Major US equity indices were higher for the holiday-shortened week, though it did end on a bit of a choppy note with SCOTUS ruling that the Trump-era tariffs were illegal, headlines around a potential new 10% tariff, and comments about a possible limited strike on Iran adding to policy and geopolitical uncertainty.

It was week 5 in the TMT earnings cycle with key prints across live entertainment, last-mile, and OTAs. We also got a first glimpse into some of the major consumer companies. As always, AI continues to be at the center of a seemingly never-ending stream of updates. See below for what we focused on in this edition.

- Earning Scorecard – Week 5

- Live Nation Cites No Pullback “Whatsoever” In Concert Demand

- AI Spooks The Media & Entertainment Industry, Along W/ Other Key AI Developments

- TMT Lost Some Favor W/ Hedge Funds In Q4…Per 13’Fs

- 2026 Will Be An Investment Year For DoorDash As It Builds The Next Version Of Itself

- Booking.com Believes That LLMs Will Stay At The Top Of The OTA Funnel

- Quick Earnings Takes – OMC, WMT, EBAY, ETSY, & W

- Grab Bag: MSG Sports Is Exploring A Spin-Off / Apple Introduces A New Video Podcast Feature / Uber Is Expanding Food Delivery In Europe

Also, on the home front, I wanted to highlight that LionTree Advisors LLC served as financial advisor to Liberty Global and Telefonica on their £2bn acquisition of Substantial Group through their existing joint venture, Nexfibre and LionTree Advisors LLC also served as financial advisor to Liberty Global on its acquisition of Vodafone’s stake in VodafoneZiggo and the creation of Ziggo Group.

Best,

Leslie

Earning Scorecard – Week 5

This was Week 5 of the TMT earnings storm. In total, 17 stocks in our LionTree Universe reported. Unlike the last 2 weeks, stock reactions skewed positive this week, with 9 stocks trading up and 8 trading down. The best performer in reaction to earnings was Omnicom, which was up +15.4% (see Theme #7), while the worst performer was Wayfair, which fell -13.0% (see Theme #7).

Live Nation had a favorable reaction to earnings (up +3.3% – see Theme #2) as did DoorDash (up +1.6% – see Theme #5). Bookings closed out the OTA earnings season, but it was on a tougher note with the stock falling -6.1% in reaction to its print (see Theme #6).

On the Consumer front, eBay, Etsy and Walmart all reported and were up +3.1%, +9.3% and down -1.4% respectively in reaction to earnings (see Theme #7).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Live Nation Cites No Pullback “Whatsoever” In Concert Demand

Live Nation closed out Q4 with a broad-based beat across rev and adj op income, and that strength has continued into 2026. Concert demand remains “extremely robust” globally, with major tours like Bruno Mars, Harry Styles, and BTS hitting record-level pre-sales, and no pullback “whatsoever” in demand for any budget-conscious fans. Ticketmaster’s GTV is expected to accelerate “a bit” from 2025, driven by concerts and improvements in the sports and other segment, and distribution partnerships with platforms like Spotify continue to expand reach for shows that might not otherwise sell out.

Looking ahead, 2026 will be a ramp year for Venue Nation investments, with pre-opening costs increasing from $25mn in 2025 to $50mn in 2026, though these costs are NOT expected to increase at that pace as the portfolio reaches a steady state. They are laying the groundwork for faster AOI growth and long-term returns, with venues opened in 2025 and 2026 expected to reach full profitability within 2–3 years and deliver 20%+ IRRs. Live Nation is also taking significant steps to curb secondary mkt, while supporting artist control and price caps, though these initiatives are expected to impact Ticketing AOI by MSD for the full yr. On the regulatory front, the recent dismissal of DOJ monopoly claims was a welcome development, with mgmt noting there is “no possible basis” for breaking up Live Nation and Ticketmaster, though the case will still proceed to trial. Despite all the aforementioned, the Co still guided to another yr of double-digit AOI growth in 2026.

All in all, investors keep waiting for a slow-down in the business trends, but that slow-down has not emerged and mgmt is investing to support continued growth expansion. Live Nation shares have also benefitted as investors rotate out of AI disrupted sectors to insulated industries like live entertainment.

See below for what we viewed as most incremental from the results and call.

-> Live Nation’s stock was up +3.3% in reaction to its Q4 report and ended the week up +2.8%; The stock is up +29.5% since hitting a low in mid-November

Q4 Was A Clean Beat For Live Nation

- Revenue – BEAT by +3.3%:

- Beat across all segments

- Adj op income BEAT by +3.7%:

- Beat across all segments but esp within Concerts

Incremental Guidance – Expect Another Yr Of Op Income And AOI Growth Amid A Step Up In CapEx

- Expect “another year” of double-digit op income and AOI growth y/y in 2026

- Op income was up +52% y/y in 2025

- AOI was up +10% y/y in 2025

- 2026 full-year AOI to FCF-adjusted conversion is expected to be higher than 2025

- CapEx is guided to slightly tick up to $1.1bn-1.2bn in 2026 (vs $1.05bn in 2025)

- ~$800-850mn is for venue expansion and enhancement projects

- Venue investment cash requirements are expected to be reduced by ~$250mn from funding by JV partners, sponsorship agreements, and other sources

- Addtl investment is allocated to their ticketing and sponsorship growth initiatives, as well as ongoing maintenance at their venues.

Concerts Biz Is Steady As It Goes As Both Demand And Supply Show No Sign Of Slowing Down

- Concerts AOI expected to be up double-digits y/y in 2026 (was up +30% y/y in 2025)

- Driven by supply/demand dynamics, as the supply pie continues to grow across mkts globally which drives increased demand

- On the concert DEMAND side…continue to see “extremely robust” demand

- Overall demand and sell-through rates are consistent w/ last yr

- Ticket sales are holding up across venue sizes and some major tours (i.e., Harry Styles, BTS, Bruno Mars) are seeing record-level demand

- Not seeing any pullback “whatsoever” in demand for any budget-conscious fans

- On the concert SUPPLY side… 80% of shows are booked

- Large venues are up vs 2024 and 2025

- Arenas are up LDD in terms of show count, which are largely US-driven (vs last yr, which was intl-driven)

- Stadiums are up double-digits, driven by intl, particularly UK and Europe (US is up “a bit”)

- Looking further ahead…continue to expect Concert biz to be a “continual growth industry” on a global basis, growing HSD industry-wide

2026 Is A Ramp Year For Investments In Venue Nation But Lays The Groundwork For Faster AOI Growth

- Venue Nation is expected to host 70mn+ fans in 2026, growing HSD to LDD

- Expect a ramp up in pre-opening costs in 2026: Increasing from $25mn in 2025 to $50mn in 2026

- In-line w/ prior commentary that ramp-up costs are going to be “large” as a %age of the benefit in its first few

- It is not expected to increase at that level as they get to more of a steady state

- Venues typically reach full profitability after ~2 yrs if they acquire it and ~3 yrs if they build it

- Profitability timeline –

- Venues opened in 2025 are on track to reach their projected run-rate annual AOI across concerts and sponsorship by 2028, delivering 20%+ IRRs

- Venues opening in 2026 are projected to reach their run-rate annual AOI across concerts and sponsorship by 2029, delivering 20%+ IRRs

- Expected build out of owned/operated fan count mix in 2026 –

- ~20% of total owned/operated fans coming from venues opened in 2025

- ~33% from venues opened in 2026

- ~50% from organic growth at existing venues

- “As you add new venues […] you’re going to accelerate your rate of increase …so would absolutely expect each year to help grow that base of fans in our operated venues”

- Essentially… more venues → more fans → more mature venues each year → faster AOI growth over time

- Also to flag…the acq of ForumNet Group in Italy was NOT an indication of a shift in strategy – “it’s just a one-off. We’re not looking to buy venue management companies”

- “We don’t love the return on those businesses as much as we like owning the venue and fully taking over the P&L. So in this case, they were added bonuses, but not a regular strategy”

Concert Demand and Ticketmaster GTV Will Drive Momentum in 2026 Despite Modest AOI Growth

- Ticketing AOI is guided to grow MSD y/y in 2026 (was up +1% y/y in 2025)

- Have some one-time headwinds; “We’re not expecting a lot there, even with some underlying health and improvement on the fundamentals”

- Expect 2026 Ticketmaster GTV to accelerate “a bit” from 2025’s +6% y/y

- Concerts will still drive most of that growth (was up +9% y/y in 2025), but sports and other categories should improve and contribute more than they did last yr (was down -1% y/y in 2025)

- So far this yr…ticket sales for 2026 Live Nation concerts are up double-digits to ~67mn fans, which is an acceleration in fan growth globally

- Fan demand “shattered” records with Bruno Mars delivering largest single-day ticket sales in Live Nation history, Harry Styles hitting 11.5mn pre-sale registrations, and BTS selling out a 41-date stadium tour

- Early indicators point to strong festival demand, with Electric Daisy Carnival sold out and ticket sales for Austin City Limits, Reading, and Leeds up double-digits

- Also this yr…Ticketmaster delivered a record January with concert ticket GTV up over 50%, led by N. America on-sales

- On reports that Spotify facilitated $1bn+ in ticket purchase activity through the platform – is it growing the industry overall or just shifting the point of discovery?

