In this second week of the year, it was off to the races, especially as it related to a landslide of impactful updates and developments within the AI sector, across models, vertical applications, chips and infrastructure. It truly reached a new level.

Meanwhile, the major market indices modestly pulled back given policy/ geopolitical volatility, plus key bank earnings, though small caps bucked the trend (Russell 2000 +2%)

This week’s key updates and developments that we focused on include:

- Impactful Developments Regarding AI Models & Applications Lead Headlines This Week

- Another Forecast Points To $3 Trillion Of New Global Datacenter Spend During The Next 5 Years + Other Key Chip/Infra Developments

- Media Entertainment Data Stats Were On A Roll This Week

- Phishing-As-A Service & AI Have Propelled Scamming Volumes To New Heights

- Short Sellers Made Money In The Most Shorted TMT Stocks In Q4…

- A New Record Is In Sight For NBA Team Valuations…

- App Revenue Climbed In 2025 Despite Fewer Downloads, As Non-Gaming Apps Take The Lead

- Chart Of The Week – Is Software’s Underperformance Overdone?

- Grab Bag: Walmart & Wing Team Up For Drone Delivery / Meta Is Considering Doubling Production Of AI Glasses / Beijing Tells Chinese Firms To Stop Using US & Israeli Software

Enjoy the long weekend and rest up for the earnings storm which kicks off next week with bellweather Netflix reporting on Tuesday evening…

Best,

Leslie

Impactful Developments Regarding AI Models & Applications Lead Headlines This Week

We could have dedicated almost an entire edition to all the impactful AI related updates that emerged left and right this week across models, chips and infrastructure! To start on the AI model side of the equation, Apple kicked off on Monday with a splash announcement that it will be using Gemini and Google cloud infrastructure to power future Apple Intelligence features, including a more personalized Siri. On the Google side, this was certainly a boost regarding Gemini’s standing in the LLM market.

Also this week, Google’s Gemini released “Personal Intelligence” which essentially makes Gemini more personal, proactive and powerful by connecting Google apps. It is being rolled out in a limited fashion in the US next week and will expand availability over time. OpenAI’s announcement to start testing ads on ChatGPT also reflects an inflection in the sector and surely, we will be hearing more about this from other chatbots as well looking ahead.

Moving onto vertical applications, AI’s push into healthcare is accelerating. Following OpenAI’s announcement last Thursday the 8th, a string of further developments emerged this week including: OpenAI acquiring health data startup Torch, NVIDIA and Eli Lilly committing $1bn to a joint AI lab aimed at accelerating drug discovery, and Anthropic launching Claude for Healthcare with HIPAA-ready infrastructure.

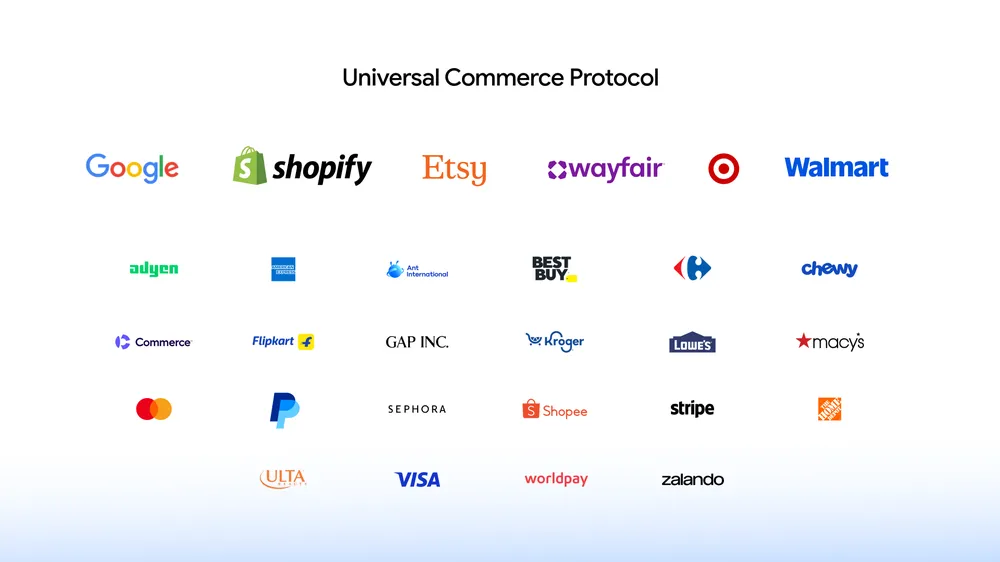

Retail is another sector in full swing with AI experimentation and implementation and along these lines, Google this week unveiled an open platform Universal Commerce Protocol (UCP), which was developed with partners including Wayfair, Shopify, Target, and Walmart. UCP allows for shoppers to move from “AI product discovery” to checkout with greater ease.

See more thoughts below on these developments and also see Theme #2 for our takeaways on the avalanche of important AI chip & infrastructure related updates and developments this week as well.

Apple & Google Both Annc’d Major AI Model Related Updates This Week

- Following speculation in August, it is now official that Apple will use Google’s Gemini to power its Foundation Models and use its cloud infrastructure (link/link/link)

- Bloomberg earlier speculated that Apple will pay $1bn per year but official terms were not disclosed for this multi-year contract

- Gemini will help power future Apple Intelligence features, including a more personalized Siri coming this year

- Apple determined that Google’s Al tech provides the “most capable foundation” for Apple Foundation Models

- Apple will run Gemini-controlled processing on its Private Cloud Compute infrastructure, ensuring user data remains under Apple’s protection, aligning with its long-standing privacy stance

-> Apple’s stock closed up +0.3% in reaction to the news, while Google’s stock closed up +1%

- Google Gemini launched “Personal Intelligence” which essentially makes Gemini more personal, proactive and powerful by connecting Google apps with a single tap (link/link/link)

- Users can control exactly which apps to link, and each one “supercharges the experience”

- Connecting apps is off by default

- But when enabled, Gemini accesses users’ data to answer their specific requests and to do things for them

- B/c this data already lives at Google securely, they don’t have to send sensitive data elsewhere

- Gemini will try to reference or explain the information it used from your connected sources so you can verify it

- It is built with privacy in mind, Gemini doesn’t train directly on Gmail inbox or Google Photos library

- Personal Intelligence has two core strengths…reasoning and retrieving specific details to answer questions

- An example mentioned was someone needing new tires for a 2019 Honda minivan. Standing in line at the shop, he realized I didn’t know the tire size. He asked Gemini. It suggested different options: one for daily driving and another for all-weather conditions, referencing a family road trip to Oklahoma found in Google Photos

- Roll-out timeline: Access is rolling out over the next week to eligible Google AI Pro and AI Ultra subscribers in the U.S

- Once enabled, it works across Web, Android and iOS and with all the models in the Gemini model picker

- They are starting with this limited group to learn, but over time we will expand to more countries and to the free tier

- It’s also coming to AI Mode in Search soon

- Users can control exactly which apps to link, and each one “supercharges the experience”

OpenAI Saying It Will Start Testing Ads On ChatGPT Is A Key Development

- On its blogpost & X, OpenAI annc’d that it will start to test ads on ChatGPT in the “coming weeks” (link/link/link)

- They will appear at the bottom of the chat window “when there’s a relevant sponsored product or service based on your current conversation”

- How will the test work and who will see ads?

- Users will be able to learn more about why they are seeing that ad, or dismiss any ad and report why

- ChatGPT will not show ads to users that say they are under 18 or who OpenAI predict is under 18

- Ads are not eligible to appear near sensitive or regulated topics like health, mental health or politics

- Only adults who use the free version of ChatGPT, or ChatGPT Go, a low-cost sub plan OpenAI announced in Aug, will be shown ads

- Higher-tier subs, including Pro, Business and Enterprise, will not see ads

- OpenAI also shared on X their principles on how they will approach ads

- Responses in ChatGPT will not be influenced by ads

- Ads are always separate and clearly labeled

- Conversations are private from advertisers

- Plus, Pro, Business, and Enterprise tiers will not have ads

The AI Push Into Healthcare Was Front & Center This Week…Again

- Following Open AI’s annce’ment last week, Anthropic is also expanding into healthcare with “Claude for Healthcare” (link/link)

- The product will allow healthcare providers, insurers, and consumers to use Claude for medical purposes through HIPAA-ready infrastructure: The launch builds on the earlier release of “Claude for Life Sciences”, which focused on research and drug discovery

- The platform is designed to reduce admin work and help both clinicians and patients better understand medical info: The tools are powered by Claude Opus 4.5

- Claude can now connect directly to several industry-standard databases, including:

- Centers for Medicare & Medicaid Services Coverage Database

- ICD-10 medical coding data

- The National Provider Identifier Registry

- PubMed’s biomedical research library

- The Co also intro’d “Agent Skills” for streamlining prior authorization requests & assisting developers in building applications using FHIR (the modern standard for exchanging healthcare data btw systems)

- On the consumer side, they are rolling out integrations that let US subs on its Pro and Max plans use Claude to access their health records

- New connectors include HealthEx and Function Health, which launched in beta on Sunday

- Apple HealthKit and Android Health Connect integrations roll out this week in beta via Claude’s mobile apps

- Anthropic said data accessed through these integrations isn’t stored in Claude’s memory or used to train its models

- Lastly, the Co is expanding Claude’s capabilities for life sciences customers as well

- They are adding connectors to platforms such as Medidata, ClinicalTrials.gov, and bioRxiv

- New agent skills support tasks like drafting FDA- and NIH-compliant clinical trial protocols or monitoring trial performance

- OpenAI buys health records startup, Torch, for an undisclosed amount (link/link/link)

- What do they do? The Co was working on an app that combined all a person’s medical information for AI use…It included things like doctor visits, lab tests, wearables, and other portals

- Torch’s 4-person team is joining OpenAI

- Speculation on price: A source reported that OpenAI paid $100mn worth of equity

- Others reported the deal size was lower, at ~$60mn

- What do they do? The Co was working on an app that combined all a person’s medical information for AI use…It included things like doctor visits, lab tests, wearables, and other portals

- NVIDIA and Lilly annc’d a joint $1bn investment in a Co-Innovation AI Lab in San Fran to accelerate drug discovery (link/link):

- The $1bn investment will be spent over 5 years on infrastructure, computing, and talent for the lab

- Nvidia’s engineers will work alongside Lilly’s experts to generate large-scale data and build AI models to advance medicine development

- The lab’s work will begin early this year

- The investment builds on Nvidia and Lilly’s existing partnership

- Lilly in Oct said it was building an AI factory with Nvidia’s AI systems to speed up drug discovery timelines

- Nvidia has also invested in biotech firm Recursion and has partnered with Novo Nordisk, the Mayo Clinic, Illumina, and IQVIA, to use AI in medical research and development.

- The $1bn investment will be spent over 5 years on infrastructure, computing, and talent for the lab

Google’s Release Of Universal Commerce Protocol (UCP) Was Also A Standout Regarding AI Retail

- Google’s new Universal Commerce Protocol (UCP) is an open standard for agentic commerce that works through the entire shopping journey, from discovery, buying and post-purchase support

- It establishes a “common language” for agents and systems to operate together across consumer surfaces, businesses and payment providers

- It was co-developed w/ retail companies that include Shopify, Etsy, Wayfair, Target and Walmart

- It was also endorsed by more than 20 others across the ecosystem like Adyen, American Express, Best Buy, Flipkart, Macy’s Inc., Mastercard, Stripe, The Home Depot, Visa and Zalando

- UCP will soon power a new checkout feature on eligible Google product listings in Search AI Mode and the Gemini app

- This allows shoppers to check-out from eligible U.S. retailers right as they’re researching on Google

- Shoppers can buy with Google Pay using payment methods and shipping info already saved in Google Wallet and soon, will be able to make a purchase with PayPal

- In the coming months, Google will work with retailers to expand globally and add more capabilities, like discovering related products, applying loyalty rewards, and powering custom shopping experiences on Google

- Google alongside UCP, also annc’d Business Agents & Direct Offers

- Business Agent: Is a new way for shoppers to chat with brands, right in Search

- It’s described as a virtual sales associate that can answer product questions in the “brand’s voice”

- It is starting this week with retailers like Lowe’s, Michael’s, Poshmark, Reebok and others

- Eligible U.S. retailers can choose to activate and customize this branded agent in Merchant Center

- In the coming months, they’ll be able to train the agent based on their data, access new customer insights

- Direct Offers: This new ad pilot allows advertisers to present exclusive offers for shoppers, like a special 20% discount

- For example, if users are searching for a new rug, Google already elevates the most relevant products to meet their search criteria

- Now relevant retailers have an opportunity to also feature a special discount

- Business Agent: Is a new way for shoppers to chat with brands, right in Search

Support of the Universal Commerce Protocol from across the ecosystem.

