There were a few strangler earnings this week (CoreWeave and several China Tech names) but it was nice to not have the onslaught! News flow started to easy but there were several key updates and developments that we focused on this week. In the background, the major market indices trended higher (the S&P 500 +0.9% and Nasdaq +0.8%).

Please see below for the key themes this week:

- Earnings Wrap – More Companies Beat Expectations In Q2 vs Q1, But Upside In Many Cases Was Priced In

- The Dial Turns Higher On Strategic Activity In The Broadcast Sector

- CoreWeave 's Q2 Is Another Sign Pointing To AI Demand Outstripping Supply

- Sports Reign in the Streaming Era

- Amazon Heats Up Competition In The US Online Grocery Segment

- Quick Takes On China Tech: Tencent, JD.com, & Tencent Music

- Grab Bag: EA's Strong BF6 Beta Reception / Netflix Upfronts / Perplexity & Google Chrome

Also, I wanted to mention that LionTree served as exclusive financial advisor to DigitalBridge and Crestview Partners on their take-private acquisition of WideOpenWest (WOW!).

**Lastly, please note that in these last 2 weeks of the August summer period, we will be sending a light version of our Weekly update. The full edition will be back post Labor Day.**

I hope that everyone will have the opportunity to take some time to recharge ahead of what is always a full steam ahead in September!

Best,

Leslie

Earnings Wrap – More Companies Beat Expectations In Q2 vs Q1, But Upside In Many Cases Was Priced In

Given that we reached the end of the Q2 earnings season (finally!), we looked across our LionTree TMT and Consumer Universe of ~200 companies covering 37 sub-sectors with market caps of $1bn+ to evaluate financial performance relative to Wall Street projections.

Overall quarterly performance relative to expectations slightly improved from Q1 in that the number of profitability and revenue beats were higher than last quarter, though there were some shifts in magnitude and distribution.

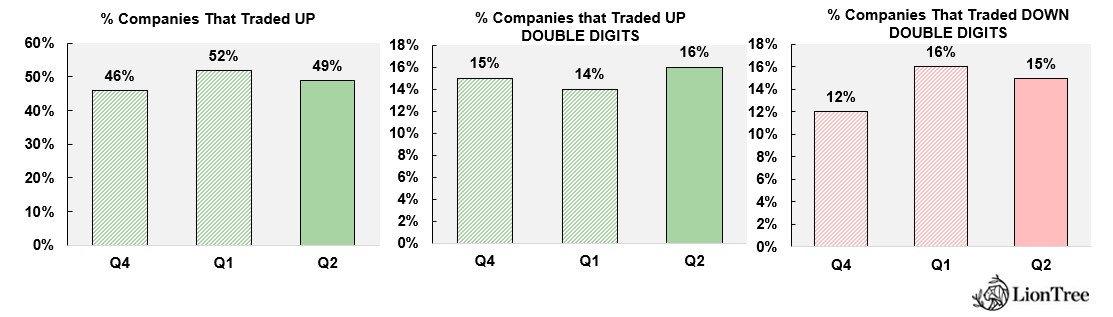

On the profitability side, 83% of companies beat consensus projections, up from 76% in Q1, and the median EBITDA beat widened to +6.2%, from +4.4% last qtr (the avg beat of +10.3% in Q2 was up from +9.7% in Q1). However, 39% of companies delivered double-digits beats which was down from last qtr’s 43%.

On the revenue side, 78% of companies topped estimates, which was above 74% in Q1, 5% of companies posted double-digit revenue beats, up slightly from 3% in Q1, and the median sales increased to +2.3% from +1.0% in Q1, while the avg ticked up to +3.2% from +2.0%.

What was the Street’s reaction to this higher level of out-performance? More of the upside was already priced in as slightly fewer companies (49%) traded up vs down (51%) following results.

See below for more on Q2 financial and stock performance of companies within our LionTree Universe of TMT and Consumer stocks relative to Street expectations.