- Distribution partnerships are helpful and incremental, as these platforms help reach more fans, especially for smaller shows

- It’s less about shifting discovery and more about expanding reach for shows that might not otherwise sell out

Taking Aggressive Steps to Curb Secondary Market Activity While Supporting Artist Control

- The Co is taking material actions after FTC lawsuit around secondary mkts

- “Dramatically” restricted brokers who can sell on Ticketmaster platform, including limiting to one broker acct per tax ID and capping the # of tickets they can sell

- Impact? Broker-listed tickets for concerts on Ticketmaster have been cut in ~ half (caveated that some of the resale activity has likely shifted to other platforms at this point, pending them taking similar steps)

- Taking addtl steps to stop the scalpers from getting the tickets in the first place: Increased identity verification during acct creation, added more verification for artist presales and queue access, expanded use of Face Value Exchange (a resale platform at original ticket price)

- “Dramatically” restricted brokers who can sell on Ticketmaster platform, including limiting to one broker acct per tax ID and capping the # of tickets they can sell

- There is “momentum in the air” around secondary both on the consumer and artist side

- Reiterated their support of giving the artist more control and implementing price caps on resale, “because we don’t seem to be getting more nuanced solutions to give the artists that control”

- More artists are adopting tools like Face Value Exchange (100+ artists now)

- The Co launched artist-specific anti-scalping programs (i.e., with Noah Kahan and Kid Rock)

- “Ultimately, I think legislation will creep in as it is state-by-state to aid in their fight against secondary”

- Reiterated their support of giving the artist more control and implementing price caps on resale, “because we don’t seem to be getting more nuanced solutions to give the artists that control”

- Impact to financials… ongoing initiatives to combat scalpers and bots are expected to limit secondary activity, which are expected to impact ticketing AOI by MSD for the full yr

Additional Incremental Commentary…Update On DOJ Case, International Buildout, And Sponsorship Biz

- Mgmt was “pleasantly surprised” that the DOJ dismissed claims that Live Nation has a monopoly in promotion and bookings / “See no possible basis for breaking up Live Nation and Ticketmaster”

- The DOJ will now need to demonstrate that Ticketmaster’s “so-called monopoly” harms BOTH venues and fans which “makes the case somewhat more difficult for them”

- International continues to be a “huge focus” and seeing that “all the countries equally have the appetite” for live shows

- Sponsorship AOI is expected to continue to be up double-digits in 2026 (grew +11% y/y in 2025)

- Over 70% of 2026 sponsorship commitments have been booked, up double-digits y/

AI Spooks The Media & Entertainment Industry, Along W/ Other Key AI Developments

Important and impactful AI updates continue at a rapid clip and this week’s most pivotal developments in our mind centered around new models, particularly those that impact the media and music entertainment industries, and new infrastructure announcements, in addition to some other notable odds and ends. On the infrastructure front, Meta expanded their deal with Nvidia to use millions of AI chips in their ongoing data center buildout and India is making a big AI buildout push as well.

Meanwhile Hollywood is fighting back against ByteDance, who last week released its new Seedance 2.0 AI platform that can basically produce Hollywood quality movie content with minimal text prompts (if you have not seen any of the clips … LINK TO YOUTUBE TRAILER). This week Netflix joined three other major studios in sending cease and desist letters to ByteDance for enabling copyright infringement through this new AI platform. Also spooking the media & entertainment industry was Google’s new Lyria 3 music model which was also released this week, dragging down music labels intra-day. However, Sony announced new tech that will identify source material of AI songs and help song writers seek compensation if their music was used by AI developers (though there wasn’t too much reaction to this).

See below for more on the above as well as a few other notable model and AI industry updates.

Key AI Infrastructure Updates…The Build-Outs Continue

- Meta expands its Nvidia deal to use millions of AI chips in data center build-out, including standalone CPUs (link/link)

- Financial terms of the deal were not provided

- “The deal is certainly in the tens of billions of dollars,” said chip analyst Ben Bajarin of Creative Strategies

- The multiyear deal is part of Meta’s overall commitment to spend $600bn in the U.S. by 2028

- Meta has plans for 30 data centers, 26 of which will be based in the U.S.

- Its two largest AI data centers are under construction now: the Prometheus 1-gigawatt site in New Albany, Ohio, and the 5-gigawatt Hyperion site in Richland Parish, Louisiana

- Financial terms of the deal were not provided

-> Meta stock was up +0.6% in reaction to the news, while NVIDIA was up +1.6%

- Anthropic may pay $6.4bn to cloud partners (link/link): The money would go to Amazon, Alphabet, and Microsoft in 2027 under revenue sharing deals tied to its Claude AI models

- Reportedly, Anthropic expects to spend ~$80bn through 2029 just to run its AI on cloud infrastructure

- Training costs could reach $100bn over the same stretch

- Revenue share payouts to cloud partners are projected at $1.9bn in 2026 and $6.4bn in 2027, up from about $360mn last year and only $1.3mn in 2024

- For context, Anthropic has forecast revenue of as much as $18bn in 2026, meaning these partner payouts could equal roughly 10% of total sales

- ~50% of Anthropic’s gross profits from AI sold via Amazon reportedly goes back to Amazon

- Google typically takes 20%-30% of net resale revenue

- Microsoft, which pledged $5bn to Anthropic, is actively pushing Claude through Azure sales channels

- Reportedly, Anthropic expects to spend ~$80bn through 2029 just to run its AI on cloud infrastructure

- AI investments surge in India as tech leaders convene for Delhi summit (link)

- Blackstone annc’d on Monday that it was leading a $600mn equity investment in Indian AI cloud startup Neysa

- It will help deploy more than 20k GPUs for AI training in India

- The Neysa investment includes participation from Teachers’ Venture Growth, TVS Capital, 360 ONE, and Nexus, with the Co also seeking an additional $600mn in debt financing

- AMD annc’d an expanded partnership with Mumbai-based Tata Consultancy Services to deploy up to 200 megawatts of AI infrastructure

- AI Cos are also using the summit to emphasize their growth beyond Western markets

- This week, Anthropic annc’d that India has become the 2nd-largest market for its Claude AI platform, with run-rate revenue doubling since October 2025

- Meanwhile, Sam Altman wrote in the Times of India that India now has 100mn weekly active ChatGPT users, making it the company’s second-largest user base after the US

- Blackstone annc’d on Monday that it was leading a $600mn equity investment in Indian AI cloud startup Neysa

-> AMD stock fell -2% in reaction to the news, while Blackstone stock was up +1.2%

AI Entertainment & Music Updates Spook The Sector

- Google brings AI music generation to Gemini with Deepmind’s Lyria 3 which caused quite a stir (link/link)

- How does it compare to earlier Lyria models?

- Lyrics will be generated based on a users’ prompt

- It provides more creative control over elements like style, vocals and tempo

- It can create more realistic and musically complex tracks

- How can it be used?

- Text to track:Describe a specific genre, mood, or memory to create tracks with lyrics or instrumental audio

- From photos and videos to track:Upload a photo or video and watch Gemini use the content to compose a track with lyrics

- Availability: Lyria 3 is on YouTube’s Dream Track; It is available in the U.S. and is now rolling out to YouTube creators in other countries

- Available in the Gemini app for all users 18+ in English, German, Spanish, French, Hindi, Japanese, Korean and Portuguese

- It rolled out on desktop (02/18) and to the mobile app over the “next several days”

- How does it compare to earlier Lyria models?

-> Alphabet’s shares were down -0.3% in reaction to the news. Spotify’s and SiriusXM’s shares modestly fell -0.6% and -0.3% on intra-day, while WMG and UMG shares were down as much as -4.7% and -3.4% intra-day, respectively, in reaction to the news as well

- US court bars OpenAI from using “Cameo” (link)

- What happened: A federal district court in Northern California ruled in favor of Cameo, a platform that allows users to get personalized video messages from celebrities, and ordered OpenAI to stop using “Cameo” in its products and features

- OpenAI was using the “Cameo” name for its AI-powered video-generation app Sora 2

- In a ruling filed Saturday, the court said the name was similar enough to cause user confusion and rejected OpenAI’s argument that “Cameo” was descriptive, finding that “it suggests rather than describes the feature”

- What happened: A federal district court in Northern California ruled in favor of Cameo, a platform that allows users to get personalized video messages from celebrities, and ordered OpenAI to stop using “Cameo” in its products and features

- Sony develops tech to identify source material for AI songs (link)

- Why does it matter: It makes it possible for songwriters to seek compensation from AI developers if their music is used

- How does it work: The tech analyzes which musicians’ songs were used in learning and generating music

- It can quantify the contribution of each original work, such as “30% of the music used by the Beatles and 10% by Queen”

- If the AI developer agrees to cooperate for the analysis, Sony Group will obtain data by connecting to the developer’s base model system

- When cooperation is not attainable, the tech estimates the original work by comparing AI-generated music with existing music

-> Sony stock was down -1.6% in reaction to the news

Entertainment Industry Fires Back Against ByteDance

- Last week ByteDance released its new Seedance 2.0 AI platform which can basically produce Hollywood quality movie content with minimal text prompts…if you have not seen this … LINK TO YOUTUBE TRAILER