Source: Google Press Release

–> Later in the week, a viral post by Groundwork Collaborative’s Lindsay Owens warned that Google’s new AI shopping features could enable “surveillance pricing,” using chat data to upsell or potentially charge consumers more, citing Google’s roadmap and technical documents. The Co pushed back, saying upselling simply means showing premium options, prices on Google cannot exceed those on merchants’ sites, and its AI agents cannot change prices based on individual user data. (link/link/link)

Another Forecast Points To $3 Trillion Of New Global Datacenter Spend During The Next 5 Years + Other Key Chip/Infra Developments

Alongside all the AI platform updates this week (see Theme #1) there was an equally long list of AI updates that were related to infrastructure and chips. First of all, it was interesting to see that Moody’s now predicts global datacenter investment to hit $3 trillion over the next 5 years. This adds more credibility to market research firm JLL, which last week, also forecasted a $3 trillion datacenter spend level for that same period. However, as a caveat, there are a few risk factors that could challenge these massive investment projections, which include public push-back and rising costs.

Also on the topic of datacenters this week, both Microsoft and Meta announced new initiatives. Regarding the former, the Co is launching a new initiative with hopes of becoming a “good neighbor” in their infrastructure expansion (trying to address the public push-back risk). Regarding the latter, details were limited, but Mark Zuckerberg posted on Threads that as part of “Meta Compute”, the Co will “build tens of gigawatts this decade, and hundreds of gigawatts or more overtime”.

Lastly, there was a critical mass of other impactful infrastructure and chip updates out this week including AMD & Intel reportedly looking into raising chip prices due to low inventory and very high demand; TSMC reporting a standout quarter with record profit and higher capx expectations given strong demand; and some chip drama with both Trump and the Chinese government putting out different statements, limiting the use of chips from each other’s respected countries.

See more details on our quick takes below of the need to knows on this topic this week.

Another Forecast Points To $3 Trillion Of Global Datacenter – Related Investments from 2025-2030

- $3 trillion will be plowed into global datacenter related investments over the next 5 years, to 2030, per a new Moody’s report (link/link/link): This includes spending on servers, computing equip, datacenter facilities, and new power capacity

- Most of the spend is anticipated to come from hyperscalers…Microsoft, Amazon, Alphabet, Oracle, Meta, & CoreWeave – projections in aggregate:

- ~$400bn in 2025

- ~$500bn in 2026

- ~$600bn in 2027

- Debt financing will be on the rise to support this spend: US data centers are anticipated to turn to asset-backed securities, commercial mortgage-backed securities, and private credit markets for refinancing, after a record US$15bn was issued in the US ABS market in 2025

- But what are the challenges with this level of investment?

- Pre-leasing capacity increases counterparty concentration risk

- Public push-back regarding power & water consumption (see below for Microsoft’s move to combat this dynamic)

- Rising costs (addtl production is expected to remain insufficient to moderate 2026 price increases)

- Most of the spend is anticipated to come from hyperscalers…Microsoft, Amazon, Alphabet, Oracle, Meta, & CoreWeave – projections in aggregate:

–> To note, last week, research firm JLL ALSO predicted the same $3 trillion global datacenter investment forecast between now and 2030 (estimating 100GW of new data center capacity globally, reaching 200GW in 2030). For their detailed report, CLICK HERE

–> Separately but related this week, New York plans to require large data center operators to either generate their own electricity or pay higher grid rates to prevent surging power demand from raising household utility bills. Governor Kathy Hochul said massive data centers are driving electricity demand faster than the grid can keep up, shifting costs onto families and small businesses. The initiative aims to protect consumers while still supporting economic (link/link)

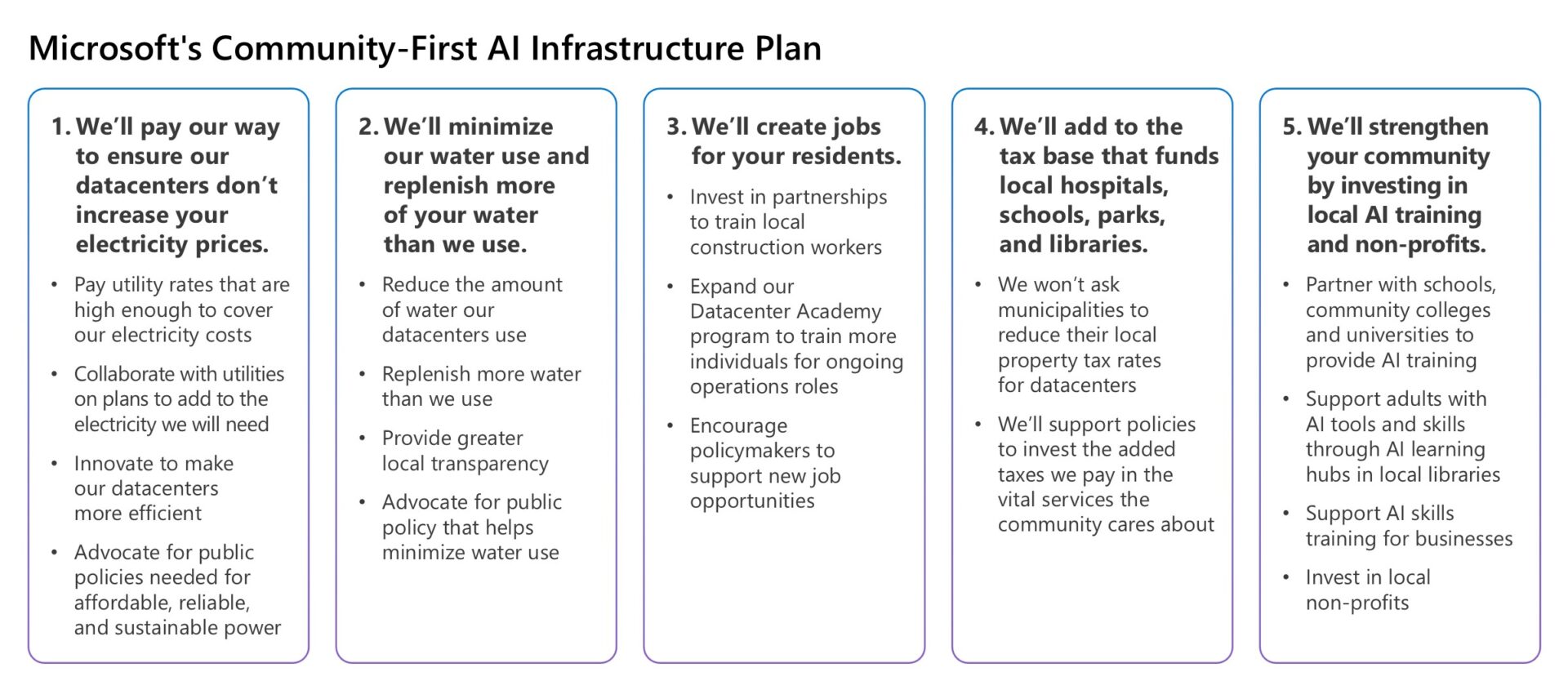

On The Topic Of Pubic Push-Back, Microsoft Announces “Community-First” AI Infrastructure

- Microsoft annc’d a new initiative in order to “be a good neighbor” in the communities they build in (link/link/link)

- Under the 5-point plan, Microsoft has committed to paying its way to ensure its data centers do not drive-up local electricity prices

- It will also minimize water use & replenish more water than it consumes by optimizing water usage across its data center operations

- In addition, Microsoft plans to create jobs for local residents, expand the tax base that supports public services, and invest in local AI training programs and non-profit organizations

- Brad Smith, vice chairman & president, emphasized that community trust will be critical to the long-term success of AI infrastructure

- Under the 5-point plan, Microsoft has committed to paying its way to ensure its data centers do not drive-up local electricity prices

Source: Microsoft Blog

Meta Is Launching Its Own AI Infrastructure…“Meta Compute”

- On a Threads post, Meta CEO Mark Zuckerberg annc’d that the Co is establishing a new top-level initiative called “Meta Compute” (link/link)

- Details are sparse but the Co is planning to build “tens of gigawatts this decade, and hundreds of gigawatts or more overtime”

- This effort will be led by Santosh Janardhan and Daniel Gross: They will both work with Dina Powell McCormick, who joined Meta as President & Vice Chairman to work on partnering with govts and sovereigns to build, deploy, invest in, and finance Meta’s infrastructure

Other Impactful Chip/Infrastructure Quick Takes This Week That Point To Cont’d Strong AI Demand

- AMD & Intel are reportedly considering raising server CPU prices (link): The reported price increase could be up to 15% for server CPUs

- Both Cos have sold their existing inventories for the rest of the year and most of the demand is cited as coming from hyperscalers

- TSMC smashed forecasts with its earnings report this week (link/link/link)…AI demand remains strong – “Looking ahead, we observe increasing AI model adoption across consumer, enterprise and sovereign AI segment. This is driving need for more and more computation, which supports the robust demand for leading edge silicon. Our customers continue to provide us with their positive outlook.”

- FQ4 net rev beat: NT$1.046T vs cons of NT$1.031T

- FQ4 op mrgn beat: 54% vs cons of 50.9%

- FQ1:26 rev and gross margins guidance beat:

- Rev $34.6-$35.8bn vs cons $32.8bn

- Gross profit margin 63-65% vs cons 59.4%

- Op profit 54-56% vs cons 49.7%

- F2026 capx guidance of $52bn-$56bn, is up from $32.8bn in F2025 and is significantly higher than the $101bn spent in the last 3 years

- CapEx in the next three years will be “significantly higher” than that, but mgmt did not provide an exact figure

–>These results drove TSMC shares up 5.3% in reaction

- OpenAI reportedly plans to launch a self-developed AI chip, codenamed “Titan,” by the end of 2026, using TSMC’s N3 process (link)

- OpenAI’s self-developed chip is expected to leverage ASIC design services from Broadcom

- Timing? Mass production is expected to begin in H2:2026, w/ development of the 2nd-gen chip, Titan 2, also slated to start in the same period

- OpenAI also signed an agreement with Cerebras to supply 750 MW of computing power, in deal worth more than $10bn (link/link): The deal will start this year and continue throughout 2028

- OpenAI said these systems would speed responses that currently require more time to process

- Donald Trump on Wednesday imposed a 25% tariff on certain AI chips (link): Nvidia’s H200 AI processor and a similar semiconductor from AMD called the MI325X are among those affected

- The action is part of a broader effort to create incentives for chipmakers to produce more semiconductors in the US

- The White House said in a fact sheet that the tariffs will be narrowly focused and will not apply to chips and derivative devices imported for U.S. data centers

- Lastly, China is reportedly drafting purchase rules for Nvidia H200 chips following Trump’s decision (link): The Chinese gov is working on rules that will likely regulate the total volume of AI chips local Cos can purchase, allowing some sales by Nvidia instead of banning them outright

- Thought Reuters could not immediately verify the report

–>NVIDIA shares closed up +2%, seemingly unaffected in reaction to the news

Media Entertainment Data Stats Were On A Roll This Week

In addition to the barrage of AI related updates (in Theme #1 & Theme #2), there were also a high concentration of noteworthy stats and developments across the media entertainment space this week, spanning record global content spending forecasts for 2026, the continued rise of ad-supported streaming tiers, and shifting audience behavior across award shows and music, among other updates.

