It doesn’t exactly feel like mid-December, with the New Year right around the corner! Activity in the space has been sky-high and the major market indices have become increasingly choppy with a rotation out of Tech (Nasdaq fell -1.6% this week) and into cyclicals (the Dow rallied +1%). Fresh concerns about the AI trade surfaced and was a big focus this week (see Theme #1) but at the same time, AI developments were also widespread. In the background, as expected the Fed cut rates by 25bp though there was some debate about the rate cut path in 2026

Our edition this week delves into the below themes/developments:

- AI Bets Come Under the Spotlight as Investors Get More Nervous

- Digging Deeper Into Enterprise AI Spend & Trends

- Less Impact From Tariffs & AI Investments Drive Global Ad Forecasts Back Up

- Roku Presents Their 2025 Trend Rewind Along With 2026 Predictions

- US Pay-TV Shows Its First Growth In Years As The Industry Continues To Shift & Adapt

- The AV Space Was Full Of New Milestone & Key Updates This Week

- 2025 Global IT Spending Growth Hits 1996 Levels Thanks To AI

- Grab Bag: TKO’s Mrgn Guidance / Millions Of Teens Lose Access To Social Media / Euro CEOs Are Looking To Invest In The US Even More Than Before

Have a restful weekend.

Best,

Leslie

AI Bets Come Under the Spotlight as Investors Get More Nervous

It’s been a rough past few weeks for the AI sector and the tone from investors has shifted. After a couple of years of giving companies the benefit of the doubt, investors have started to push back on big AI promises and ask for clearer timelines and a better sense of when all this investment will start to pay off. That pressure has been building amid shakier chatter in the sector, as reports of Microsoft missing its AI sales growth targets (which the Co refuted), and CoreWeave lowering full-year guidance due to data center construction delays are starting to temper the rose-colored views many have held on the space.

That backdrop was top of mind heading into Oracle’s earnings this week, and results added further fuel to the fire. The Co missed revenue for the past qtr, but the real hit to sentiment came from CapEx, which came in well ahead of quarterly expectations and full year guidance was unexpectedly raised by $15bn. On the heels of that, Broadcom’s beat-and-raise quarter was not enough to outweigh concerns stemming from a lack of forward visibility on the Co’s AI roadmap. The end result was double-digit post-earnings drop for both companies, and a broader sell-off across AI-exposed names including NVIDIA, CoreWeave, and AMD.

Layered on top of that, the regulatory landscape is shifting as well. The Trump administration signed an executive order this week to block states from setting their own AI rules in favor of a single national framework. Large AI players have been pushing for this, arguing it could ease compliance burdens and support innovation, but states are pushing back.

Despite all these moving parts in the sector, what has not slowed down has been the level of innovation in the sector. New partnerships and product launches continue to roll out, including OpenAI announcing a major licensing agreement with Disney alongside a $1bn investment, as well as new model releases from OpenAI and Runway. Optimism on AI’s long-term potential remains high, but investor tolerance for heavy spending without a clearer path to ROI is starting to wear thin, and how the two will intersect remains to be seen.

See below for more of what we view as the need to knows for AI developments this week.

It Was A Tough Week For Major AI Infrastructure Players As Chatter Around Oracle Added Fuel To Investor Worry Around An AI Bubble (link)

- Oracle reported FQ2 earnings on Wednesday post-close and it was a difficult print…

- FQ2 rev MISSED: Came in at $16.06bn vs cons $16.19bn (-0.8% miss)

- Driven by -0% miss in the Software segment, while Cloud, Hardware, and Services all beat

- FQ2 op margin MISSED: 9% vs cons 42.1%

- FQ2 FCF was significantly below: -$9.97bn vs cons -$5.21bn

- FQ2 rev MISSED: Came in at $16.06bn vs cons $16.19bn (-0.8% miss)

- …and of particular focus was much higher qtrly and guided CapEx

- FQ2 CapEx came in much higher than expected: $12.11bn vs cons $8.35bn

- And FY26 guidance was raised by +$15bn: Expected to come in at $50bn vs earlier guide in FQ1 of $35bn

-> Oracle shares fell -11% after its earnings report Wednesday post-close, and AI-related stocks also declined including CoreWeave falling -0.9%, NVIDIA down -1.6%, and Broadcom down -1.6%

- The next day, on Friday, it was reported that Oracle is delaying some of its data centers from 2027 to 2028…

- The delays are being attributed to labor and material shortages

- What is the scope of the Oracle-OpenAI agreement? Oracle is working to deliver a $300bn contract to supply the compute

- …BUT Oracle refuted the report: A Co spokesperson said they remain confident in their ability to meet their obligations

- “There have been no delays to any sites required to meet our contractual commitments, and all milestones remain on track”

- Broadcom also reported its FQ4 earnings Thursday post-close and it was a beat-and-raise qtr, BUT on the back of Oracle’s report the day before, investors seemed to want even more visibility on the AI roadmap ahead

- Backlog of $73bn in AI product orders that will be shipped over the next 6 qtrs was questioned by investors, despite that figure being a “minimum”

- “We do expect much more as more orders come in for shipments within that next six quarters…so our lead time, depending on the particular product it is, can be anywhere from six months to a year,” said CEO Hock Tan

- AI products tightening margins was also brought up, but mgmt responded that rev is expected to grow fast enough that op margins will continue to expand

- Mgmt also held off on giving 2026 AI rev forecast, calling it a “moving target”

- Backlog of $73bn in AI product orders that will be shipped over the next 6 qtrs was questioned by investors, despite that figure being a “minimum”

-> Broadcom fell -11% after its Q3 report, its worst day since January; Oracle continued to slide and fell a further -4.5%; CoreWeave plunged -10.1%, and NVIDIA fell a further -3.3%; AMD also fell -4.8%

At The Same Time, Trump Signed An Order This Week Seeking To Limit State-Level AI Regulation (link/link/link)

- President Donald Trump signed an executive order to create one unified set of rules for AI

- “To win, United States AI companies must be free to innovate without cumbersome regulation. But excessive State regulation thwarts this imperative,” per the Order

- The order directs the US attorney general to establish an “AI Litigation Task Force” with the responsibility of challenging state AI laws that are “inconsistent” with that policy

- It also directs the secretary of Commerce, within 90 days, to consult with other officials and “publish an evaluation of existing State AI laws that identifies onerous laws that conflict with the policy”

- As a reminder…the US currently has no national laws regulating AI

- BUT more than 1,000 separate AI bills have been introduced in states across the US

- What happens if a state continues to regulate AI? The order instructs federal agencies to explore whether they can restrict grants to that particular state, including…

- Permitting the Commerce Department to review whether federal broadband funding should be revoked

- Withholding future discretionary grants by other agencies

- The order is expected to face legal challenges, esp from states w/ provisions already in place

- California State Senator Scott Wiener said “it’s absurd for Trump to think he can weaponize the DOJ and Commerce to undermine state rights…If the Trump Administration tries to enforce this ridiculous order, we will see them in court”

- California is expected to be one of the hardest hit by the order: California has passed more laws to regulate AI than any other state, per a Stanford report from earlier this yr

- Hawaii’s Senator Brian Schatz said he has planned legislation that would seek a full repeal of the order: “Congress has a responsibility to get this technology right – and quickly – but states must be allowed to act in the public interest in the meantime”

- California State Senator Scott Wiener said “it’s absurd for Trump to think he can weaponize the DOJ and Commerce to undermine state rights…If the Trump Administration tries to enforce this ridiculous order, we will see them in court”

- White House AI Czar David Sacks defended the order, saying the provision calling for the Justice Department to sue states over AI rules was designed to go after the most burdensome regulations…

- …and that it eases the growing compliance burden

- “You have fifty different states running in fifty different directions. That type of compliance regime will be hard for small companies and startups, especially innovators…what we need is a single federal or national framework for AI regulation”

- The order culminates months of lobbying by AI companies, led by OpenAI and Google as well as VC firm Andreessen Horowitz

- The Cos have argued that differing state laws up across the country risk were holding them back and potentially harming US competitiveness with China in AI

And AI Innovation Continues At Break Neck Speed W/ Hollywood Jumping In & New AI Models Hitting The Scene This Week

- Disney and OpenAI reach an agreement whereby Disney will license its iconic characters to OpenAI + take a $1bn stake in the Co (link/link/link/link)

- Under the 3-yr licensing agreement…

- Sora will be able to generate short, user-prompted social videos from a set of ~200 animated characters from Disney, Marvel, Pixar and Star Wars

- ChatGPT Images will be able to turn a few words by the user into fully generated images in seconds, drawing from the same IP

- Sora and ChatGPT Images are expected to start generating content in early 2026

- How will it be integrated into Disney+?

- Fans will be able to watch curated selections of Sora-generated videos on Disney+

- OpenAI and Disney will collaborate to utilize OpenAI’s models to power new experiences for Disney+ subscribers

- Alongside the licensing agreement, Disney will become a “major” customer of OpenAI + make a $1bn equity investment in the Co

- Disney will use OpenAI’s APIs to build new products, tools, and experiences, including for Disney+, and deploying ChatGPT for its employees

- Along w/ the $1bn equity investment, Disney will also receive warrants to purchase addtl equity

- The deal is already getting some pushback from creatives in the industry…

- The Writers Guild of America said it would meet with Disney, as the announcement “appears to sanction its theft of our work and cedes the value of what we create to a tech company that has built its business off our backs”

- Danny Lin, president of The Animation Guild, said while animators do not own the rights to Disney characters, “we’re certainly the reason they exist and the reason that they have such earning potential.”

- SAG-AFTRA said Disney and OpenAI contacted the union to offer assurances the deal would ensure the responsible use of the tech

- …though Disney CEO Bob Iger said the collaboration with OpenAI will “thoughtfully and responsibly” extend the reach of their storytelling through genAI, while respecting and protecting creators and their works

- Disney itself has taken a more aggressive stance in going after AI Cos for copyright infringements in recent months –

- On Wednesday, Disney reportedly sent a cease-and-desist letter to Google, alleging it is infringing Disney’s copyrights on a massive scale

- In Sept, they sent a cease-and-desist letter to Character.AI with similar allegations.

- In June, Disney along w/ NBCUniversal became the first major studio to sue a genAI Co when it filed a complaint against Midjourney

- Earlier this month, Disney teamed with NBCU and WBD to sue the Chinese AI firm MiniMax, alleging large-scale piracy of their respective studios’ copyrighted works

- Under the 3-yr licensing agreement…

- OpenAI released GPT-5.2 – “the most advanced frontier model for professional work and long-running agents” (link)

- It is designed to “unlock even more economic value for people”: It is better at creating spreadsheets, building presentations, writing code, perceiving images, understanding long contexts, using tools, and handling complex, multi-step projects

- The new models that were released include –

- GPT‑5.2 Instant is a fast, capable “workhorse” for everyday work and learning, with improvements in info-seeking questions, how-tos and walk-throughs, technical writing, and translation

- GPT‑5.2 Thinking Is for coding, summarizing long documents, answering questions about uploaded files, working through math and logic step by step, and supporting planning and decisions with clearer structure and more useful detail.

