After dropping last Friday and sliding through midweek, the S&P 500 regained its footing on Thursday and Friday following the November CPI print which showed tamer inflation than expected. The S&P finished roughly flat for the week and Nasdaq climbed about +1.9%.

**Before everyone heads off for the holidays, we are publishing the Winter Edition of our LionTree’s Lens, which outlines what we view as the most important developments and themes, as well as predictions for the year ahead (see Theme #1) – feedback is always welcome!**

Elsewhere it was busy in the sector and we focused on the below in this week’s report:

- LionTree’s Lens: Winter 2025 – *NEW REPORT*

- CEOs & Investors Are Entering 2026 With “Measured Optimism And Sharpened Realism”

- More Speculation Emerges This Week That Added Fuel To The AI Infrastructure & Deal Circulatory Debate

- Short Form Video Continues To Consolidate Its Position In The Streaming Landscape

- Key Trends W/ Bots, Internet Traffic, And Global Connectivity In 2025

- FWA Speeds For The Big 3 Telcos Have Been A Little Less Speedy So Far This Year

- Grab Bag: 24 Hour Trading? / Instacart & AI Pricing Inquiry / Coinbase Also Jumps Into Predictions Markets

Lastly, on behalf of LionTree, I want to wish everyone a wonderful holiday and New Year. We look forward to engaging with all of you in the year ahead! (Also note that the next LT Weekly Update will be post the holidays).

Best,

Leslie

LionTree’s Lens: Winter 2025 – *NEW REPORT*

We are excited to share our latest LionTree’s Lens: Sector Insights & A Look Ahead, Winter 2025 perspectives, which highlights what we view as the most important market trends and thematic shifts across the TMT and consumer landscape during the last quarter, and some expectations as we look ahead.

Click HERE for our slide deck and the ~20-minute video presentation.

While headline indices have stayed modestly positive in Q4, performance has been highly concentrated beneath the surface. Healthcare has emerged as the market leader after lagging in Q3, while Information Technology has seen a sharp reversal, falling from the top-performing sector in Q3 to one of the weakest in Q4.

In this edition, AI was certainly a common thread across many themes and we offer perspectives in sub-sectors including sports/media entertainment, digital advertising, social media, connectivity, the predictions markets, and more. Overall, the industry continues to evolve and transform at a rapid clip!

-> As always, we’re happy to discuss any of these topics in more detail, and we’d appreciate your thoughts and/or feedback

Key Themes

Macro & Markets

- The Major Market Indices Hold Onto The Strong Q2 & Q3 Gains…

- …But With Concentration Of Gains & Strong Rotations Under The Hood

- The Majority Of TMT Stocks Are Underperforming Q4-To-Date

- Concerns Regarding The Jobs Picture Remains A Hot Button…

- …BUT GDP Forecasts Continue Upward Revisions, W/ AI Spend Helping

- Mega-Mergers Are Returning, With A Jump In Debt Financing

- The IPO Recovery Holds In 2025 & A Strong Pipeline Is Set To Propel 2026 Activity

Key Themes Across The Sector

- A Complicated Web Of Circular AI Ecosystem Deals Emerges

- And AI Players Are Starting To Step On Each Other’s Toes

- The AI Bubble Debate Moves Into High Gear

- Digital Advertising Continues To Consolidate At The Top, But With Some Loosening

- Momentum Is Building Around Social Media Safety, Globally

- Post A 2026 Bump, Signs Point To Growth Flattening For US Sports Media Rights

- Short Form Video Is Increasingly Taking Center Stage

- Streaming Platforms Are Pushing Harder Into Other Adjacencies

- Connectivity In Flux As The Sector Undergoes A Transformation

- New Entrants Are Flooding Into Predictions Mkts But Regulatory Remains A Wild Card

- The Push & Pull Of AI-Driven Personalized Pricing Is Likely To Gain Momentum

Wall Street Sentiment

- Wall Street’s Top TMT Picks & Pans

- Analysts See A Lot Of Upside To Company Price Targets Going Into YE

CEOs & Investors Are Entering 2026 With “Measured Optimism And Sharpened Realism”

As 2026 approaches, global CEOs and investors are entering the year with confidence intact, but measured. Insights from Teneo’s Vision 2026 survey of more than 350 CEOs and 400 institutional investors show that expectations for growth remain positive. That optimism, however, is uneven. Mid-cap CEOs are significantly more bullish than large-cap leaders, and overall sentiment is impacted by heightened political, economic and corporate uncertainty.

There was a lot covered in the report but the three areas in particular that we wanted to flag were 1) confidence in capital markets and dealmaking remains intact, and CEOs and investors continue to be optimistic on the M&A front, though there is some cautious sentiment around expected impacts from higher capital costs, tighter access to debt, and elevated investor activism; 2) the global investment map continues to evolve as the US is still viewed as the most attractive market, while India’s strategic importance is rising quickly, especially as it relates to China, though there is “no doubt” around China’s continued long-term relevance, and 3) 2026 is set to be a year of progress over perfection on the AI-front, though there is some divergence in ROI timeline expectations between mid-cap CEOs vs larger-cap CEOs vs investors.

See below for what we thought was the most incremental, and if you would like to take a deeper look into the report, you can do so HERE.

Read more below…

“Cautious Confidence” On The Global Economy Amongst CEOs Going Into 2026

- The global economic outlook for H1:26 remains positive, but has slightly tempered vs last yr

- 73% of CEOs and 82% of investors expect an improvement in 2026 (which is down from m 77% and 86% in 2025, respectively)

- What’s driving the uncertainty? “Globally, we’re seeing a high degree of political, economic and corporate complexity, and that naturally breeds uncertainty”

- Mid-cap CEOs are more bullish: 80% expect improvement in H1 2026, compared to just 31% of large-cap execs

- Notably, large-cap CEO confidence has fallen -20pts since last year, vs just -3pts for mid-cap CEOs

Source: Teneo Vision 2026

- Overall, nearly half of CEOs and investors are preparing to increase hiring as well as international and domestic investment in 2026

Sentiment Around Deal Making Is Also Optimistic, Though With Some Caveats

- CEOs & investors are also optimistic about the funding potential from equity markets and affordability of debt levels

- BUT both groups are more cautious heading into 2026 regarding access to the debt market

- “On the margins, debt markets remain open, but there is more stress in the system than there has been in many years”

Source: Teneo Vision 2026

- M&A optimism persists but is slightly down from 2025, with 78% of CEOs and 77% of investors expecting to see more activity (vs 83% and 87%, respectively, last yr)

- Both groups, across all regions, cite high capital costs as the primary headwind to M&A execution

- Large-cap CEOs are marginally more bullish vs mid-cap CEOs, w/ 81% anticipating incr’d M&A activity vs 76%, respectively

- What sector CEOs and investors are most optimistic about M&A activity in 2026? CEOs representing the healthcare and resources industries + investors with portfolios in resources, financial and industrial

- What about across regions? CEOs in LATAM, MENA and North America exhibit the strongest confidence in M&A outlook, while investors across APAC and Europe are most optimistic for deal activity heading into 2026

- Amidst the heightened deal environment, 72% of CEOs and 76% of investors globally expect a rise in investor activism through 2026 (mixed from the 80% and 74%, respectively, last yr)

Expect A Shifting Landscape Globally – US Remains On Top, But India And China Are Continuing To Rise

- The US remains the most attractive market for investment among global CEOs, but sentiment has slightly decel’d from last yr: 89% of CEOs consider the US to be an attractive investment oppty for their biz, which is slightly down from 91% last yr

- India is expected to eclipse China by 2036…

- Within 5 years, CEOs believe India will reach parity with China in terms of significance to business strategies

- More CEOs expect India to become more important for biz: 33% of CEOs expect India to be extremely important to biz, and that figure is expected to rise to 47% by 2036 (overtaking China at 44%)

- Why? CEOs cite its “massive and young consumer market” and “growing digital infrastructure and innovation momentum,” and that India has shaped into a “top strategic hub for IT and digital services”

- BUT there is still some execution risk in India, with “with social tensions at play and a quasi-federal system of government that can create operational complexities”

- Also to flag…the “shift has major implications for the Middle East, given its proximity, youth-driven consumer market and fast-growing digital infrastructure, all of which make India an increasingly critical economic and energy partner for the region and the world”

- …BUT there is “little doubt” that China will remain central to any biz and investment strategy long-term

- Driven by China’s growing middle class, production affordability, supply chain scale, energy sources and R&D investments, which “remain unmatched”

Source: Teneo Vision 2026

- CEOs (60%) and investors (57%) agree that deglobalization is accelerating but views are nuanced by geography

- Leaders in MENA and APAC see less pervasive acceleration, whereas CEOs in LATAM believe it is accelerating most rapidly

Source: Teneo Vision 2026

2026 Will Be The Year Of Progress Over Perfection On The AI Front

- Global AI spend is expected to top $2 trillion in 2026, with 68% of CEOs planning to increase spending in the yr

- AI is shifting from “an innovation line item to a core driver of competitiveness”

- It is the only technology in which CEOs plan to increase investment at a faster rate than in 2025

- BUT there is a growing gap emerging between “investor expectations and CEOs’ realism”

- 53% of investors expect new AI initiatives to deliver returns in 6 months or less, while only 16% of large-cap CEOs think that’s achievable, though mid-cap CEOs show greater confidence at 52%

- Moving to past 6 months is when we see 84% of large-cap CEOs expecting to see results from AI

Source: Teneo Vision 2026

- CEOs report fewer than half of current AI projects are ROI-positive, but they see the greatest gains across internal efficiency, administrative and customer-facing applications

- Beyond ROI, CEOs and investors are seeing the most success across marketing and customer service AI strategies

- Applications that pose the greatest potential risk and complexity (security, legal and HR) are the biggest challenges

- CEOs and investors expect AI to drive an increase in hiring across all levels in 2026

- 67% of CEOs say AI is increasing the entry level headcount and 58% expect expansion of senior leadership roles

- CEOs also rank increasing the use of AI and automation to augment the workforce (50%) and upskilling talent (46%) as the top priorities for their organizations in 2026

More Speculation Emerges This Week That Added Fuel To The AI Infrastructure & Deal Circulatory Debate

Following annc’d, and speculated, delays regarding data center builds, this week’s press that Blue Owl backed out of a Oracle datacenter deal caused a bit of angst in the market. But Oracle commented that there is a different partner involved and that their construction start is tracking as planned. At the same time, another circular deal emerged this week with Amazon reportedly in early talks to invest up to ~$10bn in OpenAI and in exchange Amazon will sell OpenAI its Trainium chips.

