It was an historic week, and one characterized by a plethora of important sector developments and updates following Trump’s presidential inauguration, coupled with the start of earnings season. Washington headlines certainly dominated the market focus and helped push the major indices up for the second straight week (S&P and Nasdaq both up ~+1.7%).

Sector-wise, we focused on the below themes and developments in this edition:

- LAST CALL… 7th Annual LionTree Sector Themes Survey - Please Participate!

- Trump JUMPS Into Action This Week…

- AI Infrastructure Gets A Huge Boost (Stargate) + Other Key AI Updates This Week

- A Knockout & Touchdown Quarter For Netflix

- TikTok’s Future Remains In Flux…

- Verizon Enters The AI Race And Posted Its Highest Quarterly Postpaid Net Adds In Over A Decade

- Key Titles Can Be “Make” Or “Break” In Gaming… EA Faced The Latter

- Huge Improvements In Non-Gaming Mobile App Monetization Drove The 2024 App Economy

- Grab Bag: TMT M&A Speculation/Comcast’s New Sports & News TV Video Package/Threads To Test Ads

Also, on the home front, over the last couple of weeks…

LionTree served as financial advisor to Bauer Media Group on its acquisition of the Northern European operations of Clear Channel Outdoor Holdings for $625mn.

LionTree served as financial advisor to Diamond Sports Group on its financial restructuring and emergence from Chapter 11 bankruptcy. Now operating as Main Street Sports Group, it owns the FanDuel Sports Network RSNs.

PS. It was also an exciting week in that I had the opportunity to ride in a Waymo for the first time (w/ my colleague Antal)! And I give it 5 stars!

Best,

Leslie

LAST CALL… 7th Annual LionTree Sector Themes Survey - Please Participate!

Our 7th Annual TMT Themes survey is closing this weekend, and we would love your participation. It includes ~20 quick questions about the market, sector, and company expectations. It should take ~5-8min to complete. Also, as a reminder, our rule is that we send the survey results ONLY to those who participate! 😊

**CLICK HERE** to participate.

We are gathering insights on the M&A and regulatory environment, the AI CapEx trajectory, the ARPU impact from a super-premium music subscription tier, Tik Tok’s future, autonomous vehicle penetration, Take-Two’s GTA launch, ESPN’s flagship DTC adoption, and more!

Trump JUMPS Into Action This Week…

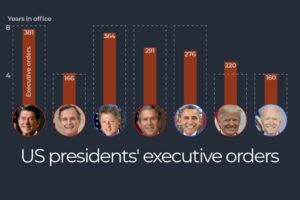

As part of his first day in office following his inauguration, President Donald Trump issued a slate of 46 presidential actions, including 26 executive orders, 12 memorandums, as well as 4 proclamations, and later in the week, Trump issued additional executive orders pertaining to crypto and AI. Notably, there is no official definition of executive orders, memoranda, or proclamations, though they are generally written directives from the President to government officials and agencies. A Congressional Research Service report (link) indicates that the only technical difference between them is that executive orders and proclamations must be published in the Federal Register, while presidential memoranda are published only when the President determines they have “general applicability and legal effect.” The report adds that executive orders have historically pertained to more controversial topics, while memoranda often deal with more routine directives to federal agencies. Proclamations tend to deal with the activities and private individuals and are more ceremonial in nature.

Procedurally, the judicial branch can review executive orders, and the legislative branch has the power to ratify or nullify them as well. Furthermore, subsequent Presidents can revoke or modify any previously issued executive order with which he disagrees – an ability that Trump took full advantage of in rolling back some of former President Joe Biden’s executive orders.

The exhaustive list of presidential actions can be found HERE, but we thought it would be helpful to outline a handful that will be most impactful to the TMT sector. We also included some highlights regarding Trump’s comments that could have broader potential implications for the US and the global economy. See below for more details:

Key Executive Actions From Trump’s First Day In Office

- Executive order RESCINDING previous executive orders (link): In total, the order revoked 78 executive orders from former President Biden’s time in office, including the following –

- The 2023 executive order on AI risk: Exec Order 14110 on the “Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence” sought to promote competition in the AI industry, preventing AI-enabled threats to civil liberties and national security, and ensuring US global competitiveness in AI

- The 2021 executive order on EV production: Exec Order 14037 “Strengthening American Leadership in Clean Cars and Trucks” set a nonbinding target that half of all new vehicles sold in 2030 would be electric; This was supported by leading automakers

- Trump’s new order also pauses the disbursement of federal funds for EV charging infrastructure

- Executive orders related to DEI initiatives: These included Exec Order 13985 “Advancing Racial Equity and Support for Underserved Communities Through the Federal Govt) and Exec Order 139888 “Preventing and Combating Discrimination on the Basis of Gender Identity or Sexual Orientation,” among others

- Executive orders related to climate issues: Such as Exec Order 13990 “Protecting Public Health and the Environment and Restoring Science to Tackle the Climate Crisis and Exec Order 14008 “Tackling the Climate Crisis at Home and Abroad,” among others

- Executive order delaying the TikTok ban (link): The US TikTok ban was effective delayed for 75 days after being shut down last weekend; The ban was passed w/ broad bipartisan support in Congress and was unanimously upheld by the Supreme Court (see Theme #5 for more important updates on TikTok this week)

- Executive order on freedom of speech (link): The order claims that the Biden Administration “trampled free speech rights by censoring Americans’ speech on online platforms, often by exerting substantial coercive pressure on third-parties, such as social media Cos,” and directs the Attorney General to investigate policies of the last four yrs

- Executive Order To End “The Weaponization of the Federal Govt” (link): Directs the Attorney General to “identify and take appropriate action to correct” alleged “politically motivated” law enforcement activity at the Dept of Justice, the SEC, and the FTC

- It also calls upon the Director of National Intelligence to do the same within the intelligence community

- Memorandum on “America First Trade Policy” (link): States that “unfair and unbalanced trade” should be addressed and directed Cabinet officials to review trade & tariff policies, including those w/ China

- Executive order titled “Declaring a National Energy Emergency” (link): To lower energy costs and to insulate the country from “hostile foreign actors,” the order calls for boosting the production of domestic oil and natural gas production as well as the review of legal environment protections that have become “obstacles to domestic energy”

- Executive order on “Unleashing American Energy” (link): Directs an immediate review of agency activities that “potentially burden” the development of domestic energy resources, specifically natural gas, coal, hydropower, biofuels, critical mineral, and nuclear energy; Agencies are required to have action plans within a month

- Executive order to tighten immigration laws (link): The order contains a handful of policies designed to curb immigration, including the identification, removal, and repatriation of illegal immigrants to “any foreign state”; Also sets up Homeland Security Task Forces in every state to ensure the ability to “faithfully execute” immigration laws

-> The US wireless industry could count 1mn fewer new customers next yr, depending on how President Trump limits immigration in the US, per some sell-side financial forecasts (link)

- Executive order to restrict visa-seekers from certain countries (link): A list identifying countries that will have immigration partially or fully suspended will be submitted within 60 days of the order

Later In The Week, Trump Issued Addt’l Actions Pertaining To Crypto And AI

- Executive order on “strengthening American leadership” in crypto (link): Establishes a working crypto group tasked w/ proposing new digital asset regulations and exploring the creation of a national crypto stockpile;

- The action also orders banking svs for crypto Cos to be protected and bans the creation of central bank digital assets that can compete w/ existing cryptocurrencies

- Executive order calling for an AI action plan (link): Directs the development of a plan aiming to retain US leadership in AI and improve the country’s economic and national security; Also revokes existing AI directives and policies that were viewed as a impediments to AI innovation; An AI action plan will be submitted within 180 days

Addt’ly, Trump Made Several Other Provocative Statements Related To The Economy This Week

- Trump will “demand that interest rates drop immediately” (link): Speaking to an assembly of global leaders at the World Economic Forum in Davos, Switzerland via a video call, Trump added, “…And likewise, they should be dropping all over the world. Interest rates should follow us all over”

- Trump threatened to impose a 10% tariff on Chinese-made goods arriving in the US (link): The tariff could be enacted as early as Feb 1, w/ any penalties on Chinese goods being “based on the fact that they’re sending fentanyl to Mexico and Canada,” per Trump

- Levies are also being considered on EU imports…: Trump highlighted that “we have a $350bn deficit w/ the European Union,” claiming that “they treat us very, very badly, so they’re going to be in for tariffs”

- … And on Mexico as well as Canada: Trump said that he was considering introducing 25% tariffs on imports from Mexico and Canada as soon as Feb 1

- Trump accused Bank of America (BofA) and JPMorgan Chase of refusing to serve conservatives (link): “I hope you start opening your bank to conservatives b/c many conservatives complain that the banks are not allowing them to do business within the bank, and that included a place called BofA,” per Trump to BofA CEO Brian Moynihan

- Trump will call on Saudi Arabia and OPEC to lower oil prices and increase a planned US investment package to $1tn (link): This followed a meeting between Trump and Saudi Arabian Crown Prince Mohammed bin Salman after which a Saudi State news agency reported the kingdom wants to invest $600bn into the US over the next four yrs

- Trump criticized EU regulators for targeting Apple, Google, Meta, and other US tech giants (link): Trump described the EU fines against the US Cos as “a form of taxation” and said that “they shouldn’t be doing that”; He has “some very big complaints w/ the EU”

AI Infrastructure Gets A Huge Boost (Stargate) + Other Key AI Updates This Week

Also, as another key event this week, OpenAI CEO Sam Altman, Softbank CEO Masayoshi Son, and Oracle Chairman Larry Ellison came together at a White House ceremony with President Trump to announce a $500bn private-sector investment into AI infrastructure. The joint venture, dubbed Stargate, will aim to create more than 100k jobs in the US as part of data center builds across the country, with the first deployments slated to occur in Texas. We included available details below; however, information surrounding the joint venture was still quite vague overall. It also wasn’t clear whether the announcement was an update to a previously announced initiative under the Biden Administration, though Altman told Trump during the event that “we wouldn’t be able to do this without you, Mr. President.” Moving forward, we expect there to be more announcements related to Stargate in the coming weeks.