Investors Were Less Impressed By Q2 Results Than Q1…

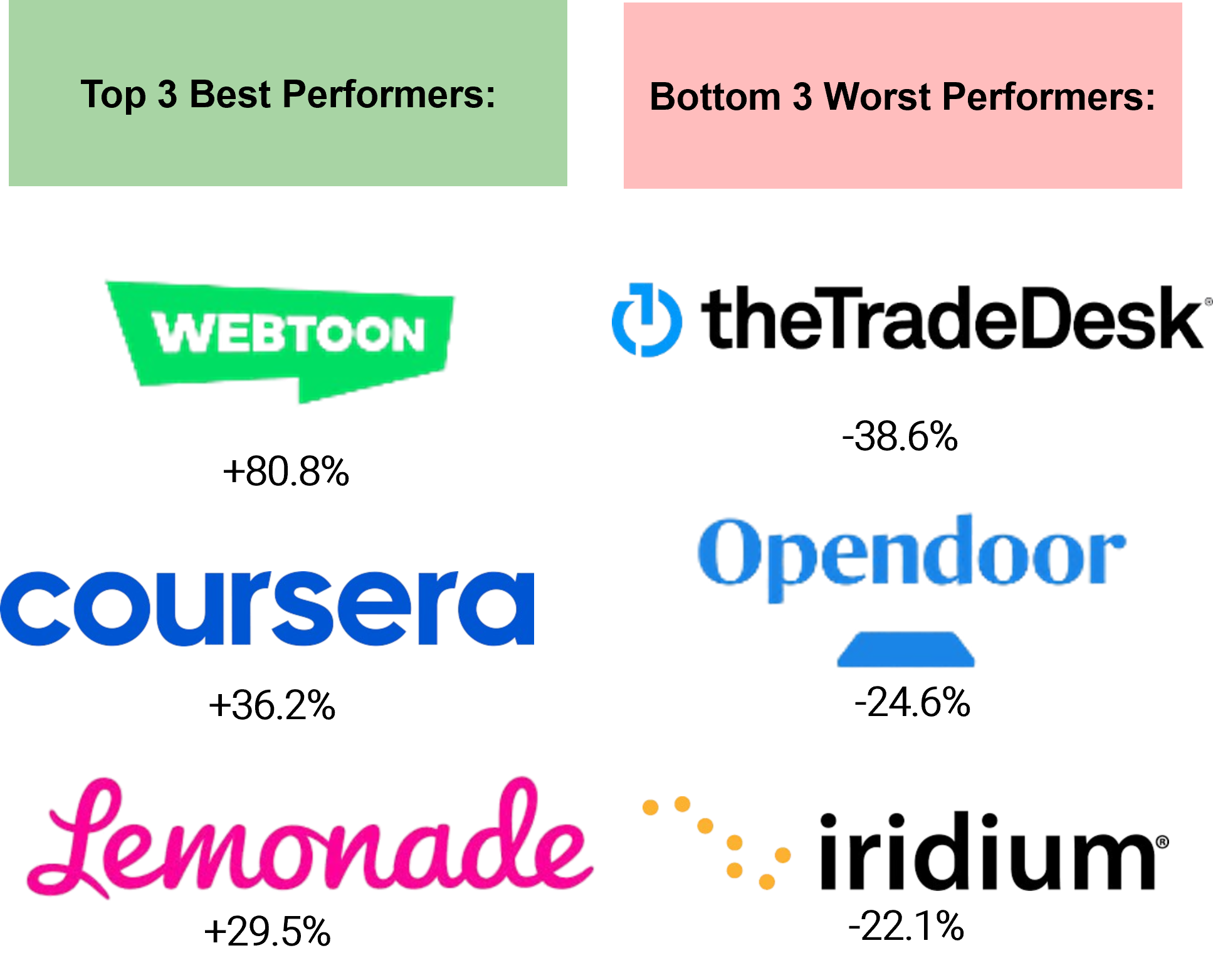

Top 3 Best & Worst Performers…

Of The Companies That BEAT Expectations In Q2…

- Criteo, Liberty Formula One and Reddit had the largest % beats on Sales

- Overall, 78% of the companies in our LionTree Universe beat consensus on revenue (about in-line w/ 74% in Q1), and 5% of those companies beat expectations by double-digits or more (up from 3% in Q1)

- That said, the median sales beat rose to +2.3%, after falling to +1.0% in Q1 (Q4 was +1.4%)

- WEBTOON, Sonos and EA had the largest % beats on adj EBITDA

- Overall, 83% of the companies in our Universe beat consensus on adj. EBITDA, (vs 76% in Q1) and 39% had double-digit beats (vs 43% in Q1)

- The median adj EBITDA rose to +6.2%, up from +4.4% in Q1 (+3.3% in Q4)

Of The Companies That MISSED Expectations In Q2…

- Coinbase, Six Flags and Block had the largest % misses on sales

- Overall, 22% of the companies in our Universe reported sales in-line/lower than consensus

- Lions Gate, Six Flags and Snap had the largest % misses on adj EBITDA

- Overall, 17% of the companies in our Universe we inline or missed consensus on adj. EBITDA

The Dial Turns Higher On Strategic Activity In The Broadcast Sector

Comcast started a trend in November last year when it announced plans to spin off its broadcast/cable nets by the end of 2025 (to be named Versant). Then in June, WarnerBrosDiscovery announced plans to separate its broadcast/cable nets by mid-2026 (to be named Discovery Global). Now this week, there were two more notable updates along these lines…1) Sinclair announced that the Co is launching a strategic review of its b-cast business; and 2) press reports emerged that Nexstar is in advanced talks with Tegna about a proposed transaction, per sources.

All these moves continue to highlight the structural challenges with traditional linear media assets given the shift in TV viewership to streaming and will ultimately provide M&A and consolidation flexibility.

See more details below.

-> Sinclair stock rose +19% in reaction to the Co’s announcement but is still down -8.8% YTD; Tegna stock rallied +30% on the back of its deal speculation while Nexstar (which also traded up +4%); Other broadcasters that rose on this week’s b-cast updates include Gray Media (+16.2%) and Scripps (+13.2%)

Details On Sinclair’s Strategic Review & Potential Ventures Spin

- Sinclair launched a strategic review of its b-cast business…it will evaluate all “value-enhancing opportunities, including acquisitions, strategic partnerships, and business combinations”

- The Co’s B-cast business operates and provides services to 178 TV stations in 81 markets

- Q2 Local Media revenue & adj EBITDA

- Revs: $679mn, down -9% y/y

- Adj EBITDA: $99mn, down -39% y/y

- 2024 Local Media revenue & adj EBITDA

- Revs: $3.25bn, up +13% y/y

- Adj EBITDA $859mn, up +56% y/y

- Q2 Local Media revenue & adj EBITDA

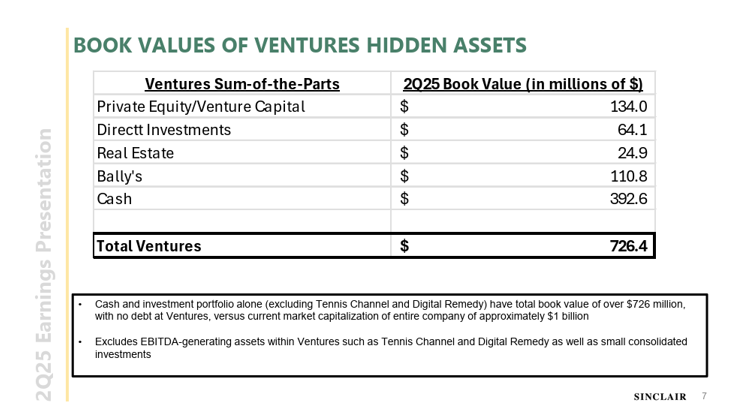

- Separately, it is also evaluating separating Ventures through a spin-off, split off or other transaction

- Along with its last earnings release, the Co broke out the book value of these assets which totaled $726mn

- Press reports emerged early this week that Nexstar is in advanced talks to acquire Tenga: Details were limited

- For reference in Feb of 2022, Tenga annc’d that it would be acquired by PE firm Standard General in a $8.6bn deal ($24/share)…but was later terminated in 2023 as the FCC effectively blocked the transaction

- Tenga shares closed last Friday at $15.31/share

- On Tegna’s earnings call last week, CEO Mike Steib didn’t comment on the press but said…“we believe deregulation is coming and will create significant opportunities…we are open to being a buyer or seller, depending on the opportunities, and are disciplined in our approach”