See more color below…

Blue Owl Reportedly Backs Out Of Oracle Data Center Deal

- Oracle said talks for an equity deal to support its Michigan data center project remain on schedule, but will not include Blue Owl, per the FT (link/link)

- The ~1-gigawatt project in Saline Township, Michigan, is part of the Stargate AI infrastructure push by Oracle and OpenAI

- The Co said in late Oct that construction is to begin in early 2026

- Blue Owl, Oracle’s largest data center partner, had been in talks to back the $10bn deal

- They reportedly failed to reach an agreement on terms that matched those of other projects it had already committed to

- Oracle responded to the news, but did not give much detail

- “Our development partner, Related Digital, selected the best equity partner from a competitive group of options, which in this instance was not Blue Owl,” an Oracle spokesperson said

- Construction is scheduled to begin Q1 2026

-> Oracle shares were down -5% on the day of the news and closed up +1% on the week

At The Same Time, Another Possible Circular Deal Is Forming

- Amazon is reportedly in early discussions to invest as much as $10bn in OpenAI and to give them their new Trainium chips to use (link/link/link)

- If it materializes, the deal will value OpenAI at ~$500bn, Bloomberg reported, citing an anonymous source

- This would mark the latest in a series of circular deals in the AI space, which include but are not limited to:

- This past March, OpenAI invested $350mn of equity into CoreWeave, which used the funds to buy chips from Nvidia

- In Oct, OpenAI signed a deal to pick up a 10% stake in AMD and committed to using the chipmaker’s AI GPUs and also signed a chip usage agreement with Broadcom that month

- In Nov, Open AI signed a $38bn cloud computing deal with Amazon

–> Amazon shares were up 1% on the day of the news and closed up +1% on the week

Short Form Video Continues To Consolidate Its Position In The Streaming Landscape

The U.S. video ecosystem saw several notable developments this week, led by TikTok’s anticipated move to formalize its U.S. operations under a new, domestically controlled joint venture. Following months of regulatory pressure and political negotiations, TikTok confirmed plans to house its U.S. business in a newly created entity backed by Oracle, Silver Lake, and MGX, with Oracle also assuming a central role in data security and compliance.

Separately, social media platform players continue to push deeper into the living room to try to take share of TV-based viewing. Meta announced the launch of Instagram for TV app on Amazon Fire TV devices, signaling an effort to scale Reels beyond mobile. In the meantime, YouTube TV continues to add subscribers at an impressive clip and the Academy deciding to air the Oscars on YT TV starting in 2029 instead of ABC is also telling.

See below for more details.

TikTok Signs Agreement To Create New U.S. Joint Venture

- TikTok CEO Shou Zi Chew told employees on Thursday that the Cos U.S. operations will be housed in a new joint venture (link/link/link/link)

- What will happen?

- The entity is named TikTok USDS Joint Venture LLC, according to a memo sent by Chew and obtained by CNBC

- As part of the JV, Chew said the Co has signed agreements with the three managing investors: Oracle, Silver Lake, and Abu Dhabi-based MGX

- The deal’s “closing date” is set for Jan. 22

- How will it be structured?

- ~50% will be held by a consortium of new investors, including Oracle, Silver Lake and MGX, with 15% each

- ~30% will be held by affiliates of certain existing investors of ByteDance

- ~19.9% will be retained by ByteDance

- Financial terms of the deal, annc’d in an internal memo by TikTok were not disclosed

- What will happen?

- In addition, Oracle will serve as the “trusted security partner” in charge of auditing and validating that it complies with “agreed upon National Security Terms,” the memo said

- U.S. data will be stored in Oracle’s U.S.-based cloud computing data centers, Chew wrote

- Shares were up 5% in after-hours trading in reaction to the news

- The new entity will also be tasked with retraining the video app’s content recommendation algorithm “on U.S. user data to ensure the content feed is free from outside manipulation”

- Former TikTok CEO Kevin Mayer said that he thinks “it is a good deal”

- It meets security regulations since ByteDance is under the 20% ownership threshold and Oracle is running the algorithm

- He has heard that the code is still owned by China and will be licensed to Oracle servers and retrained

- The training, housing and data used to train will all be housed and viewed in the US, which allows it to meet requirements

- ByteDance will also still be helping with the commercial operations such as ad sales and ecommerce, which “seems like a low security risk”

- “It is set up for success in the commercial aspect”

- The possible app redownload aspect will be a “non-issue” as it looks like a seamless approach

- When asked about the possibility of this company being sold again in the future, Kevin said “it is conceivable” but to get all the folks in line for future M&A is “relatively difficult and will probably operate as a joint venture for a long time”

- It meets security regulations since ByteDance is under the 20% ownership threshold and Oracle is running the algorithm

- This is NOT a surprise: In Sept, Trump signed an executive order approving a proposed deal that would keep TikTok operational in the U.S.

- Trump also said in Sept that Chinese President Xi Jinping agreed to move forward with the proposal

- Vance noted that there was “some resistance” from the Chinese govt to support the deal

- “We thank President Xi Jinping and President Donald J. Trump for their efforts to preserve TikTok in the United States,” ByteDance said at the time

Instagram For TVs Is Launching, Starting On Amazon

- Meta has intro’d Instagram for TV, marking the first time Instagram content has been specifically optimized for TV screens (link/link)

- The new app, available starting today on select Amazon Fire TV devices in the US, allows users to experience Instagram Reels on a larger display

- Reels are now organized into dedicated channels tailored to individual interests

- These channels cover a wide range of topics, including new music releases, sports highlights, travel discoveries, trending moments, and more

- The personalization comes from users’ existing Instagram activity

- Users can download the Instagram for TV app directly from the Amazon Appstore on compatible devices

- Supported models include the Fire TV Stick HD, Fire TV Stick 4K Plus, Fire TV Stick 4K Max (both first and second generations), Fire TV 2-Series, Fire TV 4-Series, and Fire TV Omni QLED Series

- The app allows up to five separate profiles, enabling each household member to maintain their own customized feed

- Future updates may include features like phone-based remote control, improved channel navigation, shared viewing feeds with friends, and better tools for following creators

- Reels displayed in the app align with PG-13-guidlines

- For younger users, safeguards mirror those on the main Instagram app, including restrictions on certain content, comments, and profiles

- Time spent in the TV app counts toward any existing teen account limits, with reminders for approaching usage thresholds or bedtime modes

YouTube TV Continues To Take Share Of TV Viewers With Strong Projected Adds In Q3, Though Down Y/Y

- YouTube TV is estimated have added ~750k subs in Q3, reaching a base of ~11mn (per sources) (link/link): Analysts attribute much of this growth to the timing of the quarter, which coincided with the start of the 2025 NFL season

- This is clearly strong but below last yr Q3’s 1mn adds estimate

-> Also related, the Academy annc’d that the Oscars will move to YouTube starting in 2029, marking the first time the ceremony will leave broadcast TV after more than 50 years on ABC. YouTube will stream the show live and free to its 2bn+ global users and surround it with extensive creator-driven content, including red carpet access, behind-the-scenes coverage, and year-round Oscars programming (link)

Key Trends W/ Bots, Internet Traffic, And Global Connectivity In 2025

Given the approaching year end, there are several reports that have come out, and we certainly had our pick of the lot.

The 2025 Cloudflare Radar Year in Review was another stand out report this week, offering an extremely detailed look at internet trends and patterns observed across its global network. While the report is very granular, we focused on global traffic growth, bot activity, infrastructure developments, emerging technologies, and a couple more adjacent topics.

Big picture, global internet traffic accelerated y/y, though top platforms largely held their positions. What stood out to us the most was the data on AI bots, which are increasingly crawling the web to train AI models. Other key highlights include Starlink’s substantial traffic growth, governments being the leading cause of major internet outages, Europe maintaining its position as a leader in internet speed and quality, and more.

Below we’ve highlighted the top 12 takeaways that we thought were most incremental. And if you would like to delve deeper into the detailed report, you can find it HERE, as well as the interactive version HERE.