- Netflix this week joined 3 other major studios in sending cease and desist letters to ByteDance for enabling copyright infringement through its Seedance 2.0 AI platform (link/link)

- On Tuesday, Netflix sent a letter stating that the Co remove Netflix IP from training datasets and prevent further infringement from occurring

- The letter is the first to threaten “immediate litigation,” following similar letters issued by Disney, Paramount, and Warner Bros

- Specifically, Netflix accused ByteDance of enabling infringement of “KPop Demon Hunters,” “Stranger Things,” “Squid Game,” and “Bridgerton”

- The “clip art” comparison follows that made by Disney in its cease-and-desist letter sent to ByteDance earlier this week

- Warner Bros. and Paramount have similarly issued letters accusing ByteDance of enabling infringement of their respective intellectual properties

- Netflix has given them 3 days to act to “avoid immediate litigation”

- That action includes:

- The removal of all infringing content

- An accounting of all instances where infringement has occurred

- Revoking third-party access by commercial partners or API users

- Ceasing further generative output of infringing content

- That action includes:

- ByteDance also received criticism from Hollywood accusing them of copyright infringement (link)

- The Motion Picture Association last week accused Seedance of “unauthorized use of US copyrighted works on a massive scale”

- MPA chairman Charles Rivkin — representing the likes of Disney, Universal, Warner and Netflix — said Bytedance’s new AI model “operates without meaningful safeguards against infringement” and “should immediately cease”

- The actors’ union SAG-AFTRA also condemned “the blatant infringement” and unauthorized use of its members’ voices and likenesses enabled by Seedance 2.0

- In response ByteDancestated it has “heard the concerns” and is taking steps to strengthen safeguards against the unauthorized use of intellectual property

- The Co affirmed its respect for intellectual property rights while working to address the use of protected content in its AI-generated clips

Important New AI Model Updates

- Anthropic released Claude Sonnet 4.6 which brings much-improved coding skills to more of our users and is the “most capable sonnet model yet” (link/link):

- Who gets access: For those on their Free and Pro plans, Claude Sonnet 4.6 is now the default model in claude.ai and Claude Cowork; Pricing remains the same as Sonnet 4.5, starting at $3/$15 per mn tokens

- In Claude Code, their early testing found that users preferred Sonnet 4.6 over Sonnet 4.5 ~70% of the time

- Users reported that it more effectively read the context before modifying code and consolidated shared logic rather than duplicating it

- Users even preferred Sonnet 4.6 to Opus 4.5, our frontier model from November, 59% of the time

- Alibaba unveils Qwen3.5 which is designed to execute complex tasks independently, with big improvements in performance and cost (link/link)

- Cost savings: Alibaba said Qwen3.5 is 60% cheaper to use and 8x better at processing large workloads than its immediate predecessor

- The model also comes w/ the ability to independently take actions across mobile and desktop apps, or what the company calls “visual agentic capabilities”

- The Co also released a “hosted version,” meaning the model can run on Alibaba’s own servers

- Cost savings: Alibaba said Qwen3.5 is 60% cheaper to use and 8x better at processing large workloads than its immediate predecessor

-> Alibaba stock was down -0.2%

- Gemini 3.1 Pro has been released (link/link)

- What is new?

- 1 Pro is a smarter, more capable baseline for complex problem-solving

- On ARC-AGI-2, 3.1 Pro achieved a verified score of 77.1%. This is more than double the reasoning performance of 3 Pro

- Starting 2/19, 3.1 Pro is rolling out:

- For developers in preview via the Gemini API in Google AI Studio, Gemini CLI, our agentic development platform Google Antigravity and Android Studio

- For enterprises in Vertex AI and Gemini Enterprise

- For consumers via the Gemini app and NotebookLM

- What is new?

-> Google stock flat in reaction to the news

Other Notable AI Updates This Week That We Wanted To Highlight

- OpenAI is nearing completion of the first phase of a new funding round, expected to raise over $100bn, according to Bloomberg (link)

- The round could value the Co at more than $850bn, up from a ~$730bn pre-money valuation

- The capital raise is intended to support OpenAI’s massive long-term AI infrastructure build-out, with spending expected to reach trillions over the next decade

- Reported participants in the round include major tech players such as:

- Microsoft

- NVIDIA

- Amazon

- The funding is also expected to help offset the extremely high costs of model training and development, as OpenAI has remained loss-making due to heavy compute and R&D spending

- Rackspace and Palantir annc’d a partnership…which led to a huge Rackspace stock rally (link/link/link)

- What is the partnership? Rackspace will integrate Palantir’s Foundry and AI Platform (AIP) with its managed services, targeting highly regulated industries

- Rackspace will provide implementation, data migration, private cloud and UK sovereign hosting, plus managed operations and security controls

- Rackspace currently has 30 Palantir‑trained engineers and plans to scale to ~250 in 12 months

- What is the partnership? Rackspace will integrate Palantir’s Foundry and AI Platform (AIP) with its managed services, targeting highly regulated industries

–>Rackspace’s stock was up +226% in reaction to the news, Palantir stock was up +1.7%

- Perplexity is stepping away from its in-chat advertising over concerns that ads risk eroding user confidence in AI-generated answers (link/link): The Co is focusing on monetization through subscriptions and enterprise sales, prioritizing paying users’ overgrowth metrics like total queries answered

- “A user needs to believe this is the best possible answer to keep using the product and be willing to pay for it. The challenge with ads is that a user would just start doubting everything … which is why we don’t see it as a fruitful thing to focus on right now”

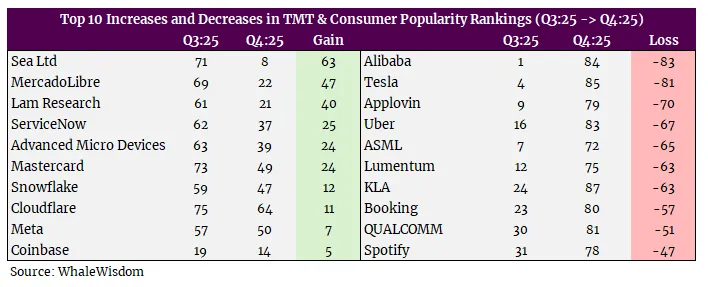

TMT Lost Some Favor W/ Hedge Funds In Q4…Per 13’Fs

The new 13F ownership changes were filed this week as well and we finally had a chance to take a closer look (as a reminder, this is for the period ending December 31, 2025).

Always dominating headlines are Berkshire Hathaway’s portfolio changes. During Q4, the fund was a net seller, divesting ~$9.54bn in equities while purchasing ~$3.56bn. The firm trimmed its largest position, which is in Apple, selling about 10.3mn shares (representing 4.3% of its stake), and more significantly sold 77% of its Amazon position (sold 7.7mn shares). Berkshire also initiated a new position in The New York Times and added to several holdings, increasing its stakes in Chevron (+6.6%), Chubb (+9.3%), and Domino’s (+12.3%). In addition to lowering its stakes in Apple and Amazon, it reduced exposure to Aon (-12.1%), Liberty Latin America (-8.9%), and Atlanta Braves Holdings (-48.4%), though it did not fully exit any positions during the period. Berkshire maintained core allocations to American Express, Coca-Cola, Moody’s, Kraft Heinz, Alphabet, Kroger, Visa, SiriusXM, Mastercard, Capital One, UnitedHealth, Formula One, Charter, and Jefferies, and as of quarter-end, its five largest holdings were Apple (22.7%), American Express (18.8%), Bank of America (10.9%), Coca-Cola (9.9%), and Chevron (7.1%).

Where Are The Top Hedge Funds Investing, In Aggregate?

Each quarter, WhaleWisdom tracks the stocks that were most bought and sold during the quarter across 150 of the top hedge funds. It ranks the “hottest” stocks based on a formula that takes into account the number of buyers adding and initiating new positions vs sellers, the change in average ranking that the stock had in the portfolios, and the number of times the stock appears in the top 10 holdings of the portfolios. The biggest takeaways were:

- TMT was less in favor…4 out of the Top 10 were TMT this quarter, down from 7 in Q3: They were Reddit (#6), Coherent Corp (#7), Sea Ltd (#8) and AppFolio Inc (#9)

- All of the MAANG stocks remained in the Top 100 BUT most fell in ranking

- Apple – decreased q/q (#21 in Q3 -> #58 in Q4)

- Alphabet – decreased (#32 -> #38)

- Netflix – decrease (#56 -> #86)

- Meta – increased (#57 -> #50)

- Amazon – decrease (#58 ->#57)

- Breakdown by sector: Information Technology continues to dominate the most owned

- Information Technologycompanies took the top spot again, as 36 of the Top 92 most popular companies were in the sector (a continued step up from 29 in Q3)

- Finance took the second spot again, w/ 19 of the top 92 Cos, up from 16 in Q3

- 11 Cos in the Communications sector, along with 10 Cos in the Consumer Discretionary, 7 in Industrial, 4 in Healthcare, 2 in Materials, 2 in Consumer Staples and 1 in Real Estate

- All of the MAANG stocks remained in the Top 100 BUT most fell in ranking

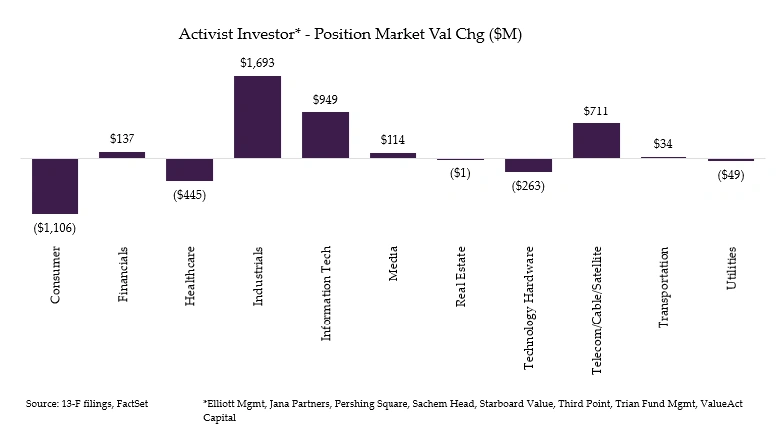

Where Are Activist/Event Investors Placing Their Bets, In Aggregate?

