Is earnings season almost over?! Not yet! Week 3 was certainly extremely busy with A LOT of key updates and developments across the sector, especially regarding Big Tech AI/CapEx, digital ad trends, music, video gaming, last mile transport, online travel, legacy media, and more. The market pulled back a bit (S&P -0.24% and Nasdaq -0.5%), as investors reacted to earnings as well as headlines coming out of the new administration regarding tariffs and concerns about potential trade wars, among other things.

We tried to capture a lot this week but as always, I’d would love to hear any thoughts or comments or other points of view.

Have a nice weekend. A snowstorm is brewing on the east coast! Stay warm.

- Earnings Scorecard – Week 3

- Alphabet… Higher CapEx + Cloud Capacity Constraints Part I

- Amazon… Higher CapEx + Cloud Capacity Constraints Part II

- Disney: Conservative Or Cautious? That Was The Key Question Regarding The Reiterated Full Year Guidance

- Fox Outshines The Field This Qtr And Looks To Make A Play Into DTC

- Snap & Pinterest: A Tale Of Two Cities In Q4

- Spotify Continues To Break Away From The Pack

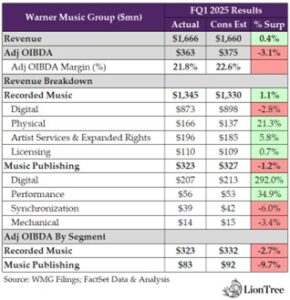

- Warner Music Group Pushes Forward Amid FX Headwinds And Streaming Shifts

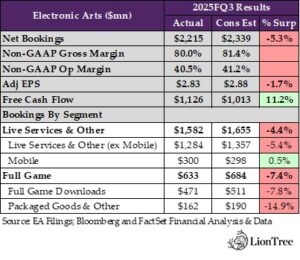

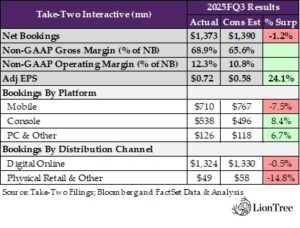

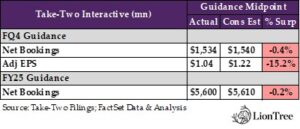

- EA & Take-Two Navigated Through Some Temporary Speedbumps In Q4

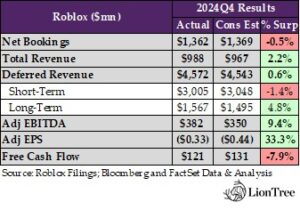

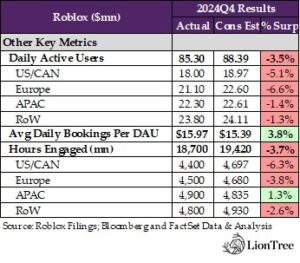

- Roblox Bets On AI And 3D Streaming To Catalyze Its Business

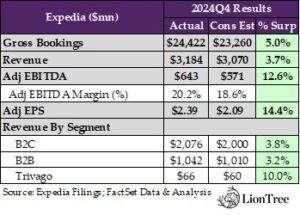

- Expedia Rides Better Than Expected Travel Demand To A Strong 2024 Finish

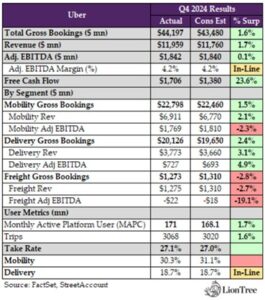

- The Bump In The Road Doesn’t Veer Uber Off The Track

Best,

Leslie

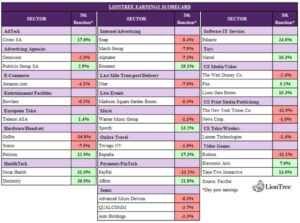

Earnings Scorecard – Week 3

There was a storm of earning prints hitting the tape this week, as 37 companies in our LionTree Universe reported fourth quarter earnings (up from last week’s 17). In a reversal from last week, stock price reactions were biased to the downside, as 21 companies (57%) traded down in reaction to results, while 16 companies (43%) traded up. GoPRO had the worst performance of the lot, falling -16.8% after its report, while Doximity was the best performer, jumping +36%.

While quarterly reports were across sub-sectors this week, arguably the most prominent were the digital advertisers. Reactions were shaky at the start of the week, as Alphabet traded down -7.3% (see Theme #2), followed by Snap, which fell a steeper -8.4%. However, Pinterest ended the week on a high note for the sub-sector, with the stock surging +19.1% (see Theme #6 for more on Snap and Pinterest).

This week also brought with it more media earnings, starting with Fox, which shared a big announcement that helped drive the stock up +5.2% (see Theme #5 for more details). That was followed by Disney, which had its stock go the other way and was down -2.4% post its print (see Theme #4). Also seeing some bifurcation in reactions was the music sub-sector, which saw Spotify jump +13.2% after its results (see Theme #7), while WMG fell -1.1% (see Theme #8).

It was also a big week for the video game companies, and while EA and Take-Two were both up +7.6% and +14.0% (see Theme #9), Roblox didn’t fare so well and fell -11.1% (see Theme #9).

On the last-mile side, Uber had a tough going, with the stock down -7.6% in reaction (see Theme #12). Expedia kicked off online travel earnings this week, with the stock leaping +17.3% in reaction (see Theme #11). Finally, rounding out the Big Tech reports was Amazon, which fell -4.1% in reaction (see Theme #3).

Alphabet… Higher CapEx + Cloud Capacity Constraints Part I

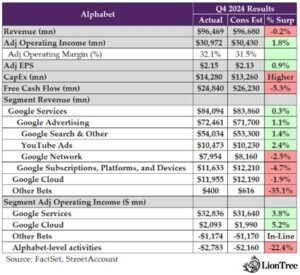

It has been a mixed bag thus far in Big Tech earnings, and this week was more of the same but with a more negative bias, as both Alphabet and Amazon shares sold off in reaction to earnings. The “higher than expected AI CapEx” theme continues to be front-and-center, but neither company significantly outperformed on the revenue side as a result of the prior spending step ups. Additionally, their respective Cloud revenue growth rates were lackluster versus expectations. However, we would note that both were negatively impacted by capacity/supply constraints in Q4, which should ease later this year. Alphabet and Amazon also continue to push hard regarding their own AI chips as part of that as well.

On Alphabet more specifically, while the company’s core advertising business performed better than expected (grew +11% y/y in Q4, which is up from +10% y/y in Q3) and it posted a slight acceleration in Search & YouTube revenue, that was overshadowed by weaker than expected revenue growth in Google Cloud (decelerated to +30% y/y in Q4 from 35% y/y in Q3) in part due to the aforementioned capacity constraints. Also, Alphabet’s full year guidance of $75bn was +43% above 2024’s $52.5bn level, so that was a hot button as well. Questions about what the normalized level of capital intensity should be were left unanswered.

The integration of AI into the company’s core ads business was a big focus on the conference call, and thus far it has been a driver for incremental search opportunities. That said, we should expect to see much more innovation with Search in 2025.

Overall, Big Tech company executives still see a massive AI land grab opportunity and want to fortify their positions, while investors want to more clearly understand the CapEx trajectory and want to see more tangible evidence of incremental growth from these investments.

See below for more of what we thought were the most important elements and themes from Alphabet’s results and earnings. Also, see Theme #3 for similar perspective on Amazon’s results.

Lastly, see Theme #6 for more on digital advertising from Snap and Pinterest results.

-> Alphabet shares fell -7.3% on the day and ended the week down -9.2%; YTD, Alphabet stock is down -2.1%

Better Q4 Margins Were Overshadowed By A Miss In Cloud Revenue & Q1:25 Revenue Will Be Impacted By Two Items

- Margins beat, while revenues missed: Headline revenues grew +12% y/y and +12% y/y ex-FX (vs +15% y/y and +16% y/y ex-FX in Q3), slightly missing cons by -0.2%; Op margins of 32.1% outperformed cons 31.5% and expanded by +4.6pts y/y; EPS beat by +0.9% and grew+31% y/y; FCF of $24.8bn missed by -5.3%

- Google Services revs (+10.2% y/y) were essentially in-line, while op income (+23% y/y) was +3.8% ahead of cons (margin rose to 39% vs 35% in Q3)

- Total Google Advertising rev rose +10.6% y/y (vs +10.4% y/y in Q3) and beat by +1.1%

- Subscription, platform, and devices revs rose +8% y/y (vs +28% y/y in Q3) and missed by -4.7%

- Network ad revs fell -4% y/y

- Cloud revs rose +30% y/y (vs +35% y/y in Q3) and missed by -1.9%;5% op margins

- Other Bets revs of $400mn was -35% below cons, but the op loss of -$1.2bn was in-line

- Google Services revs (+10.2% y/y) were essentially in-line, while op income (+23% y/y) was +3.8% ahead of cons (margin rose to 39% vs 35% in Q3)

- Outlook – Two items will impact Q1 rev

- FX – expect a larger headwind to revenue from the strengthening US dollar vs other key currencies

- The impact of 2024’s leap year means 1 fewer day in Q1:25 y/y

Google Cloud Faced Some Supply Issues In Q4, But The Co Is Working Hard To Bring On New Capacity

