It is hard to believe that we are approaching the last two weeks of the year, especially with the still high level of news flow and strategic actions! There was a lot to think about this week on that front.

Meantime, the major indices were flattish to down, especially small cap laden Russell 2000, which was down -2.6%. Looking ahead, next week’s FOMC meeting is the key event, with the market now pricing in almost a 100% probability of a -25bp rate cut following November CPI numbers, which came in-line with expectations.

- **A Technology Breakthrough**… Google Unveils It’s “Willow” Quantum Chip

- OMC + IPG: Long -Awaited Consolidation Finally Arrives For Ad Agencies But With Some Concerns

- Is WBD Setting The Stage For A Spin Or Sale Of Assets?

- Connectivity Providers See A Choppy Finish To 2024

- Gen AI Release Palooza… OpenAI’s Sora, Google’s Gemini 2.0, and Microsoft’s Phi-4

- Global Internet Traffic Growth Remains Strong But Decelerated From 2023

- The Growth Of The Advertising Industry Continues To Defy Expectations Of A Slowdown

- Grab Bag: AVs Hit A Road Bump / Amazon Auto Launches / YT Reached 1Bn TV Hours In 2024

Have a nice weekend.

Best,

Leslie

**A Technology Breakthrough**… Google Unveils It’s “Willow” Quantum Chip

While all the focus has been on gen AI (see Theme #5 for a whole host of updates out this week), Google shifted the focus this week in many regards by introducing a new quantum chip that “paves the way to a useful, large-scale quantum computer” that can perform practical, real-world computations that traditional computers cannot. The chip, called Willow, needed less than five minutes to perform a mathematical calculation that one of the world’s most powerful supercomputers could not complete in 10 septillion years, a length of time that exceeds the age of the known universe!

Quantum computing is still in its experimental stages but continues to develop as researchers address key challenges. Unlike classical computers, which process information in binary bits of 1s and 0s, quantum computers use qubits which use 1s, 0s, and both at the same time and can store and process more complex information due to their ability to represent a wider range of values.

However, the fragility of qubits has posed challenges, as errors frequently disrupt calculations. Google’s recent work has surpassed the “error correction threshold,” which is a critical milestone in improving the reliability of these systems. While practical applications of quantum computing remain in development, Google’s new chip is viewed as a huge step toward being able to supercharge artificial intelligence innovation and creating broad usability. (link/link/link)

See below for more.

-> Google closed up +4% on the day of the announcement (reaching its highest point since July) and ended the week up +8.4%

-

- Willow performed a benchmark computation test in <5 minutes, compared to the 10^25 or 10 septillion (10,000,000,000,000,000,000,000,000) years – longer than the universe’s known existence – that it would have taken one of today’s fastest supercomputers

- Believe the speed is indicative of multiple universes existing: “This mind-boggling number exceeds known timescales in physics and vastly exceeds the age of the universe. It lends credence to the notion that quantum computation occurs in many parallel universes, in line with the idea that we live in a multiverse,” per Hartmut Neven, Founder and Lead of Google Quantum AI

- Key breakthrough – The more qubits used in Willow, the more errors are reduced, and the more quantum the system becomes (increasingly exhibiting the properties and advantages of quantum mechanics)

- Errors are one of the “greatest challenges” in quantum computing, since qubits, the units of computation in quantum computers, tend to rapidly exchange information with their environment, making it difficult to protect the information needed to complete a computation

- Typically, the more qubits you use, the more errors will occur, and the system becomes classical (loses its quantum mechanical properties and behaves like a traditional computer based on classical physics)

- It is also can do real-time error correction, which is critical for any real time applications

- Use cases are still TBD…: “Many of these future game-changing applications won’t be feasible on classical computers; they’re waiting to be unlocked with quantum computing” (link)

- … Though the progress made with this chip could pave the way for future innovations (link)

- When quantum computing matures, it is expected to be useful for large-scale simulations and code breaking, but that may not be possible for years or decades

- Potential applications include drug discovery, optimization of nuclear fusion reactors, and enhanced energy storage solutions, amongst others

- Willow is the second milestone in Google’s six-step strategy to develop quantum computers that can perform useful application’

- “The next challenge for the field is to demonstrate a first ‘useful, beyond-classical’ computation on today’s quantum chips that is relevant to a real-world application. We’re optimistic that the Willow generation of chips can help us achieve this goal”

- Willow performed a benchmark computation test in <5 minutes, compared to the 10^25 or 10 septillion (10,000,000,000,000,000,000,000,000) years – longer than the universe’s known existence – that it would have taken one of today’s fastest supercomputers

Source (link)

- Google isn’t the only tech giant working on quantum computing: NVIDIA, Microsoft, Intel, IBM, and other tech Cos are also working on the technology, in addition to researchers at startups and universities

- Willow’s introduction was praised by several, including Tesla CEO Elon Musk and OpenAI CEO Sam Altman

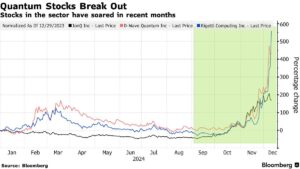

-> Other quantum-related stocks also moved in the wake of Alphabet’s announcement; Rigetti Computing jumped +45% on Tuesday (day of the announcement) while D-Wave Quantum rose as much as +16% before paring much of that advance and closed up +0.7%; IonQ fell -3.7%

-> The group has experienced a surge recently; IonQ is up ~+400% off a September low, while D-Wave is up ~+500%; Rigetti has soared more than 840% off a September low of its own

OMC + IPG: Long -Awaited Consolidation Finally Arrives For Ad Agencies But With Some Concerns

With the new administration on the way that is expected to have a more business friendly agenda, company executives have been more vocal about the potential for M&A in the sector, and that cycle appears to already be underway! While consolidation in some form amongst the ad agencies had been widely speculated, Omnicom’s move to acquire IPG in full was not amongst the envisioned transactions, so it came as a bit of a surprise.

Omnicom views this transaction as one that will “bring together the industry’s deepest bench of marketing talent as well as the broadest and most innovative services and products, driven by the most advanced sales and marketing platform.” Mgmt stressed several times the complementary nature of not only the data and technology platforms but also the cultural fit, which was something that ended up thwarting the proposed Omnicom/Publicis merger a decade back. Overall, Omnicom believes the combined company will have “an industry leading identity solutions platform with the most comprehensive understanding of consumer behaviors and transactions,” allowing it “to deliver superior outcomes for [its] clients at scale and speed.”

Analysts and investors had some concerns about the combination though. For one, the global regulatory process is difficult to assess, but it sounded like the Co will do what it takes to get the deal done. Secondly, the Co doesn’t expect the deal to close until H2 2025, which is a fair way out. There is the risk of losing employees or clients during that limbo timeframe, but mgmt would view any such moves as “short sighted”. Third, there was some concern about potential “client conflicts,” which mgmt dismissed. Lastly, while OMC expects $750mn in annual cost synergies, with most realized within 24 months after the deal closes, the transaction is margin dilutive initially (proforma adj EBITDA margin is 15.1% vs OMC 15.6%). Mgmt expects margins to improve over time but gave no further guidance or timeframe on that assertion.

All-in-all, assuming the Co can get through the regulatory process, the name of the game will come down to flawless execution and blocking and tackling.

See below for more color on the deal terms and other aspects of the transaction we wanted to highlight.

-> OMC shares fell -10% in reaction to the transaction while IPG rallied as much as 13% intra-day but was dragged down by the exchange ratio; IPG ended the week trading at a 4% discount to the offer; Publicis, WPP, and Dentsu traded up +0.3%, up +2.5%, and up +2.1%, respectively, in reaction to the transaction

-> Before the deal was announced, YTD Omnicom, IPG, Publicis, WPP and Dentsu were up +19.5%, down -8.4%, up +19.2%, up +15.9%, and up +2.7%, respectively

- Basic deal terms

- Stock for stock transaction valued IPG at $13.25bn and at a +21.6% premium to the Dec 6 closing price

- IPG shareholders receive 0.344 OMC shares for each IPG share

- Post close, OMC shareholders will own 60.6% of the combined Co

- The transaction is deleveraging for OMC

- Combined leverage ratio 2.1x before synergies (vs 2.5x OMC standalone)

- The deal is expected to close in H2:25

- No change to OMC’s capital allocation policy: The combined Co annual FCF of $3bn+

- Will continue to pay a substantial dividend (70c/shr for the combined Co), pursue accretive acqs and buyback stock

- And accretive to adj EPS for both OMC and IPG shareholders

- The combined Co will retain the Omnicom name and trade under OMC/NYSE

- OMC CEO John Wren will continue to lead the combined Co

- Stock for stock transaction valued IPG at $13.25bn and at a +21.6% premium to the Dec 6 closing price

- The deal is margin dilutive initially but expect to improve over time: Proforma adj EBITDA margin is 15.1% vs OMC 15.6%

- But expect the incremental growth and cost synergies to enable the combined Co to bring this margin “towards historical Omnicom levels and beyond” (but no time frame given)

- Expects a $750mn annual cost savings: The majority to be achieved w/in 2 years of closing with completion w/in 36 months: Will incur ~$450mn 1x cash costs to achieve the synergies

- Where do synergies come from?