Elsewhere across the AI industry, there was a barrage of headline-grabbing news this week. In addition to being a central part of the Stargate announcement at the White House, OpenAI launched Operator, an enhanced chatbot that can execute tasks on the web for users and extended a strategic partnership with Microsoft through 2030. Moreover, there were reports that OpenAI could soon release an AI super-agent capable of performing Ph.D.-level tasks. ByteDance remained in the spotlight as well as it was reported that the Co has discussed purchasing over $12bn worth of AI chips. Perplexity AI, which submitted a bid to merge with TikTok US earlier this week (see Theme #5), also launched an agent for Android devices that will compete with Apple’s Siri and Amazon’s Alexa, while Google invested another $1bn in Anthropic. Lastly, news also emerged that Mistral AI, a developer of open weight AI models based in France, is gearing up for an IPO.

See below for more details on these key AI updates.

Stargate: Leading Tech Execs Made A Big AI-Related Annc’ment At A White House Event

- OpenAI, Softbank, and Oracle pledged up to $500bn to build AI infrastructure in the US (link/link): The three Cos are planning a JV called Stargate to build data centers in the US, creating 100,000+ jobs in the process

- The investment is expected to occur over the next four yrs: The Cos are committing $100mn to the JV for immediate deployment and plan to invest the rest of the amount through 2029

- The initial $100bn includes projects that the Cos already annc’d, per sources: These were reportedly initiated under the Biden Administration

- It’s unclear how much cash each partner will contribute: OpenAI is still losing money but has raised billions of dollars, Oracle has ~$11bn in cash and mktable securities but more in debt, and SoftBank has ~$30bn of cash on hand

- Stargate will hire a new CEO and have a separate board of directors: Softbank CEO Masayoshi Son will be chairman; OpenAI said it will operate the venture, while SoftBank will finance it

- Stargate reportedly plans to bring on addt’l equity investors: Softbank is also planning to raise debt from third-parties to pay for Stargate’s projects, per sources

- Other prominent tech Cos were named “technology partners”: As tech partners, Microsoft, Arm Holdings, and NVIDIA will be involved in creating Stargate’s infrastructure

- Stargate’s first data centers will be in Texas: Oracle Chairman Larry Ellison indicated the site started construction last yr; Twenty ~500k sq ft data centers will be built, and they will be operated by Oracle and used by OpenAI

- The project could power AI for use cases in healthcare: Including analyzing electric health records and helping doctors care for their patients, per Ellison

- The investment is expected to occur over the next four yrs: The Cos are committing $100mn to the JV for immediate deployment and plan to invest the rest of the amount through 2029

-> Elon Musk responded sardonically to the annc’ment on X, claiming that “they don’t actually have the money” (link)

There Were Also A Handful Of Other Notable AI-Related Updates This Week…

- OpenAI unveiled Operator, “an agent that can go to the web to perform tasks” for users (link): OpenAI’s new chatbot can automate tasks such as planning vacations, filling out forms, making restaurant reservations, and ordering groceries

- Operator is trained to interact with the features that people use daily on the web: Including buttons, menus, and text fields; Users can take control of the screen at any time

- The tool can also ask follow questions to enhance personalization: Such as asking for login information for other websites

- BUT Operator isn’t without flaws: OpenAI noted that Operator still has trouble with some tasks, including managing calendars and creating slideshows

- It is only currently available to ChatGPT Pro users in the US: The Pro tier costs $200 per month, and the chatbot can be accessed at Operator.ChatGPT.com

- OpenAI eventually plans to expand access to Plus, Team, and Enterprise users: The Co will also integrate Operator into ChatGPT

- Users can opt out of some of the Co’s collection of training data: This can be done by turning off the “improve the model for everyone” setting in ChatGPT; Users can also delete all browsing data and log out of all sites w/ a single click in the privacy section

- Operator is trained to interact with the features that people use daily on the web: Including buttons, menus, and text fields; Users can take control of the screen at any time

-> Axios also reported this week that a top AI Co, possibly OpenAI, could announce the launch of AI super-agents in the coming weeks; The expected advancements will unleash Ph.D.-level AI agents capable of performing complex human tasks and potentially replacing mid-level software engineers and other human jobs as soon as this yr; Several OpenAI staff have been telling friends that they are both jazzed and spooked by the recent progress (link)

- Microsoft and OpenAI also extended their strategic partnership (link): This covers the duration of the two Cos’ contract through 2030

- OpenAI recently made a new, large Azure commitment: As part of this, Microsoft also approved OpenAI’s ability to build addt’l capacity, which will mainly be used for research and the training of models

- The new agreement also includes changes to exclusivity on new capacity: The deal moves the two Cos to a model where Microsoft has right of first refusal

- Otherwise, the two Cos are maintaining “key elements” of their partnership –

- Microsoft has rights to OpenAI’s IP, which includes model and infrastructure, for use within Microsoft’s products, like Copilot

- The OpenAI API remains exclusive to Azure, runs on Azure, and is also available through the Azure Open AI svs

- Microsoft and OpenAI have rev sharing agreements that flow both ways

- Microsoft remains a major investor in OpenAI

- OpenAI recently made a new, large Azure commitment: As part of this, Microsoft also approved OpenAI’s ability to build addt’l capacity, which will mainly be used for research and the training of models

-> Notably, the Stargate annc’ment could mean that OpenAI and Microsoft will be less reliant on each other in the future; The two Cos have reportedly been at odds over OpenAI’s insatiable need for computing power and inability to obtain more capacity from other sources, given the exclusive nature of their relationship; Still, OpenAI CEO Sam Altman reaffirmed that the his Co and Microsoft will have a “very important and huge partnership, for a long time to come” earlier this week (link)

- ByteDance plans to spend $12bn+ on AI chips in 2025, per the Financial Times (link): Sources indicated that ByteDance will allocate $5.5bn towards buying AI chips in China and ~$6.8bn on overseas chips this yr to build up its foundational model training capabilities

- ~60% of ByteDance’s domestic semiconductor orders would reportedly go to Chinese suppliers, like Huawei and Cambricon: The remainder would be spent on NVIDIA chips that have been watered down to adhere to US export controls, per sources

- Beijing has given informal guidance for tech Cos to purchase at least 30% of their chips from domestic suppliers, according to the report

- However, a ByteDance spokesperson refuted the report: “The anonymously sourced information about our plan is incorrect,” they noted

- ~60% of ByteDance’s domestic semiconductor orders would reportedly go to Chinese suppliers, like Huawei and Cambricon: The remainder would be spent on NVIDIA chips that have been watered down to adhere to US export controls, per sources

- Google reportedly agreed to invest another $1bn+ into Anthropic (link): The new financing adds to Google’s $2bn of past investments and 10% stake in Anthropic, which is known for its Claude AI chatbot; The two Cos also have a large cloud contract

- Anthropic is also in late stage talks to raise a separate $2bn funding round at a $60bn valuation: This round is being led by Lightspeed Venture Partners

- Anthropic has grown its top-line by ~10x y/y: A source indicated that the Co’s rev primarily comes from enterprise sales

- Amazon has been another major backer of Anthropic: Last Nov, Amazon annc’d an addt’l $4bn investment in Anthropic, bringing its total investment in the Co to $8bn; As part of that, AWS became Anthropic’s “primary cloud and training partner”

- However, Amazon remains a minority investor and doesn’t have a board seat

- Perplexity AI launched an agent for Android devices to rival Apple’s Siri and Amazon’s Alexa (link): The tool, dubbed Perplexity Assistant, can book dinner reservations, hail rides on apps, and set reminders, among other actions; It is available in 15 languages on Google’s Play store