- Q4 revenues grew +30% y/y, a deceleration from +35% in Q3: GCP grew in excess of the total, and healthy Google Workspace growth was primarily driven by an increase in avg rev per seat

- Headwinds in Q4? There were tough comps from the strong deployment base from Q4 2023 but also exited the qtr with demand exceeding available capacity

- 2025 commentary – growth rates are contingent on new capacity: They are working diligently to increase capacity w/ CapEx going up in 2025, but given that Cloud revs are correlated w/ the timing of deployment of new capacity, “we could see variability in cloud revenue growth rates depending on when new capacity comes online during 2025”

- First-time commitments more than doubled in 2024 compared to 2023 / Deals over $250mn doubled y/y

- Highlighted new cloud customers: Mercedes-Benz, Mercado Libre, and Servier

- Q4 saw significant uptake of Trillium, the Co’s sixth-generation TPU

- Offers +4x better training performance and +3x greater inference throughput than the previous generation

- But still have a cont’d strong partnership with NVIDIA

- Vertex AI (their AI developer platform), saw a +5x increase in customers y/y

- Vertex usage surged +20x in 2024, with high adoption of Gemini Flash, Gemini 2.0, Imagen 3, and VEO

- Robust growth in AI-powered databases, data analytics, and cybersecurity platforms

- Expanding portfolio of AI applications with strong customer adoption

- Launched Google Agent Space in Q4

- Helps enterprises synthesize data with Google-quality search

- Enables creation of Gemini-powered agents and automates transactions for employees

- Provided all Google Workspace business and enterprise customers access to Gemini AI capabilities to enhance productivity

- Launched Google Agent Space in Q4

CapEx Guidance Was MUCH Higher Than Expected BUT No Color On What Normalized Capital Intensity Will Be

- Q4 CapEx of $14bn was an increase from Q3’s $13bn and +7.7% higher than expectations: Continue to invest in technical infrastructure, w/ the largest component being servers, followed by data centers

- The $75bn 2025 CapEx guidance was +27% above cons and +43% above the $52.5bn spent in 2024

- Q1:25 guidance: ~$16-18bn

- Expect the growth rate in depreciation to accelerate in 2025

- The costs for AI will keep coming down, making more use cases feasible, and “that’s the opportunity space. It’s as big as it comes, and that’s why you’re seeing us invest to meet that moment”

- How do we think about long-term capital intensity for this business? Mgmt didn’t comment directly to this analyst question

- Believe the Co’s strategy to take an end-to-end AI stack approach creates a strong differentiation in optimizing cost, but also on a latency and performance basis: It is partly why they have been able to bring forward flash models at very attractive value props, which is what is driving developer growth

- Have doubled developers to 4.4mn in just ~6 months

Total Advertising Growth Remained At A Low DD Rate… 2025 Will Be The “Biggest Year” For Search Innovation & YouTube Rev Growth Accelerated

- Google Search & Other ad revs incr’d +13% y/y (slightly up from +12% y/y in Q3) with broad-based strength led by fin svs (esp insurance), followed by retail (which was the same last qtr)… Paid clicks grew +5% y/y and cost per click grew +7% y/y

- HOWEVER, that strength in fin svs will create a tough comp in 2025

- Note that Q4 total advertising growth also faced tough comps due to APAC-based retailers spending levels in Q4:23

- Rapidly integrating AI innovation into the consumer search experience

- Started testing Gemini 2.0 in AI overviews… Available in 100+ countries & plan to roll it out more broadly later in the year

- AI Overviews are driving higher usage and satisfaction

- Seeing people increasingly ask entirely new questions

- Recently launched ads w/in AI overviews on mobile in the US (previously rolled out ads above and below)… overall monetization is roughly the same rate

- Circle to Search is now available in 200mn+ Android devices: It is driving addt’l search use and leading to even more types of questions

- Those who have tried Circle to Search use it to start 10%+ of their searches

- Intro’d a reinvented Google Shopping experience rebuilt from the ground-up w/ AI

- In Dec saw ~+13% more daily active users on Google Shopping in the US y/y

- Offering new ways for people to search such as with Lens

- Lens is used for 20bn+ visual search queries every month, and most of these searches are incremental

- Believe there are many more avenues to innovate in Search looking ahead: “As AI continues to expand the universe of queries that people can ask, 2025 is going to be one of the biggest years for search innovation yet”

- Started testing Gemini 2.0 in AI overviews… Available in 100+ countries & plan to roll it out more broadly later in the year

- YT ad rev growth modestly accelerated to +14% y/y from +12% y/y in Q3; Growth was driven by brand, followed by DR

- YT usage is strong and taking streaming share:

- YouTube continues to be #1 in streaming watch time across ad-supported and premium experiences

- In the US, YT’s share of streaming is now at a record high

- Early investment in podcasts are paying off: Google is now the most frequently used svs for consuming podcasts in the US, according to a recent Edison report

- In 2024, people watched 400mn+ podcasts each month on living room devices alone.

- Making progress with YouTube shopping: Expanded at the end of last year to 3 addt’l countries

- Now have 250k+ creators in the YT Shopping affiliate program in the US and Korea alone

- YT Shorts is closing the gap with long-form: In 2024, the monetization rate of short relative to in-stream viewing incr’d by more than +30ppts in the US, and the Co expects to make additional progress in 2025

- Making it easier for advertisers to benefit from shorts on all screens: Excited by success on Connected TV, which now makes up 15% of shorts viewing in the US

- Continue to believe AI will revolutionize every part of the marketing value chain across media buying, creative, and measurement

- Media buying: Made YouTube Select Creator takeovers generally available in the US and will be expanding to more markets this year

- Creative: Intro’d new controls and made reporting easier in Pmax

- Measurement: Last week, made Meridian (their marketing mix model) generally available for customers

The Gemini App Is All About User Experience In 2025, But There Will Be Advertising Potential Over Time

- Have had strong momentum for Gemini on the app side, particularly in H2, as it became more accessible (debuted on iOS last Nov)

- Unveiled Gemini 2.0 in Dec – built for the Agentic era

- 0 Flash is one of the most capable models at the free tier

- Late last year, also debuted the experimental Gemini 2.0 flash thinking model

- Gemini Live is “definitely a hit”

- Gemini Deep Research has been well received as well for advanced users

- Focused on a free tier and subscriptions with Gemini app right now and want to lead with the user experience this year; However, the Co does have very good ideas for native ad concepts

Waymo Is Ramping Rapidly

- Served 4mn+ passenger trips in 2024 and is averaging 150k+ trips each week and growing

- Expansion plans

- Early 2025: Austin & Atlanta in the US and vehicles will arrive in Tokyo in the “coming weeks”

- 2026: Miami

- Developing the sixth-generation Waymo driver, which will significantly lower hardware costs

Amazon… Higher CapEx + Cloud Capacity Constraints Part II

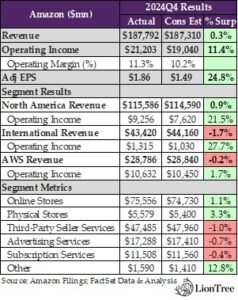

Following the above commentary on Alphabet (see Theme #1), Amazon was the other Big Tech juggernaut to report results this week, and the higher profitability in Q4 was not enough to offset concerns about the combination of: 1) weaker Q1 guidance; 2) an in-line to a slight miss on AWS revenue growth; and 3) of course, much higher CapEx. More specifically, total Q4 op income beat by +11%, given strong upside in the North America and international segments (it was the eighth consecutive quarter that the company posted a y/y margin improvement in both the North America and international segments), while revenue was more or less in-line. However, Amazon’s Q1 guidance was -12.8% lower than consensus expectations on op income and -3.3% lower on revenue at the midpoint, but it is worth noting that FX is expected to weigh on results, along with an accounting change.

On AWS, constant currency revenue growth of +19% y/y was consistent with the prior qtr. That said, and as noted for Google Cloud, AWS also was negatively impacted by supply constraints, though management sees that bottleneck improving in H2. Regarding CapEx, guidance of ~$100bn was a big step up from the ~$78bn in 2024 and ~$53bn in 2023. Nonetheless, management believes this level of spend is justified, given that “AI represents for sure the biggest opportunity since cloud and probably the biggest technology shift and opportunity in business since the Internet.” It is a “once-in-a-lifetime type of business opportunity” for the company.

In terms of the core Stores business, it is essentially “same ole, same ole”. Amazon continues to expand selection, focus on lowering prices, and increase delivery speeds, of which the investment is not seeing diminishing returns. The company continues to execute on squeezing out more cost efficiencies, and the cost of serve should further decline in 2025 despite 2 consecutive years of improvement there.

See below for more details on these key takeaways, along with some interesting updates on the Co’s advertising and video businesses, among other updates.