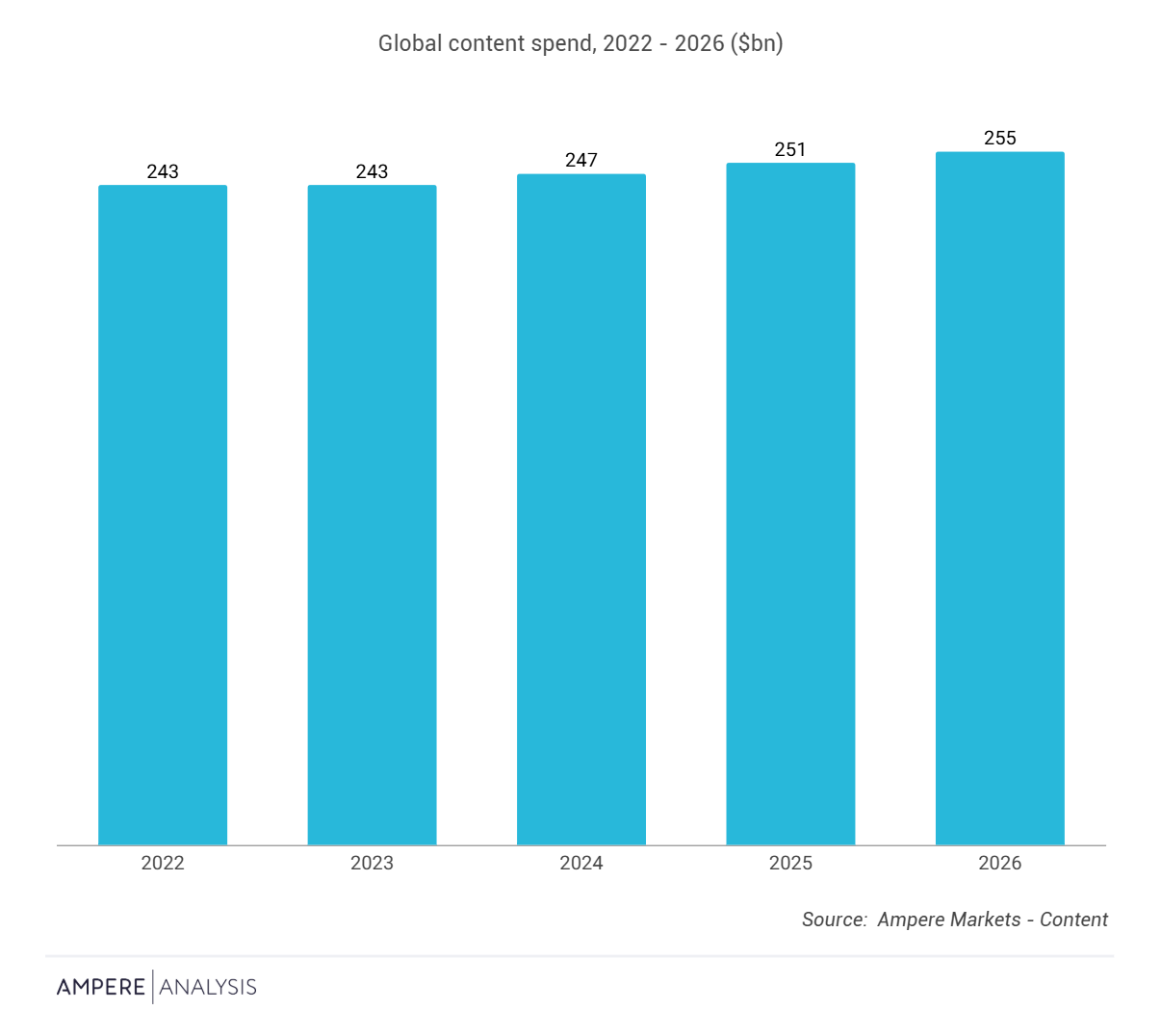

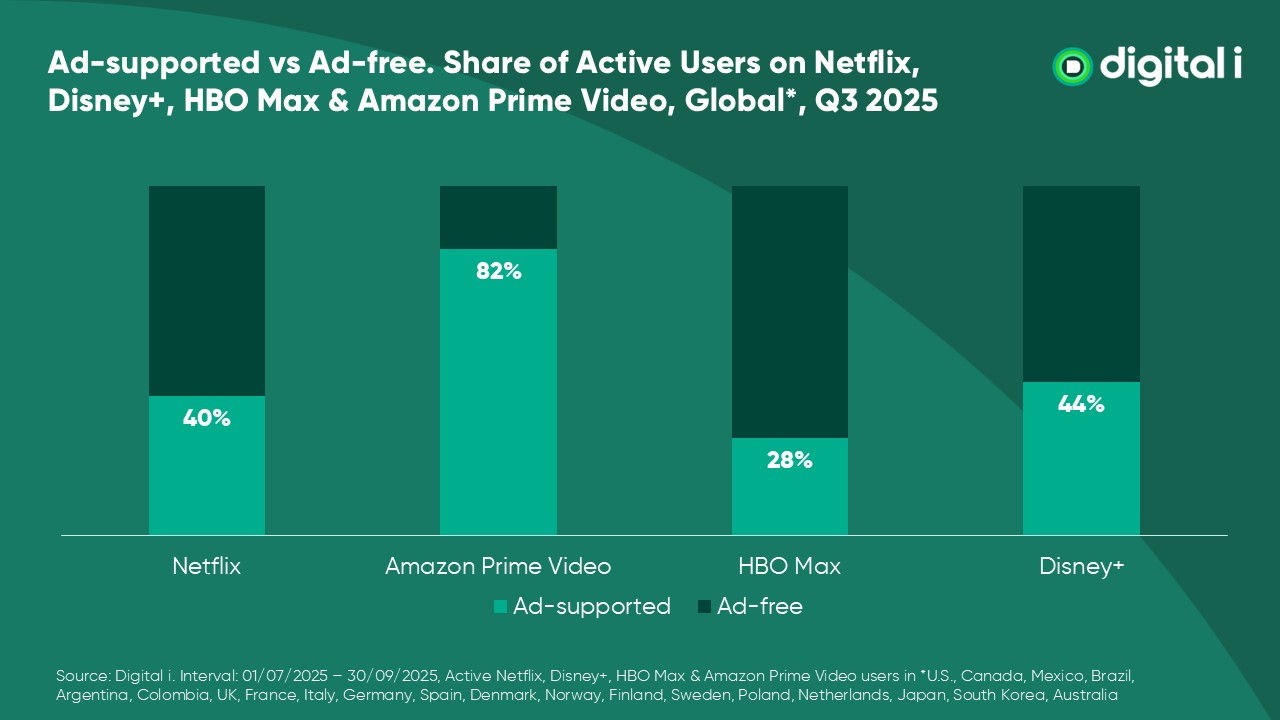

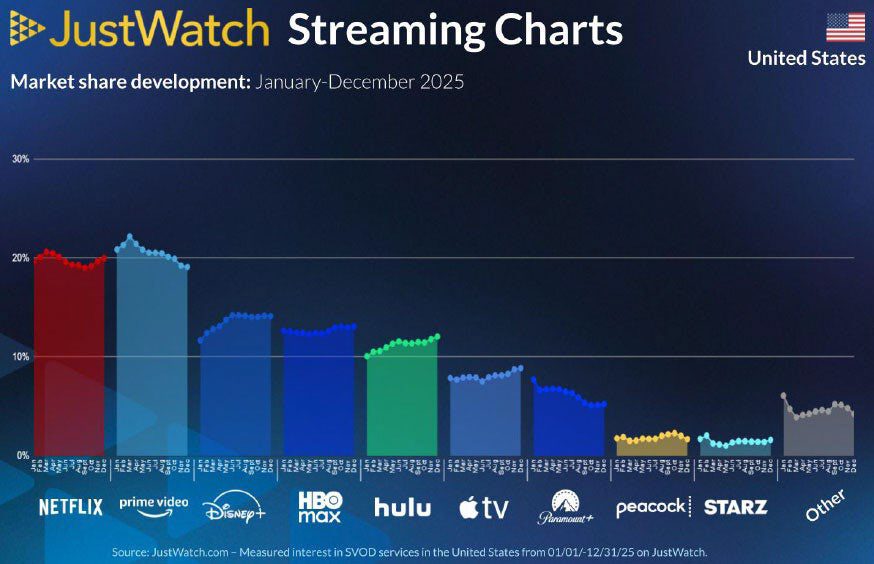

To start, on the content spend front, total global investment is projected to reach $255bn this year, with streamers expected to surpass $100bn in spend for the first time, or ~40% of the global market, further extending their lead as traditional broadcasters face flat to declining investment. That spending shift continues to be accompanied by changes in how streaming services are monetized. New data from Digital i shows that ad-supported tiers are gaining traction across most major platforms, with Netflix seeing the largest adoption increase in ad supported subscribers from Q4:24 to Q3:25. Amazon’s Prime Video was the only major service to decline in ad supported adoption, though it still has the highest overall penetration of overall ad-supported users. That said, zooming out and looking more broadly, it was interesting to see that Netflix and Prime Video traded the top spot in US engagement market share for much of the year with Netflix ultimately pulling ahead in Q4, reaching a 20% share as Prime slipped to 19%, per JustWatch Insights.

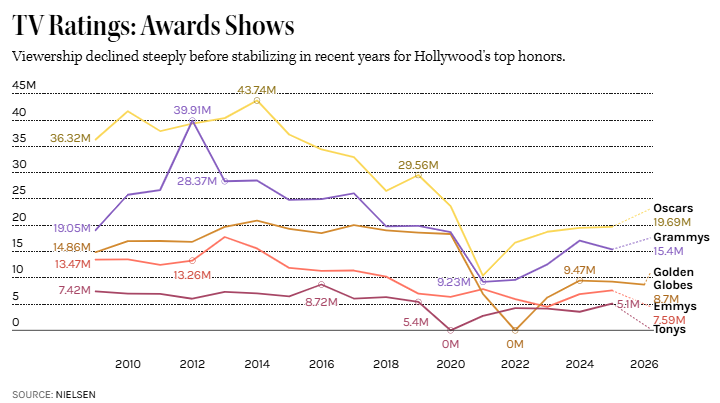

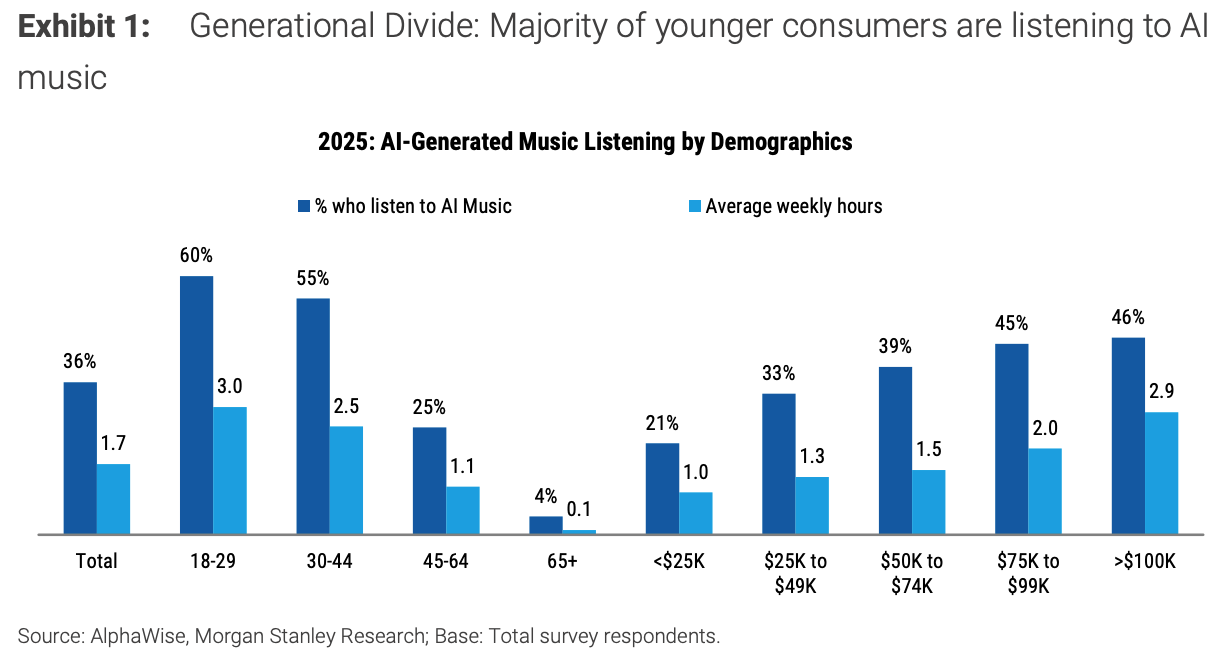

Away from video streaming, linear viewership remains under pressure at award shows. Last week’s 2026 Golden Globes telecast drew 8.7mn viewers, down y/y. At the same time, listening habits continue to evolve, with results from a Morgan Stanley survey finding that ~50–60% of listeners ages 18–44 are now spending 2.5-5 hrs per week listening to AI-generated music, most of which is on social media platforms like YouTube and TikTok vs traditional streaming services. And speaking of traditional music streaming services, Spotify announced price increases across its subscription plans in the US, set to take effect beginning in February (though the increases were to a lesser degree than some investors hoped). Finally to round out the week, Apple shared a rare update on its Services business and highlighted strong performance across Apple TV, Music, and Podcasts in 2025, including record engagement on Apple TV and its “best year ever” for both Apple Music and Apple Podcasts.