- Aligning complementary businesses

- Eliminating duplicative spend w/ 3rd party vendors

- Rationalizing the real estate footprint

- Leveraging shared service centers & driving automation and off-shoring

- Leveraging the future tech platform and AI investments across an expanded business & client base

- But $750m is ~25% of the combined SG&A expenses, i.e., high? “I’m extremely comfortable”

- Where do synergies come from?

- Some strategic rationale call-outs:

- The combined Co will have the most complete offerings across media, precision marketing, CRM, data, digital commerce, advertising, healthcare, public relations and branding

- Underpinned by Omni, Interact, Acxiom, and Flywheel…positioning the combined Co to “thrive in an AI-driven future”

- Increases exposure to higher growth disciplines and also to N. Amer (57% of revenue proforma vs 51% OMC standalone)

- Principal media buying: “That’s something that, from a very transparent and ethical point of view, we’ve perfected… We can absolutely lend to IPG’s client base that they haven’t been able”

- Principal trading has “become very important to clients”: “This meaningfully accelerates and elevates our ability to deliver that”

- Healthcare: “No one that can even come close to servicing every aspect of what a pharmaceutical or an ethical pharmaceutical company wants to do than the combination of the assets”

- “The offering on the healthcare side that we can put together is going to be extremely compelling”

- The combined Co will have the most complete offerings across media, precision marketing, CRM, data, digital commerce, advertising, healthcare, public relations and branding

- Regulatory risk to get the deal done? “Pretty confident that this is not going to create any regulatory issues” but are “prepared to do whatever we have to do” to get regulatory approval

- “We’re certainly prepared to take, if we’re required to act on that on parts of our portfolio, we would do that. But we’re not anticipating it at this point”

- Mgmt also cites the new administration’s more business-friendly attitude

- Omnicom/Public was not able to get done a decade ago so what is different this time? With IPG, “we actually share core values” and are aligned culturally

- Will “make certain that the lessons learned a decade ago are not going to be repeated” (for more on the previous Omnicom & Publicis announced deal which didn’t close as they were not able to align on control and clashed culturally… see here)

Is WBD Setting The Stage For A Spin Or Sale Of Assets?

On the heels of Comcast announcing the spin of its cable TV assets (see Theme #8 Weekly 11/22/24), Warner Bros Discovery (WBD) this week announced an action that could lead to the same. WBD is separating its businesses into 2 divisions, including: 1) the Global Linear Networks division, which will house networks of news, sports, scripted and unscripted programming, such as CNN, TBS, TNT, HGTV and the Food Network; and 2) the Streaming & Studios division, which will consist of Max and Discovery+ in addition to the film studios. Each division will also have its individual operating priorities whereby the Global Linear Networks division will focus on maximizing profitability & FCF to de-lever and the Streaming & Studios business will focus on growth and strong returns on invested capital. The implementation of the new corporate structure will be completed by mid-2025.

Why are they doing this? “To enhance its strategic flexibility and create potential opportunities to unlock additional shareholder value” as well as to “increase optionality to pursue further value creation opportunities for both divisions in an evolving media landscape.” The news was met with investor enthusiasm given it looks to be laying the groundwork for a potential sale or spinoff. Consolidation among the media conglomerates has been long hoped for, but we do seem to be getting closer vs further away from that reality.

In addition to the new corporate structure announcement, WBD was quite busy operationally this week and also announced a new distribution agreement with Comcast, plus Charter went live with offering Max w/ ads to its Spectrum Select Customers as per their recent agreement. See below for more color on those.

-> WBD shares rallied a strong +15.4% in reaction to the news; Comcast’s stock was also up +1.3%, Paramount Global’s rose +3.9%, and Fox’s shares increased +2.7%

-> Separately but as a reminder, in August this year WBD wrote down the value of its TV assets by $9bn+ (see Theme #3 Weekly 8/9/24).

WBD & Comcast Come To A New Distribution Agreement

- The agreement is for distribution across Xfinity and Sky UK & Ireland customers using Comcast’s platform across linear TV, apps, and streaming services (link)

- Contract length: Unclear…just said “long-term”

- WBD’s content included:

- Comcast will carry linear cable networks for Xfinity TV customers, including TNT, TBS, CNN, Discovery, Food Network, HGTV, TLC, and Investigation Discovery

- Comcast will also continue to carry HBO

- The deal expands Comcast’s rights to package the ad-supported versions of Max and Discovery+ in its streaming bundles

- Sky UK and WBD broadened their collaboration to bring WBD TV and movies to Sky UK & NOW customers through a new long-term partnership in the UK and Ireland

- The agreement will now include a new, non-exclusive ad-supported Max app when WBD launches the svs in the UK and Ireland in early 2026

- Comcast’s comments on the deal at the UBS Conf this week… it’s a “win win”

- Said it received “really good economics” in the renewal terms and has “flexibility” to offer WBD’s DTC apps for “certain packages” in the future; It emphasized that Comcast won’t offer DTC apps necessarily to every tier of video but that it “could make a lot of sense” for the high-end segment

-> This distribution agreement could be a precursor to a future Max + Peacock bundle…

-> Also separately but related, Charter & WBD went live with Max w/ ads for Spectrum Select Customers as per their previous agreement (link)

Connectivity Providers See A Choppy Finish To 2024

After AT&T’s Investor Day last week (see Theme #3 Weekly 12/6/24), investors got to hear from other major executives in the connectivity space, including T-Mobile CEO Mike Sievert, Comcast Cable CEO Dave Watson, and Charter CEO Chris Winfrey, at the UBS Global Media & Communications Conference this week. However, some of these updates weren’t necessarily favorable. Comcast warned of steepening sequential broadband net losses (excluding ACP) in Q4, and T-Mobile acknowledged “a lot of risk” in its postpaid phone net adds in the back half of the quarter, resulting in a drop in both companies’ share prices. In contrast, Charter’s stock traded up following the event (after falling in response to Comcast’s comments), as the company has been benefiting from a “stabilization” of the broadband industry and doesn’t see a “dramatic change” in the competitive environment over the longer-term from an acceleration of wireline overbuilds.

There were many other interesting comments from the discussion, and we highlighted the most incremental insights below:

T-Mobile CEO Mike Sievert Urged For Cautiousness Among Investors Heading Into The End Of The Yr

- “There’s a lot of risk in the back half” of Q4: Sievert cautioned investors that Q4 is back-end loaded and that most of the qtr is still in front of the Co

- BUT “it’s been a great qtr so far”: T-Mobile has cont’d w/ its strategy to “profitably systematically take share at a predictable, reliable pace,” and the Co is “confident” in its guidance of ~+3mn postpaid net adds in FY24 (which implies a -100k y/y drop in Q4 postpaid net adds)

- BUT “the upgrade rate is pretty low”: Reiterated that 80% of T-Mobile’s customers have 5G-capable phones already and that they still “love” the Co’s upgrade programs; Longer-term, more switching will “probably drive some upgrade volume” for T-Mobile

- BUT “it’s been a great qtr so far”: T-Mobile has cont’d w/ its strategy to “profitably systematically take share at a predictable, reliable pace,” and the Co is “confident” in its guidance of ~+3mn postpaid net adds in FY24 (which implies a -100k y/y drop in Q4 postpaid net adds)

- A “big secular shift” in the industry is “just kind of not happening”: Highlighted that there hasn’t been a slowdown of low-calorie net adds and that switching levels as well as port volumes are higher than three yrs ago

- The Co sees “many yrs” of share-taking ahead in rural mkts “without some secular change”: This was evidenced by the Co’s “all-time high” win share in smaller and rural mkts in Q3; Digitization should “open up new oppties” as well moving forward

- The enterprise story is “equally as exciting”: T-Mobile’s mkt share is “quite low” in the space, and the Co has “tons of room to run” b/c it’s “winning the reputation game” and isn’t the facing “the same kind of headwinds on reputation” as its peers

- There’s also “potential[ly] more room to run” in growing ARPU: T-Mobile has seen 60%+ loading rates on Go5G Next and Go5G Plus; However, the Co “didn’t reach everybody w/ that,” as only 30% of its overall base has these premium rate plans

