. CEO Reilly called it a milestone; Garcia praised the smooth, value-driven process. (Street Account)

Artificial Intelligence/Machine Learning

- California State Senator Scott Wiener, a Democrat from San Francisco, has introduced a bill requiring AI cos to publicly release safety protocols for models above a certain computing threshold. The bill mandates reporting critical safety incidents to the state attorney general. Affected cos include OpenAI, Google, and Anthropic. The legislation follows a veto by Governor Gavin Newsom last yr. (Bloomberg)

- xAI’s chatbot, Grok, recently went rogue, issuing violent ideations to users on X. Will Stancil, an attorney and urban planning advocate, discovered Grok advising millions on how to break into his house and assault him. Stancil, who often engages in political debates on social media, was targeted despite his familiarity with online contention. (WSJ)

- Amazon Web Services (AWS) is launching an AI agent marketplace next week, partnering w/ Anthropic. The marketplace will debut at the AWS Summit in NYC on Wed., Jul. 15. It aims to centralize AI agents, allowing startups to offer them directly to AWS customers. Anthropic, backed by Amazon, sees AI agents as the future. The marketplace will boost Anthropic’s rev, which hit $3bn in May. AWS will take a minimal rev cut from agent installations. (TechCrunch)

- Amazon is weighing another multibn$ investment in Anthropic to deepen their AI alliance, countering rivals like Microsoft/OpenAI & Google. The deal supports joint infra like Project Rainier (Wed, Jul.10), a 2.2GW data center using Trainium2 chips. While backing Anthropic, Amazon also develops its own AI (Nova) for Alexa+. Anthropic’s rev run rate tops $4bn, boosted by AWS sales (Winbuzzer)

- Meta hired ex-Apple AI lead Ruoming Pang w/ a pay pkg over $200mn, part of its superintelligence team push. The pkg includes salary, bonus & stock tied to performance. Meta also brought in Nat Friedman, Daniel Gross & took a 49% stake in Scale AI. Despite Altman’s claims of better culture at OpenAI, Meta has poached 10+ of its researchers (Yahoo Finance)

- Microsoft saved $500mn+ in call centers last yr using AI, per Bloomberg. AI now handles small biz interactions & generates 35% of new code, speeding launches. Despite investing $80bn in AI infra, MSFT is cutting ~4% of staff after 6,000 layoffs in May. (Reuters)

- Groq, a Silicon Valley AI chip Co backed by Cisco & Samsung, is seeking to raise $300–$500mn at a $6bn valuation to support a $1. 5bn Saudi deal. The Co expects ~$500mn in rev this yr. Its chips rival Nvidia’s in AI inference. On Wed (Jul.9), Groq was chosen by Saudi-backed HUMAIN for AI ops. In Aug.2023, it raised $640mn at $2.8bn. Earlier this month, Groq opened a European data center in Helsinki to meet rising AI demand. (Benzinga)

- Google annc’d AI upgrades to Circle to Search & Gemini Live. AI Mode now integrates into Circle to Search on Pixel & Samsung phones, enabling follow-ups via “dive deeper” prompts. Gamers get in-game help w/o exiting apps. Gemini Live adds camera-sharing to Flip 7’s cover screen & expands to Samsung apps. Wear OS 6 watches incl. Watch 8 series now support Gemini. (The Verge)

- Mistral AI is in early talks to raise up to $1bn equity funding, possibly backed by MGX. The Paris-based Co, Europe’s largest AI startup, also seeks debt funding from French banks incl. Bpifrance. Mistral, valued at €5.8bn ($6.79bn), raised €600m ($643m) in Jun.2024. It devs open-source LLMs, runs Le Chat chatbot, and partners w/ MGX, Nvidia & TotalEnergies on AI infra & low-carbon tech. (Yahoo Finance)

- Global venture funding hit $91bn in Q2, up YoY from $82bn, but down from $114bn in Q1. AI led w/ $40bn (45%), incl. $14.3bn to Scale AI. H1 2025 totaled $205bn, up 32% YoY. U.S. cos got $60bn. M&A reached $50bn in Q2. Late-stage funding rose 53% YoY to $55bn. Seed hit $10.3bn, led by Thinking Machines’ $2bn. Capital cont’d to concentrate in fewer, larger cos. (Crunchbase News)