See below for more of our takeaways.

Expect Record Content Spend In 2026, Driven By The Streamers, According To Ampere Analysis Forecasts (link)

- Total global content investment is expected to reach $255bn in 2026, up +2% y/y (consistent w/ prior yr growth)

- Driven by sustained investment from global streaming platforms, which are further increasing their share of content spend

- And streamer spend is set to top $100bn for the first time in 2026: Streamers (including both ad-funded and subscription-based platforms) are expected to see +6% growth in their content expenditure to reach $101bn in spend, or 40% of the global mkt, in 2026

- This follows 2025, when streamers surpassed commercial broadcasters in overall content spend contribution for the first time

- Meanwhile, traditional broadcasters are expected to see stagnant or declining investment in 2026

- Includes pay TV operators, commercial broadcasters and public broadcasters

- Why? Persistent advertising pressure and rising production costs, which is widening the gap between them and global streamers

- Much of the decline is driven by US-based Cos, for whom studio parents are redirecting more of their budget towards owned streaming operations

- While Cos outside the US are showing greater resilience, they are maintaining more stable investment levels through 2026

Source: Ampere Analysis

Netflix Leads Incr’d Levels Of Ad-Supported Subscription Tiers (link)

- From Q4:24 to Q3:25…Netflix had the highest increase of ad tier adoption

- Netflix Standard w/ ads plan tier: From 26% adoption -> 40% adoption (+14%)

- Disney+ ad-supported tier: From 35% -> 44% (+9%)

- HBO Max’s ad-supported tier: From 22% -> 28% (+6%)

- Amazon’s Prime Video remains the svs w/ the highest ad-supported tier usage but FELL from 88% in Q4:24 -> 82% in Q3:25 (-6%)

Source: Digital i

Netflix & Prime Video Traded Lead In Engagement Through 2025, Though Netflix Pulled Ahead In Q4 , Per JustWatch Insights (link)

- In 2025… Netflix and Amazon Prime Video continued to dominate US engagement, but lost some share to mid-sized platforms y/y

- Disney+ incr’d its US engagement market share to 14%, rising +2pp y/y, and surpassed HBO Max in March to become the 3rd-largest streaming svs in the country

- Apple TV+ added +2ppts to reach a 9% share, reflecting growing traction with high-performing originals such as Severanceand the Q4 hit Pluribus

- Peacock Premium gained +1ppt over the year

- Hulu also recorded steady progress, adding +1ppt y/y and narrowing the gap with HBO Max

- HBO Max showed no significant change y/y but lost its top three ranking earlier in the year as Disney+ continued to expand

- Netflix declined by -1ppt y/y, while Prime Video fell by -3ppts y/y

- Paramount+ saw the biggest decline, which lost -4ppts y/y

- Looking into Q4 specifically…there was some reshuffling for the top spot as Netflix overtook Amazon Prime Video in US engagement market share

- Netflix reached 20% share, beating out Amazon Prime Video, which slipped to 19%

- Netflix gained +1pp from Q3 to Q4, while Prime Video lost -1pp over the same period

Award Show Roundups…Viewership Has Been Down (link/link)

- The 2026 Golden Globes saw another y/y audience decrease, w/ 8.66mn live + same-day viewers tuning in

- How does that compare to previous telecasts?

- Down ~-7% from last yr, when ~9.27mn tuned in

- …but still better than the 2023 telecast’s all-time low of 6.3mn

- …though still well below 2020’s telecast that avg’d 18.3mn

- A viewership decline was somewhat expected, particularly b/c this yr’s Globes didn’t have the benefit of a direct lead-in from an NFL playoff game

- BUT chatter online about the Globes was up, generating 43mn interactions, up +5% y/y to a new high

- How does that compare to previous telecasts?

- How does that compare to other award shows?

- Viewership was higher than the 2025 Emmys (took place in Sept) which averaged 7.42mn viewers

- But much lower than the 2025 Oscars, which had 69mn viewers tune in (the 2026 Oscars will air on Mar 15th)

Moving Over To Music…The Majority Of Younger Consumers Are Listening To AI Music (link/link)

- 50-60% of listeners ages 18- 44 reported 2.5-3 hours per week of AI music listening

- Where are people listening to AI music? Mostly on social media rather than traditional streaming svs

- The most common sources are YouTube and TikTok

- BUT back in Nov, Deezer said that while fully AI-generated music now accounts for 34% of new tracks uploaded to its service, it is only 0.5% of its streams – up to 70% of which are fraudulent (i.e. bots)

Spotify Is Increasing The Price of Premium Subscriptions (link/link)

- Spotify will increase the price of its monthly premium subscription plan in the US, Estonia, and Latvia mkts

- The cost of the premium subscription will rise by +$1/mo in the US: Will increase from $11.99/mo

- Spotify last bumped the Premium price for US users in June 2024 to $11.99/mo; In July 2023, the price was raised to $10.99/mo

- Duo, Family, and Student plans will also see an increase –

- Duo is increasing from $16.99/mo -> $18.99/mo (+$2/mo)

- Family increasing from $19.99/mo -> $21.99/mo (+$2/mo)

- Student is increasing from $5.99/mo -> $6.99/mo (+$1/mo)

- The new pricing will take effect on consumers’ billing dates starting in Feb

-> Spotify share fell -1% on the back of the news as investors were expecting to see a higher price increase

A Rare Update From Apple…2025 Was A Standout Yr For Apple TV, Music, & Podcasts (link)

- Apple TV had a “landmark” yr, driven by F1, which was the #1 movie at the global box office, the top film on Apple TV, and the highest-grossing sports movie of all time, and the premiere of Apple TV’s biggest series to date, the widely acclaimed Pluribus

- Apple TV’s monthly engagement set a new record this past December w/ total hrs viewed up +36: Driven by “robust” audience growth across Europe and LatAm, cont’d expansion in the US, and the global streaming debuts of F1, Pluribus, and The Family Plan 2, as well as the classic A Charlie Brown Christmas

- Apple Music had its “best year ever” in 2025, breaking records across both listenership and new subscribers

- Driven by its biggest product feature release since launch, the opening of a brand-new state-of-the-art studio, and expanding its reach beyond the Apple ecosystem for the first time, partnering with companies like GM, TuneIn, Chase, and more

- Apple Podcasts also had its “best year yet”, achieving record listeners, plays, and subscribers

- Introduced new accessibility and discovery features, including enhanced dialogue, new playback speeds, automatically created chapters, timed links, and expanded transcripts to 125mn+ episodes in 13 languages

- Lastly, Apple shared some additional insights on its other Apple Services, including App Store, Apple Pay, Apple Maps, Apple Arcade, Apple Fitness+, Apple One, iCloud and more – see those HERE

Phishing-As-A Service & AI Have Propelled Scamming Volumes To New Heights

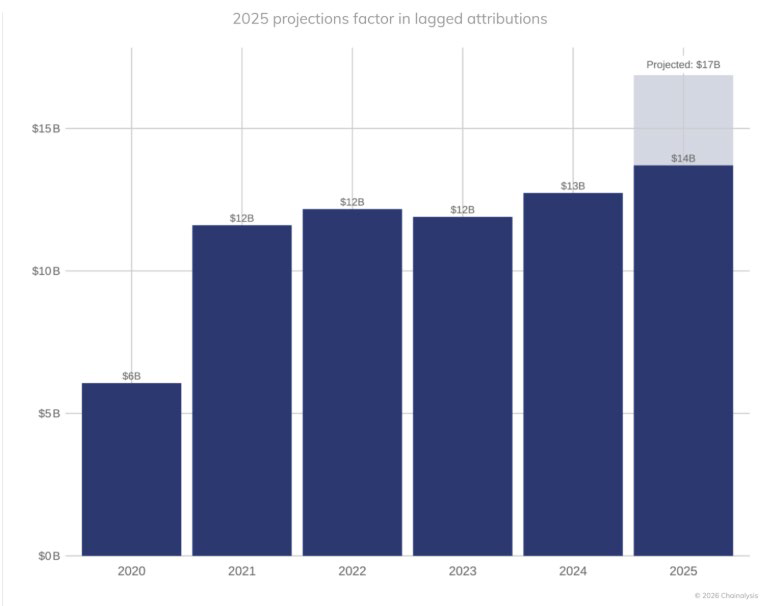

A record $17bn is estimated to have been stolen in crypto and fraud in 2025, which is a step function increase from the prior annual rate over the last few years, based on a new Chainanalysis report this week. While “pig butchering” (see below description) and high-yield investment scams are the most prevalent by volume, impersonation scams increased +1400% y/y (!) and AI-enabled scams have been 4.5x more profitable than traditional scams.

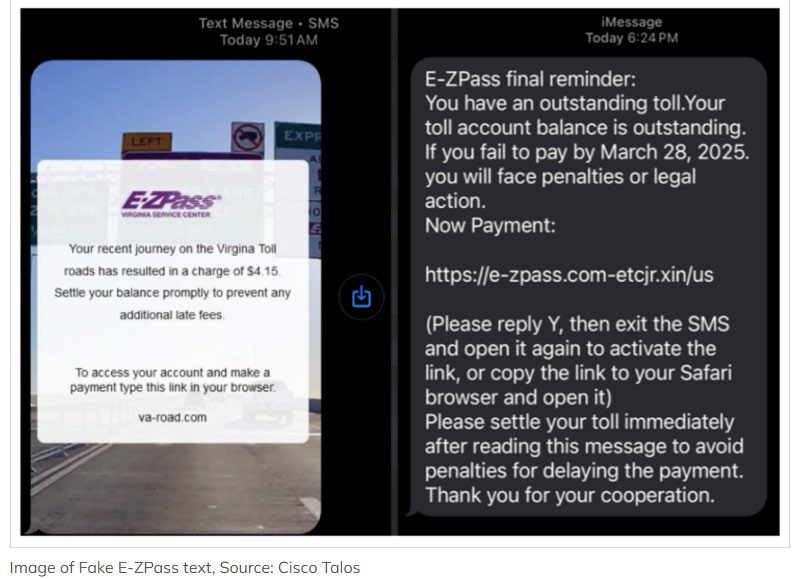

The proliferation of phishing-as-a-service platforms (that even include customer service!) and easy access to AI tools are enabling even unsophisticated scammers to conduct large-scale scam campaigns. The data in this report certainly hit close to home as we’ve received the E-ZPass scam text message on multiple occasions!

See below for more details on our takeaways from the Chainanalysis report. Looking ahead, we do not expect this trend to improve…as AI continues to become more capable, it will also unfortunately propel scamming activity as well.

