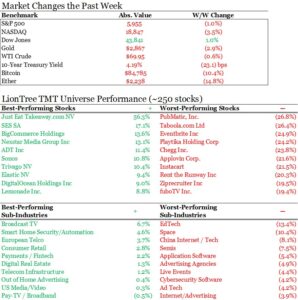

It was a rocky week and the major indices fell, and sharply in the case of Nasdaq, which was down -3.5% (the S&P 500 declined -1%). Uncertainty about Trump 2.0 policies were once again the main event and stoked fear about impacts to inflation and economic growth. February consumer confidence also posted its largest monthly drop since August 2021 but on the flipside, in-line core PCE inflation data was met with a sigh of relief on Friday.

This was the last big week for earnings in the sector and as has been the case for the last several weeks, AI related updates and developments were of particular note. This edition focuses on

- Earnings Scorecard – Week 6

- NVIDIA Continues To Clear High Revenue Growth Bars… But Margins Become A Hot Button

- WBD Has All Eyes On Its North Star…FCF

- Paramount’s Linear To Streaming Shift Will Not Be A Straight Line

- AI Developments Continue At A Fast & Furious Rate

- Instacart’s Cart Is Still Building

- TKO: The 2025 Outlook Disappoints… But All Eyes Will Be On The Upcoming Renewals

- Amazon Shows Up Fashionably Late To The AI Agent & Quantum Wars…

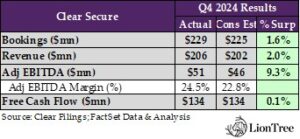

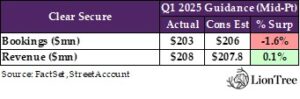

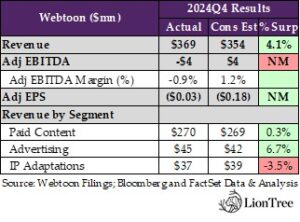

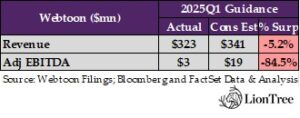

- Quick Take On Other Earnings Out This Week…CLEAR & Webtoon

- Grab Bag: The Biggest Crypto Heist Ever/ Sports Streaming Product Updates/ TikTok Reaches $6bn In 2024 In-App Purchases

Enjoy the read and have a nice weekend.

Best,

Leslie

Earnings Scorecard – Week 6

Despite being in its sixth week, the earnings calendar was intense with 56 companies in our LionTree Universe putting out their fourth quarter prints this week (more than double the 26 companies that reported last week). Stock price reactions were once again biased to the downside, with 38 companies (68%) trading down in reaction and 18 companies (32%) trading up. Chegg was the worst performer, plunging -31.4% post its report, while Nexstar Media Group was the best performer, up +11.1%.

The last of the media conglomerate reports came out this week, and results were flat to up, with Paramount trading up +0.2% post its print (see Theme #4) and Warner Bros. Discovery trading up +4.8% (see Theme #3).

That said, some of the other reports this week had a tougher showing. On the live events front, TKO fell -5.8% after its print (see Theme #7) and similarly on the semis side, NVIDIA fell -8.5% (see Theme #2). However, it was Instacart that saw the largest drop, with the stock falling -12.3% in reaction (see Theme #6).

We also took quick looks at CLEAR Secure and Webtoon, which both fell -6.5% after their respective earnings reports (see Theme #9).

NVIDIA Continues To Clear High Revenue Growth Bars… But Margins Become A Hot Button

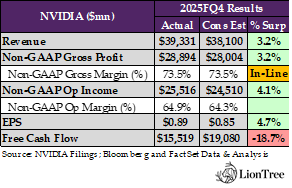

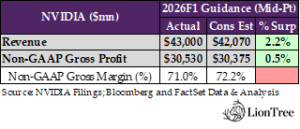

NVIDIA was easily one of the most high-flying stocks of 2024, as its share price jumped +171% over the course of the calendar year. With that comes a high bar for delivering on future growth and earnings. This dynamic was certainly evident this week, with the market reacting unfavorably to NVIDIA’s print despite it reporting top-line growth, non-GAAP gross profit, non-GAAP operating income, and EPS that were ahead of consensus expectations. The main blemish on the company’s print was related to its gross margin, which finished in-line with estimates in FQ4 but were guided lower than the Street anticipated in FQ1, as efforts to ramp up the production and distribution of the new Blackwell chips will result in gross margins remaining in the low-70s% range before rebounding back to the mid-70s% range later in FY26. Nonetheless, several sell-side analysts found the gross margin guide to be slightly concerning, given that it could be a potential sign of growing pricing pressure and competition.

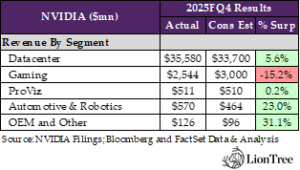

Otherwise, there was still a lot to be optimistic about regarding NVIDIA’s FQ4 earnings. Revenues generated by the company’s core Datacenter business (~90% of total revenue) surpassed consensus forecasts by a comfortable +5.6%, supported by accelerating inference demand as well as customers’ post-training and model customization efforts. CSPs continued to account for ~50% of Datacenter revenues, as Azure, AWS, GCP, and OCI have been among the first to implement GB200 Blackwell systems, utilizing the racks in cloud regions around the world. Notably, NVIDIA’s Blackwell AI GPUs generated $11bn for the company in FQ4 in what CFO Colette Kress deemed “the fastest product ramp” in its history. After the Blackwell launch was delayed by a quarter, production is now “fully ramped,” and demand for the chips has been “extraordinary,” per CEO Jensen Huang.

Additional highlights included the impact of export controls, which have resulted in sales to China tracking “well below” prior levels as a percentage of Datacenter rev, as well as some incremental comments on the Gaming and Automotive segments. The former saw strong demand over the holidays but was negatively impacted by supply constraints, while the latter posted a record quarter and is expected to reach $5bn in revenue in FY26 (a +194% y/y increase), based on recent deals that NVIDIA has signed with Hyundai, Toyota, and other auto OEMs.

See below for more details on what we thought were the most incremental takeaways and insights from NVIDIA’s FQ4 print:

-> NVIDIA shares fell -8.5% in reaction to earnings and finished the week down -7.2%; YTD, NVIDIA stock is down -7.1%

NVIDIA Posted Another Record Qtr, Though Growth Decel’d Seq Across All Metrics

- NVIDIA’s FQ4 headline results mostly surpassed consensus forecasts –

- Revenue rose +77.9% y/y (vs +93.6% y/y in FQ3) and finished +3.2% above cons

- Non-GAAP gross profit grew +70.4% y/y (vs +93.8% y/y in FQ3) and topped cons by +3.2%

- Non-GAAP gross margin of 73.5% (vs 75.0% in FQ3) was in-line w/ cons

- Non-GAAP op income was up +73.0% y/y (vs +101.4% y/y in FQ3) and beat cons by +4.1%

- Non-GAAP op margin of 64.9% (vs 66.3% in FQ3) topped cons’ 64.3%

- Adj EPS of $0.89 closed +4.7% above cons

- FCF incr’d +38.4% y/y (vs +138.4% y/y in FQ3) and missed cons by -18.7%

FQ1 Outlook – Strong Top-Line Growth Is Expected To Continue, But Blackwell’s Ramp Will Weigh On Margins

- FQ1 revenue guidance was better than the Street anticipated: Expects total rev between $42.1-43.9bn, representing a +65.1% y/y increase (vs +77.9% y/y in FQ4) and beating cons by +2.2% at the mid-pt

- BUT FQ1 non-GAAP gross margin was guided below the Street’s estimates: Forecasts non-GAAP gross margin of 71.0% (vs 73.5% in FQ4), which was below cons’ 72.2%; Gross margins are expected to remain in the low-70s% as Blackwell ramps but return to the mid-70s% later in FY26

- Still, the implied non-GAAP gross profit exceeded expectations: The projected non-GAAP gross margin suggests non-GAAP gross profit will increase +48.5% y/y in FQ1 (vs +70.4% y/y in FQ4) and top cons by +0.5%

- Other items included in the outlook –

- Non-GAAP OpEx of $3.6bn (vs $3.4bn in FQ4)

- Non-GAAP other income and expense (ex-items) of ~$400mn (vs $457mn in FQ4)

- Non-GAAP tax rate (ex-items) between 16-18%

The Datacenter Biz Continues To Click On All Cylinders W/ Blackwell Being A Key Driver

- FQ4 Datacenter rev outperformed estimates: FQ4 Datacenter rev incr’d +93.3% y/y (vs +112.0% y/y in FQ3) and topped cons by +5.6%; FY25 Datacenter rev of $115.2bn was up +142.4% y/y

- Compute rev decel’d seq but still more than doubled y/y: FQ4 compute rev of $32.6bn was up +116% y/y (vs 132% y/y in FQ3), driven by customers’ efforts to scale infrastructure to train cutting-edge AI models

- Post-training and model customization have been “fueling demand”: Sees post-training and customization driving “massive” demand, requiring “orders of magnitude” of more compute than pre-training as devs and enterprises have been tailoring models for domain-specific use cases

