Market volatility is back. After hitting a new all-time high earlier this week, the S&P 500 and other major indices traded down sharply to end the week. There was a market rotation into defensives and away from tech and cyclicals. The level of uncertainty around Trump’s plans remained the focus, and concerns about the consumer (and the economy) resurfaced following comments from Walmart this week. The TMT earnings drumbeat also continued with new updates across China Tech and Live Music, in particular.

Also, I forgot to mention this last week, but for those of you that participated in our annual 2025 Sector Themes Survey, we sent the results directly to your email on Feb 11. Let me know if you need me to resend, and thanks for participating!

Have a nice weekend.

- Earnings Scorecard – Week 5

- Alibaba & Baidu Are Making Notable Strides In The Global AI Race

- Live Nation: The "Live Music" Bandwagon Keeps On Rolling

- New 13-Fs Reveal The Most Bought TMT Stocks Among Hedge Funds In Q4... Tesla, Booking, & CrowdStrike

- The Barrage Of AI Updates & Innovations Continues

- A Highlight Reel Of This Week's Notable Sports Updates

- Booking Rounds Out A Resoundingly Strong Quarter For The OTA Industry

- Grab Bag: Details On Spotify's Upcoming Premium Tier/Microsoft's New Quantum Computing Chip/ Apple's New Lower-End iPhone 16e

Best,

Leslie

Earnings Scorecard – Week 5

Despite the shortened holiday week, there were still 26 companies in our LionTree Universe that reported their fourth quarter results this week (slightly up from 25 last week). Stock price reactions were heavily biased to the downside, with 19 companies (74%) trading down in reaction to their report and just 7 trading up. Bumble was the worst performer, down -30.3% post its print, while Unity was the best performer, up +30.4%.

China Tech was a frontrunner on the earnings circuit this week, with Alibaba and Baidu seeing opposite reactions from the Street, up +8.1% and down -7.5%, respectively (see Theme #2 for more). Live Nation was also a key report this week though the stock fell -1.9% post its print (see Theme #3). The last of the online travel names also reported this week, including Bookings Holdings, which fell -0.5% in reaction (see Theme #7).

Alibaba & Baidu Are Making Notable Strides In The Global AI Race

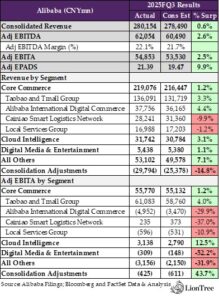

Growing optimism around AI has driven a rally in China Tech stocks recently (link), with the KWEB ETF gaining ~+24% over the past month alone, and Alibaba’s FQ3 print for its December-ended quarter this week further reinforced this trend. “Rapid adoption of AI technology across industries” led to a sequential acceleration in the Co’s Cloud Intelligence business’ top-line growth, resulting in its sixth consecutive quarter of triple-digit y/y growth in AI-related product revenue. Alibaba’s management sees a “clear and massive demand for infrastructure” in the AI era and believes this is “the kind of opportunity for industry transformation that really only comes about once every several decades.” As a result, the company is committing to its “highest-ever historical investments in CapEx” over the next three years, spending more on infrastructure over that period than it has over the past decade. Alibaba believes that AI can eventually replace 50% of global GDP, and it views infrastructure as the “clearest monetization pathway” around the technology moving forward. Otherwise, commentary on the company’s core commerce business was sparser but was still positive, as revenue growth accelerated sequentially and adj EBITDA returned to growth on a y/y basis.

Like Alibaba, Baidu’s Q4 earnings call was also heavily focused on the company’s AI Cloud segment and its ERNIE chatbot. However, unlike Alibaba, the positive commentary surrounding Baidu’s cloud business, which included strong enterprise adoption trends, didn’t necessarily spark a favorable reaction from the market. This was likely due to “near-term pressures” that caused “softness” in the company’s core online marketing business. In addition to small & medium enterprises being “particularly sensitive” to ongoing macro conditions, Baidu’s management highlighted a “persistently challenging competitive landscape.” The B2C side of the company’s business also faced challenges, which were reflected in sequential declines in Baidu App users. Still, there appears to be greener pastures on the horizon for Baidu. The company has seen encouraging early signs from its efforts to integrate AI and its ERNIE bot further into its advertising products and mobile ecosystem. Also, Baidu’s plans to expand its robotaxi business are expected to result in a “significant acceleration” in rides growth in 2025.

See below for more of what we thought was most interesting from both Alibaba and Baidu’s results.

-> Alibaba shares rose +8.1% post-earnings and ended the week up +15.2%; Baidu shares fell -7.5% following the print and closed the week down -6.4%; YTD, Alibaba stock is trading up +69.5%, while Baidu stock is still up +8.3%

1) ALIBABA – See below for our thoughts on key themes, updates, and takeaways

Alibaba’s Headline Numbers Were Propelled By “Strong Biz Fundamentals & Profit-Generating Capabilities”

- Alibaba’s results broadly exceeded estimates:

- FQ3 rev rose +7.6% y/y (vs +5.2% y/y in FQ2) and beat cons by +0.6%

- Adj EBITDA was up +4.2% y/y (vs -3.9% y/y in FQ2), topping cons by +2.6%

- Adj EBITA also finished +2.5% ahead of cons

- Adj EPADS of CNY21.39 came in +9.9% above cons

- By segment:

- Core Commerce (~78% of total rev) – BEAT:

- Rev incr’d +8.9% y/y in FQ3 (vs +7.8% y/y in FQ2) and closed +1.2% ahead of cons

- Adj EBITA grew +0.2% y/y (vs -8.2% y/y in FQ2) and beat cons by +1.2%

- Cloud Intelligence (~11% of total rev) – BEAT:

- FQ3 rev was up +13.1% y/y (vs +6.5% y/y in FQ2) and topped cons by +3.1%

- Adj EBITA rose +32.7% y/y (vs +88.9% y/y in FQ2) and ended +12.5% above cons

- Digital Media & Entertainment (~2% of total rev) – MIXED:

- Rev grew +7.9% y/y in FQ3 (vs -1.5% y/y in FQ2) and beat cons by +1.1%

- Adj EBITA of -CNY309mn (vs -CNY517mn the prior yr qtr and -CNY178mn in FQ2) missed cons by -52.2%

- All Others (~19% of total rev) – MIXED:

- FQ3 rev incr’d +12.9% y/y (vs +8.6% y/y in FQ2) and topped cons by +7.1%

- Adj EBITA of -CNY3,156mn (vs -CNY3,172mn the prior yr qtr and -CNY1,582mn in FQ2) fell short of cons by -31.9%

- Consolidation Adjustments (~-11% of total rev) – MIXED:

- Core Commerce (~78% of total rev) – BEAT:

- FQ3 rev missed by -14.8%, while adj EBITA beat cons by +43.7%

Taobao and Tmall Group Benefited From Prior Investments In User Experience

- Taobao and Tmall Group (TTG) outperformed expectations: Rev grew +5.4% y/y in FQ3 (vs +2.5% y/y in FQ2) and beat cons by +3.3%; Adj EBITA was up +1.9% y/y (vs -5.3% y/y in FQ2) and topped cons by +4.0%, benefiting from the new customer mgmt svs fee but partly offset by investments in user experience

- Customer mgmt rev growth accel’d seq: Customer mgmt rev rose +9% y/y in FQ3 (vs +2% y/y in FQ2), driven by online GMV growth and an improvement in take-rate; This also reflected the full qtr impact of the software svs fee and increasing adoption of the Quanzhantui digital mkting tool for merchants

- Efforts to grow the user base and enhance the user experience are paying off: The Co saw “strong growth in both new consumers and orders” during the qtr

- 88 VIP membership “cont’d to grow rapidly”: TTG’s core consumer group maintained double-digit growth and surpassed 49mn+ by the end of the qtr, w/ profitability increasing on a cohort basis

- Improvements in monetization have helped stabilize margins…: The Co has “done a lot to drive incr’d monetization recently,” including integrating new payment methods and charging payment processing fees; A more intelligent mkting product and a software svs fee have boosted monetization as well

- … BUT TTG “remain[s] in an investment stage”: The Co will continue to invest in user experience and acquisition to achieve “healthy, stable mkt share” moving forward

- Introducing AI features is expected to be another monetization driver in the future: Many of these projects will be launched “soon” and will increase consumer engagements as well as drive higher transaction efficiency

The AI + Cloud Strategy Continues To Drive “Robust Momentum” In The Cloud Biz

- Cloud rev growth improved seq: Alibaba Cloud rev (excluding Consolidating subsidiaries) was up +11% y/y in FQ3 (vs +7% y/y in FQ2) and was “fueled by even faster public cloud rev growth”

- AI-related product rev grew at a triple-digit rate for the sixth straight qtr: Highlighted that the “rapid adoption of AI tech across industries” has been driving surging customer demand for Alibaba Cloud products

