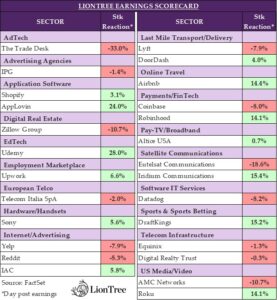

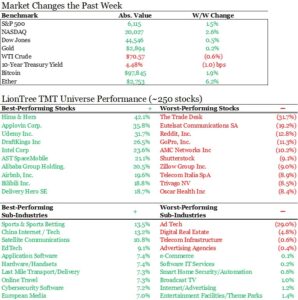

Hi everyone – what percentage of stocks in our universe traded up this week? 70%. It was another very busy week with updates across a wide range or sub-sectors within our space given the continued earnings storm (it’s now week 4). The best performing stock on the back of earnings this week was Udemy, up +28% (see Theme #1).

The overall market backdrop was favorable with Nasdaq’s +2.6% and the S&P 500’s +1.5% rally. Following the PPI numbers out on Thursday, investors shrugged off the higher-than-expected CPI print earlier in the week. Trump’s policies/tariffs remained top of mind this week as well.

An interesting FactSet stat that I saw was that 76% of S&P 500 companies have reported a positive EPS surprise and 62% have reported a positive revenue surprise. That is a rather supporting datapoint regarding fundamentals across the economy…

Enjoy the long weekend and I hope you are having a nice Valentine’s Day celebration!

- Earnings Scorecard – Week 4

- A Surprise Recalibration At The Trade Desk Surfaces In Q4

- Roku Q4 Provides A Sigh Of Relief As Its Platform Strategy Is Working

- Super Bowl LIX’s Record Viewership Didn’t Necessarily Translate Into Record Ad Revs…

- DraftKings Looks To Go Full Steam Ahead In 2025

- It’s Deja Vue To Last Qtr With DASH “Delivering”

- Airbnb Surged Across The Finish Line In 2024, Though Supply Growth Could Be A Challenge In 2025

- Lyft Flags Competitive Pricing Pressure Emerging In Ride Sharing

- Quick Takes On Prints From Other Key Stocks Across The Sectors – SHOP, RDDT, IPG, ATUS

- Grab Bag: Musk’s Bids For OpenAI / TMUS-Starlink Beta Open For All Carriers / BYD Unveils “God’s Eye”

Best,

Leslie

Earnings Scorecard – Week 4

It was another week of earnings, with 25 companies in our LionTree Universe reporting quarterly results (down from last week’s 37). In a flip from last week, stock price reactions were just barely biased to the upside, as 13 companies (52%) traded up in reaction to their print, while 12 companies (48%) traded down. Udemy was the best performer, up +28% post earnings, while The Trade Desk was the worst performer, plunging -33% (see Theme #2).

Companies reporting this week were across a plethora of sectors. Starting with the stocks that elicited the best reactions from the Street, on the media side, there was Roku, which was up +14% (see Theme #3), in sports betting, there was DraftKings, up +15% (see Theme #5), and in online travel there was Airbnb, up +14.4% (see Theme #7).

There was some divergence in the last-mile transport/delivery sub-sectors, as while DoorDash was up +4.0% (see Theme #6), Lyft went the other direction and fell -7.9% (see Theme #8).

Finally, we took a quick look at some other key reports out this week, including Altice USA and Shopify, which were up +0.7% and +3.1%, respectively, as well as Reddit and IPG, which were down -5.3% and -1.4%, respectively (more on all these in Theme #9).

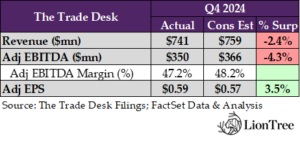

A Surprise Recalibration At The Trade Desk Surfaces In Q4

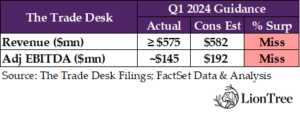

Where to start?! The Trade Desk has beaten their internal forecasts for 32 quarters in a row, but this 33rd qtr came out of left field and broke their impressive streak. Q4 revenues grew +22% y/y, which is a big deceleration from the +27.3% y/y in Q3 (and missed cons +25.3% growth forecast), while adj EBITDA fell short of estimates by -4.3%. Q1’s guidance for (as low as) +17% y/y revenue growth and only ~17% adj EBITDA margins (vs cons 33% and Q4s seasonally high 47.2%) were negative surprises as well. While margins should improve from Q1 levels, mgmt didn’t commit to a time frame for returning to a 20%+ y/y revenue growth profile. On the plus side, the Co annc’d an increase in its buyback by $564mn, bringing the total amount for future repurchases to $1bn, but that total is only 2.5% of the Co’s market cap.

The big question was obviously what happened?? While management stressed that the miss was not due to a less attractive market opportunity nor competitive issues, they were a bit vague about details of the “execution missteps” which left investors wondering what really happened. Big picture, mgmt. stressed several times that they chose to forgo short term results to prioritize establishing strong longer-term positioning, but that still lacks detail. With that said, the Co was very clear about the steps they are putting in place to address the issues and about how they are transitioning the business to capitalize on the 15 tailwinds that they outlined on last qtr’s earnings call.

See below for more of the need to knows about The Trade Desk’s Q4 and strategic plans for 2025. Needless to say, this will be a show me stock until the Co can show that the business is back on track and able to capture the big opportunities ahead of them.

-> The Trade Desk was one of the best performers for the full year 2024 (up +63.3%) but with that, came higher expectations and even last qtr the stock traded off -6% (but was down as low as -12.5%) on a sell the news mentality; This week, TTD fell -33% in reaction to earnings and closed the week down -32%

Q4 & Q1 Guidance = A Negative Surprise…The Co Hikes Its Buyback Authorization

- Total revenue & adj EBITDA missed by -2.4% & -4.3%, respectively

- Rev grew +22% y/y, which is a big deceleration from the +27.3% y/y in Q3

- Adj EBITDA margin hit 47% which missed cons 48.2%

- Adj EPS beat due to below the line items

- CTV was the main growth driver as has been the case…the percentage shr of the biz –

- Video, which includes CTV, represented a high 40s% (and continues to grow as a % of mix)

- Mobile represented a mid-30s %

- Audio represented ~5%

- Display represented a low double-digit %

- Q1 guidance was materially below consensus on both revs and adj EBITDA

- Implies revenue growth of only +17% y/y+ (also impacted by comps with leap year and political ad spend)

- And implies 25% adj EBITDA margins vs cons 33%

- 2025 will see some margins contraction for the full year with “modestly higher spend” but margins should generally improve from Q1 levels as the year progresses

- Incr’d the buyback authorization by $564mn, bringing the total amount for future repurchases to $1bn: Will be opportunistic with purchases

What Happened in Q4??? The Specifics Are A Little Unclear…But Mgmt Cites “Small Execution Issues” And That It Was Not About A Lack Of Opportunity Or Competition

- “For Q4, the reality is that we stumbled due to a series of small execution missteps while simultaneously preparing for the future. If this were a sporting event, we”d still have a championship caliber team. But in this particular game, we turned over the ball too many times”

- “And when we talk about the missteps specifically, many of them involve people, mistakes that aren’t appropriate to discuss publicly, especially when people are already learning from these mistakes”

- In Q4, there were a “series of decisions” they could have made to “enhance the short-term performance of the company and neglect the long-term” but they prioritized positioning for the long term

- “That said, we see a larger and faster growing market than we originally expected, which is why we have been making changes and will continue to do so. Simply put, as you”ve seen before, as companies grow and become increasingly complex, they need recalibration to unlock new opportunities. We are recalibrating our larger company for an even stronger future”

- “This didn’t happen because the opportunity isn’t as big as we thought. In this case, it isn’t because of our competition either”

What Are They Doing To Address The Mis-Execution??

- Undertook the largest reorganization in its history in December: This provided a clearer view of roles and responsibilities for most employees & involved changes in reporting structures; Also streamlined client-facing teams to reduce complexity and clarify responsibilities

- Shifted more focus to internal effectiveness and scalability: Over the past 2 mo, they have focused more on operational improvements than at any other point in their history

- Incr’d resource allocation on brands: They are doing so recognizing a broader shift in the industry towards more strategic and data-driven media buying decisions; They have secured joint business plans (JBPs) with over 100 of the world’s leading brands, which historically grow faster than the rest of their biz

- Revamped the product development process: The Co has shifted back to smaller agile teams that release updates weekly, moving away from less conducive waterfall methods; This chg is expected to accelerate enhancements and complete the transition of clients from Solimar to Kokai during the calendar yr

- Supply chain improvements: Initiatives aimed at creating a cleaner and more efficient supply chain include, the annc’d Ventura operating system for CTV which will create a better supply chain for all OEMs, content owners, consumers and advertisers & the Co acq’d Sincera, a metadata Co dedicated to improving the supply chain of the open Internet

- Investing in AI: It not only provides “next-level performance” in targeting and optimization, but it is also “particularly game-changing in forecasting and identity and measurement”

What Are The 15 Things They Are Doing To Capitalize On The Long-Term Tailwinds??