See more below…

- Overall, global Internet traffic grew +19% y/y in 2025, an acceleration from +17% y/y in 2024

- Top 10 most popular internet services worldwide remained consistent with 2024 BUT there was some reshuffling

- Not surprisingly Google and Facebook retained their #1 and #2 spots, respectively

- Microsoft, Instagram, and YouTube all moved higher to #4, #5, and #7, respectively; Amazon Web Services (AWS) dropped one spot lower to #6, while TikTok fell four spots to #8

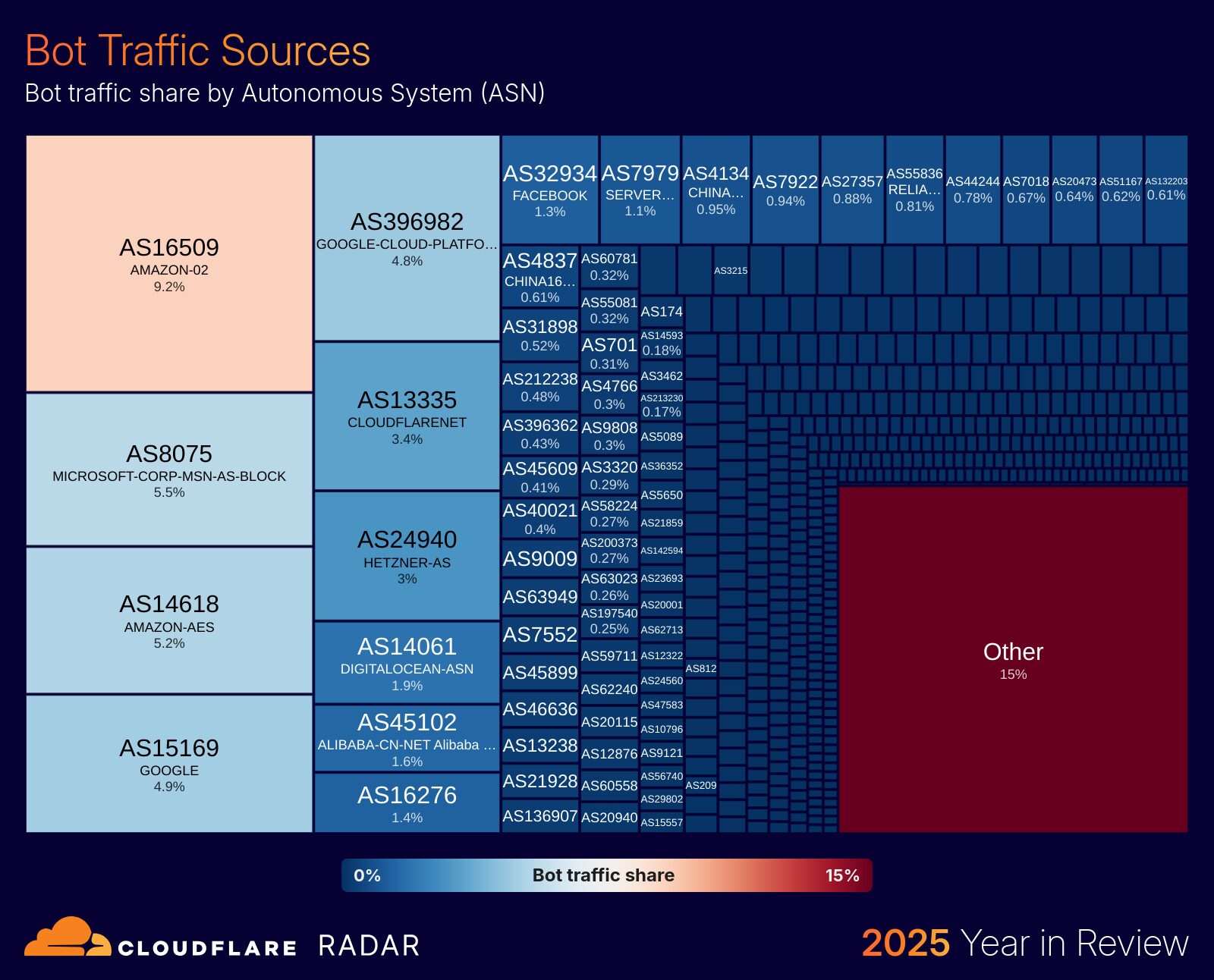

- AI bots made their presence felt this year, accounting for 4.2% of HTML request traffic as they crawl the web for content to be used in training models

- WHERE is bot traffic coming from? 40% of global bot traffic came from the US…

- This was followed by Germany at 6.5% and Singapore at 4.1%

- Globally, the top 10 countries/regions accounted for 71% of observed bot traffic

- …and Amazon Web Services, Google Cloud, and MSFT Azure originated ~30% of global bot traffic

- AWS accounted for a total of 14.4% of observed bot traffic

- Google Cloud was responsible for 9.7% of bot traffic

- Microsoft Azure originated 5.5% of bot traffic

- The remaining players all originated <3.5% each

- WHO is generating the traffic? Googlebot, which crawls for both search engine indexing and AI training, was the most active bot in 2025 and was responsible for over 28% of traffic from Verified Bots

- OpenAI’s GPTBot, which crawls content for AI training, was the next most active bot, originating about 7.5% of Verified Bot traffic

- Microsoft’s Bingbot, which crawls Web site content for search indexing and AI training, came in third and generated 6% of Verified Bot traffic throughout the year

- Anthropic had the highest crawl-to-refer ratio, while Perplexity had the lowest amongst the biggest AI and search platforms

- As a reminder, a crawl-to-refer ratio compares a bot’s page requests to the traffic it drives back

- A high ratios means lots of crawling but little referral traffic, while low ratios means crawling closely matches traffic sent

- Anthropic had the highest crawl-to-refer ratios, reaching as much as 500,000:1

- OpenAI’s ratios mainly sat around 1,500:1

- Perplexity had the lowest crawl-to-refer ratios of the major AI platforms, settling at ~200:1 from Sept onwards

- As a reminder, a crawl-to-refer ratio compares a bot’s page requests to the traffic it drives back

Source: Cloudflare Radar 2025 Year in Review

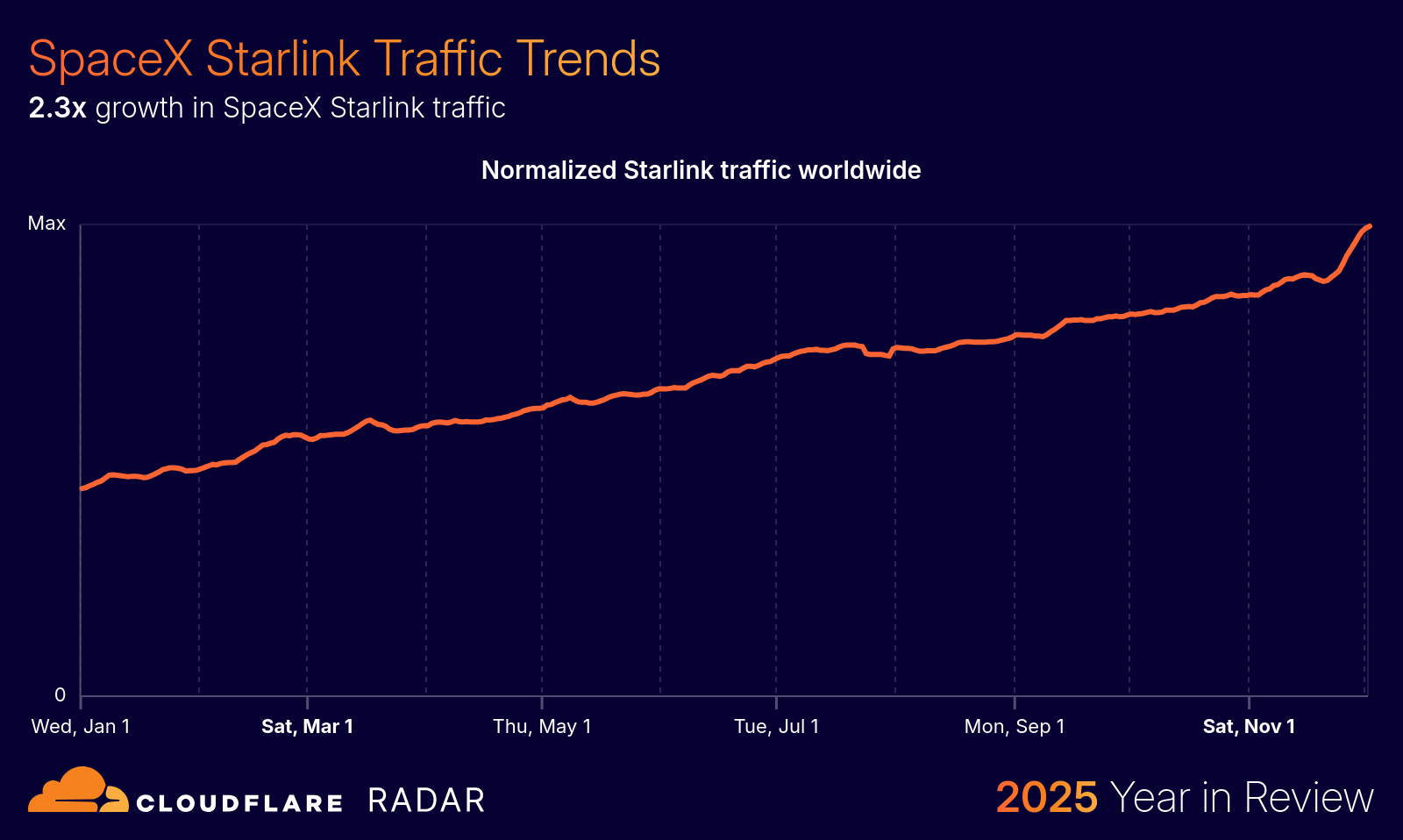

- Starlink traffic doubled in 2025, including traffic from 20+ new countries/regions