- Alibaba has plans to “aggressively invest” in AI infrastructure: Over the next three yrs, the Co will spend more on cloud & AI infrastructure than it has spent over the past decade; Spending levels will be relatively even on a y/y basis over the period but could fluctuate on q/q basis depending on supply chains

- The “clear and massive demand for infrastructure” created by AI is an oppty that “only comes about every several decades”: As a result, new capacity is expected to be “taken up very rapidly”

- Having a cloud computing network is “the clearest monetization pathway” today: Explained that the “future ways in which these [AI] models will be monetized are not necessarily clear”; Compared AI to electricity and Alibaba’s cloud computing network to a power grid

- Forward-looking comments –

- “Rev growth of Cloud Intelligence Group will continue to accel”: Cited Alibaba’s recent launch of Q1 2.5 MAX, its flagship AI foundational model; By the end of Jan, 90,000+ Q1-derivative models had been developed globally, and 290,000+ Cos and devs had accessed Q1 APIs

- Greater scale will lead to higher margins over time: “We will grow our customer base and expand industry coverage across a wider range of sectors, and all of that will certainly contribute to higher levels of margin in [the Co’s] AI svs” and enable it to “better optimize the cost of this build-out”

- At the model layer, Alibaba’s “first and foremost goal” is to pursue artificial general intelligence (AGI): More broadly, the Co’s aim is to “keep pushing out those boundaries” of AI use cases “to create more and more oppties”

- “The standard for AGI is AI that can replace or achieve 80% of our human capabilities”: AGI could “have a tremendous impact” in restructuring industries and “even replace 50% of global GDP”

- The Co will “substantially increase R&D investment in AI foundational models” moving forward: This will help it maintain its technological leadership and drive the development of AI native applications

- There are also plans to further integrate AI models within Alibaba’s B2C and B2B products: Highlighted Quark, a search product, on the B2C side as well as DingTalk, which is the Co’s “most important asset” on the B2B side, as offerings that will be further enhanced by AI

Alibaba International Digital Commerce’s Performance Was Driven By Incr’d Investments

- Alibaba International Digital Commerce (AIDC) posted mixed results: FQ3 rev rose +32% y/y (vs +29% y/y in FQ2) and beat cons by +4.4%; However, adj EBITA losses of -CNY4,952mn (vs -CNY3,146 the prior yr qtr and -CNY2,905mn in FQ2) missed cons by -29.9%

- The cross-border biz contributed to “strong growth” in the international e-commerce biz in FQ3: AIDC incr’d investments during overseas shopping festivals on a seq basis and cont’d to invest in select European mkts in the Gulf Region to acquire users

- AIDC is expected to achieve its first qtr of profitability in FY26: Unit economics have been improving on a seq basis and are expected to see a “significant increase” over the next few qtrs, driven by the Co’s focus on operating efficiency and the optimization of its B2C biz model

- Otherwise, the Co anticipates a “stable trend” in the international biz over “the next few yrs”: The Co plans to continue working towards achieving “significant profitability at scale”

Notes On Buybacks & Recent Transactions

- Alibaba repurchased $1.3bn worth of stock in FQ3: This equated to a -0.6% net reduction in share count during the Dec qtr; Over the last nine months, the Co bought back $10bn worth of shares and achieved a net -5% reduction in share count

- The divestments of Sun Art and Intime are expected to close within the next two qtrs: Both deals have already passed anti-monopoly reviews

- There are no plans to sell Freshippo as part of the effort to exit non-core bizs: That said, Alibaba has an “open attitude” to introducing a strategic investor or adopting “similar approaches that could enhance the value of Freshippo,” given the biz’s success

2) BAIDU – See below for our thoughts on key themes, updates, and takeaways

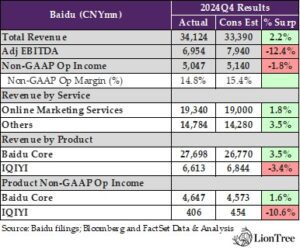

Baidu’s Headline Results Reflected Near-Term Pressures

- Q4 headline numbers were mixed, w/ top-line beating but profitability coming up short:

- Total rev fell -2.4% y/y in Q4 (vs -2.6% y/y in Q3) but still topped cons by +2.2%

- Adj EBITDA dropped -23.2% y/y (vs -8.1% y/y in Q3) and missed cons by -12.4%

- Non-GAAP op income was down -28.7% y/y (vs -7.7% y/y in Q3) and -1.8% below cons

- By segment –

- Baidu Core (~81% of total rev) – BEAT:

- Q4 rev was up +0.8% y/y (vs -0.2% y/y in Q3) and beat cons by +3.5%

- Non-GAAP op income was down -25.0% y/y (vs -0.3% y/y in Q3) but still ended +1.6% above cons

- IQIYi (~19% of total rev) – MISS:

- Rev dropped -14.2% y/y in Q4 (vs -9.6% y/y in Q3) and closed -3.4% below cons

- Non-GAAP op income fell -56.2% y/y (vs -58.7% y/y in Q3) and missed cons by -10.6%

- Baidu Core (~81% of total rev) – BEAT:

Core Ad Rev Declined For A Third Consecutive Qtr But It Is Reaching A “Low Point”

- The online marketing biz experienced “softness” in Q4: Online mkting svs rev was down -7.0% y/y in Q4 (vs -5.8% y/y in Q3); Highlighted “near-term pressures,” including small & medium enterprises being “particularly sensitive” to ongoing macro conditions as well as the “persistently challenging competitive landscape”

- Baidu believes it is “reaching a low point of [its] ad biz”: The Co is “seeing many oppties for future growth,” such as improving its app biz, and anticipates that H1:25 will play out better than Q4; H2:25 is also expected to show a further uptick over H1:25

- Recently introduced stimulus measures “eventually will benefit the economy” but “need some time to flow through”: These include monetary easing as well as other trading policies

- Efforts to enhance Search w/ gen AI transformations have been “progressing steadily”: The Co has been working to drive “deeper personalization” w/ gen AI and has been seeing “encouraging improvements in user match testing”; This is expected to drive rev growth and new monetization oppties in the longer-term

- Daily search queries per user on the Baidu App grew +2% y/y in Dec: In Jan, 83% of MAUs that conducted a search on the Baidu App engaged with gen AI content

- ~22% of all search result pages have AI-generated content currently: Baidu App users that were exposed to AI-generated search results “demonstrated higher engagement levels, conducted more search queries, and showed high orientation rates and longer time spans

- Baidu believes it is “reaching a low point of [its] ad biz”: The Co is “seeing many oppties for future growth,” such as improving its app biz, and anticipates that H1:25 will play out better than Q4; H2:25 is also expected to show a further uptick over H1:25

The AI Tech “Megatrend” Continues To Benefit Baidu’s Cloud Biz

- Baidu AI Cloud “delivered a robust performance,” as rev growth improved significantly seq: AI Cloud rev rose +26% y/y in Q4 (vs +11% y/y in Q3), primarily driven by “increasing mkt recognition” of the Co’s AI capabilities and its “expanding mkt share in China’s cloud mkt”

- Baidu has “momentum in [its] enterprise client pipeline” …: The Co partnered w/ “leading enterprises across diverse sectors” in Q4, collaborating w/ State Grid Corporation of China as well as Xiamoi and Jiku

- … And is “increasingly becoming the preferred choice for mid-tier bizs”: Reflecting the “strengthening competitiveness” of its AI infrastructure

- Gen AI-related rev nearly tripled y/y across 2024: Given “rising demand for ERNIE and [the Co’s] AI infrastructure”

- China’s AI Cloud mkt is expected “grow rapidly” in 2025 as well: Public awareness of foundational models has been increasing, and steady declines in cost have lowered the barrier to entry to utilize these models; This will enable the Co maintain “strong momentum” in AI Cloud rev growth

- “More enterprises will integrate foundational models into every aspect of their biz operations”: Ranging from R&D to production as well as other svs; This will “drive explosive growth in API cost”

- Baidu has “momentum in [its] enterprise client pipeline” …: The Co partnered w/ “leading enterprises across diverse sectors” in Q4, collaborating w/ State Grid Corporation of China as well as Xiamoi and Jiku

Businesses Are Finding More Use Cases For The ERNIE Bot

- The ERNIE bot has seen “widespread adoption across various scenarios”: The ERNIE AI chatbot svs has experienced “rapid growth across various biz sectors,” including education, e-commerce, entertainment, and recruitment

- API calls for ERNIE are “significantly growing”: Highlighted that ERNIE handled ~1.65bn API calls daily in Dec, w/ external API calls growing +178% seq, driven by falling inference costs as well as bizs finding value from integrating the chatbot into their day-to-day operations

- Recent “strategic” decisions are expected to “enable broader adoption”: Including the decision to open source the upcoming ERNIE 4.5 series and make ERNIE Bot free for end users

- 27,000+ advertisers generated ad spend through ERNIE agents daily in Dec: Advertisers have been using AI agents to “quickly master complex, non-standardized svs portfolios… while efficiently qualifying leads” from standard customer inquiries