- GPT‑5.2 Pro is their smartest and most trustworthy option for difficult questions where a higher-quality answer is worth the wait

- GPT-5.2 “sets a new state of the art” across many benchmarks, including GDPval, an eval measuring well-specified knowledge work tasks across 44 occupations

- Specifically, GPT‑5.2 Thinking beats or ties top industry professionals on 70.9% of comparisons on GDPval knowledge work tasks, including making presentations, spreadsheets, and other artifacts

- Other key use case callouts –

- GPT‑5.2 Thinking hallucinates less than GPT‑5.1 Thinking

- GPT‑5.2 Thinking is also better at front-end software engineering than GPT‑5.1 Thinking

- Price per million tokens is increasing over previous models “because it is a more capable model”

Source: OpenAI

-> Separately, OpenAI CEO Sam Altman said this week that Google’s Gemini 3 had less impact on the Co’s metrics than initially feared, and that OpenAI expects to exit its internal “code red” by January; The code red, issued in early December, paused non-core projects and redirected teams to accelerate development in response to Gemini 3, culminating in the launch of GPT-5.2 this week (link)

-> It was also reported by The Information this week that ChatGPT is nearing 900mn weekly active users, up from 800mn in October (link)

- Runway released its first-ever world model, GWM-1 + updated its Gen 4.5 video model (link/link)

- What is a world model? An AI system that learns an internal simulation of how the world works so it can reason, plan, and act without needing to be trained on every scenario possible in real life

- How does it work? Through frame-by-frame prediction it creates a simulation with an understanding of physics and how the world behaves over time, the Co said

- The model is split into 3 versions…GWM-Worlds, GWM-Robotics, and GWM-Avatars with different goals

- Worlds: Generates, predicts, and reasons about real-world dynamics from visual data

- Robotics: Made to train and stress-test robots in simulated worlds, including identifying failure modes and policy violations before deployment

- Avatars: Realistic human avatars that simulate human behavior, communication, and interaction

- The Co noted that they will eventually merge all these into one model

- Earlier this month they also launched its Gen 4.5 video model which they also updated along with the new release

- The enhanced model can now generate one-minute videos with character consistency, native dialogue, background audio, and complex shots from various angles

- Can also edit existing audio and add dialogues, and edit multi-shot videos of any length

- What can the models be used for? Game development and virtual environment creation, robotics training, digital communication, and content creation

Source: Runway

Digging Deeper Into Enterprise AI Spend & Trends

Menlo Ventures’ deep dive report “AI Boom vs Bubble” had some interesting data and analysis related to the enterprise AI spend trends that we wanted to highlight this week. The data was based on a survey of ~500 US enterprise decision makers, combined with their insights and a bottoms-up model of the generative AI market spanning model APIs, infrastructure, and applications.

Menlo Ventures estimated that overall enterprise AI spend grew +3.2x in 2025 to reach $37bn, and that these expenditures were roughly evenly split between the AI application layer and AI infrastructure. A few standouts that we’d call out from the report include: 1) coding is the biggest killer app by a long shot and is a $4bn market already; 2) healthcare scribing has been another major use case as well; 3) copilots dominate horizontal AI spend and are 10x bigger than agent spend, for now; and 4) Anthropic and Google have made huge market gains in the Enterprise LLM API space (the report has some good charts).

See more details below and we also included Menlo Ventures’ 2026 Enterprise AI predictions, plus some very handy market maps for departmental AI, vertical AI, and the AI infrastructure stack that we found helpful as well.

Enterprise AI Spend Growth Is “The Fastest Scaling Software Category In History” (Full Report)

- Overall, companies spent $37bn on gen AI in 2025, up +2x y/y (and up from $1.7bn in 2023

- It now accounts for 6% of the global Saas mkt and it is “growing faster than any software category in history”

- Total enterprise AI spend is broken down roughly 50 / 50 between the Application Layer AI ($19bn) and AI Infrastructure ($18bn)

- Within the application layer, horizontal AI spend is the largest and fastest growing (in green below)

- Within AI infrastructure, foundation model API spend is the largest (in green below)

- Coding is AI’s first killer app…it accounts for ~55% of departmental AI spend and is a $4bn market: Other areas of departmental AI spend include IT (10%), marketing (9%), customer success (9%), design (7%), and HR (5%)

- Copilots dominate horizontal AI spend, holding 86% of that spend share ($7.2bn): This is led by ChatGPT Enterprise, Claude for Work, and Microsoft CoPilot

- Agent platforms like Salesforce Agentforce, Writer, and Glean account for only 10% of the spend

- Foundation model API spend market share by provider, market share trends, and coding market share are below

- Anthropic and Google have made huge market share gains

- Startups dominate AI applications, earning nearly $2 for every $1 incumbents earn, while enterprise infrastructure spend continues to favor incumbents

- 2026 predictions…

- AI will exceed human performance in daily practical programming tasks

- Jevon’s paradox will continue to hold true…net spend on generative AI will rise further despite falling costs of inference

- With the increase in autonomy and decision-making by agents, the ability to explain and govern the decisions they’re making will increase in importance

- Models finally move to the edge…compute will continue to move on-device

- ALSO Menlo Ventures also had some helpful market maps…. for departmental AI, vertical AI, and for the AI infrastructure stack…see below:

Less Impact From Tariffs & AI Investments Drive Global Ad Forecasts Back Up

Mid-2025, WPP took a more cautious view on their full year 2025 and 2026 global ad spend forecasts due to macro/tariff concerns, but the agency giant did an about face this week when they raised those forecasts not only back up, but to levels that were above where they originally started at the beginning of the year. In its This Year Next Year (TYNY) Global End-of-Year update, the firm is now expecting 2025 global ad spend to grow +8.8% y/y and 2026 to expand +7.1% y/y (both ex-US political). The Co’s higher forecasts were largely driven by better-than-anticipated trade tariff results and AI investments.

Global content driving advertising remains the biggest spending category (58% share of global ad rev) but global commerce ad revenue surpassed that of TV for the first time.

See more color below on our key takeaways from the update…

WPP Media Revised Up Their 2025 & 2026 Global Advertising Forecasts To Levels Above Their Earlier Expectations At The Start Of The Year (link/link/link)

- During WPP’s June update, the Co cut its 2025 global ad revenue forecast from +7.7% y/y to +6% y/y (ex US political) due to disruptions to global trade and continued deglobalization pressures weighing on advertising investment

- Now, it is raising its 2025 forecast back up, but from +6% y/y to a higher +8.8% (ex-US political), reaching $1.14 trillion

- For reference, 2024 global ad rev grew +9.7% y/y (ex-US political)

- Additionally, the firm raised its 2026 global ad revenue forecast from +6.1% y/y to +7.1% y/y (which is also above its original +6.3% y/y at the start of the year)

- The drivers for the higher 2025 and 2026 growth estimates are largely attributed to trade tariff outcomes proving more favorable than expected and the AI investment boom

- Over a 5-year period, the CAGR of global ad spend is +6.3% y/y

Looking At Key Trends In Channel Dynamics, Commerce Ad Revs Is Projected To Pass That Of Total TV For The First Time

- Global content-driven advertising remains the largest category at $663.5bn (58% share of global ad rev)

- Gaming represents the fastest-growing content advertising channel and is forecast to increase +29.5% y/y to $8.5bn in 2025

- BUT…gaming is still an extremely small % of total 2025 global ad revenue (just 0.7%)

- Newspaper advertising is expected to be stable at $31.4bn in 2025 before declining

- Digital out-of-home (DOOH) is forecast to represent 43.9% of total OOH rev by 2030, reaching $31.4bn

- Gaming represents the fastest-growing content advertising channel and is forecast to increase +29.5% y/y to $8.5bn in 2025

- Global commerce ad revs are projected to reach $178.2bn in 2025 (which is an increase from the $169.9bn estimate as of June 2025 and surpasses TV ad spend for the 1st time)

- The report also included channel data on content-driven ad rev share

- Gaming and social/other digital is expected to continue to grow

- TV, audio, magazines and newspapers are continuing their declines

Source: WPP

Drilling Down Into The Top 15 Markets

- Compared to 2024, the top 10 markets remain mostly the same, except Brazil now surpassed Canada in ad rev

Source: WPP

- 2025 y/y growth is expected to:

- Accelerate in…the US, Japan, Brazil, & Australia

- Decelerate in…China, the UK, Germany, France, Canada, & India

Roku Presents Their 2025 Trend Rewind Along With 2026 Predictions

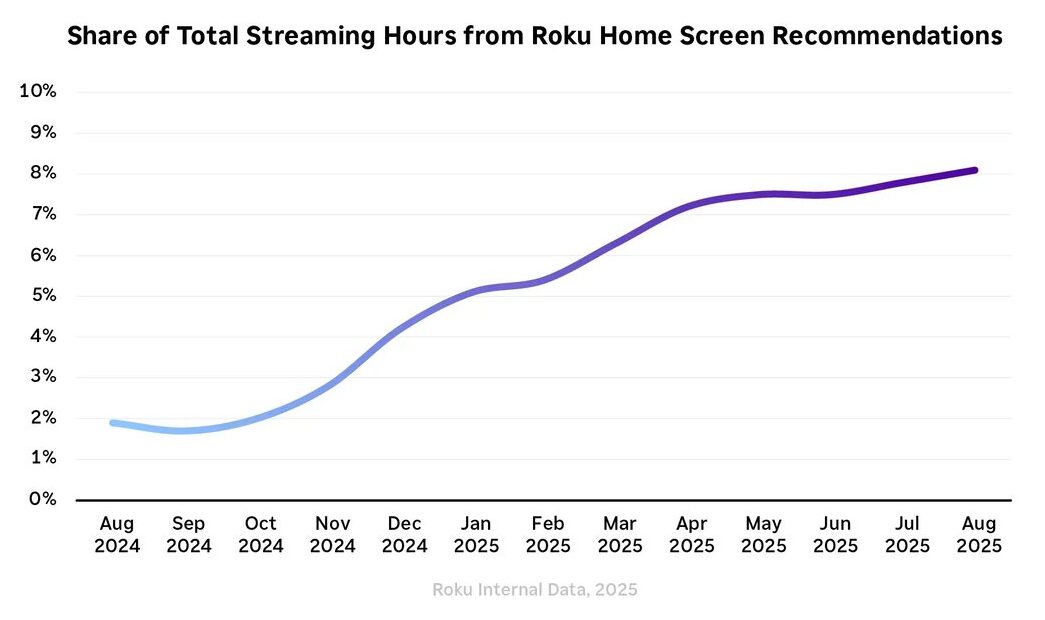

On the streaming side of things this week, Roku’s latest insights show how TV, movies, sports, Gen Z behavior, and platform-level viewing patterns shaped up 2025 and how those shifts are setting up major trends for 2026. Their findings ranged from TV moments that audiences obsessed over, to genres and stars that are driving spikes in search, to the way app-hopping and seasonal binge cycles are reshaping viewing. It also highlights the growing role of CTV as AI disrupts search, social, and the broader internet.