- Globally, traffic from Starlink continued to see consistent growth throughout 2025, with total request volume up 2.3x across the year

- Of countries/regions where service was active before 2025, Benin, Timor-Leste, and Botswana had some of the largest traffic growth, at 51x, 19x, and 16x respectively

Source: Cloudflare Radar 2025 Year in Review

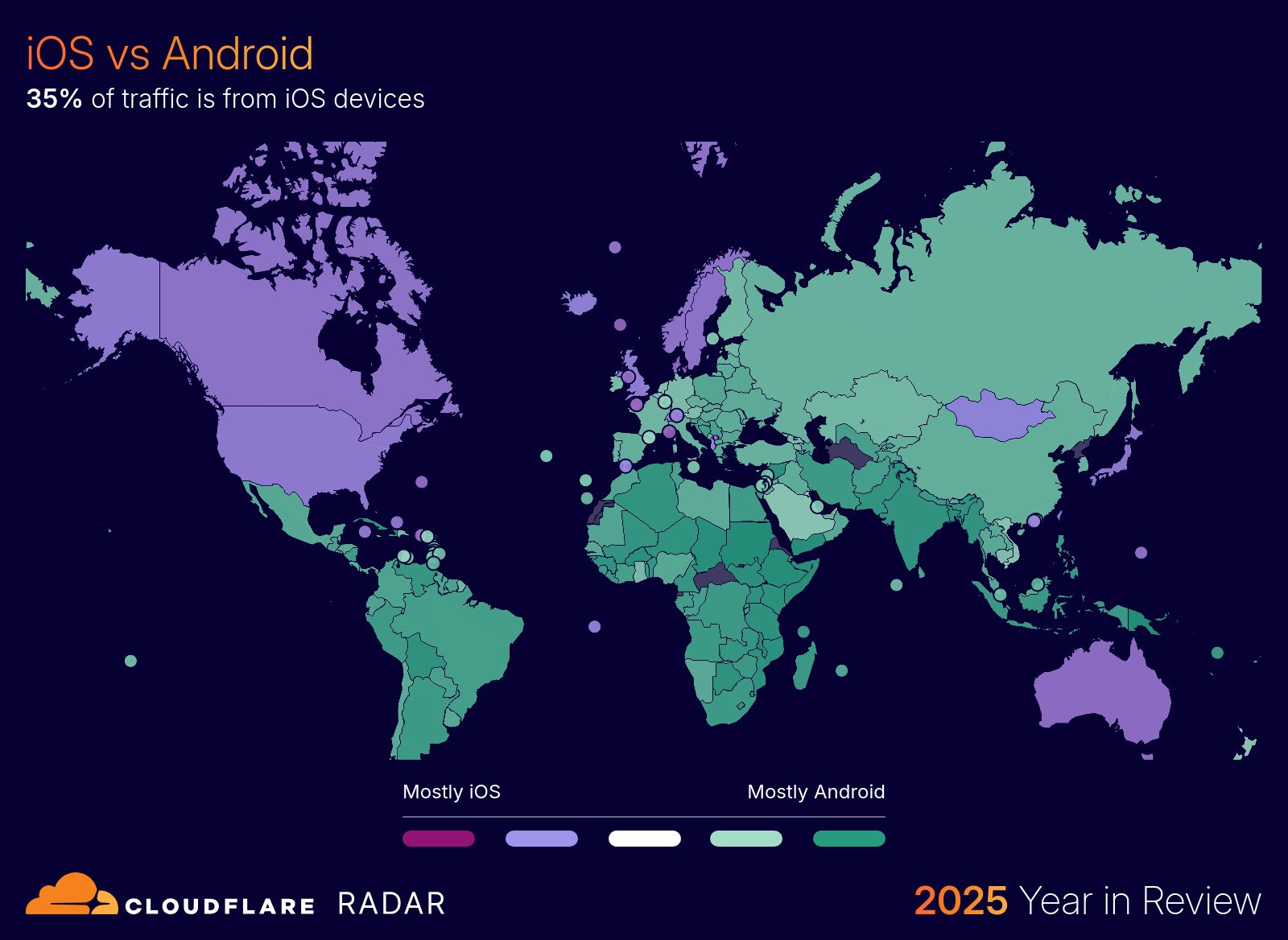

- iOS devices generated 35% of mobile device traffic globally (accel from 33% in 2024), and more than half of device traffic in many countries…

- iOS also drove 50% or more of mobile device traffic in a total of 30 countries/regions, including Denmark (65%), Japan (57%), and Puerto Rico (52%)

- …but Android continues to lead by a large margin at 65%

- Android was responsible for 50% or more of mobile device traffic in 175 countries/regions

Source: Cloudflare Radar 2025 Year in Review

- Governments lead as the top cause of major internet outages

- Nearly half of all major Internet disruptions observed globally were triggered by govt actions

- Outside of govt, outages caused by cable cuts dropped ~50%, but those linked to power failures doubled

- Europe leads the world in internet speed and quality

- For download: Spain, Hungary, Portugal, Denmark, Romania, and France were all in the top 10, with both Spain and Hungary averaging speeds above 300 Mbps

- Spain’s average grew by 25 Mbps from 2024, while Hungary’s jumped 46 Mbps

- For upload: Spain topped the list for the metric at 206 Mbps, up 13 Mbps from 2024

- For download: Spain, Hungary, Portugal, Denmark, Romania, and France were all in the top 10, with both Spain and Hungary averaging speeds above 300 Mbps

- Chrome remains the top browser across platforms and operating systems EXCEPT on iOS, where Safari has the largest share

- Globally, 66% of request traffic came from Chrome in 2025, similar to its share last yr

- Safari was the second most-popular browser (15.4% mkt shr), followed by Microsoft Edge (7.4%), Mozilla Firefox (3.7%) and Samsung Internet (2.3%)

- iOS – as the default browser on iOS, Safari is the most popular on those devices, with 79% mkt shr, four times Chrome’s 19% share

- < 1% of requests come from DuckDuckGo, Firefox, and QQ Browser (developed in China by Tencent)

- Android – in contrast, on Android, 85% of requests are from Chrome

- Samsung Internet is a distant second with a 6.6% share

- Windows – despite being the default browser on Windows, Edge’s 19% share pales in comparison to Chrome, which leads with a 69% share on that OS

- Globally, 66% of request traffic came from Chrome in 2025, similar to its share last yr