- Inference demand has been accel’ing: Test-Time Scaling and new reasoning models, such as OpenAI o3, DeepSeek R1, and Grok 3, have been drivers, given that long thinking, reasoning AI can require +100x more compute per task vs one shot inference

- Networking rev was down on both a seq and y/y basis: Networking rev of $3.0bn fell -9% y/y in FQ4 (vs +20% y/y in FQ3)

- BUT is expected to return to growth in FQ1: The Co has been transitioning from small NVLink 8 w/ InfiniBand to large NVLink 72 w/ Spectrum X and sees the latter as a “major new growth vector”

- Compute rev decel’d seq but still more than doubled y/y: FQ4 compute rev of $32.6bn was up +116% y/y (vs 132% y/y in FQ3), driven by customers’ efforts to scale infrastructure to train cutting-edge AI models

- FQ4 end mkt breakdown –

- Large CSPs represented ~half of Datacenter rev: Sales to large CSPs nearly doubled y/y, w/ Azure, AWS, GCP, and OCI purchasing GB200 Blackwell systems for cloud regions around the world

- Regional cloud providers incr’d as a % of Datacenter rev: Driven by cont’d AI factory buildouts as well as rapidly growing demand for AI reasoning models and agents

- Consumer Internet rev tripled y/y: Highlighted an “expanding set of gen AI and deep learning use cases,” including recommender systems, vision, language understanding, synthetic data, generation search, and agentic AI

- Enterprise rev nearly doubled y/y: Supported by accel’ing demand for model fine-tuning, RAG, agentic AI workflows, and GPU accel’d data processing

- The Co sees Enterprise as a “far larger” end mkt than CSPs in the longer-term: Given that heavy industries will require three types of AI – agentic AI, AI factories, and physical AI – to support their manufacturing processes as well as their end users

- FQ4 geographic color –

- The US drove the largest seq increase in Datacenter rev: Cited the initial ramp of Blackwell

- The EU is expected to become a major source of demand in the coming yrs: Given France’s €200bn AI investment and the EU’s €200bn InvestAI initiatives

- China Datacenter sales cont’d to be negatively impacted by export controls: As a % of Datacenter rev, sales to China remained “well below” levels seen before the onset of export controls and are projected to remain at roughly the same % moving forward

- Blackwell GPU sales exceeded NVIDIA’s expectations: The Co delivered $11bn in Blackwell rev in FQ4 to meet “strong demand” for the chips, which have been designed to address the entire AI mkt

- “This is the fastest product ramp in [the] Co’s history, unprecedented in its speed and scale”: Blackwell began shipping in Jan, for reference; Blackwell production is now in “full gear across multiple configurations,” and NVIDIA has been quickly increasing production

- Blackwell clusters will commonly start w/ 100,000+ GPUs: The Co has already started supplying multiple infrastructures of this size

- Blackwell is seeing “great demand for inference”: Many early GB200 deployments are “earmarked for inference,” which is a “first for new architecture”

- A “significant ramp” in Blackwell is expected in FQ1: Given “extraordinary demand” for the product as well as efforts to scale production

- AND Blackwell Ultra is coming in H2:FY26: The next iteration will come w/ “new networking, new memories, and… new processors”; Ultra will “slot right in” alongside other Blackwell chips

- “This is the fastest product ramp in [the] Co’s history, unprecedented in its speed and scale”: Blackwell began shipping in Jan, for reference; Blackwell production is now in “full gear across multiple configurations,” and NVIDIA has been quickly increasing production

- Hopper 200 sales cont’d to see seq growth as well: Highlighted that Meta’s Andromeda advertising engine runs on the Grace Hopper superchip to serve “vast quantities of ads” across Instagram and Facebook

- Hopper chips can still be used alongside Blackwell chips for “less-intensive workloads”: Given that both are CUDA-compatible; This means that customers can continue to utilize the “installed bases of the past”

Color On Other Verticals

- Gaming rev fell short of expectations: FQ4 Gaming rev was down -11.2% y/y (vs +14.8% y/y in FQ3) and missed cons by -15.2%; FY25 Gaming rev incr’d +8.6% y/y

- Supply constraints weighed on FQ4 rev: Nonetheless, demand remained strong throughout the holiday season

- “Strong seq growth” is anticipated in FQ1: Driven by increases in supply

- Professional Visualization rev was slightly better than estimated: ProViz rev grew +10.4% y/y in FQ4 (vs +16.8% y/y in FQ3) and beat cons by +0.2%; FY25 ProViz rev was up +20.9% y/y

- Automotive and healthcare were cited as key verticals that were driving demand in FQ4

- Automotive & Robotics rev finished well ahead of the Street’s forecasts: FQ4 Automotive & Robotics rev incr’d +102.8% y/y (vs +72.0% y/y in FQ3) and beat cons by +23.0%; FY25 Automotive & Robotics rev rose +55.3% y/y

- The ramp in autonomous vehicles was response for “strong growth” in the segment in FQ4

- FY26 automotive rev is expected to grow to ~$5bn from $1.7bn in FY25 –

- Hyundai Motor Group is adopting NVIDIA tech to accel AV & robotics development as well as smart factory initiatives

- Toyota will build its next-gen vehicles on NVIDIA Orin, running the safety-certified NVIDIA DriveOS

- Aurora and Continental will deploy driverless trucks at scale powered by NVIDIA DRIVE Thor

Other Highlights

- Tariffs are “a little bit of an unknown” at this point: NVIDIA is waiting for further clarity from the US govt regarding timing, the countries that will be included, and their magnitude

- An analyst meeting will be held on Mar 19: The Q&A session for analysts will follow a “news-packed” keynote address from CEO Jensen Huang the prior day

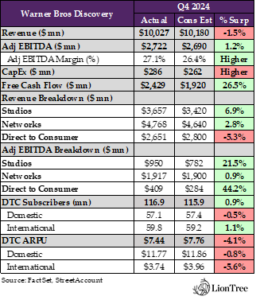

WBD Has All Eyes On Its North Star…FCF

Warner Bros. Discovery’s (WBD) report on Thursday capped off the Media conglomerate Q4 earnings cycle (Paramount also reported this week – see Theme #4). While total revenue missed due to the DTC segment, profitability came in above expectations in all three segments, with Studios and DTC in particular posting +22% and +44% profitability beats, respectively. FCF was also dramatically higher than consensus and remains a top priority.

On the DTC side of the business, Max continues to pace higher on the profitability front and is expected to surpass its 2025 adj. EBITDA target of $1bn by an additional $300mn. Total subscribers are now at 117mn (beat by +0.9%), and there is visibility toward reaching “at least” 150mn subscribers by the end of 2026. A substantial portion of that growth will come from international as they continue to roll out in new regions, which will weigh on ARPU in the near-term, but will drive rev growth in the long-term. WBD has been pushing for bundling for some time now, and they’re seeing increasing interest not only internationally, but also regionally and locally, which will be another key subscriber growth driver.

While it was a great year for Max, Studios had a tougher time in 2024, and major transformations and overhauls are currently underway across WBTV, films, and games. These include refocusing resources, creating a more balanced content portfolio, driving economic efficiencies and more. All these changes are expected to drive a “healthy” improvement in the segment’s 2025 adj EBITDA, as they aim to get Studios back to being a $3bn+ adj. EBITDA business (no exact timeline provided on when they expect to achieve that target).

Finally, it was particularly busy on the Networks side of the business in Q4, as the segment saw both some wins and losses. While Networks beat on both rev and profitability, ad revs were down -16% y/y as political ad spend came in lower than the Co anticipated, and forecasting future advertising is “challenging” given continued pressure and deterioration in linear. That said, WBD reached multi-yr affiliate renewal agreements with 5 of the 6 largest US pay-TV providers, securing rate increases across these deals, though at a slightly slower pace compared to previous agreements. The new affiliate deals feature a variety of models, including soft and hard bundles, hybrid structures with DTC access, and more packaging flexibility, which are expected to help stabilize Network’s rev over the next few yrs.

There was certainly a lot to unpack from WBD’s Q4 report…see below for more on our key takeaways.