- The top 8 activist funds were net buyers this qtr, buying $3.64bn and selling $1.86bn of stocks

- Inflows: Industrials saw the largest inflows (+$1.69bn), followed by Information Tech (+$949mn), Telecom/Cable/Satellite (+711mn) and Financials (+137mn)

- The top 3 largest inflows came from Pershing Square taking a new +$1.76bn position in Meta, Elliott increasing its position in Toyota Industriesby +$1.35bn, and Pershing Square Management increasing their position by +$873mn in Amazon

- Outflows:Consumer saw the largest outflow of (-$1.11bn) followed by Healthcare (-$445mn), Tech hardware (-$263mn), Utilities (-$49mn) and Real Estate (-$1mn)

- The top 3 largest outflows came from Pershing Square decreasing its position in Alphabet (-$1.30bn), Pershing Square selling out of its position in Chipotle (-$797mn) and Sachem Head decreasing its position in Kenvue by (-$469mn)

- Inflows: Industrials saw the largest inflows (+$1.69bn), followed by Information Tech (+$949mn), Telecom/Cable/Satellite (+711mn) and Financials (+137mn)

Drilling Deeper Into Individual Activist Funds…

- Value Act took a new position in BlackRock; The fund increased its position in Liberty Holdings Class A (+4.6%) and Class C (+2.5%) as well as Live Nation (+28.4%), Meta (+36.3%), Roblox (+39.3%), Salesforce (+3.3%), Toast (+135.9%) and Visa (+9.7%); The fund decreased its positions in Amazon (-3%), MongoDB (-33.6%), and Walt Disney (-29.9%)

- Starboard Value increased their position in Kenvue (+30.5%) and Tripadvisor (+1.4%); The fund decreased its positions in Autodesk (-23.7%), News Corp (-26.2%), Rogers (-50.2%) and Salesforce (-24.3%); lastly the fund sold out of its position in Alright Inc

-> Tripadvisor said on Tuesday that its board & mgmt have held multiple discussions with activist investor Starboard Value, which owns ~9% of the company and has accused it of failing to hold leadership accountable for “value destruction.” “Mgmt and the Board are focused on pursuing all avenues to drive value for shareholders.” (link)

- Sachem Head took new positions in Carvana, EchoStar, and Live Nation; They increased their positions in Dicks (+21%) and Warner Bros Discovery (+107.1%); The fund did not change their position in Six Flags; They decreased their positions in CVS (-17.9%), Kenvue (-89.2%) and Zoom (-3.9%)

- Trian Fund took no new positions; The fund decreased their position in Invesco (-79.7%); The fund did not sell out of any positions

- Third Point took new positions in Alibaba, Chipotle, Spotify and Wix; The fund increased their positions in Live Nation (+27.8%) and Nvidia (+3.5%); The fund did not change their position in Hertz; They decreased their positions in Amazon (-23%), Capital One (-20.6%), Kenvue (-63.9%), Microsoft (-15.9%), and Taiwan Semiconductors (-61.4%); The fund sold out of its positions in Apollo, Flutter, and Meta

- Pershing Square took a new position in Meta; The fund increased their position in Amazon (+65%); The fund did not change their positions in Hertz and UMG; It decreased its positions in Alphabet (-86%) and sold out of their position in Chipotle

- JANA Partners Increased their position in Rapid7 (+3.7%) and Six Flags (+1.6%); They decreased their position in Freshpet (-46.8%); The fund sold out of its position in Trimble

- Elliott Management increased their position in Toyota Industries (+38.4%); They did not change their positions in Crown Castle, Equinix, Etsy, Pepsico, and Pinterest; The fund decreased its potion in in Southwest Airlines (-8.9%)

2026 Will Be An Investment Year For DoorDash As It Builds The Next Version Of Itself

After suffering its biggest one-day drop ever in reaction to its print last qtr, DoorDash seems to have effectively reset expectations this qtr. The Street reaction was far more measured, as investors are now better aligned with mgmt’s message that the Co is in the midst of a significant transition. DoorDash is investing aggressively to evolve from purely a restaurant delivery platform into a global tech and infrastructure partner to merchants, building the software, logistics, and fulfillment backbone that enables local commerce at scale. As CEO Tony Xu reiterated on the call, “2026, in many ways, is like a setup year of building […] a new company that is now a global company.”

At the center of this transition is the unification of DoorDash, Wolt, and Deliveroo onto a single global tech stack, which remains a major execution priority. Most of this work is expected to be completed this year, and early benefits are already starting to show, particularly in the ability to roll out features more quickly across geographies. Mgmt also provided more detailed commentary than in prior qtrs on its autonomous strategy, describing the autonomous delivery platform as “probably the most valuable part of what we’re building.” It’s complex, but a goal in 2026 is to focus on defining the various use cases across Dashers and AVs, alongside continued development of DoorDash Dot and drone initiatives. At the same time, New Verticals and International continue to outperform, driven by continued execution. In fact, New Verticals is expected to reach gross profit positivity in H2 and International ex-Deliveroo is expected to be contribution profit positive in H2 as well.

On the near-term outlook, Q1 adj. EBITDA guidance falling -9.4% below cons was a negative focus, and was driven by incremental Deliveroo investment, higher Dasher costs tied to seasonality and growth initiatives, and weather-related impacts. That being said, the Co expects profitability to improve sequentially through the yr, with H2 expected to be “significantly higher” than H1.

Overall, the underlying fundamentals of the Co remain strong and they have not seen any competitive issues with Amazon’s grocery push. Furthermore, mgmt. believes their last -mile business model will benefit from new AI channel partner as well. After last qtr’s reset, investors appear more comfortable with the investment narrative given that the core biz continues to show strength while DoorDash builds toward its next phase.

See below for more details of what we thought was most important from DoorDash’s results and conference call.

-> DoorDash was up +1.6% after its report but is still down -36.4% since its high in Oct 2025

DoorDash Posts A Slightly Mixed Q4 Given A Lower Take Rate

- Revenue – MISSED by -0.6%: Grew +38% y/y (accel from +27% y/y in Q3)

- EBITDA BEAT by +0.8%: Grew +38% y/y (decel from +41% y/y in Q3); Margin of 19.7% also beat cons 19.4%

- Marketplace GOV BEAT by +1.8%: Grew +39% y/y (accel from +25% y/y in Q3)

- Total Orders BEAT by +2.0%: Grew +32% y/y (accel from +21% y/y in Q3)

- Contribution profit BEAT by +2.6%: Grew +45% y/y (decel from +36% y/y in Q3)

- Take rate was 13.3% and was BELOW cons 13.6%, which is down from 13.8% in Q3 and 13.5% in Q2

The Co Guides For Higher Cost/Investments In Q1, But The FY Outlook Points to Improvement Through 2026

- Q1 Marketplace GOV guidance BEAT by +2.3% at the midpt: $31.0bn-$31.8bn vs cons $30.7bn

- A caveat…while the Co has historically exceeded the high end of their guidance range for Marketplace GOV, their current operating plan for Q1:26 reflects Marketplace GOV within the guided range

- Q1 adj EBITDA guidance MISSED by -9.4% at the midpt: $675mn-$775mn vs cons $800.6mn; Highlighted three primary factors impacting adj. EBITDA…

- Incremental investments in Deliveroo, which drive an expectation for Deliveroo to contribute <$25mn to adj EBITDA in Q1:26 vs $45mn+ in Q4:25

- Q/Q increase in Dasher costs per order, which reflects seasonality, investments to increase system capacity and support growth in longer distance and higher effort deliveries, and an annual increase in cost in regulated mkts

- Estimated $20mn direct impact from severe storms Gianna and Fern in the US

- BUT H2:26 adj EBITDA is expected to be “significantly higher” vs that in H1:26, driven by:

- Investment in ROO, some of which is front-end loaded and is expected to increase going through the yr

- Pace of expansion for both New Verticals and Intl biz, ex-ROO, will also increase through the yr – expect New Verticals to be gross profit positive in H2 and Intl ex-ROO to be contribution profit positive in H2

- Looking into Q2…expect adj EBITDA as a % of Marketplace GOV to increase in Q2 from Q1, but remain “slightly below” the level achieved in Q2:25 (which was 2.7%)