- The est’d $17bn stolen in crypto scams & fraud in 2025 is a step function increase from the $12-13bn annual crypto scam & fraud losses from 2021-2024

- $14bn of the $17bn has been identified and Chainanalysis believes that an addt’l $3bn of illicit activity will be identified in the coming months

- Crime networks in East and Southeast Asian are extremely active

- Impersonation scams are up +1400% y/y (this is where fraudsters pose as legitimate organizations or authority figures to manipulate victims into transferring funds)

- The avg pmts made incr’d over +600% y/y

- AI is being utilized w/ SMS phishing and targeting victims more effectively…AI enabled scams were 4.5x more profitable than traditional scams: I.e., scams with on-chain links to AI vendors extracted $3.2mn on avg per operation vs $719k for those w/o an on-chain link…they also have:

- Dramatically higher daily rev…$4,838 vs $518 median daily revenue

- And 9x higher transaction volume…35.1 vs 3.89 avg transfers per day

- Some other stats:

- Avg scam payments is expected to be up +253% y/y in 2025, from $782 to $2,764

- The dominant scams by volume are high yield investment programs & “pig butchering”

- “Pig butchering” scams are long-term, sophisticated investment fraud where criminals build a deep emotional or friendly relationship w/ a victim before manipulating them into investing large sums of money in a fake platform, most often involving cryptocurrency

- There is a proliferation & commercialization of tools (phishing-as-a-service) that enable even unsophisticated scammers to conduct industrial-scale scams

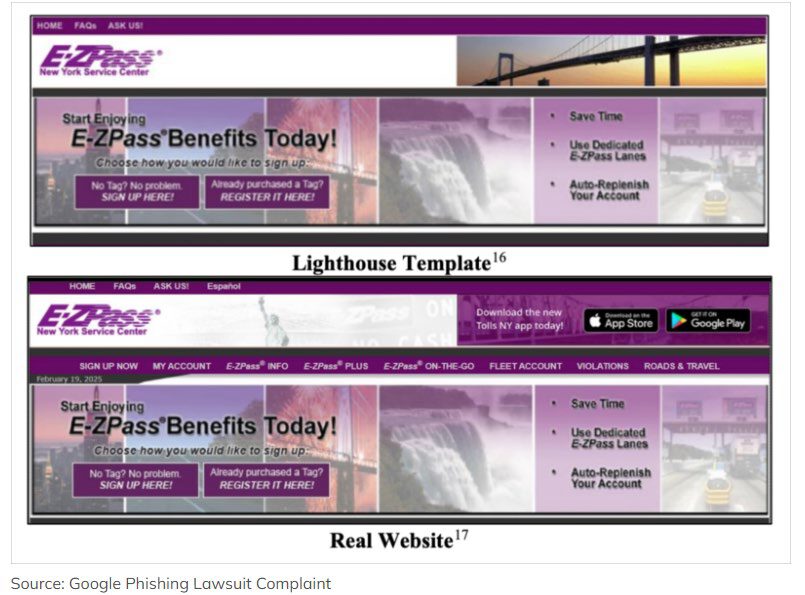

- A China based cybercriminal group called Lighthouse Enterprise is an example…they operated a multi-faceted business model that makes it even easier for scammers to execute phishing campaigns…their modular approach included:

- Developer Group – Supplied phishing software and templates

- Data Broker Group – Provided targeted lists of potential victims

- Spammer Group – Offered tools to send fraudulent text messages at scale

- Theft Group – Specialized in monetizing stolen sensitive information

- Administrative Group – Ran online recruitment and collaboration forums

- There are examples of other platforms that offer accounts for Gmail, Tinder & other services for scammers to target pig butchering victims and also offer the scammers customer svs via Telegram (!)

- A China based cybercriminal group called Lighthouse Enterprise is an example…they operated a multi-faceted business model that makes it even easier for scammers to execute phishing campaigns…their modular approach included:

- E-Pass as a case study…see examples of phishing text messages (which I’ve also received!) and a fraudulent website which is strikingly similar to E-ZPass’ real official site

- Google has been active in fighting scammers: In Nov 2025, Google sued Lighthouse for running a massive text message phishing scam impersonating legitimate companies like E-ZPass and the USPS; Google is also endorsing 3 bipartisan bills to protect against fraud and cyberattacks (link)

- Per the suit, the E-ZPass scheme allegedly reached 330k texts in a single day as part of a separate toll fee scam campaign, amassing $1bn over 3 yrs and duping over 1mn people in at least 121 countries

- On the positive side, law enforcement scam identification activity was also unprecedented in 2025

- In Nov 25, the UK Metro Police seized over 61k Bitcoin (~GBP5bn) from Chinese national Zhimin Qian who victimized 128k+ people between 2014-2017

- $15bn of illicit proceeds linked to the Prince Group criminal organization was also seized in 2025

- Chainalysis’s full report can be found HERE

Short Sellers Made Money In The Most Shorted TMT Stocks In Q4…

Q4 2025 was a better quarter for short sellers than Q3. 14 out of the top 20 most-shorted stocks underperformed the S&P 500 this past quarter. The analysis includes ~150 stocks in the LionTree Universe with $1bn+ in market cap across the tech, media, telco, and consumer sectors.

The Top 3 most shorted stocks at quarter end were Hims & Hers, AST SpaceMobile, and WEBTOON. Hims and Hers made the #1 spot again in Q4. Of the Top 20 most shorted stocks in Q4, 13 were also on the top 20 most shorted list in Q3.

In terms of the biggest changes in Q4, Opendoor Technologies saw the most short covering, while WEBTOON topped the list for largest increase in its short position.

See the bullets below and table for more detail…

Most Shorted Stocks (As % Of Float) – Hims & Hers…Again

- The Top 3 Most Shorted – #1 is Hims & Hers, #2 is AST SpaceMobile, & #3 is WEBTOON -> Hims & Hers stayed at the #1 spot in both Q3 and Q4; AST SpaceMobile rose from the #6 position last qtr to the #2 spot; WEBTOON was not included in Q3’s Top 20 list

- Lemonade was #2 last qtr and dropped to #7; The RealReal was #3 last qtr and dropped to #6

- Stocks that dropped out of the Top 20 most shorted: Opendoor Technologies, Gogo, Oscar Health, Revolve Group, Mobileye, fuboTV, and DigitalOcean

- Stocks that joined the Top 20 most shorted: WEBTOON Entertainment, Charter Communications, CoreWeave, Duolingo, Upwork, Penn National Gaming, and Teladoc Health

-> The S&P 500 was up +2.4% in Q4 making it a better qtr than Q3 for short sellers as 14 out of the top 20 most shorted stocks underperformed the S&P 500 over the period; On avg the top 20 stocks traded down -10% in Q4, compared to Q3’s average of +89% rally (skewed by Opendoor, up an astonishing +1395%)

Largest Increase In Short Interest (As % Of Float) – WEBTOON

- The largest increase in short interest was seen by WEBTOON: The Co saw a +8.9ppt increase in Q4 to 23.3% of the float short, –-> The stock fell -32.9% in the qtr, significantly underperforming the S&P 500’s +2.4% gain

- Other stocks with notable increases in short interest = Duolingo, CoreWeave & Coursera -> all of which underperformed the S&P 500 in the period

Largest Decrease In Short Interest (As % Of Float) – Opendoor Technologies

- The largest decrease in short interest was for Opendoor Technologies: The Co posted a -11.8ppt decrease in Q4 to 14.1% of the float short which caused it to fall out of the top 20 most-shorted list

- Other stocks with notable decreases in shorts interest = Oscar Health, Omnicom & Outfront Media

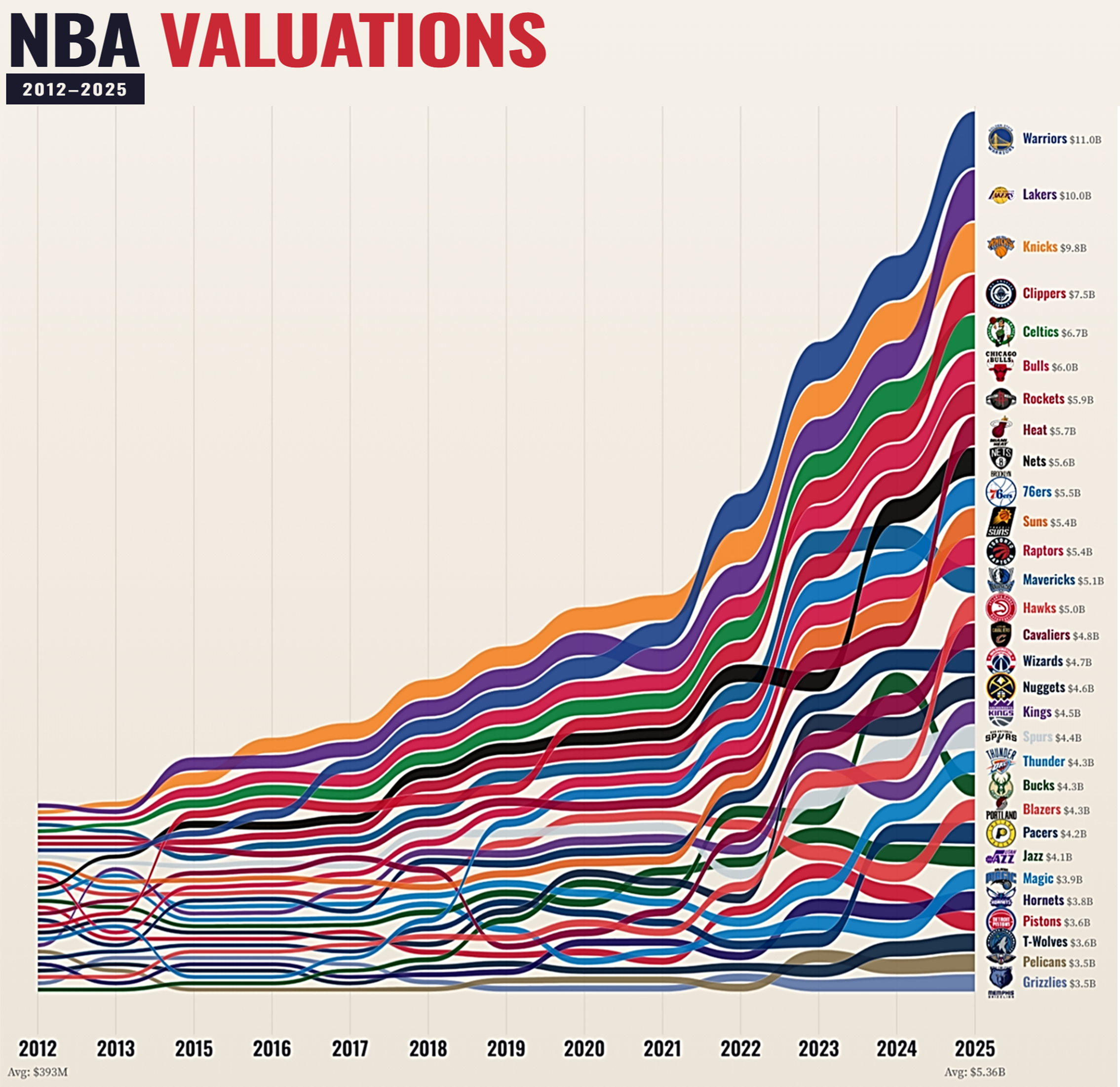

A New Record Is In Sight For NBA Team Valuations…

NBA team valuations look to be on the rise once again, as press hit this week that the Golden State Warriors is potentially selling a 5% stake at an $11bn valuation, which would be a massive increase from a reported $5.5bn valuation related to Arctos Sports Partners’ minority stake in 2021 and the $450mn valuation listed on Forbes Most Valuable NBA Team list in 2012 (i.e., the team’s value would have increased 2,344% over that time). This valuation mark would also set a record and overtake the Lakers as the most highly valued team. Bigger picture, since 2012, the average NBA team value has increased +1,263%.

This news hit at the same time that the NBA is reportedly in the process of pitching investors on the launch of a new European league, targeting team valuations of up to $1bn. London and Berlin are expected to host teams in this new league. Growth in media rights, as well as sponsorship, have certainly been key drivers to the surge in NBA team valuations and international expansion is important as it is anticipated to layer on a new source of revenue looking ahead.

See below for more of the points that we thought were most important on this theme this week.