-> Amazon shares fell -4.1% in reaction to earnings and ended the week -3.6%; YTD, Amazon stock is still up +4.4%

Higher Q4 Profitability Overshadowed By Weaker Q1 Guidance & A Slight Miss On AWS Revenue Growth

- Q4 was another qtr of a larger op income beat (by +11.4%) along with a more modest revenue beat (by +0.3%)

- Total revs rose +10% y/y (+11% ex-FX) vs +11% in Q3

- Op income grew +61% y/y (margins hit 11.3% vs cons 10.2%)

- Adj EPS beat by +25%

- Q4 by segment – Higher than expected North America revenue was mostly offset by lower than expected Intl revenue, while profitability in both segments were WELL above Street forecasts; AWS was mixed

- Amer: Revs rose +10% y/y (vs +9% y/y in Q3) with 8% op margins vs cons 6.6%

- Intl: Revs grew +8% y/y or +9% y/y ex-FX (vs +12% y/y in Q3), and profitability was much stronger than expected (up +1.7bn y/y) with a 3% op margin

- AWS: Revs grew +19% y/y was more or less in-line, while op income slightly beat

- The higher est’d useful life of servers starting in 2024 contributed ~200bp to the AWS margin increase y/y in Q4

- Q1 guidance was a disappointment in part due to expected FX hit and a chg in acct of fixed assets:

- The mid pt of rev guidance (between +5-9%) was -3.3% below cons

- Assumes a ~-$2.1bn or -150bp headwind from FX

- Also the leap year added +$1.5bn in the yr ago qtr

- The mid-pt of op income guidance was -12.8% below cons

- Guidance incls changes to the useful life of fixed assets that in aggregate will decrease full-year 2025 op income by ~-$400mn

- The mid pt of rev guidance (between +5-9%) was -3.3% below cons

Capacity Constrained In AWS But This Should Ease In H2, And Investments Will Lead To Higher Growth

- AWS revs grew +19% y/y ex-FX, which is the same rate as in Q4

- Saw growth in both generative AI and non-generative AI offerings

- AWS revenue would have grown faster if not for constraints on capacity, but mgmt expects these constraints will relax in H2:2025; What has been constrained?

- 3P chips are coming a little slower than before

- Mid-stream changes take some time

- There are some power constraints

- Motherboards are in short supply

- In AWS, the faster it grow, the more CapEx the Co ends up spending b/c it has to procure data centers, hardware, chips, and networking gear ahead of when it is able to monetize it

- “We don’t procure it unless we see significant signals of demand”

- Very bullish on the Cloud Biz: While “AWS growth will be lumpy over the next few years as enterprise adoption cycles, capacity consideration, and tech advancements impact timing… it’s hard to overstate how optimistic we are about what lies ahead for AWS customers and business””

- Mgmt believes they are very well positioned in AI, given they have capabilities in all three layers of the stack

- Intro’d new Trainium2 AI chip which is delivering much better price performance than current GPU powered instances

- Working on Tranium3, which expect to preview late in ’25 and defining Tranium4 thereafter

- Have their own foundation models in Amazon Nova and new models and features in Amazon Bedrock

- Amazon Q is helping with the migration from old platforms

- Intro’d the next edition of Amazon SageMaker to pull data, analytics, and AI together more concertedly

- Intro’d new Trainium2 AI chip which is delivering much better price performance than current GPU powered instances

- AWS op margins will fluctuate; AI initially has lower margins and heavy investment load, but over the long term, AI margins will be comparable to non-AI workloads

- New agreements with… the U.S. Army, Intuit, PayPal, Norwegian Cruise Line, Northrop Grumman, Medtronic, The Guardian Life Insurance Company of America, Reddit, Japan Airlines, Baker Hughes, The Hertz Corporation, Redfin, Chime, and Asana

- Regionally, the Co launched AWS Asia Pacific (Thailand) and AWS Mexico (Central) Region

CapEx Takes A Big Step Up In 2025 Given The “Once-In-A Lifetime” Opportunity”; AWS Will Continue To Invest In Emerging Areas

- Q4 CapEx guidance of $26.3bn is a “reasonable representative” run-rate for 2025, implying ~$100bn for the year vs ~$78bn in 2024

- Most of the spend is primarily for AWS but will also support the N. Amer and Intl segments, where the Co is investing in capacity for fulfillment and the transportation network, in addition to same day delivery and the inbound network plus robotics and automation

- “AI represents for sure the biggest opportunity since cloud and probably the biggest technology shift and opportunity in business since the Internet”

- “We think virtually every application that we know of today is going to be reinvented with AI inside of it and with inference being a core building block just like compute and storage and database”

- AI is “one of these once-in-a-lifetime type of business opportunities”

- Also will continue to invest in experiences that have a larger potential over the long-term

- Alexa

- Healthcare

- Grocery

- Kuiper (planned launches of production satellites in the “coming months”)

- Expect the cost for inference to “substantially” come down but companies will also end up “spending a lot more in total on technology once you make the per unit cost less”

- Impressed by what DeepSeek did esp w/ training techniques and inference optimizations were interesting; Everyone building frontier models today are learning from one another and a lot of innovation is to come; Ultimately think all big gen AI apps will use different models

The MO For The Stores Biz Remains The Same – Expand Selection, Lower Prices, & Improve Convenience

- Reached highest annual mix of 3P seller units at 61% of the total in 2024

- Mgmt has not yet seen diminishing returns from improving the speed of delivery: Customers more than not buy more when there is faster delivery; With Prime Air, can deliver items inside one hour

- Expanded the # of same-day delivery sites by more than 60% in 2024

- Delivered at its fastest speeds ever for Prime members in 2024

- Delivered 9bn+ units the same or next day globally

- With that said, sometime people do choose to receive packages later as well

- Paid units grew +11% y/y in Q4 (vs +8% y/y in Q3)

- The Co does not expect an impact from UPS’ decision: UPS “decided that serving Amazon is a lower margin for them. And so I think they’ve walked away from some of the volume that they otherwise could have had in the partnership. We’re able to handle it with our own logistics capability, and we’ll see how it continues to evolve”

Amazon Expects To Drive Down Cost To Serve AGAIN In 2025

- Reduced cost to serve on a per unit basis for the second year in a row while also increasing speed and increasing selection (has been a meaningful driver to the higher op income)

- Mgmt believes they can reduce cost to serve again in 2025 and beyond due to –

- On top of the regionalization they have done, recently rolled-out redesigned US inbound network which brings inventory close to end customers; It is still early days

- Also optimizing the number of items per package sent to customers

- Per unit transportation costs continue to decline

- Accelerate robotics and automation in the network

- The next tranche of robotics initiatives has started hitting production, but this will be a many-year effort:

- “We actually don’t think there are that many things that we can’t improve the experience with robotics”

Media-Related Efforts Continue To Show Success… Ad Revs Deliver Consistent Y/Y Growth & Sports Content Attracts Eyeballs

- Ad revs were up +18% ex-FX, reaching $17.3bn ($69bn annual run rate) vs +18.8% in Q4

- Sponsored products (largest portion) have more room to grow

- Wrapped up first year for Prime Video ads and “quite please”; Have momentum into 2025

- And have differentiated audience features that leverage billions of customer signals and drive returns

- Prime Video events are attracting large audiences

- Red One: 50mn worldwide viewers in its first four days (Amazon MGM Studios’ most-watched film debut ever on Prime Video)

- Third season of Thursday Night Football: Full-season avg of 13.2mn viewers on Prime Video per Nielsen, up +11% y/y and saw a peak of 24.7mn during the Wild Card playoff game btw the Steelers and Ravens

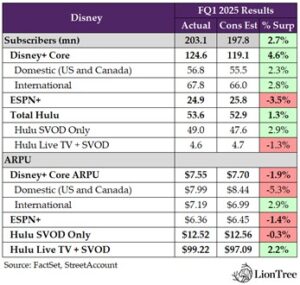

Disney: Conservative Or Cautious? That Was The Key Question Regarding The Reiterated Full Year Guidance

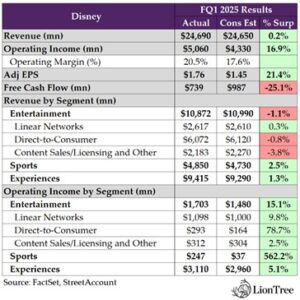

Last week, we got our first look at Media earnings with Comcast reporting, while this week, Disney and Fox (see Theme #5) were the main Media events; however, it was hit or miss. Disney’s Experiences and Sports segments topped analysts’ estimates, and profitability across the board was a standout, though the Entertainment segment and direct-to-consumer (DTC) missed top line forecasts. D+ subs are expected to fall sequentially next quarter due to a “temporary” uptick in churn from both the recent price increases as well as the end of a recent promotional offer. Notably, management didn’t raise the full year profitability guidance despite the outperformance in the quarter. Drilling down, Disney’s FQ1 adj EPS growth of +44% y/y is pacing significantly above the full year guidance of high single digit growth, and the company’s almost $300mn in DTC op income in FQ1 is tracking well vs the full year guidance of $1bn. Based on comments on the call, our take is that they are trying to create some buffer to overdeliver on the previously stated guidance, but time will tell if that is the case or if management is bracing for a softer year ahead.

While the Experiences business performed quite well vs expectations, there is some concern about Comcast’s EPIC theme park (launching in May). Management has already baked in a “small” impact to the guidance, which it is “confident” in reaching. Sports and the flagship ESPN DTC are also a key catalyst, and the new offering will be coming this fall. Disney is leaning into the product and aims for ESPN to reach customers wherever they are, including via the new skinny bundles. It was also interesting to see that Disney’s FY25 content budget is now $23bn (vs the previous $24bn), but management didn’t provide detail around that change.