See our key takes from their report below…

Roku’s Top TV Moments In 2025 (link/link)

- SNL 50 was a major moment

- Searches for the 50th Season of NBC’s Saturday Night Live peaked around its anniversary special in Feb

- The top-searched episodes were hosted by Ariana Grande, Jean Smart, and Shane Gillis

- Awards still matter

- After the Emmys, searches for award winners like The Studio (+111%), Severance (+103%), and Adolescence (+151%) more than doubled

- Love Island USA became a surprise juggernaut

- Peacock’s Love Island USA was the #1 searched show on Roku this summer, with searches growing +180% vs the prior season

How Did Movies On Their Platform Perform This Year?

- Original horror comes back…the genre grew +20% y/y

- Original horror surged in 2025, led by the breakout film Sinners, which generated more than 2x the search volume of the next highest horror title

- The new Pope drove a surge for Conclave

- In the days after the election of Pope Leo XIV, Chicago-area Roku homes were +42% more likely than the rest of the country to search for Focus Features’ Conclave

- Stars still sell

- Adam Sandler and Ariana Grande topped Roku’s most-searched actor lists due to megahits like Happy Gilmore 2 and Wicked

How Did Sports & Live Entertainment Perform?

- Scripted comedy to live sports?

- Fans of Apple TV’s golf comedy Stick also streamed real golf

- Stick viewers were 2.8x more likely than Happy Gilmore 2 to search for The Masters

- NFL & MLB ruled the Sports Zone

- NFL teams were the most favorite in 24 states on the Roku Sports Zone

- MLB loyalty dominates the coasts and across the Great Lakes

- Pro wrestling was a breakout

- Roku searches grew (+275%), outpacing auto racing (+75%) and MMA (+69%) as the fastest-growing sports on the platform

Gen Z On The Platform Is Showing A Lot Of Interest In Animation

- Gen Z adults were animation-focused

- ~2/3 of Roku searches from Gen Z were for animated titles

- The oldest Gen Z’ers are 28 years old, watching anime, adult animation, and animated films with cult-like followings

CTV Viewing Trends Across States, Months & Apps

- Viewers tend to rotate apps, switch between free and paid services, and binge in predictable seasonal cycles

- Which states streamed the most?

- In 2025, Mississippi streamed more hours per capita than any other state, followed by Alabama, Kentucky, Arkansas, and West Virginia

- Which months saw the most streaming?

- January, with more than 1/3 of sessions lasting 8 hours or longer

- The top streaming weekend of the year followed Thanksgiving, showing that people love to binge while they are home for the holidays

- Apps used per home…the median is 9

- The median Roku household streamed across nine apps in 2025, 3 of which were free to watch

- During the year, the avg home added 4 new apps and dropped four apps

Roku Also Predicted 5 Key Trends That Will Shape 2026 (link)

- TV gets way more personalized via AI: The Co is predicting that AI-driven personalization will cut the time it takes viewers to find a show

- In 2025, streaming viewers spent ~20 minutes on avg to find their next watch, up from 7.5 minutes in 2019

- In 2026, AI-driven recommendations “will reverse the trend”

- Netflix and YouTube are already doing this with their recommendation engine

- Netflix influences 80% of viewing hrs and expands its “effective product catalog” roughly 4x compared to a non-personalized system

- Netflix has also teamed up with OpenAI to improve discovery further

- YouTube’s engine drives 70% of viewing

Source: Roku

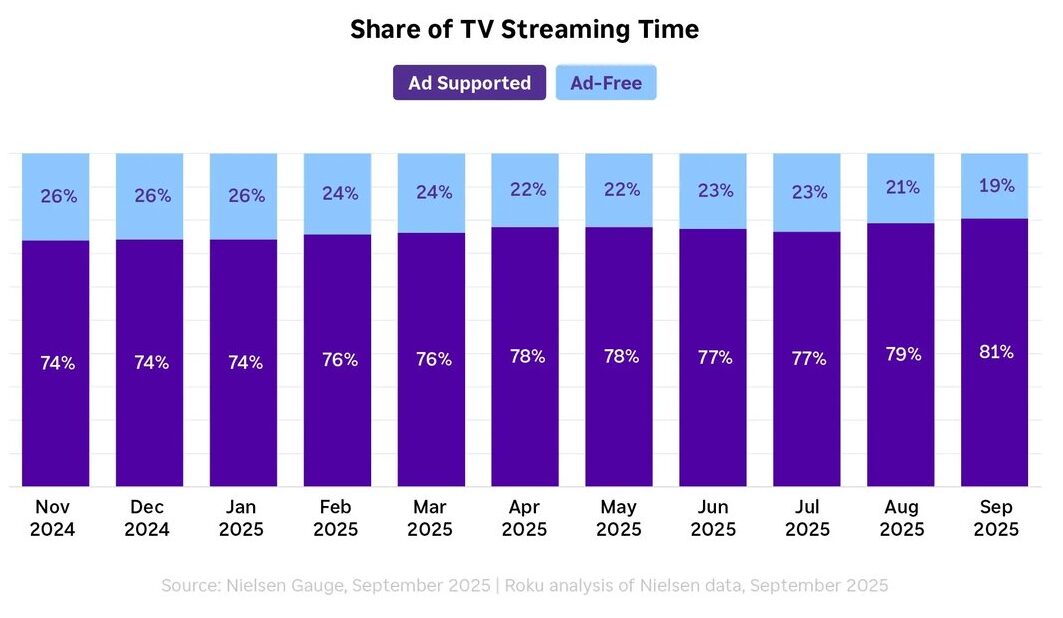

- The ad-free viewer goes extinct as 100% of audiences see video ads

- Today, most Roku streaming households (96%) see video ads and Nielsen reports that content with ads accounts for ~74% of all TV viewing

- Subscriptions to services with ads incr’d +32.7% y/y in Q2 2025

- What is driving this shift?

- Americans are watching YouTube occasionally, and most YouTube viewing includes ads

- Amazon has also contributed as the Co turned ad-free viewers into ad-supported when it began showing ads to all Prime Video users in 2024 (unless they paid $2.99 a month to continue an ad-free experience)

- Ad-supported Prime Video now reaches 130mn US customers

- How much time are viewers spending on ads? Most streaming services show ads for between 4-8 mins per hr, according to Wurl

- In August 2025, Amazon showed 2-3.5 mins per hour, but that incr’d months later to 4-6 mins per hour

- No major players have embraced the level of ad loads of linear TV, which can stretch to 16-19 mins

Source: Roku

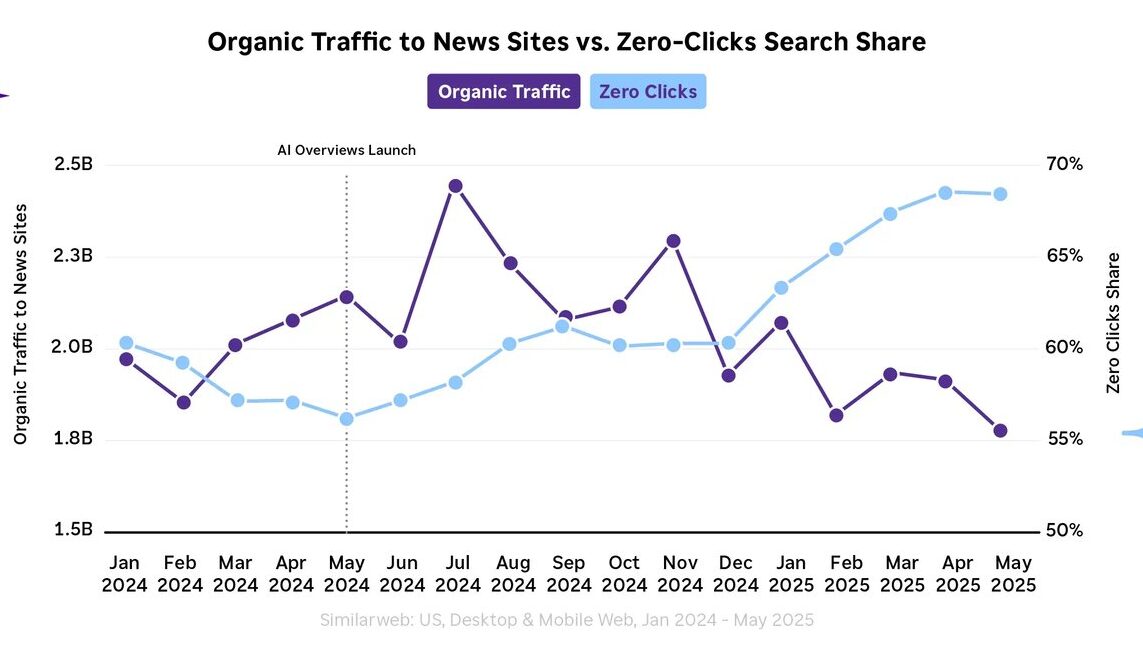

- CTV will continue to become increasingly valuable

- AI summaries are replacing the need for traditional search results, causing traffic and ad volume to decline

- Due to AI, social media is also becoming a riskier, less reliable place for marketers

- Most consumers can’t tell real content from AI content, which causes confusion and trust issues

- This led to a 72% increase in offensive or unsafe content

- AI is affecting the way people search: AI answer engines reduce clicks, which hurts both advertisers and publishers

- Advertisers lose ad effectiveness, and publishers lose traffic and rev

- In H2 2026, both marketers and publishers will look to CTV, which is mostly insulated from genAI

- They believe ~50% of streaming advertisers will subsidize CTV ad spend increases w/ budgets siphoned from search and social

Source: Roku

- TV collides with the creator economy: The creator economy is booming, with ~50mn creators making and monetizing content for 5bn social media users globally, according to Deloitte

- In 2026, creators will expand their presence on CTV through licensing, ads, and more

- At least one major streaming service beyond YouTube will add a “creator” tab

- Roku is already seeing this move: In August, viewership of creator-led content on The Roku Channel grew ~80% in streaming hrs per household y/y