NBA Team Valuations Look Set To Hit A New Record…(link/link/link/link)

- Golden State Group, the parent Co of the Golden State Warriors, is said to be selling a 5% stake at an $11bn valuation

- That would place the Warriors as the #1 most valuable NBA team based on Forbes’ annual Most Valuable NBA Teams data for 2025

- #2 would be the Lakers ($10bn) and #3 would be the Knicks ($9.8bn)

- This new valuation mark is also a huge step-up from the Golden State Warriors’ reported $5.5bn valn related to PE firm Arctos Sports Partners taking a minority stake in 2021

- It also compares to a $450mn valuation as of 2012 (when it was ranked #8 in Forbes’ report))

- More broadly, how have NBA team valuations changed over time? From 2012 to Oct 31, 2025, the avg NBA franchise has grown +1,263% (easily surpassing the S&P 500’s +384% during the period): In 2012 the avg team valuation was $393mn…in 2025 the avg team valuation was $5.4bn

- Biggest Rise: Clippers +$7.2bn (20th ➔ 4th)

- Biggest Fall: Magic +$3.5bn (11th ➔ 25th)

- Highest growth: Warriors +2,344%

- Lowest growth: Bulls +900%

…At The Same Time The League Is Reportedly Getting Ready To Pitch A European League

- The NBA is reportedly pitching investors on a new European league, targeting team valns of up to $1bn (link)

- London and Berlin are likely to host a team in the league which could debut as early as next year, as per sources

- NBA commissioner Adam Silver is expected to attend a pair of regular season games in those cities starting Thursday

- The NBA will also open its data room for the planned European league to investors in the coming days, including financial projections, the sources said

- The project would include 12 franchises and 4 addtl teams that qualify for the competition w/o owning equity

- The NBA would retain a 50% stake in the new league

- FIBA, the world governing body for basketball, will also have a stake in the new league

- The NBA will also hold a private conference in London to meet potential sponsors, media partners and investors in mid-Jan

- Existing NBA owners have expressed interest in buying stakes in European teams and the league

- BUT… NBA rules currently prohibit the ownership of more than one team

- In March last yr, Silver said it was considering a model in which NBA owners could participate as collective owners

- A spokesperson for FIBA said the new league will be a joint project with the NBA, while declining to comment on the valuation

- London and Berlin are likely to host a team in the league which could debut as early as next year, as per sources

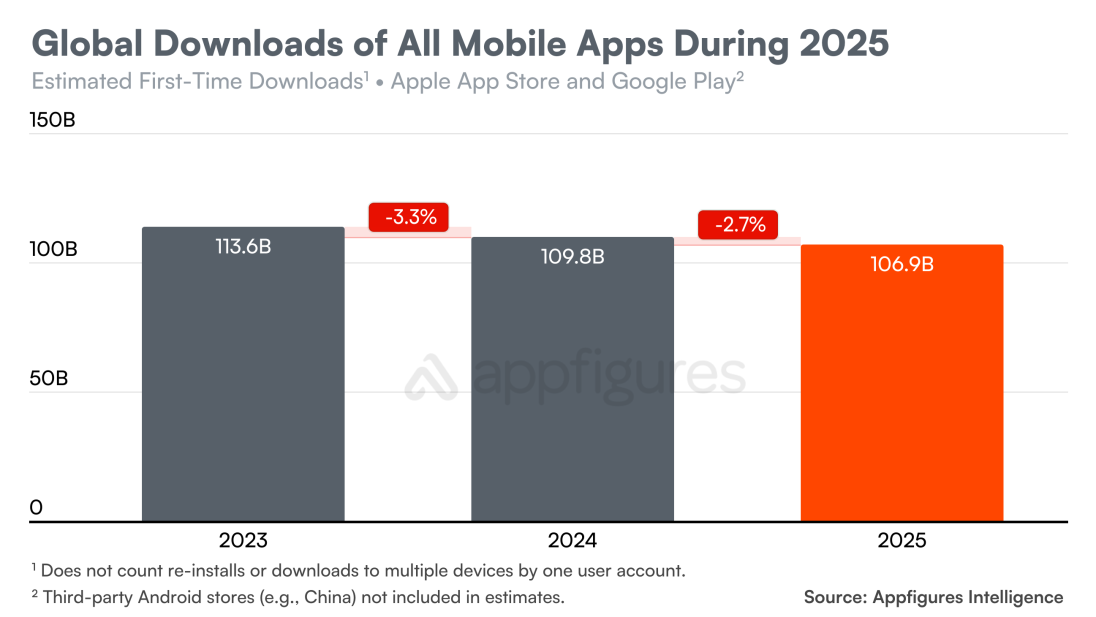

App Revenue Climbed In 2025 Despite Fewer Downloads, As Non-Gaming Apps Take The Lead

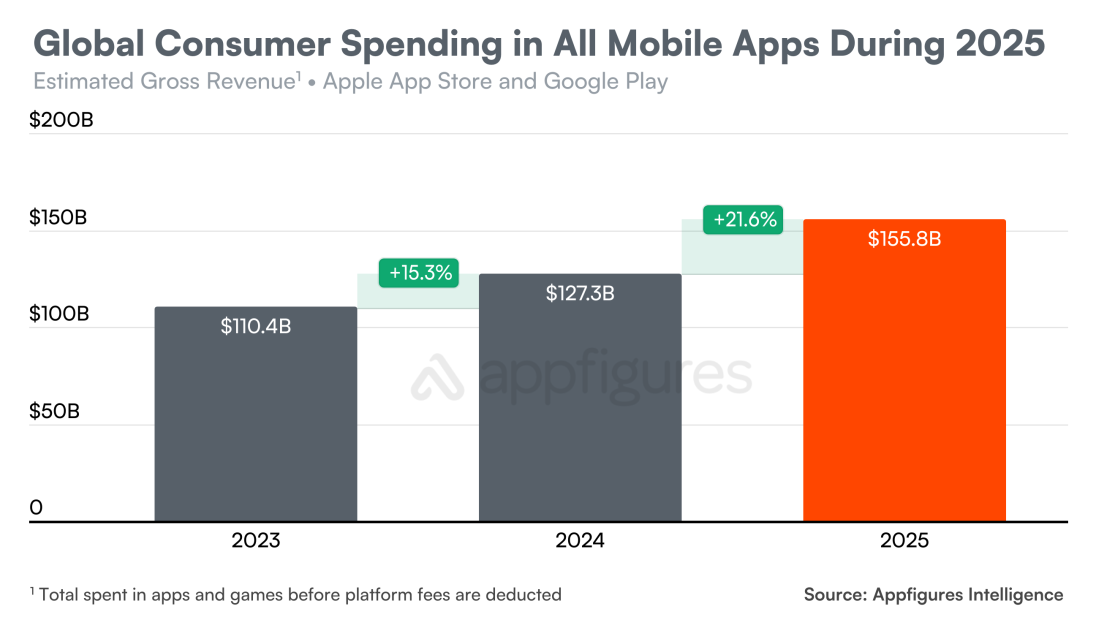

Amongst all the stats we covered across video streaming and music in Theme #3, one other entertainment area we wanted to quickly flag was gaming. There were some interesting figures out from Appfigures, which found that in 2025, while overall app downloads continued to fall, revenue climbed as subscriptions and recurring spend became more deeply embedded across the ecosystem.

That dynamic played out very differently across gaming and non-gaming apps. Mobile games experienced a steeper drop in downloads and more modest revenue growth, while non-game apps continued to add users and accounted for the bulk of app spending growth. As a result, non-gaming apps generated more revenue than games in 2025. (link)

Appfigures has yet to release the full report publicly, but you can dive deeper into the disclosed numbers below.

- Mobile app revenues grew in 2025…

- Consumer spending grew +21.6% y/y in 2025 to reach an estimated $155.8bn

- What’s driving the growth? Most apps now have in-app purchases or a subscription model built in, which has offered a more sustainable path for app developers

- …even as app downloads declined for the fifth consecutive yr

- Global downloads of mobile apps and games across the App Store and Google Play fell -2.7% y/y in 2025 to an estimated 106.9bn downloads

- Mobile game downloads in particular saw a larger decline this yr: Were downloaded 39.4bn times, down -8.6% y/y, after a -6.6% decline from 2023 to 2024

- Non-game app downloads were essentially flat: Only saw a slight increase of +1.1% y/y to reach 67.4bn

- After reaching an all-time high of 135bn in 2020 during the pandemic, downloads have been on the decline

- Global downloads of mobile apps and games across the App Store and Google Play fell -2.7% y/y in 2025 to an estimated 106.9bn downloads

- The app economy continued to move away from mobile games as its main rev driver in 2025

- Game app spending was up +10% y/y to reach $72.2bn in 2025

- Accounted for 46% of all spending within mobile apps

- Non-game app spending was up +34% y/y to reach $82.6bn in 2025

- Game app spending was up +10% y/y to reach $72.2bn in 2025

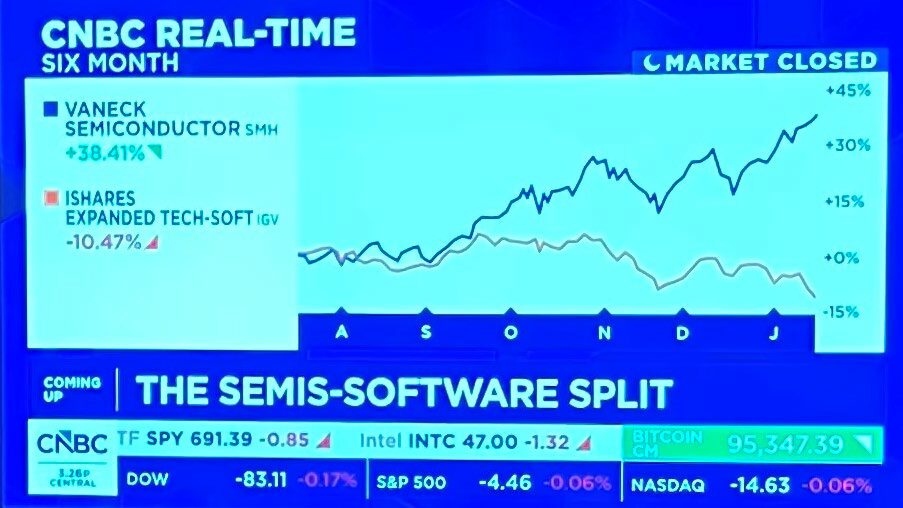

Chart Of The Week – Is Software’s Underperformance Overdone?

The chart below shows how significantly software (IGV index) has underperformed semis (SMH index) since late September 2025, which prompted some Wall Street pundits to question whether this is overdone…it is dramatic.

Grab Bag: Walmart & Wing Team Up For Drone Delivery / Meta Is Considering Doubling Production Of AI Glasses / Beijing Tells Chinese Firms To Stop Using US & Israeli Software

- Wing is expanding drone delivery to another 150 Walmart stores (link/link/link): Walmart will be able to use drones to deliver products to customers at 150 locations by the end of this yr

- The expansion follows plans shared in Jun 2025 to launch in Houston, Orlando, Tampa, and Charlotte

- Reportedly, Wing’s new chief business officer Heather Rivera said Houston will launch on Jan 15

- Once complete, Wing will operate from ~270 Walmart stores and serve ~10% of the US population

- Wing suggests that drones could serve ~40mn people by 2027

- Rivera told TechCrunch the top 25% of customers are using the service 3x a week: Some of the most ordered items are eggs, ground beef, tomatoes, avocados, limes, lunchables, and snacks

- Reportedly, Rivera would not share if its operations are profitable or when they might be: But… she did note that she was brought in to scale the biz, “volume is definitely powering our flywheel”

- The expansion follows plans shared in Jun 2025 to launch in Houston, Orlando, Tampa, and Charlotte

-> Walmart’s stock closed up +2% in reaction to the news

- Meta and EssilorLuxottica are considering doubling the production capacity of their smart glasses to 20mn units annually by the end of this year (link/link/link): Though neither company commented or confirmed

- The potential increase, driven by strong demand, could also see capacity exceed 30mn units

- EssilorLuxottica, responsible for manufacturing, is already near its current capacity target of 10mn pairs by the end of 2026

- The Cos began their partnership in 2019 and launched their Ray-Ban branded frames in 2021

- As a reminder from last week, Meta said that it paused the international expansion of the Ray-Ban Display glasses due to supply shortages and prioritizing U.S. shipments

- But trends are not as rosy on the VR side of the house as this week Meta annc’d they are cutting ~1,000 jobs from the Cos Reality Labs division

- The cuts are expected to hit ~10% of employees within the Reality Labs group, which has ~15,000 workers

-> Meta’s stock closed down -2.4% in reaction to the news

- Beijing tells Chinese firms to stop using US and Israeli cybersecurity software (link)

- The US Cos whose cybersecurity software has been banned include Broadcom-owned VMware, Palo Alto Networks, Fortinet, Alphabet owned Mandiant and Wiz, as well as CrowdStrike, SentinelOne, Recorded Future, McAfee, Claroty, and Rapid7

- The Israeli Cos also impacted include Check Point Software, two of the sources said, along with CyberArk, Orca Security, Cato Networks and Imperva

- Company responses to the matter:

- CrowdStrike said it did not sell to China and did not have offices, hire people or host infrastructure there, and thus could “only be negligibly affected”

- SentinelOne said it had “no direct revenue exposure to China,” citing similar reasons

- Claroty said it did not sell to China

- Orca Security CEO Gil Geron said his Co had not been notified of the move; He added that his Co was focused on defense and that a ban “would be a step in the wrong direction”

- Reuters was unable to establish how many Chinese Cos received the notice that the sources said were issued in recent days

- Chinese authorities expressed concern the software could collect and transmit confidential information abroad, the sources said

–>Shares of Broadcom fell more than -4% in Wednesday trading, while Palo Alto’s share price stayed virtually flat. Check Point’s shares closed up slightly. Fortinet shares fell more than -2%. Rapid7 shares fell more than -1%