-> WBD’s stock was up +4.8% post its report, and ended the week up +6.3%

Much Higher FCF, DTC Profitability, & Studio Performance Were Q4’s Highlights

- Q4 consolidated revs missed by -1.5%: Down -1% y/y (vs -3% y/y in Q3)

- Miss was driven by DTC

- Studios outperformed Street estimates while Networks was in-line to better

- Q4 adj. EBITDA beat by +1.2% (and returned to growth): Up +11% y/y (vs down -19% y/y in Q3)

- All segments beat, with DTC in particular coming in +44.2% ahead of expectations

Strong Q4 FCF Beat Underscores Continued Steady Progress Towards Deleveraging, As FCF Remains The Top Priority

- Q4 FCF was dramatically higher than cons: $2.4bn vs cons $1.9bn

- Ended Q4 at 3.8x net leverage

- FCF continues to be “one of our top priorities from a financial perspective… and that’s one of the reasons why we continue to put up these strong cash conversion rates, even with some top line pressures, especially on the linear side”

- Looking ahead – “We continue to target 2.5-3.0x gross leverage and our top priority for FCF remains paying down debt”

- Ended Q4 having paid down $19bn in debt since transaction closure, which will continue to be a focus

- But gross leverage target is not “the be all end all” for the long-term

- Key 2025 FCF focuses:

- Continue growing content investments

- “Strong” working capital (drag of ~$500mn in 2024 that isn’t expected to happen in 2025)

- Benefit from lower debt load and corresponding interest payments

- “A little more CapEx” as they expand production footprint

- Decreases in restructuring expenses

- But “the actual dollar amount in the end is going to be mostly driven by the resulting final EBITDA number”

Implemented Corporate Reorganization On January 1st And Targeting “Substantive Completion” In Early Q2

- “We continue to make meaningful progress to work through the operational and financial aspects of this new structure”

- “This new structure will provide investors with better visibilityto the strength of our streaming and studios business and will give us real strategic value and optionality into the future”

- “We don’t think, from today’s perspective, that we’re going to see a dramatic change to our segment reporting” BUT plan to provide incremental guidance beyond that in Q1 to “enhance clarity around global linear networks, streaming, and studios”

DTC Profitability Growth, Strong Subscriber Growth, Expanding Global Footprint, and Robust Content Pipeline Are Driving Long-Term Upside

- Q4 DTC saw substantial beat on profitability, despite a revenue miss

- DTC rev missed by -5.3%…: Increased +6% y/y (vs +9% y/y in Q3) to $2.7bn

- …but DTC adj. EBITDA beat by +44.2% and was the second consecutive positive qtr: Came in at $409mn, which is up from $289mn in Q3 and +$464mn in the yr-ago qt

- Guided 2025 DTC adj. EBITDA to be ~$1.3bn

- Looking ahead – “no doubt” they will “hit and exceed” 20%+ adj. EBITDA margin target in the DTC segment but will not be managing towards that goal: “I’d much rather have stronger growth in 2025, 2026, 2027, maybe at the expense of a little bit of EBITDA margin because it builds longer term asset value”

- DTC ad revs increased +27% y/y (vs +49% y/y in Q3), primarily driven by an increase in ad-lite subscribers

- Max added +6.4mn subs in Q4 to reach 116.9mn (beat by +0.9%): Down from +7.2mn adds in Q3

- Have a “clear path” to reach “at least” 150mn global subscribers by the end of 2026, “with corresponding strong DTC revenue and adj EBITDA growth”

- Expect “a large proportion” of growth to come from intl, “just because…we’ve got a material foodprint outside the US that we’re not even reaching yet”

- “US is a pretty mature market. We think that there’s still some growth given the quality of our service and we’re fighting for that”

- Intl growth will be driven by penetration growth and launching in new mkts

- In 2025 – “expect strong DTC subscriber growth to continue throughout [the yr]”

- Expect “a large proportion” of growth to come from intl, “just because…we’ve got a material foodprint outside the US that we’re not even reaching yet”

- Flagged 3 “key growth drivers” that will increase subscriber and rev growth in the near and long-term, but will weigh on near-term ARPU trends

- Continued rollouts in intl mkts

- Will see some continued pressure as they launch in intl mkts in Asia, which is a region “that has generally low ARPUs”

- Strategic distribution partnerships that help accelerate consumer adoptions

- Driving higher penetration in existing mkts, particularly with their lower priced ad-supported tier

- In the “medium to long term, we’re very confident we can get back to ARPU growth even after this expansion period here over the next sort of 12 to 18 months”

- Continued rollouts in intl mkts

- Global expansion has “significant runway as Max rolls out to over 40% of the addressable global market where it is not yet available”

- Germany and Italy launching by Q1:26: “Two important markets with strong proven appeal for our programming”

- UK and Ireland launching by Q2:26: Struck a nonexclusive agreement to launch on Sky that will bring Max to ~10mn of their current subscribers and gives WBD “the flexibility to potentially reach consumers not currently served by Sky”

- Max and HBO’s content line-up over the next 2+ years “has never looked stronger”

- In 2025, will return 15 franchises that previously ranked among the top 20 series: Include the recent debut of The White Lotus, The Righteous Gemstones, Hacks, The Last of Us, And Just Like That, The Gilded Age, and Peacemaker, as well as new series such as the recently premiered The Pitt and Task and It: Welcome to Derry to debut later in the year

- Success w/ recent S3 premiere of The White Lotus, which had an audience size “nearly double” that of S2 premiere in its first week; Globally, the show is now the second largest returning original season in platform history, behind only House of the Dragon S2

- Looking ahead – producing new seasons of some of their highest-viewed and “most resonant” series…: such as House Of The Dragon, Euphoria, and True Detective

- …as well as brand new original series, like A Knight Of The Seven Kingdoms, Lanterns, DTF St. Louis, and Harry Potter

- In 2025, will return 15 franchises that previously ranked among the top 20 series: Include the recent debut of The White Lotus, The Righteous Gemstones, Hacks, The Last of Us, And Just Like That, The Gilded Age, and Peacemaker, as well as new series such as the recently premiered The Pitt and Task and It: Welcome to Derry to debut later in the year

Continue To Get Behind Bundling – “Think There Will Be An Aggregation In A Meaningful Way Behind A Couple Of The Bigger Global Players”

- Bundling is “an exciting new growth vector for us”

- Bundling can happen both structurally (via mergers) or commercially (as product bundles)

- “We’ve seen great success with it, obviously here in the US with Disney, seeing it both drive acquisition, as well as significantly reduced churn”

- Shifting from a period of overspending and “a glut of content” to a “much more rational spend” and “and providing consumers access to all that goodness through these bundles”

- “It’s gaining a bit of a momentum across the world, not just with global players, but frankly, with regional and local players as well”

- Bundling can happen both structurally (via mergers) or commercially (as product bundles)

- Regional players are increasingly interested in bundling with WBD: “Many of the really high-quality local players have come to us now after two or two and a half years and aligned on our strategy of better together”

- Dependency on sports is becoming a pressure point for these players: “Some regional players are becoming more and more dependent on sports and rental sports, and the ability to really build a long-term platform on short-term sports rights has not been a good story in the past, and it’s unlikely to be a good story in the future”

- Skinny sports bundles are “compelling” but success will depend on consumer experience and perceived value

- “Unless it’s significantly less expensive, [consumers] opt for the bigger bundle where they could see a wealth of other quality content”

- “Ultimately everything we’re doing is going to be driven by providing a better consumer experience, and everything we do here is driven by that”

- “”That’s what we’re doing with Disney, that’s what we’re doing with Verizon when we’re together with Netflix… to create a better, more seamless experience for consumers”

Substantial Turnaround For 2025 Is In Motion In The Studios Business

- Studios beat expectations on both rev and adj EBITDA in Q4

- Studios rev beat by +6.9%: Up +16% y/y (vs -17% y/y in Q3) to $3.7bn

- Adj EBITDA beat by +21.5%: Up +78% y/y (vs -31% y/y in Q3) to $950mn

- Expect “healthy” improvement in Studios segment’s adj. EBITDA results in 2025: “WBTV will play a key role in helping to secure that momentum, with support from improved expected results from our Motion Pictures Group and Games businesses”

- “While results from these divisions were disappointing in 2024, we have taken action to improve performance and are optimistic about their long-term outlook”

- Reiterated plans to get “Studios back to a place of industry leadership and generating $3bn or more in EBITDA” …: “Studios remain one of our primary growth levers” and “delivering more consistency and profitability is a top priority”

- …BUT $3bn is “not an end state. That’s sort of fixing where we are right now and then growing from here and we believe the studio has enormous potential beyond that”

- WBTV “reclaimed its position as the industry’s #1 supplier of live action TV” in 2024, and delivered hits like –

- The Penguin, one of the top three most viewed original debut seasons on Max ever

- Presumed Innocent, one of WBTV’s three series that ranked in Apple TV+’s top 5 most watched shows in 2024

- Georgie & Mandy’s First Marriage, CBS’ #1 rated comedy this season

- Motion Picture Group’s multi-yr transformation is ongoing, and is expected to result in –

- “A more balanced portfolio of output across our creative engines”

- AND “a more economical avg cost per film, driven by a mix of high-profile, tentpole releases and more modestly budgeted films”

- Impact of these changes should be most visible at DC, and upcoming release of Superman will kick off “a thrilling new era for DC Studios”: Film releases July 11th, and kicks off a multi-yr story arc that “will showcase exciting new DC characters and reintroduce beloved icons like Supergirl, Lanterns, Batman & Robin, and Clayface, among others”

Also Within Studios Segment – Gaming Biz Overhaul Is Underway

- Implementing restructuring plan that refocuses resources and capital on “proven IP” + games from “proven, world class studios”

- Focusing Games biz around four tentpole franchises that have each generated $1bn+ in consumer sales in past yrs: They include Harry Potter, Game of Thrones, Mortal Kombat, and DC (“particularly top tier characters like Batman”)

- Expect re-focused strategy will “propel” Games division back to profit in 2025 “and emerge as a more significant contributor to growth in the years ahead”