- The Co is also aiming to Perplexity Assistant accessible on Apple’s App Store: “We’d love to make it available on iOS, and if Apple gives us the right permissions, we’ll make it happen,” a Co spokesperson said

- OpenAI launched a similar tool, Tasks, last week: The tool is available to ChatGPT Team and Pro subscribers on the web platform

- Mistral AI is gearing up for an IPO (link): A public offering remains the French Co’s primary goal, per co-founder and CEO Arthur Mensch; Mistral AI was founded in 2023 by former Google DeepMind and Meta engineers and focuses on developing open weight LLM models

- Mistral has been focused on expanding in Europe and Asia-Pacific: As part of the Co’s expansion strategy and to strengthen its presence in APAC, it plans to open an office in Singapore

- The Co is “not for sale”: This was Mensch’s response to acquisition rumors, particularly regarding Microsoft, which has invested $15.6mn in the Co

- Mistral has “plenty of capital”: As a result, the Co is currently seeking addt’l funding; Mistral has raised ~$1.14bn from investors, including Andreessen Horowitz, General Catalyst, and Lightspeed Venture Partners

- The Co has a reported valuation of ~$6bn

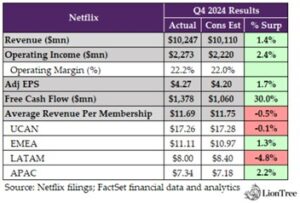

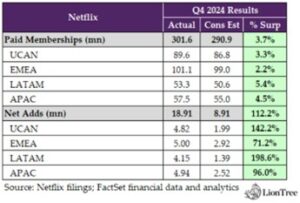

A Knockout & Touchdown Quarter For Netflix

Netflix not only beat on its top-line, but also added its biggest quarterly subscriber gain in the company’s history (18.9mn). It was a pivotal qtr for Netflix as its live strategy was truly put to the test with the Paul vs. Tyson fight and 2 NFL Christmas Day football games, and the effort paid off, with both events creating viewership records. That said, mgmt made a point to highlight that these events only drove “a small minority” of the 18.9mn subscriber adds.

Along with the strong results, Netflix also announced price increases across most of its plans in the US, Canada, Portugal and Argentina, which included the first ever price increase on its ad-supported tier. More than half (55%) of sign-ups in its ad countries are for ad-supported plans, which is a continued step up from ~50% and ~45% in Q3 and Q2, respectively. That said, while ad rev doubled in 2024 and is expected to double again in 2025, it is still not likely to be a primary revenue driver until 2026.

Looking ahead, while Q1 guidance was slightly softer than consensus estimates, Netflix raised its 2025 outlook on revenue by +$500mn at the mid-pt, which was +0.8% more than the Street’s forecasted, as well as its outlook on op margin to 29% (vs 28% prior). The Co also announced a $15bn stock buyback. As a reminder, starting with their Q1:25 earnings report in April, the Co will no longer regularly report paid membership and ARM on a quarterly basis, and instead will announced paid memberships as they cross “key milestones.”

See below for a full account of what we thought was most incremental from Netflix’s record-making qtr…

-> Netflix shares rallied +9.8% the day post earnings and closed at an all-time high (before rising further on the following day on Jan 23); The stock ended the week up +13.9%

Netflix Delivers A Strong Q4 With Headline Beats Across The Board

- Higher revenue growth was due to stronger membership additions and ad sales, more than offsetting a strengthening US dollar

- Q4 rev growth of +16% y/y (or +19% y/y ex-FX) beat consensus and accel’d seq from last qtr’s +15% y/y; Came in above guidance of +15%

- But ARM was up +1% y/y (or +3% y/y ex-FX) and missed consensus by -0.5%

- Q4 rev growth of +16% y/y (or +19% y/y ex-FX) beat consensus and accel’d seq from last qtr’s +15% y/y; Came in above guidance of +15%

- Strong operating leverage drove higher than expected Q4 op margin of 22.2% vs cons 22.0% (vs 29.6% in Q3 and 27.2% in Q2)

Netflix Had Its Largest EVER Qtr For Subscriber Net Adds

- Q4 paid net adds came in more than double consensus expectations (+112.2% beat): +91mn vs cons +8.91mn

- Strong beats across all regions, with LatAm (+199% beat) and UCAN (+142% beat) leading, while APAC and EMEA also posted strong double-digit beats (+96% and +72%, respectively)

- Membership adds were broad-based…Tyson-Paul fight, Christmas Day football games, and Squid Games S2 only represent “a small minority” of total member acquisition in the quarter”

- “As we’ve consistently seen across our history, no single title really drives a majority of our acquisition or engagement”

-> That being said, we’d also flag that research firm Antenna estimates that Netflix gained 656k signups in the 3-day window (Dec 24-26) for NFL Christmas Gameday, while with the Jake Paul vs. Mike Tyson game, which aired live on November 15, 2024, Antenna observed 1.43mn sign-ups to the svs over the 3-day period; Per the firm’s research, Netflix has consistently been w/in 50-70k signups per day for the entire 1.5 years since the password crackdown (link/link)

- “Retention behavior of those folks who did come in for those events, look a lot like the folks who came in for all of our other big titles”

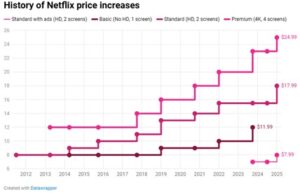

Netflix Is Increasing Prices For Most Plans, Including First-Ever Price Hike On Ad-Supported Tier

- The Co annc’d a bump in prices “across most plans in the US, Canada, Portugal and Argentina”

- Standard w/ ads increased by +$1: From $6.99 to $7.99 per month -> first ever increase in ad tier

- Standard increased by +$2.50: From $15.49 to $17.99 per month -> first increase in 3 yrs

- Premium increased by +$2: From $22.99 to $24.99 per month

- The cost of adding an Extra Member to a primary account is also increasing: From $7.99 to $8.99 per month

- Anticipate smooth adoption of price increases: “You’ve seen us take up price across a number of markets in EMEA and APAC and LatAm over the last couple of quarters across most plans and including ads, too. And those changes have gone smoothly…We certainly expect the same for these latest changes.”

- “When you’re going to ask for a price increase, you better make sure you have the goods and the engagement to back it up. And I feel like what we have going into 2025 is just that”

Q1 Guidance Was Softer Than Expected, But Raised Guidance For 2025

- Q1 guidance came in lighter than expected

- Q1 rev – missed cons by -0.7%: $10.416bn vs cons $10.49bn

- Implies rev growth of +11% y/y (+14% y/y ex-FX), which is “modestly” below 2025 guidance due to the timing of price changes and the seasonality of ads biz

- Q1 EPS – missed cons by -6.4%: $5.58 vs cons $5.96

- Q1 op income – missed by cons -5.5%: $2.94bn vs cons $3.11bn

- Q1 rev – missed cons by -0.7%: $10.416bn vs cons $10.49bn

- INCREASED 2025 rev guidance, which topped estimates: $43.5-$44.5bn, which is up +$0.5bn from prior guidance of $43-$44bn and beat cons of $43.65bn by +0.8%

- Drivers of updated guidance: Reflects improved biz fundamentals and the expected carryover benefit of stronger-than-forecasted Q4:24 performance, net of headwinds from the strengthening of the US dollar “over the past few months”

- Implies 2025 rev growth of +12-14% y/y vs 2024’s +16% y/y, which reflects an expectation of continued “healthy” member growth, “modest” F/X neutral ARM growth and a “rough doubling” of ad rev (consistent with prior ad rev guidance)

- INCREASED 2025 op margin guidance: 29% vs prior forecast of 28% and 2pts higher than the 27% op margin in 2024

- Drivers of updated guidance – balancing rev growth w/ strategic investments into the biz: Expense growth is expected to grow by ~9% in 2025, which is slower than expected rev growth of +12-14% y/y; Breaking that down –

- Content amortization growth expected to be in ~HSD, which will move around “a bit” based on timing of releases

- Also investing into growth priorities…: “Pretty heavily” investing into product and engineering teams to build out ads and live and games capabilities, as well as new user interface to enhance product discovery; Also investing in marketing and sales as they build out their ads sales organization and go-to-market capabilities

- …as well as support areas, which is growing in the low-mid single digits

- Drivers of updated guidance – balancing rev growth w/ strategic investments into the biz: Expense growth is expected to grow by ~9% in 2025, which is slower than expected rev growth of +12-14% y/y; Breaking that down –

- Strategy around FX volatility and hedging in 2025 given strengthening of US dollar?