- Incremental q/q outlook on adj EBITDA as a % of Marketplace GOV…

- From Q1:26 -> Q2:26: Expected to increase, but remain “slightly below” the level achieved in Q2:25 (which was 2.7%)

- From Q2:26 -> Q3:26: Expected to increase

- Reiterated that for FY26, expect adj EBITDA as a % of Marketplace GOV to increase “slightly” vs 2025, excluding the impact of Deliveroo in both periods

- Continue to expect Deliveroo to contribute ~$200mn to adj EBITDA in 2026, with contribution increasing through the yr

Update On Areas Of Priority Investment…2026 Is “A Setup Year Of Building […] A New Company”

- Reiterated 3 main areas of investment –

- Global tech stack

- Autonomy

- Merchant services

- Highlight 3 long-term missions – “if we can do this across every geography…I think it’s a very exciting future for DoorDash”

- “Bring you everything inside the city”: Expand beyond restaurants by delivering grocery, convenience, and retail; A big part of that is building stronger fulfillment capabilities and investment in autonomous technologies to enable fast, cost-efficient delivery

- Help merchants transition into omnichannel bizs: Build omnichannel software tools (i.e., Storefront, SevenRooms, Drive) to help merchants operate seamlessly online and offline and become full end-to-end digital bizs

- Drive in-store traffic by offering customers value deals, dining discovery, and reservation access

- In the process of building an “operating system for local commerce”: Helping physical bizs (small, medium, and large) become omnichannel bizs and be able to compete with the “behemoths”; To do this, they are investing in…

- Software: Including tools for bizs to add themselves to the DoorDash app, offer their own delivery, and/or run their own e-commerce channels

- Warehousing and physical infrastructure: DashMart Fulfillment Services and partnerships with Cos like Kroger and CVS to bring inventory closer to customers so they are able to compete and offer same-hour, same-day delivery

- Autonomous: Including investments in autonomous vehicles like DoorDash Dot, as well as some other projects that are in the works

- Dashers’ experience: Expanding the types of orders Dashers can take (grocery, retail, more complex deliveries) with a pay model that reflects that

- Cataloging physical inventory: Partnering with Dashers to document items that aren’t online, increasing accuracy of product availability

Seeing Continued Growth Across New Verticals… Focus Is Now On Getting 100% Of MAUs To Use Grocery AND Retail?

- DoorDash is now the leading and fastest-growing third-party transaction platform in the US… “and we’re growing very, very fast outside of the US as well in that dimension”

- ~30% of MAUs are ordering outside of the restaurant category

- How do they get from 30% of MAUs to 100% over time? As they improve selection and invest in making the product better, whether it’s quality or portability, more and more of DASH’s MAUs continue to order from categories outside of restaurants

- Also, the # of new consumers that join and start their journey with New Verticals is also improving y/y

- Seeing an evolution of customer behavior with respect to grocery, who are now incorporating both a “middle of the week” stock up use case and “weekend” large basket use case

- Customers are increasingly using the platform for both quick grocery trips and larger stock-up orders

- Seeing this happen “faster and faster” with each successive cohort

- And existing cohorts are actually increasing their spend and their overall share of wallet when it comes to grocery with DASH

- The Co has also made “really good” progress in unit economics y/y and expect Retail and Grocery bizs to be unit-economic position in H2:26

- Driven by continued execution and improvements in the product

- Is grocery biz seeing any impact from Amazon doubling down on groceries? No: “We haven’t seen an impact on our growth. In fact, we continued very high growth rates…as fast as we’ve seen in the grocery sector not just in Q4, but also for this year as well”

- What’s driving the growth? Their avg consumer tends to buy from a couple different grocery stores and DoorDash aggregates many grocers in one place “at the best possible price and the highest quality of delivery”; New capabilities (like DashMart Fulfillment Service) help grocers compete more effectively, including against Amazon.

- “As long as you believe that customers are going to want choice [there] will continue to be very strong interest in the DoorDash product”

On Deliveroo And Wolt…“Feel Really Strong About Our Position Overseas”

- Seeing faster growth outside of the US vs in the US, even as the US had two of the Co’s fastest growing qtrs in 2025 in the last four yrs

- …and continuing to improve unit economics “across the board”

- Feel “really great” about their position in Europe…: “We’re the leading player in many of the countries in that continent”

- …and “off to a really great start” w/ Deliveroo acq…: “We are growing much faster at the same profit contribution that we expected before the acquisition. We’re gaining share in its largest markets”

- Accelerated y/y growth in total orders in Q4, driven by improvements across the product

- …“and we’re doing the same on the Wolt side”

- Where are the oppties to improve? Across the board: “There’s a ton of things we kind of have identified… it’s really a bunch of small things that add up to make the difference”

DoorDash’s Positioning Within An Agentic Future Is Not A Cause Of Concern…“Whoever Solves The End-To-End Job Wins”

- DoorDash is “well-positioned” because they are solving the end-to-end job for a customer… “to get them some item brought to them in the condition they expect, on time, every time”

- …and historical precedent supports that

- Amazon gained product search share in the 2010s by owning the entire purchase-to-return experience

- Google Food Ordering launched back in 2016 drove traffic that was “multi-fold” what DoorDash could have generated for those restaurants, but retention and frequency was “a fraction” of DoorDash’s due to weaker post-checkout execution (i.e., a driver might be late, an item might be missing, exact brand is not available, etc.)

- DoorDash also collects its data in a proprietary way… “that information does not exist anywhere on the internet”

- “That’s actually really hard to do. You got to map the physical world… You have to be excellent at collecting all the metadata as well for all of these different items, as well as the personalization you can perform if you actually have all […] of the customer information”

- … “And so long as we are that best place, we will also attract all of the audience and all of the advertiser dollars that comes from that audience”

- So, what is DASH’s view on AI assistants? They are channel partners

- “We’ll see how much traffic they can drive in a very similar way to how companies like Facebook and Google did the same for DoorDash in the past”

- “I kind of view them very much as almost like the new forms of the Googles or other large kind of top-of-funnel channel”

- Quick comment on coding agent use internally at DoorDash: Seeing 90%+ daily active usage of coding agents across their engineers; “The question now is…what is the right new environment for them to kind of keep up that sustained productivity gain?”

Investments In Overhauling The Tech Platform Are Expected To Drive Significant Increases In Efficiency

- The Co’s major execution priority continues to be bringing the three bizs together into a single tech stack

- “We operate on three tech platforms, pretty much a very similar business”

- “That means that you’re going to be slowed down because in order to ship one feature, you have to ship that three times”

- “We’re making this pretty big investment in order to both improve the velocity in which we ship […] and also just be more efficient with our global footprint”

- The majority of the tech stack work will be completed this yr, but benefits are already showing through

- For example, features built in one country can now be rolled out faster in other mkts

- In terms of cost, expect some redundancy as they run both tech stacks in parallel

- Majority of that will be in 2026, and “some” will be in 2027, “that that will come off and you should expect that to be a smaller component”

Mgmt Also Provided More Color Than They’ve Historically Given On Their Autonomous Efforts

- “The autonomous delivery platform is probably the most valuable part of what we’re building”

- Focus is on solving for…

- “There are certain times where you’re going to see handoffs between Dashers and AVs”

- “At other times, you’re going to see AVs perform deliveries that Dashers don’t want to do”

- “At other times, you’re going to see Dashers perform deliveries that AVs are not well equipped to do”

- And so the goal for 2026 is to “really figure out what are all of these different use cases?”

- “We actually have real live deliveries happening right now with AVs, and we’re very excited about the future”

- Looking ahead…expect that delivery vehicles will be able to address both suburbs and cities

- Dot was constructed in a “purposeful” way to “serve many of the suburbs”

- Drone projects can even go “beyond suburbs” to “even more rural regions” where distances traveled are much farther and its faster to travel by air vs on land

Addtl Incremental Updates On The US Restaurant Biz, Integration With SevenRooms, DashPass, And Advertising

- Performance of US restaurant biz continues to be “quite strong”

- Contribution margin for the segment was up y/y in Q4

- Grew faster at a larger scale in 2025 vs 2024

- Also hit an all-time high in MAUs

- Expect to continue to improve margins in 2026 but at a lower pace vs prior yrs

- Will continue to invest behind the biz across selection, quality, and affordability

- Integration w/ SevenRooms has been going “really well” and have already been able to “tremendously” speed up their work

- Now adding venues 50% faster post-acquisition than before DoorDash partnered w/ them

- Performance is in-line w/ their thesis that a best-in-class CRM software (SevenRooms) + demand generator platform (DoorDash) creates strong value for restaurants by helping them build repeat customers and direct relationships

- Mainly serving higher-end restaurants today, but as features are simplified, it can expand to more restaurants and ultimately support both in-restaurant dining and the off-premise / takeaway biz

- Continue to add more benefits to DashPass while maintaining the same membership price

- Added a record # of subscribers in both Q4 and 2025

- Expanding perks across non-restaurant categories like retail and grocery by offering more discounts and preferential delivery pricing, even for more complicated deliveries and discounts on key value items

- Also seeing “significant” growth oppty in their in-store business, by driving traffic and offering members either access or value to restaurants that they couldn’t get otherwise if they were not members

- “I think the DashPass ecosystem has a long runway ahead of it… I think we’re a fraction or a single-digit percentage of what DashPass could actually achieve”

- Ads biz is growing “really, really” fast and Symbiosys acq is “off to a great start”: Doubled the number of advertisers for Symbiosys, as well as tripled the spend from those advertisers

Booking.com Believes That LLMs Will Stay At The Top Of The OTA Funnel

Following Expedia and Airbnb results, Booking.com wrapped up OTA Q4 earnings season, though on a sorer note with the stock trading down in reaction. A better-than-expected Q4 has been a consistent theme across the group though forward guidance has been mixed. Along this vein, Booking.com’s gross bookings growth stepped up to +16% y/y from +14% y/y in Q3 and revenue reaccelerated sharply to +16% y/y, driven by better-than-expected room night growth (despite tough comps). Adj EBITDA also grew +19% y/y and margins expanded +80bp y/y despite marketing running +24bp higher as a percent of gross bookings. As a caveat, mgmt did highlight that US consumers continue to be “thoughtful” about discretionary spend.