- UK publishers, led by the Independent Publishers Alliance, are urging Google to offer an opt-out from AI Overviews, claiming it cannibalizes traffic by summarizing content w/o click-throughs, hurting ad rev. They argue it’s unfair use of their work w/o consent or compensation. Google says AI Overviews boost clicks, but publishers cite rising zero-click searches. Unlike Gemini/Vertex, no opt-out exists for Overviews, intensifying global publisher concerns (MSN)

- At least 36 new tech unicorns have emerged in 2025 so far, driven largely by AI investment. While many are AI-focused, others span sectors like robotics (Gecko), satellite tech (Loft Orbital), and blockchain (Kalshi). Notable names include Thinking Machines ($10bn valuation), Meter ($1.38bn), and Decagon ($1.5bn). The trend reflects investor appetite for innovation beyond AI, with startups raising major rounds from top VCs (TechCrunch)

- OpenAI’s stock-based comp surged over 5x to $4. 4bn last yr, making up 119% of rev, as Meta poached at least 9 AI researchers. OpenAI had forecasted this would drop to 45% in 2025 and <10% by decade’s end. But w/ recent exits, Chief Research Officer Mark Chen hinted the Co may boost stock offers to retain talent (Investing.com)

Audio/Music/Podcast

- Spotify is threatening to pull out of Turkey over playlists mocking President Erdogan’s wife, Emine, and her alleged lavish spending. The Turkish govt accused Spotify of hosting content that insults national values. The govt also demanded Spotify open a physical office in Turkey and is investigating the co for anti-competitive practices. Spotify, which launched in Turkey in 2013, is evaluating all scenarios, including exiting the market. (The Times)

Cable/Pay-TV/Wireless

- The US Department of Justice has approved T-Mobile’s $4. 4bn acquisition of UScellular, allowing T-Mobile to take over UScellular’s wireless operations, including customers, stores, and 30% of its spectrum assets. The clearance follows T-Mobile’s decision to end diversity programs under pressure from the Trump administration. The Justice Department’s investigation found no evidence of competition harms but warned of further spectrum consolidation among the Big 3 (Verizon, AT&T, T-Mobile). (Reuters)

- Blackstone may bid for SFR in a deal worth up to $35bn incl. debt, teaming w/ rivals due to operational complexity. The move aligns w/ plans to deploy $500bn in Europe over 10yrs. Altice France, SFR’s owner, seeks to cut debt after an $8.6bn restructuring. Local & Middle Eastern buyers also show interest, signaling intensifying PE activity in EU telecom. (Yahoo Finance)

- Reliance Jio has delayed its IPO beyond 2025, aiming to grow rev & user base before listing. Valued at $100bn+, Jio wants maturity across telecom & digital biz. Parent Reliance lost $6bn in mkt value post-news. Jio faces rising costs, Starlink rivalry & has 488mn+ users. (Yahoo Finance)

- AT&T has exited media by selling its remaining 70% stake in DirecTV to TPG for $7. 6bn. The deal, separate from DirecTV’s failed Dish merger, marks AT&T’s full retreat after spending $49bn on DirecTV in 2015 and $85bn on Time Warner in 2018. The Co now focuses solely on connectivity, ending its costly media experiment (Axios)

Cloud/DataCenters/IT Infrastructure

- Under CEO Rene Haas, Arm Holdings has seen a 14-fold increase in data center customers since 2021, reaching 70,000. The Co’s growth is driven by AI computing demand. Arm chips, known for high performance and low energy use, are now widely adopted in data centers by giants like Amazon, Google, and Microsoft. Despite challenges in PC and mobile mkts, Arm has doubled apps running on its tech to 9mn and increased its developer base by 1.5 times to 22mn since 2021. (Reuters)

- Google will heavily discount cloud computing svs for the US govt, w/ a deal likely finalized within weeks, amid President Trump’s efforts to minimize federal spending. Oracle will offer federal agencies a 75% discount on its license-based software and a substantial discount on its cloud svs through Nov. Google’s cloud contract is expected to follow suit, w/ similar discounts from Microsoft’s Azure and Amazon Web Svcs. In Apr., Google agreed to offer a 71% discount till Sept. 30 for its biz apps package. (Yahoo)