- One-time impacts are expected to weigh on wholesale rev in 2025: Anticipates that Verizon buying TracFone as well as Dish building out its own network will result in “some of that volume [coming] off,” though these headwinds have already been accounted for in T-Mobile’s guidance

- Fixed wireless is “absolutely” here to stay: Cited that both “demand for speed and capacity is increasing” and that wireless tech is “improving at… the rate that demand is increasing”

- A lot of T-Mobile’s spectrum “hasn’t been put into the fight”: Thus far, T-Mobile has only 60% of its mid-band spectrum but none of its C-band deployed on 5G

- “Our biz model for fixed wireless focuses on fallow capacity”: The Co has been finding pockets all over the country “where no normal amount of mobile usage will take up [its] capacity”

-> On a somewhat related note to Sievert’s comments on spectrum, it was annc’d this week that the FCC unanimously adopted new rules to expand very-low-power device operations across all 1,200 MHz of the 6-GHz band, alongside other unlicensed and Wi-Fi-enabled devices; The FCC’s intention is to bolster cutting-edge applications like wearable technologies and augmented and virtual reality, which will enhance learning opportunities, improve healthcare outcomes, and bring new entertainment experience (link)

- Early penetration curves on T-Mobile’s pilot fiber mkts “look very promising”: These mkts have yet to achieve full penetration, though the thesis that “terminal penetration for T-Mobile would be noticeably higher than for a pure standalone no-name fiber Co” remains

- There’s an “ongoing appetite” for more fiber partnerships: This appetite is currently “limited,” and the Co is “going to be smart about it,” looking for deals that will be “win-win” in nature

-> T-Mobile shares fell -6.1% in response to the event, finishing the week down -4.9%; YTD, T-Mobile stock is still trading up +44.7%

Comcast Cable CEO Dave Watson Anticipates A Seq Slowdown In Broadband Net Adds (Excluding ACP) In Q4

- The broadband mkt “remains competitively intense”: This “has not changed” in Q4TD; Competition levels have been “pretty consistent throughout the yr,” particularly at the more price-sensitive end of the mktplace, where FWA “has had some success”

- Q4 is playing out similarly to the slow H1:24: Expects “just over” -100k broadband losses in Q4 (vs -120k in Q2 and -65k in Q1) and ARPU to come in at the low-end of the guided 3-4% range; Although the Olympics, back-to-school tailwinds, and AT&T’s work stoppage benefited Q3, these benefits have subsided

- Q4 has been affected by two hurricanes: Estimated ~-10,000 broadband losses and a “slight impact” to ARPU from hurricane-related rebates

- Mix changes have also been a headwind to ARPU: Noted “a little bit more activity around the price-conscious segments,” including a “swirl of lower-end activity… related to the timing of ACP and mktplace dynamics there”

- Still, “churn has remained stable and near record lows” in premium segments: Refers specifically to plans where Comcast sells 500+ Mbps, including 1 gig svs; Selling wireless w/ broadband has helped churn as well

- Q4 is playing out similarly to the slow H1:24: Expects “just over” -100k broadband losses in Q4 (vs -120k in Q2 and -65k in Q1) and ARPU to come in at the low-end of the guided 3-4% range; Although the Olympics, back-to-school tailwinds, and AT&T’s work stoppage benefited Q3, these benefits have subsided

- Comcast’s network capabilities are “ahead of the curve” competitively: The Co can “match any competitor whether that’s fiber”; Comcast’s WiFi product can beat FWA in terms of speed, and the DOCSIS 4.0 rollout will make it even harder for lower-end competitors to catch up

- Comcast has completed ~50% of its mid-splits: The Co is largely done w/ mid-splits in major mkts and plans to finish the “vast majority” within the next couple of yrs; DOCSIS 4.0 will follow to provide multi-gig symmetrical speeds

- BUT the Co walked back guidance on 2024 home passings: On its Q3 call, Comcast indicated it would pass 1.2mn homes in 2024, but Watson indicated that the Co is now looking at a little over 1mn this yr

- Comcast has no plans to build out its own wireless network as of right now: The Co is “well-positioned” w/ its core MVNO agreement currently, though there could be oppties to improve economics via CBRS offload moving forward

- AI has also helped w/ network performance…: Highlighted that 60% of alerts pertaining to problems w/ the network are self-healed b/c of AI

- … And could be a “terrific addition to margin improvement”: Particularly on the customer svs and repair side of things; Believes AI will help take out unnecessary transactions and also amplify good transactions

-> Comcast shares dropped -9.5% following the event and closed the week down -7.5%; YTD, Comcast stock is trading down -9.0%

Charter CEO Chris Winfrey Sees A “Stabilization” Of The Broadband Industry

- Excluding one-time impacts, the “underlying trend for subscribers is actually slightly better y/y”: A “stabilization” of the mkt has occurred, and Charter’s pricing and packaging has been performing “really well”; The Co is optimistic heading into 2025

- Charter has lost -30k broadband customers due to the impact from the hurricanes: A good number of these will come back over time as flooded homes are remodeled and rebuilt

- There haven’t been any major changes in ARPU: The pricing strategy remains unchanged, as the Co remains focused on avoiding take rate increases “at all costs,” and is instead focused on growing gig penetration as well as leveraging pricing and packaging to drive ARPU

- Wireline overbuilds won’t result in a “dramatic change” in the competitive environment: Emphasized that the telcos’ fiber expansion plans only cover “a fraction of their footprint” and that some of these passings might be duplicative, which could eventually result in competitors backing off in some markets

- The “vast majority” of Charter’s ACP sign-ups are still w/ the Co: Estimated that the incremental loss (in addition to the normal rate of churn) of the Co’s ~5mn ACP signups should be around or under 10% and maintained expectations of -100k ACP-related disconnects in Q4

- ACP’s conclusion hasn’t had a major impact on ARPU: Acknowledged “some” impact, but this was already reflected in Q2 and Q3 results

- Progress updates on launching the new video offering –

- Step one – Launching DTC apps: The Co just launched Max, and now, Peacock is the only other major streaming platform that it has yet to launch

- Step two – Making sure that our customers can upgrade to the ad-free versions of these DTC apps: Alternatively, the Co wants to provide the option for customers to manage their existing account and determine addt’l DTC inclusion vs the incremental cost of the ad-free offerings

- Step three –Ensuring DTC is available for non-video broadband customers: Could include both à la carte offerings or packages; Emphasized that this piece isn’t necessarily less important than the prior steps but is just a function of timing and how the Co is setting things up

- Step four – Creating a “video store”: This would allow a customer to manage all of their svs, including DTC inclusion, ad-free upgrade, existing account alignment, as well as add-ons for skinny packages in a single place

- Charter’s rate of home passings will normalize after 2025: The Co plans to pass ~1.2mn homes in 2024, though much of those will be rural and subsidized rural constructions that have a “finite timeline” and a limited oppty set; Moving forward, Charter will return “back to [its] historical construction rate” of 500-600k homes “over time”

- BEAD funding “looks to be a lot less” than originally anticipated: The “oppty set is less for Charter,” and “the number of passings is a lot lower than what was originally intended”

- Only “a fraction” of the states in the Charter’s territory have attractive returns on private capital: Given the program’s policies around rate regulation and labor

- “Not a dollar has flowed to construct actual passings” yet: In the meantime, Charter used state grants, ARPA grants, and RDOF funds to buildout rural passings

- Satellite has proven to be a “viable” alternative in low-density environments: Believes that LEO satellites could svs areas w/ below 5-6 homes per mile in a less capital-intensive manner than passings, while Charter has been building in areas w/ 10 homes per mile in its subsidized rural footprint

-> Charter shares rose +3.3% in reaction to the event, ending the week but still ended the week down -5.8%; YTD, Charter stock is trading down -2.3%

Gen AI Release Palooza… OpenAI’s Sora, Google’s Gemini 2.0, and Microsoft’s Phi-4

The AI landscape is evolving at quantum speed (see Theme #1 for a literal quantum-related update in the space), and the race to train faster, generate smarter, and scale broader continues to accelerate. This week, there were substantial updates out from the biggest players in the AI space.

Starting with OpenAI, after sharing a public preview back in February, the Co finally released its AI video generator, called Sora, to the public this week. Sora not only allows users to create videos in multiple aspect ratios, but also incorporates features for mixing existing assets with AI-generated content. While demand for the new tool exceeded expectations as users were temporarily unable to access it due to “heavy traffic”, there was some disappointment with the limitations of the platform. OpenAI is limiting Sora’s ability to generate videos involving human subjects while OpenAI refines its deepfake prevention systems.