See below for more on what we thought were the most important takeaways and updates from Disney’s earnings and conference call.

-> Disney share fell -2.4% in reaction to earnings and is now flat for the year

The Experiences & Sports Businesses & Profitability Were The Upside Areas In FQ1

- Total consolidated FQ1 revs were up +5% y/y, essentially in-line w/ cons, while op income (up +31% y/y) was +17% ahead of consensus & adj EPS (+44% y/y) was +21% ahead

- Experiences & Sports posted the biggest upside vs the Street

- Experiences revs beat by +1.3% and op income beat by +5.1%

- Sports revs beat by +2.5% and op income beat by +$210mn

- Operating income upside was across all segments

Reiterated FY25 Adj EPS Growth Guidance Despite Pacing Ahead

- Q2 FY25 guidance:

- Entertainment DTC: Modest decline in Disney+ subscribers vs Q1

- Sports: Op income adversely impacted by ~-$100mn due to college sports and one addt’l NFL game, plus ~-$50mn from exiting the Venu Sports JV

- Experiences: Disney Cruise Line pre-opening expense of ~-$40mn

- FY25 guidance: Reiterated ~+hsd% y/y adj EPS growth DESPITE the +44% y/y adj EPS growth in FQ1

- Mgmt commented that the higher-than-expected FQ1 adj EPS growth rate “certainly gives us confidence, and even higher level of confidence than we probably even had before, as we get into the balance of the year. At the same time, given the rapidly evolving macro environment, we think it would be premature at this point to change the guidance, but obviously the results were certainly in excess of expectations in the first quarter”

- FY25 guidance by segment:

- Entertainment: ~+double-digit% y/y segment op income growth, w/ an increase in Entertainment DTC op income of ~+$875mn, which includes a comp to an adverse impact of their India DTC biz of ~-$200mn in FY24

- Growth will be weighted to the H1 due to timing of theatrical releases compared to FY24

- Sports: +13% segment op income growth

- Experiences: +6-8% segment operating income growth

- Expects FY25 CapEx of ~$8bn vs $5bn in FY24, driven primarily by fleet expansion at Disney Cruise Line and new guest offerings at our theme parks around the world

- India business is expected to:

- Contribute +$73mn to Entertainment op income in FY25 vs +$254mn in FY24

- Contribute $9mn to Sports op income in FY25 vs a -$636mn loss in FY24

- Equity loss from the India JV of -$33mn in Q1 primarily due to the impact of purchase accounting

- FY25: expect an equity loss of ~-$300mn, driven by purchase accounting

- Lowered the content cost budget in FY25 to $23bn from the previous $24bn but did not provide any color around that

Profitability Improved In DTC At A Faster Pace Than The Qtrly Rate Implied In The Full Year Guidance

- DTC op income incr’d by +$431mn to $293mn, which is tracking on a qtrly rate ahead of the FY profit target of $1bn; However, the Co is not changing the guidance now

- “We’re out of the blocks very, very quickly. As I mentioned earlier in this call, we’re certainly not afraid to over-deliver if the business momentum gives us that”

- DTC ad rev fell -2%, but ex D+ Hotstar, it was up +16% y/y (FQ4 +14% y/y)

- More than half of new US Disney+ subscribers are choosing the ad tier

- “The only way you succeed in global streaming, both from a subscription perspective and a profitability perspective, is with a great combination of high-quality product with volume and technology”; They believe they are well positioned here

- Already made the business more economical

- And with the tech that they have in place, combined with their content,” we actually are bullish about our ability to grow subs too”

D+ Subscriber Adds Top Expectations But Will Decline Seq Next Qtr /Nonetheless, Expects Subs Growth For the Full Year

- D+ Core subs net adds of 4.4mn was stronger than expected, and the Co ended the period with 125mn total subs (+4.6% ahead of cons)

- Bundle subscriptions continued to grow with Hulu on Disney+

- But expect a modest seq decline in D+ Core subs in FQ2: Driven by the “temporary” uptick in churn from both the recent price increases and the end of a recent promotional offer

- With that said, Paid sharing is starting to “take hold,” and as they add more of the movie slate that they produced in the back half of ’24 into the streaming service in ’25, that “will drive sub growth as well” for the full year

Remain Confident In The Experiences Full Year Guidance Despite EPIC Launching In May

- FQ1 Experiences rev rose +3% y/y

- Domestic parks rose +2% y/y

- International parks rose +12% y/y

- FQ1 Experiences op income was impacted by several one-time impacts: Hurricanes Milton and Helene (~-$120mn impact) & pre-opening expenses (~-$75mn impact) related to the launch of the Disney Treasure

- Domestic parks fell -5% y/y

- International parks incr’d +28% y/y

- Feel very confident in the full year guidance despite EPIC opening: A small impact from EPIC is already built into the existing guidance, which the Co feels very confident about (performance in FQ1 increases confidence in the FY guidance even more)

- Mgmt reiterated summer bookings are up y/y, despite Epic

- Will also have easier comps in H2, esp FQ4, given their ship is coming on as of this quarter, which supports the results from FQ2 going forward

- Update on new experiences:

- Disney Treasure is off to a “spectacular” start w/ selling out rooms: A high % of people are rating it excellent; Expect this ship to be profitable in its first quarter in the water

- Lightning Lane is launching, but it’s a product that “we are learning how to use, so we are marketing it very gently initially”: It is in line w/ expectations, but “we are moving slowly”; It’s going to build over time

Lays Out More Details On Flagship ESPN DTC Timing

- FQ1 Sports revs were ~flattish y/y

- Domestic ESPN ad revs +15% y/y

- FQ1 Sports op income incr’d +$350mn y/y to $247mn

- Flagship ESPN DTC is still slated for “fall” 2025 – the goal is to make ESPN as accessible as possible: The Co is “leaning in”; Enhancements include “some form of betting, and fantasy, a high degree of customization and personalization, and essentially a much bigger offering in terms of product programming than the linear channels currently offer”

- Have opportunity to bundle it with Disney+ and Hulu

- Will be “really smart and strategic about pricing there”

- If users happen to subscribe to Disney+ and Hulu, then they can experience ESPN flagship in a one-app experience

- “Flagship is not really designed to preserve a business. It’s designed to grow a business”

- Impact of skinny bundles? “Plan to take advantage of the emergence of these bundles because it is a great way to distribute ESPN”

- There were some analyst concerns about the cost of the NBA rights, given the weaker season to date ratings and the step-up next season, but mgmt. reiterated its optimism about the rights and that economics are baked into the ESPN guidance, which they are committed to

Not Ruling Out M&A Of Small Cable Networks But Linear Networks Are Viewed As “Assets”

- View linear networks as “assets”: Linear networks at our company “are not a burden at all”; The Co is programming them and funding them at levels that actually give them the ability to enhance the overall TV business

- M&A? “Won’t rule out the possibility some of the smaller networks in some form or another in being configured differently in terms of how we bring them to market, maybe even ownership, but we’re not right now”

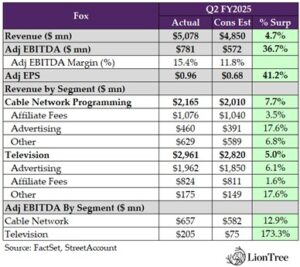

Fox Outshines The Field This Qtr And Looks To Make A Play Into DTC

Unlike the debate following Disney’s results (see Theme #4), Fox’s FQ2 delivered a landslide victory across all fronts, as higher political advertising, strong MLB postseason ratings and NFL pricing, continued growth at Tubi, and robust news ratings and pricing all helped drive an easy beat across revenue and adj EBITDA. The outperformance was driven by both segments, as Cable Networks and TV Stations posted sequential accelerations and topped both revenue as well as adj EBITDA estimates.

On the advertising side, y/y growth accelerated sequentially across both the segments, and that momentum has been continuing into FQ3 across the portfolio. Most timely is the upcoming Sunday Super Bowl 59, which sold out ad slots and saw “record pricing.” Notably, Tubi is set to stream the Super Bowl for the first time (alongside the regular broadcast) after the service posted a +31% y/y increase in ad rev in FQ2, which was an acceleration even when excluding political revenue. Despite plans to “step on the gas a little bit” for the Super Bowl in terms of investments, it remains on track to meet its profitability goals.

FOX News was also particularly strong in the quarter, given the election, and those share and ratings gains have sustained. To capitalize on the strength, the focus remains on expanding distribution of not only FOX News, but the other core FOX channels as well as across traditional, digital, and DTC. The rise of “skinny bundles” has been a key avenue to accomplish that. The company is “very pleased” with the ride of the “skinny bundle,” as it works out to be both “financially and economically a positive.”

Finally, and arguably the biggest announcement out of the call, was that Fox would be launching its own DTC streaming service by the end of 2025. While they continue to remain “huge supporters” of the traditional cable bundle, the goal of the new streaming service will be to reach the “large population” of cord-cutters and cord-nevers.