- US utilities are seeking regulatory approval for $29bn in rate increases in the first half of 2025, driven by booming data centre demand. This 142% rise over the same period last yr highlights the debate over who should bear the cost of AI’s energy burden. Utilities argue the increases are needed for infrastructure upgrades and climate change repairs. Consumer advocates question if households should pay for the US’s AI dominance. (Financial Times)

- America’s largest power grid, PJM, is under strain as data centers and AI chatbots consume power faster than new plants can be built. Electricity bills in PJM territory are projected to surge over 20% this summer. Pennsylvania’s governor threatens to leave PJM if costs aren’t reduced. PJM’s CEO announced his departure, and the board faced upheaval. Despite reforms, PJM struggles with delays in new plant applications and rising demand, especially from data centers. (Reuters)

- Trump pressures Google, Amazon, Microsoft to cut cloud prices for US govt, aiming to slash IT procurement costs. Oracle sets precedent w/ 75% discounts on software contracts. Google’s cloud contract expected to follow suit. Amazon AWS, Microsoft Azure negotiations ongoing. Oracle’s deals could generate $30bn rev by fiscal 2028. (MSN)

- Amazon Web Services (AWS) has developed the In-Row Heat Exchanger (IRHX) to cool Nvidia GPUs used for AI workloads. AWS opted for this solution over liquid-cooled data centers due to space and water usage concerns. The IRHX can be integrated into existing and new data centers, enhancing cooling efficiency for Nvidia’s power-hungry GPUs. AWS’s custom hardware approach reduces reliance on third-party suppliers, benefiting its bottom line. AWS’s P6e computing instances now utilize this tech. (CNBC)

- CoreWeave to acquire Core Scientific in all-stock deal. Deal, valued at ~$9bn, aims to verticalize data center ops, cut $10bn+ lease overhead, and add $500mn in annual cost savings by 2027. CoreWeave to gain ~1.3GW power capacity, boosting AI/HPC deployment. Deal expected to close in Q4 (Street Account)

- Groq, backed by Samsung and Cisco, annc’d its 1st European data center in Helsinki via Equinix, aiming to meet rising AI demand in the region. The $2.8bn Co designs LPUs for inference, not training, offering faster deployment and simpler supply chains vs Nvidia. CEO Ross said the site was decided 4 weeks ago and will serve traffic by week’s end. EU’s push for sovereign AI also supports move (CNBC)

Crypto/Blockchain/web3/NFTs

- Crypto firms are fast-tracking listings via SPACs to bypass IPO hurdles. ProCap BTC raised $750mn+ post-merger, buying 3,724 BTC. Reserve One to list via MBAV, backed by Galaxy & Kraken. SPACs offer faster access, valuation control & BTC exposure. VivoPower pivoted to XRP after a $100mn Saudi investment. (Brave New Coin)

- NFT sales fell 4. 61% to $2.82bn in H1 2025 vs H2 2024, despite Jan hitting $679mn. Q2 saw $1.24bn vs. $1.59bn in Q1. Sales counts rose 78% QoQ to 12.5mn despite lower volumes, showing growing affordability. (AI Invest)

eCommerce/Social Commerce/Retail

- Bain Capital is considering selling its remaining stake in Canada Goose Holdings, which it acquired in 2013 and took public in 2017. Bain holds 60.5% of the co’s multiple voting shares, giving it 55.5% voting power. Canada Goose reported C$1.3bn in rev and ~C$95mn in net income for the fiscal yr ending Mar. 2025. The stock price rose 5.5% to $13.64 on the news. Discussions are in early stages, and no transaction is guaranteed. (Ainvest)

- China’s e-commerce Cos JD. com, Alibaba, and Meituan are locked in a fierce price war in the “instant commerce” sector, offering massive subsidies to attract consumers.com’s entry into food delivery sparked competition, leading to billions in subsidies and rapid delivery promises. Despite benefits for consumers, the price war has negatively impacted cos’ share prices and earnings outlook. Regulators have urged fair competition, but the battle continues. (CNBC)

- Jefferies flagged Lululemon’s rising markdowns & inconsistent pricing as momentum fades. The Co’s shift from yoga roots to bold, logo-heavy styles aims to attract younger shoppers but risks earnings. US sales, mall traffic & China growth are weakening. Competitors like Vuori & Athleta show stronger store/digital traction. LULU plans 40–45 new stores in 2025 despite margin pressure. (Retail Drive)