- Baidu will focus on performance improvements and cost-cutting in future iterations of the ERNIE bot: The Co is also committed to an application-driven approach in “continuously iterating ERNIE, so that it can “effectively address real-world problems at scale”

- API calls for ERNIE are “significantly growing”: Highlighted that ERNIE handled ~1.65bn API calls daily in Dec, w/ external API calls growing +178% seq, driven by falling inference costs as well as bizs finding value from integrating the chatbot into their day-to-day operations

Ongoing Investments In AI Are Also “Propelling Significant Progress” In The Robotaxi Biz

- Apollo Go’s domestic robotaxi operations cont’d to “show robust momentum” in Q4: Apollo Go provided ~1.1mn rides to the public in China in Q4, representing a +36% y/y increase

- Jan saw the Co achieve further milestones: Apollo Go transitioned to 100% fully driverless operations and surpassed 9mn+ cumulative rides provided to the public

- Apollo Go rides have accumulated 130mn+ autonomous kms to-date: And have done so w/ “an outstanding svs record”

- Baidu anticipates “a significant accel” in Apollo Go’s ride volumes in 2025: Driven by efforts to further scale operations

- The Co is “confident” in its plan to expand beyond Mainland China: Apollo Go secured permits to conduct open road testing in Hong Kong last Nov, making it the only Co to receive robotaxi testing authorization in the region

- Apollo Go has “established a path to profitability” within the autonomous driving industry: The Co remains focused on narrowing losses w/ better operational efficiency and an improved user experience; It is also exploring innovative operational models, including asset-light models

- Jan saw the Co achieve further milestones: Apollo Go transitioned to 100% fully driverless operations and surpassed 9mn+ cumulative rides provided to the public

Other Highlights

- User growth remained a challenge across the mobile ecosystem: Q4 Baidu App MAUs of 679mn were up +2% y/y but down -4% seq, as difficulties associated w/ user engagement persisted

Managed page accounted for 48% of Baidu’s online mkting rev in Q4: Vs 51% in Q3

Live Nation: The "Live Music" Bandwagon Keeps On Rolling

2024 was “live music’s biggest year yet,” and 2025 is “shaping up to be even bigger”. That’s per Live Nation, which reported a solid Q4 print this week, with revenue beating consensus by +1.5% and AOI beating by a more substantial +20%. AOI grew +35% y/y in the qtr and is expected to continue growing at a double-digit rate in 2025.

Stadium shows will be a big driver in the year ahead, and both sides of the supply & demand equation are looking strong. The pipeline is up +60% y/y, and sell through rates at the stadium level are higher than are previous year, with 75%+ of tickets sold in the first week of sales. That dynamic is not just limited to stadium shows, as strong demand is being seen across the business, including across geographies. International continues to be a substantial oppty, not only on the show/touring side, but also on the venue expansion front. An increasing amount of capital is being directed towards international arena oppties, and the Co is on track to add 20 large venues globally through 2026, which is expected to add an incremental +6-7mn fans.

An interesting update to flag was commentary around DSP partnerships. While Live Nation has had discussions with Spotify, Apple, Amazon, and is open to exploring a partnership if the economics align, scaling the offering is challenging, especially for high-demand events, where only a limited number of customers can secure tickets despite early access.

There were additional comments that we thought were incremental on ticket pricing strategy, regulatory updates, CapEx strategy, and more. See below.

-> Live Nation shares fell -1.9% post-earnings and closed the week down -2.8%; YTD, Live Nation stock is still trading up +15.4%

Solid Q4 With Much Stronger Profitability To End The Year / Expect Continued AOI Growth In Q1, Though FX Will Be A Headwind

- Revenue – Beat by +1.5%: Down -2% y/y or +0.2% y/y CC (accel from -6% y/y and -6% y/y CC in Q3)

- Concerts and Ticketing segments beat by +1.9% and +2.1%, respectively, while Sponsorship & Advertising missed by -2.2%

- Adj op income – Beat by a wide +19.9%: Grew +35% y/y or +60% y/y CC (big accel from +4% y/y or +5% y/y CC in Q3)

- Beat across all segments, with Concerts biz coming in the most ahead of expectations

- Looking ahead, the Co expects to continue to deliver double-digit AOI growth across the biz, BUT FX will be a headwind (on AOI, as well as op income and rev)

- FX movement, primarily in LatAm currencies, is expected to impact Q1 op income by low-teens and rev and AOI by mid-to-high single digits, based on current rates

The magnitude of impact is expected to be the greatest in Q1, given seasonality and timing of activity in LatAm mkts

Global Oppties, Particularly Venue Expansion, Will Be Central To Growth Strategy Over The Next Decade

- 2025 CapEx is expected to be b/w $900mn-$1bn (vs $633mn in 2024)

- $700-$800mn is related to venue expansion and enhancement plans, while maintenance CapEx spend to remain consistent with historical levels

- Cash flow requirements will be reduced by ~$250mn of funding from joint-venture partners, sponsorship agreements, and other sources

- Expect to see “a trend towards more of the capital being deployed internationally because of the attractiveness and volume of those arena opportunities”

- Oppties in intl continue to ramp up on both sides – Live Nation tends to be the “first, second phone call if you are a developer” and Live Nation’s own appetite “still remains very large to expand in that platform”

- “Live has a real global unlock”

- Coldplay show in India was their largest single concert in history and sold out “instantly” with 125k attendees

- Have 100 offices in ~40 countries, will focus on growing mkt share in underdeveloped mkts

- Global venue expansion will “not just deliver attractive returns, but also move some reasonable volume of fans, expand out shows, growth the markets”

- “Heavily focused internationally at the arena level, globally focused on these large theaters”

- Timing of returns will vary by project, but strategy is aligned with ongoing thesis of growing to 200mn fans globally

- Preliminary timeline of incremental fan adds –

- “At least” 5mn more fans expected to attend shows in operated venues in 2025, benefiting from the addition of new venues in 2024 and 2025

- Expect to add 20 large venues globally through 2026, delivering run-rate of 6-7mn incremental fans: Major projects include stadiums in Bogotá and Toronto, seven amphitheaters, and nine large theaters

2025 Will See Strong Stadium Growth

- Q2 and Q3 stadium show activity expected to be the primary growth driver for 2025…

- Stadium show pipeline is up +60% YTD vs the same time last yr

- …though pace of rev and AOI growth will depend on mix of stadiums vs owned venues

- Mix shift towards stadiums in 2025 will drive “some good revenue growth”

- Ticketmaster “will be a big beneficiary”

- But b/c stadium shows don’t capture ancillary rev (i.e., food, drinks, parking), rev and AOI growth will depend on the performance of owned venues (i.e., amphitheaters, festivals, theaters, etc.)

- Mix shift towards stadiums in 2025 will drive “some good revenue growth”

- Sell through rates at the stadium level are higher than any previous yr – “lots of inventory, but equally great demand”

- Selling through 75%+ of tickets in the first week on sales, “and that’s much higher than the last year”

- “Seeing consumers buying up those stadium dates faster than ever, up year over year, or any comparable base”

- “Selling most of these stadiums out or close to being sold out by the time we get to the show dates”

Seeing No Slowdown In Demand / Artists Are Optimizing Ticket Prices For Accessibility While Shifting Sales Away From Secondary Markets

- Seeing no pullback across the board – “whether it’s geographical, whether it’s venue type or whether it’s festival, we’re still seeing strong, strong consumer across the board in terms of buying tickets for the 2025 season”

- “Beyoncés are always going to have incredible demand”

- Club biz is up +17% y/y – “that’s kind of the simplest way to say, bottom end, on a Tuesday in Indianapolis, my business is doing better”

- Festivals are selling at “record levels”

- 65mn tickets sold for Live Nation concerts in 2025, up double-digits led by stadium and intl activity

- Given the strong pipeline of events, why is YTD Ticketmaster transacted ticketing volume up just +3% y/y vs event-related deferred rev up +11% y/y?