Google also debuted Gemini 2.0, which is twice as fast as its predecessor and is all about reaching the next level with AI agents. It can generate images, audio, and assist with tasks such as coding and complex search queries. The update includes features like an AI-powered research assistant, a chat-optimized version of Gemini 2.0 Flash, and experimental agents for gaming and shopping, with more in the works over the coming months.

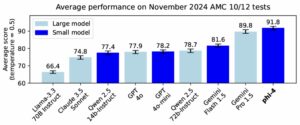

Finally, Microsoft introduced Phi-4, a 14bn parameter small language model, that not only outperformed other small language competitors, but also larger models, challenging the AI industry’s “bigger is better” philosophy. Unlike competitors like OpenAI’s GPT-4o and Google’s Gemini, which operate with hundreds of billions or trillions of parameters, Phi-4 excels in mathematical reasoning while using far fewer computational resources. This could have significant implications as the industry navigates the balance between cost and energy consumption.

See below for more on all the above.

OpenAI Releases AI Video Generator Sora For The Public (link/link/link)

- What kind of videos can Sora generate? Users can generate videos up to 1080p resolution, up to 20 sec long, and in widescreen, vertical or square aspect ratios

- Several inputs and use cases to generate a video clip –

- Uses text to type out a desired scene

- Generates video clips inspired by still images

- Extends existing videos

- Fillis in missing frames

- Along with several features (link) –

- “Remix” allows users to replace, remove, or re-imagine elements in their clips

- “Re-cut” lets users find and isolate the best frames, and extend them in either direction to complete a scene

- “Storyboard” allows users to organize and edit unique sequences from their videos on a personal timeline

- “Loop” trims down and creates clips which repeat seamlessly

- “Blend” combines two videos into a single, seamless clip

- “Presets” allows users to create and share styles to capture imagination

- Also has a “Featured” and “Recent” feed of Sora-made videos that are constantly updated with creations from the community

- How does it compare to the February preview? Back in February, OpenAI introduced Sora in preview; The new version, called Sora Turbo, is “significantly” faster than that model

- Highlighted that “the version of Sora we are deploying has many limitations”: “It often generates unrealistic physics and struggles with complex actions over long durations”; Also noted that “we’re still working to make the technology affordable for everyone”

- The Co is currently limiting Sora’s ability to generate videos of people: At launch, uploads involving human subjects face restrictions while OpenAI refines its deepfake prevention systems; The platform also blocks content involving CSAM and deepfakes

- Have implemented multiple safeguards to identify Sora-generated content and provide transparency

- All Sora-generated videos come with C2PA metadata, which will identify a video as coming from and can be used to verify origin

- Have also added safeguards like visible watermarks by default, and built an internal search tool that uses technical attributes of generations to help verify if content came from Sora

- Moderation of user content in Sora will be “starting a little conservative,” but if it “doesn’t quite get it right, just give us that feedback,” said CEO Sam Altman

- Available in most countries, with the exception of Europe: Rolled out to US and “most countries internationally”, though “no timeline” yet for launching in Europe, UK, and some other countries, likely because of stringent EU privacy laws

- Varying availability across plans –

- Plus ($20/mo): Can generate up to 50 videos at 480p resolution or “fewer” videos at 720p each month

- Pro ($200/mo): Includes 10x more usage, higher resolutions, and longer durations

- Working on tailored pricing for different types of users, which are expected to be available early next year

- Saw a surge of activity when Sora first came out: On early Monday (Dec 9th) afternoon, when the model was released, users trying to access the tool were presented with a message that that “sign ups are temporarily unavailable” due to “heavy traffic”

- OpenAI CEO Sam Altman wrote on social network X that “we significantly underestimated demand for Sora”

- That being said…the competitive landscape is quickly evolving: Google last week rolled out its Veo video generator to business partners, and Meta is developing Movie Gen, though neither is yet available to the general public

Google Introduces Gemini 2.0 – “Our New AI Model For The Agentic Era” (link/link/link)

- Starts with experimental release of Gemini 2.0 Flash: The model family can generate text, images, and speech while processing multiple types of input including text, images, audio, and video (similar to multimodal AI models like GPT-4o, which powers OpenAI’s ChatGPT)

- How does it differ from Gemini 1.0? “If Gemini 1.0 was about organizing and understanding information, Gemini 2.0 is about making it much more useful,” Google CEO Sundar Pichai said

- Outperforms its predecessors in the majority of user request areas, such as code generation and the ability to provide factually correct responses from user requests

- Will be rolled out across Google products over the next few months: Users can now use the chat version of Gemini 2.0 Flash (a lighter version of Gemini 2.0) via the Gemini app on their phones; Gemini 2.0 will expand to more Google products early next year

- Have begun using for Search and AI Overviews: Leveraging the “advanced reasoning capabilities” of Gemini 2.0 to AI Overviews to tackle more complex topics and multi-step questions, including advanced math equations, multimodal queries and coding; Have begun limited testing and will be rolling it out more broadly early next year

- Will also continue to bring AI Overviews to more countries and languages over the next year

- Several improvements to Project Astra (Google’s research prototype exploring future capabilities of a universal AI assistant), driven by Gemini 2.0 –

- Better dialogue: Project Astra now has the ability to converse in multiple languages and in mixed languages, with a better understanding of accents and uncommon words

- New tool use: With Gemini 2.0, Project Astra can use Google Search, Lens and Maps, making it more useful as an assistant in everyday life

- Better memory: Now has up to 10 minutes of in-session memory and can remember more conversations the user had with it in the past, making it more personalized to the user

- Improved latency: With new streaming capabilities and native audio understanding, the agent can understand language at about the latency of human conversation.

- Also introduced research projects that showcase the model family’s capabilities in context –

- Deep Research, a “personal AI research assistant”

- After entering a question, Deep Research creates a multi-step research plan for the user to either revise or approve; Once the user approves, it begins deeply analyzing relevant information from across the web on the user’s behalf, and creates a detailed report with source links, exportable to Google Docs

- Project Mariner, which “explores the future of human-agent interaction”

- As a research prototype, it’s able to understand and reason across information in a user’s browser screen (including pixels and web elements like text, code, images and forms), and then uses that information via an experimental Chrome extension to complete tasks for the user

- “It’s still early, but Project Mariner shows that it’s becoming technically possible to navigate within a browser, even though it’s not always accurate and slow to complete tasks today, which will improve rapidly over time

- Jules, an AI-powered code agent for developers

- Experimental AI-powered code agent that integrates directly into a GitHub workflow

- Can tackle an issue, develop a plan and execute it, all under a developer’s direction and supervision

- Deep Research, a “personal AI research assistant”

- Exploring use cases for agents in games and other domains

- Have built agents using Gemini 2.0 that can help navigate the virtual world of video games: These can reason about the game based solely on the action on the screen, and offer up suggestions for what to do next in real time conversation

- Collaborating with game developers like Supercell to explore how these agents work, testing their ability to interpret rules and challenges across a diverse range of games, from strategy titles like “Clash of Clans” to farming simulators like “Hay Day”

- Beyond acting as virtual gaming companions, these agents can even tap into Google Search to connect users with the plethora of gaming knowledge on the web

- Beyond the virtual world, also exploring oppties in the physical world with robotics: Also experimenting with agents that can help in the physical world by applying Gemini 2.0’s spatial reasoning capabilities to robotics, though it’s still early days

- Have built agents using Gemini 2.0 that can help navigate the virtual world of video games: These can reason about the game based solely on the action on the screen, and offer up suggestions for what to do next in real time conversation

- Additionally…Google unveiled Trillium, its 6th-gen AI accelerator chip that powers the training of Gemini 2.0 (link)

- Key improvements include –

- Over 4x improvement in training performance

- Up to 3x increase in inference throughput

- A 67% increase in energy efficiency

- These enhancements enable Trillium to excel across a wide range of AI workloads, including –

- Scaling AI training workloads

- Training LLMs including dense and Mixture of Experts (MoE) models

- Inference performance and collection scheduling

- Embedding-intensive models

- Parallel processing of large models in a cost effective manner and optimizing performance per dollar

- Key improvements include –

Microsoft Introduces Small Language Model Phi-4 (link)

- Newest addition to Microsoft’s Phi family of small language models

- Phi-4 “outperforms comparable and larger models on math related reasoning”

- Compared to other smaller models like GPT-4o mini and Google’s Gemini 2.0 Flash, Phi-4 competes aggressively in functionality and speed while requiring fewer computational resources

- See below chart for benchmarks for Phi-4 on math competition problems

- Uses just 14bn parameters, which is well below LLMs like GPT-4 and Gemini Pro, which often require hundreds of billions of parameters to achieve high performance

- Drivers: Advancements throughout the processes, including the use of high-quality synthetic datasets, curation of high-quality organic data, and post-training innovations”

-

- Compared to other smaller models like GPT-4o mini and Google’s Gemini 2.0 Flash, Phi-4 competes aggressively in functionality and speed while requiring fewer computational resources

- Available in very limited access only on Microsoft’s recently launched Azure AI Foundry development platform, and only for research purposes under a Microsoft research license agreement

Global Internet Traffic Growth Remains Strong But Decelerated From 2023

The 2024 Cloudflare Radar Year in Review had some interesting data on global internet trends and patterns. There was a lot of fanfare in the press that global internet traffic was up +17.2% y/y in 2024 (ending Dec 1), which is strong growth. That said, we checked out last year’s report and found that growth was +25% y/y in 2023, so there has been some deceleration. See below for the stats we thought were most interesting, and the full report details can be found here: Cloudflare 2024 report blog / Cloudflare Radar 2024 Year in Review.