Looking ahead, the Co is making $700mn in incremental investments above its baseline but a large chunk is being funded by savings from the Transformation Program and other cost efficiencies. These investments are anticipated to drive incremental revenue and adj EBITDA in the year ahead, though the 2026 guidance was largely in-line with existing expectations. For Q1, guidance was more of a mixed bag with the gross bookings and revenue outlook ahead of consensus, helped in part by strength in FX, but y/y room night growth is expected to decelerate sharply from Q4 levels and adj EBITDA growth guidance also missed expectations.

As expected, AI was a point of conversation and mgmt has been integrating Agentic capabilities into its user experience with encouraging results thus far (seeing more engagement, faster search, better conversion, and lower cancellation rates and higher customer satisfaction). Mgmt believes that Booking.com is structurally insulated from AI disruption given the view that the large LLMs will stay at the top of the funnel (like where Google has been with Search) and NOT move downstream given the complexities with managing supply, servicing partners, and being the merchant of record for payments.

All in all, it was a solid qtr with largely expected forward 2026 guidance but given the secular concerns with AI’s impact and a more mixed Q1 outlook, it was not enough to ease investor concerns.

-> Bookings stock was down -6.1% in reaction to earnings and is down -29% since its high in Aug. 2025

Strong Q4 W/ Revenue Accelerating & Margins Expanding Despite Higher Marketing Spend

- Gross Bookings BEAT by +2.5%: Up +16% y/y or +11% FXN vs +14% y/y or +10% FXN in Q3

- Driven by better-than-expected room night growth

- Revenue BEAT by +3.4%: Up +16% y/y or +13% FXN vs +8% y/y or +10% FXN in Q3

- Marketing expense as a % of gross bookings was 24bp higher y/y in Q4…due to: 1) strong performance marketing; 2) 13% increase in social media spend; and 3) higher brand marketing (can be lumpy)

- But the Co also realized savings elsewhere to more than offset, and expanded margins (adj EBITDA 34.6% margin, up +80bp y/y)

- Adj EBITDA BEAT by +4.3%: Up +19% vs +15% y/y in Q3

- Adj EPS marginally BEAT by +0.2%: Up +17% y/y vs +19% y/y in Q3

- BUT FCF MISSED by -21.1%: Up +120% y/y vs -40% y/y in Q3

- Q4 shareholder returns were $2.4bn (buyback + dividends)

- The Board approved a 9.4% increase in the qtrly cash div/shr and a 25:1 stock split (taking effect on April 2nd)

US Room Night Growth Accelerated Y/Y Despite Tough Comps, Though US Consumers Are Still Being “Thoughtful” About Discretionary Spend

- Q4 room nights growth of +9% y/y BEAT cons +6.5%: This compared to +8% y/y in Q3 (it accelerated each qtr in 2025)…the bookings window was also “more expanded” than anticipated

- Asia & the US: Both grew low double-digit

- Europe & RoW: Rose high single digits

- The Co also posted an acceleration in US room night growth despite a tough y/y comp…driven by –

- Targeted investment (incl brand & tradtl performance marketing)

- Momentum in B2B business

- Growth of direct channels in the US was also a driver

- However, note that the US is still seeing some “thoughtful”-ness regarding discretionary spend –

- The booking window in the US “remained steady in Q4” though the Co is “seeing slightly lower ADR and a slightly shorter length of stay y/y, which may indicate that some consumer segments are continuing to be thoughtful on their discretionary spending”

BUT Q1 Room Night Y/Y Growth Is Guided To Decelerate & 2026 Guidance Was In-Line

- Q1 guidance was a mixed bag –

- Gross bookings & revenue guidance BEAT consensus

- Gross Bookings guidance includes ~1% of positive impact from higher flight ticket and other verticals growth

- Expect FXN ADR to be flat y/y

- But room night growth guidance MISSED expectations and growth y/y is expected to decelerate sharply from Q4

- And adj EBITDA y/y growth guidance of +12% y/y at the md-pt MISSED cons +15% y/y

- FX also has a positive impact: Estimate changes in FX to positively impact Q1 reported growth rates by ~7% for gross bookings and rev, and by ~8% for adj EBITDA

- Gross bookings & revenue guidance BEAT consensus

- 2026 guidance was IN-LINE TO LOWER than consensus (on adj EPS growth)

- Guidance does reflect adj EBITDA margins expanding y/y by ~ 50bps while the top line grows 100bp faster than their overall algorithm

- FX to positively impact results: Estimate changes in FX will positively impact 2026 reported growth rate by ~2.5ppts for gross bookings, ~2ppts for revenue, and by ~1.5ppt for adj EBITDA and adj EPS

- Cost efficiencies are anticipated to come from the Transformation Program and addtl operational Improvements

- At YE2025, reached ~$550mn in annual run rate savings at YE25 (high-end of prev guidance)

- In 2026, expect the transformation program to deliver in-year savings of $500-550mn which is $250mn+ higher than in 2025

- Aim to drive additional efficiencies in our ongoing operations through both marketing and fixed operating expense leverage

- The Co plans to reinvest ~$700mn above baseline investments in 2026 given these savings and efficiencies

- Investing into areas such as progressing our GenAI capabilities, advancing our Connected Trip vision, growing in Asia and the U.S., growing our advertising business, OpenTable’s international expansion, and expanding our FinTech and loyalty offerings

- Mgmt expects these initiatives will generate ~ $400mn in incremental revenue in 2026, resulting in a net impact of ~ $300mn to adj EBITDA for the year

Mgmt Views Gen AI As A “A Major Opportunity” For The Co… And DOES NOT THINK LLMs Will Choose To Move Down The Funnel

- In 2025, the Co rolled out agentic capabilities across brands to enhance the full traveler journey…such as:

- Helping customers discover & plan trips through natural-language search

- Make more informed booking decisions w/ smart filters and summaries

- Get better, faster support before and during their trip through interactive AI agents

- Its early but have seen “more engagement from our traveler customers, faster search, better conversion, lower cancellation rates, and positive customer satisfaction”

- The Co also realized a ~10% decline in customer service cost per booking given implementation of AI

- In 2026, the Co will focus on offering a more unified & personalized experience via agentic capabilities

- AND the Co does NOT believe LLMs will focus on the lower funnel given…

- …Managing their supply network is very complex: Almost 90% of their accommodation biz is from independent hotels or homes, or small brands and these are “not sophisticated”…Bookings has over 4m properties to keep updated

- Independent partners choose to work with them not just for the demand they deliver, but for the broader set of technological capabilities they provide

- They have dedicated partner services teams on the ground across the world

- The Co has several thousand service people including those that support partners

- “The idea that the large language players are going to be doing that, I don’t know about that”

- …Payments also creates another level of complexity and regulation surrounding payments is “tremendous”

- “That’s another issue of complexity that I don’t think – my opinion, I don’t think that the large language models are going to want to enter that whole space and all that issue”

- “So do we think that the large language models are going to be entering – want to enter down the funnel down to where we are? I don’t think so. And then, even if that did happen, even if they were thinking about going in there, the question is will the customer want to be there”

- “Google has made great money at the top of the funnel” and “some of these other large language models when I look at this, they may say, you know, that’s the right way to do it. Not go down the funnel. Don’t become merchant of record. Take it high above. Don’t deal with the mess of the day-to-day in and out that we have to deal with all the time”…”I think that’s the way it’s probably going to go in the end. But that’s my opinion”

A Few Other Key Updates On Other Key 2025 Stats, Connected Trips, Alt Accommodations, & Genius Loyalty

- 2025 regional breakdown

- Bookers from Europe represented ~50% of the room nights booked

- Bookers from Asia were ~25% and US bookers were a low double-digit percentage

- 2025 B2C direct mix was in the mid 60% range (similar to last year)

- 2025 connected trip transactions (customers book more than one vertical for the same trip) grew in the high 20% range and represented a low dd % of Booking.com total transactions

- Q4 alternative accommodations room night growth slowed a little to +~9% y/y in Q4 vs +10% y/y in Q3: This remains an important area and are not where they want to be with inventory so will continue to work hard on

- 2025: the global mix of alternative accommodation nights was ~36% (up 1ppt from last year)

- Supply growth was up ~8% y/y (at 8.6mn listings) and it is growing faster in the US

- “We are quite optimistic about the outlook for alternative accommodations”

- The mix of higher tiers Genius loyalty program is increasing: The mix of Booking.com room nights booked by travelers in the higher Genius tiers of Levels 2 and 3 was in the high 50% range in 2025 (up from mid-50% range in 2024)

- “We see additional opportunities to further strengthen the Genius offering in 2026”

Quick Earnings Takes – OMC, WMT, EBAY, ETSY, & W

There were a few other important earnings prints on which we wanted to provide our quick takeaways. See below for thoughts on Omnicom, Walmart, EBAY, ETSY, and Wayfair.