- Ticketmaster transacting volume is up +3% y/y BUT Live Nation concert ticket sales are up +10% y/y: Live Nation’s concerts are driving higher growth in concert ticket sales vs Ticketmaster’s overall ticket volume; B/c Ticketmaster sells a mix of tickets and Ticketmaster’s overall volume is still early in the year, more growth is expected

- “Bit early to read too much into that number”

- Deferred rev growth is up +11% due to differences in on-sales timing y/y: Strong stadium lineup drove higher deferred rev in the qtr, vs last yr’s qtr, which saw fewer stadium sales but earlier on-sales for arenas and amphitheaters, which spread out deferred rev more evenly

- Ticketmaster transacting volume is up +3% y/y BUT Live Nation concert ticket sales are up +10% y/y: Live Nation’s concerts are driving higher growth in concert ticket sales vs Ticketmaster’s overall ticket volume; B/c Ticketmaster sells a mix of tickets and Ticketmaster’s overall volume is still early in the year, more growth is expected

- Artists are becoming more strategic with ticket pricing, balancing accessibility for fans while preventing scalpers from buying up high-demand seats

- “We love seeing the stadium sitting somewhere around 95% sold out right now. The instant we sold out at 10:00 AM means we’ve transferred a lot of wealth to the scalper”

- Artists are also adding more venues, “so they’re helping consumers get to more shows at a good price, but also making sure that it’s priced closer to market, which means you’ll have a few high-end tickets sit around in the rim until we get closed to show date”

- “So finding that right combination where you’re making sure demand and supply kind of march along on the way to the show date versus the 10:00 AM buy or sell”

- As a result, more ticket sales are shifting from secondary platforms to primary: “Every tour is looking at that P1 and making sure that if their fans are going to buy it, they would rather buy it from them direct on show date than two days later from a secondary site, ours included”

- “Artists are going to figure out how to keep price in the P1s a little more aggressively, price the bottom back end of the house lower, so we’ve got a great sell through”

- On Lawnie Pass discontinuation in 2025 – “it was a pull back and relaunch”: Program was “very small”, and new venue leadership decided that “we were discounting too much too early”; Instead will focus and consolidate around larger sales events like Concert Week

Exploring DSP Partnerships For Ticket Presales, But Mutually Beneficial Economics Are A Challenge

- Actively monetizing ticket inventory through sponsorships: Have several presale programs in place with partners like Verizon, Citibank, etc.

- “Our job is always to look at that show, work with the artist and figure out if there are ways to maximize that inventory to business as well as consumers”

- Have been approached by all the DSPs (Spotify, Apple, Amazon) and open to working with them IF the economics make sense

- Have discussed potential deals with DSPs but ultimately artists control how their tickets are distributed; B/c they want to maximize their revenue, and they tend to be particular about how much of the ticket inventory is given away at a discount/for free

- DSPs can explore ticket presale access as part of premium subscription tiers, but scaling the offering is challenging

- High-demand events (i.e., Beyoncé presales) are difficult to distribute at scale; When competition for tickets is high, even if a subscription model offers early access, only a few customers will actually get tickets

New Administration Brings About Some Possibility Of Settling DOJ Case (But Still Too Early To Tell)

- Trial “continues to move at pace as it has” and is on track for early next year

- “Hoping that this DOJ returns to a more traditional approach” and is open to discussing a settlement (which the previous administration had “really no interest in”)

- BUT have not have any discussions yet b/c “the person that you would discuss it with has not been approved yet, not been appointed”

- “Until that happens, there’s nothing we can do and we’ll see how that plays out in the coming months”

New 13-Fs Reveal The Most Bought TMT Stocks Among Hedge Funds In Q4... Tesla, Booking, & CrowdStrike

Amidst the earnings whirlwinds, the first 13-F filings of 2025 were also released last week, and as usual, we took a look at stock ownership changes across the sector. As a reminder, this is for the period ending Dec 31, 2024.

To start with, we took a deep dive into Warren Buffet’s Berkshire Hathaway, which was once again a net seller across its portfolio in Q4, selling ~$10.4bn of stocks while purchasing only ~$2.9bn. The fund initiated a position in just one new stock last quarter, which was Constellation Brands. After taking new positions in Domino’s Pizza and Pool Corp. in the prior qtr, Berkshire increased its position in both stocks last qtr by +87% and +48%, respectively. It also increased its position in Occidental Petroleum and Verisign (both by +4%) and further increased its position in SiriusXM (+4% increase on top of a +691% increase the prior qtr) while it decreased its position in Citi by -74%, Liberty Formula One by -12%, and T-Mobile by -7% (after maintaining positions in all three in the prior qtr) and further decreased its positions in Bank of America, Capital One, and Charter (after decreasing positions in all three in the prior qtr). Berkshire also sold out of its position in Ulta Beauty (after cutting its position by ~97% in the prior qtr) and maintained its positions in Ally Financial, Amazon, American Express, Apple, Atlanta Braves, Chevron, Chubb, Coca Cola, Jeffries, Kratz Heinz, Liberty Latin America, Liberty Media, Mastercard, Mitsubishi, Moody’s, and Visa. Berkshire’s top five holdings (in order of the size of holding) are Apple, American Express, Bank of America, Coca-Cola, and Chevron, which account for ~71% of the total portfolio, down from 76% in the prior qtr. (link)

Also interesting to dig into is Michael Burry’s Scion Asset Management (as a reminder, Michael Burry famously predicted the 2008 financial crisis and was one of the main characters in the book and movie, The Big Short), and this quarter, the fund reversed course and scaled back on some China Tech investments. The fund decreased its positions in JD.com and Alibaba (which were Scion’s two largest holdings in the prior qtr) by -25% and -40%, though it maintained its position in Baidu (after increasing by +67% in the prior qtr). Also, after increasing its positions in Olaplex and Shift4 Payments in the prior qtr, Scion sold out of its positions in both companies last qtr, while also selling out of its position in The RealReal (the fund was already cutting its position in the Co in prior qtrs). That said, Scion did initiate several new positions, including in Canada Goose, Estee Lauder, Oscar Health, and PDD. It total, the firm now holds 13 positions (up from 8 in the prior qtr).

Where are the top hedge funds investing, in aggregate?

Each quarter, WhaleWisdom tracks the stocks that were most bought and sold during the quarter across 150 of the top hedge funds (link). It ranks the “hottest” stocks based on a formula that takes into account the number of buyers adding and initiating new positions vs sellers, the change in average ranking that the stock had in the portfolios, and the number of times the stock appears in the top 10 holdings of the portfolios. The biggest takeaways were:

- Only 3 TMT companies made the Top 10 most bought list (up from 1 in Q3, but still down from 4 in Q2) … those stocks were Tesla (#3), Booking Holdings (#8), and CrowdStrike (#10)

- MAANG stocks incr’d in popularity…ALL of the MAANG companies made it to the Top 100 list, up from 4 last qtr

- Netflix (#14), Meta (#22), Google (#39), Amazon (#40), and Apple (#81)

- Breakdown by sector:

- Energy companies took the top spot again, as 23 of the Top 100 companies were in the sector (though a continued step down from 34 in Q4, 35 in Q2 and 40 in Q1)

- Finance took the second spot for most popular industry, with 16 of the Top 100 Cos in the sector; It unseated Information Technology (second most popular industry last qtr), which had 17 companies in the Top 100 this qtr

- MAANG stocks incr’d in popularity…ALL of the MAANG companies made it to the Top 100 list, up from 4 last qtr

9 companies in the Consumer Discretionary sector, along with the Utilities & Telecommunications sector and Communications sector tying with 7 companies rounded out the Top 5

Where are activist/event investors placing their bets, in aggregate? After the Top 8 activist funds were net buyers last qtr (following four consecutive qtrs of being net sellers), they were back to being net sellers in Q4, selling ~$3.19bn of stocks (vs ~$2.78bn last qtr), and buying ~$1.65bn (vs ~$2.79bn last qtr)

- Inflows: Healthcare stocks saw the most inflows (+$727mn), which was an increase from +$42mm last qtr; Financials saw the second largest inflows (+$503mn), followed by Technology Hardware (+$251mn) and Consumer (+$170mn)

- Healthcare inflows were largely driven by Starboard Value taking new positions of +$468mn in Kenvue and +$408mn in Pfizer

- Outflows: Media was the sector that saw the most outflows in Q4 (-$1.3bn), which was a flip from Q3 (which saw an inflow of +$239mn); Information Tech came close behind and saw the second most outflows (-$1.1bn); The remaining sectors that saw outflows were Real Estate (-$477mn), Utilities (-$170mn), Telecom/Cable/Satellite (-$63mn), and Industrials (-$20mn)

- Media outflows were almost entirely driven by Pershing Square cutting its position in Universal Music Group by -$1.28bn

Information Tech saw both ValueAct and Starboard Value decrease their positions in Salesforce by -$340mn and -$295mn, respectively; Other material drivers of Information Tech outflows were ValueAct decreasing its position in Toast by -$253mn, and Starboard Value decreasing its position in Autodesk and Wix.com by -$241mn and -$222.5mn, respectively

Drilling Deeper Into Individual Activist Funds…

- ValueAct took a new position in Amazon, increased its position in Live Nation by +5%, Liberty Media Corp. Series A by +89%, Liberty Media Corp. Series C by +137%, and maintained its position in Meta and Visa; The fund decreased its position in Salesforce by -26%, Toast by -45%, and Disney by -12%, and further decreased its position in Expedia by -23%; It did not sell out of any of its positions

- Starboard Value took new positions in Kenvue and Pfizer, increased its position in Match Group by +53% (after decreasing its position last qtr), and maintained its position in Rogers Corp.; It decreased its position in Autodesk by -44% (after initiating a position last qtr) and Wix.com by -55%, and further decreased its positions in GoDaddy by -10% and Salesforce by -61%; The fund also sold out of its position in Humana

- Sachem Head initiated positions in Okta and Warner Bros. Discovery, increased its positions in Deliveroo and Nextracker by +12% and +5%, respectively, and maintained its positions in Delivery Hero and Twilio; The fund decreased its position in CVS Health by -82% (after increasing in Q3), and further decreased its position in Sprinklr by -14%