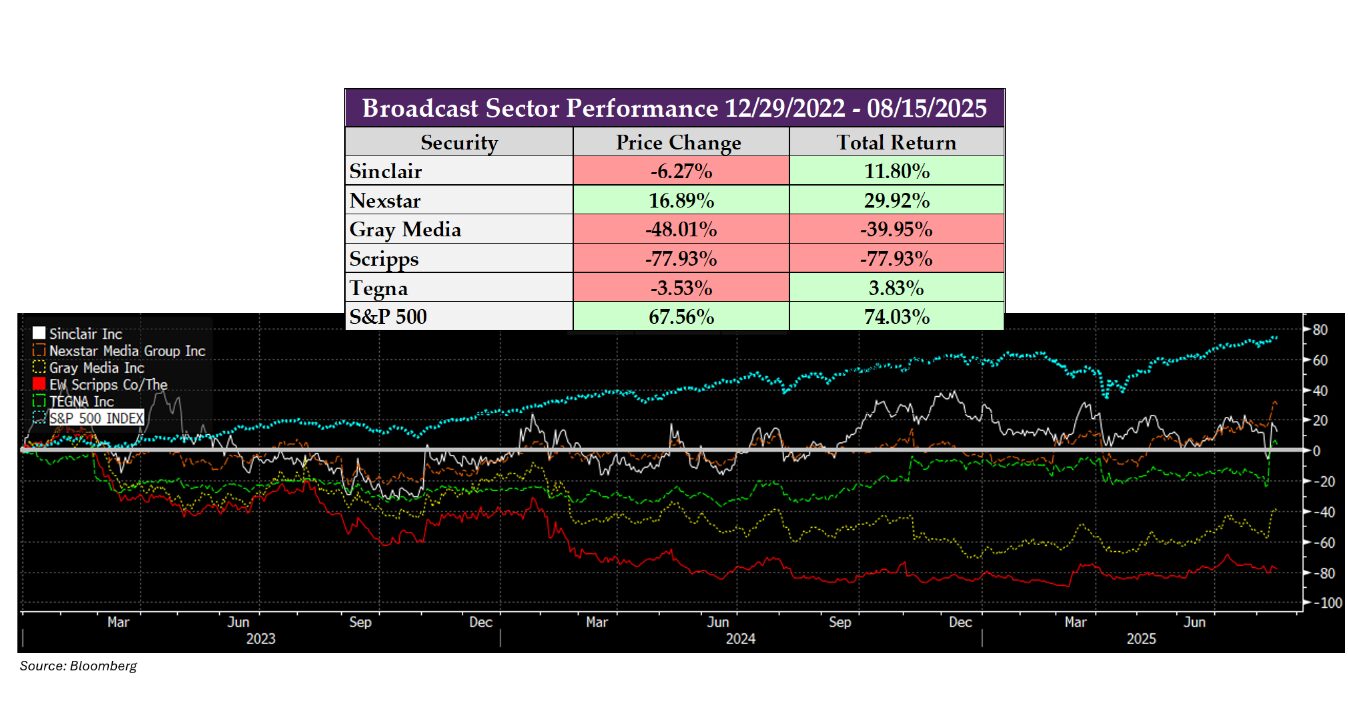

The Broadcast Sector Has Significantly Lagged The Broader Market Since The End Of 2022

- The S&P 500 index from the end of 2022 to date is up 68% (+74% total return), while all broadcasters have underperformed.

CoreWeave 's Q2 Is Another Sign Pointing To AI Demand Outstripping Supply

In addition to Chinese tech companies at the tail-end of the TMT earnings (see Theme #6), CoreWeave was another late reporter this week. Q2 results were quite strong and the Co raised the full year 2025 revenue guidance for the second quarter in a row but near-term investments will weigh on operating income. CoreWeave needs to spend now in order to support the demand levels that are currently out-stripping supply (which mgmt. talked a lot about).

Separate from earnings, the lock-up expired today (Friday) and news circulated of insiders selling $1bn+ worth of shares in blocks priced in the mid-90s (per sources –link).

-> CoreWeave shares fell -20.8% in reaction to earnings and is down -28.5% on the week; The stock is still up 150% since the IPO price of $40/share

CoreWeave Delivers A Better Than Expected Q2

- Q2 was much better than expected with a ~12% beat on both revenue and adj EBITDA

- Revenues grew +207% y/y (down from the +420% y/y in Q1)

- Adj EBITDA grew +201% y/y (down from the +477% y/y in Q1)

- Cash from operations missed cons by -273%

- But Q3 guidance was mixed vs the Street’s view

- Rev guidance BEAT cons by 2.4%

- Adj op income MISSED cons by -12.2%

- The co is “quickly ramping up our capacity to meet demands”

- Interest expense is projected at $370mn at the mid pt: Due to “incr’d debt to support our demand-led CapEx growth, partly offset by increasingly lower cost of capital”

- Capx at mid pt is $3.2bn

- And while the Co raised the FY25 revenue guidance (for 2nd time in a row), op income guidance was maintained

- The new rev guidance was 5% ahead of the Street at the mid-pt

- Re-affirmed operating income ($800-830mn vs cons $819mn) and capx ($20-23bn) guidance

- Continue to target 900 megawatts of active power at the end of the yr (ended Q2 w/ nearly 470 megawatts)

- CapEx will also be back-end loaded in Q4

- Mgmt reiterated several times that demand exceeds supply

- “We are still operating in a structurally supply-constrained environment, where demand far outstrips supply for our products and services. Our operations and engineering teams are working relentlessly to deploy more capacity faster for our customers”

- “We are seeing unprecedented demand environment”

- “Our growth continues to be capacity-constrained with demand outstripping supply”

- “We are seeing an acceleration of customer demand”

- The pipeline remains strong – contracted revenue backlog of $30bn was up +86% y/y (doubled YTD): Includes the $4bn expansion w/ OpenAI plus new customer wins ranging from large enterprise to AI start-ups

- Signed expansion contracts w/ both hyperscale customers in the past 8 weeks

- “Our pipeline remains robust, growing and increasingly diverse, driven by a full range of customers from media and entertainment, to healthcare, to finance, to industrials and everything in between”

- There was quite a bit of focus on the call explaining the Core Scientific acquisition

- The rationale behind the deal is “quite simple and powerful”

- “Verticalization creates tremendous operational and financial efficiencies that will strengthen our ability to serve our customers at scale”

- “Owning the infrastructure will allow CoreWeave to scale faster and more efficiently”

- “The integration of Core Scientific meaningfully advances our capacity to operate one of the largest and most sophisticated AI cloud platforms in the world”

- “Upon closing, CoreWeave would own ~ 1.3 gigawatts of gross power capacity across Core Scientific’s national data center footprint, with an incremental 1 gigawatt or more available for future expansion”

- “This scale enhances our flexibility to take on new projects and meet accelerated customer demand”

- “Anticipate $500mn in fully ramped annual run rate cost savings by the end of 2027, benefiting both the Core Scientific and CoreWeave shareholders directly”

- Reaffirmed strategic direction: “Will continue to verticalize our platform and enhance our control, efficiency and differentiation fueled by our investment both up the stack as you saw with our acquisition of Weights & Biases last quarter, and down the stack as highlighted by our proposed acquisition of Core Scientific last month”

- Mgmt also highlighted that they have executed on accessing new pools of capital and driving down their cost of capital

Sports Reign in the Streaming Era

On the back of Disney and Fox both announcing that their respective sports streaming services will be launched on August 21st and both talked about openness to partner, it wasn’t exactly shocking to see news this week that they are now planning to offer a combined bundle, which would provide a $10/mo savings for subscribers.

Also, on the topic of key updates in sports streaming, last week on its earnings call TKO said that a UFC deal is “in the homestretch” …and voila, this week a $7.7bn deal was announced with Paramount. The $1.1bn avg annual revenue (ARR) from this new agreement was a sizable increase from the $500mn ARR deal with the ESPN deal, which expires this year (link).

All in all, sports content remains critical for media companies and continues to drive up value for sports owners. And as TV viewership shifts to streaming platforms, so must sports.

See below for more details.