Networks Advertising Disappointed In Q4, Particularly On The Political Front, And Is Expected To Continue To Face Headwinds In The Near-Term

- Networks beat on both revenue and adj. EBITDA in Q4

- Networks rev beat by +2.8%: Fell -4% y/y (vs +3% y/y in Q3) to $4.8bn

- Networks adj EBITDA beat by +0.9%: Decreased -13% y/y (vs -12% y/y in Q3) to reach $1.9bn

- “We are responding tenaciously and creatively to the secular headwinds we face in the broader linear television market, and we are squarely focused on maximizing our Networks’ ongoing cash generation potential”

- Networks ad revs were down -16% y/y (vs -13% y/y in Q3), driven by domestic networks audience declines of -28% and the continuing softness in the domestic linear ad mkt

- Saw weaker ad sales in Q4 “than we had hoped for and what we had expected”

- “We didn’t expect a ton of political advertising but…we had hoped for a greater benefit from the elections, which didn’t come in”

- Called out forecasting Networks’ advertising is “challenging,” given reduced subscribers combined with further pressure on linear viewership, particularly for general entertainment content

- Looking into Q1 – seeing “some mild positive signals” from the ad mkt: “It’s not a sea change but we’re seeing less upfront cancellations than in the prior year. We’re seeing scatter CPMs up moderately, but we also acknowledge that we have some work to do in terms of our linear portfolio ratings and delivery”

Strategic Affiliate Renewals Drove Rate Increases (Though At A Slightly Lower Pace) With Flexible Deal Structures To Support Long-Term Networks Stability

- Reached multi-year renewal agreements with 5 of the 6 largest pay TV providers domestically, many of which were renewed “significantly ahead of schedule” and “all of which commanded overall rate increases”

- Rate increases in new set of deals will be “slightly slower” y/y”: Saw “close to” 6% rate increases in Q4:24 in their domestic affiliate biz; With the new set of deals, those rate increases are going to be “more in the low-single-digit versus a mid-single-digit” rate

- “But as we laid out, we have also, as an industry, I think, come together and created some flexibility that will drive the sustainability and longevity of that ecosystem

- New affiliate deals are not “one size fits all” and have a variety of different models in play globally

- Soft bundles: “There’s no penetration or carriage commitments”

- Hard bundles: “There’s plenty that do have carriage for penetration commitments, and then there’s others that don’t”

- Case-by-base: Some include obligations where a partner agrees to distribute WBD’s content to a fixed portion of their subscriber base (i.e., Sky in the UK)

- In certain cases, some renewals include hybrid structures with DTC app access and/or greater packaging flexibility in line with industry trends

- “While these attributes may put pressure on near-term linear trends, they may support longer-term health and sustainability of the overall ecosystem”

- Already seeing positive net rev impact from affiliate renewals: In many of the renewals, working w/ affiliate partners to make “some” concessions on the linear side, which are facing “not as pronounced, but similar pressures” as domestically being seen here, but cooperating through software hard bundles on the DTC side

- “Net-net, in the aggregate, we’re growing”

- International trends are “much better” and pressure is “much more moderate” vs domestic, but “there’s some uncertainty there as well”

- International affiliate portfolio is up in rev y/y “and that’s the kind of crossing of the line that we’re looking for” but “we’re not there in the US yet”

- Looking ahead – “these agreements will deliver overall affiliate rate increases, helping to stabilize our Networks segment’s revenue over the next few years”

- Clarified that the stabilization being referred to means “stabilizing out position within the industry trends” NOT “zero growth or a decline”

Strategy Around Sports And News Streaming Is Still A Work In Progress / Sports Rights Cost Will Be A Profitability Drag In 2025 (But Will Reverse Course In 2026)

- “Continuing to experiment on what the right model is” on the sports and news front: Balance of driving engagement and first views while also figuring out a biz model that works

- Have a variety of different models in operation around the world –

- In the US, announced plans to move sports and news out of the ad-lite and into the premium and standard ad-free

- In LatAm, available across all packages

- In Europe, upsell it as an add-one and a buy-through

- Keep an eye on CNN – “oppty to build a completely separate digital and subscription line of bizs”: Over the next few months, Mark Thompson and Alex McCallum (build the digital bizs at The New York Times) will share “what we’re doing to build a sustainable digital business out of [CNN]”

- Have a variety of different models in operation around the world –

- Sports rights costs will weigh on 2025 adj. EBITDA, due to overlapping costs of newly acquired rights and the remaining portion of their current NBA deal that ends after H1:25

- BUT these costs will “more than reverse” in 2026, in what will be the first full year without the NBA

- Expect to see “several hundred millions of dollars of sports expense come out in 2026”

- Investing with “fiscal discipline” in adding new rights to their sports portfolio…: Which now includes the U.S. rights for the French Open, Unrivaled, NASCAR, multiple college sports assets, including the College Football Playoffs, on top of March Madness, MLB, and NHL

- …and will continue to “opportunistically” consider sports rights as they become available: “Don’t need any more sports anywhere in the world” but would buy “if we think it would enhance our business”

- BUT these costs will “more than reverse” in 2026, in what will be the first full year without the NBA

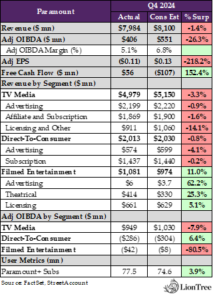

Paramount’s Linear To Streaming Shift Will Not Be A Straight Line

Ahead of the pending close of the SkyDance merger (still slated for a H1:2025), Paramount’s Co-CEOs are moving quickly to shore up the balance sheet and drive FCF while also transitioning the business to be better positioned in this streaming era. Q4 showed some signs of progress, with FCF coming in materially above expectations (positive $56mn vs cons loss of -$107mn) and FCF for 2025, even including the tough comps from the Super Bowl and political ad spend, will be higher y/y. Improvements in Paramount+ were the key highlight as not only did subscriber adds come in solidly ahead of expectations but engagement and watch time was also materially up which is a good leading indicator for retention and further monetization. The Co’s strategy of “fewer bigger breakthrough series with big movie stars” is yielding results (P+ ranking as the #2 domestic SVOD service for hours watched across all Original Series in Q4). While the division’s adj OIBDA swung into a loss in Q4 due to seasonality of the content slate, it was by a lesser degree than analysts were forecasting and improved by more than $200mn y/y. The Co reiterated guidance that domestic streaming profitability will break into the black in 2025. To flag though, P+ subs growth in Q1 is expected to be below that of Q4 given the timing of content releases.

While progress is being made on streaming, challenges on the linear side remain a headwind. TV Media revenue fell -4% y/y with ad revs down -4% y/y and affiliate & subscription revenue down -6.7% y/y. The Co will feel more pressure in Q1 with reported ad revs facing tough comps with the Super Bowl and the affiliate revenue decline worsening on the back of recent deal renewals. Longer term, mgmt does expect net growth in affiliate & subscription revs as D2C scales.

The film business generated higher than expected revenue due to Gladiator II and Sonic the Hedgehog 3 but higher marketing spend weighed on profits. Looking ahead, the Co has several high-profile films on the docket, with Mission Impossible: The Final Reckoning being one of them.

Overall, shifting the business from linear to streaming while also driving more cost efficiency remains the name of the game for Paramount.

-> Paramount was up +0.2% the day after its report and ended the week down -1.1%

Stronger Than Anticipated FCF, Lower Loss In DTC, & Better Film Revs Were The Main Highlight W/ Q4 Results While TV Media & Adj OIBDA Solidly Disappointed

- Total revs (+5% y/y) missed consensus by -1.4% while adj OIBDA at $406mn was -26% below consensus

- Adj OIBDA was impacted by Co-wide variable comp and actions taken to mitigate energy exposure (resulted in $90mn higher expenses)

- The biggest portion of the comp increase was incurred at TV media

- Segments performance vs the Street…

- TV Media posted much weaker performance overall: Revs missed by -3.3% and adj OIBDA missed by -8% (note comment above)

- DTC’s lower loss on inline revs were notable: Lost $286mn in Q4 vs cons loss of $304mn

- Filmed Entertainment revs were better than expected but generated a greater than expected loss

- FCF was much better at $56mn vs cons loss expectation of -$107mn

- Achieved annual run rate savings of $500mn as targeted

Content Spend Overall Should Be Flat In 2025 & FCF Should Increase Y/Y In 2025 Despite Super Bowl & Political Benefit In 2024

- 2025 content spend overall is expect it to be “relatively flat” y/y on a total company basis: This is a more normalized level of content spend

- But there will be a “remixing” in favor of streaming

- Q1 adj OIBDA will decline y/y, reflecting the underlying business trends and the Super Bowl comp

- Adj OIBDA will be back-half weighted given the Super Bowl and addtl cost reductions planned for the H2

- 2025 OIBDA will grow on an underlying basis though will likely still be “slightly down” including Super Bowl and political

- Q1 FCF will be lower y/y given it will include~$150mn in cash restructuring pmts + lapping last yr’s Super Bowl