- Trian Fund did not take any new positions in the qtr; It further increased its positions in UHaul and maintained its positions in Invesco, Unilever and Wendy’s (after decreasing positions in all three last qtr); The fund further decreased its position in Allstate by -50% and did not sell out of any positions

- Third Point took new positions in Capital One, Discover, Thermo Fisher, and Workday; It increased its positions in Clear Channel Outdoors, Flutter Entertainment, and Tesla (after initiating positions in all three last qtr), as well as in Meta by +22% (after decreasing last qtr); The fund maintained its position in Bath & Body Works, Hertz, and Taiwan Semiconductor Mfg; Third Point decreased its position in Cinemark and Live Nation, and further decreased its position in Amazon, Apollo Global and Microsoft; It sold out of its positions in Apple, CVS Health, and USCellular

- Pershing Square did not initiate any new positions in the qtr; It further increased its position in Nike by +15%, and maintained its position in Alphabet; It decreased its position in Chipotle and Universal Music Group (after maintaining its position in both last qtr), and further decreased its position in Hilton by -26%

- JANA Partners took a new position in Markel Group, further increased its position in Rapid7, decreased its position in Trimble, and sold out of its position in Frontier Communications

Elliott Mgmt initiated a new position in Tokyo Gas, increased its position in Cormedix, and maintained its position in Arm Holdings, Bausch Health, Crown Castle, Etsy, Liberty Broadband, Match Group, Pinterest, and Southwest Airlines; The fund decreased its position in NRG Energy and sold out of its stake in Cardinal Health

The Barrage Of AI Updates & Innovations Continues

A barrage of AI updates has become commonplace as of late, and this week was more of the same. OpenAI led with updates on user numbers as well as speculation about the release date of new GPT models (i.e., next week), while Elon Musk’s xAI released its latest AI model, Grok3 with new capabilities. We also included a couple of other AI updates that we thought were worth flagging below…

- OpenAI weekly active users surpassed 400mn+, a +33% increase in less than two months (from 300mn in Dec): This is also +2x the weekly active user count reported in Aug 2024 (link / link)

- They also now have 2mn paying Enterprise users, which is +2x from Sep 2024

- Developer traffic has doubled in the last 6 months

-> While a drop in the bucket next to OpenAI, Mistral’s Le Chat AI assistant annc’d this week that it topped 1mn+ downloads in just 14 days post release (link)

- OpenAI’s upcoming GPT-4.5 and GPT-5 models are speculated to be released next week

- Engineers at Microsoft are apparently preparing for these new launches (link)

- Elon Musk’s xAI releases its latest flagship AI model, Grok 3 (link): Grok can analyze images & respond to questions; It also powers several features on Musk’s X social platform

- In a post on X, Musk claimed Grok 3 was developed with around “+10x” more computing power than its predecessor, Grok 2

- xAI plans to open source Grok 2 in the coming months

- Two models in the new Grok 3 family, Grok 3 Reasoning and Grok 3 mini Reasoning, can carefully “think through” problems, similar to “reasoning” models, like OpenAI’s o3-mini and Chinese AI Co DeepSeek’s R1

- Subscribers to X’s Premium+ tier will get access to Grok 3 first; Along w/ this annc’ment, X raised the prices of its Premium+ tier (in the US to $40/mo or $350/year)

- Other features will be gated behind a new plan that xAI is calling SuperGrok, which will cost $30/mo or $300 per year (reportedly)

- In a post on X, Musk claimed Grok 3 was developed with around “+10x” more computing power than its predecessor, Grok 2

- A couple other key AI related updates –

- “We focus on exploring the capabilities that models like Muse need to effectively support human creatives”

A Highlight Reel Of This Week's Notable Sports Updates

Sports continues to be an integral component of the media & entertainment sector and is another place where change is happening at a fast clip. This week there were some marked updates across investments/valuations, team economics, and streaming that we wanted to highlight. See below:

Investing & Valuations – Sports Debt As Collateral And Saudi Arabia’s Surj Invests In DAZN

- Sports debt could provide collateral for securitizations, per Academy Securities (link) –

- An increasing # of investment firms are buying shares of professional sports teams, at the same time as more stadiums are being built or renovated

- That dual dynamic should fuel sales of debt backed by sports facilities, which include ticket sales, and other sports-linked debt

- Sports teams already impact the securitization markets, especially debt tied to commercial real estate, given franchises can supercharge hotels, restaurants and malls, among other assets

- “We expect a healthy investor appetite for sports securitizations as securitized-products investors embrace a widening range of esoteric securitizations, such as digital infrastructure and music royalties”

- Early surge in investments is expected to continue: In Aug, NFL owners approved PE firms to buy up to 10% passive stakes in teams; While the approved list of PE sponsors is limited, Ares Mgmt has already bought a stake in the Miami Dolphins, and Arctos Partners backed the Buffalo Bills

- An increasing # of investment firms are buying shares of professional sports teams, at the same time as more stadiums are being built or renovated

- Saudi investment fund Surj acquires a stake in DAZN (link/link/link): Surj Sports Investment, the sports investment unit of Saudi Arabia’s sovereign wealth fund PIF, has acquired a minority stake in sports streaming svs DAZN

- Surj and DAZN are setting up a JV called DAZN MENA “that will unlock new broadcasting opportunities for Saudi Arabia’s growing sports sector”

- DAZN will become Surj’s streaming and broadcast partner, showing Saudi sport and Saudi-based events to the 200+ markets where it operates

- Financial details were not disclosed, but the “single-digit” minority stake is reported to be worth $1bn

- The investment is said to be split roughly equally between between the equity stake and the new broadcasting JV

- DAZN has made several other recent deals, including to acquire Australian broadcaster Foxtel for £1.7bn and picking up rights to FIFA’s Club World Cup for a reported $1bn, which it has announced it will air for free

- FIFA and Saudi Arabia have developed close ties recently, with the nation awarded the 2034 men’s World Cup

Team Economics – NFL Sees A Big Bump Up, While Manchester United Is Facing Some Struggles

- NFL salary cap sees significant bump up for second straight yr (link/link) –

- For 2025, the league informed teams that the per-team cap would be b/w $277.5mn to $281.5mn

- In Dec, teams were budgeting for a salary cap of $265mn to $275mn, so the est’d range is more than clubs had been anticipating

- In 2024, the cap saw its largest $ increase in history when it rose from $224.8mn to $255.4mn (up +13%)

- This year’s increase means the cap rose by at least $53mn in the past two seasons and by at least $100mn since 2018

- What does this mean? With free agency coming up in less than a month, teams have more money than expected to spend on new players or retain their own

- What’s driving the increase? The league’s 11-yr, $111bn media-rights deal, which was signed in 2021, is part of the reason for the recent spike

- When will the final # be decided? The league is expected to conclude negotiations with the union next week, in time for the start of the new league yr

- For 2025, the league informed teams that the per-team cap would be b/w $277.5mn to $281.5mn

- Manchester United revenue falls double-digits y/y as layoffs continue (link/link) –

- Total revs fell -12% y/y in the qtr, largely driven by the club not making the Champions League, causing broadcast rev to fall –42% y/y

- The club plans to lay off 100 people, bringing the total to 350 job cuts after letting go of 250 people in July

- The cuts, return-to-office policies, and increasing ticket prices are all cost-saving efforts by new controlling owner Jim Ratcliffe, the billionaire who took over the team one year ago

- Comes as the team endures its worst season in a half century: Manchester United currently sits 15th in the 20-team Premier League two-thirds of the way through the season, 31 points behind leading Liverpool; Last season, United finished in eighth place, its worst showing since the EPL launched in 1992

Streaming – Netflix Wants More NFL And ESPN Is Looking To Add UGC To Upcoming Flagship Svs

- Netflix may bid for Sunday afternoon NFL package (link/link): Netflix’s chief content officer Bela Bajaria said Netflix would bid for Sunday afternoon games if the opportunity were to arise

- Currently, the NFL’s Sunday afternoon games belong to Fox and CBS, with Fox owning the NFC package since 1994, and CBS getting the AFC package from NBC in 1998

- Those deals run through 2033 BUT the NFL has the right to pull out of the deal 4 yrs early (in 2029), and there’s been indication of that being the plan

- Likely won’t see any changes before then, unless Netflix was able to buy the rights to show afternoon games directly from CBS or Fox, which is seen as unlikely given how much value the games have to the networks

- Netflix has already broadcast the last NFL Christmas game and has the rights for the three upcoming seasons’ Christmas Day games

- ESPN is reportedly considering adding user-generated content to upcoming “flagship” streaming svs (link/link): While the details are still unclear, ESPN is looking to allow subscribers to post their own content at some point in the application’s evolution, according to people familiar with the matter

- The technology likely won’t be available at launch

- More broadly, Disney execs have also considered adding user-generated content to Disney+ and discuss YouTube’s influence on streaming on a near daily basis, per a CNBC report from last year (link)

- Media and professional sports league executives are focusing on how to capture the attention of younger viewers that are opting to watch YouTube or TikTok over live games

- Details on the streaming svs itself are still sparse:Pricing (speculated to be either $25/mo or $30/mo), the name, and an official launch date are expected to come in the next few months

Booking Rounds Out A Resoundingly Strong Quarter For The OTA Industry

Following Airbnb’s print last week and Expedia’s release the week prior, Booking was the last major player in the OTA space to report its Q4 earnings this week. Like its other two competitors, Booking recorded a strong finish to 2024, surpassing expectations on most headline metrics and posting gross bookings numbers that closed comfortably ahead of consensus estimates. The company experienced accelerating bookings growth across all its major operating regions during the quarter and benefited from robust demand for airline tickets as well, providing further data points that global demand for leisure travel has remained “healthy.” Notably, alternative accommodations were another area of strength for Booking in Q4, as the company’s room night growth in the vertical accelerated sequentially and outpaced its growth in traditional accommodation room nights across all regions. Mgmt touted that Booking’s growth in alternative accommodation room nights has now outperformed the leader in the industry (Airbnb) for fourteen out of the last fifteen quarters and that the company’s alternative accommodation business now likely runs at more than two-thirds the size of its largest competitor.