Source: Roku

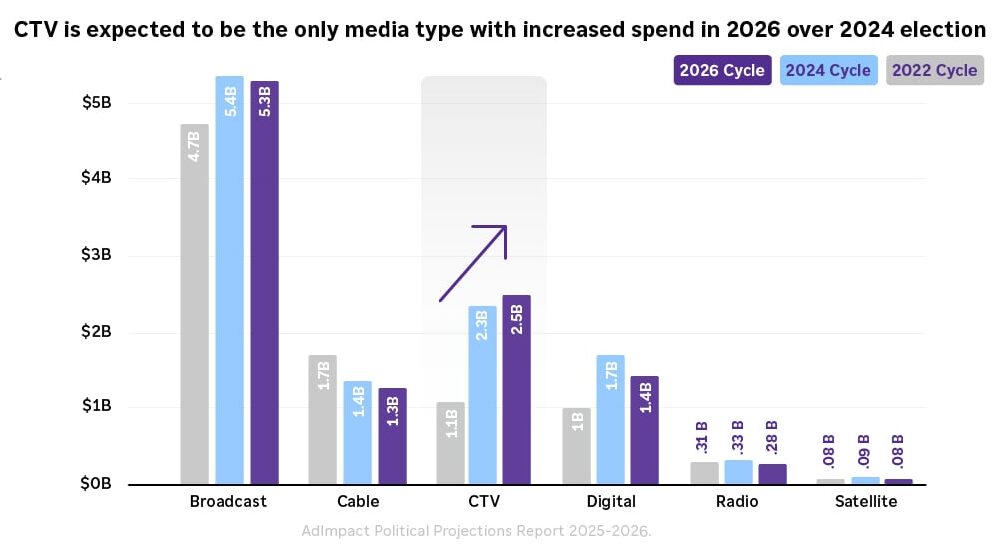

- Hyperlocal advertisers embrace CTV, following the lead of political campaigns…2026 will be a tipping point for locally targeted campaigns thanks to the midterm elections

- Political campaigns will lead the way, proving that self-serve TV ads combined with AI-generated creative can help candidates turn out the vote

- “Law firms, hair salons, real estate agencies, and other regional businesses will follow”

- Local ad dollars are already flowing to CTV, reaching ~$2.8bn in 2025, ~8% of all local video advertising

- In 2026, they predict that genAI will help many local advertisers boost the effectiveness of their ads by 30% compared to linear

- Political campaigns will lead the way, proving that self-serve TV ads combined with AI-generated creative can help candidates turn out the vote

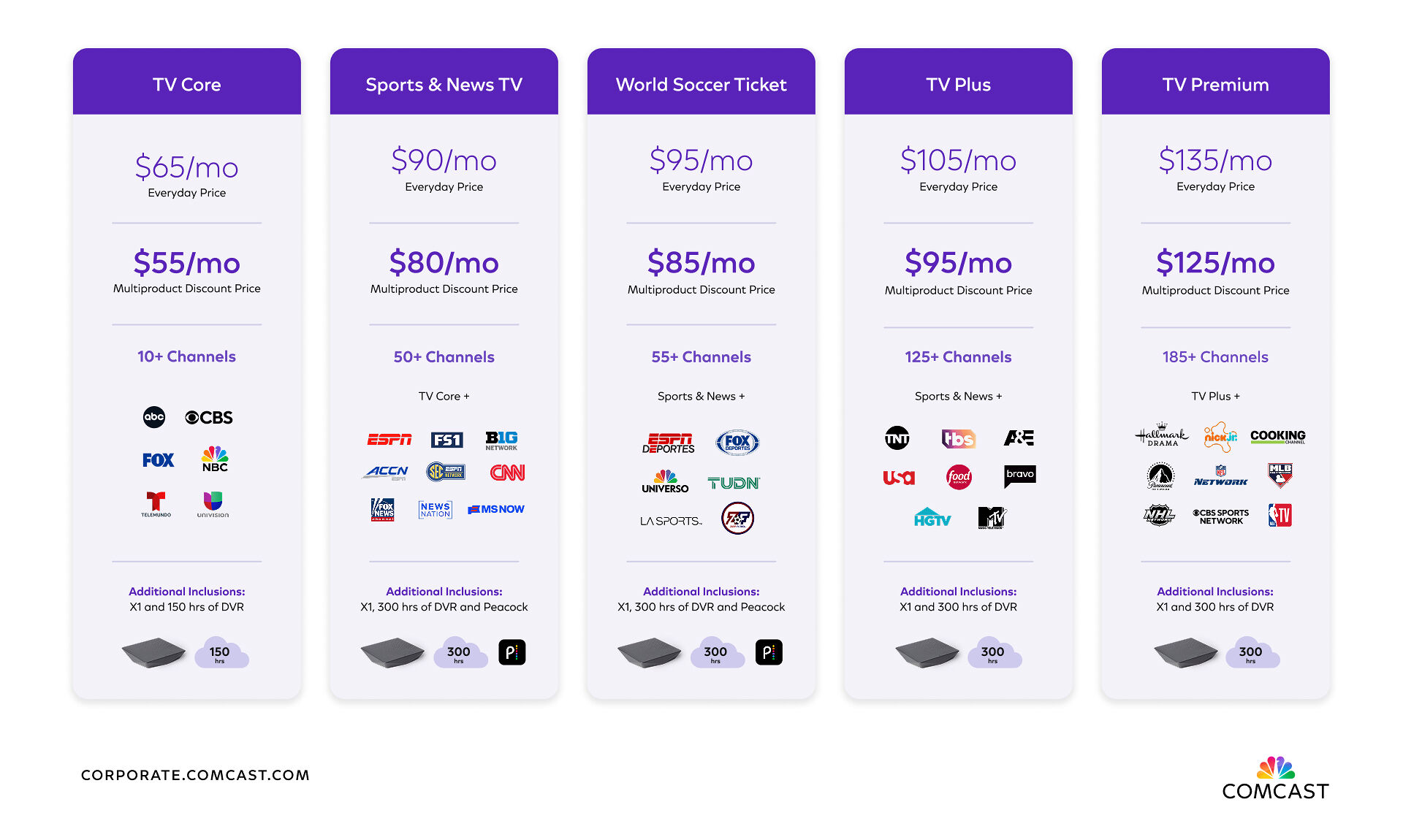

US Pay-TV Shows Its First Growth In Years As The Industry Continues To Shift & Adapt

It is interesting timing that just as linear cable networks are being separated or spun, Wall Street research out this week found that Q3 was the first time in eight years that pay-TV subscribers in total actually grew, with 300k+ new subs in the quarter. While the pay-TV mkt is still shrinking y/y, the rate of decline has continued to ease. What is driving the improvement? A seasonal lift in vMVPDs due to the start of football season plus Charter’s better-than-expected video performance in Q3.

Against this backdrop, Charter CEO Chris Winfrey shared some initial insights this week on the Co’s’s recently launched Spectrum App Store, which expands its video offering with SVOD-bundled packages. Nearly half of eligible video customers who access the App Store are using it, indicating meaningful runway for adoption ahead, and users typically activate several apps once engaged. Comcast is also making changes with its plans, rolling out simplified, all-in Xfinity TV pricing that includes equipment, removes annual contracts, and offers additional savings for existing internet customers.

Elsewhere, YouTube TV is projected to become the largest US pay-TV provider by 2027, surpassing both Charter and Comcast, marking the first time a vMVPD would lead the market.

While everyone has been calling for the death of the linear cable nets, it’s also a reminder that the industry isn’t standing still. Traditional operators are experimenting with new ways to engage subscribers, while to be fair, virtual providers like YouTube continue to gain ground.

See below for of what we thought were key developments in the pay-TV sector this week.

- Total pay-TV subscribers grew for the FIRST TIME in 8 yrs, per MoffettNathanson’s “Cord-Cutting Monitor” report (link/link): PayTV added +303k net subs in Q3

- BUT y/y, overall Pay-TV is still declining (though at a lesser qtrly %age): It was down -5.8% y/y overall in Q3, versus yr-ago qtr’s -6.7% y/y

- What drove the improvement? vMVPDs saw a big seasonal surge + Charter’s improved video performance

- The start of the NFL season in Q3 drove a +1.43mn increase in total vMVPD additions in Q3 (up from +1.36mn in prior yr qtr)

- Charter also shrank its video losses dramatically (-70K vs -294K last yr) driven by its new SVOD-bundled cable package, which reduced drag in the category

- Traditional pay-TV still fell q/q in Q3, but again, by less: Down -10.2% y/y in Q3 vs -12.4% y/y in Q3:24

- This is the 3rd consecutive qtr of improvement in the decline rate of traditional pay-TV

-> Separately, but related, Nielsen also found that ad-supported TV viewing in Q3 peaked in September, driven by the start of the football season; After peaking in July with 48% of the overall ad supported pie, streaming lost 3.6 share pts, down to 44.4% in September, while broadcast gained 4.4 share pts, jumping to 29.1% thanks to a strong sports slate, while cable remained fairly consistent (link)

- On this topic…Charter this week provided an update on its recently launched Spectrum App Store – seeing early traction with much more room to grow (link)

- But it will take some time for the adoption curve to improve: The Co is finding that it is taking some time for customers to realize that these apps are part of their pay-TV svs and not a short-term promo

- “So why wouldn’t it be 100% [participation]…customers have become so accustomed to a promotional offer…that getting them to understand and buy in that this is permanently included as part of your subscription is included for free … It’s not a gimmick,” said CEO Chris Winfrey

- But once customers activate the first app, they tend to quickly activate more

- Nearly half of Charter video customers who have access to the App Store are using it

- Amongst those users, most are now activating “well over” three apps at this point

- As a reminder… Charter currently offers about a dozen ad-supported apps from programmers for no extra cost to video customers who subscribe to eligible video plans; Combined, they represent $125 in value

- But it will take some time for the adoption curve to improve: The Co is finding that it is taking some time for customers to realize that these apps are part of their pay-TV svs and not a short-term promo

Source: Charter

- YouTube TV is on track to become the largest US pay-TV operator by 2027, per Omdia (link)

- It is set to surpass Charter and Comcast (end of 2025 -> 2027 forecast)

- Charter: 11.4mn subscribers -> 10.0mn subscribers (-1.4mn)

- Comcast: 10.6mn subscribers -> 9.2mn subscribers (-1.4mn)

- YouTube: 9.3mn subscribers -> 10.4mn subscribers (+1.1mn)

- This will mark the first time a virtual pay-TV provider will claim the top spot

- It is set to surpass Charter and Comcast (end of 2025 -> 2027 forecast)

Source: Omdia

- Comcast revamps its Xfinity TV plans w/ simplified, all-in pricing and no annual contracts (link/link)

- Every new package now comes standard with an included X1 4K TV box, an X1 4K TV box, Xfinity’s voice remote, Multiview, Enhanced 4K, StreamStore and Fan View

- How does it work? Customers pay a single rate that rolls in all associated fees, w/o worrying about renting equipment, breaking contracts or special promos that expire

- Customers who already have Xfinity Internet will save an extra $10/mo for bundling w/ their video package

- New Xfinity TV plans come a couple of months after Comcast similarly relaunched its Xfinity Internet packages with streamlined, all-in pricing and includes a year of unlimited mobile

- How does this compare to the competition? When bundled together w/ internet and mobile, Customers could save over $70/mo for a yr when compared to AT&T and Verizon

- To flag…the cost of Comcast’s skinny sports bundle somewhat incr’d in the overhaul: Comcast launched its Sports & News TV bundle in January at a discounted $70/mo when paired with internet; It now costs $80/mo for the same bundle

- BUT there are no major extra fees or extra costs for the X1 set-top box, which is valued at $14/mo

Source: Comcast

The AV Space Was Full Of New Milestone & Key Updates This Week

The AV industry reached several new milestones this week, led by Waymo crossing 450k weekly paid rides, which is nearly double its April level, per CNBC citing a letter from Waymo’s investor Tiger Global. The Co is rapidly expanding into new cities and freeways and logged 14mn robotaxi trips in 2025, tripling last year’s level and implying ~$286mn in revenue. But at the same time, safety scrutiny has been on the rise and Waymo this week also issued a voluntary software recall after investigations found its vehicles illegally passed stopped school buses in Austin and Atlanta. This prompted an active NHTSA review of ~700 incidents this year, though no injuries have been reported.