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Omnicom annc’d next-gen Omni platform & Walmart tie-up to link purchase data w/ influencer efforts on Instagram. New move tackles TV freq capping by integrating Roku viewing, Acxiom audience & Amazon Ads shopper insights into Omni. Acxiom, now part of Omnicom post-IPG merger, boosts closed-loop attribution to cut ad waste. (Cynopsis)

- OpenAI will air a 60-sec Super Bowl LX ad on NBC, marking its 2nd yr of paid ads as AI cos escalate marketing battles. Ad costs exceed $8mn per 30-sec slot, w/ millions more for production. AI firms spent $333.6mn on TV ads in 2025 (+43% YoY) and $426mn on digital, tripling 2024 outlays. (The Wall Street Journal)

- WPP faces fresh challenges as major clients like Nestle, Mondelez & Unilever explore rival deals, signaling doubts over CEO Cindy Rose’s turnaround plan. Rose, who took over in Sept., hired McKinsey in Nov. to reverse falling profits & shares. (MSN)

Artificial Intelligence/Machine Learning

- OpenAI annc’d ChatGPT Translate, a standalone web tool competing w/ Google Translate. The service supports 50+ languages and mirrors Google’s two‑box layout but currently limits desktop use to text-only input. Mobile browsers add voice input, while image support is listed but not yet available. (The Verge)

- Chinese tech firms have become global leaders in patents for physical AI used in humanoid robots, vehicles and other machines, reflecting Beijing’s push for homegrown tech. A Nikkei analysis w/ LexisNexis data found Baidu, Huawei and Tencent ranked top by patent quantity and quality, w/ Huawei nearing U.S. peers’ quality levels. (Nikkei Asia)

- AI is touted as a productivity booster, but a Workday survey shows a paradox: while 85% of employees save 1–7 hrs/wk, ~37% of that is lost to “rework” like fixing errors. Only 14% report consistent positive outcomes. CEOs hope AI cuts labor costs, w/95% expecting layoffs in 5 yrs, though real gains remain elusive. (Axios)

- Big Tech is on an energy hiring spree to tackle AI’s biggest bottleneck: power access. Energy-related hires surged 34% YoY in 2024, w/ MSFT adding 570+ staff since 2022, AMZN 605, and GOOGL 340. Firms are acquiring energy cos, signing PPAs, and even seeking trader status. Data centers use ~1.5% of global electricity, up 12% in 5 yrs. (CNBC)

- Microsoft is set to spend ~$500mn annually on Anthropic’s AI svs, deepening use of its tech across products. The move diversifies MSFT’s AI partnerships beyond OpenAI, whose models power MSFT 365, Azure & Copilot. Anthropic’s Claude AI aids new MSFT infra & apps. (Yahoo Finance)

- Microsoft warned that US AI cos risk losing ground as China’s subsidized open-source models gain traction in emerging mkts. DeepSeek’s R1 model, launched last yr, boosted adoption in Africa due to low cost, securing ~18% share in Ethiopia and 17% in Zimbabwe. (Investing.com)

- CoreWeave CEO Intrator rejected claims of “circular financing” w/ Nvidia, calling them “ridiculous. ” Nvidia’s ~$300mn stake is minor vs CoreWeave’s $25bn capital and $42bn valuation. Expansion uses debt via “boxes,” securing rev from investment-grade contracts (e.g., MSFT, META) to pay lenders first. (Yahoo Finance)

- Executives from Home Depot, Wayfair & PayPal discussed agentic AI at NRF. Home Depot is in “get out & try” mode, expanding Magic Apron tools for project guidance in-store, w/ nationwide rollout planned. Wayfair focuses on on-site & off-site AI journeys. PayPal sees slow adoption due to trust; AI will assist but not replace human shopping. (Customer Experience Dive)

- Matthew McConaughey is tackling AI misuse by trademarking his likeness and voice, incl clips and his iconic “Alright, alright, alright. ” His team aims to enforce consent and attribution norms, using federal trademark law to deter unauthorized AI fakes. While state publicity laws exist, McConaughey’s approach tests broader protection. (The Wall Street Journal)

Broadcast/Cable Networks

- Sinclair, Inc. filed w/ the SEC letters detailing cont’d merger proposal talks w/ The E.W. Scripps Co. Sinclair said it reinforced willingness to engage, but Scripps declined discussions, favoring a standalone plan. Sinclair’s latest offer implied a >240% premium to Scripps’ unadj share price, incl a 32.7% cash premium. (Sinclair Broadcast Group)

- An analysis showed ABC, CBS, FOX, and NBC lost over 3mn prime-time viewers from 2020–2025 as Americans shifted to streaming. CBS fell ~1.16mn (21%), NBC 782k (15.6%), ABC 480k (10.6%), and FOX ~1.02mn (24.5%). (Cord Cutters News)

Cable/Pay-TV/Wireless

- A widespread Verizon outage began ~12:00 p. m. ET on Tue., Jan. 14, disrupting wireless svs across New York, Washington, D.C., New Jersey and other areas. Downdetector showed a surge in reports, w/ some 911 access affected. Verizon said engineering teams were fully deployed to restore svs. (Fierce Network)

- Array Digital Infrastructure, Inc annc’d the close of its deal w/ AT&T to sell select spectrum licenses for $1.018bn, cont’d from its May 2024 plan to monetize assets post-T-Mobile sale. Board declared a special dividend of $10.25/share, payable Feb. 2 to holders as of Jan. 23. Advisors included Citigroup Global Mkts, Centerview, TD Securities, and Wells Fargo. (PR Newswire)

Capital Market Updates

- Private credit firms seeking to capture leveraged debt biz from Wall St are weakening safeguards that once made them more resilient in downturns. As competition intensifies, terms resembling those long common in leveraged loans are spreading across the ~$1.7bn private credit mkt. (Bloomberg)

- Bank CEOs said Wall Street’s big five posted a record $134bn trading rev in 2025 and expect momentum to cont’d. Morgan Stanley and Goldman Sachs execs cited volatile mkts, Trump policy shifts and rate cuts lifting client activity and M&A pipelines, though risks persist. (Yahoo Finance)

- Wall Street firms are ramping up hiring for prediction mkts desks, targeting arbitrage on platforms like Polymarket & Kalshi. Trading vol surged from <$100mn/mo in early 2024 to >$8bn by Dec. 2025. DRW offers $200K base pay; Susquehanna, Tyr Capital & start-ups join in. Focus is on spreads, not odd bets. Liquidity gaps keep big hedge funds cautious, but mkts-makers like Jump & Flow Traders are active. (MSN)

- Liftoff Mobile, Inc, a global leader in mobile app performance marketing, annc’d filing a Form S-1 w/ SEC for a proposed IPO. Terms incl. share count & price range remain undetermined. If completed, stock will list on Nasdaq under “LFTO.” Goldman Sachs, Jefferies & Morgan Stanley lead book-running; other cos incl. Barclays, UBS & Wells Fargo join. (PR Newswire)

- JPMorgan annc’d ~$1. 1bn loan to Altice USA (now Optimum Communications) to refinance $1bn asset-backed facility from Goldman & TPG before call protection kicks in. Move aims to preserve cash amid heavy debt, antitrust suit vs creditors over alleged cartel. Altice earlier raised $2bn from JPM for 2028 loan refi, boosting JPM’s seniority. (Yahoo Finance)

- In 2025, private equity backers offloaded a record $110bn in ageing fund stakes, driven by challenges in the buyout industry and difficulty in exiting investments. Secondary deals, where investors sell their fund stakes, surged ~25% from 2024’s $89bn. The boom reflects the maturing $22tn private capital sector and increased demand for liquidity. (Financial Times)

Crypto/Blockchain/web3/NFTs

- US spot Bitcoin ETFs saw $697mn inflows on Jan. 5, strongest since Oct. crash. BlackRock’s IBIT led w/ $372mn; Fidelity FBTC added $191mn. BTC gained ~7.5% past wk, now ~$93,800, facing resistance near $93K before $100K. CryptoQuant notes cost basis at $100K; move above turns bullish. (Yahoo Finance)

- Polymarket, backed by ICE, has annc’d contracts on active wars, incl. China-Taiwan and Russia-Ukraine, w/ one US-Iran strike mkts topping $18mn. Critics, incl. 12 senators and AGA, say such bets violate law and pose security risks. CFTC may bar war-related contracts under Commodity Exchange Act; proposed rules in 2024 remain unfinalized. (MSN)

- Eric Adams’ NYC token, launched to fund charitable causes and fight antisemitism, surged to ~$600mn mkt cap before crashing to ~$110mn. On-chain data shows wallet linked to deployer removed $2.43mn USDC liquidity, added back $1.5mn, leaving ~$932K unaccounted. Token price fell 81% from $0.58 to $0.11. (Decrypt)

Cybersecurity/Security

- The U.S. urged UN states to crack down on North Korea’s IT worker scams and crypto thefts funding weapons programs. A report shows >40 countries hit by schemes, w/ crypto heists topping $2bn last yr. NK uses stolen funds via Chinese banks to buy arms, fuel. ~2k IT workers operate abroad despite UN bans. (The Record)

- Malwarebytes annc’d a leak exposing sensitive info of ~17. 5mn Instagram users, incl. usernames, emails, phone nos., and addresses, claiming data is for sale on dark web. Instagram denied breach, stating accounts are secure and issue was tied to password reset emails triggered by an external party. (Engadget)

eCommerce/Social Commerce/Retail

- Uber and Kroger annc’d nationwide availability of ~2,700 Kroger Family of Cos stores across Uber Eats, Uber, and Postmates apps. Customers can order full grocery assortments, including fresh food and household essentials, w/ on-demand or same-day delivery. (Kroger)

- NPR checked 114 items at a Georgia Walmart and found prices rose ~5% in 2025, even as inflation slowed to 2. 7%. Nearly half of items cost more, linked to tariffs and extreme weather that hit food and imports, while ~25% got cheaper, incl eggs and butter. (NPR)

- Holiday retail sales grew 4. 1% for Nov.–Dec., near NRF’s forecast (3.7–4.2%). Dec. core sales rose 1.6% MoM, 3.58% YoY; total retail up 1.26% MoM, 3.54% YoY. 2025 sales gained 4.93% overall, 5.08% core. Categories led by sporting goods (+3.52% MoM), clothing (+2.05%), and general merchandise (+2.9%). (Chain Store Age)

- India’s govt urged quick-commerce cos to drop “10-min delivery” after a strike over unsafe conditions. Platforms like Zomato, Blinkit, Zepto face scrutiny as riders report stress, penalties, and low pay (~₹20k/mo). Blinkit removed the promise; others may follow. Gig economy is booming, but workers lack social security and career growth. (BBC)

- Italy’s antitrust authority cut Amazon’s record fine to €752mn ($878mn) from €1. 128bn after a regional court ruling. The penalty, imposed in 2021 for abusing its dominant position in logistics svs, was recalculated per the Sept. decision. (Reuters)

EdTech

- Duolingo annc’d CFO transition. Gillian Munson, Board member & Audit Chair, to become CFO effective Feb 23, 2026; Matt Skaruppa steps down after 6 yrs, moving to advisory role. Munson brings prior CFO experience at Vimeo, Iora Health & XO Group. Co also shared prelim Q4’25 update: DAU growth ~30% YoY; bookings near high end of $329.5mn–$335.5mn guidance. (Duolingo)

Electric & Autonomous Vehicles

- Waymo is accelerating plans to launch driverless svs in Australia, with Sydney eyed this yr. The Co has sought office space, held talks w/ NSW officials and EV makers incl China’s Geely, and hired a lobbyist to push testing approvals. Waymo already runs ~25,000 robotaxis across five US states and is expanding partners beyond Jaguar as it races Tesla and Amazon. (Australian Financial Review)

Film/Studio/Content/IP/Talent

- A. film, TV and commercial production showed no rebound in Q4 2025, per FilmLA data. Production days fell 12.3% q/q, extending a decline cont’d since 2022, w/ total shoot days stagnant since 2021. Despite $771mn in state incentives annc’d and allocated, impacts aren’t visible yet, as overall volume is ~50% of 2019 levels, subsidies rose in TV, but film and TV metrics remain sharply below 5-yr averages. (Variety)