- ~60% of rev is in non-US dollar currencies, and ~50% of the exposure is hedged on a rolling forward 12-month basis

- Hedging is viewed as a “short to medium term solution, at best” and used as a price averaging program to smooth the impact of FX, reduce the volatility from big near-term FX moves, and avoid short term swings to the biz

- Long-term strategy prioritizes managing underlying operating results through natural hedges, pricing adjustments, and cost structure mgmt

The Co’s Content Spend Is Still Going Up & They Are A “Long Way From Equilibrium”

- 2025 cash content spend expected to come in at $18bn, up from 2024’s $17bn: “It’s really about where do we put the next $1 billion and then beyond that to work in the most impactful way”, which “over the year or so” includes –

- “Continuing to build into big, scripted TV series”

- “Continuing to build out live”

- “Continuing to build out our original programming in each of our regions around the world”

- “Seeing more and more kind of impactful licensing opportunities”

- On long-term cash content spend strategy – “we have a long way to grow”: Given that they’re only capturing ~ 6% of their estimated rev market. “think we’re a long way from equilibrium”

- Any disruption to LA based productions due to wildfires? “Nothing meaningful”: No “meaningful” delays in project deliveries, and no “meaningful” impact to cash content spend in 2025

- “But this industry has been through a really tough couple of years, starting with COVID, going into the strikes and now this. So, it’s really important that we try not to delay anything and try to make sure that these jobs stay safe”

Sports Offerings Were A Resounding Success in Q4 (But That Doesn’t Change Views On Acquiring Full Season Sports Packages)

- Record-making quarter in sports

- Jake Paul vs. Mike Tyson fight became the most-streamed sporting event ever

- Taylor-Serrano undercard became the most-watched professional women’s sports event in US history

- NFL Christmas Day games were “the two most streamed NFL games ever”: Avg minute audience was 30-31mn

- WWE is “off to a great start”

- Outperforming vs prior linear broadcast: Had ~5mn view in the first week, which is ~2x the audience that Monday Night Raw was getting in linear TV; In the US, viewing of Monday Night Raw was as big as the Monday Night Raw viewing has been in 5 yrs

- Non-live viewing was also up: Grew by 25%, mostly outside US time zones (i.e., UK, Canada, Mexico, Australia, Brazil, etc.)

- Does success of WWE influence decision process on UFC rights? “Not going to comment anything specifically like the UFC”

- But the success of NFL Christmas Day games does NOT change their view on full season sports rights: Underlying economics of full-season Big League sports are still “extremely challenging”

- But still open to the right oppty…: “If there was a path where we can actually make the economics work for both us and the League, we certainly would explore”

- …that reflects the value of the “big”, “young”, “more global” audience (vs linear tv) that Netflix provides: “We want to be able to bring value to the sport like we have…with WWE…with the NFL, too…but that has to be reflected in the deal”

- “We’re not focusing on acquiring rights to large regular season sports packages; rather, our live strategy is all about delivering can’t-miss, special event programming”

- On the decision to buy rights to FIFA Women’s World Cup in 2027 and 2031 – it “fits perfectly into the strategy”

- “Is a real TV event”

- “Matches set a bunch of viewing records in 2023”

- “Women’s sports have only become more interesting and more popular since”

- “We’re thrilled to have the time to start telling the stories of these teams and these athletes like we’ve done so well with other sports, with our series and our documentaries”

Advertising Focus Is Shifting From Scale To Monetization – “2025 Is The Year That We Transition From Crawl To Walk”

- 55% of sign-ups in ads countries were for ad-supported plans in Q4, vs “over 50%” in Q3 and “over 45%” in Q2

- Memberships on ad plans are up “nearly 30%” q/q in Q4, vs +35% q/q in Q3 and +34% q/q in Q2

- View hours per member on ad-supported plans is similar to engagement on standard non-ads plan in ads country

- Are in the early innings of shifting advertising strategy focus from scale to monetization: “This is going to remain a priority and part of our roadmap for at least the next several years, likely years to come after that”

- Met scale goals for advertisers in 2024

- Making “solid progress” on monetization

- Exceeded ads rev target in Q4

- Doubled ads rev y/y in 2024 and expect to double it again in 2025

- “There’s considerable work ahead of us for sure, but we don’t see specific hurdles…we think our path is relatively straightforward”

- Netflix ad stack will roll out across all 12 ads countries in 2025

- Launched and testing in Canada and “that’s done well…we’re learning quickly”

- Will launch in US next in April

- Biggest initial benefit of having their own ad serve is improving the overall buyer experience: Enables them to offer more flexibility, more ways of buying for advertisers, and fewer activation hurdles, which drives increased sales

- “We’re already seeing the impact of those benefits in the revenue growth in Canada”

- Over time, expect to offer even more capabilities: Including more programmatic availability, enhanced targeting, leveraging more data sources, more measurement more reporting, more incrementality studies

User Engagement Remains A Top Priority

- Is engagement growth a strategic priority for Netflix? Absolutely: “Our average member is watching for about two hours a day. So we’ve still got plenty of work to do to grow that, and that’s what the team is very highly focused on”

- On competing w/ short-form video platforms for engagement – “think we see ourselves as playing a specific and differentiated role in the ecosystem”: “Our core is in kind of professional longer-form storytelling, and that’s a very big and enduring business. But again, as things get pulled – as eyeballs get pulled into other places, we definitely want to be there for them as well”

- “Find that the short-form services also are a great breeding ground for new storytellers”…Netflix is “a place where those great storytellers…can graduate to”

- Regarding Narnia debuting in theaters in 2026 – it’s a “release tactic”: Routinely release movies in theaters a few weeks before to “quality for awards…meet festival requirements, and to prime the publicity pump a bit”

- Narnia will be a two-week special event and will release in IMAX theaters

- Overall, there is “no change at all” in theatrical strategy: Core strategy remains giving members exclusive first-run movies on Netflix

Still “Just Scratching The Surface Today In Terms Of What We Can Ultimately Do” In Video Games And Are “Refining” Their Strategy

- Squid Game: Unleashed is on pace to become their most downloaded game: Reached #1 in action games in the app stores in 107 countries

- On video game impact on subscribers – The Co “see[s] positive impacts in acquisition and retention” BUT “those effects are relatively small”

- That said, investment in games relative to overall content budget is also “relatively small,” so will “stay disciplined about scaling that investment as we see continued scaling and member benefits”

- Continue to “refine” strategy based on synergies that reinforce both interactive and non-interactive content – What’s coming up next?

- Focusing on more narrative games based on Netflix IP: “These are consistent fan favorites and we’ve got a lot in the library to work with there”

- Introducing party and couch co-op games on TV delivered from the cloud: “We think of this as a successor to family board game night or an evolution of what the game show on TV used to be”

- Games for kids: “No ads, no in-app payments. It’s a safe space for kids just included with your subscription”

- More recognizable mainstream titles, including both licensed titles and homegrown titles based on their IP

- Moving beyond mobile: “While we started in mobile, our goal is to make our games accessible on all device types over time and in 2025 we’ll continue to test and expand our offering of cloud games on TV”

- “We’re iteratively showing our members that we are a place to discover and play games, and we look forward to continuing to launch bigger and bigger games every year”

TikTok’s Future Remains In Flux…

After much chatter and deliberation last week around the fate of TikTok in the face of a possible shutdown in operations on Jan 19, the “ban” was ultimately implemented on Saturday night (Jan 18). However, service was shortly brought back on Sunday afternoon (Jan 19), with a pop-up message crediting Trump for the app’s return – “Thanks for your patience and support. As a result of President Trump’s efforts, TikTok is back in the US!”

Since then, there have been a plethora of updates out, including an executive order delaying enforcement of the ban, a signal from China on willingness to strike a deal, several potential buyer names, and the possibility of alternative non-selling solutions, all while Meta is taking steps to capitalize on the uncertainty around TikTok’s future.

See below for the most recent developments.

Trump Signals Support For TikTok

- On Jan 19, Trump said on a Truth Social post that he would issue an executive order on Monday (Jan 20), his first day in office, “to extend the period of time before the law’s prohibitions take effect, so that we can make a deal to protect our national security”

- And there would no liability for companies preventing TikTok’s shutdown: Trump also said that “the order will also confirm that there will be no liability for any company that helped keep TikTok from going dark before my order”

- But there were conditions to his support – 50% US ownership of the app (link): Trump said he wants “the United States to have a 50% ownership position in a joint venture” between the current owners and new owners

- An executive order was signed on Jan 20 to delay enforcement of the federal ban on TikTok in the US for 75 days – see Theme #2 (link):

- “I intend to consult with my advisors, including the heads of relevant departments and agencies on the national security concerns posed by TikTok, and to pursue a resolution that protects national security while saving a platform used by 170 million Americans,” Trump said in the executive order; “My Administration must also review sensitive intelligence related to those concerns and evaluate the sufficiency of mitigation measures TikTok has taken to date”

China Also Seems To Be Softening Its Stance And Has Signaled An Openness To Strike A Deal

- China previously said it “firmly opposes” and would block any forced sale of the app (link)

- But on Jan 20, the Chinese Foreign Ministry said that private companies CAN make their own decisions about whether to sell or merge, which was a divestiture from its previous stance