- ESPN DTC & Fox One to launch combined bundle offer (link/link):

- ESPN’s DTC offering will give fans access to all of ESPN’s linear networks, in addition to ESPN on ABC, ESPN+, SECN+, and ACCNX

- FOX One will bring all of FOX’s News, Sports and Entertainment branded content into one streaming platform

- Those who sign up for the bundle will get access to a wide-ranging portfolio of content, including the NFL, NBA, WBNA, MLB, NHL, college football and basketball, NASCAR, IndyCar, as well as next summer’s FIFA World Cup

- Timing availability? The bundle will be available starting Oct 2

- The ESPN DTC offering and FOX One svs will both individually become available to consumers beginning Aug 21

- The bundle price is $39.99/mo, which is a $10/mo savings

- Standalone, ESPN will cost $29.99/mo, while Fox One will cost $19.99/mo

-> Bundling has become more and more of a topic as it relates to streamers and reducing churn…and alone those lines this week, Hub Research’s “2025 Monetization of Video” report found that 42% of users said they’re much more likely to keep bundled services compared to individual subscriptions (link)

- Paramount & UFC announce a $7bn US media rights deal (link/link)

- Starting in 2026, Paramount will exclusively distribute UFC’s full slate of 13 marquee numbered events and 30 Fight Nights via its DTC streaming platform, Paramount+, w/ select numbered events to be simulcast on its CBS broadcast network

- UFC events currently air on ESPN, as UFC’s partnership with ESPN runs through the end of 2025

- Deal length: 7-yrs

- Deal size: The ARR is $1.1bn, w/ an overall value of $7.7bn, which is up from the $500mn ARR ESPN deal

- The contract’s payment schedule is “weighted more towards the back end of the deal

- As part of the agreement, UFC and Paramount will move away from UFC’s existing Pay-Per-View model and instead it will be made available at no addtl cost to Paramount+’s US subscribers

- Plans for intl rights? Paramount said it intends to explore UFC rights outside the US “as they become available in the future”

- Starting in 2026, Paramount will exclusively distribute UFC’s full slate of 13 marquee numbered events and 30 Fight Nights via its DTC streaming platform, Paramount+, w/ select numbered events to be simulcast on its CBS broadcast network

Amazon Heats Up Competition In The US Online Grocery Segment

Amazon made a splash this week, announcing a big expansion of its grocery effort by offering same day delivery in more than 2.3k cities and towns by the end of the year. On Amazon.com, customers “can now order milk alongside electronics; oranges, apples, and potatoes with a mystery novel; and frozen pizza at the same time as tools for their next home improvement project—and check out with one cart and have everything delivered to their doorstep within hours”. The services is included for Prime members (for orders over $25) and available for a flat fee of ~$13/order for non-Prime Members.

US online grocery sales are estimated to reach $327.7bn in 2025, up from $257.5bn in 2024, with Walmart leading market share at an estimated 29%, followed by Amazon’s 22%. Clearly Amazon is trying to take more share of household spend and offering a seamless and integrated way to buy all the goods one needs, including perishable grocery items, should lead to more adoption.

-> Walmart traded down -2.5% and Kroger down -4.4% on the back of the announcement while Instacart also traded down -11.5% on the day.

Amazon’s Big Push In Grocery…

- Amazon.com expands same-day delivery to include fresh groceries

- Scope: Now available in 1k+ U.S. cities and towns, w/ plans to reach 2.3k+ by the end of 2025; Continue rollout to addtl cities & towns in 2026

- New Markets: Includes Raleigh (NC), Milwaukee (WI), Tampa (FL), Columbus (OH), among others

- Service integrates w/ existing grocery options: Which includes Amazon Fresh, Whole Foods Market, and local/specialty retailers

- Pricing:

- Prime members: Free Same-Day Delivery on orders overs $25…a $2.99 fee otherwise

- Non-Prime members: $12.99 fee per delivery, regardless of order size

- Positive early feedback: Early pilots in Phoenix, Orlando, and Kansas City saw first-time grocery customers shop 2x as often w/ Same-Day Delivery

- Fresh items like strawberries have entered the top 5 best sellers, surpassing products like AirPods

- In 2024, Amazon generated $100bn+ in grocery & household essentials sales (ex Whole Foods and Amazon Fresh)

US Online Grocery Is Expected To Grow @ A +12.3% CAGR from 2024-29 – A Few Key Market Stats…(link)

- U.S. online grocery sales numbers/estimates

- 2024: $175.6bn

- 2025E: $327.7bn

- 2026E: $363.8bn

- The US online grocery market is expected to grow at a CAGR of 12.3% from 2024 to 2029

- Market share estimates of US online grocery sales:

- Walmart: 29%

- Amazon: 22%

- Kroger: 9.9%

- Target: 4.5%

- Albertsons: 3.2%

- Other: 31.4%

Quick Takes On China Tech: Tencent, JD.com, & Tencent Music

Just as US TMT companies finish their earnings cycle, China Tech giants report. Tencent, JD.com, and Tencent Music Entertainment (TME) all reported this week! All in all, Tencent and TME surprised on the upside, especially the latter and outlined a bullish view. JD.com’s core retail fundamentals were strong, but a step-up in investments in newer initiatives, especially in food delivery, were a hot button for investors especially given heightened competition.

See below for our quick takes on all 3 China tech giants’ results.

->In reaction to their respective earnings, Tencent traded up +7.4% and TME rallied +11.8%, while JD.com fell -2.9%%; YTD, Tencent and TME are up +43.2%, +126.8%, respectively while JD.con is down -5.6%; Alibaba and Bidu are also up +45.3% and +6.6% respectively, YTD

Tencent: Strong Quarter As The Co Still Benefits From Easy Domestic Gaming Comps

- Tencent delivered stronger than expected revenue & profitability:

- Total rev BEAT by +3.0%

- Non-IFRS op profit BEAT by +3.6%

- Non-IFRS EPS BEAT by +4.6%

- All divisions beat consensus expectations

- Domestic Games rev (22% of total revenue) growth is still benefitting from easy comps: Q2 revs were up +17% y/y (vs +24% y/y in Q1), driven by the recently released game, Delta Force, and growth from evergreen games HoK, VALORANT and Peacekeeper Elite

- Delta Force: Added underwater combat and dynamic weather features which drove monthly avg DAU above 20mn in July, ranking top 5 industry-wide by DAU and top 3 by gross receipts in China

- Peacekeeper: Avg DAU rose over 30% y/y in Q2, driven by strong growth in extraction shooter mode popularity

- Valorant: Avg DAU hit a record high in Q2, boosted by an eSports tournament and the new large-scale map Corrode; VALORANT MOBILE is set to launch on Aug 19

- International Games rev growth accel’d seq: Q2 rev grew +35% y/y (vs +23% y/y in Q1), or +33% y/y ex-FX; Cited contributions from Dune: Awakening, Clash Royal, and PUBG Mobile