- However, expect FCF to increase in 2025, even when including the impacts of the Super Bowl and political advertising in 2024

- Will see a significant improvement in FCF conversion: FCF conversion has been diluted by cash restructuring payments and for 2025, ~10 ppt of conversion will be impacted by restructuring; That is “obviously something that goes away in the future”

P+ Subscriber Gains In Q4 Stand Out & DTC Is On Track For Domestic Profitability In 2025

- DTC revs rose +8% y/y and DTC adj OIBDA improved by $204mn in Q4 (from rev growth + cost efficiencies) and improved by nearly $1.2bn for the FY

- DTC subscriber revs grew +7% and ads revs grew +9% (driven by P+, Pluto and higher political)

- While the integration of Showtime into P+ has temporarily diluted D2C subscription rev growth, it has been a “key enabler of the significant improvement in D2C profitability we’ve delivered over the past several quarters”

- P+ total revs rose +16% y/y due to strong subs growth and P+ subscription revs rose +14% y/y due to a combo of subs growth, churn reduction & ARPU improvement

- Strong sub adds- beat cons by ~4%: P+ subs adds hit 5.6mn, reaching to 77.5mn (best qtr of adds in 2 years)

- P+ subscriber growth “benefited from a particularly high volume of acquisition-oriented content, including a robust slate of originals, theatricals, the NFL and college football”

- Modest ARPU increase: P+ global ARPU incr’d +1% y/y reflecting the lapping of the 2023 price increase and a cont’d mix of the subs base to the Essential tier

- Note that when the Co implemented the most recent price increase in Aug 2024 to existing Essential tiers, subscribers were grandfathered so as a result, it will take longer for this most recent price change to flow through to overall Paramount+ ARPU

- Focused on driving engagement as that is the key driver for ARPU growth and subscriptions:

-

- In Q4, global watch time per user rose 20%, driving a +100bps y/y improvement in churn

- P+ domestic watch time/user reached a record high and incr’d +22% y/y

- Global viewing hours incr’d 28% y/y across Paramount+ & Pluto TV

- Pluto TV also had a record year, growing 16% in hours watched for Q4 y/y

- Q4, Paramount+ saw the highest level of engagement yet and achieved a new record, ranking as the #2 domestic SVOD service for hours watched across all Original Series

-

- What to expect for streaming in Q1?

- P+ subs: Will see growth in subs but NOT at the same level as Q4 given the timing of content releases

- P+ ARPU: Growth should accelerate as they fully lap the 2023 price increase and see a full qtr impact from Q4’s sub-additions, which skewed heavily toward direct subscribers (generate attractive ARPU)

- 2025 Outlook – “great confidence Paramount+ will achieve full year domestic profitability for 2025”

Paramount+, Strategy Of “Fewer Bigger Breakthrough Series With Big Movie Stars Is Setting Us Apart In A Crowded Space”

- In Q4

- Landman, Lioness and Tulsa King all scored as Top 10 original series across all SVOD svs in the US

- Also launched 2 new Showtime series which “scored”…Dexter: Original Sin & the Agency

- These shows are also performing “exceptionally well” at Paramount+ internationally along w/ Yellowstone & South Park (have exclusively for SVOD)

- Q1 thus far:

- Launched Season 3 of Yellowjackets Feb 14th… up 50%+ vs prev season

- Launched Season 2 of Yellowstone’s 1923 this past Sunday…was the most watched original premiere in Paramount+ history

- Called out two series later this qtr:

- Mob Land from Guy Ritchie

- Happy Face from exec producers Robert and Michelle King

But TV Media Remains Under-Pressure From Linear Eco-System Trends

- TV Media revs fell -4% y.y (vs down -6% y/y in Q3)

- TV media ad revs fell -4% y/y (declines in linear ad mkt & fewer sporting events on CBS, partially offset by higher political)

- TV Media affiliate & subscription revs fell -6.7% y/y

- TV Media licensing and other revs fell -3% y/y (primarily driven by secondary licensing growth, partially offset by fewer made for third-party productions)

- TV Media adj OIBDA fell -17% y/y (cost reduction initiatives were offset by higher content costs from a new fall slate and variable compensation costs)

Affiliate Growth Will Decline In Q1 Due To New Deals But Expect Net Growth As D2C Scales In 2025 / Still Not Convinced By Skinny Bundles But Are Experimenting

- Recent deal renews are impacting affiliate growth: In Q4, renewed Comcast deal and last week renewed YouTube deal

- Q1 outlook – Expect rate of decline in affiliate revs to increase due to the full effect of recent renewal deals as well as an evolving pay-TV ecosystem

- 2025 – Expect net growth in total affiliate & subscriptions revs as D2C scales

- Impact from skinny sports & news bundles? “Hard to imagine” a sports bundle w/out CBS being a part of it; They are part of Comcast’s and are in discussions with DTV regarding theirs

- PARA will join bundles “when it makes business sense for us”

- “We’re going to continue to experiment with skinny bundles. We know they’re here, but we’re just not at this point convinced there’s a compelling value proposition relative to the full bundle”

Tough Sports Comps Impact Q4 & Q1 Ad Trends

- The ad biz in Q4 saw a 350bp headwind from fewer NFL & college football games y/y & were impacted by softer college football ratings & intl advertising, including FX headwinds

- In Q1, expect similar underlying advertising trends in linear and digital vs Q4 but reported ad growth in TV media and D2C will be impacted by the Super Bowl comp in 2024

Theatrical Profitability Was Weighed Down In Q4 By Higher Marketing Costs But The Slate Drives Top Line

- Filmed Ent revs rose +67% y/y

- Theatrical revs rose $336mn due to Gladiator II and Sonic the Hedgehog 3

- Licensing and other revs rose +17% y/y

- Filmed Ent ad OIBDA fell $66mn (to a loss of -$42mn) due to film marketing costs for 5 films vs 1 in the prior yr period as well as the timing of Sonic 3, which was released late in the qtr

- “We’re excited for a dynamic and robust 2025 slate”…includes:

- Mission Impossible: The Final Reckoning

- An original live action comedy coming from the creators of South Park and Kendrick Lamar

- Edgar Wright’s The Running Man

- An animated Smurfs film

- An all new SpongeBob SquarePants film

- Licensing still remains “an essential component of what we do”: Do a “great deal” of licensing internally which will “pay real dividends downstream” in the growth of the D2C platforms; This is why they are making fewer originals for third parties; Additionally, “we believe there’s real room for innovation in windowing strategy and deal structures that could unlock even more value from our content in the future”

AI Developments Continue At A Fast & Furious Rate

It appears that those with an appetite for AI-related news and developments will not have to worry about going hungry, as this week saw a plethora of new updates hit the tape. One notable theme surrounding AI has been the sheer amount of capital needed to finance the technology’s immense infrastructure requirements, and it looks like Apple and Alibaba will be stepping up their spending accordingly, committing to $500bn+ and $52bn in investments, respectively, over the next few years.

This week also was also filled with updates on new and upcoming AI models, which looks to be an increasingly crowded space. Anthropic launched Claude 3.7 Sonnet, which it has deemed as the industry’s first hybrid-frontier AI model and is capable of both reasoning as well as outputting answers in real-time. OpenAI also made its Deep Research feature accessible to all paying users and rolled out GPT-4.5 to Pro users. In terms of other new AI models and products on the horizon, DeepSeek is reportedly accelerating the development of its next R2 model after its predecessor, R1, shook up the markets in January. Additionally, Meta is planning a standalone AI app, and Perplexity has a web browser for agentic AI search in the works. Finally, third-party research firms found that xAI’s launch of Grok 3 last week was highly successful in driving new user growth on the Grok app.

See below for more details and also note Theme #8 for some AI-oriented updates out of Amazon:

Big Tech Cos Annc’d Big AI Infrastructure Spending Plans

- Apple plans to spend $500bn+ on domestic infrastructure and add 20,000 jobs over the next four yrs (link/link): The investment and pledge represents Apple’s largest US commitment to-date

- The scope of Apple’s investments and hiring plans:

- A new, 250k sq ft server manufacturing facility in Houston that will produce the servers powering the cloud component of Apple Intelligence, a system called Private Cloud Compute; This would insource some production from overseas

- Existing data center capacity expansions in Arizona, Oregon, Iowa, Nevada, and North Carolina

- A supplier academy in Detroit, Michigan that will help smaller Cos w/ manufacturing

- Addt’l spending w/ existing US suppliers

- Doubling of the Co’s US Advanced Manufacturing Fund to $10bn

- The 20,000 new jobs will focus on R&D, silicon engineering, and AI

- BUT this only represents a slight accel over Apple’s prior investments and annc’d plans: Over the last five yrs, Apple has hired 20,000 R&D workers and previously said that it would invest $430bn in the US over the next half-decade back in 2021

- President Trump’s tariffs may have influenced the decision: Apple’s annc’ment came days after a meeting between CEO Tim Cook and Trump; Previously, Trump has traded investment in the US for relief from tariff policies

- The scope of Apple’s investments and hiring plans:

-> On a related note, Alibaba annc’d this week that it will invest at least 380bn yuan ($52.4bn) in cloud computing and AI infrastructure over the next three yrs; The total investment amount exceeds the Co’s spending on AI and cloud infrastructure over the past decade (link)

There Was Also A Flurry Of Updates Pertaining To New AI Models This Week

- Anthropic unveiled Claude 3.7 Sonnet, its “most intelligent” AI model (link): Anthropic calls Claude 3.7 Sonnet the industry’s first hybrid frontier model, as it combines the ability to reason, or stopping to consider more complex answers, w/ a traditional model that generates answers in real time

- Users have the option to choose whether to activate Claude 3.7 Sonnet’s reasoning abilities: This is part of Anthropic’s broader effort to simplify the user experience; Many other AI models force users to choose from a daunting model picker w/ several different options that vary in cost and capability

- The Co eventually wants Claude to determine how long to “think” about answers on its own: “Similar to how humans don’t have two separate brains for questions that can be answered immediately versus those that require thought,” per a blog post

- Claude 3.7 Sonnet will refuse to answer questions less than previous models: The model can make more nuanced distinctions between harmful and benign prompts; It has reduced unnecessary refusals by -45% compared to its predecessor Claude 3.5

- Claude 3.7 Sonnet launched to all users and devs: However, only those paying for Anthropic’s premium Claude chatbot plans have access to the model’s reasoning features, while free users get the standard non-reasoning version

- The model costs just “a few tens of millions of dollars” to train (link): This is cheaper than the $100mn needed to train OpenAI’s GPT-4 model and the nearly $200mn to train Google’s Gemini Ultra model

- Users have the option to choose whether to activate Claude 3.7 Sonnet’s reasoning abilities: This is part of Anthropic’s broader effort to simplify the user experience; Many other AI models force users to choose from a daunting model picker w/ several different options that vary in cost and capability

-> It was reported this week that Anthropic is discussing a $3.5bn capital raise at a $61.5bn valuation; Lightspeed Venture Partners is leading the round, and General Catalyst as well as others are also participating; The funding round is substantially more than the $2bn that Anthropic originally set out to raise, per sources; The deal would also roughly triple the Co’s valuation from its last private mkt valuation of $18bn (link)

-> Separately and also this week, Anthropic released an agentic coding tool called Claude Code, which enables developers to run specific tasks through Claude directly from their terminal; Claude Code will initially be available to a limited number of users on a “first come, first serve” basis link)

- OpenAI rolled out Deep Research all paying ChatGPT users (link): Earlier this week, OpenAI made the feature, which enables users to create in-depth reports on nearly any subject, available to Plus, Team, Edu, and Enterprise users; Previously, only $200/mo Pro users could access Deep Research

- Usage limits for different tiers of users –

- Plus, Team, Edu, and Enterprise users will be limited to 10 queries per month

- Pro users will see their access expand to 120 queries per month from their original 100 query allotment

- OpenAI also made a couple of improvements to Deep Research’s functionality: ChatGPT now embeds images alongside citations to provide “richer insights”; The system also has a better understanding of file types, resulting in better document analysis and improved accuracy

- Usage limits for different tiers of users –

-> OpenAI CEO Sam Altman also annc’d this week that the Co is “out of GPUs,” forcing it to stagger the launch of its newest GPT-4.5 model; The “giant” and “expensive” GPT-4.5 started rolling out to ChatGPT Pro users this week and ChatGPT Plus users next week but will require “tens of thousands” of addt’l GPUs before addt’l ChatGPT users gain access; Notably, GPT-4.5 users will be charged 30x the input cost and 15x the output cost of OpenAI’s GPT-4o model (link)

- DeepSeek is reportedly accel’ing the launch of its next AI model, R2 (link): After launching its R1 model and shaking up the mkts in Jan, sources indicate that DeepSeek is now planning to release its next R2 model as soon as possible after initially planning for a launch in May

- Upgrades to the new R2 model: Include better coding as well as the ability to reason in languages beyond English

- R2’s launch could be a “pivotal moment” in the AI industry: As DeepSeek’s cost-effective models could result in others to accel their own efforts and result in more players entering the increasingly crowded market for AI models; R2 is also likely to raise some concerns within the US govt

- DeepSeek also introduced off-peak pricing for devs (link): Between 1630 GMT and 0030 GMT, the cost of using the API for DeepSeek’s R1 and V3 models would be -75% and -50% cheaper, respectively, per a table on the Co’s website; Notably, the timeframe is daytime hours for those in the US and Europe

- Meta reportedly has a standalone AI app in the works (link): Meta AI would join Facebook, Instagram, and WhatsApp as another one of the Co’s standalone apps

- The Co is planning to debut the Meta AI standalone app in FQ2: “This is going to be the yr when a highly intelligent and personalized AI assistant reaches 1bn+ people, and I expect Meta AI to be that leading AI assistant,” per CEO Mark Zuckerberg on the Co’s recent earnings call

- Potential benefits of creating a standalone app –

- Deeper user interactions w/ the AI assistant: Given that Meta AI is currently only available to users via a website and the company’s apps such as Facebook and WhatsApp

- A more unified experience across devices: Bridging Meta AI across smartphones and other platforms, such as the Ray Ban Meta smart glasses, would help users organize their conversational histories w/ the digital assistant and allow for deeper personalization and customization

- Meta plans to test a paid subscription svs for Meta AI: On the Co’s last earnings call, Meta CFO Susan Li said that there are “pretty clear monetization oppties here over time, including paid recommendations and including a premium offering”

- Perplexity is developing a web browser for agentic AI search (link): The Co posted a sign-up list for the browser, dubbed Comet, earlier this week, though it’s still unclear when the launch will occur and what the browser will look like

- Perplexity’s browser will enter a very competitive space: In addition to incumbents like Chrome and Microsoft Edge, the browser will have to contend w/ other third-party alternatives that also offer AI-powered features, such as the upcoming Dia browser from The Browser Company

- This annc’ment follows a string of recent product releases from Perplexity: The Co launched a “deep research” product to compete w/ offerings from OpenAI, Google, and xAI earlier in Feb and debuted an AI product assistant for Android as well as an API for AI search in Jan

-> Perplexity is also reportedly creating a $50mn venture fund that will focus on investments in pre-seed and seed AI startups based in the US; The Co will be an anchor investor in the fund, though most of the capital will be sourced from outside limited partners, including f7 Ventures’ Kelly Graziadei and Joanna Lee Shevelenko, per sources (link)

- The launch of Grok 3 by Elon Musk’s xAI was highly successful, per third-party research Cos (link): Preliminary estimates by Sensor Tower showed that both worldwide and US mobile app downloads of Grok incr’d more than tenfold last week over the prior week following the launch of the third iteration of xAI’s flagship AI model

- The Grok app’s DAU growth soared last week: Daily active users for Grok’s US app incr’d over +260% w/w, while global daily active users jumped fivefold w/w, per Sensor Tower

- BUT the expansion of the app to new mkts likely caused some noise in the numbers: Grok 3’s release coincided w/ the Grok app’s expansion to several mkts in Europe, LatAm, and Southeast Asia

- The web version of Grok also saw an uptick in traffic: According to Simliarweb, US daily visits to the Grok web app (independent of the mobile app) rose to 900,000+ in the days following Grok 3’s release from ~189,000 prior; Globally, daily visits incr’d to 4.5mn from 627,000

- BUT there have been some recent controversies surrounding Grok 3: The weekend after its release, users found Grok 3 censored unflattering mentions of President Trump and Musk, while a few days earlier, Grok 3 consistently said that both deserved the death penalty; Both issues were quickly patched

- The Grok app’s DAU growth soared last week: Daily active users for Grok’s US app incr’d over +260% w/w, while global daily active users jumped fivefold w/w, per Sensor Tower

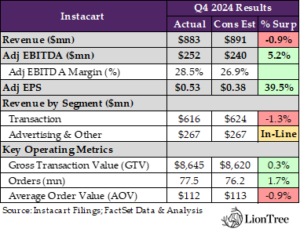

Instacart’s Cart Is Still Building

On the online grocery side of the equation, Instacart was the big event this week and there were some puts and takes with results, which disappointed Street expectations in aggregate, especially given the stock appreciation YTD ahead of results (was up +17.8%). Overall Q4 GTV y/y growth slightly decelerated (10.8% in Q3 ->10% in Q4) though was still a tad ahead of consensus and adj EBITDA beat previously lowered expectations, however Q1 adj EBITDA guidance fell short of Street forecasts by -5% at the mid-pt. Silver lining is that mgmt. is committed to annual margin expansion (even with continued aggressive investment) though it might not be linear.

Two key platform developments that are helping to drive order volume are 1) reducing the minimum free delivery threshold for Instacart+ subscribers to $10 and 2) also adding the restaurant use case. As a result, order growth rose +11% y/y in Q4 BUT this was partially offset by a -1% y/y decline in AOV given the smaller restaurant basket sizes and the Co also had some impact of smaller orders in the lead up to holidays. This dynamic is expected to continue in Q1 as well. However, it is worth noting that the new use case of restaurants is driving a “halo effect” for the company and adding new demand for the core grocery business. Given their scale and ability to bundle orders, the Co can make the economics work even at smaller basket sizes.