- “For such actions as corporate operations and acquisitions, we always believe that they should be decided independently by companies based on market principles,” Chinese foreign ministry spokeswoman Mao Ning said; “If Chinese companies are involved, they should comply with Chinese laws and regulations”

Several Names Are Reportedly Being Floated As Potential Buyers (link/link)

- Tesla and SpaceX owner Elon Musk

- Chinese govt officials had reportedly considered selling TikTok’s US operations to Musk ahead of the first ban deadline of Jan 20

- When asked if he would be open to Musk buying TikTok, Trump said, “I would be if he wanted to buy it, yes”

- Oracle Chairman Larry Ellison (see Theme #3 for more)

- Trump has said he’d “like” to see Ellison purchase the platform

- At a press conference on AI infrastructure investment plans under the Trump Administration, which Ellison joined –

- Trump said, “What I’m thinking about saying to somebody is, buy it, and give half to the United States of America. Half and we’ll give you the permit”

- To which Ellison responded, “Sounds like a good deal to me Mr. President”

- Ellison had bid for TikTok, along with Walmart, back in 2020 when Trump first pushed for a ban on the platform, and while Trump had approved the deal in principle, the attempt to ban TikTok at the time fell through in the face of legal challenges

- Oracle is currently at the center of the TikTok dilemma, as it operates as a cloud infrastructure provider for ByteDance in the US

- YouTube creator Jimmy Donaldson aka MrBeast

- Posted on Jan 13 on X that he would “buy TikTok so it doesn’t get banned”

- On Jan 14, he followed up with another post on X that “unironically I’ve had so many billionaires reach out to me since I tweeted this, let’s see if we can pull this off”

- On Jan 23, a spokesperson for Donaldson said that “several potential buyers are in ongoing discussions with Jimmy, but he has no exclusive agreements with any of them”

- The People’s Bid for TikTok, a group formed by billionaire Frank McCourt in partnership with his nonprofit organization Project Liberty + Shark Tank star and investor Kevin O’Leary (link/link)

- “I’ve spoken to all the potential bidders, and it’s clear to me that Frank McCourt and Project Liberty are the team to get this done. This is the bid that can save TikTok. Project Liberty has brought together the right people, the right vision and the right technology to avoid a ban. It is a win for all Americans,” O’Leary said in a statement

- The consortium said that it delivered a proposal to ByteDance on Jan 23rd to acquire TikTok’s US assets

- Perplexity AI (link)

- The Co reportedly submitted a bid to merge w/ TikTok US which would create a new combined entity consisting of Perplexity, TikTok US, and new capital partners, per sources

- Perplexity believes its bid has a chance b/c it is proposing a merger vs a sale of the Co

- The new structure would allow for most of ByteDance’s existing investors to retain their equity stakes: In turn, the deal would bring more video to Perplexity, according to sources

- The final price would be determined by what ByteDance’s existing shareholders decide: Including whether they choose to remain part of the new equity or decide to cash out; Sources believe a fair price is “well north of $50bn”

There Is Also Some Chatter That TikTok Is Weighing Non-Sale Options (link)

- ByteDance is exploring a deal to keep TikTok running in the US without selling its operations there, according to General Atlantic CEO and ByteDance board member Bill Ford

- General Atlantic, a private equity firm, holds a stake in ByteDance

- The Co is looking at options for TikTok that could involve a change of control locally to ensure it complies with US legislation and “we are optimistic we will find a solution”

- “There are a number of alternatives we can talk to President Trump and his team about that are short of selling the company that allow the company to continue to operate, maybe with a change of control of some kind, but short of having to sell”

- “I’m optimistic about the dialog that is emerging between President Trump and President Xi…That might help create a much more constructive environment, a much higher level of engagement that could lead to a positive solution” Ford said

Meta Is Capitalizing Off Of The Uncertainty In TikTok’s Future (link)

- Over the weekend when TikTok temporarily shut down, Meta began contacting TikTok creators with a new offer, which it’s calling the “Breakthrough Bonus” program

- Who is the program for and what does it offer?

- Who: “Creators who are new to Facebook or Instagram”; Must be 18+, based in the US, and have an existing presence on a “third party social app”

- The incentive…: “Accepted creators will immediately be able to earn money across reels, longer videos, photos and text posts through Facebook’s invite-only Content Monetization program”

- …along with a $ bonus: “Plus earn up to $5,000 in extra Breakthrough bonuses to help you get off the ground during the first 90 days”

- Creators who apply for the program will be able to share details of their presence in other apps, with the size of their following/s on those other platforms dictating how much Meta will pay each participant in bonuses (Meta will calculate individual bonuses “based on an evaluation of your social presence”)

- Requirements of the program –

- Content minimum: Creators will have to share at least 20 reels on Facebook, and 10 reels on Instagram, within each 30-day bonus period

- Exclusivity: Content posted must be original and not available on other apps

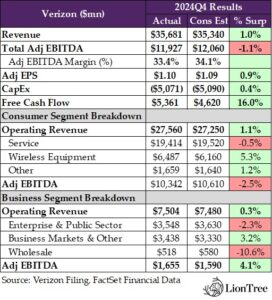

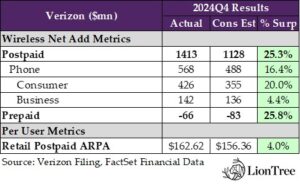

Verizon Enters The AI Race And Posted Its Highest Quarterly Postpaid Net Adds In Over A Decade

Jumping the queue ahead of next week earnings rush in the connectivity industry, Verizon was the first major player in the sector to report its Q4 earnings this week, and the company’s print will certainly be a tough act to follow as it relates to net add metrics and free cash flow performance, in particular. Verizon’s postpaid phone net adds closed a wide +16.4% ahead of the Street’s forecasts, driven by better than anticipated performances across both its Consumer and Business segments. Notably, the company’s consumer segment has been picking up market share in Tier 1 cities and benefited from a “concerted effort” to target the Latino population. Looking ahead, the momentum in the company’s mobility business is expected to carry into 2025, and a “gradual improvement” in the handset upgrade rate should add some fuel to the fire as well.

On the broadband side of the equation, dynamics have been equally favorable for Verizon, as the company continued to take market share in the space. Q4 fixed wireless access (FWA) and Fios both came in ahead of expectations with a combined +408k net adds. Verizon is “very comfortable” that this trend of +350-400k broadband net adds will continue in 2025, though there will likely be some mix changes on the horizon. Given the company’s shifting focus to tier 2 and 3 markets with its C-band deployments, it expects that its traditional FWA will slow somewhat from the pace seen in 2024. However, this will be offset by a new FWA MDU product as well as accelerated expansion of the Fios footprint to an additional +650k open-for-sale locations after passing ~+500k in 2024.

From a financial perspective, there were some put and takes with Verizon’s FY25 outlook, as adj EBITDA growth is projected to accelerate, but wireless service growth is expected to decelerate. That said, part of the slowdown in wireless service revenue growth was explained by an accounting change as well as a peak impact from ongoing promo amortization efforts. Nonetheless, Verizon still has irons in the fire that could drive upside to these forecasts, and the most prominent of these is its newly introduced AI Connect suite of offerings. With an estimated TAM of $40bn+, AI Connect could be a significant growth driver for Verizon in FY25 and beyond.

See below for more on what we thought was most incremental from Verizon’s Q4 print:

-> Verizon shares were up +1.0% in reaction to the print and ended the week up +2.0%; YTD, Verizon stock is trading down -1.1%

Headline Numbers Were Mixed… BUT Verizon Added Its Most Qtrly Postpaid Subs In Over a Decade

- Verizon posted mixed headline results, w/ a beat on rev but a miss on adj EBITDA: Q4 rev grew +1.6% y/y (vs ~flat y/y in Q3) and topped cons by +1.0%; Adj EBITDA was up +2.1% y/y (vs (+2.1% y/y in Q3), missing cons by -1.1%; Adj EPS of $1.10 beat by +0.9%; FCF was a wide +16.0% above cons

- Consumer (~77% of total rev) – MIXED: Rev incr’d +2.2% y/y in Q4 (vs +0.4% y/y in Q3) and beat cons by +1.1%; Adj EBITDA was down -0.4% y/y (vs +1.8% y/y in Q3) and missed cons by -2.5%

- Business (21% of total rev) – BEAT: Q4 rev decr’d -1.5% y/y (vs -2.3% y/y in Q3) and closed +0.3% ahead of cons; Adj EBITDA rose +3.0% y/y (vs -3.7% y/y in Q3) and topped cons by +4.1%

FY25 Guidance Reflected Some Puts & Takes And Moving Parts In Wireless Svs Rev

- 2025 total wireless svs rev growth is expected to decel: Sees +2.0-2.8% y/y growth in FY25 (vs +3.1% y/y in FY24); The mid-pt of the guide assumes ~+$2bn of addt’l growth off of a base of $82bn