- PUBG Mobile: Players’ engagement in the UGC-powered World of Wonder sandbox grew, w/ April monthly gross receipts hitting a record high driven by popular ancient Egyptian-themed outfits

- Clash Royale: More frequent content updates, optimized rewards, & incr’d community events drove higher DAU and influencer attention, pushing June monthly gross receipts to a 7-year high

- Dune: Awakening: Reception was positive for Funcom’s open-world survival game based on the Dune IP which was launched in June; It ranked as the top pay-to-own game by revenue on Steam worldwide during its launch period

- Updates on social networks & AI features in Weixin

- Mini Programs: GMV from Mini Programs rose by a “teens %” y/y in Q2, driven by stronger support for financial services, dine-in ordering, and transportation

- Mini Games gross receipts grew 20% y/y, aided by tech upgrades that improved engine compatibility, graphics, and load times, enabling easier porting of complex app-based games

- Mini Shops: Enabled brands to port SKU libraries from Mini Programs to Mini Shops and unify loyalty programs, expanded gifting to Mini Programs, Video Accounts, and Official Accounts

- launched a “shop with friends” feature for social sharing and group discounts

- AI Updates: Intro’d AI-powered citations for contextual commentary in Official Accounts and Video Accounts, upgraded Mini Shops customer service with LLM-driven responses and personalized recommendations, and enabled Yuanbao to interpret and summarize Video Accounts content

- Mini Programs: GMV from Mini Programs rose by a “teens %” y/y in Q2, driven by stronger support for financial services, dine-in ordering, and transportation

JD.com: Top Line Growth Accelerated Due To Strength In Core Retail, But Investments To Support Newer Initiatives Like Food Delivery Will Continue To Weigh On Operating Profits

- Headline revs and non-GAPP EPADS surpassed expectations but adj EBITDA fell well below Street projections

- Core retail was strong as Q1 rev growth accelerated to +22% y/y (vs +15.8% y/y in Q1): The revenue beat was mainly driven by upside in Electronics & Home Appliance rev (+6.1% above cons) but Net Services revenue was also 13.4% better than expected

- But Operating losses in food delivery and other strategic investments weighed on profitability

- Focused on JD Supermarket expansion by adding unique products during the JD 618 Grand Promotion: Introd’d custom-sized dairy products and liquor

- Through six specialized product portfolios, the Co helped suppliers avoid price-driven competition while showcasing supply chain advantages

- The Co has strong momentum in food delivery and investments continue, but competition has heated up

- JD Food Delivery has maintained “healthy order volume growth, especially for meal orders in Q3 QTD

- Mgmt stressed synergies of the biz: “I want to reiterate that we do not view our food delivery as a stand-alone business, as it’s deeply integrated with JD’s broader ecosystem”

- JD Food Delivery’s daily orders surpassed 25mn during the JD 618 Grand Promotion, supported by over 1.5mn merchants and 150k full-time riders

- The July launch of 7Fresh Kitchen aims to drive high-quality industry growth through supply chain innovation

- Competition has been “intensifying since July” but “low value competition doesn’t create value for the industry”

- Approach to improve profitability in the biz? A more refined and targeted subsidy programs & improving fulfilment efficiency

- Will continue to invest: “Despite near-term financial impact, this food delivery business has driven meaningful traffic and user growth and significantly boost user shopping frequency. We have also observed a visible uplift in conversion and cross-selling with our core retail business. Moving forward, we will continue to focus on merchants supply, delivery efficiency, and user experience for food delivery business.”

- JD.com launched “One Step Ahead – Accelerated Upgrade Program” to boost sales of 3C electronics and emerging categories like AI glasses and intelligent robots

- JD MALL also opened new locations in key cities, reaching 24 stores by June 2025, offering an immersive, digitally integrated shopping experience

- JDL expanded its Global Smart Supply Chain Network: Opened new overseas warehouses in multiple countries, reaching over 130 facilities across 23 regions with ~1.3mn sqm managed area

- Also launching its JoyExpress delivery service in Saudi Arabia to provide end-to-end local logistics capabilities

- JD Health reinforced its role as China’s leading online marketplace for new and specialty medicine launches, adding products such as Innovent Biologics’ weight-loss drug Xin Er Mei and Qingfeng Pharmaceutical’s anti-influenza drug Yi Su Da to its platform

Tencent Music Entertainment (TME): Strong Qtr & Bullish Outlook…Advertising, Artist Related Merch & Concerts/Live Events Drove Upside In the Qtr Along With Further Traction Of Its Premium Subscription Tier

- TME delivered stronger than expected Q2 headline numbers: Total rev beat by 6% and non-IFRS EPADS beat by 12% w/ the biggest upside coming from “Other” revenue (advertising, artist related merch and concerts/live events) which beat cons by 19%

- The Co has a positive outlook and expects accelerated full-year y/y growth & margin expansion – drivers include:

- Healthy subscription growth (supported by SVIP offerings like artist merchandise, long-form audio, and concerts)

- Steady non-subscription gains from improved advertising and product innovation

- Deeper partnerships w/ music labels & artists to grow merchandise and concert revenues

- Online Music Services total revs grew +26% y/y (81% of total revs) & beat cons by +6.5% given upside in Other revenue (advertising, artist related merch and concerts/live events) which beat cons by 19%)

- Music subscription revenues (52% of total revs) grew +17% y/y: Mainly driven by a strong +9% increase in monthly ARPPU (beat cons by +0.9%)

- Growth of monthly ARPPU was due to expansion of the SVIP membership program

- Other revenue (advertising, artist related merch and concerts/live events) grew +47% y/y: Launched ad-supported membership, along with optimized ad formats and incentives, enhanced user engagement and ad effectiveness, driving strong y/y growth in advertising revenue’ Artist related merch sales and offline performances weer also robust

- Music subscription revenues (52% of total revs) grew +17% y/y: Mainly driven by a strong +9% increase in monthly ARPPU (beat cons by +0.9%)

- Social Entertainment Services revs fell -9% y/y (19% of total revs) but still beat cons estimates by +2.6%: This is also an improvement from -12% y/y in Q1

- TME continues to see strong adoption of its premium SVIP tier

- SVIP subscribers topped 15mn in Q2 (out of total 124mn subs)

- Both ARPPU & retention rates for SVIP are ramping up and are “in line” w/ mgmt’s expectations

- Subscription drivers: Premier sound quality plus long-form audio content; Priority access to concert tickets for in-demand events and exclusive digital album releases (e.g., Jolin Tsai’s album as an SVIP sign-up privilege) have significantly boosted SVIP conversions; Features like the “bubble” community, livestreamed concerts with dedicated SVIP access, and personalized virtual fan communities (e.g., Penguin Island) further drive SVIP adoption & engagement