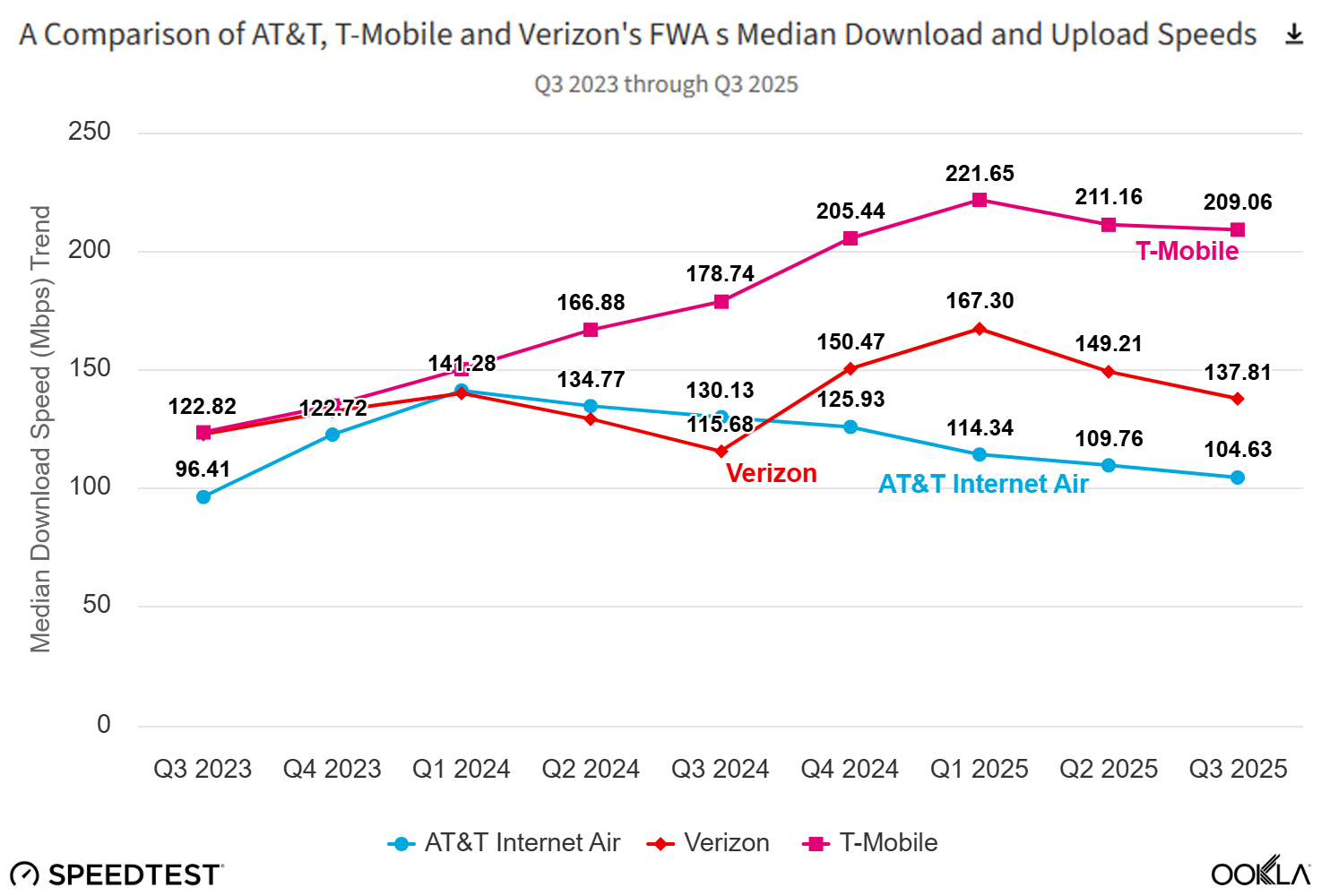

FWA Speeds For The Big 3 Telcos Have Been A Little Less Speedy So Far This Year

While innovation has been happening at breakneck speed across many parts of the TMT space, one area that has seen slower momentum and has been in a bit of “flux” is the connectivity sector (more on this theme in our LionTree Len’s deck that we just published HERE). In Ookla’s updated US FWA report this week, T-Mobile continues to lead the pack in FWA speeds, but all three of the big telcos saw declines in both download and upload speeds in Q2 and Q3 2025. Seasonal factors, such as trees at their leafiest, and potential network congestion may have contributed to these shifts.

There were also a few other key stats that we pulled out of the report around latency, urban vs rural FWA performance, and predictions on overall FWA sub additions for 2026. What we did find is that in addition to speed, T-Mobile remains at the top of the pack amongst the three with the lowest latency and the highest % of FWA users across suburban and rural that meet the FCC’s minimum 100/20 Mbps standard.

See the full report HERE and more on the above, below…

T-Mobile Remains The FWA Speed Leader…But All Three Providers Saw A Decline In Speed

- All 3 telcos experienced a decline in median DOWNLOAD speeds in Q2 and Q3 2025 (though T-Mobile maintained its FWA leadership position)

- T-Mobile’s median download speeds dipped from 221.65 Mbps in Q1 2025 to 209.06 Mbps in Q3 2025

- Verizon’s declined from 167.30 Mbps in Q1 2025 to 137.81 Mbps in Q3 2025

- AT&Ts dropped from 114.34 Mbps to 104.363 Mbps over the same period

- As well as a decline in median UPLOAD speeds

- T-Mobile’s median upload speed dropping from 24.03 Mbps in Q1 2025 to 15.49 Mbps in Q3 2025

- Verizon’s median upload speed declined from 15.23 Mbps in Q1 2025 to 11.40 Mbps in Q3 2025

- AT&Ts dropped from 13.13 Mbps to 9.25 Mbps during the same time

- What’s driving the fluctuations in speed? It could be seasonality or an indicator of network congestion

- Foliage reduces FWA speeds, especially in spring and summer (Q2 and Q3) when trees are the most leaf-dense, affecting mmWave most but also mid-band in tree-dense areas like suburbs and urban streets

- Network congestion may also impact FWA and mobile performance since both share 5G spectrum

Source: Ookla Research

Some Additional Quick Callouts On Latency, Urban Vs Rural FWA, And Overall FWA Sub Adds Expectations

- AT&T’s latency remains the highest amongst the 3 but has been trending down

- In Q3, AT&T’s median latency was 67 milliseconds (ms) compared to Verizon at 54 ms and T-Mobile at 50 ms.

- But AT&T’s latency has been improving every qtr from a high of 78 ms in Q3 2024

Source: Ookla Research

- Urban FWA users consistently outperform rural FWA users in meeting the FCC standard (min. 100/20 mbps speeds)…and the gap is most pronounced for VZ

- Verizon shows the largest urban–rural gap with 25.7% of urban users meeting the standard vs 14.7% of rural users

- T-Mobile FWA leads significantly in urban areas with 42% of users meeting the standard, almost double Verizon and AT&T

- In rural areas, T-Mobile also performs best at 26.9%

- Why the gap? Likely due in part to urban users having closer proximity to cell sites than rural users

Source: Ookla Research

- Analysts at New Street Research predict a slowdown in overall FWA sub additions in 2026 to around 3.6mn for the year, down from the 3.7-3.8mn/yr that the US has experienced over the past 3 yrs…

- New Street said it expects Verizon and T-Mobile’s subs adds to slow but AT&T’s will hold steady since it’s a newer entrant in the market

- … but did caveat that the FCC’s proposed auction of the upper C-band spectrum could provide addtl capacity for another +4mn FWA subs

- That C-band spectrum auction isn’t expected to occur until 2027 so the impact of this new spectrum may still be several years away

- As a reminder, both T-Mobile and Verizon have increased their long-term FWA targets

- T-Mobile predicts 12mn customers by 2028

- Verizon predicts 8-9mn FWA subs by 2028

Grab Bag: 24 Hour Trading? / Instacart & AI Pricing Inquiry / Coinbase Also Jumps Into Predictions Markets

- Nasdaq is planning to submit paperwork w/ the SEC to roll out nearly 24-hour trading, 5 days aa week (link/link): If approved, the new schedule would launch in H2 2026

- What is the new proposal?

- Nasdaq would expand trading hours to 23 hours each weekday from the current 16 hours

- Stocks would trade in a “day session” from 4 a.m. to 8 p.m. Eastern time, followed by a 1-hr pause for maintenance, testing and clearing

- A “night session” would then run from 9 p.m. to 4 a.m. the following morning

- But there was some backlash …

- “This is literally the worst thing in the world,” the Wells Fargo trading desk wrote in a note to clients. “I cannot think of an action that single-handedly gamifies the stock market even more than it has already become”

- Jay Woods, chief market strategist at Freedom Capital Markets and a former market maker, said “listed companies need a time to break and release news events and to have meetings where they’re not moving markets, and now we’re taking that away from them,”

- Although Nasdaq is not alone

- The NYSE is pursuing its own extended-hours model, with plans for 22 hours of weekday trading that won initial SEC approval in February, contingent on data-feed upgrades

- And… Robinhood, has already rolled out extended or near-24-hour trading for certain U.S. stocks and cryptocurrencies

- What is the new proposal?

- The U.S. FTC is reportedly probing Instacart as the retail platform faces criticism over its AI-driven pricing tool (link/link)

- What happened?

- The FTC has sent the Co a civil investigative demand, Reuters sources said

- They are seeking info about Instacart’s Eversight pricing tool

- The software allows retailers on Instacart to experiment with different prices using AI

- What was the study?

- It involved 437 shoppers viewing Instacart prices in 4 cities

- On avg, there was a 7% difference in the total cost for the same grocery list at the same store

- “Some shoppers found grocery prices that were ~23% higher than prices available to other shoppers for the exact same items, in the exact same store, at the exact same time,” the study’s authors wrote

- Grocers who use Eversight see revenue growth of 1-3%, according to Instacart’s website

- Instacart does not set prices for the items available on its platform, the Co said at the time

- Except for Target, retailers set the prices shoppers encounter, and Instacart provides the tools to do so

- Target is not affiliated with Instacart and does not control the prices it sets, a spokesperson said; Instead, Instacart scrapes publicly available Target prices and adds margin to cover its costs

- This is not the FTC’s first investigation into AI and data-driven pricing practices

- Last year, the FTC demanded info from Mastercard, JPMorgan Chase, Accenture, McKinsey & Co., and 4 other Cos about tools they sell to other biz to analyze data and set prices or tailor discounts

- What happened?

-> Instacart shares were down -10% in after-hours trading

- Coinbase is expanding into stocks, more sophisticated trading tools, and prediction markets, as part of a broader “single app” play (link/link)

- While many of these offerings have been telegraphed for months, Coinbase says the products are now built, and ready to go

- These new updates include:

- Stock Trading & Tokenization

- They rolled out stock trading to Coinbase users in the US

- You will now be able to buy, sell, and manage leading stocks and ETFs alongside your crypto portfolios, with USD or USDC, all within one Coinbase app and account

- With tokenized stocks, you’ll be able to trade 24/7 anywhere in the world, use the stocks you own on chain, and even make instant payments

- Prediction Markets

- They rolled out access to prediction markets on Coinbase in the US

- You will soon be able to trade on the outcomes of real-world events with prices of the event contracts determined by the collective trading activity of market participants

- All market flow will come from Kalshi at launch

- Futures & Perpetual Futures Trading

- Allows users of the app to trade futures and perpetual futures in the US

- Solana DEX Trading

- They are expanding their DEX trading integration to include access to Solana tokens

- Coinbase Business

- Available to all eligible businesses in the U.S. and Singapore

- They are empowering users to send and receive payments globally with payment links and invoices, manage crypto assets via Coinbase Advanced, earn rewards on USDC they hold, and automate financial workflows with access to Coinbase’s regulated infrastructure

- Coinbase Advisor

- Users can simply tell the AI their goals and questions – “Build me a portfolio,” “What’s the latest market news and how does it impact me?” – and get a personalized answer with recommendations powered by the products, data, and tools available on Coinbase