- Focus on scale: Obsessed about scale; TTD only controls $12bn of ad spend in a $1 trillion industry

- Preparing for Google’s exit from the open internet: This will open a big oppty

- Will promote their objectivity against “cheap reach”: This is in contrast to Amazon who “competes with its ad clients”

- Will leverage the supply demand imbalance: It’s a buyer’s mkt and TTD’s exclusive focus on the buy side puts them in a strong position

- Expect 2025 to be the year OpenPath enters steep acceleration

- Make CTV the most effective channel in programmatic advertising: Mgmt believes if they can expand Sincera’s charter and capabilities to CTV and audio, CTV and premium video can reach half the pie of the advertising TAM

- “CTV is the kingpin of the open Internet”

- “CTV should be the first place all brand advertiser spend, not walled gardens”

- Make 2025 the best year for audio: Audio is the most “on sale” component of the internet – this is one of the biggest opportunities in programmatic and for SPOT

- Move 100% of clients to Kokai this year: The majority already have but TTD is maintaining two systems, Solimar and Kokai, which “slows us down”

- “Well before the end of this year, I expect that all of our clients will be using Kokai exclusively”

- Will change the way the industry manages deals: Will use AI-powered forecasting to help advertisers and agencies avoid bad deals

- To do this, they are enhancing Kokai w/ some of the most “game-changing parts”, like Deal Manager

- Will continue to invest in AI, focusing on provable upgrades and auditable results: Hundreds of enhancements recently shipped and that are coming in 2025 would not be possible without AI

- Will simplify the Retail offering in 2025: Their Retail offering has been a significant growth driver for them but “it has often been too complicated”

- “We’ve studied what works and understand the changes needed to help retail media continue to meaningfully outpace our business”; This will require a closer collaboration with retail partners

- Are working to simplify the platform: Finding ways to improve the experience and make decisions easier and also more intuitive for users

- Will use more data: Enhancing decision-making with AI across the platform

- Will expand JBPs (as previously mentioned)

- Have revised and will continue to revise the product development process (as also mentioned)

- Hiring senior leadership; Over the next few years, will 2x the number of senior leaders in the Co at the VP level and above and this will include “some very key senior level appointments”

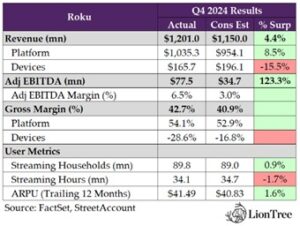

Roku Q4 Provides A Sigh Of Relief As Its Platform Strategy Is Working

After The Trade Desk’s negative surprise on Wednesday night (see Theme #2), investors were concerned that TTD’s issues might not solely be company specific and could reflect a broader issue related to CTV…but Roku’s results on Thursday night pulled through with very strong performance in its Platform business and very strong performance in adj. EBITDA margins relative to Street estimates.

While the Q1 guidance was a bit mixed and 2025 revenue guidance was in-line, the Co expects a much higher level of profitability for the year vs expectations (2025 adj EBITDA guidance was $350mn vs cons $287.5mn…that implies a 130bp improvement y/y).

Overall, the Co’s Home Screen has become quite an asset, as it is driving higher ad demand through enhanced integrations and partnerships, and it is also helping to grow subscription revenue. And looking ahead, there is “more room to grow”. The Co has also done a good job at reallocating capital to grow the Platform side of the business while keeping overall opex in check and finding new areas of cost efficiency via hiring in lower cost regions and leveraging automation and AI across the business.

Overall, it was a solid qtr and the outlook remains favorable.

-> Roku shares rallied +14.1% post results and ended the week up +16.6%

Strong Q1 Performance Was Driven By Upside In Platform Revenue & MUCH Stronger Adj EBITDA Margins While Key Performance Metrics Were Mixed

- Total revs rose +22% y/y and beat cons by +4.4% with Platform rev topping estimates by +8.5% (grew +25% y/y and ex political it was up +19% y/y), more than offsetting weaker Device rev (grew +7% y/y)

- Adj EBITDA margins at 6.5% were much better than cons 3%

- But KPMs were mixed –

- Streaming households at 89.8mn was nearly 1% ahead of est (and was up +12% y/y) and APRU beat by +1.6% (was up +4% y/y)

- BUT Streaming Hours missed by -1.7% (but up +18% y/y)

Mixed Q1 Guidance, But Inline-To-Better 2025 Guidance

- Q1 guidance: Mixed w/ revs & adj EBITDA a tad below expectations but GP ahead

- Revenue (up +14% y/y) was a tad below ests

- Platform revs up +16% y/y

- Device revs flat y/y due to elevated inventory from lower holiday sales

- Gross profit beat by +4.5%

- Adj EBITDA also a tad below ests

- 2025 guidance: In-line to better w/ revs as expected and GP & adj EBITDA ahead of expectations

- Revenue in-line

- Platform revs up +12% y/y or +15% ex political which is slightly above 2024 growth

- Device revs up +12% y/y

- Gross profit +2.3% above cons

- Platform gross margins btw 52-53%; Expect to grow platform gross profit as much as Platform rev ex ASC 606

- Adj EBITDA a huge 22% above cons (implies 130bp improvement y/y)

- FCF & FCF/share “is our north star metric”: Mgmt expects FCF to be higher than adj EBITDA guide for 2025

- On the 2025 guide… “it’s not a guide out there that we would say is conservative. It’s our view of what we would expect for 2025”

- Remain on path to become operating income positive in 2026

The Co’s Strategy To Grow Platform Revenue Is Working…Subscriptions & 3P Partnerships Have Been Key Drivers

- Seeing strength in both streaming service distribution (SSD) & advertising: Both grew strongly in Q4

- Making a better Home Screen “has been key”

- Video on the home screen is in beta but they are being very careful about putting ads on the home screen; It is strategic

- Added row of content recommendations which is driving more engagement and subscriptions

- Subscriptions are driving SSD and mgmt is continuing to focus on that area: Have “tens of millions” of subscribers, both through Premium subscriptions and also through DTC subscriptions

- Q4 was the highest quarter of Premium Subscription net adds since its launch in 2019

- Subscription is “a good business”; Will continue to add more partners

- Note that the Co will start to comp avg price increases in H2:25

- DSP partners & integrations are helping drive ad revs

- Q1 & 2025 outlook: Expect ad business to grow faster than SSD

- SMB response to self servs ad manager has been great; The Co will continue to invest in this

- Q1 & 2025 outlook: Expect ad business to grow faster than SSD

- Q4 political was a positive upside surprise to ad revs in the qtr (and it was still strong excluding that): Political was 6% of ad revs (vs at TTD was 5%); They have been more actively pursuing political ad dollars as see it as a big oppty

- This particular vertical will be a strength going forward

- “We’ve already started talking about 2026 and even 2028 and how we’re going to prepare for it”

A Few Other Key Comments

- Mgmt talked down the potential impact from the Walmart/Vizio deal

- The weakness in the Devices business was due to excess inventory in Q4, which will also impact Q1 (primarily in the 1P TV business)

- But device margins will normalize as per the guidance

- International expansion? Still mostly focused on scaling vs monetization

- “Pleased” with progress (regionally focused on the Americas, N. Amer, C. Amer, LatAm and the UK)

- In most markets, except for Canada, the Co is still focused primarily on scale of streaming households & less so on monetization of that

- BUT starting to turn focus on monetization in Mexico

- Intl is a key part of reaching the target of 100mn streaming households in the next 12-18 months

- Strong usage growth of The Roku Channel: Q4 streaming hours on The Roku Channel rose +82% y/y in the US and reached HHs w/ 145mn people

- In Dec, more than 80% of Streaming Hours on The Roku Channel originated from the Roku Experience (not a Roku Channel app tile), a 15-pt increase y/y

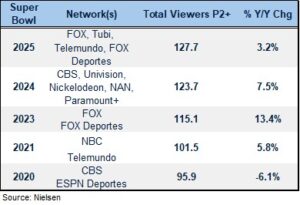

Super Bowl LIX’s Record Viewership Didn’t Necessarily Translate Into Record Ad Revs…

The main event last weekend was most certainly Super Bowl LIX as the Philadelphia Eagles ended up breaking the Kansas City Chief’s winning streak by a wide margin (40-22). It went down as one of the most one-sided games in Super Bowl history (the biggest gap was actually when the San Francisco 49ers defeated the Denver Broncos by 55-10 in 1990).

The key question Monday morning was, how were the viewership numbers? It was a new record high for overall viewership (rising +3% y/y), not only on linear but also on streaming with Fox’s Tubi airing the event for the first time. Did this record viewership translate into record ad dollars? In that case, no. $800mn was spent on the day, in total, as per Fox but that was down -2.4% from the estimated spend in 2024 as last year benefitted from overtime (i.e., more ad spots).

Regardless, the numbers are big and the Super Bowl remains le crème de la crème for sports events in the US. See below for more details on viewership and ad revenue.