- The Co is bundling bubble w/ the subscription and SVIP business, aiming to make it a key growth driver for future SVIP growth, especially among young, highly active users

- Expect SVIP to further penetrate the base: “The penetration ratio will continue to go up, including the ARPPU and retention”; “The growth trajectory is in line with our expectation”

- Future plans: “We will keep focusing on expanding our SVIP membership, introducing more and enhanced SVIP privileges such as high-quality content, artist-centric ticket privileges, including early access to artist merchandise and the concerts

Grab Bag: EA's Strong BF6 Beta Reception / Netflix Upfronts / Perplexity & Google Chrome

- Battlefield 6‘s open beta weekend drew in 521,079 people concurrently per press reports, smashing the all-time concurrent player record of Call of Duty: CoD’s record was 491,670 for Black Ops 6 and Warzone combined (link/link/link)

- The previous Battlefield, BF 2042, reached a concurrent player count of 156,665 at its highest

- BF6 also lit up Twitch: More than 870k viewers watching live (12mn hours watched), over twice the viewership peak of the previous game, which topped out around 350k

- This open beta has driven usage on older Battlefield games (link)

- Battlefield 2042— gained 128.6% players, moved from #57 > #22

- Battlefield 4— gained 210.2% players, moved from #130 > #46

- Battlefield 1— gained 86.6% players, moved from #103 > #68

- Battlefield V— gained 86.5% players, moved from #119 > #78

- Battlefield 3— gained 167.1% players, moved from #634 > #361

- Battlefield Hardline— gained 59.9% players, moved from #556 > #417

- Reminder that BF6 official release date is Oct 10th (competitively, CoD Black Ops 7 has an end of year release, but no date yet)

- Netflix announced that it more than doubled U.S. Upfront commitments for 2025–2026 (link)

- This was in-line w/ their expectations

- Saw y/y growth across all key categories like Retail, CPG, Telco, Health & Wellness, Entertainment and Tech

- For the two NFL games this December, Netflix sold out of all available in-game inventory & closed sponsorships w/ multiple partners like Accenture, FanDuel, Google, and Verizon on in-game and broadcast features

- New features that have helped them gain traction with advertisers include enhanced data capabilities, expanded buying and measurement solutions and new creative formats

- Perplexity AI reportedly makes $34.5bn unsolicited bid for Google Chrome (link)

- That level actually exceeds its own $18bn valuation from July; Several investors have reportedly agreed to back the deal

- The bid follows the DOJ’s proposal that Google divest Chrome after losing an antitrust case, with the agency calling it a critical step to level the playing field in search

- Perplexity, known for its AI-powered search and recently launched Comet browser, previously considered a merger with TikTok but did not finalize it

- Meta reportedly approached Perplexity earlier in 2025 about a potential acquisition, but no deal was reached

- That level actually exceeds its own $18bn valuation from July; Several investors have reportedly agreed to back the deal

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- TTD’s Q2 earnings call triggered a ~10% drop across ad tech stocks after CEO Jeff Green downplayed Amazon’s competitive threat, calling it a “potential partner. ” Investors found the stance unconvincing, especially as Amazon Ads hit $15.7bn in Q2. (Adexchanger)

- TV/streaming upfront rev rose 5% y/y to $31bn for 2025–26, driven by 17. 9% growth in streaming ($13.2bn). Broadcast fell 2.5% to $9.1bn; cable dropped 4.3% to $8.7bn. CPMs declined: streaming -8% to $27.25, broadcast -4.1% to $43.50, cable -6% to $19.35. FASTs helped lower CPMs; sports content buoyed linear demand. (Media Post)

Artificial Intelligence/Machine Learning

- Perplexity is raising funds at a $20bn valuation, up from $18bn in Jul. and $520mn in Jan. 2024. Backed by SoftBank, Nvidia & Bezos, the AI search Co’s ARR surged to $150mn+ in mid-2025. It recently bid $34.5bn for Google Chrome and launched its AI-native browser, Comet. (Business Insider)

- Apple is plotting an AI comeback w/ new devices incl. a tabletop robot (2027), lifelike Siri, smart speaker w/ display (2026), & home-security cams. These aim to boost its smart-home ecosystem & challenge rivals like Samsung & Meta. (Yahoo Finance)

- Google’s Gemini update enables automatic memory of past chats to personalize responses, expanding on last yr’s manual memory feature. Users can disable it via settings. Gemini 2.5 Pro rolls out in select countries, w/ Gemini 2.5 Flash to follow. (The Verge)

- AI search engine Perplexity annc’d a $34. 5bn cash offer to buy Chrome from Google, pledging $3bn to Chromium and keeping Google as default search. The bid follows DOJ’s Mar. proposal to force Chrome’s sale over monopoly concerns. (Tech Crunch)

- Anthropic annc’d it will offer its Claude AI model to the US govt for $1, aiming to secure federal contracts. This follows Claude, ChatGPT, and Gemini being added to the govt’s approved AI vendor list. CEO Amodei emphasized secure AI access for institutions. (Reuters)

- Character AI, once focused on AGI, has shifted to entertainment under new CEO Karandeep Anand. The Co now has ~20mn users, including kids engaging w/ chatbots like Sherlock Holmes to create stories. The Co’s pivot reflects a broader trend in AI svs, prioritizing user engagement over superintelligence goals. (Wired)

- AI boom is fueling historic wealth creation, minting dozens of new billionaires via massive fundraises by Anthropic, OpenAI, Anysphere & others. There are now 498 AI unicorns worth $2.7tn. Liquidity is growing via secondary mkts, M&A, and IPOs. SF leads in AI wealth, surpassing NY. (CNBC)

Audio/Music/Podcast

- Spotify and Kobalt have signed a direct and multi-yr licensing agreement in the United States. The agreement will expand the licensing framework to allow and protect songwriters’ participation on streaming platforms. (Variety)

Broadcast/Cable Networks

- Rogers Communications has agreed to sell its nine Rogers Business data centres to InfraRed Capital Partners, part of Sun Life. While continuing to provide network connectivity and sell services post-closing; the deal, part of Rogers’ plan to divest non-core assets and repay debt, is expected to close by year-end 2025 pending regulatory approval. (Yahoo Finance)

Cable/Pay-TV/Wireless

- Netflix more than doubled U. S. Upfront commitments for 2025–2026, securing major advertiser deals across key categories and selling out live event inventory. While expanding its Ads Suite, programmatic integrations, measurement partnerships, and multilingual targeting to enhance global reach and ROI.(Netflix )

- CNMC has fully deregulated Spain’s wholesale fibre mkts, ending Telefónica’s NEBA Local & NEBA Fibra obligations after a six-month phase-in. The move, annc’d on [Tue., Aug. 13], follows rising competition, w/ FTTH coverage at ~90% & retail share falling below 50%. Altnets like MásOrange, Digi & Onivia have reshaped the landscape. MARCo rules for ducts/poles remain, though rates rose 11–14.6%, sparking legal pushback. (Mobile Europe)