- Global Internet traffic grew 17.2% y/y in 2024, which is up nicely but down from the +25% y/y the Co reported in 2023

- Android had a >90% share of mobile device traffic in 29 countries/regions

- 41.3% of global traffic comes from mobile devices

- In nearly 100 countries/regions, the majority of traffic comes from mobile devices

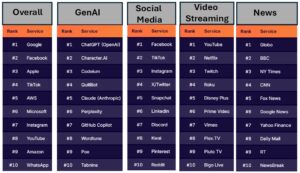

- Most popular platforms:

- Google maintained its position as the #1 most popular Internet service overall

- Facebook & Apple stood at #2 & #3, respectively

- See tables below for the Top 10 platforms across Gen AI, Social Media, Video Streaming, News, E-Commerce, Messaging, Metaverse/Gaming, Financial Services, and Crypto

- Google maintained its position as the #1 most popular Internet service overall

- Global traffic from Starlink grew 3.3x in 2024, in line with last year’s growth rate: See below for a call out to a few service launches that have seen dramatic traffic growth:

- Malawi service started in July 2023, and throughout 2024, Starlink traffic from the country grew 38x

- In the Eastern European country of Georgia, service became available on Nov 1, 2023 and after a slow ramp, traffic began to take off growing over 100x through 2024

- In Paraguay, service availability was annc’d on Dec 21, and began to grow at the beginning of Jan, registering an increase of over 900x across the year

- There were 225 major Internet disruptions that Cloudflare observed globally in 2024: Most were due to government-directed regional and national shutdowns of Internet connectivity; Cable cuts and power outages were also leading causes

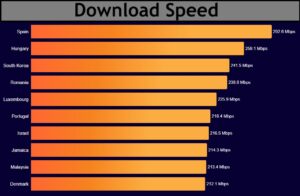

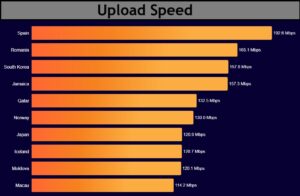

- Spain was consistently among the top location across the measured Internet quality metrics with the highest download speeds (293Mbps) and highest upload speeds (193Mbps)

- The top 10 countries ranked by Internet speed all had avg download speeds above 200 Mbps

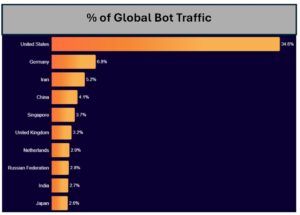

- The US was responsible for over a third of global bot traffic which was dramatically higher than any other country (Germany was #2 at < 7% of global bot traffic)

- 12.7% of global bot traffic came from AWS & 7.8% came from Google

- Globally, Gambling/Games was the most attacked industry, slightly ahead of 2023’s most targeted industry, Finance

The Growth Of The Advertising Industry Continues To Defy Expectations Of A Slowdown

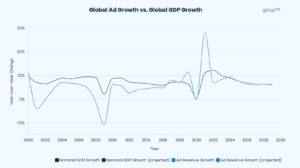

After Dentsu published its latest advertising forecasts last week (see Theme #5 Weekly 12/6/24), GroupM followed suit with its own revised advertising outlook for 2024 & 2025 this week. Similar to Dentsu, GroupM also raised its estimates for global ad revenue growth for both years and now anticipates a +9.5% y/y jump in 2024 as well as a +7.7% y/y rise in 2025, which compares to its previous mid-year forecast of +7.8% y/y and +6.8% y/y respective increases. Geographically, the improved outlook was most evident in the US, UK, and Canada, though expectations for all of the industry’s top 10 markets were more constructive, with the exception of China. However, the ad agency didn’t provide much color on the 2025 estimate changes below the headline numbers. Beyond 2025, GroupM anticipates relatively consistent growth, ranging from +5.9-6.3% y/y through 2029.

Interestingly, a key takeaway was the need for marketers to adopt a balanced approach across channels. Although the ongoing shift to digital channels is expected to continue driving rapid growth in pureplay digital advertising in the coming years, increasing scrutiny and regulation will create a more complex environment. Meanwhile, TV advertising, which includes streaming, is forecasted to grow at a slower rate than the overall advertising market, but its effectiveness in reaching viewers “remains undeniable.” All said, the forward picture for the advertising industry appears to be brightening.

Click HERE to access the report and see below for our takeaways:

- Raised 2024 global ad growth forecasts: Excluding the impact of US political advertising, global advertising rev is expected to grow +9.5% y/y to $1.04tn (vs prior mid-yr forecast of a +7.8% y/y increase to $989.8bn)

- Raised 2025 global ad growth forecasts, but growth is still down from 2024: Projects global advertising rev to climb +7.7% y/y to $1.1tn (vs prior mid-yr forecast of a +6.8% y/y increase); The Co did not detail the underlying estimates changes for the major ad mediums but see below for their current forecasts

- Digital ad rev is expected to grow +10.0% y/y to $813.3bn, which is consistent with their expectations for 2024

- “Pure-play” digital will account for 72.9% of total advertising in 2025 and 76.8% in 2029: This excludes the digital extensions of traditional media, such as CTV and digital out-of-home (DOOH), but includes YouTube and TikTok, which is the largest segment of ad rev globally

- TV ad rev is expected to grow +1.9% y/y to $169.1bn, which was a touch slower the est’d +2.7% y/y in 2024

- TV remains the most effective form of advertising, per research: Still, GroupM expects global TV (including both linear and streaming, but excluding political revenue) to grow at just a +2.4% CAGR between 2024-2029, significantly slower than total ad rev growth of +6.4%

- OOH ad rev is expected to grow +7.2% y/y to $56.1bn which is a deceleration from the +11.5% y/y jump expected for 2024: OOH is expected to account for 5.0% of total ad rev in 2025

- OOH has maintained its share of the global ad industry in the face of the digital onslaught better than any other channel: The channel benefited from its “unskippable” nature in more recent yrs, its location-based value proposition, and its rapid digitalization and innovation

- Audio ad rev is expected to grow +0.3% y/y to $27.0bn, which would be a touch slower than the +0.8% y/y expected for 2024

- Streaming audio will see double-digit growth in 2024 and grow at a +4.4% CAGR through 2029

- BUT traditional audio will see its share drop: From 1.8% of global ad rev in 2024 to 1.2% in 2029 (although it will still account for 60%+ of total audio ad rev)

- Print ad rev is expected to decrease -3.0% y/y to $48.1bn, following a -4.5% y/y drop in 2024

- This includes all traditional and digital formats across both newspapers and magazines; By 2029, their combined share will represent just 3.0% of total ad rev, down from 10.7% in 2019 and 35.1% in 2009

- Cinema ad rev is projected to rise +5.9% y/y to $2.3bn, a decel from 2024’s projected +5.2% y/y increase: However, the $2.3bn expected in 2025 will fall short of 2019’s $3.0bn global figure

- Some mkts will have surpassed 2019 levels by 2025: Though of the world’s five largest cinema ad mkts, including the US, Brazil, the UK, India, and South Korea, only Brazil will have completed its recovery by 2025

- Digital ad rev is expected to grow +10.0% y/y to $813.3bn, which is consistent with their expectations for 2024

- Expectations for the top 10 mkts were mostly adjusted upwards: Note, the list below is ranked in descending order, and prior refers to estimates included in the mid-yr forecast –

- 2025 ad rev breakdown by category: Note, the mid-yr forecast did not include this data

- Digital Endemics: 12.8% (median ad rev as a percentage of rev)