Amazon’s Zoox is also pushing ahead and announced plans to begin charging for rides in Las Vegas in early 2026 and later in the Bay Area. Zoox surpassed 1mn autonomous miles and is shifting focus toward moving more people. With that said, meaningful revenue remains years away. And on the OEM front, Nissan and Wayve signed a major agreement to integrate Wayve’s AI Driver into Nissan’s next-gen ProPILOT system, making it the first large-scale commitment to deploy Wayve AI across mass-produced vehicles beginning in 2027.

Read more of what we thought was more important below this week…

Waymo Hit A New Milestone, But Could They Be Moving Too Fast? (link/link/link/link)

- Waymo crossed 450k weekly paid rides, according to a letter from investor Tiger Global that was viewed by CNBC

- This is up +200k since April, when they hit 250k weekly rides

- In the letter Tiger Global wrote: “Waymo is the clear leader in autonomous driving…with a product that is 10x safer than human drivers”

- Waymo is one of Tiger’s largest positions in their 2024 fund

- Waymo declined to comment on the matter

- As a recap for this year: Waymo’s expansions include its debut on freeways in 3 cities, and autonomous driving in cities including Miami, Dallas, Houston, San Antonio and Orlando

- Where is Tesla? They have run limited pilots in Austin and operate a ride-hailing service in the Bay Area

- BUT… at the same time, Waymo launched a software recall

- The Co is issuing a voluntary recall after school bus safety concerns came to light earlier this year

- The recall won’t pull cars from the road but will instead see them updated

- It comes after an investigation by Nexstar’s KXAN found the Cos vehicles illegally passed school buses with their stop arms out in Austin, Texas

- The Austin Independent School District said similar incidents occurred ~19x this school year

- The National Highway Traffic Safety Administration (NHTSA) opened an investigation in October

- No injuries have been reported, but parents and law enforcement alike are raising red flags about the vehicles’ programming

- Austin isn’t the only place this is happening: Atlanta Public Schools said it recorded ~6 similar stop-arm violations between May-December

- NHTSA has been reviewing ~700 Waymo-related incidents since January 2025

- The Co said these incidents make up a tiny fraction of its service

- The Co is issuing a voluntary recall after school bus safety concerns came to light earlier this year

-> Waymo reported completing 14mn robotaxi trips in 2025, triple its 2024 volume; With an avg ride price of $20.43, the company could have generated over $286mn in revenue, before taxes and ride-hailing fees; Despite currently operating in only 5 US cities, Waymo plans to expand to 20 international cities; The Co also projects reaching 20mn trips by the end of 2026 (Dec 10th)

Amazons Zoox Will Start Charging For Rides In 2026, Shifting Their Focus On People Not Packages (link/link)

- Zoox expects to start charging passengers for rides in Las Vegas in early 2026, with paid rides in the San Francisco Bay Area coming later next yr, a company executive said on Monday

- CTO Jesse Levinson said that Zoox is “laser focused” on moving people around cities

- He sees the addressable marketplace as being “just profoundly huge”

- This directive came “all the way from the very top” at Amazon, despite the retailer’s significant interest in driverless package delivery

- “It’s harder to move people around than packages in terms of what you have to do with your vehicle,” Levinson said

- On the other hand, “automating package delivery is rife with its own challenges because the boxes have to get in and out of the vehicle”

- Zoox crossed the 1mn mile technical threshold for autonomous rides last week, Levinson said

- They currently provide rides to passengers free of charge in portions of Las Vegas

- Zoox is opening the wait list to use the service in San Francisco

- Despite the progress to start charging fares, Zoox won’t generate revs that are “meaningful” for at least several more yrs

- He added that the revenue you can generate from the robotaxi is “quite a bit more” than the expense to run robotaxis

- How can they stand out from the competition?

- A competitive element for Zoox is its battery, said Levinson

- It’s more environmentally and economically friendly because it requires less charging

-> Separately but related, Uber expects it will take 5–10 years before self-driving vehicles make up more than 10% of global trips on its network. Additionally, Uber annc’d that by the end of 2026, robotaxi services will be available in over ten markets, with potential markets including Hong Kong and Japan (link/link)

A New Nissan & Wayve Deal Was Another Notable Development

- Nissan and Wayve annc’d an agreement to collaborate on integrating the next-gen ProPILOT series with Wayve AI tech across Nissan vehicles (link)

- Under the new agreement, Nissan and Wayve will integrate “Wayve AI Driver” into the next generation ProPILOT series, enabling deployment in mass-produced vehicles

- Nissan plans to introduce the first model equipped with this new gen of ProPILOT in Japan in fiscal year 2027

- Under the new agreement, Nissan and Wayve will integrate “Wayve AI Driver” into the next generation ProPILOT series, enabling deployment in mass-produced vehicles

- Nissan intro’d ProPILOT in 2016 for single-lane highway assistance and launched ProPILOT 2.0 in 2019, adding multi-lane support and hands-off functionality

- These features are now available across multiple Nissan models

- Building on this foundation, Nissan is developing its next-generation ProPILOT integrated with Wayve AI

- In September 2025, Nissan unveiled a prototype featuring Wayve’s AI software, “Wayve AI Driver” integrated with Nissan’s “Ground Truth Perception“ tech

- Nissan is the first automaker to commit to deploying Wayve AI systems at scale across a broad range of vehicles

- Wayve’s end-to-end embodied AI can adapt efficiently to new cities and vehicle platforms with minimal additional development

- When combined with ProPILOTvarious sensor configurations including cameras, radar and LiDAR, it can deliver intelligent driving across many vehicles

- Deploying the system into mass-produced vehicles will allow Nissan and Wayve to learn from diverse real world conditions

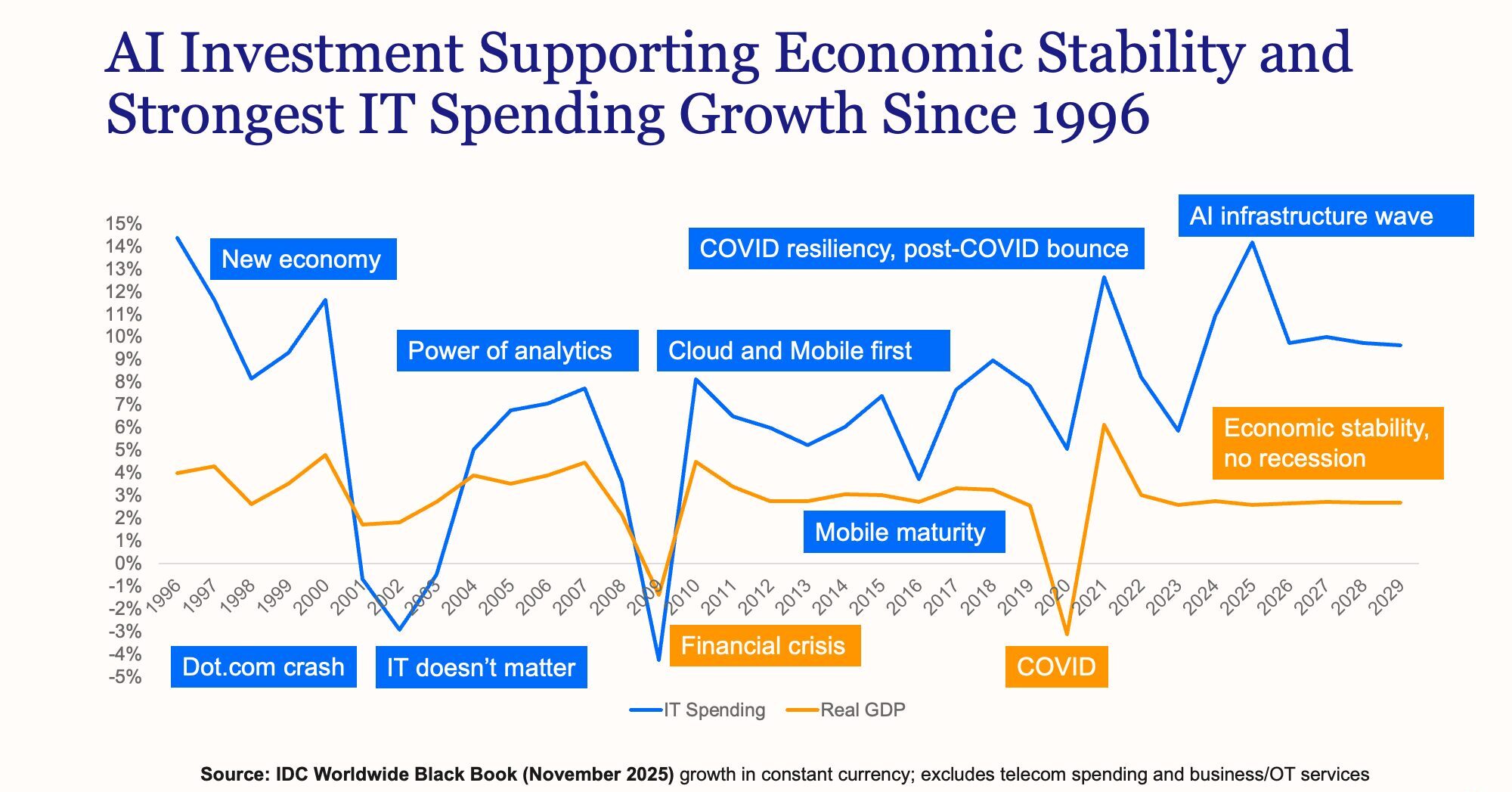

2025 Global IT Spending Growth Hits 1996 Levels Thanks To AI

IDC’s newest global IT spend (hardware, software, and IT services) projections, which were released this week, point to a whopping +15% y/y growth rate in 2025. The last time growth was that strong was in 1996 when Windows 95 was launched and expanded PC usage and internet adoption. What is the driver of this new super cycle this go around? AI, of course. Total IT spending is slated to reach $4.25 trillion this year and this forecast has essentially been revised up 7x!

Will this level of spending hit a wall? IDC does not see that on the horizon. Their surveys indicate that most businesses plan to increase IT budgets again in 2026. IDC itself now forecasts a decelerating, but still healthy growth of +10% y/y in 2026. This would still represent one of the strongest years for the industry since the 1990s. However, one potential risk to be aware of is that an expected memory component shortage could drive up PC prices next year. Even so, expectations are optimistic… “even in a moderate recession, most IT spending would continue. The likelihood of a ‘perfect storm’ similar to the IT market crash of 2001 remains low” (link)

While IDC remains bullish, the debate regarding future IT spending trends will likely continue to be top of mind.