- The FY25 wireless svs rev guide should be viewed in the context of a higher base of rev: In Q1:25, the Co is reclassifying $2.9bn+ of annual recurring device protection and insurance-related planned revs from other rev into wireless svs rev

- $1bn+ of svs rev growth has already been “baked in” from the two price-ups annc’d so far in 2025 (link) –

- Some customers will see a hike of $3/line per month starting on Feb 20

- Shared data plans are also seeing an increase, w/ single-line accounts being charged an extra $4 per month and multi-line accounts seeing a $15 per month increase; Fees for exceeding data limits are also rising to $20 per GB from $15

- Promo amortization will peak in FY25: However, “customer economics are very healthy,” and this headwind is expected to ease towards the end of the yr and into FY26

- 2025 adj EBITDA growth is projected to accel: Expects +2.0-3.5% y/y growth in FY25 (vs +2.1% y/y in FY24)

- 2025 EPS growth guidance is lower than the Street anticipated: Projects flat to +3.0% y/y growth in FY25, falling short of cons’ +3.1% y/y at the mid-pt

Verizon Fired On All Cylinders Regarding Postpaid Phone Net Adds

- Q4 postpaid phone net adds were MUCH stronger than anticipated: Total retail postpaid phone net adds incr’d +26.5% y/y to +568k in Q4 (vs +239k in Q3) and beat cons by +16.4%

- Consumer postpaid phone net adds BEAT: Net adds were up +34.0% y/y to +426k in Q4 (vs +81k in Q3), finishing +20.0% above cons

- Gross adds growth was ~flat seq: Q4 gross adds grew +5.5% y/y (vs +5.9% y/y in Q3 and +12.0% y/y in Q2), marking eight consecutive qtrs of y/y gross adds growth

- Drivers: The “unique” value prop has been “resonating very well,” “local mkting is starting to pay off,” the Co is gaining mkt share in tier 1 cities, and a “concerted effort” to pursue the Latino mkt is bearing fruit

- Verizon sees this trend continuing into FY25

- There was a “modest” +10bps y/y increase in the upgrade rate: Customers continue to hold onto devices for 40+ months, and many are locked into 3-yr device protection plans (DPPs) through 2025

- A ~+msd% y/y improvement in upgrades is projected for FY25: A large cohort is coming off of their 3-yr DPP, and, “at some point, customers will want new devices”

- Postpaid phone net adds ended FY24 in positive territory: This result held true both w/ and w/out the contribution from the second number offering

- Gross adds growth was ~flat seq: Q4 gross adds grew +5.5% y/y (vs +5.9% y/y in Q3 and +12.0% y/y in Q2), marking eight consecutive qtrs of y/y gross adds growth

- Business “had another solid qtr,” w/ “cont’d healthy biz phone volumes”: Business postpaid phone net adds rose +8.4% y/y to +142k, topping cons by +4.4%, w/ “strong growth across all three customer groups”

- Postpaid phone churn was higher seq and exceeded estimates: Total retail postpaid phone churn was flat y/y at 0.93% (vs 0.89%) but worse than cons’ 0.92%

- Consumer postpaid phone net adds BEAT: Net adds were up +34.0% y/y to +426k in Q4 (vs +81k in Q3), finishing +20.0% above cons

Wireless Service Rev Growth Was A Bright Spot

- Q4 wireless svs rev growth accel’d seq: Wireless svs rev incr’d +3.1% y/y in Q4 (vs +2.7% y/y in Q3); The Co ended 2024, w/ “industry-leading total wireless svs rev of $20bn”

- Consumer wireless svs rev growth accel’d slightly seq: Q4 consumer wireless svs rev grew +3.0% y/y (vs +2.9% y/y in Q3 and +3.7% y/y in Q2)

- Business wireless svs rev growth also improved seq: Business wireless svs rev was up +3.4% y/y in Q4 (vs +2.9% y/y in Q3 and +2.4% y/y in Q2)

Multiple Factors Contributed To Stronger Than Anticipated ARPA Numbers

- Q4 postpaid ARPA surpassed expectations: Q4 total retail postpaid ARPA of $162.62 was up +3.9% y/y (vs +3.8% y/y in Q3) and beat cons by +4.0%

- Pricing was an “important component”: The Co had 4 major price-ups throughout 2024, targeting areas where w/ lower churn and higher input prices as well as areas where it is providing more value to customers

- Customers are “stepping up” to more premium plans: There has started to be a “little bit of a tailwind” from upselling customers in areas where C-band has been rolled out, and Fios customers have been upgrading to gig plans; Customers are also buying more perks from the Co

- The Co has “started exploring aggressively” other ways to monetize the network: Launched its first network slice in Q4 and has begun to see more monetization in “enhanced satellite connectivity”

The “Turnaround” In Prepaid Cont’d, W/ Strong Momentum Heading Into 2025

- Q4 prepaid net losses were better than feared: Total prepaid net losses of -66k in Q4 (vs the prior yr qtr’s -289k and Q3’s -69k) were better than cons’ -83k

- The Co saw a “really strong performance” in its value biz: The Co’s “operational rigor… cont’d to pay off”; The “refreshed value brands,” the value prop, the relationship w/ Walmart, as well as “expanded total wireless distribution” have all been “working very well”

- Excluding SafeLink, prepaid net adds were positive for the yr: This was the first time that has occurred since the TracFone acquisition, reflecting a “great turnaround” by the consumer team

- Verizon is “very comfortable” that prepaid net adds “can continue to grow… in this environment”: As a result, the rev headwind “will become a tailwind on prepaid” in FY25

Broader Commentary On The Mkt & Verizon’s Go-To-Mkt Strategy Was Constructive

- Overall wireless mkt growth has been “robust” and “very resilient”: The Co expects the overall postpaid mkt to grow between 8-8.5mn lines in 2025, w/ prepaid to postpaid migration comprising almost half of that

- Verizon’s “customer-first” offerings are “resonating”: The Co continues to invest in the biz and make “strategic moves for long-term growth”

- MyPlan has been seeing “growing adoption”: More than half of the Co’s base is now on MyPlan, and the offering’s accompanying perks have been seeing strong uptake as well

- MyHome is “working very well”: This has helped segment the mkt “very well” between fiber and FWA customers, driving “cont’d success”

- The brand refresh is “really paying off”: But still acknowledged that “it’s early” after launching just six months ago

- There’s nothing new in the competitive environment: The market has remained competitive, but Verizon has just been “performing way better”

- Verizon’s “customer-first” offerings are “resonating”: The Co continues to invest in the biz and make “strategic moves for long-term growth”

Mkt Share Gains Drove “Cont’d Success” In Broadband

- Q4 broadband net adds improved seq and topped the Street’s forecasts: Total broadband net adds fell -1.2% y/y to +408k in Q4 (vs +389k in Q3) and beat cons by +2.8%; The Co “cont’d to take mkt share,” adding nearly 1.6mn broadband subs across 2024 and ending the yr w/ 12.3mn+ total broadband subs

- FWA net adds BEAT, stepping up slightly seq: Q4 FWA n et adds were down -0.5% y/y to +373k (vs +363k in Q3) and topped cons by +2.2%; Consumer FWA net adds of +216k were +2.9% above cons, and business net adds of +157k were +1.3% ahead of cons

- The Co is “off to a great start” to hit its next milestone of 8-9mn FWA subs by 2028: Verizon ended Q4 w/ almost 4.6mn FWA subs and $2.1bn+ of FWA rev

- There will be “a little bit less” traditional FWA oppties going into H1:25: Given that the Co is now deploying C-band and opening up FWA in less dense tier 2 and 3 suburban-rural mkts

- BUT a new FWA MDU solution should help offset that: Expects this start scaling into 2025 but didn’t provide more specific estimates

- Fios net adds were better seq and ahead of expectations: Q4 Fios net adds were down -7.3% y/y to +51k (vs +43k in Q3) but beat cons by +4.1%; This was a “solid result, given challenges noted by… competitors”

- The Co plans to ramp up Fios net adds in FY25: Cited the previously outlined initiative to expand Fios to up to 650k open-for-sale locations as well as a better economic situation in the US, where people have more purchasing power

- Verizon is “very comfortable” w/ a target range of +350-400k broadband net adds each qtr of FY25: Assuming some fluctuations

- FWA net adds BEAT, stepping up slightly seq: Q4 FWA n et adds were down -0.5% y/y to +373k (vs +363k in Q3) and topped cons by +2.2%; Consumer FWA net adds of +216k were +2.9% above cons, and business net adds of +157k were +1.3% ahead of cons

AI Connect Is Poised To Be A Major Future Growth Driver For Verizon

- Verizon introduced a new suite of offerings, AI Connect: This solution is meant to address the “enormous capacities” required by new applications powered by gen AI and LLMs, especially as compute begins to occur closer to the network edge

- The Co is “utilizing existing assets in new ways” to svs the offering: Including its “unmatched fiber assets,” both inside its ILEC footprint and outside of it via its 71-city One Fiber buildout; Prior investments in the Converged Intelligent Edge Network will also pay dividends