- Paris-based Banijay Group, the world’s largest independent TV producer, confirmed it is in advanced talks to merge w/ UK producer All3Media, owned by RedBird IMI. The deal, first reported by Reuters, could create a European TV production behemoth combining franchises incl. Peaky Blinders, MasterChef and Big Brother w/ The Traitors, Call the Midwife and Fleabag. (The Guardian)

- Fanatics & OBB Media annc’d launch of Fanatics Studios, a global sports-entertainment JV. It aims to create, finance & distribute premium content incl. films, docs, scripted/unscripted originals, live specials & digital series. Fanatics brings vast sports reach, athletes & biz assets; OBB adds award-winning storytelling. (Fanatics)

FinTech/InsurTech/Payments

- Online prediction mkts are seeing heavy betting on actions President Trump may take, from Greenland to Fed leadership and shutdown risks, w/ millions wagered. Notable payouts include ~$410,000 on Venezuela politics. Donald Trump Jr. sits at the center of this biz, serving as investor or adviser to Polymarket and Kalshi, and as a director of the Trump family’s social media Co, which annc’d plans to launch its own platform, Truth Predict. (The New York Times)

- Goldman Sachs CEO David Solomon said the Co is actively exploring involvement in prediction mkts, reflecting rising institutional interest. Speaking on the Co’s Q4 earnings call, Solomon said he recently met w/ leaders of two major platforms and assigned internal teams to study potential opportunities. (CNBC)

Handheld Devices & Accessories/Connected Home

- Schools are cracking down on cellphone use, but teens’ views differ. Pew survey (Sept.–Oct. 2025) shows 41% of U.S. teens ages 13–17 support classroom bans, while ~50% oppose; only 17% back full-day bans. Support varies by race—White teens (46%) more favorable than Hispanic/Black (~33%). (Pew Research Center)

- Global smartphone shipments grew 2% YoY in 2025, driven by premiumization and 5G adoption in emerging mkts. Apple led w/20% share, 10% growth; Samsung followed at 19%, up 5%. Xiaomi held 13%, vivo rose 3%, while OPPO fell 4%. Nothing and Google surged 31% and 25%. (Counterpoint Research)

Macro Updates

- The six largest US banks cut ~10,600 jobs in 2025, marking the biggest workforce reduction since 2016 as firms focused on efficiency amid slower biz activity. Combined staff fell to ~1.09mn, the lowest since 2021. Wells Fargo drove most cuts, reducing headcount by 12,000+, while Citigroup cut ~3,000 and plans more. (Yahoo Finanzas)

- Grocery prices rose 0. 7% in Dec., fastest pace in 3 yrs, pressuring household budgets as overall inflation stayed flat. Food-at-home costs up ~2.4% YoY, w/ staples like coffee (+20%), beef (+16%), candy (+10%) seeing double-digit hikes. Dining out also saw biggest gain in 3 yrs. Tariff rollbacks eased some items—bananas down ~2% MoM but still +6% YoY. (Axios)

- Oklo, a California-based nuclear Co, warned that skilled labor shortages could hinder new plant projects. CEO Jacob DeWitte said on Bloomberg TV that Oklo plans a 1.2-gigawatt power campus in Ohio, chosen partly for worker availability. The first small reactor may go into service by 2030. (Bloomberg)

- Core CPI for Dec. rose 0.2% m/m and 2.6% y/y, both 0.1 pt below forecasts; headline CPI up 0.3%, annual rate 2.7%. Shelter climbed 0.4%, food +0.7% (eggs -8.2%), energy +0.3%. Fed likely holds rates till Jun.; mkts expect no cut soon. Trump urged Powell for meaningful cuts citing “LOW” inflation. (CNBC)

- T-Mobile quietly cont’d layoffs in Dec, mainly sales roles, w/ rumors of more in Jan. Co didn’t disclose job cuts but confirmed “some changes” as it shifts to digital svs via T-Life app (90mn+ downloads, 70% upgrades digital). AI adoption (IntentCX) drives fewer stores & calls. Verizon annc’d 13,000 layoffs in Nov., tied to restructuring & AI, plus $20mn reskilling fund. (Fierce Network)

Metaverse/AR & VR

- Meta annc’d it will discontinue Horizon Workrooms, its metaverse-for-work app, effective Feb. 16, 2026, and stop selling business headsets and managed svs by Feb. 20. The Co is shedding ~10% of Reality Labs jobs and closing multiple VR studios as it rethinks its metaverse push, prioritizing mobile, AI tools and smart glasses over VR-focused biz. (The Verge)

Regulatory

- Oracle was sued by bondholders claiming losses after the Co failed to disclose plans for major debt sales to fund AI infra. Investors bought $18bn notes post-Oracle’s $300bn, 5-yr OpenAI deal, then were blindsided by $38bn loans for data centers. Bondholders allege offering docs misled them, citing false “may borrow more” statements. (Reuters)

- Gov’t dropped plans for mandatory digital ID for UK workers; existing checks via biometric passports to go fully online by 2029. U-turn follows backlash, falling public support, and ~3mn petition signers. Ministers cite need for better policy comms; critics call move “car crash.” Digital ID still planned for svs access via Gov.uk One Login & Wallet. (BBC)

- FCC granted Verizon a waiver from the 60-day phone unlocking rule, allowing longer lock periods per CTIA code. Prepaid devices unlock after 1 yr; postpaid after contract or fees. FCC cited fraud prevention and law enforcement concerns, saying 60 days was insufficient. Consumer groups opposed, arguing auto-unlocking boosts competition, reduces e-waste, and lowers switching costs. (Ars Technica)

- Newsom vowed to fight a proposed CA wealth tax, calling it harmful as billionaires flee ahead of Jan 1 retroactive deadline. The ballot measure seeks 5% levy on assets >$1bn, w/rev mainly for public health svs. SEI-UHW backs it to offset rising health costs post-Obamacare subsidy loss. (Forbes)

Satellite/Space

- AST SpaceMobile annc’d it was awarded a prime position on the U.S. Missile Defense Agency’s SHIELD IDIQ contract, validating its on‑orbit, dual‑use tech for comms and defense apps. The award enables the Co to compete for future task orders across R&D, engineering, prototyping, and ops supporting U.S. national security. (Business Wire)

- SpaceX got FCC approval to deploy 7,500 more Gen2 Starlink satellites, totaling 15,000. This expansion enables high-speed, low-latency Internet globally w/ fixed & mobile svs. FCC waived old rules, allowing new orbital shells (340–485 km) & advanced tech upgrades. SpaceX also plans another 15,000 satellites for MSS connectivity after a $17bn spectrum deal w/ EchoStar. (Ars Technica)

- Eutelsat annc’d procurement of 340 OneWeb LEO satellites from Airbus, adding to 100 ordered in Dec. 2024, totaling 440 units. Delivery starts end-2026 from Airbus’ Toulouse facility. New sats feature tech upgrades incl. digital channelizers for enhanced processing & flexibility, ensuring service continuity as older batches retire. (Business Wire)

Social/Digital Media

- YouTube annc’d new parental controls to manage kids’ Shorts viewing. Parents can set timers, block Shorts permanently or temporarily, and add Bedtime/Break reminders. Features aim to curb mindless scrolling and improve safety. Upcoming updates will ease account toggling. (TechCrunch)

- US vows to use “full range of tools” vs Labour’s censorship plans after PM Keir Starmer warned X could lose self-regulation amid Ofcom probe into Grok AI abuse. Sarah B Rogers said threats to ban X are politically driven, citing US efforts for uncensored net in Iran via Starlink. She stressed free speech priority, noting Trump’s past Twitter ban and warned Labour’s stance shows pro-censorship inclinations. (GB News)

Software

- Apple annc’d Apple Creator Studio, a subscription bundling Final Cut Pro, Logic Pro, Pixelmator Pro, Motion, Compressor & MainStage w/ new AI tools. Features include Transcript Search, Beat Detection, Magnetic Mask, AI Session Player, Chord ID & Content Hub for Keynote, Pages & Numbers. (Apple)

Sports/Sports Betting

- The number of illegal sports streams in Britain has more than doubled to 3. 6bn over the past three yrs, exposing growing challenges for broadcasters and leagues, according to a new report annc’d. The Campaign for Fairer Gambling said piracy and unlicensed betting are closely linked, with 89% of illegal streams carrying black‑market bookmaker ads. (The Guardian)

- Kalshi and Polymarket are racing to add parlay-style sports bets as they seek liquidity to challenge the $14bn US sports gambling mkts. Prediction mkts rely on binary bets and need separate liquidity pools, making parlays harder than for sportsbooks such as DraftKings or Flutter. (Financial Times)

Tech Hardware

- Micron, after killing its Crucial brand in Dec., clarified it’s not abandoning consumers, citing LPDDR5 supply to OEMs. The Co is pivoting to AI-focused DRAM/SSD, w/new fabs in NY ($100bn) and Idaho, but real output won’t impact mkts until 2028. Current capacity meets only ~50–66% demand, so shortages and high prices for PC builds will cont’d for yrs. (Tom’s Hardware)

- DC reports PC shipments grew ~10% YoY in Q4’25 to 76mn units, driven by holiday demand, Windows 10 support ending, and cos pulling inventory amid RAM shortages. AI-driven data center demand has spiked RAM/NAND prices, prompting makers like Lenovo, HP to stockpile. (The Verge)

- Apple faces a critical glass cloth shortage, a key chip substrate material, due to AI-driven demand from Nvidia, Google, Amazon, etc. Supply crunch may cont’d till H2 2027 as Nittobo, the main supplier, lacks capacity. Apple, AMD, Nvidia sought Japanese govt aid and alternative sources like China’s GFT, but quality hurdles persist. (9to5Mac)

Towers/Fiber

- Crown Castle annc’d DISH Wireless defaulted on payment obligations, leading to termination of its wireless infra agreement. DISH owes Crown Castle >$3.5bn after ceasing its network biz post FCC actions and spectrum sales to AT&T & SpaceX (~$40bn). Crown Castle aims to recover dues and enforce rights, noting no impact on full-yr 2025 results. (Crown Castle)

Video Games/Interactive Entertainment

- Saudi Arabia’s PIF is transferring ~$12bn in gaming shares, incl. Nintendo Co. & Bandai Namco, to subsidiary Savvy Games Group. Savvy will hold ~10% in firms like Koei Tecmo, NCSoft, Nexon & Square Enix post-transfer. Established in 2021 w/ $38bn for gaming biz, Savvy acquired Scopely, Niantic & esports cos. (Bloomberg)

- Ubisoft annc’d new layoffs at Massive & Stockholm studios, cutting 55 jobs as part of its cont’d restructuring plan to reduce costs. This follows the voluntary leave program in fall 2025 & Tencent’s $1bn investment in Vantage Studios, focusing on Assassin’s Creed, Far Cry & Rainbow Six Siege. Despite cuts, updates for The Division 2 & dev of The Division 3 will proceed. (Kotaku)

Video Streaming

- Netflix and Sony Pictures Entertainment annc’d a landmark, multi‑yr global Pay‑1 deal making Netflix the exclusive streaming home for SPE feature films after theatrical and home entertainment runs. The rollout begins later this yr, reaching full global availability in early 2029. (Netflix)

- WWE’s “Monday Night Raw” on Netflix hit 340mn viewing hrs in its first yr since Jan 2025 debut, part of 525mn hrs of WWE content streamed in 2025. Raw ranked in Global Top 10 English TV chart 47 of 52 weeks, averaging 3mn viewers weekly. WWE events like WrestleMania, Royal Rumble added 185mn hrs. (Variety)

- YouTube TV’s Live Guide redesign is rolling out on Android & iOS, mirroring the 2023 TV version. It adds higher info density, channel icons on the left, swipe to see upcoming shows, and a red “Jump to live” button. Users can long-press for previews, descriptions, and actions like adding to library or setting reminders. (9to5Google)

- Netflix’s push into live events began in 2022 as subs stalled, adding an ad tier and cracking down on password sharing. It struck a 10-yr WWE deal worth $5bn and streamed 200+ events since Mar. 2023, but faced tech hurdles like the Nov. 2024 Paul-Tyson fight w/65mn viewers. Netflix built a live ops center, improved algorithms, and plans intl expansion in 2026. (The Wall Street Journal)

- HBO Max annc’d expansion into 8 new mkts—Italy, Germany, Austria, Switzerland, Luxembourg, Liechtenstein, Israel & Greece, bringing WBD’s streaming reach to 100+ countries. Launch includes partnerships w/ Amazon, RTL+, TIM & others. (Warner Bros. Discovery)