Fox Reported “Record-Setting” Viewership Numbers For Super Bowl LIX Both On Linear & On Tubi (link/link)

- The avg audience hit 127.7mn viewers across all platforms (+3.2% y/y): This number, which includes fans that watched across both TV (FOX, FOX Deportes, and Telemundo) and digital channels (Tubi and NFL digital properties) marked a new all-time high for Super Bowl viewership

- The big game peaked at 137.7mn viewers: This occurred in the game’s second qtr, per Nielsen Media Research

- Pregame coverage (1:00-6:30pm) avg’d 23.4mn viewers: This ranks as the most-watched Super Bowl pregame on record that started at 1:00pm

- The pre-kick portion avg’d 82.5mn viewers: An increase of +9% y/y

- The Apple Music Super Bowl Halftime Show garnered an avg of 133.5mn viewers across TV and digital platforms (+3% y/y)

- Tubi’s simulcast of the Super Bowl LIX broadcast also broke streaming records: Tubi’s simulcast reached 15.5mn peak concurrent streaming viewers as well as a 13.6mn avg minute audience, which was “up by a decisive margin from prior Super Bowls”

- Tubi saw 24mn unique viewers access the platform across game day programming

HOWEVER, This Didn’t Necessarily Translate To Record Ad Rev Figures

- Gross ad rev generated by Super Bowl LIX topped $800mn+ across all platforms, per Fox (link): This represented a -2.4% y/y decline from the est’d $819.5mn in total day ad revs realized by CBS’ broadcast of last yr’s Super Bowl LVIII, per EDO Ad EnGage (though last yr’s big game also featured an overtime period that brought in an addt’l $60mn in ad rev)

- BUT top pricing for a 30-sec ad spot rose to $8mn from $7.5mn last yr (link)

- National ad revs for the actual game reached $652.2mn via 70 commercials airing that yielded 9.0bn impressions (per EDO Ad EnGage estimates)

- This compares to CBS at $708.2mn via 80 commercial airings that yielded 9.6bn impressions

- The biggest ad categories during the game (also per EDO) –

- Beer/Cider/Hard Seltzer: $56.7mn from nine airings

- Streaming platforms aired 4 spots, spending $26.8mn

- Snack brands and AI services each with 4 spots and $35mn in spend

- Mobile/wearable devices, social media categories each with three spots, and $28mn and $21mn, respectively

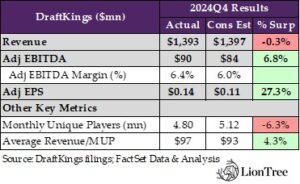

DraftKings Looks To Go Full Steam Ahead In 2025

After DraftKings slashed its FY24 guidance on its last earnings call following “the most customer-friendly stretch of NFL sport outcomes [it has] ever seen,” the discussion surrounding the company’s Q4 results took on a much more optimistic tone. DraftKings reported mixed headline numbers relative to consensus estimates that were eased after the previous call, with revenue coming in a slight -0.3% below sell-side forecasts and adj EBITDA finishing +6.8% above expectations. Despite the unfavorable sport outcomes that once again weighed on the quarter, DraftKings’ structural hold percentage was a bright spot, as efforts to market and merchandise higher hold products, such as parlays, resulted in bet mix improvements in both the NFL and the NBA. Otherwise, the company’s MUPs fell short of estimates, and ARPMUP, while topping expectations, still declined on a y/y basis, even when excluding the impact of the Jackpocket due to “distraction around the election.” Handle was also negatively impacted by one fewer NFL game occurring in Q4 vs the prior year quarter as well as lower engagement with the NBA.

Interestingly and perhaps most incrementally for investors, all the headwinds that DraftKings faced in Q4 have appeared to reverse direction thus far in 2025. NFL sport outcomes, which are generally “customer-friendly” when favorites win and more prominent players score, started to benefit the house, and the company’s NBA handle has “bounced back quite a bit” in Q1TD. Furthermore, DraftKings anticipates a “pretty meaningful decline in promo intensity” in 2025, which should provide an uplift to margins throughout the year. On the regulatory side, management believes that this year will also be “a little bit better in terms of legalization,” given that politicians won’t be as distracted by campaigns and more willing to take up controversial issues. The company now views further legalization of online gaming as “inevitable”. Beyond all these tailwinds, DraftKings’ launch in Missouri, which is expected to occur in the summer, and the company’s plans to increase investment in its live betting offerings will be additional needle-movers to monitor in 2025 as well. All said, DraftKings has a lot of wind behind its sails this year.

-> DraftKings shares soared +15.2% post-earnings and closed the week up +26.5%; YTD, DraftKings stock is trading up +43.8%

Q4 Headline Results Were Solid Relative To Tempered Expectations

- DraftKings printed MIXED headline numbers –

- Q4 rev incr’d +13.2% y/y (vs +38.7% y/y in Q3) but closed a narrow -0.3% below cons

- Q4 adj EBITDA fell -40.8% y/y to $89.5mn (vs -$58.5mn in Q3) but beat cons by +6.8%

- Adj EPS of $0.14 (vs $0.29 the prior yr qtr and -$0.17 in Q3) topped cons by +27.3%

- The FY25 outlook was raised on the top-line and maintained for adj EBITDA: Notably, the outlook doesn’t include the tailwind of favorable NFL sport outcomes in early 2025, nor the Co’s launch of mobile sports betting in Missouri; The Co also wants to wait for longer before raising guidance to “see how the yr progresses”

- Rev guidance was incr’d above the Street’s forecasts: Now expects FY25 rev between $6.3-6.6bn (vs $6.2-6.6bn prior), beating cons by +0.8% at the mid-pt; Cited the Co’s “excellent” performance across core value drivers thus far in 2025 as well as investments in live betting

- Adj EBITDA guidance was reaffirmed: Still anticipates an adj EBITDA range of $900mn to $1bn in FY25, which was above cons by +0.8%

- FCF is still expected to be $850mn: Assuming a $100mn bridge between adj EBITDA and FCF

Structural Sportsbook Hold Continues To Rise / Actual Sportsbook Hold Has Reversed Direction In 2025 YTD

- DraftKings’ structural sportsbook hold percentage has been “a little bit better than expectations”: Structural sportsbook hold incr’d +80bps y/y to 11.2% in Q4 (the Co didn’t provide figures in Q3 but reported a hold of ~10% in Q2 and 9.8% in Q1)

- Structural hold has benefited from improving bet mix: Driven by efforts to mkt and merchandise products w/ higher hold “in a more effective way”

- NFL structural hold was better than the Co forecasted before the season: Flagged that NFL parlay handle mix rose more than +600bps y/y in Q4

- There’s also been “great bet mix improvement y/y in the NBA”

- The Co is “very bullish on the outlook for structural [hold] for 2025”: DraftKings’ “long-term feeling” is that hold “could prove higher than [it] forecast”; Still, the Co maintained its forecast of an 11% structural sportsbook hold in 2025

- Structural hold has benefited from improving bet mix: Driven by efforts to mkt and merchandise products w/ higher hold “in a more effective way”

- Actual sportsbook has exceeded expectations in 2025 YTD: The Co’s actual sportsbook hold ended Jan at 11% and was tracking at 13% in Feb MTD through Feb 11; After being hit w/ unfavorable “customer-friendly sport outcomes” in Q4, NFL sport outcomes were favorable throughout the rest of the 2024-25 season

There Were Some Puts & Takes On User Growth/Monetization Trends In Q4… BUT 2025 Is Looking Strong

- Monthly Unique Payers (MUPs) fell short of the Street’s estimates: MUPs of 4.8mn grew +36% y/y in Q4 (vs +55% y/y in Q3) and missed cons by -6.3%; Excluding the impact of the acquisition of Jackpocket, MUPs incr’d ~+16% y/y

- Still, “customer acquisition exceeded [the Co’s] expectations”: Newly acquired Sportsbook as well as iGaming customers cont’d to increase on a y/y basis w/ expansion into new territories, and the Jackpocket digital lottery courier app benefited from the Mega Millions jackpot reaching $1.2bn in late Dec

- User penetration has still been growing in mature mkts: DraftKings still doesn’t know where their ceiling could be

- Super Bowl LIX was a “bright spot” for 2025 customer acquisition efforts: Super Bowl Sunday was a “successful event for the Co,” as the DraftKings sportsbook app reached the number one spot in the App Store in the sports category and was number three across all apps

- Still, “customer acquisition exceeded [the Co’s] expectations”: Newly acquired Sportsbook as well as iGaming customers cont’d to increase on a y/y basis w/ expansion into new territories, and the Jackpocket digital lottery courier app benefited from the Mega Millions jackpot reaching $1.2bn in late Dec

- User monetization outperformed the Street’s forecasts: Avg rev per MUP (ARPMUP) decr’d -16% y/y in Q4 (vs -10% y/y in Q3) but still topped cons by +4.3%; Excluding the impact of the Jackpocket acquisition, ARPMUP was down ~-4% y/y

- Drivers behind the y/y decline: Consisted of the inclusion of lower ARPMUP Jackpocket customers as well as lower actual sportsbook hold due to “customer-friendly sport outcomes,” though these factors were partly offset by improved structural sportsbook hold and promo reinvestment in sportsbook and iGaming

- “Customer engagement and retention were strong”: The Co set its own daily record for sportsbook handle at $436mn; This was helped by a ~+40% y/y increase in Same Game Parlay handle

- BUT external several factors weighed on handle during the qtr: Acknowledged that “distraction around the election” had this biggest impact; Q4 also had one fewer NFL game vs 2023, and the “NBA was down a little bit” but has since bounced back in 2025