- US back-to-school spending is set to hit $33. 3bn, up 3.3% YoY, per Coresight. Despite inflation concerns (68.8%) and expected price hikes from tariffs/supply issues (73%), 90%+ plan to spend same or more. Avg spend per child is $378, up 21.5%. Shoppers are buying early, seeking deals, and switching to private labels. Retailers like Amazon, Walmart, and Target launched summer sales to meet early demand (Retail Drive)

Electric & Autonomous Vehicles

- Tesla plans to expand its robotaxi svs to the SF Bay Area in 1–2 months, pending regulatory nods. A limited rollout began in Austin last month. Unlike Texas, CA requires DMV & CPUC permits. Waymo remains the only firm w/ paid driverless ops in SF. Musk aims to scale robotaxis rapidly across US cities. (Reuters)

- Waymo annc’d teen accounts for riders aged 14–17 in Phoenix, letting them ride solo via Waymo One if linked to a parent’s acct. Parents can track rides in real time, and trained remote operators can assist if needed. The move, tested for months, mirrors Uber’s teen strategy. Though risks remain, Waymo cites safety data and Gen Z’s shift from driving. No rollout date for other mkts yet. (The Verge)

- Waymo launched road trips to Philly and NYC. Fleets will map and test in complex zones like downtown Philly and Manhattan to The Battery, plus parts of NJ. Though not a commercial launch, it mirrors past trips that led to ops in LA. Waymo awaits NYC AV test permit; current laws bar driverless deployment. Miami and D.C. launches are next (Yahoo News)

Film/Studio/Content/IP/Talent

- James Gunn’s Superman is projected to open w/ $130mn domestically, though DC Studios conservatively forecasts $100mn+. The film, starring David Corenswet, opens Wed., Jul. 10 in North America and 78 overseas mkts. Previous Superman films had varied openings, w/ Man of Steel at $116mn. (The Hollywood Reporter)

FinTech/InsurTech/Payments

- Lemonade cont’d US expansion by launching Lemonade Car in Indiana. With this addition, Lemonade Car is now available in states representing approximately 42% of the U.S. car insurance market. Car was LMND’s fastest-growing product in Q1. (Street Account)

Handheld Devices & Accessories/Connected Home

- IKEA is launching new smart home products designed for ease of use. The lineup includes smart lighting, blinds, and air purifiers, all integrated with the IKEA Home smart app. These products aim to simplify home automation and enhance user experience. The design focuses on accessibility and functionality, ensuring that even those new to smart tech can easily operate them. (Fast Company)

Last Mile Transportation/Delivery

- Alibaba shares fell after JD. com annc’d a $1.4bn program to boost its food delivery biz, JD Delivery. This move aims to compete w/ Meituan and Alibaba’s Taobao Instant Commerce. Beijing may not favor this expansion of consumer svs, as it could lead to irrational consumption. Earlier, Alibaba integrated its food delivery and online travel svs into its core e-commerce unit and added rapid-delivery for Taobao Instant Commerce. (Sherwood)

- Amazon launched 10-min delivery in Delhi via its “Now” svs, expanding from Bangalore. Competing w/ Blinkit, Instamart & Zepto, the move targets India’s booming quick-commerce mkts. Amazon has invested $11bn+ in India since 2013, adding $233mn last month to boost infra. Five new fulfillment centers aim to speed up deliveries in smaller cities. (Yahoo Finance)

Live Entertainment/Theme Parks/Concerts/Experiential

- Live Nation has submitted a proposal to the Trump administration, DoJ, and FTC to address secondary ticket mkts. The Co suggests 20% caps on resale prices, more control for artists, and stronger enforcement of the 2016 BOTS Act. (Variety)

Macro Updates

- Japan’s NTT sold $17. 7bn of dollar and euro bonds, marking the largest-ever offering by an Asian corporate in the global debt market. NTT Finance Corp. priced $11.25bn of dollar-denominated notes in seven tranches and €5.5bn ($6.5bn) of euro bonds in four parts. The deal, driven by investor demand for diversification, will help refinance loans for NTT’s data-center unit acquisition. This sale is part of a broader trend of Japanese companies increasing global bond sales. (The Edge Communications)

Media Conglomerates

- Disney & Hearst are exploring a sale of A+E Global Media, parent of A&E, History & Lifetime. Wells Fargo is advising on options incl. partnerships. The move follows industry trends as linear TV declines. A+E has ~58mn U.S. subs & global reach in 200+ regions. Despite falling income, it remains cash-generative. No deal is guaranteed. (Deadline)