- Thousands of distributed telco facilities will serve as the foundation for edge computing: Many of these sites already have the power space and cooling needed for this

- Verizon also has extensive connectivity of third-party data centers ranked third in the mkt: Addt’ly, the Co has 100-200 acres of undeveloped land, some of it currently zoned for data center development and “much of it in prime data center-friendly areas”

- AI Connect already had a positive impact on rev and adj EBITDA in Q4: The Co has a pipeline of $1bn+ of sales, w/ major players such as Google and Meta having purchased capacity

- The Co estimates a TAM of $40bn+

- The Co is “utilizing existing assets in new ways” to svs the offering: Including its “unmatched fiber assets,” both inside its ILEC footprint and outside of it via its 71-city One Fiber buildout; Prior investments in the Converged Intelligent Edge Network will also pay dividends

Verizon Continues To March Forward W/ Previously Outlined Investment Initiatives

- C-band and Fios remain Verizon’s primary investment priorities: Though the Co will continue to look for oppties to efficiently deploy capital

- The Co plans to deploy 80-90% of C-band sites in FY25: Reiterated these will be focused in rural as well as suburban mkts and that mkts w/ C-band have higher premium sell-through, lower churn, and can offer FWA; The previous milestone was 70% coverage by the end of 2024

- Verizon has been finding ways to deploy fiber more cheaply: This will help the Co maintain its ROI as it looks to expand the Fios footprint to 650k open-for-sale locations (vs the previous target of ~500k in 2024)

- There are still plans to participate in BEAD, but there have been “very little” oppties: Mgmt indicated that the states are still in the process of figuring out plans

CapEx Was Lower Than Anticipated But Is Still Expected To Step Up In FY25

- Q4 CapEx levels came in below the Street’s estimates: CapEx was up +10.2% y/y to $5.07bn but still a slight +0.4% better than cons; Total FY24 CapEx finished at $17.1bn, which was at the low-end of the initial $17.0-17.5bn guidance range and down -8.9% y/y

- Reaffirmed FY25 CapEx range of $17.5-18.5bn (the mid pt is 0.3% below cons)

Verizon Cont’d To Demonstrate “Strong Cash Generation” In Its Biz

- FCF finished well above forecasts: FCF of $5.4bn was up +31.6% y/y in Q4 (vs -10.8% y/y in Q3) and beat cons by a wide +16.0%; The Co closed FY25 w/ $19.8bn in FCF, a +6.0% y/y increase

- Q4 FCF was affected by a couple of one-time items, including –

- ~$2bn in proceeds from the Vertical Bridge tower transaction

- ~$600mn in severance payments, which represents ~half of the total payments expected under the voluntary separation program

- FY25 FCF is projected to be slightly below the Street’s expectations: Anticipates FCF between $17.5-18.5bn, missing cons by -0.3%

- Interest expense continues to imp rove heading into FY25: The Co paid down $7bn in total debt in 2024

- There has been no changes from last qtr regarding cash taxes: Still sees pressure from bonus depreciation but noted some chance for a legislative change, given the new presidential administration

- Q4 FCF was affected by a couple of one-time items, including –

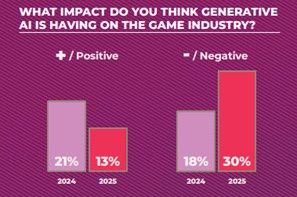

Key Titles Can Be “Make” Or “Break” In Gaming… EA Faced The Latter

The last year has been tough for the video game industry as it relates to title release schedules being delayed and new title performance lagging expectations. Along these lines, Electronic Arts surprised investors by cutting its FY25 net bookings guidance this week, which was driven by underperformance of EA SPORTS FC 25 and Dragon Age: The Veilguard, causing a massive sell-off in the stock. The update comes ahead of EA’s FQ3 earnings report on Feb 4th so more to come on this later.

Meanwhile, GDC came out with its 2025 State of the Game Industry report this week as well, which had some interesting insights across engines and platforms (PC development has “skyrocketed”), AR/VR (Meta continues to be the platform that developers are most interested in), genAI (which is actually becoming more unpopular with developers), industry layoffs (1 in 10 developers have lost their jobs in the past yr), and more.The data is based on responses from 3,000+ developers across the gaming industry. You can access the report HERE.

See below for more of our takeaways.

EA Cuts Guidance Due To Underperforming Titles

- EA cut its FY25 net bookings guidance by -7.5% at the mid-pt due to underperforming titles: The Co now anticipates FY25 net bookings between $7.00-7.15bn (vs prior $7.50-7.80bn), missing cons by -8.0% and implying a -4.8% y/y decline at the mid-pt

- The Co now projects a ~+msd% y/y decline in live svs net bookings: EA initially forecasted a ~+msd% y/y rise in live svs and maintained this guidance through the end of FQ2

- EA expects a “return to growth” in FY26 as it launches more “iconic franchises”

- The Global Football franchise accounted for most of the change in guidance: After two consecutive fiscal yrs of double-digit net bookings growth, the franchise “experienced a slowdown as early momentum in FQ3 did not sustain through to the end”

- EA now expects Global Football to finish FY25 down ~-msd% at the mid-pt of the new outlook: Exiting FQ2, Global Football was projected to grow net bookings over a “record prior yr”

- A “comprehensive gameplay refresh” has shown “encouraging” early results: This includes the Co’s annual Team of the Year update in FC 25; These efforts have generated “positive player feedback”

- Dragon Age also underperformed EA’s expectations by nearly -50%: The game engaged ~1.5mn players in FQ3

- The Co now projects a ~+msd% y/y decline in live svs net bookings: EA initially forecasted a ~+msd% y/y rise in live svs and maintained this guidance through the end of FQ2

-> EA shares fell -16.7% in reaction the news and ended the week down -17.9%

Some Key Insights From GDC’s 2025 State Of The Game Industry Report…

- Dominance of PCs in gaming continues to increase: 80% of developers said they’re currently making games for PC (up from 66%); This was followed by PlayStation 5 (38%) and Xbox Series X/S (34%)

- PlayStation continues its console lead over Xbox: About 38% of developers are currently making games for PS5 hardware (compared to 34% for Xbox Series X/S)

- Mobile game development has increased for the first time since 2020: 29% of developers are currently making games for Android and 28% for iOS (up from 24% and 23% respectively)

- Much of that is in Brazil and the East and South / Central / West Asia regions, where over half of developers say they work on mobile games

- Browser games have reached the highest %age of developers in a decade: 16% of developers are working on releases for web browsers, which is up from 9% last yr and 11% the yr before

- Meta Quest / Horizon Store remains the dominant space for VR/AR developers, with 59% currently making games for the platform, followed by Steam VR (31%) and PlayStation VR/VR2 (16%)

- Meta Quest / Horizon Store also tops the list in developer interest and beats Apple by a wide margin: 63% of developers said Meta Quest / Horizon Store is the VR/AR platform they are most interested in right now, vs Apple visionOS at 26% and Apple ARKit at 12%

- Hollywood is adapting more video games: 13% of developers have worked on games that are being (or have been) adapted into movies, shows, or other media, up from 10% in last yr

- The number jumps to 36% for AAA developers, which is a 10-pt increase from last yr

- Gaming workforce trends – 1 in 10 game developers have been laid off in the past year

- Top 3 reasons Cos gave for layoffs: Restructuring (22%), Declining Revenue (18%), and Market Shifts/Industry Trends (15%)

- Sentiment towards GenAI is generally souring: Last year, developers were more favorable than opposed to generative AI, which is no longer the case

Specific concerns developers pointed to included intellectual property theft, energy consumptions, quality of AI-generated content, potential biases, and regulatory issues

Huge Improvements In Non-Gaming Mobile App Monetization Drove The 2024 App Economy

If you are interested in the app economy, you will be interested in Sensor Tower’s 2025 State of Mobile Consumers report which was out this week. Saying that it includes a lot of data on iOS and Google Play in-app purchase trends for both gaming and non-gaming is an understatement. The overall punchline is that while overall global mobile app downloads remain slightly down y/y, overall time spent is still increasing (though at a decelerated rate). That said, monetization growth is the shining star, in particular with non-gaming apps (though mobile gaming in app revenue (IAP) did re-bound back to growth.

See below for our quick takes but if you want to delve in more, click here to access their full 95 page deck. Also, see Theme #7 for some more key developments this week as it related to the gaming sector.