DraftKings’ Promo Strategy Is Becoming More Effective & Efficient

- Promo reinvestment outperformed DraftKings’ expectations in dollar terms in Q4: Given the Co’s “optimization of promo offers”

- A “pretty meaningful decline in promo intensity” is anticipated in 2025: Driven by the maturation of the online sports betting mkt as well as the Co’s internal efforts to become more efficient w/ promos

There Is Optimism Surrounding Legislative Trends In 2025

- DraftKings anticipates 2025 will be “a little bit better in terms of legalization”: Highlighted that “last yr was a tough yr b/c it was the election and typically getting votes during an election yr is hard… people are just distracted w/ campaigns and also don’t want to take up any sort of issue that may even be mildly controversial”

- “Addt’l online gaming legalization in the US appears inevitable”: Views further iGaming legalization as “more a question of when, not it”; Highlighted that online gaming is “large and growing industry w/ secular tailwinds behind it”

- DraftKings is “well-positioned to capture significant share” in iGaming: Indicated that expansion of its online gaming biz outside the US and Canada could be explored as a longer-term oppty

- The Co has a “keen interest” in prediction mkts: There will be a “CFTC ruling and all sorts of things” within the next 60 days, and DraftKings will be “watching it very actively… and seeing how it plays out”

Capital Allocation Notes

- DraftKings will be “fairly programmatic” w/ buybacks in 2025: The Co plans to be “very consistent q/q” w/ its repurchases and will look to tie them to FCF

- The Co will look towards “exploring oppties in the debt mkts” in 2025: Indicated this will be for “general corporate purposes and just to establish a presence in the debt mkt w/ no specific focus in mind”

Other Highlights

- “There’s really not like a burning need to rush international expansion”: The Co still believes that it has a “huge runway” in the US as well as Canada and will continue to focus on these mkts unless “the right oppty is out there”

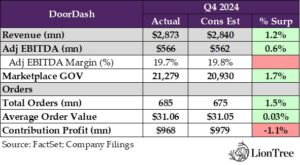

It’s Deja Vue To Last Qtr With DASH “Delivering”

DoorDash delivered in the quarter, with both revenue and adj. EBITDA beating and orders also coming in above expectations. While AOV was in-line and contribution profit slightly missed, mgmt highlighted significant runway across all business segments, reiterating their strategy of driving compounding growth through incremental improvements across their portfolio rather than relying on a single driver.

The quarter was characterized by a continuation of recent trends, with MAUs growing double-digits and order frequency at all-time highs levels. The Co continues to acquire new users at a healthy pace, while retention and frequency amongst older cohorts has been improving over time. New vertical builds are gaining momentum, with frequency of orders and overall spend per MAU growing as they add selection and improve quality. The international business is also gaining further momentum, with Wolt outperforming early DashPass adoption, and several markets exceeding the US’s grocery penetration levels.

Looking ahead, also similar to the past quarter, Q1 is expected to see more progress on initiatives already in place, with a focus on scaling the business by enhancing the user experience to drive frequency and drive greater penetration. While profitability guidance was a little light for Q1 versus consensus estimates (-1.4% below the midpt), the low-end of Marketplace GOV guidance came in ahead of expectations. Though there wasn’t much guidance beyond Q1 provided, the Co did flag that they expect 2025 adj. EBITDA margin to trend up through 2025.

Overall, it was another solid quarter of execution. See below for our key highlights from the call…

-> DASH’s stock was up +4.0% the day post earnings and built on those gains through the week to end up +9.1%

- Q4 results mostly beat expectations (contribution profit was a little light)

- Revenue – BEAT by +1.2%: Grew +25% y/y (in-line w/ +25% y/y in Q3)

- EBITDA – BEAT by +0.6%: Great +56% y/y (accel from +55% y/y in Q3)

- Total Orders – BEAT by +1.5%: Grew +19% y/y (accel from +18% y/y in Q3)

- Marketplace GOV – BEAT by +1.7%: Grew +21% y/y (accel from +19% y/y in Q3)

- Contribution Profit – MISSED by -1.1%: Grew +41% y/y (decel from +45% y/y in Q3)

- Q1 profitability guidance disappointed, thought Marketplace GOV came in well ahead

- ETBIDA – MISSED by -1.4% at midpt: $550-600mn vs cons $583.3mn

- Marketplace GOV – BEAT by +1.6% at midpt: $22.6-23.0bn vs cons $22.43bn

- Guided 2025 adj. EBITDA margin to trend up through 2025: Expect adj. EBITDA as a %age of Marketplace GOV to increase from Q1 to Q2 and again from Q2 to Q3

- Capital allocation strategy will remain largely unchanged from 2024 to 2025

- Continued investments in core biz areas: S. restaurants, international markets, non-restaurant commerce, and advertising

- Approach to buybacks remains “opportunistic”, “conservative”, and focused on long-term shareholder returns

- Q4 take rate of 13.5% was flat seq: Impact was largely seasonal due to Dasher pay; Q4 tends to be a higher growth qtr, “so we lean into Dasher pay in order to support the growth”

- Despite challenging weather/natural disaster, Dash Supply continues to look “really, really healthy”: “Obviously, there has been some challenging circumstances with weather in different parts of the world as well as, unfortunately, different natural disasters that have also occurred”; But outside of those anomalies, Dasher Supply looks “really good”

- Incremental platform stats –

- Reached 42mn+ MAUs, and is growing double-digits

- Order frequency “continues to be at an all-time high”

- Not taking the segmentation approach of other delivery Cos: Unlike Uber and Lyft, which are segmenting delivery, in-store, and pick-and-pack tasks, DoorDash has always tried “to construct the maximum flexible set of opportunities for Dashers” that focuses on maintaining a flexible and adaptable network without such segmentation

- Underlying cohort strength is “strong” for both new and existing users

- Still acquiring new users at “a pretty healthy clip”

- Older cohorts “continue to be very strong…continue to increase their engagement [and] order frequency over

- While order frequency among new users starts lower, retention and order frequency across all cohorts continue to improve over time

- Seeing repeat buying and engagement in new verticals, as focus remains on scaling

- Increasing engagement, with repeat purchasing behavior

- Frequency of orders and overall spend per MAU is growing as they add selection and improve quality

- On profitability: Continue to focus on overall dollar growth vs targeting specific margin percentages

- Grocery delivery in the US and globally is “still quite nascent” w/ significant room for improvement; Focusing on product enhancements to drive growth

- Penetration levels are lagging behind other categories of e-commerce and delivery

- Biggest problem – “customers today are asked to pay a premium, but they don’t always receive the items that they order”

- Focused on improving product quality by expanding catalog, ensuring accurate deliveries, and matching the right type of Dashers who want to do grocery deliveries with actual grocery orders

- Finding that customers who started with small, top-up grocery orders are now purchasing larger baskets and are using the product across use cases

- More retailers are also recognizing the incremental customers DoorDash brings

- Quick callouts on intl biz –

- “Gaining share in virtually every country that we operate in”

- Reached all-time high in intl MAUs

- Order frequency “continues to grow,” driven by improvement in selection, quality, and driving affordability

- Wolt+ is growing faster than DashPass was in its early years

- “Several countries” where new verticals and grocery penetration in the intl portfolio is higher than that in the US

- Overall intl portfolio is gross profit positive

- On growing DashPass – “it’s a pretty straightforward playbook”

- DoorDash has 100mn+ users, while DashPass has subscribers “only in the tens of millions”

- “We have a large fraction of our customer base within our own ecosystem that are not subscribers”

- Solved by…making the product better -> increases frequency -> makes it more obvious the value of being a subscriber -> increased likelihood of becoming a DashPass subscriber

- “Don’t think that we have to do anything unnatural to see growth in our subscriber programs. We feel really good about where we’re at, and we just have to keep going”

- Partnership with The Trade Desk is part of a broader strategy to integrate with external ad ecosystems

- “There are a lot of different partners that existing merchants and advertisers work with”

- “We’ll likely have more partnerships where we’ll just kind of keep solving for what I think advertisers are somewhat accustomed to”

- Reiterated commentary on challenges around autonomous vehicles and delivery

- Delivery-focused AVs differ from robotaxis since they lack passengers to assist with first/last-mile logistics

- Have been exploring AV delivery “for years” but no major announcements yet

- Cost structure of AV delivery is also still uncertain and evolving

- Success will depend on aligning AV technology with operational needs to create a viable cost structure

- AI agents are very valuable but are not a panacea for all challenges

- “…they certainly don’t solve the tasks in the physical world, such as providing the logistics infrastructure, understanding how to do it at the highest quality, the lowest cost with the greatest accuracy”

- BUT, will “make sure that we take advantage of these technologies, especially as the costs continue to scale down quite quickly… think there’s great opportunity for much better personalization…to virtually improve every part of our operations”

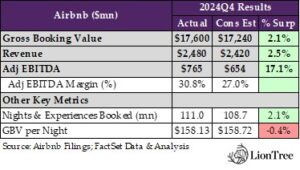

Airbnb Surged Across The Finish Line In 2024, Though Supply Growth Could Be A Challenge In 2025

On the heels of Expedia’s strong print last week, the online travel space notched another win this week, as Airbnb’s Q4 earnings provided further testament to the strength of travel demand across the world and sparked another favorable reaction from the market. Benefiting in particular from a “strong” North American consumer that has been “contemplating future travel,” Airbnb saw growth in its gross bookings value accelerate to +13.5% y/y (vs +8.3% y/y in Q3) and in its Nights & Experiences Booked to +12.3% y/y (vs +8.5% y/y in Q3) in Q4, with both surpassing consensus estimates by +2.1%. Beyond just North America, Airbnb’s growth in nights booked also stepped up sequentially across all other regions, and the company highlighted that growth in its newer geographies doubled that of its more mature markets, though off a smaller base. These factors translated into Airbnb’s +2.5% beat on revenue and contributed to an adj EBITDA that finished a wide +17.1% ahead of expectations.