- Automotive: 9.3%

- Luxury: 9.0%

- Media & Entertainment: 5.9%

- Consumer Packaged Goods: 5.3%

- Pharma: 2.8%

- Technology: 2.1%

- Financial Svs: 1.9%

- Retailers: 0.8%

- Forecasts for ad rev growth beyond 2025 –

- 2026: +6.3%

- 2027: +6.0%

- 2028: +6.3%

- 2029: +5.9%

Grab Bag: AVs Hit A Road Bump / Amazon Auto Launches / YT Reached 1Bn TV Hours In 2024

- Autonomous vehicles players hit a road bump this week…

- General Motors cuts funding to Cruise and cuts robotaxi plans (link/link):

- What drove the move? Cited “considerable time and resources that would be needed to scale the business, along with an increasingly competitive robotaxi market”

- Expects restructuring to reduce spending by $1bn+ annually, after the proposed plan is completed, which is expected in H1:25

- GM had invested $10bn in development since it acquired Cruise in March 2016 for $1bn

- What happens to Cruise? GM said it owns about 90% of Cruise and intends to buy out the remaining investors; It plans to combine the technical teams from Cruise and GM into a single effort to advance autonomous and assisted driving

- Will still work on other AV initiatives: GM will continue to develop fully autonomous technology for personal vehicles, and build on the progress of its Super Cruise system, a hands-off, eyes-on driving feature that the company introduced several years ago

- Not the only traditional automaker to shut down AV initiatives: Ford Motors shut down its autonomous venture in October 2022

- A Waymo robotaxi got stuck in a roundabout loop (link): A video was posted on social Reddit (link) showing a Waymo robotaxi continuously circling a roundabout

- Waymo responds: A spokesperson said there were no passengers onboard the vehicle in the video and said the company has already addressed the issue by deploying a software update to its fleet

- General Motors cuts funding to Cruise and cuts robotaxi plans (link/link):

- Amazon enters online car sales market with the launch of Amazon Autos (link/link)

- What does the process look like?

- To buy a car: Customers can filter cars by make, model, trim, color, and features; Once they choose a car, they can “secure financing (handled by dealership), electronically sign paperwork, and place their orders with just a few clicks”; Once the order is complete, buyers can schedule their vehicle pick-up at their chosen dealership

- To trade in an old car: Can receiving instant trade-in valuation (calculated by independent third-party) and schedule drop-off with the dealership when collecting their new cars

- Model diverges significantly from the classic dealership format

- Fixed pricing on cars: The system doesn’t offer negotiation on car prices, which is notable difference from the usual back-and-forth seen at car dealerships

- No oppty to test drive, so buyers will need to rely on reviews and specifications rather than direct experience

- Currently available for consumers in 48 cities, including major hubs such as Atlanta, New York, Los Angeles, and Chicago

- The primary focus at launch is on Hyundai models…: Such as the Palisade, Kona, Elantra, Venue, Sonata, Ioniq 5, Ioniq 6, Santa Cruz, Tucson, and Santa Fe

- Only new vehicles are being sold at this time

- … With plans to introduce additional brands and models next year

- Who are the other big players in the space? Costco and Walmart also offering car buying services that offer both new and used cars

- What does the process look like?

- YouTube viewers streamed 1bn+ hours of content daily on TVs in 2024 (link): This was according to the Co’s 2024 recap of YouTube on TV; Other notable highlights include –

- Viewers watched 400mn+ hours of podcasts monthly on living room devices: More creators are turning to a multimedia storytelling approach to deepen connections w/ their audiences on YouTube, blurring the lines between audio-only podcasts and videos

- The share of videos uploaded to YouTube in 4K is up by over +35% y/y: Creators have been increasingly prioritizing high-quality viewing experiences that shine on TV screens

- Thenumber of creators making a majority of their revenue from TV is up more than +30% y/y

- Watch time of sports content on YouTube TV has grown +30% y/y: Users have been visiting YouTube to access clips, highlights, and post-game interviews all in one place

- New features will drive further engagement: Including –

- Watch With: Will enable creators to provide live commentary, analysis, and real time reactions to sports games and events for their audience

- A new parent code feature: Gives parents the power to prevent kids from accessing content that might not be age-appropriate; Currently in pilot

- The subscribe button has been added directly to the video player: Early tests of this streamlined button show more than a +40% increase in net subscribers through TVs

-> YouTube TV also annc’d a major price increase this week, raising the monthly price of its base plan by +$10/mo to $82.99; The hike is effective starting on Jan 13, 2025; As justification for the increase, the company cited “the rising cost of content and the investments [it] make[s] in the quality of [its] svs”; It was a little over a yr and a half ago that YouTube TV raised its price from $64.99 to $72.99 in March 2023 (link)

Stock Market Check

This Week's Other Curated News

- Amazon’s head of AI, Rohit Prasad, confirmed that Jeff Bezos remains deeply involved in Amazon’s AI efforts, despite no longer being CEO. Bezos spends 95% of his time at Amazon on AI-related projects. Prasad also dismissed concerns that large language models have “hit a wall,” stating that AI devs continually overcome technical barriers. Amazon recently released new LLM models called Nova and is developing a more conversational version of Alexa. (Fortune)

- Harvard University and Google are set to release a dataset of ~1mn public-domain books for AI training. This dataset includes works from authors like Dickens, Dante, and Shakespeare. The initiative, part of Harvard’s Institutional Data Initiative (IDI), aims to make AI training data more accessible. The project is financially backed by Microsoft and OpenAI, and the dataset will be available to research labs and AI startups. (TechCrunch)

- OpenAI released real-time video capabilities for ChatGPT, initially demoed seven months ago. The new feature, Advanced Voice Mode w/ vision, allows users to point their phones at objects and receive real-time responses. It can also understand what’s on a device’s screen via screen sharing. This feature is available to ChatGPT Plus, Team, and Pro subs, w/ a broader rollout planned. (TechCrunch)

Audio/Music/Podcast

- Canal+ and Apple expanded their partnership, offering Canal+ subs in mainland France an individual Apple Music subs for €7.69/mo, a 30% discount from the regular price. This offer includes access to 100mn+ songs, curated playlists, artist interviews, original content, and immersive sound with Spatial Audio and Dolby Atmos. Canal+ will promote this new offer w/ a national advertising campaign by BETC. (ADVANCED-TELEVISION)

Cable/Pay-TV/Wireless

- Airtel identified and flagged a staggering 8bn spam calls and 0.8bn spam SMSes within just two and a half months of launching its AI-powered spam detection system. The advanced algorithm-driven solution identified nearly 1mn spammers daily, marking 6% of all calls and 2% of all SMSes on Airtel’s network as spam. According to the Co, this initiative has resulted in a 12% drop in the number of answered spam calls. (CNBCTV18)

- Axiata Group and Sinar Mas are finalising talks to merge their Indonesian mobile bizs, per Bloomberg. This would give XL Axiata the scale to better compete w/ the country’s two largest players. The pair are working out details of a deal to merge XL and Smartfren, which Bloomberg wrote involves a mix of cash and shares and could be completed this week. The news comes days after long-serving XL president director Dian Siswarini stepped down. (Mobile World Live)

- Gigs partnered w/ Vodafone UK to empower startups and large tech Cos across the UK to launch their own mobile svs. Together, Gigs and Vodafone UK are drastically lowering the barriers to entry and reducing operational overhead for bizs to launch their own Mobile Virtual Network Operator (MVNO). Through a seamless integration, Gigs’ platform will enable bizs of all sizes to allow their customers to tag on connectivity when making purchases. (THEFASTMODE)

- Verizon has annc’d the launch of Enhanced Video Calling powered by network slicing, currently available on iPhone. Enhanced Video Calling is a new technology feature allowing Verizon’s network to intelligently adapt and manage data from video communication applications like Facetime, WhatsApp and Zoom to provide an even better experience for iPhone users. (THEFASTMODE)

Cloud/DataCenters/IT Infrastructure

- Google is partnering w/ Intersect Power and TPG Rise Climate to build data centers powered by on-site renewable energy. This $20bn initiative aims to develop “industrial parks” across the US by 2027. The goal is to reduce reliance on fossil fuels and connect directly to solar and wind farms. This approach could shift data center locations to areas w/ abundant renewable energy, addressing climate concerns and reducing pressure on local utilities. (The Verge)

- Microsoft is introducing zero-water data centers to reduce the climate impact of its AI-driven data center expansion. The new design, launched in Aug, uses a closed-loop system to recycle water, eliminating the need for fresh supplies. This will save 125mn+ liters of water per year per data center. The first zero-water data centers will be in Phoenix, Arizona, and Mount Pleasant, Wisconsin, starting in 2026. (Yahoo Finance)