See below for our key highlights and takeaways from the call…

-> Fox shares rallied +4.8% post results and is the best performing media conglomerate YTD, up +8.7%

Fox Unilaterally Beat Expectations In FQ2

- It was knockout qtr across the board in FQ2, w/ profitability being the standout

- Total revs – beat by +4.7%: Grew +20% y/y (accel from +11% y/y in FQ1)

- Adj EBITDA – beat by +36.7% (and was an FQ2 record): Grew +123% y/y (accel from +21% y/y in FQ1)

- Adj EPS – beat by +41.2%

- Cable Networks – rev beat by +12.5% and adj EBITDA by +18.5%

- Rev grew +31% y/y

- Adj EBITDA grew +16% y/y

- TV Stations – rev beat by +1.7% and adj EBITDA beat by +7.3%

- Rev grew +16% y/y

- Adj EBITDA grew to $205mn from -$138mn in the prior year’s qtr

Demand For News & Sports Has Not Abated… FOX News Viewership Shows No Signs Of Slowing Down & Expectations Are High For The Super Bowl

- FOX News once again ended the qtr as the most watched cable network in total day and in primetime, growing total day audience by ~+40% y/y, and prime time audience by +45%y/y

- FOX News saw 4.5bn hours of content consumed across its platform in FQ2

- FOX News posted its highest qtrly share of primetime cable news audience in its history, at over 60%, which includes a 70% share in December

- This was more than double the viewing of its closest competitor

- Saw an uptick in “non-traditional media sources” during the past election cycle – “We view these new media markets opportunistically and as central to our growth strategy”

- Increase in consumers who either supplement or solely accessed their news and information from “non-traditional media sources”

- On YouTube, FOX News generated ~410mn views in January, beating their closest competitor, NBC, by ~2.5x

- Looking into FQ3 – Momentum has cont’d w/ FOX News FQ3-to-date ratings are up over +50%, prime time ratings are up over +40%, delivering FOX News a 69% share of prime time cable news audience

- On sports… “Autumn is traditionally the strongest time of year for FOX Sports, and 2024 was no exception”: Driven by Major League Baseball World Series, college football expanding to Friday nights, and the NFL (which “remaining the most watched content in all of television)

- FOX was the leader in consumption of live sports events in FQ2

- Next big event is this Sunday’s Super Bowl LIX

Tubi Continues To Be A Big Driver To Overall Ad Revenue & Super Bowl Streaming Is The Next Catalyst

- Tubi’s audience reaches those viewers not in the traditional cable universe: Audience is 65%+ cordless, made up of cord-nevers and cord cutters

- Tubi was a “strong” contributor ad rev growth, up +31% y/y and accelerated even when excluding political rev

- Tubi will livestream the Super Bowl for the very first time, which will afford Tubi “an opportunity to engage a large cohort of new users”

- After the game viewers will have access to Tubi’s library of 275k+ movies and TV episodes

- Cost? “There’s some technology streaming costs, obviously, but it’s tiny compared to the opportunity in front of us. So, very low incremental costs”

- Benefit? “Tremendous exposure”; “A lot of first-party data….[which] is really critically…and will help us drive our CPMs”

- “It’s not necessarily a big change in strategy, but it’s a huge opportunity for Tubi, and it’s something we were very keen to focus very intensely on”

- On the road to profitability: Investment in Tubi has reduced this yr as the biz continues to scale; Will continue to invest throughout this year and next before it reaches profitability

- Will “step on the gas a little bit” when investing for Super Bowl in FQ3 “to take max advantage of the marketing and user acquisition that comes with that”

- “To the extent that we see more opportunities and we’ll remain opportunistic, but at the moment, we’re bang on track”

- “On schedule to meet our breakeven profitability as per our […] business plans and expectations for the business”

Broad-Based Strength Across Advertising In FQ2 Is Expected to Continue Into FQ3

- Total ad revs were up +21% y/y (accel from +11 y/y in FQ1), with broad-based strength across their portfolio, including “significant” political ad spend collected at their local stations, “strong” MLB ratings and “robust” pricing across key sports properties, continued growth at Tubi and “strong” engagement at News

- Cable ad revs grew +32% y/y (accel from +11% y/y in FQ1) driven by the strength in FOX News linear ratings and digital engagement and supported by “healthy” pricing in both national and direct response; Additionally, Sports ad revs benefited from higher MLB postseason ratings

- TV ad revs grew +19% y/y (accel from +11% y/y in FQ1), boosted by political ad revs, “strong” MLB ratings and pricing strength across their sports schedule, and continued growth at Tubi

- FOX News, in particular, is seeing “really a tremendous amount” of new advertisers come to the platform, driven by strength in ratings and momentum post the presidential election and inauguration

- “We’ve seen over 100 new clients who have not been FOX News advertisers with major national clients come on to the platform…that’s driving demand and driving pricing”

- Looking into FQ3 – Ratings and revenue are accelerating from FQ2; “Advertising strength has continued into our fiscal third quarter, where we are seeing very healthy trends across our portfolio”

- NFL postseason broadcast of the Wild Card Divisional and NFC Championship saw their “highest ever” unit pricing and demand for these matches

- Super Bowl 59 saw “record” pricing and is sold out

- FOX News ad trends across DR and national ad categories are “strong”; Seeing increased demand from both existing blue-chip advertisers and new clients due to FOX News record share of audience

- In entertainment, scatter pricing is tracking at HSD above upfront levels, and cancellation options are at “historical lows”

Announced Plans To Launch A DTC Product By YE To Reach Cord-Cutters And Cord-Nevers

- Continue to remain “huge supporters” of the traditional cable bundle: “We see the traditional cable bundle as still the most value for our consumers, and frankly, the most value for the company”

- “This service will be a package of our existing content on existing brands targeted at consumers that are not currently in the bundle”

- Do not expect to have any exclusive rights costs or additional incremental rights costs

- Offering is meant to target cord cutters and cord-nevers “that are not traditionally in the cable bundle”

- “So, the incremental cost will be relatively low, certainly relative to what our peers have spent in this space”

- Subscriber expectations will be “modest” and will price the service “accordingly”, given that “we don’t want and we have no intention of churning our traditional distribution customer into our D2C customer”

- Targeting launch by end of this calendar year

Pricing Gains And Subscriber Declines Are Helping Drive Affiliate Growth

- Total affiliate revs grew +6% y/y (in-line w/ FQ1)

- Cable affiliate revs grew +4% y/y (vs +3% y/y in FQ1) as pricing gains from affiliate renewals outpaced the impact from net subscriber declines

- TV affiliate revs grew +9% y/y (vs +10% y/y in FQ1), as healthy growth in fees across FOX owned and affiliated stations more than offset the impact from industry subscriber declines

- Have completed all affiliate renewals that will impact FY25

- Subscriber declines improved for the second consecutive qtr: Went from “a touch under 8%” last qtr to ~7%

- “I think there probably is some seasonality in subscriber trends with, obviously, being in the middle of an energized and exciting sports season…but we are very heartened by the trends moving in the right direction”

- “Hopefully, the skinny bundles continue to see that trend continue…but it’s too early really to say that’s having a major impact”

- What’s driving the pricing gains? “A very focused portfolio of channels that distributors really want” AND a “distribution strategy that prioritizes the bundle”

- “As we’ve said for the last five years, we think that strategy of both content and distribution should lead us to take share of wallet. And I think we’re starting to see that”

Growing Adoption Of “Skinny Bundles” Is A Net Positive For Fox

- “Only disappointment” in sports was that they were not moving forward with Venu…: “In the end, the legal distractions around the business became increasingly difficult to bear”

- …BUT “continue to be focused on maximum distribution of our content, whether that be traditional, digital streaming or our own D2C offering in the near future”

- Bullish on growth in skinny bundles: “Encouragingly, the distribution market has made some major strides recently”; Have seen the launch of several smaller, lower cost bundles of sports, news and broadcast networks “and we expect this trend to continue”

- “We’re very pleased with this trend of the bundle. It’s financially and economically a positive for us”

- Stronger economics vs what Venu could have given them: Inclusion of FOX’s Sports and News channels in new skinny bundles is “a real economic benefit to us, even more so than the sports-specific Venu”

- Financial benefits from skinny bundles are about the same as traditional bundles, as nearly all of Fox’s core channels (FOX Network, FOX News, FOX Business, FS1, FS2, and Big Ten Network) are included

Sports Betting Licensing Will Take Some Time, But Also Have Plenty Of TIme

- Sports betting licensing process is “a relatively complicated one, but it’s moving forward”: Talking to ~26 states for licensing; “We expect there to be sort of no significant hurdles with that process, but it will take time”

- Option is not due for another 5 yrs (end of 2030) BUT “we would expect to get licenses very significantly before that”

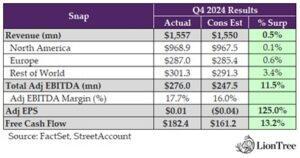

Snap & Pinterest: A Tale Of Two Cities In Q4

After updates out of Alphabet and Amazon that highlighted strong digital ad growth amongst these market share leaders (see Theme #2 and Theme #3) as well as previous volatility with Pinterest and Snap’s results, it was hard to gauge what to expect this week from the latter, and it ended up being a tale of two cities. Starting with Pinterest, after two quarters in a row of double digit sell-offs post earnings, this quarter’s strong Q4 and solid Q1 guide was very favorably received. The company reached key milestones, including its first-ever $1bn+ revenue quarter, a record high in MAUs, and its highest-ever user engagement.