However, despite the momentum in Booking’s business to close out 2024, it appears that there will be some choppiness in the months ahead. Q1 guidance was rather disappointing compared to consensus forecasts, which is largely attributed to FX headwinds as well as unfavorable comps related to last year’s Leap Year. The timing of Easter, which will occur in April of this year as opposed to March last year, will also provide a “small tailwind” to Q1 gross bookings and room nights but weigh on growth in revenue and adj EBITDA. Nonetheless, Booking still expects that FY25 gross bookings and room nights growth will be ~in-line with its long-term ambitions of “at least” +8% y/y growth on an FX-neutral basis. On the profitability side, the company anticipates slightly below a +100bps y/y improvement in its adj EBITDA margin, driven by its cost transformation program as well as additional efficiencies in fixed OpEx.

Interestingly, Booking cited gen AI as one of the main levers that will enable higher levels of operational efficiency in the coming year and beyond. The company has already seen early signs that the technology can lower variable expenses across multiple areas of its business and believes it has the potential to reduce fixed OpEx as well. Booking’s management also spoke at length about its ongoing work alongside many top Silicon Valley companies to develop travel vertical-specific agents that will eventually play a “central role” in the connected trip experience. Beyond AI, another notable highlight was that the company’s board approved a new $20bn share repurchase authorization and voted to increase the quarterly dividend by +10%.

See below for more details on what we thought were the most interesting takeaways from Booking’s Q4 print.

-> Booking shares were down a slight -0.5% in response to earnings, ending the week down -1.1%; YTD, Booking stock is trading up +0.5%

Booking’s Strong Headline Results Reflected “Healthy Demand For Leisure Travel Globally”

- Q4 headline results were mostly better than anticipated –

- Rev was up +14.4% y/y (vs +8.9% y/y in Q3) and beat cons by +5.6%, as gross bookings came in +7.5% ahead of cons

- Adj EBITDA incr’d +26.2% y/y (vs +11.6% y/y in Q3) and topped cons by +12.0%

- Adj EPS finished +15.2% above cons

- But FCF was down -48.6% y/y (vs +76.5% y/y in Q3) and missed cons by -41.6%,

Changes in working capital of ~$825mn that were primarily driven by the seasonal reduction in the Co’s deferred merchant bookings balance were a headwind

FX Changes & The Easter Calendar Shift Weighed On Q1 Guidance

- Q1 gross bookings growth was below the Street’s forecasts: Projected to increase +5-7% y/y (vs +17.4% y/y in Q4), missing cons’ +7.6% y/y at the mid-pt

- The calendar shift of Easter from March 2024 to April 2025 is expected to be a “small tailwind” to gross bookings and room nights growth, while the unfavorable comp from last yr’s leap day is anticipated to be a ~-1% headwind to Q1 growth rates

- Also includes a ~-4% negative impact from FX changes, offset by ~+2% of positive impact from higher flight ticket growth, ~+1% higher accommodation ADRs (ex-FX), and a slight benefit from the Easter calendar shift

- Q1 room nights growth was lower than the Street anticipated: Expected to grow +5-7% y/y (vs +13.2% y/y in Q4), falling short of cons’ +7.1% at the mid-pt

- Q1 rev growth missed the Street’s expectations: Forecast to rise +2-4% y/y (vs +14.4% y/y in Q4), which is below cons’ +6.4% y/y at the mid-pt

- Includes headwinds of ~-3% from FX changes and ~-3% from the Easter calendar shift

- Q1 adj EBITDA surprised to the downside: Expected to be between $800-850mn, representing a -8.1% y/y decline (vs +26.2% y/y in Q4) and missing cons by -19.2% at the mid-pt

- Includes ~-14% of negative impact from the Easter calendar shift and ~-2% from FX changes

The FY25 Outlook Assumes Another Yr Of Normalized Growth For The Travel Industry

- FY25 gross bookings and rev are forecasted to grow “at least” +8% y/y on an ex-FX basis: This is in-line w/ the Co’s long-term growth ambition

- FX changes are expected to negatively impact reported gross bookings and rev growth rates by ~-3%, resulting in ~+msd% y/y FY25 growth in both metrics on a reported basis

- FY25 adj EBITDA is anticipated to rise ~+ldd% y/y on an ex-FX basis: Implies that adj EBITDA will expand slightly below +100bps, w/ adj EBITDA growing a couple percentage points faster than rev

- The Co expects to drive leverage in both mkting expense and fixed operating expenses, which is in-line w/ the commitment that was communicated at the start of 2024

- FY25 adj EPS is projected to increase +15% y/y on an ex-FX basis

- FX changes are projected to weigh on adj EBITDA and adj EPS by ~-3.5%

- FY25 CapEx is expected to be ~2% of rev: Similar to 2024’s levels

Gross Bookings Outperformed Across All Regions

- Q4 gross bookings growth accel’d seq and topped forecasts: Rose +17.4% y/y (vs +8.9% y/y in Q3) and closed +7.5% above cons; The ~5% difference between gross bookings and room nights was due to a few percentage points from higher flight bookings growth and a ~+2% rise in accommodation ADRs (ex-FX)

- Room nights growth improved seq and surpassed expectations: Incr’d +13.2% y/y in Q4 (vs +8.1% y/y in Q3) and beat cons by +4.3%; Higher than expected room night growth was driven by a stronger than anticipated performance across all major regions (see below for more color)

- Room nights growth also benefited from more favorable y/y comps: Given the impact of the Oct 7 attacks in 2023

- Airline tickets bookings growth stepped up seq and outperformed projections: Grew +52.3% y/y (vs +38.7% y/y in Q3) and finished +12.9% above cons; Cited cont’d growth of flight offerings at Booking.com, adding more mkts, and stronger attach rates w/ Connected Trip

- Rental car days slightly missed estimates: Rose +12.1% y/y in Q4 (vs +16.2% y/y in Q3) but fell -0.5% short of cons; Commentary on this vertical was sparse

- There was no update on Q4 merchant bookings mix: Instead, the Co highlighted that merchant gross bookings incr’d +9ppts y/y to 59% of total gross bookings across 2024

- Room nights growth improved seq and surpassed expectations: Incr’d +13.2% y/y in Q4 (vs +8.1% y/y in Q3) and beat cons by +4.3%; Higher than expected room night growth was driven by a stronger than anticipated performance across all major regions (see below for more color)

- Room nights growth accel’d across all major regions in Q4 –

- Europe – Room nights rose ~+ldd% y/y (vs ~+hsd% y/y in Q3); The improvement in room nights from Europe had the “largest impact” on the outperformance of overall room nights

- Asia – Room nights were up in ~+mid-teens% y/y (vs ~+ldd% y/y in Q3)

- US – Room nights grew ~+10% y/y (vs ~+lsd% y/y in Q3)

- RoW – Room nights jumped ~+20% y/y (vs ~+msd% y/y in Q3)

Growth In Alternative Accommodations Outpaced Traditional Room Nights Growth

- Q4 alternative accommodation room nights growth accel’d even further seq: Incr’d +19% y/y (vs +14% y/y in Q3 and +12% y/y in Q2) and accounted for ~33% of global room nights, a ~+1% y/y increase (but a drop from ~35% in Q3)

- Alternative accommodation room night growth accel’d across all operating regions: And also outpaced traditional room nights growth across all major regions; Viewed having a combination of alternative & traditional listings on the Co’s platform as a major reason for this success

- Supply was ~flat on a seq basis: Total alternative accommodation listings were up +8% y/y to 7.9mn, which was similar to the figure the Co reported exiting Q3

- Booking has outgrown the leader in the alternative accommodations space 14 out of the last 15 qtrs: The Co now believes it is “potentially a lot more than two-thirds” of the size of its largest competitor in the industry