Cybersecurity/Security

- Yahoo has laid off around 25% of its cybersecurity team, known as The Paranoids, over the past year. This includes the complete elimination of the red team, which conducted cyberattack simulations. The layoffs are part of broader changes under new CTO Valeri Liborski, who annc’d adjustments across the tech unit. Yahoo’s spokesperson stated that the Co is transitioning offensive security operations to an outsourced model to focus resources on critical security priorities (TechCrunch)

eCommerce/Social Commerce/Retail

- A federal judge has blocked Kroger’s bid to merge with Albertsons, citing concerns over market concentration and reduced competition. The ruling follows a trial where the FTC argued the merger would harm consumers and workers. Kroger and Albertsons can appeal but face significant challenges. The companies had planned to divest 600 stores to address regulatory concerns. Kroger must pay Albertsons a $600m termination fee if the merger fails. (Grocery Dive)

- Activist investor Barington Capital revealed a stake in Macy’s. Barington has pushed Macy’s to consider options for its Bloomingdale’s and Bluemercury bizs and create a separate real estate unit within the Co. The exact size of Barington’s hold in Macy’s is unclear. Barington partnered w/ real estate firm Thor Equities on its investment, per a presentation for Macy’s shareholders. (New York Post)

- Amazon expanded into online car sales with the launch of Amazon Autos, an e-commerce biz that lets customers find, order, and buy new cars, trucks, and SUVs from dealerships. Amazon is kicking off the new endeavor with Hyundai in 48 US cities, including Atlanta, Boston, Chicago, Los Angeles, and New York. Amazon said it will add more cities and addt’l auto manufacturers in 2025. (SLASHDOT)

- Amazon is testing a 15-minute delivery service in Bangalore, India, to compete in the quick-commerce mkt. Amazon plans to experiment w/ the new initiative in some areas of Bangalore, the southern Indian tech hub, as a potential precursor to a broader rollout. The product catalog on offer will vary from groceries to household items, depending on the neighborhood being served. (Yahoo Finance)

- Figs received a takeover offer from PE firm Story3 Capital Partners that valued the Co at $1bn+. Story3 offered $6 a share for the common shares outstanding of Figs that it doesn’t already own. Story3 and affiliated funds own a little over 1% of the Co’s shares. An offer of $6 represents an 18% premium to the stock’s closing price on Dec 6 of $5.09. Fortress Investment Group, a strategic limited partner, is prepared to provide debt financing. (Yahoo Finance)

- Inditex, owner of Zara, missed Q3 revenue forecasts with €9.36bn in sales, as growth slowed due to competition from low-cost brands like Shein. Net profit rose 5.8% to €1.7B but fell short of expectations. Shares dropped 6.1%, erasing €9B in market value. Inditex plans a €900M logistics upgrade to counter challenges. Despite setbacks, its autumn-winter sales grew 9%, and annual forecasts remain intact. (THETIMES)

- Party City is considering options including a sale or a potential bankruptcy filing, just over a yr after it emerged from Chapter 11. The Co, which sells balloons and other party supplies, is behind on rent at some locations and running out of cash to maintain operations. Party City’s struggles stem from yrs of lagging sales that have left it unable to keep pace with a sizable debt load. It entered bankruptcy in 2023 w/ ~$1.8bn in debt. (Yahoo Finance)

- Rent the Runway enhanced its customer onboarding experience to drive loyalty and engagement. New subs can now book styling appointments via phone, text, or Zoom, and replace any item within the first 60 days. These initiatives have already shown positive results, contributing to a 4.7% rev increase in Q3. The Co aims to break even on cash flow by the end of the fiscal year, leveraging customer data to improve inventory and product availability. (CX Dive)

- Shein’s planned London IPO, estimated at £50bn, is delayed as the UK’s Financial Conduct Authority (FCA) reviews supply chain oversight following allegations of forced labor linked to Xinjiang cotton. Advocacy group Stop Uyghur Genocide and the UK’s Anti-Slavery Commissioner raised concerns. China’s securities regulator approval is also pending. The IPO is targeted for early 2025. (Retail Gazette)

- The 2024 holiday shopping season is five days shorter, prompting earlier spending, with Black Friday and Cyber Monday sales up over 10% and 7% year-over-year, respectively. Retailers face challenges with the shorter timeframe but benefit from extended shopping trends. Investments in supply chain efficiency, AI, and logistics are helping companies like Walmart and J.C. Penney adapt to heightened demand and delivery pressures. (Retail Dive)

- TikTok is offering users hundreds of dollars in TikTok Shop credits to spend time in the app, invite friends, and purchase products. This promotion aims to boost user engagement and shopping habits ahead of a potential US ban. Users can earn $50 for recruiting new users and up to $350 in bonuses for more recruits. Addt’l incentives include daily check-ins and browsing TikTok Shop items. This move follows a court ruling that could ban TikTok nationwide in Jan. (Yahoo Finance)

- US TikTok users have spent heavily to buy merchandise from a range of vendors on TikTok Shop so far this holiday shopping season, per TikTok estimates and a Reuters analysis of spending patterns measured by data from Facteus. The patterns show that TikTok Shop, which launched in the US in Sept 2023, has likely gained mkt share in e-commerce at a critical moment. TikTok Shop said that its sales had reached $100mn on Black Friday. (AOL)

- Walgreens shares soared 20% after reports of talks to go private with Sycamore Partners. The deal, potentially closing early next yr, follows a significant decline in Walgreens’ market value from over $100bn in 2015 to around $7.5bn. Sycamore may sell parts of Walgreens or collaborate with partners. Walgreens has struggled with competition and financial strains since merging with Alliance Boots in 2015. (New York Post)

Electric & Autonomous Vehicles

- Archer raised $430mn in equity funding to support its collab w/ Anduril Industries on the development of hybrid vertical take-off and landing (VTOL) aircraft for defense applications and for other general corporate purposes. The new partnership with Anduril targets a potential program w/ the US Department of Defense and aims to deliver cutting-edge capabilities w/ accel’d timelines and reduced costs. (AviTrader Aviation News)

- GM is ending funding for its Cruise robotaxi service to focus on autonomous vehicle development for personal use. Cruise employees will join GM’s internal teams working on advanced driver assist systems. The robotaxi svs, which lost $3.48bn in 2023, became too costly to maintain. GM will repurchase its remaining shares of Cruise, and the board will decide on restructuring or shutting down. (The Verge)

FinTech/InsurTech/Payments

- Ebay and Klarna expanded their partnership to offer buy now, pay later options in new European mkts. Following a successful launch in Germany, these flexible payment options are now available in the UK, Austria, France, Italy, the Netherlands, and Spain. Shoppers can choose from interest-free pay in 3, pay in 30 days, or financing for larger purchases. This expansion aims to provide greater payment flexibility and choice for Ebay customers. (Retail Gazette)

Handheld Devices & Accessories/Connected Home

- Apple plans to introduce satellite connectivity and blood pressure monitoring to its Apple Watch Ultra in 2025. The satellite feature will allow off-the-grid text messaging via Globalstar’s satellites, while the blood pressure tool will alert users to potential hypertension. These updates aim to enhance the health and safety features of the Apple Watch, making it more appealing to hikers and health-conscious consumers. (CNBCTV18)

HealthTech/Wellness

- Microsoft’s AI head, Mustafa Suleyman, is recruiting former Google DeepMind staff to boost Microsoft’s AI healthcare efforts. Key hires include Dominic King, ex-head of DeepMind’s health unit, and Christopher Kelly, a clinical research scientist. This new AI health team in London aims to leverage gen AI for health applications, addressing the growing trend of consumers seeking health info online. (Benzinga)

- Peloton Strength+ is now available as Peloton’s new, standalone app dedicated solely to strength training. W/ the app, subscribers can access workout guidance from Peloton’s strength coaches, exercise tracking, and a library of instructional videos. The Co is offering select customers access to the app for $1 per month during an introductory period, but it will charge $9.99 per month after that period ends. (Retail Dive)

Last Mile Transportation/Delivery

- Talabat is set to start trading in Dubai next week, solidifying a yrs-long turnaround for the city’s bourse. Talabat’s $2bn IPO, the largest in the Middle East this yr and the biggest tech listing globally, could also help kickstart a new chapter in the emirate’s push for private listings. The UAE as a whole is set to be the busiest venue for listings in the broader EMEA region for the third yr in a row. (Yahoo Finance)

Macro Updates

- China plans to boost consumer spending in 2025 by increasing public borrowing and spending as well as shifting its policy focus to consumption. President Xi Jinping and top officials annc’d plans to raise the fiscal deficit target and strengthen the social safety net, including healthcare and pensions. While lacking concrete policy details, they emphasized the need to enhance domestic demand amid external uncertainties and domestic challenges. (Fortune)