- And the new Base App that turns “scrolling into earning”

- Officially available in 140+ countries

- It brings social, trading, payments, app discovery, and earning into one place

- Content in the Base App is tokenized and tradeable and value is set in an open market, which means your posts and creativity can become real assets you control

-> Coinbase shares were up +1.5% in after-hours trading

Stock Market Check

This Week's Other Curated News

Artificial Intelligence/Machine Learning

- Meta is prepping next-gen AI models—image/video-focused “Mango” and text-based “Avocado”—to rival OpenAI & Google. Launch set for H1 2026, marking a shift beyond Llama. Effort led by CEO Zuckerberg & Chief AI Officer Wang after $14bn Scale AI stake. Avocado targets advanced coding; Meta also exploring “world models” for physical reality. (Yahoo Finance)

- GPT‑ 2-Codex is OpenAI’s most advanced agentic coding model for real-world SWE and defensive cybersecurity. It improves long-horizon coding, large refactors, Windows support, and vision for UI mocks. Stronger cyber capabilities enable faster vulnerability research, as seen in recent React disclosures. (OpenAI)

- DOE annc’d agreements w/24 orgs to advance Genesis Mission, a national AI effort to boost discovery science, strengthen security & drive energy innovation. Backed by Trump’s AI Action Plan, the initiative unites cos, academia & labs to build scalable AI infra for R&D. (U.S. Department of Energy)

- Amazon’s Alexa Plus now has a web interface live for some users, offering features like smart home control, calendar, lists, reminders, and file uploads. Menus include prompts for planning trips, creating study guides, and shopping. This move aims to integrate Alexa into daily workflows and compete w/ AI rivals. (The Verge)

- Gemini annc’d Gemini 3 Flash, delivering frontier intelligence w/ speed, efficiency & low cost. Built on Gemini 3’s reasoning, it’s 3x faster than 2.5 Pro, uses 30% fewer tokens, and excels in multimodal tasks. Rolling out globally via Gemini app, AI Mode in Search, and for enterprises on Vertex AI. Pricing: $0.50/1M input tokens, $3/1M output tokens. (Google)

- Apple delayed its major Siri AI upgrade to 2026 after annc’d plans for 2025, aiming for a “10/10” launch. While rivals like Google, Microsoft, and Meta surged ahead in AI, Apple focused on iPhone 17 success and modest AI features via Apple Intelligence. (CNBC)

- Google annc’d “TorchTPU” to boost TPU compatibility w/ PyTorch, aiming to erode Nvidia’s CUDA edge in AI mkts. TPUs, key to Google Cloud rev, face adoption hurdles due to Jax reliance. Partnering w/ Meta, Google plans open-source elements to cut switching costs. Move follows rising demand for AI infra, w/ TPUs now sold beyond Google Cloud. (Reuters)

- China secretly built a prototype EUV lithography machine in Shenzhen, completed early 2025, aiming for chip production by 2028 though insiders expect 2030. The project, led by ex-ASML engineers and Huawei, mirrors a “Manhattan Project” for semiconductor independence. Despite progress, challenges remain in optics and precision parts. (Reuters)

- OpenAI, Google & Perplexity are battling for AI users in India w/ freebies to harvest multilingual data. India, w/ 730mn smartphones & low data rates, is key for AI training. ChatGPT daily users surged 607% YoY to 73mn, Gemini hit 17mn; both surpass U.S. usage. Google offers $400 Gemini Pro free for 18 mos to Jio users; OpenAI’s ChatGPT Go free for 1 yr; Perplexity’s $200 Pro free via Airtel. (Reuters)

- DoorDash annc’d Zesty, an AI-driven app for local restaurant discovery, now in beta in SF Bay Area & NY. Users can enter prompts for tailored suggestions, view/share photos & comments, and follow others. Zesty pulls data from DoorDash, Google Maps, TikTok & more, adding social-network-style features. (Yahoo Tech)

- OpenAI struck a landmark deal w/ Walt Disney Co to license 200+ iconic characters for its Sora video app, using stock warrants instead of cash. Disney also annc’d a $1bn stake in OpenAI at a $500bn valuation, marking the largest equity investment by a major studio in an AI model maker. (Yahoo Finance)

- OpenAI annc’d removal of its vesting cliff, letting new hires access equity immediately, aiming to boost talent retention amid fierce AI hiring wars. Earlier, it cut the cliff to 6 mos from the 12-mo norm. Rival xAI made similar changes after facing recruiting hurdles. (MSN)

- Tether, issuer of USDT, annc’d plans to acquire Juventus FC by buying Exor’s 65% stake in an all-cash deal and later making a public offer for remaining shares. Juventus has a $925mn mkt cap; Tether aims to invest $1bn post-acquisition. The Co posted >$10bn net profit this yr, holds $188bn USDT mkt cap and 116 tons of gold. (CoinDesk)

Audio/Music/Podcast

- Podcasts surged on YouTube in 2025, w/ living room viewership hitting 700mn hrs in Oct. up from 400mn last yr. To support this, YouTube updated its TV interface w/ Creator Shows & annc’d 1bn monthly active podcast viewers. A new US Podcast chart launched to boost discovery. (YouTube)

- Spotify annc’d a major milestone in Korea by partnering w/ NAVER Corp to integrate music features across NAVER’s platform, incl Search, Maps, and NAVER+ Membership. NAVER Maps now supports Spotify playback, while NAVER+ members get Spotify Premium Basic at no extra cost, offering ad-free listening and better audio. (Spotify)

Broadcast/Cable Networks

- DirecTV’s antitrust suit vs Nexstar was revived by the 2nd U.S. Circuit, reversing a prior dismissal. DirecTV alleges Nexstar, Mission & White Knight schemed to inflate retransmission fees, harming competition. DirecTV claims lost profits & ~1mn subscribers after refusing high rates. Nexstar disputes ruling, vows to cont’d fight. (Reuters)

- Sinclair Inc annc’d disappointment over Scripps’ rejection of its merger proposal despite prior encouragement. Sinclair claims the offer provides strategic, financial benefits and a substantial premium over Scripps’ share price, urging engagement for fair evaluation. (Sinclair)

Cable/Pay-TV/Wireless

- Optimum (NYSE: OPTU) cont’d its stance against TEGNA’s 30% hike on major networks and 50% on CW, calling demands egregious and tied to a looming Nexstar merger. Optimum argues these rates ignore mkts reality, inflate bills, and limit choice. (Optimum)

- Lawmakers raised concerns over EchoStar’s deals to sell spectrum to AT&T ($23bn) and SpaceX ($17bn), warning it may cut competition in wireless & satellite mkts. They urged FCC & DOJ for robust review, citing risks of consolidation harming consumers w/ higher costs & less innovation. (Reuters)

- US pay-TV posted its first sub gain in 8 yrs, adding 303K in Q3 2025 per MoffettNathanson. Total subs hit 64.77mn as losses slowed (-5.8% vs -6.4%). Traditional cos still lost 1.12mn, but vMVPDs added 1.42mn, led by YouTube TV (+750K). Gains tied to NFL season may reverse in early 2026. (Light Reading)

- Verizon annc’d a multi-yr partnership w/ Array Digital Infrastructure to boost 5G flexibility & customer experience. Deal enables Verizon to collocate on Array’s 4,400 towers nationwide, streamlining pricing for cost efficiency & long-term stability. Execs highlight enhanced agility for advanced wireless tech deployment. (Verizon)

- Liberty Global annc’d sale of UPC Slovakia to O2 Slovakia (e&PPF Telecom) for ~€95mn ($110mn), valuing UPC at ~7x 2025 adj EBITDA. Deal subject to regulatory approval. UPC serves 600K+ households in 80 cities w/ speeds up to 2.5Gbps. (Liberty Global)

- AT&T, T-Mobile & Verizon’s wireless war has escalated. T-Mobile’s “Easy Switch” tool, launched to lure rivals’ customers, sparked AT&T’s lawsuit alleging system intrusion & data harvesting. Verizon’s “Bring Your Bill” promo also targets AT&T/T-Mobile users. NAD disputes over deceptive ads add fuel, w/ AT&T suing BBB National Programs. (The Wall Street Journal)

- Orange annc’d a binding deal w/ Lorca to acquire the remaining 50% stake in MasOrange for €4. 25bn cash, gaining full ownership of Spain’s leading operator by customer base. The move, aligned w/ Orange’s “Lead the Future” plan, strengthens its position in Spain—its 2nd-largest mkt in Europe. (Orange)

- KPN & trade unions reached a CAO deal effective Jan 1, 2026 for 18 months. Includes 5% salary hike (3% Feb. 2026, 0.5% Oct., 1.5% Jan. 2027) + €500 bonus Jul. 2026. Offers €1,000/yr childcare aid, €2,000/yr student debt repayment, home sustainability support, flexible leave, caregiving benefits, reservist options, inclusive holidays, and new training for tech & soft skills. (KPN)

Cloud/DataCenters/IT Infrastructure

- Telefónica Tech cont’d its leadership in Spanish IoT mkts, reaching 17mn lines by Nov. , up 240% YoY from 5.018mn in 2024. Growth driven by V16 connected beacons, mandatory from Jan., and digitisation in health, industry, water & gas. Movistar beacon sales rose 52% on Black Friday. (Telefónica)