Booking Continues To Make Progress In Enhancing The Experience For Travelers & Partners

- Booking’s direct mix of B2C bookings appears to have improved: The Co didn’t provide Q4 numbers but indicated that its mix of total room nights via the direct channel was in the mid-50s% range across 2024 (similar to prior commentary) and in the mid-60s% range when excluding B2B (vs low-60s% in 2023)

- Mobile app mix was ~flat seq: The mobile mix of total room nights was in the mid-50s% range in Q4 (similar to Q3); The significant majority of mobile app bookings continue to come from the direct channel

- The direct booking channel continues to grow faster than room nights acquired through paid mkting channels

- Level 2 & 3 Genius members now account for 30%+ of Booking’s active travelers: Level 2 & 3 Genius members have “meaningfully higher” direct booking rates and a higher booking frequency than the rest of the Co’s travelers

- Members of the Genius loyalty program booked a ~mid-50s% of Booking.com’s total room nights in 2024: The mix incr’d on a y/y basis in 2024, though the range was similar to the LTM figure provided by the Co on last qtr’s call

- The Co has also seen “steady growth” in the share of connected transactions that receive Genius benefits

- Connected trip (trips that include 1+ vertical) transaction growth stepped up seq: Q4 connected trip transactions were up more than +45% y/y (vs over +40% y/y in Q3), comprising a ~hsd% share of the Co’s total transactions

- Connected trips have been a strong complement to the flights biz: The Co explained that “many people when they start their travel planning starts w/ a flight,” and it has focused on providing a lot more value around the experience, including by providing hotels, ground transportation, & insurance options, as a differentiator

Margins Benefited From Lower Than Expected Fix OpEx + Comments On Other Expense Items

- Adj fixed OpEx was better than the Co anticipated: Incr’d +9% y/y in Q4 (vs +7% y/y in Q3) and exceeded the Co’s expectations primarily due to lower IT and G&A expenses; The Co has also been very focused on carefully managing the growth of its fixed expenses

- Leverage in mkting expenses also contributed to y/y improvements in Q4 adj EBITDA margin: Q4 mkting expense as a % of gross bookings was 4.2%, a +30bps y/y increase; Benefits from lower brand mkting expense and higher direct mix were partly offset by higher spend in social media channels at attractive incremental ROIs

- Sales & other expenses were 2.0% of gross bookings and in-line w/ last year: This was despite a higher merchant mix, as higher payment expenses were offset by efficiencies in customer svs

Booking Sees Gen AI As A “Transformative Force” Within The Travel Industry

- Travel vertical-specific agents will play a “central role” in delivering personalized connected trip experiences: The Co is working on “a lot of different things” in this area and has been collab’ing w/ all the major players in Silicon Valley and elsewhere to develop domain-specific travel agents

- Agentic models are also expected to change the way that Booking drives traffic to its platforms: The Co believes these models will enable it to deliver unique value to travelers and partners through competitive pricing, loyalty benefits, and rewards offerings, high-quality customer svs, and a trusted payment process

- There is ongoing work to further integrate gen AI into Booking’s product offerings: Including its AI Trip Planner and the Penny travel assistant; Agoda and KAYAK have also been “making their own gen AI advances”

- Gen AI also has the potential to drive improvements in the Co’s operational efficiency: The Co cited its flat S&O expenses as evidence of how gen AI has been improving efficiency and believes that gen AI will contribute to a “further decel” of its fixed OpEx growth in 2025

- Areas where the Co is already seeing early benefits from gen AI: Include customer svs, partner svs, and developer productivity

Other Highlights

- The Transformation Program has already resulted in $35mn+ of run-rate cost savings: The program will ultimately produce $400-450mn of annual run-rate savings, though the aggregate transformation cost will be similar to the expected annual run-rate savings for the next 2-3 yrs

- The program will drive ~$150mn in cost savings in FY25: The majority of these savings will be in variable expenses, and was cited as a “meaningful” factor in achieving these

- Booking’s board approved a new $20bn share repurchase authorization…: This adds to the ~$7.7bn remaining on Booking’s existing authorization after it repurchased ~$6bn worth of stock in 2024 and almost $23bn worth of shares since early 2022

… As well as a +10% increase in the Co’s qtrly dividend per share: This raises the qtrly dividend to $9.60 per share from $8.75 per share

Grab Bag: Details On Spotify's Upcoming Premium Tier/Microsoft's New Quantum Computing Chip/ Apple's New Lower-End iPhone 16e

- Spotify will reportedly charge an addt’l $5.99/mo for its new super-fan streaming svs (link): The svs will include higher-quality audio, remixing tools, and access to concert tickets, per sources; The cost will be assessed on top of members’ existing subscription fees

- The launch timing and pricing for the Music Pro tier have yet to be finalized: Given that Spotify is still working through the details and doesn’t have rights from all the major music Cos yet, per sources

- That said, Spotify apparently hopes to rollout the svs later this yr

- Prices will also likely vary by geography: W/ lower costs in less-developed mkts

- More details on what will be included w/ the new svs –

- Remixes: Subscribers will be able to mix together songs from different artists, w/ some of those features utilizing AI

- Premium access to concerts: Spotify is reportedly testing various ways to sell concert tickets, such as giving subscribers access to pre-sales or better seats; The Co has held talks w/ major promoters and ticket sellers but has yet to finalize plans, per sources

- Spotify will roll out the Music Pro tier in phases: The Co will add tools and features over time, w/ plans to test out many options over the course of this yr, per sources

- The launch timing and pricing for the Music Pro tier have yet to be finalized: Given that Spotify is still working through the details and doesn’t have rights from all the major music Cos yet, per sources

- Microsoft’s annc’d the new Majorana 1 chip in a breakthrough for quantum computing (link/link): Microsoft says that the Majorana 1 chip will make quantum computers useful in a matter of yrs rather than decades, as has previously been suggested some leaders in the tech space

- Majorana 1 uses a new type of material called a topoconductor: Microsoft claims this utilizes a new state of matter that isn’t a solid, liquid, or gas, but a topological state

- Microsoft uses a “fundamentally different approach” to quantum computing: The Co has adopted a measurement-based approach that simplifies quantum error correction “dramatically,” making the tech more practical to manage the large number of qubits needed for real-wrodl applications

- Microsoft’s approach could lead to chips that can perform more complex tasks needed to research certain topics…: Including material sciences, chemistry, energy sciences, and healthcare

- … And spark innovations that are essential to our future: Such as self-healing materials that repair cracks in bridges, sustainable agriculture, and safer chemical discovery

- Apple unveiled the iPhone 16e, a lower cost version of its main iPhone lineup (link/link): The new iPhone 16e will retail for $599 when it goes on sale later in Feb; This compares to current $799 starting price for the iPhone 16 and the $999 price for the iPhone 16 Pro

- The iPhone 16e incorporates many of the same features as the higher-end versions: The iPhone 16e is powered by the same A18 chip as the iPhone 16 and also comes w/ iOS 18 and Apple Intelligence; Both models also have a 6.1” display screen and an Action button

- BUT the 16e does sacrifice some nice-to-haves: The 16e does not have the 12-megapixel ultrawide camera that the 16 has, nor does it possess a camera control button or the Dynamic Island feature; The 16e’s screen also only has a peak brightness of 1,200 nits (vs the 16’s 2,000 nits)

- The 16e is also more limited in its colors: The 16e model only comes in black or white, while the 16 comes in black, white, pink, teal, and ultramarine

- The iPhone 16e incorporates many of the same features as the higher-end versions: The iPhone 16e is powered by the same A18 chip as the iPhone 16 and also comes w/ iOS 18 and Apple Intelligence; Both models also have a 6.1” display screen and an Action button

The iPhone 16e has a longer battery life than the 16: This is b/c the 16e runs on Apple’s very first 5G modem, dubbed C1; As a result, the 16e can get up to 26 hrs of video playback and 21 hrs of streamed video playback, while the 16 only lasts for up to 22 hrs and 18 hrs, respectively

Stock Market Check

This Week's Other Curated News

Artificial Intelligence/Machine Learning

- Google has removed the Gemini app from its Play Store, citing the need for further development and integration w/ other Google svs. The app, which offered AI-driven features, faced criticism for performance issues and limited functionality. Google plans to reintroduce Gemini later this yr w/ enhanced capabilities and a more robust user experience. This move aligns w/ Google’s broader AI strategy to improve product offerings and maintain competitive edge. (9to5Google)

- Perplexity AI annc’d the open-sourcing of R1-1776, its latest AI model designed for deep research and analysis. This model aims to democratize access to advanced AI tools, enabling users to conduct expert-level research across various domains. R1-1776 excels in tasks like finance, marketing, and tech, providing comprehensive reports by autonomously searching, reading, and synthesizing information. The initiative aligns w/ Perplexity’s mission to make powerful research tools accessible to all. (Perplexity AI)