Capital Market Updates

- US CEOs mentioned recession <300 times in Q2 earnings calls—near a record low—despite tariff, inflation, and demand concerns. Stocks hit highs as EPS rose 10.5% vs. 2.8% est. Consumers remain cautious but resilient. Fed rate cuts of 100bps by mid-2026 are expected. Recession odds fell to 35%. (AInvest)

Cloud/DataCenters/IT Infrastructure

- Google pledged $9bn to expand AI & cloud infra in Oklahoma, incl. a new data center in Pryor. The investment supports Gemini AI & sustainability goals, w/ plans to use geothermal energy. (Reuters)

- ST Telemedia may sell its 34% stake in China’s GDS Holdings, ahead of a potential $5bn sale of STT GDC to KKR. STT, which is owned by Singapore’s state-owned sovereign wealth fund Temasek Holdings, develops and operates data centers through its STT GDC division. (Data Centre Dynamics)

- Rumble is weighing a ~$1. 17bn deal to acquire Germany’s Northern Data, gaining control of GPU-rich Taiga cloud and Ardent data centers. Tether, owning 54% of Northern Data, backs the move and may become Rumble’s top shareholder post-deal. Northern Data plans to sell its crypto biz to repay a €575mn Tether loan. Offer values shares at $18.3, a 32% discount. (Reuters)

Crypto/Blockchain/web3/NFTs

- eToro CEO said retail investors seized Apr. mkts dip post-tariff annc’t, boosting trading in Google, Nvidia & Tesla. Despite adj profit of $0.56/share vs. est. $0.50, shares fell 8% as trading normalized by Jul. Crypto svs surged w/ bitcoin highs & clearer U.S. regulation. Co plans AI-driven expansion beyond retail. (CNBC)

- Circle Internet Group stock fell >5% in extended trading after annc’d offering of 10mn Class A shares—2mn by the Co, 8mn by existing holders. Shares have surged 450% since IPO. Underwriters have 30-day option for 1.5mn more. Despite a $4.48/share loss due to IPO charges, Q2 rev rose 53% w/ strong stablecoin growth. Shares closed up 1.3% before the annc. (CNBC)

Earnings Scorecard & Analysis

- Singtel’s Q1 net profit surged 317% y/y to S$2. 88bn, driven by S$2.2bn in gains from Airtel stake sale (S$1.47bn) & Intouch-Gulf merger (S$746mn). Optus & NCS posted strong rev/EBIT growth; Airtel & AIS boosted regional profits. (Mini Chart)

eCommerce/Social Commerce/Retail

- On’s Q2 net sales rose 32% YoY to ~CHF 749. 2mn, led by 47.2% DTC growth. Despite a CHF 40.9mn net loss due to currency shifts, the Co raised its full-yr outlook to 31% growth and improved margin guidance to 60.5–61%. Footwear grew ~30%, apparel 67.5% to CHF 36.7mn, and accessories 133.3% to CHF 7.7mn. (Retail Dive)

- Skechers annc’d Q2 rev of $2. 44bn, up 13.1% YoY, ahead of its $9.4bn go-private deal w/ 3G Capital. Wholesale grew 15% to $1.3bn; DTC rose 11% to $1.1bn. EMEA led mkts w/ 48.5% growth; China fell 8.2%. No exec call or full-yr outlook was provided. (Retail Dive)

- Cava lowered its full-yr same-store sales forecast to 4–6% (prev. 6–8%) after Q2 growth of just 2.1%, missing Wall St. est. of 6.1%. Q2 rev hit $280.6mn vs. $285.6mn expected; EPS was $0.16. Net income fell to $18.4mn. Despite 20% rise in restaurant sales, stock dropped 23%. Co also annc’d $25mn investment in Hyphen to boost tech automation and order accuracy. (CNBC)

- Restaurant chains like McDonald’s, Wendy’s, Chipotle, and Denny’s face declining sales as US consumers shift to home-cooked meals amid economic uncertainty and high prices. Fast-food visits fell 1% in 2025, w/value meals like McD’s $5 deals seeing mixed results. (Seeking Alpha)

Electric & Autonomous Vehicles

- Pony. ai is on track to hit its 2025 goal of 1,000 Gen-7 robotaxis, w/ 200+ units already deployed. It’s expanding into Europe via Luxembourg trials and has permits in South Korea. Partnerships w/ Uber & Dubai’s RTA support Middle East entry. (Yahoo Finance)

- Ford Motor Co annc’d a ~$2bn revamp of its Louisville plant to produce EVs, starting w/ a midsize electric pickup in 2027. The new platform cuts costs, speeds assembly by 15%, and reduces parts by 20%. Powered by low-cost Michigan-made batteries, the truck targets a ~$30,000 price. (NBC News)

- Revel shut down its NYC ride-hail biz to focus on EV charging, annc’d that Co will sell its fleet and 165 license plates worth ~$20K–$25K each. Charging utilization rose from 21% in early 2023 to 45% in 2025, aided by Uber’s 2024 deal. Revel plans 400+ stalls in LA, NYC & SF by end of 2026. (Tech Crunch)

- GM is reviving its autonomous driving program, led by ex-Tesla exec Sterling Anderson. Plans include rehiring Cruise staff and expanding its Mountain View office. LiDAR cars are collecting data to build simulation models. GM shut down its Cruise robotaxi biz after a pedestrian accident, pivoting to hands-free personal vehicles. (MSN)

Film/Studio/Content/IP/Talent

- Disney inked a multiyear deal w/Webtoon to bring ~100 titles featuring characters from Marvel, Star Wars, and more to its webcomics app. Launching w/Spider-Man in Aug., titles will include Avengers, Alien, and Belle-themed stories. Webtoon, w/~155mn monthly users, will host both reformatted and original content. (Variety)

FinTech/InsurTech/Payments

- Adyen shares plunged 18% after warning that the end of the U. S. “de minimis” shipping exemption (items <$800) will hit APAC-based cos using its platform. The rule change, adds tariffs/taxes, impacting rev growth. Adyen now guides FY growth to match H1’s 21%, down from prior acceleration hopes.. (Morning Star)

- SoftBank has selected Goldman Sachs, JPMorgan, Mizuho, and Morgan Stanley to lead a potential US IPO for its payments app PayPay, sources said. The offering, possibly in Q4, may raise over $2bn. PayPay, which helped shift Japanese consumers from cash, also offers banking and credit card svs. This would mark SoftBank’s first U.S. listing since Arm’s $54.5bn IPO in 2023, now valued at $145bn. (Reuters)

Live Entertainment/Theme Parks/Concerts/Experiential

- Sphere Ent. sold 120K+ tickets for immersive “Wizard of Oz” screenings at Vegas Sphere, aiming for 200K. CEO Dolan called it “groundbreaking,” using AI “outpainting” to expand 1939 film frames. The 4D experience includes 167K speakers, haptic seats & scents. (CNBC)