Online Marketplaces/Learning (Real Estate/Education/Jobs)

- Indeed and Glassdoor, owned by Recruit Holdings Co. , are cutting ~1,300 jobs to consolidate operations and focus on AI. The layoffs will primarily impact US-based teams in research, development, and sustainability. CEO Hisayuki “Deko” Idekoba emphasized the need to adapt to AI advancements to enhance product experiences. (Bloomberg )

Regulatory

- Trump’s antitrust enforcers have recently cleared several multibillion-dollar deals, marking a shift from Biden’s stricter policies. The FTC and DOJ approved three deals worth $63bn in June, including Ferrero’s $3.1bn acquisition of WK Kellogg. This approach, favoring settlements and shorter reviews, aims to provide certainty to dealmakers. Notable deals include Mars’ $36bn takeover of Kellanova and Omnicom’s $13.5bn acquisition of Interpublic. (Reuters)

- Trump confirmed no further delay on tariffs starting Thu(Aug. 1), vowing a 50% tariff on copper & up to 200% on drug imports if production isn’t moved to the U.S. He also threatened new levies on the EU & India, citing BRICS ties & digital taxes. Copper futures surged. Pharma stocks dipped. Trump aims to reshape trade via Section 232 probes & unilateral tariff letters (Japan Times)

Satellite/Space

- SpaceX plans a share sale valuing the Co at ~$400bn, surpassing its Dec. buyback valuation of $350bn, per Bloomberg. The raise includes a primary round & secondary sale of insider shares. Growth in Starlink—now over 50% of rev—and Starship milestones drive the valuation. (MSN)

- Globalstar annc’d a launch svs agreement w/ SpaceX to deploy satellites supporting its next-gen terrestrial spectrum strategy. The deal includes a planned launch in 2026 and options for up to three add’l missions. The Co aims to enhance its satellite constellation to support growing demand for mobile satellite svs and terrestrial spectrum use. (Business Wire)

Social/Digital Media

- TikTok has rejected a Reuters report claiming it is laying the groundwork for a potential sale, calling the report “factually inaccurate. ” The statement, posted on TikTok’s official website, refutes the claim based on anonymous sources. Reuters reported TikTok plans to launch a standalone app for US users, separate from its global app, amid ongoing discussions w/ China. (Global Times)

- TikTok is restructuring its US operations, including revamping its trust and safety team and its e-commerce arm, TikTok Shop. The changes involve layoffs and are partly in preparation for the spin-off of TikTok’s US operations, as mandated by the Trump administration. The restructuring also follows TikTok Shop’s failure to meet performance goals. ByteDance has until Sept. to divest TikTok’s U.S. operations or face a ban. (Asia Nikkei)

- TikTok is halting sponsorships in Canada incl TIFF, Junos & MusiCounts as it complies w/ Ottawa’s order to shut down ops over security concerns. The move ends millions in creator support & affects programs like the Indigenous Accelerator. TikTok is challenging the order in court but warns of job losses & cultural impact if shutdown proceeds. (CBC News)

- TikTok is building a new US-specific app ahead of a planned sale to US investors, per The Information. Launch is targeted for Sept 5, w/ current app support ending by Mar next yr. Trump said a deal is “pretty much” done and talks w/ China begin Mon or Tue (Jul 7 or Jul 8). ByteDance must divest US assets by Sept 17. Users will need to download the new app to continue access (Reuters)

Software

- Autodesk is evaluating a cash-and-stock deal to acquire rival PTC, per Bloomberg. The Co is working w/ advisers, but no final decision has been made. PTC is also drawing interest from other players. Autodesk’s AI-driven cloud tools are seeing strong adoption, while PTC benefits from rising demand for product design & svs software. (Reuters)

- Gemini is rolling out to Wear OS, replacing Assistant on Pixel Watch, Samsung & others. On Wed(9 Jul), Google began enabling natural prompts, memory, Workspace, YouTube Music & more via voice or app tap. Users can say “Hey Google” or long-press to launch. Gemini supports tasks like “remind me to shop” or “summarize last email.” Full rollout coming weeks; Wear OS 6 to support brand-specific apps. (9to5Google)