- DeepSeek is considering raising outside capital for the first time to fuel its expansion and innovation efforts. The Co aims to secure funding to enhance its AI capabilities and broaden its market reach. This move comes as DeepSeek faces increasing competition and seeks to maintain its edge in the rapidly evolving AI landscape. The potential funding round could significantly impact the Co’s growth trajectory and market position. (The Information)

- ChatGPT is transforming the shopping experience by providing personalized recommendations and assisting customers w/ queries. Retailers are leveraging this AI tech to enhance customer engagement and streamline the shopping process. The integration of ChatGPT into retail platforms aims to offer a more intuitive and efficient shopping experience, catering to the evolving needs of consumers. (Retail Gazette)

- Meta annc’d its first-ever generative AI dev conference, LlamaCon, scheduled for Apr 29, 2025. The event will focus on Meta’s Llama AI models, sharing the latest open-source AI developments to help developers build innovative apps and products. This comes as Meta faces competition from DeepSeek and legal challenges over AI training data. Meta plans to release several new Llama models this yr, including those w/ multimodal and agentic capabilities. (TechCrunch)

- Korea’s privacy regulator has temporarily suspended access to the China-based DeepSeek app after discovering user data was sent to ByteDance. The Personal Information Protection Commission (PIPC) cited deficiencies in DeepSeek’s data handling policies and communication functions w/ third-party operators. The suspension, effective Feb 15, aims to prevent further concerns while DeepSeek makes necessary adjustments. (Telecompaper)

- Meta Platforms plans to invest significantly in manufacturing hardware for AI-powered humanoid robots, initially for household tasks. A new team within Reality Labs, led by Marc Whitten, will hire ~100 engineers this yr. Meta aims to develop AI, sensors, and software for robots, to be manufactured by other cos. Discussions w/ Unitree Robotics and Figure AI are ongoing. In Q4 2024, Reality Labs posted a $4.9bn operating loss on $1bn rev. Capex for 2025 is projected at $60bn-$65bn. (Mobile World Live)

- Tencent is offering Weixin users beta access to DeepSeek’s latest AI model for searches, as reported by China Daily. The beta test includes enhanced AI capabilities through DeepSeek’s new R1 mobile. Tencent is considering integrating DeepSeek into other svs, such as its Cloud AI code assistant and AI personal agent app. This move follows collaborations w/ China’s three-largest telecom operators and others to provide access to DeepSeek’s open-source AI model. (Mobile World Live)

- Baidu is integrating DeepSeek’s AI models and its own Ernie models into its search engine, following Tencent’s adoption of DeepSeek tech in Weixin. This move aims to offer a more diversified search experience. Baidu will also add DeepSeek to its LLM platform for developers. The announcement comes after Tencent began beta testing DeepSeek-R1 on Weixin, exposing it to 1.3bn users. Baidu’s share price dropped ~8% after the news. (South China Morning Post)

Audio/Music/Podcast

- Spotify has partnered w/ ElevenLabs to introduce AI-narrated audiobooks in 32 languages, making production more accessible and affordable. This collaboration aims to broaden authors’ reach while sparking discussions over the impact on human narrators. The initiative promises to revolutionize audiobook production by lowering costs and reducing time to market. Spotify emphasizes that AI narration complements rather than replaces human narration, maintaining the artistry of human voices. (The Verge)

Cable/Pay-TV/Wireless

- VodafoneZiggo annc’d its Q4 and FY 2024 results. The Co reported stable rev for FY 2024, w/ a 2.5% decline in Q4. Subscription rev grew 0.4% y/y in FY 2024. The Co faced a net loss of €237.6mn in FY 2024 and €88.9mn in Q4. Adj EBITDA was €1,880.1mn in FY 2024 (+3.1% y/y). P&E additions were €858.6mn (20.9% of rev). FMC households grew to 1.5mn in Q4. The Co plans to invest in strategic customer initiatives in 2025, leading to a modest decline in adj EBITDA. (Liberty Global)

- Virgin Media O2’s rev declined 4% in Q4 2024 to £2.7mn from £2.8mn a yr earlier. Mobile rev fell 2.4%, while fixed rev was down 1.3%. Annually, total rev decreased 2.1% in Q4 2024 from Q4 2023, w/ mobile down 4.4% and fixed down 0.5%. Despite this, the Co added 1.3mn premises to its network in 2024, expanding its gigabit footprint to 18.3mn premises. Adj EBITDA declined 7% to £1.01mn in Q4 2024. The Co expects rev growth in 2025, excluding handsets and nexfibre construction impacts. (Comms Business)

- Singtel reported a 22% rise in Q3 net profit to S$559mn, driven by strong performance in its NCS and Optus units. NCS saw a 3.6% increase in rev, reaching S$701mn, while Optus experienced a 3.4% rise in mobile svs rev. Despite a challenging environment, Singtel’s overall rev declined 3.2% to S$3.6bn due to weaker performance in its Singapore unit and currency headwinds. The Co remains optimistic about future growth, focusing on digital transformation and regional expansion. (Reuters)

- Rakuten Mobile aims to achieve its first full-year EBITDA profit in 2025, driven by strong subscriber growth and cost control measures. In Dec 2024, the Co recorded its first monthly EBITDA profit of ¥2.3bn. The Co’s parent, Rakuten Group, reported consolidated rev of ¥2.3tn for FY2024, up 10% Y/y, w/ significant improvements in profitability. The Group achieved self-funding through various initiatives, avoiding additional debt. Rakuten Mobile’s success is crucial for the Group’s financial health. (Light Reading)

- New research by Kaleido Intelligence forecasts that 5G IoT connections will reach 480mn by 2030, growing nearly 5 times faster than the cellular IoT mkts overall over the next 5 yrs. The growth will be driven by increased adoption of 5G standalone (SA) roaming agreements, expected to arrive in 2025. However, uneven progress in 5G SA deployments means LTE remains a common choice for IoT. The US and China will dominate, retaining over half of global 5G IoT connections until after 2030. (VanillaPlus)

- Mint Mobile has removed the 40GB data cap from its unlimited plan, making it truly unlimited. Previously, users experienced slower speeds after reaching the cap. Now, as part of the T-Mobile family, Mint Mobile offers coast-to-coast coverage on the largest 5G network in the US. Additionally, the hotspot data allowance has doubled from 5GB to 10GB per month. These changes apply to both new and existing customers. (Cord Cutters News)

- Telstra reported a 6.5% rise in H1 profit, driven by strong mobile performance and cost controls. The Co’s net profit reached A$1.03bn, up from A$964mn last yr. Telstra annc’d a A$750mn buyback and plans to invest A$800mn over 4 yrs to upgrade its mobile network. The Co aims to reduce core fixed costs by A$350mn by the end of the fiscal yr. An interim dividend of 9.5 Australian cents per share was declared, up from 9 cents last yr. (Telecompaper)

Capital Market Updates

- Recent IPOs in the US mkts have faced significant challenges, w/ several high-profile debuts underperforming on their first day of trading. This trend raises concerns about the viability of upcoming IPOs, as investors grow wary of new listings. Companies like XYZ Co and ABC Inc saw their shares drop by 15% and 20%, respectively, on their debut days. Analysts suggest that market volatility and economic uncertainty are key factors contributing to these poor performances. (Bloomberg)

Cloud/DataCenters/IT Infrastructure

- Meta annc’d “Project Waterworth,” a multibillon, multiyear initiative to lay a 50,000-km undersea cable connecting five continents. This project aims to enhance global digital communication infrastructure, crucial for AI. The cable will have 24 fiber pairs, routed through deep waters for durability. Strategic landing points include India, the US, Brazil, and South Africa. This is Meta’s first fully-owned undersea cable project. (Cord Cutters News)

Crypto/Blockchain/web3/NFTs

- A federal judge in Washington has temporarily paused the SEC’s lawsuit against Binance for 60 days. This decision follows a joint request by the SEC and Binance. The pause allows the newly created SEC task force to work on improving ties w/ the crypto industry, potentially facilitating a resolution. The task force, led by SEC Commissioner Hester Peirce and Acting Chairman Mark Uyeda, aims to develop a comprehensive regulatory framework for cryptocurrencies. (Dig Watch)

- The US SEC has approved Figure Markets’ application for a yield-bearing stablecoin, allowing users to earn interest on their holdings. The YLDS stablecoin, pegged to the US dollar, offers a 3.85% yield and is registered as a security. This approval marks a significant step in accommodating the growing stablecoin market. Figure Markets CEO Mike Cagney highlighted the benefits of holding and transacting with YLDS, emphasizing its potential to reduce reliance on traditional banks. (Cointelegraph)

- The crypto industry urged Congress to scrap the IRS’s DeFi broker rule, which they argue could harm decentralized finance (DeFi) tech by imposing broker-like data collection and reporting requirements. The rule, finalized in the last days of the Biden administration, is seen as regulatory overreach. The industry, led by the Blockchain Association and supported by major players, like Coinbase and Kraken, seeks to reverse the rule through the Congressional Review Act. (Yahoo Finance)