Source: IDC

Grab Bag: TKO’s Mrgn Guidance / Millions Of Teens Lose Access To Social Media / Euro CEOs Are Looking To Invest In The US Even More Than Before

- TKO shares fell -2.4% after the Co provided margin guidance that fell short of expectations (link/link)

- TKO execs stated on the Wall Street conference circuit that they expect adj EBITDA margins “in excess of 35%” next yr, vs consensus 37.5% per Bloomberg

- The Co also discussed an upcoming UFC event scheduled to take place at the White House on June 14

- They described the event as “a spectacle on steroids” compared to previous productions at venues like the Sphere

- However, they acknowledged that “there will be no ticket sales,” which “will hurt us financially”

-> Despite the knee jerk sell-off, TKO shares closed up +3% this week and is up +48% YTD

- Millions of teens lose access to their accounts as Australia’s world-first social media ban begins (link/link)

- Australia’s world-first ban on social media for users aged under 16 came into effect this week

- Who is involved? Facebook, Instagram, Threads, X, YouTube, Snapchat, Reddit, Kick, Twitch and TikTok are expected to have taken steps from Wednesday to remove accounts

- Platforms that do not comply with the rules risk fines of up to $32.09mn (A$49.5mn)

- Guardian Australia has received several reports of those under 16 passing the facial age assurance tests

- The gov flagged it is not expecting the ban will be perfect from day one

- Polling has consistently shown that 2/3 of voters supported raising the minimum age for social media to 16

- The opposition, including leader Sussan Ley, recently voiced alarm about the ban, despite waving the legislation through parliament

- The ban has garnered worldwide attention, with several nations indicating they will adopt a ban of their own, including Malaysia, Denmark and Norway

- The European Union passed a resolution to adopt similar restrictions

- A spokesperson for the British government told Reuters it was “closely monitoring Australia’s approach to age restrictions”

- A recent survey showed that European CEOs are downbeat on Europe & favor US investment (link/link)

- What was the survey? It was of the European Round Table for Industry, which comprises about 60 CEOs and chairs of companies such as ASML, BASF and Vodafone

- What was found? Respondents found that the biz case for investing in Europe was weakening further and that the European Union was too slow to implement required reforms

- ~38% said they would invest less than they had planned 6 months earlier in Europe or had put decisions on hold

- ~8% said their European investments would increase

- ~45% said they intend to invest more in the US

- A “large majority” of survey respondents said they had seen little or no positive impact from EU initiatives in critical areas

- These included regulatory simplification, single market completion, competition policy and energy affordability

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Telemundo annc’d its 104-match World Cup slate is ~90% sold out, w/ ad pricing sharply higher vs. 2022 Qatar. The network expects record ad rev as demand surges ahead of the event. Peacock will stream matches, boosting NBCU’s sports biz reach. Strong mkts interest signals continued growth for FIFA-related media svs. (Sportico)

Artificial Intelligence/Machine Learning

- Broadcom CEO Hock Tan revealed that AI lab Anthropic is the mystery customer behind a $10bn chip order annc’d in Sept. Anthropic also placed an extra $11bn order in Q4 for Google TPUs, which Broadcom helps build. Broadcom now has five XPU customers, incl. a new $1bn deal. (CNBC)

- Gemini Deep Research, powered by Gemini 3 Pro, is now live via Interactions API, enabling devs to embed advanced autonomous research in apps. It features improved multi-step reasoning, reduced hallucinations, and state-of-the-art results on HLE (46.4%) and DeepSearchQA (66.1%). (Google)

- OpenAI marks 10 yrs since annc’d mission to build AGI for humanity. From early uncertainty w/15 staff, cont’d breakthroughs incl. 2017 RL wins, sentiment neuron, and human-preference alignment. ChatGPT launch 3 yrs ago, GPT‑4 scaled tech globally. Co adopted iterative deployment, now optimistic on superintelligence by 2035. (OpenAI)

- Google Labs annc’d Disco, a new platform to reimagine web browsing, featuring GenTabs built w/ Gemini 3. GenTabs helps users manage complex tasks by creating interactive web apps from natural language, linking back to sources. Early testers use it for trip planning, meal prep, and learning. A waitlist is open for macOS; feedback will shape future Google products. (Google)

- Microsoft research on 37.5mn Copilot chats (Jan.–Sept. 2025) shows users treat it as a productivity tool on desktop but as a conversational partner on mobile. Late-night queries skew philosophical. While bots offer guidance, risks include errors, bias, and lack of legal confidentiality. MS aims to add guardrails after past failures (e.g., Tay). (Axios)

- OpenAI warns upcoming frontier AI models may pose “high” cybersecurity risk as their autonomous capabilities grow, enabling brute force attacks. GPT-5 scored 27% on a CTF in Aug., while GPT-5.1-Codex-Max hit 76% last month. Co plans for “high” risk levels under its Preparedness Framework, forming a Frontier Risk Council and testing Aardvark to detect security gaps. (Axios)

- OpenAI & Deutsche Telekom annc’d a multi-yr collaboration to co-develop AI products for everyday use. Deutsche Telekom gains early access to an alpha-phase model, w/ pilots planned for Q1 2026. Focus: simple, privacy-first AI for millions, enhancing communication & productivity. ChatGPT Enterprise will roll out internally, boosting svs, workflows & innovation. (Telekom)

- OpenAI annc’d Denise Dresser as Chief Rev Officer, aiming to scale its fast-growing biz platform. Denise, ex-CEO of Slack and former Salesforce exec, brings deep customer insight and global sales expertise. She’ll drive rev strategy as cos adopt AI broadly, w/ 75% reporting improved work speed/quality. (OpenAI)

- Enterprise AI spend surged to $37bn in 2025 (up 3. 2x YoY), now 6% of global SaaS mkts. Apps dominate w/$19bn, led by coding tools ($4bn) as AI’s first killer use case. Vertical AI hit $3.5bn, w/healthcare at $1.5bn. Horizontal AI copilots captured $7.2bn. Infra spend reached $18bn, w/Anthropic leading LLM share at 40%. (Menlo Ventures)

- Mistral annc’d state-of-the-art open-source agentic coding models and CLI agent, branded as Devstral, aiming to redefine SOTA coding. The launch includes Mistral Vibe CLI for streamlined dev workflows. Co highlights ease of install via bash script and invites devs to explore, build, and join its growing team. (Mistral AI)

- Microsoft annc’d a US$17.5bn investment in India (CY2026–2029) to expand cloud & AI infra, skilling, and sovereignty solutions, building on its earlier $3bn spend. Plans include hyperscale datacenters (Hyderabad mid-2026), AI integration into e-Shram & NCS for 310mn workers, and doubling skilling to 20mn by 2030. (Microsoft)

- Beijing plans to limit access to Nvidia’s H200 AI chips despite Trump’s approval to export w/ a 25% fee. Regulators aim for restricted use, adding hurdles for U.S. cos in China mkts. Nvidia shares rose 2% premarket but closed up ~0.6%. Earlier U.S. bans hit rev growth in China. (Reuters)

- Google denied reports that ads will appear in its Gemini AI app, stating there are “no current plans” for such changes. While ads exist in AI Overviews in the US and tests continue in AI Mode, Gemini remains ad-free. The rumor stemmed from claims Google told ad clients about 2026 plans, which it calls inaccurate. (9to5Google)

- OpenAI’s survey of 9,000 workers across 100 cos shows AI tools save ~40–60 mins daily on tasks, w/ data science, engineering & comms roles seeing most gains. 75% report improved speed or quality. Despite skepticism—MIT, Harvard & Stanford cite low ROI & “workslop”—OpenAI claims enterprise adoption is accelerating. (Bloomberg)

- Limitless has been acquired by Meta to align w/ its vision of personal superintelligence and AI-enabled wearables. Existing Pendant customers will be supported for ~1 yr, get Unlimited Plan free, and no longer pay subscriptions. Pendant sales stop; non-Pendant features like Rewind will be sunset. Users can export or delete data easily. (Limitless)

- Sensor Tower data suggests ChatGPT is still the mobile AI leader (about 50% of global downloads and 55% of global MAUs). Its growth is slowing—MAUs rose only ~6% from Aug–Nov 2025 to ~810M, while Google Gemini grew faster (~30% in the same period), boosted by its viral image model “Nano Banana” and deeper **Android OS integration that drives usage beyond the standalone app. (TechCrunch)

Audio/Music/Podcast

- UMG annc’d two new UMusic Shops in NY & London expanding its global retail footprint. NY’s 2 Penn Plaza store offers exclusive artist merch, vinyl, and collabs like UMG x Awake NY. London’s Camden Market shop opens, featuring immersive installations, live sets, and a Vinyl Lounge. (Universal Music)

- Spotify annc’d Prompted Playlist, a beta feature launching Dec. 11 for Premium users in NZ. It lets listeners steer the algorithm w/ custom prompts, creating playlists based on taste, history, and world trends. Users can fine-tune, refresh daily/weekly, and access curated ideas. (Spotify)

- Spotify annc’d beta rollout of music videos for Premium users in U. S. & Canada. Feature offers official videos incl. live & cover versions, w/ limited catalog initially but set to expand in coming months. Users can switch between audio/video on TV, desktop & mobile. Burson survey shows 70% want more video; engagement boosts streams by 34% & saves/shares by 24%. (Spotify)

Cable/Pay-TV/Wireless

- AT&T annc’d Wi-Fi Personalization, an AI-powered feature for All-Fi Pro & fiber-wireless combo customers at no extra cost. It lets users set priorities for work, gaming, or streaming via Smart Home Manager app or rely on AI to auto-optimize speeds. Data stays secure locally. Early results show better home Wi-Fi & lower latency. (AT&T)

Capital Market Updates

- T-Mobile US annc’d its board approved a new shareholder return program of up to $14. 6bn running through Dec. 31, 2026. The plan includes stock repurchases and cash dividends, funded by cash and potential debt. It follows an existing $14bn program expiring in 2025. Timing depends on mkts and cos performance; repurchases may use open mkts, 10b5-1 plans, or private deals. (Investing.com)

- Massive debt-fueled deals are back on Wall Street. Financing from banks & private-credit funds fuels bold bets, w/ mkts showing signs of overexuberance. (The Wall Street Journal)

- More than half of Intercontinental Exchange Inc.’s institutional clients show interest in prediction-mkt data from its new Polymarket partnership, per CEO Jeffrey Sprecher. The exchange operator’s 10,000 customers, who trade oil, gas & cocoa, now eye prediction mkts to gauge impact on current & future positions, Sprecher said at Goldman Sachs financial svs conf. (Bloomberg)

- CoreWeave annc’d plans to offer $2bn convertible senior notes due Dec 2031 in a private deal, w/ option for $300mn more. Notes guaranteed by subs, accrue semi-annual interest, convertible into cash, stock or both. Proceeds to fund capped call transactions & general corp purposes. (CoreWeave)