- Apple appealed a €500mn EU fine over its App Store, calling it “unprecedented” and accusing the EC of overreach. The fine stemmed from Apple blocking developers from steering users to cheaper deals outside its store, violating the Digital Mkts Act. Apple claims the EC forced “confusing” biz terms and unlawfully expanded the definition of “steering.” An appeal was filed to EU’s general court on July 7th. (The Guardian)

Sports/Sports Betting

- The UK’s Competition and Markets Authority (CMA) has opened a consultation period for the proposed merger between Sportradar and IMG Arena. The regulatory body is seeking public input on whether the combination would substantially reduce competition in the mkt. The CMA has issued a statement inviting comments from interested parties regarding the potential competitive impact of the merger. (Investing.com)

- Boyd Gaming Corp is selling its 5% stake in FanDuel Group to Flutter Entertainment plc for $1. 755bn. The sale, expected to close in Q3 2025, will help Boyd pay down debt and strengthen its financial position. Boyd’s online gaming and sports betting rev in 2024 was $606.2mn, contributing to its total annual rev of $3.9bn. The new agreements will extend market-access terms through 2038, with Boyd receiving fixed fees from FanDuel’s operations in several states. (Las Vegas Review-Journal)

Tech Hardware

- Super Micro CEO Charles Liang annc’d plans to increase investment in Europe, incl ramping up AI server manufacturing. Despite weaker-than-expected guidance for the current quarter, Liang emphasized strong growth due to rising demand in Europe and globally. The co’s stock, boosted by Nvidia chip demand, hit a record high in Mar. 2024 but is now 60% off that peak. (CNBC)

- Global PC shipments rose 7. 4% to 67.6mn in Q2 2025, per Canalys. Notebook shipments increased 7% YoY to 53.9mn, including mobile workstations. Desktop shipments grew 9% to 13.7mn. The growth is driven by remote work, learning solutions, and supply chain recovery. (Telecompaper)

- Apple is set to launch new products by early 2026, including the budget-friendly iPhone 17e, several iPads, and upgraded Macs. The lineup will feature updates to the entry-level iPad and iPad Air, an external Mac monitor, and new MacBook Pros and Airs. The iPhone 17e will include the A19 processor. This wave of products follows the typical fall upgrade cycle, which will introduce a slimmed-down iPhone 17, redesigned Pro models, new Apple Watches, and a faster Vision Pro headset. (Mac Daily News)

- TSMC’s June qtr rev rose 39% to $32bn, beating forecasts & signaling strong AI demand. Sales to Nvidia & Apple drove growth. CEO Wei reaffirmed 2025 rev growth in mid-20% range. TSMC plans $100bn+ in global expansion incl. AZ, JP & DE. Despite mobile softness, AI chip demand keeps momentum strong. Tariff risks still cloud 2025 outlook. (Yahoo Finance)

- Samsung annc’d Galaxy Z Flip 7 FE at $899, offering a budget foldable w/ Exynos 2400, 8GB RAM & up to 256GB storage. On Wed(9 Jul), it revealed a 6.7″ AMOLED inner display, smaller outer screen, 4,000mAh battery, 25W fast charging, & dual rear cams (50MP+12MP). Ships w/ Android 16. Pre-orders open w/ perks incl. $50 credit, boosted trade-ins & free storage upgrade. (9to5Google)

- Samsung annc’d Galaxy Watch 8 & Watch 8 Classic w/ new “cushion” design, slimmer build & Wear OS 6. It revealed 2GB RAM, Exynos W1000 chip, sapphire display, & up to 64GB storage. Features include GPS upgrades, Bedtime Guidance, Vascular Load, & Antioxidant Index. Gemini AI & Now Bar included. Watch 8 starts at $349 (40/44mm), Classic at $499 (46mm). Pre-orders offer $50 credit & trade-in deals. (9to5Google)

- Samsung annc’d Galaxy Z Fold 7 w/ major upgrades incl. 8.9mm closed thickness, 8″ inner & 6.5″ outer displays, & IP48 rating. On Wed(9 Jul), it revealed a 200MP main cam, Snapdragon 8 Elite, up to 16GB RAM & 1TB storage. S Pen support dropped for durability. Ships w/ Android 16 & One UI 8. Starts at $1,999.99. Pre-orders offer up to $1,150 off via trade-ins & $50 credit via 9to5Google links. (9to5Google)