The advertising business was also a focal point and y/y growth remained in the +10% range as their vertical of food & beverage is still being negatively held back by macro. The Co is using this time to continue to improve its advertising offering via performance gains, innovation, scale, and diverisification. In Q1, ad revenue & other growth is expected to grow faster than GTV guidance, hence implies an expected acceleration which will be a plus.

Overall, the Co is blocking and tackling and in 2025, we’d expect to see continued investment in the core across selection (restaurants, affordability, convenience, speed) as well as in enterprise solutions (Caper is one of them). The online grocery and adjacency opportunity remains large.

See below for more detail and color on what we thought was most important from Instacart’s results and outlook.

-> CART shares fell -12.3% in reaction to results and guidance and is down -0.8% YTD; The stock was up +76.5% in 2024

-> Also in online delivery this week, Prosus agreed to acquire European food delivery group Just Eat Takeaway for $4.3bn (link)

Q4 Margins Were A Shining Star (Though On Lowered Expectations)

- Q4 GTV grew +10% y/y which was at the top end of guidance (8-10%) and a tad above consensus

- Total revs missed expectations by ~-1%…it grew +10% y/y (vs +11.5% in Q3)

- Transactions revs (~70% of total) – MISSED by -1.3%: Grew +10% y/y vs +11.8% in Q3; Represented 7.1% of GTV (7.3% in Q3); Continue to drive shopper efficiencies and reinvest in affordability initiatives

- Advertising & Other revs (~30% of total) – INLINE: Grew +10% y/y vs +10.8% in Q3 (3.1% of GTV)

- Adj EBITDA margins of 28.5% easily topped cons 26.9% and exceeded the high end of the Co’s guidance range (which at the time issues was below Street forecasts)

- Adj EPS was 40% ahead of consensus

- But the buyback was limited in Q4: Bought back $5mn worth of shares in Q4 bringing the cumulative total in 2024 to ~$1.4bn; Have $312mn of capacity remaining

While Upside In Q4 Margins Didn’t Lead To Upside In Q1 Margin Guidance, Mgmt Is Committed To Annual Margin Expansion

- Q1 GTV guidance range is a tad above cons at the mid-point ($9.00-9.15bn vs cons $9bn)

- Represents 8-10% growth and includes 1ppts+ headwind from leap year

- Q1 adj EBITDA -5% below cons ($12mn below): Decls seq primarily due to seasonality in advertising & other revenue

- For 2025…remain committed to delivering steady annual adj EBITDA expansion (“even as we maintain an aggressive approach to reinvesting in growth initiatives”) but there will be fluctuations on a qtrly basis

- Targeting 2025 stock-based comp to be < $425mn, w/Q1 being the lowest quarter of SBC, followed by an anticipated step up in Q2 due to the timing of the annual refresh grant

Ramp Of Restaurant Orders Is Weighing On Average Order Value But Drives A “Halo Effect” / Orders Will Grow Faster Than GTV In Q1

- GTV growth at +10% y/y was a slightly tick down from +10.8% y/y in Q3 but also a tad ahead of cons

- Order growth rose +11% y/y (due to both growth in users and order frequency)

- Partially offset by a -1% y/y decline in AOV due to smaller restaurant order size and also had some impact of smaller orders in the lead up to holidays

- Outlook – Orders will grow faster than GTV in Q1; Restaurant will impact AOVs in Q1 and they will also see the impact from the $10 min basket (most of these orders come from IC+ members)

- While small order sizes of restfaurnat weighs on AOVs, it is helping drive the grocery business as well and having a “Halo effect”

- Restaurant adoption is still very early, and mgmt sees a logn runway “throughout 2025 and beyond”.

- Shopper supply is “very healthy”: They have a wait list in most cities and are seeing good retention of shoppers

The Ad Business Is Still Held Back By Macro But This Co Is Making Investments To Position For An Acceleration

- Advertising & Other revs rose +10% y/y in Q1 vs +10.8% y/y in Q3…seeing strong performances from emerging brands and many large brand partners

- Q1 outlook – Advertising & Other revenue growth should outpace anticipated GTV growth (+8-10%)

- Why isn’t ad revenue growing faster than 10%?? Macro factors: Many retail media plaltform have more demand outside of just food and beverage and “the macro on food and beverage is still challenged”; Over time this will change and in the meatime the Co has been leaning into ad performance, innovation (new formats, new measurement capabilities, new metrics, incorporating AI into ad products), scale (caper ads is part of that) and diversification (emerging brands growing faster)

- “Very confident in our long term target range of ads being between 4% to 5% of DTV”

Strong Trends On User Engagement And On Instacart+ Subscribers & Economics

- The Co bought in more new users and GTV in 2024 than they did pre-pandemic: The “2024 cohort delivered the strongest engagement we’ve seen in recent years” and at the same time “existing cohorts are stable and existing users continue to increase their order, frequency and spend per user over time, including in the last year”

- Bullish on Instacart+ subscriber trends: Mgmt doesn’t break out the number of subscribers but did convey that they are seeing “deeper penetration of Instacart+ members among our overall user base”

- Engagement of members “has been strong”, especially w/ the launch of new use cases like restaurants and $10 minimum basket

- What are you seeing in response to reducing the free delivery threshold for IC+?

- An increase in order frequency, an increase in total GTV, and higher Instacart+ adoption w/out seeing any impact on bigger basket orders

- Mgmt is able to make the economics work since they can bundle some of these orders given the high order density of stores

- “Excited about what we are seeing with this change and that’s why we are leaning into it”

A Few Other Key Call-Outs On Affordability Push, AI, & Caper Carts

- The Co is still very focused on driving down affordability of online grocery: Grocery prices have incr’d “over 25%” since 2019, so they are working hard to find ways to save money; They have been pushing grocers to move to price parity between online and their stores given the data shows they can do so while preserving margins

- Hy-Vee stop loyalty and digital fliers, each re now at more than 80% of GTV coverage

- Using AI in “everything” they do: From things like tracking store inventory to substitution and reducing order rates of ordering

- Called out improvements in replacements: 2024, had 300mn replacements w/ a high 95% satisfaction rate; AI helps find great replacements with accuracy

- Caper Carts are a win-win with customers and retailers but takes time to role out

- Seeing very good results from the pilot

- Customers “love the product”…they are “fun”

- For retailers, it leads into larger baskets and they also share in the ad revs from these carts

- Ad engagement w/ caper hasw been inline with online ad engagement

- Caper carts will also help customers reorder online as well

- “Have thousands” of cart commitments in the works right now but these are physical products and the roll-outs take time

TKO: The 2025 Outlook Disappoints… But All Eyes Will Be On The Upcoming Renewals

TKO has officially reached its one-year milestone, with Q4 marking the first like-for-like financial comparison since the September 2023 merger of UFC and WWE that formed TKO and the combined Co delivered a strong quarter. TKO beat the Street across the topline as a y/y decline at WWE due to the transition of WWE Raw from USA Network to Netflix was more than offset by growth at UFC. That said, 2025 guidance, which does NOT include the acquisitions of IMG, On Location, and PBR (which are expected to close in Q1) widely disappointed, with both revenue and adj. EBITDA missing consensus by -9.3% and -7.4%, respectively.

That said, TKO has big plans for the upcoming year. In addition to closing the deal to acquire Endeavor’s assets, discussions are currently ongoing with Disney ESPN around UFC, and renewal talks with Peacock regarding WWE are expected to begin in H2:25. Honing in on a $5bn rights deal that has already been agreed and sign on, the Netflix-Raw partnership officially kicked off in January and it is off to a roaring start. Netflix has exceeded expectations on the promotional front, and ratings are up +13% from the yr-ago qtr when the program was on USA Network. When asked about the potential for an ancillary programming deal w/ Netflix, mgmt responded to “assume there’s more cooking in the pipeline.”

While UFC and WWE remain the top and primary priorities, TKO confirmed that it is also entering a new sports arena – boxing. TKO is “close to an agreement” with Saudi Arabia to create a boxing league. The Co is not making any investment but rather will be a promoter of the league and responsible for all day-to-day operations, for which it will receive a fee. In addition to the creation of the boxing league, bigger picture, international is viewed as a material oppty, with plans to host “a higher number” of international events in 2025 vs 2024. While these events may have a lower margin profile in the near-term, the “massive investment” is made with a long-term view in mind “to ensure that we continue to reach fans all over the globe.”

There were a whole host of other updates out of the call…see below for what we thought was most incremental and important.