Omnicom Surprises With Higher Deal Synergies + A Large Buyback: The Co initiated a major post-acq restructuring, targeting $1.5bn in run-rate synergies (double initial projections) w/ a near-term focus on realizing $900mn in 2025;. The Co’s core retained business generated $23.1bn in LTM revenue, supported by +4% organic growth and a plan to divest $2.5bn of lower-margin, nonstrategic operations; An immediate $2.5bn ASR was launched as part of a $5bn buyback, with mgmt projecting a 9-11% YE reduction in shares outstanding; More guidance will be provided at the upcoming Investor Day on March 12th

-> Omnicom stock was up +15.4% in reaction to earnings and is up +20.6% on the week

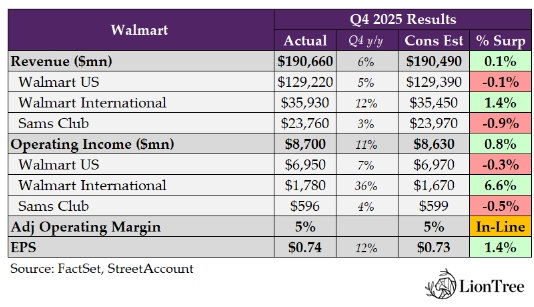

Walmart’s Disappoints W/ A Cautious Outlook: Despite losing its title as the country’s largest Co by revenue to Amazon, Walmart did still manage to beat Street expectation on revenue, in addition to op income; That being said, it was a bit of a mixed bag under the hood, with both beats being entirely driven by the International biz; In the US, the customer is being “choiceful” in their spending, and the majority of share gains in Q4 came from $100k+ households, while those earnings <$50k have wallets that are more stretched; Looking ahead, Q1 and FY27 guidance for EPS both missed consensus estimates at the midpt by -5.9% and -5.7%, respectively, as mgmt takes a “measured’ approach with the outlook, and while they haven’t seen any consumer behavior or macro KPIs that would make them more cautious than they have been in the past, “there are certainly indicators out there” (citing slow hiring, student loan delinquencies, and other factors) that makes them want to be “more balanced” in their guidance; Separately, the Co also annc’d a new $30bn share repurchase authorization.

-> Walmart fell -1.4% post its print and ended the week down -8.1%; Despite that the stock is still up +10.4% YTD

Ebay Beats Expectations & Expands Into 2nd Hand: Ebay’s Q4 results were overshadowed by the Co’s acq announcement of second-hand marketplace Depop from Etsy for ~$1.2bn (for context, Etsy bought Depop in 2021 for $1.6bn); Ebay plans to cross-list Depop products on its platform and expects the acq will expand its mkt shr; Depop’s seller and buyer cohorts will gain access to eBay’s financial svs, shipping and cross-border trade solutions, as well as its authenticity guarantee; Looking into the Co’s results, it was a strong qtr with both rev, EPS, and GMV coming in ahead of expectations (op margin missed by a hair); But Q1 guidance was the highlight, with both rev and EPS beating expectations by +8.4% and +5.4%, respectively, at the midpt; The Co also incr’d its qtrly dividend from 29c to 31c and authorized an incremental $2bn under their stock repurchase program.

-> Ebay’s stock was up more than 8% aftermarket when the Co announced the acq along with its Q4 results; It closed the day post the announcement up +3.1% and ended the week up +6.9%

Etsy Refocuses On Core Mktplace But Q1 GMS Disap: Similar to Ebay, the big news out from Etsy was its sale of Depop; Etsy CEO Kruti Patel Goyal said selling the platform would allow the Co to focus on growing its core marketplace; Etsy will use the proceeds from the sale to invest in its own marketplace and repurchase its own shares; Regarding the qtr, rev was ~inline w/ cons, though adj EBITDA and EPS beat by +4.2% and +8.2%, respectively; Marketplace active buyers decr’d y/y but waa nearly flat q/q, while US buyer GMS grew for the first time in 4 yrs; On the guidance front, the Co forecast Q1 GMS at $2.38bn- 2.43bn, which was well-below cons of $2.68bn (-10.3% miss at the midpt), implying growth b/w +2-4% y/y (vs +2.4% y/y in Q4); That is also expected to be the strongest growth of the yr, due to FX tailwinds that are likely to moderate and comparisons that get less favorable beyond Q1; Importantly, for FY26, Etsy expects GMS to achieve “slight” growth in 2026 after falling -6% y/y in 2024 and -4% y/y in 2025.

-> Etsy was up +9.3% on the back of its report and the Depop acq announcement; The stock ended the week up +14.1% for the week but is still down -5.9% YTD

Wayfair’s Q4 Profitability Stands Out But A Dip In GM in 2026 Plus Macro Concerns Overshadow: The Co delivered a strong Q4 especially on profitability w/ gross margin +20bps ahead and EBITDA +11.4% higher (margins +60bps above); Adj EPS beat consensus by +23.2%; Revenue upside was more subdued (+1.2% above cons) supported by orders +36bps higher and AOV +1.1% stronger, though ending active customers missed by -1.4%; Guidance for Q1 was largely in line on revenue and gross margin, with EBITDA margin guided +20bps above consensus at the midpoint, BUT mgmt signaled gross margin could dip below 30% in FY26 as it prioritizes gross profit dollars over margin rate which was a focus; Concerns about the macro backdrop also persist

-> Wayfair fell -13% post its print and ended the week down -1.2%

Grab Bag: MSG Sports Is Exploring A Spin-Off / Apple Introduces A New Video Podcast Feature / Uber Is Expanding Food Delivery In Europe

- MSG Sports annc’d that it is exploring a potential spin-off that would separate its two major franchises: (link/link)…the post-spin company structures…

- Knicks Company:

- New York Knicks (NBA franchise)

- Westchester Knicks (NBA G League affiliate)

- Rangers Company:

- New York Rangers (NHL “Original Six” franchise)

- Hartford Wolf Pack (AHL affiliate)

- The spin-off remains exploratory with no timeline set, and would require:

- League approvals

- Tax opinion from counsel

- Final board approval

- If completed, the transaction is expected to be:

- Structured as a tax-free spin-off

- Distributed pro rata to existing Class A and Class B shareholders

- Shareholders would receive 100% of the new company’s stock

- Knicks Company:

-> MSG stock was up +16.3% in reaction to the news

- Apple introduces a new video podcast experience on Apple Podcasts (link/link): The Co will launch advanced video podcast capabilities in Apple Podcasts this spring, marking a major expansion of the platform beyond audio

- The new experience is powered by HTTP Live Streaming (HLS), enabling:

- Adaptive streaming quality based on network conditions

- Smooth playback on Wi-Fi or cellular

- Seamless switching between watching and listening

- Users will be able to:

- Watch video directly inside the Apple Podcasts app

- Rotate to full-screen landscape viewing

- Download video episodes for offline viewing

- Creators gain new monetization tools, including:

- Ability to distribute video through participating hosting providers

- Dynamic insertion of video ads (including host-read placements)

- Access to the broader video advertising market while retaining content control

- Apple will not charge creators or hosting providers for video distribution, but:

- The Co will charge ad networks an impression-based fee for dynamic video ad delivery starting later this year

- Launch partners supporting HLS video include:

- Acast

- ART19 (Amazon)

- Triton Omny Studio

- SiriusXM (including AdsWizz and Simplecast)

- The new experience is powered by HTTP Live Streaming (HLS), enabling:

-> Apple stock was up +3.2% in reaction to the news

- Uber expands into 7 new European markets this year in food delivery (link/link)

- Countries they are expanding to:

- Czech Republic

- Greece

- Romania

- Austria

- Denmark

- Finland

- Norway

- The rollout is expected to generate roughly $1bn in incremental gross bookings over the next three years, according to the FT

- Susan Anderson, Uber’s Global Head of Delivery, said the company aims to “raise the bar, shake things up, and deliver better value across the category”

- Separately, Uber recently agreed to acquire the delivery arm of Getir in Turkey from Mubadala, further strengthening its regional delivery footprint

- Countries they are expanding to:

-> Uber stock was up +0.8% in reaction to the news

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Havas cont’d to beat its 2025 outlook w/3. 1% organic rev growth and sees 2026 at 2–3%. Q4 rose 3.7%. NA grew 4.6%, Europe 3.5%, APAC & Africa ~2%, LatAm 3.2% in Q4. Net rev reached €2.783bn. The Co bought stakes in 11 agencies and plans 5–10 in 2026. Its Horizon Global venture shows early promise. (MediaPost)