- Donald Trump has annc’d several key appointments, including Andrew Ferguson as the next chair of the FTC, Ronald Johnson as ambassador to Mexico, and Kimberly Guilfoyle as ambassador to Greece. Trump also nominated Tilman Fertitta as ambassador to Italy and Tom Barrack as ambassador to Turkey. These appointments are subject to Senate approval. The new FTC leadership is expected to be more business-friendly, potentially reviving blocked mergers. (CBSNEWS)

- Europe is bracing itself for another round of economic challenges, this time spurred by the impending reintroduction of tariffs under the presidency of Donald Trump. W/ 2025 on the horizon and expectations of significant IPOs lined up, potential trade hostilities have cast shadows on what was previously seen as an optimistic financial forecast. This anticipated shift can be linked back to Trump’s proposal for universal tariffs between 10-20%. (The New York Times)

- Goldman Sachs CEO David Solomon predicts a surge in M&A by 2025, potentially surpassing 10-yr avgs. This optimism follows Donald Trump’s election, which is expected to bring pro-growth policies and regulatory changes. Goldman Sachs has already benefited from a rebound in investment banking, advising on major deals like Kellanova’s $36bn acquisition by Mars. While PE buyouts have been slow, they are expected to increase next yr. (Devdiscourse)

- The annual inflation rate in the US accel’d to 2.7% in Nov, w/ the CPI rising 0.3% m/m. Core CPI, excluding food and energy, remained at 3.3% annually. These figures align with forecasts and increase the likelihood of a Federal Reserve rate cut at their upcoming meeting. Shelter costs, a significant inflation component, rose 0.3%, contributing to the overall increase. The report further solidified the mkt outlook for a cut. (CNBC)

- US household net worth rose by nearly $4.8tn (2.9%) to a record $168.8tn in Q3, driven by a $3.8tn increase in stock values. Real estate values fell by almost $200bn. Consumer borrowing grew, while business borrowing slowed, with mortgage debt up 3.1%. Household deposits rose by $379.5bn to $18.9tn. Despite this wealth increase, economists expect demand to moderate due to higher borrowing costs and living expenses. (OC Register)

Media Conglomerates

- Paramount Global is bracing for a major overhaul under the leadership of incoming CEO David Ellison. Following the Co’s merger w/ Ellison’s Skydance Media next yr, Ellison plans to implement sweeping changes, including significant cuts to Paramount’s TV networks and a renewed focus on streaming. Ellison also is reportedly exploring a consolidation of Paramount’s TV networks, including CBS and MTV, into a single unit. (Cord Cutters News)

- Rupert Murdoch’s attempt to amend his family trust was blocked by a Nevada commissioner on Dec 10, potentially hindering his plan to consolidate control of his media empire under his son Lachlan. This was according to the New York Times, which cited a sealed court document. Nevada Commissioner Edmund Gorman ruled that Rupert Murdoch and his son Lachlan acted in “bad faith” in attempting to modify the family’s irrevocable trust. (WIONEWS)

- Sony has confirmed its intention to acquire Kadokawa Group, the parent Co of FromSoftware. Some Kadokawa employees are excited about the acquisition, hoping for changes in mgmt. However, an analyst warns that Kadokawa could lose its independence and face stricter mgmt under Sony. Discussions between Sony and Kadokawa are ongoing, w/ no detailed comments from Sony. (TechRadar)

- The New York Times Tech Guild has reached a tentative agreement with management on a three-yr contract after a two-year bargaining process. This follows a week-long strike during the 2024 election week. The contract includes “just cause” protections, guaranteed wage increases up to 8.25%, additional compensation for on-call work, and improved protections for workers on visas. The agreement also ensures flexible hybrid work schedules and transparency in career growth and performance reviews (Fox News)

- The proposed $8bn merger between Paramount Global and Skydance Media is encountering significant obstacles as it seeks US regulatory approval, w/ complications arising from both political and labor fronts. Trump’s claim is that the interview was manipulated to favor Harris, which could now influence the FCC review of the merger. Skydance’s plan to save $2bn, w/ half expected in the first yr, has raised fears of significant layoffs. (Cord Cutters News)

Metaverse/AR & VR

- Apple’s Vision Pro could gain support for Sony PSVR 2 controllers soon, per Bloomberg. Apple and Sony apparently planned to announce support for the controllers “weeks ago” but pushed back the rollout. Under this rumored partnership, Apple would begin selling Sony’s controllers, which aren’t currently available on their own. Sony has been working on adding the support for months, while Apple has been gauging receptiveness from third-party devs. (The Verge)

- Google is launching Android XR, a new mixed reality OS for headsets and smart glasses. At a demo, Google showcased features like real-time translation and AI-powered interactions. The platform, powered by Gemini, aims to enhance user experiences w/ natural language processing and multimodal AI. On top of that, the platform will work with any mobile and tablet app from the Play Store out of the box. (The Verge)

Regulatory

- The US Supreme Court dismissed a case against NVIDIA, allowing a shareholder lawsuit to proceed. Shareholders claim NVIDIA misled investors about its reliance on the crypto-mining industry before a 2018 crash. The court’s unanimous dismissal reflected its aversion to the case’s complex technical details. Justices expressed frustration with the arguments, indicating they were not well-equipped to handle the technical analysis required. This decision follows a similar dismissal in a case against Meta. (Engadget)

Satellite/Space

- SpaceX is raising $1.25bn through a Tender Offer, pricing new shares at $185 each and valuing the Co at ~$350bn. This offer is open to accredited investors and existing employees. SpaceX itself is purchasing up to $500mn worth of common stock. Demand for shares has been overwhelming. Addt’ly, SpaceX continues to expand its Starlink svs, now available in Timor-Leste, marking its presence in 116 countries. (ADVANCED-TELEVISION)

- AST SpaceMobile signed a commercial agreement w/ longtime investor Vodafone Group that lasts through 2034. This agreement establishes the framework for Vodafone to offer space-based cellular broadband connectivity in its home mkts and for other operators through its partner mkts program. Vodafone also placed an order for its first Block 1 BlueBird gateway. AST SpaceMobile annc’d the agreement on Dec 9, but financial terms were not disclosed. (Via Satellite)

Social/Digital Media

- A new Pew Research Center survey reveals that US teens remain highly connected to social media and smartphones. YouTube is the most popular platform, used by 90% of teens, followed by TikTok, Instagram, and Snapchat. Facebook and X have seen significant declines in usage. Nearly half of teens report being online almost constantly. Usage patterns vary by gender, race, and income, with older teens and those from lower-income households spending more time online. (Pew Research Center)

- Amazon and Meta each plan to donate $1mn to Donald Trump’s inauguration. Previously critical of Trump, Bezos and Zuckerberg now express optimism about his deregulation focus. This marks a shift in their relationship, with both tech Cos seeking to mend ties with the president-elect. (Business Insider)

- Australia will introduce new rules requiring big tech Cos like Facebook, TikTok, and Instagram to pay local publishers for news. This follows a 2021 law aimed at making Meta and Google pay for hosting news. The new rules, starting in Jan 2025, will apply to firms earning over A$250mn annually. If they don’t enter commercial deals w/ media organizations, they risk higher taxes. This move aims to ensure tech Cos contribute to Australian journalism. (BBC)

- California Attorney General Rob Bonta and Assemblymember Rebecca Bauer-Kahan have proposed a new bill, AB 56, that would require social media Cos to put a warning label on their platforms to disclose their mental health risks. Citing social media platforms’ “harnessing of addictive features and harmful content for the sake of profits,” Bonta says that consumers should have access to info about platforms that could impact their mental health. (Engadget)

- Chelsea football club owner Todd Boehly has made a late move to acquire The Telegraph, offering to help finance the £550mn acquisition of the 169-yr-old British newspaper. Boehly is considering partnering w/ or replacing US media exec Dovid Efune, who has been in exclusive negotiations to secure the purchase for more than a month. “Boehly is interested and engaged in conversations,” said a person close to the situation. (The Guardian Nigeria News – Nigeria and World News)

- Efforts by tech billionaires Patrick Soon-Shiong and Jeff Bezos to overhaul two of America’s most storied newspapers to “restore trust” in the news media are raising alarm among press advocates. Soon-Shiong said this week he had been “quietly building” an AI-powered “bias meter” to attach to the newspaper’s stories. However, press advocates and journalists fear these moves undermine trust in newsrooms and the fragile newspaper industry. (FUN The first AI powered news website to automatically publish articles)