Looking ahead, momentum should continue into Q1, given the “strong demand” that it has been experiencing thus far in 2025. That said, there will be a couple of dynamics outside of Airbnb’s control that will weigh on growth during the quarter. For one, the strong US dollar, while fueling Americans’ desire to travel overseas, will pose a ~-2% headwind to revenue growth in Q1. Secondly, the timing of Easter, which will occur in April this year as opposed to in March last year, as well as the unfavorable comparison created by last year’s Leap Day, are expected to lower y/y revenue growth by another ~-3%. As it pertains to the whole of 2025, Airbnb didn’t issue a full-year outlook on its top-line growth but guided for an adj EBITDA margin of 34.5%, marking a decline from its 36.0% adj EBITDA margin in 2024. Notably, the forecast includes $200-250mn of planned investments for scaling and launching new businesses and products. One of the most interesting items in the pipeline is an AI-powered customer service agent that is expected to be part of the company’s summer release, as it will enable the company to operate more efficiently and could eventually become a full-service travel and living concierge when combined with Airbnb search over the coming years.

Nonetheless, despite all the room for optimism in Airbnb’s print, there were some lingering causes for concern on the supply side given that supply growth decelerated for a fourth consecutive quarters and grew only +4% y/y to 8mn+ listings in 2024. Moreover, Airbnb closed out 2024 with roughly the same number of hosts (5mn+) at the end of the year that it had on its platform at the beginning of it. With other alternative accommodations platforms, such as Vrbo, starting to close the competitive gap, the slowdown in supply growth could hurt Airbnb in the medium- to longer-term.

-> Airbnb shares jumped +14.5% in reaction to earnings, ending the week up +19.6%; YTD, Airbnb stock is trading up +22.8%

Airbnb Ended 2024 On A Strong Note

- Q4 headline numbers beat across the board

- Q4 gross booking value grew +13.5% y/y (vs +8.3% y/y in Q3) and exceeded cons by +2.1%

- Rev incr’d +11.8% y/y in Q4 (vs +9.3% y/y in Q3) and topped cons by +2.5%

- Q4 adj EBITDA rose +3.7% y/y (vs +6.8% y/y in Q3) and beat cons by a wide +17.1%

Trends Are Projected To Be Mostly Similar In Q1, Excluding FX & Calendar Factors + Color On FY25 Margins

- AQ1 rev guidance came in below the Street’s forecasts: Between $2.23-2.27bn, which represents +5.0% y/y growth (vs +11.8% y/y in Q4) but missed cons by -2.1% at the mid-pt; Ex-FX, rev is projected to grow +7-9% y/y, and w/out the impact of calendar factors and FX, rev is expected to grow +10-12% y/y

- Y/Y growth in Q1 Nights & Experiences Booked is expected to be “relatively stable” vs Q1:24: Excludes the impact of Leap Day in 2024, which added ~+1ppt of growth in Q1:24’s +12.0% y/y increase in room nights

- Q1 ADR is projected to “decline slightly” on a y/y basis: “Largely driven by FX headwinds,” and when excluding these, the Co would have anticipated a slight y/y increase in Q1 ADR

- Q1 adj EBITDA and adj EBITDA margin is forecasted to decline y/y: Cited one-time calendar factors, including the timing of Easter and the inclusion of the leap yr in last yr’s results, as well as FX headwinds (same as the drivers behind rev); Excluding these, Q1 adj EBITDA margin would be ~flat y/y

- FY25 adj EBITDA margin is expected to be at least 34.5%: Including $200-250mn of planned investments towards launching and scaling new bizs, the impact of which will be most pronounced in the first nine months of 2025; Rev from new product launches won’t scale until the end of Q2

- Highlighted Brazil and Japan as two mkts that the Co will be investing in: The bulk of the Co’s investment will hit both its mkting and product development line items

Airbnb Sees A Strong Travel Demand Environment

- Benefited from “organic tailwinds” in demand “across the industry”: “The North American consumer has been strong” and has also “been strong in terms of contemplating future travel” following “initial uncertainty leading into the election”; The Co has been seeing “strong demand” early in 2025 as well

- The Co continues to gain mkt share on a y/y basis from hotels: This has been “true both from a traffic share as well as a nights/day perspective” and has occurred both at a regional level and globally

- Airbnb has been doing “quite well” vs Vrbo: Highlighted that non-urban US mkts, where the Co tends to compete against Vrbo, have been one of Airbnb’s fastest-growing segments in the US

- The Co also saw a “notable accel” in the number of first-time bookers on its platform

- North America will represent a major oppty in 2025: Given that the region is still “dominated by hotels” and that Airbnb’s biz is still a fraction of the overall lodging industry; Certain demos, including the Latino population, as well as states, such the heartland states outside of the coast, are also underpenetrated

- The Co continues to gain mkt share on a y/y basis from hotels: This has been “true both from a traffic share as well as a nights/day perspective” and has occurred both at a regional level and globally

Q4 Was Airbnb’s Highest Y/Y Growth Qtr For GBV And Nights & Experiences Booked In 2024

- Airbnb – Gross bookings value growth accel’d seq and surpassed expectations: GBV rose +13.5% y/y in Q4 (vs +8.3% y/y in Q3) and topped cons by +2.1%

- Growth in Nights & Experiences Booked also improved seq and outperformed forecasts: Q4 Nights & Experiences Booked were up +12.3% y/y (vs +8.5% y/y in Q3) and came in +2.1% ahead of cons; Dec had the highest y/y growth in nights booked of any month in 2024

- Nights booked on the Co’s app incr’d +22% y/y in Q4 (vs +18% y/y in Q3): App bookings accounted for 60% of total nights booked in Q4 (vs 55% in the prior yr qtr and 58% in Q3)

- Product optimizations contributed ~+200bps to the exit growth rate of the biz: These included enhanced search functionality, better merchandising, suggested destinations, etc.

- The implied take rate (rev divided by GBV) of 14.1% was down slightly y/y: Primarily driven by unfavorable comps to Q4:23, which included one-time benefits recognized from unused gift cards; Otherwise, the Co cont’d to benefit from the cross-currency transaction svs fee introduced in Q2:24

- ADR growth decel’d seq and was lower than anticipated: Q4 GBV per night incr’d +0.9% y/y (vs +1.4% y/y in Q3) and missed cons by -0.4%; Ex-FX, ADR grew +2% y/y (+2% y/y in Q3), w/ increases across all regions being driven by price appreciation

- Growth in Nights & Experiences Booked also improved seq and outperformed forecasts: Q4 Nights & Experiences Booked were up +12.3% y/y (vs +8.5% y/y in Q3) and came in +2.1% ahead of cons; Dec had the highest y/y growth in nights booked of any month in 2024

- Airbnb saw accel’ing growth across all regions: W/ new geos growing at double the rate of the Co’s five core mkts in Q4

- Asia Pacific and LatAm, again, led the way, each w/ ~+low-20s% y/y growth in nights booked in Q4 (vs +19% y/y and +15%, respectively, in Q3)

- North America nights booked incr’d ~+msd% y/y in Q4 (vs “cont’d growth” in Q3), driven by “broad strength of underlying trends within the region”; Growth in short-term stays cont’d to outpace growth in long-term stays

- EMEA nights booked rose ~+ldd% y/y in Q4 (comp vs Q3 is unclear), w/ accel’ing growth across domestic and cross-border travel, as well as urban and non-urban mkts; There was also an accel of growth across all age ranges

BUT Supply Growth Has Cont’d To Stagnate

- Supply growth slowed further and significantly seq: Q4 supply on the Co’s platform grew +4% y/y in Q4 (vs +10% y/y in Q3, +14% y/y in Q2, and +17% y/y in Q1); Exited 2024 w/ 8mn+ listings after entering the yr w/ 7.7mn

- Airbnb removed ~100,000 low-quality listings in Q4: Maintaining a similar pace from Q3, when it had removed ~300,000 listings YTD by the end of the Qtr

- The number of hosts on Airbnb’s platform was ~flat y/y: The Co both entered and exited 2024 w/ 5mn+ hosts

AI Has Yet To Have A Material Impact On The OTA Industry

- Regarding AI trip planning – “It’s still really early”: Airbnb believes Agentic AI will have a “profound impact on travel” but caveated that it’s not quite ready for “prime time” and indicated that has yet to fundamentally change any of the large travel platforms

- The Co’s work w/ AI is “starting w/ customer support”: The Co plans to launch an AI-powered customer svs agent as part of its summer release and eventually combine it w/ Airbnb search “over the coming yrs” to create a “travel and living concierge”

- AI has already been leading to some op efficiencies: In addition to customer svs, the Co has been “seeing some productivity gains” in engineering functions but hasn’t seen a “fundamental step-change in productivity yet”; Anticipates a +30% increase to tech & engineering productivity in a few yrs

Lyft Flags Competitive Pricing Pressure Emerging In Ride Sharing

Following somewhat mixed results from Uber last week with its disappointing Q1 guidance calling out to FX headwinds, Lyft similarly disappointed regarding next qtr’s gross bookings guidance, but this time called out pressure from low pricing in the industry (which didn’t come up on the Uber call).