- Raymour & Flanigan annc’d PHD USA as its new media agency after a fall review. The incumbent was Dentsu. The Co spends ~$120mn on measured media/yr. Pres. Seth Goldberg said PHD showed strong ability to track mkts and link media to biz results. The Co operates 147+ locations across seven Northeast states, serving ~1.1mn customers/yr. (MediaPost)

Artificial Intelligence/Machine Learning

- China’s humanoid robots wowed the Spring Festival Gala, showing major leaps vs last yr’s stumbles. Startups like Unitree displayed fluid flips and dances, boosting public interest and raising concerns over labor + U.S.-China tech rivalry. Analysts say despite rapid gains and low-cost production, long-term impact hinges on AI models, reliability + real-world task performance. (CNBC)

- Microsoft’s blueprint aims to verify real vs manipulated content online. Its AI safety team tested ~60 methods combining provenance, watermarks, and fingerprints, finding which reliably flag AI edits. While not judging truth, the tools show origins. (MIT Technology Review)

- Microsoft annc’d it’s on pace to invest $50bn by decade-end to expand AI across the Global South. At the New Delhi AI summit, leaders emphasized boosting emerging mkts w/ infra and tech dev. The Co earlier unveiled $17.5bn AI plans in India, underscoring its push to accelerate the region’s rapid digital growth and broader AI adoption. (Reuters)

- Reliance chair Ambani annc’d a ₹10tn (~$110bn) plan to build gigawatt-scale AI infra incl. data centers, edge network & AI svs w/ Jio. First ~120MW goes live in 2H26. Move follows Adani’s $100bn push as India targets $200bn AI spend. Ambani said AI costs must drop, backed by green power & partnerships across mfg, agri, health, finance, plus AI in local langs. (TechCrunch)

- AI adoption among 12k+ EU firms boosts labour productivity ~4% w/out short‑run job loss. Gains skew to medium/large firms able to invest in data, software and training. Smaller firms lag due to lower AI uptake and fewer complementary assets. (CEPR VoxEU)

- World Labs, led by Fei-Fei Li, annc’d raising $1bn to speed spatial‑intel tech. Investors include AMD, Nvidia, Autodesk, Fidelity and others; Autodesk added $200mn and will advise the Co. The startup builds 3D world models for AR/VR and robotics. Its Marble model creates 3D worlds, competing w/ Google DeepMind and similar cos. (Reuters)

- Pentagon may cut ties w/Anthropic after cont’d disputes over limits on military AI use Anthropic rejects “all lawful purposes,” keeping bans on mass domestic surveillance & fully autonomous weapons. Tensions rose after questions on Claude’s role in a Venezuela raid. Pentagon says constraints hinder ops, though Claude is key in gov’t tech. (Axios)

- AI chatbots now show ads as OpenAI seeks new rev sources to balance huge spend, sparking privacy worries. Rival Anthropic mocked the move, while Google, MSFT, Perplexity also test ad models. OpenAI says ChatGPT replies won’t be altered and no user data will be sold. (Yahoo Finance)

- SpaceX and its subsidiary xAI are competing in a secret Pentagon contest for voice‑controlled autonomous drone‑swarm tech, per a Bloomberg report. The $100mn, six‑mo challenge aims to build systems that turn voice commands into digital instructions. SpaceX’s recent xAI acquisition came ahead of its planned IPO this yr. (Reuters)

Audio/Music/Podcast

- Apple annc’d a major update bringing HLS video to Apple Podcasts, letting users switch between watching/listening, use full‑screen, and download offline. The cont’d upgrade boosts creators’ control, enabling dynamic video ads and new rev options. (Apple)

Broadcast/Cable Networks

- TV viewing hit a 12‑mo high in Jan. per Nielsen’s The Gauge, up 3.7% vs Dec. Cable rose 9% as ESPN’s CFP coverage drove big gains and news lifted FOX News/CNN. Broadcast grew 4.2% w/ NFL anchoring top telecasts and dramas up 24%. Streaming held 47% of TV as Netflix stayed strong and Peacock, Tubi, Roku Channel posted gains across mkts. (Nielsen)

Cable/Pay-TV/Wireless

- Orange annc’d cont’d cash-flow and dividend growth, driven by acquisitions, organic growth, mkts expansion and capex savings after its fibre and 5G rollout across most of Europe. Under its ‘Trust the future’ plan, organic cash flow is set to rise from €3.65bn last yr to ≥€4bn in 2026 and €5.2bn in 2028. (Telecompaper)

- Telstra posted stronger results for the half yr to 31 Dec. 2025, as lower costs and reduced staff boosted perf. Income excl. finance edged up 0.2% to AUD11.85bn, while profit attributable to equity holders rose 9.4% to AUD1.12bn. EBITDA after leases grew 4.9% to AUD4.16bn and EBIT climbed 9.2% to AUD2.02bn, underscoring improved ops. (Telecompaper)

- AT&T filed a new suit vs T‑Mobile, alleging the carrier’s “Switching Made Easy” promo is deceptive, w/ claims of “illusory” savings and unrealistic 15‑min switching. AT&T says T‑Mobile uses non‑comparable plans to show ~$1k/yr savings and that actual switching takes hrs/days. (Fierce Network)

Capital Market Updates

- The U. S. posted a $901.5bn trade deficit in 2025, barely changed as Trump’s tariffs cont’d to reshape mkts. Dec. deficit jumped to $70.3bn after cos front‑loaded imports early in the yr following annc’d 10% duties. Biggest goods gaps were w/ EU, China and Mexico. Exports rose to $3.43tn while imports hit $4.33tn, underscoring persistent imbalance despite shifting policy. (CNBC)

- Atlassian’s founders Cannon-Brookes and Farquhar saw their wealth drop ~1/3 as a global tech rout hit SaaS cos, w/ shares down 50% YTD, pushing them out of the Billionaires Index. Despite losses, they say AI is a major boost and Atlassian cont’d heavy R&D spend. Both had sold billions in stock until sales halted on Feb. 6 when shares fell below $100. (MSN)

- IPO mkts slowed as new issuances hit a seasonal lull. Clear Street Group Inc. and Blackstone-backed Liftoff Mobile Inc. postponed listings, while volatility hurt growth investors. w/ the audit-window closing last wk, delayed deals and choppy 2026 debuts capped momentum despite the busiest start to a yr since 2021’s go-go period. (Bloomberg)

Cloud/DataCenters/IT Infrastructure

- Ormat annc’d a long‑term geothermal PPA w/ NV Energy to supply Google up to 150MW clean‑firm power under the CTT, starting as early as 2028 and cont’d thru 2030. The 15‑yr portfolio deal supports Ormat’s growth strategy, enabling multi‑site dev and stable rev, while boosting Nevada’s clean‑energy mkts and Google’s reliable carbon‑free ops. (Ormat Technologies)

- Telefónica annc’d it closed 2025 w/12 Level 4 autonomous network use cases, boosting its ANJ program and advancing toward level 3. 75 by 2028 and level 4 by 2030. Ops in Spain, Brazil & Germany drove progress across domains. (Telefónica)

Crypto/Blockchain/web3/NFTs

- Polymarket annc’d acquisition of Dome, a YC Fall 2025 startup offering unified prediction mkts API. Dome, which raised $500k from YC and $4.7mn seed, enables devs to build cross‑platform tools. The deal supports Polymarket’s U.S. expansion after its QCEX buy and adds to its growing distribution deals across major sports leagues and media platforms. (The Block)

- Vitalik Buterin warned prediction mkts risk collapse due to reliance on retail gamblers. He said platforms like Polymarket have unhealthy product–mkt fit, prioritizing short‑term bets over societal info value. He urged a shift toward hedging models that insure real‑world risks and suggested AI‑driven systems could even replace fiat‑pegged stablecoins. (Yahoo Finance)

Cybersecurity/Security

- PANW beat Q2 est w/ $2. 59bn rev and $1.03 EPS, yet shares slid 7% after Q3 EPS guide of 78–80c lagged the 92c est. Q3 rev outlook of $2.94–$2.95bn topped views as rev grew 15% yr/yr. Co cont’d its AI-led strategy, closing the $25bn CyberArk deal, the $3bn Chronosphere buy and annc’d Koi. (CNBC)

eCommerce/Social Commerce/Retail

- TikTok Shop reversed its plan to end seller‑fulfilled shipping in the U. S., telling merchants to operate as usual as deadlines won’t take effect. The move follows backlash from brands citing higher costs, margin pressure and fulfillment issues. (Modern Retail)

- Amazon topped Walmart as the world’s largest Co by 2025 sales, posting $717bn vs Walmart’s $713bn. Amazon’s growth came from AWS, ads and Prime, while retail remained key. AWS drove profits, bringing ~$129bn. Walmart, despite 90% of rev from stores, is strengthening US biz, gaining mkts and hitting a $1tn valuation as it positions itself as a tech Co. (CNN)

- Reddit annc’d a test for U. S. users showing AI-powered product carousels in search for queries like “best noise-canceling headphones.” The feature surfaces top-mentioned items from community posts, w/ pricing, images & retailer links. The initial electronics-focused test aims to streamline discovery while keeping community insights central. (Reddit)