- Overall global mobile app downloads in 2024 have stabilized at roughly flat y/y (-1%) to 136bn

- Downloads have hovered ~ 135-140bn a year since 2020

- And while people are spending more time on their phone, there are some signs of slowing in certain markets

- Growth in time spent on mobile apps decelerated to +5.8% y/y in 2024 from +7.7% y/y in 2023 as time spent leveled out in several key mkts including the US, Japan, South Korea, and China

- The 4.2 trillion hours spent across iOS and Google Play apps translates into ~ 3.5 hours/day/ mobile user

- BUT monetization on mobile accelerated due to strong growth in non-gaming apps revenue

- In 2024, global in-app purchase (IAP) rev across iOS and Google Play reached $150bn (+13% y/y), the highest growth seen since 2021; This includes spending on in-app purchases, subscriptions, and paid apps and games

- Non-gaming drove most of this growth (+23% y/y), while gaming saw a bounce back (+4% y/y) following back-to-back years of declines

- Global Mobile Gaming App downloads in 2024 fell -6% y/y (to 49.6bn) BUT revenue returned to growth in 2024 (+4% y/y to $81bn) after 2 consec periods of declines: Driven by Strategy, Puzzle, and Action games in particular

- Regional performance diverged: Most mkts across AMER and EMEA saw strong growth return in 2024, though this was pulled down by lagging growth across the largest markets in APAC like Japan, China, and South Korea

- Despite the lower downloads, consumers are spending more time on mobile devices and increasingly making purchases, driven by enhanced gaming experiences and better monetization strategies

- Global Mobile NON-Gaming App revenue in 2024 rose +25% y/y (added $14bn in addtl IAP rev vs the $9bn added in 2023)

- What’s driving the growth? Entertainment, Productivity, and Photo & Video led the way in 2024

- The US remained the leading market in 2024 with $52bn in IAP revenue (or more than a third of the global total) and this was up +16% y/y, outpacing the worldwide rate

- Europe contribution was smaller but IAP revenue across the continent rose +24% y/y (almost 2x the global figure); This included strong growth in the region’s top markets like the UK, Germany, France, and Italy

- Mobile users spent nearly 2.4 trillion hours on Social Media apps in 2024, +6% y/y and TikTok was the #1 app in the category: That amount of time spent equates to 6.6bn hours/day or ~50 minutes for every person on Earth

- Messaging apps were a distant second in terms of time spent at 607bn hours (WhatsApp was #1): Followed by browsers at 330bn hours (Google Chrome)

- Time spent growth in AI Chatbot apps was hyper growth at 300+% y/y: Consumers spent 7bn+ hrs in apps like Character AI and ChatGPT

- Another fast-growing subgenre was Digital Wallets & P2P Payments, which saw time spent climb +21% y/y

- AI Apps are already a billion industry – IAP rev in AI Chatbot and AI Art Generator apps reached ~$1.3bn in 2024 from just over $400mn in 2023

- The US accounts for 45% of Gen AI apps revenue, followed by UK (but only 4% of total revenue)

- Expect many more apps to launch new AI features in 2025

Grab Bag: TMT M&A Speculation/Comcast’s New Sports & News TV Video Package/Threads To Test Ads

- M&A speculation took center stage this week…

- Paramount Global was hit w/ a last-minute $13.5bn competing bid (link): The all-cash offer from Project Rise Partners (PRP), a consortium of investors that previously bid on the Co, is vastly superior to Skydance and Redbird’s $8bn, all-cash deal w/ Paramount, per the group

- PRP is offering $19 per Class B share: This compares to the Redbird-Skydance bid of $15 per share

- PRP’s bid for the Class A shares remains the same as the Skydance offer

- PRP will add +$2bn to Paramount’s balance sheet

- It is unclear which investors are in the PRP group: Outside of Daphna Edwards Ziman, co-chairman of Cinémoi, and Moses Gross, CEO of Malka Equities, sources indicate that PRP is backed by titans of industry, at least one of the richest men in the world, and a Co partner that is a pioneer in the satellite industry

- Paramount Global was hit w/ a last-minute $13.5bn competing bid (link): The all-cash offer from Project Rise Partners (PRP), a consortium of investors that previously bid on the Co, is vastly superior to Skydance and Redbird’s $8bn, all-cash deal w/ Paramount, per the group

- TripAdvisor received an indication of interest regarding a third-party takeover (link): This was revealed in a SEC filing by holding Co Liberty TripAdvisor Holdings, which showed this interest was initiated last Oct

- The non-binding proposal initially offered $17.50 per share in cash on Oct 18, 2024…: Subject to diligence and other customary conditions

- … BUT this was raised to $18-19 per share of TripAdvisor not held by Liberty TripAdvisor on Jan 17, 2025: Implies a +14-21% premium to the closing price on Jan 22

- The revised offer also includes acquiring outstanding shares of Liberty TripAdvisor for $0.3080 per share in cash: As well as Liberty TripAdvisor preferred stock for an aggregate $102mn

- Liberty TripAdvisor’s board is against the deal: The board counseled TripAdvisor’s special committee that it “determined that it was not in the best interest of TripAdvisor and its shareholders to engage” w/ the party that submitted the indication of interest

- The non-binding proposal initially offered $17.50 per share in cash on Oct 18, 2024…: Subject to diligence and other customary conditions

-> Paramount Global shares rose +1.8% following the news and ended the week up +7.8%; TripAdvisor shares surged +13.9% in reaction to the news and closed the week up +10.2%

- Comcast’s Xfinity launches $70/mo “Sports and News TV” video package (link/link)

- What is included in the package? The package includes 50+ broadcast, cable news and sports channels, a subscription to Peacock, 300 hours of cloud DVR storage, and access to 100+ free streaming channels

- Who is the package available to? The $70 price is available only to customers who also have Xfinity internet service

- How does pricing compare to other offerings?

- The same as DirecTV’s MySports bundle (which was introduced just earlier this month) -> MySports does not include CBS as of now (Xfinity’s package does)

- Cheaper than YouTube TV — which now costs $82.99/mo after a price hike in December — as well as Disney’s Hulu + Live TV service, which starts at $81.99/mo for live TV only

- Meta plans to begin testing ads on Threads (link): The experiment, which marks Meta’s first attempt at generating rev from Threads, will begin w/ a few Cos in the US and Japan; Threads currently has 300mn+ users, and ~75% of people follow at least one biz on their personal feeds

- The test ads will look like sponsored content on Facebook and Instagram: During the test, a small number of Threads users will see ads w/ large images within their feeds

- Bizs participating in the test will be able to access Meta’s brand-safety tool: This is also used in Facebook, Instagram, and Reels products so that brands’ sponsored content doesn’t run alongside offensive content

- “We’ll closely monitoring this test before scaling it more broadly,” per Instagram head Adam Mosseri: The goal is to get ads on Threads “to a place where they are as interesting as organic content,” per Mosseri

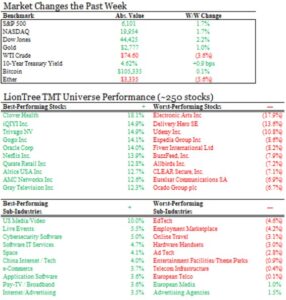

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Amazon is pushing to make its DSP the top choice in programmatic advertising. The Co is enhancing its ad tech to attract advertisers beyond its own media. Recent efforts include upgrading integrations w/ SSPs to secure better access to premium inventory and improve signal capture for in-app and CTV inventory. These moves aim to provide advertisers w/ more buying options and enhance performance. Amazon’s focus on in-app and CTV deals highlights its commitment to expanding its programmatic ad reach (Digiday Media)

Artificial Intelligence/Machine Learning

- Google’s Gemini virtual assistant is set to rival Samsung’s Bixby, Apple’s Siri, and Amazon’s Alexa. Gemini, powered by advanced AI, aims to offer seamless integration across Google’s ecosystem, enhancing user experience w/ personalized recommendations and improved natural language understanding. The assistant will be available on various devices, including smartphones and smart home gadgets, positioning Google as a strong competitor in the virtual assistant mkts (The Verge)

- Consumer spending on AI apps reached nearly $1.1 bn in 2024, driven by the popularity of generative AI apps like ChatGPT and Google Gemini. This represents a 200% year-over-year increase. The “State of Mobile” report by Sensor Tower highlights that AI apps saw 7.7 bn hours of usage and 17 bn downloads in 2024. The surge in demand for AI apps contributed to a global increase in mobile app spending, which totaled $150 bn, up 13% from the previous yr (Slashdot)

- Google reportedly collaborated directly w/ Israel’s military to provide advanced AI tools. Documents reveal that Google employees facilitated access to AI tech for the Israel Defense Forces (IDF) and Israel’s Defense Ministry (IDM) starting in 2021. The collaboration aimed to enhance military operations and included a $1.2 bn cloud computing contract. Despite internal protests, Google continued to support the IDF, highlighting the Co’s strategic priorities (Slashdot)

- Meta annc’d plans to launch new hardware, including AR glasses, smartwatches, and earbuds to rival Apple. The AR glasses, codenamed “Orion,” are expected to compete w/ Oakley. Meta’s smartwatch will feature health tracking and integration w/ its ecosystem, while the earbuds aim to rival AirPods. These products are part of Meta’s strategy to diversify its biz and reduce reliance on ad rev (Bloomberg)