Aside from that, pluses that we would highlight are the strong rides and active rider trends, as well as stronger than expected margin and FCF performance in Q4. The Co’s initiatives such as reducing Primetime (i.e., when surge pricing comes into play) and expanding Price Lock have been working to attract and retain riders, while incentives and new features have been successful at attracting and retaining drivers. Maintaining strong market share dynamics remains a key KPI for investors and thus far Lyft appears to be delivering on this front. Like Uber, Lyft is positioning for a future of robotaxis with a launch planned in Dallas in 2026, in partnership with Marubeni/Mobileye. Ultimately, mgmt. sees AVs as a catalyst to expand the overall TAM for ride sharing, but that is still a ways off.

See below for what we thought were the most incremental updates from Lyft’s earnings and investor call.

-> The stock fell -2.5% in reaction to earnings, but that was an improvement from the almost -10% post close the night prior

- Mixed Q4 – Gross bookings performance fell short of estimates while profitability & FCF performance was better than expected (see chart)

- Q4 gross bookings grew +15% y/y vs +16% in Q3 – the weaker performance was due to pricing pressures (see more below), tougher comps, and the loss of the Delta partnership

- Q4 adj EBITDA margin of 2.6% of GB hit an all-time high (was 1.8% in Q4:23)

- Trailing 12M FCF was $766mn

- Authorized a $500mn buyback…represents ~9% of Lyft’s mkt cap

- Have seen some pricing pressure in the industry, which is persisting into Q1: At the end of January, price on a per-mile basis to remain competitive was at the “lowest point it’s been in the last five quarters”

- Q1 gross bookings guidance disappoints as a result

- Gross booking guidance of +10-14% was below cons +15% and implies a deceleration from the +15% in Q4 and +16% in Q3

- 2024 leap year also creates a headwind of ~1 ppt y/y to gross bookings growth

- Mid pt of adj EBITDA guidance is ~1% ahead of cons

- Adj EBITDA as a % GB guidance is 2.2-2.3% (down from Q4 2.6%): Despite the pricing issue, mgmt remains confident in reaching this Q1 margin guidance

- Drivers increasingly want to work with Lyft: The Co’s Q4 survey suggests that there is now a 16-point preference gap between them and Uber vs 12-point gap in Q3

- The Co has seen a significant increase in driver sign-ups, attributed to improved driver incentives and support programs; Lyft is focused on ensuring that drivers have a positive experience on the platform

- Rides & rider engagement remains strong into January

- The # of rides in Q4 was up +15% y/y vs +16% in Q3

- Q1:25 commentary: Rides growth should be in the mid-teens y/y …In January specifically, rides growth was high-teens due to growth in active riders and cont’d growth in frequency

- Active riders in Q4 were up +10% y/y vs +9% y/y in Q3

- Exiting the year, the Co has the most high-frequency riders in 5 yrs

- Believes autonomous cars will ultimately expand the market for ride share

- Lyft is not seeing a negative impact to mkt share in robotaxi markets: Its mkt share in San Fran has been stable and has actually gone up in Pheonix

- Mgmt believes they are unlocking new demand or taking share from someone else

- Will see Lyft’s platform expand to include AVs in 2025 via the partnership May Mobility in Atlanta

- Annc’d a new partnership with Marubeni: Will use Mobileye’s Lyftready AV technology to deploy a fleet of “thousands of vehicles” on Lyft’s platform

- Starting in Dallas as early as 2026 with other cities to follow

-> Note that last week, Uber opened an “interest list” in the Uber app for customers in Austin to receive updates about the upcoming Waymo robotaxi launch and increase their chances of being matched with one (link); Uber will also bring autonomous ride-hailing to Atlanta in September as well; Additionally, Elon Musk has said Tesla will launching a robotaxi svs in Austin in June of this year

-> Also, Baidu in talks with UAE officials to launch its Apollo Go robotaxi service in Dubai as early as H1 of this year (link)

Quick Takes On Prints From Other Key Stocks Across The Sectors – SHOP, RDDT, IPG, ATUS

There were a few addtl earnings prints across the sector that we took a deeper look into as well. See below for more on why Shopify and Altice USA shares were up post their results, while Reddit and IPG’s shares fell.

SHOPIFY – Incremental Updates From Its Q4 Earnings: Shopify recorded a strong a finish to 2024, posting a record Q4 GMV as well as other headline numbers that broadly exceeded consensus expectations. The company appears to be executing on two of its major growth initiatives, namely enterprise and international. Nonetheless, Shopify guided for decelerating growth in revenue and gross profit in Q1:25 with investments poised to tick up, though many sell-side analysts viewed this as the company taking a more conservative approach.

-> Shopify shares were up +3.1% in reaction to the print and finished the week up +9.3%; YTD, Shopify stock is trading up +20.7%

- Shopify’s headline results broadly outperformed expectations in Q4 –

- GMV beat estimates: GMV grew +25.7% y/y in Q4 (vs +24.0% y/y in Q3) and topped cons by +1.9%

- Rev was better than anticipated: Q4 rev incr’d +31.2% y/y (vs +26.1% y/y in Q3) and beat cons by +3.0%

- Adj op income surprised to the upside: Adj op income was up +47.7% y/y to $585mn in Q4 and finished +5.7% ahead of cons; The adj op margin of 20.8% was above cons’ 20.3%

- Q1 guidance: For context, Q1 is Shopify’s lowest GMV qtr seasonally

- Rev is expected to grow in the ~mid-20s% y/y range: A decel from +31.2% y/y in Q4 and ~in-line w/ cons’ +24.6% y/y

- Gross profit is projected to increase at a ~low-20s% y/y rate: Down from +27.3% y/y in Q4

- OpEx is expected to be 41-42% of rev: Up from 31.5% of rev in Q4

- Stock-based comp is forecasted to be $120mn: Up from $109mn in Q4

- FCF margin is expected to be in the ~mid-teens%: An uptick from 12% in Q1:24 but down from 22% in Q4:24

- Shopify continues to gain traction w/ “larger, high volume global brands”: “At the high-level, the enterprise is migrating to Shopify” Including Cos in the following categories over the past qtr –

- Retail, apparel, & accessories: Karl Lagerfeld, Reebok, Champion, Westwing, BarkBox, Reitmans, David’s Bridal, Uncommon Goods, Dooney & Bourke, and Goop

- High-profile professional sports teams: FC Barcelona, which joined European football giants Real Madrid and Newcastle United, NBA teams such as the LA Lakers, Miami Heat, Dallas Mavericks, and Sacramento Kings, as well as the Toronto Maple Leafs and Red Bull Racing as enterprise users

- Global e-sports teams: Team Liquid and Shopify Rebellion

- Newer verticals: Music label Warner Music Group as well as window covering Co Hunter Douglas

- The Co has been seeing “cont’d strength internationally”: GMV outside North America grew +33% y/y in Q4, outpacing growth in North America GMV, led by +37% y/y growth in EMEA; Japan was another area highlighted as a rapid growth mkt

- 50% of Shopify’s merchant base is now located outside of North America: But the Co still has less than 1% of global mkt share

- Investments in product are helping to drive international adoption of Shopify: Highlighted offerings such as frictionless sign up to drive adoption, localization f Shopify.com, compliance, new local shipping methods that has been integrated w/ Shopify POS in more countries, and rolling out Klarna as a local payment method

- Merchant Solutions rev outpaced growth in Subscription Solutions rev in Q4…: Merchant Solutions rev rose +33% y/y in Q4, while Subscription Solutions rev was up +27% y/y

- … AND this dynamic is expected to continue through 2025 –

- Merchant Solutions rev growth will continue to be driven by increasing penetration of Shopify Payments and growing adoption of other offerings for merchants

- Subscription solutions rev growth is expected to be slowed by a move to three-month trials and a lack of “substantive pricing changes” in 2025

- This dynamic is projected to weigh on FQ1 gross margins in Q1, given the mix shift: Shopify’s Q1 guidance of gross profit dollars growth in the ~+low-20s% accounts for the mix shift towards Merchant Solutions rev growth as well as overall rev growth in the ~+mid-20s% in Q1:25

- … AND this dynamic is expected to continue through 2025 –

- Q4 FCF margin was better than Shopify anticipated: Q4 FCF incr’d +37% y/y to $611mn (vs +53% y/y in Q3), representing a margin of 22% (vs 19% in Q3); Upside to Shopify’s estimates was primarily due to its outperformance on rev

- BUT moving forward, the priority will be “investing further in key areas… as opposed to driving higher FCF margins”

- Shopify will “continue to embrace the transformative potential of AI”: The Co plans to deepen its investment in Sidekick and other AI capabilities to help make its merchants more successful, its developers more effective, and its customer support interactions more efficient

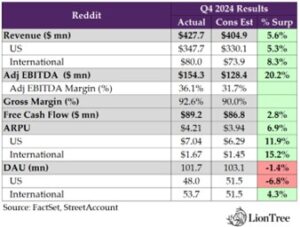

REDDIT – Incremental Updates From Its Q4 Earnings: Despite delivering a strong Q4, with rev growth accelerating sequentially and posting a second consecutive qtr of profitability, Reddit’s miss on DAUs in the US due to Google search volatility was a negative surprise. However, the impact was mostly limited to logged out users, and traffic has since recovered in Q1 but the event still surfaces a risk factor going forward. While the Co didn’t provide Q1 DAU guidance, both rev and adj. EBITDA guidance both came in ahead of consensus.