The holiday season was a key contributor to those results, as Pinterest hit a record revenue volume during Cyber 5, while simultaneously reducing CPAs by over -30% y/y. The company has also made significant progress in filling gaps in its auction, advancing its ability to ingest demand from a variety of sources. This improvement, coupled with a strong focus on lower-funnel tools, is expected to drive continued growth in 2025. A major focus remains on the development and adoption of Performance+, with new features and functionality set to be released in 2025. Pinterest anticipates the role of third-party demand will continue to decrease as its core first-party business grows, which strengthens direct advertiser relationships and is a positive dynamic for the platform. Looking ahead, the company pointed to all the aforementioned levers as drivers behind continued growth in 2025 as well as further share gains in key verticals, including retail and emerging categories like financial services and technology,

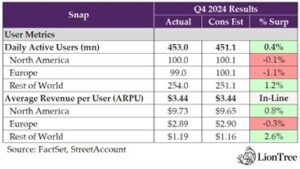

On the other hand, Snap’s Q4’s beat across the top-line and across all geo segments was overshadowed by weak Q1 guidance, especially a -27% miss on adj EBITDA due to investment plans. Q4 DAUs also beat by a hair, with almost all the growth coming from RoW, and the outlook for next qtr was ~in-line with the Street’s expectations. The company is focused on building “a more resilient”, “performance-based,” and “diversified business,” with investments planned, including an +8-10% increase in headcount through 2025.

The advertising business continued to show resilience, with SMB adoption and improved ad products driving direct response ad growth, though brand-oriented ad revenue remains a challenge. New ad formats like Sponsored Snaps and Promoted Places are showing promising early results. Outside of advertising, Snapchat+ subscriptions more than doubled y/y, net adds accelerated q/q to reach 14mn total subscribers, and price increases are being explored to drive ARPU growth in the long term. Also in the works is Simple Snapchat, which is being used by 25mn+ Snapchatters in almost every country. Engagement trends are encouraging, but there are things that need to be worked on before a broader rollout over the coming year.

There was a whole lot that was discussed across the two companies…see below for our takes on the most incremental updates and developments.

-> Pinterest jumped +19.1% on the back of its report and ended the week up +21.4%; On the other hand, after initially surging ~12% after hours, Snap’s stock ended the day post earnings down -8.7%, It slightly rebounded over the next few days and closed the week down -3.3%

Starting off with Pinterest’s Report…

PINS – Posted A Strong Q4 And Achieved Its First $1bn+ Rev Qtr

- Q4 rev – BEAT by +1.2% (and was PINS first ever $1bn+ rev qtr): Grew +18% y/y (in-line w/ Q3) to reach $1.2bn

- UCAN – ~IN-LINE: Grew +16% y/y, with strength coming from retail and emerging categories, including technology and financial svs

- Europe – BEAT by +3.4%: Grew +21% y/y (+20% ex-FX), with strength driven by retail

- RoW – BEAT by +8.0%: Grew +44% y/y (+53% ex-FX)

- Q4 adj EBITDA – BEAT by +5.6%: Reached $471mn (41% margin, ~+300bps y/y)

PINS – Q4 Net Adds Drove MAUs to a Record High, While Strengthening Engagement Among the Most Mature Users

- Global MAUs reached another record high of 553mn, growing +11% y/y (in-line w/ +11% y/y in Q3)

- WAU/MAU ratio reached an all-time high of 62%

- “Sign of deepening engagement even at record number of users”

- Ratio is highest in more mature regions, like UCAN and Europe

- Users continues to grow y/y across all geographies in Q4

- US and Canada MAU +4% y/y

- Europe MAU +7% y/y

- RoW MAU +15% y/y

- Gen Z is increasingly their largest and fastest-growing audience

- ARPU also grew seq and beat expectations across all regions

- Looking ahead… “while we don’t guide to users, I think the effects that we see, we believe, are durable and based on the uniqueness of our platform and we continue to focus on that as we look ahead”

PINS – Q1 Guidance Came In Well Above Expectations (Profitability Was A Standout)

- Q1 rev guidance – BEAT by +1.1% @ midpt: $837mn-$852mn vs cons $835.7mn

- Q1 adj EBITDA guidance – BEAT by +15.2% @ midpt: $155mn-$170mn vs cons $141mn, implying 13-15% y/y growth (+15-17% ex-FX)

- Reflects the effects of lapping Leap Day and the earlier Easter timing in Q1:24

PINS – Looking Ahead To 2025…Doubling Down On Several Multi-Year Initiatives To Continue To Drive Growth

- Will continue to grow the user base and deepen engagement and bring back users more frequently through efforts in actionability and curation

- Will continue to leverage AI and “unique” first-party signal to drive “a more personalized and relevant” experience for users

- Will continue to complement their “strong and growing” first-party business through new sources of demand, as they’ve done through the launch of resellers and 3P partners

- See room to further grow ad load, particularly in high-intent surfaces and verticals on the platform, and for users that are in a commercial mindset

- Will invest in curation experiences and the shop-ability of the platform to allow users to move more seamlessly from inspiration to action

- Will continue to innovate and improve lower funnel tools, allowing advertisers to successfully reach customers who are demonstrating high commercial intent

PINS – Q4 Ad Trends Highlight Continued Impression Growth, Record Holiday Revenue and Accelerating Lower-Funnel Adoption

- Q4 ad impressions grew +43% y/y (vs +41% y/y in Q3), and ad pricing declined -18% y/y (vs -17% y/y in Q3)

- Efforts to begin serving ads and monetize intl markets or previous gaps in their auction have been accretive to net revenue

- HOWEVER, as these initiatives have scaled, it has naturally led to an increase in ad impressions growth and downward pressure on overall global platform pricing due to this ongoing mix shift

- Saw over +90% y/y growth in clicks to advertisers, even after lapping the initial impact of direct links from Q4:23 that drove four consecutive qtrs of more than +100% growth

- Saw largest-ever rev volume over the Cyber 5 holiday shopping period WHILE simultaneously decreasing CPAs by 30%+ y/y

- Created personalized gift guides across 27 categories with 40k+ products, resulting in +40% higher click-through rates via personalized recommendation modules

- Retailers who showcased special offers by including a promotion for their conversion saw an +18% increase in conversion rate compared to those ads w/o a promotion

- Lower-funnel adoption is accelerating, particularly amongst their bigger advertisers

- For some of Pinterest’s largest advertisers, 80%+ of their spend is now tied to lower-funnel objectives, which is up “significantly” over the last two years and “significantly” higher than the overall platform mix

- Have been steady gaining share of performance-driven budgets amongst their “most sophisticated advertisers,” capturing ~5% of total ad budgets and 10%+ of digital ad budgets

PINS – Retail And Emerging Verticals Were Strong, Partially Offset By Softness Within Food & Beverage

- Retail: “Continue to see broad-based strength”; “Been strong for us in 2025, and there’s certainly more room to grow there in 2025”

- “Emerging verticals” – financial svs and technology: “Continue to be a nice driver for us”

- Saw strength in both categories in Q4 “and really much of 2024”

- These are ad verticals with bns of dollars in digital ad spend, “and we still have a very small percentage market share today. So, we see lots of opportunity there”

- Food and beverage: Was softer in 2024 due to category-specific headwinds, but are now lapping the early stages of that softness, which started in Dec 2023

- Expect overall drag to top line rev to “lessen slightly” in Q1 “as we start to see very early signs of green shoots in that category…it’s too early to say the headwind is fully behind us”

- Did not see benefit from election-related spend in Q4, as PINS does not accept political advertising

PINS – Growth In First-Party Demand Is Reducing The Need For Third-Party Partnerships

- 3P demand “was targeted at rounding out gaps” in their auction, “with a particular focus on improving shop-ability as a complement to our first-party sales effort”

- Have seen “great progress” on multiple fronts in rounding out those gaps

- “Our platform is more shoppable than ever”

- “Driving strong first-party demand…and new demand efforts providing a complement when needed”

- “Enhanced our ability to bring in programmatic demand as well as demand through resellers”

- As a result – search results are +2x as relevant as they were two yrs ago

- “As the core first-party business grows, it reduces the need for third-party demand…that’s a very healthy dynamic for our overall business”

- Advertisers are coming to them directly, “which is what we want,” and “we’re finding we have fewer gaps in our auction, especially in our more mature markets”

- “Capability to ingest demand from many sources…and thereby reduce gaps in our auction, is more advanced than it’s ever been, which allows us to respond more dynamically when and if there are shifting demand patterns. So, this is an area that we’ll continue to optimize and advance as we move forward”

- Will NOT break out rev from 3P partners or resellers separately: “We’ve noted these initiatives were new and began to scale in 2024 with each quarter ramping sequentially. And we’ll continue to test and optimize as we move forward”

“More Of The Opportunity Is In Front Of Us Than Behind Us” On Performance+

- As a reminder, “Performance+ is a key advancement in our lower funnel ad product suite that utilizes AI to bring greater performance and better efficiency to our advertisers while automating much of the campaign setup process”