- Oilfield svs cos like Baker Hughes, Halliburton & SLB are pivoting to the fast-growing data centre biz as drilling demand weakens. They’re leveraging expertise to supply gas turbines, power gen systems, batteries & cooling tech. W/ data centres seeking alt power sources beyond grids, these cos also design & maintain energy-efficient systems, snapping up related businesses to expand in this sector. (Financial Times)

- Databricks annc’d a $4bn Series L raise, valuing the Co at $134bn, up 34% from summer. Rev run rate hit $4.8bn in Oct., +55% YoY, w/ its AI-ready data platform driving growth. Funding led by Insight Partners, Fidelity & J.P. Morgan; cash to boost core data-analytics, AI svs, and hiring thousands globally incl. 600 grads next yr. (The Wall Street Journal)

Cybersecurity/Security

- ServiceNow is in advanced talks to acquire cybersecurity startup Armis for up to $7bn, marking its largest deal yet. Armis, founded by Israeli cyber intelligence veterans, posted ~$300mn annual recurring rev and targets a 2026 IPO. ServiceNow, valued at ~$179.5bn, seeks to expand AI and security offerings, following peers like Alphabet and Palo Alto Networks in embedding cybersecurity into enterprise tech platforms. (MSN)

eCommerce/Social Commerce/Retail

- Nike posted Q2 rev of $12.43bn, beating estimates, but net income fell 32% YoY. Sales in China dropped 17% for the 6th straight quarter. Tariffs from SE Asia added $1.5bn in costs. Gross margin slid 300 bps, w/ further decline expected. CEO Hill said recovery is “middle innings,” focusing on core sports, retail ties, and new lines like NikeSKIMS. (Reuters)

- Holiday returns fell 2.5% from Nov. 2–Dec. 12, w/ a slight 0.1% drop post-Cyber Week, per Adobe. Mobile drove 42.4% of spend vs. 39.1% of returns. Consumers spent $187.3bn (+6.1% YoY) so far; full-yr online spend projected >$250bn (+5.3%). BNPL hit $13.9bn (+6%). (MediaPost)

- NRF annc’d a record ~158.9mn consumers expected to shop on Super Saturday, up from 158.5mn in 2022. Survey of 8,005 adults (Dec. 1–10) shows 63% plan to shop; 45% both online & in-store, 29% in-store only. Top spots: e-commerce, dept. stores, discount retailers. 31% gifting experiences vs. 22% in 2015. (Retail Dive)

- Apparel sales rebounded in 2025 despite tariffs and consumer anxiety, rising monthly through Oct. except Feb., per U.S. Commerce Dept. Q3 results from Gap, Urban Outfitters, Abercrombie & Fitch Co., and American Eagle beat expectations, aided by strong social media campaigns (e.g., Gap’s denim ad, AE’s celeb collabs). (Retail Dive)

- Walmart’s latest earnings call highlights a major shift: affluent households now drive growth, w/ ~75% of share gains from those earning $100k+. Sam’s Club memberships rose 9%, and online sales in toys, electronics, apparel grew 40% YoY. Fashion, home, and wellness posted strong gains. (Quartz)

- Retail sales for Oct hit $265.75B, up 6.2% YoY; e-commerce surged 9%. All categories posted gains: apparel +6.3%, electronics +5.4%, sporting goods +5.7%, home goods +0.7%. Dept. stores spiked 7.4%, partly inflation-driven. Analysts warn momentum may slow amid job mkts moderation and price pressures. (Retail Dive)

EdTech

- Coursera & Udemy annc’d an all-stock merger, creating a leading AI-driven skills platform. Combined Co aims for >$1.5bn annual rev & $115mn cost synergies w/in 24 mos. Udemy holders get 0.800 Coursera shares per share (26% premium); equity value ~$2.5bn. Closing expected 2H 2026, pending approvals. (Coursera)

Electric & Autonomous Vehicles

- Rivian annc’d update 2025. 46, expanding Universal Hands-Free from 135k to 3.5mn miles across U.S. & Canada, now usable on/off highways. Adds Autonomy Drive Styles—Mild, Medium, Spicy—for personalized assist behavior. Enhances Autonomy View, speed control via thumbwheel. Launches Rivian Digital Key for iPhone, Pixel, Samsung, enabling wallet-based access. (Rivian)

- NTT plans to deploy 1,000+ autonomous buses & vehicles across Japan by the 2030s to tackle driver shortages and expand automated transport svs nationwide, Nikkei reports. The Co formed a wholly owned unit, NTT Mobility, to manage deployment and operations of self-driving fleets in collaboration w/ local govts and transport operators. (Telecompaper)

- Waymo, Alphabet’s autonomous driving unit, is in talks to raise >$15bn at a valuation near $100bn, per Bloomberg. The round, involving external investors and Alphabet, could hit $110bn. This marks a sharp rise from Oct. 2024’s $45bn valuation. Waymo leads U.S. robotaxi mkts, surpassing rivals like Tesla w/ more driverless miles, paying customers, and permits. (Yahoo Finance)

- China’s industry regulator annc’d approval of two level-3 autonomous EV sedans from state-owned cos Changan Auto and BAIC BluePark, marking the first national clearance for mass adoption. The models can operate w/ conditional autonomy in Chongqing (50km/h) and Beijing (80km/h) via ride-hailing trials. (Reuters)

- Tesla annc’d driverless Robotaxi tests in Austin, nearly 6 mos after launching a limited ridehail svc w/ safety drivers. Fleet of ~30 cars may double to 60 by end-2025. Musk posted “testing underway w/ no occupants.” Shares closed at $475.31, up 18% YTD. Texas allows AV tests under traffic laws; stricter rules start May 28, 2026. (CNBC)

Film/Studio/Content/IP/Talent

- Sony Music Entertainment Japan (SMEJ), Sony Pictures Entertainment (SPE) & WildBrain annc’d a definitive agreement for SMEJ & SPE to acquire WildBrain’s ~41% stake in Peanuts Holdings LLC. Post-deal, SMEJ & SPE will own 80%, Schulz family retains 20%. SMEJ will lead mgmt w/ SPE. Goal: expand “PEANUTS” IP biz leveraging Sony Group’s global network. (Sony Pictures)

- FreeWheel annc’d an exclusive partnership w/ Lionsgate to serve ads across its U. FAST channels, giving buyers direct or programmatic access via FreeWheel SSP. Lionsgate’s portfolio includes MovieSphere and 50 Cent Action, leveraging its vast film/TV library. The deal aims to unify ad decisions, boost rev, and scale premium streaming. (Business Wire)

- Cinema United’s annual report hows Gen Z defied trends w/ a 25% rise in theater visits in 2025. 41% saw films ≥6 times vs 31% in 2024; avg attendance hit 6.1 vs 4.9 last yr. Hits like “Minecraft Movie,” “Demon Slayer,” & “FNAF 2” drove under-30 crowds. (Yahoo)

FinTech/InsurTech/Payments

- PayPal annc’d plans to establish PayPal Bank, a Utah-chartered industrial loan co, filing apps w/ Utah regulators & FDIC. The bank aims to expand access to svs for U.S. small biz, offering lending solutions & interest-bearing savings accounts, plus FDIC-insured deposits. Since 2013, PayPal has provided ~$30bn in loans to 420,000 biz accounts. (PayPal)

Handheld Devices & Accessories/Connected Home

- True Digital Group annc’d a strategic collab w/ VNPT Tech & T3 Tech to build AI Home ecosystem in Vietnam. The partnership focuses on AI Home platform, devices, and biz model innovation, integrating AI solutions w/ broadband & TV svs. True Digital leverages TrueX experience (2.2M downloads, 800K MAUs) to expand into Vietnam’s fast-growing digital economy, aiming for smarter, safer, and more convenient living for millions of households. (True )

Last Mile Transportation/Delivery

- FedEx CEO Raj Subramaniam told CNBC that FedEx is “the heartbeat of the industrial economy,” citing strong B2B biz, which drives 66% of rev. FedEx beat on top/bottom lines and raised its full-yr forecast after earnings, w/ shares up 2% post-market. Growth seen in healthcare, aerospace, defense, and AI-driven data centers. (CNBC)

Macro Updates

- Economists questioned the delayed Nov. CPI report showing 2.7% headline and 2.6% core inflation, both below est. (3.1%, 3%). Skepticism stems from BLS methodology, esp. OER calc, where some prices may have been set to zero, creating downward bias. Shutdown-related quirks and holiday discounting added noise. (CNBC)

- U.S. CPI likely rose 3.1% YoY in Nov., the biggest gain since May 2024, amid tariff-driven price hikes, per economists. Govt shutdown halted Oct. data collection, so only YoY CPI/core CPI will be published. Tariffs passed to consumers (~40% by Sept., seen at 70% by Mar.), hitting low-income households hardest. Fed cut rates to 3.50%-3.75% but sees limited further easing. (Reuters)

- U.S. Trade Rep Jamieson Greer signaled support for keeping CUSMA intact during closed-door briefings, despite Trump hinting at letting it lapse or splitting into two deals. The accord faces a mandatory review as it nears its 6th yr, allowing signatories to extend, revise or end it. Lawmakers viewed hearings as positive, noting potential revisions for state industries. (Financial Post)