- Samsung Electronics expects Q2 op profit to fall 39% YoY to 6. 3trln won (~$4.62bn), hit by delays in supplying advanced AI chips to Nvidia. HBM rev stayed flat as US curbs on China sales persist. Samsung’s HBM3E chips still await Nvidia certification, though AMD began receiving supply in Jun. Smartphone sales held steady ahead of potential US tariffs. Uncertainty over US trade policy remains a risk (Reuters)

Towers/Fiber

- Mitratel is considering reviving a merger with rival PT Tower Bersama Infrastructure. This would be their second attempt in a decade. The companies have held early talks with advisers about the potential combination, which could create an entity worth $5.7bn. The discussions are private, and no final decision has been made. (Bloomberg )

- Cablevision Lightpath LLC, majority controlled by Altice USA, plans to sell up to $2. 8bn of asset-backed securities, backed by fiber networks and customer agreements. This move comes as Altice USA faces $7.2bn of debt due in 2027 and $5.4bn in 2028. Earlier debt restructuring talks were shelved in April due to market volatility. (MSN)

- Vodacom’s $743mn bid for 30% of fiber operator Maziv is back on track after South Africa’s Competition Commission dropped its opposition ahead of the Tue(Jul. 22–24) court hearing. Revised terms incl. capital pledges, low-cost broadband, and protections for smaller rivals. Minister Parks Tau backed the appeal. Vodacom shares rose 1.4% on the news. Final ruling pending. (Yahoo Finance)

Video Games/Interactive Entertainment

- EA’s 2017 Star Wars Battlefront 2 surged to #12 in May’s best-sellers, up from #135 in Apr. , driven by Andor hype, Revenge of the Sith 20th, promos & discounts. On PC, it hit #5. Despite past backlash over loot boxes, fans now praise it. Jefferies noted EA hasn’t matched its success since. No sequel is planned as EA shifts focus to Battlefield (Kotaku)

- Activision took down Call of Duty: WWII (Microsoft Store/Game Pass ver. ) after PC players were hacked via an RCE flaw, per TechCrunch. The flaw, patched in other vers., let attackers control devices. The Co is working on a fix. Past hacks incl. anti-cheat exploits and malware. Layoffs have impacted Activision’s cybersecurity teams. Game remains offline. (TechCrunch)

- Nintendo Switch 2 is now listed on Amazon U. S., but buyers must request an invite to purchase. The $450 base model & $500 Mario Kart World bundle are both available. Amazon was absent from Apr.24 pre-orders amid rumored disputes w/ Nintendo. The listing marks a shift after limited availability of Nintendo products on Amazon. No official reason for the delay (Kotaku)

- Epic has cont’d its legal fight vs Google but dropped claims vs Samsung after a mystery settlement just 2 days before Samsung’s Unpacked event (Wed, Jul 10). Epic CEO Tim Sweeney said Samsung will address Epic’s concerns, but no details were shared. Epic had earlier criticized Samsung’s Auto Blocker for hindering 3rd-party app stores. It’s unclear if Samsung made changes or offered other concessions (The Verge)

Video Streaming

- Disney and ITV have signed a “first-of-its-kind” deal to share content across their streaming platforms. Disney+ will feature a “Taste of ITVX” selection, including shows like “Mr. Bates vs The Post Office” and “Love Island.” ITVX will offer a “Taste of Disney+” with titles like “The Bear” and “Andor.” The service, launching [Wed., Jul. 16], will be free for customers and refreshed every few months. This partnership aims to attract new audiences and drive subscriptions. (Variety)

- ESPN is in talks w/ Verizon, T-Mobile, Roku, Take-Two, Walmart & others to support its $29. 99/mo streaming svc offering live ESPN channels & exclusive content. Launch aims to shift 65mn cable users to digital. Deals may incl. bundling, trials, or wholesale access. ESPN is also negotiating w/ Charter, Hulu + Live TV & Cox to expand reach (Cord Cutters News)

- YouTube is facing a surge in full-length pirated movies uploaded by users exploiting its copyright system. These uploads often use deceptive thumbnails and titles to evade detection. Despite takedowns, many reappear quickly. Studios and copyright holders are pressuring YouTube to enhance enforcement. The Co said it’s investing in AI and human review to combat piracy, but challenges persist due to the scale and speed of uploads (New York Times)