- “We’re at the beginning of a multi-year product cycle for Performance+”: “Don’t think of these as moments in time or as a hockey stick in a given moment. These have a steady build over time and a compounding effect of these things as they build on each other”

- Looking into 2025… “Will continue to release new features and functionality while simultaneously continuing to drive adoption and increase the percent of revenue eligible to take advantage of key features within the automation suite”

- Will roll out Performance+ to the lower funnel with more granular bidding functionality, allowing advertisers to effectively bid on a “wider swath” of their catalogs

- Advertisers will require 50% less inputs to create a campaign, “and that’s a significant improvement in campaign setup”

- “Doubling down” to give advertisers more creative control: Including automated cropping, adjusting image brightness, and adding logo overlays so their brand is present, all of which is expected to roll out in H1:25

Shifting Over To Snap’s Earnings Print…

SNAP – Beats Across The Business In Q4 (With Adj EBITDA & EPS Particularly Standing Out)

- Q4 rev – BEAT by +0.5%: Grew +14% y/y (a slight decel from +15% y/y in Q3)

- Amer rev grew +8% y/y (vs +9% y/y in Q3) with the relatively lower rate of growth due to the impact of weaker large client upper funnel demand being relatively concentrated in the region

- Europe rev grew +20% y/y (vs +24% y/y in Q3)

- RoW rev grew +35% y/y (vs +32% y/y in Q3), driven by the continued progress with their DR ad platform and investments in go-to-market operations

- Q4 adj EBITDA – BEAT by +11.5%: Reached $276mn compared to $159mn in the prior-yr qtr, reflecting higher rev and OpEx discipline (similar commentary last qtr)

- Adj EBITDA flow-through was 60% in Q4 (up from 50% in Q3), reflecting seasonally higher rev in Q4 and continued prioritization of investments to drive topline growth and deliver improved financial performance

- Q4 FCF – BEAT by +13.2%: Reached $182.4mn vs cons $161.2mn

SNAP – But Q1 Guidance Beat On Rev But Missed Big On Profitability Expectations + Preliminary Plans To Invest “Productively” In 2025

- Q1 rev guidance – BEAT @ the midpt: $1.325bn-$1.36bn vs cons $1.33bn, implying +11%-14% y/y growth (but seq decel at midpt from +14% y/y in Q4)

- Q1 adj EBITDA –MISS: $40-$75mn, which was well below cons $78.7mn due to some investment plans

- Some preliminary 2025 guidance… “Our investment plans for 2025 reflect… optimism, alongside a strong commitment to make further financial progress towards profitability as we scale”

- Expect to grow full time headcount by +8-10% over the course of 2025

- Infrastructure cost per DAU will be b/w $0.82-$0.87 per quarter in 2025 (was $0.84 in Q4)

- Expected to rise through the year driven by planned investments to move toward even larger models and near real time model refreshes

- FY OpEx b/w $2.7-$2.75b, driven by higher legal costs associated w/ litigation and compliance

SNAP – Focused On 5 Key Initiatives In 2025 “To Build On The Momentum We Established In 2024”

- New ad placements – Sponsored Snaps and Promoted Places

- Provide advertisers w/ incremental reach while enabling them to connect with the Snap community “in unique and personalized ways

- Improving go to market process

- By providing advertising partners with actionable insights and introducing automated campaign optimization tools to enhance performance

- Rolling out a simplified Snapchat experience

- Designed to improve accessibility and usability for Snap users

- Continue to advance machine learning infrastructure

- To drive higher-quality ad interactions

- Expand developer ecosystem

- By enhancing tools to simplify AR creation, and increase the number of Spectacles experiences that can bring AR into everyday life

SNAP – DAUs Were Mostly In-Line, With Majority Of Net Adds Coming From RoW / Continue To Prioritize User Engagement And Creator Onboarding + Monetization Opptys

- Q4 – DAUs BEAT by +0.4%: Grew +9% y/y (in-line w/ Q3) to reach 453mn (incr’d +10mn seq); Overall ARPU was in-line with estimates

- Amer DAUs were ~flat q/q and y/y at 100mn

- Europe DAUs were ~flat q/q and up +3mn y/y to reach 99mn

- RoW DAUs were up +10mn q/q and up +36mn y/y to reach 254mn

Q4 – DAUs outlook was ~in-line: Expected to grow +6mn q/q or +37mn to reach 459mn vs cons 458.3mn

- Global time spent watching grew y/y (did not specify exactly how much vs +25% y/y last qtr), driven primarily by strong growth in total time spent watching Spotlight

- For users – introduced new features in Q4 to “inspire creation and help our community strengthen their relationships through Snapping”

- Launched new Bitmoji stickers based on new trends for Snapchatters to react and express themselves visually

- Announced new location sharing features in Family Center, Snap’s in-app hub for parental tools and resources, making it easier for families to stay connected while on the move

- Launched new and early access Snapchat+ features including Footsteps, which helps Snapchatters keep track of the places they’ve visited on the Snap Map and new app themes and custom backgrounds

- For creators – continued to invest in content creation tools and a “diverse” set of monetization oppties in Q4

- Prioritized “authentic creators and timely original content”

- e., comments on Spotlight videos within 24 hours of submission increased “significantly” in Q4, driven primarily by fresher content, leading to “deep” engagement b/w Snapchatters and content creators

- New unified Monetization Program that allows eligible creators to monetize Spotlight videos

- Builds on existing Stories Revenue Share Program that helps creators monetize their Stories

- # of creators posting content grew 40%+ y/y in Q4 (vs +50% y/y in in Q3)

- 1bn+ Snaps were shared publicly on Snapchat every month in Q4 from Snap’s community, creators, and media partners

- Prioritized “authentic creators and timely original content”

SNAP – SMB Adoption & Improved Ad Products Drove DR Performance, While Brand-Oriented Is Still On The Road To Recovery

- Q4 total ad rev grew +10% y/y (in-line w/ Q3): Driven primarily by growth from DR ad rev (similar commentary in Q3)

- Q4 direct response ad rev increased +14% y/y (vs +16% y/y in Q3)

- Q4 brand-oriented rev was down -1% y/y (in-line w/ the prior two qtrs), driven by continued weakness concentrated among “a relatively small” group of large clients focused largely in North America

- Continue to be focused on reaccelerating demand for upper funnel brand rev (similar commentary last qtr)

- SMB active advertisers doubled y/y in Q4 and were the largest contributors to ad rev growth in 2024, driven by a combination of more performant DR products, improved go-to-market operations optimized for SMB customers, and a simplified buying experience

- More broadly – “the overall growth in revenue […] is going to come even more from folks as they either grow into the medium advertiser segment or that start out there. And the key there is really about ease of getting started”

- Strong demand for Pixel Purchase and App Purchase Optimizations continues, which are becoming a more meaningful contributor to topline growth

- Began testing Sponsored Snaps and Promoted Places in Q4 and seeing promising results

- Looking into Q1… plan to roll out Sponsored Snaps and Promoted Places to addtl markets; Will also begin limited testing of Pixel Purchase optimization for Sponsored Snaps as the placement is made available for lower funnel bidding objectives

- Best ad performance has been coming from verticals where they’ve built “great” product market fit

- Retail, CPG and health and wellness are seeing “really good results” after rollout of 7-0 pixel purchase optimization a year and a half ago, and that’s been a “very big” driver of the DR biz over the last yr

- Gaming, retail, e-commerce, and financial services saw increased adoption following mid-2024 updates to app-based optimizations, which leveraged a new ML architecture and product stack and drove 70% YoY growth in app purchase optimizations in Q4

SNAP – Simple Snapchat Is Showing Promising Trends In Engagement, But Still Some Work Required Before A Broader Rollout

- Expanded test of Simple Snapchat in Q4: To 25mn+ Snapchatters “in nearly every country” Snapchat is offered (up from ~10mn across “dozens” of countries last qtr)

- “Continue to see encouraging trends in engagement metrics,” including –

- Increased content active days among less frequent and more casual users

- Greater share of time spent watching content vs than scrolling to find something to watch

- Preparing for a broader roll out over the coming year

- “Two big puzzle pieces that we’re still working on” –

- Migrating Story ad demand from the Stories page tiles to in-feed or Sponsored Snap units

- Addressing engagement losses among users who prefer the tile-based Stories page

- “We’ve got a number of ideas on how we can solve both of those pieces, and we’re going to work on rolling those out in the coming weeks and month”

- No material impact included in Q1 revenue and user growth forecasts

Snapchat+ Subscribers Growth Accelerated Seq, And Price Increases May Be A Consideration In The Future

- Other rev “more than doubled” y/y (in-line w/ commentary last qtr) to reach $143mn: Includes all non-advertising rev, the majority of which is Snapchat+ subscription rev

- Snapchat+ subscribers reached 14mn (up from 12mn+ in Q3 and 11mn+ in Q2)

- “Think there will be room for some price increases”: “And I think folks have indicated that they’re getting a lot of value from Snapchat+. So that may be another avenue in terms of growing ARPU over the longer term.”