- Amazon is set to lay off 370 staff at its European HQ in Luxembourg, ~8. 5% of workforce, down from 470 initially planned due to EU rules requiring talks w/ employee reps. Cuts mainly hit software developers as tech shifts to AI. Amazon annc’d in Oct. plans to cut 14,000 jobs globally amid AI adoption. Despite layoffs, Co remains 5th-largest employer in Luxembourg. (Engadget)

- McKinsey & Co plans major layoffs amid a consulting slowdown, targeting ~10% headcount reduction. Leadership cites declining demand for advisory svs as clients curb spending. Cuts may impact thousands globally, marking one of the firm’s largest workforce adjustments in yrs. The move reflects broader mkts pressure on biz models reliant on discretionary corporate rev. (Financial Post)

Media Conglomerates

- CNBC spoke w/16 media execs for 2026 predictions: major M&A bets incl. Paramount buying WBD, Apple or Amazon acquiring NBCU assets, and Comcast possibly buying Roku. Sports forecasts: NFL to extend media deals, Amazon to grab intl. NFL rights, March Madness & CFP to expand. (CNBC)

Metaverse/AR & VR

- Apple’s Vision Pro, priced at $3,500, is evolving beyond hardware updates w/ immersive content creation. At an Oct. Cupertino event, Apple shared best practices for devs and filmmakers, boosting momentum over the past 12–18 mos. (Fast Company)

Online Marketplaces/Learning (Real Estate/Education/Jobs)

- Airbnb’s bid to ease NYC short-term rental rules failed as the bill didn’t make the council’s final voting agenda. The proposal, opposed by hotel union, aimed to let single-/two-family homeowners rent primary residences w/o being present and raise guest limit to 4. (Bloomberg)

Regulatory

- Brendan Carr told senators the FCC is “not an independent agency,” after the term was removed from its mission statement, sparking fears of Trump’s power-grab since his Jan. Carr, a Trump ally, faced criticism for allegedly threatening TV networks over satire, citing vague “public interest” rules. (The Guardian)

- FTC has annc’d a probe into Instacart’s AI-driven Eversight pricing tool after a study showed shoppers paid up to 23% more for identical items. Shares fell ~10%. The tool lets retailers run price tests, boosting rev by 1–3%. Critics, incl. Sen. Schumer, demand transparency. FTC seeks info via civil demand; investigation doesn’t confirm wrongdoing. (Reuters)

- US Trade Rep warned retaliation vs EU over “discriminatory” lawsuits, taxes, fines under DSA hitting US tech giants incl Google, Apple, Amazon, Microsoft, Meta; X fined $140mn earlier this mo. Post named EU cos like SAP, Siemens, Spotify. Threat cites US law allowing fees/restrictions on foreign svs if cont’d. (The Verge)

Satellite/Space

- SpaceX plans a blockbuster IPO, targeting an $800bn valuation, potentially joining the trillion-dollar club if mkts respond strongly. Elon Musk’s rocket & satellite biz could reshape tech and finance landscapes. The move, signals cont’d investor appetite for space ventures amid growing global interest in innovation and infrastructure. (The New York Times)

Social/Digital Media

- Meta is testing a limit on link posts for Facebook professional mode and Pages. Users can post only 2 links unless subscribed to Meta Verified at $14.99/month. Affiliate links, comments, and Meta platform links remain allowed. Publishers excluded. Test aims to add value for subscribers as 98% U.S. feed views lack links. (TechCrunch)

- Meta tolerated high levels of ad fraud from China to protect billions in rev. Internal docs show ~19% of its $18.4bn China ad biz in 2024 came from scams, illegal gambling & banned svs. After a brief crackdown cut fraud to 9%, Meta pivoted, disbanded its anti-fraud team & lifted restrictions, letting violations rebound to 16% by mid-2025. (Reuters)

Software

- Accenture beat Q1 rev estimates at $18.74bn vs $18.52bn forecast, driven by strong AI svs demand. CEO Julie Sweet highlighted $21bn in new bookings, incl. 33 clients >$100mn. Co partnered w/ Anthropic & OpenAI to upskill staff. Despite uneven public sector demand, it forecast Q2 rev of $17.35–$18bn, slightly below analyst midpoint. (Reuters)

- Apple annc’d it will allow alt app stores in Japan and enable devs to process payments outside its system to comply w/ MSCA. Similar to EU’s DMA and U.S. court rulings, these changes impact App Store rev. Apple warns of malware risks, introducing “Notarization” for security. Epic Games criticized Apple’s 21% fee on 3rd-party purchases. (TechCrunch)

Sports/Sports Betting

- ESPN annc’d MNF Playbook w/ Next Gen Stats, for 49ers-Colts on ESPN2 & App. This alt telecast uses TruPlay AI for real-time predictive analytics, advanced metrics & live probabilities. Runs through ESPN’s Divisional Round, w/ 5 games total. Luke Kuechly, Dan Orlovsky & Field Yates lead early editions; rotating cos join later. (ESPN)

- NFL viewership hit a 35-yr high through Week 14, avg 18. 7mn per telecast window, per Nielsen & Adobe. Up 7% YoY, 8% vs 2023, aided by out-of-home tracking & new data methods combining smart TVs, set-top boxes, and provider data. FOX’s Packers-Bears drew 27.94mn, NBC SNF hit 24.2mn w/ streaming, MNF at 20.4mn. (Yahoo Sports)

- FanDuel Sports Network, formerly Bally Sports, annc’d cost-cutting changes to pre/postgame coverage. NBA & NHL shifts to on-site productions now extend to MLB, reducing studio costs. Cardinals’ home games keep full crew; road games combine host/reporter roles, trimming staff. Alexa Datt takes expanded duties; Jim Hayes focuses on home contests. (Cord Cutters News)

- DAZN is in advanced talks to acquire a majority stake in Main Street Sports Group, a major U. S. regional sports broadcaster. A deal could be annc’d as soon as Jan. if talks don’t hit snags. DAZN plans a sizable cash investment and aims to integrate both live-sports platforms. Exact terms remain undisclosed. (The Wall Street Journal)

- Big 12 is close to a deal w/ RedBird & Weatherford for a strategic biz partnership, offering up to $500mn in capital to member schools via credit lines (~$30mn each) at reduced rates. No equity will be given up. The pact aims to boost rev streams, create new biz ops, and professionalize the league office. (Yahoo Sports)

Tech Hardware

- Micron annc’d upbeat Q2 forecast citing AI-driven memory demand. Rev projected at $18.3–$19.1bn vs est. $14.4bn; adj EPS $8.22–$8.62. Shares rose 10%, up 168% YTD. CEO Mehrotra called Micron an “essential AI enabler,” investing $20bn this yr to boost supply amid shortages. Q1 rev jumped 57% to $13.6bn. (MSN)

Video Games/Interactive Entertainment

- Riot Games annc’d a major overhaul of League of Legends, dubbed League Next, set for 2027. Update will revamp visuals, UI, and tech to ease updates and attract new players. Riot is reorganizing staff and improving new-player experience. Despite ~100mn monthly users, player base declined; Valorant earns more. (Bloomberg)

- Kick annc’d an Xbox app, sparking controversy due to its gambling ties and lax moderation. Xbox clarified no official partnership; the app was self-published and under review for policy compliance. Kick, linked to Stake, hosts banned Twitch streamers and high-profile creators like xQc, Nickmercs, and Amouranth. (Kotaku)

- Spending on video game hardware in Nov. hit $695mn, down 27% YoY — lowest since 2005, per Circana. Unit sales were 1.6mn, lowest since 1995. Price hikes pushed avg. hardware cost to $439 (+11% vs. 2024). PS5 led in units & dollars; Switch 2 ranked 2nd, Nex Playground 3rd in units, Xbox Series 3rd in dollars. (The Verge)

- Amazon Luna cloud gaming svc launched on Comcast’s X1 & Xumo Stream Box in US; Rogers users in Canada also gain access. Prime members get 50+ AAA & family titles at no extra cost, incl. “Hogwarts Legacy” & “Indiana Jones.” Luna redesigned for ease, playable w/ mobile phones. (Variety)

- Ubisoft annc’d acquisition of March of Giants from Amazon’s Montreal Games studio. The free-to-play 4v4 MOBA blends real-time strategy w/ lane combat, featuring giant heroes and Battleworks like tanks, turrets, and bunkers. Led by ex-Ubisoft veterans Alex Parizeau and Xavier Marquis, dev team aims to elevate the title’s potential under Ubisoft, following a successful closed alpha milestone. (Ubisoft)

Video Streaming

- Netflix annc’d ESPN’s Elle Duncan as its first sports anchor, marking a major shift for the streamer now holding NFL, MLB, WWE & Women’s World Cup rights. Duncan, known for “SportsCenter” & “College GameDay,” signed a multiyr deal to host sports & cultural live events. Her debut in early 2026 will be “Skyscraper Live,” featuring Alex Honnold’s climb of Taipei 101. (Variety)

- Netflix annc’d a reimagined FIFA football game for its Games platform ahead of FIFA World Cup 2026. Developed by Delphi Interactive, the game offers fast, accessible play for solo or online modes using phones as controllers. Free for Netflix members, it aims to bring football back to its roots and reach billions globally. (Netflix Tudum)

- Netflix annc’d a multi-yr deal w/ Barstool Sports to stream video versions of top podcasts — Pardon My Take, The Ryen Russillo Podcast, and Spittin’ Chiclets — exclusively on its platform starting early 2026. Audio remains on all major platforms. Launch begins in U.S., more mkts to follow. (Netflix Tudum)