- StubHub resumed IPO plans after Apr pause due to Trump tariffs, filing an updated prospectus. The Co aims for a Sept. debut on NYSE under “STUB.” (CNBC)

Macro Updates

- The U. S. extended its pause on extra tariffs for China imports, per an exec. order signed by Trump, citing China’s “significant steps” in trade talks. U.S. imposed a 30% duty; China cut its 34% rate to 10% and dropped other duties. Talks in Stockholm led to the extension. In 2024, China made up 10.9% of U.S. trade; the U.S. had a ~$295bn deficit. (Retail Dive)

- CPI rose 0. 2% in Jul. and 2.7% YoY, below est. of 2.8%. Core CPI up 0.3% MoM, 3.1% YoY. Shelter costs rose 0.2%, energy fell 1.1%. Tariff-linked items showed mixed impact. Traders expect Fed rate cut in Sept. amid labor mkts concerns. BLS faces scrutiny after Trump fired its chief; new nominee annc’d. (CNBC)

- Cash allocations by US corps halved since 2021, falling to 20% by end-Jul. from 40%, per Clearwater Analytics. Firms shifted to longer-duration treasuries for higher yields amid high rates. Median portfolio duration rose to 0.61 yrs. (Reuters)

Media Conglomerates

- AMC CEO Adam Aron expects Paramount to ramp up theatrical releases under Skydance, which acquired the studio last week. Aron praised past leadership but noted Paramount’s cash constraints limited its output. (Deadline)

- Skydance’s takeover of Paramount has reshaped Hollywood’s power structure. David Ellison now leads the studio, while ESPN’s Mark Shapiro is rumored to be eyeing WWE/UFC-style sports-entertainment ventures. Analysts expect Paramount to lean into live sports & IP-driven content. The $8bn merger, approved by the FCC, ends a year-long saga. Industry watchers see more consolidation ahead. (NYT)

Regulatory

- Apple & Google lost a landmark Australian court case, found to have abused market power by limiting app store competition. While Epic’s consumer law claims were rejected, the ruling may trigger a major class action payout. (The Sunday Morning Herald)

Satellite/Space

- Amazon annc’d the launch of 24 Kuiper satellites aboard a SpaceX Falcon 9, boosting its LEO constellation past 100. The $10bn+ project aims to deliver affordable broadband via 3,236 satellites. Beta testing starts in early 2026. S (Cord Cutters News)

- PLDT Enterprise annc’d a deal to resell Starlink’s LEO satellite broadband in the Philippines, targeting underserved areas. The Co aims to enhance connectivity for sectors like logistics, banking, agriculture, disaster response, education & healthcare. Starlink will support ops, boost productivity & offer backup during outages. (Developing Telecoms)

- AST SpaceMobile (ASTS) shares surged 12% premarket after the Co annc’d plans to launch 45–60 satellites by 2026, w/ five orbital launches by Q1 2026. Despite a Q2 loss of $0.41/share and $1.16mn rev, up 29% YoY, the Co expects $50–$75mn H2 rev. Operating costs hit $74mn. ASTS secured eight U.S. govt contracts and aims to serve mkts in the U.S., Europe, Japan & more. (Yahoo Finance)

Social/Digital Media

- Publisher groups in the U. S., UK, and EU report double-digit declines in Google Search referral traffic. Median YoY drops of 10% overall, 7% for news, and 14% for non-news—blaming Google’s AI Overviews for reduced clicks despite stable rankings, and are pushing regulators, including the U.S. DOJ and EU authorities, to allow blocking Google’s AI crawler without losing search visibility. (Digiday )

- YouTube rolled out AI-based age verification in the U. S. to auto-restrict users estimated to be under 18, regardless of stated birthdate. Teens will get non-personalized ads, privacy reminders, and limited video recs. Creators may see lower teen ad rev. Users can verify age via ID, selfie or card. The model uses signals like activity & account age. (Variety)

- Meta’s Threads hit 400mn MAUs, up from 350mn in Apr, per Instagram head Mosseri. Threads saw 115.1mn daily mobile users in Jun., a 127.8% YoY rise, nearing X’s 132mn (down 15.2%). Web visits lag: Threads at 6.9mn vs. X’s 145.8mn. Growth driven by new features incl. DMs, fediverse, custom feeds, AI. (Tech Crunch)

Sports/Sports Betting

- NBC extended its U. S. Open media rights deal through 2032 in a six-yr pact starting 2027, involving NBCUniversal & Versant. NBC retains rights to U.S. Women’s & Senior Opens; Golf Channel & USA Network will cover other USGA events. (Front Office Sports)

- NBA approved the Boston Celtics’ $6. 1bn sale to William Chisholm’s group, marking the second-highest NBA team valuation. Chisholm replaces Wyc Grousbeck as governor. Stakeholders incl. Aditya Mittal & Sixth Street. The Grousbecks bought the team for $360mn in 2002. The sale follows Boston’s 18th title & Tatum’s injury. (Yahoo Finance)

Tech Hardware

- Trump said he initially asked Nvidia for a 20% cut of China sales for H20 chips, later settling at 15% after talks w/ CEO Huang. He called H20 “obsolete” and noted Huawei has a similar chip. Nvidia hopes to sell ~$8bn in H20s. Trump won’t allow Blackwell chips to China w/o 30–50% performance cuts. (CNBC)

Video Games/Interactive Entertainment

- Sony’s Crunchyroll annc’d layoffs amid a global restructuring to focus on high-growth mkts like India, Brazil & Mexico. The move, not driven by financials, aims to empower regional teams. Crunchyroll plans new tech hubs in the U.S., Mexico & India, and will expand into manga, merchandise & collectibles. (Cord Cutter News)

- Take-Two CEO Strauss Zelnick expressed high confidence GTA 6 will launch on its intended release date, despite past delays. In a CNBC interview, he said Rockstar aims to exceed expectations but acknowledged dev challenges. GTA 6, set in Vice City, is slated for Xbox Series X/S, PS5 & PC. (Kotaku)

Video Streaming

- Fubo is prepping a sports-only plan for the 2025 season, aiming to differentiate amid rising content costs. The move follows its lawsuit against WBD & Disney over the sports JV, which led to losing WBD channels. (MSN)

- A Cord Cutters News survey reveals 43% of cord cutters prefer YouTube over paid platforms like Disney+, HBO Max & Netflix. Viewers cite free access, vast content, & ease of use. (Cord Cutters News)

- Sling TV annc’d new Day ($4. 99), Weekend ($9.99) & Week ($14.99) Passes for short-term access to Sling Orange’s 30+ channels incl. ESPN, Disney & CNN. Ideal for sports fans, each pass offers flexible viewing options. Add-ons like Sports Extra or Entertainment Extra cost $1–$3 based on pass type. (USA Today)