SNAP – Mostly Optimistic Views On Emergence Of DeepSeek And Uncertainty Around TikTok

- View on DeepSeek – “It’s been really inspiring to see the innovation there”

- “It just further validates our view that a lot of these models are going to continue to become commoditized over time and, obviously, are going to become more and more efficient to run”

- “I think right now, we’re just sort of in early experimentation phase with some of their open-source work”

- View on TikTok – “The overall environment of uncertainty is benefiting our business”

- Any benefit from blackout? “Some of the changes with TikTok, they’ve sort of been an imperfect experiment. So, we’re not trying to draw too many conclusions from some of the engagement that we saw when the app went dark for that brief period of time”

- “A big priority for us is really just helping make sure we support advertisers and creators during this period of uncertainty”

- Advertisers – “very focused on contingency planning and diversifying their spend”

- Creators – “are really thinking hard about how they can build the most diversified engagement with their fan base across various platforms, including Snapchat”

Continue To Make Headway In AI And AR Initiatives, Particularly On Lens

- Developed “groundbreaking” AI model capable of generating high-resolution images on mobile devices “in just seconds”: The on-device model can produce images in 1.4 seconds on an iPhone 16 Max

- Will bring this technology into production in the coming qtr

- Expanded Lens Creator Rewards program and introduced new Lens Challenges: Designed to reward the top Lenses built by the community and help AR creators monetize their AR Lenses

- Introduced the first two-person genAI Lens, which uses generative AI to create a personalized selfie together with a friend

- Also introduced the new Me in the 60’s Lens, which enables Snapchatters to transform into a ‘60’s version of themselves

- Was viewed 900mn times

- Launched Easy Lens in Lens Studio 5.4, an AI-powered tool that simplifies creation by enabling users to create and customize Lenses through text prompts

- 3k+ Lenses have been published using Easy Lens within a month of launch with Snapchatters engaging with these Lenses ~300mn times

Spotify Continues To Break Away From The Pack

After ending the year with a better-than-expected set of Q4 results, Spotify now moves into a year of “accelerating execution.” It will all be about pumping out new products and features at a swifter pace, and profitably. The company is doubling down in music and will invest more in video, hence while margins are targeted to be up again in 2025 vs 2024, the level of improvement will be at a moderated rate vs what they delivered y/y in 2024. Price adjustments are part of the toolkit looking ahead, and the new super premium tier will be a key catalyst when it launches this year (no official date set but expected in H1). The next phase for the music industry will be launching other types of segmented tiers, meaning pricing plans will no longer be a one-size-fits-all.

For the quarter itself, the +555bp y/y improvement in gross margins (especially driven by the Premium business and lower content costs) was a key highlight on the back of better-than-expected revenues. MAUs and ARPU were both better than anticipated (the company posted an impressive ~+double-digit% y/y growth in MAU and subs in Q4). That is all a good formula. “Wrapped,” as usual, was a big contributor to Q4 performance with 245mn users engaged, surpassing 2023’s record. Management also called out a competitor exiting select “developing” markets as a MAU driver in the quarter. On the ad-supported side, the build remains a work in progress, and it will become more of a 2026 story.

See below for more of our thoughts and perspectives regarding the key themes from Spotify’s earnings update.

–> SPOT shares rallied strongly at +13.2% on the day (this is the 5th qtr in a row of strong stock reaction to results), and ended the week up +13.6%; YTD the shares are up +39%

It Is Hard To Argue With The Q4 Headline Results & Q1 Guidance Was Constructive Though A Seasonally Slower Qtr

- Total revs BEAT cons by +2.2% and grew +17% y/y (+16% y/y ex-FX) vs +19% y/y in Q3

- Q1 outlook – Rev of €4.2bn was +1% ahead of cons; Assumes ~+90bp y/y benefit from FX

- Operating income beat by cons +2%, though margins were a tad light, given Social Charges were +€80mn above forecast due to share price appreciation during the quarter

- Q1 outlook – Op income of €548mn was a sizeable +19% ahead of cons; Includes -€18mn in Social Charges

- Big step up in FCF… reached €877mn in Q4, bringing 2024 FCF to €2.3bn

- 2025 outlook – Expect FCF to “meaningfully exceed” 2024 levels

- What about cash returns to shareholders?

- The top priority is investing in “sustainable growth opportunities” with “attractive return potential” but “to the extent capacity rises, we will, of course take our shareholders into consideration”

- Total MAUs beat cons by +1.6%

Margin Expansion Was A Key Positive & Expect More Of The Same In 2025, Though At A More Moderate Rate, Given Planned Investments

- Notable upside in the Q4 gross margin was due to upside vs cons in Premium (primarily due to content cost favorability): 2% vs cons 31.9% (+555bps y/y)

- Premium posted very strong improvements due to Audiobooks, music, and Other cost of revenue

- Ad-supported gains (but missed), driven by music and podcast (partially offset by real estate impairment activity)

- Q1 outlook – Gross margin at 31.5%, topped cons 31%

- 2025 gross margin & operating margin are guided to improve y/y “albeit at a more moderated pace relative to last year’s exceptional levels”

- Plan to make targeted investments in core offerings

- May make seq gross margin cadence “a bit more variable” over the course of this year

- But Q4:25 is expected to be higher than Q1 due to seasonality

- Expect more of the profitability growth to come from developed markets vs emerging markets, but over time emerging market like India will be profitable

A Competitor Exiting Select “Developing” Markets Helped Drive MAUs

- Total MAUs rose +12% y/y and grew +5.5% q/q… 35mn total MAU net adds was largest Q4 in history (beat guidance by +10mn)

- Wrapped campaign ~+double-digit% y/y growth in user engagement across 184 mkts

- Had an exceptionally strong Q4 w/ outperformance driven by developing markets

- Grew in all regions, led by RoW and LatAm

- Aided by a “shift in competitor dynamics in select developing markets”

- Q1 outlook – MAUs at 678mn were line w/ cons 678.3mn (implies +3mn new MAUs)

- The Co is “not prioritizing retention of the recent influx of lower engagement users in Q1 as we continue to focus on growing higher-value users”

- This will amplify typical Q1 seasonality

- 2025 MAU commentary – Expect net additions to be w/in the range of the last four years

Premium Business Was Much Stronger Across The Board & Focused On Customer Quality

- Q1 Premium business delivered much stronger across the board with especially strong performance with gross margins

- Revenue (87% of the total) rose +17% y/y (+19% CC) vs +21% in Q3 and beat cons by 1.5%

- Gross margin was stronger than expected at 34.7% vs cons 33.9%

- Subscribers grew +11% y/y to 263mn vs cons 259.93mn (+4.4% seq) led by RoW

- Q1 outlook…total Premium subs of 265mn (implies 2mn net new subs vs 3mn in Q4 due to Q1 seasonality)

- “Expect another year of healthy growth with a focus on customer quality and improving LTVs”

- ARPU grew +5% y/y (+7% CC) and beat cons (€4.85 vs cons €4.73)

- Price increase partially offset by product/mix shift

Ad-Supported Business Is Making Progress With The Build But It Is Still A 2026 Story

- Q1 Ad-Supported revenue (13% of the total) is still in only growing ~+msd% y/y: Rose +7% y/y (+6% CC) vs +6% in Q3 but still beat cons by +6.7% due to higher-than-expected ARPU and MAUs

- Both music and podcast ad revs were driven by impressions sold partially offset by pricing softness; Automated sales channels were the largest driver of overall ad growth

- MAUs BEAT: 425mn vs cons 419.1mn (+5.7% q/q)

- ARPU BEAT: €0.43 vs cons €0.40

- But ad-supported gross margins were below expectations (15.1% vs cons 16.2%)

- Expected roadmap for the ads business… Reiterated that 2025 will be the year of building, and 2026 is “when we think we’re going to get scale”

- Moved from brand to performance sales, but “were late on the ball” and it takes time

- “Saw some early positive progress in our automated sales efforts”

- The technical build is largely complete

- Getting unified supply on their server

- Are opening up from more demand on bidding

- Will look to add more partners (in addition to The Trade Desk)

Pushing Harder Into Video, Making Progress In Education, & The Next Phase Of New Pricing Tiers

- Pushing harder into video podcast

- Seeing higher engagement w/video podcasts… now have 330k video podcasts globally & 270mn users have streamed one

- In Nov, launched uninterrupted video podcasts for premium subs

- Evolved Spotify for Podcasters into Spotify for Creators and introduced Spotify Partner Program

- Intr’d new efforts and tools to help video creators turn their shows into a sustainable businesses

- Seeing a big uptake on video podcasters coming to the platform and adopting the partner program

- Investing heavily in the TV experience for several years, which is an important part of their strategy

- Making progress in the Education category, but it is early days

- Regarding the education & courses product initially launched in the UK, it is “early days,” but they are passionate about the category and “pleased” with developments

- The global entertainment industry is estimated to be btw $2-2.5tn vs the global education marketplace, ex K-12, at the same size

- “We’re not a pure-play entertainment platform. We are also a platform where people spend a lot of time educating themselves already with podcast, with audiobooks. So education is really a quite natural step and extension into that journey”

- The next version of the music industry will tailor the Spotify experience to different subgroups

- Moving from a one-size-fits-all approach to a more specialized experience for users