-> Reddit fell -5.3% in reaction to its print and fell further through the week to end down -12.8%

- A strong Q4 top-line ….

- Q4 rev grew +71% y/y (accel from +68% y/y in Q3) and beat cons by +5.6%

- Second consecutive qtr of being GAAP profitable – adj. EBITDA beat by +20.2%

- ARPU grew +23% (accel from +14% y/y in Q3) and beat cons by +6.9%, w/ upside in both the US and international

- …was weighed down by a miss on US DAUs (intl DAUs beat)

- Total DAUs were up +39% y/y (decel from +47% y/y in Q4) to 101.7mn and missed cons by -1.4% (driven by US miss of -6.8%; Intl beat by +4.3%)

- What drove the miss in DAUs? Experienced some volatility from Google search late in Q4, triggered by a periodic algorithm change

- “What happened wasn’t unusual. Referrals from search fluctuates from time to time, and they primarily affect logged-out users”

- No impact to revenue, as the change primarily affected logged-out users in the US

- “Our teams have navigated many algorithm updates over the years and did an excellent job adapting to these latest changes effectively”

- “Our relationship with [Google] is great”

- Looking into Q1… traffic from search has recovered so far in the qtr and they have regained momentum

- Q1 guidance came in ahead of consensus estimates

- Revenue – BEAT by +1.8% at midpt: $360mn-$370mn vs cons $358.4mn

- EBITDA – BEAT by +17.1% at midpt: $80mn-$90mn vs cons $72.6mn

- Q4 ads rev grew +60% y/y (vs +56% y/y in Q3) driven by broad based strength across objectives, channels, verticals and geographies

- Saw “really healthy” y/y and q/q growth in monthly active advertiser count and “that diversification continues”, driven by a focus on ease of use (i.e., AI-driven headline generation, automation for ad optimization)

- Grew across the funnel –

- Saw strength in brand advertising, with top of the funnel rev growing the fastest rate in 3+ yrs

- Mid and lower funnel rev accounted for ~60% of total ad rev and drove more than half of the y/y growth in Q4

- 10 of their top 15 verticals grew 50%+ y/y

- Led by finance, retail, auto, pharma, gaming and tech

- Focus is on expanding managed mid-market and SMB advertisers

- “Not focused on self-serve right now”

- Very large oppty to unlock in international

- Reddit is ~50% US and ~50% intl vs peers in the space that are 80-95% non-US

- “We have no reason to believe that we won’t be in that range, because Reddit is universal, because communities are universal”

- Machine translation (MT) has been a key driver for international user growth

- MT drove between 40-50% of international user growth in Q4

- MT id available in 8 languages – French, Spanish, Italian, Portuguese, German, Swedish, Dutch, and Filipino – and are on track to expand to addtl mkts in 2025

- Community-building efforts, including in-country teams identifying topic areas, recruiting/training moderators, organizing meetups, etc.

- Reddit is ~50% US and ~50% intl vs peers in the space that are 80-95% non-US

- Open-source models (like DeepSeek) are NOT a threat to oppties in licensing

- The value Reddit provides is ongoing access to up-to-date, user-generated content, which remains essential for AI models to stay relevant over time

- “It’s actually no change from the situation we are already experiencing, and we’re very excited about the open-source models”

- Product spotlight: Launched beta for Reddit Answers in the US, an AI-powered search tool

- Provides curated summaries of community discussions and helps users search and discover content, including the best product recommendations and advice from across the platform

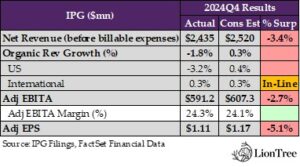

IPG – Incremental Updates From Its Q4 Earnings: IPG’s struggles from prior quarters largely continued in Q4, as its clients maintained a “somewhat more cautious and deliberate approach to budgeting” and account losses from a lackluster principal trading practice were reflected in underwhelming headline results. Moving forward, the loss of a significant healthcare client and other account losses were expected to result in y/y declines in organic revenue in Q1:25 as well. Otherwise, the acquisition by Omnicom is still expected to close in H2:25, and IPG is planning to undergo a business restructuring that will eventually result in ~$250mn of in-year cost savings.

-> IPG shares were down -1.4% in reaction to earnings and closed the week down -1.6%; YTD, IPG stock is trading down -3.5%

- IPG’s headline numbers mostly disappointed w/ the exception of margins –

- Rev before billable expenses fell short of forecasts: Q4 rev before billable expenses was down -5.9% y/y (vs -2.9% y/y in Q3) and missed cons by -3.4%

- Organic rev growth was also underwhelming: Organic rev declines of -1.8% y/y in Q4 (vs ~flat y/y in Q3) was below cons’ +0.3%

- Adj EBITA missed expectations: Q4 adj EBITA before restructuring charges fell -5.9% y/y (vs -2.9% y/y in Q3) and missed cons by -2.7%

- BUT margins beat: Adj EBITA margin of 24.3% in Q4 (vs 17.2% in Q3) was better than cons’ 24.1%

- Rev before billable expenses fell short of forecasts: Q4 rev before billable expenses was down -5.9% y/y (vs -2.9% y/y in Q3) and missed cons by -3.4%

- Global macroeconomic and geopolitical uncertainty remains an ongoing theme: Resulting in the Co’s clients in certain industry sectors maintaining a “somewhat more cautious and deliberative approach to budgeting”

- BUT the impact has been “nothing dramatic”: Acknowledged a “slight downshift” from a handful of client categories but also emphasized that people are “beginning to really get by w/ the reality that they [need] to just start to make plans and invest and grow”

- Rev headwinds from account activity picked up “broadly across a number of disciplines and geographic regions” in Q4: Though this was partly offset by “notably strong growth” in the food & bev sector, plus a return to solid growth in tech and telecom

- Principal media was a “decisive factor” in losing a “very significant” number of media accounts: In contrast to some of its competitors, IPG has been building a media biz that uses “a consultative, highly database” approach

- The combination w/ Omnicom will help address shortcomings in the principal media biz: Omnicom is “sophisticated in that regard” and has that capability “globally”

- 2025 organic rev is forecasted to decline -1-2% y/y: This accounts for the trailing impact of client losses, but the Co sees an “otherwise sound underlying performance” ahead

- The loss of a big client in healthcare is expected to negatively impact growth by -4.5-5%: Excluding this, IPG sees its healthcare biz growing in 2025

- The acquisition by Omnicom is still expected to close in H2:25: The regulatory process is “moving forward,” and the Co is also progressing in the HSR review; Addt’ly, foreign filing processes are “well underway”

- Special shareholder meetings to approve the transaction are scheduled for March 18

- Shareholder repurchases were suspended in Q4: Due to the pending merger

- Dividends also weren’t incr’d: Although the Co typically raises its dividend per share at this time of the yr, the Co and Omnicom agreed to no increases during the pre-merger period

- IPG’s new programming restructuring is projected to generate in-yr savings of ~$250mn in 2025: The initiative includes ramping up progress on the strategic centralization of many corporate functions, greater offshoring and near-shoring in both corporate svs and certain areas of client svs delivery, as well as other efficiency improvements

- The charge/costs associated w/ the program should be of an equal amount: A significant portion of these expenses will be non-cash and recognized in Q1 and Q2; Addt’l details on the plan will be provided on the Q1 call

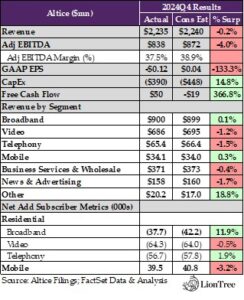

ALTICE USA – Incremental Updates From Its Q4 Earnings: Altice USA was the last connectivity company to report, and there were puts & takes with its Q4 print. Although the company missed consensus estimates on all headline metrics, it stemmed net account losses across both its broadband and video businesses and recorded its highest-ever quarter of fiber net adds as well. The mobile segment also ended the quarter with its best net adds performance within the last five years, as new converged offerings are starting to resonate with customers, but mobile net adds still fell short of expectations.