-> TKO fell -5.8% in reaction to its report and ended the week down -5.2%

TKO Delivers Solid Results Relative To Expectations

- Rev – beat by +6.4%: Grew +5% y/y, reflecting an increase in rev at UFC, partially offset by a decrease at WWE, which was primarily related to the previously disclosed timing of the transition of WWE’s weekly flagship program, Raw

- Adj EBITDA – beat by +1.7%: Increased +7% y/y, due to an increase in UFC rev and a decrease in corporate expenses, partially offset by a decrease at WWE, which was primarily related to the previously disclosed timing of the transition of WWE’s Raw

But 2025 Guidance Stumbled In The Ring

- Rev – missed by -9.3% at the midpt: $2.93bn-$3.00bn vs cons $3.27bn

- EBITDA – missed by -7.4% at the midpt: $1.35bn-$1.39bn vs cons $1.48bn

- Highlighted 4 “notable drivers” of 2025’s outlook –

- Netflix-Raw deal: Will include the step up, as well as a full year of media rights fees, from long-term agreement for Raw (began in Jan 2025)

- Y/Y decrease in PLEs: Will have only one PLE in Saudi Arabia compared to two PLEs in 2024, which will have an unfavorable impact of ~$55mn to total Co rev, equating to ~200bps of rev growth and ~50bps on FY total Co adj. EBITDA margin

- “For the avoidance of doubt, this item is purely timing related, as we expect to host three PLEs in Saudi Arabia in 2026, including Royal Rumble”

- Site fees: Anticipate “meaningful” growth in site fees in 2025

- UFC domestic vs. intl event mix: Expect to host fewer events at Apex in Las Vegas and host a higher # of intl events in 2025 vs 2024; While it will lead to an increase in rev, these events have a lower margin profile

- Decision to move more events out of Las Vegas “is with a long-term view in mind”: “Apex events obviously coming out of COVID carry a lower cost structure and a higher margin profile. But we view this more holistically and are making investments in the long run”

- Incremental 2025 FCF commentary: Expect an unfavorable impact of $250mn of payments related to the UFC antitrust lawsuit settlements, as well as payments for professional fees related to the acquisition of IMG, On Location, and PBR

- Excluding those ~$300mn of non-recurring amounts, targeted FCF conversation rate would be “in excess” of 60%

WWE Revs Took A Hit In Q4 Due To Media Rights Transitions And Timings

- Q4 WWE rev fell -10% y/y, reflecting the short-term domestic rights deal reached for Raw, which had an unfavorable impact of ~$50mn on rev vs Q4:23

- Media Rights & Content rev fell -26% y/y, primarily related to the short-term deal for Raw, as well as a decrease in 3P original programming due to the timing of delivery.

- On timing of content deliveries: “Will sort itself out over the course of a year or any quarter…nothing that is of concern or structurally problematic, just timing”

- Live Events rev incr’d +13% y/y, primarily related to an increase in ticket sales

- Sponsorship rev incr’d +48% y/y, due to new partnerships and renewals across multiple categories, including gaming and retail, among others

- Media Rights & Content rev fell -26% y/y, primarily related to the short-term deal for Raw, as well as a decrease in 3P original programming due to the timing of delivery.

- Q4 WWE adj EBITDA fell -19% y/y, reflecting the decrease in rev, partially offset by a decrease in expenses, which primarily reflected lower personnel and production costs related to planned cost reduction initiatives implemented following the formation of TKO

- WWE’s adj EBITDA margin was 38%, down from 43% in the prior-yr period

- Q4 event highlights – set 40+ individual market records for ticket sales and paid attendance in Q4

- Bad Blood in Atlanta delivered the largest gross ticket sales for a US arena event in WWE history

- Survivor Series in Vancouver set the largest North American arena gate in WWE history, since topped by Raw’s “blockbuster” debut with Netflix at the Intuit Dome

- Saturday Night’s Main Event returned with a sold-out crowd that set a WWE gate record for New York’s Nassau Coliseum and reached 3mn+ US households across NBC and Peacock

- Q1 WWE outlook –

- Live Events and Sponsorship rev will continue to reflect the momentum in the biz

- Media Rights & Content rev is expected to reflect the expansion of SmackDown to a 3-hr format for the H1:25, which is purely timing related and results in a shift in quarterly rev recognition but has no impact on the full-year amount

- WWE expenses: Expected to reflect the impact of addtl intl events compared to the prior-yr period (i.e., for the first time ever, the road to WrestleMania will include an 11-city tour across the UK and Europe over 3 weeks in March)

High Praise For Netflix Partnership, With More WWE Programming Likely Coming Soon

- Netflix has “been phenomenal to deal with and they promoted us in a way that we hope [we] would be promoted, even more so than we had hoped”

- “Seeing a great take-up on Netflix with Raw”

- Ratings (total viewed minutes divided by run time) are up +13% from Q1:24 avg on USA Network

- Monday night episodes have consistently landed in Netflix’s weekly top 10 “across the US and the globe”

- Also have been “getting some new audience”

- How to think about growth in Media Rights & Content rev as more Netflix mkts get turned on?

- Will retain income from intl distributors that have deals that do NOT term out on Jan 1st

- As they roll into the Netflix deal, they roll in at rates similar to economics in the Netflix deal

- “No real impact from who the distributor is because we’re economically indifferent in the first year”

- Potential for ancillary programming deals w/ Netflix? “All we’ve seen from Netflix is an appetite for more WWE”

- Announced a WWE behind-the-scenes show w/ Netflix a few weeks ago, which will come out later this yr

- “Assume there’s more cooking in the pipeline”

UFC Returned To Growth & Surpassed Estimates In Q4 / Negotiations For Domestics Rights Are Ongoing

- Q4 UFC rev inc’d +22% y/y (vs -11% y/y in Q3) and benefited from the timing of the events calendar (had 10 total events in Q3 vs 9 in the yr-ago qtr)

- Media Rights & Content rev inc’d +18% y/y, primarily driven by the addtl numbered event, as well as the contractual escalation of media rights fees

- Live Events rev incr’d +24% y/y, primarily due to the addtl numbered event as well as higher ticket sales as compared to the prior-yr period, as well as “strong” underlying trends in pricing and attendance for high profile events

- Sponsorship rev incr’d +39% y/y, driven by new partnerships and an increase in fees from renewals compared to the prior-yr period, as well as the favorable event mix

- Q4 UFC adj EBITDA incr’d +25% y/y (vs falling -18% y/y in Q3) – adj EBITDA margin was 52%, up from 51% in the prior-yr period

- Q4 event highlights –

- Hosted highest grossing North American Fight Night ever in Tampa

- UFC 309 at Madison Square Garden “cemented UFC’s place as a cornerstone franchise for the world’s most famous arena”

- UFC now holds 7 of the top 10 highest grossing event records in MSG history

- Q1 UFC outlook: Results will reflect the mix of events in the qtr

- Live events rev will include a site fee from the Fight Night help in Saudia Arabia earlier this month

- Expenses will reflect two addtl intl Fight Nights and two fewer Apex events compared to the prior-yr period

- Ongoing UFC domestic deal negotiations – “we’re focused on doing what’s best for the business in the long term…a balance between maximizing our reach and engagement and monetization”

- Highlighted “unique” value prop: “Not only do we own and control it, but it’s year out. There is no off-season. Our content…has the urgency, and the urgency allows us to attract subs and viewers and also gives us a consistency to retain subs and viewers, reduce churn”

- Implied openness to deal structures: “When it comes to our overall deal, one package, two packages, half packages, four packages, NASCAR style, whatever it might be…”

- Currently in exclusive negotiating window with Disney/ESPN: Window opened Jan 15th and will last 90 days

- “Disney ESPN has been a great partner”: “Enjoy” partnering with them; UFC has helped Disney w/ its transition from linear to streaming and “just keeping linear strong”, and also “helped [UFC’s] brand”

- “We like where we’re at. We love to stay with them as long as we’re realizing fair value for our content, and we think in this window, our content is premium plus”

“Really Not Seeing Any Signs Of A Slowdown” In Live Events And Viewership

- Demand is not abating – “always mindful of the macroeconomic uncertainty and we’re always keeping an eye on those trends, we’re really not seeing any signs of a slowdown”

- Ticket yield is “strong”

- Dynamic pricing is “strong”

- “We’re exercising AI opportunities and we’re monitoring pacings in advanced sales very closely for any signs of a falloff, not seeing it”

- “On Location is off to a roaring start with both WWE and UFC, and we’re bullish about where that goes”

- NXT, which moved from USA Network to The CW, “has been a real winner for us” and driven “significant audience growth”

- The CW’s Tuesday night timeslot saw a ~100% increase y/y in Q4 total viewership, with “even stronger gains” in the 18-34 yr-old demographic

- Premiere to date, NXT is up +12% compared to USA’s 2024 avg

- Also coming up – PLEs + Peacock renewal: Deal for the PLEs with Peacock is up in March of 2026; Expect to begin renewal discussions with them in H2:25

Seeing Strength Across All 3 Leagues On The Sponsorship Front, But Lots Of Room For Continued Runway

- Reiterated guidance for $375mn in sponsorship rev (inclusive of digital) for the yr: “We’re on track to hit that number”

- Seen “tremendous success” selling all three leagues

- UFC: “A lot of renewals because they have a lot of traction and incumbent deals”

- WWE: “…this is all fertile ground for Nick Khan and what he’s trying to accomplish here in selling different parts of the ring, the arena, and really, outdoor activations and retail. So, we see there’s huge opportunity there”

- PBR: “Not even closed on PBR yet” have but already closed 2-3 deals