- Altice International asked its secured creditors for a copy of their cooperation pact and member identities before any talks on restructuring its balance sheet. The pact binds lenders to act jointly, limiting direct negotiations w/ the Co. Altice seeks clarity on “future engagement” terms. (Bloomberg)

Cloud/DataCenters/IT Infrastructure

- SoftBank is exploring acquisitions to boost its AI infrastructure push, including Switch, a data-center operator valued at ~$50bn w/debt. Talks also involve DigitalBridge, a major digital infra investor w/$108bn AUM. Switch may IPO early next yr at ~$60bn valuation. Recent SoftBank moves include $6.5bn Ampere buy, $30bn OpenAI commitment, and Stargate project. (The Japan Times)

- Boom Supersonic annc’d Superpower, a 42MW natural gas turbine leveraging its Symphony supersonic engine core to tackle AI data center power shortages. Unlike legacy turbines, Superpower delivers full output even at 110°F, operates water-free, and offers cloud-native monitoring. (Boom Supersonic)

- Big tech hyperscalers plan >$400bn capex on AI data centres, but face a severe power crunch. By 2028, ~44GW extra capacity is needed vs 25GW available, leaving a 19GW gap. Five US sites will each draw >1GW by 2026. Grid delays, ageing infra, and equipment shortages hinder expansion, risking AI “bubble” deflation. (Financial Times)

- IBM is in advanced talks to acquire Confluent Inc for ~$11bn, per WSJ. Confluent shares surged 28.1% premarket. The deal, possibly annc’d today, would be IBM’s largest in yrs, expanding its software stack into real-time data streaming and boosting AI capabilities. (Investing.com)

Crypto/Blockchain/web3/NFTs

- Coinbase Global, the US’s biggest crypto exchange, plans to annc’d prediction mkts and tokenized equities at a showcase, per a source. Tokenized stocks will be launched in-house, not via partners. These products aim to tap two of the hottest trends in financial mkts, signaling Coinbase’s push to expand its biz beyond traditional crypto svs. (Bloomberg)

- Kalshi & Crypto. com annc’d formation of Coalition for Prediction Mkts (CPM) w/ Coinbase, Robinhood & Underdog to promote safe, federally supervised access. Prediction mkts, w/ ~$28bn trading vol in 2025, outperform polls by ~30%, aiding insight into econ & cultural trends. (PR Newswire)

Cybersecurity/Security

- CLEAR annc’d a contract w/ CMS to integrate its CLEAR1 secure identity platform into Medicare. gov by early 2026. The move aims to modernize account creation/recovery, reduce fraud, and improve access for millions of beneficiaries. (Clear)

eCommerce/Social Commerce/Retail

- Walmart annc’d its historic transfer from NYSE to Nasdaq, ending 53 yrs on NYSE since 1972. WMT’s stock grew 536,000% over that period. As of its last NYSE day, WMT had a $905bn market cap, making this the largest exchange transfer ever. (Yahoo Finance)

- Best Buy annc’d holiday deals for last-minute shoppers. Apple Sales Event runs till Dec. 11 w/ savings on Mac, iPad, AirPods. 3-Day Sale starts, up to 50% off TVs, laptops, games. Last-Minute Savings on Dec. 15. Doorbusters every Fri.; members earn up to $25 rewards. Trade-in offers up to $400 off PS5. (Best Buy)

- Costco beat Wall Street’s Q1 expectations w/ rev of $67. 31bn vs $67.14bn est. Sales rose 8.2%, digital up 20.5%. EPS hit $4.50 vs $4.27 est. Net income grew to $2bn. Comparable sales: U.S. +5.9%, global +6.4%. Black Friday e-comm rev topped $250mn. Memberships up 5.2% to 81.4mn; renewal rate 92.2% in U.S./Canada. (CNBC)

- Lululemon shares jumped ~10% after CEO Calvin McDonald annc’d he’ll step down Jan. 31, staying as advisor till Mar. 31. Co posted Q3 EPS $2.59 vs $2.25 est., rev $2.57bn vs $2.48bn est. FY sales outlook raised to $10.96–$11.05bn; EPS $12.92–$13.02. Americas rev fell 2%, intl up 33%. (CNBC)

- Amazon annc’d Same-Day perishable grocery delivery now in 2,300+ cities, w/ cont’d expansion in 2026. Fresh items make up 9 of top 10 orders; bananas, avocados lead. Perishable selection grew 30% since Aug., incl. Whole Foods favorites. Prime offers free delivery on $25+ orders; non-members pay $12.99. Amazon Grocery private brand tops 1,000 items, most <$5. (Amazon)

- Shopify annc’d Product Network, enabling US merchants to expand catalogs instantly w/ zero inventory risk. Merchants access products from thousands of brands, earn commission on sales, and retain customer data. Integration is quick—placements customizable across search, thank-you pages, etc. (Shopify)

- Study by Groundwork & Consumer Reports found Instacart prices vary for same items in same store/time, w/diffs up to 20%. Tests in 4 cities showed ~7% basket variance. Instacart said stores set prices, citing short-term tests to gauge consumer prefs. Dynamic pricing via algorithms, rising post-pandemic, adds volatility, may push costs higher. (The New York Times)

- Home Depot annc’d fiscal 2026 outlook w/ flat–2% same-store sales growth and adj EPS up 0–4%, both below estimates. CFO cited persisting pressure from high home prices, unemployment, and weak housing activity despite easing rates. Big-ticket spending remains sluggish; cos expect recovery once housing mkts stabilize. Stock down ~10% YTD vs S&P 500’s 16% rise. (Reuters)

- Retail job cuts hit 3,290 in Nov, up 35% from Oct, per Challenger report. YTD layoffs total 91,954, nearly 140% higher vs. 2024, driven by soft demand, tariffs & shifting consumer prefs. Across all industries, 71,321 jobs cut in Nov., 24% YoY rise. Major cos like Target (1,000 roles), Amazon (14,000) & Yankee Candle (900) annc’d cuts. (Retail Dive)

- Instacart annc’d it’s the first grocery tech Co to launch an app on ChatGPT, enabling embedded shopping and Instant Checkout w/ AI-powered support. Users can plan meals, build carts, and pay securely in-chat via Stripe, w/ Apple Pay & Google Pay coming soon. (Instacart)

Electric & Autonomous Vehicles

- Rivian annc’d major tech strides at its Autonomy & AI Day, unveiling custom RAP1 silicon powering Gen 3 ACM3 w/1600 sparse TOPS and RivLink interconnect. LiDAR integration for R2 models ships end-2026. Software roadmap includes LDM for autonomy, UHF on 3.5mn miles, and Autonomy+ subscription ($2,500 or $49.99/mo) in early 2026. (Rivian)

- Uber spent yrs pushing drivers toward EVs w/ promos. Levi Spires, a 51-yr-old driver in Syracuse, took a $2,000 offer after his Prius was damaged, buying a Tesla. Over 23 mos., he earned ~$3,500 in EV bonuses driving ~139,000 miles. These efforts were part of Uber’s goal to shift drivers into cleaner cars. (Bloomberg)

Film/Studio/Content/IP/Talent

- Cinema attendance remains at 64% of pre-COVID levels, per Bain & Co.’s report. Streaming surged since 2010 while box-office rev fell; rising concession costs make theaters seem pricey. Bain urges cos to invest in premiumization, personalization, and partnerships. Recommendations include premium auditoriums, social spaces, community events, and fresh content beyond big IP. (The Hollywood Reporter)

- Disney’s Zootopia 2 eyes No. 1 w/~$26M (-40% from $43.4M) in its 3rd wknd, nearing $1bn WW sans Russia—3rd film YTD to hit that mark. Universal’s Five Nights at Freddy’s 2 targets $16M–$20M, stands at $71M, heading for $100M+. Brooks’ dramedy Ella McCay opens at $4M vs $35M cost; reviews poor (23% RT). (Deadline)

- Netflix annc’d Steps, an animated film reimagining Cinderella’s stepsisters. Directed by Alyce Tzue & John Ripa, voiced by Ali Wong & Stephanie Hsu, it follows Lilith, who accidentally turns her sis into a frog, forcing a team-up w/ Cinderella to save the kingdom. Produced by Amy Poehler & team, the story explores belonging & kindness. (Netflix)

FinTech/InsurTech/Payments

- Mastercard’s Board annc’d a quarterly cash dividend of $0.87/share, up 14% from $0.76. Payment set for Feb. 9, 2026 to holders as of Jan. 9, 2026. The Board also approved a new share repurchase program authorizing up to $14bn of Class A stock, effective after completion of its prior $12bn program. As of Dec. 5, 2025, ~$4.2bn remained under the current plan. (Business Wire)

Handheld Devices & Accessories/Connected Home

- AT&T annc’d Connected Life, a smart home security svc powered by Google Home & Abode, offering cellular backup to stay online during outages. Starter kit costs $399 incl. Nest Doorbell, Abode hub, sensors; advanced kit at $699 adds Nest cam & keypad. Plans start at $10.99/mo for 30-day video history & smart alerts; $21.99/mo adds 24/7 monitoring. (The Verge)

- Pixel Watch 4 brings AI-powered Gemini features w/ two major updates: 1) New one-handed gestures like Double pinch & Wrist turn let users scroll, dismiss notifications, snooze alarms, manage timers, pause music, and handle calls w/o touching the screen. 2) Enhanced Smart Replies use Gemma-based model for faster, efficient on-device responses even untethered from phone—ideal for multitasking during holidays. (Google)

Investor & Market Sentiment

- Survey by European Round Table shows CEOs of major cos like ASML, BASF, Vodafone remain downbeat on EU prospects, citing slow reforms and weak biz case. ~38% plan reduced or delayed EU investment; only 8% expect increase. Meanwhile, 45% aim to invest more in U.S. Leaders urge EU to act on Draghi/Letta reports for competitiveness, but most see little impact from initiatives on regulation, mkts, energy. (Reuters)

Live Entertainment/Theme Parks/Concerts/Experiential

- Venu Holding Corp entered into a 5-yr Operator Agreement w/ Live Nation for The Sunset McKinney amphitheater in Texas. Live Nation will lease the premises, hold exclusive booking rights, and share rev via profit-sharing, per-ticket rent, and concession splits. Co retains naming rights; Live Nation gets ROFO on sale. (SEC.gov)

Macro Updates

- U. S. trade deficit in goods & svs narrowed >10% from Aug. to Sept., as Trump tariffs cont’d to weigh on trade, per Commerce Dept. Imports rose 0.6% to $342.1bn, exports up 3% to $289.3bn. Deficit fell to $52.8bn, lowest since Jun. 2020 amid Covid-19. Experts caution trend may not persist; trade patterns distorted by cos avoiding tariffs. (The New York Times)

- Worldwide IT spend is projected to grow 14% in 2025, driven by AI infra investments, per IDC. This marks the fastest growth since 1996 when PCs & internet adoption surged. Total IT outlays to hit $4.25tn this yr, while overall ICT spend incl. telecom & biz svs will near $7tn. (Telecompaper)