-> Altice shares were up +0.8% following earnings but closed the week down -1.1%; YTD, Altice stock is trading up +17.0%

- Altice’s headline results were mostly worse than anticipated –

- Rev was slightly below expectations: Q4 rev was down -2.9% y/y (vs -3.9% y/y in Q3) and missed cons by a narrow -0.2%

- Adj EBITDA surprised to the downside: Adj EBITDA fell -7.3% y/y in Q4 (vs -5.8% y/y in Q3) and closed -4.0% below cons

- FCF was better than projected: Q4 FCF dropped -75.2% y/y (vs -36.6% y/y in Q3) but still came in well above cons’ -$19mn

- Key priorities for 2025 were outlined: Executing on these will help the Co stabilize adj EBITDA, enhance capital efficiency, and increase FCF

- Improve broadband subscriber trends: A focus on increasing value-added svs, growing mobile penetration, and expanding the B2B product portfolio will be integral to this initiative

- Examples of new products on the horizon: Include whole home Wi-Fi solutions w/ svs protection add-on, advanced Wi-Fi, and billing on behalf of partnerships w/ third-party OTT app providers and subscription svs to sell-in Optimum packages

- Driving higher efficiency and product margins across operations: Primarily by continuing to leverage AI, digital solutions, and self-svs tools ‘

- Altice has identified efficiencies that are expected to reduce other OpEx by -4-6% by the end of 2026: More detail will be provided on future calls

- Accel’ing the pace of fiber migrations and penetration: In addition to cont’ing to grow total passings, the Co also plans to increase the availability of multi-gig speeds across its footprint w/ new fiber builds and updates to its HFC network

- Improve broadband subscriber trends: A focus on increasing value-added svs, growing mobile penetration, and expanding the B2B product portfolio will be integral to this initiative

- Broadband net losses weren’t as steep as forecasted: Q4 residential bband sub net losses of –37.7k (vs -27.0k the prior yr qtr and -49.2k in Q4) were better than cons by +11.9%

- Multiple factors weighed on the Co’s performance during the qtr: Including the hurricane in North Carolina as well as various new go-to-mkt strategies and base mgmt programs

- Low move activity also pressured gross adds: Highlighted that home sales fell to the lowest levels in nearly 30 yrs

- Intense competition cont’d to be a headwind: Specifically, the Co’s West footprint remained “more challenged,” particularly in the income-constrained segment, by incremental fiber overbuilders and fixed wireless provider

- BUT there were “many positive trends” heading into 2025 –

- Q4 marked the Co’s best-ever qtr for fiber net adds w/ +57k: This marked a +22% y/y increase and was driven by more than double the pace of fiber migrations

- Churn remained low and improved y/y in the East footprint: As a result of the Co’s focus on implementing strong base mgmt strategy

- The Co “saw stronger win rates” in mature mkts across its footprint: Particularly against established ILEC and overbuild fiber operators

- Multiple factors weighed on the Co’s performance during the qtr: Including the hurricane in North Carolina as well as various new go-to-mkt strategies and base mgmt programs

- Mobile net adds were below expectations but still represented Altice’s best performance in the last five yrs: Q4 mobile net adds grew +16.2% y/y to +39.5k (vs +35.5k in Q3) but missed cons by -3.2%

- Mobile line growth is projected to continue to accel in 2025: Mgmt referenced the fact that the Co’s pace of mobile net adds grew by nearly +70% throughout 2024

- The Optimum Complete converged package is “really starting to resonate”: Altice’s new offers are generating +60% growth in the avg number of lines that each customer takes; Scaling up the salesforce behind the offering has helped as well

- The Co has also “evolved [its] mobile strategy a bit” by simplifying the pricing: This is “really helping [it] compete effectively in the East”

- Video net losses improved seq but were slightly worse than anticipated: Residential video net losses of -64.3k in Q4 (vs -62.2k in the prior yr qtr and -77.0k in Q3) were slightly below cons’ -64.0k

- Altice’s three new video offerings have been “seeing early success”: Highlighted that video attach rates have improved to up to 20% on gross adds and that customers have become stickier w/ a higher CLV since launching the products, which are just starting to scale

- Video gross margins were a bright spot: Video ARPU was up +7% y/y in Q4 due to the Co’s “much more disciplined approach to passing along the annual programming cost increases” as well as through its new packaging; The Co also saw more than a -$200mn y/y decline in programming costs

Grab Bag: Musk’s Bids For OpenAI / TMUS-Starlink Beta Open For All Carriers / BYD Unveils “God’s Eye”

- Elon Musk-led consortium of investors makes $97.4bn bid for control of OpenAI (link/link/link)

- Musk and OpenAI CEO Sam Altman have history: Both were co-founders of OpenAI back in 2015, but since then have had disputes over several issues, including whether OpenAI should be run for profit; Musk resigned from its board in 2018

- Why does the group want to buy OpenAI? To revert it back to its original charitable mission as a nonprofit research lab; “It’s time for OpenAI to return to the open-source, safety-focused force for good it once was”

- Altman has pledged to transform OpenAI LLC from a subsidiary into a standalone, for-profit corporation by 2026: He had to accept this term in return for a $6.5bn investment made last yr by investors including Microsoft and NVIDIA

- Altman quickly rejected the unsolicited bid and said that the Co is not for sale

- Altman also said the move is just an effort by Musk to “slow down a competitor”: The bid is being backed by Musk’s artificial intelligence company xAI, which could merge with OpenAI following a deal

- In addition to Altman, OpenAI’s board also shared on Friday that it unanimously rejected the bid, saying it was “not in the best interest” of the Co’s mission and reiterated Altman’s point that the Co is not for sale (link)

- Musk has said he would pull the offer IF OpenAI remains a nonprofit: “If OpenAI Inc.’s Board is prepared to preserve the charity’s mission and stipulate to take the ‘for sale’ sign off its assets by halting its conversion, Musk will withdraw the bid,” the court filing said. “Otherwise, the charity must be compensated by what an arms-length buyer will pay for its assets”

- Regardless of whether the bid is accepted or not, the offer could challenge OpenAI’s transition from a non-profit to a for-profit and make equity distribution more complex

- OpenAI’s transition from a nonprofit to a for-profit company involves selling its nonprofit assets to the new for-profit entity

- OpenAI has been reportedly negotiating a price of ~$40bn, but Musk’s bid suggests that OpenAI might be undervaluing its assets, which could force a reassessment from California regulators who are responsible for protecting the value of assets of non-profit entities and complicate the transaction

- OpenAI already has to divide ownership among its investors (like Microsoft, employees, etc.); If the nonprofit’s val’n increases due to Musk’s big, it would demand a larger stake in the new for-profit Co, leaving less equity for existing investors

- Mobile + Satellite…T-Mobile USA annc’s Starlink beta for free through July, which is open to customers of ANY carrier (i.e., AT&T & Verizon), not just T-Mobile (link)

- Pricing: The svs will be included in T-Mobile’s Go5G Next plans at no extra cost; For other T-Mobile plans, it will be an add-on svs for $15/month

- Non-T-Mobile customers can access it for $20/month

- Coverage: The svs targets the 500k square miles in the US not covered by any w-less company

- Service capability: Currently supports texting, w/ plans to add voice calls and data service later

- Devices: Supports at least 50 device models; Some notable omissions incl Google Pixel 8 (though Pixel 9 is supported) and certain Motorola, OnePlus, and Xiaomi devices (link to list here)

- Pricing: The svs will be included in T-Mobile’s Go5G Next plans at no extra cost; For other T-Mobile plans, it will be an add-on svs for $15/month

-> T-Mobile shares rallied up +3.9% on the back of the news

- China vs the US in self-driving cars…Chinese electric vehicle Co BYD annc’d the rollout of its new “God’s Eye” driver-assist system that will be installed across 21 different EV models (even cheaper ones) at no extra cost: (link/link)

- DeepSeek AI will power the technology

- Very cheap pricing: Models priced as low as $9,600 (but can also sell for as high as ~$150k)

- To compare, Tesla pricing starts higher at ~$30k and the most expensive model can exceed $120k

- Per Chairman Wang Chuanfu…”2025 will be the first year of intelligent driving for all,” predicting the self-driving feature will become something as normal as seat belts within three years.

-> Overall, this will bring self-driving capabilities to a much lower price point and brings more competition into the advanced driver-assistance tech market; BYD shares were up +7.9% on the back of the news, while Tesla fell -6.3%

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Apple has resumed advertising on X after a 15-month pause. The Co had halted ads in Nov. 2023 following controversial remarks by X’s owner, Elon Musk. Apple is now promoting Safari’s privacy features and the Apple TV+ show “Severance” on the platform. This move aligns w/ other major brands like Disney and IBM, which have also returned to X. (MacRumors)

- Disney+ has updated its subscriber agreement to include ads during live sports and 24/7 channels, even for ad-free tiers. This change, effective from Jan. 27,2025 for new subscribers and Mar. 24,2025 for existing ones, aligns w/ industry trends seen in platforms like Peacock and Paramount+. The move aims to expand Disney+’s content library and integrate ESPN+ programming, which includes over 30,000 live sports events annually. (AdWeek)

Artificial Intelligence/Machine Learning

- Google has introduced a new feature for its Gemini AI, allowing it to recall past conversations. This enhancement enables users to create new chats based on previous ones or request summaries of old conversations. Initially, this feature is exclusive to Google One AI Premium subscribers and supports only English, with more languages to be added soon. (The Verge)