Media Conglomerates

- Shares of Mexican media conglomerate Grupo Televisa SAB hit a 2-wk high after reports it’s eyeing AT&T’s Mexico unit. Columnist Dario Celis said Televisa’s cable arm Izzi is in final stages of a possible deal, competing w/ Cerberus Capital Mgmt. Televisa’s local shares rose 2.2% to 10.19 pesos per share. (Bloomberg)

- Gedi Gruppo Editoriale SpA, a media group controlled by the Agnelli family, is in talks w/ Greece’s Antenna Group for a potential sale of its editorial assets. A spokesperson for Exor NV-owned Gedi annc’d late Sunday that discussions, which began last summer, are cont’d positively, but no further details were provided. (Bloomberg)

- Global M&A is on track for its best yr since 2021, w/ late-yr deals pushing volumes past $3tn. (Bloomberg)

Online Marketplaces/Learning (Real Estate/Education/Jobs)

- Lai Sun Dev. annc’d sale of 50% stake in HK office tower to JD.com for HK$3.5bn ($450mn) to bolster cash flow amid financial stress. Deal covers 12 floors + parking, closing in Jan. Net proceeds HK$2.4bn; Lai Sun expects HK$261mn loss (non-cash). Price at 6.7% discount to Jul. valuation. Shares up 3.2%; JD.com down 0.8%. (Reuters)

Online Travel

- Expedia Group annc’d agreement to acquire Tiqets, an Amsterdam-based platform for museums, attractions & experiences, aiming to expand global travel offerings. Deal enhances Expedia’s B2B tech ecosystem, integrating curated activities w/ its scale to deliver full-trip solutions. Expected close in Q1 2026, subject to customary conditions. Tiqets operates in 60+ countries & 1,000+ cities, boosting Expedia’s reach & innovation. (Expedia Group)

Regulatory

- Gov. Hochul signed first-in-nation laws to boost AI transparency in film. Bill S.8420-A/A.8887-B mandates ads disclose AI-generated synthetic performers; S.8391/A.8882 requires heirs’ consent for post-mortem name/image use. Officials cite rising deepfakes harming consumers, jobs. (Governor of New York)

- Gov. Hochul plans to replace NY’s RAISE Act w/ SB 53 language, shifting AI regulation to a lighter-touch model. Proposal drops key RAISE provisions like bans on risky models, stricter incident reporting, and higher fines ($10–30mn vs. $1mn). SB 53 applies only to cos w/ rev >$500mn, unlike RAISE’s $100mn compute spend rule. (Transformer)

- Google faces a potential EU fine in Q1 2026 if Google Play doesn’t meet DMA rules for fair access. Tweaks annc’d in Aug. still fall short, w/ issues on devs steering users to cheaper channels and high svs fees. Apple’s App Store overhaul post €500mn fine sets benchmark. Google may offer more changes; fines can reach 10% of global rev. (Reuters)

Satellite/Space

- Bezos’ Blue Origin and Musk’s SpaceX are racing to move AI data centers into orbit. Blue Origin has worked >1 yr on tech for orbital AI hubs, while SpaceX plans upgraded Starlink satellites for AI computing, pitching a share sale valuing the Co at ~$800bn. Challenges include cost, engineering hurdles, and matching ground-based performance. (The Wall Street Journal)

- SpaceX plans an IPO in mid-to-late 2026 aiming to raise >$30bn, targeting ~$1. 5tn valuation—near Saudi Aramco’s 2019 record. Timing may shift to 2027. Growth driven by Starlink svs and Starship dev. Rev forecast: $15bn in 2025, rising to $22–24bn in 2026. Funds to support space-based data centers. (Yahoo Finance)

Social/Digital Media

- Reddit filed a lawsuit in Australia’s High Court, seeking to overturn the nation’s social media ban for under-16s, calling it a threat to free speech. The Co argues the law impedes political discourse and claims it doesn’t meet the definition of social media. Govt compares Reddit’s move to Big Tobacco tactics, vowing to fight. Platforms face fines up to A$49.5mn for non-compliance. (Reuters)

- Reddit annc’d a limited alpha test of verified profiles, adding grey checkmarks to usernames for individuals & cos to confirm identity. This opt-in feature aims to boost clarity, aid moderators, and preserve pseudonymity. Initial rollout targets public figures & trusted partners; users can’t request verification yet. Verified accounts must follow all rules. (Reddit)

- Adults in the UK spend avg 4. 5 hrs online daily, mostly via smartphones using 41 apps/month. Alphabet & Meta svs dominate, w/ YouTube (94%) & Facebook/Messenger (93%) leading. AI reshapes search: 30% queries show AI overviews; ChatGPT hits 1.8bn visits in 8 mos. Only 33% see internet as good for society. (Ofcom)

- Teens’ online habits show stability w/ new trends: 97% go online daily, 40% almost constantly. YouTube leads use (90%), followed by TikTok (61%) & Instagram (55%). WhatsApp grew to 24%, while X & Facebook declined. 64% use AI chatbots; 31% daily, w/ ChatGPT most popular (59%). (Pew Research)

- Reddit annc’d global teen safety updates as Australia enforces a social media ban for kids <16. Changes include stricter chat settings, no NSFW content, no personalized ads, and birthdate verification. AU users face an age-prediction model; under-16 accounts suspended. Law fines cos up to $32.9mn for non-compliance. (Yahoo Finance)

Software

- Adobe annc’d upbeat FY2026 outlook, projecting rev of ~$25. 90–26.10bn and adj EPS of $23.30–23.50, beating Wall St. estimates. Q4 rev hit $6.19bn vs. $6.11bn forecast. Growth driven by strong demand for Creative Cloud, Photoshop, Lightroom, and AI tools like Firefly. Monthly active users rose 35% YoY to 70mn. (Reuters)

Sports/Sports Betting

- Wrexham AFC annc’d Apollo Sports Capital as minority investor, fueling growth on/off pitch. ASC will finance STōK Cae Ras redevelopment incl. new Kop Stand, part of Wrexham Gateway Project to boost city’s economy. Co-chairs Rob Mac & Ryan Reynolds aim for Premier League while preserving heritage. (Apollo)

Tech Hardware

- Appeals court ruled against Apple in its cont’d legal fight w/ Epic, affirming contempt finding over a 27% fee on external transactions. The 9th Circuit said the fee had a “prohibitive effect,” violating an injunction allowing devs to link outside App Store. Judge must reconsider commission for Apple’s IP use. (Investing.com)

- Memory prices are projected to surge in 1Q26, adding cost pressure on global device makers, says TrendForce. Smartphone & notebook brands will raise prices and downgrade specs; shipment forecasts face downward revision. DRAM costs dominate BOM, forcing Apple to rethink pricing and Android brands to hike launch prices. (TrendForce)

- Meta plans price hikes on VR devices to ensure long-term sustainability, per an internal memo. Execs said the biz will shift by raising prices, extending device replacement cycles, and focusing on high-quality software. Quest 3 retails at $499.99; entry-level at $299.99. Mixed reality glasses launch pushed to 1H 2027. (Business Insider)

- EssilorLuxottica’s Ray-Ban Meta AI glasses, launched in 2021, delivered first meaningful rev boost this yr, driving a 14% rally for the €140bn Co despite only 2% of global sales. Features like photo/video capture and AI assistant spark EU privacy concerns under GDPR. EssilorLuxottica holds 60% mkts share but faces rising competition from Alibaba, Apple, Google, Amazon. (Reuters)

- Nintendo’s shares fell 4.7% to their lowest since May, as surging component costs threaten profits. Memory prices for Switch 2 soared: 12GB RAM up 41% this qtr per TrendForce, NAND storage nearly 8% pricier, impacting add-on cards. Rising accessory costs may curb mkts demand, squeezing margins for the Kyoto-based gaming pioneer amid escalating chip expenses. (Bloomberg)

- Warby Parker annc’d collab w/ Google to launch lightweight AI-powered glasses in 2026, revealed at The Android Show | XR Edition. Google aims to re-enter wearable tech after shelving Glass a decade ago, leveraging Android XR & Gemini AI for multimodal intelligence. (Reuters)

- ByteDance annc’d tighter controls on its AI-powered Nubia M153 phone after major apps restricted Doubao’s voice functions. Measures include disabling svs on banking, payments, and games to ensure fair play. Issues w/ WeChat caused login blocks; Alipay, Taobao, Pinduoduo also limited use. Phone, priced at ~$494, sold out on launch as a tech preview. (Yahoo Tech)

Video Games/Interactive Entertainment

- Amazon Game Studios & Crystal Dynamics annc’d “Tomb Raider: Catalyst,” launching 2027 for PS5, Xbox Series X|S & Steam, w/ Lara Croft voiced by Alix Wilton Regan. Set post-cataclysm in N. India, Lara faces rivals to stop misuse of ancient power. A remake, “Tomb Raider: Legacy of Atlantis,” arrives 2026 w/ Unreal Engine 5 visuals, honoring 1996 debut. (Variety)

- Epic Games’ Fortnite returned to Google Play in the U. S. after Google complied w/ a court injunction. Epic is working w/ Google to seek court approval for a settlement in their yrs-long antitrust dispute over app store practices. Fortnite was removed in 2020 after Epic bypassed Google billing. (Reuters)

- Hollywood and gaming are increasingly intertwined, w/ Fortnite leading the charge. Epic annc’d major collabs like “Simpsons,” “Star Wars,” and now Tarantino’s “Kill Bill” short, marking its first scripted content launch. Studios see gaming as vital for younger audiences, w/ Roblox enabling IP-based games and boosting monetization. (Yahoo)

- GameStop posted Q3 rev of $821mn, missing est. of $987.3mn, as it cont’d to struggle w/ its digital pivot. Shares fell 5.8% after-hours. Once a leader in physical game sales, the Co faces pressure as gamers shift to online purchases & subscription svs. Hardware/accessories rev dropped ~12%. Efforts incl. (Reuters)

Video Streaming

- Netflix House venues in Dallas (Galleria) and Philadelphia (King of Prussia) are now open, offering immersive fan experiences like Stranger Things: Escape the Dark, Squid Game: Survive the Trials, Wednesday: Eve of the Outcasts, and ONE PIECE: Quest for the Devil Fruit. Attractions include VR games, mini-golf, arcade RePlay, screenings, dining at Netflix Bites, and merch. (Netflix)

- YouTube TV, currently $82. 99/mo, will roll out 10+ cheaper genre-specific plans in early 2026, incl. Sports Plan w/ ESPN Unlimited, Fox Sports 1, NBC Sports & add-ons like NFL Sunday Ticket. Plans keep core features like unlimited DVR & multiview. Pricing & full channel details TBD. (Variety)

- Crunchyroll will end its ad-supported free tier, requiring paid subs starting Jan. 1, 2026. Current plans remain: Fan $7.99/mo, Mega Fan $11.99, Ultimate Fan $15.99; annual options unchanged. Move aligns w/ streaming industry’s retreat from ad models. Free tier once offered older titles w/ ads; its removal leaves piracy as only zero-cost option. (Cord Cutters News)